China Aviation Oil (CAO) - International Insolvency Institute

18

1 Some Recent Some Recent Insolvencies Insolvencies in Singapore in Singapore Kannan Ramesh Kannan Ramesh Senior Partner Senior Partner Tan Kok Quan Partnership Tan Kok Quan Partnership

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of China Aviation Oil (CAO) - International Insolvency Institute

11

Some Recent Some Recent InsolvenciesInsolvenciesin Singaporein Singapore

Kannan RameshKannan Ramesh

Senior PartnerSenior Partner

Tan Kok Quan PartnershipTan Kok Quan Partnership

22

China Aviation OilChina Aviation Oil (CAO)(CAO)

PwC appointed by the CAO on the direction of the Stock Exchange of Singapore to investigate CAO�s oil trading losses of about USD550 million and to report its findings to SGX.

TKQP retained by PWC as counsel to advise and assist PWC in the investigation.

33

Events Leading to CAOEvents Leading to CAO��s Lossess Losses

CAO took a bearish view of oil prices after 3 Q 2003.

4Q 2003 � Marked-to-Market (�MTM�) value of CAO�s speculative options deteriorated as oil prices rose.

Options maturing in 1Q 2004 � CAO�s view was that if losses were not realized, no requirement to account for losses in its financial statements. This was incorrect.

First restructuring of options on 26 January 2004.

44

Restructurings (1)Restructurings (1)

Restructuring effected by the purchase of option contracts to close out the loss making options. CAO financed this by selling longer dated options with higher strike prices and volumes which stretched out to 4Q 2005.

Intent was to achieve zero net cashflow.

However, MTM value of new options also deteriorated as oil prices continued to rise. Margin calls made against CAO from May 2004 onwards.

55

Restructurings (2)Restructurings (2)

Second restructuring undertaken in June 2004 with same intent of achieving zero net cashflow.

However, the continued rise in oil prices resulted in a further deterioration of the MTM. Further margin calls were made.

Third restructuring exercise was undertaken in September 2004.

CAO eventually ran out of funds to meet the margin calls.

66

Critical FailuresCritical FailuresCritical failures at every tier of CAOCritical failures at every tier of CAO��s risk control structure:s risk control structure: Front office Middle Office Back Office Risk Management Committee (�RMC�) Internal Audit Division (�IAD�) Managing Director (�MD�) and Chief Executive Officer

(�CEO�) Audit Committee (�AC�) Other DirectorsIn this presentation, we will look specifically at the IAD, the MDand CEO, the AC and the other Directors.

77

IADIAD

IADIAD eexisted in name only and did not make regular reports to the AC. Its reports were repetitive and perfunctory. They were inaccurate in giving the impression that CAO�s internal controls were operating satisfactorily.

88

MD and CEOMD and CEO

Mr Chen Jiulin bore primary responsibility for: commencing options trading without understanding

precisely what it entailed and without ensuring there was proper and prior evaluation of the risks involved

committing CAO to imprudent risks in the restructurings failing to report CAO�s MTM losses in its financial reports fostering a culture of secrecy.

Impression of those working with Mr Chen was that he waspropelled by a need to surpass past achievements. Evidencesuggested that he was motivated to conceal the MTM lossesas a matter of personal ambition.

99

ACAC

Amongst other things, AC failed to ensure that there was an effective system of internal controls and risk management to identify, evaluate and manage the business risks for speculative trading of options after being told of such activity. AC did not request for regular management reports and monitor periodically CAO�s speculative derivatives positions, its financial exposure to such positions and the MTM value of such positions.

1010

Other DirectorsOther Directors

Nominee directors on the Board knew or ought to have known of the fact that the CAO was speculating in futures and swaps. They could have learnt of the options trading from information that was publicly available. However, they did not take steps to enforce controls on such trading. This was a serious corporate governance failure.

1111

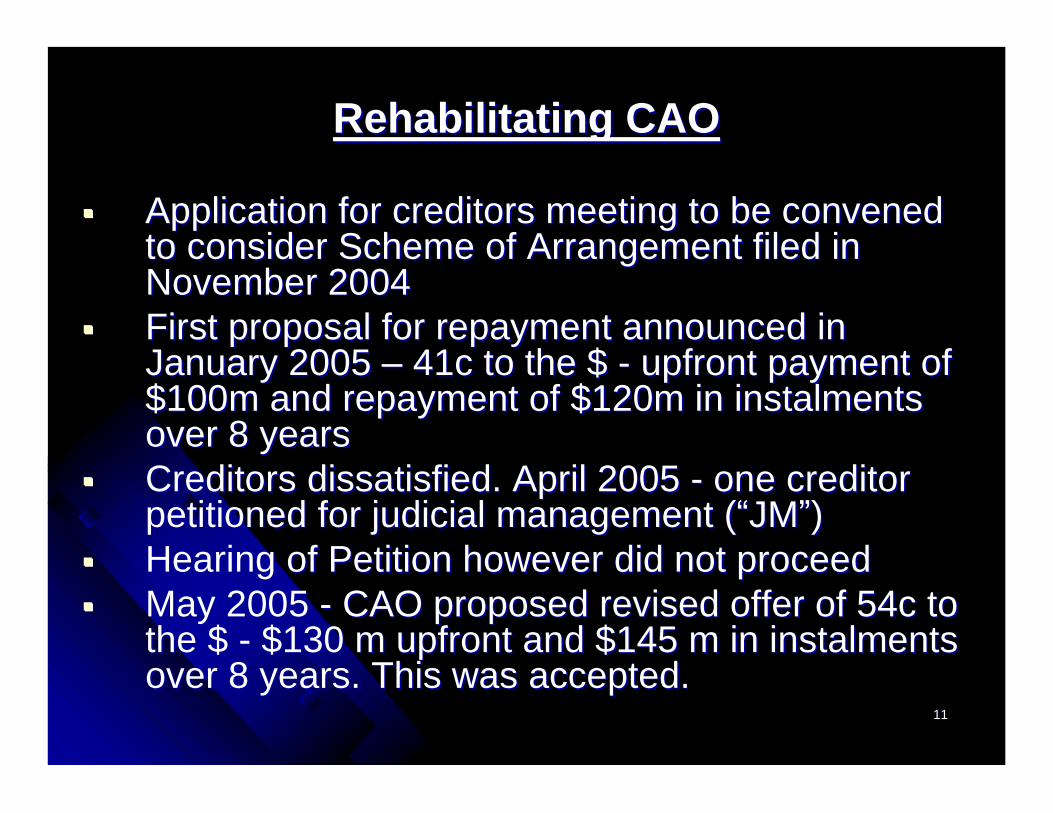

Rehabilitating CAO Rehabilitating CAO

Application for creditors meeting to be convened Application for creditors meeting to be convened to consider Scheme of Arrangement filed in to consider Scheme of Arrangement filed in November 2004November 2004

First proposal for repayment announced in First proposal for repayment announced in January 2005 January 2005 �� 41c to the $ 41c to the $ -- upfront payment of upfront payment of $100m and repayment of $120m in instalments $100m and repayment of $120m in instalments over 8 yearsover 8 years

Creditors dissatisfied. April 2005 Creditors dissatisfied. April 2005 -- one creditor one creditor petitioned for judicial management (petitioned for judicial management (��JMJM��))

Hearing of Petition however did not proceedHearing of Petition however did not proceed May 2005 May 2005 -- CAO proposed revised offer of 54c to CAO proposed revised offer of 54c to

the $ the $ -- $130 m upfront and $145 m in instalments $130 m upfront and $145 m in instalments over 8 years. This was accepted.over 8 years. This was accepted.

1212

Need for Cross Border Insolvency LawNeed for Cross Border Insolvency Law

With SGX�s push for overseas companies to list in Singapore, the potential for insolvencies with cross border elements has increased dramatically. CAO is one example of a overseas company that listed in Singapore and was subsequently insolvent. Asia Pulp & Paper Co Ltd Asia Pulp & Paper Co Ltd ((��APPAPP��) ) is another. In APP, the need for the law to provide for cross border insolvency elements was amply demonstrated.

1313

Asia Pulp & Paper Co Ltd (APP)Asia Pulp & Paper Co Ltd (APP)

APP, which was controlled by the Widjaja family, APP, which was controlled by the Widjaja family,

had more than 150 subsidiaries worldwidehad more than 150 subsidiaries worldwide

had debts in excess of US$13 bn as of 2001had debts in excess of US$13 bn as of 2001

was the biggest debt defaulter in Asiawas the biggest debt defaulter in Asia

was the largest debtor in emerging marketswas the largest debtor in emerging markets It made a Debt Standstill Announcement on 12

March 2001 which creditors called �unilateral� Deutsche Bank and BNP Paribas petitioned for

JM.

1414

In responding to the petition, APP in essence argued that:In responding to the petition, APP in essence argued that:

Its operating subsidiaries located in Indonesia and China Its operating subsidiaries located in Indonesia and China would ring fence its assets, stop paying APP management would ring fence its assets, stop paying APP management fees, enter into separate restructuringsfees, enter into separate restructurings

JM would not be able to discharge their duties to take JM would not be able to discharge their duties to take control of the companycontrol of the company��s assets outside Singapores assets outside Singapore

JM had no rights under Indonesia and Chinese lawJM had no rights under Indonesia and Chinese law JM could not secure cooperation from the groundJM could not secure cooperation from the ground JM would jeopardize the JM would jeopardize the ��cheapcheap�� supply of wood from supply of wood from

Sinar Mas companies which were associated with the Sinar Mas companies which were associated with the Widjaja familyWidjaja family

JM would not have specialized knowledgeJM would not have specialized knowledge IBRA, owed US$604 m of debt by the operating IBRA, owed US$604 m of debt by the operating

subsidiaries, would enforce its security over the assets of subsidiaries, would enforce its security over the assets of the subsidiaries if JM appointedthe subsidiaries if JM appointed

Appointment of JM would sound APPAppointment of JM would sound APP��s death knell.s death knell.

1515

At first instance, High Court of Singapore At first instance, High Court of Singapore disallowed the Petitiondisallowed the Petition

Court of Appeal Court of Appeal agreed but pointed out the agreed but pointed out the difficulties faced by the JM could not be a difficulties faced by the JM could not be a permanent barrier to a JM order if the consensual permanent barrier to a JM order if the consensual restructuring stalled or questionable transactions restructuring stalled or questionable transactions continued to be entered into by the APP group.continued to be entered into by the APP group.

1616

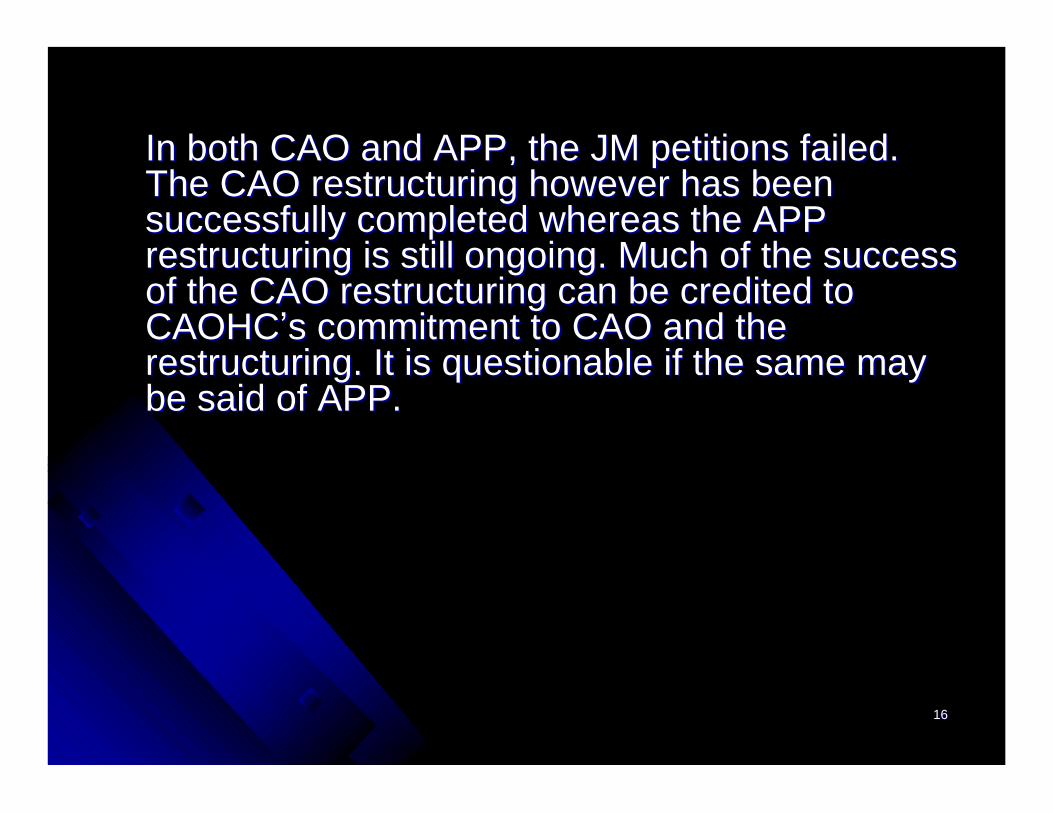

In both CAO and APP, the JM petitions failed. In both CAO and APP, the JM petitions failed. The CAO restructuring however has been The CAO restructuring however has been successfully completed whereas the APP successfully completed whereas the APP restructuring is still ongoing. Much of the success restructuring is still ongoing. Much of the success of the CAO restructuring can be credited to of the CAO restructuring can be credited to CAOHCCAOHC��ss commitment to CAO and the commitment to CAO and the restructuring. It is questionable restructuring. It is questionable if the same may if the same may be said of APP.be said of APP.

1717

The Company Legislation and Regulatory The Company Legislation and Regulatory Framework Committee has considered the Framework Committee has considered the UNCITRAL Model Law but has decided to adopt UNCITRAL Model Law but has decided to adopt a a ��wait and seewait and see�� approach. It stated that:approach. It stated that:

��In the course of our review we have also In the course of our review we have also reviewed developments relating to the UNCITRAL reviewed developments relating to the UNCITRAL Model Law on Insolvency and would recommend Model Law on Insolvency and would recommend that we await further developments which would that we await further developments which would indicate how these would impact the insolvency indicate how these would impact the insolvency legislation of the major common law jurisdictions.legislation of the major common law jurisdictions.��

1818

THE ENDTHE END

Thank youThank you

Kannan RameshKannan RameshTan Kok Quan PartnershipTan Kok Quan Partnership

May 2006May 2006