Buckling Testing and Analysis of Honeycomb Sandwich Panel ...

Upload

independentCategory

view

1download

0

Analysis of Panel Data

Panel data models have become increasingly popular among applied re-searchers due to their heightened capacity for capturing the complexity ofhuman behavior as compared to cross-sectional or time-series data mod-els. As a consequence, more and richer panel data sets also have becomeincreasingly available. This second edition is a substantial revision of thehighly successful first edition of 1986. Recent advances in panel data re-search are presented in a rigorous and accessible manner and are carefullyintegrated with the older material. The thorough discussion of theory andthe judicious use of empirical examples will make this book useful to grad-uate students and advanced researchers in economics, business, sociology,political science, etc. Other specific revisions include the introduction ofBayes method and the notion of strict exogeneity with estimators presentedin a generalized method of moments framework to link the identificationof various models, intuitive explanations of semiparametric methods ofestimating discrete choice models and methods of pairwise trimming forthe estimation of panel sample selection models, etc.

Cheng Hsiao is Professor of Economics at the University of SouthernCalifornia. His first edition of Analysis of Panel Data (EconometricSociety Monograph 11, Cambridge University Press, 1986) has beenthe standard introduction for students to the subject in the economicsliterature. Professor Hsiao is also a coauthor of Econometric Models,Techniques, and Applications, Second Edition (Prentice Hall, 1996, withM. Intriligator and R. Bodkin), coeditor of Analysis of Panels and LimitedDependent Variable Models (Cambridge University Press, 1999, withK. Lahiri, L.F. Lee, and M.H. Pesaran), and coeditor of Nonlinear Stati-stical Inference (Cambridge University Press, 2001, with K. Morimuneand J.L. Powell). He is a Fellow of the Econometric Society and coeditorand Fellow of the Journal of Econometrics.

Analysis of Panel DataSecond Edition

C H E N G H S I A OUniversity of Southern California

Cambridge, New York, Melbourne, Madrid, Cape Town, Singapore, São Paulo

Cambridge University PressThe Edinburgh Building, Cambridge , United Kingdom

First published in print format

isbn-13 978-0-521-81855-1 hardback

isbn-13 978-0-521-52271-7 paperback

isbn-13 978-0-511-06140-0 eBook (NetLibrary)

© Cheng Hsiao 2003

2003

Information on this title: www.cambridge.org/9780521818551

This book is in copyright. Subject to statutory exception and to the provision ofrelevant collective licensing agreements, no reproduction of any part may take placewithout the written permission of Cambridge University Press.

isbn-10 0-511-06140-4 eBook (NetLibrary)

isbn-10 0-521-81855-9 hardback

isbn-10 0-521-52271-4 paperback

Cambridge University Press has no responsibility for the persistence or accuracy ofs for external or third-party internet websites referred to in this book, and does notguarantee that any content on such websites is, or will remain, accurate or appropriate.

Published in the United States of America by Cambridge University Press, New York

www.cambridge.org

-

-

-

-

-

-

Econometric Society Monographs No. 34

Editors:Andrew Chesher, University College LondonMatthew O. Jackson, California Institute of Technology

The Econometric Society is an international society for the advancement of economic theory inrelation to statistics and mathematics. The Econometric Society Monograph Series is designed topromote the publication of original research contributions of high quality in mathematicaleconomics and theoretical and applied econometrics.

Other titles in the series:

G. S. Maddala Limited-dependent and qualitative variables in econometrics, 0 521 33825 5Gerard Debreu Mathematical economics: Twenty papers of Gerard Debreu, 0 521 33561 2Jean-Michel Grandmont Money and value: A reconsideration of classical and neoclassical

monetary economics, 0 521 31364 3Franklin M. Fisher Disequilibrium foundations of equilibrium economics, 0 521 37856 7Andreu Mas-Colell The theory of general economic equilibrium: A differentiable approach,

0 521 26514 2, 0 521 38870 8Truman F. Bewley, Editor Advances in econometrics – Fifth World Congress (Volume I),

0 521 46726 8Truman F. Bewley, Editor Advances in econometrics – Fifth World Congress (Volume II),

0 521 46725 XHerve Moulin Axioms of cooperative decision making, 0 521 36055 2, 0 521 42458 5L. G. Godfrey Misspecification tests in econometrics: The Lagrange multiplier principle and

other approaches, 0 521 42459 3Tony Lancaster The econometric analysis of transition data, 0 521 43789 XAlvin E. Roth and Marilda A. Oliviera Sotomayor, Editors Two-sided matching: A study in

game-theoretic modeling and analysis, 0 521 43788 1Wolfgang Hardle, Applied nonparametric regression, 0 521 42950 1Jean-Jacques Laffont, Editor Advances in economic theory – Sixth World Congress (Volume I),

0 521 48459 6Jean-Jacques Laffont, Editor Advances in economic theory – Sixth World Congress (Volume II),

0 521 48460 XHalbert White Estimation, inference and specification, 0 521 25280 6, 0 521 57446 3Christopher Sims, Editor Advances in econometrics – Sixth World Congress (Volume I),

0 521 56610 XChristopher Sims, Editor Advances in econometrics – Sixth World Congress (Volume II),

0 521 56609 6Roger Guesnerie A contribution to the pure theory of taxation, 0 521 23689 4, 0 521 62956 XDavid M. Kreps and Kenneth F. Wallis, Editors Advances in economics and econometrics –

Seventh World Congress (Volume I), 0 521 58011 0, 0 521 58983 5David M. Kreps and Kenneth F. Wallis, Editors Advances in economics and econometrics –

Seventh World Congress (Volume II), 0 521 58012 9, 0 521 58982 7David M. Kreps and Kenneth F. Wallis, Editors Advances in economics and econometrics –

Seventh World Congress (Volume III), 0 521 58013 7, 0 521 58981 9Donald P. Jacobs, Ehud Kalai, and Morton I. Kamien, Editors Frontiers of research in economic

theory: The Nancy L. Schwartz Memorial Lectures, 1983–1997, 0 521 63222 6, 0 521 63538 1A. Colin Cameron and Pravin K. Trivedi, Regression analysis of count data, 0 521 63201 3,

0 521 63567 5Steinar Strøm, Editor Econometrics and economic theory in the 20th century: The Ragnar Frisch

Centennial Symposium, 0 521 63323 0, 0 521 63365 6Eric Ghysels, Norman R. Swanson, and Mark Watson, Editors Essays in econometrics: Collected

papers of Clive W. J. Granger (Volume I), 0 521 77496 9Eric Ghysels, Norman R. Swanson, and Mark Watson, Editors Essays in econometrics: Collected

papers of Clive W. J. Granger (Volume II), 0 521 79649 0

To my wife, Amy Mei-Yunand my children,

Irene ChiayunAllen ChenwenMichael ChenyeeWendy Chiawen

Contents

Preface to the Second Edition page xiiiPreface to the First Edition xv

Chapter 1. Introduction 11.1 Advantages of Panel Data 11.2 Issues Involved in Utilizing Panel Data 8

1.2.1 Heterogeneity Bias 81.2.2 Selectivity Bias 9

1.3 Outline of the Monograph 11

Chapter 2. Analysis of Covariance 142.1 Introduction 142.2 Analysis of Covariance 152.3 An Example 21

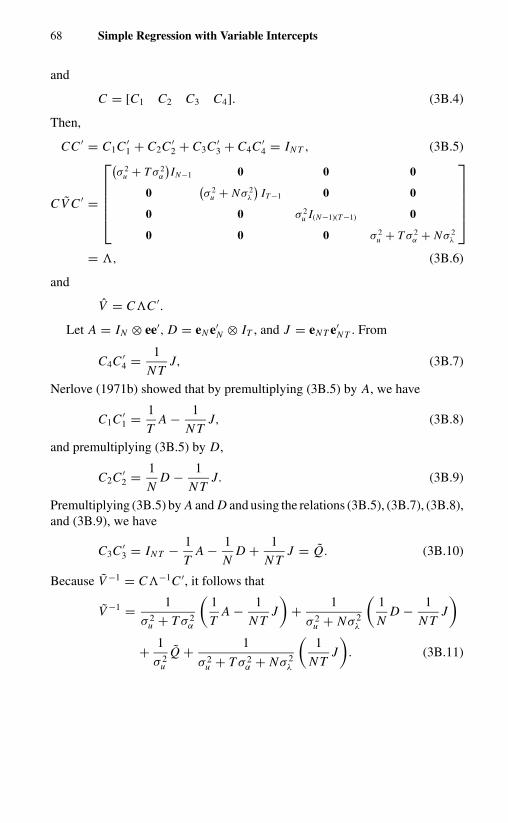

Chapter 3. Simple Regression with Variable Intercepts 273.1 Introduction 273.2 Fixed-Effects Models: Least-Squares Dummy-Variable

Approach 303.3 Random-Effects Models: Estimation of

Variance-Components Models 343.3.1 Covariance Estimation 353.3.2 Generalized-Least-Squares Estimation 353.3.3 Maximum Likelihood Estimation 39

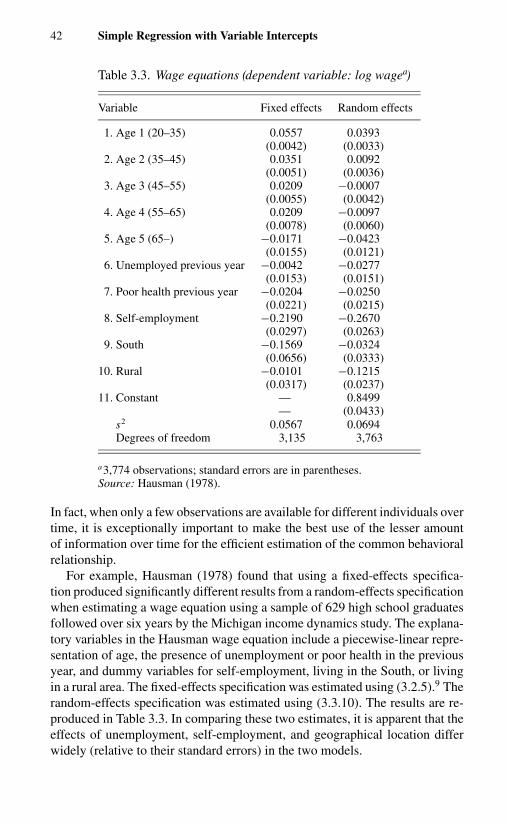

3.4 Fixed Effects or Random Effects 413.4.1 An Example 413.4.2 Conditional Inference or Unconditional (Marginal)

Inference 433.4.2.a Mundlak’s Formulation 443.4.2.b Conditional and Unconditional Inferences in the

Presence or Absence of Correlation betweenIndividual Effects and Attributes 46

viii Contents

3.5 Tests for Misspecification 493.6 Models with Specific Variables and Both Individual- and

Time-Specific Effects 513.6.1 Estimation of Models with Individual-Specific

Variables 513.6.2 Estimation of Models with Both Individual and

Time Effects 533.7 Heteroscedasticity 553.8 Models with Serially Correlated Errors 573.9 Models with Arbitrary Error Structure – Chamberlain π

Approach 60Appendix 3A: Consistency and Asymptotic Normality of the

Minimum-Distance Estimator 65Appendix 3B: Characteristic Vectors and the Inverse of the

Variance–Covariance Matrix of aThree-Component Model 67

Chapter 4. Dynamic Models with Variable Intercepts 694.1 Introduction 694.2 The Covariance Estimator 714.3 Random-Effects Models 73

4.3.1 Bias in the OLS Estimator 734.3.2 Model Formulation 754.3.3 Estimation of Random-Effects Models 78

4.3.3.a Maximum Likelihood Estimator 784.3.3.b Generalized-Least-Squares Estimator 844.3.3.c Instrumental-Variable Estimator 854.3.3.d Generalized Method of Moments

Estimator 864.3.4 Testing Some Maintained Hypotheses on Initial

Conditions 904.3.5 Simulation Evidence 91

4.4 An Example 924.5 Fixed-Effects Models 95

4.5.1 Transformed Likelihood Approach 964.5.2 Minimum-Distance Estimator 984.5.3 Relations between the Likelihood-Based

Estimator and the Generalized Method ofMoments Estimator (GMM) 99

4.5.4 Random- versus Fixed-Effects Specification 1014.6 Estimation of Dynamic Models with Arbitary Correlations

in the Residuals 1034.7 Fixed-Effects Vector Autoregressive Models 105

4.7.1 Model Formulation 1054.7.2 Generalized Method of Moments (GMM) Estimation 107

Contents ix

4.7.3 (Transformed) Maximum Likelihood Estimator 1094.7.4 Minimum-Distance Estimator 109

Appendix 4A: Derivation of the Asymptotic Covariance Matrixof the Feasible MDE 111

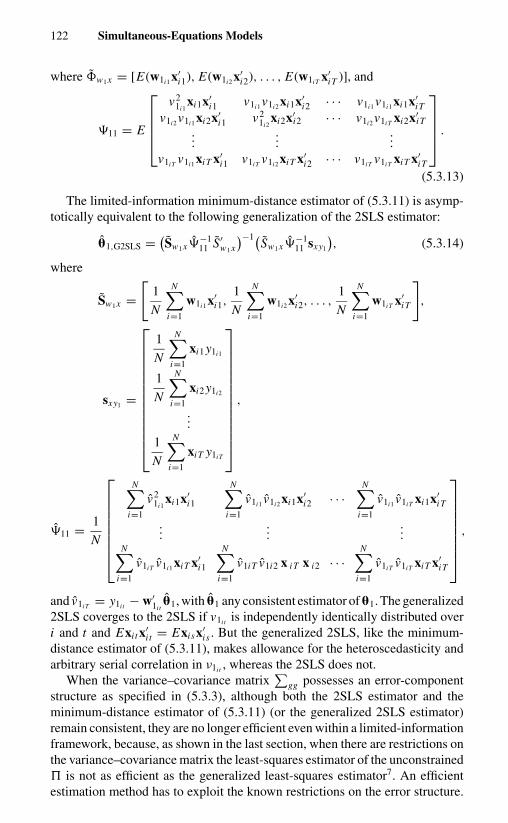

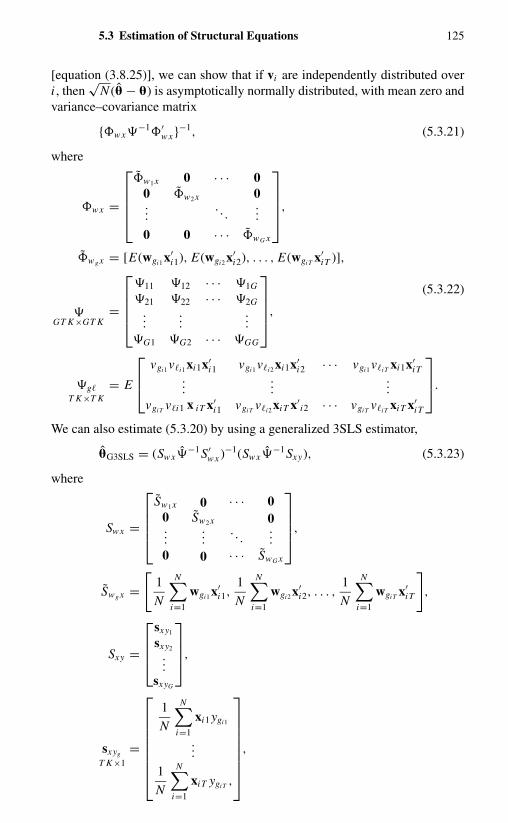

Chapter 5. Simultaneous-Equations Models 1135.1 Introduction 1135.2 Joint Generalized-Least-Squares Estimation Technique 1165.3 Estimation of Structural Equations 119

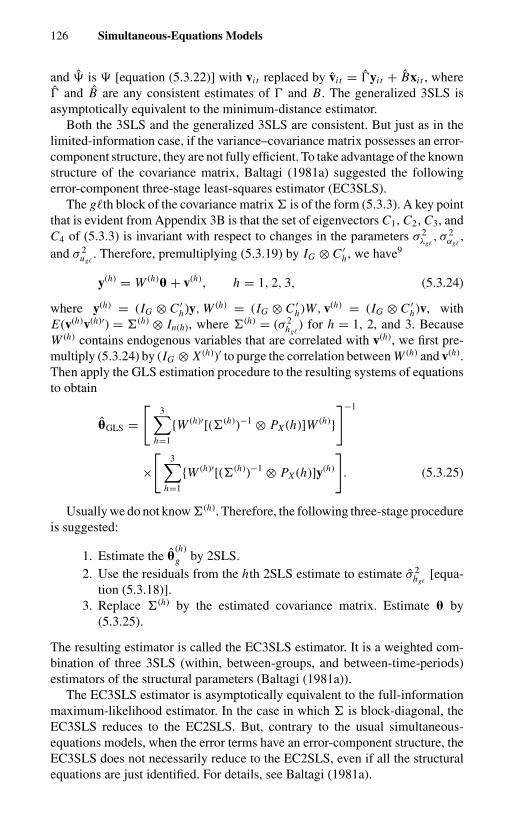

5.3.1 Estimation of a Single Equation in the Structural Model 1195.3.2 Estimation of the Complete Structural System 124

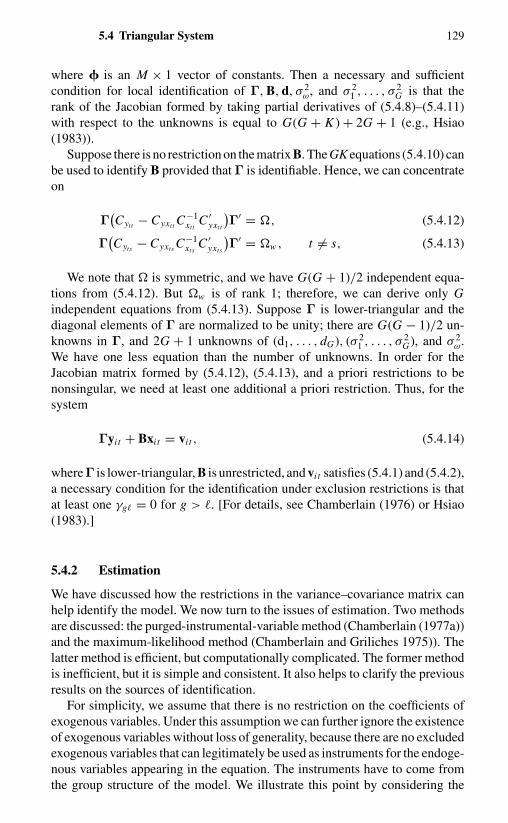

5.4 Triangular System 1275.4.1 Identification 1275.4.2 Estimation 129

5.4.2.a Instrumental-Variable Method 1305.4.2.b Maximum-Likelihood Method 133

5.4.3 An Example 136Appendix 5A 138

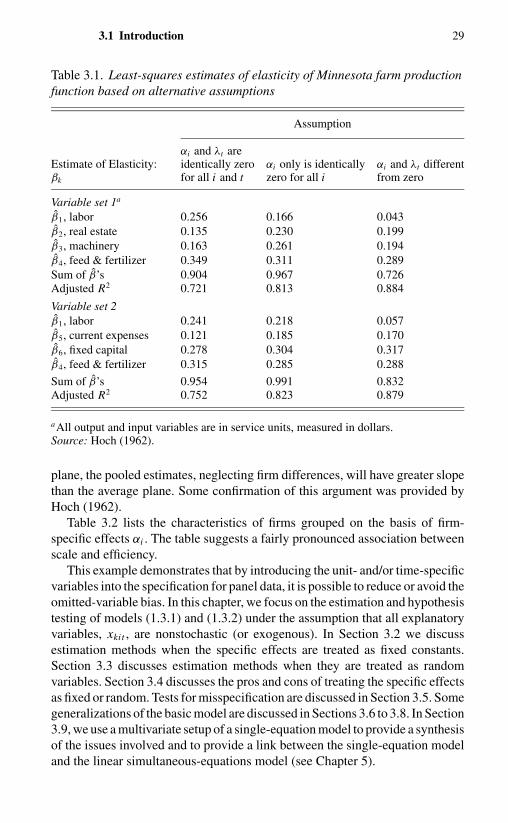

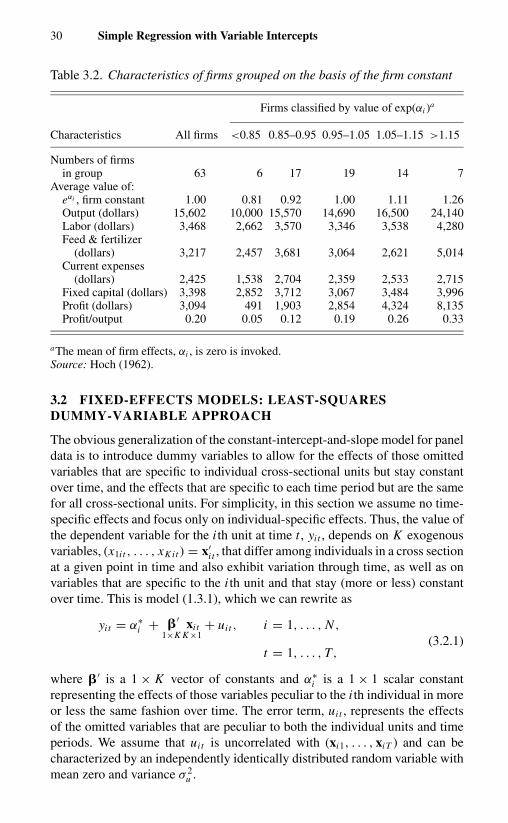

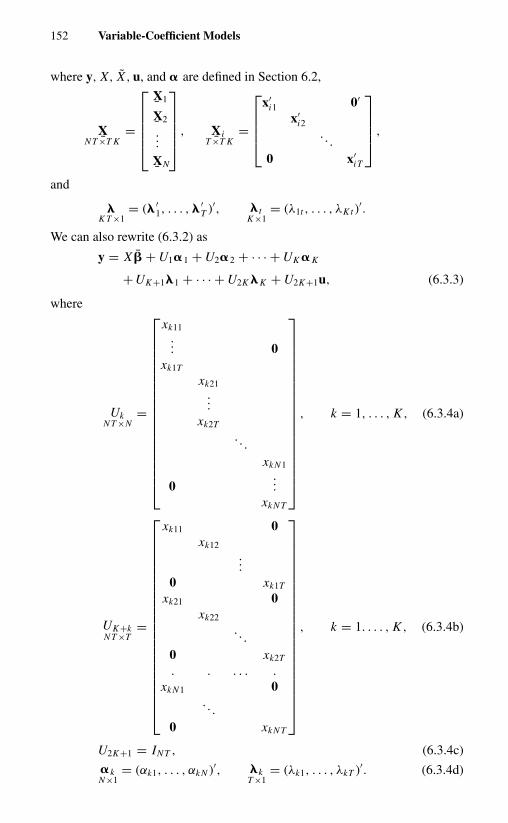

Chapter 6. Variable-Coefficient Models 1416.1 Introduction 1416.2 Coefficients That Vary over Cross-Sectional Units 143

6.2.1 Fixed-Coefficient Model 1446.2.2 Random-Coefficient Model 144

6.2.2.a The Model 1446.2.2.b Estimation 1456.2.2.c Predicting Individual Coefficients 1476.2.2.d Testing for Coefficient Variation 1476.2.2.e Fixed or Random Coefficients 1496.2.2.f An Example 150

6.3 Coefficients That Vary over Time and Cross-Sectional Units 1516.3.1 The Model 1516.3.2 Fixed-Coefficient Model 1536.3.3 Random-Coefficient Model 153

6.4 Coefficients That Evolve over Time 1566.4.1 The Model 1566.4.2 Predicting �t by the Kalman Filter 1586.4.3 Maximum Likelihood Estimation 1616.4.4 Tests for Parameter Constancy 162

6.5 Coefficients That Are Functions of Other ExogenousVariables 163

6.6 A Mixed Fixed- and Random-Coefficients Model 1656.6.1 Model Formulation 1656.6.2 A Bayes Solution 1686.6.3 An Example 170

x Contents

6.6.4 Random or Fixed Parameters 1726.6.4.a An Example 1726.6.4.b Model Selection 173

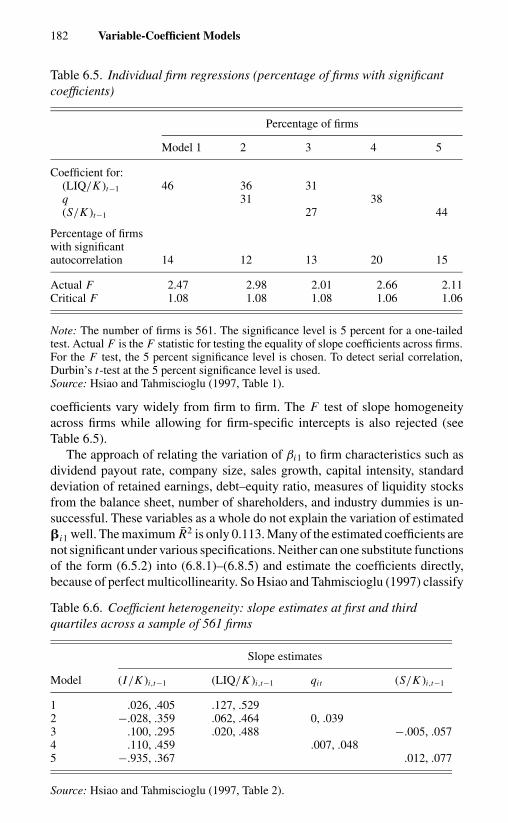

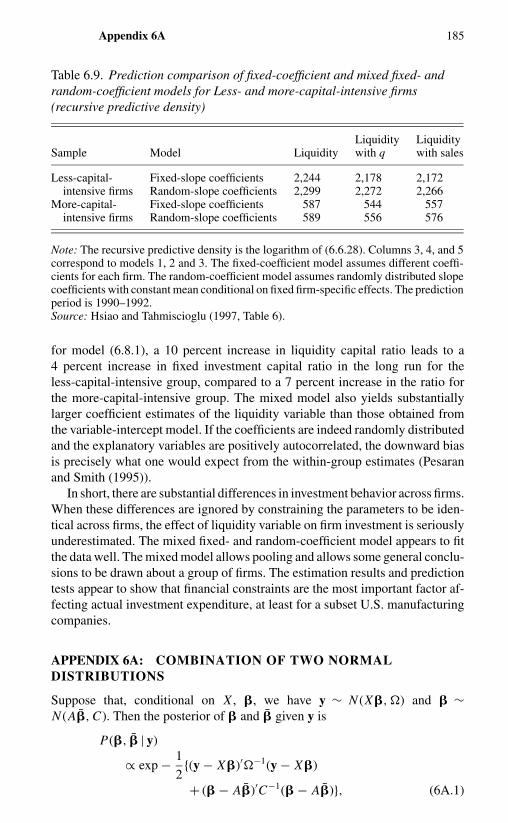

6.7 Dynamic Random-Coefficient Models 1756.8 An Example – Liquidity Constraints and Firm Investment

Expenditure 180Appendix 6A: Combination of Two Normal Distributions 185

Chapter 7. Discrete Data 1887.1 Introduction 1887.2 Some Discrete-Response Models 1887.3 Parametric Approach to Static Models with Heterogeneity 193

7.3.1 Fixed-Effects Models 1947.3.1.a Maximum Likelihood Estimator 1947.3.1.b Conditions for the Existence of a Consistent

Estimator 1957.3.1.c Some Monte Carlo Evidence 198

7.3.2 Random-Effects Models 1997.4 Semiparametric Approach to Static Models 202

7.4.1 Maximum Score Estimator 2037.4.2 A Root-N Consistent Semiparametric Estimator 205

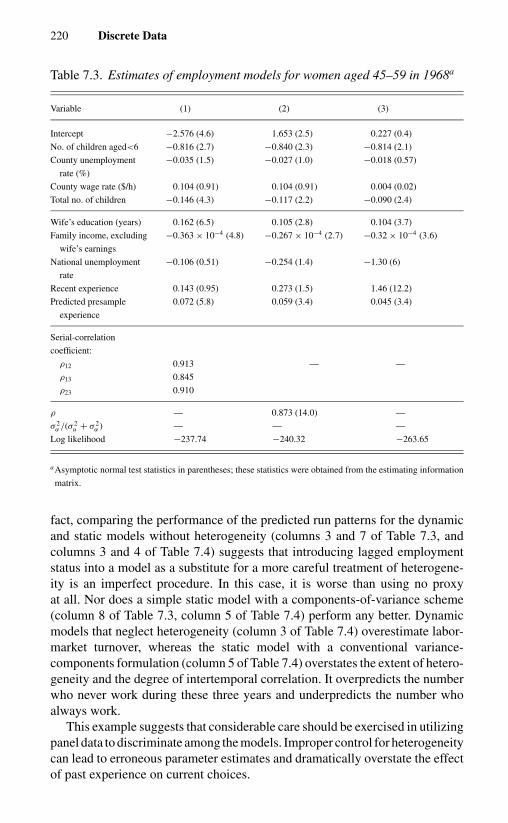

7.5 Dynamic Models 2067.5.1 The General Model 2067.5.2 Initial Conditions 2087.5.3 A Conditional Approach 2117.5.4 State Dependence versus Heterogeneity 2167.5.5 Two Examples 218

7.5.5.a Female Employment 2187.5.5.b Household Brand Choices 221

Chapter 8. Truncated and Censored Data 2258.1 Introduction 2258.2 An Example – Nonrandomly Missing Data 234

8.2.1 Introduction 2348.2.2 A Probability Model of Attrition and Selection Bias 2358.2.3 Attrition in the Gary Income-Maintenance Experiment 238

8.3 Tobit Models with Random Individual Effects 2408.4 Fixed-Effects Estimator 243

8.4.1 Pairwise Trimmed Least-Squares andLeast-Absolute-Deviation Estimators forTruncated and Censored Regressions 243

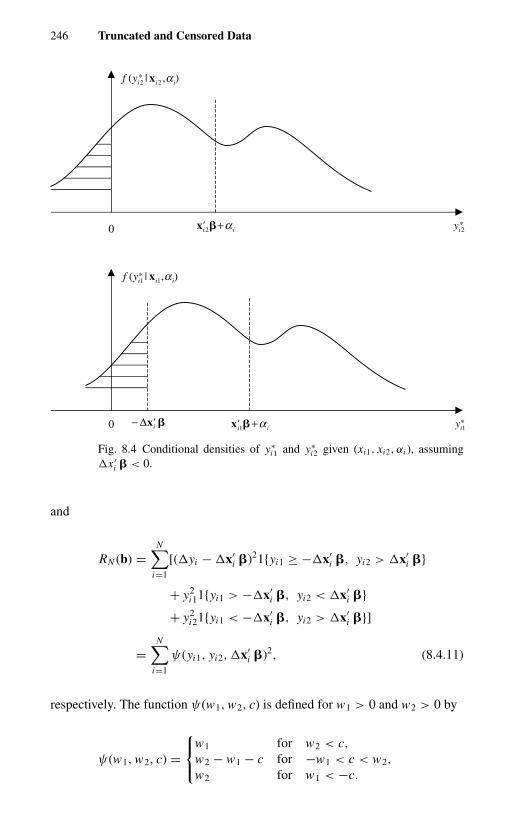

8.4.1.a Truncated Regression 2438.4.1.b Censored Regressions 249

8.4.2 A Semiparametric Two-Step Estimator for theEndogenously Determined Sample Selection Model 253

Contents xi

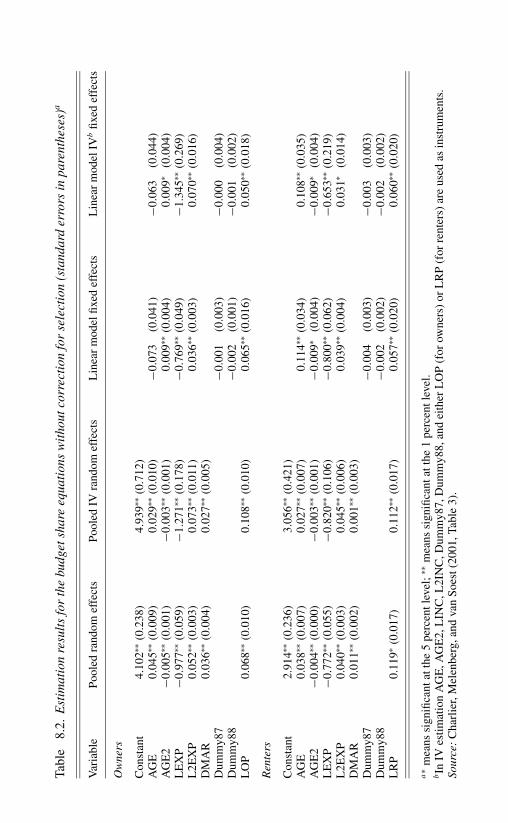

8.5 An Example: Housing Expenditure 2558.6 Dynamic Tobit Models 259

8.6.1 Dynamic Censored Models 2598.6.2 Dynamic Sample Selection Models 265

Chapter 9. Incomplete Panel Data 2689.1 Estimating Distributed Lags in Short Panels 268

9.1.1 Introduction 2689.1.2 Common Assumptions 2709.1.3 Identification Using Prior Structure of the Process

of the Exogenous Variable 2719.1.4 Identification Using Prior Structure of the Lag

Coefficients 2759.1.5 Estimation and Testing 277

9.2 Rotating or Randomly Missing Data 2799.3 Pseudopanels (or Repeated Cross-Sectional

Data) 2839.4 Pooling of a Single Cross-Sectional and a Single

Time-Series Data Set 2859.4.1 Introduction 2859.4.2 The Likelihood Approach to Pooling Cross-Sectional

and Time-Series Data 2879.4.3 An Example 288

Chapter 10. Miscellaneous Topics 29110.1 Simulation Methods 29110.2 Panels with Large N and T 29510.3 Unit-Root Tests 29810.4 Data with Multilevel Structures 30210.5 Errors of Measurement 30410.6 Modeling Cross-Sectional Dependence 309

Chapter 11. A Summary View 31111.1 Introduction 31111.2 Benefits and Limitations of Panel Data 311

11.2.1 Increasing Degrees of Freedom and Lesseningthe Problem of Multicollinearity 311

11.2.2 Identification and Discrimination betweenCompeting Hypotheses 312

11.2.3 Reducing Estimation Bias 31311.2.3.a Omitted-Variable Bias 31311.2.3.b Bias Induced by the Dynamic Structure

of a Model 31511.2.3.c Simultaneity Bias 31611.2.3.d Bias Induced by Measurement Errors 316

xii Contents

11.2.4 Providing Micro Foundations for Aggregate DataAnalysis 316

11.3 Efficiency of the Estimates 317

Notes 319References 331Author Index 353Subject Index 359

CHAPTER 1

Introduction

1.1 ADVANTAGES OF PANEL DATA

A longitudinal, or panel, data set is one that follows a given sample of individualsover time, and thus provides multiple observations on each individual in thesample. Panel data have become widely available in both the developed anddeveloping countries. For instance, in the U.S., two of the most prominent paneldata sets are the National Longitudinal Surveys of Labor Market Experience(NLS) and the University of Michigan’s Panel Study of Income Dynamics(PSID).

The NLS began in the mid-1960s. It contains five separate longitudinal databases covering distinct segments of the labor force: men whose ages were 45to 59 in 1966, young men 14 to 24 in 1966, women 30 to 44 in 1967, youngwomen 14 to 24 in 1968, and youth of both sexes 14 to 21 in 1979. In 1986, theNLS expanded to include surveys of the children born to women who partici-pated in the National Longitudinal Survey of Youth 1979. The list of variablessurveyed is running into the thousands, with the emphasis on the supply sideof the labor market. Table 1.1 summarizes the NLS survey groups, the sizes ofthe original samples, the span of years each group has been interviewed, andthe current interview status of each group (for detail, see NLS Handbook 2000,U.S. Department of Labor, Bureau of Labor Statistics).

The PSID began with collection of annual economic information from arepresentative national sample of about 6,000 families and 15,000 individualsin 1968 and has continued to the present. The data set contains over 5,000variables, including employment, income, and human-capital variables, as wellas information on housing, travel to work, and mobility. In addition to the NLSand PSID data sets there are several other panel data sets that are of interestto economists, and these have been cataloged and discussed by Borus (1981)and Juster (2000); also see Ashenfelter and Solon (1982) and Becketti et al.(1988).1

In Europe, various countries have their annual national or more frequentsurveys – the Netherlands Socio-Economic Panel (SEP), the German SocialEconomics Panel (GSOEP), the Luxembourg Social Economic Panel (PSELL),

Tabl

e1.

1.T

heN

LS:

Surv

eygr

oups

,sam

ple

size

s,in

terv

iew

year

s,an

dsu

rvey

stat

us

Age

Bir

thye

arO

rigi

nal

Initi

alye

ar/

Num

ber

Num

ber

atSu

rvey

grou

pco

hort

coho

rtsa

mpl

ela

test

year

ofsu

rvey

sla

stin

terv

iew

Stat

us

Old

erm

en45

–59

4/2/

07–4

/1/2

15,

020

1966

/199

013

2,09

21E

nded

Mat

ure

wom

en30

–44

4/2/

23–4

/1/3

75,

083

1967

/199

919

2,46

62C

ontin

uing

You

ngm

en14

–24

4/2/

42–4

/1/5

25,

225

1966

/198

112

3,39

8E

nded

You

ngw

omen

14–2

419

44–1

954

5,15

919

68/1

999

202,

9002

Con

tinui

ng

NL

SY79

14–2

119

57–1

964

12,6

863

1979

/199

818

8,39

9C

ontin

uing

NL

SY79

child

ren

birt

h–14

——

419

86/1

998

74,

924

Con

tinui

ngN

LSY

79yo

ung

adul

ts15

–22

——

419

94/1

998

32,

143

Con

tinui

ng

NL

SY97

12–1

619

80–1

984

8,98

419

97/1

999

38,

386

Con

tinui

ng

1In

terv

iew

sin

1990

wer

eal

soco

nduc

ted

with

2,20

6w

idow

sor

othe

rne

xt-o

f-ki

nof

dece

ased

resp

onde

nts.

2Pr

elim

inar

ynu

mbe

rs.

3A

fter

drop

ping

the

mili

tary

(in

1985

)an

dec

onom

ical

lydi

sadv

anta

ged

non-

Bla

ck,n

on-H

ispa

nic

over

sam

ples

(in

1991

),th

esa

mpl

eco

ntai

ns9,

964

resp

onde

nts

elig

ible

for

inte

rvie

w.

4T

hesi

zes

ofth

eN

LSY

79ch

ildre

nan

dyo

ung

adul

tsam

ples

are

depe

nden

ton

the

num

ber

ofch

ildre

nbo

rnto

fem

ale

NL

SY79

resp

onde

nts,

whi

chis

incr

easi

ngov

ertim

e.So

urce

:N

LS

Han

dboo

k,20

00,U

.S.D

epar

tmen

tof

Lab

or,B

urea

uof

Lab

orSt

atis

tics.

1.1 Advantages of Panel Data 3

the British Household Panel Survey (BHPS), etc. Starting in 1994, the NationalData Collection Units (NDUs) of the Statistical Office of the European Com-munities, “in response to the increasing demand in the European Union forcomparable information across the Member States on income, work and em-ployment, poverty and social exclusion, housing, health, and many other diversesocial indicators concerning living conditions of private households and per-sons” (Eurostat (1996)), have begun coordinating and linking existing nationalpanels with centrally designed standardized multipurpose annual longitudinalsurveys. For instance, the Manheim Innovation Panel (MIP) and the ManheimInnovation Panel – Service Sector (MIP-S) contain annual surveys of innova-tive activities (product innovations, expenditure on innovations, expenditureon R&D, factors hampering innovations, the stock of capital, wages, and skillstructures of employees, etc.) of German firms with at least five employees inmanufacturing and service sectors, started in 1993 and 1995, respectively. Thesurvey methodology is closely related to the recommendations on innovationsurveys manifested in the OSLO Manual of the OECD and Eurostat, therebyyielding international comparable data on innovation activities of German firms.The 1993 and 1997 surveys also become part of the European Community Inno-vation Surveys CIS I and CIS II (for detail, see Janz et al. (2001)). Similarly, theEuropean Community Household Panel (ECHP) is to represent the populationof the European Union (EU) at the household and individual levels. The ECHPcontains information on demographics, labor-force behavior, income, health,education and training, housing, migration, etc. The ECHP now covers 14 of the15 countries, the exception being Sweden (Peracchi (2000)). Detailed statisticsfrom the ECHP are published in Eurostat’s reference data base New Cronosin three domains, namely health, housing, and income and living conditions(ILC).2

Panel data have also become increasingly available in developing countries.In these countries, there may not have a long tradition of statistical collection.It is of special importance to obtain original survey data to answer many sig-nificant and important questions. The World Bank has sponsored and helpedto design many panel surveys. For instance, the Development Research Insti-tute of the Research Center for Rural Development of the State Council ofChina, in collaboration with the World Bank, undertook an annual survey of200 large Chinese township and village enterprises from 1984 to 1990 (Hsiaoet al. (1998)).

Panel data sets for economic research possess several major advantages overconventional cross-sectional or time-series data sets (e.g., Hsiao (1985a, 1995,2000)). Panel data usually give the researcher a large number of data points,increasing the degrees of freedom and reducing the collinearity among explana-tory variables – hence improving the efficiency of econometric estimates. Moreimportantly, longitudinal data allow a researcher to analyze a number of im-portant economic questions that cannot be addressed using cross-sectional ortime-series data sets. For instance, consider the following example taken fromBen-Porath (1973): Suppose that a cross-sectional sample of married women

4 Introduction

is found to have an average yearly labor-force participation rate of 50 per-cent. At one extreme this might be interpreted as implying that each womanin a homogeneous population has a 50 percent chance of being in the laborforce in any given year, while at the other extreme it might imply that 50 per-cent of the women in a heterogeneous population always work and 50 percentnever work. In the first case, each woman would be expected to spend halfof her married life in the labor force and half out of the labor force, and jobturnover would be expected to be frequent, with an average job duration oftwo years. In the second case, there is no turnover, and current informationabout work status is a perfect predictor of future work status. To discriminatebetween these two models, we need to utilize individual labor-force historiesto estimate the probability of participation in different subintervals of the lifecycle. This is possible only if we have sequential observations for a number ofindividuals.

The difficulties of making inferences about the dynamics of change fromcross-sectional evidence are seen as well in other labor-market situations. Con-sider the impact of unionism on economic behavior (e.g., Freeman and Medoff1981). Those economists who tend to interpret the observed differences betweenunion and nonunion firms or employees as largely real believe that unions andthe collective-bargaining process fundamentally alter key aspects of the employ-ment relationship: compensation, internal and external mobility of labor, workrules, and environment. Those economists who regard union effects as largelyillusory tend to posit that the real world is close enough to satisfying the con-ditions of perfect competition; they believe that the observed union–nonuniondifferences are mainly due to differences between union and nonunion firms orworkers prior to unionism or postunion sorting. Unions do not raise wages inthe long run, because firms react to higher wages (forced by the union) by hiringbetter-quality workers. If one believes the former view, the coefficient of thedummy variable for union status in a wage or earning equation is a measure ofthe effect of unionism. If one believes the latter view, then the dummy variablefor union status could be simply acting as a proxy for worker quality. A singlecross-sectional data set usually cannot provide a direct choice between thesetwo hypotheses, because the estimates are likely to reflect interindividual dif-ferences inherent in comparisons of different people or firms. However, if paneldata are used, one can distinguish these two hypotheses by studying the wagedifferential for a worker moving from a nonunion firm to a union firm, or viceversa. If one accepts the view that unions have no effect, then a worker’s wageshould not be affected when he moves from a nonunion firm to a union firm,if the quality of this worker is constant over time. On the other hand, if unionstruly do raise wages, then, holding worker quality constant, the worker’s wageshould rise as he moves to a union firm from a nonunion firm. By followinggiven individuals or firms over time as they change status (say from nonunionto union, or vice versa), one can construct a proper recursive structure to studythe before–after effect.

1.1 Advantages of Panel Data 5

Whereas microdynamic and macrodynamic effects typically cannot be es-timated using a cross-sectional data set, a single time-series data set usuallycannot provide precise estimates of dynamic coefficients either. For instance,consider the estimation of a distributed-lag model:

yt =h∑

τ=0

βτ xt−τ + ut , t = 1, . . . , T, (1.1.1)

where xt is an exogenous variable and ut is a random disturbance term. Ingeneral, xt is near xt−1, and still nearer 2xt−1 − xt−2 = xt−1 + (xt−1 − xt−2);fairly strict multicollinearities appear among h + 1 explanatory variables,x1, xt−1, . . . , xt−h . Hence, there is not sufficient information to obtain preciseestimates of any of the lag coefficients without specifying, a priori, that eachof them is a function of only a very small number of parameters [e.g., Almonlag, rational distributed lag (Malinvaud (1970))]. If panel data are available, wecan utilize the interindividual differences in x values to reduce the problem ofcollinearity; this allows us to drop the ad hoc conventional approach of con-straining the lag coefficients {βτ } and to impose a different prior restriction toestimate an unconstrained distributed-lag model.

Another example is that measurement errors can lead to unidentification of amodel in the usual circumstance. However, the availability of multiple observa-tions for a given individual or at a given time may allow a researcher to identifyan otherwise unidentified model (e.g., Biørn (1992); Griliches and Hausman(1986); Hsiao (1991b); Hsiao and Taylor (1991); Wansbeek and Koning (1989)).

Besides the advantage that panel data allow us to construct and test more com-plicated behavioral models than purely cross-sectional or time-series data, theuse of panel data also provides a means of resolving or reducing the magnitudeof a key econometric problem that often arises in empirical studies, namely, theoften heard assertion that the real reason one finds (or does not find) certaineffects is the presence of omitted (mismeasured or unobserved) variables thatare correlated with explanatory variables. By utilizing information on both theintertemporal dynamics and the individuality of the entities being investigated,one is better able to control in a more natural way for the effects of missing orunobserved variables. For instance, consider a simple regression model:

yit = α∗ + �′xi t + �′zi t + uit , i = 1, . . . , N ,

t = 1, . . . , T,(1.1.2)

where xi t and zi t are k1 × 1 and k2 × 1 vectors of exogenous variables; α∗,�, and � are 1 × 1, k1 × 1, and k2 × 1 vectors of constants respectively; andthe error term uit is independently, identically distributed over i and t , withmean zero and variance σ 2

u . It is well known that the least-squares regressionof yit on xi t and zi t yields unbiased and consistent estimators of α∗, �, and�. Now suppose that zi t values are unobservable, and the covariances betweenxi t and zi t are nonzero. Then the least-squares regression coefficients of yit on

6 Introduction

xi t are biased. However, if repeated observations for a group of individuals areavailable, they may allow us to get rid of the effect of z. For example, if zi t = zi

for all t (i.e., z values stay constant through time for a given individual but varyacross individuals), we can take the first difference of individual observationsover time and obtain

yit − yi,t−1 = �′(xi t − xi,t−1) + (uit − ui,t−1), i = 1, . . . , N ,

t = 2, . . . , T .

(1.1.3)

Similarly, if zi t = zt for all i (i.e., z values stay constant across individuals at agiven time, but exhibit variation through time), we can take the deviation fromthe mean across individuals at a given time and obtain

yit − yt = �′(xi t − xt ) + (uit − ut ), i = 1, . . . , N ,

t = 1, . . . , T,(1.1.4)

where yt = (1/N )∑N

i=1 yit , xt = (1/N )∑N

i=1 xi t , and ut = (1/N )∑N

i=1 uit .Least-squares regression of (1.1.3) or (1.1.4) now provides unbiased and con-sistent estimates of �. Nevertheless if we have only a single cross-sectionaldata set (T = 1) for the former case (zi t = zi ), or a single time-series data set(N = 1) for the latter case (zi t = zt ), such transformations cannot be performed.We cannot get consistent estimates of � unless there exist instruments that arecorrelated with x but are uncorrelated with z and u.

MaCurdy’s (1981) work on the life-cycle labor supply of prime-age malesunder certainty is an example of this approach. Under certain simplifying as-sumptions, MaCurdy shows that a worker’s labor-supply function can be writtenas (1.1.2), where y is the logarithm of hours worked, x is the logarithm of thereal wage rate, and z is the logarithm of the worker’s (unobserved) marginalutility of initial wealth, which, as a summary measure of a worker’s lifetimewages and property income, is assumed to stay constant through time but to varyacross individuals (i.e., zit = zi ). Given the economic problem, not only is xit

correlated with zi , but every economic variable that could act as an instrumentfor xit (such as education) is also correlated with zi . Thus, in general, it is notpossible to estimate � consistently from a cross-sectional data set,3 but if paneldata are available, one can consistently estimate � by first-differencing (1.1.2).

The “conditional convergence” of the growth rate is another example (e.g.,Durlauf (2001); Temple (1999)). Given the role of transitional dynamics, it iswidely agreed that growth regressions should control for the steady state levelof income (e.g., Barro and Sala-i-Martin (1995); Mankiew, Romer, and Weil(1992)). Thus, a growth-rate regression model typically includes investmentratio, initial income, and measures of policy outcomes like school enrollmentand the black-market exchange-rate premium as regressors. However, an im-portant component, the initial level of a country’s technical efficiency, zi0, isomitted because this variable is unobserved. Since a country that is less efficient

1.1 Advantages of Panel Data 7

is also more likely to have lower investment rate or school enrollment, one caneasily imagine that zi0 is correlated with the regressors and the resulting cross-sectional parameter estimates are subject to omitted-variable bias. However,with panel data one can eliminate the influence of initial efficiency by takingthe first difference of individual country observations over time as in (1.1.3).

Panel data involve two dimensions: a cross-sectional dimension N , and atime-series dimension T . We would expect that the computation of panel dataestimators would be more complicated than the analysis of cross-section dataalone (where T = 1) or time series data alone (where N = 1). However, incertain cases the availability of panel data can actually simplify the computationand inference. For instance, consider a dynamic Tobit model of the form

y∗i t = γ y∗

i,t−1 + βxit + εi t (1.1.5)

where y∗ is unobservable, and what we observe is y, where yit = y∗i t if y∗

i t > 0and 0 otherwise. The conditional density of yit given yi,t−1 = 0 is much morecomplicated than the case if y∗

i,t−1 is known, because the joint density of(yit , yi,t−1) involves the integration of y∗

i,t−1 from −∞ to 0. Moreover, whenthere are a number of censored observations over time, the full implemen-tation of the maximum likelihood principle is almost impossible. However,with panel data, the estimation of γ and β can be simplified considerably bysimply focusing on the subset of data where yi,t−1 > 0, because the joint den-sity of f (yit , yi,t−1) can be written as the product of the conditional densityf (yi,t | yi,t−1) and the marginal density of yi,t−1. But if y∗

i,t−1 is observable,the conditional density of yit given yi,t−1 = y∗

i,t−1 is simply the density of εi t

(Arellano, Bover, and Labeager (1999)).Another example is the time-series analysis of nonstationary data. The large-

sample approximation of the distributions of the least-squares or maximum like-lihood estimators when T → ∞ are no longer normally distributed if the dataare nonstationary (e.g., Dickey and Fuller (1979, 1981); Phillips and Durlauf(1986)). Hence, the behavior of the usual test statistics will often have to beinferred through computer simulations. But if panel data are available, and ob-servations among cross-sectional units are independent, then one can invokethe central limit theorem across cross-sectional units to show that the limitingdistributions of many estimators remain asymptotically normal and the Wald-type test statistics are asymptotically chi-square distributed (e.g., Binder, Hsiao,and Pesaran (2000); Levin and Lin (1993); Pesaran, Shin, and Smith (1999),Phillips and Moon (1999, 2000); Quah (1994)).

Panel data also provide the possibility of generating more accurate predic-tions for individual outcomes than time-series data alone. If individual behaviorsare similar conditional on certain variables, panel data provide the possibilityof learning an individual’s behavior by observing the behavior of others, inaddition to the information on that individual’s behavior. Thus, a more accuratedescription of an individual’s behavior can be obtained by pooling the data

8 Introduction

(e.g., Hsiao and Mountain (1994); Hsiao and Tahmiscioglu (1997); Hsiao et al.(1989); Hsiao, Applebe, and Dineen (1993)).

1.2 ISSUES INVOLVED IN UTILIZINGPANEL DATA

1.2.1 Heterogeneity Bias

The oft-touted power of panel data derives from their theoretical ability to iso-late the effects of specific actions, treatments, or more general policies. Thistheoretical ability is based on the assumption that economic data are gener-ated from controlled experiments in which the outcomes are random variableswith a probability distribution that is a smooth function of the various vari-ables describing the conditions of the experiment. If the available data were infact generated from simple controlled experiments, standard statistical methodscould be applied. Unfortunately, most panel data come from the very compli-cated process of everyday economic life. In general, different individuals maybe subject to the influences of different factors. In explaining individual behav-ior, one may extend the list of factors ad infinitum. It is neither feasible nordesirable to include all the factors affecting the outcome of all individuals in amodel specification, since the purpose of modeling is not to mimic the realitybut is to capture the essential forces affecting the outcome. It is typical to leaveout those factors that are believed to have insignificant impacts or are peculiarto certain individuals.

However, when important factors peculiar to a given individual are left out,the typical assumption that economic variable y is generated by a parametricprobability distribution function P(y | �), where � is an m-dimensional realvector, identical for all individuals at all times, may not be a realistic one.Ignoring the individual or time-specific effects that exist among cross-sectionalor time-series units but are not captured by the included explanatory variablescan lead to parameter heterogeneity in the model specification. Ignoring suchheterogeneity could lead to inconsistent or meaningless estimates of interestingparameters. For example, consider a simple model postulated as

yit = α∗i + βi xi t + uit , i = 1, . . . , N ,

t = 1, . . . , T,(1.2.1)

where x is a scalar exogenous variable (k1 = 1) and uit is the error term withmean zero and constant variance σ 2

u . The parameters α∗i and βi may be differ-

ent for different cross-sectional units, although they stay constant over time.Following this assumption, a variety of sampling distributions may occur. Suchsampling distributions can seriously mislead the least-squares regression of yit

on xit when all N T observations are used to estimate the model:

yit = α∗ + βxit + uit , i = 1, . . . , N ,

t = 1, . . . , T .(1.2.2)

1.2 Issues Involved in Utilizing Panel Data 9

For instance, consider the situation that the data are generated as either in case1 or case 2.

Case 1: Heterogeneous intercepts (α∗i �= α∗

j ), homogeneous slope(βi = β j ). We use graphs to illustrate the likely biases due to theassumption that α∗

i �= α∗j and βi = β j . In these graphs, the broken-

line ellipses represent the point scatter for an individual over time,and the broken straight lines represent the individual regressions.Solid lines serve the same purpose for the least-squares regression of(1.2.2) using all N T observations. A variety of circumstances mayarise in this case, as shown in Figures 1.1, 1.2, and 1.3. All of thesefigures depict situations in which biases arise in pooled least-squaresestimates of (1.2.2) because of heterogeneous intercepts. Obviously,in these cases, pooled regression ignoring heterogeneous interceptsshould never be used. Moreover, the direction of the bias of thepooled slope estimates cannot be identified a priori; it can go eitherway.

Case 2: Heterogeneous intercepts and slopes (α∗i �= α∗

j , βi �= β j ). InFigures 1.4 and 1.5 the point scatters are not shown, and the cir-cled numbers signify the individuals whose regressions have beenincluded in the analysis. For the example depicted in Figure 1.4, astraightforward pooling of all N T observations, assuming identicalparameters for all cross-sectional units, would lead to nonsensicalresults because it would represent an average of coefficients that dif-fer greatly across individuals. Nor does the case of Figure 1.5 makeany sense in pooling, because it gives rise to the false inference thatthe pooled relation is curvilinear. In either case, the classic paradigmof the “representative agent” simply does not hold, and pooling thedata under homogeneity assumption makes no sense.

These are some of the likely biases when parameter heterogeneities amongcross-sectional units are ignored. Similar patterns of bias will also arise if theintercepts and slopes vary through time, even though for a given time period theyare identical for all individuals. More elaborate patterns than those depicted hereare, of course, likely to occur (e.g., Chesher and Lancaster 1983; Kuh 1963).

1.2.2 Selectivity Bias

Another frequently observed source of bias in both cross-sectional and paneldata is that the sample may not be randomly drawn from the population. Forexample, the New Jersey negative income tax experiment excluded all familiesin the geographic areas of the experiment who had incomes above 1.5 times theofficially defined poverty level. When the truncation is based on earnings, usesof the data that treat components of earnings (specifically, wages or hours) asdependent variables will often create what is commonly referred to as selectionbias (e.g., Hausman and Wise (1977); Heckman (1976a, 1979); Hsiao (1974b)).

10 Introduction

Fig. 1.1 Fig. 1.2 Fig. 1.3

Fig. 1.4 Fig. 1.5

L

Fig. 1.6

For ease of exposition, we shall consider a cross-sectional example to getsome idea of how using a nonrandom sample may bias the least-squares esti-mates. We assume that in the population the relationship between earnings (y)and exogenous variables (x), including education, intelligence, and so forth, isof the form

yi = �′xi + ui , i = 1, . . . , N , (1.2.3)

where the disturbance term ui is independently distributed with mean zero andvariance σ 2

u . If the participants of an experiment are restricted to have earnings

1.3 Outline of the Monograph 11

less than L , the selection criterion for families considered for inclusion in theexperiment can be stated as follows:

yi = �′xi + ui ≤ L, included,

yi = �′xi + ui > L, excluded.(1.2.4)

For simplicity, we assume that the values of exogenous variables, except forthe education variable, are the same for each observation. In Figure 1.6, we letthe upward-sloping solid line indicate the “average” relation between educationand earnings and the dots represent the distribution of earnings around this meanfor selected values of education. All individuals with earnings above a givenlevel L , indicated by the horizontal line, would be eliminated from this experi-ment. In estimating the effect of education on earnings, we would observe onlythe points below the limit (circled) and thus would tend to underestimate the ef-fect of education using ordinary least squares.4 In other words, the sample selec-tion procedure introduces correlation between right-hand variables and the errorterm, which leads to a downward-biased regression line, as the dashed line inFigure 1.6 indicates.

These examples demonstrate that despite the advantages panel data maypossess, they are subject to their own potential experimental problems. It isonly by taking proper account of selectivity and heterogeneity biases in thepanel data that one can have confidence in the results obtained. The focus ofthis monograph will be on controlling for the effect of unobserved individualand/or time characteristics to draw proper inference about the characteristics ofthe population.

1.3 OUTLINE OF THE MONOGRAPH

Because the source of sample variation critically affects the formulation andestimation of many economic models, we shall first briefly review the clas-sic analysis of covariance procedures in Chapter 2. We shall then relax theassumption that the parameters that characterize all temporal cross-sectionalsample observations are identical and examine a number of specifications thatallow for differences in behavior across individuals as well as over time. Forinstance, a single-equation model with observations of y depending on a vectorof characteristics x can be written in the following form:

1. Slope coefficients are constant, and the intercept varies over individu-als:

yit = α∗i +

K∑k=1

βk xkit + uit , i = 1, . . . , N ,

(1.3.1)t = 1, . . . , T .

12 Introduction

2. Slope coefficients are constant, and the intercept varies over individu-als and time:

yit = α∗i t +

K∑k=1

βk xkit + uit , i = 1, . . . , N ,

(1.3.2)t = 1, . . . , T .

3. All coefficients vary over individuals:

yit = α∗i +

K∑k=1

βki xkit + uit , i = 1, . . . , N ,

(1.3.3)t = 1, . . . , T .

4. All coefficients vary over time and individuals:

yit = α∗i t +

K∑k=1

βki t xkit + uit , i = 1, . . . , N ,

(1.3.4)t = 1, . . . , T .

In each of these cases the model can be classified further, depending on whetherthe coefficients are assumed to be random or fixed.

Models with constant slopes and variable intercepts [such as (1.3.1) and(1.3.2)] are most widely used when analyzing panel data because they providesimple yet reasonably general alternatives to the assumption that parameterstake values common to all agents at all times. We shall consequently devotethe majority of this monograph to this type of model. Static models with vari-able intercepts will be discussed in Chapter 3, dynamic models in Chapter 4,simultaneous-equations models in Chapter 5, and discrete-data and sampleselection models in Chapters 7 and 8, respectively. Basic issues in variable-coefficient models for linear models [such as (1.3.3) and (1.3.4)] will be dis-cussed in Chapter 6. Chapter 9 discusses issues of incomplete panel models,such as estimating distributed-lag models in short panels, rotating samples,pooling of a series of independent cross sections (pseudopanels), and the pool-ing of data on a single cross section and a single time series. Miscellaneoustopics such as simulation methods, measurement errors, panels with large Nand large T , unit-root tests, cross-sectional dependence, and multilevel panelswill be discussed in Chapter 10. A summary view of the issues involved inutilizing panel data will be presented in Chapter 11.

The challenge of panel data analysis has been, and will continue to be, thebest way to formulate statistical models for inference motivated and shapedby substantive problems compatible with our understanding of the processesgenerating the data. The goal of this monograph is to summarize previous workin such a way as to provide the reader with the basic tools for analyzing and dra-wing inferences from panel data. Analyses of several important and advanced

1.3 Outline of the Monograph 13

topics, such as continuous time-duration models (e.g., Florens, Fougere, andMouchart (1996); Fougere and Kamionka (1996); Heckman and Singer (1984);Kiefer (1988); Lancaster (1990)), general nonlinear models (e.g., Abrevaya(1999); Amemiya (1983); Gourieroux and Jasiak (2000); Hsiao (1992c);Jorgenson and Stokes (1982); Lancaster (2001); Wooldridge (1999)),5 countdata (Cameron and Trevedi 1998), and econometric evaluation of social pro-grams (e.g., Angrist and Hahn (1999); Hahn (1998); Heckman (2001); Heckmanand Vytlacil (2001); Heckman, Ichimura, and Todd (1998); Hirano, Imbens, andRidder (2000); Imbens and Angrist (1994)), are beyond the scope of this mono-graph.

CHAPTER 2

Analysis of Covariance

2.1 INTRODUCTION1

Suppose we have sample observations of characteristics of N individuals over Ttime periods denoted by yit , xkit , i = 1, . . . , N , t = 1, . . . , T , k = 1, . . . , K .Conventionally, observations of y are assumed to be the random outcomes ofsome experiment with a probability distribution conditional on vectors of thecharacteristics x and a fixed number of parameters �, f (y | x, �). When paneldata are used, one of the ultimate goals is to use all available information tomake inferences on �. For instance, a simple model commonly postulated isthat y is a linear function of x. Yet to run a least-squares regression with allN T observations, we need to assume that the regression parameters take valuescommon to all cross-sectional units for all time periods. If this assumption isnot valid, as shown in Section 1.2, the pooled least-squares estimates may leadto false inferences. Thus, as a first step toward full exploitation of the data,we often test whether or not parameters characterizing the random outcomevariable y stay constant across all i and t .

A widely used procedure to identify the source of sample variation is theanalysis-of-covariance test. The name “analysis of variance” is often reservedfor a particular category of linear hypotheses that stipulate that the expectedvalue of a random variable y depends only on the class (defined by one or morefactors) to which the individual considered belongs, but excludes tests relatingto regressions. On the other hand, analysis-of-covariance models are of a mixedcharacter involving genuine exogenous variables, as do regression models, andat the same time allowing the true relation for each individual to depend onthe class to which the individual belongs, as do the usual analysis-of-variancemodels.

A linear model commonly used to assess the effects of both quantitative andqualitative factors is postulated as

yit = α∗i t + �′

i t xi t + uit , i = 1, . . . , N ,

t = 1, . . . , T,(2.1.1)

where α∗i t and �′

i t = (β1i t , β2i t , . . . , βK it ) are 1 × 1 and 1 × K vectors of

2.2 Analysis of Covariance 15

constants that vary across i and t , respectively, x′i t = (x1i t , . . . , xK it ) is a 1 × K

vector of exogenous variables, and uit is the error term. Two aspects of the esti-mated regression coefficients can be tested: first, the homogeneity of regressionslope coefficients; second, the homogeneity of regression intercept coefficients.The test procedure has three main steps:

1. Test whether or not slopes and intercepts simultaneously are homoge-neous among different individuals at different times.

2. Test whether or not the regression slopes collectively are the same.3. Test whether or not the regression intercepts are the same.

It is obvious that if the hypothesis of overall homogeneity (step 1) is ac-cepted, the testing procedure will go no further. However, should the overallhomogeneity hypothesis be rejected, the second step of the analysis is to decideif the regression slopes are the same. If this hypothesis of homogeneity is notrejected, one then proceeds to the third and final test to determine the equalityof regression intercepts. In principle, step 1 is separable from steps 2 and 3.2

Although this type of analysis can be performed on several dimensions,as described by Scheffe (1959) or Searle (1971), only one-way analysis ofcovariance has been widely used. Therefore, here we present only the proceduresfor performing one-way analysis of covariance.

2.2 ANALYSIS OF COVARIANCE

Model (2.1.1) only has descriptive value. It can neither be estimated nor beused to generate prediction, because the available degrees of freedom, N T ,is less than the number of parameters, N T (K + 1) + (number of parameterscharacterizing the distribution of uit ). A structure has to be imposed on (2.1.1)before any inference can be made. To start with, we assume that parameters areconstant over time, but can vary across individuals. Thus, we can postulate aseparate regression for each individual:

yit = α∗i + �′

i xi t + uit , i = 1, . . . , N ,

t = 1, . . . , T .(2.2.1)

Three types of restrictions can be imposed on (2.2.1). Namely:

H1: Regression slope coefficients are identical, and intercepts are not.That is,

yit = α∗i + �′xi t + uit . (2.2.2)

H2: Regression intercepts are the same, and slope coefficients are not.That is,

yit = α∗ + �′i xi t + uit . (2.2.3)

H3: Both slope and intercept coefficients are the same. That is,

yit = α∗ + �′xi t + uit . (2.2.4)

16 Analysis of Covariance

Because it is seldom meaningful to ask if the intercepts are the same when theslopes are unequal, we shall ignore the type of restrictions postulated by (2.2.3).We shall refer to (2.2.1) as the unrestricted model, (2.2.2) as the individual-meanor cell-mean corrected regression model, and (2.2.4) as the pooled regression.

Let

yi = 1

T

T∑t=1

yit , (2.2.5)

xi = 1

T

T∑t=1

xi t (2.2.6)

be the means of y and x, respectively, for the i th individual. The least-squaresestimates of �i and α∗

i in the unrestricted model (2.2.1) are given by3

�i = W −1xx,i Wxy,i , αi = yi − �′

i xi , i = 1, . . . , N , (2.2.7)

where

Wxx,i =T∑

t=1

(xi t − xi )(xi t − xi )′,

Wxy,i =T∑

t=1

(xi t − xi )(yit − yi ), (2.2.8)

Wyy,i =T∑

t=1

(yit − yi )2.

In the analysis-of-covariance terminology, equations (2.2.7) are called within-group estimates. The i th-group residual sum of squares is RSSi = Wyy,i −W ′

xy,i W−1xx,i Wxy,i . The unrestricted residual sum of squares is

S1 =N∑

i=1

RSSi . (2.2.9)

The least-squares regression of the individual-mean corrected model yieldsparameter estimates

�w = W −1xx Wxy,

(2.2.10)α∗

i = yi − �′w xi , i = 1, . . . , N ,

where

Wxx =N∑

i=1

Wxx,i and Wxy =N∑

i=1

Wxy,i .

Let Wyy = ∑Ni=1 Wyy,i ; the residual sum of squares of (2.2.2) is

S2 = Wyy − W ′xy W −1

xx Wxy . (2.2.11)

2.2 Analysis of Covariance 17

The least-squares regression of the pooled model (2.2.4) yields parameterestimates

� = T −1xx Txy, α∗ = y − �′x, (2.2.12)

where

Txx =N∑

i=1

T∑t=1

(xi t − x)(xi t − x)′,

Txy =N∑

i=1

T∑t=1

(xi t − x)(yit − y),

Tyy =N∑

i=1

T∑t=1

(yit − y)2,

y = 1

N T

N∑i=1

T∑t=1

yit , x = 1

N

N∑i=1

T∑t=1

xi t .

The (overall) residual sum of squares is

S3 = Tyy − T ′xy T −1

xx Txy . (2.2.13)

Under the assumption that the uit are independently normally distributedover i and t with mean zero and variance σ 2

u , F tests can be used to test therestrictions postulated by (2.2.2) and (2.2.4). In effect, (2.2.2) and (2.2.4) canbe viewed as (2.2.1) subject to various types of linear restrictions. For instance,the hypothesis of heterogeneous intercepts but homogeneous slopes [equation(2.2.2)] can be reformulated as (2.2.1) subject to (N − 1)K linear restrictions:

H1 : �1 = �2 = · · · = �N .

The hypothesis of common intercept and slope can be viewed as (2.2.1) subjectto (K + 1)(N − 1) linear restrictions:

H3 : α∗1 = α∗

2 = · · · = α∗N ,

�1 = �2 = · · · = �N .

Thus, application of the analysis-of-covariance test is equivalent to the ordi-nary hypothesis test based on sums of squared residuals from linear-regressionoutputs.

The unrestricted residual sum of squares S1 divided by σ 2u has a chi-square

distribution with N T − N (K + 1) degrees of freedom. The increment in theexplained sum of squares due to allowing for the parameters to vary acrossi is measured by (S3 − S1). Under H3, the restricted residual sum of squaresS3 divided by σ 2

u has a chi-square distribution with N T − (K + 1) degrees offreedom, and (S3 − S1)/σ 2

u has a chi-square distribution with (N − 1)(K + 1)degrees of freedom. Because (S3 − S1)/σ 2

u is independent of S1/σ2u , the F

18 Analysis of Covariance

statistic

F3 = (S3 − S1)/[(N − 1)(K + 1)]

S1/[N T − N (K + 1)](2.2.14)

can be used to test H3. If F3 with (N − 1)(K + 1) and N (T − K − 1) degreesof freedom is not significant, we pool the data and estimate a single equationof (2.2.4). If the F ratio is significant, a further attempt is usually made tofind out if the nonhomogeneity can be attributed to heterogeneous slopes orheterogeneous intercepts.

Under the hypothesis of heterogeneous intercepts but homogeneous slopes(H1), the residual sum of squares of (2.2.2), S2 = Wyy − W ′

xy W −1xx Wxy , divided

by σ 2u has a chi-square distribution with N (T − 1) − K degrees of freedom.

The F test of H1 is thus given by

F1 = (S2 − S1)/[(N − 1)K ]

S1/[N T − N (K + 1)]. (2.2.15)

If F1 with (N − 1)K and N T − N (K + 1) degrees of freedom is significant, thetest sequence is naturally halted and model (2.2.1) is treated as the maintainedhypothesis. If F1 is not significant, we can then determine the extent to whichnonhomogeneities can arise in the intercepts.

If H1 is accepted, one can also apply a conditional test for homogeneousintercepts, namely,

H4 : α∗1 = α∗

2 = · · · = α∗N given �1 = · · · = �N .

The unrestricted residual sum of squares now is S2, and the restricted residualsum of squares is S3. The reduction in the residual sum of squares in movingfrom (2.2.4) to (2.2.2) is (S3 − S2). Under H4, S3 divided by σ 2

u is chi-squaredistributed with N T − (K + 1) degrees of freedom, and S2 divided by σ 2

u ischi-square distributed with N (T − 1) − K degrees of freedom. Because S2/σ

2u

is independent of (S3 − S2)/σ 2u , which is chi-square distributed with N − 1

degrees of freedom, the F test for H4 is

F4 = (S3 − S2)/(N − 1)

S2/[N (T − 1) − K ]. (2.2.16)

We can summarize these tests in an analysis-of-covariance table (Table 2.1).Alternatively, we can assume that coefficients are constant across individuals

at a given time, but can vary over time. Hence, a separate regression can bepostulated for each cross section:

yit = α∗t + �′

t xi t + uit , i = 1, . . . , N ,(2.2.17)

t = 1, . . . , T,

where we again assume that uit is independently normally distributed withmean 0 and constant variance σ 2

u . Analogous analysis of covariance can thenbe performed to test the homogeneities of the cross-sectional parameters over

Tabl

e2.

1.C

ovar

ianc

ete

sts

for

hom

ogen

eity

Sour

ceof

vari

atio

nR

esid

uals

umof

squa

res

Deg

rees

offr

eedo

mM

ean

squa

res

With

ingr

oup

with

hete

roge

neou

sin

terc

epta

ndsl

ope

S 1=

∑ N i=1

( Wyy

,i−

W′ xy,

iW−1 xx,

iWx

y,i

)N

(T−

K−

1)S 1

/N

(T−

K−

1)

Con

stan

tslo

pe:h

eter

ogen

eous

inte

rcep

tS 2

=W

yy−

W′ xyW

−1 xx

Wx

yN

(T−

1)−

KS 2

/[N

(T−

1)−

K]

Com

mon

inte

rcep

tand

slop

eS 3

=T

yy−

T′ xyT

−1 xx

T xy

NT

−(K

+1)

S 3/[N

T−

(K+

1)]

Not

atio

n:C

ells

orgr

oups

(or

indi

vidu

als)

i=

1,..

.,N

Obs

erva

tions

with

ince

llt=

1,..

.,T

Tota

lsam

ple

size

NT

With

in-c

ell(

grou

p)m

ean

y i,x i

Ove

rall

mea

ny,

xW

ithin

-gro

upco

vari

ance

Wyy

,i,

Wyx

,i,

Wx

x,i

Tota

lvar

iatio

nT

yy,

Tyx

,T x

x

20 Analysis of Covariance

time. For instance, we can test for overall homogeneity (H ′3 : α∗

1 = α∗2 = · · · =

α∗T , �1 = �2 = · · · = �T ) by using the F statistic

F ′3 = (S3 − S′

1)/[(T − 1)(K + 1)]

S′1/[N T − T (K + 1)]

(2.2.18)

with (T − 1)(K + 1) and N T − T (K + 1) degrees of freedom, where

S′1 =

T∑t=1

(Wyy,t − W ′

xy,t W−1xx,t Wxy,t

),

Wyy,t =N∑

i=1

(yit − yt )2, yt = 1

N

N∑i=1

yit ,

(2.2.19)

Wxx,t =N∑

i=1

(xi t − xt )(xi t − xt )′, xt = 1

N

N∑t=1

xi t ,

Wxy,t =N∑

i=1

(xi t − xt )(yit − yt ).

Similarly, we can test the hypothesis of heterogeneous intercepts, but homoge-neous slopes (H ′

1 : α∗1 �= α∗

2 �= · · · �= α∗T , �1 = �2 = · · · = �T ), by using the

F statistic

F ′1 = (S′

2 − S′1)/[(T − 1)K ]

S′1/[N T − T (K + 1)]

(2.2.20)

with (T − 1)K and N T − T (K + 1) degrees of freedom, where

S′2 =

T∑t=1

Wyy,t −(

T∑t=1

W ′xy,t

)(T∑

t=1

Wxx,t

)−1 (T∑

t=1

Wxy,t

),

(2.2.21)

or test the hypothesis of homogeneous intercepts conditional on homogeneousslopes �1 = �2 = · · · = �T (H ′

4) by using the F statistic

F ′4 = (S3 − S′

2)/(T − 1)

S′2/[T (N − 1) − K ]

(2.2.22)

with T − 1 and T (N − 1) − K degrees of freedom. In general, unless bothcross-section and time-series analyses of covariance indicate the acceptanceof homogeneity of regression coefficients, unconditional pooling (i.e., a singleleast-squares regression using all observations of cross-sectional units throughtime) may lead to serious bias.

Finally, it should be noted that the foregoing tests are not independent. Forexample, the uncomfortable possibility exists that according to F3 (or F ′

3),we might find homogeneous slopes and intercepts, and yet this finding couldbe compatible with opposite results according to F1(F ′

1) and F4(F ′4), because the

alternative or null hypotheses are somewhat different in the two cases. Worse

2.3 An Example 21

still, we might reject the hypothesis of overall homogeneity using the test ratioF3(F ′

3), but then find according to F1(F ′1) and F4(F ′

4) that we cannot reject thenull hypothesis, so that the existence of heterogeneity indicated by F3 (or F ′

3)cannot be traced. This outcome is quite proper at a formal statistical level,although at the less formal but important level of interpreting test statistics, itis an annoyance.

2.3 AN EXAMPLE4

With the aim of suggesting certain modifications to existing theories of invest-ment behavior and providing estimates of the coefficients of principal interest,Kuh (1963) used data on 60 small and middle-sized firms in capital-goods-producing industries from 1935 to 1955, excluding the war years (1942 to1945), to probe the proper specification for the investment function. He ex-plored various models based on capacity accelerator behavior or internal fundsflows, with various lags. For ease of illustration, we report here only functionalspecifications and results based on profit theories, capacity-utilization theories,financial restrictions, and long-run growth theories in arithmetic form (Table2.2, part A), their logarithmic transformations (part B), and several ratio models(part C). The equations are summarized in Table 2.2.

There were two main reasons that Kuh resorted to using individual-firmdata rather than economic aggregates. One was the expressed doubt about thequality of the aggregate data, together with the problems associated with es-timating an aggregate time-series model when the explanatory variables arehighly correlated. The other was the desire to construct and test more compli-cated behavioral models that require many degrees of freedom. However, asstated in Section 1.2, a single regression using all observations through timemakes sense only when individual observations conditional on the explanatoryvariables can be viewed as random draws from the same universe. Kuh (1963)used the analysis-of-covariance techniques discussed in Section 2.2. to test foroverall homogeneity (F3 or F ′

3), slope homogeneity (F1 or F ′1), and homoge-

neous intercept conditional on acceptance of homogeneous slopes (F4 or F ′4) for

both cross-sectional units and time-series units. The results for testing homo-geneity of time-series estimates across cross-sectional units and homogeneityof cross-sectional estimates over time are reproduced in Tables 2.3 and 2.4,respectively.

A striking fact recorded from these statistics is that except for the time-seriesresults for equations (2.3.1) and (2.3.3) (which are in first-difference form), allother specifications failed the overall homogeneity tests.5 Furthermore, in mostcases, with the exception of cross-sectional estimates of (2.3.17) and (2.3.18)(Table 2.4), the intercept and slope variabilities cannot be rigorously separated.Nor do the time-series results correspond closely to cross-sectional results forthe same equation. Although analysis of covariance, like other statistics, is nota mill that will grind out results automatically, these results do suggest thatthe effects of excluded variables in both time series and cross sections may be

22 Analysis of Covariance

Table 2.2. Investment equation forms estimated by Kuh (1963)

Part AIit = α0 + β1Ci + β2Kit + β3Sit (2.3.1)Iit = α0 + β1Ci + β2Kit + β4Pit (2.3.2)Iit = α0 + β1Ci + β2Kit + β3Sit + β4Pit (2.3.3)Iit = α0 + β1Ci + β2 Kit + β3 Sit (2.3.4)Iit = α0 + β1Ci + β2 Kit + β4 Pit (2.3.5)Iit = α0 + β1Ci + β2 Kit + β3 Sit + β4 Pit (2.3.6)Iit = α0 + β1Ci + β2 Kit + β3 Si,t−1 (2.3.7)Iit = α0 + β1Ci + β2 Kit + β4 Pi,t−1 (2.3.8)Iit = α0 + β1Ci + β2 Kit + β3 Si,t−1 + β4 Pi,t−1 (2.3.9)Iit = α0 + β1Ci + β2 Kit + β3[(Sit + Si,t−1) ÷ 2] (2.3.10)Iit = α0 + β1Ci + β2 Kit + β4[(Pit + Pi,t−1) ÷ 2] (2.3.11)Iit = α0 + β1Ci + β2 Kit + β3[(Sit + Si,t−1) ÷ 2] (2.3.12)

+ β4[(Pit + Pi,t−1) ÷ 2][(Iit + Ii,t−1) ÷ 2] = α0 + β1Ci + β2 Kit + β3[(Sit + Si,t−1) ÷ 2] (2.3.13)[(Iit + Ii,t−1) ÷ 2] = α0 + β1Ci + β2 Kit + β4[(Pit + Pi,t−1) ÷ 2] (2.3.14)[(Iit + Ii,t−1) ÷ 2] = α0 + β1Ci + β2 Kit + β3[(Sit + Si,t−1) ÷ 2] (2.3.15)

+ β4[(Pit + Pi,t−1) ÷ 2]

Part B log Iit = α0 + β1 log Ci + β2 log Kit + β3 log Sit (2.3.16)log Iit = α0 + β1 log Ci + β2 log Kit + β3 log Sit (2.3.17)log Iit = α0 + β1 log Ci + β2 log Kit + β3 log Si,t−1 (2.3.18)log Iit = α0 + β1 log Ci + β2 log[(Kit + Ki,t−1) ÷ 2] (2.3.19)

+ β3 log[(Sit + Si,t−1) ÷ 2]

Part CIit

Kit= α0 + β1

Pit

Kit+ β2

Si,t−1

Ci · Ki,t−1(2.3.20)

Iit

Kit= α0 + β1

Pit

Kit+ β2

Si,t−1

Ci · Ki,t−1+ β3

Sit

Ci · Kit(2.3.21)

Iit

Kit= α0 + β1

Pit + Pi,t−1

Kit · 2+ β2

Si,t−1

Ci · Ki,t−1(2.3.22)

Iit

Kit= α0 + β1

Pit + Pi,t−1

Kit · 2+ β2

Si,t−1

Ci · Ki,t−1+ β3

Sit

Ci · Kit(2.3.23)

Note: I = gross investment; C = capital-intensity index; K = capital stock; S = sales;P = gross retained profits.

very different. It would be quite careless not to explore the possible causes ofdiscrepancies that give rise to the systematic interrelationships between differentindividuals at different periods of time.6

Kuh explored the sources of estimation discrepancies through decompo-sition of the error variances, comparison of individual coefficient behavior,assessment of the statistical influence of various lag structures, and so forth. Heconcluded that sales seem to include critical time-correlated elements commonto a large number of firms and thus have a much greater capability of annihilatingsystematic, cyclical factors. In general, his results are more favorable to the ac-celeration sales model than to the internal-liquidity/profit hypothesis supported

Tabl

e2.

3.C

ovar

ianc

ete

sts

for

regr

essi

on-c

oeffi

cien

thom

ogen

eity

acro

sscr

oss-

sect

iona

luni

tsa

F3

over

allt

est

F1

slop

eho

mog

enei

tyF

4ce

llm

ean

sign

ifica

nce

Deg

rees

offr

eedo

mD

egre

esof

free

dom

Deg

rees

offr

eedo

m

Equ

atio

nN

umer

ator

Den

omin

ator

Act

ual

Fs

Num

erat

orD

enom

inat

orA

ctua

lF

sN

umer

ator

Den

omin

ator

Act

ual

Fs

(2.3

.1)

177

660

1.25

118

660

1.75

c57

660

0.12

(2.3

.2)

177

660

1.40

b11

866

01.

94c

5766

00.

11(2

.3.3

)23

660

01.

1317

760

01.

42b

5660

00.

10(2

.3.4

)17

784

02.

28c

118

840

1.58

c57

840

3.64

c

(2.3

.5)

177

840

2.34

c11

884

01.

75c

5784

03.

23c

(2.3

.6)

236

780

2.24

c17

778

01.

76c

5678

03.

57c

(2.3

.7)

177

720

2.46

c11

872

01.

95c

5772

03.

57c

(2.3

.8)

177

720

2.50

c11

872

01.

97c

5772

03.

31c

(2.3

.9)

236

660

2.49

c17

766

02.

11c

5666

03.

69c

(2.3

.10)

177

720

2.46

c11

872

01.

75c

5772

03.

66c

(2.3

.11)

177

720

2.60

c11

872

02.

14c

5772

03.

57c

(2.3

.12)

236

660

2.94

c17

766

02.

49c

5666

04.

18c

(2.3

.16)

177

720

1.92

c11

872

02.

59c

5772

00.

55(2

.3.1

7)17

784

04.

04c

118

840

2.70

c57

840

0.39

(2.3

.18)

177

720

5.45

c11

872

04.

20c

5772

06.

32c

(2.3

.19)

177

720

4.68

c11

872

03.

17c

5772

07.

36c

(2.3

.20)

177

720

3.64

c11

872

03.

14c

5772

03.

66c

(2.3

.21)

236

660

3.38

c17

766

02.

71c

5666

04.

07c

(2.3

.22)

177

600

3.11

c11

860

02.

72c

5760

03.

22c

(2.3

.23)

236

540

2.90

c17

754

02.

40c

5654

03.

60c

aC

ritic

alF

valu

esw

ere

obta

ined

from

A.M

.Moo

d,In

trod

ucti

onto

Stat

isti

cs,T

able

V,p

p.42

6–42

7.L

inea

rin

terp

olat

ion

was

empl

oyed

exce

ptfo

rde

gree

sof

free

dom

exce

edin

g12

0.T

hecr

itica

lF

valu

esin

ever

yca

seha

vebe

enre

cord

edfo

r12

0de

gree

sof

free

dom

for

each

deno

min

ator

sum

ofsq

uare

sev

enth

ough

the

actu

alde

gree

sof

free

dom

wer

eat

leas

tfou

rtim

esas

grea

t.T

heap

prox

imat

ion

erro

rin

this

case

isne

glig

ible

.bSi

gnifi

cant

atth

e5

perc

entl

evel

.c Si

gnifi

cant

atth

e1

perc

entl

evel

.So

urce

:K

uh(1

963,

pp.1

41–1

42).

Tabl

e2.

4.C

ovar

ianc

ete

sts

for

hom

ogen

eity

ofcr

oss-

sect

iona

lest

imat

esov

erti

mea

F′ 3

over

allt

est

F′ 1

slop

eho

mog

enei

tyF

′ 4ce

llm

ean

sign

ifica

nce

Deg

rees

offr

eedo

mD

egre

esof

free

dom

Deg

rees

offr

eedo

m

Equ

atio

nN

umer

ator

Den

omin

ator

Act

ual

Fs

Num

erat

orD

enom

inat

orA

ctua

lF

sN

umer

ator

Den

omin

ator

Act

ual

Fs

(2.3

.1)

5278

42.

45b

3978

42.

36b

1078

42.

89b

(2.3

.2)

5278

43.

04b

3978

42.

64b

1078

44.

97b

(2.3

.3)

6577

02.

55b

5277

02.

49b

977

03.

23b

(2.3

.4)

6495

22.

01b

4895

21.

97b

1395

22.

43b

(2.3

.5)

6495

22.

75b

4895

22.

45b

1395

23.

41b

(2.3

.6)

8093

51.

91b

6493

51.

82b

1293

52.

66b

(2.3

.7)

5684

02.

30b

4284

02.

11b

1184

03.

66b

(2.3

.8)

5684

02.

83b

4284

02.

75b

1184

03.

13b

(2.3

.9)

7082

52.

25b

5682

52.

13b

1082

53.

53b

(2.3

.10)

5684

01.

80b

4284

01.

80b

1184

01.

72d

(2.3

.11)

5684

02.

30b

4284

02.

30b

1184

01.

79d

(2.3

.12)

7082

51.

70b

5682

51.

74b

1082

51.

42

(2.3

.13)

5684

02.

08b

4284

02.

11b

1184

02.

21c

(2.3

.14)

5684

02.

66b

4284

02.

37b

1184

02.

87b

(2.3

.15)

7082

51.

81b

5682

51.

76b

1082

52.

35c

(2.3

.16)

5684

03.

67b

4284

02.

85b

1184

03.

10b

(2.3

.17)

6495

21.

51c

4895

21.

1413

952

0.80

(2.3

.18)

5684

02.

34b

4284

01.

0411

840

1.99

c

(2.3

.19)

5684

02.

29b

4284

02.

03b

1184

02.

05c

(2.3

.20)

4285

54.

13b

2885

55.

01b

1285

52.

47b

(2.3

.21)

5684

02.

88b

4284

03.

12b

1184

02.

56b

(2.3

.22)

4285

53.

80b

2885

54.

62b

1285

51.

61b

(2.3

.23)

5684

03.

51b

4284

04.

00b

1184

01.

71b

aC

ritic

alF

valu

esw

ere

obta

ined

from

A.M

.Moo

d,In

trod

ucti

onto

Stat

isti

cs,T

able

V,p

p.42

6–42

7.L

inea

rin

terp

olat

ion

was

empl

oyed

exce

ptfo

rde

gree

sof

free

dom

exce

edin

g12

0.T

hecr

itica

lF

valu

esin

ever

yca

seha

vebe

enre

cord

edfo

r12

0de

gree

sof

free

dom

for

each

deno

min

ator

sum

ofsq

uare

sev

enth

ough

the

actu

alde

gree

sof

free

dom

wer

eat

leas

tfou

rtim

esas

grea

t.T

heap

prox

imat

ion

erro

rin

this

case

isne

glig

ible

.bSi

gnifi

cant

atth

e1

perc

entl

evel

.c Si

gnifi

cant

atth

e5

perc

entl

evel

.dSi

gnifi

cant

atth

e10

perc

entl

evel

.So

urce

:K

uh(1

963,

pp.1

37–1

38).

26 Analysis of Covariance

by the results obtained using cross-sectional data (e.g., Meyer and Kuh (1957)).He found that the cash-flow effect is more important some time before the actualcapital outlays are made than it is in actually restricting the outlays during theexpenditure period. It appears more appropriate to view internal liquidity flowsas a critical part of the budgeting process that later is modified, primarily inlight of variations in levels of output and capacity utilization.