An internship report on A STUDY ON “WORKING CAPITAL ...

84

An internship report on A STUDY ON “WORKING CAPITAL MANAGEMENT “ AT DILIP MARETRIAL HANDLING EQUIPMENT BY SHARATH KUMAR CE 1NZ13MBA35 Submitted to VISVESVARAYA TECHNOLOGICAL UNIVERSITY, BELAGAUM In partial fulfillment of requirement for the award of degree of MASTER OF BUSINESS ADMINISTRATION Under the guidance of INTERNAL GUIDE EXTERNAL GUIDE Mrs.Sayantani banerjee Ms.Smitha Asst.professor finance manger DEPARTMENT OF MBA NEW HORIZON COLLEGE OF ENGINEERING, OUTER RING ROAD, MARATHALLI, BANGALORE-560103. 2014-2015

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of An internship report on A STUDY ON “WORKING CAPITAL ...

An internship report on

A STUDY ON “WORKING CAPITAL MANAGEMENT “

AT DILIP MARETRIAL HANDLING EQUIPMENT

BY

SHARATH KUMAR CE

1NZ13MBA35

Submitted to

VISVESVARAYA TECHNOLOGICAL UNIVERSITY, BELAGAUM

In partial fulfillment of requirement for the award of degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

INTERNAL GUIDE EXTERNAL GUIDE

Mrs.Sayantani banerjee Ms.Smitha

Asst.professor finance manger

DEPARTMENT OF MBA

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI, BANGALORE-560103.

2014-2015

ACKNOWLEDGEMENT

I wish to place on record my deep sense of appreciation to all those who made this project

come into existence and guide me from the start to finish. I express my sincere gratitude to

institution of New Horizon College of Engineering, Bangalore.

I would like to thank Dr. Manjunath, principal of New Horizon College of Engineering,

Bangalore for giving me opportunity to prove my caliber by submitting this project report.

I am very grateful to Dr.sheelanmishra, Head of department of management studies, New

Horizon College of Engineering, and Bangalore for her support in to formatting and

completion of this project.

I am indebted to my sincere gratitude to Prof. Sayantani banerjee for his support from the

beginning till completion of this study.

I extend my sincere gratitude to Ms. SMITHA, finance manager of dilip material equipment,

Bommasandra industrial area, Bangalore for giving me the time and information needed for

making this assignment successful.

SHARATH KUMAR CE

1NZ13MBA35

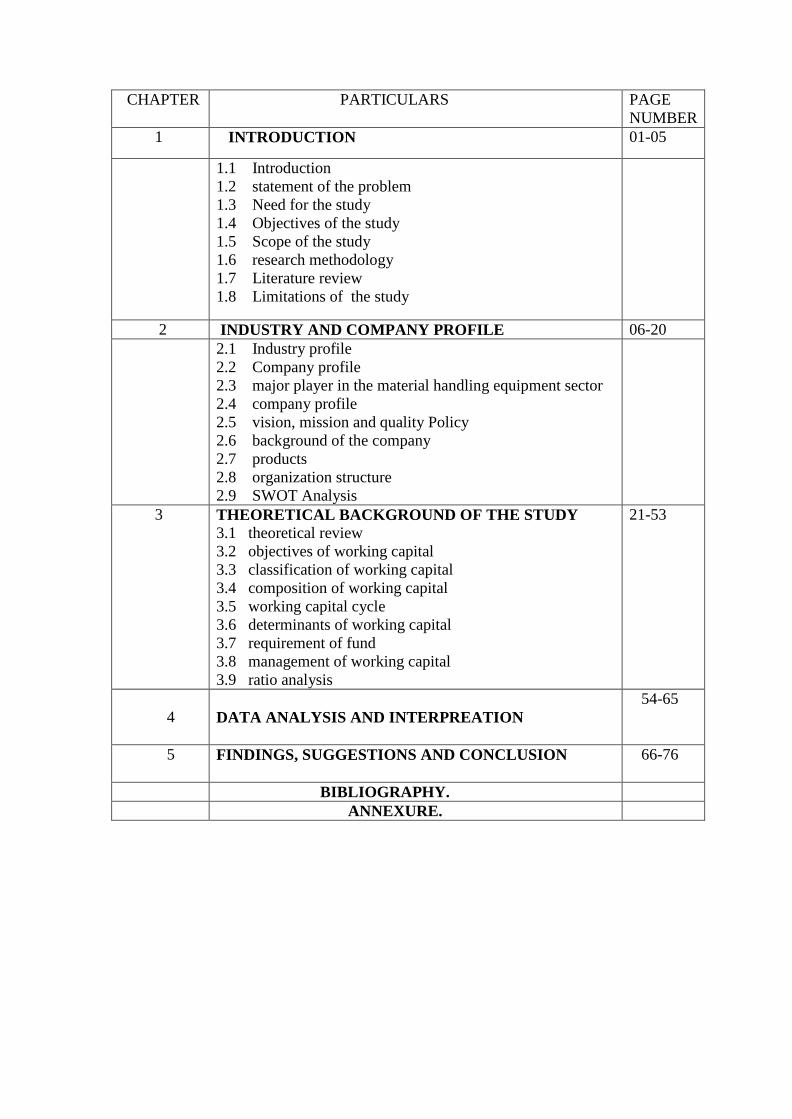

CHAPTER PARTICULARS PAGE

NUMBER

1 INTRODUCTION 01-05

1.1 Introduction

1.2 statement of the problem

1.3 Need for the study

1.4 Objectives of the study

1.5 Scope of the study

1.6 research methodology

1.7 Literature review

1.8 Limitations of the study

2 INDUSTRY AND COMPANY PROFILE 06-20

2.1 Industry profile

2.2 Company profile

2.3 major player in the material handling equipment sector

2.4 company profile

2.5 vision, mission and quality Policy

2.6 background of the company

2.7 products

2.8 organization structure

2.9 SWOT Analysis

3 THEORETICAL BACKGROUND OF THE STUDY

3.1 theoretical review

3.2 objectives of working capital

3.3 classification of working capital

3.4 composition of working capital

3.5 working capital cycle

3.6 determinants of working capital

3.7 requirement of fund

3.8 management of working capital

3.9 ratio analysis

21-53

4

DATA ANALYSIS AND INTERPREATION

54-65

5

FINDINGS, SUGGESTIONS AND CONCLUSION 66-76

BIBLIOGRAPHY.

ANNEXURE.

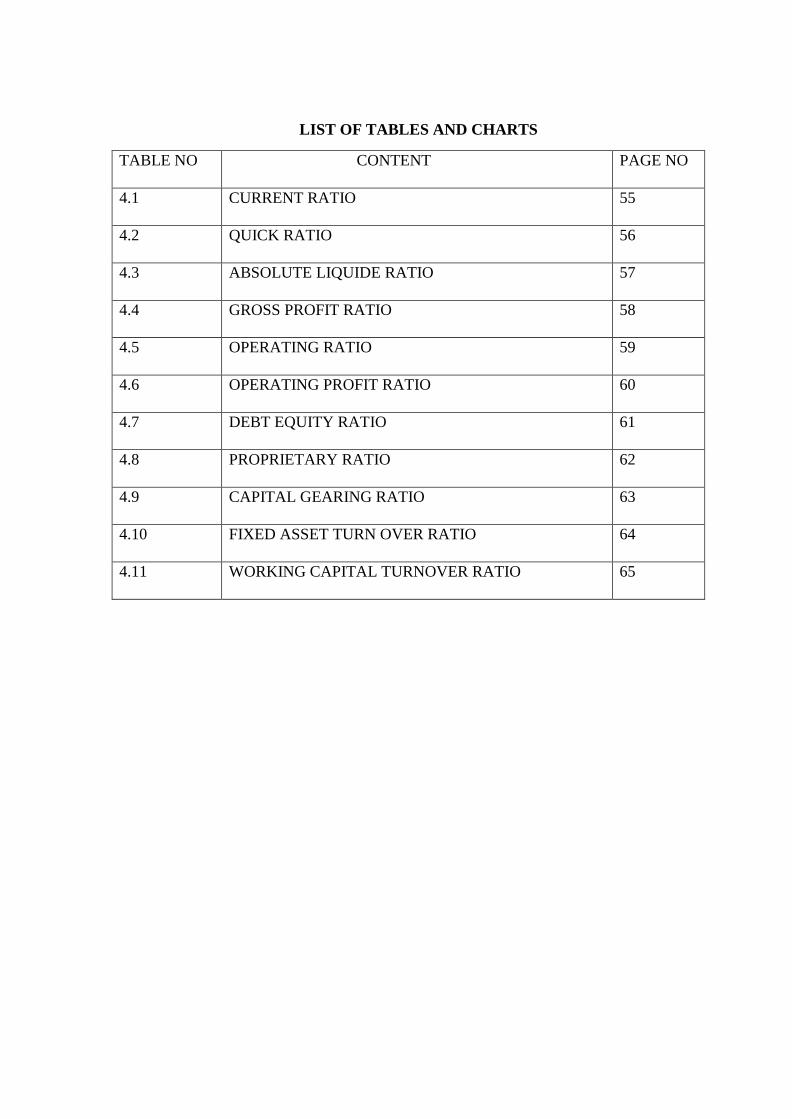

LIST OF TABLES AND CHARTS

TABLE NO CONTENT

PAGE NO

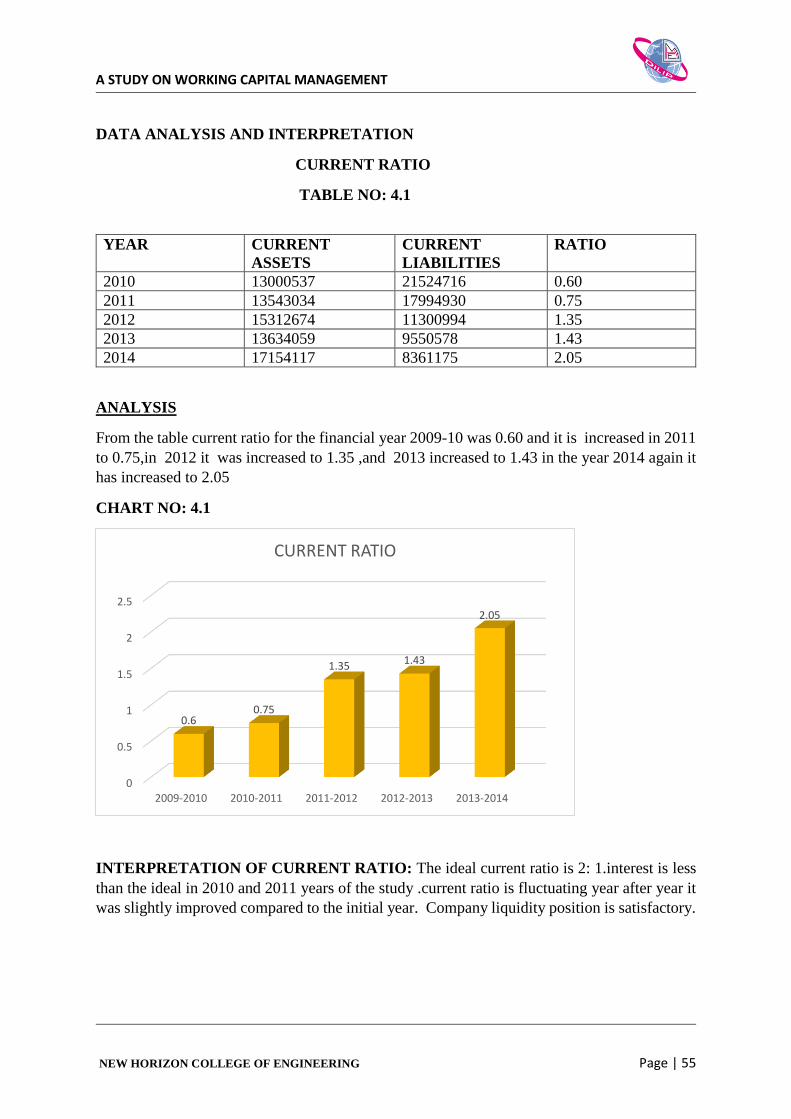

4.1 CURRENT RATIO

55

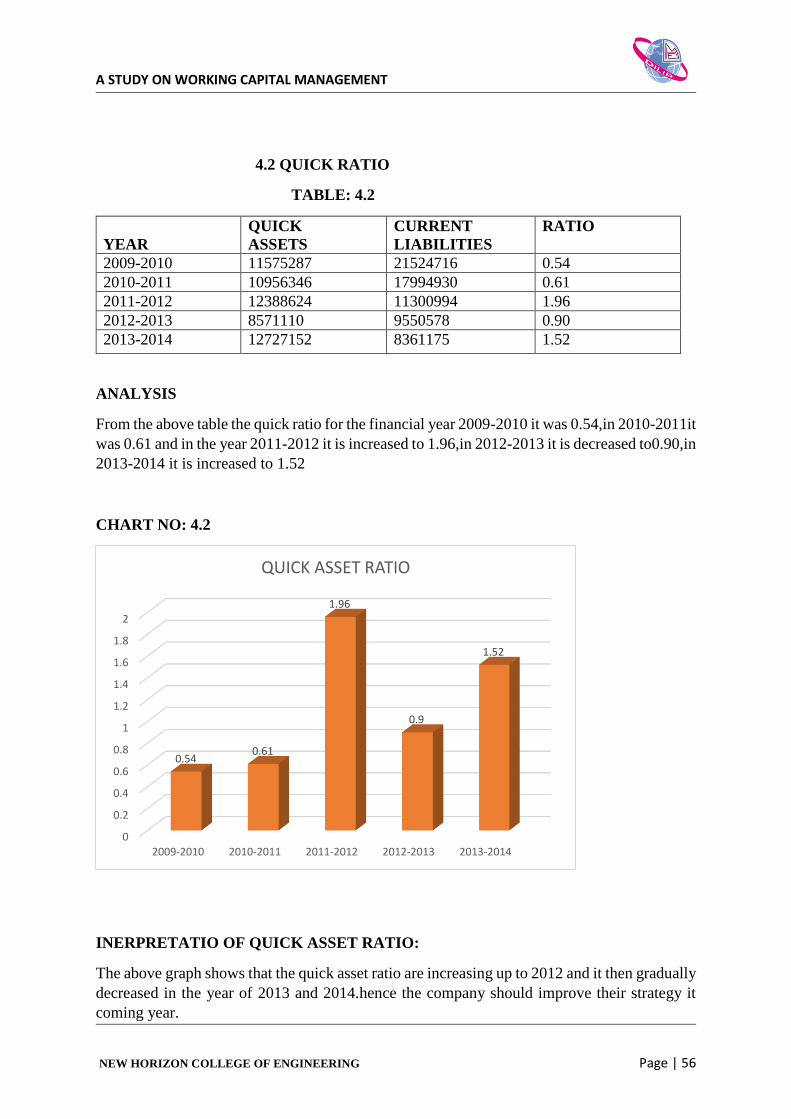

4.2 QUICK RATIO

56

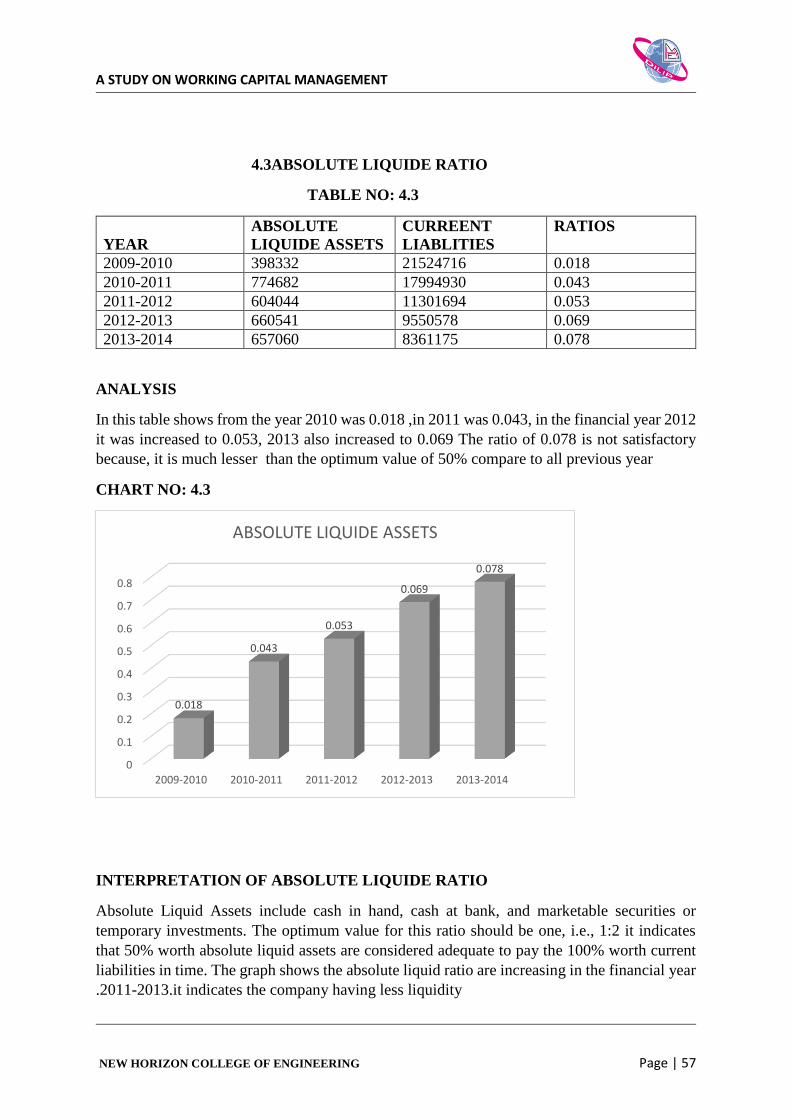

4.3 ABSOLUTE LIQUIDE RATIO

57

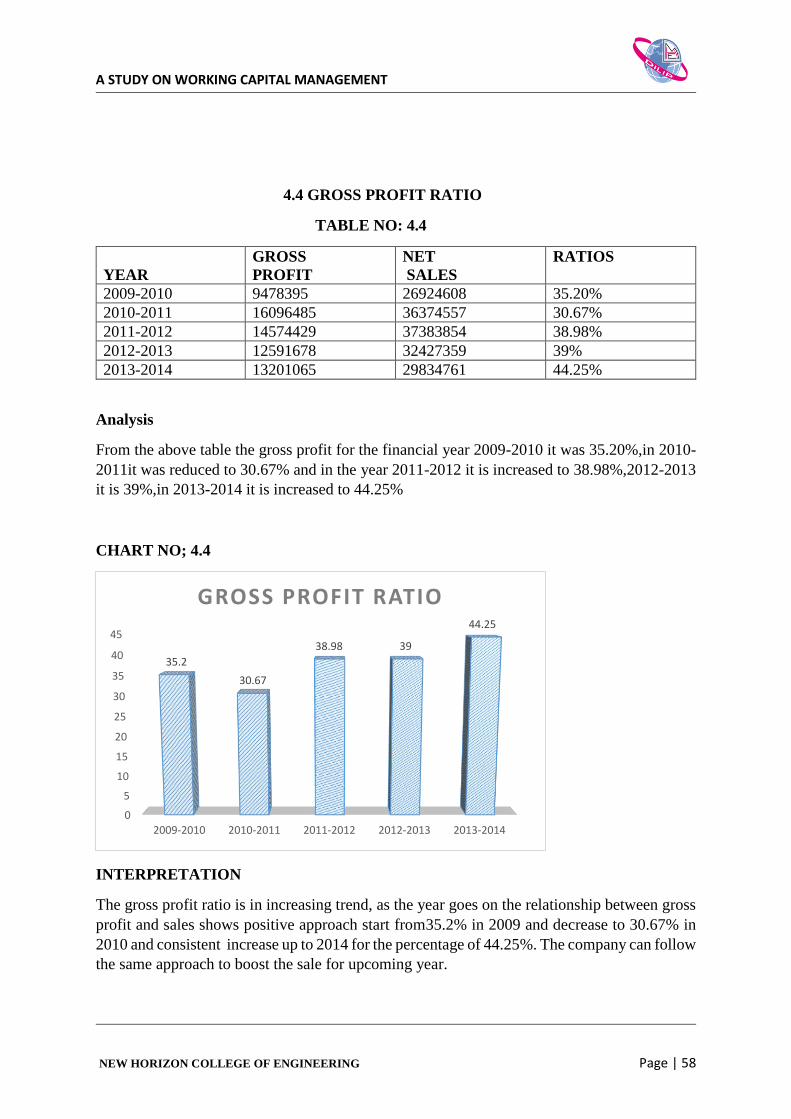

4.4 GROSS PROFIT RATIO

58

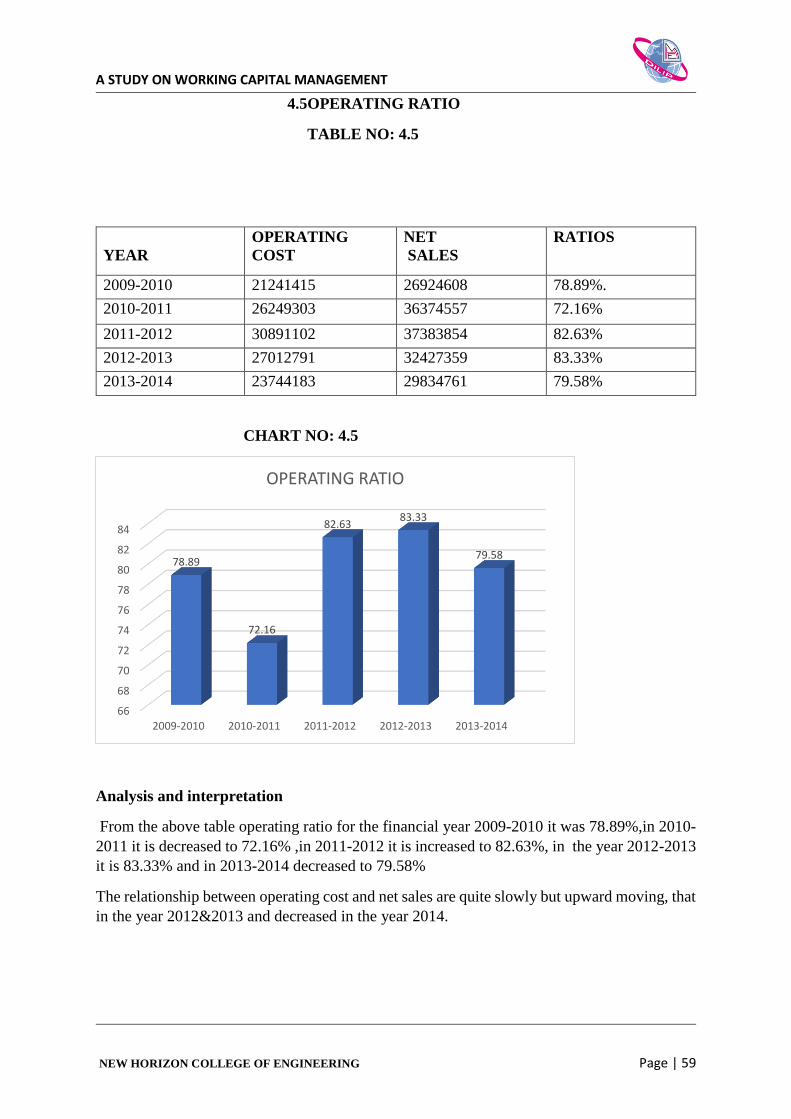

4.5 OPERATING RATIO

59

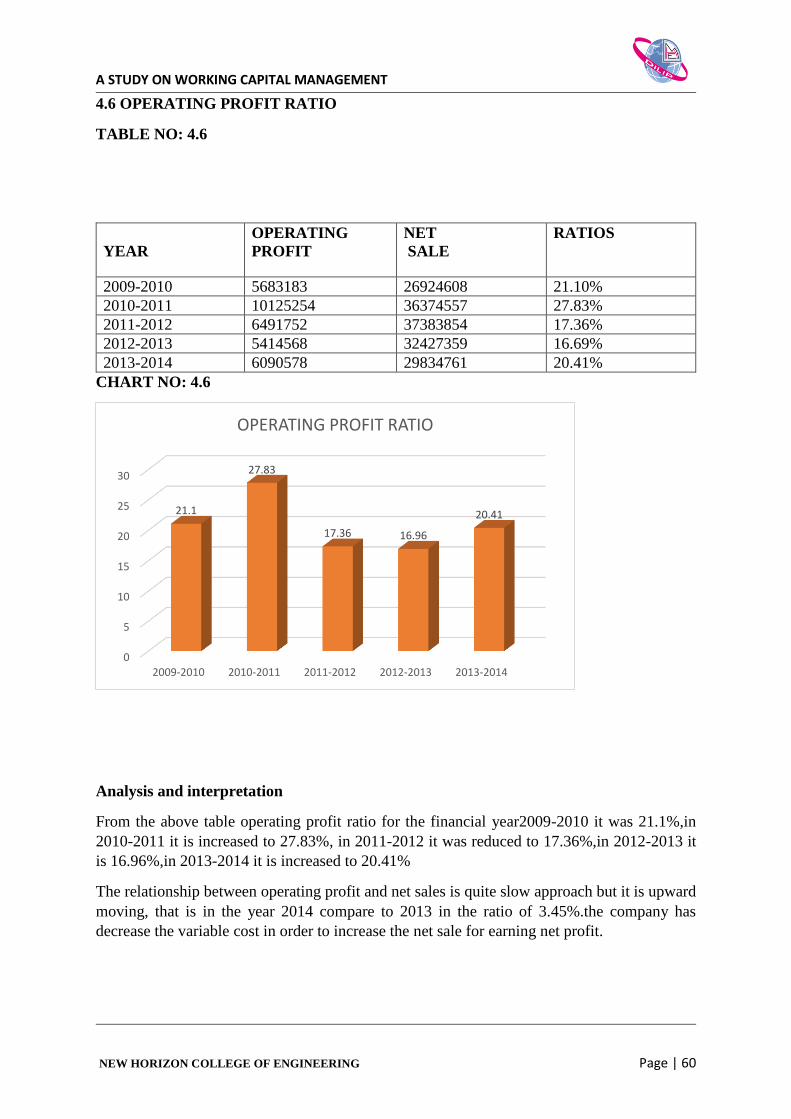

4.6 OPERATING PROFIT RATIO

60

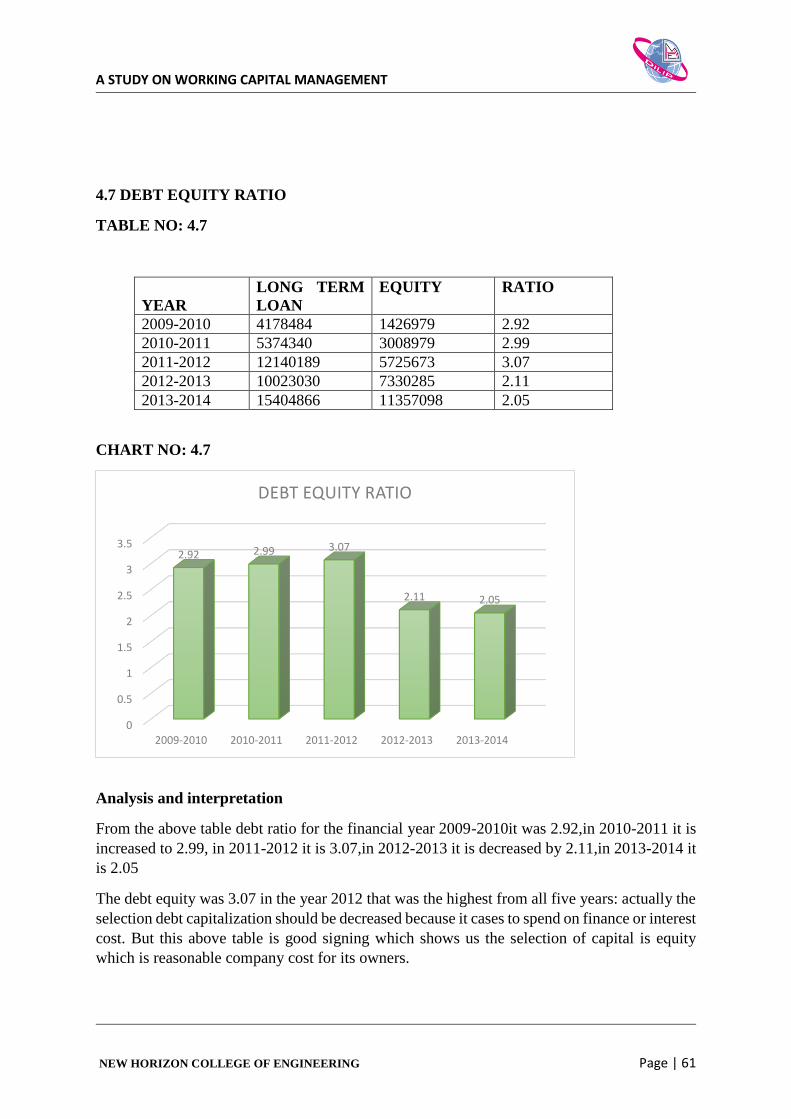

4.7 DEBT EQUITY RATIO

61

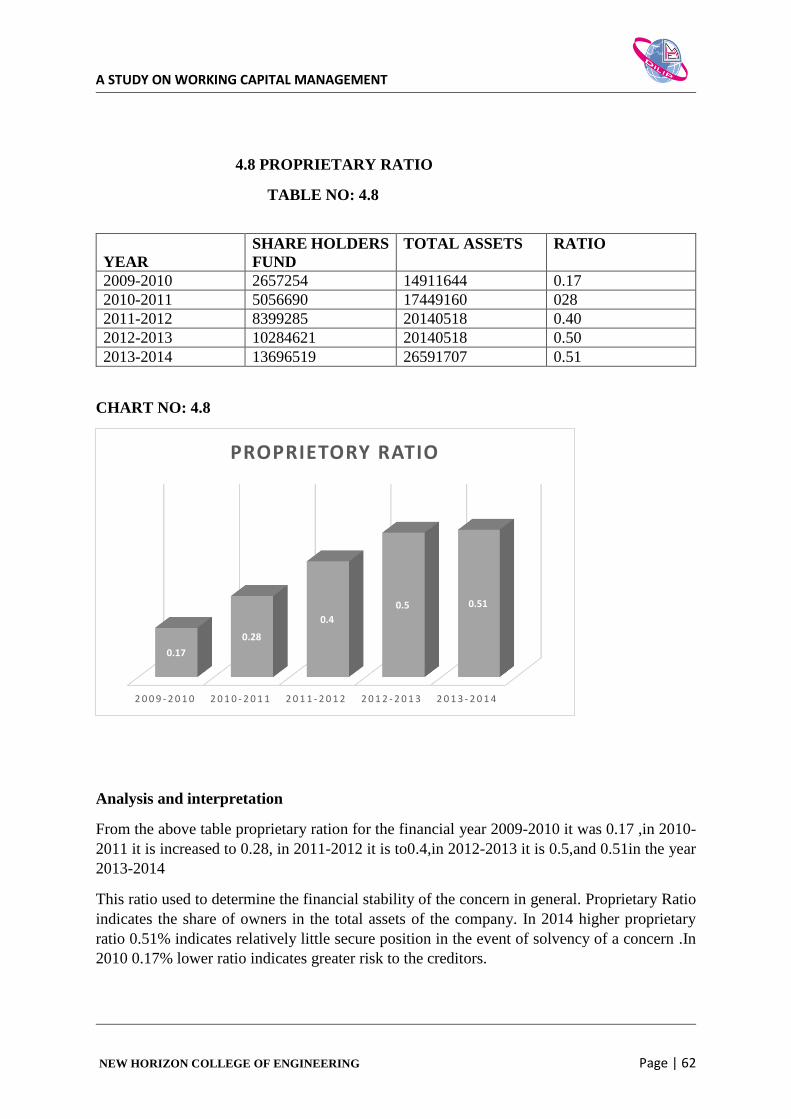

4.8 PROPRIETARY RATIO

62

4.9 CAPITAL GEARING RATIO

63

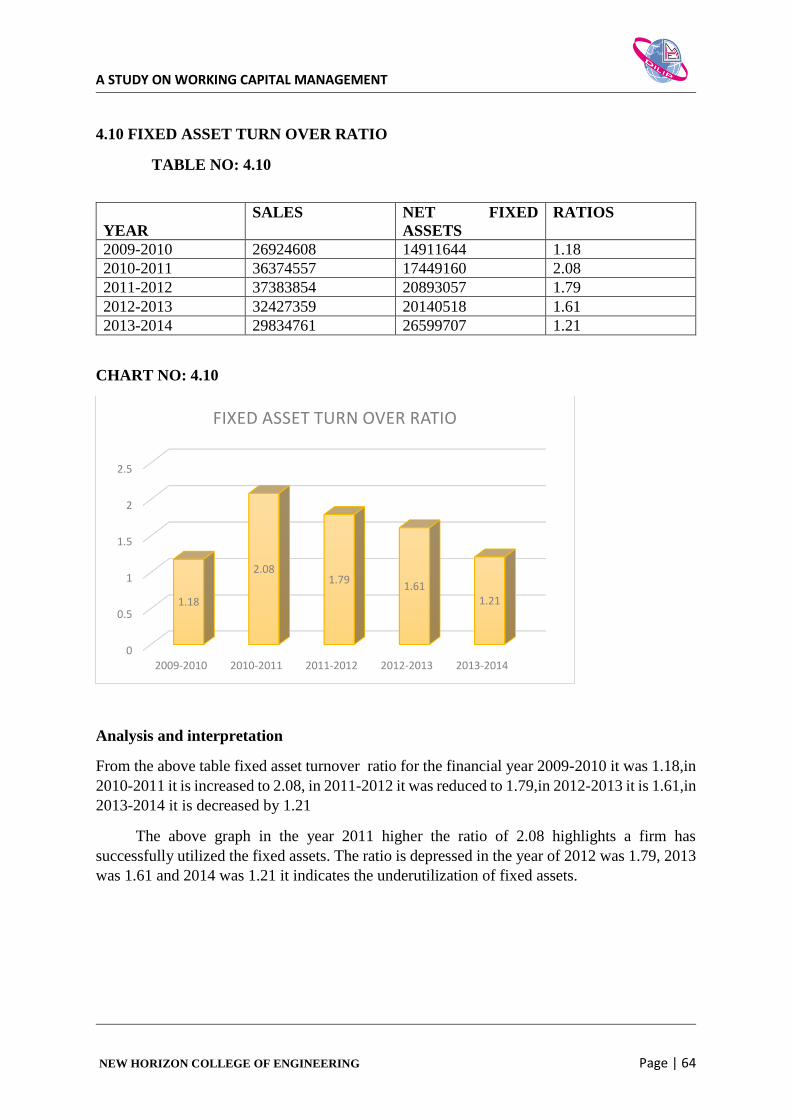

4.10 FIXED ASSET TURN OVER RATIO

64

4.11 WORKING CAPITAL TURNOVER RATIO

65

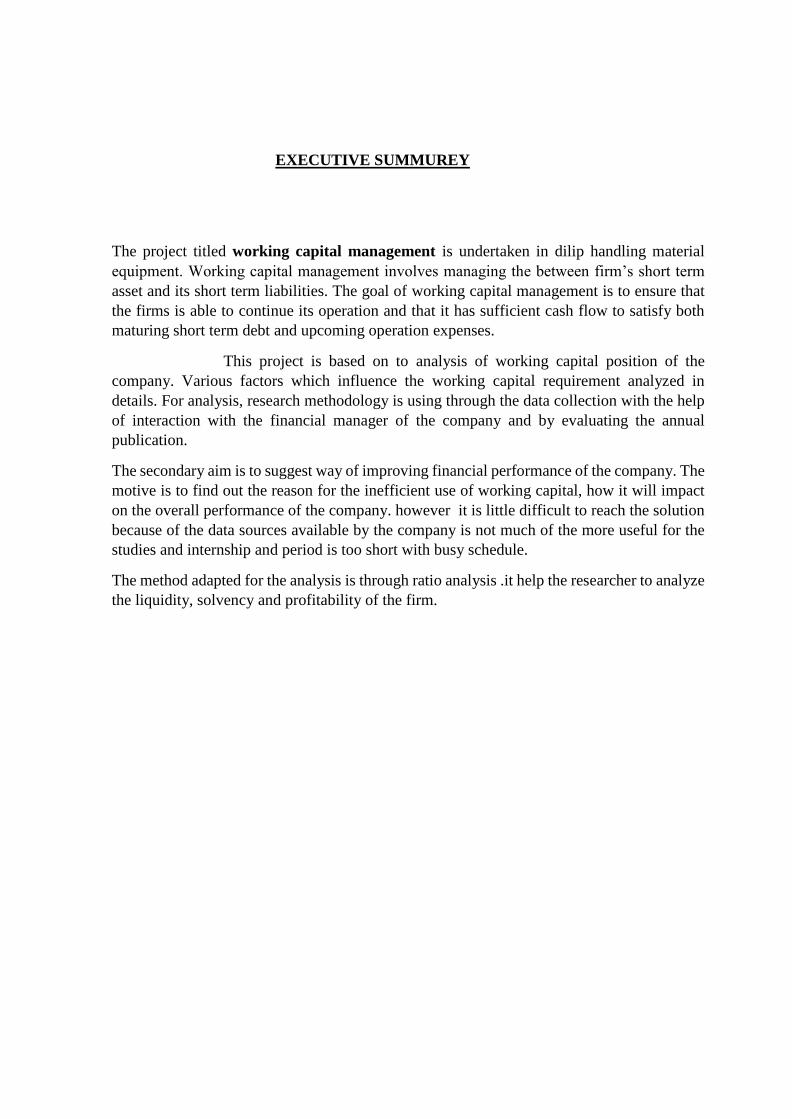

EXECUTIVE SUMMUREY

The project titled working capital management is undertaken in dilip handling material

equipment. Working capital management involves managing the between firm’s short term

asset and its short term liabilities. The goal of working capital management is to ensure that

the firms is able to continue its operation and that it has sufficient cash flow to satisfy both

maturing short term debt and upcoming operation expenses.

This project is based on to analysis of working capital position of the

company. Various factors which influence the working capital requirement analyzed in

details. For analysis, research methodology is using through the data collection with the help

of interaction with the financial manager of the company and by evaluating the annual

publication.

The secondary aim is to suggest way of improving financial performance of the company. The

motive is to find out the reason for the inefficient use of working capital, how it will impact

on the overall performance of the company. however it is little difficult to reach the solution

because of the data sources available by the company is not much of the more useful for the

studies and internship and period is too short with busy schedule.

The method adapted for the analysis is through ratio analysis .it help the researcher to analyze

the liquidity, solvency and profitability of the firm.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 1

CHAPTER 1

INTRODUCTION

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 2

1.1 INTRODUCTION

Capital is what makes or breaks a business, and no business can run successfully without

enough capital to cover both short and long-term needs. Maintaining sufficient levels of short-

term capital is a constantly ongoing challenge, and in today’s turbulent financial markets and

uncertain business climate external financing has become both harder and more costly to

obtain. Companies are therefore increasingly shifting away from traditional sources of external

financing and turning their eyes towards their own organizations for ways of improving

liquidity. One efficient but often overlooked way of doing so is to reduce the amount of capital

tied-up in operations, that is, to improve the working capital management of the company.

Working capital is a financial metric of operating liquidity which describes the amount of cash

tied up in operations and defines the short term condition of a company. A positive working

capital position is required for the continuous running of a company’s operations, i.e. to pay

short term debt obligations and to cover operational expenses. A company with a negative

working capital balance is unable to cover its short-term liabilities with its current assets.

Working capital is calculated with the following formula:

Working Capital = Current Assets1 - Current Liabilities2

The above formula includes three important balance sheet accounts which all have a direct

impact on the business, namely accounts receivable (A/R), accounts payable (A/P) and

inventory. These accounts are often referred to as the three areas of working capital.

● Accounts Receivable – Money owed to the company for products/services that have been

delivered to customers but not yet paid for.

● Inventory – The raw materials, work-in-progress goods and finished goods that are ready or

will be ready for sale. Inventory represents a key asset to most businesses as the turnover of

inventory is a primary source of revenue generation and subsequently earnings for the

Shareholders/owners of the company.

● Accounts Payable – Money owed to suppliers for goods and services that the company has

purchased on credit.

Clearly, the importance of the above components differs between companies and industries,

and whereas for example retailers and manufacturers often have large inventories of finished

goods, work-in-progress (WIP) and raw materials, banks and insurance companies do not hold

any traditional inventory. However, regulation requires both banks and insurance companies

to maintain certain reserve levels. In addition to the required reserves, these types of businesses

typically hold major positions of liquid assets and large portfolios of interest-bearing

investments in which deposits and premiums received from customers are invested. The

uncertainty of cash

1. Current Assets = Cash, Accounts Receivable (A/R) and Inventory

2. Current Liabilities = Short term debt, Accounts Payable (A/P), Accrued Liabilities and Other

Debts flows also varies significantly between industries, and many retailers have little to worry

about when it comes to accounts receivables as the customer pays on site at the time of

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 3

purchase. On the other hand, banks and insurance companies are privileged by the fact that

they receive deposits and premiums before having to make any payments, but are also subject

to unpredictable cash outflows when customers decide to withdraw their funds or when

insurance claims come in.

Why do companies need to Manage Working Capital?

Just as the importance of the working capital components depends on the nature of a company,

so does the optimal level of working capital. Even in a given industry, companies may have

very different working capital needs, and it is therefore impossible to determine an overall

optimal working capital level without considering a company’s specific situation.

“Just as the importance of the working capital components differ between companies and

industries, so does the optimal level of working capital.”

The appropriate level of working capital depends on both macro factors, such as the market

conditions in which a company operates, and micro factors, such as the set-up of the value

chain within the company. As working capital spans over a wide range of different business

activities, the parameters in the equation must be set in relation to the overall strategy and

business model to determine the optimal level of working capital. For example retailers with a

fast turnover of cash, or insurance companies that receive cash (premiums) before having to

settle possible claims, have much lower working capital requirements than manufacturing

companies that can experience substantial material and labor costs long before receiving

payment.

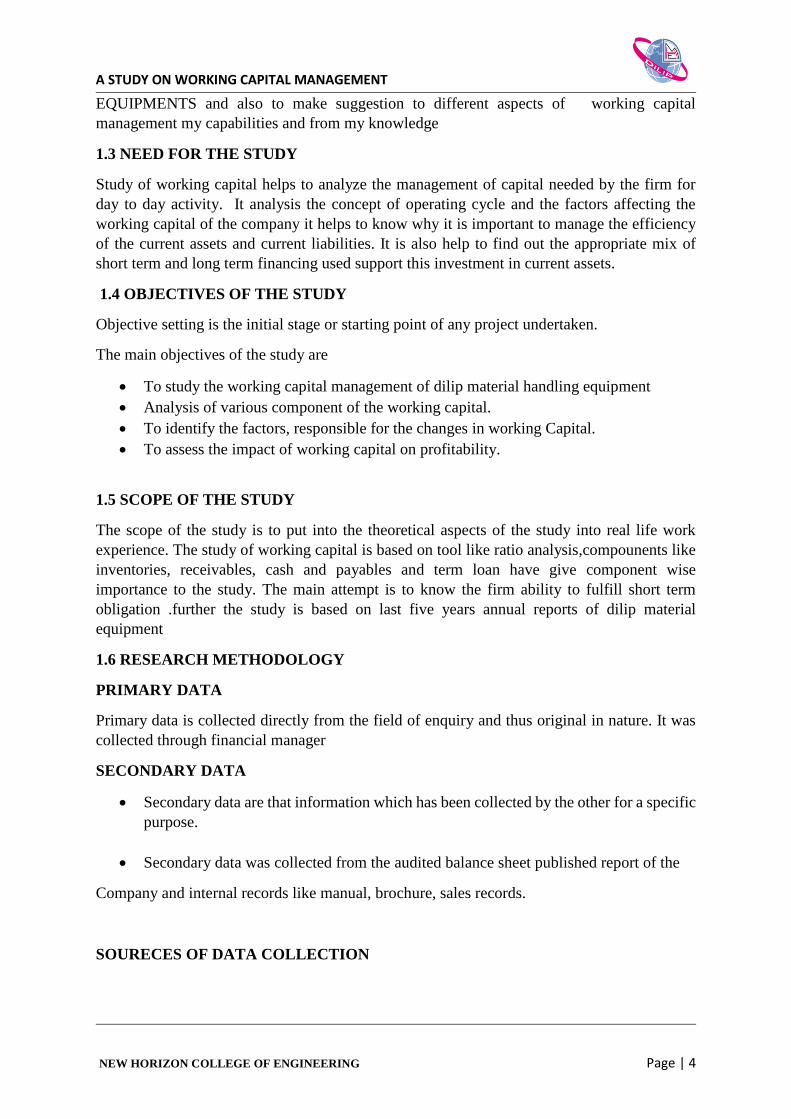

1.2 STATEMENT OF THE PROBLEM

The project titled WORKING CAPITAL MANAGEMENT OF DILIP MATERIAL

HANDLING EQUIPMENTS is mainly focused on evaluating the financial status of the

company and analyzing the working capital management of DILIP MATERIAL HANDLING

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 4

EQUIPMENTS and also to make suggestion to different aspects of working capital

management my capabilities and from my knowledge

1.3 NEED FOR THE STUDY

Study of working capital helps to analyze the management of capital needed by the firm for

day to day activity. It analysis the concept of operating cycle and the factors affecting the

working capital of the company it helps to know why it is important to manage the efficiency

of the current assets and current liabilities. It is also help to find out the appropriate mix of

short term and long term financing used support this investment in current assets.

1.4 OBJECTIVES OF THE STUDY

Objective setting is the initial stage or starting point of any project undertaken.

The main objectives of the study are

To study the working capital management of dilip material handling equipment

Analysis of various component of the working capital.

To identify the factors, responsible for the changes in working Capital.

To assess the impact of working capital on profitability.

1.5 SCOPE OF THE STUDY

The scope of the study is to put into the theoretical aspects of the study into real life work

experience. The study of working capital is based on tool like ratio analysis,compounents like

inventories, receivables, cash and payables and term loan have give component wise

importance to the study. The main attempt is to know the firm ability to fulfill short term

obligation .further the study is based on last five years annual reports of dilip material

equipment

1.6 RESEARCH METHODOLOGY

PRIMARY DATA

Primary data is collected directly from the field of enquiry and thus original in nature. It was

collected through financial manager

SECONDARY DATA

Secondary data are that information which has been collected by the other for a specific

purpose.

Secondary data was collected from the audited balance sheet published report of the

Company and internal records like manual, brochure, sales records.

SOURECES OF DATA COLLECTION

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 5

The data are collected mainly from the annual reports of the company. In addition to this,

different websites of the company, circulars, and company manuals has also been used together

for the information .and also used both secondary and primary data.

1.7 LITERATURE REVIW

MANAGEMENT OF WORKING CAPITAL

NANDINI SHARMA

Management of short term asset and short run sources of finance is described as working capital

management. Working capital management is concerned with all decision and acts that

influence the size and effectiveness of working capital. The goal of working capital

management is to manage is to manage each of firm current assets and current liabilities in

such a way that an acceptable level of working capital is maintained.it is concerned with the

determination of appropriate level of current assets and their efficient use as well as the choice

of financing mix for raising for the current resources. 'Proper management of working capital

is very important of success of the concern. It aims at protecting the purchase power of assets

and maximizing return of on investment. The manner of management of working capital to a

very large extent determination the success of operation of the concern. Failure of business is

undoubtedly due to poor management of working capital. Shortage of working capital is so

often advanced as the main cause of failure of an individual concern.

Mr.J. Aloy Niresh (2012)In his study reveals that ,there is a negative relationship between cash

conversion cycle and performance measuring among manufacturing firm in srilanka the study

recommends the manufacturing firms to manage the working capital efficiently to achieve

optimal profitability . By improving the inventory control process, collecting receivables in

line with the agreed credit terms and by delaying payments to suppliers. Manufacturing firm in

srilanka follow conservative policy. Which is contrary to the traditional belief, more investment

in current assets might also increase profitability

1.8 LIMITATION OF THE STUDY

The study only covers the accounting period of the last years and current year was

excluded on account of non-availability of data.so the current position of the firm was

not taken into consideration.

The study is mainly based on secondary data drawn from the secondary sources

connected to the topic. So errors are it may possible.

The main interaction with the management personnel was difficult in nature due to their

busy schedule.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 6

CHAPTER 2

INDUSTRY AND COMPANY PROFILE

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 7

2.1 INDUSTRY PROFILE

Introduction

According to Construction World update, it has been projected that the present € 1.6 billion

construction equipment industry in India is expected to touch about € 10.3 billion. While the

current size is just a fraction of the world market, it has been growing between 10-15 %

compared to the global growth of around 5%. India is one among the top 10 markets for

construction equipment and is one of the key international markets. The prospects of the

construction equipment industry look attractive with a projected investment of € 212.5 billion

in the infrastructure sector over the next few years. The Indian market is catered by about 200

domestic manufacturers (small, medium & large).

Industrial goods

Machinery, manufacturing plants, materials, and other goods or component parts for use or

consumption by other industries or firms. Demand for industrial goods they help to produce

called derived demand

Material Handling Equipment’s Sector

Material handling equipment is equipment that relate to the movement, storage, control and

protection of materials, goods and products throughout the process of manufacturing,

distribution, consumption and disposal. Material handling equipment is the mechanical

equipment involved in the complete system.

The demand of construction and material equipment is correlated with the growth of

Infrastructure sector. India still needs to develop it in a big way. There is substantial scope for

the growth of the infrastructure sector viz., Roads, Steel, Coal, Cement, Power etc.

The continuing investments in these sectors will support demand of these products. Also, with

increased need of mechanization and shrinking timelines of infrastructures projects, the

demand for equipment’s should see a definitive upward trend. The demand is largely from

F&B, retail and automobile sectors. Palletisation and containerization are also expected to

increase demand. Although, it may be worthwhile to note that the global recession and

slowdown in India as well as the rise in input prices may act as major threat to this sector.

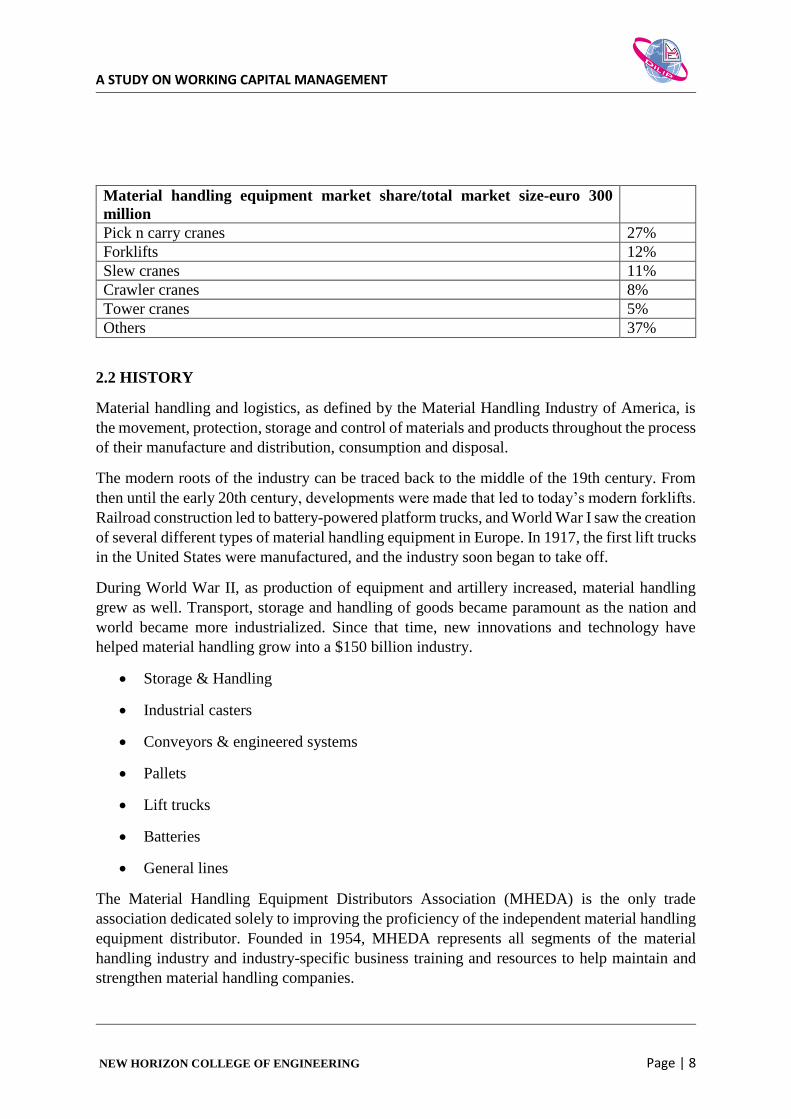

Market Size and Segmentation

The present market size is estimated to be around € 300 million. The table below explains the

different material handling equipment and their market share. The material handling equipment

is dominated by cranes and forklifts. Pick and carry cranes is the largest segment with 27 %

share of the material handling equipment market. Slew cranes, crawler cranes and tower cranes

together account for another 24 percent. Forklifts have 12 percent share.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 8

Material handling equipment market share/total market size-euro 300

million

Pick n carry cranes 27%

Forklifts 12%

Slew cranes 11%

Crawler cranes 8%

Tower cranes 5%

Others 37%

2.2 HISTORY

Material handling and logistics, as defined by the Material Handling Industry of America, is

the movement, protection, storage and control of materials and products throughout the process

of their manufacture and distribution, consumption and disposal.

The modern roots of the industry can be traced back to the middle of the 19th century. From

then until the early 20th century, developments were made that led to today’s modern forklifts.

Railroad construction led to battery-powered platform trucks, and World War I saw the creation

of several different types of material handling equipment in Europe. In 1917, the first lift trucks

in the United States were manufactured, and the industry soon began to take off.

During World War II, as production of equipment and artillery increased, material handling

grew as well. Transport, storage and handling of goods became paramount as the nation and

world became more industrialized. Since that time, new innovations and technology have

helped material handling grow into a $150 billion industry.

Storage & Handling

Industrial casters

Conveyors & engineered systems

Pallets

Lift trucks

Batteries

General lines

The Material Handling Equipment Distributors Association (MHEDA) is the only trade

association dedicated solely to improving the proficiency of the independent material handling

equipment distributor. Founded in 1954, MHEDA represents all segments of the material

handling industry and industry-specific business training and resources to help maintain and

strengthen material handling companies.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 9

Importance of Material handling Equipment

When materials in the warehouse are being managed well, there will be an increase in

efficiency. On the other hand, without MHE, it will eventually lead to poor material

handling.

Some of the poor materials handling effects include confusion on product storage, too much

walking, cluttered aisles, lack of standardization, as well as high losses and damages.

Guidelines for Basic Handling

Standardize equipment by using equipment that can be deployed as many areas as possible.

Maximize continuous flow rather than intermittent or one-way flow.

Focus on handling rather than stationary Minimize ratio of dead-weight to payload of

handling equipment and not wasting unnecessary capacity of equipment’s

2.3 Major Players in the Material Handling Equipment Sector:

� Godrej & Boyce Mfg. Co.

� McNally Bharat Energy Co.

� Mukand Ltd.

� Escorts Ltd.

� Ahluwalia Contracts [India] Ltd.

� Saico Engineers & Fabricators Ltd.

� Elecon Engineering Co.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 10

� Electrometer

� ACE

� OMEGA

� Voltas

� TIL

� TELCON

Pick & Carry Cranes

Some of the typical uses include loading, unloading, moving, shifting and erecting material.

The pick-n-carry crane segment in India has an estimated market size of € 57.76 million (3698

units), and these cranes comprise 27 % of the overall material handling market and over 50 %

of the cranes market. The market has grown at a CAGR of 72 % in volume terms in the last 3

years. Going forward, the growth rate is expected to be in the range of 15-20 % over the next

few years. The key drivers are the construction and industrial sectors. Within the construction

sector the key demand driver is urban infrastructure (expected investment growth of 13 %

annually).

Within industrial applications, the key demand drivers are steel and power industries (growing

at around 9 % annually). The major players in this segment are ECEL and Actions Construction

Equipment (ACE). While ECEL has been the traditional leader in this segment, ACE has been

gaining share. A third player – Omega – has been able to capture 2.5 % of the market within

one year of commencing production. The barriers of entry in this segment are low. The first

movers have the added advantage of established sales, service and distribution network along

with an existing component supplier.

Other Cranes

Other cranes consist of slew cranes, crawler cranes and tower cranes. These are higher value,

more sophisticated cranes than pick-n-carry cranes and are typically used for heavier duty

work. The market for slew cranes is about € 23.24 million (300 numbers) with about € 8.6

million (180 numbers) of this being accounted for by imported used equipment.

Within slew cranes, yard cranes are the most prominent, comprising 65 % of all new slew

cranes. The crawler cranes market is about € 16.6 million (210 numbers) with imported used

cranes comprising about € 6.3 million (110 numbers). Tower cranes are about € 10.35 million

(175 numbers). In volume terms other cranes comprise about 16 % of the overall cranes

Market in India, but in value terms these cranes account for almost 47 % of the market. While

slew cranes have witnessed a CAGR of 34 % over the last 2 years, tower cranes have grown at

71 % CAGR in the same period. Industry sources indicate a growth rate of between 15-20 %

over the next few years.

Demand for other cranes is driven primarily by the construction and industrial sectors. Within

industrial applications, the key demand drivers going forward are likely to be the power,

refinery and mining sectors. With increasing average scale of infrastructure and construction

projects, the growth rate of slew (specifically yard/rough terrain) and tower cranes is likely to

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 11

surpass the average growth rate of the overall cranes segment. With improved road networks

by 2010, demand for truck mounted cranes may also witness a spike. In the slew cranes

segment, used imports dominate the market, with Tractors India Limited (TIL) being the

market largest domestic player. TIL and ECEL have a market share of around 32 % and 6 %

in terms of volumes. Telco is the sole player in the crawler cranes segment with a share of

approximately 50 % by volume (balance is accounted for by used imports). Shrike Petain is the

market leader in the Tower crane category with 50 % market share followed by ACE at 25 %

market share.

ACE plans to widen its product portfolio in the cranes segment through manufacture of Truck

Mounted and Tower cranes. Electromech will ramp up the production of cranes at its Pune

plant in order to increase its market share from 10% to 25% in the next three years.

Forklifts

Forklifts are low tonnage vehicles used to transport materials stored in pallets, within limited

spaces. Most forklifts are in the 1 tons–5 tones range, though equipment up to 20 tones are

available. The flexibility and speed these equipment offer make them ideal for repetitive

material handling tasks especially in restricted areas like warehouses and yards .There are 3

types of forklifts based on fuel input - Diesel, Liquefied Petroleum Gas (LPG) and Battery.

Each variant finds application in different industries based on the load factor determined by the

power inputs pollution etc.

The current market is approximately of 2150 units per annum for forklifts with a market size

of approximately € 25.23 million. The segment has been on a 20 % growth trajectory year-on-

year and is estimated to grow at a CAGR between 10-20 %. Diesel powered forklifts comprise

a bulk of the market size at 83 % and are likely to drive growth going forward. Demand for

forklifts will be driven primarily by new capacity creation and increased automation in the

manufacturing and logistics (warehousing) sectors. Forklifts contribute to making the end user

industry organized and less labor intensive (in material handling). It has also increased the

levels of palletisation and containerization. Godrej and Voltas are the two major players having

around 80 % market share, with Godrej having 48 % share. The forklifts market is highly price

sensitive. Technology is presently not seen as a differentiator, but with the end user industries

becoming more organized and competitive, it would become increasingly important.

Opportunities in the Sector:

The construction equipment industry is primarily driven by two key sectors: Construction and

Manufacturing

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 12

CONSTRUCTION INVESTMENT

As of 2009, the Indian construction industry, at current prices, contributed more than US$ 91

billion to the country’s gross domestic product (GDP). It employs more than 18 million people.

Construction investments accounted for 11 % of GDP and 50 per cent of gross fixed capital

formation. Construction activity has grown at 11 % over the period 2006 to 2009. Construction

equipment accounts for around 5–24 % of the total cost incurred in any construction project.

Increasing mechanization of industry and construction facilitates greater penetration of

construction equipment. Recent Government policies around tax benefits for infrastructure

ventures have boosted equipment usage.

• Ports: the projected investment for improving major and minor ports in India is around €

11.95 billion over the next four to six years. A major portion of the investment for improving

the major ports is expected to come from private players. Privatization has been regard as one

of the key avenues for increasing investments in this segment. Another pertinent factor is the

expected growth in the cargo handled at all Indian ports, which is expected to grow at a CAGR

of 8 %. These developments would drive demand for material handling equipment such as

cranes for handling cargo and construction equipment for infrastructure development in the

ports.

• Railways: the investment in this segment is expected to be focused on relaying of tracks and

improving the existing network. The Government has awarded € 544.4 billion of projects to

private firms.

MANUFACTURING SECTOR INVESTMENT

The index of industrial production has displayed healthy growth trend. India’s industrial GDP

has grown at a CAGR of 12.6 % over the last five years. The industrial sector is a primary

demand driver for material handling equipment.

• Steel: Steel majors in India have undertaken large capacity expansion projects with an

expected outlay of € 10.22 billon. The industry is estimated to grow at 9-10 % over the next 5

years. The production and consumption have experienced steady growth over the period

considered.

• Power: Investment to the tune of about € 64 billon is expected in India’s power sector in the

next 10 years, for adding generation capacity. The installed capacity in India is projected to

grow to 212,000 MW by 2012 as against current level of 115,000 MW. This translates to a

growth of 86 % over a period of 7 years, or a CAGR of 9.3 %.

• Refineries: India’s refining throughput as also oil consumption is expected to chart out a

steady growth path. It is expected to reach approximately 187 million tonnes by 2010. The

estimated throughput growth is at 10 % over 2006-10.

• Engineering /Automobiles /Food & Beverages: An estimated € 45.14 billion is projected

for capital investment for the engineering industry in India, over key manufacturing sectors

such as automobiles and food & beverages. In turn, this would drive demand for material

handling equipment in the new capacities coming up. Diesel forklifts find particular application

in the automobile industry which has been growing at close to 15 %. The total automobile

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 13

production is set to cross 10 million units. Estimated CAGR for key segments is 15-18 % with

an overall outlook for the future pegged at 16 %. LPG forklifts find particular application in

food & beverages industry. Led by processed foods, wine, ice cream and edible oil, the € 53.12

billion food and beverages industry registered an 8.5 % growth during the 2005-06 fiscal.

• Retail: Exponential growth and emerging competition in organized retail in India is expected

to drive the organized logistics and warehousing industries. India’s organized chain store retail

is at the inflection point. The estimated potential market size is € 39.83 billion by 2015 implying

a CAGR of 32 % over next 10 years. This would drive the construction of new stores, in turn

leading to demand for construction equipment.

2.4 COMPANY PROFILE

Address of the company:

DILIP MATERIAL HANDLING EQUIPMENT

#83/A, 3rd cross, 8thmain,

Bommasandra industrial area,

Bangalore

Tele fax: +91 80 2783 9025

E-mail: [email protected]/[email protected]

Dilip material handling started in 1998 is the result of Mr. Chalapathy desire to provide

industry cost effective material handling solutions. Drawing on the hands-on experience he

gained working in the material handling equipment industry, he came up with a range of tough

but easy to operate equipment that even small industries could afford.

Today Dilip material handling equipment’s., unit at Bommasandra on the outskirts of

Bangalore, Dilip material handling equipment’s Is on ISO 9001:2000 certified company that

produces material handling products a range of Hydraulic Hand Pallet Trucks, High Lifting

Hand Pallet Trucks, Manual Trolleys, Hydraulic Floor Cranes, Hydraulic Hand Stackers, Semi-

Electric Stackers, Electric Stackers, Electric Platform Trucks, Manual Mobile Lift Platform,

Order picker, Hydraulic Lift Tables, Hydraulic Dock Leveler, Racking and storage solutions

with load capacities from 500KGS to 2500KGS. A well-equipped infrastructure and all India

sales and service network has helped us to be recognized as a mainstay in the India subcontinent

market. Dilip’s have always placed safety as top priority.

It also has the distinction of being the country’s only manufacturing of Hydraulic Hand Pallet

Trucks with Lift, neutral & lower. The superior

Performance of the equipment has seen dilip become a name that is gaining rapid popularity in

Karnataka and tamilnadu.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 14

The rust proof and scratch resistant equipment has been designed and built to offer long years

of trouble-free services, Manufacturing from high quality materials, they are light and

maneuverable besides being silent in operation. The Principle of ergonomics have been to

ensure ease of operation and low operation fatigue requiring minimal maintenance, the

equipment has proved its worth in a host of industries. Dilip’s now manufacturing more than

20 different products in India.

2.5VISION, MISSION AND QUALITY POLICY

VISION:

The Company wants to develop its products to global standards.

The Company also want to get quality standard certified to ensure its customers about the

quality of the product.

The Company wants to reduce the cost by introducing substitutes without comprising

on quality.

MISSION:

The Company is striving to develop new lift trucks with latest technologies.

The Company wants to improve the existing product in terms of quality.

ISO 9001: 2000

ISO Certificate Registration No. 44 100 114088-E3

QUALITY POLICY:

“Dilip material handling equipment's commits to design, produce and dispatch products of

consistent quality through continual improvements of process, products and satisfaction by

involving everyone in the organization

Range of Products:

Hydraulic Hand Pallet Trucks

Manual Stackers

Semi Electric Stackers

Electric Stackers

Electric Pallet Trucks

Mini Fork Lift

Tow Tractors

Electric Platform Trucks

Scissor Lift Tables

Dock Levelers

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 15

Order Pickers

Goods Lift

Floor Cranes

Storage Systems

New Products:

Towing tractors

Counter Panel

Competitors in Dilip material handling equipment’s:

Maine Material Movement PVT. Ltd.

Marathi Handling

puma Material Handling Equipment

Elite Material Handling

Acer Engineers PVT Ltd

Dock Lift

Aditya material Handling

Josts

Nilkiamal

Patel Handling

Ferrow foundries

Marketing branches of Dilip:

Bangalore

Chennai

COMPANY OBJECTIVES:

Introduce 3 new products to the market.

Making 350 new customers.

Adopt A.C technology to the equipment.

Extend sales network to 3 states.

Major customers of Dilip’s material handling:

Amara raja Batteries, Tirupathi

Arriva T& D India Ltd. Bangalore/Chennai

Ashok Leyland Ltd. Bangalore

Biocon Limited, Bangalore

Coca-Cola India PVT Ltd, Pune

Dauber pharms

Mysore Paper Mills Ltd ,Bangalore

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 16

Max India Ltd, Punjab

Eastern Groups of companies, Ernakulum

FDC limited, Mumbai

S.K.F India Ltd, Bangalore

TVS Ltd, Madurai

Kingfisher Ltd, Mumbai

Hindustan Lever Ltd, Pondicherry

M.T.R Foods limited, Bangalore

Mahindra & Mahindra company, Bangalore

2.6 BACK GROUND OF THE COMPANY

2.7 PRODUCTS

SEMI-ELECTRIC STACKER

MODEL; DES 5E/8E/10E CAPACITY: 800/1000kg

Ergonomically designed steering handle

For easy operation from all angle

1 Name of the company DILIP MATERIAL HANDLING

EQUIPMENT

2 Year of establishments 1998

3 Company registration No. U 29199KA2001PTC029595

4 Ownership Pattern PVT. LTD

5 Registered address NO 83/A, 4th phase, Bommasandra

industrial area, Bangalore.

Bangalore

6 Telephone No +91 80 2783 9026

7 Fax No. +91 80 2783 9025

8 Website Www. Dilip. [email protected]

www.diliplifttruck.com

9 Name of the directors and manager Mr. A V CHALAPATHY

Ms.SMITHA(manager)

10 Branch offices in India Chennai only

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 17

Effortless operation

Robust stability

HYDRALIC DOCK LEVER SPECIFICATION

MODEL -30-90

Capacity: 3000-9000kg

Quality dock leveler

Easy to install

Long lasting

safe

HYDRALINC HAND PALLET TRUCK

MODEL: DP-25/30 Capacity: 2500/3000kg

No oil leakage

Minimum maintenances

Easy to operate

Requires minimum pulling power

HIGH LIFTING PALLET TRUCK

MODEL; DH-8/10 capacity: 800/100 kg

Versatile

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 18

Compact

Economical

Light and maneuverable

HAND OPERATED STACKER

MODEL: DS -5/8/15 capacity: 500/800/1500kg

To ensure the long life of the hydraulic system

Ergonomically designed steering handle

For easy operation from all angle

Light and compact construction

BATTERY OPERATED STACKER

MODEL; DPS-10/12/15 capacity; 1000/1200/1500kg

High quality ,imported drive motor for battery and constant road grip

Heavy duty structure robust , long lasting design

Electric break acting on drive motor is an added features

BATTERY OPERATED PALLET TRUCK

MODEL –dpp-22/30 capacity;2200/3000

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 19

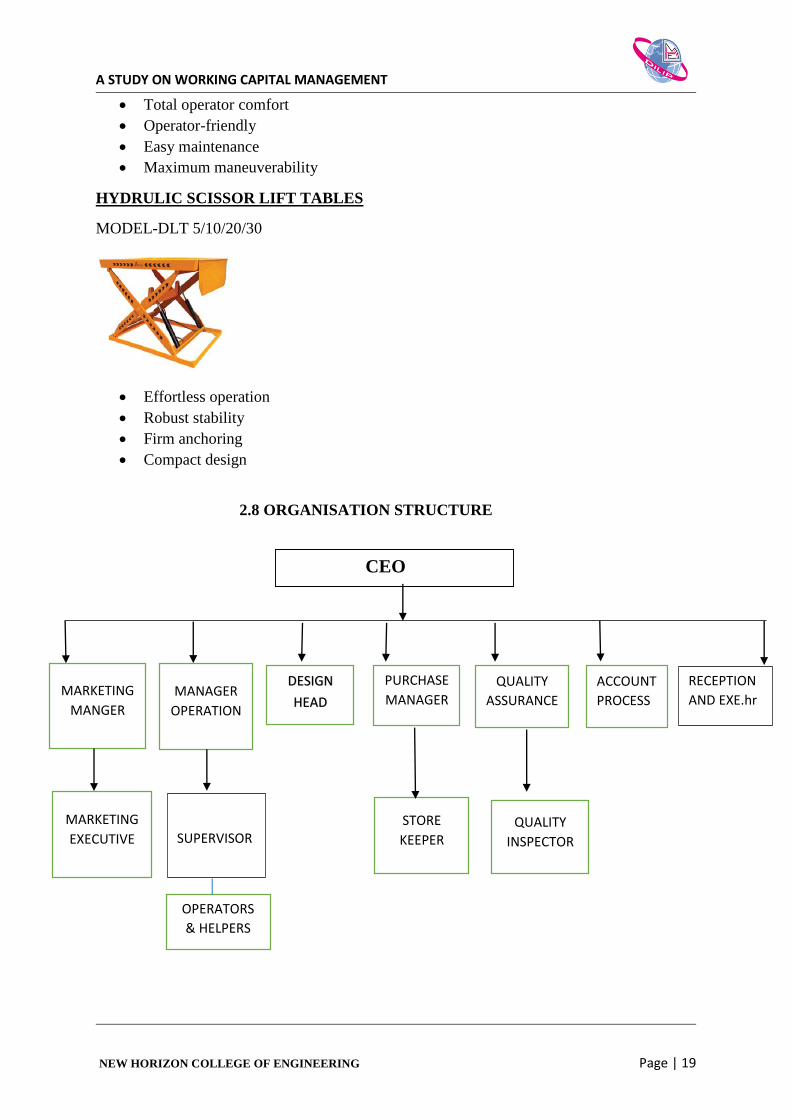

Total operator comfort

Operator-friendly

Easy maintenance

Maximum maneuverability

HYDRULIC SCISSOR LIFT TABLES

MODEL-DLT 5/10/20/30

Effortless operation

Robust stability

Firm anchoring

Compact design

2.8 ORGANISATION STRUCTURE

CEO

MARKETING

MANGER

MANAGER

OPERATION

DESIGN

HEAD

PURCHASE

MANAGER

QUALITY

ASSURANCE

ACCOUNT

PROCESS

RECEPTION

AND EXE.hr

MARKETING

EXECUTIVE

SUPERVISOR

OPERATORS

& HELPERS

STORE

KEEPER QUALITY

INSPECTOR

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 20

2.9 SWOT ANALYSIS

STREANTH

o The brand has its presence in srilanka and Nepal including India.

o Huge demand for Domestic Industrial goods.

o Avail of Low-cost, Skilled Human Resources

o The company has a well-established R&D unit one of the best kinds in the material

handling equipment.

o The company dully equipped to develop a new products to meet the requirements of

the market.

o The company has been maintaining a quality products and as it is products are well

accepted in the market by quality conscious customer, it does not anticipate any

marketing problem.

o The products of WIP are certified by ISO

WEAKNESS

o The distribution &after sales system is still not as superior as national or global leaders

o There is an actual shortage of good raw material which has forced the company to

import a raw material which has focused the company to import a sustain portion of its

main raw material viz., which has also seen a considerable increase in price.

o Lack of distribution network as compared to its competitor.

OPPORTUNITIES

o Growing Competition of Indian industry due to focus on efficient and quality

o Marketing tie-ups with leading foreign companies which facilitate the availability of

latest technology and machine from around the world could makes it R&D stronger

manifold.

o Growing demand for the material handling equipment’s.

o when company invent a new product it helps to increase market share

o Income level at consistent growing level

THEATES

o Increasing cost of raw material so the company also increase product price when

increase product price sales level will be fall down.

o Government regulation is to be when changes in new government they should adapt

new certain regulation

o Heavy competition in manufacturing field from Bengaluru

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 21

CHAPTER 3

THEORATICAL REVIEW

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 22

3.1 THEORETICAL REVIEW

Working capital is the key difference between the long term financial management and short

term financial management in tern of the timing of cash. Long term financial involves the cash

flow over the extended period of the time i.e. 5 to 15 years, while short term financial decision

cash with in a years or with in operating cycle. Working capital management is a short term

financial management.

Management of working capital is very much important for the success of the business. It has

been emphasized that a business should maintained should working capital position and also

that there should not be an excessive level of investment in the working capital component. As

pointed out of by rlph kenned and steavart MC Muller, “the inadequacy or miss-management

of working capital is one of a leading cause of business failure.

Working capital management concerned with the problem that arise in attempting to manage

the current asset, the current liabilities & in inter relationship that exits between them. The

current asset refers to those assets which can be easily converted in to cash in ordinary course

of business, without disturbing the operation of firm,

Current assets in fact, account for a very large portion of the total investment of the firm.

DEFINITION:

In accounting, “working capital is the difference between the inflow and outflow of funds. In

other words, it is the net cash inflow. It is defined as the excess of current assets over current

liabilities and provisions”.

3.2 Objectives of working capital

Explain how the definition of “working capital “differences between financial analysts and

accountants.

Understand the two fundamental decision issues in working capital management-and the

trade-offs involved in making these decisions.

Discuss the how to determine the optimal level of current assets.

Describe the relationship between profitability, liquidity, and risk in the management of

working capital.

Explain how to classify working capital according it its “components” and according to

“time” (i.e., either permanent or temporary).

Describe the hedging (maturity matching) approach to financing and the

advantages/disadvantages of short -term versus long-term financing.

Explain how the financial manager combines the current asset decision with the liability

structure decision.

Maintenance of working capital at appropriate level, and Availability of ample funds as

and when they are needed.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 23

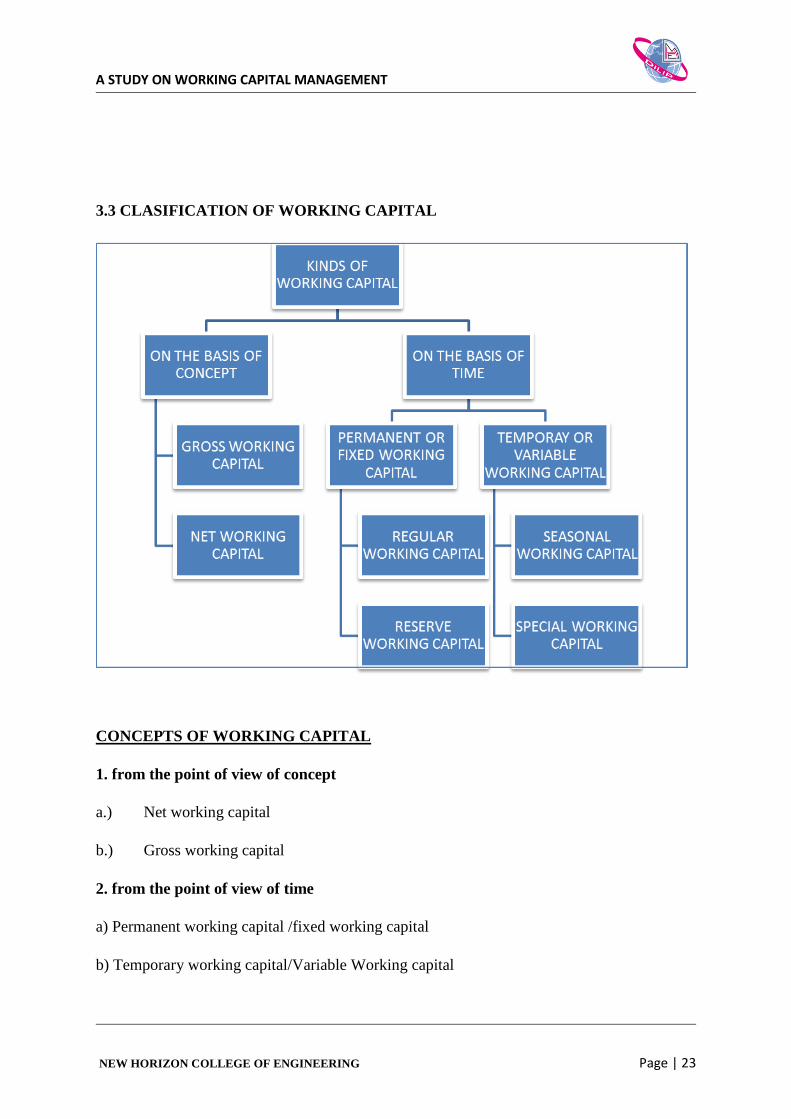

3.3 CLASIFICATION OF WORKING CAPITAL

CONCEPTS OF WORKING CAPITAL

1. from the point of view of concept

a.) Net working capital

b.) Gross working capital

2. from the point of view of time

a) Permanent working capital /fixed working capital

b) Temporary working capital/Variable Working capital

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 24

1. ON THE BASIS CONCEPT

a.) NET WORKING CAPITAL

This is the difference between current assets and current liabilities . Current

liabilities are those that are expected to mature within on accounting year and include

creditors , bills payable and outstanding expenses.

Investments in current assets represents a very significant portion of the total

investment in assets .

The working capital needs increase as the firm’s grows as sales grow , the

firm needs to invest more in debtors and inventories .

B.)GROSS WORKING CAPITAL

Gross working capital refers to the firm’s investment in current assets . Current

assets are the assets which can be converted into cash within a short period say , an

accounting year . Current assets include cash , debtors , bills receivables , short term

securities etc. .

It is equal to the total sum of the current assets and may represent both

owned capital and loan capital .

2. ON THE BASIS OF TIME

a.) PERMANENT WORKING CAPITAL

Permanent working capital is permanently locked up in the circulations of current

assets . It covers the minimum amount requested for maintaining the circulation of

current assets .

1. INITIAL WORKING CAPITAL

At its inception and during the formative period of funds to meet its

obligations. The need for initial working capital is for every company to consolidate its

position

2. REGULAR WORKING CAPITAL

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 25

It refers to the medium amount of liquid capital required to keep up the circulation

of the capital from the cash inventories to accounts receivable and from accounts

receivables to back again cash .

b)VARIABLE WORKING CAPITAL

It refers to the past of the working capital which changes with the volume of

business , it may be divided into two classes.

1. SEASONAL WORKING CAPITAL

There are many lines of business where the volume of operations is different and

hence the amount of working capital varies with the seasons . The capital required to meet

the seasonal working capital.

2. SPECIAL WORKING CAPITAL

The capital required to meet any special operations such as experiments with new

products or new technique of production and making interior advertising campaign etc

are also known as special working capital.

3.4 COMPOSITION OF WORKING CAPITAL

MAJOR CURRENT ASSET

Cash

Account receivable

Inventory

Marketable securities

MAJOUR CURRENT LIABILITIES

Bank over draft

Outstanding expenses

Accounts payable

Bill payable

Working capital refers to the cash a business requires for day to day operations or more

specifically, for financing conversion of raw material in to finished goods, which company

sells for payment. Among the most important item of the working capital are levels of

inventory, debtor ad creditor. These items are looked at for signs of a company efficiency and

financial strength.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 26

The better a company manager is working capital, the less the company needs to borrow. Even

companies with cash surpluses needs to manage working capital to ensure that those surpluses

are invested in ways that will generate suitable returns for investors.

Working capital management is very important to ensure that the company has enough fund to

carry on with its day to day operation smoothly. A business should not have a very long cash

conversion cycle. A cash conversion cycle measures the time period for which a firm will be

deprived of funds if its increase its investment as a part of its business growth strategies. For

this company has to take certain measures such as reduce the credit period of the customer,

negotiate with the supplier and increase its own credit period with them, maintaining the right

level of the inventory which reduce the raw material cost and proper cash management which

ensures that cash holding cost are reduced. If these measures are followed, the working capital

requirement automatically comes down.

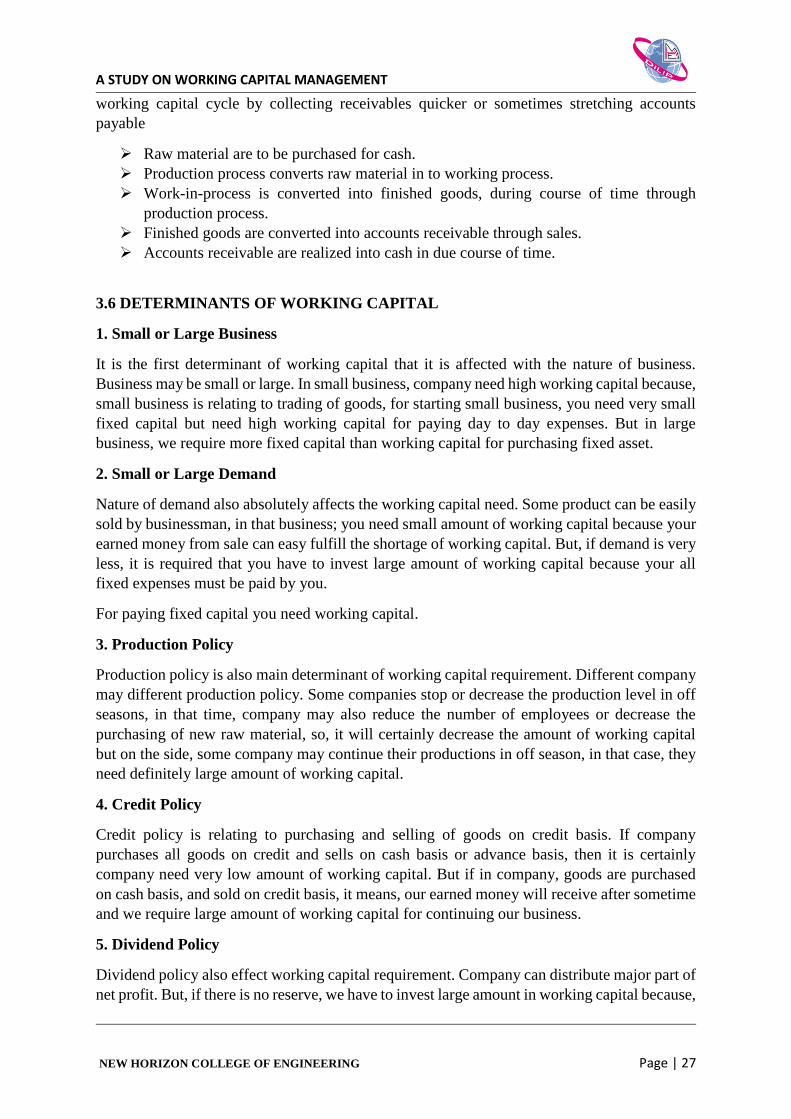

3.5 WORKING CAPITAL CYCLE

The working capital requirement of a firm depended to a great extent upon the operating cycle

of the firm. The duration of time required to complete the sequence of events right from

purchase of raw material /goods for cash to the realization of cash is called the operating cycle

or working capital cycle.it can be determined by the adding the number of days required for

each stage in cycle. In case of manufacturing concerns, working capital is required to cater to

the following needs of business in order:

The working capital cycle (WCC) is the amount of time it takes to turn the net current assets

and current liabilities into cash. The longer the cycle is, the longer a business is tying up capital

in its working capital without earning a return on it. Therefore, companies strive to reduce its

Raw Materials

Work In Process

Finished Goods

Sales

Debtors

Cash

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 27

working capital cycle by collecting receivables quicker or sometimes stretching accounts

payable

Raw material are to be purchased for cash.

Production process converts raw material in to working process.

Work-in-process is converted into finished goods, during course of time through

production process.

Finished goods are converted into accounts receivable through sales.

Accounts receivable are realized into cash in due course of time.

3.6 DETERMINANTS OF WORKING CAPITAL

1. Small or Large Business

It is the first determinant of working capital that it is affected with the nature of business.

Business may be small or large. In small business, company need high working capital because,

small business is relating to trading of goods, for starting small business, you need very small

fixed capital but need high working capital for paying day to day expenses. But in large

business, we require more fixed capital than working capital for purchasing fixed asset.

2. Small or Large Demand

Nature of demand also absolutely affects the working capital need. Some product can be easily

sold by businessman, in that business; you need small amount of working capital because your

earned money from sale can easy fulfill the shortage of working capital. But, if demand is very

less, it is required that you have to invest large amount of working capital because your all

fixed expenses must be paid by you.

For paying fixed capital you need working capital.

3. Production Policy

Production policy is also main determinant of working capital requirement. Different company

may different production policy. Some companies stop or decrease the production level in off

seasons, in that time, company may also reduce the number of employees or decrease the

purchasing of new raw material, so, it will certainly decrease the amount of working capital

but on the side, some company may continue their productions in off season, in that case, they

need definitely large amount of working capital.

4. Credit Policy

Credit policy is relating to purchasing and selling of goods on credit basis. If company

purchases all goods on credit and sells on cash basis or advance basis, then it is certainly

company need very low amount of working capital. But if in company, goods are purchased

on cash basis, and sold on credit basis, it means, our earned money will receive after sometime

and we require large amount of working capital for continuing our business.

5. Dividend Policy

Dividend policy also effect working capital requirement. Company can distribute major part of

net profit. But, if there is no reserve, we have to invest large amount in working capital because,

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 28

lacking of reserve will effect on adversely on fulfill our liabilities. In that case, we have to yield

working capital by taking short term loan for paying uncertain liability.

6. Working Capital Cycle

Working capital cycle shows all steps which starts from cash purchasing of raw material and

then this converted into finished product, after this it is converted into sale, if it is credit sale,

debtors will also the part of working capital cycle and when we gets money from our debtors,

it is the final part of working capital cycle. If we receive fastly from our debtors, we need small

amount working capital. Otherwise, for purchasing new raw material, we need more amount

of working capital.

7. Manufacturing Cycle

Manufacturing cycle means the process of converting raw material into finished product. Long

manufacturing cycle will create the situation in which we require large amount of working

capital. Suppose, we have to construct the building, for constructing colony of buildings, it may

consume the time more than 5 years, so according to this we need working capital.

8. Business Cycle

There are two main part of business cycle, one is boom and other is recession. In boom, we

need high money or working capital for development of business but in recession, we need

only low amount of working capital.

9. Price Level Changes

If there is increasing trend of products prices, we need to store high amount of working capital,

because next time, it is precisely that we have to pay more for purchasing raw material or other

service expenses. Inflation and deflation are two major factors which decide the next level of

working capital in business.

10. Effect of External Business Environmental Factors

There are many external business environmental factors which affect the need of working

capital like fiscal policy, monetary policy and bank policies and facilities

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 29

3.7 REQUIREMENTS OF FUNDS

Fund requirements of company

FIXED CAPITAL WORKING CAPITAL

o Preliminary expenses Raw material

o Purchase of fixed assets Inventories

o Establishment work expenses Goods in progress

o Fixed working capital Others

Every company requires funds for investing into types of capital i.e. fixed capital, which

requires long term funds, and working capital, which requires short term funds.

Sources of working capital

Long term sources short term

sources

(Fixed working capital) (Temporary working

capital)

Loan from financial institution Factoring

Floating of debenture Invoice discounting

Accepting public depositing Bank over draft

Issue of shares Trade credit

Cash credit Instalment Credit

Income received

Commercial Papers

Trade finance

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 30

Sources of additional working capital include the following:

Existing cash reserves

Profit (when you secure it as cash)

Payable (credit from supplier)

New equity or loans from shareholders

Bank overdraft or lines of credit

Term loans

If we have insufficient working capital and try to increase sales, you can easily over-stretch the

financial resource of the business. This is called overtrading. Early warning signs include:

Pressure on existing cash

Bank overdraft exceeds authorized limit

Seeking greater overdraft or lines or credit

Part-paying suppliers or other creditors

Management pre occupation with surviving rather than managing

Frequent short term emergency request to the bank.

Long term sources of working capital

Issue of shares

The number of authorized shares that is sold to and held by the shareholders of a company,

regardless of whether they are insiders, institutional investors or the general public.

Issued shares is a term of law and finance for the quantity of shares of a corporation, which

have been allocated (allotted) and are subsequently held by shareholders. The act of creating

new issued shares is called issuance, allocation or allotment. Allotment, in simplicity, is the

creation of shares and their transfer to a subscriber. After allotment, a subscriber becomes a

shareholder. The number of issued shares is a subset of the total authorized shares. It is that

amount which the board of directors and/or shareholders have agreed to allocate. Issued shares

are the sum of outstanding shares and treasury shares.

Debentures

A type of debt instrument that is not secured by physical assets or collateral. Debentures are

backed only by the general creditworthiness and reputation of the issuer. Both corporations and

governments frequently issue this type of bond in order to secure capital. Like other types of

bonds, debentures are documented in an indenture

Debentures have no collateral. Bond buyers generally purchase debentures based on the belief

that the bond issuer is unlikely to default on the repayment. An example of a government

debenture would be any government-issued Treasury bond (T-bond) or Treasury bill (T-bill).

T-bonds and T-bills are generally considered risk free because governments, at worst, can print

off more money or raise taxes to pay these type of debts.

Loan from financial institution

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 31

The term debenture is a strictly legal term but there are other forms of loan or loan stock. A

loan is for a fixed amount with a fixed repayment schedule and mat appear on a balance sheet

with a specific name telling the reader exactly what the loan is and its main details.

Short Term Sources of Working Capital

Factoring

Factoring is a traditional source of short term funding. Factoring facility arrangements tend to

be restrictive and entering into a whole-turnover factoring facility can lead to aggressive

chasing of outstanding invoices from clients, and a loss of control of a company’s credit

function.

Instalment Credit

Instalment credit is a form of finance to pay for goods or services over a period through the

payment of principal and interest in regular payments.

Invoice Discounting

Invoice Discounting is a form of asset based finance which enables a business to release cash

tied up in an invoice and unlike factoring enables a client to retain control of the administration

of its debtors.

Income received in advance

Income received in advance is seen as a liability because it is money that does not correlate to

that specific accounting or business year but rather for one that is still to come. The income

account will then be credited to the income received in advance account and the income

received in advance will be debited to the income account such as rent.

Advances received from customers

A liability account used to record an amount received from a customer before a service has

been provided or before goods have been shipped.

Bank Overdraft

A bank overdraft is when someone is able to spend more than what is actually in their bank

account. The overdraft will be limited. A bank overdraft is also a type of loan as the money is

technically borrowed.

Commercial Papers

A commercial paper is an unsecured promissory note. Commercial paper is a money-market

security issued by large corporations to get money to meet short term debt obligations e.g.

Payroll, and is only backed by an issuing bank or corporation’s promise to pay the face amount

on the maturity date specified on the note. Since it is not backed by collateral, only firms with

excellent credit ratings will be able to sell their commercial paper at a reasonable price

Trade finance

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 32

An exporter requires an importer to prepay for goods shipped. The importer naturally wants to

reduce risk by asking the exporter to document that the goods have been shipped. The

importer’s bank assists by providing a letter of credit to the exporter (or the exporter’s bank)

providing for payment upon presentation of certain documents, such as a bill of lading. The

exporter’s bank may make a loan to the exporter on the basis of the export contract.

Letter of Credit

A letter of credit is a document that a financial institution issues to a seller of goods or services

which says that the issuer will pay the seller for goods/services the seller delivers to a third-

party buyer. The issuer then seeks reimbursement from the buyer or from the buyer’s bank.

The document is essentially a guarantee to the seller that it will be paid by the issuer of the

letter of credit regardless of whether the buyer ultimately fails to pay. In this way, the risk that

the buyer will fail to pay is transferred from the seller to the letter of credit’s issuer.

3.8 Management of working capital

Guided by the above criteria, management will use a combination of policies and techniques

for the management of working capital. These policies aim at managing the current assets

(generally cash and cash equivalents, inventories and debtors) and the short term financing,

such that cash flows and returns are acceptable.

Cash management.

WHAT IS CASH?

The term cash with reference to cash management is used in two sense .in a narrow sense it

include ,coins, currency notes, cheque, bank draft held by a firm with it and the demand deposit

held by it in bank . in broader sense it also include near cash assets such as marketable securities

and time deposit with banks .such deposit can immediately be sold or converted into cash if

the circumstances so require .the term cash management is generally used for management of

both cash and near current assts.

FACTS OF CASH MANAGEMENT

Management of cash is concerned with the managing of

a. cash inflow and outflow of firm

b. cash flows within the firms and

Cash balances needed by the firm at a point of time by the financing of deficit or of investing

surplus cash. but it is difficult to predict cash flows accurately .hence ,in order to resolve the

uncertainty about cash flow prediction and lack of synchronization between cash receipts and

payments ,the firm should develop some strategies regarding the following four factor of cash

management.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 33

1. CASH PLANNING

It is a technique to plan and control the use of cash it protects the financial condition of

the firm by developing projected cash statement from forecasting of expected cash in flows

and out flows for a given period the forecasts may be used on the present operation or the

anticipated future operations .cash planning is very crucial in developing the overall operating

plans of the firm.

2. CONTROLLING THE LEVEL OF CASH BALANCES

As one of the basic objectives of cash management is to minimize the level of cash

balance, controlling the level of cash balance does not mean just minimizing the level of cash

balance within the firm .it means neither ensuring that the level of cash balance is neither

excessive nor inadequate .(i.e. .optimum).

3. OPTIMUM CASH LEVEL

Company must decide about the appropriation level of cash balances to be maintained. Both

the cost of excess cash and danger of cash deficiency have to be matched to arrive at optimum

level of cash balance.

4. INVESTMENT SURPLUS CASH

All surplus cash has been properly invested so as to earn profit .the company has to decide

about the division of such cash balance borrowed from bank deposit ,marketable securities on

inter corporate loan.

An idea cash management system depends on the company’s product, organization structure,

culture and option available

MANAGEMENT OF INVENTORY

In dictionary meaning of inventory is a “detailed list of goods, furniture etc.” Many

understand the word inventory, as a stock of goods, but the generally accepted meaning of the

word ‘goods’ in the accounting language, is the stock of finished goods only. In a

manufacturing organization, however, in addition to the stock of finished goods, there will be

stock of partly finished goods, raw materials and stores. The collective name of these entire

items is ‘inventory’.

The term ‘inventory’ refers to the stockpile of production a firm is offering for sale and the

components that make up the production.

Identify the level of inventory which allows for uninterrupted production but reduces the

investment in raw material – and minimizes recording costs - and hence increases cash flow.

Besides this, the lead times in production should be lowered to reduce work in progress (WIP)

and similarly, the Finished Goods should be kept on as low level as possible to avoid over

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 34

production – see supply chain management ;Just in Time (JIT); Economic order quantity

(EOQ); Economic quantity.

Inventories occupy the most strategic position in the structure of working capital of most

business enterprises. It constitutes the largest component of current asset in most business

enterprises. In the sphere of working capital, the efficient control of inventory has passed the

most serious problem to the cement mills because about two-third of the current assets of mills

are blocked in inventories. The turnover of working capital is largely governed by the turnover

of inventory. It is therefore quite natural that inventory which helps in maximize profit occupies

the most significant place among current assets

Inventories consist of raw materials, stores, spares, packing materials, coal, petroleum

products, works-in-progress and finished products in stock either at the factory or deposits. It

is most important component of current assets in the cement industry and was 42 per cent of

total current assets for sample companies as on March 31, 2004. In other industries too it is

very important component of total investment.

The maintenance of inventory means blocking of funds and so it involves the interest and

opportunity cost to the firm. In many countries especially in Japan great emphasis is placed on

inventory management. Efforts are made to minimize the stock of inputs and outputs by proper

planning and forecasting of demand of various inputs and producing only that much quantity

which can be sold in the market.

The inventory cost is not only interest on stocks but also cost of store building for storage,

insurance and obsolesce and movement of inputs from place of storage to the factory where the

materials have to be finally used to convert them into finished goods. In japan industries have

adopted concept of JIT (Just in Time) and components, materials are received when required

for which detailed instructions are given to suppliers.

There are many engineering companies who receive components directly at assembly point and

that too only for 3-4 hours requirements at a time. Even in case of bulk materials like iron ore,

which is imported from abroad, the minimum possible inventory is kept.

As against this by and large in India the inventory of coal, raw materials and packing materials

is very high and many items become junk or obsolete causing heavy loss to the enterprise. Lack

of inventory planning in India has been pointed out by various committees but due to

uncertainties in supplies, problem of timely receipt of railway wagons, lack of planning and

unreliable suppliers the investment in inventories is quit high.

Objectives of Inventory Management

The primary objectives of inventory management are:

(i) To minimize the possibility of disruption in the production schedule of a firm for want of

raw material, stock and spares.

(ii)To keep down capital investment in inventories.

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 35

So it is essential to have necessary inventories. Excessive inventory is an idle resource of a

concern. The concern should always avoid this situation. The investment in inventories should

be just sufficient in the optimum level. The major dangers of excessive inventories are:

(i) The unnecessary tie up of the firm’s funds and loss of profit.

(ii) Excessive carrying cost, and

(iii) The risk of liquidity.

The excessive level of inventories consumes the funds of business, which cannot be used for

any other purpose and thus involves an opportunity cost. The carrying cost, such as the cost of

shortage, handling insurance, recording and inspection, are also increased in proportion to the

volume of inventories. This cost will impair the concern profitability further.

On the other hand, a low level of inventories may result in frequent interruptions in the

production schedule resulting in under-utilization of capacity and lower sales. The aim of

inventory management thus should be to avoid excessive inventory and inadequate inventory

and to maintain adequate inventory for smooth running of the business operations. Efforts

should be made to place orders at the right time with the right source to purchase the right

quantity at the right price and quality. The effective inventory management should

(i) Maintain sufficient stock of raw material in the period of short supply and anticipate price

changes.

(ii) Ensure a continuous supply of material to production department facilitating uninterrupted

production.

(iii) Minimize the carrying cost and time.

(iv)Maintain sufficient stock of finished goods for smooth sales operations.

(v) Ensure that materials are available for use in production and production services as and

when required.

(vi) Ensure that finished goods are available for delivery to customers to fulfil orders, smooth

sales operation and efficient customer service.

(vii) Minimize investment in inventories and minimize the carrying cost and time.

MANAGEMENT OF RECEIVABLE

INTRODUCTION:

Management of trade credit is commonly known as Management of Receivables. Receivables

are one of the three primary components of working capital, the other being inventory and cash,

the other being inventory and cash. Receivables occupy second important place after

inventories and thereby constitute a substantial portion of current assets in several firms. The

capital invested in receivables is almost of the same amount as that invested in cash and

inventories. Receivables thus, form about one third of current assets in India. Trade credit is an

important market tool. As, it acts like a bridge for mobilization of goods from production to

distribution stages in the field of marketing. Receivables provide protection to sales from

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 36

competitions. It acts no less than a magnet in attracting potential customers to buy the product

at terms and conditions favorable to them as well as to the firm. Receivables management

demands due consideration not financial executive not only because cost and risk are associated

with this investment but also for the reason that each rupee can contribute to firm's net worth.

MEANING AND DEFINITION:

When goods and services are sold under an agreement permitting the customer to pay for them

at a later date, the amount due from the customer is recorded as accounts receivables; So,

receivables are assets accounts representing amounts owed to the firm as a result of the credit

sale of goods and services in the ordinary course of business. The value of these claims is

carried on to the assets side of the balance sheet under titles such as accounts receivable, trade

receivables or customer receivables. This term can be defined as "debt owed to the firm by

customers arising from sale of goods or services in ordinary course of business." 1 According

to Robert N. Anthony, "Accounts receivables are amounts owed to the business enterprise,

usually by its customers. Sometimes it is broken down into trade accounts receivables; the

former refers to amounts owed by customers, and the latter refers to amounts owed by

employees and others".

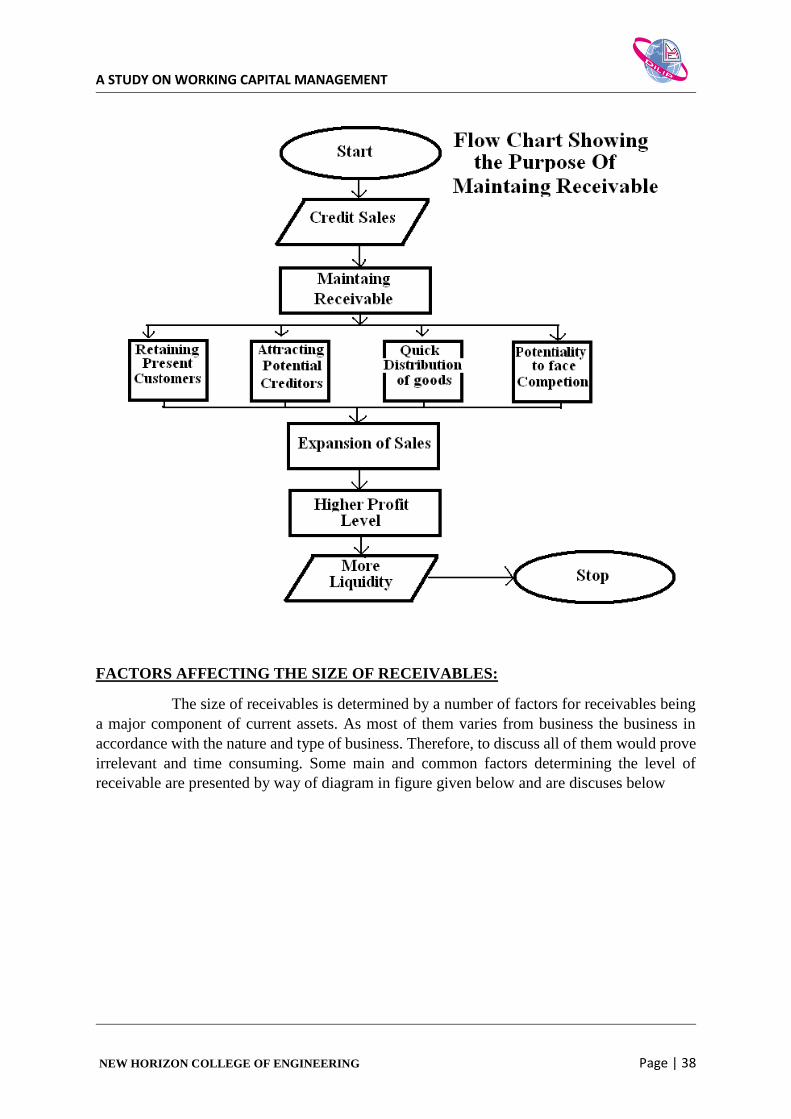

Generally, when a concern does not receive cash payment in respect of ordinary sale of its

products or services immediately in order to allow them a reasonable period of time to pay for

the goods they have received. The firm is said to have granted trade credit. Trade credit thus,

gives rise to certain receivables or book debts expected to be collected by the firm in the near

future. In other words, sale of goods on credit converts finished goods of a selling firm into

receivables or book debts, on their maturity these receivables are realized and cash is generated.

According to prasanna Chandra, "The balance in the receivables accounts would be; average

daily credit sales x average collection period."

The book debts or receivable arising out of credit has three dimensions:

It involves an element of risk, which should be carefully assessed. Unlike cash sales credit

sales are not risk less as the cash payment remains undeceived.

It is based on economics value. The economic value in goods and services passes to the

buyer immediately when the sale is made in return for an equivalent economic value expected

by the seller from him to be received later on.

plies futurity, as the payment for the goods and services received by the buyer is made

by him to the firm on a future date.

The customer who represent the firm's claim or assets, from whom receivables or book-debts

are to be collected in the near future, are known as debtors or trade debtors. A receivable

originally comes into existence at the very instance when the sale is affected. But the funds

generated as a result of these ales can be of no use until the receivables are actually collected

in the normal course of the business. Receivables may be represented by acceptance; bills or

notes and the like due from others at an assignable date in the due course of the business. As

sale of goods is a contract, receivables too get affected in accordance with the law of contract

A STUDY ON WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE OF ENGINEERING Page | 37

e.g. Both the parties (buyer and seller) must have the capacity to contract, proper consideration

and mutual assent must be present to pass the title of goods and above all contract of sale to be

enforceable must be in writing. Moreover, extensive care is needed to be exercised for

differentiating true sales form what may appear to be as sales like bailment, sales contracts,

consignments etc. Receivables, as are forms of investment in any enterprise manufacturing and

selling goods on credit basis, large sums of funds are tied up in trade debtors. Hence, a great

deal of careful analysis and proper management is exercised for effective and efficient

management of Receivables to ensure a positive contribution towards increase in turnover and

profits.

When goods and services are sold under an agreement permitting the customer to pay for them

at a later date, the amount due from the customer is recorded as accounts receivables; so,