Carbon8 Systems

21

Carbon8 Systems Developing an innovative and profitable process that combines waste CO 2 and thermal residues, to create a carbon negative aggregate for construction and lock CO 2 in for good within our built environment. Dr Paula Carey Managing Director

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Carbon8 Systems

Carbon8 Systems Developing an innovative and profitable process that

combines waste CO2 and thermal residues, to create a carbon negative aggregate for construction and lock CO2 in for good

within our built environment.

Dr Paula Carey Managing Director

Content

• Company Background • Technology • Route to commercialisation • Costs involved in process • Development potential

Who we are

• Company based in the UK, at the University of Greenwich, South East England

• Formed in Feb 2006 to commercialise a patented technology developed within the University of Greenwich

• Result of >20 years of research into solidification/stabilisation of wastes and soils.

• Exclusive world wide licence from the university for the use of the technology: Accelerated Carbonation (ACT) - treatment of wastes with carbon dioxide.

3

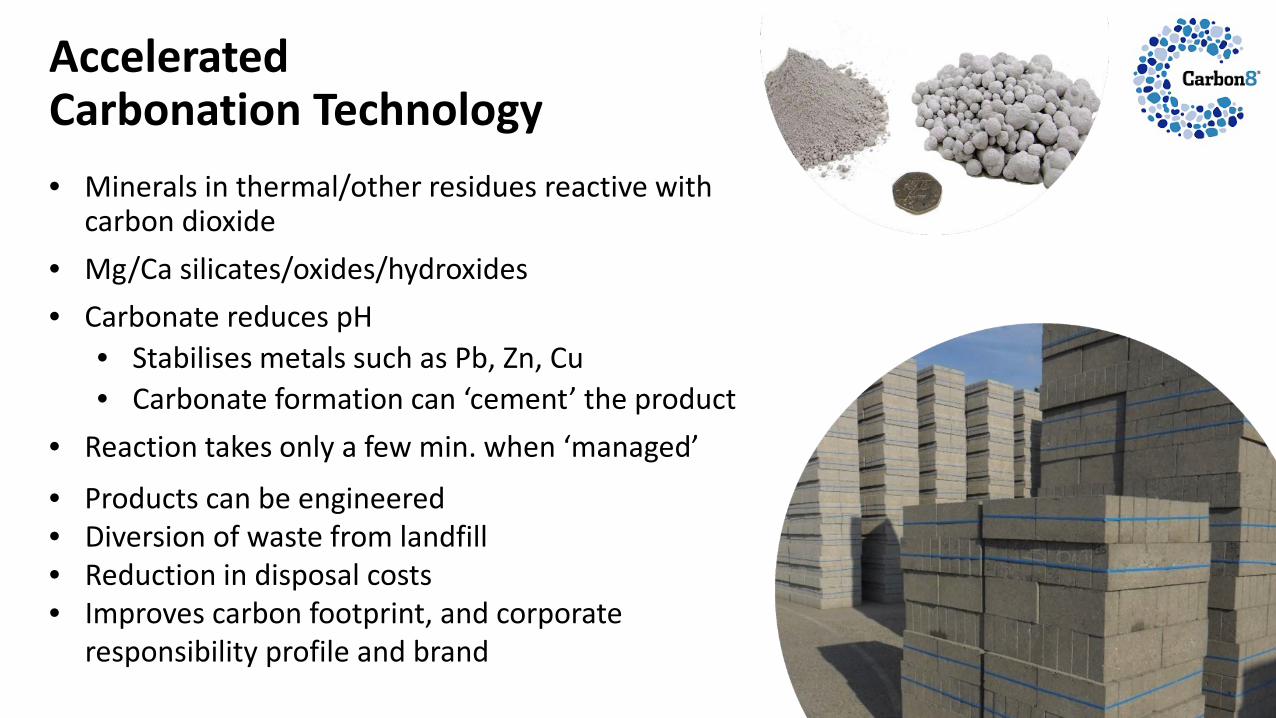

Accelerated Carbonation Technology • Minerals in thermal/other residues reactive with

carbon dioxide • Mg/Ca silicates/oxides/hydroxides • Carbonate reduces pH

• Stabilises metals such as Pb, Zn, Cu • Carbonate formation can ‘cement’ the product

• Reaction takes only a few min. when ‘managed’

• Products can be engineered • Diversion of waste from landfill • Reduction in disposal costs • Improves carbon footprint, and corporate

responsibility profile and brand 4

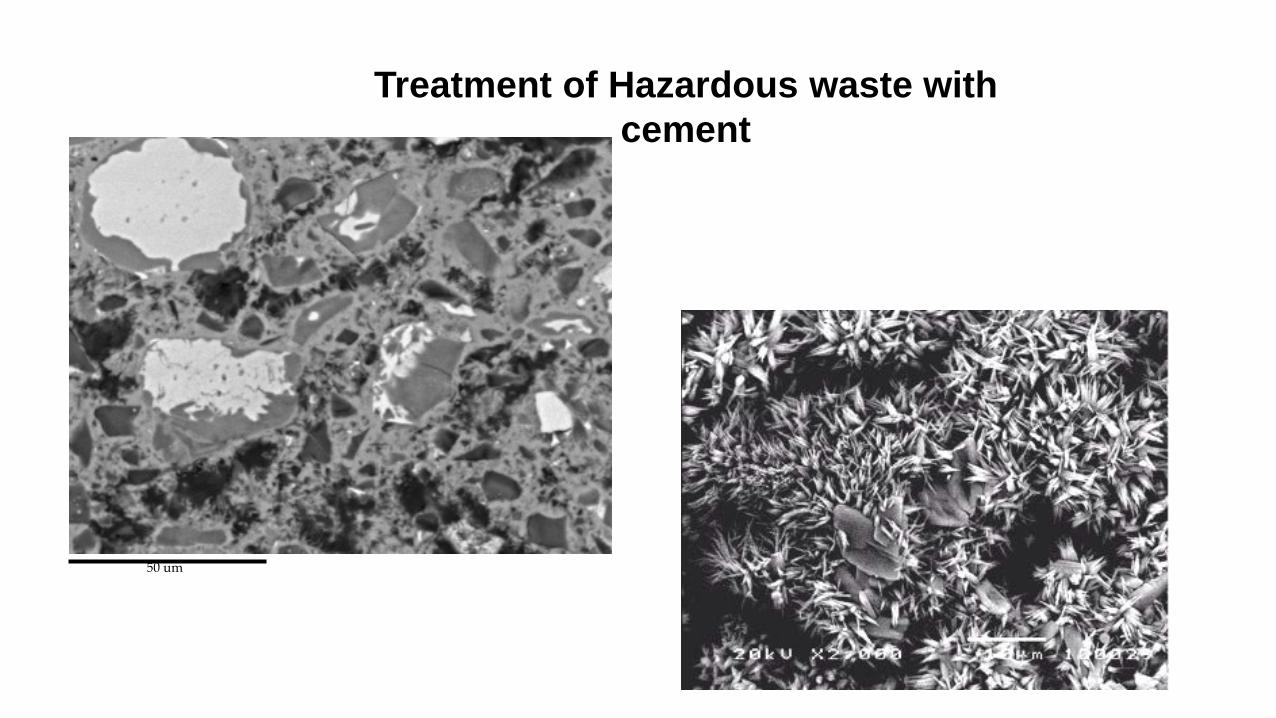

200 um

Treatment of Hazardous waste with cement

50 um

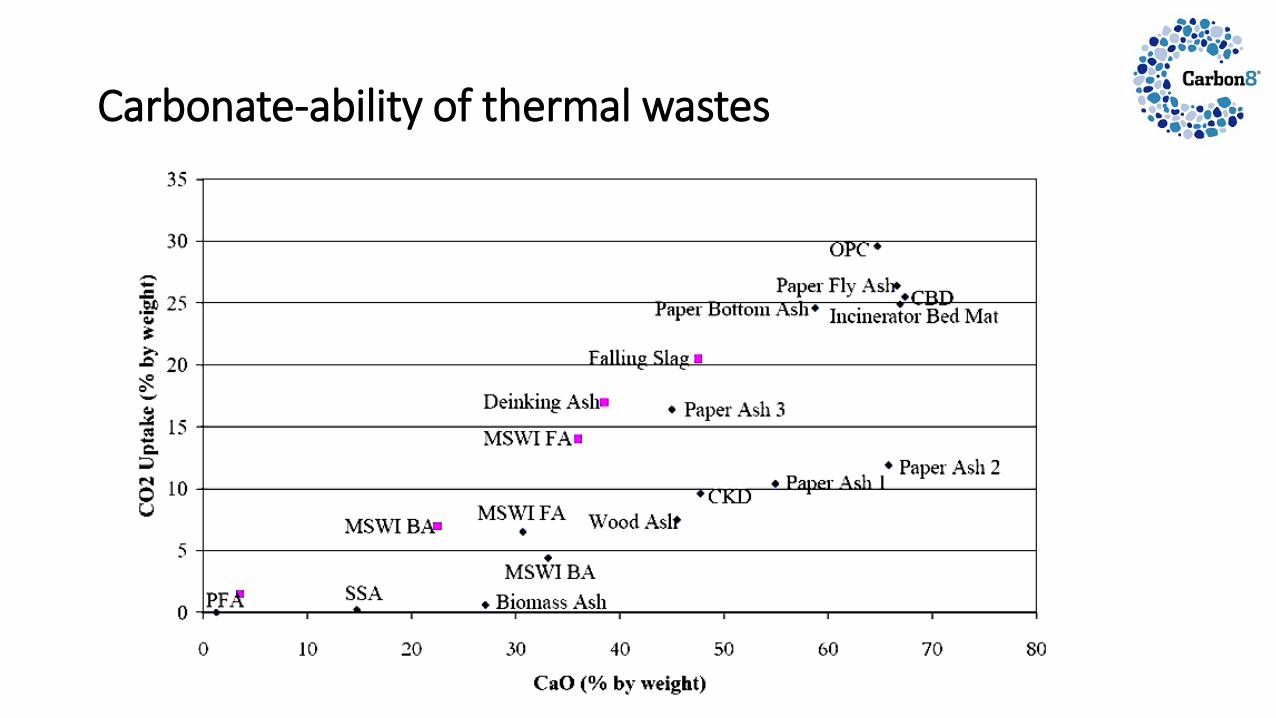

Carbonate-ability of thermal wastes

Steel Wastewater Sludge Quarry Fines

Bauxite

Wood Ash

Paper Ash

Metal Dust

Treatment of wastes • Thermal residues – contain reactive Calcium and Magnesium phases

• Air Pollution Control Residues • Stainless Steel Slags • Cement By-pass dust • Biomass ash

• Hazardous non-reactive wastes – need to add a reactive binder • Contaminated soils • Thermal desorption residues

• Bulk difficult to handle non-reactive wastes – need to add a reactive binder

• Marine dredging fines • Quarry fines

Route to commercialisation • Selected Air Pollution Control Residues for first

commercial development • Drivers:

• High landfill Costs – landfill tax plus gate fees - £100 / tonne

• Increasing number of EfWs • Potential change in regulation stopping APCr

disposal to landfill • Lack of other sustainable solutions for APCr

• 2009 – set of small-scale trials to develop treatment process and manufacture aggregate

• Manufacture of first carbonated aggregate block

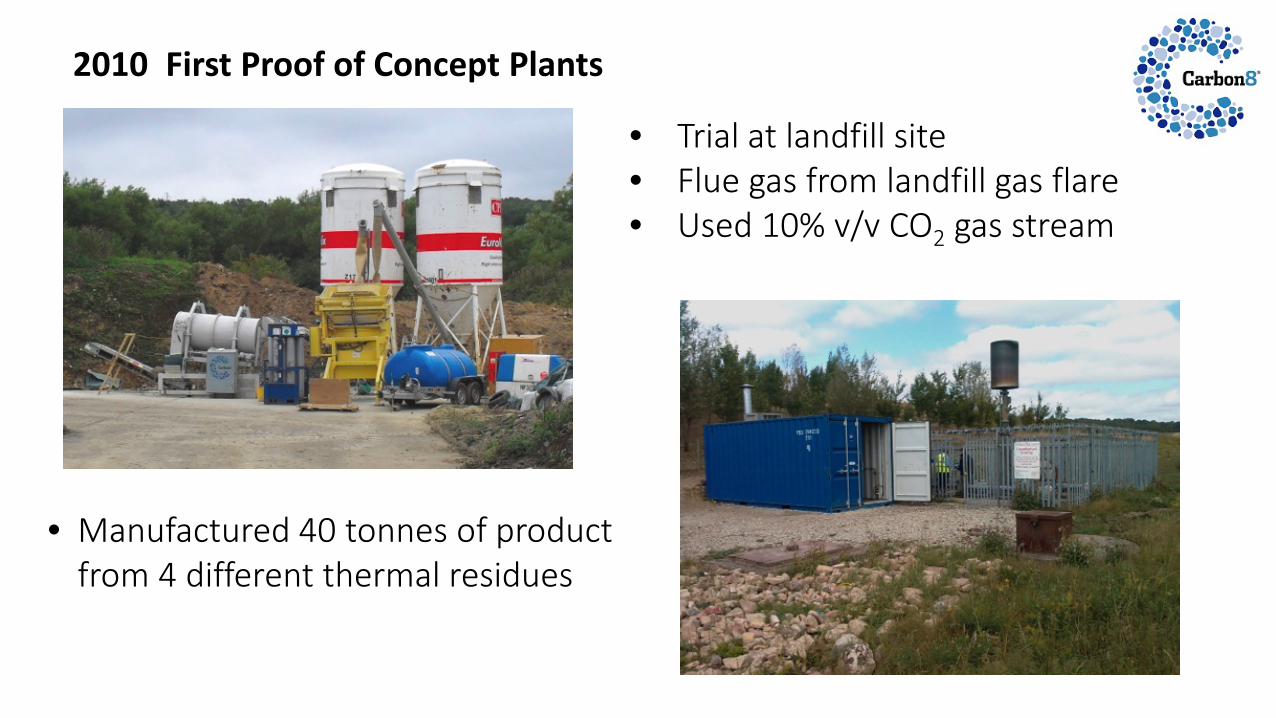

2010 First Proof of Concept Plants

• Trial at landfill site • Flue gas from landfill gas flare • Used 10% v/v CO2 gas stream

• Manufactured 40 tonnes of product from 4 different thermal residues

2010

• Formed Carbon8 Aggregates Limited • Licence to treat APCr in the UK • Gained first round investment – to fund larger scale pilot plant • Manufactured sufficient aggregate (200 tonnes) for manufacture of full

run of aggregate blocks • Data for submission to regulator for “end of waste”

Success of pilot led to: • Investment in Carbon8 Aggregate by a waste management company • Building of first fully commercial plant on block makers site • Plant commissioned in February 2012 • Launch of “Carbonbuster” first carbon negative block

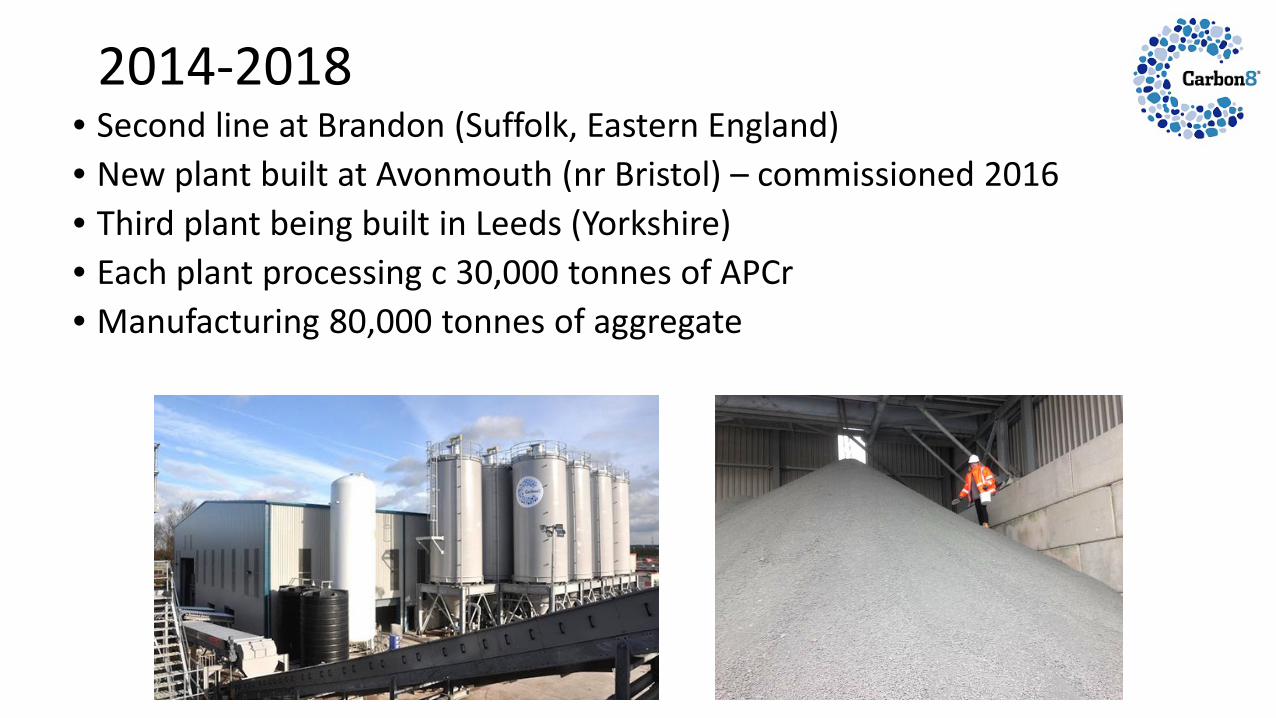

2014-2018 • Second line at Brandon (Suffolk, Eastern England) • New plant built at Avonmouth (nr Bristol) – commissioned 2016 • Third plant being built in Leeds (Yorkshire) • Each plant processing c 30,000 tonnes of APCr • Manufacturing 80,000 tonnes of aggregate

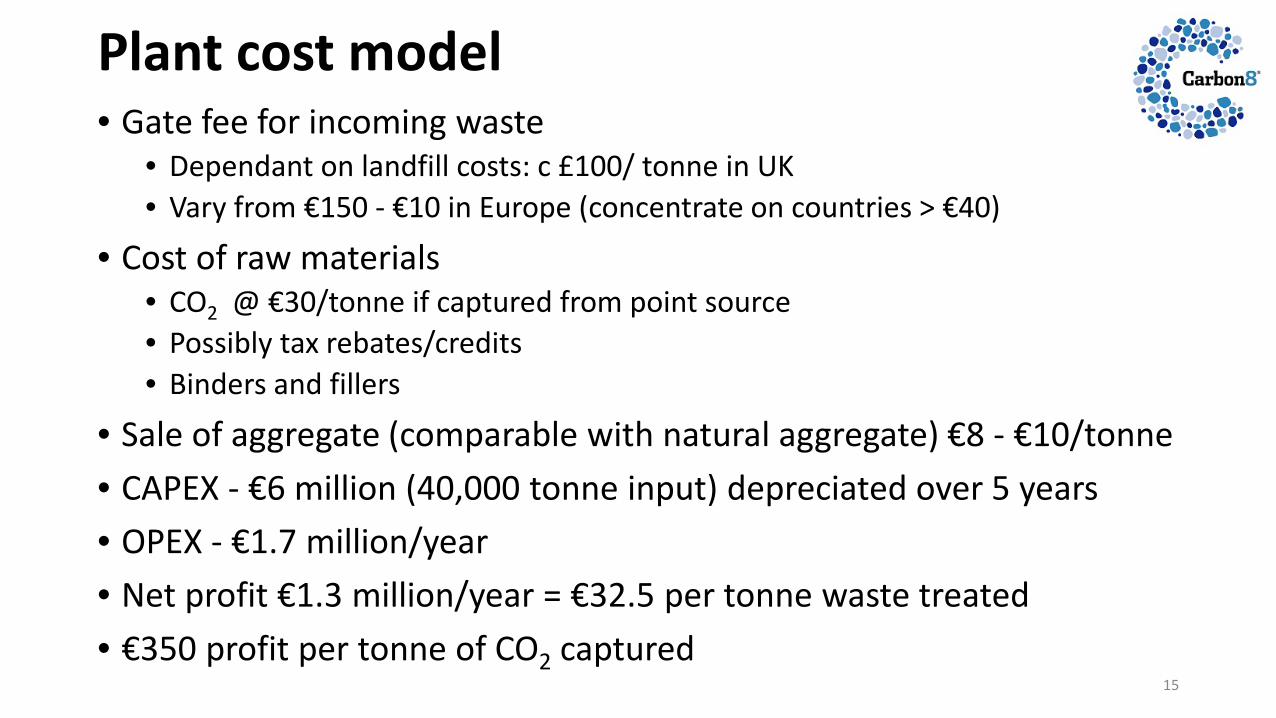

Plant cost model • Gate fee for incoming waste

• Dependant on landfill costs: c £100/ tonne in UK • Vary from €150 - €10 in Europe (concentrate on countries > €40)

• Cost of raw materials • CO2 @ €30/tonne if captured from point source • Possibly tax rebates/credits • Binders and fillers

• Sale of aggregate (comparable with natural aggregate) €8 - €10/tonne • CAPEX - €6 million (40,000 tonne input) depreciated over 5 years • OPEX - €1.7 million/year • Net profit €1.3 million/year = €32.5 per tonne waste treated • €350 profit per tonne of CO2 captured

15

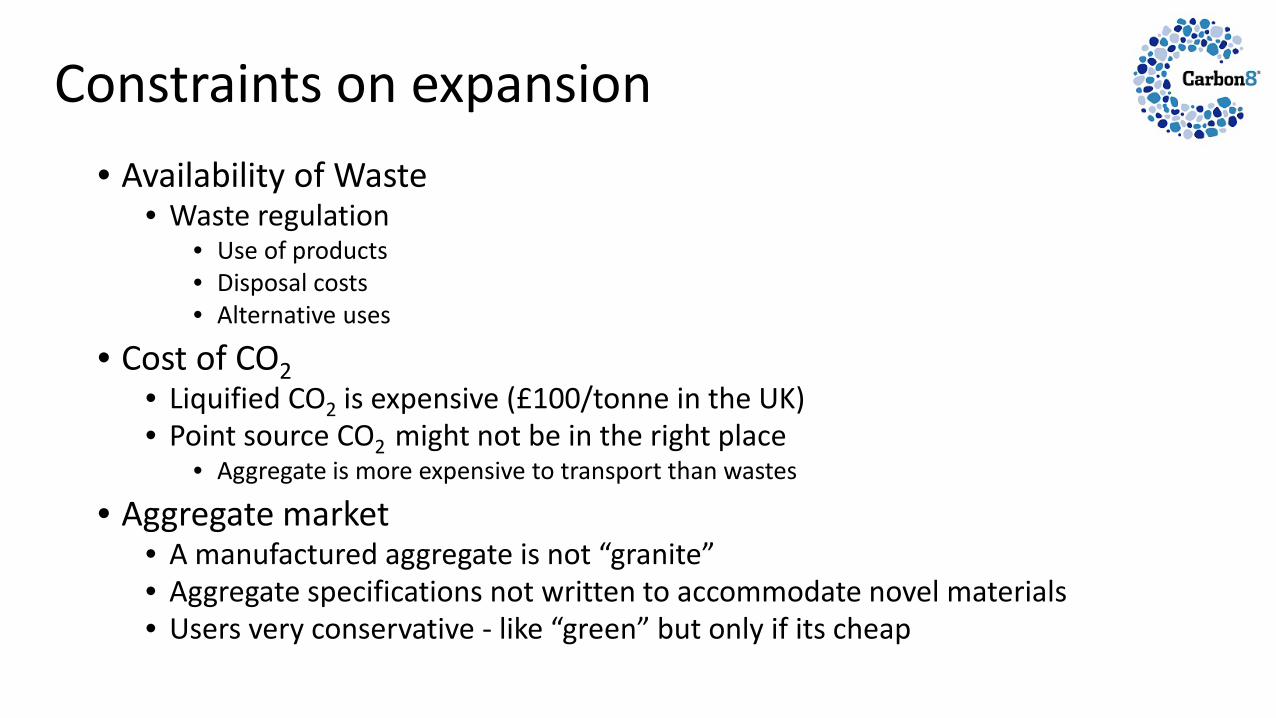

Constraints on expansion • Availability of Waste

• Waste regulation • Use of products • Disposal costs • Alternative uses

• Cost of CO2 • Liquified CO2 is expensive (£100/tonne in the UK) • Point source CO2 might not be in the right place

• Aggregate is more expensive to transport than wastes

• Aggregate market • A manufactured aggregate is not “granite” • Aggregate specifications not written to accommodate novel materials • Users very conservative - like “green” but only if its cheap

Scale of CO2 capture in aggregate

• The Global CO2 initiative (GCI) predicted that carbonate aggregates could store up to 3.6 Gt/yr by 2030

• This figure included mineralisation of virgin materials as well as the carbonation of industrial wastes.

• Other researchers have suggested that there are up to 10Gt of mineral wastes available for carbonation worldwide

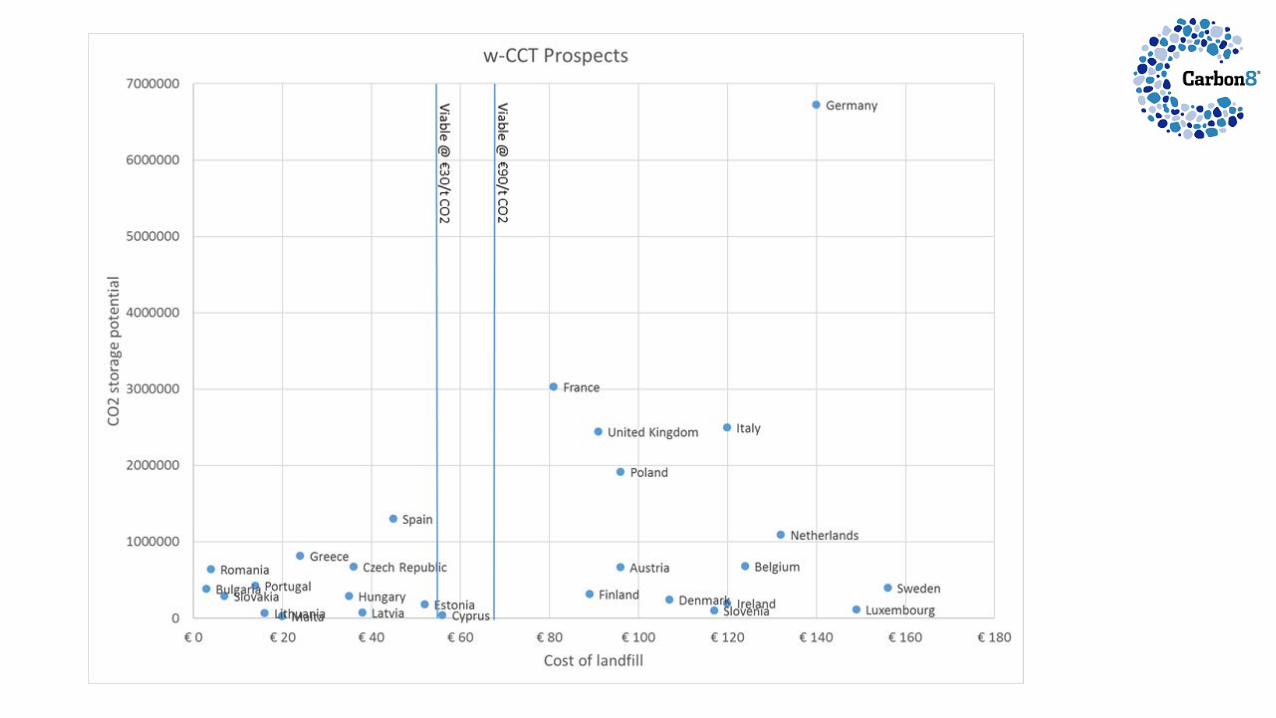

• Carbon8 Systems has looked at the potential for CO2 sequestration in Europe

• Euro statics for quantities of waste • Laboratory data on CO2 uptake of each type of waste • Considered the availability of each waste stream – alternative uses etc • Considered only countries in Europe where landfill costs provide an incentive

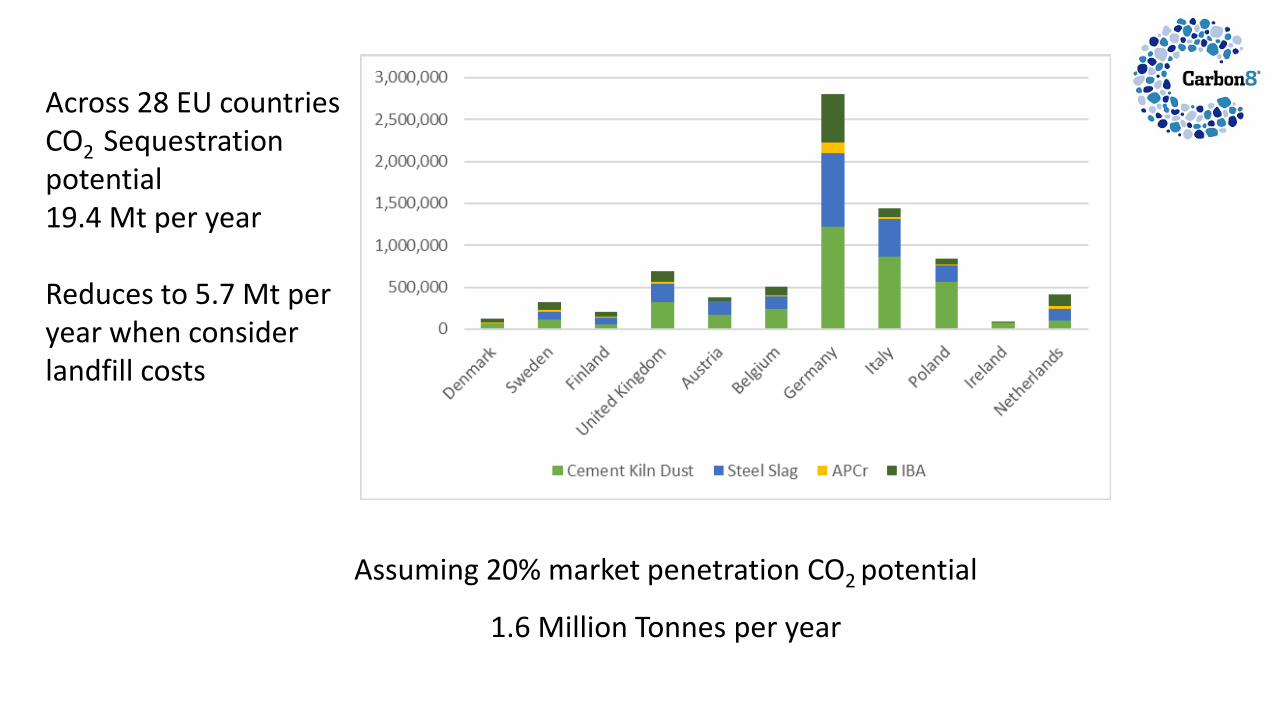

Assuming 20% market penetration CO2 potential

1.6 Million Tonnes per year

Across 28 EU countries CO2 Sequestration potential 19.4 Mt per year Reduces to 5.7 Mt per year when consider landfill costs

Current Scale of CO2 capture • Thermal residues uptake CO2 at 5-20% w/w, depending on

chemistry/mineralogy

• MSW APCr is quite reactive (10% w/w), but bulk CO2 is expensive and so the amount used in current plants is minimised

• CO2 applied at 7-10% w/w, and is enough to stabilise and carbonate-cement the product

• Three plants capturing 7,700 t/year bulk CO2

• If a value for carbon is realised, then more CO2 could be used

• Globally, circa 1Gt (suitable) waste, with potential to sequester >100Mt CO2