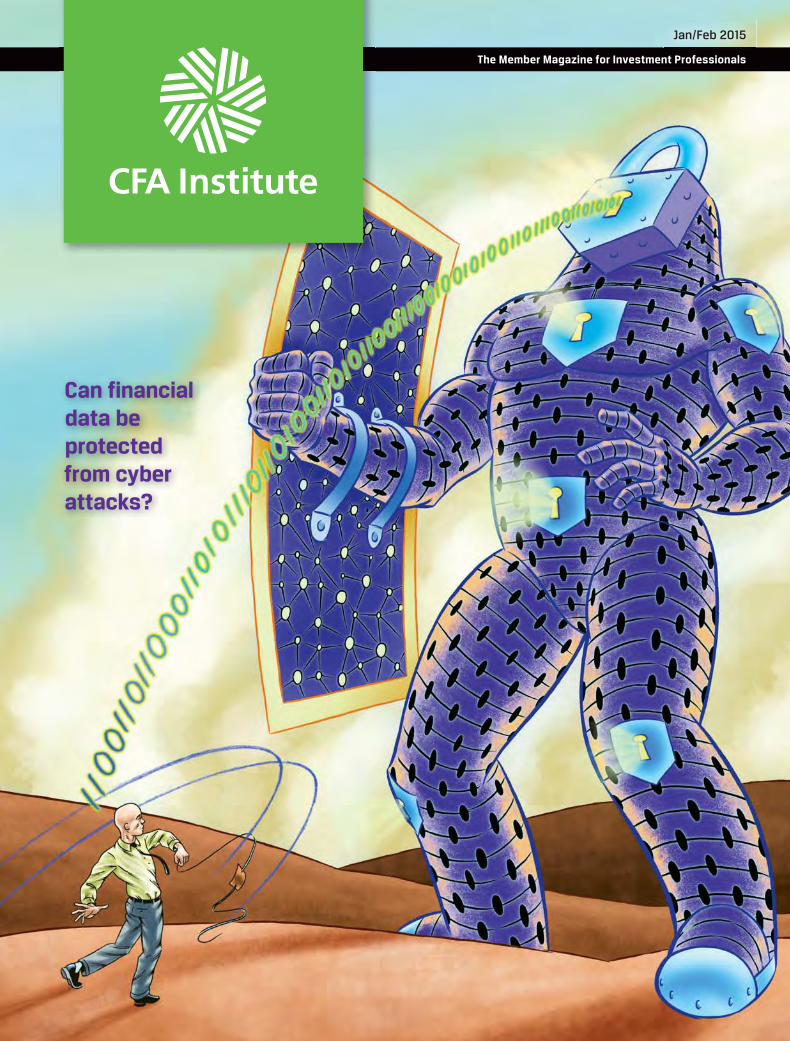

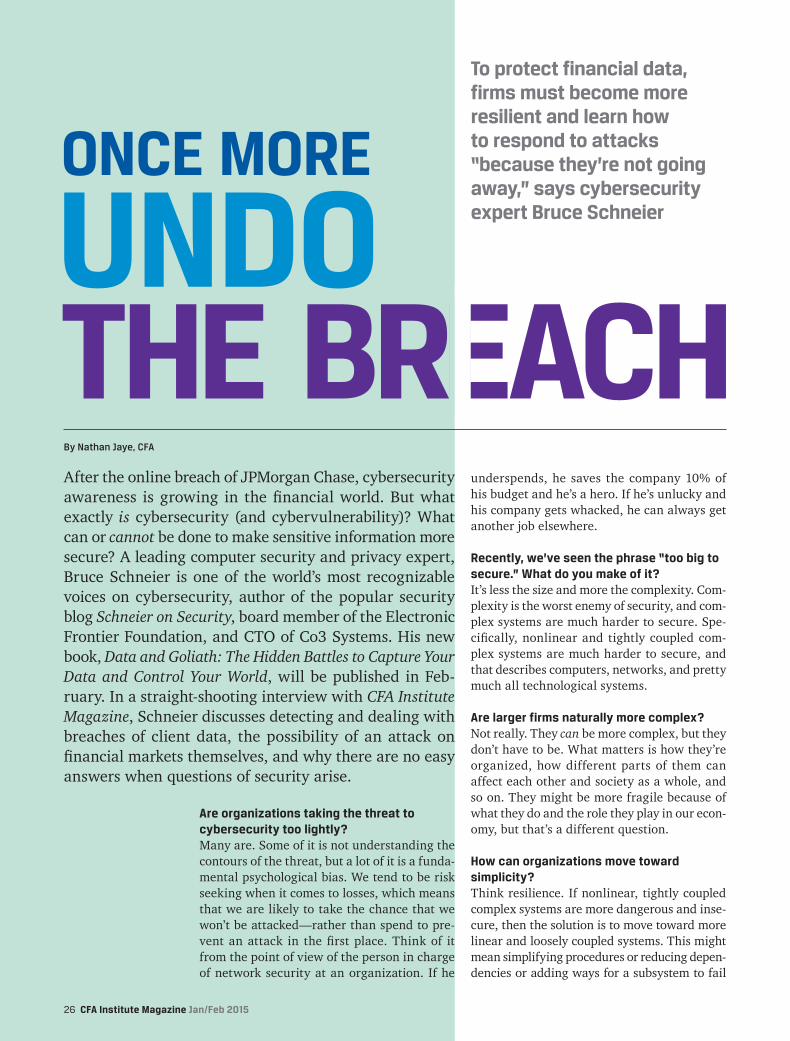

Can financial data be protected from cyber attacks? - CFA ...

44

Can financial data be protected from cyber attacks? The Member Magazine for Investment Professionals Jan/Feb 2015

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Can financial data be protected from cyber attacks? - CFA ...

Can financial

data be

protected

from cyber

attacks?

The Member Magazine for Investment Professionals

Jan/Feb 2015

•

•

•

•

•

•

• •

•

•

•

•

•

• 1

Interactive Brokersfor Institutions

1 1

cfa

stocks • options • futures • forex • bonds — on over 100 markets worldwide from one account

1 1

Jan/Feb 2015

COVER STORY

26 Once More Undo the BreachTo protect financial data, firms

must learn how to survive

cyberattacks and respond to them

more effectively because prevention

is an obsolete concept, says

cybersecurity expert Bruce Schneier.

By Nathan Jaye, CFA

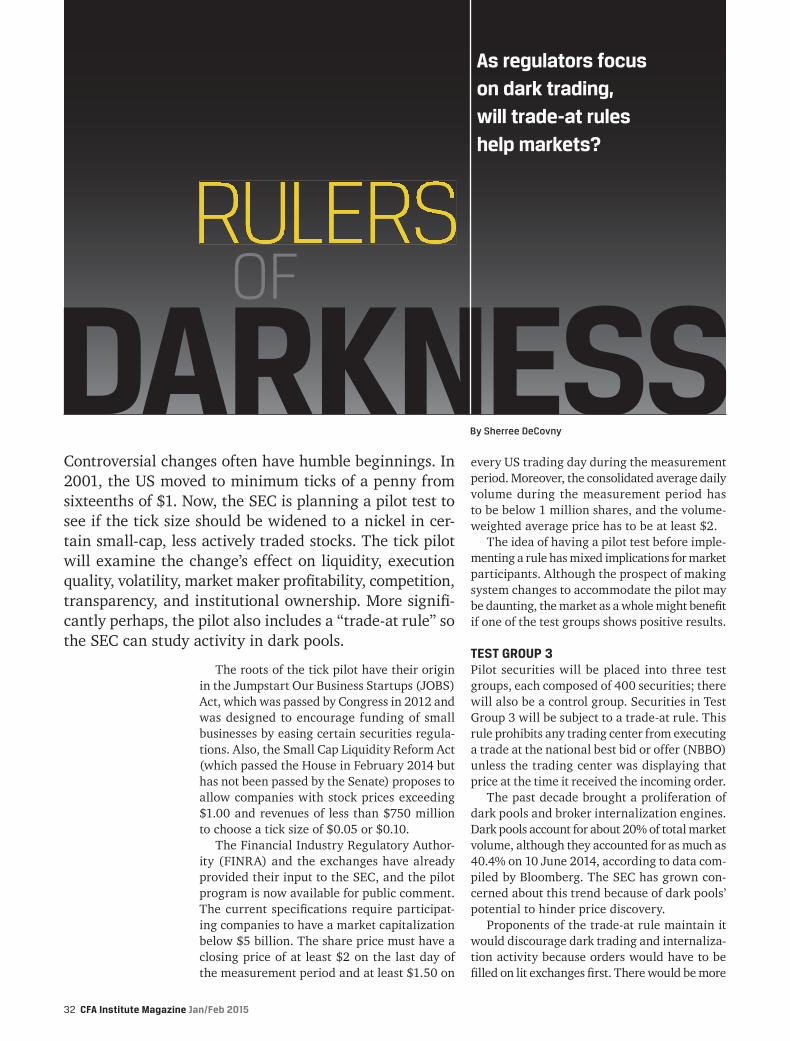

32 Rulers of DarknessAre trade-at rules the best way

for regulators to shed light on

dark trading?

By Sherree DeCovny

CFA INSTITUTE NEWS

8 EMEA Voice

ESG in Investing: Highlights from EuropeBy Usman Hayat, CFA

9 APAC Focus

The ROI of Learning and DevelopmentBy Richard McGillivray

11 Miscellaneous Briefs

VIEWPOINT

13 Toward a New Framework for Private WealthTo improve performance, better structures

and investment processes are needed

By Pranay Gupta, CFA

15 The Decisive Advantage of DecisivenessOverlooked skills can help an investment

manager stand out from the crowd

By Jason Voss, CFACOVER ILLUSTRATION

Kelly Alder

11

12

13

26

AlphaSense is a registered service mark of AlphaSense, Inc. | www.alpha-sense.com

AlphaSense is , including some of the world’s largest investment rms and anks, managing over $3 trillion in AUM.

AlphaSense is a game changer for research. Everyone will need it.

Portfolio ManagerNew York

“I spent a week building a report that this tool built in a minute.

Research AnalystSan Francisco

“

ith one search, AlphaSense helps you nd key information uried in roker research, S lings, call and event transcripts, IR presentations and your own proprietary content.

With AlphaSense, you can:

Keyword search millions of documents and use uni ue lters to hone results

Search across all public companies worldwide and know exactly who said what

Get email alerts every time a company mentions “X” (any keyword or theme)

Upload your own content – AlphaSense will index it and make it searcha le

Annotate content, take notes and access your intel on the companies and themes you track – even at a meeting or on the road

AlphaSense helps you nd what others miss on pu lic companies worldwide

The New Search Engine for Analysts

Request a free trial today. Visit www.alpha-sense.com or call 212.203.2799

Introducing AlphaSense

No More R -F AlphaSense eliminates the need to search documents one at a time.

LEARN MORE.FactSet.com/advise

Data and Analytics to Advise with Confidence You can’t predict what’s going to happen in the future, but you can use the right tools to determine the best asset allocation strategy. Incorporate custom capital market assumptions and simulate portfolio performance of various asset allocation strategies so you can advise your clients on an optimal path to reach their unique goals.

PROFESSIONAL PRACTICE

18 Investing with “impaired vision”

20 A new era of investment potential for solar power?

22 How Social Security benefits boost optimization

24 Demonstrating added value

ETHICS AND STANDARDS

36 Market Integrity and Advocacy

• “An ideal platform for influencing policy”

• Beyond Bitcoin: crypto 2.0 vs. regulators

• Closing the gap for non-GAAP performance measures

• Will Hong Kong lose its special status?

40 Professional Conduct

Notices of disciplinary action

5 In Summary

Jan/Feb 2015

36

CFA Institute Magazine (ISSN 1543-1398, CPM 400314-55) is published bimonthly—in January, March, May, July, September, and November—by CFA Institute. Periodicals postage paid at Charlottesville, VA, and additional mailing offices. POSTMASTER: Send address changes to CFA Institute Magazine, 915 East High Street, Charlot-tesville, VA 22902.

Statements of fact and opinion are the responsibility of the authors alone and do not imply an endorsement by CFA Institute.

Copyright 2015 by CFA Institute. All rights reserved. Materials may not be reproduced or translated without written permission. CFA®, Chartered Financial Analyst®, the CFA Institute logo, Claritas®, GIPS®, and CIPM® are just a few of the trademarks owned by CFA Institute. See www.cfainstitute.org for a complete list.

Annual subscription rate for CFA Institute members is US$40, which is included in the membership dues. Annual nonmember subscription rate is US$50.

THE AMERICAS915 East High StreetCharlottesville, VA 22902USAPhone: (800) 247-8132 or

+1 (434) 951-5499

477 Madison Avenue, 21st floorNew York, NY 10022 USAPhone: +1 (212) 754-8012

EUROPE, MIDDLE EAST & AFRICA131 Finsbury Pavement, 7th FloorLondon EC2A 1NTUnited KingdomPhone: +44 (20) 7330-9500

ASIA–PACIFIC23/F, Man Yee Building68 Des Voeux RoadCentral, Hong KongPhone: +852 2868-2700

BRUSSELSNCI LOCARTIS European ParliamentSquare de Meeûs 38/401000 Brussels (Belgium)Phone: +32 (02) 401-6828

Jan/Feb 2015 Vol. 26, No. 1

EDITORIAL ADVISORY TEAMShanta AcharyaBashir Ahmed, CFAJim Allen, CFAJonathan Boersma, CFAJarrod Castle, CFAMichael Cheung, CFAJosephine Chu, CFAFranki Chung, CFADarrin DeCosta, CFANick Dinkha, CFAJerry Donohue, CFAAlison Durkin, CFAKenneth Eisen, CFAWilliam Espey, CFAJulie Hammond, CFABurnett Hansen, CFAM. Mahboob Hossain, CFAVahan Janjigian, CFAAndreas Kohler, CFAAaron Lai, CFA

Kate Lander, CFACasey Lim, CFAMichael Liu, CFABob Luck, CFAFarhan Mahmood, CFADennis McLeavey, CFASudip Mukherjee, CFAJerry Pinto, CFALinda RittenhouseCraig Ruff, CFAChristina Haemmerli Schlegel, CFADavid Shen, CFAArjuna Sittampalam, ASIPLarry Swartz, CFAJacky Tsang, CFAGary Turkel, CFARaymond Wai Pong Yuen, CFAJames Wesley Ware, CFAJean Wills

CFA INSTITUTE PRESIDENT AND CEODwight D. Churchill, CFA

MANAGING EDITORRoger [email protected]

ONLINE PRODUCTION COORDINATORKara Hite

ADVERTISING MANAGERTom [email protected]

ASSISTANT EDITORMichele Armentrout

GRAPHIC DESIGNCommunication Design, [email protected]

CIRCULATION COORDINATORJennette [email protected]

4 CFA Institute Magazine Jan/Feb 2015

Jan/Feb 2015 CFA Institute Magazine 5

Let There Be Light

The characters of Charles Dickens’ classic yuletide tale A Christmas Carol are so vivid and familiar that they seem like old acquaintances, from the miserly Ebenezer Scrooge

-ures lurks in the shadows. It is the darkness.

This darkness is more than the absence of illumination. It seems to be a mysterious presence that slithers into every scene and coils itself around any source of light. Along the street at night, a multitude of candles are “like ruddy smears upon the palpable brown air.” Even when a lamp is held up to the dark, the “scanty light” is constricted.

People instinctively distrust any lack of visibility. This is -

parency” in a variety of forms has become a common refrain. Terms such as “dark pools” and “dark trading” have an omi-nous sound. For more substantial reasons, concerned reg-ulators have begun to peer into the dark and develop poli-cies (“Rulers of Darkness,” 32). They are also trying to shed light on shadowy crypto-currencies (“Beyond Bitcoin,” 37).

But Scrooge prefers poor visibility. “Darkness is cheap, and Scrooge liked it,” writes Dickens. Scrooge has a point.

-sive, and likely to burn the house down. Modern methods demand vast electric grids. To lower his electric bill, maybe

a modern Scrooge would invest in trends with potential to make solar power inexpensive and practical (“Solar Flair,” 20). The Scrooge in the story certainly believes in the advan-tages of impaired property, for he lives in “a gloomy suite of rooms, in a lowering pile of building up a yard, where it has so little business to be” (“Impaired Vision,” 18).

Scrooge not only makes his residence in an isolated, fore-boding place but also double-locks himself inside two sets of doors. Like modern computer networks, however, the system is easily penetrated by “hackers”—a ghost and three Christ-

-vention is futile against virtual intruders. The trick is to “fail gracefully” through resilient adaptation, says cybersecurity expert Bruce Schneier (“Once More Undo the Breach,” 26).

Graceful failure for Scrooge means going through a pain-ful process of enlightenment about his inner darkness. With the help of three spirits, he sees his former life carrying him “through the lonely darkness over an unknown abyss.” When his black heart is illuminated by compassion like “a

-

Roger Mitchell, Managing Editor ([email protected])

IN SUMMARY

Literature Review

ISLAMIC FINANCE: ETHICS, CONCEPTS, PRACTICE

Usman Hayat, CFAAdeel Malik, PhD

This review will clarify misconceptions and serve as a rich and nuanced introduction to

© 2014 CFA Institute

For more information or to download a free copy, visit www.cfainstitute.org/islamic_finance.

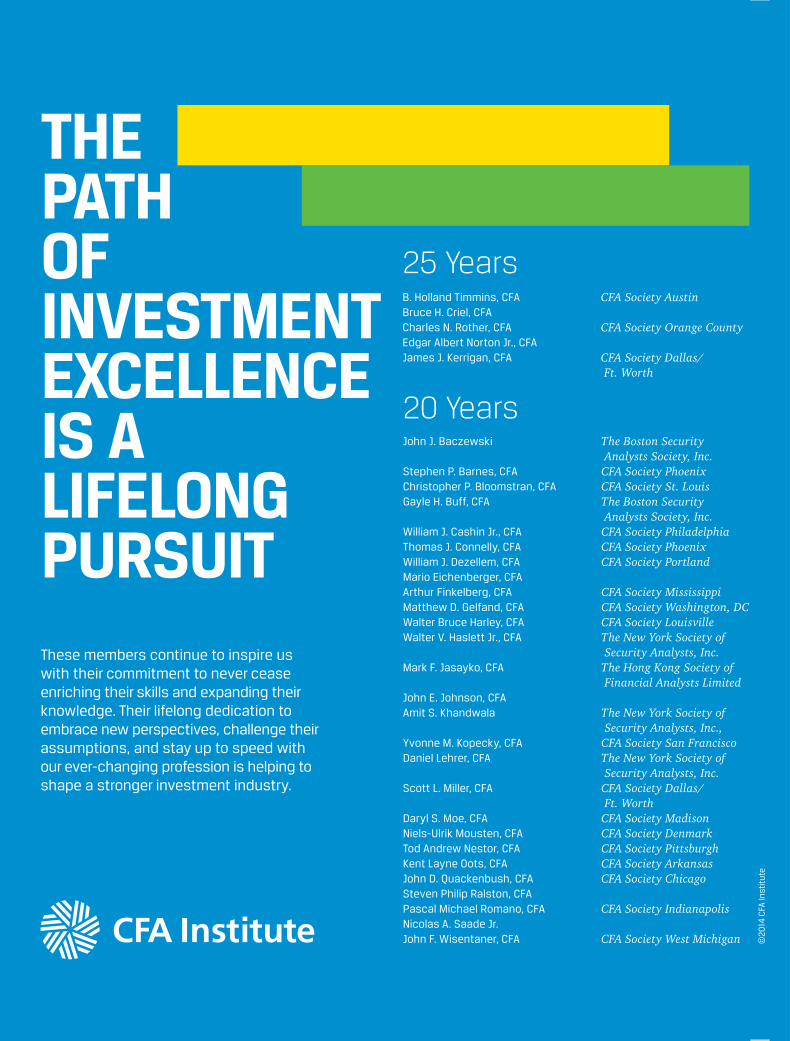

25 YearsB. Holland Timmins, CFA CFA Society AustinBruce H. Criel, CFACharles N. Rother, CFA CFA Society Orange CountyEdgar Albert Norton Jr., CFAJames J. Kerrigan, CFA CFA Society Dallas/

Ft. Worth

20 YearsJohn J. Baczewski The Boston Security

Analysts Society, Inc.Stephen P. Barnes, CFA CFA Society PhoenixChristopher P. Bloomstran, CFA CFA Society St. LouisGayle H. Buff, CFA The Boston Security

Analysts Society, Inc.William J. Cashin Jr., CFA CFA Society PhiladelphiaThomas J. Connelly, CFA CFA Society PhoenixWilliam J. Dezellem, CFA CFA Society PortlandMario Eichenberger, CFAArthur Finkelberg, CFA CFA Society MississippiMatthew D. Gelfand, CFA CFA Society Washington, DCWalter Bruce Harley, CFA CFA Society LouisvilleWalter V. Haslett Jr., CFA The New York Society of

Security Analysts, Inc.Mark F. Jasayko, CFA The Hong Kong Society of

Financial Analysts LimitedJohn E. Johnson, CFAAmit S. Khandwala The New York Society of

Security Analysts, Inc., Yvonne M. Kopecky, CFA CFA Society San FranciscoDaniel Lehrer, CFA The New York Society of

Security Analysts, Inc.Scott L. Miller, CFA CFA Society Dallas/

Ft. WorthDaryl S. Moe, CFA CFA Society MadisonNiels-Ulrik Mousten, CFA CFA Society DenmarkTod Andrew Nestor, CFA CFA Society PittsburghKent Layne Oots, CFA CFA Society ArkansasJohn D. Quackenbush, CFA CFA Society ChicagoSteven Philip Ralston, CFAPascal Michael Romano, CFA CFA Society IndianapolisNicolas A. Saade Jr.John F. Wisentaner, CFA CFA Society West Michigan

These members continue to inspire us with their commitment to never cease enriching their skills and expanding their knowledge. Their lifelong dedication to embrace new perspectives, challenge their assumptions, and stay up to speed with our ever-changing profession is helping to shape a stronger investment industry.

THE PATH OF INVESTMENT EXCELLENCE IS A LIFELONG PURSUIT

©20

14 C

FA In

stit

ute

15 YearsCraig D. Allen, CFA CFA Society San DiegoJoseph A. Anglin, CFA CFA Society ColoradoFrancois E. Aubert CFA Society SwitzerlandMichael D. Axel, CFALaurent A. Bachmann, CFA CFA Society SwitzerlandMark W. Bodie, CFA The New York Society of

Security Analysts, Inc. Pui Wah Regina Chan, CFA CFA Society TorontoDon M. Chance, CFAAlina Chiew, CFADouglas Sherman Cronk, CFA CFA Society OkanaganRobert James Denoo CFA Society ChicagoBeverly A. Durston CFA Society SydneyAlain Eckmann, CFA CFA Society SwitzerlandJoseph D. Eskridge Jr., CFATheo Evangelakos, CFA CFA MontrealChristian Faitz, CFA CFA Society GermanyMichael P. Fogarty, CFA CFA Society Kansas CityMichael K. Frommelt, CFA CFA Society LiechtensteinJean-Pierre Galichon The New York Society of

Security Analysts, Inc.Gary E. Gordon, CFA CFA Society BaltimoreJohn F. Gualy, CFA CFA Society HoustonSteven Philip Habegger, CFAMatthew John Haertzen, CFA CFA Society PhoenixCraig Hicklin Harrel, CFA CFA Society HoustonWarren Huang, CFAAndrew J. Hutton, CFA CFA Society United KingdomFuminori Imura, CFAShirin Ismail, CFAPaul Timothy Kaspar, CFA CFA Society MinnesotaMark J. Kavaloski CFA Society Los AngelesJason Kiss, CFA CFA Society San FranciscoHendrik A. Klein Haneveld, CFAHenry Chi-Yin Lam, CFA The Hong Kong Society of

Financial Analysts LimitedDirk E. Laschanzky, CFA CFA Society IowaMattias Ledunger, CFA CFA Society SwitzerlandDerrick Hong-Peng Lee, CFANelson Cheong Wing Lee, CFA The Hong Kong Society of

Financial Analysts LimitedSean Anthony Lynch, CFA CFA Society NebraskaThomas P. Madsen, CFA CFA Society ChicagoZenon Andrzej MarciniakWilliam Gordon McBean, CFA CFA Society Orange CountyJ.R. Melikian, CFA CFA Society JacksonvilleDaren E. Miller, CFA CFA Society CalgaryGeorge L. Montgomery, CFA CFA Society PhiladelphiaRonald L. Moy, CFAConor Savio Muldoon, CFA CFA Society Los AngelesRaymond L.H. Murphy III, CFA The Boston Security

Analysts Society, Inc.Alan F. Niederer, CFA CFA Society Switzerland

Ana Dolores Novaes, CFA CFA Society BrazilDaniel Doyce Payne, CFA CFA Society JacksonvilleRobert Matthew Peets, CFA CFA Society VancouverCraig P. Prall, CFA CFA Society Atlantic CanadaPaul William Reisz, CFA CFA Society Los AngelesMario Ruiz, CFA CFA Society OttawaPierre Saint-Laurent, CFA CFA MontrealRoelof M. Salomons, CFA CFA Society NetherlandsRobert A. Seiler, CFA CFA Society SwitzerlandWilliam A. Shahriari, CFA CFA Society Tampa BayJohn Simmons, CFA CFA Society ChicagoRaymond J. Slatter, CFAKaj Mikael Somerkoski, CFAKanna Sriskanthan, CFA CFA Society StamfordCraig B. Stanford, CFA CFA Society CalgarySuzanne D. Stepan, CFA CFA Society West MichiganRehaz N.M. Subdar, CFA CFA Society TorontoPaul Victor Temperton, CFA, CIPM CFA Society United KingdomIsabelle Juillard Thompsen, CFA CFA Society United KingdomMatthew Irvin Walter, CFA CFA Society South CarolinaWataru Watanabe, CFARichard J. Wayman, CFA CFA Society ColumbusKevin J. Williams, CFA CFA Society HawaiiDaniel A. Xystus, CFA The Hong Kong Society of

Financial Analysts LimitedClay H. Young, CFA CFA Society North CarolinaE. A. Tony Zaremba, CFA CFA Society CalgaryJoseph M. Zuiker, CFA CFA Society Bermuda

Join us in applauding the energy, effort,

and perseverance of these members in

achieving these Continuing Education

milestones in 2013.

CFA INSTITUTE NEWSEMEA VOICE

ESG in Investing: Highlights from Europe

By Usman Hayat, CFA

When a large company, such as British Petroleum, Lonmin, or GlaxoSmithKline, makes headlines for the wrong reasons, the underlying cause is often linked to envi-ronmental, social, or governance (ESG) factors. Examples of ESG issues include cli-mate change, environmental degradation, water stress, human rights, employee rela-tions, corruption, and executive compen-sation. Fortunately, ESG issues in invest-

ing are not all negative. Within the past year, a host of pos-itive developments have occurred in the wider ESG space.

GROWTH OF GREEN BONDS

The era of green bonds has come, claims a 2014 report by the Climate Bonds Initiative, which estimates that the green bonds market “stood at $35.8bn outstanding on 10 June 2014, with issuance in 2013 ($11bn) and 2014 ($18.3bn) accounting for over 80% of the total outstanding.” The report describes these as bonds “where the use of proceeds is for climate or environmental projects and they are labelled as ‘Green’” and attributes their growth to rising interest in ESG issues. A major concern about green bonds is whether they are merely a strategic re-branding of what would otherwise have been conventional bonds. In 2014, 13 commercial and investment banks, along with the IFC and the World Bank, launched a set of voluntary guidelines to bring clarity to the processes involved in issuing and managing such bonds. For the long-term sustainability of the green bond segment,

EXCLUSIONARY SCREENING

Different methodologies are used by investors to consider ESG issues in investing, but the oldest methodology—exclu-sionary screening—is the most widely used. Exclusionary screening means not investing in companies because what they do is against the investor’s values. According to the 2014 European Sustainable and Responsible Investment Study published by Eurosif, exclusionary screening covers “about 41% (€7 trillion) of European total professionally managed assets.” Thus, exclusionary screening accounts

-ing may come as a surprise to those who argue for moving away from exclusionary screening to ESG integration or those who consider ESG issues strictly as economic risks

FOSSIL FUEL DIVESTMENT

That climate change may have a “serious, pervasive and irreversible” impact on human society and nature is at the

heart of the fossil fuel divestment campaign. Many inves-tors have pledged to withdraw from fossil fuel investments

series of small moral victories for the campaigners, such as

impact? Some observers believe that the divestment cam-paign relating to apartheid in South Africa shows that such

discourse. Others are cautioning investors that some fossil

on investors.

IMPACT INVESTING

beyond its size, attracting the attention of investors, entre-preneurs, politicians, and even the pope. According to the 2014 report of the Social Impact Investment Taskforce (established under the UK’s presidency of the G–8), “social impact investments are those that intentionally target spe-

-sure the achievement of both.” Capturing data and market perspectives from 125 impact investors, the 2014 impact-investment survey by the Global Impact Investing Network and J.P. Morgan Social Finance states that “shortage of high quality investment opportunities with track record” is the single most important challenge facing impact investments.

ESG EDUCATION AND CFA INSTITUTE

CFA Institute continues to offer a variety of educational opportunities regarding ESG issues in investments. In Sep-tember 2014, we launched a free e-course, ESG-100, which offers a comprehensive introduction to ESG issues in invest-ing. The course is accessible at cfa.is/ESG100. In addition, as part of a wider practice-analysis process, our curricu-lum team has conducted focus groups with ESG specialists in London, New York, Amsterdam, and Hong Kong to keep the ESG-related content in the CFA Program curriculum up to date with industry practice. The 2015 CFA Institute Annual Conference in Frankfurt this April will have more than one session dedicated to ESG issues in investing. Our member societies also continue to hold such events as the “Alpha from Sustainability” conference organized by CFA Society Netherlands in October 2014. If you are a member of CFA Institute and would like to offer your expertise in ESG issues in investing for our educational efforts, please email me at [email protected].

Usman Hayat, CFA, is director of Islamic finance and ESG at CFA Institute.

8 CFA Institute Magazine Jan/Feb 2015

The ROI of Learning and Development

By Richard McGillivray

Measuring the return on investment of learning and devel-opment (L&D) programs has been one of the major chal-

past year, the CFA Institute institutional partnerships team -

als about this question, particularly as it relates to the appli-cation of knowledge-based curricula, such as the Claritas®

In our experience, L&D ROI is more often evaluated sub-jectively in the workplace rather than measured empiri-cally. There are many reasons for this tendency, including the challenge of isolating the impact of training as a vari-able in the performance and contribution of employees who are complex social beings working in complex social teams and workplaces. Drawing on insights gained from speaking

--

ing and learning.First, when customers know they are dealing with a com-

pany that invests in high-quality, reputable training, it gives --

company’s commitment to delivering consistent high-quality services throughout the customer journey and across geo-graphic regions. Thus, to ensure that ROI in training is effec-tive for client acquisition and retention, companies value partnering with L&D providers that are well known, reputa-ble, and supportive (in branding terms) of their businesses.

Second, employer brand is increasingly a key factor in companies’ ability to attract talent. The most talented profes-sionals favor employers known to invest in their employees, both in structured development and practical opportunity. Such professionals recognize that having worked at a top employer brand enhances their appeal to future employers, particularly because of the training investments that have been made. L&D providers that are reputable and have a

-tribute to this perception when their brands are also visible to individuals and carry their own intrinsic value.

In modern, knowledge-based workplaces, learning hap-

with which we are able to learn things because they are close to what we already know. For example, a person who under-stands the fundamentals of accounting will more quickly assimilate International Financial Reporting Standards than

and concepts. Through horizontal (broader, more general) learning, such as the knowledge-based Claritas Program,

a wide range of other possible learning can become prox-imal. In L&D terms, this effect is one of the reasons why horizontal learning is an effective and necessary founda-tion for vertical (deeper, more expert) learning.

Because so much of learning in the workplace is now social and project based, some of the most valuable com-petencies for individuals to have are those that help them quickly become more proximal to knowledge that they need. This capacity includes the ability to identify, seek out, accu-

--

spear, an independent learning strategist, researcher, and innovator, refers to this as “learning agility.”

Learning agility requires competencies that support immediate, project-based, and social learning. Three com-

to reach out to others, to contribute, to understand the context of a project in which

, which means “I used this approach in a previous project, and I think we

and (3) , which means reaching out to people within one’s organiza-

that’s needed for a particular task.We are encouraged by two key pieces of feedback in our

review of participants in our clients’ Claritas programs. First, they report that their employees have increased their

-lated into willingness among employees to contribute pro-

and its clients.Many of our clients arrange their learning support of the

Claritas curriculum in two important ways. First, learning support groups are arranged to enable individuals to form cross-organizational bonds with colleagues in other func-tional areas. Second, input is provided to learning support groups by in-house subject matter experts. These structures have enabled the movement of expertise between indi-viduals and teams, and the curriculum has provided the common professional language and mutual respect neces-sary for this exchange to happen. In doing so, these clients have succeeded in fostering competencies that are support-

L&D investment.

Richard McGillivray is director of institutional partnerships in Asia Pacific at CFA Institute.

CFA INSTITUTE NEWSAPAC FOCUS

Jan/Feb 2015 CFA Institute Magazine 9

Research Foundation

Aliber Ad

Congratulations to the

newest CFA charterholders

Your CFA designation sets you apart—focused on investment knowledge, committed to integrity. Employers around the world turn to CFA charterholders for the value they bring to clients and for the highest standards of excellence they bring to the industry.

Meet the new charterholders at cfainstitute.org/newclass.

ARE THE FUTURE OF FINANCE

©2014 CFA Institute. CFA®, CFA Institute® and Chartered Financial Analyst® are registered trademarks of CFA Institute in many countries around the world.

Jan/Feb 2015 CFA Institute Magazine 11

Charterholders Ride for PeaceBy Michele Armentrout

When Ahmed Olayinka Sule, CFA, and Uchenna Ndu, CFA, -

working event, they quickly made the connection that they were fellow Nigerians who grew up in two distinctly dif-

Igbo ethnic group, and Sule, in western Nigeria, from the Yoruba ethnic group.

“Nigeria encompasses over 100 different ethnicities, and unfortunately, in many parts of Africa, members of these

Sule said.As their friendship

grew stronger and they began to discuss trib-alism issues in Africa, they often wondered what they could do to impact change in the region for the greater good. (The pair are equally pas-

and tennis, but their exchanges on world matters and social

activism often dominated.) It was during one of these dis-cussions that the investment professionals came up with a novel idea for promoting solidarity and cooperation among

The friends embarked on their journey on 22 August 2014 and raised £535.33 (US$837) for the AET to help children

access education and training.

“It was a great feeling arriving in Paris on 24 August and knowing we achieved our goal without any punctures, bike problems, or accidents,” Ndu said. “And what a wonderful way to get away from technology and clear the head while taking in the beautiful French and English countryside.”

Overall, the trip renewed their faith in the human spirit.“In the course of our ride, we were generously helped

by many people, some of whom donated to our cause when

-phones while others helped with directions when we got off track,” Sule said.

If you are interested in donating to Ndu and Sule’s cause, including upcoming bicycle rides that they are currently planning, contact [email protected] for details.

Michele Armentrout is a communications specialist at CFA Institute.

IN MEMORIAM

Michael O’Loughlin Burpee

Bermuda

Pascale Nadine Canova-Aeberli, CFA

Feusisberg, Switzerland

G. Raymond Chang, CFA

Toronto

Anne B. Dewey, CFA

San Carlos, California

Michael Scott Fuller, CFA

Richmond, Virginia

Anne M. Grichuhin

Bainbridge Island, Washington

Robert H. Harper, CFA

Chicago

Nathan L. Hutson, CFA

Dallas, Texas

Emiel Roland Mahler

South Melbourne, Australia

Mark Rowland, CFA

Atlanta

Christopher Michael Shawe, CFA

London

Samuel H. Talley, CFA

Fairfax, Virginia

Joseph M. Wikler, CFA

Silver Spring, Maryland

Jayne S. Wong, CFA

Lafayette, California

Uchenna Ndu, CFA, continues the 500-kilometer bike ride on Day 2 under sunny

skies, rested and ready to ride to his next destination. Ndu and his fellow

cyclist, Ahmed Sule, CFA, departed from the London Eye on 22 August 2014.

Ahmed Sule, CFA, pauses for a break in the

French countryside en route to Beauvais, a

historic cathedral city in the Northern French

region of Picardy.

CFA INSTITUTE NEWS

CFA INSTITUTE NEWS

Society Leadership Conference

Focuses on Partnerships

The 23rd annual CFA Institute Society Leadership Conference was held in London at Park Plaza West-minster Bridge in September, with more than 350 delegates attending the three-day event that fea-tured seminars, panel discussions, and educational opportunities focusing on the theme “Shaping our Future Together.”

William McGinnis, CFA, of CFA Society Milwaukee, and Sharon Criswell, CFA,

of CFA Society Austin, take advantage of a networking opportunity following

a work session on “Partnership and the Bigger Community.” Both profes-

sionals were awarded a Volunteer of the Year Award for their respective

society engagement.

Maria Barabash and

Elena Matviychuk of

CFA Society Ukraine

celebrate their Most

Outstanding Society

Excellence Award with

Ray DeAngelo, senior

advisor at CFA Insti-

tute, who presented

the award to the

energetic duo.

CFA Institute Board of Governor Member Colin McLean, FSIP, addresses

the audience during a panel discussion with delegates as CFA Institute

CEO Dwight Churchill, CFA, looks on.

CFA Institute Holds Annual Global Policy Summit

In mid-November, CFA Institute hosted a Global Policy Summit in Char-lottesville, Virginia. The event brought together approximately 120 CFA Institute volunteers, society leaders, and staff members from around the world to dis-cuss industry issues and strategies for gener-ating more member and society engagement in advocacy worldwide.

Members of five CFA Institute policy councils—the Corporate Disclosure Policy Council, the Capital Markets Policy Council, the GIPS® Executive Committee, the Standards of Practice Council, and the Asset Manager Code Advisory Committee—were on hand for the two-day event, as were volun-teers from CFA Institute societies who are actively advocating for ethics and CFA Institute standards and policy positions in their local markets.

Ph

oto

by

Mic

hae

l Bai

ley

In the “Ethical Behavior vs. Regulation: Solving the Lack

of Trust” debate (left to right) Samuel Jones Jr., CFA,

member of the Standards of Practice Council, argued the

importance of ethics while Christopher Addy, CFA, chair of

the Capital Markets Policy Council (CMPC) and fellow CMPC

member Bruce Tomlinson, CFA, discussed the merits of

industry regulation.

12 CFA Institute Magazine Jan/Feb 2015

Volunteer with the DRC

If you have an interest in helping to uphold ethical conduct in the investment profes-sion, are a CFA charterholder with no pend-ing professional conduct issues, have a fair and impartial temperament, and have knowledge of or a desire to learn more about the CFA Institute disciplinary process, the Disciplinary Review Committee (DRC) would like to hear from you.

The DRC, a committee of CFA Institute member volunteers who decide disciplin-ary cases, is accepting nominations. Email DRC Administrator Ange Hansen at [email protected] to request an application. Application deadline is 28 February.

For details, visit the “Integrity and Stan-dards” section of www.cfainstitute.org and select “Professional Conduct Program.”

Jan/Feb 2015 CFA Institute Magazine 13

VIEWPOINT

Toward a New Framework for Private WealthTO IMPROVE PERFORMANCE, BETTER INVESTMENT PROCESSES ARE NEEDED

By Pranay Gupta, CFA

Institutional investment management has evolved over the years to become a more transparent product indus-try. Competitive pressures have led to

-cesses, better risk management, lower fees, and greater alignment of inter-est between the asset owner and the asset manager. But private wealth man-agement has been driven historically by the need for privacy, legal struc-tures to protect ownership, and inter-generational transfer of assets. In this framework, the client had a relation-ship with the individual banker rather than with the banking institution. The result was a less effective investment structure for client assets because both the client and the banking institution did not consider management of the assets as a prime objective.

As the legal environment has evolved, the situation for private wealth has also

privacy is no longer possible, (2) global legal structures are more readily avail-able in a cost-effective manner, and (3) strength of institutions has become a bigger factor for a banking relationship. Consequently, the value of the invest-ment proposition for private wealth assets has come into focus. For client

-cient investment proposition, changes will be necessary in the private wealth investment industry. What changes are needed, and what would be the chal-lenges of making such changes? This article outlines possible solutions.

THE INVESTMENT PROBLEM

The requirements of a private client are exactly the same as for any kind

-

real return with a constraint on the

would seem that this requirement can be tackled in exactly the same way as a

traditional institutional plan sponsor’s portfolio problem. But eight key differ-ences make the private wealth invest-

and implement.

(1) A TRUE ABSOLUTE-RETURN REQUIREMENT. Private wealth portfolios come with a constraint on maximum use of hedge funds, implying that the requirement of absolute return has to be met by a solu-tion in which one is long market risk in all asset classes at all times. This is

Institutional asset management sidesteps the abso-lute-return long-market investment problem in three di f ferent ways. First, for long-only products, the solu-tion is having a long market index as a benchmark. Second, for abso-lute-return prod-ucts, the approach is to use the ability to short. Third, for multi-asset prod-ucts, a hybrid of asset class market indexes is used as the benchmark. Plan sponsors do the same by creating a “policy portfolio,” which they use to transform the absolute-return problem of the plan into a relative-return prob-lem to be followed by the managers.

In the private wealth world, however, because discretionary mandates give full control of the investment process to the asset manager, the difference in risk exposure between long-only invest-ments and an absolute-return require-ment falls within direct responsibility of the manager and cannot be sidestepped to a policy portfolio or a hybrid bench-mark. This constraint imposes a true absolute-return investment problem,

the institutional investment manage-ment problem.

(2) CUSTOMIZATION. Institutional invest--

work in which assets are invested in multiple commingled fund structures (internal or external). Private wealth is distinguished by the fact that every

preferences to be incorporated into the portfolio, resulting in limits on invest-ments, liquidity, leverage, single stock holdings, home bias, intergenerational

large number of accounts in private wealth, the customization requirement is a problem for large-scale implemen-tation. Even though the manager may have a single market view, all accounts are different and each one needs a dif-ferent portfolio.

(3) ACCOUNT SIZE. The investment pro-cess in an institutional product can be created for a single portfolio size, at any given time, be it a large or small asset base. In the private wealth setting, however, there can be accounts of dra-matically different sizes that need to be managed at the same time. Accord-ingly, the investment process needs to be simultaneously applicable and Ill

ust

rati

on b

y Ti

mo

thy

Co

ok

14 CFA Institute Magazine Jan/Feb 2015

VIEWPOINT

relevant to very large and very small account sizes.

(4) DEFINED TIME HORIZON. In institutions, although intra-horizon drawdowns are painful, the agency structure serves to delink any emotional attachment to the assets, thereby decreasing behavioral biases in investment decisions. Because private wealth is very much an emo-tional attachment for the owner, the tolerance for intra-horizon drawdowns

-itive impact on the possibilities of the portfolio that are feasible or optimal for private wealth clients.

(5) LIMITATION ON DERIVATIVES. The seg-regated legal structure of institutional assets affords their use as collateral for non-delta-one derivative investments. In the private client world, trying to make such an arrangement for every single client account is cumbersome and limits the types of instruments that can be used to gain or hedge exposure in a private client portfolio.

(6) COST OF MANAGEMENT. The business model of private wealth relies on sourc-ing revenue from multiple points of

the total account, transaction fees for every trade or investment, wider bid–ask spreads, and a management and performance fee for investment prod-ucts. Because of the multiple levels of fees, private wealth assets must clear a higher hurdle than institutional assets (which don’t have these costs) to deliver a similar net-of-fees return.

(7) DIRECT STOCK HOLDING. Private clients have a bias in favor of direct holding of stocks rather than investment in funds. Although this bias is mostly emotional, a rational argument can be made for it. Directly holding a stock is appropri-ate if the objective is an absolute return (and a drawdown is acceptable), rather than holding a stock inside a fund (for which the objective is market-relative performance).

(8) THE BUSINESS MODEL. Private wealth has always had a service-oriented business model in which a critical

component is to include services from other parts of the bank in the asset structure. This kind of arrangement can take the form of using internally man-aged funds from the bank’s own asset management division or using “favored” external managers. Both approaches lead to incurring higher trading and implementation costs. In institutional asset management, the economic inter-ests of the client and asset manager are aligned toward minimizing fric-tional costs, but in private wealth man-agement, these interests diametrically oppose each other because higher imple-mentation costs are direct revenue for the asset manager. Furthermore, the fact that private wealth is a service business means that the relationship manager for the client is more central to all portfolio decisions than is the portfolio manager.

Given these eight structural differ-ences, a standard institutional invest-ment process cannot be directly imported to solve a private wealth problem.

INCUMBENT INVESTMENT

FRAMEWORKS

The traditional investment solution for private wealth assets was based on the concept of a 60/40 balanced portfolio, with some variations. The risk level of the portfolio could be varied to cater to the asset owner’s risk aversion, allow-ing for conservative and aggressive portfolio solutions. Based on this con-ventional framework, four investment approaches have been tried in private wealth. First, in decentralized portfolio management, each relationship team manages its portfolios independently. This approach dilutes investment uni-formity but brings the portfolio closer to the client. Second, in a core–satel-lite portfolio structure, every account invests in a single, core investment product that is internally managed. The remainder (or “satellite”) of an account is managed on an basis. A third approach is the core packaged set of internal funds, in which a core set of in-house investment products is used for all accounts but the account itself is

left to be managed by the relationship manager on an advisory or discretion-ary basis. Finally, with the standardized house view, a single investment view is recommended and implemented with different degrees of rigidity, depend-ing on the account mandate.

All four models fail to tackle the structural problems described earlier in this article. Moreover, they have the

-sion on the percentage of equity expo-sure in the portfolio, driven by a single investment process, dictates the success or failure of the portfolio. Given that market timing cannot be done sustain-ably, the portfolio is therefore always prone to failure at some point.

ALTERNATIVE INVESTMENT

FRAMEWORKS

three alternative frameworks offer the potential to address many of the chal-lenges in private wealth.

(1) A PRIVATE WEALTH MANAGER PLATFORM. Consider a private wealth platform in which professional fund managers make their full portfolio holdings avail-able on a live basis. Through the plat-form, clients would have the ability to invest in any of the funds or directly in the underlying assets of any fund. The fees should be the same, so the man-

as to the implementation choice. The client’s portfolio could be rebalanced according to the client’s choice or the bank’s advice (depending on the man-date), and the client could choose to

taken into account. Although portfolio holding replication would not be feasi-

funds and illiquid funds, this structure would solve a number of critical issues. It would allow full client customiza-tion, facilitate direct stock holding,

taken by a professional fund manager (yet leave the implementation control with the relationship manager), allow a single investment platform for advisory

Jan/Feb 2015 CFA Institute Magazine 15

The Decisive Advantage of DecisivenessOVERLOOKED SKILLS CAN HELP AN INVESTMENT MANAGER STAND OUT FROM THE CROWD

By Jason Voss, CFA

Some of the skills most investment man-agers look for are obvious. You proba-bly recognize these skills as necessary because they permeate the mythology of the investment business. Yet many of the critical skills needed for a suc-cessful investment management career are not taught in business schools, dis-cussed in the business press, or under-

Having hired research analyst interns, research analysts, a portfolio manager, and even my own successor when I retired from investment man-agement in 2005, I have gained a fair amount of knowledge about which skills separate you as an investment manager. Distinctive skills include such attributes as creativity and intuition, which were

If you would like to separate your-self from the crowd of highly motivated and highly intelligent candidates, try adding these to your arsenal of skills. In the second part of the series, I will

decisiveness, absolute versus relative decision making, and forthrightness.

DECISIVENESS

The difference between a research ana-lyst and a portfolio manager is that an analyst aims a gun but the burden of

on the manager. This difference under-scores not only the grave stresses that can come with responsibility but also the need for decisiveness in investment management.

I have worked with analysts whose experience in the investment business was greater than mine as a portfolio manager. Even so, when I would ask these analysts for their opinion about a business and a prospective investment in that business—“Would you buy at the current price?”—they would answer the question with loads more data. While

This article is adapted from an ongoing series of posts being published on the Enterprising Investor blog. To date, installments in the Skills That Separate You as an Investment Manager series have addressed the following topics: introspection (April), creativity (May), intuition (June), decisiveness (July), absolute versus relative decision making (August), forthrightness (September), discernment (October), and scaling (November). All posts in the series are available at blogs.cfainstitute.org/investor.

and discretionary clients, and reduce the bias toward in-house funds. This structure is already present in institu-tional asset management for large cus-tomized managed accounts (as well as in the alternatives world), where it facilitates greater transparency and better risk management. There seem

-

wealth asset management.

(2) A GROUP OF THEMATIC PORTFOLIOS. First-generation wealth creators often have

dynamics that are better articulated as trends or themes rather than as equity–bond allocation decisions or stock selec-tions. With this kind of client in mind, what if a private bank’s investment team were to create and manage trans-parent security portfolios that capital-

an advisory mandate, the client could choose the theme that seems likely to play out and allocate (and rebalance) assets accordingly. In a discretionary mandate, the bank portfolio manag-ers could take the allocation decision as well. This approach would offer three advantages. First, equity–bond allocation decisions would be taken at

multiple times and for differing reasons

client’s views would be incorporated while the investment team’s expertise still would be used. Finally (and most importantly), an implicit time horizon would be created for each theme, lead-ing to more realistic risk–reward trade-offs for the client.

(3)ALLOCATING TO CLIENT OBJECTIVES. Institutional allocation frameworks often begin with asset class alloca-tion (an approach also followed in pri-vate wealth), but several plan sponsors have a liability-driven investment (LDI) approach. Although the LDI framework cannot be explicitly followed in private wealth because there may be no spe-

by allocating to client objectives rather than to asset classes. Such objectives could include liquidity, yield to matu-rity, growth, short-term asset selec-tion, illiquidity premium, active allo-cation, and stable shareholding. Each

investment horizon and an inclina-tion as to the equity–bond decision. Again, although this framework may not solve all the problems of private wealth management, it could help align

the expectations of the client with the realities of the portfolio and allow the implementation of client objectives while retaining account control with the relationship manager, supported by the investment strength of the invest-ment manager.

PRACTICAL SOLUTIONS

Investment processes followed by pri-vate wealth need to improve to deliver better performance and risk manage-ment but must do so in a manner that does not compromise customization and service quality. I have proposed some potential solutions that would satisfy

private clients for their assets and also would enable the formation of portfo-lios with the institutional strength of investment decision making. Because these frameworks would be minimally disruptive to organizational structures, I believe these approaches are potential options for private banks to consider.

Pranay Gupta, CFA, has more than 20 years of experience in asset management. He is a member of the CFA Institute Research Founda-tion’s Board of Trustees and a visiting research fellow at the Centre for Asset Management Research and Investment at the National Uni-versity of Singapore.

16 CFA Institute Magazine Jan/Feb 2015

VIEWPOINT

this response was sometimes helpful, it was, I think, an example of that most

paralysis. Their lack of decisiveness was shrouded in a cloak of data.

Analysis paralysis happens for several reasons. For starters, most analysts and portfolio managers have yet to realize or come to grips with one of the great les-

things that have occurred in the past, but investment results unfold in the future.

-sions are always leaps of faith. No fact can make a decision for you. First, you must come to grips with this reality.

Second, I have found that underneath the carefully constructed veneer of ana-lytical rigor that many analysts wear is a person out of touch with his or her emo-tional state. One way to overcome this problem is by using meditation because it can provide valuable insights into one’s emotional state and the underly-ing causes of emotional states.

Third, if you catch yourself in anal-ysis paralysis, try making decisions of less consequence under uncertainty as practice. Start with very small deci-sions and work your way up. For exam-ple, start by being deliberate and con-scious about what apples to buy at the grocery store and eventually advance to decisions with much higher stakes.

When I retired from money man-agement, I had the unique privilege of hiring my successor. He and I shared an

acquainted with the many choices I had made during my tenure as well as with my models. As you might expect, he asked numerous questions about my pro-cess, my relationships, and my choices.

All of the questions were of the knowledge-seeking sort until one day he asked me a very different type of

green earth are you doing that when you could be doing thisbig smile, and my successor immedi-ately apologized, saying, “I’m sorry, that was out of line.” I replied, “Quite the contrary, this is the moment I have been waiting for, and the fund is

now yours.” The transition was sealed -

ing and able to question my judgment.With that simple act of decisiveness,

the responsibility was his and I was able to quietly retire a couple of weeks later.

ABSOLUTE VS. RELATIVE

DECISION MAKING

A lack of decisiveness can be cured by the careful application of a medita-tion practice that leads to greater intu-itive insights. Your outward appear-ance becomes one of a person making “snap decisions” of the sort that Daniel Kahneman calls System 1 decisions. But inwardly, the architecture is entirely different. It is not prefrontal cortex vs.

waves vs. beta brain waves. In this way, your attunement to the environment around you allows you to make absolute decisions rather than relative ones—not always, mind you, but in cases

and the facts do not determine your answer.

Put another way, you do not need to reference data, other experiences, or consult others when making your decisions. Instead, you are able to make decisions because you have developed direct perception of the truth. This abil-

-ization of “the calculus,” which then took two years to describe mathemat-ically. The mathematical proof was for all of the rest of us, as Newton

.Of all the skills I have enumerated

in this series, this one is rarest. I have seen only a handful of people capable of making decisions of this quality. To be clear, I am not talking about the

-sion gun willy-nilly to take on the out-ward appearance of decisiveness. No, I am talking about the person that rou-tinely makes absolute decisions whose

-ably smart.

In the state of absolute decision making, judgment is purer and free of prejudices and the decision maker is seeing things others cannot see. We have all witnessed athletes “in the

zone” who make decisions absolutely that result in brilliant outcomes. Scien-tists like to poke holes in the hot-hand fallacy by looking at more extended sample sizes, but they do not take into account the self-reports of the athletes themselves who say that they are “in the zone.” Instead, scientists assume a constant state of mind in the athlete across the entire sample.

in dangerous situations also report sim-ilar experiences. Many of these types of heightened “in the zone” experi-ences are described in the book On

by Dave Grossman and Lauren Chris-tensen. Through meditation, people can develop the ability to tap this deep state of mental awareness in which people report seeing the spin of bullets caused

at them. Most importantly, in the state of heightened awareness, many report doing extraordinary things to avoid the

Times such as 9 March 2009, when the

are an example of when the ability to decide absolutely (from heightened awareness), rather than relatively, is critical to long-term outperformance.

of meditation for making decisions, I am not aware of another way to develop this skill set. On the other hand, self-con-fessed meditator Ray Dalio of Bridge-water Associates has said that any alpha he has ever generated is attributable to his meditation practice.

In my discussion of creativity in the November/December issue of CFA Insti-

(also available on the blog), I mentioned

my purchase of AES Corporation (AES). What I did not state then was that I pur-chased the majority of the shares on a day in which my trader at Lehman Brothers warned me against buying because it was a day when most of the market feared the company was going bankrupt. In fact, the trader pleaded with me, “Are you sure you want to buy more? You are the only bidder today!”

Jan/Feb 2015 CFA Institute Magazine 17

Behavioral economics folks will tell you that I only remember this story because it worked out for me in the end, that I have buried the pain of other failed “guesses” deep within my subcon-scious mind. But I keep an investment thesis for every business I do analysis on, including those that I do not buy. Further, at least quarterly, I review my decisions, even those I do not purchase and hence have no opportunity to sell. My records show that this instance was one of only a few times I ever acted in this way during my career. It was an absolute decision. AES had released appallingly bad news and appeared likely to go bankrupt, so the decision was not made relative to fundamentals.

My other decisions of this kind were purchases of Bank of America and Gen-eral Electric and a sale of Kmart. These decisions also turned out to be “cor-rect” decisions as evaluated by future market success or failure.

FORTHRIGHTNESS

You may have mastered all other skills necessary for successful investment management, but knowing and com-municating that you know something are entirely different skill sets. Trans-lating the insights of the right brain into language—a more linear form—takes tremendous skill. With this skill, investment professionals are able to

speak the truth of what they think and know in such a way that the often abstruse thought processes of invest-ment analysis are made clear for listeners, such as portfo-lio managers, chief invest-

of directors. Forthright-ness differs from honesty in that it insists that invest-ment managers speak the truth as they see it and vol-unteer their opinions with-out heavily filtering the message. When you consis-tently take this approach, decisions become easier to make because people seem to have an innate sense of the truth of your statements.

If you want to be more forthright and for your

words to ring with truth, try working with the following mental framework. Words are typically perceived as authen-

imagination, thought, word, and deed.

• is the “aha!” or “eureka!” quality that comes with true discovery.

• is inspiration combined with knowledge and experiences to

this as creativity.

• is the creation of architec-ture meant to make the initial inspi-ration and commensurate imagina-tion a structured reality.

• (as in “I give you my word”) is a meaningful commitment and responsibility to make real the orig-inal inspiration.

• is doing the hard work to make an originally intangible idea a tan-gible reality.

working together seamlessly, then mag-ical things can happen for investment managers. Such things include chang-ing the asset allocation of a portfolio, creating an ideal set of questions with which to pepper an intransigent busi-ness management so you get to the truth of a situation, developing a new way

of looking at all businesses that leads to new analytical insights, or divining what to write to your shareholders in your semiannual report so it conveys your true regret at a bad decision but doing so in such a way that you get to keep your job and restore trust.

As a part of the original job candi-

of my master’s thesis, in which I con-cluded that active managers outperform passive managers (contrary to popular opinion) so long as you use downside measures of risk and not measures of volatility in calculating Sharpe and Treynor ratios. During a subsequent in-person interview for that research analyst job, my interviewer turned to me and said, “You know, I think your thesis is a load of bull!”

I took a deep breath to dissipate my emotions and to center on some inspi-ration. Namely, I did not feel that my

inspired insight. Knowing what I knew

managers), I could not imagine that he had read the thesis. I then remembered

interview, he was on a conference call with a company and that he was then busy checking emails for a while, keep-ing our interview at bay. This was the “thought” stage of forthrightness. I also committed myself to challenge him on whether or not he read the thesis (the word phase) and then replied (deed phase), “I don’t think you read it all the way through, because it actually advo-cates strongly for the power of active management.”

Normally, the advice given to inter-view candidates is to be a shrinking violet and not to challenge the inter-viewer. In this case, however, my words resulted in the interviewer blushing and then saying, “Well, you are right. Why don’t you tell me what your thesis is about?” I eventually received a job offer, which I accepted. This is the nature of

abstruse layers of conversational and intellectual confusion.

Jason Voss, CFA, a former mutual fund manager, is a content director at CFA Institute.

Illu

stra

tion

by

Tim

oth

y C

ook

18 CFA Institute Magazine Jan/Feb 2015

PROFESSIONAL PRACTICEPORTFOLIO PERFORMANCE

Impaired VisionINVESTORS IN IMPAIRED REAL ESTATE SEE A SILK PURSE INSTEAD OF A SOW’S EAR

By Sherree Decovny

As an alternative investment, impaired real estate isn’t a

opportunities. Moreover, investors can now participate in structured transactions than could potentially achieve high returns over a short time period.

Real estate is impaired when its fair value is less than the carrying value recorded on the owner’s balance sheet. Impairment can be caused by factors such as environmental or physical damage, weak rental demand, low occupancy rates,

pressure to offer concessions to tenants, a high number of leases due to expire, bank-ruptcy, and legal matters.

There is no scarcity of impaired properties, accord-ing to Brent Anderson, CEO at International Risk Group (IRG) in Littleton, Colorado. But investing in impaired real estate requires specialized technical, legal, financial, real estate, and risk man-agement expertise. Ander-son estimates that about 13% of the US commercial and industrial real estate market has some form of impair-ment, but only a small por-tion of properties will trans-

with investors to rehabilitate and sell them. Ultimately, value is created by taking a site that has perceived (and to some extent real) problems and returning it to productive reuse.

“Like all real estate, it’s got to have fundamental value, and a number of these properties have the wrong attributes for any potential redevelopment,” Anderson says. “They may

or their former use is not conducive to being repurposed for a future use.”

THE DRIVERS

The US real estate market is in recovery, but investment in impaired real estate is not driven by economic conditions. In good times and bad, there are typically good purchase

it comes to exiting the deal. That being said, other factors currently support the market for these properties.

One is reshoring activity in the US, particularly from the Far East. Companies that want to come to the US need a

transactions are driven by foreign companies that want to exit the US market and need to sell an impaired property.

Another factor is the desire to invest in green and sus-tainable projects and to address land scarcity. Impaired real estate may be reused in different ways. An environmental issue on the land can be cleaned up, the buildings on the property can be left in their existing state, and the property can be sold or leased. As an alternative, the buildings can be rehabilitated, sold, or leased, or they can be torn down. Some properties have excess land that can be developed. One advantage is that it is often possible to use the exist-ing infrastructure, including roads and sewer and power lines, to support the site instead of building from scratch.

Demographics also play a role, especially in the residential sector. According to a 2013 survey conducted by the Urban

-ment in the Digital Age,” 39% of respondents (all US residents) born during the 1980s and early 1990s said that they were city people. Furthermore, 14% live either downtown or near downtown, 34% live in a city neighborhood outside of down-town, and 13% live in a dense, older suburb. The demand is

locations, but the current owner can’t execute because they can’t solve an impairment issue,” says Adam Margolin, man-aging partner at Structured Finance Solutions in Denver, Colorado. “By dealing with the impairments, you can turn an unattractive, vacant piece of property into something useful as well as a revenue producer for the municipality. That in itself is of great value.”

THE RISK

The deal structures almost always involve multiple types of documents and relationships with an array of parties,

uncertainty and transaction costs. In addition to the tradi-tional buyer, seller, equity investor, and lender documents that go along with any transaction, documents must be sub-mitted to federal and state regulatory agencies. Depending on the deal, specialized insurance contracts and bonding documents may be necessary to protect against unknown environmental risks.

A lack of understanding of the market vernacular pre-vents some investors from identifying and taking advan-tage of good opportunities. Often, they are scared away by the term “impairment” because they conjure up images of polluted sites, costly cleanup jobs, and legal complications.

Investment in impaired real estate is being driven by reshoring, green/sustain-ability project activity, and demographic trends.

Cost overruns and extensions are key risks; environmental risk can be mitigated through specialized insurance and bonding contracts.

Impairment analysis, fair value determination, and tax implications are critical to the investment decision.

KE

Y P

OIN

TS

Jan/Feb 2015 CFA Institute Magazine 19

The perceived risk may differ from the reality. Impair-ments can be relatively minor. Certain risks are associated with every real estate deal. For example, building supply costs could increase, or the municipality or governmental entity may change its standards and building codes. Cost overrun risk in an impaired real estate transaction is typ-ically managed through due diligence and underwriting.

“The potential outcomes need to be measured in the con-text of the greater transaction. If half the cost of a transac-tion is environmental-related issues and you miss that by 100%, your deal is in serious trouble,” says Anderson. “If you have 10% of your cost involved in that and you miss by 100%, you’re going to be unhappy but you’re not going to be dead.”

In addition, the deal could take longer than expected, which is known as extension risk. Yet the potential high return associated with impaired real estate transactions may give them a distinct advantage over more traditional transactions.

“If the transaction takes longer than expected, cost over-runs will affect the IRR [internal rate of return],” Margo-lin explains. “But when you have higher IRRs and higher returns, you have much more latitude to deal with that kind of volatility.”

THE OPPORTUNITY

Not all investors are natural players in the impaired real estate market. Individual transactions tend to require an equity cap-ital investment ranging from $3 million to $20 million. Thus, they attract smaller institutions, real estate funds, foreign

-tion, density, zoning, credit enhancements, and risk in valu-ing real estate and that can execute quickly. These investors recognize that the market is tight

traditional property assets.Spreads in impaired real estate

transactions are as high as 1800–2000 bps over US Treasuries, Mar-golin points out. In comparison, the

real estate mezzanine transactions are currently about 800–1200 bps over Treasuries. Two of IRG’s recent deals have turned over and paid off in less than a year, yielding a triple-digit IRR. Generally, the company underwrites to a three-year holding period and aims to achieve a return of 20–22%, depending on the particular deal parameters.

It is possible to enhance the credit rating on a portfolio of impaired property assets using securitization and insur-ance. For example, the fact that the properties in the port-folio may be rehabilitated and monetized in different ways makes it more challenging to securitize impaired assets than commercial properties in commercial mortgaged-backed securities, for example.

to look at the characteristics of the property and due dili-gence work that has already been done to understand the risks and estimated returns. “There’s a certain amount of judgment involved in the impairment analysis and fair value determination, and there are various valuation approaches,”

Hughes Goodman in Tysons, Virginia. “One needs to know how the real estate that has been impaired is being used by its current owner to better understand the inputs taken into consideration in determining the level of that impairment.”

The fair value of the asset is judged based on its current use. The cost approach looks at the cost of both the land and the reconstruction of the assets on it. The relative sales value approach compares the impaired real estate to the selling price of similar assets in the market. The income approach, which is probably the most judgmental, looks at the income generated from the real estate asset over time.

It is also important to look at the tax implications, notes

estate practice. Real estate professionals may want to make an impaired real estate investment for future appreciation and use some tax losses up front. But Gilman warns against phantom income scenarios, in which the asset is generat-

the income. That income could be offset against other loss-making assets. Additionally, if the investor expects to make

and a day, the time needed to qualify as long-term capital gains. It might be worth paying the tax on phantom income

capital gains rates on the appreciation.

this asset class is not for everyone.“The most useful investment partner is one who is not

just looking to create value on a piece of paper but truly cre-ating some value on the ground,” says Anderson. “It’s someone who believes it’s possible to make a silk purse from a sow’s ear.”

Sherree DeCovny is a freelance journal-ist specializing in finance and technology.

“Bricks and Clicks,” CFA Institute Magazine (July/August 2014) [www.cfapubs.org]

“Cultivating Returns,” CFA Institute Magazine (September/October 2012) [www.cfapubs.org]

KEEP GOING

NOT ALL INVESTORS ARE NATURAL PLAYERS IN THE IMPAIRED REAL ESTATE MARKET. INDIVIDUAL TRANSACTIONS TEND TO REQUIRE AN EQUITY CAPITAL INVESTMENT RANGING FROM $3 MILLION TO $20 MILLION. THUS, THEY ATTRACT SMALLER INSTITUTIONS, REAL ESTATE FUNDS, FOREIGN INVESTORS, AND FAMILY OFFICES.

20 CFA Institute Magazine Jan/Feb 2015

PROFESSIONAL PRACTICEANALYST AGENDA

Solar FlairIS SOLAR POWER ENTERING A NEW ERA OF INVESTMENT POTENTIAL?

By John Rubino

of cost cutting and innovation (largely fueled by subsidies from governments trying to move beyond fossil fuels), gen-erating electricity from sunshine is economically viable. And as solar power’s cost continues to fall, solar appears ready not only to participate in tomorrow’s global energy market

but also to lead it.According to a 26 October

2014 report by Deutsche Bank analyst Vishal Shah, solar is at grid parity (the point at which rooftop solar panels provide electricity as cheaply as the local utility under cur-rent subsidy regimes) in 10 US states. Over the next two years, says Shah, “solar has the potential to reach grid parity in 12 additional states. In those markets, we expect installed [solar] capacity growth of ~400%–500% within 3–4 years.”

And the US isn’t even the main growth story. China (because its energy needs and pollution problems are both immense) and Japan

(because its commitment to nuclear power culminated in the Fukushima disaster) are poised to lead the world in solar installations through the balance of the decade.

Extrapolating today’s near-parabolic trend out to 2050, the International Energy Agency now predicts that solar’s share in the global electricity market will rise from the current 1% to 26%, making it the world’s single largest energy source.

Three developments have been key for solar’s sudden

changing customer behavior. First, as to costs, solar power keeps getting cheaper. “In recent years, the main focus has been on reducing costs,” says Treasa Ni Chonghaile, port-folio manager with Bethesda, Maryland–based Calvert Global Alternative Energy Fund. “They’re using less silver in solar cells, for instance, and developing better invert-ers [which convert DC current from solar arrays into AC current that can power appliances].” She predicts that the likely result will be a further 10% drop in solar panel pro-duction costs in 2015.

Even bigger savings are being realized in “balance-of-system costs,” such as installation, says Edward Guinness,

portfolio manager of London-based Guinness Atkinson’s Alternative Energy Fund. “A few years ago, the modules were more than half the total cost of a system, let’s say $4 per watt [of generating capacity] for the module and $8 for the installed system. Now the module is $0.60 and in Europe the installation costs another $0.60–$1.00. Best prac-

lowering the cost of capital. System installers, such as Solar-City and Vivint, offer to build and maintain solar arrays on homeowners’ rooftops in return for lease or loan payments that are typically less than current utility bills. The installer then sells these income streams to securitizers who bundle them—just like mortgages or credit card balances—into asset-backed bonds and sell them to institutional investors.

Meanwhile, “yieldcos” have emerged that own solar farms

approach is similar to the model used by real estate invest-ment trusts (REITs) for commercial property or by master limited partnerships (MLPs) for gas pipelines. “Yieldcos are driving the cost of capital down and creating a visible benchmark for other sources of capital to come in at attrac-tive prices,” says Guinness.

Finally, customers are noticing the past declines in module costs. “This is an ocean liner beginning to respond to the price points for modules that have already been reached,” says Guinness. “Many countries are waking up to the poten-tial of solar, and [as they expand their installed base] much fat is being taking out of the non-module piece. The differ-ence between the cost of installation in China and Germany versus the US or the Middle East is huge.” So, increasing demand begets economies of scale and lower prices, which ramps up demand even further.

Add it all up, and “the cost of producing electricity with solar will continue to decline while the cost of other energy sources goes up. I’m hopeful that we’ll see grid parity in a majority of markets by the end of the decade,” says Chonghaile.

SPEED BUMPS AND COMPLICATIONS

Soaring demand, although far better than the alternative, does not market nirvana make. There are always potential com-

MARGIN COMPRESSION. Falling prices and fast growth are great for generating sales but can be problematic for earnings. “Many of the [solar panel makers] that were used to higher margins are having to absorb lower markups and narrower margins,” says Pavel Molchanov, energy analyst with Tampa, Florida, brokerage house Raymond James & Associates.

The International Energy Agency has predicted that solar energy’s share of the global electricity market will rise from 1% currently to 26% by 2050.

To benefit from this trend, investors will have to avoid a variety of pitfalls, from margin compres-sion to shifting government policies.

Despite difficulties, “this is a story that will become more rather than less com-pelling over time,” predicts one analyst.

KE

Y P

OIN

TS

Jan/Feb 2015 CFA Institute Magazine 21

Installers tend to book the costs of customer acquisition and system construction up front and accrue the result-ing revenues over time. SolarCity, for instance, generated 20% higher revenues year over year in 2014’s third quar-ter but saw its operating expenses rise by 119%, produc-ing a substantial loss.

Chonghaile. “The strongest panel makers will be those that eke out the most power from every panel and participate in the fastest-growing markets.”

Chinese panel makers boast the industry’s lowest pro-duction costs. And given their home country’s solar ambi-tions, they’re positioned perfectly. “A lot of China’s tier-1 manufacturers are at full utilization and can’t keep up with local demand,” says Chonghaile.

CONSOLIDATION. Most parts of the solar ecosystem are highly fragmented and thus ripe for a wave of M&A as stronger

to roll up (or over) weaker competitors, notes Chonghaile.Ditto for the installer market, where “the companies with

the necessary scale to facilitate tax equity funds, asset-backed securities, and economies of scale in a post-ITC [investment tax credit] environment gain market share,” observes Shah.

CAPACITY CONSTRAINTS. “The Chinese government is acting like an OPEC, not allowing its solar companies to build new manufacturing capacity unless it comes with mean-

adding new plants, the Chinese companies are upgrad-ing and improving what they’ve got.” Other things being

risks turning glut into shortage, temporarily constraining sales growth.

UNPREDICTABLE REGULATIONS AND SUBSIDIES. Despite the approach of grid parity, this is still a market in which subsidies and trade barriers play huge and occasionally decisive roles. The US recently imposed antidumping duties on Chinese solar modules, and Japan is rumored to be considering cuts in its perhaps overgenerous subsidy regime. And the US Solar Investment Tax Credit, which shaves 30% from the upfront price of a solar array, is due to expire in 2016, effectively raising the cost of solar power by nearly a third.

So, even as solar panels become commodities and bal-ance-of-system best practices become the norm, geogra-phy still matters. The companies headquartered in markets where demand is growing fastest or subsidies are most gen-erous will continue to have big advantages.

FLUCTUATING FOSSIL FUEL PRICES. In late 2014, the price of oil plunged by nearly 20%, which spooked the energy market in general and con-tributed to a painful correction in solar equities. Not to worry, says

price of electricity. The econom-ics of solar have zero connection

to oil in North America and Europe and only a very tenu-ous one in Japan.”

Coal is a different story and could, by declining in price, delay solar grid parity in many markets. But fossil fuel price volatility also works in solar’s favor because sunshine is always free and solar panel long-term costs are well under-stood. As a result, solar farms “are very stable, predictable assets,” says Guinness. So, even where solar is a bit more expensive than coal, solar power’s predictability could make it attractive on a risk-adjusted basis.

In any event, as solar becomes ubiquitous, it will begin

markets, displacing fossil fuels and limiting their pricing power. “Solar puts a ceiling on where electricity prices should be able to go,” says Guinness.

THE STORAGE SPEED BUMP. Solar appears to be guaranteed a great few years. After that initial period, however, “a hurdle pops up,” says Molchanov. Because solar is an “intermittent” source of electricity that works only when the sun is shin-

problem might limit solar’s long-term growth prospects.“This point is a ways away in markets like the US, where

solar has a less than 1% share. But in Germany, where it’s 8%, [potential grid destabilization] is a big deal,” says Mol-chanov. “By the end of the decade, there will be many coun-tries where solar is above 10% of the electricity mix, and at that point, it will be vital for the industry to develop cost-effective storage solutions.”

Consequently, one key to mainstreaming renewables is a battery capable of storing excess power during the day and then feeding it to the grid at night, effectively convert-ing intermittent technologies like solar and wind into much more attractive “baseline” power sources.

“Right now, the emerging battery market is dominated by big, familiar names,” says Chonghaile. “Samsung and Panasonic are each developing battery types, some focus-ing more on the automobile market and some on renew-ables themselves. Siemens has a battery that can be used for wind power. Johnson Matthey in the UK is buying up various battery tech companies. They’re each making big strides.”

LONG LEGS

Nothing is guaranteed of course, but if the right pieces—including cheap capital, continued cost reduction, favorable government policies, and viable storage solutions—fall into place, solar’s current momentum appears to have very long legs indeed. “This is a story that will become more rather

than less compelling over time,” says Guinness.

John Rubino, a former financial analyst, is author of The Money Bubble.“Global Energy: The Private Equity Opportunity

of the Century,” summarized in CFA Digest (October 2014) [www.cfapubs.org]

“The Global Impact of the U.S. Shale Energy Boom,” CFA Institute Take 15 Series (17 April 2013) [www.cfainstitute.org]

KEEP GOING

22 CFA Institute Magazine Jan/Feb 2015

PROFESSIONAL PRACTICEPRIVATE CLIENT CORNER

The Accidental Optimization BoosterSOCIAL SECURITY BENEFITS CAN HAVE SURPRISING VALUE FOR WEALTHY CLIENTS

By Ed McCarthy

--

tainly sensible for most retirees to maximize what they can earn from the system, but does it matter to the very wealthy?

Consider the example of one such client who easily

Charles Bennett Sachs, CFA, with Private Wealth Counsel in Miami, Florida, learned that the client had decided to start his Social Security

(without consulting Sachs), he asked why. The client cer-tainly didn’t need the extra income, and wasn’t he con-cerned that early claiming probably wasn’t the optimal decision?

That’s when Sachs learned that his client viewed the

an extra thousand dollars or so that “popped” into his account each month, and he

enjoyed “blowing it.” That attitude didn’t completely sur-prise Sachs, who notes that at some point the extra monthly

Security is just a complete non-issue,” he says. “It doesn’t make or break or change one iota one way or the other.”

Sachs doesn’t tell clients to waste the money, but he does