State of Economy: An Overheating Economy?

39

Transcript of State of Economy: An Overheating Economy?

Foreword

The Social Policy and Development Centre is pleased to presentits annual review of the state of the economy in the light of thePakistan Economic Survey 2004-05 and the Federal Budget

2005-06. As soon as the Survey and the Budget are released, theSPDC team goes to work in analyzing the new data, assessing themacroeconomic and fiscal policies, and examining the implications forthe macroeconomic situation and for the poverty and socialdevelopment picture. Our goal is to conduct a thorough and detailedanalysis, including inputting the new data into our large-scaleIntegrated Social Policy and Macro model and conducting any modelsimulations and other econometric work that are necessary to shedlight on the major issues that we see as being pertinent. The researchhas been conducted over a period of two to three weeks, and theReview has been completed within a month of the release of theSurvey and the Budget.

The Review is an effort to objectively present the situation withrespect to the state of the economy. It highlights the impressivegrowth performance and the Government's role in achieving that. Butit also emphasizes that some signs of overheating and stress are nowemerging in the economy that policy makers and other economicparticipants would be ill-advised to ignore. We hope that allstakeholders will find this annual review of Pakistan's economy useful.

Dr. Shaghil Ahmed Acting Managing Director

(i)

SPDC Team

Shaghil Ahmed Haroon Jamal Qazi Masood Ahmed Kalim Hyder Iffat Ara Amir Jahan Khan Farhan Sami KhanAurangzeb Tabinda Areeb Haider Hussain Abdul Aleem Khan

Rizwanullah Khan

Research

Computer Graphics & Designing

(iii)

C o n t e n t s

MACROECONOMIC ANALYSIS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7Inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10External Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14Poverty and Social Development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

FISCAL ANALYSIS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21Budget Deficit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22Revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23Current and Development Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . .26Intergovernmental Relations and Regional Development . . . . . . . . . . . . . . .29

CONCLUSIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

(v)

List of Tables and ChartsTable 1: Growth by Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2Table 2: Growth by Expenditure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3Table 3: Growth Accounting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5Table 4: Current Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14Table 5: Major Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17Table 6: Major Imports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18Table 7: Imports by Economic Categories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19Table 8: Components of SDI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20Table 9: The Federal Budget . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22Table 10: Fiscal Deficit Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23Table 11: Target and Actual Federal Receipts . . . . . . . . . . . . . . . . . . . . . . . . . . . .23Table 12: CBR Tax Collections . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24Table 13: Growth in Custom Duties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Table 14: Non-Tax Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Table 15: Budgeted and Actual Federal Expenditures . . . . . . . . . . . . . . . . . . . . . .26Table 16: Current Expenditure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Table 17: Subsidies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28Table 18: Targeted and Actual Development Expenditure . . . . . . . . . . . . . . . . . . .29Table 19: Provincial Transfers to Federal Government . . . . . . . . . . . . . . . . . . . . .30Table 20: Financing of Provincial Development Prgramme . . . . . . . . . . . . . . . . . .31

Chart 1: Sectoral Contribution to Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3Chart 2: Contribution to Growth of Selected Expenditure Components . . . . . . . . .4Chart 3: Actual and Trend Real GDP Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . .6Chart 4: Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6Chart 5: Interest Rate (T-Bill Rate) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7Chart 6: Dynamics of Employed Labour Force . . . . . . . . . . . . . . . . . . . . . . . . . . .7Chart 7: Sectoral Growth 2002-2004 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8Chart 8: Change in Labour Force 2002-2004 . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Chart 9: Trend in Unemployment Rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Chart 10: CPI Inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10Chart 11: Contributions of Components to 12-month CPI Inflation . . . . . . . . . .10Chart 12: Contribution Shares of Increase in CPI Inflation from 2004 to 2005 . .11Chart 13: Relationship between Output Gap and Inflation . . . . . . . . . . . . . . . .12Chart 14: Sources of CPI Inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13Chart 15: Real Credit to the Private Sector . . . . . . . . . . . . . . . . . . . . . . . . . . .14Chart 16: International Reserves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15Chart 17: Exchange Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16Chart 18: Economic and Social Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20Chart 19: Components of Social Development Index . . . . . . . . . . . . . . . . . . . .21Chart 20: Tax Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24Chart 21: Composition of Expenditure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27

(vii)

An Overheating Economy?

Research Report No. 62 1

MACROECONOMIC ANALYSIS

According to data reported in theGovernment of Pakistan's EconomicSurvey 2004-05, Pakistan's economy

grew a solid 8.4 percent in FY 2005, one ofthe highest growth rates in the world andsurpassing expectations for the third straightyear. Unlike last year, the growth is morebalanced, with the agriculture,manufacturing, wholesale and retail trade,and services sectors all making significantcontributions. Our analysis, suggests thatthere have been some gains in productivityand, to some extent, in employment as well.The performance is impressive and nodoubt is bolstered by the macroeconomicstability that the government hasengendered over the past few years.

However, there are signs of stress and,in particular, overheating now emerging inthe economy that policy makers and otherparticipants in the economy would be ill-advised to ignore. The most obvious one isinflation, which, based on 12-monthchanges in consumer prices, surpassed 11percent in April. Although supply-sidefactors, which have kept food prices andworld oil prices high, account for asignificant chunk of the increase in inflation,there are underlying demand-sidepressures building up as well, which wedocument in this report. The State Bank ofPakistan seems well aware of thesepressures, and the loose stance ofmonetary policy has begun to reverse--appropriately to us--and more tightening isprobably in order. The provisions in theFederal Budget 2005-06 announced onJune 6 also pose a significant challenge forthe macroeconomic situation. In particular,the proposed increase in the budget deficitexacerbates inflationary pressures andmakes the central bank's task all the moredifficult over the coming quarters.

Another development to keep awatchful eye on is the widening trade deficit,which has turned a current account surplus

into a deficit in FY 2005. Some outpacing ofexports by imports is to be expected in aneconomy which is growing faster than itstrading partners and in which the growth isnot being led by exports. But the differencebetween the growth rate of real imports inthe national income accounts (44 percent)and real exports (8 percent) seemsexcessive and is also suggestive of anoverheating economy. Financing of thecurrent account deficit is not an issue in theshort run, but a continuing trend of awidening current account deficit will haveadverse effects on expectations that couldthreaten the hard-earned credibility on themacroeconomic front. The argument thatmuch of the increase in imports is goingtowards buying up of machinery and othercapital goods which will engineer futuregrowth and future exports is only partlycomforting. This is because the overallinvestment position does not look all thatrosy with real private investment as a shareof real GDP continuing to fall. With risinginterest rates and a continued increase inthe relative price of capital, a reversal in theinvestment-output ratio does not appear tobe on the cards any time soon.

The long-term prospects of theeconomy depend, of course, on how muchof the growth momentum is sustainable.Only per capita growth that results from anincrease in the productive capacity of aneconomy can, and should be, sustained.Quantifying the notion of productivecapacity--in other words, potential output--isnotoriously difficult for any economy.Qualitatively, in the case of Pakistan, onecan discern a combination of transient, e.g.the contribution of weather to a bumpercotton crop, and more persistent, e.g. policystability, in the recent surge in economicactivity. Some illustrative quantitativeestimates that we have made usingstatistical techniques suggest a significantgain in the growth rate of Pakistan'spotential output over the past few years, forwhich the present government deserves

An Overheating Economy?

Research Report No. 622

due credit. But the estimates also suggestthat potential growth may not quite havereached 7 percent yet. While admittedlythese estimates are highly uncertain, weemphasize that overestimating potentialgrowth runs the risk of allowing aggregatedemand, particularly consumption demand,to elevate to a level that cannot bemaintained in the long run with its attendantproblems.

On the poverty front,in the absence of up todate data, it is difficult tosay what the recentacceleration in per capitareal income has done topoverty. The forces atwork in the Social Policyand Development Centre's(SPDC's) Integrated SocialPolicy and Macro (ISPM)model suggest only amodest net reduction inpoverty as a result of thehigh per capita growthrate--the gains from the size of the pieincreasing are being partially offset byfactors such as rapid increases in foodprices and a decrease in the investment-output ratio, which our model documents tobe poverty-increasing. Moreover, we havealso computed a new Social DevelopmentIndex based on indicators of health,education, and access to services such astelephones and electricity. Unfortunately,the growth in this Social Development Indexhas been relatively weak over the 2000-2004 period, despite remarkable progresson the growth front.

We continue to maintain, based on ourmodel simulations, that direct interventionsto reduce income and asset inequality arerequired to make a significant dent intopoverty at an acceptable pace. Whileimprovements have been made in thisregard by budgeting additional developmentoutlays in the new Federal Budget, there isstill a long way to go down the road of

utilizing these effectively and channelingthem to the components, e.g. education andhealth, which matter most for povertyreduction and social sector development.

Growth

Output accelerated significantly inFY2005, with real GDP at factor cost

measured in FY2000 prices expanding by8.4 percent, compared with 6.4 percent the

previous year (Table 1). The growth is well-balanced with the manufacturing andwholesale and retail trade sectors growingat double-digit rates, agricultural outputincreasing by 7.5 percent, and other sectorsalso expanding significantly.

The supply-side sectoral contributions togrowth (in percentage points) are shown inChart 1. These are obtained by multiplyingthe sectoral growth rates by their respectiveshare in total output. The manufacturingsector adds the same, about 2¼ percentagepoints, to total output growth in each of thepast two years. However, the contribution ofagriculture has more than tripled from ½percentage points of growth last year toabout 1¾ percentage points this year, andthe contribution of wholesale and retail tradehas also increased by ¾ percentage points.Thus, manufacturing has continued toperform, and output in agriculture, wholesaleand retail trade, and in other (primarilyservice-oriented) sectors has accelerated.

TABLE 1GROWTH BY SECTOR

Growth Rates (Percent)At constant factor cost of FY 2000

Sector FY 2001 FY 2002 FY 2003 FY 2004 FY 2005Total (GDP at Factor Cost) 1.8 3.1 4.8 6.4 8.4Agriculture -2.2 0.1 4.1 2.2 7.5Manufacturing 9.3 4.5 6.9 14.1 12.5Transport and Communication 5.3 1.2 4.3 5.5 5.6Wholesale and Retail Trade 4.5 2.8 6.0 8.1 12.0Others -1.2 5.9 3.8 5.0 5.4

Source: Pakistan Economic Survey 2004-05

Table 2 reports the demand-sidecomponents of real GDP measured atmarket prices. Real private consumptiongrew a striking 16.8 percent in FY2005,according to data reported in the EconomicSurvey, double the rate posted last year.Real imports, after declining significantly lastyear surged 44.1 percent this year. By

contrast, private fixed investment increasedonly a modest 4.8 percent from the ratherlow base implied by last year's 11 percentcontraction. And, with the decline in publicinvestment of more than 5 percent, theoverall investment picture is a cause forconcern. The very high growth rates ofprivate consumption and imports in FY2005

relative to those of privatefixed investment andexports are suggestive ofan overheating economy.

The decline of 11percent in private fixedinvestment in FY2004shown in Table 2 ispuzzling, as against the 8percent expansionreported for the same yearin the previous EconomicSurvey (not shown here).Similarly, a decline of

An Overheating Economy?

Research Report No. 62 3

TABLE 2GROWTH BY EXPENDITURE

Growth Rates (Percent)At constant market prices of FY 2000

Sector FY 2001 FY 2002 FY 2003 FY 2004 FY 2005Total (GDP at market price) 1.7 3.1 4.8 6.4 7.9Private Consumption 2.3 1.2 0.8 8.2 16.8Public Consumption -20.1 15.0 7.2 2.1 2.3Private Fixed Investment 2.9 13.2 5.7 -11.0 4.8Public Fixed Investment 7.4 -24.5 -0.2 14.0 -5.6Exports 12.2 10.0 28.4 -1.5 7.6Imports 2.2 3.0 11.2 -8.6 44.1

Source: Pakistan Economic Survey 2004-05

CHART 1SECTORAL CONTRIBUTION TO GROWTH

Total (GDP at FC) 100

Agriculture 23

Manufacturing 18

Transport and Communication 11

Wholesale and Retail Trade 18

Others 29

9

8

7

6

5

4

3

2

1

0

Others1.5

Agriculture1.7

Others1.6

Sectoral Shares(%)

Transport & Comm.0.6

Transport & Comm.0.6

Agriculture0.5

Wholesale &Retrail Trade

1.5

Wholesale &Retrail Trade

2.2

Manufacturing2.3

Manufacturing2.2

Perc

enta

gePo

ints

FY 2004 FY 2005

Source: SPDC estimates based on data from Pakistan Economic Survey 2004-05

6.4

8.4

nearly 6 percent in private consumption inFY2004 reported last year has been revisedto an expansion of more than 8 percent, asreported in this year's Economic Survey. Itseems difficult to rationalize such large datarevisions in a single year.

Chart 2 depicts the contributions togrowth of different types of expenditure.

The contribution of final private domesticdemand--the sum of the privateconsumption and private investment bars--is about 12½ percentage points of growth inFY2005, of which only about ½ percentagepoints is accounted for by private fixedinvestment. With the growth in real importssurpassing that of exports by a wide margin,

real net exports shaved off almost 5percentage points from growth. Themagnitude of growth in private consumptionrecorded in FY2005 is likely not sustainableand, in fact, attempts to sustain it mightprove counterproductive.

As part of SPDC's large-scale ISPMmodel, we have estimated aggregate and

sectoral production functions. Theestimates can be used to do agrowth accounting exercise thatdecomposes growth into that due tochanges in the quantity of inputsused and that which can beattributed to shifts in the productionfunction (i.e. productivity gains--theability to get more output from anygiven amount of inputs). In principle,shifts to the production function canbe a result of both transient factors(such as weather-related shocks)and more permanent gains inproductivity (such as due totechnological improvements andgovernment policies).

The results of the growthaccounting exercise for overallgrowth and for agricultural growthare presented in Table 3. Theincrease in inputs added 2.1percentage points to overall growthin FY2005, three-fourths of whichwas the contribution of capital. Theshifts in production functionaccounted for 6.2 percentage pointsof the growth, of which almost a halfcan be attributed to the increase incotton production. In the case ofagricultural output, all but about 1percentage point of the 7.5 percent

growth in FY2005 resulted from productionfunction shifts, of which cotton productioncontributed 5 percentage points. However,the contribution of inputs--specificallylabour--to agricultural growth was asubstantial at 2.6 percentage points ofgrowth during the previous year.

An Overheating Economy?

Research Report No. 624

CHART 2CONTRIBUTION TO GROWTH OF SELECTED

EXPENDITURE COMPONENTS

14

12

10

8

6

4

2

0

-2

-4

-6

FY 2004 FY 2005

Net Exports-4.7

Net Exports1.1

Private FixedInvestment

0.5

Private FixedInvestment

-1.3

PrivateConsumption

12.1

PrivateConsumption

5.8

Perc

enta

gePo

ints

Source: SPDC estimates based on data from Pakistan Economic Survey 2004-05

An Overheating Economy?

Research Report No. 62 5

The large share of growth accountedfor by production function shifts this yearindicates significant gains in total factorproductivity. A substantial portion of theseshifts, however, came in the shape of abumper cotton crop. To the extent that thisis plausibly partly a result of transientfactors, such as good weather and arelatively favourable virus position, it shouldnot lead to excessive euphoria or misplacedcomplacency.

This brings us to a key question aboutthe state of the economy: How much of thegrowth momentum is sustainable goingforward? Ideally one would want to computethe productive capacity (or potential output)of an economy under the assumption of fullemployment of all available factors ofproduction and with all the policy andstructural changes that have taken place built

in. The growth rate of thispotential output could thenbe interpreted as thesustainable rate ofeconomic growth. This is adifficult exercise toaccomplish, particularly fordeveloping countries. Onecrude alternative that isoften used is to determine,using statistical methods,where the long-run trend inoutput seems to he headed,given the actual historicalbehavior. Assuming thegovernment's achievementof the target growth rate of7 percent for 2006 and2007, the picture thatemerges from such anexercise for Pakistan isdepicted in Chart 3.

Several features ofthis chart are noteworthy.First, the actual growthpattern for Pakistan hasbeen quite volatile.

Second, during the 1980s and 1990s, trendgrowth appears to have declined, fromabout 6 percent in 1981 to just 4 percent in2000. There has been a notable shifttoward growth since then, which has pulledup potential growth from its low point of 4percent to about 5½ percent. The exactnumbers here are highly uncertain and onlymeant to be illustrative. The main point isthat while it seems very plausible that thegovernment has facilitated a turnaround inpotential growth in recent years, it seemsequally plausible that potential growth hasnot quite reached rates of 7 percent to 8percent yet.

Some other telling evidence that itmight be difficult to immediately sustaingrowth rates in the range of 7 percent to 8percent from now onwards comes from thebehaviour of the investment-to-GDP ratio,

TABLE 3GROWTH ACCOUNTING

Sector FY 2001 FY 2002 FY 2003 FY 2004 FY 2005Total Growth (%) 1.8 3.1 4.8 6.4 8.4

Contribution (%Points) of:Inputs 2.8 3.2 2.6 2.9 2.1

Of whichCapital 2.4 2.2 2.2 1.9 1.6Labor 0.5 0.9 0.5 1.0 0.5

Production function shifts -1.0 -0.1 2.2 3.5 6.2Of which:

Change in cotton production -0.3 -0.1 -0.2 -0.1 2.8

Agricultural Growth (%) -2.2 0.1 4.1 2.2 7.5

Contribution (% Points) of :

Inputs 1.3 -3.4 0.4 2.6 0.8Of which

Capital 0.0 0.0 0.0 -0.1 -0.1Labor 0.9 -3.7 0.8 2.6 0.9

Production function shifts -3.5 3.5 3.7 -0.4 6.6Of which:

Change in cotton production -0.5 -0.1 -0.4 -0.2 5.0

Source: SPDC estimates.

displayed in Chart 4. Investment, which washovering at an already modest 12½ percentof GDP during the 1990s, has declinedfurther, to about 11 percent of GDP, onaverage, during the period 2003-05. This

has occurred despite strong imports ofmachinery and capital goods. The fall isprobably due in part to an increase ininterest rates, from a low of 2 percent inFY2003 to more than 7 percent in FY2005,

An Overheating Economy?

Research Report No. 626

CHART 3ACTUAL* AND TREND REAL GDP GROWTH

*For 2006, 2007 projected growth of 7% has been usedSource: Actual is from Pakistan Economic Surve 2004-05

Trend is SPDC estimate based on popular statistical filter (Hodrick-Prescott Filter)

10

9

8

7

6

5

4

3

2

1

0

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Perc

ent Ac

tual

Trend

CHART 4INVESTMENT

Source: SPDC estimates based on data from Pakistan Economic Survey, 2004-05 and 2002-03.

13.0

12.5

12.0

11.5

11.0

10.5

10.0

1.20

1.15

1.10

1.05

1.00

0.95

0.90

0.85

0.80

Perc

ent R

atio

1991-93 1994-96 1997-99 2000-02 2003-05

Relative Price of Investment

Private Investment-to-GDP

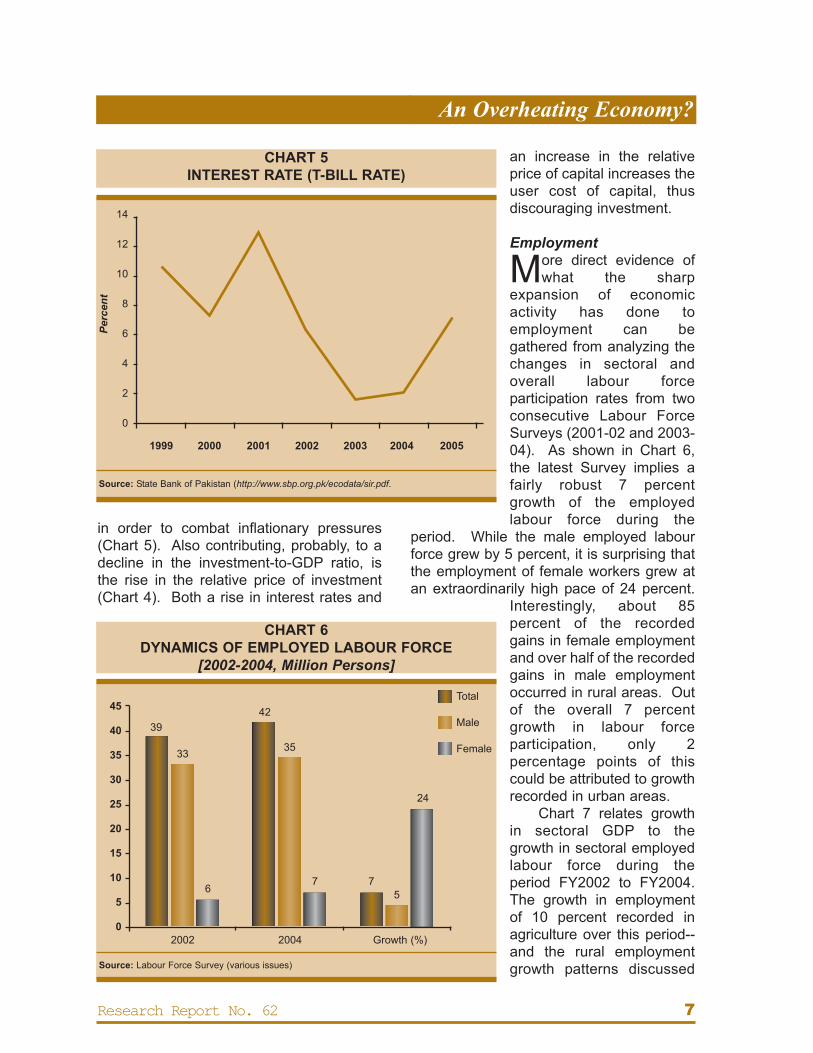

in order to combat inflationary pressures(Chart 5). Also contributing, probably, to adecline in the investment-to-GDP ratio, isthe rise in the relative price of investment(Chart 4). Both a rise in interest rates and

an increase in the relativeprice of capital increases theuser cost of capital, thusdiscouraging investment.

Employment

More direct evidence ofwhat the sharp

expansion of economicactivity has done toemployment can begathered from analyzing thechanges in sectoral andoverall labour forceparticipation rates from twoconsecutive Labour ForceSurveys (2001-02 and 2003-04). As shown in Chart 6,the latest Survey implies afairly robust 7 percentgrowth of the employedlabour force during the

period. While the male employed labourforce grew by 5 percent, it is surprising thatthe employment of female workers grew atan extraordinarily high pace of 24 percent.

Interestingly, about 85percent of the recordedgains in female employmentand over half of the recordedgains in male employmentoccurred in rural areas. Outof the overall 7 percentgrowth in labour forceparticipation, only 2percentage points of thiscould be attributed to growthrecorded in urban areas.

Chart 7 relates growthin sectoral GDP to thegrowth in sectoral employedlabour force during theperiod FY2002 to FY2004.The growth in employmentof 10 percent recorded inagriculture over this period--and the rural employmentgrowth patterns discussed

An Overheating Economy?

Research Report No. 62 7

CHART 5INTEREST RATE (T-BILL RATE)

Source: State Bank of Pakistan (http://www.sbp.org.pk/ecodata/sir.pdf.

14

12

10

8

6

4

2

0

Perc

ent

1999 2000 2001 2002 2003 2004 2005

CHART 6DYNAMICS OF EMPLOYED LABOUR FORCE

[2002-2004, Million Persons]

Source: Labour Force Survey (various issues)

45

40

35

30

25

20

15

10

5

0

39

33

42

35

67 7

5

24

2002 2004 Growth (%)

Total

Male

Female

above--translated into only a 6 percentincrease in agricultural sector GDP. Thissuggests that other factors, such as capital,might have been lagging behind in theagriculture sector over the period. Bycontrast over the same period of 2002-2004,while the employed labour force inmanufacturing grew only about 7 percent,real GDP of manufacturing increased a solid22 percent, the highest gain of all the majorsectors shown. This is suggestive of higherproductivity and/or more capacity utilizationin this sector, which were also hinted at byour growth accounting exercise discussedearlier. However, the phenomenon meritsfurther detailed investigation and research.Another interesting aspect of the dynamicbehaviour of employment and GDP is visiblein the construction sector. Despite 4 percentgrowth in the labor force from 2002 to 2004in this sector, a decline in real GDP isrecorded.

Growth of the non-agricultural labourforce disaggregated into formal and informal

sectors, exposes another area of concern.For statistical purposes, the non-agricultureinformal sector in Pakistan is defined asfollows: all household enterprises ownedand operated by own-account workers,irrespective of the size of the enterprises; orhousehold enterprises owned and operatedby employers with less than 10 personsengaged. As shown in Chart 8, all non-agriculture formal sectors registereddeclines in employment over the period2002-2004. Apparently, all of the growth inthe non-agriculture employed labor force(about 2 million) is recorded in the informalsector. Thus the employment-generatingpart of the high GDP growth in themanufacturing and service sectorsobserved during the period appears to bedue to expansions in informal sectors only,which raises some questions.

There is an evident decline in theunemployment rate, as depicted in Chart 9.The data show that the overallunemployment rate has decreased from 8.3

An Overheating Economy?

Research Report No. 628

CHART 7SECTORAL GROWTH 2002-2004

[Percentage]

Source: SPDC estimates

25

20

15

10

5

0

-5

Labor Force Real GDP

10

22

15

1012

6 7 74

-3

4 4

Agriculture Manufacturing Trade Construction Transport & CommunityCommunication Services

An Overheating Economy?

Research Report No. 62 9

CHART 8CHANGE IN LABOR FORCE 2002-2004

[Million Persons]

Source: Labour Force Survey (various issues)

CHART 9TREND IN UNEMPLOYMENT RATE

Source: Pakistan Economic Survey (various issues)

9.0

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.01980s 1990-94 1995-99 2000-01 2001-02 2002-03 2003-04

GDP

Unemployment

6.1

4.9

4.0

1.8

3.1

4.8

6.4

7.77.8

8.3

6.06.06.2

3.4

4

3

2

1

0

-1

1.61

0.39

0.82

0.23 0.150.37

3.56

-0.04-0.41

-0.13 -0.05 -0.12

-0.76Agriculture Manufacturing Trade Construction Transport & TotalCommunity

Communication Services

Formal Informal

Perc

ent

percent in 2001-02 to 7.7 percent in 2003-04. Thus, the high GDP growth recordedover the period is making a dent intounemployment, but it should be noted thatthe unemployment rate still remains farabove the average rate of 3.4 percent thatprevailed in the 1980s.

Inflation

Following a generally declining trendsince about the mid-1990s, inflation has

picked up sharply since last year, reachingdouble-digit levels in April on the basis of12-month changes in consumer prices(Chart 10). The chart also demonstratesthat the rise in inflation has not just beenrestricted to increases in food and transportand communications prices (which includethe price of oil). A measure of CPI inflationthat excludes these two components (alsographed in Chart 10) still shows a doublingfrom about 4 percent to 8 percent over thepast year.

The contributions to inflation of thedifferent components of the CPI are shownin Chart 11. Of the 8.5 percent rise inconsumer prices from June 2003 to June

An Overheating Economy?

Research Report No. 6210

CHART 10CPI INFLATION (12-MONTH CHANGES)

Source: Based on data from SBP Annual Report (various issues)

14

12

10

8

6

4

2

0

Perc

ent

Jul

Oct

Jan

Apr Ju

l

Oct

Jan

Apr Ju

l

Oct

Jan

Apr Ju

l

Oct

Jan

Apr Ju

l

Oct

Jan

Apr Ju

l

Oct

Jan

Apr Ju

l

Oct

Jan

Apr Ju

l

Oct

Jan

Apr Ju

l

Oct

Jan

Apr

CPI Inflation

CPI Inflationexcluding Foodand Transport &Communication

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

CHART 11CONTRIBUTIONS OF COMPONENTS TO

12-MONTH CPI INFLATION

12

10

8

6

4

2

0

Food,Beverages

and Tobacco5.2

Food,Beverages

and Tobacco6.4

House Rent1.9

House Rent2.8

Others0.8

Others1.1

Transpt. & Comm.0.6

Transpt. & Comm.0.8

Perc

enta

gePo

ints

June 03 - June 04 April 04 - April 05

Source: SPDC estimates based on data from SBP Annual Report(various issues)

8.5%

11.1%

2004, 5.2 percentage points (or 63 percent)was accounted for by rises in food pricesand another 1.9 percentage points byincreases in the house rent component.Between April 2004 and April 2005, foodprice increases continued to be a heavycontributor to inflation, adding 6.4percentage points to CPI inflation, but thehouse rent component and othercomponents also added significantly, 2.8percentage points and 1.1 percentagepoints, respectively.

Chart 12 displays the proportion of thechange in CPI inflation between FY2004and FY2005 that can be accounted for bythe different components. Together, foodprices and transportation andcommunications prices account for a littleover a half of the increase in inflation inFY2005. In other words, nearly half of therise in inflation from the previous year isaccounted for by an increase in the houserent and other components. This suggeststhat demand-side pressures to inflationhave now built up significantly in addition tosupply-side pressures that work throughvolatile oil and food prices.

This merits further investigation.According to macroeconomic theory, one ofthe key determinants of fundamentalinflationary pressures in the economy is theoutput gap, the deviation of actual outputfrom potential output. If the output gap ispositive--that is, the actual output of theeconomy is above the level that can besustained in the long run--there is atendency for inflation to increase due tocapacity constraints, overtime shifts,bottlenecks, running down of inventories,etc. On the other hand, if there is sparecapacity and actual output is belowpotential, there is a tendency for the rate ofinflation to decline. This does not, of course,mean that higher growth rates lead to higherinflation necessarily. If actual growth is high,but the productive capacity of the economyis keeping pace and the extra output beingdemanded is being produced easily, thereshould be no pressure on inflation toincrease. Or, if actual growth is high relativeto potential growth, but the economy hadbeen mired in a recessionary situationwhere the actual level of output to begin withwas much lower than the level of potential

output, then actual output growingfaster is just a catching up processand should not lead to higherinflation.

So what does the output gapsituation of Pakistan look like, andwhat implications does this havefor inflation? Based on theestimates of potential output thatwe obtained earlier (which weagain emphasize are meant to beillustrative only), since the mid-1990s, Pakistan's output gap hasgenerally been falling and inflationhas shown a tendency to fall withit (Chart 13). In 2003, the outputgap turned around and started torise, and it is about the same timethat inflation also turned aroundand started to pick up. However,the output gap was still negative

An Overheating Economy?

Research Report No. 62 11

CHART 12CONTRIBUTION SHARES OF INCREASE IN

CPI INFLATION FROM 2004 TO 2005

Source: SPDC estimates

Transporation &Communication

10%

Food, Beverages& Tobacco

43%

House Rent33%

Others14%

until last year. Now it has turned positive inFY2005 and, with forecasted growth of 7percent in 2006 and 2007, the output gapwill pick up further. On this count,inflationary pressures, unless checkedappropriately will become more severe.

We have also estimated aneconometric equation for inflation based ondeterminants that are suggested byeconomic theory. The model incorporatesthe effects of the output gap as mentionedabove, expectation or inertial effects throughthe previous year's inflation rate, pass-through from nominal exchange ratechanges, the impact of the world price ofimports (including oil imports), and theinfluence of changes in excess liquidity inthe market, proxied by the lagged value ofgrowth in the money supply-to-GDP ratio.The model fits fairly well on statistical criteriaand is able to explain about two-thirds of thevariation in the CPI inflation rate.

The sources of inflation based on thismodel for FY2004 and FY2005 are shown in

Chart 14. The contribution of the world priceof imports was quite large in FY2004--themodel's predicted effect on inflation fromchanges in world price of our imports was 62percent of the actual inflation rate for thatyear. Changes in the money supply-to-GDPratio have made less of a contribution toinflation this year than last year, but thecontribution is still positive. The model alsohelps us to assess price pressures for nextyear. First, with a rise in inflation this year,the expectations effects which are quitelarge will only exacerbate. Second, if therupee depreciates more, this will have somepass through effects on inflation. Third, theoutput gap turned positive this year with theimplication that it has now become a sourceof inflationary pressure. These three factorswill not necessarily automatically dissipatewith a deceleration of food prices and worldoil prices, and the now tightening stance ofmonetary policy needs to be maintained.

Chart 14 also shows that about a third ofthe inflation rate in FY2005 is not explained by

An Overheating Economy?

Research Report No. 6212

CHART 13RELATIONSHIP BETWEEN OUTPUT GAP* AND INFLATION

*Output Gap is percent deviation of actual output from potential output. Potential output is computed from a statistical filter (Hodrick PrescottFilter). Growth of 7% is assumed in 2006 and 2007 in working the projections of output gap for these years.

Source: SPDC estimates

14

12

10

8

6

4

2

0

5

4

3

2

1

0

-1

-2

-3

-4

-5

Perc

ent Percent

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Output Gap

Inflation (CPI)

the variables in our equation but accountedfor by other factors not modeled, i.e. theresidual. One of these non-modeled factorsmight be the recent expansion of real credit tothe private sector, for which we do not haveconsistent data for a long enough period to beable to incorporate this variable directly in ourequation.

As can be seen from Chart 15, realcredit to the private sector has certainly

expanded sharply over the past two years.No doubt this growth in credit hascontributed to the recent strength of theeconomy, but the relationship betweencredit and growth can be tricky one. Cross-country evidence establishes a positiverelationship between financial developmentand growth. But, this holds only up to apoint. There is also evidence that oncecredit goes beyond the point that can be

An Overheating Economy?

Research Report No. 62 13

CHART 14SOURCES OF CPI INFLATION

Source: SPDC estimates

Growth in Money-to-GDP Ratio (Lagged)

38%

Growth in Money-to-GDP Ratio (Lagged)

11%

Output Gap(Demand Relative toSupply Pressures)

-15%

Nominale ExchangeRate Depreciation

-8%

Nominale ExchangeRate Depreciation

8%

Other Factors(Residual)

-22%

Other Factors(Residual)

33%

ExpectationsIntertia45%

Expectations(Intertia)

33%

Import PriceDollars62%

( F Y 2 0 0 4 )

( F Y 2 0 0 5 )

Output Gap(Demand Relative toSupply Pressures)

2%

Import Pricein Dollars

13%

safely supported by thebanking system and the existingregulatory environment, it canhave adverse effects on theeconomy. Of course, whencredit growth becomesexcessive is in the eye of thebeholder and, clearly, moreresearch needs to be done onthis issue.

On balance, the aboveevidence appears to suggest aneed for some cooling off ofdemand in the short run, whileat the same time continuingpolicies and changes thatwould in the long run create anenabling environment forgrowth in the range of 7percent to 8 percent to becomesustainable.

External Sector

The trade deficitwidened to $3.4

billion during the periodof July 2004 to March2005 from its value of$0.6 billion over thesame nine months ayear ago (Table 4).This reflected importgrowth of about 40percent (from about$10 billion to $14billion), which outpacedexport growth of 15percent (from $9 billionto about $10½ billion).With the deficit on theservices balance alsodoubling, the currentaccount during theperiod registered adeficit of $1.4 billioncompared to a surplus

An Overheating Economy?

Research Report No. 6214

CHART 15REAL CREDIT TO THE PRIVATE SECTOR

Source: SPDC estimates based on data from SBP, Annual Report (various issues)

300

250

200

150

100

50

0

Rup

ees

Billio

n

1995

9476 71

83

18

54 49

151

279

107

1996 1997 1998 1999 2000 2001 2002 2003 2004

TABLE 4CURRENT ACCOUNT

(US $ Million)

Trade Balance -444 -1212 -645 -3378Exports (f.o.b) 10889 12395 9175 10572Imports (f.o.b) -11333 -13607 -9820 -13950

Services (Net) -2128 -3585 -2240 -4238Receipts 2967 2914 2382 2660Payments -5095 -6499 -4622 -6898

Shipment -951 -1241 -887 -1266Investment Income -2381 -2392 -1691 -1884Others -1763 -2866 -2044 -3748

Private Unrequited Transfers (net) 5737 6110 4390 6258(Workers Remittances) 4237 3871 2875 3051

Current Account Balance 3165 1313 1505 -1358

Trade Balance as % of GDP 1.3 3.4 - -

Current Account Balance 3.8 1.4 - -as % of GDP

Source: Pakistan Economic Survey, 2004-05

FY 2003 FY 2004 FY 2004 FY 2005July - March

of $1.5 billion over the same months a yearago. However, the current account deficit

was much less than the deficit onmerchandise trade and services combined($7.6 billion) during the July 2004 to March2005 period because net private unrequitedtransfers were positive to the tune of $6.2billion. In particular, workers' remittancesfrom abroad have started to increase again,rising to about $3 billion during the period.

Even though the current account hasdipped into the red, financing it is not anissue at the moment. The central bank'swar chest of international reserves, graphedin Chart 16, has continued to rise and stoodat nearly $14 billion in March 2005.However, expressed in relation to imports,reserves have fallen to about 9 months ofimports from 12 months of imports inFY2004. The government also has beenable to tap international markets at betterterms and should be able to continue to do

so in the near future. That said, if thecurrent account deficit gets much worse and

persists, this could havecredibility effects that couldjeopardize macroeconomicstability and make it'sfinancing more difficultthrough an increase in thecountry risk premium.

Over the past year orso, the rupee hasdepreciated more than 3percent against the dollar(Chart 17). However, thisdevelopment by itself isunlikely to improve ourcompetitiveness and boostour exports relative toimports because ourinflation rate has been muchhigher than that of ourtrading partners. Adjustingfor this price differential, atrade-weighted real effectiveexchange rate (REER) thatwe have computed showsan appreciation, on balance,over the past year (Chart

17). However, the REER remains at adepreciated level, relative to historicalaverages.

The behavior of major exports is shownin Table 5. Over the nine-month period fromJuly 2004 to March 2005, total exports grewabout 15 percent compared with the sameperiod a year earlier. This was higher thangrowth of 10 percent in exports recorded inFY2004 relative to FY2003. Note thatexports of textiles manufactures, which lastyear constituted about two-thirds of totalexports, increased just 2.1 percent.However this slow growth was made up by23.4 percent growth in exports of primarycommodities (led by raw cotton), 22.4percent growth in exports of othermanufactures, and 90.3 percent growth inexports of other goods. While thediversification of Pakistan's export base is a

An Overheating Economy?

Research Report No. 62 15

CHART 16INTERNATIONAL RESERVES*

*Gold and Foreign Exchange Reserves**End of periodSource: SBP Annual Report (various issues)

16

14

12

10

8

6

4

2

0

US

$Bi

llion

3.8

7.1

11.5

13.213.7

FY 01** FY 02** FY 03** FY 04** Mar. 05

welcome development, the relatively weakperformance of textiles manufactures doesnot augur well for making inroads in thepost-textile quota environment, although it isprobably too early to tell just yet. Onepossible reason for the relatively weakperformance of textiles in value terms mightbe that gains in export volume (quantity) arebeing offset by decreases in export unitvalues. In that case, we should see higher(and positive) growth rates of volumescompared to those of values, which doesnot appear to be the case generally, exceptfor towels and ready-made garments.

Table 6 reveals that total imports rosenearly 40 percent during the July 2004 toMarch 2005 period, relative to their valueduring the same months a year ago. Thiscame on the heels of strong import growthlast year as well. Strong increases wererecorded in nearly all major groups withgrowth of 20.8 percent in food imports (ledby wheat), 54.9 percent in machineryimports (which constitute about a third of allimports), 30.9 percent in petroleum and

petroleum products, and 32.9 percent inimports of agriculture and chemical goods(including fertilizer and insecticides).Considering components within the broadgroups, the increases in import volumegrowth are generally less pronounced thanthat of import value growth, reflectingincreases in unit values of imports as well.

As shown in Table 7, the growth rates ofimports by type of good during the July 2004to December 2004 period from a year earlierwere 30.9 percent for capital goods, 57.7percent for raw material for capital goods,and 32.9 percent for raw material forconsumer goods. Consumer goods importshave also been strong, rising 41.5 percent,but they have a share of only 10 percent.There is, thus, much to the argument thatimports are of the productive kind and couldlead down the road to much stronger exportperformance. However, it is not hearteningthat despite strong imports of capital goods,including machinery, the performance ofprivate fixed investment (discussed earlier)has been rather weak.

An Overheating Economy?

Research Report No. 6216

CHART 17EXCHANGE RATES

Source: Nominal: from SBP Statistical BulletinREER (Real Effective Exchange Rate):SPDC estimates

Note: A rise in exchange rate represents a depriciation of the rupee.

60.0

59.5

59.0

58.5

58.0

57.5

57.0

56.5

56.0

101.5

101.0

100.5

100.0

99.5

99.0

98.5

98.0

Mar

. 04

Apr

. 04

May

. 04

Jun.

04

Jul.

04

Aug

. 04

Sep

. 04

Oct

. 04

Nov

. 04

Dec

. 04

Jan.

05

Feb.

05

Mar

. 05

Rup

ees

perU

S$

Index(M

ar.04=

100)

REER

Nominal

An Overheating Economy?

Research Report No. 62 17

Prim

ary

Com

mod

ities

1012

9.1

1017

8.3

0.5

-74

48.

491

99.

023

.4-

Ric

e55

663

514

.20.

246

160

230

.431

.0R

aw c

otto

n49

48-2

.7-3

2.3

3594

171.

419

0.0

Fish

& F

ish

Pre

para

tion

135

153

13.7

10.8

115

98-1

5.4

-24.

0Fr

uits

8310

323

.436

.977

71-7

.8-2

1.0

Vege

tabl

es32

31-0

.6-1

1.4

1817

-5.6

-48.

0To

bacc

o5

1110

6.1

-9

7-2

2.2

-27.

0W

heat

130

6-9

5.4

-96.

26

--

-Sp

ices

1619

20.0

17.2

1510

-35.

9-3

2.0

Oil

seed

s, n

uts

and

kern

als

711

55.6

34.4

821

162.

524

7.0

Text

ile M

anuf

actu

res

7264

65.1

8073

65.6

11.1

-58

5065

.759

7258

.52.

1-

Cot

ton

Yarn

928

1127

21.4

-3.9

848

729

-13.

9-9

.0C

otto

n C

loth

1346

1712

27.2

18.3

1221

1333

9.2

5.0

Kni

twea

r11

4714

5927

.227

.310

3112

6522

.810

.0B

edw

ear

1329

1383

4.1

1.0

1008

910

-9.7

-1.0

Tow

els

375

404

7.7

1.2

277

345

24.5

32.0

Rea

dym

ade

Gar

men

ts10

9399

3-9

.1-2

4.3

733

754

2.9

11.0

Syn

thet

ic T

extil

e57

447

1-1

8.0

-16.

937

522

1-4

1.1

-39.

0O

ther

s47

252

511

.2-

359

415

15.6

-

Oth

er M

anuf

actu

res

2043

18.3

2149

17.5

5.2

-15

9017

.919

4619

.122

.4-

Car

pets

, Rug

s &

Mat

s22

123

14.

8-2

.616

418

814

.39.

0P

etro

luem

& P

etro

luem

Pro

duct

s24

929

518

.5-1

.819

431

662

.936

.0Sp

orts

Goo

ds33

532

5-3

.1-

229

212

-7.6

-Le

athe

r Tan

ned

235

252

7.2

4.6

177

202

14.7

11.0

Leat

her M

anuf

actu

res

387

414

7.2

-31

134

711

.6-

Foot

wea

r12

11-1

3.6

27.7

6583

27.7

53.0

Sur

gica

l Goo

ds &

Inst

rum

ents

150

133

-11.

6-

100

118

17.9

-C

utle

rry

3030

0.3

24.0

2120

-4.8

-O

nyx

Man

ufac

ture

d12

12-1

.82.

08

7-1

2.5

-15.

0C

hem

ical

s &

Pha

rmac

eutic

als

261

263

0.8

-19

625

630

.5-

Eng

inee

ring

Goo

ds74

100

35.1

-69

115

66.9

-G

ems

& J

ewel

ry25

2813

.8-

2017

-15.

0-

Furn

iture

810

15.5

-7

928

.6-

Mol

asse

s45

473.

114

.529

5693

.111

.0

Oth

ers

841

7.5

1075

8.7

27.7

-72

0.6

8.1

1371

13.4

90.3

-

Tota

l11

160

100.

012

313

100.

010

.3-

8905

100.

010

207

100.

014

.6-

Sour

ce:P

akis

tan

Eco

nom

ic S

urve

y 20

04-0

5, S

BP

Ann

ual R

epor

t (20

03-0

4), a

nd S

BP

Third

Qua

rterly

Rep

ort 2

004-

05

TAB

LE 5

MA

JOR

EXP

OR

TS(V

alue

s in

US

$ M

illio

n)Ju

ly-M

arch

July

-Mar

chJu

ly-M

arch

FY20

03FY

2004

Gro

wth

(%)

FY20

04FY

2005

Gro

wth

(%)

Valu

e%

Sha

reVa

lue

% S

hare

Valu

eQ

uant

ityVa

lue

% S

hare

Valu

e%

Sha

reVa

lue

Qua

ntity

An Overheating Economy?

Research Report No. 6218

Food Group

9788.0

10336.6

5.7-

7817.4

9426.5

20.6-

Wheat U

nmiled

2924

-17.8-27.0

1556

271.5306.0

Tea173

19311.5

7.2151

17515.7

15.0S

oyabean Oil

4846

-4.02.3

4049

21.3-22.0

Palm

Oil

539613

13.75.7

466478

2.52.0

Pulses

11675

-35.233.7

5383

56.850.0

Others

7484

12.856

10282.4

-

Machinery G

roup2942

24.14220

27.143.4

-2513

23.93892

26.954.9

-P

ower G

enerating269

2783.5

-205

27332.7

-Textile

532598

12.4-

419697

66.3-

Construction &

Mining

101102

0.2-

73112

53.6-

Electrical &

apparatus217

25819.1

-180

22827.0

-R

oad Motor Vehicles

501653

30.2-

482706

46.5-

Others

13232332

76.3-

11531876

62.7-

Petroleum G

roup3066

25.13167

20.33.3

-2108

20.12761

19.130.9

-P

etroleum P

roducts1700

1401-17.6

35.9936

114922.9

8P

etroleum C

rude1367

176529.2

16.21173

161137.4

19

Textile Group

2221.8

2611.7

17.6194

1.8238

1.622.6

Agri/O

ther Chem

ical Group

216117.7

279817.9

29.5-

197218.8

262118.1

32.9-

Fertilizer240

28518.7

4.1191

26237.5

10.0Insecticides

59124

112.186.2

78107

37.229.0

Plastic M

aterial421

54930.4

18.0387

58150.1

33.0M

edicinal Products

222275

23.88.9

201200

-0.517.0

Other

12191565

28.3-

11151471

31.9-

Metal G

roup507

4.2688

4.435.5

-477

4.5857

5.979.6

-Iron &

Steel402

51227.3

15.0351

62578.1

84.0other

105176

67.2-

126232

83.7-

Miscellaneous/O

thers2344

19.23426

22.046.2

-2452

23.43158

21.828.8

-

Total12220

100.015592

100.027.6

-10497

100.014469

100.037.8

-

Source:Pakistan E

conomic S

urvey 2004-05, SB

PA

nnual Report (2003-04), and S

BP

Third Quarterly R

eport 2004-05

TAB

LE 6M

AJO

R IM

POR

TS(Values in U

S $ Million)

July-March

July-March

July-March

FY2003

FY2004

Grow

th (%)

FY2004

FY2005

Grow

th (%)

Value%

ShareValue

% Share

ValueQ

uantityValue

% Share

Value%

ShareValue

Quantity

An Overheating Economy?

Research Report No. 62 19

Poverty and Social Development

The recent Pakistan Economic Surveyenlightens us that "Readers would have

to wait till December 2005 to get estimatesof poverty from the Provincial level survey ofthe PSLM which is focusing on householdconsumption and expenditure…. Theestimates of poverty for 2004-05 would thenbe available for all of us."

SPDC's large-scale ISPM model has apoverty and inequality module in it. Povertyis estimated to be a function of per capitaincome and income inequality; inequality, inturn, is estimated to be function of variablessuch as per capita income, food prices,investment-output ratio, and developmentexpenditures as a share of GDP, etc. Inprinciple, therefore, we have the expertise toforecast poverty for 2005 but, in practice,this requires us to take a stand on what ishappening to inequality or how therelationship between per capita income andinequality has changed recently. If we takethe historical relationship between percapita growth and inequality, then our modelpredicts poverty to have gone up becausehistorically per capita growth has beenaccompanied by significant increases inincome inequality. On the other hand, if weassume that the recent per capita growth isdistribution-neutral, then poverty isprojected to have gone down, but only

modestly because thep o v e r t y - r e d u c i n geffects of growth arepartially offset by thep o v e r t y - i n d u c i n geffects of increases infood prices and a fallin investment as ashare of GDP.

We would preferto let the data speakfor itself about howthe relationshipbetween per capitagrowth and inequality

has changed and, therefore, eagerly awaitthe new PSLM/HIES survey. Meanwhile,let's focus on social development and relateit to economic performance. There is nowwidespread dissatisfaction with per capitaincome as the sole indicator to measure thewell-being of a nation in any case. Theemphasis has now shifted to alternativemeasures of development. Socialindicators, quality of life, basic needs,human development, and standard of livingare the new approaches, which are beingdiscussed and propagated by internationalinstitutions and concerned scholars. Interestin social development as a developmentpolicy objective appears to have beenpromoted by the observed unevenness inthe economic performance of developingcountries. In many cases, despite positiveand high GDP growth rates, economicdevelopment has failed to reach allsegments of society and the poorest havehardly reaped any of the benefits ofdevelopment.

To summarize various social indicators,we constructed a Social Development Index(SDI) for Pakistan using the "PrincipalComponent" statistical technique for theperiod 1960-2004. The choice ofcomponent variables for forming thecomposite SDI is primarily governed by theavailability of consistent time series data.Individual indicators used to create the

TABLE 7IMPORTS BY ECONOMIC CATEGORIES

(US $ Million)

FY 2004 FY 2005 (July - December) (July - December)Value % Share Value % Share % Change

Categories (1) (2) (3) (4) (3 over 1)Capital Goods 2084 32 2729 31 31

Raw Material for Capital Goods 450 7 710 8 58

Raw Material for Consumer Goods 3418 52 4542 51 33

Consumer Goods 658 10 932 10 42

Total 6611 100 8913 100 35

Source: SPDC estimates based on data from Pakistan Economic Survey 2004-05

components of the SDI represent healthservices, education facilities, andconsumption of durable goods and energy.The constituent variables of the SDI are

listed in Table 8. All data on these variablesare taken from various issues of thePakistan Economic Surveys.

The comparison between growth in theSDI index and per capita real GDP growth isdepicted in Chart 18. From the 1960s untilthe 1980s, changes in per capita growth andgrowth in social development are positivelyrelated. In particular, the 1970s period ofproclaimed trickle-up policies led to slippagein per capita growth, which was alsoaccompanied by slippage in growth of socialdevelopment. This bolsters the argumentthat higher growth in income is aprerequisite for higher achievement in socialand human development. Nevertheless, thepositive relationship between growth andimprovements in social development doesnot hold strongly in the fourth period. Duringthe 1990s, a decrease in per capita GDPgrowth did not significantly affect SDIgrowth. This is perhaps indicative of theSocial Action Programme's (SAP) successin improving access to basic public social

An Overheating Economy?

Research Report No. 6220

TABLE 8COMPONENTS OF SDI

Consumption:Cars Per Million PopulationTelephone Per Million PopulationProportion of Non-Agriculture Labor ForceElectricity Generation Per Million Population

Education:Primary Male Enrollment Rate Primary Female Enrollment RateSecondary Male Enrollment RateSecondary Female Enrollment RateTertiary MaleEnrollment RateTertiary Female Enrollment Rate

Health:Physicians Per Million PopulationHospital Beds Per Million PopulationInfant Survival Rate Per 1000 Live Births

CHART 18ECONOMIC AND SOCIAL GROWTH

[Average Annual Growth Rates]

Source: SPDC estimates

4

3

2

1

0

2.89

1.531.64

3.02

1.792.01 1.92

2.04

0.95

2.36

1.48

60’s 70’s 80’s 90’s 2000-2004 1960-2004

1

Per Capita GDP

Social Development Index

An Overheating Economy?

Research Report No. 62 21

services and the dynamism demonstratedby the private sector in filling the gap indemand.

The last period exhibits a completelydifferent and rather disconcerting picture.Despite sizable gains in per capita real GDPduring the 2000-2004 period, the averagegrowth in SDI is quite low, compared withthe 1980s and 1990s. The componentanalysis (Chart 19) clearly revealscontinued solid performance in theconsumption component of the SDI (whichmeasures availability of cars, telephones,and electricity), but average growth ineducation and health indicators since 2000has been visibly inglorious. However, to befair, the year-wise growth rates in the healthand education components of SDI doindicate some upward trend after 2002.

The evidence, based on the selectedindictors and methodology suggest thateconomic growth is a pre-requisite for socialdevelopment. Nevertheless, over the past

few years, the gap between economicperformance and social development,especially human development as it relatesto health and education, has widened, whichneeds to be redressed on an urgent basis.

FISCAL ANALYSIS

Unencumbered by IMF pressures forfiscal restraint, the Federal Budget2005-06 turns the stance of fiscal

policy significantly more expansionary. Thishas both positive and negative aspects.The substantial increases in developmentexpenditures, which can potentially helpalleviate poverty and foster social andhuman development are to be lauded. Alsoto be commended, in principle, are the taxincentives being provided to exporters in anattempt to broaden the source of growth toinclude exports.

CHART 19COMPONENTS OF SOCIAL DEVELOPMENT INDEX

[Average Annual Growth Rates]

Source: SPDC estimates

4

3

2

1

0Per Capita GDP Social Development Education Health Consumption

Index

2.89

1.64

3.02

2.01 2.04

1.53

1.79 1,

92

0.95

2.05

0.46

1.96

2.33

0.34

0.97

1.81

2.19

0.95

0.21

1.74

1.05

1.58

1.85

1.69

1

1960s 1970s 1980s 1990s 2000-2004

But the widening gap between totalexpenditures and total revenues, leading toan increase in the budget deficit, may not bewise in an economy which is experiencingdouble-digit inflation and is showing signs ofoverheating. Adjusted for the businesscycle, the budget is even moreexpansionary than it might appear at first.More efforts should be made to finance therequisite increase in developmentexpenditures through some expenditureswitching and through more targetedmeasures to increase tax revenues andexpand the tax base. Moreover, theexperience from last year suggests that thePublic Sector Development Programme(PSDP) needs considerable improvement tomore effectively channel and utilize theexpenditures. Otherwise, the government'sintentions underlying the increasedallocation of development expenditures maynot have the desired results in addressingthe problems of poverty, inequality, and lackof social development more generally.

Budget Deficit

The revised fiscal deficit of Rs. 246 billionfor FY2005 is Rs. 33 billion (or 15½

percent) more than budgeted, as reported inTable 9. Moreover, in FY2006, the budgetdeficit is slated to increase further by nearly20 percent from this revised estimate. As ashare of GDP, the revised budget deficit of3.8 percent of GDP is projected to increaseto 4 percent of GDP in FY2006, if weassume economic growth of 7 percent andinflation of 6 percent for that year. To theextent that the deficit is being fueled by theprojected increase of nearly 35 percent indevelopment expenditures, it should beexpected to spur growth further. But notethat development expenditures start off froma low base, with their share in totalexpenditure being just 20 percent.Moreover, even though currentexpenditures are expected to rise only 5.3percent from the revised estimates forFY2005, the revised estimates of theseexpenditures were 12.4 percent higher thanbudgeted for that year. Compared tobudgeted values for FY2005, the budget forFY2006 implies an increase in current

An Overheating Economy?

Research Report No. 6222

TABLE 9THE FEDERAL BUDGET

(Rs. Billion)

FY 2005 FY 2006Budgeted Revised Growth (%) Budgeted Growth (%)

Categories (1) (2) (2 over 1) (3) (3 over 2)

Current Expenditures 700.8 784.7 12.0 826.5 5.3Minus Repayment of Foreign Loans 51.1 54.3 6.2 65.3 20.4

Current Expenditures (excludingRepayments of Foreign Debt) 649.7 730.4 12.4 761.2 4.2

Plus Development Expenditures 202.0 202.0 0.0 272.0 34.7Minus Net Revenue Receipts 557.2 630.0 13.1 643.1 2.1Minus Self-Financing of PSDP by Provinces 33.1 38.4 16.0 41.0 6.7Minus Recovery of Loans from Provinces 13.2 28.7 116.5 14.4 -49.6Minus Provincial Surplus 31.6 6.2 -80.5 33.5 442.5Minus Net Lending to others 3.6 -16.9 -565.8 6.2 -136.5

FISCAL DEFICIT 213.0 246.0 15.5 295.0 19.9 FISCAL DEFICIT as % of GDP 3.3 3.8 - 4.0p -

Source: Federal Budget in Brief 2005-06p = Projected

expenditures of about $125 billion, while theincrease in development expenditures is$70 billion. Net revenue receipts, on theother hand, increase relatively less fromtheir budgeted amount by about $85 billion.

The financing of the budget deficit isshown in Table 10. The dependence onexternal sources to finance the budgetdeficit has increased in recent years, with ashare in financing of more than 55 percentin the revised estimates for FY2005. InFY2006, this dependence is expected to godown some, but remain over 40 percent.Another important source of financing forthe deficit is bank borrowing. In FY2005,such borrowing was budgeted to finance Rs.45 billion of the deficit, but ended upfinancing more than Rs 80 billion and againis expected to finance Rs. 98 billion of thedeficit in FY2006. This is an alarming trendin the prevailing inflationary environment.

Revenues

Table 11 provides a comparison ofbudgeted and revised figures of gross

revenue receipts and their components.The table indicates that gross revenuereceipts were 10 percent higher than thebudgeted figure for FY2005. However, thislargely reflects an increase of $107 billion(or 71 percent) relative to target in non-tax

An Overheating Economy?

Research Report No. 62 23

FINANCING OF THE DEFICIT 213.1 246.0 15.5 295.0 19.9Non-Bank Borrowings 74.7 13.3 -82.2 55.4 315.3Share (%) 35.1 5.4 - 18.8 -

Net External Resources 78.2 141.9 81.5 121.6 -14.3Share (%) 36.7 57.7 - 41.2 -

Bank Borrowings 45.1 80.8 78.9 98.0 21.4Share (%) 21.2 32.8 - 33.2 -

Privatization Proceeds 15.0 10.0 -33.3 20.0 100.0Share (%) 7.0 4.1 - 6.8 -

Source: Federal Budget in Brief 2005-06

TABLE 10FISCAL DEFICIT FINANCING

(Rs. Billion)

2004-05 Growth 2005-06 GrowthHeads Budgeted Revised (%) Budgeted (%)

(1) (2) (2 over 1) (3) (3 over 2)

TABLE 11TARGET AND ACTUALFEDERAL RECEIPTS

(Rs. Billion)2001-02 2002-03* 2003-04* 2004-05**

Gross Revenue ReceiptsTarget 643.8 674.9 728.4 796.3 Actual 618.9 703.3 769.9 875.3 Actual as % of Target 96.1 104.2 105.7 109.9

Tax Revenues (CBR)Target 457.7 460.6 510.0 580.0Actual 404.1 460.6 518.9 590.0 Actual as % of Target 88.3 100.0 101.7 101.7

Direct TaxesTarget 149.8 148.4 161.1 181.9Actual 142.5 151.9 165.3 182.7Actual as % of Target 95.1 102.4 102.6 100.4

Indirect TaxesTarget 307.9 312.2 348.9 398.1Actual 261.6 308.7 353.6 407.3 Actual as % of Target 85.0 98.9 101.3 102.3

Import DutiesTarget 69.6 56.5 78.1 103.2Actual 47.8 68.8 89.9 113.9Actual as % of Target 68.7 121.8 115.1 110.4

Federal ExciseTarget 53.1 50.0 47.7 45.7Actual 47.2 44.8 44.6 54.4Actual as % of Target 88.9 89.6 93.5 119.0

Sales TaxTarget 185.2 205.7 223.1 249.2Actual 166.6 195.1 219.1 239.0Actual as % of Target 89.9 94.8 98.2 95.9

SurchargesTarget 47.0 60.5 61.1 65.3Actual 54.9 66.9 64.4 27.1Actual as % of Target 116.7 110.5 105.3 41.6

Non-Tax RevenuesTarget 139.1 153.8 157.2 151.0 Actual 159.9 175.8 186.6 258.2 Actual as % of Target 115.0 114.3 118.7 170.9

Sources: Targets and Revised Estimates are from Federal Budget in Brief (various issues)Actuals are from SBP Annual Report (various issues) and SBP Website

Note: Non-Tax Revenues for 2003-04 & 2004-05 also includes Workers' ProfitParticipation Tax, Foreign Travel Tax and Airport Tax.* Revised Estimates for Surcharges and Non Tax Revenue, otherwise Actuals** All Revised Estimates

revenues. According to the revisedestimates, CBR tax revenue was Rs. 10billion (or 1.7 percent) higher than the target.Collection from surcharges amounted toonly about 42 percent of the budgetedamount, largely because of the shortfall inthe petroleum development levy resultingfrom an increase in international oil prices.The sales tax target was again missed by asignificant amount, as in recent years.

CBR tax collections for FY2006 areanalyzed in Table 12. Revised figuresindicate that CBR tax collections rose nearly14 percent in FY2005 over the previousyear and are projected to increase about 17percent in FY2006. Considering thecomposition of taxes, revenues from indirecttaxes, which constitute about 70 percent oftotal tax revenues, increased 15 percent inFY 2004; whereas direct taxes, which

constitute about 30 percent oftotal tax revenues, increasedrelatively less, by 10 percent.Thus, the share of direct taxesin total taxes, depicted in Chart20 has fallen in recent years.This has made a tax system,which already lacks enough taxprogressivity, even lessprogressive (Note thatprogressivity measures theextent to which the rich bear agreater burden of taxes as ashare of their income than thepoor do). The projected growthof nearly 18 percent in direct taxrevenue in FY2006 versus 16½percent in indirect tax revenue

An Overheating Economy?

Research Report No. 6224

TABLE 12CBR TAX COLLECTIONS

(Rs. Billion)

A C T U A L Revised Budgeted

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06TAX REVENUES 392 404 461 519 590 690

Growth (%) 13.0 3.0 14.0 12.7 13.7 16.9

Direct Taxes 125 143 152 165 183 215Growth (%) 10.3 14.4 6.6 8.8 10.5 17.9

Indirect Taxes 268 262 309 354 407 475Growth (%) 14.3 -2.3 18.0 14.5 15.2 16.5Customs 65 48 69 90 114 121Growth (%) 5.5 -26.5 43.9 30.7 26.7 6.4Federal Excise 49 47 45 45 54 59Growth (%) -12.0 -3.9 -5.1 -0.4 22.0 9.2Sales Tax 154 167 195 219 239 294Growth (%) 31.6 8.5 17.1 12.3 9.1 23.0

Source: SBP website and Federal Budget in Brief 2004-05

CHART 20TAX SHARES

Source: SPDC estimates based on data from Pakistan Economic Survey 2004-05,SBP website and Federal Budget in Brief 2005-06

36

35

34

33

32

31

30

29

28

161514131211109876

2000-01 2001-02 2002-03 2003-04 2004-05

Direct Tax as % of Total Tax

Total Tax-to-GDP Ratio

31.8

35.3

33.0

31.9

31.0

9.09.49.69.29.4

will make only a minoradjustment to thecomposition of taxes.

Moreover, theoverall tax-to-GDP ratio,also depicted in Chart20, has also fallenslightly in recent yearsand, at less than 10percent, remains verylow even by developingcountry standards.Better tax performanceis needed if the increasein developmentexpenditures projectedin the FY2006 Budget isto be sustained withoutadding to concernsabout the budget deficit.

According torevised data, revenuesfrom custom dutiesincreased 32 percent inFY2005 over FY2004,reflecting a surge ofimports last year (Table13). However, it seemsrather strange that evenfor revised data 10 out of13 items display exactlythe same rate of growthof 27 percent. Thisraises some questionsabout the plausibility ofthe data.

Another notableaspect of the budget isthe build-up of non-taxrevenues, from aboutRs 165 billion in FY2002to Rs. 258 billion inFY2005 (Table 14),representing an annualcumulative growth rateof 16 percent. Itemswith a major share innon-tax receipts are

An Overheating Economy?

Research Report No. 62 25

Chemical & Chemical Products 27% 27% 6%Dyes, Colors, Paints & Varnishes 27% 27% 6%Iron, Steel & Manufactures 27% 27% 6%Machinery 27% 16% 6%Metals (Other than Gold) 27% 27% 6%Minerals, Fuel Oils (POL) 27% 27% 6%Rubber & Rubber Products 27% 27% 6%Plastic Resins etc. 27% 27% 6%Vehicles 27% 2% 6%Wood Pulp & Papers 27% 27% 6%Yarn & Fabrics 27% 27% 6%Medical & Photographic Equip. 27% 27% 6%Other Items 30% 35% 26%Gross Collection 28% 28% 16%Less: Refund / Rebates 11% 11% 6%CUSTOM DUTIES (Net) 32% 32% 17%

B.E. Budget Estimate, R.E. Revised Estimate

Source: SPDC estimates based on Explanatory Memorendum on Federal Receipts (various issues)

TABLE 13GROWTH IN CUSTOM DUTIES

Growth in B.E Growth in R.E Growth in R.E(FY 2005 over FY 2005 over (FY 2006 over

FY 2004) FY 2004) FY 2005)

Interest 54.2 54.0 67.3 61.1 4.1Provinces 29.5 28.0 26.4 24.3 -6.3Local Bodies 19.6 10.7 12.4 13.1 -12.7Financial Insitutions 5.4 4.2 5.4 5.3 -0.9Non- Financial Institutions 18.8 29.8 29.8 25.6 10.9

WAPDA 16.4 26.5 27.6 23.6 12.9Other Autonm. Bodies/Corp. 2.4 3.2 2.1 2.0 -5.7

Govt. Servants, Commercial Deptt.,AJK & Others 3.9 3.5 4.7 6.9 20.8Less: Estimated Shortfall -23.0 -22.2 -11.4 -14.0 -15.3

Dividends & Returns 26.5 27.7 33.4 57.5 29.5Defence 26.0 56.3 42.9 61.4 33.1

Effective & Non-Effective 2.5 2.5 2.5 2.9 4.9Receipts from UN and Misc. Receipts 23.5 53.8 40.4 58.5 35.5

Miscellaneous and Others 58.0 37.8 43.0 78.2 10.5TOTAL NON-TAX REVENUE** 165 176 187 258 16.2

Source: SPDC estimates based on Explanatory Memorendum on Federal Receipts (various issues)Note: *Annual cumulative growth rate**Non-Tax Revenue for 2003-04 & 2004-05 also includes Workers' Profit Participation Tax, ForeignTravel Tax and Airport Tax

TABLE 14NON-TAX REVENUE

(Rs. Billion)

Revised Estimates ACGR*FY 2002 FY 2003 FY 2004 FY 2005 (%)

interest receipts, dividends from non-financialinstitutions (OGDC and PTCL being the maincontributors), and defence earnings. Defenceearnings have registered an annualcumulative growth rate of 33 percent sinceFY2002, largely being driven by receipts fromthe U.N. and miscellaneous receipts, whichappear to have been bolstered by Pakistan'srole as an ally against the war on terrorism.The main concern about the recent surge innon-tax revenues is whether this can berelied upon as a source of revenue on asustained basis.

Current and DevelopmentExpenditures

Table 15 provides a comparisonof budgeted and actual federal

expenditures. In the currentexpenditures category, there wasoverspending of 12 percent inFY2005 relative to the target level.Debt servicing was over thebudgeted amount by 3.5 percent,an improvement over FY2004when the target was overshot by24 percent. Defence spendingincreased 12 percent in FY2005relative to the budgeted amount forthe year and the category "OtherCurrent Expenditures" exceededits target by 33 percent. On apositive note, the developmentexpenditures target was fulfilled forthe first time in at least 5 years.That said, it seems as though theextra fiscal space created byhigher-than-expected GDP growthwent towards extra currentexpenditures rather than extradevelopment expenditures.

One should not feel toocomplacent about developmentexpenditures in any case becausetheir relative share is very low tobegin with. As shown in Chart 21,the share of developmentexpenditures in total expenditurewas budgeted to be just 22 percentin FY2005 and the revised

estimates indicate that the actual shareturned out to be even a bit less at 20 percent.On the other hand, defence expenditure anddebt servicing and repayment account forabout half of total expenditure. It isimperative to shift the composition ofexpenditures more toward developmentexpenditures to combat poverty and createan enabling environment for socialdevelopment, and the projected increase ofthe share of development expenditures intotal spending to 25 percent implied by theBudget FY2006 is a welcome development.

An Overheating Economy?

Research Report No. 6226

TABLE 15BUDGETED AND ACTUALFEDERAL EXPENDITURES

(Rs. Billion)

2001-02 2002-03* 2003-04* 2004-05*Current Expenditures

Budget Estimates 621.7 608.0 645.2 700.8 Actual 650.4 673.3 714.0 784.7 Actual as % of B.E. 104.6 110.7 110.7 112.0

DefenceBudget Estimates 131.6 146.0 160.3 193.9 Actual 149.3 160.1 180.5 216.3 Actual as % of B.E. 113.4 109.7 112.7 111.5

Debt ServicingBudget Estimates 329.2 289.7 256.0 265.3Actual 318.7 257.4 317.7 274.7Actual as % of B.E. 96.8 88.9 124.1 103.5

SubsidiesBudget Estimates 20.7 20.8 - 59.5 Actual 25.5 49.8 - 51.4 Actual as % of B.E. 123.1 239.4 - 86.3

Other Current ExpendituresBudget Estimates 140.2 151.4 229.0 182.0 Actual 156.9 205.9 215.8 242.3 Actual as % of B.E. 111.9 136.0 94.2 133.2

Public Sector Development Program (PSDP)Budget Estimates 130.0 134.0 160.0 202.0Actual 126.3 131.6 154.4 202.0Actual as % of B.E. 97.1 98.2 96.5 100.0

Federal Current Expenditure + PSDPBudget Estimates 751.7 742.0 805.2 902.8 Actual 776.6 804.9 868.4 986.7 Actual as % of B.E. 103.3 108.5 107.8 109.3

Source: SBP Annual Report and Federal Budget in Brief (various issues)Note: Subsidy figures are not available for 2003-04* Revised Estimates

Estimated current expenditures in thenew FY2006 Budget and a comparison ofthese with the previous year's figures arereported in Table 16. The total of theseexpenditures is expected to grow a bit more

than 5 percent over the next year. This is arelatively restrained growth rate but followshigher-than-budgeted spending in FY2005,as noted above. Note that the growth rateof spending on transfer payments,

An Overheating Economy?

Research Report No. 62 27

CHART 21COMPOSITION OF EXPENDITURE

2004-05 Budgeted 2004-05 Revised 2005-06 Budgeted

Source: SPDC estimates based on Federal Budget in Brief 2005-06

Develop-ment22%

Other27%

Defence21%

DebtServicing &Repayment

30%

Develop-ment20%

Other30%