Application of binary classifiers to filter transactions on the financial market

41

Running head: FILTERING TRADING SYSTEM TRANSACTIONS 1 Application of binary classifiers to filter transactions on the financial market Andrzej Endler Quants Technologies S.A. ,ul.Getta Żydowskiego 16,98-220 Zduńska Wola, Poland [email protected]

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Application of binary classifiers to filter transactions on the financial market

Running head: FILTERING TRADING SYSTEM TRANSACTIONS 1

Application of binary classifiers to filter transactions

on the financial market

Andrzej Endler

Quants Technologies S.A. ,ul.Getta Żydowskiego 16,98-220 Zduńska Wola, Poland

FILTERING TRADING SYSTEM TRANSACTIONS 2

Abstract

One of the key problems relating to concluding transactions on financial markets is the

definition of whether or not, in given market conditions, we should conclude a specific

transaction. This problem applies to all transactions irrespective of whether they are

concluded in a discretionary manner by a person, or by the appropriate software. The subject

of research presented in this document was practical verification of the hypothesis that the use

of filters composed of classifiers independent of the main algorithm of the strategy may

improve the characteristics of this strategy. This means constructing an additional filter,

independent of the main logic and algorithm of the strategy, either allowing the transaction to

be conducted or not. The strategy being examined is a real strategy used in trading in shares

on the American market. Many various classifiers based on various algorithms, as well as sets

of classifiers composed of them, were examined.

As a consequence of this research interesting results were obtained, noticeably improving the

various characteristics of an automatic strategy for which the filters had been created. The

research confirmed the justification for using classifiers as a filter for transactions for the

automatic strategy under examination.

Keywords: Data Mining, Classification, Classifiers, Trading Systems, Stocks, Filtering transactions, Data mining techniques, real-world applications

FILTERING TRADING SYSTEM TRANSACTIONS 3

Application of binary classifiers to filter transactions

on the financial market

The objective of this study is to present the results of research relating to the use of binary

classifiers to filter transactions of the existing automatic trading strategy on the American

shares market. As will be indicated at a later stage in this paper, the use of such classifiers

may bring very positive results which clearly improve the characteristics of the trading

strategy.

1. Introduction

Many studies have been devoted to various methods of anticipating the returns on financial

markets using various Data Mining methods. For example (AL-RADAIDEH, ASSAF,

&ALNAGI, 2013) discusses the use of decision trees for this purpose, (Soni, 2010) in his

paper presents literature devoted to use of neural networks to anticipate returns on the shares

market. There are considerably fewer works devoted to the application of methods of learning

and classification for additional filtering of automatic strategy principles. (Varutbangkul,

2013) discusses the use of decision trees to filter signals in six simple ‘traditional’ trading

systems. Most often, in available studies simple, somewhat ‘academic’ trading strategies are

used, such as intersection of moving averages, and not ‘real-life’, more complicated strategies

actually used on the financial market. The aim of my study is to present the research for

which the input data was taken from a strategy applied ‘live’ on the American shares market.

FILTERING TRADING SYSTEM TRANSACTIONS 4 Automatic systems analyse market data, and then with the use of an implemented

algorithm take a decision on the purchase or sale of given financial assets e.g. shares. Such

systems base their operating principles on extremely varied algorithms based on the classical

technical analysis, or various types of data analysis, including the use of statistical tools and

data exploration. Most frequently a set of input data is checked, for which the conditions are

defined which – if they are satisfied – make the system take up a certain market position.

Next, the position is managed in accordance with the assigned algorithm and finally closed

with either a profit or a loss.

The problem of a good system (somewhat simplified of course) involves in fact

finding a system with a positive expected value of the transaction and at the same time trading

as often as possible. An ideal situation is a presence of as great a volume as possible of

transactions and, in addition, only profit-making ones, however such situations practically do

not exist in conditions of real market trading.

I decided to examine whether it was possible to ‘improve’ the existing system

operating on the market so as to improve its characteristics by eliminating those transactions

which did not bring any profit, and at the same time by preserving the maximum possible

volume of transactions which resulted in earing a profit. I narrowed the task down to the

problem of binary classification. Transactions which achieved a profit were included in one

class (positive class), and those which did not achieve a profit into another class (negative

class).

Usually, every automatic strategy already contains some type of filters in the form of

e.g. trend filters based on moving averages or similar. However, we want to find additional

variables /attributes, not dependent on the main logic of the strategy. Obviously, we do not

know what variables, e.g. price or derivative indices, are significant and how to define this

filter.

FILTERING TRADING SYSTEM TRANSACTIONS 5 The strategy which is the source of data on transactions is described in chapter 2. The

first step was to prepare the data for all assets present in the transactions, which I will be

discussing in chapter 3. The next step was the selection of attributes which will constitute

good input data for the classifiers. The choice of attributes will be discussed in chapter 4. In

chapter 5 I will present the choice of classifiers found to be the most suitable for our data. In

chapter 6 I will describe the construction of sets of classifiers used later on for research, and

chapter 7 sets out the procedure for this research. Finally, in chapter 8 I will set out the results

of research of individual classifiers and their groups, and in chapter 9 I am applying models

obtained for filtering automatic strategy transactions. Chapter 10 contains brief conclusions

and suggestions for further studies.

2. Strategy for which we define filters

The strategy for which we define filters admitting/eliminating transactions is a trading

strategy on the American shares market. The strategy opens the position at the opening of the

stock exchange session if the defined conditions are satisfied, mainly if a considerable

deviation between the opening price and the closing price (a gap) occurs. The strategy is

trading only on the “long” side, taking up a position in the opposite direction to the gap,

expecting it to decrease. The time spent on the market is fairly short and amounts to an

average of 20 minutes.

The results set out in the table below are results of the backtest strategy from February

2009 to April 2014. A commission of 0.005$ on share was included. The strategy is used to

trade on the Nasdaq market on a composite basket of 95 assets, using 33.33% of the capital

available at any given moment for each transaction.

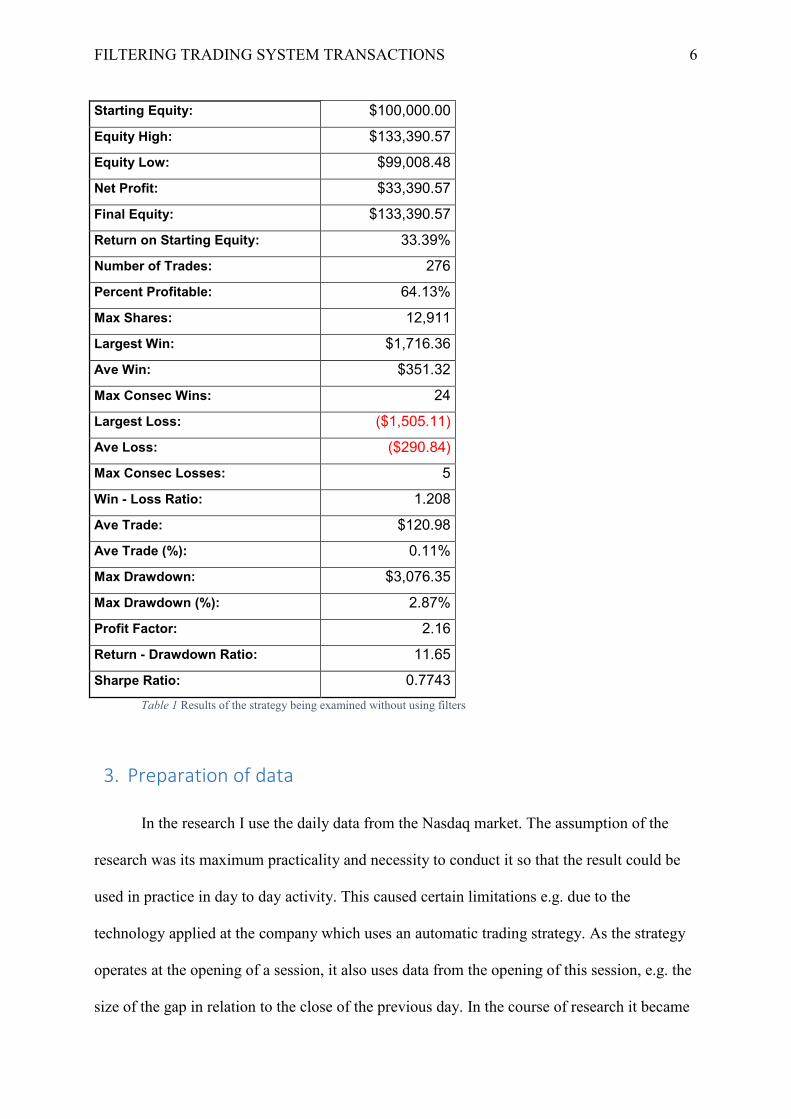

FILTERING TRADING SYSTEM TRANSACTIONS 6

Starting Equity: $100,000.00

Equity High: $133,390.57

Equity Low: $99,008.48

Net Profit: $33,390.57

Final Equity: $133,390.57

Return on Starting Equity: 33.39%

Number of Trades: 276

Percent Profitable: 64.13%

Max Shares: 12,911

Largest Win: $1,716.36

Ave Win: $351.32

Max Consec Wins: 24

Largest Loss: ($1,505.11)

Ave Loss: ($290.84)

Max Consec Losses: 5

Win - Loss Ratio: 1.208

Ave Trade: $120.98

Ave Trade (%): 0.11%

Max Drawdown: $3,076.35

Max Drawdown (%): 2.87%

Profit Factor: 2.16

Return - Drawdown Ratio: 11.65

Sharpe Ratio: 0.7743 Table 1 Results of the strategy being examined without using filters

3. Preparation of data

In the research I use the daily data from the Nasdaq market. The assumption of the

research was its maximum practicality and necessity to conduct it so that the result could be

used in practice in day to day activity. This caused certain limitations e.g. due to the

technology applied at the company which uses an automatic trading strategy. As the strategy

operates at the opening of a session, it also uses data from the opening of this session, e.g. the

size of the gap in relation to the close of the previous day. In the course of research it became

FILTERING TRADING SYSTEM TRANSACTIONS 7

evident that due to the required speed of the system’s reaction and other technical conditions,

I had to limit myself only to the data at the close of the previous day (not taking into account

the data from the opening of the session). Creating models, making calculations and

classifications took place in the period between sessions.

As I did not know what attributes (variables) actually conveyed the information

allowing to increase the probability of a successful transaction, I decided to use a large group

of technical analysis indices, prices, sales volumes and their values shifted in time (delayed)

and differences. Data on values and indices for stock market indices and gold, oil and

American bonds were added as potential indicators defining the state of the market. In total

there were 39,886 attributes. All attributes were numeric attributes – continuous ones. All data

was subject to the ‘Z’ transformation (by subtracting the average and dividing by the standard

deviation) for time windows of a period of 100 days. I carried out a simple data cleansing

removing all observations with an undefined value. After completing all data cleansing

operations, I was left with 551 transactions / observations on 89 assets.

4. Selection of significant variables

Due to the very substantial number of attributes it was necessary to select the

significant attributes. I tried to select those attributes by applying 3 methods:

a) Random forest

b) Tree from the C5.0 algorithm

c) Rough Sets – reduct

I carried out an assessment of the behaviour of individual sets of parameters by

comparing the results of classifications for several selected classification methods – C5.0,

SVM Radial Basis Function kernel and Naive Bayes. As a result of conducting many tests for

FILTERING TRADING SYSTEM TRANSACTIONS 8

various numbers of attributes and methods of defining significant variables, I decided to use

attributes defined by the random forest (10,000 trees). For the purposes of further

examination, I assumed the first 60 variables from the list sorted by the significance of

variables provided by this model. In the future it is worth considering using various sets of

variables/attributes and creating sets of classifiers with various sets of input data. An

interesting fact relating to the selected variables is that a large part of them constitute

variables which are derivatives of indices, gold, oil and bonds – that is, variables defining the

state of the market in general and not the price of the asset itself.

5. Selecting classifiers

My next step was to examine the behaviour of various types of classifiers towards the

data. I selected parameters for each classifier using the Cross Validation procedure 10, and

then averaged out the results obtained. I chose parameters of the model maximizing the F

coefficient. In the examination I used the caret package (Kun et al., 2014) and other R

packages (R Core Team, 2014) described in chapter 11.

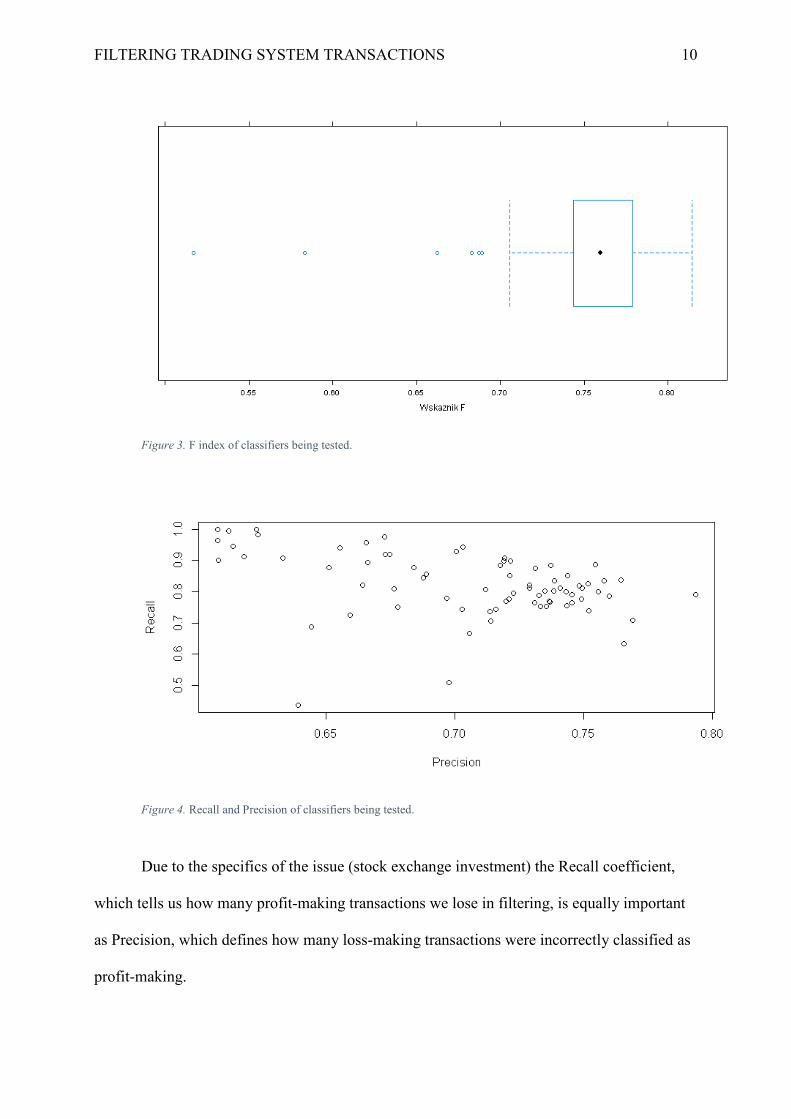

I checked a total of 76 various classifiers, defining for each one the average parameters

of classification quality for my data. The results are presented in the following diagrams, and

detailed values for individual classifiers in appendix 1.

FILTERING TRADING SYSTEM TRANSACTIONS 9

Figure 1. Recall of classifiers being tested.

Figure 2. Precision of classifiers being tested.

FILTERING TRADING SYSTEM TRANSACTIONS 10

Figure 3. F index of classifiers being tested.

Figure 4. Recall and Precision of classifiers being tested.

Due to the specifics of the issue (stock exchange investment) the Recall coefficient,

which tells us how many profit-making transactions we lose in filtering, is equally important

as Precision, which defines how many loss-making transactions were incorrectly classified as

profit-making.

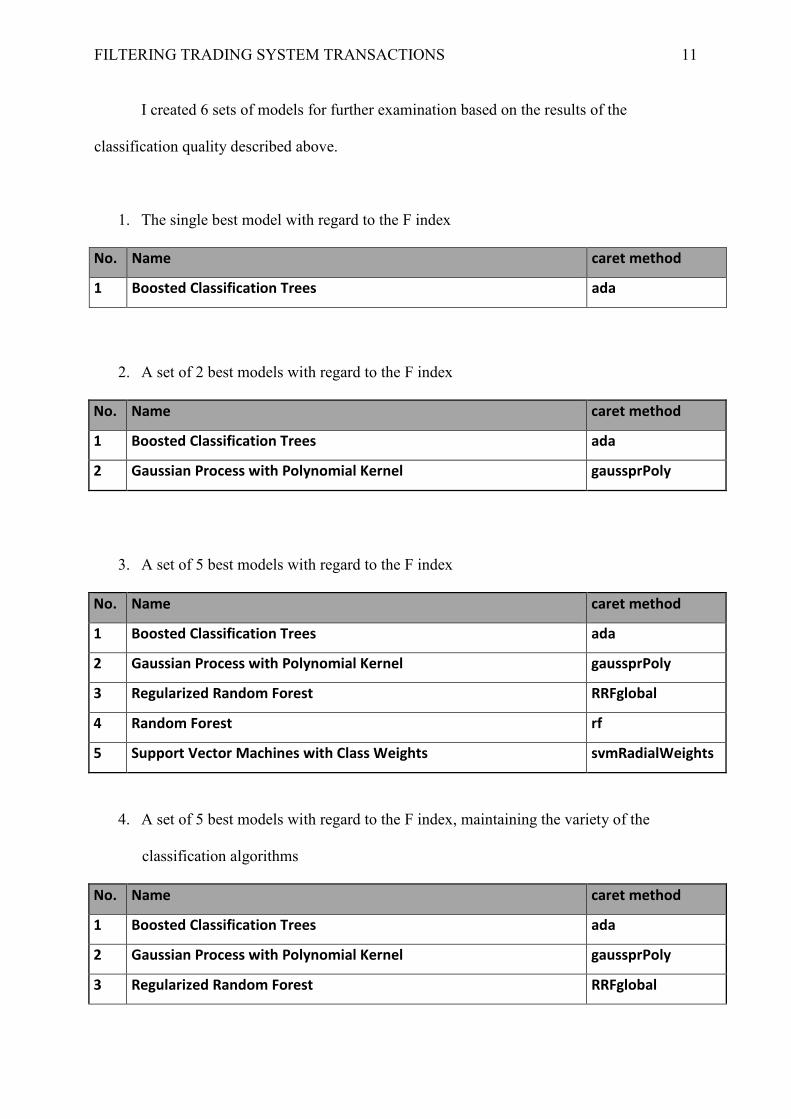

FILTERING TRADING SYSTEM TRANSACTIONS 11 I created 6 sets of models for further examination based on the results of the

classification quality described above.

1. The single best model with regard to the F index

No. Name caret method

1 Boosted Classification Trees ada

2. A set of 2 best models with regard to the F index

No. Name caret method

1 Boosted Classification Trees ada

2 Gaussian Process with Polynomial Kernel gaussprPoly

3. A set of 5 best models with regard to the F index

No. Name caret method

1 Boosted Classification Trees ada

2 Gaussian Process with Polynomial Kernel gaussprPoly

3 Regularized Random Forest RRFglobal

4 Random Forest rf

5 Support Vector Machines with Class Weights svmRadialWeights

4. A set of 5 best models with regard to the F index, maintaining the variety of the

classification algorithms

No. Name caret method

1 Boosted Classification Trees ada

2 Gaussian Process with Polynomial Kernel gaussprPoly

3 Regularized Random Forest RRFglobal

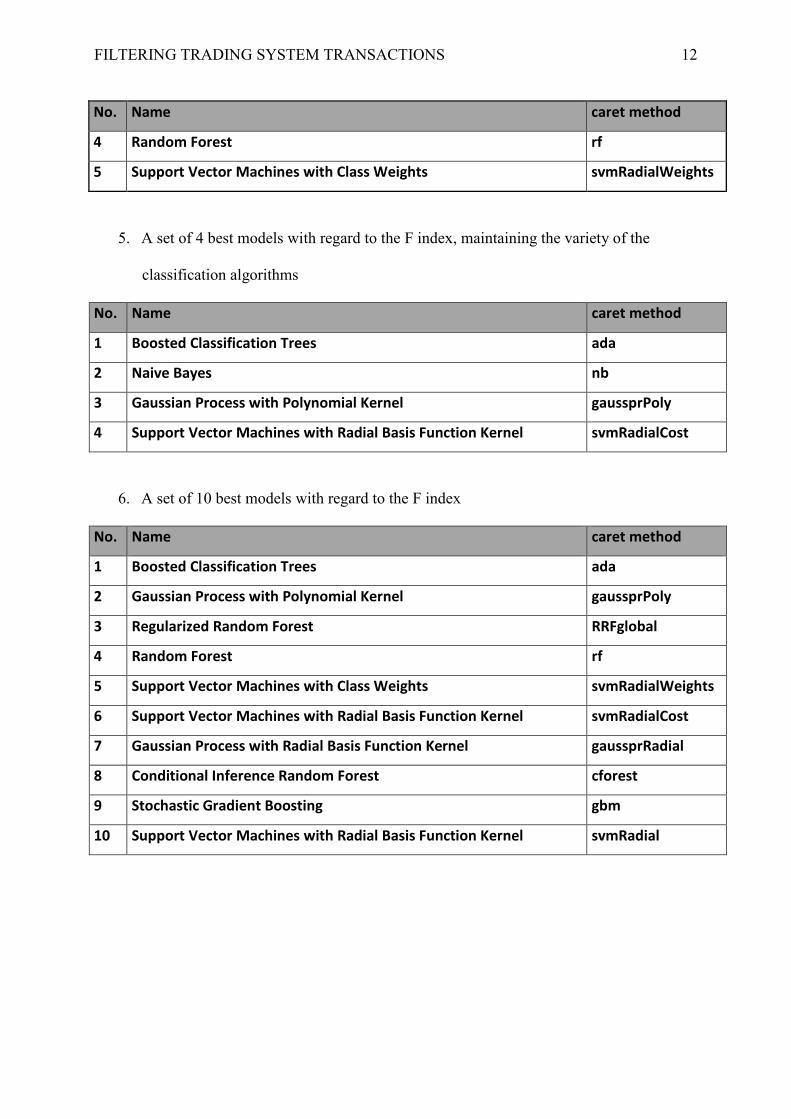

FILTERING TRADING SYSTEM TRANSACTIONS 12

No. Name caret method

4 Random Forest rf

5 Support Vector Machines with Class Weights svmRadialWeights

5. A set of 4 best models with regard to the F index, maintaining the variety of the

classification algorithms

No. Name caret method

1 Boosted Classification Trees ada

2 Naive Bayes nb

3 Gaussian Process with Polynomial Kernel gaussprPoly

4 Support Vector Machines with Radial Basis Function Kernel svmRadialCost

6. A set of 10 best models with regard to the F index

No. Name caret method

1 Boosted Classification Trees ada

2 Gaussian Process with Polynomial Kernel gaussprPoly

3 Regularized Random Forest RRFglobal

4 Random Forest rf

5 Support Vector Machines with Class Weights svmRadialWeights

6 Support Vector Machines with Radial Basis Function Kernel svmRadialCost

7 Gaussian Process with Radial Basis Function Kernel gaussprRadial

8 Conditional Inference Random Forest cforest

9 Stochastic Gradient Boosting gbm

10 Support Vector Machines with Radial Basis Function Kernel svmRadial

FILTERING TRADING SYSTEM TRANSACTIONS 13

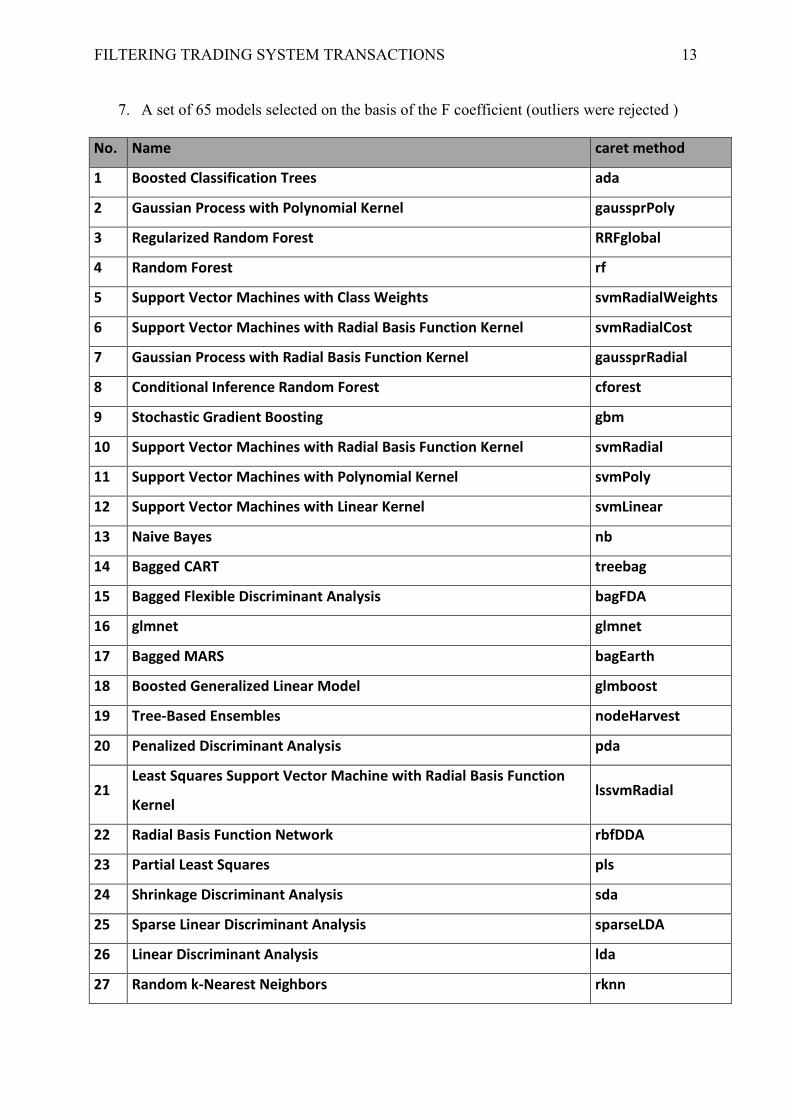

7. A set of 65 models selected on the basis of the F coefficient (outliers were rejected )

No. Name caret method

1 Boosted Classification Trees ada

2 Gaussian Process with Polynomial Kernel gaussprPoly

3 Regularized Random Forest RRFglobal

4 Random Forest rf

5 Support Vector Machines with Class Weights svmRadialWeights

6 Support Vector Machines with Radial Basis Function Kernel svmRadialCost

7 Gaussian Process with Radial Basis Function Kernel gaussprRadial

8 Conditional Inference Random Forest cforest

9 Stochastic Gradient Boosting gbm

10 Support Vector Machines with Radial Basis Function Kernel svmRadial

11 Support Vector Machines with Polynomial Kernel svmPoly

12 Support Vector Machines with Linear Kernel svmLinear

13 Naive Bayes nb

14 Bagged CART treebag

15 Bagged Flexible Discriminant Analysis bagFDA

16 glmnet glmnet

17 Bagged MARS bagEarth

18 Boosted Generalized Linear Model glmboost

19 Tree-Based Ensembles nodeHarvest

20 Penalized Discriminant Analysis pda

21 Least Squares Support Vector Machine with Radial Basis Function

Kernel lssvmRadial

22 Radial Basis Function Network rbfDDA

23 Partial Least Squares pls

24 Shrinkage Discriminant Analysis sda

25 Sparse Linear Discriminant Analysis sparseLDA

26 Linear Discriminant Analysis lda

27 Random k-Nearest Neighbors rknn

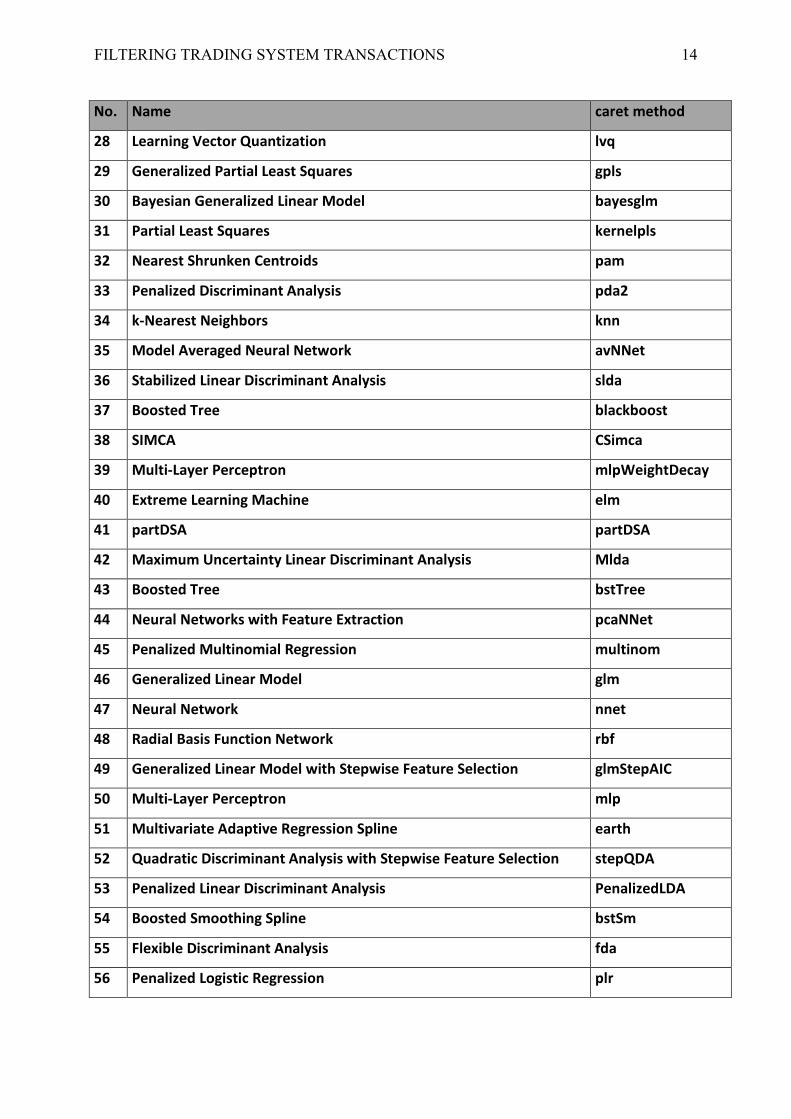

FILTERING TRADING SYSTEM TRANSACTIONS 14

No. Name caret method

28 Learning Vector Quantization lvq

29 Generalized Partial Least Squares gpls

30 Bayesian Generalized Linear Model bayesglm

31 Partial Least Squares kernelpls

32 Nearest Shrunken Centroids pam

33 Penalized Discriminant Analysis pda2

34 k-Nearest Neighbors knn

35 Model Averaged Neural Network avNNet

36 Stabilized Linear Discriminant Analysis slda

37 Boosted Tree blackboost

38 SIMCA CSimca

39 Multi-Layer Perceptron mlpWeightDecay

40 Extreme Learning Machine elm

41 partDSA partDSA

42 Maximum Uncertainty Linear Discriminant Analysis Mlda

43 Boosted Tree bstTree

44 Neural Networks with Feature Extraction pcaNNet

45 Penalized Multinomial Regression multinom

46 Generalized Linear Model glm

47 Neural Network nnet

48 Radial Basis Function Network rbf

49 Generalized Linear Model with Stepwise Feature Selection glmStepAIC

50 Multi-Layer Perceptron mlp

51 Multivariate Adaptive Regression Spline earth

52 Quadratic Discriminant Analysis with Stepwise Feature Selection stepQDA

53 Penalized Linear Discriminant Analysis PenalizedLDA

54 Boosted Smoothing Spline bstSm

55 Flexible Discriminant Analysis fda

56 Penalized Logistic Regression plr

FILTERING TRADING SYSTEM TRANSACTIONS 15

No. Name caret method

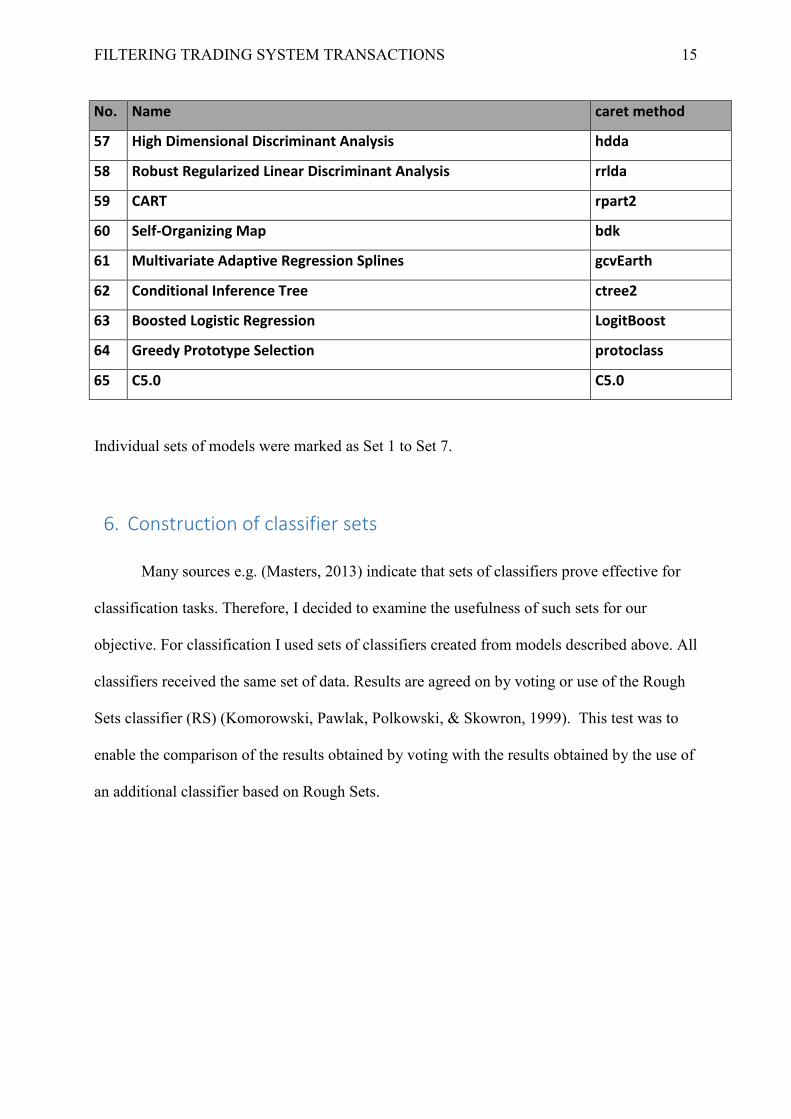

57 High Dimensional Discriminant Analysis hdda

58 Robust Regularized Linear Discriminant Analysis rrlda

59 CART rpart2

60 Self-Organizing Map bdk

61 Multivariate Adaptive Regression Splines gcvEarth

62 Conditional Inference Tree ctree2

63 Boosted Logistic Regression LogitBoost

64 Greedy Prototype Selection protoclass

65 C5.0 C5.0

Individual sets of models were marked as Set 1 to Set 7.

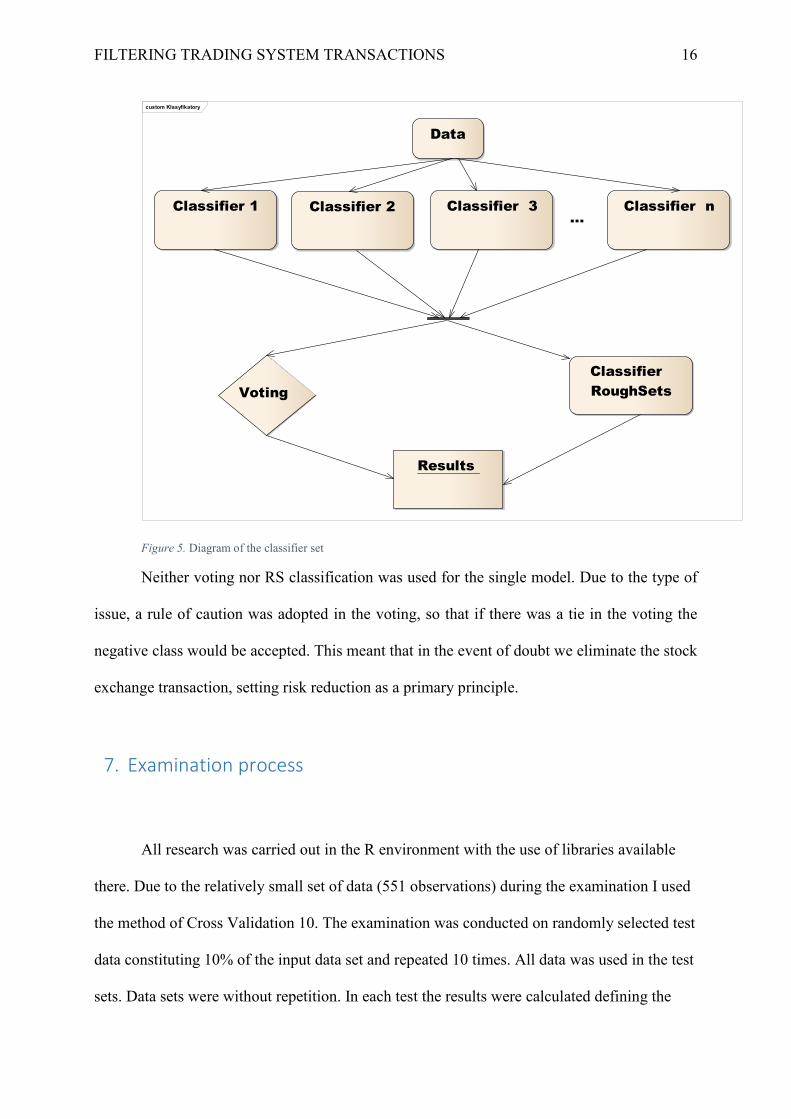

6. Construction of classifier sets

Many sources e.g. (Masters, 2013) indicate that sets of classifiers prove effective for

classification tasks. Therefore, I decided to examine the usefulness of such sets for our

objective. For classification I used sets of classifiers created from models described above. All

classifiers received the same set of data. Results are agreed on by voting or use of the Rough

Sets classifier (RS) (Komorowski, Pawlak, Polkowski, & Skowron, 1999). This test was to

enable the comparison of the results obtained by voting with the results obtained by the use of

an additional classifier based on Rough Sets.

FILTERING TRADING SYSTEM TRANSACTIONS 16

custom Klasyfikatory

...

Voting

Classifier 1 Classifier 2 Classifier 3 Classifier n

Classifier RoughSets

Results

Data

Figure 5. Diagram of the classifier set

Neither voting nor RS classification was used for the single model. Due to the type of

issue, a rule of caution was adopted in the voting, so that if there was a tie in the voting the

negative class would be accepted. This meant that in the event of doubt we eliminate the stock

exchange transaction, setting risk reduction as a primary principle.

7. Examination process

All research was carried out in the R environment with the use of libraries available

there. Due to the relatively small set of data (551 observations) during the examination I used

the method of Cross Validation 10. The examination was conducted on randomly selected test

data constituting 10% of the input data set and repeated 10 times. All data was used in the test

sets. Data sets were without repetition. In each test the results were calculated defining the

FILTERING TRADING SYSTEM TRANSACTIONS 17

classification quality. Models were trained on sets containing 90% of data. After creating all

models for a given sequence, the prediction was carried out for this data, which constituted a

training set for the Rough Set based classifier used to resolve conflicts between classifiers.

The results of the classification then created an initial set of the classified data containing 551

observations, which were compared with the known set. The indices defining the

classification quality are calculated on the basis of this data.

FILTERING TRADING SYSTEM TRANSACTIONS 18

custom Proces

ActivityFinal

sav e result and calculate indices

sav e results - test data

classify using RoughSets model

Vote

make prediction using test data

create Rough Sets model

make prediction using training data

create models

Split data into train and test data

ActivityInitial

All test setsdone ?

YES NO

Figure 6. The course of the examination process

FILTERING TRADING SYSTEM TRANSACTIONS 19

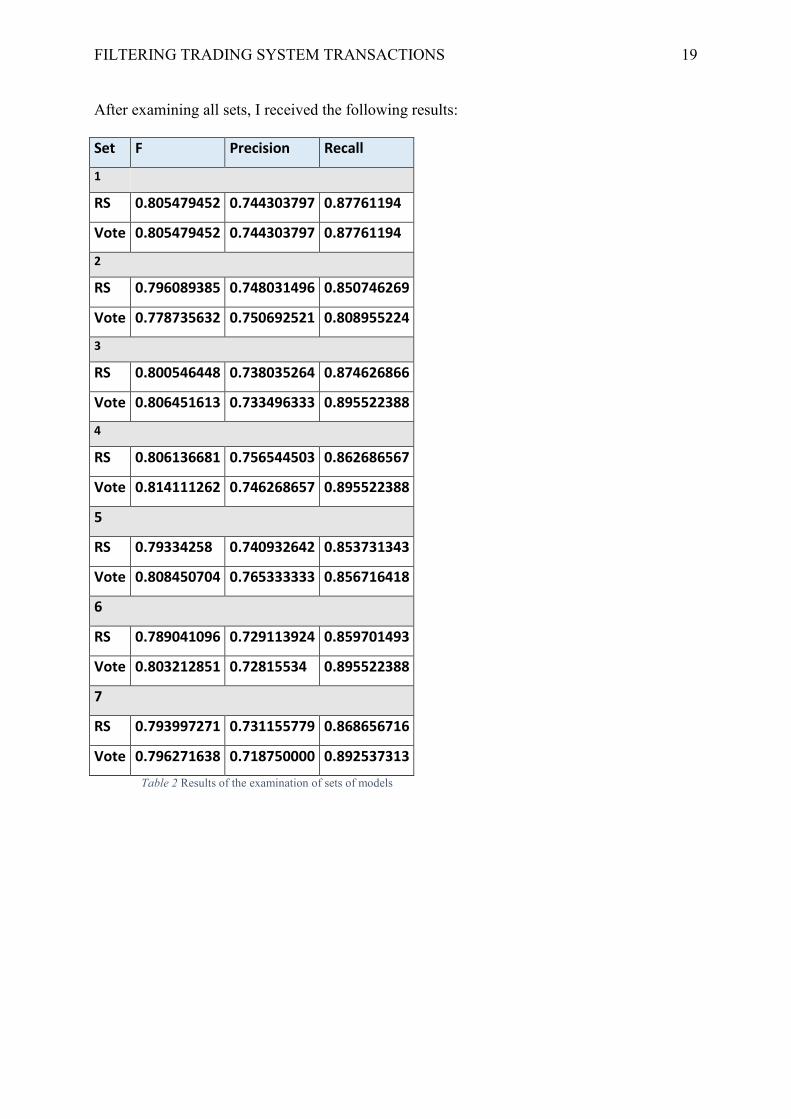

After examining all sets, I received the following results:

Set F Precision Recall

1

RS 0.805479452 0.744303797 0.87761194

Vote 0.805479452 0.744303797 0.87761194

2

RS 0.796089385 0.748031496 0.850746269

Vote 0.778735632 0.750692521 0.808955224

3

RS 0.800546448 0.738035264 0.874626866

Vote 0.806451613 0.733496333 0.895522388

4

RS 0.806136681 0.756544503 0.862686567

Vote 0.814111262 0.746268657 0.895522388

5

RS 0.79334258 0.740932642 0.853731343

Vote 0.808450704 0.765333333 0.856716418

6

RS 0.789041096 0.729113924 0.859701493

Vote 0.803212851 0.72815534 0.895522388

7

RS 0.793997271 0.731155779 0.868656716

Vote 0.796271638 0.718750000 0.892537313

Table 2 Results of the examination of sets of models

FILTERING TRADING SYSTEM TRANSACTIONS 20

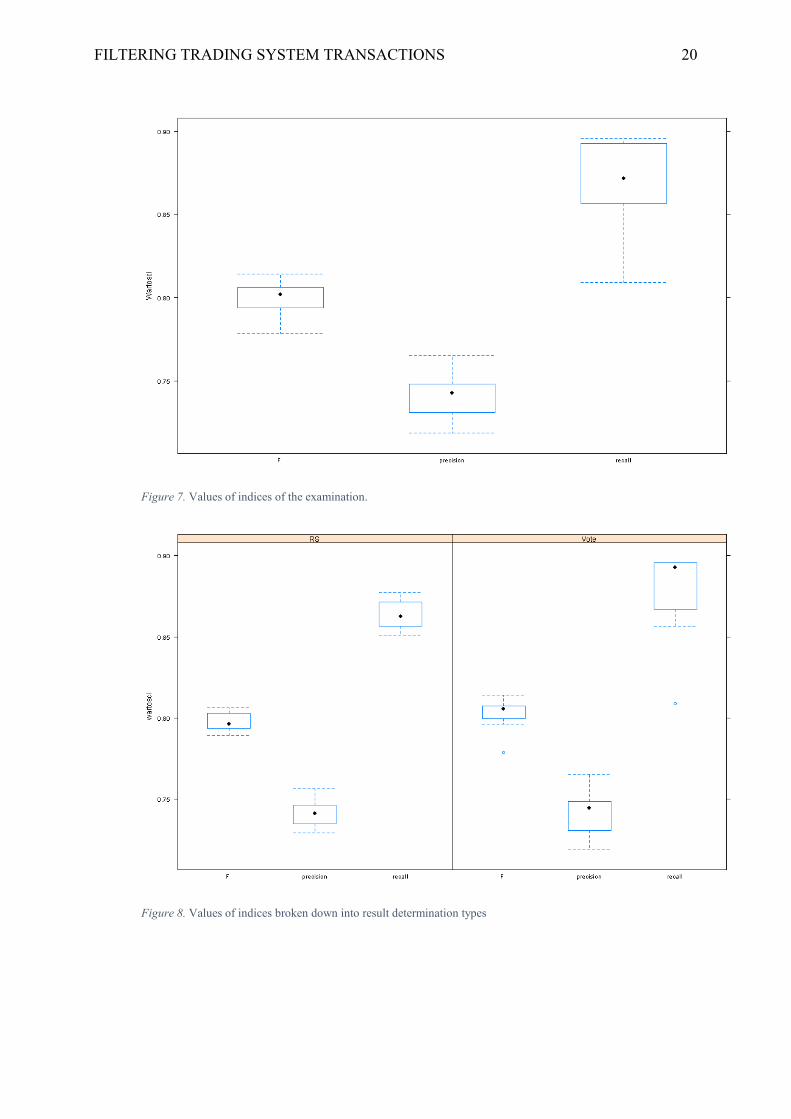

Figure 7. Values of indices of the examination.

Figure 8. Values of indices broken down into result determination types

FILTERING TRADING SYSTEM TRANSACTIONS 21

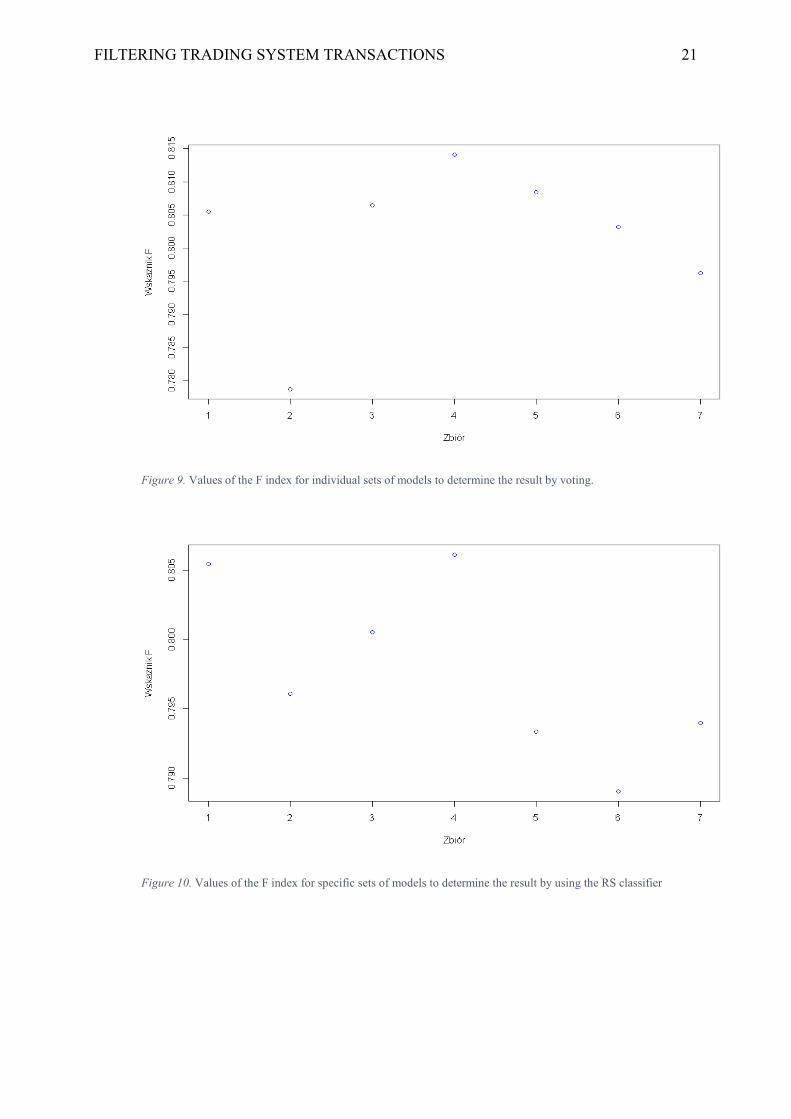

Figure 9. Values of the F index for individual sets of models to determine the result by voting.

Figure 10. Values of the F index for specific sets of models to determine the result by using the RS classifier

FILTERING TRADING SYSTEM TRANSACTIONS 22

7.1. Conclusions drawn from examining various classifiers

The research conducted shows that the best results were achieved for model set no. 4

where the results were determined by voting. Use of the RS classifier does not significantly

improve results, however it changes their characteristics slightly. Further (in relation to set 4)

increase of the number of classifiers in the set does not improve the results. It should be

added, however, that the results for various sets are similar, there are no significant

differences.

For further research I selected set 4, comprising 5 classifiers.

8. Application of the chosen set of models to filter transactions in the

automatic strategy

In the next step I used the selected models to filter transactions in the automatic

strategy. I carried out two tests. The first uses the Cross Validation procedure leaving 10 test

transactions for the set of classifiers described above (set 4). In the second test I used a single

model with the best parameters (set 1 described above) and used the backtest procedure.

Initially half of the data was used as a training set with a test on a single observation, which in

the next step was included in the training set, increasing it etc.

8.1. Application of filters using a set of classifiers (set 4)

Due to the relatively small amount of data I used the method of leaving 10 transactions

for the test set, and treated the remainder as a training set. The data was downloaded in

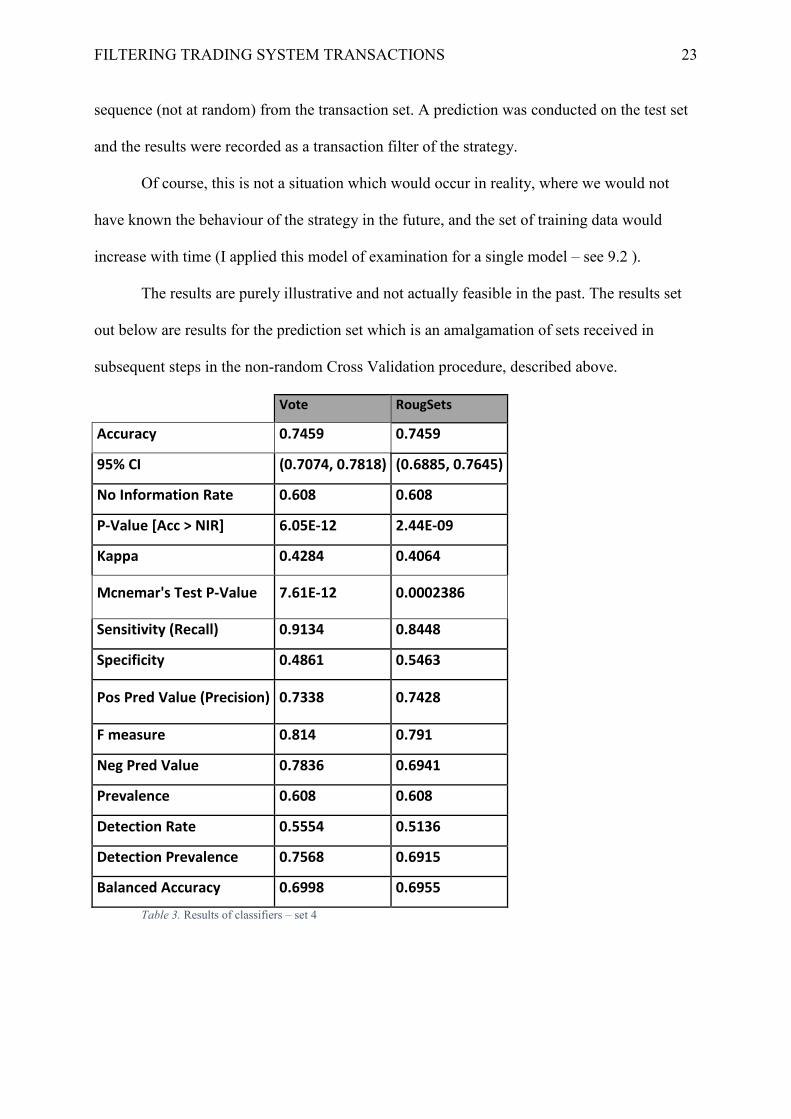

FILTERING TRADING SYSTEM TRANSACTIONS 23

sequence (not at random) from the transaction set. A prediction was conducted on the test set

and the results were recorded as a transaction filter of the strategy.

Of course, this is not a situation which would occur in reality, where we would not

have known the behaviour of the strategy in the future, and the set of training data would

increase with time (I applied this model of examination for a single model – see 9.2 ).

The results are purely illustrative and not actually feasible in the past. The results set

out below are results for the prediction set which is an amalgamation of sets received in

subsequent steps in the non-random Cross Validation procedure, described above.

Vote RougSets

Accuracy 0.7459 0.7459

95% CI (0.7074, 0.7818) (0.6885, 0.7645)

No Information Rate 0.608 0.608

P-Value [Acc > NIR] 6.05E-12 2.44E-09

Kappa 0.4284 0.4064

Mcnemar's Test P-Value 7.61E-12 0.0002386

Sensitivity (Recall) 0.9134 0.8448

Specificity 0.4861 0.5463

Pos Pred Value (Precision) 0.7338 0.7428

F measure 0.814 0.791

Neg Pred Value 0.7836 0.6941

Prevalence 0.608 0.608

Detection Rate 0.5554 0.5136

Detection Prevalence 0.7568 0.6915

Balanced Accuracy 0.6998 0.6955

Table 3. Results of classifiers – set 4

FILTERING TRADING SYSTEM TRANSACTIONS 24 As you will have noticed from the results presented above, slightly better results with

regard to the F coefficient were achieved by the set of classifiers with the use of voting to

determine the result. In voting we achieve a better Recall parameter – that is, we lose less

transactions which are in fact profit-making, but also a somewhat worse Precision – so that

we are classifying more loss-making transactions as profit-making ones. In case of RS

classification the result is reversed, i.e. we lose more profit-making transactions, but we are

more accurate in filtering off the loss-making ones. The number of admitted transactions is

also different (our positive class) – in the first case there are 417, and in the second 381. It is

not easy to establish which of these classifiers is better in practice; it depends on various

factors and criteria chosen.

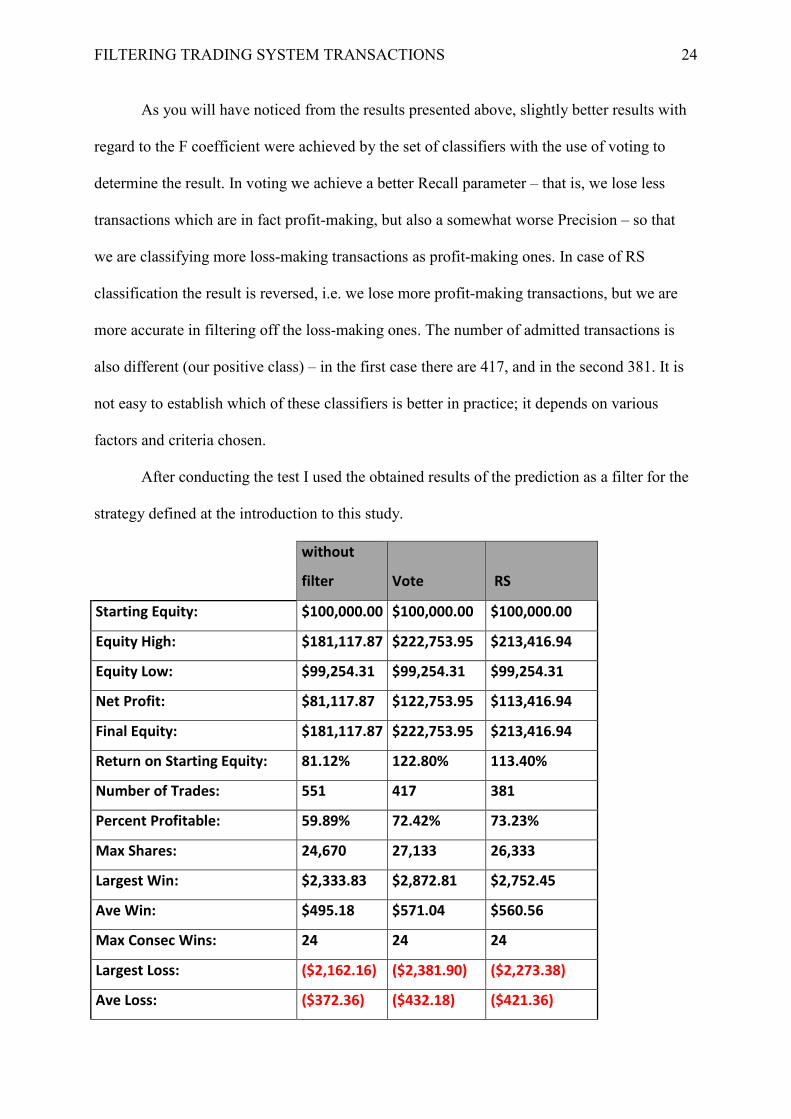

After conducting the test I used the obtained results of the prediction as a filter for the

strategy defined at the introduction to this study.

without

filter Vote RS

Starting Equity: $100,000.00 $100,000.00 $100,000.00

Equity High: $181,117.87 $222,753.95 $213,416.94

Equity Low: $99,254.31 $99,254.31 $99,254.31

Net Profit: $81,117.87 $122,753.95 $113,416.94

Final Equity: $181,117.87 $222,753.95 $213,416.94

Return on Starting Equity: 81.12% 122.80% 113.40%

Number of Trades: 551 417 381

Percent Profitable: 59.89% 72.42% 73.23%

Max Shares: 24,670 27,133 26,333

Largest Win: $2,333.83 $2,872.81 $2,752.45

Ave Win: $495.18 $571.04 $560.56

Max Consec Wins: 24 24 24

Largest Loss: ($2,162.16) ($2,381.90) ($2,273.38)

Ave Loss: ($372.36) ($432.18) ($421.36)

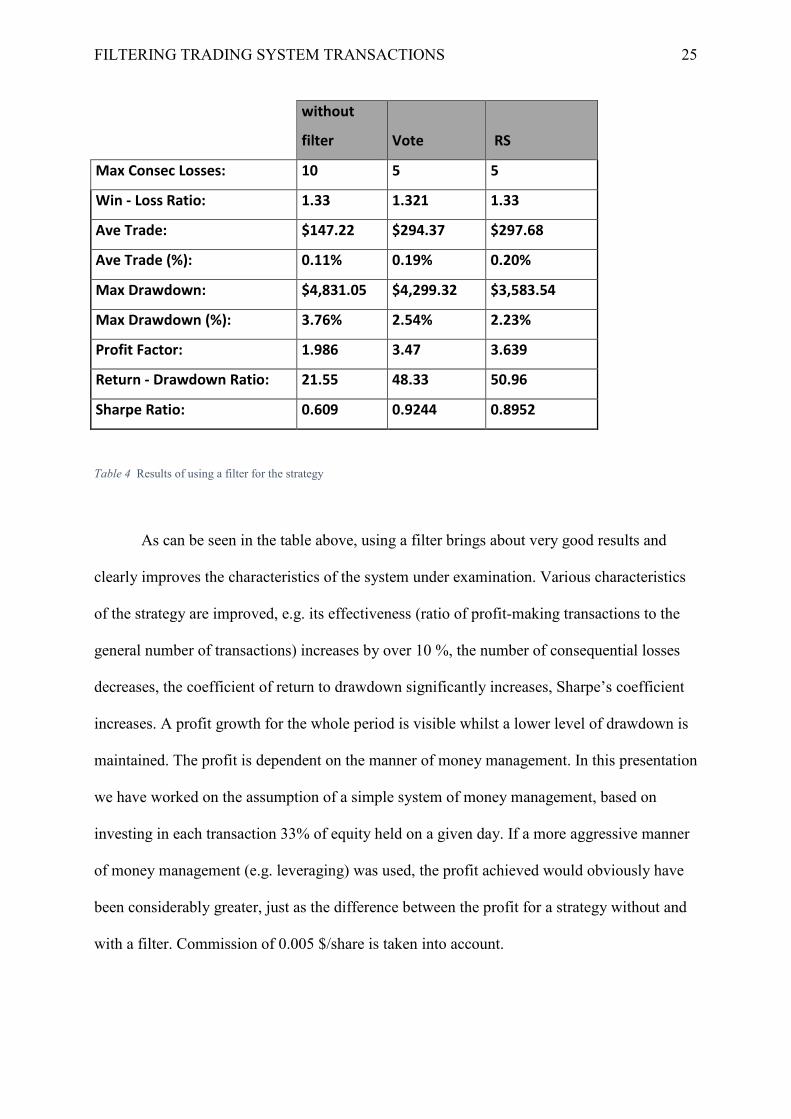

FILTERING TRADING SYSTEM TRANSACTIONS 25

without

filter Vote RS

Max Consec Losses: 10 5 5

Win - Loss Ratio: 1.33 1.321 1.33

Ave Trade: $147.22 $294.37 $297.68

Ave Trade (%): 0.11% 0.19% 0.20%

Max Drawdown: $4,831.05 $4,299.32 $3,583.54

Max Drawdown (%): 3.76% 2.54% 2.23%

Profit Factor: 1.986 3.47 3.639

Return - Drawdown Ratio: 21.55 48.33 50.96

Sharpe Ratio: 0.609 0.9244 0.8952

Table 4 Results of using a filter for the strategy

As can be seen in the table above, using a filter brings about very good results and

clearly improves the characteristics of the system under examination. Various characteristics

of the strategy are improved, e.g. its effectiveness (ratio of profit-making transactions to the

general number of transactions) increases by over 10 %, the number of consequential losses

decreases, the coefficient of return to drawdown significantly increases, Sharpe’s coefficient

increases. A profit growth for the whole period is visible whilst a lower level of drawdown is

maintained. The profit is dependent on the manner of money management. In this presentation

we have worked on the assumption of a simple system of money management, based on

investing in each transaction 33% of equity held on a given day. If a more aggressive manner

of money management (e.g. leveraging) was used, the profit achieved would obviously have

been considerably greater, just as the difference between the profit for a strategy without and

with a filter. Commission of 0.005 $/share is taken into account.

FILTERING TRADING SYSTEM TRANSACTIONS 26 The strategy which uses classifiers with determination by voting is somewhat more

‘aggressive’, involves more transactions, a larger drawdown, more consequential losses. The

strategy which uses classifiers with determination by the RS classifier is more conservative,

operates less frequently and has a better ratio of profit-making transaction to the general

number of transactions. However, the results do not vary significantly.

8.2. Application of filters in the backtest convention for the

single model

Due to slight differences between the results of individual sets of models I decided to

check the behaviour of strategies for the simplest, single model from the ada package (Culp,

Johnson, & Michailidis, 2012) (Boosted Classification Trees). The research was conducted in

a manner considerably closer to reality. The first 265 transactions of the strategy (half of the

available data) were treated as a training set and then the classifier was activated on the next

data record (transaction), in the next step the training set increased by one record (to 276), and

the next record was included in the tests etc. until the end of the set of strategy transactions.

This means that the training set increased with each transaction. At every step, an examination

referred to above was carried out, i.e. new model parameters were selected.

The results again confirmed a considerable advantage of using a classifier for the

strategy. The results obtained are clearly better than those achieved by the strategy without a

classifier. Commission of 0.005 $ per share was taken into consideration . The results for the

strategy without and with a filter are set out below (there is no division into Vote and RS with

regard to the single model, and no mechanism of result determination is used ).

FILTERING TRADING SYSTEM TRANSACTIONS 27

Value

Accuracy 0.7355

95% CI (0.6793, 0.7866)

No Information Rate 0.0019

P-Value [Acc > NIR] 0.0019

Kappa 0.3662

Mcnemar's Test P-Value 0.0002

Sensitivity (Recall) 0.8889

Specificity 0.4479

Pos Pred Value (Precision) 0.7512

F measure 0.8143

Neg Pred Value 0.6825

Prevalence 0.6522

Detection Rate 0.5797

Detection Prevalence 0.7717

Balanced Accuracy 0.6684

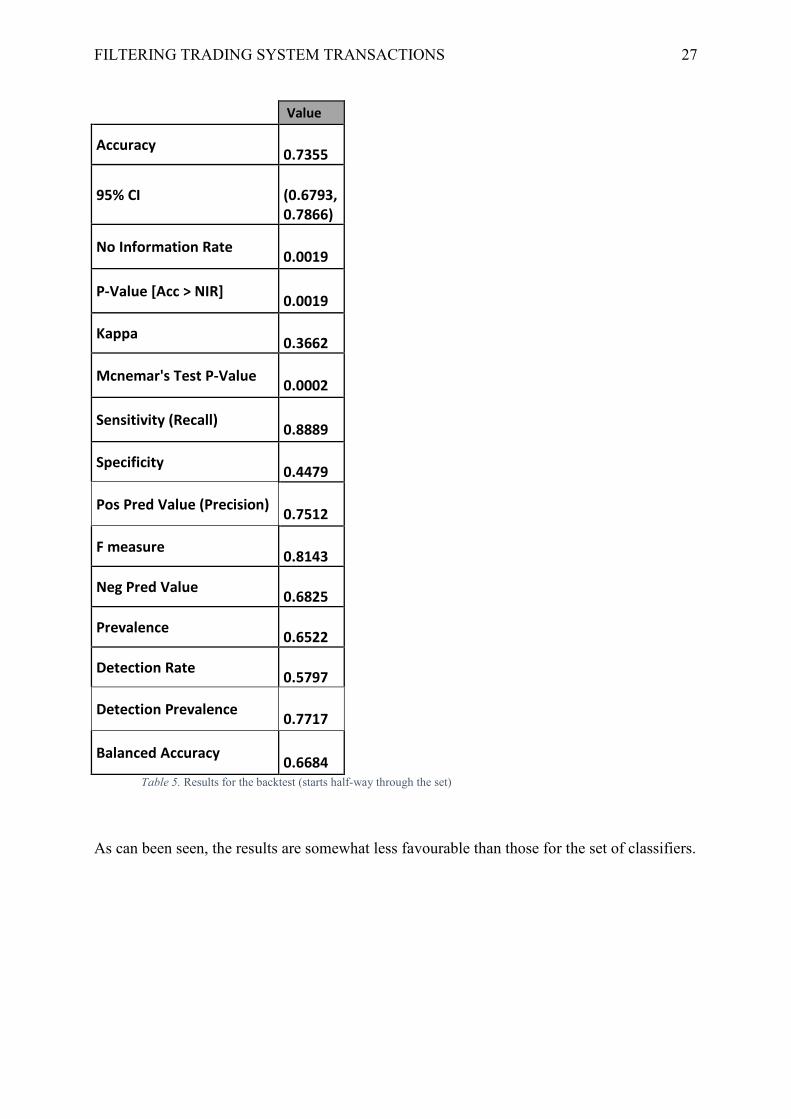

Table 5. Results for the backtest (starts half-way through the set)

As can been seen, the results are somewhat less favourable than those for the set of classifiers.

FILTERING TRADING SYSTEM TRANSACTIONS 28

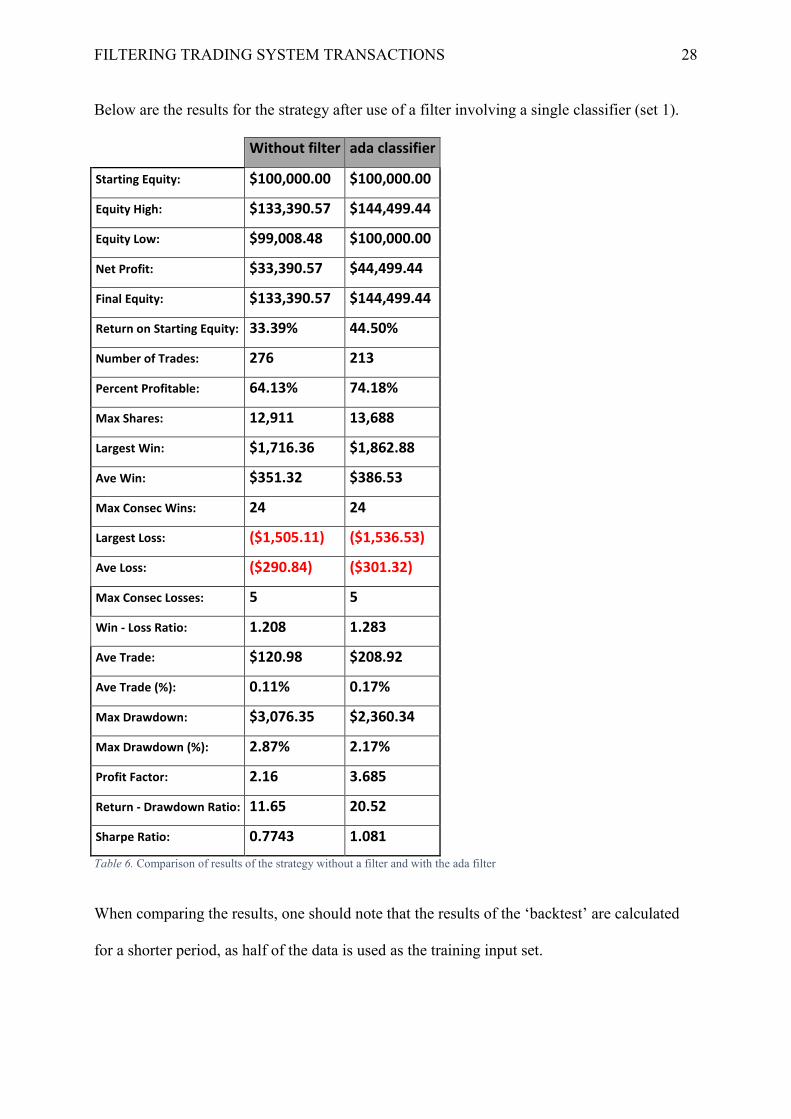

Below are the results for the strategy after use of a filter involving a single classifier (set 1).

Without filter ada classifier

Starting Equity: $100,000.00 $100,000.00

Equity High: $133,390.57 $144,499.44

Equity Low: $99,008.48 $100,000.00

Net Profit: $33,390.57 $44,499.44

Final Equity: $133,390.57 $144,499.44

Return on Starting Equity: 33.39% 44.50%

Number of Trades: 276 213

Percent Profitable: 64.13% 74.18%

Max Shares: 12,911 13,688

Largest Win: $1,716.36 $1,862.88

Ave Win: $351.32 $386.53

Max Consec Wins: 24 24

Largest Loss: ($1,505.11) ($1,536.53)

Ave Loss: ($290.84) ($301.32)

Max Consec Losses: 5 5

Win - Loss Ratio: 1.208 1.283

Ave Trade: $120.98 $208.92

Ave Trade (%): 0.11% 0.17%

Max Drawdown: $3,076.35 $2,360.34

Max Drawdown (%): 2.87% 2.17%

Profit Factor: 2.16 3.685

Return - Drawdown Ratio: 11.65 20.52

Sharpe Ratio: 0.7743 1.081

Table 6. Comparison of results of the strategy without a filter and with the ada filter

When comparing the results, one should note that the results of the ‘backtest’ are calculated

for a shorter period, as half of the data is used as the training input set.

FILTERING TRADING SYSTEM TRANSACTIONS 29

9. Final conclusions

This research has proved the great advantage of using binary classifiers to filter

transactions of the system under examination. The research brought very good results and

should be continued.

In the future it is worth considering the use of additional attributes and methods, which

may enable even better results to be achieved. One could, for example, consider the method of

selecting classifiers with regard to their accuracy on the training data which is similar to that

examined (e.g. because of the cosine similarity). In other words, a classifier might be selected

at a given moment which was the most suitable one for similar data in the past (Masters,

2013).

It should also be established how often the models should be taught on new data, and

also whether to continue adding new data (increasing the training set with time), or to use the

flexible time window for training data.

An important aspect is the model’s ability to adapt to the changing market – and

therefore in the production framework, besides selection of model parameters (e.g. with each

transaction), also periodical selection of significant attributes and perhaps even control of

model effectiveness should be taken into account.

10. Calculations

All computations and graphics in this paper have been obtained using R version 3.1.0

(R Core Team, 2014) using packages: ada (Culp et al., 2012), arm (Gelman & Su, 2014),

blotter (Carl & Peterson, 2014), bst (Wang, 2013),C50 (Kuhn, Weston, & Quinlan, 2014, p.

50), caTools (Tuszynski, 2014), chron(James & Hornik, 2014), class (Venables & Ripley,

FILTERING TRADING SYSTEM TRANSACTIONS 30

2002), compiler (R Core Team, 2014), earth (S. M. D. from mda:mars by T. Hastie &

wrapper, 2014), elmNN (Gosso, 2012), extraTrees (Simm & Abril, 2013),

FinancialInstrument (Carl et al., 2012), foreach (Analytics & Weston, 2014), gbm (Ridgeway,

2013), glmnet (Simon, Friedman, Hastie, & Tibshirani, 2011), gpls (Ding, n.d.), HDclassif

(Bergé, Bouveyron, & Girard, 2012), HiDimDA(Silva, 2012), ipred (Peters & Hothorn,

2013), kernlab (Karatzoglou, Smola, Hornik, & Zeileis, 2004), klaR (Weihs, Ligges, Luebke,

& Raabe, 2005), kohonen(Wehrens & Buydens, 2007), lattice (Sarkar, 2008),

MASS(Venables & Ripley, 2002), mboost(Hothorn, Buehlmann, Kneib, Schmid, & Hofner,

2013),mda (Leisch, Hornik, & Ripley, 2013),nnet (Venables & Ripley, 2002),

nodeHarvest(Meinshausen, 2013), pamr(T. Hastie, Tibshirani, Narasimhan, & Chu, 2013),

partDSA(Molinaro, Olshen, Lostritto, Ryslik, & Weston, 2014),party (Hothorn, Hornik, &

Zeileis, 2006), penalizedLDA (Witten, 2011), PerformanceAnalytics (Carl & Peterson,

2013), pls (Mevik, Wehrens, & Liland, 2013), plyr (Wickham, 2011), pracma (Borchers,

2014), proxy (Meyer & Buchta, 2014), quantmod (Ryan, 2013), quantstrat (Carl, Peterson,

Ulrich, & Humme, 2014), randomForest (Liaw & Wiener, 2002), rknn (Li, 2013), RoughSets

(Riza et al., 2014), rpart (Therneau, Atkinson, & Ripley, 2014), rrcovHD (Todorov, 2013),

RRF (Deng, 2013), rrlda (Gschwandtner, Filzmoser, Croux, & Haesbroeck, 2012), RSNNS

(Bergmeir & Benítez, 2012), RWeka (Hornik, Buchta, & Zeileis, 2009), sda (Ahdesmaki,

Zuber, Gibb, & Strimmer, 2014), SDDA (Bioinformatics & Stone, 2010), sparseLDA

(Clemmensen & Kuhn, 2012), stats (R Core Team, 2014), stepPlr (Park & Hastie, 2010),

TTR (Ulrich, 2013), xts (Ryan & Ulrich, 2014)

FILTERING TRADING SYSTEM TRANSACTIONS 31

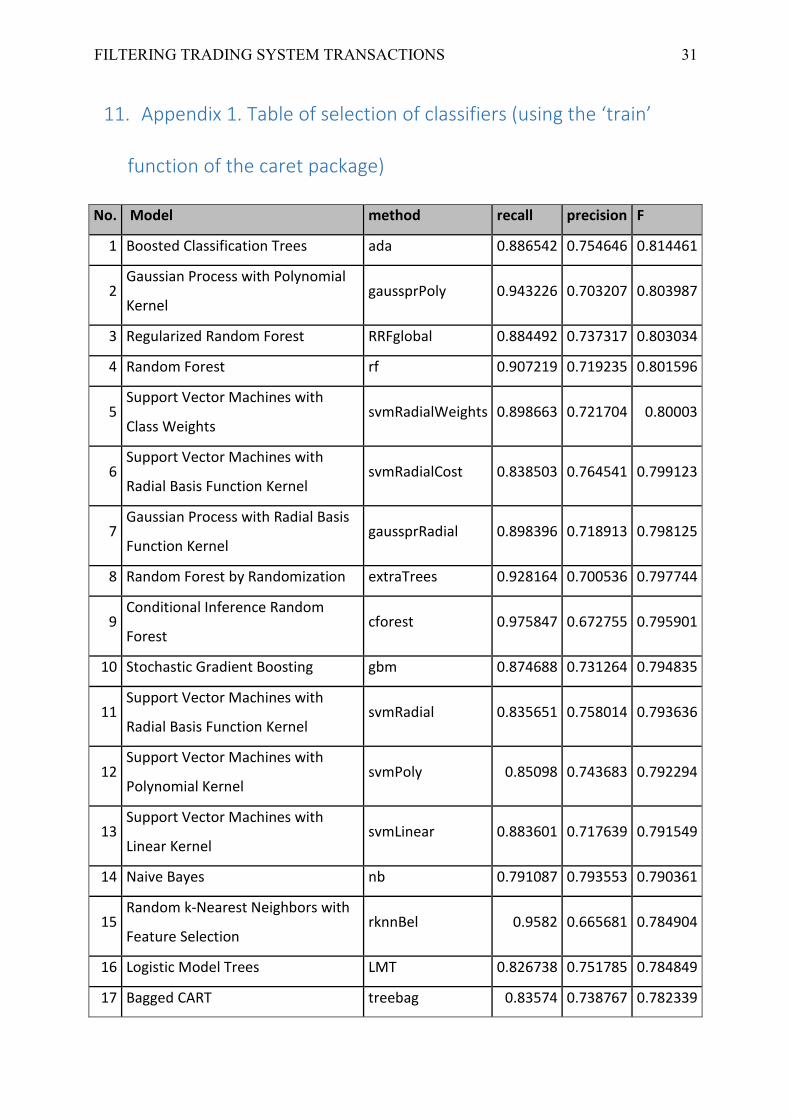

11. Appendix 1. Table of selection of classifiers (using the ‘train’

function of the caret package)

No. Model method recall precision F

1 Boosted Classification Trees ada 0.886542 0.754646 0.814461

2 Gaussian Process with Polynomial

Kernel gaussprPoly 0.943226 0.703207 0.803987

3 Regularized Random Forest RRFglobal 0.884492 0.737317 0.803034

4 Random Forest rf 0.907219 0.719235 0.801596

5 Support Vector Machines with

Class Weights svmRadialWeights 0.898663 0.721704 0.80003

6 Support Vector Machines with

Radial Basis Function Kernel svmRadialCost 0.838503 0.764541 0.799123

7 Gaussian Process with Radial Basis

Function Kernel gaussprRadial 0.898396 0.718913 0.798125

8 Random Forest by Randomization extraTrees 0.928164 0.700536 0.797744

9 Conditional Inference Random

Forest cforest 0.975847 0.672755 0.795901

10 Stochastic Gradient Boosting gbm 0.874688 0.731264 0.794835

11 Support Vector Machines with

Radial Basis Function Kernel svmRadial 0.835651 0.758014 0.793636

12 Support Vector Machines with

Polynomial Kernel svmPoly 0.85098 0.743683 0.792294

13 Support Vector Machines with

Linear Kernel svmLinear 0.883601 0.717639 0.791549

14 Naive Bayes nb 0.791087 0.793553 0.790361

15 Random k-Nearest Neighbors with

Feature Selection rknnBel 0.9582 0.665681 0.784904

16 Logistic Model Trees LMT 0.826738 0.751785 0.784849

17 Bagged CART treebag 0.83574 0.738767 0.782339

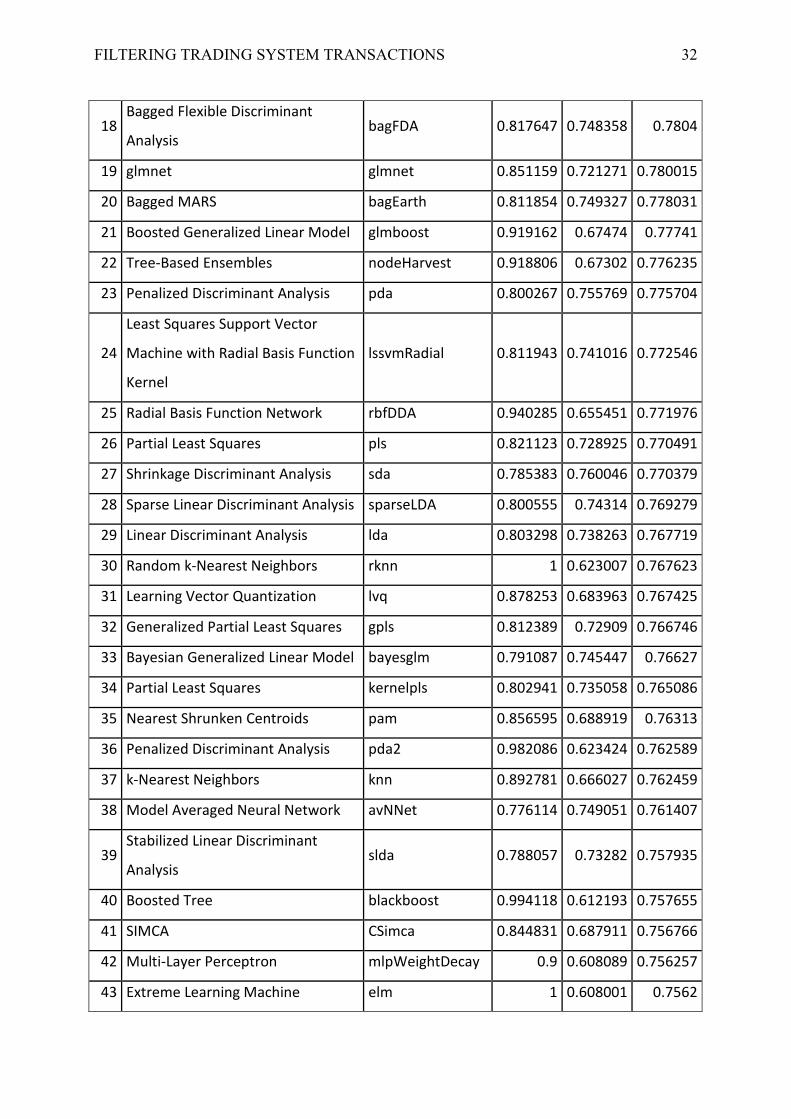

FILTERING TRADING SYSTEM TRANSACTIONS 32

18 Bagged Flexible Discriminant

Analysis bagFDA 0.817647 0.748358 0.7804

19 glmnet glmnet 0.851159 0.721271 0.780015

20 Bagged MARS bagEarth 0.811854 0.749327 0.778031

21 Boosted Generalized Linear Model glmboost 0.919162 0.67474 0.77741

22 Tree-Based Ensembles nodeHarvest 0.918806 0.67302 0.776235

23 Penalized Discriminant Analysis pda 0.800267 0.755769 0.775704

24

Least Squares Support Vector

Machine with Radial Basis Function

Kernel

lssvmRadial 0.811943 0.741016 0.772546

25 Radial Basis Function Network rbfDDA 0.940285 0.655451 0.771976

26 Partial Least Squares pls 0.821123 0.728925 0.770491

27 Shrinkage Discriminant Analysis sda 0.785383 0.760046 0.770379

28 Sparse Linear Discriminant Analysis sparseLDA 0.800555 0.74314 0.769279

29 Linear Discriminant Analysis lda 0.803298 0.738263 0.767719

30 Random k-Nearest Neighbors rknn 1 0.623007 0.767623

31 Learning Vector Quantization lvq 0.878253 0.683963 0.767425

32 Generalized Partial Least Squares gpls 0.812389 0.72909 0.766746

33 Bayesian Generalized Linear Model bayesglm 0.791087 0.745447 0.76627

34 Partial Least Squares kernelpls 0.802941 0.735058 0.765086

35 Nearest Shrunken Centroids pam 0.856595 0.688919 0.76313

36 Penalized Discriminant Analysis pda2 0.982086 0.623424 0.762589

37 k-Nearest Neighbors knn 0.892781 0.666027 0.762459

38 Model Averaged Neural Network avNNet 0.776114 0.749051 0.761407

39 Stabilized Linear Discriminant

Analysis slda 0.788057 0.73282 0.757935

40 Boosted Tree blackboost 0.994118 0.612193 0.757655

41 SIMCA CSimca 0.844831 0.687911 0.756766

42 Multi-Layer Perceptron mlpWeightDecay 0.9 0.608089 0.756257

43 Extreme Learning Machine elm 1 0.608001 0.7562

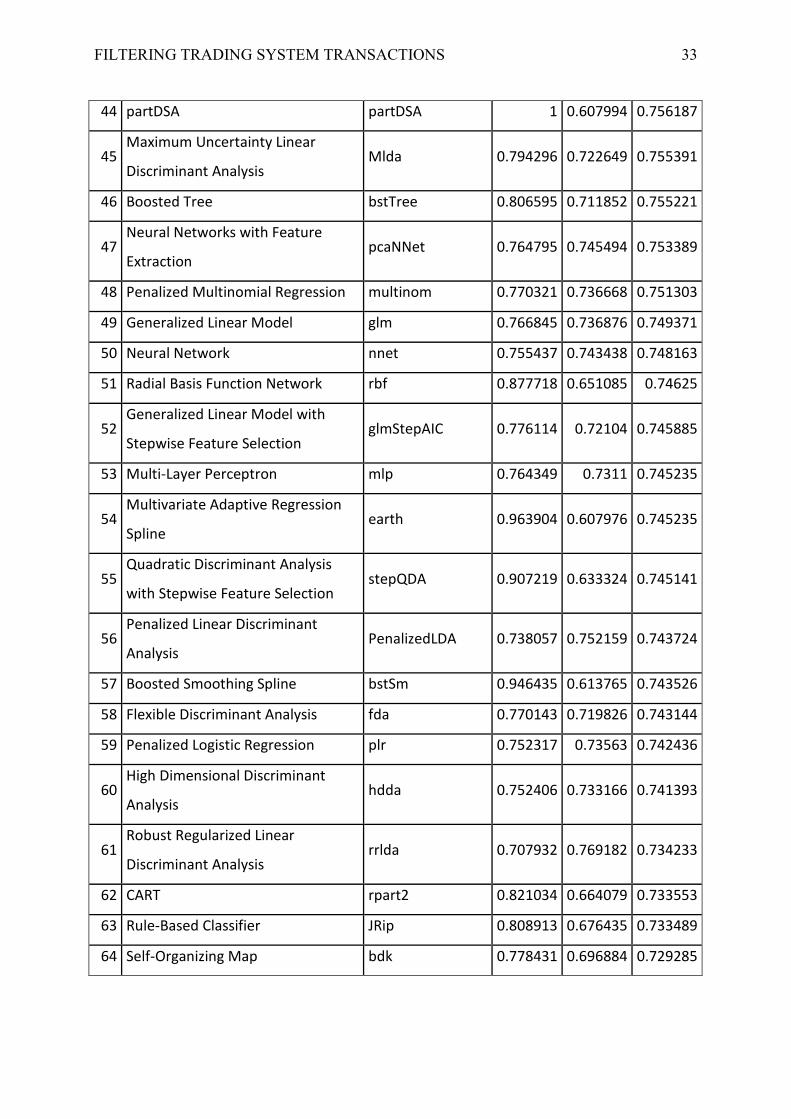

FILTERING TRADING SYSTEM TRANSACTIONS 33

44 partDSA partDSA 1 0.607994 0.756187

45 Maximum Uncertainty Linear

Discriminant Analysis Mlda 0.794296 0.722649 0.755391

46 Boosted Tree bstTree 0.806595 0.711852 0.755221

47 Neural Networks with Feature

Extraction pcaNNet 0.764795 0.745494 0.753389

48 Penalized Multinomial Regression multinom 0.770321 0.736668 0.751303

49 Generalized Linear Model glm 0.766845 0.736876 0.749371

50 Neural Network nnet 0.755437 0.743438 0.748163

51 Radial Basis Function Network rbf 0.877718 0.651085 0.74625

52 Generalized Linear Model with

Stepwise Feature Selection glmStepAIC 0.776114 0.72104 0.745885

53 Multi-Layer Perceptron mlp 0.764349 0.7311 0.745235

54 Multivariate Adaptive Regression

Spline earth 0.963904 0.607976 0.745235

55 Quadratic Discriminant Analysis

with Stepwise Feature Selection stepQDA 0.907219 0.633324 0.745141

56 Penalized Linear Discriminant

Analysis PenalizedLDA 0.738057 0.752159 0.743724

57 Boosted Smoothing Spline bstSm 0.946435 0.613765 0.743526

58 Flexible Discriminant Analysis fda 0.770143 0.719826 0.743144

59 Penalized Logistic Regression plr 0.752317 0.73563 0.742436

60 High Dimensional Discriminant

Analysis hdda 0.752406 0.733166 0.741393

61 Robust Regularized Linear

Discriminant Analysis rrlda 0.707932 0.769182 0.734233

62 CART rpart2 0.821034 0.664079 0.733553

63 Rule-Based Classifier JRip 0.808913 0.676435 0.733489

64 Self-Organizing Map bdk 0.778431 0.696884 0.729285

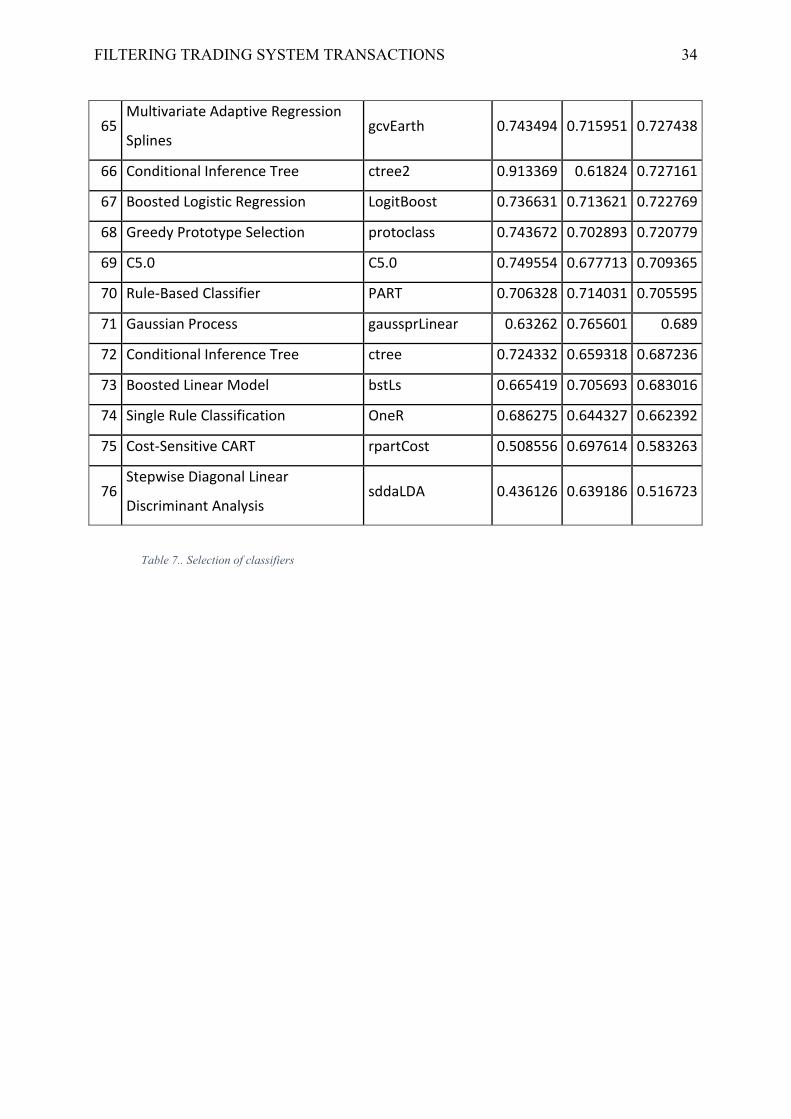

FILTERING TRADING SYSTEM TRANSACTIONS 34

65 Multivariate Adaptive Regression

Splines gcvEarth 0.743494 0.715951 0.727438

66 Conditional Inference Tree ctree2 0.913369 0.61824 0.727161

67 Boosted Logistic Regression LogitBoost 0.736631 0.713621 0.722769

68 Greedy Prototype Selection protoclass 0.743672 0.702893 0.720779

69 C5.0 C5.0 0.749554 0.677713 0.709365

70 Rule-Based Classifier PART 0.706328 0.714031 0.705595

71 Gaussian Process gaussprLinear 0.63262 0.765601 0.689

72 Conditional Inference Tree ctree 0.724332 0.659318 0.687236

73 Boosted Linear Model bstLs 0.665419 0.705693 0.683016

74 Single Rule Classification OneR 0.686275 0.644327 0.662392

75 Cost-Sensitive CART rpartCost 0.508556 0.697614 0.583263

76 Stepwise Diagonal Linear

Discriminant Analysis sddaLDA 0.436126 0.639186 0.516723

Table 7.. Selection of classifiers

FILTERING TRADING SYSTEM TRANSACTIONS 35

12. References

Ahdesmaki, M., Zuber, V., Gibb, S., & Strimmer, K. (2014). sda: Shrinkage Discriminant

Analysis and CAT Score Variable Selection. Retrieved from http://CRAN.R-

project.org/package=sda

AL-RADAIDEH, Q. A., ASSAF, A. A., & ALNAGI, E. (2013). PREDICTING STOCK

PRICES USING DATA MINING TECHNIQUES.

Analytics, R., & Weston, S. (2014). foreach: Foreach looping construct for R. Retrieved from

http://CRAN.R-project.org/package=foreach

Bergé, L., Bouveyron, C., & Girard, S. (2012). HDclassif: An R Package for Model-Based

Clustering and Discriminant Analysis of High-Dimensional Data. Journal of

Statistical Software, 46(6), 1–29.

Bergmeir, C., & Benítez, J. M. (2012). Neural Networks in R Using the Stuttgart Neural

Network Simulator: RSNNS. Journal of Statistical Software, 46(7), 1–26.

Bioinformatics, C., & Stone, G. (2010). SDDA: Stepwise Diagonal Discriminant Analysis.

Retrieved from http://CRAN.R-project.org/package=SDDA

Borchers, H. W. (2014). pracma: Practical Numerical Math Functions. Retrieved from

http://CRAN.R-project.org/package=pracma

Carl, P., Eddelbuettel, D., Ryan, J., Ulrich, J., Peterson, B. G., & See, G. (2012).

FinancialInstrument: Financial Instrument Model Infrastructure for R. Retrieved from

http://CRAN.R-project.org/package=FinancialInstrument

Carl, P., & Peterson, B. G. (2013). PerformanceAnalytics: Econometric tools for performance

and risk analysis. Retrieved from http://CRAN.R-

project.org/package=PerformanceAnalytics

FILTERING TRADING SYSTEM TRANSACTIONS 36

Carl, P., & Peterson, B. G. (2014). blotter: Tools for transaction-oriented trading systems

development. Retrieved from http://R-Forge.R-project.org/projects/blotter/

Carl, P., Peterson, B. G., Ulrich, J., & Humme, J. (2014). quantstrat: Quantitative Strategy

Model Framework. Retrieved from http://R-Forge.R-project.org/projects/blotter/

Clemmensen, L., & Kuhn, contributions by M. (2012). sparseLDA: Sparse Discriminant

Analysis. Retrieved from http://CRAN.R-project.org/package=sparseLDA

Culp, M., Johnson, K., & Michailidis, G. (2012). ada: ada: an R package for stochastic

boosting. Retrieved from http://CRAN.R-project.org/package=ada

Deng, H. (2013). Guided Random Forest in the RRF Package. arXiv:1306.0237.

Ding, B. (n.d.). gpls: Classification using generalized partial least squares.

Gelman, A., & Su, Y.-S. (2014). arm: Data Analysis Using Regression and

Multilevel/Hierarchical Models. Retrieved from http://CRAN.R-

project.org/package=arm

Gosso, A. (2012). elmNN: Implementation of ELM (Extreme Learning Machine ) algorithm

for SLFN ( Single Hidden Layer Feedforward Neural Networks ). Retrieved from

http://CRAN.R-project.org/package=elmNN

Gschwandtner, M., Filzmoser, P., Croux, C., & Haesbroeck, G. (2012). rrlda: Robust

Regularized Linear Discriminant Analysis. Retrieved from http://CRAN.R-

project.org/package=rrlda

Hastie, S. M. D. from mda:mars by T., & wrapper, R. T. U. A. M. F. utilities with T. L. leaps.

(2014). earth: Multivariate Adaptive Regression Spline Models. Retrieved from

http://CRAN.R-project.org/package=earth

Hastie, T., Tibshirani, R., Narasimhan, B., & Chu, G. (2013). pamr: Pam: prediction analysis

for microarrays. Retrieved from http://CRAN.R-project.org/package=pamr

FILTERING TRADING SYSTEM TRANSACTIONS 37

Hornik, K., Buchta, C., & Zeileis, A. (2009). Open-Source Machine Learning: R Meets Weka.

Computational Statistics, 24(2), 225–232. doi:10.1007/s00180-008-0119-7

Hothorn, T., Buehlmann, P., Kneib, T., Schmid, M., & Hofner, B. (2013). mboost: Model-

Based Boosting, R package version 2.2-3. Retrieved from http://CRAN.R-

project.org/package=mboost.

Hothorn, T., Hornik, K., & Zeileis, A. (2006). Unbiased Recursive Partitioning: A

Conditional Inference Framework. Journal of Computational and Graphical Statistics,

15(3), 651–674.

James, D., & Hornik, K. (2014). chron: Chronological Objects which Can Handle Dates and

Times. Retrieved from http://CRAN.R-project.org/package=chron

Karatzoglou, A., Smola, A., Hornik, K., & Zeileis, A. (2004). kernlab – An S4 Package for

Kernel Methods in R. Journal of Statistical Software, 11(9), 1–20.

Komorowski, J., Pawlak, Z., Polkowski, L., & Skowron, A. (1999). Rough sets: A tutorial.

Rough Fuzzy Hybridization: A New Trend in Decision-Making, 3–98.

Kuhn, M., Weston, S., & Quinlan, N. C. C. code for C. 0 by R. (2014). C50: C5.0 Decision

Trees and Rule-Based Models. Retrieved from http://CRAN.R-

project.org/package=C50

Kun, M., Weston, S., Williams, A., Keefer, C., Engelhardt, A., Cooper, T., … Wing, J.

(2014). caret: Classification and Regression Training. Retrieved from

http://CRAN.R-project.org/package=caret

Leisch, S. original by T. H. & R. T. O. R. port by F., Hornik, K., & Ripley, B. D. (2013).

mda: Mixture and flexible discriminant analysis. Retrieved from http://CRAN.R-

project.org/package=mda

Li, S. (2013). rknn: Random KNN Classification and Regression. Retrieved from

http://CRAN.R-project.org/package=rknn

FILTERING TRADING SYSTEM TRANSACTIONS 38

Liaw, A., & Wiener, M. (2002). Classification and Regression by randomForest. R News,

2(3), 18–22.

Masters, T. (2013). Assessing and Improving Prediction and Classification (1 edition.).

CreateSpace Independent Publishing Platform.

Meinshausen, N. (2013). nodeHarvest: Node Harvest for regression and classification.

Retrieved from http://CRAN.R-project.org/package=nodeHarvest

Mevik, B.-H., Wehrens, R., & Liland, K. H. (2013). pls: Partial Least Squares and Principal

Component regression. Retrieved from http://CRAN.R-project.org/package=pls

Meyer, D., & Buchta, C. (2014). proxy: Distance and Similarity Measures. Retrieved from

http://CRAN.R-project.org/package=proxy

Molinaro, A., Olshen, A., Lostritto, K., Ryslik, G., & Weston, S. (2014). partDSA:

Partitioning using deletion, substitution, and addition moves. Retrieved from

http://CRAN.R-project.org/package=partDSA

Park, M. Y., & Hastie, T. (2010). stepPlr: L2 penalized logistic regression with a stepwise

variable selection. Retrieved from http://CRAN.R-project.org/package=stepPlr

Peters, A., & Hothorn, T. (2013). ipred: Improved Predictors. Retrieved from http://CRAN.R-

project.org/package=ipred

R Core Team. (2014). R: A Language and Environment for Statistical Computing. Vienna,

Austria: R Foundation for Statistical Computing. Retrieved from http://www.R-

project.org/

Ridgeway, G. (2013). gbm: Generalized Boosted Regression Models. Retrieved from

http://CRAN.R-project.org/package=gbm

Riza, L. S., Janusz, A., Cornelis, C., Herrera, F., Slezak, D., & Benitez, J. M. (2014).

RoughSets: Data Analysis Using Rough Set and Fuzzy Rough Set Theories. Retrieved

from http://CRAN.R-project.org/package=RoughSets

FILTERING TRADING SYSTEM TRANSACTIONS 39

Ryan, J. A. (2013). quantmod: Quantitative Financial Modelling Framework. Retrieved from

http://CRAN.R-project.org/package=quantmod

Ryan, J. A., & Ulrich, J. M. (2014). xts: eXtensible Time Series. Retrieved from

http://CRAN.R-project.org/package=xts

Sarkar, D. (2008). Lattice: Multivariate Data Visualization with R. New York: Springer.

Retrieved from http://lmdvr.r-forge.r-project.org

Silva, A. P. D. (2012). HiDimDA: High Dimensional Discriminant Analysis. Retrieved from

http://CRAN.R-project.org/package=HiDimDA

Simm, J., & Abril, I. M. de. (2013). extraTrees: ExtraTrees method. Retrieved from

http://CRAN.R-project.org/package=extraTrees

Simon, N., Friedman, J., Hastie, T., & Tibshirani, R. (2011). Regularization Paths for Cox’s

Proportional Hazards Model via Coordinate Descent. Journal of Statistical Software,

39(5), 1–13.

Soni, S. (2010). Applications of ANNs in Stock Market Prediction: A Survey.

Therneau, T., Atkinson, B., & Ripley, B. (2014). rpart: Recursive Partitioning and

Regression Trees. Retrieved from http://CRAN.R-project.org/package=rpart

Todorov, V. (2013). rrcovHD: Robust multivariate Methods for High Dimensional Data.

Retrieved from http://CRAN.R-project.org/package=rrcovHD

Tuszynski, J. (2014). caTools: Tools: moving window statistics, GIF, Base64, ROC AUC, etc.

Retrieved from http://CRAN.R-project.org/package=caTools

Ulrich, J. (2013). TTR: Technical Trading Rules. Retrieved from http://R-Forge.R-

project.org/projects/ttr/

Varutbangkul, E. (2013). Integrating Traditional Stock Trading Systems: A Data Mining

Approach.

FILTERING TRADING SYSTEM TRANSACTIONS 40

Venables, W. N., & Ripley, B. D. (2002). Modern Applied Statistics with S (Fourth.). New

York: Springer. Retrieved from http://www.stats.ox.ac.uk/pub/MASS4

Wang, Z. (2013). bst: Gradient Boosting. Retrieved from http://CRAN.R-

project.org/package=bst

Wehrens, R., & Buydens, L. M. C. (2007). Self- and Super-organising Maps in R: the

kohonen package. J. Stat. Softw., 21(5). Retrieved from

http://www.jstatsoft.org/v21/i05

Weihs, C., Ligges, U., Luebke, K., & Raabe, N. (2005). klaR Analyzing German Business

Cycles. In D. Baier, R. Decker, & L. Schmidt-Thieme (Eds.), Data Analysis and

Decision Support (pp. 335–343). Berlin: Springer-Verlag.

Wickham, H. (2011). The Split-Apply-Combine Strategy for Data Analysis. Journal of

Statistical Software, 40(1), 1–29.

Witten, D. (2011). penalizedLDA: Penalized classification using Fisher’s linear discriminant.

Retrieved from http://CRAN.R-project.org/package=penalizedLDA

FILTERING TRADING SYSTEM TRANSACTIONS 41