Cambodian agriculture in transition

248

Agriculture Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

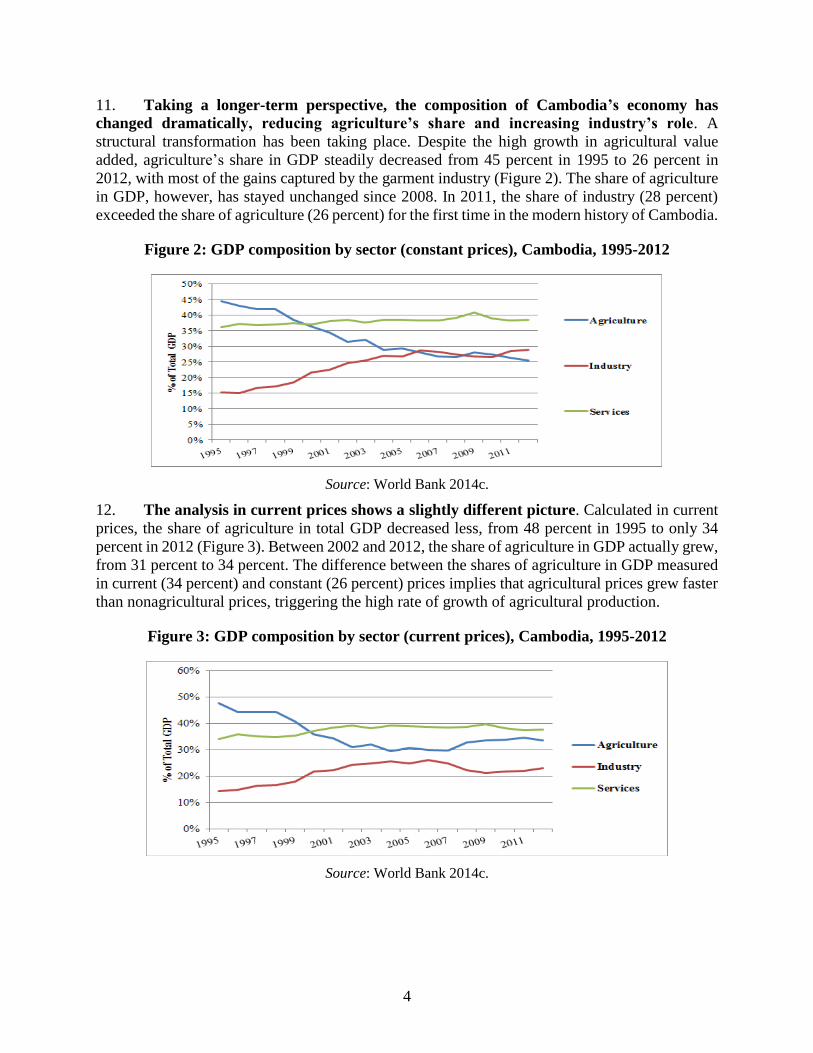

download

0

Transcript of Cambodian agriculture in transition

Agriculture

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

i

Economic and Sector Work, Report No. 96308-KH

CAMBODIAN AGRICULTURE IN TRANSITION:

OPPORTUNITIES AND RISKS

May 19, 2015

Agriculture Global Practice

East Asia and Pacific Region

________________________________________

ii

© 2015 The International Bank for Reconstruction and Development / The World Bank

1818 H Street, NW, Washington, DC 20433

All rights reserved:

This volume is a product of the staff of the International Bank for Reconstruction and

Development/ The World Bank. The findings, interpretations, and conclusions expressed in this

paper do not necessarily reflect the views of the Executive Directors of The World Bank or the

governments they represent. The World Bank does not guarantee the accuracy of the data

included in this work. The boundaries, colors, denominations, and other information shown on

any map in this work do not imply any judgment on the part of The World Bank concerning the

legal status of any territory or the endorsement or acceptance of such boundaries.

Rights and Permission

The material in this publication is copyrighted. Copying or transmitting any of this work without

permission may be a violation of applicable law. The International Bank for Reconstruction and

Development/The World Bank encourages dissemination of its work and will normally grant

permission to reproduce portions of the work promptly.

For permission to photocopy or reprint any part of this work, please send a request with

complete information to the Copyright Clearance Center, Inc., 222 Rosewood Drive,

Danvers, MA 01923, USA, telephone 978-750-8400, fax 978-750-4470,

www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed

to the Office of the Publisher, The World Bank, 1818 H Street NW, Washington, DC

20433, USA, fax 202-522-2422, e-mail [email protected].

iii

Table of Contents

ACRONYMS AND ABBREVIATIONS .................................................................................... X

ACKNOWLEDGMENTS .......................................................................................................... XI

EXECUTIVE SUMMARY ...................................................................................................... XII

1. INTRODUCTION................................................................................................................. 1

2. A DECADE OF AGRICULTURAL TRANSFORMATION IN CAMBODIA .............. 3

2.1. AGRICULTURAL GROWTH ................................................................................................ 3

2.2. AGRIBUSINESS DEVELOPMENT ........................................................................................ 8

2.3. AGRICULTURAL GROWTH AND POVERTY REDUCTION ................................................... 10

2.4. AGRICULTURAL TRANSFORMATION ............................................................................... 13

3. CHANGES IN AGRICULTURE: EVIDENCE FROM THE FIELD ........................... 18

3.1. INTRODUCTION .............................................................................................................. 18

3.2. CROP PRODUCTION ........................................................................................................ 19

3.3. FARMLAND .................................................................................................................... 25

3.4. AGRICULTURAL LABOR FORCE ...................................................................................... 29

3.5. USE OF AGRICULTURAL INPUTS ..................................................................................... 32

3.6. USE OF AGRICULTURAL MACHINERY ............................................................................ 40

3.7. AGRICULTURAL SERVICES ............................................................................................. 42

3.8. FARMERS’ ORGANIZATIONS ........................................................................................... 50

3.9. AGRICULTURAL INFRASTRUCTURE ................................................................................ 52

4. CHANGES IN FARM BUDGETS AND FARM PROFITABILITY ............................ 55

4.1. INTRODUCTION .............................................................................................................. 55

4.2. RESULTS OF THE 2013 SURVEY ...................................................................................... 58

4.3. COMPARISON OF THE 2005 AND 2013 SURVEY RESULTS ............................................... 63

5. COMPETITIVENESS OF CAMBODIAN FARMS ....................................................... 69

5.1. INTRODUCTION .............................................................................................................. 69

5.2. DOMESTIC RESOURCE COST FOR RICE ........................................................................... 70

5.3. DOMESTIC RESOURCE COST FOR CASSAVA AND MAIZE ................................................ 72

5.4. SUMMARY ...................................................................................................................... 73

6. DRIVERS OF PAST GROWTH ....................................................................................... 74

7. DRIVERS OF FUTURE GROWTH ................................................................................. 80

8. A LONG-TERM VISION FOR CAMBODIAN AGRICULTURE ............................... 86

9. OPTIONS FOR SUPPORTING A LONG-TERM VISION FOR AGRICULTURE .. 93

iv

9.1. INTRODUCTION .............................................................................................................. 93

9.2. SCENARIOS FOR ENVIRONMENTAL SUSTAINABILITY ..................................................... 93

9.3. SCENARIOS FOR PRODUCTIVITY GROWTH ...................................................................... 98

9.4. SCENARIOS FOR IMPROVED COMPETITIVENESS ............................................................ 105

9.5. SCENARIOS FOR INCOME GROWTH ............................................................................... 108

9.5 SUMMARY OF SIMULATIONS’ RESULTS ........................................................................ 113

10. POLICY AGENDA TO SUPPORT A LONG-TERM VISION FOR CAMBODIAN

AGRICULTURE....................................................................................................................... 115

10.1. MAINTAINING A PRIVATE SECTOR FRIENDLY AGRICULTURAL POLICY ENVIRONMENT 115

10.2. STRENGTHENING THE ENVIRONMENTAL SUSTAINABILITY ........................................... 117

10.3. IMPROVING THE AGRICULTURAL “PUBLIC GOODS” INVESTMENTS .............................. 118

10.4. HELPING DEVELOP THE AGROPROCESSING AND AGRIBUSINESS INDUSTRY ................. 127

11. CONCLUSIONS AND POLICY RECOMMENDATIONS ..................................... 132

12. REFERENCES .............................................................................................................. 139

ANNEX 1: ANALYTICAL WORK FROM THE WORLD BANK AND AUSAID

PARTNERSHIP ........................................................................................................................ 143

ANNEX 2: METHODOLOGY FOR THE 2013 FARM SURVEY...................................... 144

ANNEX 3: DETAILED FARM BUDGETS BY CROP ........................................................ 152

ANNEX 4: PROJECTION OF SELECTED ECONOMIC INDICATORS, CAMBODIA 184

ANNEX 5: RESULTS OF POLICY SIMULATIONS .......................................................... 186

v

Boxes

Box 1: Rural Population in Cambodia .......................................................................................... 14

Box 2: Rice Yields in Cambodia .................................................................................................. 24

Box 3: Gender Dimensions of Cambodian Agriculture ................................................................ 31

Box 4: Farmers’ Organizations in Cambodia ............................................................................... 51

Box 5: Factor Analysis and Modern versus Traditional Farmers ................................................. 57

Box 6: Gross Margin versus Value Added ................................................................................... 58

Box 7: Driving Forces Underpinning Future Agricultural Transformation in Cambodia ............ 85

Box 8: Indicators of Agricultural Transformation ........................................................................ 87

Box 9: Importance of Fiscal Sustainability for Pro-Poor Agricultural Growth .......................... 119

Box 10: Fertilizer Subsidy in Sri Lanka ..................................................................................... 126

Box 11: Food Safety Investments in Thailand ............................................................................ 128

Box 12: Requirements for an Increase in Cambodian Rice Exports to China ............................ 129

Figures

Figure 1: Agricultural GDP growth (constant prices), Cambodia, 2002-2012 ............................... 3

Figure 2: GDP composition by sector (constant prices), Cambodia, 1995-2012 ........................... 4

Figure 3: GDP composition by sector (current prices), Cambodia, 1995-2012 ............................. 4

Figure 4: Growth of agricultural subsectors (constant prices), Cambodia, 2002-2012 .................. 5

Figure 5: Share of subsectors in agricultural GDP, Cambodia, 2002-2012.................................... 6

Figure 6: Contribution to turnover of different types of agribusinesses, Cambodia, 2011 ............ 9

Figure 7: Poverty rate by region, Cambodia, 2004-2011.............................................................. 11

Figure 8: Drivers of poverty reduction in Cambodia, 2004-2011 ................................................ 12

Figure 9: Crop production and cultivated land areas, Cambodia .................................................. 20

Figure 10: Regional distribution of aromatic paddy production (% of farmers), 2013 ................ 21

Figure 11: Contribution of land and yield to average ag. production growth, 2003-2012 ........... 22

Figure 12: Projections for land expansion and yield changes, Cambodia, 2013 .......................... 25

Figure 13: Private land markets, Cambodia, 2013 ........................................................................ 27

Figure 14: Change in the perception about women’s role in agriculture, Cambodia, 2013 ......... 30

Figure 15: Impact of youth migration on agricultural households, Cambodia, 2013 ................... 31

Figure 16: Access to inputs, Cambodia, 2013 .............................................................................. 33

Figure 17: Access to improved seeds, Cambodia, 2013 ............................................................... 34

Figure 18: Use of manure, Cambodia, 2013 ................................................................................. 36

Figure 19: Use of fertilizers, Cambodia, 2013 .............................................................................. 37

Figure 20: Trends in chemical fertilizer use (kg nutrient/ha), select countries, 2005-2011 ......... 38

Figure 21: Use of pesticides, Cambodia, 2013 ............................................................................. 39

Figure 22: Use of agricultural equipment, Cambodia, 2013 ......................................................... 41

Figure 23: Access to extension services, Cambodia, 2013 ........................................................... 44

Figure 24: Access to financial services, Cambodia, 2013 ............................................................ 47

vi

Figure 25: Access to information, Cambodia, 2013 ..................................................................... 49

Figure 26: Reasons for creation of FOs and their perceived benefits, Cambodia, 2013 .............. 51

Figure 27: Irrigation, Cambodia, 2013 ......................................................................................... 53

Figure 28: Agricultural facilities, Cambodia, 2013 ...................................................................... 54

Figure 29: Average land by farm size and crop, Cambodia, 2013 ............................................... 56

Figure 30: Gross revenues ($/ha) by crop and farm practice, Cambodia, 2013 ........................... 59

Figure 31: Total variable costs ($/ha) by crop and farm practice, Cambodia, 2013 ..................... 60

Figure 32: Breakdown of cost structure by crop, Cambodia, 2013 .............................................. 60

Figure 33: Comparison of nominal gross margins ($/ha), Cambodia, 2005 and 2013 ................. 65

Figure 34: Farm wage, off-farm wage, and returns to agricultural labor ($/day), Cambodia ...... 67

Figure 35: CPI and food price index in Cambodia, 2002-2012 .................................................... 75

Figure 36: Transportation costs in Cambodia and neighboring countries, $/100 km/ton ............. 77

Figure 37: Value of the projected food demand in East Asia, $ billion, 2030.............................. 82

Figure 38: Perspectives on the possibility of change in cultivated areas by crop, Cambodia ...... 94

Figure 39: Labor use in production (days/ha), Cambodia .......................................................... 100

Figure 40: Return to labor ($/day), Cambodia ............................................................................ 100

Figure 41: Shift in land used by traditional and modern farmers, Cambodia ............................. 101

Figure 42: MOWRAM’s projected investments, $ million, 2014-2018 ..................................... 121

Figure 43: Structure of MOWRAM’s projected investments by source .................................... 121

Tables

Table 1: Impact of lower agric. growth on selected agriculture sector indicators, Cambodia .... xvi

Table 2: Summary of the report’s key policy recommendations based on the time of impacts’

realization .................................................................................................................................... xvii

Table 3: Gross agricultural production, annual growth, selected countries, 2002-2012 ................ 5

Table 4: Production, area, yields, and growth of major crops, Cambodia, 2002-2012 .................. 7

Table 5: Irrigated areas, selected countries ..................................................................................... 7

Table 6: Production, area, yield, and export of rubber, Cambodia, 2002-2011 .............................. 8

Table 7: Evolution of formal trade of select commodities, Cambodia, 1996-2011 ........................ 8

Table 8: Agribusiness industry in Cambodia, 2002-2012 .............................................................. 9

Table 9: Rice commodity balance (‘000 tons), Cambodia, 2008-2013 ........................................ 10

Table 10: Growth elasticity of poverty, selected countries in Asia .............................................. 11

Table 11: Indicators of structural transformation, Cambodia, 2004 and 2012 ............................. 13

Table 12: Country groups based on the role of agriculture in the economy ................................. 14

Table 13: Selected economic indicators, Cambodia, 2004 and 2012 ........................................... 15

Table 14: Labor use for rice production in Central Luzon, Philippines, 1966/67-2011/12 .......... 16

Table 15: Diversification in cultivated area, Cambodia, 2002-2011 ............................................ 19

Table 16: Change in farm size, Cambodia, 2008-2012 ................................................................ 23

Table 17: Average crop yields in selected countries (tons/ha), 2010-2013 .................................. 23

Table 18: Wages of labor hired for rice production, selected countries, 2013 ............................. 28

Table 19: Changes in land prices between 2005 and 2013, Cambodia ........................................ 28

vii

Table 20: Use of labor in farm production by crop, Cambodia, 2005 and 2013 .......................... 29

Table 21: Use of labor in dry season paddy production, selected countries, 2013 ....................... 30

Table 22: Illustrative use of fertilizers, Cambodia, 2005 and 2013 .............................................. 38

Table 23: Number of agricultural equipment units, Cambodia, 2006-2010 ................................. 40

Table 24: Average costs of and difficulty finding agricultural machinery, Cambodia, 2013 ...... 42

Table 25: Categorization of farm size by cultivated crop areas, Cambodia ................................. 55

Table 26: Gross margin ($/ha) by crop, technology use, and farm size, Cambodia, 2013 ........... 61

Table 27: Returns to labor ($/day) by crop, technology use, and farm size, Cambodia, 2013 ..... 62

Table 28: Comparison of key farm budget indicators, $/ha, Cambodia, 2005 and 2013 ............. 64

Table 29: Comparison of total crop budgets, Cambodia, 2005 and 2013..................................... 65

Table 30: Changes in crop margins in nominal and real terms, Cambodia, 2005 and 2013 ........ 66

Table 31: Annual changes in crop margins in real terms, Cambodia, 2005 and 2013 ................. 66

Table 32: Changes in returns to labor in nominal and real terms, Cambodia, 2005 and 2013 ..... 67

Table 33: DRCs for selected agricultural crops, Cambodia, 2013 ............................................... 70

Table 34: Sensitivity analysis of impacts of changes of production costs on DRC for rice ......... 71

Table 35: Sensitivity analysis of impacts of changes in prod costs on cassava and maize DRCs 72

Table 36: Sensitivity analysis of impacts of changes in input and output prices on DRCs .......... 73

Table 37: Drivers of agricultural growth during 2002-2012 ........................................................ 74

Table 38: Global agricultural prices, selected commodities, $/ton (in real 2010 prices) ............. 75

Table 39: Selected economic projections, Cambodia, 2012-2030 ................................................ 80

Table 40: Caloric food demand projections, world and selected regions/countries ..................... 81

Table 41: Global rice demand projections (kg per capita) per year .............................................. 82

Table 42: Global agricultural terms of trade, index projections (in real 2010$) .......................... 83

Table 43: Indicators of agricultural transformation at 5 percent agricultural growth ................... 87

Table 44: Changes of indicators of ag transformation at 3 percent comp. with 5 percent growth 88

Table 45: Proposed indicators and targets for a Long-Term Vision for Cambodian Agriculture 91

Table 46: Assumptions about land expansion for Env. Sustainability scenarios L1-L3 .............. 95

Table 47: Simulation results for Weak Environmental Sustainability scenarios L1-L3 .............. 96

Table 48: Simulation results for Strong Environmental Sustainability scenarios L4-L6 ............. 98

Table 49: Assumptions about Productivity Growth scenarios P1-P3 ......................................... 102

Table 50: Simulation results for Productivity Growth scenarios P1-P3 ..................................... 103

Table 51: Simulation results for Productivity Growth scenario P4 ............................................ 104

Table 52: Assumptions about Competitiveness scenarios C1-C6 .............................................. 105

Table 53: Simulation results for the Competitiveness scenarios C1-C6..................................... 107

Table 54: Assumptions about rice variety changes under Income Growth scenarios I1-I2 ....... 109

Table 55: Simulation results for Income Growth scenarios I1-I2 ............................................... 110

Table 56: Assumption about cassava processing under Income Growth scenarios I3-I4 ........... 110

Table 57: Assumptions about Income Growth under scenarios I5-I6 ........................................ 112

Table 58: Summary of the simulations’ results .......................................................................... 114

Table 59: Key issues and options to reform the seed sector in Cambodia ................................. 117

viii

Table 60: Agricultural research intensity .................................................................................... 123

Table 61: Yield response for supplementing nitrogen to soil, Cambodia................................... 125

Table 62: Prices and logistics costs of rice in Cambodia, Vietnam, and Thailand ..................... 130

Table 63: Time and cost in rice export procedures, Cambodia, 2012-2013 ............................... 130

Table 64: Summary of the report’s key policy recommendations by implementing agency ..... 138

Table 65: Product selection for the 2013 field survey ................................................................ 144

Table 66: Selected locations for 2013 field work ....................................................................... 146

Table 67: Matrix of size x technology ........................................................................................ 148

Table 68: List of respondents to 2013 survey ............................................................................. 150

Table 69: Comparison of key indicators across type of commercial cassava ............................. 157

Table 70: Wet season rice farm budget by technology and farm size ........................................ 161

Table 71: Wet season rice farm budget by farm size .................................................................. 162

Table 72: Wet season rice farm budget by technology use ........................................................ 163

Table 73: Wet season rice farm budget by province ................................................................... 164

Table 74: Dry season rice farm budget by technology and farm size ......................................... 165

Table 75: Dry season rice farm budget by farm size .................................................................. 166

Table 76: Dry season rice farm budget by technology use ......................................................... 167

Table 77: Dry season rice farm budget by province ................................................................... 168

Table 78: Cassava farm budget by technology and farm size .................................................... 169

Table 79: Cassava farm budget by farm size .............................................................................. 170

Table 80: Cassava farm budget by technology use ..................................................................... 171

Table 81: Cassava farm budget by province ............................................................................... 172

Table 82: Maize farm budget by technology and farm size ........................................................ 173

Table 83: Maize farm budget by farm size ................................................................................. 174

Table 84: Maize farm budget by technology use ........................................................................ 175

Table 85: Maize farm budget by province .................................................................................. 176

Table 86: Vegetable (mix) farm budget by technology and farm size ....................................... 177

Table 87: Vegetable (mix) farm budget by farm size ................................................................. 178

Table 88: Vegetable (mix) farm budget by technology use ........................................................ 179

Table 89: Vegetable (mix) farm budget by province .................................................................. 180

Table 90: Changes in prices of commodities, Thailand and Cambodia ..................................... 181

Table 91: Change in the prices of inputs, services, and labor, Cambodia .................................. 182

Table 92: Average use of inputs, Cambodia, 2013 ..................................................................... 182

Table 93: Farm budget indicators by crop, farm size, and technology use, Cambodia, 2013 .... 183

Table 94: Results of simulations on land use (baseline) ............................................................. 186

Table 95: Results of simulations on land use (scenario L1) ....................................................... 187

Table 96: Results of simulations on land use (scenario L2) ....................................................... 188

Table 97: Results of simulations on land use (scenario L3) ....................................................... 189

Table 98: Results of simulations on land use (scenario L4) ....................................................... 190

Table 99: Results of simulations on land use (scenario L5) ....................................................... 191

ix

Table 100: Results of simulations on land use (scenario L6) ..................................................... 192

Table 101: Demand for labor for environmental sustainability scenarios .................................. 193

Table 102: Demand for fertilizers for environmental sustainability scenarios ........................... 194

Table 103: Demand and average return to labor ($/day) for scenarios with env sustainability . 195

Table 104: Farm budget data comparing traditional and modern technology users (revenue and

modern inputs) ............................................................................................................................ 196

Table 105: Farm budget data comparing traditional and modern technology users (labor,

services, and gross margins) ....................................................................................................... 197

Table 106: Gross margins and NPV (million $) for TFP scenario (baseline) ............................ 198

Table 107: Gross margins and NPV (million $) for TFP scenario (scenario P1) ....................... 199

Table 108: Gross margins and NPV (million $) for TFP scenario (scenario P2) ....................... 200

Table 109: Gross margins and NPV (million $) for TFP scenario (scenario P3) ....................... 201

Table 110: Summary of gross margins for TFP scenarios .......................................................... 202

Table 111: Examples of costs of irrigation investment (per unit and total investment) ............. 202

Table 112: Demand for labor and return to labor for TFP scenarios .......................................... 203

Table 113: Demand for fertilizers for TFP scenarios ................................................................. 204

Table 114: Cultivated land and gross margins for scenario P4 (TFP through irrigation) ........... 205

Table 115: Gross margins on competitiveness (scenarios C1-C6) ............................................. 206

Table 116: Summary of gross margins and NPV for Competitiveness scenarios (C1-C6) ........ 207

Table 117: Return to labor for Competitiveness scenarios (C1-C6)........................................... 208

Table 118: Demand for labor and demand for fertilizers with Competitiveness scenarios ........ 210

Table 119: Characteristics of rice production: fragrant vs. IRRI ................................................ 211

Table 120: Cultivated land areas for fragrant rice Income Growth scenarios ............................ 212

Table 121: Gross margins for fragrant rice Income Growth scenarios ....................................... 213

Table 122: Summary of gross margins for fragrant rice Income Growth scenarios ................... 214

Table 123: Demand for labor, return to labor and demand for fertilizers for fragrant rice Income

Growth scenarios ........................................................................................................................ 214

Table 124: Cultivated land areas for cassava processing Income Growth scenarios ................. 215

Table 125: Gross margins for cassava processing Income Growth scenarios (million $) .......... 216

Table 126: Comparison between fresh cassava and dry chips production ................................. 217

Table 127: Demand for and return to labor for cassava processing Income Growth scenarios . 218

Table 128: Distribution and farm budget by farm size ............................................................... 219

Table 129: Gross margins with Farm Size Distribution scenario (baseline) .............................. 221

Table 130: Gross margins with Farm Size Distribution scenario (I5) ........................................ 222

Table 131: Gross margins with Farm Size Distribution scenario (I6) ........................................ 223

Table 132: Summary of gross margins from changes on Farm Size Distribution ($ million).... 224

Table 133: Demand for labor and return to labor for Farm Size Distribution scenarios ............ 225

x

ACRONYMS AND ABBREVIATIONS

ADB Asian Development Bank

ASEAN Association of Southeast Asian Nations

CARDI Cambodian Agricultural Research and Development Institute

CCSF Cambodian Community Savings Federation

CDRI Cambodia Development Resource Institute

CICP Cambodian Institute for Cooperation and Peace

CPI Consumer price index

DAP Diammonium phosphate

DRC Domestic resource cost

EBA Everything but Arms

FAO Food and Agriculture Organization of the United Nations

FAOSTAT Food and Agriculture Organization Corporate Statistical Database

FGD Focus group discussion

FO Farmers’ organization

FWUC Farmer Water User Communities

GDP Gross domestic product

ha Hectares

IFC International Finance Corporation

IRR Internal rate of return

MAFF Ministry of Agriculture, Forestry, and Fisheries

MFI Microfinance institution

MOWRAM Ministry of Water Resources and Meteorology

NGO Nongovernmental organization

NIS National Institute of Statistics, Cambodia

NPV Net present value

O&M Operation and maintenance

PDA Provincial Departments of Agriculture

PPP Purchasing power parity

RGC Royal Government of Cambodia

SOWS-REF Secretariat of One Window Service for Rice Export Formality

SNEC Supreme National Economic Council

TFP Total factor productivity

TOT Terms of trade

tph Tons per hour

USAID United States Agency for International Development

WDI World Development Indicators

WRS Warehouse Receipt System

xi

ACKNOWLEDGMENTS

This report was prepared by the World Bank’s Agriculture Global Practice, with financial

support from Australian Aid. The report preparation was initiated by Paavo Eliste (Lead Rural

Development Specialist, GFADR) and completed by Sergiy Zorya (Senior Economist, GFADR).

The team included Mudita Chamroeun (Senior Rural Development Specialist, GFADR) and

Munichan Kung (Rural Development Officer, GSURR). The team was supported by Narya Ou

(Program Assistant, EACSF) in Phnom Penh.

Primary data were collected and background reports were prepared by AgriFood

Consulting International, with the team composed of Francesco Goletti, Jean Claude

Randrianarisoa, and Cheng Vanny.

The report benefited from comments from its peer reviewers: Madhur Gautam (Lead

Economist, GFADR), Enrique Aldaz-Caroll (Senior Economist, GMFDR), and Hendericus

Bastiaan Rozemuller (Operations Officer, CMGSB/IFC). Helpful guidance and supports was also

received from Ulrich Zachau (Country Director, EACTF), Alassane Sow (Country Manager,

Cambodia, EACSF), Louise Scura (Program Leader, EACTF), Nathan Belete (Practice Manager,

GFADR), and Steven Jaffee (Lead Rural Development Specialist, GFADR).

The task team is grateful to H.E. Dr. Hang Chuon Naron, Minister of Education, Youth

and Sports for initiating this analytical work and H.E. Dr. Ouk Rabun, Minister of Agriculture,

Forestry and Fisheries (MAFF) for taking ownership and support; H.E. Ty Sokhun, Secretary of

State, MAFF, and Co-Chair of the Technical Working Group for Agriculture and Water, who

supported and coordinated the consultation process with government agencies and other

stakeholders; H.E. So Khanrithykun, General Director of the MAFF’s General Directorate of

Agriculture, and other MAFF staff for the time they devoted to provide information, discussions,

and support during preparation of the report. We would also like to acknowledge valuable

comments and contributions from government agencies in Phnom Penh and in provinces, from the

donor community, including those received through the joint Government-Donors Technical

Working Groups, and from the many representatives of the private sector, research institutes and

NGOs, who contributed their views and feedback on the initial drafts, background reports, and the

2013 survey. The excellent comments and feedback from the participants of the consultative

workshops held in May 2014, January 2015, and May 2015 in Phnom Penh are particularly

appreciated.

We are grateful to Nicholas Wolf and other Australian Aid staff for support for preparation

of this report provided under the Cambodia Food Crisis Capacity Support Partnership Trust Fund

and the preparation of many other reports produced under this partnership that fed into this

strategic analytical work.

The document was edited by Amy Gautam and Tiina Joosu-Palu assisted with the

preparation of communication materials and dissemination.

xii

EXECUTIVE SUMMARY

This report seeks to understand the

successes, challenges and opportunities of

Cambodia’s agricultural transformation over the

past decade to derive lessons and insights on how to

maintain future agricultural growth, and

particularly on the government’s role in facilitating

it. It is prepared per the request of the Supreme

National Economic Council and the Ministry of

Agriculture Forestry and Fisheries and is based on the

primary farm data surveys from 2005 and 2013, and

the secondary data from various sources. In 2013-

2014, the agricultural growth slowed down to 1 percent from its average of 5.3 percent over 2004-

2012. Is the country in transition to a slower agricultural growth? Cambodia can ill afford it

because agricultural growth will be critical to continued poverty reduction in the country, given its

large size in the economy. Market and private investment friendly policies and targeted public

sector investments in irrigation, extension, and other “public good” agricultural services, as

feasible within the government’s total budget, can help secure continued robust agricultural

growth.

KEY FINDINGS

THE PAST DECADE’S AGRICULTURAL GROWTH IS A STORY OF MANY SUCCESSES

In the last decade, Cambodia’s agriculture sector has undergone significant

structural transformation. Although still playing a large role, the agriculture sector became

relatively less “important” in overall GDP and the total labor force, but more “productive”, i.e.

agricultural land and labor productivity has increased. This transformation was driven by vibrant

and pro-poor agricultural growth.

The agricultural growth in Cambodia was high. During 2004-2012, the annual growth

in agricultural gross production was 8.7 percent. Agricultural value added1 grew by 5.3 percent

during this period. This exceptional growth, among the highest in the world, was driven by crop

production, mainly of paddy rice (annual growth of 9 percent), but also maize (20 percent), cassava

(51 percent), sugarcane (22 percent), and vegetables (10 percent). The growth in livestock and

fisheries was modest.

The agricultural growth was also pro-poor. Cambodia’s poverty headcount declined

from 50 percent in 2007 to 21 percent in 2011, with the number of poor declining from 7 million

to 3 million. Most poverty reduction took place in rural areas. More than 60 percent of the poverty

reduction was attributed to the agriculture sector: higher rice prices stimulated the larger rice

production that increased farm wages. Further poverty reduction will continue to depend on the

success of agriculture for many years to come, due to its large role in the labor force, value added,

and exports, as well as the fact that many farmers are among the poor and vulnerable.

1 The agricultural value added is defined as the value of gross production less the value of intermediate farm inputs.

xiii

Agricultural wages have been converging with nonagricultural wages. Agricultural

wages grew by 206 percent between the surveys conducted in 2005 and 2013, while nonfarm

wages increased by 60 percent. As a result, the ratio between per worker nonagricultural to

agricultural valued added in current prices fell to 2.1 in 2012 from 3.2 in 2004. Returns to farm

labor have been increasing.

The diversification of crop production has started. Although crop production is still

mainly focused on paddy, the crop mix has been

changing, driven by higher profitability of non-rice

crops. In 2013, average farm gross margins (and

returns to labor) were $506/ha ($9.4/day) for

cassava, $303/ha ($8.8/day) for maize, and

$1,393/ha ($7.2/day) for vegetable production,

compared to $245/ha ($4.6/day) for wet season rice

and $296/ha ($9.6/day) for dry season rice. Dry

season rice competes with non-rice crops in terms of

returns to labor but its expansion is constrained by

limited irrigation. The share of total area planted

under paddy declined from 86 percent in 2002 to 74 percent in 2011, while the share of planted

area for maize and cassava production increased significantly.

Even the paddy sector has started to diversify. Triggered by the demand from

modernized rice mills, more farmers grow more profitable aromatic paddy, estimated at 10 percent

of rice cultivated area and 30 percent of total production. Further expansion of farmland under

aromatic paddy is possible with improvements in quality seed supply, agricultural extension, and

irrigation.

Yields increased for most crops. With the annual growth in cultivated land areas at 4.7

percent and agricultural gross production at 8.7 percent, the average growth of yields was 4 percent

during 2004-2012. This growth in yields was triggered by wide adoption of improved technologies,

expanded (yet still limited) irrigation, more use of modern inputs, and better access to mechanized

services, pointing to the advances in commercialization. Farmers also have better access to

markets.

Cambodian farm products remain price competitive at farm gate. A domestic resource

cost analysis of competitiveness shows that despite rising labor costs and prices of farm inputs, the

value added generated by farmers exceeds the costs of domestic factors of production (land, labor,

and capital). This high competitiveness explains the large increase in agricultural exports in the

recent decade. However, the competitiveness of ordinary rice produced during the wet season has

xiv

worsened in recent years and many small farmers producing ordinary rice started to lose their

competitive edge.

Past agricultural growth was driven by several factors. Among the major ones were

open trade and, in general, market-oriented agricultural policy. Cambodia was one of the few

developing countries that did not overact to the 2008 global food price spike but actually saw

higher food prices as an opportunity to leverage agricultural growth. Other net-exporting countries

such as India and Vietnam used export restrictions to limit transmission of the global food price

spike into their markets. Higher agricultural prices in Cambodia made farmland expansion

profitable. In addition, the agriculture sector benefited from: (i) improved access to overseas

markets through the Everything but Arms Agreement with the European Union and open cross-

border trade with neighbors; (ii) better availability and wider use of mechanization services

triggered by the higher cost of rural labor; (iii) better farm access to finance; and (iv) the private

sector investments in rice mills.

BUT THERE ARE CHALLENGES

A large share of the past agricultural growth was driven by farmland expansion. The

average contribution (weighted by crop areas) of land expansion to the change in farm gross

margins in real terms between 2005 and 2013 was about 60 percent. Farmland expanded annually

by 4.7 percent, with very large increases (128 percent) for cassava. This farmland expansion has

contributed to accelerated deforestation, especially in upland areas.

The average increase in per hectare gross

margin2 was good, at 3.4 percent per year. But it

varied between 2.1 percent for dry season rice to 44.5

percent for vegetables. Maize’s per hectare margin

even declined. In many cases, farmers who expanded

their land areas received higher incomes, but farmers

with unchanged land areas were not able to

substantially increase their incomes. The period of

relatively high food prices was largely used to expand

land areas rather than to build a strong foundation

through productivity increases.

While poverty reduced significantly, the number of vulnerable people also increased

significantly. Most people who escaped poverty did so by a small margin. The loss of only 1,200

Riels per day (the cost of two small water bottles) would cause Cambodia’s poverty rate to double

to 40 percent. This high rate of vulnerability is the sign of still modest agricultural productivity

increases. Nutritional security has also lagged behind the reduction in poverty: although the

prevalence of stunting among children under five has declined by 7 percent between 2010 and

2014, it remained at the high rate of 33 percent.

2 Gross margin is defined as gross revenue less intermediate inputs, including hired labor. The farm gross margin

estimated in this report includes major, but not all crops, i.e. rice, cassava, maize, and vegetables.

Changes in farm gross margins, real terms, 2005-2013, %

Change in Cultivated

Area

Change in Gross Margin

per Hectare

Change in Total

Gross Margin

Wet season rice 2.1 2.4 4.5

Dry season rice 6.7 2.1 8.8

Cassava 128.1 15.1 143.2

Maize 17.2 -10.3 6.9

Vegetables 6.4 44.5 50.9

Weighted average 4.7 3.4 8.1

Source: 2005 and 2013 surveys.

xv

Poor are those living below $1.15 per day (poverty line) Near poor or vulnerable are those living above $1.15 per

day, but below $2.30 per day

Vulnerability is greatest among the smallest farms. Small farmers, with land area less

than a hectare, reported finding it difficult to expand and integrate into the emerging modern food

value chains. The share of such farms in total number of rural households owning land was 48

percent in 2011. In the last decade, there has been the trend in Cambodia for large farms (above 3

ha) to become larger and small farms (less than 1 ha) to become smaller.3 The average size of the

interviewed farms4 with less 1 ha declined from 0.99 ha in 2008 to 0.88 ha in 2012, while the

average size of medium farms (between 1 and 3 ha) increased from 1.55 ha to 2.38 ha and the

larger farms (above 3 ha) from 3.61 ha to 7.03 ha. In spite of the productivity improvements of

some small farms in the past, the productivity of most small traditional farms has remained low,

as agricultural extension and other public services have not reached them at a large scale. It appears

that the income increase for this group of farmers in the last decade largely came from higher

production values, driven by high agricultural prices, and the sale of their labor to larger farms at

higher wages, rather than higher land and labor productivity.

Except for rice, the agroprocessing industry has played a limited role in agricultural

growth. Almost all crops were exported to neighboring countries unprocessed. This indicates

serious weaknesses in the value chain, particularly in the post-harvest system of supply chain

management (collection of raw material, storage, finance, logistics, transportation, and

information).

WHAT WORKED IN THE PAST WILL NOT BE SUFFICIENT IN THE FUTURE

With global food prices declining and the land frontier diminishing, Cambodian

agriculture is losing its two major growth drivers. Moreover, agricultural labor is becoming

scarcer and more expensive, adding to production costs. Global agricultural prices are projected to

continue their decline in the next decade, and selling low-quality ordinary rice on domestic and

foreign markets will be less and less profitable. Relying on higher domestic demand driven by the

increase in GDP and higher import demand alone, without more efficient use of resources, will not

be enough to maintain the high rate of past growth. Cambodia would need to find other drivers of

growth to help maintain agricultural growth at or near 5 percent and make it more sustainable.

The recent slowdown in agricultural growth in Cambodia may signal a potential

longer-term decline. As global food prices gradually declined and the global rice market became

more competitive with the reentry of Thailand and Myanmar, rice production in Cambodia stalled.

And with it, total crop value added declined, from 4.9 percent in 2012 to 0.6 percent in 2013. The

3 This change in distribution of farmland is occurring independently of economic land concessions. 4 The farm survey was carried out for this report in 2013, see Annex 2 for details.

xvi

growth in agricultural value added slowed down to 1.6 percent in 2013 after average growth of 5.3

percent between 2004 and 2012.

Returning to a high agricultural growth rate is important. Agriculture still maintains a

large share in GDP, trade, and the labor force, which means that it will remain the key to further

reduction in poverty and vulnerability in the upcoming decade. If Cambodia’s structural

transformation continues, with agricultural growth averaging 5 percent, by 2030 Cambodia will

have relatively smaller but more productive agriculture sector. The agriculture’s share in GDP and

total labor force are projected to go down respectively to 17 percent and 31 percent in 2030, from

26 percent and 51 percent in 2012, while land productivity would increase from $1,300/ha to

$2,700/ha and labor productivity would rise from $1,200/person to $3,700/person (Table 1).

By contrast, the cost of slow agricultural growth would be huge. If average agricultural

growth is only 3 percent between 2012 and 2030, agricultural value added would be 29 percent

lower by 2030 compared with a 5 percent growth scenario, slicing overall GDP by 18 percent,

keeping more people in agriculture, reducing agricultural labor productivity by 34 percent, and

slowing any further income convergence between farmers and nonfarmers. Lower agricultural

growth would also lead to a much slower reduction in poverty.

Table 1: Impact of lower agricultural growth on selected agriculture sector indicators,

Cambodia Indicators 2012 2030

3% Ag GDP growth 5% Ag GDP growth

Share of agriculture in GDP, % 26 15 17

Share of agriculture in labor force, % 51 34 31

Agricultural labor productivity, $/person 1,200 2,450 3,700

Agricultural land productivity, $/ha 1,300 1,900 2,700

Labor productivity ratio of agricultural to

nonagricultural workers

2.1 2.1 1.6

A long-term vision for Cambodian agriculture would need to encompass elements of

sustainability, productivity, competitiveness, and income growth, shifting from still strong

focus on production. Simulation of different scenarios for future agricultural development reveals

that a rise in farm productivity would have the largest positive effect on farm incomes, especially

if the shift from traditional to modern technologies is accompanied by higher efficiency of modern

input use and irrigation. Farmers producing fragrant rice, processing cassava into dry chips, and

undertaking other value addition activities can further increase their incomes, illustrating the

importance of the agroprocessing industry. Lowering production costs through better use of

existing resources (e.g., productivity increase) and minimizing drops in farm output prices through

lower logistics costs are the keys to maintaining farm competitiveness. Continued land expansion

also provides additional income but sustainability considerations will limit large expansions in the

future. This constraint makes agricultural productivity, commercialization, and diversification

even more critical for ensuring future agricultural growth that reduces poverty and boosts shared

prosperity in Cambodia.

RECOMMENDATIONS

Continued rapid agricultural growth and further structural transformation in the

agriculture sector are possible in Cambodia. Four sets of policies together can help support such

continued agricultural growth during the next five years (short-to medium run). The first is

xvii

maintaining a private sector friendly agricultural policy environment, with added attention to lower

the regulatory burden in farm input sectors. The second is strengthening the environmental

sustainability of agricultural production. The third is improving the quality of agricultural public

programs and, as feasible within Cambodia’s total government budget, increasing allocations to

more effective programs. And the fourth is helping develop the agribusiness and agroprocessing

industry.

Investments and policy improvements are needed immediately but not all will show

immediate results. For some of them, more time and effort are required to have an impact on the

ground. Table 2 summarizes key policy recommendations that need to be set in motion

immediately to produce impacts in the short to medium run that would help reverse the recent

slowdown in agricultural growth and help fully utilize the significant potential of Cambodia’s

agriculture.

Table 2: Summary of the report’s key policy recommendations based on the time of

impacts’ realization

Policy recommendations Impacts

realizable

in Short

Run

Impacts

realizable in

Medium-to-

Long Run

Maintaining a private sector friendly agricultural policy environment

Continue the open trade policy and non-distortive agricultural policy X

Reduce the regulatory costs of importation of fertilizers X

Open up seeds sector for private investments through deregulation and

institutional strengthening X

Strengthening the environmental sustainability

Improve land use planning and better enforce land laws/regulations X

Strengthen land tenure security X

Promote sustainable land management practices X

Promote the safe use of agricultural chemicals X

Improving agricultural “public good” investment programs

As feasible within Cambodia’s total government budget, increase the

budget for core agricultural public goods, especially irrigation, applied

research, extension, soil nutrient management, input quality control,

food safety, vocational training, and rural roads

X

In irrigation, pay more attention to upgrades and rehabilitation of

existing systems and participatory management of irrigation

infrastructure

X

Improve the quality of agricultural public programs X

Facilitate integration of small farms into food value chains X

Helping develop agribusiness and agroprocessing industry

Improve access to and reduce electricity costs X

Invest in food safety public infrastructure X

Improve rice trade logistics, including cost reduction X

Remove barriers for introduction of warehouse receipts X

xviii

សេចក្ដីេសខេបរួម

របាយការណ៍ស េះ បា ព្យាយាមស្េែខយលព់្យសីោគជយ័ បញ្ហា ប្បឈម ខិកាលា ុវត្ដភាព្យន បម្លា េប់ដរូក្នខុវេិយ័ក្េកិ្មម សៅក្មពុោ

សៅក្នខុទេវត្សរក៍្ ាខសៅស េះ ស ើមបីទាញ បា ោសមសរៀ ខិគ ំតិ្េំខា ់ៗ េប្ម្លបរ់ក្ាក្សំណើ ក្េកិ្មម នាសព្យលអនាគត្ ោព្យិសេេ

ត្នួាទីរបេ់រដ្ឋា ភបិាល សៅក្នខុការបខកលក្េណៈ ឱ្យម្ល ក្សំណើ ស្បបស េះ។ របាយការណ៍ស េះប្ត្ូវបា សរៀបចំស ើខ សៅតាម ការសេនើេំុរបេ់ឧត្ដមប្ក្ុមប្បឹក្ាសេ ាក្ិចចោត្ ិ ិខប្ក្េួខក្េិក្មម រុកាេ ប្បម្លញ់ ិខស សាទ សដ្ឋយស្អែក្សៅតាមការអសខកត្ប្បមូលទិ ន ័យផ្ទា ល់ព្យីក្េិដ្ឋា ព្យីឆ្ន ២ំ០០៥ ល់២០១៣ ិខទិ ន ័យស្ លបា ព្យីប្បភព្យសអសខៗ។ សៅក្ំ ុខឆ្ន ំ ២០១៣-២០១៤ ក្ំសណើ ក្េិក្មមម្ល ការថមថយមក្សៅប្ត្ឹម ១ភាគរយ

ព្យីក្ំសណើ ោមធ្យម ៥,៣ភាគរយ សៅក្ំ ុខឆ្ន ំ ២០០៤-២០១២។ សត្ើប្បសទេក្មពុោ េថិត្សៅក្នុខអ ដរកាលសៅរក្ក្ំសណើ សេ ាក្ិចចយឺត្ោខមុ ឬ? ប្បសទេក្មពុោមិ អាចបសដដ យឱ្យម្ល បញ្ហា ស្បបស េះ ប ដសក្ើត្ម្ល ស ើខស ើយ សដ្ឋយសេត្ុថាក្ំសណើ ក្នុខវិេ័យក្េិក្មមម្ល សារៈេំខា ់ េប្ម្លប់ប ដការកាត្់ ប ថយភាព្យប្ក្ីប្ក្សៅក្នុខប្បសទេស េះ ិខសដ្ឋយសារស្ត្ក្េិក្មមម្ល េម្លេភាគធ្ំ សៅក្នុខសេ ាក្ិចចរបេ់ប្បសទេក្មពុោ។ សោល សយាបាយ ស្ លបខកភាព្យងាយប្េួល ល់ទីអារ ិខការវិ ិសយាគឯក្ជ ិខការវិ ិសយាគក្នុខវិេ័យសាធារណៈ ស្ លសផ្ទដ ត្ចំសោលសៅ ូចោ

វិេ័យធារាសាស្ដេដ អសព្យែអាយបសចចក្សទេក្េិក្មម ិខ សេវាក្េិក្មមោ “ប្បសយាជ ៍សាធារណៈ” នទសទៀត្ សៅតាមលទធភាព្យស្ លអាចសធ្ែើបា ក្នុខរខែខ់លទធភាព្យថវិកាេរុបរបេ់រដ្ឋា ភិបាល អាច ឹខជួយរក្ាឱ្យវិេ័យក្េិក្មមសៅស្ត្ប ដក្ំសណើ រឹខម្លបំា ។

លទធអលរក្ស ើញេខំា ់ៗ

ក្សំណើ ន វេិយ័ក្េកិ្មមសៅក្នខុទេវត្សរក៍្ ាខសៅ បា បងាា ញព្យីសោគជយ័ោសប្ចើ

សៅក្នខុទេវត្សរច៍ខុសប្កាយស េះ វេិយ័ក្េកិ្មមរបេ់ប្បសទេក្មពោុ បា ឆ្ាខកាត្ប់ម្លា េប់ដូររចនាេមព ័ធេំខា ់ៗ គួរឱ្យក្ត្េ់ម្លា ល។់ សបើសទាេះបីោសៅម្ល ត្ួនាទី ៏ធ្ំយា៉ា ខដក្៏សដ្ឋយ វិេ័យក្េិក្មមមិ េូវម្ល “សារៈេំខា ់” សៅក្នុខ អេេ

ិខក្ម្លា ខំព្យលក្មមេរុបស ើយ ប៉ាុស្ ដម្ល “អលិត្ភាព្យ” ោខមុ សោលគឺអលិត្ភាព្យរបេ់ ីក្េិក្មម ិខក្ម្លា ខំព្យលក្មម ម្ល ការសក្ើ ស ើខ។ បម្លា េ់បដូរស េះប្ត្ូវបា ជប្មុញ សដ្ឋយសារស្ត្ក្ំសណើ ក្នុខវិេ័យក្េិក្មម ស្ លោបំ្ទ ល់ជ ប្ក្ីប្ក្។

ក្សំណើ វេិ័យក្េកិ្មម សៅក្នខុប្បសទេក្មពុោម្ល ក្ប្មតិ្ខ្ពេ។់ ចសនាា េះព្យីឆ្ន ២ំ០០៤ ល់២០១២ ក្ំសណើ ប្បចឆំ្ន នំ អលិត្ក្មមក្េិក្មមេរុបម្ល ៨,៧ភាគរយ។ ត្នមាបស្ ថមរបេ់វិេ័យក្េិក្មម5 ម្ល ការសក្ើ ៥,៣ភាគរយ សៅក្នុខរយៈសព្យលស េះ។ ក្ំសណើ ព្យិសេេ ស្ លេថិត្សៅក្នុខចំសដមក្ំសណើ ខ្ពេ់ោខសគ សៅក្នុខព្យិភព្យសលាក្ស េះ ប្ត្ូវបា ជប្មុញសដ្ឋយអលិត្ក្មម ំដ ំោព្យិសេេប្េូវ (ក្ំសណើ ប្បចឆំ្ន ំ៩ ភាគរយ) ិខសោត្ (២០ ភាគរយ) ំ ូខមី (៥១ ភាគរយ) អំសៅ (២២ ភាគរយ) ិខបស្ ា (១០ ភាគរយ)។ ក្ំសណើ សៅក្នុខវិេ័យបេុេត្ែ ិខស សាទ ម្ល ក្ប្មិត្មធ្យម។

ក្សំណើ ក្នខុវេិយ័ក្េកិ្មមស េះ ក្ោ៏ំប្ទ លប់្បោព្យលរ ាប្ក្បី្ក្អខស្ រ។ អប្តាន ភាព្យប្ក្ីប្ក្របេ់ប្បសទេ ក្មពុោ ម្ល ការថយចុេះព្យី ៥០ភាគរយ សៅក្នុខឆ្ន ២ំ០០៧ មក្សៅ ២១ភាគរយ សៅក្នុខឆ្ន ២ំ០១១ សដ្ឋយចំ ួ ប្បោជ ប្ក្ីប្ក្ថយចុេះព្យី ៧លា នាក្់ មក្សៅ ៣លា នាក្់។ ការកាត្់ប ថយភាព្យប្ក្ីប្ក្ភាគសប្ចើ សក្ើត្ម្ល ស ើខសៅតាមត្ំប ់ជ បទ។ ការកាត្់ប ថយ ភាព្យប្ក្ីប្ក្ោខ ៦០ភាគរយ សក្ើត្ស ើខសដ្ឋយសារវិេ័យក្េិក្មម៖ ត្នមាអខករខ្ពេ់ោខមុ បា ជប្មុញឱ្យអលិត្ក្មមប្េូវ សក្ើ ស ើខ ស្ លជួយបសខកើ ប្បាក្់ចំណូល ល់អនក្ស្ លសធ្ែើស្ប្េ ិខក្េិដ្ឋា ប្េូវនានាស្ រ។ ការកាត្់ប ថយភាព្យប្ក្ីប្ក្បស្ ថមសទៀត្ សៅប ដព្យឹខអាប្េ័យសលើសោគជ័យន វិេ័យក្េិក្មមសប្ចើ ឆ្ន ំសៅមុខ្សទៀត្ សដ្ឋយសារស្ត្ត្ួនាទី ៏ធ្ំរបេ់វិេ័យស េះ ចំសោេះ ក្ម្លា ខំព្យលក្មម ត្នមាបស្ ថម ិខការនាសំចញ

ក្៏ ូចោសដ្ឋយសារស្ត្ក្េិក្រោសប្ចើ េថិត្សៅក្នុខចំសដមអនក្ស្ លប្ក្ីប្ក្ ិខ ងាយរខសប្ោេះោខសគ។

ប្បាក្ឈ់នលួក្នខុវិេយ័ក្េកិ្មម សក្ើ ស ើខសៅសក្ៀក្ ខឹប្បាក្ឈ់នលួក្នខុវេិ័យម ិស្ម ក្េកិ្មម។ ប្បាក្់ឈនួលក្នុខ វិេ័យក្េិក្មមម្ល ការសក្ើ ស ើខ ២០៦ភាគរយ សៅក្នុខការអសខកត្ស្ លសធ្ែើស ើខចសនាា េះ ឆ្ន ២ំ០០៥ ិខ២០១៣ ខ្ណៈសព្យល

ស្ លប្បាក្់ឈនួលក្នុខវិេ័យមិ ស្ម ក្េិក្មម ម្ល ការសក្ើ ស ើខ ៦០ភាគរយ។ ូសចនេះ អលសធ្ៀបរវាខត្នមាបស្ ថម េប្ម្លប់អនក្ សធ្ែើការក្នុខវិេ័យមិ ស្ម ក្េិក្មមម្លន ក្់ សធ្ៀបោមួយ ឹខអនក្សធ្ែើរបរក្េិក្មម គិត្ោត្នមាបចចុបប ន ម្ល ការថយចុេះព្យី ៣,២ សៅក្នុខឆ្ន ២ំ០០៤ មក្ ២,១ សៅក្នុខឆ្ន ២ំ០១២។ ចំណូលស្ លបា មក្ព្យីការសធ្ែើការងារសៅក្នុខក្េិដ្ឋា ម្ល ការសក្ើ ស ើខ។

5 ត្នមាបស្ ថមក្នុខវិេ័យក្េិក្មម ប្តូ្វបា សគកំ្ណត់្ ិយម ័យឱ្យថាោត្នមាេរុបរបេ់អលិត្ក្មម ក្ត្នមាធាតុ្ចូលក្េិក្មមសចញ។

xix

ព្យពិ្យធិ្ភាព្យអលតិ្ក្មម ំដបំា ចប់សអដើម ខិក្ពំ្យខុប ត។ សបើសទាេះបីោអលិត្ក្មម ំដ ំ សផ្ទដ ត្ោចមបខសលើ ំដបំ្េូវក្តី មុខ្ ំដកំ្ំព្យុខម្ល ការស្ប្បប្បួល សដ្ឋយសារស្ត្លទធភាព្យចំសណញ ខ្ពេ់ន ប្បសភទ ំដសំប្ៅព្យីប្េូវ។ សៅឆ្ន ២ំ០១៣ អលចំណូល េរុបគិត្ោមធ្យម (រួមទាខំក្ំនរព្យលក្មម) របេ់ក្េិដ្ឋា រួមម្ល ៥០៦ ុលាា រ/េិចតា (៩,៤ ុលាា រ/នថៃ) េប្ម្លប់ ំ ូខមី, ៣០៣ ុលាា រ/េិចតា

(៨,៨ ុលាា រ/នថៃ) េប្ម្លប់សោត្ ិខ ១៣៩៣ ុលាា រ/េិចតា (៧,២ ុលាា រ/នថៃ) េប្ម្លប់ ំដបំស្ ា សបើសធ្ៀប ោមួយ ឹខ ២៤៥ ុលាា រ/េិចតា (៤,៦ ុលាា រ/នថៃ) េប្ម្លប់ប្េូវ វេា ិខ ២៩៥ ុលាា រ/េិចតា (៩,៦ ុលាា រ/នថៃ) េប្ម្លប់ប្េូវប្បាខំ។ ប្េូវរ ូវប្បាខំប្ត្ូវប្បស្ជខោមួយ ឹខ ំដមំិ ស្ម ប្េូវ នទសទៀត្ សបើគិត្ព្យីចំណូលរបេ់ក្ម្លា ខំព្យលក្មម ប៉ាុស្ ដការព្យប្ខីក្អលិត្ក្មមប្េូវរ ូវប្បាខំប្ត្ូវជួបឧបេគា សដ្ឋយសារស្ត្ ប្បព្យ័ ធធារាសាស្ដេដសៅម្ល ក្ប្មិត្សៅស ើយ។ ភាគរយន នអា ីេរុបស្ លសប្បើប្បាេ់ េប្ម្លប់បខកបសខកើ អលប្េូវ ម្ល ការ ថយចុេះព្យី ៨៦ភាគរយ សៅក្នុខឆ្ន ២ំ០០២ រេូត្ ល ់ ៧៤ភាគរយ សៅក្នុខឆ្ន ំ២០១១ ខ្ណៈសព្យលស្ លភាគរយន នអា ីេប្ម្លប់ដ្ឋសំោត្ ិខ ំ ូខមី ម្ល ការសក្ើ ស ើខគួរឱ្យក្ត្់េម្លា ល់។

េមូបសី្ត្វេិ័យប្េូវក្ច៏ប់សអដើមសធ្ែើព្យពិ្យធិ្ក្មមអខស្ រ។ សដ្ឋយសារស្ត្ម្ល ត្ប្មូវការព្យីសរាខម្ល៉ា េីុ ក្ិ ប្េូវទំស ើប ក្េិក្រ កា ់ស្ត្សប្ចើ ោខមុ នាោំន បសខកើ ការអលិត្ប្េូវប្ក្អូបស្ លអដល់ប្បាក្់ចំសណញខ្ពេ់ោខមុ ប្បម្លណោ១០ភាគរយ ន នអា ី ដ្ឋបំ្េូវេរុប ិខប្បម្លណោ ៣០ភាគរយន អលិត្ក្មមេរុប។ ការព្យប្ខីក្ ីស្ប្េបស្ ថមសទៀត្ េប្ម្លប់ប្េូវប្ក្អូបស េះ គឺអាច សធ្ែើសៅបា ោមួយ ឹខការស្ក្លំអការអាត្់អាខ់ប្ោប់ព្យូជប្បក្បសដ្ឋយគុណភាព្យ ការអសព្យែអាយក្េិក្មម ិខប្បព្យ័ ធធារាសាស្ដេដ។

ទ ិនអលម្ល ការសក្ើ ស ើខ េប្ម្លប ់ដំភំាគសប្ចើ ។ ោមួយ ឹខក្ំសណើ ប្បចឆំ្ន នំ នអា ីដ្ឋ ំុេះ ៤,៧ភាគរយ ិខអលិត្ក្មមក្េិក្មមេរុប ៨,៧ភាគរយ ទិ ន ័យម្ល ក្ំសណើ ោមធ្យមប្បចឆំ្ន ំ ៤ភាគរយ ចសនាា េះព្យីឆ្ន ២ំ០០៤ ល់២០១២។ ក្ំសណើ ទិ នអលទាខំស េះប្ត្ូវបា ជប្មុញ សដ្ឋយការសប្បើប្បាេ់បសចចក្វិទាថមីៗសប្ចើ ោខមុ ការព្យប្ខីក្ប្បព្យ័ ធធារាសាស្ដេដ (សបើសទាេះបីោសៅម្ល ក្ប្មិត្សៅស ើយក្៏សដ្ឋយ) ការសប្បើប្បាេ់ព្យូជ ិខជីរក្េិក្មមលែៗកា ់ស្ត្សប្ចើ ោខមុ ិខលទធភាព្យ ទទួលបា សេវាសប្គឿខយ ដលែប្បសេើរោខមុ ស្ លទាខំស េះេុទធស្ត្បងាា ញព្យីភាព្យសជឿ សលឿ ន ោណិជផូ ីយក្មម។ ក្េិក្រ ក្៏ម្ល លទធភាព្យទទួលបា ទីអារកា ់ស្ត្ប្បសេើរោខមុ អខស្ រ។

ត្នមាអលតិ្អលក្េកិ្មមរបេក់្មពោុសៅម្ល ភាព្យប្បក្តួ្ប្បស្ជខសៅ ខឹក្េិដ្ឋា ផ្ទា ល។់ ការវិភាគសលើភាព្យប្បក្ួត្ ប្បស្ជខន ត្នមាអលិត្អលក្នុខប្េុក្ បងាា ញថាសបើសទាេះបីោត្នមាក្ម្លា ខំព្យលក្មម ិខត្នមាធាត្ុចូលស្ លសប្បើប្បាេ់េប្ម្លប់ដ្ឋ ំុេះ ម្ល ការសក្ើ ស ើខយា៉ា ខដក្តី ត្នមាបស្ ថមស្ លគិត្សដ្ឋយក្េិក្រសៅខ្ពេ់ោខត្នមា ន ក្តាដ អលិត្ក្មមក្នុខប្េុក្ ( ី ព្យលក្មម ិខស ើមទុ )។ ភាព្យប្បក្ួត្ប្បស្ជខខ្ពេ់ស េះ អាចោមូលសេត្ុនាឱំ្យម្ល ការសក្ើ ស ើខការនាំសចញក្េិអល ៏សប្ចើ សៅក្នុខ ទេវត្សរ៍ក្ ាខសៅស េះ។ ប៉ាុស្ ដភាព្យប្បក្ួត្ប្បស្ជខន ប្េូវធ្មមតាស្ លអលិត្សៅរ ូវវេា ម្ល ការថយចុេះក្នុខរយៈប៉ាុនាម ឆ្ន ំចុខសប្កាយស េះ សេើយ ក្េិក្រខាន ត្ត្ូចោសប្ចើ ស្ លអលិត្ប្េូវធ្មមតា បា ចប់សអដើមបាត្់បខ់ភាព្យប្បក្ួត្ប្បស្ជខរបេ់ខ្ាួ ។

ក្សំណើ សៅក្នខុវេិយ័ក្េកិ្មមក្ ាខមក្ ប្ត្វូបា ជប្មុញសដ្ឋយក្តាដ ោសប្ចើ ។ ក្នខុចំសដមក្តាដ ធ្ំៗ រួមម្ល ការ សបើក្ចំេរការសធ្ែើោណិជផក្មម ិខសោល សយាបាយក្េិក្មមសផ្ទដ ត្សលើទីអារោទូសៅ។ ប្បសទេក្មពុោ ោប្បសទេមួយ ក្នុខ ចំសដមប្បសទេក្ំព្យុខអភិវឌ្ឍនានា ស្ លមិ បា ប្បត្ិក្មមប្ជុលខាា ខំសព្យក្សៅ ឹខការសលាត្ ស ើខ ូវត្នមាសេបៀខអាហារ ោេក្លសៅក្នុខឆ្ន ំ២០០៨ ប៉ាុស្ ដចត្់ទុក្ការស ើខនថាសេបៀខអាហារស េះ ថាោឱ្កាេមួយស ើមបីទាញប្បសយាជ ៍ េប្ម្លប់ ក្ំសណើ វិេ័យក្េិក្មម។ ប្បសទេនានាស្ លម្ល ការនាសំចញសប្ចើ ោខការនាចំូល ូចោឥដា ិខសវៀត្ដម ោស ើម បា ដ្ឋក្់ក្ំេិត្សលើការនាសំចញ ស ើមបីទប់ឥទធិព្យលន ការស ើខនថាសេបៀខអាហារោេក្ល មក្សលើទីអាររបេ់ព្យួក្សគ។ ត្នមា អលក្េិក្មមខ្ពេ់សៅក្នុខប្បសទេក្មពុោ

បា សធ្ែើឱ្យការព្យប្ខីក្ ីក្េិក្មម អដល់អលចំណូលមក្វិញខ្ពេ់។ សលើេព្យីស េះ វិេ័យក្េិក្មមបា ទទួលប្បសយាជ ៍ព្យី (i) ការទទួលបា ទីអារសៅបរសទេសប្ចើ ោខមុ តាមរយៈក្ិចចប្ព្យមសប្ព្យៀខទំ ិញប្គប់ស្បបយា៉ា ខសលើក្ស្លខស្ត្អាវុធ្សចញ ោមួយ ឹខេេភាព្យអឺរ ុប ិខការសបើក្ចំេោណិជផក្មមឆ្ាខស្ ោមួយ ឹខប្បសទេ ជិត្ខាខ (ii)ការទទួលបា ិខការសប្បើប្បាេ់យា៉ា ខទូលាយ ូវសេវាសប្គឿខយ ដ ជំ ួេសអាយការចំដយកា ់ស្ត្ខ្ពេ់សលើក្ម្លា ខំព្យលក្មមសៅជ បទ (iii)ការទទួលបា ឥណទា ប្បសេើរោខមុ ិខ (iv)ការវិ ិសយាគរបេ់វិេ័យឯក្ជ សលើម្ល៉ា េីុ ក្ិ ប្េូវខាន ត្ធ្ំ។

បញ្ហា ប្បឈមនានា

ភាគរយ ខ៏្ពេ់ន ក្សំណើ ក្នខុវេិយ័ក្េកិ្មមក្ ាខសៅស េះ ប្ត្វូបា ជប្មញុសដ្ឋយសារស្ត្ការព្យប្ខកី្នអា ីដ្ឋ ំេុះ។ ការរួមចំស្ណក្ោមធ្យម ន ការព្យប្ខីក្នអា ីដ្ឋ ំុេះ ចំសោេះការស្ប្បប្បួលអប្តាចំណូលេរុបរបេ់ក្េិក្មម គិត្ោត្នមាព្យិត្ ចសនាា េះព្យីឆ្ន ២ំ០០៥ ល់២០១៣

គឺប្បស្េលោ ៦០ភាគរយ។ ីក្េិក្មម ប្ត្ូវបា ព្យប្ខីក្ប្បម្លណោ ៤,៧ភាគរយ ក្នុខមួយឆ្ន ំ សដ្ឋយម្ល ការសក្ើ ស ើខយា៉ា ខសប្ចើ (១២៨ភាគរយ) េប្ម្លប់ ំ ូខមី។ ការព្យប្ខីក្ ីក្េិក្មមស្បបស េះ បា រួមចំស្ណក្ សធ្ែើឱ្យម្ល ការបាត្់បខ់នប្ព្យសឈើកា ់ស្ត្សលឿ ោព្យិសេេ

សៅត្ំប ់ខ្ពខ់រាប។

ក្សំណើ ោមធ្យមន អប្តាចំសណញក្នខុមយួេចិតា6 ម្ល ក្ប្មតិ្ លែប្បសេើរ គឺ៣,៤ភាគរយក្នខុមយួឆ្ន ។ំ ប៉ាុស្ ដ វាម្ល ការស្ប្បប្បួលចសនាា េះព្យី ២,១ភាគរយ េប្ម្លប់ប្េូវរ ូវប្បាខំ សៅ៤៤,៥ភាគរយ េប្ម្លប់បស្ ា។ អប្តា ចំសណញេប្ម្លប់សោត្ក្នុខមួយេិចតាម្ល ការថយចុេះ។ សៅក្នុខក្រណីោ សប្ចើ ក្េិក្រស្ លបា ព្យប្ខីក្នអា ីរបេ់ខ្ាួ បា ទទួលប្បាក្់ចំណូលខ្ពេ់ ោខមុ ប៉ាុស្ ដក្េិក្រស្ លរក្ានអា ីដ្ឋ ំុេះ ស្ លមិ អាចបសខកើ ប្បាក្់ចំណូលរបេ់ខ្ាួ ឱ្យបា សប្ចើ ស ើយ។ ក្ំ ុខសព្យលស្ ល ត្នមាសេបៀខស ើខខ្ពេ់ ប្ត្ូវបា ជំរុញសលើការព្យប្ខីក្នអា ី ោោខការក្សាខមូលដ្ឋា រឹខម្លំ តាមរយៈការបសខកើ អលិត្ភាព្យ។

សព្យលស្ លភាព្យប្ក្បី្ក្ម្ល ការថយចេុះគួរឱ្យក្ត្េ់ម្លា ល់ ច ំ ួប្បោជ ស្ លងាយរខសប្ោេះក្ម៏្ល ការសក្ើ ស ើខ សប្ចើ អខស្ រ។ ភាគសប្ចើ ន ប្បោជ ស្ លសខើបសចញព្យីភាព្យប្ក្ីប្ក្ សៅមិ ទា ់សៅអុត្ឆ្ៃ យព្យីវាសៅស ើយ។ ការបាត្់បខ់ ចំណូលប្ត្ឹមស្ត្១២០០សរៀល ក្នុខមួយនថៃ (ត្នមាទឹក្េុទធព្យីរ បត្ូច) ឹខសធ្ែើឱ្យអប្តា ន ភាព្យប្ក្ីប្ក្របេ់ប្បសទេក្មពុោ សក្ើ ស ើខ សទែ ខ ល់៤០ភាគរយ។ អប្តាន ភាព្យងាយរខសប្ោេះ ៏ខ្ពេ់ស្បបស េះ គឺោេញ្ហា ស្ លបងាា ញថា

ក្ំសណើ អលិត្ភាព្យក្េិក្មម សៅម្ល ក្ប្មិត្ត្ិចត្ួចសៅស ើយ។ េ ដិេុខ្អាហារូបត្ថមភ ក្៏សៅម្ល សលបឿ យឺត្ោខការកាត្់ប ថយភាព្យប្ក្ីប្ក្អខស្ រ៖ សទាេះបី ោសប្បវា ខ់ន ភាព្យប្ក្ិ របេ់ក្ុម្លរអាយុសប្កាម៥ឆ្ន ំ បា ថយចុេះ៧ភាគរយ សៅចសនាា េះព្យីឆ្ន ២ំ០១០ ិខ២០១៤ក្តី អប្តា ស េះសៅស្ត្ម្ល ក្ប្មិត្ខ្ពេ់ (៣៣ ភាគរយ)

សៅស ើយ។

6 អប្តាចំណូលេរុប ោចំណូលេរុប ក្ធាតុ្ចូលប្បសយាលសចញ រាប់ទំាខព្យលក្មមស្ លប្តូ្វបា ជួលអខ។ អប្តាចំសណញរបេ់ក្េិដ្ឋា ស្ លប្តូ្វបា បា៉ា ់ប្បម្លណសៅក្នុខរបាយការណ៍ស េះ រាប់បញ្ចូលស្ត្ ំដំេំខា ់ៗ ូចោ ប្េូវ ំ ូខមី សោត្ ិខបស្ ា ោស ើម។

Changes in farm gross margins, real terms, 2005-2013, %

Change in Cultivated

Area

Change in Gross Margin

per Hectare

Change in Total

Gross Margin

Wet season rice 2.1 2.4 4.5

Dry season rice 6.7 2.1 8.8

Cassava 128.1 15.1 143.2

Maize 17.2 -10.3 6.9

Vegetables 6.4 44.5 50.9

Weighted average 4.7 3.4 8.1

Source: 2005 and 2013 surveys.

xx

ប្បោជ ប្កី្ប្ក្ ស្ លកំ្ពុ្យខរេ់សៅសប្កាម ១,១៥ ុលាា រ ក្នុខមួយនថៃ (បនាា ត់្ន ភាព្យប្កី្ប្ក្) ប្បោជ ស្ លសក្ៀក្ប្ក្ ឬងាយរខសប្ោេះ គឺោអនក្ស្ លរេ់ សៅសលើ ១,១៥ ុលាា រ ក្នុខមួយនថៃ ប៉ាុស្ ដសប្កាម ២,៣០ ុលាា រ ក្នុខមួយនថៃ

ភាព្យងាយរខសប្ោេះម្ល ក្ប្មតិ្ខ្ពេោ់ខ ក្នខុចសំដមក្េដិ្ឋា ស្ លម្ល ទេំតំ្ចូៗ។ ក្េិដ្ឋា ត្ូចៗ ស្ លម្ល ទំេំ ី ត្ិចោខ១េិចតា ប្ត្ូវបា រក្ស ើញថាជួប ឹខការលំបាក្ ស ើមបីព្យប្ខីក្ខ្ាួ ិខសធ្ែើេម្លេរណក្មម ចូលសៅក្នុខស្ខ្សេងាែ ក្់ អាត្់អាខ់អាហារស្ លម្ល លក្េណៈទំស ើប។ ន ក្េិដ្ឋា ទាខំស េះ គិត្ោចំ ួ ប្គួសារេរុបស្ លម្ល ីោក្មមេិទធិផ្ទា ល់ខ្ាួ គឺ ៤៨ភាគរយ សៅក្នុខឆ្ន ២ំ០១១។ សៅក្នុខទេវត្សរ៍ចុខសប្កាយស េះ សៅក្នុខប្បសទេក្មពុោ ម្ល ិនាន ការស្ លក្េិដ្ឋា ធ្ំៗ (សលើេ៣េិចតា)កា ់ស្ត្រីក្ធ្ំសៅៗ សេើយក្េិដ្ឋា ត្ូចៗ (ត្ិចោខ១េិចតា)កា ់ស្ត្រួញត្ូចសៅៗ។7 ទំេំមធ្យមរបេ់ក្េិដ្ឋា ខាន ត្ត្ូច8 បា ថយចុេះព្យី០,៩៩េិចតាក្នុខឆ្ន ២ំ០០៨ មក្សៅ០,៨៨េិចតាក្នុខឆ្ន ២ំ០១២ សេើយក្នុខសព្យលោមួយោន សនាេះ ទំេំ ោមធ្យមរបេ់ក្េិដ្ឋា ខាន ត្មធ្យម (ចសនាា េះព្យី១ សៅ៣េិចតា) បា សក្ើ ស ើខព្យី១,៥៥េិចតា ល់២,៣៨េិចតា សេើយក្េិដ្ឋា ធ្ំៗ (សលើេព្យី ៣េិចតា) បា សក្ើ ស ើខព្យី ៣,៦១េិចតា ល់៧,០៣េិចតា។ សបើសទាេះបីោអលិត្ភាព្យរបេ់ក្េិដ្ឋា ត្ូចៗម្ល ការសក្ើ ស ើខខ្ាេះក្តី ក្៏សៅម្ល ក្ំរិត្ទាប សដ្ឋយភាគសប្ចើ ន ក្េិដ្ឋា ត្ូចសៅមិ ទា ់បា ទទួល សេវាអសព្យែអាយ ក្េិក្មម ិខសេវាសាធារណៈ នទសទៀត្ ក្នុខប្ទខ់ប្ទាយធ្ំស ើយ។ ការសក្ើ ស ើខ ូវប្បាក្់ចំណូលរបេ់ក្េិក្រក្នុខប្ក្ុមស េះ សៅក្នុខទេវត្សរ៍ចុខសប្កាយស េះ ហាក្់បី ូចោសក្ើត្ស ើខសដ្ឋយសារស្ត្ត្នមាអលិត្ក្មមខ្ពេ់ោខមុ ិខការលក្់ព្យលក្មមសអាយ ក្េិដ្ឋា ធ្ំៗបា ប្បាក្់ឈនួលខ្ពេ់ោខមុ ោោខសដ្ឋយសារការសក្ើ ស ើខន អលិត្ភាព្យ ី ិខគុណភាព្យព្យលក្មម។

សលើក្ស្លខស្ត្អខករសចញ ឧេាេក្មមស្ក្នចនក្េអិលបា បសំព្យញត្ួនាទតី្ចិត្ចួ សៅក្នខុក្ំសណើ វេិ័យក្េកិ្មម។ ក្េិអលសេាើរស្ត្ទាខំអេ់ប្ត្ូវបា នាសំចញសៅប្បសទេជិត្ខាខ សដ្ឋយព្យុំម្ល ការស្ក្នចន។ ស េះបងាា ញព្យីចំណុចសខ្ាយធ្ៃ ់ធ្ៃរ សៅក្នុខស្ខ្សេងាែ ក្់ត្ំនល

ោព្យិសេេសៅក្នុខប្បព្យ័ ធប្គប់ប្គខស្ខ្សេងាែ ក្់អាត្់អាខ់សប្កាយប្បមូលអល (ការប្បមូលក្េិអល មិ ទា ់ស្ក្នចន ការរក្ាទុក្ ការអដល់េិរញ្ាបបទា ភេដុភារ ការ ឹក្ជញ្ផូ ិខព្យ័ត្៌ម្ល )។

អែសី្ លម្ល ប្បេទិធភាព្យក្ ាខមក្ ខឹម ិប្គបប់្ោ ់ េប្ម្លបអ់នាគត្ស ើយ

ោមួយ ខឹត្នមាសេបៀខអាហារម្ល ការថយចេុះ សេើយនអា ីដ្ឋ ំេុះស្លខសក្ើ ស ើខ វេិ័យក្េកិ្មមសៅក្មពោុ ក្ពំ្យខុ បាត្ប់ខ ់ក្តាដ ជប្មញុក្ំសណើ ធ្ំៗ របេខ់្ា ួច ំ ួព្យរី។ សលើេព្យីស េះ ក្ម្លា ខំព្យលក្មមក្នុខវិេ័យក្េិក្មមកា ់ស្ត្ខ្សត្់សៅៗ ិខម្ល ត្នមាកា ់ស្ត្ខ្ពេ ់

ស្ លនាឱំ្យចំដយនថាស ើមអលិត្ក្មមកា ់ស្ត្សក្ើ ស ើខ។ ត្នមាក្េិអលោេក្ល ប្ត្ូវបា សគព្យាក្រថា ឹខ ប ដថយចុេះសៅក្នុខទេវត្សរ៍ខាខមុខ្ស េះ សេើយការលក្់អខករធ្មមតាស្ លម្ល ត្នមាទាប សៅក្នុខទីអារក្នុខប្បសទេ ិខអ ដរោត្ិ ឹខទទួលបា ចំសណញត្ិចោខមុ ។ ការព្យឹខអាប្េ័យសលើត្ប្មូវការក្នុខប្េុក្ស្ លសក្ើ ស ើខ សដ្ឋយសារស្ត្ក្ំសណើ ន អេេ ិខក្ំសណើ ត្ប្មូវការន ការនាចំូល សដ្ឋយមិ ម្ល ការសប្បើប្បាេ់ធ្ ធា ឱ្យកា ់ស្ត្ម្ល ប្បេិទធភាព្យសទសនាេះ ឹខមិ ប្គប់ប្ោ ់ ស ើមបីរក្ាក្ំសណើ ខ្ពេ់ ូចសព្យលក្ ាខស ើយ។ ប្បសទេក្មពុោចបំាច់ប្ត្ូវស្ត្ស្េែខរក្ ក្ម្លា ខំចលក្រក្ំសណើ សអសខសទៀត្ ស ើមបី ជួយរក្ាក្ំសណើ ក្នុខវិេ័យក្េិក្មមឱ្យបា សេមើ ឬសក្ៀក្ ឹខ៥ភាគរយ ិខសធ្ែើឱ្យក្ំសណើ ស េះម្ល ិរ ដរភាព្យបស្ ថមសទៀត្។

ការថមថយ ូវក្សំណើ ក្នខុវិេយ័ក្េកិ្មមរបេក់្មពោុកាលព្យសីព្យលថមីៗ ស េះ អាចោេញ្ហា បងាា ញព្យកីារថយចេុះ ស្ ល អាចសក្ើត្ស ើខក្នខុរយៈសព្យលស្វខ។ ខ្ណៈសព្យលស្ លត្នមាសេបៀខអាហារម្ល ការថយចុេះោប ដបនាា ប់ សេើយទីអារអខករ េក្សលាក្ កា ់ស្ត្ម្ល ការប្បក្ួត្ប្បស្ជខោមួយ ឹខការចូលមក្ក្នុខទីអារសារោថមីរបេ់ប្បសទេនថ ិខមីយា៉ា ់ម្ល៉ា អលិត្ក្មម ប្េូវសៅក្នុខប្បសទេក្មពុោសៅប្ទឹខ។ ោមួយោន ស េះ ត្នមាបស្ ថមេរុបរបេ់ ំដមំ្ល ការថយចុេះព្យី ៤,៩ភាគរយ សៅក្នុខឆ្ន ំ ២០១២ មក្០,៦ភាគរយ

សៅក្នុខឆ្ន ២ំ០១៣។ ក្ំសណើ ន ត្នមាបស្ ថមរបេ់វិេ័យក្េិក្មមបា ថយមក្សៅ ១,៦ភាគរយ សៅក្នុខឆ្ន ំ២០១៣ សប្កាយសព្យលស្ លម្ល ក្ំសណើ ោមធ្យម ៥,៣ ភាគរយ ចសនាា េះព្យីឆ្ន ំ២០០៤ ល់ ២០១២។

ការវិលប្ត្លបស់ៅរក្អប្តាក្សំណើ ក្េកិ្មមក្ប្មតិ្ខ្ពេ ់ម្ល សារៈេខំា យ់ា៉ា ខខាា ខំ។ វិេ័យក្េិក្មម សៅស្ត្រក្ា ចំស្ណក្មួយ ៏ធ្ំន អេេ ោណិជផក្មម ិខក្ម្លា ខំព្យលក្មម ស្ លម្ល ័យថា វិេ័យស េះសៅស្ត្ម្ល សារៈេំខា ់ចំសោេះ ការកាត្់ប ថយភាព្យប្ក្ីប្ក្ ិខភាព្យងាយរខសប្ោេះ ក្នុខទេវត្សរ៍ខាខមុខ្ស េះ។ ប្បេិ សបើបស្ប្មបប្មួលក្នុខប្បសទេក្មពុោ សៅស្ត្ប ដម្ល សទៀត្ ោមួយ ឹខក្ំសណើ ោមធ្យមក្នុខវិេ័យក្េិក្មម៥ភាគរយ ប្ត្ឹមឆ្ន ២ំ០៣០ ប្បសទេក្មពុោ ឹខម្ល វិេ័យក្េិក្មម ស្ លម្ល ទំេំត្ូចោខស េះ ប៉ាុស្ ដម្ល អលិត្ភាព្យខ្ពេ់ោខមុ ។ ចំស្ណក្ន វិេ័យក្េិក្មម សៅក្នុខ អេេ ិខ ក្ម្លា ខំព្យលក្មមេរុប ប្ត្ូវបា ព្យាក្រថាថយចុេះមក្សៅប្ត្ឹម ១៧ភាគរយ ិខ ៣១ភាគរយ សៅក្នុខឆ្ន ំ២០៣០ ព្យី ២៦ភាគរយ ិខ ៥១ភាគរយ សៅក្នុខឆ្ន ២ំ០១២ ខ្ណៈសព្យលស្ លអលិត្ភាព្យ ីធ្ាី ឹខម្ល ការសក្ើ ស ើខព្យី ១៣០០ ុលាា រ/េិចតា ល់ ២៧០០ ុលាា រ/េិចតា សេើយអលិត្ភាព្យព្យលក្មម ឹខម្ល ការសក្ើ ស ើខព្យី ១២០ ុលាា រ/នាក្់ ល់ ៣៧០០ ុលាា រ/នាក្់ (តារាខ ទី ១)។

អាយុសៅវញិ ការខាត្បខ់សដ្ឋយសារស្ត្ក្ំសណើ ក្េកិ្មមម្ល សលបឿ យតឺ្ ខឹម្ល ទេំធំ្ំសធ្ខ។ ប្បេិ សបើ ក្ំសណើ ោមធ្យមន វិេ័យក្េិក្មមម្ល ប្ត្ឹមស្ត្ ៣ភាគរយ ចសនាា េះព្យីឆ្ន ២ំ០១២ ល់២០៣០ សនាេះត្នមាបស្ ថម ន វិេ័យក្េិក្មម ឹខម្ល ការថយចុេះោខមុ ២៩ភាគរយ សៅឆ្ន ២ំ០៣០ សបើសធ្ៀបោមួយ ឹខសេដរីយ៉ាូ ក្ំសណើ ៥ភាគរយ ស្ លសធ្ែើឱ្យ អេេ ោរួមថយចុេះប្ត្ឹម១៨ភាគរយ សេើយទ ាឹមោន សៅស្ត្រក្ាប្បោោជ សប្ចើ នាក្់សៅក្នុខវិេ័យក្េិក្មម អលិត្ភាព្យព្យលក្មម ក្នុខវិេ័យក្េិក្មមថយចុេះ៣៤ភាគរយ ិខសធ្ែើឱ្យការខ្ិត្មក្ជិត្ោន ន ចំណូលរវាខក្េិក្រ ិខអនក្មិ ប្បក្បរបរក្េិក្មម កា ់ស្ត្ម្ល ភាព្យយឺត្យា៉ា វ។ ក្ំសណើ ក្នុខវិេ័យក្េិក្មមទាបោខមុ ឹខនាឱំ្យការកាត្់ប ថយភាព្យប្ក្ីប្ក្ម្ល សលបឿ យឺត្ខាា ខំ។

តារាខទី ១ ៖ អលប៉ាេះោលន់ ក្ំសណើ ក្េកិ្មមទាបមក្សលើេចូនាក្រវិេយ័ក្េកិ្មមមយួច ំ ួ ប្បសទេក្មពុោ េចូនាក្រ ២០១២ ២០៣០

៣% ន ក្សំណើ អេេ ក្នខុវេិ័យក្េកិ្មម ៥% ន ក្សំណើ អេេ ក្នខុវេិយ័ក្េកិ្មម េម្លេភាគន ក្េិក្មមសៅក្នុខ អេេ គិត្ោ % ២៦ ១៥ ១៧

េម្លេភាគន ក្េិក្មមសៅក្នុខក្ម្លា ំខព្យលក្មម គិត្ោ % ៥១ ៣៤ ៣១

អលិត្ភាព្យក្ម្លា ំខព្យលក្មមក្នុខវិេ័យក្េិក្មម គិត្ោ ុលាា រ/នាក់្ ១២០០ ២៤៥០ ៣៧០០

អលិត្ភាព្យ ីក្េិក្មម គិត្ោ ុលាា រ/េិចតា ១៣០០ ១៩០០ ២៧០០ អលសធ្ៀបន អលិត្ភាព្យក្ម្លា ំខព្យលក្មមរវាខ អនក្សធ្ែើការងារ ក្នុខ វិេ័យក្េិក្មម ោមួយ ឹខអនក្សធ្ែើការងារក្នុខវិេ័យសអសខសទៀត្ ២,១ ២,១ ១,៦

7 ការស្ប្បប្បួលរបាយ ីក្េិក្មមស េះ សក្ើត្ស ើខសដ្ឋយមិ ោក់្ព័្យ ធោមួយ ឹខេមបទា ីសេ ាកិ្ចចស ើយ។

8 ការអសខកត្សលើក្េិដ្ឋា ប្តូ្វបា សធ្ែើស ើខ សៅក្នុខឆ្ន ំ ២០១៣ េប្ម្លប់របាយការណ៍ស េះ។ េូមសមើលឧបេមព័ ធទី ២ េប្ម្លប់ព័្យត៌្ម្ល លំអិត្។

xxi

ចក្េវុិេយ័រយៈសព្យលស្វខេប្ម្លបវ់ិេយ័ក្េកិ្មមសៅក្មពោុ ចំបាចប់្ត្វូសកាដ បសលើេម្លេធាត្ុន ិរ ដរភាព្យ ទ ិនអល ភាព្យប្បក្តួ្ប្បស្ជខ ខិក្សំណើ ប្បាក្ច់ណូំល សដ្ឋយេរំាលព្យកីារសផ្ទដ ត្ខាា ខំសព្យក្ស្ត្សលើអលតិ្ក្មម។ ការគណនាបា៉ា ់សាម តាម សេដរីយ៉ាូសអសខៗ េប្ម្លប់ការអភិវឌ្ឍវិេ័យក្េិក្មមនាសព្យលអនាគត្ បងាា ញថាការសក្ើ ស ើខ ូវអលិត្ភាព្យក្េិក្មម នាសព្យល អនាគត្ ឹខម្ល អលោវិជផម្ល ខាា ខំមក្សលើចំណូលរបេ់ក្េិក្រ ោព្យិសេេ ប្បេិ សបើម្ល ការផ្ទា េ់បដូរព្យីការដ្ឋ ំុេះតាមស្បប ប្បនព្យណី សៅោការសប្បើប្បាេ់បសចចក្វិទាទំស ើប សដ្ឋយអមោមួយ ឹខការសក្ើ ស ើខ ូវប្បព្យ័ ធធារាសាស្ដេដ ិខការសប្បើប្បាេ់ េំភារៈក្េិក្មមថមីៗស្ លម្ល ប្បេិទធភាព្យខ្បេ់។ ក្េិក្រស្ លដ្ឋំប្េូវប្ក្អូប ស្ក្នចន ំ ូខមីោចំណិត្ ំ ូខមីសប្ក្ៀម ិខសធ្ែើ ការបស្ ថមត្នមាសអសខសទៀត្សលើក្េិអល ឹខអាចទទួលបា ចំណូលខ្ពេ់ោខមុ ិខបងាា ញចាេព់្យីសារៈេំខា ់ន ការស្ក្នចន ក្េិអល។ ការកាត្់ប ថយចំដយអលិត្ក្មម តាមរយៈការសប្បើប្បាេ់ឱ្យបា ប្បសេើរោខមុ ូវធ្ ធា ស្ លម្ល ប្សាប់ (តាមរយៈការបសខកើ ទិ នអល) ិខការកាត្់ប ថយការធាា ក្់ចុេះត្នមាក្េិអល តាមរយៈការកាត្់ប ថយត្នមា ឹក្ជញ្ជូ គឺោគ ាឹេះ េប្ម្លប់រក្ាភាព្យប្បក្ួត្ប្បស្ជខន ក្េអិលនានា។ ការប ដព្យប្ខីក្នអា ី ក្៏អដល់ ូវចំណូលបស្ ថមអខស្ រ ប៉ាុស្ ដភាព្យក្ំណត្់ន ធ្ ធា ី ឹខកាត្់ប ថយការព្យប្ខីក្ ីក្នុខប្ទខ់ប្ទាយធ្ំនាសព្យលអនាគត្។ បញ្ហា ប្បឈមស េះ សធ្ែើឱ្យការបសខកើ ទិ នអលក្េិក្មម ោណិជផូប ីយក្មម ិខការសធ្ែើព្យិព្យិធ្ក្មម រឹត្ស្ត្ម្ល សារៈេំខា ់ខាា ខំស ើខ ក្នុខការធានាឱ្យម្ល ក្ំសណើ ក្េិក្មម កាត្់ប ថយភាព្យ ប្ក្ីប្ក្ ិខសលើក្ក្មពេ់វិបុលភាព្យរួម សៅក្នុខប្បសទេក្មពុោ នាសព្យលអនាគត្។

អនុសាសន៍ ការប ដក្សំណើ ក្េកិ្មមយា៉ា ខសលឿ ខិការផ្ទា េប់ដូររចនាេមព ័ធន វេិ័យក្េកិ្មមបស្ ថមសទៀត្ គអឺាចសធ្ែើសៅបា េរំាបប់្បសទេក្មពោុ។ េំណុំសោល សយាបាយរួមោន ចំ ួ ៤ អាចជួយអដល់ការោបំ្ទ ល់ការប ដក្ំសណើ ក្េិក្មមស្បបស េះ

សៅក្នុខរយៈសព្យល៥ឆ្ន ខំាខមុខ្ (រយៈសព្យលខ្ាី ិខមធ្យម)។ ទី១ គឺប្ត្ូវរក្ាបរិយាកាេសោល សយាបាយក្េិក្មម ស្ លបខកភាព្យ ងាយប្េួល ល់វិេ័យឯក្ជ សដ្ឋយសផ្ទដ ត្ការយក្ចិត្ដទុក្ដ្ឋក្់បស្ ថមសលើការកាត្់ប ថយប ាុក្ស្អនក្ ិត្ិក្មម សៅក្នុខវិេ័យ េំភារៈក្េិក្មម។ ទី២

គឺការព្យប្ខឹខ ិរ ដរភាព្យបរិសាថ េប្ម្លប់អលិត្ក្មមក្េិក្មម។ ទី៣ គឺការបសខកើ គុណភាព្យ ក្មមវិធ្ី អសព្យែអាយក្េិក្មមសាធារណៈ ិខវិភាជ ៍ថវិកាបស្ ថម ល់ក្មមវិធ្ីទាខំឡាយស្ លម្ល ប្បេិទធភាព្យខ្ពេ់ សៅតាមលទធភាព្យ ន ថវិកាេរុបរបេ់រដ្ឋា ភិបាលក្មពុោ។ ទី៤ គឺការជួយអភិវឌ្ឍវិេ័យក្េិោណិជផក្មម ិខឧេាេក្មមស្ក្នចនក្េអិល។

ការបសខកើ ទ ុវ ិសិយាគ ខិស្ក្លអំសោល សយាបាយ ចំបាចប់្ត្វូសធ្ែើោបនាា ់ ប៉ាសុ្ ដ ខឹម ិបា ស ើញលទធអល ភាា មៗស ើយ។ េប្ម្លប់ការស្ក្លំអមួយចំ ួ ចបំាច់ប្ត្ូវម្ល ការចំដយសព្យល ិខក្ិចចប្បឹខស្ប្បខបស្ ថមសទៀត្ ស ើមបីឱ្យស ើញ

អលោក្់ស្េដខសៅ ឹខមូលដ្ឋា ។ តារាខទី២ េសខេបព្យីអ ុសាេ ៍សោល សយាបាយេំខា ់ៗ ស្ លចបំាច់ប្ត្ូវអ ុវត្ដភាា មៗ ស ើមបីបា ទទួលលទធអលក្នុខរយៈសព្យលខ្ាីសៅមធ្យម សេើយស្ ល ឹខជួយទប់ ិនាន ការថយចុេះ ន ក្ំសណើ វិេ័យក្េិក្មម បចចុបប នស េះ ប្ព្យមទាខំជួយសប្បើប្បាេ់េកាដ ុព្យលន វិេ័យក្េិក្មមរបេ់ប្បសទេក្មពុោឱ្យបា សព្យញសលញ។

តារាខទ២ី៖ េសខេបអ សុាេ ៍េខំា ់ៗ ន របាយការណ ៍សដ្ឋយស្អែក្សៅតាមសព្យលសវលា ស ើមបីេសប្មចលទធអល

អ ុសាេ ស៍ោល សយាបាយ លទធអលស្ ល េសប្មចបា

ក្នខុរយៈសព្យល ខ្ា ីលទធអលស្ ល េសប្មចបា ក្នខុរយៈសព្យលព្យី

មធ្យម សៅស្វខ រក្ា វូបរយិាកាេសោល សយាបាយក្េកិ្មម ស្ លបខកភាព្យងាយប្េលួ លវ់េិយ័ឯក្ជ ប ដសោល សយាបាយោណិជផក្មមសបើក្ចំេរ ិខសោល សយាបាយក្េិក្មមស្ លមិ នំាឱ្យខូ្ចប្ទខ់ប្ទាយរបេ់វិេ័យ X កាត់្ប ថយចំដយសលើស្បបបទការនំាចូលជីក្េិក្មម X សបើក្ចំេរវិេ័យប្ោប់ពូ្យជ េប្ម្លប់ការវិ ិសយាគពី្យវិេ័យឯក្ជ តាមរយៈការសធ្ែើ ប ិបបញ្ាត្ដិក្មម ិខការព្យប្ខឹខសាថ ប័ X ព្យប្ខឹខ រិ ដរភាព្យបរសិាថ ស្ក្លំអការសរៀបចំស្អ ការសប្បើប្បាេ់ ីធ្ាី បសខកើ ប្បេិទធភាព្យការុេះ ុវត្តចាប់ ីធ្ាី ិខបទដ្ឋា គតិ្យុត្ដិោក់្ព័្យ ធនានា X ព្យប្ខឹខេិទធិកា ់កាប់ ីធ្ាី X សលើក្ក្មពេ់ការប្គប់ប្គខ ីធ្ាីប្បក្បសដ្ឋយ ិរ ដរភាព្យ X សលើក្ក្មពេ់ការសប្បើប្បាេ់ជី ិខថាន ំគីមីក្េិក្មមប្បក្បសដ្ឋយេុវត្ថិភាព្យ X ស្ក្លអំក្មមវធិ្វីិ សិយាគសលើ “ប្ទព្យយសាធារណៈ” ន វេិយ័ក្េកិ្មម

បសខកើ ថវិកាេប្ម្លប់ប្ទព្យយសាធារណៈក្េិក្មមេំខា ់ៗ សៅតាមលទធភាព្យថវិកា របេ់រដ្ឋា ភិបាល ោពិ្យសេេ សលើប្បព័្យ ធធារាសាស្ដេដ ការេិក្ាប្សាវប្ោវ ការអសព្យែអាយ ការប្គប់ប្គខជីោតិ្ ី ការប្តួ្ត្ពិ្យ ិត្យគុណភាព្យេំភារៈក្េិក្មម េុវត្ថិភាព្យចំណីអាហារ ការបណដុ េះបដដ លវិោផ ជីវៈ ិខអាូវជ បទ។

X

េប្ម្លប់វិេ័យធារាសាស្ដេដ សផ្ទដ ត្ការយក្ចិត្ដទុក្ដ្ឋក់្ឱ្យបា កា ់ស្ត្សប្ចើ ោខមុ សលើការស្ក្លំអ ិខការសាដ រប្បព័្យ ធស្ លម្ល ប្សាប់ ិខការប្គប់ប្គខសេដ្ឋា រចនាេមព័ ធធារាសាស្ដេដ សដ្ឋយម្ល ការចូលរួម។ X បសខកើ គុណភាព្យន ក្មមវិធី្ក្េិក្មមសាធារណៈ X េប្មបេប្មួលការសធ្ែើេម្លេរណក្មមក្េិដ្ឋា តូ្ចៗ ចូលសៅក្នុខស្ខ្សេងាែ ក់្តំ្នលន សេបៀខ X ជយួអភវិឌ្ឍក្េោិណជិផក្មម ិខឧេាេក្មមស្ក្នចនក្េអិល បសខកើ លទធភាព្យទទួលបា អគាិេ ីសប្បើប្បាេ់ ិខកាត់្ប ថយចំដយសលើការសប្បើប្បាេ់អគាិេ ី X វិ ិសយាគសលើសេដ្ឋា រចនាេមព័ ធសាធារណៈ ស្ លោក់្ព័្យ ធោមួយ ឹខេុវត្ថិភាព្យចំណីអាហារ X សធ្ែើឱ្យកា ់ស្ត្ប្បសេើរ ូវសេវា ឹក្ជញ្ជូ ន ជំ ួញប្េូវអខករ រួមទំាខកាត់្ប ថយចំដយ X លុបសចលរបំាខនានា ស ើមបីដ្ឋក់្ឱ្យសប្បើប្បាេ់ ូវប្បព័្យ ធទទួលយក្ទំ ិញក្នុខឃ្ា ំខោវត្ថបុញ្ហច ំ (warehouse receipts) X

1

1. INTRODUCTION

1. Cambodian agriculture is in the midst of a rapid transformation. Its annual production

growth during 2002-2012 averaged 9.6 percent, far exceeding agricultural production growth in

Asia and around the world. This high agricultural growth has greatly contributed to poverty

reduction, exports, agribusiness development, and farm commercialization in the last decade.

While the Royal Government of Cambodia (RGC)’s agricultural policy focus has mainly been on

rice production and exports, it is increasingly recognized that the current rice-based traditional

agriculture would need to transform into modern, diversified agriculture to generate the returns

necessary to keep farming an attractive source of income and a contributor to economic

development. Cambodian agriculture is still a long way from being an economic activity

indistinguishable from other sectors, at least in terms of productivity of labor and capital or in the

location of poverty, which would be the final outcome of a structural transformation. The

agricultural growth has recently slowed down to about 1 percent, from 5.3 percent during 2004-

2012. Still, the last decade has seen significant positive changes.

2. How can Cambodia build on this positive development? While there is a wealth of

literature on smallholder farming systems in Cambodia and sectoral information from the national

accounts, the existing analytical work lacks a systematic analysis of changes in farming systems.

Combined with the lack of information on related changes in farm versus nonfarm incomes, this

has limited Cambodia’s ability to have an informed agricultural policymaking process and has

hampered efforts to compare and contrast the impacts and effectiveness of alternative policies and

programs for long-term agricultural development.

3. Further, little empirical knowledge has been generated about past and future sources

of agricultural growth and the government’s role in facilitating growth. Why did agriculture

grow so rapidly and will this growth last? What made that growth pro-poor and how can Cambodia

keep its strong pro-poor impact? How would farming systems need to look to ensure continuation

of the 5 percent growth in agricultural value added? What forces will shape an enabling

environment for agriculture in the future and how different will they be from those that drove

development in the past? And how can the government facilitate future growth, helping farmers

overcome challenges and capitalize on opportunities?

4. This report addresses this knowledge gap. It was requested by the Supreme National

Economic Council (SNEC) and the Ministry of Agriculture Forestry and Fisheries (MAFF). The

report uses primary data on farming systems collected in 2013, and compares them to comparable

data from 2005. It also uses evidence from interviews with villages and experts, discussions with

government staff, and analytical work carried out by the World Bank Group and other development

partners in the recent decade, including the analytical work resulting from the five-year

collaboration between the World Bank and Australian Aid under the Cambodia Food Crisis

Capacity Support Partnership Trust Fund (Annex 1).

5. The report covers the main crops with the largest changes in the past decade and

focuses on smallholders, including small farms (up to 1 hectare), medium farms (from 1 to 3

hectares), and large farms (above 3 hectares). It does not cover the livestock and fisheries sector,

nor does it cover in detail economic land concessions.

6. The remaining report is organized as follows. Chapter 2 presents key facts about

Cambodia’s recent agricultural development using data from national accounts and various

2