City of Edmond

222

City of Edmond NOTICE OF PUBLIC MEETING The City of Edmond encourages participation from all its citizens. If participation at any Public meeting is not possible due to a disability, notification to the City Clerk at least 48 hours prior to the scheduled meeting is encouraged to make the necessary accommodations. The City may waive the 48-hour rule if signing is not the necessary accommodation. AGENDA Finance/Audit Committee Wednesday, March 19, 2014 4:00 p.m. City Council Chambers 20 S. Littler, Edmond, OK CITY COUNCIL WORKSHOP 1. Call to Order. 2. Approve the minutes from February 19th, 2014. 3. Discussion and consideration of the responses to the 2014 request for internal audit services. 4. Discussion and consideration of the arbitrage rebate calculations by EideBailly of the EPWA Sales Tax & Utility System Revenue Bonds, Series 2004. 5. Discussion and consideration of the annual review of the 457(b) and 401(a) deferred compensation plans and the funds performances for year 2013 presented by Great-West Retirement representative Gary Wilkins and Chara Green. 6. Discussion and consideration of the analysis by DiMeo Schneider & Associates, LLC, of the 457 Deferred Compensation Plan as of December, 2013. 7. Accept the City Treasurer's month end investment reports for January 31st and February 28th, 2014. 8. New Business - (In accordance with the Open Meeting Act, new business is defined as any matter not known about or which could not have been reasonably foreseen prior to the time of posting of the agenda.) 9. Adjournment.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of City of Edmond

City of EdmondNOTICE OF PUBLIC MEETING

The City of Edmond encourages participation from all its citizens. If participation at any Public meetingis not possible due to a disability, notification to the City Clerk at least 48 hours prior to the scheduledmeeting is encouraged to make the necessary accommodations. The City may waive the 48-hour rule ifsigning is not the necessary accommodation.

AGENDA

Finance/Audit CommitteeWednesday, March 19, 2014

4:00 p.m.City Council Chambers

20 S. Littler, Edmond, OK

CITY COUNCIL WORKSHOP

1. Call to Order.

2. Approve the minutes from February 19th, 2014.

3. Discussion and consideration of the responses to the 2014 request for internal audit services.

4. Discussion and consideration of the arbitrage rebate calculations by EideBailly of the EPWA SalesTax & Utility System Revenue Bonds, Series 2004.

5. Discussion and consideration of the annual review of the 457(b) and 401(a) deferredcompensation plans and the funds performances for year 2013 presented by Great-WestRetirement representative Gary Wilkins and Chara Green.

6. Discussion and consideration of the analysis by DiMeo Schneider & Associates, LLC, of the 457Deferred Compensation Plan as of December, 2013.

7. Accept the City Treasurer's month end investment reports for January 31st and February 28th,2014.

8. New Business - (In accordance with the Open Meeting Act, new business is defined as any matternot known about or which could not have been reasonably foreseen prior to the time of posting ofthe agenda.)

9. Adjournment.

Finance/Audit Committee 2. Meeting Date: 03/19/2014

InformationAgenda ItemApprove the minutes from February 19th, 2014.

Background

AttachmentsFeb 2014 Minutes

Page 1 of 2

FINANCE/AUDIT COMMITTEE

February 19, 2014 1. Call to Order. Chairman Stephen Schaus called a regular Finance/Audit Committee meeting to order at 4:00 pm in the City Council Chambers on Wednesday, February 19, 2014. Present were Charles Lamb, Nick Massey, Larry Stevens, City staff, and guests. 2. Approve the minutes of January 14, 2014. Motion made by Massey, seconded by Lamb, to approve the minutes. Motion carried unanimously. Chairman Schaus stated the following three items would be discussed at one time. Chris Gander, Bond Advisor with BOSC-Oppenheim, .addressed the Committee and stated the three following outstanding bonds will be combined into the “Sales Tax and Utility System Revenue Refunding Bonds, Series 2014 in the aggregate amount not to exceed $25,000,000. He stated the savings on Series 2003B (Sr. Bonds) will be $140,000, the 2004 (Sr. Bonds) will be $850,000 and the 2004 (Jr. Bonds, the callable portion) will be $1,200,000. He noted the average interest rate will be approximately 2.75%. The Bonds will be sold on March 6th and close soon after April 1st due to the call date. 3. Discussion and Consideration of refunding the Utility System Revenue Bonds, Series 2003B (Sr. Bonds). Motion by Lamb, seconded by Massey, to approve refunding of the above Bonds. Motion carried unanimously. 4. Discussion and Consideration of refunding the Utility System Revenue Bonds, Series 2004 (Sr. Bonds). Motion by Massey, seconded by Lamb, to approve refunding the above Bonds. Motion carried unanimously. 5. Discussion and Consideration of refunding the Sales Tax and Utility System Revenue Bonds, Series 2004 (Jr. Bonds – the callable portion). Motion by Lamb, seconded by Massey, to approve refunding the above Bonds. Motion carried unanimously. 6. Discussion and Consideration of the analysis by DiMeo Schneider & Associates, LLC, of the 457 Deferred Compensation Plan as of December, 2013. In 2012 the Committee approved a budget of $14,950 for one-time investment consulting services. In 2013 the City hired DiMeo Schneider as the Pension Plan Fund Manager, to perform an analysis of the 457 Plan investment options, fee, and fund performance. DiMeo Schneider also re-negotiated the City’s costs with the current service providers, Great-West Retirement (record-keeper) and its affiliate, Advised Asset Group (investment advisors), with annual savings of $8,302 for administrative fees and the reduction of asset-based fees for managed accounts of approximately $4,000 to $5,000 annually.

Page 2 of 2

Holly Wescott, Treasury Coordinator, addressed the Committee and stated as a result of the negotiations, new contracts with both entities will need to be formally approved by Council. In addition, the Committee will need to discuss and determine if the City wants to offer different funds or move to lower-cost shareclasses. DiMeo recommended to terminate without replacement Davis NY Venture A and to discuss termination of Heartland Value and OakMark. Other issues recommended for discussion was whether to replace Risk based funds with Target Date Funds and replacing AAG with a non-affiliated group acting in an advising/consulting capacity because AAG is not independent of Great-West and DiMeo advocated independent services. She stated Great-West representatives will attend the next meeting to present the annual review of the 457 Plan. She noted during the last discussion with Gary Wilkins, the regional director, he indicated they wanted to accommodate whatever direction the City chooses to go regarding these issues. Great West is not suggesting adding any additional funds, but are willing to offer substitutions. Consensus of the Committee was to continue this item until the next meeting in order to further discuss the recommendations from DiMeo Schneider with Great-West. 7. Acceptance of the City Treasurer’s Investment Report for month ending December 31, 2013. Motion by Lamb, seconded by Massey, to accept the Treasurer’s investment report for December, 2013. Motion carried unanimously. 8. New Business: Holly Wescott, Treasury Coordinator, addressed the Committee and stated a team has been created to work on a new RFP for merchant services. 9. Adjournment. The meeting adjourned at 4:30 pm.

Finance/Audit Committee 3. Meeting Date: 03/19/2014

InformationAgenda ItemDiscussion and consideration of the responses to the 2014 request for internal audit services.

Background

AttachmentsCrawford RFP ResponseCompass RFP Response

PROPOSAL FOR INTERNAL AUDIT SERVICES

FOR

THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012 CLOSING DATE MARCH 4, 2014 AT 2:00 PM CST

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

2

TABLE OF CONTENTS

Description

Page

LETTER OF INTRODUCTION – TRANSMITTAL LETTER

3

I. COMPANY BACKGROUND INFORMATION:

PROFILE OF THE FIRM FINANCIAL SOUNDNESS PERSONNEL INTERNAL AUDIT TEAM FOR CITY OF EDMOND EXPERIENCE LIST OF CLIENTS & CONTACTS

4-13

II. ENGAGEMENT STRATEGY

PREPARATION AND START-UP GOALS, OBJECTIVES AND SCOPE

13-14

METHODOLOGY

III. FEES AND COSTS

14

ATTACHMENT A – FIRM ORGANIZATION CHART

ATTACHMENT B – CITY COUNCIL & MANAGEMENT RISK SURVEY ATTACHMENT C – RISK ASSESSMENT ATTACHMENT D – ENGAGEMENT PROFILE ATTACHMENT E – INTERNAL AUDIT PLAN ATTACHMENT F – INTERNAL AUDIT REPORTS ATTACHMENT G – CALCULATION OF ESTIMATED HOURS & FEES ATTACHMENT H – FIRM PEER REVIEW ATTACHMENT I – PROOF OF PROFESSIONAL LIABILITY INSURANCE ATTACHMENT J – FIRM OAB ANNUAL PERMIT Firm Contact Person: Frank Crawford, CPA Firm President Crawford & Associates, P.C. 10308 Greenbriar Place Oklahoma City, OK 73159 Phone: (405) 691-5550 Cell Phone: (405) 229-9084 Fax: (405) 691-5646 Email: [email protected]

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

3

March 4, 2014 Ms. Brenda Mayer, CPPO Purchasing Manager City of Edmond 100 East First Edmond, Oklahoma 73034 Dear Ms. Mayer: Crawford & Associates, P.C. is pleased to provide the enclosed response to your request for internal audit services. As you may already know, we are a very unique Firm in that since 1984 we have provided accounting, auditing and consulting services exclusively to state and local governments. We are recognized throughout Oklahoma and the Nation as the leader in this field by both our CPA peers and the various governmental entities in the State and the Country. We have been recognized by the Governmental Accounting Standards Board (GASB) as the first auditing Firm in the United States to have audited a local government which early implemented the provisions of GASB Statement 34, The New Reporting Model. In addition, Firm Chairman Emeritus Mike Crawford is the AICPA national representative and past Vice Chairman of the Governmental Accounting Standards Advisory Council (GASAC) that advises the GASB; and Firm President Frank Crawford is the past Chairman of the AICPA National Government Expert Panel that works directly with the GASB and leads the accounting profession nationally in governmental auditing. In 1997, the Firm recognized a need for providing expert internal auditing and related consulting services. Therefore, the practice was expanded to meet this need by adding professional staff that had specific internal auditing and related consulting experience to provide those services to our clients. As a result, we have experienced significant growth in the demand for those services and continue to welcome opportunities to provide these specialized services to assist our clients in meeting their needs. In addition, we place the utmost importance on maintaining and enhancing the integrity and objectivity of the accounting and audit profession. In fact, Firm Chairman Emeritus, Mike Crawford, is the co-author of the national publication, The CPAs’ Multistate Guide to Ethics and Professional Conduct, and annually provides ethics training to other CPAs across the country. We feel strongly that, when acquiring internal audit services of such a specialized nature, the most important factors to consider in relation to fees are qualifications, experience and level of available services. We believe when you compare the qualifications, experience and service of our Firm in relation to that of any other Firm, you will agree that Crawford & Associates, P.C., is the best Firm available to the City of Edmond. We encourage you to learn more about Crawford & Associates and our proud history and exciting future at our web site www.crawfordcpas.com. We are very excited about the opportunity to serve the City of Edmond as internal auditor and would be more than happy to meet with you to further discuss our proposal. Respectfully submitted, Crawford & Associates, P.C

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

4

I. COMPANY BACKGROUND INFORMATION: PROFILE OF THE FIRM OVERVIEW – HISTORY OF THE FIRM Crawford & Associates, P.C. is a 20-person Firm headquartered in Oklahoma City, Oklahoma. Since its creation in 1984, the Firm has earned an international, national and statewide reputation second to none in the area of governmental accounting and consulting. Our vision in 1984 to establish a CPA Firm to exclusively serve governments has proven to be ahead of its time, as many professional service Firms are now learning the value of specialization. Crawford & Associates, established by brothers Mike and Frank Crawford, specializes in providing consulting and accounting services solely to governmental entities and training and consultation to other CPA Firms that provide accounting and auditing services to governmental entities. We offer a variety of services including annual financial statement preparation, accounting and reconciliation assistance, accounting and financial management technical assistance, internal control analysis and design, data-mining analysis, accounting policy and procedure development, contract internal auditing, fraud and other special investigations, quality assurance reviews, training, and expert witness testimony in litigation and labor arbitration matters. In addition, the Firm is nationally recognized for its financial analysis tool, the Performeter®, used by government entities around the world as a measure of the government’s financial health and performance. FINANCIAL SOUNDNESS Crawford and Associates is celebrating its 30th year in business, has no long-term debt, owns title to all its assets, and is 100% owned by five local shareholders. The Firm in its 30 year existence has never had any litigation filed against it, nor has the Firm ever been subject to an investigation by a regulatory authority. Furthermore, the Firm has no contingent liabilities. PERSONNEL – FIRM ASSOCIATES (See Organization Chart at Attachment A) INDIVIDUAL POSITION YEARS WITH FIRM LOCATION Mike Crawford, CPA Chairman Emeritus 30 Oklahoma City Frank Crawford, CPA President/Shareholder 28 Oklahoma City Deanna Crawford, CPA Manager/ Shareholder 22 McAlester, OK Marcy Twyman, CPA Manager/Shareholder 12 Oklahoma City G. Dwayne Tate, CPA Manager/Shareholder 9 Oklahoma City Brenda Wright, CPA Manager/Shareholder 12 Oklahoma City Justin Kersey, CPA, CFE Manager 6 Oklahoma City Richard Rose, CPA Manager 5 Oklahoma City Chris Pembrook, CPA Manager 3 Oklahoma City Stephanie Ballard, CPA Manager 3 Oklahoma City Joni Parker, CPA Consultant 12 Davis, OK Amanda Copeland, CPA Consultant 12 Oklahoma City Tammy Hunt Consultant 26 Oklahoma City Kristy Awtry Consultant 10 Oklahoma City Kimberly Green Consultant 10 Oklahoma City Andrea Depee Consultant 9 Oklahoma City Jennifer Traxler Consultant 8 Oklahoma City D. Ann Matthews Consultant 6 Durant, OK Kristin Lamar, CFE Consultant 7 Oklahoma City Courtney Crowder Consultant 9 Oklahoma City Wendy Moreno Quality Control Manager 21 Oklahoma City Candy Dow Office Administrator 10 Oklahoma City Debbie Crawford Office Staff 21 Oklahoma City

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

5

PRESIDENT FRANK CRAWFORD, CPA Frank Crawford is President of Crawford & Associates, P.C., Certified Public Accountants, an accounting Firm located in Oklahoma City, OK. The Firm specializes in providing auditing, consulting and accounting services solely to governmental entities and is a member of the AICPA’s. Over the last 30 years, Crawford & Associates has provided a variety of audit and accounting services to all sizes of government including many types of financial statement audits and attestation services, fraud investigations, internal control analysis, accounting policy and procedure development, contract internal auditing and internal monitoring, developing management anti-fraud programs and controls, quality assurance reviews, training, and expert witness testimonies.

Mr. Crawford recently completed a 4 year term as Chairman of the AICPA Government Expert Panel, and is currently the Chairman of the Oklahoma Society of CPAs Government Accounting and Auditing Committee (15 years), and has also been involved in a number of other AICPA committees and task forces as they relate to governmental accounting and auditing, including the AICPA Governmental Accounting and Auditing Committee, the AICPA Government and Not-For-Profit Expert Panel, the AICPA Government Performance and Accountability Committee, and the AICPA GASB 34 Audit Guide Revision Task Force.

Mr. Crawford is also currently the Chairman of the AICPA National Governmental Accounting and Conference Planning Task Force (10 years), and is also a member and co-chair of the Planning Committee of the AICPA’s Government and Not-For-Profit Training Conference (14 years).

Over the years, Mr. Crawford has assisted both the AICPA and GASB in the development of several implementation guides as a member of an advisory group, task force or technical content provider. His experience with GASB 34 implementation and audit issues dates back to June 30, 1999, as auditor of the first general-purpose government in the United States to implement the requirements of GASB 34.

Mr. Crawford is also currently working with many of the territories, commonwealths and freely-associated states on audit finding resolution and financial analysis projects and serves as a technical consultant and advisor to a number of Federal Government Agencies.

Frank is a frequent lecturer, trainer and discussion leader for numerous groups, including U.S. Federal Government Agencies, various local and national CPA Firms, a number of State Societies, and has appeared in several AICPA continuing professional education videos and live satellite CPE broadcasts and Webcasts related to governmental accounting and auditing.

MANAGING SHAREHOLDER MARCY TWYMAN, CPA Marcy Twyman, CPA, joined Crawford & Associates in March 2002 as Audit and Consulting Manager. Before coming to the Firm, Marcy was Finance Director at the City of Guymon, Oklahoma for 11 years. The City of Guymon was the first city in the United States to implement GASB 34. She was key in the implementation of GASB 34 and has taught various classes and seminars on the subject. Marcy is a frequent lecturer, trainer, and discussion leader for various groups including the Oklahoma Society of CPAs, Oklahoma Municipal League, and Oklahoma Municipal Clerks, Treasurers, and Finance Officers Association related to governmental accounting and management. She has also served on task forces and participated in field tests for the Governmental Accounting Standards Board in their standards-setting process. She was recognized as the 2000 Outstanding CPA in Business and Industry by the Oklahoma Society of CPAs. In 2004, Marcy became a shareholder of Crawford & Associates and currently serves as managing shareholder. She is a graduate of Panhandle State University. She has managed multiple internal audit engagements including several State colleges and universities and State agencies.

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

6

SHAREHOLDER BRENDA WRIGHT, CPA Brenda Wright, CPA, rejoined Crawford & Associates in February 2009 as Consulting Manager and became a shareholder in 2011. From 1991 to 2001, she worked for the Firm in financial statement auditing, internal auditing, and consulting divisions. Prior to rejoining the Firm, she served as Finance Director for the City of Mustang, Oklahoma, for seven years. Brenda has over 20 years of governmental accounting, auditing, and consulting experience. She is a frequent lecturer, trainer, and discussion leader for various groups including the Oklahoma Society of CPAs, Oklahoma Municipal League, and Oklahoma Municipal Clerks, Treasurers, and Finance Officers Association related to governmental accounting and management. She is a graduate of East Central University. She has managed multiple internal audit engagements including several State colleges and universities and State agencies. THE INTERNAL AUDIT TEAM FOR THE CITY OF EDMOND The internal audit team assembled for the City of Edmond is unparalleled in its qualifications, experience and reputation. The team’s knowledge of state and governmental accounting principles and Oklahoma State law, combined with their experience in Oklahoma State government and Oklahoma Higher Education is second to none. Under the guidance of Firm President Frank Crawford, CPA, the internal audit practice is headed by Dwayne Tate, CPA, with over 20 years’ experience with Oklahoma Higher Education institutions. Dwayne has an unprecedented understanding of colleges and universities which stems from his prior roles as Assistant Controller for the University of Central Oklahoma, Controller for Rose State College, Director of Finance for Oklahoma City Community College, and as Director of Internal Auditing for the Board of Regents for Oklahoma Colleges and Universities. To complement Dwayne Tate is a seasoned senior manager, Chris Pembrook, CPA, CGAP, Cr.FA, MBA, who has over 7 years’ experience with state agencies through his former position as Deputy Director of the Local Government and Special Services Division for the Office of State Auditor and Inspector, in addition to severing as CFO for the Oklahoma Police Pension System. Also, Chris has extensive knowledge and experience using the professional data base mining software, ACL, for audit, financial, risk and compliance data analysis. From his use of the ACL software, Chris has identified multiple instances of non-compliance with college and university pro-card purchasing policies and procedures. The internal audit team also includes Justin Kersey, CPA, CFE, and Richard Rose, CPA, both of whom have five or more years’ experience performing internal audits and financial consulting services for many Oklahoma Higher Education institutions. Brief profile descriptions are listed below. SHAREHOLDER G. DWAYNE TATE, CPA Dwayne Tate, CPA, joined Crawford & Associates in April 2005 as Consulting Manager and became shareholder in 2008. He was hired to head up the Oklahoma Higher Education Internal Audit, Consulting, and Special Projects division of the Firm. Prior to joining the Firm, he was Controller for Rose State College and Director of Finance for Oklahoma City Community College, and has a combined total of thirteen years financial management experience in Oklahoma Higher Education. He also has three years’ experience as Director of Internal Audit for the Board of Regents of Oklahoma Colleges and Universities, and two years’ experience as staff auditor with KPMG Peat Marwick. He is a graduate of the University of Oklahoma. He has managed multiple internal audit engagements including several State colleges and universities and State agencies.

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

7

MANAGER CHRIS PEMBROOK, CPA, CGAP, Cr.FA, MBA Chris Pembrook joined Crawford & Associates in September 2011. He has a degree in accounting from East Central University and an MBA from Oklahoma Christian University. Prior to joining the Firm, he served as the Chief Financial Officer of the Oklahoma Police Pension & Retirement System. He also worked for the Oklahoma State Auditor’s Office for seven years, two of the years serving as the Deputy Director of the Local Government and Special Services Division. During that time, he was responsible for all audit engagements for that division and supervised a staff of 54 employees. He was key in the implementation of division-wide use of ACL data-mining analysis software which helped decrease audit budgets from 35% - 50%. He is a graduate of East Central University. He has worked on various internal audit engagements including several State colleges and universities and State agencies. MANAGER JUSTIN KERSEY, CPA, CFE

Justin is a Certified Public Accountant and Certified Fraud Examiner, and joined Crawford & Associates in July 2008 and serves as accountant and consultant. He is a 2005 graduate of the University of Central Oklahoma with a bachelor's degree in accounting. Prior to joining the Firm, Justin worked as a fleet accountant in the international department of Hertz. He is a graduate of the University of Central Oklahoma. He has worked on various internal audit engagements including several State colleges and universities and State agencies. MANAGER RICHARD ROSE, CPA

Richard joined Crawford & Associates in January 2009 as a professional accountant and consultant. He is a 2000 graduate of the Southwestern Oklahoma State University with a bachelor's degree in accounting. Prior to joining the Firm, Richard worked as an auditor and staff accountant for Hunter & Gibbins, P.C., in Elk City, Oklahoma. He is a graduate of Southwestern Oklahoma State University. He has worked on various internal audit engagements including several State colleges and universities and State agencies. EXPERIENCE Crawford & Associates is a properly licensed CPA Firm in good standing with the Oklahoma Accountancy Board (license # 743). All of the Crawford & Associates staff that provide professional services meet or exceed all continuing education requirements of the Oklahoma Accountancy Board and the Governmental Accountability Office to the extent applicable. In addition, the Firm’s audit and attest practice undergoes a peer review once every three years as required. A copy of our most recent peer review report is attached (See Attachment H), and is also available on our web site at www.crawfordcpas.com. Crawford and Associates currently provides internal audit and consulting services to 20 of the 28 public colleges and universities in the State of Oklahoma. Eleven of those 18 are our internal audit clients, including the Six Regional Universities, Oklahoma City Community College, Rose State College, Western Oklahoma State College, Murray State College, and Eastern Oklahoma State College. We also currently provide internal audit services for the Oklahoma Firefighters Pension System and the Oklahoma Law Enforcement Retirement System. We are proud of our relationship with the numerous governmental clients we have served over the past 30 years. The majority of our clients are Oklahoma municipalities, 60 plus and counting in total. We have also served State agencies, colleges and universities, and other government trusts or organizations. Over the past thirty years we have served over 100 different state and local governments in Oklahoma and around the world. Below is a list of our State and Local Government clients with references including contact information:

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

8

LISTING OF CITY & TOWN CONSULTING CLIENTS:

Contact Title

Client Address

Phone number/Email

Donna Doolen, Finance Director/Treasurer

City of Ada 231 S Townsend Ada, OK 74821

(580) 436-6300 [email protected]

Amy Lucas, Sr. Accountant

City of Altus 509 S. Main Altus, OK 73521

(580) 481-2202 [email protected]

Joe Don Dunham, Business Manager

City of Alva 415 4th Street Alva, OK 73717-2340

(580) 327-1340 [email protected]

Betty Koehn, Finance Director

City of Bixby PO Box 70 Bixby, OK 74008-0070

(918) 366-4430 [email protected]

Robert Floyd, City Manager

City of Blanchard PO Box 480 Blanchard, OK 73010

(405) 485-9392 [email protected]

Sandy Gaches, Clerk

Town of Byars PO Box 251 Byars, OK 74831-0251

(405) 783-4255 [email protected]

Coleen Bishop, Clerk/Treasurer

Town of Byng 110 Byng Avenue Byng, OK 74820

(580) 436-2545 [email protected]

Jennifer Firgard, Clerk/Treasurer

Town of Cashion 102 S. Main Cashion, OK 73016-0027

(405) 433-2243 [email protected]

Bette Sanders, Finance Director

City of Checotah 414 W Gentry Checotah, OK 74426-2444

(918) 473-5411 [email protected]

Pam Polk, City Manager

City of Collinsville 106 N 12th St Collinsville, OK 74021-0730

(918) 371-1010 [email protected]

Janice Goins, Dep Clerk/Treasurer

City of Commerce PO Box 99 Commerce, OK 74339-0099

(918) 675-4373 [email protected]

Sondra Easterly, Clerk

Town of Covington 224 W Main Covington, OK 73730-0078

(580) 864-7428 [email protected]

Ed Stanton, City Manager

City of Crescent PO Box 561 Crescent, OK 73028-0561

(405) 969-2538 [email protected]

Brenda Wadsworth, Clerk/Treasurer

Town of Dewar PO Box 7 Dewar, OK 74431-0007

(918) 652-4042 [email protected]

Earlene Walker, Treasurer

City of Durant PO Box 578 Durant, OK 74702-0578

(580) 924-7222 [email protected]

Ross Vanderhamm, Finance Director

City of Edmond PO Box 2970 Edmond, OK 73083-2970

(405) 348-8830 [email protected]

Gayla Duke, Finance Director

City of El Reno 101 N Choctaw El Reno, OK 73036-0700

(405) 262-4070

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

9

Luena King, Clerk/Treasurer

City of Elgin PO Box 310 Elgin, OK 73538-0310

(580) 492-5777 [email protected]

Donna Hysell, Clerk/Treasurer

City of Eufaula PO Box 684 Eufaula, OK 74432

(918) 689-2534 [email protected]

Fabian Reyes, Finance Director/Treasurer

City of Frederick PO Box 399 Frederick, OK 73542-0399

(580) 335-7551 [email protected]

Mary Hays, Clerk/Treasurer

City of Geary PO Box 125 Geary, OK 73040-0125

(405) 884-54665 [email protected]

Wanda Calvert, Clerk/Treasurer

City of Guthrie PO Box 908 Guthrie, OK 73044-0908

(405) 282-2489 [email protected]

Kimberly Meek, City Manager/ Finance Director

City of Guymon 219 NW 4th St. Guymon, OK 73942-4708

(580) 338-0137 [email protected]

Tiffany Tilman, Clerk/City Manager

Town of Hennessey PO Box 306 Hennessey, OK 73742-0306

(405) 853-2416 [email protected]

Donna White, Clerk/Treasurer

City of Henryetta PO Box 608 Henryetta, OK 74437-0608

(918) 652-3348 [email protected]

Lorrie Brittian, Clerk/Treasurer

City of Holdenville PO Box 789 Holdenville, OK 74848-0789

(405) 379-3397 [email protected]

Tina Foshee, City Manager

City of Idabel 201 E Main Idabel, OK 74745-4875

(580) 286-7608 [email protected]

Tom Trueblood, Mayor

City of Kaw City PO Box 30 Kaw City, OK 74641-0030

(580) 269-2525 [email protected]

Linda Betts, Clerk

Town of Keyes PO Box 121 Keyes, OK 73947-0121

(580) 546-7651 [email protected]

Anita James, Treasurer

City of Kingfisher 301 N Main Kingfisher, OK 73750-2795

(405) 375-3705 [email protected]

Sherry Pierce, Clerk

Town of Kiowa PO Box 69 Kiowa, OK 74553-0069

(918) 432-5621

Rick Endicott, Finance Director

City of Lawton 103 SW 4th Street Lawton, OK 73501-4031

(580) 581-3305 [email protected]

Kathy Griffith, Clerk

City of Lindsay PO Box 708 Lindsay, OK 73052-0708

(405) 756-2019 [email protected]

Toni Ervin, CFO

City of McAlester PO Box 578 McAlester, OK 74502-0578

(918)423-9300 [email protected]

Barbara Bush, Clerk/Treasurer

City of Medford PO Box 123 Medford, OK 73759-0123

(580) 395-2823

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

10

Lindsay Schnakenberg, Finance Director

City of Miami PO Box 1288 Miami, OK 74355-1288

(918) 542-6685 [email protected]

Judy Redman, Finance Director/Treasurer

City of Midwest City 100 N Midwest Blvd. Midwest City, OK 73110

(405) 732-2281 [email protected]

Dawn Vieregge, City Clerk

City of Minco PO Box 512 Minco, OK 73059-0512

(405) 352-4274 [email protected]

Kim Johnson, Clerk/Treasurer

City of Morris 501 S. Hughes Morris, OK 74445

(918) 733-4222 [email protected]

Janet Watts, Finance Director

City of Mustang 1501 N Mustang Rd Mustang, OK 73064

(405) 376-4521 [email protected]

Sharon Ferguson, Treasurer

City of Newcastle PO Box 179 Newcastle, OK 73065-0179

(405) 387-4427 [email protected]

Cathy Keller, Finance Director

City of Nichols Hills 6407 Avondale Nichols Hills, OK 73116

(405) 843-6637 [email protected]

Evelyn Atkinson, Clerk/Treasurer

City of Okemah 502 W Broadway Okemah, OK 74859-2400

(918) 623-1050 [email protected]

Ronnia Andrews, Clerk

City of Okmulgee PO Box 250 Okmulgee, OK 74447-0250

(918) 756-4060 [email protected]

Sherry Bishop, Clerk

City of Owasso PO Box 180 Owasso, OK 74055-0180

(918) 376-1500 [email protected]

Jennifer Smith, Clerk

City of Piedmont PO Box 240 Piedmont, OK

(405) 373-2621

Donna Mobly, Clerk/Treasurer

City of Prague 1116 N Jim Thorpe Blvd. Prague, OK 74864-3523

(405) 567-2270 [email protected]

Kelly Lamberson, Finance Director

City of Sand Springs PO Box 338 Sand Springs, OK

(918) 246-2500 [email protected]

Pam Vann, Treasurer

City of Sapulpa PO Box 1130 Sapulpa, OK 74067-1130

(918) 224-3040 [email protected]

Joan Johnson, Clerk/Treasurer

Town of Shattuck PO Box 670 Shattuck, OK 73858-0670

(580) 938-2916 [email protected]

Brian McDougal City Manager

City of Shawnee PO Box 1448 Shawnee, OK 74802

(405) 878-1601 [email protected]

Shirley Lett, Clerk/Treasurer

Town of Skiatook PO Box 399 Skiatook, OK 74070-0399

(918) 396-2797 [email protected]

Heather Shelley, Clerk/Treasurer

Town of Springer PO Box 368 Springer, OK 73458

(580) 653-2500

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

11

Cheryl Monks, Clerk/Treasurer

City of Stigler 115 S Broadway Stigler, OK 74462-2318

(405) 372-0025 [email protected]

Shelldon Miggletto, Clerk/Treasurer

City of Stilwell 503 W Division Stilwell, OK 74960-2811

(918) 696-8111

Cheryl LaFerney, Clerk

City of Tuttle PO Box 10 Tuttle, OK 73089-0010

(405) 381-2335 cheryl.laferney@tuttle_ok.gov

Dollie Glenn, Clerk

City of Walters PO Box 485 Walters, OK 73572-0485

(580) 875-3337 [email protected]

Pamela Ramirez, Clerk/Treasurer

City of Warr Acres 5930 NW 49th St. Warr Acres, OK 73122

(405) 789-2892 cityclerk@warracres_ok.gov

Karen Johnson, Clerk/Treasurer

City of Wewoka PO Box 1497 Wewoka, OK 74884-1497

(405) 257-2413 [email protected]

Tennie Clark, Clerk/Treasurer

City of Wilburton 300 W Main St. Wilburton, OK 74578-4048

(918) 465-5361 [email protected]

Doug Haines, Finance Director/Treasurer

City of Woodward 1219 8th St. Woodward, OK 73801-3287

(580) 256-2280 [email protected]

Beverly Badgley, Clerk/Treasurer

City of Wynnewood 207 W Robert S Kerr Wynnewood, OK 73098-7603

(405) 665-2307 [email protected]

LISTING OF INTERNAL AUDIT CLIENTS:

Contact Title

Client Address

Phone number/Email

Sheridan McCaffree Executive Director

Regional University System of Oklahoma 3555 Northwest 58th Street, Suite 320 Oklahoma City, Oklahoma 73112

(405) 942-8817 [email protected]

Charlie Babb General Counsel

Regional University System of Oklahoma 3555 Northwest 58th Street, Suite 320 Oklahoma City, Oklahoma 73112

(405) 942-8817 [email protected]

Dr. Steve Turner President

Northeastern State University 600 North Grand Avenue Tahlequah, Oklahoma 74464

(918) 458-2030 [email protected]

David Koehn Vice President for Administration and Finance

Northeastern State University 600 North Grand Avenue Tahlequah, Oklahoma 74464

(918) 458-2030 [email protected]

Sue Catron Director of Business Affairs

Northeastern State University 600 North Grand Avenue Tahlequah, Oklahoma 74464

(918) 456-5511 [email protected]

Jessica Boles Vice President for Administration and Finance

East Central University 1100 East 14th Street Ada, Oklahoma 74820

(580) 559-5539 [email protected]

Susie Shockey Controller

East Central University 1100 East 14th Street Ada, Oklahoma 74820

(580) 559-5216 [email protected]

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

12

David Pecha Vice President for Administration

Northwestern Oklahoma State University 709 Oklahoma Boulevard Alva, Oklahoma 73717

(580) 327-8528 [email protected]

Ross Walkup Vice President for Business Affairs

Southeastern Oklahoma State University 1405 North 4th Avenue Durant, Oklahoma 74701

(580) 745-2148 [email protected]

Kay Lynn Roberts Controller

Southeastern Oklahoma State University 1405 North 4th Avenue Durant, Oklahoma 74701

(580) 745-2977 [email protected]

Tom Fagan Vice President for Administration and Finance

Southwestern Oklahoma State University 100 Campus Drive Weatherford, Oklahoma 73096

(580) 774-3000 [email protected]

Brenda Burgess Controller

Southwestern Oklahoma State University 100 Campus Drive Weatherford, Oklahoma 73096

(580) 774-3021 [email protected]

Lisa Harper Assistant Vice President for Financial Operations

University of Central Oklahoma 100 North University Drive Edmond, Oklahoma 73034

(405) 974-2753 [email protected]

Dr. Paul Sechrist President

Oklahoma City Community College 7777 South May Avenue Oklahoma City, Oklahoma 73159

(405) 682-1611 [email protected]

Dr. John Boyd, Vice President for Business and Finance

Oklahoma City Community College 7777 South May Avenue Oklahoma City, Oklahoma 73159

(405) 682-7501 [email protected]

Brenda Carpenter Director of Finance

Oklahoma City Community College 7777 South May Avenue Oklahoma City, Oklahoma 73159

(405) 682-1611 ext.367 [email protected]

Ray Blanke Controller

Rose State College 6420 S.E. 15th Midwest City, Oklahoma 73110

(405) 733-7314 [email protected]

Tricia Latham Vice President for Business Affairs

Western Oklahoma State College 2801 North Main Altus, Oklahoma 73521

(580) 477-7725 [email protected]

Heather Hood Controller

Western Oklahoma State College 2801 North Main Altus, Oklahoma 73521

(580) 477-7725 [email protected]

Dr. Steve Smith President

Eastern Oklahoma State College 1301 West Main Street Wilburton, OK 74578

(918) 465-1723 [email protected]

LaDonna Howell Vice President for Business & Finance

Eastern Oklahoma State College 1301 West Main Street Wilburton, OK 74578

(918) 465-1753 [email protected]

Alaina Bray Controller

Eastern Oklahoma State College 1301 West Main Street Wilburton, OK 74578

(918) 465-1895 [email protected]

Joy McDaniel President

Murray State College One Murray Campus Tishomingo, Oklahoma 73460

(580) 371-2371 [email protected]

Dennis Westman Assistant Vice President of Administrative Services

Murray State College One Murray Campus Tishomingo, Oklahoma 73460

(580) 371-2371, ext. 121 [email protected]

Ginger Poplin, Executive Director

Oklahoma Law Enforcement Retirement System 421 NW 13TH ST., SUITE 100 Oklahoma City, OK 73103

(405) 522-4932 [email protected]

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

13

Bob Jones, Executive Director

Oklahoma Firefighters Pension and Retirement System 4545 North Lincoln Blvd., Suite 265 Oklahoma City, OK 73105-3414

(405) 522-4600 [email protected]

Duane Michael, Chief Financial Officer / Assistant Executive Director

Oklahoma Firefighters Pension and Retirement System 4545 North Lincoln Blvd., Suite 265 Oklahoma City, OK 73105‐3414

(405) 522-4600 [email protected]

II. ENGAGEMENT STRATEGY – GOALS, OBJECTIVES, and SCOPE: PREPARATION AND START-UP The goal of the Internal Audit Firm is to function as an essential component of the City’s internal control process by striving to assist the City council, management, and staff in providing reasonable assurance of achieving the three primary objectives of the internal control process:

1. Financial reports are reliable and resources/assets are adequately safeguarded; 2. Operations are conducted in an effective and efficient manner, relatively free of waste and abuse; and

3. Compliance with applicable provisions of laws, regulations, grants and contracts is achieved.

In accordance with the Standards for the Professional Practice of Internal Auditing, “The objective of internal auditing is to assist management and staff of an organization in the effective performance of their responsibilities. To accomplish this objective, internal auditing provides analysis, appraisals, recommendations, counsel, and information regarding the activities reviewed. The ultimate objective of an internal audit is to promote effective internal controls at a reasonable cost. The scope of internal auditing encompasses the examination and evaluation of the adequacy and effectiveness of the organization’s system of internal control and the quality of performance in carrying out assigned responsibilities. The scope of internal auditing includes: Reviewing the reliability and integrity of financial and operating information and the means used to

identify, measure, classify, and report such information.

Reviewing the systems established to ensure compliance with those policies, plans, procedures, laws, and regulations which could have a significant impact on operations and reports, and determining whether the organization is in compliance.

Reviewing the means of safeguarding assets and, as appropriate, verifying the existence of such assets. Appraising the effectiveness and efficiency of operations within the organization. Reviewing operations or programs to ascertain whether results are consistent with established goals and

objectives, and whether the operations or programs are being implemented or performed as planned.”

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

14

METHODOLOGY To accomplish the stated goals, objectives, and scope of internal audit, Crawford & Associates, P.C., uses a six step approach which results in a risk-based long-term audit plan approved by the City in which a list of internal audit areas are identified, assessed for risk, and determined for frequency of review based on input from the City Council and Finance/Audit Committee, City management and staff, and Crawford & Associates, P.C. Listed below is our Six Step Approach:

STEP 1. Identify potential internal audit areas for audit planning purposes through City

Council/Management Survey of Importance, ranking areas for importance by High, Medium, or Low. (See example at Attachment B)

STEP 2. Perform an independent risk analysis to identify high risk audit areas for audit

planning purposes, based on the following risk factors: Materiality, Internal Controls, Public Exposure, Complexity, Change, and Pressures (See example at Attachment C)

STEP 3. Develop engagement profile forms for each audit area to include the audit area’s risk

score and estimated hours. (See example at Attachment D) STEP 4. Prepare an annual written internal audit plan based upon the priorities determined by

the risk analysis and City Council/Management input. (See example at Attachment E) STEP 5. Perform an annual internal audit in accordance with the plan and professional

standards. STEP 6. Report the results of the internal audit and any recommendations in writing to the City

Council and Finance/Audit Committee. (See examples at Attachment F)

The internal audit will be performed in accordance with generally accepted accounting principles (GAAP) and auditing standards as set forth by the American Institute of Certified Public Accountants (AICPA), and other applicable professional standards. We will also utilize professional auditing software, such as ACL data-mining analysis software, to perform the internal audit in an efficient and effective manner. III. Fees and Costs Fees and out-of-pocket expenses for this engagement will be billed monthly as the work progresses and are payable upon receipt of our invoices. Out-of-pocket expenses include such costs incurred by our Firm in providing the services including travel, lodging, telecommunications, printing, document reproduction, and the like, excluding any such expenses incurred directly by the City on behalf of our staff. Our fees for these services will be billed at our standard hourly rates, as follows, for the individual performing such services based on the actual number of hours of work, including travel time, performed by that individual. Standard Hourly Rates:

Firm Chairman $225 Firm President $225 Shareholders $155 Consulting Managers $140 Consulting Staff $100 Clerical Staff $35

The estimated fees for this internal audit engagement have been summarized at Attachment G – Statement of Fees and Calculation of Estimated Hours.

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

15

ATTACHMENT A – ORGANIZATION CHART

Frank Crawford, CPA Firm President

& Majority Shareholder

Marcy Twyman, CPA Minority & Managing

Shareholder

Brenda Wright, CPA Minority Shareholder

Dwayne Tate, CPA Internal Audit & Minority

Shareholder

Deanna Crawford, CPA Minority Shareholder

Wendy Treadwell

Quality Assurance

Tammy Hunt Quality Assurance, Client Support

Richard Rose, CPA* IT

Andrea Depee CIC Support

Kimberly Green Customer Service

Candy Dow Administrator Assistant

Justin Kersey, CPA Internal Audit &

Consulting Manager

Chris Pembrook, MBA, CPA, CGAP, CR.FA

Internal Audit & Consulting Manager

Richard Rose, CPA* Internal Audit &

Consulting Manager

Joni Parker, CPA Consulting Manager

Stephanie Ballard, CPA

Consulting Manager

D. Ann Matthews Consulting Staff

Courtney Crowder Consulting Staff

Jennifer Traxler Consulting Staff

Andres Numez Consulting Staff

Kristin Lamar, MBA Consulting Staff

Amanda Copeland, CPA

Consulting Manager

Kristy Awtry Consulting Staff

*Denotes Dual Role Yellow highlight denotes staff assigned directly to the City of Edmond internal audit proposal

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

ATTACHMENT B – CITY COUNCIL/MANAGEMENT SURVEY

CRAWFORD & ASSOCIATES LIST OF INTERNAL AUDIT AREAS

CITY COUNCIL / MANAGEMENT SURVEY OF IMPORTANCE

Instructions: The purpose of this Survey of Importance is to facilitate a risk-based approach to the performance of internal audit type monitoring procedures on an annual basis. The summary of this Survey’s results will be considered in conjunction with our Firm’s assessment of risk and the amount of resources made available for internal audit type monitoring activities to determine the frequency of audit for each potential internal audit area. Please indicate your assessment of the importance for each of the following Engagement Areas by circling the appropriate letter (H = High, M = Medium, or L = Low).

Engagement Name

Engagement Description

Board/Mgmt.Importance

(H,M,L,)

1. Sales Tax Revenue Collection and Usage Review and evaluate internal controls, policies and procedures, and records for ensuring accurate and complete revenue collection and timely deposit, and to ensure compliance with approved use of sales tax revenues.

H M L

2. Utility Billing System and Revenue Collection

Review and evaluate the internal controls, policies and procedures for utility billing, and compare to actual accounts and billings and approved rate schedules, to determine the level of compliance with those policies and procedures, and to determine the accuracy and completeness of the assessment of utility billings.

H M L

3. Hotel/Motel Tax Revenue Collection Review and evaluate the internal controls, policies and procedures, and records for ensuring accurate and complete revenue collection and timely deposit. H M L

4. Municipal Court Revenue Collection Review and evaluate the internal controls, policies and procedures, and records for ensuring accurate and complete revenue collection and timely deposit. H M L

5. Parks & Recreation – Operations & Revenue Collections

Review and evaluate the internal controls, policies and procedures for operations and evaluate the adequacy and effectiveness for proper safeguarding of assets and the accuracy and completeness of revenue collections.

H M L

6. Human Resources and Payroll

Review and evaluate the internal controls, policies and procedures, and records for payroll expenditures, and test for accuracy and existence. Also, review and evaluate the internal controls, procedures, and records documenting the process of hiring new employees, terminations and retirements, and determine compliance with the established design of internal controls.

H M L

7. Purchasing, Payables, & Expenditures

Review and evaluate internal controls, policies and procedures, and records for purchasing and payables/expenditures to verify accuracy, completeness, and evidence of proper approval, and to ascertain compliance with all applicable laws, regulations, and procedures for purchasing and payables.

H M L

8. Procurement/Purchasing Card (Pro-Card) Review and evaluate the internal controls, policies and procedures for the City’s use of the Pro-Card and determine the level of compliance with those policies and procedures (using Data Analysis/Mining software - ACL).

H M L

9. Grants and Contracts

Review and evaluate the internal controls, policies and procedures for administering grants and contracts and evaluate the adequacy and effectiveness for proper safeguarding of assets. Also, review related expenditure records to verify evidence of proper approval and verification of allowable costs, and ascertain compliance with all applicable laws and regulations relating to grants and contracts.

H M L

10. Fleet Management

Review/Performance of preventive maintenance practices, fleet availability, cost effectiveness, and fuel usage.

H M L

11. Cash-on-Hand Review and evaluate the internal controls and procedures for safeguarding cash, and perform cash counts to verify existence. H M L

12. Capital Assets Review and evaluate the internal controls, procedures, and records for receiving, recording, disposing, and tracking capital assets. H M L

CRAWFORD & ASSOCIATES LIST OF INTERNAL AUDIT AREAS

CITY COUNCIL / MANAGEMENT SURVEY OF IMPORTANCE

Instructions: The purpose of this Survey of Importance is to facilitate a risk-based approach to the performance of internal audit type monitoring procedures on an annual basis. The summary of this Survey’s results will be considered in conjunction with our Firm’s assessment of risk and the amount of resources made available for internal audit type monitoring activities to determine the frequency of audit for each potential internal audit area. Please indicate your assessment of the importance for each of the following Engagement Areas by circling the appropriate letter (H = High, M = Medium, or L = Low).

Engagement Name

Engagement Description

Board/Mgmt.Importance

(H,M,L,)

13. General Ledger Account Reconciliations

Review and evaluate the internal controls, procedures, and records documenting the performance of the account reconciliations (e.g., cash), including outstanding reconciling items, and determine compliance with the established design of internal controls.

H M L

14. Information Technology – General Controls

Review and evaluate the general internal controls, policies and procedures regarding the information system (e.g., passwords, segregation of duties, data protection).

H M L

15. Disaster Recovery Plan Review and evaluate the internal controls, policies and procedures, for administering the City’s Disaster Recovery Plan and determine compliance thereof.

H M L

16. Police – Seized Property Inventory Review and evaluate the internal controls & policies and procedures as it relates to compliance with applicable laws & regulations. H M L

17. Follow-up on Prior Year Audit Findings Review and evaluate the City’s implementation of its corrective action plan to the prior year audit findings, as documented in the City’s Management Responses.

Required Annually

1. Please list below your top three areas from the listing above, those that are most important to you: 1.

2.

3.

2. Please list below any additional areas you would like the internal audit function to consider:

1.

2.

3. 4.

5.

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

ATTACHMENT C – RISK ASSESSMENT

CRAWFORD & ASSOCIATES INDEPENDENT INTERNAL AUDIT SERVICE

RISK ASSESSMENT FORM

AUDIT AREA: Human Resources and Payroll

Risk Factor Evaluation

Weight Score

1. Materiality The measure of the exposure to loss or embarrassment due to the relative dollar significance of the audit area to the budget or financial statements as a whole.

3 Over 10% of base 2 Between 2-10% of base 1 Under 2% of base Value selected: 3

x 4

12 2. Internal Controls The measure of the quality of the existing internal controls over the audit area based on existing knowledge and past audits.

3 Known to be weak 2 Acceptable 1 Known to be strong Value selected: 1

x 3

3

3. Public Exposure The measure of the likely political exposure and adverse publicity resulting from public perception or regulatory impact.

3 Major impact 2 Minor impact 1 No impact Value selected: 3

x 4

12 4. Complexity The measure of the overall complexity of the audit area including: degree of regulation, degree of automation, and number of transactions and processes.

3 Very complex 2 Moderately complex 1 Not complex Value selected: 3

x 1

3

5. Change The measure of the degree of changes in the audit areas operations in the last 12 months, including: changes in key personnel, changes in systems, and reorganization.

3 Major changes 2 Moderate changes 1 Little or no changes Value selected: 1

x 2

2

6. Pressures The measure of the degree of internal and/or external pressures on management or employees of the audit area to meet certain objectives, either personal or professional.

3 Significant pressures 2 Moderate pressures 1 Little or no pressure Value selected: 1

x 3

3

Total Score For Audit Area

35

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

ATTACHMENT D – ENGAGEMENT PROFILE

CRAWFORD & ASSOCIATES INDEPENDENT INTERNAL AUDIT SERVICE

ENGAGEMENT PROFILE FORM AUDIT AREA: Human Resources and Payroll RISK SCORE: 35 ESTIMATED AUDIT HOURS: 24-32 ENGAGEMENT FREQUENCY: Every 2 - Years INTERNAL CONTROL OBJECTIVE(S) AFFECTED:

X Financial Reporting Reliability and/or Safeguarding of Resources

Effective and Efficient Operations, Controls over Waste and Abuse

X Compliance with Laws, Regulations, Grants and Contracts ENGAGEMENT DESCRIPTION:

The system of internal control and administrative procedures surrounding the payroll process will be reviewed and evaluated for adequacy and effectiveness. Considering that payroll expenditures comprise approximately 80 % of the College’s Educational and General Budget, internal controls must be adequate and effective to properly safeguard College assets. A random sample of payroll records will be selected for testing to verify accuracy, existence, and completeness, and to ascertain compliance with applicable laws and regulations. ANTICIPATED ENGAGEMENT BENEFITS:

Deterrent to or Detection of Waste and Abuse

X Improved Policies, Programs or Controls

X Enhanced Reliability of Financial Reports X Enhanced Compliance

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

ATTACHMENT E – INTERNAL AUDIT PLAN

CRAWFORD & ASSOCIATES INTERNAL AUDIT PLAN

FY 2014

Engagement Name Risk Score

City Council/Mgmt. Importance

(H,M,L,)

Estimated Hours

1. Sales Tax Revenue Collection and Usage 40 M 16-24

2. Utility Billing System and Revenue Collection 40 M 16-24

3. Human Resources and Payroll 35 H 16-24

4. Purchasing, Payables, & Expenditures 35 H 16-24

5. Procurement/Purchasing Card (Pro-Card) 35 H 16-24

6. Grants and Contracts 35 M 16-24

7. Follow-up on Prior Year Audit Findings N/A N/A 16-24

8. Report Writing, Meetings, and Presentations -- -- 24-32

Total Planned Hours 136-200

CRAWFORD & ASSOCIATES

LIST OF INTERNAL AUDIT AREAS & PROPOSED SCHEDULE ASSESSMENT OF RISK & IMPORTANCE

Engagement Name Risk Score

City Council/Mgmt.

Importance (H,M,L,)

Estimated Hours

Planned

Frequency Proposed Schedule per Fiscal Year

2014 2015 2016 2017 2018

1. Sales Tax Revenue Collection and Usage 40 M 16-24 2 years

2. Utility Billing System and Revenue Collection

40 M 16-24 2 years

3. Hotel/Motel Tax Revenue Collection 25 L 16-24 4 years

4. Municipal Court Revenue Collection 25 L 16-24 4 years

5. Parks & Recreation – Operations & Revenue Collections

25 L 16-24 4 years

6. Human Resources and Payroll 35 H 16-24 2 years

7. Purchasing, Payables, & Expenditures 35 H 16-24 2 years

8. Procurement/Purchasing Card (Pro-Card) 35 H 16-24 2 years

9. Grants and Contracts 35 M 16-24 3 years

10. Fleet Management 35 M 16-24 3 years

11. Cash-on-Hand 30 M 16-24 3 years

12. Capital Assets 25 L 16-24 4 years

13. General Ledger Account Reconciliations 25 L 16-24 4 years

14. Information Technology – General Controls

35 H 16-24 2 years

15. Disaster Recovery Plan 35 H 16-24 2 years

16. Police – Seized Property Inventory 30 M 16-24 3 years

17. Follow-up on Prior Year Audit Findings N/A N/A 16-24 Annual

PROPOSAL FOR INTERNAL AUDIT SERVICES FOR THE CITY OF EDMOND

INTERNAL AUDIT SERVICES RFP14-012

ATTACHMENT F – INTERNAL AUDIT REPORTS

[Date] [Example Council] [Address] [City], OK [Zip code] Re: Report on Internal Audit Type Monitoring Activities – [Example Entity] Members of the Council: The [Example] engaged Crawford and Associates, P. C. to provide certain professional services as identified in the Scope and Objectives of Our Services section below with regards to [Example Entity (EE)]. This report describes the scope and objectives of our services, the specific procedures we performed, our findings and recommendations, and (EE) management’s responses to our findings and recommendations. Scope and Objectives of Our Services The scope of our professional services was limited to performing certain consulting services designed to assist the [Example Council] in meeting its fiduciary responsibilities. These services were performed in accordance with the standards applicable to consulting engagements of the American Institute of Certified Public Accountants. With regards to this specific engagement, the scope of our services included certain internal audit type monitoring procedures in the following areas at (EE):

Purchasing Procurement Card Human Resources/Employment Services & Payroll Capital Assets Cash-on-hand Grants & Contracts

The objectives of our services in this engagement were to obtain information and review selected accounting records to determine whether any recommendations are warranted regarding the design of established internal control policies and procedures, and to report on the level of compliance with those policies and procedures as designed based on our test work. Purchasing Procedures Performed: To accomplish the stated objectives, we performed the following procedures:

Obtained and reviewed (EE) and [Example Council] policies and procedures regarding purchasing. We also conducted interviews with appropriate management and personnel.

Selected a random sample of 34 purchase orders processed during the audit scope period of January 1, 2013 through December 31, 2013. To ensure a proportionately representative selection, we stratified the sample in the following manner:

o Five (5) purchase orders greater than $2,500, but less than or equal to $10,000 – those requiring a minimum of three verbal quotes;

Procedures Performed – continued:

o Four (4) purchase orders greater than $10,000, but less than or equal to $25,000 – those requiring a minimum of three written quotes;

o Six (6) purchase orders greater than $25,000, but less than or equal to $100,000 – those requiring competitive bids and must be reported to the [Example Council] ;and

o Nineteen (19) purchase orders greater than $100,000 – those requiring [Example Council] approval before purchase.

For each purchase order selected, we verified there was properly documented approvals and compliance with

purchasing policies and procedures including but not limited to quote, competitive bid, and/or [Example Council] notification or approval requirements.

Findings: All purchase orders tested were properly approved in accordance with (EE) and [Example Council] policies

and procedures.

All purchase orders tested complied with all quote, competitive bid, and/or [Example Council] notification or approval requirements.

Recommendations: We have no recommendations at this time. Procurement Card Procedures Performed: To accomplish the stated objectives, we performed the following procedures:

Obtained and reviewed (EE) policies and procedures, and laws and regulations regarding the use of the procurement card. We also conducted interviews with appropriate management and personnel.

Performed data analysis of procurement card transactions for the audit scope period of January 1, 2013

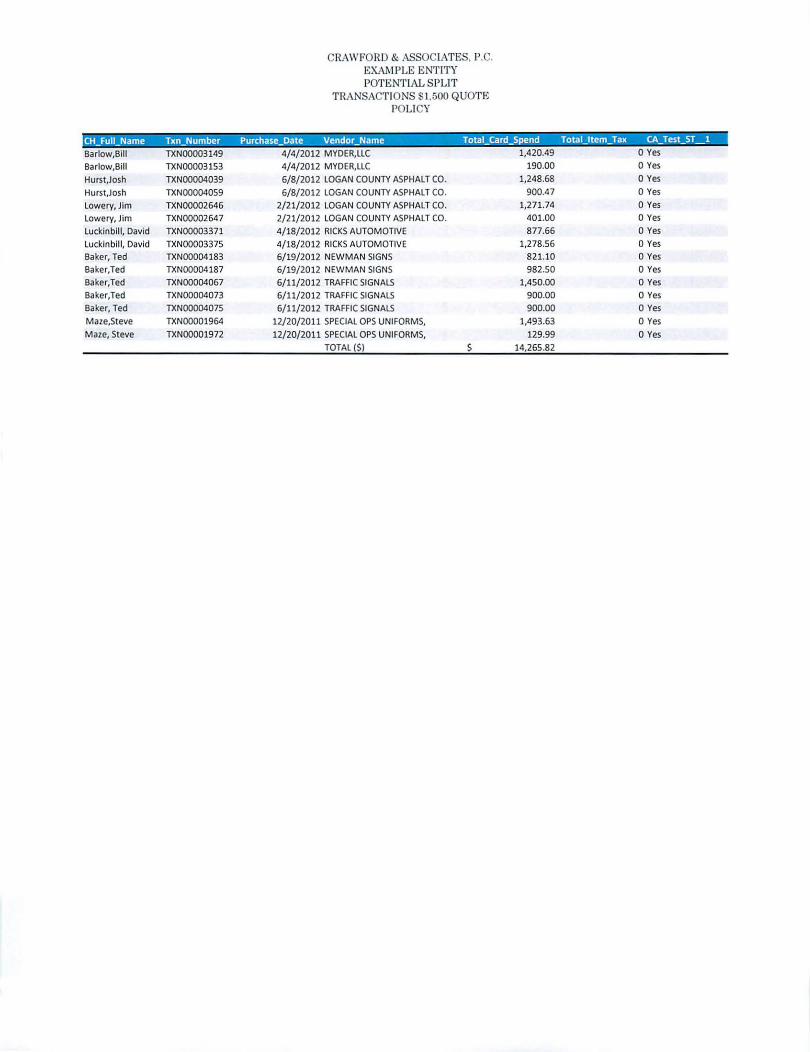

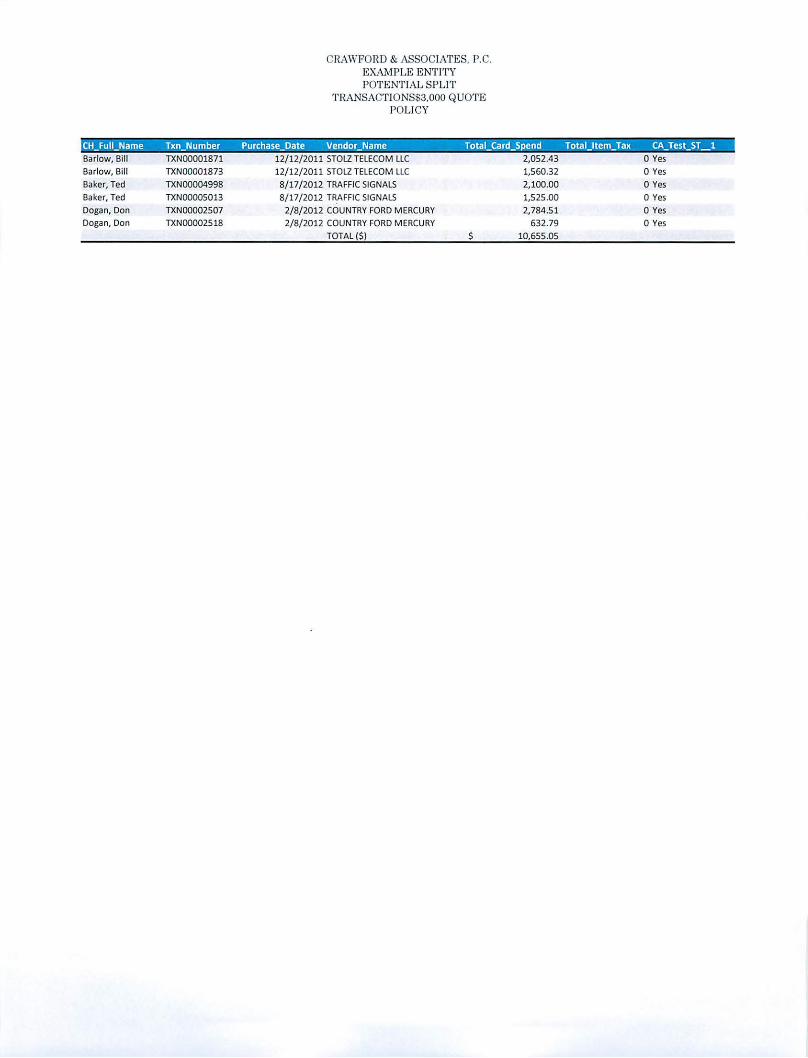

through December 31, 2013, for 190 cards with 12,655 transactions, to ensure that no single purchase exceeded the individual purchase amounts set forth by (EE) policies and the individual card limit, to ensure cardholders did not split transactions in order to make purchases in excess of their single transaction limit, and to ensure that the monthly billing cycle purchase limit did not exceed the card limit as set forth by (EE) policies and the individual card limit.

Through the use of data analysis procedures we judgmentally selected monthly billing cycles for twenty one

(21) cardholders from the audit scope period of January 1, 2013 through December 31, 2013. For each monthly billing cycle selected, we verified whether supporting documentation indicated the following:

o All charges were properly supported by invoices or other supporting documentation.

o All charges were properly approved.

o All charges appear to be for a public purpose.

o All charges were for allowable purchases set by (EE) policy.

Findings:

All procurement card transactions tested were properly within cardholder limits for monthly billing cycle limits.

All procurement card transactions tested were properly approved.

12,654 of the total 12,655 transactions tested were properly supported by invoices or other supporting documentation. The following is the one charge noted that was not properly supported:

o One purchase only had a total charge receipt and not a detail receipt. So testing of public purpose and what was actually purchased could not be determined.

12,651 of the 12,655 transactions tested were expended for a public purpose. The following are the four (4) charges noted that were not for a public purpose:

o One (1) purchase of personal shoes o Two (2) purchases of funeral flowers o One (1) purchase of a sympathy card

12,650 of the 12,655 transactions tested were in compliance with (EE) policy regarding charges for allowable

purchases. The following are the five (5) charges noted that were not allowable purchases according to (EE) policy:

o Two (2) purchases of computer monitors o One (1) purchase of a printer over $500 o One (1) purchase of gasoline o One (1) purchase of travel-related (i.e., parking) expense

12,647 of the total 12,655 transactions tested were in compliance with (EE) policy regarding split purchasing.

We identified four (4) instances involving eight (8) transactions in which a cardholder split a purchase and exceeded the individual transaction limit. Of the four (4) instances noted, two (2) of the transactions had been identified and addressed by the procurement card administrator prior to our beginning the internal audit.

Recommendations: We recommend (EE) management provide additional training to cardholders who have violated (EE) policies, specifically addressing split purchase transactions and unallowable purchases. We also recommend (EE) management update the Procurement Card policy to reflect current practices on campus. Human Resources/Employment Services and Payroll Procedures Performed: To accomplish the stated objectives, we performed the following procedures:

Obtained and reviewed (EE) policies and procedures regarding Human Resources/Employment Services and Payroll. We also conducted interviews with appropriate management and personnel to gain an understanding of and to document the internal controls surrounding the employment services and payroll processes. We then conducted a walkthrough of the employment services and payroll processes, and evaluated the established internal controls as designed, noting any recommendations for strengthening those controls.

Procedures Performed – continued:

Selected a random sample of 20 new hires (8%) from a total of 266 newly hired employees for the audit

scope period of January 1, 2013 through December 31, 2013. For each new employee selected, we reviewed their personnel file to verify that all required documentation for processing a new hire was present and properly completed. We also reviewed the FLSA Exempt or Nonexempt classification for each new employee selected to verify the proper classification. We recalculated and compared the salary or hourly rate paid per the monthly payroll to the authorized pay rate per the Employee Transaction Form or Contract. We also compared the W-4 information in the payroll system to the W-4 Form.

Selected a random sample of 15 additional employees (2%) from a total of 703 active employees hired before the audit scope period of January 1, 2013 through December 31, 2013. For each employee selected we reviewed the FLSA Exempt or Nonexempt classification to verify the proper classification. We recalculated and compared the salary or hourly rate paid per the monthly payroll to the authorized pay rate per the Employee Transaction Form or Contract. We also compared the W-4 information in the payroll system to the W-4 Form.

Selected a random sample of 5 terminated employees (13%) from a total of 40 terminations (i.e., retirements, resignations, discharges, other) for the audit scope period of January 1, 2013 through December 31, 2013. For each terminated employee selected, we reviewed their personnel file to verify that all required documentation for processing a termination was present and properly completed.

Verified the proper display of Workplace Posters as required by the U.S. Department of Labor and the State of

Oklahoma Department of Labor.

Requested copies of any amended W-2’s and supporting documentation of changes for the audit scope period of January 1, 2013 through December 31, 2013.

Requested any unclaimed payroll checks and supporting documentation of follow-up for the audit scope period of January 1, 2013 through December 31, 2013.

Findings:

From the review of existing internal controls surrounding the employment services and payroll processes, we

noted that the HR Director obtains the required documentation necessary to hire a new employee (i.e., create a new record) or make changes to an existing employee’s record, and then the payroll accountant enters that information into the HR/Payroll System. There is no subsequent independent review within the HR and Payroll Office of the data entry to the source documentation to verify the completeness and accuracy of that information entered into the payroll system. However, a system-generated Payroll Reconciliation Report for Gross Amounts is run by the payroll accountant who provides explanations for changes and submits said Report to the Vice President for Administration for their review.

For the new employees hired during the audit scope period and selected for testing:

o Nineteen (95%) of the twenty new hires selected for testing had all of the required documentation for

processing a new hire (e.g., Employee Transaction Form or Contract, I-9, E-Verify, W-4, Drug-Free Workplace Policy, Loyalty Oath, insurance forms) present and properly completed. One of the new hires’ files did not contain a completed Drug-Free Workplace Policy form.

o All FLSA Exempt or Nonexempt positions were properly classified. o All salary and hourly rate amounts paid, per the monthly payrolls selected, properly agreed to the

authorized pay rate per the Employee Transaction Form or Contract. o All W-4 information in the payroll system properly agreed to the W-4 Form.

Findings – continued:

For the active employees hired prior to the audit scope period and selected for testing:

o All FLSA Exempt or Nonexempt positions were properly classified. o All salary and hourly rate amounts paid, per the monthly payrolls selected, properly agreed to the

authorized pay rate per the Employee Transaction Form or Contract. o All W-4 information in the payroll system properly agreed to the W-4 Form.

For the terminated employees, terminated during the audit scope period and selected for testing, all required

documentation for processing a termination was present and properly completed.

All Workplace Posters as required by the U.S. Department of Labor and the State of Oklahoma Department of Labor were properly displayed.

There were no amended W-2’s noted for the audit scope period.

There were no unclaimed payroll checks noted for the audit scope period. Recommendations:

1. We recommend (EE) management implement an independent review process within the HR and Payroll Office to ensure the accuracy and completeness of data entry to the source documentation for either creating a new payroll record or modifying an existing record. We further recommend that the independent review be performed by the HR Director prior to submitting the Payroll Reconciliation Report for Gross Amounts to the Vice President for Administration.

2. We recommend (EE) management reinforce with staff compliance with the designed internal control procedure to properly maintain all required supporting documentation and forms in the personnel files. We further recommend that documentation supporting staff’s due diligence and good-faith efforts or attempts to obtain the required forms also be maintained in the personnel files.

Capital Assets Procedures Performed: To accomplish the stated objectives, we performed the following procedures:

Obtained and reviewed (EE) policies and procedures regarding capital assets. We also conducted interviews with appropriate management and personnel.

Selected a random sample of 10 capital asset additions (66.7%) from a total of 15 capital assets added during

the audit scope period of January 1, 2013 through December 31, 2013. For each of the additions selected, we verified the asset was properly located, properly tagged, and agreed to the invoice regarding description, date acquired, and amount.

Selected a random sample of 20 capital assets from the capital assets listing and traced them to the floor. For

each of the capital assets selected, we verified the asset was properly located, properly tagged, properly included in the inventory records, and had a matching description in the inventory records.

Selected a random sample of 5 capital assets from the floor and traced them to the capital assets listing. For each of the capital assets selected, we verified the asset was properly located, properly tagged, properly included in the inventory records, and had a matching description in the inventory records.

Procedures Performed – continued:

Selected a random sample of 10 capital asset disposals (91%) from a total of 11 capital assets disposed during the audit scope period of January 1, 2013 through December 31, 2013. For each of the disposals selected, we verified the asset was properly disposed or deleted from the capital assets listing in compliance with asset disposal policies and procedures.

Findings:

For the capital asset additions selected for testing:

o All capital assets were properly located. o All capital assets were recorded with the correct description and date acquired.

o Eight (80%) of the 10 capital assets were recorded at the correct amount or invoice cost. The

following two capital assets were not recorded at the correct amount:

Asset ID Asset Reported Actual

Item # Number Description Amount Cost

1 013099 Latitude E5520 Laptop $ 10,208.37 $ 1,208.37 2 N/A ST Imaging Digital Printer $ 8,975.00 $ 9,195.00

o Six (60%) of the 10 capital assets were properly tagged. The following four capital assets were not tagged:

Asset ID Asset Dollar Item # Number Description Location Amount 1 Not Tagged Cybex 770T-CT Treadmill WC $ 10,538.50 2 Not Tagged ST Imaging Digital Printer LB $ 9,195.00 3 Not Tagged Z925A MN $ 8,947.00 4 Not Tagged John Deere Gator TX AGE $ 6,555.00

For the capital assets selected for list to floor testing:

o Sixteen (80%) of the 20 capital assets could be located. The following four capital assets could not be located:

Asset ID Asset Reported Dollar

Item # Number Description Location Amount

1 010691 Polycom BS4000 CODEC H.323 IE-129 $ 7,049.53 2 4-28622 1996 Chevy Van MN-SHED $ 21,525.00 3 008288 Alpha Server 400 SH-203 $ 9,434.00 4 006867 Treadmill WC-206 $ 6,140.00

Findings – continued:

o All sixteen of the capital assets that were located had a matching description in the inventory records.

o Twelve (75%) of the 16 capital assets located were properly tagged. The following four capital

assets did not have a tag number issued:

Asset ID Asset Dollar Item # Number Description Location Amount 1 N/A Kwikgoal Pro Premier Goal 2B8 Field $ 5,500.00 2 N/A Sewer machine Mongoose 184 Fleet Building $ 37,840.00 3 N/A Polycom VS4000 CODEC H.323 EN-220 $ 7,049.00 4 N/A Polycom VS4000 CODEC H.323 EN-208 $ 8,050.00

o Twelve (75%) of the 16 capital assets located were located in the proper location according to inventory records. The following four capital assets were found, but were not located in their proper location according to inventory records:

Asset ID Asset Reported Dollar

Item # Number Description Location Amount

1 N/A Polycom VS4000 CODEC H.323 EN-220 $ 7,049.00 2 N/A Polycom VS4000 CODEC H.323 EN-208 $ 8,050.00 3 011341 Viewstation 82033034C3DM7 EN $ 10,949.00 4 010366 Polycom VS400 CODEC H.323 WW-B $ 8,400.00

For the capital assets selected for floor to list testing:

o All five of the capital assets had a proper matching description in the inventory records.

o Three (60%) of the 5 capital assets were properly tagged. The following two capital assets did not have a tag number recorded in the inventory listing:

Asset ID Asset Dollar Item # Number Description Location Amount 1 13474 Elmo Projector WW-116 $ 1,964.00 2 12561 IETV Camera EN-220 $ 3,499.30

o Four (80%) of the 5 capital assets were located in the proper location according to inventory records.

The following capital asset did not have a room location recorded in the inventory records:

Asset ID Asset Dollar Number Description Location Amount 13474 Elmo Projector WW-116 $ 1,964.00

Findings – continued:

All ten of the capital asset disposals selected for testing were traced to the appropriate documentation to support the deletion.

Recommendations: We recommend (EE) management and staff responsible for maintaining the capital assets inventory system and accounting for capital assets ensure that:

All capital asset additions are properly recorded at actual cost; All capital assets are properly located; All capital assets are properly tagged; and Inventory records are updated on a regular basis to remain current.

Cash-on-Hand Procedures Performed: To accomplish the stated objectives, we performed the following procedures:

Obtained and reviewed (EE) policies and procedures regarding cash-on-hand. We also conducted interviews with appropriate management and personnel to gain an understanding of and to document the internal controls for safeguarding cash-on-hand.

Obtained a complete listing of cash-on-hand, noting locations and authorized amounts. We then conducted a walkthrough of certain selected locations and evaluated the established internal controls, as designed for safeguarding cash-on-hand, noting any recommendations for strengthening those controls. We also conducted unannounced or surprise cash counts at certain selected locations to verify the accuracy and completeness of cash-on-hand.

Obtained daily cashier checkout (end of day balancing) forms for certain selected days during the audit scope period of January 1, 2013 through December 31, 2013, to test compliance with the internal control policies and procedures as designed.

Findings: