Great apes and FSC: Implementing ‘ape friendly’practices in central Africa’s logging concessions

Upload

khangminh22Category

view

0download

0

1

Challenges in Accessing

the Small Business CGT

Concessions

Tom Delany

Principal, Tax Partner Pty Ltd

Small Business Concessions - Overview

• The small business concessions are set out in Division 152 ITAA 97

• Basic conditions (Subdivision 152-A ITAA 97)

• CGT event leading to a capital gain has happened

• SBE (turnover test), or maximum net asset value test (s 152-15 ITAA 97) or other tests related to assets used by connected entities or affiliates s 152-10(1A) and (1B) ITAA97

• Active asset test (s 152-35 ITAA 97)

• Ownership rules for shares/trust interests (s 152-10(2) ITAA97) (New rules since 8 February 2018).

• Concessions

• 15 year exemption (Subdivision 152-B ITAA 97)

• 50% reduction (Subdivision 152-C ITAA 97)

• Retirement concession (Subdivision 152-D ITAA 97)

• Roll-over (Subdivision 152-E ITAA 97)

2

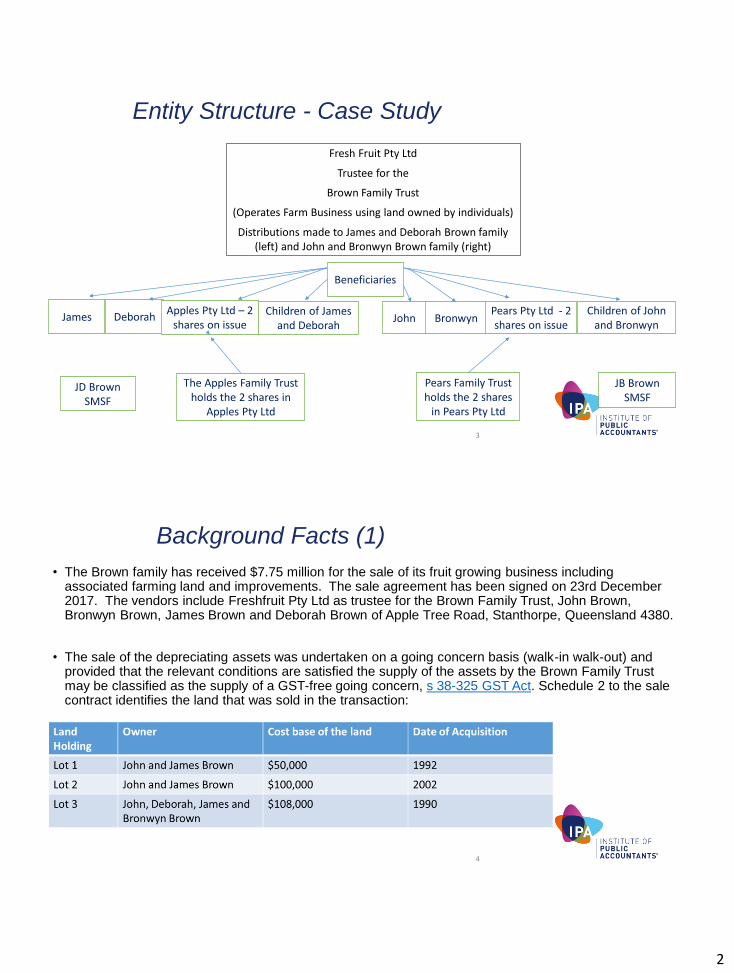

Entity Structure - Case Study

3

Fresh Fruit Pty Ltd

Trustee for the

Brown Family Trust

(Operates Farm Business using land owned by individuals)

Distributions made to James and Deborah Brown family (left) and John and Bronwyn Brown family (right)

The Apples Family Trust holds the 2 shares in

Apples Pty Ltd

James DeborahApples Pty Ltd – 2

shares on issue

Beneficiaries

John BronwynPears Pty Ltd - 2 shares on issue

Pears Family Trust holds the 2 shares

in Pears Pty Ltd

JB Brown SMSF

JD Brown SMSF

Children of James and Deborah

Children of John and Bronwyn

Background Facts (1)

• The Brown family has received $7.75 million for the sale of its fruit growing business including associated farming land and improvements. The sale agreement has been signed on 23rd December 2017. The vendors include Freshfruit Pty Ltd as trustee for the Brown Family Trust, John Brown, Bronwyn Brown, James Brown and Deborah Brown of Apple Tree Road, Stanthorpe, Queensland 4380.

• The sale of the depreciating assets was undertaken on a going concern basis (walk-in walk-out) and provided that the relevant conditions are satisfied the supply of the assets by the Brown Family Trust may be classified as the supply of a GST-free going concern, s 38-325 GST Act. Schedule 2 to the sale contract identifies the land that was sold in the transaction:

4

3

Background Facts (2)

• Trust distributions from the Brown Family Trust have in the main been made over time to equalize the distributions to the John and Bronwyn Brown family (including Pears Pty Ltd) and the James and Deborah Brown family (including Apples Pty Ltd). The turnover of the trust was over $4 million in the 2017 and 2018 years. Trust distributions have been made to the following beneficiaries in the 2015, 2016 and 2017 income years. A similar pattern existed in earlier years.

• The retained earnings in Apples Pty Ltd and Pears Pty Ltd is $2.7million each.

5

Trust Distribution 2017 2016 2015

John Brown $20,000 (5.5%) $55,000 (4.19%) $12,000 (1.33%)

Bronwyn Brown $20,000 (5.5%) $45,000 (3.43%) $10,000 (1.11%)

James Brown $15,000 (2.1%) $65,000 (4.95%) $20,000 (2.21%)

Deborah Brown $15,000 (2.1%) $65,000 (4.95%) $20,000 (2.21%)

Pears Pty Ltd $324,380.99 (39%) $556,100.90 (42.38%) $429,479.32 (47.56%)

Apples Pty Ltd $334,380.99 (45.8%) $526,100.89 (40.09%) $411,482.74 (45.57%)

Total Distributions $728,761.98 (100.00%) $1,312,201.79 (100.00%) $902,962.06 (100.00%)

Meaning of Connected EntitySection 328-125 provides that an entity is connected with another entity if:

• (a) either entity controls the other entity in a way described in this section; or

• (b) both entities are controlled in a way described in this section by the same third entity.

• Entity other than a discretionary trust - beneficially ownership, or have the right to acquire the beneficial ownership to receive a percentage (the control percentage) that is at least 40% of:

(i) any distribution of income by the other entity; or

(ii) if the other entity is a partnership--the net income of the partnership; or

• (iii) any distribution of capital by the other entity; or

• if the other entity is a company - beneficially own, or have the right to acquire the beneficial ownership of at least 40% of the voting power in the company.

• Direct control of a discretionary trust – (1) An entity (the first entity ) controls a discretionary trust if a trustee of the trust acts, or could reasonably be expected to act, in accordance with the directions or wishes (Gutteridge v FCT [2013] AATA 947); and (2) An entity (the first entity ) controls a discretionary trust for an income year if, for any of the 4 income years before that year the trustee of the trust paid to, or applied at least 40% of the income or capital of the trust.

• Section 328-125(7) provides that a series of entities can be controlled where each entity is connected to another entity.

4

Meaning of Affiliate

Section 328-130 defines an affiliate to mean -

• (1) An individual or a company is an affiliate of yours if the individual or company acts, or could

reasonably be expected to act, in accordance with your directions or wishes, or in concert with you, in

relation to the affairs of the business of the individual or company.

• (2) However, an individual or a company is not your affiliate merely because of the nature of the

business relationship you and the individual or company share.

• Example: A partner in a partnership would not be an affiliate of another partner merely because the first

partner acts, or could reasonably be expected to act, in accordance with the directions or wishes of the

second partner, or in concert with the second partner, in relation to the affairs of the partnership. Directors

of the same company and trustees of the same trust, or the company and a director of that company,

would be in a similar position.

Capital Gains Tax – Family Members (1)

• As the Brown family has entered into a contract for the sale of their CGT assets all calculations related to the sale will need to be performed on that date (CGT event A1) including the determination of net asset values, turnover and any capital gains tax apportionments.

• The apportionment of the sale price and initial capital gains calculations are as follows:

• The balance of the sale price has been attributed to depreciating assets.8

Land Holding

Owner Cost base of the land

Date of Acquisition

Sale Price Capital Gain

Discount Gain

Lot 1 John and James Brown

$50,000 1992 $2 million $1.95million

$975,000

Lot 2 John and James Brown

$100,000 2002 $1.76 million

$1.66 million

$830,000

Lot 3 John,Deborah, James and Bronwyn Brown

$108,000 1990 $3.45million

$3.342million

$1,671,000

$7.21 M $6.952 M $3.476 M

5

Capital Gains Tax – Family Members (2)

• The approximate CGT liability in the absence of the small business CGT concessions is shown in the following table:

9

Land Holding

Owner Sale Price Capital Gain Discount Gain

Income Tax Payable

Lot 1 John and James Brown

$2 million $1.95 million $975,000 $477,750

Lot 2 John and James Brown

$1.76 million $1.66 million $830,000 $406,700

Lot 3 John, Deborah, James and Bronwyn Brown

$3.45 million $3.342 million $1,671,000 $818,790

$7.21 M $6.952 M $3.476 M $1,703,240

Small Business Concessions (1)

• Basic conditions (Subdivision 152-A ITAA 97)

1. CGT event leading to capital gain has happened

• CGT event D1 has special conditions (s 152-12 ITAA 97)

• CGT event K7 is not eligible for the small business concessions

• CGT events J2, J5 and J6 are not eligible for the 15-year exemption

• CGT events J5 and J6 are not eligible for the rollover

2. Entity qualifies as a “CGT small business entity”, net asset value test or similar test (s 152-10 ITAA97)

• There are 4 ways to satisfy this condition

• The first way to satisfy the condition is if the taxpayer is a CGT small business entity

• Generally, the taxpayer carries on a business with a turnover under $2m (Subdivision 328-C ITAA 97)

6

An entity's "aggregated turnover" is the sum of the relevant "annual turnovers", but excluding certain

amounts, s 328-115 ITAA97.

• The relevant "annual turnovers" are the entity's annual turnover, any connected entity's annual turnover

and any affiliate's annual turnover (based on an arm’s length methodology), s 328-120(4) ITAA97.

Three classes of related party ordinary income are excluded from aggregated turnover to avoid double-

counting (s 328-115(3) ITAA97).

The following amounts are excluded from annual turnover (s 328-120 ITAA97)

• any GST-related amounts that are non-assessable non-exempt income under s 17-5; and

• any ordinary income derived from the sale of retail fuel (a retail sale requires the transfer of property in

the fuel from the seller to the buyer).

• If an entity carries on a business for part of the income year only, its turnover must be worked out using

a reasonable estimate of what the turnover would have been if the entity had carried on a business for

the whole of the income year: s 328-120(5).

Aggregated Turnover

Small Business Concessions (2)

• Basic conditions (Subdiv 152-A ITAA 97) cont.

2. Entity qualifies as a “CGT small business entity”, net asset value test or similar test (s 152-10 ITAA97)

The second way to satisfy the condition is the maximum net asset value test

• Net value of CGT assets of the taxpayer, affiliates, connected entities and their affiliates is less than $6m (s 152-15 ITAA 97)

• Net value includes some CGT assets that are normally disregarded eg trading stock, but excludes many personal assets (s 152-20 ITAA 97)

• Net value is reduced for liabilities related to CGT assets and provisions for leave and tax (s 152-20 ITAA 97)

• Affiliates are entities that act in accordance with the taxpayer’s wishes or in concert with them (s 328-130), see also s 152-47 ITAA97

• Connected entities are entities that control each other or have common control (s 328-125 ITAA 97). For discretionary trusts, see also s 152-78 ITAA 97.

7

Market Value

• Market Value for Taxation Purposes - guidance has been provided by the ATO and in that material the ATO advises that the meaning of the term will depend on the statutory context. Where a statutory definition is provided for a particular context, it must be used. Otherwise the term 'market value' usually takes its ordinary meaning.

• Business valuers in Australia typically define market value as:

• the price that would be negotiated in an open and unrestricted market between a knowledgeable, willing but not anxious buyer and a knowledgeable, willing but not anxious seller acting at arm's length.

• The High Court in Spencer v The Commonwealth of Australia (1907) 5 CLR 418 provided guidance on the meaning … the test of value of land is to be determined, not by inquiring what price a man desiring to sell could have obtained for it on a given day, i.e. whether there was, in fact, on that day a willing buyer, but by inquiring: What would a man desiring to buy the land have had to pay for it on that day to a vendor willing to sell it for a fair price but not desirous to sell?

Is the Sale Price always “Market Value”?

In Excellar Pty Ltd v FCT [2015] AATA 282 the taxpayer sold a property for $5,500,000 but argued that the market value was $3.72 million. The AAT held that the best indication of the value of a property was its selling price on the basis that:

• The parties to the transaction were acting at arm’s length and were willing, but not anxious, to sell or buy and had freely negotiated that price; and

• Evidence existed to suggest that the methodology used in determining the market value by the taxpayer was flawed.

• In Miley v FCT 2017 ATC ¶20-640) the Federal Court concluded that despite the fact that a discount is normally applied to minority interests held in companies when valuing those interests it is not possible to ignore the fact that just before the sale, there was a buyer in the market who was ready and willing to purchase all the shares for $17.7 million and there was nothing to suggest that the parties were not willing and knowledgeable, or anxious or that the price that was struck between the parties was not the product of an arm's length negotiation.

8

Market Value – Other Issues

• In Excellar the AAT held that cash held in a bank account was an asset.

• Breakwell v FCT [2015] FCA 1471 discussed the concept of whether the value of a statute barred loan should be included - held that even if a remedy is not available (recovery is constrained because the debt is statute barred) the debt still exists and should be included the market value (note that fiduciary issues also arose in this case as well as the fact that the signing of the financial statements may represent acknowledgement of the debt).

• If the asset is not being used solely for personal use and enjoyment then the total market value of the asset must be included. The case of Altnot Pty Ltd v FCT [2013] AATA 140 provides us with guidance that the asset must actually be used for personal use and enjoyment.

• Does the market value mean the GST inclusive or exclusive value of the asset or the liability? Consider s 960-405 ITAA97 – Generally the market value of an asset is based on the GST exclusive value while the market value of a liability is based on a GST inclusive value (Byrne Hotels).

Market Value – Related Liabilities• In Excellar the AAT held that the liability for land tax did not exist just before the CGT event

because the land tax liability came into being on a later date. However the AAT held that the liability for paying rates by instalments was incurred despite the fact that payment was deferred.

• In Scanlan v FCT [2014] AATA 725 the AAT held that a resolution to pay leave entitlements did not result in a liability being incurred.

• In Bell v FCT [2013] FCAFC 32 the Full Federal Court concluded that borrowing made to make a cash distribution did not relate to the acquisition of an asset of the trust and so was not a liability related to the assets of the trust. Note that in Bell the taxpayer borrowed an exact amount to make the distribution. Would it have been different if the borrowing and the distribution were not the same amount?

• In FCT v Byrne Hotels Qld Pty Ltd [2011] FCAFC 127 the court held that contingent liabilities generally did not count but that where services were performed but unbilled the requirement to pay for those services is a liability, (for example the services of a real estate agent).

9

Satisfying the basic conditions• Maximum Net Asset Value Test - A taxpayer satisfies the maximum net asset value test if, just before

the time of the CGT event, the net value of the CGT assets of the taxpayer and connected entities/affiliates is not more than $6m.

• Having reviewed the distributions for the past 4 years from the Brown Family Trust it is evident that none of the individual members of the family received a distribution of at least 40% so they are not connected under this rule whereas Pears Pty Ltd and Apples Pty Ltd have received distributions in these years to the extent of 40% or more and accordingly are connected with the Brown Family Trust.

• As the Pears Family Trust is connected to Pears Pty Ltd (shareholding) and John and Bronwyn are in a position to control the Pears Family Trust (appointors) then John and Bronwyn are connected with the Brown Family Trust, Pears Pty Ltd and the Pears Family Trust. Similarly James and Deborah will be indirectly connected with the B Brown Family Trust, Apples Pty Ltd and the Apples Family Trust.

• In satisfying the net asset value test (market value less related liabilities) each individual must include the value of all connected entities.

Issues in Satisfying the NAV (1)Land

• The land had two main residences, there was some borrowing related to the land and commission will be paid on the sale of the properties.

• How are the main residences treated when constructed on the primary production land?

• Do joint owners of the land need to include the full value of the asset in determining their NAV?

• Should borrowing expenses and loans be applied to reduce NAV?

• Given that the Commission is not payable until after settlement is it a liability?

Brown Family Trust

• The Brown Family Trust had prepared a set of financial statements to 20 December 2017 which indicated an interim profit amount of $1.2 million and on that date the trustee of the trust made an interim distribution of $1.2 million of income being 50% each to Apples Pty Ltd and Pears Pty Ltd.

• Assuming that it is possible to make an interim distribution in accordance with the trust deed, what are the consequences of making the interim distribution?

10

Issues in Satisfying the NAV (2)Direct Property

• Bronwyn had a rental property with a market value of $410,000 with no borrowing.

Pears Family Trust

• The Pears Family Trust had net value of just over $300,000.

• What is the consequence of this for each of John and Bronwyn?

Pears Pty Ltd

• The financial statements of Pears Pty Ltd indicates that the company has advanced $2.7 million to John and Bronwyn – Division 7A loan.

• What is the consequence of this for John and Bronwyn?

• What is the consequence of the interim distribution from the Brown Family Trust? Should the provision for income tax be considered to be a liability?

Issues in Satisfying the NAV (3)Direct Property

• James and Deborah had a residential property in Brisbane that was used by their children while attending university at the time of the CGT event. The property has been held for around 8 years with it being used by their children for 84% of the time and the rest of the time to earn assessable income. They also held other real property assets that were rented and shares and had related borrowing.

• What is the consequence of this for each of James and Deborah?

Apples Family Trust

• The Apples Family Trust had net negative equity of $10,000.

• What is the consequence of this for each of James and Deborah?

Apples Pty Ltd

• The financial statements of Apples Pty Ltd indicates that the company has advanced $2.7 million to James and Deborah – Division 7A loan.

• What is the consequence of this for James and Deborah?

11

Satisfying the basic conditions (4)• The net asset value of each of the individuals is as follows (after all calculations undertaken):

• The above table provides us with a determination of the net asset values of each of the individuals and based on this analysis all family members are below the $6 million maximum net asset value test. In other words on the basis of this analysis we can conclude that condition 2 can be satisfied.

• However a significant amount of work had to be undertaken in determining each of the parties NAV and appropriate market valuations prepared.

John Brown Bronwyn Brown

James Brown Deborah Brown

Net Asset Value $5,126,085 $3,949,049 $5,217,511 $3,630,475

Small Business Concessions (3)• Basic conditions (Subdivision 152-A ITAA 97) cont.

2. Entity qualifies as a “CGT small business entity”, net asset value test or similar test (s 152-10 ITAA97)

• The third way to satisfy the condition is if the CGT asset is a partner’s interest in a partnership which is a small business entity

• The fourth way to satisfy the condition is if the CGT asset is a passively held asset and one of the following applies:

• the CGT asset is an active asset used in an associated/connected small business entity’s business (s 152-10(1A) ITAA 97); or

• the CGT asset is an active asset used in the taxpayer’s partnership (s 152-10(1B) ITAA 97)

12

Small Business Concessions (4)• Basic conditions (Subdivision 152-A ITAA 97) cont.

3. Active asset test (s 152-35 ITAA 97)

• The CGT asset must be “active” for the lesser of

• half the period of ownership and

• 7 ½ years.

• An asset is “active” if it is:

• used or held ready for use in carrying on, or

• an intangible asset owned by the taxpayer and inherently connected with

a business carried on by the taxpayer, their affiliate or connected entity.

• A share or trust interest is “active” if:

• 80% of the company or trust’s assets by market value are active (see TD 2006/65 for chains of entities); and

• The taxpayer is a CGT concession stakeholder in the company/trust.

• Assets used to derive passive income such as rent or interest do not qualify

Satisfying the basic conditions – Active Assets• A CGT asset satisfies the active asset test if the asset was an active asset of the taxpayer:

• for a total of at least half the period from when the asset is acquired until the CGT event, or

• if the asset is owned for more than 15 years, for a total of at least 7½ years during that period.

• A CGT asset is an active asset if the taxpayer owns the asset (whether it is tangible or intangible) and: • uses it, or holds it ready for use, in the course of carrying on a business; or

• it is used in the course of carrying on a business by an affiliate or another entity that is connected with the taxpayer (includinga business carried on by the taxpayer's spouse or child under 18).

• The earlier analysis in this case study concluded that the Brown Family Trust is connected with the four individual family members and that it has been connected since the trustee was incorporated in 1995 and so each parcel of land may be considered to be active for at least half of the period of ownership or at least 7.5 years.

• It is recognized that in relation to the land that was purchased in 1990 and 1992 were used by a family partnership up to the time that the Brown Family Trust was established may have had up to 5 or 3 years respectively of active holding during that period.

13

Small Business Concessions (5)• Basic conditions (Subdivision 152-A ITAA 97) cont.

4. If the CGT asset is a share in a company or an interest in a trust, then one of the ownership tests must be satisfied (s 152-10(2) ITAA 97):

• Taxpayer is a CGT concession stakeholder in the company / trust; or

• CGT concession stakeholders in the company / trust together hold a small business participation percentage of at least 90% in the taxpayer

• A “CGT concession stakeholder” is a “significant individual” in the company / trust or the spouse of a “significant individual” who also has an interest in the company / trust (s 152-60 ITAA 97)

• A “significant individual” is an individual with a “small business participation percentage” in the company / trust of at least 20% (s 152-55 ITAA 97)

• A “small business participation percentage” is a direct or indirect interest of the prescribed type in the company / trust (s 152-65 ITAA 97)

Changes - Shares and Units• To be eligible to apply the CGT small business concessions, a taxpayer must satisfy the basic conditions

set out in s 152-10(2) in relation to the capital gain. Changes applicable from 8 February 2018.

Additional basic conditions apply for capital gains relating to shares in a company or interests in a trust. These are:

• either:

– the taxpayer must be a CGT concession stakeholder in the object entity; or

– broadly, entities that are CGT concession stakeholders in the object entity must have small business participation percentages totalling at least 90 per cent in the taxpayer;

• unless the taxpayer satisfies the maximum net asset value test, the taxpayer must have carried on a business just prior to the CGT event;

• the object entity must be a CGT small business entity for the income year or satisfy the maximum net asset value test; and

• the shares or interests in the object entity must satisfy a modified active asset test that looks through shares in companies and interests in trusts to the activities and assets of the underlying entities.

14

15-Year Exemption - Conditions

Concessions

1. 15 year exemption (Subdiv 152-B ITAA 97)

• This concession makes the whole capital gain exempt from CGT. There is no need to apply capital losses or discounts first.

• Proportionate payments of the capital gain to CGT concession stakeholders within 2 years are also exempt (s 152-115 ITAA 97)

• The special conditions are:

• The taxpayer owned the asset for 15 years before the CGT event (roll-overs may extend the period of ownership);

• If the taxpayer is an individual, they are either (a) over 55 and retiring or (b) permanently incapacitated (s 152-105 ITAA 97);

• If the taxpayer is a company or trust, the taxpayer had a significant individualfor at least 15 years during which it owned the asset and that individual is either (a) over 55 and retiring or (b) permanently incapacitated (s 152-110 ITAA 97)

• This exemption has priority over the other small business concessions.

15-Year Exemption (1)• A capital gain that qualifies for the 15-year exemption is disregarded entirely if the basic conditions are

satisfied and the asset has been held for 15 years and the disposal of the asset is in connection with the person’s retirement or the person is permanently incapacitated.

• As the properties acquired in 1990 and 1992 have been held for 15 years then a consideration of whether it would be possible to elect to use the 15 year exemption and exempt all the capital gains from the disposal of this land. For CGT events that happen in the 2006/07 income year and later income years, the exemption applies where:

• the basic conditions in Subdivision 152-A are satisfied for the gain.

• the individual continuously owned the CGT asset for the 15-year period ending just before the CGT event, and

• at the time of the CGT event, the individual is either:

• (i) 55 years of age or over and the event happens in connection with retirement, or

• (ii) permanently incapacitated.

15

15-Year Exemption (2)• All four taxpayers are over 55 years at the time of the CGT event. James and John have agreed to stay

on to manage the property for the new owners – does this cause a problem?

• Whether a CGT event happens in connection with an individual's retirement depends on the particular circumstances of each case. There would need to be at least a significant reduction in the number of hours the individual works or a significant change in the nature of their present activities to be regarded as a retirement. However, it is not necessary for there to be a permanent and everlasting retirement from the workforce.

• A CGT event may be ‘in connection with your retirement’ even if it occurs at some time before or after retirement provided there is a clear connection between retirement and the sale of the CGT asset.

• The term permanent incapacity is not defined in ITAA97 but an indicative description is ill health (whether physical or mental), where it is reasonable to consider that the person is unlikely, because of ill health, to engage again in gainful employment for which the person is reasonably qualified. The incapacity does not necessarily need to be permanent in the sense of everlasting.

Small Business 50% Reduction - Conditions

2. 50% reduction (subdiv 152-C ITAA 97)

• This concession is a 50% discount, which is applied after any capital losses and the general CGT discount (s 152-205 ITAA 97)

• There are no special conditions – it is available if the basic conditions are satisfied

• If the 15-year exemption is available, apply that exemption instead (s 152-215 ITAA 97)

• If the small business retirement exemption and small business roll-over are available, the 50% reduction may be applied as well (s 152-210 ITAA 97)

• If the concession is being considered in a company or unit trust explore using the other concessions first.

16

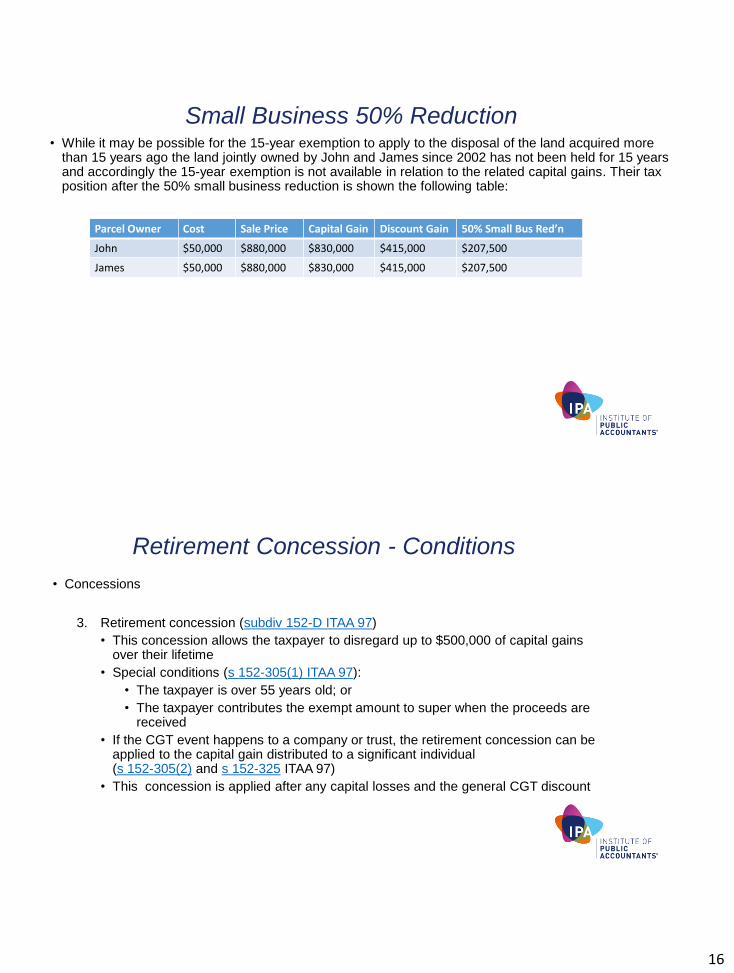

Small Business 50% Reduction• While it may be possible for the 15-year exemption to apply to the disposal of the land acquired more

than 15 years ago the land jointly owned by John and James since 2002 has not been held for 15 years and accordingly the 15-year exemption is not available in relation to the related capital gains. Their tax position after the 50% small business reduction is shown the following table:

Parcel Owner Cost Sale Price Capital Gain Discount Gain 50% Small Bus Red’n

John $50,000 $880,000 $830,000 $415,000 $207,500

James $50,000 $880,000 $830,000 $415,000 $207,500

Retirement Concession - Conditions

• Concessions

3. Retirement concession (subdiv 152-D ITAA 97)

• This concession allows the taxpayer to disregard up to $500,000 of capital gains over their lifetime

• Special conditions (s 152-305(1) ITAA 97):

• The taxpayer is over 55 years old; or

• The taxpayer contributes the exempt amount to super when the proceeds are received

• If the CGT event happens to a company or trust, the retirement concession can be applied to the capital gain distributed to a significant individual (s 152-305(2) and s 152-325 ITAA 97)

• This concession is applied after any capital losses and the general CGT discount

17

Retirement Concession

• Under the retirement exemption in Subdivision 152-D ITAA97, a taxpayer can choose to disregard all or part of a capital gain made from a CGT event. The taxpayer can be an individual, a company or a trust.

• However, a lifetime maximum limit of $500,000 applies to amounts that qualify for the exemption, ss 152-315 and 152-320 ITAA97. It is assumed for the purpose of this case study that John, and James have not utilised any of their $500,000 retirement exemption limit to date.

• As John and James are over 55 years at the time of the CGT event then they can elect to use the retirement exemption and no amount needs to be contributed to superannuation.

Small Business Roll-Over• A taxpayer can choose to roll over all or part of a capital gain under Subdivision 152-E ITAA97 if the basic

conditions in Subdivision 152-A ITAA97 are met.

• If the taxpayer does not acquire a "replacement asset" by the end of the "replacement asset period", or other replacement asset conditions are not met by that time (eg the asset is not an active asset by that time), then CGT Event J5 will apply to reinstate the rolled over gain.

• Likewise, if the taxpayer has not acquired a replacement asset or incurred "fourth element" capital expenditure on an existing CGT asset by the end of the replacement asset period to cover the amount of the rolled over gain, CGT Event J6 will apply to reinstate the gain to the extent of the difference between the gain rolled over and the expenditure incurred.

• On the other hand, CGT Event J2 will apply to reinstate the rolled over gain if, after the end of the "replacement asset period", an acquired replacement asset ceases to qualify as a replacement asset (egif it ceases to be an active asset).

• The "replacement asset period" is the period beginning one year before, and ending 2 years after, the last CGT event in the income year for which the roll-over is available, s 104-190 ITAA97. If any of the parties choose to apply the small business roll-over relief they will have to acquire a replacement asset prior to 23 December 2017 or the date when the contract to sell the land was signed.

18

Questions / Discussion

35

Copyright © 2022 FDOKUMEN