Company Valuation Report 2013 - Sonic Healthcare Limited (Produced by: Brent Alan Hood, Callan Ross...

87

Company Valuation Report (2013) Group Members Brent Alan Hood (S3196824) Thomas Kingsley Martin Lackmann (S3167966) Brendan Pillai (S3261463) Callan Ross Thornton (S3285971) 1 | Page

Transcript of Company Valuation Report 2013 - Sonic Healthcare Limited (Produced by: Brent Alan Hood, Callan Ross...

Company Valuation Report

(2013)

Group MembersBrent Alan Hood (S3196824)

Thomas Kingsley Martin Lackmann (S3167966)Brendan Pillai (S3261463)

Callan Ross Thornton (S3285971)

1 | P a g e

Table of Contents

1. Introduction to Sonic Healthcare Limited4

1.1 Company Analysis4

1.2 Overview4

1.3 History4

1.4 Share Price Performance5

1.5 Corporate Strategy and Objectives6

1.6 Sources of Competitive Advantage7

1.7 Ownership Structure8

2. Industry Analysis9

2.1 Overview92.2 Segmentation92.3 Key Competitors102.4 Porter's Analysis

112.5 Industry Outlook

123. Economic Environment

2 | P a g e

133.1 Micro-economic Analysis133.2 Federal Funding for Medicare

143.3 Private Health Insurance Membership

143.4 Real Household Disposable Income

153.5 Population Growth & Average Age of the Population

163.6 Broader Economic Outlook and Expected Stock Market Returns

183.7 Macro-economic Analysis203.8 Forecast213.9 Expected Return on the Market

214. Financial Analysis

224.1 Financial Statement and Company Risk Analysis

224.2 Peer Analysis234.3 Financial Risk234.4 Extended DuPont Return on Equity (ROE)

264.5 Operating Profit Margin

284.6 Total Asset Turnover284.7 Return on Assets

294.8 Interest Expense Rate

294.9 Net Before Tax/Total Assets

294.10 Financial Leverage Multiplier

304.11 Net Before Tax/Common Equity

3 | P a g e

304.12 Return on Equity (ROE)

304.13 Growth Rate31

5. Valuation Assumptions32

5.1 The Required Rate of Return (CAPM)32

5.2 Calculating Systematic Risk (Beta)33

5.3 Determining the Risk Free Rate of Return (RFR)34

5.4 The Required Rate of Return35

5.5 Sensitivity Analysis (RRR)35

6. Valuation Analysis366.1 Dividend Discount Model (DDM)376.1.1 Sensitivity Analysis (DDM)

396.2 Free Cash Flow to Equity Model (FCFE)

416.2.1 Cash Flow Forecast416.2.2 Estimating the FCFE Growth Rate

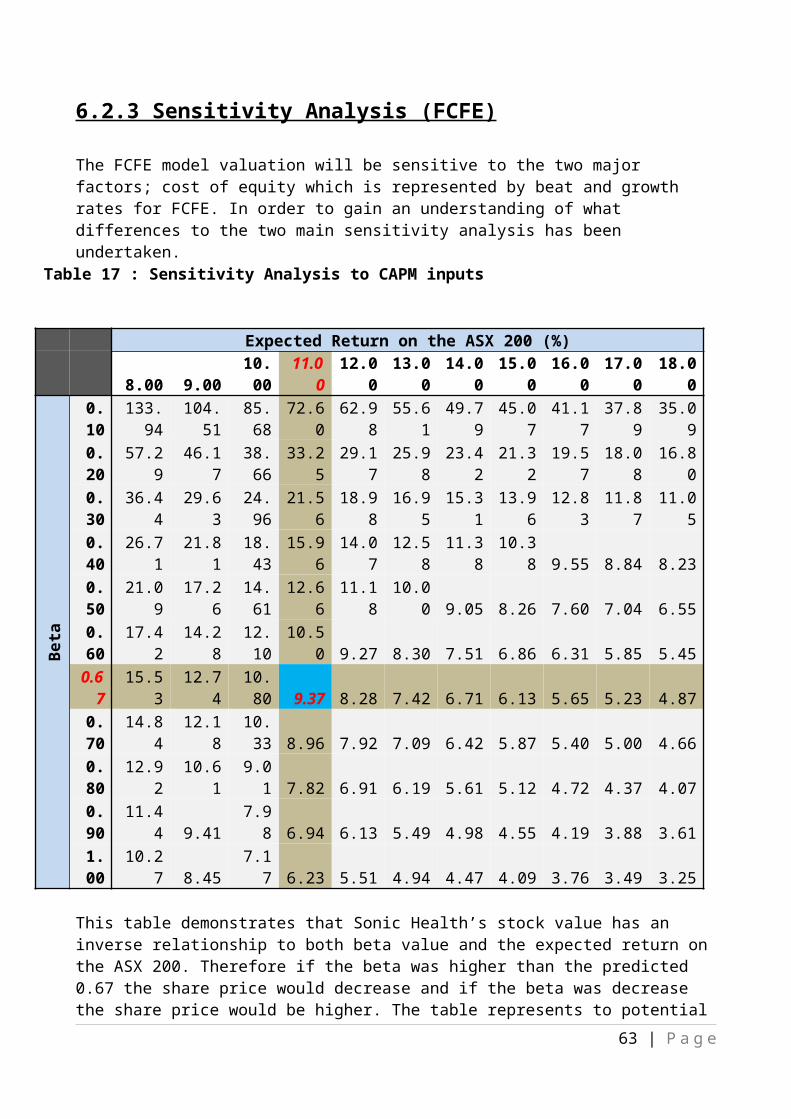

426.2.3 Sensitivity Analysis (FCFE)

436.3 Price/Earnings (P/E) Ratio

456.3.1 Comparison: Sonic Healthcare Limited vs Primary Health

Care Limited 466.3.2 Sensitivity Analysis (P/E Ratio)

476.4 Price/Book Value (P/BV) Ratio

476.4.1 Sensitivity Analysis (P/BV Ratio)

496.5 Net Tangible Asset Backing Model (NTAB)

4 | P a g e

497. Valuation Summary

507.1 Dividend Discount Model (DDM)507.2 Free Cash Flow to Equity Model (FCFE)

517.3 Price/Earnings (P/E) Ratio

527.4 Price/Book Value (P/BV) Ratio

537.5 Net Tangible Asset Backing Model (NTAB)

537.6 Preferred Valuation Method

548. Conclusion & Recommendation

559. Appendix 5610. References

57

5 | P a g e

1. Introduction to Sonic Healthcare Limited____________________________________________________________

1.1 Company Analysis

Sonic Healthcare Limited ASX Listing Details*

Issuer Code SHLOfficial Listing

Date30 June, 1987

GICS IndustryGroup

Health Care Equipment & Services

Exempt Foreign NoInternet Address http://www.sonichealthcare.com.au/ Registered Office

Address14 Giffnock Avenue, Macquarie Park, NSW, Australia, 2113

Current SharePrice

$13.41 (as of COB 03/05/2013)

*Source: Australian Securities Exchange (ASX) 20131.2 Overview

Sonic Healthcare Limited (ASX: SHL) is a company that specialises in the pathology and radiology sectors of the medical diagnostics industry. The company is headquartered in Sydney, NSW, Australia and was formerly known as Sonic Technology Australia Ltd before changing its name to Sonic Healthcare Limited in 1995.

The company operates pathology and clinical laboratories in 6 | P a g e

countries such as Australia, New Zealand, United Kingdom, United States, Germany, Switzerland, Belgium and Ireland while focusing its radiology and diagnostic imaging operations within Australia and New Zealand. Their services are provided to a multitude of clients such as medical practitioners, hospitals and patients. Germany, United States and Australia are seen as Sonic Healthcare Limited's largest markets as the company's growth over the years can be attributed to their acquisitions in the aforementioned countries.

Sonic Healthcare Limited has a current market capitalisation of US$5.315 Billion (as of 3rd May 2013) and is a market leader in its relevant fields. The company holds an estimated market share of 43.6% in the medical diagnostics industry and its main competitors would be Primary Health Care Limited, Healthscope Limited and Cochlear Limited.

1.3 History

Sonic Healthcare Limited was listed on the Australian Securities Exchange in 1987 under the name Sonic Technology Australia Ltd andmade Douglass Laboratories of Sydney their first pathology acquisition in the same year. Douglass Laboratories was then merged with a number of other acquisitions around the country before finally adopting the Sonic Healthcare Limited name in 1995.

The company's strategy of acquisitions and mergers continues into the new millennium and results in them adopting a decentralised structure so as to grant a level of autonomy and authority to their local interests. The creation and implementation of Sonic Healthcare Limited's core values across the company also allowed for a level of standardisation to take root.

In 2004, Sonic Healthcare Limited moved towards international partnerships and acquisitions by first creating a partnership between one of their subsidiaries, The Doctors Laboratory, and University College of London Hospital. They then moved to acquire majority control of the Schottdorf Group in Germany and Clinical Pathway Laboratories Inc of the United States. Further acquisitions over the next few years in the United States,Switzerland and Germany allowed Sonic to build their internationalportfolio to a point where they become the largest medical laboratory group in Europe and the third largest in the United

7 | P a g e

States by 2007. This is followed by further acquisitions in Belgium and Ireland over the next few years to strengthen their position in Europe (Sonic Healthcare Limited 2013).

The company's policy of acquisition has allowed it to record consistently growing revenue over the last 20 years and has also contributed to investor confidence within the financial sector as it has provided value for its shareholders through its strong performances year on year.

1.4 Share Price Performance

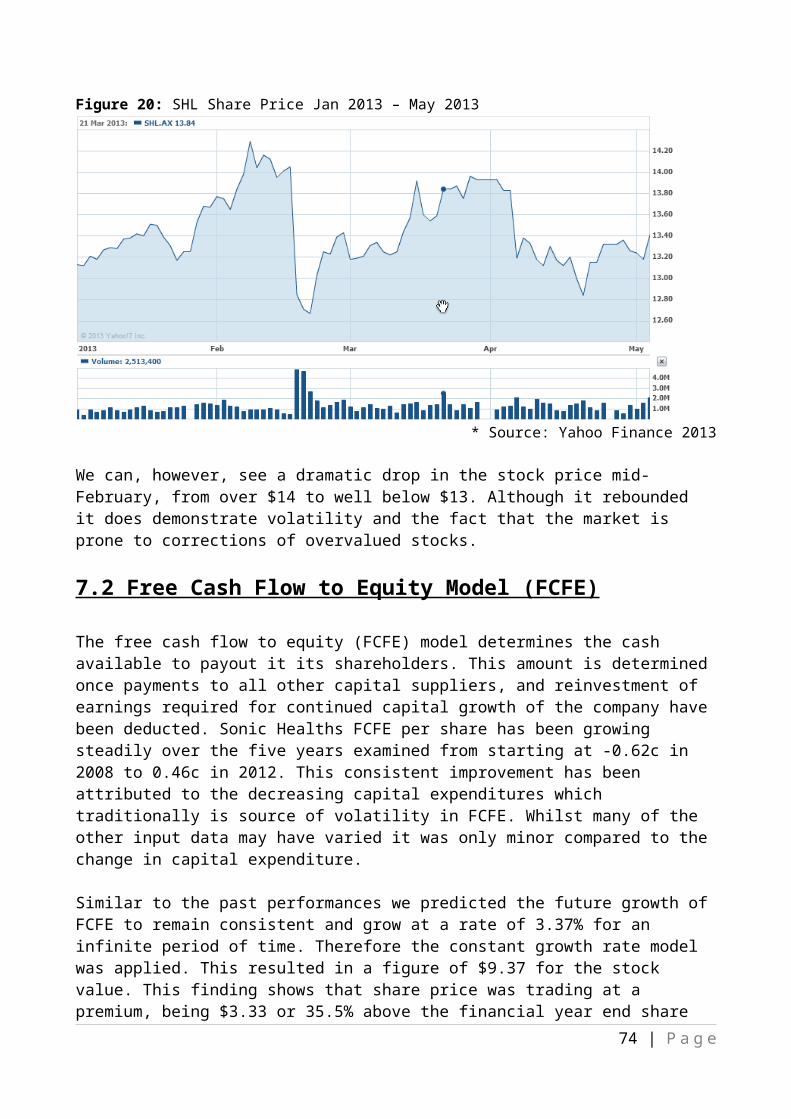

Sonic Healthcare Limited (SHL) has experienced fluctuating share prices in the last 5 years, with have included periods of high performance and dramatic declines. The following charts show the performance of Sonic Healthcare Limited (SHL) shares in relation to the Healthcare Index (XHJ).

Figure 1 shows a moderately strong level of appreciation in the share price of the company over the last 2 years, which occurred after a series of peaks and troughs in the 3 years before that. There have been two periods of relative stability in terms of the share price:

June 2008 to December 2008 when SHL stock was fluctuating in its middle price range

July 2009 to March 2010 when SHL stock was fluctuating in itstop price range

There have been 3 periods of sharp decline during the last 5 years(December 2008 to February 2009, March 2010 to June 2010 and June 2011 to September 2011) which have resulted in share prices declining significantly, although it did eventually recover to a fairly stable level. Every $1 that was invested in SHL shares in June 2009 and held until now is worth $0.96, which amounts to a decline of approximately 4% in the nominal share value for that 5 year period.

8 | P a g e

Figure 1: Historical Share Price Performance (Average Monthly Prices) for Sonic Healthcare Limited (SHL) Ordinary Shares vs Healthcare Index (XHJ)

*Source: Australian Securities Exchange (2013)The share price appreciation for Sonic Healthcare Limited (SHL) inthe last 2 years mirrors that of the Healthcare Index (XHJ). Therehave also been periods where the SHL and the XHJ prices have movedin similar upward and downward trends. This is supported by the analysis in Figure 2 which seems to indicate that there is a positive correlation between the share price movement of SHL and that of the XHJ, especially in the last 2 years.

Figure 2: Recent Share Price Performance (June 2011 – May 2013) of9 | P a g e

Sonic Healthcare Limited (SHL) vs Healthcare Index (XHJ)

*Source: Australian Securities Exchange (2013)

1.5 Corporate Strategy and Objectives

Sonic Healthcare Limited's corporate strategy has focused on the acquisition of firms within the industries in which they operate so as to allow for the expansion of the business into new territories. Based on the information provided by the company during its Annual General Meeting (AGM) in 2012, it can be ascertained that it will be focusing on the following objectives (Aspect Huntley 2012):

a) Consistent application of proven model

The company intends to continue utilising its existing business model of acquiring firms both nationally and internationally so asto better benefit its bottom line. As this model has proven itselfto be a viable and profitable means of generating revenue and profits for the company, the intention to continue on the same path would be of benefit for their long term growth both in terms of profits and size.

b) Growth in terms of Return on Invested Capital (ROIC) and Earnings per Share (EPS)

The company has recorded a 9.8% return on invested capital in the financial year ended 31st June 2012 and it is their intention to increase that margin for the year ahead through the use of their business model. Earnings per share for the same period amounted to

10 | P a g e

80.7 cents for every ordinary issued share and the company hopes that higher revenue and profitability would allow them to grow that figure in the year ahead (Sonic Healthcare Limited 2012).

c) Increasing market share

d) Increasing efficiency through control of expenditure

e) Utilisation of existing infrastructure to encourage business growth

f) The employment of acceptable expansion and acquisition strategies

g) Leveraging off the strong growth drivers in their relevant industries

The company has experienced strong growth across all the sectors relevant to their operations and the general consensus would be tocontinue focusing on that growth so as to reach new heights in thefuture. It can be assumed that the company will seek to extend their market share lead in the pathology sector while aiming to take the lead in the radiology sector through ongoing operations as well as the continuation of their acquisition strategy in the years ahead.

1.6 Sources of Competitive Advantage

Sonic Healthcare Limited enjoys a fair amount of competitive advantage due to their position in the medical diagnostics business and its relevant industries. The company currently has a 43.6% market share in the pathology industry and a 12.8% market share in the radiology industry.

In terms of overall market share within the healthcare industry, Sonic Healthcare Limited is considered to be one of the major players, commanding a 1.5% overall market share and directly competing with other major players such as Primary Health Care Limited, Healthscope Limited and Cochlear Limited (IBISWorld Pty Ltd 2013).

Sonic Healthcare Limited is also able to depend on their network of subsidiaries both nationally and internationally in terms of

11 | P a g e

establishing a level of competitive advantage. Due to the company's acquisitive nature over the last 25 years, it has been able to build a network of subsidiaries in the key industry areas in which they operate and these subsidiaries are responsible for alarge portion of the company's yearly revenue.

It has also been mentioned by Gluyas (2010) that Sonic Healthcare Limited's commitment to recruiting their senior management from the medical industry as well as their view that the delivery of their services is more important that their profitability is a major source of competitive advantage as it sets them apart from their competitors and also builds brand loyalty and recognition.

It has also been mentioned that the aforementioned factors that constitute their competitive advantage has also allowed them to look beyond Australia in terms of expansion as this approach provides them with an image of credibility within the various industries that the operate in. This would then allow them to be seen as a suitable investor in overseas medical diagnostic firms, thus contributing to their rapid acquisition and accumulation of awhole network of subsidiaries (Gluyas 2010).

Their acquisition of trusted medical diagnostic companies is another source of competitive advantage as it allows them access to technologies and patents which their competitors may not possess. By doing so, they would be able to place themselves at the forefront of their various industries and exert a level of control over the business and its resources.

1.7 Ownership Structure

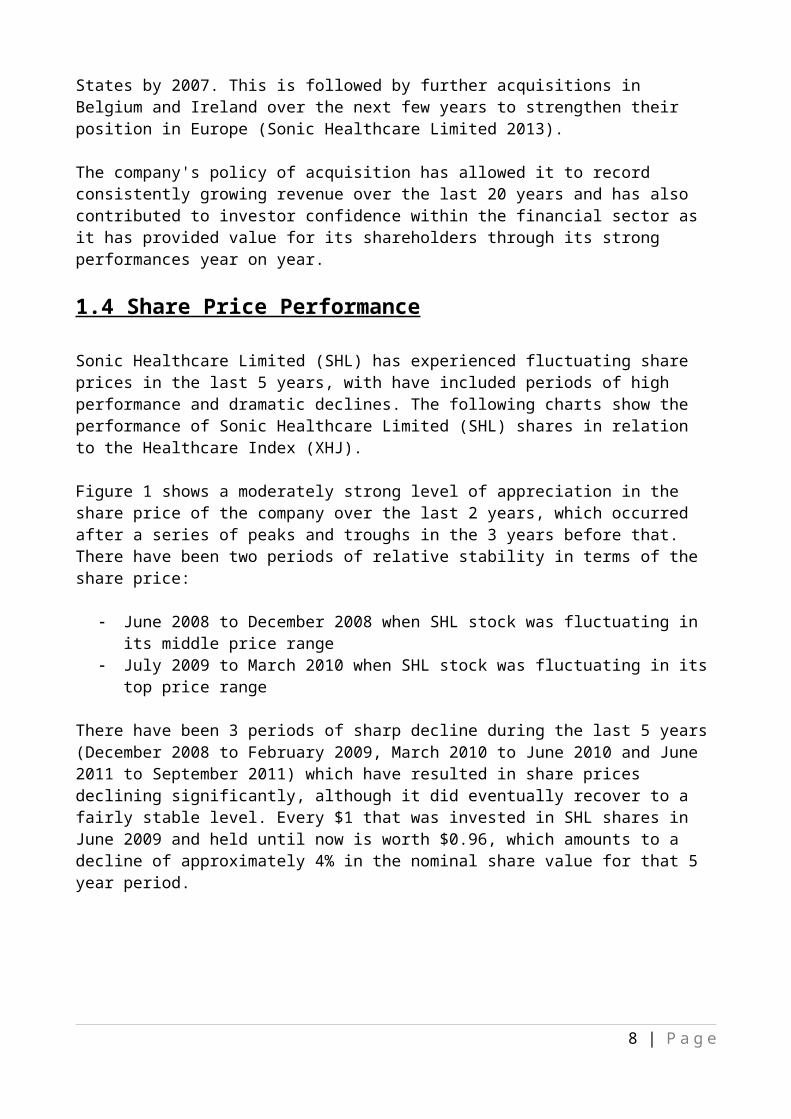

Sonic Healthcare Limited has a large shareholder base that consists of 34,590 registered entries. The 20 largest shareholdersaccount for 77.93% of the total capital of the company as at 14 September 2012 and consist of companies such as J P Morgan Nominees Australia Limited, HSBC Custody Nominees (Australia) Limited and National Nominees Limited. The aforementioned companies together control a 58.59% share in the company.

Table 1: Sonic Healthcare Limited Equity Securities & Major Shareholders*

Total number of (ordinary) 389,835,777

12 | P a g e

sharesTotal number of shareholders 34,590

Largest Shareholders % of ordinary sharesJ P Morgan Nominees Limited Australia 22.88

HSBC Custody Nominees (Australia) Limited 19.81National Nominees Limited 15.90

Jardvan Pty Ltd 4.06Citicorp Nominees Pty Limited 3.03

JP Morgan Nominees Australia Limited <CashIncome A/C>

2.31

Citicorp Nominees Pty Limited <ColonialFirst State Inv A/C>

1.74

BNP Paribas Noms Pty Ltd <Master Cust DRP> 1.58Perpetual Trustee Company Limited 1.09

*Source: Sonic Healthcare Limited Annual Report 2012 (Correct as at 14 September 2012)

2. Industry Analysis_________________________________________________________

2.1 Overview

The health services industry is a $116bn dollar industry and is the largest employer in Australia. Due to the ageing population inAustralia creating an increase in demand for products and the continued increase of government spending, the health services industry is expected to grow steadily at 4.2% per annum for at least the next 5 years (IBISWorld Pty Ltd 2013). The Government isexpected to make reforms that divert spending away from cost heavyinstitutional care to the less expensive community alternative.

2.2 Segmentation

13 | P a g e

Sonic Healthcare Limited's revenue and industry segmentation is spread across the countries and sectors in which they operate. As the company has a large number of subsidiaries in 8 countries across 3 continents, the revenue that they generate tends to vary based on sector as well as country.

As seen in Figure 3 below, the vast majority of revenue is generated by the pathology industry while the radiology and medical practice sectors provide the rest of the revenue for the company. This revenue generation is also segmented according to country, as shown in Figure 4. It can be ascertained that Australia is the largest source of revenue for the company, with the United States and Germany the next largest sources.

Figure 3: Sonic Healthcare Limited Figure 4:Sonic Healthcare Limited

Industry Segmentation

Geographical Segmentation (% of Total Revenue) (%

of Total Revenue)

*Figures 3 & 4 have been sourced from IBISWorld Pty Ltd (2013)

The Diagnostic Imaging and Pathology sector equates to 4.7% of the

14 | P a g e

total health services industry (IBISWorld Pty Ltd 2013). Sonic Healthcare operates mainly within two distinct segments. Its primary source of revenue is in pathology services, which makes upalmost 80% of its annual revenue. The other is in diagnostic imaging services, specifically radiology, which makes up 11% of its revenue (IBISWorld Pty Ltd 2013)

The pathology industry is a $2.7 billion industry and with an aging population and an increase of 5% to government funding via Medicare, the industry is expected to continue growing by 2.2% perannum for the next 5 years. Despite a lowering of prices industry wide the revenue generated is expected to grow because of the increase in demand for services and increased efficiency. Due to past government funding cuts after industry deregulation in 2010 (Urban 2012), the pathology industry has become highly concentrated because smaller businesses have either failed or beenabsorbed by larger companies. In 2012 the Australian Competition &Consumer Commission stepped in to block the sale of some of Healthscope, a pathology company, to SHL siting “competition concerns” (Urban 2012). SHL’s major competitor in the pathology industry is Primary Health Care Limited (PRY), together they control 70% of the market with SHL controlling over 42%. (IBISWorld Pty Ltd 2013).

2.3 Key Competitors

Primary Healthcare is a leading Australian healthcare company. It specializes in four main areas; Medical centers, pathology, healthtechnology and diagnostic imaging. It is SHL’s largest competitor and in 2012 posted revenues of over $1.3bn and a profit of $119m (Primary Health Care Limited 2012). Other competitors in the Pathology industry are St John of God Health Care Inc and Healthscope Limited as show in the image below.

Figure 5: Major Competitors in the Healthcare industry

*Source: IBISWorld Pty Ltd 201315 | P a g e

The other arm of SHL’s operations is in the diagnostic imaging services industry. This industry provides medical practitioners with many different kinds of diagnostic information to help them prevent, treat, diagnose and monitor all sorts of ailments and illnesses. This industry is a cornerstone in the heathcare system,generating $3.2bn in revenue and this is recognized by the Medicare system which funds around 70% of all diagnostic imaging services (IBISWorld Pty Ltd 2013). The industy looks set to grow by 3.3% per annum over the next 5 years due to an increase in demand for services by the ageing population.

There are three major companies in the industry but together they control less than 50% of the market, which make it far more segmented than the pathology industry. The two main competitors to SHL in regards to diagnostic imaging services are I-Med Holdings Limited and Primary Health Care Limited.

I-Med Holdings is a large privately owned radiology company which generates most of its revenue from diagnostic imaging services. Ithas struggled in recent years as it has been unable to manage its high level of debt, which in 2011 amounted to over $1bn dollars (Rochfort 2011).

Cochlear, albeit not a direct competitor of SHL, is a market leader within the Australian health care industry. It makes audio implants, which provide hearing solutions to the hearing impaired and exports them all over the world. In 2012 the company generatedover $780m in revenue and before 2012 had consistantly posted growing yearly profits. (IBISWorld Pty Ltd 2012).

2.4 Porter's Analysis

The porter's five forces analysis is used as a means of ascertaining and evaluating the overall profitability of the healthcare industry in which Sonic Healthcare Limited operates. From the analysis, it can be ascertained that the healthcare industry is fairly stable and not subject to many threats from substitutes or new entrants due to the high level of specialisation and differentiation as well as the high barriers toentry into the relevant segments. It is also apparent that the

16 | P a g e

industry exhibits a fairly high level of competitive rivalry, but it would be dependent on the specific segments as the level of competition tends to vary from one to another. Industry concentration is also rather low, with the major competitors only commanding 10.7% of total revenue.

Threat of new entrants

The threat of new entrants to the healthcare industry is low. This would be due to the high barriers of entry being present in the industry. The cost of entry into any of the participating segmentsof the healthcare industry would be prohibitively high due to highstart-up costs and the level of expertise and qualifications needed to effectively run a business within any of the segments would also be restrictive (IBISWorld Pty Ltd 2013). Any new business would also be subject to a multitude of regulations imposed by the Government.Supplier Power

Supplier power in the healthcare industry is high. As there are only a handful of companies which are able to provide the necessary equipment or services for each segment, it is not easy to find substitutes for these companies. Moreover, the presence ofGovernment restrictions and the need for regulatory approval meansthat the pool of companies within the relevant segments is rather small and may display a significant amount of differentiation fromone another (IBISWorld Pty Ltd 2013).

Buyer Power

Buyer power in the healthcare industry is medium. While consumers have a choice over the products and services they would want to buy, it is restricted to the options that are available. The Insurance industry is a key buyer for this industry as they tend to form partnerships with companies within relevant segments to present consumers with competitive products. Consumers would be able to choose their desired products which give them a host of options, but the diversification in offerings means that they would have to pick the product that best suits their needs (IBISWorld Pty Ltd 2013).

Threat of Substitutes

17 | P a g e

The threat of substitutes in the healthcare industry is low. While it may be prevalent in some segments where alternative forms of therapy could be utilised, such as physiotherapy and massage therapy, it is generally accepted that the threat of substitutes within the healthcare industry is limited due to the highly specialised nature of the segments that it consists of. The presence of Government restrictions and the need for regulatory approval also make it difficult for there to be many variations within the industry (IBISWorld Pty Ltd 2013).

Competitive Rivalry

Competitive rivalry in the healthcare industry is medium to high. As there are a number of companies within the relevant segments whichprovide similar products and services, the level of competitive rivalry would be dependent on the type of product or service provided and the level of demand that it exhibits. Some segments are more likely to be highly competitive due to the presence of a large number of substitutes and the lack of differentiation, but others are less likely to exhibit a significant level of differentiation and are more likely to be highly specialised (IBISWorld Pty Ltd 2013).

2.5 Industry Outlook

The healthcare sector is resilient in the face of financial turmoil because illness, like the demand for consumer staples, will be prevalent in any state – however, when the outlook is prosperous (or at least there is some projected growth in economicindicators) demand will accelerate as consumers become less pessimistic about the state of their finances. The major economic influence in the sector is government spending on health-related services and as noted, there is no sign of slowing. With an ageingpopulation that is relatively wealthy compared to with previous generations of the same age group it can be expected that private expenditure will also increase – with the insurance industry expected to play a huge role in the coming years.

Table 2: Revenue Growth for the Health Services Industry

18 | P a g e

* Source: Fitzpatrick, 2013

In 2012-13, revenue in the sector is expected to grow by 4.1% to $116.5 billion. Revenue growth seems to be relatively stable, withslightly subdued activity in the years after the financial crisis.Employment in the industry is expected to grow by 3.0% p.a. up from 2.8% in the past (employment is a critical factor in determining the health of an economy). With jobs becoming available, there is higher propensity to satisfy demand and generate revenues (Fitzpatrick 2013).Overall it can safely be asserted that the Healthcare industry will continue to grow for reasons above. Governments have an incentive to make the health system more flexible and efficient for the purpose of alleviating the federal budget of financial strain. The government’s response to the ageing population issue was to release a healthcare reform agenda which is expected to influence the sector’s profitability by directing resources to more efficient institutions and more efficient means of dealing with illness and invalidity (Fitzpatrick 2013).

3. Economic Environment____________________________________________________________

19 | P a g e

3.1 Micro-economic Analysis

As a member of the ASX top 100 listed Health Care companies, SHL will be affected by microeconomic variables that affect the wider Healthcare sector. These variables are outside the control of the organisation and affect the industry’s returns.

Figure 6: Performance of SHL Relative to the ASX 200 and the ASX 200 Health Care Indices

* Source: Morningstar DatAnalysis, 2013

Over the past 6 months, the Health Care index has tended to move in line with movements in the wider market (here using the ASX 200as a market proxy for illustrative purposes). SHL’s returns have proven more volatile than the wider Australian market, particularly since mid-February, reasons for which will most likely be reflected in firm-specific factors. It should be noted that comparisons are being drawn against Australian benchmarks. Sonic Healthcare is headquartered in Australia and derives approximately 50% of its sales revenue from Australian operations (see geographical breakdown below), and it is therefore appropriate to perform the economic analysis using Australian indicators.

Table 3: Geographical breakdown of SHL sales revenues

20 | P a g e

* Source: Sonic Healthcare Limited Annual Report, 2012

Some of the key economic drivers for the Health Care industry as awhole, as recognised by Fitzpatrick (2013), are the average age ofthe population, federal funding for Medicare, private health insurance membership, and real household disposable income. What are the implications of changes in these variables to the performance of the Health Care sector? The ensuing subsections deal with these variables individually.

3.2 Federal Funding for Medicare

Medicare is Australia’s national health insurance system funded bythe federal government. It covers medical services, prescription pharmaceuticals and public hospital visits (Australian Bureau of Statistics 2013). The health of the population is recognised by the Australian government as a crucial factor in determining the strength of the economy. Whilst the government uses a flat tax levy to supplement taxation revenues to assist in its commitment to the health of the populace (an increase in which diminishes household income), Medicare is a vital source of revenue for the health care industry (IBISWorld Pty Ltd 2013).

Table [4] below illustrates yearly funding for the Australian healthcare industry broken down into government and non-governmentfunding. Total expenditure has increased more than two-fold over the 10 years to 2011 with government expenditure as a proportion of the total steadily increasing over this period. With governmentexpenditure on healthcare accounting for close to 70% of total industry revenue, any budget cuts to healthcare would severely impact upon sector revenue.

Table 4: Funding for Health Expenditure 2000-01 to 2010-11 ($M)

21 | P a g e

* Source: Australian Institute of Health and Welfare, 2012

Fitzpatrick (2013) predicts government expenditure on Medicare to increase by 6.7% over 2012-13. Furthermore, fiscal changes to the Medicare levy will see taxation revenues increase by an estimated $20b over the next 5 years with the Medicare levy increasing to 2%(ABC News 2013). From this perspective, with the government makingthe necessary changes to meet the ever-increasing demand for healthcare services, it is not expected that there will be any subdued growth in the sector due to government policy.

3.3 Private Health Care Membership

The proportion of Australia’s population that is covered by private health insurance is one factor influencing the demand for private hospital and health services among the population. The graph below shows that, over the past four years, the proportion of Australia’s population with some form of health cover has increased from slightly below 52% up to 54.6%.

Figure 7: Private Health Insurance Membership to September 2012

22 | P a g e

* Source: Private Healthcare Australia, 2012

There is a very prominent upward trend in private health insuranceparticipation. With the Australian government also offering incentives for individuals to get health cover (in the form of thePrivate Health Insurance Rebate and the Medicare Levy Surcharge) this trend is expected to continue, and this will be accompanied by an increase in the demand of private health services. Additionally, the 65-69 age bracket had the largest annual increase (September 2011 – September 2012) in private health insurance membership (Private Healthcare Australia, 2012). Given that this is the age bracket most susceptible to illness and invalidity (see above), it follows that the health care sector is likely to see revenue growth aligned with this trend.

3.4 Real Household Disposable Income

The more disposable income Australians have, the less reliance 23 | P a g e

they will have on the government to subsidise their medical expenses, and the higher will be private spending in the health sector.

Figure 8: Household Final Consumption Expenditure on Health (1990 – 2012)

* Source: Australian Bureau of Statistics

Figure [8] shows the trend in household consumption expenditure onhealth. This directly correlates with the growth in real householddisposable income over the years. Fitzpatrick forecasts real household disposable income growth of 3.4% over 2013 which would be the highest rate in 5 years. It can thus be predicted that thiswill also buoy demand for health services.

3.5 Population Growth & Average Age of the Population

Population growth and an ageing population drive demand for healthservices (particularly the latter). Naturally, an increase in the population will be followed by an increase in the number of patients demanding output from the health care sector. Figure [9]

24 | P a g e

shows an increasing gap of quarterly births over deaths (natural growth) whilst Figure [10] compares both natural population growthand population growth from overseas immigration. From September 2011 to September 2012 Australia’s population grew by 1.7% - 40% of which was attributable to natural growth and 60% to net overseas migration (Australian Bureau of Statistics 2013).

Figure 9: Domestic Population Growth (Natural Increase)

* Source: Australian Bureau of Statistics, 2013

Figure 10: Composition of Australia’s Population Growth

25 | P a g e

* Source: Australian Bureau of Statistics, 2013

Perhaps more significant, however, is the fact that Australia is experiencing an ageing population. In the early 1970s, 31% of Australians were aged 15 years and younger – this dropped to 22% by the early 2000s. Over the same period of time, the proportion of Australians aged 65 years or older has increased from 8% to 13%. The Australian government predicts that by the 2040s, the elderly population (65 and over) will occupy approximately 25% of the total population (The Treasury 2004). This forecast is illustrated in Figure [10] whereby population growth in the 65-84 age bracket and (even more evidently in) the 85+ age bracket far outstrips that of the younger age groups.

Figure 11: Population Growth Indices by Age Group

26 | P a g e

* Source: The Treasury Department, 2004

The elderly population are more susceptible to illness and invalidity. Consequently, a growth in this segment of the population drives demand for health care. According to Fitzpatrick(2013), the baby boomer generation entering this age bracket are considerably wealthier than previous generations, and thus have the ability (and willingness) to spend on health care products andservices. As can be seen from Figure [12] there is a distinct upward trend in the average age of all persons in the population,and as this trend continues, so too will the demand for health care services continue to grow.

Figure 12: Depiction of Advancing National Age

* Source: Australian Bureau of Statistics, 2010

3.6 Broader Economic Outlook and Expected Stock 27 | P a g e

Market Returns

Gross Domestic Product (GDP), as a measure of aggregate economic output, is expected to be a reflection of business performance over the period for which output is measured (Reilly and Brown 2012). The ensuing section will first detail which economic indicator is considered to be a sound measure of aggregate stock market performance, followed by a brief outlook on the economy andhow this indicator is expected to be affected.

GDP is a measure of an economy’s performance and due to the fact that it is driven in part by corporate earnings, one might expect that GDP growth is a good measure of stock market performance. However, stock prices generally reflect investor expectations of future corporate earnings – meaning that the stock market, in theory, should already be reflective of expected future economic performance. Much research has been conducted into the effect on consumption expenditure of a change in household wealth. The stockmarket is one factor affecting net household wealth. The consensusamong researchers is that rising/falling stock prices can increase/reduce consumers’ sense of financial wellbeing which directly influences their spending on final goods and services. This has been termed “the wealth effect” which is a component of consumer confidence (Holger 2012).

Holger (2012) argues that there is virtually no statistical relationship between the change in GDP and the change in the overall market index (he uses US GDP to explain the returns on theS&P 500). To reinforce his findings, a statistical analysis of theeffect of quarterly changes in Australian GDP on quarterly changesin the ASX 200 was conducted for the period December 2007 – December 2012. The findings were remarkably similar with a Coefficient of Determination (R-Square value) of 0.0107 for the Australian economy compared with 0.0146 for the US economy.

The other economic indicator mentioned above – consumer confidence– lends itself to a more promising trend. The Consumer Sentiment Index, as compiled and reported by Australia’s Westpac Banking Corporation, measures consumer optimism towards both the state of the economy and their financial position. According to Trading Economics (2013), consumer confidence is one of the key determinants of the overall performance of the economy.

28 | P a g e

Figure 13: WBC Consumer Sentiment Index 2002-2013

* Source: Trading Economics, 2013

Figure [14] below shows the relationship between monthly ASX 200 closing prices and the monthly Consumer Sentiment Index values from May 2011 to April 2013.

Figure 14: ASX 200 in relation to Australian consumer confidence May 2011– April 2013

* Source: Trading Economics, 2013

29 | P a g e

Comparing this R-Square value to that obtained using GDP as the explanatory economic indicator a remarkable increase in predictionstrength is witnessed. The model here indicates that approximately30% of the movement in the ASX 200 is explained by changes in consumer sentiment. While this may appear to be a weak predictor, it has been stated by WestLB Asset Management’s chief economist Holger Sandte (2012) that finding an economic indicator with any meaningful strength for predicting the future market performance is extremely difficult – even going so far as to say that searching for one is futile.

Given this line of thought and the fact that interpreting the strength of a regression is extremely circumstantial, the model above is strong enough to justify using consumer confidence to determine the expected return of the market.

3.7 Macro-economic Analysis

First on a global outlook, the Reserve Bank of Australia (RBA) predicts global GDP growth of 3.5% over 2013 and 4% over 2014. It is predicted that the US will manage to avoid severe fiscal tightening measures and that US monetary policy will be in line with fiscal economic objectives, fostering a continuation of the moderate economic growth that has been witnessed of late. While there is no doubt Europe’s woes will continue to weigh on global confidence, the RBA acknowledges that policymakers are working hard to alleviate the strain of fiscal and structural instability in the euro area, minimising near-term risks. Consumer and business confidence will continue to be tested by these global issues – particularly the ongoing risk of severe destabilisation in the Euro zone area due to economic and social shocks in the crises countries, and question marks over the sustainability of current levels of US debt (Reserve Bank of Australia 2013).

In view of the Australian economy, the RBA forecasts GDP growth tobe below the long-term trend (of just over 3%) at 2.5% for 2013 and then picking up to 3.5% for 2014. Consumption expenditure is expected to be the component holding growth back as wage and employment growth soften (Reserve Bank of Australia 2013). FederalTreasury recently cut its growth forecast from 3% to 2.75%, notingthat an overvalued Australian dollar is eroding corporate profits and thus federal tax revenue (Financial Review, 6 May 2013, p. 1).

30 | P a g e

Senior economists point to the fragility of consumer confidence after the most recent figures show that confidence plummeted unexpectedly by 5.1% from March to April. This is particularly disappointing given that there has been a modest upward trend since Feb/March 2012. This does not, however, detract from the long term downward trend in consumer confidence over the period before and after GFC (see Fig. [13] above). Economists note such factors as expectations of declining stock prices, domestic repercussions of distressed global economies (mentioned above) andthe prospect of higher domestic interest rates being the culprits of substandard consumer sentiment (The Age, 10 April 2013).

Over the same period that consumer confidence slumped, so too did the stock market. Share market performance was weighed on heavily by the news emanating from Europe that Cypriot policymakers would cause a run on the banking system due to potential deposit taxes. Another important factor noted by economists is interest rate expectations. It appears consumers are anticipating future rate rises given that interest rates are currently at extremely low levels (The Age, 10 April 2013).

3.8 Forecast

Based on the above analysis, it is expected that GDP growth will be between 2.5% and 3% - below the long-term trend. This is reflective of the uncertainty of current economic conditions and the impact on the job market of suffering corporate profits. This is a prediction of virtually no change from last year in economic activity over 2013.

However, the RBA’s announcement of a 25 basis point cut in the official cash rate in May indicates that there is little chance ofany drastic interest rate rises before the end of the year as it takes time to see the effects of monetary easing run through the economy. Due to this it is forecast that consumer confidence will end the year above its January index level of 105.65 (i.e. very low chance of there being an annual decline in consumer sentiment based on the index provided by Westpac).

In line with modest economic growth forecasts over the coming years, while consumer confidence is not expected to slump in annual terms, it is not expected to be an exceptional outcome. In fact, from December 2012 to March 2013 there was disproportionate

31 | P a g e

growth in sentiment of 10% - so it doesn’t appear that the recent dive of 5.1% between March and April was anything more than a correction and that the index should continue its short-term upward trend. The most likely range of growth in consumer sentiment over 2013 is between 2% and 3%.

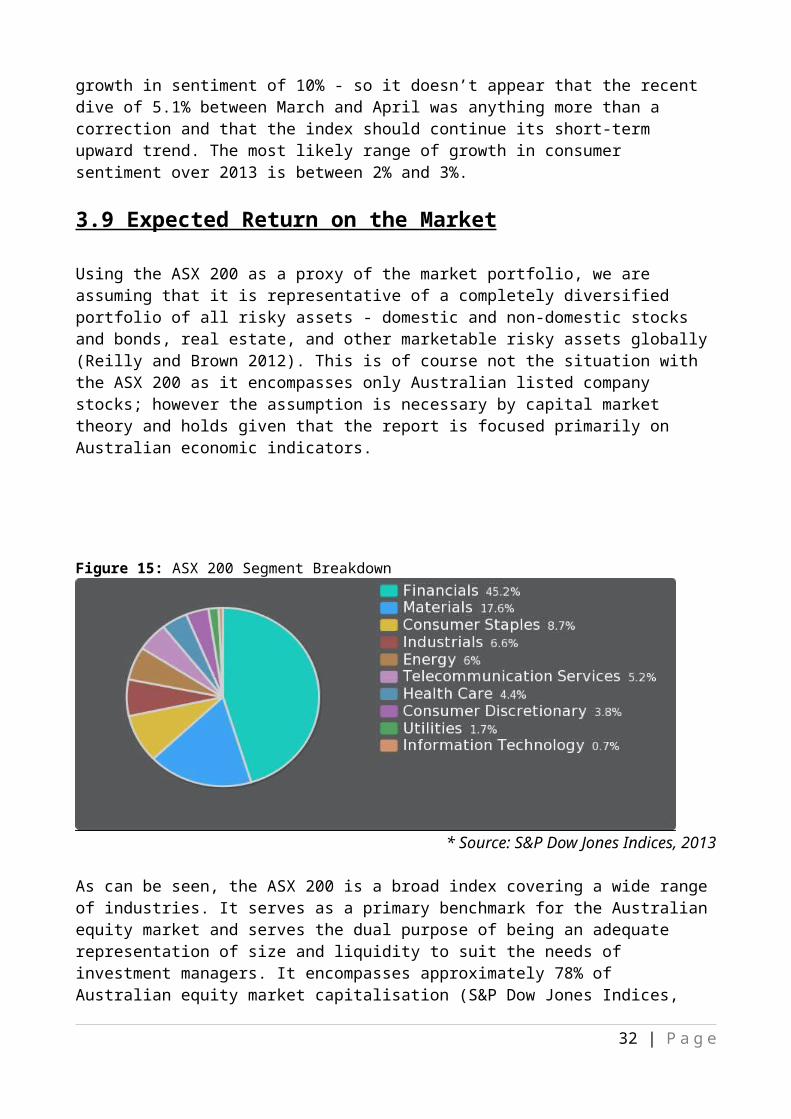

3.9 Expected Return on the Market

Using the ASX 200 as a proxy of the market portfolio, we are assuming that it is representative of a completely diversified portfolio of all risky assets - domestic and non-domestic stocks and bonds, real estate, and other marketable risky assets globally(Reilly and Brown 2012). This is of course not the situation with the ASX 200 as it encompasses only Australian listed company stocks; however the assumption is necessary by capital market theory and holds given that the report is focused primarily on Australian economic indicators.

Figure 15: ASX 200 Segment Breakdown

* Source: S&P Dow Jones Indices, 2013

As can be seen, the ASX 200 is a broad index covering a wide rangeof industries. It serves as a primary benchmark for the Australianequity market and serves the dual purpose of being an adequate representation of size and liquidity to suit the needs of investment managers. It encompasses approximately 78% of Australian equity market capitalisation (S&P Dow Jones Indices,

32 | P a g e

2012). For this reason, it will serve as the market proxy for the valuation of SHL.

Based on the economic analysis above, the following table providesa probability-weighted expected return on the market where the weights are attributable to the particular economic scenario considered. Four scenarios are considered using potential growth rates of the Consumer Sentiment Index (the preferred economic indicator as justified above).

Table 5: Expected Market Return

4. Financial Analysis________________________________________________________________________________

4.1 Financial Statement and Company Risk Analysis

The comparative analysis of a company’s past financial statements allows us to gain an insight to their projected future performance. In order to complete this comparative analysis, various financial ratios denoting Sonic Health Care’s position have been calculated overtime using financial statements from the past 5 financial years (2008-2012).

Furthermore, financial ratios have also been compiled for Primary Health Care and Cochlear two peer companies competing within the industry. The companies manufacture and sell similar products operating with the same sector and it appears that customer demandcomes from the same industry sectors.4.2 Peer Analysis

Primary Health Care LimitedPrimary Health Care is a service company within the Health Care Equipment and Services sector. They offer a range of medical and related services in its network of medial and pathology centres

33 | P a g e

across Australia. They are also a provider of healthcare technology solutions to medical practitioners, medical practices and hospitals. Primary Health care competes directly with sonic health and has therefore been chosen as an appropriate peer.

Cochlear LimitedCochlear is also part of the Health Care Equipment and Services sector. For this reason they have been chosen as an appropriate peer even though they are a manufacturer and distributor of cochlear implantable devices for the hearing impaired. Whilst would not directly compete with Sonic Healthcare they do provide an indicator of the sectors performance.

4.3 Financial Risk

Financial risk is dependent on the nature of the business risk of a company. If a company is able to rely on consistent operations and earnings, it is more likely to provide investors with the confidence and the ability to accept greater financial risk. Financial risk also refers to additional risk that shareholders are exposed to due to the structure and nature of the debt that the company holds, which is why it is imperative that investors assess the amount of long-term debt that the company holds as wellas its interest obligations and repayment schedule in order to make an informed decision.

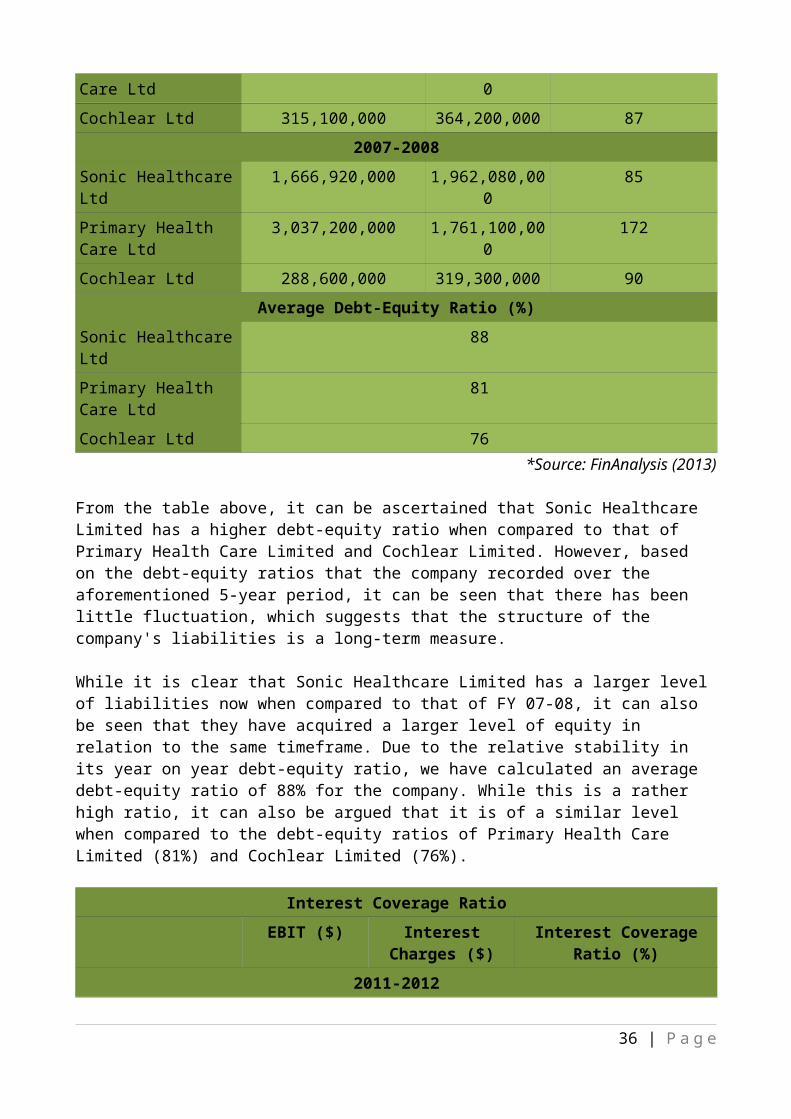

For the purpose of this assessment, we have utilised the debt-equity ratio and the interest coverage ratio as a means of calculating Sonic Healthcare Limited's financial risk. The inclusion of the debt-equity and interest coverage ratios for two of the company's competitors, Primary Health Care Limited and Cochlear Limited, have also been included so as to provide a meansof comparison.

34 | P a g e

Debt-Equity RatioTotal Long-Term

Debt ($)Total Equity

($)Debt-EquityRatio (%)

2011-2012Sonic HealthcareLtd

2,318,610,000 2,610,200,000

89

Primary Health Care Ltd

1,288,800,000 2,573,100,000

50

Cochlear Ltd 317,700,000 384,900,000 832010-2011

Sonic HealthcareLtd

2,196,460,000 2,516,440,000

87

Primary Health Care Ltd

1,321,300,000 2,504,400,000

53

Cochlear Ltd 237,800,000 503,300,000 472009-2010

Sonic HealthcareLtd

2,304,980,000 2,558,740,000

90

Primary Health Care Ltd

1,226,000,000 2,470,200,000

50

Cochlear Ltd 313,400,000 438,300,000 722008-2009

Sonic HealthcareLtd

2,229,160,000 2,532,080,000

88

Primary Health 1,661,800,000 2,116,700,00 79

35 | P a g e

Care Ltd 0Cochlear Ltd 315,100,000 364,200,000 87

2007-2008Sonic HealthcareLtd

1,666,920,000 1,962,080,000

85

Primary Health Care Ltd

3,037,200,000 1,761,100,000

172

Cochlear Ltd 288,600,000 319,300,000 90Average Debt-Equity Ratio (%)

Sonic HealthcareLtd

88

Primary Health Care Ltd

81

Cochlear Ltd 76*Source: FinAnalysis (2013)

From the table above, it can be ascertained that Sonic Healthcare Limited has a higher debt-equity ratio when compared to that of Primary Health Care Limited and Cochlear Limited. However, based on the debt-equity ratios that the company recorded over the aforementioned 5-year period, it can be seen that there has been little fluctuation, which suggests that the structure of the company's liabilities is a long-term measure.

While it is clear that Sonic Healthcare Limited has a larger levelof liabilities now when compared to that of FY 07-08, it can also be seen that they have acquired a larger level of equity in relation to the same timeframe. Due to the relative stability in its year on year debt-equity ratio, we have calculated an average debt-equity ratio of 88% for the company. While this is a rather high ratio, it can also be argued that it is of a similar level when compared to the debt-equity ratios of Primary Health Care Limited (81%) and Cochlear Limited (76%).

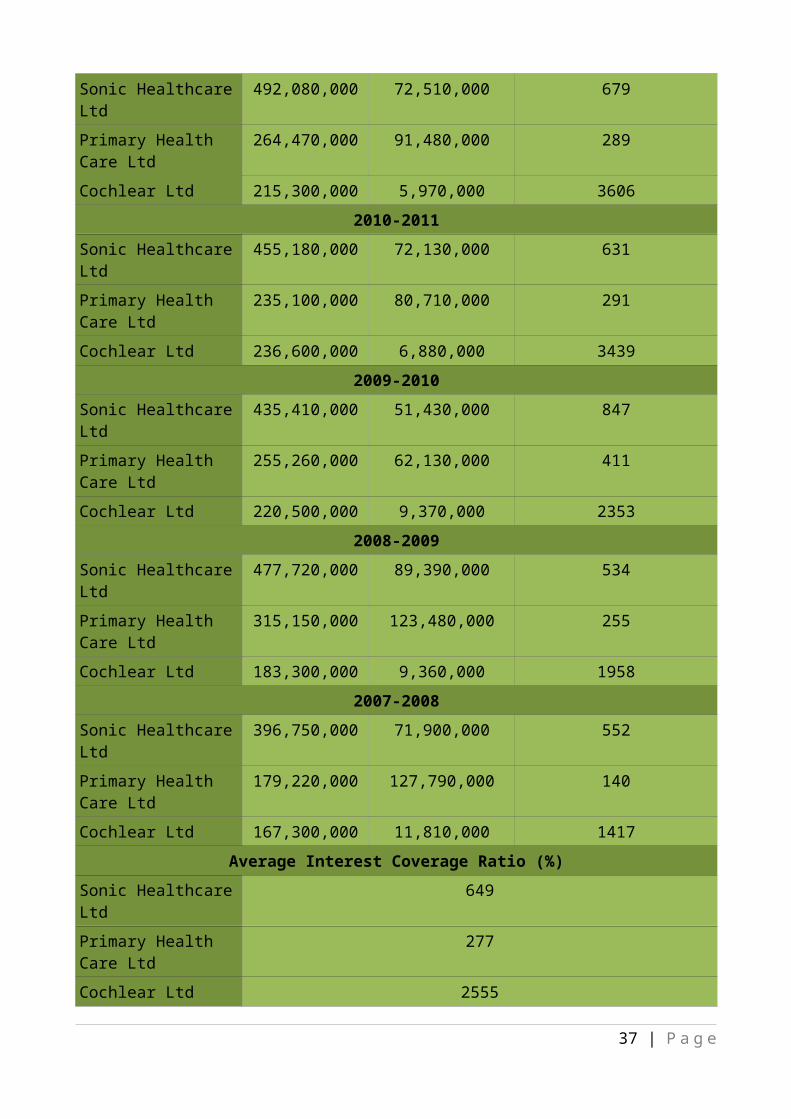

Interest Coverage RatioEBIT ($) Interest

Charges ($)Interest Coverage

Ratio (%)2011-2012

36 | P a g e

Sonic HealthcareLtd

492,080,000 72,510,000 679

Primary Health Care Ltd

264,470,000 91,480,000 289

Cochlear Ltd 215,300,000 5,970,000 36062010-2011

Sonic HealthcareLtd

455,180,000 72,130,000 631

Primary Health Care Ltd

235,100,000 80,710,000 291

Cochlear Ltd 236,600,000 6,880,000 34392009-2010

Sonic HealthcareLtd

435,410,000 51,430,000 847

Primary Health Care Ltd

255,260,000 62,130,000 411

Cochlear Ltd 220,500,000 9,370,000 23532008-2009

Sonic HealthcareLtd

477,720,000 89,390,000 534

Primary Health Care Ltd

315,150,000 123,480,000 255

Cochlear Ltd 183,300,000 9,360,000 19582007-2008

Sonic HealthcareLtd

396,750,000 71,900,000 552

Primary Health Care Ltd

179,220,000 127,790,000 140

Cochlear Ltd 167,300,000 11,810,000 1417Average Interest Coverage Ratio (%)

Sonic HealthcareLtd

649

Primary Health Care Ltd

277

Cochlear Ltd 2555

37 | P a g e

*Source: FinAnalysis (2013)

The interest coverage ratio is used as a means of identifying the level of coverage a company possesses to pay the interest expensesit incurs in relation to its earnings. It is generally accepted that a company that possesses a higher interest coverage ratio is more desirable as it shows that it possesses a larger amount of earnings in proportion to interest expenses while a lower interestcoverage ratio indicates that a company might be holding on to a higher debt load.

Sonic Healthcare Limited's interest coverage ratio for FY 11-12 was 679%, which means that the company is in a strong position to cover any interest payments more than six times over. On average, the company has recorded an interest coverage ratio is 649%, whichis a good level of coverage in general, while its competitor Primary Health Care Limited has recorded a much lower average figure of 277%. Both these figures pale in comparison to that of Cochlear Limited though, which has an average interest coverage ratio of 2555%.

However, this can be attributed to the fact that the company has consistently accrued small interest charges year on year in comparison to its EBIT. It can be ascertained that Sonic Healthcare Limited's high interest coverage ratio means that the company could afford earnings to fall dramatically and significantly before it would be unable to meet interest payment obligations.

4.4 Extended DuPont Return on Equity (ROE)

Return of equity (ROE) measures the rate of return that managementhas earned on the capital provided by stockholders after accounting for payments to all other capital suppliers. This is an important indicator of a firms operating performance. The Dupont framework used to calculate ROE provides insight into additional factors that affect ROE, including profitability, effective asset management, shareholder returns and the effects ofleverage and income tax (Hitchner 2006).

Figure 16: The components of the extended Dupont ROE framework.*Source: Reilly & Brown 2012

38 | P a g e

39 | P a g e

Table 6:

Ext

ended

Dupont ROE C

alculation

for Sonic

Healt

h Ca

re,

Primar

y He

alth C

are

& Cochlear

Limited (

2008 to 20

12)

4.5 Operating Profit Margin

The operating profit margin represents the ratio of a company’s operating profit (before interest and taxes) on net sales, indicating the proportion of a company’s revenue remaining after the variable costs of production. Furthermore this ratio allows analysts to gain an understanding of a company’s profitability prior to interest and taxes on each dollar of sale. It is desirable for the operating profit margin to be as high as this would indicate high profitability from each dollar of sale (Reilly& Brown 2012). Whilst this ratio provides an indication of operating profit it should not be looked at in isolation. The ratio does not consider expenses in other areas such as investmentor financing which can heavily impact on the companies operating profits.

Result findings: Sonic Health Care: The operating profit margin has remained

relatively consistent from 2010 to 2012. This indicates that the operating cost have been maintained at a similar level over this duration as the increase in operating profit has been matched with the increase in sales.

Primary Health Care: Has had an overall fall in their operating profit margin 21.6% in 2009 to 17.99% in 2012. The data shows that the increase in sales has not been matched byan increase in profit which had led this decline.

Cochlear: Whilst providing the highest margin for four of thefive years examined their percentage fall becomes of note in 2012. This fall is due to the huge decrease in operating profit with sales remaining relatively consistent. This indicates Cochlear has not been able to control costs of goods sold which is heavily impacting on the operating profit.

40 | P a g e

4.6 Total Asset Turnover

Total asset turnover measures the amount of sales for every dollarof assets. This ratio indicates how effectively the business is using assets to generate sales revenue. Therefore, based on net sales, we can see how frequently assets are turned over. A high asset turnover suggests that assets are being used productively and that fewer assets are required to generate sales revenue (Reilly & Brown 2012). However, if this figure is too high it may also indicate that the firm’s assets are not enough to cover theirexisting sales revenue.

Result findings: Sonic Health Care: The five year examination again shows a

relatively consistent performance from Sonic Health Care. Over the five year the ratio remained within a range of 0.752to 0.840. The growth over the last two years is a positive indicator as productivity has improved. This is a far better result than that of Primary Health who provide a similar service.

Primary Health Care: Following an increase from 0.135 in 2008to 0.352 Primary Health has remained around this mark. This figure remains low in comparison to fellow review.

Cochlear: Having the highest asset turnover rate indicating their ability to use their assets productively. However therewas a large fall from the 2008 financial year it has since remained consistent and above its peers.

4.7 Return on Assets

Return on total assets is a measure of operating profit relative to the firm’s total assets. This measure is used to indicate how effectively the company is using their assets to generate profits.The operating profit taken into calculation does not include interest or tax expenses. Interest expenses are a result of a firmfinancing practises and the fluctuation of tax demonstrate why these expenses are not included in operating profit. A firm will

41 | P a g e

desire to have a high return on assets.

Result findings: Sonic Health Care: Since 2009 Sonic Health care has been able

to use their assets more efficiently to generate profits. Whilst the total assets figure has remained relatively constant the growth in operating profit is evident.

Primary Health Care: Similar improvement to that of Sonic Health however from 2008. However this has been achieved froma reduction in assets whilst still improving operating profitagain demonstrating the efficiency improvement in generating profit from their assets.

Cochlear: Provided by far the highest return on asset resultsfor four out of the five years however the fall of 25% from 2011 to 2012 outlines a large impact. With total assets remaining consistent Cochlear was unable to provide similar operating profit leading to the large fall.

4.8 Interest Expense Rate

The interest expense rate measures the negative effect of financial leverage in utilising borrowed money by looking at the impact of interest expense as a percentage of total assets.

Result findings: Sonic Health Care: Has been able to reduce their rate over

the five years. This has been achieved by maintaining a similar interest expense as assets increase providing a positive result within a range similar to the other firms.

Primary Health Care: Had the highest rate for each of the five year examined. As interest expense decreased for one period as did total assets and visaverser.

Cochlear: Was the best performed out of it peers being able to reduce their rate whilst total assets increased and interest expense decreased in all but one year.

42 | P a g e

4.9 Net Before Tax/Total Assets

This ratio examines the return on assets prior to the effect of taxes. This ratio dismisses the impacted of tax which is then useful for comparing different companies which may be subject to different tax rates.

Result findings: Sonic Health Care: This ratio has remained relatively

consistent from 2010 to 2012. The 2012 result was far better than that of the two peer compared.

Primary Health Care: The worst performed in this indicator asthe profit prior to tax remained low relative to the assets.

Cochlear: Provided by far the highest ratio results for four out of the five years however there large fall in 2012. This fall is due to the profit before tax falling significantly whilst assets remained relative to previous years.

4.10 Financial Leverage Multiplier

The financial leverage multiplier is a used as a way to determine how a company uses debt to finance its assets. The multiplier takes the firms total assets and divides it by its to show the company’s total assets per dollar of common equity.

Result findings: The firms provided similar results in this field. This

indicates a similar use of the firm’s debt to finance their assets. Sonic Health has shown a consistent rise however thisremain relatively small and with the range of its peers.

4.11 Net Before Tax/Common Equity

This ratio gives an indication of pre-tax return on equity. It represents the return that common equity holders receive prior to the payment of tax.

Result findings:

43 | P a g e

Sonic Health Care: Again the most consistent performer with the only obvious variation in 2009 due to the increase in common equity which was not matched by the operating profit before tax.

Primary Health Care: Since 2008 has improved in this field and remained consistent since. This movement in 2008 was due to the large increase in operating profit before tax.

Cochlear: Provided by far the highest best results for four out of the five years however again there was a large fall in2012. This fall was due to the large fall in operating profitfrom the previous year.

4.12 Return on Equity (ROE)

Return on Equity (ROE) is a measure of the rate of return that management generates on capital provided by common shareholders. (Reilly & Brown 2012)

44 | P a g e

Figure 17: Historical ROE

Result findings: Sonic Health Care: The average ROE for Sonic Health Care is

consistent with the collective average of the companies examined. The results show a much more consistent performancefor the years 2010-2012. These consistent years have led to the company being consistent with the collective average taken.

Primary Health Care: The average shows a consistently weaker performance than that of Sonic Health Care. This is consistent within the yearly findings with a top ROE being of7.18%. However the ROE like Sonic Health has been more consistent from 2009-2012 and improved performance from 2008.

Cochlear: Clearly leading and well above the collective average and fellow competitors. However this overall average does not show the decline in performance from 2008 to 2012. Cochlear had the lowest ROE for 2012 out of all companies dueto the reason of performance outline above.

4.13 Growth Rate

The analysis of sustainable growth potential examines ratios that indicate how fast a firm should grow. This potential growth is an important figure for both owners and lenders. This growth rate is crucial to owners as providing insight into future earnings, cash flows and dividends. It is of equal importance to creditors in

45 | P a g e

determining a firm’s ability to pay obligations.

Sonic Health Care Short – Medium Run Growth RateWhereas the long run growth rate will consider previous financial performances to predict the long run growth rate it will not consider the impact of future macro-economic factors. As stated inthe above forecast with a GDP rise between 2.5% and 3% due to the uncertainty in the economy which is reflective of last year’s results. On this basis it can be predicted that the impact will cause similar result to that of the previous year. Sonic health is relatively stable being well established within the industry and having a highly experienced management team it isunlikely that there will be drastic internal changes that impact on the growth rate. It is expected that the company will continue to be acquisitive purchasing relevant companies around the world to continue building upon its market share.

Determinants of GrowthUltimately the growth of a company will depend on two factors: theamount of resources retained and reinvested and the rate of returnfor reinvested funds. The growth rate can be indicated by the formula g =RR x ROE. This formula takes into account these two factors. The retention rate (RR) indicates the percentage of earnings that has been paid in dividends or reinvested into the company. The return on equity (ROE) suggests the earnings generated from those reinvested funds.

Sonic Health Care Long Run Growth Rate The above formula has been applied to Sonic Health in order to determine their long run growth rate. The input figures for the ROE have been taken from the extended ROE dupoint findings and theretention rate has been determined from the dividend ratios found with annual reports.

YearRetention Rate

Return on Equity Growth Rate

Average growth rate

2008 0.339 23.80% 8.07%

3.37%2009 -0.118 7.34% -0.87%2010 0.218 14.76% 3.22%2011 0.222 12.50% 2.77%2012 0.272 13.47% 3.66%

46 | P a g e

Table 7: Growth Rate for Sonic

This growth rate can be consider as a constant for an infinite period as it has taken into account the business cycle over the 5 year period and varying performance. Additionally the established management with Sonic Health will are likely to continue the dividend payment technique. This is a manageable growth rate for the company with existing assets and a retention rate allowing this trend to continue

5. Valuation Assumptions________________________________________________________________________________

5.1 The Required Rate of Return (CAPM)

The following section uses four of the most common valuation models to determine the intrinsic value of SHL: (1) the Dividend Valuation Model; (2) the Free Cash Flow to Equity Model; (3) the Price/Earnings Ratio Model; and (4) Price/Book Ratio Model. All these models require that we discount future expected returns at the discount rate determined (Reilly and Brown 2012).

Underpinning this analysis is the required rate of return, which will be used to discount future earnings/cash flows/dividends backto the present in order for us to compare the present value of SHL’s stock to the market price. It is important to note that the intrinsic value will depend on the estimates which this analysis provides, specifically the forecast future returns and the required rate of return.

The Capital Asset Pricing Model (CAPM) has been developed in accordance with capital market theory (an extension of portfolio theory) where an individual asset’s required rate of return can be determined. This required rate of return assumes that the asset (the common stock of SHL) is incorporated into a completely diversified portfolio and is determined based on its systematic risk (i.e. that portion of total risk which the investor cannot diversify away).

It is necessary to review some of the critical assumptions associated with the use of CAPM. Firstly, investors are assumed tobe able to borrow and lend any amount of money at a certain risk-

47 | P a g e

free rate of return (RFR). Secondly, all investments are priced inaccordance with the risk attributable to that asset. The model relies heavily on the determination of a rate of return consideredto be that attributable to a risk-free asset (such as a governmentbond) – there is no uncertainty for an investor in this asset. Additionally, the return on the market portfolio is crucial as it determines the risk premium that maximises an investor’s compensation for bearing risk (Reilly and Brown 2012).

CAPM uses a risk measure universally known as beta (β). β measures the asset’s systematic risk relative to the market portfolio. The brief overview of CAPM has illustrated three important inputs: therisk-free rate of return, the expected return on the market portfolio, and an index of an individual security’s risk to the market. The risk premium for an individual asset is thus simply the expected return of the market over and above the risk-free rate of return scaled for how this asset moves with the market. Therefore, the required rate of return is the RFR plus this risk premium.

Recall that the ASX 200 is considered to be representative of a completely diversified portfolio and will therefore be used as theproxy for the market portfolio defined by CAPM. Therefore, for thepurpose of SHL valuation, the formula can be written as:

5.2 Calculating Systematic Risk (Beta)

Conveniently, betas are able to be calculated using a simple linear regression. SHL’s monthly holding period yields (HPY) will be the independent variable and corresponding monthly yields for the ASX 200 will be the dependent variable. Regression line produced is known as the characteristic line. The time frame used for this analysis is January 2007 to March 2013 corresponding to 74 observations, a substantial sample to provide a reliable beta coefficient and a time period over which no drastic changes have occurred in SHL. The slope of the line will be the systematic riskof SHL.

The regression produced the following raw beta:48 | P a g e

Figure 18: Sonic Healthcare Limited’s Characteristic Line

This can be interpreted as SHL being 49% less risky than the market. This is very much in line with the Healthcare industry beta of the same value (CommSec 2013) We can be assured of the fitof this model because, based on the t-test for the population slope, we can be 99% confident that the there is a linear relationship between SHL monthly returns and monthly returns on the ASX 200 (the p-value for the beta of SHL is 0.00055 so we can reject the notion that there is no observable linear relationship between the two variables at a 99% level of confidence).

49 | P a g e

Blume (1971) in his assessment of risk noted through empirical studies that there was a tendency of risk measures to regress towards the mean over time. Betas on individual assets move towardthe market beta of 1. The explanation behind this phenomenon is that, as all information becomes known over time, individual assetreturns that are out of line with the market will be pulled back in line with market returns (Bredenkamp 2010). Blume noted that adjusting for this mean-reversion phenomenon would produce a higher degree of accuracy in the determination of future risk.

There is an adjustment to be performed on the raw beta calculated from the slope of the characteristic line such that we have a forward looking beta. The formula for this is given by:

The beta of the market is, by definition, 1. This is because any variable is perfectly correlated with itself. Therefore, the beta that will be used to calculate the expected return of SHL is:

5.3 Determining the Risk Free Rate of Return (RFR)

The risk-free rate of return (RFR) is the return on a risk-free asset. This asset has no variance in terms of the returns an investor can expect and therefore there is no uncertainty associated with it. This asset has no correlation with any other risky assets (Reilly and Brown 2012). The best proxy for the riskyasset that will be used to determine the RFR is Australian government bonds. Government bonds are inherently near-zero risk because of the ability for governments to print money in the event they couldn’t raise enough funds to repay debt holders.

The proxy used in the determination of SHLs expected return will be the yield on 10-Year Australian Government Bonds. The average over the month of April 2013 will be used.

Table 8: Risk Free Asset Proxy Yields Over April 2013

50 | P a g e

* Source: The Reserve Bank of Australia 2013

The table above shows the market yields for 10-year Australian Governments Bonds over the month of April 2013. The average is 3.25% and this will be used as the RFR in the model.

5.4 The Required Rate of Return

We have now determined all the components of CAPM that are necessary to calculate the required rate of return on SHL. Recall that the expected return on the market has already been determinedbased on the macroeconomic analysis above.

Therefore:

5.5 Sensitivity Analysis (RRR)

51 | P a g e

Understandingly, the model is going to be sensitive to the inputs as determined by the analysis in this report. The table below details the sensitivity of to the two inputs most susceptible to change.

Table 9: Sensitivity Analysis (RRR)

It is perhaps the market return that is most subjective in this analysis. The market return of the ASX 200 was determined to be 11% based on potential changes in consumer sentiment over the year. If, assuming the beta remains unchanged, the expected returnon the market was determined to be, say, 15% (perhaps by giving more weight to an optimistic growth scenario), then the required rate of return would be almost 3% higher at 11.12%.

Also, if no adjustment had been made to beta in line with Blume’s mean reversion analysis, we would have a required return of around7.13% at an expected rate of return on the market of 11% and a required return of approximately 9.13% at a expected rate of return on the market of 15%. The impact of these differences will only become apparent when we consider them in the ensuing valuation models. However, the authors are content with the inputsas already determined as they are backed by strong macroeconomic analysis.

6. Valuation Analysis________________________________________________________________________________

Figure 19: Approaches to the Valuation of Common Stock

52 | P a g e

* Source: Reilly and Brown, 2012

Discounted cash flow valuation techniques require discounting of future expected cash flows back to present using the required rateof return. The techniques used in this analysis will be the present value of dividends model and the present value of free cash flow to equity model.Relative valuation techniques use ratios based on the current price of the stock in question. The techniques used in this analysis will be the P/E ratio and the P/BV ratio.All valuation techniques rely on the required rate of return (which has been determined by CAPM) and the growth rate used (which will differ per model) (Reilly and Brown 2012).

6.1 Dividend Discount Model (DDM)Present Value of DividendsThis is the most straightforward way to calculate the value of thecompany. It is most tangible to equity holders because it represents the cash flow that they receive for holding the stock.

Reilly and Brown (2012) note that the ‘reduced form of the dividend discount model is very useful when discussing valuation for a stable, mature entity where the assumption of relatively constant growth of dividends for the long term is appropriate’. This is convenient because, recapping on a few of the points made so far regarding Sonic Healthcare, they are a mature business withsignificant competitive advantage in the healthcare industry. Their business model has been effective and they intend to maintain a consistent strategic framework allowing them to

53 | P a g e

leverage off growth drivers effectively and maintain control over their growth.

There are strong entry barriers to a sector in which they hold a rather large share, and the threat of substitutes is low, meaning they are not under any significant risk of revenue erosion due to the introduction of alternative and more efficient forms of their services. Additionally, SHL’s stock price tends to move in line with the industry. We have already discerned that the industry outlook is rather stable with no adverse shocks foreseeable – government policy being a crucial factor to this conclusion – and therefore the industry will continue in line with its long-term upward trend. Thus, if SHL moves with the industry, we can expect that it too will follow a stable long-term upward growth trend.

The Dividend Discount Model (DDM) is based on the classic present value of future cash flows formula, which is given in its simplest form below:

Where: = value of the asset = life of the asset = cash flow at Period

= discount rate

For reasons above we will assume the SHL’s future dividend stream will grow at a constant rate. Here we introduce a growth constant. This will be given the value as determined by average growth

rate from the financial year ended 2008 through to the financial year ended 2012.

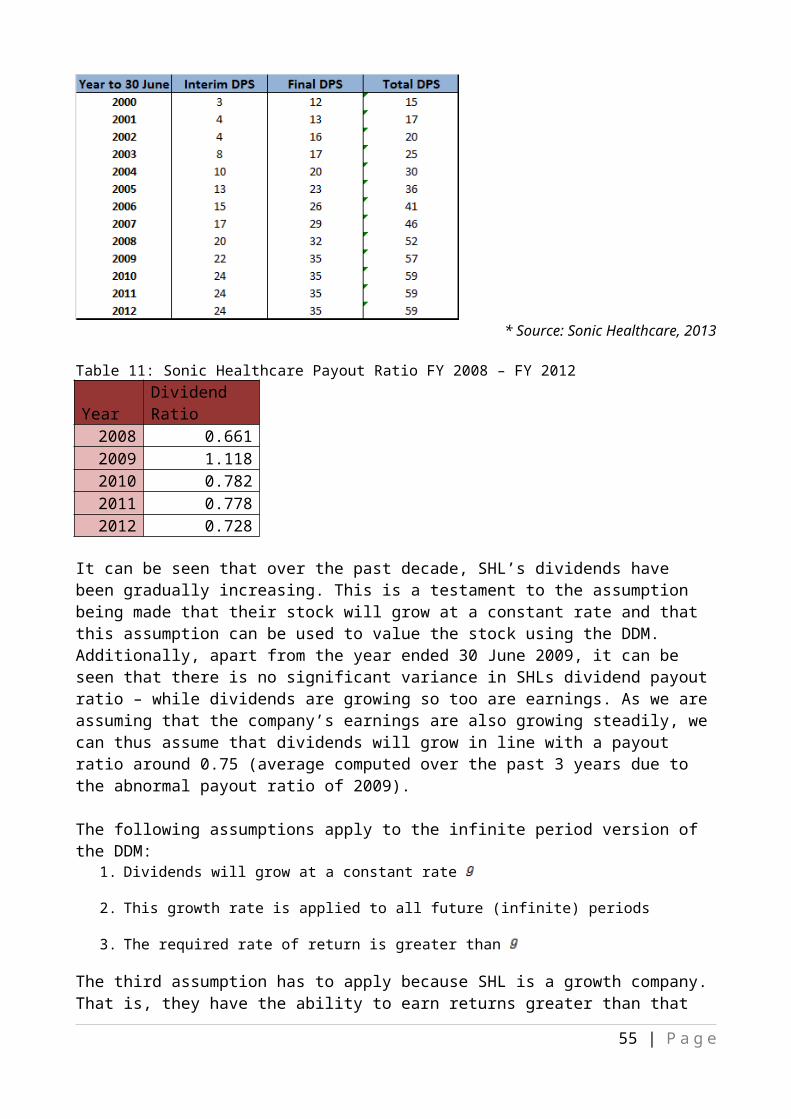

The table below details SHL’s dividend history:

Table 10: Sonic Healthcare Dividends per Share FY 2000 – FY 2012

54 | P a g e

* Source: Sonic Healthcare, 2013

Table 11: Sonic Healthcare Payout Ratio FY 2008 – FY 2012

YearDividend Ratio

2008 0.6612009 1.1182010 0.7822011 0.7782012 0.728

It can be seen that over the past decade, SHL’s dividends have been gradually increasing. This is a testament to the assumption being made that their stock will grow at a constant rate and that this assumption can be used to value the stock using the DDM. Additionally, apart from the year ended 30 June 2009, it can be seen that there is no significant variance in SHLs dividend payoutratio – while dividends are growing so too are earnings. As we areassuming that the company’s earnings are also growing steadily, wecan thus assume that dividends will grow in line with a payout ratio around 0.75 (average computed over the past 3 years due to the abnormal payout ratio of 2009).

The following assumptions apply to the infinite period version of the DDM:

1. Dividends will grow at a constant rate

2. This growth rate is applied to all future (infinite) periods

3. The required rate of return is greater than

The third assumption has to apply because SHL is a growth company.That is, they have the ability to earn returns greater than that

55 | P a g e

required by investors to buy their stock (Reilly and Brown 2012).

Recall:

The infinite period model is given the formula:

Where represents the most recent dividend paid by the company.

This model will calculate the price of SHL based on the total dividend for the most recent financial (FY 2012). This is because,as can be seen, the interim period dividend is always less than the final period dividend, which will skew if we annualised the very last dividend paid.

Therefore:

Before commencing the sensitivity analysis, there is another method of calculating the growth rate to be applied in the DDM which involves using the actual growth of the dividend stream. Theformula is given below:

This should only be used if the dividend growth has been fairly consistent over the time period used in the formula. This formula should thus be applicable to SHL. The formula accounts for compounding growth. If the past five years of total dividend data were used (in line with the time horizon used for the preceding analysis of SHL) then the average dividend growth rate would be 0.0256 (see below).

Obviously, a different value for SHL will be attained based on this growth rate. By using the infinite period growth of dividendsform of DDM we would get a stock value of $10.29 with equal to 0.0256. Thus the DDM is very sensitive to the growth rate used.

56 | P a g e

6.1.1 Sensitivity Analysis (DDM)

It has already been stressed that the intrinsic value determined by the models relies heavily upon the two main inputs of the required rate of return and the growth rate. These have different meanings in the model. In isolation, an increase in the growth translates to an increase in the value of the company (so long as the growth rate does not exceed the required rate of return).

On the other hand, as investors’ required rate of return increasesholding constant, the intrinsic value of the company decreases. It has already been discerned that the required rate of return produced by CAPM is sensitive to the Beta and market risk premium – this flows on to the dividend discount model. Also, the growth rate used is the expected growth rate. It has been attained by observing past management performance in generating a return on the assets the company employs, as well as earnings that the company has retained in the past to help grow its assets.

While it has been justified that SHL are a growth company in a mature stage which allows the use of the constant growth rate methodology – it is an assumption inherent in the model. Thereforeit is crucial to analyse how the valuation will change based on the required rate of return and on the growth rate.

Table 12: SHL Stock Value Sensitivity to Required Rate of Return (CAPM Inputs) Based on DDM

57 | P a g e

Table 13: SHL Stock Value Sensitivity to Required Rate of Return and Growth Rate Based on DDM

* Note: the shaded grey section in the table above corresponds to a combination of and where the and thus violates a major assumption of the model

Firstly, consider the first table. If the beta had not been adjusted and remained at 0.51 and the expected return on the market is held constant, the value of the stock would be more the $4 higher by the infinite period DDM. Consider the original hypothetical of having the expected return on the market at 15% instead of 11%. Holding the beta constant, this would translate toan intrinsic value of $7.87 – more than $4 lower than the currently estimated intrinsic value. This accentuates the vitalityof having a solid backing for the CAPM input estimates.