CHAPTER 7 – Audit of Property, Plant, & Equipment - 1 File ...

34

1 CHAPTER 7 – Audit of Property, Plant, & Equipment Problem 1 The trial balance of Aguilar Enterprises on December 31, 2006 shows P350,000 as the unaudited balance of the Machinery account. On April 1, 2006, a Jucuzzi machine costing P40,000 with accumulated depreciation of P30,000 was sold for P20,000, which proceeds was credited to the Machinery account. On June 30, 2006, a Goulds machine, costing P50,000 and with accumulated depreciation of P22,000 was traded in for a new Pioneer machine with an invoice price of P100,000. The cash paid of P90,000 for the Pioneer machine (P100,000 less trade-in allowance of P10,000 was debited to the Machinery account). Company policy on depreciation which you accept, provides an annual rate of 10% without salvage value. A full year’s depreciation is charged in the year of acquisition and none in the year of disposition. Question 1 The adjusted balance of the Machinery account at December 31, 2006 is: a. P 290,000 b. P 370,000 c. P 260,000 d. P 300,000 2 The correct depreciation expense for the machinery for the year ended December 31, 2006 is: a. P 37,000 b. P 29,000 c. P 30,000 d. P 26,000 Solution OE: Cash 20,000 Machinery 20,000 CE: Cash 20,000 Accumulated dep’n. 30,000 Machinery 40,000 Gain on sale 10,000 Adj: Accumulated dep’n 30,000 Machinery 20,000 Gain on sale 10,000 --------------------------------------------- OE: Machinery 90,000 Cash 90,000 CE: Machinery 100,000 Accumulated dep’n 22,000 Loss on sale 18,000 Machinery 50,000 Cash 90,000 Adj: Machinery 10,000 Accumulated dep’n 22,000 Loss on sale 18,000 Machinery 50,000 --------------------------------------------- 1 A P350,000 – P20,000 + P10,000 -P50,000 2 B P290,000 x 10%

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of CHAPTER 7 – Audit of Property, Plant, & Equipment - 1 File ...

1

CHAPTER 7 – Audit of Property,

Plant, & Equipment

Problem 1

The trial balance of Aguilar Enterprises on December 31, 2006 shows P350,000 as the

unaudited balance of the Machinery account. On April 1, 2006, a Jucuzzi machine costing

P40,000 with accumulated depreciation of P30,000 was sold for P20,000, which proceeds

was credited to the Machinery account. On June 30, 2006, a Goulds machine, costing

P50,000 and with accumulated depreciation of P22,000 was traded in for a new Pioneer

machine with an invoice price of P100,000. The cash paid of P90,000 for the Pioneer

machine (P100,000 less trade-in allowance of P10,000 was debited to the Machinery

account).

Company policy on depreciation which you accept, provides an annual rate of 10% without

salvage value. A full year’s depreciation is charged in the year of acquisition and none in

the year of disposition.

Question

1 The adjusted balance of the Machinery account at December 31, 2006 is:

a. P 290,000 b. P 370,000 c. P 260,000 d. P 300,000

2 The correct depreciation expense for the machinery for the year ended December 31,

2006 is:

a. P 37,000 b. P 29,000 c. P 30,000 d. P 26,000

Solution OE: Cash 20,000 Machinery 20,000 CE: Cash 20,000 Accumulated dep’n. 30,000 Machinery 40,000 Gain on sale 10,000 Adj: Accumulated dep’n 30,000 Machinery 20,000 Gain on sale 10,000 --------------------------------------------- OE: Machinery 90,000 Cash 90,000 CE: Machinery 100,000 Accumulated dep’n 22,000 Loss on sale 18,000 Machinery 50,000 Cash 90,000 Adj: Machinery 10,000 Accumulated dep’n 22,000 Loss on sale 18,000 Machinery 50,000 --------------------------------------------- 1 A P350,000 – P20,000 + P10,000 -P50,000 2 B P290,000 x 10%

2

Problem 2

The Land account was debited for P300,000 on March 31, 2006 for an adjoining piece of

land which was acquired in exchange for 15,000 shares of Rizal Corporation’s own stock

with a par value of P10. At the time of the exchange, the shares were selling at P24.

Transfer and legal fees of P20,000 were paid and charged to Professional Fees.

1. The adjusting entry required is:

DEBIT CREDIT

a. Land 140,000 Prem. on cap. stock 140,000

b. Land 160,000 Capital stock 150,000

Cash 10,000

c. Land 80,000 Professional fees 20,000

Prem. on cap. stock 60,000

d. None of these

2. On the Land acquired in No. 6, real estate taxes of P20,000 were paid in December,

2006, including P5,000 for the first quarter of the year. (Ignore penalty for delayed

payment). Land account was debited for the taxes paid.

The adjusting entry is:

DEBIT CREDIT

a. Taxes 15,000 Land 15,000

b. Taxes 5,000 Land 5,000

c. Land 5,000 Cash 20,000

Taxes 15,000

d. None of these

Solution

1. C OE: Land 300,000 Common Stock 150,000 APIC 150,000 Professional fees 20,000 Cash 20,000 CE: Land 380,000 Common stock 150,000 Cash 20,000 APIC 210,000 Adj: Land 80,000 APIC 60,000 Professional fees 20,000 2. A OE: Land 20,000 Cash 20,000 CE: Land 5,000 Taxes 15,000 Cash 20,000 Adj: Taxes 15,000 Land 15,000

Problem 3

Two independent companies, KAYA and MUYAN, are in the home building business. Each

owns a tract of land for development, but each company would prefer to build on the other’s

land. Accordingly, they agreed to exchange their land. An appraiser was hired and from

the report and the companies records, the following information was obtained:

KAYA Co.’s Land MUYAN Co.’s Land

Cost (same as book value) P 800,000 P 500,000

Market value, per appraisal 1,000,000 900,000

3

The exchange of land was made and based on the difference in appraised values, MUYAN

Company paid P100,000 cash to KAYA Company.

Question

1. For financial reporting purposes, KAYA Company would recognize a pretax gain on the

exchange in the amount of:

a. P 20,000 b. P 60,000 c. P 100,000 d. P 200,000

2. For financial reporting purposes, MUYAN Company recognize a pretax gain on the

exchange in the amount of:

a. P 0 b. P 100,000 c. P 300,000 d. P 400,000

3. After the exchange, KAYA Company record its newly acquired land at:

a. P 700,000 b. P 720,000 c. P 800,000 d. P 900,000

4. After the exchange, MUYAN Company record its newly acquired land at:

a. P 1,000,000 b. P 900,000 c. P 600,000 d. P 500,000

Solution Muyan Kaya Land 1,000,000 Cash 100,000 Cash 100,000 Land 900,000 Land 500,000 Land 800,000 Gain 400,000 Gain on sale 200,000 1 D 2. D 3. D 4. A

Problem 4

On an audit engagement for 2007, you handled the audit of fixed assets of Esmedina

Copper Mines. This mining company bought the exploration rights of Maharishi Exploration

on June 30, 2007 for P7,290,000. Of this purchase price, P4,860,000 was allocated to

copper ore which had remaining reserves estimated at 1,620,000 tons. Esmedina Copper

Mines expects to extract 15,000 tons of ore a month with an estimated selling price of P50

per ton. Production started immediately after some new machines costing P600,000 was

bought on June 30, 2007. These new machineries had an estimated useful life of 15 years

with a scrap value of 10% of cost after the ore estimated has been extracted from the

property, at which time the machineries will already be useless.

Among the operating expenses of Esmedina Copper Mines at December 31, 2007 were:

Depletion expense P 405,000

Depreciation of machineries 40,000

Questions

1. Recorded depletion expense was

a. Overstated by P90,000 c. Overstated by P135,000

b. Understated by P90,000 d. Understated by P135,000

2. Recorded depreciation expense was

a. Overstated by P10,000 c. Overstated by P20,000

b. Understated by P10,000 d. Understated by P20,000

4

3. The adjusted depletion at year-end amounted to:

a. P 270,000 b. P 315,000 c. P 495,000 d. P 540,000

4. The adjusted depreciation at year-end amounted to:

a. P 20,000 b. P 30,000 c. P 50,000 d. P 60,000

Solution P4,860,000/1,620,000 x 15,00o tons x 6 months = P270,000 P600,000 – P60,000/9 years * x 6/12 = P30,000 *1,620,000 tons/180,000 = 9 years 1. C P405,000 - (4,860,000/1,620,000 x 90,000 units) = P135,000 overstated 2. A P40,000 - (600,000 - 60,000)/1,620,000 x 90,000 = P10,000 overstated 3. A 4. B

Problem 5

In connection with your examination of the financial statements of the Maraat Corporation

for the year 2007, the company presented to you the Property, Plant and Equipment section

of its balance sheet as of December 31, 2006, which consists of the following:

Land P 400,000

Buildings 3,200,000

Leasehold improvements 2,000,000

Machinery and equipment 2,800,000

The following transactions occurred during 2007:

1. Land site number 5 was acquired for P4,000,000. Additionally, to acquire the land,

Maraat Corporation paid a P240,000 commission to a real estate agent. Costs of

P60,000 were incurred to clear the land. During the course of clearing the land, timber

and gravel were recovered and sold for P20,000.

2. The second tract of land (site number 6) with a building was acquired for P1,200,000.

The closing statement indicated that the land value was P800,000 and the building value

was P400,000. Shortly after acquisition, the building was demolished at a cost of

P120,000. The new building was constructed for P600,000 plus the following costs:

Excavation fees P 44,000

Architectural design fees 32,000

Building permit fees 4,000

Imputed interest on funds used during construction 24,000

The building was completed and occupied on September 1, 2007.

3. The third tract of land (site number 7) was acquired for P2,400,000 and was put on the

market for resale.

5

4. Extensive work was done to a building occupied by Maraat Corporation under a lease

agreement. The total cost of the work was P500,000, which consisted of the following:

Particular Amount Useful life

Painting of ceilings P 40,000 one year

Electrical work 140,000 Ten years

Construction of extension to current

working area 320,000 Thirty years

The lessor paid one-half of the costs incurred in connection with the extension to the

current working area.

5. A group of new machines was purchased under a royalty agreement which provides for

payment of royalties based on units of production for the machines. The invoice price of

the machines was P300,000, freight costs were P8,000, unloading charges were P6,000,

and royalty payments for 2007 were P52,000.

Question

1. Land at year-end is

a. P 5,480,000 b. P 5,900,000 c. P 6,000,000 d. P 8,400,000

2. Buildings at year-end is

a. P 3,800,000 b. P 3,880,000 c. P 4,200,000 d. P 4,280,000

3. Leasehold improvements at year-end is

a. P 2,300,000 b. P 2,560,000 c. P 2,600,000 d. P 2,720,000

4. Machinery and equipment at year-end is

a. P 3,100,000 b. P 3,108,000 c. P 3,114,000 d. P 3,166,000

Solution 1. Land 4,300,000 Cash 4,300,000 Cash 20,000 Land 20,000 2. Land 1,320,000 Cash 1,320,000 Building 680,000

Cash 680,000 3. Land - investment 2,400,000 Cash 2,400,000 4. Operating expenses 40,000 Leasehold improvements 300,000 Cash 340,000 5. Machinery 314,000 Royalty expenses 52,000 Cash 366,000 Answer: 1. C 2. B 3. A 4. C

6

Problem 6

Norie Company’s property, plant and equipment and accumulated depreciation balance at

December 31, 2005 are:

Accumulated

Cost Depreciation

Machinery and equipment P 1,380,000 P 367,500

Automobiles and trucks 210,000 114,320

Leasehold improvements 432,000 108,000

Additional information:

Depreciation methods and useful lives:

Machinery and equipment – straight line; 10 years

Automobiles and trucks – 150% declining balance; 5 years, all acquired after 2000.

Leasehold improvements – straight line

Depreciation is computed to the nearest month.

Salvage values are immaterial except for automobiles and trucks, which have an estimated

salvage values equal to 10% of cost.

Other additional information:

- Norie Company entered into a 12-year operating lease starting January 1, 2003. The

leasehold improvements were completed on December 31, 2002 and the facility was

occupied on January 1, 2003.

- On July 1, 2006, machinery and equipment were purchased at a total invoice cost of

P325,000. Installation cost of P44,000 was incurred.

- On August 30, 2006, Norie Company purchased new automobile for P25,000.

- On September 30, 2006, a truck with a cost of P48,000 and a carrying amount of

P30,000 on December 31, 2005 was sold for P23,500.

- On December 30, 2006, a machine with a cost of P17,000, a carrying value of P2,975 on

date of disposition, was sold for P4,000.

Questions

1. The gain on sale of truck on September 30, 2006 is:

a. P 0 b. P 250 c. P 2,680 d. P 6,500

2. The gain on sale of machinery on December 30, 2006 is:

a. P 0 b. P 13,000 c. P 2,725 d. P 1,025

3. The adjusted balance of the property, plant, and equipment as of December 31, 2006 is:

a. P 1,813,000 b. P 2,351,000 c. P 2,387,000 d. P 2,388,500

4. The total depreciation expense to be reported on the income statement for the year

ended December 31, 2006 is:

a. P 138,000 b. P 185,402 c. P 221,404 d. P 245,065

7

5. The carrying amount of property, plant, and equipment as of December 31, 2006 is:

a. P 1,290,547 b. P 1,578,545 c. P 1,587,497 d. P 1,617,322

Solution Entries: Machinery and equipment 369,000 Cash 369,000 Automobile and trucks 25,000 Cash 25,000 Cash 23,500 Accumulated depreciation 24,750 Automobile and trucks 48,000 Gain on sale 250 Accumulated deprecation - 12/31/02 18,000 Depreciation - 9 mos. (P30,000 x 30% x 9/12) 6,750 Total 24,750 Cash 4,000 Accumulated depreciation 14,025 Machinery and equipment 17,000 Gain on sale 1,025 Depreciation 221,404 Accumulated depreciation - mach. 156,450 Accumulated depreciation - auto. 28,954 Accumulated depreciation - improv. 36,000 Machinery and equipment - P1,380,000/10 years = P 138,000 P 369,000/10 years x 6/12 = 18,450 P 156,450 Leasehold improvement - P432,000/12 years = 36,000 Automobile and trucks - CV of unsold item P 65,680 x 30% = 19,704 Sold item - 30,000 x 30% x 9/12 = 6,750 Current purchase P25,000 x 30% x 4/12= 2,500 28,954 Answer: 1. B 2. D 3. B 4. C 5. B

Problem 7

Information pertaining to Highland Corporation’s property, plant and equipment for 2005 is

presented below:

Account balances at January 1, 2005:

Debit Credit

Land P 150,000

Buildings 1,200,000

Accumulated depreciation – Buildings P263,100

Machinery and equipment 900,000

Accumulated depreciation – Machinery and equipment 250,000

Automotive equipment 115,000

Accumulated depreciation – Automotive equipment 84,600

Depreciation data:

Depreciation method Useful life

Buildings 150% declining-balance 25 years

Machinery and equipment Straight-line 10 years

Automotive equipment Sum-of-the-years’-digits 4 years

Leasehold improvements Straight-line -

8

The salvage values of the depreciable assets are immaterial. Depreciation is computed to

the nearest month.

Transactions during 2005 and other information are as follows:

a. On January 2, 2005, Highland purchased a new car for P20,000 cash and trade-in of a 2-

year-old car with a cost of P18,000 and book value of P5,400. The new car has a cash

price of P24,000; the market value of the trade-in is not known.

b. On April 1, 2005, a machine purchased for P23,000 on April 1, 2000, was destroyed by

fire, Highland recovered P15,500 from its insurance company.

c. On May 1, 2005, costs of P168,000 were incurred to improve leased office premises. The

leasehold improvements have a useful life of 8 years. The related lease terminates on

December 31, 2011.

d. On July 1, 2005, machinery and equipment were purchased at a total invoice cost of

P280,000; additional costs of P5,000 for freight and P25,000 for installation were

incurred.

e. Highland determined that the automotive equipment comprising the P115,000 balance

at January 1, 2005, would have been depreciated at a total amount of P18,000 for the

year ended December 31,2005.

Questions

Based on the information above, answer the following questions:

1. The adjusted balance of Machinery and Equipment (at cost) at December 31, 2005 is:

a. P 1,180,000 b. P 1,187,000 c. P 1,202,500 d. P 1,210,000

2. The adjusted balance of Automotive Equipment (at cost) at December 31, 2005 is:

a. P 139,000 b. P 121,000 c. P 115,000 d. P 109,000

3. The adjusted balance of Accumulated Depreciation of Building at December 31, 2005 is:

a. P 72,000 b. P 263,100 c. P 335,100 d. P 319,314

4. The adjusted balance of Accumulated Depreciation of Machinery and Equipment at

December 31, 2005 is:

a. P 330,775 b. P 342,275 c. P 351,475 d. P 353,775

5. The adjusted balance of Accumulated Depreciation of Automotive Equipment at

December 31, 2005 is:

a. P 90,600 b. P 96,000 c. P 103,200 d. P 108,600

6. The adjusted balance of Accumulated Depreciation of Leasehold Improvements at

December 31, 2005 is:

a. P 0 b. P 14,000 c. P 14,700 d. P 16,800

7. The total adjusted balance of Accumulated Depreciation of Property and Equipment at

December 31, 2005 is:

a. P 534,375 b. P 698,475 c. P 774,389 d. P 804,475

9

8. The total gain(loss) from disposal of assets at December 31, 2005 is:

a. P 5,400 b. P 4,000 c. P 2,600 d. P 1,400

9. The adjusted book value of Building at December 31, 2005 is:

a. P 1,128,000 b. P 936,900 c. P 880,686 d. P 864,900

10. The adjusted book value of Leasehold Improvement at December 31, 2005 is:

a. P 168,000 b. P 154,000 c. P 153,300 d. P 151,200

Solution

Entries: a. Automobile Equipment 24,000 (cash paid, P20,000 plus P4,000 trade-in allow.)

Accum. Depreciation 12,600 Loss on trade-in 1,400 Automobile Equipment 18,000 Cash 20,000 * Trade in allowance is the difference between the cash price and the purchase price of the equipment. b. Cash 15,500 Accum. Depreciation 11,500 Machinery and equipment 23,000 Gain on asset disposal 4,000 c. Leasehold improvements 168,000 Cash 168,000 d. Machinery and equipment 310,000 Cash 310,000 Computation of the Depreciation Expense and Accumulated Depreciation: Building: Book value 1/1/05 (P1,200,000 - P263,100) - P936,900

X declining rate (1/25 x 150%) 6% . Depreciation for the year P 56,214 Plus; Accum. Depreciation - 1/1/05 263,100

Accum. Depreciation - 12/31/05 P319,314 Machinery and Equipment: Balance - 1/1/05 P900,000 Less: machine destroyed by fire 23,000 P877,000 Divided by 10 yrs. P 87,700 Dep’n of the Machine destroyed by fire: (P23,000/10 x 3/12) 575 Dep’n of the machine purchase for the year: (P310,000/10 x 6/12) 15,500 Total Depreciation P103,775 Plus: Accum. Dep’n - 1/1/05 250,000 Less: Accum. Dep’n - destroyed by fire ( 11,500) Accum. Depreciation - 12/31/05 P342,275 Automotive Equipment: Depreciation on P115,000 balance, 1/1/05 P 18,000 Less: Depreciation on car traded in (P18,000 x 2/10) 3,600 Adjusted depreciation on the beg. Bal. P 14,400 Dep’n on the 1/2/05 Purchase: (P24,000 x 4/10) 9,600

Total Depreciation expense P 24,000 Plus: Accum. Depreciation - 1/1/05 84,600 Less: Accum. Dep’n - traded equipment ( 12,600) Accumulated depreciation - 12/31/05 P 96,000 Leasehold Improvements: P168,000/80 months x 8 mos. for 2005 P 16,800 ANSWER: 1. B 2. B 3. D 4. B 5. B 6. D 7. C 8. C 9. C 10. D

10

Problem 8

The schedule of Gerasmo Company’s property and equipment prepared by the client

follows:

PLANT ASSETS

Land P 320,000

Building 540,000

Machinery and Equipment 180,000

Total 1,040,000

ACCUMULATED DEPRECIATION

Building P 81,000

Machinery and Equipment 54,000

Total P 135,000

Further examination revealed the following:

1. All property and equipment were acquired on January 2, 2003.

2. Assets are depreciated using the straight-line method. The building and equipment are

expected to benefit the company for 20 years and 10 years respectively. Salvage values

of the assets are negligible.

3. An equipment with an original cost of P40,000 was sold on December 30, 2005 for

P32,000. The proceeds were credited to other operating income account.

4. In 2005, The company recognized an appreciation in value of land and building as

determined by the Company’s engineers. The appraisal was recorded as follows:

Debit Credit

Land 70,000

Building 60,000

Accum. depreciation 6,000

Revaluation increment 124,000

Questions

1. Property and equipment at year-end is:

a. P 753,000 b. P 870,000 c. P 910,000 d. P 990,000

2. Accumulated depreciation at year-end is:

a. P 114,000 b. P 117,000 c. P 123,000 d. P 135,000

Solution OE: Cash 32,000 Other ope. income 32,000 CE: Cash 32,000 Accumulated dep’n 12,000 Property & equip. 40,000 Other ope. income 4,000 Adj: Accum. dep’n 12,000 Other ope. income 28,000 Property & equip. 40,000 ----------------------------------------------- Adj: Revaluation increment 124,000 Accumulated dep’n 6,000 Property & equipment 130,000 ----------------------------------------------- Per book depreciation - bldg 75,000 Per audit depreciation - bldg 72,000 (540,000-60,000/20 x 3 yrs) Adjustment 3,000

11

Adj: Accum. Depreciation 3,000 Operating expenses 3,000 Answer: 1. B 2. A

Problem 9

The following information pertains to Marlisa Company’s delivery trucks:

Date Particulars Debit Credit

1/1/04 Trucks 1, 2, 3, & 4 3,200,000

3/15/05 Replacement of truck 3 tires 25,000

7/1/05 Truck 5 800,000

7/10/05 Reconditioning of truck 4, which was

damaged in a collision 35,000

9/1/05 Insurance recovery on truck 4 accident 33,000

10/1/05 Sale of truck 2 600,000

4/1/06 Truck 6 1,000,000 150,000

5/2/06 Repainting of truck 4 27,000

6/30/06 Truck 7 720,000

12/1/06 Cash received on lease of truck 7 22,000

ACCUM. DEPRECIATION - DELIVERY EQUIPMENT

Date Particulars Debit Credit

12/31/04 Depreciation expense 300,000

12/31/05 Depreciation expense 300,000

12/31/06 Depreciation expense 300,000

a. On July 1, 2005, Truck 3 was traded-in for a new truck. Truck 5, costing P850,000; the

selling party allowed a P50,000 trade in value for the old truck.

b. On April 1, 2006, Truck 6 was purchased for P1,000,000; Truck 1 and cash of P850,000

being given for the new truck.

c. The depreciation rate is 20% by unit basis.

d. Unit cost of Trucks 1 to 4 is at P800,000 each.

Questions

1. What is the loss on trade-in of truck 3?

a. P 50,000 b. P 430,000 c. P 510,000 d. P 560,000

2. The correct cost of truck 5 is

a. P 560,000 b. P 610,000 c. P 800,000 d. P 850,000

3. The book value of truck 5 at December 31, 2006 is

a. P 850,000 b. P 595,000 c. P 560,000 d. P 510,000

4. What is the loss in trade-in of Truck 1?

a. P 150,000 b. P 250,000 c. P 290,000 d. P 410,000

5. The correct cost of truck 6 is

a. P 590,000 b. P 800,000 c. P 850,000 d. P 1,000,000

12

6. The carrying value of Truck 6 at December 31, 2006 is

a. P 501,500 b. P 680,000 c. P 850,000 d. P 1,100,000

7. The gain (loss) on sale of truck 2 is

a. P 80,000 b. P 331,600 c. P 495,000 d. P 496,200

8. The book value of truck 4 at December 31, 2006 is

a. P 320,000 b. P 331,600 c. P 495,000 d. P 496,200

9. The 2000 depreciation expense is understated by

a. P 92,000 b. P 252,000 c. P 292,000 d. P 372,000

10. The cost of repainting truck 4 should have been charged to:

a. Claims receivable - insurance company

b. Retained earnings

c. Accumulated depreciation

d. Repairs and maintenance

11. Which of the following controls would most likely allow for a reduction in the scope of the

auditor’s tests of depreciation expense?

a. Review and approval of the periodic property depreciation entry by a supervisor who

does not actively participate in its preparation.

b. Comparison of property account balances for the current year with the current year

budget and prior-year actual balance.

c. Review of the miscellaneous revenue account for salvage credits and scrap sales of

partially depreciated property.

d. Authorization of payment of vendors’ invoices by a designated employee who is

independent of the property receiving functions.

Solution 1. C

Cost of truck 3 800,000 Accumulated depreciation (P800,000 x 20% x 1.5) 240,000 Net book value 560,000 Trade-in allowance 50,000 Loss on trade-in 510,000 2. D 3. B (P850,000-(P850,000x20%x1.5) 4. B Cost of truck 1 800,000 Less: Accumulated depreciation (P800,000 x 20% / 12 mos. x 27 mos.) 360,000 Net book value 440,000 Trade-in allowance 150,000 Loss on trade-in 290,000 5. D 6. C [P1,000,000 - (1,000,000 x 20% x 9/12)] 7. A Cost of truck 2 800,000 Accumulated depreciation (P800,000 x 20% / 12 mos. x 21 mos.) 280,000 Net book value 520,000

Selling price 600,000 Gain on sale 80,000 8. A ([P800,000 - (P800,000 x 20% x 3)] 9. C Truck 1 (P800,000 x 20% 3/12) 40,000 - Truck 2 - - Truck 3 - - Truck 4 (P800,000 x 20%) 160,000 800,000 Truck 5 (P850,000 x 20%) 170,000 850,000

13

Truck 6 (P1,000,000 x 20% x 9/12) 150,000 1,000,000 Truck 7 (P720,000 x 20% x 6/12) 72,000 720,000 Depreciation per audit 592,000 3,370,000 Depreciation per records 300,000 Understatement 292,000 10. D 11. B

Problem 10

Information pertaining to SAILADIN CORPORATION’s property, plant and equipment for

2006 is presented below.

Account balances at January 1, 2006

Debit Credit

Land 6,000,000

Buildings 48,000,000

Accumulated depreciation – bldg. 10,524,000

Machinery and equipment 36,000,000

Accumulated depreciation – mach. & equip. 10,000,000

Automotive equipment 4,600,000

Accumulated depreciation – auto. Equip. 3,384,000

Depreciation data:

Depreciation method Useful life

Buildings 150% declining-balance 25 years

Machinery and equipment Straight-line 10 years

Automotive equipment Sum-of-the-years-digits 4 years

Leasehold improvements Straight-line -

The salvage values of the depreciable assets are immaterial. Depreciation is computed to

the nearest month.

Transactions during 2006 and other information are as follows:

(a) On January 2, 2006, Sailadin Corporation purchased a new car for P800,000 cash and

trade-in of a 2-year car with a cost of P720,000 and a book value of P216,000. The new

car has a cash price of P960,000; the market value of the trade-in is not know.

(b) On April 1, 2006, a machine purchased for P920,000 on April 1, 2001, was destroyed by

fire. Sailadin Corporation recovered P620,000 from its insurance company.

(c) On May 1, 2006, costs of P6,720,000 were incurred to improve leased office premises.

The leasehold improvements have a useful life of 8 years. The related lease terminates

on December 31, 2012.

(d) On July 1, 2006, machinery and equipment were purchased at a total invoice cost of

P11,200,000; additional costs of P200,000 for freight and P1,000,000 for installation

were incurred.

(e) Sailadin Corporation determined that the automotive equipment comprising the

P4,600,000 balance at January 1, 2006, would have been depreciated at a total amount

of P720,000 for the year ended December 31, 2006.

14

Questions

1. What is the depreciation on building for 2006?

a. P 2,998,080 b. P 2,880,000 c. P 2,248,560 d. P 1,499,040

2. What is the book value of the building at December 31, 2006?

a. P 35,976,960 b. P 35,227,440 c. P 34,596,000 d. P 34,477,920

3. What is the depreciation on machinery and equipment for 2006?

a. P 4,220,000 b. P 4,197,000 c. P 4,151,000 d. P 4,128,000

4. What is the gain on machine destroyed by fire?

a. P 620,000 b. P 460,000 c. P 300,000 d. P 160,000

5. What is the balance of the Accumulated Depreciation – Machinery and Equipment at

December 31, 2006?

a. P 13,777,000 b. P 13,760,000 c. P 13,691,000 d. P 13,231,000

6. What is the depreciation on automotive equipment for 2006?

a. P 1,104,000 b. P 960,000 c. P 816,000 d. P 720,000

7. What is the gain (loss) on car traded-in?

a. P 240,000 b. P (240,000) c. P 56,000 d. P (56,000)

8. What is the book value of automotive equipment at December 31, 2006?

a. P 1,720,000 b. P 1,144,000 c. P 1,000,000 d. P 712,000

9. What is the depreciation on leasehold improvements for 2006?

a. P 756,000 b. P 672,000 c. P 630,000 d. P 560,000

10. What is the book value of leasehold improvements at December 31, 2006?

a. P 6,160,000 b. P 6,090,000 c. P 6,048,000 d. P 5,964,000

Solution 1. C

Book Value, 1/1/06 (P48,000,000 - P10,524,000) P 37,476,000 150% declining-balance rate (1/25 x 150%) x 6% Depreciation on building P 2,248,560

2. B Cost of building P 48,000,000 Less: Accumulated depreciation (P10,524,000 + P 2,248,560) 12,772,560 Book value of building, 12/31/06 P 35,227,440

3. C Balance, 1/106 P 36,000,000 Less: Machine destroyed by fire 920,000 Balance P 35,080,000 Depreciation 10% 3,508,000 Machine destroyed by fire (P920,000 x 10% x 3/12) 23,000 Purchased 7/1/06 (P12,400,000 x 10% x 6/12) 620,000 Total depreciation on machinery and equipment 4,151,000

4. D Insurance recovery 620,000 Less: Book value of machine destroyed

(Cost 920,000 - Accum. dep’n (P 920,000 x 10% x 5) 460,000 Gain on recovery from insurance company 160,000

5. C Balance, 1/1/06 10,000,000 Add: depreciation for 2006 4,151,000

15

Total 14,151,000 Less: Machinery destroyed by fire (P920,000 x 10% x 5) 460,000 Accumulated depreciation - machinery and equip. 13,691,000

6. B Depreciation on P4,600,000 balance on 1/1/06 (given) 720,000 Less: Depreciation on car traded-in, 1/1/06 (P720,000 x 2/10) 144,000 576,000 Car purchased, 1/2/06 (P960,000 x 4/10) 384,000 Total depreciation on automotive equipment for 2006 960,000

7. C Book value of car traded-in (given) 216,000 Less: Trade-in allowance (P960,000 - P800,000) 160,000 Loss on trade-in 56,000

8. C Cost of the machinery and equipment: Balance, 1/1/06 4,600,000 Car purchased, 1/2/06 960,000 Car traded in (720,000) 4,840,000 Accumulated depreciation: Balance, 1/1/06 3,384,000 Depreciation for 2006 960,000 Car traded in (P720,000 - P216,000) ( 504,000) 3,840,000 Book value of automotive equipment, 12/31/06 1,000,000

9. B Cost of leasehold improvements 6,720,000 Divide by term of lease, 5/1/06 - 12/31/2012 80 mos Depreciation per month 84,000

Depreciation, 5/1 - 12/31 (P84,000 x 8 mos) 672,000 10. C

Cost of leasehold improvements 6,720,000 Less: Accumulated depreciation (see No. 9) 672,000 Book value, 12/31/06 6,048,000

Problem 11

You are engaged to audit the financial statements of TRIUMPH CORPORATION for the year

ended December 31, 2006. You gathered the following information pertaining to the

company’s Equipment and Accumulated Depreciation accounts.

EQUIPMENT

1.1.06 Balance P 446,000 9.1.06 No. 6 sold P 9,000

6.1.06 No. 12 36,000 12.31.06 Balance 474,000

9.1.03 Dismantling

of No. 6 1,000 ______

P 483,000 P 483,000

ACCUMULATED DEPRECIATION – EQUIPMENT

12.31.06 Balance P 271,400 1.1.06 Balance P 224,000

______ 12.31.06 2006 Dep’n 47,400

P 271,400 P 271,400

The following are the details of the entries above:

1. The company depreciates equipment at 10% per year. The oldest equipment owned is

seven years old as of December 31, 2006.

2. The following adjusted balances appeared on your last year’s working papers:

Equipment P 446,000

Accumulated depreciation 224,000

16

3. Machine No. 6 was purchased on March 1, 1999 at a cost of P30,000 and was sold on

September 1, 2006, for P9,000.

4. Included in charges to the Repairs Expense account was an invoice covering installation

of Machine No. 12 in the amount of P2,500.

5. It is the company’s practice to take a full year’s depreciation in the year of acquisition

and none in the year of disposition.

Questions

1. The gain/(loss) on sale of Machine 6 is:

a. P 1,000 b. P 500 c. P (1,000) d. P (500)

2. The Equipment balance of TRIUMPH CORPORATION at December 31, 2006 is:

a. P 446,000 b. P 452,000 c. P 454,500 d. P 475,500

3. The Depreciation expense – Equipment of TRIUMPH CORPORATION at December 31,

2006 is:

a. P 45,200 b. P 45,450 c. P 46,525 d. P 53,525

4. The entry to correct the sale of Machine 6 is:

a. Loss on sale of equipment 1,000

Accumulated depreciation 21,000

Equipment 22,000

b. Accumulated depreciation 22,500

Equipment 22,000

Gain on sale 500

c. Accumulated depreciation 21,500

loss on sale of equipment 500

Equipment 22,000

d. Accumulated depreciation 23,000

Equipment 22,000

Gain on sale of equipment 1,000

5. The Depreciation Expense at December 31, 2006 is:

a. Overstated by P6,125 c. Understated by P1,950

b. Understated by P6,125 d. Overstated by P1,950

Solution OE: Cash 9,000

Equipment 1,000 Equipment 9,000 Cash 1,000

CE: Cash 9,000 Accum. dep’n 21,000 Loss on sale 1,000

Equipment 30,000 Cash 1,000

------------------------------------------- Adj: Accum. dep’n 21,000

Loss on sale 1,000 Equipment 22,000

------------------------------------------- Adj: Equipment 2,500

Repairs expense 2,500

17

------------------------------------------- Adj: Accum. dep’n 1,950

Depreciation 1,950 Answer: 1. C 2. C 3. B 4. A 5. D

Problem 12

Information pertaining to Eddie Vic Corporation’s property, plant and equipment for 2005 is

presented below:

Account balances at January 1, 2005

Debit Credit

Land P 1,500,000

Building 12,000,000

Accum. depreciation-building P 2,631,000

Machinery and equipment 9,000,000

Accum. depreciation-Mach. and Eqpt 2,500,000

Automotive Equipment 1,150,000

Accum. depreciation-Automotive Eqpt 846,000

Depreciation method and useful life

Building – 150% declining balance; 25 years

Machinery and equipment – Straight-line; 10 years

Automotive equipment – Sum-of-the-years’-digits; 4 years

The salvage value of the depreciable assets is immaterial

Depreciation is computed to the nearest month.

Transactions during 2005 and other information:

On January 2, 2005, Eddie Vic purchased a new car for P350,000 cash and trade-in of a 2-

year old car with a cost of P490,000 and a book value of P147,000. The new car has a cash

price of P520,000; the market value of the trade-in is not known.

On April 1, 2005, a machine purchased for P230,000 on April 1, 2000, was destroyed by

fire. Eddie Vic recovered P155,000 from its insurance company.

On July 1, 2005, machinery and equipment were purchased at a total invoice cost of

P2,800,000; additional costs of P50,000 for freight and P250,000 for installation were

incurred.

Eddie Vic determined that the automotive equipment comprising the P1,150,000 balance at

January 1, 2005, would have been depreciated at a total amount of P180,000 for the year

ended December 31, 2005.

Questions

1. Depreciation expense for building at December 31, 2005 is:

a. P 749,520 b. P 720,000 c. P 682,150 d. P 562,140

2. Depreciation expense for machinery and equipment at December 31, 2005 is:

a. P 1,049,250 b. P 1,037,750 c. P 1,032,000 d. P 877,000

3. Depreciation expense for Automobile equipment at December 31, 2005 is:

a. P 388,000 b. P 312,000 c. P 290,000 d. P 180,000

18

4. Total depreciation expense for 2005 is:

a. P 2,047,750 b. P 2,009,900 c. P 1,978,770 d. P 1,889,890

5. Total gain on asset disposal for 2005 is:

a. P 63,000 b. P 40,000 c. P 23,000 d. P 17,000

6. Total accumulated depreciation of building at December 31, 2005 is:

a. P 3,380,520 b. P 3,351,000 c. P 3,313,150 d. P 3,193,140

7. Total book value of property, plant, and equipment at December 31, 2005 is:

a. P 19,141,110 b. P 19,021,100 c. P 18,983,250 d. P 18,953,730

8. The property, plant and equipment at December 31, 2005 is:

a. P 19,141,110 b. P 19,021,100 c. P 18,983,250 d. P 18,953,730

9. The total cost of property, plant and equipment at December 31, 2005 is:

a. P 26,670,010 b. P 26,579,520 c. P 26,550,000 d. P 26,459,510

10. Total accumulated depreciation of property, plant, and equipment at December 31, 2005

is:

a. P 7,648,910 b. P 7,596,270 c. P 7,506,300 d. P 7,408,890

Solution Schedule of Accumulated Depreciation December 31, 2005 Building Mach.&

Equipment Auto. Eqpt. Total

Balance, 1.1.05 P2,631,000 P2,500,000 P846,000 P5,977,000 Add depreciation for 2005 562,140 1,037,750 290,000 1,889,890 P3,193,140 P3,537,750 P1,136,000 P7,866,890 Deduct acc. depr. related to Mach, destroyed by fire (5 x 10% x P230,000) 115,000 Car traded in (490,000 - 147,000) _________ _________ 343,000 458,000 Balance, 12.31.05 P3,193,140 P3,422,750 P 793,000 P7,408,890 SCHEDULE OF DEPRECIATION EXPENSE For the Year Ended December 31, 2005 Building Book value , 1/1/05 (P12,000,000 - P2,631,000) P9,369,000

150% declining balance rate (100% / 25) x 1.5 x 6% Total depreciation on building P562,140 Machinery and Equipment Balance, 1.1.05 less machine destroyed by fire P8,770,000 Depreciation x 10% 877,000 Depr. on Machine destroyed by fire, 4.1.05 (P230,000 x 10% x 3/12) 5,750 Depr. on machine purchased on 7.1.05 (P3,100,000 x 10% x 6/12) 155,000 Total depreciation on mach. and equipment P1,037,750 Automotive Equipment Depreciation on P1,115,000 bal. on 1.1.05 P180,000 Deduct depr. on car traded in , 1.2.05 (SYD 3rd year 2/10 x P490,000) (98,000) 82,000 Depr. on car purchased , 1.2.05 (P520,000 x 4/10) 208,000 Total depreciation on automotive equipment 290,000 Total depreciation expense for 2005 P1,889,890

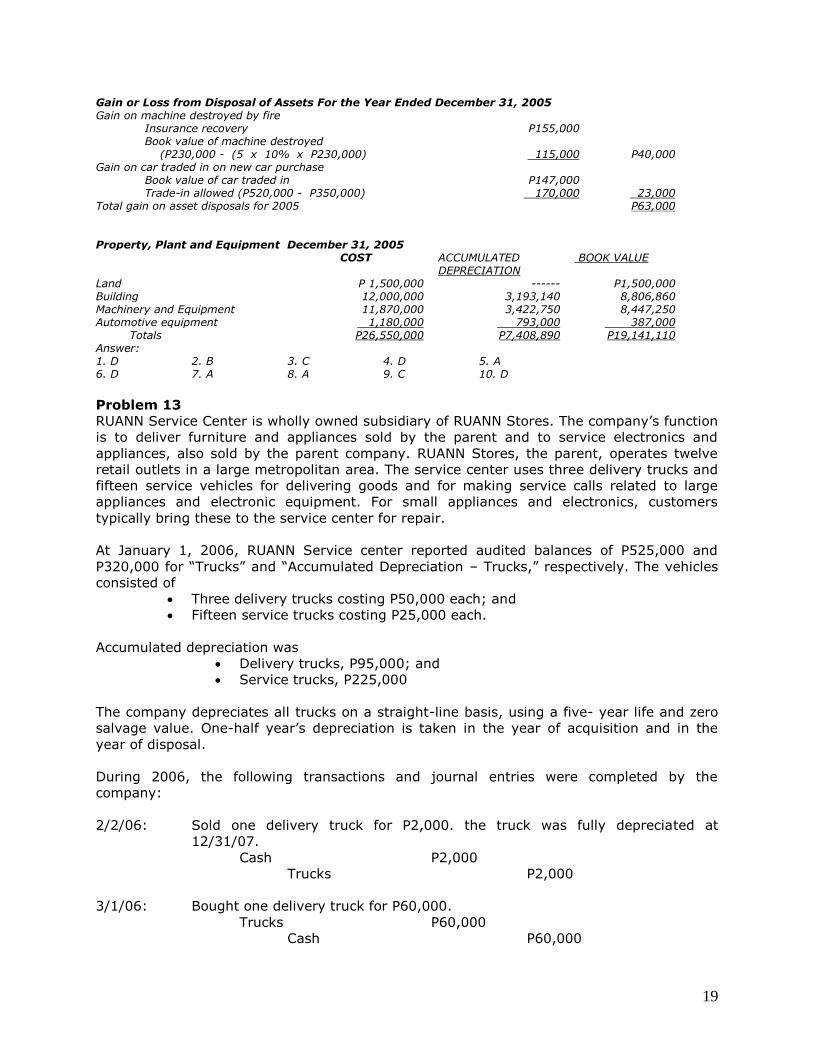

19

Gain or Loss from Disposal of Assets For the Year Ended December 31, 2005 Gain on machine destroyed by fire Insurance recovery P155,000 Book value of machine destroyed (P230,000 - (5 x 10% x P230,000) 115,000 P40,000 Gain on car traded in on new car purchase Book value of car traded in P147,000 Trade-in allowed (P520,000 - P350,000) 170,000 23,000 Total gain on asset disposals for 2005 P63,000 Property, Plant and Equipment December 31, 2005 COST ACCUMULATED

DEPRECIATION BOOK VALUE

Land P 1,500,000 ------ P1,500,000 Building 12,000,000 3,193,140 8,806,860 Machinery and Equipment 11,870,000 3,422,750 8,447,250 Automotive equipment 1,180,000 793,000 387,000 Totals P26,550,000 P7,408,890 P19,141,110 Answer: 1. D 2. B 3. C 4. D 5. A 6. D 7. A 8. A 9. C 10. D

Problem 13

RUANN Service Center is wholly owned subsidiary of RUANN Stores. The company’s function

is to deliver furniture and appliances sold by the parent and to service electronics and

appliances, also sold by the parent company. RUANN Stores, the parent, operates twelve

retail outlets in a large metropolitan area. The service center uses three delivery trucks and

fifteen service vehicles for delivering goods and for making service calls related to large

appliances and electronic equipment. For small appliances and electronics, customers

typically bring these to the service center for repair.

At January 1, 2006, RUANN Service center reported audited balances of P525,000 and

P320,000 for “Trucks” and “Accumulated Depreciation – Trucks,” respectively. The vehicles

consisted of

Three delivery trucks costing P50,000 each; and

Fifteen service trucks costing P25,000 each.

Accumulated depreciation was

Delivery trucks, P95,000; and

Service trucks, P225,000

The company depreciates all trucks on a straight-line basis, using a five- year life and zero

salvage value. One-half year’s depreciation is taken in the year of acquisition and in the

year of disposal.

During 2006, the following transactions and journal entries were completed by the

company:

2/2/06: Sold one delivery truck for P2,000. the truck was fully depreciated at

12/31/07.

Cash P2,000

Trucks P2,000

3/1/06: Bought one delivery truck for P60,000.

Trucks P60,000

Cash P60,000

20

3/15/06: Sold one service truck for P8,000. This truck was purchased 6/15/03 for

P25,000 and the accumulated depreciation, according to RUANN’s subsidiary

ledger, at the date of sale was P12,500

Cash P8,000

Trucks P8,000

7/25/06: Bought one service truck for P27,500.

Truck P27,500

Cash P27,500

12/31/06: Recorded depreciation for 2006:

Two delivery trucks @ P10,000 each = P20,000

Fifteen service trucks @ P5,000 each = 75,000

Total P95,000

Depreciation Expense – Trucks P95,000

Accumulated depreciation P95,000

Questions

1. The adjusted balance of Delivery Truck at December 31, 2006 is:

a. P 537,500 b. P 217,500 c. P 210,000 d. P 160,000

2. The adjusted balance of Service Truck at December 31, 2006 is:

a. P 537,500 b. P 402,500 c. P 377,500 d. P 217,500

3. The Accumulated Depreciation – Delivery Truck at December 31, 2006 is:

a. P 86,000 b. P 76,000 c. P 75,000 d. P 65,000

4. The Accumulated Depreciation – Service Truck at December 31, 2006 is:

a. P 300,000 b. P 285,250 c. P 285,000 d. P 284,750

5. The Carrying Value of Delivery Truck at December 31, 2006 is:

a. P 461,500 b. P 145,000 c. P 142,500 d. P 74,000

6. The Carrying Value of Service Truck at December 31, 2006 is:

a. P 237,500 b. P 117,500 c. P 92,250 d. P 67,250

7. The Gain/Loss on Disposal of Trucks at December 31, 2006 is:

a. P 10,000 b. P 8,000 c. P 2,000 d. P 0

8. The Depreciation Expense of Trucks at December 31, 2006 is:

a. P 106,250 b. P 101,250 c. P 98,750 d. P 95,000

Solution 2/2/06 OE: Cash 2,000 Delivery truck 2,000 CE: Cash 2,000 AD - Del. truck 40,000 Loss on sale 8,000 Delivery truck 50,000 Adj: AD - del. truck 40,000 Loss on sale 8,000 Delivery truck 48,000 3/15/06 OE: Cash 8,000 Service truck 8,000

21

CE: Cash 8,000 AD - ser. truck 15,000 Loss on sale 2,000 Service truck 25,000 Adj: AD - serv. truck 15,000 Loss on sale 2,000 Service truck 17,000 12/31/06 Depreciation 11,250 AD - del. truck 11,000 AD - service truck 250

Del. truck Serv. truck Per book 95,000 20,000 75,000 Per audit 106,250 31,000 75,250 Adjustment 11,250 11,000 250 Depreciation - Delivery truck Disposed truck 5,000 Undisposed truck 20,000 (2 x P10,000) Purchased during the year 6,000 (P60,000/5 x 1/2) ______ Total 31,000

Depreciation - service truck Disposed truck 2,500 Undisposed truck 70,000 (14 x P5,000) Purchased during the year 2,750 (P27,500/5 x 1/2) ______ Total 75,250

Answer: 1. D 2. C 3. A 4. B 5. D 6. C 7. A 8. A

Problem 14

You are engaged in the examination of the financial statements of the PAUL COMPANY and

are auditing the Machinery and Equipment Account and the related depreciation accounts

for the year ended December 31, 2005. Your permanent file contains the following

schedules:

MACHINERY AND EQUIPMENT

Year Balance 2004 2004 Balance

________ 12.31.03 Retirements Additions 12.31.04

1991-1994 P 800,000 P 210,000 P 590,000

1995 40,000 40,000

1996

1997

1998 390,000 390,000

1999

2000 530,000 530,000

2001

2002 420,000 420,000

2004 ________ _________ P 570,000 570,000

P 2,180,000 P 210,000 P 570,000 P 2,540,000

22

ACCUMULATED DEPRECIATION

Year Balance 2004 2004 Balance

________ 12.31.03 Retirements Additions 12.31.04

1991-1994 P 784,000 P 210,000 P 16,000 P 590,000

1995 34,000 4,000 38,000

1996

1997

1998 214,500 39,000 253,500

1999

2000 185,500 53,000 238,500

2001

2002 63,000 42,000 105,000

2003

2004 ________ _________ 28,500 28,500

P 1,281,000 P 210,000 P 182,500 P 1,253,500

A transcript of the Machinery and Equipment account for 2005 follows:

MACHINERY AND EQUIPMENT

Date Item Debit Credit

2005

Jan. 1 Balance forwarded P 2,540,000

Mar. 1 Burnham grinder 120,000

May 1 Air compressor 750,000

June 1 Power lawnmower 60,000

June 1 Lift truck battery 32,000

Aug. 1 Rockwood saw 15,000

Nov. 1 Electric spot welder 450,000

Nov. 1 Baking oven 280,000

Dec. 1 Baking oven 32,500 __________

P 4,264,500 P 15,000

_________ 4,249,500

P 4,264,500 P 4,264,500

Your examination reveals the following information:

a. The company uses a ten-year life for all machinery and equipment for depreciation

purposes. Depreciation is computed by the straight-line method. Six month’s

depreciation is recorded in the year of acquisition or retirement. For 2005, the company

recorded depreciation of P280,000 on machinery and equipment.

b. The Burnham grinder was purchased for cash from a firm in financial distress. The chief

engineer and a used machinery dealer agreed that the practically new machine was

worth P180,000 in the open market.

c. For production reasons, the new air compressor was installed in a small building that

was erected in 2005 to house the machine and will also be used for general storage.

The cost of the building, which has a 25-year life, was P500,000 and is included in the

P750,000 voucher for the air compressor.

d. The power lawnmower was delivered to the house of the company president for personal

use.

23

e. On June 1, the battery in a battery powered lift truck was accidentally damaged beyond

repair. The damaged battery was included at a price of P60,000 in the P420,000 cost of

the lift truck purchased on July 1, 2002. The company decided to rent a replacement

battery rather than buy a new battery. The P32,000 expenditure is the annual rental for

the battery paid in advance, net of a P4,000 allowance for the scrap value of the

damaged battery that was returned to the battery company.

f. The Rockwood saw sold on August 1 had been purchased on August 1, 2001, for

P150,000. The saw was in use until it was sold.

g. On September 1, the company determined that a production casting machine was no

longer needed and advertised it for sale for P180,000, after determining from a used

machinery dealer that its market value. The casting machine had been purchased for

P500,000 on September 1, 2000.

h. The company elected to exercise the option under a lease-purchase agreement to buy

the electric spot welder. The welder had been installed on February 1, 2005, at a

monthly rental of P10,000.

i. On November 1, a baking oven was purchased for P1,000,000. A P280,000 down

payment was made and the balance will be paid in monthly installment over a three year

period. The December 1 payment included interest charges of P12,500. Legal title to

the oven will not pass to the company until the payments are completed.

Questions

1. The entry to record the adjustment of depreciation expense at December 31, 2005 is:

a. Depreciation expense 19,500

Accumulated depreciation 19,500

b. Depreciation expense 37,250

Accumulated depreciation 37,250

c. Accumulated deprecation 19,500

Depreciation expense 19,500

d. Accumulated depreciation 37,250

Depreciation expense 37,250

2. Depreciation Expense at December 31, 2005 is:

a. P 260,500 b. P 262,500 c. P 280,000 d. P 342,500

3. The entry to record the adjustment in “item c” at December 31, 2005 is:

a. Building 500,000

Machinery and equipment 500,000

b. Machinery and equipment. 750,000

Building 750,000

c. Machinery and equipment 500,000

Building 500,000

d. No adjustment

4. The total Loss on disposal of equipment at December 31, 2005 is:

a. P 38,000 b. P 70,000 c. P 93,000 d. P 108,000

5. The total rental expense in item “h” at December 31, 2005 is:

a. P 45,000 b. P 90,000 c. P 125,000 d. none

24

6. The total interest expense at December 31, 2005 is:

a. P 10,000 b. P 12,500 c. P 25,000 d. P 50,000

7. The total accumulated depreciation of the machinery and equipment at December 31,

2005 is:

a. P 773,000 b. P 791,000 c. P 816,000 d. P 855,000

8. The accumulated depreciation of the machinery and equipment at December 31, 2005 is

overstated by:

a. P 480,500 b. P 462,500 c. P 437,500 d. P 398,500

9. The Total Machinery and Equipment (gross) at December 31, 2005 is:

a. P 3,740,000 b. P 2,310,500 c. P 2,030,500 d. P 1,940,500

10. The net book value of Machinery and Equipment at December 31, 2005 is:

a. P 1,518,000 b. P 1,494,500 c. P 1,503,000 d. P 2,924,000

Solution a. Accumulated Depreciation 19,500 Depreciation Expense 19,500 Correct depreciation expense for 2005 1995 acquisition : 40,000 x 10% x ½ P2,000 1998 “ : 390,000 x 10% 39,000 2000 “ : (500,000 x 10% x ½) + (30,000 x 10%) 28,000 2002 “ : (60,000 x 10% x ½) + (360,000 x 10%) 39,000 2004 “ : 570,000 x 10% 57,000 2005 “ : (120,000 + 250,000 + 540,000 + 1M) x 10% x ½ 95,500 P260,500 Amount recorded 280,000 Overstatement P 19,500 b. No AJE necessary c. Buildings 500,000 Machinery & Equipment 500,000 d. Receivable from Officers 60,000 Machinery & Equipment 60,000 e. 1 Accumulated Depreciation 18,000 Loss on Disposal of Assets 42,000 Machinery & Equipment 60,000 Cost P60,000 Less acc. Depreciation (60,000 x 10% x 3) 18,000 Book value P42,000 Trade in value 4,000 Loss P38,000 e.2 Equipment rental expense (7/12) 21,000 Prepaid equipment rental 15,000 Machinery & Equipment 32,000 Loss on Disposal of Assets 4,000

f. Accumulated Depreciation 150,000 Machinery & Equipment 135,000 Gain on Disposal of Assets 15,000 g. Other Assets - Mach. Held for sale 180,000 Accumulated depreciation 250,000 Loss on Disposal of Assets 70,000 Machinery & Equipment 500,000

25

BV ( P500,000 x 5/10) P250,000 Estimated selling price 180,000 Loss P70,000 h. Machinery & Equipment 90,000 Equipment Rental Expense 90,000 Rental for the period Feb. 1 to October 31. i. Machinery & Equipment 687,500 Interest expense 12,500 Equipment contract payable 700,000

Answer: 1. C 2. A 3. A 4. D 5. D 6. B 7. C 8. C 9. A 10. D

Problem 15

You are engaged in the examination of the financial statements of PATIENCE CORPORATION

for the year ended December 31, 2005. The chief accountant of the client has prepared the

accompanying analyses of the Property, Plant, and Equipment and related accumulated

depreciation accounts. You have traced the beginning balances to your prior year’s audit

working papers.

All plant assets are depreciated on the straight-line basis (no residual value taken into

consideration) based on the following estimated service lives: building, 25 years, and all

other items, 10 years. The company’s policy is to take one-half year’s depreciation on all

assets additions and disposals during the year.

PATIENCE CORPORATION

Analysis of Property, Plant, and Equipment, and

Related Accumulated Depreciation Accounts

Year Ended December 31, 2005

Description Final

12/31/04

Assets

Additions

Assets

Retirements

Per ledger

12/31/05

Land P 4,225,000 P 500,000 P 0 P 4,725,000

Buildings 1,200,000 475,000 0 1,675,000

Machinery & Equipment 3,850,000 404,000 260,000 3,994,000

P 9,275,000 P 1,379,000 P 260,000 P 10,394,000

Description Final

12/31/04

Assets

Additions

Assets

Retirements

Per ledger

12/31/05

Buildings P 600,000 P 51,500 P 651,500

Machinery & Equipment 1,732,500 392,200 2,124,700

P 2,332,500 P 443,700 P 2,776,200

Your examination revealed the following information:

1. On April 1, the company entered into a 10-year lease contract for a die-casting machine,

with annual rentals of P50,000 payable in advance every April 1. The lease is cancelable

by either party (60 day’s written notice is required), and there is no option to renew the

lease or buy the equipment at the end of the lease. The estimated service life of the

machine is 10-years with no residual value. The company recorded the die casting

machine in the Machinery and Equipment account at P404,000, the present value at the

26

date of the lease, and P20,200 applicable to the machine has been included in

depreciation expense for the year.

2. The company completed the construction of a wing on the plant building on June 30.

The service life of the building was not extended by this addition. The lowest

constructions bid received was P475,000, the amount recorded in the Building account.

Company personnel constructed the addition at a cost of P460,000 (materials,

P175,000; labor, P155,000; and overhead, P130,000).

3. On August 18, P500,000 was paid for paving and fencing a portion of land owned by the

company and used as a packing lot for employees. The expenditure was charged to the

Land account.

4. The amount shown in the Machinery and Equipment asset retirement column represents

cash received on September 5 upon disposal of a machine purchased in July, 1998 for

P480,000. The chief accountant recorded depreciation expense of P35,000 on this

machine in 2005.

5. Davao City government donated land and building appraised at P1,000,000 and

P4,000,000, respectively, to PATIENCE CORPORATION for a plant. On September 1, the

company began operating the plant. Since no costs were involved, the chief accountant

made no entry for the above transaction.

Questions

1. PATIENCE CORPORATION’s Land balance at December 31, 2005 is:

a. P 5,725,000 b. P 5,225,000 c. P 4,725,000 d. P 4,225,000

2. PATIENCE CORPORATION’s Building balance at December 31, 2005 is:

a. P 5,690,000 b. P 5,675,000 c. P 5,660,000 d. P 5,645,000

3. PATIENCE CORPORAITON’s Machinery and Equipment balance at December 31, 2005 is:

a. P 4,090,000 b. P 3,590,000 c. P 3,370,000 d. P 3,110,000

4. PATIENCE CORPORATION’s Accumulated Depreciation – Building at December 31, 2005

is:

a. P 766,000 b. P 747,000 c. P 737,500 d. P 651,500

5. PATIENCE CORPORATION’s Accumulated Depreciation – Machinery and Equipment at

December 31, 2005 is:

a. P 1,819,900 b. P 1,788,700 c. P 1,757,500 d. P 1,752,700

6. PATIENCE CORPORATION’s Depreciation Expense – Building at December 31, 2005 is:

a. P 227,000 b. P 211,500 c. P 147,000 d. P 137,500

7. PATIENCE CORPORATION’s Depreciation Expense – Machinery and Equipment at

December 31, 2005 is:

a. P 372,000 b. P 361,000 c. P 337,000 d. P 276,000

8. PATIENCE CORPORATION’s Depreciation Expense – Land Improvements at December

31, 2005 is:

a. P 50,000 b. P 25,000 c. P 18,750 d. P 0

27

9. PATIENCE CORPORATION’s Net Book Value of Building at December 31, 2005 is:

a. P 5,023,500 b. P 4,924,000 c. P 4,913,000 d. P 4,907,500

10. PATIENCE CORPORATION’s Net Book Value of Machinery and Equipment at December

31, 2005 is:

a. P 2,332,500 b. P 1,770,100 c. P 1,612,500 d. P 1,357,300

Solution Adjusting Journal Entries as of December 31, 2005 (1) Equipment Rental Expense (P50,000 x 9/12) 37,500 Prepaid Equipment Rental 12,500 Obligations under Capital Lease 354,000 Machinery and Equipment 404,000 (2) Profit on Construction 15,000 Buildings ( 475,000 - 460,000) 15,000 (3) Land Improvements 500,000 Land 500,000 (4) Accumulated Depreciation - Mach. & Eqpt. 336,000 Machinery & Equipment 220,000 Gain on sale of machinery 116,000 P260,000 - (480,000 x 3/10) = P116,000 gain (5) Land 1,000,000 Building 4,000,000 Gain from Donation 5,000,000 (6) Depreciation Expense 95,667 Accumulated Depreciation - Buildings 95,667 Depreciation Expense for 2005

1,200,000 x 4% P48,000 460,000 / 12 years x ½ 19,167 4,000,000 x 4% x ½ 80,000 P147,167 Amount recorded 51,500 Adjustment to be made P95,667 (7) Accumulated Depreciation - Mach. & Equipment 31,200 Depreciation Expense 31,200 Depreciation expense for 2005 (3,850,000 - 480,000) x 10% P337,000 480,000 x 10% x ½ 24,000 P361,000 Amount recorded 392,200 Adjustment to be made (P31,200) (8) Depreciation Expense 25,000 Accumulated Depreciation - Land Improvements 25,000 (P500,000 x 10% x 6/12) Answer: 1. B 2. C 3. C 4. B 5. C 6. C 7. B 8. B 9. C 10. C

28

Problem 16

You are engaged to examine the financial statement of the Rabago Manufacturing

Corporation for the year ended December 31, 2004. The following schedules for property,

plant, and equipment and the related accumulated depreciation accounts have been

prepared by your client. The opening balances agree with your prior year’s audit working

papers.

Rabago Manufacturing Corporation

Analysis of Property, Plant, and Equipment and

Related Accumulated Depreciation Accounts

Year Ended December 31, 2004

COST

Final Per Books

12/31/03 Additions Retirements 12/31/04

Land P 450,000 P 100,000 P P 550,000

Buildings 2,400,000 350,000 2,750,000

Machinery/Equip 2,770,000 808,000 520,000 3,526,000

P 5,620,000 P1,258,000 P 520,000 P 6,826,000

ACCUMULATED DEPRECIATION

Final Per Books

12/31/03 Additions Retirements 12/31/04

Buildings P 1,200,000 P 103,000 P 1,303,000

Machinery/Equip 546,500 313,600 860,100

P 1,746,200 P 416,600 P 2,163,100

Further investigation revealed the following:

a. All equipment is depreciated on the straight-line basis (with no salvage value) based on

the following estimated lives: Building – 25 years, all other items 10 years.

b. The company entered into a 10-year lease contract for a derrick machine with annual

rental of P100,000, payable in advance every April 1. The parties to the contract

stipulated that a 30-day written notice is required to cancel the lease. Estimated useful

life is 10 years. The derrick was recorded under machinery and equipment at P808,000

and P60,000 applicable to the machine was included in the depreciation expense during

the year.

c. The company finished construction of a new building wing in June 30. The useful life of

the main building was not prolonged. The lowest construction bid was P350,000 which

was the amount recorded. Company personnel constructed the building at a total cost

of P330,000.

d. P100,000 was paid for the construction of a parking lot which was completed on July 1,

2004. The expenditure was charged to land.

e. The P520,000 equipment under retirement column represent cash received on October

1, 2004 for a machinery bought in October 1, 2000 for P960,000. The bookkeeper

recorded depreciation expense of P72,000 on this machine in 2004.

f. Mr. Rabago, the company’s president donated land and building appraised at P200,000

and P400,000 respectively to the company to be used as plant site. The company began

29

operating the plant on September 30, 2004. Since no money was involved, the

bookkeeper did not make any entry for the above transaction.

Questions

1. The balance of rent expense as of December 31, 2004 is:

a. P 0 b. P 25,000 c. P 75,000 d. P 100,000

2. The balance of prepaid rent as of December 31, 2004 is:

a. P 0 b. P 25,000 c. P 75,000 d. P 100,000

3. The life of the building wing is

a. 25 years b. 11 years c. 12 years d. 13 years

4. The carrying value of the building as of December 31, 2004 is

a. P 1,447,000 b. P 1,816,250 c. P 1,820,250 d. P 1,827,400

5. The value of the land account for balance sheet presentation as of December 31, 2004

is:

a. P 450,000 b. P 545,000 c. P 650,000 d. P 750,000

6. The loss on the disposal of the machinery sold for P520,000 is

a. P 0 b. P 30,000 c. P 56,000 d. P 152,000 Solution 1. C

The lease is considered as operating lease since it is cancelable. Equipment rental expense - P100,000 x 9/12 = P P75,000 2. B

Prepaid rental expense - P100,000 x 3/12 = P 25,000 3. C

Age of the building as of December 31, 2003 P1,200,000/P2,400,000 = 50% x 25 years = 12.5 years

Expired life for the current year = .5 year Remaining life of the building wing = 12.5 - .5 = 12 years 4. B

Building per schedule 2,400,000 Accumulated depreciation (1,296,000) 1,104,000 Building wing 330,000 Accumulated depreciation (P330,000/12 x 6/12) ( 13,750) 316,250

Building - donation 400,000 Accumulated depreciation (P400,000/25 x 3/12) ( 4,000) 396,000 Total carrying value 1,816,250 5. C

Land per schedule 450,000 Land - donation 200,000

650,000 6. C

Cost of the machine sold 960,000 Accumulated depreciation (P960,000/10 x 4) 384,000 Book value 576,000 Proceeds from sale 520,000 Loss on sale 56,000

30

Problem 17

On an audit engagement for calendar year 2003, you handled the audit of Fixed Assets of

Crame Corporation. Plant assets consists of:

Land P 100,000

Leasehold improvements 190,000

Equipment 450,000

Total per WBS P 740,000

The land was acquired on October 1, 2003, at a cost of P500,000. Crame Corporation made

a cash downpayment of P100,000 and signed a 18% mortgage note payable in four equal

annual installments of P100,000. The first interest and principal payment is due on October

1, 2004. No interest has been accrued as of December 31, 2003.

In October 1, 2003, a lawyer was engaged to title the property at a fee of P10,000 which

was charged to operating expenses.

You ascertained that due to obsolescence, computer equipment with an original cost of

P80,000 and accumulated depreciation of P16,000 at January 1, 2003 had suffered a

permanent impairment in value and, as a result, should have a carrying value of only

P40,000 at the beginning of the year. In addition, the remaining useful life of the

equipment was reduced from 4 to 2 years. No entry has yet been made in the books. For

2003, the company recorded depreciation of P16,000 for the said equipment.

At present, Crame Corporation’s office and warehouse are located in a rented building. The

rental contract was signed on July 1, 2003 and has a term of five (5) years renewable for

another five (5) years. On October 1, 2003, Crame Corporation spent P190,000 to install

walls and fixtures. The leasehold improvements have a useful life of five years. No

amortization has been booked as of December 31, 2003.

Questions

1. The adjusted cost of land amounted to:

a. P 528,000 b. P 510,000 c. P 500,000 d. P 410,000

2. The carrying value of leasehold improvements as of December 31, 2003 amounted to:

a. P 190,000 b. P 183,000 c. P 180,500 d. P 180,000

3. Audit adjustments will increase depreciation/amortization expense by:

a. P 38,000 b. P 24,000 c. P 14,000 d. P 13,500

4. Loss due to impairment in value amounted to:

a. P 30,000 b. P 28,000 c. P 24,000 d. P 20,000

Solution 1. B

Cost of the land 500,000 Add: tilting cost 10,000 Total 510,000 2. C

Land improvement 190,000 Less: Accumulated depreciation 10,000 (P190,000/57 mos. x 3 mos.) Carrying value 180,000 3. C

Depreciation - leasehold improvement 10,000 Depreciation - Equipment (P40,000/2) 20,000

31

Total per audit 30,000 Total per book 16,000 Understatement of depreciation 14,000 4. C

Net book value 64,000 Less: CV after impairment 40,000 Loss on impairment 24,000

Problem 18

On January 1, 2003, BLESSING COMPANY signs a 10-year noncancelable lease agreement

to lease a storage building from GRACE COMPANY. The following information pertains to

this lease agreement:

a. The agreement requires equal rental payments of P720,000 beginning on January 1,

2003.

b. The fair value of the building on January 1, 2003, is P4,400,000.

c. The building has an estimated economic life of 12 years, with an unguaranteed residual

value of P100,000. BLESSING COMPANY depreciates similar buildings on the straight-

line method.

d. The lease is nonrevnewable. At the termination of the lease, the building reverts to the

lessor.

e. BLESSING COMPANY’s incremental borrowing rate is 12% per year. The lessor’s implicit

rate is not known by BLESSING COMPANY.

f. The yearly rental payment includes P24,705.10 of executory costs related to taxes on

the property.

The following present value factors are for 10 periods at 12% annual interest rate:

Present value of an annuity due of 1 6.32825

Present value of an ordinary annuity of 1 5.65022

Present value of 1 0.32197

Questions

1. The minimum annual lease payment is:

a. P 744,705.10 b. P 720,000.00 c. P 695,294.90 d. P 0

2. The present value of minimum lease payments is:

a. P 0 b. P 4,400,000 c. P 4,207,747.65 d. P 3,928,569.15

3. The interest expense at December 31, 2003 is:

a. P 0 b. P 414,476.98 c. P 444,564,61 d. P 528,000.00

4. The depreciation expense at December 31, 2003 is:

a. P 0 b. P 420,774.76 c. P 440,000.00 d. P 471,268.00

5. The Book Value of Leased Building at December 31, 2004 is:

a. P 3,520,000.00 b. P 3,786,972.89 c. P 3,979,225.24 d. P 3,960,000.00

32

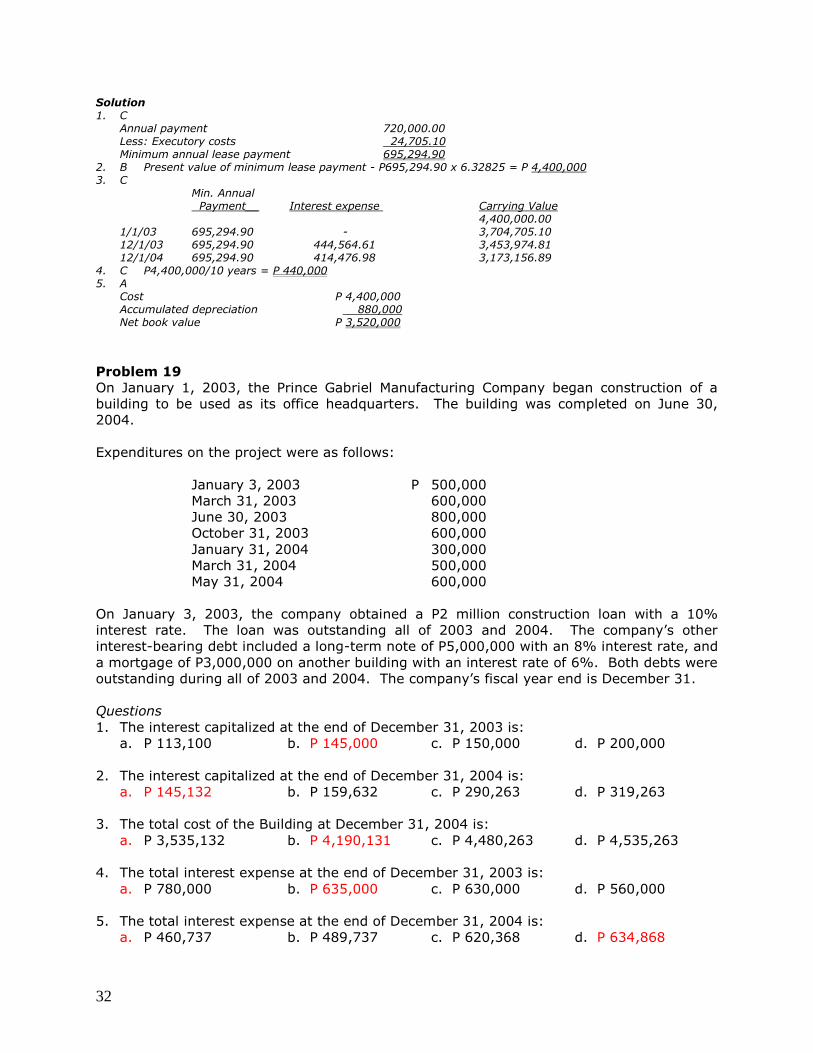

Solution 1. C

Annual payment 720,000.00 Less: Executory costs 24,705.10 Minimum annual lease payment 695,294.90 2. B Present value of minimum lease payment - P695,294.90 x 6.32825 = P 4,400,000 3. C

Min. Annual Payment__ Interest expense Carrying Value 4,400,000.00 1/1/03 695,294.90 - 3,704,705.10 12/1/03 695,294.90 444,564.61 3,453,974.81 12/1/04 695,294.90 414,476.98 3,173,156.89 4. C P4,400,000/10 years = P 440,000 5. A Cost P 4,400,000 Accumulated depreciation 880,000 Net book value P 3,520,000

Problem 19

On January 1, 2003, the Prince Gabriel Manufacturing Company began construction of a

building to be used as its office headquarters. The building was completed on June 30,

2004.

Expenditures on the project were as follows:

January 3, 2003 P 500,000

March 31, 2003 600,000

June 30, 2003 800,000

October 31, 2003 600,000

January 31, 2004 300,000

March 31, 2004 500,000

May 31, 2004 600,000

On January 3, 2003, the company obtained a P2 million construction loan with a 10%

interest rate. The loan was outstanding all of 2003 and 2004. The company’s other

interest-bearing debt included a long-term note of P5,000,000 with an 8% interest rate, and

a mortgage of P3,000,000 on another building with an interest rate of 6%. Both debts were

outstanding during all of 2003 and 2004. The company’s fiscal year end is December 31.

Questions

1. The interest capitalized at the end of December 31, 2003 is:

a. P 113,100 b. P 145,000 c. P 150,000 d. P 200,000

2. The interest capitalized at the end of December 31, 2004 is:

a. P 145,132 b. P 159,632 c. P 290,263 d. P 319,263

3. The total cost of the Building at December 31, 2004 is:

a. P 3,535,132 b. P 4,190,131 c. P 4,480,263 d. P 4,535,263

4. The total interest expense at the end of December 31, 2003 is:

a. P 780,000 b. P 635,000 c. P 630,000 d. P 560,000

5. The total interest expense at the end of December 31, 2004 is:

a. P 460,737 b. P 489,737 c. P 620,368 d. P 634,868

33

Solution 1. B Jan. 3 500,000 x 12/12 = 500,000 March 31 600,000 x 9/12 = 450,000 June 30 800,000 x 6/12 = 400,000 AAE Oct 31 600,000 x 2/12 = 100,000 1,450,000 x 10% = P145,000 (Lower than the

actual cost of P580,000) 2. A Beg bal. 2,500,000 x 6/6 = 2,500,000 145,000 x 6/6 = 145,000 Jan. 31 300,000 x 5/6 = 250,000 Mar 31 500,000 x 3/6 = 250,000 May 31 600,000 x 1/6 = 100,000 3,245,000 AAE Specific borrowing - P2,000,000 x 10% x 6/12 = 100,000 General borrowing - 1,245,000 x 7.25% x 6/12 = 45,132 Interest to be capitalized 145,132 (Lower than the actual cost of P580,000) Average rate (general) 5,000,000 x 8% = P 400,000 3,000,000 x 6% = 180,000 580,000 / 8,000,000 = 7.25% 3. B

Total cost in the construction - P 3,900,000 Interest capitalized - 290,132 Total cost – building - P 4,190,132 4. B Interest expense – 2003 Specific borrowing P 2,000,000 x 10% = 200,000 General borrowing P 5,000,000 x 8% = 400,000 P 3,000,000 x 6% = 180,000 Less: Interest capitalized = (145,000) Total interest expense – 2003 = 635,000 5. D Interest expense – 2004 Specific borrowing P 2,000,000 x 10% = 200,000 General borrowing P 5,000,000 x 8% = 400,000 P 3,000,000 x 6% = 180,000 Less: Interest capitalized = (145,132) Total interest expense – 2003 = 634,868

Problem 20

In connection with your audit of Bing-Bong Corporation, you noted that on January 2, 2002,

the corporation purchased a building site for its proposed research and development

laboratory at a cost of P2,400,000. Construction of the building was started in 2002. The

building was completed on December 31, 2003, at a cost of P11,200,000 and was placed in

service on January 1, 2004. The estimated useful life of the building for depreciation

purposes was 20 years; the straight-line method of depreciation was to be employed and

there was no estimated salvage value.

Management estimates that about 50% of the projects of the research and development

group will result in long-term benefits to the corporation. The remaining projects either

benefit the current period or are abandoned before completion. A summary of the number

of projects and the direct costs incurred in conjunction with the research and development

activities for 2004 appears below.

34

No. of Salaries and Other expenses

Projects employees benefits (excluding dep’n.)

Completed projects with

long-term benefits 60 3,600,000 2,000,000

Abandoned projects that

benefit the current year 40 2,600,000 600,000

Projects in process – results

indeterminate 20 1,600,000 480,000

Upon the recommendation of the research and development group, Bing-Bong Corporation

acquired a patent for manufacturing rights at a cost of P3,200,000. The patent was

acquired on March 31, 2003, and has an economic life of 10 years.

Questions

1. Carrying value of the patent as of December 31, 2004 is:

a. P 3,600,000 b. P 3,200,000 c. P 2,880,000 d. P 2,640,000

2. Carrying value of the building as of December 31, 2004 is:

a. P 5,320,000 b. P 10,640,000 c. P 10,080,000 d. P 0

3. Carrying value of the land as of December 31, 2004 is:

a. P 1,200,000 b. P 2,400,000 c. P 2,160,000 d. P 0

4. Research and development expense for 2004 is:

a. P 5,280,000 b. P 10,880,000 c. P 11,440,000 d. P 11,760,000

Solution 1. D Cost of patent - P 3,200,000 Amortization – 2003 - 240,000 Amortization – 2004 - 320,000 Net carrying value - P 2,640,000 2. B Cost of building - P 11,200,000 Depreciation – 2004 - 560,000 Net carrying value - P 10,640,000 3. B cost of the land – P 2,400,000 4. C Salaries and benefits - P 7,800,000

Other expenses - 3,080,000 Depreciation - 560,000 Total R and D Cost - P11,440,000