Arabtec Holding - GulfBase.com

34

www.hc-si.com On Top Of The Game Arabtec is actively diversifying its portfolio to include more infrastructure and utilities works in high spending GCC countries, mainly Abu Dhabi, Saudi Arabia and Qatar. We project Arabtec’s backlog to double between 2009 and 2013 from around AED20.2 billion to AED40.4 billion at the beginning of 2013. We project FCF to grow by 45% (09e-13f). We resume coverage on Arabtec with a “Buy” recommendation based on a fair value/share of AED4.17, implying an upside potential of 51.0%. The GCC has proven to be resilient compared to other parts of the world thanks to high levels of reserves from accumulated revenues which support the region’s spending program. We view the infrastructure and energy (utilities) sectors as essential to the region’s economy as they will boost non hydrocarbon revenues. We believe Arabtec will take part of the planned projects as it chases new contracts in 2009 and 2010 in order to restore its backlog to previous levels and secure a revenue stream for the next three to four years. We view Arabtec’s strategy of diversifying its backlog portfolio as positive given that: (i) the company will focus more on infrastructure works which yield higher margins compared to Arabtec’s previous focus on commercial projects, and (ii) the company will benefit from high infrastructure spending in its targeted markets specifically Qatar, Saudi Arabia and Abu Dhabi. Arabtec is already an established contractor in Qatar and has smoothly penetrated the Saudi Arabian market through its Joint Venture (JV) with one of Saudi’s biggest players, Saudi Bin Laden Group. We expect Arabtec EBITDA to grow at a CAGR of 5.5% (09e-13f) with an FCF CAGR of 45% over the same forecasted period. The growth is mainly attributed to geographical expansion which will boost the company’s backlog with high margin projects in high spending MENA countries. The company is resisting the slowdown in Dubai by utilizing its idle capacity to penetrate new markets with minimum spending. Moreover, FCF growth will come from the improving working capital going forward, resulting in lower interest expense. We expect the company to maintain a decent net income margin at an average of 8.4%, with net income growing at a CAGR of 2.5% (09e-13f). We assumed no dividends in 2009 and 2010 as the company will rely on self financing and borrowing to support expansions and payables. However, we maintained a dividend payout (DPO) of 40% beyond 2010. We resume coverage on Arabtec with a "Buy" recommendation based on a DCF value of AED4.17/share, which implies an upside potential of 51%. Arabtec is trading at a PER (09e) of 4.68x (45% discount to peers) and an EV/EBITDA (09e) of 4.49x (37.8% discount). We believe the stock is undervalued at current levels. Buy Price Performance Chart 0 0.5 1 1.5 2 2.5 3 3.5 4 D-08 D-08 J -09 M-09 M-09 A-09 M-09 DFMGI ARTC *All prices & multiples are based on June 25th, 2009 closing prices. Target Price (AED) 4.17 Market Price (AED) 2.76 Upside 51% Listed On DFM Bloomberg Code ARTC UH RIC ARTC.DU Enterprise Value (AEDm) 4,902 Net Debt (AEDm) 745.8 Market Cap. (AEDm) 3,301 Market Cap. (USDm) 899.4 Number of Shares (m) 1,196.0 Foreign Ownership Limit 49.0% Foreign Ownership Level 26.5% Daily Turnover (AEDm) 133.5 Daily Turnover (USDm) 36.4 Ownership Structure* Riad Kamal 7.74% Hashem Al Safi 6.54% Others 30.7% Free Float 55.0% *Source: Zawya Key Performance Indicators *Excluding unusual items and discontinued operations A = Actual; E/F = HC's Estimates/Forecasts; C = Consensus Estimates Fiscal Year 08A 09E 09C 10F 10C Revenues (USD Mil.) 9,722 8,391 8,228 8,821 8,347 EBITDA (USD Mil.) 1,293 1,091 1,000 1,182 1,128 EBITDA Margin 13.3% 13.0% 13.3% 13.4% 13.5% Net Income (USD Mil.)* 957 705 743 754 771 EPS (USD)* 0.80 0.59 0.62 0.63 0.64 EPS Growth 78.0% -26.3% -22.4% 6.8% 3.8% DPS (USD) 0.25 0.00 0.50 0.00 0.47 Net Debt/EBITDA (x) 0.39x 0.68x 0.41x 0.73x -0.11x P/E 3.45x 4.68x 4.44x 4.38x 4.28x EV/EBITDA 2.94x 4.49x 3.43x 4.24x 2.82x Dividend Yield (%) 9.1% 0.0% 18.1% 0.0% 17.0% UAE – Construction Research Department 1 July 2009 Company Report Arabtec Holding Roaa Alian +2 02 3332 8612 [email protected] Menna El Hefnawy +2 02 3332 8632 [email protected] Disclaimer: See Page 33

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Arabtec Holding - GulfBase.com

www.hc-si.com

On Top Of The Game Arabtec is actively diversifying its portfolio to include more infrastructure

and utilities works in high spending GCC countries, mainly Abu Dhabi, Saudi Arabia and Qatar.

We project Arabtec’s backlog to double between 2009 and 2013 from

around AED20.2 billion to AED40.4 billion at the beginning of 2013. We project FCF to grow by 45% (09e-13f).

We resume coverage on Arabtec with a “Buy” recommendation based on

a fair value/share of AED4.17, implying an upside potential of 51.0%. The GCC has proven to be resilient compared to other parts of the world thanks to high levels of reserves from accumulated revenues which support the region’s spending program. We view the infrastructure and energy (utilities) sectors as essential to the region’s economy as they will boost non hydrocarbon revenues. We believe Arabtec will take part of the planned projects as it chases new contracts in 2009 and 2010 in order to restore its backlog to previous levels and secure a revenue stream for the next three to four years. We view Arabtec’s strategy of diversifying its backlog portfolio as positive given that: (i) the company will focus more on infrastructure works which yield higher margins compared to Arabtec’s previous focus on commercial projects, and (ii) the company will benefit from high infrastructure spending in its targeted markets specifically Qatar, Saudi Arabia and Abu Dhabi. Arabtec is already an established contractor in Qatar and has smoothly penetrated the Saudi Arabian market through its Joint Venture (JV) with one of Saudi’s biggest players, Saudi Bin Laden Group.

We expect Arabtec EBITDA to grow at a CAGR of 5.5% (09e-13f) with an FCF CAGR of 45% over the same forecasted period. The growth is mainly attributed to geographical expansion which will boost the company’s backlog with high margin projects in high spending MENA countries. The company is resisting the slowdown in Dubai by utilizing its idle capacity to penetrate new markets with minimum spending. Moreover, FCF growth will come from the improving working capital going forward, resulting in lower interest expense. We expect the company to maintain a decent net income margin at an average of 8.4%, with net income growing at a CAGR of 2.5% (09e-13f). We assumed no dividends in 2009 and 2010 as the company will rely on self financing and borrowing to support expansions and payables. However, we maintained a dividend payout (DPO) of 40% beyond 2010.

We resume coverage on Arabtec with a "Buy" recommendation based on a DCF value of AED4.17/share, which implies an upside potential of 51%. Arabtec is trading at a PER (09e) of 4.68x (45% discount to peers) and an EV/EBITDA (09e) of 4.49x (37.8% discount). We believe the stock is undervalued at current levels.

Buy

Price Performance Chart

0

0.5

1

1.5

2

2.5

3

3.5

4

D-08 D-08 J-09 M-09 M-09 A-09 M-09

DFMGI ARTC

*All prices & multiples are based on June 25th, 2009 closing prices.

Target Price (AED) 4.17 Market Price (AED) 2.76 Upside 51% Listed On DFM Bloomberg Code ARTC UH RIC ARTC.DU Enterprise Value (AEDm) 4,902 Net Debt (AEDm) 745.8 Market Cap. (AEDm) 3,301 Market Cap. (USDm) 899.4 Number of Shares (m) 1,196.0 Foreign Ownership Limit 49.0% Foreign Ownership Level 26.5% Daily Turnover (AEDm) 133.5 Daily Turnover (USDm) 36.4 Ownership Structure* Riad Kamal 7.74% Hashem Al Safi 6.54% Others 30.7% Free Float 55.0% *Source: Zawya

Key Performance Indicators

*Excluding unusual items and discontinued operations A = Actual; E/F = HC's Estimates/Forecasts; C = Consensus Estimates

Fiscal Year 08A 09E 09C 10F 10C Revenues (USD Mil.) 9,722 8,391 8,228 8,821 8,347 EBITDA (USD Mil.) 1,293 1,091 1,000 1,182 1,128 EBITDA Margin 13.3% 13.0% 13.3% 13.4% 13.5% Net Income (USD Mil.)* 957 705 743 754 771 EPS (USD)* 0.80 0.59 0.62 0.63 0.64 EPS Growth 78.0% -26.3% -22.4% 6.8% 3.8% DPS (USD) 0.25 0.00 0.50 0.00 0.47 Net Debt/EBITDA (x) 0.39x 0.68x 0.41x 0.73x -0.11x P/E 3.45x 4.68x 4.44x 4.38x 4.28x EV/EBITDA 2.94x 4.49x 3.43x 4.24x 2.82x Dividend Yield (%) 9.1% 0.0% 18.1% 0.0% 17.0%

UAE – Construction Research Department

1 July 2009Company Report

Arabtec Holding

Roaa Alian +2 02 3332 8612 [email protected]

Menna El Hefnawy +2 02 3332 8632 [email protected] Disclaimer: See Page 33

UAE – Construction

2

Financial Statements and Ratios

AED Million 2008 2009e 2010f 2011f 2012f 2013f

Income Statement Revenues 9,722 8,391 8,821 9,254 9,359 9,718 Growth in Revenue (%) 127.5% -13.7% 5.1% 4.9% 1.1% 3.8% Cost of Goods Sold 8,010 6,922 7,339 7,699 7,730 8,007 SG&A Expense 586 545 529 555 562 583 Other operating income 167 168 229 259 234 224 EBITDA 1,293 1,091 1,182 1,259 1,301 1,351 EBITDA Margin 13.3% 13.0% 13.4% 13.6% 13.9% 13.9% Depreciation & Amortization 220 277 291 332 388 437 Operating Profit 1,073 814 891 926 913 913 Operating Margin 11.0% 9.7% 10.1% 10.0% 9.8% 9.4% Net Interest (3) (19) (26) (15) (12) (8) Investment Income 6.0 12.4 18.9 19.5 19.6 20.1 Net Other non operating items 19 22 27 31 33 34 Profit Before Taxes (PBT) 1,095 829 910 962 953 960 Taxes 16 19 46 48 55 61 Net Profit PM 1,079 810 864 914 898 898 Net Profit Margin (pre minority) 11.1% 9.7% 9.8% 9.9% 9.6% 9.2% Minority Interest 122 105 110 116 117 121 Net Profit 957 705 754 798 781 777 Net Profit Margin 9.8% 8.4% 8.5% 8.6% 8.3% 8.0% Earnings Per Share (EPS) 0.80 0.59 0.63 0.67 0.65 0.65 Growth in EPS (%) 78.0% -26.3% 6.8% 5.9% -2.1% -0.5% Dividends Per Share (DPS) 0.25 0.00 0.00 0.27 0.26 0.26 Dividends Payout (%)** 31.2% 0.0% 0.0% 40.0% 40.0% 40.0% Dividends Yield 9.1% 0.0% 0.0% 9.7% 9.5% 9.4% Balance Sheet Total Fixed Assets 2,173 2,511 2,822 3,037 3,259 3,496 Total Current Assets 7,286 7,640 8,129 8,534 8,155 8,277 Total Current Liabilities 7,010 6,784 7,075 7,391 6,802 6,967 Total Long Term Liabilities 557 889 947 1,011 1,287 1,325 Total Shareholder’s Equity 1,893 2,477 2,930 3,169 3,325 3,481 Key Ratios Net Debt/EBITDA 0.39x 0.68x 0.73x 0.52x 0.39x 0.30x RoA 11.4% 8.0% 7.9% 7.9% 7.9% 7.6% RoE 48.3% 26.9% 24.2% 23.2% 21.1% 19.8% Capex to Sales 8.8% 6.0% 5.5% 5.5% 6.5% 7.0%

UAE – Construction

3

Investment Case

Arabtec is changing its strategy to become more of a regional player and is diversifying its portfolio in terms of both project type and country exposure to include high spending MENA countries, as well as high margin infrastructure projects.

Arabtec is disproving rumors doubting the sustainability of its operations and is successfully

managing its payables and receivables, reaching agreements with government and quasi government clients to receive due payments.

We resume coverage on Arabtec with a “Buy” recommendation based on a fair value/share of

AED4.17, implying an upside potential of 51%.

We resume coverage on Arabtec with a “Buy” recommendation, 51% upside potential We assign a "Buy" recommendation to Arabtec based on a DCF target price of AED4.17/share, which implies an upside potential of 51%. We have applied a WACC of 11.76% in our DCF that is derived from a cost of equity of 15.5% and a cost of debt of 4.36%. We used a Beta of 1.45 and a perpetual growth of 2%.

Table 1: WACC calculation

Debt Weight 33.52%Pre-Tax Cost of Debt 4.46%Effective Tax Rate * 2.17%After-Tax Cost of Debt 4.36%Equity Weight 66.48%Risk Free Rate* 4.62%Beta 1.45 Equity Risk Premium 7.50 Cost of Equity 15.49%WACC 11.76%* Based on a weighted average risk free according to the main countries where Arabtec operates.

Source: HC Brokerage

Table 2: Valuation

AED Million 2009e 2010f 2011f 2012f 2013f NOPLAT 795.7 845.2 879.6 860.3 855.2 Depreciation 276.7 291.4 332.3 388.1 437.4 CAPEX (583.3) (461.5) (485.2) (601.5) (655.1) Change in Working capital (432.3) (396.9) (108.2) 86.0 20.9 Change in other assets – Net 127.3 88.2 93.4 146.8 146.3 Free Cash Flow 184.1 366.4 711.9 879.8 804.7 Present Value of FCFs 169.3 301.6 524.4 579.8 474.6 Terminal Value 8,246 Enterprise Value 7,505 Net Debt (1,665) Minority Interests (855.0) Equity Value 4,985 Value per ordinary share (AED) 4.17 Source: HC Brokerage

UAE – Construction

4

Table 3: Sensitivity analysis of value per share to WACC and perpetual growth rate

WACC (%) Perpetual Growth Rate (%) 10.76% 11.76% 12.76%

1.0 4.40 3.79 3.29

2.0 4.88 4.17 3.59 3.0 5.49 4.63 3.95

Source: HC Brokerage

Table 4: Sensitivity analysis of value per share for 2009e-2013f

New Awards Growth EBITDA Margin (%) DCF Value

Worst Case -48% to 5% 12.0% - 12.8% 3.67

Base Case -39% to 7% 13.0%-13.9% 4.17 Best Case -28% to 20% 13.6% -14.5% 5.64

Source: HC Brokerage

Despite the slowdown, we still remain positive on the GCC construction sector We are positive that expenditure plans in the construction and infrastructure sectors will stay relatively intact in the GCC as governments are committed to mitigate against the slowdown and boost their economies through strategic infrastructure developments given:

• The expected increasing population in the region which puts extra burden on infrastructure facilities, demanding spending on meeting infrastructure needs. With more businesses going bankrupt in Europe and the US, highly skilled calibers have been eyeing the move to the GCC, where the market is still rather intact. Population in the GCC is expected to grow by 2% in 2009, mainly driven by growth in Qatar, Abu Dhabi and Saudi Arabia where thriving expansionary plans are underway.

• The construction sector is considered a relatively low risk sector and was assigned a stable credit outlook in the GCC by Fitch Ratings in January 2009.

The high levels of reserves and accumulated revenues from previous years when oil prices were at their peak. As a result, GCC countries have the financial ability to support their spending programs and boost their economies through non oil dependant revenues.

The continuing drop in construction costs within the region, which encourages construction and infrastructure investments.

Arabtec well- positioned to resist the meltdown

With a rather positive outlook on the GCC construction sector and global contractors eyeing the region to benefit from the significant expansionary plans currently underway, we firmly believe that Arabtec is in a strong position to compete with global and regional contractors over the projects in the GCC given the company’s:

• Solid reputation and sound track record: Arabtec is one of the largest civil construction companies in the Middle East, tracing its roots to 1975. It has expertise in residential construction and the oil and gas sector and a strong presence in Dubai, Abu Dhabi and Sharjah. Arabtec has an excellent track record and the capacity to handle a sizable backlog.

• Strong ties with developers: Arabtec is the preferred contractor for big developers such as Emaar properties, Nakheel and Dubai properties in the UAE.

• Partnership & JVs with regional players that facilitate smooth penetration of different markets. Arabtec has successfully penetrated the highly competitive Saudi Arabian market by venturing with one of the Kingdom's big players, Saudi Bin Laden Group. Arabtec has already won two contracts in the Kingdom worth around AED3.5 billion in 1H09. In Qatar, Arabtec has strong ties with Naser bin Khaled & Sons and is the main contractor for their AED4 billion project, Al Wa’ab City.

• Acquisitions to gain new competencies: In order to gain competency in infrastructure work, the company has acquired stakes in pure infrastructure players over the past couple of years to be able to bid for infrastructure projects in Abu Dhabi and other GCC countries.

UAE – Construction

5

Diversifying business and capitalizing on a strong reputation Arabtec is changing its strategy and capitalizing on its expertise and strong reputation in the UAE; the company is expanding its focus and diversifying its business to alleviate the repercussions of the financial crisis. This is mainly through changes in its backlog nature which include: (i) diversifying its exposure to high spending GCC markets through its planned regional expansions; (ii) shifting focus from commercial and residential projects to infrastructure and energy and utilities, especially after gaining expertise in this area through the acquisition of 60% of Abu Dhabi-based Target Engineering, a pure infrastructure player in 2007; (iii) building strong ties with creditworthy clients and business partners in new markets such as Qatar and Saudi Arabia, and (iv) looking for new markets to penetrate in the MENA region such as Algeria, Libya and Egypt.

Backlog to double by 2013

We based our assumptions on the company's 1Q09 backlog of AED18.8 billion which excludes the AED10 billion Okhta Center project in Russia. Nonetheless, we project that Arabtec’s backlog will double from AED20.2 billion in 2009e to AED40.4 billion at the beginning of 2013f.

Chart 1: Arabtec’s Estimated Backlog

25,592

35,106

13,030 14,092 14,515 15,53120,152

30,452

40,437

13,682

0

6,000

12,000

18,000

24,000

30,000

36,000

42,000

48,000

2009e 2010f 2011f 2012f 2013f

USD

Mil.

-50%

-40%

-30%

-20%

-10%

0%

10%

20%Backlog (at the begining of the year) New Awards During the Year% YoY Change in New Awards

Source: HC Brokerage

FCF to grow at a CAGR of 45% (09f-13f)

The company will be able to generate a positive free cash flow over our forecasted horizon with an FCF CAGR of 45% (09e-13f) on the back of improving working capital, hence lower interest expenses going forward. With the company expanding into the region and managing its working capital, we assumed that the company will not pay out dividends over the next two years. Meanwhile, we expect the company to start paying dividends in 2011; accordingly we maintained a dividend payout ratio of 40% until 2013 given that the company has no plans for high borrowings as short term borrowings will come down after 2011. We expect FCF yield in 2009e would be 5.6% compared to peers and increase to 11.1% in 2010.

Chart 2: Arabtec’s FCF yield vs. Peers 2009e

10.0%8.0% 7.0%

5.6%4.0% 3.0% 3.0% 2.0% 2.0% 2.0% 1.0%

-2.0% -3.0%-5.0% -5.0%

-7.0%

-15%

-5%

5%

15%

Teke

fen

GSEC

Vinvi

SA

Arab

tecGalf

ar

Samsu

ng En

g

Hende

rson D

ev OCI

HOCHIE

F

China

CCC

Larse

n & To

urbo

Hindus

tan Co

nst.

Mitsub

ishi H

eavy

Kajim

a Corp

Leigh

ton H

olding

s

Grupo F

errov

ial

Source: Reuters, Bloomberg, HC Brokerage

UAE – Construction

6

Aarbtec looks attractive on multiples Based on our valuation, Arabtec looks attractive in terms of multiples trading at an EV/EBITDA of 4.49x for 2009e, implying a discount of 37.8% to peers. Moreover, it trades at a discount of 45.0% on a PER 2009e of 4.68x. We believe that the stock is undervalued at current levels.

Chart 3: Arabtec vs. Peers

EV/EBITDA (2009e)

OCI

Arabtec

Galfar

Tekfen Holding

Enka InsaatGSEC

Samsung Eng. Huyndai Eng.

Hyundai Dev.Nagarjuna

IVRCL

IJM

China Com. Const.

-

2

4

6

8

10

12

14

16

-10% -5% 0% 5% 10% 15% 20% 25%

EBITDA CAGR (09-12)

EV/E

BITD

A (0

9)

PER (2009e)

OCI

Arabtec

Galfar

Tekfen HoldingEnka Insaat

GSEC

Samsung Eng.

Huyndai Eng.Hyundai Dev.

NagarjunaIJM

IVRCL

China Com. Const.

-

5

10

15

20

25

30

-10% 0% 10% 20% 30% 40%

EPS CAGR (09-12)

PER

(09)

Source: Bloomberg and HC Brokerage

UAE – Construction

7

Risks to our Valuation We believe risks to our valuation would be:

• Further cancellations and/or delays in projects, specifically out of Arabtec's backlog in Dubai which currently accounts for 49% of total backlog excluding Russia.

• Lower than expected growth in new awards, leading to slower growth in backlog. • Higher than expected defaults on receivables, this is likely, given current tight liquidity conditions. • Further renegotiation of contracts as developers try to make use of lower construction costs to bring down

the value of new projects.

Upside to our valuation

On the other hand, there are also factors that may provide an upside to our valuation:

• Suspended/ delayed projects coming back on stream: Since Arabtec’s backlog has already been slashed from AED57 billion to AED28.8 billion (including Russia) as a result of suspended or delayed projects, we would expect a decent upside to our valuation in case some of these projects come back on stream.

• Accounting for Russia’s Okhta project in our valuation: We note that due to our conservative approach to valuation, we have excluded the AED10 billion Okhta Centre project in Russia from our backlog assumptions given that it accounted for one third of the AED28.8 billion reported backlog and yet no ground work has been confirmed on the project. As the Russian project becomes active, we would expect an upside to our current valuation. We based our assumptions on a backlog of AED18.8 billion as of 1Q09 instead.

• More awards than expected in KSA, Qatar and other GCC countries: Arabtec’s management has revealed recently that it expects to be awarded close to AED22 billion worth of projects by the end of 2009. Although this maybe achievable, we chose to be conservative in our assumptions and divided the anticipated new awards amount (as per company announcement) over the two years of 2009 and 2010.

UAE – Construction

8

GCC remains most resilient

GCC countries are adhering to their earlier announced economic stimulus packages, supported by their accumulated revenues and benefiting from the decline in building materials prices

Government spending is expected to focus on the infrastructure and energy (utilities) sectors in

an attempt to accommodate the growing population, secure the private sector and encourage non hydrocarbon revenues.

Arabtec is taking solid moves to diversify its backlog away from Dubai through regional

expansions, starting with its smooth penetration of the Saudi Arabian market through its JV with Saudi Bin Laden Group. The company is seeking other partners in neighboring countries to further expand its exposure.

GCC well positioned to shield its economy

Post the financial crisis, the MSCI World GDP index lost 35.5% during the second half of 2008 and the International Monetary Fund (IMF) estimated that global GDP is to decline by 1.3% in 2009 in its April 2009 update, versus its previous estimate of 0.5% growth in 2009. Global GDP grew by 3.4% in 2008.

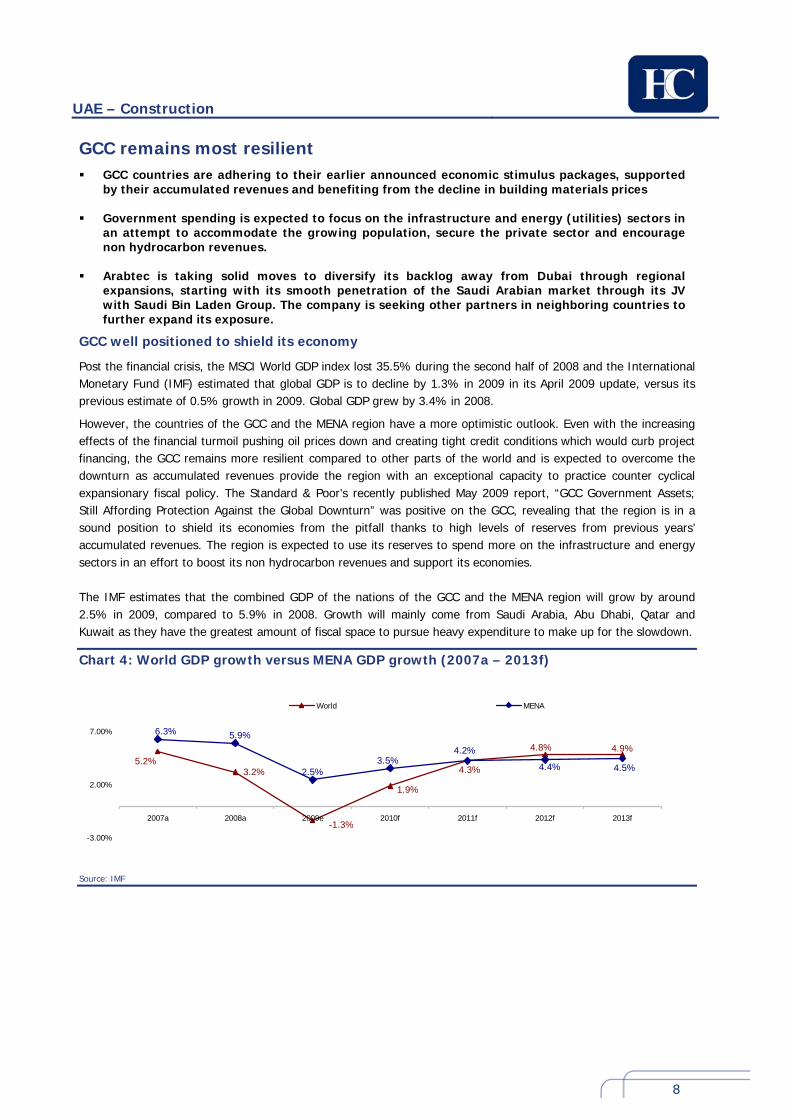

However, the countries of the GCC and the MENA region have a more optimistic outlook. Even with the increasing effects of the financial turmoil pushing oil prices down and creating tight credit conditions which would curb project financing, the GCC remains more resilient compared to other parts of the world and is expected to overcome the downturn as accumulated revenues provide the region with an exceptional capacity to practice counter cyclical expansionary fiscal policy. The Standard & Poor’s recently published May 2009 report, “GCC Government Assets; Still Affording Protection Against the Global Downturn” was positive on the GCC, revealing that the region is in a sound position to shield its economies from the pitfall thanks to high levels of reserves from previous years’ accumulated revenues. The region is expected to use its reserves to spend more on the infrastructure and energy sectors in an effort to boost its non hydrocarbon revenues and support its economies. The IMF estimates that the combined GDP of the nations of the GCC and the MENA region will grow by around 2.5% in 2009, compared to 5.9% in 2008. Growth will mainly come from Saudi Arabia, Abu Dhabi, Qatar and Kuwait as they have the greatest amount of fiscal space to pursue heavy expenditure to make up for the slowdown.

Chart 4: World GDP growth versus MENA GDP growth (2007a – 2013f)

3.2%

4.9%4.8%

4.3%5.2%

-1.3%

1.9%

4.5%4.4%

4.2%3.5%

2.5%

5.9%6.3%

-3.00%

2.00%

7.00%

2007a 2008a 2009e 2010f 2011f 2012f 2013f

World MENA

Source: IMF

UAE – Construction

9

Saudi Arabia, Qatar and Abu Dhabi are key markets

According to Standard &Poor’s May 2009 report, Saudi Arabia, Abu Dhabi and Qatar are the most resilient in the GCC given their high reserves from petrodollars accumulated over previous years. These countries are most likely to overcome the global meltdown through spending reserved petrodollars in developing their non oil dependant sectors to help support their economies. GCC governments are committed to supporting the private sector and encouraging non hydrocarbon revenues; accordingly each government is adhering to the stimulus packages announced earlier this year, with investments focused on infrastructure spending in transportation, utilities and construction. This focus on infrastructure spending is essential for GCC countries given the increasing interest in the region, as more and more people are escaping the meltdown in the US and Europe to come to the GCC.

Chart 5: GDP Growth of selected GCC countries (2007a – 2013f)

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

2007a 2008a 2009e 2010f 2011f 2012f 2013f

UAE Qatar Saudi Arabia

Source: IMF

Table 5: Foreign Reserves and Budget Surplus

USD Bil. KSA UAE Qatar

Foreign Reserves 2008 27.6 34.8 9.6 Foreign Reserves as % of GDP 7.2% 26.9% 22.5% Budget Surplus (Deficit) 2008 157.3* 59.9* 10.5~

Cumulative Fiscal Surplus since 2003 350 221.9 34.1

Estimated Oil Price for 2009 Budgets (USD/B) 40 45 35

Budgeted Total Expenditure in 2009 (USD billion) 126.7 25.9

Allocated to infrastructure spending (USD billion) 61 168** 10.4 *Estimates ~As of April 2008 ** Abu Dhabi spending until 2010 Source: Bloomberg, IMF, Central Banks, Newspapers, HC Brokerage, QCB, BMI,

Healthy demographics drive spending

We believe that construction activity in the GCC is sustainable as the commercial viability of infrastructure and utility projects is determined by future demand, and demand for these services in emerging markets is essentially driven by demographic trends.

Population in the GCC is expected to grow in 2009 at a slower rate of 2% compared to 4% in 2008. According to our estimates, the UAE population is expected to decline by 1.2% in 2009 as a result of expatriates leaving Dubai either due to being laid off or seeking another stable working environment in neighboring countries. On the other hand, the IMF estimates that Qatar's population is to increase by 4%, a much slower rate compared to previous years of double digit growth of 18% and 23% in 2007 and 2008, respectively. Also, Saudi Arabia has an annual demographic growth of 3% .

UAE – Construction

10

Chart 6: Population growth in selected GCC countries (2007a – 2012f)

-3%

1%

5%

9%

13%

17%

21%

25%

2007a 2008a 2009e 2010f 2011f 2012f

UAE Qatar Saudi Arabia

Source: IMF, HC Brokerage

New contracts awarded in the MENA region grow significantly in June 2009

In an attempt to boost their economies, governments of the GCC announced various stimulus packages and decided to heavily invest in construction, specifically in the infrastructure and energy sectors. According to MEED, project contracts awarded in the MENA region in June 2009 (until 22 June 2009) were worth approximately USD9.8 billion compared to USD4.5 billion awarded in May 2009.

Chart 7: Growth in value of contracts awarded in MENA region (per month)

-5% 2%

343%

51%

-44%

41%-1%

80%

184%226%

196%

78%

25%

-44%-2%

67%

118%

-22%

62%

-13%

30%15%29%

-50%-10%30%70%

110%150%190%230%270%310%350%390%

Jan-07

Feb-07

Mar-07

Apr-07

May-07

Jun-07

Jul-07

Aug-07

Sep-07

Oct-07

Nov-07

Dec-07

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Contracts awarded growth %

Source: MEED

GCC projects reach USD2.1 trillion mainly on the back of infrastructure projects

The MEED Projects index reported a 3% drop M-o-M in total value of planned and underway projects in the GCC, coming in at USD2.145 trillion as of 22 June 2009 compared to USD2.204 trillion as of 30 May 2009. Planned and underway projects, however, are up 8.9% YoY from USD1.98 trillion.

Chart 8: MEED Gulf Projects in June 2009

0400

800

1,2001,6002,000

2,400

2,8003,200

Bahrain Kuwait Oman Qatar SaudiArabia

UAE GCC total Iran Iraq Gulf to tal-30%

20%

70%

120%

170%

220%Jun-09 Jun-08 % YoY Growth

Source: MEED

UAE – Construction

11

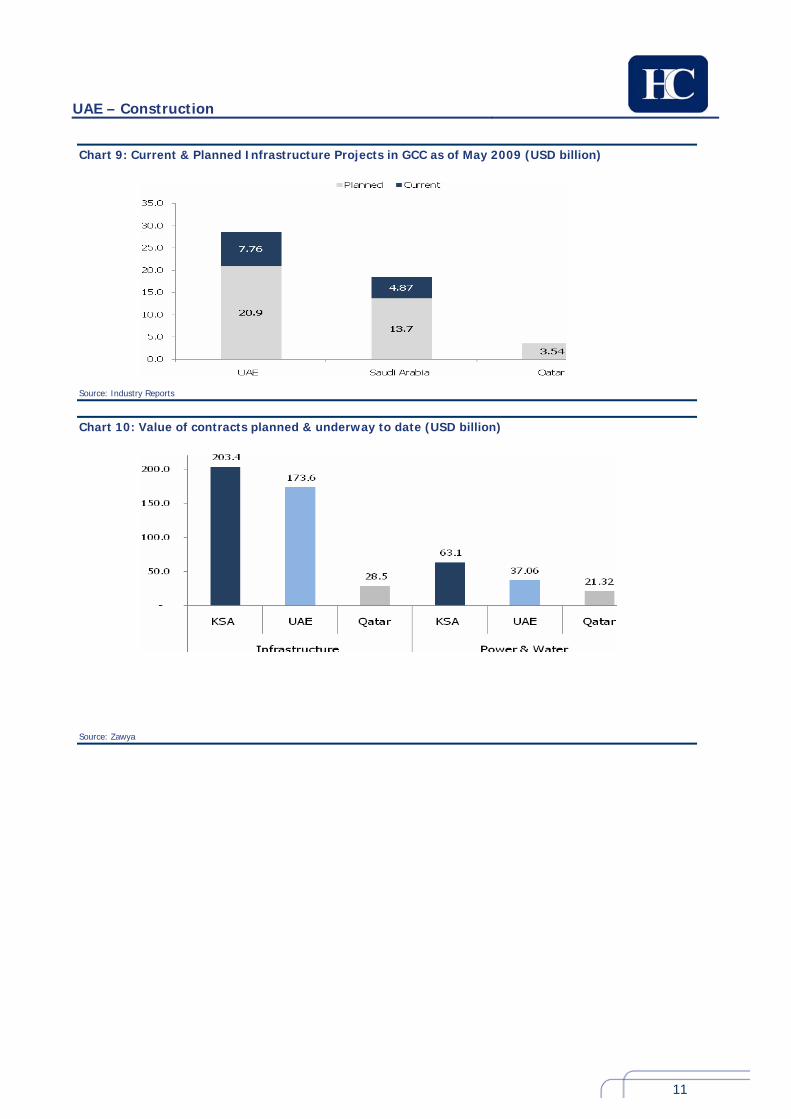

Chart 9: Current & Planned Infrastructure Projects in GCC as of May 2009 (USD billion)

Source: Industry Reports

Chart 10: Value of contracts planned & underway to date (USD billion)

Source: Zawya

UAE – Construction

12

Table 6 : Main Highlights in Regional Infrastructure

UAE KSA • The UAE government plans to invest up to USD272 billion

in infrastructure projects over the next five to seven years. • The government of Dubai has recently announced its 2009

budget which revealed that the government will allocate around AED17.1 billion (USD4.7 billion) to infrastructure spending. Dubai alone will witness 11 road & bridge projects costing USD1 billion by mid of 2009.

• UAE utilities industry, which includes water services, power generation, and power transmission infrastructure, is estimated to increase by 90% between 2007 and 2012.

• More than USD10 billion will be spent to meet soaring power demand in the UAE, which is expected to account for 5.77 % of regional power generation by 2011.

• The Dubai Electricity and Water Authority (DEWA) plans to invest AED13 billion (USD3.5 billion) in 2009 in new projects as part of its AED75 billion (USD20.4 billion) spending plan to build capacity to match the emirate's future economic growth.

• In April 2008, Dubai’s government completed the issuance of AED6.5 billion (USD1.8 billion), representing the first tranche of its AED15 billion (USD4.1 billion) Medium Term Note (MTN) program to raise funds for various infrastructure projects.

• The Saudi government announced its plans to spend USD400 billion on infrastructure projects over the next five years as it seeks to benefit from lower construction costs.

• In January 2009, the Saudi government announced that it will earmark SAR11.5 billion (USD3.1 billion) in 2009 and 2010 for road construction projects with total length of 8,250 km, representing a 4.7% increase over its current roads’ length of 175,000 km.

• Persistent demand for electric utilities is growing by 5-7% annually mainly driven by rapidly expanding population, growth in the industrial sector, and low power tariffs.

• The Saudi Ministry of Water and Electricity projected

that the country will require at least 35 GW of additional power generating capacity by 2023 at an estimated cost of USD120 billion.

• Zawya Projects reports that the Saudi Arabian

investments cluster in infrastructure, real estate and power and water sectors exceeds USD350 billion to be completed over the next eight years.

Algeria Qatar

• The Algerian government is to announce the new

infrastructure and public works plan (2009-2013) which is expected to be around USD150 billion to be spent on infrastructure, construction, transportation, and water sectors.

• It announced the upgrading of 1,200 miles of railway with an estimated cost of USD1.5 billion. The government also intends to allocate around USD5.5 billion to the oil and gas projects, where the national oil company Sonatrach is planning to invest USD45 billion over five years.

• In addition to its investments in the oil and energy

sector, the Qatari government intends to invest USD130 billion to develop the state’s infrastructure and diversify its economy in line with its ambitious target of zero dependence on oil by 2020.

Source: BMI, Zawya Projects, Foreign Affairs & International Trade Canada, Various Newspapers

UAE – Construction

13

Arabtec can weather the storm

We believe Arabtec’s excellent track record, sizable capacity and strong ties with clients give it an edge over other competitors in the GCC and makes it more likely to overcome the slowdown.

Arabtec has added to its expertise through vertical integration, and is able to provide other services related to civil construction.

Arabtec extended its expertise to areas other than civil construction through the acquisition of pure infrastructure companies over the past couple of years, giving it an edge to compete for the increasing infrastructure projects in the region.

A reputable company with a strong track record… Arabtec’s excellent track record and capacity to handle a sizable backlog give it an edge over other contractors in the UAE and the region to land mega contracts in current times; when funding is limited, quality and reputation become more imperative. Arabtec Holding is one of the leading civil contractors in the Middle East and one of the largest UAE-based construction companies, extending back to 1975. The company was founded to offer construction services in the UAE, specifically in Dubai, Abu Dhabi and Sharjah. Through its various subsidiaries, Arabtec is primarily engaged in the construction of high rise towers, buildings and residential villas. Arabtec Holding’s backbone is its wholly owned subsidiary, Arabtec Construction (started in 2005) which has a remarkable track record of constructing several of the most renowned projects in the UAE. Some of Arabtec’s recognized projects are:

• In Dubai: the Burj Dubai which is still under execution, Jumairah beach resort towers and hotel, the Fairmont Hotel, Lexus tower, the 21st Century tower, DIFC Gate Village, Sky Gardens, and the interiors and fit out of Burj Al Arab.

• In Abu Dhabi: the new Abu Dhabi Investment Authority headquarters (ADIA), ADNEC, and Emirate

Palace.

• In Sharjah: Sharjah Art Gallery.

The company's major assets are its large number of employees and equipment, which give the company the capacity, means and facilities to complete mega projects punctually and with high quality. Currently, Arabtec’s workforce exceeds 70,000 employees.

… maintaining strong ties with clients & suppliers A key to every successful contractor is its relationship with clients and suppliers. Arabtec has earned being the preferred contractor to the Emirates' big developers, such as Emaar Properties, Nakheel, and Dubai properties. Good ties with clients provide Arabtec the advantage of being awarded new contracts in the region. One highlight is Emaar Properties' strong presence in Saudi Arabia, which we believe is positive for Arabtec as its potential contractor. Moreover, during current times, a history of trustworthiness and healthy relationships with clients provides Arabtec with an edge over competitors when getting paid for due contracts. Suppliers also favor Arabtec, as the company manages to consistently be on top of payments. Emaar used to account for the lion’s share in Arabtec’s backlog prior to the financial crisis, which led to delays/cancellations of a number of Emaar’s Dubai-based projects. Emaar Properties has a strong presence in Saudi Arabia and is assigned the supervision of the Kingdom City and Kingdom Tower project, worth SAR100 billion (USD26.7 billion). With Arabtec penetrating the Saudi Arabian market and its strong ties with Emaar, we believe it has a higher chance of being awarded a portion of the contract. Arabtec has already entered the Saudi market through a joint venture with Saudi Bin Ladin Group earlier this year. According to our estimates to date, backlog from the JV accounts for 16.6% of total backlog, up from 8% in 1Q09. This increase is mainly due to the recently awarded contract to build a luxury tower worth AED2 billion (USD533 million) in the Kingdom. According to our estimates as of June 2009, Nasser Bin Khaled & Sons –NBKS project Wa’ab City in Qatar is now the biggest single project on Arabtec’s backlog, accounting for 17.8% of the backlog.

UAE – Construction

14

Chart 11: Backlog as of June 2009 by client

Others33%

ICT 4%

NBKS Wa'ab City18%

Zabeel Inv9%

KSA Bin Laden, 16.60%

Emaar6%

Emirates Sunland4%

Nakheel4%

Cayan Inv5%

Source: Arabtec, HC Broerage

Expanding expertise by acquisitions and vertical integration Since its foundation, Arabtec has specialized in oil and gas as well as civil construction, benefiting from increasing developments of large scale villas and high rise towers. Arabtec has expanded vertically to add to its service; through its subsidiaries, the company is capable of executing several construction related activities, from being awarded MEP contracts to manufacturing ready mix concrete, pre-cast concrete and structural steel works. Since Arabtec is mainly a pure construction player and did not have high expertise in infrastructure works, in 2007 it acquired 60% of Abu Dhabi-based Target Engineering Construction Company, a pure infrastructure playe, in order to gain competency in this area. This strengthens Arabtec‘s position to compete for infrastructure projects as government spending focuses on infrastructure works rather than real estate construction amid the financial crash.

Arabtec’s backbone is Arabtec Construction, which accounts for 82% of the company’s work, and its main focus is civil construction. Meanwhile, Target Engineering accounts for 12% of the company’s backlog and is an infrastructure focused subsidiary. This is justified as Arabtec’s current backlog remains skewed to residential and mixed development projects compared to infrastructure. We believe that as Arabtec lands more infrastructure projects in Abu Dhabi, Target’s share in the projects will increase.

Table 7: Subsidiaries & Joint Ventures

Subsidiary Country Ownership% Principal Activity 2005

Arabtec Construction Dubai/ Abu Dhabi - UAE 100% Civil Construction & related works

Austrian Arabian Ready Mix Dubai - UAE 100% Manufacture & transport ready mix concrete products

2006 House of Equipment Dubai - UAE 33.3% Trading & leasing of construction equipment Arabtec Construction Qatar 49% Civil Construction & related works

Arabtec Precast Dubai - UAE 100% Manufacture of Pre-cast panels 2007

Nasser Bin Khaled Factory Ready Mix Concrete Qatar 49% Manufacture & transport of ready mix concrete

products Emirate Falcon Electromechanical –

EFECO Dubai - UAE 55% Electrical mechanical & plumbing contracts

Arabtec Engineering Services Dubai - UAE 100% Infrastructure construction works Arabtec Pakistan Pakistan 60% Civil Construction & related works

Target Engineering Construction Abu Dhabi - UAE 60% Infrastructure & Civil construction works 2008

Gulf Steel Industries Sharjah – UAE 55% Fabrication of steel structures Arabtec WCT (JV) Dubai – UAE 51% Infrastructure construction works

Arabtec International Mauritius 100% Civil Construction & related works Arabtec Engineering Enterprise Jordan 50%

Source: Arabtec

UAE – Construction

15

Chart 12: Backlog as of 1Q09 by subsidiary

Arabtec Construction

82%

Target Engineering

12%

Arabtec Engineering

3%

ECC1%

Arabian Business

2%

Source: Arabtec, HC Brokerage

UAE – Construction

16

Regional expansion - Building a more stable backlog

We believe Arabtec will be building on backlog to safeguard itself against further project cancellations or contract renegotiations in Dubai. We estimate a 39% drop in new awards in 2009 with a pick up expected as of 2010 to have new awards grow at a CAGR of 4% (09e-13f).

Accordingly, we estimate revenues to grow at a CAGR of 3.7% (09e-13f) on the back of anticipated increase in new contracts awarded in highly liquid new markets such as Saudi Arabia, Qatar and Abu Dhabi.

We expect EBITDA margins to be in the range of 13.0-13.9% over the forecasted horizon due to more exposure to high margin infrastructure projects within the region.

Arabtec is diversifying its portfolio away from Dubai Amid the financial turmoil which led to major project cancellations in the UAE, Arabtec’s backlog has been slashed and questions regarding the sustainability of the remaining projects were raised. This called for a change of plans and strategy to accommodate the new situation and boost confidence in the company’s operations. In order to mitigate the hit the company is moving in steady steps to have a more diversified portfolio in terms of location and project type. The company managed to:

• Smoothly penetrate the highly competitive Saudi Arabian market by venturing with one of the Kingdom's big players, Saudi Bin Laden Group. Accordingly, the company will have exposure to the market and a very good chance of winning big contracts. Arabtec has already won two contracts in the Kingdom worth around AED3.5 billion in 1H09.

• Have a strong presence in Qatar, where it is expected to win more contracts by the end of 2009. • Expand its operations in Abu Dhabi capitalizing on its 2007 acquisition of the Abu Dhabi-based

infrastructure company, Target Engineering, which adds to Arabtec’s expertise in infrastructure and utilities works.

• Currently be in negotiations with other quasi government bodies in neighboring countries as potential business partners to facilitate smooth penetration of new markets.

We have taken a conservative approach by which we excluded the Okhta project in Russia from our backlog calculation, as the project has been witnessing some execution risks and work on it has not yet begun. The Okhta project accounted for one third of Arabtec’s backlog of AED28.8 billion. Accordingly, we built our assumptions on a backlog as of 1Q09 worth AED18.8 billion which excludes the AED10 billion value of the Okhta center project. According to our estimates, Arabtec’s backlog as of June 2009 totals to AED21.1 billion excluding Russia and including the newly awarded contract in Abu Dhabi (AED800 million) and that in Saudi Arabia (AED2 billion).

Chart 13: Arabtec’s Backlog by Exposure as of June 2009 (excluding Russia)

Dubai 49.9%

Abu Dhabi 12.9%

Qatar 18.5%

KSA16.6%

Others 2.1%

Source: Arabtec, HC Brokerage

UAE – Construction

17

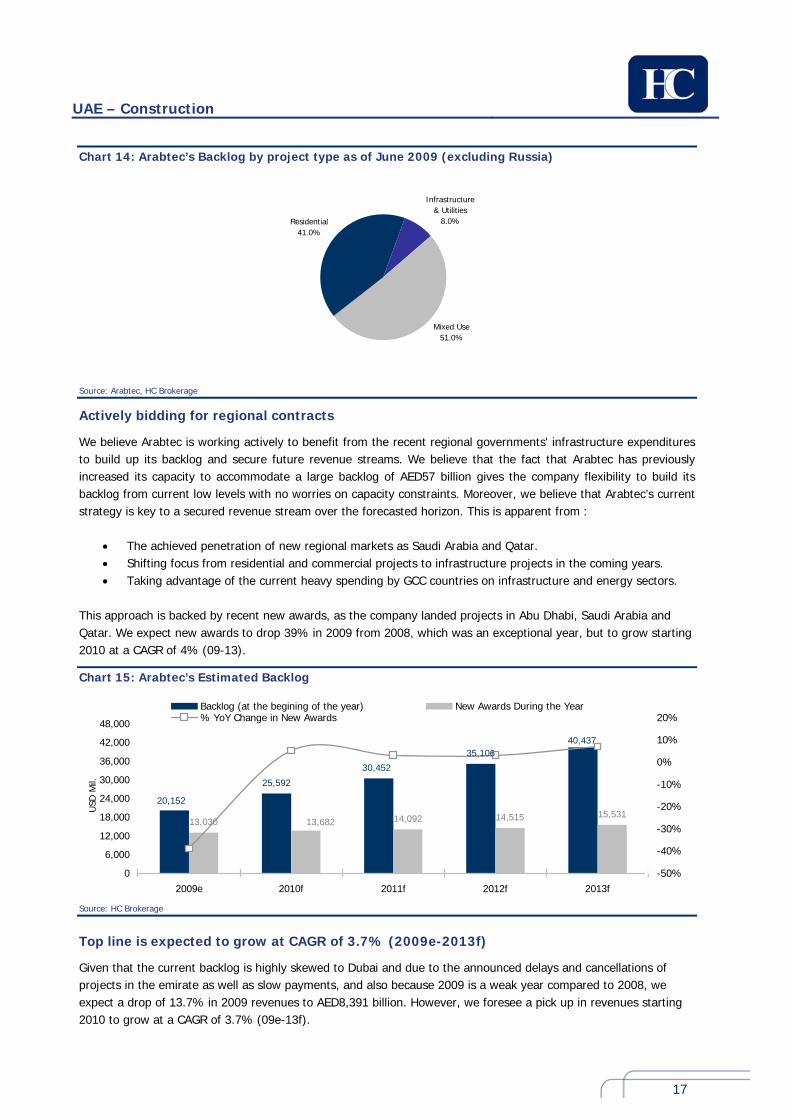

Chart 14: Arabtec’s Backlog by project type as of June 2009 (excluding Russia)

Infrastructure & Utilities

8.0%

Mixed Use51.0%

Residential 41.0%

Source: Arabtec, HC Brokerage

Actively bidding for regional contracts

We believe Arabtec is working actively to benefit from the recent regional governments' infrastructure expenditures to build up its backlog and secure future revenue streams. We believe that the fact that Arabtec has previously increased its capacity to accommodate a large backlog of AED57 billion gives the company flexibility to build its backlog from current low levels with no worries on capacity constraints. Moreover, we believe that Arabtec’s current strategy is key to a secured revenue stream over the forecasted horizon. This is apparent from :

• The achieved penetration of new regional markets as Saudi Arabia and Qatar. • Shifting focus from residential and commercial projects to infrastructure projects in the coming years. • Taking advantage of the current heavy spending by GCC countries on infrastructure and energy sectors.

This approach is backed by recent new awards, as the company landed projects in Abu Dhabi, Saudi Arabia and Qatar. We expect new awards to drop 39% in 2009 from 2008, which was an exceptional year, but to grow starting 2010 at a CAGR of 4% (09-13).

Chart 15: Arabtec’s Estimated Backlog

25,592

35,106

13,030 14,092 14,515 15,53120,152

30,452

40,437

13,682

0

6,000

12,000

18,000

24,000

30,000

36,000

42,000

48,000

2009e 2010f 2011f 2012f 2013f

USD

Mil.

-50%

-40%

-30%

-20%

-10%

0%

10%

20%Backlog (at the begining of the year) New Awards During the Year% YoY Change in New Awards

Source: HC Brokerage

Top line is expected to grow at CAGR of 3.7% (2009e-2013f)

Given that the current backlog is highly skewed to Dubai and due to the announced delays and cancellations of projects in the emirate as well as slow payments, and also because 2009 is a weak year compared to 2008, we expect a drop of 13.7% in 2009 revenues to AED8,391 billion. However, we foresee a pick up in revenues starting 2010 to grow at a CAGR of 3.7% (09e-13f).

UAE – Construction

18

Chart 16: Revenues

8,3919,2549,722

8,821 9,3599,718

0

2,000

4,000

6,000

8,000

10,000

12,000

2008a 2009e 2010f 2011f 2012f 2013f

USD

Mil.

-30.00%

10.00%

50.00%

90.00%

130.00%

Revenues % YoY Change in New Awards

Source: HC Brokerage

Costs increase on the back of geographical expansions

Building material costs account for approximately 30% of total direct costs and with building materials prices going down, this should reflect positively on margins. However, we still assumed tight COGS/revenue as a result of higher costs attributed to current regional expansions and higher labour costs due to more spending on labour camps to meet human rights regulations. The status of labour camps has become a major human rights issue and accordingly GCC contractors are faced by regular inspections of their labour camps and are obligated to maintain certain specs to comply with regulations. Arabtec has announced on several occasions that it is undergoing labor camp expansions and upgrading, in addition to new camps being built in the newly penetrated markets in the region. We have assumed COGS/revenue to remain close to the 82.4% - 83% level.

EBITDA margin to hover around the 13.0%-13.9% levels (2009e-2013f)

As the current backlog which is heavily weighted on Dubai starts to deplete, and with more spending in the region on infrastructure and energy works, we expect Arabtec’s backlog to shift from being focused in Dubai on commercial and residential works to focus on infrastructure and energy projects in other GCC countries. Arabtec has already penetrated the Saudi Arabian market through a JV with Saudi Bin Ladin Group. The company also has a strong presence in Qatar and sound ties with the Qatari government. We estimate the company’s EBITDA margin level to remain around 13.0%-13.9% over the forecasted horizon, with higher levels beyond 2010 as more commercial projects would have been depleted and more infrastructure projects would dominate the backlog. Although we expect lower level of EBITDA compared to 2007 level at 15%, Arabtec is still expected to yield higher margins versus its peer average of 10.2% - 10.6% (09-11). Although margins are benefiting from lower construction costs as a result of deflation, labor costs are increasing due to recent strikes and human rights lookout on the welfare of labor forces. There is and will continue to be decent spending on maintaining certain specs in labor camps anywhere in the GCC.

UAE – Construction

19

Chart 17: EBITDA Growth (in AED billion)

1,293

1,0911,182

1,259 1,3011,351

6.47%8.39%

3.37%

3.84%

-15.63%

98.91%

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2008a 2009f 2010f 2011f 2012f 2013f-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%EBITDA % YoY Growth

Source: Arabtec and HC Brokerage

Table 8: Key Performance Indicators

USD Million 2008a 2009e 2010f 2011f 2012f 2013fRevenues 9,722 8,391 8,821 9,254 9,359 9,718 YoY change 127.52% -13.69% 5.13% 4.90% 1.14% 3.84% EBITDA 1,293 1,091 1,182 1,259 1,301 1,351 YoY change 98.91% -15.63% 8.39% 6.47% 3.37% 3.84% EBITDA margin 13.30% 13.00% 13.40% 13.60% 13.90% 13.90% Net Income 957 705 754 798 781 777 YoY change 78% -26% 7% 6% -2% -1% NPM 9.8% 8.4% 8.5% 8.6% 8.3% 8.0% Source: Arabtec, HC Brokerage

Table 9: Arabtec ‘s Margins vs. Peers

Country Company EBITDA Margin % NPM %

2008 2009e 2010f 2011f 2008 2009e 2010f 2011f

EGYPT OCI (Construction LoB)* 12.9% 13.3% 12.8% 13.5% 11.6% 8.7% 8.6% 8.9% Oman Galfar 11.47% 13.48% 13.19% 13.35% 7.93% 5.52% 6.43% 5.79% India Larsen & Tourbo 11.53% 11.80% 11.80% 11.18% 10.76% 8.25% 9.05% 9.05% Turkey Tekfen Holding 13.95% 10.57% 10.65% 11.36% 7.31% 6.70% 6.43% 6.57% Turkey Enka Insaat 14.37% 14.68% 15.12% 15.56% 5.78% 5.92% 5.58% 5.86% South Korea Samsung Eng. 6.95% 7.40% 7.05% 7.17% 8.55% 7.82% 8.83% 9.23% South Korea Hyundai Eng 7.59% 6.67% 6.66% 6.90% 6.97% 5.51% 5.14% 5.35% South Korea Hyundai Dev. 10.59% 10.86% 11.67% 11.99% 5.86% 2.99% 3.28% 3.30% South Korea GSEC 7.47% 6.92% 6.95% 6.99% 3.45% 3.60% 3.73% 3.97% Malaysia Gamuda 10.00% 12.20% 13.80% 10.00% 1.76% 2.24% 2.40% 2.47% India Hindustan Construction 9.64% 12.03% 12.11% 12.37% 4.51% 4.75% 5.00% 0.00% China China Com. Const. Co. 7.96% 8.24% 8.38% 8.35% 42.30% 41.91% 40.40% 36.42% China China Railway Construction 4.27% 4.75% 4.94% 4.85% 2.90% 2.48% 2.35% 2.71% Malaysia IJM Corporation 16.60% 16.00% 17.20% 16.60% 1.91% 0.60% 0.33% 0.89% India IVRCL Infrastructure &

Projects 9.30% 9.50% 9.50% 9.30% 1.90% -0.34% 0.91% 1.01% India Nagarjuna Construction 9.50% 10.30% 10.40% 9.50% 15.60% -6.57% 4.12% 16.42%

Average 10.26% 10.51% 10.75% 10.56% 8.50% 6.09% 6.93% 7.27% UAE Arabtec 13.30% 13.03% 13.40% 13.60% 9.8% 8.4% 8.5% 8.6% Source: Arabtec, HC Brokerage

UAE – Construction

20

Net income affected by increase in minority & taxes

We expect minority interest to increase going forward given the company’s acquisitions to enhance vertical integration. Moreover, we also expect the effective tax rates to increase gradually when more of the backlog is located in tax paying countries. Currently, Arabtec’s backlog is more skewed to UAE projects, which is a free tax environment. We project that net income after minority will grow at a CAGR of 2.5% between 2009 and 2013.

Chart 18: Net Income Growth (in AED billion)

957

705754

798 781 777

6%7% -2% -1%

-26%

78%

200

400

600

800

1,000

1,200

2008a 2009f 2010f 2011f 2012f 2013f-45%

-25%

-5%

15%

35%

55%

75%

Net Income % YoY Growth

Source: Arabtec and HC Brokerage

Delayed payments trigger short term financing

Following the credit crunch, clients delayed due payments and some may very well fail to meet their payments at all. Arabtec resorted to short term financing to manage its payables in order not to compromise its operations. Its is worth noting that historically, the company followed a “pay when paid” scheme with suppliers.

In 1Q09, as a result of delayed payments, receivables more than double compared to 1Q08 to reach AED4.7 billion versus AED2.3 billion, while payables were increasing as well to reach AED5.1 billion in 1Q09 compared to AED3.2 billion in 1Q08. This triggered the company to take on short term debt to finance its payables. Short term debt in 1Q09 increased to AED1.3 billion compared to AED291 million in 1Q08. We expect that Arabtec will continue to take on short term debt to finance its working capital requirements going forward, especially since the company is aggressively targeting new contracts, naturally adding to its receivables and leading to increasing inventory to accommodate new projects. As receivables form old contracts start to deplete and are replaced by more “liquid” receivables from new contracts, short term borrowing would drop as the company would be able to manage its payables through cash as was the case in previous years.

Chart 19: Working Capital versus Short Term Financing

2,315

4,6794,983 5,116 5,275 5,147 5,209

3,241

5,024

5,7325,244 5,469 5,460 5,316 5,452

4,992

3%-42%19%

426%

4%0%

500

1,500

2,500

3,500

4,500

5,500

6,500

1Q08 1Q09 2008a 2009f 2010f 2011f 2012f 2013f-60%

0%

60%

120%

180%

240%

300%

360%

420%

480%Receivables Payables STD growth%

Source: Arabtec , HC Brokerage

UAE – Construction

21

Qatar: One of the world’s highest GDPs per capita

Qatar would be the first GCC country to overcome the effects of the global slowdown, with GDP to sustain a double digit growth in 2009 and 2010 driven by construction activity.

Based on 2009/10 budget, the government is committed to investing up to USD25.9 billion in

the infrastructure and energy sectors to accommodate the growing population and encourage non hydrocarbon revenues.

Arabtec already has a strong presence in Qatar, and according to management is expected to

land more projects in the country as part of its strategy to diversify its exposure in high spending MENA countries.

The only GCC country expected to witness double digit growth in 2009

Qatar is expected to sustain growth against the slowdown as it is one of the richest countries per capita in the world. Qatar posts one of the highest GDPs per capita, estimated at USD58, 585 for 2009. Moreover, the country has locked in huge surplus from both oil exports and LNG exports in 2008. The country’s reserves of natural gas is the third in the world and is expanding heavily in mega LNG projects which provide much higher return than gas. Based on Standard & Poor’s recent Credit Survey on the GCC in 2009, it estimates that a big portion of previous surpluses have been and will be re-invested in productive infrastructure, particularly in the expansion of LNG production capacity. The IMF estimates that Qatar's GDP is to grow by 18% in 2009 compared to the expected contracting economies in neighboring countries. Moreover, the country has healthy demographics as population has been growing by double digits over the past four years to reach 1.6 million in 2008. The IMF estimated population to grow by 4% in 2009 to reach 1.67 million.

Qatar allocates USD10.4 billion for infrastructure developments

In April 2009, Qatar approved its 2009/10 budget based on a budgeted oil price of USD40/ barrel. The budget was characterized as an expansionary plan despite the financial crisis, allocating USD25.9 billion for total spending out of which USD10.4 billion will be allocated for strategic infrastructure projects. This positively reflects the government’s commitment to infrastructure spending to meet the increasing needs of the country as well as its support for the private sector’s activities, which we believe will present great opportunities for construction companies. The Governor of the Qatar Central Bank, Sheikh Abdullah bin Saud al-Thani, reaffirmed that the government would continue public spending on development projects to accommodate increasing interest in the country and the growing population. Moreover, it is estimated that around USD120 billion will be invested in Qatar’s energy and infrastructure over the next five years.

Qatar construction industry to grow by 14.6% in 2009

Construction activity in Qatar is at a peak with long term, large scale projects planned and underway, including airport, power and rail projects. However, there is always a risk due to the global slowdown which impacts the level of foreign investments in the country due to financing difficulties, as well as falling demand on residential properties in the GCC which has already hit the UAE, slowing down its construction of large scale projects. However, government will support spending, which will mainly be directed towards:

• Transportation: Most of the country’s available transportation infrastructure is operating close to capacity, which calls for the need to expand. There is no rail network, thus the country is relying heavily on roads and straining the transportation infrastructure. Current underway and planned projects amount to approximately USD28.5 billion.

• Energy & Utilities: Although Qatar has a well established power sector, electricity consumption is currently exceeding electricity generation and is expected to further increase with the increasing population and scale of projects. The main problem is that the power sector is wholly reliant on one generating source, that being gas. The country is still looking to diversify its reliance and sources of generating capacity by looking into nuclear power. Qatar is continuing to expand its power sector through the

UAE – Construction

22

construction of more power plants, which will help combat the power shortages in the country. This is being combined with the issue of water demand, which is being tackled through developing Independent Water and Power Projects (IWPPs).

• Construction: Expected to benefit from the attempts to develop the non oil and gas sector in Qatar. The construction of education and sports facilities has been forthcoming and there has been a drive in residential construction. One of the largest projects in Qatar is Diar’s Lusail Development, with a total cost of USD5.5 billion.

Arabtec well-positioned to compete against local players

With so many global players in the market and other Qatari companies in the picture, competition is very high. In 2006, 53% of contracts launched were awarded to Qatari companies, suggesting some bias to local contractors. However, we believe Arabtec has a much higher chance of landing projects in Qatar versus other competitors in the market especially after being awarded one of the county’s biggest projects, “Al Wa’ab City”, valued at AED4 billion. Also, Arabtec is a favored contractor in Qatar given its competency gained from high scale projects completed in Dubai and Abu Dhabi. Qatar is a booming country in its development phase, Arabtec’s experience in shaping the image of developments and construction in Dubai has a magnet effect, attracting other countries and governments to make use of it. Arabtec’s management has recently announced its expectations to land more projects in Qatar by the end of 2009.

Chart 20: Underway & Planned Spending in Qatar

Transportation 21%

Oil & Gas 79%

Airports50%

Ports29%

Roads&Bridge10%

Rail4%

Other7%

Source: Zawya Projects

Table 10: Qatar Population & Economic Indicators

2007e 2008e 2009e 2010f 2011f 2012f

Population (million) 1.30 1.60 1.67 1.75 1.78 1.82 YoY % 18% 23% 4% 5% 2% 2% Nominal GDP (USD bn) 71.10 102.30 73.60 83.00 101.30 122.10

GDP per capita PPP (USD) 85,199 85,868 92,121 97,001 95,711 90,458

Real GDP Growth % 15.3% 16.4% 18.0% 16.4% 3.3% 3.3%

Construction value (USD bn) 4.02 4.99 6.27 6.94 7.69 8.51

Construction real growth % 8.3% 12.4% 14.57% 6% 7% 8%

Construction as % of GDP 5.7% 4.9% 8.5% 8.4% 7.6% 7.0% Source: IMF, Central Banks, BMI, & HC Brokerage

UAE – Construction

23

Saudi Arabia: Largest construction market in MENA region

Although the Saudi Arabian economy is expected to contract by 0.9% in 2009, it remains the largest construction sector in the MENA region.

Government is expected to spend up to USD61 billion in 2009/2010 on infrastructure

development to accommodate the growing population in the Kingdom. Arabtec penetrated the Saudi Arabian market through its JV with big player, Saudi Bin Laden

Group, and was awarded two projects worth USD3.5 billion in 1H09.

Saudi Arabia represents the largest construction market in the MENA region Saudi Arabia is the largest economy in the Middle East, accounting for almost half the GCC's GDP and more than one third of the MENA region's GDP. It is the world’s largest producer and exporter of oil, benefiting from buoyant oil prices in 2003 – 2007. As is the case with other GCC countries, the Saudi Arabian government revealed that it is to use petrodollars to foster the Kingdom’s economic diversification and sustain growth, which now comes as a priority given the global slowdown and dropping oil prices which will downsize revenues. The IMF estimates that Saudi's GDP will contract by 0.9% in 2009, starting to pick up in 2010 by 2.9%. Meanwhile, Saudi Arabia remains the largest construction market in the Middle East but as the industry is heavily dependent on oil revenues, construction spending may be inconsistent. However, the Saudi government announced that no reduction in infrastructure spending will take place even if oil prices fall below the budgeted prices for 2009. In fact, the Kingdom recently revealed an additional USD10 billion to be spent on infrastructure and construction.

Plans to spend USD61 billion on infrastructure Saudi Arabia’s population is expected to grow 3% annually until 2012, which is a key driver for growth in infrastructure spending. The government is encouraging privatization and public-private partnerships and plans to invest USD300 billion in infrastructure development between 2008 and 2010, focusing on expanding and modernizing key sectors such as education and healthcare.

Based on a budgeted oil price of USD40/b for 2009, total expenditure for 2009/10 was estimated at SR475 billion (USD126.7 billion), 16% higher than the 2008 budgeted expenditure of SR410 billion (USD109 billion), thus implying a fiscal deficit of SR65 billion (USD17.3 billion). Of the total spending, a remarkably high 47% (USD61 billion) is expected to be capital expenditure, emphasizing the government’s willingness to improve critical infrastructure and to continue to boost non-oil sector growth in the short run.

Chart 21: Saudi Arabia plans to spend USD61 billion on Infrastructure

Education&Manpower

26%

Health&Social 11%

Transport &Telecom

4%

Water&Utility7%

Other52%

Source: BMI & EIU

UAE – Construction

24

Saudi Arabia’s construction industry growth drivers Government spending will be mainly directed to developing the kingdom’s infrastructure and energy sectors to meet the growing needs of the population. The main areas of investments will be in : Transportation: Saudi Arabia’s transport infrastructure not only services the Saudi population but also the tourist industry. The country’s tourist industry is based around religious pilgrimage. The annual hajj – the Muslim pilgrimage to Mecca – places intense pressure on Saudi infrastructure as an estimated 1.9 million overseas visitors and 500,000 domestic pilgrims make the trip. During the hajj, the country’s airports and roads are put under increasing strain. Projects underway and planned in the Kingdom include:

• Airports projects worth USD3.3 bn (allocated budget is USD5.12 bn) • Ports worth USD876 mn • Railways worth USD10.7 bn • Roads worth USD448.9 mn (allocated budget is USD3 bn)

Energy and Utilities: Gulf Power Transmission Saudi Arabia is part of the GCC transmission project. The GCC-integrated power grid project is in two phases and will link Saudi Arabia, Qatar, Bahrain, UAE, Oman, and Kuwait in an integrated power grid system. The Saudi-based GCC Interconnection Authority (GCCIA) is supervising the project and the USD1.2bn investment necessary for its initial phase. This grid will provide adequate supplies of electricity for the GCC and will reduce the cost of power generation. Saudi Arabia suffers from water shortages and so has turned to desalination plants to meet growing demand from a rising population. Combining water with power plants through independent water and power projects (IWPPs) has been a popular means to meet demand in the Middle East. It is expected that over USD200bn is needed to be invested in water and power projects to meet the forecasted demand over the next 15 years.

Construction: In October 2008, it was reported that in Saudi Arabia more than 285 civil construction projects worth over USD260 billion were presently in progress or in design phase. Proleads' database of civil construction projects, including the ones in design phase, estimates that the top ten projects are worth over USD200 billion combined. The top three largest projects in KSA are

• King Abdullah Economic City worth USD93 billion. • Prince Abdul Aziz Bin Mousaed Economic City worth USD53 billion • Jizan Economic City worth USD30 billion

Moreover, the kingdom is expected to build 1.3 million houses over the next seven years to accommodate for shortages in houses along with the growing population.

Arabtec penetrates Saudi Arabia's highly competitive market As part of its strategy to diversify exposure, Arabtec managed a smooth penetration into the highly competitive Saudi Arabian market by venturing with one of the Kingdom’s big players, Saudi Bin Laden Group. Accordingly, the company will have exposure to the market and a very good chance of winning big contracts. Arabtec has already won two contracts in the Kingdom worth around AED3.5 billion in 1H09. Another advantage of penetrating the Saudi Market is Emaar properties’ strong presence in the Kingdom, handling mega projects. Arabtec is very likely to capture a share of the contracts given its long history as Emaar's preferred contractor.

UAE – Construction

25

Table 11: Saudi Arabia Population & Economic Indicators

2007e 2008e 2009e 2010f 2011f 2012f Population (million) 24.3 24.9 25.5 26.2 26.8 27.6 YoY % 2% 3% 2% 3% 3% 3% Nominal GDP (USD bn) 356.6 381.9 481.6 374.0 423.8 468.7 GDP per capita PPP (USD) 22,852 23,834 23,255 23,448 24,020 24,833 Real GDP Growth % 3.52% 4.63% -0.91% 2.90% 4.40% 4.94% Construction value (USD bn) 16.7 18.0 19.4 20.2 20.8 21.4 Construction real growth % 2.00% -0.24% -0.71% -0.55% -0.54% -0.38% Construction as % of GDP 4.38% 3.75% 5.18% 4.77% 4.45% 4.17% Source: IMF, Central Banks, BMI, & HC Brokerage

UAE – Construction

26

UAE: construction activity supported by Abu Dhabi

UAE's GDP is estimated to contract by 0.6% in 2009, mainly driven by the slowdown in Dubai. The UAE economy remains somewhat intact, supported by Abu Dhabi.

Population growth in the UAE will come from Abu Dhabi, and accordingly the Abu Dhabi

government is committed to invest up to USD168 billion in capital expenditure until 2010, which will be the main driver to the growth in the UAE.

In an attempt to soften the effects of the slowdown in Dubai, Arabtec has shifted its focus from

Dubai and residential works to Abu Dhabi and infrastructure works, which yield higher margins.

Although Dubai pressures the UAE economy …

According to IMF estimates, the UAE's GDP will drop by 0.6% in 2009 compared to a healthy 7.4% growth in 2008, mainly driven by a drop in Dubai which was the worst affected by the economic crash. Meanwhile, GDP is expected pick up again in 2010 by a meager 1.6%

Real estate projects were hit the hardest and given that 74% of the UAE construction portfolio is comprised of real estate projects, the UAE was most hurt by the economic turmoil compared to neighboring GCC countries. The slowdown called for many real estate developers in the region to cancel or reschedule several projects.

According to an industry report by Proleads, around 53% of total projects (USD1.3 trillion) being developed in the UAE, worth USD582 billion, have been either cancelled or put on hold. This means that approximately USD700 billion worth of projects are still underway, which remains optimistic unless further cancellations take place. Moreover, Dubai alone accounted for c91% of the 31% of total projects suspended in the GCC, worth approximately USD249 billion.

…but Abu Dhabi would save the day

Abu Dhabi, which constitutes 55% of UAE’s GDP, is expected to invest heavily in real estate and infrastructure to accommodate for the rising population from expatriates as there are major shortages in the Emirate that need to be met. Even with the expected decline in population in Dubai, we expect population in the UAE to grow driven by an increase in Abu Dhabi's population by a CAGR of 4% (08 -12f). Even with the spending, Abu Dhabi is well positioned to register double digit growth in 2010 and 2011 in pursuit of achieving its 2030 vision as reported by Abu Dhabi Economic Planning Unit earlier in May 2009. Financial strength in Abu Dhabi is further boosted by global investors’ confidence and their appetite to invest in the country.

The Abu Dhabi government is expected to invest up to USD168 billion in development projects until 2010 to diversify its macro economy and boost non oil revenues. The sectors of focus will be infrastructure works, to accommodate for the witnessed expansions in the country. The government is committed to spend on construction and building, tourism, utilities, industrials and oil and gas sectors.

Chart 22: Abu Dhabi to invest up to USD168 billion on different sectors until 2010 Water & Electricity

6%Industrials

10%

Oil&Gas13%

Tourism 20%

Construction 51%

Source: Abu Dhabi Chamber of Commerce & Industry

UAE – Construction

27

UAE construction industry driven by infrastructure spending mainly in Abu Dhabi BMI estimates that the value of the construction industry in the Emirates will continue to grow, yet at a much slower rate compared to the 8.87% in 2008. It estimates that the construction industry will sustain its growth at a weak 0.87% in 2009 and pick up gradually going forward; however, a level similar to that of 2008 is not likely to reoccur. We believe the sustained growth in the construction industry comes from the government’s commitment to support infrastructure spending, especially in Abu Dhabi. Spending will mainly be focused on:

• Transportation: In an attempt to achieve its 2030 plan, the Abu Dhabi government plans to launch a long-term investment program to upgrade its airports, ports and public transportation system to accommodate for an increasing population which is pressuring the transport infrastructure in the emirate. Some of the projects it announced are the construction of a USD7bn international airport (2010-2012), and a new port facility at the Khalifa Port and Industrial Zone. The emirate plans for the metro, a high-speed rail with Dubai, and new roads. Planned expansions in Dubai and Abu Dhabi airports are underway as well as construction of the third phase of Ras Al Khaimah saqr port.

• Energy and Utilities: To accommodate for the increasing demand on water and electricity, the local water and electricity authorities have plans to raise their capital investments in infrastructure. The value of investments in water projects in the UAE has increased by 20% from USD11.62bn in 2007 to USD14bn in 2008. Given that natural gas supply in the UAE is insufficient and the country imports around 9 cubic meters of gas form Qatar, there is a plan to change the energy mix in the UAE. This will be through adopting nuclear power for electricity generation. France and the UAE agreed to jointly develop the UAE’s nuclear power sector. New and ongoing projects in the energy and utilities sector around the emirates amount to approximately USD31.5 billion, with USD22 billion going to the Mastar City project by Masdar in Abu Dhabi, a long term project to be completed in 2016.

• Construction: Even with the slowdown, the UAE government is committed to developing its non hydrocarbon economy through developing its commercial, residential and tourism needs. New and ongoing projects around the emirates include: i) residential projects worth USD21.4 billion, ii) commercial projects worth USD39.4 billion, iii) industrial projects worth USD7.0 billion, and iv)Hotels & Resorts worth USD14.7 billion.

Table 12: UAE Population & Economic Indicators

2007e 2008e 2009e 2010f 2011f 2012f

Dubai 1,478 1,646 1,510 1,518 1,565 1,615 Abu Dhabi 1,493 1,556 1,587 1,647 1,713 1,788 Rest of Emirates 1,516 1,565 1,613 1,664 1,732 1,806 Total UAE Population 4,487 4,767 4,711 4,829 5,011 5,209 YoY % 6.1% 6.2% -1.2% 2.5% 3.8% 4.0% Nominal GDP (USD bn) 180.18 260.14 215.20 235.52 256.10 280.83 GDP per capita PPP (USD) 37,941 39,077 40,039 40,534 41,256 42,065 Real GDP Growth % 6.34 7.41 -0.60 1.55 3.29 4.65 Construction value (USD bn) - 19.04 20.90 22.27 23.95 25.74 Construction real growth % - 8.87% 0.87% 1.11% 3.58% 3.47% Construction as % of GDP - 7.3% 9.7% 9.5% 9.4% 9.2% Source: IMF, Central Banks, BMI, & HC Brokerage

1Q09 confirms Abu Dhabi’s sound position Construction contracts awarded in the UAE in the first four months of 2009 were valued at USD10.6 billion (AED39 billion) with Abu Dhabi accounting for 58% of total contracts awarded, while 33% were awarded in Dubai. Contracts awarded in 1Q09 were 75% lower than those awarded in 1Q08, which is only natural given the slowdown. Lower contracts are mainly due to lack of liquidity in the emirates and the renegotiation of contracts as a result of plummeting construction costs. Although Dubai has recently announced a cutback on spending to manage its debt and restructure its system, the UAE in general is expected to continue spending on infrastructure developments in other emirates, especially in Abu Dhabi. The slowdown anticipated in Dubai has triggered local contractors to look into diversifying their portfolios away from Dubai and focus more on Abu Dhabi.

UAE – Construction

28

Chart 23: Projects awarded in UAE by Emirate (1Q09)

Abu Dhabi58%Dubai

33%

Other Emirates9%

Source: Zawya

Chart 24: Projects awarded in UAE by sector

1Q09 1Q08

Commercial /Industrials

72%

Energy22%

Infrastructure6%

Commercial /Industrials

76%

Energy11%

Infrastructure13%

Source: Zawya

Arabtec shifts focus to Abu Dhabi Arabtec has always been a dedicated civil contractor with expertise in residential construction and the oil and gas sector, with a strong presence in Dubai, Abu Dhabi and Sharjah. We believe Arabtec will benefit from the infrastructure spending in Abu Dhabi, utilizing its competency in this area gained following the acquisition of a 60% stake in Abu Dhabi-based pure infrastructure company, Target Engineering Company, in 2007 which also solidified its presence in Abu Dhabi and added 4,000 employee to its workforce. We believe this comes as a smart management call to diversify the company’s focus from Dubai and residential works to Abu Dhabi and infrastructure works. The company has already been awarded a project worth AED800 million in Abu Dhabi in May 2009, and management expects to land around AED4.5 billion worth of projects by the end of the year.

UAE – Construction

29

Declining construction costs; a double edged weapon

After reaching high peaks in 2008, construction costs plummeted as a result of the slowdown in real estate which led to declining global demand on materials.

On one hand, lower construction costs serve as a stimulus by supporting infrastructure spending in the region; on the other hand, declining costs suggest that new and existing contracts will be subject to re-negotiations and value revisions.

We believe that the drop in construction costs will impact the pricing mechanism of contracts as developers will seek more favorable agreements.

Dropping construction costs serve as spending stimulus…

Construction costs have witnessed significant declines thanks to the credit crunch, lack of available funds, and the cancellation and rescheduling of many real estate projects which heavily impacted the global demand on building materials. This decline in construction costs serves as a stimulus, supporting infrastructure spending and making 2009 a prime time for governments’ expenditures.

Chart 25: Steel World Prices UAE Portland Cement Price (AED/ton)

500

600

700

800

900

1,000

1,100

1,200

1,300

Jan-

08

Mar-08

May-0

8Ju

l-08

Sep-

08

Nov-0

8

Jan-

09

Mar-09

May-0

9

USD

/ton

MEPS CARBON STEEL PRODUCTS-WORLD PRICE- USD/TONNE

100

150

200

250

300

350

400

2000

2001

2002

2003

2004

2005

2006

2007

2008

1Q20

09

2Q20

09

UAE Portland Cement Price

Source: Bloomberg, Dubai Statistic Centre, News & Industry reports

… but are also a double edged weapon for contractors