a-survey-report-on-chinese-consumers-purchase-preference ...

58

Chinese Consumers’ Purchase Preference on Foreign and Local Brands SURVEY REPORT

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of a-survey-report-on-chinese-consumers-purchase-preference ...

Chinese Consumers’ PurchasePreference on Foreign and Local Brands

SURVEY REPORT

PREFACE

CATEGORY ANALYSIS

ABOUT THE SURVEY

CONCLUSIONS AND IMPLICATIONS

PART 1 PART 2

PART 3 PART 4

PREFACE

PART 1

For a long time, Foreign-branded products have held an elevated status in the Chinese market as the hallmark of a comfortable, modern, and middle-class lifestyle. In contrast, local products’ frequent safety and quality scandals have made Chinese consumers lack trust in domestic brands. They are ambitious and hungry for imported consumer goods, often the expensive and premium ones for themselves, their families, and their pets. China is, therefore, becoming a magnet for international brands and is viewed by them as a must-win market.

However, recently, the Swedish fast-fashion brand H&M’s statement on refusing to use Xinjiang cotton has triggered widespread denunciation and resis-tance from the Chinese public. H&M’s online and offline businesses have been hit hard. Uniqlo, Nike, Adidas, and other brands have also been implicated in the boycott, resulting in a massive celebrity contract termination wave. Besides boycotting those foreign brands, Chinese netizens turn to support domestic brands such as Lining which use Xinjiang cotton to show their support for the region.

Before the anti-Xinjiang cotton controversy, Chinese local brands are actually already on the rise in terms of brand influence and recognition. While foreign brands continue to lead in a number of product cate-gories, domestic brands are making a name for themselves, highlighting the intense competition for consumers’ mind share.

01

As COVID-19 is yet to be brought under full control at the global level, the world economy is likely to remain in the doldrums. The headwinds against globalization further overshadow the recovery of international trade and investment. In 2020, China proposed a new economic development pattern of "dual circulation", defined as a policy that "takes the domestic market as the mainstay while letting internal and external markets boost each other." The new development pattern is poised to inject new momentum into the growth of local brands.

Under this circumstance, many foreign stakeholders are worried about whether the Chinese government would give more support to the local brands and whether Chinese consumers would tend to choose more domestic brands in the future. Although local brands face historic development opportunities, they still need to work hard in terms of product innovation and brand value enhancement. In this respect, foreign brands have always had an advantage in.

ChemLinked organized a consumer survey and analyzed foreign and domestic brands’ purchase preferences across a number of product categories. We write this report to help foreign brands gain an insight into the evolving competitive scenario in China and search for new strategies for continuous growth.

The rise of domestic brands is due to the following reasons:

The improvement of China's overall national might has boosted consumer confidence. In the past, consumers lack confidence in the poor quality or backward design of many local products. However, with the continuous development of China's economy and the strengthening of cultural confidence, quality, service, reputation, and cultural identity have become the new labels of local brands. The “made in China” technology, products and services have become increasingly sought after by Chinese consumers.

The new generation of consumer group is more receptive to domestic brands. The Post-90s and post-00s have become the consumer market’s main force. Different from previous generations, they are born against rapid national economic development and have more cultural confidence and a sense of national pride. They care more about the embodiment of personality and values instead of brands.

New sales channels help the rise of domestic brands. In the past decades, the Chinese consumption market has flipped from the old brand-building model to a digital ecosystem, from bricks and mortar to e-commerce. Domestic brands have taken advantage of online channels such as e-commerce and social media to occupy more market share. According to the 2020 China Consumer Brand Development Report by AliResearch, Chinese brands’ online market shares reached 72% in 2019.

02

ABOUT THE SURVEY

PART 2

Income87.12% of respondents have a monthly income above 5,000 yuan. Those with a monthly income of 5,000-10,000 account for the largest share of 43.56%.

Survey content

Respondent profile

Gender & Age

Survey information

Time period

Region

Survey subject

Form

Sample conditions

Sample size

Categories involved

Description

March 22 to April 9 2021

Nationwide

Chinese consumers

Questionnaire

Chinese consumers with FMCG purchase demand

3000 sent, 2640 valid

Health food, pet food, infant formula, dairy, baby food, cosmetics

Most respondents are females, with a proportion of 74.62%.Most respondents are between 18 and 50 years old. The 18 -28 age group and the 29-50 age group account for nearly 50%, respectively.

Region80% of respondents live in the first-tier cities and new first-tier cities.

NoteFirst-tier cities: Beijing, Shanghai, Guangzhou, ShenzhenNew first-tier cities: Chengdu, Chongqing, Hangzhou, Wuhan, Xi’an, Tianjin, Suzhou, Nanjing, Zhengzhou, Changsha, Dongguan, Shenyang, Qingdao, Hefei, Foshan.Source: 2020 Ranking of Cities’ Business Attractiveness, Yicai

010102020303

03

Want to support domestic products(patriotism)

Survey result overview

The survey shows that regardless of other factors, respondents are more likely to buy imported products.

Better product quality is the top reason for choosing foreign brands, accounting for 72.83%, followed by brand fame (67.39%) and superior experience (28.80%).

Reasons for Choosing Foreign Brands Reasons for Choosing Local Brands

More than 90% of respondents show willingness to increase consumption frequency of domestic brands in the future.

Patriotic sentiment dominates most respondents’ shopping choices for local brands, accounting for 81.25%.

Are you Willing to Increase the Consumption Frequency of Domestic Brands?

High quality Brand fame

Superior experience

Others

Highly cost effective Good service

Easy access

30.30%

69.70%

6.44%

93.56%

25.54%28.80% 5.43%

72.83%67.39%

32.50%

56.25%

57.50%

81.25%

04

Foreign brands Local brands

Good serice

YES NO

In the Case of Similar Prices, Domestic Brands and Foreign Brands Choose Preference

Respondents also pay more attention to new foreign brands in the sectors of food & beverage, cosmetics, fashion clothing, shoes and bags.

Online channels represented by e-commerce and social media platforms, friend recommendation and KOL/celebrity/influencer endorsement are the leading information channels for them to know these brands.

They show a willingness to buy foreign brands they newly know except for H&M because the brand enraged Chinese consumers amid the anti-Xinjiang cotton controversy.

Health food

Beverage

Cosmetics

Shoes

Clothes

Clothes

Cosmetics

New Zealand

Sweden

U.S.

UK

South Korea

South Korea

UK

Taobao

Friend recommendation

Friend recommendation

Celebrity

Celebrity

Douyin

Yes

Yes

Yes

Yes

Yes

Yes

Yes

05

Brands Category Origin Future purchaseintention

Sources of information

Clothes

Clothes

Shoes

Coffee

Cosmetics

Cosmetics

Bag

Clothes

Beverage

Sweden

South Korea

Italy

Italy

U.S.

Italy

U.S.

UK

U.S.

/

Online store

Friend recommendation

Little Red Book

KOL

Friend recommendation

Youtube

Friend recommendation

No

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

06

Brands Category Origin Future purchaseintention

Sources of information

Get the most of your Food Digital Week experience! Join us for CLFDW 2021.

5000+Viewers

Sidestep travel restrictions for attendees to share knowledge and connect with global

entrepreneurs, opinion leaders and more peers.

6+Thematic Sessions

Focus on Health Food, Infant Formula, Pet Food, CBEC, and more Imported Food

Compliance policies and tips

15+Speakers

A unique opportunity to communicate with regulatory experts, government

officials, and industry leaders.

E-mail: [email protected]: (+86)571-8609-4444

21-25 June 2021 | Time (GMT+8): 10:00 am - 12:15 pm

X

ABOUT

ChemLinked Food Digital Week, organized by ChemLinked and REACH24H, will feature one week of informative sessions on China latest food regulatory changes, policy and trend interpretations, and marketing strategies. From health food or infant formula to cross-border ecommerce, we will have industry experts and government officials present on all the key topic areas to enable you receive updates on these regulations in China and speak directly to professionals.

WHO SHOULD ATTEND

Embassy of the Czech RepublicEvent Partners:

FOOD DIGITAL WEEK2021 CHEMLINKED

Food Import & Export Food TraceabilityFood Marketing Food Regulatory Affairs

Food Safety Management & Supervision

Food Production, Processing & Packaging

Government Food Regulatory & Policy Making

Compliance Management

CATEGORY ANALYSIS

PART 3

Health foods in China shift from high-end consumer goods and gifts to daily nutrition supplement options for many people.

Health foods produced by local brands are relative single nutritional supplements such as the VC, VE, calcium tablet, etc. In contrast, foreign brands bring more segmented and functional products, such as cranberry tablets for urinary tract health, and deep-sea cod liver oil for blood pressure adjustment, etc.

Foreign health food brands are the first shopping choice of most respondents, accounting for nearly 80%.

Local vs. Foreign Health Food Brand Purchase Preference

Foreign brands Local brands

HEALTH FOOD

Key takeaways

Consumer preference

20.08%

79.92%

07

Low market concentration is a prominent feature of China's health food industry. In 2020, the CR3 (market share of the top three companies), CR5 (market share of the top five companies) and CR10 (market share of the top 10 companies) in China’s health food market were 13.9%, 19.9%, and 30.4% respectively. BYHEALTH is the company with the largest market share of 6.4%.

Better and safer ingredients (76.14%), more premium brand position (51.14%), and better efficacy (37.12%) are the top 3 factors driving respondents to choose foreign health food brands.

Reasons for Choosing Foreign Health Food Brands

Market Share of Major Companies in China's Health Food Industry in 2020

[Data source: Euromonitor, Qianzhan Industry Research Institute]

Competitive landscape

76.14%Better and safer ingredients

More premium brand position

Better efficacy

Social media impact

Better packaging design

Others

51.14%

37.21%

33.33%

11.36%

4.92%

6.4%

BYHEALTH Infinitus Amway CR3 CR5 CR10

3.9% 3.6%

13.9%

19.9%

30.4%

08

Foreign health food brands deliver outstanding performance on the e-commerce platform. During the Tmall Double 11 Shopping Festival in 2019 and 2020, foreign brands accounted for nine and seven spots of the top-selling lists, respectively.

BYHEALTH's brand influence index also ranked first, followed by NUTRILITE and Yang Sheng Tang.

[Data source: Chinapp.com, Qianzhan Industry Research Institute]

[Data source: ChemLinked]

Top 10 Selling Health Food Brands During the Tmall Double 11 Shopping Festival

Impact Index of Major Brands in China's Health Food Industry in 2020

BYHEALTH NUTRILITE Yang ShengTang

DEEJ Centrum Caltrate Sanchine Tong RenTang

GNC 21 Super Vita

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Swisse

BYHEALTH

Move Free

SIMEITOL

MUSCLETECH

GNC

Keylid

Myprotein

BLACKMORES

CENTRUM

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Swisse

BYHEALTH

Move Free

MUSCLETECH

BLACKMORES

GNC

POLA

NUTREND

Doppel Herz

Myprotein

2020 2019

09

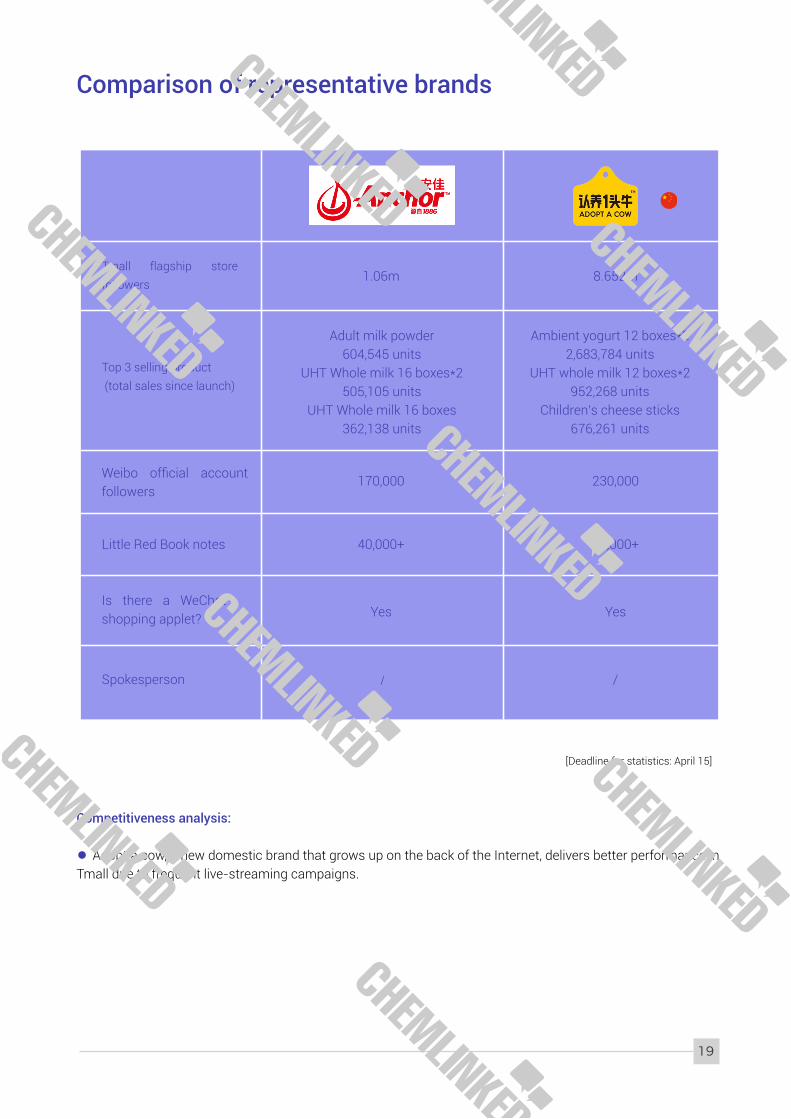

[Deadline for statistics: April 15]

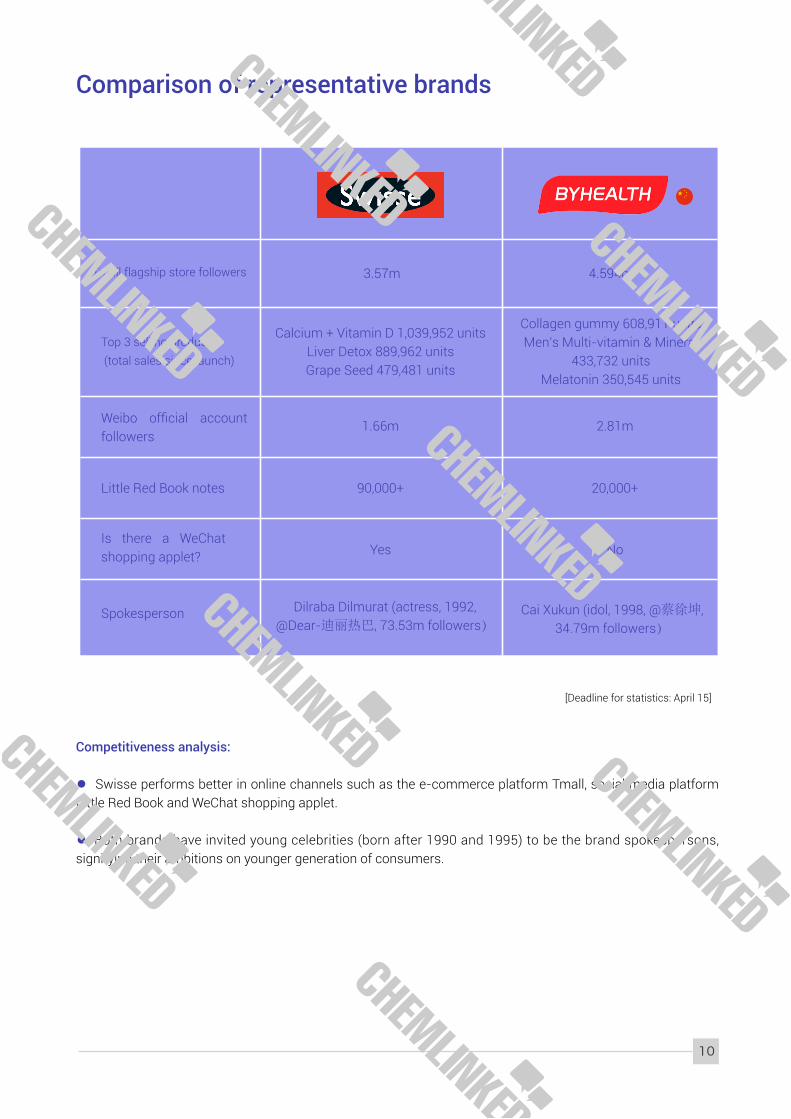

Comparison of representative brands

10

Competitiveness analysis:

Swisse performs better in online channels such as the e-commerce platform Tmall, social media platform Little Red Book and WeChat shopping applet.

Both brands have invited young celebrities (born after 1990 and 1995) to be the brand spokespersons, signifying their ambitions on younger generation of consumers.

3.57m

1.66m

90,000+

Yes

Top 3 selling product (total sales since launch)

Calcium + Vitamin D 1,039,952 unitsLiver Detox 889,962 unitsGrape Seed 479,481 units

Dilraba Dilmurat (actress, 1992, @Dear-迪丽热巴, 73.53m followers)

4.594m

2.81m

20,000+

No

Collagen gummy 608,911 unitsMen’s Multi-vitamin & Mineral

433,732 unitsMelatonin 350,545 units

Cai Xukun (idol, 1998, @蔡徐坤, 34.79m followers)

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

Tmall flagship store followers

Increasing local competition puts pressure on international brands, as Chinese-grown brands represented by Feihe (Firmus) have begun to clash head on with them.

The biggest advantage of most domestic brands is their ability to organize channel services in lower-tier cities. The COVID-19 outbreak has also brought some changes to China’s infant formula market because of quarantine measures, production issues, and interrupted logistics.

Foreign infant formula brands are the first shopping choice of most respondents, accounting for 76.89%.

Local vs. Foreign Infant formula Brand Purchase Preference

Foreign brands Local brands

INFANT FORMULA

Key takeaways

Consumer preference

23.11%

76.89%

11

Domestic brands Foreign brands

Domestic infant formula used to dominate the market and accounted for 60% market share in 2007, then dropped significantly from 2008 due to the Melamine scandal. The scandal-induced trust crisis has given foreign brands excellent opportunities for expansion since then.

However, in recent two years, the market proportion of Chinese domestic milk powder brands has rebounded to a half-half situation, and by 2020, domestic stakeholders have controlled more than 50% of the market.

The survey found that the factors most likely to lead respondents to buy foreign infant formulas were better and safer milk source (85.61%), more scientific formulation (54.17%), and more enriched nutrition (42.42%).

Reasons for Choosing Foreign Infant formula Brands

Infant Formula Market Share in China

[Data source: Euromonitor]

Competitive landscape

85.61%Better and safer milk source

More scientific formulation

More enriched nutrition

More premium brand position

Social media impact

Others

54.17%

42.42%

39.02%

15.53%

7.58%

12

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

40%

60%

48%

52%

50%

50%

52%

48%

53%

47%

55%

45%

58%

42%

59%

41%

60%

40%

58%

42%

56%

44%

55%

45%

51%

49%

100%

80%

60%

40%

20%

0%

First-tier Second-tier Third-tier Fourth-tier

Domestic brands Foreign brands

[Data source: Euromonitor, ECdataway]

Market Share of Top 10 Infant Formula Companies in China

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Nestlé

Danone

Firmus

Abbott

Mead Johnson

Friso

Yili

Yashili

Ausnutria

H&H group

13.90%

8.10%

8.60%

6.80%

6.50%

5.30%

5.00%

4.80%

3.90%

3.20%

Nestlé

Firmus

Danone

Abbott

Mead Johnson

Junlebao

Yili

Friso

Ausnutria

H&H group

2018 2019

Domestic brands have more advantages in the lower-tier markets.

Foreign Brands vs. Domestic Brands Market Share Comparison Across Cities in 2019

13

Despite the heated competition, foreign brands still have a strong presence, which occupied seven positions in the top 10 baby food brands by market share in 2020 H1. Aptamil had the largest share, accounting for 13.0%.

[Data source: Nielsen, Qianzhan Industry Research Institute]

13.50%

13.30%

10.10%

6.70%

6.10%

5.50%

5.30%

5.10%

5.00%

4.90%

Aptamil

Mead Johnson

Friso

Firmus

Wyeth

Abbott

Yili

Junlebao

Nestlé

a2

2020H1

13.0%

8.0%

7.4%

6.9%

6.0%

4.7%

3.5%

3.5%

3.2%

3.1%

74%

26%

55%

45%

46%

54%

34%

66%

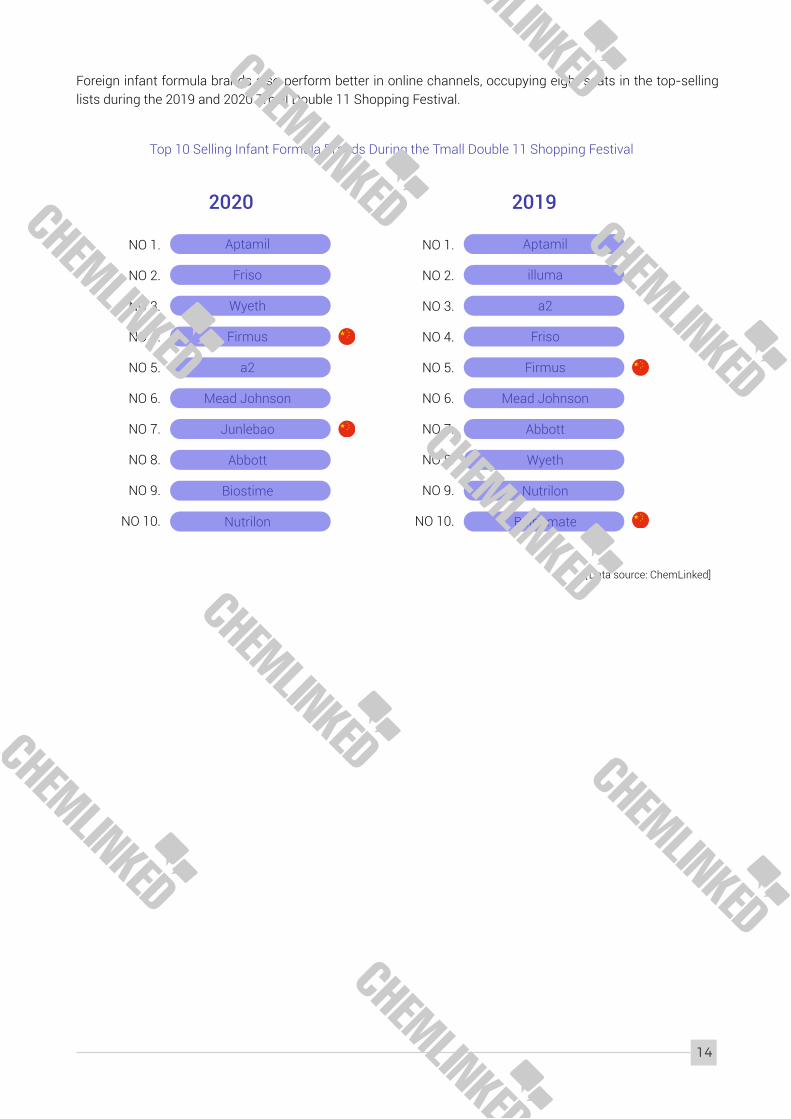

Foreign infant formula brands also perform better in online channels, occupying eight seats in the top-selling lists during the 2019 and 2020 Tmall Double 11 Shopping Festival.

[Data source: ChemLinked]

Top 10 Selling Infant Formula Brands During the Tmall Double 11 Shopping Festival

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Aptamil

Friso

Wyeth

Firmus

a2

Mead Johnson

Junlebao

Abbott

Biostime

Nutrilon

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Aptamil

illuma

a2

Friso

Firmus

Mead Johnson

Abbott

Wyeth

Nutrilon

Beingmate

2020 2019

14

[Deadline for statistics: April 15]

Comparison of representative brands

15

Competitiveness analysis:

Aptamil performs better in online channels such as the e-commerce platform Tmall and social media platform Little Red Book.

Both brands have launched WeChat shopping applet, which is regarded as a promising sales channel for brands.

Tmall flagship store followers

1.27m

50,000

30,000+

Yes

Top 3 selling product (total sales since launch)

Classic version stage3 800g 244,211 units

Classic version stage1 800g 156,136 units

Profutura stage1 380g 153,795 units

Li Na (tennis star, @李娜, 22.49m followers)

1.94m

810,000

10,000+

Yes

ASTROBABY Stage1 300g 117,126 units

ASTROBABY Stage1 700g 98,717 units

Super Feifan Stage3 400g*6 84,234 units

Wu Jing (actor and director, @吳京, 13.93m followers)

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

UHT milk, which consists of UHT white milk and ambient yogurt, occupies a dominant part in the Chinese dairy consumption market.

Domestic brands are keen on rolling out ambient yogurts. The three leading brands of Ambrosial (Yili), Chunzhen (Mengniu), and Momchilovtsi (Bright Dairy) occupy 70%-80% of the market share.

66.67% of respondents are more willing to choose local milk brands.

Local vs. Foreign UHT Milk Brand Purchase Preference

(UHT white milk and ambient yogurt)

Foreign brandsLocal brands

UHT MILK

Key takeaways

Consumer preference

66.67%

16

33.33%

Domestic Foreign

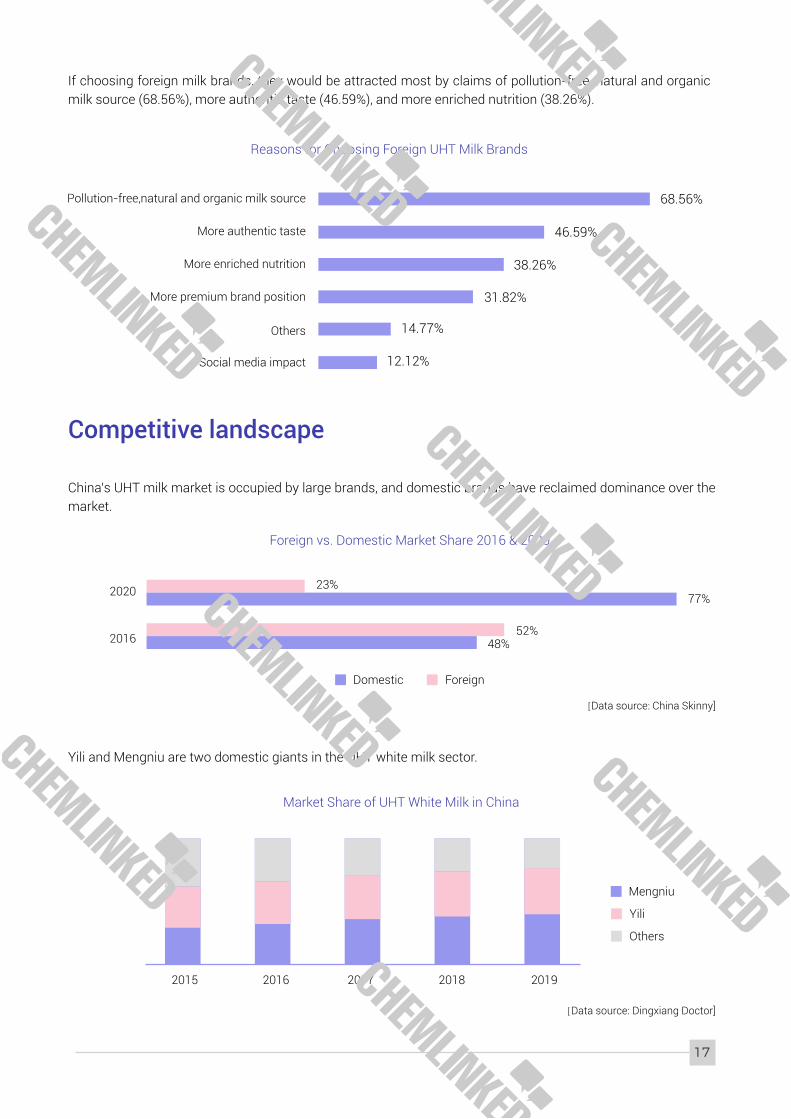

Yili and Mengniu are two domestic giants in the UHT white milk sector.

Market Share of UHT White Milk in China

China’s UHT milk market is occupied by large brands, and domestic brands have reclaimed dominance over the market.

If choosing foreign milk brands, they would be attracted most by claims of pollution-free, natural and organic milk source (68.56%), more authentic taste (46.59%), and more enriched nutrition (38.26%).

Reasons for Choosing Foreign UHT Milk Brands

Foreign vs. Domestic Market Share 2016 & 2020

[Data source: China Skinny]

Competitive landscape

68.56%

46.59%

38.26%

31.82%

14.77%

12.12%

17

Pollution-free,natural and organic milk source

More authentic taste

More enriched nutrition

More premium brand position

Social media impact

Others

2016

2020 77%23%

52%48%

[Data source: Dingxiang Doctor]

20162015 2018 20192017

Mengniu

Yili

Others

Chunzhen

Momchilovtsi

[Data source: ChemLinked]

Top 10 Selling UHT Milk Brands During the Tmall Double 11 Shopping Festival

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Mengniu

Yili

Adopt a Cow

Deluxe Milk

Weidendorf

Australia’s Own

Theland

Bai Fei Lao

Sanyuan

Anchor

Mengniu

Deluxe Milk

Yili

Weidendorf

Theland

Adopt a Cow

Australia’s Own

Bai Fei Lao

Anchor

Xiao Xi Niu

2020

UHT white milk Ambient yogurt

2019

In the ambient yogurt sector, the three leading local brands of Ambrosial (Yili), Chunzhen (Mengniu), and Momchilovtsi (Bright Dairy) occupy 70%-80% of the market share.

Market Share of Ambient Yogurt in China

18

Local UHT milk brands occupied dominant positions in the top-selling lists in the past two years of Tmall Double 11 Shopping Festival.

[Data source: Dingxiang Doctor]

Adopt a Cow

Yili

Mengniu

Ambrosial

Junlebao

Bright Dairy

Pom’ Potes

Weidendorf

WAHAHA

Jinghe

2020

Mengniu

Adopt a Cow

Yili

Pom’ Potes

Weidendorf

WAHAHA

Junlebao

Jelley Brown

COOL

MOMCHILOVTSI

2019

Ambrosial

Others

[Deadline for statistics: April 15]

Comparison of representative brands

19

Competitiveness analysis:

Adopt a cow, a new domestic brand that grows up on the back of the Internet, delivers better performance in Tmall due to frequent live-streaming campaigns.

Tmall flagship store followers

1.06m

170,000

40,000+

Yes

Top 3 selling product (total sales since launch)

Adult milk powder 604,545 units

UHT Whole milk 16 boxes*2 505,105 units

UHT Whole milk 16 boxes 362,138 units

/

8.652m

230,000

10,000+

Yes

Ambient yogurt 12 boxes*2 2,683,784 units

UHT whole milk 12 boxes*2 952,268 units

Children’s cheese sticks 676,261 units

/

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

Imported brands dominate China’s baby food market, and the market concentration is relatively high.

In recent two years, there emerged several new local brands focusing on the e-commerce channel.

75.38% of respondents are more willing to buy foreign baby food brands.

Local vs. Foreign Baby Food Brand Purchase Preference

(complementary food and snacks)

Foreign brands Local brands

BABY FOOD

Key takeaways

Consumer preference

75.38%

20

24.62%

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Engnice

Beingmate

Andros

Eastwes

Fangguang

HEINZ

Gerber

Hipp

Happy Baby

Earth’s Best

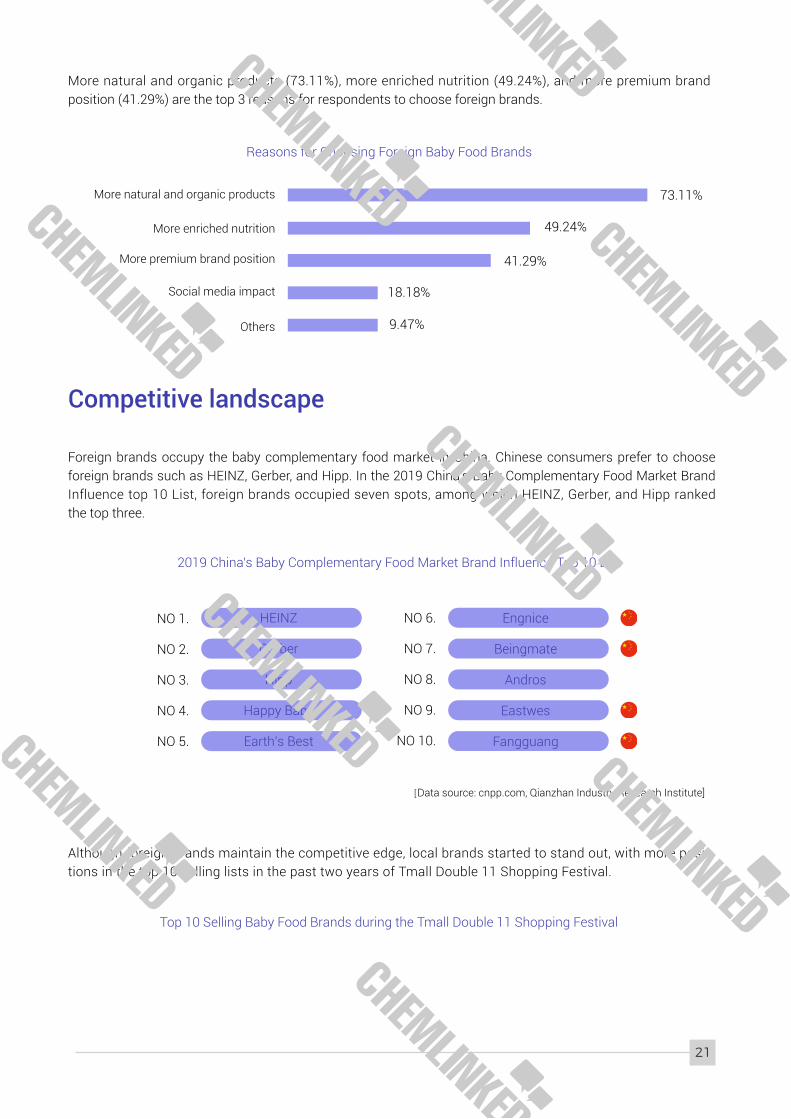

Foreign brands occupy the baby complementary food market in China. Chinese consumers prefer to choose foreign brands such as HEINZ, Gerber, and Hipp. In the 2019 China's Baby Complementary Food Market Brand Influence top 10 List, foreign brands occupied seven spots, among which HEINZ, Gerber, and Hipp ranked the top three.

More natural and organic products (73.11%), more enriched nutrition (49.24%), and more premium brand position (41.29%) are the top 3 reasons for respondents to choose foreign brands.

Reasons for Choosing Foreign Baby Food Brands

2019 China's Baby Complementary Food Market Brand Influence Top 10 List

Competitive landscape

73.11%

49.24%

41.29%

18.18%

9.47%

21

Although foreign brands maintain the competitive edge, local brands started to stand out, with more posi-tions in the top 10 selling lists in the past two years of Tmall Double 11 Shopping Festival.

Top 10 Selling Baby Food Brands during the Tmall Double 11 Shopping Festival

More natural and organic products

More enriched nutrition

More premium brand position

Social media impact

Others

[Data source: cnpp.com, Qianzhan Industry Research Institute]

Since 2020, domestic brands, represented by Deer Blue and Baobao Chanle, have emerged as strong rivals of foreign brands in this sector.

22

New domestic baby food brands

[Data source: ChemLinked]

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Gerber

Little Freddie

Baobao Chanle

Engnice

HEINZ

Fangguang

Earth’s Best

RIVSEA

Deer Blue

Happy Baby

Gerber

Little Freddie

HEINZ

Earth’s Best

Happy Baby

Engnice

Bellamy’s

Fangguang

Eastwes

RIVSEA

Deer Blue

Baobao Chanle

Gerber

Engnice

Beakid

RIVSEA

Happy Baby

Qiutian Manman

Little Freddie

Polysun

Gerber

Happy Baby

Little Freddie

Polysun

SunRype

Richfield

Engnice

Little remedies

Beakid

maxigenes

2020

Complementary food Snacks

2019 2020 2019

Bestore Fairy Yummy 2020 Be&Cheery Tong An An Little Friend 2020

Beingmate KidsClub 2020Three Squirrels Deer Blue 2020

Shamba Star, 2021Qixu Duo Mao Mao 2020

[Deadline for statistics: April 15]

Comparison of representative brands

23

Competitiveness analysis:

As an emerging local baby food brand, Baobao Chanle has ushered in explosive growth since 2020. Although the upstart shows strong growth momentum, it still lags behind the foreign brands in online sales and marketing.

Tmall flagship store followers

882,000

28496

1.4m+

No

Top 3 selling product (total sales since launch)

Baby rice 1,364,128 units

Fruit puree 100g*10 191,110 units

Yogurt fruit puree 100g*10 158,493 units

/

640,000

317

30,000+

Yes

Sesame sea moss floss 709,954 units

Sesame sea moss 660,953 units

Cod puffs 528,539 units

/

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

Lyfen Yizai, June, 2020 Yellow Elephant, 2019

2021 will witness the explosive growth of China’s pet food market, with more imported new entrants.

Domestic pet food brands also emerge with eye-catching sales performance on the e-commerce channel.

Respondents' preferences for domestic and imported pet food brands were relatively equal, with a little more preference for foreign brands (53.79%).

Local vs. Foreign Pet Food Brand Purchase Preference

Foreign brands Local brands

PET FOOD

Key takeaways

Consumer preference

46.21%

53.79%

24

The survey found that the factors most likely to lead respondents to buy foreign pet food brands were better and safer ingredients (70.83%), more scientific formulation (58.33%), and more premium brand position (32.58%).

25

Reasons for Choosing Foreign Pet Food Brands

Competitive landscape

70.83%Better and safer ingredients

More scientific formulation

More premium brand position

Social media impact

More appealing packaging design

Others

58.33%

32.58%

21.21%

13.26%

10.23%

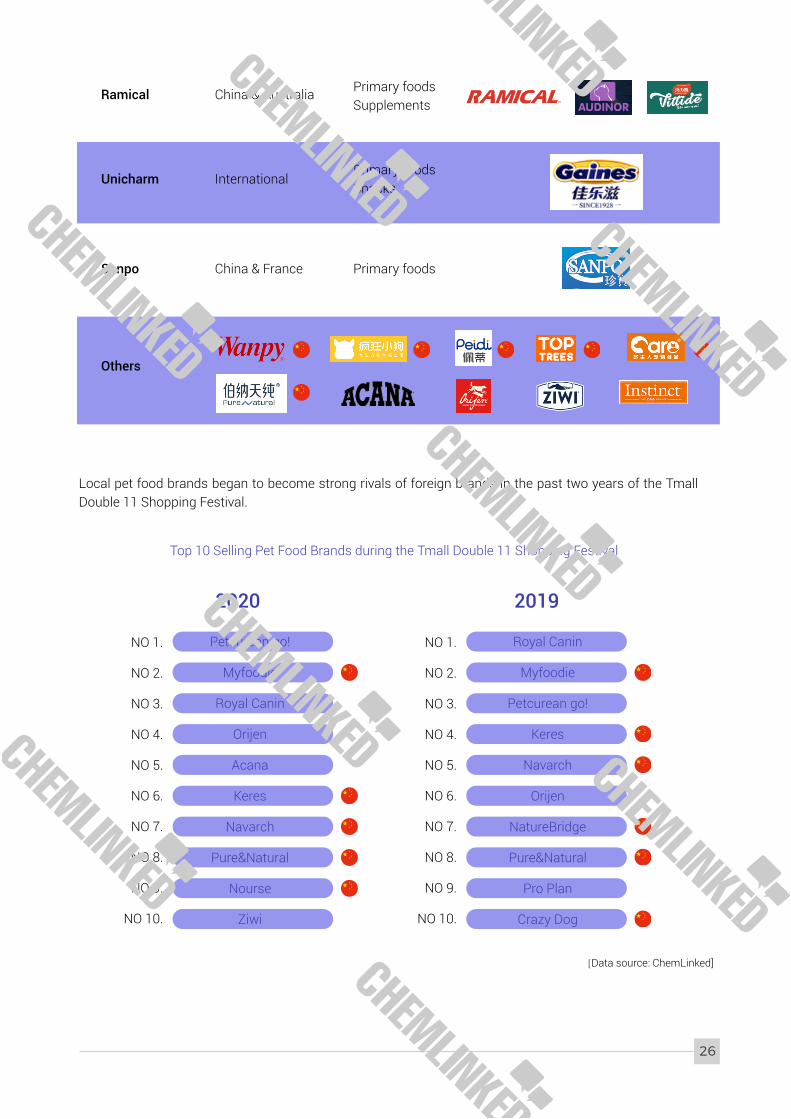

Foreign brands take the lead in entering the domestic pet food market and occupy an important position. In recent years, the market shares of domestic brands, represented by NatureBridge, Gambol, and Crazy Dog, have increased substantially.

Major Players in the Chinese Pet Food Market

Company

Mars

Nestle

NatureBridge

Gambol

International

International

China

China

Primary foods SnacksSupplements

Primary foods Snacks

Primary foods

Primary foods SnacksSupplements

Type Categories Top brands

26

Local pet food brands began to become strong rivals of foreign brands in the past two years of the Tmall Double 11 Shopping Festival.

[Data source: ChemLinked]

Top 10 Selling Pet Food Brands during the Tmall Double 11 Shopping Festival

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Petcurean go!

Myfoodie

Royal Canin

Orijen

Acana

Keres

Navarch

Pure&Natural

Nourse

Ziwi

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Royal Canin

Myfoodie

Petcurean go!

Keres

Navarch

Orijen

NatureBridge

Pure&Natural

Pro Plan

Crazy Dog

2020 2019

Ramical

Unicharm

Sanpo

Others

China & Australia

International

China & France

Primary foods Supplements

Primary foods Snacks

Primary foods

[Deadline for statistics: April 15]

Comparison of representative brands

27

Competitiveness analysis:

Domestic brand Myfoodie is more sophisticated in local marketing through building presence in mainstream social media platforms and enlarging brand influence with celebrity endorsement.

Tmall flagship store followers 188,000

/

400+

No

Top 3 selling product (total sales since launch)

Grain free small breed petite 11,768 units

Grain free adult cat 9,178 units

Grain free kitten 8,208 units

/

1.81m

170,000

4800+

Yes

Dog snack dried chicken meat 1,248,157 units

Small breed petite meal 673,016 unitsMeat package 603,384 units

Nicholas Tse (singer, @谢霆锋, 12.17m followers)

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

International brands still dominate the Chinese market, and more brands are accelerating their pace to enter the Chinese market. The cross-border e-commerce channel represented by Tmall Global becomes their first choice.

Local brands with unique focuses are rising, such as brands focusing on sensitive skin.

Foreign brands (85.98%) are more popular in the skincare sector.

Local vs. Foreign Skincare Brand Purchase Preference

Foreign brands Local brands

SKINCARE

Key takeaways

Consumer preference

14.02%

85.98%

28

Respondents choose foreign skincare brands mainly due to more potent efficacy (73.11%), brand fame and position (63.64%), and social media impact (30.68%).

Reasons for Choosing Foreign Skincare Brands

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

LA MER

Olay

Kiehl's

HFP

Proya

L'Oréal

SK-II

Lancome

The history of whoo

Estee Lauder

International brands still dominate the skincare sector but local brands are also emerging. For example, HFP, Chinese version of The Ordinary, gains traction because of its simple packaging and highlight of ingredients.

Top 10 Selling Skincare Brands on Taobao in 2020

[Data source: Cyanhill Capital]

Competitive landscape

73.11%More technology-based

with stronger efficacy

More premium bramd position

Social media impact

Celebrity endorsement

Others

63.64%

30.68%

18.18%

10.61%

29

In 2020 Double 11, 9 of top 10 best-selling skincare brands were international brands. Winona was only local brand to enter the list. The brand is regarded as the representative of functional skincare brands by consumers.

Top 10 Selling Skincare Bbrands during the Tmall Double 11 Shopping Festival

NO 1.

NO 2.

NO 3.

Estee Lauder

L'Oréal

Lancome

NO 1.

NO 2.

NO 3.

L'Oréal

Lancome

Estee Lauder

2020 2019

New domestic functional skincare brands

30

[Data source: ChemLinked]

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

The history of whoo

Olay

SK-II

SULWHASOO

Shiseido

Winona

LA MER

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Olay

SK-II

PECHOIN

The history of whoo

CHANDO

Shiseido

Winona

Winona Dr. Yu

Biohyalux (Bloomage Biotech)Voolga

QuadHA (Bloomage Biotech)MedRepair (Bloomage Biotech)

HBNDr. Alva

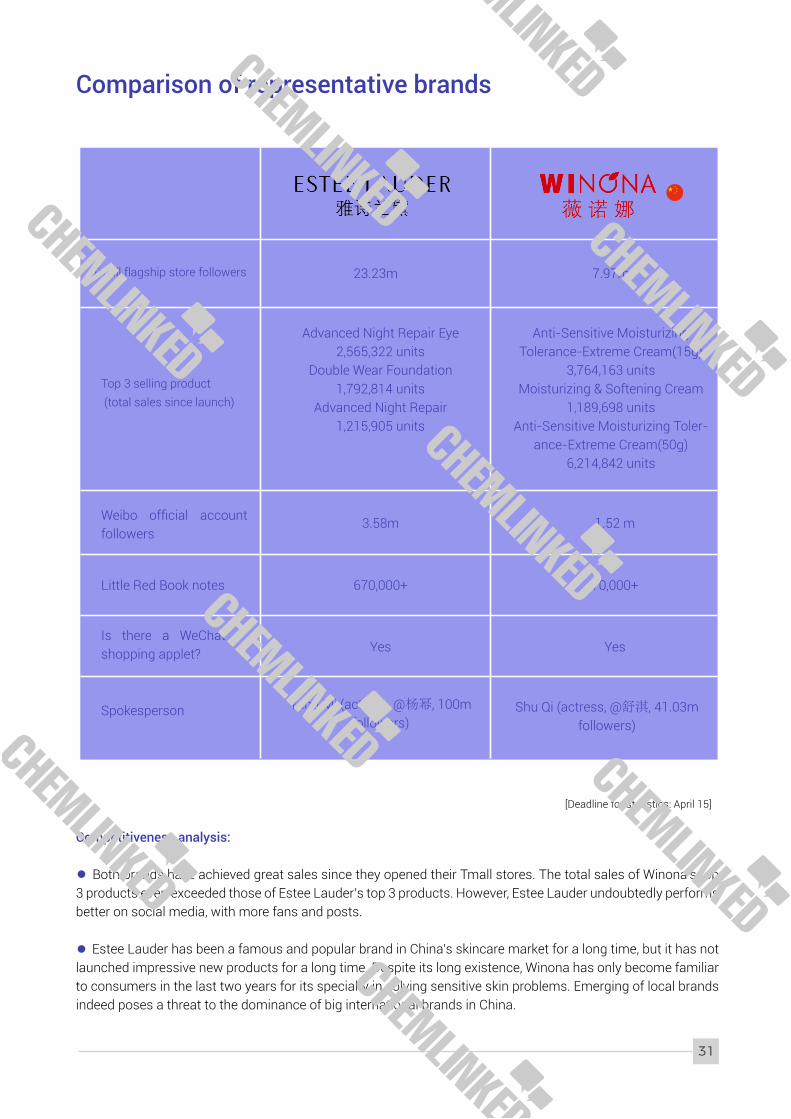

[Deadline for statistics: April 15]

Comparison of representative brands

31

Competitiveness analysis:

Both brands have achieved great sales since they opened their Tmall stores. The total sales of Winona’s top 3 products even exceeded those of Estee Lauder’s top 3 products. However, Estee Lauder undoubtedly performs better on social media, with more fans and posts.

Estee Lauder has been a famous and popular brand in China’s skincare market for a long time, but it has not launched impressive new products for a long time. Despite its long existence, Winona has only become familiar to consumers in the last two years for its specialty in solving sensitive skin problems. Emerging of local brands indeed poses a threat to the dominance of big international brands in China.

23.23m

Top 3 selling product (total sales since launch)

Advanced Night Repair Eye 2,565,322 units

Double Wear Foundation 1,792,814 units

Advanced Night Repair 1,215,905 units

7.97m

Anti-Sensitive Moisturizing Tolerance-Extreme Cream(15g)

3,764,163 unitsMoisturizing & Softening Cream

1,189,698 unitsAnti-Sensitive Moisturizing Toler-

ance-Extreme Cream(50g) 6,214,842 units

3.58m

670,000+

Yes

Yang Mi (actress, @杨幂, 100m followers)

1.52 m

70,000+

Yes

Shu Qi (actress, @舒淇, 41.03m followers)

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

Tmall flagship store followers

International brands have dominated this sector for a long time, but local brands represented by Perfect Diary and Florasis have stood out as strong rivals in the last three years.

In Chinese consumers’ eyes, international brands represent high reputation and local brands represent high price-performance ratio.

In our survey, foreign brands (78.41%) are more popular in the makeup category.

Local vs. Foreign Makeup Brand Purchase Preference

Foreign brands Local brands

MAKEUP

Key takeaways

Consumer preference

21.59%

78.41%

32

Local Japan & Korea

Europe & the U.S. Others

Respondents choose foreign makeup brands for their stronger efficacy (69.70%), more premium brand position (61.36%) and social media impact (33.71%).

Reasons for Choosing Foreign Makeup Brands

Competitive landscape

69.70%Stronger efficacy

More premium bramd position

Social media impact

More appealing packaging design

Celebrity endorsement

Others

61.36%

33.71%

27.27%

24.64%

6.44%

33

In recent years, local makeup brands become increasingly popular among consumers under the tide of China Chic (国潮). Many new local brands emerged and grew quickly to clash head on with international brands. According to EqualOcean, in 2019, local makeup brands accounted for 61% of the total sales of makeup products on Tmall, and its growth rate reached 82%.

In 2020, consumers pay more attention to domestic brands than those from Europe, the United States, Japan and South Korea. Seven of the Top 10 brands are domestic brands, and Perfect Diary's attention is far ahead.

Country Distribution of Top 100 Brands with Most Attention

[Data source: QuestMobile]

29%

30%

37%

4%

Perfect Diary FlorasisLittleDreamGarden

MACGIORGIOARMANI

CHIOTURE EsteeLauder

CHANDO WIS ZEESEA

Perfect Diary also clinched the No.1 place of the makeup category in the Tmall Double 11 Shopping Festival for two consecutive years from 2019 to 2020.

Top 10 Selling Makeup Brands during the Tmall Double 11 Shopping Festival

NO 1.

NO 2.

Perfect Diary

Florasis

NO 1.

NO 2.

Perfect Diary

MAC

2020 2019

16.3%

7.0% 6.8% 6.7% 6.3% 6.1% 5.9% 5.1% 4.9% 4.7%

Top 10 Brands with Most Attention by Makeup Consumers

[Data source: QuestMobile]

34

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

3CE

Lancome

Colorkey

Dior

Estee Lauder

Perfect Diary

Florasis

YSL

GIORGIO ARMANI

MAC

Local rising stars Perfect Diary and Florasis have surpassed foreign brands to become the top 2 best-selling brands on Taobao in 2020.

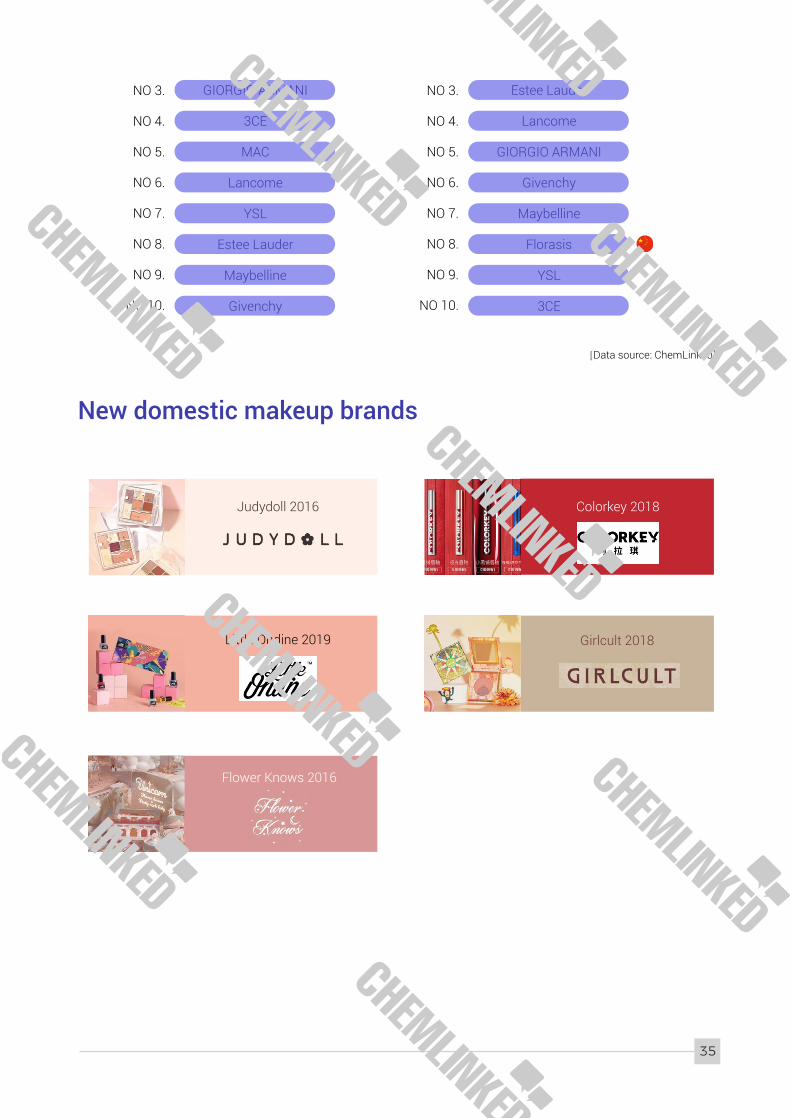

Top 10 selling makeup brands on Taobao in 2020

[Data source: Cyanhill Capital]

Girlcult 2018Little Ondine 2019

Flower Knows 2016

35

[Data source: ChemLinked]

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

GIORGIO ARMANI

3CE

MAC

Lancome

YSL

Estee Lauder

Maybelline

Givenchy

Estee Lauder

Lancome

GIORGIO ARMANI

Givenchy

Maybelline

Florasis

YSL

3CE

New domestic makeup brands

Judydoll 2016 Colorkey 2018

[Deadline for statistics: April 15]

Comparison of representative brands

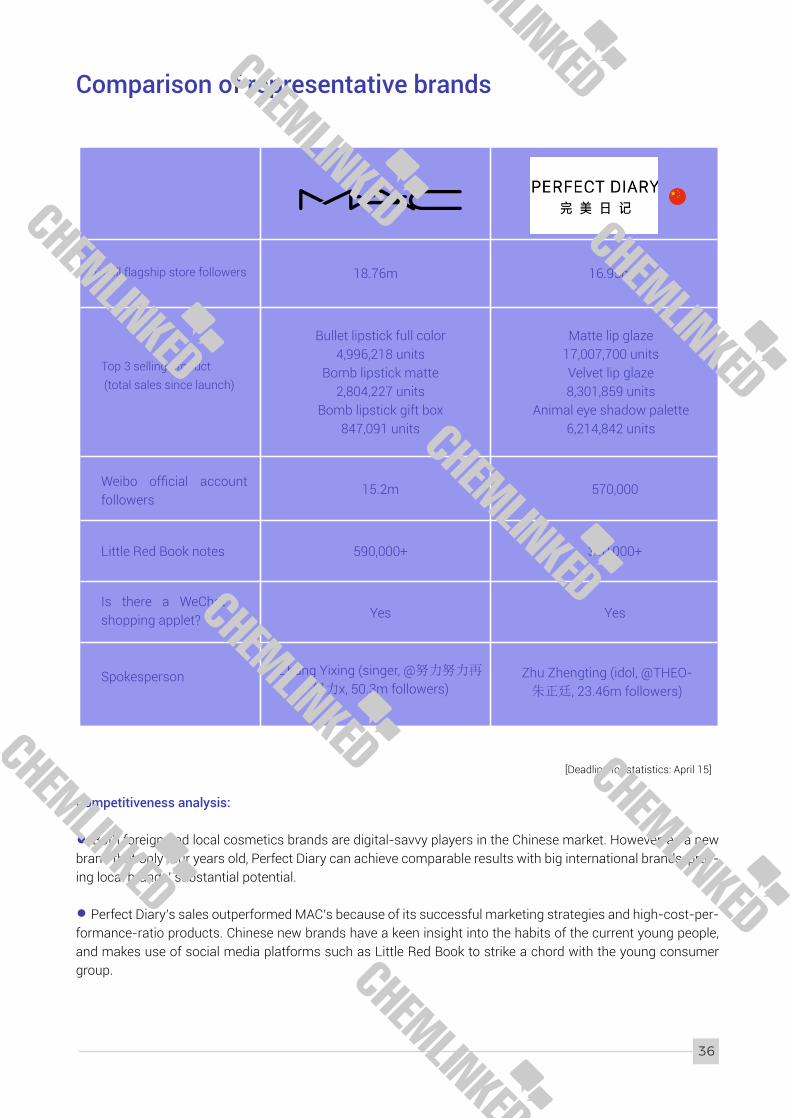

36

Competitiveness analysis:

Both foreign and local cosmetics brands are digital-savvy players in the Chinese market. However, as a new brand that only four years old, Perfect Diary can achieve comparable results with big international brands, prov-ing local brands’ substantial potential.

Perfect Diary’s sales outperformed MAC’s because of its successful marketing strategies and high-cost-per-formance-ratio products. Chinese new brands have a keen insight into the habits of the current young people, and makes use of social media platforms such as Little Red Book to strike a chord with the young consumer group.

18.76m

Top 3 selling product (total sales since launch)

Bullet lipstick full color 4,996,218 units

Bomb lipstick matte 2,804,227 units

Bomb lipstick gift box 847,091 units

16.95m

Matte lip glaze 17,007,700 unitsVelvet lip glaze 8,301,859 units

Animal eye shadow palette 6,214,842 units

15.2m

590,000+

Yes

Zhang Yixing (singer, @努力努力再努力x, 50.3m followers)

570,000

310,000+

Yes

Zhu Zhengting (idol, @THEO-朱正廷, 23.46m followers)

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

Tmall flagship store followers

More niche brands enter China’s e-commerce platform like Tmall and deliver excellent performance.

Classic luxury perfumes continue to grow in popularity.

Local brands still lack competitive advantages.

Foreign brands obtain a landslide advantage in consumer preference with a high proportion of 86.74%.

Local vs. Foreign Perfume Brand Purchase Preference

Foreign brands Local brands

PERFUME

Key takeaways

Consumer preference

86.74%

37

13.26%

Baidu Search Comparison in Perfume Industry in 2019

The Chinese perfume market has a high degree of brand concentration, and international brands dominate the market. Luxury-based players perform well and niche brands are growing at an accelerated pace.

According to the 2019 Baidu Perfume Industry Report, 80% of Baidu (Chinese searching engine equivalent to Google) searches were for big-brand perfumes, and 17% searches were for niche brands.

With the rapid growth of China's perfume market, a group of fledgling domestic perfume brands with affordable prices and local stories have taken a 3% share in the search of perfume brands.

Better experience (73.11%), more premium brand position (46.21%), and social media impact (20.08%) are the top 3 factors attracting respondents to choose foreign fragrance brands.

Reasons for Choosing Foreign Perfume Brands

Competitive landscape

73.11%

46.21%

20.08%

14.39%

11.36%

38

Better experience

Celebrity endorsement

More premium brand position

Social media impact

Others

Foreign designer perfume Foreign niche perfume Domestic perfume

80%

17%

3%

39

Top searched CHANEL

DIOR

Jo Malone

LOEWR +27%

LOUIS VUITTON +21%

CELINE +27%

Diptyque

Serge Lutens

Creed

Le Labo +50%

Acqua Di Parma +47%

L’Artisan Parfumeur +47%

Scent Library

Boitown

Fenshine

Boitown +96%

Barrio +76%

Vivinevo +47%

Top rising

Foreign designer perfume Foreign niche perfume Domestic perfume

[Data source: ChemLinked]

Top 10 Selling Perfume Brands during the Tmall Double 11 Shopping Festival

Boitown was the only local brand thrusting into the top 10 selling brand lists in the last two years of Tmall Double 11 Shopping Festival.

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

GIORGIO ARMANI

Boitown

Jo Malone

YSL

Tom Ford

Bvlgari

Atelier Cologne

Calvin Klein

Versace

Dior

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Boitown

Jo Malone

Dior

Tom Ford

Atelier Cologne

YSL

Bvlgari

Anna sui

Elizabeth Arden

Hermes

2020 2019

[Deadline for statistics: April 15]

Comparison of representative brands

40

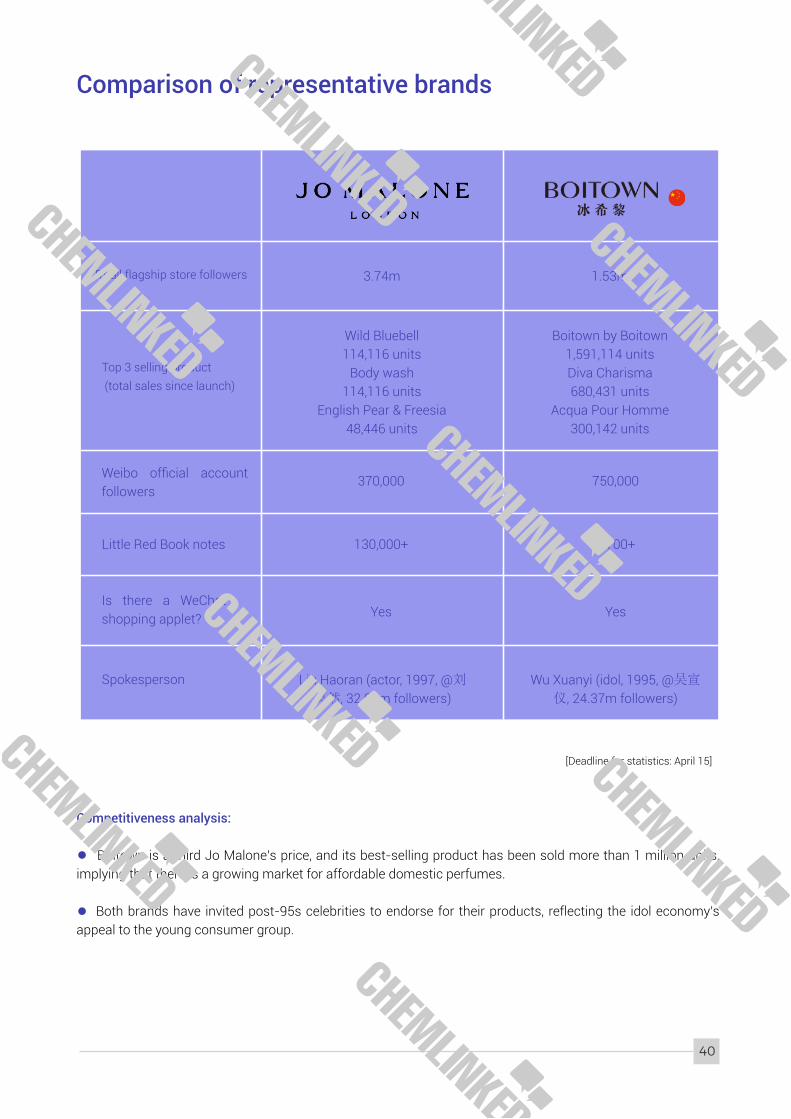

Competitiveness analysis:

Boitown is a third Jo Malone’s price, and its best-selling product has been sold more than 1 million units, implying that there is a growing market for affordable domestic perfumes.

Both brands have invited post-95s celebrities to endorse for their products, reflecting the idol economy's appeal to the young consumer group.

3.74m

370,000

130,000+

Yes

Top 3 selling product (total sales since launch)

Wild Bluebell 114,116 units

Body wash 114,116 units

English Pear & Freesia 48,446 units

Liu Haoran (actor, 1997, @刘昊然, 32.08m followers)

1.53m

750,000

9,700+

Yes

Boitown by Boitown 1,591,114 unitsDiva Charisma 680,431 units

Acqua Pour Homme 300,142 units

Wu Xuanyi (idol, 1995, @吴宣仪, 24.37m followers)

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

Tmall flagship store followers

International brands dominate this category, and most brands are from P&G.

New domestic personal care brands are springing up and gaining popularity by innovative product and package designs.

75% of respondents are inclined to opt for foreign personal care brands.

Local vs. Foreign Perfume Brand Purchase Preference

Foreign brands Local brands

PERSONAL CARE

Key takeaways

Consumer preference

25%

75%

41

Like perfume, respondents are more likely to buy foreign brands for a better experience (73.11%), more premium brand position (46.21%), and social media impact (20.08%).

Reasons for Choosing Foreign Personal Care Brands

Competitive landscape

73.11%Better experience

More premium bramd position

Social media impact

Celebrity endorsement

Others

46.21%

20.08%

14.39%

11.36%

42

Foreign brands, most of which belong to multinational groups P&G and Unilever, occupy most top-selling seats during the Tmall Double 11 Shopping Festival. Chinese new brand Triptych of Lune (founded in 2016) shows promising growth potential.

Top 10 Selling Body Wash & Hair Care Brands during the Tmall Double 11 Shopping Festival

International brands dominate China’s personal care industry, and the monopoly situation expects to continue for a long time.

China's Personal Care Market Share in 2018

[Data source: huaon.com]

35%

12%

29%

5%

4%

3%

2%

2%

1%

1%

6%

P&G

Uniever

Henkel

L'Oréal

Beiersdorf

UNIASIA

Shiseido

Laf

Youngrace

Amore Pacific

Others

New domestic personal care brands

43

NO 1.

NO 2.

NO 3.

NO 4.

NO 5.

NO 6.

NO 7.

NO 8.

NO 9.

NO 10.

Safeguard

LUX

Dove

Kuyura

Olay

Dettol

Walch

Femfresh

Opal

Kustie

Safeguard

Kuyura

Dove

LUX

Olay

Little Dream Garden

Walch

Dettol

The Face Shop

Tesori D’oriente

2020

Body wash Hair care

2019

Head&Shoulders

VS

Pantene

CLEAR

Shiseido

REJOICE

Triptych of Lune

Adolph

Selsun

Moroccanoil

2020

Head & Shoulders

VS

Pantene

Adolph

Triptych of Lune

CLEAR

REJOICE

Dove

Shiseido

LUX

2019

[Data source: ChemLinked]

Triptych of Lune (2016)Effortless (2018)

Nattitude (2015) TTOUCHME (2017)

Storymix (2020)

[Deadline for statistics: April 15]

Comparison of representative brands

44

Competitiveness analysis:

Head&Shoulders has been a household name for Chinese consumers, and some may even mistake it for a domestic brand. Although there emerged several domestic brands which achieved brilliant results through online marketing, it’s not going to happen overnight for these new brands to take over the national status of the established ones.

Besides, the domestic brand Triptych of Lune is suspected of copying the design of the foreign customized hair care brand Functional of Beauty, and passing off as a foreign brand, reflecting the lack of indigenous innovation and brand confidence of domestic brands.

11.76m (P&G flagship store)

Top 3 selling product (total sales since launch)

Whisper liquid sanitary napkin 9,369,100 units

Tide laundry detergent 4,402,100 units

Head&Shoulders shampoo 4,292,600 units

1.53m

Fluffy hair shampoo 993,720 units

Oil-control shampoo 745,592 units

Mousse shower gel 421,546 units

1.44m

10,000+

Yes

Wang Yibo (idol, @UNIQ-王一博, 38.2m followers)

20,000

10,000+

Yes

/

Weibo official account followers

Little Red Book notes

Is there a WeChat shopping applet?

Spokesperson

Tmall flagship store followers

WHO WE ARE

We provide one-stop e-commerce solutions for Chinese market covering market research, digital mar-keting, e-commerce operation, IT solutions, and brand management.

We have supported brands establish and grow their online sales across a variety of sectors such as Food & Beverage, Cosmetics & Person Care, Pet Products, Kid and Mother products.

As a strategic partner trusted by international brands, our mission to provide diversified and precise services for overseas brands entering China, cultivating the brand value, and achieving sustained sales growth.

WHY CHOOSE US

OUR PARTNERS

One-stop, all-in-one market entry solution

Customized localization marketing strategy

High Efficiency and Quality

WHAT WE PROVIDE

KOL/KOC CampaignLivestreaming e-commerce; Endorsements; Offline Events

Market ResearchMarket Investigation; Industry Report; Strategy Consulting

Technology SolutionsBaidu SEO; WeChat Applet

Brand LocalizationCompany Establishment; Trademark & IP Registration; Brand Image Design

Social Media MarketingWeChat; Weibo; Red Book; TikTok etc.

E-commerce Store Setup & OperationOpen an Online Store; Channel Matchmaking; Operation &Management

CONTACT US Jocelyn Sun, Brand Strategist

14th Floor, Building 3, Haichuang Technology Center, Hangzhou, China (311121)

[email protected]+86 571 8700 7503

Helping You Win in ChinaEnd-to-end China Market Entry Lifecycle Management

CONCLUSIONS AND IMPLICATIONS

PART 4

Conclusions

The survey shows that perfume, skincare products, health food, makeup, baby food (including milk powder, complementary food, and snacks), and personal care are the sectors in which respondents are more willing to buy foreign brands. Foreign brands have an absolute advantage in these categories. In the pet food sector, foreign brands win by a narrow margin. The UHT milk is the only category where domestic brands surmount foreign brands.

It is evident that foreign brands have pulled ahead in brand value building, and they have left a deep impression as a representative of high-end and high-quality life for Chinese consumers. In the food sector, foreign products’ ingredients and formulations are competitive edges. In the cosmetics sector, social medial marketing plays an increasingly vital role in driving consumers’ decisions.

In the cosmetics sector, stronger efficacy, more premium brand position, and social impact are the top 3 factors driving respondents to opt for foreign brands. In the food sector, respondents choose foreign brands mainly due to better and safer ingredients, brand fame and position, and more scientific formulations.

45

Perfume

Cosmetics (skincare)

Health food

Cosmetics (makeup)

Infant formula

Baby food (complementary food and snacks)

Personal care

Pet food

UHT milk (UHT white milk and ambient yogurt)

Foreign

86.74%

85.98%

79.92%

78.41%

76.89%

75.38%

75%

53.79%

33.33%

Local

13.26%

14.02%

20.08%

21.59%

23.11%

24.62%

25%

46.21%

66.67%

46

Implications

The rise of new local brands, the booming China Chic tide (国潮), and Chinese consumers’ willingness to purchase more local brands in the future have brought substantial potential for local brands. Intensified competition from local counterparts put pressure on foreign brands. Therefore, foreign brands should take the Chinese market more seriously by carefully understanding Chinese culture and Chinese consumers’ habit. The time when Chinese consumers pursue international brands unconditionally and blindly has passed.

Foreign brands should get to grips with the online channels and digital ecosystem when strategizing marketing and branding plans because online marketing has been proven to be an effective method to create word of mouth and build up hype around a brand. A large proportion of new domestic cosmetics brands rely on online marketing and gain quicker recognition. Cooperation with KOL is the most common marketing modes.

Foreign brands would lose out by politicizing business in China. The misguided and baseless boycott of Xinjiang cotton has put foreign brands which heavily depend on the Chinese market, including H&M, Adidas, and Nike, under fire. There's no room for compromise when it comes to national dignity for Chinese people, especially the young generation, who have a stronger sense of national pride than their parents.

China is always committed to opening to the world. Although the government has proposed the new economic development pattern of "dual circulation," it is by no means a closed domestic loop. The survey also embodies that Chinese consumers are more receptive to foreign brands in some categories that can lead them to a better life. There is no need to worry about state-level policy obstacles.

Most Likely Situation for the Relationship Between Local and Foreign Brands in the Next Five Years of Market Competition

39.39%

32.58%

28.03%

Consumer’s awareness of product country origin would diminish, and they would pay more attention to product quality and cost-effectiveness

Chinese people are more willing to choose Chinese brands and domestic brands occupy more market

Foreign brands still have their advantages in innovation and creativity, and they are on a par with Chinese brands with their respective advantage

1

2

3

4

Disclaimer

This report has been prepared by ChemLinked as general information only for study and research in the industry, and shall not be used for any commercial purposes.

Some of the text and data in this report are collected from public information and are owned by the original author. The brand logo and product pictures in the report are all from the official website of the brand or its Tmall official flagship store, and the pictures are only used for demonstration. It does not specifically refer to any relationship between the brand and this report.

Copyright: unless otherwise stated all contents of this website are ©2021 - REACH24H Consulting Group - All Rights Reserved - For permission to use any content on this site, please contact [email protected]

47

The following individuals contributed to the production of this report.

Content Manager, Research Specialist

Research Analyst

Research Analyst

Acknowledgements

Chris Wang

Shine Hu

Ye Chen

Value-Added

Regulatory SolutionNews, Regulatory Analysis & Market Insights, Reports , Wikipedia-Style Guides of APAC Regulations

Compliance Consultation, Ingredient Review, Product Registration, Tailored Report/Training

Webinars (Web-Based Seminar), O�ine Events, Tailored Training Courses Consultation Service, Advertising

Opportunities, 1-1 Customer Service On-Demand Translation Service

Regulatory Database, Ingredient Search Tools, English Translations of Regulatory Standards

Product Registration and Consulting Services Conferences, Workshops and Webinars

· Chemical Regulatory Annual Conference (CRAC)

· QSAR Training Courses

· Lifecycle Management of Chemicals Open Courses

· OECD GLP Training Courses

Regulatory Data and News Alerts

· Continous News Monitoring · Substance Database

· Comprehensive Regulatory Database · Webinars

· Translation of Relevant Regulations

· Expert Analysis and Regulatory Reports

Software and Information Services

· NEWRSCC · SDS Cloud · KR Cloud

· Newchem Cloud · iMeeton

· ZFR Textile Regulation & RSL Searching Database

Washington D.C.USA

DublinIreland London

UK

HangzhouChina

SeoulSouth Korea

TaiwanChina

global branches providing 24-hour service

High-level technical expertise to ensure professional support

Industry-specific services to meet client's expectations

Supported by internationally certified toxicologists, safety and risk assessment professionals

Longstanding partnership with government agencies and leading industry associations

Successful completion of 10s of thousands of regulatory cases

First choice of over 9,000 companies for our regulatory expertise and experience

REACH24H offers one-stop global market access

services for businesses in the industrial chemicals,

pesticides and disinfectants, cosmetics, food and food

contact materials as well as pharmaceutical industries.

Taiwan, China

9th Floor, 898 Jing Guo Road, Luzhu District, Taoyuan, TaiwanTel: +886-3-3466936 Fax: +886-3-5167038

China

14th Floor, Building 3, Haichuang Technology Center, 1288 West Wen Yi Road, Hangzhou, China (311121)Tel : +86-571-8700-7555 Fax: +86-571-8700-7566

UK

20-22 Wenlock Road, London, N17GU, EnglandTel: +44-203-582-2996

South Korea

Room 908-909, 7, Heolleungno, Seocho-gu, Seoul, 06792, Republic of Korea Tel: +82-2-3497-1610

USA

11921 Freedom Drive, Suite 550, Reston, Virginia 20190 USATel: +1-703-596-8055 Fax: +1-703-776-9462

Ireland

Paramount Court, Corrig Road Sandyford, Dublin 18, Ireland Tel: +353-1-8899-951 Fax: +353-1-6865-683

REACH24H Consulting Group [email protected] www.reach24h.comContact Us

market.chemlinked.com

Add: 14th Floor, Building 3, Haichuang Technology Center, 1288 West Wen Yi Road, Hangzhou, China

Tel: +86 571 8710 4444

E-mail: [email protected]

Scan for LinkedIn Scan for WeChat