Aspen Real Estate Trust - Nickel Financial

204

| | CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 1 Nge ratio Aspen Real Estate Trust STRENGTH IN NUMBERS

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Aspen Real Estate Trust - Nickel Financial

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 1

Nge ratio

Aspen Real Estate Trust S T R E N G T H I N N U M B E R S

CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES I

AND

CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES II

AND

CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES III

AND

CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES IV

AND

CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES 5

AND

CLEAR SKY SUNGATE LIMITED PARTNERSHIP

NOTICE OF SPECIAL MEETINGS OF UNITHOLDERS

TO BE HELD ON DECEMBER 1, 2020 - AND -

JOINT MANAGEMENT INFORMATION CIRCULAR

November 5, 2020

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 3

LETTER TO UNITHOLDERS

Dear fellow Unitholders,

You have the opportunity to enhance overall returns from your investment in Clear Sky Capital Strategic Asset Fund – Series I (“Fund 1”), Clear Sky Capital Strategic Asset Fund – Series II (“Fund 2”), Clear Sky Capital Strategic Asset Fund – Series III (“Fund 3”), Clear Sky Capital Strategic Asset Fund – Series IV (“Fund 4”), Clear Sky Capital Strategic Asset Fund – Series 5 (“Fund 5”, and collectively with Fund 1, Fund 2, Fund 3 and Fund 4, the “Trusts”) and/or Clear Sky Sungate Limited Partnership (“Sungate” and, together with the Trusts, the “Funds” and each, a “Fund”) through a consolidation of the Funds that we believe will provide:

(i) more effective access to the accumulated equity of the properties held by each of the Funds;

(ii) more geographic and asset class diversification and size; and

(iii) greater cost efficiencies.

Clear Sky invites you to participate in Aspen Real Estate Trust, a new open-ended, unincorporated investment trust to be formed under the laws of Alberta (“New Fund”) that will be a consolidation of all multi-family properties currently held in the six separate Funds into one fund. The properties are located throughout Arizona, New Mexico and Texas (the “Properties”), and almost all of the Properties have experienced overall operational improvements and valuation gains since acquisition.

Please review the accompanying joint management information circular (the “Circular”) which provides details on how you can benefit from participating in New Fund and, if applicable, submit your proxy today (or ask your dealing representative to assist you) voting FFOR the proposed consolidation.

| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 4

It is expected that, as a result of the consolidation, overall

Unitholder returns will be enhanced in the following ways:

1. Potential to increase overall

return by accessing currently

inaccessible equity. ________________________________________________

Overall there has been significant value creation within the

Funds; however, interest rates have declined since the

Properties were acquired by the Funds. With current

interest rates being lower than those under the existing

loans for the Properties, the costs associated with pre-

paying the loans make refinancing any of the loans on a

per loan basis or disposing of any of the Properties on a

per property basis, financially inefficient and impractical.

Due to the current ultra-low interest rate environment,

defeasance costs have increased, causing penalties

imposed upon pre-payment of the loans to rise sharply.

As a result, the equity appreciation in the Properties since

the initial investment or acquisition by the applicable Fund

is currently inaccessible. It is expected that, as New Fund

will have a larger portfolio of Properties, Clear Sky Capital,

Inc., an Arizona corporation, as manager and/or

administrator of the Funds (the “Manager” or “Clear Sky”),

will have more leverage to negotiate with the lenders under

the loans. Alternatively, the Manager may be better

positioned to pursue alternative methods to unlock the

equity appreciation in the Properties by pledging minority

interests in one or more of such Properties. The proposed

consolidation is expected to address these funding

limitations and provide the Manager with increased

financing flexibility by consolidating the Properties under

New Fund.

2. Superior investment in a larger,

more diversified Fund with further

upside potential. ________________________________________________

Upon completion of the proposed consolidation, it is

expected that New Fund’s portfolio will be comprised of

the current Properties contributed from each of the Funds.

With the potential to access currently inaccessible equity,

as discussed above, New Fund may also acquire or

develop additional properties to provide further

diversification and growth potential.

It is expected that New Fund will indirectly own seven

Properties comprising 1,159 multi-family units, appraised

in the aggregate at approximately US$122.4 million, and is

expected to benefit from increased geographical diversity

across metropolitan areas exhibiting population growth,

including in Arizona, New Mexico and Texas. The Manager

believes that additional growth remains to be realized in

the U.S. Sun Belt rental real estate markets and further

diversification across the property portfolio, including

geographical diversification, mitigates the risk and

exposure to any one property or market.

Additionally, the COVID-19 pandemic has caused

economic turmoil. While each of the Funds is positioned to

operate independently, the Manager believes that

investors in the Funds will be better positioned to achieve

higher returns and weather the economic storm by

combining into New Fund.

| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 5

3. Potential to lead to greater cost

efficiencies. ________________________________________________

The proposed consolidation is expected to provide

economies of scale by eliminating duplicative general and

administrative costs, including legal, accounting and

auditing fees, and costs associated with operating the

Funds as separate funds.

In addition, holders of units (“Units”) of the Funds

(“Unitholders”) will receive units of New Fund that have an

aggregate asset management fee that is likely to be lower

than that charged in the aggregate in respect of the Units

that they currently hold, an acquisition fee that is lower

than that charged in respect of Units that they currently

hold (other than for the Class A units of Sungate (the

“Sungate Units”)), and a disposition fee that is equal to or

lower than that charged in respect of units that they

currently hold (other than for the Sungate Units). In

addition, the annual fee paid to the non-management

trustees of New Fund will be lower than that currently

charged in the aggregate in respect of the Funds. New

Fund will also have a Development Fee and a Construction

Fee, which is not currently charged in respect of Units that

Unitholders currently hold.

4. Provide optionality in disposition

strategy. ________________________________________________

Often times market conditions provide for a value premium

for larger, bulk sale transactions. Consolidating the

Properties into New Fund will provide the optionality to

take advantage of this, if available, or to sell the Properties

on an individual basis.

Other factors that Unitholders should consider in

assessing the proposed consolidation are:

Thorough process, Fairness Opinion and procedural

protections consistent with corporate governance best

practices - Evans & Evans, Inc. has provided a fairness

opinion to the independent member of each of the board of

trustees and board of directors of the general partner of

each of the Funds, as applicable, stating that as of

November 3, 2020, and based upon and subject to the

assumptions, limitations and qualifications set out therein,

the consolidation is fair, from a financial point of view to

Unitholders. Additionally, the proposed consolidation has

procedural measures to protect the interests of

Unitholders. Specifically, (i) in the case of each Trust, each

of the resolutions approving the proposed consolidation

must be approved by at least 66 2/3% of the votes cast by

applicable Unitholders virtually or represented by proxy at

the applicable Meeting, and (ii) in the case of Sungate, the

written resolutions approving the proposed consolidation

must be approved by holders of Sungate Units (the

“Sungate Unitholders”) holding more than 66 2/3% of the

issued Sungate Units. Furthermore, any registered

Unitholder of a Trust as of the Record Date (as defined in

the Circular) can exercise dissent rights and may, on strict

compliance with certain conditions, receive the fair value of

their Units in the applicable Fund.

Tax deferral - It is expected that, if approved, the proposed

consolidation will be completed on a tax deferred “rollover”

basis to Unitholders for Canadian income tax purposes,

provided that, in the case of a qualifying holder of Sungate

Units, the holder of Sungate Units elects to receive units of

a newly formed limited partnership subsidiary of New Fund

(“New LP”) in exchange for their Sungate Units and the

holder of Sungate Units makes the necessary joint tax

election with the general partner of New LP. See “Certain

Canadian Federal Income Tax Considerations” in the

accompanying Circular.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 6

ABOUT CLEAR SKY CAPITAL REAL ESTATE INVESTMENTS

Continued commitment of experienced management with a track record of value creation. ________________________________________________

Clear Sky is a private equity investment management firm specializing in the acquisition and management of real estate assets in the United States.

Clear Sky was founded in 2009 by Marcus Kurschat and is led by an executive management team consisting of Marcus Kurschat (Founder and Chief Executive Officer), Matthew Collins (Chief Financial Officer) and Matt Mason (General Counsel). Clear Sky is currently comprised of a team of 13 investment professionals with experience in multi-family real estate asset management in the United States.

Clear Sky is an active investor in value-added real estate opportunities throughout the United States. Since its inception in 2009 through to December 31, 2019, Clear Sky has acquired or developed approximately US$771 million of real estate and operating assets, investing in excess of US$270 million of equity through various investment vehicles. Clear Sky’s real estate investments are diversified across real estate sectors including multi-family, self-storage and manufactured housing.

Clear Sky’s multi-family investments are primarily located in Arizona, California, Florida, New Mexico and Texas. Since inception, Clear Sky and its affiliates have successfully invested in 48 properties with invested equity in excess of US$194 million towards the acquisition or development of US$594 million in multi-family assets. Of the 48 properties, as of December 31, 2019, 28 properties have been realized, generating an aggregate realized gross internal rate of return of 30.9% and gross equity multiple of 2.2x.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 7

The independent member of each of the board of trustees and board of directors of the general partner of each of the Funds, as applicable, has determined that the Transaction is advisable and in the best interest of the respective Fund and rrecommends that Unitholders of the Fund vote FOR or approve in writing, as applicable, the Transaction.

Special meetings of Unitholders of each of the Trusts will be held beginning at 9:00 a.m. (Mountain time) on December 1, 2020. Out of an abundance of caution, to proactively deal with the public health impact of the novel coronavirus disease, also known as COVID-19, and to mitigate risks to the health and safety of our communities, Unitholders, employees and other stakeholders, we will be holding the Meetings in a virtual-only format, which will be conducted via live audio webcast online at https://web.lumiagm.com. The accompanying Circular and Virtual Meeting User Guide provide important and detailed instructions about how to participate at the applicable virtual Meeting(s).

The consolidation is subject to the approval (i) in the case of each Trust, by at least 66 2/3% of the votes cast by Unitholders of each Trust, virtually or represented by proxy at the Meeting of such Trust, or any adjournment(s) or postponement(s) thereof, and (ii) in the case of Sungate, by Sungate Unitholders holding more than 66 2/3% of the issued Sungate Units.

Your participation in the applicable Meeting(s) is important to us. We encourage all Unitholders to take the opportunity to read the accompanying Circular in full and in advance of the applicable Meeting(s) or approval of the Sungate Resolution, as applicable, as it details important information that will assist you in exercising your right to vote as a Unitholder.

Sincerely, Marcus Kurschat P R E S I D E N T

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 8

Falling Interest Rates

When each of the Properties was acquired, a 10-

year term mortgage was secured on the Property.

A 10-year term would typically mitigate against

rising interest rate risk for a normal economic

cycle, allowing for a sale of the Property, either by

a small prepayment penalty or an attractive

mortgage for the acquirer to assume.

Prior to the fall of 2018, the general market

consensus was that interest rates would rise;

however, they instead took an unconventional

turn and began to drop. They continued to drop to

the point where one could borrow for a 10-year

term for less than a 2-year term (see chart below).

Falling interest rates have given rise to enormous

prepayment penalties on long-term debt, which

makes any consideration of selling a property not

financially viable.

N E W F U N D

7Properties comprising of

1,159 units

$122.4Million in Value (USD)

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 9

Clear Sky Fund Properties

STRATEGIC ASSET FUND – SERIES I: Silverado Apartments

Location Albuquerque, NM Purchase Price $19,500,000

Unit Count 256 Current Value $28,050,000 / 43.8%

Year Built 1985 Loan Amount $14,653,638

Acquisition Date January 2015 Defeasance $2,438,241

STRATEGIC ASSET FUND – SERIES II: Villas at Helen of Troy

Location El Paso, TX Purchase Price $10,750,000

Unit Count 108 Current Value $12,700,000 / 18.1%

Year Built 2013 Loan Amount $7,800,000

Acquisition Date January 2016 Defeasance $1,936,662

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 10

Clear Sky Fund Properties

STRATEGIC ASSET FUND – SERIES III: Casas de Soledad

Location Las Cruces, NM Purchase Price $15,550,000

Unit Count 256 (176 rental units, 80 units owned individually) Current Value $18,950,000 / 21.8%

Year Built 2004 Loan Amount $11,467,082

Acquisition Date February 2016 Defeasance $3,052,533

STRATEGIC ASSET FUND – SERIES III: Rancho Verde

Location Albuquerque, NM Purchase Price $5,465,787

Unit Count 65 Current Value $7,300,000 / 33.5%

Year Built 1985 Loan Amount $4,162,000

Acquisition Date June 2016 Defeasance $980,828

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 11

Clear Sky Fund Properties

STRATEGIC ASSET FUND – SERIES IV: Tesoro on Spain

Location Albuquerque, NM Purchase Price $22,762,383

Unit Count 267 Current Value $29,300,000 / 28.7%

Year Built 1986 Loan Amount $17,100,000

Acquisition Date January 2016 Defeasance $3,801,980

STRATEGIC ASSET FUND – SERIES 5: North Park Apartments

Location Houston, TX Purchase Price $14,500,000

Unit Count 192 Current Value $12,850,000 / 11%

Year Built 1978 Loan Amount $10,116,482

Acquisition Date February 2018 Defeasance $3,412,544

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 12

Clear Sky Fund Properties

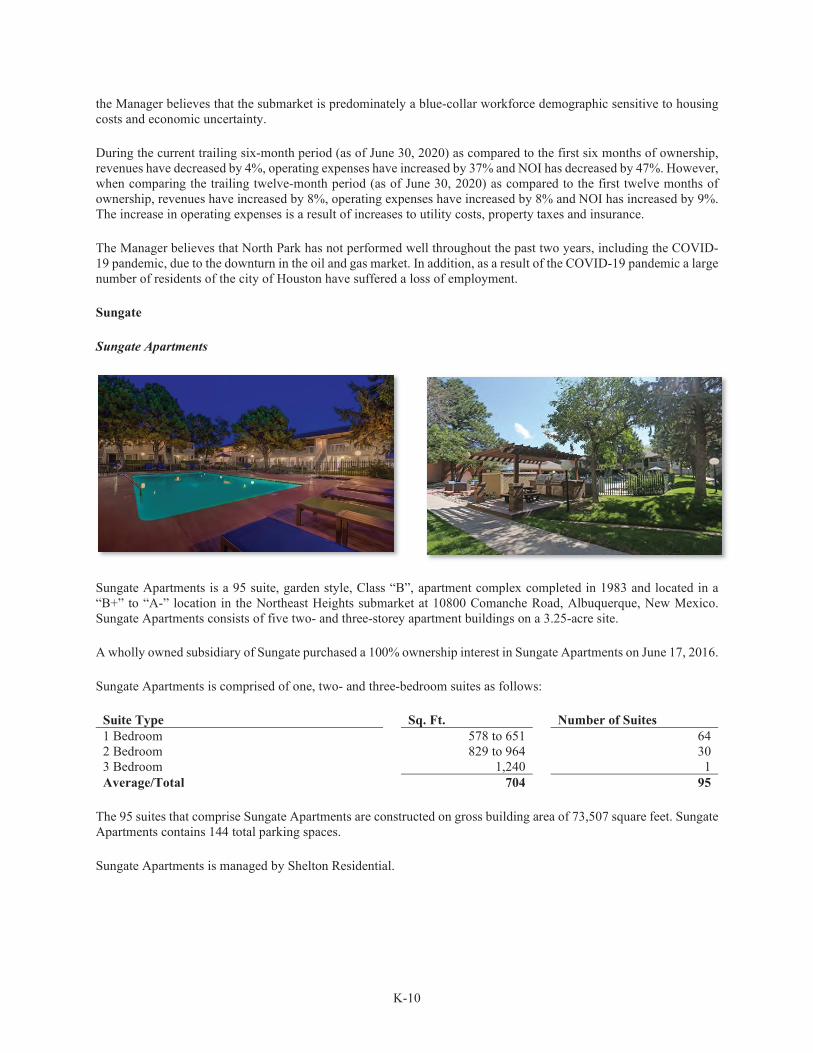

SUNGATE LIMITED PARTNERSHIP: Sungate Apartments

Location Albuquerque, NM Purchase Price $6,972,430

Unit Count 95 Current Value $10,300,000 / 48%

Year Built 1983 Loan Amount $5,272,000

Acquisition Date June 2016 Defeasance $1,200,950

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 13

NOTICE OF SPECIAL MEETINGS OF UNITHOLDERS

OF CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES I CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES II CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES III CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES IV CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES 5

(collectively, the “Trusts”)

For each Trust, NOTICE IS HEREBY GIVEN that a special meeting (the “Meeting”) of holders (“Trust Unitholders”) of units (“Trust Units”) of the Trust will be held for the following purpose:

1. to consider and, if thought advisable, to pass, with or without variation, a special resolution of the Trust (the “Trust Resolution”), the full text of which is set forth in the applicable Schedule to the accompanying joint management information circular dated as of November 5, 2020 (the “Circular”), authorizing and approving an amendment to the declaration of trust to provide for the transfer of all of the assets of the applicable Trust (other than a nominal amount of cash) to Aspen Real Estate Trust, an open-ended, unincorporated investment trust to be formed under the laws of Alberta (“New Fund”), in consideration for the assumption of liabilities of the applicable Trust and units of New Fund (“New Fund Units”) and the redemption of all units of the applicable Trust (other than one unit of such Trust to be held by New Fund) in exchange for such New Fund Units (together with the Sungate Matters (as defined below), the “Transaction”), as more particularly described in the accompanying Circular; and

2. to transact such further or other business as may properly come before the Meeting or any adjournment(s) or postponement(s) thereof.

Each Meeting will be held consecutively beginning at 9:00 a.m. (Mountain time) on December 1, 2020 as a virtual-only Meeting by way of a live audio webcast utilizing the LUMI meeting platform at https://web.lumiagm.com. Please refer to the accompanying Circular and Virtual Meeting User Guide for access details with respect to the applicable Meeting(s), including the Meeting ID(s).

The holders (the “Sungate Unitholders” and, together with the Trust Unitholders, “Unitholders”) of Class A units (“Sungate Units” and, together with the Trust Units, “Units”) of Clear Sky Sungate Limited Partnership (“Sungate” and, together with the Trusts, the “Funds” and each, a “Fund”) are requested to pass the applicable special resolution (the “Sungate Resolution” and, together with the Trust Resolutions, the “Transaction Resolutions”) authorizing and approving an amendment to the limited partnership agreement of Sungate to provide for (i) the redemption of the Sungate Units held by certain Sungate Unitholders (being Sungate Unitholders who do not elect to exchange their Sungate Units for units of a limited partnership subsidiary of New Fund to be formed under the laws of British Columbia (“New LP”)) in consideration for New Fund Units, and (ii) the transfer of all remaining Sungate Units to New LP in exchange for Class B limited partnership units of New LP that are, to the greatest extent practicable, economically equivalent to, and exchangeable for, New Fund Units (the “Sungate Matters”) by written resolution.

The accompanying Circular provides important and detailed information relating to the matters to be dealt with at the Meetings and forms part of this notice.

Out of an abundance of caution, to proactively deal with the public health impact of the novel coronavirus disease, also known as COVID-19, and to mitigate risks to the health and safety of our communities, Trust Unitholders, employees and other stakeholders, the Meetings will be held in a virtual-only format, which will be conducted via live audio webcast online at https://web.lumiagm.com. During the audio webcast, Trust Unitholders will be able to listen to the applicable Meeting live, and registered Trust Unitholders and duly appointed and registered proxyholders will be able to submit questions and vote while the applicable Meeting is being held. We hope that hosting the Meetings virtually helps enable greater participation by Trust Unitholders by allowing Trust Unitholders that might not

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 14

otherwise be able to travel to a physical meeting to attend online, while minimizing the health risk that may be associated with large gatherings. Please refer to the accompanying Circular and Virtual Meeting User Guide for access details with respect to the applicable Meetings, including the Meeting ID(s).

Registered Trust Unitholders and duly appointed and registered proxyholders will be able to virtually attend, participate in and vote at their respective Meeting(s) at https://web.lumiagm.com, using password “clearsky2020” (case sensitive). Non-registered Trust Unitholders who receive this notice of special meetings of Trust Unitholders and related materials through their broker, investment dealer, bank, trust company, custodian, nominee or other intermediary, should carefully follow the instructions of their intermediary to ensure that their Trust Units are voted at the applicable Meeting in accordance with such Trust Unitholders’ instructions. Please refer to the accompanying Circular and Virtual Meeting User Guide for access details with respect to applicable Meeting(s), including the Meeting ID(s).

Registered Trust Unitholders as of the record date of November 3, 2020 may exercise their right to vote at their respective Meeting(s) by completing and submitting a form of proxy. To be effective, the form of proxy, properly completed and duly signed, must be received by the proxy agent of the Trusts, Computershare Trust Company of Canada, prior to 9:00 a.m. (Mountain time) on November 27, 2020 or, in the case of any adjournment or postponement of a Meeting, not less than 48 hours, Saturdays, Sundays and holidays excepted, prior to the time of the adjournment or postponement. Detailed instructions on how to complete and return proxies are provided in the accompanying Circular.

Non-registered Trust Unitholders (being Trust Unitholders who hold their units through an investment dealer, trust company, custodian, nominee or other intermediary) are advised that voting through a proxyholder at the applicable Meeting will include, as a result of the virtual nature of the Meetings, the additional step of registering proxyholders with the proxy agent of the Trusts, Computershare Trust Company of Canada, after submitting their form of proxy or voting instruction form, as applicable. Failure to register the proxyholder with the proxy agent will result in the proxyholder not receiving a “Control Number” to participate in the applicable Meeting and only being able to attend as a guest. Non-registered Trust Unitholders who have not duly appointed themselves as proxyholder will be able to attend the applicable Meeting as guests but will not be able to vote or submit questions at the applicable Meeting. Please refer to the instructions provided in the Circular under “General Proxy Matters – Non-Registered Holders”.

If you plan to vote at a Meeting, it is important that you are connected to the internet at all times during such Meeting in order to vote when balloting commences. It is your responsibility to ensure internet connectivity for the duration of the applicable Meeting. You should allow ample time to login to the applicable Meeting online and complete the check-in procedures.

Trust Unitholders are encouraged to express their vote in advance of their respective Meeting(s) by completing the form of proxy or voting instruction form provided to them.

The Trust Units represented by properly executed proxies given in favour of the persons named in the form of proxy will be voted at the applicable Meeting in accordance with the instructions indicated thereon. If no instructions are given, the Trust Units represented by properly executed proxies given in favour of the persons named in the form of proxy will be voted FOR the applicable Trust Resolution.

DATED the 5th day of November, 2020.

BY ORDER OF THE BOARD OF TRUSTEES OF CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES I

BY ORDER OF THE BOARD OF TRUSTEES OF CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES II

(signed) “Kevin Kinnear” (signed) “Kevin Kinnear”Kevin Kinnear Independent Trustee

Kevin Kinnear Independent Trustee

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 15

BY ORDER OF THE BOARD OF TRUSTEES OF CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES III

BY ORDER OF THE BOARD OF TRUSTEES OF CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES IV

(signed) “Kevin Kinnear” (signed) “Kevin Kinnear”Kevin Kinnear Independent Trustee

Kevin Kinnear Independent Trustee

BY ORDER OF THE BOARD OF TRUSTEES OF CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES 5

(signed) “Kevin Kinnear”Kevin Kinnear Independent Trustee

TABLE OF CONTENTS Page

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 16

LETTER TO UNITHOLDERS .................................................................................................................................. 3 NOTICE OF SPECIAL MEETINGS OF UNITHOLDERS ................................................................................. 13 JOINT MANAGEMENT INFORMATION CIRCULAR ..................................................................................... 17 FORWARD-LOOKING STATEMENTS ............................................................................................................... 17 ELIGIBILITY FOR INVESTMENT....................................................................................................................... 18 CURRENCY AND EXCHANGE RATE ................................................................................................................. 19 NON-IFRS MEASURES ........................................................................................................................................... 19 QUESTIONS AND ANSWERS ................................................................................................................................ 20 GENERAL PROXY MATTERS .............................................................................................................................. 27 THE TRANSACTION .............................................................................................................................................. 30 SPECIAL BUSINESS OF THE MEETINGS ......................................................................................................... 50 RISK FACTORS ....................................................................................................................................................... 52 CERTAIN CANADIAN FEDERAL INCOME TAX CONSIDERATIONS ........................................................ 63 CERTAIN U.S. FEDERAL INCOME TAX CONSEQUENCES .......................................................................... 74 VOTING SECURITIES AND PRINCIPAL HOLDERS THEREOF .................................................................. 79 INTERESTS OF CERTAIN PERSONS OR COMPANIES IN MATTERS TO BE ACTED UPON ............... 79 AUDITORS ................................................................................................................................................................ 79 OTHER MATTERS .................................................................................................................................................. 80 GLOSSARY OF TERMS.......................................................................................................................................... 81 APPROVAL OF THE BOARDS ............................................................................................................................. 93 SCHEDULE “A” TEXT OF FUND 1 RESOLUTION ....................................................................................... A-1 SCHEDULE “B” TEXT OF FUND 2 RESOLUTION ........................................................................................ B-1 SCHEDULE “C” TEXT OF FUND 3 RESOLUTION ....................................................................................... C-1 SCHEDULE “D” TEXT OF FUND 4 RESOLUTION ....................................................................................... D-1 SCHEDULE “E” TEXT OF FUND 5 RESOLUTION ........................................................................................ E-1 SCHEDULE “F” TEXT OF SUNGATE RESOLUTION ................................................................................... F-1 SCHEDULE “G” DISSENT RIGHTS ................................................................................................................. G-1 SCHEDULE “H” FAIRNESS OPINION ............................................................................................................ H-1 SCHEDULE “I” FORM OF TRANSACTION AGREEMENT .......................................................................... I-1 SCHEDULE “J” VOTING SECURITIES ........................................................................................................... J-1 SCHEDULE “K” DESCRIPTION OF THE EXISTING PROPERTIES ........................................................ K-1 SCHEDULE “L” INFORMATION RELATING TO NEW FUND ................................................................... L-1 SCHEDULE “M” PRO FORMA FINANCIAL STATEMENTS...................................................................... M-1

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 17

JOINT MANAGEMENT INFORMATION CIRCULAR

CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES I CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES II CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES III CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES IV CLEAR SKY CAPITAL STRATEGIC ASSET FUND – SERIES 5

(collectively, the “Trusts”)CLEAR SKY SUNGATE LIMITED PARTNERSHIP

(“Sungate” and, together with the Trusts, the “Funds” and each, a “Fund”)

This joint management information circular (this “Circular”) is provided by Clear Sky Capital Inc., an Arizona corporation, as manager and/or administrator of the Funds (the “Manager” or “Clear Sky”).

For each Trust, the Manager will hold a special meeting of holders of Trust Units (the “Meeting”) beginning at 9:00 a.m. (Mountain time) on December 1, 2020 in virtual-only format, which will be conducted by way of a live audio webcast at https://web.lumiagm.com for the purposes set forth in the enclosed Notice of Special Meetings of Unitholders of the Trusts (the “Notice of Meetings”), as more particularly described, with respect to each Meeting, under “General Proxy Matters – Meeting Information”. The holders (the “Sungate Unitholders”) of Class A units (“Sungate Units”) of Clear Sky Sungate Limited Partnership (“Sungate” and, together with the Trusts, the “Funds” and each, a “Fund”) are requested to pass the Sungate Resolution by written resolution. Please refer to the this Circular and the accompanying Virtual Meeting User Guide for access details with respect to the applicable Meeting(s), including the Meeting ID(s).

The Manager, as manager and/or administrator of the Funds, is providing this Circular in connection with the solicitation of proxies for use at the Meetings or at any adjournment(s) or postponement(s) thereof. No person has been authorized to give any information or to make representations in connection with the Transaction or any other matters to be considered at the Meetings other than those contained in this Circular and, if given or made, any such information or representation should not be considered to have been authorized by the Funds or the Manager.

This Circular does not constitute the solicitation of an offer to acquire any securities or the solicitation of a proxy by any person in any jurisdiction in which such solicitation is not authorized or in which the person making such solicitation is not qualified to do so or to any person to whom it is unlawful to make such solicitation.

All capitalized terms used in this Circular but not otherwise defined herein shall have the meanings set forth under “Glossary of Terms”.

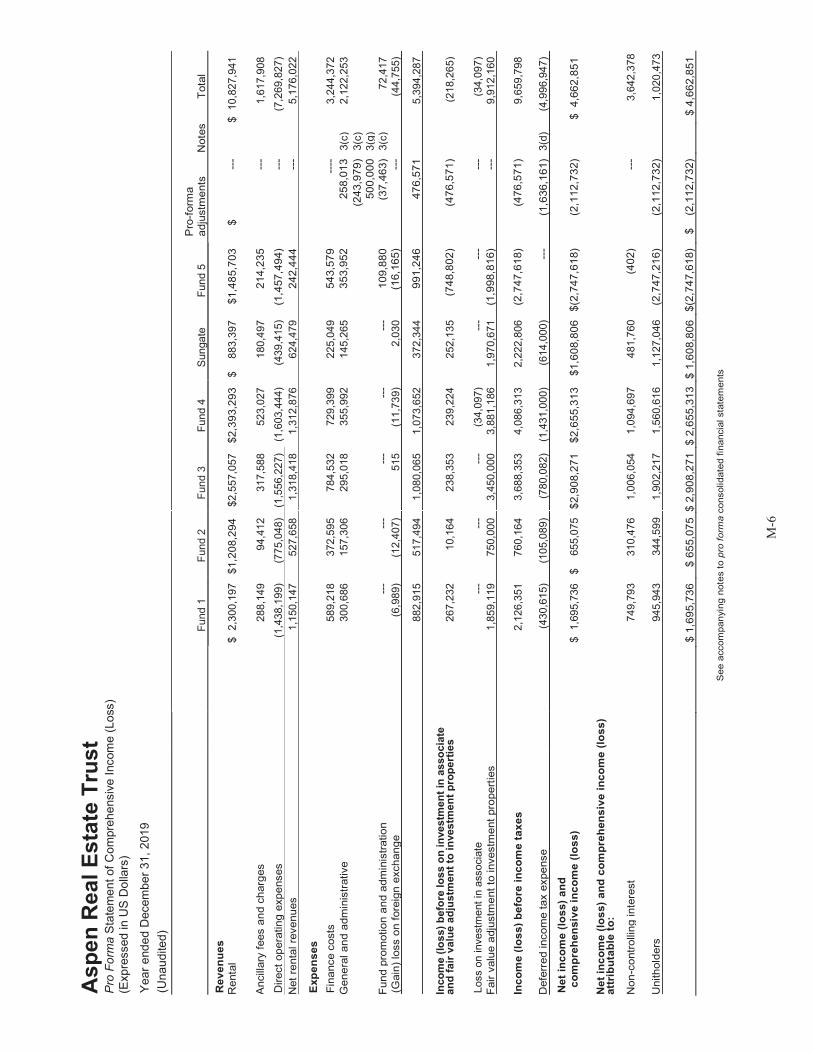

Each Funds’ financial statements and the pro forma financial statements of New Fund that are included herein are reported in United States dollars and have been prepared in accordance with International Financial Reporting Standards (“IFRS”).

You should not construe the contents of this Circular as legal, tax or financial advice and should consult with your own professional advisors as to the relevant legal, tax, financial or other matters in connection herewith.

FORWARD-LOOKING STATEMENTS

Certain statements contained in this Circular may constitute forward-looking statements and forward-looking information (collectively, “forward-looking statements”) within the meaning of Canadian securities laws, which are based on opinions, estimates and assumptions of the Manager and are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. Forward-looking statements may include, but are not limited to, statements with respect to: the completion of the Transaction; the expected benefits of the Transaction; the Exchange Ratios; the timing of the Meetings; the anticipated Effective Date; the effects of the Transaction on Unitholders; opportunities in the U.S. multi-

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 18

family real estate market; expectations regarding the U.S. economy; the anticipated and potential impact of the novel coronavirus disease (“COVID-19”) on the Funds, including rent collection; the treatment of Unitholders under tax laws, the expected future quarterly cash distributions of New Fund, and other expectations of the Manager and are often, but not always, identified by terminology such as “may”, “might”, “will”, “could”, “should”, “would”, “occur”, “expect”, “plan”, “anticipate”, “believe”, “intend”, “seek”, “aim”, “estimate”, “target”, “project”, “predict”, “forecast”, “potential”, “continue”, “likely”, “schedule”, or the negative thereof or similar expressions concerning matters that are not historical facts.

Forward-looking statements are provided for the purpose of presenting information about management’s current expectations and plans relating to the future and readers are cautioned that such statements may not be appropriate for other purposes. Although the Manager believes that the expectations reflected in such forward-looking statements are reasonable, such statements are not guarantees of future performance and are subject to certain risks, uncertainties and assumptions, including those discussed below. Many factors could cause actual results, performance or achievements to differ materially from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking statements prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, believed, estimated or expected.

Material factors or assumptions that were applied in drawing a conclusion or making an estimate set out in the forward-looking statements include, among other things, obtaining Unitholder approval of the Transaction Resolutions; assumptions made in connection with the anticipated benefits of the Transaction; the timing of the Meetings; assumptions made in connection with the preparation of the pro forma financial statements included herein; the impact of the current economic climate and the current global financial condition the Funds’ operations; vacancy and rental growth rates in the U.S. multi-family property market; demand for multi-family properties in the U.S.; demographic and economic trends in the U.S.; the realization of property value appreciation and timing thereof; the availability of properties for acquisition and the price at which such properties may be acquired; the price at which Properties may be disposed of and the ability and timing thereof; the availability of mortgage financing and current interest rates; the capital structure of New Fund; expenditures and fees in connection with the maintenance, operation and administration of the Properties; the ability of the Manager to manage and operate the Properties; actual or threatened epidemics, pandemics, outbreaks, or other public health crises, including the recent global outbreak of COVID-19; foreign currency exchange rates; governmental regulations and tax laws; and general global economic, market and business conditions. Risks and uncertainties regarding the Transaction are discussed under the “Risk Factors” section of this Circular.

Investors are cautioned against placing undue reliance on forward-looking statements. Except as required by law, the Manager undertakes no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

ELIGIBILITY FOR INVESTMENT

In the opinion of Blake, Cassels & Graydon LLP, counsel to the Funds, subject to the restrictions, limitations and assumptions set out under the heading “Certain Canadian Federal Income Tax Considerations”, provided that New Fund is a “mutual fund trust” for the purposes of the Tax Act on the Effective Date, New Fund Units will be, on that date, qualified investments under the Tax Act for trusts governed by registered retirement savings plans (“RRSPs”), registered retirement income funds (“RRIFs”), deferred profit sharing plans (“DPSPs”), registered education savings plans (“RESPs”), registered disability savings plans (“RDSPs”) and tax-free savings accounts (“TFSAs” and, together with RRSPs, RRIFs, DPSPs, RESPs and RDSPs, “Plans”).

Notwithstanding that New Fund Units may be qualified investments as discussed above, if New Fund Units are a “prohibited investment” (as defined in the Tax Act) for an RRSP, RRIF, TFSA, RDSP, or RESP, the annuitant of the RRSP or RRIF, the holder of the TFSA or RDSP, or the subscriber of the RESP, as the case may be, will be subject to a penalty tax as set out in the Tax Act if New Fund Units are held in a trust governed by such Plan. New Fund Units will not be a prohibited investment provided the annuitant, holder, or subscriber, as the case may be, deals at arm’s length with New Fund for purposes of the Tax Act and does not have a “significant interest” (as defined in the Tax Act) in New Fund. In addition, a New Fund Unit will not be a “prohibited investment” if the New Fund Unit is

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 19

“excluded property” (as defined for purposes of the prohibited investment rules in the Tax Act) for a trust governed by an RRSP, RRIF, TFSA, RDSP, or RESP, as applicable. Annuitants, holders, and subscribers of such Plans should consult their own tax advisors to ensure that New Fund Units would not be a prohibited investment in their particular circumstances.

Redemption Notes and other property which may be received in connection with an in specie redemption of New Fund Units may not be qualified investments for trusts governed by Plans. Accordingly, Unitholders should consult with their own tax advisors before deciding to exercise redemption rights in connection with New Fund Units held in a trust governed by a Plan.

New LP Units are not expected to be qualified investments for trusts governed by Plans.

CURRENCY AND EXCHANGE RATE

Unless otherwise indicated, all references to “dollars”, “$” or “US$” in this Circular refer to United States dollars and all references to “C$” in this Circular refer to Canadian dollars.

The daily average exchange rate as reported by the Bank of Canada for conversion of United States dollars to Canadian dollars on November 4, 2020 was US$1.00 = $1.3138.

NON-IFRS MEASURES

In this Circular, the Funds use certain non-International Financial Reporting Standards (“IFRS”) financial measures, which include Net Operating Income (NOI). These terms are not measures recognized under IFRS as prescribed by the International Accounting Standards, do not have standardized meanings prescribed by IFRS and should not be compared to or construed as alternatives to profit/loss, cash flow from operating activities or other measures of financial performance calculated in accordance with IFRS. Net Operating Income, as computed by the Funds, may not be comparable to similar measures as reported by other trusts or companies in similar or different industries. The Funds use these measures to better assess their underlying performance and provide these additional measures so that investors may do the same. NOI is presented in this Circular because management considers this non-IFRS measure to be an important measure of operating performance and uses this measure to assess each Property’s operating performance on an unlevered basis. In this Circular, “Net Operating Income” or “NOI” means all Property revenue, less direct Property costs such as utilities, realty taxes, repairs and maintenance, on-site salaries, insurance, bad debt expenses, Property management fees, and other Property specific administrative costs.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 20

QUESTIONS AND ANSWERS

The following are some questions that you may have relating to the Transaction, and the answers to those questions. These questions and answers do not provide all the information relating to the Transaction and are qualified in their entirety by the more detailed information contained elsewhere in this Circular. Unitholders are urged to read this Circular in its entirety before making a decision related to their Units.

Q: What is the Transaction?

A: If the Transaction is consummated, among other things:

(i) with respect to each of the Trusts, all of the assets of the Trust (other than a nominal amount of cash) will be transferred to New Fund in consideration for the assumption of liabilities of the Trust and New Fund Units, and all of the Units of the Trust (other than one Unit of the Trust to be held by New Fund) will be redeemed in exchange for such New Fund Units;

(ii) with respect to Sungate, (i) all of the Sungate Units held by Non-Electing Sungate Unitholders will be redeemed in consideration for New Fund Units, and (ii) all of the Sungate Units held by Electing Sungate Unitholders will be transferred to New LP in exchange for New LP Units; and

(iii) as a result of the foregoing, the Funds will effectively be consolidated into New Fund which will continue to carry on, directly or indirectly, the business carried on by the Funds.

For further details of the Transaction, see “The Transaction”.

Q: What approval is required to pass the Transaction Resolutions of each of the Funds?

A: At each Meeting, Trust Unitholders will be asked to pass the applicable Trust Resolution, in each case approving the Transaction, including an amendment to the applicable Declaration of Trust. Each of the Trust Resolutions must be approved by at least 66 2/3% of the votes cast by applicable Trust Unitholders virtually or represented by proxy at the applicable Meeting.

The Sungate Resolution must be approved by Sungate Unitholders holding more than 66 2/3% of the issued Sungate Units. Sungate Unitholders are requested to pass the Sungate Resolution in writing.

See “The Transaction – Termination of the Transaction”.

Q: Does each of the Trust Boards and the Sungate GP Board support the Transaction?

A: Having received a Fairness Opinion and having considered a number of other factors, each Trust Board and the Sungate GP Board concluded (with the Conflicted Trustees or Conflicted Directors, as applicable, declaring their interest and refraining from consideration and voting) that the Transaction is fair from a financial point of view and is in the best interests of each of the Funds. Accordingly, the Independent Trustee of each Trust Board and the Independent Director of Sungate GP Board approved the Transaction and recommends that the Unitholders of each respective Fund vote FOR or approve in writing, as applicable, the applicable Transaction Resolution.

Q: What are the reasons for the recommendation of the Trust Boards and Sungate GP Board to approve the Transaction?

A: The Independent Trustee of each Trust Board and the Independent Director of Sungate GP Board identified a number of factors set out below as being most relevant to its recommendation to Unitholders to vote FORor approve in writing, as applicable, the applicable Transaction Resolution that will implement the Transaction, including the following:

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 21

Potential to increase overall return by accessing currently inaccessible equity: Overall there has been significant value creation within the Funds, however interest rates have declined since the Existing Properties were acquired by the Funds. With current interest rates being lower than those under the Loans, the costs associated with pre-paying the Loans make refinancing any of the Loans on a per Loan basis, or disposing of any of the Existing Properties on a per property basis, financially inefficient and impractical. Due to the current ultra-low interest rate environment, defeasance costs have increased, causing the penalties imposed upon pre-payment of the Loans to rise sharply.

As a result, the equity appreciation in the Existing Properties since the initial investment or acquisition by the applicable Fund is currently inaccessible. It is expected that, as New Fund will have a larger portfolio of Properties, the Manager will have more leverage to negotiate with the lenders under the Loans. Alternatively, the Manager may be better positioned to pursue alternative methods to unlock the equity appreciation in the Existing Properties by pledging minority interests in one or more Properties. The Transaction is expected to address these funding limitations and provide the Manager with increased financing flexibility to access such equity by consolidating the Existing Properties under New Fund. Access to equity can then be used by the Manager to increase the value of the Existing Properties through additional improvements or for the acquisition and development of new assets.

Superior investment in a larger, more diversified fund with further upside potential: Upon completion of the Transaction, it is expected that New Fund’s portfolio will be comprised of the Existing Properties contributed from each of the Funds. With the potential to access currently inaccessible equity, as discussed above, New Fund may also acquire or develop additional properties to provide further diversification and growth potential.

It is expected that New Fund will indirectly own seven Existing Properties comprising 1,159 multi-family units, appraised in the aggregate at approximately US$122.4 million and is expected to benefit from increased geographical diversity across metropolitan areas exhibiting population growth, including in Arizona, New Mexico and Texas. The Manager believes that additional growth remains to be realized in the U.S. Sun Belt rental real estate markets and that further diversification across the property portfolio, including geographical diversification, mitigates the risk and exposure to any one property or market.

Additionally, the COVID-19 pandemic has caused economic turmoil. While each of the Funds is positioned to operate independently, the Manager believes that investors in the Funds will be better positioned to achieve higher returns and weather the economic storm by combining into New Fund.

Potential to lead to greater cost efficiencies: The Transaction is expected to provide economies of scale by eliminating duplicative general and administrative costs, including legal, accounting and auditing fees, and costs associated with operating the Funds as separate funds.

In addition, Unitholders will receive New Fund Units that have an aggregate Asset Management Fee with respect to the Existing Properties that is likely to be lower than that charged in the aggregate in respect of the Units that they currently hold, an Acquisition Fee that is lower than that charged in respect of Units that they currently hold (other than for the Sungate Units), and a Disposition Fee that is equal to or lower than that charged in respect of Units that they currently hold (other than for the Sungate Units). In addition, the annual fee paid to the non-management New Fund Trustees will be lower than that currently charged in the aggregate in respect of the Funds. New Fund will also have a Development Fee and a Construction Fee, which is not currently charged in respect of the Units. See “Management Fees” in Schedule “L” to this Circular for additional details regarding the proposed Fees.

Provide optionality in disposition strategy: Often times market conditions provide for a value premium for larger, bulk sale transactions. The Transaction will provide the optionality to take advantage of this, if available, or to sell the Properties on an individual basis.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 22

Thorough process, Fairness Opinion and procedural protections consistent with corporate governance best practices: Evans & Evans, Inc. (“E&E”) has provided a fairness opinion to the Independent stating that as of November 3, 2020, and based upon and subject to the assumptions, limitations and qualifications set out therein, the Transaction is fair, from a financial point of view, to Unitholders.

Additionally, the Transaction has procedural measures to protect the interests of Unitholders. Specifically, (i) in the case of each of the Trusts, the Trust Resolutions must be approved by at least 66 2/3% of the votes cast by applicable Unitholders virtually or represented by proxy at the applicable Meeting, and (ii) in the case of Sungate, the Sungate Resolution must be approved by Sungate Unitholders holding more than 66 2/3% of the issued Sungate Units.

Furthermore, any registered Unitholder of a Trust as of the Record Date can exercise Dissent Rights and may, on strict compliance with certain conditions, receive the fair value of their Units. See “The Transaction – Dissent Rights”.

Tax deferral: It is expected that, if approved, the Transaction will be completed on a tax deferred “rollover” basis to Unitholders for Canadian income tax purposes, provided that, in the case of a qualifying Sungate Unitholder, the Sungate Unitholder elects to receive New LP Units in exchange for their Sungate Units and the Sungate Unitholder makes the necessary joint tax election with New LP GP. See “Certain Canadian Federal Income Tax Considerations”.

Continued commitment of experienced management with track record of value creation: Clear Sky is a private equity investment management firm specializing in the acquisition and management of real estate assets in the United States. Clear Sky’s multi-family investments are primarily located in Arizona, California, Florida, New Mexico and Texas. Since inception, Clear Sky and its affiliates have successfully invested in 48 properties with invested equity in excess of US$194 million towards the acquisition or development of US$594 million in multi-family assets. Of the 48 properties, as of December 31, 2019, 28 properties have been realized, generating an aggregate realized gross internal rate of return of 30.9% and gross equity multiple of 2.2x.

See “The Transaction – Reasons for the Recommendation of the Trust Boards and Sungate GP Board”.

Q: How was the Exchange Ratio determined and what will I receive as consideration for my Units?

A: The Exchange Ratio for each class of Units for a particular Fund is determined to be the quotient equal to:

(i) the Net Equity Value of such Fund attributable to such class of Units, determined by:

(a) allocating the Net Equity Value to each applicable class of Units, calculated on the basis of the corresponding “proportionate share for each outstanding Participating Unit” as described in the applicable Declaration of Trust, Sungate LPA and Fund Offering Documents (provided that, in the case of Canadian dollar Units, the value is first determined in US dollars and converted to Canadian dollars using the Effective Exchange Rate);

(b) divided by the total outstanding Units of such class;

(ii) divided by the issue price of the corresponding class of New Fund Units (being C$ in the case of New Fund Class A Units and US$ in the case of New Fund Class B Units).

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 23

Based on the Effective Exchange Rate, Unitholders of each class of Units of a particular Fund would be entitled to receive for each Unit, approximately the following corresponding number and class of New Fund Units, or in the case of Electing Sungate Unitholders, the same number of New LP Units:

New Fund

Fund 1 Fund 2 Fund 3 Fund 4 Fund 5 Sungate

Class Class Ratio Class Ratio Class Ratio Class Ratio Class Ratio Class Ratio

A (C$)

A 0.925541 A 0.533480 A 0.648237 A 0.682402 A, Series A1

0.208417 A 797.163691

B N/A1 B N/A B N/A C N/A A, Series F1

N/A - -

Special N/A Special N/A Special N/A Special N/A - - - -

B (US$)

- - - - C 0.648237 B 0.682402 A, Series A2

0.208417 - -

- - - - - - - - A, Series F2

N/A - -

1 “N/A” is used to indicate that no units of such class are issued and outstanding as of the date of this Circular.

See “The Transaction – Process of Determination of Exchange Ratios”.

Q: Is the completion of the Transaction subject to any conditions?

A: The completion of the Transaction is subject only to the approval of Trust Resolutions by at least 66 2/3% of the votes cast by applicable Trust Unitholders virtually or represented by proxy at the applicable Meeting and approval of the Sungate Resolution by Sungate Unitholders holding more than 66 2/3% of the issued Sungate Units.

Q: What if the approval level required to pass the Transaction Resolutions is not obtained for one or more Funds?

A: If the Unitholders of a Fund do not approve the applicable Transaction Resolution, such Fund will not participate in the Transaction.

At any time before or after the Meetings or the passing of a written resolution by Sungate Unitholders, any of the Trust Boards or the Sungate GP Board, as applicable, may in their sole discretion delay or terminate the implementation of the Transaction, including any or all ancillary changes to the Declarations of Trust or Sungate LPA, as applicable, without further notice to, or action on the part of, the Unitholders. See “The Transaction – Termination of the Transaction”.

Q: When will the Transaction become effective?

A: Subject to having obtained the approval of the Transaction Resolutions by Unitholders, the Trust Boards and Sungate GP Board, as applicable, expect to consummate the Transaction as soon as practicable following the date of the Meetings, subject to the discretion of the Trust Boards and Sungate GP Board.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 24

Q: Are there any risks that I should consider in deciding whether to vote for or approve in writing, as applicable, the applicable Transaction Resolution?

A: Yes. There are a number of risks you should consider in connection with the Transaction and the ownership of New Fund Units or New LP Units, which are described in this Circular under “Risk Factors”.

Q: Do I have Dissent Rights?

A: Pursuant to the Declarations of Trust, registered Trust Unitholders on the Record Date have the right to dissent with respect to the applicable Trust Resolution subject to the below conditions.

The Dissent Rights are subject to strict compliance with the following conditions: (i) the Trust Unitholder’s written objection to the applicable Transaction Resolution is sent to the applicable Trust, c/o Computershare Trust Company of Canada by fax at 1-866-249-7775 or by mail or hand delivery to 100 University Avenue, 8th Floor, Toronto, Ontario M5J 2Y1, Canada, prior to 9:00 a.m. (Mountain time) on the second Business Day prior to the applicable Meeting or, if any Meeting is adjourned or postponed, not less than 48 hours prior to such adjourned or postponed meeting; (ii) the Dissenting Unitholder does not vote his, her or its Trust Units at the applicable Meeting either virtually or represented by proxy, in favour of the applicable Trust Resolution; and (iii) the Dissenting Unitholder exercises the Dissent Rights in respect of all of the Trust Units that he, she or it holds on behalf of the beneficial holder. See “The Transaction – Dissent Rights”.

A Non-Registered Holder who wishes to exercise its Dissent Rights in respect of its Trust Units should immediately contact the intermediary with whom the Non-Registered Holder deals. Trust Unitholders are advised that voting against the applicable Trust Resolution does not qualify as an exercise of Dissent Rights.

Sungate Unitholders do not have any right to dissent with respect to the Sungate Resolution.

Q: What if I have other questions?

A: Unitholders who have additional questions about the Transaction may contact Kevin Wheeler, Investor Relations, 120 Varsity Estates Bay NW, Calgary, Alberta T3B 2W4 at [email protected] or (403) 354-5274. Unitholders who have questions about deciding how to vote should contact their professional advisors.

The following are some questions that a Trust Unitholder may have relating to the Meetings, and the answers to those questions. These questions and answers do not provide all the information relating to the Meetings or the matters to be considered at the Meetings and are qualified in their entirety by the more detailed information contained elsewhere in this Circular. Unitholders are urged to read this Circular in its entirety before making a decision related to their Units.

Q: When and where will the Meetings be held?

A: Each Meeting will be held beginning at 9:00 a.m. (Mountain time) on December 1, 2020 in a virtual-only format, unless adjourned or postponed, as more particularly described, with respect to each Meeting, under “General Proxy Matters – Meeting Information”.

Out of an abundance of caution, to proactively deal with the public health impact of COVID-19 and to mitigate risks to the health and safety of our communities, Trust Unitholders, employees and other stakeholders, the Meetings will be held in a virtual-only format, which will be conducted via live audio webcast. Trust Unitholders will have an equal opportunity to participate in their respective Meeting(s) online, regardless of their geographic location. The live audio webcast will be accessible online at https://web.lumiagm.com, password “clearsky2020” (case sensitive). Please refer to this Circular and the accompanying Virtual Meeting User Guide for access details with respect to the applicable Meeting(s), including the Meeting ID(s).

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 25

Q: How can I vote?

A: If you are eligible to vote at the applicable Meeting and your Trust Units are registered in your name, you can vote your Trust Units by signing and returning your form of proxy to Computershare by telephone at 1-866-732-VOTE (8683) or online at www.investorvote.com or by fax to 1-866-249-7775 or by mail or hand delivery to 100 University Avenue, 8th Floor, Toronto, Ontario M5J 2Y1, Canada, prior to 9:00 a.m. (Mountain time) on November 27, 2020 or, in the case of any adjournment or postponement of a Meeting, not less than 48 hours, Saturdays, Sundays and holidays excepted, prior to the time of the adjournment or postponement. The time limit for the deposit of proxies may be waived or extended by the Chair of the applicable Meeting at his or her discretion without notice. Voting procedures for Non-Registered Holders are described below.

Q: Am I a Non-Registered Holder?

A: You are a Non-Registered Holder if your Trust Units are registered in the name of an Intermediary that you deal with in respect of the Trust Units, such as, among others, a trust company, securities dealer, director or administrator of RRSPs, RRIFs, RESPs and similar plans.

Q: How can a Non-Registered Holder vote?

A: If your Trust Units are not registered in your name but are held in the name of an Intermediary, your Intermediary is required to seek your instructions as to how to vote your Trust Units in advance of the applicable Meeting. Every Intermediary has its own mailing procedures and provides its own return instructions, which should be carefully followed in order to ensure that your Trust Units are voted at the applicable Meeting.

If you are a Non-Registered Holder and wish to attend and participate at a Meeting, you should carefully follow the instructions set out on your voting information form and in this Circular relating to the applicable Meeting, in order to appoint and register yourself as proxy.

The following are some questions that you may have relating to New Fund, and the answers to those questions. These questions and answers do not provide all the information relating to New Fund and are qualified in their entirety by the more detailed information contained elsewhere in this Circular. Unitholders are urged to read this Circular in its entirety before making a decision related to your Units.

Q: If a Property indirectly held by New Fund is sold, how will that impact me as a New Fund Unitholder?

A: It is generally contemplated that the net proceeds from the sale of any Property indirectly held by New Fund will be distributed amongst New Fund (through New LP), the other partners of New LP (including Electing Sungate Unitholders) and the general partner(s) of the applicable Property LP. The portion of net proceeds that will be available for distribution will depend on, among other things, the ongoing financial requirements of the other properties in the portfolio. Upon any reinvestment of such net proceeds in New Fund, it is expected that the general partner(s) of the applicable Property LP will reinvest any net proceeds it receives from the sale proportionately. The general partner(s) of the applicable Property LP has an economic interest in the applicable Property LP and is aligned with New Fund Unitholders in the distribution of such proceeds. For Canadian federal income tax purposes, New Fund Unitholders and New LP Unitholders will generally be required to recognize their share of any gain realized on a sale of a Property regardless of whether the proceeds of such sale are distributed by New Fund and New LP. See “Certain Canadian Federal Income Tax Considerations”.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 26

Q: What right will I have to redeem my New Fund Units?

A: In accordance with the terms of the New Fund Declaration of Trust, New Fund Unitholders are entitled to receive cash upon the redemption of their New Fund Units; provided that, the Redemption Limit of US$100,000 per calendar quarter in respect of all New Fund Units is not exceeded. See “Description of New Fund Units – Redemption of New Fund Units” in Schedule “L” to this Circular.

New LP Units are not directly redeemable, but may be exchanged at the option of the holder for New Fund Units.

Q: How will the Net Asset Value of each Unitholder’s investment be impacted by the Transaction?

A: Each Trust intends to transfer substantially all of its assets and liabilities to New Fund and New Fund intends to acquire all of the Sungate Units, such that the assets and liabilities of the Funds combined will form the assets and liabilities of New Fund. The combined NAV may initially be decreased due to the costs of the Transaction; however the combined NAV is expected to increase over time as a result of the efficiency of New Fund and additional value created by carrying out New Fund’s investment objectives.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 27

GENERAL PROXY MATTERS

Solicitation of Proxies

The solicitation of proxies will be primarily by mail, but proxies may also be solicited in person, by telephone, by facsimile, by email or by other form of electronic communication. If you have any questions about or require assistance completing the form of proxy, please contact Kevin Wheeler, Investor Relations, 120 Varsity Estates Bay NW, Calgary, Alberta T3B 2W4 at [email protected] or (403) 354-5274.

Each Trust has fixed the close of business (Mountain time) on November 3, 2020 as the record date (the “Record Date”) for determining the Trust Unitholders entitled to receive notice of, and to vote at, the Meetings or any adjournment(s) or postponement(s) thereof.

Meeting Information

Each Meeting will be held beginning at the time set forth below (all times Mountain time) on December 1, 2020 in a virtual-only format, unless adjourned or postponed, as follows:

Clear Sky Capital Strategic Asset Fund – Series I 9:00 a.m.

Clear Sky Capital Strategic Asset Fund – Series II 10:00 a.m.

Clear Sky Capital Strategic Asset Fund – Series III 11:00 a.m.

Clear Sky Capital Strategic Asset Fund – Series IV 12:00 p.m.

Clear Sky Capital Strategic Asset Fund – Series 5 1:00 p.m.

Out of an abundance of caution, to proactively deal with the public health impact of COVID-19 and to mitigate risks to the health and safety of our communities, Trust Unitholders, employees and other stakeholders, the Meetings will be held in a virtual-only format, which will be conducted via live audio webcast. Trust Unitholders will have an equal opportunity to participate in their respective Meeting(s) online, regardless of their geographic location. The live audio webcast will be accessible online at https://web.lumiagm.com, password “clearsky2020” (case sensitive). Please refer to this Circular and the accompanying Virtual Meeting User Guide for access details with respect to the applicable Meeting(s), including the Meeting ID(s).

Sungate Unitholders are requested to pass the Sungate Resolution in writing.

Participation at the Meetings

The Meetings will be hosted online by way of a live audio-only webcast. Trust Unitholders will not be able to attend any Meeting in person. Please refer to the accompanying Virtual Meeting User Guide for access details with respect to the applicable Meeting(s), including the Meeting ID(s).

Registered Trust Unitholders and duly appointed and registered proxyholders will be able to virtually attend, participate and vote at the applicable Meeting(s). Registered Trust Unitholders and duly appointed and registered proxyholders who participate in a Meeting online will be able to listen to such Meeting, submit questions and vote, all in real time, provided they are connected to the Internet and comply with all of the requirements set out below under “– Registered Trust Unitholders – Voting at the Virtual Meetings”.

Non-Registered Holders who have not duly appointed themselves as proxyholders may still attend their respective Meeting(s) as guests. Guests will be able to listen to a Meeting but will not be able to submit questions or vote at such Meeting. See “– Non-Registered Holders”.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 28

Registered Trust Unitholders, duly appointed and registered proxyholders and guests, including Non-Registered Holders who have not duly appointed themselves as proxyholder, can log in to a Meeting as set out below. Guests can listen to a Meeting but are not able to vote.

1. Log in online at https://web.lumiagm.com. We recommend that you log in at least 15 minutes before the applicable Meeting starts. Please refer to the accompanying Virtual Meeting User Guide for access details with respect to the applicable Meeting(s), including the Meeting ID(s).

2. Read and accept the Terms and Conditions.

3. Click “Login” and then enter your Control Number (see below) and password “clearsky2020” (case sensitive).

OR click “Guest” and then complete the online form.

Registered Trust Unitholders and duly appointed proxyholders may ask questions at the applicable Meeting and vote by completing a ballot online during the applicable Meeting.

Registered Trust Unitholders

The control number located on the form of proxy or in the email notification you received is your “Control Number” for the purposes of logging in to the applicable Meeting(s).

Duly Appointed Proxyholders

The proxy agent will provide proxyholders with a Username by email after the proxyholder has been duly appointed and registered in accordance with the instructions provided in the form of proxy.

If you attend a Meeting, it is important that you are connected to the Internet at all times during the Meeting in order to vote when balloting commences. It is your responsibility to ensure connectivity for the duration of the Meeting. You should allow ample time to check into the applicable Meeting(s) online and complete the related procedures.

Appointment of Proxyholder

The individuals named in the accompanying form of proxy are trustees or officers of the Trusts. A registered Trust Unitholder has the right to appoint as proxyholder a person or company (who need not be a Trust Unitholder), other than the persons already named in the form of proxy, to represent such Trust Unitholder at the applicable Meeting, as the case may be. Such right may be exercised by crossing out the names the printed in the form of proxy and inserting the name of the person or company in the blank space provided or by completing another proper form of proxy, and in either case returning the proxy as instructed below.

Trust Unitholders who wish to appoint a third party proxyholder to represent them at the applicable Meeting must submit their proxy or voting instruction form (as applicable) prior to registering their proxyholder. Registering the proxyholder is an additional step once a Trust Unitholder has submitted their proxy/voting instruction form. Failure to register a duly appointed proxyholder will result in the proxyholder not receiving a Username to participate in the applicable Meeting. To register a proxyholder, Unitholders MUST visit the website indicated in the accompanying Virtual Meeting User Guide by November 27, 2020 and provide Computershare with their proxyholder’s contact information, so that Computershare may provide the proxyholder with a Username via email.

To be valid, the proxy must be received by Computershare by telephone at 1-866-732-VOTE (8683), by fax at 1-866-249-7775, by Internet at www.investorvote.com, or by mail or hand delivery to 100 University Avenue, 8th Floor, Toronto, Ontario M5J 2Y1, Canada, prior to 9:00 a.m. (Mountain time) on November 27, 2020 or, in the case of any adjournment or postponement of a Meeting, not less than 48 hours, Saturdays, Sundays and holidays excepted, prior to the time of the adjournment or postponement. The time limit for the deposit of proxies may be waived or extended by the Chair of the Meeting at his or her discretion without notice.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 29

Voting by Proxyholder

A form of proxy confers discretionary authority upon the persons named therein with respect to amendments or variations to matters identified in the accompanying Notice of Meetings and with respect to other matters which may properly come before a Meeting or any adjournment(s) or postponement(s) thereof. As of the date of this Circular, the Manager was not aware of any amendment, variation or other matter to come before any of the Meetings; however, if any amendments or variations to matters identified in the accompanying Notice of Meetings or any other matters should properly come before a Meeting, or any adjournment(s) or postponement(s) thereof, the Units represented by properly executed proxies given in favour of the persons named in the form of proxy will be voted on such matters pursuant to the discretionary authority provided for in the form of proxy. If no instructions are given, the Trust Units represented by properly executed proxies given in favour of the persons named in the form of proxy will be voted FOR the applicable Trust Resolution.

Registered Trust Unitholders

If you are a registered Trust Unitholder as of the Record Date, a form of proxy for the applicable Meeting is enclosed with this Circular and you may, and you are encouraged to appoint a proxy by completing, dating and signing the enclosed form of proxy and returning it to Computershare by telephone at 1-866-732-VOTE (8683) or online at www.investorvote.com or by fax to 1-866-249-7775 or by mail or hand delivery to 100 University Avenue, 8th Floor, Toronto, Ontario M5J 2Y1, Canada, ensuring that the proxy is received on November 27, 2020 not later than 9:00 a.m. (Mountain time) or in the case of any adjournment or postponement of a Meeting, not less than 48 hours, Saturdays, Sundays and holidays excepted, prior to the time of the adjournment or postponement. The time limit for the deposit of proxies may also be waived or extended Chair of the applicable Meeting at his or her discretion without notice.

Voting at the Virtual Meetings

You do not need to complete or return your form of proxy if you plan to vote at the applicable Meeting(s). Simply follow the instructions set out under “– Meeting Information – Participating at the Meetings” above and in the accompanying Virtual Meeting User Guide, to attend the applicable Meeting(s) online and complete a ballot virtually during the Meeting(s).

Non-Registered Holders

A Trust Unitholder is a non-registered (or beneficial) Trust Unitholder (a “Non-Registered Holder”) if the Trust Unitholder’s Trust Units are registered in the name of an intermediary that the Non-Registered Holder deals with in respect of the Trust Units, such as, among others, a trust company, securities dealer, director or administrator of RRSPs, RRIFs, RESPs and similar plans (in each case, an “Intermediary”).

Applicable regulatory policy requires Intermediaries to seek voting instructions from Non-Registered Holders in advance of the applicable Meeting(s). Every Intermediary has its own mailing procedures and provides its own return instructions, which should be carefully followed by Non-Registered Holders in order to ensure that their Trust Units are voted at the applicable Meeting(s). Often, the form of proxy supplied to a Non-Registered Holders by its Intermediary is identical to that provided to registered Trust Unitholders. However, its purpose is limited to instructing the registered Trust Unitholders how to vote on behalf of the Non-Registered Holder. A Non-Registered Holder receiving a voting instruction form cannot use that form to vote his, her or its Trust Units directly at the applicable Meeting(s). Rather, the Non-Registered Holder must return the voting instruction form, or otherwise indicate his, her or its voting wishes, to its Intermediary in accordance with such Intermediary’s procedures well in advance of the applicable Meeting(s) to have the Non-Registered Holder’s Trust Units voted.

Should a Non-Registered Holder who receives a voting instruction form wish to attend and vote at a Meeting (or have another person attend and vote on behalf of the Non-Registered Holder), the Non-Registered Holder should follow the corresponding instructions on the voting instruction form. Non-Registered Holders should carefully follow the instructions of their Intermediaries and their service companies.

|| CLEAR SKY CAPITAL – ASPEN REAL ESTATE TRUST 30

Revocation of Proxy

In addition to revocation in any manner permitted by law, a registered Trust Unitholder as of the Record Date who has returned a form of proxy may revoke it by:

(a) completing and signing a form of proxy bearing a later date, and delivering it to Computershare, 100 University Avenue, 8th Floor, Toronto, Ontario M5J 2Y1, Canada and depositing it in accordance with the instructions (including the submissions deadlines) set out above;

(b) delivering a written statement expressly revoking such proxy, signed by the registered Trust Unitholder, who is authorized in writing, to:

(i) Kevin Wheeler, Investor Relations, at 120 Varsity Estates Bay NW, Calgary, Alberta T3B 2W4, at any time up to and including the day that is 48 hours, Saturdays, Sundays and holidays excepted, prior to the day to which such Meeting is adjourned or postponed;

(ii) the Chair of the applicable Meeting prior to the start of such Meeting; or

(c) attending and voting at the applicable Meeting virtually.

A Non-Registered Holder who wishes to revoke his or her voting instructions must contact his or her Intermediary in respect of such instructions and comply with any applicable requirements imposed by such Intermediary. An Intermediary may not be able to revoke such instructions if it receives insufficient notice of revocation.

Questions

If you have questions or need assistance with the completion and delivery of your form of proxy, you may contact Kevin Wheeler, Investor Relations, 120 Varsity Estates Bay NW, Calgary, Alberta T3B 2W4, at [email protected] or (403) 354-5274.

THE TRANSACTION

The Funds

The Trusts