ANNUAL REPORT - Central Bank of Eswatini

216

UMNTSHOLI WEMASWATI ANNUAL REPORT APRIL 2016 - MARCH 2017 CENTRAL BANK OF SWAZILAND UMNTSHOLI WEMASWATI

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of ANNUAL REPORT - Central Bank of Eswatini

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

i

UMNTSHOLI WEMASWATI

ANNUAL REPORTAPRIL 2016 - MARCH 2017

CENTRAL BANK OF SWAZILANDUMNTSHOLI WEMASWATI

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

ii

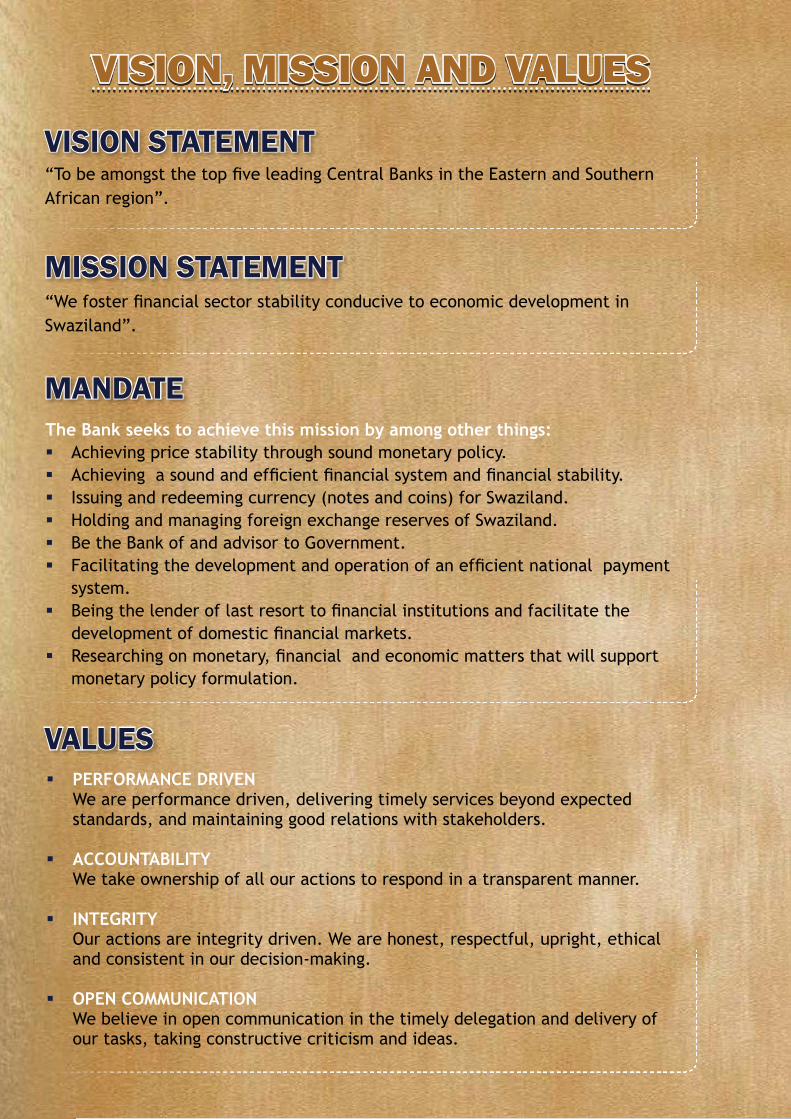

VISION, MISSION AND VALUES

VISION STATEMENT

MISSION STATEMENT

MANDATEThe Bank seeks to achieve this mission by among other things: � Achieving price stability through sound monetary policy.� Achievingasoundandefficientfinancialsystemandfinancialstability.� Issuing and redeeming currency (notes and coins) for Swaziland.� Holding and managing foreign exchange reserves of Swaziland.� Be the Bank of and advisor to Government.� Facilitatingthedevelopmentandoperationofanefficientnationalpayment

system.� Beingthelenderoflastresorttofinancialinstitutionsandfacilitatethe

developmentofdomesticfinancialmarkets.� Researchingonmonetary,financialandeconomicmattersthatwillsupport

monetary policy formulation.

“WefosterfinancialsectorstabilityconducivetoeconomicdevelopmentinSwaziland”.

“TobeamongstthetopfiveleadingCentralBanksintheEasternandSouthernAfrican region”.

� PERFORMANCE DRIVEN We are performance driven, delivering timely services beyond expected

standards, and maintaining good relations with stakeholders. � ACCOUNTABILITY We take ownership of all our actions to respond in a transparent manner. � INTEGRITY Our actions are integrity driven. We are honest, respectful, upright, ethical

and consistent in our decision-making. � OPEN COMMUNICATION We believe in open communication in the timely delegation and delivery of

our tasks, taking constructive criticism and ideas.

VALUES

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

1

EXECUTIVE BOARD MEMBERS

Mr. Majozi V. SitholeGovernor and Chairman

MrSitholeistheGovernoroftheCentralBankofSwaziland,aposition he has held since November 2013. Prior to this current position he held the political positions of: Minister for Finance (2001–2013); Minister of Economic Planning and Development(1998-2001); Elected Member of Parliament for MafutseniInkhundla (1998 – 2008); Appointed Member of Parliament (2008–2013).

Prior to engaging in a political career he was an academician and held the following positions: Research Assistant at University of Swaziland (UNISWA) 1981–1983, Research Fellow at UNISWA (1986–1994); Lecturer in Economics Department (1986–1998);Research Associate in Women and Law in Southern Africa. Majozi is a Fulbright Scholar (Iowa State University 1996/97) and holds academic qualifications which include a B.A. Social SciencesinEconomicsandAccountingfromUNISWA,1981andanM.Sc.AgriculturalEconomicsfromtheUniversityofAlberta,Canada,1986; and a few post graduate diplomas. He has attended many LeadershipTrainingPrograms,EmotionalIntelligenceWorkshopsand Strategy Formulation Workshops both locally and externally. He has done consultancy work while working at UNISWA. His area ofspecializationisTransportationEconomics,ProjectEvaluation,andAgriculturalEconomics.

Mr Sithole has an extensive administration experience including being Head of the Department of Economics at UNISWA,ChairmanandSecretaryGeneraloftheAssociationofLecturersand Academic Personnel of the UNISWA, Governor of IMF/WB and Governorof theAfricanDevelopmentBank. Hehasproducedover 40 papers, some of which have been published in research journals,referredjournalsandforspecificconferencepapers.

He is currently a board member of the Swaziland Revenue Authority,SwazilandEconomicPolicyandResearchCentreandalso serves as an Executive Committee Member of the MEFMISecretariat.

Mr. Mhlabuhlangene P. DlaminiDeputy Governor

Mr Dlamini is the Deputy Governor of the Central Bank ofSwaziland, a position he has held since November, 2015. Prior to this current position he has held the following:-BoardSecretaryandHeadLegalattheCentralBankofSwazilandfrom2008–2015;LegalOfficerattheCentralBankofSwazilandfrom 2007 – 2008; Partner at Magagula & Hlophe Attorneys; ManagerLegalComplianceStandardBank(Swaziland)Limited;CompanySecretary,Stanlib(Swaziland)andCandidateAttorneyatMillin&CurrieAttorneys.Mr Dlamini was a part-time Law Lecturer at the Universityof Swaziland Distance Education Unit. He holds professionaladmissionasanAttorneyoftheSupremeCourtofSwazilandandthefollowingacademicqualifications:• ABritishScheveningScholar;• MasterofLawsinBankingandFinancialRegulation(Kings

College–UniversityofLondon)–(Non-degreed);• MasterofLawsMerchantileLaw(StellenboschUniversity)–

(Degreed);• BachelorofLaws(RhodesUniversity-(Degreed);• BachelorofArtsinLaw–UniversityofSwaziland–(Degreed,

1994; Currently, he is a board member of the Swaziland RevenueAuthority;SwazilandPostandTelecommunicationsCorporation;and Lomati Mine (Pty) Ltd.

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

2

Ms. Refiloe M. Mamogobo Board Secretary

Ms Mamogobo is the Head Legal and Secretary to the Board of DirectorsoftheCentralBankofSwaziland.SheholdsaBachelorof LawsDegree (LLB) awarded in 2000andaBachelor ofArtsDegree(B.ALaw)awardedin1998.

She was admitted and enrolled as an attorney of the High CourtofSwazilandinOctober,2001.ShewasalsoadmittedandenrolledasaConveyancerJune,2006andfurtheradmittedandenrolled as a Notary Public in March, 2011.

She has served in several boards and including being President of theMalkernsTownBoardEvaluationCourt,MatsaphaTownBoardEvaluationCourtandNgwenyaTownBoardEvaluationCourt.

She has also served as a board member of the Swaziland Railways, RoyalSwaziNationalAirwaysCorporationandthePrinceLindaniFoundation.

ShehasalsoservedasProBonoCounselfortheSavetheChildrenFund and prosecutor for the Premier League of Swaziland. Ms MamogobowasfurtherappointedtotheCommissionofEnquirytolookintotheaffairsoftheMunicipalCouncilofMbabaneandservedasanExecutiveMemberoftheCounciloftheLawSocietyof Swaziland – 2001/2002 : 2004/2005 and 2007/ 2008.

ABRIDGED PROFILE OF BOARD MEMBERS

Mr. Bheki S. BhembeEx-Officio Member, Principal Secretary Ministry of FinanceNon-Executive Board Director

Mr Bhembe has been the Principal Secretary for the Ministry of Finance since 2014. Prior to his appointment as the Principal Secretary, he held the position of Budget Director within theMinistry of Finance between 2009 and 2014. Mr Bhembe is an economist by profession with extensive experience in the public sector having served over seven years as a planning officer oreconomist in various departments of the Ministry of EconomicPlanningandDevelopment.Hehasalsoworkedasaneconomistand statistician for the Central Bank of Swaziland and theSwaziland Railway respectively.

HeholdsaMasterofArtsdegreeinDevelopmentEconomicsfromWilliamsCollege,MA,USA,completedinJune2005.Hecompletedhis Bachelor of Arts’ Degree in 1997 from the University ofSwaziland.MrBhembecurrentlyservesasanAlternateExecutiveDirectorintheAfricanDevelopmentBankrepresentingLesotho,Swaziland and South Africa in the Board and as an ExecutiveCommitteeMemberoftheMEFMISecretariat.Healsohasservedin various boards within the country such as the Swaziland Development and Savings Bank, Swaziland Revenue Authority,NationalEmergencyResponseCouncilonHIV/AIDS,UniversityofSwazilandandSwazilandEnvironmentAuthority.

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

3

Mr. Daniel M. ShabanguNon-Executive Board Director

Mr Shabangu began his career as an Investment Analyst with BakerWilliams&AssociatesinCapeTown,whereheacquiredallroundskillsincorporatefinanceadvisory,dealingprimarilywithlisted companies. He has been exposed to the practical aspects ofpublicfinance,handlingSOEsatthePEU,MinistryofFinance.HewasHead of loans& Equities at SIDCwith responsibilitiesin origination, structuring and execution of project financetransactions.

Mr Shabangu holds a BSc (Maths & Physics) from UNISWA and a BBusSci(Finance)fromtheUniversityofCapeTown(UCT)andanMBA(finance)fromMaastrict,Holland.HewonaCASHPrizeineconomicsatUCTandhisMBAwasawardedwithdistinction.HeisanAlumniofINSEADBusinessSchoolinParis,France.

He has served in a number of Boards of companies locally, including Swazican, then Protea Hotel, Swaziland Water Services Corporation,Swaprop,SwaziPlazaProperties,tonameafew. MrShabanguhasadvisedbroadlyongreenfieldtransactionsacrossvarious industries including telecommunications, pulp & paper, insuranceandWaterreticulation(SD),oil&gas(Mozambique),mining(Zimbabwe)andOilRefining(Namibia).HeispresentlyaDirectorofSalueloCapital,aspecialistprojectFinanceadvisorycompany focusing on the origination, preparation and capital raisingforimpactfulgreenfieldprojectsregionally.

Mrs. Adelaide S. DlaminiNon-Executive Board Director

Mrs Dlamini is recently retired from the employ of TibiyoTakaNgwane having served the organization and its affiliatedcompanies for thirty years, entering at grass-roots level and culminating in the management cadre. She serves in various companies’BoardsofDirectors,rangingfromagriculture,leisure,propertyandfinanceindustries.SheoftensitsintheRemCoandAuditSub-Committeesofthese,mainly,asChairmanormember.She has a robust knowledge of retirement funds having served as a Trustee for both pension and provident funds for over twenty years.

SheholdsaBachelor’sDegreeinAccountingwhichsheobtainedin1976fromCuttingtonUniversityinLiberia,anMBAinCorporateFinance in 1986 from the Adelphi University, Long Island, New York and a Chartered Global Management Accountant (CGMA)obtainedin2010fromCIMA,UnitedKingdom.

She received with honour His Majesty’s 45th Anniversary Medal for Good National Service bestowed at the Lozitha Royal Residence in 2014byHisMajestyKingMswatiIII.

ABRIDGED PROFILE OF BOARD MEMBERS

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

4

Dr. Khanyisile D. DlaminiNon-Executive Board Director

Dr. Dlamini is passionate in nurturing small businesses andentrepreneurs to reach their full potential. She is the founder and director of TOWAK Consultancy, a financial andbusiness management consulting firm that has footprintsin Swaziland and South Africa. She specializes in designing funding models, conducting financial due diligence, financialwellness, training on managing finance, mentorship, as wellas conducting commissioned market surveys. She mainly works with government departments, private companies, non-governmental organisations and micro small and medium enterprises. Previously, she was a lecturer at the University of SwazilandandUniversityofDerby,UKandhasbeenavisitinglecturer at California State Polytechnic University, Pomona,USA.

Dr Dlamini completed her Bachelor of Commerce Degree in1990 from the University of Swaziland and a Master of Business Administration from De Montfort University, Leicester, UK in1994.ShefurtherobtainedaGraduateDiplomainMarketingin1995fromTheCharteredInstituteofMarketing,London,UK.In2006shecompletedaDegreeofDoctorofPhilosophyinSMEandEconomicDevelopmentfromAstonUniversity,Birmingham,UK.Dr Dlamini sits in several boards including, Central Bank ofSwaziland, Greystone Partners Limited, Central TransportOrganisation and a Trustee for the Swaziland Royal Insurance Corporation Preservation Provident Fund and Swaziland RoyalInsurance Pension Fund.

ABRIDGED PROFILE OF BOARD MEMBERS

Professor Mike S. MatsebulaNon-Executive Board Director

Professor Matsebula is an independent economist, having retired fromthepositionofCEOattheSwazilandSugarAssociationwhereheservedfor19years.Previously,hewasanEconomicsProfessorat the University of Swaziland. He completed his Bachelor’s Degreein1972atthethenUniversityofBotswana,LesothoandSwaziland (now National University of Lesotho); completed his Master’s Degree in Economics at theUniversity ofManitoba inWinnipeg,Canadain1975;andcompletedhisDoctorateDegreeinEconomicsatQueen’sUniversity,Ontario,Canadain1981.

Professor Matsebula has published extensively on various issues related to the Swazi economy, regional economic integration as well as international economic relations. He has made several presentations at national and international conferences. He subscribes to the King Code of Corporate Governance and hasbeen involved with its application in a few enterprises. He is a non-executive director of a few companies.

Professor Matsebula has been decorated twice with national honours in recognition of his meritorious efforts. These are the Royal Order of Sobhuza II, Chief Counsellor (awarded in 1992)and the Order of Eswatini, Rank of Commander (awarded inSeptember 2008).

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

5

ABRIDGED PROFILE OF BOARD MEMBERS

Dr. Sikhomba C. Gumbi Non-Executive Board Director

DrGumbiistheChiefExecutiveofREDI,aleadingmanagementconsulting services company based in Swaziland but with a regional footprint. He specializes in Leadership, Strategy and Governance.HeisaCertifiedProjectManagerandAccreditedCorporate Governance Facilitator. He has served as ProjectDirectorforlongtermassignmentsfortheAfDB,COMESAandUSAfricanDevelopmentFoundation.InadditiontoseveralDiplomacertificates mainly in management and human resources, heholdsaBachelorofScience inAgricultureEducation,aMasterof Science (UNISWA), and aDoctor of Philosophy in EducationManagement (Walden). He has studied Quality ManagementProgrammes at the University Sians Malaysia, the World Bank Institute,UniversityofIllinois,Urbana-Champaign,USAandtheAsia Institute of Technology in Bangkok, Thailand. He has also done short term training in Finance and Strategy at Wits Business School and the Gordon Institute of Business Studies (GIBS). DrGumbi’spreviousboards’appointmentsincludeSwazilandPostandTelecommunicationsCorporation,ConciliationMediationandArbitrationCommission,theUniversityofSwaziland,SwazilandStandards Authority, the Scholarship Selection Board as well as Boards of Non-Governmental Organisations: SHAPE, CitizenEmpowermentCentreandGoneRuralBoMake.HeisaRotarianandpastPresidentof theMbabane-MbuluziRotaryClubwherehe is a Paul Harris Fellow. He was honoured for exceptional nationalservicebyHisMajestyKingMswatiIIIandbestowedwithHis Majesty’s 45th Anniversary Medal in 2014.

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

6

CENTRAL BANK OF SWAZILAND UMNTSHOLI WEMASWATI

OfficeoftheGovernorMahlokohla Street Tel: (+268) 2408 2111P.O.Box546 Telex:2029WD:MONASMbabane, Swaziland Fax: (+268) 2404-0013

10th August, 2017

SenatorMartinG.DlaminiHonourable MinisterMinistry of FinanceP.O. Box 443MBABANEH100

DearMinister

InaccordancewithSection52(1)oftheCentralBankOrderof1974,Ihavethehonourtotransmit:-

(i). A copy of the Financial Statements for the year ended 31stMarch,2017certifiedbyAuditors;and

(ii). AreportoftheCentralBankoperationsandactivitiesincludingcoverageofeconomicdevelopmentsduringthefinancialyear2016/17.

Yours faithfully

MajoziV.SitholeGovernor

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

7

DEPARTMENT MANAGEMENT

EXECUTIVE COMMITTEEGovernor

DeputyGovernorAssistant Governor

GM, Financial MarketsGM, Finance

GM, OperationsGM,EconomicPolicyResearch&Stats

GM, Financial Regulation Head of Internal Audit

Head of Risk Head of HR & Administration

Secretary to the Board & Head of Legal

M.V. SitholeM.P. DlaminiM.E. Dlamini M.M. Khomo P. NxumaloL.G. Dlamini S.S. DlaminiM.T. NkambuleR.T. Manyathi J.S. DlaminiVacantR.M. Mamogobo

HeadofICTHeadofStrategy&Communication

Head, Internal Affairs & SecurityManager, Statistics & Publications

Manager, BOP & International Affairs Manager, PRAMA

Manager, Settlements Manager,Compliance&Risk

Manager,Investments&DomesticMarketsManager, National Payments Systems

Manager,CurrencyManager, Banking

Manager, Bank Supervision Manager,Policy&Enforcement

Manager,ExchangeControlManager,ICT(Systems)

Manager, IT Infrastructure & Security Manager, Facilities

Manager, Human Resources Manager,Learning&OD

Manager, Financial Accounting Manager, Management Accounting

Manager,SupplyChain Manager, Financial Stability

Manager,Compliance&EthicsManager, Security & Protection Services

DeputyHeadofLegal

S.N. DlaminiZ.M. GinaS.G. FakudzeA.M. DlaminiJ.C. DlaminiP.B. NdzinisaS.M. NxumaloO.Z. MakhanyaN.I. MthethwaM.L. DlaminiZ.F. NkambuleR.M. MambaB.A. DlaminiM.A. MathunjwaB. N. GilbertS. K. GamaL. D. SacoloS. N. MotsaG.C. DlaminiP. K. Mthupha S.M. ManyatsiQ.T. JeleB.O. MotsaW.L. MotsaZ.N. SimelaneN.J. HlatshwayoS. N. Jele

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

8

TABLE OF CONTENTS

Acronyms & Abbreviations .............................................................................................. 12

1. Governor’s Statement .............................................................................................. 15

PART A - REVIEW OF THE ECONOMY ................................................................................... 19

2. Global Economic Developments ................................................................................. 202.1 Overview ........................................................................................................ 202.2 IndustrializedCountries ...................................................................................... 212.3 EmergingMarkets&DevelopingEconomies ............................................................... 232.4 EconomicDevelopmentsinSouthAfrica ................................................................... 252.5 RegionalDevelopments ....................................................................................... 26

2.5.1 Common Monetary Area ............................................................................. 262.5.2 Southern African Customs Union .................................................................. 262.5.3 Southern African Development Community ...................................................... 272.5.4 Common Market for Eastern and Southern Africa ............................................. 272.5.5 Other Regional & International Arrangements .................................................. 27

3. Domestic Economy .................................................................................................. 293.1 AnnualRealGDPDevelopments ............................................................................ 29

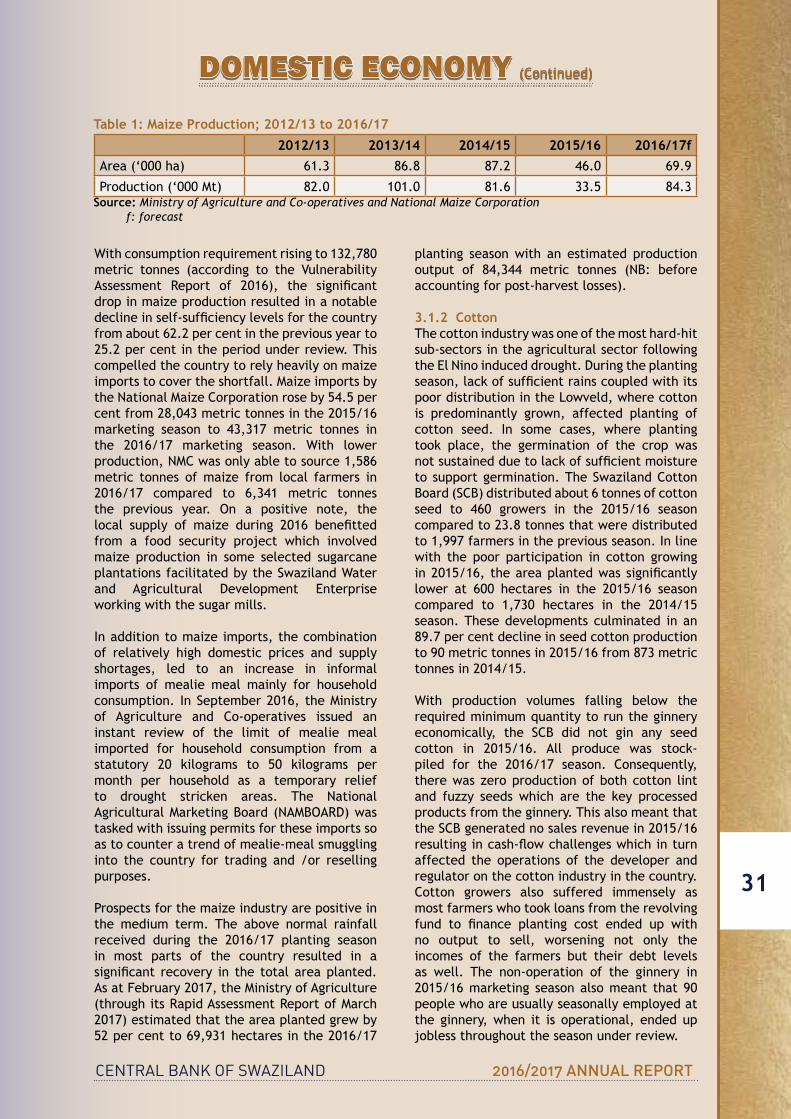

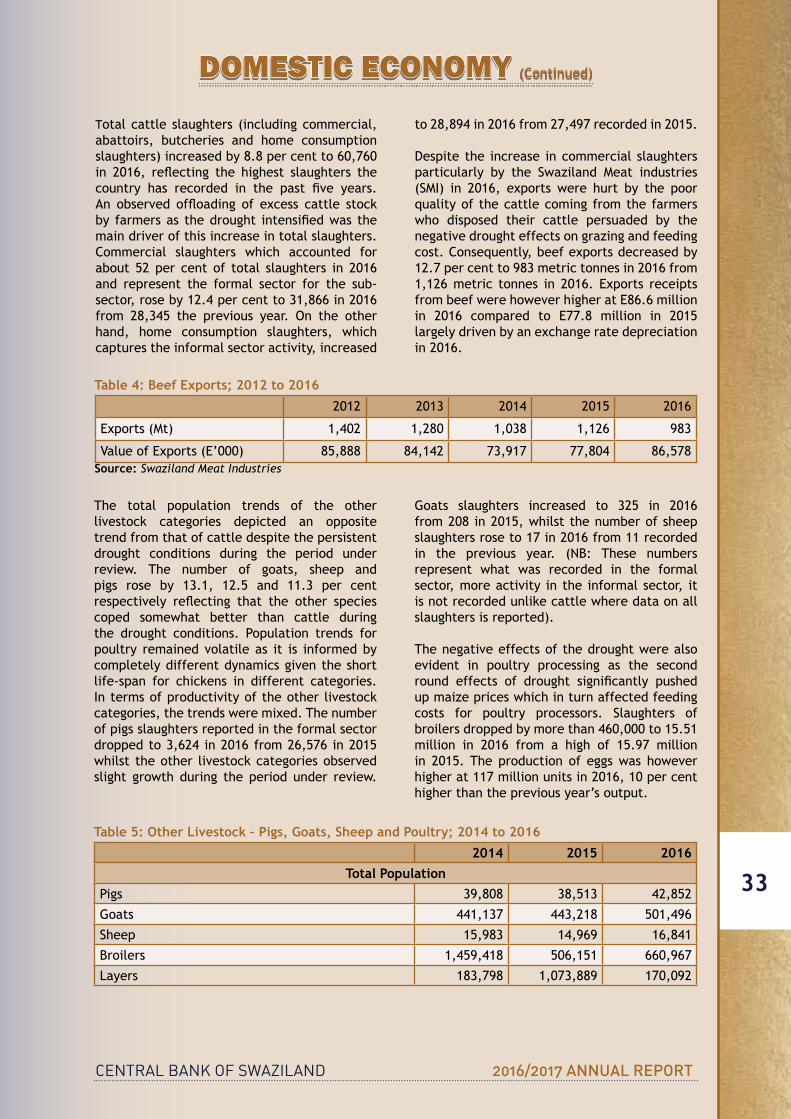

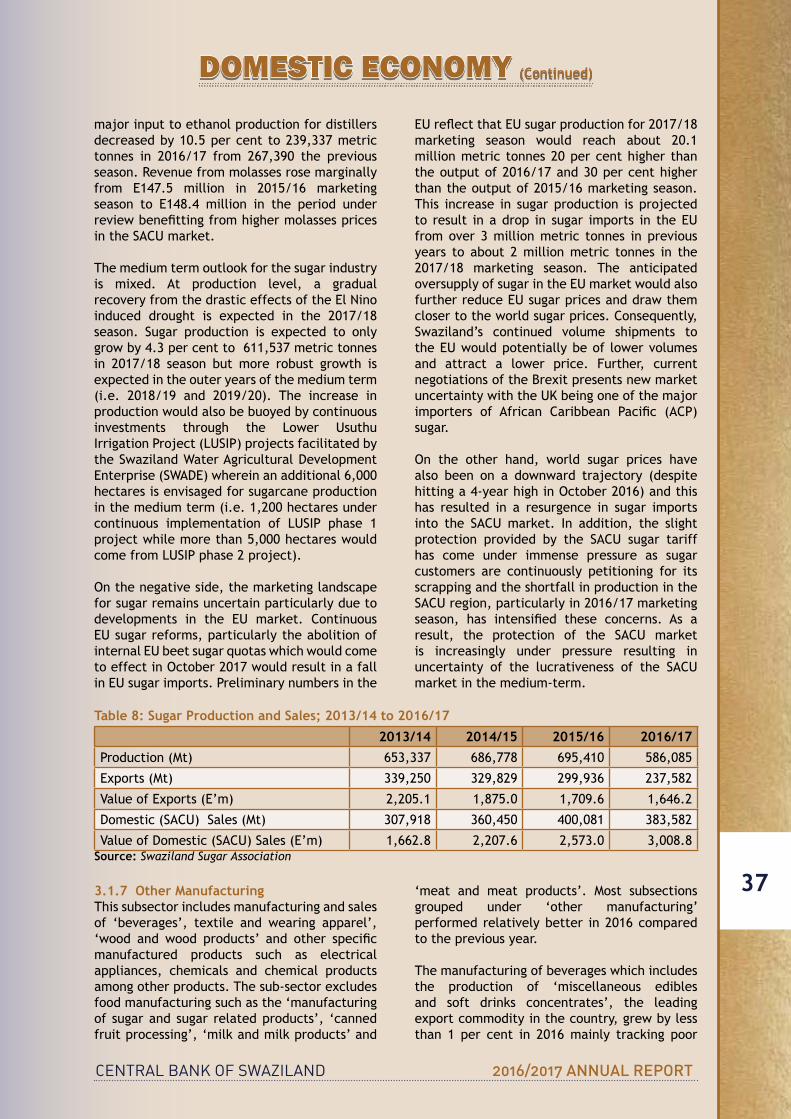

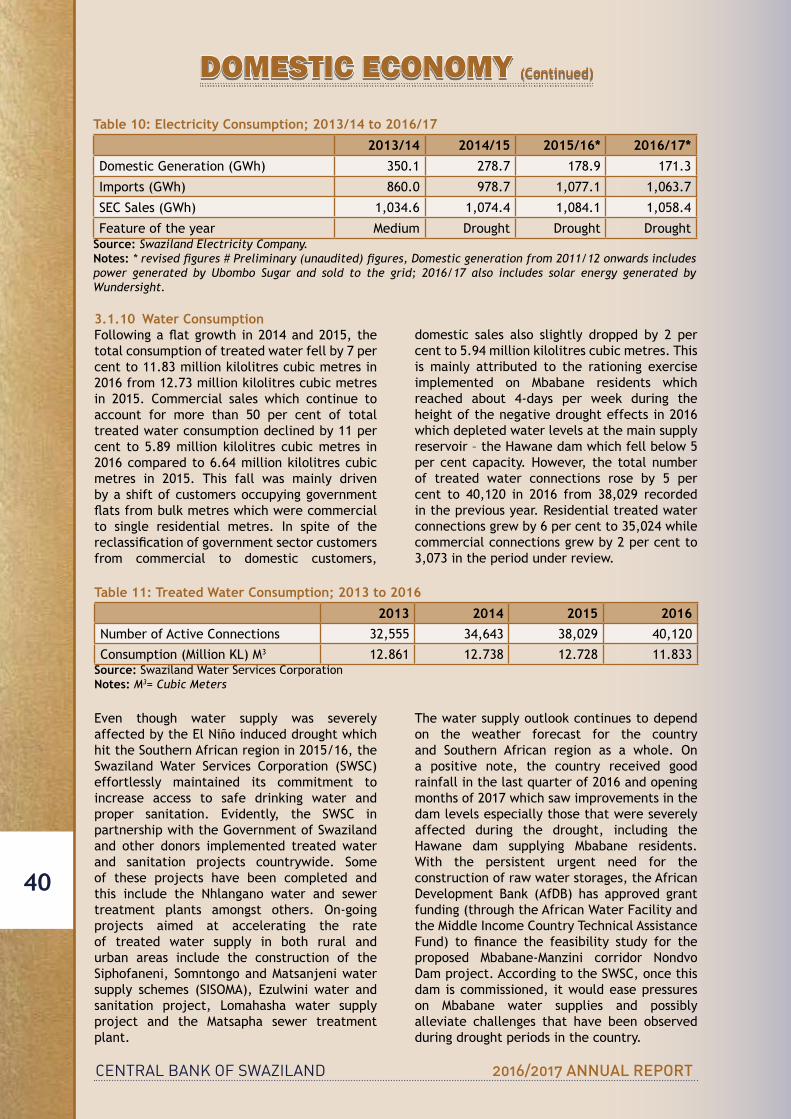

3.1.1 Maize .................................................................................................. 303.1.2 Cotton .................................................................................................. 313.1.3 Livestock ............................................................................................... 323.1.4 Milk/Dairy Production ............................................................................... 343.1.5 Mining and Quarrying ................................................................................ 353.1.6 Sugar ................................................................................................... 363.1.7 Other Manufacturing ................................................................................ 373.1.8 Construction .......................................................................................... 383.1.9 Electricity Consumption ............................................................................. 393.1.10 Water Consumption .................................................................................. 40

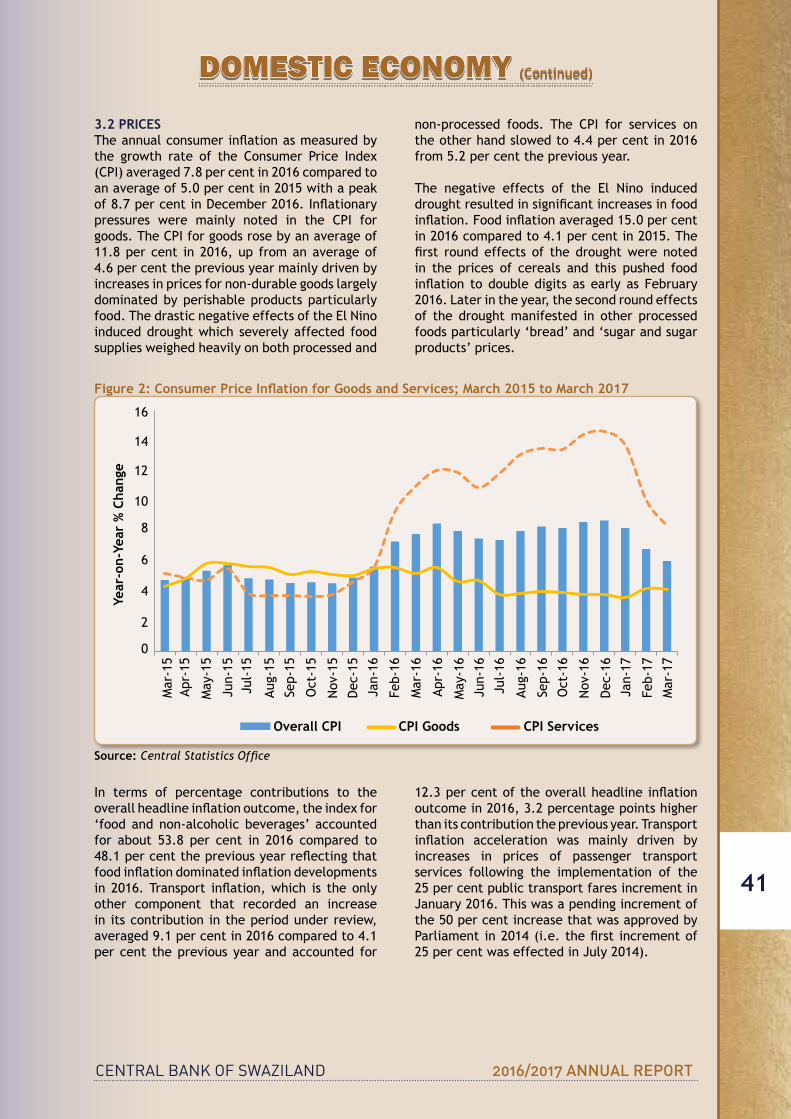

3.2 Prices ............................................................................................................ 41

4. Balance of Payments ............................................................................................... 434.1 ChangesintheBalanceofPaymentsandInternationalInvestmentPositionMethodology ........ 444.2CurrentAccount ................................................................................................ 45 4.2.1 Trade Account......................................................................................... 46

4.2.2 Services Account ...................................................................................... 464.2.3 Primary Income ....................................................................................... 464.2.4 Secondary Income .................................................................................... 46

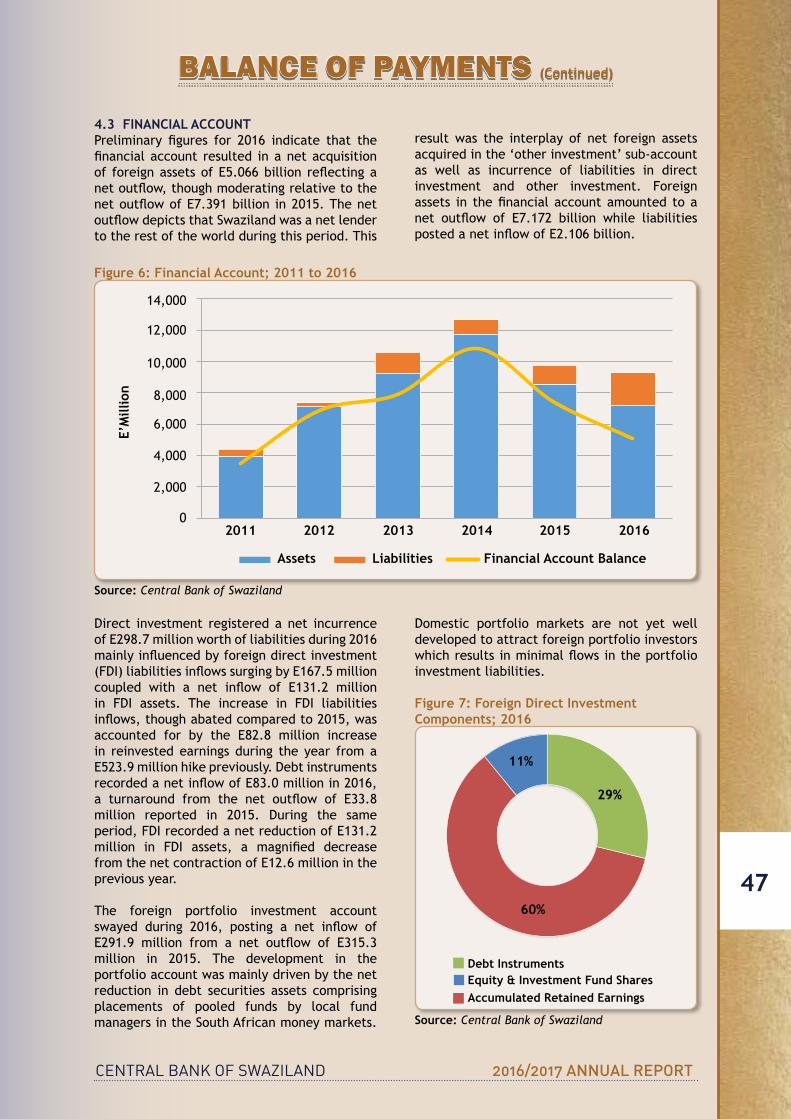

4.3 Financial Account ............................................................................................. 474.4 International Investment Position ........................................................................... 484.5 ExchangeRateDevelopments ................................................................................ 48

5. Monetary Developments ........................................................................................... 515.1 Overview ........................................................................................................ 51 5.2 Interest Rates .................................................................................................. 51 5.3 Statutory Reserve and Liquidity Requirements ............................................................ 525.4 DepositoryCorporationsSurvey ............................................................................ 53

5.4.1 Net Foreign Assets ................................................................................... 535.4.2 Domestic Claims (Net) ............................................................................... 535.4.3 Money .................................................................................................. 55

6. Public Finance ...................................................................................................... 576.1 The 2017/18 Government Budget Review and Analysis ................................................. 57

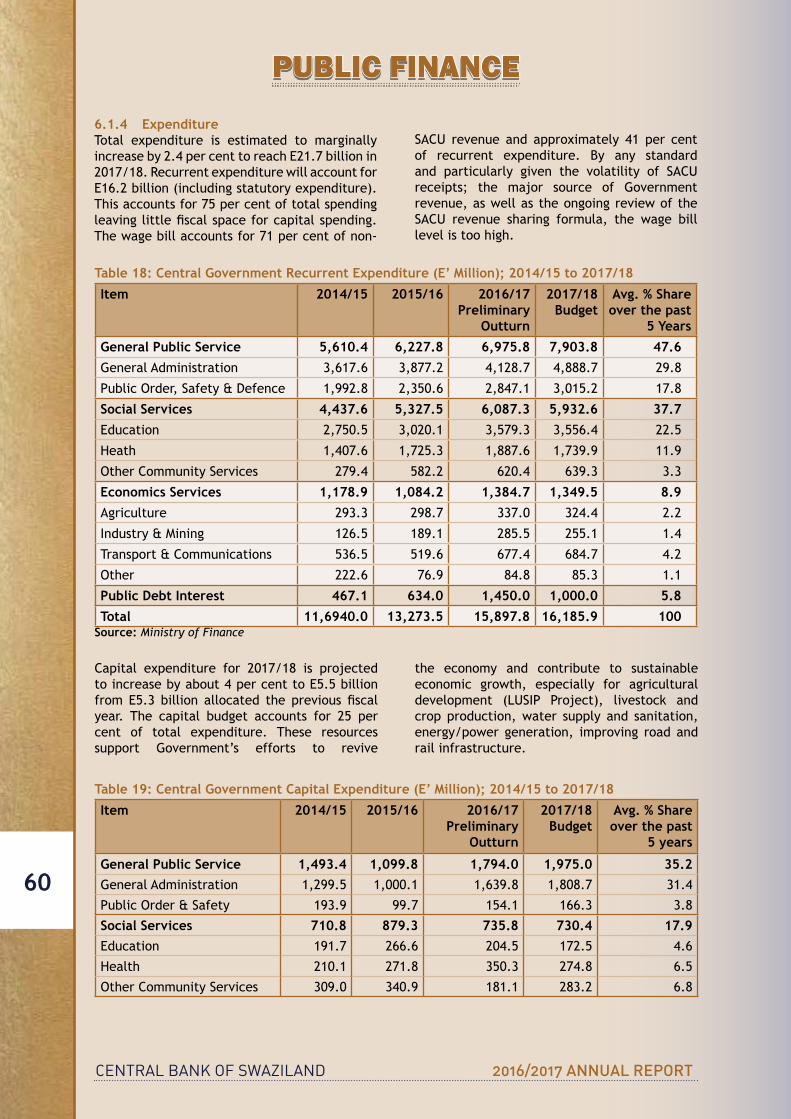

6.1.1 Introduction ........................................................................................... 576.1.2 Summary of Budget Estimates ..................................................................... 576.1.3 Revenue ................................................................................................ 586.1.4 Expenditure ........................................................................................... 60

6.2 BudgetDeficitFinancing ...................................................................................... 61

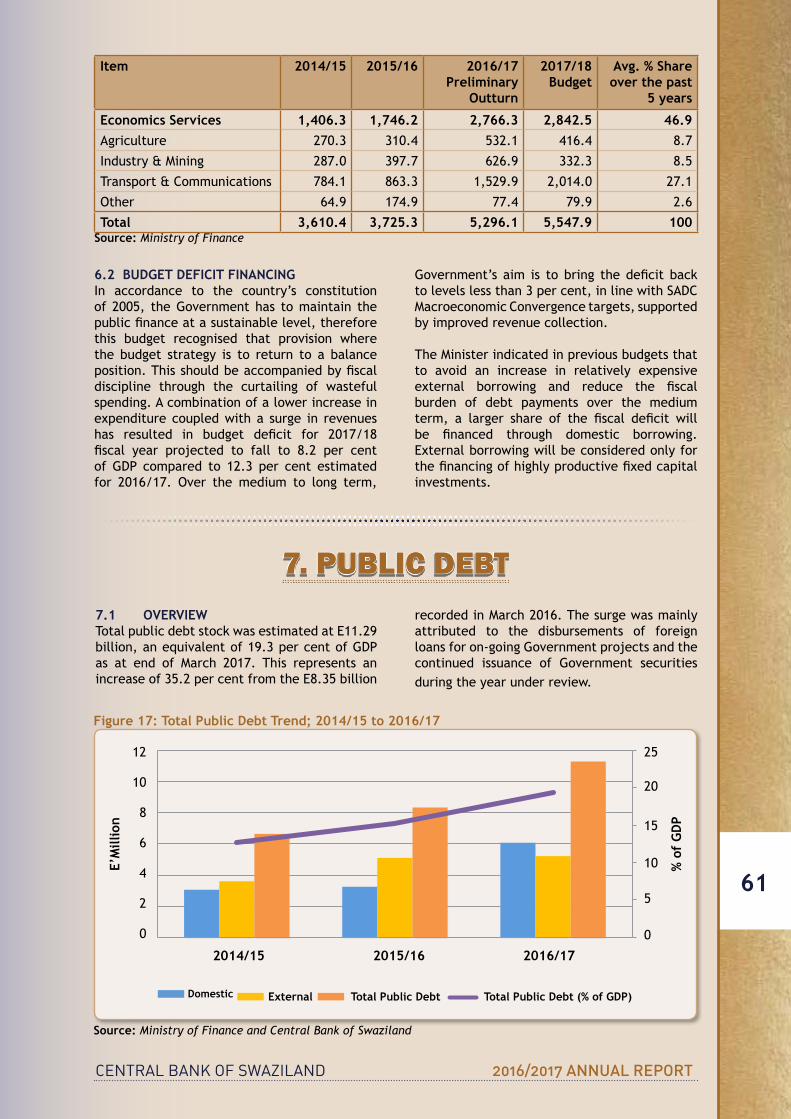

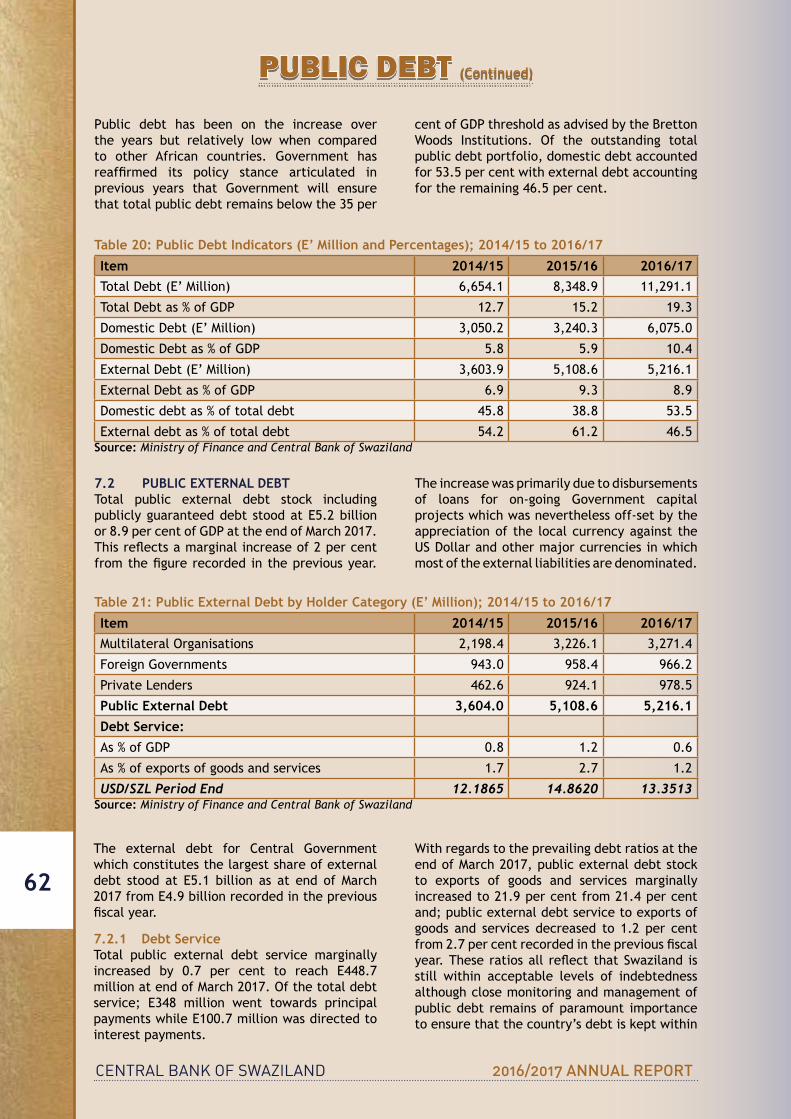

7. Public Debt......... .................................................................................................. 617.1 Overview ....................................................................................................... 617.2 PublicExternalDebt .......................................................................................... 62

7.2.1 Debt Service ........................................................................................... 627.2.2 Disbursements ........................................................................................ 63

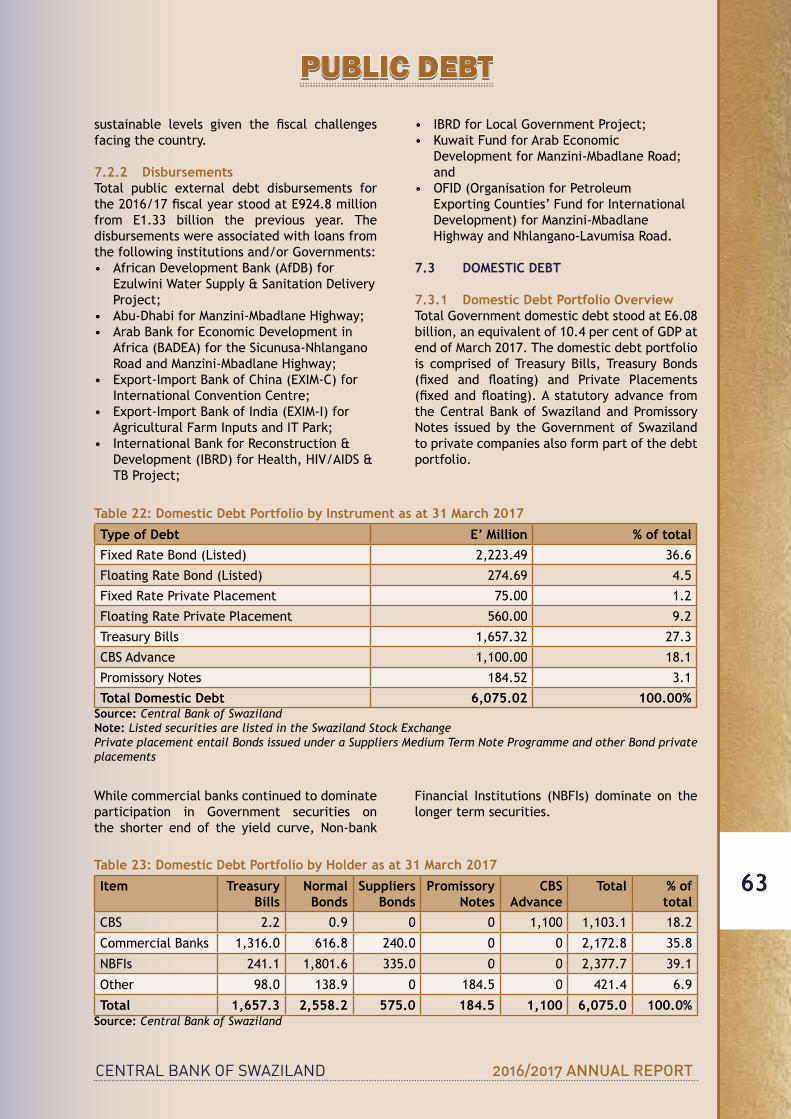

7.3 DomesticDebt ................................................................................................. 637.3.1 Domestic Debt Portfolio Review ................................................................... 63

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

9

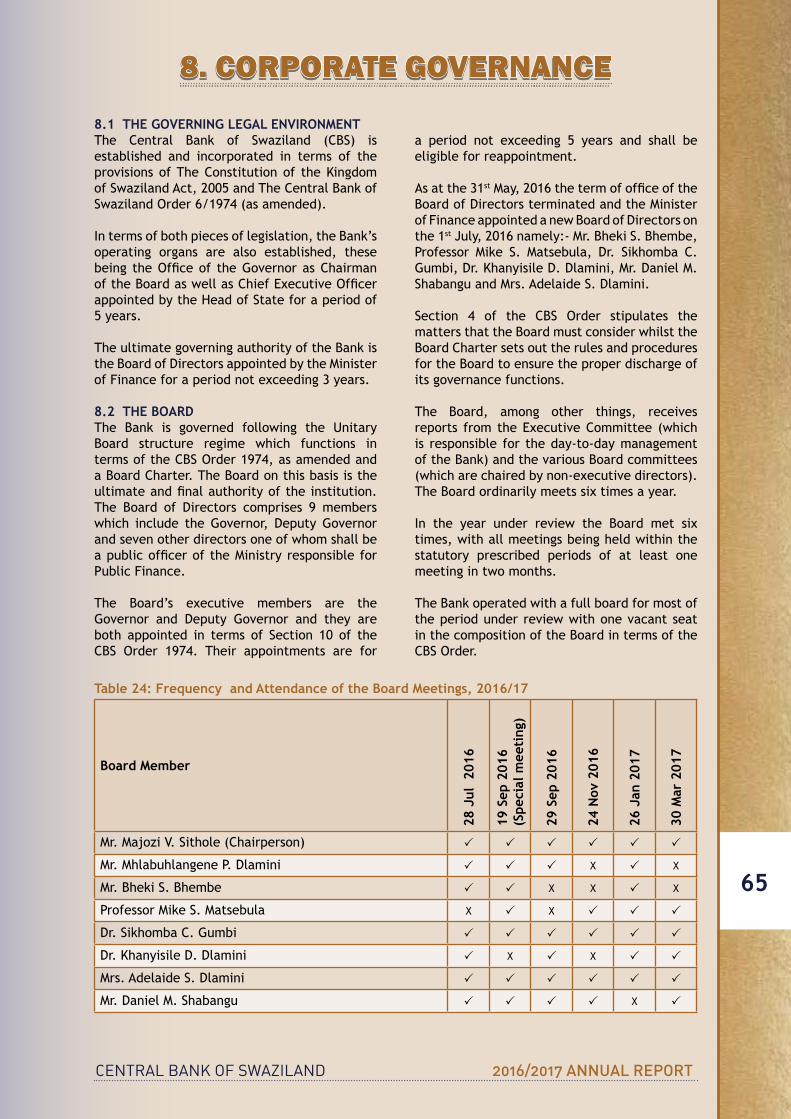

TABLE OF CONTENTSPART B - REPORT ON OPERATIONS ..................................................................................... 64 8. Corporate Governance ............................................................................................. 65

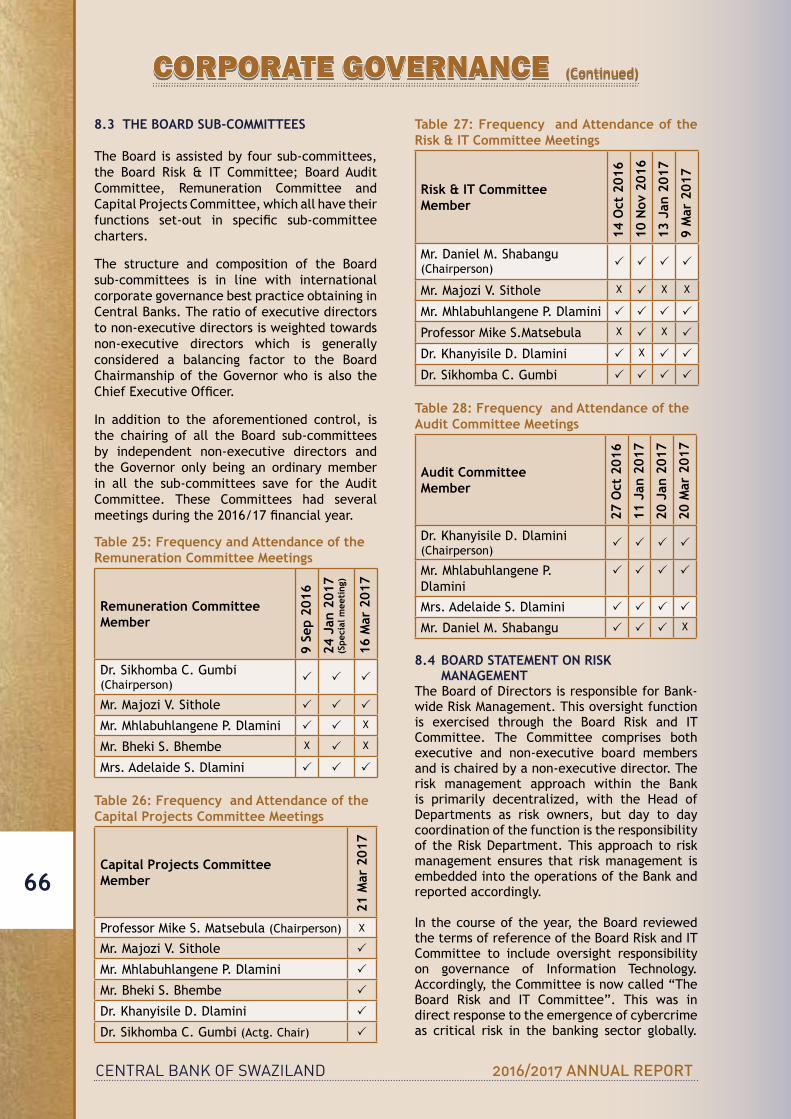

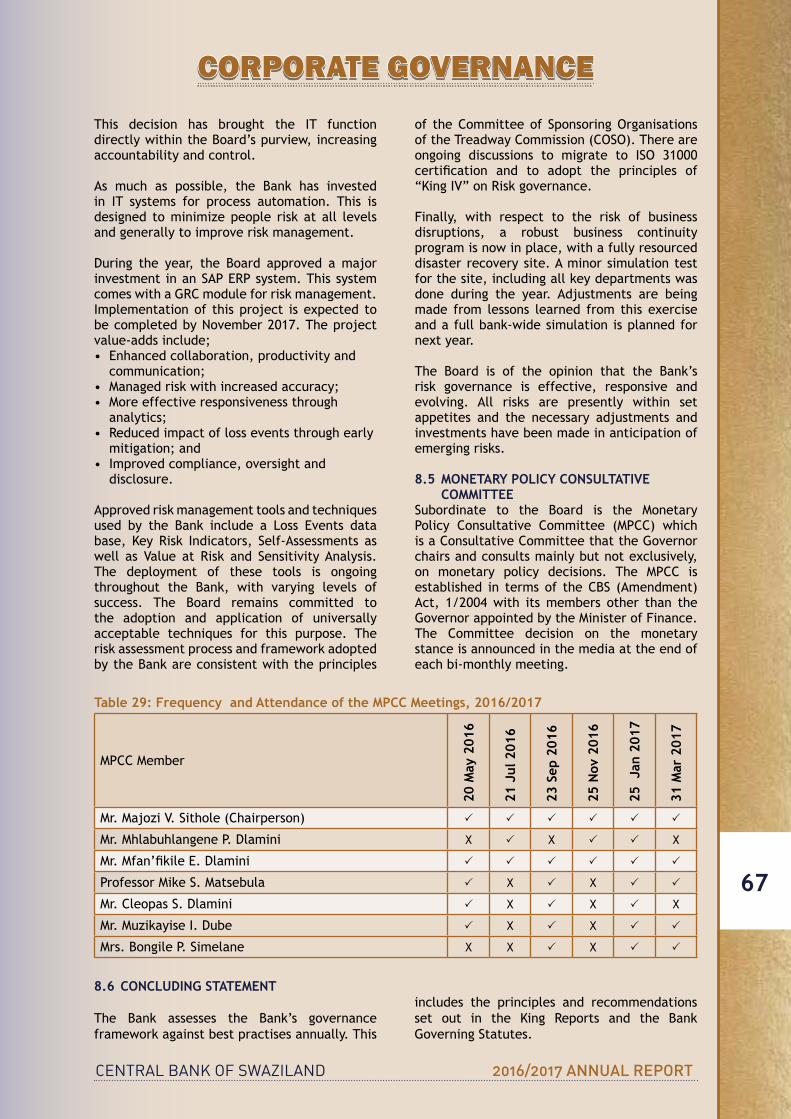

8.1 TheGoverningLegalEnvironment ......................................................................... 658.2 The Board ....................................................................................................... 658.3 TheBoardSub-Committees .................................................................................. 668.4 Board Statement on Risk Management ..................................................................... 668.5 MonetaryPolicyConsultativeCommittee .................................................................. 678.6 ConcludingStatement ......................................................................................... 67

9. Corporate Strategy and Communication ....................................................................... 689.1 Strategy Implementation ..................................................................................... 689.2 Performance Indicators ....................................................................................... 689.3 Progress Made................................................................................................... 68

9.3.1 SWOT Analysis ........................................................................................ 689.3.2 Excellence & Organizational Transformation .................................................... 689.3.3 Innovation & High Performance .................................................................... 689.3.4 Top 10 Risks ........................................................................................... 689.3.5 Performance Standards ............................................................................. 68

9.4 Branding and Image ............................................................................................ 68 10. Financial Markets Department ................................................................................... 69

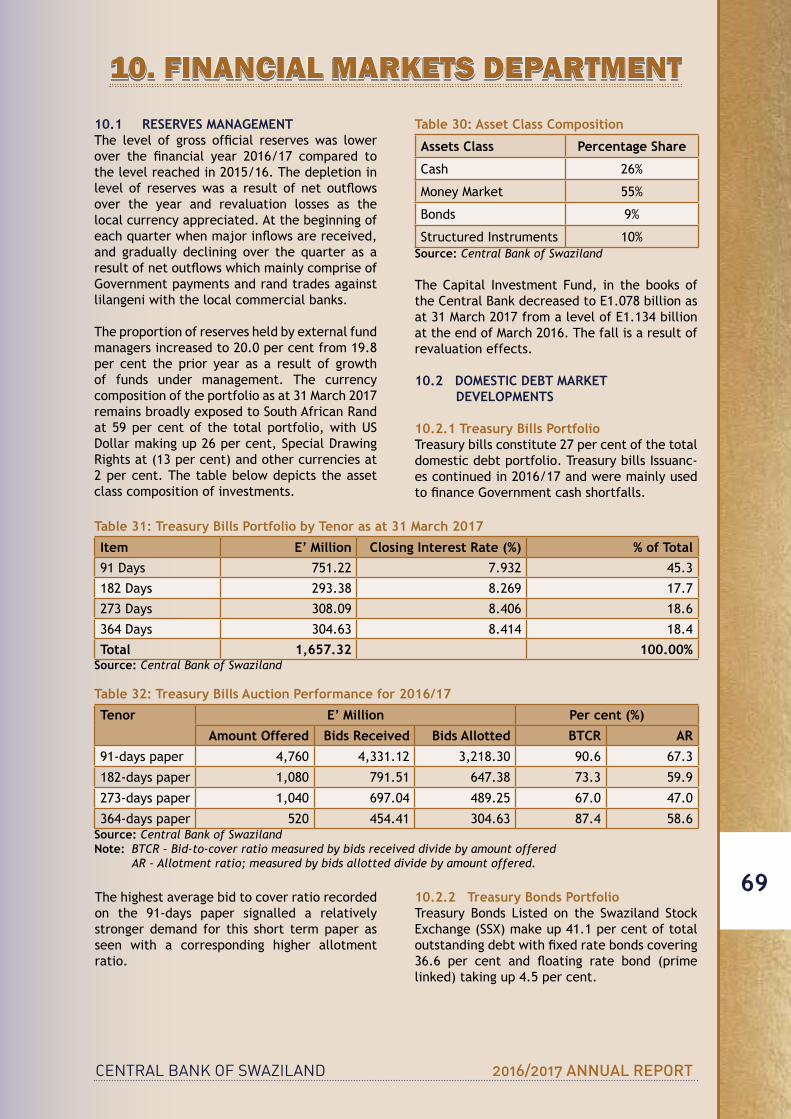

10.1 Reserves Management ......................................................................................... 6910.2DomesticDebtMarketDevelopments ....................................................................... 69

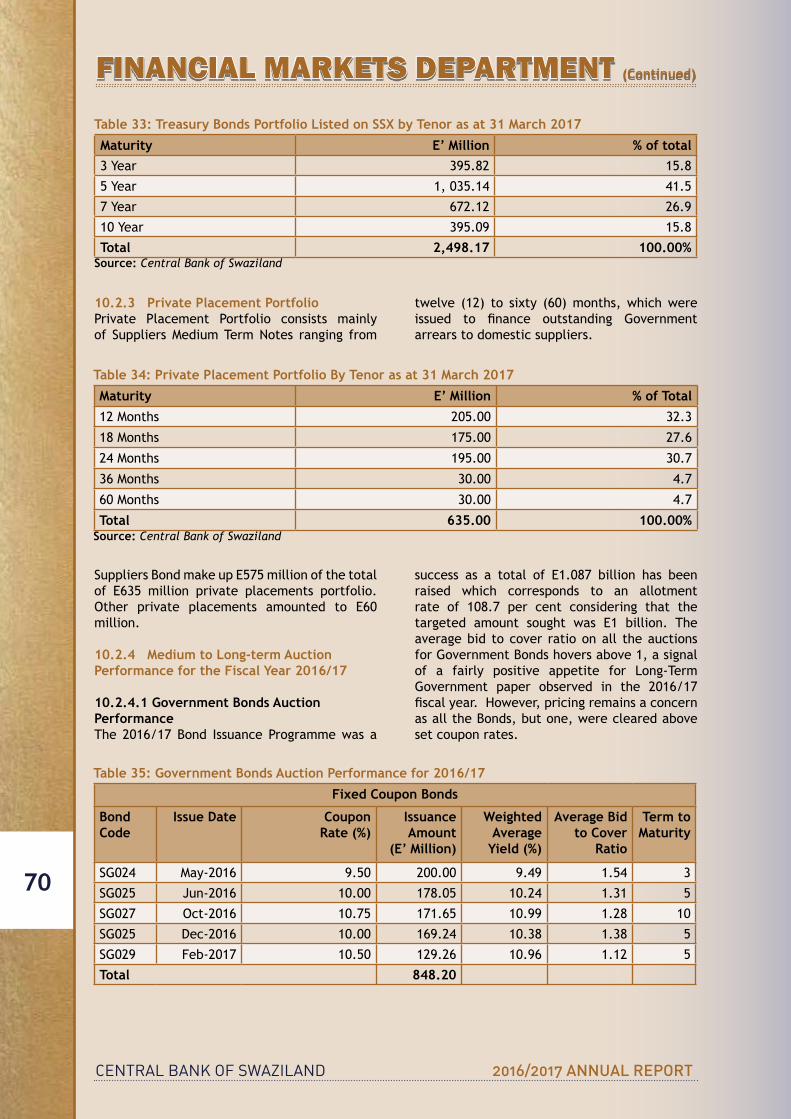

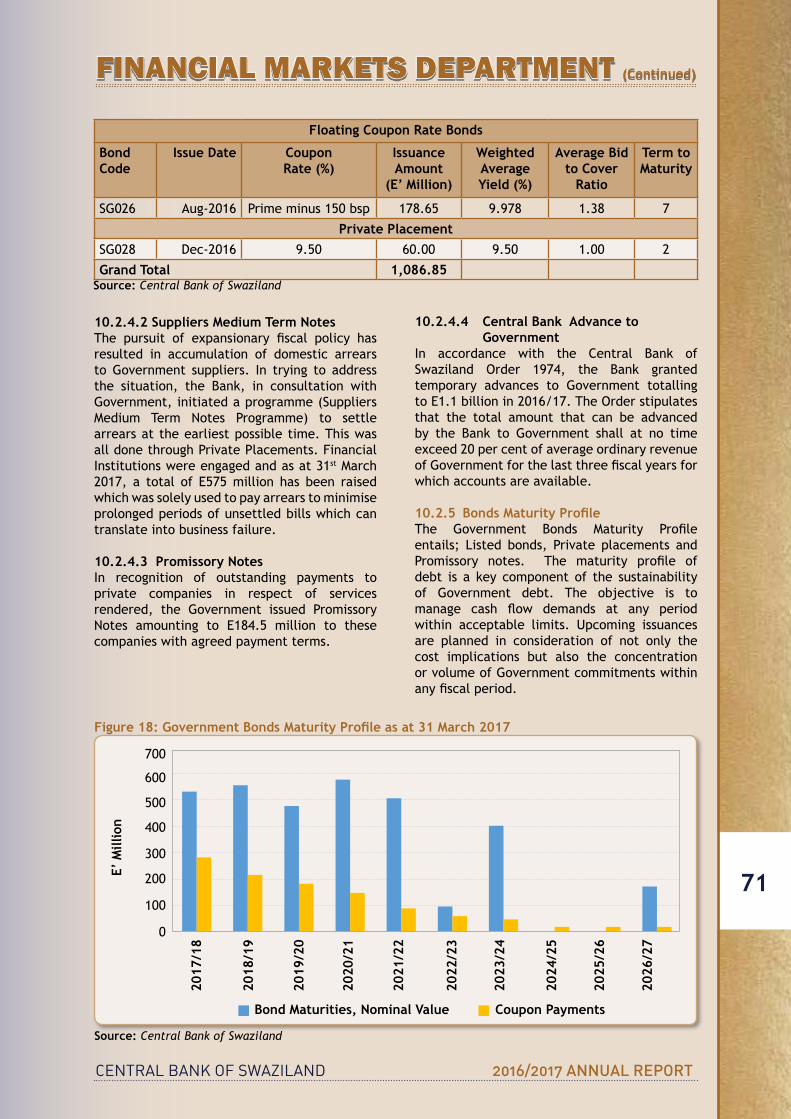

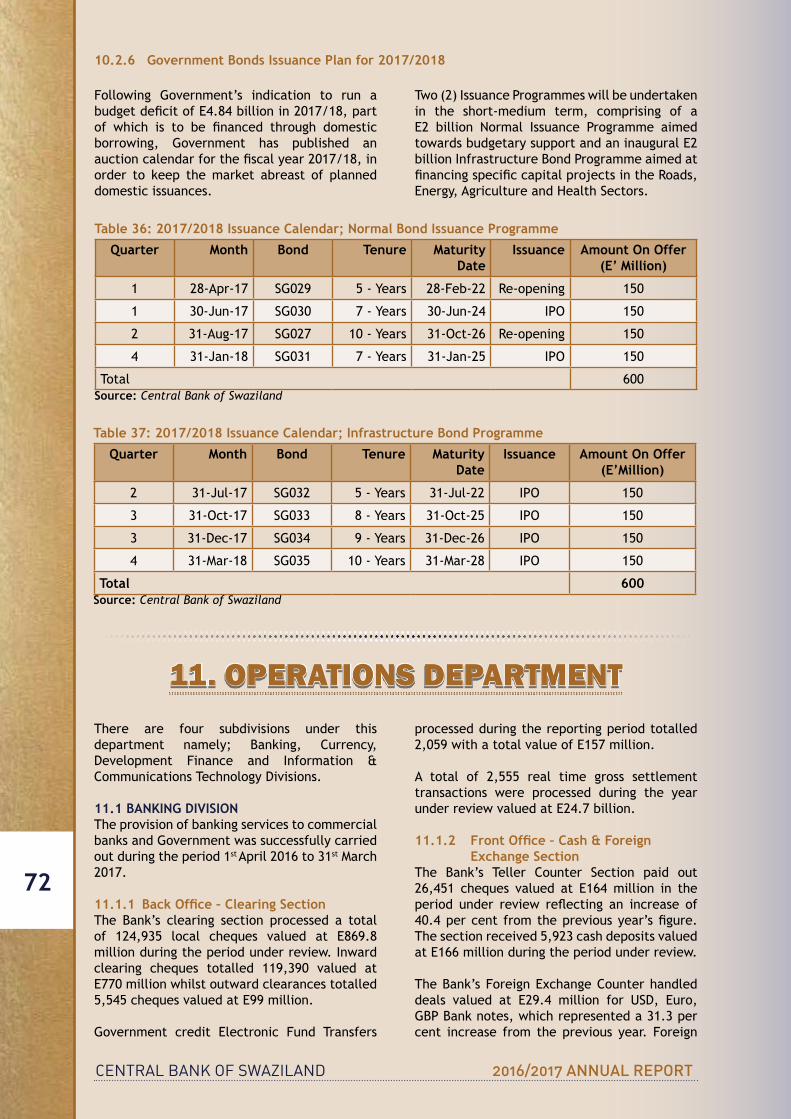

10.2.1 Treasury Bills Portfolio .............................................................................. 6910.2.2 Treasury Bonds Portfolio ............................................................................ 6910.2.3 Private Placement Portfolio ........................................................................ 7010.2.4 Medium to Long-Term Auction Performance for the Fiscal Year 2016/17 ................... 7010.2.5 BondsMaturityProfile ............................................................................... 7110.2.6 Government Bonds Issuance Plan for 2017/18 ................................................... 72

11. Operations Department ........................................................................................... 7211.1BankingDivision ................................................................................................ 72

11.1.1 BackOffice-ClearingSection ...................................................................... 7211.1.2 FrontOffice-Cash&ForexSection ............................................................... 72

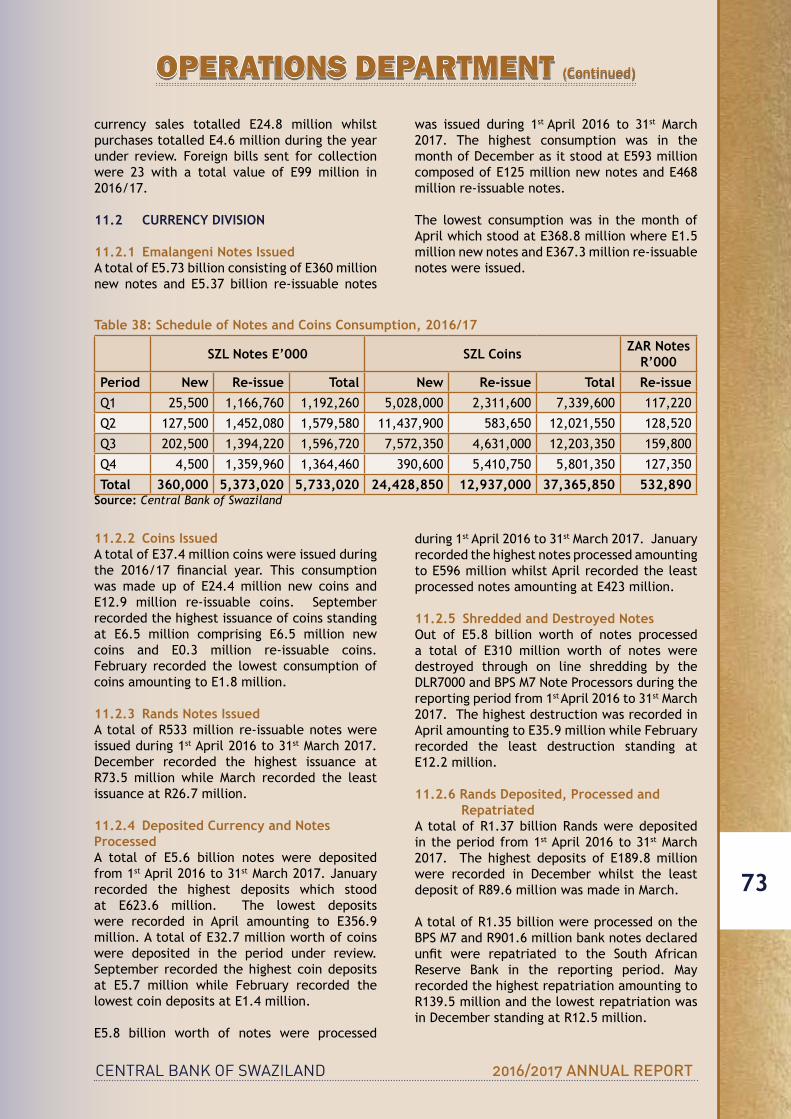

11.2CurrencyDivision .............................................................................................. 7311.2.1 Emalangeni Notes Issued .......................................................................... 7311.2.2 Coins Issued ......................................................................................... 7311.2.3 Rands Notes Issued ................................................................................. 7311.2.4 Deposited Currency and Notes Processed ...................................................... 7311.2.5 Shredded and Destroyed Notes ................................................................... 7311.2.6 Rands Deposited, Processed and Repatriated ................................................... 7311.2.7 Currency in Circulation ............................................................................. 7411.2.8 New Coins Series .................................................................................... 7411.2.9 Old Coins Series ..................................................................................... 7511.2.10 Coin Destruction .................................................................................... 7511.2.11 Commemorative Coins ............................................................................. 7511.2.12 New Notes ........................................................................................... 75

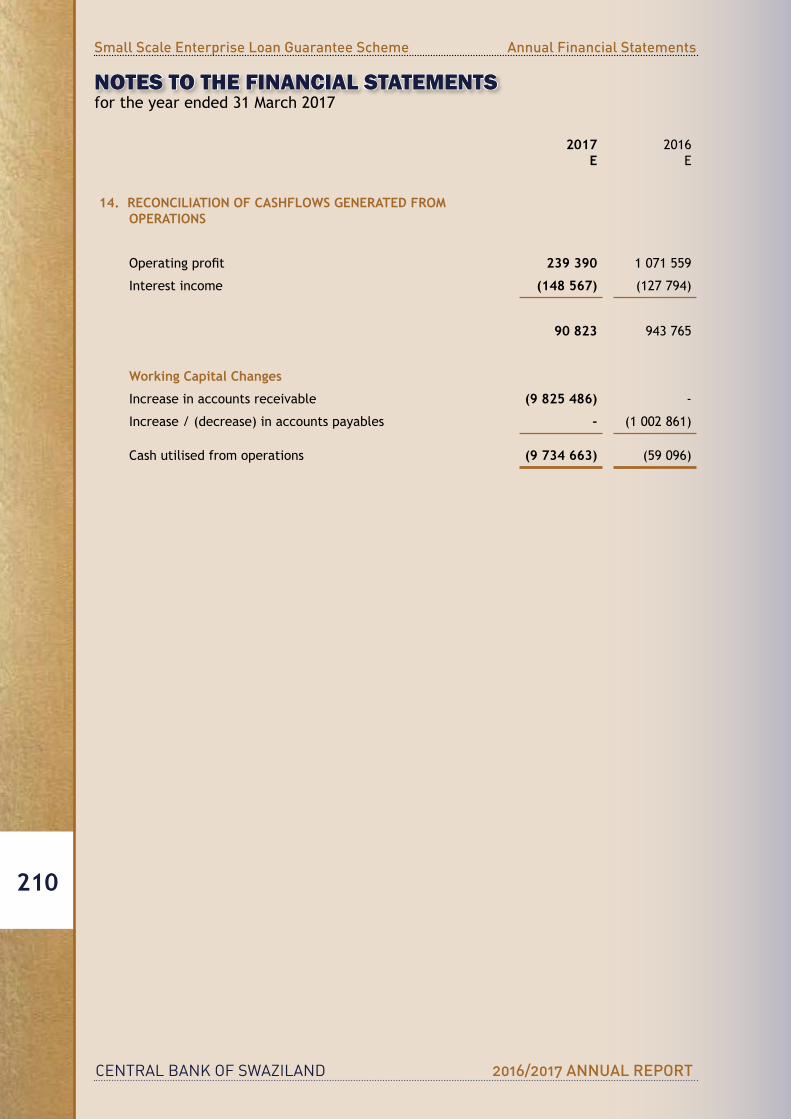

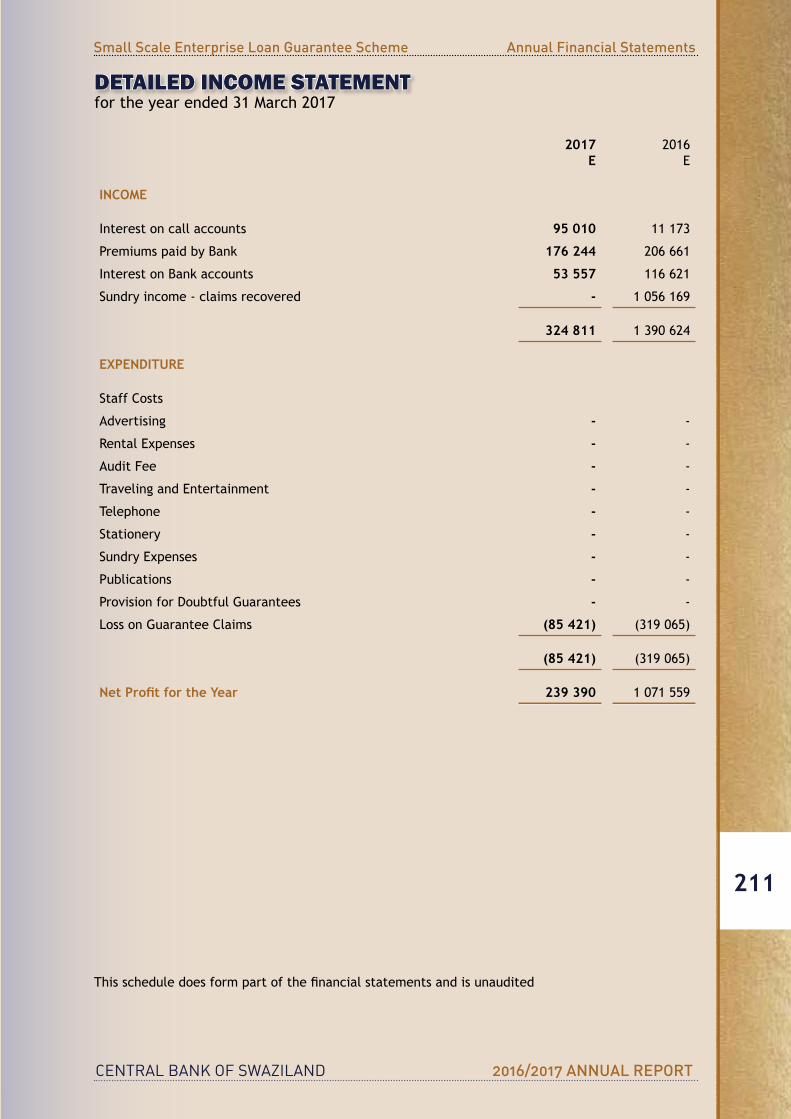

11.3DevelopmentFinanceDivision ............................................................................... 75 11.3.1 Overview ............................................................................................... 75

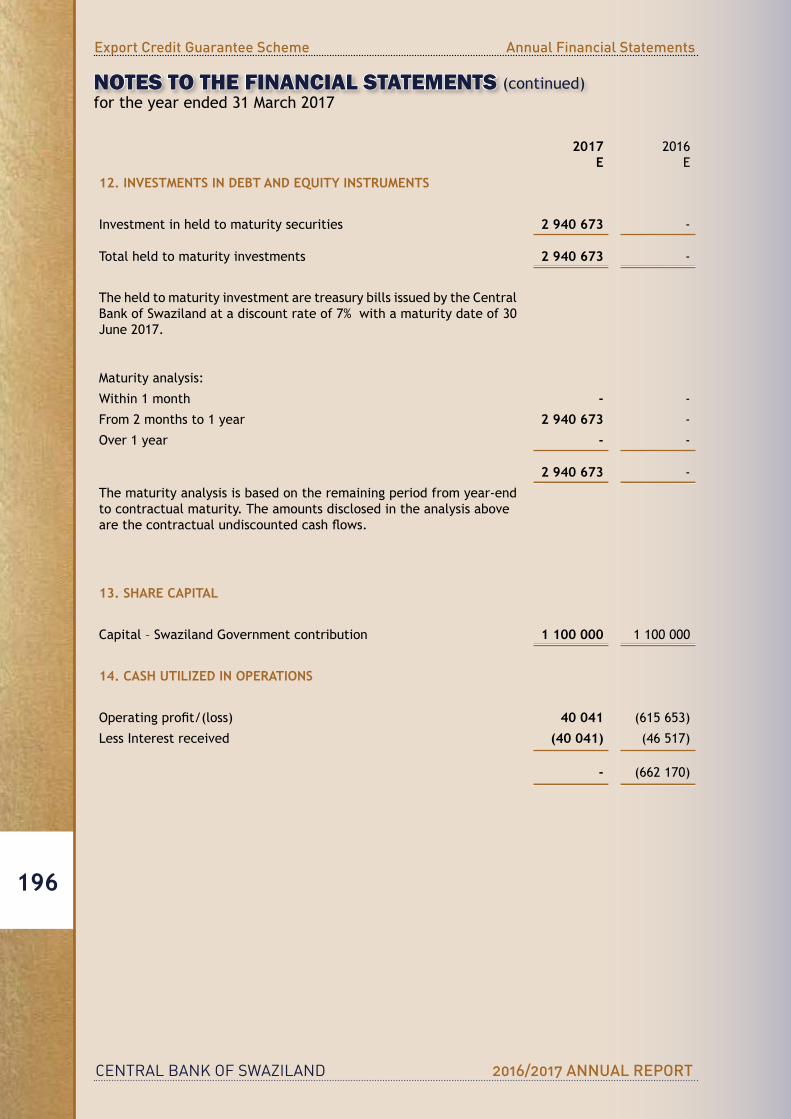

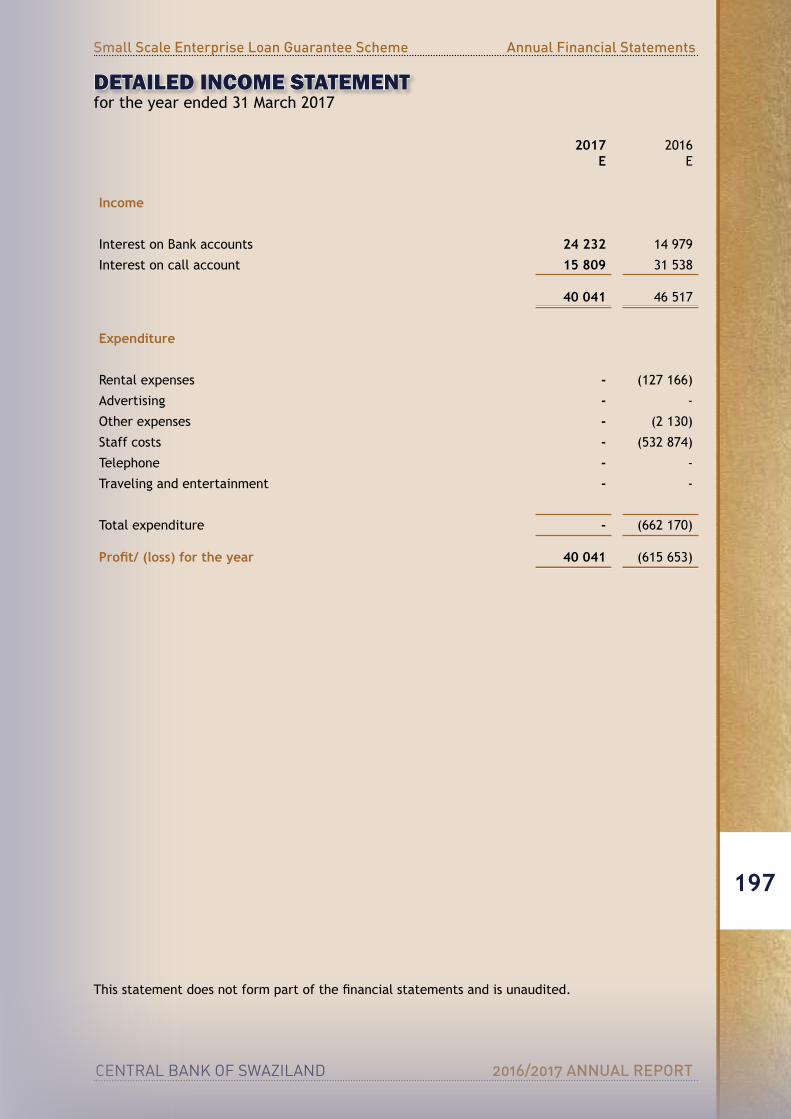

11.3.2 Small Scale Enterprise Loan Guarantee Scheme ................................................ 75 11.3.3 Export Credit Guarantee Scheme .................................................................. 7611.4Information&CommunicationTechnologyDivision ...................................................... 76 11.4.1 SAP Enterprise Resource Planning Update ....................................................... 76

12. Report on National Payments & Settlements Systems.............. ......................................... 7712.1 Introduction .................................................................................................... 7712.2CentralBankOversightofPaymentSystems .............................................................. 7712.3 Operational Activities ......................................................................................... 7812.4Cross-BorderPayments ....................................................................................... 7812.5FutureDevelopments ......................................................................................... 78

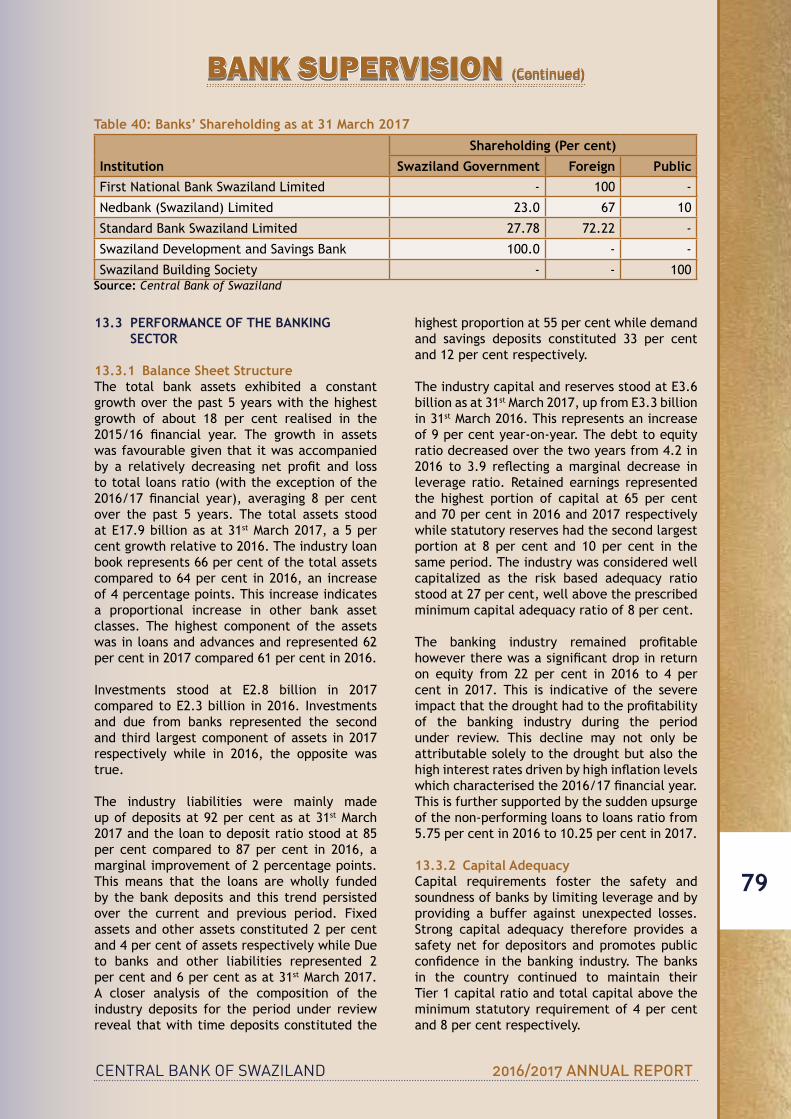

13. Bank Supervision .................................................................................................... 7813.1 Introduction .................................................................................................... 7813.2 Overview of the Banking System ............................................................................ 7813.3 Performance of the Banking Sector ........................................................................ 79

13.3.1 Balance Sheet Structure ............................................................................ 7913.3.2 Capital Adequacy ..................................................................................... 8013.3.3 Earnings Performance ............................................................................... 8013.3.4 Assets Quality ........................................................................................ 80

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

10

TABLE OF CONTENTS13.3.5 Liquidity Management ............................................................................... 80

13.4 Off-site Surveillance........................................................................................... 8013.5 On-site Inspection Supervision ............................................................................... 8113.6RegulatoryDevelopments .................................................................................... 81

13.6.1 Legal Notice on Bank Charges ...................................................................... 8113.6.2 Basel II Implementation ............................................................................. 8113.6.3 IFRS 9 Implementation .............................................................................. 81

14. Exchange Control and Anti-Money Laundering ................................................................ 8114.1ExchangeControl .............................................................................................. 81

14.1.1 Applications Approved ............................................................................... 8114.1.2 Out-Payments ......................................................................................... 8114.1.3 Import Permits Granted & Out Payments ........................................................ 8214.1.4 Analysis of Import Permits Granted ............................................................... 8214.1.5 Total In-Payment ..................................................................................... 82

14.2 Anti-Money Laundering ........................................................................................ 8214.2.1 Introduction ........................................................................................... 8214.2.2 Overview of the Regulated Industry .............................................................. 8214.2.3 Regulatory Developments ........................................................................... 8314.2.4 National Risk Assessment ........................................................................... 8414.2.5 Challenges ............................................................................................. 8414.2.6 Future Outlook ....................................................................................... 84

15. Internal Audit ........................................................................................................ 85

15.1OverviewandAuditCoverage ................................................................................ 8515.2 Achievements ................................................................................................... 85

15.2.1 Audits Covered ....................................................................................... 8515.2.2 Continuous Internal Assessments .................................................................. 8515.2.3 Anti-fraud & Logs Monitoring System ............................................................. 85

15.3 Future Outlook ................................................................................................ 8515.3.1 Combined Assurance Audit .......................................................................... 8515.2.2 Anti Fraud & Lock Monitoring System............................................................. 8515.2.3 Upgrade of TeamMate ............................................................................... 85

16. Risk Management Function ....................................................................................... 8616.1 Risk Management Framework ................................................................................ 8616.2 Top 10 Risks ..................................................................................................... 8616.3Safety,Health,Risk&Quality..... ........................................................................... 86

16.3.1 Compliance with the Occupational Safety and Health Act of 2001 ......................... 8716.3.2 Environmental Survey ............................................................................... 8716.3.3 Stakeholder Engagement ............................................................................ 87

16.4BusinessContinuityManagement ............................................................................ 87

17. Economic Policy Research and Statistics Department....... ................................................ 8717.1 Major Highlights ................................................................................................ 87

17.1.1 Monetary Policy Framework ........................................................................ 8717.1.2 Research Bulletin ..................................................................................... 8717.1.3 FinancialSectorDevelopmentImplementationPlan ........................................... 8817.1.4 Post Budget Seminar ................................................................................. 88

17.2ActivitiesEarnmarkedfor2017/18.......................................................................... 88

18. Human Resource Management ................................................................................... 8818.1HumanResourceDivision ..................................................................................... 88

18.1.1 Staff Compliment .................................................................................... 8818.1.2 Induction ............................................................................................... 8818.1.3 Salary Review ......................................................................................... 8818.1.4 Talent Management Strategy ....................................................................... 88

18.2LearningandOrganisationalDevelopment ................................................................ 8818.2.1 Specialized Training .................................................................................. 8818.2.2 General Training ...................................................................................... 8818.2.3 Change Management ................................................................................. 89

18.3 Facilities......................................................................................................... 8918.4EmployeeAssistanceProgramme ............................................................................ 89

PART C - FINANCIAL STATEMENTS ..................................................................................... 90CentralBankofSwaziland ................................................................................................ 90CapitalInvestmentSpecialFund ........................................................................................ 169ExportCreditGuaranteeScheme ....................................................................................... 184SmallScaleEnterpriseLoanGuaranteeScheme ...................................................................... 198

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

11

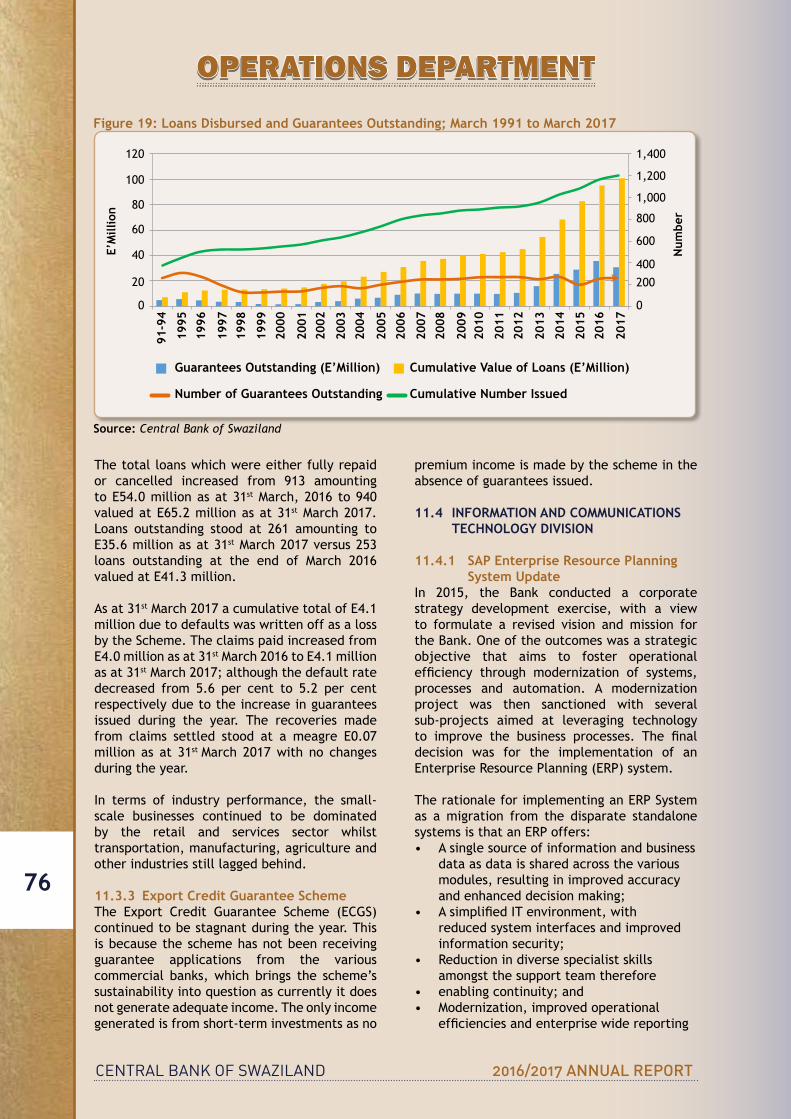

LIST OF FIGURESFigure 1: WorldEconomicOutlook–GDPProjections(revised):2015-2018 .................................... 20Figure 2: ConsumerPriceInflationforGoodsandServices ........................................................ 41Figure 3: ContributiontoAnnualConsumerInflationbyCOICOPCategory ..................................... 42Figure 4: OverallInflationversusCoreInflation ..................................................................... 42Figure 5: CurrentAccount .............................................................................................. 45Figure 6: Financial Account ............................................................................................. 47Figure 7: ForeignDirectInvestmentComponents,2016 ........................................................... 47Figure 8: MonthlyLilangeni’sExchangeRate-2016 ................................................................ 49Figure 9: NominalEffectiveandRealEffectiveExchangeRateIndices ......................................... 50Figure 10: NetForeignAssets&GrossOfficialReserves ............................................................. 53Figure 11: PrivateSectorLoansandDeposits ......................................................................... 55Figure 12: Loans by Type of Business ................................................................................... 55Figure 13: Money Supply .................................................................................................. 56Figure 14: MoneySupply:AnnualChanges ............................................................................. 56Figure 15: ComparativeBudgetSummary ............................................................................. 58Figure 16: GovernmentRevenueMajorComponents ................................................................. 59Figure 17: TotalPublicDebtTrend ...................................................................................... 61Figure 18: GovernmentBondsMaturityProfile ........................................................................ 71Figure 19: LoansDisbursedandGuaranteesOutstanding ........................................................... 76

LIST OF TABLESTable 1: Maize Production ............................................................................................. 31Table 2: CottonProduction ............................................................................................ 32Table 3: LivestockProduction-Cattle ............................................................................... 32Table 4: BeefExports ................................................................................................... 33Table 5: Other Livestock – Pigs, Goats, Sheep and Poultry ....................................................... 33Table 6: DairyProductioninMillions–LiquidMilkEquivalent(LME) ............................................ 34Table 7: Minerals - Production and Sales ............................................................................ 35Table 8: Sugar Production and Sales ................................................................................. 37Table 9: ConstructionIndicators ...................................................................................... 39Table 10: ElectricityConsumption ..................................................................................... 40Table 11: TreatedWaterConsumption ................................................................................ 40Table 12: Bank Liquidity ................................................................................................. 52Table 13: TotalClaimsonOtherSectors(PrivateSector)byCategoryofBorrower ........................... 54Table 14: Business: Loans and Advances by Type of Industry ...................................................... 54Table 15: OwnershipofDepositswithOtherDepositoryCorporationsinSwaziland ........................... 57Table 16: Budget Summary .............................................................................................. 58Table 17: CentralGovernmentRevenue .............................................................................. 59Table 18: CentralGovernmentRecurrentExpenditure ............................................................. 60Table 19: CentralGovernmentCapitalExpenditure ................................................................ 60Table 20: PublicDebtIndicators ....................................................................................... 62Table 21: PublicExternalDebtbyHolderCategory ................................................................. 62Table 22: DomesticDebtPortfoliobyInstrument ................................................................... 63Table 23: DomesticDebtPortfoliobyHolder ........................................................................ 63Table 24: Frequency and Attendance of Board Meetings ........................................................... 65Table 25: FrequencyandAttendanceofRemunerationCommitteeMeetings ................................... 66Table 26: FrequencyandAttendanceofCapitalProjectsCommitteeMeetings ................................ 66Table 27: FrequencyandAttendanceofRisk&ITCommitteeMeetings ......................................... 66Table 28: FrequencyandAttendanceofAuditCommitteeMeetings ............................................. 66Table 29: FrequencyandAttendanceofMPCCCommitteeMeetings ............................................. 67Table 30: AssetClassComposition ..................................................................................... 69Table 31: Treasury Bills Portfolio by Tenor ........................................................................... 69Table 32: Treasury Bills Auction Performance for 2016/17 ......................................................... 69Table 33: Treasury Bonds Portfolio Listed on SSX .................................................................... 70Table 34: Private Placement Portfolio By Tenor ..................................................................... 70Table 35: Government Bonds Auction Performance for 2016/17 .................................................. 70Table 36: 2017/2018IssuanceCalendar;NormalBondIssuanceProgramme.................................... 72Table 37: 2017/2018IssuanceCalendar;InfrastructureBondProgramme ...................................... 72Table 38: ScheduleofNotesandCoinConsumptionfor2016/17 ................................................. 73Table 39: RandsDepositedandRepatriated .......................................................................... 74Table 40: Banks’ Shareholdings ......................................................................................... 78Table 41: RegulatedEntities ............................................................................................ 82Table 42: Top 10 Risks ................................................................................................... 86

LIST OF FIGURES AND TABLES

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

12

ACRONYMS AND ABBREVIATIONS

AACB - AssociationofAfricanCentralBanks

ACH - AutomatedClearingHouse

AfDB - AfricanDevelopmentBank

AGOA - African Growth Opportunity Act

AIDS - AcquiredImmuneDeficiencySyndrome

AU – African Union

AML - Anti-Money Laundering

BCM - BusinessContinuityManagement

BOE – BankofEngland

BOJ - BankofJapan

BOP - Balance of Payments

BPM - Balance of Payments Manual

BRC - BoardRiskCommittee

BRICS - Brazil,Russia,India,ChinaandSouthAfrica

BSD – BankSupervisionDivision

CAATS - ComputerAssistedAuditTechniques

CBS - CentralBankofSwaziland

CCBG - CommitteeofCentralBankGovernors(SADC)

CFT - CombatingFinancingofTerrorism

CFTA - ContinentalFreeTradeArea

CIEA - CompositeIndicatorforEconomicActivity

CMA - CommonMonetaryArea

COMESA - CommonMarketforEasternandSouthernAfrica

COMSEC - CommonwealthSecretariat

CPI - ConsumerPriceIndex

CSO - CentralStatisticalOffice

EAC - EastAfricanCommunity

ECB - EuropeanCentralBank

ECGS - ExportCreditGuaranteeScheme

EFT - ElectronicFundsTransfers

EFTA - EuropeanFreeTradeAssociation

EPA - EconomicPartnershipAgreement

EPRS - EconomicPolicyResearchandStatisticsDepartment

ERM - EnterpriseRiskManagement

EU - EuropeanUnion

FDI - ForeignDirectInvestment

FIP - Finance and Investment Protocol

FOMC - FederalOpenMarketCommittee

FSC - FinancialStabilityCommittee

FSDIP - FinancialSectorDevelopmentImplementationPlan

FSRA – Financial Services Regulatory Authority

FSU - Financial Stability Unit

FTA - Free Trade Area

GBP - Great Britain Pound

GDP - GrossDomesticProduct

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

13

ACRONYMS AND ABBREVIATIONS

GM - GeneticallyModified

GSP - Generalised System of Preferences

HIV - HumanImmunoVirus

IAA - Internal Audit Activity

ICCFISH - InternationalConventionCentreandFiveStarHotel

IBRD - InternationalBankforConstruction&Development

ICT – InformationandCommunicationTechnology

IFRS - International Financial Reporting Standards

IIP - International Investment Position

IMF - International Monetary Fund

IPPs - Individual Power Producers

IT - Information Technology

JPY - JapaneseYen

LME - LiquidMilkEquivalent

LUSIP - Lower Usuthu Smallholders Irrigation Project

M2 - Broad Money Supply

MEPD - MinistryofEconomicPlanning&Development

MEFMI - MacroeconomicandFinancialManagementInstituteofEastern

MMA - Multilateral Monetary Agreement

MMT - Mobile Money Transfer

MPC – MonetaryPolicyCommittee

MPCC - MonetaryPolicyConsultativeCommittee

Mt - Metric Tonnes

NAMBOARD - National Agricultural Marketing Board

NBFIs – Non–Bank Financial Institutions

NCDs - Non-CommunicableDiseases

NEER - NominalEffectiveExchangeRate

NMC - NationalMaizeCorporation

NPSS - National Payments and Settlements System

OHS - Occupational Health and Safety

PAYE – PayAsYouEarnTax/PersonalIncomeTax

PBOC - People’sBankofChina

PPI - Producer Price Index

PPPs - Private-Public Partnerships

PRAMA - Policy Research and Macroeconomic Analysis

PTA – Preferential Trade Agreement

RBIA - Risk Based Internal Audit

REC – RegionalEconomicCommunity

REER - RealEffectiveExchangeRate

RISDP - RegionalIndicativeStrategicDevelopmentPlan

RSA - Republic of South Africa

RSF – Revenue Sharing Formula

RTGS - Real Time Gross Settlement

SACU - SouthernAfricanCustomsUnion

SADC - SouthernAfricanDevelopmentCommunity

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

14

SARB - South African Reserve Bank

SCB - SwazilandCottonBoard

SEC - SwazilandElectricityCompany

SG - Swaziland Government

SIDC – SwazilandIndustrialDevelopmentCompany

SIRESS – SADCIntegratedRegionalElectronicSettlementSystem

SMEs – SmallandMediumEnterprises

SMI - Swaziland Meat Industries

SNHB – Swaziland National Housing Board

SNL – Swazi Nation Land

SRA - Swaziland Revenue Authority

SSA - Swaziland Sugar Association

SSELGS - SmallScaleEnterpriseLoanGuaranteeScheme

SSX - SwazilandStockExchange

STA - Swaziland Tourism Authority

SWIPSS - Swaziland Inter-Bank Payment and Settlement System

SWSC – SwazilandWaterServicesCorporation

TFTA - Tripartite Free Trade Area

TIDCA – Trade,InvestmentandDevelopmentCooperationAgreement

TLC - TechnicalLiaisonCommittees

UCT - UniversityofCapeTown

UNISWA - University of Swaziland

UK - UnitedKingdom

USA/US - United States of America

USD - UnitedStatesDollar

VAT - ValueAddedTax

WCO - WorldCustomsOrganisation

WEO – WorldEconomicOutlook

ACRONYMS AND ABBREVIATIONS

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

15

1. GOVERNOR’S STATEMENT

� Mr. Majozi SitholeGovernor

According to the IMF April 2017 World Economic Outlook, global growth wassubdued in 2016, with the world economy

advancing by a lower 3.1 per cent compared to3.2percentrecordedin2015.Contributingto the lagging growth in the global economy was a slump in private consumption mostly in the advanced economies as well as sluggish performance in commodity markets, which in turn also affected emerging markets, who have been the anchor of positive and higher source of growth in previous years. Advanced economies grew by a paltry 1.7 per cent in 2016 compared to 2.1 per cent in 2015, whilst emerging market economies grew by 4.1 per cent in 2016 unchanged from the previous year. However, going forward there seems to be optimism with the buoyant financial marketscombined with a recovery in manufacturing and a pick-up in global trade. Synchronised growth in world output is expected to persist in 2017 withconfidencesurveysandmarketssignallingbetter prospects for global expansion. Global growth is expected to rise to 3.5 per cent in 2017 and 3.6 per cent in 2018. Risks, however, to the global outlook still remains a heightened possibility with political uncertainty playing a big part especially given the developments in theUSandEurope.

On the other hand, monetary policy conditions changed in 2016 with global consumer price

inflation increasing as the retail prices ofgasoline and other energy related products slightly rose. The uptick has been especially strong for advanced economies, where 12-month consumer price inflation in the year stoodslightly above 2 per cent - more than double the averageannualinflationrateof0.8percentin2016. In many emerging market and developing economies headline inflation picked up dueto higher commodity prices. Annual headline inflationin2016forEMDEswasrecordedat4.4per cent in 2016 and is expected to edge up to4.7percentin2017(IMFWEOReport,April2017).

The sluggish global growth and commodity markets negatively affected Swaziland’s leading trading partner, South Africa, in 2016; and this combined with rising prices. Again according to the International Monetary Fund’s April 2017 World Economic Outlook Report,South African national output declined by 0.3 percentin2016comparedtoaGDPgrowthof1.3 per cent in 2015. South Africa experienced atechnicalrecessionforthefirsttimeineightyears after recording two consecutive quarterly economic growth contractions in the period 2016 to first quarter of 2017. However, goingforward a modest recovery is expected in 2017, with growth rising to 0.8 per cent as commodity prices rebound, drought conditions ease, and electricity capacity expands; for 2018, GDP

A tight monetary policy stance was pursued by the Bank during the financial year ended March 2017. The broad objective of the stance was to contain rapidly intensifying inflationary pressures while cautious not to further weaken economic growth prospects.

“

“

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

16

growth is projected at 1.6 per cent. This glossy outlook though is likely to be affected by sovereign credit ratings downgrade on domestic private sectorgrossfixedcapital formation inparticular(IMFWEOReport,April2017).

The South African Reserve Bank (SARB) weighed in to assist the situation by loosening its monetary policy to shore up economic growth in mid-2016. However, the Bank found itself having to backtrack after its hand was forced by rising consumer prices, taking CPI outsidethe target range especially in the latter part of2016.Inthefirstquarterof2017,theSARBincreased the benchmark repo rate, taking it back to 7 per cent where it was early in 2016. However, inflation pressures are expected toimprove with headline inflation expected toreturn to within the target range during the second quarter of 2017 (South African Reserve Bank,27June2017).

In Swaziland, revised estimates indicate that the economy grew by 1.3 per cent in 2016, an upward revision from the September 2016 estimate of -0.6 per cent, but remained marginally lower than the revised estimate of 1.5 per cent growth in 2015. The improvement in economic performance (relative to the previous projection) mainly benefited frombetter output in the secondary sector due to lower-than-anticipated effects of the ElNino induced drought on food manufacturing, electricity generation and water supply.

The real output of the secondary sector contracted by 0.8 per cent in 2016 compared to a growth of 2.8 per cent in 2015. The reduction in output for the secondary sector was accounted for by the manufacturing sector whose output declined by 1.3 per cent in 2016 compared to a growth of 2.5 per cent in 2015. The tertiary sector grew by 3.7 per cent in 2016 compared to a slower pace of 1.3 per cent the previous year, mainly supported by an expansionary fiscal policy (following theimplementation of a salary review exercise) in the second half of 2016. Other sectors that recorded growth include ‘wholesale and retail’,

‘tourism’, ‘financial services’, ‘transport’,‘communication’ and ‘real estate’ subsectors. The primary sector shrank by 2.4 per cent in 2016 compared to another contraction of 3.5 per cent in 2015. The performance of the primary sector was mainly affected by the negativeeffectsoftheElNinoinduceddroughtparticularly the growing of crops both for rain-fed crops and irrigated farms.

Swaziland’s headline consumer inflationincreased from an average of 5.0 per cent in 2015 to an average of 7.8 per cent in 2016, with a peak of 8.7 per cent reached in December2016. The rise in overall consumer inflationmainly benefitted from a notable growth infoodinflationlargelydrivenbyasevereElNinophenomenon that affected the entire Southern Africa region. However, inflationary pressuressubsided in the opening months of 2017, with headline inflation slowing to 7.1 per cent inApril 2017, as favourable weather conditions reversed the effects of the drought that prevailed in the 2015/16 season.

Swaziland’sinflationoutlookisexpectedtobecontained in the short to medium term due to a combination of factors that include declining food prices, a relatively stronger Rand/Lilangeni against major trading partners and containedinternationaloilprices.TheCentralBank inflation forecasts reflect that inflationwill close the year on a downward trajectory with an average of 7.0 per cent in 2017. The mediumtermforecastsalsoshowthatinflationwill average 5.8 per cent in 2018 and 5.6 per cent in 2019.

A tight monetary policy stance was pursued by the Bank during the financial year endedMarch 2017. The broad objective of the stance wastocontainrapidlyintensifyinginflationarypressures while cautious not to further weaken economic growth prospects. The policy (bank) rate increased by 75 basis points from 6.50 per cent in March 2016 to 7.25 per cent at the endofMarch2017.Correspondingly,theprimelending rate increased from 10.00 per cent in March 2016 to 10.75 per cent in March 2017.

Revised estimates for GDP growth indicate that the economy grew by 1.3 per cent in 2016, an upward revision from the September 2016 estimate of -0.6 per cent, but remained

marginally lower than the revised estimate of 1.5 per cent growth in 2015.

GOVERNOR’S STATEMENT (Continued)

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

17

GOVERNOR’S STATEMENT (Continued)

International reserves reached 3.4 months of imports of goods and services at the end of March 2017, notably lower than the level of 3.9 months at the end of March 2016. The deterioration in reserves was largely attributed totheconsiderabledeclineinSACUreceiptsforthefiscalyear2016-17.Theshorttomedium-term prospects for the country’s reserves remainpositivewitharecoveryinSACUreceiptsfor 2017/18 expected to improve the reserves level. The Bank will thus continue to monitor and provide appropriate advice to government to ensure that the reserves are sustained at a healthy position. This would go a long way in safeguarding the market’s confidence in thecountry’s ability to meet its external obligations and to withstand external shocks.

With the new balance of payments compilation format of BPM6 the preliminary data indicate that in 2016, the current account recorded a E5.923billionsurplus,downfromasurplusofE9.379billioninthepreviousyear.Thedeclinewas a turnaround from the 52.9 per cent increase in the surplus reported in 2015. The current account in 2016 was equivalent to 10.8 percentofGDPfrom17.9percentin2015.Thebalance in the current account was explained by a narrow trade balance and a reduction in the net receipts posted in the secondary income account.

The financial account resulted in a netacquisition of foreign assets of E5.066 billionreflecting a net outflow, though moderatingrelativetothenetoutflowofE7.391billionin2015.The net outflow depicts that Swazilandwas a net lender to the rest of the world during this period. This result was the interplay of net foreign assets acquired in the ‘other investment’ sub-account as well as incurrence of liabilities in direct investment and other investment.

The international investment position (IIP) for Swaziland indicates that external financialassets continued to surpass external financial

liabilities. At the end of 2016, Swaziland’s IIP recorded a net asset position amounting to E21.698 billion, an increase of 21.7 per centfrom the net asset position posted in 2015. The net position in the IIP was sustained by a 21.6 per cent increase in foreign assets while liabilities grew 21.4 per cent.

The Minister of Finance presented the 2017/18 National Budget to Parliament under the theme: “Rising Above Adversity to Create Prosperity for All”. The Budget was in line with His Majesty’s Speech from the Throne when opening the 4th session of the 10th Parliament. The key objectives of this Budget were highlighted as reducing reliance on SACUreceipts,fiscalconsolidationandinfrastructuredevelopment to build Government’s preparedness and resilience against future adversities.

Thebudgetshowedadeficitof8.2percentofGDP (E4.8billion) for 2017/18 compared to adeficitof12.3percentestimatedfor2016/17.The improvement in the budget deficit willbenefitfromacombinationofalowerincreasein expenditure coupled with a surge in revenues for2017/18fiscalyear.Overthemediumtolongterm,Government’saimistobringthedeficitback to levels less than 3 per cent, in line with SADC Macroeconomic Convergence targets,supported by improved revenue collection.

The Minister indicated in previous budgets that to avoid an increase in relatively expensive external borrowing and reduce the fiscalburden of debt payments over the medium term, a larger share of the fiscal deficit willbe financed through domestic borrowing.Externalborrowingwillbeconsideredonlyforthefinancingofhighlyproductivefixedcapitalinvestments.

The Swaziland banking sector was stable, financially sound and conformed to statutory

In line with the Bank’s mandate of promoting a sound and safe banking system and ensuring confidence in the domestic banking sector, the Central Bank increased the

minimum liquidity requirement for commercial banks with effect from 1st July 2016 while the reserve requirement remained unaltered. The liquidity requirement for all banks

went up from 20 per cent to 25 per cent of domestic liabilities while for the Swazi Bank it was increased from 17 per cent to 22 per cent of domestic liabilities.

The reserve requirement remained unchanged at 6 per cent.

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

18

prudential requirements in terms of capital adequacy and liquidity. The asset quality of banks deteriorated notably during the year with non-performing loans and advances expressed as a percentage of gross loans at 10.25 per cent inMarch2017, representinga significantincrease from the 5.0 per cent recorded in March 2016. Furthermore, their profitability showedsignificantdeteriorationwhencomparedtotheprevious year, mainly due to the severe drought that impacted negatively on economic growth, the volatile exchange rate market and increased cost of borrowing which resulted in low credit extension and high non-performing loans The banking sector assets grew by 5.0 per cent to E17.9billionduringtheyearendedMarch2017fromE17.0billionattheendofMarch2017.Netloans and advances consisted of 62.0 per cent of the banking sector assets, rising marginally from 61.0 per cent reported at the end of March 2016.

In line with the Bank’s mandate of promoting a sound and safe banking system and ensuring confidenceinthedomesticbankingsector,theCentral Bank increased theminimum liquidityrequirement for commercial banks with effect from 1stJuly2016whilethereserverequirementremained unaltered. The liquidity requirement for all banks went up from 20 per cent to 25 per cent of domestic liabilities while for the Swazi Bank it was increased from 17 per cent to 22 per cent of domestic liabilities. The reserve requirement remained unchanged at 6 per cent.

TostrengthenthefinancialsectorinSwazilandtheMinistryofFinance, theCentralBankandFinancial Services Regulatory Authority have collaborated to develop Swaziland’s Financial Sector Development Implementation Plan(FSDIP). The FSDIP was formulated with the

To strengthen the financial sector in Swaziland, the Ministry of Finance, the Central Bank and Financial Services Regulatory Authority have collaborated to develop Swaziland’s

Financial Sector Development Implementation Plan (FSDIP). The FSDIP was formulated with the support of the World Bank which provided the expertise and assisted in ensuring it has latest international best practice in financial sector development.

GOVERNOR’S STATEMENT

support of the World Bank which provided the expertise and assisted in ensuring it has latest international best practice in financial sectordevelopment. This is a three-year strategy which will be implemented from 2017 to 2019.

The objective of the strategy is to have a stable, diversified, modern and competitive financialsystem that provides quality, affordable and accessible financial services to all people inthe economy in an effort to support economic growth. This national strategy was launched byHis Excellency theRightHonourablePrimeMinister Dr. Barnabas Sibusiso Dlamini on13th April 2017. The Bank is on course with the implementation of its own strategy and continues to be guided by best practice in corporate governance.

In an endeavour to foster cooperation and monetary integration at the regional level, the Bank continues to participate in the meetings of theCommitteeofCentralBankGovernorsintheCMA,SADC,COMESAandAfricaasacontinent.

I would like to extend my sincere thanks to theMinisterofFinanceandhisOfficials,Boardof Directors, all staff of the Central Bank ofSwazilandaswell asfinancial institutions andother key stakeholders for their cooperation, commitment and dedication to the attainment offinancialstabilityinSwaziland.

..................................M.V.SitholeGovernor

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

19

PART A

CENTRAL BANK OF SWAZILAND

REVIEW OF THE ECONOMY

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

20

2. GLOBAL ECONOMIC DEVELOPMENTS

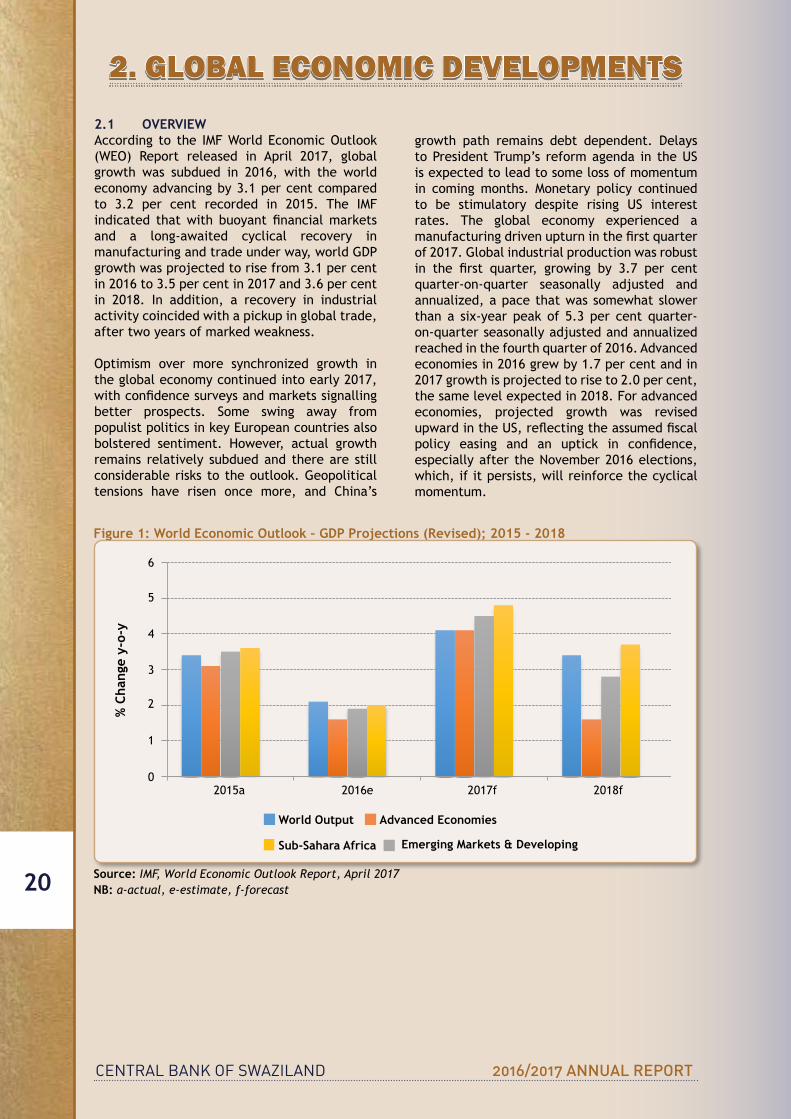

Figure 1: World Economic Outlook – GDP Projections (Revised); 2015 - 2018

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1 2 3 4 5 2015a

% C

hang

e y-

o-y

6

5

4

3

2

1

02016e 2017f 2018f

World Output Advanced Economies

Emerging Markets & DevelopingSub-Sahara Africa

Source: IMF, World Economic Outlook Report, April 2017NB: a-actual, e-estimate, f-forecast

2.1 OVERVIEWAccording to the IMFWorldEconomicOutlook(WEO) Report released in April 2017, globalgrowth was subdued in 2016, with the world economy advancing by 3.1 per cent compared to 3.2 per cent recorded in 2015. The IMF indicated thatwith buoyant financialmarketsand a long-awaited cyclical recovery in manufacturingandtradeunderway,worldGDPgrowth was projected to rise from 3.1 per cent in 2016 to 3.5 per cent in 2017 and 3.6 per cent in 2018. In addition, a recovery in industrial activity coincided with a pickup in global trade, after two years of marked weakness.

Optimism over more synchronized growth in the global economy continued into early 2017, withconfidencesurveysandmarketssignallingbetter prospects. Some swing away from populistpoliticsinkeyEuropeancountriesalsobolstered sentiment. However, actual growth remains relatively subdued and there are still considerable risks to the outlook. Geopolitical tensions have risen once more, and China’s

growth path remains debt dependent. Delaysto President Trump’s reform agenda in the US is expected to lead to some loss of momentum in coming months. Monetary policy continued to be stimulatory despite rising US interest rates. The global economy experienced a manufacturingdrivenupturninthefirstquarterof 2017. Global industrial production was robust in the first quarter, growing by 3.7 per centquarter-on-quarter seasonally adjusted and annualized, a pace that was somewhat slower than a six-year peak of 5.3 per cent quarter-on-quarter seasonally adjusted and annualized reached in the fourth quarter of 2016. Advanced economies in 2016 grew by 1.7 per cent and in 2017 growth is projected to rise to 2.0 per cent, the same level expected in 2018. For advanced economies, projected growth was revised upwardintheUS,reflectingtheassumedfiscalpolicy easing and an uptick in confidence,especially after the November 2016 elections, which, if it persists, will reinforce the cyclical momentum.

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

21

TheoutlookhasalsoimprovedforEuropeandJapan based on a cyclical recovery in globalmanufacturing and trade that started in the second half of 2016. The main forces shaping the outlook differ, to some extent, between advanced economies and emerging market and developing economies. Among the advanced economies group, the US economy is projected togathersteambecauseofexpansionaryfiscalpolicy. Elsewhere, especially in Europe, thecyclical recovery from the crises of 2008/09 and 2011/12 will help keep growth modestly above potential over the next few years. Looking to the medium term, however, demographic headwinds and weak trend productivity are likely to restrain growth. Risks to the global outlook remain tilted to the downside. These include increased trade protectionism, elevated economic policy uncertainty, the possibility offinancialmarket disruptions, and, over thelongerterm,weakerpotentialgrowth(IMFWEOReport, April 2017).

2.2 INDUSTRIALISED COUNTRIES Growth in major advanced economies strengthened, and their short-term outlook has improved, despite elevated policy uncertainty. A modest recovery should continue, with output gaps narrowing and inflation graduallyconverging toward central bank targets. US monetary policy normalization is expected to proceed at a measured pace. China’s policyguided gradual transition to slower but more sustainable growth continues as expected.

Advanced economies started the year on a solid note, with investment and exports regaining momentum after subdued growth in 2016. Private consumption decelerated somewhat in early 2017, but has been supported by labour market improvements. Import demand has strengthened, further contributing to a recovery in global trade.

Advanced economies consumer price inflationhas ticked up as the retail prices of gasoline and other energy related products have increased. Consumerinflationadvancedto0.8percentin2016 up from 0.3 per cent in 2015.The uptick is expected to continue in 2018, where it will reach 2.0 per cent before remaining somewhat steady at 1.9 per cent in 2018. The world also needs a renewed multilateral effort to tackle a number of common challenges in an integrated global economy. Many of the challenges that the global economy confronts call for individual country actions to be supported by multilateral cooperation. Key areas for collective action

include preserving an open trading system, safeguarding global financial stability,achieving equitable tax systems, continuing to support low-income countries as they pursue their development goals, and mitigating and adapting to climate change (IMFWEOReport,April 2017).

In the United States:In2016,USGDPexpandedby 1.6 per cent after growing by 2.6 per cent in 2015, the lowest since 2011. This was due toaslumpinprivateinvestment,thefirsttimesince 2009, dragged down by structures and equipment.For2017,projectedUSGDPgrowthbytheIMFassumesafiscalstimulusthatleadsgrowth to rise to 2.3 per cent and further advanceby2.5percentin2018.Thefiscalpolicyeasingandanuptick inconfidence,especiallyafter the November 2016 US elections, which, if it persists, will reinforce the observed cyclical momentum(IMFWEOReport,April2017).

TheUSFederalReserve(USFED)raisedinterestratesby25basispointstwiceinearly2017,firstin Januaryand inMarch respectively. Interestrates were raised from a range of between 0.25 per cent and 0.5 per cent in December 2016to a range of 0.75 per cent to 1.00 per cent in March2017.Thismarkedoneof theUSFED’smost convincing steps yet in the effort to return monetary policy to a more normal stance (US Federal Reserve, April 2017).

USinflationforthefullyearof2016ranatthefastestpace infiveyears,climbingto2.1percent,propelledbyfivestraightmonthsofcostof living increase compared to 0.1 per cent in 2015. For the period ending March 2017, US consumer prices increased by 2.4 per cent year-on-year, lower than 2.7 per cent in February and below market expectations of 2.6 per cent. This was the lowest inflation rate in threemonthsdue to a slowdown in energy and services cost (USBureauofEconomicAnalysis,April2017).

According to the US Bureau of Labour Statistics, US unemployment rate in 2016 averaged 4.9per cent, and in thefirstquarter of 2017unemployment declined rapidly. As at end March 2017 US unemployment was recorded at 4.5 per cent from 4.7 per cent in the previous month, as the number of unemployed persons declined.

In the Eurozone: According to the IMF World EconomicOutlook,over thewhole year2016,EurozoneGDPadvancedby1.7percentaftergrowing by 2 per cent in 2015. The IMF projected

GLOBAL ECONOMIC DEVELOPMENTS (Continued)

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

22

thatEurozoneGDPin2017and2018willgrowby1.7 per cent and 1.6 per cent, respectively. In thefirstquarterof2017theEurozoneeconomyexpanded by 0.6 per cent, following a 0.5 per cent advance in the previous quarter. This was thestrongestgrowthratesincethefirstquarterof 2015, mainly boosted by fixed investmentand household consumption. Growth picked up in Germany, Spain, Italy and Finland but slowed in France.

Following the European Central Bank’s (ECB)decision to lower its benchmark-refinancingrate to 0.0 per cent and increase its asset purchase programme to €80 billion a month in March 2016, the ECBmaintained the samepolicy stance until end of March 2017. Both the deposit rate and the lending rate were also left steady at -0.4 per cent and 0.25 per cent, respectively.ECBpolicymakersconfirmedthatthe monthly asset purchases will run at the current monthly pace of €80 billion until March 2018, and from April 2018, they are intended to continue at a monthly pace of €60 billion until the end of the year 2018 (European CentralBank, April 2017).

Eurozone inflation rate rose to 1.1 per centyear-on-year in December 2016, compared to0.2 per cent in December 2015. The surge ininflation was the highest in more than threeyears, driven by increased prices for energy, food, alcohol and tobacco. In the three months toMarch2017,consumerpricesintheEurozonerose by 1.5 per cent year-on-year, easing from a 2 per cent increase in February and below marketexpectationsof1.8percent(Eurostat,April 2017).

Eurozone unemployment rate averaged 10per cent in 2016 and has been steadily on a downward trend. The unemployment rate came in at 9.5 per cent in March 2017, unchanged from the previous month and was the lowest unemploymentratesinceApril2009(Eurostat,April 2017).

In the United Kingdom: Looking at 2016 as a whole,UKGDPgrowthslowedto1.8percentfrom 2.2 per cent in 2015. Fixed investment and government spending went up at a slower pace while household consumption grew further. In the first quarter of 2017, the UKeconomy grew by only 2.2 per cent, the lowest quarter-on-quarter growth in a year, after expanding by 0.7 per cent in the fourth quarter of 2016. The slowdown was mainly driven by

the service sector on weak performances of consumer-focused industries, such as retail and accommodation(IMFWorldEconomicOutlook,April 2017).

The Bank of England cut its interest rates to0.25 per cent from 0.5 per cent in August 2016 and introduced a package of measures designed to provide additional monetary stimulus. The Bank of England has kept interest rates atrecord low for the whole of 2016 and including thefirstquarterof2017,inordertomeetits2percentinflationtarget.TheBank’sobjectiveis to achieve sustainable economic growth and fullemployment(BankofEngland,April2017).

UK inflation averaged 0.67 per cent in 2016compared to 0.2 per cent in 2015. The Bank ofEnglandexpects inflation to riseabove the2 per cent target over the short-term, before peaking at around 2.75 per cent in early 2018 and drifting gradually back down towards the target thereafter. The projected overshoot reflectstheexpectedeffectsofthedropinthevalue of the Pound Sterling. Wages and salary growth remained subdued, while measures of inflationexpectationsremainatlevelsbroadlyconsistentwiththeachievementoftheinflationtarget(Eurostat,April2017).

Average annual unemployment rate in the UK was recorded at 4.9 per cent in 2016and has been on a declining trend since. UKunemployment rate fell to 4.6 per cent in the three months to March 2017 from 4.7 per cent inthepreviousperiod(Eurostat,April2017).

In Japan:Japan’sGDPgrewby1.0percentin2016 compared to 0.5 per cent in 2015. The growth momentum, fuelled by stronger-than-expected net exports in 2016, will continue into 2017, with growth forecast at 1.2 per cent. The pace of expansion is expected to weaken thereafter to 0.6 per cent in 2018, with the assumed withdrawal of fiscal support and arecovery of imports offsetting the impact of stronger anticipated foreign demand and Tokyo Olympics–relatedprivateinvestment(IMFWEOReport, April 2017).

FollowingtheBankofJapan’sdecisiontoadopta negative interest rate policy, the Bank has maintained this rate for the whole of 2016. Further, the Bank of Japan left its key short-term interest rate unchanged at -0.1 per cent at its March 2017 meeting. Policymakers also decided to keep its 10-years government

GLOBAL ECONOMIC DEVELOPMENTS (Continued)

CENTRAL BANK OF SWAZILAND 2016/2017 ANNUAL REPORT

23

bond yield target around zero per cent and maintaining their upbeat economic view (Bank ofJapan,April2017).

Japanconsumerinflationin2016averaged-0.1per cent following 0.2 per cent recorded in 2015. Higher energy prices, the recent weakening in the yen, and slowly building wage-price pressuresareexpectedtoliftinflationinJapan.However,withinflationexpectationsrisingonlyslowly,theincreaseininflationisprojectedtobequite subdued,with inflation rates stayingwellbelowtheBankofJapan’spricestabilitytarget of 2 per cent throughout the forecast horizon(StatisticsBureauofJapan,April2017).On an average basis the unemployment rate in Japan was recorded at 3.1 per cent in 2016,declining from 3.3 per cent recorded in 2015. The unemployment rate at the end of March 2017 stood at 2.8 per cent, the same as in February2017.Thefigurecameslightlybelowmarket consensus of 2.9 per cent (Statistics BureauofJapan,April2017).

2.3 EMERGING MARKET AND DEVELOPING ECONOMIES