Awareness, perceptions and purchase intentions towards Islamic general and life insurance products:...

108

1 Awareness, perceptions and purchase intentions towards Islamic general and life insurance products: An empirical study of Australian Muslim consumers Muhammad Abdulsater A thesis submitted to the University of New South Wales In partial fulfilment of the requirement for the degree of Bachelor of Commerce (Honours) University of New South Wales Business School School of Marketing

Transcript of Awareness, perceptions and purchase intentions towards Islamic general and life insurance products:...

1

Awareness, perceptions and purchase intentions towards Islamic

general and life insurance products:

An empirical study of Australian Muslim consumers

Muhammad Abdulsater

A thesis submitted to the University of New South Wales

In partial fulfilment of the requirement for the degree of

Bachelor of Commerce (Honours)

University of New South Wales Business School

School of Marketing

2

ORIGINALITY STATEMENT

I hereby declare that this submission is my own work and to the best of my knowledge it

contains no materials previously published or written by another person, or substantial

proportions of material which have been accepted for the award of any other degree or

diploma at UNSW or any other educational institution, except where due

acknowledgement is made in the thesis. Any contribution made to the research by others,

with whom I have worked at UNSW or elsewhere, is explicitly acknowledged in the

thesis.

I also declare that the intellectual content of this thesis is the product of my own work,

except to the extent that assistance from others in the project's design and conception or

in style, presentation and linguistic expression is acknowledged.

---------------------------------

Muhammad Abdulsater

3

Acknowledgements

I feel grateful to the Milesian wench who, seeing the philosopher Thales continually

spending his time in contemplation of the heavenly vault and always keeping his eyes

raised upwards put something in his way to make him stumble, to warn him that it

would be time to amuse his thoughts with things in the clouds when he had seen to

those at his feet. Indeed she gave him good counsel, to look rather to himself than to the

sky – Michel de Montaigne.

There were many difficulties I faced during the production of this thesis, from the

personal battles fought right through to the unexpected deaths of my grandfather,

uncle and two cousins all within the space of a few months. If this thesis were to be

dedicated to anybody, it would be dedicated to them. Having reached the end of a

seemingly endless journey, I feel a sense of relief, achievement, and personal

satisfaction knowing that I pushed myself and came through triumphant. However,

around me I was surrounded by some of the greatest people I have had the privilege to

meet for whom words cannot do any justice.

First and foremost I would like to acknowledge my supervisor Associate Professor Dr

Mohammed Abdur Razzaque for everything he has done for me. He was like a father

figure who guided me and continually pushed me to greater heights. I thank him for all

the fun and engaging conversations we had about politics and religion and especially for

his help and expertise in enhancing the quality of my work. I would also like to

acknowledge and thank Associate Professor Dr Jack Cadeaux, Dr Rahul Govind and

Associate Professor Dr Nitika Garg for their advice, ideas, suggestions and help during

the course of my studies. I enjoyed studying under their expertise very much indeed and

found their courses a delight to sit in.

Secondly, I would like to acknowledge my fellow honours and PhD friends whom I have

had the utmost privilege and honour to meet this year. My good friends Anthony, David,

Edwina, Michael and Shachi, you guys are incredible. I mean what can I say? I had an

awesome time this year with you all, enjoyed every second with you and learnt so much

from you all. From the PhD peeps, it was a pleasure spending time with you all. I

certainly benefited tremendously from speaking and engaging with you. A special ‘thank

you’ to David Lie, my good friend and brother from another mother, for answering all of

my questions and always being there for me, I appreciate it all. It was a pleasure sharing

the office with Christopher, Jeenat and Yutian. I learnt so much from you all and I

especially enjoyed talking politics with Chris

4

I would like to thank my friends Fatima and Mariam Bazzi and also Mohammed Daher

for supporting me during the journey and always being there for me.

Last but not least, I would like to acknowledge and thank my parents and brothers, for

without them I would not be the man I am today. A special thank you to my mum and

dad, who have always nurtured me, loved me and taught me the value of education and

wisdom. They sacrificed a lot for me and my brothers and I hope to repay them by

making them proud. This is for you. God bless you.

5

Table of Contents

Glossary of Arabic Terms

Abstract

1. Overview 9

1.1. Islamic insurance products …………………………………………………………………………. 9

1.2. Purpose of research ……………………………………………………………………… 10

1.3. Potential contributions of study ……………………………………………………………... 11

1.4. Organization of the thesis ……………………………………………………………. 12

2. Literature review 14

2.1. Rationale and focus ……………………………………………………………………. 14

2.2. Culture and consumer behaviour ………………………………………………………. 15

2.3. Religion and its impacts on consumer behaviour …………………………………. 16

2.4. The nature of Islamic insurance (Takaful) ……………………………….... 18

2.5. Nature of conventional vs. Islamic insurance …………………………………. 20

2.6. Conventional insurance in the light of Islamic principles,

the Sharia law and Muslim Scholars …………………………………………………….. 24

2.7. Does Takaful provide a solution to this problem? ………………. 32

2.8. Consumer attitudes, perceptions and awareness of Islamic

insurance products ………………………………………………………………………….. 38

2.9. Determinants of Islamic insurance demand: General and life ……………… 42

3 The Conceptual Model and the Hypotheses 44

3.1. The conceptual model …………………………………………………………………….. 44

3.2. Formulation of hypotheses …………………………………………………………………. 45

4. Methodology ………………………………………………………………… 48

4.1. Research design ……………………………………………………………….. 48

4.2. Selection of sample ……………………………………………………………….. 48

4.3. Questionnaire design ……………………………………………………………….. 49

4.4. Data reduction ……………………………………………………………….. 52

4.5. Moderation, mediation and moderated mediation …………………………. 54

4.6. Correlation and regression ………………………………………………………………. 55

5.0. Results ……………………………………………………………… 57

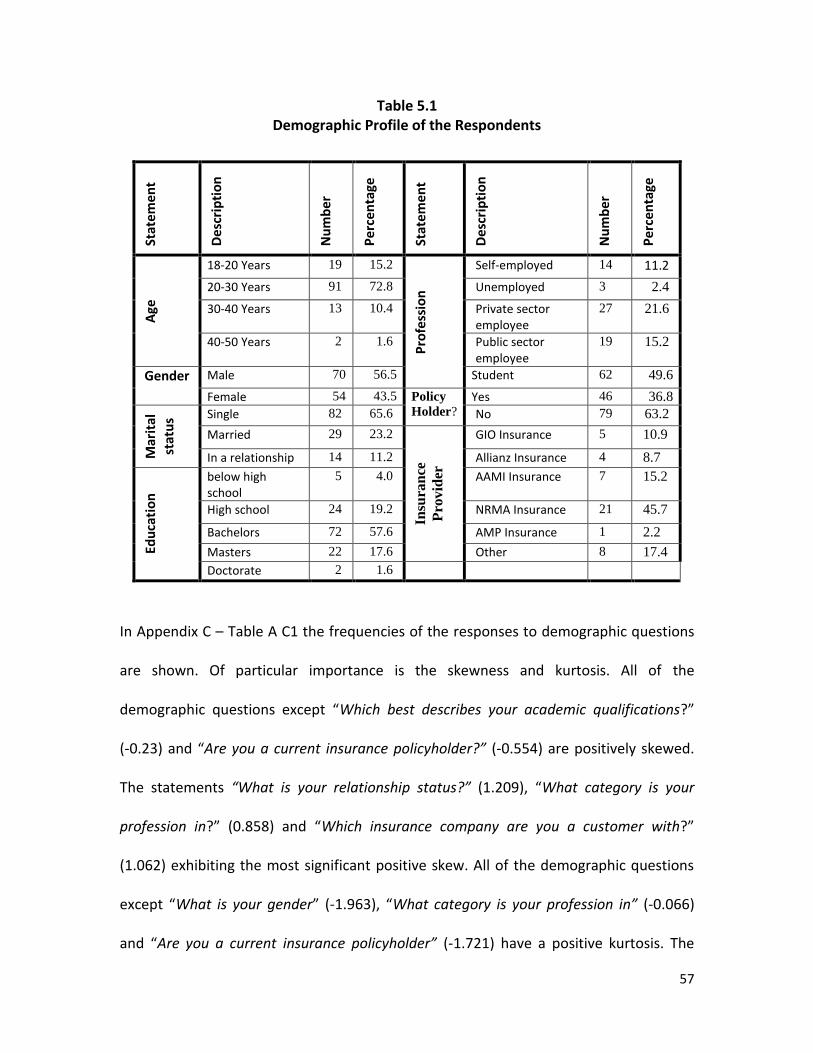

5.1. Descriptive statistics for demographic questions …………………………. 57

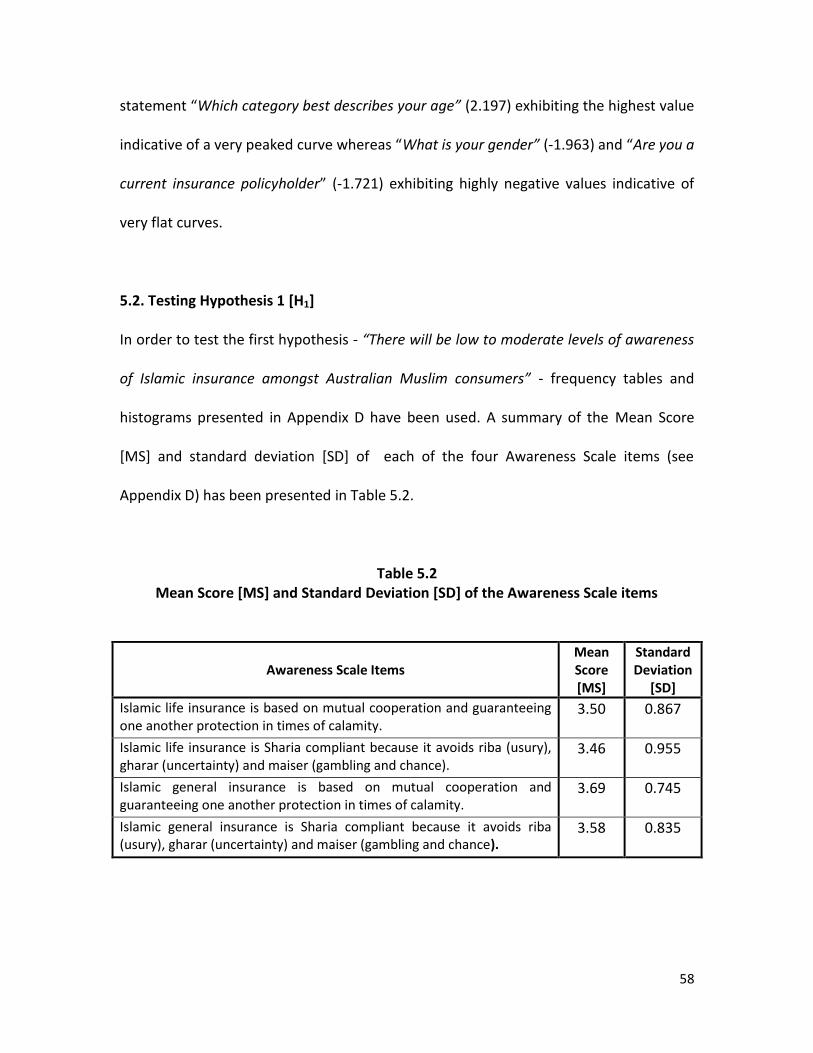

5.2. Testing hypothesis 1 ……………………………………………………………… 59

5.3. Principal component factor analysis ………………………………………….. 60

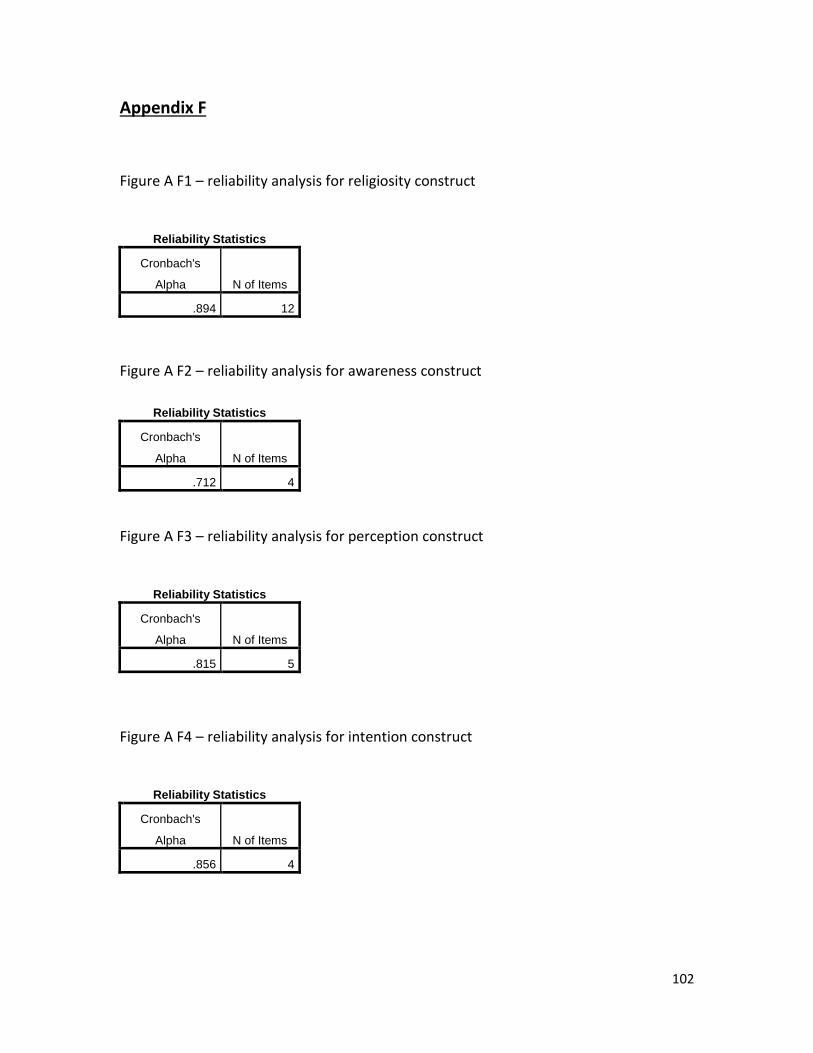

5.4. Reliability analysis …………………………………………………………….. 62

5.5. Moderated mediation analysis ………………………………………. 62

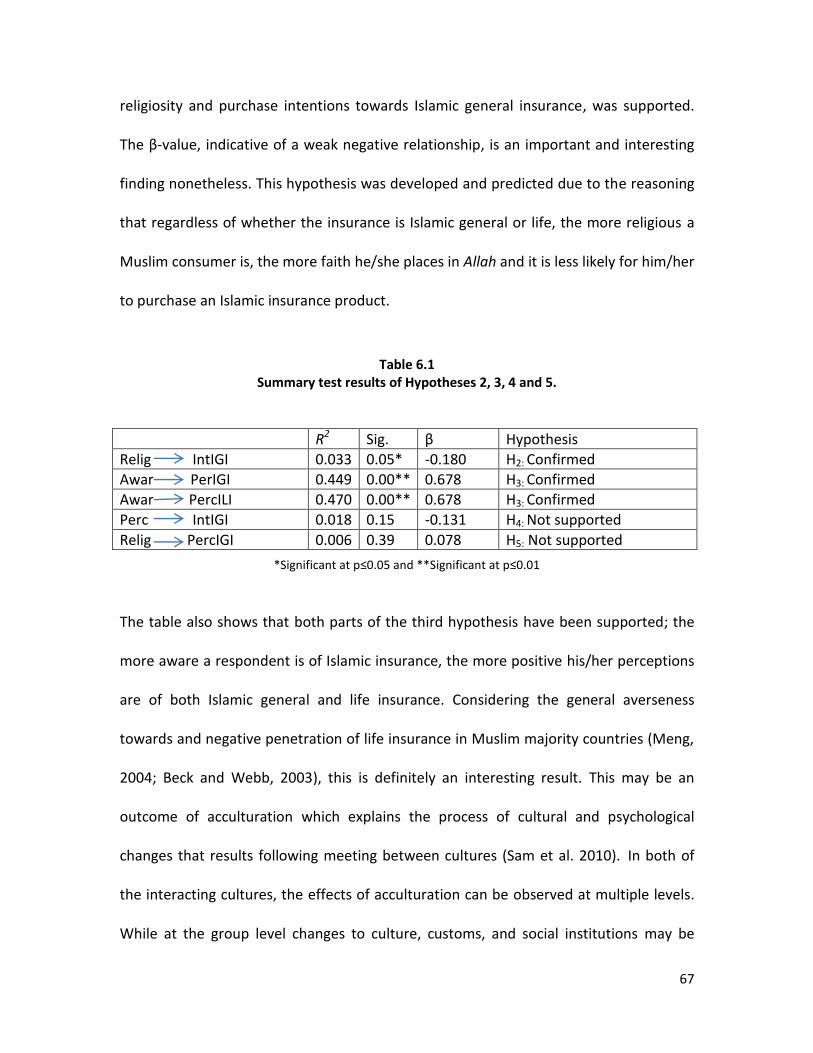

5.6. Testing hypothesis 2, 3, 4 and 5 ………………………………………. 64

6

6.0. Discussion and Conclusion ……………………………………………………………… 67

6.1. Interpreting results ……………………………………………………………… 67

6.2. Implications of the study ……………………………………………………………… 70

6.3. Limitations of the study ……………………………………………………………… 71

6.4. Future research ……………………………………………………………… 72

Bibliography ……………………………………………………………. 73

APPENDIX ……………………………………………………………. 86

7

Glossary of Arabic Terms used in this Thesis

Abu Bakr: Senior companion and father in law of Prophet Muhammad; first caliph of Islam.

Ali: Cousin and son in law of Prophet Muhammad. First caliph according to Shia

Muslims and fourth caliph according to Sunni Muslims

Allah: God

Gharar: Uncertainty

Gharar Fahish: Excessive uncertainty

Gharar Yasir: Minor uncertainty

Hadith: Traditions of Prophet Muhammad (pbuh); includes his sayings and actions

Haram: Prohibited for use or consumption by Muslims

Ijtihad: Independent reasoning to deduce religious edicts

Kafala: To guarantee each other against risk and damage through a joint agreement

based on the “law of large numbers”

Maiser: Gambling or activity involving chance

Mudaraba: A trustee-financing contract where one partner, the financier, gives money to

another the entrepreneur for the purpose of commercial investments

Muhammad: Believed by Muslims to be the last and final prophet and messenger of God.

pbuh: Peace be upon him, mandatory for Muslims to say this whenever Prophet

Muhammad’s name is mentioned.

Quran: Muslims consider the Quran to be the word of Allah revealed to Prophet

Muhammad (pbuh) through the archangel Gabriel

Riba: Interest, usury

Shariah: The moral code and religious law of a prophetic religion.

Shia: Represent the second largest denomination of Islam; it is the short form of the

historic phrase Shīʻatu ʻAlī, meaning followers of Ali who believe Ali should have

been the rightful successor to Prophet Muhammad

Sunni: The largest denomination of Islam. Sunnis are people of the tradition of

Muhammad and the consensus of the Muslim Ummah or ahl as-sunnah

Tabaru: Donation

Takaful: Islamic insurance

Umar: Companion of Prophet Muhammad and second caliph

Uthman: Companion of Prophet Muhammad and third caliph

Wakala: A fee based financing model based on an agency contract whereby the

participant nominates a person or agent to manage his business or right

8

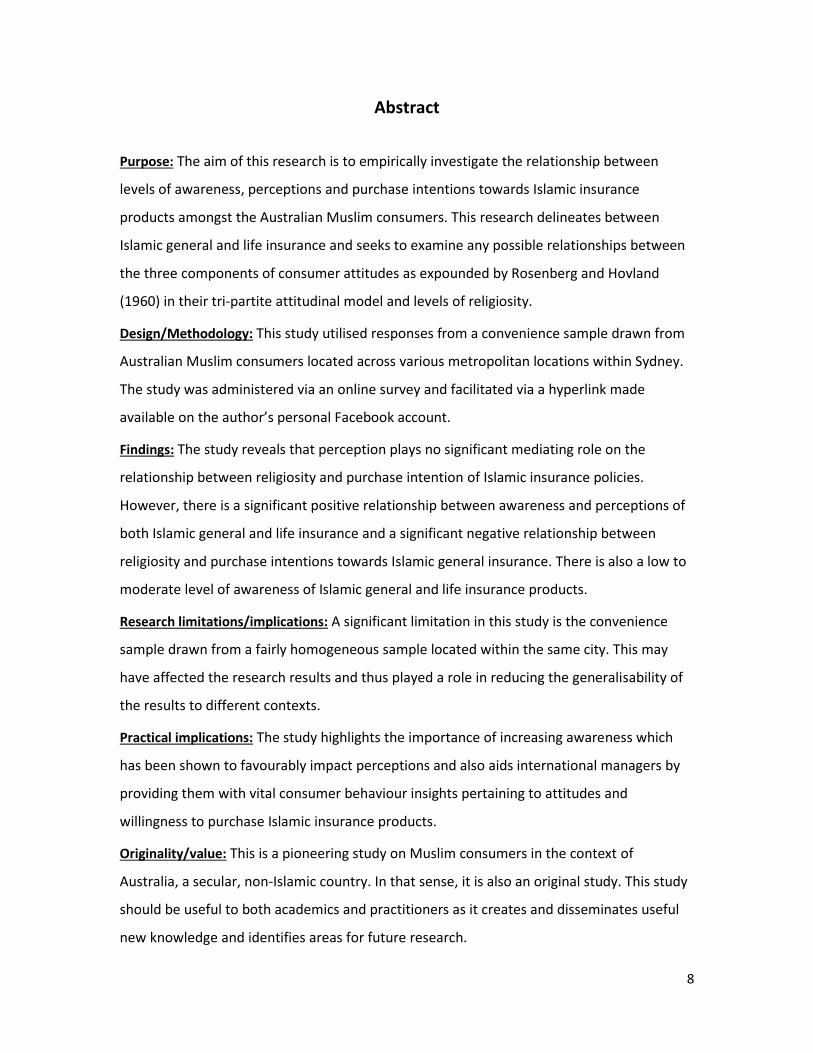

Abstract

Purpose: The aim of this research is to empirically investigate the relationship between

levels of awareness, perceptions and purchase intentions towards Islamic insurance

products amongst the Australian Muslim consumers. This research delineates between

Islamic general and life insurance and seeks to examine any possible relationships between

the three components of consumer attitudes as expounded by Rosenberg and Hovland

(1960) in their tri-partite attitudinal model and levels of religiosity.

Design/Methodology: This study utilised responses from a convenience sample drawn from

Australian Muslim consumers located across various metropolitan locations within Sydney.

The study was administered via an online survey and facilitated via a hyperlink made

available on the author’s personal Facebook account.

Findings: The study reveals that perception plays no significant mediating role on the

relationship between religiosity and purchase intention of Islamic insurance policies.

However, there is a significant positive relationship between awareness and perceptions of

both Islamic general and life insurance and a significant negative relationship between

religiosity and purchase intentions towards Islamic general insurance. There is also a low to

moderate level of awareness of Islamic general and life insurance products.

Research limitations/implications: A significant limitation in this study is the convenience

sample drawn from a fairly homogeneous sample located within the same city. This may

have affected the research results and thus played a role in reducing the generalisability of

the results to different contexts.

Practical implications: The study highlights the importance of increasing awareness which

has been shown to favourably impact perceptions and also aids international managers by

providing them with vital consumer behaviour insights pertaining to attitudes and

willingness to purchase Islamic insurance products.

Originality/value: This is a pioneering study on Muslim consumers in the context of

Australia, a secular, non-Islamic country. In that sense, it is also an original study. This study

should be useful to both academics and practitioners as it creates and disseminates useful

new knowledge and identifies areas for future research.

9

CHAPTER 1

Overview

1.1 Islamic Insurance Products

Islam is a complete code of life for Muslims. For everything they do, purchase, use or

consume, Muslims seek to learn if their proposed action is permissible from the

viewpoint of Islam. Purchasing a conventional insurance policy, a common practice in

modern times, has long been a contestable issue in Islam as religious scholars interpret

it differently. Most Islamic scholars, however, tend to consider it un-Islamic. But given

the nature of the modern economic system, it often becomes mandatory for Muslims to

purchase certain types of insurance policies, particularly policies involving automobiles,

home and contents, boat etc. especially if they are living in non-Muslim countries. There

has also been a latent demand for an ‘Islamic’ type of insurance among the new

generation of Muslims. Consequently, there have been efforts to ‘Islamise’ insurance

which resulted in the development of ‘Takaful’ - a co-operative system of reimbursing

people and companies concerned about hazards when they incur loss out of a fund to

which they agree to donate small regular contributions managed on behalf by an

operator (Bhatti, 2011). Entrepreneurs offering these products claim that these are

permissible according to Islamic tenets. However, talking to the prospective buyers of

such products, the researcher tends to believe that there is lack of understanding and

knowledge of these products among Muslims which may have affected their perception

of these products and their subsequent adoption.

10

1.2 Purpose of the research

The purpose of this research is to gain an empirical understanding of knowledge,

perceptions and attitudes of Australian Muslim consumers towards Islamic insurance

products and to examine any possible relationships between these constructs (i.e.,

knowledge, perceptions and attitudes) and consumer’s level of religiosity. The current

research diverges from previous studies as it deliberately distinguishes between

attitudes and subsequent purchase intention for general non-life insurance and that for

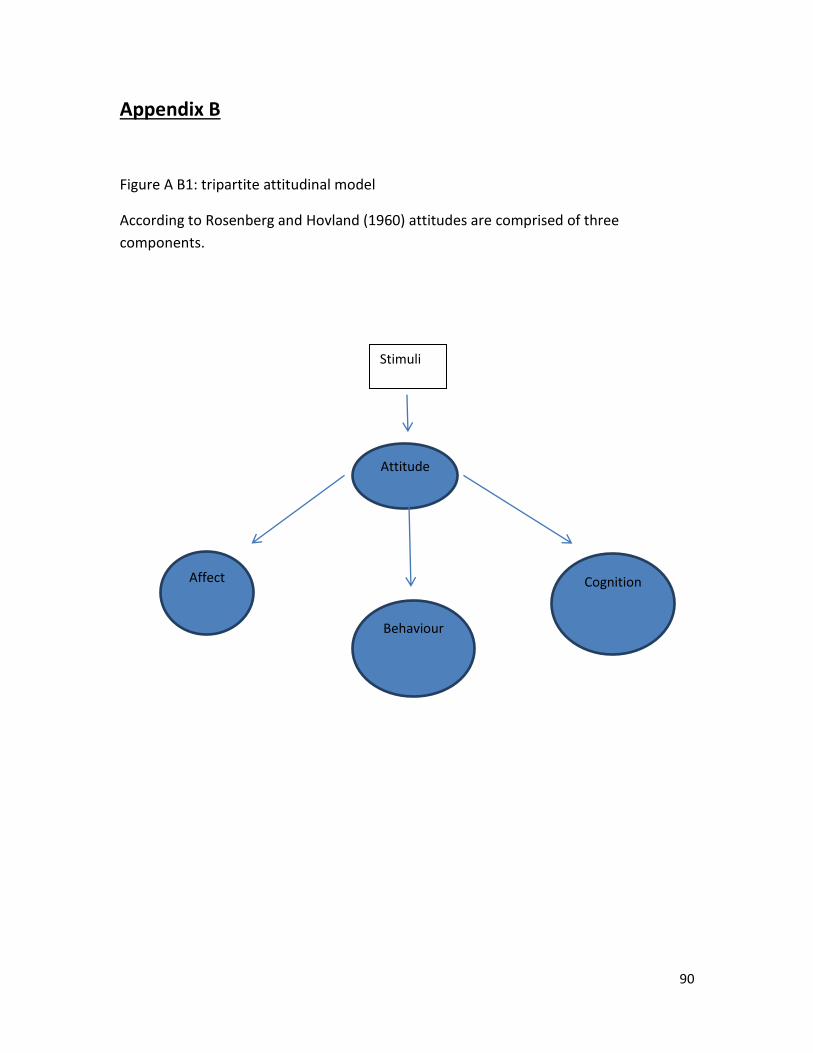

life insurance. To measure consumer attitudes the current study uses Rosenberg and

Hovland’s (1960) (Appendix B, Figure B1) tri-partite model that views attitude as a

composite of a cognitive component (knowledge and awareness of a product), an

affective component (emotions and feelings about a product) and a conative or

behavioural component (likelihood or tendency to act or behave with regard to the

product). It must, however, be noted that this study is focused on the measurement of

consumer knowledge (cognitive component) and consumer perceptions (affective

component). The study also measures consumers’ level of religiosity using a religious

commitment inventory scale adapted from Razzaque and Chaudhry (2013) to examine a

possible link between higher levels of religiosity and willingness - current or potential -

to consume both Islamic general and life insurance products.

Muslims constitute about a quarter of world’s total population and therefore gaining a

better understanding of the consumption behaviour of Muslims cannot be

overemphasised (Shafie and Othman, 2006). While there has been an increased

11

research interest in ‘Halal’ meat and food products (Harran and Low, 2008) in recent

times, many other products/services, particularly financial products that have become

part and parcel of secular contemporary living have received little research attention. It

is not clear if consumption or use of these products is permissible for Muslims. The

current research makes a modest attempt to shed some light on one such financial

product – Islamic insurance.

1.3 Potential Contributions of the Study

The current research is likely to make both theoretical and practical contributions

towards the understanding of Islamic insurance as a phenomenon; resolution of the

conflict between the Muslim consumer psyche; and its adoption and diffusion as a

popular component of contemporary living. A new generation of researchers have

become engaged in understanding what makes different secular products/services such

as financial products non-permissible for Muslim consumers and what can be done to

make them permissible (and if launched, to make them popular). The current study

would definitely fall in that category. From a theoretical standpoint, the research is

likely to generate new knowledge about a topic hitherto neglected by the researchers

and motivate new researchers to take interest in this area.

Islamic insurance is a relatively new concept. This research can be of practical

importance to multinational companies seeking to expand their Islamic finance

products, particularly Islamic insurance (Takaful) into developed countries such as the

12

USA, the UK and Australia where there is a sizeable Muslim market. By providing insights

into perceptions, attitudes and willingness of Muslim consumers towards the purchase

of Islamic insurance products this empirical research may provide some food for

thought for managers seeking expansion into those non-Muslim countries.

1.4 Organisation of the Thesis

The thesis is organised in six chapters. This introductory chapter (Chapter 1) is followed

by Chapter 2 which presents a critical review of the literature and discusses issues such

as religion and its impacts on the behaviour of Muslim consumers; nature of Islamic

insurance commonly known as ‘Takaful’ in Arabic (لتكافل) and conventional insurance

products. It also highlights relevant Islamic principles and presents a scholarly debate on

the permissibility of conventional insurance in Islam. It then discusses if Islamic

insurance or Takaful is a solution to this problem. The remaining parts of the chapter

discusses extant literature on consumer attitudes, perceptions and awareness of Islamic

insurance products and ends with reviewing the determinants of Islamic insurance

demand and the delineation between demand for general and life insurance.

Chapter 3 discusses the conceptual model used in the research and the five hypotheses

developed on the basis of the literature analysed in Chapter 2. The Research

methodology has been discussed in Chapter 4. This chapter discusses the research

design including the sampling procedure, data collection method, operationalisation of

variables, the research instrument and data cleaning and data reduction procedures.

13

The questionnaire discusses the principal component factor analysis, moderation,

mediation followed by correlation and regression analyses of the research data. Chapter

5 is devoted to the presentation of the results of the study. Finally, Chapter 6, the

concluding chapter of the thesis is devoted to discussing the results, practical

implications of the study, limitations of the study and possible future research in this

area.

14

CHAPTER 2

Literature Review

2.1 Focus and Rationale This chapter reviews extant literature with a view to explore several key facets within

the marketing and Islamic finance field of inquiry. As the research focuses on Muslim

consumers’ attitudes, perceptions and awareness of Islamic insurance products, the

review specifically looks at those research undertakings that are of particular relevance

to this investigation both in terms of consumer behaviour and Islamic insurance.

In order facilitate a comprehensive and holistic understanding of the research topic;

consumer behaviour literature will be examined to show the influence of religion on

consumer decision making behaviour. This might reflect the attitude of Australian

Muslim consumers towards a secular financial product, generally viewed as

controversial and un-Islamic by Muslims, that has been made compliant to Islamic

tenets and as such, permissible for Muslims. A review of the Islamic finance, banking

and insurance literature will foster an understanding of what it is exactly that results in

positive consumer attitudes. This includes defining Takaful, understanding why

conventional insurance has been viewed as non-permissible for Muslim consumers and

also looking at how Takaful overcomes the controversy and presents a permissible

alternative. Finally, after providing a contextual backdrop to our research, the literature

review looks at studies measuring individual consumer attitudes, knowledge and

perceptions of Islamic finance products.

15

2.2 Culture and Consumer Behaviour

The body of literature dealing with the definitions and influence of culture and

subculture are both vast and well researched in fields such as psychology (Allport, 1967)

and sociology (Anderson, 1970). Extant consumer psychology research discuss the

impacts of culture on cognitive processes (independent versus interdependent self-

construal) which form the basis of consumer choice (risk seeking versus risk averse),

judgments and decision making (cultural influence through reasons offered to justify

choice) (Mandel, 2003; Briley, Morris and Simonson, 2000). Ever since Johar et al (2006)

urged academic researchers to inquire further into the impacts of culture on consumer

behaviour there has been a plethora of literature devoted to examining the influence of

culture on the consumption of consumer goods (De Mooij, 2001), services (Kwok and

Tadesse, 2006) and life insurance (Chui and Kwok, 2008). Although researchers (e.g.,

Browne and Kim, 1993; Beck and Webb, 2003; Outreville, 1996) have comprehensively

shown the many determinants of life insurance demand around the world, there is a

lack of research examining the relationship between religion and consumer attitudes

towards both general and life insurance. This is precisely the contribution that this

research intends to make to the relevant literature. Previous investigators such as

Crosby and Stephens (1987) maintain that life insurance is inherently a difficult-to-

evaluate product even after consumption and is inherently complex and abstract. Leung

et al (2005) have shown that under conditions of uncertainty, cultural affiliation has a

strong impact on consumer behaviour. Based on these two studies, it makes sense to

argue that religion just like culture (in Leung et al 2005) is likely to have a strong impact

16

on consumer intentions and behaviour towards Islamic insurance consumption,

particularly life insurance. This postulation has been confirmed by Chui and Kwok (2008)

who noted that religious people tend to purchase less life insurance if they believed

they were going against God’s decree or not having faith in God’s protection.

No research in consumer behaviour is complete without a thorough investigation into

the influence of culture and subculture on consumer psychology and purchase decisions

(Shaw and Clarke, 1998; Schouten and McAlexander, 1995). These influences also

extend into affecting consumer motives (Chang, 2005). Culture includes beliefs, values,

customs, technologies and knowledge that one generation passes onto the next and

subculture is comprised of nationality, race, geography and religion (Otts, 1989; Alam,

Mohammed and Hisham, 2011).

2.3 Religion and Consumer Behaviour

Religion yields the greatest influence over consumer decisions and actions on an

individual and societal level (Kotler, 2000; Mokhlis, 2009). This notion has been further

reinforced by the fact that Islam is not strictly a doctrinal religion based on a set of

beliefs (Ozalp, 2004). For Muslims, Islam is a complete way of life that governs and

guides each and every action of its adherents (Ozalp, 2004). According to Quranic

injunctions chapter 17 verses 26-27 Muslims are implored and encouraged to spend

only in the way of God and be not excessive in expenditure or consumption (Alam,

Mohammed and Hisham, 2011). Exploring the influence of religion on purchase decision

17

making and levels of involvement, Yousaf and Malik (2012) show that consumer

behaviour pertaining to the level of involvement will vary according to the degree of the

consumer’s religiosity. It is now known that highly religious Muslim consumers are less

fashion conscious, less recreational and less impulsive in their shopping behaviour

(Yousaf and Malik, 2012). They are also more likely to be influenced in their purchase

decisions by social factors and are more conscious about the lifestyle they lead (Yousaf

and Malik, 2012). This means they are less confused by factual information over choices

when comparing alternatives in their considered set. These results are starkly

juxtaposed to less religious consumers who appear to be less conscious about their

lifestyles and more confused by information over choices (Yousaf and Malik, 2012).

Further research on the relationship between religious consumers and their interaction

with monetary cost (Yousaf and Malik, 2013) is also quite illuminating. According to

Kamaruddin and Kamaruddin (2009) and Sood and Nasu (1995) consumers who exhibit

higher degrees of religiosity tend to struggle to achieve fair value for their money spent

and also spend considerably more on products that are on sale. Research has shown

that deeply religious consumers also tend to actively seek out and propagate

consumption related information before making final purchase decisions (Hirschman,

1981; Afshan et al, 2011; Razzaque and Chaudhary, 2014). More religious consumers

also tend to be more brand loyal as they try to build environments that foster certitude

and risk aversion which serves to lower brand switching behaviour (Swimberghe et al,

2009; Fontaigne et al, 2005). The interrelationship between deeply religious consumers

and their interaction and tolerance of certain types of appeals in advertisements has

18

also been investigated. Religious consumers have been found to display annoyance

towards sexually charged advertisements featuring nudity and profanity (De Run et al,

2010). Furthermore, consumer behaviour research has extended into the domain of

family decision making dynamics and reported that deeply religious households tend to

exhibit conventional gender roles while the less religious households exhibit joint

decision making (Delener, 1994; Kahle et al, 2005).

2.4 The nature of Islamic insurance (Takaful).

For many people in both the Muslim and non-Muslim world, Islamic finance continues

to be a poorly understood concept despite its rapid advancement into a multi-billion

dollar growing segment (Hamid and Nordin, 2001). In 1997 a nationwide survey was

carried out in Britain and the results showed that 74% of respondents considered their

religion important with 80% reporting visiting religious centres every week (Modood et

al, 1997). With over 1.3 billion adherents to the Islamic faith representing 20% of the

world’s population expected to reach 30% by 2025 (Shafie and Othman, 2006) it is

important that alternative religiously compliant financial products and services are

considered, developed and offered to Muslims. There is no reason why insurance

cannot be presented as an alternative for the modern Muslim consumers looking to

engage themselves in the financial community whilst not foregoing central religious

principles (Zaher and Hassan, 2001). There are currently over 200 Islamic banks

functioning over 70 countries sprawled across both Muslim and non-Muslim markets

with the first operator established in Sudan (Hassan and Lewis, 2007; Ahmad, 1991;

19

Jaffer, 2007). As of 2005, the Islamic insurance industry was worth over $2 billion

growing at a rate of over 20% annually in recent years and projected to reach $7 billion

by 2015 (Jaffer, 2007). According to reports from Ernst and Young and Bank Negara

Malaysia premiums surpassed $8.9 billion in 2010 and are expected to reach $12.5

billion by 2015 with $30 billion in funds (Hamid, 2010). There are now an estimated 150

Islamic insurance companies operating across 22 nations (Hassan and Lewis, 2007;

Archer, Karim and Nienhaus, 2011). Takaful may be viewed as an unconventional form

of insurance or “cooperative mutual insurance” where members are both the insured

and the insurers (Anwar and Hussain, 1994; Monger and Rawashdeh, 2008). Takaful, a

derivative of the Arabic word kafala, means to guarantee each other against risk and

damage through a joint agreement based on the “law of large numbers” whereby

shared responsibility is used to hedge against risk. Hence, Takaful is mutual protection

and indemnity, implying that one party (insurer) provides help to the other party

(insured) but is also indemnified by them (Bakar, 2011). This interpretation has been

endorsed by many notable scholars such as Bekkin (2007), Garigiparthy (2007), Anwar

and Hussain (1994), Siddiqi (1985) and Maysami and Kwon (1999). The primary function

of Takaful is to protect people from risk and conduct business transactions according to

Sharia principles. Furthermore, these business transactions are to be conducted on a

cooperative basis whereby all functions including underwriting, reinsurance, marketing,

management and corporate governance are to be strictly executed according to the

spirit of Sharia principles (Garigiparthy, 2007; Bakar, 2011).

20

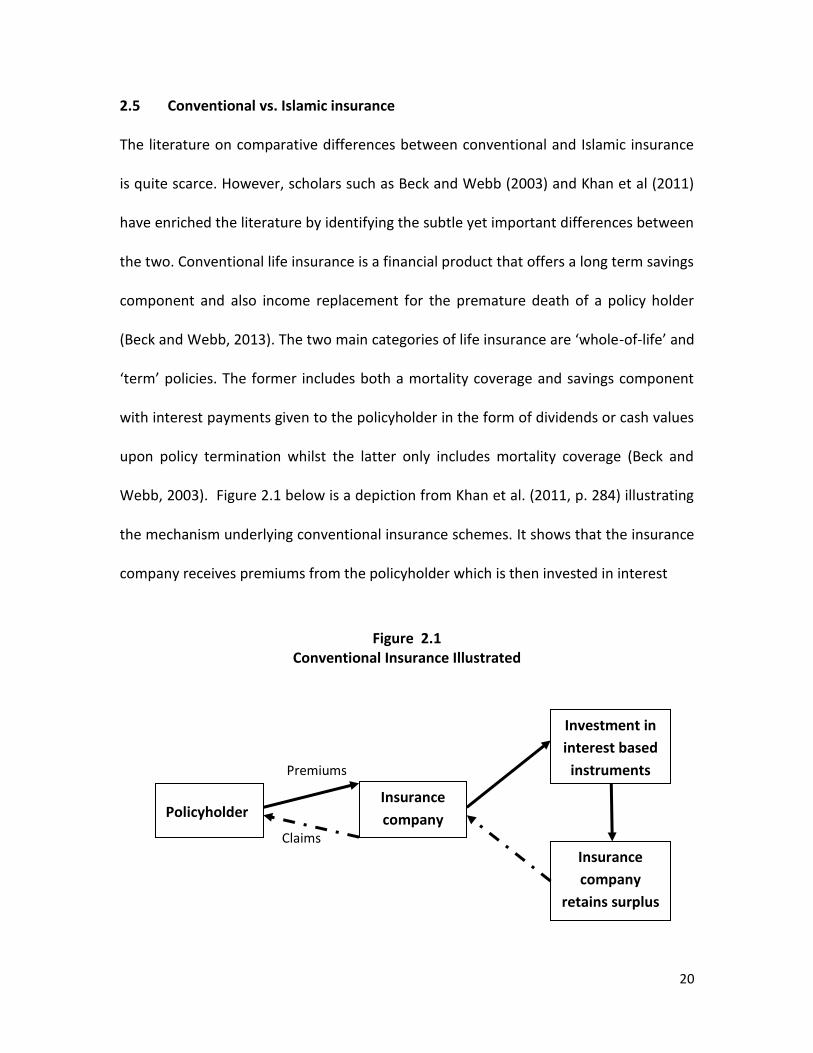

2.5 Conventional vs. Islamic insurance

The literature on comparative differences between conventional and Islamic insurance

is quite scarce. However, scholars such as Beck and Webb (2003) and Khan et al (2011)

have enriched the literature by identifying the subtle yet important differences between

the two. Conventional life insurance is a financial product that offers a long term savings

component and also income replacement for the premature death of a policy holder

(Beck and Webb, 2013). The two main categories of life insurance are ‘whole-of-life’ and

‘term’ policies. The former includes both a mortality coverage and savings component

with interest payments given to the policyholder in the form of dividends or cash values

upon policy termination whilst the latter only includes mortality coverage (Beck and

Webb, 2003). Figure 2.1 below is a depiction from Khan et al. (2011, p. 284) illustrating

the mechanism underlying conventional insurance schemes. It shows that the insurance

company receives premiums from the policyholder which is then invested in interest

Figure 2.1 Conventional Insurance Illustrated

Premiums

Claims

Investment in

interest based

instruments

Insurance

company

retains surplus

Policyholder Insurance

company

21

bearing financial instruments that provide a profit which is retained by the company as

surplus to be used to meet claims made against the company.

By contrast, in general or non-life Islamic insurance diagrammatically illustrated

(Maysami and Kwon, 1999) in Figure 2.2 below, coverage is offered on fire, liability, car,

marine, fidelity and even crop insurance whereby premiums are pooled into a fund

managed by the insurer. Funds are then invested in islamically permitted financial

instruments and institutions with the investment income less the investment expenses

Figure 2.2 Islamic Insurance Illustrated – 1

Insured Insurer

Premiums Fund managed by

insurer

Net investment income

Payments, expenses and

reserves

Surplus

Shareholders

50%

50%

22

channelled back into the fund. Expenses are then deducted by the insurer with the

remaining funds allocated to reserves. Any balance remaining is surplus and is shared

on an agreed 50-50 basis between the insured and the insurer (Maysami and Kwon,

1999).

The obvious difference being that Islamic life insurance in both the joint venture

mudarabah and fee based waqala financing models, surplus is distributed back to the

policyholder and funds are invested cautiously into non-interest bearing financial

instruments. This is evident in Figure 2.3 (Maysami and Kwon 1999, pp. 116) which

depicts the mechanisms of Islamic life insurance policies.

Figure 2.3 Islamic life Insurance Illustrated – 2

-

-

Insured Insurer

Premiums Fund managed by

insurer

Individual account

Special account

Net investment

income

Payments, expenses

and reserves

Surplus Shareholders 30%

70%

23

One can clearly see that premiums are deposited into two separate accounts, an

individual one for savings and investment and a special one where premiums are built

up as reserves for the heir of the insured in the case of premature death. Funds from

the individual and special account are then invested in the form of mutual funds,

primarily the stock of Islamic financial institutions. Exceptions are, however, made

pertaining to non-Islamic financial institutions so long as their goods and/or services are

permitted within Islamic law. When sharing profits from investments, the insurer only

receives a share from the net income whilst the special and individual accounts remain

untouched. Operating and administrative expenses are deducted from investment

income and upon the death of the insured; the beneficiaries receive the sum of the

funds deposited in the special and individual accounts plus the 70% of the surplus.

Finally, in order to claim death benefits, only the proof of death is required to be

submitted whereas the cause of death is of little importance within this context as death

from the Islamic standpoint is considered to be the decree of God which lies outside

one’s direct loci of control (Maysami and Kwon, 1999).

2.6 Conventional insurance in the light of Islamic principles, the Sharia law and Muslim Scholars

Ever since the Islamic scholar and jurist Muhammad Amin Ibn Abidin (1783-1836 AD)

wrote about the legality and meaning of insurance, the status and permissibility of

insurance within Islam has been thoroughly discussed (Anwar and Hussain 1994, pp. 13-

15; Mankabady, 1989). Conventional insurance involves an exchange contract whereby

24

the policyholder, i.e., the insured, pays the insurer an amount of money called the

premium which provides protection and coverage of up to a certain amount in the case

of unforeseen circumstance. The premiums accumulated are then reinvested in several

asset classes in which their returns are used to make payments to insured parties.

Depending on the risk underwritten, most insurance companies reinvest premiums in

highly liquid asset classes that are also highly marketable securities such as bills of

exchange and certificates of deposit (Viney, 2007). It is clear that conventional insurance

is a form of risk management whereby the insured is essentially purchasing peace of

mind and security by paying money in exchange for coverage against an uncertain and

contingent loss (Maysami and Williams, 2006). Hence, the way insurance practices are

carried out by modern conventional insurance companies is not permissible for

consumption or use by the Muslim consumer because it violates Islamic principles. What

is permissible, however, is cooperative insurance (Mankabady, 1989) whereby the

member is also the owner of the fund whereby if one member were to suffer an

expected loss or damage, he/she receives financial benefit from a common pool of

funds. This pool is comprised of individual contributions of all the participating members

(Abdul-Wahab, Lewis and Hassan, 2007). Islamic insurance is expected to influence the

demand and supply for insurance in Muslim communities.

Early Islamic scholars such as Ibn Abidin rejected the concept of insurance on the basis

of the mode of exchange, the possibility of riba, gharar and maisir (Anwar and Hussain

1994, pp. 1316; Mahmoud, 1991; Khan et al, 2011). This has also been endorsed by

25

Khorshid (2013) who viewed insurance not only unnecessary but also un-Islamic for the

same reasons indicated above. Furthermore, Archer, Abdel-Karim and Nienhaus (2011)

contend that any contract must avoid uncertainty in the buying and selling of assets and

also usury which involves lending and borrowing of money for a premium. According to

Khan and Porzio (2010) gharar is an outcome linked to purchasing or consumption

which is ambiguous or uncertain like the sale of a fish still in the ocean. For Muslims, this

issue is only compounded when they lack the relevant product knowledge or have little

control over the purchase outcome. A re-examination of the consumer behaviour

literature reveals that the requirement for seeking certitude and developing risk

aversion behaviour is very much a fact within highly religious Muslim communities

(Miller, 2000). This view has also been supported by Mokhlis (2008) and Saroglou and

Dupuis (2006) who found highly religious consumers to be more risk averse, meaning

they are less likely to engage in risk taking behaviour and subscribe to certain values

that ensure more certitude is practiced. Finally, this view is further reinforced by the

fact that according to the Hadith of Muslim (10:3614) and Muwatta (31:75) (Tarjumana

and Johnson, 1982), Muslim consumers are discouraged from taking unnecessary risks.

If a contract does not avoid the characteristics mentioned above then it violates sharia

principles making the conventional insurance policy unacceptable to Muslim consumers.

When the legality, i.e., meaning and status of insurance within Islamic tradition, is

examined, one must refer to the two most fundamental and authoritative sources

within Islam, the Quran and the Hadith. Muslims consider the Quran to be the word of

Allah revealed to Prophet Muhammad through the archangel Gabriel and as such,

26

infallible, while the Hadiths are the collected sayings, actions and traditions of the

Prophet Muhammad (pbuh) (Arham, 2010).

Any attempt to understand the role and place of insurance within the Islamic tradition

requires attention to a basic dimension that characterises the followers of Islam:

Muslims do not represent a homogeneous religious group. Just like other major religious

traditions, for example Protestantism and Catholicism within Christianity or Hinayan and

Mahayan in Buddhism, Islam also has many schools of thoughts. The main two are the

Sunni’s and the Shiite’s. According to comparative religion expert and theologian

Mehmet Ozalp (2004) approximately 85% of the Muslims are Sunni; only 13% are Shiites

with the remaining 2% classified as small groups of fringe adherents. Both the Sunni and

the Shiite schools of thought are unanimous in accepting the fact that the Quran is the

ultimate authoritative text in Islam followed by the traditions of Prophet Muhammad

(pbuh). They both share similarities in practically all the essential articles of faith

including prayer, fasting, giving of alms, pilgrimage to Mecca and belief in the unity of

Allah, all his messengers and the divine books sent to mankind (Ozalp, 2004). However,

these similarities notwithstanding, there is a serious theological chasm and ritualistic

differences between the two major sects that go back to early Islamic history. After the

demise of Prophet Muhammad (pbuh), the Shiites took the prophet’s son-in-law and

cousin Ali to be his successor and thus, the legitimate leader of the Muslims. However,

the Sunni’s claim that the community had arrived at a consensus and selected the

prophet’s companion Abu Bakr to be the legitimate leader of the Muslims (Ozalp, 2004).

27

Further discussion on the specifics of this split is beyond the scope and focus of the

current research; but it is important to note that due to this division, major

jurisprudential issues arise pertaining to every fine detail that governs the life of a

Muslim.

According to Muslehuddin (1979), insurance is based on usury and thus clashes with the

Quranic injunctions and prophetic traditions. Permissible financial or business

transactions within the framework of Islamic law must be interest free (Ahmad, 1967).

According to the Quran in chapter 2 verse 275 “those who swallow down usury cannot

arise except as one whom satan has prostrated by his touch does rise. This is because

they say that trading is like usury and God has allowed trading and forbidden usury”;

several subsequent verses (i.e., 276, 278, 280 and 282) in the same chapter clearly show

that usury is forbidden. Having a conventional life insurance policy for a Muslim is not

permissible because the beneficiary of that policy will receive more than what the

original insured paid up until the time of death (Wahab, Lewis and Hassan, 2007).

Furthermore, this is evident when conventional insurance companies use premiums to

re-invest in interest based financial instruments or institutions or even loan their funds

for interest income (Wahab, Lewis and Hassan, 2007). This occurs because all insurance

policies have an inbuilt savings and investment component whereby the insurer

reinvests the insured’s premiums (Wahab, Lewis and Hassan, 2007). The Quran in

chapter 2 verse 219 also forbids gambling and activities involving chance and

uncertainty: “they ask you about games of chance and intoxicants: say in both of them

28

there is a great sin and means of profit for men and their sin is greater than their profit”.

Life insurance resembles a gamble or activity of chance whereby the family of the

deceased expects a large enough pay out. This expectation and hope for such a windfall

violates Quranic injunctions against partaking in activities of chance or gamble

(Mohammad, 1993). Furthermore the interests of both parties (i.e. the insurer and

insured) are utterly opposed and both parties are oblivious to their respective

responsibilities and rights up until the occurrence of the indemnified incident (Lewis,

2005). The insured is betting his/her premiums on the condition that the insurer will

make a payment should a covered event occur. Conventional life insurance is

considered impermissible in Islamic law because it places a value on something that is

invaluable or in other words is paying for a loss of human life (Ali, 1989). According to

Mohammad (1980) life insurance is antagonistic towards the fundamental and central

Muslim belief of pre-destination or fate. By insuring one’s life, the insured is actually

involved in pre-determining his/her death and future earnings by hoping a large payout

will be made to his/her heirs (Siddiqi, 1980). The Quran makes it clear in chapter 31

verse 34 that “Only Allah is the determiner and knower of all things including what one

will earn in the future and also their time and place of death”. Hence, it is clear that

both the concepts of riba and maiser are clearly and explicitly forbidden in the Quran.

Both the Sunni and the Shiite schools of thought are unanimous on this and agree on

forbidding business transactions involving usury and gambling and/or chance because

the Quran is the ultimate source of jurisprudence and authority for Muslims. Gharar,

the last element in this discussion explaining the unacceptability of conventional

29

insurance for Muslims, has its roots in the Hadith. According to the Hadith compilations

namely, Sahih Muslim, Sunan Abu Daud and Malik’s Muwatta, prophet Muhammad

(pbuh) forbade the Muslims in selling anything with elements of uncertainty (Anwar and

Hussain 1994, pp. 1316; Yousaf and Malik, 2012). According to Sahih Muslim (10:3614)

the prophet forbade transactions involving ambiguity and chance while according to

Malik’s Muwatta (31:75) (Tarjumana and Johnson, 1982) the prophet forbade a

transaction between two men over the price of a sheep due to the risk and uncertainty

in the conditions stipulated. Siddiqi (1985) contends that life insurance involves gharar

and maintains that any transaction involving elements of uncertainty is forbidden in

Islam.

Muslim individuals, businesses and even states and nations are discouraged from

engaging in transactions involving ambiguous and ill-defined outcomes whilst expecting

predefined financial gains (Maysami and Kwon, 1999). This stems from the knowledge

that the benefits to be received by the insured depend upon the occurrence of an event

which is simply not known at the time of signing the contract. Hence, it is clear that

according to Sunni traditions, conventional insurance is not permissible for Muslims. The

Shia school of thought, on the other hand, defines gharar differently. The Shiites view

gharar as a concept on a continuum ranging anywhere between ‘gharar yasir’ or

tolerable/minor uncertainty and ‘gharar fahish’ or excessive uncertainty and the

legitimacy of a business transaction is decided depending on the degree of uncertainty

(Rashid, 1993). This explanation is acceptable to the Shia Muslims as it is in line with the

30

Shia tradition of ijtihad, meaning independent reasoning to arrive at religious edicts and

conclusions. It is, however, important to note that the prophetic tradition does not

forbid transactions that are indispensable to human needs and which cannot be free

altogether from hazard, therefore these minor uncertainties are “tolerated” and

deemed permissible (Jensen, 2008). Muhammad Hussein Fadlallah, a leading Lebanese

religious scholar and jurist, was of the opinion that if the riba and maiser components of

insurance were fully removed, the presence of gharar yasir would not make insurance

unacceptable (Jensen, 2008). When Islamic jurists distinguish between the types of

gharar they also pay attention to four conditions which invalidate a contract. These

conditions are:

1) Uncertainty is excessive;

2) The contract must be a sale and not a gift;

3) If the uncertainty affects principal components of the contract and

4) If the contract meets a need that cannot otherwise be met then the contract

will not be deemed invalid based on that level of uncertainty.

Jensen (2008) also cites previous studies (p.827) where religious edicts issued by

prominent scholars including Sunni Jurist Yusuf Al-Qaradawi and Iraq’s most prominent

Shiite cleric Ali Sistani allow Muslims living in non-Muslim countries to get involved in

many forms of conventional finance. Therefore as mentioned before, insurance is a

form of risk management strategy whereby the insured is paying money to receive a

certain level of coverage against a contingent and uncertain loss. There is no guarantee

of a return for the insured, what is being paid for is intangible peace of mind. In the case

of no claims being made to the insurer, from one point of view a tragedy has been

31

avoided but it also means that the insurer receives money from the insured without

having to make payment (Korshid, 2013).

Khan (1979) has argued that according to some Hadith such as the one present in Sahih

Al Bukhari (8:725) it is preferred and highly recommended that one leave his/her family

in a healthy financial position as opposed to leaving them needy and destitute. Many

scholars such as Mohammad (1993) have noted that according to some Muslim scholars

conventional insurance products including life insurance are all about safeguarding the

financial interests and security of those dearest to you so as not to leave them destitute

or in need after the primary income earners demise. Furthermore, life insurance does

not contain gharar because the major elements underlying the contractual agreement

are known and that surely one day the insured will pass away (Mohammad, 1993). Life

insurance does not involve maiser or does not contradict the insured person’s belief in

pre-determination/fate because the former one is hoping for a gain in something and

the latter one is trying to pre-determine something; also it does not contain riba. The

primary objective of life insurance is not to gamble or pre-determine anything but

rather through the depositing of premiums, the individual is, in fact, protecting his/her

family against adverse future risk.

2.7 Does Islamic Takaful provide a solution to this problem?

Takaful, unlike the primarily profit-oriented conventional insurance, is interested in

sharing the risks associated with business transactions equally (Monger and Rawashdeh,

2008). This form of Islamic insurance covers both life and general insurance and

32

operates very similarly to conventional insurance (Anwar and Hussain, 1994). Takaful

exists primarily to cover and protect the insured against potential loss resulting from

specified calamities. It is based upon a financial philosophy of co-operation, mutual

assistance and shared and equal responsibility (Ahmad, 1991). The tabaru that the

insured contributes will vary according to the value of the asset under coverage. The

operator (Islamic insurance company, directors and shareholders) will then reinvest the

tabaru funds with the profits allocated between the fund and management according to

principles of mudaraba (a trustee-financing contract where one partner, the financier

gives money to another the entrepreneur for the purpose of commercial investments)

(Monger and Rawashdeh, 2008). In the case of indemnity, the money will come out of

the tabaru fund. In fact, this is how gharar and riba are avoided. Through tabaru, each

member sincerely pledges to transfer a portion of their insurance instalments to

another member as a donation in order to pay out a compensation claim. This way, the

funds are transferred to the other indemnified party free of charge (Bekkin, 2007). All

operational expenditure pertaining to the insurance policy including reinsurance fees

will be subtracted from the tabaru fund (Anwar and Hussain, 1994).

Takaful is considered to be a solution and Sharia compliant alternative to conventional

insurance because it avoids riba by reinvesting funds in Sharia compliant financial

instruments. It also avoids gharar through compensations and subscription; avoids

maiser by dividing losses amongst members through fund pooling; policyholders

33

cooperate together for mutual good and no advantage is derived at the loss of another

member (Garigiparthy, 2007).

Islam is a tremendously powerful subcultural factor that influences Muslim consumer

behaviour on both the macro societal and governmental level and the micro individual

level (Schiffman et al, 2011). With the Quran being the ultimate root of all Islamic law,

Islamic religious law governs and guides literally all facets of a Muslim’s life including

economic, social, political and legal affairs (Monger and Rawashdeh, 2008).

Unfamiliarity with Islamic principles may prompt one to erroneously conclude that Islam

prohibits profit oriented transactions or may even be anti-business. The truth, however,

is that Islam encourages trade and business but cautions against uncertain transactions

that may unduly advantage one party over another and thus pose an issue of inequality

due to the uncertain, speculative or hidden nature of the outcome (Maysami and Kwon,

1999; Ismail, 1997). Islam seeks to put in place fair systems for all parties to thrive;

Prophet Muhammad (pbuh) himself was a successful businessman of considerable

repute (Trim, 2009; Antonio, 2007). Islam does not prohibit businesses to innovate and

experiment with products and services that ensure profitability of businesses whilst

providing consumers with benefits permissible under Islamic tenets. Seen from this

standpoint, insurance does not have to violate any Quranic injunctions if considered

thoroughly and adjusted to comply with sharia principles, insurance can become central

to the life of the modern Muslim consumer (Khorshid, 2013).

34

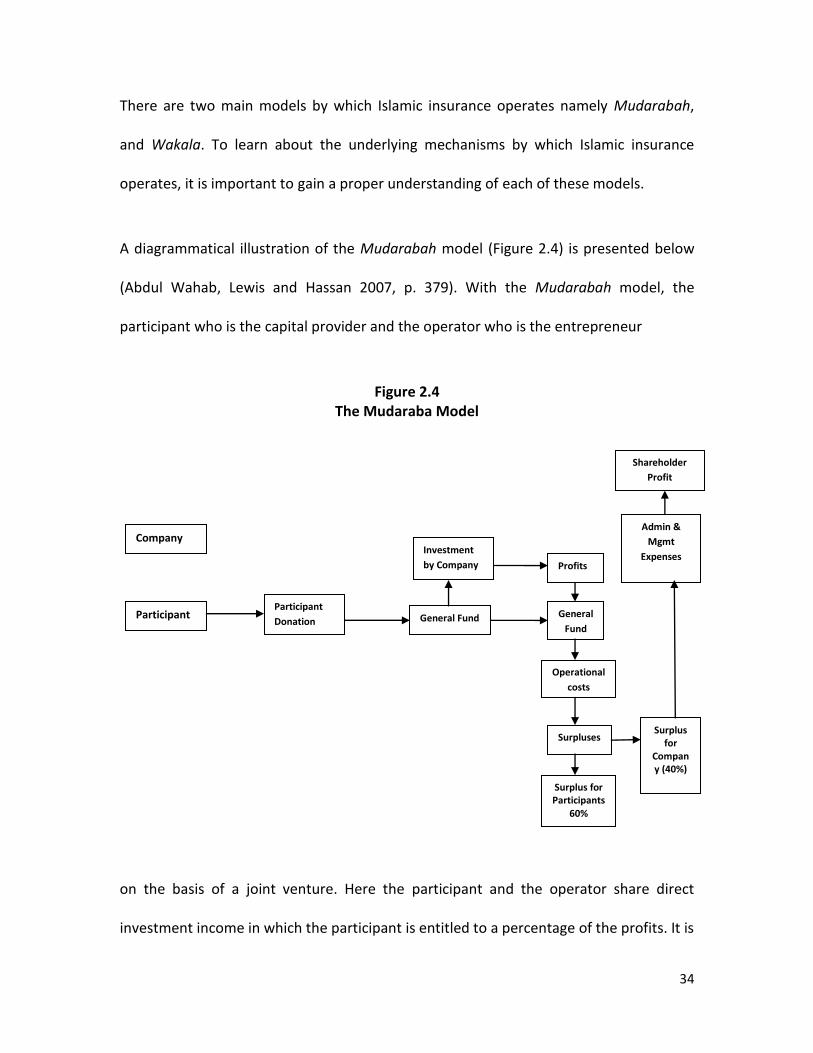

There are two main models by which Islamic insurance operates namely Mudarabah,

and Wakala. To learn about the underlying mechanisms by which Islamic insurance

operates, it is important to gain a proper understanding of each of these models.

A diagrammatical illustration of the Mudarabah model (Figure 2.4) is presented below

(Abdul Wahab, Lewis and Hassan 2007, p. 379). With the Mudarabah model, the

participant who is the capital provider and the operator who is the entrepreneur

Figure 2.4 The Mudaraba Model

on the basis of a joint venture. Here the participant and the operator share direct

investment income in which the participant is entitled to a percentage of the profits. It is

Company

Participant

Donation Participant General Fund

Shareholder

Profit

Investment

by Company

Surplus for Participants

60%

Surpluses

General

Fund

Profits

Admin &

Mgmt

Expenses

Operational

costs

Surplus for

Company (40%)

35

evident that the participant’s contributions and investment income are being used to

cover the operational costs associated with re-insurance and cover payments for claims.

The surplus is then divided between participants and the company according to a

defined proportion, 60% allocated to the former party and 40% allocated to the latter

party. The surplus allocated to the company is then used to cover management and

marketing related expenses with the remainder used as shareholder profit (Wahab,

Lewis and Hassan, 2007).

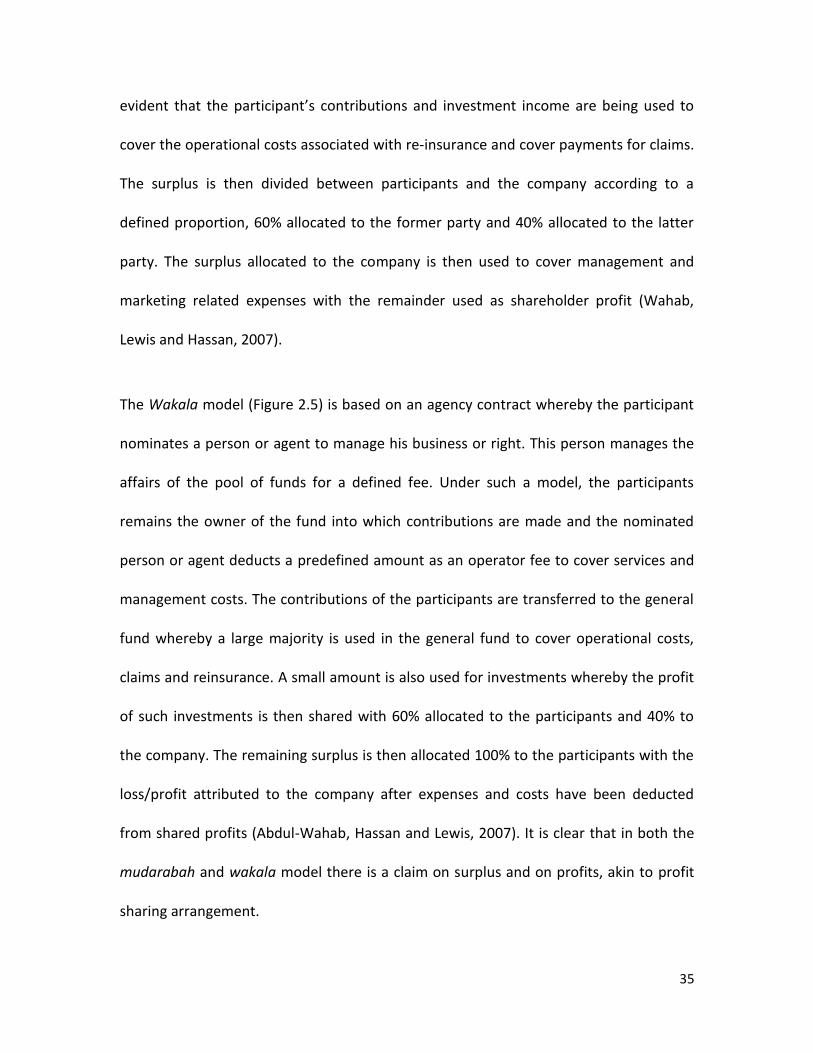

The Wakala model (Figure 2.5) is based on an agency contract whereby the participant

nominates a person or agent to manage his business or right. This person manages the

affairs of the pool of funds for a defined fee. Under such a model, the participants

remains the owner of the fund into which contributions are made and the nominated

person or agent deducts a predefined amount as an operator fee to cover services and

management costs. The contributions of the participants are transferred to the general

fund whereby a large majority is used in the general fund to cover operational costs,

claims and reinsurance. A small amount is also used for investments whereby the profit

of such investments is then shared with 60% allocated to the participants and 40% to

the company. The remaining surplus is then allocated 100% to the participants with the

loss/profit attributed to the company after expenses and costs have been deducted

from shared profits (Abdul-Wahab, Hassan and Lewis, 2007). It is clear that in both the

mudarabah and wakala model there is a claim on surplus and on profits, akin to profit

sharing arrangement.

36

Figure 2.5 The Wakala Model

Source: Abdul Wahab, A, Lewis, M and Hassan, M, (2007, pp. 382)

This is permissible within the framework of Islamic insurance because the profit sharing

ratio is predetermined and thus is permitted in Islam (Maysami and Kwon, 1999).

Company

Participant Contribution by

participant

General fund 70-75%

General fund

Operational cost

Surplus

Share of surplus for participants 100%

Share of profit for company

Management

expenses

Profit/loss for shareholders

Investment by fund

Profit from

investment

Profit sharing basis 40%

60%

Operator fee for

admin expenses

25%-30%

37

2.8 Consumer attitudes, perceptions and awareness of Islamic insurance products.

An examination of the literature on consumer attitudes, perceptions and awareness of

Islamic finance products reveals that it is not as voluminous or rich as the literature on

conventional financial products and institutions. With the growth of Takaful worldwide,

it is imperative to increase awareness and education of such a product amongst both

Muslim and non-Muslim consumers (Wyman, 2009). A 1997 study conducted in

Malaysia revealed that only 45% of respondents actually had some knowledge about life

insurance and it was very little (Asian Insurance Review, 1997).

As the Islamic financial sector continues to grow from an estimated $822 billion in 2009

with Shariah compliant assets to an estimated $1.6 trillion in 2012, the importance of

measuring consumer attitudes towards these products, especially Islamic insurance

cannot be ignored (Wyman, 2009). Keeping this in view, this study investigates this

empirically and aims to enrich the marketing literature, in particular the literature

pertaining to marketing to Muslim consumers. The major shortcoming discovered in the

literature pertains to the lack of balance between the well-researched area of Islamic

banking compared to conventional banking and the under researched area of Islamic

insurance.

It appears that the earliest study on individual consumer attitudes towards Islamic

financial products was conducted by Erol and El-Bdour (1989). The study did not find

any influence of religious motivation on the patronage of either Islamic or conventional

banks. However, efficiency, reputation, image and confidentiality were found to be the

38

decisive variables in purchase decisions. The study also revealed that there was a

moderate level of awareness of Islamic banks amongst the sample of 434 Jordanians

with information coming from the reference group including family and friends. A later

study by Erol et al (1990), however, found that religious factors play a small role on

overall patronage of Islamic finance products. Other research corroborating similar

findings include Gerrard and Cunningham (1997) and Haron et al (1994) who found

religious motivation to be a non-significant factor in determining patronage of Islamic

finance products. However, the former study reported a high level of unawareness of

Islamic methods of finance amongst both the Muslim and non-Muslim samples whereas

the latter study reported moderate levels of awareness. A recent study by Yaacob et al

(2012) also reports an insignificant relationship between religiosity and Islamic

insurance patronage with 19.1% ascribing their patronage due to religious reasons. A

further 42% cite “easiness of damages” which means the ease and efficiency in which

claims are paid out as the reason for patronage. This is contrary to the findings of Husin

and Rahman (2013) who reported consumer intentions to purchase family Takaful

products to be heavily influenced by religious motivations, awareness and perceptions

including behavioural control, norms and attitudes.

Hamid and Nordin (2001) also found that the majority of Malaysian customers sampled

in their study possessed sufficient knowledge of Islamic finance products, however not

enough to say they understood particular intricacies. Omer (1992) also reported that

Muslims living in the United Kingdom have a high level of unawareness of Islamic

39

finance products. Similar findings were reported by Akbar, Shah and Kalmadi (2012),

Maturi (2013) and Othman and Hamid (2009) whereby respondents exhibited low to

moderate awareness of Islamic banking practices. It was not surprising that due to this

lack of knowledge they also expressed negative perceptions regarding Islamic finance

ethical frameworks. In another study Maysami and Williams (2006) found 47.7% of

Muslim respondents to be aware of the existence of non-life Islamic insurance products;

however, less than 30% of these respondents seemed to have favourable dispositions

towards such products. Maysami and Williams (2006) note that the relationship

between awareness and perception is not uniform and the two constructs are not

independent. They found lower levels of awareness to be associated with having

perceptions of Islamic insurance as being encompassing of both religious and social

goals. It is only with higher a level of awareness does the perception of Islamic insurance

being compatible with profit making become apparent (Maysami and Williams, 2006; p.

231). In the study by Maturi (2013) it was found that the majority of sampled

participants were unaware of particular Takaful concepts; they did not know whether

Takaful was really Sharia compliant or not. Hamid and Othman (2009) and Yaacob et al

(2012) also observed a deep level of unawareness amongst Muslim participants in

regards to the main principles of Takaful such as gharar, maiser and tabaru. However,

what was interesting in the Yaacob et al (2012) study was that a high proportion of

participants (61.8%) expressed their preference of Islamic insurance over conventional

insurance. Despite their lack of awareness most participants in the Maturi (2013) study

indicated their willingness to purchase Takaful products provided the coverage of

40

Takaful was similar to that of conventional insurance and at a competitive price.

However, there have been contrary research findings indicating negative perceptions

towards these products. For example, in a study by Dar (2005) more than 82% of the

respondents did not think that Islamic financial products were really Sharia compliant.

Furthermore, this phenomenon is ascribed to the fact that there is a deep unawareness

of Islamic financial products which may adversely affect potential demand and

consumption of such products if no substantial marketing effort is taken to increase

awareness (Dar, 2005).

A large number of research investigations by scholars such as Khan et al (2007), Husin

and Rahman (2013, Hegazy (1995), Metwally (1996), Omer (1992), Naser et al (1999),

Zainuddin et al (2004), Metawa and Almossawi (1998), Okumkus (2005), Sultan (1999)

and Bley and Keuhn (2004) also reported strong inter-relationship between religious

motivation and patronage of Islamic finance products. This is also supported by Siala

(2013) who reports strong relationships between the influence of religious motivation

and consumption of religiously-compliant high involvement indemnity services. The

findings include a positive relationship between religiosity and attitudinal and

behavioural loyalty manifested through repeat patronage, positive word of mouth and

price tolerance. This may be viewed as a reflection of consumers’ positive

perceptions/emotions and affective attachments towards religiously compliant

products. Contrary to the findings reported by Gerrard and Cunningham (1997), Haron

et al (1994), Hamid and Nordin (2001), Omer (1992), Dar (2005), Maturi (2013) and

41

Hamid and Othman (2009) concerning the low and moderate levels of awareness, a

study by Bley and Keuhn (2004) reported otherwise. They reported high levels of

awareness of Islamic finance products amongst the Arab-Muslim sample and

significantly lower levels of awareness amongst the non-Arab-Muslim sample.

The literature cited in this section has shown mixed results. However, the majority of

the studies seem to have corroborated the view that Muslims living in a non-Muslim

country exhibit a lower level of awareness of Islamic finance products as compared to

Muslims living in Muslim countries (Gait and Worthington, 2007).

2.9 Determinants of demand for Islamic insurance: general and life

In their study aimed at identifying the determinants of demand for Islamic insurance

Yazid et al (2012) found nine (9) socio-economic factors namely income, inflation,

interest rates, stocks and price, savings, pension and financial development. They also

found seven (7) socio-demographic factors including age, education, household size,

dependency ratio, life expectancy, urbanization and employment as the major

determinants of demand for family non-life Islamic insurance products. Beck and Webb

(2003) also endorsed price as being an important factor influencing demand for these

products. Exclusion of price from the conceptual framework will subject the empirical

test to omitted variable bias.

Religious convictions may also affect attitudes towards insurance and subsequently risk

aversion. The degree of risk aversion towards insurance may be related to the dominant

42

religion of the country (Outreville, 1996). Muslim consumers typically disapprove of life

insurance because it is perceived to be a hedge against the decree of Allah. Research

has revealed that in Islamic countries there is a negative correlation between religiosity

and demand for life insurance (Browne and Kim, 1993; Meng, 1994). This is further

supported by the fact that penetration of life insurance as opposed to nonlife insurance

such as home, business or motor vehicle which may be mandatory in some countries is

much lower due to religious reasons (Rahim, 2006). According to Rahim (2006) in a

research publication by Swiss Re SITC, insurance penetration in Muslim dominant

countries such as those in the Middle East is generally low with only 1% of total GDP per

capita being spent on insurance premiums (Rahim, 2006). In countries such as

Indonesia, Pakistan and Bangladesh, percentage of GDP per capita spent on insurance

premiums ranges from 0.1 to 0.3%, whilst in India where 15-20% of the total population

is Muslim, percentage spent on insurance premiums again is low at 0.6% (Rahim, 2006).

43

CHAPTER 3

The Conceptual Model and the Hypotheses

3.1 The conceptual Model

This chapter discusses the conceptual model used in the current research followed by

the hypotheses formulation. The model has been developed based on the

comprehensive literature survey presented in Chapter 2. The basic premise of the model

is that intention to purchase Islamic insurance products is a function of four composite

variables namely levels of religiosity, awareness of Islamic insurance, perception of

Figure 3.1 The Conceptual Model

H2

H5

H4

H3

Levels of Religiosity

Awareness of Islamic insurance

Perception of Islamic insurance

Intention to purchase Islamic

insurance

Type of insurance

44

Islamic insurance and purchase intention of Islamic insurance policies. Levels of

religiosity and awareness are the exogenous independent variables (or predictor

variables). Perception is the mediator between religiosity, awareness and purchase

intention and purchase intention is the endogenous dependent variable (or outcome

variable). The type of insurance (whether general or life) is the moderator between

religiosity and perception, perception and intention and religiosity and intention. The

indirect effect of religiosity and awareness on purchase intention which is mediated by

perception is conditional upon whether the type of insurance is general or life, therefore

creating a conditional indirect effect, or otherwise known as a moderated mediation.

3.2 Formulation of Hypotheses

Hypothesis 1: From the literature review it appears that the majority of the studies

conducted on Muslim consumers living in Muslim majority countries yield results quite

contrary to the results obtained from studies on Muslim consumers residing in Muslim

minority countries. With the exception of Maturi (2013), Akbar, Shar and Kalmadi (2012)

and Omer (1992), who conducted their investigations in the UK, all the studies reviewed

in the literature review were conducted in Muslim majority countries where awareness

and knowledge of Islamic methods of finance is higher. Since Muslims in Australia

constitute less than 2.5% of the total national population (ABS, 2012), It is quite likely

that there is a lack of awareness of Islamic insurance products amongst the Australian

Muslim consumers. Therefore the first hypothesis is:

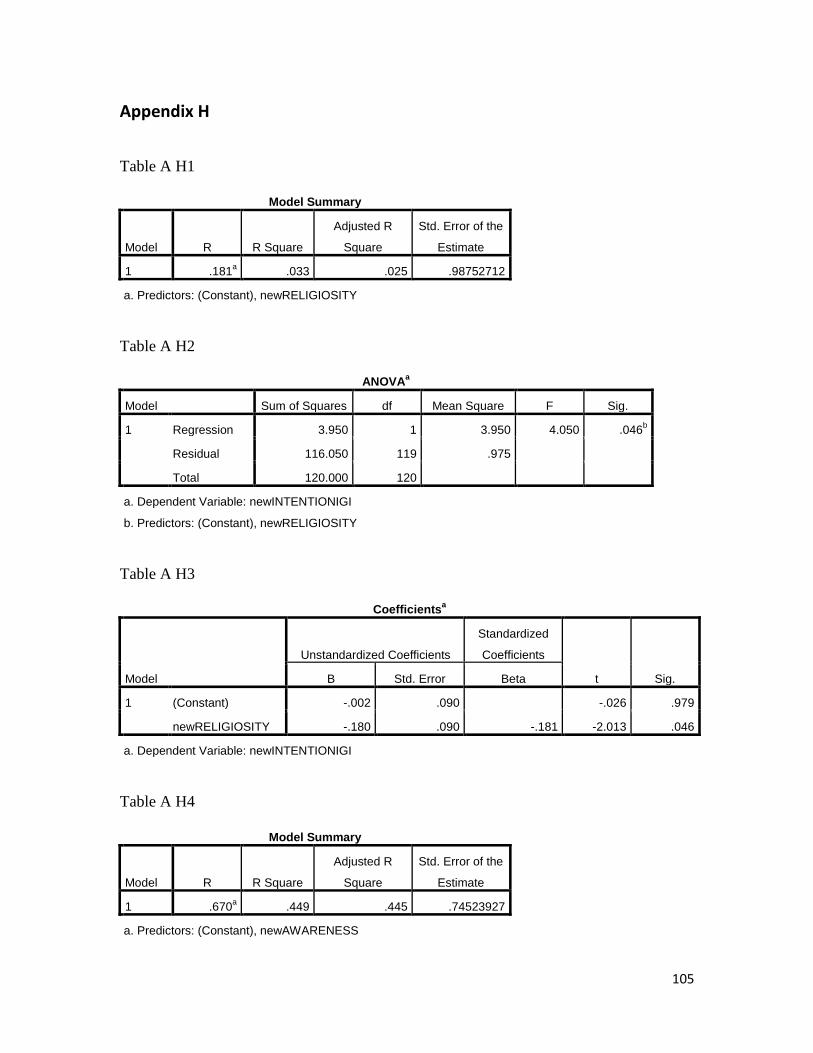

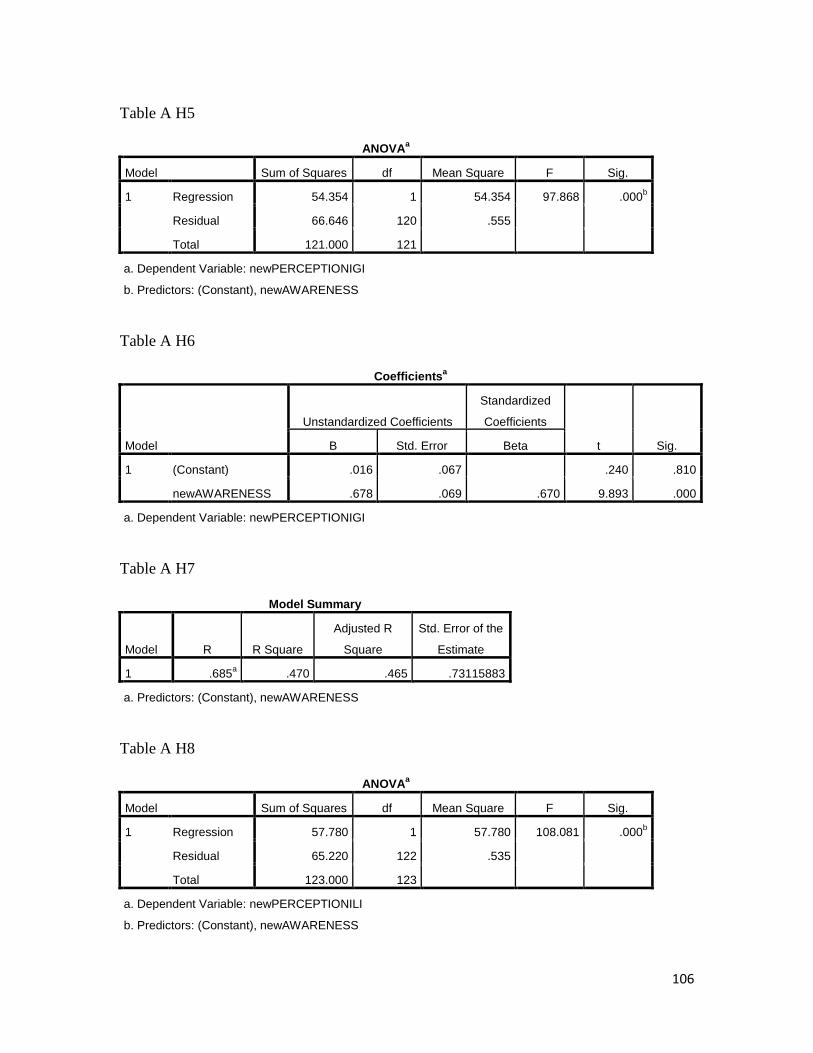

H1: There will be low to moderate levels of awareness and knowledge about Islamic insurance products amongst the Australian Muslim consumers.

45

Hypothesis 2: The literature review established that there is an averseness of religious

Muslim consumers towards risk taking and gravitation towards certitude in purchasing

behaviour when it comes to purchasing a life insurance policy. However, purchase of

Islamic general insurance for boat, business, public liability, home and contents

insurance which are not compulsory or statutory also present theological dilemmas to

the religious Muslim consumers. Although extant research did not corroborate any

significant role of religiosity on the patronage of Islamic financial products; the

researcher argues that religious controversy involving the very notion of ‘insurance’

makes it more likely that Muslim consumers would view insurance products less

favourably than other financial products. This leads to the formulation of the following

hypothesis:

H2: There is a negative relationship between religiosity and willingness to purchase Islamic general insurance products.

Hypothesis 3: Siala (2013) reported an intimate relationship between religiosity and

religiously compliant high involvement services. Given the strict principles of Islam and

somewhat controversial nature of insurance products, the decision to purchase an

insurance policy will be viewed as a high-involvement decision. Hence, it is logical to

assume that consumers with higher levels of awareness and knowledge of Islamic

insurance will demonstrate more positive perceptions towards the purchase of Islamic

insurance products. Therefore, the third hypothesis can be formulated as follows:

H3: There is a positive relationship between awareness and perceptions towards both Islamic general and life insurance.

46

Hypothesis 4: Siala (2013) also indicated a positive relationship between positive

perceptions/emotions consumers have towards a religiously compliant product and the

development of attitudinal/behavioural brand loyalty. In the light of this finding, it

seems likely that in the context of purchasing an Islamic insurance product, there will be

a strong positive relationship between positive perceptions and emotions about the

products and willingness to purchase Islamic insurance. Hence the following hypothesis

is posited.

H4: There is a positive relationship between perceptions and increased willingness to purchase Islamic general insurance products.

Hypothesis 5: It is further assumed that in hypothesis 4 (H4) there must be an

underlying cause that drives the consumers to have this positive perception and/or

strong emotional attachment towards Islamic insurance and that in turn leads to high

levels of loyalty. This research argues that religiosity, more specifically, high levels of

religiosity is the cause of such positive perceptions which in turn drives the decision

makers’ behaviour. Thus, the final hypothesis of this study may be formulated as:

H5: There is a positive relationship between religiosity and perceptions towards Islamic general insurance products.

47

CHAPTER 4

Research Methodology

4.1 Research Design

This chapter discusses the research design including sampling, data collection method

and questionnaire design. It also explains how the variables used in the study have been

operationalized.

Given the very nature of the current research and the intended respondents, i.e., young

Australian Muslim consumers, a descriptive research involving an on-line survey was

deemed to be an appropriate method. Popularity of online survey stems from its ability

to obtain many responses from a wide variety of people that fit a certain profile

reasonably quick, easily and relatively cheap.

4.2 Selection of the Sample

A total of 150 Australian Muslim individuals over the age of 18 who are either born in

Australia or are citizens of Australia were approached to participate in the study by

completing a self-administered questionnaire delivered via the researcher’s personal

Facebook account. One hundred forty (140) of those approached participated in the

study. However, 15 of the responses were unusable as they were not completed

properly. As such the study was based on the responses of 125 valid respondents and

represented a high response rate of 83.3%.

48

4.3 The Questionnaire Design

The questionnaire used in the study (see Appendix A) comprised four (4) sections. The

first section (Table A1) had a total of seven (7) questions, first five of which sought to

develop the participant’s demographic profile and requested each participant to state

his/her age, gender, marital status, academic qualifications and profession. The

remaining two questions asked if the respondent was an insurance policyholder, and the

company from which that policy was bought. The analysis of the demographic variables

was required to relate the profiles of the sampled respondents with their religiosity

(Section 2); levels of awareness of Islamic insurance products, perceptions (Section 3)

and their willingness to purchase or switch to Islamic insurance (section 4) depending on

whether or not they were policyholders.

Section two (Table A2) contained twenty (20) Likert type statements seeking the

respondents’ level of agreement or disagreement on a 5-point scale (5 - strongly agree,

3 – neither agree nor disagree and 1 - strongly disagree) with a view to measure their

religiosity. These statements have been taken from the religious commitment inventory

scale used by Razzaque and Chaudhary (2013) in their research on Australian Muslims.

The major reasons underlying the use of this scale were two-fold. First, the items used in

the scale reflect a holistic Islamic orientation; second, all the scale items were tested on

Muslim consumers in the Australian context and showed high reliability and validity.

In Section 3 of the questionnaire, there were thirteen Likert type statements (5 -

strongly agree, 1 - strongly disagree and 3 – neither agree nor disagree) (see Table - A3)

49

intended to measure the sampled respondents’ awareness (9 statements) as well as

perceptions of Islamic insurance products (4 statements). These statements have been

specifically developed for the current study based on the knowledge gained from the

literature review. Through these statements, the researcher seeks to determine one of

two things about Islamic insurance products. First, if the participants are aware of the

permissibility of these products for Muslims as they are Sharia compliant; avoid riba,

gharar and maiser. Second, how the participants perceive these products. Keeping this

objective in view, each of the thirteen statements in this section have been worded in a

simple, unambiguous, easy to understand manner that can extract the participant’s

honest responses. Furthermore, in order to adequately reflect the differing levels of

religiosity of the sampled respondents, some of the statements were negatively framed

[e.g., Insurance is altogether (conventional and Islamic) haram or prohibited] in order to

elicit stronger emotional responses. Questions such as “I feel like the religious benefits

of consuming Islamic general insurance products outweigh the costs of having to switch

insurance” have been included to examine the participants’ affective attachment or lack

thereof similar to the research carried out by Siala (2013). This question in particular

intends to measure perception by way of understanding whether the participant views

Islamic insurance to be more beneficial religiously than costly monetarily or vice versa.

Due to the scarcity and lack of appropriate and reliable scales in the extant literature,

the questionnaire items regarding the measurement of awareness, perception and

purchase intentions towards Islamic general and life insurance have been specifically

50