Audit and Risk - UK.COM

348

Audit and Risk Date: Thursday, 13 February 2014 Time: 18:30 Venue: Supper Room Address: Town Hall, Hall Plain, Great Yarmouth, NR30 2QF AGENDA Open to Public and Press DECLARATIONS OF INTEREST You have a PERSONAL INTEREST in a matter being discussed at a meeting IF • It relates to something on your Register of Interests form; or • A decision on it would affect you, your family or friends more than other people in your Ward. You have a PREJUDICIAL INTEREST in a matter being discussed at a meeting IF • It affects your financial position or that of your family or friends more than other people in your Ward; or • It concerns a planning or licensing application you or they have submitted • AND IN EITHER CASE a reasonable member of the public would consider it to be so significant that you could not reach an unbiased decision. If your interest is only PERSONAL, you must declare it but can still speak and vote. If your interest is PREJUDICIAL, you must leave the room. However, you have the same rights as a member of the public to address the meeting before leaving. TRAINING ON INTERNAL AUDIT PLANNING PROCESS Training will take place at 6pm prior to the meeting. Page 1 of 348

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Audit and Risk - UK.COM

Audit and Risk

Date: Thursday, 13 February 2014

Time: 18:30

Venue: Supper Room

Address: Town Hall, Hall Plain, Great Yarmouth, NR30 2QF

AGENDA

Open to Public and Press

DECLARATIONS OF INTEREST You have a PERSONAL INTEREST in a matter being discussed at a meeting IF • It relates to something on your Register of Interests form; or • A decision on it would affect you, your family or friends more than other people in your

Ward. You have a PREJUDICIAL INTEREST in a matter being discussed at a meeting IF • It affects your financial position or that of your family or friends more than other people

in your Ward; or • It concerns a planning or licensing application you or they have submitted • AND IN EITHER CASE a reasonable member of the public would consider it to be so

significant that you could not reach an unbiased decision. If your interest is only PERSONAL, you must declare it but can still speak and vote. If your interest is PREJUDICIAL, you must leave the room. However, you have the same rights as a member of the public to address the meeting before leaving.

TRAINING ON INTERNAL AUDIT PLANNING PROCESS

Training will take place at 6pm prior to the meeting.

Page 1 of 348

1 MINUTES

To confirm the minutes of 19 September 2013.

5 - 8

2 GROUP MANAGERS RISK REPORTS

The Committee will consider the Area of Risk reports from the Group Manager's for Customer Services, Resources, Environmental Services and Tourism & Communications.

9 - 38

3 ANNUAL AUDIT LETTER 2012-13

The Committee will consider the attached report.

39 - 50

4 ANNUAL CERTIFICATION REPORT 2012-13

The Committee will consider the attached report.

51 - 58

5 AUDIT AND CERTIFICATION FEES 2013-14

The Committee is requested to note the briefing report which is for information only.

59 - 61

6 LOCAL GOVERNMENT AUDIT COMMITTEE BRIEFING

The Committee will consider the attached report.

62 - 70

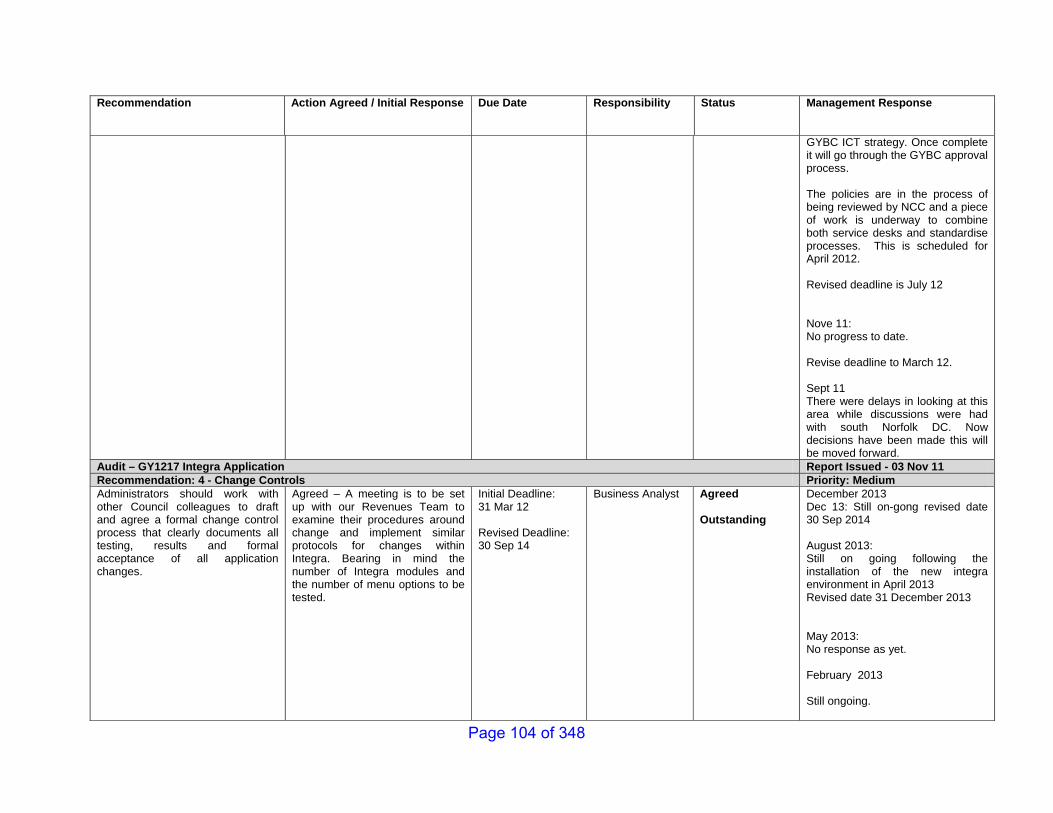

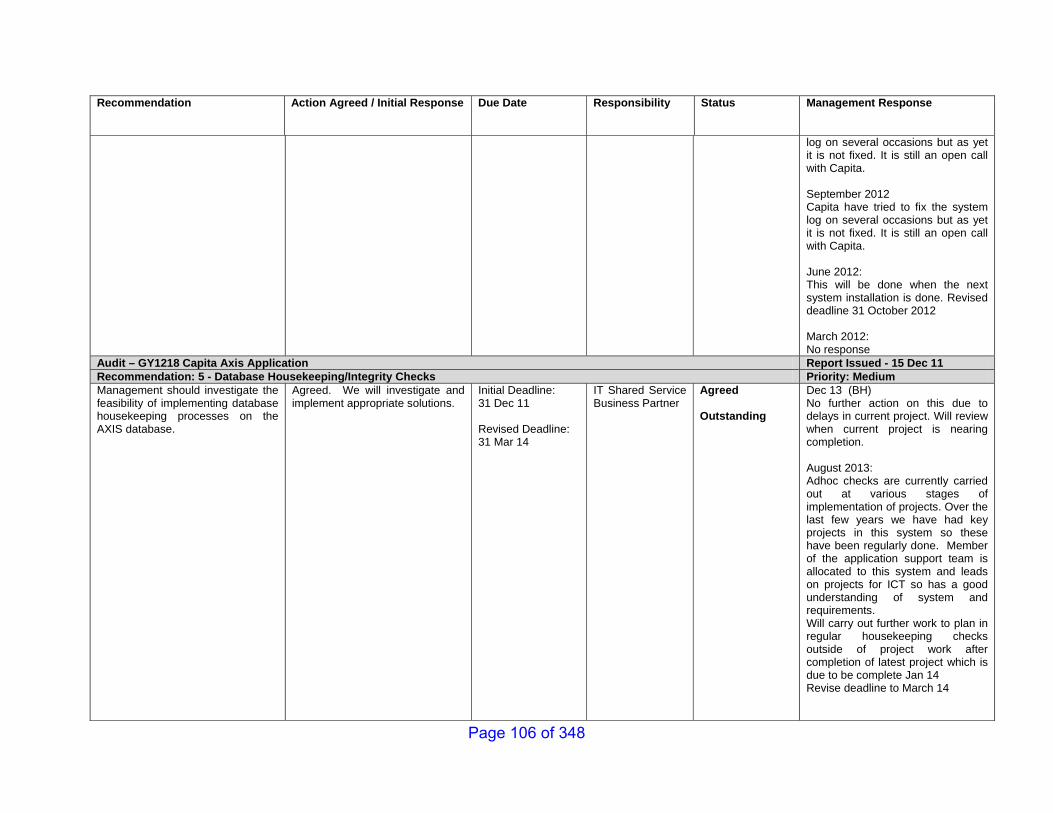

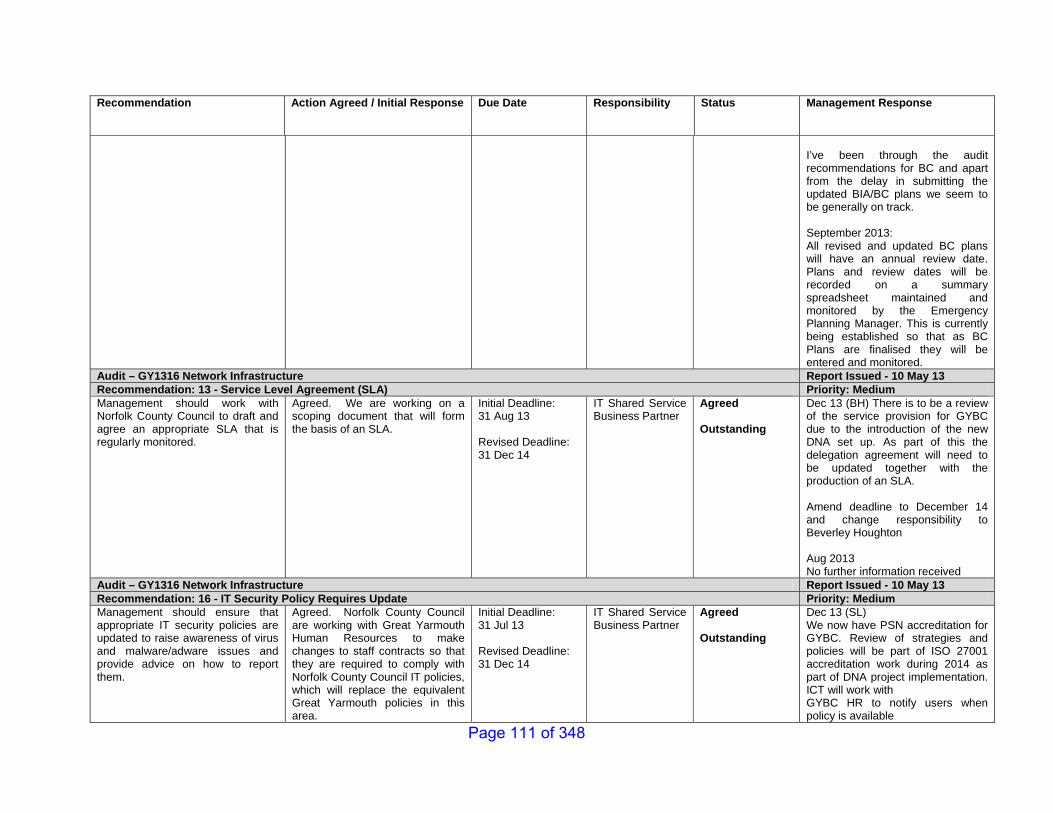

7 FOLLOW UP ON EXTERNAL AUDIT RECOMMENDATIONS

The Committee will consider the report.

71 - 75

8 FOLLOW UP ON INTERNAL AUDIT RECOMMENDATIONS

The Committee will consider the attached report.

76 - 115

9 PROGRESS REPORT 2013-14

The Committee will consider the attached report.

116 - 155

10 INTERNAL AUDIT CHARTER

The Committee will consider the attached report.

156 - 197

11 WORKING PROTOCOL BETWEEN INTERNAL AUDIT AND

EXTERNAL AUDIT

The Committee will consider the attached report.

198 - 218

12 TREASURY MANAGEMENT STRATEGY MID YEAR REPORT

The Committee will consider the attached report.

219 - 234

13 TREASURY MANAGEMENT STRATEGY

The Committee will consider the attached report.

235 - 264

14 RISK MANAGEMENT FRAMEWORK

The Committee will consider the attached report.

265 - 280

15 CORPORATE PROCUREMENT STRATEGY

The Committee will consider the attached report.

281 - 295

16 REVISED CONTRACT STANDING ORDERS

The Chairman has requested that the Committee's attention be brought to this report.

296 - 325

Page 2 of 348

17 CODE OF CORPORATE GOVERNANCE

The Committee will consider the attached report.

326 - 349

18 ANY OTHER BUSINESS

To consider any other business as may be determined by the Chairman of the meeting as being of sufficient urgency to warrant consideration.

19 DATE AND TIME OF NEXT MEETING

To confirm that the next meeting will be held on Thursday, 17 April 2014.

Page 3 of 348

AUDIT AND RISK COMMITTEE

19 September 2013 – 6.30 pm

PRESENT: Councillor Sutton (in the Chair); Councillors T Coleman, Marsden, Pettit, A Smith and B Walker. Councillor M Coleman attended as substitute for Councillor Hanton. Mrs J Beck (Director of Customer Services), Mr R Hodds (Cabinet Secretary), Mrs L Mockford (Group Manager Governance), Mrs V George (Group Manager Housing Services for the Elderly), Mr R Gregory (Group Manager Neighbourhoods and Communities) and Mr D Minns (Group Manager Planning and Building Control). Ms E Hodds (Deputy Audit Manager) and Mr D Riglar (External Audit Manager). Apologies for absence had been received from Councillors Hanton, Holmes and Stone. 1. MEMBERS MEETING WITH REPRESENTATIVES FROM INTERNAL AUDIT AND

AUDIT COMMISSION The Committee agreed that there were no relevant issues to be discussed in private with the Deputy Audit Manager. 2. MINUTES The minutes of the meeting held on the 27 June 2013 were confirmed. 3. AREAS OF RISK (a) Governance The Committee considered the Group Manager (Governance) report with regard to the areas of risk in respect of service areas relating to Corporate Governance, Electoral Services, Information, Licensing, Member Services and nplaw client. The Corporate Risk Assessment had identified three specific areas within Governance relating to information security, data quality and non compliance with legislation.

LARGER PRINT COPY AVAILABLE

PLEASE TELEPHONE: 01493 846325

Page 4 of 348

Audit and Risk Committee 19 September 2013 (b) Housing, Health and Wellbeing The Committee considered the Group Manager (Housing, Health and Wellbeing’s) Service Risk Assessment relating to services in respect of Private Sector Housing and Renewal Services and services for older people. Members were advised that the purpose of this group of services was to help older and vulnerable people live the way they want through the provision of support services, advice and information and adaptations to their homes. (c) Neighbourhoods and Communities The Committee considered the Group Manager (Neighbourhood and Communities) report on areas of risk relating to functions including Community Centres, Partnerships, Indoor and Outdoor Leisure, Sports Development, Arts and Culture Development and youth engagement. (d) Planning and Building Control The Committee considered the Group Manager (Planning’s) report on areas of risk relating to Planning and Development Control. The Group Manager’s report identified the key risks, the potential impact of the risks and which service area could be affected and what action could be taken to address such risks. In particular the Group Manager referred to risks relating to new legislative implications for Development Control and on issues with regard to the delivery of the new Local Plan. Members noted that the reports were new to the committee but wanted to see a consistent approach in reporting. Reports to focus on key risks and unmitigated risks. RESOLVED: That the Group Manager’s reports in relating to (a) to (d) above be noted. 4. STATEMENT OF ACCOUNTS 2012/13 The Committee was advised that the Accounts and Audit (England) Regulations 2011 require the approval of the Council’s Statement of Accounts 2012/13 by the statutory deadline of the 30 September 2013. In discussing the report, the Committee expressed their concern with regard to the lack of financial officer support at this meeting. However, Members were assured by External Audit that the Statement of Accounts had not materially changed since they reviewed the draft version at the previous committee meeting. RESOLVED: That Council be recommended to approve the audited annual Statement of Accounts

2012/13. 5. ANNUAL FINANCIAL REPORT The external Audit Manager presented his annual financial report for the year ended 31 March 2013. Mr Riglar reported that his report summarised the findings from the 2012/13 audit which was substantially complete. It included the messages arising from the audit of the financial statements and the results of the work undertaken to assess the Council’s arrangements to secure value for money in the use of resources. As from the 17 September 2013 the external auditors expected to issue an un-qualified opinion. The external audit demonstrated that the Council has prepared its financial statements well. Mr Riglar reported

Page 5 of 348

Audit and Risk Committee 19 September 2013 that appropriate arrangements were in place to secure economy, efficiency and effectiveness in the use of resources. Mr Riglar also noted the improvement journey that the Council had made of the past six years in completing a clean set of accounts. One matter that was reported with the Annual Financial Statement was in relation to the Councils Financial Regulations and standing orders and that these had not been formally reviewed since 2006. RESOLVED: (i) That Council be recommended to approve the annual results report for the year ended 31 March 2013. (ii) That Cabinet be recommended to approve a review of the current standing orders for procurement. 6. LETTER OF REPRESENTATION The Committee considered the letter of representation for the 2012/13 financial statements audit for the Borough Council audit for the year ended 31 March 2013. RESOLVED:

That a letter of representation to be signed on behalf of the Council by the Chairman and the Chief Finance Officer prior to the audit opinion and conclusion being issued be agreed.

7. REPORT ON THE STATUS OF AUDIT RECOMMENDATIONS DUE FOR IMPLEMENTATION BETWEEN THE 1 APRIL AND 31 JULY 2013 The Committee considered the internal audit consortium manager’s report which informed Members as to the latest progress made in relation to the management’s implementation of agreed audit recommendations falling due between the 1 April and 31 July 2013. The Committee noted that steady progress has been made by management in relation to the implementation of audit recommendations and were encouraged to note that responses had been received from all managers and that reasons for delay were justified. RESOLVED: That the Committee receive a note the current position in relating to the completion of agreed audit recommendations. 8. PROGRESS REPORT ON INTERNAL AUDIT ACTIVITY 1 APRIL – 31 AUGUST 2013 The Committee considered the internal audit consortium manager’s report which examined progress made between the 1 April and 31 August 2013 in relation to delivery of the Annual Audit Plan for 2013/14, and included abbreviated management summaries in respect of four audit reviews which have been finalised during this period. In discussing the report Members recorded their concern in relation to the rescheduling of the Tourism and Marketing audit to October as this was when work would be underway with regard to the Seafront BID. Members were assured by the Director of Customer Services that there is capacity to do both.

Page 6 of 348

Audit and Risk Committee 19 September 2013

RESOLVED: (i) That the Committee receive a note the outcomes of those audits finalised during the first five months of the financial year. (ii) That the Committee note the current status of the Annual Plan for 2013/14 and where the re-timetabling of some work has proved necessary. 9. CORPORATE RISK REGISTER The Committee considered the Corporate Risk Officer’s report which asked Members to review the Corporate Risk Register to determine whether the register correctly reflects the risk affecting the authority. Members were advised that the register was reviewed. The Deputy Audit Manager assured the Committee that the changes to the timing of the audit had been agreed with the Group Manager and the Director of Customer Services also confirmed that this would not be an issue. The Chairman queried the limited assurance level awarded to Print and Design as this had previously been awarded such an opinion. The Chairman was assured by the Deputy Audit Manager that the action plan had been agreed and the Director of Customer Services assured the Chairman that management of the area has now settled down and due progress would be made against the recommendations. RESOLVED: That the Corporate Risk Officer’s report on the Corporate Risk Register be noted. 10. DATE AND TIME OF NEXT MEETING Members noted that the next meeting of the Committee will take place on the 13 February 2014 at 6.30 pm. 11. CLOSURE OF THE MEETING The meeting ended at 8.05 pm.

Page 7 of 348

Subject: Customer Services – Areas of Risk

Report to: Audit and Risk Date: 13th February 2014

Report by: Group Manager Customer Services

1. Introduction

Customer Services consists of the following service areas:

Administration of Housing Benefit and Local Council Tax Reduction Scheme Customer Service – telephony, face to face and online including Corporate

Website Support Services including Reception and Cashiers Bereavement Services –Crematorium Parking Services ICT Client – Shared Service

2. Corporate risks

The corporate risk assessment already identifies the following risks within the Customer Services Group:

Economy - Increased workload Housing Benefit & Council Tax Reduction Administration

Business Continuity – Loss of IT Systems Information Security – Electronic Access to key DWP systems Customer Needs – Failure to deliver expectations of customers

3. Other identified risks within the service group There are two further main areas of risk within the group: Introduction and national rollout of Universal Credit

Housing costs to be included within Universal Credit Original migration plan for transfer of Housing Benefit caseload to Universal

Credit has been delayed No replacement migration plan available yet Uncertainty for Housing Benefit and Customer Service staff, have already started

to lose experienced staff at a time when demand is still high and the caseload unchanged

Inability to forward plan effectively Uncertainty over future funding Ultimately facing staff redundancy through migration to end of legacy Housing

Benefit Support and assistance for customers moving on to Universal Credit

Page 8 of 348

Bereavement Services – Replacement Cremators

Crawfords Europe Ltd, contracted by Morgan Sindall on GYBC behalf Crawfords Europe Ltd now in liquidation Installation of new cremators incomplete – Abatement system not operational No ongoing maintenance contract in place Emergency remedial work following fire in place with temporary maintenance

agreement Need to tender for new maintenance contract to complete works and comply with

legislation Legal action ongoing with GYBC contractor, Morgan Sindall

Page 9 of 348

Customer Service – Service Risk Assessment

Service Function

Risks associated with service

Likelihood

Impact

Action taken/To be taken

Comments

Housing Benefit Administration And Customer Services

A-Very High B-High C-Significant D-Low E- Very Low F- Almost Impossible

1- Catastrophic 2- Critical 3-Marginal/Moderate 4-Negligible

Housing Benefit Delivery & Customer Service

Introduction of Universal Credit

Timescales and Migration Plan for Housing Benefit Caseload to transfer to Universal Credit

A

3

Engagement with DWP and JobCentre Plus/ attendance to workshops/seminars – access to web pages for communication updates

The national roll out of UC has been delayed and timescales for migration are yet to be finalized. Difficulties for service planning Some certainty around Pensioner Cased which will remain until at least 2017 - Housing costs for supported accommodation to remain with local authorities

Loss of key resource insufficient to meet continued demand due to uncertainty of timescales, impact on quality and subsidy audit

A

2

Ongoing overtime to help meet demand Intensive training for new inexperienced staff

The service has already experienced a loss of experience staff due to opportunities within the council following restructures – caseload has remained stable but workload remains high Page 10 of 348

Staff redundancy due to loss of Housing Benefit Caseload

A

3

Vacant posts have been and will be filled on a temporary basis

GYBC will retain responsibility for the assessment and delivery of Local Council Tax Reductions Scheme, Housing Costs for those in supported accommodation and other Discretionary schemes like Discretionary Housing Payments

Local support for Customers claiming Universal Credit including Housing Costs

A

3

Multi agency approach already in place for wider welfare reform changes with referral for money management and debt advice in place Continued encouragement for customers to access services online in readiness for claiming UC – development of interactive services on GYBC website Continued engagement with DWP and Job centre plus at a local level

The Government has produced a draft Local Support Services Framework which gives information relating to how customers claiming Universal Credit can be supported locally through the process. The document outlines best practice from a selection of organizations supporting customers through the welfare changes The document also outlines some certainty around Local Authority involvement with support for customers at least in the short term including working jointly with other agencies and voluntary organizations although funding is yet to be further defined Page 11 of 348

Service Function

Risks associated with service

Likelihood

Impact

Action taken/To be Taken

Comments

Bereavement Services

A-Very High B-High C-Significant D-Low E- Very Low F- Almost Impossible

1- Catastrophic 2- Critical 3-Marginal/Moderate 4-Negligible

Cremations Crematorium

No current maintenance contract in place for the completion and ongoing maintenance of the new cremators

A

2

Emergency maintenance agreement in place to keep operational until maintenance contract can be tendered for

Following fire above Cremator 1, ATI were appointed to make remedial works to get cremators operational – they have agreed to a temporary emergency maintenance arrangement

Inability to complete works on and have operational cremator abatement system

B

3

This will not be investigated until maintenance contract has been retendered and awarded

Failure to get Abatement system operation : Two options: a) Purchase new Abatement System (£3-400k Approx) b) Enter into National or Local Burden Sharing Scheme (£100k PA Approx)

Completion of successful legal action against Contractor

C

3

GYBC and Contractors Legal teams are in communication

Page 12 of 348

Subject: Resources – Areas of Risk

Report to: Audit and Risk Date: 13.February 2014

Report by: Group Manager - Resources

1. Introduction

Resources consists of the following service areas:

Finance – Treasury Management, Systems, Creditors, Budgets, Annual Accounts, Internal and External Audit

HR Revenues – Council Tax, NNDR, Systems & Fraud

2. Corporate risks

The corporate risk assessment already identifies the following risks within the Resources Group:

Delivery of Long Term Strategic Objectives – Medium Term Financial Strategy Lack of Resources – Medium Term Financial Strategy Limited Capacity – Medium Term Financial Strategy Business Continuity – Business Continuity Plans Reliance on Key Individuals – Job Evaluation

3. Other identified risks within the service group There are three further main areas of risk within the group:

Introduction and national rollout of Universal Credit and Single Fraud Investigation Service (SFIS) Uncertainty for Revenues System staff, who maintain the system for the Housing

Benefits Team The SFIS is due to come into existence by March 2015, which means a difficult

and uncertain year for the Revenues Fraud team Inability to forward plan effectively Uncertainty over future funding Ultimately facing staff redundancy through migration to end of legacy Housing

Benefit

Staff Resourcing and Skills The HR team have recently been through a restructure which resulted in

compulsory redundancies and therefore, loss of skills and knowledge The Revenues team have been through a period of turmoil and have suffered

with vacancies and staff illness

Page 13 of 348

Bank Contract

The Co-operative Bank have informed all local authorities that once their banking contract comes to the end of its term, the bank will not renew the contract

GYBC will need to find another bank to deliver its banking services by April 2016 Significant volumes of transactions go through the main bank account and there

are risks involved in transferring information GYBC last changed bank accounts approximately 10 years ago

Page 14 of 348

Customer Service – Service Risk Assessment

Service Function

Risks associated with service

Likelihood

Impact

Action taken/To be taken

Comments

Revenue Services – Systems team and Fraud team

A-Very High B-High C-Significant D-Low E- Very Low F- Almost Impossible

1- Catastrophic 2- Critical 3-Marginal/Moderate 4-Negligible

Introduction of Universal Credit

Timescales and Migration Plan for Single Fraud Investigation Service (SFIS)

A

3

Engagement with DWP

The national roll out of SFIS is programmed to be completed by March 2015. Details of ‘how and when’ are limited which will cause difficulties for service planning

Staff redundancy due to loss of Housing Benefit Systems support

A

3

Vacant posts will be filled on a temporary basis

The impact on the systems team is unknown as GYBC will retain responsibility for the assessment and delivery of Local Council Tax Reductions Scheme, Housing Costs for those in supported accommodation and other Discretionary schemes like Discretionary Housing Payments, all of which will require systems support staff. Page 15 of 348

Service Function

Risks associated with service

Likelihood

Impact

Action taken/To be Taken

Comments

Staffing

A-Very High B-High C-Significant D-Low E- Very Low F- Almost Impossible

1- Catastrophic 2- Critical 3-Marginal/Moderate 4-Negligible

HR

The HR team have gone through a restructure which resulted in two compulsory redundancies and one voluntary redundancy. The loss of knowledge and skill at a senior HR level may leave the organization vulnerable. Two members of the team will be on maternity leave during 2014 leaving the team further exposed.

A

3

After the process an experienced HR Business Partner commenced with the team to cover the interim period. The team has only been covering the day to day operational and the development of the team, policies, etc. will commence once the team is fully resourced. One of the maternity posts has been covered by an experienced HR administrator, therefore, reducing the risk. An internal appointment has been made to the vacant HR Officer post and the new post-holder will strengthen the team.

The agency person has settled well into the team and operationally the team is delivering.

Page 16 of 348

Service Function

Risks associated with service

Likelihood

Impact

Action taken/To be Taken

Comments

Revenues

The Revenues team have had several vacancies throughout the year, and several incidences of staff sickness. The key post of Local Taxation Team Manager has been vacant since August and despite being advertised we have been unsuccessful in making a new appointment. This post is currently being covered by agency.

A

3

The post for Local Taxation Team Manager will be re-advertised. Some minor changes to line management have taken place and this will hopefully make the post more attractive to candidates.

The agency person has settled well into the team and operationally the team is delivering.

Co-Operative Bank Account

A-Very High B-High C-Significant D-Low E- Very Low F- Almost Impossible

1- Catastrophic 2- Critical 3-Marginal/Moderate 4-Negligible

The transfer of the bank account will require a significant amount of staff time to prepare and transfer the information accurately. There are costs associated with this -transfer of staff time, tender process costs for consultant, legal fees, IT support.

A 2 We are currently working with all Norfolk local authorities to pursue the option of a group tender.

Page 17 of 348

Page 18 of 348

Environmental Services Group – Service Risk Assessment

Page 1 of 6

ENVIRONMENTAL SERVICES - SERVICE RISK ASSESSMENT Introduction The Environmental Services Group comprises of the following services: Environmental Health:

o Food Safety o Internal & External Health and Safety o Port Health o Licensing (Animal, Scrap Metal & Skin Piercing) o Environmental Protection o Nuisance & ASB o Private Sector Housing Enforcement

Environmental Rangers & Waste & Recycling Communications:

o Enviro Crime Enforcement o Waste & Recycling Communications o Environmental Policy o Stray Dogs

Emergency Planning Coastal Management Client Services - GYBServices

The purpose of this group of services is to protect the health, safety and environment of residents, employees and visitors within the Borough

Page 19 of 348

Environmental Services Group – Service Risk Assessment

Page 2 of 6

SERVICE FUNCTION RISKS ASSOCIATED WITH SERVICE

FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

Environmental Health

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

To protect the health, safety and environment of residents, employees and visitors within the Borough by

Investigating requests for service

Undertaking proactive inspections

Inspecting under the relevant licensing framework

Increase in demand during summer months often means officer resources are stretched resulting in

Backlog of service requests

Inspections not completed by due dates – backlogs created

Licensing inspections and issuing delayed

C

2

Risk assessment of service requests undertaken, all high risk or related to a vulnerable group are prioritised. Customers notified of expected response times. Additional support during the summer months has been brought in for the last two years under an existing budget provision. Some licence work has been rescheduled for winter months. Any proactive project work across health is planned for quieter periods. Ongoing systems thinking work to continue to drive out any

This is an annual risk and one that can be planned for so that the steps to mitigate the risks are put in place at the start of each season.

Page 20 of 348

Environmental Services Group – Service Risk Assessment

Page 3 of 6

waste from the system. SERVICE FUNCTION RISKS

ASSOCIATED WITH SERVICE

FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

Environmental Rangers and Waste & Recycling Communication

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

To protect the health, safety and environment of residents, employees and visitors within the Borough by

Investigating requests for service

Undertaking proactive inspections

Providing effective communication around waste & recycling issues

3 Rangers and 1 Waste Communication & Recycling Officer permanently employed (2 further through DCLG funding) results in a relatively small team covering the Borough, so officer absence could impact on service delivery.

D

2

All officers in Environmental Health and now Civil Enforcement officers are authorised to issue FPN’s for dog fouling and littering. All officers in Environmental Health can undertake most of the Rangers work so resources can be moved around during times of need. Forward planning for waste communications work currently taking place to plan for reduction of staff when DCLG funding expires.

The actions outlined help to mitigate this risk.

Page 21 of 348

Environmental Services Group – Service Risk Assessment

Page 4 of 6

SERVICE FUNCTION RISKS

ASSOCIATED WITH SERVICE

FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

Emergency Planning & Coastal Management

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

To protect the health, safety and environment of residents, employees and visitors within the Borough by

By planning for and responding in emergency situations

By producing and implementing the Shoreline Management Plan

Loss of key staff as there are two post holders who hold technical and specific information in each of these specialist areas.

B

2

Movement into Environmental Services has allowed for some resilience to be established, mainly through the Community Protection Manager.

Further work needs to be undertaken to build on this resilience and succession planning for these areas of work, currently resources are the barrier to this progressing.

Page 22 of 348

Environmental Services Group – Service Risk Assessment

Page 5 of 6

SERVICE FUNCTION RISKS ASSOCIATED

WITH SERVICE FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

Client services - GYBServices

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

To protect the health, safety and environment of residents, employees and visitors within the Borough by

Ensuring GYB Services undertake their functions as specified in the JV Contract and Service Level Agreements

Pressure to make financial savings having a potential to impact on service delivery.

C

3

Close working relationships with GYBServices when dealing with budget pressures. Ongoing liaison with members when saving options are considered. Liaison Board meetings monitor ongoing performance and service delivery of GYB Services.

Minimal impact from ongoing savings provided by GYBServices already.

Reduced contract management as part of the change in the contract with GYBServices, which has now moved to a Joint Venture with the Authority

D

2

As part of the Joint venture GYBServices now operates as an extension of this Authority, developing stronger working relationships with this Authority. Liaison Board meetings

The actions outlined help to mitigate this risk

Page 23 of 348

Environmental Services Group – Service Risk Assessment

Page 6 of 6

are held, and chaired by the Environmental Portfolio holder where contract and financial issues can be raised and discussed.

Page 24 of 348

DCLG Project Work Plan

Green – Completed

Yellow – Started

Date Work to be Started by

Task Working with Key Milestones Date Completed

Task Lead Cost Notes

1/1/13 - Implement weekly collections for 4,500 properties

GYB Services Environmental Services Residents Press Councillors

- Mass implementation for 4,500 properties

12/8/13 Simon Mutten – GYBS

£151,967 for vehicle (actual) £330,000 depot staff running costs for 3 years

Weekly Collection list provided by GYBS details weekly collection rounds

12/8/13 - Implement weekly collections for a further 2,500 properties

GYB Services Environmental Services Residents

- Year 2 implementation for ? properties - Year 3 implementation for ? properties

Simon Mutten – GYBS

N/A Met with Simon Mutton 14/1/14 to progress lists for year 2 & 3

1/8/13 - Vehicle livery advertising recycling

GYB Services Environmental Services

- New dustcart livery in place

1/9/13 Paul Shucksmith – GYBC

£773.00

1/9/13 - Purchase of recycling facilities in communal areas

GYB Services Environmental Services Community Housing

- Identify facilities to be purchase - Identify suitable

Paul Shucksmith – GYBC

£45,000 Mapping currently being undertaken in these areas to determine what facilities will be

Page 25 of 348

Residents installation sites - Installation

provided

1/1/13 - Ongoing recycling promotion in areas of weekly collections

GYB Services Environmental Services

- Ongoing general comms - Comms project around MRF -Comms project around new recycling facilities

1/1/13 – Ongoing

Paul Shucksmith – GYBC

£100,000 waste comms officers for one & three years £5,000 promotional materials

Ongoing – Comms team respond to all requests for service and contaminated bin info

1/1/13 -Work with community housing /neighbourhoods & community & voluntary organisations re recycling promotion

Environmental Services Community Housing Neighbourhood & Communities

- Ongoing general comms - Comms project around MRF -Comms project around new recycling facilities

1/1/13 – Ongoing

Paul Shucksmith – GYBC

£100,000 waste comms officers for one & three years £5,000 promotional materials

Ongoing – through Comms team

1/9/13 -Recycling promotion in schools

Environmental Services

- Ongoing general comms - Comms project around MRF -Comms project around new recycling facilities

Paul Shucksmith – GYBC

£100,000 waste comms officers for three years £5,000 promotional materials

Promotional events completed in five schools – all schools in DCLG areas will be visited

1/3/13 -Increase in Garden waste recycling

GYB Services Environmental Services

-Delivery of promotional campaigns/deals

Paul Shucksmith – GYBC

£100,000 waste comms

Successful promotion of a free brown bin

Page 26 of 348

Borough wide officers for three years£5,000 promotional materials

1/6/13 – 31/7/13

1/1/13 -Work to reduce fly tipping in areas of weekly collections

Environmental Services

- Ongoing investigation of complaints by Env Rangers

1/1/13 – Ongoing

Paul Shucksmith – GYBC

£0 Ongoing –Rangers respond to all requests for service. Also trialing a project to highlight fly tips in areas prior to collection.

1/8/13 - Work to improve route for weekly collections in target areas

GYB Services Environmental Services Community Housing Residents

- Identify structural changes & feasibility - Implement changes

Paul Shucksmith – GYBC

£42,500 Mapping currently being undertaken in these areas to determine what facilities will be provided. Discuss potential financial contribution from community Housing

Estimated Total £675,240

Original Bid £675,625

Page 27 of 348

1

Subject: Tourism and Communications – Areas of Risk Report to: Audit & Risk Date: 13th February 2014 Report by: Group Manager: Tourism and Communications

1. Introduction a. Tourism and Communications consists of the following service areas.

i. Tourism and Corporate Marketing ii. Print & Design iii. Events and Town Hall Function Rooms including portering services iv. Tourist information Services v. Mayoral and Civic Events vi. Communications and Media vii. Greater Yarmouth Tourist Authority

2. Corporate Risks

a. The corporate risk assessment identifies no specific areas within Tourism & Communications but several risks could be applied in general terms including

i. Climate change (1) ii. Changes in local and national economy (2) iii. Lack of financial resources (5) iv. Infra-structure not being able to meet demand (13) v. Partnership working (27)

b. The tourism industry in particular has built up a degree of resilience to changes in the economy and climate change (adverse weather)

3. Other risks within the group of services a. Tourism and Corporate Marketing

i. Resources is always a key issue in order to remain competitive amongst strong competition from the UK and overseas destinations. Once approved the Great Yarmouth Business Improvement District will mark the start of a new era for destination marketing.

b. Print & Design i. Loss of key staff and key equipment is the main risk although a

failure to generate outside work to help support the operation may impact on its potential to deliver services in the future.

ii. Combining a range of skills within the department will help ensure that staff retain and develop the necessary skills and continue to develop their commercial activities.

c. Events and Town Hall Function Rooms including portering services i. The greatest risk revolves around accident or incidents which result

in injury or death and would leave a damaging impact on the reputation of the Borough Council.

Page 28 of 348

2

ii. All events follow a set of procedures which include event management planning, risk assessment and health & safety checks to minimise the potential risk.

d. Tourist information Services i. The biggest risk is the prospect of future funding cuts and a

subsequent inability to continue with the service and its potential damage to the reputation of Great Yarmouth as a premier visitor destination.

ii. The new BID project may deem it necessary to underpin the work of the TIC to secure the future of the service.

e. Mayoral and Civic Events i. In addition to potential funding cuts the main risk is the protection of

the civic regalia; protocols surrounding the safe-keeping of the civic regalia are documented in the new civic protocols.

f. Communications and Media i. Communications become a vital tool during any crisis so the

importance of the use of several different communications channels is very importance. Total reliance on one type of communication channel is therefore avoided.

g. Greater Yarmouth Tourist Authority (GYTA) i. Insolvency is always a major risk for the GYTA; most critically the

risk; albeit minimised, of bad weather during the annual Maritime Festival affecting attendance levels and thus voluntary contributions.

ii. Failure to deliver the Business Improvement District may prompt a gradual downturn of GYTA voluntary membership making its long term survival unlikely. A lack of tourism leadership absence of any partnership working will inevitably lead to a gradual decline in the local tourism industry.

iii. However all the current indications are that the GYTA will succeed in the effort to form a new BID.

Page 29 of 348

Tourism and Communications – Service Risk Assessment

Page 1 of 8

TOURISM AND COMMUNICATIONS - SERVICE RISK ASSESSMENT

1. Introduction Tourism and Communication Group comprises of the following Services:-

a. Tourism Marketing & Corporate Marketing b. Print and Design c. Events and Town Hall Function Rooms including portering services d. Tourist Information Services e. Mayoral and Civic Events f. Communications and Media g. Greater Yarmouth Tourist Authority

2. The purpose of the group of services is to harness the skills of Marketing, PR, Event Management in order to add to the

quality of life of residents and visitors by ensuring that they are made fully aware of the range of leisure and cultural activities and Council services available within the Borough and subsequently acting as a stimulus to the local economy and towards the creation of jobs

Page 30 of 348

Tourism and Communications – Service Risk Assessment

Page 2 of 8

SERVICE FUNCTION

RISKS ASSOCIATED WITH SERVICE

FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

(1) Marketing: Tourism & Corporate

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

-To develop and implement a dynamic marketing mix to promote Greater Yarmouth as a Tourism Destination. -To manage and develop the marketing of Great Yarmouth Borough Council across all section (in conjunction with the Communications Officer)

Limited financial resources in order to compete with UK and European destinations.

C

2

Working in partnership with GYTA

Working towards the creation of a Borough-wide Tourism Business Improvement District

The new BID should start in the spring for a five-year period

Loss or further reduction of key staff or insufficient staff to meet demand

C

2

Monthly monitoring of workload

Industry expectations of an effective support mechanism is very high; outcomes constantly monitored through GYTA Working Groups and Board of Directors

Inconsistent message from Council departments that may damage reputation of the Borough Council

C 2 Already have a Communication protocols document

Working on a Social Media strategy & a corporate marketing strategy

Negative publicity about Great Yarmouth causing damage to its reputation as a visitor destination

D 2 The department has key staff who have experience in handling the media including negative PR

Page 31 of 348

Tourism and Communications – Service Risk Assessment

Page 3 of 8

SERVICE FUNCTION

RISKS ASSOCIATED WITH SERVICE

FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

(2) Print and Design

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

-To develop the Print & Design team to provide essential services to Council functions and increase income from external jobs.

Loss of key staff D

2

To some degree support staff can cover any loss of staff in the short term although existing workloads would place unacceptable pressure on remaining staff in the medium and long term

Failure of essential print and design equipment & software

D

3

Service contracts are in place covering our main equipment.

Injury to staff by printing machinery

D 2 All staff are fully trained before they are permitted to work any of the equipment.

Page 32 of 348

Tourism and Communications – Service Risk Assessment

Page 4 of 8

SERVICE FUNCTION

RISKS ASSOCIATED WITH SERVICE

FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

(3) Events and Town Hall Functions

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

Compiling, scheduling and managing an indoor/ outdoor events programme and civic events programme in accordance with current Health & Safety legislation and event management guidelines. To manage the Town Hall porters; work in a team to promote and manage functions as the Town Hall.

Loss of key staff D

2

Monthly monitoring of workload

Reduced funding or complete cut in funding

C

3

Attempts are made to make all events self-financing.

It is hoped that through the Business Improvement District the events programme will be greatly enhanced. Events play a crucial and growing role as an economic driver.

Major incident at a Council-organised event

D

2

All events are thoroughly planned and risked assessed.

Event Management Plans are always present to the Event Safety Advisory Group

Major incident in Town Hall function Room; ie accident or food poisoning resulting in damage to reputation of the function venue and the Council.

D 2 Following a formal tendering procedure GYBC now have a sole caterer.

All events within the function room are risk assessment to limit to likelihood of any incidents.

Injury to Porters during normal working or working alone

D 2 Regular training given to Porters on areas such as manual handling

A risk assessment for the porters role is being constantly reviewed.

Page 33 of 348

Tourism and Communications – Service Risk Assessment

Page 5 of 8

SERVICE

FUNCTION RISKS ASSOCIATED

WITH SERVICE FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

(4) Mayoralty & Civic Events

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

To co-ordinate all aspects of the Mayors engagements and Civic events.

Reduced funding or complete cut in funding

D

2

Staff are able to demonstrate the importance of the ambassadorial role both inside and outside the Borough

The Mayor also promotes the Borough of Great Yarmouth in a positive manner and acts as a link between the Council and various local groups and organisations.

Loss of key staff D 3 Monthly monitoring of workload

Continued training and development of staff.

The department has support staff that are able to cover the absence of principle officers

Loss of Civic Regalia D

2

Mayor is advised not to take any unnecessary risks with the Civic Regalia.

Whilst the Civic Regalia is irreplaceable the extent to which should be protected is detailed in the Mayoral and Civic Protocols.

Page 34 of 348

Tourism and Communications – Service Risk Assessment

Page 6 of 8

SERVICE FUNCTION

RISKS ASSOCIATED WITH SERVICE

FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO

MITIGATE THE RISK

COMMENTS

(5) Tourist Information Services

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

To act as a support mechanism and as a ‘signpost’ for a range of services, amenities and attractions to encourage both residents and visitors to gain maximum enjoyment.

Loss of key staff D

2

Monthly monitoring of workload

Staff carry a wealth of experience and knowledge of the local area.

Reduced funding or complete cut in funding

C

2

Possible financial support through the Business Improvement District

The TIC is arguably the shop-window of the Borough tourism industry. All year opening demonstrates the authorities commitment to becoming an all-year visitor destination

Page 35 of 348

Tourism and Communications – Service Risk Assessment

Page 7 of 8

SERVICE FUNCTION

RISKS ASSOCIATED WITH

SERVICE FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO MITIGATE THE RISK

COMMENTS

(6) Communications and Media

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

To work with media and public relations matters to promote the work and reputation of the council

Loss of key staff D

2

Limited backup is available within the department in the absence of the Communications Manager

Monthly monitoring of workload

Reduced funding or complete cut in funding

C

2

Service is able to demonstrate its key outcomes in promoting the reputation of the Council through enhanced press and media coverage

The Communications role supports all departments in promoting their services to local residents

Inconsistent message from Council departments that may damage reputation of the Borough Council

D

3

The communications team have already published a set of media protocols and are currently working on a Social Media protocol in order to ensure a consistent message is maintained.

Breakdown of communication channels during a local crisis (ie flood alert)

C 2 To avoid sole reliance on one channel a range of communication channels are used during an emergency situation

Page 36 of 348

Tourism and Communications – Service Risk Assessment

Page 8 of 8

SERVICE FUNCTION

RISKS ASSOCIATED WITH SERVICE

FUNCTION

LIKELIHOOD IMPACT ACTIONS TAKEN OR BEING TAKEN TO MITIGATE THE

RISK

COMMENTS

(7) Greater Yarmouth Tourist Authority

A: Very High B: High C: Significant D: Low E: Very Low F: Almost Impossible

1: Catastrophic 2: Critical 3: Marginal/Moderate 4: Negligible

To work with media and public relations matters to promote the work and reputation of the council.

Loss of key staff D

2

GYTA employed their own Project Manager and GYBC support the work of the GYTA through the GYBC Tourism Staff

GYTA is externally funded. GYBC makes no financial contribution to the GYTA.

GYTA becoming insolvent due to the collapse of a particular project

E 2 All GYTA projects are risked assessed.

The GYTA Board take full responsibility for approving critical projects aware of the potential scale of the risk

The Maritime Festival is perhaps the biggest ‘risk’ project undertaken by the GYTA. The Board of aware of the potential financial impact of very bad weather.

Council\Meetings\Audit & Risk\Tourism and Communications

Page 37 of 348

Great Yarmouth Borough Council

Year ending 31 March 2013

Annual Audit Letter

31 October 2013

Page 38 of 348

DELIBERATELY LEFT BLANK FOR PRINTING PURPOSES

Page 39 of 348

Ernst & Young LLP One Cambridge Business Park Cambridge CB4 0WZ

Tel: + 44 1223 394400 Fax: + 44 1223 394401 ey.com

Tel: 023 8038 2000 Fax: 023 8038 2001 www.ey.com/uk

The Members Great Yarmouth Borough Council Town Hall Hall Plain Great Yarmouth Norfolk, NR30 2QF

16 October 2013

Dear Members,

Annual Audit Letter

The purpose of this Annual Audit Letter is to communicate to the Members of Great Yarmouth Borough Council and external stakeholders, including members of the public, the key issues arising from our work, which we consider should be brought to their attention.

We have already reported the detailed findings from our audit work to those charged with governance of Great Yarmouth Borough Council in the 2012/13 Audit results report, issued 19 September 2013. The matters reported here are the most significant for the Council. I would like to take this opportunity to thank the officers of Great Yarmouth Borough Council for their assistance during the course of our work.

Yours faithfully

Mark Hodgson Director For and behalf of Ernst & Young LLP Enc

Page 40 of 348

DELIBERATELY LEFT BLANK FOR PRINTING PURPOSES

Page 41 of 348

EY i

Contents

1. Executive summary .......................................................................... 1

2. Key findings ...................................................................................... 3

3. Control themes and observations .................................................. 6

In March 2010 the Audit Commission issued a revised version of the ‘Statement of responsibilities of auditors and audited bodies’ (Statement of responsibilities). It is available from the Chief Executive of each audited body and via the Audit Commission’s website.

The Statement of responsibilities serves as the formal terms of engagement between the Audit Commission’s appointed auditors and audited bodies. It summarises where the different responsibilities of auditors and audited bodies begin and end, and what is to be expected of the audited body in certain areas.

The Standing Guidance serves as our terms of appointment as auditors appointed by the Audit Commission. The Standing Guidance sets out additional requirements that auditors must comply with, over and above those set out in the Code of Audit Practice 2010 (the Code) and statute, and covers matters of practice and procedure which are of a recurring nature.

This Audit Results Report is prepared in the context of the Statement of responsibilities. It is addressed to the Members of the audited body, and is prepared for their sole use. We, as appointed auditor, take no responsibility to any third party.

Our Complaints Procedure – If at any time you would like to discuss with us how our service to you could be improved, or if you are dissatisfied with the service you are receiving, you may take the issue up with your usual partner or director contact. If you prefer an alternative route, please contact Steve Varley, our Managing Partner, 1 More London Place, London SE1 2AF. We undertake to look into any complaint carefully and promptly and to do all we can to explain the position to you. Should you remain dissatisfied with any aspect of our service, you may of course take matters up with our professional institute. We can provide further information on how you may contact our professional institute.

Page 42 of 348

Executive summary

Ernst & Young 1

1. Executive summary

Our 2012/13 audit work has been undertaken in accordance with the Audit Plan we issued on 28 March 2013 and is conducted in accordance with the Audit Commission’s Code of Audit Practice, International Standards on Auditing (UK and Ireland) and other guidance issued by the Audit Commission. The Council is responsible for preparing and publishing its Statement of Accounts, accompanied by the Annual Governance Statement. In the Annual Governance Statement, the Council reports publicly on an annual basis on the extent to which they comply with their own code of governance, including how they have monitored and evaluated the effectiveness of their governance arrangements in the year, and on any planned changes in the coming period. The Council is also responsible for putting in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources. As auditors we are responsible for:

► forming an opinion on the financial statements;

► reviewing the Annual Governance Statement;

► forming a conclusion on the arrangements that the Authority has in place to secure economy, efficiency and effectiveness in its use of resources; and

► undertaking any other work specified by the Audit Commission. Summarised below are the conclusions from all elements of our work:

Audit the financial statements of Great Yarmouth Borough Council for the financial year ended 31 March 2013 in accordance with International Standards on Auditing (UK & Ireland)

On 30 September 2013 we issued an unqualified audit opinion in respect of the Council.

Form a conclusion on the arrangements the Council has made for securing economy, efficiency and effectiveness in its use of resources.

On 30 September 2013 we issued an unqualified value for money conclusion.

Issue a report to those charged with governance of the Council (the Audit and Risk Committee) communicating significant findings resulting from our audit.

On 19 September 2013 we issued and presented our report in respect of the Council to the Audit and Risk Committee.

Report to the National Audit Office on the accuracy of the consolidation pack the Council is required to prepare for the Whole of Government Accounts.

We reported our findings to the National Audit Office on 30 September 2013

Consider the completeness of disclosures in the Council’s Annual Governance Statement, identify any inconsistencies with the other information of which we are aware from our work and consider whether it complies with CIPFA / SOLACE guidance.

No issues to report.

Consider whether, in the public interest, we should make a report on any matter coming to our notice in the course of the audit.

We did not issue such a report.

Determine whether any other action should be taken in relation to our responsibilities under the Audit Commission Act.

We did not take such action.

Issue a certificate that we have completed the audit in accordance with the requirements of the Audit Commission Act 1998 and the Code of Practice issued by the Audit Commission.

On 30 September 2013 we issued our audit completion certificate.

Page 43 of 348

Executive summary

Ernst & Young 2

Issue a report to those charged with governance of the Council summarising the certification (of grants claims and returns) work that we have undertaken.

We plan to issue our annual certification report to those charged with governance with respect to the 2012/13 financial year by 31 January 2014.

1.1 Audit fees

The table below sets out the scale fee and our final proposed audit fees.

Planned fee Scale fee Final

Code audit work £73,500 £73,500 £73,500

Certification of claims and returns

£37,100 £37,100 see note below

Non-Code work Nil Nil Nil

Our actual fee is in line with the agreed fee for the Code audit work. Work on the certification of claims and returns is not yet complete. We will report our final fee for the certification work in our report to be issued by 31 January 2014. We confirm that we have not undertaken any non-audit work outside of the Audit Commission’s Audit Code requirements.

Page 44 of 348

Key findings

EY 3

2. Key findings

2.1 Financial statement audit

We audited the Council’s Statement of Accounts in line with the Audit Commission’s Code of Audit Practice, International Standards on Auditing (UK and Ireland) and other guidance issued by the Audit Commission. We issued an unqualified audit report on 30 September 2013. In our view, the quality of the process for producing the accounts, including the supporting working papers was good, which was reflected in the low number of errors reported. The main issues identified as part of our audit were:

Significant risk 1: Valuation of property, plant and equipment assets

We concluded that valuations of non-current assets are free from material misstatement and that non-current asset additions were capital in nature.

Significant risk 2 – HRA self financing

The government reformed local authority housing finance by adopting a self-financing model from 1 April 2012. This involved a one-off settlement payment to central government in March 2012.

The in year accounting for self-financing commenced in 2012/13 and required changes in accounting practices for HRA depreciation and the allocation of debt charges between housing and general fund services.

We tested HRA depreciation and confirmed the accuracy of the charge.

We concluded that the Council adopted the approach recommended by Cipfa to record general fund and HRA debt, and the associated financing costs.

Other risk 1 - Weak journal processing controls

We identified journals that were prepared and authorised by the same person. Sample testing of these journals did not identify errors.

Other risk 2 – Jobs processed between Norse and Anite

We tested property maintenance expenditure to underlying evidence. We concluded that the job had occurred and was correctly charged.

Other risk 3 - Housing rents debtor and creditor balances at the year end

We concluded that adequate audit trails were provided to support debtor and creditor housing rents.

Other risk 4 – Exit packages and termination benefits

We concluded that exit packages and termination benefits recorded were complete and correctly disclosed in the accounts.

Other risk 2: Risk of misstatement due to fraud and error.

We carried out the following audit procedures and did not identify any specific fraud risks: ► made enquiries and assessed management’s response about risks of fraud and the controls put in place to

address those risks; ► assessed the oversight given by the Audit and Risk Committee, as those charged with governance, of

management’s processes over fraud; ► performed mandatory procedures regardless of specifically identified fraud risks; and ► considered the results of the Audit Commission’s National Fraud Initiative.

Other key findings:

We identified one material misstatement during our audit. This related to a disclosure error in the note for Property Plant and equipment. It did not change the net present value of property, plant and equipment.

Management have corrected all misstatements. The impact of audit changes was increased usable reserves by £0.14 million.

Page 45 of 348

Key findings

EY 4

2.2 Value for money conclusion

We are required to carry out sufficient work to conclude on whether the Council has put in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources. In accordance with guidance issued by the Audit Commission, in 2012/13 our conclusion was based on two criteria:

► The organisation has proper arrangements in place for securing financial resilience; and

► The organisation has proper arrangements for challenging how it secures economy, efficiency and effectiveness.

We issued an unqualified value for money conclusion on 30 September 2013. Our audit did not identify any significant matters. The following is a brief summary of our findings against each of these criteria.

Criteria and findings

1. Financial resilience

The Council has robust arrangements in place to ensure its financial resilience. The Council has a history of good financial management and delivery of budgets.

At 31 March 2013, the Council’s general fund balance which is available to meet unforeseen circumstances stood at £5.70 million, while earmarked reserves were £4.10 million. Although the majority of these are earmarked for specific purposes, they do provide the Council with enhanced flexibility to manage its financial position in the current economic environment.

In 2012/13 the council achieved a surplus of £0.12 million on the general fund that was used to increase general fund reserve balances.

Following confirmation that the Council would receive the Efficiency Support Grant, the Council is planning on a contribution to general fund reserves of £0.50 million in 2013/14.

The Council’s general fund reserves are planned to be £6.00 million at 31 March 2014. Without further savings, or receipt of additional funding the Council would need to draw £2.00 million from reserves in 2014/15 to balance the budget. This would lower general fund reserves to £4.00 million at 31 March 2015, but they would still be above the minimum set level approved by the Council of £1.90 million.

The Council is developing plans to address the savings requirement identified in 2014/15 and 2015/16.

2. Securing economy efficiency and effectiveness

The Council has demonstrated that it has effective arrangements in place for securing economy, efficiency and effectiveness.

The Council has a record of prioritising its resources within tighter budgets through the achievement of cost

reductions, e.g. a management restructure, procurement reviews, and by improving efficiency and productivity. The

Council has plans to meet further budget gaps through increasing income streams and through the better use of

council assets.

2.3 Whole of government accounts

We reported to the National Audit office on 30 September 2013 the results of our work performed in relation the accuracy of the consolidation pack the Council is required to prepare for the whole of government accounts. We did not identify any areas of concern.

2.4 Annual governance statement

We are required to consider the completeness of disclosures in the Council’s Annual Governance Statement, identify any inconsistencies with the other information of which we are aware from our work, and consider whether it complies with CIPFA / SOLACE guidance. Page 46 of 348

Key findings

EY 5

We completed this work and did not identify any areas of concern.

2.5 Certification of grants claims and returns

We have not yet completed our work on the certification of grants and claims. We will issue the Annual Certification Report for 2012/13 in January 2014.

Page 47 of 348

Control themes and observations

EY 6

3. Control themes and observations

As part of our audit of the financial statements, we obtained an understanding of internal control sufficient to plan our audit and determine the nature, timing and extent of testing performed. Although our audit was not designed to express an opinion on the effectiveness of internal of internal control we are required to communicate to those charged with governance at the Council any significant deficiencies in internal control.

We had no such matters to report.

Page 48 of 348

EY | Assurance | Tax | Transactions | Advisory

Ernst & Young LLP

© Ernst & Young LLP. Published in the UK. All rights reserved.

The UK firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with registered number OC300001 and is a member firm of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

ey.com

Page 49 of 348

The UK firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with registered number OC300001 and is a member firm of Ernst & Young GlobalLimited. A list of members’ names is available for inspection at 1 More London Place, London SE1 2AF, the firm’s principal place of business and registered office.

Ernst & Young LLPOne Cambridge Business ParkCambridgeCB4 0WZ

Tel: + 44 1223 394400Fax: + 44 1223 394401ey.com

Tel: 023 8038 2000

The MembersGreat Yarmouth Borough CouncilTown HallHall PlainGreat YarmouthNorfolk,NR30 2QF

27 January 2013

Direct line: 01223 394547

Email: [email protected]

Dear Member

Certification of claims and returns annual report 2012-13Great Yarmouth Borough Council

We are pleased to report on our certification work. This report summarises the results of our work onGreat Yarmouth Borough Council’s 2012-13 claims and returns.

Scope of workLocal authorities claim large sums of public money in grants and subsidies from central government andother grant-paying bodies and are required to complete returns providing financial information togovernment departments. In some cases these grant-paying bodies and government departmentsrequire certification from an appropriately qualified auditor of the claims and returns submitted to them.

Under section 28 of the Audit Commission Act 1998, the Audit Commission may, at the request ofauthorities, make arrangements for certifying claims and returns because scheme terms and conditionsinclude a certification requirement. When such arrangements are made, certification instructions issuedby the Audit Commission to appointed auditors of the audited body set out the work they must undertakebefore issuing certificates and set out the submission deadlines.

Certification work is not an audit. Certification work involves executing prescribed tests which aredesigned to give reasonable assurance that claims and returns are fairly stated and in accordance withspecified terms and conditions.

In 2012-13, the Audit Commission did not ask auditors to certify individual claims and returns below£125,000. The threshold below which auditors undertook only limited tests remained at £500,000. Abovethis threshold, certification work took account of the audited body’s overall control environment forpreparing the claim or return. The exception was the housing and council tax benefits subsidy claimwhere the grant paying department set the level of testing.

Where auditors agree it is necessary, audited bodies can amend a claim or return. An auditor’scertificate may also refer to a qualification letter where there is disagreement or uncertainty, or theaudited body does not comply with scheme terms and conditions.

Statement of responsibilitiesIn March 2013 the Audit Commission issued a revised version of the ‘Statement of responsibilities ofgrant-paying bodies, authorities, the Audit Commission and appointed auditors in relation to claims andreturns’ (statement of responsibilities). It is available from the Chief Executive of each audited body andvia the Audit Commission website.

Page 50 of 348

2

The statement of responsibilities serves as the formal terms of engagement between the AuditCommission’s appointed auditors and audited bodies. It summarises where the different responsibilitiesof auditors and audited bodies begin and end, and what is to be expected of the audited body in certainareas.

This annual certification report is prepared in the context of the statement of responsibilities. It isaddressed to those charged with governance and is prepared for the sole use of the audited body. We,as appointed auditor, take no responsibility to any third party.

Summary

Section 1 of this report outlines the results of our 2012-13 certification work and highlights the significantissues.

We checked and certified three claims and returns with a total value of £82.148 million. We met thesubmission deadlines for the housing and council tax benefits subsidy claim and the pooling of capitalreceipts.

The audit submission of the national non-domestic rates return was late. This was due to Council’sinability to produce supporting audit trails for the claim.

We issued two qualification letters, one for the housing and council tax benefits subsidy claim and onefor the national non-domestic rates return. Details of the qualification matters are included in section 1.Our certification work found errors which the Council corrected. The amendments had a marginal effecton the grant due.

Fees for certification work are summarised in section 2. The Audit Commission applied a generalreduction of 40% to certification fees in 2012-13. We have included the actual fees for 2011-12 to assistyear on year comparisons.

We welcome the opportunity to discuss the contents of this report with you at the February 2014 Auditand Risk Committee.

Yours faithfully

Mark HodgsonDirectorErnst & Young LLPEnc

Page 51 of 348

Contents

Certification of claims and returns annual report 2012-13

Contents

1. Summary of 2012-13 certification work ..................................................................... 12. 2012-13 certification fees ........................................................................................... 33. Looking forward ......................................................................................................... 4

Page 52 of 348

Summary of 2012-2013 certification work

EY ÷ 1

1. Summary of 2012-13 certification work

We certified three claims and returns in 2012-13. The main findings from our certification work are providedbelow.

Housing and council tax benefits subsidy claim

Scope of work Results

Value of claim presented for certification £53,039,434

Amended Yes – subsidy increased by £5,670 to £53,045,104

Qualification letter Yes

Fee - 2012-13Fee - 2011-12

£35,130£67,361

Councils run the Government's housing and council tax benefits scheme for tenants and council taxpayers.Councils responsible for the scheme claim subsidies from the Department for Work and Pensions (DWP)towards the cost of benefits paid.

The certification guidance requires auditors to complete more extensive ‘40+’ testing (extended testing) ifinitial testing identifies errors in the calculation of benefit or compilation of the claim. We found errors andcarried out extended testing in several areas.

Extended ‘40+’ testing and other testing identified errors which the Council amended. They had a small netimpact on the claim. We have reported underpayments, uncertainties and the extrapolated value of othererrors to the DWP in a qualification letter. The following are the main issues which was included in ourqualification letter:

o Income assessment errors across all four main benefit types, Non HRA Rent Rebates, HRARent Rebates, Rent Allowance and Council Tax Benefit. Extended 40+ testing was applied toquantify results and report.

o Incorrect classification of eligible overpayments for Rent Allowances and Council Tax Benefits.Extended 40+ testing was applied to quantify results and report.

o Errors in the disregard applied and income assessment for Rent Rebate, Rent Allowance andCouncil Tax Benefit modified scheme cases.

National non-domestic rates return

Scope of work Results

Value of return presented for certification £27,985,239

Limited or full review Full review

Amended Yes – payments to the pool increased by £7,314 to£27,992,553

Qualification letter Yes

Fee – 2012-13Fee – 2011-12

£3,140 (Additional fee raised)£2,002

Page 53 of 348

Summary of 2012-2013 certification work

EY ÷ 2

The Government runs a system of non-domestic rates using a national uniform business rate. Councilsresponsible for the scheme collect local business rates and pay the rate income over to the Government.Councils have to complete a return setting out what they have collected under the scheme and how muchthey need to pay over to the Government.

We found three errors in the national non-domestic rates return and we certified the amount payable to thepool with qualification. The issues found were:

· The audit trail totals did not agree to the draft return. Four entries in the claim were amended.

· The date the last VO direction has been taken into account was amended to 27/2/2013.

· Testing of transitional relief cases identified one error. The failure related to the base liability used tocalculate the transitional relief. As we were unable to quantify the overall impact, this was reportedin our qualification letter.

An additional fee of £2,310 was discussed and agreed with officers for this additional work.

Pooling of housing capital receipts

Scope of work Results

Value of return presented for certification £1,110,289

Limited or full review Full review

Amended No

Qualification letter No

Fee – 2012-13Fee – 2011-12

£1,140£1,640

Councils pay part of a housing capital receipt into a pool run by the Department of Communities and LocalGovernment. Regional housing boards redistribute the receipts to those councils with the greatest housingneeds. Pooling applies to all local authorities, including those that are debt-free and those with closedHousing Revenue Accounts, who typically have housing receipts in the form of mortgage principal and rightto buy discount repayments.

We found no errors on the pooling of housing capital receipts return and we certified the amount payable tothe pool without qualification.

Page 54 of 348

2012-13 certification fees

EY ÷ 3

2. 2012-13 certification fees

For 2012-13 the Audit Commission replaced the previous schedule of maximum hourly rates with acomposite indicative fee for certification work for each body. The indicative fee was based on actualcertification fees for 2010-11 adjusted to reflect the fact that a number of schemes would no longer requireauditor certification. There was also a 40 per cent reduction in fees reflecting the outcome of the AuditCommission procurement for external audit services.

The indicative composite fee for Great Yarmouth Borough Council for 2012-13 was £37,100. The actual feefor 2012-13 was £39,410. This compares to a charge of £71,003 in 2011-12.

Claim or return 2011-12 2012-13 2012-13

Actual fee

£

Indicative fee

£

Actual fee

£

Certification of claims and returnsincluding the annual report

71,003* 37,100 39,410

*Adjusted for fees charged in 2011-12 for claims and returns not audited in 2012-13

Fees for annual reporting and for planning, supervision and review have been allocated directly to theclaims and returns.

The fees for 2012-13 were calculated based on those for 2010-11 less 40%.

Fees fell overall compared to 2010-11 because of the Audit Commission’s 40% reduction. However, afterallowing for the 40% reduction there was a small increase in fees for the following claims and returns:

The actual fee is £2,310 higher than the indicative fee due to the additional fee reported in section1 for theaudit of the NNDR return.

Page 55 of 348

Looking forward

EY ÷ 4

3. Looking forward

For 2013-14, the Audit Commission has calculated indicative certification fees based on the latest availableinformation on actual certification fees for 2011-12, adjusted for any schemes that no longer requirecertification. The Audit Commission has indicated that the national non-domestic rates return will not requirecertification from 2013-14.

The Council’s indicative certification fee for 2013-14 is £39,700. The actual certification fee for 2013-14 maybe higher or lower than the indicative fee, if we need to undertake more or less work than in 2011-12 onindividual claims or returns. Details of individual indicative fees are available at the following link:[http://www.audit-commission.gov.uk/audit-regime/audit-fees/201314-fees-and-work-programme/individual-certification-fees/]