CFA Society Indonesia Universitas Prasetiya Mulya - CFA ...

31

CFA Institute Research Challenge Hosted by CFA Society Indonesia Universitas Prasetiya Mulya The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and presentation skills of university students. The following report was submitted by a team of university students as part of this annual education initiative and should not be considered a professional report. Disclosures: Ownership and material conflicts of interest: The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company. The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the content or publication of this report. Receipt of compensation: Compensation of the author(s) of this report is not based on investment banking revenue. Position as a officer or director: The author(s), or a member of their household, does not serve as an officer, director or advisory board member of the subject company. Market making: The author(s) does not act as a market maker in the subject company’s securities. Disclaimer: The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by any individual affiliated with CFA Society Indonesia, CFA Institute or the CFA Institute Research Challenge with regard to this company’s stock.

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of CFA Society Indonesia Universitas Prasetiya Mulya - CFA ...

CFA Institute Research Challenge Hosted by

CFA Society Indonesia

Universitas Prasetiya Mulya

The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and

presentation skills of university students. The following report was submitted by a team of university students as part of this annual education

initiative and should not be considered a professional report.

Disclosures: Ownership and material conflicts of interest:

The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company.

The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the

content or publication of this report.

Receipt of compensation:

Compensation of the author(s) of this report is not based on investment banking revenue.

Position as a officer or director:

The author(s), or a member of their household, does not serve as an officer, director or advisory board member of the subject company.

Market making:

The author(s) does not act as a market maker in the subject company’s securities.

Disclaimer:

The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be

reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information

is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment

advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by

any individual affiliated with CFA Society Indonesia, CFA Institute or the CFA Institute Research Challenge with regard to this company’s stock.

1

Universitas Prasetiya Mulya

This report is published for educational purposes only by

students competing in CFA Institute Research Challenge 2018

Date : February 15th, 2019 Current Price : IDR 2,460 Recommendation : BUY

Ticker : PGAS IJ (Bloomberg) Upside Potential : 20.73% Target Price : IDR 2,970

MARKET PROFILE 52-Wk Price Range (IDR) 1,505 – 2,860

Avg. Trading Volume 90,396,068

Shares Outstanding (Bn) 24.24

Free Float 43,04%

Market Cap. (Tn) IDR 59.63

P/E (ttm) 16.35x

P/BV 1.21x

USD/IDR 14,160

Share Price Information (IDR)

Source: Bloomberg

Upside Potential in 2019F

Source: Bloomberg

Time for the Giant to Break-Free Backed by a favourable gas distribution industry outlook, PGAS is well positioned as a market leader to achieve growth and further market penetration. We believe PGAS can overcome insecurity of supply and high capital expenditure, through capital expenditure efficiency and securing gas supply through Pertamina’s gas holding. After considering the investment risks and future growth prospects, we arrived at a BUY recommendation on PGAS with a 12-month target price of IDR2,970/share, reflecting a 20.73% upside potential from its IDR2,460 closing price on 15/02/2019 based on our sum of the parts valuation model. Our recommendation lays on the following key catalysts:

Strong Upcoming Demand from Gas Infrastructure Projects Government have set a target on gas power plant installation of 47.7 GW by 2030 vs current 13.98 GW (growing 9.2% CAGR) (IRENA, 2017). The growing capacity will lead to a growing gas demand. However, inadequate pipeline network is currently a setback as it only provides 20-30% of the needed infrastructure (Ministry of SOE, 2018). Therefore, government is expected to ramp up this figure up to

80-100% by 2030F. Since this government-led plan will involve high expertise to be executed, the

government will turn its favours on PGAS as the government’s leader in the gas sub-holding to deliver this product. On the other hand, PGAS will gain benefits from this, as the government will give incentives for construction in new market area in the form of 20 years monopoly rights (resulting in maximized margins as there will be no margin sharing between distributors) and IRR at 12% in that new market area (Company Presentation, 2019).

Secured Supply from Gas Holding to Fulfil Enormous Potential Demand To fulfil the high potential demand, gas supply comes into the equation. The establishment of the government’s oil and gas holding will align Pertamina’s gas supply chain, securing more supply for PGAS. The oil and gas holding means that Pertamina will turn in PGAS’ favour more as the leader in the gas sub-holding, in terms of transporting and distributing its gas. We expect more secured supply for PGAS to be realized soon. To start with, PGAS will benefit from Pertamina’s 6 gas fields with a total potential of 281 mmscfd which are expected to fully commercialize by 2021 (Ministry of SOE, 2018). We see this holding initiative as a mutualism between Pertamina and PGAS. Pertamina can have more ease at bringing more blocks to the commercialization process due to assurance of distribution through PGAS, while PGAS can benefit from the opportunity in transporting the potential supply.

PGAS-Pertagas Pipeline Integration to Boost Synergic Value With a secure potential supply and huge potential demand, PGAS will need the infrastructure to match the supply and demand’s region. Currently, gas production in Indonesia aggregately is above gas demand (7,453 mmscfd vs 7,318 mmscfd), but lack of infrastructure has created gas supply imbalances in several regions (Ministry of EMR, 2018). This is most evident in Region II and III (Figure 8) which runs a gas supply deficit while Region IV has a gas supply surplus. The acquisition of Pertagas will solve this uneven supply problem. PGAS’ and Pertagas’ pipeline will be integrated, which will connect Region II, III, and IV’s pipeline network with a 576 km pipeline costing US$213.25 mn of CAPEX. The plan, expected to finish by 2020, will bring an additional revenue of US$342.85 mn by 2023F. Revenue synergy along with cost savings from CAPEX duplication avoidance and SG&A savings will bring NPV of total synergic value at US$582.14 mn.

Attractive Valuation with Strong Cash Flow Generator PGAS is trading at an attractive 12.7% 2019F FCF Yield and 5.9x 2019F EV/EBITDA (-1 std of 5-yrs historical average). With a turnaround performance, we believe incremental downside risk remains limited as there will also be lower dependency on upstream oil and gas portfolio post Pertagas acquisition. Therefore, PGAS’ developed infrastructure earnings characteristic will resurface.

Key Financial Highlights 2016A 2017A 2018F 2019F* 2020F Revenue Growth -4.37% 1.19% 11.88% 20.29% 7.41%

Gross Margin 30.22% 26.85% 27.09% 27.29% 27.78%

EBITDA Margin 26.23% 28.12% 26.68% 27.36% 27.62%

EPS (IDR) 182.0 85.6 171.1 179.4 232.2

ROE 9.73% 4.63% 8.65% 9.18% 10.61%

ROA 4.52% 2.35% 4.44% 4.44% 5.25%

Interest Coverage 3.9 2.9 3.2 3.1 3.9

Debt/Equity 0.92 0.75 0.72 0.81 0.74

Source: Company Reports, Team Estimates *Acquisition of Pertagas

1000

1500

2000

2500

3000

3500

Feb

ruar

y-1

6

Jun

e-1

6

Oct

ob

er-1

6

Feb

ruar

y-1

7

Jun

e-1

7

Oct

ob

er-1

7

Feb

ruar

y-1

8

Jun

e-1

8

Oct

ob

er-1

8

Feb

ruar

y-1

9

PGASCurrent PriceTarget Price

2,970

2,460

PT Perusahaan Gas Negara Tbk. Infrastructure, Utilities, Transportation, and Energy Sectors

Indonesia Stock Exchange

0

200

400

600

Feb

ruar

y-1

6

Jun

e-1

6

Oct

ob

er-1

6

Feb

ruar

y-1

7

Jun

e-1

7

Oct

ob

er-1

7

Feb

ruar

y-1

8

Jun

e-1

8

Oct

ob

er-1

8

Feb

ruar

y-1

9

Vo

lum

e (M

illio

n)

1000

2000

3000

4000

5000

6000

7000

IDR

/Sh

are

PGAS JCI

20.73%

2

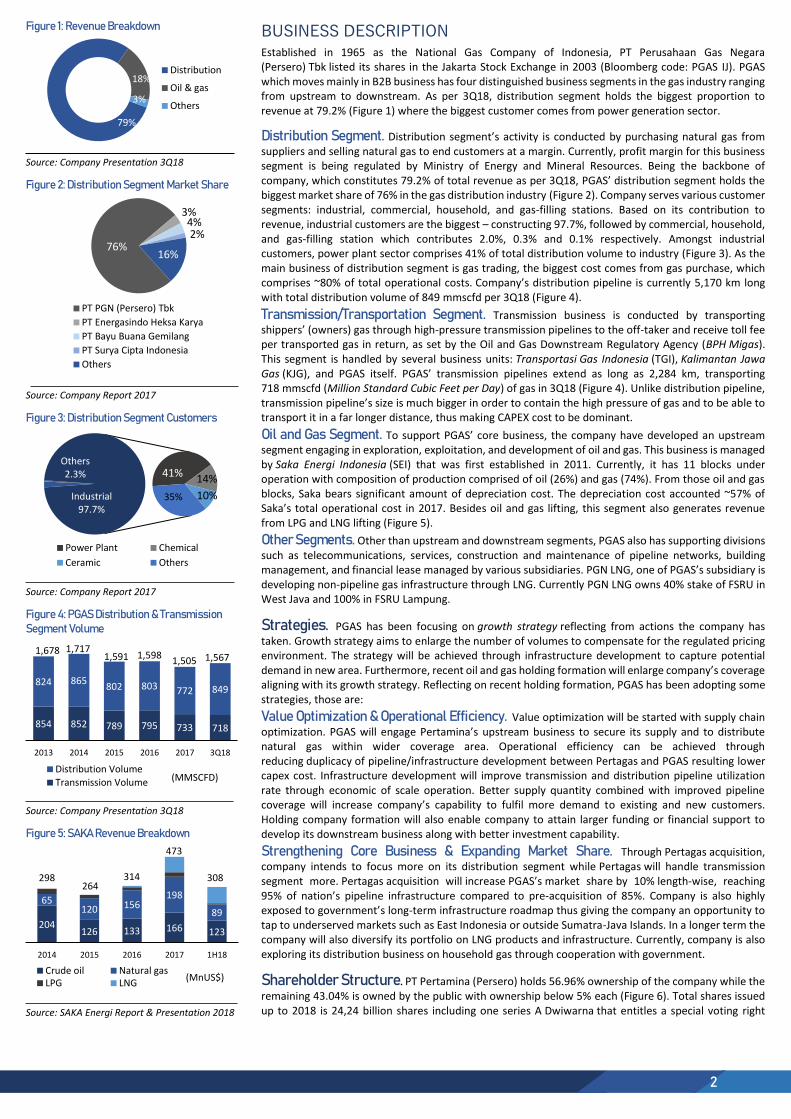

Figure 1: Revenue Breakdown

Source: Company Presentation 3Q18

Figure 2: Distribution Segment Market Share

Source: Company Report 2017

Figure 3: Distribution Segment Customers

Source: Company Report 2017

Figure 4: PGAS Distribution & Transmission Segment Volume

Source: Company Presentation 3Q18

Figure 5: SAKA Revenue Breakdown

Source: SAKA Energi Report & Presentation 2018

BUSINESS DESCRIPTION Established in 1965 as the National Gas Company of Indonesia, PT Perusahaan Gas Negara (Persero) Tbk listed its shares in the Jakarta Stock Exchange in 2003 (Bloomberg code: PGAS IJ). PGAS which moves mainly in B2B business has four distinguished business segments in the gas industry ranging from upstream to downstream. As per 3Q18, distribution segment holds the biggest proportion to revenue at 79.2% (Figure 1) where the biggest customer comes from power generation sector.

Distribution Segment. Distribution segment’s activity is conducted by purchasing natural gas from suppliers and selling natural gas to end customers at a margin. Currently, profit margin for this business segment is being regulated by Ministry of Energy and Mineral Resources. Being the backbone of company, which constitutes 79.2% of total revenue as per 3Q18, PGAS’ distribution segment holds the biggest market share of 76% in the gas distribution industry (Figure 2). Company serves various customer segments: industrial, commercial, household, and gas-filling stations. Based on its contribution to revenue, industrial customers are the biggest – constructing 97.7%, followed by commercial, household, and gas-filling station which contributes 2.0%, 0.3% and 0.1% respectively. Amongst industrial customers, power plant sector comprises 41% of total distribution volume to industry (Figure 3). As the main business of distribution segment is gas trading, the biggest cost comes from gas purchase, which comprises ~80% of total operational costs. Company’s distribution pipeline is currently 5,170 km long with total distribution volume of 849 mmscfd per 3Q18 (Figure 4).

Transmission/Transportation Segment. Transmission business is conducted by transporting shippers’ (owners) gas through high-pressure transmission pipelines to the off-taker and receive toll fee per transported gas in return, as set by the Oil and Gas Downstream Regulatory Agency (BPH Migas). This segment is handled by several business units: Transportasi Gas Indonesia (TGI), Kalimantan Jawa Gas (KJG), and PGAS itself. PGAS’ transmission pipelines extend as long as 2,284 km, transporting 718 mmscfd (Million Standard Cubic Feet per Day) of gas in 3Q18 (Figure 4). Unlike distribution pipeline, transmission pipeline’s size is much bigger in order to contain the high pressure of gas and to be able to transport it in a far longer distance, thus making CAPEX cost to be dominant.

Oil and Gas Segment. To support PGAS’ core business, the company have developed an upstream segment engaging in exploration, exploitation, and development of oil and gas. This business is managed by Saka Energi Indonesia (SEI) that was first established in 2011. Currently, it has 11 blocks under operation with composition of production comprised of oil (26%) and gas (74%). From those oil and gas blocks, Saka bears significant amount of depreciation cost. The depreciation cost accounted ~57% of Saka’s total operational cost in 2017. Besides oil and gas lifting, this segment also generates revenue from LPG and LNG lifting (Figure 5).

Other Segments. Other than upstream and downstream segments, PGAS also has supporting divisions such as telecommunications, services, construction and maintenance of pipeline networks, building management, and financial lease managed by various subsidiaries. PGN LNG, one of PGAS’s subsidiary is developing non-pipeline gas infrastructure through LNG. Currently PGN LNG owns 40% stake of FSRU in West Java and 100% in FSRU Lampung.

Strategies. PGAS has been focusing on growth strategy reflecting from actions the company has taken. Growth strategy aims to enlarge the number of volumes to compensate for the regulated pricing environment. The strategy will be achieved through infrastructure development to capture potential demand in new area. Furthermore, recent oil and gas holding formation will enlarge company’s coverage aligning with its growth strategy. Reflecting on recent holding formation, PGAS has been adopting some strategies, those are:

Value Optimization & Operational Efficiency. Value optimization will be started with supply chain optimization. PGAS will engage Pertamina’s upstream business to secure its supply and to distribute natural gas within wider coverage area. Operational efficiency can be achieved through reducing duplicacy of pipeline/infrastructure development between Pertagas and PGAS resulting lower capex cost. Infrastructure development will improve transmission and distribution pipeline utilization rate through economic of scale operation. Better supply quantity combined with improved pipeline coverage will increase company’s capability to fulfil more demand to existing and new customers. Holding company formation will also enable company to attain larger funding or financial support to develop its downstream business along with better investment capability.

Strengthening Core Business & Expanding Market Share. Through Pertagas acquisition, company intends to focus more on its distribution segment while Pertagas will handle transmission segment more. Pertagas acquisition will increase PGAS’s market share by 10% length-wise, reaching 95% of nation’s pipeline infrastructure compared to pre-acquisition of 85%. Company is also highly exposed to government’s long-term infrastructure roadmap thus giving the company an opportunity to tap to underserved markets such as East Indonesia or outside Sumatra-Java Islands. In a longer term the company will also diversify its portfolio on LNG products and infrastructure. Currently, company is also exploring its distribution business on household gas through cooperation with government.

Shareholder Structure. PT Pertamina (Persero) holds 56.96% ownership of the company while the remaining 43.04% is owned by the public with ownership below 5% each (Figure 6). Total shares issued up to 2018 is 24,24 billion shares including one series A Dwiwarna that entitles a special voting right

79%

18%

3%

Distribution

Oil & gas

Others

76%

3%4%2%

16%

PT PGN (Persero) Tbk

PT Energasindo Heksa Karya

PT Bayu Buana Gemilang

PT Surya Cipta Indonesia

Others

Others 2.3% 41% 14%

10%35%Industrial97.7%

Power Plant Chemical

Ceramic Others

854 852 789 795 733 718

824 865802 803 772 849

2013 2014 2015 2016 2017 3Q18

(MMSCFD)Distribution VolumeTransmission Volume

1,678 1,7171,591 1,598

1,505 1,567

204126 133 166 123

65120 156

198

89

2014 2015 2016 2017 1H18

(MnUS$)Crude oil Natural gasLPG LNG

298264

314

473

308

3

Figure 6: Shareholder Structure

Source: Company Report 2017

Table 1: PGAS Board of Director

Board of Director

Name Title

Gigih Prakoso President Director

Said Reza Pahlevi Director of Finance

Dilo Seno Widagdo

Director of Infrastructure & Technology

Danny Praditya Director of Commercial

Desima E. Siahaan Director of HR & General

Affairs

Source: Company Press Release 2018

Table 2: PGAS Board of Commissioner

Board of Commissioner

Name Title IGN Wiratmaja

Puja President Commissioner

Mohamad Ikhsan Comissioner

Paiman Raharjo Independent Comissioner

Kiswodarmawan Independent Comissioner

Hambra Commissioner

Source: Company Press Release 2018

Figure 7: Natural Gas Industry Customer

Source: Ministry of Energy and Mineral Resources 2018

Figure 8: Indonesia Gas Network Region

Source: Ministry of Energy and Mineral Resources 2018

owned by the government. Previously there was transfer of ownership from Indonesian government as controlling shareholder to PT Pertamina (Persero) align with government’s vision to form a holding company for oil and gas sector. The transfer is legalized in April 2018 allowing Pertamina to be the parent company and create integration towards a vision amongst oil and gas enterprises.

CORPORATE GOVERNANCE

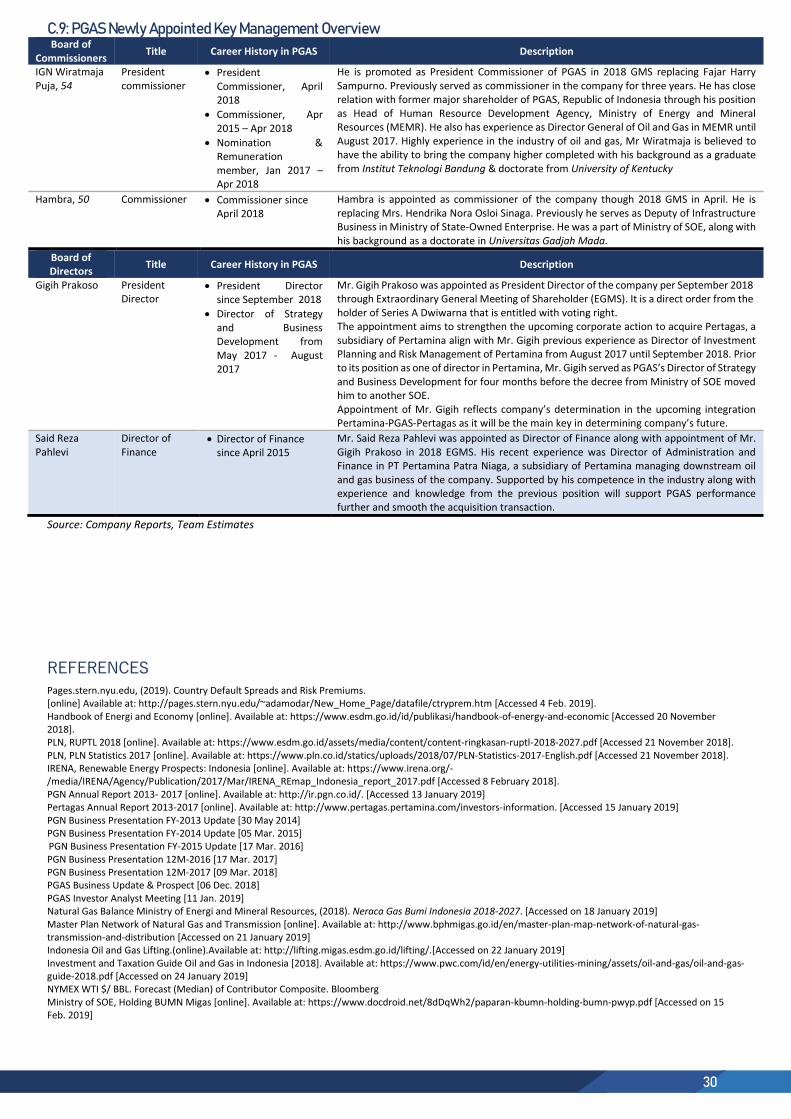

Corporate Management. PGAS’ management is comprised of highly-experienced board of commissioners and directors with widely known skills and competence relevant to the industry. Related to the nature of the company as an SOE, several members of the company’s key management have been directly appointed by the government (Appendix C.8, C.9). Placement of several commissioners in the company from the government’s side is aimed to increase the monitoring function and helps align the company’s visions towards the government’s objectives for the natural gas industry. The company is also channelling their focus to human resource quality as the industry only prevails to human resource with high technical skills to be able to operate the complex pipeline infrastructure. Director of Human Resources and General Affairs, Mrs. Desima Equalita is known to have deep understanding to the company’s human resources as she has been in every stage of the company from low-mid-high management and has a tenure for almost 10 years in the company.

Oil and gas holding company formation. PGAS, under government’s decree is experiencing some degree of changes in the organization structure (Appendix A.5). Major shareholder of PGAS has moved from the government to PT Pertamina (Persero), making PGAS to be Pertamina’s sub-holding. PGAS will be handling the midstream and downstream natural gas business while the upstream business will be handled by Pertamina directly. This will help the company to enhance its focus on distribution segment and further improve synergy. In line with the holding company formation, the company has acquired PT Pertamina Gas, one of Pertamina’s subsidiaries working on midstream and downstream business of natural gas. With that strategy, the company placed Mr. Gigih Prakoso and Mr. Said Reza Pahlevi as President Director and Director of Finance, both has previously served as Director of Investment Planning and Risk Management of Pertamina, and Director of Administration and Finance of PT Pertamina Patra Niaga respectively. Placement of two Pertamina’s top management in PGAS has clearly translated the company’s strategy to align PGAS vision to the parent company, Pertamina.

Social responsibility. PGN implemented a holistic approach to the society by practicing ISO 2600: 2010 which enables them to contribute in seven core subjects: organizational governance, human rights, labour practices, environment, fair operating practices, consumer issues, and community involvement and development. This is evident with the company’s contribution towards the success of the Nawacita program to realize economic independence by driving strategic sectors in the domestic economy. One of them is the Village Development Program which aims to build community independence around the PGN Offtake Station. As of 2017, the company received 2 awards for the perseverance of corporate social responsibility act.

INDUSTRY OVERVIEW & COMPETITIVE POSITIONING

Indonesian gas transportation and distribution industry is known as a quasi-monopoly market. This is mainly due to its capital intensive nature, tight permit approvals, and relations needed to secure supply. The several players in this industry serves 3 main segments: industry (40%), electricity (24%), and fertilizer (18%) (Figure 7). In these segments, there are shifts towards a higher gas usage, driven by gas’ clean emission, competitive price, and reliable source of power at peak hours.

Natural Gas Industry: Ample Room for Growth

Countries Indonesia Malaysia Thailand Philippines Vietnam GDP/capita (USD) 3,847 9,945 6,594 2,989 2,343 Natural gas consumption (m3/capita) 204 1,296 1,678 31 161 Gas in energy mix 22% 50% 59% 22% 22% Power plant capacity (GW) 62 34 44.6 20.1 59.4 Total gas pipelines length (km) 11,702 6,439 5,900 576 955 Gas Reserves (TSCF) 142.72 134.45 6.80 4.91 10.11

Source: Countries’ Energy Handbook 2018, Ministry of Energy and Minerals, OPEC Annual Statistic Bulletin 2018, US Energy Information Administration, Statistical Review of World Energy

Indonesia is ranked 1st in terms of gas reserves among other ASEAN emerging countries. This shows that Indonesia still has much room and opportunity for natural gas industry to develop further. Also, Indonesia has a rather low natural gas consumption per capita of 204 m3 compared to other countries and only accounts for 22% of the energy mix by 3Q18 while Thailand is at 59% and Malaysia is at 43%. Those data translate that higher natural gas consumption in Indonesia is still within reach for improvement and will boost the industry’s performance even further. However, domestic natural gas hasn’t been utilized properly due to the lack of infrastructure development. For Indonesia to reach the same level of gas consumption, it will require the development of infrastructure to supply the high potential demand – as Indonesia currently only cover 20-30% of the needed infrastructure (Ministry of SOE, 2018).

57%

43%

Pertamina

Public

40%

24%

18%

5%

14%

Industry

Power sector

Petrochemical

Oil lifting

Others

4

Figure 9: Natural Gas Supply and Demand per Region 2019F

Source: Ministry of Energy and Mineral Resources 2018

Figure 10: Natural Gas Potential Demand

Source: Ministry of Energy and Mineral Resources 2018

Figure 11: Natural Gas Demand in Java and Outside Java

Source: Ministry of Energy and Mineral Resources 2018

Figure 12: Indonesian Energy Mix

Source: PLN Statistics, PLN RUPTL 2018-2027

Government’s Support in Securing Gas Supply A total gas reserve of 142.72 TSCF puts Indonesia in a secure position in terms of gas supply. This reserve, able to fulfil 54 years of current total annual consumption, is expected to be utilized even more efficiently as upstream regulations are being streamlined. However, Indonesia is expected to run a gas supply deficit by 2025 due to lack of encouragement from gas lifters because of uncertain regulations. To enlighten the situation, Ministry of Energy and Mineral Resources is gradually simplifying its notorious oil and gas regulations which is previously considered as unfavourable for investors. One such incentive is the rise of baseline company-take of profits from 30% to 48% for upstream gas companies. The ministry of EMR is also constantly simplifying regulations, most recently in 12/02/2019, where 10 oil and gas regulations are condensed into only 7. With these steps, we believe upstream lifting environment to welcome more investors and thus securing more domestic supply.

Indonesian Gas Network Region Given the nature of being an archipelagic country, it is indeed harder to build adequate gas infrastructure that could cover the whole country. Inadequate gas infrastructure has caused uneven gas supply despite of abundant natural gas reserves. Most players in the gas distribution industry has their own pipeline built near the supply of natural gas blocks. This aims to simplify the distribution process with no additional transportation costs but discourages companies to build pipelines far away from gas supply. As a result, Indonesia is lacking gas infrastructure, especially in regions where gas supply is absent. Based on the available gas distribution network, the Ministry of Energy and Mineral Resources divides the Indonesian archipelago into 6 regions: (I) Aceh and North Sumatra, (II) Central Sumatra, South Sumatra, Riau Islands, Natuna and West Java, (III) Central Java, (IV) East Java, (V) Kalimantan and Bali, (VI) Sulawesi, Nusa Tenggara, Maluku, and Papua (Figure 8). Overall, Region II and Region III are facing gas shortages (2019F: Aggregate supply: 3,141 mmscfd vs. aggregate demand: 3,370 mmscfd), while other regions are left with more supply but no adequate infrastructure to distribute them (2019F: Aggregate supply: 5,085 mmscfd vs aggregate demand: 4,230 mmscfd) (Figure 9).

Gas Infrastructure Masterplan, a Key to Develop Industry One of the government’s long-term goal regarding the distribution industry is to construct gas infrastructure based on a roadmap to be achieved by 2030 (Appendix C.3). It aims to maximize domestic gas utilization by connecting gas infrastructure throughout all regions in Indonesia and to increase distribution coverage to suppliers and customers, as well as to capture new potential demand. Potential demand will reach 8,255 mmscfd in 2023F based on EMR Ministry (2018) forecast on each region’s demand (Figure 10). The plan will include the construction of West Java-East Java pipeline by 2020 to address regional supply imbalance problems. The two regions will be connected by pipeline with a length of 567-667 km with 850 mmscfd capacity. Those pipelines will be completed by 2020 and start operating at full capacity by 2021. Once the pipeline starts to operate, it will capture new demand for natural gas that has been highly anticipated by local consumers in Sumatera-Java area (Region II-IV), demand will be as high as 4,070 mmscfd in 2019F compared to other regions of 3,530 mmscfd (Figure 11). While these plans will take some time to realize, other forms of gas distribution will still take place.

New Market Potentials in the Household Segment Households in Indonesia currently procure their gas supply through LPG tubes that are delivered to each household through non-pipeline distribution networks. With the ongoing construction of city gas pipelines, households can now acquire gas at a price of IDR 4,500-IDR 6,500/m3, compared to the 12 kg LPG tubes sold at Rp155,000, or IDR 23,919/m3. The absence of gas pipeline infrastructure connecting households to gas supply is a new potential market for the Indonesian natural gas industry. Even though the average household consumes much less gas (0.005 MMSCF/year) than industries (157.24 MMSCF/year), the potential number of customers to be reached is enormous. There are 69.5 million household in Indonesia, and only 192,489 being PGAS’ current household consumers. City gas projects still offer a good deal as it will help the industry to connect with thousands of new consumers and gain new potential revenue that is promising and sustainable.

Higher Demand from Core Customers Await Apart from the potential from household sector, higher demand from power generation and petrochemical is expected to take place in 2019F afterwards. MEMR has proposed higher electricity demand as designed in RUPTL 2018-2027 with sustainable gas proportion in the energy mix of 23% in 2019F (Figure 12). Gas demand from electricity is expected to increase up to 1,581 mmscfd by 2023F. Fertilizer sector will also increase their production capacity according to government’s vision to revitalize the industry. Gas as its raw material, will experience an increase along with the increase in production. Combined with tax holiday policy for petrochemical industry, it is expected that natural gas demand as raw material for fertilizer will soar up to 1,470 mmscfd applying the best scenario in 2023 (Figure 13).

Regulations to Secure Bargaining Power to Consumer There are times where players in the gas transportation business were not able to pass through gas acquisition cost increase to major customers. However, under EMR Ministerial Regulation No. 58/2017, price to end consumers are set at a formula of gas buying price, infrastructure costs, and a 7% margin. While this regulation may limit margins, players within this sector is assured to be able to pass through the gas acquisition cost to customers. This situation will protect margins which will not fall below the

240

3250

120

700

16901600

423

3088

53

914

2152

1596

Region 1 Region 2 Region 3 Region 4 Region 5 Region 6

(MMSCFD)Demand Supply

7318

7600

7896

8255

6800

7200

7600

8000

8400

2018F 2019F 2020F 2021F 2022F 2023F

(MMSCFD)

3515 35303791

3865

38044070 4105

4390

2500

3100

3700

4300

4900

2018F 2019F 2020F 2021F 2022F 2023F

(MMSCFD)Demand outside Java

Demand in Java

25% 23% 21% 23% 24%

12%6% 4% 4% 2%

51% 58% 62% 60% 61%

7% 7% 7% 6% 6%

4% 5% 5% 6% 6%

2016 2017 2018 2019 2020

Gas Oil

Coal Hydro

Geothermal

5

Figure 13: Natural Gas Demand from Core Customers

Source: PLN RUPTL 2018-2027, Ministry of Energy and Mineral Resources

Figure 14: Potential Demand from Oil Lifting

Source: Ministry of Energy and Mineral Resources 2018

Figure 15: Potential Gas Supply from Gas Holding

Source: Ministry of SOE 2018

Figure 17: EV/EBITDA Band

Source: Bloomberg, Team Estimates

regulated margin spread. Having the regulation set into place gives gas transportation players an extra bargaining chip to determine price to consumers.

COMPETITIVE POSITIONING PGAS is currently the market leader in the Indonesian gas distribution industry. High barriers to entry such as its capital intensive nature, tight permit approvals, and the relations required to secure supply, has deterred new entrants to enter and survive, leaving PGAS alone to be dominant in the industry. Combined with Pertagas acquisition and oil and gas holding formation, PGAS’ position as a market leader will be enhanced through several ways:

Potential New Demand from Parent Company PGAS has just moved under the wing of Pertamina, Indonesia’s oil and gas holding company. It will bring integration between upstream and downstream, creating higher effectiveness and efficiencies in natural gas management. Moreover, PGAS will also be able to capture potential deals inside Pertamina group. Currently Pertamina is engaging many diverse projects, for instance Refinery Development Master Plan (RDMP) to reduce Indonesia’s dependency to oil import. RDMP projects consist of five oil refineries project: Cilacap, Balikpapan, Balongan, Tuban, and Bontang. Those oil refineries are expected to generate additional gas demand of 765 mmscfd for oil lifting (Figure 14). Other projects such as LPG terminal or pipeline construction projects, will surely benefit PGAS compared to other players in industry.

Gas Holding to Secure Supply Contracts Oil and gas holding formation will allow Pertamina to directly provide its natural gas supply into PGAS’ supply chain. According to Indonesian Ministry of SOE’s plan, all Pertamina’s gas contracts will be given to PGAS along with its supply infrastructure (transmission and distribution pipeline). Currently Pertamina produces gas 1,785 mmscfd domestically and another potential additional gas supply with 6 blocks commencing with total amount 281 mmscfd up to 2021F (Figure 15). Pertamina’s natural gas production is expected to increase due to viability from additional exploration and extraction using PGAS’ infrastructure, likewise improving PGAS’s supply. Infrastructure will increase revenue when demand soars high, mutually benefitting both sides.

More Developed Infrastructure to Access End Customers Improved gas infrastructure comes from PGAS-Pertagas' pipeline integration and various government projects regarding gas infrastructure roadmap. Currently PGAS holds 85% nation’s gas infrastructure (7,454 km). Post-acquisition of Pertagas, PGAS has 95% of nation’s infrastructure (9,677 km). Pipeline integration between both companies will also excel the distribution process from supplier to customer, for example SSWJ and East Java pipeline integration. Next, government also incessantly enforcing its infrastructure roadmap project. As an SOE, PGAS has an advantage and received more exposure towards various government’s infrastructure projects. Nation’s long-term masterplan to support gas infrastructure (Appendix C.3) will increase company’s coverage to new demand and supply. Even more, company’s position as market leader with extensive pipeline will ease the bidding process over a project, making it easier for company to grow larger.

INVESTMENT SUMMARY Figure 16: PGAS’s Share Price and News Flows since February 2016 (Stock Price in IDR)

We issue a BUY recommendation on PGAS with a 12-month target price of IDR2,970/share implying 7.66x EV/EBITDA and 1.18x EV/IC. This represents a potential 20.73% upside from its closing price of IDR2,460/share on 15/02/2019. We derived our target price using a sum of the parts method, employing the following methodologies: Discounted Cash Flow to the Firm and Trading Multiples. Our recommendation is based on these key drivers:

Key Drivers Growth Opportunity in Indonesia’s Gas Market Despite its abundant gas reserve (largest in Asia), Indonesia's gas hasn’t been utilized properly due to a lack of infrastructure. This is evident with Indonesia having one of the lowest gas consumptions per capita

1368

1560 1581

1125

1470 1470

600

900

1200

1500

1800

2018F 2019F 2020F 2021F 2022F 2023F

(MMSCFD)Power Generation

Fertilizer

206

229

80

125

125

Cilacap

Balikpapan

Balongan

Tuban

Bontang

(MMSCFD)

10

10

20

15

40

186

Simenggaris

Bambu Besar

Salawati

Cikarang Tegal

Puspa

Cepu

(MMSCFD)

3

4

5

6

7

8

9

10

2/1

8/20

16

5/1

8/20

16

8/1

8/20

16

11/

11

/20

16

8/2

/201

7

12/

5/20

17

8/1

6/20

17

11/

13

/20

17

9/2

/201

8

9/5

/201

8

8/1

5/20

18

12/

11

/20

18

12/

2/20

19

EV/EBITDA PGAS IJ

Average EV/EBITDA

EV/EBITDA STD+1

EV/EBITDA STD+2

EEV/EBITDA STD-1

EV/EBITDA STD-2

9.34

8.24

7.15

6.05

4.96

Appointment of new President Director,

Gigih Prakoso

Natural gas pricing formula announcement

ConocoPhillips increased its gas selling price

Government capped gas selling price of

$1.8/MMBTU in North Sumatra

PLN proposed DMO at $6/MMBTU

PGAS acquired 51% ownership of Pertagas

PGAS's ownership was transferred to Pertamina

First time recorded loss in quarter report

6

Figure 18: Distribution Volume and Margin Spread under Pertagas (PTG) Consolidation

Source: Team Estimates

Figure 19: Cash Flow

Source: Team Estimates

Figure 20: Fixed Asset Turnover

Source: Team Estimates

compared to other emerging Asian countries. The lack of infrastructure has resulted in gas supply deficits in several regions, despite aggregate supply being above aggregate demand. This situation is due to the tight permit nature of the industry and high capital intensity resulting an underdeveloped gas pipelines. But with better connectivity and recovering industrial demand, a great potential is to be seen from PGAS.

Gas Infrastructure Development to Boost Potential Demand To fulfil the increasing electricity demand, the government have set an ambitious plan to expand Indonesian gas infrastructure up to 80%-100% of needed infrastructure to achieve energy mix target by 2030 (compared to current condition of 20%-30%). The government-backed PGAS which controls the gas-sub holding will be favoured in building and operating the humongous planned network of pipeline with a 20 years monopoly rights and higher margin at 12% IRR.

Gas Sub-Holding Formation to Secure PGAS’ Supply The gas sub-holding will bring a security of supply for PGAS. Pertamina can have more ease at commercializing blocks, and PGAS can transport the potential supply. PGAS being under Pertamina also means that Pertamina will favour PGAS more in terms of distributing its gas. One impact of the mutualism can be felt soon from Pertamina’s 6 gas fields with a total capacity of 281 mmscfd which is expected to commercialize by 2021.

PGAS to Benefit from Acquisition Synergy Acquisition of Pertagas will provide substantial synergy for PGAS. From this initiative, PGAS will strengthen its market share of pipeline into 95% length-wise, allowing the company to grab more customers. Revenue synergy will occur from the plan to integrate both companies’ pipelines across Java, allowing the gas surplus from Region IV to be channelled into the gas deficit Region II and III. This will pump up the available supply that can be distributed by PGAS to meet the demand. Apart from revenue, cost synergies will also transpire from lower SG&A expenses, as well as capex duplication avoidance. Following the acquisition, PGAS will obtain a synergic value of US$582.14 mn.

Value Opportunity: Strong Cash Generator Trading at Discount With a turnaround performance and limited incremental risks, PGAS is currently trading at a 12.7% 2019 FCF Yield and 5.9x EV/EBITDA (-1 standard deviation based on 5 years historical average). We believe that this attractive valuation and brighter outlook will not only provide an adequate margin of safety, but also create a top- notch investment opportunity.

Valuation Methodology We used sum of the parts approach, employing the following methodologies: Discounted Cash Flow to the Firm and Trading Multiples to arrive at our 12-month target price of IDR 2,970/share, which presents an upside potential of 20.73% from 15/02/2019 closing price of IDR 2,460.

Key Risk Delay in Pipeline Integration The pipeline integration bound to be finished by 2020 will cover the gas shortage in Region II and III. Any delay in this pipeline integration means that these two regions will run a gas deficit for a longer time, eliminating the potential revenue of US$342.85 mn.

Change in Gas Pricing Regulation Being a highly regulated industry, gas pricing is very dependent on new regulations, the newest being EMR Ministerial Regulation No. 58/2017 which sets the price downstream gas price. While this recent regulation is also beneficial seeing that margin is guaranteed, future regulations may affect PGAS’ profitability negatively.

Gas Demand from Power Plant Muted Power Plant Sector remain as the largest customer of PGAS, contributing 41% of its total distribution volume. With natural gas bearing one of the higher costs compared to other energy alternatives (coal and renewable energy), PLN have indicated some interest to lower gas proportion in the national energy mix. Although it has been rejected by the Minister of Energy, this have marked an uncertainty in the natural gas market, especially for PGAS.

FINANCIAL ANALYSIS

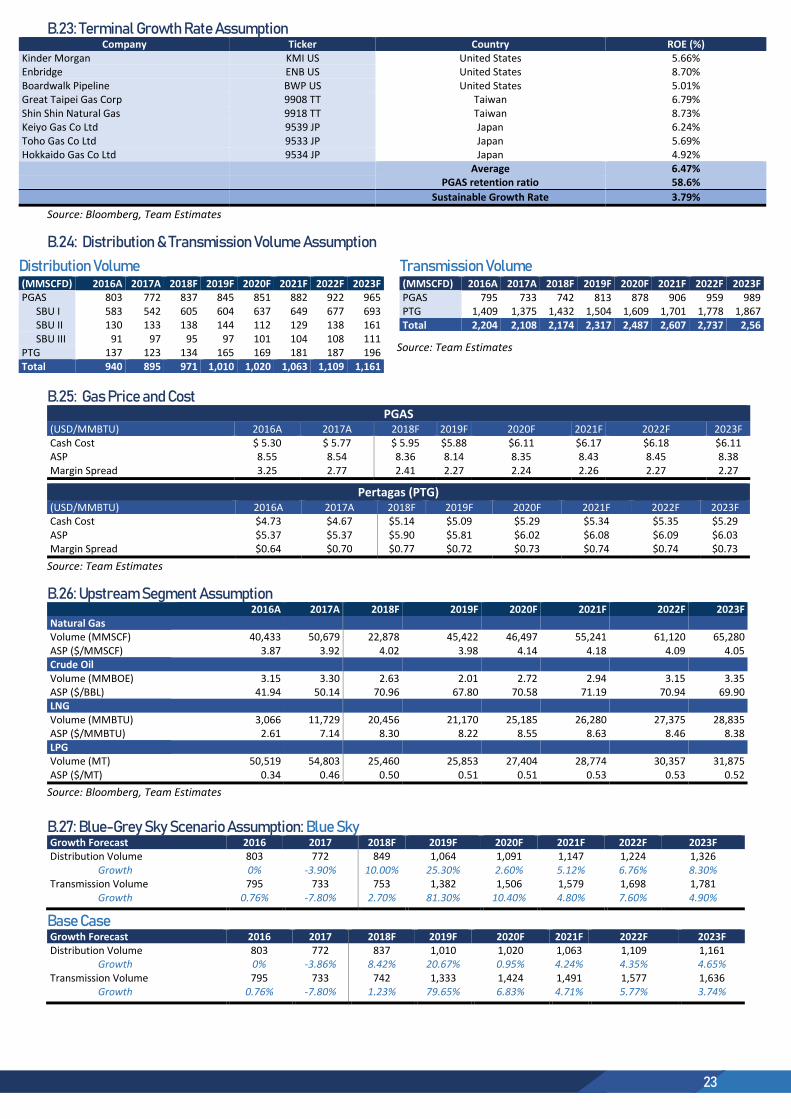

Lower Margins to be Accommodated with Higher Sales Volume Even though the upcoming government regulation (Appendix C.5, C.6) will diminish PGAS’ gas distribution margin arriving at a cheaper gas price, we believe that this factor, along with infrastructure integration will boost natural gas demand and distribution volume. The cheaper gas price will make gas more attractive, while the infrastructure will support the increase in demand. Therefore, we expect revenue trend to be upward with 8.65% CAGR for 2018-2023 supported by higher growth in distribution and transmission volume of 16.96% CAGR and 5.61% CAGR respectively. Whereas previous trend of revenue is rather stagnant at 0.02% CAGR over the past 5 years, due to a falling distribution and transmission volume at -1.03% CAGR and -1.96% CAGR respectively. This resulted in a revenue slowdown as reflected by lower revenue/km of US$478,000/km in 2013 to US$322,000/km in 2017 (Figure 18).

Strong cash generating abilities Throughout 2013 until 2017, PGAS presented positive OCF and negative FCF in 2013 to 2015 due to company’s strategy in acquiring oil and gas blocks through Saka Energi and higher CAPEX is required in the early production stage in 2014. However, as SAKA undergoes the middle production stage, PGAS has showed a positive FCF with increasing trends. We expect this trend to continue as PGAS will most likely

971 1,001 1,135

1,174

2.18

2.01 2.00 2.012.02 2.01

1.9

2

2.1

2.2

-

400

800

1,200

1,600

2018F 2019F 2020F 2021F 2022F 2023F

Distribution Volume Margin Spread

1.83

2.14 2.15 2.2113.5%

11.8%10.9% 10.6%11.3%

13.4% 12.5%12.8%

0%

4%

8%

12%

16%

0

0.5

1

1.5

2

2.5

2018F 2019F 2020F 2021F 2022F 2023F

OCF/Capex

Capex/Sales

FCF Margin

2.01

1.29 1.35 1.4 1.45 1.49

0

1

2

3

2018F 2019F 2020F 2021F 2022F 2023F

7

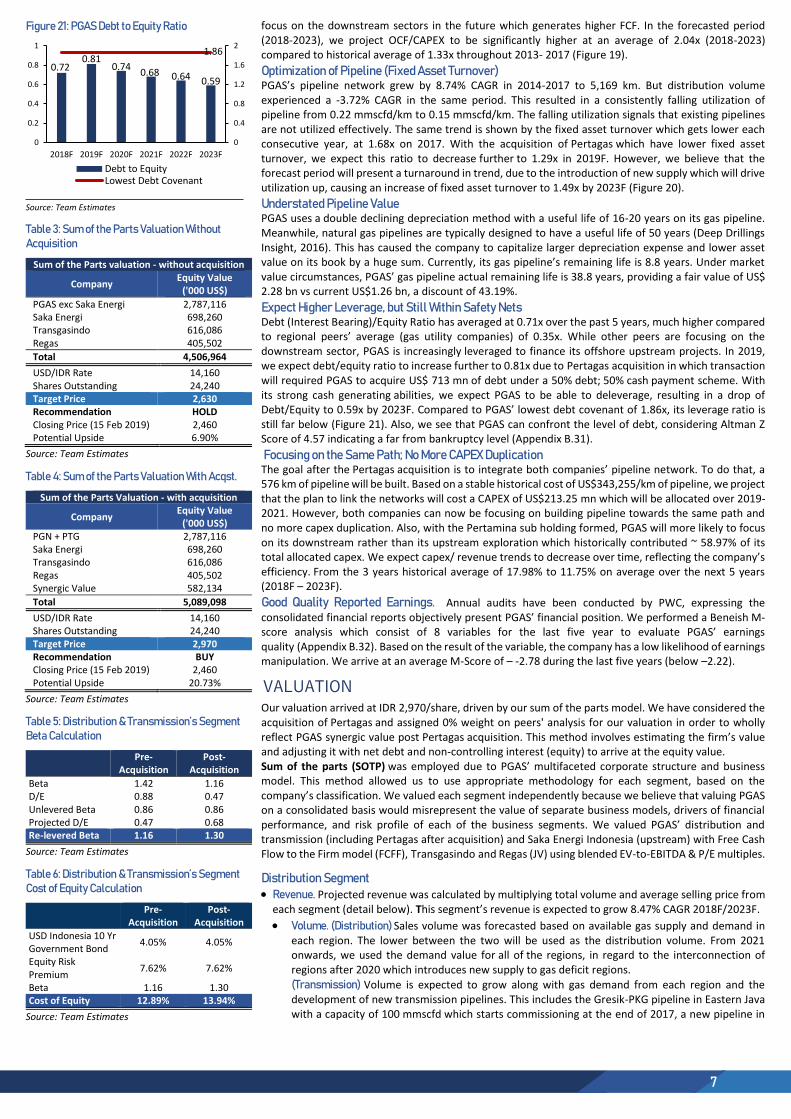

Figure 21: PGAS Debt to Equity Ratio

Source: Team Estimates

Table 3: Sum of the Parts Valuation Without Acquisition

Sum of the Parts valuation - without acquisition

Company Equity Value

('000 US$)

PGAS exc Saka Energi 2,787,116 Saka Energi 698,260 Transgasindo 616,086 Regas 405,502

Total 4,506,964

USD/IDR Rate 14,160 Shares Outstanding 24,240 Target Price 2,630 Recommendation HOLD Closing Price (15 Feb 2019) 2,460 Potential Upside 6.90%

Source: Team Estimates

Table 4: Sum of the Parts Valuation With Acqst.

Sum of the Parts Valuation - with acquisition

Company Equity Value

('000 US$) PGN + PTG 2,787,116 Saka Energi 698,260 Transgasindo 616,086 Regas 405,502 Synergic Value 582,134

Total 5,089,098

USD/IDR Rate 14,160 Shares Outstanding 24,240 Target Price 2,970 Recommendation BUY Closing Price (15 Feb 2019) 2,460 Potential Upside 20.73%

Source: Team Estimates

Table 5: Distribution & Transmission’s Segment Beta Calculation

Pre-Acquisition

Post-Acquisition

Beta 1.42 1.16 D/E 0.88 0.47 Unlevered Beta 0.86 0.86 Projected D/E 0.47 0.68 Re-levered Beta 1.16 1.30

Source: Team Estimates

Table 6: Distribution & Transmission’s Segment Cost of Equity Calculation

Pre-Acquisition

Post-Acquisition

USD Indonesia 10 Yr Government Bond

4.05% 4.05%

Equity Risk Premium

7.62% 7.62%

Beta 1.16 1.30 Cost of Equity 12.89% 13.94%

Source: Team Estimates

focus on the downstream sectors in the future which generates higher FCF. In the forecasted period (2018-2023), we project OCF/CAPEX to be significantly higher at an average of 2.04x (2018-2023) compared to historical average of 1.33x throughout 2013- 2017 (Figure 19).

Optimization of Pipeline (Fixed Asset Turnover) PGAS’s pipeline network grew by 8.74% CAGR in 2014-2017 to 5,169 km. But distribution volume experienced a -3.72% CAGR in the same period. This resulted in a consistently falling utilization of pipeline from 0.22 mmscfd/km to 0.15 mmscfd/km. The falling utilization signals that existing pipelines are not utilized effectively. The same trend is shown by the fixed asset turnover which gets lower each consecutive year, at 1.68x on 2017. With the acquisition of Pertagas which have lower fixed asset turnover, we expect this ratio to decrease further to 1.29x in 2019F. However, we believe that the forecast period will present a turnaround in trend, due to the introduction of new supply which will drive utilization up, causing an increase of fixed asset turnover to 1.49x by 2023F (Figure 20).

Understated Pipeline Value PGAS uses a double declining depreciation method with a useful life of 16-20 years on its gas pipeline. Meanwhile, natural gas pipelines are typically designed to have a useful life of 50 years (Deep Drillings Insight, 2016). This has caused the company to capitalize larger depreciation expense and lower asset value on its book by a huge sum. Currently, its gas pipeline’s remaining life is 8.8 years. Under market value circumstances, PGAS’ gas pipeline actual remaining life is 38.8 years, providing a fair value of US$ 2.28 bn vs current US$1.26 bn, a discount of 43.19%.

Expect Higher Leverage, but Still Within Safety Nets Debt (Interest Bearing)/Equity Ratio has averaged at 0.71x over the past 5 years, much higher compared to regional peers’ average (gas utility companies) of 0.35x. While other peers are focusing on the downstream sector, PGAS is increasingly leveraged to finance its offshore upstream projects. In 2019, we expect debt/equity ratio to increase further to 0.81x due to Pertagas acquisition in which transaction will required PGAS to acquire US$ 713 mn of debt under a 50% debt; 50% cash payment scheme. With its strong cash generating abilities, we expect PGAS to be able to deleverage, resulting in a drop of Debt/Equity to 0.59x by 2023F. Compared to PGAS’ lowest debt covenant of 1.86x, its leverage ratio is still far below (Figure 21). Also, we see that PGAS can confront the level of debt, considering Altman Z Score of 4.57 indicating a far from bankruptcy level (Appendix B.31).

Focusing on the Same Path; No More CAPEX Duplication The goal after the Pertagas acquisition is to integrate both companies’ pipeline network. To do that, a 576 km of pipeline will be built. Based on a stable historical cost of US$343,255/km of pipeline, we project that the plan to link the networks will cost a CAPEX of US$213.25 mn which will be allocated over 2019-2021. However, both companies can now be focusing on building pipeline towards the same path and no more capex duplication. Also, with the Pertamina sub holding formed, PGAS will more likely to focus on its downstream rather than its upstream exploration which historically contributed ~ 58.97% of its total allocated capex. We expect capex/ revenue trends to decrease over time, reflecting the company’s efficiency. From the 3 years historical average of 17.98% to 11.75% on average over the next 5 years (2018F – 2023F).

Good Quality Reported Earnings. Annual audits have been conducted by PWC, expressing the consolidated financial reports objectively present PGAS’ financial position. We performed a Beneish M-score analysis which consist of 8 variables for the last five year to evaluate PGAS’ earnings quality (Appendix B.32). Based on the result of the variable, the company has a low likelihood of earnings manipulation. We arrive at an average M-Score of – -2.78 during the last five years (below –2.22).

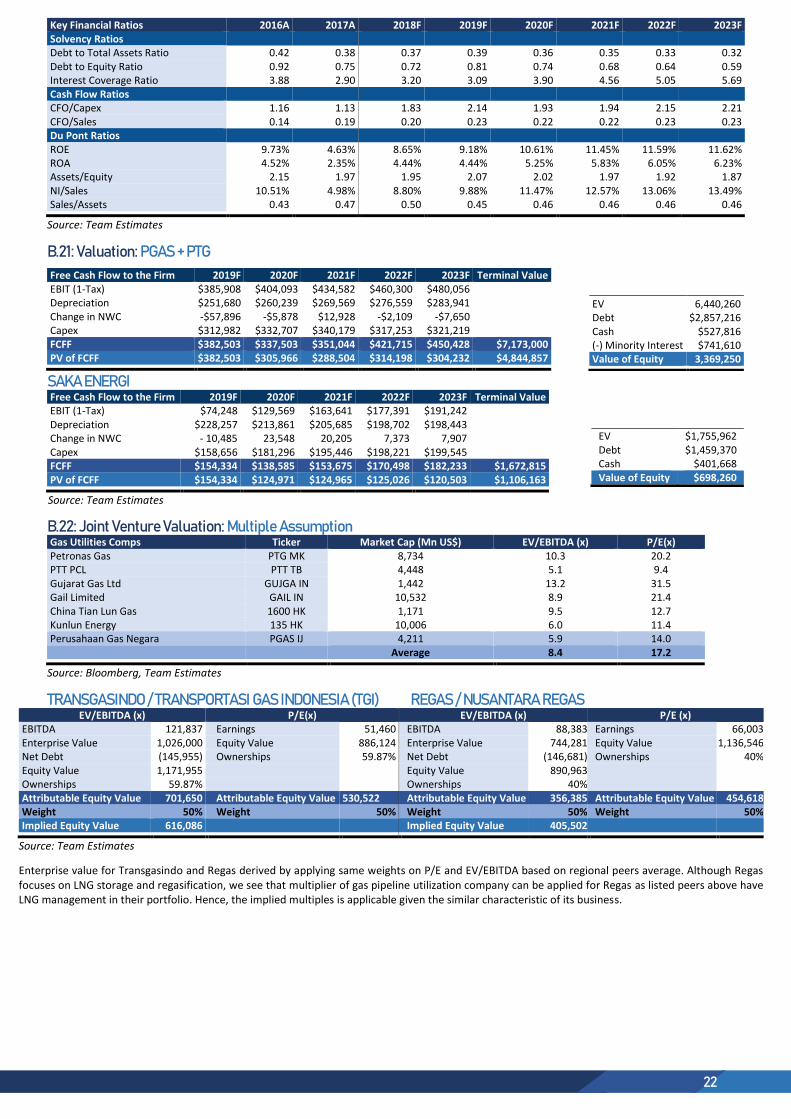

VALUATION Our valuation arrived at IDR 2,970/share, driven by our sum of the parts model. We have considered the acquisition of Pertagas and assigned 0% weight on peers' analysis for our valuation in order to wholly reflect PGAS synergic value post Pertagas acquisition. This method involves estimating the firm’s value and adjusting it with net debt and non-controlling interest (equity) to arrive at the equity value. Sum of the parts (SOTP) was employed due to PGAS’ multifaceted corporate structure and business model. This method allowed us to use appropriate methodology for each segment, based on the company’s classification. We valued each segment independently because we believe that valuing PGAS on a consolidated basis would misrepresent the value of separate business models, drivers of financial performance, and risk profile of each of the business segments. We valued PGAS’ distribution and transmission (including Pertagas after acquisition) and Saka Energi Indonesia (upstream) with Free Cash Flow to the Firm model (FCFF), Transgasindo and Regas (JV) using blended EV-to-EBITDA & P/E multiples.

Distribution Segment Revenue. Projected revenue was calculated by multiplying total volume and average selling price from

each segment (detail below). This segment’s revenue is expected to grow 8.47% CAGR 2018F/2023F.

Volume. (Distribution) Sales volume was forecasted based on available gas supply and demand in each region. The lower between the two will be used as the distribution volume. From 2021 onwards, we used the demand value for all of the regions, in regard to the interconnection of regions after 2020 which introduces new supply to gas deficit regions.

(Transmission) Volume is expected to grow along with gas demand from each region and the development of new transmission pipelines. This includes the Gresik-PKG pipeline in Eastern Java with a capacity of 100 mmscfd which starts commissioning at the end of 2017, a new pipeline in

0.720.81

0.740.68 0.64 0.59

1.86

0

0.4

0.8

1.2

1.6

2

0

0.2

0.4

0.6

0.8

1

2018F 2019F 2020F 2021F 2022F 2023F

Debt to EquityLowest Debt Covenant

8

Table 7: Distribution and Transmission’s Segment Cost of Debt Calculation

Pre-Acquisition

Post-Acquisition

Cost of Debt 5.05% 6.67% After-Tax Cost of Debt 3.79% 5.00%

Source: Team Estimates

Table 8: Distribution and Transmission’s Segment WACC Calculation

Pre-Acquisition

Post-Acquisition

Cost of Equity 12.89% 13.94% Weight of Equity 68% 59% After-Tax Cost of Debt

3.79% 5.00%

Weight of Debt 32% 41% WACC 9.98% 10.31%

Source: Team Estimates

Table 9: Upstream Segment Beta Calculation Oil & Gas peers Beta Debt/MCap Guanghui Energy 1.01 0.11 Medco Energi Internasional

1.71 2.79

Oil and Natural Gas Corp 1.04 0.36 Bharat Petroleum Corp 1.43 0.39 Median 1.24 0.37

Source: Team Estimates

Table 10: Upstream Segment WACC Calculation Cost of Equity – CAPM 13.46% Market Risk Premium 7.62% Risk Free Rate 4.05% Beta 1.24 Cost of Debt 4.01% Target D/E 0.37 WACC 10.89%

Source: Team Estimates

Table 11: Joint Venture Valuation Assumption Peers Valuation

Multiples Computation EV/EBITDA 8.4 P/E 17.2

Transgasindo (TGI) Enterprise Value 1,026,000 Net Debt (145,955) Value from EV/EBITDA (50%) 585,978 Value from P/E (50%) 443,062 Equity Value 1,029,039 Ownerships 59.87% Attributable Equity Value 616,086

Regas Enterprise Value 744,281 Net Debt (146,681) Value from EV/EBITDA (50%) 445,481 Value from P/E (50%) 568,273 Equity Value 1,013,754 Ownership 40% Attributable Equity Value 405,502

Source: Team Estimates

Figure 22: Synergic Value Up To 2023F

Source: Team Estimates

Southern Sumatera transmitting 126 mmscfd for ConocoPhillips is expected to be completed by the end of 2018, and Semarang-Gresik pipeline that will start transmitting 100 mmscfd by 2020. Thus we arrive at a projection of 6.96% and 30.93% CAGR (due to consolidation of Pertagas) from 2018 to 2023 of distribution volume and transmission volume respectively.

Price. (Distribution) To set the selling price, we considered gas pricing formula (Apendix C.9) set by the EMR Ministerial Regulation No. 58/2017 which consists of cost of gas, infrastructure management cost, and trading margin (7% cash cost) for industrial customers. This gas pricing formula will be effectively implied in July 2019. We also consider gas price forecast, which is implied in our cash cost, to administer the selling price used.

(Transmission) Selling Price is forecasted based on average toll fees charged in each region (Northern Sumatera, Southern Sumatera, Western Java, Eastern Java, and Kalimantan). We expect toll fees to be sustained as toll fees are stable for the last 3 years in the nature of it being highly affected by regulations specific for each region.

Cost. Cost is mostly derived from the purchase of gas. We made a projection of purchase of gas price following the movement of global natural gas price as its benchmark. Infrastructure management cost is calculated by the cost of services divided by volume, in which we take several items into account: depreciation expense, general and administrative expenses, repair and maintenance cost, tax and levy, and other operational expenses. Operational cost is expected to increase by 7.80% CAGR 2018- 2023.

Capital Expenditures. In the forecast period, CAPEX will be driven to meet the volume growth and maintenance of assets. We forecast CAPEX with some adjustments after the acquisition takes place in which PGAS’ downstream segment will require additional CAPEX to integrate its pipelines with Pertagas’, which is estimated to be US$213.25 mn over the course of 5 years (2018-2023). Following the acquisition, there will be CAPEX savings from CAPEX duplication avoidance. CAPEX is forecasted with normalized CAPEX to sales ratio ranging between 7.72% to 9.14% for the next 5 years.

Oil and Gas Sales Segment (Upstream) Revenue. Revenue from Saka is calculated by considering the lifting volume and selling price from each

commodity. Revenue from oil and gas sales is expected to grow 6.94% CAGR from 2018F/2023F.

Volume. The growth of volume is forecasted for each block that the company owns, factoring in the capacity utilization level and production stages (and permits). Currently, most of SAKA Energi’s blocks are at an early production stage and 2 blocks (East Kalimantan and Sanga-Sanga) have reached its expiration year. We also estimated Sidayu (under Pangkah) block to commence its operation in the end of 2019 which will contribute 15.7% in oil lifting volume and 28.2% in gas lifting volume. Hence, from the 2018-2023 period, oil lifting volume and gas lifting volume are expected to grow by 4.98% CAGR and 8.72% respectively.

Price. Selling price is set based on the assumptions of commodity forecasts (Appendix B.26) for each type of commodity sold, namely LNG, LPG, Oil, and Natural Gas.

Cost. We estimate cash cost by converting gas and oil to the same units (mmboe). This cost will Increase (decrease) in line in a ratio of 55% with the movement of commodity forecast as contractors will increase its service cost during commodity price hike and decrease its service cost when commodity price fall. Operational cost (including depreciation) is expected to increase by 3.26% CAGR 2018-2023.

Capital Expenditures. CAPEX is required to continue Saka Energi’s exploration and operational activities. In the forecast period, we adjusted based on the blocks’ production stage and its revenues. CAPEX is expected to grow by 3.37% CAGR for the next 5 years with CAPEX/sales ratio between 0.26-0.30.

Joint Ventures (Midstream Segment) – Trading Multiples While accounting classification excludes profit from joint ventures from EBIT, we still acknowledge 2 of PGAS’ JVs contribution to PGAS valuation as it cannot be left out. This is due to their large contribution for the company’s earnings (18.2%) and the nature of operations which are comparable to PGAS’ core business. We derived the target price based on the average gas infrastructure industry’s EV/EBITDA of 8.42x and P/E of 17.3x. In computing the valuation, we equally weight both variables (50%;50%). It was selected since (1) It is a proper metric for gas distribution company in measuring operating performance, by adjusting peers’ tax rate (due to lack of comparison in Indonesia) and depreciation method accounting adjustment (2) the Joint Ventures attribute PGAS based on its earnings, thus earnings performance will affect PGAS’ bottom line. Thereafter, we multiply it by PGAS’ ownership (%) to reflect its value for PGAS.

Synergic Value We foresee PGAS-PTG synergy would take place in the form of additional operating income (Business alignment & optimization and business expansion in gas sub holding) and cost savings. By acquiring Pertagas, PGAS can capture potential deals inside Pertamina group, align Pertagas’ and PGAS’ infrastructure to reach gas supply site and boost sales volume. Also, both companies can avoid pipeline construction duplication and therefore being more efficient on capital expenditure. We then compare the equity value of PGAS with and without the synergy. From this analysis, we conclude that there is a synergic value of US$582 million, which contributes to an upside potential from target price of IDR2,630/share without acquisition into IDR2,970/share with acquisition.

Weighted Average Cost of Capital (WACC) Downstream Segment. The cost of equity is calculated through the Capital Asset Pricing Model adjusted to the country risk premium. As for the risk-free rate, we used the 10Y Indonesia Government Dollar-

2,787 3,3691,425 5821,425

PG

AS

(par

ent

on

ly)

Acq

uis

itio

n C

ost

Per

taga

s

Syn

ergi

c V

alu

e

Tota

l Val

ue

(USD Mn)

9

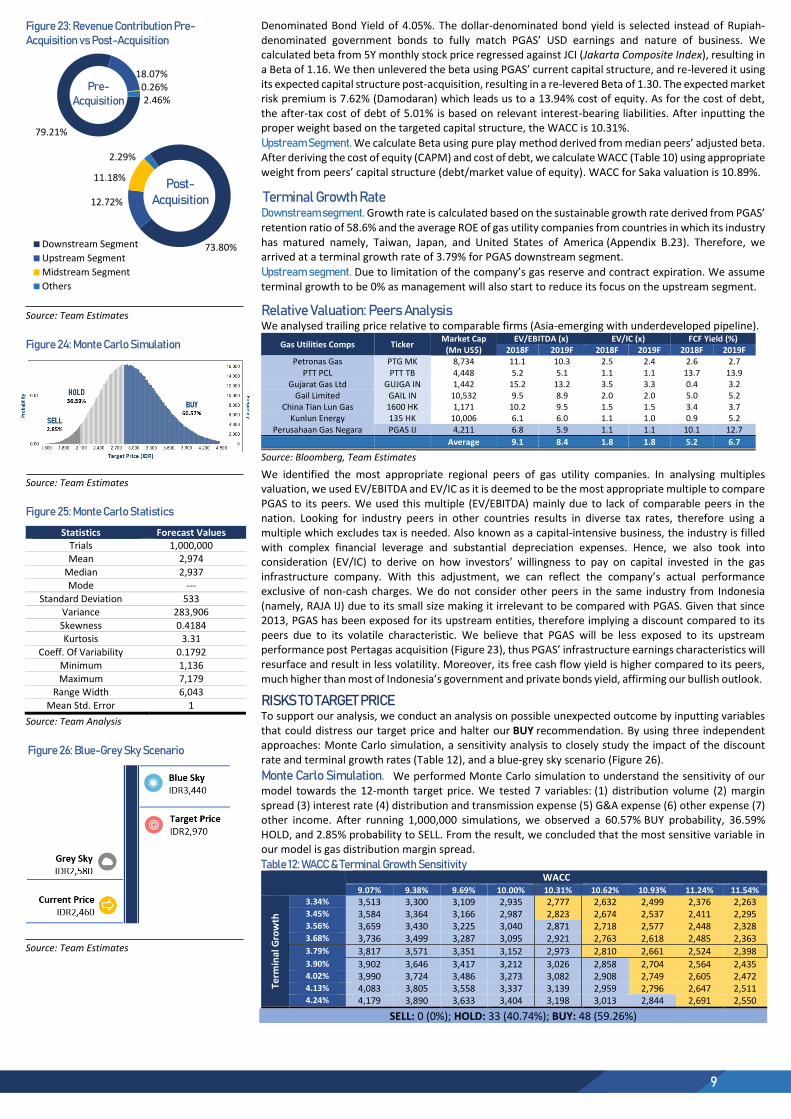

Figure 23: Revenue Contribution Pre-Acquisition vs Post-Acquisition

Source: Team Estimates

Figure 24: Monte Carlo Simulation

Source: Team Estimates

Figure 25: Monte Carlo Statistics

Statistics Forecast Values Trials 1,000,000 Mean 2,974

Median 2,937 Mode ---

Standard Deviation 533 Variance 283,906

Skewness 0.4184 Kurtosis 3.31

Coeff. Of Variability 0.1792 Minimum 1,136

Maximum 7,179 Range Width 6,043

Mean Std. Error 1

Source: Team Analysis

Figure 26: Blue-Grey Sky Scenario

Source: Team Estimates

Denominated Bond Yield of 4.05%. The dollar-denominated bond yield is selected instead of Rupiah-denominated government bonds to fully match PGAS’ USD earnings and nature of business. We calculated beta from 5Y monthly stock price regressed against JCI (Jakarta Composite Index), resulting in a Beta of 1.16. We then unlevered the beta using PGAS’ current capital structure, and re-levered it using its expected capital structure post-acquisition, resulting in a re-levered Beta of 1.30. The expected market risk premium is 7.62% (Damodaran) which leads us to a 13.94% cost of equity. As for the cost of debt, the after-tax cost of debt of 5.01% is based on relevant interest-bearing liabilities. After inputting the proper weight based on the targeted capital structure, the WACC is 10.31%.

Upstream Segment. We calculate Beta using pure play method derived from median peers’ adjusted beta. After deriving the cost of equity (CAPM) and cost of debt, we calculate WACC (Table 10) using appropriate weight from peers’ capital structure (debt/market value of equity). WACC for Saka valuation is 10.89%.

Terminal Growth Rate Downstream segment. Growth rate is calculated based on the sustainable growth rate derived from PGAS’ retention ratio of 58.6% and the average ROE of gas utility companies from countries in which its industry has matured namely, Taiwan, Japan, and United States of America (Appendix B.23). Therefore, we arrived at a terminal growth rate of 3.79% for PGAS downstream segment.

Upstream segment. Due to limitation of the company’s gas reserve and contract expiration. We assume terminal growth to be 0% as management will also start to reduce its focus on the upstream segment.

Relative Valuation: Peers Analysis We analysed trailing price relative to comparable firms (Asia-emerging with underdeveloped pipeline).

Gas Utilities Comps Ticker Market Cap

(Mn US$) EV/EBITDA (x) EV/IC (x) FCF Yield (%)

2018F 2019F 2018F 2019F 2018F 2019F Petronas Gas PTG MK 8,734 11.1 10.3 2.5 2.4 2.6 2.7

PTT PCL PTT TB 4,448 5.2 5.1 1.1 1.1 13.7 13.9 Gujarat Gas Ltd GUJGA IN 1,442 15.2 13.2 3.5 3.3 0.4 3.2

Gail Limited GAIL IN 10,532 9.5 8.9 2.0 2.0 5.0 5.2 China Tian Lun Gas 1600 HK 1,171 10.2 9.5 1.5 1.5 3.4 3.7

Kunlun Energy 135 HK 10,006 6.1 6.0 1.1 1.0 0.9 5.2 Perusahaan Gas Negara PGAS IJ 4,211 6.8 5.9 1.1 1.1 10.1 12.7

Average 9.1 8.4 1.8 1.8 5.2 6.7

Source: Bloomberg, Team Estimates

We identified the most appropriate regional peers of gas utility companies. In analysing multiples valuation, we used EV/EBITDA and EV/IC as it is deemed to be the most appropriate multiple to compare PGAS to its peers. We used this multiple (EV/EBITDA) mainly due to lack of comparable peers in the nation. Looking for industry peers in other countries results in diverse tax rates, therefore using a multiple which excludes tax is needed. Also known as a capital-intensive business, the industry is filled with complex financial leverage and substantial depreciation expenses. Hence, we also took into consideration (EV/IC) to derive on how investors’ willingness to pay on capital invested in the gas infrastructure company. With this adjustment, we can reflect the company’s actual performance exclusive of non-cash charges. We do not consider other peers in the same industry from Indonesia (namely, RAJA IJ) due to its small size making it irrelevant to be compared with PGAS. Given that since 2013, PGAS has been exposed for its upstream entities, therefore implying a discount compared to its peers due to its volatile characteristic. We believe that PGAS will be less exposed to its upstream performance post Pertagas acquisition (Figure 23), thus PGAS’ infrastructure earnings characteristics will resurface and result in less volatility. Moreover, its free cash flow yield is higher compared to its peers, much higher than most of Indonesia’s government and private bonds yield, affirming our bullish outlook.

RISKS TO TARGET PRICE To support our analysis, we conduct an analysis on possible unexpected outcome by inputting variables that could distress our target price and halter our BUY recommendation. By using three independent approaches: Monte Carlo simulation, a sensitivity analysis to closely study the impact of the discount rate and terminal growth rates (Table 12), and a blue-grey sky scenario (Figure 26).

Monte Carlo Simulation. We performed Monte Carlo simulation to understand the sensitivity of our model towards the 12-month target price. We tested 7 variables: (1) distribution volume (2) margin spread (3) interest rate (4) distribution and transmission expense (5) G&A expense (6) other expense (7) other income. After running 1,000,000 simulations, we observed a 60.57% BUY probability, 36.59% HOLD, and 2.85% probability to SELL. From the result, we concluded that the most sensitive variable in our model is gas distribution margin spread.

Table 12: WACC & Terminal Growth Sensitivity

WACC 9.07% 9.38% 9.69% 10.00% 10.31% 10.62% 10.93% 11.24% 11.54%

Term

inal

Gro

wth

3.34% 3,513 3,300 3,109 2,935 2,777 2,632 2,499 2,376 2,263 3.45% 3,584 3,364 3,166 2,987 2,823 2,674 2,537 2,411 2,295 3.56% 3,659 3,430 3,225 3,040 2,871 2,718 2,577 2,448 2,328 3.68% 3,736 3,499 3,287 3,095 2,921 2,763 2,618 2,485 2,363 3.79% 3,817 3,571 3,351 3,152 2,973 2,810 2,661 2,524 2,398 3.90% 3,902 3,646 3,417 3,212 3,026 2,858 2,704 2,564 2,435 4.02% 3,990 3,724 3,486 3,273 3,082 2,908 2,749 2,605 2,472 4.13% 4,083 3,805 3,558 3,337 3,139 2,959 2,796 2,647 2,511 4.24% 4,179 3,890 3,633 3,404 3,198 3,013 2,844 2,691 2,550

SELL: 0 (0%); HOLD: 33 (40.74%); BUY: 48 (59.26%)

79.21%

18.07%0.26%2.46%

Pre-Acquisition

73.80%

12.72%

11.18%

2.29%

Downstream Segment

Upstream Segment

Midstream Segment

Others

Post-Acquisition

10

Risks Mitigating Factors

Regulatory Risk Downstream Gas Price Amendment Offset the risk in margin spread with a strategy to boost distribution volume (e.g. Pipeline Integration)

National Energy Policy Grab customers in other industrial segments

Operational Risk Delay in Pertagas Integration Integrate pipeline network in several areas Pipeline Leakage Set operating procedures, maintenance, and repairs to ensure pipeline installation quality Losing Supply Contracts Secure supply contracts through Pertamina holding

Market Risk Slowdown in Indonesia Industrial Growth Have consumers in other segments and constantly develop other household segments Interest Rate Hike Acquire fixed rate debt with a proportion of 95% fixed and 5% floating

Oil and Gas Price Fluctuations Focusing on midstream and downstream segment

Source: Team Estimates

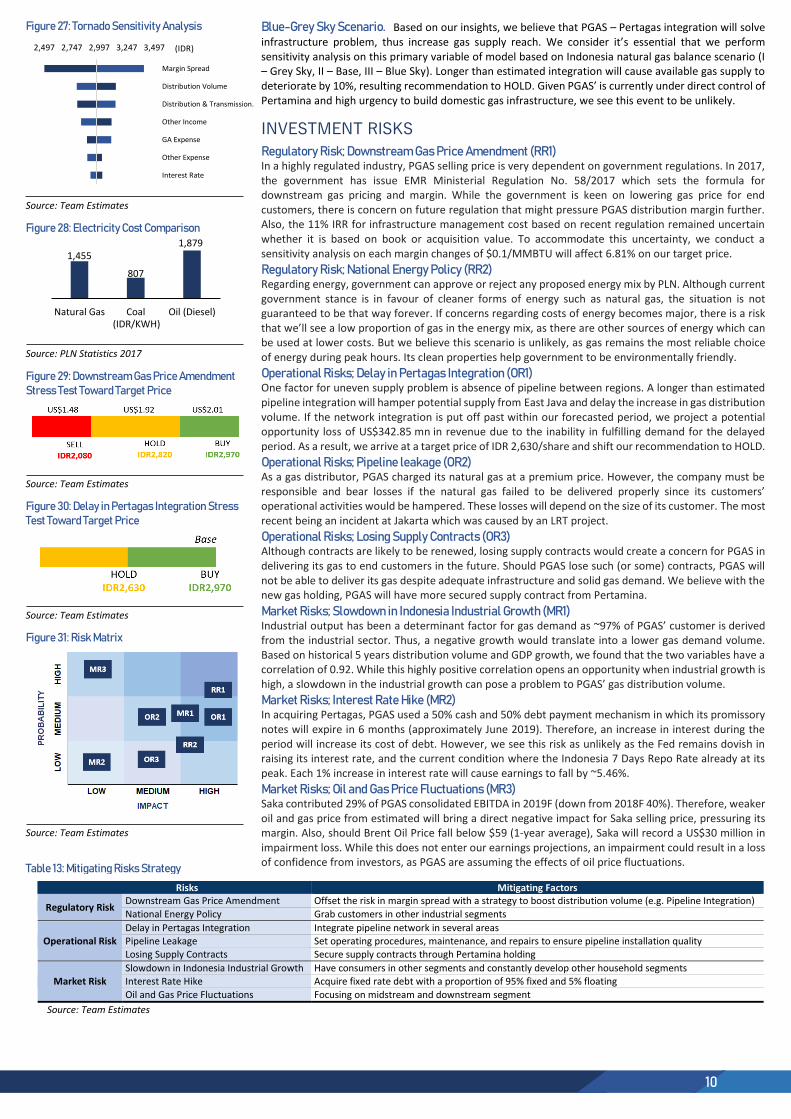

Figure 27: Tornado Sensitivity Analysis

Source: Team Estimates

Figure 28: Electricity Cost Comparison

Source: PLN Statistics 2017

Figure 29: Downstream Gas Price Amendment Stress Test Toward Target Price

Source: Team Estimates

Figure 30: Delay in Pertagas Integration Stress Test Toward Target Price

Source: Team Estimates

Figure 31: Risk Matrix

Source: Team Estimates

Table 13: Mitigating Risks Strategy

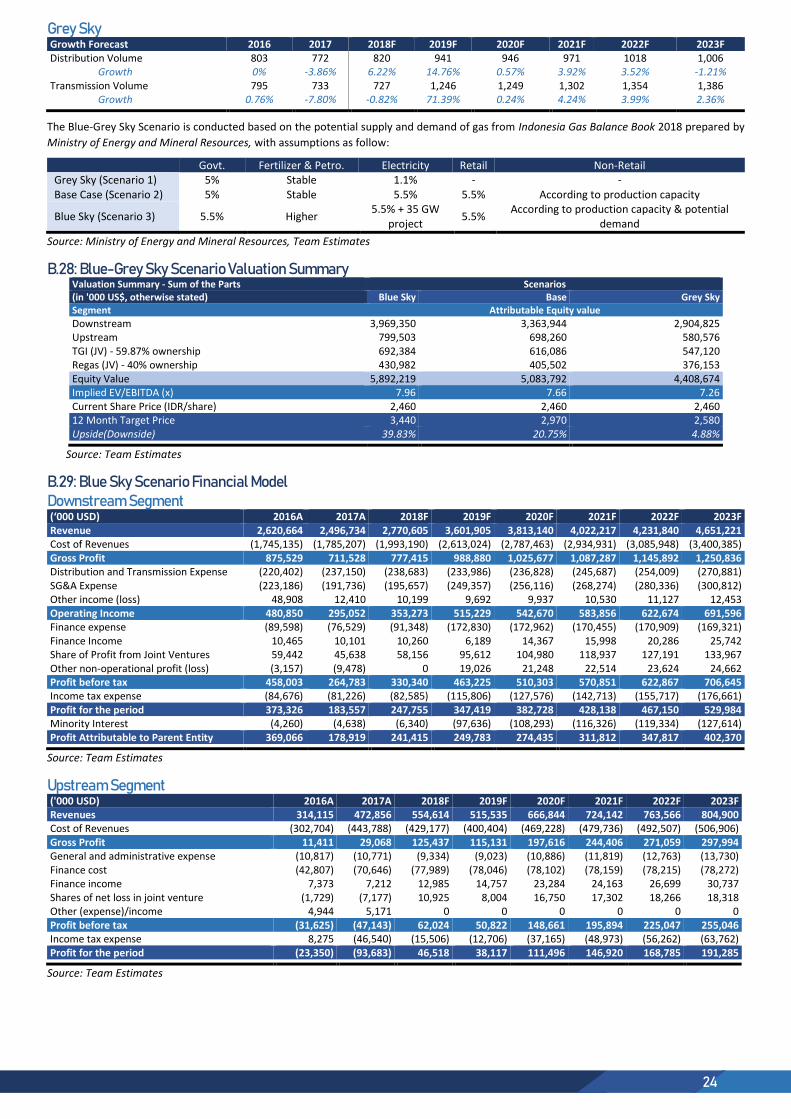

Blue-Grey Sky Scenario. Based on our insights, we believe that PGAS – Pertagas integration will solve infrastructure problem, thus increase gas supply reach. We consider it’s essential that we perform sensitivity analysis on this primary variable of model based on Indonesia natural gas balance scenario (I – Grey Sky, II – Base, III – Blue Sky). Longer than estimated integration will cause available gas supply to deteriorate by 10%, resulting recommendation to HOLD. Given PGAS’ is currently under direct control of Pertamina and high urgency to build domestic gas infrastructure, we see this event to be unlikely.

INVESTMENT RISKS

Regulatory Risk; Downstream Gas Price Amendment (RR1) In a highly regulated industry, PGAS selling price is very dependent on government regulations. In 2017, the government has issue EMR Ministerial Regulation No. 58/2017 which sets the formula for downstream gas pricing and margin. While the government is keen on lowering gas price for end customers, there is concern on future regulation that might pressure PGAS distribution margin further. Also, the 11% IRR for infrastructure management cost based on recent regulation remained uncertain whether it is based on book or acquisition value. To accommodate this uncertainty, we conduct a sensitivity analysis on each margin changes of $0.1/MMBTU will affect 6.81% on our target price.

Regulatory Risk; National Energy Policy (RR2) Regarding energy, government can approve or reject any proposed energy mix by PLN. Although current government stance is in favour of cleaner forms of energy such as natural gas, the situation is not guaranteed to be that way forever. If concerns regarding costs of energy becomes major, there is a risk that we’ll see a low proportion of gas in the energy mix, as there are other sources of energy which can be used at lower costs. But we believe this scenario is unlikely, as gas remains the most reliable choice of energy during peak hours. Its clean properties help government to be environmentally friendly.

Operational Risks; Delay in Pertagas Integration (OR1) One factor for uneven supply problem is absence of pipeline between regions. A longer than estimated pipeline integration will hamper potential supply from East Java and delay the increase in gas distribution volume. If the network integration is put off past within our forecasted period, we project a potential opportunity loss of US$342.85 mn in revenue due to the inability in fulfilling demand for the delayed period. As a result, we arrive at a target price of IDR 2,630/share and shift our recommendation to HOLD.

Operational Risks; Pipeline leakage (OR2) As a gas distributor, PGAS charged its natural gas at a premium price. However, the company must be responsible and bear losses if the natural gas failed to be delivered properly since its customers’ operational activities would be hampered. These losses will depend on the size of its customer. The most recent being an incident at Jakarta which was caused by an LRT project.

Operational Risks; Losing Supply Contracts (OR3) Although contracts are likely to be renewed, losing supply contracts would create a concern for PGAS in delivering its gas to end customers in the future. Should PGAS lose such (or some) contracts, PGAS will not be able to deliver its gas despite adequate infrastructure and solid gas demand. We believe with the new gas holding, PGAS will have more secured supply contract from Pertamina.

Market Risks; Slowdown in Indonesia Industrial Growth (MR1) Industrial output has been a determinant factor for gas demand as ~97% of PGAS’ customer is derived from the industrial sector. Thus, a negative growth would translate into a lower gas demand volume. Based on historical 5 years distribution volume and GDP growth, we found that the two variables have a correlation of 0.92. While this highly positive correlation opens an opportunity when industrial growth is high, a slowdown in the industrial growth can pose a problem to PGAS’ gas distribution volume.

Market Risks; Interest Rate Hike (MR2) In acquiring Pertagas, PGAS used a 50% cash and 50% debt payment mechanism in which its promissory notes will expire in 6 months (approximately June 2019). Therefore, an increase in interest during the period will increase its cost of debt. However, we see this risk as unlikely as the Fed remains dovish in raising its interest rate, and the current condition where the Indonesia 7 Days Repo Rate already at its peak. Each 1% increase in interest rate will cause earnings to fall by ~5.46%.

Market Risks; Oil and Gas Price Fluctuations (MR3) Saka contributed 29% of PGAS consolidated EBITDA in 2019F (down from 2018F 40%). Therefore, weaker oil and gas price from estimated will bring a direct negative impact for Saka selling price, pressuring its margin. Also, should Brent Oil Price fall below $59 (1-year average), Saka will record a US$30 million in impairment loss. While this does not enter our earnings projections, an impairment could result in a loss of confidence from investors, as PGAS are assuming the effects of oil price fluctuations.

2,497 2,747 2,997 3,247 3,497

Margin Spread

Distribution Volume

Distribution & Transmission…

Other Income

GA Expense

Other Expense

Interest Rate

(IDR)

1,455

807

1,879

Natural Gas Coal Oil (Diesel)(IDR/KWH)

11

APPENDICES

SECTION A: BUSINESS OVERVIEW

A.1: PGAS’s Business Process

Source: Company Reports, Team Analysis

A.2: PGAS Transmission Business Segment PGN TGI KJG

Length (km) 1041 1006 201 Off-taker PLN, BBG CPI, Gas Supply P.LTD, PGN, PLN PLLN

Pipelines Wampu-Belawan;

SSWJ Phase I; SSWJ Phase II Grissik – Duri;

Grissik – Batam - Singapore Kepodang – Tambak Lorok

(Kalimantan Jawa I)

Volume (MMSCFD) 8 645 76 2017 Revenue (MN US$) 2.5 151.62 55.46

Pipeline Operator Length (km)

Shippers Off-taker Toll Fee (US$/MMSCFD)

Wampu Belawan PGN 37 PLN PLN 0.400

SSWJ Phase I PGN 378 PGN PGN – West Java Distribution 1.550

SSWJ Phase II PGN 626 PGN ; PLN PGN – West Java Distribution;

PLN – Muara Tawar 1.470

Grissik – Duri TGI 536 ConocoPhillips; PGN; PLN;

Pertamina; GEI; PT Energasindo Heksa Karya

Chevron; PLN; PGN 0.466

Grissik – Batam – Singapore

TGI 470 ConocoPhillips; PetroChina; PGN;

PLN Batam; PT Inti Daya Latu Prima; PDPDE South Sumatra

Gas Supply Pvt Ltd; PGN; PLN Batam; Tanjung Ucang power

plant 0.740

Kepodang – Tambak Lorok

KJG 201 PLN PLN Tambak Lorok 2.326

Source: Company Reports 2018

A.3: PGAS Subsidiaries and Affiliates Company Name Entity Ownership Line of Business

PT Saka Energi Indonesia (SEI) Subsidiary PGN 99.997%; PGASSOL 0.003% Upstream oil & gas

PT PGN LNG Indonesia (PGN LNG) Subsidiary PGN 99.999%; GEI 0.000% LNG PT Gagas Energi Indonesia (GEI) Subsidiary PGN 99.88%; PGASSOL 0.12% Downstream

PT PGAS Solutions (PGASSOL) Subsidiary PGN 99.91%; Yayasan Kesejahteraan Pegawai dan Pensiunan Gas Negara (YKPP Gas) 0.09%

Engineering

PT PGAS Telekomunikasi Nusantara Subsidiary PGN 99.93%; YKPP Gas 0.07% Telecommunication

PT Permata Graha Nusantara (PERMATA) Subsidiary PGN 99.989%; PGASSOL 0.011% Property management

PT Nusantara Regas Joint

Venture PGN 40%; Pertamina 60%

Floating storage and regasification terminal

PT Transportasi Gas Indonesia (TGI) Joint

Venture PGN 59.87%; Transasia Pipeline 40%; YKPP Gas 0.13% Gas transportation

PT Kalimantan Jawa Gas (KJG) Affiliation Permata 80%; PT Bakrie & Brothers 20% Gas transportation

PT Permata Karya Jasa (PERKASA) Affiliation Permata 75%; YKPP Gas 25% Oil and gas supporting services PT Solusi Energi Nusantara (SENA) Affiliation PGASSOL 99.9%; Permata 0.1% Engineering

PT Widar Mandripa Nusantara (WIDAR) Affiliation GEI 99.996%; Perkasa 0.004% Power plant and trade

PT Namtem Gas Synergi Joint

Venture

PT Andiracitra Grahawira 68.43%; PT Banten Global Synergi 14.14%; PT Banten Global Development 8.57%; Izma Agyano Bursman 8.71%; Perseroan 0.14%

Services, transportation, trade and mining

Source: Company Reports 2018

Midstream

Gathering

Pipelines

Natural Gas Transmission

Pipeline

Storage Natural Gas Transmission Pipeline

Gas

Processing

Upstream

Exploration

Exploitation

Development of oil

and gas

Downstream

Distribution of natural gas to

end-customers:

Industrial

Commercial

Household

Gas-filling stations

12

A.4: PGAS’s Source of gas

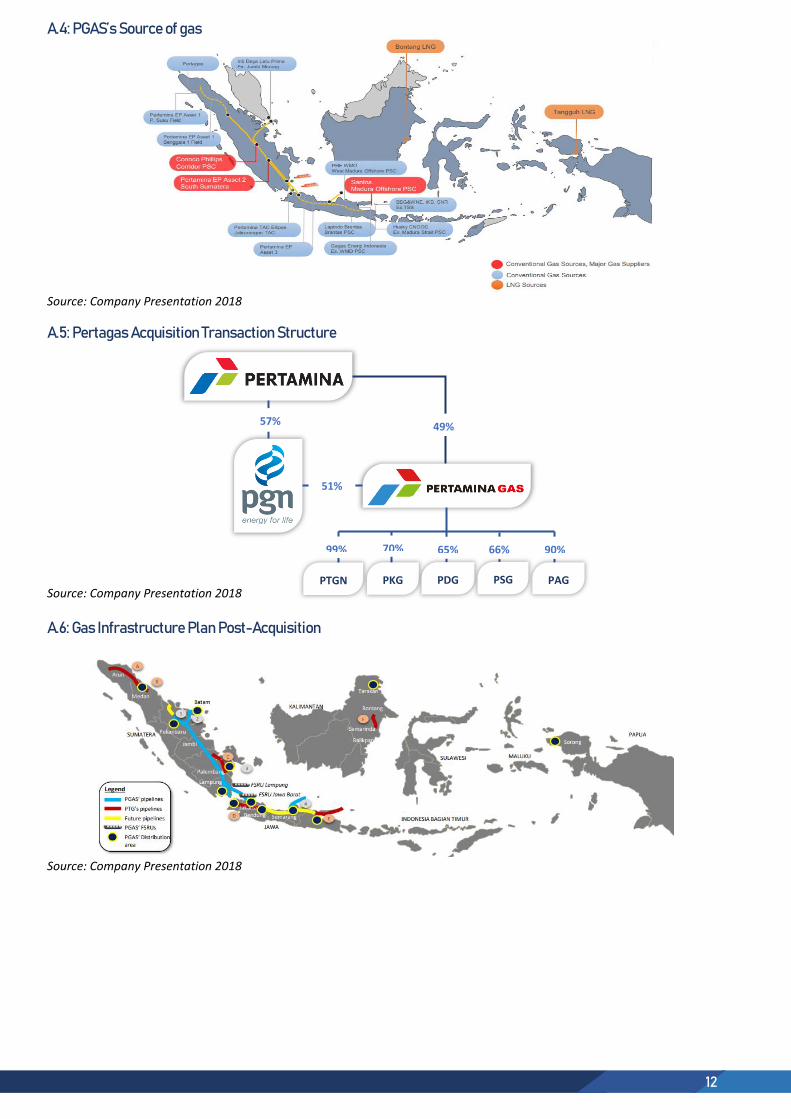

Source: Company Presentation 2018

A.5: Pertagas Acquisition Transaction Structure Source: Company Presentation 2018

A.6: Gas Infrastructure Plan Post-Acquisition

Source: Company Presentation 2018

57%

51%

99% 70% 65% 66% 90%

PTGN PKG PDG PSG PAG

49%

13

A.7: SAKA’s asset summary Assets Ownership Reserves (MMBOE) Type(s) of Resources Year Acquired Contract expiration

Fasken (US) 36% 15.2 Gas 2014 2050

Pangkah 100% 28.5 Gas, LPG, and Crude Oil 2013 2026

Bangkanai 30% 10.9 Gas 2013 2033

West Bangkanai 30% N/A Gas 2015 2043

Muara Bakau 11.70% 9.9 LNG 2015 2032

Sanga- Sanga 37.80% 12 Gas, LPG, LNG, and Crude Oil 2016 2018

Wokam 100% N/A Gas 2016 2040

SES 8.90% 1.6 Gas 2014 2018

Ketapang 20% 5.8 Gas, Crude Oil 2013 2028

South Sesulu 100% 33.5 Gas Development 2014 2039

Muriah 20% 4.7 Gas 2014 2026

Source: SAKA Energi Reports 2018

A.8: SWOT Analysis SWOT ANALYSIS

Strengths Weaknesses

Market leader with vast spread gas infrastructure, constructing 85% of nation’s gas infrastructure

Backed with government support as nation’s gas distributor company

Security of supply and long-term contract customers

Integrated upstream-downstream business model and value chain of natural gas

Strong reputation and highly experienced

Dependency to suppliers’ natural gas

Fragmented geographical presence complicate infrastructure development

Exposure to commodity price fluctuations

Opportunities Threat

Abundant resources of natural gas

Growing preference towards clean environment

Lack of gas distribution and infrastructure provide more room for company to grow

Horizontal acquisition of Pertagas will strengthen company’s position

Potential in developing new products to non-conventional gas sources

Construction of non-pipe gas infrastructure utilizing LNG and FSRU

Tight government’s regulation

More competitive energy alternatives and other substitute product

Weaker Indonesian economic growth and domestic industrial growth

High capital requirement to develop infrastructure

Source: Team Analysis

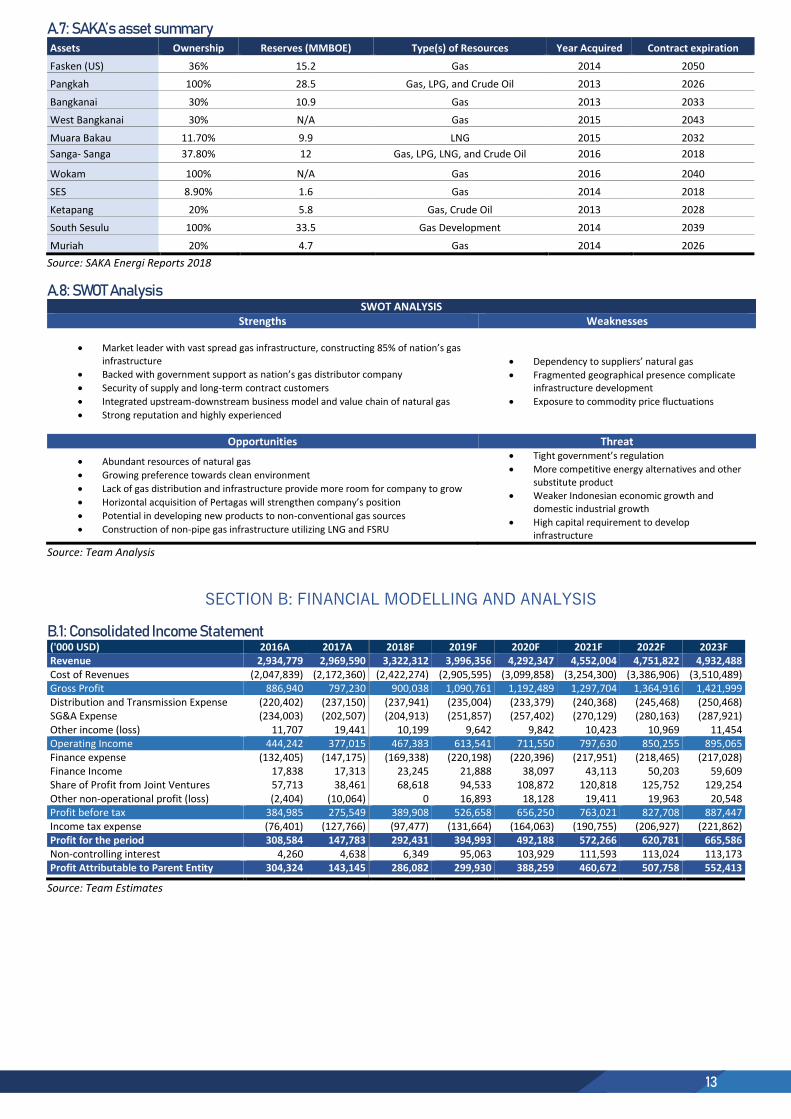

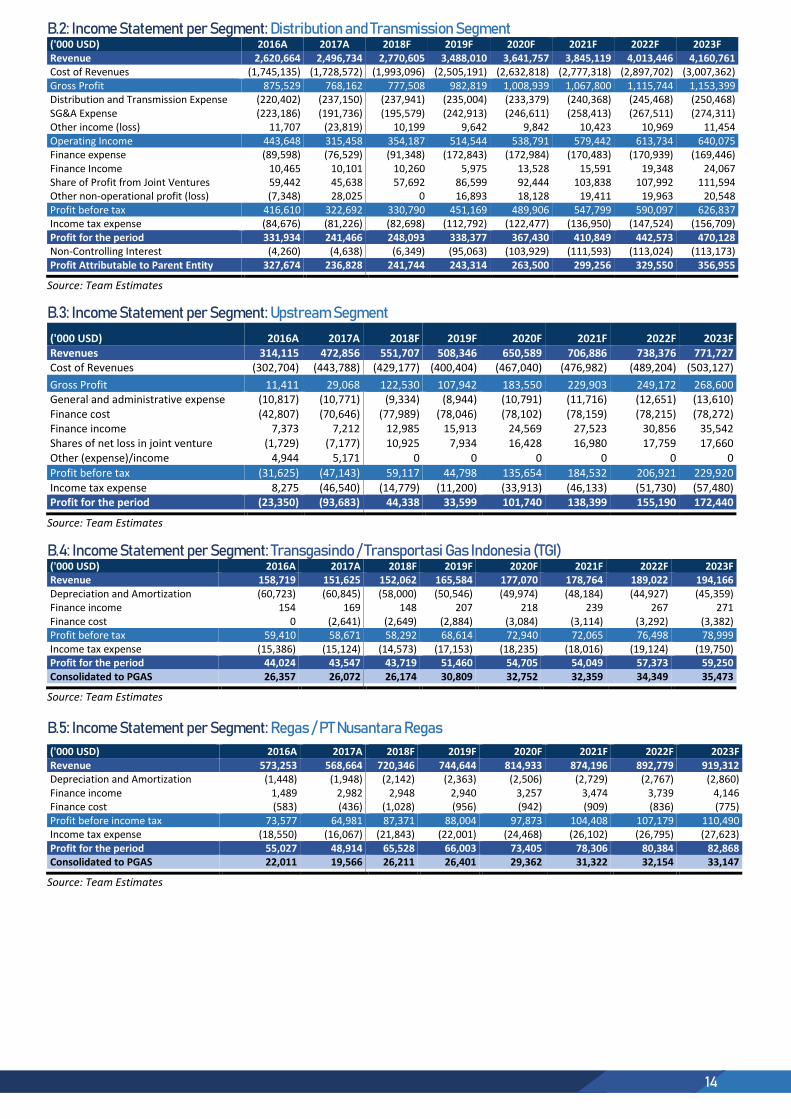

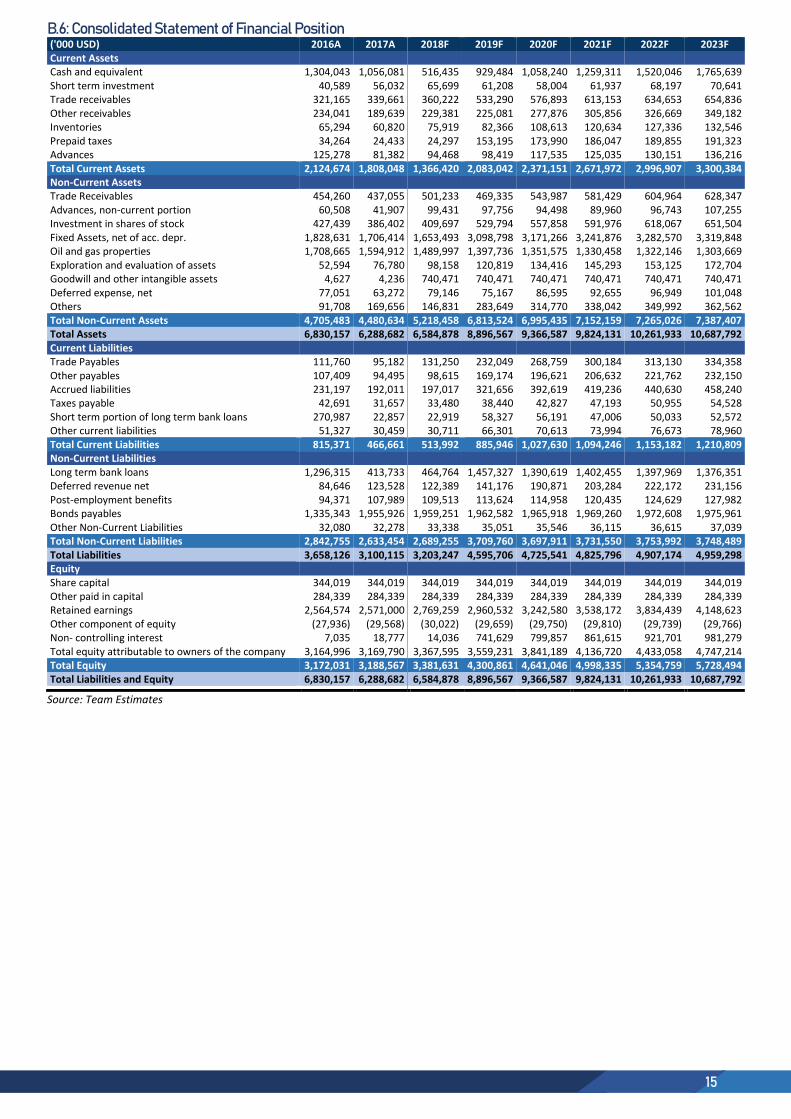

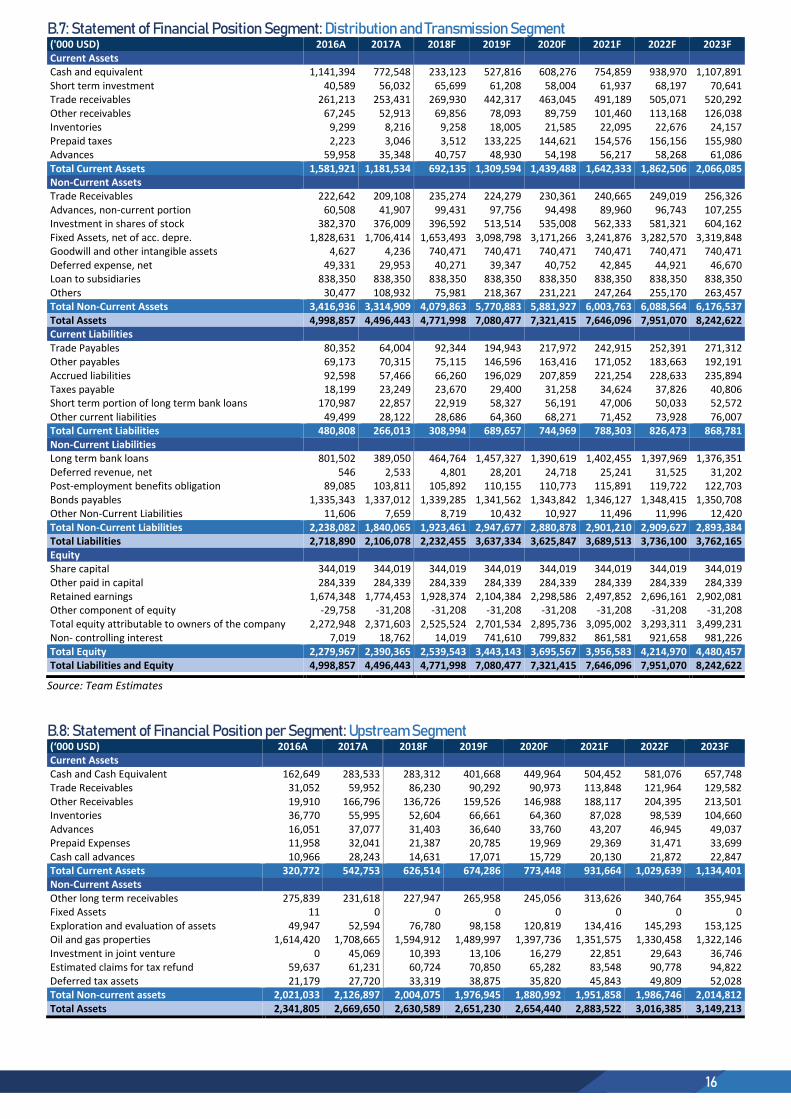

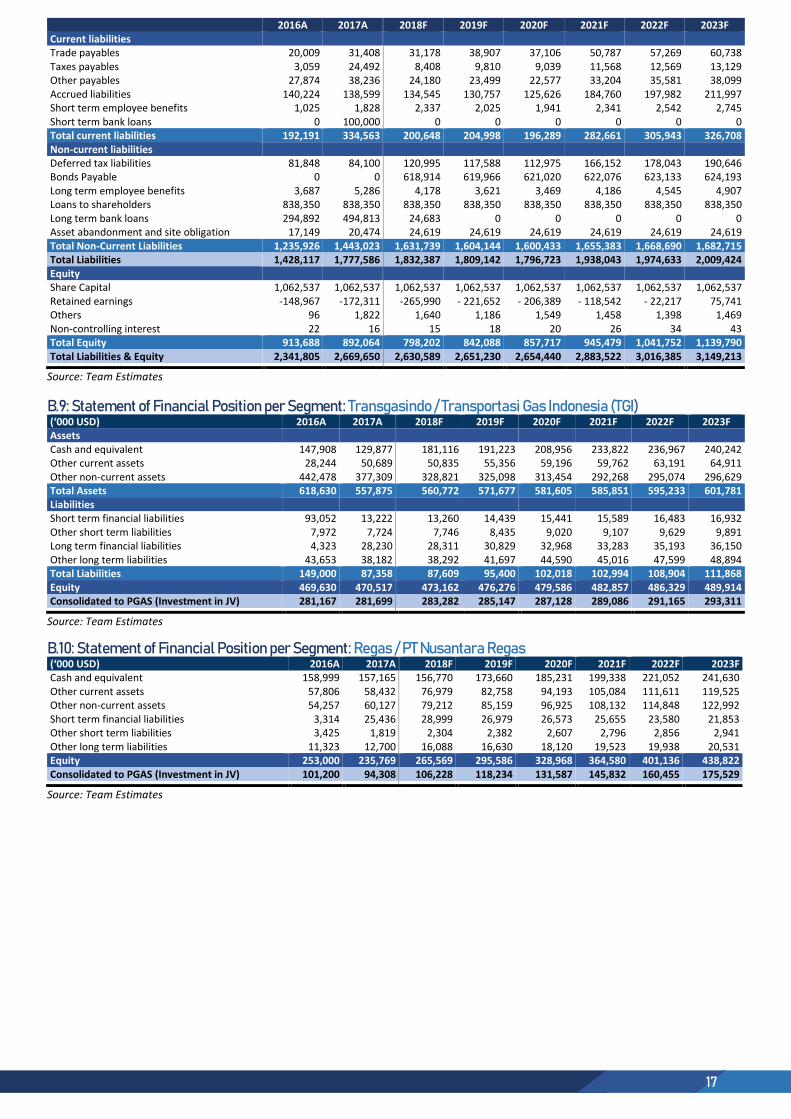

SECTION B: FINANCIAL MODELLING AND ANALYSIS

B.1: Consolidated Income Statement