International Corporate Governance and Corporate Cash Holdings

Upload

khangminh22Category

view

1download

0

New Rules, New Roles: Does PSP Benefit the Poor?

The Corporate Muddle of Manila's Water Concessions

Jude Esguerra

Since this study was written, many events have unfolded. A rate rebasing process approved tariffincreases in late 2002, but these were below what one of the companies, Maynilad Water ServicesIncorporated, petitioned for. As a result, Maynilad pulled out of the concession. An arbitration case hasfollowed to resolve the controversy over Maynilad’s claims for reimbursement.

The analysis and position in this study are those of the author’s. Nevertheless, WaterAid is publishingthis study as it focuses on key issues in the water privatisation debate that are not discussed elsewhere.Contentious arguments are raised here against the companies, hence, WaterAid has included textboxes that provide space for the responses of Ondeo, one of the companies involved.

Jude Esguerra is an economist of the nongovernment Institute for Popular Democracy in Manila. He is the spokesman of Bantay-Tubig (Water Watch) a coalition of consumer groups and activistorganisations. Eric Gutierrez edited the text. Gordon McGranahan provided commentaries.

© WaterAid and Tearfund 2003

New Rules, New Roles: Does PSP Benefit the Poor?

Contents

I. Executive summary of synthesis report ..................................................................................... 4

II. Case Summary .......................................................................................................................... 6

III. Introduction .............................................................................................................................. 10

IV. Ondeo’s response to this case study ....................................................................................... 12

V. Context and the Contract ......................................................................................................... 13A Bidder's Bag of Tricks........................................................................................................... 15Maynilad's Story....................................................................................................................... 17

(a) Maynilad only had its reputation, not its money, at stake ............................ 19(b) Maynilad underestimated operating costs ................................................... 19(c) Maynilad overestimated revenues............................................................... 20(d) A mechanism is in place to cover foreign exchange losses ........................ 21

Manila Water's challenge......................................................................................................... 21The Mangling of the Concession Agreement ........................................................................... 24Consequences and Analysis of the Amendments to the Concession Agreement.................... 28

(a) The amendment increases the bankability of Maynilad and gave the company an undeserved bailout ................................................................. 28

(b) The integrity of the original bidding has been undermined .......................... 29(c) The new mechanism for foreign exchange cost recovery (FCDA)

reduces efficiency........................................................................................ 29(d) The task of hedging against future foreign exchange fluctuations is

taken off the shoulders of the private sector but it is not assigned to anyone ........................................................................................................ 30

(d) The regulatory office has been given new powers and assigned newtasks despite the weakness of the regulatory system ................................. 30

VI. Ondeo’s specific responses ..................................................................................................... 31

VII. Conclusions and Recommendations ....................................................................................... 31

VII. Conclusions and Recommendations ....................................................................................... 32

VII. Conclusions and Recommendations ....................................................................................... 33

References............................................................................................................................................. 38

Meetings and Interviews ........................................................................................................................ 38

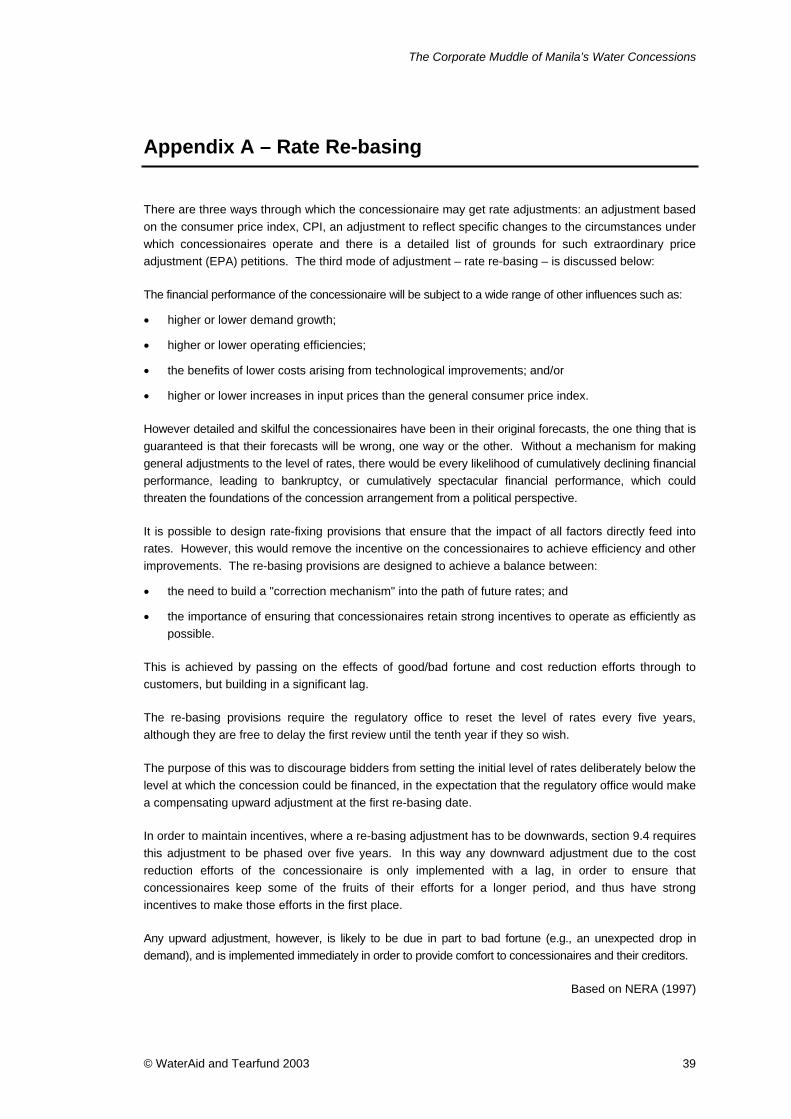

Appendix A – Rate Re-basing................................................................................................................ 39

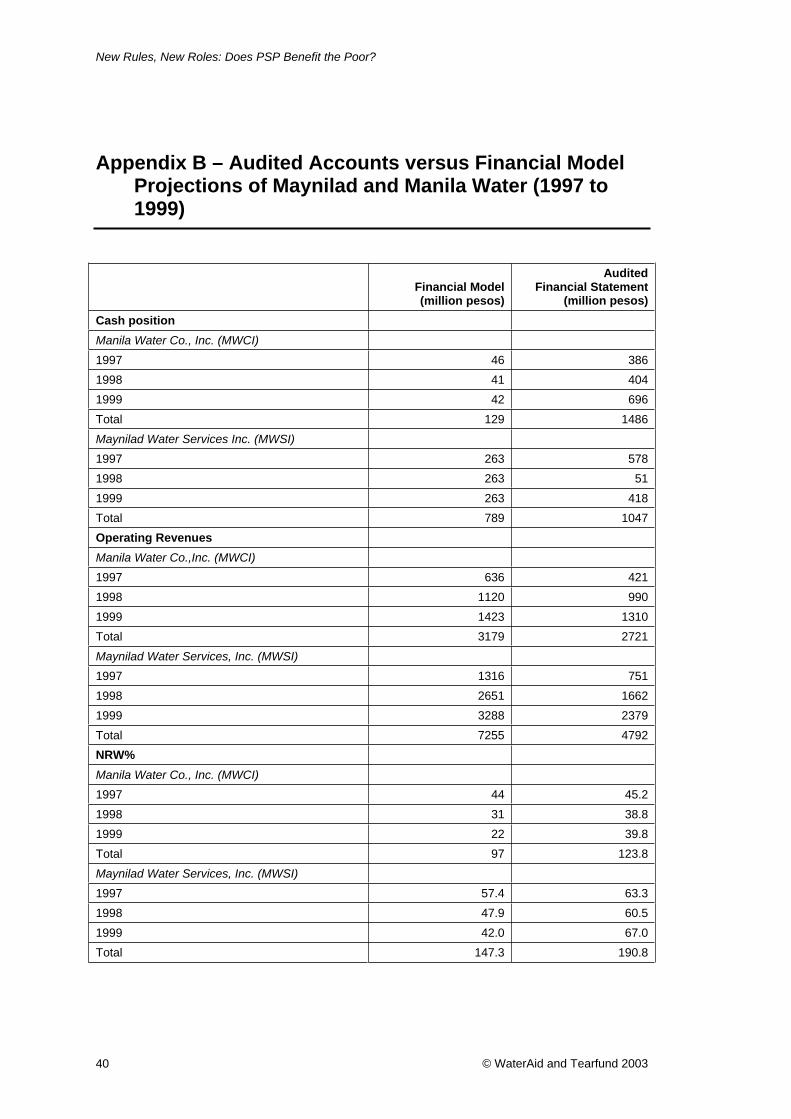

Appendix B – Audited Accounts versus Financial Model Projections of Maynilad and ManilaWater (1997 to 1999) ............................................................................................................... 40

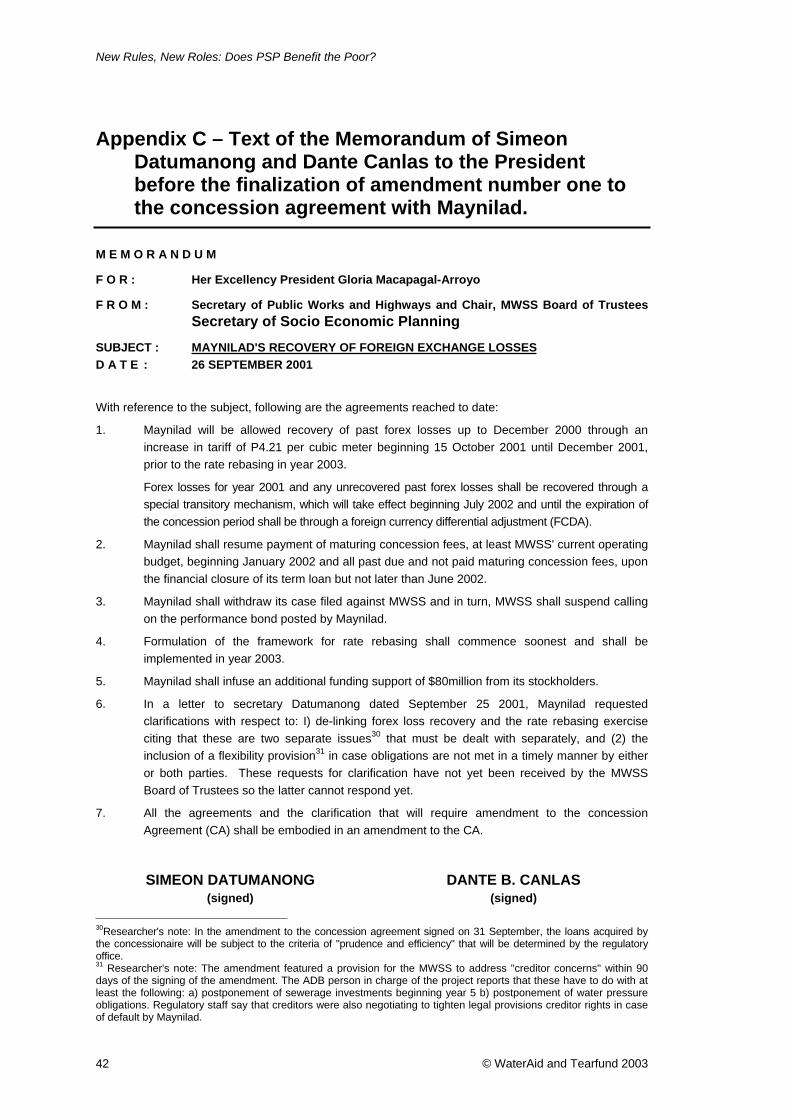

Appendix C – Text of the Memorandum of Simeon Datumanong and Dante Canlas to the President before the finalization of amendment number one to the concessionagreement with Maynilad. ........................................................................................................ 42

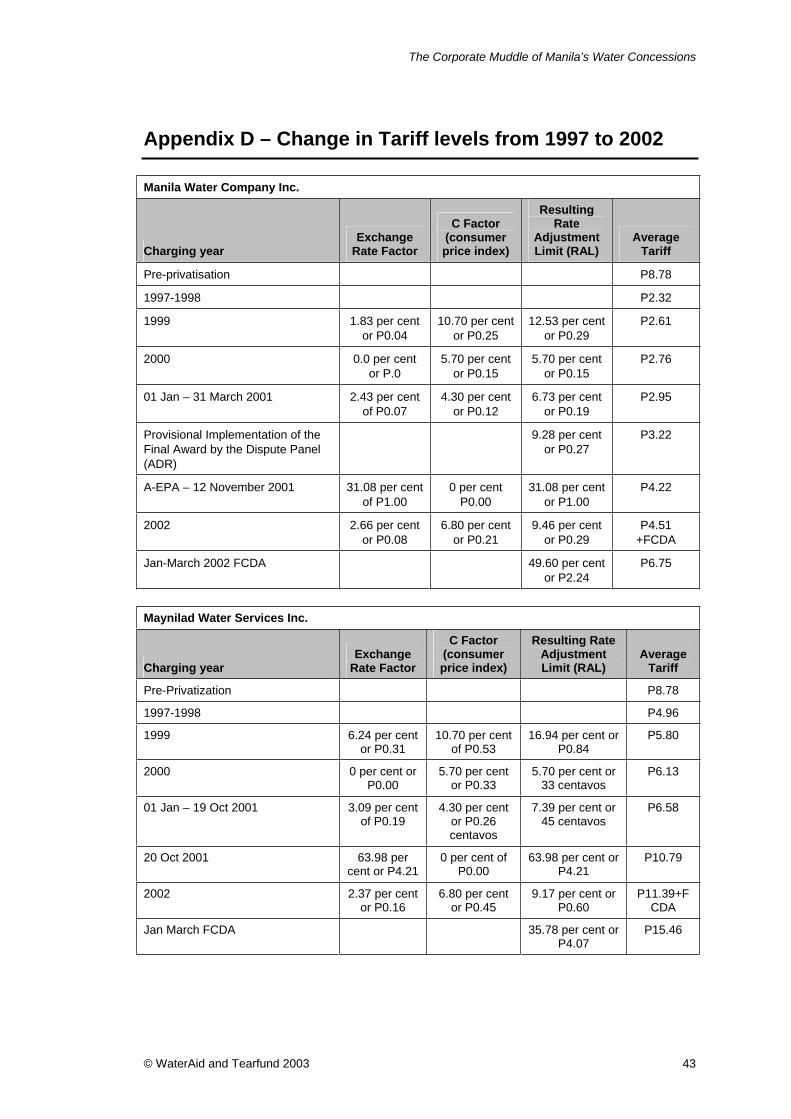

Appendix D – Change in Tariff levels from 1997 to 2002 ....................................................................... 43

Figure 1 – The Manila water concession's problems and the range of solutions ..................................22

© WaterAid and Tearfund 20032

The Corporate Muddle of Manila's Water Concessions:

Acronyms

ADB Asian Development Bank

ADR Automatic Discount Rate

BHC Benpres Holding Company

CERA Currency Exchange Rate Adjustment

EPA Extraordinary Price Adjustment

FCDA Foreign Currency Differential Adjustment

IFC International Finance Corporation – World Bank arm providing financing for privatesector projects

LDP Lyonnaise des Eaux Philippine

LYSA Lyonnais des Eaux Services Association

MWCI Manila Water Company Incorporated

MWSI Maynilad Water Services Incorporated

MWSS Metropolitan Water and Sewerage Systems – a government owned corporation that is the utility delivering water and sanitation services in Metro Manila

MWSS-RO MWSS Regulatory Office

NEDA National Economic Development Authority – the economic planning body of the nationalgovernment

NERA National Economic Research Associates – founded in 1961, a firm of consultingeconomists specialising in markets and how they work

NGO Non governmental organisation

pcm Per cubic metre

PHP Philippine peso

SLDE Suez Lyonnais des Eaux

© WaterAid and Tearfund 2003 3

New Rules, New Roles: Does PSP Benefit the Poor?

I. Executive summary of synthesis report

Governments, both northern andsouthern, have rightly placedthemselves under much pressure to

achieve better water and sanitation coverage.The Millennium Development Goals aim to halvethe proportion of people without access to waterand sanitation services by 2015. Millions dieevery year from lack of access to safe water andadequate sanitation. On one hand there is anundeniable urgency about these issues thatmakes prolonged discussion frustrating and aquestionable use of resources. But on the other,the risk of the blanket promotion of onedebatable method of reform is an unnecessarywaste of scarce resources.

Most southern governments have consistentlyfailed to deliver affordable and sustainable waterand sanitation to the poor. It is difficult to summarise the causes for this failure as eachsituation is different and complex. However,some broad problems cut across many publicutilities and municipal services: bad financialmanagement, low funding priority, lack of staff experience and qualifications, absent or weakcustomer service orientation, politicalinterference, little or no independent regulationand an absence of civil society consultation.Many of these problems have been described asattributable to weak government capacity –equally acute in urban and rural contexts.

Our research shows that the policy of privatesector participation (PSP) does notcomprehensively tackle the underlying causes ofwater utilities’ failure to serve the poor. In fourkey areas capacity building, communityparticipation, finance and institutional reform,major problems persist, making it unlikely thatthe multinational private sector is going to playany significant role in achieving the MillenniumDevelopment Goals.

Currently the pursuit of a policy of PSP generally undermines local and national governmentcapacity. For one, it limits the ability of the publicsector to take services back should PSP fail orwhen contracts end. Private sector contractingmust not result in irreversible dependence on

private companies, and there must be clauses incontracts to prevent this dependence.

Without adequate government capacity, noreform processes can be successful. The privatesector cannot be contracted without tacklingfailing government. The government’s role tofacilitate, monitor and regulate is as much anessential element in PSP as in public and user-managed utilities. Yet, it seems that this requirement is being practically ignored in therush to establish PSP. It is essential that donorsrefocus efforts to building government capacity atlocal and central levels.

The involvement of local communities is oftenlacking in PSP reform programmes. Where PSPhas failed to deliver the promised gains, the caseoften is that the poor are seen mainly asrecipients, rather than contributors todevelopment. Whether projects involve large orsmall-scale PSP, the focus is on giving contractsor concessions to the private sector. Socialmobilisation and community participation, proventime and again as prerequisites for sustainabledevelopment, are seen as burdens and non-essential components of the task. Failure toconsult communities means that the interests of the poor are often not being represented. It results in a lack of ownership over projects andan absence of accountability between users andservice providers. It seems that the lack ofcommunity involvement that led to previousfailures is continuing, raising serious doubts overthe sustainability of PSP projects.

Cost recovery and capital cost contributions arein most cases necessary for water services to besustainable. However, there are problems in theapplication of these principles, which oftenresults in denying the poor access to services.Expensive technology choices and a failure toconsider the non-cash contribution of the poorare widespread in PSP contracting. Donors are guilty of promoting an approach that is narrowand mechanistic, allowing for little flexibility andabsence of perspectives incorporatingcommunity action and considering thecomplexities of poverty.

© WaterAid and Tearfund 20034

The Corporate Muddle of Manila’s Water Concessions

Changing the role of government, by effectivelyreducing its capacity through reductions at central level, but not increasing personnel atlocal government levels, erases benefits that could be gained from decentralisation per se (such as responsiveness to people’s needs,greater accountability etc.). Weak decentralisedagencies cannot be expected to quickly learnabout tenders or forms of contracting and keeptrack, monitor and supervise the activities of contractors fanning beyond provincial capitals.

With these findings, we are opposed to donorspressuring developing countries to accept PSP inwater services as a condition of aid, trade or debtrelief. To promote a policy regardless of specificcontexts increases the likelihood of failureespecially when the likelihood of success of thatpolicy is intensely contested. Furthermore, theenforcement of PSP as the central policy reformlimits the options for governments and civil society to improvise and innovate using the bestpossible arrangements. We believe rather thatpolicies should be used to ensure that in anyreform process the poor will be protected, theiraccess to services increased, and the processitself actively seeks the opinion of civil society.

In the rural areas that were studied, reducedgovernment roles had a detrimental impact as work was often sub-standard leaving thecommunities with a costly and unreliable service.The rural case studies also show that there are, so far, no improvements in accountability. In some respects, accountability was compromised inthe dilution of responsibilities that accompanied thechange in roles. Because projects are betweengovernments and contractors (communities aretypically not a party in the contract), thesupposed beneficiaries are in no position to seekredress for sub-standard work. Accountability islost in the commercial/ contractual, quick-fixarrangements of private sector involvement.

This does not mean that we are rejecting privatesector involvement. The private sector has a rolethat should not be denied. But, where there iscorruption and/or political resistance to serve thepoor, the private sector can do very little and can,in fact, compound the problem. Where there islack of information, participation and democraticprocesses, the situation is thrown wide open toopportunistic behaviour from the private sector.However, given a situation with stable rules,enough political commitment to address theunderlying causes, good governance and aninformed and active citizenry, the private sectorcan be a responsible partner in development andan important player in reforming and improvingwater services.

Political interference has been seen ascontributing to the failure of many public utilitiesto deliver to the poor. In establisheddemocracies there is ‘interference’ in the runningof utilities but this is seen as governmentexercising its duty to keep institutions to account.There is a fine line between ‘interference’ and theneed for accountability, the difference seems tobe the depth and strength of democraticinstitutions in individual countries.

In order to move forward on this contentiousissue, a multi-stakeholder review should beundertaken. We believe that it is only throughsuch a review (similar to the World Commissionon Dams) that the final, authoritative word can bemade on whether PSP benefits the poor. We alsobelieve in the necessity of building the capacity ofcivil society actors to influence privatisationprocesses and to hold governments and theprivate sector to account. This needs to start withimproving their knowledge and understanding ofthe issues surrounding failing water services, andenabling civil society groups around the world tolearn from each other’s experiences ofintervention in privatisation processes.

Civil society working to strengthen the hand ofgovernment through, for example, commentingon tender documents prepared by externaladvisors, increases the likelihood that reformswill further the concerns of the poor. It is in theinterests of government to involve a broadconstituency, especially one that represents the interests of the poor and poor people themselvesin the shaping of privatised basic services. Pro-active openness and transparency bygovernment in reform processes lessens thepossibility of civil strife.

© WaterAid and Tearfund 2003 5

II. Case Summary

The privatisation of Manila’s waterutilities to two companies, which tookthe East and West zones of the city,

was originally regarded as a model ofsuccess, with an open and competitivebidding process, followed by a tight andreasonable Concession Arrangement thatsharply reduced prices. However, less thanthree years into the contract, one of thecompanies was in dire financial straits, andthe other was challenging one of thefundamental tenets of the agreement. Both ofthe companies appeared to have madeparticularly low bids, on poor foundations,with the assumption they would change theterms of the contract once it was won.Crucially, the contract administrators allowedthat to happen. The result is a corporatemuddle, whereby the supposed benefits of PSP disappear, and government and publicadministrators are seemingly unable toprevent it.

Background

Following the major power crisis of the early1990s in the Philippines that was successfullydealt with by initially privatising the power sector,then President Fidel Ramos wanted the samemodel adopted to resolve Manila’s growing watercrisis. Selected for privatisation was the hugely-indebted and grossly inefficient MetropolitanWater and Sewerage Services (MWSS), whichserved nearly 12 million residential, commercialand industrial customers. Congress gave Ramosthe power to enter into private contracts to dealwith the problems of MWSS. Though passingmuch of the technical work to aides, the President retained a direct hand in the decisions.What emerged was a privatisation and biddingprocess that was hailed as a significantimprovement over previous similar deals.

What went wrong?

A few months after signing, a series of eventsstarted that sent the Concession Agreementseriously floundering. Maynilad Water ServicesInc (MWSI) found itself in dire financial straits. It

first threatened to, and then eventually walkedout of the 25-year concession, blaming the Asianfinancial crisis and the intransigence of government to grant them a bailout throughhigher prices. Manila Water Company Inc (MWCI) mounted a legal challenge to re-interpret the Concession Agreement to allow it tohave increased discounts before the five yearrate re-basing process.

Initial suspicion is that the bids made by the twowinning companies were unsustainable. Theywere ‘dive bids’, where the companies went inwith extremely low bids just to win the contract.Dive bids are not unusual, and nor is it unusualfor companies to operate at significant loss for the first few years, as long as they forecasthigher returns later. But in this case it seems the companies submitted dive bids with the assumption they could later change the terms of the contract in their favour. A lack of attention to dive bidding on the part of those crafting the contract can result when the priority is to conclude the bidding process, rather than to ensure the contract is viable. To reject ManilaWater’s lower bid, for example, would have beencontroversial, delaying and unacceptablepolitically. The bid was accepted, despite somereservations by experts about its financialviability.

One of the contributing problems was that the government had no sound studies on which to measure water demand for Metro Manila. Theyhad no basis on which to judge the feasibility ofnon-revenue water reduction, such as repairingthe network. Thus the financial modelssubmitted in the bids made by the companiescould be nothing more than a corporate muddle,with unreliable figures and unsound businesspropositions.

Maynilad

By the end of December 2000 Maynilad was indeep financial distress. It made heavy lossesbecause it was made to assume 90% of theestimated US$800 million debt of the MWSS, and the Asian financial crisis massively reduced the

© WaterAid and Tearfund 2003

The Corporate Muddle of Manila’s Water Concessions

Maynilad put little of its own money at stake.worth of the peso. These losses led to weakrevenues, which meant banks and financiers wouldnot lend the company the money needed toimprove the network or make the capital outlaysnecessary to increase its income. Repairing anddeveloping broken networks, which brought in littleshort term revenue, would have been hugely costly.The only solution, the company argues, was to increase tariffs.

The company drastically underestimated its operating costs.

Maynilad employed expensive partners andtechnical assistance.

The company overestimated the revenues itcould earn.

The Concession Agreement actuallyassured Maynilad’s currency losses. Maynilad’s officials claim that none of the

problems are the results of the company’s ownfault, but rather with the Asian financial crisis.This study argues Maynilad’s inability to containcosts and to realise the revenue potentials of the network was a cause of its problems, not aneffect of them. This study argues that:

Manila Water

While Manila Water suffered little of the economic muddle Maynilad experienced, it still launched a legal bid to interpret the Concession

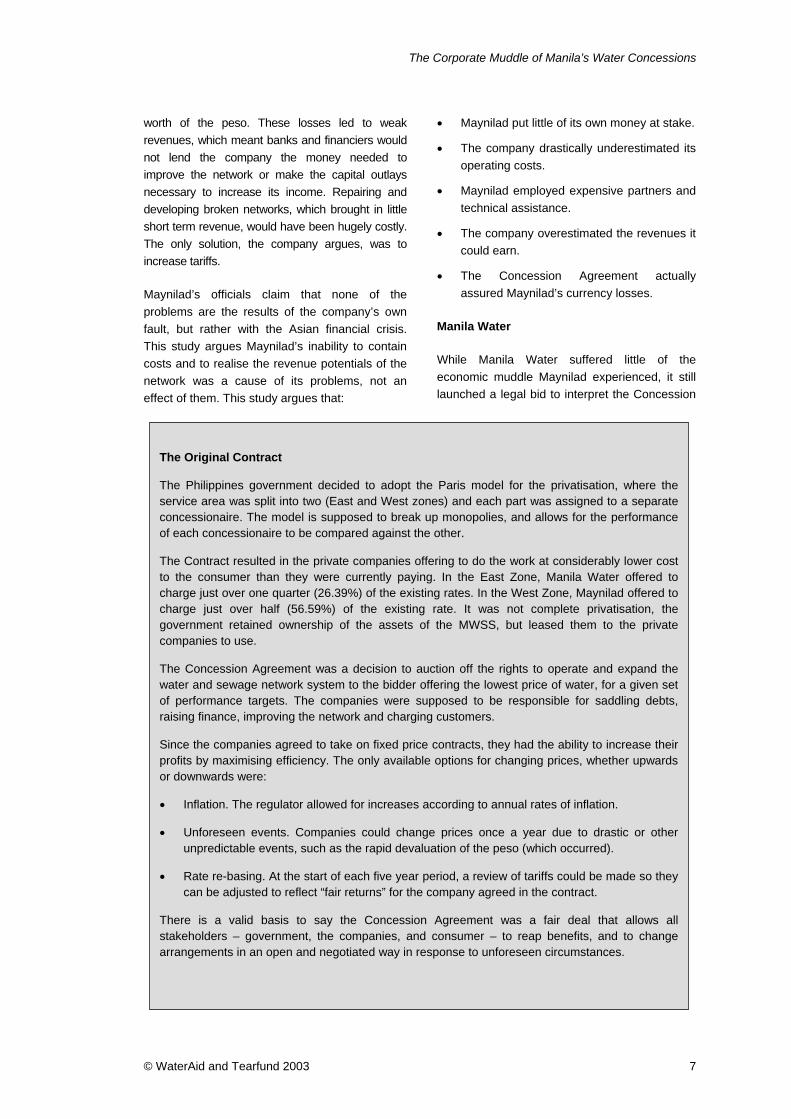

The Original Contract

The Philippines government decided to adopt the Paris model for the privatisation, where theservice area was split into two (East and West zones) and each part was assigned to a separateconcessionaire. The model is supposed to break up monopolies, and allows for the performanceof each concessionaire to be compared against the other.

The Contract resulted in the private companies offering to do the work at considerably lower costto the consumer than they were currently paying. In the East Zone, Manila Water offered tocharge just over one quarter (26.39%) of the existing rates. In the West Zone, Maynilad offered tocharge just over half (56.59%) of the existing rate. It was not complete privatisation, thegovernment retained ownership of the assets of the MWSS, but leased them to the privatecompanies to use.

The Concession Agreement was a decision to auction off the rights to operate and expand thewater and sewage network system to the bidder offering the lowest price of water, for a given setof performance targets. The companies were supposed to be responsible for saddling debts,raising finance, improving the network and charging customers.

Since the companies agreed to take on fixed price contracts, they had the ability to increase theirprofits by maximising efficiency. The only available options for changing prices, whether upwardsor downwards were:

Inflation. The regulator allowed for increases according to annual rates of inflation.

Unforeseen events. Companies could change prices once a year due to drastic or otherunpredictable events, such as the rapid devaluation of the peso (which occurred).

Rate re-basing. At the start of each five year period, a review of tariffs could be made so theycan be adjusted to reflect “fair returns” for the company agreed in the contract.

There is a valid basis to say the Concession Agreement was a fair deal that allows allstakeholders – government, the companies, and consumer – to reap benefits, and to changearrangements in an open and negotiated way in response to unforeseen circumstances.

© WaterAid and Tearfund 2003 7

New Rules, New Roles: Does PSP Benefit the Poor?

Agreement to change the key parameter on rate re-basing. This parameter was the appropriatediscount rate (ADR): the amount the companycould claim as profits resulting from efficiencies it has created.

The amendment was a bailout to Maynilad, andbenefited Manila Water as well. Maynilad is closer now to realising its debts, and beingregarded as a bankable prospect by creditors,but these things are by no means assured.Creditors are still concerned about the company’s financial viability, especially since if itfails to meet its service obligations, it could loosea US$200m bond put up as a guarantee.However, Maynilad seems to have significantenough political clout to get its serviceobligations postponed.

Manila Water wanted to raise the ADR to 18 percent, while only 5.2 percent was implied in theoriginal contract. The regulators refused, and thedispute was brought to the Appeals Panel, whichwas created as part of the ConcessionAgreement. It eventually led to the granting of anew ADR of 9.3 percent. But the regulators andMWSS board challenged the decision at the Court of Appeals, arguing the Appeals Panel hadoverstepped its powers. A legal wrangle followed,which remains unresolved in the courts. They areyet to decide which body had the appropriatepowers. Crucially, Manila Water won its originalbid on financial projections based at the 5.2percent ADR. Other companies were rejectedbecause their projected cost to the consumer,based on a 10 percent ADR, were higher. ManilaWater had won by projecting a small ADR, then attempted to have it changed once the contractwas theirs.

The integrity of the original bidding has beenundermined. Had the other bidders guessed that the technical parameters that imposed an upperlimit on their bids could be falsified and then latertreated with forbearance by the government,they too could have made very low, butunrealistic bids.

The new mechanism for foreign currencyexchange cost recovery reduces efficiency. Nowthe lengthily waiting period is gone, the cost are passed immediately to consumers. Thecompanies will have no incentives foreconomising on buying materials from abroad or in foreign borrowing.Consequences

This study concludes that the relevant publicauthorities appear to have played into the scheme laid out by the companies, whetherknowingly or unwittingly. They never entertainedthe idea that Maynilad could have beenincompetent, or had the right incentives in placeto make the scheme viable. Manila Water’s legalchallenge and the government’s stutteredresponse showed it was not ready to deal withsuch a challenge. The private companies mayhave muddled the PSP process, but theresponse of public institutions and officials –those tasked to uphold the public interest –constitutes half the blame.

The private companies have managed to disownthe risk associated with foreign exchangefluctuations, but it has not been passed ontoanyone else. Only the private sector has accessto sophisticated financial mechanisms to shoulder this risk.

The regulatory office was given, as a result oflegal wrangles, different and wider powers thanwas intended under the original contract. Thereremains a lack of clarity about its terms of reference.

Conclusion

The original bidding process for Manila’s waterconcessions was a success, along with the allocation of risk. The impact on the poor hasbeen positive, bringing greater access to betterquality water. But while PSP may have broughtefficiencies, the result was a corporate muddlewhich finally makes the Manila experience a failure. It was turned primarily into a tool foradvancing and preserving private, not public,

Thanks to Manila Water’s legal wrangling, andMaynilad’s financial difficulties, the Governmentwere forced to negotiate amendments to theConcession Agreement which many had hailedas water tight and effective. The mainamendment led to the cost of foreign exchangerecovery being completely and immediatelypassed to consumers.

© WaterAid and Tearfund 20038

The Corporate Muddle of Manila’s Water Concessions

interest. Some of the lessons to be learned fromManila’s experience are:

Regulatory arrangements in one countrymay not be applicable in another.

It is necessary to do rigorous homeworkbefore the tendering process, creatingforecasts which can be used to eliminatebids that have unrealistic or optimisticprojections of sales.

Corporate sponsors should put their ownbalance sheets on the line, at least duringthe first couple of years.

The government must clarify right from thebeginning that it will not tolerate divebidding.Rate re-basing on a set timeframe will install

discipline in companies, but the threat of delayed rate re-basing is not always deemedto be credible.

This paper concludes that the Manila waterexperience shows a corporate muddle to get away from the disciplines of a deal which at thebeginning is fair to all stakeholders, and withgovernment, public authorities, donors and lenders allowing this to happen.

In no circumstances should the regulator seeits role as bailing out companies if they sufferfrom their own unrealistic bids.

© WaterAid and Tearfund 2003 9

New Rules, New Roles: Does PSP Benefit the Poor?

III. Introduction

When the winning bids were announced on6 January 1997, a sense of excitement andvindication swept through the public officials andconsultants who made it happen. Particularlybuoyant was Philippine President Fidel Ramos.Flushed by the success of a privatisationprogramme that ended a crippling andeconomically devastating power crisis early in histerm, Ramos gambled on a similar process doingthe same for Metro Manila's growing water crisis.Now he had plenty of reasons to be happy.

The award of East-Zone and West-Zone waterconcessions to two foreign-backed companiesnot only reduced the cost of water to theconsumer by an amazing 50 per cent and 75 percent (roughly), it also offered a number ofpolitically attractive promises. These promiseswere contract-mandated obligations that, forinstance, made the private companiesresponsible for over US$7 billion in investmentsto be sunk into the water utility over the life of thecontracts. The private companies also assumedthe huge US$880 million debt of the MetropolitanWater and Sewerage Service (MWSS), the government-owned utility, thus removing asizeable chunk of a crippling burden ongovernment finances. And the deal was asignificant improvement over past privatisationselsewhere in the world, as it contained morespecific guidelines for the protection of consumerinterests while ensuring that proper incentiveswere in place so that the new private operatorswill consistently strive for efficiency: thisconstituted a most decisive response to the hugeand seemingly intractable problems of the MWSS in serving nearly 12 million customers.The MWSS privatisation was no meanaccomplishment; it was a coup of sorts for theRamos administration. Not only did it remove ahuge drain on government resources whilebringing real promise of a more efficient serviceat significantly lower costs, it also went throughsmoothly, with almost no opposition, especially inCongress. Even the MWSS unions barely raiseda cry.

Yet, barely just three years later, the deal wasseriously foundering. One of the companies –

Maynilad Water Services Inc. – found itself indire financial straits. It threatened to walk out ofthe 25-year concession contract, citing hugelosses resulting from a force majeure – the July1997 Asian financial crisis that among otherthings caused the devaluation of the peso. It petitioned the Regulatory Office for a 70 per centincrease in tariff to bail it out of its mess. Meanwhile, the other company opened adifferent but related legal battle with the Regulatory Office. Manila Water Company Inc.wanted to interpret the Concession Agreement ina manner that will allow it to have increaseddiscounts (in the form of interest to be paid for byconsumers) before the mandatory rate re-basingprocess is held. This basically meant changingthe terms of the Concession Agreement.

From Maynilad's financial woes and ManilaWater's legal challenge emerges an intricate andcomplex debate on the status of the world'sbiggest privatisation. The bottom line is that theprocess that initially appeared to be an extremelysuccessful solution now lies in serious doubt.What emerges from an investigation of this debate is a corporate muddle – a process thatwas not the winning solution it was hyped to beafter all. Rather, it could well be a case of street-smart companies making unrealistic andunsustainable bids just to win the tender, andgambling on the possibility that the rules of thegame may be changed later on in their favour: ashrewd gamble given the weakness of regulationin the Philippines and the state's historicalpermeability to private interests.

These companies' confidence in makingapparently unrealistic bids may be bolstered bythe fact that the Philippines' two wealthiestfamilies were behind the two winning companies,and they were backed by the biggest water and sanitation multinationals in the world. The Lopezfamily's Benpres Holding Company (BHC) is themajority owner of Maynilad. The Frenchmultinational Suez Lyonnaise des Eaux SLDE (now Ondeo), is the minority owner. ManilaWater is owned mainly by the Ayala family, andbacked by Bechtel and United Utilities. It appears that the two companies' approach was

© WaterAid and Tearfund 200310

The Corporate Muddle of Manila’s Water Concessions

to win the bid at all costs, and then deal with the problems of profitability later. The result is aprivatisation that has failed to impose marketdiscipline on the companies, and which,ironically, presents striking parallels to problemsof under-performing state corporations undersocialist states or petty dictatorships.

This study argues a number of points to untanglethis corporate muddle:

The two companies submitted bids for highservice qualities at a low price, and thenonce the contract was written, tried to re-negotiate, to chisel down quality, to scaledown and postpone targets, and to exploitthe loosely defined regulatory rules for priceadjustments.

Maynilad's inability to contain costs and torealise the revenue potential of the assetsassigned to it is more a cause, rather thanan effect as it claims to be, of the problemsof creditworthiness and cash flow of the firm. It tried to put the blame on the Asianfinancial crisis, which while no doubt led toserious foreign exchange losses, had little todo with water delivered to customers that isnot billed due to metering mistakes, stealing,tampering, etc. These accounted for nearlyhalf the non-revenue water it was trying to reduce. In short, the Asian financial crisismerely provided the smokescreen to the morereal problems created by the company's owninefficiency and dive-bidding.

Manila Water was in a better positionfinancially, but also had the same efficiencyproblems. For instance, it had equallyserious problems of inability to deal with

non-revenue water. Manila Water used alegal challenge in the Appeals Panel tochange the rules of regulation in its favour.

Both companies, in striving to move out ofthe contract terms they originally agreed to,have in effect caused long-term damage to the credibility and viability not only ofregulatory processes that were mandatedwhen the concession agreements weresigned, but also of private sectorparticipation in general.

The next section of this study will sketch anoutline of what has happened with the Manilawater concessions in order to describe thecircumstances and context in which this corporate muddle took place. It will then discussseparately the arguments it is making andprovide supporting evidence to go with it. A review of the lessons learned from thisexperience follows. In particular, it looks at thelessons on risk mitigation in concessioncontracts, the setting up of tenders andevaluation of bids, the problems of limited-recourse financing, and the consequences of tampering with regulatory processes. Throughthis discussion of the lessons, a number ofalternatives are recommended. This concludesthat while private sector involvement offers a realpromise of efficiency and decisiveness in dealingwith intractable problems of water and sanitation services delivery in a huge metropolis, thecontext in which these happen to a large extentdetermines whether the benefits can actually bedelivered. The key then is to understand thefinancial, political and social contexts well – thebest defence against the corporate muddle of an otherwise desirable mechanism for efficiency.

© WaterAid and Tearfund 2003 11

New Rules, New Roles: Does PSP Benefit the Poor?

© WaterAid and Tearfund 200312

IV. Ondeo’s response to this case study

This study is almost entirely built up on a concept it calls ‘dive-bidding’. It paints a picture where all theproblems are due to a tactic of deliberate under-pricing. This is an allegation that is completelyunfounded. There were four bidders each for the two concessions. The bids of Anglian Water, theVivendi and the Ondeo consortia were separated by the narrowest of margins. This clearly indicates thatall the bidders at this level had interpreted the information in very much the same way. The remainingbids from the IWL/Ayala consortium were both at a level of about half the price of the others -- if therewere ‘dive bids’, it was these. Nevertheless, the government accepted this very low bid for one of the twoconcessions awarded. This was done once the government had received confirmation from IWL/Ayalathat they stood by their bid.

Several important differences between the two concessions need to be noted. The most significant isthat the government ‘loaded’ the majority (90%) of the historic debt of MWSS onto the West Concession(awarded to Maynilad) through the concession fee. It is quite likely that government did this as it saw therisk it ran of non-recovery if it shared the debt burden more equitably between the two contracts. In laterevents, this decision hugely penalised Maynilad: it left Manila Water virtually unexposed to the hugedevaluation that devastated Maynilad.

This problem was compounded by the difference in the nature of the two contract areas. The Mayniladzone contains infrastructure in a much worse state, and a large un-connected and low-incomepopulation. In comparison, the Manila Water zone has a much more viable situation.

In addition, the accuracy of the technical and operational data provided for the Maynilad zone has provedto be very inaccurate. Major elements such as the length of the distribution network were greatlyunderstated. In the bid documents, it was stated that the length of the network to be maintained was2534 kilometres – but the actual length on the ground has now been determined to be 3880 kilometres.

There is a strong likelihood that had Maynilad not had to unilaterally support the historic debt of almostthe whole of Manila’s water system, and with the huge foreign exchange losses due to the devaluation ofthe Peso, these difficulties might have been overcome.

Maynilad has made great efforts to both negotiate a reasonable solution that would enable it to operatethe contract in a stable and sustainable way, and has also achieved some real improvements in servicedelivery and coverage. For example, the service coverage has been improved from 58% in 1997 to 84%today. Some 144,000 new connections have been completed. In particular, these have provided firsttime access to over 500,000 urban poor. The study makes scant reference to these facts.

The real situation is that Maynilad and its sponsors have been ‘bled’ excessively for reasons that aretotally beyond their control. They have negotiated in good faith, and proposed many solutions. They havenot been able to secure any workable solutions from the client or the Philippine government. Havingfaced this situation for a long period, they have been left with no realistic alternative to giving notice toterminate the contract.

From our point of view, this is certainly a failure. It is however very unfair to lay the blame of this on theprivate sector. There are obviously problems with a bidding process that relies on incomplete informationand the selection of an operator on the basis of the lowest price alone. These problems have beenrecognised for many years, yet persist. Many of these problems can, and in the case of Manila, couldhave been overcome. The main lesson however must be that the private sector should not be expectedto take responsibility for risks that it has no means to manage. Almost important is the necessity for the public sector client to maintain an equitable and constructive attitude to problem solving.

The Corporate Muddle of Manila’s Water Concessions

V. Context and the Contract

In the early 1990s, the Philippines suffered its worst power crisis. For nearly three years, powerblackouts were to hit Manila and its industrialareas, sometimes for as long as eight hours aday. The effect on production was tremendous,and contributed to a significant shrinking of theeconomy. When a new president, Fidel Ramos,took office in 1992, he vigorously pursued withvigour a policy response to the crisis – theprivatisation of the power sector. In a fewmonths' time, the power crisis was substantiallyresolved.

The quick response of private investors to thepower blackouts convinced Ramos of theefficacy of private sector involvement even inareas once thought to be the exclusive domain ofprovision by the public sector1. This rapid end to the power outages led the Ramos administrationto make a deliberate effort to bring the privatesector into the urban water sector of the countryas well. And first to be selected for privatisationwas one of the government's biggest headaches– the hugely-indebted and grossly inefficientMetropolitan Water and Sewerage Services(MWSS), a utility started in 1878 that by the1990s had expanded to serve nearly 12 millionresidential, commercial and industrial customers.

Ramos played his cards well in organising thismove. His first step was to get Congress to givehim the authority to enter into contracts (withprivate companies) that would deal with theproblems of the MWSS. This authorisation wasone of the most important provisions of the WaterCrisis Act. The bill was certified as urgent by thePresident, and passed through Congress withlittle opposition in 1995, largely because it waspresented as a strategic response to the El Ni ophenomenon that by then was ravagingagriculture. While Ramos delegated the task of contract-making to his Public Works Secretary,Gregorio Vigilar, who concurrently served as

chair of the MWSS, the President himself took adirect hand in many of the decisions (Dumol,2000). They took steps to ensure that they gotthe best advice by hiring consultants from theWorld Bank's International Finance Corporation(IFC). The details of a contract attractive toprivate investors and which took intoconsideration the lessons learned in other waterprivatisation deals (eg Buenos Aires, Englandand Wales) were soon crafted. Among otherthings, this contract sought to achieve thefollowing:

identification of concessionaire serviceobligations

identification of tasks assigned to the MWSS– mainly as parties to the agreement anddevelopment of a major water supply source

setting up of a regulatory office that wouldmonitor compliance with contract obligationsand determine rate adjustments based onguidelines set in the contract

setting up of a dispute resolution mechanism

identification of rights of creditors

specification of grounds and procedures forcontract amendment and termination

recommendation of a mechanism for publicperformance appraisal

The IFC-led team of consultants also played animportant role in providing prospective bidderswith the assurances and information they neededif they wanted to bid, in collecting data that wouldbe the basis for profit forecasts, in identifying theeligible bids and in identifying the winningbidders.

What emerged was a privatisation and biddingprocess that was hailed internationally as asignificant improvement over previous similardeals. For instance, the government decided toadopt the Paris model, where the service area

1 However, later problems of overcapacity andextravagantly high and rising prices would lead many towithdraw their effusive praise for the private sector'srole in the electricity sector.

© WaterAid and Tearfund 2003 13

New Rules, New Roles: Does PSP Benefit the Poor?

was split into two (East and West Zone) andeach part was assigned to a separateconcessionaire. In theory, this model is ameasure intended to break up the monopolypowers that a concessionaire would otherwisehave after winning the bid. The regulators cancheck the performance of one concessionaireagainst that of the other. It also providesleverage with which to judge petitions for possible price increases2. But the mostimportant measure was price. Compared for instance to the experience in Buenos Aires,Metro Manila's privatisation resulted insignificantly lower prices. The winning companyin Buenos Aires, Aguas Argentinas (partly ownedby Suez Lyonnaise) offered to run the concession by charging a price that was 75 percent of pre-privatisation rates. In Manila, the company that won the East Zone offered to runthe concession by charging a price that was only26.39 per cent of existing rates. Manila Wateroffered to charge only PHP 2.32 per cubic metre(pcm), as compared to the PHP 8.78 pcm beingcharged by MWSS. The West Zone was given tothe next lowest bidder, Maynilad, which offeredto charge only PHP 4.96 pcm, which is around56.59 per cent of then current prices3.

The MWSS deal was not a full privatisationarrangement, similar to what happened inEngland and Wales where the governmentdivested itself of ownership of its water utilities,transformed these utilities into corporations, andsold shares of stock to private individuals andcompanies. The Philippine government retainedownership of MWSS assets. What the Concession Agreement provided was to give theprivate sector the right to use these assets. It also imposed an obligation on the concessionaireto maintain and expand these assets at the

companies' own expense. At the end of 25years, everything including all the improvementspaid for by the company reverts back to thegovernment. In return for all these, the privatecompanies are given the right to collect a fee from users, which is to be regulated by anMWSS Regulatory Office (MWSS-RO).

In sum, the Concession Agreement was adecision to auction off the rights to operate andexpand the water and sewerage network systemto the bidder offering the lowest price of water,for a given set of performance parameters.These parameters included the expansion of service coverage, and the maintenance of theassets, both of which require large sunkinvestments. The Agreement can thus be seenas a procurement contract. The government,saddled by rising debts and inefficiencies, asks acompany to run and operate the network and beresponsible for getting the investments needed to expand coverage and improve serviceexpansion. The company spends its ownmoney, or uses its credit worthiness to borrowmoney from the banks, which will be sunk asinvestments into the network. It is then given theright to reimburse these investments and expenses they have made, via the collection of aregulated fee from users.

The implicit reimbursement rules provideincentives for increased efficiency because theytake on the character of fixed price contracts orprice caps. Since the prices are essentially fixedand could not easily be moved, the only way aprofit-maximising company can gain greaterprofits is to improve efficiency, ie reduce costs,reduce non-revenue water, improve billing andexpand the service to get more customers. Thecontract allows the company to keep the rewardsof being efficient.

2 It was however up to the ingenuity of regulators to develop the guidelines and find practical use of this arrangement. The first five years did not see theregulatory office taking full advantage of thepossibilities that this arrangement held. It became clearthat what was applicable to Paris was not necessarilyautomatically applicable to Manila.

Mechanisms have been provided in the contractto adjust prices, whether upwards or downwards.There are three grounds on which rates may beadjusted. First is inflation. The regulatorautomatically allows for increases to the standardrates annually based on changes in theconsumer price index. The concessionairestherefore have some protection against inflation– their revenues grow with the pace of inflation.Second is Extraordinary Price Adjustment (EPA),

3 It should be noted though that the price reductionswould not have been as dramatic when compared withthe August 1996 MWSS price of PHP 6.43 pcm.MWSS increased its prices in August 1996 to PHP 8.78pcm, using the tariff trend since 1990, which is a 38 percent jump. It may be that the tariff was increased tominimise the shock should water rates increasefollowing privatisation.

© WaterAid and Tearfund 200314

The Corporate Muddle of Manila’s Water Concessions

adjustments that may be initiated once a year tocapture the financial effects of certain unforeseenevents applicable to the concessionaire. Hence,should there be a drastic devaluation of the peso(as actually happened) extraordinary priceadjustments may be made. The EPA essentiallyprovides protection to the company against a force majeure, or unanticipated costs arisingfrom, for instance, new health or environmentalstandards that may be legislated in the future.This mechanism is well defined by theConcession Agreement. There is a strict set ofvalidation procedures and needs evaluation to beconducted by the MWSS-RO to determinewhether an extraordinary event has indeedhappened that necessitates price increases.Inflation adjustments and EPAs may also bemade quarterly, and are covered by rules in the Agreement.

The third mechanism for price adjustment is ratere-basing. At the start of every five-year period,the Concession Agreement provides for a reviewof tariffs so that they can be adjusted in casethey exceed the definition of "fair returns"stipulated in the contract. The company reapsthe higher profits they make as a result of improved efficiency, but these are reviewed atthe end of every five years. This gradualreadjustment (in this case a lowering of tariffs) atthe end of every five-year cycle simply meansthat consumers also subsequently benefit fromthe concessionaire's efficiency gains.

The Concession Agreement also had provisionsfor a performance bond – US$200 million – putup by each of the concessionaires andaccessible by the MWSS. The performancebond serves as a kind of insurance money – incase a concessionaire reneges on its contractobligations, the government can forfeit this bondand use it to finance the unfulfilled contractobligation, like hiring another company to do it.

In general, these mechanisms have establishedprocedures that leave little room for discretion.But there are also certain soft targets – decisionsthat can be made which involve greaterdiscretion by the MWSS-RO or the authoritiesconcerned. For instance, it was initiallypublicised that prices in real terms cannotexceed the public sector's last price before the

contract was awarded. This is a soft target – theMWSS-RO can allow for an increase in pricesbeyond the public sector's last price if they seethat this is necessitated by extraordinarycircumstances. The idea for the ConcessionAgreement was to make the arrangement asunambiguous as possible, i.e. to reduce thenumber of soft targets and therefore leave lessroom for discretion or political interference.

In short, there are plenty of valid bases to saythat the Concession Agreement was indeed asuccess. It was a fair deal that allows all stakeholders – government, the companies, andconsumer – to reap benefits, and moreimportantly, to change the arrangements in anopen and negotiated process should unforeseenor extraordinary events happen. There aresufficient guarantees for a fair return for efficiency-maximising companies, and adequateprotection against risks that the companies mayface. The deal therefore left little room for it toturn into a losing business venture for theconcessionaire. Ramos was rightfully happyover the arrangement they had crafted. But asevents would later show, the success wastheoretical and largely on paper. Whathappened in practice, particularly the movestaken by the companies, would turn a successfulprivatisation into what can be justly called afailure.

A Bidder's Bag of Tricks

There is a joke among consultants that disparagesome of multinational companies that dominatethe world's privatised water and sanitationmarket. The joke goes that these companies'executives only start to be serious the day after a contract is won. They would then plan torenegotiate the contract or change the rules ofthe game . As a result, the seemingly enviousconsultants say, three French companies alone –Vivendi, Ondeo, and Saur – control nearly 75 percent of the world's privatised market. Theirclosest rival is Thames Water, formerly British-owned but now controlled by the Germanmultinational RWE, which controls 10 per cent ofthis market (PSIRU, 2001). Dumol himselfrecounted how the filing of petitions fortemporary restraining orders in courts around the

© WaterAid and Tearfund 2003 15

New Rules, New Roles: Does PSP Benefit the Poor?

world was Standard Operating Procedures ofcompanies who lose bids.

Hence, the initial suspicion is that the bids madeby the two winning companies for the ManilaWater concessions were unsustainable – thesewere dive bids that were meant to win the tender,not to provide a realistic assessment of how thecompanies would actually operate the Manilaconcessions if they won the contracts.

Aggressive dive bidding, or bidding at such a lowlevel that will require the company to operate at aloss, is not irrational behaviour, at least when thebidder expects to be able to renegotiate once thecontract is signed. Bidding for a concession isitself costly. The losses incurred at the start of the contract need not be permanent. Thegamble will have a greater propensity of eventually paying off if regulatory structures areweak, or if there is a greater role for non-formal political interference to play a role in futuredecisions. Similarly, the more ambiguous thecontract (ie more rather than less soft targets), the greater the incentive there are for dive bidding.

The responsibility for protecting all otherstakeholders against dive bidding therefore lieswith the crafters of the contract agreement, whomust themselves take the political context intoaccount. The Ramos administration took stepsto get the best possible advice – by hiring theInternational Finance Corporation and itsconsultants. The assumption was that theseconsultants were in possession of cutting-edgeinformation that enables them to give the best possible economic, financial and technicaladvice. But as the experience of Manila shows,there is actually no guarantee that the advice andinformation even from the best of experts is always correct.

A lack of attention to dive bidding on the part of those crafting the contract can result when theirpriority is to conclude the bidding process, ratherthan to ensure the contract is viable. In thetender for the Manila water concessions,rejecting the lowest bids would undoubtedly havebeen controversial (leading to delays), wouldprobably have been unacceptable politically, andmight have resulted in the executive losing itscongressional authorisation to enter into a

contract. As two University of the Philippineseconomists, Solon and Pamintuan pointed out,the IFC accepted the bid of Manila Water asfeasible, despite the observations of its ownconsultants that:

Manila Water's consumer demandprojections were 45 per cent higher than theearlier study made by the French consultingfirm SOGREAH.

Manila Water was optimistic that it couldreduce by half non-revenue water in fiveyears' time. (This would have meant hugecapital investments to repair leaks, and would have meant a general overhaul of theunderground pipe system that would resultin further traffic problems for already-congested Manila. This also would havemeant aggressive prosecution for watertheft.)

Manila Water assumed that it would be ableto secure yen-denominated project financeat a very low rate of 2.79 per cent (which didnot happen).

It had a gearing ratio of 87 per cent, ie 87per cent of its operating capital is borrowedmoney, which therefore incurs more costs.

Its capital spending in the first five years waslow — at least 25 per cent less than theamount earmarked by the other bidders.

Its projected internal rate of return was set at3.6 per cent, whereas the other bidders had9 to 11 per cent.

Cash flow was projected to be negative forthe first ten years — the company would beoperating at a cumulative loss of US$496million. (The IFC expressed concern overhow MWCI would gain access to debtfunding under these terms to finance thisnegative cash flow.)

In the case of the bid of Maynilad, fewer doubtswere raised about its feasibility mainly because itwas closer to the bids submitted by the otherlosing companies. But a short IFC review citedconcerns over Maynilad's highly aggressive and

© WaterAid and Tearfund 200316

The Corporate Muddle of Manila’s Water Concessions

optimistic projections about the reduction of non-revenue water, and the consequent rapidincremental increase in the volume of water thatthe company assumed it could automaticallycollect revenues from. The review pointed outthat this was no more aggressive than ManilaWater's own plan. The IFC and the governmentdid not appear to have any technical studies that would assist them in judging the feasibility of the non-revenue water reduction assumptions in thefinancial models of the bidders. Cristina David ofthe Philippine Institute for Development Studiesreveals that no studies on water demandprojections for Metro Manila existed4. The onlytechnical study that could have been used — theone done by SOGREAH — clearly warned aboutthe assumptions of the bidders (David, 2001).

The IFC review may not have been as thoroughas it needed to be. Subsequent performance of the two companies showed how far off the mark they were in their non-revenue water reductiontargets. Actual billed water volumes andrevenues reported by Manila Water from 1997 to2000 were PHP 586 million (12 per cent) belowprojections. In the case of Maynilad, it was PHP2,789 million or 25 per cent below financialmodel expectations, although the companyexplain this as being a result of the Asianfinancial crisis. The concerns in the IFC reviewshowed that the consultants had suspected thatthe targets for non-revenue water reduction, andtherefore revenue generation, were unrealistic.But they did not pursue that suspicion, andinstead merely hoped for the best.

Thus, the financial models submitted in the bidsmade by the companies could be nothing morethan a corporate muddle. The figures wereunreliable, and the bids were therefore not soundbusiness propositions being offered to thegovernment. More evidence of a muddle hasbeen made clear recently. Staff at the financialregulation division of the MWSS-RO pointed outthat the debt assumed by Maynilad (a part of itsservice obligations in the contract) was PHP 3.9billion shy of what it was instructed to assume.

Could this have been a mistake, or a deliberateeffort to make the company's financial positionlook better so that it could obtain projectfinancing? Also, if this were detected early onwhen the bids were being considered, is this not sufficient grounds for rejecting Maynilad's bidaltogether?

Maynilad's Story

By the end of December 2000, Maynilad founditself in deep financial distress. Its revenueswere down and its costs had risen beyond theexpectations found in its financial model. Its lenders would not approve the term loan ofUS$350 million that it needed to fulfil its plannedcapital investments for the first five years of its concession contract (see Alunan 2001). What itwas able to assemble were bridge-financingarrangements to keep the company going while itwas trying to achieve financial closure on theterm loan.

Maynilad blamed its problems on the Asianfinancial crisis which triggered a fall in the peso'svalue from PHP26:US$1 to PHP50:US$1 by2000. It announced losses of PHP 2.7 billion inadditional and unanticipated foreign exchangecosts by the end of the year 2000. Theimmediate impact of the peso's fall was muchgreater on Maynilad than Manila Water becausethe former inherited 90 per cent of the foreignindebtedness of the MWSS. Maynilad had to nearly double its peso payments on the dollarloans it assumed (Alunan 2001)5.

This triggered a cycle of problems for thecompany. Foreign exchange losses led to weakrevenues. Weak revenues, in turn, made thecompany ineligible for the loans it was applyingfor — it lost credit worthiness as a result.Inability to get the loans, as well as the lack ofrevenues itself, prevented the company frommaking capital outlays that it needed to reducenon-revenue water, improve billing and expandits income-generating base. It was stuck in a rut, and the only way to get out of this rut, the

4 Had these studies been made, they could havewarned not only the consultants but, more importantly,the regulatory office to be set up, about the extent towhich sales could decline as a result of the jump in tariff levels arising from the amendment to theconcession agreements.

5 Project loans that were to be disbursed after thecontract signing, however, were destined for the EastZone (Manila Water) and would reduce this percentageshare of Maynilad's inherited loans to 80 per cent.

© WaterAid and Tearfund 2003 17

New Rules, New Roles: Does PSP Benefit the Poor?

company argued, was to increase the tariff it collected.

Thus, it is a force majeure that is pinpointed asthe source of the problem — an event beyondthe control of anyone — argued Maynilad. TheAsian financial crisis could not have beenforeseen, and was therefore uninsurable. OnDecember 2000, it submitted proposals to thegovernment that would:

Allow for an accelerated recovery ofunanticipated foreign exchange coststhrough an automatic currency exchangerate adjustment (auto-CERA). This cost recovery mechanism allows for water ratesto immediately adjust on a monthly basis (upor down) for foreign exchange losses. It is 'automatic' because it does not needevaluation and approval by the MWSS-RO— the costs or gains are automaticallypassed on to consumers as reflected inmonthly bills. Auto-CERA is a new

mechanism not covered by the ConcessionAgreement.

Postpone some service obligations.Lenders, including the Asian DevelopmentBank, would not release the US$350 millionMaynilad is applying for unless the MWSS-RO allowed the company to postpone someservice obligations as enshrined in thecontract. These are water pressure targetsand investments in new sewerage networks.Essentially, the lenders were worried thatMaynilad would not meet these obligations,risking the event of forfeiting its performancebond, which places the company in an evenmore uncreditworthy position.

Alter the volume of water that the companyis expected to bill. This means that thecompany will not be able to meet its targetson billing and non-revenue water reduction,and will consequently have a smallerrevenue intake.

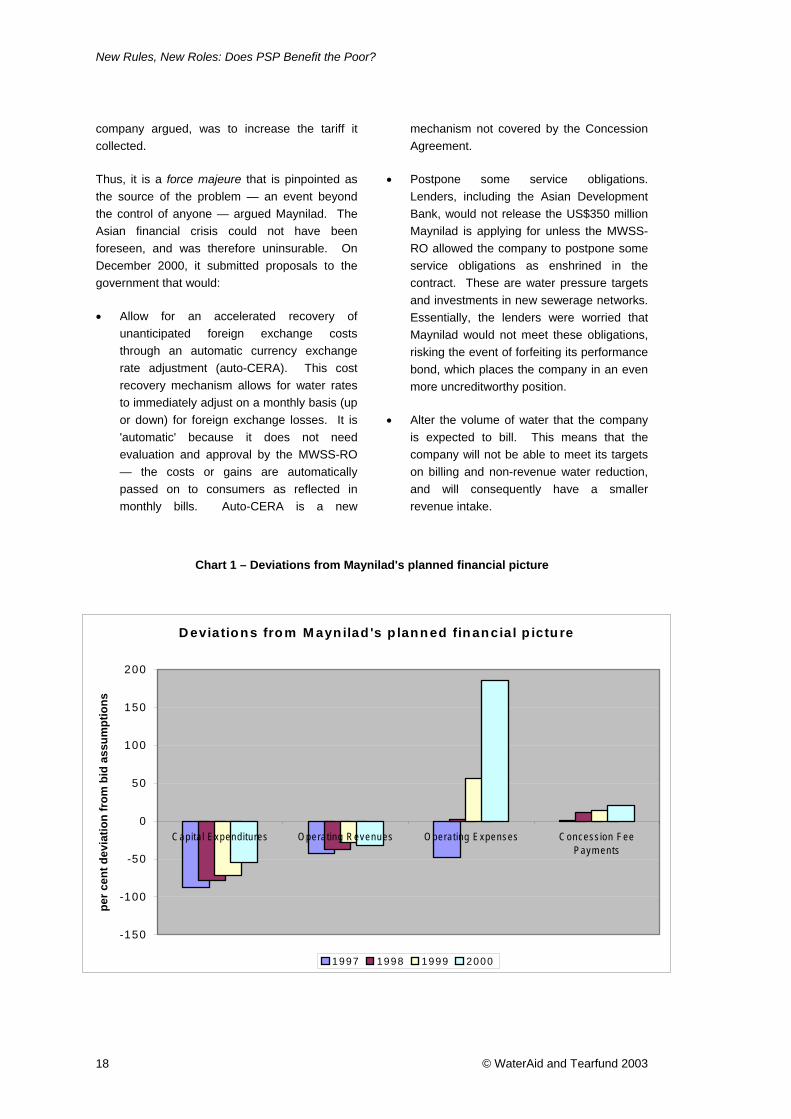

Chart 1 – Deviations from Maynilad's planned financial picture

D eviations from M ayn ilad 's p lann ed fin ancia l p ictu re

-150

-100

-50

0

50

100

150

200

C apita l E xpenditu res O pera ting R evenues O perating E xpenses C oncess ion F eeP aym ents

per c

ent d

evia

tion

from

bid

ass

umpt

ions

1997 1998 1999 2000

© WaterAid and Tearfund 200318

The Corporate Muddle of Manila’s Water Concessions

One spectre raised in the event of governmentnot agreeing to these proposals was a potentialdomino effect on the financial system that animpasse would cause. It was feared thatbecause BHC was highly leveraged and sufferingthe effects of bad performance of other affiliates,a call on its guarantees on the bridge loanswould have acted as the proverbial last strawthat would cause BHC to default on its loanobligations. In other words, government couldnot allow BHC to go under because of its size,which it was claimed would have potentiallydisastrous effects on the economy. There is noclear indication, however, of exactly how a BHCdefault would actually rock the financial system.But the raising of this spectre alone would havehad a profound effect on the decision-makingprocess.

Maynilad's arguments to support these proposalsare convincing, except for one key flaw —Maynilad officials claim that none of the problemsare the results of the company's own fault.Everything is blamed on the Asian financialcrisis. This study argues the opposite:Maynilad's inability to contain costs and to realisethe revenue potentials of viable assets assignedto it is a cause and not an effect of the problemsof creditworthiness and cash flow of the firm. A different diagnosis and explanation is possible.The evidence to support this argument is as follows:

(a) Maynilad only had its reputation,not its money, at stake

There is a major difference in the financingmodel adopted by Maynilad in contrast to ManilaWater. This may also account for the difficultyencountered by Maynilad in securing its termloan of US$350 to finance its investment plans inthe first five years. Maynilad used a limitedrecourse financing scheme for its US$350 millionterm loan. This means that the collateral onwhich the loan is secured is the receivables ofthe project itself, unlike Manila Water, which put the assets of its owners Bechtel and AyalaCorporation at stake.

Other things being equal, the risk premium that creditors would assign to Maynilad would behigher and this raises the financing cost.

Maynilad's creditors would also be far moremeticulous than Manila Water's creditors when itcame to rights of third parties (eg, creditors)which claims on Maynilad's assets and futureincome streams, especially in case of bankruptcyor default. Such things added tremendously tothe difficulty of achieving financial closure forMaynilad's US$350 million term loan. In themeantime, it transpired that the limited recoursefinancing could not be secured, Maynilad had tosecure bridge financing backed by the equity of the French and Filipino partners, and simplypostpone payments due to its suppliers andsubcontractors.

That project finance is inherently more technically demanding than corporate financedoes not mean that it is less desirable. But thisraises the question of whether Maynilad'ssponsors were unwilling to bet on the success oftheir own project. There is also anotherconsequence arising from this mode of finance.The creditors wanted the MWSS to allowMaynilad to postpone service obligations onwater pressure targets and investment in newsewerage networks.

With its own money not at stake, it makes iteasier for Maynilad to risk bankruptcy, unlikeprojects where financing is mobilised by puttingthe corporate balance sheets of the sponsors onthe line.

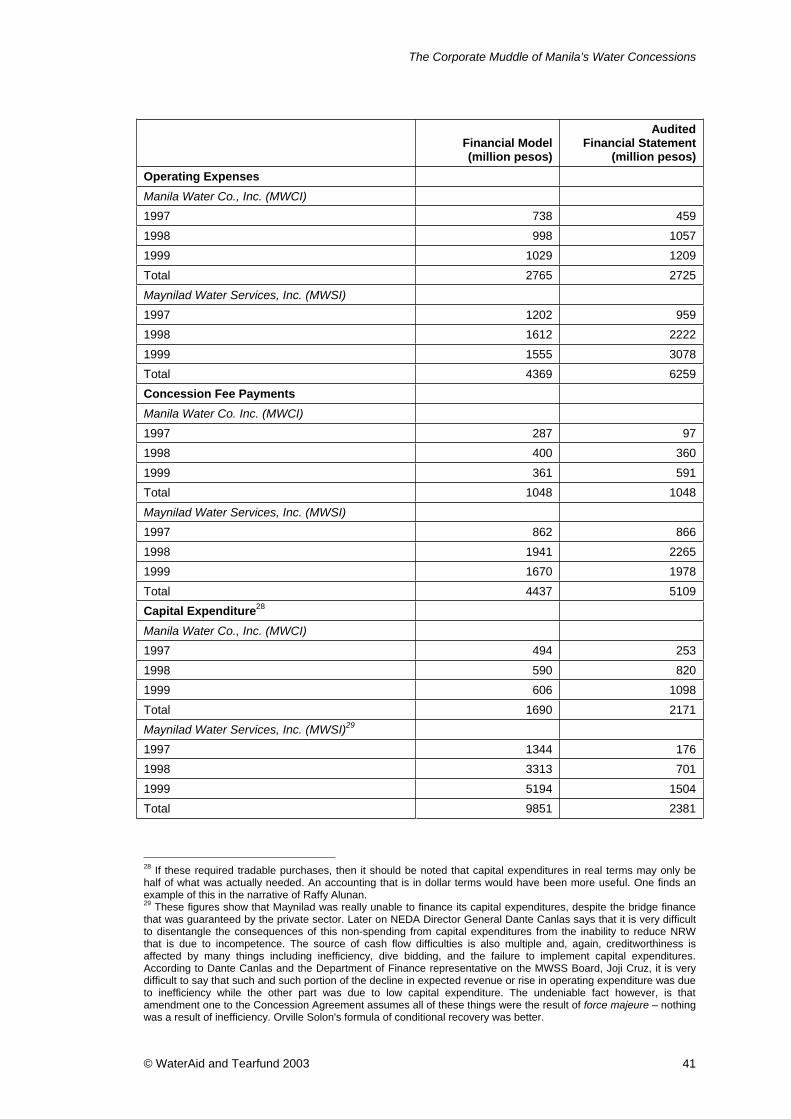

(b) Maynilad underestimatedoperating costs

In the financial model it submitted, Mayniladestimated operating expenses for 1997, 1998and 1999 to be PHP 4,369 million. Actualoperating expenses for this period were PHP6,259 million, or 43 per cent more. This studyhas not been able to access sufficientinformation to fully explain the overestimation ofcosts. It learned from Maynilad's disclosure in a28 May 2001 meeting with Public Works andHighways Secretary Simeon Datumanong thatthe pipe network is actually much more extensivethan it thought it was. But there are also claimsfrom disgruntled employees at Maynilad andfrom an MWSS source that the company hadvery expensive contracts with the affiliatecompanies of the French and Filipino corporate

© WaterAid and Tearfund 2003 19

New Rules, New Roles: Does PSP Benefit the Poor?

sponsors. This included a managementconsultancy contract with Lyonnaise des EauxPhilippine (LDEP), and interest bearing advancesfrom BHC as well as from LDEP for bidding andstart-up costs. There was also a technicalassistance and service agreement with both BHCand LDEP. Maynilad also paid charges for guarantee fees related to loans and standbyletters of credit guaranteed by BHC and SLDE.Then, there was an interim programmemanagement deal with Safage Consulting andMontgomery Watson, an affiliate of SLDE.Finally, there was a technical assistanceagreement with Lyonnaise des Eaux ServicesAssociation (LYSA) for the revenue enhancement programme of reducing the non-revenue water. All of these deals aredenominated in foreign currency and thusbecame inflated as a result of the pesodevaluation.

However, there is no easy way of verifying theseallegations and of arriving at a judgement of whether these costs may have been imprudent.Ordinarily, the magnitude of operatingexpenditures need not be a public concernbecause of the presumption that the company isinterested in reducing costs whenever it can.However, there are certain accountingprocedures that cleverly pass on some of thecosts to the consumers, rather than to the company. For instance, there is an allegationthat costs for the deals enumerated in thepreceding paragraph were accounted for not asoperating costs but as capital expenditures. If these were treated as operating costs, then itwould mean a reduction in the company's profits.If accounted for as capital expenditures,however, these costs are passed on to consumers. Hence, Maynilad had no incentive tominimise these costs. Thus, the presumptionthat companies are cost-minimising has to beapplied with care when the procurementrelationship is with affiliate companies.

(c) Maynilad overestimated revenues

In its financial model, Maynilad expectedrevenues totalling PHP 7,255 million for the years 1997 to 1999. Actual revenues were onlyPHP 4,729 million, which is 33 per cent off target.This serious underestimation was clearly seen in

1997, before the effects of the Asian financialcrisis set in. Maynilad expected to collect PHP 1,316 million in 1997; actual collections that yearwere only PHP 751 million, which was 43 percent off target.

Maynilad claims that because it did not get theloan it applied for, it had to postpone urgentcapital expenditures that had direct negativeconsequences on its non-revenue waterreduction programme and therefore on itsrevenues. These claims are only partiallycorrect. Addressing physical losses needs a lotof capital expenditure as it means expensiverepairs and replacement of pipes and mains(although some leaks do not entail huge costs).But Maynilad itself reported that leaks accountedfor only one half of its non-revenue waterproblems. Water delivered to customers that is not billed due to illegal connections, meteringmistakes, tampering, etc make up the other half,and these do not require high capitalinvestments, and deliver high returns. One is ledto doubt whether Maynilad had the will to deal atall with these latter problems.

Thus, whether Maynilad's own numbers arereliable or not, one may reasonably expect thateven without capital expenditures, palpablereduction in non-revenue water could have beenachieved. This in turn would have improvedMaynilad's creditworthiness and its ability to raisefunds through means other than the US$350million term loan.

World Bank data from various countries showthat loss of revenue due to physical losses is generally less than losses due to ineffectivemonitoring by the water concessionaire. It notesthat "lack of accountability and managerialincentives to deal with the problem" have beenoffered as the main factor to explain6 whyprogrammes to reduce non-revenue water arelargely frustrating experiences. If theseobservations apply to Maynilad, then its growingrather than decreasing non-revenue waterproblems can only be interpreted as badmanagement. At present, for every three cubicmetres of water it produces, Maynilad earns from

6 Yepes, Guillermo (1995) "Reduction of unaccountedfor water : the job can be done!" Working Paper. TheWorld Bank

© WaterAid and Tearfund 200320

The Corporate Muddle of Manila’s Water Concessions

only one. Yet it has to use up resources for storing, purifying and pumping not just for one cubic metre of water but for three. The sameproblem can be seen in sewerage; Maynilad isable to bill for only one-half of the volume of sewage that it had originally intended to bill. Thissituation is clearly unsustainable.

(d) A mechanism is in place to cover foreign exchange losses

Article 9.3.1 of the Concession Agreementassures Maynilad that it will be able to recoveradditional costs incurred as a result of thedevaluation of the peso from the reference rate(P26:US$1) in December 1996. Thus, strictlyspeaking, there can be no foreign exchangelosses as the Concession Agreement guaranteesthat Maynilad will be paid for all such losses.The problem for the company however is timing.The agreement states that it is the obligation of the concessionaires to pay unanticipated forexcosts on any given year up-front. Theconcessionaires will then be allowed to collectthese with interest and on instalment fromconsumers over the life of the contract. ButMaynilad needed the "losses" recoveredimmediately to improve its credit rating andqualify for the US$350 million loan it is applyingfor. The recovery of the unanticipated foreignexchange "losses" only became an issuebecause banks would not lend to Maynilad onthe basis of the assured but gradual recovery ofthese costs over the life of the contract. EvenMaynilad officials readily acknowledge this. Inother words, if creditors saw Maynilad as a viableconcern despite the company's own immediatecash problems it should have been possible to"convert" at least some of the future revenuestream on unanticipated foreign exchange lossrecovery into cash.

Practitioners in the business community call this conversion "securitisation". Private placementsof securities of this type are common in thePhilippines, especially with highly liquidinsurance companies as holders of thesecurities. However, it is not all that easy to assign future income streams from consumers tothe holders of the security. The legal issuesaside (these may be manageable), one financialanalyst, Gina Ledesma, says that the difficulty

about securitising revenue from water tariffs is that the company will have to collect the tariffs first (interview). This is one important matter thatcreditors would have to worry about, especially ifthe company they are dealing with is Maynilad.

Also, while no one could have anticipated a fall ofthe peso from P26:US$1 to P50:US$1 by end-2000, the concessionaires were expected toanticipate some fall in the exchange rate, fromP26:US$1 in 1996 to P35:US$1 in 2000. Forsuch a contingency the company would alsohave been expected to be ready to respond tocapital calls by bringing in additional equity7 as needed or by tapping credit lines if the peso fell.

The bottom line is, as far as the banks areconcerned, Maynilad lacked creditworthiness.

Manila Water's challenge

Manila Water, for its part, opened a separate butrelated legal battle with the regulatory office onanother front. As shown by the diagram below,Manila Water wanted to interpret the ConcessionAgreement in a manner that allowed it to changea key bid parameter before rate re-basing. Thisbid parameter is the appropriate discount rate (ADR). The ADR determines the interest rate that consumers must pay for the deferredrecovery by the concessionaires of costs that areapproved during Extraordinary Price Adjustmentpetitions.

The ADR implicit in the original bid was 5.2 percent. Manila Water wanted this raised to 18 percent but the regulators refused. The dispute wasbrought to the Appeals Panel (a body createdunder the terms of the Concession Agreement)

7 In a meeting with economic planning secretary DanteCanlas, (on 4 October 2001 immediately before he wasto give official acknowledgment of the amendment tothe concession agreement), he said that it did not seem reasonable to require the private sector to put in morecapital than it had originally expected to put in,especially because the cost of capital has risen since the Asian financial crisis, while the returns to capital are regulated and limited under the contract. This is onlypartly true. The returns to the concessionaires are onlypartly regulated (see appendix on rate re-basing). Mostrecently, in a ruling favouring Manila Water the international arbitration panel also allowed for the use of a market-based discount rate in the calculation ofannual tariff escalation due to the protracted recoveryof unanticipated costs such as those arising fromadditional foreign exchange costs.

© WaterAid and Tearfund 2003 21

New Rules, New Roles: Does PSP Benefit the Poor?

and it led to a grant of a new ADR at 9.3 percent. The regulators and the MWSS Boardresponded by sending a certiorari petition beforethe Court of Appeals, arguing that the Appeals

Panel overstepped its powers. The AppealsPanel, the MWSS petition argued, can only judgeon whether proper procedures were followed,and not act like it was the Regulatory Office itself.

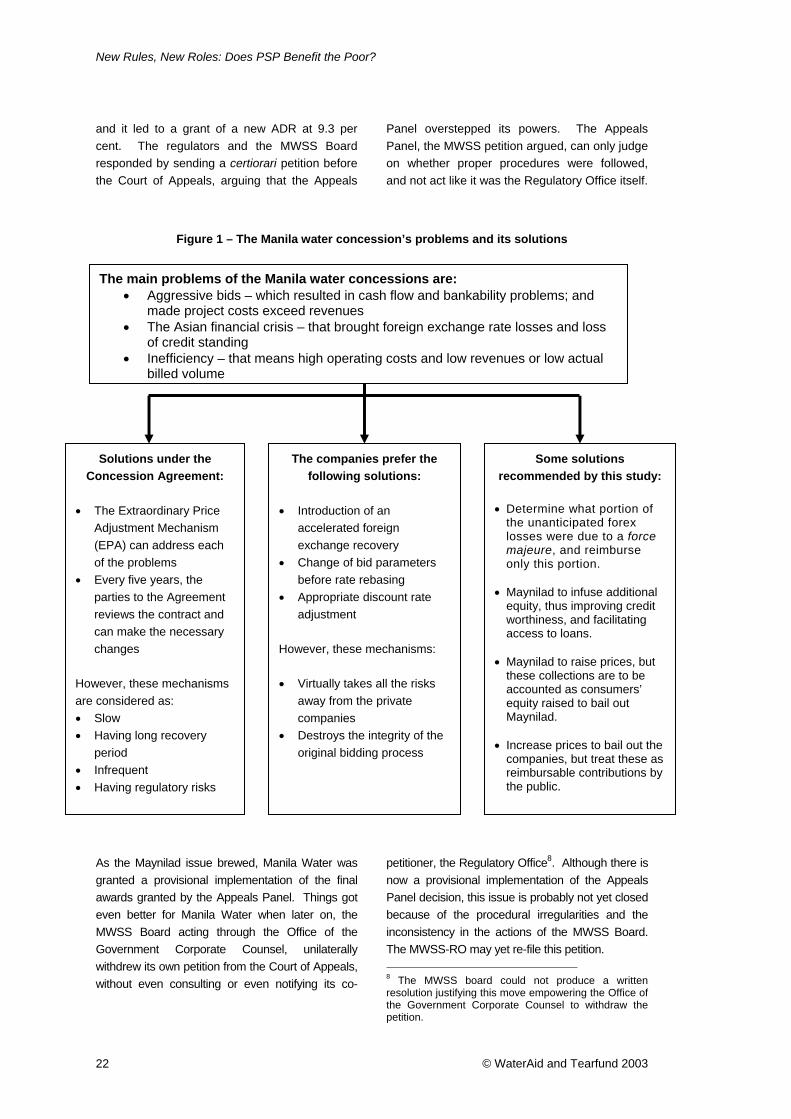

Figure 1 – The Manila water concession’s problems and its solutions

The main problems of the Manila water concessions are: Aggressive bids – which resulted in cash flow and bankability problems; and made project costs exceed revenuesThe Asian financial crisis – that brought foreign exchange rate losses and loss of credit standingInefficiency – that means high operating costs and low revenues or low actualbilled volume

Solutions under theConcession Agreement:

The Extraordinary PriceAdjustment Mechanism (EPA) can address each of the problemsEvery five years, the parties to the Agreementreviews the contract and can make the necessarychanges

However, these mechanisms are considered as: Slow

Having long recoveryperiod

InfrequentHaving regulatory risks

The companies prefer thefollowing solutions:

Introduction of an accelerated foreignexchange recoveryChange of bid parametersbefore rate rebasing

Appropriate discount rateadjustment

However, these mechanisms:

Virtually takes all the risks away from the privatecompaniesDestroys the integrity of the original bidding process

Some solutionsrecommended by this study:

Determine what portion of the unanticipated forexlosses were due to a forcemajeure, and reimburseonly this portion.

Maynilad to infuse additionalequity, thus improving creditworthiness, and facilitatingaccess to loans.

Maynilad to raise prices, but these collections are to be accounted as consumers’equity raised to bail outMaynilad.

Increase prices to bail out the companies, but treat these as reimbursable contributions bythe public.

As the Maynilad issue brewed, Manila Water wasgranted a provisional implementation of the final awards granted by the Appeals Panel. Things got even better for Manila Water when later on, theMWSS Board acting through the Office of the Government Corporate Counsel, unilaterallywithdrew its own petition from the Court of Appeals,without even consulting or even notifying its co-

petitioner, the Regulatory Office8. Although there is now a provisional implementation of the AppealsPanel decision, this issue is probably not yet closed because of the procedural irregularities and the inconsistency in the actions of the MWSS Board. The MWSS-RO may yet re-file this petition.

8 The MWSS board could not produce a writtenresolution justifying this move empowering the Office of the Government Corporate Counsel to withdraw thepetition.

© WaterAid and Tearfund 200322

The Corporate Muddle of Manila’s Water Concessions