CAUSES AND CONSEQUENCES FOR POLITICAL ECONOMY

255

TAX PILFRAGE IN PAKISTAN – CAUSES AND CONSEQUENCES FOR POLITICAL ECONOMY PhD Dissertation To be presented at the Faculty of Contemporary Studies National Defence University, Islamabad in partial fulfillment for the degree of Doctor of Philosophy in Government and Public Policy Asad Kamal Registration No: NDU-GPP-PhD/S-13/015 Supervisor Dr. Muhammad Bashir Khan Faculty of Contemporary Studies, Department of Government and Public Policy, National Defence University, Islamabad, Pakistan. 2020

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of CAUSES AND CONSEQUENCES FOR POLITICAL ECONOMY

TAX PILFRAGE IN PAKISTAN – CAUSES

AND CONSEQUENCES FOR POLITICAL

ECONOMY

PhD Dissertation

To be presented at the Faculty of Contemporary Studies National

Defence University, Islamabad in partial fulfillment for the degree of

Doctor of Philosophy in Government and Public Policy

Asad Kamal

Registration No: NDU-GPP-PhD/S-13/015

Supervisor

Dr. Muhammad Bashir Khan

Faculty of Contemporary Studies, Department of

Government and Public Policy,

National Defence University, Islamabad, Pakistan.

2020

Acknowledgement

First of all I would thank the ALMIGHTY without whose blessings this degree would not have

been possible.

I would like to acknowledge my parents and siblings who have supported throughout my life and

are the main reason I have reached this stage in my life, who have also been my motivational

source throughout this journey.

I would also like to acknowledge my supervisor Dr. Muhammad Bashir Khan from National

Defence University; Dr Sarfraz Hussain Ansari as a teacher of doctoral studies; Dr. Shahzad

Hussain for overall guidance throughout the PhD studies – all of whom were an infinite support

and motivation throughout my doctoral degree. Other faculty member od National Defence

University on the whole for their support as well as all my PhD classmates.

I would also like to support my current organzationa – PAF – that enabled me to continue my

studies. in this regard I highly appreciate the efforts of Air Marshall Arsha Malik Chairman PIA

who enabled my to continue my studies. I would also like to thank Muhammad Zafar Khan of PAF

for giving me support during the course of my degree.

I would also thank my collegues from NDU who helped me as required. Dr. Fiaz Kazmi, Dr Naila

Erum, Dr. Shahzad Rao and Dr. Muhammad Zaheer Khan who motivated me in tough times and

also assisted me in times of need.

Dedication

This thesis is dedicated to my parents, siblings and daughter.

i

ABSTRACT

Taxation and pilferage are very old phenomena and were there in ancient civilizations as well. Tax evasion

is widespread in Pakistan and is a significant cause of poor tax collection since inception that has led to

inadequate provision of public services. The study measured attitude towards tax evasion, their

demographic profile and tax morale through a survey. The study included a sample of 400 potential

taxpayers who were randomly selected and their responses were taken on a carefully constructed

questionnaire. The questions measured evasion behavior, tax morale and demographic indicators.

Responses of questions were taken on a six point likert scale. The data was analyzed using using Linear

Regression and Chi Square Test (wherever applicable).

The results of the survey suggest that in terms of demographic variables, income level and age both had

significantly positive relationship with tax evasion while gender and educational level had insignificant

relationship. Similarly, in terms of tax morale, perceived penalties and elements of shame had significantly

inverse relationship with tax evasion while perceived extent of utilization of tax money on public services

had significantly positive relationship. However, Gender, Educational level, perceived corruption and

element of guilt had insignificant relationship with tax evasion in the country. The findings were robust at

95% level of significance.

The study also touched upon some political and economic consequences of tax evasion that has affected the

economic growth of Pakistan. the first issue is related to inflation. Tax evasion leads to too much money

held by the private sector causing price hike. Another important consequence of tax evasion is related to

public debt where the government - in order to fulfill its responsibilities – has to borrow from internal and

external sources to finance its expenditures. This borrowing is done to fulfill certain government

requirements like provision of basic public services to its citizens that has political repercussions as most

citizens in developing nations like Pakistan depend on such public services. Secondly, due to lack of

finances, the government is unable to finance PSEs and so the government has to go for borrowing.

The study concludes by giving some policy implications which includes progressive fines on evasion, public

awareness regarding tax payment, depicting payment as a social norm and control of corruption in tax

administration. Use of media in this regard is of much importance.

ii

Table of Contents

ABSTRACT .................................................................................................................................... i

LIST OF TABLES ........................................................................................................................... v

LIST OF FIGURES ....................................................................................................................... vi

.......................................................................................................................................... 1

INTRODUCTION ........................................................................................................................... 1

Historical Background ................................................................................................................. 1

Tax System of Pakistan ................................................................................................................ 3

Tax Collection in Pakistan ....................................................................................................... 4

Types of Taxes ......................................................................................................................... 5

Direct Taxes ............................................................................................................................. 5

Tax Evasion and Underground Economy in Pakistan................................................................ 10

Tax Collection Profile for the Years 2010 – 2015 ..................................................................... 11

Tax Collection FY 2012 – 13 ................................................................................................. 15

Tax Collection FY 2013-14 .................................................................................................... 17

Tax Collection FY 2014-15 .................................................................................................... 18

Initiatives by Government as of 2015 to 2018 ....................................................................... 19

Statement of the Problem ........................................................................................................... 20

Objectives of the Study .............................................................................................................. 21

Significance of the Study ........................................................................................................... 21

Organization of the Study .......................................................................................................... 23

........................................................................................................................................ 24

LITERATURE REVIEW .............................................................................................................. 24

Role of Taxation in Economic Growth ...................................................................................... 24

Tax Collection in Developing Countries ................................................................................... 26

Tax Issues in Pakistan ................................................................................................................ 28

Determinants of Tax Evasion ..................................................................................................... 29

Hypothesis .................................................................................................................................. 58

........................................................................................................................................ 65

METHODOLOGY ........................................................................................................................ 65

Research Methods ...................................................................................................................... 65

Type of Data (Primary VS Secondary) ...................................................................................... 66

iii

Approach used to Measuring Tax Evasion ................................................................................ 66

Questionnaire Development ....................................................................................................... 70

Rationale behind integrative research design / methods ............................................................ 72

Figure 3-1: Conceptual Framework of the Study ....................................................................... 73

Operationalization of Concepts .................................................................................................. 73

Selection of Appropriate Scale .................................................................................................. 78

Pilot Testing ............................................................................................................................... 82

Rectification of questionnaire .................................................................................................... 83

Re-testing ................................................................................................................................... 83

Population and Sample Size ....................................................................................................... 84

Rationale behind Target population –The Salaried Class .......................................................... 85

Study Area .................................................................................................................................. 87

Data Analysis ............................................................................................................................. 87

Research paradigms ................................................................................................................... 95

........................................................................................................................................ 97

DEMOGRAPHIC PROFILE OF RESPONDENTS ..................................................................... 97

Gender of Respondents ............................................................................................................ 100

Income Level of Respondents .................................................................................................. 101

Educational Qualification......................................................................................................... 102

Ethnic Background of the Respondents ................................................................................... 105

...................................................................................................................................... 119

FINDINGS AND ANALYSIS .................................................................................................... 119

Demographic Variables and Tax Evasion ................................................................................ 119

Age and Tax Evasion ........................................................................................................... 119

Gender and Tax Evasion ...................................................................................................... 122

Income Level of Respondents .............................................................................................. 124

Educational Qualification of Respondents ........................................................................... 128

Tax Morale and Tax Evasion ................................................................................................... 131

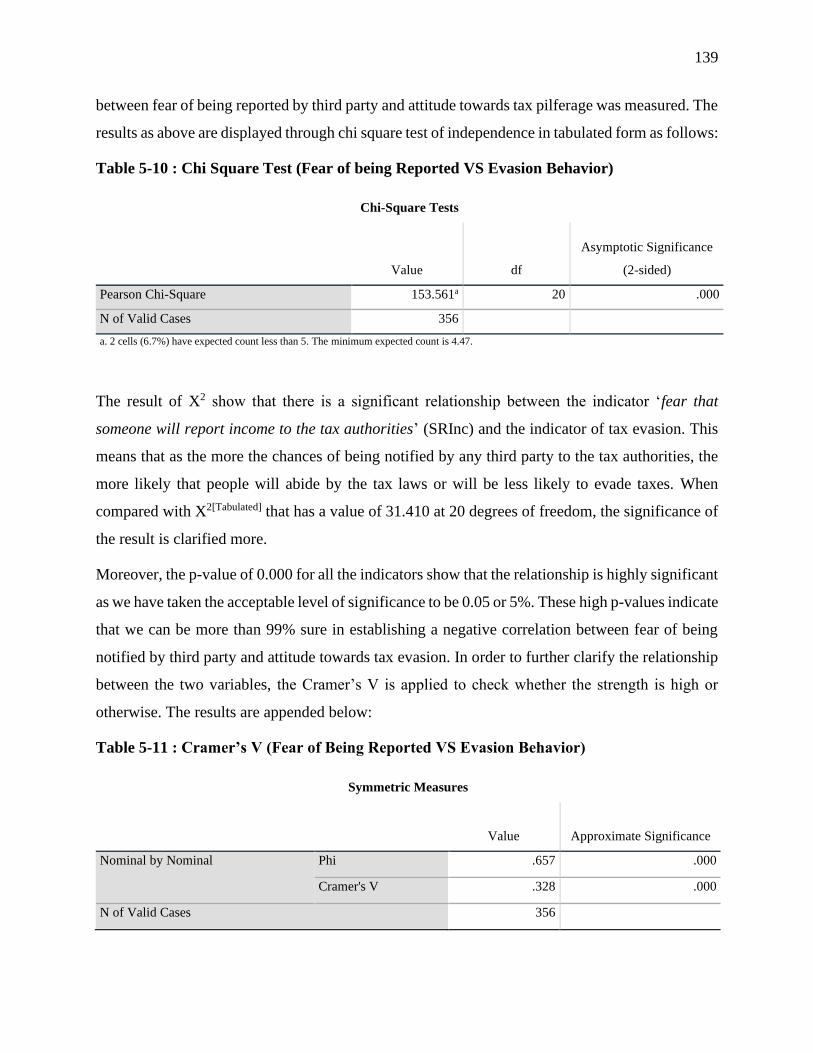

Perceived Shame and Guilt .................................................................................................. 133

Trust in Government ............................................................................................................ 144

Perception about others paying taxes ................................................................................... 150

Penalties on of Tax Evasion ................................................................................................. 153

Summary of Key Findings ....................................................................................................... 156

iv

...................................................................................................................................... 157

CONSEQUENCES OF EVASION ON POLITICAL ECONOMY ........................................... 157

Political Economy .................................................................................................................... 157

Consequences of Tax Evasion on Political Economy .............................................................. 161

...................................................................................................................................... 165

CONCLUSION AND POLICY IMPLICATIONS ..................................................................... 165

Conclusion ............................................................................................................................... 165

Policy Implications .................................................................................................................. 167

Implication for Stakeholders .................................................................................................... 178

...................................................................................................................................... 185

FUTURE RECOMMENDATIONS ............................................................................................ 185

Limitations of The Study ......................................................................................................... 185

Recommendations for Future Research ................................................................................... 185

REFRENCING ............................................................................................................................ 187

APPENDICES ............................................................................................................................. 235

Appendix A .............................................................................................................................. 235

Appendix B .............................................................................................................................. 236

Appendix C .............................................................................................................................. 238

v

LIST OF TABLES

Table 1-0-1 : Tax Collection FY 2010 – 11 .................................................................................. 12 Table 1-0-2 : Tax Collection FY 2011 - 12 ................................................................................... 14 Table 3-1: First indicator of Tax Evasion ...................................................................................... 92 Table 3-0-2 : Second indicator of Tax Evasion ............................................................................. 93 Table 3-0-3 : Third Indicator of Tax Evasion ................................................................................ 93

Table 4-1 : Age of the Respondent ................................................................................................ 97 Table 4-2 : Gender of Respondents ............................................................................................. 100 Table 4-3 : Education-wise roportion of Pakistan ....................................................................... 101 Table 4-4: Income Level .............................................................................................................. 102 Table 4-5 : Education Qualification ............................................................................................ 103

Table 4-6: Provincial Share of Survey Population ...................................................................... 106 Table 4-7 : Province wise Population as in 1998 Census ............................................................ 107

Table 4-8 : Area-wise represenatation of respondents ................................................................ 108 Table 4-9 : Percentage of Response on first indicator of Evasion ............................................... 112

Table 5-1: Chi Square Test (Age Vs Tax Evasion Behavior) ..................................................... 120 Table 5-2 : Cramer’s V : Age Vs Tax Evasion Behavior ............................................................ 121 Table 5-3 : Chi Square Test (Gender and Evasion Behavior) ..................................................... 123

Table 5-4 : Cramer’s V (Gender VS Evasion Behavior) ............................................................. 123 Table 5-5 : Chi Square Test (Income Level VS Evasion Behavior) ............................................ 126

Table 5-6 : Craver’s V (Income Level VS Evasion Behavior) .................................................... 127 Table 5-7 : Chi Square Test (Education VS Evasion Behavior) ................................................. 130 Table 5-8 : Chi Square Test (Fear of being listed VS Evasion Behavior) ................................... 136

Table 5-9 : Cramer’s V (Fear of being listed VS Evasion Behavior) .......................................... 136

Table 5-10 : Chi Square Test (Fear of being Reported VS Evasion Behavior) ........................... 139 Table 5-11 : Cramer’s V (Fear of Being Reported VS Evasion Behavior) ................................. 139 Table 5-12 : Chi Square Test (Perceived Guilt VS Evasion Behavior) ....................................... 143

Table 5-13 : Chi Square Test (responsibility towards Others VS Evasion Behavior) ................. 143 Table 5-14 : Chi Square Test (Perceived Service Delivery VS Evasion Behavior) .................... 148

Table 5-15 : Cramer’s V (Peerceived Service Delivery VS Evasion Behavior) ......................... 148

Table 5-16 : Chi Square Test (Perceived Corruption VS Evasion Behavior) ............................. 150 Table 5-17 : Chi Square Test (Perceived Social Norms VS Evasion Behavior) ......................... 152

Table 5-18 : Cramer’s V (Perceived Social Norms VS Evasion Behavior) ................................ 152 Table 5-19 : Chi Square Test (Perveiced Penalties VS Evasion Behavior) ................................ 154 Table 5-20 : Cramer’s V (Perceived Penalties VS Evasion Behavior) ....................................... 155

vi

LIST OF FIGURES

Figure 3-1: Conceptual Framework of the Study .......................................................................... 73 Figure 3-2: Graphical Representtion of Tax Evasion indicators ................................................... 94 Figure 3-3 : Fiscal Psychological Theory ...................................................................................... 96

Figure 4-1 : Age Profile of Pakistan .............................................................................................. 99 Figure 4-2: Geographical Representation of Population as per 1998 Census ............................. 107 Figure 4-3 : Depiction of Central Punjab Area ............................................................................ 109 Figure 5-1 : Response of Fear of Being included in Defaulters List ........................................... 135

Figure 5-2: Perception regarding being reported on evasion ....................................................... 138 Figure 5-3 : Graphical Representation of Responses on Guilt .................................................... 142 Figure 5-4: Response Chart for Social Norm and Rax Evasion .................................................. 151

1

TAX EVASION IN PAKISTAN – CAUSES AND CONSEQUENCES

FOR POLITICAL ECONOMY

INTRODUCTION

Historical Background

“Nothing is certain but death and taxes” - Benjamin Franklin. Taxes trace their origin as old as

3000 BC when in ancient Egypt, Pharaohs used to take part of harvest as taxes. As mentioned in

the bible, Chapter 47, Verse 33, Pharaohs used to send his commissioners to collect one-fifth of

grains harvested as taxes. According to archeological records, the first available records of taxation

can be traced to The Egyptian King Scorpion the First who ruled the Southern Egypt between 3300

and 3200 BC (Samsun 2002). Taxation existed in the ancient times in other empires outside Egypt

also. Taxes also existed in the region of Mesopotamia dating back to 2500 BC where citizens of

Babylonia paid taxes to the government for many purposes the foremost of which being enabling

the government to spend on maintaining the irrigation canals from Euphrates and the Tigris rivers

(Garbutt 1984).

Taxation was also found in the Achaemenid Empire between 538 and 330 BC where the central

government in collaboration with the provincial governments levied taxes on the citizens as the

King’s share (Kleber 2015). Similarly taxation was also found out to be a major object recorded

by archeologists in the Inca civilization in the present day Peru. The empire flourished during the

1500 century AD where taxation was an integral part of the economic and social development of

the rising empire (Yeakel 1983). The conquered tribes were required to pay taxes to the central

government that in turn provided them with road infrastructure and protection and also provided

food in case of famine like situation in a particular tribe or area. Similarly China and Greece also

imposed war taxation on their citizens while the Roman Empire were pioneers in levying customs

duties on imports and exports that was known as Portoria (Adams 1993).

2

Like taxation, tax evasion also has its roots deeply entrenched in history. In Ancient Egypt, the

Pharaohs had employed their representatives called ‘Scribes’ who were responsible to collect tax

on their behalf. These scribes were empowered to collect tax and had their own tax courts that

could not be challenged by the taxmen (Rostovtzeff 1953). As the Pharaohs were perceived by

their citizens as God therefore they did not want to press their masses to an extent where they start

revolting against them. The Pharaohs would even let those citizens go untaxed whose harvest was

poor (Ehrenberg 1960). Moreover, given much powers, even the scribes were not given autonomy.

These administrators were also kept under surveillance. Special agents were employed who had

been tasked to keep a check on overtaxing by the scribes and were also authorized to spy on the

scribes to ensure any corrupt practice was not being carried out (C. Adams 2001).

The first available record of corruption and tax heavens can also be seen form the ancient Egypt.

According to (Adams, 2001), as scribes were given tremendous judicial and executive powers over

taxation they indulged in unfair practices of overtaxing the masses. The special agents who were

tasked to restrict such practices and listen to tax related complaints. Although these agents were

subject to extreme punishments (having his nose cut off) on non-compliance still they collaborated

with the scribes and both parties shared the tax money generated. Similarly during the 17 year

reign of Akhenaten, all the temples and religious buildings were exempted from taxation that

provided a tax heaven for tax evaders. That practice enabled many evaders to get away from the

scribes that ultimately resulted in the decline of tax revenue during that time period.

In Ancient Greece, the tax money collected was used for the construction of road and other public

facilities (Viljoen 2016). All the rich members of the society were approached to forcefully fund

projects and it had become a status symbol in Greece at that time that proved a person to be wealthy

(Frank 2012). Apart from such funding, other taxes were also there in Greece. Like the Egyptian

Scribes, The Greek government also had agents who were responsible to collect taxes as part of

harvest (Viljoen, 2016). Such taxes were easier to evade as agents were not there at the time of

harvesting. In order to compensate for the lost revenue as a result of evasion in harvesting, foreign

merchants in Athens were levied with Poll Tax (Roberts 2002). People also tried to evade poll tax

by forging their birth certificates as a person having both parents form Greece were exempt from

such tax. Such practices of evasion on harvesting and poll tax were there despite the fact that heavy

punishments were there for non-compliance (Adams, 2001).

3

The Roman empire that boasted off being the greatest civilization of that time and were confident

of having a strong army that could never be defeated was defeated by Odovacor and his army in

the year 476 AD. The main cause of that invasion was attributable to tax evasion by some

historians. The Roman empire did not have enough revenue available to sustain its military that

led to the invasion by Odovacor (Cousin 2015). During the third century AD, Diocletian, the then

emperor of the Roman Empire tried to build his empire such that it could not be defeated easily

(Cousin, 2015). However, in order to persue his goals, he taxed his masses heavily in the form of

harvest tax. He also employed tax agents who would use harsh techniques to receive taxes that

resulted in poor farmers selling their lands to the rich ones (Viljoen, 2016).

The rich farmers in turn started bribing the agents and hence tax evasion rose in the empire that

ultimately led to lower revenue collections (Pope 2010) and ultimately a hindrance in fulfilling the

desired goal of Diocletian. When Julian assumed power, he determined higher taxes as the main

reason of poor tax collection and reduced taxes. However, the taxes were again doubled to support

the Roman Army at that time that again led to the previously deteriorated situation. People could

not bear the burden of those taxes and after selling their lands, the farmers also sold their slaves

who were useless for them to fight in the military (Viljoen, 2016) that ultimately led to the demise

of the great Roman Empire (Adams, 2001).

Tax System of Pakistan

The system of Pakistan is based on the revenue-sharing structure provided under the Government

of India Act 1935 that served as a guideline for future constitutions of the country in distributing

financial powers between the Federation and provinces (Khan A. , 1992). The 1973 Constitution

of Islamic Republic of Pakistan empowers the Federal government to levy and collect taxes on

personal income, corporate income, sales tax, import and export duties, excise duties and any other

tax med necessary by the President of Pakistan.1 FBR, previously known as the Central Board of

Revenue (CBR) which works under the Ministry of Finance is vested with the responsibility to

collect taxes on behalf of the Federal Government.2

The government relies mostly on indirect taxes which comprise 55% of total tax revenue generated

by the Federal Government (Sherani, Pakistan's Taxation Crisis, 2015). The main reason to rely

1 Clause 3, Chapter 1, Part VI of the Constitution of 1973 2 FBR website: http://www.fbr.gov.pk/ShowArticle.aspx?actionID=57

4

on indirect taxes is that direct taxes that include income taxes are mostly evaded due to corruption

and collusion of tax officers with the tax payers – a fact that was admitted by Mr. Haroon Tareen,

Director Intelligence and Investigation, FBR (Ansaari, 2015).

Tax Collection in Pakistan

Federal Government levies taxes on income, customs, sales tax on goods and FED etc. while

income tax on agriculture and property taxes among others have been given to provinces (Pasha

& Pasha, 2015). After 18th Amendment the sales tax on services has also been given to the

provinces (pp. 175).

Pakistan is a developing country and 79%3 of the total revenue by the Federal Government is

generated through taxes. According to a report published by the UK Parliament’s International

Development Committee in 2013, only 0.57% of Pakistanis paid their share of taxes and that the

tax to GDP ratio of Pakistan was around 10% that was the lowest compared to countries of its per

capita income group. The report also showed Pakistan’s VAT performance to be just 25% which

was 45% for Sri Lanka and 90% for New Zealand. It should be noted that Sales Tax comprises the

largest proportion of Pakistani Tax structure.

Pakistan’s tax collection has remained a point of concern since the 1970s a period that was marked

with nationalization of assets without downsizing of public servants while at the same time

regional conflicts called for increasing defense expenditures all that led to deficit financings

through external borrowings (Cashin, Haq, & Olekalns, 1999). Similarly during the 1980s due to

huge aid coming by the west during Afghan war and also the military government wanted to protect

itself from the wrath of the masses and maintain its legitimacy (Chaudhary & Munir, 2010).

The budget deficits of the country remained between 5.4 to 8.7% of GDP with around 6% in 1970s,

7.6% in 1980s and again souring to 7% in the first decade of the 21st century. The era of 1990s

saw decline in the deficit due to lack of investments by the government in development projects

hence affecting long term development (Chaudhary & Shabbir, 2005).

3 FBR Annual Budget FY 2015-16 Revised

5

Types of Taxes

In Pakistan, a total of 70 different types of taxes are being levied and are administered by 37

government agencies (Horrigan, 2010). According to FBR, the federal taxes imposed in Pakistan

are mainly divided into Direct and Indirect taxes. Direct taxes include Income Tax, Workers

Welfare Fund and Capital Value Tax while indirect taxes include Customs, Sales and Excise ies.

There are, however, other taxes included in the federal budget that comprise Airport Tax, Gas

Development and Petroleum levy.

Direct Taxes

a. Income Tax

Income Taxes comprise the largest part of direct taxes and constitute more than 40% of the total

direct taxes4. Income Tax is regulated under the provision of the Income Tax Ordinance, 2001. At

the time of independence, Pakistan adopted the Income Tax Act, 1922 but soon afterwards, the

Central Board of Revenue was tasked with devising a new framework as new forms of income

emerged ending in enactment of the Income Tax Ordinance of 1979 that enabled enhance tax net

and increase the tax base (Ahmed & O'Donoghue, 2009). 21 years later the Income Tax Ordinance

2001 was enacted that is still prevalent in Pakistan with certain amendments made in it through

different Finance Acts the latest being Finance Act 2016. The heads of income specified in the

Income Tax Ordinance 2001 are as follows:

i. Salaries

ii. Income from Property

iii. Income from Business

iv. Capital Gains

v. Income from other Sources

According to the federal Board of Revenue (FBR)5, entities subject to income tax are as follows:

Companies

4 FBR Documents and Author’s own computations 5 FBR Website:

http://www.fbr.gov.pk/OfficeHomePage.aspx?view=Office%20Home%20Page&ActionID=40&ArticleID=149

6

a. Association of Persons (AOPs)

b. Non salaried Persons

c. Salaried Persons

a. Personal Income Tax

Personal income tax includes income of salaried persons, non salaried persons and unincorporated

firms (including AOPs). The personal income tax system of Pakistan has its roots in the mid 19th

century British India and is one of the oldest tax income tax system in the world and is very close

to India and other developing countries (Klevin & Waseem, 2011).

The income tax of Pakistan is divided into different notches. As per the Income Tax Ordinance

2001 (Amended till 30 August, 2016) the income tax of salaried persons has been divided into 12

notches while the income tax for all other individuals is divided into 8 notches.

b. Corporate Tax

Corporate tax in Pakistan is divided into 3 main categories namely Banking Sector, Public

Companies and Private limited Companies. Tax rates as in 2016 are 40%, 35% and 45%

respectively6. There are however, small companies that –according to Section 2 of Income Tax

Ordinance, 2001 – should not have paid up capital of more than 50 million, a workforce of less

than 250 people and its annual turnover should not increase PkR. 250 million. Tax rate on such

companies has been 25%.

In September, 2015, the Federal Government through finance Act, 2015 imposed Super tax over

and above the normal tax rates applied to the companies at the rate of 4% for Banking companies

and 3% for all other persons whose income exceeds PkR. 500 million in the fiscal year 2015 – 16.

c. Workers Welfare Fund

Workers Welfare Fund is governed under the provisions provided by the Workers Welfare Fund

Ordinance 1971. WWF was established in 1971 by the Federal Government with an initial capital

paid by the federal Government amounting to Rs. 100 million while the rest is to be paid by the

industrial sector while income generated from investments by the WWF and voluntary

contributions may also be used as sources of income for the fund7.Section 4 of the ordinance states

6 Finance Act 2016 7 Section 3 (2)a & b of Workers Welfare fund Ordinance

7

that the industrial sector8 firms having annual income of more than PkR. 500,000 would pay

amount at the rate of 2% of the total income. WWF had been established with the aim to provide

low cost housing, marriage and educational grants and scholarships for the industrial workers9.

d. Capital Value Tax

Capital Value Tax (CVT) is the tax levied on the capital value of the immovable property. The

Constitution of 1973 authorized the Federal government to levy CVT on immovable property

while the provision was abolished after the 18th amendment to the Constitution of Islamic Republic

of Pakistan in 2010. According to the Finance Act 2012, CVT has been made provincial subject

while the Federal Legislature is only allowed to levy such tax on immovable property within the

Islamabad Capital Territory at the rates given in Table II. CVT constitutes a fraction of the total

budget contributing around 0.02 – 0.04 % of the annual Federal Tax revenue.10

Indirect Taxes

Indirect taxes are common in countries like Pakistan that affect the poor to due their regressive

nature which affects the poor more especially when such taxes are implemented on necessity items

(Empirical Analysis of Tax Revenues and Its Impact on Economic Groeth of Pakistan, 2015).

Indirect taxes imposed in Pakistan are of the following types:

a. Sales Taxes

Sales Tax in Pakistan is governed under the provisions provided in the Sales Tax 1990 that keeps

on being amended from time to time by different governments. In Pakistan, sales tax constitutes

the largest proportion of the federal taxes comprising more than 41% of the total taxes.11 Sales tax

is a regressive tax and in Pakistan it is known as GST or Generalized Sales Tax which is levied at

the rate of 17% on all goods and services (Ahmad E. , 2010). GST performance in Pakistan is one

of the worst in the world (i.b.i.d. p. 11). The sales tax remained at 16% from 2006 – 2016 and was

raised to 17% through the Finance Act, 2016.

b. Customs Duties

Customs Duties are enforces and implemented in Pakistan under the Customs Act, 1969 with

certain amendments from time to time by the Federal Government. Section 1 of the act authorizes

8 Definition provided in Section 2(f) of Workers Welfare Fund Ordinance 1971 9 WWF Website: http://www.wwf.gov.pk/ 10 Authors computations for the FY 2014-16 11 FBR Budget documents of FY 1991 - 2016

8

the Federal Government to enact laws as and when required to make amendments as it deems

necessary from time to time. Total share of Customs duty in the total federal tax revenue has

remained less than 7% in the last two fiscal years.

c. Federal Excise Duty

The Federal Excise Duty of FED was named as Central Excise Duty and was governed under the

provisions of the ‘Central Excise Act, 1944’12. FED was enforced in wef 1 July, 2005 and was

extended in the entire country under the provisions of federal Excise Act, 2005. According to

Section 3 of the act, FED is applicable to goods manufactured or imported in Pakistan and also on

services provided in the country irrespective of whether these services originate within the country

of abroad. Clause‘d’ has specified the rate of FED at 15% and FED applicable on imported goods

has to be paid at the time of import by the import. The total share of FED in total revenue generation

has been just 6 – 6.5% of the total federal tax revenue in FY 2014 – 16.

Other Taxes

Other taxes include the Airport Tax, Gas Infrastructure, Natural Gas Development Surcharge and

Petroleum and constitute 10 – 11 % of the total federal tax collection as evident from the federal

budget documents of the last 02 years.

National Finance commission

Pakistan is a federation that is divided into four provinces. The majority of tax revenue generated

in Pakistan is done at the Federal level. According to the Federal budget analysis, around 95% of

the total tax revenue is generated at federal level that includes taxes on income, customs and excise

duties and other taxes as mentioned above. While the provinces generate only 5% of the total tax

revenue that does not suffice their requirements. Provincial taxes include sales tax on services,

stamp duty, vehicle tax, capital value tax etc. The constitution of Islamic Republic of Pakistan lays

down procedure of distribution of federal income from tax collection to the provinces through the

National Finance Commission (NFC).

Article 160(1) of the Constitution of Islamic Republic of Pakistan 1973 clearly explains the

distribution of federal revenue to provinces in a systematic manner through the constitution of

12 FBR website:

http://www.fbr.gov.pk/OfficeHomePage.aspx?view=Office%20Home%20Page&ActionID=49&ArticleID=160

9

National Finance Commission having federal and provincial Finance ministers as its members and

is proposed to be held at intervals of every five years (Constitution of Pakistan 1973). The aim,

according to the constitution is to distribute federal tax revenue to the provinces

History of NFC Awards

The redistribution of federal resources was never the same as of today in Pakistan. After

independence, Pakistan adopted the Neimeyer Award for the distribution of resources between the

Federal and the provincial governments based on the Government of India act. During that time

sales tax was a provincial subject while income tax was a federal subject that was distributed

between the federation and the provinces in equal ratio with some additional grants for Sindh and

NWFP (Ahmed, Mustafa, & Khalid, 2007).

Soon after independence, the Prime Minister conferred Sir Jeremy Raisman with the responsibility

of preparing another feasible system of income redistribution. Raisman awards were presented in

1948 and were enforced with effect from 1 April 1952 with certain amendments like the provinces

gave 50% of their share of sales tax collection to the Federal Government while the federal

government distributed half of its income and other taxes collected to the provinces in the ratio of

45% and 55% to East and West Pakistan respectively. the share of West Pakistan was further

distributed among the provinces with special grants for the NWFP (Government of Pakistan ,

1991).

After Pakistan was divided into two units namely East and the West Unit, all the provinces in the

West Pakistan were amalgamated into one unit. Under this system two awards were presented.

Under the 1961 awards divisible pool comprising of income taxes and 70% of the sales tax

proceeds were distributed between East Pakistan and West Pakistan in the ratio of 54% and 46%

share. The remaining 30% sales tax proceeds were distributed to provinces according to their share

of sales tax collection. Other duties were distributed between the units on the basis of their

collection (Government of Pakistan , 1991).

The next national Finance Commission was setup in 1964 under the provisions of article 144 of

the Constitution of 1962. Sales tax, income tax, exercise and export duties were included in the

divisible pool and the share was distributed between federal government and both units in the

ration 35:65 with the same proportion for both the units including the provision of 30% sales tax

as per collection by the province. However, after the abolishing of one unit concept, the share of

10

West Pakistan was further divided in the ratio 56.5, 23.5, 15.5 and 4.5for Punjab, Sindh, NWFP

and Baluchistan respectively (Bilgrami Jaffery & Sadaqat, 2006).

In April 1970, a National Finance Committee was formed under the Federal Finance Minister to

distribute the resources. The share of provinces and units remained the same as of 1964 but the

Federal share was reduced to 20%. After the separation of West Pakistan (Now Bangladesh) the

provincial share in West Pakistan remained the same but the volume of their share increased

(Ahmed, Mustafa, & Khalid, 2007).

After the separation of East Pakistan and the promulgation of a new constitution of 1973, the

financial distribution between the Federal and Provincial governments was amended. Under the

article 160 of the constitution, the President was bound to form a committee consisting of the

Federal and Provincial Finance Ministers and the the government was obliged to compose NFC

at an interval of maximum five years for a fair distribution of resources between the Federal and

provincial Governments (Bilgrami Jaffery & Sadaqat, 2006).

Since that time a total of seven NFC Awards have been setup. All the NFCs redistributed income

to the provinces mainly in accordance with the population share with certain grants also provided

to under developed provinces. The matter was resolved in the seventh NFC award that was

population was not made the main criterion for income distribution rather backwardness, tax effort

and inverse population density were also included as a proportion for income distribution

(Mustafa, 2011).

Tax Evasion and Underground Economy in Pakistan

According to Saqib Sherani13, out of seven million eligible taxpayers only five hundred thousand

pay their taxes that constitutes 0.3% of the population making this proportion as the lowest in the

world (Sherani, Pakistan's Taxation Crisis, 2015). IMF in its report14 termed Pakistan’s tax-to-

GDP at around 11% in FY 2014-15 that was far below the potential ratio of 22% while the potential

tax base was much less as compared to the potential figures15. The NFC report finalized in a

13 Saqib Sherani is the former economic advisor to the Government and presently heads a macroeconomic

consultancy based in Islamabad, Pakistan 14 IMF ninth Review Report (IMF Country Report No 16/1) 15 According to the report, a total of Registered Income Tax filers were only 970,000 against the potential

figure of 5.7 million while the number of Corporate income tax filers was less than 1% of commercial

electricity users

11

meeting held on 28 November, 2015 revealed that Pakistan lagged much behind the promised tax

to GDP ratio of 15% in the FY 2014 – 15 in the 7th NFC Award (Kayani, 2016).

According to one study tax evasion in Pakistan increased from PkR. 1.5 Billion in 1973 to PkR.

152 Billion in 1996 (Iqbal, Qureshi, & Mehmood, The Underground Economy and Tax Evasion

in Pakistan : A Fresh Assessment, 1998) while according to another estimate tax evasion grew

from PkR. 405 Million in 1960 to Rs. 123.6 Billion in 1998 that was 84% of the total budget deficit

of the country (Aslam S. , 1998). The World Bank report also claimed that the tax gap of Pakistan

in 2008-09 was 79% amounting to Rs. 796 billion in total or Rs. 4800 evaded by every Pakistani

on an average (Government of Pakistan, World Bank, Georgia State University, 2009).

Similarly Underground Economy has a positive and highly positive correlation with tax evasion

(Kemal, 2007). Underground Economy in Pakistan grew from 29% in 1960 to 43% of the total

GDP of Pakistan in 1998 (Aslam S. , 1998).

Tax Collection Profile for the Years 2010 – 2015

According to the Fiscal Policy statements issued by the Ministry of Finance, Government of

Pakistan the tax collection by the Federal Government during the Fiscal Years 2009-2010 through

2015- 16 has been calculated. The collection figures are appended below:

Tax Collection during FY 2009-10

During the FY 2009 – 10, total tax collection was estimated to be Rs. 1380 Billion in the federal

Budget. Of which actual collection amounted to Rs. 1327.4 Billion with a shortfall of Rs. Rs. 52.6

billion. The total tax collection during the year was 9% of the total DGP.

a. Direct Taxes

Direct taxes amounted to Rs. 528.6 Billion against estimated 540.4 Billion constituting 40% of the

total tax collection during the year. Withholding Taxes constituted the largest portion of the direct

taxes amounting to Rs. 298.4 Billion. Voluntary payments that included payments with returns

and advances generated Rs. 165.8 Billion in the total Tax revenue.

b. Indirect Taxation

Sales Tax collection constituted around 65% of the total indirect tax collection while 39% of the

total tax collection during the said period. A total of Rs. 516 Billion were collected as sales tax

12

during FY 2009-10. Sales tax is sub categorized into Domestic GST and GST on imports with Rs.

269 Billion coming from domestic while the remaining Rs. 247 generated through imports.

Customs duty contributed 20.2% of the total indirect tax while 12.2%of the total tax collection in

FY 2010 with Rs. 161.5 Billion against budgeted estimates of Rs. 164.9 billion. The reason as

stated in the FBR report was mainly due to 0.3% reduction in dutiable imports. Similarly the FED

contributed Rs. 121.2 billion in total tax collection that made 9.1% of the total tax collected.

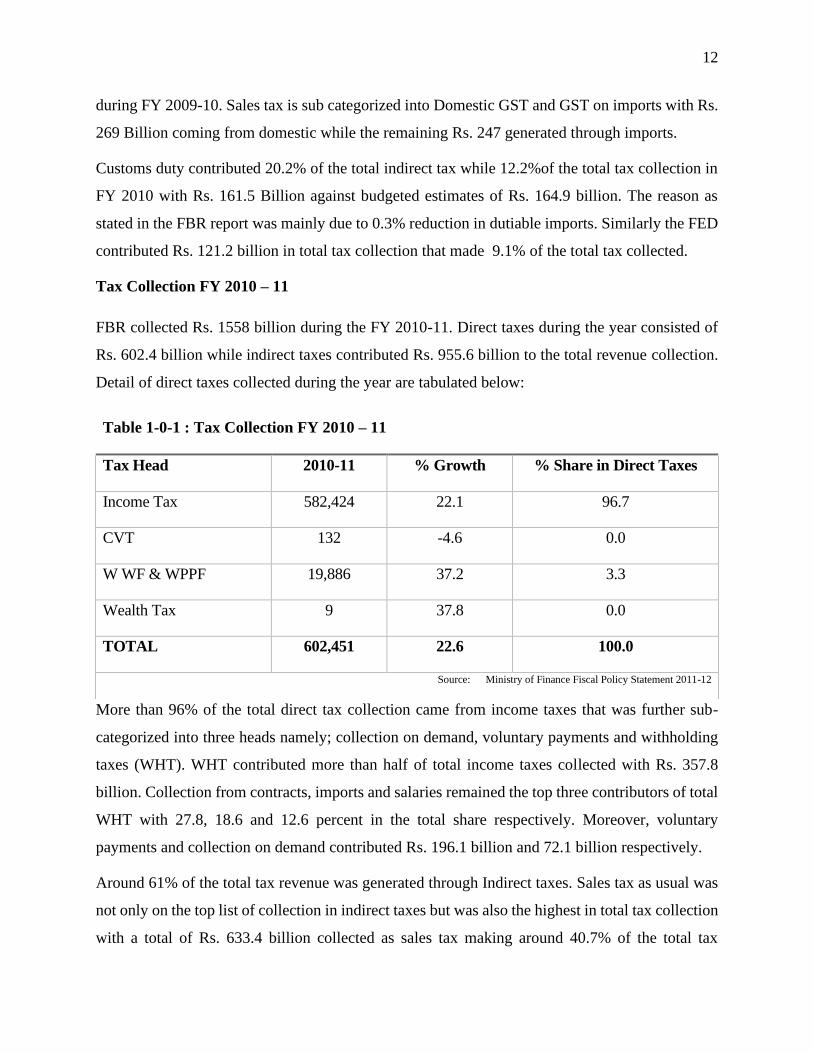

Tax Collection FY 2010 – 11

FBR collected Rs. 1558 billion during the FY 2010-11. Direct taxes during the year consisted of

Rs. 602.4 billion while indirect taxes contributed Rs. 955.6 billion to the total revenue collection.

Detail of direct taxes collected during the year are tabulated below:

More than 96% of the total direct tax collection came from income taxes that was further sub-

categorized into three heads namely; collection on demand, voluntary payments and withholding

taxes (WHT). WHT contributed more than half of total income taxes collected with Rs. 357.8

billion. Collection from contracts, imports and salaries remained the top three contributors of total

WHT with 27.8, 18.6 and 12.6 percent in the total share respectively. Moreover, voluntary

payments and collection on demand contributed Rs. 196.1 billion and 72.1 billion respectively.

Around 61% of the total tax revenue was generated through Indirect taxes. Sales tax as usual was

not only on the top list of collection in indirect taxes but was also the highest in total tax collection

with a total of Rs. 633.4 billion collected as sales tax making around 40.7% of the total tax

Table 1-0-1 : Tax Collection FY 2010 – 11

Tax Head 2010-11 % Growth % Share in Direct Taxes

Income Tax 582,424 22.1 96.7

CVT 132 -4.6 0.0

W WF & WPPF 19,886 37.2 3.3

Wealth Tax 9 37.8 0.0

TOTAL 602,451 22.6 100.0

Source: Ministry of Finance Fiscal Policy Statement 2011-12

13

collection while 66% of the indirect taxes were collected as sales tax. Of the total sales tax more

than half of the sales tax collected during the year amounted to Rs. 357.5 billion were collected

from the domestic products while the remaining Rs. 308.7 billion was collected through sales tax

on imports. POL products remained at the top of both domestic and imports component of sales

tax with a contribution of 41.2 and 36.8 percent of the total collection in both components

respectively.

Customs duty collected during the FY 2010-11 amounted to Rs. 184.9 billion making around 12%

of the total tax revenue and 19% of the indirect collection. Imported vehicles, POL products and

Edible oil remained at the top of total customs duty collection with a share of 14.5, 11.1 and 8.9

percent of total customs duty collection respectively.

Another Rs. 137.4 billion were collected as Federal Excise Duty (FED) the major portion of which

came from FED on cigerattes with more than 34% share in total FED collection. Cement remained

the second top contributor with 11.2 percent share while 1% special FED also enabled to collect

more than 18% of the total FED during the year. Natural gas, POL, Services, beverages and

perfumes & cosmetics also contributed in FED collection.

Tax Collection FY 2011-12

The Federal Government of that time brought many changes in the tax structure during the FY

2011 – 12 that included reduction on GST on goods from 17% to 16%, abolishment of special

Excise duty, abolished regulatory duties on many products and enhanced exemption limit on

income tax.16

Total Taxes collected in FY 2012 amounted to Rs. 1882.7 billion against the target of Rs. 1952

billion adding Rs. 324. 7 billion from the previous year that was termed as the highest growth in

the history of FBR by the Government of Pakistan.17 The distribution of total tax collected during

FY 2011 along with growth rate has been appended in the following Table:

1616 FBR Fiscal Policy Statement 2012-13 (pp. 7) 17 FBR Year Book 2011-12 (pp. 9)

14

Table 1-0-2 : Tax Collection FY 2011 - 12

Description 2011-12 2010-11 Change

(%) Direct Taxes 738.4 602.4 22.6

Sales Tax (Total) 804.9 633.4 27.1

Federal Excise 122.5 137.4 -10.8

Customs Duty 216.9 184.8 17.3

All Taxes 1,882.7 1,558.0 20.8

Source: Ministry of Finance Fiscal Policy Statement 2012-13

a. Direct Tax Collection

Tax Head 2011-12 2010-11 % Growth

% Share in Direct Taxes

2011-12 2010-11

Income Tax 711,017 582,424 22.1 96.3 96.7

CVT 126 132 -4.6 0.0 0.0

W WF & WPPF 27,275 19,886 37.2 3.7 3.3

Wealth Tax 5.6 9 37.8 0 0.0

TOTAL 738,424 602,451 22.6 100.0 100.0

Source: Ministry of Finance Fiscal Policy Statement 2012-13

b. Income Taxes

Tax Head

2011-12 2010-11 %

Growth

% Share in Direct

Taxes

2011-12 2010-11

(A) Out of Demand 130,054 72,182 80.2 16.0 11.5

(B) Voluntary payments 237,366 196,065 21.0 29.2 31.2

(C) Withholding Taxes 420,088 357,836 17.5 51.8 56.9

Miscellaneous 24,016 3,019 696.5 3.0 0.5

15

Gross 811,524 629,102 29.0 100.0 100.0

Refund 91,560 46,678 96.2

Net 719,964 582,424 23.6

Source: Ministry of Finance Fiscal Policy Statement 2012-13

c. Indirect Tax Collection

Indirect tax collected included Sales Tax, Customs Duty and FED. Sales tax contributed the largest

portion of total tax collected in FY 2011-12 with a total of 42.8% of the total tax collected during

the year. Rs. 805 billion were collected as sales tax that was further divided into two sources.

Domestic GST constitution 46.5% of the total sales tax collected while the remaining included

GST on imports. POL products were the main contributors in sales tax collection with 40.9% and

36.5% of the total domestic sales tax and sales tax on imports collection respectively.

Another Rs. 217 billion were collected as Customs Duty that was 18.9% of the total indirect tax

and 11.5% of the total federal taxes collection in FY 2012. The largest share in customs duty was

from imported vehicles that was 19.1% of the total Customs duty.

The remaining Rs. 122.5 billion were collected as FED and the major share was from cigarettes

that constituted 43.6% of the total FED making around Rs. 53.5 Billion during FY 2011-12.

Tax Collection FY 2012 – 13

The financial Year 2012 – 13 brought with it more reliance on non-tax revenue to compensate for

the rationalization of tax revenues by the government that included reducing tax slabs to only 5

and raising tax on dividend from 25% to 35% while reducing tax on company profits from 1% to

0.5%. Similarly, zero-rated products were taxed to enhance tax base and all tax rates were unified

to 16% to avoid multiplicity. However, sales tax on may products was reduced from 16% to 5%

to discourage the trend of smuggling. Furthermore, FED was on construction material was reduced

from Rs. 500 to Rs. 400 per metric ton and maximum rate of customs tariff was reduced.

The total tax collected by the FBR during the FY 2012-13 was Rs. 1936.1 billion against the

estimated target of Rs. 2381 billion achieving around 81% efficiency. Direct tax collection stood

at Rs. 735.8 billion that contributed 38% of the total tax collected during the year. Direct tax

collection stood at 79% of the amount estimated in the federal budget. The breakdown of direct

16

taxes during the year as provided by Ministry of Finance in th Fiscal Policy Statement of 2013 -

14 is as follows:

Tax-wise Analysis

Direct Taxes

A total of 38% of the total taxes collected during the FY 2013-13 were collected as direct taxes

that amounted to Rs. 735.8 Billion. The maximum chunk of the direct taxes came from

Withholding Taxes (WHT) comprising 57% of the total direct tax collection. There was 3%

increase in WHT collection because of many reasons namely; 8% increase in imports of dutiable

products resulting in 21% increase in WHT from imports. Similarly, increased dividends due to

lack of investment opportunities, increased electricity tariffs and increased bank interests led to

increase in WHT collection. On the contrary, due to increase in tax free band of salary and cash

withdrawal limits, WHT collection on salary and cash withdrawal decreased.

Voluntary payments that comprised 29% of the total direct taxes also showed an increase from the

previous year. An amount of Rs. 245billion of which Rs. 230 billion was collected as advance

payments and the remaining was collected as payments with returns. Collection on demand

showed a decrease by 31% from the previous year due to lack of audit by the government that

failed to produce demand for new taxpayers. Around 11% of the total direct taxes were collected

on demand.

Indirect taxes

Around 62% of the total taxes collected in FY 2012-13 were indirect taxes amounting to Rs. 841.3

billion. Sales tax had been the biggest contributor that comprised 44% of the total tax collected

showing an increase of 4.5% entirely due to increase in sales tax from domestic market. The share

of both domestic and imports components in sales tax were approximately equal during the year.

POL comprised the largest contributor in sales tax collection both from domestic and import

components comprising 36.3 and 42.3% of their total contribution respectively.

Customs duty collection stood at Rs. 239 billion comprising 12% of the total tax revenue collected

during the year. This head showed an increase of 10% with 11% increase in import of dutiable

products achieving around 97% of the target. As far as FED was concerned, a total of Rs. 119.6

Billion were collected comprising 6% of the total tax revenue. The major portion of Fed was

17

collected from domestic sources and cigarettes contributed more than 50% of the total revenue

collected as FED.

Tax Collection FY 2013-14

In the FY 2013-14, FBR achieved 92% of the estimated budget by collecting Rs. 2266.3 billion as

federal taxes. Of this total amount, 61% were collected as indirect taxes including sales tax,

customs duty and FED while the remaining 39% were collected as direct taxes. The tax-to-gdp

ration stood at 8.9% during the said year.

Tax-wise Collection

Direct Taxes

An amount of Rs. 884.1 billion was collected as direct taxes 97% of which comprised of income

tax (voluntary payments Rs. 262.6 billion, collection on demand Rs. 80.6 billion and WHT Rs.

578.6 billion) during the year. Another Rs. 26.1 billion were collected under the miscellaneous

head of direct taxes.

Voluntary payments during the year grew by 7% with advance tax increasing by 8.1% and

payments with returns reducing by 6.8% from the previous year. Overall voluntary payments

consisted of 28% of the total direct tax collection. Collection on demand again decreased by 10%

and the reason attributed to was the lack of audit, cases under litigation and ineffectiveness of the

tax administration in the Fiscal Policy statement 2014-15.

The major share of direct taxes (61%) came from WHT that grew by 33% from the previous year.

Contracts, Imports and Salaries were the top three contributors of WHT with collection of Rs.

136.6, 123.8 and 64.6 billion respectively. Another measure by the government to enhance WHT

during the year was introduction of WHT on marriage halls., hotels, restaurants, educational

institutions with fees above Rs. 200,000, foreign movies and dramas moreover, FBR claimed and

attributed the overall growth in WHT to effective monitoring and rationalization of tax rates.

Indirect Taxes

Indirect taxes that included sales tax, customs duties and FED comprised 61% of the total tax

collection during the year. Sales tax that has been the major source of tax collection accounted for

44% of the total tax revenue. Sales tax grew by 19% from previous year mainly due to increase in

18

domestic sales tax collection as a result of fixing sales tax at from 16% to 17%. Sales tax on

domestic products was 52% of the total sales tax collection and petroleum contributed the major

portion in both domestic and import components of the sales tax with 45.6 and 34.2 percent of the

total collection respectively.

Customs duties contribution in indirect and total tax collection was around 17% and 11%

respectively. dutiable imports consisted only 38% of the total imports that grew by 7.6%. customs

duty collection grew by only 0.8% from previous year and the main reason attributed to it was

appreciation in Pak Rupee during the year. Vehicles remained the top contributor in Customs duty

despite decline in imports by 18% from the last year causing a decline in revenue of 14%. Edible

oil and POL products remained the second and third contributor of Customs duties collection

resepecitely. POL products duty fell by 18% due to exemption of crude oil, furnance oil and motor

spirit from customs duty.

FED contributed 6% of the total tax revenue that was the same as in the previous year. Major

contribution of FED was collected through the domestic component of FED while cigerattes

remained at the top in FED collection with more that 51% of the total FED. Collection on services

surpassed the target by 39% and reached an amount of Rs. 20 billion.

Other taxes imposed by the Federal government also include petroleum levy, airport taxes and

other taxes. Collection from petroleum levy amounted to Rs.104 billion showing a decline of 6

percent against previous year. Other taxes registered growth of 73 percent owing to small base

year collection and stood at Rs.5 billion.

Tax Collection FY 2014-15

Tax collection ratio registered consistency in FYs 2014 and 2015 at 92% of budget estimate while

showing growth by 14% of the last year collection. The Tax to GDP ratio during the year was

14.4%.with an improvement to 9.5% against last year’s improvement of 8.9%.

Direct Taxes

The share of direct taxes in total tax revenue collection increased to 40% and income tax that

included voluntary payments, collection on demand and WHT contributed 99% in the total direct

tax collection. Direct tax collection achieved 87% achievement of targets against 91% in the

previous year.

19

WHT witnessed a growth of 21% and contributed 62% of the total share in direct tax collection.

The top three contributors in WHT again remained Contracts, Imports and Salaries with maximum

growth witnessed in electricity bills from the last year. Voluntary payment share in total direct tax

collection reduced by 2% from previous year to 26% while payments with returns increased by

30%. Collection on demand grew to Rs. 116 billion from 89 billion of last year. This increase in

collection after many years was attributed to fresh audits and effective administrative system of

the tax agencies.

Indirect Taxes

Indirect taxes, as usual, provided 60% share in the total tax collection in the year of which sales

tax contributed 42%, Customs Duty 12% and FED 6% in total tax collection. Sales tax grew by

9% while more than half of the share came from sales tax on domestic products while the

remaining was collected through sales tax on imports. Majority of share in both domestic and

import components of sales tax came from POL which was was 43.9 and 30 percent for domestic

and imports respectively.

Customs duty comprised 20% and 12% of indirect tax and total tax collection respectively.

Dutiable imports consisted of 57% of the total imports during the year and custom duties grew by

27% achieving 119% of the budgeted estimates of FY 2014-15. Customs duty on vehicles and

POL products remained at the top of the list with share of 15.7 and 7.7 percent of total custom duty

collection respectively.

FED contributed 6% in the total tax revenue achieving 91% of the target. Again cigarettes

remained as the top contributor of FED collection with around 51% and international travel

segment scoring second position with 17.1% share in total FED collection. Overall FED collection

recorded an increase of 17% from the previous year.

Initiatives by Government as of 2015 to 2018

The Government of Pakistan took certain steps in order to enhance tax base and increase tax

collection. Three major steps in this regards included:

a. CNIC to be NTN

Previous NTN or the National Tax Number was issued for registration with FBR. However, the

present Federal government took the initiative of replacing National Tax Number (NTN) with

20

Computerized National Identity Card (CNIC). According to an SRO18 issued by FBR any

individual having a valid CNIC will be able to file returns manually without prior registration.

However, online enrollment would be required through FBR website. However, any person

without a CNIC would be required to register on application. The SRO empowered the Income

Tax Commissioner to register or enroll any individual provided he is satisfied that the person falls

into tax bracket.

b. Withholding Tax on Banking Transaction

The government also introduced 0.6% WHT on banking transactions exceeding Rs. 50,000 by

non-filers vide section 236P of Income Tax Amendment Ordinance 2015. However the WHT rate

was reduced to 0.3% for a period of four months and was later increased again to 0.6%.19

c. Discriminatory WHT Rates by FBR

Apart from the above, the government has made discriminatory rates on withholding Tax (WHT)

for filers and non-filers on different transactions including registration and transfer of cars import

of goods, dividends and profits on bonds and shares as well as on profits on bank savings etc. 20

Statement of the Problem

Pakistan is one of the worst countries hit by the menace of tax evsion. According to the

International Development Committee of British Parliament in 201321, just under 0.79 million

Pakistanis or 0.57% of the total population paid taxes. According to the Current Prime Minister

of the Country Mr. Imran Khan, the country was collecting PkR 3.8 trillion as tax revenues while

it has the potential to generate around PkR 8 trillion (Hassan, 2018). According to the Federal

Board of Revenue (FBR), Pakistan is generating taxes from only 0.5% of the entire population and

pakistan generates only 9% of GDP from taxes as opposed to countries of the same per capita

income who generate approximately 14% (Khan, 2014) This is despite the fact that pakistan is

listed amonsgt the top nations in terms of generocity. According to studies, Pakistanis pay around

PkR 240 billion or US$ 2 Billion annually in some sort of charity while approximately 98% of the

population of Pakistan pays voluntarily either in cash or in kind (Amjad and Ali 2018). The same

study also reveals that Pakistan contributes 1 percent of GDP as charity which brings it at par with

18 S.R.O. 1076(I)/2015 dated 02 November, 2015 19 DG (WHT) FBR letter No DO.No.1 (1) DG (WHT)/2015/103767/2015-R dated 03 August, 2015 20 FBR Withholding Tax Card 2017/2018 21 BBC website : http://www.bbc.co.uk/news/uk-politics-22017091

Invalid source specified.

21

nations like Canada and the UK while the proportionate contributions is twice as much as that of

India. On the other hand, the Tax-to-GDP ratio of the country for the Fiscal years 2017 – 2019

remained around 11 percent22 as compared to Tax-to-GDP ratios of 33.4% and 33% for UK and

Canada (OECD 2020). The ratio of India and Pakistan during the same period remained the same.

One of the main cause of this reluctance to pay taxes is lack of trust on the government. This is

evident from the fact that in 2014, a large gathering of people followed his disovbedience

movement and burned their utility bills in an attempt to describe the government of the country as

corrupt and having no return for the taxes paid by the public (Tahir 2019). It is because of this

reason that the tax gap of the country stands at 22.3% which is about PkR 3.3 trillion as estimated

by the World Bank. The main cause of this poor tax collection in the country is tax evasion that

needs to be addressed on priority in order to stabilize the economic situation of the country

(Hassan, 2018). The World Bank has suggested that all Pakistan needs is to enhance its revenue

generation without imposing any additional taxes by eliminating evasion (Ahmed 2019).

Objectives of the Study

The study aims at finding the main causes of tax evasion in Pakistan and also tries to study the

consequences of tax evasion on the political economy. Based on the aim, possible objectives of

the study are as follows:

1. To determine the relationship of demographic variables and behavior towards tax evasion

in Pakistan

2. To analyze attitudes of taxpayers towards tax system of the country

3. To measure the association of different indicators of tax morale with tax evasion in

Pakistan

4. To analyze the consequences of tax evasion on the political economy of Pakistan

5. To find out the policy implications of tax evasion in Pakistan

Significance of the Study

Although scholars have investigated many determinants of tax evasion from political and

economic determinants (Becker, 1968) and (Allingham and Sandmo 1972) to lack of Deterrence

22 Ministry of finance, Government of Pakistan

22

(Anderson, 1977) to psychological factors (Robben et al., 1990) to personal characteristics

(Recardson, 2008). However, there is a list of determinants of tax evasion as described by (Jackson

& Milliron, 1986) and explained by (Recardson, 2006) that include personal characteristics like

age, gender, education, income level, income source, while other determinants like marginal tax

rates, fairness, complexity, revenue authority initiated contact and tax morale. The causes have not

also been confined to issues like lack of audit, lack of documentation (Bilqees, 2004) and economic

issues like higher tax rates, high unemployment rates by prominent scholars like (Kemal, 2006) as

in case of Pakistan. Scholars at international level have taken up issues like impact of gender and

other demographic variables (Slemrod, 2007), tax morale (Torgler & Schneider, 2007) and the

like.

The current study has taken up the challenge of finding relation of tax evasion with determinants

that include demograhpic variables of age, gender, income level and education level. While

different indicators of tax morale have also been included in the study. At policy level, the study

will be of prime importance to policy makers and legislators as the study incluldes non-monetary

variables that are different from typical stereotype economic variables. the findings of the study

will be useful in handling different segments of society based on age, gender and income level in

order to get rid of the menace of tax evasion from the society. Similarly, tax morale that inlucdes

intrincic motivation to pay taxes would be useful for the policy makers in tackling the minds of

individuals and changing minds of the people to curb the evil of non-compliance form pakistan.

The study will be a great source of help for policymakers in that it pakistan in getting pakistan out

of the menace of poor tax collection tht has the following repurcussions for the country:

Increasing Tax Revenue

Pakistan’s budget deficit for the year 2019 remained 3.4 trillion that could have been overcome

through tax compliance as the tax gap during the same year was Rs. 3.3 trillion. World Bank has

already termed tax non-compliance as a major hurdle in the economic development of the country.

Public Service Delivery

The aim of government is to provide better public services to the citizens which is only possible if

the government has revenue to provide such services. in case of Pakistan where the 90% of revenue

of government is generated through taxes, tax compliance is very much necessary

23

Countering Money Laundering

Curbing tax evasion would further have an indirect benefit to the economy. Presently, Pakistan is

also on the watch list of FATF (Financial Action Task force) who has placed Pakistan in the grey

list since June 2018. Motivating citizens to pay taxes and bring them into the tax net would have

an added advantage that their assets would be declared to the government. This will enable the

government to further track their transaction to a greater extent and ultimately would also enable

the government to watch out for unwanted transaction, if any.

Organization of the Study

In the first chapter, the study includes introduction and background of the study. In this section

history of tax evsion worldwide and in Pakistan has been discussed. This will be followed by

introduction to taxes being enforced in the country and the tax collection profile of Pakistan for

the last five years starting from 2010 upto 2015. Afterwards, the chapter includes statement of

problem, objectives and significance of the study. The second chapter discusses the review of

existing literature in which literature containing evasion at global and national level has been

discussed. All possible causes of tax evasion have been discussed in this chapter. Methodogoly

has been discussed in the third chapter while fourth chapter contains the demographic profile of

the respondents and some of the impacts of demographic characteristics on tax evasion in Pakistan.

The fifth chapter includes determining relationship of some demographic factors including age,

gender, income and education level with tax evasion. Similarly different indicators of tax morale

and their impact on tax evsion in Pakistan have also been been observed in the chapter. The sixth

chapter involves provididing a comprehensive discussion regarding impacts of tax evasion on the

political economy of the country. The last chapter includes policy implications and

recommendations have been discussed in the same chapter followed by conclusions.

24

LITERATURE REVIEW

Literature has been speaking much on the issue of tax evasion since very long. The first available

evidence of mentioning of tax evasion as a reason of currency holding was presented by (Cagan

1965) who claimed that higher tax rates led people to keep their cash undocumented hence evading

their share of tax payment (Chapter iv). The argument was taken further by Baker who placed tax

evasion under the umbrella of crime and stated that tax evasion along-with other crimes – apart

from felonies – had erupted as a result of increase in the circulation of currency since the late 1920s

up to 1960 (Baker 1968).

Role of Taxation in Economic Growth

This is a quote by a Roman. Cicero who was a Roman Statesman, orator, Philosopher and lawyer,

Marcus Tullius Cicero and remained part of the Roman Council in the year 63 BC. He stated that

“Taxes are the Sinews of the State” and was of the view that taxes played crucial role in the Roman

Empire and that the state could not flex its muscles till the time they abstract revenue from the

private sector (Winer, Profeta, & Hettich, 2013). James and Nobes presented the definition of

taxation in the year 1997 which states that, ‘Taxation is a levy that is paid by a person who does

not receive anything directly in return” (Obasa, 2018). Taxation is a main source of government

revenue that is used by the government for the purpose of growth and development (Edame &

Okoi, 2014). If this source of government revenue is not available in sufficient quantity, the

government will not be able to spend in areas necessary to address and hence the economic growth

and development of the country will be hampered (Martinez-Vazquez, Vulovic, & Liu, 2011).

Taxes play an important role in the economic development of a country. According to Prammer,

Taxes enable a government to collect funds for utilization for provision of necessary public

services, redistribution of income in the society, and overall stabilization of economy as a whole

(Prammer, 2011). The study also claimed that revenue generation through taxing items like

tobacco and alcohol and other environmental related taxes helps the government to address issues

related to externalities. However, literature has suggested that there are different types of taxes and

impact of each type of tax is different on the economic growth. However, literature also suggests

25

that taxation alters the economic decisions regarding investment the three factors of production

namely labor, capital and entrepreneurship.

A study by (Zipfel & Heinrichs, 2012) taking 27 European countries concluded that all factors of