Complexity, compliance costs and non compliance with VAT by small and medium enterprises in...

48

281 Complexity, compliance costs and non compliance with VAT by small and medium enterprises in Bangladesh: is there a relationship? Nahida Faridy, a Richard Copp, b Brett Freudenberg c,* and Tapan Sarker d Abstract Similar to many developing nations, Bangladesh’s small and medium sector enterprises (SMEs) constitute some 90% of all businesses and play an important role in the country’s economic growth and employment. 1 This study investigates the nature and extent of the relationships between the complexity of Bangladesh’s Value Added Tax (VAT) legislation, the costs of compliance with VAT in Bangladesh, and non-compliance (either intentional or unintentional) with the VAT legislation by Bangladeshi SMEs. These results could be important as it appears that SMEs are under-represented in terms of their contribution to Bangladesh’s VAT revenue 1 Mintoo, A. A. (2004). SMEs in Bangladesh. TECH MONITOR, Sep-Oct, 44-56. is paper was accepted for publication on 3 May 2014. a,b,c Department of Accounting, Finance and Economics, Griffith Business School, Griffith University d Department of International Business & Asian Studies, Griffith Business School, Griffith University * Corresponding author, E-mail: b.freudenberg@griffith.edu.au, Tel.: +61 7 373 58071

Transcript of Complexity, compliance costs and non compliance with VAT by small and medium enterprises in...

281

Complexity, compliance costs and non compliance with VAT by small and medium enterprises in Bangladesh: is there a relationship?

Nahida Faridy,a Richard Copp,b Brett Freudenbergc,* and Tapan Sarkerd

Abstract

Similar to many developing nations, Bangladesh’s small and medium sector enterprises (SMEs) constitute some 90% of all businesses and play an important role in the country’s economic growth and employment.1 This study investigates the nature and extent of the relationships between the complexity of Bangladesh’s Value Added Tax (VAT) legislation, the costs of compliance with VAT in Bangladesh, and non-compliance (either intentional or unintentional) with the VAT legislation by Bangladeshi SMEs. These results could be important as it appears that SMEs are under-represented in terms of their contribution to Bangladesh’s VAT revenue

1 Mintoo, A. A. (2004). SMEs in Bangladesh. TECH MONITOR, Sep-Oct, 44-56.

This paper was accepted for publication on 3 May 2014.

a,b,c Department of Accounting, Finance and Economics, Griffith Business School, Griffith University d Department of International Business & Asian Studies, Griffith Business School, Griffith University * Corresponding author, E-mail: [email protected], Tel.: +61 7 373 58071

282 (2014) 29 AUSTRALIAN TAX FORUM

collection, which if other foreign studies2 are relevant could be due in part to compliance costs. The current study is the first to empirically examine the relationships between the complexity of VAT legislation, compliance costs and non-compliance for SMEs in Bangladesh context. The study involved firstly a series of focus group interviews involving different types of SMEs taxpayers in Bangladesh. This was then followed by survey through a purposive sample of SMEs taxpayers in Bangladesh. The results suggest that a majority of the compliant SMEs taxpayers listed complexity in VAT law and compliance costs as the two important factors influencing VAT non-compliance in SMEs. On the other hand, non-compliant taxpayers emphasised more about the positive relationship between taxpayers and VAT officials for compliant behaviour. The likelihood of audits, penalties and sanctions were found to have less effect on VAT non-compliance for non-compliant taxpayers. In comparison, such monitoring and penalties would apparently improve compliant behaviour by compliant taxpayers. The findings of this research have practical policy implications, in that they can assist policy makers and administrators in their understanding of the potential interrelationships between legislative and regulatory complexity, the costs of complying with VAT legislation, and non-compliance with VAT legislation by SMEs. Having a robust and functioning VAT system is seen as an important attribute for a developing economy, so these findings may be important not only for Bangladesh, but also similar developing economies.

Key words: Compliance Costs, VAT, Small and Medium Enterprises (SMEs), Bangladesh

2 Ritchie, K. (2001). The Tax Compliance Costs of Small Business in New Zealand. In Chris Evans, Jeff Pope and John Hasseldine (Eds.), Tax Compliance Costs: A Festschrift for Cedric Sandford (pp. 297-315).Prospect Media Pty Ltd, St. Leonards, Australia. Abdul Jabbar, H. (2009). Income tax non-compliance of small and medium enterprises in Malaysia: Determinants and tax compliance costs. Degree of Doctor of Philosophy, Curtin University of Technology, Curtin.

283COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

1 Introduction

Small and Medium Enterprises (SMEs) are considered as a key engine of economic growth in developing countries.3 Due to the importance of the SMEs sector to a country’s economy, governments around the world have commonly emphasised the importance of a healthy SME sector and geared public policy toward fostering SME development and growth.4 Bangladesh is no exception where SMEs5 create large scale and low-cost employment opportunities using mainly locally available inputs and technologies and develops entrepreneurship by mobilising small and scattered private savings.6

In Bangladesh, the 79,754 enlisted SMEs establishments7 account for about 45% of the total value-added in manufacturing; 80% of industrial employment and about 25% of the total labour force.8 Although SMEs constitute some 90% of all businesses9 and play an important role in the country’s economic growth and employment, SMEs appear to be under-represented in terms of their registration for Value Added Tax (VAT)10 and their contribution to VAT revenue collected. For instance, only 11% of

3 Shome, P. (2004). Tax Administration and the Small Taxpayer. Policy Discussion Paper No. PDP/04/2, The International Monetary Fund, Fiscal Affairs Department: Washington, D. C.

4 Hansford, A., Hasseldine, J. D., and Horworth, C. (2003). Factors affecting the costs of UK VAT compliance for small and medium-sized enterprises. Environment and Planning : Government and Policy, 21, 479-492.

5 In Bangladesh, SMEs are defined for governmental statistical purposes in terms of whether they are manufacturing-based or non-manufacturing-based. A “medium”-sized enterprise in a manufacturing sector in Bangladesh means an enterprise in which the value/replacement cost of durable resources other than land and factory buildings is between 15 million to 100 million taka ( as at 10/2/2014 exchange rates, one AUD is approximately equivalent to 70 taka). A “small” enterprise means an industry in which the value/replacement cost of durable resources other than land and factory building is less than 15 million taka. In a non-manufacturing context, a “medium”-sized enterprise means an enterprise in which 25 to 100 people work; and a “small” enterprise means an enterprise in which fewer than 25 people work (eg. family members working together in a cottage industry). See Bangladesh Bureau of Statistics (2005).

6 Bangladesh Bank (2006-2007). Annual Report, Security Printing Press, Dhaka.

7 Asian Development Bank. (2004). Report and Recommendation of the President to the Board of Directors on proposed Loans and Technical Assistance Grant to the People’s Republic of Bangladesh for SMEs Development Program, Retrieved from the world wide web: www.adb.org/Documents/RRPS/BAN/rrp-ban-35225.pdf

8 Government of Bangladesh (2011). Bangladesh Economic Review, Ministry of Finance, Dhaka

9 Alam, S., and Ullah, A. (2006). SMEs in Bangladesh and Their Financing: An Analysis and Some Recommendations. The Cost and Management, 34(3), 57-72.

10 Conceptually, a Value Added Tax is an indirect tax on consumption that is levied on the value addition of goods or services at each point in the supply chain from the raw material or input stage to final consumption. Bangladesh in fact has two conceptually distinct taxes which are, in common business nomenclature in Bangladesh, referred to as “VAT”. The first is the official

284 (2014) 29 AUSTRALIAN TAX FORUM

total VAT revenue come from SMEs, while SMEs’ share of revenue collected from turnover tax is a mere 0.03% of total VAT revenue collected.11 To date there has been no study in Bangladesh concerning the low representation of SMEs in terms of VAT. It is important to understand this low participation as having an effective VAT system is seen as an important attribute to assist developing nations.12

The reminder of the paper is organised as follows. The next section provides an overview of VAT in Bangladesh. Section three briefly reviews the literature regarding the role of complexity and compliance costs in VAT non-compliance studies. This discussion is then followed by the outline of the methods used in this study comprising of focus group discussions and surveys. Next the findings of the study for both methods are provided. The subsequent section provides a general discussion of the overall findings. The final section concludes the paper and provides suggestions for future research.

2 Value Added Tax (VAT) in Bangladesh: An Overview

From the time of independence in 1971 until 1991, Bangladesh had a relatively complicated indirect tax system. Domestically produced goods were subject to a Bangladeshi excise system, which only taxed goods and not services. The excise tax base was very narrow, and there were a multitude of rates and exemptions. In addition there was tax cascading, as excise was payable at every stage of value adding in the supply chain, with no offsets for the tax payable at prior stages of production on those goods. Imports of raw materials and intermediate goods were also subject to an indirect sales tax. This sales tax on imports performed two main functions: revenue-raising and protecting local industries. This protection led to considerable economic inefficiencies, exacerbating Bangladesh’s already adverse export and balance of payments position.13

In recognition of the complexity of this indirect taxation system in April 1979 the Government of Bangladesh established the Taxation Enquiry Commission (TEC), with a view to investigate and recommend viable alternatives to existing sales taxes and excise duties in Bangladesh. The TEC proposed introducing a VAT in Bangladesh

VAT; the second is a turnover tax imposed on small business. There are two key differences between these two taxes. First, the official or true VAT in Bangladesh is generally imposed on all firms at 15%, subject to an exception for small businesses, who have the option of instead paying a turnover tax at the rate of 3%. Second, VAT taxpayers in Bangladesh can generally claim input tax credits to offset their VAT payable, whereas small businesses paying turnover tax generally cannot.

11 National Board of Revenue (2011). Annual Report 2009-2010. Security Printing Press, Dhaka.

12 IMF (2007).Taxation of Small and Medium Enterprises, Background Paper for International Tax Dialogue Conference, Buenos Aires, October 2007.

13 World Bank (1989). Bangladesh: An Agenda for Tax Reform. The World Bank, Washington, D.C.

285COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

to (a) bring transparency in the taxation system; (b) prohibit cascading taxation at different stages of production; (c) consolidate the tax administration; (d) activate the overall economy by mobilising more in internal resources; and (e) bring a consistency in the tax-GDP ratio. This led to the introduction of a VAT in Bangladesh as per The VAT Act 1991 and The VAT Rules 1991. Initially VAT was extended to importation and manufacturing of goods and a handful of services and remained so until 1996 when the term ‘supply’ was re-defined to include all business transactions. In 1997 the VAT was then extended to cover the whole range of business transactions in an incremental way. Now in Bangladesh, all goods except those mentioned in the First Schedule to the VAT Act and all services except those mentioned in the Second Schedule14 are taxable goods and services. It is mandatory for any business or a person dealing in any taxable goods and services and having an annual turnover of BDT 6 million (USD$80,000) or more to register for VAT.15

In Bangladesh the standard rate of VAT for home consumption goods and services is 15% and exports and deemed exports are zero rated. However there are some other rates in practice that emerge due to different methods of calculation. The tax is generally imposed on the invoiced price, although where invoices are unavailable, a so-called ‘fixed value addition’ on a ‘truncated base’ (in effect, a notional value-added) is used to assess the appropriate VAT. For those businesses at the wholesale and retail levels that do not declare any input tax credits, a deemed 1.5% VAT (that is the so-called ‘Trade VAT’) is imposed, in lieu of the standard 15% VAT, on the total value of the goods or services sold.

Another variation is for small business suppliers (defined as those with an annual turnover is less than 6 million Taka - equivalent to approximately USD$ 80,000 as of 2013) have the option of paying a tax of 3% on their annual turnover, in lieu of 15% VAT. Choosing this option excludes the claiming of input tax credits.

Also, small business ‘consumers’ (that is purchasers) at the wholesale and retail level pay a fixed annual dollar amount of VAT, the quantum of which depends on the geographic location of their business. For example, if a small retail shop is based in the capital city – Dhaka - or one of the two major port cities, it would pay 6,000 Taka (USD$76) per year in deemed VAT. In contrast, a small retail shop based in a remote small town would pay 2,400 Taka (USD$30) per year in deemed VAT. Firms in cottage industries (defined as those firms with annual turnover of less than 2.4 million Taka (USD$ 31,000) and capital machinery of up to 300,000 Taka (USD$4,000) in value) and their consumers are exempt from VAT and turnover tax.

14 The First Schedule is the list of exempt goods which are basically unprocessed agricultural products such as cattle, crops, fruits, seeds and primary products (raw hides and natural sand). Exempt services mentioned in the Second Schedule in belong to the following categories-basic services for living; social welfare services; culture related services; finance and financial activities related services; transport service; and other services.

15 Starting with a threshold of BDT 0.5 million in 1991, the VAT threshold underwent a number of upward revisions in last 20 years.

286 (2014) 29 AUSTRALIAN TAX FORUM

Finally, for some taxable products listed in the National Board of Revenue’s (NBR) ‘special regulatory orders’, if the NBR considers that market prices have increased too much, the NBR can determine and set a lower so-called ‘tariff value’ so that relevant market prices (and the VAT payable) are artificially reduced. Businesses which pay VAT on the basis of this tariff value are not entitled to claim input tax credits. Consequently, it can be appreciated that there are numerous methods in calculating the VAT, which may of itself add to the complexity of the system.

The usual practice of paying VAT due (that is, the excess of output tax over input tax) to the government is through a return at the end of the tax period on a self-assessment basis by the registered taxpayers. The Bangladesh VAT has four distinct methods of paying VAT for different business transactions: advance payment through an Account Current, payment along with VAT returns, advance VAT for commercial goods at the importation stage and finally, withholding.

VAT has existed for 22 years in Bangladesh and collecting on an average 37% of total tax revenue in last 15 years.16 While the introduction of a VAT in Bangladesh has proved to be successful in terms of increasing tax revenues as well as expanding the tax base,17 some evidence suggests that there is the potential for improvement. For example, the tax base is narrow in Bangladesh compared to other developing countries and the tax revenue in Bangladesh is still very low as a percentage of GDP. In 2005, the average tax/GDP ratio in the developed world was approximately 35%, in developing countries it was equal to 15% and in the poorest of these countries, the low income countries tax revenue was 12% of GDP.18 In 2005, the tax/GDP ratio was less than 10% in Bangladesh and in 2011-2012 the ratio was 11%.19 Still now the gap between potential VAT revenue and actual VAT revenue is estimated to be more than 40%.20 Compared to other low-income countries the C-efficiency ratio21 is very low in Bangladesh. In low income countries the average C-efficiency ratio is 38.0% but in Bangladesh it is only 23.4%.22 The VAT efficiency (or Productivity) ratio is 15.92% in Bangladesh, whereas, according to International Monetary Fund (IMF) the average

16 Faridy, N. (2011). Progressivity of Value Added Tax (VAT) in Bangladesh, Unpublished Master’s Dissertation, Keio University, Japan.

17 Saleheen, A. M. (2012). Presumptive Taxation under Bangladesh. INTERNATIONAL VAT MONITOR, 23 (5),316-321.

18 Fuest, C., and Riedel, N. (2009). Tax evasion, tax avoidance and tax expenditures in developing countries: A review of the Literature, Paper prepared for UK DFID, Oxford University Centre for Business Taxation, Oxford.

19 Government of Bangladesh (2012). Bangladesh Economic Review. Ministry of Finance, Dhaka

20 Faridy, above n 16, at 45.

21 C-efficiency ratio is defined as a share of the VAT in consumption divided by the standard VAT rate.

22 IMF (2011). Revenue Mobilization in Developing Countries. International Monetary Fund , Washington, D.C.

287COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

worldwide VAT efficiency ratio is 34%.23 These figures would tend to indicate that there is potential for greater VAT collections.

According to the 2003 economic census the total number of Bangladeshi businesses was 3,674,971 of which 1,127,613 were registered with the trade licensing authorities.24 In 2011, the number of businesses registered under VAT system was 480,467, which is very low compared to the above figures.25 Of the 480,467 registered VAT payers, only 16.15% of registered VAT payers (or 77,615 firms) submitted their monthly VAT returns to local VAT authority on time. This means that approximately 84% of VAT taxpayers failed to lodge their returns on time. Anecdotal evidence suggests that only large VAT taxpayers registered with the NBR’s Large Taxpayer Unit (LTU) regularly submit their VAT returns. Overall, these figures suggest an under-representation by SMEs in the VAT revenue collected by government may be due to significant non-compliance by SMEs with Bangladesh’s VAT Law. In addition to that, there is some 60.24 billion Taka (USD$0.8 billion) in outstanding VAT yet to be collected from the VAT payers in respect of the 2009-10 fiscal years.26

Whether SMEs’ non-compliance with the VAT legislation is intentional or unintentional is unclear. One possible cause of SMEs’ non-compliance with the VAT legislation could be that Bangladesh’s VAT Law is too complex, so that they find the (private) costs of compliance (to them) to be excessive. Another cause of SMEs’ non-compliance could be the fact that under the legislation the Bangladeshi Government has power to determine and set regulated prices, and therefore affect VAT amounts for many products. Thus many taxpayers may fail to pay VAT initially themselves, simply because they know that the government will dictate to them how much to pay later. A further cause could be a lack of monitoring or enforcement on the part of authorities27 such as the NBR. To date there has been no study to explore the specific reasons of non-compliance with VAT by SMEs in Bangladesh. Against this backdrop, this paper aims to explore the reasons of non-compliance of VAT by SMEs in Bangladesh and examines whether complexity of VAT law and compliance costs lead to SMEs taxpayers’ non-compliance. The findings of this research may be insightful for other developing nations trying to ensure that their VAT system is robust.

23 Smith, A. M. C., Islam, A. and Moniruzzaman, M. (2011) “Consumption Taxes in Developing Countries – The Case of the Bangladesh VAT, Working Paper No. 82.” Victoria University of Wellington, available at http://www.victoria.ac.nz/sacl/cagtr/working-papers/WP82.pdf.

24 BBS. (2012). “Statistical Highlights of Economic Census, 2001 & 03, Bangladesh.” Retrieved November 21, 2013, from http://www.bbs.gov.bd/WebTestApplication/userfiles/Image/Economic%20Census/h_b_new.pdf.

25 NBR, above n 11, at 51.

26 NBR, above n 11, at 59.

27 Kirchler, E.(2007). The Economic Psychology of Tax Behaviour. Cambridge University Press Cambridge, UK.

288 (2014) 29 AUSTRALIAN TAX FORUM

3 Complexity, Compliance Costs and Non-compliance of VAT

Simplicity is one of the commonly accepted key tenets of any sound taxation system. Simplicity – or conversely, reducing complexity – in a taxation system cet. par. reduces compliance costs, administrative costs, and thereby taxpayer uncertainty. Such an outcome could lead to improved levels of voluntary compliance.28 Highlighting the importance of simplicity in a tax system, the report of The Australian Government Tax Road Map29 stated:

Simplicity is the major aim of the Governments tax reform. A tax system buried in red tape and complexity will reduce investment, stifle innovation and risk taking and ultimately reduce productivity and economic growth. Complexity in the tax system will reduce the time an individual or company has for other pursuits, and detract from further participation in the work force. It also makes the system unfair, as it imposes a higher burden on lower income households.

Miller30 points to three main types of complexity inherent in many taxation systems: technical complexity, compliance complexity and structural complexity. The first two types of complexity in particular would appear to be problems in Bangladesh, given the general population’s relatively low educational standards and low levels of financial literacy.31 Complexity is a universal problem and has been cited as the most serious problem by the United States of America (USA) income taxpayer.32 Excessive complexity increases filing and administrative costs and it has impact on voluntary compliance,33 although several studies have failed to document such a relationship.34 In a recent empirical study in Australia (albeit in the context of personal income tax), the level of complexity was found to be directly related to taxpayer compliance costs

28 Kasipillai, J.(2005). A Comprehensive Guide to Malaysian Taxation: Current Year Assessment, McGraw-Hill, Kuala Lumpur.

29 The Treasury. (2012). Tax Reform: Road Map. Commonwealth of Australia (available at www.budget.gov.au),p.5.

30 Miller, A. J. (1993). Indeterminacy, Complexity, and Fairness: Justifying Rule Simplification in the Law of Taxation. Washington Law Review, 68(1),1-78.

31 Government of Bangladesh (2009). Bangladesh Economic Review. Ministry of Finance, Dhaka.

32 Oveson, W. V. (2000). National Taxpayer Advocate’s Annual Report to Congress. Office of Taxpayer Advocate, Washington D. C.

33 Collins, J. H., Milliron, V. C., and Toy, D. R. (1992). Determinants of tax compliance: A contingency approach. Journal of the American Taxation Association, 14, 1–29. Vogel, J. (1974). Taxation and Public Opinion in Sweden: An Interpretation of Recent Survey data. National Tax Journal, 27( 4), 449-513.

34 Porcano, T. M. (1988). Correlates of Tax Evasion. Journal of Economic Psychology, 9, 47-67. Yankelovich, S., and White, I. (1984). Taxpayer Attitudes Study: Financial Report. Public Opinion Survey Prepared for the Public Affairs Division, Internal Revenue Service, New York.

289COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

and thence to taxpayers’ commitment to compliance.35 A similar empirical result was found in a Malaysian income tax context by Pope and Abdul-Jabbar.36

It is argued that complexity has a greater effect on small businesses, as they can be more severely affected by red tape than large businesses.37 This can be due to small businesses being less proficient in dealing with the complexities of regulations and are unable to spread the costs of compliance across large-scale operations.38 However, to-date the role of complexity (perceived or actual) in explaining taxpayer non-compliance with the VAT Law in Bangladesh has not yet been investigated.

It has been stated that the more complex the tax legislation and regulation the greater the knowledge gap – or information asymmetry – between legislators and taxpayers, and the greater the costs to the taxpayer of complying with the legislation.39 However the costs of complying with taxation legislation are not limited to taxpayers. Where the tax authorities have a legal duty to monitor and enforce the legislation (as does the NBR in Bangladesh), the tax authorities themselves face costs of discharging their duties in accordance with the legislation. In a very real sense, these too can be regarded as compliance costs, not the ‘private’ compliance costs of the taxpayer, but the publicly funded compliance costs for the tax regulator.

In the context of the Bangladeshi VAT, the private costs to a taxpayer of complying with the VAT Law can encompass not only the direct costs of collecting documentation; accounting for VAT; the fees paid to professional tax advisers; and remitting VAT on products but also indirect costs. These indirect costs include the value of labour time associated with the completion of VAT returns; the investment costs associated with acquiring intellectual capital necessary to enable this work to be done and even psychological costs that many taxpayers experience when trying to comply with tax legislation and regulation.40

35 McKerchar, M. (2003). The Impact of Complexity upon Tax Compliance: A Study of Australian Personal Taxpayers, Australian Tax Research Foundation, Sydney.

36 Pope, J., and Abdul-Jabbar, H. (2007). Tax Simplification and Small Business in Malaysia: Past Developments and The Future, 19th Conference of Australian Tax Teachers Association, Brisbane.

37 Shome, above n 3.

38 Chittenden, F., Kauser, S. and Poutziouris, P.(2003). Tax Regulation and Small Business in the USA, UK, Australia and New Zealand. International Small Business Journal, 21 (1), 93-115.

39 Sandford, C. (Ed.). (1995). Taxation Compliance Costs: Measurement and Policy. Fiscal Publications, Bath, UK.

40 Sandford, C. (1973). Hidden Costs of Taxation. University of Bath, Institute for Fiscal Studies, Bath, UK. Cléroux, P. (1992). Small business and the cost of paperwork: the goods and service tax. Journal of Small Business and Entrepreneurship, 9(4), 27-40. Evans, C. (2003). Studying the Studies: An Overview of Recent Research into Taxation Operating Costs. e-Journal of Tax Research, 1(1), 64-92. Klun, M. (2004). Compliance Costs for Personal Income Tax in a Transition Country: The Case of Slovenia. Fiscal Studies, 25(1), 93-104. O’Keefe, J.,

290 (2014) 29 AUSTRALIAN TAX FORUM

The first comprehensive study on the compliance costs of VAT was conducted by Sandford et al.41 for the year 1977-78 in the United Kingdom. However, the first modern study of compliance cost was conducted by Haig42 in the USA about the federal taxes separated from the states and local government taxes. In terms of empirical studies about VAT, the international evidence suggests that in most countries the introduction of a VAT results in significantly higher compliance costs for taxpayers than other forms of taxation; and that VAT compliance costs are disproportionately higher for small businesses than large businesses.43

The World Bank Group (WBG) conducted large-scale semi-structured questionnaire-based studies into tax compliance costs in transitional and developing countries (e.g., South Africa, Vietnam, Ukraine, Yemen, Peru, Nepal, Uzbekistan, Kenya) from 2006 - 2011, not only in relation to the time and costs spent on compliance with VAT, but also with income tax and payroll tax. Semi-structured questions were used to ask taxpayers about their bookkeeping practices; computer and internet access; experience with tax inspections and audits; taxpayer morale; their reasons for any non-compliance (including failure to register for VAT); and their perceptions of the competence, fairness, consistency and integrity of tax authorities and tax officers. These studies also found that tax compliance costs are regressive in nature. 44

In Bangladesh, Saleheen conducted a field survey in 2012 and showed that 49% of the surveyed population considered that VAT Law in Bangladesh were not clear at all and 45% of them found VAT law is not trade friendly and complex. Furthermore, 41% respondents claimed that VAT is a complicated process. However, this study didn’t explore the relationship between complexity and non-compliance.45

The regressivity in tax compliance costs may influence the competition of SMEs with large businesses, as small businesses may have compliance cost around 2% of their

and O’Hare, P. (2008). Increased compliance costs: VAT and place of supply of services. International Tax Review, 27-31. Barbone, L., Bird, R., and Vázquez- Caro, j. ( 2012). The Costs of VAT: A Review of the Literature, CASE Network Report No. 106/2012, Warsaw, Poland.

41 Sandford, C., Godwin, M., Hardwick, P., Butterworth, M. (1981). Costs and Benefits of VAT. London, UK: Heinemann Educational Books.

42 Haig, R. M. (1935). The cost to business concerns of compliance with tax laws. Management Review, November, 232–333.

43 Cnossen, S. (1994). Administrative and Compliance Costs of VAT- a review of the evidence. Tax Notes International, 8, 1649-1668. Coolidge, J. (2012). Finding of tax compliance cost surveys in developing countries. Paper presented at the 10th International Tax Administration Conference, Sydney,2nd & 3rd of April, 2012, at p. 13-28.

44 IFC (2011). IFC Tax Perception and Compliance Cost Surveys: A Tool for Tax Reform, World Bank Group, March 2011. Available at: https://www.wbginvestmentclimate.org/uploads/TPCCS_Consolidated_Web.pdf. (Accessed 14.3.13).

45 Saleheen, A.M. (2013). Taxation and Good Governance: The Case of Value Added Tax in Bangladesh. Unpublished PhD Thesis, Flinders University, Australia.

291COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

total turnover, where it can be lower as a fraction for the large businesses.46 Therefore, higher compliance costs and complex tax legislations can discourage voluntary compliance and encourage tax non-compliance among SME sector.

Franzoni47 identified that businesses may create a kind of resentment against tax authorities for high levies and too complex of a tax system. These may cause intentional non-compliance activities by the taxpayers. Furthermore, because of the complexity of the tax system, the businesses may engage expert tax professionals to help them with sophisticated tax planning to minimize tax payments. While there is some research into compliance with consumption taxes in developed economies, there is a paucity of research into VAT compliance generally in developing countries, and in particular in Bangladesh. The study outlined in this paper seeks to explore whether complexity - perceived or actual - plays a role in explaining taxpayer non-compliance with the VAT Law in Bangladesh. These results may be relevant to other developing nations, as a sound VAT system is seen as a fundamental cornerstone to provide adequate tax revenue for public spending.

4 Methodology

The overarching research problem which underlies this study is to ascertain why some SMEs comply with the VAT Law in Bangladesh, while others do not. In order to undertake this investigation, the research explores the extent of any associations between the complexity of the VAT Law, VAT compliance costs and SME non-compliance with the VAT in Bangladesh. A mixed methods approach was adopted utilising quantitative and qualitative methods. This type of mixed methods approach is most likely to maximize, as far as is practically possible, the internal and external validity of the results.48 While much of the earlier empirical literature on tax compliance costs and tax non-compliance utilised quantitative research methods, more recent studies have used a combination of quantitative and qualitative methods.49

46 Pope, J. (2001). Estimating and Alleviating the Goods and Services Tax Compliance Cost burden upon Small Business. Revenue Law Journal, Volume 11(1), 2- 23.

47 Franzoni, L. (1999), Tax Evasion and Tax Compliance. in Bourckaert, E. (Ed.), Encyclopaedia of Law and Economics (pp. 52-94), University of Bologna, Edward Elgar, Italy.

48 Huck, S. W., Cormier, W. H., and Bounds W.G. (1974). Reading Statistics and Research, Harper & Row, New York.

49 Tran-Nam, B., and Glover, J. (2002). Estimating the Transitional Compliance Costs of the GST in Australia: a Case Study Approach. Australian Tax Forum, 17(4), 499- 536. Glover, J., and Tran-Nam, B. (2005). The GST recurrent compliance costs/benefits of small business in Australia: a case study approach. Journal of Australasian Tax Teachers Association, 1(2), 237-258. McKerchar, M. (2003). The Impact of Complexity upon Tax Compliance: A Study of Australian Personal Taxpayers, Australian Tax Research Foundation, Sydney. Loo, E. C. (2006). Tax knowledge, tax structure and compliance: A report on a quasi-experiment. New Zealand

292 (2014) 29 AUSTRALIAN TAX FORUM

Permission was obtained from the NBR to obtain lists of SMEs taxpayers that filed monthly VAT returns in financial year 2011-12. Participants were divided into three groups:

i. The SMEs taxpayers who have no non-compliance history and registered with VAT for at least three years (Referred to as Compliant VAT payers, and abbreviated to CT);

ii. SMEs taxpayers who have a completed and decided VAT non-compliance cases against them and already paid the fines and penalties imposed on them (Referred to as Non-Compliant VAT payers, and abbreviated to NCT); and

iii. NBR’s VAT officials from field level to policy level and who have been working with the NBR at least for eight years (Referred to as VAT Officials, and abbreviated to VO).

The study was conducted in two stages. Stage 1 involved focus group discussions with VAT payers of the SME sector (both CT and NCT) and VAT officials. Stage 2 involved the mailing of a questionnaire, seeking qualitative and quantitative data, to both complying and non-complying SMEs taxpayers. Early versions of the survey materials were used in both a pre-test and pilot-test and the content of the survey was submitted to independent readers for checking before commencing the actual survey. Participation was voluntary and no financial incentives were given for their time. As this study used human subjects, it was necessary to ensure that ethics approval was received before commencement of the focus groups and survey.

It needs to be acknowledged that surveys relating to tax non-compliance are complicated by the sensitive nature of topic and the threat of penalties, prosecution and stigmatization, which can induce taxpayers either to lie about their tax evasion behaviour, or refusal to take part in the study.50 A number of strategies were adopted to try to minimise this. For example many questions were raised as the 3rd person rather than directly at the taxpayer, also any personal identification of participants were removed from the transcripts and responses.

4.1 Focus group discussions

The power of focus group discussions as a research tool lies in its group dynamics. Advantages such as synergy, snowballing, stimulation, spontaneity and serendipity can occur as part of a focus group.51 As a fast and cost-effective technique for eliciting

Journal of Taxation Law and Policy, 12(2), 117–140. Yesegat, W.A. (2008). Value added tax in Ethiopia: A study of Operating costs and Compliance. Unpublished PhD Dissertation, University of New South Wales.

50 Houston, J., and Tran, A. (2001). A Survey of Tax Evasion Using the Randomized Response Technique. Advance Taxation, 13, 69-94.

51 Stewart, D. W., and Shamdasani, P. N. (1990). Focus Groups: Theory and Practice. SAGE Publications, Newbury Park.

293COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

views and opinions, focus group has been found appropriate for obtaining insights into target audience perceptions. Discussions were conducted with focus groups of SME taxpayers about their perceptions of why some SME taxpayers comply with the VAT Law in Bangladesh, and others do not.

The focus group were conducted in Dhaka, the capital city of Bangladesh because of the respondents, location. A total of 45 participants participated the focus group discussions consisting of 15 from compliant taxpayers (11 were business owners and 4 were Director VAT of the enterprises), 15 from the non-compliant taxpayers (12 were business owners and 3 were VAT consultants from the selected enterprises) and 15 from tax officials (9 were Joint Commissioners of VAT and 6 were Second Secretaries of VAT from the NBR). For many of them, the topic being researched was a matter of great interest for its potential to contribute to the improvement of the Bangladesh’s tax culture and they also considered it an opportunity to share their opinion on the different aspects of VAT with a researcher. However, a couple of VAT officers declined to participate in the discussions as they thought that they should not talk ‘on the record’ to a researcher.

Because very few participants were fluent in English language, the discussions were conducted mainly in Bangla the common language especially among SMEs. The discussions were recorded for transcription and any identifying names or references were removed from the transcription. The confidentiality and anonymity of the recorded data was confirmed by coding the participant and not using the participants’ names. The findings of the focus groups are presented later in this article.

4.2 Survey development

Focus group discussions with VAT payers’ and VAT officials helped to improve the wording of, and the meaningfulness of the survey questions (to both researcher and respondents) in the subsequent questionnaire mailed to taxpayers of both compliant and non-compliant. The completion of focus group in this way also served to maximise response rates and ensure that meaningful data are recorded at Stage 2 of the study.52 In Stage 2 a questionnaire was mailed to compliant and non-compliant SME taxpayers, with a view to gathering both quantitative and qualitative information on factors affecting VAT non-compliance, and to gather data necessary for the estimation of VAT compliance costs. The questionnaire was designed using mainly closed-ended questions in order to gather numerical data, in the form of information which could be verified against documentation (such as, the value of fees paid to professional advisers); in categorical form (such as, tax rates applicable to different product categories); or in integer format (such as, taxpayers’ ratings of their perceptions on a 1-6 Likert scale). Other open-ended questions were also included in the questionnaire, to enable the gathering of information which was not readily reducible to numerical form. These types of questions included those relating to

52 Robson, C. (2002). Real world research: a resource for social scientists and practitioner researchers(2nd ed.). Blackwell Publishers, Oxford, UK.

294 (2014) 29 AUSTRALIAN TAX FORUM

taxpayer’s perceptions of the integrity of the VAT officials; suggestions for improving the ways in which VAT in Bangladesh is designed or administered; and suggestions for the other reforms of law and practice. A summary of the English version of survey questionnaire is presented in Appendix A. Another version was also distributed that was written in Bangla, the official language of Bangladesh.

Before the final survey was undertaken 20 questionnaires were sent to SMEs taxpayers as a pilot survey to determine if the drafted questions were easily understandable to the respondents or not. After a two week period, eight completed responses were received, a response rate of 40%. After the pilot test and refinement of the survey instrument, a total of 500 questionnaires were then distributed to SMEs VAT payers from June 2013 to September 2013. The SME VAT payers were selected based on purposive sampling from NBR’s taxpayers list. Out of this total, 200 questionnaires were distributed to non-compliant taxpayers group and remaining 300 questionnaires were distributed to compliant taxpayers. Two reminders were sent to the taxpayers to improve the response rate. Finally the usable responses were 240 (152 from compliant taxpayers and 88 from non-compliant taxpayers). Giving an overall response rate was 48%, representing 51% response rate from CT and 44% response rate from NCT. .

Since VAT extends to the whole of Bangladesh, mail survey data were collected from the target population resident in the business regions of city corporation area, district town and Upazilla area. A summary of the participants’ characteristics is shown in Table 1. Most of the respondents of mail survey were well qualified in terms of academic qualifications, 35% holding a Masters and 38% holding a bachelor degree. 50% of the respondents were from manufacturing business unit and an average of 45% were a sole proprietorship business. Regarding the manner of keeping accounting records, 43.1% from compliant group and 34.1% from non-compliant group of respondents in the mail survey indicated that their systems were fully manual. The rest noted that either their accounting systems were fully or partially computerised or their external accountants or tax advisors kept their accounting records.

295COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

Table 1: Summary of participants’ characteristics

CharacteristicsCompliant (N=152)n (%)

Non-Compliant (N=88)n (%)

Location of business / enterprise

City corporation area (Dhaka) 33 (21.7) 35 (39.8)City corporation area (Other) 60 (39.5) 26 (29.6)District town 33 (21.7) 15 (17.1)Upazilla area 26 (17.1) 12 (13.6)Primary business / enterprise

Manufacturing 75 (49.7) 44 (50.0)Construction and real estate 16 (10.6) 12 (13.6)Wholesale, retail trade, hotels and restaurants 28 (18.5) 19 (21.6)Professional services 3 (2.0) 4 (4.6)Transport, storage and communication 18 (11.9) 2 (2.3)Others 11 (7.3) 7 (8.0)Business form

A sole proprietorship 63 (42.6) 40 (45.5)A cooperative 1 (0.7) 0 (0.0)A partnership 10 (6.7) 8 (9.1)A private limited company 65 (43.9) 35 (39.8)A share company 2 (1.4) 3 (3.4)Others (public limited company) 7 (4.7) 2 (2.3)VAT related record keeping practice

A manual / paper system 65 (43.1) 30 (34.1)A partially computerized system 58 (38.41) 39 (44.3)A fully computerized system 18 (11.9) 18 (20.5)Tax adviser / external accountant 10 (6.6) 1 (1.1)Average monthly VAT paid in 2011-12 (in BDT)

Under 400,000 45 (29.6) 28 (31.81)400,001 to 500,000 23 (15.1) 15 (17.1)500,001 to 600,000 10 (6.6) 4 (4.6)600,001 to 700,000 3 (2.0) 5 (5.7)800,001 to 900,000 3 (2.0) 2 (2.3)900,001 to 10,00,001 19 (12.5) 5 (5.7)More than 10,00,001 49 (32.2) 29 (33.0)Education level

Junior high school 0 0SSC 0 1 (1.14)HSC 19 (12.5) 14 (15.90)Certificate 2 (1.32) 3 (3.41)Diploma 11 (7.24) 7 (7.95)Bachelor degree 58 (38.15) 33 (37.50)Masters degree or above 60 (39.47) 24 (27.27)Others (CA, LLB, MBA, PHD) 2 (1.32) 5 (5.68)

296 (2014) 29 AUSTRALIAN TAX FORUM

4 Findings

The findings for both the focus groups (stage 1) and the survey (stage 2) are presented below.

5.1 Focus Groups

There can be a perception that taxation in general will always have the problem of compliance,53 with people generally not liking to pay tax. However, the findings from the compliant taxpayers revealed that the duties as a citizen to the country and the contribution to build-up the state can be one of the main factors in influencing them to comply with the VAT law:

It’s our duty as citizens and also our responsibility to The State to comply with the VAT Law as The State is providing us necessary services. I see paying VAT and comply with the VAT Law as a duty of a business man. (CT 8)The State has provided us with some opportunities which enable us to do our business such as infrastructure. Even if you think the State as a company, it has provided some services and facilities for us. We need to pay the price for the State’s services. If we pay the right amount of VAT, it’s a contribution to The State to build its future. (CT 15)

In comparison, the most common influence for complying with the VAT from the non-compliant taxpayers was that VAT as an obligation to the businessmen and to avoid conflict with the VAT officials. Three female enterprise owners gave their opinion that most of the business person want to run his or her business according to the law, to avoid any hazard and obstruction from the tax officials. This was especially the case as a large percentage of their wealth is invested in the business, so it may be very costly if they are subjected to any penalties from the tax officers:

I don’t want any conflict with my local VAT offices and also I want to avoid any sort of legal WURXEOH with the NBR which may be very costly for me. So I try to pay my VAT timely. (NCT 13)I firstly understand my duty when any kind of tax is mentioned. Paying VAT and abiding by the VAT Law cannot be enjoyable for people but if I can calculate my VAT correctly, paying the rightful amount of the taxes is a good job actually. I feel secure if I maintain a good relationship with the VAT offices. I think some SMEs taxpayers comply with the VAT law to maintain a good relationship with VAT offices and to get co-operation from them. (NCT 9)

53 Adams, C., and Webley, P. (2001). Small business owners’ attitudes on VAT compliance in the UK. Journal of Economic Psychology, 22, 195-216.

297COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

Kirchler54 stated that a positive relationship between the tax authority and taxpayer may influence the level of voluntary compliance. However, in developing countries an antagonistic relationship may exist between these two groups, similar to a ‘cops and robbers’ game. Tax authorities perceive the taxpayers as ‘robbers’ who try to evade whenever they can and need to be monitored all time. Similarly taxpayers perceive tax authorities as ‘cops’ and feel it their right to hide.55 Supporting this literature, participants from VAT officials’ considered better enforcement and strong monitoring by NBR is the most influencing factor to improve VAT compliance, not the civic duty:

Civic duty or contributions to The State are not the main factors. The most important things are strong monitoring and enforcement. They are tax fearing people; they are not tax loving people. (VO 3)

Participants were then asked to discuss the reasons for non-compliance with the VAT Law by Bangladesh SMEs. Some non-compliant taxpayers considered VAT as a burden and extra costs for SMEs. In addition to that, the higher VAT rate (15%) with supplementary duty and tariff value make VAT costly to the SMEs taxpayer in Bangladesh. Seven non-compliant participants stated that VAT rate is very high in Bangladesh and the business owners outside the VAT net are in a better position than the taxpayers within the VAT net. Majority of the non-compliant participants expressed that they are aware of VAT that they are obliged to pay, but considered that the government is not using taxpayers’ money wisely and taxpayers are not getting sufficient return from the government in terms of infrastructure or social security schemes. These various perceptions were used as justification to non-comply:

VAT is an extra cost for my business. I always want to minimise my cost. The VAT becomes a burden for me. (NCT 1)I am not paying the VAT from my own pocket. I am collecting VAT from the customers. If I collect it and do not deposit the right amount to the Treasury I can make 15 percent more profit than my business competitors. So why do I have to pay VAT and comply with the Law? (NCT 11) Businesses that do not file or pay taxes are in a much better situation than businesses that pay regular taxes. Businesses registered for VAT are often subjected to NBR’s audits and inspections but the NBR do not give extra effort for the businessmen who are not registered for VAT. (NCT 4)

Some of the non-compliant VAT participants’ expressed that they are aware about their duties and they have sufficient knowledge about the VAT Law. A few of the non-compliant taxpayers admitted that the unfairness in the tax system encourage them to get involve with tax evasion and tax avoidance schemes. Furthermore, they complained about VAT authorities’ attitude that is affecting the fairness in the tax system:

54 Kirchler, above n27, at 189.

55 Braithwaite, V. (2003). A New Approach to Tax Compliance. In V. Braithwaite (Ed.), Taxing Democracy: Understanding Tax Avoidance and Tax Evasion (pp. 1-11). Ashgate Publishing, Aldershot.

298 (2014) 29 AUSTRALIAN TAX FORUM

VAT officials are unfriendly, unfair and corrupt. They maintain unlawful relationship with the powerful businesses and give more cooperation to large enterprises - big businesses can pay less VAT than SMEs. Some of the VAT officials behave so badly with us, that we feel afraid to go to the VAT offices. If I saw less corruption by the VAT officials, I would actually comply more with the VAT Law and pay more VAT. (NCT 5)

Literature56 supports this, as if taxpayers find the burden of taxes unfair, he or she is more likely to evade. In contrast with the non-compliant participants, compliant participants pointed that complex tax system, multiple rates of VAT, highly complicated language and frequent changes in the VAT Law all around the financial year discourage taxpayers to comply with the VAT law. Literature suggests that simplifying tax systems and improving taxpayers’ knowledge about tax laws can encourage voluntary compliance.57 Participants from both groups of taxpayers (CT and NCT) also mentioned that NBR is not providing sufficient induction or educational programs for SMEs taxpayers to raise awareness and to inform them of changes in VAT law. Therefore, SMEs are mainly relying on themselves, their tax advisors, professional bookkeepers and accountants or common practices of market:

The NBR and local VAT offices are not informing us enough about the VAT Law. We do not know about our responsibilities and the new things about the VAT Law. To be honest it is (the VAT law) changing very frequently, so it is hard for us to track changes. If the VAT authority does not inform us properly about the changes in the VAT Law how can we comply the Law properly and accurately? We want to comply the VAT Law but the communication gap between taxpayers and the VAT offices makes us un-intentionally non-compliant. (CT 15)

The above comments demonstrate that there could be multiple of reasons for non-compliance by SME VAT payers in Bangladesh. The VAT officials stressed that SMEs taxpayers do not comply with the tax law and not pay the right amount of VAT on their extra business profit. Compliant taxpayers find complex tax system; multiple rates of VAT, highly complicated language and frequent changes in the VAT Law discourage taxpayers to comply with the VAT Law. Compliant taxpayers also expressed that the discretionary power of NBR and VAT officials are an important factors contributing to complexity and thereby non-compliance. On the other hand non-compliant taxpayers pointed that along with higher VAT rate, an unfriendly attitude of the VAT offices, corruption, red tape are the main reasons behind non-compliance with VAT Law in Bangladesh.

Complexity of the VAT Law was also considered one of the main reasons of non-compliance by most of the participants. The compliant taxpayers group gave their opinion that VAT Law in Bangladesh is very complex and difficult to understand. Few compliant participants stressed that they cannot cope up with the changes in the law.

56 Andreoni, J., Erard, B., and Feinstein, J. (1998). Tax compliance. Journal of Economic Literature. 36, 818-860. Kirchler, above n27, at 87.

57 Lewis, A. (1982). The Psychology of Taxation. St. Martin’s Press, New York.

299COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

Price declarations, complicated rebates and refund procedures which required many books to be maintained make the VAT Law very complex and costly for the SMEs:

The multiple VAT rates, frequent changes in VAT law and its highly complicated language make the law complex. The VAT law has given discretionary power to NBR and VAT officials to exempt any goods or services for any special purpose, fix tariff value of any goods for theassessment of VAT, to select goods or services for withholding and advance payment of VAT or to determine turnover threshold and bring any goods or services under VAT irrespective of their turnover. These discretionary powers are misused by the NBR officials. Continuous changes in the law also make the VAT Law complex. (CT 5)

Both compliant and non-compliant VAT payers discussed that that sometimes the law itself, the rules, office orders and Statutory Regulatory Orders (SRO) are inconsistent and contradictory. However, the majority of non-compliant participants expressed that the VAT Law in Bangladesh is not very complex and difficult to understand. They indicated that if someone gave extra effort to understand the VAT Law and track the changes, then the law is reasonably understandable to the taxpayers:

The VAT Law is not too complex as we think. If we have sufficient tax education and we give some extra effort to understand the VAT Law, the VAT Law seems easier to understand for the SMEs. (NCT 8)

On the other hand, a majority of participants from the VAT officials expressed that the VAT Law in Bangladesh is reasonably understandable. This may be because the VAT Law is drafted by the VAT officials and they work with the law consistently. Some of the compliant and non-compliant participants raised the point that VAT officials should be more knowledgeable and should have clear concept about the VAT Law. They explained that, sometimes the law is not so complex but the lack of in-depth knowledge about the law and misinterpretation of law by the VAT officials make the VAT system complex in Bangladesh. On the other hand, VAT officials claimed that the taxpayers are sufficiently aware of their liabilities though they are unaware about the VAT incentives:

SMEs taxpayers believe that they are only paying VAT. Most of them don’t have a clear idea that they are only collecting VAT as an agency from the customers. They are also unaware about the VAT incentives that they are enjoying from the NBR. They should think positively about the incentives or the opportunities that the government provides for SMEs. Always thinking negatively about paying the VAT makes the law complex and unfriendly for them. (VO 3)

The impact of complexity on compliance decision was also acknowledged by most of the participants. Consistent with the literature, many of them believed that complexity of the VAT Law affects the SMEs taxpayers more than the large taxpayers and complexity increases the cost of complying with tax laws and therefore may

300 (2014) 29 AUSTRALIAN TAX FORUM

increase the non-compliance.58 However the awareness on VAT compliance costs seems to be lower among the participants. In other words, their association of their costs to comply with VAT law is not evaluated collectively. The majority of them admitted they have not considered these compliance costs with VAT before and they

usually calculate the costs related to tax for their own business planning. These costs include customs duty, income tax and VAT altogether. Some argued that they couldn’t remember the exact figure about VAT compliance costs but felt that VAT compliance costs was higher compared to other taxes.

Most of the participants stated that they employed a VAT adviser and/or accountant to assist with VAT which increased their VAT compliance costs. VAT advisors are considered as an effective figure with SME’s tax compliance.59 Studies suggest that tax advisors can act as advocates to their clients and also as an intermediary to the government.60 Moreover, as a result of complexity of tax legislation, tax advisors might become an enforcer or exploiter of the tax law.61 A majority of the participants agreed that they could not give exact figure about the VAT compliance costs as their VAT advisor or VAT consultant would calculate such cost. However, some of that commented that their costs are not lower than 2% their annual turnover. While some of them claimed that it might be more than 1% of their annual turnover but not more than 5%. Obviously these are not exact estimates and are at best a rough estimate:

I never thought about these costs in this way before; I basically calculate all the costs related to customs duty, income tax and VAT together. (CT 10)My VAT advisor looks after everything about my VAT affairs and all the costs related to VAT. But I think that the extra cost related to VAT is higher than other tax related payments. Although my advisor is helping me to keep away from tensions and anxiety, I think I would have invested more money into my business If I didn’t have to pay my VAT advisor. (CT 4)

58 Lignier, P., and Evans, C. (2012), The rise and rise of tax compliance costs for the small business sector in Australia, Paper presented at the 10th International Tax Administration Conference, Sydney, 2nd & 3rd of April, at 5-7. The survey was completed by 159 small businesses in Australia.

59 Jackson, B. R., and Milliron, V. C. (1986). Tax compliance research: findings, problems and prospects. Journal of Accounting Literature, 5, 125-161. Richardson, M. and Sawyer, A. (2001). A Taxonomy Of Tax Compliance Literature: Further Findings Problems And Prospects. Australian Tax Forum, 16(2), 137-320.

60 Tan, L. M., and Sawyer, A. J. (2003). A synopsis of taxpayer compliance studies: overseas vis-a-vis New Zealand. New Zealand Journal of Taxation Law and Policy, 9(4), 431-454. Tomasic, R., and Pentony, B. (1991). Taxation law compliance and the role of professional tax advisers. Australia & New Zealand Journal of Criminology, 24, 241-257.

61 Klepper, S., and Nagin, D. (1989). The Role of Tax Preparers in Tax Compliance. Policy Sciences, 22,2167-194.

301COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

Jenkins and Forlemu62 stated that reducing compliance costs through simplification of the tax system and enhanced taxpayer services would reduce the level of taxpayer non-compliance and would increase voluntary compliance. Although 11 out of 15 of the compliant VAT payers agreed that SMEs would pay more VAT if the costs of complying with VAT were less, some of them argued that some SMEs taxpayers will never pay more VAT even if VAT compliance costs are less:

Taxpayers who want to pay less tax will never pay more tax if compliance cost is less than before. They will search for new ways for tax evasion. Paying more or less never depends on tax compliance costs. It depends on tax morale. It should come from within. (CT 7)

However some non-compliant participants considered that higher VAT compliance costs have an impact on tax compliance attitudes, most of them (12 out of 15) agreed that there are other factors that influenced the compliance decision. The positive attitude of VAT officials’ towards SMEs was considered an important factor for compliance:

Compliance cost is not a leading factor about paying taxes. There are other factors with compliance costs. Audit, penalties and sanctions play a vital role in changing their [taxpayers] attitude towards VAT non-compliance. It also serves as a deterrent to them. So after auditing, penalties and sanctions taxpayers have been exposed and they will give a second thought of being intentionally non-compliant. (NCT 11)SMEs taxpayers are not big shots. They always try to listen to the VAT officials. An Assistant Commissioner is enough to motivate SMEs taxpayers of his or her jurisdiction to pay right amount of VAT. It depends on his or her efficiency to motivate taxpayers. (NCT 9)

A majority of the VAT Officials participants (12 out of 15) argued that the threat of punishment, fines and penalties, cancellation of VAT registration, likelihood of audits and surprise check-up by VAT officials are more influential factors for compliance decisions rather than compliance costs:

Audit can make the taxpayers realise if there is any weakness in their understanding and record keeping for VAT. Again, penalties and sanctions have deterrent effect for the taxpayers concerned and other taxpayers. The result is a better understanding and better compliance of VAT Law. (VO 10)

Almost all the participants from VAT Officials group agreed there is no strong relationship between complexity of law, compliance costs and VAT non-compliance. The strong beliefs to pay VAT and positive tax paying attitude are emphasised to be the dominant factor to increase voluntary compliance. In contrast, some of the non-compliant VAT payers considered that being highly positive mentality does not necessarily guarantee that they would voluntarily comply with the VAT Law. The non-

62 Jenkins, G. P., and Forlemu, E. N. (1993). Enhancing voluntary compliance by reducing compliance costs: A taxpayer service approach. Development discussion paper No. 448, International Tax Program, Harvard Law School, Harvard University.

302 (2014) 29 AUSTRALIAN TAX FORUM

compliant VAT payers strongly argued that most of the VAT payers are intentionally or un-intentionally non-compliant, and it is the failure of NBR and local VAT administration that they can’t find out the non-compliant taxpayers efficiently.

On the other hand, compliant participants claimed that complexity of the VAT and compliance costs have a positive relationship with VAT non-compliance. Most of them believed that larger firms don’t bother about complexity of law and compliance costs as they have different strategies to evade VAT. However, evidence demonstrates that larger firms are more compliant with tax laws due to better internal control, proper accounting system and higher tax knowledge as compared to smaller firms and their compliance costs are proportionally lower compared to SMEs.63 Table-2 illustrates the possible relationships between complexity, compliance costs and VAT non-compliance as raised in the focus group discussions.

The focus group findings show that differentiated rates and undermining the statutory single rates of 15%, value declaration, complicated rebates and refund system and frequent changes in VAT Law could be the main reasons behind VAT complexity in Bangladesh. The findings from non-compliant VAT payers indicate that there is an apparent lack of trust between the VAT authority and taxpayers in SME sector. Despite many negative features of VAT system of Bangladesh mentioned by the compliant and non-compliant participants, majority of them agreed the situation is improving and prejudice of VAT authority is easing (although fairly slow). Finally some participants admitted government’s attitude towards SME sector is changing positively in last few years. Nevertheless, despite the government’s intention to support SME sector, the goal is not yet realised, because they claimed VAT officials is not familiar with the SME environment.

63 Juahir, M. N., Norsiah, A., and Norman, M.S. (2010). Fraudulent financial reporting and company characteristics: Tax audit evidence. Journal of Financial Report and Accounting, 8(2), 1985-2517. Tedds, L. M. (2010). Keeping it off the books: An empirical investigation of firms that engage in tax evasion. Applied Economics, 42(19),2459-2473.

303COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

4ABLE�����0OSSIBLE�2ELATIONSHIP�BETWEEN�COMPLEXITY�OF�6!4�LAW��compliance costs and non-compliance

Theme Sub-Theme Example Quotations

Civic Duty and positive tax mentality

“Not all VAT payers who are highly compliant have lower compliance costs. They also face complexity with the law. But their strong civic duty influences more than the compliance costs and complexity of law. To me, the biggest reason of paying VAT and being compliant is to contribute the State”. (CT 2)

“Paying VAT is a duty of citizenship rather than the outcome of a cost benefit calculation for my business”. (CT 11)

Apparent Weak or No Relationship

Demonstration and Deterrent Effect

“It’s not complexity and compliance costs. Significant promotion of the NBR’s prosecutions of non-compliant taxpayers increases psychological pressure among other SME taxpayers and therefore increases voluntary compliance and enforced compliance among other SME taxpayers”. (VO 13)

Fair tax system

“If I believe the VAT system is fair and neutral, I would be willing to pay more VAT though the Law is complex. I want to add, business friendly relationships between taxpayers and VAT officials are the most important factor than others”. (NCT 14)

“If I saw less corruption by the NBR officials and Local VAT administration, I would be willing to pay the correct amount of VAT. To me, corruption is more important than complexity or compliance costs”. (NCT 4)

Record keeping

“If VAT record keeping was less complicated with simpler payment system, compliance costs will be lower and business people would be willing to deposit the right amount of VAT”.(CT 6)

Apparent Strong Relationship

External Advice

“Professional VAT experts, bookkeepers and accountants are too expensive. If the VAT law was less complex and we would not need to keep so many books and records for VAT purpose - we don’t need to hire professionals. This would decrease our compliance costs and would make us more compliant”. (NCT 11)

Statutory or regulatory language

“The Bangladeshi VAT Law is full of complicated and cumbersome language and there are some inconsistencies between Law/Rules/SROs/Office orders. All these make the law complex and results in higher compliance cost. I think if we can draft a law with simplified language, this will increase voluntary compliance and decrease unintentional non-compliance”. (VO 9)

304 (2014) 29 AUSTRALIAN TAX FORUM

5.2 Findings: Survey

Based on the findings of the focus groups and to test some of notions raised, stage 2 involved the mailing of a questionnaire, seeking qualitative and quantitative data, to both complying and non-complying SME taxpayers. Alm et al. stated that people comply with the obligation to pay taxes as they understand that the public goods they receive need to be financed by their taxes.64 Aaron and Slemrod argued that people pay taxes and comply with the tax law as a duty of citizenship.65 On the other hand, Cowell argued that a taxpayer’s motivation to pay taxes comes not only from their rational equation of outcome maximisation, but also from evaluation of the extent to what the exchange between taxes and services are equitable.66 However, as demonstrated in the focus group, the compliant and non-compliant VAT payers appeared to have different opinions about the reasons for compliance. This potential difference was further explored in the survey as can be shown in Table 3. For example, 97% of compliant VAT payers strongly agreed or agreed that paying the correct amount of VAT is their civic duty, while only 24% of non-compliant VAT payers thought similarly.

One of the key findings of this study is that the perceptions of fines and penalties with compliance behaviour. Allingham and Sandmo predict that both probability of detection and the severity of penalties will affect evasion; if detection is likely and penalties are severe people will be more compliant.67 This positive relationship between penalties and non-compliance appears to contradict with the non-compliant VAT payers in Bangladesh.

Only 32% of non-compliant VAT payers strongly agreed or agreed that the likelihood of penalties and sanctions encourage them to comply with the VAT law. This may be due to the fact that non-compliant taxpayers tend to be risk-takers in making compliance decision, as penalties and fines imposed by the VAT authority is not serious. Alternatively, it may be because non-compliant VAT payers do not think there is a great risk of detection from the NBR, as less than 28% thought the likelihood of audits would encourage compliance. In comparison, 73% of compliant VAT payers considered the likelihood of penalties and sanctions influence to compliance behaviour positively.

64 Alm, J., McClelland, G. and Schulze, W. D. (1992). Why do people pay taxes? Journal of Public Economics. 48, 21-38.

65 Aaron, H. J. and Slemrod, J. Eds. (2004). The Crisis in Tax Administration. Brookings Institution Press, Washington D.C.

66 Cowell, F. A. (1992). Tax Evasion and Inequity. Journal of Economic Psychology, 13(4), 521-543.

67 Allingham, M. G., and Sandmo, A. (1972). Income tax evasion: A theoretical analysis. Journal of Public Economics, 1(3/4), 323-338.

305COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

Table 3: Reasons for Compliance

Why do SMEs comply with VAT Law?CT (N=152)n (%)

NCT (N=88)n (%)

Paying the correct amount of VAT is our civic duty

Not Sure 1 (0.65) 3 (3.41)Strongly Disagree 0 0Disagree 0 53 (60.23)Neutral 3 (1.97) 11(12.5)Agree 90 (59.21) 21 (23.86)Strongly Agree 58 (38.15) 0

Paying the correct amount of VAT is an important

contribution to the development of Bangladesh

Not Sure 1 (0.66) 9 (10.22)Strongly Disagree 0 6 (6.82)Disagree 0 10 (11.36)Neutral 4 (2.63) 14 (15.91)Agree 90 (59.21) 30 (34.10)Strongly Agree 57 (37.50) 19 (21.59)

Taxpayers paid the correct amount of VAT when there was

greater enforcement and monitoring by VAT Authority

Not Sure 10 (6.58) 6 (6.82)Strongly Disagree 9 (5.92) 20 (22.73)Disagree 15 (9.87) 20 (22.73)Neutral 14 (9.21) 8 (9.09)Agree 71 (46.71) 23 (26.13)Strongly Agree 33 (21.71) 11 (12.50)

The likelihood of penalties and sanctions encourage me to

comply with the VAT law

Not Sure 3 (1.97) 6 (6.82)Strongly Disagree 2 (1.32) 19 (21.59)Disagree 11 (7.24) 23 (26.14)Neutral 24 (15.79) 12 (13.64)Agree 78 (51.32) 24 (27.27)Strongly Agree 34 (22.36) 4 (4.54)The likelihood of audits encourage me to comply with the

VAT law

Not Sure 9 (5.92) 6 (6.82)Strongly Disagree 2 (1.32) 22 (25.00)Disagree 8 (5.27) 27 (30.68)Neutral 26 (17.10) 8 (9.09)Agree 71 (46.71) 20 (22.73)Strongly Agree 36 (23.68) 5 (5.68)

306 (2014) 29 AUSTRALIAN TAX FORUM

In terms of whether the complexity of the Bangladesh VAT influences compliance, the findings from the survey provides some evidence of the importance of less complexity. Similarly, both a large percentage of compliant (67.1%) and non-compliant VAT payers (78.42%) considered that the VAT Law in Bangladesh is overly complex: Table 4. 45.47% of non-compliant VAT payers strongly agreed or agreed that their core business suffered as VAT is complicated in Bangladesh, fewer non-compliant VAT payers agreed (30%). This may be because compliant VAT payers are generally compliant and have a concept in their mind that the law requires payment of taxes as wilful failure to pay taxes warrants penalty.

Perceptions about unregistered VAT businesses seem an important factor for non-compliance. 70% of the non-compliant VAT payers believed that businesses that are not registered with VAT and don’t pay VAT are in a better situation than registered businessman. Similarly 75% of non-compliant and 55% of compliant VAT payers agreed that businesses registered for VAT are often subject to NBR’s audits and objections: Table 4. Literature states that if taxpayer find the burden of taxes are unfair and a non-compliant taxpayer is in a better position than compliant taxpayers, the former may be discouraged to pay taxes.68 It appears that non-compliant VAT payers consider that by becoming VAT registered, businesses are more likely to come to the attention of the NBR, whereas it may be better to stay outside of the VAT system altogether and operate in the ‘cash economy’.

The discretionary and judicial power of VAT Authority is considered an important factor of non-compliance. 69.07% of compliant taxpayers and 59.01% of non-compliant taxpayers agreed or strongly agreed that the discretionary and judicial power of VAT Authority discourages them to pay VAT. Saleheen shows that the presence of excessive discretionary powers in Bangladeshi VAT law creates lack of trust between taxpayers and tax officials.69 Therefore business organisations are always vocal to a reduction of the discretionary power of VAT officials to reduce burdens on their business and to improve voluntary compliance.70

68 Kirchler, above n 27, at 77-79.

69 Saleheen, A.M. (2013). Reigning Tax Discretion: A Case Study of VAT in Bangladesh. Asia-Pacific Journal of Taxation, 16(2),77-91.

70 Financial Express. (2012). FBCCI for Reducing VAT Officials’ Discretionary Power. Retrieved May 12, 2013, from http://www.thefinancialexpress-bd.com/more.php?page=detail_news&date=2013-05-12&news_id=129179.

307COMPLEXITY, COMPLIANCE COSTS AND NON-COMPLIANCE WITH VAT BY SMALL AND MEDIUM ENTERPRISES (SMES) IN BANGLADESH: IS THERE A RELATIONSHIP?

Table 4: Possible reasons for non-compliance

Why do SMEs not comply with the VAT Law in Bangladesh?

CT (N=152)n (%)

NCT (N=88)n (%)

VAT is just an expense of the business that we try

to minimiseNot Sure 7 (4.61) 1 (1.14)Strongly Disagree 39 (25.66) 6 (6.81)Disagree 59 (38.81) 40 (45.45)Neutral 17 (11.18) 8 (9.09)Agree 23 (15.13) 24 (27.27)Strongly Agree 7 (4.61) 9 (10.59)The VAT rate is highNot Sure 0 1 (1.14)Strongly Disagree 2 (1.32) 0Disagree 39 (25.66) 4 (4.56)Neutral 12 (7.89) 3 (3.42)Agree 39 (25.66) 33 (37.50)Strongly Agree 60 (39.47) 47 (53.38)The VAT Law and regulation is overly complexNot Sure 0 1 (1.14)Strongly Disagree 4 (2.64) 5 (5.68)Disagree 34 (22.37) 6 (6.81)Neutral 12 (7.89) 7 (7.95)Agree 68 (44.73) 45 (51.14)Strongly Agree 34 (22.37) 24 (27.28)#VTJOFTTFT�UIBU�EP�OPU�ÆMF�PS�QBZ�7"5�BSF�JO�B�NVDI�CFUUFS�ÆOBODJBM�TJUVBUJPONot Sure 15 (9.86) 13 (14.77)Strongly Disagree 6 (3.96) 1 (1.14)Disagree 56 (36.84) 9 (10.23)Neutral 17 (11.18) 3 (3.41)Agree 26 (17.11) 20 (22.73)Strongly Agree 32 (21.05) 42 (47.72)Businesses registered for VAT are often subject to

NBR’s audits and objectionsNot Sure 11 (7.24) 4 (4.55)Strongly Disagree 4 (2.63) 1 (1.13)Disagree 48 (31.58) 4 (4.55)Neutral 5 (3.29) 4 (4.55)Agree 59 (38.81) 33 (37.50)Strongly Agree 25 (16.45) 42 (47.72)Other aspects of our business suffer due to

pressure of VAT, as VAT is complicatedNot Sure 6 (3.95) 2 (2.27)Strongly Disagree 12 (7.89) 6 (6.81)Disagree 75 (49.34) 30 (34.09)Neutral 14 (9.21) 10 (11.36)Agree 39 (25.66) 25 (28.41)Strongly Agree 6 (3.95) 15 (17.06)The discretionary and judicial power of VAT

Authority discourages me to pay VATNot Sure 18(11.84) 10(11.36)Strongly Disagree 2(1.32) 7(7.95)Disagree 16(10.55) 8(9.09)Neutral 11(7.24) 11(12.50)Agree 67(44.07) 25(28.41)Strongly Agree 38(25.00) 27(30.68)

308 (2014) 29 AUSTRALIAN TAX FORUM

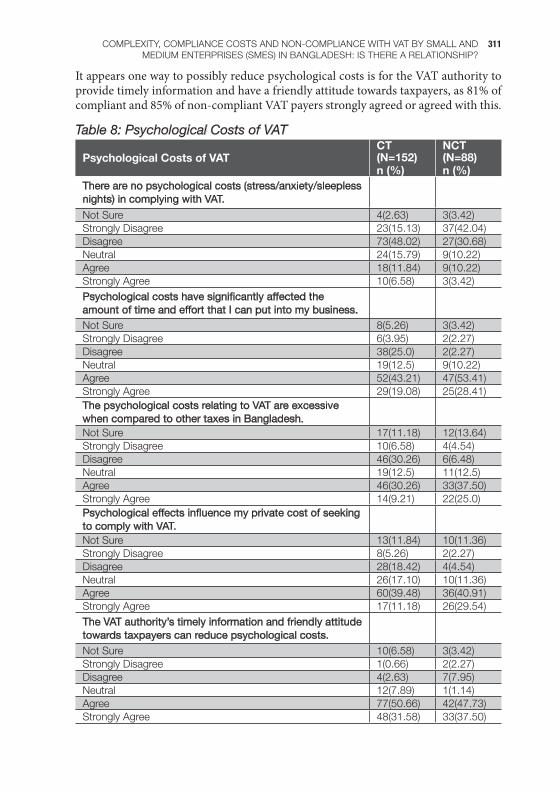

A main aim of this study was to consider whether compliance costs lead to SMEs taxpayers’ to non-comply with the VAT Law. It has mentioned earlier that compliance costs71 include three major components, namely monetary costs, time costs and psychological costs to the taxpayers where monetary costs include money spent on tax professionals and expenses relating to taxation guides, books, communication and other incidental costs. Time costs are incurred by the taxpayer mainly on record keeping for tax purposes, completing the tax return and preparation of tax details for the tax authorities or for tax professionals. The psychological costs of taxation are the net economic costs of the pressure, anxiety and stress encountered when taxpayers seek to submit their tax returns in a timely and correct manner.72

Empirical indicators of VAT compliance costs for this study are the average monthly value (in Taka) and average monthly hours spent for accountants’, bookkeepers’ and VAT advisors’ fees paid to ensure compliance with the legislation; the average monthly taka costs and hours used to produce VAT returns; the value of time taken to complete VAT returns each month; the average taka value and average hours spent travelling to the local VAT Office to file returns; and the monthly average costs and hours of audits and appeals. The monthly average compliance costs based on monthly VAT paid by compliant and non-compliant VAT payers is presented in Table 5, 6 and 7 respectively.