Transactions with Partners

46

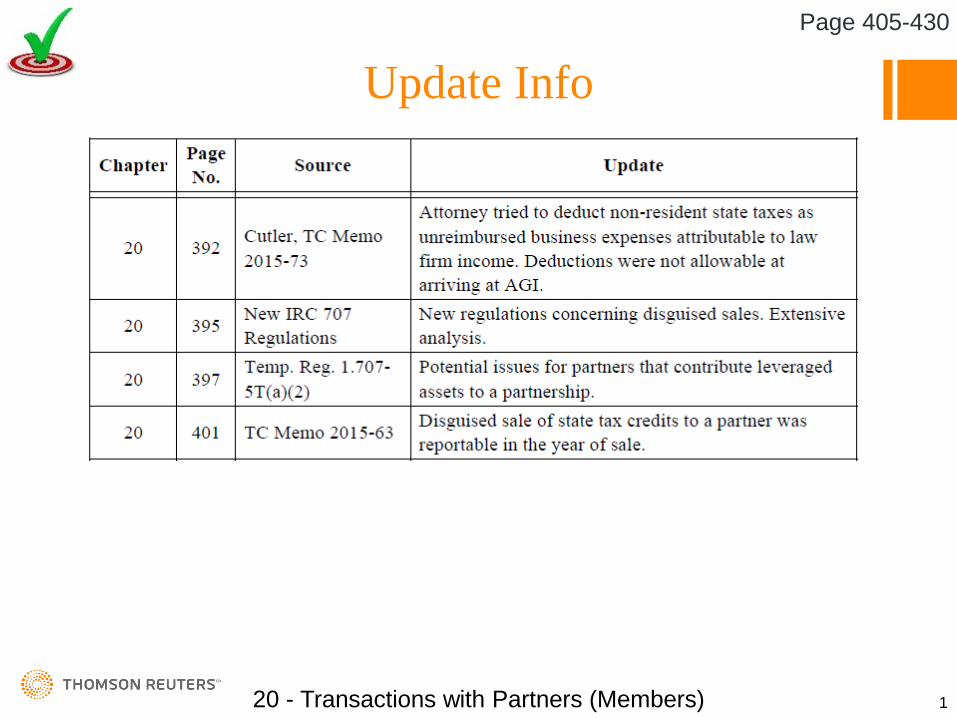

Update Info 20 - Transactions with Partners (Members) 1 Page 405-430

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Transactions with Partners

Update Info

20 - Transactions with Partners (Members) 1

Page 405-430

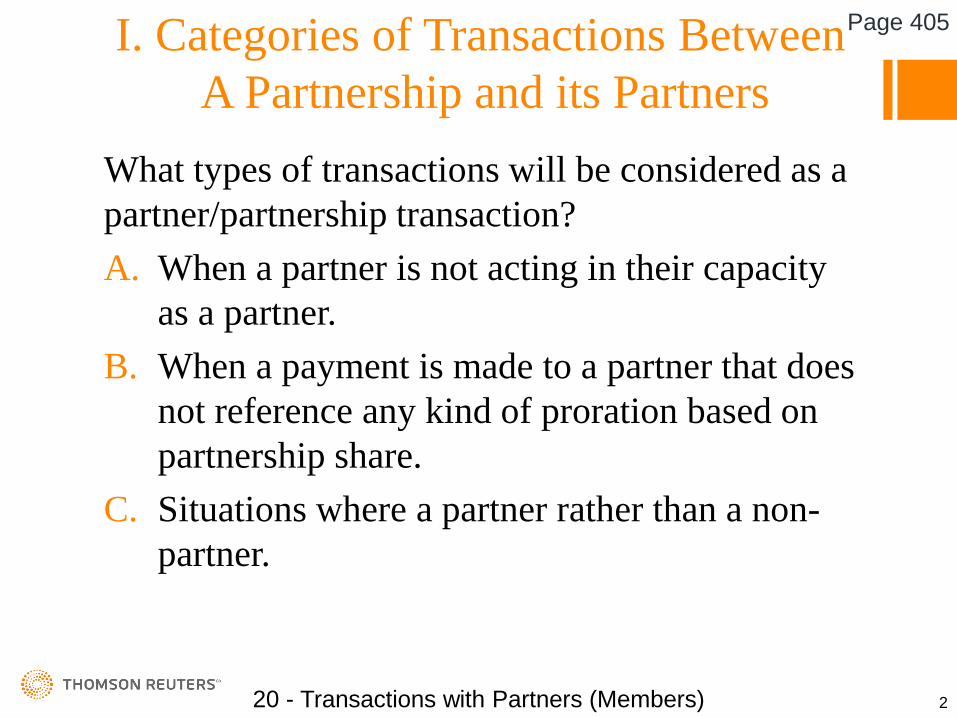

I. Categories of Transactions BetweenA Partnership and its Partners

What types of transactions will be considered as a partner/partnership transaction?A. When a partner is not acting in their capacity

as a partner.B. When a payment is made to a partner that does

not reference any kind of proration based on partnership share.

C. Situations where a partner rather than a non-partner.

20 - Transactions with Partners (Members) 2

Page 405

II. Guaranteed Payments

Be cautious of “guaranteed payment agreements” that may have unintended results:

These payments were then governed by the rules of termination or liquidation payments to partners –Chapter 21

20 - Transactions with Partners (Members) 4

Page 405

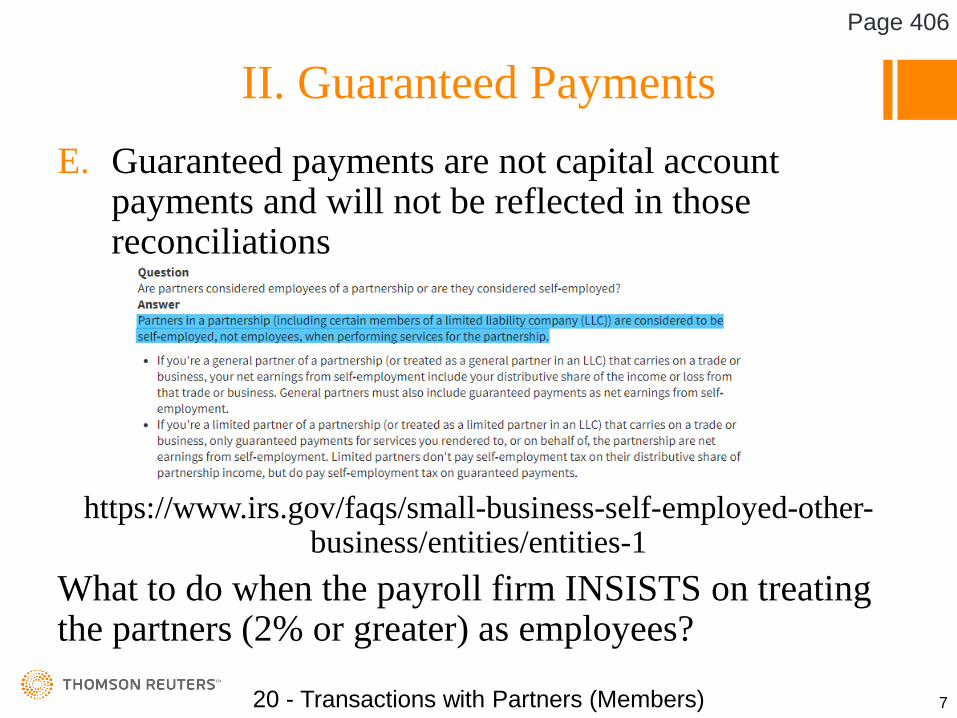

II. Guaranteed PaymentsE. Guaranteed payments are not capital account

payments and will not be reflected in those reconciliations

Bona-fide Partners ARE NOT EMPLOYEES Rev. Rul. 69-184 – Doing so could be a fraudulent act under the social security rules as well.

Reg. § 301.7701-2 – IRS clarifies that an LLC while for payroll purposes is treated as a corporation, bona-fide partners are not employees, even when the LLC is a SMLLC, i.e. disregarded entity.

20 - Transactions with Partners (Members) 5

Page 406

II. Guaranteed PaymentsE. Guaranteed payments are not capital account

payments and will not be reflected in those reconciliations

Bona-fide Partners ARE NOT EMPLOYEES Rev. Rul. 69-184 – Doing so could be a fraudulent act under the social security rules

20 - Transactions with Partners (Members) 6

Page 406

II. Guaranteed PaymentsE. Guaranteed payments are not capital account

payments and will not be reflected in those reconciliations

https://www.irs.gov/faqs/small-business-self-employed-other-business/entities/entities-1

What to do when the payroll firm INSISTS on treating the partners (2% or greater) as employees?

20 - Transactions with Partners (Members) 7

Page 406

II. Guaranteed PaymentsWhile Rev. Proc. 2001-43 specifically dealt with the issues of “unvested profits interests” it does shed light on the IRS vision and distain for partners that are treated as employees.

For the practitioner there is the very real threat of NO SUBSTANTIAL AUTHORITY and the attaching penalties under IRC 6694

20 - Transactions with Partners (Members) 8

Page 406

II. Guaranteed PaymentsTemp. Reg. § 301.7701-2TThere is little doubt that IRS plans on making this a center issue of its current assault on partnerships. Play the payroll game at your own risk. It is likely fatal.

Positive – With the release of the Temp. Reg. payroll companies seem to be more willing to move off their payroll position.

Chapter 20: Transactions with Partners (Members)20 - Transactions with Partners (Members) 9

Page 406

III. Partnership Expenses Paid by Partners

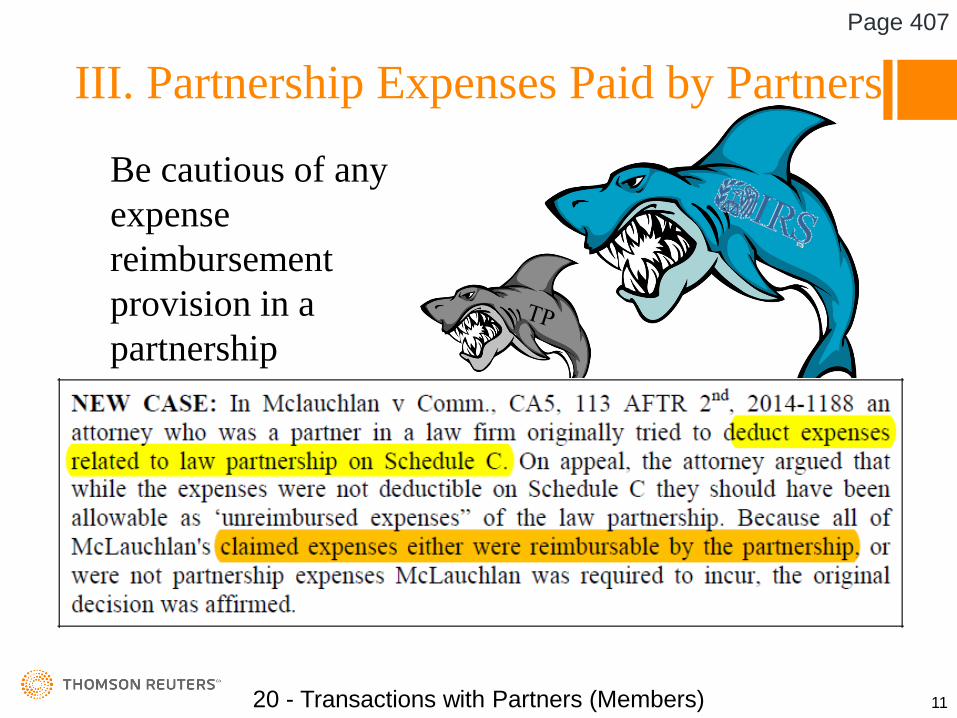

Be cautious of any expense reimbursement provision in a partnership agreement.

20 - Transactions with Partners (Members) 11

Page 407

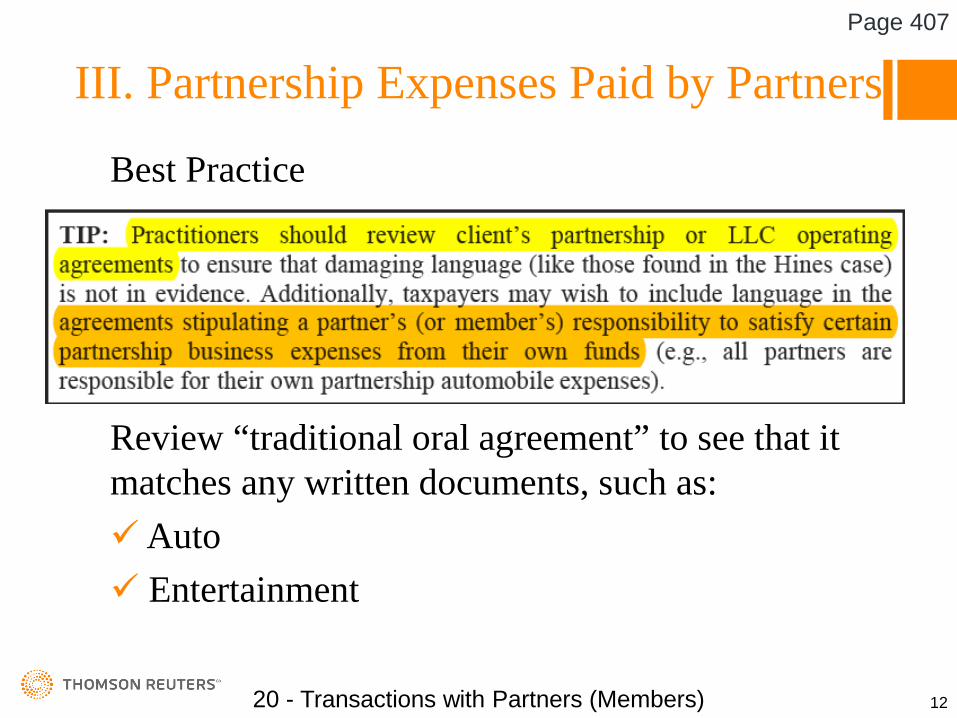

III. Partnership Expenses Paid by Partners

Best Practice

Review “traditional oral agreement” to see that it matches any written documents, such as:Auto Entertainment

20 - Transactions with Partners (Members) 12

Page 407

III. Partnership Expenses Paid by Partners

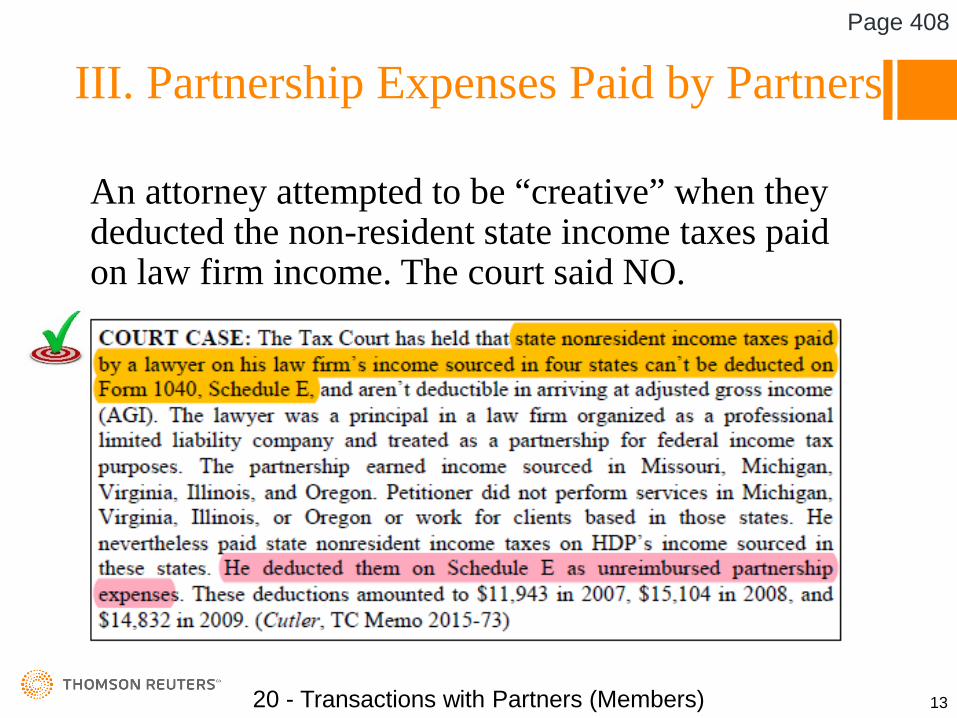

An attorney attempted to be “creative” when they deducted the non-resident state income taxes paid on law firm income. The court said NO.

20 - Transactions with Partners (Members) 13

Page 408

Note This:Item B – Listing of Non-Excludable Fringes

Item C – Listing of Excludable Fringes

Non-Excludable Items will be guaranteed payments.Excludable Items will be ordinary expenses of the partnership.

IV. Fringe Benefits

20 - Transactions with Partners (Members) 15

Page 408-409

V. Introduction to Special Rules forCertain Sales or Distributions

Some anti-abuse rules exist to prevent a partner from avoiding taxation in an “abusive” manner by “swapping” property for cash:

20 - Transactions with Partners (Members) 18

Page 410-411

VI. Disguised Sale Rules

Heads Up

With the release of the final regulations the rules we have been dealing with for the last several years will mostly stay in place with some modifications

20 - Transactions with Partners (Members) 19

Page 411

VI. Disguised Sale Rules

What is a disguised sale?

B. When a partner contributes property and receives a distribution within two years as defined:

1. Money or other consideration paid to the contributor of the property that would not have been paid except for the transfer.

2. If the transfers are not made simultaneously and the later transfers is made without regard to partnership operations.

20 - Transactions with Partners (Members) 20

Page 411

VI. Disguised Sale Rules

C. Determining factors as defined by Reg. §1.707-3(b), these are facts and circumstances test:

1. Determination of the subsequent transfer at the time of the original transfer.

2. Receiving an enforceable right as part of the initial transfer

3. Legal obligations by others to make contributions or loans.

4. Holding funds in excess of current business needs to make the transfer.

20 - Transactions with Partners (Members) 21

Page 411

VI. Disguised Sale RulesTypes of transactions that can be a disguised sale and it works in multiple directions:

20 - Transactions with Partners (Members) 22

Page 411-412

VI. Disguised Sale Rules

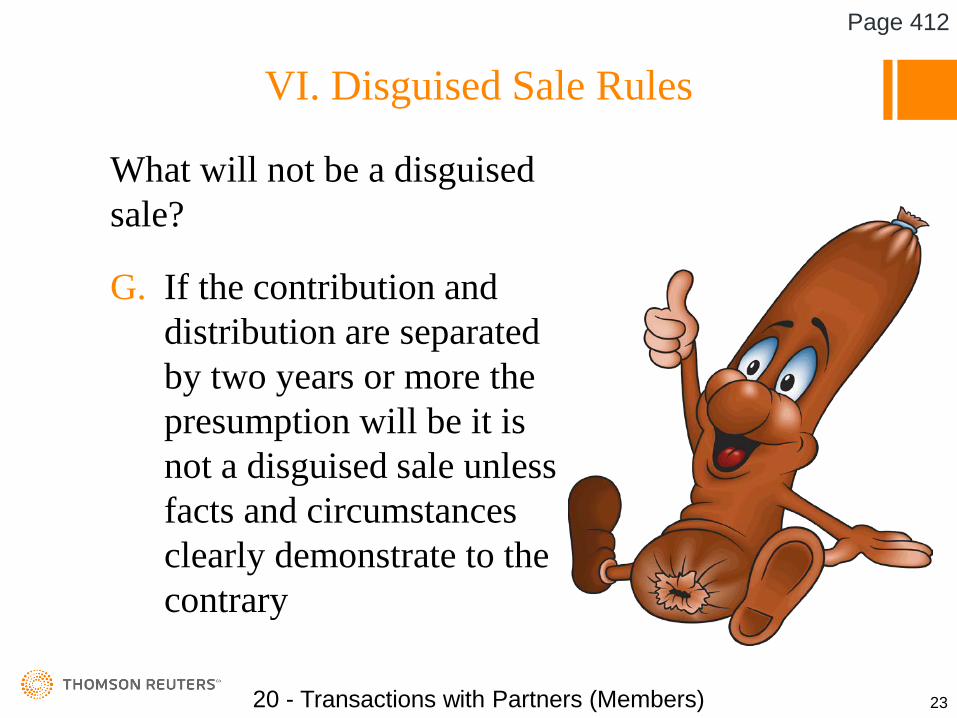

What will not be a disguised sale?

G. If the contribution and distribution are separated by two years or more the presumption will be it is not a disguised sale unless facts and circumstances clearly demonstrate to the contrary

20 - Transactions with Partners (Members) 23

Page 412

VI. Disguised Sale Rules

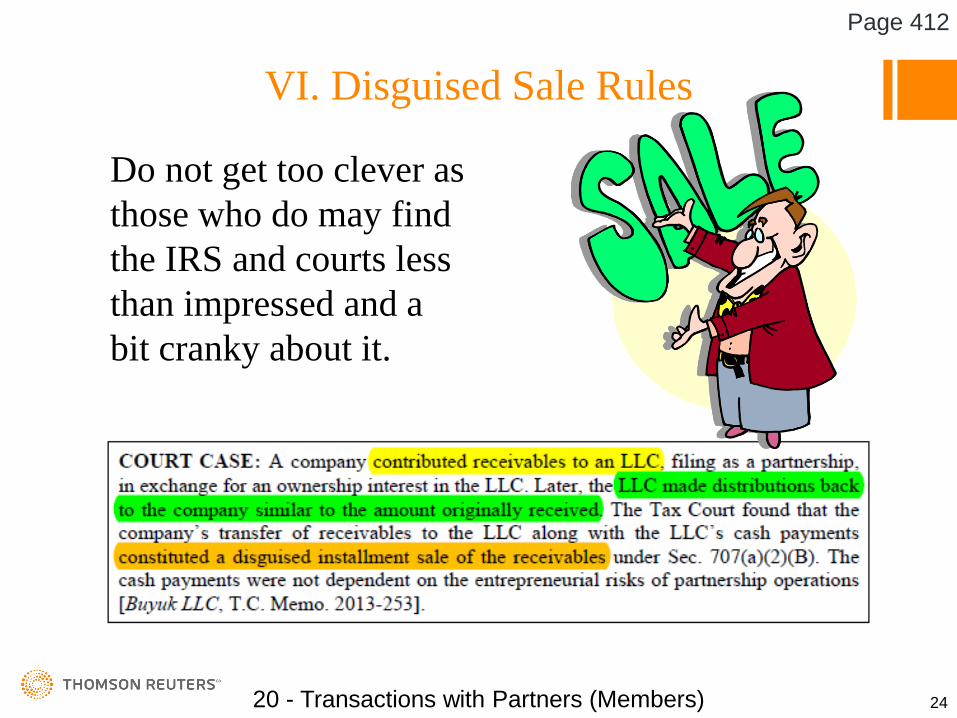

Do not get too clever as those who do may find the IRS and courts less than impressed and a bit cranky about it.

20 - Transactions with Partners (Members) 24

Page 412

VI. Disguised Sale Rules

J. The rules are not meant to prevent future payments to the contributing partner if:

20 - Transactions with Partners (Members) 25

Page 413

VII. 2016 Amendments to Disguised Sale Rules Treatment of Debt

The final rules are designed to separate types of debt associated with disguised sales:

Qualified DebtNon-Qualified Debt

20 - Transactions with Partners (Members) 26

Page 413

VII. 2016 Amendments to Disguised Sale Rules Treatment of Debt

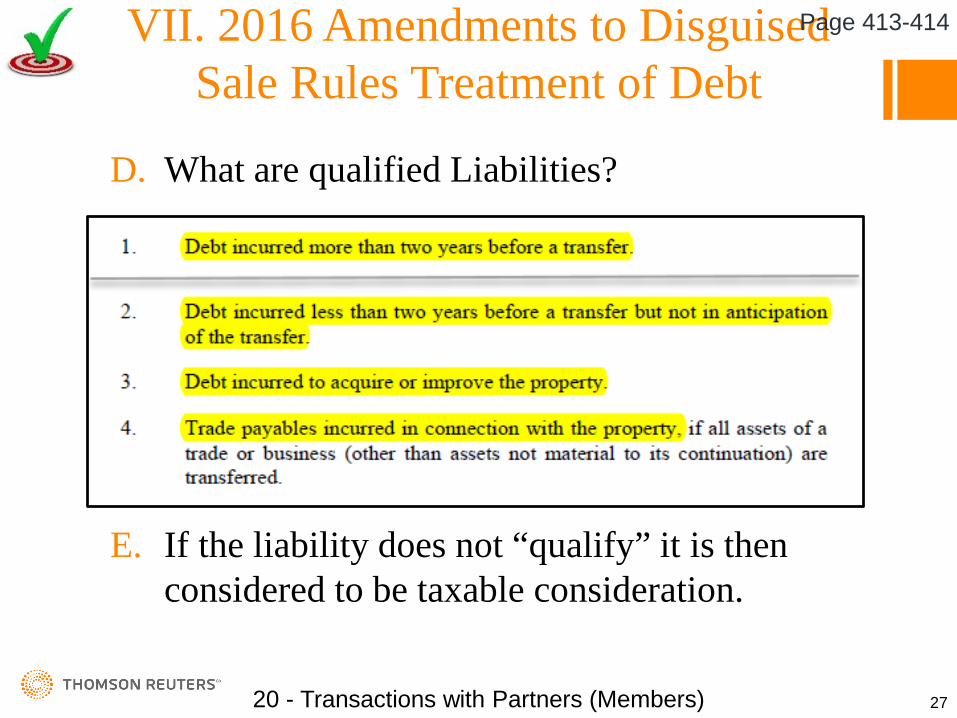

D. What are qualified Liabilities?

E. If the liability does not “qualify” it is then considered to be taxable consideration.

20 - Transactions with Partners (Members) 27

Page 413-414

VII. 2016 Amendments to Disguised Sale Rules Treatment of Debt

What happens with liabilities?F. Recourse liabilities are qualified only to the

extent of the FMV of the property.G. Debt within two years of transfer is presumed

to be non-qualified.H. Disguised sales from partnership to partner

qualified liabilities are those older than two years.

I. Qualified debt is the lesser of the debt transferred or FMV of the property transferred.

20 - Transactions with Partners (Members) 28

Page 413

VII. 2016 Amendments to Disguised Sale Rules Treatment of Debt

What happens with liabilities?J. Non-qualified liabilities transferred are

disguised sale consideration.

20 - Transactions with Partners (Members) 29

Page 414-415

VII. 2016 Amendments to Disguised Sale Rules Treatment of Debt

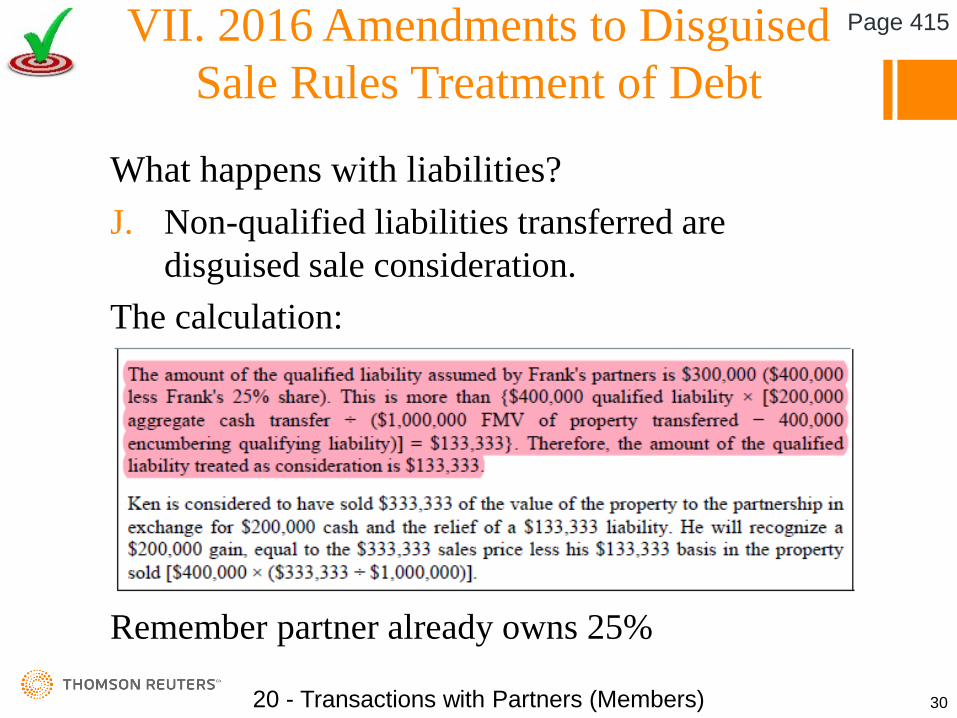

What happens with liabilities?J. Non-qualified liabilities transferred are

disguised sale consideration.The calculation:

Remember partner already owns 25%

20 - Transactions with Partners (Members) 30

Page 415

VII. 2016 Amendments to Disguised Sale Rules Treatment of Debt

The cautionary issues:K. Liabilities are based on

partnership interestsM. A partner cannot be allocated

100% of liabilities encumbering contributed property.

N. Qualified liabilities will NEVER be taken into account as consideration taxable by the transferor.

20 - Transactions with Partners (Members) 31

Page 415

VII. 2016 Amendments to Disguised Sale Rules Treatment of Debt

The Bad News:Contribution of leveraged assets that were subject to disguised sale rules must be determined by PIP

20 - Transactions with Partners (Members) 32

Page 416

VIII. Disguised Sale Tax Return Disclosure Requirements

A. Disclosure is required if:1. Transfer of property occurs within two years

and is not treated as a disguised sale.2. The transferor partner treats debt incurred

within two years of the transfer as qualified debt.

B. Disclosure is made in one of two manners: Form 8275-R On a statement attached to the return

20 - Transactions with Partners (Members) 33

Page 416

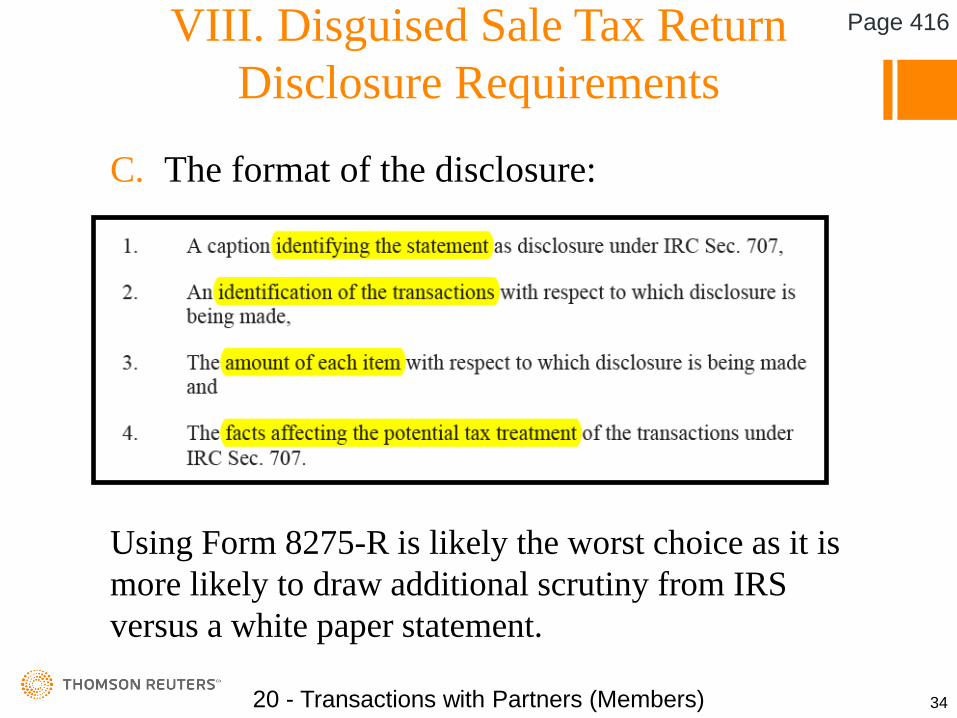

C. The format of the disclosure:

Using Form 8275-R is likely the worst choice as it is more likely to draw additional scrutiny from IRS versus a white paper statement.

20 - Transactions with Partners (Members) 34

Page 416VIII. Disguised Sale Tax Return Disclosure Requirements

In an attempt to sell tax credit to a partner the court found the transfer of credits from the partnership to a partner was in fact a disguised sale.An attempt to defer the credits also failed.

20 - Transactions with Partners (Members) 35

Page 417VIII. Disguised Sale Tax Return Disclosure Requirements

VIII. Related Party Transactions

Date of beneficial interest is controlling not when you “received” property in community property state:

20 - Transactions with Partners (Members) 38

Page 419

X. Gain (Loss) Triggered by Distributionof Precontribution Gain (Loss) Property

If IRC 704(c) property is distributed by partnership prior to 7 years then gain is recognized by contributing partner based on FMV on date of distribution.

The good news step up in basis for the partner.

20 - Transactions with Partners (Members) 39

Page 419

X. Gain (Loss) Triggered by Distributionof Precontribution Gain (Loss) Property

How it works:

20 - Transactions with Partners (Members) 40

Page 420

X. Gain (Loss) Triggered by Distributionof Precontribution Gain (Loss) Property

When there is a pre-contribution loss that loss can only be recognized by the partner contributing that loss:

20 - Transactions with Partners (Members) 42

Page 405

XI. Precontribution Gains onCertain Partnership Distributions

The provisions of IRC 737 do not apply if: Cash distributions exceed a partner’s outside

basis. IRC 737 is only triggered by non-cash

distributions. Property with “built in losses” that is distributed

is not subject to these rules.

20 - Transactions with Partners (Members) 43

Page 421-422

XII. IRC 754 Election

The election to bring inside and outside basis together

20 - Transactions with Partners (Members) 44

Page 422

XII. IRC 754 Election

A. Allows the partnership to elect to adjust the basis of its property when:

1. A distribution is made of the property of the partnership or

2. There has been a transfer of a partnership interest

20 - Transactions with Partners (Members) 45

Page 422

XII. IRC 754 Election

B. The election will require that:1. Once made its provisions are

mandatory for BOTH transfers of interest AND distributions of property

2. Will apply for the year of the election is made and all future years until the election is revoked with the permission of the commissioner

20 - Transactions with Partners (Members) 46

Page 422

XII. IRC 754 Election

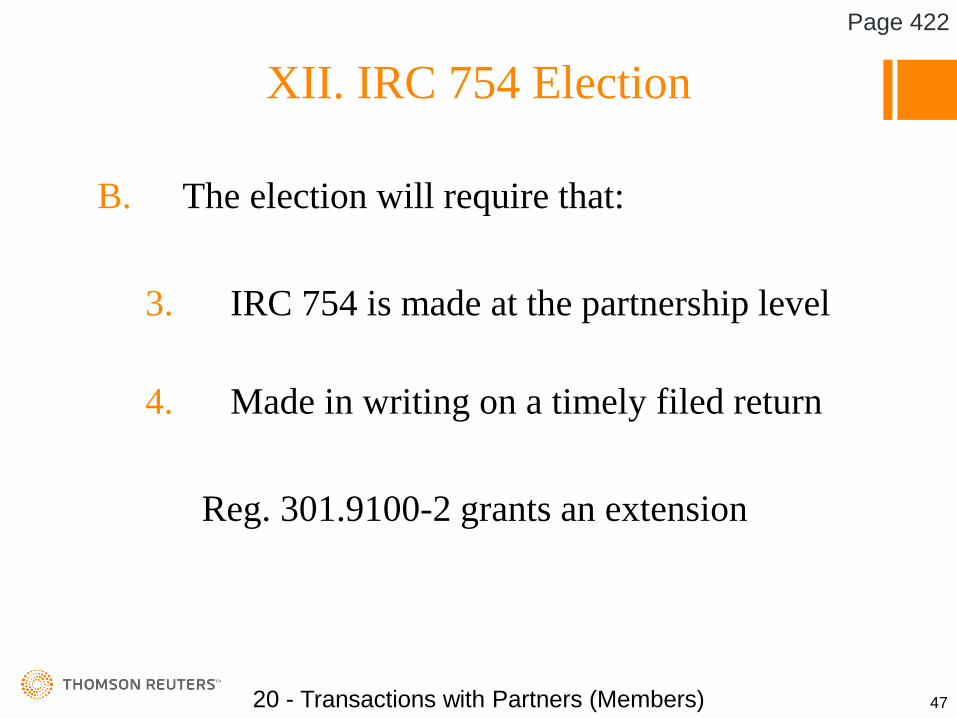

B. The election will require that:

3. IRC 754 is made at the partnership level

4. Made in writing on a timely filed return

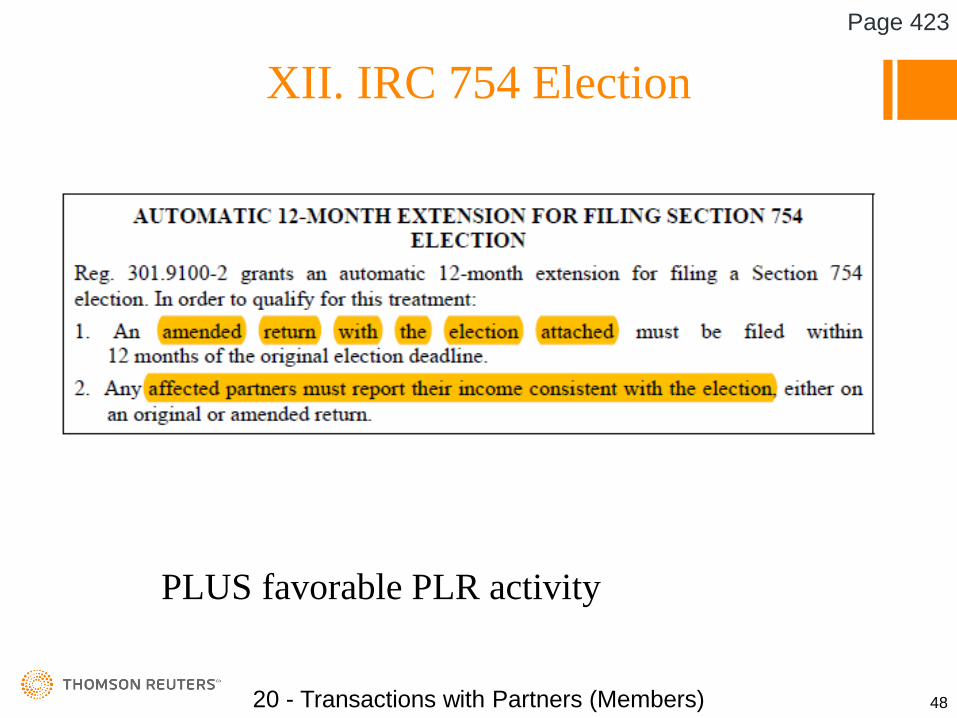

Reg. 301.9100-2 grants an extension

20 - Transactions with Partners (Members) 47

Page 422

PLUS favorable PLR activity

XII. IRC 754 Election

20 - Transactions with Partners (Members) 48

Page 423

Note that the election must be attached to both the 1065 and Affected Partner’s 1040 in the year of

election

XII. IRC 754 Election

20 - Transactions with Partners (Members) 49

Page 423

XII. IRC 754 Election

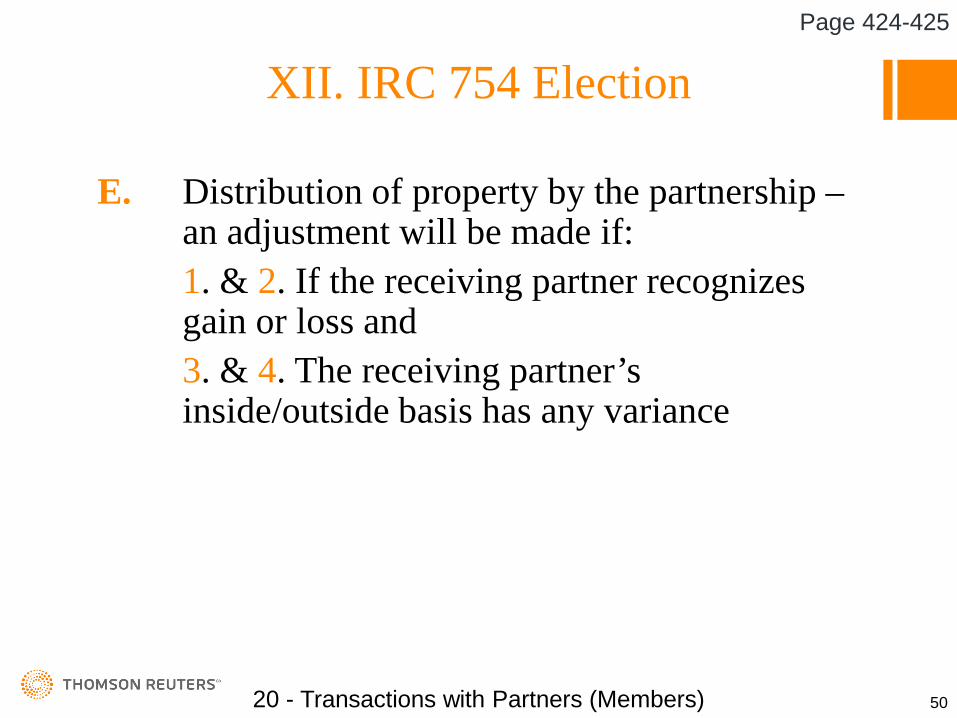

E. Distribution of property by the partnership –an adjustment will be made if:1. & 2. If the receiving partner recognizes gain or loss and 3. & 4. The receiving partner’s inside/outside basis has any variance

20 - Transactions with Partners (Members) 50

Page 424-425

XII. IRC 754 Election

F. Consider prior to making election

1. Increased bookkeeping

2. Adjustments are required for both positive and negative of any sales or liquidations of partner interestsNote the comprehensive examples

Page 425-426

20 - Transactions with Partners (Members) 51

Page 425

XII. IRC 754 Election

The most prevalent adjustment is that made when a partner dies and his/her interest is adjusted to reflect the FMV at the date of death

The assets of the partnership should be appraisedAn adjustment will be made to the partner’s share of

the asset on the books of the partnershipAny step-up on depreciable property will be taken

on the partnership’s books and allocated to the partner as an IRC 754 adjustment

20 - Transactions with Partners (Members) 52

Page 405

XII. IRC 754 Election

< $700,000=< $300,000=

20 - Transactions with Partners (Members) 53

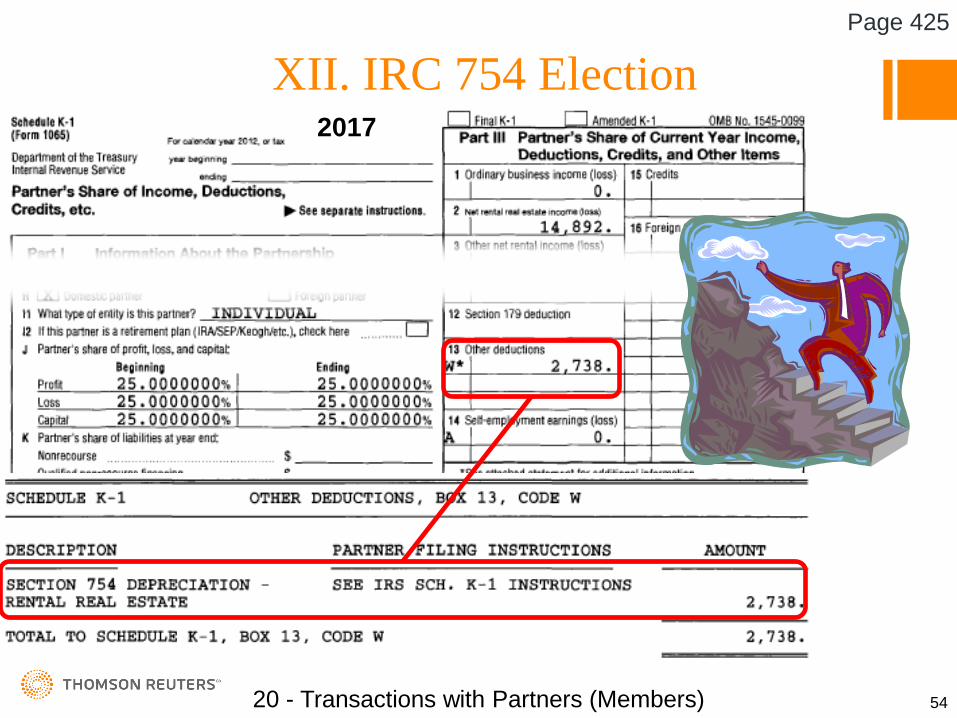

Page 425

XII. IRC 754 Election2017

20 - Transactions with Partners (Members) 54

Page 425