Annual Report - Blocked - Pomegranate

61

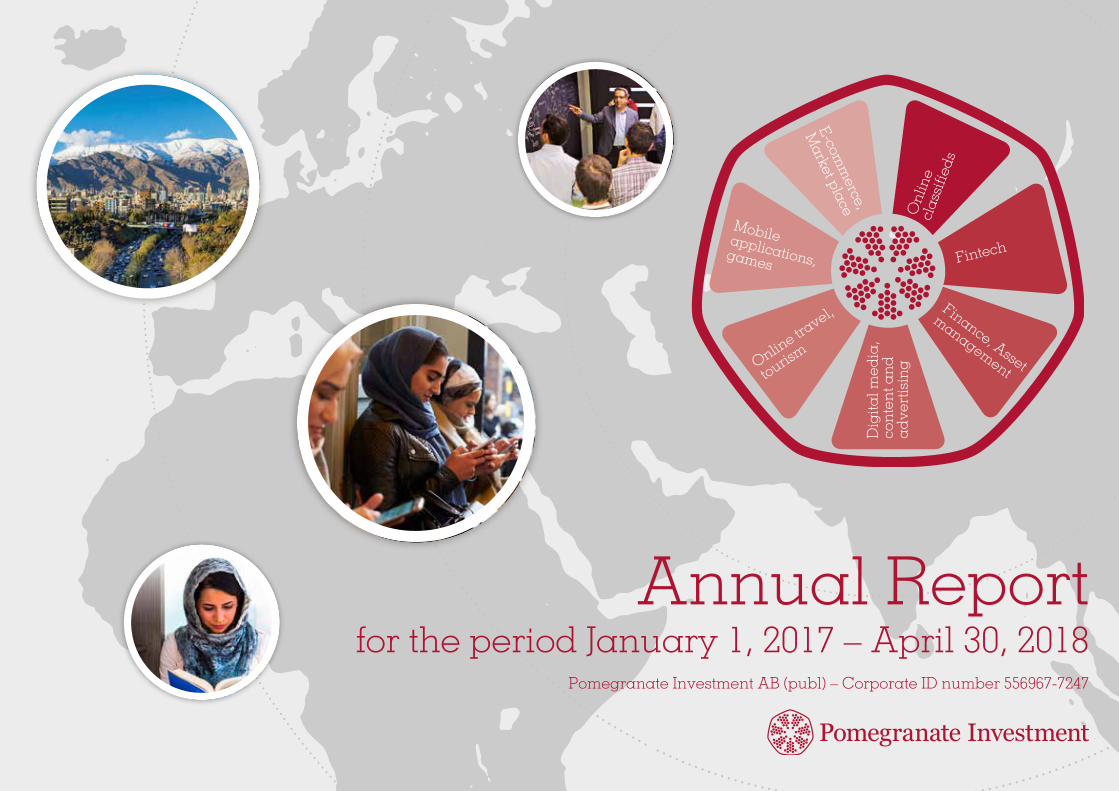

Pomegranate Investment AB (publ) – Corporate ID number 556967-7247 Annual Report for the period January 1, 2017 – April 30, 2018 Online classifieds Fintech Finance, Asset management Digital media, content and advertising Online travel, tourism Mobile applications, games E-commerce, Market place

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Annual Report - Blocked - Pomegranate

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

1

Pomegranate Investment AB (publ) – Corporate ID number 556967-7247

Annual Reportfor the period January 1, 2017 – April 30, 2018

Onl

ine

clas

sifie

ds

Fintech

Finance, Asset

management

Dig

ital m

edia

, co

nte

nt a

nd

a

dve

rtis

ingOnlin

e travel,

tourism

Mobileapplications,games

E-comm

erce,

Market place

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

2

Important Information

NOT FOR DISTRIBUTION IN THE UNITED STATES OR TO ANY U.S. PERSON

This report does not constitute an offer of any securities of Pomegranate Investment. This report may not be distributed in the United States or to any “U.S. person”, including any U.S. citizen or permanent resident (‘green card holder’) or any entity organised in the United States, whether located inside or outside the United States. Pomegranate shares represent an investment in Iran that is not suitable for U.S. persons.

This report contains forward-looking statements. All statements other than statements of historical facts included in this presentation, including without limitation, those regarding the Company’s financial position, business strategy, plans, objectives, goals, strategies and future operations and performance and the assumptions underlying these statements are forward-looking statements. Such forward-looking statements involve known and unknown risks and uncertainties and other factors which are or may be beyond the Company’s control, which may cause the actual results, performance or achievements of the Company, or industry results, to be materially different from any future results, performance or achievements ex-pressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strat-egies and the environment in which the Company will operate in the future. Some numerical figures included in this Presentation have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in certain graphs or tables may not be an exact arithmetic aggregation of the figures that preceded them.

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

3

OVERVIEWPomegranate Investment in Brief 5Reporting period in Brief 6Key Drivers 7Portfolio Overview 8Letter from the Managing Director 9-11Summary of the EU Blocking Regulation 2018 12Market Overview 13-15

INVESTMENT PORTFOLIOPomegranate invests in market leaders 17Sarava (and Sarava Holdings) 18 Digikala 19 Café Bazaar 20 Alibaba 20 Alopeyk 21 PPG 21 Avatech 21Sheypoor 22Griffon Capital 23-24Navaar 25Bahamta 26

CORPORATE GOVERNANCECompany and Share Information 28Board of Directors 29Group Management and Auditors 30Auditor 31Risks and uncertainty factors 32-34

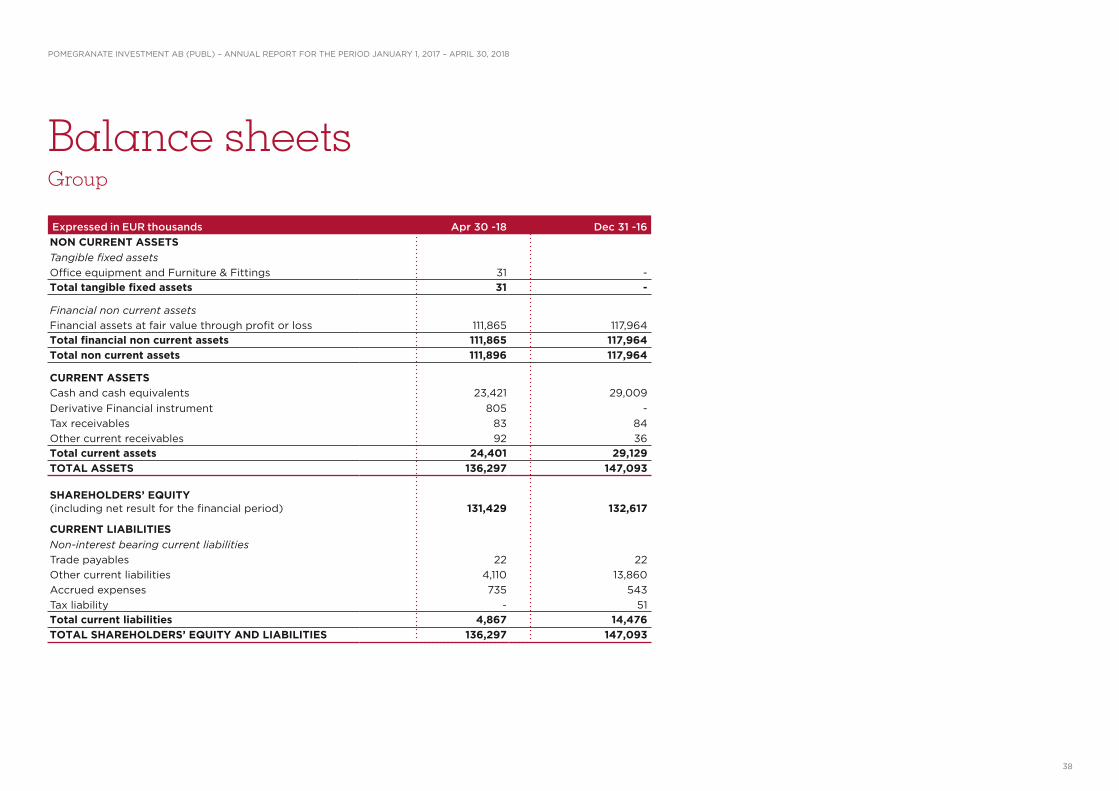

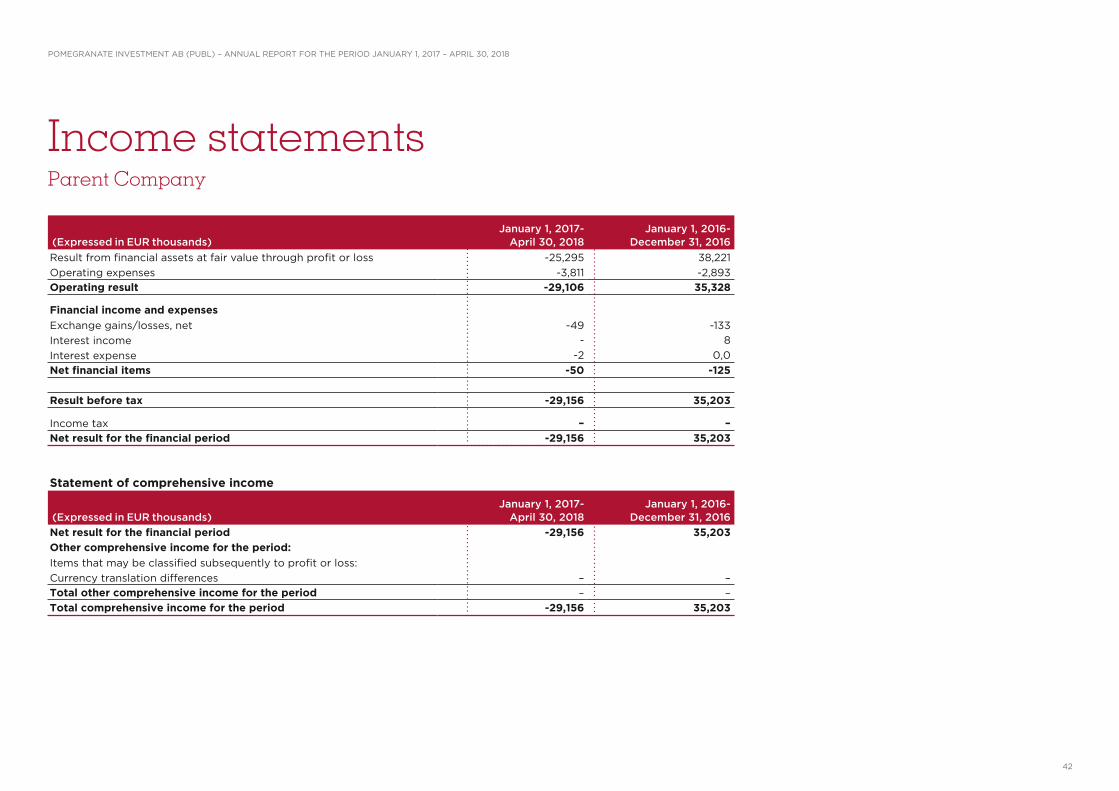

FINANCIAL INFORMATIONAdministration Report 36Income Statements – Group 37Balance Sheets – Group 38Statement of changes in Equity – Group 39Cash Flow Statements – Group 40Alternative Performance measures – Group 41Income Statements – Parent 42Balance Sheets – Parent 43Statement of changes in Equity – Parent 44Notes to the Financial Statements 45-57Independent auditors Report 58-59

INFORMATION Annual General Meeting 60Contact 60

Table of contents

The company’s accounting currency is EUR.All amounts are reported in EUR, unless otherwise specified.This report is a translation from the Swedish original.In case of any discrepancies, the Swedish versionshall prevail.

Corporate websitewww.pomegranateinvestment.com

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

4

Overview

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

5

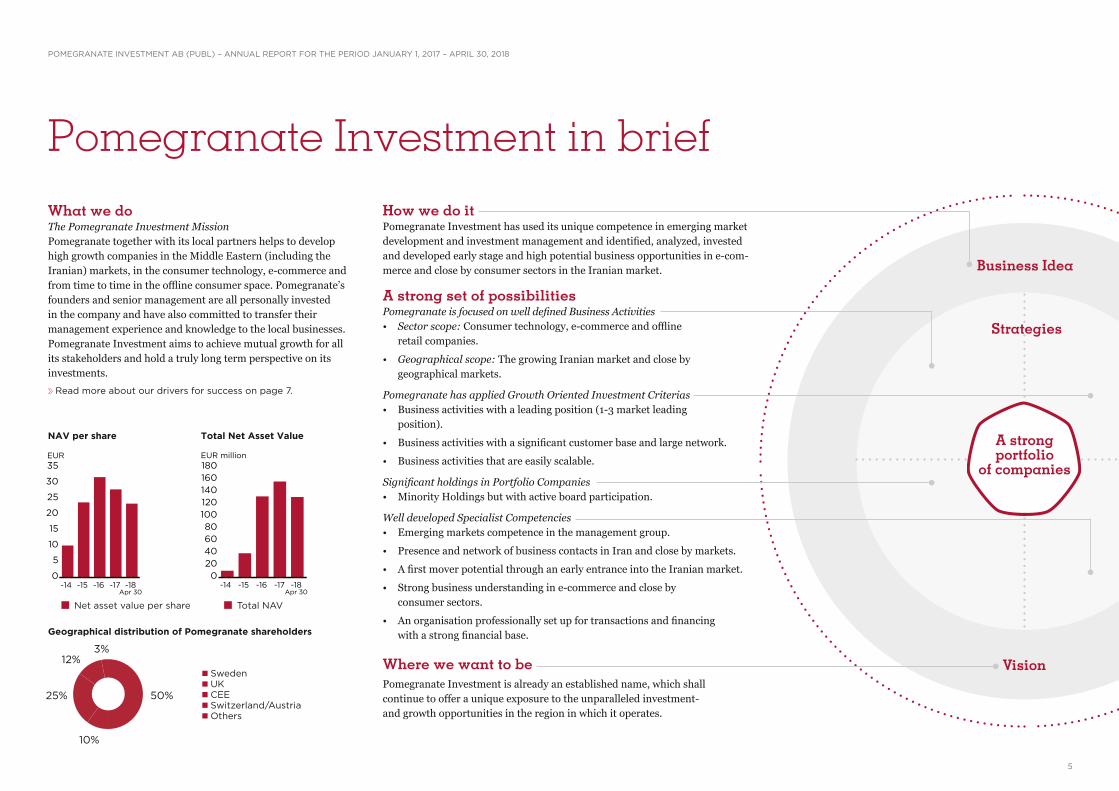

Pomegranate Investment in briefWhat we doThe Pomegranate Investment MissionPomegranate together with its local partners helps to develop high growth companies in the Middle Eastern (including the Iranian) markets, in the consumer technology, e-commerce and from time to time in the offline consumer space. Pomegranate’s founders and senior management are all personally invested in the company and have also committed to transfer their management experience and knowledge to the local businesses. Pomegranate Investment aims to achieve mutual growth for all its stakeholders and hold a truly long term perspective on its investments. Read more about our drivers for success on page 7.

Business Idea

Vision

Strategies

Net asset value per share Total NAV

NAV per share Total Net Asset Value

How we do itPomegranate Investment has used its unique competence in emerging market development and investment management and identified, analyzed, invested and developed early stage and high potential business opportunities in e-com-merce and close by consumer sectors in the Iranian market.

A strong set of possibilitiesPomegranate is focused on well defined Business Activities• Sector scope: Consumer technology, e-commerce and offline

retail companies.

• Geographical scope: The growing Iranian market and close by geographical markets.

Pomegranate has applied Growth Oriented Investment Criterias• Business activities with a leading position (1-3 market leading

position).

• Business activities with a significant customer base and large network.

• Business activities that are easily scalable.

Significant holdings in Portfolio Companies• Minority Holdings but with active board participation.

Well developed Specialist Competencies• Emerging markets competence in the management group.

• Presence and network of business contacts in Iran and close by markets.

• A first mover potential through an early entrance into the Iranian market.

• Strong business understanding in e-commerce and close by consumer sectors.

• An organisation professionally set up for transactions and financing with a strong financial base.

Where we want to bePomegranate Investment is already an established name, which shall continue to offer a unique exposure to the unparalleled investment- and growth opportunities in the region in which it operates.

A strong portfolio

of companiesEUR

0

5

10

15

20

25

30

35

-15-14 -16 -17 -18Apr 30

EUR million

020406080

100120140160180

-15-14 -16 -17 -18Apr 30

Geographical distribution of Pomegranate shareholders

50%

10%

25%

12%3%

SwedenUKCEESwitzerland/AustriaOthers

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

6

Reporting period in BriefJanuary 1, 2017 – April 30, 2018

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

Carvanro follow up round

CFO recruited

30 MEURPomegranate fundraising

At the AGM in May the financial year was changed to May 1 – April 30

Submitted formal listing application to NGM Equity

Follow up invest-ment in Sheypoor

First investment in Bahamta, peer to peer monetary transfers

Pomegranate formally became a group and started to apply IFRS

First investment in Navaar, leading audio book provider

Start of negotiations for Sarava follow up round

Signed MOI for Sarava new funding round

IPO preparations

Safi negotiations

Strengthening Pomegranate’s local brand and network

Legal Counsel recruited

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

7

Pomegranate has applied Growth Oriented Investment Criterias

First mover advantagePomegranate was established in 2014 by emerging market specialists with a strong track record in emerging and frontier markets. Since 2014, Pome-

granate’s investment portfolio has grown significantly. Pomegranate believes

that by having entered Iran earlier than most, it has established a critical head-start in

the country and is well-positioned to continue expanding in Iran’s rapidly evolving consumer technology end e-commerce sectors.

A diversified economy enabling growthDespite being an energy-rich country with the world’s second larg-est reserves of natural gas and the fourth largest reserves of crude oil, the Iranian economy is highly diversified with the oil and gas sector accounting for only 23 percent of Gross Value Added (GVA) in 2014, compared to 30 percent in the United Arab Emirates and 50 percent in Kuwait. Other significant sectors include retail, trade, real estate, construction and professional services, which together make up a larger share of the economy apart from oil and gas.

A diversified economy has enabled a growing consumer market – over 55 percent of the Iranian population has an annual purchas-ing power parity adjusted income above USD 20,000, twice as high as in China or India, and second only to Russia among the BRIC-economies. Additionally, retail sales per capita in Iran is larger than in Turkey, Malaysia or Mexico, adjusted for purchas-ing power parity.

Unique demographicsIran’s population of approx-imately 82 million is one of the largest demographics

in the region, equivalent to the size of Germany. The

population is young, with more than 65 percent of the population

currently under the age of 35, in the beginning or in the middle of their careers. Furthermore, the Iranian labor force is highly educated with the highest literacy rate in the MENA region, secondary school participation is almost 80 percent and tertiary education participation is among the highest in the world, ahead of the UK, France and Germany. Iran’s urbanisation rate of 73 percent is twice that of India (33 percent), well ahead of Italy (69 percent) and close to the levels of Germany (75 percent) and France (80 percent) – a good starting point for roll-ing out new infrastructure.

The unique demographics of Iran with a large, young, well-educated and central and urbanised population supports Pomegranate’s investments in the chosen sectors of consumer technology, e-commerce and offline retail.

Strong growth in internet and smartphone penetrationIranian internet penetration represents 52 percent (from 16 percent) and is still relatively low but outperforming countries like India (26 percent) and Egypt (36 percent). The growth rate in this sector is rather significant with an an-nual growth rate of 11 percent over the last two-year period. The 3G/4G availability was 60 percent at the end of 2015, a thirty-fold increase compared to 2013, which can be seen as an indicator of Iran advancing into modern ICT infrastructure. As opposed to internet penetration, mobile penetration is well developed with 142 phones per 100 people. Smartphone penetration in Iran has been growing at significant rates from 50.4 percent in Q1 of 2016 to 56.4 percent in Q3, an increase of 12 percent in just nine months.

With growing internet and smartphone penetration and a developing domestic regulatory environment for the space it is reasonable to assume an accelerated online consumption behavior.

Strategic location, already strong exportsIran’s central location in the Middle East, bordering countries with a

total population in excess of 400 million, including almost 40 million consuming households who are projected to grow at 5.2 percent

annually until 2025, provides the opportunity for the country to become a regional trading hub.

Despite the effects of sanctions and constrained stock and flow of foreign direct investments, Iran today exports more than Egypt, Pakistan and Morocco combined.

7

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

8

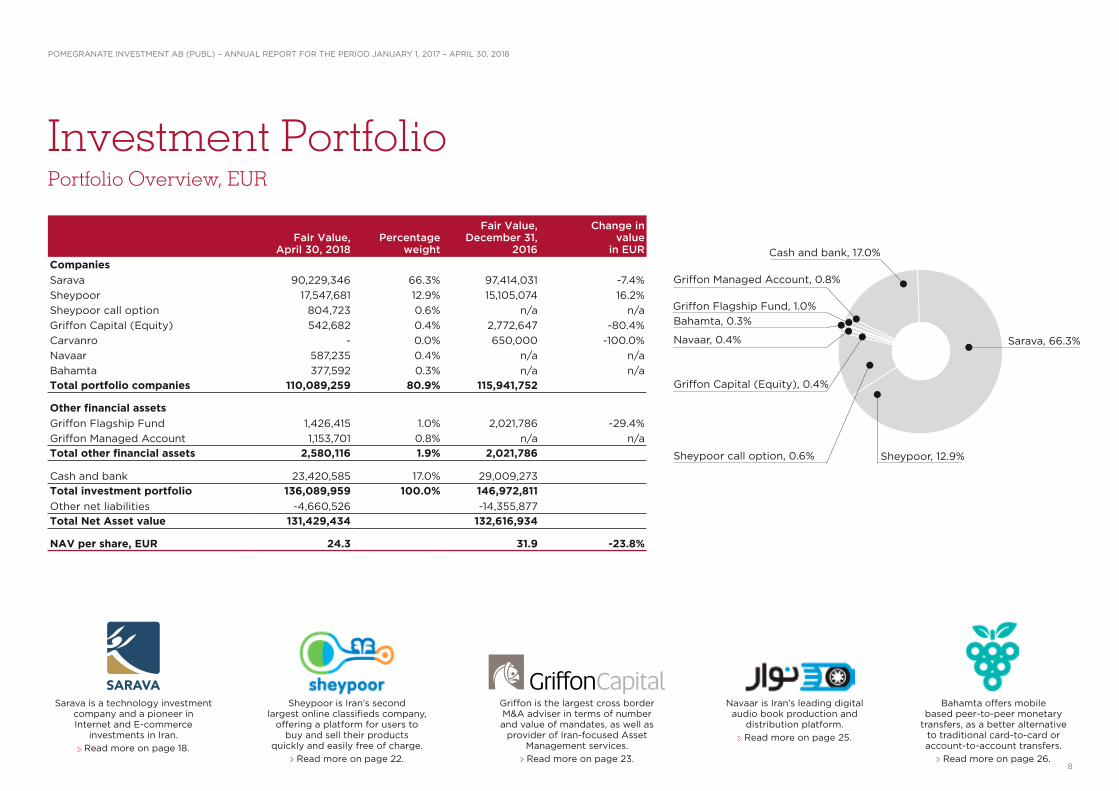

Investment PortfolioPortfolio Overview, EUR

Fair Value, April 30, 2018

Percentage weight

Fair Value, December 31,

2016

Change in value

in EUR

Companies

Sarava 90,229,346 66.3% 97,414,031 -7.4%Sheypoor 17,547,681 12.9% 15,105,074 16.2%Sheypoor call option 804,723 0.6% n/a n/aGriffon Capital (Equity) 542,682 0.4% 2,772,647 -80.4%Carvanro - 0.0% 650,000 -100.0%Navaar 587,235 0.4% n/a n/aBahamta 377,592 0.3% n/a n/aTotal portfolio companies 110,089,259 80.9% 115,941,752

Other financial assets

Griffon Flagship Fund 1,426,415 1.0% 2,021,786 -29.4%Griffon Managed Account 1,153,701 0.8% n/a n/aTotal other financial assets 2,580,116 1.9% 2,021,786

Cash and bank 23,420,585 17.0% 29,009,273Total investment portfolio 136,089,959 100.0% 146,972,811

Other net liabilities -4,660,526 -14,355,877Total Net Asset value 131,429,434 132,616,934

NAV per share, EUR 24.3 31.9 -23.8%

Griffon Capital (Equity), 0.4%

Sheypoor call option, 0.6%

Navaar, 0.4%

Cash and bank, 17.0%

Sarava, 66.3%

Sheypoor, 12.9%

Bahamta, 0.3%Griffon Flagship Fund, 1.0%

Sarava is a technology investment company and a pioneer in Internet and E-commerce

investments in Iran. Read more on page 18.

Sheypoor is Iran’s second largest online classifieds company,

offering a platform for users to buy and sell their products

quickly and easily free of charge. Read more on page 22.

Griffon is the largest cross border M&A adviser in terms of number and value of mandates, as well as

provider of Iran-focused Asset Management services. Read more on page 23.

Navaar is Iran’s leading digital audio book production and

distribution platform. Read more on page 25.

Griffon Managed Account, 0.8%

Bahamta offers mobile based peer-to-peer monetary

transfers, as a better alternative to traditional card-to-card or account-to-account transfers.

Read more on page 26.

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

9

Dear fellow share owners, In the first half of 2018, we have seen a period of trade and economic chang-es in Iran caused by the US announcing its unilateral withdrawal from the JCPOA in May and declaring its intention to reimpose sanctions on Iran. The first round of these sanctions, in the financial and non-petrochemical sectors (automobile and metals) were reintroduced in August, with the second round, affecting oil and gas, set to follow in November. Whilst they have no direct bearing on Pomegranate’s business, due to the lack of any US nexus or dependency on the US financial systems, we are not immune to the severe macro disruption the Iranian economy is facing as a result. The EU’s response to all of this has been relatively strong and clear – along with the other JCPOA signatories the EU has declared its firm commitment to the preservation of the JCPOA accord. In an effort to mit-igate the effect of the reimposed US sanctions, the EU has implemented a Blocking Regulation aimed at protecting the interest of European com-panies doing business with Iran. The force in this blocking statute is that once EU companies decide to do business with Iran, they are prohibited from complying with US extraterritorial sanctions. This grandfathering mechanism encourages predominantly small and medium size companies to increase their trade and business activities with and inside Iran. From what we can tell so far, this provides an even stronger protection for companies like Pomegranate. Further details are set out in the section below ‘Summary of the EU Blocking Regulation 2018.’ As a company we have gone from a period of sanctions lifting and fund raising in 2016-17, that allowed us to deploy capital into new and existing investments to strengthen our ownership and boost growth in our portfo-lio companies, to a more uncertain climate in 2018 against the backdrop outlined above. Given this sea change, we have had to make some prudent interim adjustments and we continue to work steadfastly to protect capital and cut costs. The good news is that our portfolio companies are doing very well despite the challenging external environment and our strategic foresight to raise capital in early 2017 has given us an even stronger foundation in regards to securing our market position, growth potential and avoiding being diluted. If necessary, we can steer the company to last beyond 2025, which marks the termination of the JCPOA.

The purpose of this report is to satisfy our annual report which has moved to the summer period as the company’s financial year was amended last year to comprise 1 May to 30 April. This move was devised to maximise our alignment with our Iranian business partners and portfolio companies. This report therefore covers the period between 1 January 2017 to 30 April 2018. The financial period is the same as last reporting period (January – April 2018). A new report will follow on 20th September 2018 and this report is effectively closing the “transition period of reporting” requirements. From the beginning of 2018, all of our attention has been focused to remain as liquid and well financed as possible during stormy days ahead. We are well equipped and prepared for capital protection and OPEX cuts. We have risk adjusted our NAV taking into account the changed macro envi-ronment which we accounted for in our previous report adjusted from EUR 29.4 to EUR 24.3 per share which is roughly where we started this reporting window in January 2017. Since this is an annual report, I would like to take the opportunity to highlight some key achievements. Corporate and organisational changesThe EUR 30 million fund raising which was carried out in the spring of 2017, assisted in securing funding for the company’s investments for a few years ahead and also contributed to diversifying our shareholder base to over 400 shareholders. The largest shareholder has just under 10% own-ership making our shareholder based balanced, including predominantly Nordic (approx. 50%) followed by Russia/CEE (approx. 33%). We still have a total sum of cash and short term investments of EUR 26 million at the end of the reporting period. Our efforts further consisted by strengthening the core team with em-ployment of our CFO and Legal Counsel in addition to the second Invest-ment Manager that came on board just before the start of this reporting period. Our core team was completed which was one of our preconditions before our own IPO, followed by IFRS implementation and first reporting in accordance with those standards, another IPO precondition. It was also our goal that our portfolio companies would eventually follow-on track in accordance with IFRS standards (for example Digikala is now 95% IFRS compliant).

Letter from the Managing Director

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

10

We proceeded to change our financial calendar to the Iranian financial calendar to be able to communicate more efficiently with our portfolio companies and their KPI’s in a timely and strategic manner and as a result increase transparency substantially.

Investment portfolio activities We have completed our target of 3-5 investments comprising 2 new invest-ments, 3 follow-on investments and 1 investment closed. We decided to discontinue the Hard Discount venture for partnership reasons and project Safi for compliance reasons. There was some M&A activity on the Iranian start up scene as well as some activity in Sarava that firmed up their strong position in the digital economy. There were follow on offerings to increase stakes in Café Bazaar, Alibaba and above all secure funding for Digikala, all motivated by strong growth and new market opportunities. We are particularly pleased with the increased indirect exposure to Café Bazaar, Iran’s largest app store, which we firmly believe is going to be a significant value driver, as many inter-national competitors cannot operate in Iran. Sheypoor secured additional funding at the end of 2017 with prominent new investors coming on board. Digikala continued to grow significantly, with 60% GMW growth year-on-year. Sheypoor continued to grow in excess of 100%. Digikala’s Market Place segment has really taken off, Café Bazaar is broadening its offering of digital services, and consumer behaviour in travel continues to move online. The local stock market is warming up to the new tech scene and consequent-ly so are IPO discussions and preparations among the local companies. We were pleased to report our first Fintech investment in Bahamta aswell as our first digital content/streaming investment in the audio book company Navaar. As a direct consequence of the recent events, we have performed renewed sanctions compliance checks of all our investment structures and sharehold-ers in target companies that have been re-approved by internal and external legal counsels. This was a compliance exercise we felt was necessary in relation to all our direct and indirect portfolio companies to make sure that no stakeholders were listed as Specially Designated Nationals on US or European sanctions lists. Q4 2017 was a key period for Pomegranate as we continued to report on a number of investments and significant developments to underpin our presence in Iran’s most exciting tech growth sectors. To round up the year, we solidified our strategy of exposure to market leadership, directly as well

as indirectly, across the E-Commerce, Classified/Mobile, Sharing Economy, Digital Content & Marketing as well as Payment/Financial Services sectors.

NAVIn general the year concluded by an upward effect in the Sarava portfolio driven by strong underlying growth, a financing round in Sheypoor at a higher valuation driven by underlying growth, and for the rest of the port-folio we had fairly recent transactions. However, due to the reimplementa-tion of US secondary sanctions and the effect the anticipation of the same had already had on the economy and currency, we performed a broad risk adjusted valuation update of all recent transaction valuations in portfolio companies. As a result, the company’s net asset value per share in EUR decreased by 24% over the period January 1, 2017– April 30, 2018. This is not the development we had wished for but we continue to strongly believe in and support the long term potential of our portfolio companies, and as experienced investors in emerging markets we have seen the volatility and swings before in many other markets and luck favours the bold and prepared in the end. At present, Pomegranate might look like a different company (compared to last year) in a different environment. We had not anticipated make adjustments so shortly after the implementation of the JCPOA. Needless to say, the company is currently too big for what the market is – we will need to be flexible around that but equally make sure the team (and portfolio teams) remain motivated.

IPOLast year we submitted our formal listing application to the regulated exchange NGM Equity. Whilst the timing of the IPO has not been right, we have completed all the formal corporate preparations for a listing in the near future. The external environment is not IPO friendly at the present time. We are technically ready to proceed with an IPO and will further explore what it would all mean together with the EU’s blocking mechanism to use to our advantage. In the interim, it is very exciting that we expect local listings of one or two companies from our portfolio within the next 6-8 months. We are confident that our local portfolio companies and their teams will come out stronger from this process given the lack of foreign competition and capital scarcity to a strong shift in online economy. Interestingly, we have observed unusually high growth rates during Q1 of the Iranian year

Completed target of 3-5 investments. 2 new investments, 3 follow investments, 1 investment closed.

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

11

which is now tailing off somewhat. It remains to be seen how these growth rates evolve over time. We are going to report more operational data again in our next report in September 2018.

Concluding remarks It has been an incredible reporting period to say the least. It started with the full impact of sanctions being rolled back, to raising EUR 30 million for con-tinued growth and offline consumer business diversification and ended with the US unilateral withdrawal from the JCPOA just after the period closed. It is worth a reminder that as a company we are not directly effected by the restoration of these sanctions and we navigated the company in 2014 before the JCPOA was born. This message is even stronger in a context where the EU actively encourages EU companies to do business with Iran and putting in place measures to facilitate that and to protect them from reimposed US sanctions. However our strategic fund raising at the beginning of 2017 is to our distinct advantage now. Protecting our existing growth investments is key, as well as, allowing ourselves to cut OPEX to last beyond 2025. Last but not least, we have provided the legal and technical summary of the current EU Blocking Regulation similarly to what we have done in our previous report. The compliance work is a day-to-day aspect of our business, which is carried out internally by our General Counsel who works alongside external legal advisors to make sure that we are compliant with the remaining Eu-ropean and UN sanctions. This work is of outmost important to us to make sure that we understand the current sanctions regime before committing to any transactions and to protect the interest of our share owners, stake holders as well as counterparties.

Greeting from Stockholm,Florian Hellmich

We are confident that our companies, and their teams will come out stronger from this process.

12

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

Summary of the EU Blocking Regulation 2018US withdrawal from the JCPOAThe US announced on 8 May 2018 that it would reinstate all previ-ously lifted sanctions removed under the JCPOA and the re-impo-sition would come into effect after a “wind-down” period of 90 days (ending 6 August 2018) and 180 days (ending 4 November 2018).

EU and E3 commitment to the JCPOAIn response to this, the European Commission initiated several steps to preserve the interest of European businesses and persons investing or doing business with Iran. On 6 June 2018, the Commis-sion adopted updates to the Council Regulation from 1996, a statute which, provided protection against the effects of extra-territorial application of US sanctions laws affecting Cuba, Libya and Iran (“the Blocking Regulation”). The updated statute entered into force on 7 August 2018. This is the first time the Blocking Regulation has been extended and it applies more broadly to US extra-territorial sanctions against Iran as specified in its annex. The basic principle of the statute is that the EU does not rec-ognise the applicability of US extra-territorial sanctions and in connection with this decisions of any nature by foreign courts and bodies will be challenged and nullified. The Blocking Regulation acts to prohibit EU Operators (as defined below) from complying with US secondary sanctions against Iran as its application will have legal repercussions including sanctions determined by each member state. Those protected under the Blocking Regulation are referred to as the ‘EU Operators’ and include, inter alia, natural persons being a resident in the European Union and a national of a member state as well as legal persons incorporated within the European Union. EU Operators are free to choose whether to start working, continue or cease business operations in Iran. The purpose of the Blocking Reg-ulation, however, is to ensure that such business decisions remain free, i.e., are not forced upon EU Operators by the US secondary sanctions. There is also a procedure for seeking authorisation from the European Commission to comply with specific US legislation on the basis that not doing so would seriously damage the EU Opera-tors’ interests, or those of the EU. One aspect of the Blocking Regulation, which is less certain, is the extent to which damages may be claimed as a result of the actions and effects of US secondary sanctions and authorities. The

Guidance Note published alongside the statute states that the scope of the damages and the defendant that the EU Operators can claim against is very broad, but ultimately leaves it to competent courts of the member states of the EU to determine the kind of damage caused and the procedure for recovery. This is an important step by the EU in demonstrating its com-mitment to the continued implementation of the JCPOA. However, it is uncertain how this legislation will be enforced and applied in practice given that this is the responsibility of each member state.

JCPOA developmentsOn 6 August 2018, Iran, China, Russia, France, Germany, the United Kingdom, and the EU High Representative reaffirmed their commitment to full and effective JCPOA implementation, and recognized that the lifting of sanctions in exchange for Iran’s imple-mentation of its nuclear-related commitments remains an essential part of it. Also on 6 August 2018, the EU High Representative and the Foreign Ministers of France, Germany and the United Kingdom issued a statement expressing their deep regret regarding the re-im-position of the US sanctions against Iran. The statement confirms that EU efforts to engage with third countries to ensure JCPOA support and to maintain economic relations with Iran will intensify in the coming weeks.

Practical use of the Blocking Regulation since 1996The praxis of the Blocking Regulation previously applied mostly to extra territorial sanctions against Cuba. There are further only few examples of Blocking regulation enforcements in the member states. According to the Commission’s Guidance Note, the benefit of the statute resulted in that in 1998 the EU and the US entered into a Memorandum of Understanding subject to which the US suspended the application of certain sanctions in return for the EU and other countries continuing their efforts to promote democracy in Cuba. The use of the statute was more limited to Iran because firstly, it applied to one US extra-territorial sanctions against Iran and Libya, and secondly, those sanctions applied for a period of 12 months.

What this means for the banking sectorOne of the restrictive effects of the US secondary sanctions return-ing is sanctions on transactions with foreign financial institutions

with the Central Bank of Iran and designated Iranian financial institutions. This also includes state owned banks. Under the Blocking Regulation, there is no requirement for EU Operators and EU banks to comply with this extra-territorial sanction. However, it is noteworthy that even before the restoration of the US secondary sanctions, money transfer to and from Iran was limited as larger banks were still reluctant to do business with Iran. This situation is likely to worsen, even with the EU Blocking Regulation, as the restoration of US sanctions have removed corresponding banking relationships between US banks and foreign banks with an existing correspondent relationships with Iranian institutions. Since the US announced its withdrawal from the JCPOA, certain banks that previously processed Iran-related payments in the past have announced that they will discontinue those facilities in the future. It remains to be seen how the EU and the Member States will continue their efforts to remove banking obstacles. On 7 August 2018, the European Commission published a decision adding Iran to the list of countries eligible for European Investment Bank (EIB) financing under EU guarantee. This means that EIB loans, loan guarantees and debt capital market instruments for the benefit of investment projects in Iran are eligible for such EU guarantee, sub-ject to a signed agreement and further conditions and ceilings. The banks will however take their own views on risk and compliance, especially when having international banking structure, notwith-standing the protection afforded to EU banks under the Blocking Regulation.

Our external sanctions counsel Freshfields Bruckhaus Deringer has contributed to this section.

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

13

A brief look at digital economy in emerging markets, MENA and IranMany countries including China and South Korea have forward-looking plans to be realized by 2020. Among these plan, South Korean Yonhap news agency reported the launch of the Ministry of SMEs and Startups (MSS) in July 2017, a government body recognizing the increased importance of startups and small businesses and their impact on the entire business ecosystem. Some of the Ministry’s objectives comprise promoting business growth, strengthening startups and supporting Small and Medium-sized Enterprises (SMEs) and Micro Enterprises (MEs). In addition, the gov-ernment of South Korea intends to launch 1,200 incubators by 2020 and allocate 4.3 billion dollars to support 100 firms, calling them “global star ventures.” Like South Korea, China is developing its technological infrastructure. It is projected that Internet penetration rate in this country will reach 70 percent and nearly half of its rural region will have access to broadband In-ternet coverage (50 Mbs) by 2020. Russia also plans to grow the technology share of its GDP from 1.1% to 8-10%. This quick glance around the world reveals that plenty of countries have serious intentions and plans to develop their digital economies. What these countries all seem to have in common is a strong focus on facilitating and preparing the essentials of the digital economy in order to enhance the startup ecosystem. In what follows, five important digital industries will be reviewed; (i) e-commerce, (ii) mobile applications, (iii) online travel, (iv) sharing econo-my, and (v) digital advertising. These factors play crucial roles in the growth of the digital economy. Subsequent to looking at these factors, we will also explore and discuss the future trends of these industries in the world, in the Middle East and in Iran.

Continuous growth of e-commerce turnover in the world and a faster growth rate forecast for developing countriesOnline shopping is among the most popular e-commerce activities in the world. Based on Ecommerce Foundation’s 2016 report, there are 5.6 billion people in the world who are over 15 and 45% of them use internet. In MENA

Market Overview

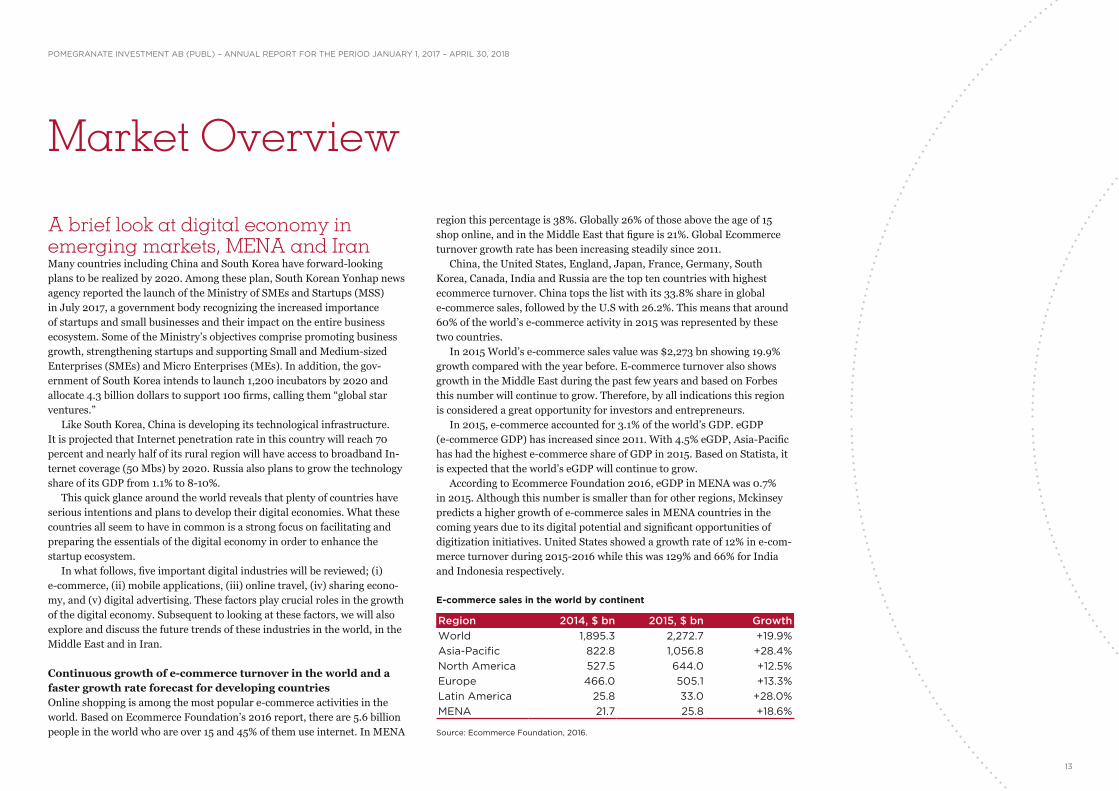

region this percentage is 38%. Globally 26% of those above the age of 15 shop online, and in the Middle East that figure is 21%. Global Ecommerce turnover growth rate has been increasing steadily since 2011. China, the United States, England, Japan, France, Germany, South Korea, Canada, India and Russia are the top ten countries with highest ecommerce turnover. China tops the list with its 33.8% share in global e-commerce sales, followed by the U.S with 26.2%. This means that around 60% of the world’s e-commerce activity in 2015 was represented by these two countries. In 2015 World’s e-commerce sales value was $2,273 bn showing 19.9% growth compared with the year before. E-commerce turnover also shows growth in the Middle East during the past few years and based on Forbes this number will continue to grow. Therefore, by all indications this region is considered a great opportunity for investors and entrepreneurs. In 2015, e-commerce accounted for 3.1% of the world’s GDP. eGDP (e-commerce GDP) has increased since 2011. With 4.5% eGDP, Asia-Pacific has had the highest e-commerce share of GDP in 2015. Based on Statista, it is expected that the world’s eGDP will continue to grow. According to Ecommerce Foundation 2016, eGDP in MENA was 0.7% in 2015. Although this number is smaller than for other regions, Mckinsey predicts a higher growth of e-commerce sales in MENA countries in the coming years due to its digital potential and significant opportunities of digitization initiatives. United States showed a growth rate of 12% in e-com-merce turnover during 2015-2016 while this was 129% and 66% for India and Indonesia respectively.

Region 2014, $ bn 2015, $ bn Growth

World 1,895.3 2,272.7 +19.9%

Asia-Pacific 822.8 1,056.8 +28.4%

North America 527.5 644.0 +12.5%

Europe 466.0 505.1 +13.3%

Latin America 25.8 33.0 +28.0%

MENA 21.7 25.8 +18.6%

E-commerce sales in the world by continent

Source: Ecommerce Foundation, 2016.

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

14

Based on a McKinsey paper that was published in 2016, the retail sector ac-counted for 8% of Iran’s GDP in 2014 and ranked fourth after oil, gas, public sector and agriculture. It is expected that in the next fifteen years, after oil and gas, e-commerce will have the largest impact on GDP growth and job creation in Iran. The United Nations Conference on Trade and Development (UNCTAD) listed Iran among the 10 most susceptible countries for e-commerce in Asia- Pacific. The other countries on the list are: Korea, Hong Kong, Singapore, Malaysia, China, Thailand, Vietnam, Philippines and India. Digikala is the largest e-commerce platform in Iran which has been showing high growth rate in the past few years and is well expected to continue its positive trend into the future.

Mobile App IndustryThere were two app downloads per person per month in the world in 2017With 175 billion app downloads in 2017, users downloaded 60% more apps in 2017 than in 2015. Total consumer spend on Google Play, iOS app store and other third party Android stores has more than doubled over the past two years (over $86 bn).

Global app downloads will reach 258 billion by 2022It is anticipated that global app download will grow at a compound annual growth rate (CAGR) of 7.7% by 2022 and global consumer spend in the app industry will grow at a CAGR of 13.95%. During 2017-2022 EMEA region is expected to reach 3.3% CAGR in the number of app downloads and a 14.3% CAGR in consumer spending. Ukraine and Netherlands are among the markets that experienced high growth rates in this region. Russia is also a large market that has already witnessed a large increase in the number of app downloads. It is predicted that China, the United states, Japan, Korea and England, will have 24%, 19%, 9%, 10% and 15% CAGR respectively while the rest of the world will witness a 6% CAGR until 2021. Given the unlimited access to high speed internet(4G), India has grown significantly in the number of app downloads up to a point that it has sur-passed United States and become the world’s second largest country. India stands first by Android apps download frequency. An interesting point is that games generate higher revenues compared to other mobile applications. Large companies like Google and Apple face restrictions to operate in Iran due to the sanctions. Therefore, there is a dire need for the Iranian companies’ presence in the industry to meet the demand. Cafe Bazaar is the most reputable Android mobile app company in Iran with robust annual

growth over the past few years. Iranian application developers have made high incomes through Café Bazaar. Number of active developers in Café Bazaar has been on the increase since its inception reaching over 21,000 at the end of 1396. Compared to the previous years, app users have also started downloading paid apps. The main source of revenue for app stores is user transactions, transactions for app purchases, and in-app purchase transactions. Accord-ing to Café Bazaar, in Iranian year 1396, transactions hit its highest point whereby more than 14 million transactions were made. The number of transactions has increased by a CAGR of 38% over the last five years.

Online travelThe market size globally of online travel agency is estimated to be $855 bn in 2021. Increasing Internet penetration rate and fast embrace of social media by growing number of individuals are seen to be the main factors of this industry’s growth. Online travel sales witnessed a noteworthy rate of growth in the past few years and it is predicted that it will continue to grow in the future. In 2017 global online travel sales was $613 billion and is expected to reach $855 billion dollars by 2021. Based on eMarketer, online travel sales in MENA region was $26 billion in 2017 and is expected to reach $41 billion by 2020. In Iran, Alibaba is one of the leading companies in this industry. Alibaba started its business by selling offline airplane tickets. As it spotted potential opportunities in online travel industry, Alibaba expanded its business and in a short period could gain a significant market share.

Digital Advertising50% of the world’s advertising expenditure is expected to be on digital advertising in 2019. Revenues from Offline advertising is decreasing every day in favour of online advertising. Digital advertising has five different categories i.e. display or banner advertising, video advertising, search advertising, social media advertising, and classified advertising. In 2014, the world’s total spending on digital advertising experienced an 11.2% growth rate which accounted for 46.2% of the total advertising spend. On the other hand, offline advertising had 1% growth in 2014. High growth rate in digital advertising spend is expected by McKinsey for the next few years to be at a point that in 2019, half of the total ad spend would be in digital advertising. Based on Statista, in recent years, search advertising category has accounted for the highest revenue in digital advertising while display adver-tising and social media advertising came in second place.

Game

Game

2018

Apps

Apps

2022

Worldwide app download broken down by Games and other Apps

Worldwide consumer spend broken down by Games and other Apps

Digital advertising revenue in the world by category ($ bn)

%

0

20

40

60

80

100

20182017

36.1 35.0 33.9

63.9 65.0 66.1

2022

%

0

20

40

60

80

100

20182017

78.8 76.7 72.5

21.2 23.3 27.5

2022

Source: Market prediction report, 2016-2022, App Annie

Source: Statista, 2018

$ billion

0

40

80

120

160

200

Displayadvertising

Videoadvertising

Searchadvertising

Social mediaadvertising

Classifiedadvertising

5170

3151

127

174

51

77

20 27

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

15

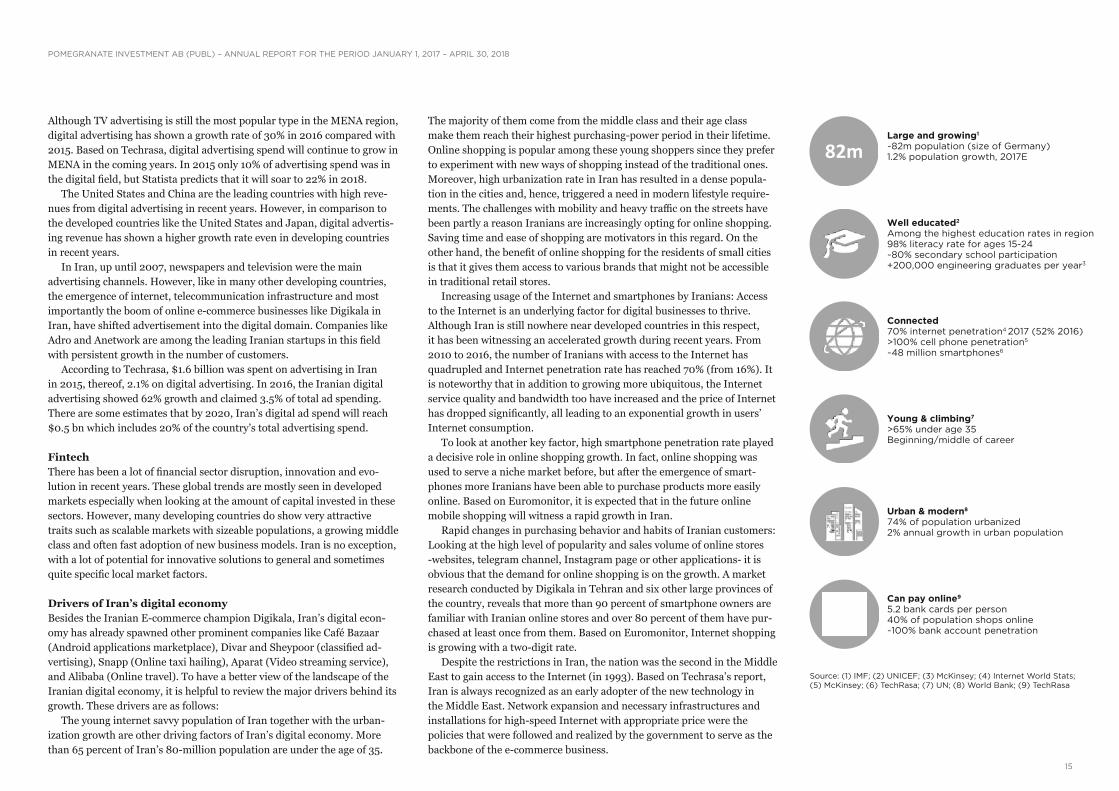

82m

Although TV advertising is still the most popular type in the MENA region, digital advertising has shown a growth rate of 30% in 2016 compared with 2015. Based on Techrasa, digital advertising spend will continue to grow in MENA in the coming years. In 2015 only 10% of advertising spend was in the digital field, but Statista predicts that it will soar to 22% in 2018. The United States and China are the leading countries with high reve-nues from digital advertising in recent years. However, in comparison to the developed countries like the United States and Japan, digital advertis-ing revenue has shown a higher growth rate even in developing countries in recent years. In Iran, up until 2007, newspapers and television were the main advertising channels. However, like in many other developing countries, the emergence of internet, telecommunication infrastructure and most importantly the boom of online e-commerce businesses like Digikala in Iran, have shifted advertisement into the digital domain. Companies like Adro and Anetwork are among the leading Iranian startups in this field with persistent growth in the number of customers. According to Techrasa, $1.6 billion was spent on advertising in Iran in 2015, thereof, 2.1% on digital advertising. In 2016, the Iranian digital advertising showed 62% growth and claimed 3.5% of total ad spending. There are some estimates that by 2020, Iran’s digital ad spend will reach $0.5 bn which includes 20% of the country’s total advertising spend.

FintechThere has been a lot of financial sector disruption, innovation and evo-lution in recent years. These global trends are mostly seen in developed markets especially when looking at the amount of capital invested in these sectors. However, many developing countries do show very attractive traits such as scalable markets with sizeable populations, a growing middle class and often fast adoption of new business models. Iran is no exception, with a lot of potential for innovative solutions to general and sometimes quite specific local market factors.

Drivers of Iran’s digital economyBesides the Iranian E-commerce champion Digikala, Iran’s digital econ-omy has already spawned other prominent companies like Café Bazaar (Android applications marketplace), Divar and Sheypoor (classified ad-vertising), Snapp (Online taxi hailing), Aparat (Video streaming service), and Alibaba (Online travel). To have a better view of the landscape of the Iranian digital economy, it is helpful to review the major drivers behind its growth. These drivers are as follows: The young internet savvy population of Iran together with the urban-ization growth are other driving factors of Iran’s digital economy. More than 65 percent of Iran’s 80-million population are under the age of 35.

The majority of them come from the middle class and their age class make them reach their highest purchasing-power period in their lifetime. Online shopping is popular among these young shoppers since they prefer to experiment with new ways of shopping instead of the traditional ones. Moreover, high urbanization rate in Iran has resulted in a dense popula-tion in the cities and, hence, triggered a need in modern lifestyle require-ments. The challenges with mobility and heavy traffic on the streets have been partly a reason Iranians are increasingly opting for online shopping. Saving time and ease of shopping are motivators in this regard. On the other hand, the benefit of online shopping for the residents of small cities is that it gives them access to various brands that might not be accessible in traditional retail stores. Increasing usage of the Internet and smartphones by Iranians: Access to the Internet is an underlying factor for digital businesses to thrive. Although Iran is still nowhere near developed countries in this respect, it has been witnessing an accelerated growth during recent years. From 2010 to 2016, the number of Iranians with access to the Internet has quadrupled and Internet penetration rate has reached 70% (from 16%). It is noteworthy that in addition to growing more ubiquitous, the Internet service quality and bandwidth too have increased and the price of Internet has dropped significantly, all leading to an exponential growth in users’ Internet consumption. To look at another key factor, high smartphone penetration rate played a decisive role in online shopping growth. In fact, online shopping was used to serve a niche market before, but after the emergence of smart-phones more Iranians have been able to purchase products more easily online. Based on Euromonitor, it is expected that in the future online mobile shopping will witness a rapid growth in Iran. Rapid changes in purchasing behavior and habits of Iranian customers: Looking at the high level of popularity and sales volume of online stores -websites, telegram channel, Instagram page or other applications- it is obvious that the demand for online shopping is on the growth. A market research conducted by Digikala in Tehran and six other large provinces of the country, reveals that more than 90 percent of smartphone owners are familiar with Iranian online stores and over 80 percent of them have pur-chased at least once from them. Based on Euromonitor, Internet shopping is growing with a two-digit rate. Despite the restrictions in Iran, the nation was the second in the Middle East to gain access to the Internet (in 1993). Based on Techrasa’s report, Iran is always recognized as an early adopter of the new technology in the Middle East. Network expansion and necessary infrastructures and installations for high-speed Internet with appropriate price were the policies that were followed and realized by the government to serve as the backbone of the e-commerce business.

Large and growing1

~82m population (size of Germany)1.2% population growth, 2017E

Young & climbing7

>65% under age 35Beginning/middle of career

Well educated2

Among the highest education rates in region98% literacy rate for ages 15-24~80% secondary school participation+200,000 engineering graduates per year3

Urban & modern8

74% of population urbanized2% annual growth in urban population

Connected70% internet penetration4 2017 (52% 2016)>100% cell phone penetration5

~48 million smartphones6

Can pay online9

5.2 bank cards per person40% of population shops online~100% bank account penetration

Source: (1) IMF; (2) UNICEF; (3) McKinsey; (4) Internet World Stats; (5) McKinsey; (6) TechRasa; (7) UN; (8) World Bank; (9) TechRasa

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

16

InvestmentPortfolio

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

17

Pomegranate invests in market leaders

SectorsTop companies in selected markets

Leading companies in Iran

Pomegranate invested directly or indirectly2

E-commerce; General merchandise Amazon; JD.com Digikala

E-commerce; Marketplace Alibaba; Rakuten Digikala4

E-commerce; Fashion Zalando; Asos Digistyle

Appstore Apple App Store; Google Play Cafe Bazaar

Online Classifieds Blocket; Avito Divar; Sheypoor

Digital advertising WPP, Axel Springer PPG5

Online travel Booking, Hotels Alibaba

On-demand delivery GO-JEK, Deliveroo Alopeyk

Fintech – peer to peer Swish Bahamta

Emerging-/Frontier markets financial services (M&A, research, AM, Brokerage)

Avior, Renessaince Capital Griffon Capital

Pomegranate invested (direct or indirectly)

18

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

Sarava is a consumer technology investment company and a pioneer in Internet and

e-commerce investments in Iran. The Company has established a unique track record in supporting local entrepre-neurs to build some of the most suc-cessful consumer technology compa-nies in the country and region.

Sarava’s investment focus is on companies operating in the universe

of internet, mobile, e-commerce, games, cloud computing and software as a service

(“SaaS”). The company is one of the very few technology investment companies in the region and

particularly the only one of its size in Iran. Sarava currently has invested in more than 35 companies, among others – Iran’s leading E-commerce company Digikala, the largest Persian Android marketplace – Café Bazaar, including the online classifieds company Divar, the first digital marketing holding in Iran– PPG (which includes A-Network, ADRO, and ADAD and Digital marketing Agencies)), Online Travel Agency (“OTA)” Alibaba and technology accelerators such as Avatech and many more. Sarava is an active investor in its portfolio companies and a sig-nificant part of Sarava’s operations is focused on providing support and knowledge-sharing within the company’s network. In Q4 2017 Sarava was involved in two larger transactions connected to Café Bazaar and OTA Alibaba, which included merger of Zoraq. In February 2018 Sarava initiated a funding round in which Pomegranate committed to invest EUR 12.7 million, out of which EUR 8.9 million had already been transferred as per 30 April 2018 and another EUR 3.8 is committed through signed Memorandum of Investment. Pomegranate’s stake in Sarava amounts to 15.7% as per 30 April 2018. As per April 30, 2018 Pomegranate’s holding in Sarava is valued based on the local currency/IRR NAV of Sarava, which in turn is established based on a combination of valuation models and last transaction of its portfolio companies. Lastly Pomegranate trans-lates the IRR NAV of Sarava into EUR based on the Central Bank of

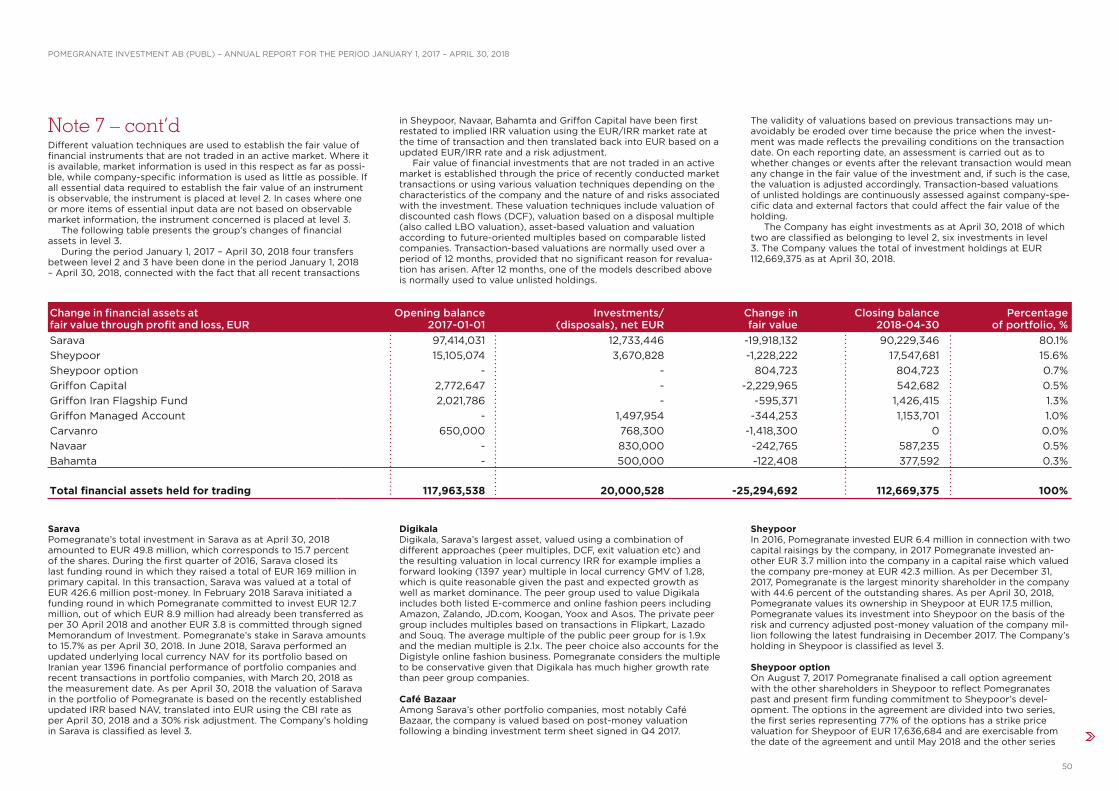

Sarava

66.3%

For more information, please visit the company’s website: www.saravapars.com/en

% of investment portfolio

Sector Internet & E-commerceCompany founded 2011First investment 2014Board representation 1 out of 7Investment Board representation 1 out of 5

Key Investment Data

90.2 mEURFair value in portfolio, April 30, 2018

-8.3 %Change in company fair value,January – April, 2018

15.7 %Pomegranate’s ownership

-7.4 %Change in company fair value, since December 31, 2016

Valuation breakdown, % Sector breakdown, %

Valuation modelLast transaction

78

75

16

3112 322

E-commerceMobile apps & classifiedsOnline travelOnline logisticsDigital/online mediaAccelerator, innovation factoryOther

Iran EUR/IRR spot rate of 50,930 on 30 April 2018, Pomegranate also applies a 30% risk adjustment to the valuation. Following the conclusion of annual performance of portfolio companies in the Iranian financial year 1397 which ended 20 March

2018, Sarava performed updated NAV review of its portfolio. All the model valuations and last transactions were determined in local currency – Iranian rial and total NAV was established at IRR 38,063 billion. The main component and driver of value in Sarava is its holding in Digikala Group.

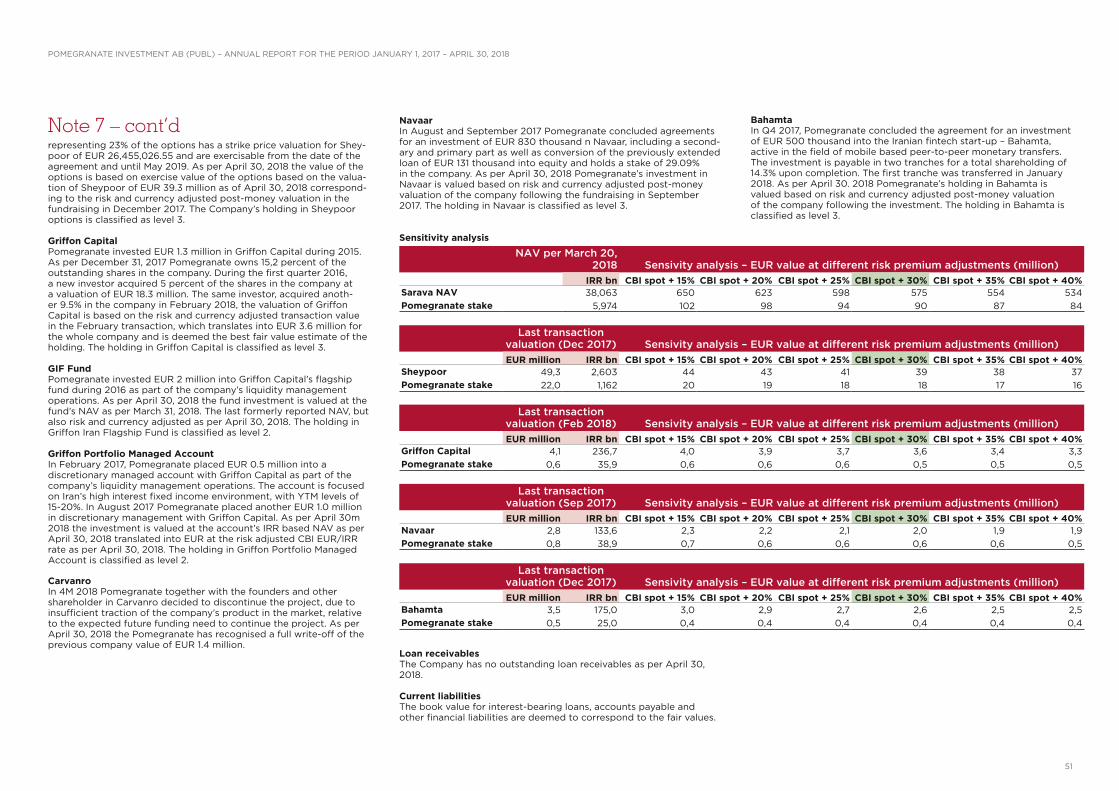

NAV Sensivity analysis – EUR value at different risk premium adjustments (millions)

IRR bn CBI spot + 15% CBI spot + 20% CBI spot + 25% CBI spot + 30% CBI spot + 35% CBI spot + 40%Sarava NAV 38,063 650 623 598 575 554 534Pomegranate stake 5,974 102 98 94 90 87 84

19

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

Sarava Holdings

For more information, please visit the company’s website: www.digikala.com

thousands

Q1 Q2Q3Q4 Q1 Q2 Q1 Q2Q3Q4Q3Q4139613951394

0

9,000

18,000

27,000

36,000

45,000thousands

139613951394139313920

500

1,000

1,500

2,000

2,500

1395/1396139413930123456789

10111213

#3

#7

#13#12#11#10#9#8#7#6#5#4#3#2#1

#13#12#11#10#9#8

#6#5#4#3#2#1

#7

#13#12#11#10#9#8

#6#5#4

#2#1

thousands

1395 13961394139313920

3,000

6,000

9,000

12,000

15,000

Traffic1)4)Number of active customers3)4)

Sales volume/Items Sold2)4) (after rejections) Alexa web traffic rank in Iran4)

1) Unique visitors: Standard definition – unique customers identified in the reporting period (Unique visitors refers to the number of distinct individuals requesting pages from the website during a given period, regardless of how often they visit).2) Sales volume: Items dispatched to customers (non-GAAP sales) after rejections made. 3) Number of active customers: Total customers having recorded a purchase in the TT12M.

4)Iranian year Starts Ends1392 mar 2013 mar 20141393 mar 2014 mar 20151394 mar 2015 mar 20161395 mar 2016 mar 20171396 mar 2017 mar 2018

SECTOR: E-COMMERCE

Digikala is a general e-commerce com-pany with an estimated market share of

over 90%. It is also Iran’s largest internet company. Today, Digikala ranks as the second and third most visited web-site in Iran according to Alexa and SimilarWeb, respectively. Digikala has a fully vertically integrated, wholly-owned logistics setup, delivering next day in the majority of the provinces in Iran, offering the best e-commerce customer experience in the country. Digikala continues strategic focus with c-level management with international experience, marketplace expansion which is now already at 32% of GMV, category expansion such as FMCG products which together with marketplace has led to the increase in the num-ber of SKUs in excess of 300 thousand and 70% of transactions are now conducted on mobile. In the current environment working capital, imports and inven-tory management are of special importance to manage but technolo-gy as well as Digikala’s scale enables them to manage this quite well.

Market placeEspecially the new market place platform has shown very strong results in terms of client acceptability with a growing selection of products, and now represents about 32% of GMV, with about 2,300 active sellers and more than 140 thousand SKUs offered on market-place. The amount of monthly items sold on market place has grown from a marginal number in beginning of 1396 to more than 735 thousand in the last month of 1396.

DigistyleIn the fall of 2016 Digikala launched Digistyle, an online fashion store. Digistyle is offering a large variety of international and local brands and has exclusive partnerships with a number of large global brands. Digikala's fulfilment centre is providing for storing, packag-ing and shipping Digistyle orders. Digistyle continues to add brands to its product portfolio and has managed to get several exclusive partnerships with well-known international brands.

The traffic to Digikala.com and number of customers have increased continuously and in the last quarter of the year 1396, spanning from March 2017 – March 2018, the number of unique visitors amounted to 41.3 million, compared with 26.8 million in the end of the third quarter 1396 and by end of year 1396 the number of active custom-ers in the last twelve months amounted to 1.5 million, with over 100 thousand new customers added in the last few months of the year. GMV grew with just below 60% in local currency in 1396 and similar growth is expected in 1397. The valuation of Digikala in local currency IRR in the NAV of Sarava is based on an average of a combination of valuation meth-ods, publicly listed peers, private transactions of peer companies, DCF and exit valuation. Public and private peer group multiples have been applied to both Last Twelve Months (1396) and Next Twelve Months (1397), GMV, NMV and Gross Profit. Generally we

IRR million Mar 16–Mar 17 1395 Mar 17–Mar 18 1396

GMV (incl VAT) 13,995,566 21,912,692

EUR/IRR 40,380 49,639

EUR millionGMV 347 441

y-on-y growth in IRRGMV 100% 57%

observe a big shift towards online vis a vis off-line retail which is DK’s biggest competition. The enormous challenges for off-line re-tail in combination with automatic repricing strategies and product offering is very favourable for the company which is gaining market share from already very elevated levels.

20

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

0 20 40 60 80

Domestic flights

International flights 12.0%

Hotel 5.5%

Walking o�ce 2.5%

Train 12.5%

67.5%

Sarava HoldingsSECTOR: ONLINE TRAVEL

In the 4th quarter of 2017, the largest online travel business in Iran (Aliba-

ba Travel) and one of the pioneers in that space (Zoraq) merged to form the largest Online Travel Agency (“OTA”) in the country. The merged company has about 45% market share of online travel in Iran, with a dominant position in online domestic travel. Alibaba GMV grew by 158% in Iranian year 1396 compared with 1395 and triple digit growth is expected in 1397 as well. This merger between the leaders of Iran’s online travel, “Alibaba” and “Zoraq”, and integration with Alibaba’s other businesses such as “Jabama”, a hotel booking website, will further lead to growth and expansion in the field of online travel booking in the Country. The merged entities will be consolidated under a holding company called “Tousha”. The valuation of Tousha online travel holding is approx-imately EUR 82 million after investment of EUR 18.5 million into the holding. Pomegranate is holding an indirect see-through stake of 3.3% in this business post the merger. The merger between Alibaba Travel and Zoraq was facilitated by Griffon Capital, another of Pomegranate’s portfolio companies, which had exclusive fundraising mandate with the online travel booking site Alibaba. The valuation of Alibaba/ Tousha in local currency IRR in the NAV of Sarava is based on underlying IRR valuation in last transac-tion from Dec 2017.

SECTOR: CLASSIFIEDS & MOBILE

Café Bazaar is a leading consumer internet company in Iran that runs the largest local Android application

marketplace for Persian speaking countries. It owns 100 percent of Iran’s largest online classifieds company, Divar. Café Bazaar was established in 2010/2011 and was the first com-pany to enter the mobile application distribution business in Iran. The Company’s service is now installed on more than 35 million Android phones and has over 26 million monthly active users. Café Bazaar has started monetizing its appstore and the company main-tains its market share at about 85 percent, with 190 K published apps and over 77 K monetising apps. Café Bazaar is also focusing on micro-payments and Instant messaging, a “WeChat” type ecosys-tem. Pomegranate has increased its indirect see-through economic interest in Café Bazaar group, from 3% to 4.5%, following a fund-raising deal in Q4 2017. The deal included EUR 38 million for a 10 per cent increase in shareholding in Café Bazaar group for investors, with a corresponding 1.5% increase in indirect shareholding for Pomegranate. The deal was made in order to raise capital for expan-sion into new areas such as micro payments and new urban services as well as strengthening of their current businesses. Café Bazaar and Divar continue to develop their well-known online services. The valuation of Café Bazaar in local currency IRR in the NAV of Sarava is based on underlying IRR valuation in the last transaction from Dec 2017.

For more information, please visit the company’s website: www.cafebazaar.ir/en

For more information, please visit the company’s website: www.alibaba.ir

Sector breakdown of sales, %

21

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

Sarava Holdings

SECTOR: DIGITAL ADVERTISEMENT & MEDIA

Company DescriptionPishgaman Pejvak Pardis group

(PPG) is a digital advertisement and media holding company, that has consolidated several online advertising brands. PPG has now consolidated a number of prominent Iranian Adtech companies, including ADRO, A-Network, and ADAD and a host of other successful content and digital brand agencies including Final Target. PPG has undergone substantial restructuring and is now run by high profile marketeers and is re-focusing on their core client busi-ness. We are following with high interest how Alibaba and now also Amazon have become substantial online-ad businesses. There is an opportunity here in our point of view. The valuation of PPG in local currency IRR in the NAV of Sarava is based on underlying IRR valuation in last transaction from May 2018.

For more information, please visit the company’s website: http://ppg.media

For more information, please visit the company’s website: https://alopeyk.com

SECTOR: ONLINE LOGISTICS

Alopeyk Iran’s leading online courier and motorbike taxi, targeting to execute the GoJek model in Iran.

Having launched about a year ago with just motor bike couriers, it has already grown to over 50,000 filled orders per day and expand-ed its fleet from motorbikes only into vans and motorbike taxis as well. The valuation of Alopeyk in local currency IRR in the NAV of Sarava is based on underlying IRR valuation in the last transaction from Dec 2017.

For more information, please visit the company’s website: www.avatech.ir

SECTOR: ACCELERATION & INNOVATION

Ashena GroupAshena Group is being formed as a

consolidation of the following companies into a group;

Avatech & Avagames – Iran’s most successful start-up accelerator program. Mentorship, entrepreneurial training, seed funding, a creative workspace, and investor demo days are a few of the services provided by Avatech.

Avatech’s network is one of the main channels for sourcing early stage start-ups in Iran for Sarava VC fund. As the start-ups mature, Sarava might do follow-on investments in the companies. Over the last two years, more than 50 start-ups have graduated from Avatech.

Avagames – is a start up incubator focused on mobiles game devel-opment.

Also included in Ashena group is Shezan –a NBIC accelerator, Noua-va – which performs consultancy services to the start-up community and Hamava – which operates the new innovation factory. The valuation of Ashena in local currency IRR in the NAV of Sara-va is based on model valuation of the groups entities.

22

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

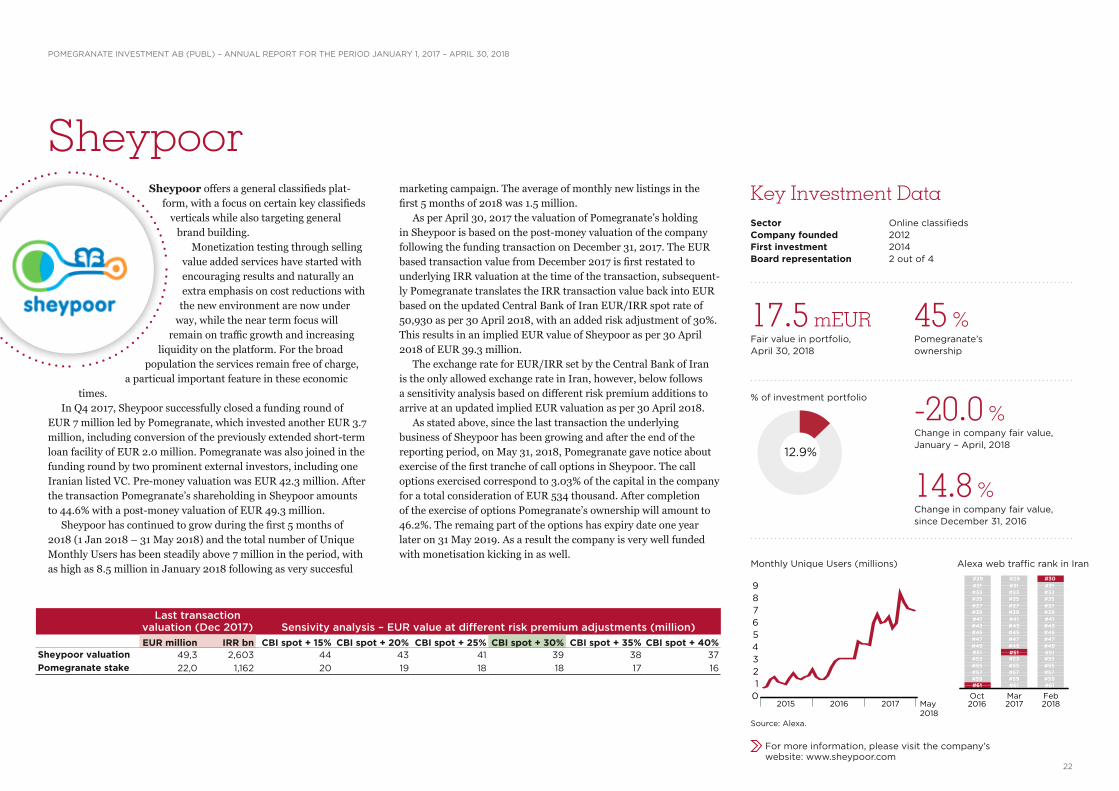

SheypoorSheypoor offers a general classifieds plat-

form, with a focus on certain key classifieds verticals while also targeting general

brand building. Monetization testing through selling value added services have started with encouraging results and naturally an extra emphasis on cost reductions with

the new environment are now under way, while the near term focus will

remain on traffic growth and increasing liquidity on the platform. For the broad

population the services remain free of charge, a particual important feature in these economic

times. In Q4 2017, Sheypoor successfully closed a funding round of EUR 7 million led by Pomegranate, which invested another EUR 3.7 million, including conversion of the previously extended short-term loan facility of EUR 2.0 million. Pomegranate was also joined in the funding round by two prominent external investors, including one Iranian listed VC. Pre-money valuation was EUR 42.3 million. After the transaction Pomegranate’s shareholding in Sheypoor amounts to 44.6% with a post-money valuation of EUR 49.3 million. Sheypoor has continued to grow during the first 5 months of 2018 (1 Jan 2018 – 31 May 2018) and the total number of Unique Monthly Users has been steadily above 7 million in the period, with as high as 8.5 million in January 2018 following as very succesful

marketing campaign. The average of monthly new listings in the first 5 months of 2018 was 1.5 million. As per April 30, 2017 the valuation of Pomegranate’s holding in Sheypoor is based on the post-money valuation of the company following the funding transaction on December 31, 2017. The EUR based transaction value from December 2017 is first restated to underlying IRR valuation at the time of the transaction, subsequent-ly Pomegranate translates the IRR transaction value back into EUR based on the updated Central Bank of Iran EUR/IRR spot rate of 50,930 as per 30 April 2018, with an added risk adjustment of 30%. This results in an implied EUR value of Sheypoor as per 30 April 2018 of EUR 39.3 million. The exchange rate for EUR/IRR set by the Central Bank of Iran is the only allowed exchange rate in Iran, however, below follows a sensitivity analysis based on different risk premium additions to arrive at an updated implied EUR valuation as per 30 April 2018. As stated above, since the last transaction the underlying business of Sheypoor has been growing and after the end of the reporting period, on May 31, 2018, Pomegranate gave notice about exercise of the first tranche of call options in Sheypoor. The call options exercised correspond to 3.03% of the capital in the company for a total consideration of EUR 534 thousand. After completion of the exercise of options Pomegranate’s ownership will amount to 46.2%. The remaing part of the options has expiry date one year later on 31 May 2019. As a result the company is very well funded with monetisation kicking in as well.

Last transaction valuation (Dec 2017) Sensivity analysis – EUR value at different risk premium adjustments (million)

EUR million IRR bn CBI spot + 15% CBI spot + 20% CBI spot + 25% CBI spot + 30% CBI spot + 35% CBI spot + 40%Sheypoor valuation 49,3 2,603 44 43 41 39 38 37Pomegranate stake 22,0 1,162 20 19 18 18 17 16

0123456789

2015 2016 2017 May2018

Sector Online classifiedsCompany founded 2012First investment 2014Board representation 2 out of 4

Key Investment Data

17.5 mEURFair value in portfolio, April 30, 2018

-20.0 %Change in company fair value,January – April, 2018

45 %Pomegranate’s ownership

% of investment portfolio

14.8 %Change in company fair value, since December 31, 2016

Source: Alexa.

12.9%

Oct2016

Mar2017

Feb2018

0123456789

10111213141516171819

2021222324252627282930313233

#51

#61#59#57#55#53#51#49#47#45#43#41#39#37#35#33#31

#30#29

#61#59#57#55#53

#49#47#45#43#41#39#37#35#33#31#29

#51

#61#59#57#55#53

#49#47#45#43#41#39#37#35#33#31

Monthly Unique Users (millions) Alexa web traffic rank in Iran

For more information, please visit the company’s website: www.sheypoor.com

23

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

Griffon CapitalGriffon Capital ("Griffon") is an Iran-focused group

providing Asset Management (Capital Markets & Private Eqity) as well as Investment Banking

Advisory. Among Griffon’s primary objectives is to enable institutional investors the ability to seamlessly access and maximise opportu-nities in Iran through purpose-built vehicles and investment products spanning traditional

and alternative assets. The Group’s strength is rooted in a robust operating platform developed

with the expressed aim of serving institutional in-vestors. Griffon’s platform consists of a high calibre

team with deep local market expertise and internation-al financial pedigree blended at the board, management

and execution levels. Griffon is also distinguished by unmatched local research and primary thinking and a governance culture defined by global best practices in risk management, compliance and reporting. During the recents months of increased uncertainty and volatility in local markets in Iran, Griffon has proven to be an especially effective and useful partner for analysis and information for Pomegranate. Griffon has been the largest cross border M&A adviser in terms of num-ber and value of mandates. In 2017 Griffon has sucessfully been strengthening its local asset man-agement offering, catering to the avalaible pools of money in Iran, which are less susceptible to international headlines.

While cross border M&A activities will certainly suffer in the current envi-ronment, post US withdrawal from the JCPOA, the strategy for the last year or so to focus more on local asset management has proven to be the right decision. In 2018 Griffon will be launching various local commodity funds and ETF’s to cater to local clients. In February 2018, there was a transaction among shareholders in Griffon whereby a shareholder owning 5% increased its ownership to 14.5% through a combination of new subscription, secondary and treasury share purchase at a valuation of the company of USD 5 million. As per April 30, 2017, Pomegranate values its investment into Griffon Capital on the basis of the recent transaction in February, first restated to underlying IRR valuation at the time of the transaction, subsequently Pome-granate translates the IRR transaction value back into EUR based on the updated Central Bank of Iran EUR/IRR spot rate of 50,930 as per 30 April 2018, with an added risk adjustment of 30%. This results in an implied EUR value of Griffon Capital as per April 30, 2018 of EUR 3.7 million, and the value of Pomegranate’s stake at EUR 542 thousand. While given the current climate we are taking a conservative approach and revising our valuations downwards based on the most recent transac-tion, it is likely that growth in local asset management business will make up for the shortfall in cross-border activity and the valuations could be revised upwards before end of the year. Also further certainty with regards to macro economic environment would allow us to move on to a DCF model again for future valuations.

For more information, please visit the company’s website: www.griffoncapital.com

Sector Asset management & advisoryCompany founded 2014First investment 2014Board representation 1 out of 6

Key Investment Data

0.5 mEURFair value in portfolio, April 30, 2018

-50.7 %Change in company fair value, January – April, 2018

2.6 mEUR, 1.9 % of investment portfolio

15 %Pomegranate’s ownership

% of investment portfolio

-80.4 %Change in company fair value, since December 31, 2016

0.4%

GIF Fund & PMALast transaction valuation (Feb 2018) Sensivity analysis – EUR value at different risk premium adjustments (million)

EUR million IRR bn CBI spot + 15% CBI spot + 20% CBI spot + 25% CBI spot + 30% CBI spot + 35% CBI spot + 40%Griffon Capital 4,1 236,7 4,0 3,9 3,7 3,6 3,4 3,3Pomegranate stake 0,6 35,9 0,6 0,6 0,6 0,5 0,5 0,5

24

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

GIF FUNDThe GIF Fund launched in April 2016 to unlock value from Iran’s public equity market. It is a Cayman domiciled open ended fund, primarily investing in the equity securities of companies listed on the TSE and the IFB. The GIF fund has outperformed local peers since its inception. Q4 2017 was generally a strong period for the Fund in terms of local currency returns with the TEDPIX reaching consistently new all time highs in November and December 2017, however, in the first months of 2018 the local stock market declined and given the recent waekness of the rial especially against the EUR, the Fund’s euro-denominated Initial Series NAV decreased by 14.8% January 1, 2018 until the last reported NAV on March 31, 2018. As per notifica-tion to shareholders of the fund in May 2018, EUR NAV determina-tion, redemption and subscription has been temporarily suspended due to uncertainty about the exchange rate. As per April 30, 2018 the investment in the GIF Fund is valued at the Fund's last reported EUR NAV as per March 31, 2018 also adjusted for the updated risk adjusted CBI EUR/IRR spot rate as per April 30, 2018. Traditionaly, due to high concentration of exporters and comod-ity based companies in the index, the local equity markets have rallied post CBI currency devaluation on April 10, 2018, albeit with a lag. Since April 30th the TEDPIX has rallied from ca 93k to 108k as of the day of sending this report. Therefore we anticipate that above NAV calculations will be revised upwards in future reports.

GRIFFON PMAThe Portfolio Managed Account ("PMA") is a local currency denominated managed account. The placing of funds in the PMA was mainly as a short term investment in the attractive Iranian yield levels at 15-20% YTM. Pomegranate has recently decided to unwind most of the fixed income positions. As per April 30, 2018 the investment is valued at the accountsreported IRR NAV as per the end April 30, 2018 translated into EUR at the updated risk adjusted CBI EUR/IRR spot rate as per April 30, 2018.

25

POMEGRANATE INVESTMENT AB (PUBL) – ANNUAL REPORT FOR THE PERIOD JANUARY 1, 2017 – APRIL 30, 2018

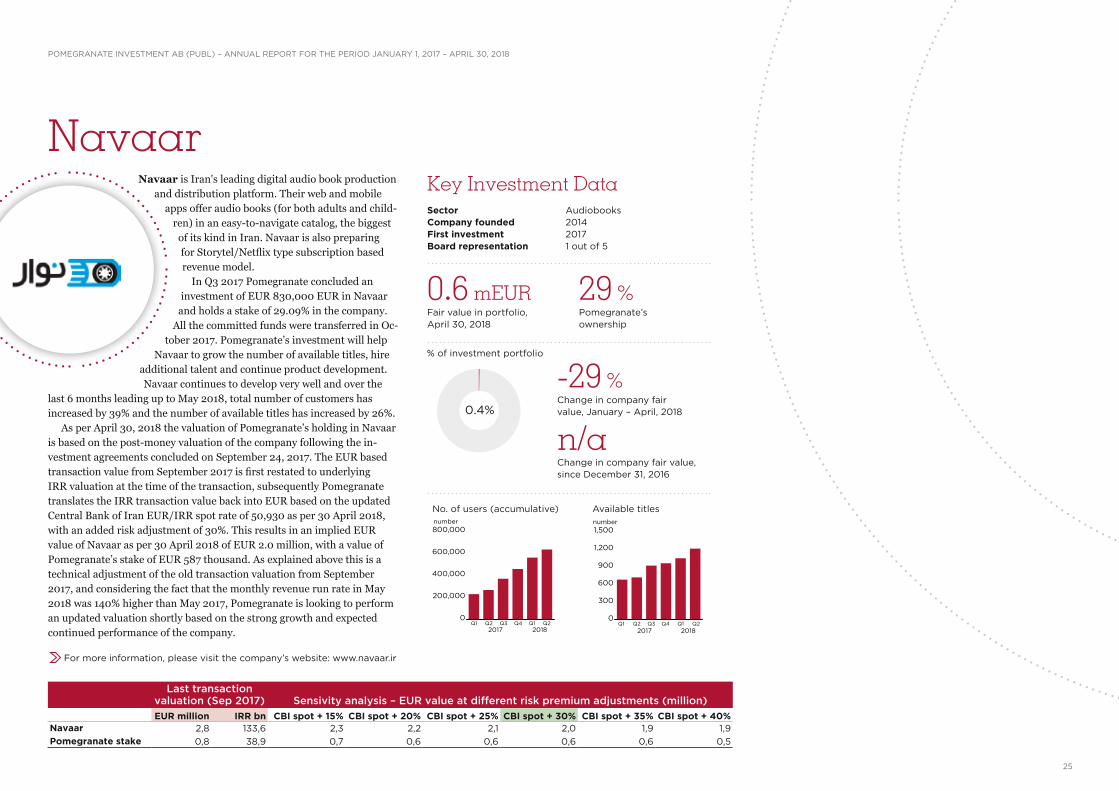

NavaarNavaar is Iran's leading digital audio book production

and distribution platform. Their web and mobile apps offer audio books (for both adults and child-

ren) in an easy-to-navigate catalog, the biggest of its kind in Iran. Navaar is also preparing for Storytel/Netflix type subscription based revenue model. In Q3 2017 Pomegranate concluded an investment of EUR 830,000 EUR in Navaar

and holds a stake of 29.09% in the company. All the committed funds were transferred in Oc-

tober 2017. Pomegranate’s investment will help Navaar to grow the number of available titles, hire

additional talent and continue product development. Navaar continues to develop very well and over the

last 6 months leading up to May 2018, total number of customers has increased by 39% and the number of available titles has increased by 26%. As per April 30, 2018 the valuation of Pomegranate’s holding in Navaar is based on the post-money valuation of the company following the in-vestment agreements concluded on September 24, 2017. The EUR based transaction value from September 2017 is first restated to underlying IRR valuation at the time of the transaction, subsequently Pomegranate translates the IRR transaction value back into EUR based on the updated Central Bank of Iran EUR/IRR spot rate of 50,930 as per 30 April 2018, with an added risk adjustment of 30%. This results in an implied EUR value of Navaar as per 30 April 2018 of EUR 2.0 million, with a value of Pomegranate’s stake of EUR 587 thousand. As explained above this is a technical adjustment of the old transaction valuation from September 2017, and considering the fact that the monthly revenue run rate in May 2018 was 140% higher than May 2017, Pomegranate is looking to perform an updated valuation shortly based on the strong growth and expected continued performance of the company.

For more information, please visit the company’s website: www.navaar.ir

Sector AudiobooksCompany founded 2014First investment 2017Board representation 1 out of 5

Key Investment Data

0.6 mEURFair value in portfolio, April 30, 2018

-29 %Change in company fair value, January – April, 2018

29 %Pomegranate’s ownership

% of investment portfolio

n/aChange in company fair value, since December 31, 2016

0.4%

number

Q3 Q4Q1 Q2 Q1 Q22017 2018

0

200,000

400,000

600,000

800,000number

Q3 Q4Q1 Q22017

Q1 Q22018

0

300

600

900

1,200

1,500