Connect. Create. Innovate. India Mobile Congress 2018

104

New Digital Horizons Connect. Create. Innovate. India Mobile Congress 2018 October 2018 KPMG.com/in

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Connect. Create. Innovate. India Mobile Congress 2018

New Digital HorizonsConnect. Create. Innovate.

India Mobile Congress 2018

October 2018

KPMG.com/in

New digital horizons: connect, create, innovate

1 Current state

1.1+ billion subscribers

512 million internet subscribers

FDI ~ USD5.9 billion during Apr-Dec 2017

Teledensity at 89.72 per cent

Government initiatives driving digital growth

3 Challenges

2 Where we want to be

Trillion dollar digital economy dream:

Convergence of connectivity and advanced technologies like AI, M2M, IoT, analytics is bringing India closer to its trillion dollar digital economy dream. Telecom companies (telcos) having a direct interface with end users, can play a central role in the digital revolution by moving beyond connectivity. It can be the platform to allow the interplay of these advanced technologies to create digital solutions across varied industries. In the next few years, a significant portion of revenue will be growing from digital initiatives enabled by 5G network.

Falling revenues (ARPUs)

Huge capex requirement (USD17 billion FY19-20)

Debt repayment of USD119.44 billion as against its annual revenue of around USD38 billion

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

5 Need of the hour

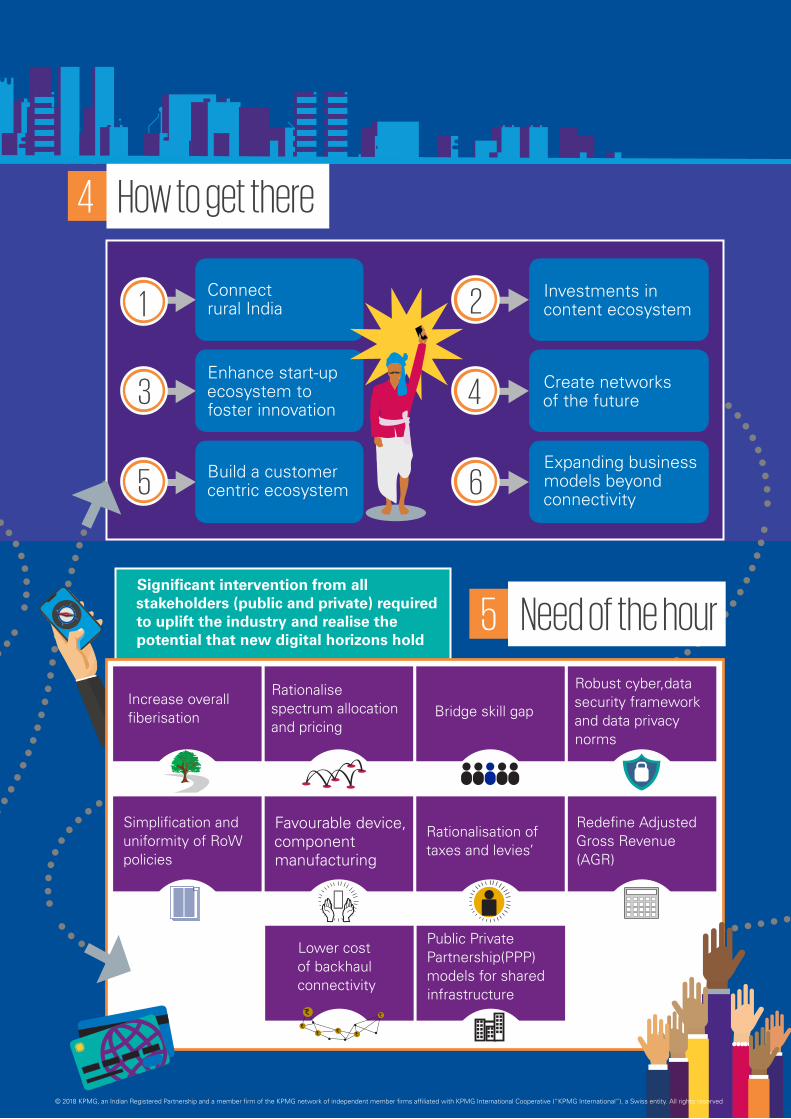

4 How to get there

1

3

5

2

4

6

Connect rural India

Enhance start-up ecosystem to foster innovation

Build a customer centric ecosystem

Investments in content ecosystem

Create networks of the future

Expanding business models beyond connectivity

Significant intervention from all stakeholders (public and private) required to uplift the industry and realise the potential that new digital horizons hold

Increase overall fiberisation

Rationalise spectrum allocation and pricing

Bridge skill gap

Robust cyber, data security framework and data privacy norms

Simplification and uniformity of RoW policies

Favourable device, component manufacturing

Rationalisation of taxes and levies’

Redefine Adjusted Gross Revenue (AGR)

Lower cost of backhaul connectivity

Public Private Partnership(PPP) models for shared infrastructure

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

ForewordIndian Telecom Industry has witnessed one of the fastest paces of expansion in the recent years. The government and the industry have worked together to make Indian Telecom Network, the 2nd largest in the world with a total subscriber base of over 1.1 billion and an overall tele density of close to 90 per cent. The government has a digital vision for India and the strategy is premised on access and inclusion, giving a digital identity to everyone and delivering next generation goods and services to all citizens.

The National Digital Communications Policy (NDCP) 2018, was approved by the cabinet this year to lay out policy and principles framework that will enable creation of a vibrant competitive telecom market. The key themes that the policy aims to look at include, the regulatory and licensing framework impacting the sector, connectivity for everyone, ease of doing business and adoption of new technologies including 5G and the IoT to accomplish the mission to connect, propel and secure India. The common underlying themes of ‘Make in India’ and ‘Skill India,’ would be inclusive elements of the above.

In a connected era, easy access to information should be enabled for all citizens. We have begun a number of initiatives like BharatNet, Network for Left Wing Extremism Areas, connecting remote areas of the North East

including over 8600 villages and installation of over 300 mobile tower sites. We are into the 4th year of Digital India initiative, in this period we have tripled our telecom infrastructure, we are spending 9 billion in providing optic fiber in rural areas. The government will be setting up over 2.5 million Wi-Fi hotspots across the country to enable connectivity covering the urban and rural areas.

Adaption of technology, whether applications or services, is best understood in the local languages. We are also working on a mass digital literacy program so that people at the bottom of the pyramid will not merely have access to technology but also will be able to leverage technology in their local language. This will enable this section of the society to stay connected and digitally informed.

While digitalization is progressive, the connected space comes with challenges and there should be a strong focus on security. Every nation faces cyber security challenges. Countries like India, where digital growth has been exponential, the magnitude and complexity of these challenges become multi-fold. A comprehensive cyber security policy along with the sectoral CERTs are the key building blocks of India’s cyber security infrastructure. India is currently working towards putting a comprehensive data protection framework in place.

I am happy to be part of the IMC meet this year, with a theme of connect, create and innovate that resonates well with the direction that the industry is headed towards. I trust a meet like this will provide an opportunity for all the stakeholders involved – big or small to showcase their expertise and be part of the larger system that drives India forward, digitally. Wishing you all the very best.

Aruna SundararajanTelecom Secretary and Chairman of the Telecom Commission

Government of India

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

ForewordIt gives me immense pleasure to bring to you IMC 2018. IMC with its vast range of dignitaries, speakers and attendees is playing a crucial role by bringing all the players in our telecom ecosystem together on a single platform. The future of our industry is defined in platforms like these where all stakeholders connect, create and innovate which strongly aligns with our central theme this year.

Telecom provides connectivity that fosters inclusion, drives empowerment and enables transformation. The near ubiquitous reach of the mobile makes it the best tool to deliver development to the very last mile through ‘Digital India’ and a ‘mobile first’ approach. It is important for the future of India to have a robust telecom network as India has an opportunity to power ahead of the rest of the world as a digital economy. The promise of 5G is tremendous and it will be a catalyst in the evolution of new

services and revenue streams for all players in the ICT ecosystem. However, to untap its true potential it is important that due emphasis is given by the government and industry on spectrum harmonization, infrastructure creation and introducing relevant regulatory measures.

IMC 2018 plans to focus on how the trinity of regulators, academia and industry can collaborate to CONNECT India, CREATE an ecosystem for ICT players to thrive and contribute to the growth of digital India and INNOVATE to bring a faster growth in technology adoption, network solutions that will allow an unforeseen socio economic development of India.

I am pleased to inform you that IMC, Cellular Operators Association of India (COAI) along with KPMG in India has brought out a comprehensive report on how the New Digital Horizon is un-flolding for India. I would like to

acknowledge the efforts made by IMC and KPMG in India’s team in making this report insightful.

Thank you.

Rajan S MatthewsDirector General

COAI

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Welcome to the 2nd edition of IMC 2018: New Digital Horizons: Connect. Create. Innovate. The event is aimed to explore the current dynamism in the telecommunications sector which has become a catalyst for a digitally empowered and connected India.

With the stupendous success from last year, IMC has become South Asia’s largest digital technology forum bringing together the congregation of regulators, academia, researchers, industry leadership under one roof. It is aimed to bring together the converging communication industry on one platform in India, to showcase emerging opportunities and trends, technologies, business opportunities, applications, platforms, government policies and initiatives.

India has the world’s 2nd largest telecommunications network and internet user base. It is becoming the hotbed for innovations in telecom services, equipment and network technologies. As new technologies like 5G and IoT are ready to usher an industrial revolution, building a collaborative framework between regulators,

academia, industry would be a key differentiator that will make India a digital leader.

Our research paper, written by our knowledge partner KPMG in India, studies the evolution of networks of the future and dwells into how technology will be shaping our lives. It identifies some of the trends on customer expectations and how telecom companies are evolving their business models to meet those expectations. It is clear from the report that only companies which thrive on innovation and cutting edge technology are the ones which will be able to leapfrog the exponential growth offered by the sector.

I conclude by thanking the team at IMC, COAI, and KPMG in India for working together to successfully deliver this program to you. Our aim is to be a one-stop-shop expo destination for the mobile industry in India and South Asia and ultimately, gain from the insights and partnerships forged this year in India.

Thank you.

P RamakrishnaCEO

India Mobile Congress

Foreword

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

ForewordThe amalgamation of players in the ICT sector is creating new landscapes. Technology is fuelling the shift and shaping a new narrative of the ICT ecosystem which in my view has assumed critical propositions with the market boundaries dissolving and changing operating models. High-speed connectivity, strategic collaborations and altering growth strategies might well determine the next phase of growth of the industry.

In association with the IMC and COAI, KPMG in India is pleased to present the report – ‘New digital horizons - Connect, create and innovate’. This report traces the evolution of various network enabled services over time and helps understand how telecom services consumption has been changing over the years and how it is likely to impact the larger ecosystem of telecommunications in our country.

The growth of the Indian economy is closely linked to the rise of the telecommunications sector as they are intricately linked to connectivity as a fundamental requirement for driving businesses. The telecom sector in India has witnessed immense disruption in the last few years. This phenomenon has propelled a shift in the user behaviour with the passive consumers of voice and SMS services becoming active participants. They are now one of the largest consumers of mobile data and high bandwidth applications like video streaming and social media. The consumers have benefited immensely from discounted pricing due to hyper competition, availability of affordable smart phones and evolving ICT infrastructure.

Furthermore, the operators are going the innovative way to offer

media content to the end consumer either by way of collaboration or through creation of their own. The industry overall, while experiencing disruptive innovations is also witnessing the slow convergence of the telecom industry with media, using technology to drive costs down. It is undisputed that the ability of ICT companies to adapt to the continuously evolving technologies to suit the changing needs and preferences of consumers is all good news for them but, it could leave the telecom operators in a precarious situation, where only those players with deep pockets could survive.

The market has already witnessed the consolidation of two major players while, the other four players are unable to sustain their businesses and are on the verge of exit. The industry might see only 4-5 main players in an aggressive telecom market of the future. To conquer this frontier, the operators will have to be ready for the ‘Digitally Native’ consumers who expect innovative, converged services of impeccable quality delivered to them seamlessly. Enhanced customer experience coupled with exceptional quality of services shall act as the key differentiators, which would help the operators not only retain their existing customers, but also acquire the new ones.

The next phase of growth in the industry is hinged on convergence of ICT. Digital technology, coupled with radical shifts in consumption patterns have undeniably resulted in the blurring of boundaries that define the ICT sectors. ICT convergence is now a reality and is expected to cause significant disruptions across the entire value chain. Very soon, the traditional ways of media consumption shall make way for on-demand and dynamic consumption

of media. Rapid use of machines to augment human intelligence in creating a new paradigm of opportunities impacting consumers and enterprises. As we look into the future, networks have the potential to be an intelligent platform to aid consumers and enterprises to reap benefits of new age technologies. ICT businesses would need to re-evaluate their existing strategies and operating models to leverage the emerging opportunities and sustain against new evolving challenges.

Mritunjay KapurNational Head Markets and StrategyHead - Technology, Media and Telecom

KPMG in India

Arun M. Kumar Chairman and CEOKPMG in India

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Table of

contents

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

1. Executive summary

2. Telecom sector - the ground covered so far

3. Connect the unconnected

4. Create an ecosystem for digital enablement

5. Networks for the future

6. Innovate beyond connectivity

7. Technology shaping our lives

8. Challenges to digital penetration and way forward

01

05

11

21

27

39

47

77

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Executive summary

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

01

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

02

The Indian telecom sector has charted an unparalleled growth story. With over 1.1 billion subscribers, overall teledensity around 90 per cent and 512 million internet subscribers01 as on June 2018, it stands tall as second largest in the world. In FY17, the Indian telecom sector contributed about 6.5 per cent of Gross Domestic Product (GDP)02 and plays a pivotal role in creating the building blocks of the digital economy which is estimated to be USD280 billion as of FY1803.

The telecom sector is at the forefront of the digital revolution and the dream of a trillion digital dollar economy will be achieved through convergence and capitalisation of multiple technologies such as AI, Machine-to-Machine (M2M) and IoT and collaboration between government and industry players. While the growth story has so far been stupendous and holds enormous potential, the sector currently faces an uphill task of debt repayment of about USD119.44 billion as against its annual revenue of USD38.78 billion03. Given the industry’s average return of capital employed at 1 per cent, there is a dearth of funds for the huge capital expenditure that lies in store for the sector.

This situation is further compounded by disruption of traditional voice and messaging revenue streams because of digitalisation. While the exponential rise in data consumption (wireless: 4026 PB during the quarter April-June 2017 to 10418 PB in April-June 2018)01,04 has provided some relief, it has not been enough to uplift the overall Average revenue per user (ARPU), which stands at USD1.25 (INR80.97) in FY18 (USD1.79 or INR117.37 in FY17)05. The ongoing price war and lack of adequate monetisation of content delivery coupled with increasing costs from bandwidth and speed upgrades have put the telecom sector in a precarious situation. It will take the collective will and action from all stakeholders, private and public to reinvigorate the sector. Lack of immediate action on this will risk the derailment of the vision of Digital India and the socio-economic development that it promises.

Telecom companies (telcos) need to think of new avenues for growth as legacy revenues are under pressure. This could mean expanding their existing solutions to newer markets while realigning their business models to cater to emerging opportunities. The following are the three themes that telcos need to focus on: connect, create and innovate.

Connect the unconnectedWith around 67 per cent of our population06 living in rural areas and the rural teledensity is 57.99 per cent as on June 201801, rural India presents a gigantic opportunity for growth. The stark digital divide is evident by the low internet penetration of 19.48 per cent in rural areas01.

However, rural telecom will require a serious revamp of backhaul connectivity and fiberisation. Fiberisation of backhaul will increase the capacity and reduce the latency period and is critical before 5G deployment. In India, about 80 per cent of cell sites are connected through microwave backhaul and only 20 per cent through fibre07. However, 70-80 per cent fiberisation is required for effective network roll-out for 4G and 100 per cent fiberisation for 5G08.

In regions where fibre backhaul is not possible, higher-capacity microwave links will have to be installed. E-band and V-band spectrum needs to be allocated to telcos at the earliest so that they can utilise them for low-cost, high last-mile connectivity to base stations. While some telcos are currently focusing on expanding the reach of fibre network to homes, policy amendments encouraging active infrastructure sharing will shape fibre leasing and renting dynamics in India.

To build a diversified and digital ecosystem, the fundamentals of conventional network and business architecture need to be revised. Therefore, ICT, infrastructure providers (IP), Telecom Service Providers (TSP), Internet Service Providers (ISP), and content providers will play an important role in paving the way for digitisation in a reliable and sustainable fashion.

Create a start-up ecosystemThe technology landscape in India has seen a rapid transformation in recent years because of the strong emergence of various start-ups. This has created a momentum for a plethora of new ideas fuelling disruption, innovation and investments across verticals. Riding on the pillars of future technologies like AI, IoT, robotics and analytics, the Indian start-up ecosystem is shaping up in positive light.

01. The Indian Telecom Services Performance Indicators April – June, 2018. FX Conversion Rate for FY18 - 64.46

02. https://www.investindia.gov.in/sector/telecom, Accessed on 25 September 2018

03. COAI Annual Report, 2017-18

04. The Indian Telecom Services Performance Indicators April – June, 2017. FX Conversion Rate for FY17 - 64.46

05. The Indian Telecom Services Performance Indicators Quaterly reports for FY17 and FY18

06. http://www.worldometers.info/world-population/india-population/

07. 5G a distant dream for India when backhaul takes a back-seat: Experts, The Economic Times, 11 August 2017

08. Why India must get fiberised to leapfrog to 5G, The Financial Express, 17 February 2018

However, to drive and nurture a strong entrepreneurial culture, the government has to address a series of roadblocks related to administrative and economic areas for start-ups.

Create networks of the futureWhile the Indian telecom sector has come a long way and has experienced tremendous growth in the past decade, it is lagging on quality parameters like network throughput and 4G coverage. With data surge and increasing use of IoT and M2M applications, the telecom ecosystem will have to boost its network capacity to offer high-speed data access and minimum latency. Although 5G is likely to be the key enabler of the fourth industrial revolution and an integrated ecosystem across business-to-business (B2B), business-to-consumer (B2C), and business-to-government (B2G), until it is launched, the telcos will have to improve on their existing networks to enhance their performance.

Software Defined Networks (SDN) and Network Function Virtualisation (NFV) are examples of cloud-based technologies. These can replace complex network functions with customisable virtualised software. It is estimated that SDN and NFV could generate significant savings in overall operator operating expenditure and will be the main drivers of adoption of these technologies in an otherwise financially constrained industry.

To unleash the full potential of Digital India, an investment of USD17 billion is required over the next two years. Significant investments are required over the next two years to unleash the full potential of Digital India. However, this can only happen when adequate Return on Investments (RoI) is enabled through a facilitative policy and regulatory environment.

Innovate beyond connectivity As per KPMG Technology Innovations Lab’s findings through a web survey comprising of 15 countries and 15 countries and more than 750 technology leaders, India is ranked third in the tech leadership charts for countries showing most promise for disruptive technology breakthrough that will have a global impact. It will take the collective will and action from the entire ICT ecosystem along with adequate government support to unearth the true potential of the Indian digital economy. With connectivity and the promise of 5G being the most critical enabler to the vision of digital India, Telcos will have an important role to play.

Further, the survey also indicates IOT followed by AI and robotics are identified as the leading game changers over the next three years globally.

As India stands at the cusp of transforming into one of the world’s fastest growing digital economies, these emerging technologies have started traversing across businesses accelerating their growth journeys. Telecom, despite being central to this digital evolution, has so far not been able to reap benefits from this growth. Instead, we are seeing a sect of new agile digital businesses emerge which are not only creating an intermediate layer between connectivity providers and the end users but also increasingly making customers agnostic of which network to choose.

To outpace the digital disruption and ensure that they remain the epicentre of the growth, telcos will have to innovate on two fronts i.e., redesign their business models beyond connectivity and enhance their customer experience.

Redesigning the business models

With traditional revenue streams maturing, redesigning business models is the need of the hour. Industry players are already commercialising consumer behaviour, trends and innovative technologies to create new paths to outpace the competition. Telcos should leverage this gold mine of data and move up the technology stack by providing platforms and applications to create industry-specific solutions using emerging technologies. This will help telcos transition from just being communication providers and become core to the enterprise and consumer digital transformation.

The adoption of 5G will drive demand from enterprises and allied industries such as e-commerce, healthcare and automotive. Though the potential opportunities for collaboration are unlimited, telcos will have to develop vertical specialisations in these industries to understand the enterprise solution requirements and collaborate with tech companies and innovators to provide a holistic solution.

Telcos will have to develop some of these capabilities in-house or acquire through partnership and collaboration with other ICT players.

Enhancing customer experience

The rapid change in consumer demand, led by enhanced network connectivity and improved speeds has increased on-the-go consumer count. They are becoming accustomed to accessing information, retail, financial and entertainment services across

03

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

devices. Consumers are demanding more from their network providers and are looking for personalised service offerings. The existing high customer churn indicates that telcos need to work on increasing customer loyalty which includes the following:

• Telcos need to differentiate beyond networks and deploy disruptive technologies that will act as a catalyst to provide a better customer experience

• Use advanced analytics to understand customer preferences based on their digital behaviour

• Adopting an organisation-wide cultural change and build customer centricity across all functions.

Challenges and way forwardThe telecom sector’s current structure is weighing on its growth. Moreover, its burgeoning debt, falling revenue and constrained margins leave little room for further investments. The government has set the tone of a progressive policy framework with the National Digital Communication Policy 2018. The policy promotes the judicious use of Universal Service Obligation Funds (USOF) and public private partnership to promote connectivity through its Bharat Net, Gram Net, Nagar Net and JanWifi initiatives. However, monetisation models and financial viability of these initiatives need to be well defined to make the public-private partnership successful.

Some of the potential areas, which could be looked at with respect to promoting an investor-friendly environment in the telecom sector are as follows:

• Spectrum management, its pricing and future availability roadmap

• Redefine Adjusted Gross Revenue (AGR)

• Bring down levies such as Spectrum Usage Charge (SUC) and Licence Fee (LF)

• Reduce the tax burden

• Lowering the cost of backhaul connectivity

• Development of the start-up ecosystem

• Data privacy

• Favourable device and component manufacturing

• Robust cyber and data security framework

• Bridging skill gap

• Public Private Partnership (PPP) models for shared infrastructure

04

ConclusionIndia is at the helm of a new revolution ‘Industry 4.0’, as digital transformation makes inroads across sectors altering the modus operandi for businesses. The enhancement of features in affordable smartphones, constant connectivity and 5G’s potential will position the telecom sector uniquely in this transformation.

Being the key stakeholder with an obvious path to full connectivity for the consumer makes telcos a necessary part of any future consumer proposition regardless of who owns the platform. The path forward is leveraging this strength while navigating the challenges in regulation, changing technology and changing consumer dynamics.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Telecom sector - the ground covered so far

05

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

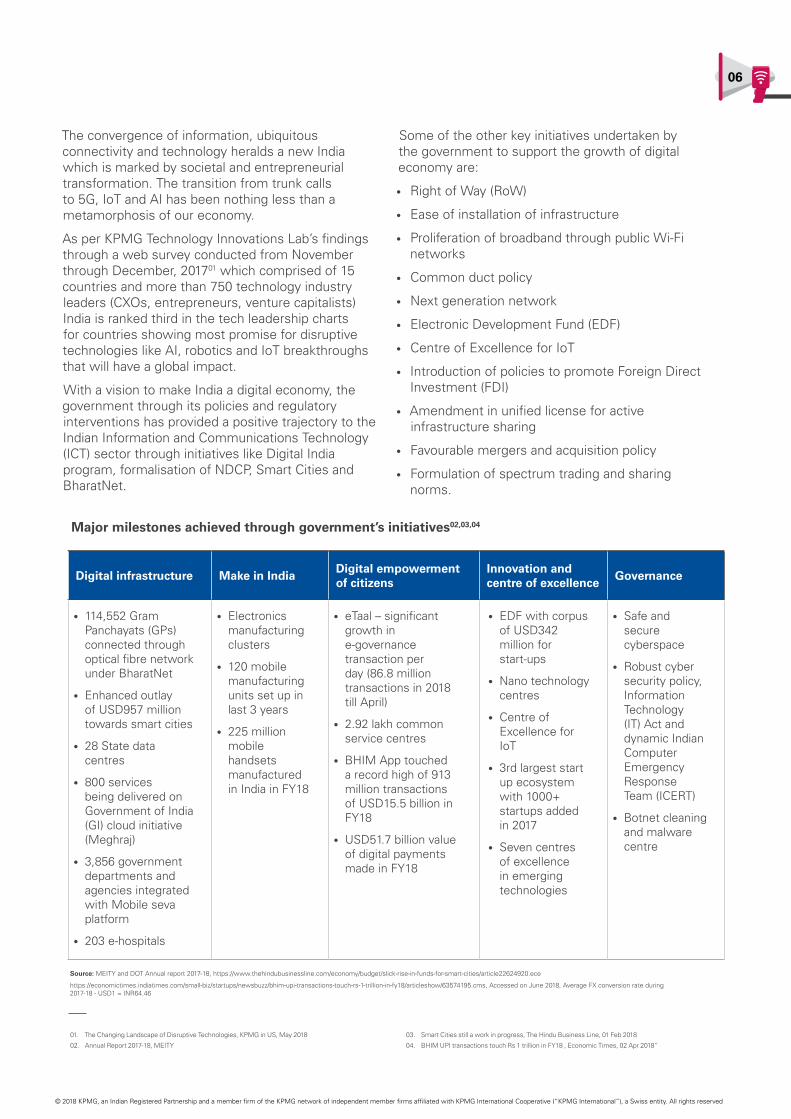

The convergence of information, ubiquitous connectivity and technology heralds a new India which is marked by societal and entrepreneurial transformation. The transition from trunk calls to 5G, IoT and AI has been nothing less than a metamorphosis of our economy.

As per KPMG Technology Innovations Lab’s findings through a web survey conducted from November through December, 201701 which comprised of 15 countries and more than 750 technology industry leaders (CXOs, entrepreneurs, venture capitalists) India is ranked third in the tech leadership charts for countries showing most promise for disruptive technologies like AI, robotics and IoT breakthroughs that will have a global impact.

With a vision to make India a digital economy, the government through its policies and regulatory interventions has provided a positive trajectory to the Indian Information and Communications Technology (ICT) sector through initiatives like Digital India program, formalisation of NDCP, Smart Cities and BharatNet.

Some of the other key initiatives undertaken by the government to support the growth of digital economy are:

• Right of Way (RoW)

• Ease of installation of infrastructure

• Proliferation of broadband through public Wi-Fi networks

• Common duct policy

• Next generation network

• Electronic Development Fund (EDF)

• Centre of Excellence for IoT

• Introduction of policies to promote Foreign Direct Investment (FDI)

• Amendment in unified license for active infrastructure sharing

• Favourable mergers and acquisition policy

• Formulation of spectrum trading and sharing norms.

06

Digital infrastructure Make in IndiaDigital empowerment of citizens

Innovation and centre of excellence

Governance

• 114,552 Gram Panchayats (GPs) connected through optical fibre network under BharatNet

• Enhanced outlay of USD957 million towards smart cities

• 28 State data centres

• 800 services being delivered on Government of India (GI) cloud initiative (Meghraj)

• 3,856 government departments and agencies integrated with Mobile seva platform

• 203 e-hospitals

• Electronics manufacturing clusters

• 120 mobile manufacturing units set up in last 3 years

• 225 million mobile handsets manufactured in India in FY18

• eTaal – significant growth in e-governance transaction per day (86.8 million transactions in 2018 till April)

• 2.92 lakh common service centres

• BHIM App touched a record high of 913 million transactions of USD15.5 billion in FY18

• USD51.7 billion value of digital payments made in FY18

• EDF with corpus of USD342 million for start-ups

• Nano technology centres

• Centre of Excellence for IoT

• 3rd largest start up ecosystem with 1000+ startups added in 2017

• Seven centres of excellence in emerging technologies

• Safe and secure cyberspace

• Robust cyber security policy, Information Technology (IT) Act and dynamic Indian Computer Emergency Response Team (ICERT)

• Botnet cleaning and malware centre

Source: MEITY and DOT Annual report 2017-18, https://www.thehindubusinessline.com/economy/budget/slick-rise-in-funds-for-smart-cities/article22624920.ece

https://economictimes.indiatimes.com/small-biz/startups/newsbuzz/bhim-upi-transactions-touch-rs-1-trillion-in-fy18/articleshow/63574195.cms, Accessed on June 2018, Average FX conversion rate during 2017-18 - USD1 = INR64.46

01. The Changing Landscape of Disruptive Technologies, KPMG in US, May 2018

02. Annual Report 2017-18, MEITY

03. Smart Cities still a work in progress, The Hindu Business Line, 01 Feb 2018

04. BHIM UPI transactions touch Rs 1 trillion in FY18 , Economic Times, 02 Apr 2018”

Major milestones achieved through government’s initiatives02,03,04

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

07

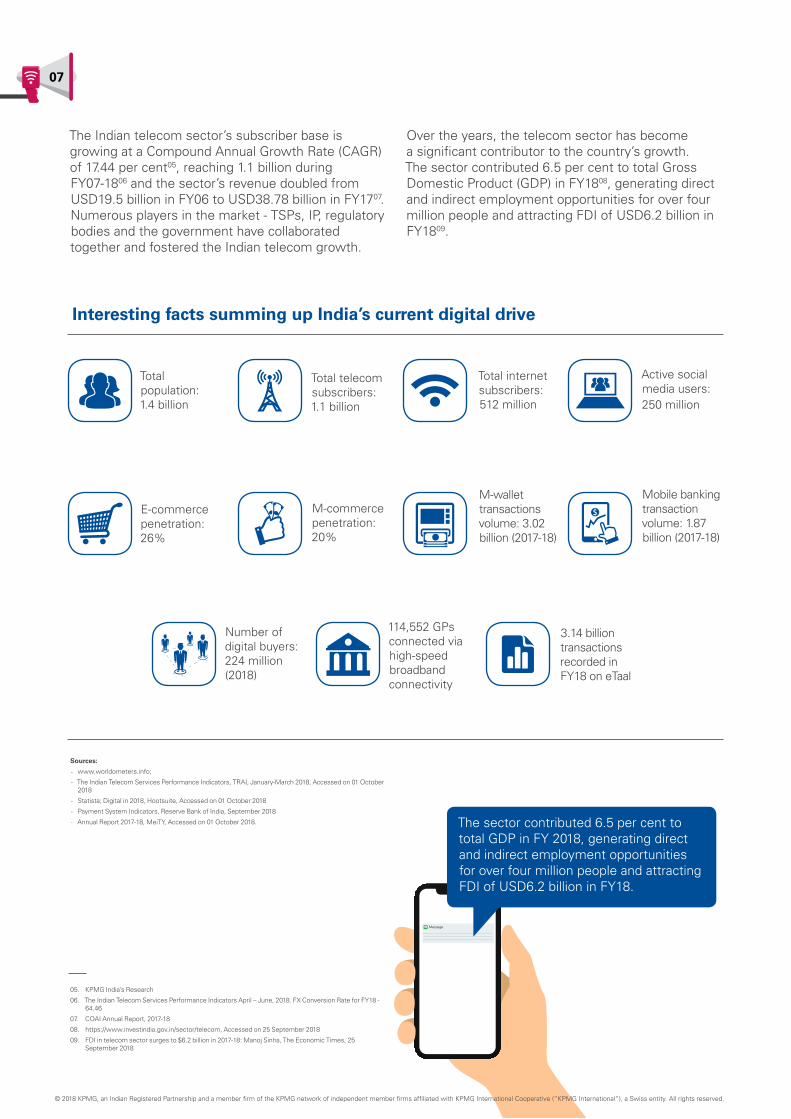

The Indian telecom sector’s subscriber base is growing at a Compound Annual Growth Rate (CAGR) of 17.44 per cent05, reaching 1.1 billion during FY07-1806 and the sector’s revenue doubled from USD19.5 billion in FY06 to USD38.78 billion in FY1707. Numerous players in the market - TSPs, IP, regulatory bodies and the government have collaborated together and fostered the Indian telecom growth.

Over the years, the telecom sector has become a significant contributor to the country’s growth. The sector contributed 6.5 per cent to total Gross Domestic Product (GDP) in FY1808, generating direct and indirect employment opportunities for over four million people and attracting FDI of USD6.2 billion in FY1809.

Interesting facts summing up India’s current digital drive

05. KPMG India’s Research

06. The Indian Telecom Services Performance Indicators April – June, 2018. FX Conversion Rate for FY18 - 64.46

07. COAI Annual Report, 2017-18

08. https://www.investindia.gov.in/sector/telecom, Accessed on 25 September 2018

09. FDI in telecom sector surges to $6.2 billion in 2017-18: Manoj Sinha, The Economic Times, 25 September 2018

Sources:

- www.worldometers.info;

- The Indian Telecom Services Performance Indicators, TRAI, January-March 2018, Accessed on 01 October 2018

- Statista; Digital in 2018, Hootsuite, Accessed on 01 October 2018

- Payment System Indicators, Reserve Bank of India, September 2018

- Annual Report 2017-18, MeiTY, Accessed on 01 October 2018.

Total population: 1.4 billion

Number of digital buyers: 224 million (2018)

114,552 GPs connected via high-speed broadband connectivity

E-commerce penetration: 26%

Total telecom subscribers: 1.1 billion

3.14 billion transactions recorded in FY18 on eTaal

M-commerce penetration: 20%

Total internet subscribers: 512 million

M-wallet transactions volume: 3.02 billion (2017-18)

Active social media users: 250 million

Mobile banking transaction volume: 1.87 billion (2017-18)

The sector contributed 6.5 per cent to total GDP in FY 2018, generating direct and indirect employment opportunities for over four million people and attracting FDI of USD6.2 billion in FY18.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

08

Internet penetration by country

Average fixed internet speed in Mbps

Average mobile internet speed in Mbps

Mobile’s share of web traffic

Unique mobile user penetration

Ecommerce annual ARPU: consumer goods (in USD)

Worldwide average 53% 40.7 21.3 52% 68% 833

Highest 99% 161.2 54.2 83% 84% 2,062

India 39.32% 19.7 9.1 79% 63% 113

Sources: Digital in 2018: Hootsuite report 2018; TRAI- performance indicator report June 2018

Sources: GSMA’s mobile connectivity index accessed on 16 October 2018

India Mobile connectivity index

The journey of the industry from being a communication provider to becoming an important economic enabler has passed significant milestones. The telecom sector has undergone radical transformations in the past few years and it stands as one of the most disruptive and customer focused industries today. India adopted the third generation mobile network (3G) in 2010 which introduced India to fast data speed and played a significant role in the path towards the transformation of sector from voice-centric to data-centric05.This received a further stimulus with the launch of the fourth generation of mobile networks (4G) and Voice over Long Term Evolution (VoLTE) services in the year 201505.Today, most TSPs in the country boast of providing 4G services to their subscribers and the industry is seeing a steady rise in the number of 4G customers. In addition to VoLTE, the industry has also rolled out the optical fibre network in excess of 2.8 million kms10 to provide reliable, secure, reasonable and high Quality of Service (QoS) to all citizens.

Today, the business is no longer only dependent on technology. Sure, that remains a driver; but only one of the many including asset-light business models and rapidly changing hyperlocal consumer preferences. Emerging technologies like 5G, IoT, M2M and cloud technologies have created a new paradigm to develop sophisticated, sustainable and scalable infrastructures to pave the way for ‘Digitalisation’. Hence, the ICT industry will be at the forefront of the newly emerging environment and help give a global competitive edge to the Indian economy. And that’s the threshold from which the next quantum leap – or the roll-out of 5G services – will occur.

05. KPMG India’s Research

10. Status of BharatNet, Bharat Broadband Network Limited, Accessed on 10 October 2018

Overall index 53.7

Infrastructure41.1

Affordability77.3

Consumer readiness

50.3

Content and services

51.8

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

09

Sources: Crisil Research, Accessed Date, 08 October 2018

IPTV

Industry 4.0

<1 4.7 10

Video conference

10% 73% 98%4K HD videos

Rural 2.0

12% 19% <50%

Cloud computing

% 4G datasubscribers

Rural internet penetration

% 4G data revenue

Data usage per subscriber per month (GB)

AI, AR, Big Data, IoT

2% 50% 83%

4G launch

5G launch

2013-14

233

905

283

970

322

1,034

401

1,170

473

1,183

488

1,196

520

1,234

580

1,263

663

1,287

2016-17 2019-20F2014-15 2017-18E 2020-21F2015-16 2018-19F 2021-22F

2016: Entry of a new player trigger high data usage; 60% spectrum unsold in auctions

Riding on technology wave, video OTT revenues to grow at a CAGR of 45% during 2018-2023

Deployment of IoT, AI, VR/AR across businesses

Significant infrastructure upgrade planned through NDCP 2018

2017: Data share in non-voice revenue reach 84% compared to 23% in 2013

2018: Consolidation amongst existing players

Total data subscribers Total subscribers

Growth of telecom industry

10

Despite the rapid subscriber base growth, the Indian telecom growth story is in distress. In particular, in 2017, telecom companies (telcos) faced financial woes with a price war, which resulted in a sharp decline in ARPU. The decline was so sharp that it reached USD1.25 in 2017-1813 and USD1.13 in April-June 2018, the lowest level since 2010. Nonetheless, the industry is shifting gears to ride over the issue by varying its pricing and bundling strategy, consolidating synergies and expanding its footprint in the ICT ecosystem through acquisition. However, these initiatives are yet to show results. The government will play a critical role in re-energising and funding the sector to shape India’s digital landscape.

The road ahead

As disruptive technologies develop and consumer expectations evolve, most industries in India are facing a triad of change relating to technology, competition and consumers, bringing the telecom industry at the forefront of this tectonic change. With economic activities relying on information, communication and technology more than ever, the opportunity for the sector is vast.

The convergence between telecom operators, ICT infrastructure providers and content providers is set to generate prodigious opportunities to connect, create and innovate.

11. State/UT wise Aadhaar Saturation, 30 Sep 2018

12. Press Information Bureau ,Government of India, Ministry of Finance, March 2018

13. The Indian Telecom Services Performance Indicators Quaterly reports for FY17 and FY18

Connect, create and innovate

CONNECT the unconnected

• Total subscriber base is expected to reach 1.28 billion in FY22• By 2022, 10 million public Wi-Fi hotspots will be deployed• Aims to provide 1 Gbps connectivity to all gram panchayats by

2020 and 10 Gbps by 2022.

CREATE an ecosystem for digital enablement

• Telecom sector to create 11-12 million job opportunities in the services sector

• Attract USD100 billion of investment to the telecom sector by 2022

• Telecom industry to contribute an additional 3.5 per cent to the GDP from 6.5 per cent in FY18

• 5,000+ tech start-ups including 300+ ICT start-ups in FY17, estimated to reach 10,500 by 2020.

INNOVATE beyond connectivity

• Potential USD1 trillion of revenues for digitally enabled businesses by 2022 and USD1.8 trillion by 2025

• Cumulative USD1 trillion 5G economic impact in India by 2035• 2.7 billion IoT units and a market size of USD15 billion by FY20.

Sources:

- Readying India for a USD 1 trillion opportunity through Digital, Nasscom, December 2017 - 5G to offer $27 bn biz opportunity for India by 2026, The Economic Times, 22 May 2018 - Panel on 5G deployment in India predicts ‘$1 trillion impact on economy’, Hindustan Times, 23 August

2018 - INDIAN IOT MARKET SET TO GROW UPTO USD 15 BILLION BY 2020, Nasscom, 05 October 2016 - Digital India: Telecom skills group sees surge in job opportunities, The Economic Times, 25 November 2016 - Indian Start-up Ecosystem-Traversing the maturity cycle, Edition 2017, Nasscom, Accessed Date 08

October 2018 - Pradhan Mantri Digital Saksharta Abhiyan (Gramin), Pradhan Mantri Yojana, Accessed Date, 08 October

2018 - 5 Crore Rural Indians to Get Wi-Fi, Thanks to Union Budget Scheme, Daily Hunt, 02 February 2018 - Expect India mobile sector to create $217 bn value by 2020:Min, Business Standard, 27 September 2017 - National Digital Communications policy 2018, Department of Telecommunications, 01 May 2018.

CONNECT

CREATE

INNOVATE

The trinity of increasing mobile penetration, 1.2 billion aadhar cards11 and over 312 million Jan Dhan accounts12 enable real time direct benefit transfers and provide digital delivery of services like education, healthcare etc.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Connect the unconnected

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

11

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Today the Indian telecom industry is at a crossroad, where it needs to meet the basic connectivity requirement of rural India including 4G proliferation

and the changing consumer requirements of urban and semi-urban India which demands next generation solutions through emerging technologies.

12

State-wise urban-rural teledensity - The stark urban-rural divide

And

hra

64.4

180.

4

134.

8162.

4

174.

0

167.

3

133.

3

165.

3

140.

5

313.

9

158.

4

145.

2

176.

5

141.

1

147.

5

177.

0

264.

8

153.

9

43.2

43.6

75.9

66.3

117.

7

56.0

63.6

76.7

44.6

74.3

49.4 58

.8 80.7

59.1

87.8

48.4 60

.7

Mah

aras

htra

Him

acha

l Pr

ades

h

Tam

il N

adu

Ass

am

Nor

th E

ast

J&K

Utt

ar P

rade

sh

Bih

ar

Oris

sa

Kar

nata

ka

Wes

t B

enga

l

Guj

arat

Punj

ab

Mad

hya

Prad

esh

Kera

la

Har

yana

Raj

asth

an

All India - June 2018 89.72

Urban teledensity 158.16

Rural teledensity 57.99

Rural teledensity

Urban teledensity

Source: The Indian Telecom Services Performance Indicators, January-March 2018, TRAI

While India’s overall teledensity stood at 89.72 per cent, rural teledensity remained low at 57.99 per cent in June 2018. Internet penetration in rural India has been at just about 19.48 per cent. As around 67 per cent of the country’s population lives in rural areas, the digital divide between urban and rural India is significant.

156.

9

The Indian telecom sector is going through an invigorating journey and it is exciting to be a part of it. As the Indian economy is leapfrogging towards digital growth, the telecom sector will play a critical role in not only enhancing the penetration of emerging technologies like IOT, AI, M2M through connectivity but also provide a platform to create solutions for consumers, enterprises and government to deploy these technologies to foster growth in different sectors. However, to unlock the true potential, it would be critical that all stakeholders in the sector, government and industry, work cohesively in addressing some of the pertinent challenges to ensure that the best of the services can be provided to the Indian telecom consumers at par with their global counterparts.

We assure the government of full support and look forward to be a path of the growth story.

Balesh Sharma

CEO Vodafone Idea Limited

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

13

Vectoring on rural IndiaWhile India’s overall teledensity stood at 89.72 per cent, rural teledensity remained low at 57.99 per cent in June 201801. Internet penetration in rural India has been at just about 19.48 per cent01. As more than 66 per cent of the country’s population lives in rural areas, the digital divide between urban and rural02 India is significant.

Not surprisingly, the focus of telcos has been shifting away from urban circles, which has hit or is hitting saturation levels. The rural sector is coveted despite infrastructure hurdles such as lower bandwidth and coverage, high upfront investment cost, low pricing power, and high customer switching among service providers. In the hinterland, aggressive expansion by operators and the launch of 4G (VoLTE) services has improved penetration. Similarly, the availability of local-language apps and devices have increased smartphone adoption, especially in rural areas.

On its part, the government has also been making facilitative investments. Its digital literacy drive is expected to reach 60 million rural households with an investment of around USD350 million by FY1903.

The phase 1 of the BharatNet project resulted in 1.1 lakh villages being connected and service ready04. In the recent fiscal budget, the government proposed an investment of about USD1.5 billion in FY1905 to develop additional telecom infrastructure.

Additionally, Public Private Partnership (PPP) models are also evolving such as Google’s partnership with RailTel as a backhaul provider for enabling public Wi-Fi hotspots at 400 railway stations. Eventually, these services will cover 6,000 railway stations06. Also, BSNL is partnering with Facebook to set-up community public Wi-Fi hotspots in rural India.

However, significant efforts from all stakeholders are required in broadband expansion and fiberisation which will be critical to eliminate the digital divide.

01. The Indian Telecom Services Performance Indicators April – June, 2018. FX Conversion Rate for FY18 - 64.46

02. http://www.worldometers.info/world-population/india-population/

03. Pradhan Mantri Digital Saksharta Abhiyan (Gramin), Pradhan Mantri Yojana, Accessed Date, 08 October 2018

04. “BharatNet Phase 1: Target Achieved Through Meticulous Planning and Focused Implementation at Ground Level; Press Information Bureau ,Government of India, Ministry of Communications, Accessed in June 2018”

05. 10,000 crore to boost telecom infrastructure , The Hindu, 01 Feb 2018

06. 6000 railway stations will be Wi-Fi-enabled in next 6 months, Economic Times, 28 August 2018

Fixed and mobile broadband subscriptions per 100 inhabitants, in 2017

Fixed-Broadband Mobile-Broadband

Fran

ce

Finl

and

Finl

and

U.K

.

U.K

.

U.S

.

Chi

na

Fran

ce

Bra

zil

Chi

na

Kore

a (R

ep)

Sin

gapo

re

Sin

gapo

re

Bra

zil

U.S

.

Kore

a (R

ep)

Arg

entin

a

Arg

entin

a

Indi

a

Indi

a

Average of 27.5

Average of 100.1

43.8 153.841.6 148.239.3

132.9112.8

90.2 88.1

87.5 83.678.1

25.8

33.930.9

26.9

25.8

17.813.7

1.3

Source:The State of Broadband: Broadband catalyzing sustainable development, September 2018

The government has also been making facilitative investments. BharatNet and NDCP are aimed to provide the required momentum to the sector in terms of infrastructure and investment push however speedy implementation of these initiatives would be key.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

14

India’s low broadband penetration compared to global peers signifies a huge potential for the industry. The NDCP released in September 2018, which aims to provide fixed-line broadband access to 50 per cent of households by 2020 and universal broadband coverage of 50 Mbps for every citizen07, should also boost broadband expansion. Moreover, the BharatNet project (phase 2) under the Digital India initiative aims to connect additional 150,000 Gram Panchayats (GPs) through high-speed optical fibres by end of 201808.

Currently, the average speed of Indian operators is below 10 Mbps09 and if we have to achieve

the 50 Mbps per citizen target, the government has to provide five times the spectrum and the telecom network has to grow from the present two million Base Transceiver Stations (BTS) deployed to 10 million. This will require focused and timely provisioning of resources. It will be important that the government intervenes to provide the requisite resources in terms of spectrum, right of way permissions, financial incentives and an implementation monitoring system to achieve the targets defined in NDCP 2018.

New asset-light operating models of fibre leasing and renting may be explored in view of declining profitability and stretched balance sheets. While some of the operators are currently focusing on expanding fibre home reach, policies and schemes encouraging active infrastructure sharing will shape up fibre leasing and renting dynamics in India.

07. “National Digital Communication Policy, 2018 - Draft For Consultation, Department of Telecommunication – Ministry of Communication, Government of India, 1 May 2018”

08. KPMG India’s Research

09. State of Mobile Networks: India (April 2018), OpenSignal, Accessed on 18 October 2018

Source: Status of BharatNet, Bharat Broadband Network Limited, Accessed on 11 September 2018

Status of BharatNet project

Sr. No. Description of work

Status as on Status as on Status as on

2 September 2018 3 September 2017 21 August 2016

1. Optical Fibre Communication (OFC) pipe laid

2,79,346 kms (1,20,713 Gram

Panchayats)

2,43,590 kms (1,08,275 Gram

Panchayats)1,55,398 kms

2. Optical fibre laid 2,87,878 kms (1,19,036 Gram

Panchayats)

2,25,475 kms (100,768 Gram

Panchayats)1,31,494 kms

3. Tenders finalised 3,291 blocks / 1,22,828 Gram

Panchayats

3,326 blocks /1,24,291 Gram

Panchayats

2,541 blocks /95,242 Gram Panchayats

4. Work started* 3,281 blocks / 1,22,305 Gram

Panchayats

3,242 blocks / 1,21,328 Gram

Panchayats

2,430 blocks /87,176 Gram Panchayats

5. Current weekly performance of optical fibre laying 386 kms 971 kms 1,089 kms

6. Current weekly performance of OFC pipe laying 194 kms 615 kms 830 kms

7. Optical fibre cable delivered on site 3,41,568 kms 2,86,944 kms 1,77,998 kms

8. Service-ready Gram Panchayats 1,14,552 Gram Panchayats

32,715 Gram Panchayats

8,472 Gram Panchayats

15

Urban India and the surge of data usageData consumption in India has grown exponentially over the past few years due to increased smartphone penetration and improved coverage of high-speed data network coupled with low data tariffs. September 2016 was a watershed moment when the arrival of a new greenfield operator resulted in a steep drop in data prices and subsequently resulted in an increase in average wireless data usage per

subscriber per month to 4.7 GB01 as of June 2018 (up from 420 MB in FY16)10. With continued operator investments in 4G roll-outs and aggressive operator data plans, there is an inherent shift in consumer data usage patterns. Incumbents followed suit and introduced aggressive 4G data plans, leading to a fundamental shift in the way consumers use data.

Falling data tariffs have led to rapid data uptake10

FY15

310

420

1,360

4,708

256229

68.5

16.4

Average realisation (Paise/MB)

Data usage/ subscriber/ month (MB)

Increase in data revenue has been offset by fall in data realisation

~7,000 MB

12.4 Paise/MB

FY18 FY20FY16 FY17

Source: Crisil Research, Accessed Date, 08 October 2018

Increased competition has led to commoditisation of voice revenue and emergence of data services as the primary driver of potential revenue growth for

telecom operators - average voice revenue per user declined about 30 per cent in FY18 and is expected to further decline by 15-20 per cent in FY1911.

01. The Indian Telecom Services Performance Indicators April – June, 2018. FX Conversion Rate for FY18 - 64.46

10. Crisil Research, Accessed Date, 08 October 2018

11. CRISIL Research, 01 June 2018

With continued operator investments in 4G rollouts and aggressive operator data plans, there is an inherent shift in consumer data usage patterns

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

16

Demand for mobility, app-based and OTT services to spawn bundled services opportunitiesPersonalised 5+ inch screens in the form of smartphones and tablets have emerged as the preferred entertainment mode. Around 95 per cent of households12 in India own just one TV making smartphones the second screen for users. The low price of an entry-level 4G enabled device — starting at around USD21 for 4G feature phones and

approximately USD40 for a 4G smartphone13 has also contributed to increased use of mobile devices with 4G capable device penetration reaching 22 per cent at a pan-India level in 2017 from 12 per cent in 201614. Consequently, mobile as a medium has become the most popular and adopted device for consuming online content.

Source: Mobile data traffic in India to grow 5 times by 2023: Ericsson report, The Economic Times, 12 June 2018

Rise of digital media proliferation to drive future adoption

Share of average time spent

Share of time spent on digital mediums- 2017

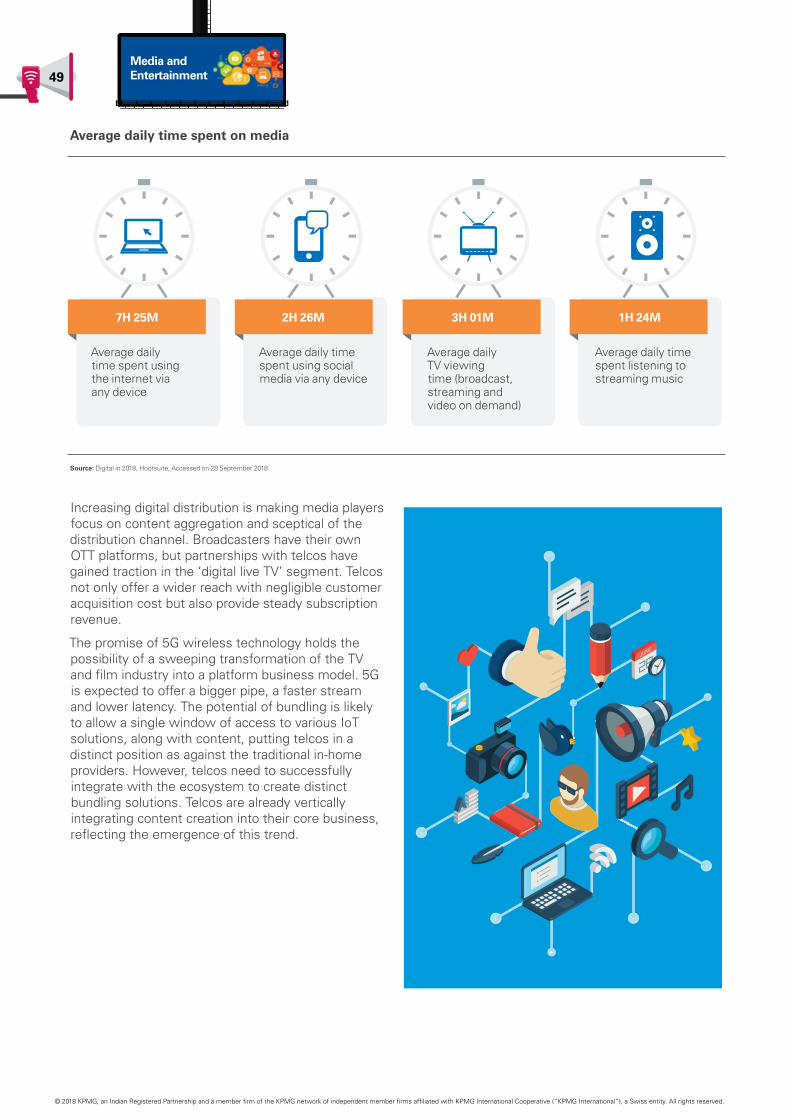

Desktop/laptop Mobile devices

17.9%

30.8%72.6% 27.4%

67.8%

56.9%

Digital TV

2013

2018

390 mn 975 mn

~100 mn 800 mn

5.7 GB 13.7 GB

2017 2023

Smartphone subscription

VoLTE connections

Average monthly data usage per smartphone

12. India Trends 2018: Trends shaping digital India, KPMG, May 2018

13. CRISIL Research, 20 July 2018

14. India Mobile Broadband Index 2018, Nokia, Accessed Date, 20 Sep 2018

With expected exponential rise in data usage, telcos need to find new ways of monetising data.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

17

Video streaming has the biggest share in media consumption

Active users (in mn) of OTT platforms

Online video audience (millions) Video OTT revenues (INR billion)

4-8% Others

8-10%Social Media

15-18%Browsing

65-75%Video streaming

Online video consumption grew 5X in 2017

YouTube 225

Operators’ OTT 50-100

Hotstar 75

ALT Balaji 2

TVF Play 4

Sony LIV 5

Netflix 5

Amazon 13

Voot 30

FY18E FY23P

225

550

FY23P

4.3

44.9

17.2

93.2

FY23P

CAGR – 50%CAGR – 60%

Advertisement Subscription

2017

2023

Sources:

- India Mobile Broadband Index 2018, Nokia, Accessed Date, 20 Sep 2018

- Media ecosystems: The walls fall down, KPMG, September 2018 Mobile data usage in India rose to the levels of a few developed markets in 2017 and is expected to surge 5x by 2023.

Video streaming contributed 65-75 per cent to total mobile data traffic in 2017 in India, driven by 4G uptake, the emergence of OTT players and availability of content in Hindi and regional languages.

CAGR – 20%

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

18

With this shift to a data-centric revenue driver, operators across the globe are exploring further data monetisation opportunities. Given the potential of the content market, operators are investing in content ecosystems (creation, curation and distribution) to provide further data value-adds. Operators like Telefonica, BT, AT&T are investing in developing content and evolving into digital media franchises with a sharp focus on bundled offerings including bundled TV, wireline and wireless phone services. Operators in India have also pursued different strategies with respect to defining and developing their content portfolios (from sourcing original content to being an aggregator of video and content platforms). The trend of investing in content can be expected to continue as operators strive to provide differentiated experiences to the end consumer with respect to content, media and video consumption.

The boundaries between Technology, Media and Telecommunications (TMT) sector are increasingly blurring across the globe with connectivity being the catalyst for this disruption and driving convergence of business models. As this convergence starts to play out across the globe, India is not likely to remain far behind.

Benefits and opportunities abound for the stakeholders of the TMT ecosystem as a result of the convergence theme.

• The convergence of traditional content-led organisations with telcos and technology led platforms results in content reaching a wider

audience base through a distribution medium which is increasingly becoming digital

• Convergence and digital distribution mediums also open up monetisation avenues for content creators – which have traditionally been led through advertisements. Convergence opens up a monetisation outlet, especially for a subscription-based revenue

• For the telecom operators, content becomes more important and has the potential to act as a key differentiator eventually helping with customer stickiness on their network

• Telcos can also look to monetise the projected surge in data traffic (by 2021, 82 per cent of all IP traffic is expected to be video)15 at scale.

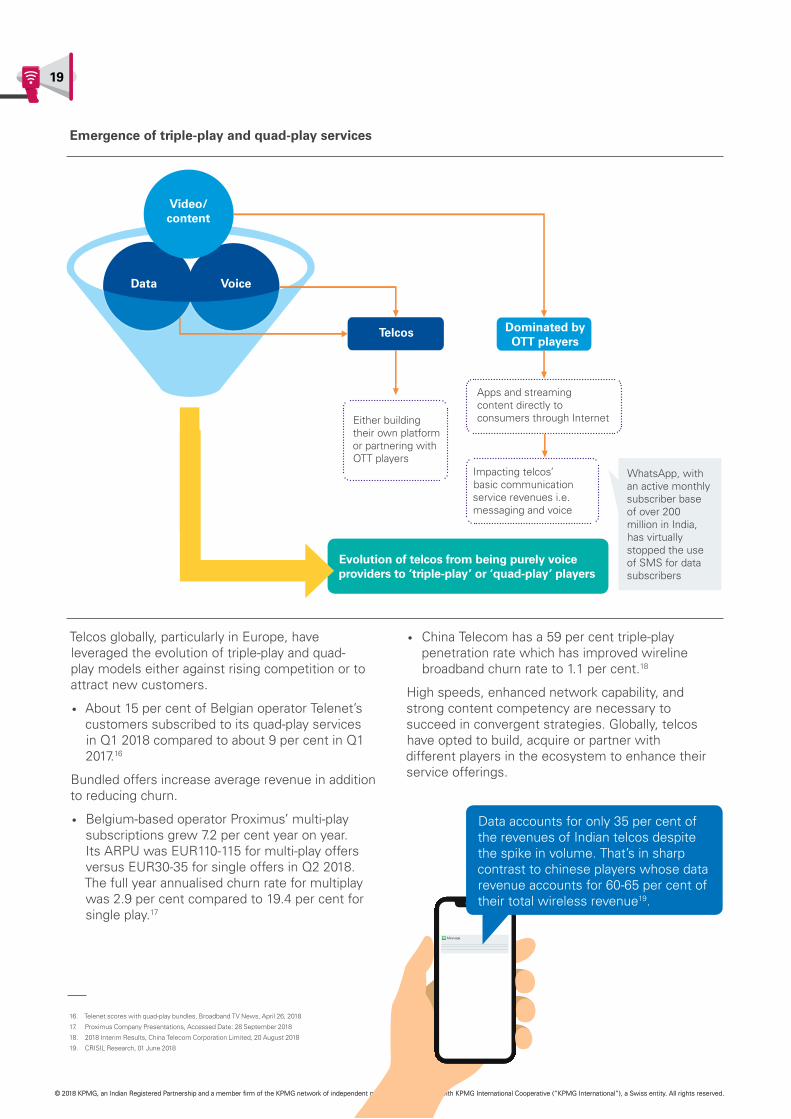

Capitalising on this opportunity, telcos are changing their business models and are coming up with lucrative bundled offers and free subscriptions to certain OTT apps to drive ARPU. Telcos are evolving from pure voice providers to ‘triple-play’ or ‘quad-play’ players integrating their voice, data, and content offerings.

• Airtel launched Airtel Home, a digital quad-play platform bundling home broadband, fixed line, post-paid mobile and digital TV in June 2018

• Jio is betting on bundled OTT and Internet Protocol TV services along with voice and data.

15. Fast Data Use Cases for Telecommunications, Voltdb, September 2017, Accessed on 01 October, 2018

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

19

Telcos globally, particularly in Europe, have leveraged the evolution of triple-play and quad-play models either against rising competition or to attract new customers.

• About 15 per cent of Belgian operator Telenet’s customers subscribed to its quad-play services in Q1 2018 compared to about 9 per cent in Q1 2017.16

Bundled offers increase average revenue in addition to reducing churn.

• Belgium-based operator Proximus’ multi-play subscriptions grew 7.2 per cent year on year. Its ARPU was EUR110-115 for multi-play offers versus EUR30-35 for single offers in Q2 2018. The full year annualised churn rate for multiplay was 2.9 per cent compared to 19.4 per cent for single play.17

• China Telecom has a 59 per cent triple-play penetration rate which has improved wireline broadband churn rate to 1.1 per cent.18

High speeds, enhanced network capability, and strong content competency are necessary to succeed in convergent strategies. Globally, telcos have opted to build, acquire or partner with different players in the ecosystem to enhance their service offerings.

Emergence of triple-play and quad-play services

Video/content

Data

Telcos Dominated by OTT players

Voice

WhatsApp, with an active monthly subscriber base of over 200 million in India, has virtually stopped the use of SMS for data subscribers

Either building their own platform or partnering with OTT players

Apps and streaming content directly to consumers through Internet

Impacting telcos’ basic communication service revenues i.e. messaging and voice

Evolution of telcos from being purely voice providers to ‘triple-play’ or ‘quad-play’ players

16. Telenet scores with quad-play bundles, Broadband TV News, April 26, 2018

17. Proximus Company Presentations, Accessed Date: 28 September 2018

18. 2018 Interim Results, China Telecom Corporation Limited, 20 August 2018

19. CRISIL Research, 01 June 2018

Data accounts for only 35 per cent of the revenues of Indian telcos despite the spike in volume. That’s in sharp contrast to chinese players whose data revenue accounts for 60-65 per cent of their total wireless revenue19.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

20

Control over content is driven by collaborations and investment models

Content

Partnerships Strategic investments

• Airtel, Vodafone Idea aggregating content

• Airtel partnered with Hotstar for content comprising live sports, movies and TV shows

• Airtel partnered with Netflix.

• Reliance Jio aggregating content and investing in original and exclusive content

• Acquired digital rights for Winter Olympics 2018, EFL Cup and T20 cricket series

• Acquired 5 per cent stake in Eros International and 25 per cent stake in Balaji Telefilms20

• Announced merger of its music app with Saavn.

20. Reliance Industries to buy 5% stake in Eros for over Rs 340 crore, Times News Network, 21 February 2018

Multi-play strategies in India are still in their infancy. Telcos face a number of challenges related to infrastructure and digital literacy in rural areas, and most importantly, content including the availability of regional language content. However, monetisation opportunities have encouraged some players to take initiatives on the infrastructure and content fronts to strengthen their position as multi-play providers.

Create an ecosystem for digital enablement

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

21

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

As the digital revolution continues to accelerate and expand at an astonishing pace, business leaders are grappling with emerging technologies, fuelling simultaneous disruptions across all aspects of the enterprise. The transition from an industrial economy that favoured mass production and scale to a digital economy that favours information, is challenging the existing ecosystems. The fourth industrial revolution is quickly unfolding as the evolution of AI, IoT and

robotics move firmly into the mainstream and upturn businesses like media and entertainment, transportation, healthcare, security and retail. This places the ICT sector at the heart of this revolution, with telecom being the essential lifeline.

It is evident from a recent KPMG survey that companies which are able to deploy some of these new edge technologies are the ones driving business transformation.

22

The road to growth: Disruptive business models

List of several companies named by tech industry leaders as companies they believe are most likely to disrupt their business.

Source: KPMG Technology Innovation Findings, The Changing Landscape of Disruptive Technologies, KPMG US, 2018. The figures are based on responses provided by global industry leaders across 15 countries

Source: KPMG Technology Innovation Findings, The Changing Landscape of Disruptive Technologies, KPMG US, 2018

Alibaba

12%

11%

Airbnb

10%

Amazon

9%

9%

The survey also indicated that over the next three years, IoT is identified as the leading game changer and e-commerce as the biggest disrupter globally.

IoT AI Robotics

17% 13% 8%

23

The road to growth: Disruptive business models Based on KPMG Technology Innovations Lab’s findings through a global web survey of more than 750 technology industry leaders (CXOs, entrepreneurs, venture capitalists), e-commerce is seen as the top disruptor in the next three years.

Top disruptive business models by country to drive growth in futureEven though e-commerce would be a top disruptor globally, social networking platforms would be the top disruptor for India.

E-commerce platforms are transforming at the speed of light, from fast deliveries to highly efficient logistics and supply chain operations along with new mobile payment services and digital assistants. This top ranking is consistent with the tech industry leaders’ responses in identifying Alibaba and Amazon as top companies to watch as disruptors of their business.

Social networking platforms ranked second. These platforms are known to have a strong influence

on people’s life, behaviour and choices. Social network platforms also play an important role in the distribution of innovative technologies. Disruption resulting from transportation as a service and self-driving vehicles is reflected in the ranking of autonomous transportation platforms. Entertainment platforms ranked fourth as the shake-ups in traditional entertainment companies are expected to continue.

Social networking platforms

19%

Autonomoustransportation

platforms

14%

Entertainmentplatforms

11%

E-Commerceplatforms

26%

Source: KPMG Technology Innovation Findings, The Changing Landscape of Disruptive Technologies, KPMG US, 2018. The figures are based on responses provided by global industry leaders across 15 countries.

Source: KPMG Technology Innovation Findings, The Changing Landscape of Disruptive Technologies, KPMG US, 2018. The figures are based on responses provided by global industry leaders across 15 countries.

Autonomoustransportation

platforms

China India Japan U.K. U.S.

E-commerceplatforms

Entertainmentplatforms

Social networking

platforms

18%

16%

12%

12%

9%

20%

20%

10%

17%

15%

19%

19%

15%

12%

23%

29% 17% 30% 26% 24%

To reap the true benefits of technology for the socio- economic development of the country, it is important that all stakeholders come together and contribute towards providing an environment that will foster innovation, entrepreneurship and investments.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

24

However, for India to emulate similar success in these businesses as its global counter parts, there is a lot that needs to be done. As per CISCO’s Digital readiness research released in May 2018, India’s score of digital readiness is 10.54, a little lower than the global average of 11.96, but with a vast difference with the highest score of 20.101, achieved by the U.S. The government is cognizant of the significant efforts required to make a digital India and NDCP 2018 is a progressive step towards the digital empowerment of India. NDCP 2018 has also outlined the following strategies to strengthen India’s digital footprint and coverage with the aim to achieve the following objectives by 202202:

1. Provisioning of broadband for all

2. Creating four million additional jobs in the Digital Communications sector

3. Enhancing the contribution of the Digital Communications sector to 8 per cent of India’s GDP from ~ 6 per cent in 2017

4. Propelling India to the Top 50 Nations in the ICT Development Index of International Telecommunications Union (ITU) from 134 in 2017

5. Enhancing India’s contribution to Global Value Chains

6. Ensuring Digital Sovereignty.

To reap the true benefits of technology for the socio-economic development of the country, it is important that all stakeholders come together and contribute towards providing an environment that will foster innovation, entrepreneurship and investments. It is believed that the two most important focus areas would be:

• Creation of a conducive environment for innovators and entrepreneurs to thrive

• Creating networks for the future, to support the functioning and adoption of the new edge technologies.

01. “Country Digital Readiness: Research to Determine a Country’s Digital Readiness and Key Interventions, Cisco, May 2018 “

02. National Digital Communication Policy, 2018

25

Start-ups adding significant value across industries India’s start-up ecosystem has grown at a rapid pace (1,000 tech start-ups added in 2017)03 and have played a big role in the growth of the Indian economy. Backed by improved connectivity and internet penetration, start-ups are building solutions across industries such as healthcare, banking, insurance, travel, agriculture and education.

India Start-up landscape

largest startup ecosystem

3rd

1

invested in 2017

USD 13.7 billion

6

Number of tech startups (2017)

5,200

2

YoY growth in top verticals

(2017) Health-tech

Fintech E-commerce

7

startups in the B2B segment

40%

3

accelerators and incubators

+190

4

active investors

+500

5

Tier II and Tier III cities

gaining momentum

828% 31% 13%

Sources:

- Over 1,000 tech start-ups added in 2017, says Nasscom, The Indian Express, 2 Nov 2017

- Indian start-up ecosystem- Traversing the maturity cycle, Edition 2017, NASSCOM, Accessed Date, 21 September 2018

- The YourStory 2017 Startup Funding Report – $13.7 billion invested across 820 deals, YourStory, 23 December 2017

- Business incubators leading growth of startups in India’s tier II/III cities: NASSCOM report, The Economic Times, 05 Dec 2017

Government backing has come in the form of the Start-up India programme, setting up an investment fund of USD1.38 billion04 to support development and growth of innovation-driven enterprises, tax incentives, patent right reforms, single-window clearances and easing of restrictions on foreign venture capitalists.

Incubators/accelerators play an important role by providing mentorship, nurturing ideas and extending technical support and providing access to funding. To encourage innovation, Niti Aayog as part of its Atal Innovation Mission (AIM) will provide USD1.49 million to 100 new incubators and USD30,000 to 500 tinkering labs in schools05.

However, despite the positive economic growth and government policies, India faces an uphill task to become a mature start-up community – mainly owing to skill-gap, lack of robust regulatory framework around data, compliance and Intellectual Property Rights (IPR), lower connectivity in rural areas and limited awareness in tier III cities that may contribute immensely to their ability to scale

and grow. For innovation to thrive, a multi-pronged approach has to be taken i.e. funding support, infrastructure support, tax and surcharge relief, regulatory and compliance support and enterprise level adoption.