“Financial Literacy Levels of Small Businesses Owners and it ...

Upload

banasthaliCategory

view

0download

0

Trends in Global Financial Literacy and the lessons for the emerging economies

Invitation LectureRefresher programme for Senior faculty members

NITI AAYOG Chair, University of Rajasthan Jaipur, India

[Speaker

Prof. Harsh Purohit (Ph.D.)Centre for Financial Planning Training

and Research for Women, Dean FMS- WISDOM,

Banasthali Vidyapith

1CFPTRW9/21/2015

CFPTRW 2

We thank Bank of America for generous CSR Support

9/21/2015

CFPTRW 3

Presentation Outline

• Concept of Financial Literacy (FL) and role played by Banasthali Vidyapith

• What needs to be improved in the OECD definition of FL.

• FL Trends in 2012/ 13/ 14 as per Mastercard and other international reports across the world including India.

9/21/2015

CFPTRW 4

Presentation Outline

• Financial Literacy in India: NCFE 2015

• Learning for the Emerging Economies

• Universities should spread Financial Literacy in India

9/21/2015

CFPTRW 5

What is Financial Literacy ?

• “FL is a combination of – awareness, knowledge, skill, attitude and

behavior; • those remain essential aspects to make

– a sound financial decision in general • that eventually secure

– financial welfare also for an individual”

OECD Definition

9/21/2015

CFPTRW 6

What is Financial Literacy ?

• “FL is to possess – the skills and knowledge on financial matters

• so that – effective actions can be taken efficiently

• that best fulfills – first an individual’s personal and family goals,

• thereby – meeting community goals at large”.

National Financial Educators Council (NFEC) of USA

9/21/2015

CFPTRW 7

CFPTRW @ Banasthali Spreading Financial Literacy among

women at all levels in Rajasthan

9/21/2015

CFPTRW 10

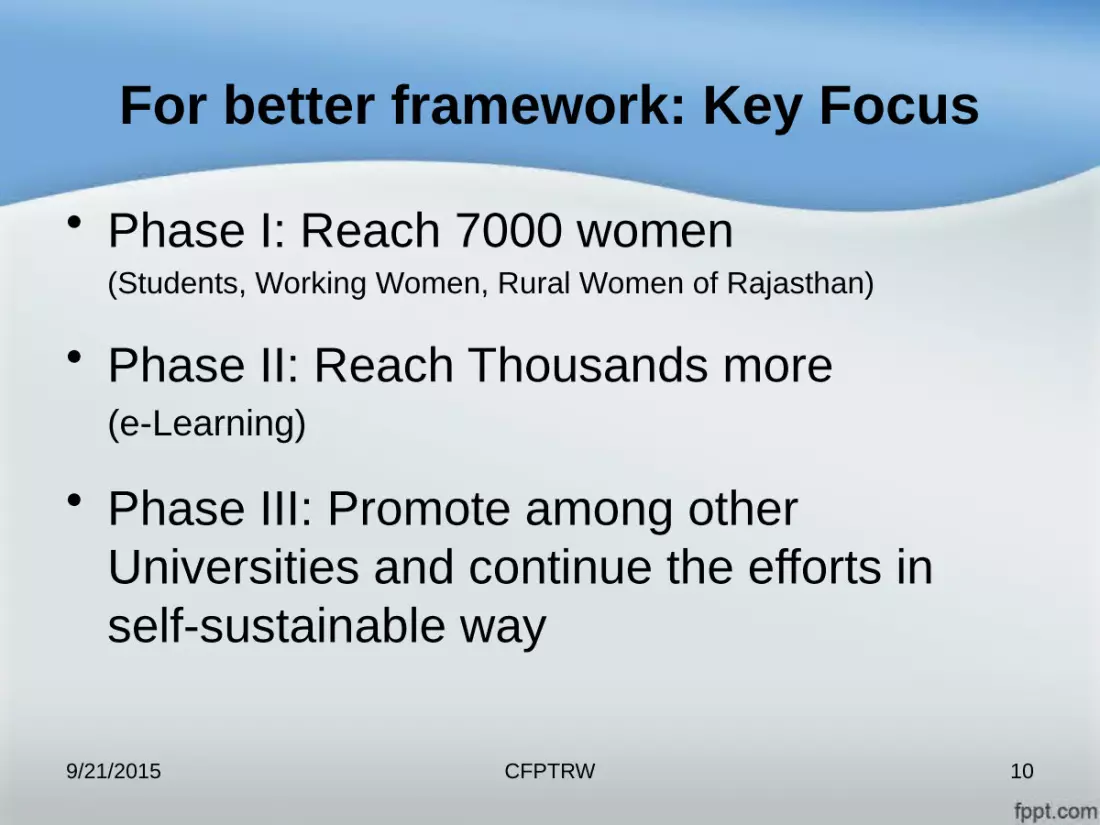

For better framework: Key Focus

• Phase I: Reach 7000 women(Students, Working Women, Rural Women of Rajasthan)

• Phase II: Reach Thousands more(e-Learning)

• Phase III: Promote among other Universities and continue the efforts in self-sustainable way

9/21/2015

CFPTRW 11

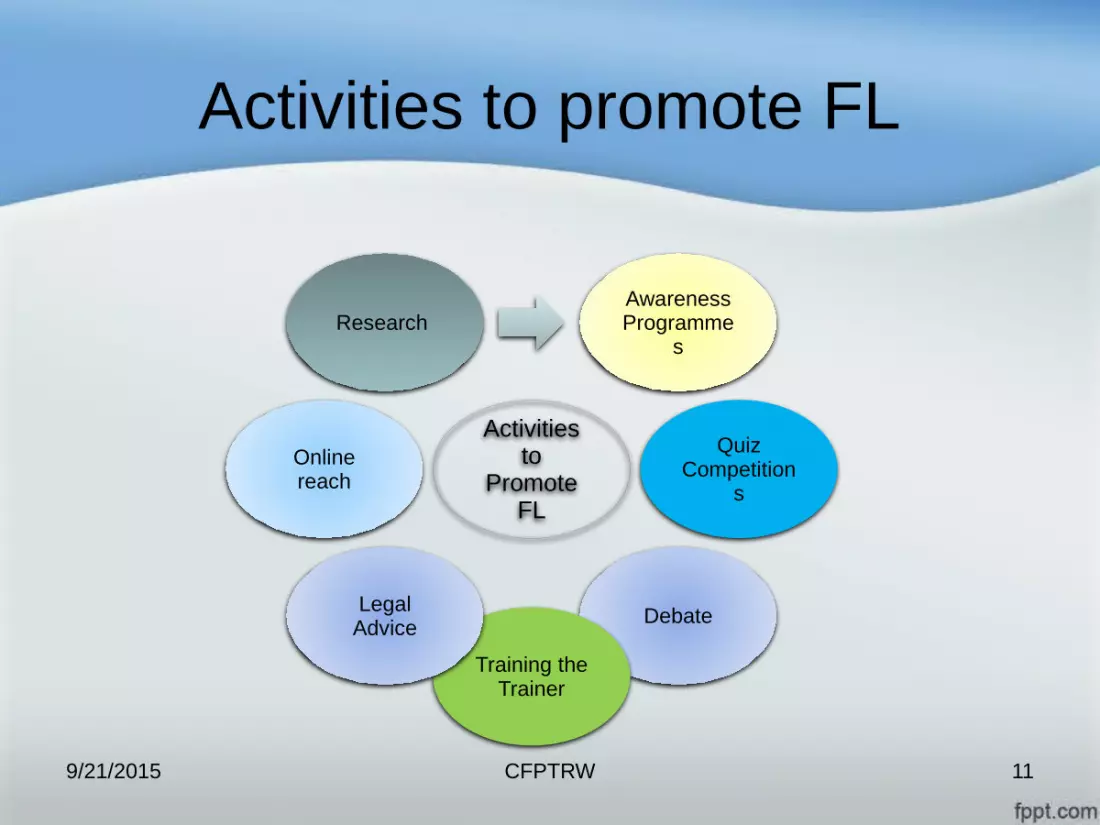

Activities to promote FL

9/21/2015

Activities to

Promote FL

Awareness Programme

s

Quiz Competition

s

Debate

Training the Trainer

Legal Advice

Online reach

Research

CFPTRW 12

FL in India: some fresh thoughts

• India has its own indigenous system– Need a definition that captures its essence in

the Indian context and culture

• Is this concept new to India?– Certainly not

9/21/2015

CFPTRW 13

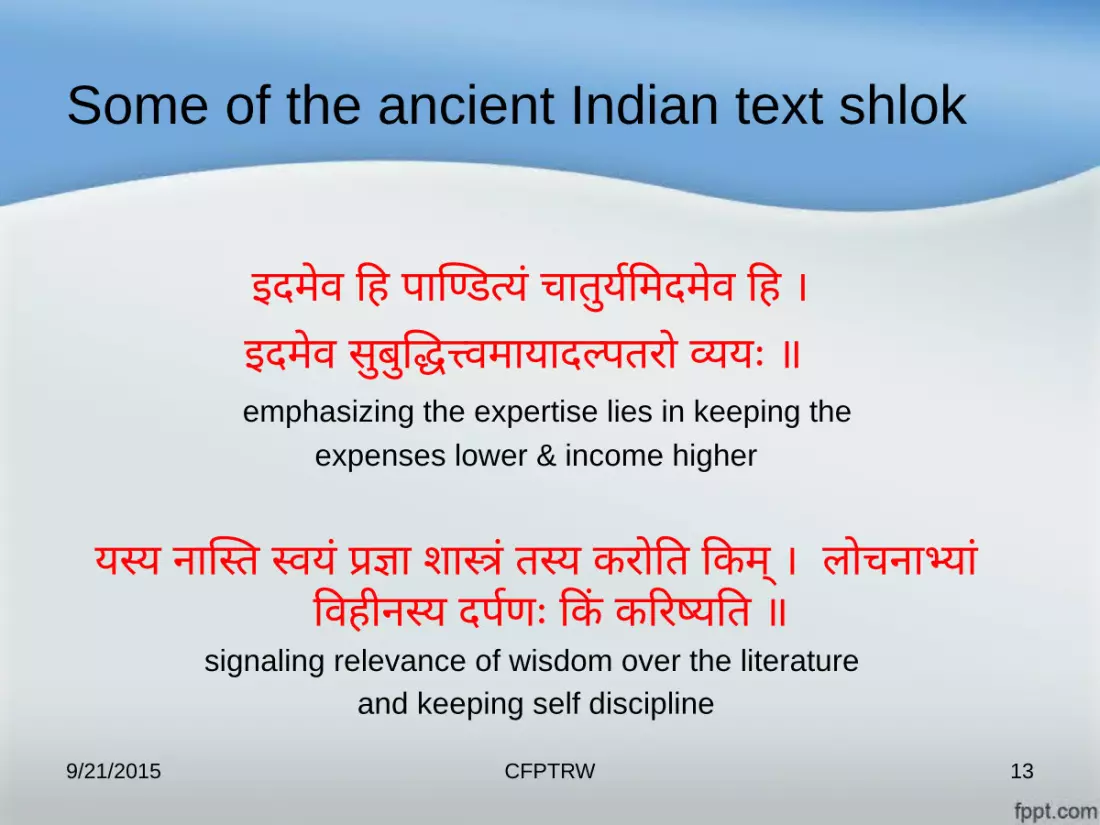

Some of the ancient Indian text shlok

इदमेव हि� पाण्डि��त्यं चातुय�मिमदमेव हि� । इदमेव सुबुद्धि�त्त्वमायादल्पतरो व्ययः ॥

emphasizing the expertise lies in keeping the expenses lower & income higher

यस्य नास्तिस्त स्वयं प्रज्ञा शास्त्रं तस्य करोहित हिकम् । लोचनाभ्यां हिव�ीनस्य दप�णः किकं करिरष्यहित ॥

signaling relevance of wisdom over the literature and keeping self discipline

9/21/2015

CFPTRW 14

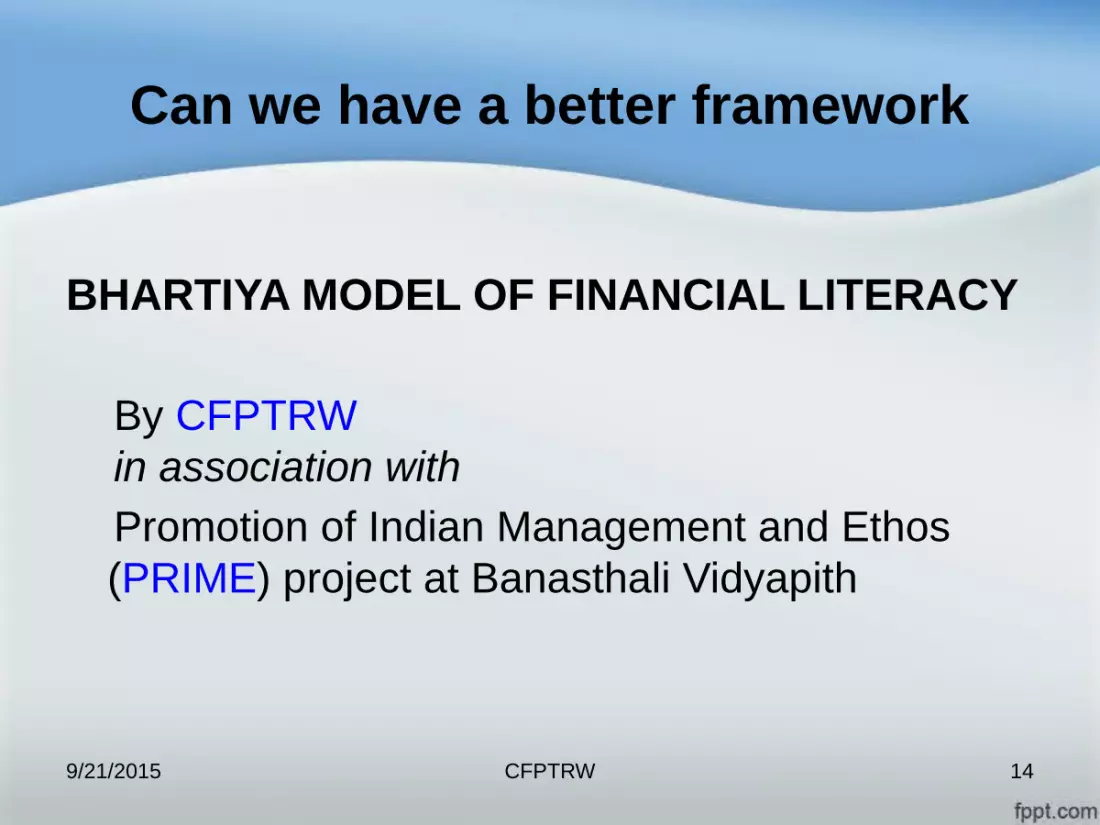

Can we have a better framework

BHARTIYA MODEL OF FINANCIAL LITERACY

By CFPTRW in association with Promotion of Indian Management and Ethos

(PRIME) project at Banasthali Vidyapith

9/21/2015

CFPTRW 15

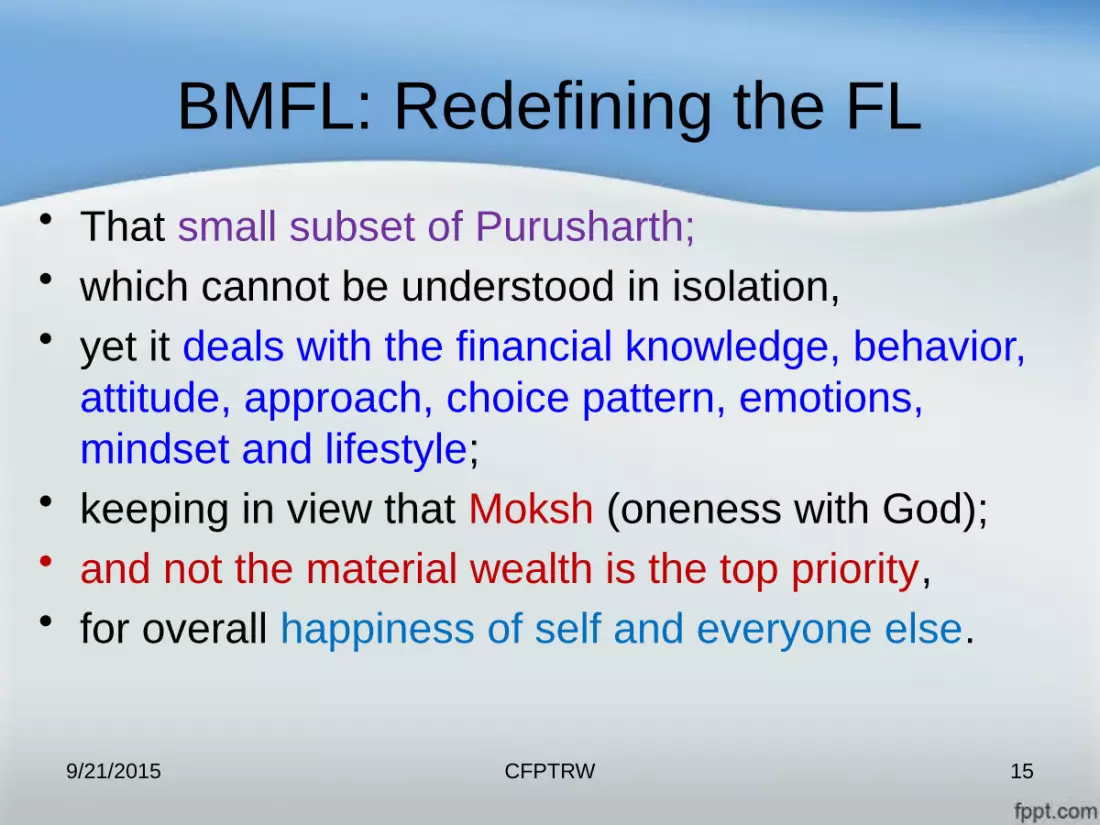

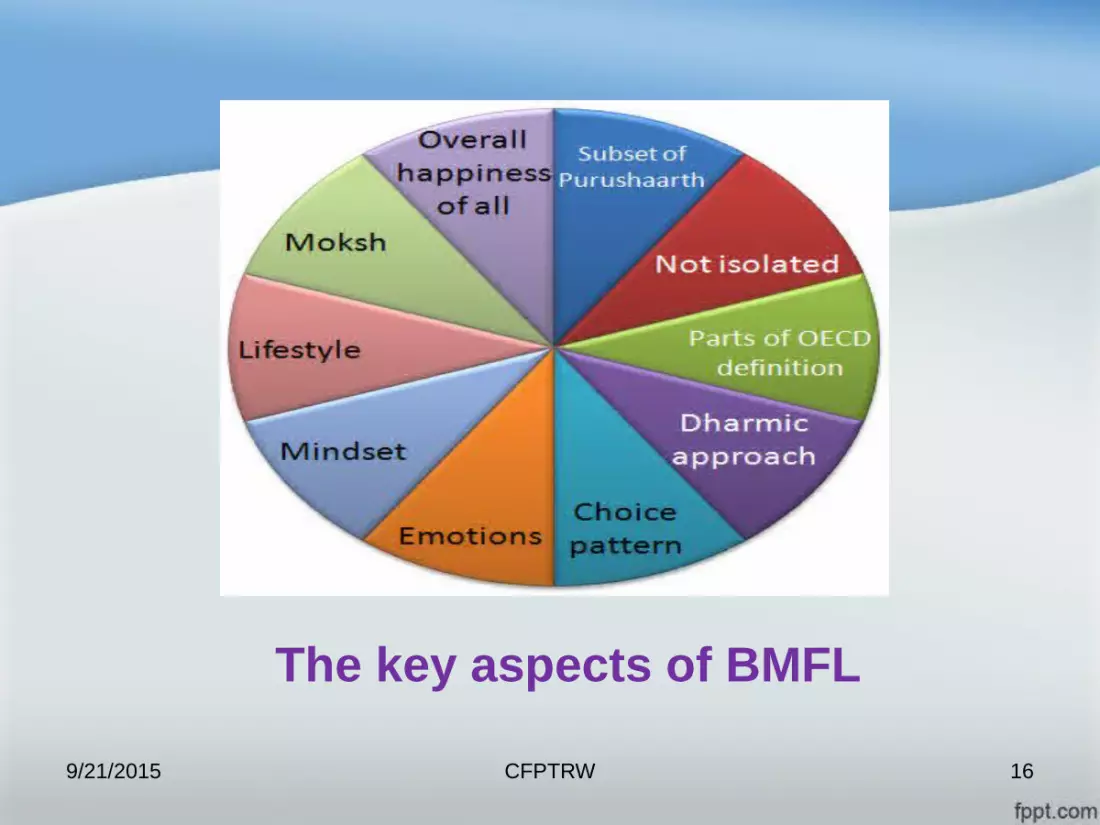

BMFL: Redefining the FL• That small subset of Purusharth; • which cannot be understood in isolation, • yet it deals with the financial knowledge, behavior,

attitude, approach, choice pattern, emotions, mindset and lifestyle;

• keeping in view that Moksh (oneness with God); • and not the material wealth is the top priority, • for overall happiness of self and everyone else.

9/21/2015

CFPTRW 16

The key aspects of BMFL

9/21/2015

CFPTRW 17

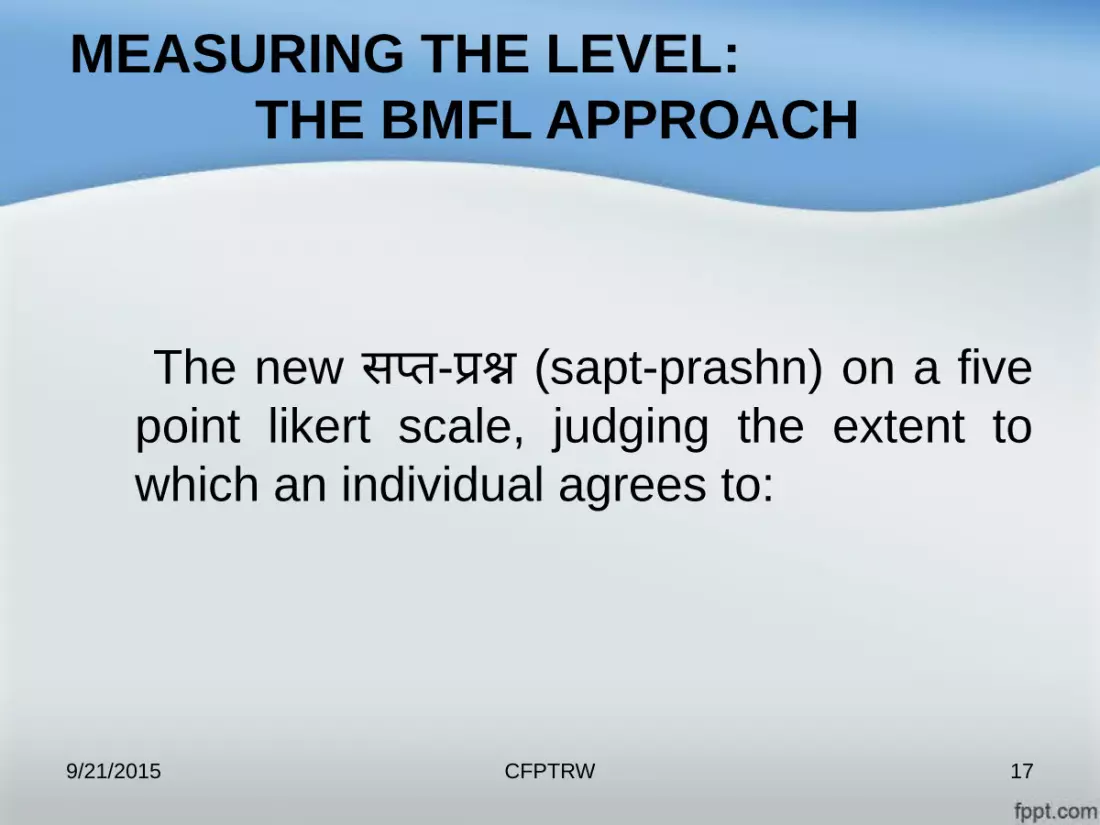

MEASURING THE LEVEL: THE BMFL APPROACH

The new सप्त- प्रश्न (sapt-prashn) on a five

point likert scale, judging the extent to which an individual agrees to:

9/21/2015

CFPTRW 18

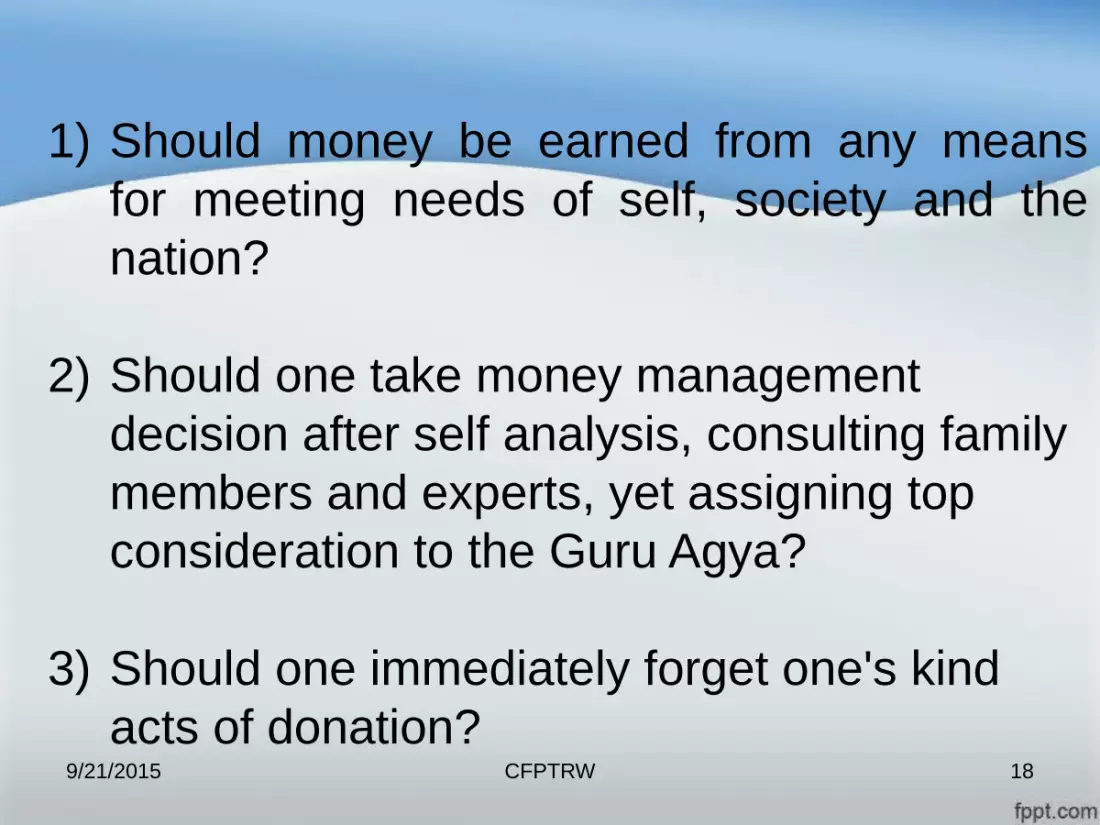

1) Should money be earned from any means for meeting needs of self, society and the nation?

2) Should one take money management decision after self analysis, consulting family members and experts, yet assigning top consideration to the Guru Agya?

3) Should one immediately forget one's kind acts of donation?

9/21/2015

CFPTRW 19

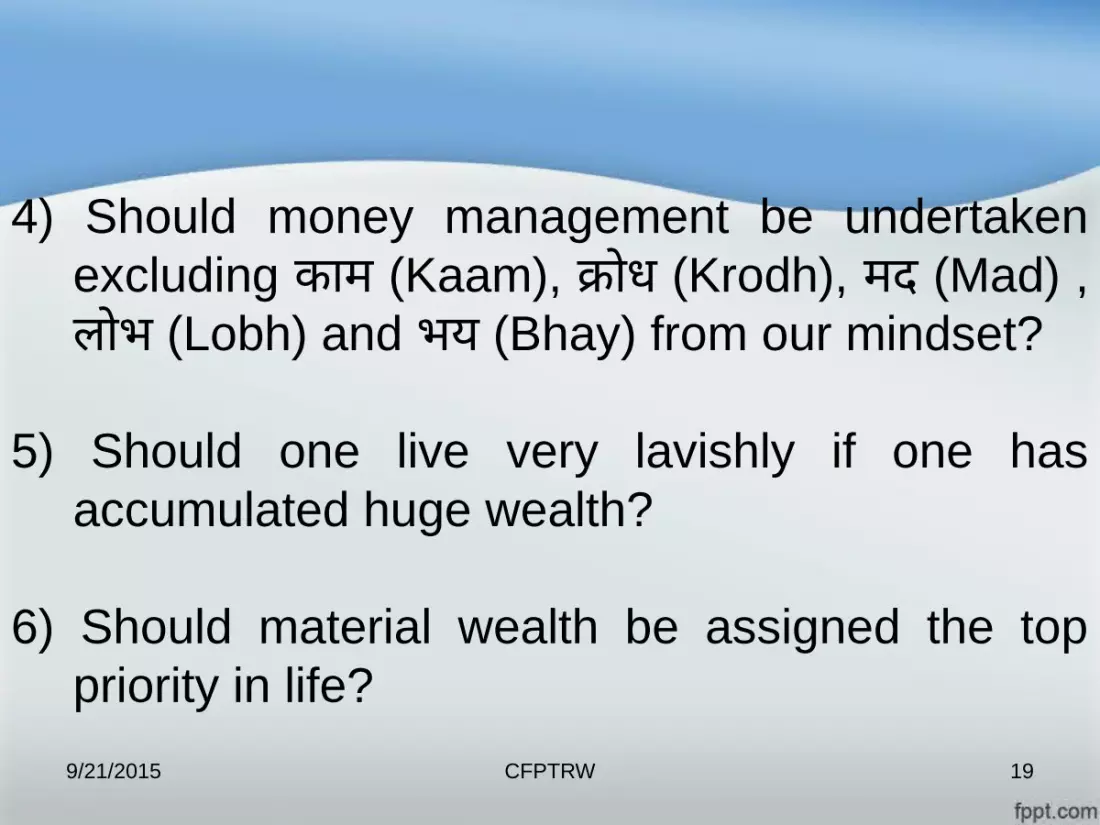

4) Should money management be undertaken excluding काम (Kaam), क्रोध (Krodh), मद (Mad) ,

लोभ (Lobh) and भय (Bhay) from our mindset?

5) Should one live very lavishly if one has accumulated huge wealth?

6) Should material wealth be assigned the top priority in life?

9/21/2015

CFPTRW 20

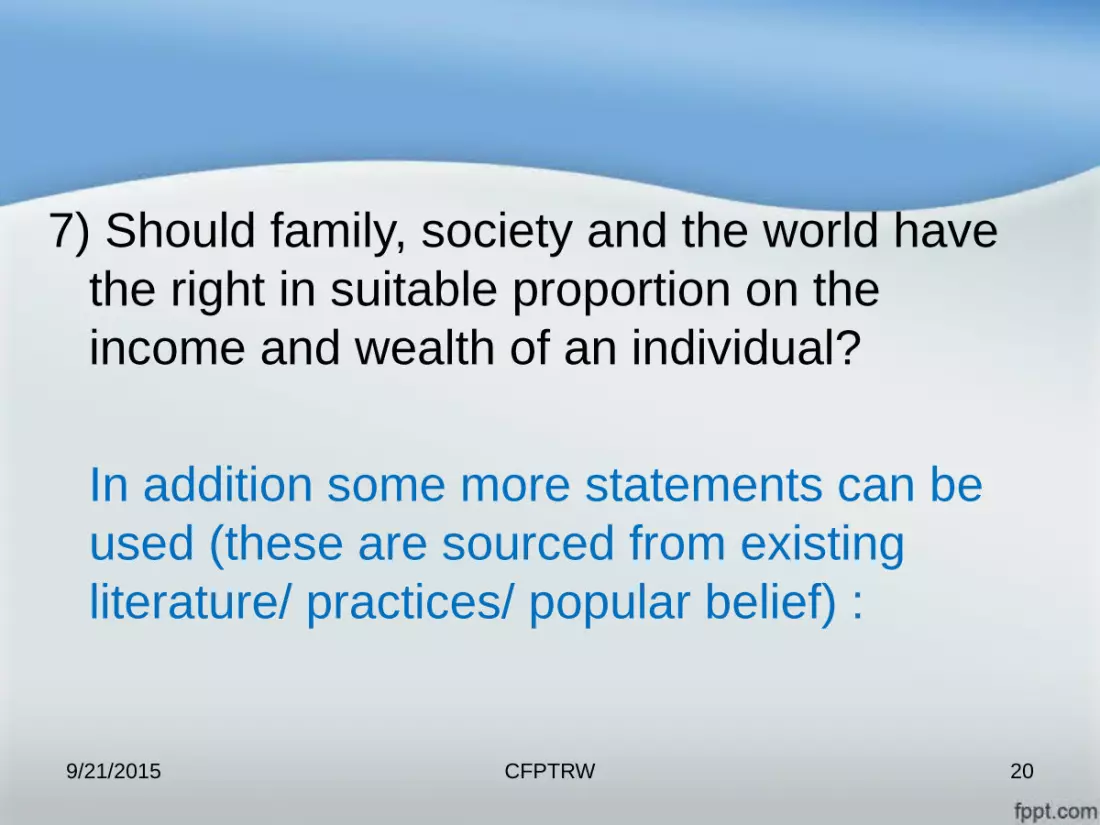

7) Should family, society and the world have the right in suitable proportion on the income and wealth of an individual?

In addition some more statements can be used (these are sourced from existing literature/ practices/ popular belief) :

9/21/2015

CFPTRW 219/21/2015

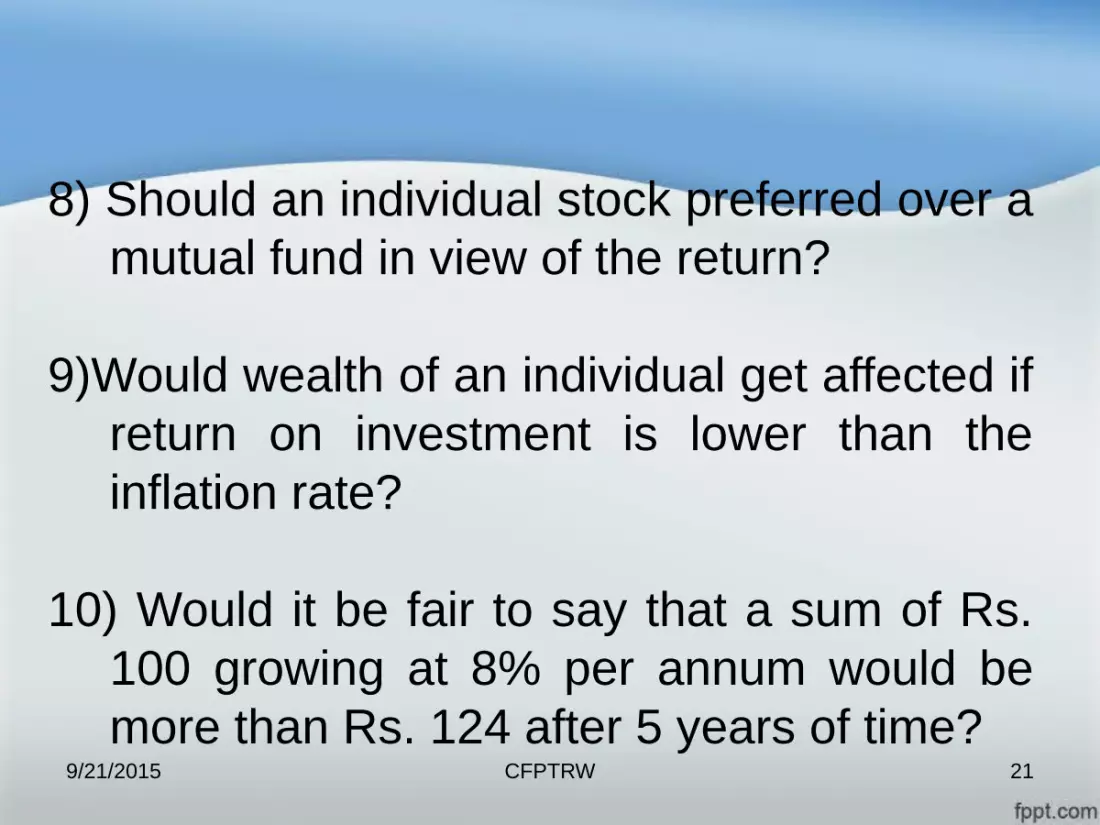

8) Should an individual stock preferred over a mutual fund in view of the return?

9)Would wealth of an individual get affected if return on investment is lower than the inflation rate?

10) Would it be fair to say that a sum of Rs. 100 growing at 8% per annum would be more than Rs. 124 after 5 years of time?

CFPTRW 229/21/2015

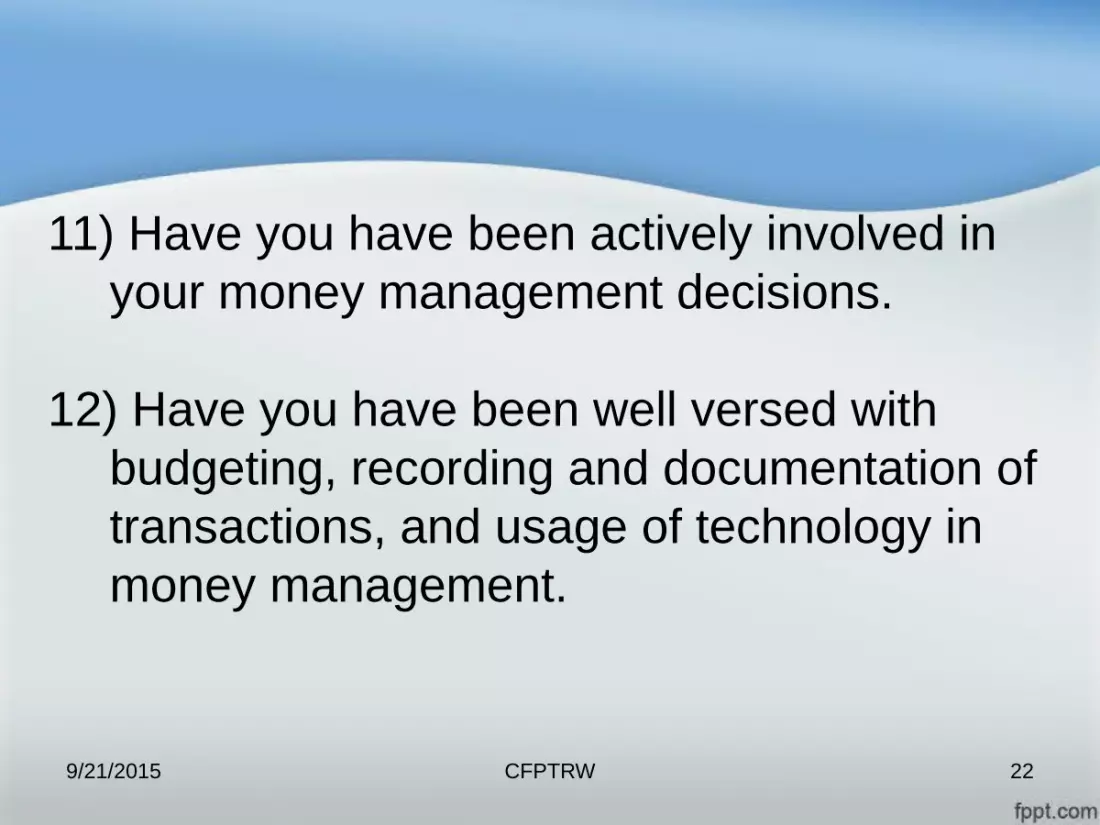

11) Have you have been actively involved in your money management decisions.

12) Have you have been well versed with budgeting, recording and documentation of transactions, and usage of technology in money management.

CFPTRW 239/21/2015

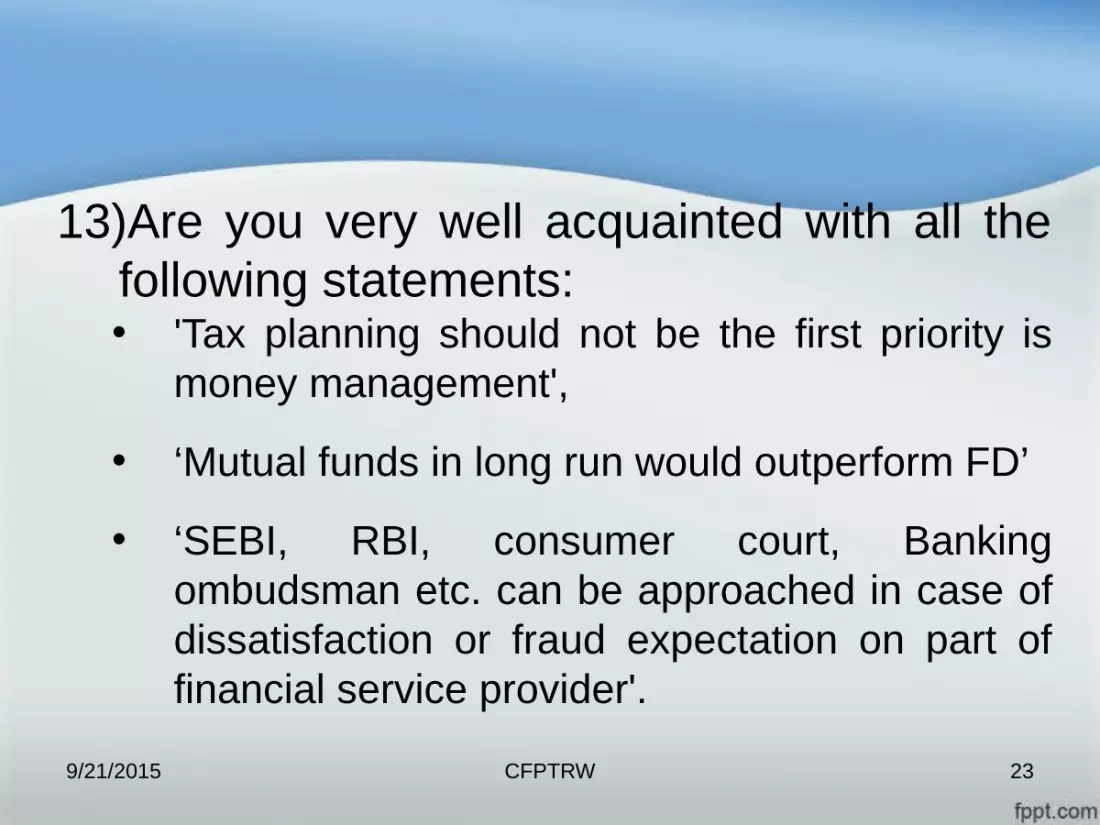

13)Are you very well acquainted with all the following statements:• 'Tax planning should not be the first priority is

money management',

• ‘Mutual funds in long run would outperform FD’

• ‘SEBI, RBI, consumer court, Banking ombudsman etc. can be approached in case of dissatisfaction or fraud expectation on part of financial service provider'.

CFPTRW 249/21/2015

14) Are you very well acquainted with the terms IPO, ETF, diversified mutual fund, Term insurance plan and PPF.

CFPTRW 25

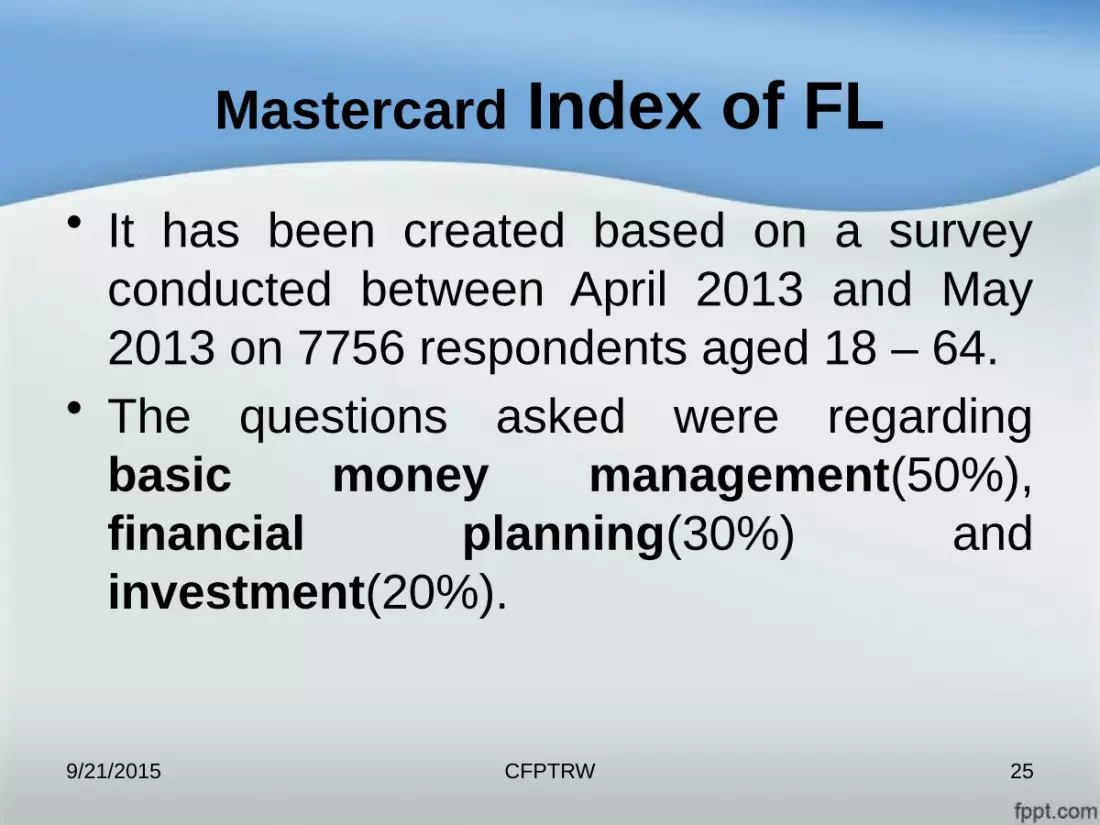

Mastercard Index of FL• It has been created based on a survey

conducted between April 2013 and May 2013 on 7756 respondents aged 18 – 64.

• The questions asked were regarding basic money management(50%), financial planning(30%) and investment(20%).

9/21/2015

CFPTRW 26

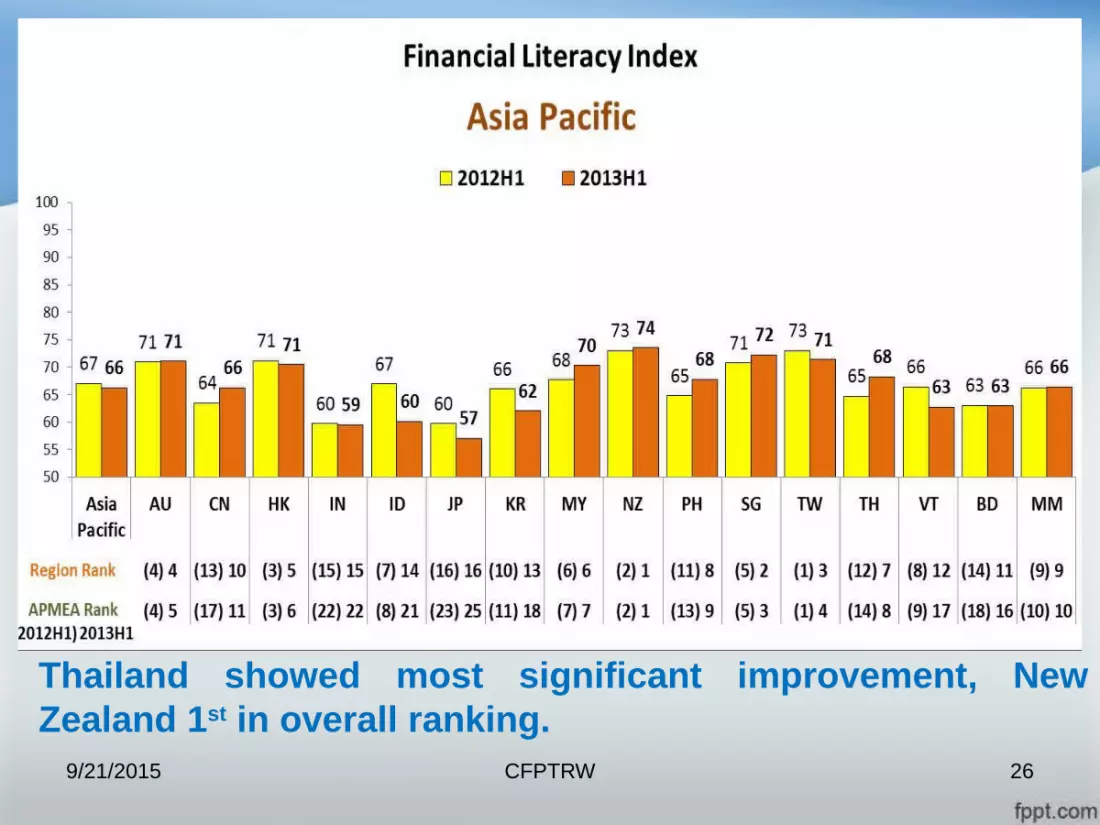

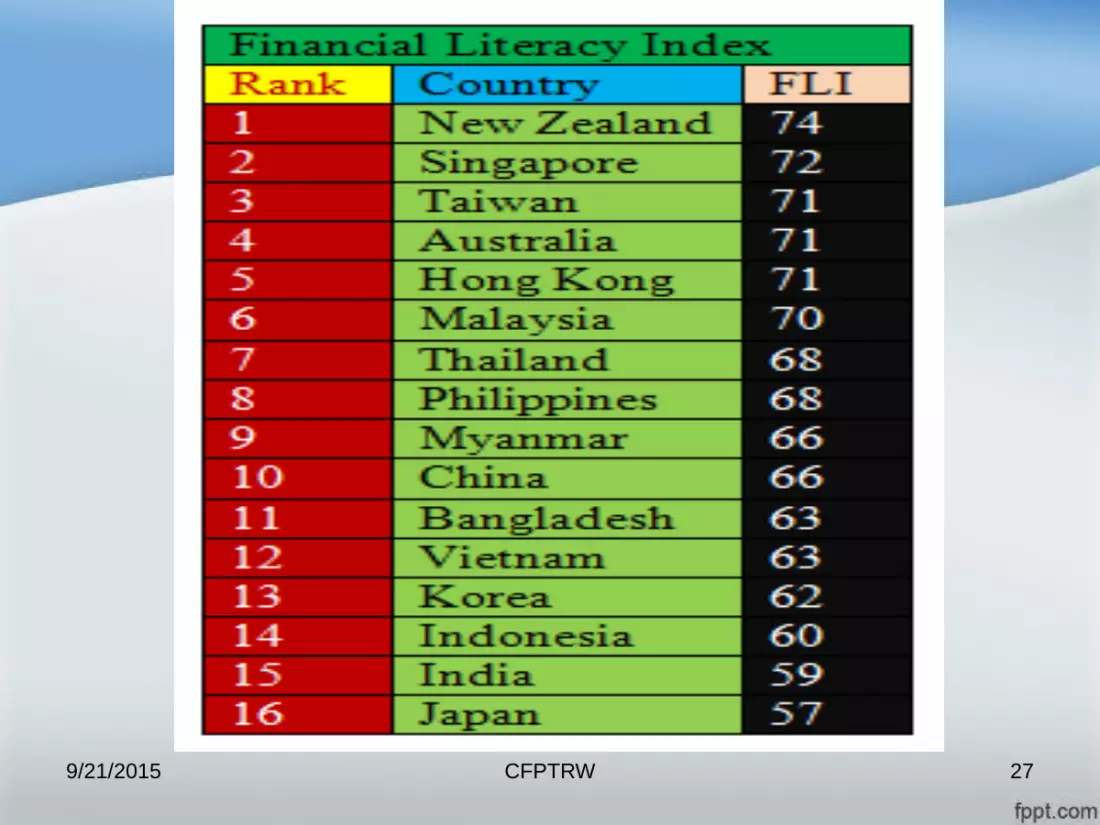

Thailand showed most significant improvement, New Zealand 1st in overall ranking.

9/21/2015

CFPTRW 279/21/2015

CFPTRW 28

In context of India• Poor FL index.

• Only 22% of adult Indians saved in the 2011 (World Bank’s Global Financial Inclusion Index 2012)

• This may be due to the fact that they were simply not earning enough to set aside money for savings, big purchases, and credit commitments.

9/21/2015

CFPTRW 29

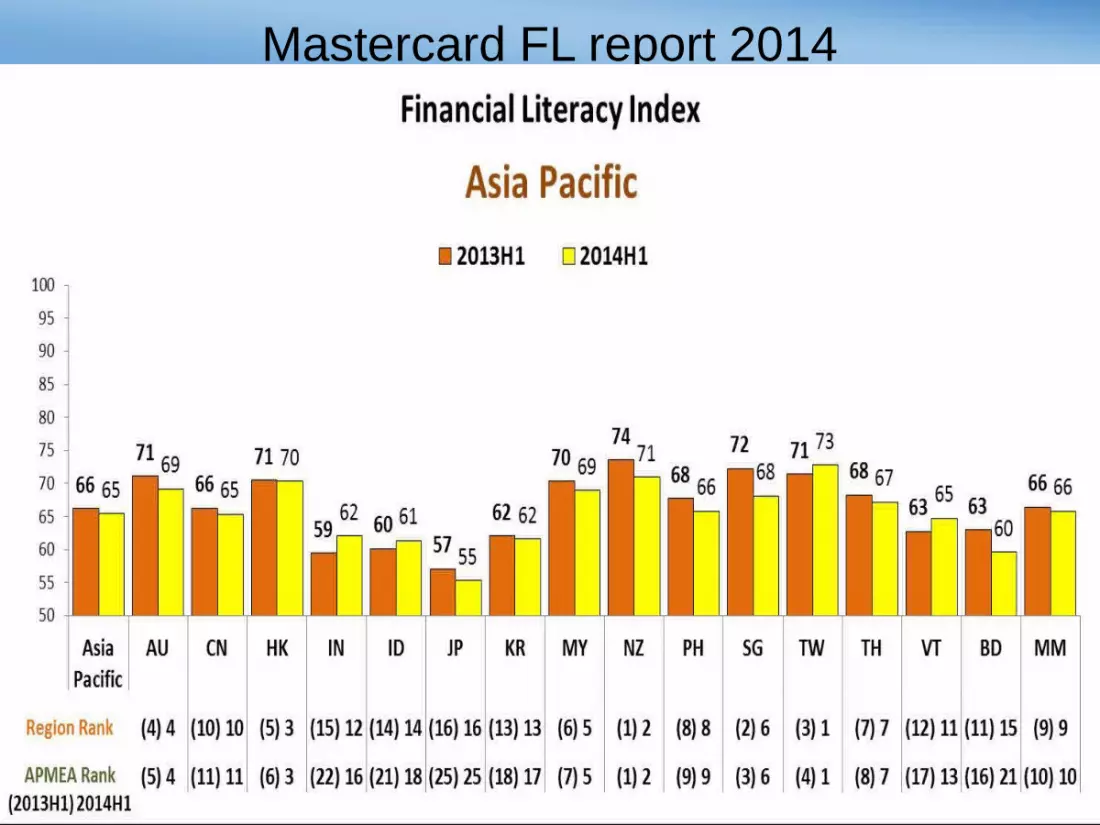

Mastercard FL report 2014

9/21/2015

CFPTRW 30

• Among the emerging Asia Pacific markets India advanced the most, gaining 3 points to 62.

• This year survey shows disappointing results in developed countries like Singapore, Australia, Japan, Korea.

9/21/2015

CFPTRW 31

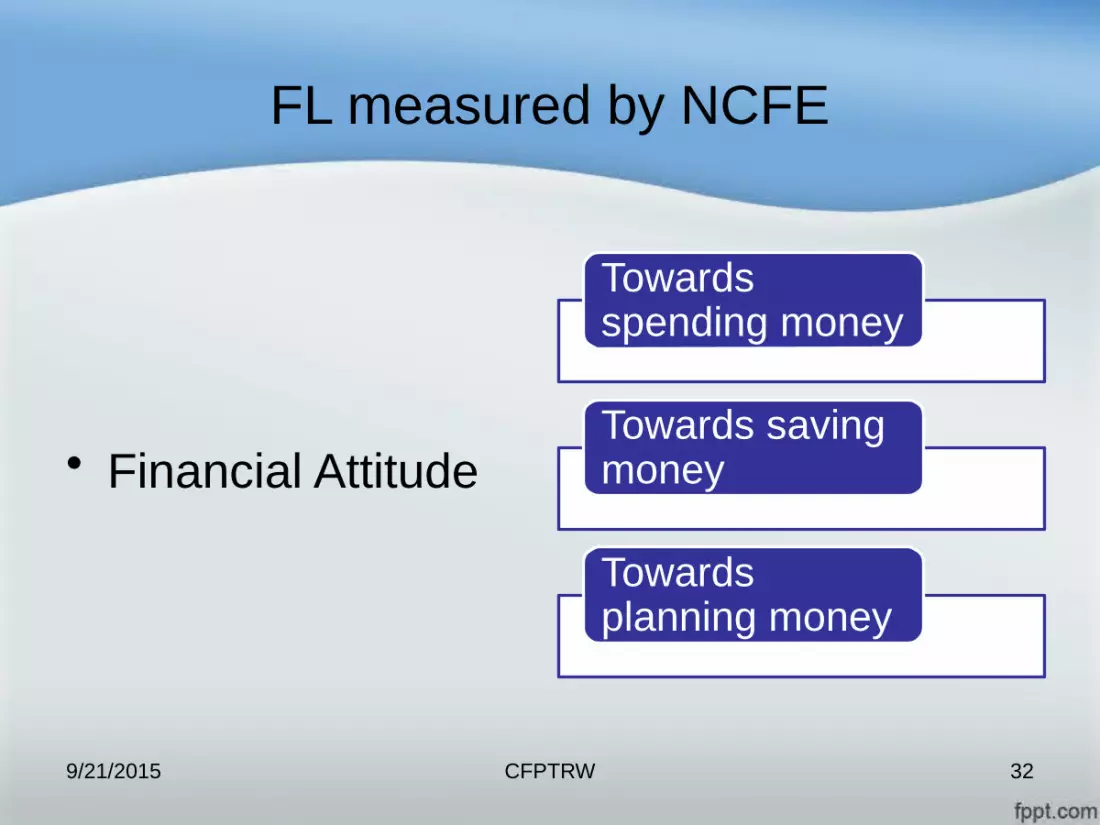

NCFE 2015 report of FL in India

• National Institute of Security Market (NISM) has conducted a survey regarding Financial Literacy and Inclusion in India.

• Survey contains sample size of 75000+ from 35 states in India, 50 questions (about financial attitude, behavior and knowledge).

9/21/2015

CFPTRW 32

FL measured by NCFE

Towards spending money

Towards saving money

Towards planning money

9/21/2015

• Financial Attitude

CFPTRW 33

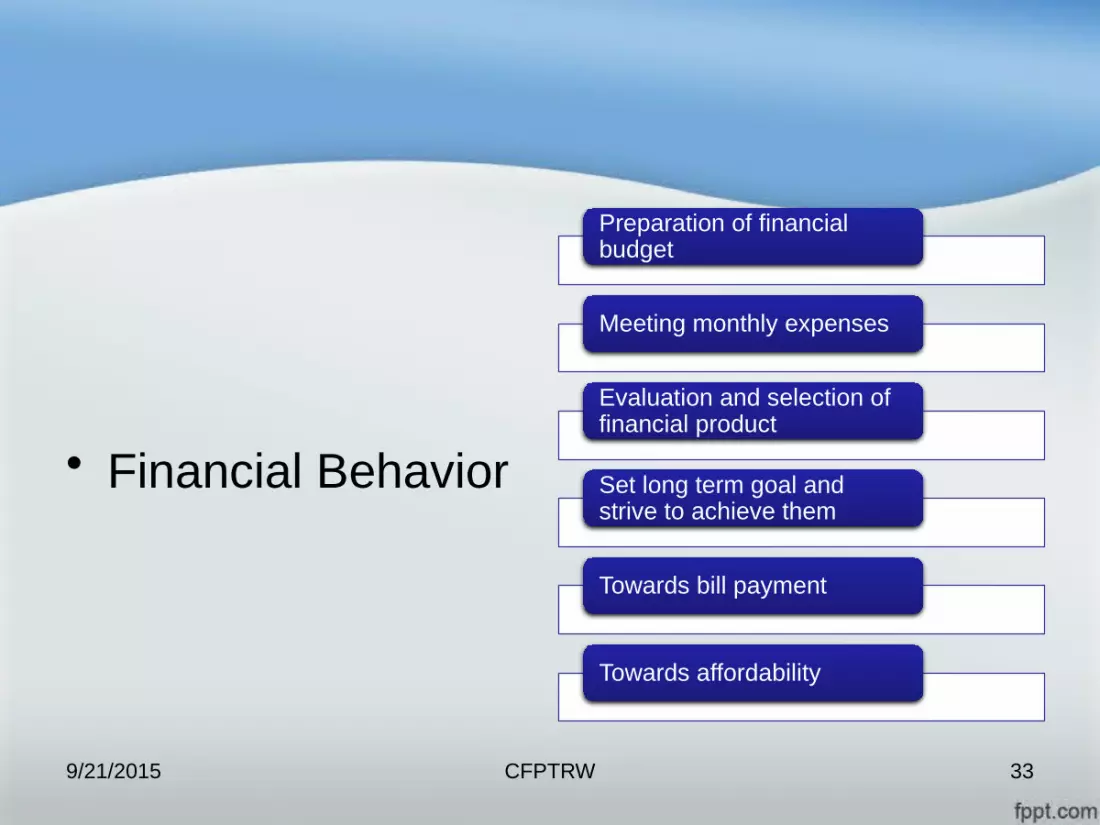

• Financial Behavior

Preparation of financial budget

Meeting monthly expenses

Evaluation and selection of financial product

Set long term goal and strive to achieve them

Towards bill payment

Towards affordability

9/21/2015

CFPTRW 34

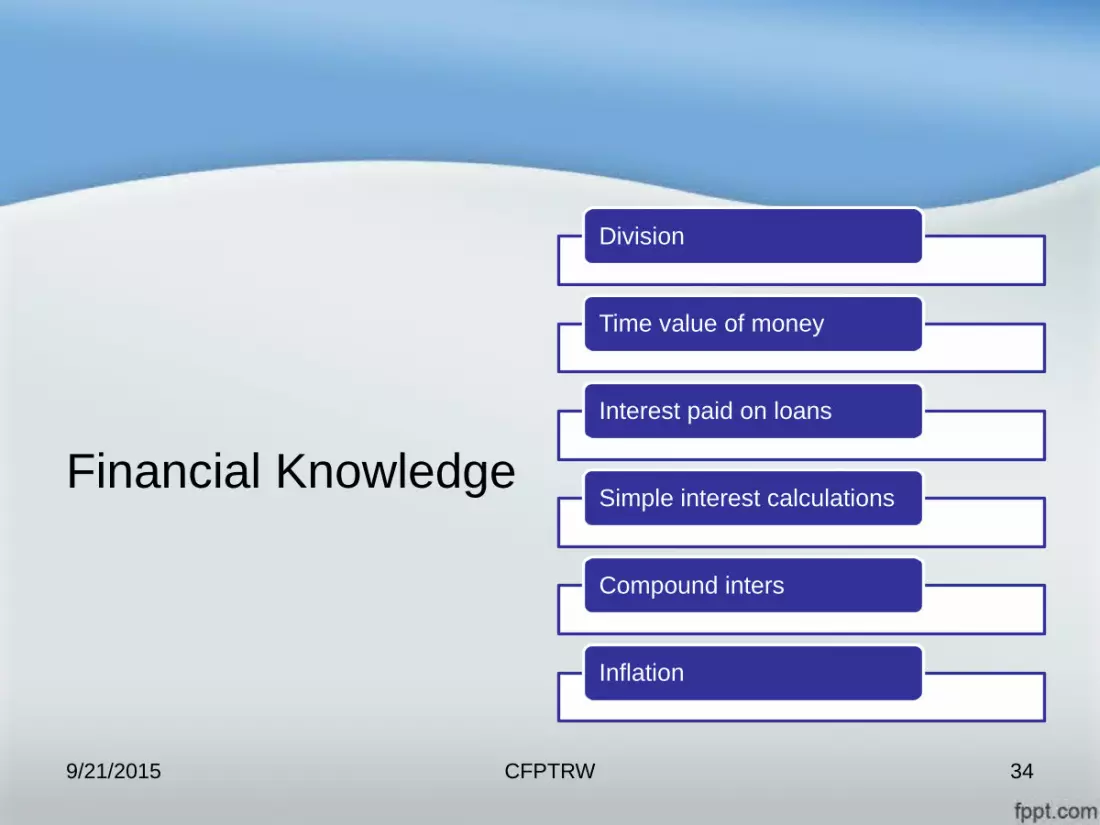

Financial Knowledge

Division

Time value of money

Interest paid on loans

Simple interest calculations

Compound inters

Inflation

9/21/2015

CFPTRW 35

For Instance

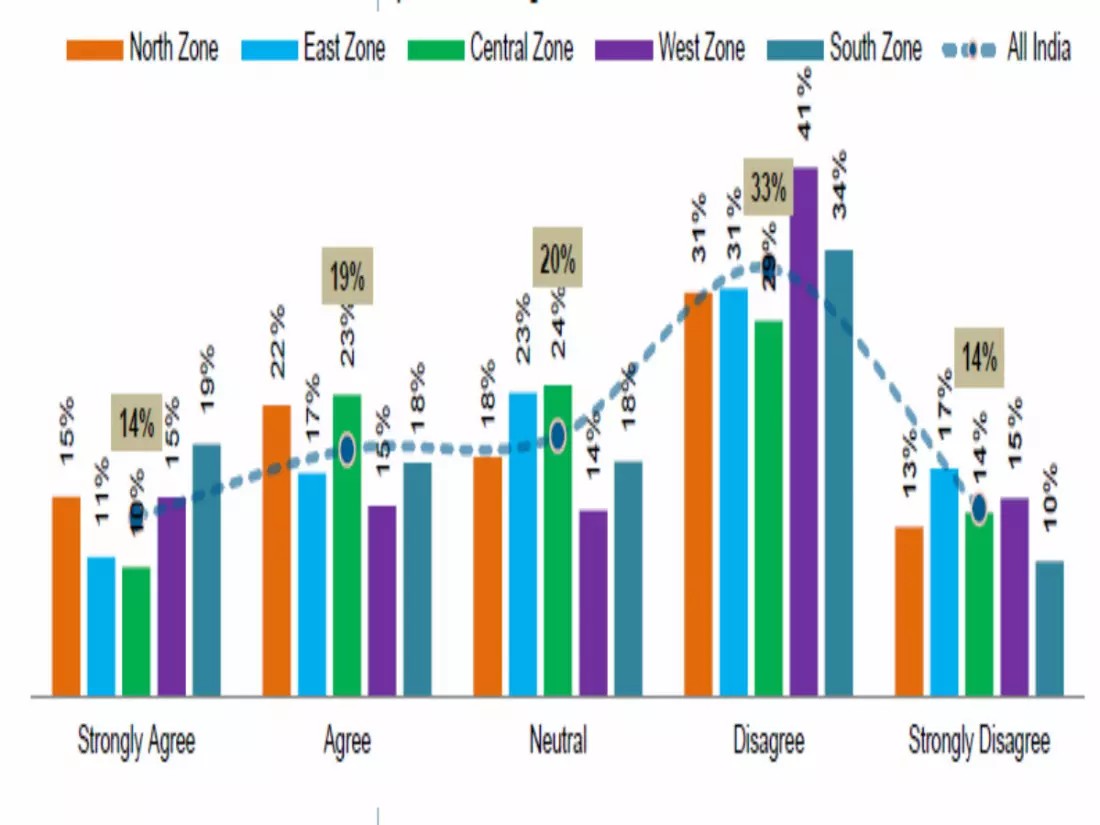

• The question asked towards spending of money -“I tend to live for today and let tomorrow take care of itself”.

• Let us see the Zone wise views of various respondents on the statement

9/21/2015

CFPTRW 369/21/2015

CFPTRW 37

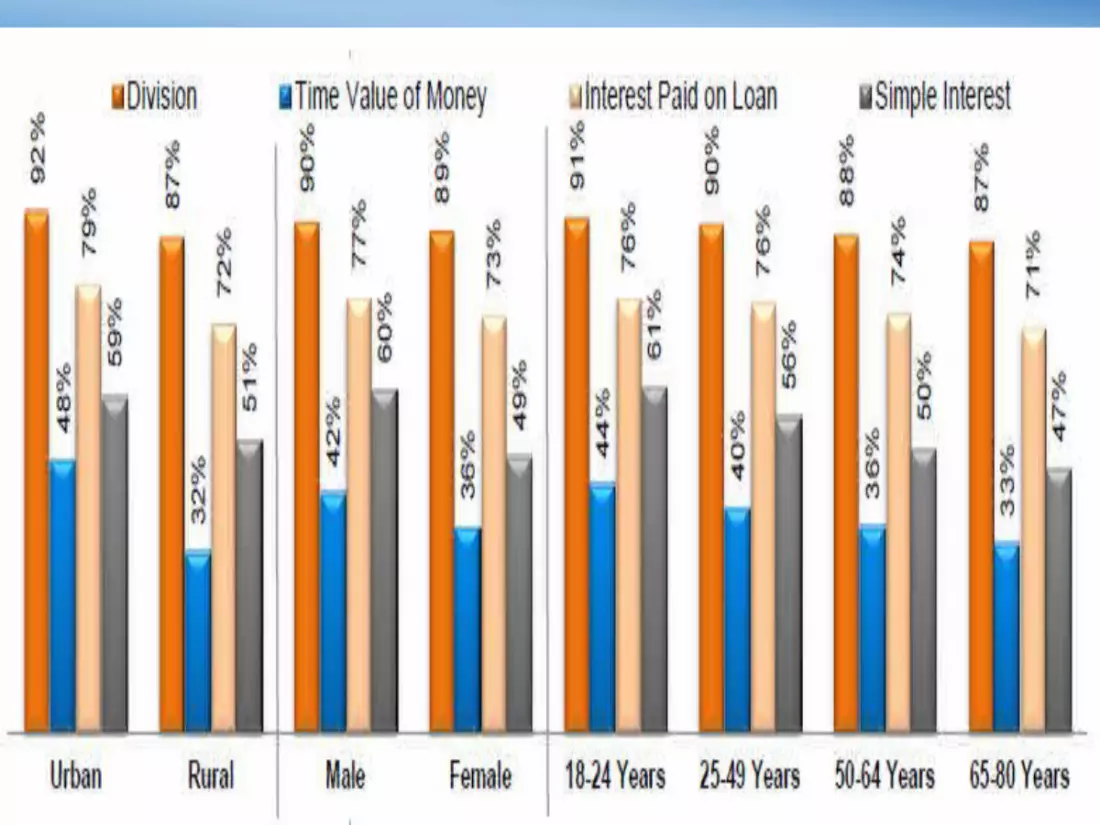

Results about Financial Knowledge

9/21/2015

For evaluation of basic financial knowledge of the respondents, it was divided into seven categories:

– Ability of Division– Understanding about Time Value of Money– Understanding about Interest component on Loan

Knowledge on Simple Interest– Knowledge about Compound Interest– Understanding about Risk – Return relationship– Knowledge about Inflation

•

CFPTRW 38

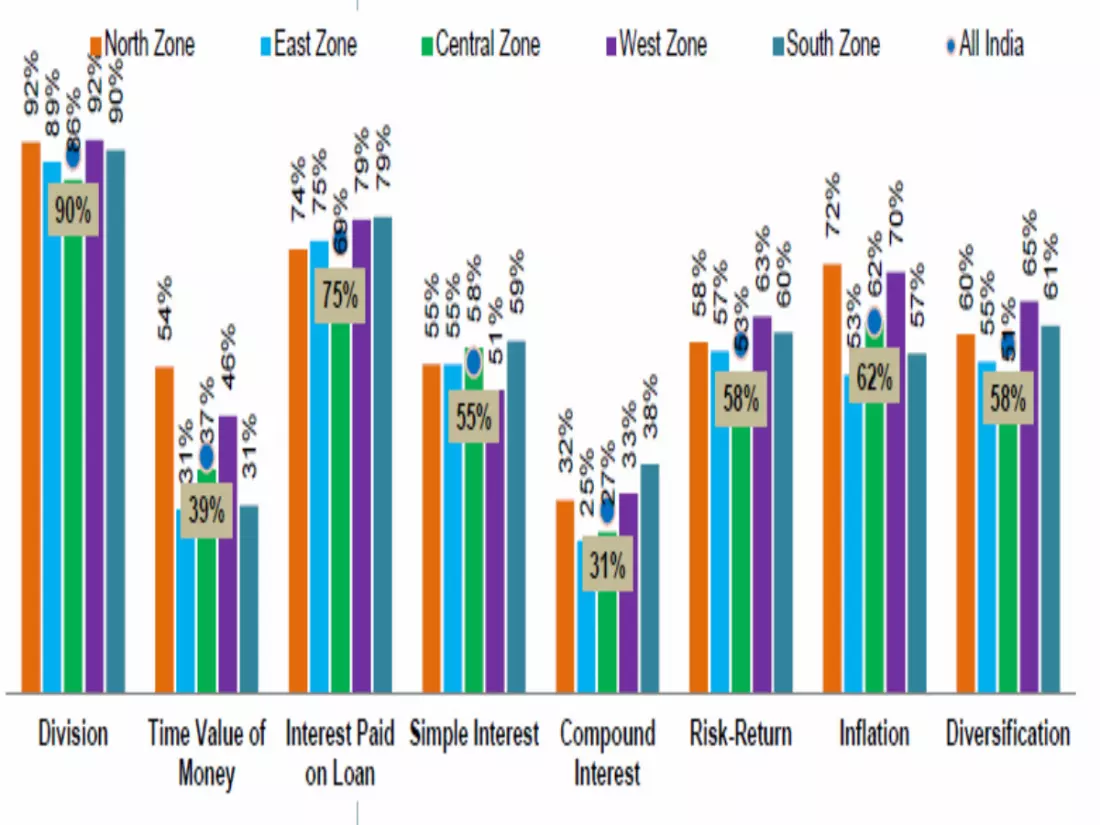

• The respondents were asked various questions about their basic financial knowledge. The zone wise details of their responses are

9/21/2015

CFPTRW 399/21/2015

CFPTRW 409/21/2015

CFPTRW 41

• It was observed that most of the respondents were comfortable in financial calculations like Division, Interest paid on Loan but had difficulty in calculations of Simple Interest and understanding about Time Value of Money.

9/21/2015

CFPTRW 42

Learning for Emerging Economies

• Measure FL in cultural context• Focus on FL programmes for Women• Prosperity of nation is linked to FL and

hence there is need to take strong steps• Several useful prescriptions by the World

Bank and OECD should be implemented• Recognize that the role of Universities is

significant in promoting FL9/21/2015

CFPTRW 43

Learning for Emerging Economies

• Do not neglect the merit of promoting mutual funds and risk management through insurance

• FL programmes are not an expense but an investment for prosperity of the world

• Special recognition to all who support FL• Promote continuous research coordinating

with stakeholders

9/21/2015

CFPTRW 44

Do Universities have a role to play?

YES, in fact we can play the key role

9/21/2015

CFPTRW 45

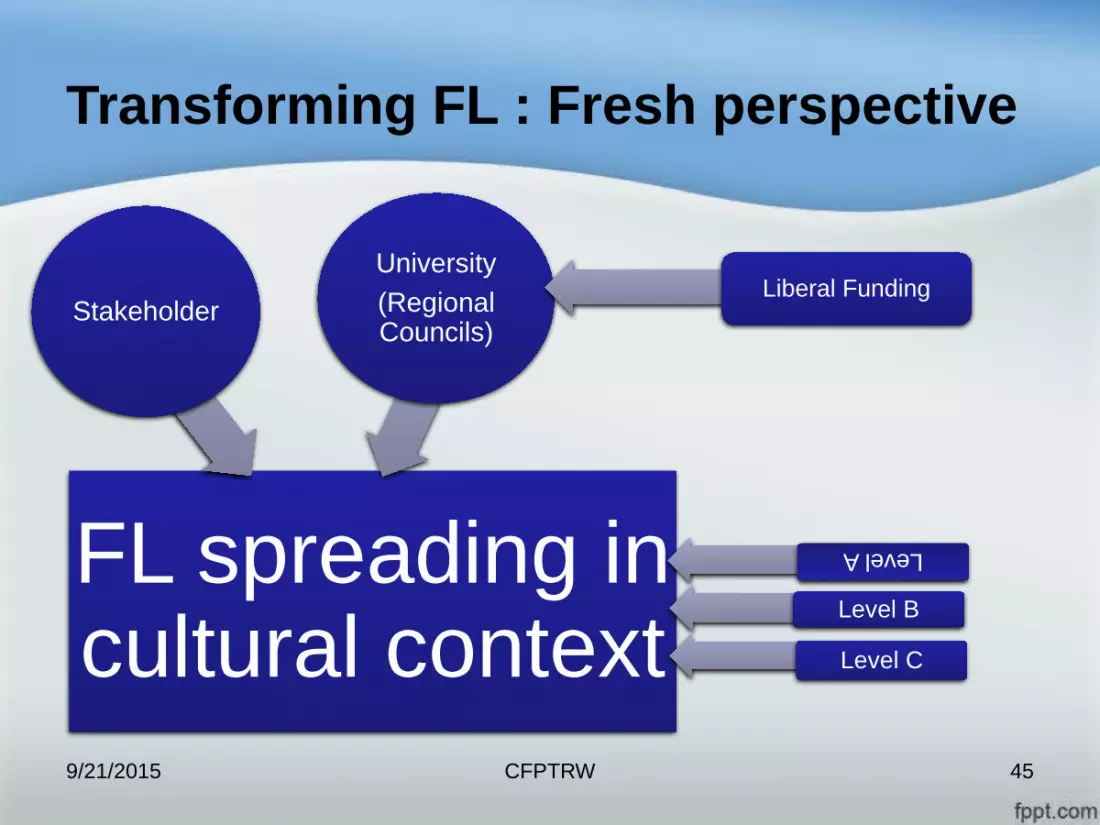

Transforming FL : Fresh perspective

9/21/2015

FL spreading in cultural context

Stakeholder

University(Regional Councils)

Liberal FundingLevel A

Level B

Level C

CFPTRW 46

Together we can play a strong role in improving Financial Literacy of India, and provide a new thinking

to the world….

What can be a better place to discuss this

9/21/2015

Copyright © 2022 FDOKUMEN

![Bhartiya Purattava: Nai Khojein, (in Hindi) [Indian Archaeology: New Discoveries]](https://static.fdokumen.com/doc/165x107/63236ea348d448ffa006abd0/bhartiya-purattava-nai-khojein-in-hindi-indian-archaeology-new-discoveries.jpg)