BMJ Open is committed to open peer review. As part of this ...

96

BMJ Open is committed to open peer review. As part of this commitment we make the peer review history of every article we publish publicly available. When an article is published we post the peer reviewers’ comments and the authors’ responses online. We also post the versions of the paper that were used during peer review. These are the versions that the peer review comments apply to. The versions of the paper that follow are the versions that were submitted during the peer review process. They are not the versions of record or the final published versions. They should not be cited or distributed as the published version of this manuscript. BMJ Open is an open access journal and the full, final, typeset and author-corrected version of record of the manuscript is available on our site with no access controls, subscription charges or pay-per-view fees (http://bmjopen.bmj.com ). If you have any questions on BMJ Open’s open peer review process please email [email protected] on February 2, 2022 by guest. Protected by copyright. http://bmjopen.bmj.com/ BMJ Open: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. Downloaded from

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of BMJ Open is committed to open peer review. As part of this ...

BMJ Open is committed to open peer review. As part of this commitment we make the peer review history of every article we publish publicly available. When an article is published we post the peer reviewers’ comments and the authors’ responses online. We also post the versions of the paper that were used during peer review. These are the versions that the peer review comments apply to. The versions of the paper that follow are the versions that were submitted during the peer review process. They are not the versions of record or the final published versions. They should not be cited or distributed as the published version of this manuscript. BMJ Open is an open access journal and the full, final, typeset and author-corrected version of record of the manuscript is available on our site with no access controls, subscription charges or pay-per-view fees (http://bmjopen.bmj.com). If you have any questions on BMJ Open’s open peer review process please email

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review onlyHealth-related outcomes among female informal workers in debt: Retrospective quasi-experimental study on the impact

of microfinance health interventions in Pakistan

Journal: BMJ Open

Manuscript ID bmjopen-2020-043544

Article Type: Original research

Date Submitted by the Author: 09-Aug-2020

Complete List of Authors: Jafree, Sara; Forman Christian CollegeZakar, Rubeena; The University of LahoreAhsan, Humna; Forman Christian CollegeMustafa, Mudasir; Utah State UniversityFischer, Florian; Charité Universitätsmedizin Berlin, Institute of Public Health; University of Applied Sciences Ravensburg-Weingarten, Doggenriedstraße

Keywords: Health policy < HEALTH SERVICES ADMINISTRATION & MANAGEMENT, PUBLIC HEALTH, EPIDEMIOLOGY

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open on F

ebruary 2, 2022 by guest. Protected by copyright.

http://bmjopen.bm

j.com/

BM

J Open: first published as 10.1136/bm

jopen-2020-043544 on 5 January 2021. Dow

nloaded from

For peer review onlyI, the Submitting Author has the right to grant and does grant on behalf of all authors of the Work (as defined in the below author licence), an exclusive licence and/or a non-exclusive licence for contributions from authors who are: i) UK Crown employees; ii) where BMJ has agreed a CC-BY licence shall apply, and/or iii) in accordance with the terms applicable for US Federal Government officers or employees acting as part of their official duties; on a worldwide, perpetual, irrevocable, royalty-free basis to BMJ Publishing Group Ltd (“BMJ”) its licensees and where the relevant Journal is co-owned by BMJ to the co-owners of the Journal, to publish the Work in this journal and any other BMJ products and to exploit all rights, as set out in our licence.

The Submitting Author accepts and understands that any supply made under these terms is made by BMJ to the Submitting Author unless you are acting as an employee on behalf of your employer or a postgraduate student of an affiliated institution which is paying any applicable article publishing charge (“APC”) for Open Access articles. Where the Submitting Author wishes to make the Work available on an Open Access basis (and intends to pay the relevant APC), the terms of reuse of such Open Access shall be governed by a Creative Commons licence – details of these licences and which Creative Commons licence will apply to this Work are set out in our licence referred to above.

Other than as permitted in any relevant BMJ Author’s Self Archiving Policies, I confirm this Work has not been accepted for publication elsewhere, is not being considered for publication elsewhere and does not duplicate material already published. I confirm all authors consent to publication of this Work and authorise the granting of this licence.

Page 1 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 1 -

Health-related outcomes among female informal workers in debt:

Retrospective quasi-experimental study on the impact of microfinance health

interventions in Pakistan

Sara Rizvi Jafree, Rubeena Zakar, Humna Ahsan, Mudasir Mustafa, Florian Fischer

Dr. Sara Rizvi JafreeDepartment of Sociology, Forman Christian College University, Lahore, Pakistan; [email protected]

Prof. Dr. Rubeena ZakarInstitute of Social and Cultural Studies, University of the Punjab, Lahore, Pakistan; [email protected]

Dr. Humna AhsanDepartment of Economics, Forman Christian College University, Lahore, Pakistan; [email protected]

Mudasir MustafaDepartment of Sociology, Social Work, and Anthropology, Utah State University, Logan, United States of America; [email protected]

Dr. Florian Fischer 1) Institute of Public Health, Charité – Universitätsmedizin Berlin, Germany; [email protected] 2) Institute of Gerontological Health Services and Nursing Research, Ravensburg-Weingarten University of Applied Sciences, Germany; [email protected]

Corresponding author:Dr. Florian FischerCharité – Universitätsmedizin BerlinInstitute of Public HealthCharitéplatz 1 10117 BerlinE-Mail: [email protected]

Word count: 4,259

Page 2 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 2 -

1 Abstract

2 In countries where dependable public health service structure and universal financial protection

3 for health coverage is missing, particularly impoverished families are at risk. In the past years,

4 different kinds of microfinance health interventions were established to promote health among

5 disadvantaged population groups. The purpose of this study is to assess the impact of microfinance

6 health interventions (health insurance and health awareness programs) on health-related outcomes

7 of female informal workers in Pakistan. We conducted a retrospective quasi-experimental study

8 among a total of 447 female borrowers from seven microfinance providers (MFPs) in 2018. A

9 standardized tool was used for data collection. Probit regression has been used to identify the

10 probability of female borrowers gaining improvement in health outcomes based on their socio-

11 demographic characteristics. Propensity score matching (PSM) has been used to assess the overall

12 impact of health interventions. Results show that women receiving health insurance and health

13 awareness programs had greater probability of better health outcomes when they were from

14 Punjab, borrow in groups, and attend monthly meetings at MFPs. The results of the PSM show

15 significant improvements in overall perceived health status when women received health insurance

16 and improvement in the purchase of prescribed medicine when women received a health awareness

17 program. Health and social policies are vital to secure health and wellbeing of poor women

18 working in the informal sector of the economy. Targeting improved equity across female

19 population groups for health intervention will in the long run improve women’s health, capacity

20 expansion and income-earning abilities.

21

22 Keywords: borrow, informal sector, health insurance, health awareness, microfinance

23

Page 3 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 3 -

24 Strengths and limitations of the study

25 This study is part of a larger mixed-methods study on the well-being of female

26 microfinance borrowers.

27 Potentially the first study which focuses on female microfinance borrowers in Pakistan to

28 assess the impact of health interventions on health-related outcomes of poor women.

29 Although a quasi-experimental analysis framework has been used, the two-group cross-

30 sectional designs suffers from the limitations related to a single measurement for all

31 subjects.

32 Future studies need to consider additional burdens of loan repayment and small business

33 investment.

34

Page 4 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

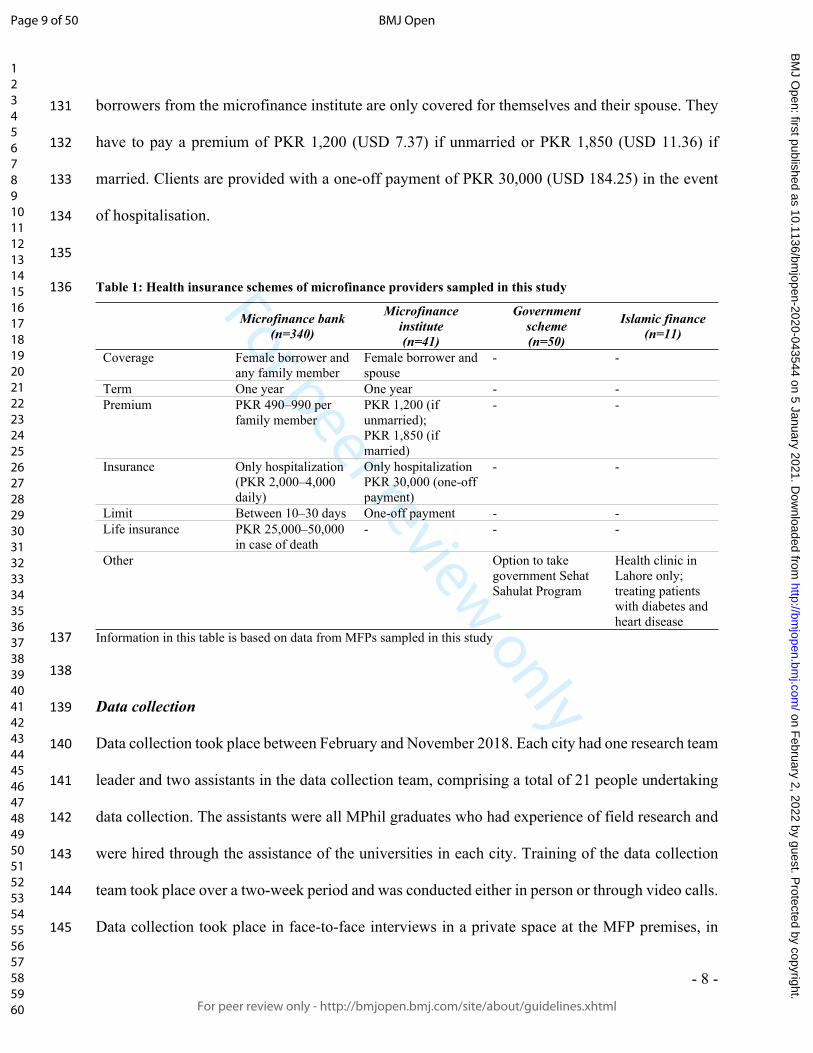

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 4 -

35 Introduction

36 More than half (57%) of the female population in Pakistan is illiterate. Less than a quarter (23%)

37 of women is employed, with a majority working in the informal sector [1]. There are several

38 problems to consider with regard to the health of female informal workers in Pakistan, including

39 high rates of poverty and low health literacy, as well as inadequate access to public health services

40 [2], reinforced by low government health budget allocation for this population group [3]. In

41 addition to the overall absence of universal health coverage, there are limited coverage for public

42 health emergencies like pandemics [4] and greater risks for acquiring infectious diseases in female

43 informal workers due to mostly unsanitary living conditions in disadvantaged communities [5].

44 Pakistan has one of the largest out-of-pocket healthcare expenditures globally, with an

45 overwhelming proportion of 90% [6]. Although health insurance can become an important support

46 system for buffering the poor in out-of-pocket payments, it covers only 1% of health expenditure

47 in the country yet [2]. This is because health insurances are mainly used by richer and urban

48 populations.

49 The efficacy and limitations of private providers for health interventions in Pakistan are not clear.

50 One of the few private providers offering health interventions to women employed in the informal

51 sector are microfinance providers (including banks, institutes and non-governmental organizations

52 [NGOs]) [7]. Microfinance providers (MFPs) are mainly operational in under-developed

53 communities providing loans to the poorest women for small business development [8]. There are

54 50 MFPs operating in Pakistan, with nearly 40 reporting some form of health intervention for

55 clients, including health insurance and health awareness programs [9]. The MFPs are regulated

56 either by the State Bank of Pakistan or the Securities Exchange Commission Pakistan. An inherent

57 function of the original model of microfinance was to catalyze wider social development for

Page 5 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 5 -

58 women, including improved health behavior and, therefore, better health-related outcomes [10]. It

59 is in the interest of MFPs to couple health interventions with loan services as healthy clients are

60 more likely to return loans and run successful businesses [11].

61 The role of microfinance health interventions is even more critical for countries like Pakistan,

62 where poverty is high and out-of-pocket payments are not possible for impoverished families.

63 Additionally, the public sector did not have a dependable service structure for complete or quality

64 healthcare and universal financial protection for health coverage is absent [4]. More than 2 million

65 poor women are loan-takers of microfinance in the country [12]. As poor populations do not have

66 the money to take traditional health insurance, microfinancing for health insurance becomes the

67 only option for them. However, small health insurance schemes have been severely criticized for

68 their minimal impact on clients lives due to minimal coverage and large burden of disease faced

69 by poor populations [13]. Evidence also suggests that poor populations receiving minimal health

70 insurance, in the event of sustaining large health costs, may resort to damaging practices such as

71 reducing household nutrition, removing children from school, and taking more loans [14]. In the

72 most recent times of the corona pandemic, debt-ridden poor women attempting to repay loans are

73 facing even more challenges in generating income from small businesses due to social isolation

74 and lockdown [15]. Therefore, health security is a major concern in women borrowers and there

75 is a need to improve research and policy to financially protect poor women and also improve their

76 health literacy [16].

77 To the best of our knowledge, there are no studies which have used female microfinance borrowers

78 as a sample to assess the impact of health interventions on health-related outcomes of poor women

79 [17]. Using a sample of female microfinance borrowers who are availing health insurance from a

80 private provider will help to identify suited policies for disease prevention and health promotion

Page 6 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 6 -

81 in Pakistan. The following research questions are addressed in this study include: 1) Do female

82 borrowers of microfinance who are provided with health interventions show improved health-

83 related outcomes?, and 2) What are the socio-demographic, household, and loan portfolio

84 characteristics of female borrowers of microfinance that are associated with improved health-

85 related outcomes?

86

87 Methods

88 This study is part of a larger mixed-methods study on the wellbeing of female microfinance

89 borrowers. The qualitative part has already been published [18]. The results presented here are

90 based on a cross-sectional survey, in which females who have been borrowers of microfinance for

91 more than one year were interviewed with a structured quantitative questionnaire. We used the

92 framework of a quasi-experimental study to estimate the impact of microfinance health

93 interventions.

94

95 Sampling

96 First, seven MFPs were sampled randomly through a list available on Pakistan Microfinance

97 Network. All MFPs were asked for permission to interview their clients. Afterwards, 500 women

98 borrowing money from these MFPs were contacted to participate in the study. The sampling took

99 place in all four provinces of Pakistan (Punjab, Sindh, Balochistan, and Khyber Pakhtunkhwa

100 [KPK]), not considering the two autonomous territories and the federal territory of Islamabad. The

101 sampling frame at the level of individual women took the population weightage of the provinces

102 into account. A total of 442 women were willing to participate in the study and provided informed

103 written consent, which is a response rate of 88.4%. These women were sampled from seven cities

Page 7 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 7 -

104 within the four provinces (Punjab: n=252 [cities: Gujranwala, Lahore, Khanewal, Sheikhapura];

105 Sindh: n=100 [city: Matiari]; Balochistan: n=50 [city: Lasbela]; KPK: n=40 [city: Abbottabad].

106 Study participants received financial support from the following types of MFPs: four microfinance

107 banks (n=340), one microfinance institute (n=41), one government microfinance scheme (n=50),

108 and one Islamic microfinance organization (n=11),

109

110 Data collection

111 Data collection took place between February and November 2018. Each city had one research team

112 leader and two assistants in the data collection team, comprising a total of 21 persons for data

113 collection. The assistants were all MPhil graduates who had experience in field research and were

114 hired through the assistance of universities in each city. Training of the data collection team took

115 place over a two-week period and was done either in person or through video calls. The structured

116 surveys were completed on behalf of the female respondents with the assistance of the trained

117 research team, as most of the women were illiterate or semi-literate. Data collection took place in

118 face-to-face-interviews in a private space at the MFP premises, in order to preserve the privacy of

119 women in lieu of the personal questions.

120

121 Measures

122 A structured interview schedule was used for data collection (see Supplementary Appendix).

123 Questions in this tool were taken from instruments used in various studies, such as Women’s

124 Healthcare Experiences Survey [19], Baseline Nutrition and Food Security Survey by UNICEF

125 [20], WHO Multi-country Study on Women’s Health and Domestic Violence against Women [21],

126 and WHO Survey on Workplace Violence [22].

Page 8 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 8 -

127 This study assesses the association of health interventions offered by MFPs on four dependent

128 health-related variables: 1) women perceive health to be good overall, 2) women visit a general

129 practitioner in the last year, 3) women have the ability to purchase prescribed medicine in the last

130 year, and 4) women’s intake of multivitamins has improved in the last year. The four dependent

131 variables have been categorized as binominal and coded as either “Yes” (1) or “No” (0).

132 Several socio-demographic variables such as age (0=less than 30 years; 1=30 years and older),

133 religion (0=Muslim; 1=Other than Muslim), literacy of the female borrower (0=Illiterate;

134 1=Literate), literacy of the spouse (0=Illiterate; 1=Literate), house ownership (0=Yes; 1=No), and

135 number of depending children living in the house (0=None; 1=One or more) have been assessed

136 as confounding variables. It is necessary to control for these variables as they have an impact on

137 each of the dependent variables mentioned above. Province is also controlled as the region is a

138 proxy for socio-cultural norms which would impact how women perceive their health and whether

139 they are able to visit a general practitioner or to purchase medicine (0=Other than Punjab [Sindh,

140 Balochistan, or KPK]; 1=Punjab).

141 The other set of variables related to microfinance provider services such as loan amount

142 (0=10,000–20,000 PKR; 1=21,000 PKR and more), monthly meetings (0=No; 1=Yes), interest

143 rate, which is the amount charged on top of the principal by a lender to a borrower (0=2.5–10%;

144 1=11% and more), group loan, meaning that a group of customers are willing to guarantee each

145 other for the repayment of loan (0=No; 1=Yes), and debt age (0=1–2 years; 1=3 or more years)

146 have been included as they assess the impact of the provision of non-financial services on each of

147 the dependent variables.

148

Page 9 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 9 -

149 Intervention

150 Using a quasi-experimental framework, the study estimates the impact of getting access to health

151 interventions against the counterfactual of those women who are receiving the loan for small

152 business mobilization in the absence of health interventions. The control group ( consists 𝑇 = 0)

153 of women who have been provided the loan but lack the provision of health intervention and the

154 treatment group ( includes women who will have provision of both, the loan as well as 𝑇 = 1)

155 health intervention.

156 The three independent variables for microfinance health intervention are: 1) receiving health

157 insurance, 2) attended at least one health workshop, and 3) received health-related talks by loan

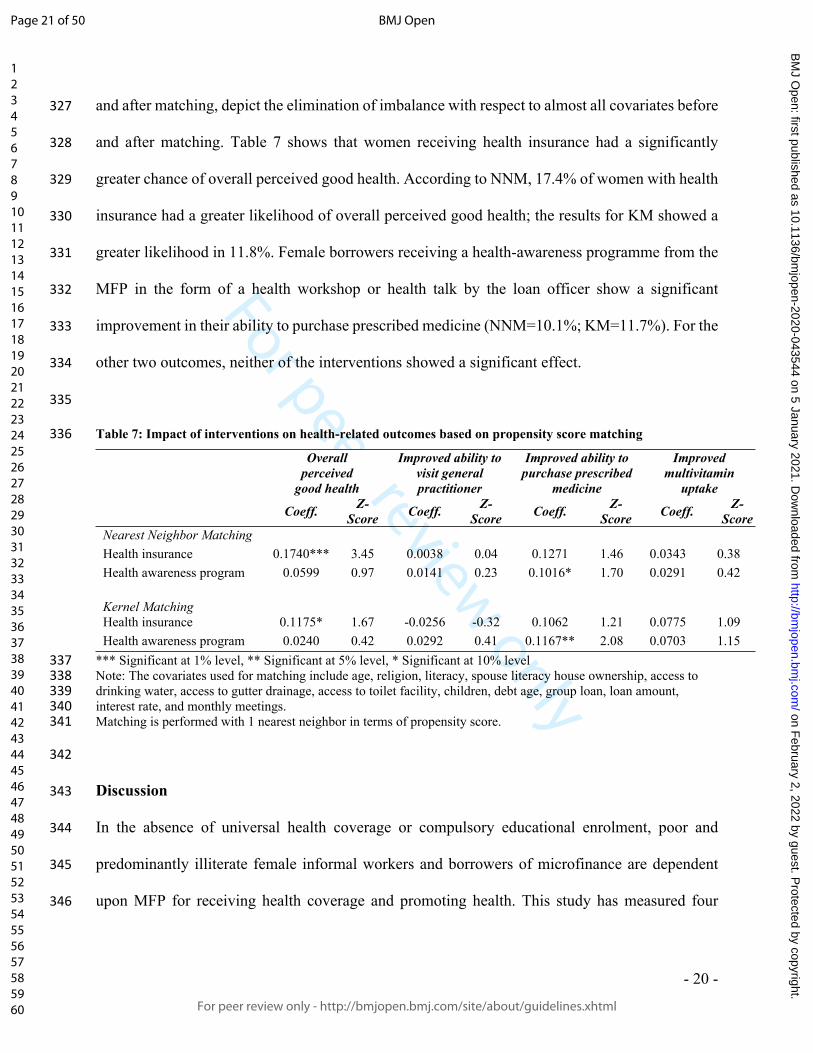

158 officers. The last two independent variables of health workshop and health-related talks by loan

159 officers were compounded to make one variable indicating whether the women received a health

160 awareness program (0=No; 1=Yes).

161

162 Data analysis

163 Data were analyzed using SPSS and STATA. The impact of health insurance and health awareness

164 programs provided by the MFP on the four dependent health-related variables will first be

165 estimated using a Probit estimation for the following linear regression equation:

166 𝑌𝑖 = 𝛽0 + 𝛽1𝑇 + 𝛽2𝑋𝑖 + 𝛽3𝑍𝑖 + 𝛽4𝐿𝑖 + 𝜀𝑖

167 where is the dependent variable measuring the four health-related outcomes. T is the treatment 𝑌𝑖

168 variable (1 if “yes”, and 0 otherwise) measuring the three microfinance health interventions. is 𝑋𝑖

169 a set of socio-demographic characteristics including age, religion, province, and literacy; is a 𝑍𝑖

170 set of household characteristic including house ownership and number of dependent children living

Page 10 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 10 -

171 in the house; is a set of loan portfolio characteristics including debt age, group loan, loan amount, 𝐿𝑖

172 interest rate, and monthly meetings; and is the error term. 𝜀𝑖

173 Following Rosenbaum and Rubin, we used Propensity Score Matching (PSM) to estimate the

174 unobserved counterfactuals and make an impact analysis of health interventions. PSM is a non-

175 parametric statistical method which matches the treated (those receiving health intervention) and

176 the controlled on the basis of conditional probability of participation, given observable

177 characteristics [23]. As we only have cross-sectional data, we can compare the dependent variables

178 related to women’s health and wellbeing in terms of those who have access to non-financial health-

179 related services provided by the microfinance provider (in this study called “health awareness

180 program”) and those who do not, as long as these services are randomly distributed and there is no

181 selection bias. The estimation of instrumental variables is one technique that is frequently used

182 within PSM. However, these results are only robust if a valid instrument is being used. As it not

183 easy to find a valid instrument in our study, we used statistical matching which has been widely

184 used before as well [24-26].

185 Our study satisfies the main conditions of PSM, which are 1) using a rich set of control variables,

186 which are observable characteristics, 2) using the same survey for treated and control groups, and

187 3) having the same community belonging to treated and control group [27]. The PSM model

188 constructs a statistical comparison group based on the probability of participating in the treatment

189 T, conditional on observed characteristics, X or the propensity score,

190 𝑝(𝑋) = 𝑃𝑟(𝑇 = 1│𝑋).

191 where T = {0, 1} is the indicator of exposure to treatment and X is the multidimensional vector of

192 pre-treatment characteristics. Following the estimation for the propensity score, the region for

193 common support is defined where distributions of the propensity score for the treatment and

Page 11 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 11 -

194 comparison group overlap. Observations within the control and treatment group that lie outside

195 the common support are eliminated [28]. As PSM is intended to help in identifying the impact of

196 the health intervention, we used the computation of ‘average treatment effect on the treated’

197 (ATT). We used two matching criteria (Nearest Neighbor Matching [NNM] and Kernel Matching

198 [KM]), to assess statistical significance from different perspectives and to test the robustness of

199 the results [24]. NNM is used to evaluate absolute differences between propensity scores and KM

200 is used to compare each treated unit to a weighted average of the outcomes of all untreated units.

201

202 Patient and Public Involvement

203 This research was conducted without involvement of public or patients. However, the view of

204 females was already included in the qualitative part of this mixed-methods approach, which has

205 already been published elsewhere [18].

206

207 Results

208 Sample characteristics

209 All women in our sample earned less than $4.82 per day and belonged to the poorest strata of

210 society. They were taking loans for small business mobilization to improve their life opportunities.

211 The majority of women were Muslim, from Punjab, and illiterate. About three quarters had been

212 borrowers for more than 3 years, were attending monthly meetings with loan officers, and were

213 paying interest rates less than 10%. Out of the 442 women borrowers in the sample, 64.2% (n=284)

214 were taking health insurance and 71.0% (n=314) have participated in a health awareness program

215 by attending a health workshop or receiving health talks by loan officers (Table 1).

216

217

Page 12 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 12 -

218 Table 1: Descriptive statistics of women borrowers receiving health interventions (n=442)

Variable

Receiving health insurance

n (%)(N=284)

Chi-square test1

Receiving health awareness program

n (%)(N=314)

Chi-square test1

Age <29 years ≥30 years

165 (58.1%)119 (41.9%)

0.557 177 (56.4%)137 (43.6%)

0.077

Religion Muslim Other

254 (89.4%)30 (10.6%)

0.740 276 (87.9%)38 (12.1%)

0.337

Province Punjab Other

197 (69.4%)87 (30.6%)

37.977*** 203 (64.6%)111 (35.4%)

16.372***

Literacy Illiterate Literate

195 (68.7%)89 (31.3%)

3.770* 219 (69.7%)95 (30.3%)

9.109**

Spouse literacy Illiterate Literate

191 (67.3%)93 (32.7%)

7.135** 199 (63.4%)115 (36.6%)

0.231

House ownership Other Owned

225 (79.2%)59 (20.8%)

9.583** 233 (74.2%)81 (25.8%)

0.030

Children None One or more

116 (40.8%)168 (59.2%)

1.907 121 (38.5%)193 (61.5%)

0.002

Debt age 1–2 years ≥3 years

75 (26.4%)209 (73.6%)

15.755*** 83 (26.4%)231 (73.6%)

21.342***

Group loan No Yes

168 (59.2%)116 (40.8%)

0.102 173 (55.1%)141 (44.9%)

5.480**

Loan amount (in PKR) 10,000–20,000 ≥21,000

123 (43.3%)161 (56.7%)

25.096*** 121 (38.5%)193 (61.5%)

6.515**

Interest rate 2.5–10% ≥11%

202 (71.7%)82 (28.9%)

1.044 237 (75.5%)77 (24.5%)

18.527***

Monthly meeting No Yes

70 (24.6%)214 (75.4%)

0.091 73 (23.2%)241 (76.8%)

2.005

Overall perceived good health No Yes

185 (65.1%)99 (34.9%)

5.545** 216 (68.8%)98 (31.2%)

0.023

Improved ability to visit general practitioner No Yes

124 (43.7%)160 (56.3%)

0.065 127 (40.4%)187 (59.6%)

3.383*

Improved ability to purchase prescribed medicine No Yes

152 (53.5%)132 (46.5%)

19.127*** 175 (55.7%)139 (44.3%)

13.073***

Improved intake of multivitamins No Yes

182 (64.1%)102 (35.9%)

6.6040** 214 (68.2%)100 (31.8%)

0.015

219 1 *** Significant at 1% level, ** Significant at 5% level, * Significant at 10% level

Page 13 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 13 -

220

221 Women taking loans from the Government Scheme or Islamic Finance Provider were not receiving

222 health insurance interventions. However, both the Government Scheme and Islamic Finance

223 Provider were giving health awareness interventions. The Government Providers offered the

224 women a separate government health insurance scheme, called Sehat Sahulat Program, but none

225 of the study participants was availing this scheme. The Islamic Finance provider was supporting

226 Lahore-based women clients with a free medical camp for diabetes and heart disease (Table 2).

227

228 Table 2: Health insurance schemes of microfinance providers sampled in this study

Microfinance Bank(n=340)

Microfinance Institute(n=41)

Government Scheme(n=50)

Islamic Finance(n=11)

Coverage Female borrower + any family member

Female borrower + spouse

- -

Term One year One year - -Premium PKR 490–990 per

family memberPKR 1,200 (if unmarried);PKR 1,850 (married)

- -

Insurance Only hospitalizationPKR 2,000–4,000 daily

Only hospitalizationPKR 30,000

- -

Limit Between 10–30 days One-off payment - -Life insurance PKR 25,000–50,000

in event of death- - -

Other Option to take government Sehat Sahulat Program.

Health clinic in Lahore only; treating patients with diabetes and heart disease

229 Information in this table is based on data from microfinance provider loan officers

230

231 Women borrowing from the banks can take insurance for themselves and any family member.

232 They have to pay a premium ranging from PKR 490–990 per person and are insured only in the

233 event of hospital admission. However, the insurance does not cover hospital costs and instead pays

234 the client the amount of daily wages lost, ranging from PKR 2,000–4,000 daily. The scheme also

235 covers a one-off payment in the event of death ranging from PKR 25,000–50,000. Female

Page 14 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 14 -

236 borrowers from the microfinance institute are only covered for themselves and spouse. They have

237 to pay a premium of PKR 1,200 if unmarried or PKR 1,850 if married. Clients are provided with

238 a one-off payment of PKR 30,000 in the event of hospitalization.

239

240 Determinants of health-related outcomes after health insurance intervention

241 Table 3 presents the determinants of health-related outcomes for recipients of a health insurance.

242 Overall perceived good health was significantly associated with group borrowers, small loan

243 amount, and smaller interest rate. Improved ability to visit a general practitioner shows a positive

244 correlation with women borrowers from Punjab province, attending monthly meetings, group loan,

245 and smaller loan amount. Women had a significantly improved ability to purchase prescribed

246 medicine when they were from Punjab, took smaller loans, owned a house. The uptake of

247 multivitamins was increased in women with smaller loans, owning a house, being borrowers since

248 no longer than two years, and attending monthly meetings. Therefore, only a small loan amount

249 was a significant determinant in all four health-related outcomes among recipients of a health

250 insurance.

Page 15 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 15 -

251 Table 3: Probit analysis on determinants of health-related outcomes among recipients of health insurance

Overall perceivedgood health

Improved ability to visit general practitioner

Improved ability to purchase prescribed

medicine

Improvedmultivitamin

uptake

Coeff. Z-Score Coeff. Z-

Score Coeff. Z-Score Coeff. Z-

ScoreAge -0.2588 -1.43 0.2754 1.39 -0.2915 -1.51 0.0703 0.36Religion 0.4079 1.37 -0.2711 -0.97 0.4165 1.46 -0.0102 -0.03Province -0.2676 -1.04 0.9990*** 4.05 1.043*** 4.21 0.0315 0.12Literacy -0.0999 -0.49 0.2018 0.96 0.0828 0.42 0.1994 0.98Spouse literacy 0.2410 1.18 0.1779 0.85 0.2424 1.20 0.1323 0.64House ownership 0.1550 0.69 -0.3397 -1.45 -0.6825** -2.65 -0.5699** -2.17Children 0.2094 1.15 0.2213 1.20 0.1530 0.85 0.2829 1.54Debt age -0.4130 -0.16 0.1650 0.63 0.3807 1.50 -0.6088** -2.41Group loan 0.8582*** 3.76 0.4813** 2.25 0.1567 0.73 -0.3705* -1.69Loan amount -0.7765*** -3.27 -0.8863** -3.50 -1.2028*** -5.05 -1.9933*** -4.13Interest rate 0.7250** 2.94 0.2777 1.12 -0.0691 -0.28 0.2345 0.98Monthly meetings 0.1370 0.61 0.7753*** 3.58 0.0166 0.08 -0.4233* -1.84No. of observationsWald Chi2

Prob> Chi2

Log likelihood

28442.740.0001

-158.6116

28476.930.0000

-146.0385

28464.570.0000

-157.5241

28453.150.0000

-153.7125252 *** Significant at 1% level, ** Significant at 5% level, * Significant at 10% level

253

254 Determinants of health-related outcomes after health awareness intervention

255 In Table 4, the determinants for all four health-related outcomes among recipients of a health

256 awareness program are presented. Women with the following characteristics have a greater

257 probability of overall perceived good health: group borrowers, smaller loans, smaller interest rates,

258 younger women, and those with literate spouses. The ability of visiting the general practitioner for

259 regular checkups in the last year was higher in women from Punjab province, with smaller loans,

260 attending monthly meetings, above 29 years of age, and non-Muslim women. Similarly, women

261 from Punjab province, having smaller loans, owning their house, and younger women had a higher

262 probability of improved ability to purchase prescribed medicine. The probability of increased

263 uptake of multivitamins was greater in women who took smaller loans, had not been in debt for

264 more than 2 years, were group borrowers, and who attended monthly meetings. As for health

265 insurance, the only variable significantly associated with all health-related outcomes among

266 recipients of a health awareness program was the small loan amount.

Page 16 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 16 -

267

268 Table 4: Probit analysis on determinants of health-related outcomes among recipients of health awareness 269 programs

Overall perceivedgood health

Improved ability to visit general practitioner

Improved ability to purchase prescribed

medicine

Improvedmultivitamin

uptake

Coeff. Z-Score Coeff. Z-

Score Coeff. Z-Score Coeff. Z-

ScoreAge -0.3747* -1.70 0.3781* 1.70 -0.4329* -2.02 0.1058 0.48Religion 0.5185 1.59 -0.5503* -1.76 0.3880 1.24 0.1904 0.56Province -0.3898 -1.24 1.3048*** 4.39 1.029*** 3.83 0.1983 0.65Literacy -0.1537 -0.65 0.2229 0.91 0.1405 0.61 0.3411 1.43Spouse literacy 0.4163* 1.80 0.2546 1.09 0.0860 0.38 0.2310 1.00House ownership 0.3495 1.42 -0.2453 -0.96 -0.6360** -2.48 -0.4271 -1.54Children 0.3209 1.55 0.2765 1.33 0.2424 1.21 0.2833 1.36Debt age -0.0066 -0.02 0.4529 1.49 0.3817 1.36 -0.7164** -2.51Group loan 0.8817*** 3.33 0.3640 1.51 0.1030 0.43 -0.6352** -2.55Loan amount -0.7199** -2.65 -0.6511** -2.28 -1.9361*** -3.52 -0.9170*** -3.35Interest rate 0.6739** 2.23 0.3860 1.28 0.2428 0.83 0.3726 1.26Monthly meetings 0.2357 0.88 0.7689** 3.08 -0.0556 -0.22 -0.5816** -2.10No. of observationsWald Chi2

Prob> Chi2

Log likelihood

31435.680.0004

-126.4054

31464.570.0000

-116.6811

31453.250.0000

-128.2105

31448.790.0000

-121.2616270 *** Significant at 1% level, ** Significant at 5% level, * Significant at 10% level

271

272 Impact of interventions on health-related outcomes

273 The results from the PSM model (Table 5) show that women receiving health insurance had a

274 significantly greater chance of overall perceived good health. According to NNM, 17.4% of

275 women with health insurance had greater likelihood for overall perceived good health; the results

276 for KM showed a greater likelihood in 11.8%. Female borrowers receiving a health awareness

277 program from the MFP in the form of health workshop or health talk by loan officer show

278 significant improvement in their ability to purchase prescribed medicine (NNM=10.1%; KM

279 =11.7%). For the two other outcomes, neither of the interventions showed a significant effect.

280

Page 17 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 17 -

281 Table 5: Impact of interventions on health-related outcomes based on propensity score matching

Overallperceived

good health

Improved ability to visit general practitioner

Improved ability to purchase prescribed

medicine

Improved multivitamin

uptake

Coeff. Z-Score Coeff. Z-

Score Coeff. Z-Score Coeff. Z-

ScoreNearest Neighbor MatchingHealth insurance 0.1740*** 3.45 0.0038 0.04 0.1271 1.46 0.0343 0.38Health awareness program 0.0599 0.97 0.0141 0.23 0.1016* 1.70 0.0291 0.42

Kernel MatchingHealth insurance 0.1175* 1.67 -0.0256 -0.32 0.1062 1.21 0.0775 1.09Health awareness program 0.0240 0.42 0.0292 0.41 0.1167** 2.08 0.0703 1.15

282 *** Significant at 1% level, ** Significant at 5% level, * Significant at 10% level

283

284 Discussion

285 In the absence of universal health coverage and compulsory educational enrollment, poor and

286 predominantly illiterate female informal workers and borrowers of microfinance are dependent on

287 MFP for receiving health coverage and promoting health. This study has measured four health-

288 related outcomes in female borrowers. The results show that there is inequity in uptake of health

289 insurance and health-related outcomes.

290 Women from Punjab have better health-related outcomes compared to women from Sindh,

291 Balochistan and KPK. National health surveys of Pakistan also report that Punjab has better health-

292 related outcomes compared to other provinces, as the provincial government of Punjab has greater

293 budget allocation for running health awareness campaigns [29]. The fact that our results show that

294 older women and non-Muslim women have higher likelihood of improved ability to visit general

295 practitioner after receiving health awareness intervention indicates that younger Muslim women

296 face barriers to health access due to regressive norms [30]. Muslim families are known to prevent

297 fertile women from accessing healthcare in an attempt to control their reproductive choices and

298 health options. Our results align with other research which suggests that Muslims suffer from

299 health disparities due to religious fallacies [31].

Page 18 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 18 -

300 Conversely, younger women show better overall perceived health and ability to purchase

301 prescribed medicine This may be because at a younger age less health issues occur and also

302 because of greater state and NGO efforts for maternal healthcare [32]. Our results confirm that

303 women under the age of 29 years receive privileged support in a patriarchal society during prime

304 childbearing years to consume maternal health related medication [33]. Women with literate

305 spouses are also showing improvement in overall general health after receiving health insurance.

306 This may be because spouse literacy has a direct effect on women’s improved health behavior and

307 mental health [34].

308 Women who borrow the loan in groups show better health-related outcomes compared to women

309 who are single borrowers. Our results suggest that women in groups share their health knowledge

310 and encourage each other toward improved health behavior [35]. Similarly, women who attend

311 monthly meetings with loan officers have better health-related outcomes. The results suggest that

312 caring loan officers are fulfilling an important responsibility in supporting women borrowers in

313 improved health behavior and health-related outcomes. Given the conservative culture of Pakistan

314 and the disadvantaged background of the female borrowers, loan-taking women might not be able

315 to utilize health services due to issues of permission or ignorance.

316 Women who receive smaller microfinance loans and do not have a long debt age show improved

317 health-related outcomes. This finding suggests that women with debt burden over a longer period

318 of time may be suffering from debt fatigue converting to declined health-related outcomes [36].

319 Women and their families who live in owned houses also have better health-related outcomes,

320 specifically related to the ability to visit general practitioners and improved uptake of

321 multivitamins. The results imply that provision of health insurance and not having to pay

322 household rents on a monthly basis translates to better health-related outcomes. Impoverished

Page 19 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 19 -

323 families that have to pay high rents for accommodation are usually employed in multiple jobs and

324 have little time for health and wellbeing [37].

325 The impact of microfinance is only visible on two health-related variables. Although there are no

326 effects on general practitioner visitation and uptake of multivitamins, we found that a microfinance

327 health insurance has an impact on an improved perception of general health. This shows that being

328 insured is an emotional support and wellbeing facilitator for poor women. The emotional buttress

329 provided by health insurance can go a long way in improving perceived wellbeing, which can

330 translate to greater commitment to self, family, and business development in poor women from

331 disadvantaged backgrounds [38]. In addition, microfinance health awareness interventions have

332 an impact on improved purchase of prescribed medicine. Many poor women in Pakistan do not

333 take prescribed medicine unless it is freely available due to the greater need to prioritize purchase

334 of basic necessities and household consumption [39]. The impact of microfinance interventions is

335 comparable to previous research. A review highlighted that most interventions combined

336 microfinance with health education. However, positive effects were mainly found for health

337 knowledge and behavior, but not health status [40]. A meta-analysis indicated the potential for

338 females, as microfinance may lead to changes in the use of contraceptives, strengthen female

339 empowerment and improve children’s nutrition [41].

340 However, for female borrowers of microfinance, there might be additional burdens of loan

341 repayment and small business investment. Our results suggest that illiterate and poor women of

342 the country are benefiting from health awareness in recognizing that if they do not consume

343 prescribed medicine for chronic ailments (heart disease, cholesterol, or diabetes) it can have

344 serious consequences for their own life and the future livelihood of their families. There needs to

345 be urgent recognition that a triadic health insurance safety net is necessary, instead of dependency

Page 20 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 20 -

346 on private providers to protect informal working women in Pakistan. Employers and the

347 government must join forces to ensure universal health insurance and – particularly in times of the

348 corona pandemic – infectious disease outbreak insurances for health emergencies. State financing

349 of healthcare is essential through increased allocations of gross domestic product (GDP),

350 government-run business profits, and increasing income and corporate tax base from the elite.

351 With regard to women microfinance borrowers, we recommend microfinance regulatory bodies to

352 urgently legislate the following reforms: (i) coverage of children and other dependents, maternity

353 costs, and non-hospitalization costs, (ii) expand coverage for religious and ethnic minorities, (iii)

354 reduce interest rates for those paying high house rents and introduce house ownership loans, (iv)

355 introduce mandatory group borrowing and monthly meetings with loan officers, and (iv) alter

356 repayment timelines and interest rate packages for women taking bigger loans.

357 We recommend the following urgent social policy improvements, which would adjoin in helping

358 health policy efforts: (i) development of public primary healthcare services for women in the

359 communities with mandatory quarterly General Practitioner meeting, (ii) upgrading of poverty

360 alleviation programs for support of poor women, (iii) capping for housing rents and improvement

361 of neighborhood sanitation to curb infection, (iv) advancement of home-based business

362 opportunities for informal women workers for income maintenance, including digitalization and

363 internet access in the homes, and (v) income supplementation and cash transfers for multivitamin

364 and food nutrition intake for immunity and health overall [42].

365

366 Limitations

367 This study has some limitations, most important the cross-sectional design. Although we were able

368 to compare the effects of an intervention because of the quasi-experimental analysis framework,

Page 21 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 21 -

369 two-group cross-sectional designs are suffering from the limitations related to a single

370 measurement for all subjects. Therefore, within-person changes over time are not observable.

371 Without repeated measures in a two-group design, causality cannot be identified, because temporal

372 sequencing on the intervention and outcomes cannot be established. For that reason, we

373 recommend longitudinal data collection in future studies. Furthermore, the results need to be

374 interpreted with caution, because the four health-related outcomes are non-homogenous and

375 dependent on socio-environmental factors specific to the region and community where the

376 interventions are taking place. Despite the limitations, we feel this study is significant for the

377 development of microfinance health services in Pakistan and the role of state and interest-free

378 microfinance health interventions.

379

380 Conclusion

381 It is critical to assess the health needs of women employed in the informal sector. As primary

382 caregivers at home as well as primary contributors for household income, the health of women

383 assumes a salience that would place both structures of the family and the economy at risk. Health

384 policy must consider several social policies for protecting disadvantaged women, who are poverty-

385 ridden, illiterate or semi-literate, and loan takers. Health insurance schemes and health promotion

386 at the workplace must be made mandatory by employers, microfinance providers, and the

387 government, given the cultural barriers of uptake for women. Targeting improved equity across

388 female population groups for health intervention will in the long run improve women’s health,

389 capacity expansion and income-earning abilities.

390 Designing and implementing a health and social policy protection net for female informal workers

391 requires empirical evidence regarding health interventions and socio-demographic characteristics

392 impacting on health outcomes. Since public sector health sector shortages and inefficiencies are a

Page 22 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 22 -

393 concern in Pakistan, the ‘health card’ must be accepted in both the private and public sector,

394 whichever is able to serve the poor first. As Pakistan is struggling with low GDP and tax collection

395 base, we recommend more research into options for social franchising, and partnership with

396 independent health insurance companies to serve disadvantaged women.

397

398 Acknowledgements

399 We thank the female borrowers who consented and gave their time to participate in the study. We

400 are grateful to our research team members in charge of logistical planning and coordination for

401 data collection across Pakistan including Rizwan Haider and Amir Naseem. Individual data

402 collection heads for each city are thanked for their efforts, especially for resolving gate keeping

403 issues, including Nida Abbas (Lahore), Zainab Asif (Abbotabad), Hina Bukhari (Gujranwala),

404 Sadia BiBi (Khanewal), Ansari Abbass (Sheikhapura), Azra Shakeel and Shumaila Sadique

405 (Matari), and Javaria Imran (Lasbela). The research assistant Bilal Asghar is also thanked for

406 entering all data.

407 We acknowledge support from the German Research Foundation (DFG) and the Open Access

408 Publication Fund of Charité – Universitätsmedizin Berlin.

409

410 Competing interests

411 The authors declare that no competing interests exist.

412

413 Funding

414 This study received funding by the Office of Research, Innovation and Commercialization at

415 Forman Christian College.

416

417 Data sharing

418 Data is available upon reasonable request from the corresponding author.

419

Page 23 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 23 -

420 Ethical considerations

421 Ethical approval for this study was taken from the Institutional Review Board of the Forman

422 Christian College University. Study participants were informed about the aims of the study and

423 provided informed consent either in written form or through thumb impression.

424

425 Author’s contributions

426 SRJ designed the study and was responsible for the research project, including data collection and

427 analysis; FF supervised this process. HA and MM supported in data collection. RZ and FF

428 contributed to the interpretation of the data. SRJ drafted the manuscript; all authors revised it

429 critically for important intellectual content. All authors approved the final version of this

430 manuscript.

431

432 References

433

434 1. United Nations Pakistan. One United Nations Programme III 2018-2022. United Nations

435 Sustainable Development Framework for Pakistan; 2018.

436 2. Malik MA. Universal health coverage assessment Pakistan. Karachi: Aga Khan University;

437 2015.

438 3. Nishtar S. Choked pipes: reforming Pakistan’s mixed health system: Oxford University

439 Press Karachi; 2010.

440 4. Nishtar S, Bhutta ZA, Jafar TH, et al. Health reform in Pakistan: a call to action. Lancet

441 2013;381(9885):2291–7.

442 5. Nishtar S, Boerma T, Amjad S, et al. Pakistan’s health system: performance and prospects

443 after the 18th Constitutional Amendment. Lancet 2013;381(9884):2193–206.

444 6. Pakistan Bureau of Statistics. Pakistan National Health Accounts 2013-14. Islamabad:

445 Pakistan Bureau of Statistics; 2014.

446 7. Garikipati S, Johnson S, Guérin I, Szafarz A. Microfinance and gender: Issues, challenges

447 and the road ahead. The Journal of Development Studies 2017;53(5):641–8.

448 8. Salim MM. Revealed objective functions of microfinance institutions: evidence from

449 Bangladesh. Journal of Development Economics 2013;104:34–55.

Page 24 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 24 -

450 9. Saba A, Saquiba A. Conceptualizing Health and Microfinance Nexus in Pakistan; 2017.

451 URL: http://www.pmn.org.pk/assets/articles/69106cec5d4f0132b45673990ab4622d.pdf

452 (accessed August 1, 2020).

453 10. Al-Shami SSA, Majid IBA, Rashid NA, Hamid MSRBA. Conceptual framework: The role

454 of microfinance on the wellbeing of poor people cases studies from Malaysia and Yemen.

455 Asian Social Science 2014;10(1):230.

456 11. Leatherman S, Dunford C. Linking health to microfinance to reduce poverty. Bull World

457 Health Organ 2010;88(6):470-1.

458 12. Zulfiqar G. Does microfinance enhance gender equity in access to finance? Evidence from

459 Pakistan. Feminist Economics 2017;23(1):160–85.

460 13. Escobar M-L, Griffin CC, Shaw RP. The impact of health insurance in low-and middle-

461 income countries. Brookings Institution Press; 2011.

462 14. Heltberg R, del Ninno C, Dorosh P, et al. Social protection in Pakistan: Managing

463 household risks and vulnerability. Washington, DC: Human Development Unit, South Asia

464 Region, World Bank; 2007.

465 15. Malik K, Meki M, Morduch J, Ogden T, Quinn S, Said F. COVID-19 and the Future of

466 Microfinance: Evidence and Insights from Pakistan. Oxford Review of Economic Policy;

467 2020

468 16. Mersland R, Strøm RØ. Microfinance: Costs, lending rates, and profitability. In: Caprio G,

469 Arner DW, Beck T, et al., eds. Handbook of key global financial markets, institutions, and

470 infrastructure. London: Academic Press 2016:489–99.

471 17. O’Malley T, Burke J. A systematic review of microfinance and women’s health literature:

472 Directions for future research. Global Pub Health 2017;12(11):1433–60.

473 18. Jafree SR, Mustafa M. The triple burden of disease, destitution, and debt: Small business-

474 women’s voices about health challenges after becoming debt-ridden. Health Care Women

475 Int Published Online First: 30 January 2020. doi: 10.1080/07399332.2020.1716236.

476 19. Women’s and Children’s Health Policy Center. Women’s Health Care Experiences Survey.

477 Baltimore: Hopkins University Bloomberg School of Public Health; 2000.

478 20. Quinn VJ, Kennedy E. Food security and nutrition monitoring systems in Africa: A review

479 of country experiences and lessons learned. Food Policy 1994;19(3):234–54.

Page 25 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 25 -

480 21. World Health Organization. WHO multi-country study on women's health and domestic

481 violence against women: summary report of initial results on prevalence, health outcomes

482 and women's responses. Geneva: World Health Organization; 2005.

483 22. Di Martino V. Relationship between work stress and workplace violence in the health

484 sector. Geneva: World Health Organization; 2003.

485 23. Rosenbaum PR, Rubin DB. The central role of the propensity score in observational studies

486 for causal effects. Biometrika 1983;70(1):41–55.

487 24. Becker SO, Ichino A. Estimation of average treatment effects based on propensity scores.

488 The Stata Journal 2002;2(4):358–77.

489 25. Dehejia R. Practical propensity score matching: a reply to Smith and Todd. Journal of

490 Econometrics 2005;125(1-2):355–64.

491 26. Dehejia RH, Wahba S. Propensity score-matching methods for nonexperimental causal

492 studies. Review of Economics and Statistics 2002;84(1):151–61.

493 27. Abadie A, Imbens GW. Matching on the estimated propensity score. Econometrica

494 2016;84(2):781–807.

495 28. Caliendo M, Kopeinig S. Some practical guidance for the implementation of propensity

496 score matching. Journal of Economic Surveys 2008;22(1):31–72.

497 29. Akram M, Khan FJ. Health care services and government spending in Pakistan. PIDE-

498 Working Papers 32. Pakistan Institute of Development Economics.

499 30. Mumtaz Z, Salway S. ‘I never go anywhere’: extricating the links between women's

500 mobility and uptake of reproductive health services in Pakistan. Soc Sci Med

501 2005;60(8):1751–65.

502 31. Padela AI, Zaidi D. The Islamic tradition and health inequities: A preliminary conceptual

503 model based on a systematic literature review of Muslim health-care disparities. Avicenna

504 J Med 2018;8(1):1–13.

505 32. Bhutta ZA, Hafeez A, Rizvi A, et al. Reproductive, maternal, newborn, and child health in

506 Pakistan: challenges and opportunities. Lancet 2013;381(9884):2207–18.

507 33. Hafeez A, Mohamud BK, Shiekh MR, Shah SAI, Jooma R. Lady health workers

508 programme in Pakistan: challenges, achievements and the way forward. Journal of the

509 Pakistan Medical Association 2011;61(3):210.

Page 26 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

- 26 -

510 34. Hamid SA, Roberts J, Mosley P. Evaluating the health effects of micro health insurance

511 placement: Evidence from Bangladesh. World Development 2011;39(3):399–411.

512 35. Prost A, Colbourn T, Seward N, et al. Women’s groups practising participatory learning

513 and action to improve maternal and newborn health in low-resource settings: a systematic

514 review and meta-analysis. Lancet 2013;381(9879):1736–46.

515 36. Jacoby MB. Does indebtedness influence health? A preliminary inquiry. The Journal of

516 Law, Medicine & Ethics 2002;30(4):560–71.

517 37. Taylor L. Housing and Health: An Overview Of The Literature. Health Affairs Health

518 Policy Brief. 7 June 2019. doi: 10.1377/hpb20180313.396577.

519 38. Bauhoff S, Hotchkiss DR, Smith O. The impact of medical insurance for the poor in

520 Georgia: a regression discontinuity approach. Health Economics 2011;20(11):1362–78.

521 39. Zaidi S, Bigdeli M, Aleem N, Rashidian A. Access to essential medicines in Pakistan:

522 policy and health systems research concerns. PloS One 2013;8(5):e63515.

523 40. Lorenzetti LMJ. Evaluating the effect of integrated microfinance and health interventions:

524 an updated review of the evidence. Health Policy Plan 2017;32(5):732–56.

525 41. Gichuru W, Ojha S, Smith S, Smyth AR, Szatkowski L. Is microfinance associated with

526 changes in women's well-being and children's nutrition? A systematic review and meta-

527 analysis. BMJ Open 2019;9(1):e023658.

528 42. Saha S. Provision of health services for microfinance clients: Analysis of evidence from

529 India. International Journal of Medicine and Public Health 2011;1(1):1–5.

Page 27 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

Relationship between Microfinance, Social Development and Women’s Health

Cover Letter for Participants Questionnaire Information for Women Microfinance Borrowers Researcher: Dr. Sara Rizvi Jafree, e-mail: [email protected]; 0300 400 5740

Thank you for your valuable time! Your name is not required and all research analysis will be undertaken with confidentiality and complete anonymity. At any point during the interview you may leave, if you wish to do so. (Translation in Roman Urdu: Apka Bohat Shukirya apke eemtay waat ke liye! Apke Nam Ka Bharna Zaruri Nahi Hai Aur Yeh Tehkeek Ko Khoofiya Rakha Jaye Ga. Interview ke doran ap kabhi bhi uth ke jaana chahey to apko puri ijazat hai.) The questionnaire has been designed to collect information about your loan portfolio and your self-rated health. Our aim is to understand your needs and challenges, and ultimately try to improve your loan portfolio and health access and services. ((Translation in Roman Urdu: Is questionnaire Ka Masad Hai ke apse chand sawal loan aur sehat ke bare mein puchna. Humara masad ye hai ke apke arze ki sahuliyat aur sehat dono ko behtar kiya jaye.) Your honest and reliable answers will be appreciated, so that we can recommend the best solutions with regard to optimal loan portfolios and health satisfaction. ((Translation in Roman Urdu: Apke Sache Aur Ba Aitibar Jawab Ke Shukarguzar Honge, Thake loan aur sehat ke hawale se hum apke mushkilay ya rukawaton ko Samajh Sake.) In the event that you feel disturbed or upset after answering questions or recalling memories related to health problems or experiences of violence/ harassment, you may call or text the researcher for free consultation services from trained female psychologists. ((Translation in Roman Urdu: Agar apko in sawal aur jawab ki wajeh se koi preshani ho ya koi aisa waiya yad a jaye jo apki zehni pareshani mein izafa kare, tho ap upar diye gaye number par call ya text kar ke rabta kar le. Hum apki muft mein madat zanana mahir-e-nafsiyat se karwayenge.)

Page 28 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

Instrument The questionnaire will be read out and completed by the researcher, on behalf of the participant. Province/City: ____________________________ Microfinance Provider:________________________ Area/locality: Participant Code:

SECTION A: SOCIO-DEMOGRAPHIC CHARACHTERISTICS

Code Entry

Q1.Age Umar?

1.20-29 2.30-39 3.40-49 4.50+

Q2.Religion Mazhab

1.Muslim 2.Christian 3.Hindu 4.Other

Q3.Province Sooba?

1.Punjabi 2.Sindhi 3.Baluchi 4.KPK

Q4.City Shehr?

1.Lahore 2.Islamabad

3.Karachi 4.Hyderabad

1.Quetta 1.Peshawar

Q5.City-Area Q6.Language spoken at home with family Madri zubaan?

Q7.Race (β) Zaat

Q8.Marital Status Kya ap shadi shuda hain?

1.Married 2.Single 3.Divorced 4.Seperated

Q9.Literacy Taleem-i-qabiliyat

1.None 2.Primary 3.Secondary 4.Graduate

Q10.Occupation Pesha

Q10.Spouse literacy Aapkay khaawand ki taleemi qabiliyat kya hai?

1.None 2.Primary 3.Secondary 4.Graduate

Q12.Spouse Occupation Apkay khawand ka pesha kya hai?

Q13.Your earning in last month Pichlay mahinay aap ki kamai kitni thi?

1.Less than 5k 2.>5k-10k 2.>10k-20k 4.Other

Q14.Your earning in last year Pichlay saal apki kitni kamai thi?

1.Less than 50k 2.>50k-70k 2.>70k-90k 4.Other

Q15.Combined household income in a month (on average) Tamaam ghar ki amdani kitni hai?

1.Less than 10k 2.>10k-15k 2.>15k-20k 4.Other

Q16.House Ownership Ghar ka malik kaun hai?

1.Owned 2.Rented 3.Living with someone

4.Other

Q17.Number of children Apkay kitnay bachay hain?

1. None 2. 1-2 3. 3-5 4. >6

Q18.Age of last child Akhri bachay ki umar?

Q19.Number of people living in house Ghar mai kitnay afraad rehte hain?

1. 1-2 2. 3-5 3. 6-9 4. >10

Sign or Thumb Impression for Written Consent

Page 29 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

Q20.Number of rooms in house Ghar mai kitnay kamray hain?

1. 1 2. 2-3 3. 4-5 4. >6

Q21.Are you currently taking care of a disabled/ dependent family member Kya apkay ghar mai koi mazoor/jiska ap par inhasaar ho, shakhs hai?

1.No 2.Yes If Yes, who:

Q22.Source of drinking water Pani penay ka kya zarya hai?

1.Plain Tap 2.Filtered 3.Local Pump

4.Other

Q23.Type of energy used for cooking in house Ghar mai khana pakanay ke liye kis chiz ka istemaal kartay hain? (gas, coal, electric etc.)

1.Gas 2.Wood 3.Electricity 4.Other

Q24.Do you have toilet facility in house Apkay ghar mai bait-ul-khala hai?

1.Yes 2.No If No, what do you use

Q25.How many toilets in the house Ghar mai kitnay bait-ul-khala hain?

1. None 2. 1-2 3. 3-5 4. >6

Q26.Does the toilet have a flush Bait-ul-khala mai flush hai?

1.Yes 2.No If No, what do you use

Q27.Is the drainage and gutter system of your house satisfactory Ganday pani ke ikhraj ka nizaam darust hai?

1.Yes 2.No

Q28.How do you dispose of the garbage Ghar ki gandagi kahan phenkhtay hain?

1.Throw it on street/ far away

from home

2.Garbage collectors come to house

3.Set Fire 4.Other

Q29.Are you taking any health insurance (not provided by the microfinance provider)? (If so, from where, how much installment) Sehat ke liye insurance le rae hain?

1.Yes 2.No If Yes, who

SECTION B: MICROFINANCE LOAN CHARACHTERISTICS

Q30.Why are you taking loan (describe your work type, hours of work, working conditions in detail) Aap karz kyun le rahe hain? (kis tarah ka kaam hai, kitnay ghantay kaam kartay hain, jahan kaam kartay hain uskay halaat)

Q31.What type of loan are you currently taking/ duration Kis tarah ka karz le rahay hain/kitnay arsay se?

Q32.How long have you been a microfinance borrower for Kitne arsay se karz le rahay hain?

1. 1-2 years 2. 3-5 years 3. 6-9 years 4. >10 years

Q33.Is it a group loan Kya ap ne kisi ke sath mil ke karz liya hai?

1.Yes 2.No If Yes, who

Q34.How much is the loan for Kitna karz liya hai?

Q35.What is the installment rate per month Karz ko ada karnay ki mahana kist kya hai?

Q36.Do you attend monthly meetings with loan officers Karz denay walay officer se kya apki mahwar mulakaat hoti hai?

1.Yes 2.No

Q37.Do you attend weekly meetings with loan officers Karz dene walay officer se kya apki haftawar mulkaat hoti hai?

1.Yes 2.No

Q38.Who helps you in loan repayment Karz ada karnay mai kya koi apki madad karta hai?

1.No one 2.Husband 3.Parents 4.Other

Q39.What exactly has the loan been used for Ap karz kis liye istemal karti hain?

1.Business 2.Household expenditure

3.Old Loans

4.Health Costs

4.Other

Page 30 of 41

For peer review only - http://bmjopen.bmj.com/site/about/guidelines.xhtml

BMJ Open

123456789101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657585960

on February 2, 2022 by guest. P

rotected by copyright.http://bm

jopen.bmj.com

/B

MJ O

pen: first published as 10.1136/bmjopen-2020-043544 on 5 January 2021. D

ownloaded from

For peer review only

Q40.How much of the loan taken has been invested in business Karz ka kitna hissa karobar mai kharch kiya hai?

1.All 2.Half 3.Quarter 4.Other

Q41.Are you satisfied with loan amount Kya aap karz ki rakam se mutmaeen hai?