Internship Report On Performance Appraisal and its Effect on ...

Upload

khangminh22Category

view

1download

0

INTERNSHIP REPORT ON

A STUDY ON INSURANCE POLICIES AT

LIFE INSURANCE CORPORATION OF INDIA

BY

PRADEEP.R

1NZ14MBA08

SUBMITTED TO

VISVESVARAYA TECHNOLOGICAL UNIVERSIYTY, BELGAUM

In partial fulfilment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

INTERNAL GUIDE EXTERNAL GUIDE

Dr. RAVICHANDRA REDDY Mr. GOPAL REDDY

PROFESSOR SENIOR GRADE FDA

NEW HORIZON COLLEGE OF ENGINEERING

DEPARTMENT OF MANAGEMENT STUDIES

OUTTER RING ROAD, BELLANDUR POST, NEAR

MARARTHATAHLLI, BENGALURU 560103

2014-2016

2014-2016

ACKNOWLEDGEMENT

I wish to pledge and reward my deep sense of gratitude for all those who have made this

project come alive.

I would like to express my heart-felt gratitude to Dr. MANJUNATHA, Principal, New

Horizon College of Engineering, for his moral support throughout the course of my project.

I would like to express my heart-felt gratitude to Dr. SHEELAN MISRA, Head of

Department of Management Studies, New Horizon College of Engineering for her valuable

suggestions and moral support throughout the course of my project.

I am gratefully indebted to my internal faculty guide, Dr. RAVICHANDRA REDDY,

Professor, Department of Management Studies, New Horizon College of Engineering, for

encouraging me and for her constant support throughout the course of the project and helping

me complete it successfully.

A special note of gratitude goes to my external guide Mr. GOPAL REDDY, general

manager at The Elite Ford for providing me an opportunity to work in this corporate exposure

and for his support and guidance in this endeavor.

I wish to thank all the people who have helped me to work on my project. I finally thank my

family and friends for their constant support and guidance.

Regards,

PRADEEP.R

TABLE OF CONTENT

CONTENT PAGE NO

CHAPTER 01 INTRODUCTION

1.1 Introduction of the Study 01

1.2 Objectives of the Study 01

1.3 Problem Statement 02

1.4 Scope of the Study 02

1.5 Research Methodology 02

1.6 Literature Review 03

1.7 Limitations of the Study 05

CHAPTER 02 INDUSTRY AND COMPANY PROFILE

2.1 Industry Profile 06

2.2 Company Profile 09

2.3 Mission and Vision 12

2.4 Infrastructure and Network 13

2.5 Competitors Information 14

2.6 Future Growth 15

2.7 SWOT Analysis 16

CHAPTER 03 THEORITCAL BACK GROUND OF THE STUDY

3.1 Meaning of Insurance 18

3.2 Features of Insurance 18

3.3 Types of Insurance Policies at LIC 19

3.4 Claim Settlement procedure of insurance policies 35

CHAPTER 04 DATA ANALYSIS AND INTERPRETATION 39-58

CHAPTER 05 FINDINGS SUGGESTIONS AND CONCLUSION 59-61

BIBLIOGRAPHY

ANNEXTURE

LIST OF TABLES

TABLE

NO PARTICULARS

PAGE

NO

4.1 TABLE SHOWING FIRST YEAR PREMIUM IN INDIVIDUAL

ASSURANCE 39

4.2 TABLE SHOWING NET PREMIUM INCOME

41

4.3

TABLE SHOWING FIRST YEAR PREMIUM OF INDIVIDUAL

PENSION SCHEMES 43

4.4 TABLE SHOWING GROUP INSURANCE PREMIUMS 45

4.5 TABLE SHOWING GROUP SUPERANNUATION PREMIUM

47

4.6 TABLE SHOWING JEEVAN AROGYA

49

4.7 TABLE SHOWING HEALTH PROTECTION PLUS

51

4.8 TABLE SHOWING MATURITY AND DEATH CLAIMS

53

4.9

TABLE SHOWING DISCONTINUED POLICIES IN THE YEAR

2014-15 55

4.10

TABLE SHOWING INDIVIDUAL NEW BUSINESS

PRODUCED AS PER CHANNEL WISE 57

LIST OF GRAPHS AND CHARTS

GRAPH

NO PARTICULARS

PAGE

NO

4.1 GRAPH SHOWING FIRST YEAR PREMIUM IN INDIVIDUAL

ASSURANCE 40

4.2 GRAPH SHOWING NET PREMIUM INCOME

42

4.3

GRAPH SHOWING FIRST YEAR PREMIUM OF

INDIVIDUAL PENSION SCHEMES 44

4.4 GRAPH SHOWING GROUP INSURANCE PREMIUMS 46

4.5 GRAPH SHOWING GROUP SUPERANNUATION PREMIUM

48

4.6 GRAPH SHOWING JEEVAN AROGYA

50

4.7 GRAPH SHOWING HEALTH PROTECTION PLUS

52

4.8 GRAPH SHOWING MATURITY AND DEATH CLAIMS

54

4.9

GRAPH SHOWING DISCONTINUED POLICIES IN THE

YEAR 2014-15 56

4.10

GRAPH SHOWING INDIVIDUAL NEW BUSINESS

PRODUCED AS PER CHANNEL WISE 58

EXECUTIVE SUMMARY

Life Insurance Corporation (India) is an Indian state-owned insurance group and investment

company headquartered in Mumbai. It is the largest insurance company in India with an

estimated asset value of ₹1560482 crores, The Life Insurance Corporation of India was founded

in 1956 when the Parliament of India passed the Life Insurance of India Act that nationalized the

private insurance industry in India. Over 245 insurance companies and provident societies were

merged to create the state owned Life Insurance Corporation.

I have taken past five years data for this project. This study has been made entirely on insurance

policies and to give suggestions for the problems like fluctuations in the revenue from premiums

and discontinuing policies at Life Insurance Corporation of India.

The suggestion to the company has been given on trend and comparative analysis of the certain

plans and policies, it is noticed that the company’s revenue and policyholders will be changing

due to external factors. The company should also have to do individual promotion of the

insurance plans for people to attract them, and it should not depend more on one channel of

marketing, it should follow up on the insurance premium to be paid and this study also tells it

can improve and overcome its problems

And finally it can be concluded that the LIC is leading life insurance company in the India, and

even though company is facing problems in certain plans/schemes, the company has been

generating its revenue at good level and it can also be overcome by the company if they take

proper measures based on suggestion

1

CHAPTER-01

INTRODUCTION

1.1 INTRODUCTION OF THE STUDY

The report basically deals with “Insurance policies of LIC (India)”. The insurance policies play a

very important role in generating revenue for the insurance company, in this report I have tried to

study the different types of insurance policies and their individual revenue, comparative study of

past 5 years revenue generation contribution to the organization and also insurance settlement

procedure in the organization.

TITLE OF THE STUDY

A study on insurance policies at Life Insurance Corporation of India

1.2 OBJECTIVES OF THE STUDY

The present study has being under taken to meet the following objectives

To analyze the insurance policies premium’s from over the period of 5 years.

To understand and eligibility and condition’s of different types of insurance plans at Life

Insurance Corporation of India.

To analyze and understand about the death insurance policy claim settlement

procedure/process at Life Insurance Corporation of India.

To analyze on discontinued policies at life insurance Corporation of India.

To provide suggestions to overcome the problems faced by Life Insurance Corporation of

India

2

1.3 PROBLEM STATEMENT

In life insurance corporation of India the company is getting less premium amount from past five

year in some of the plans and also the policies were discontinued by the policy holders and in the

2014-15 the company has lost around 6 % of market, it has been focused to give suggestion to

overcome the problems and to improve company’s performance.

1.4 SCOPE OF THE STUDY:

The scope of the study is to know and understand the different insurance plans at Life Insurance

Corporation of India and their eligibility criteria, terms and conditions of plans and also to study

about the death settlement claim procedure in the company.

1.5 RESEARCH MTHODOLOGY

The project was carried based on descriptive research, to some extent it there was a casual

research to and also the available resources, facts, information and analyze this to make a critical

evaluation of the materials.

Data collection

Primary Information:

Primary information was been collected in the method of personal interview with direct contact

technique, the method which was used to gather the information is “Personal interview" method.

The personal interview and discussion was made with Manager, Agents and other personnel

within the organization for this purpose

.

Secondary Information:

Manuals

Annual Reports

Company Brochures

3

1.6 Review of Literature

M.K Khan. (1978) accomplishments was made to understand the open doors and prediction

within the career of an additional security half. Khan clarifies regarding what a good career is

and the way a good career have to be compelled to be for giving of additional security things.

there's no age barrier what is more, it needs no past word connected expertise nevertheless one

should be associate professional what is a lot of, equipped for creating opportunity in structure

identity. The link of life policy operators with customers isn't impermanent and also the

management rendered has no substitute. He likewise sees that disaster policy operators stays, one

would possibly say, lasting server to the insurers.

Raj Kumar (1985) sees that promoting is to impact a client, who has a constrained spending

force and it appears to work through acquainting spreading news over gear-tooth latency and

picture building enhancing piece of the overall industry, instructing, useful and to have

employees support. To the extent insurance business cares, confusion may be a typical issue and

therefore the pre-testing uncovered that the overwhelming majority of the made people square

measure connected with insurance and Raj saw that the behavior of insurance business to the

overall population is consistently uncalled for.

V. Shesha (1986) in his editorial entitled "Policy Development" has examined different

problems associated with growing latest polices, for example, the significance of growing latest

plans & different issues included in the advancement of new plans in Company. He proposed the

requirement for including auxiliary advantages, for example, mischance advantages,

hospitalization and disablement advantages.

Ashis Roy (1987) in his editorial entitled "We Take Care for our Customers" has inspect the

nature and characters of improved client administration to policyholders conjointly, has

underscored the requirement for the quality in management. Roy has proposed a point note on

the various strides to be taken by the Life Insurance Companies to enhance the client

4

administration, for instance, developing the programs as directed by Company to its operators

and representatives ect, opening new branches and arranging of PCs in insurance branch

workplaces.

B.S.R Rao and Appa Machiraju (1988) in their article entitled " Insurance and Emerging

Trends in Financial Services Market", battles that the specialists of additional security got to

enhance their administrations to the extent of cash related specialist. The creators felt that the

adjustment within the financial scenario would facilitate the organization in higher

administrations field.

M. Seetaramaiah. (1992) in his article entitled "Vacillations in New Business" distinguished the

need behind substantial work load on new business amid the year finishing term. He planned a

many stages to overcome them. They’re motility the 6 months records in September, giving

substantial rebate for the premium got in to the start with quarter, giving an uncommon rebate of

premium in the incline months, and finishing the advancement and posting of authorities by the

principal week of April. Done

Shesha Ayyer, V. (1999) in his article entitled "New Insurance Products in the Next Century"

communicated his perspectives about new items. The likelihood of the matured living too long

has turned out to be genuine due to headway in therapeutic offices. Annuity plans have along

these lines gotten to be prominent however at a moderate pace. Separation rates are expanding

and the guarantor can investigate the issue and acquaint new plans with fit them.

A study led by Rajesham and K Rajender. (2006) article "Changing Scenario of Insurance

Sector" Indian Journal of showcasing uncovered that insurance organizations of India are

required to think of multi-advantage approaches counting tax cuts with quality based convenient

client administrations and need to center on medical coverage which is one of the undiscovered

zones of insurance including administrations through creative items, savvy advertising and

forceful conveyance with web office with much individual consideration straightforwardness and

5

adaptability to increment the quality and volume of insurance business. Today, the emphasis is

on offering more items to existing clients to enhance benefit, along these lines client - centered

techniques require a compelling CRM guaranteeing insurance firms screen the ebb and stream of

client conduct, giving them an all encompassing 360-degree view for their clients.

1.7 Limitations of the study

Company policy has restricted to access of vital information.

Trend analysis explains the relationship based on past information while users are more worried

about current and future information.

It was difficult to study all the types of insurance policies because of time constrain.

6

CHAPTER-02

INDUSTRY AND COMPANY PROFILE

2.1.1 INDUSTRY PROFILE

A insurance industry which deals with transfer of risk, it is an risk-transfer method that ensures

completely or partial monetary damage or loss occurred by any incident that is on the far side the

management of the insured party , typically insurance a contract (policy) during which a private

receives monetary policy against losses from associate degree insurer.

2.1.2 INSURANCE DEFNITION

American Risk and Insurance Association as given the defined as process of pooling the

expected losses by transmit of such risk to insurer financial institution who comply with

indemnify insured for such loss, to supply the opposite primary edges on their incidence or to

provide the services linked with the chance.

2.1.3 INSURANCE MEANING

A agreement of compensation for particular upcoming losses in return for a periodic payment.

Insurance is constructed to defend the monetary well being of a human being, company or any

other body in the case unpredictable loss. If the insurer Is going agree up on the terms of an

insurance policy then it creates a contract among the insured and insurer for that the insurer

should pay the premiums and company/insurer agrees to pay the sum of amount to the insurer

upon the occurrence of a particular event or events.

7

2.1.3 INSURANCE INDUSTRY IN INDIA

Life as well as general insurance in Bharat is incredibly giant area with the insurance premiums

volume for two.5% of the country's Gross domestic product whereas general insurance premiums

to zero.64% of India's GDP. The Insurance business in Bharat has versed variety of changes,

notably in from twenty years back once the government of Bharat in 1999 started the insurance

business by permitting non-public firms to control insurance and additionally granting FDI up to

twenty sixth. Indian insurance business is set to be a booming market were each international

insurance underwriter wanting to get the shares.

The Insurance business composed primarily of Insurance carriers, Insurance agencies,

brokerages, unremarkably Insurance carriers are larger firms that give insurance and takes the

risks coated by policy. Insurance brokerages and agencies are selling insurance policies for the

insurers and a few of those institutions are directly connected with explicit insurers and sell those

carrier's policies, several are freelance and that they are unengaged to market type of insurance

carriers. Additionally they additionally give supporting services i.e. alternative insurance-related

services, like claims adjustment, third party insurance services and pension funds.

The insurance business in Bharat have fifty three insurance firms of that twenty four firms ar in

insurance business and twenty nine are in non-life insurers, Among the insurance, insurance

corporation of India is that the just one public sector in India. Excluding that, the non-life

insurers there are half-dozen public sector insurers. Additionally to those, there's one national re-

insurance, viz. General Insurance of Bharat.

Out of twenty nine non-life insurance firms, 5 non-public sector firms are registered to

underwrite policies notably in personal accident, health and travel insurance segments. they're

Allied insurance company and Star health inc underwriter restricted, Phoebus Apollo Munich

insurance Company restricted, gamma hydroxybutyrate Bupa health Co restricted, Religare

insurance Co. restricted and Cigna TTK insurance Company restricted and there are a pair of

additional specialized insurers that comes beneath public sector they're credit Guarantee

Corporation of Bharat and Agriculture insurance underwriter restricted.

8

HISTORY OF INSURANCE INDUSTRY IN INDIA

In India, Insurance trade has the implanted history, we tend to perceive by the writings of

Yagnavallkya, Kautillya, and Manusmethi. The writings talks regarding pooling of

resources/wealth that might be re-distributed in times of events like fireplace, floods epidemics

and famine. We will say this was the model of contemporary day insurance within the sort of

marine trade loans and insurance contracts. Insurance in India has been evolved quickly over the

period.

In 1818 the Oriental Life Insurance Co was established with Advent of life insurance Company

in India. However the company was failed to operator successfully and ended its operation in the

year 1834, but in the year 1829 the Madras Equitable had started to operate through life

insurance operations, British Insurance act came into force in India in the 1870 and in that

movement the Foreign insurances offices played a dominated role, some of the foreign

companies are as follows Liverpool, Albert Life Insurance, London Global Insurance and Royal

Insurance, so it was very hard for Indian companies to face the competition.

The Indian Life Assurance Companies Act, 1912 is the first constitutional measure which was

enacted to standardize the life insurance operations and Indian Insurance companies Act was

came into force to enable the government to collect the statistical data about life and other

insurances which was carried out by Indian as well as foreign insurance companies in India, with

the view to protect the interest of the Insurance public they consolidated and amended by the

insurance Act, so that makes ample provisions for successful control on operations of the

insurance behavior.

The Insurance amendment Act of 1950 was terminated principal agencies, but there was a huge

figure of insurance business were operating and the competition level was high and there was

also allegation that some of the insurance companies are doing illegal practices, so they decided

to nationalize the insurance operations.

In the year 1956 the Life insurance business was nationalized and in the same year the Life

Insurance Corporation was started and LIC acquired 153 Indian, 17 foreign insurers and also 75

provident society’s, totally it was 245 insurers in all.

9

The Life insurance Corporation of India was playing as monopoly in insurance industry in India

till 1990's

The Government of India then introduced the Insurance regulatory and development authority

Act in the year 1999, in that way de-regulating the insurance business and permitting non-public

firms into the operations of insurance. In recent years several non-public firms entered within the

Insurance sector of India. Firms with equal strength competitive within the Indian insurance

market. Currently, in India solely two million folks (0.2 % of total population of one billion), ar

coated beneath Medi claim, whereas in developed countries like America regarding seventy five

take advantage of the population ar coated beneath some insurance policies. With additional and

additional non-public players within the sector this situation could amendment at a speedy pace.

2.2.1 COMPANY PROFILE

Introduction to Life Insurance Corporation of India

Life Insurance Corporation of India (LIC) was started within the year 1956, by an Act of

legislature, namely, Insurance Corporation Act 1956, with complete capital involvement from

Government of Republic of India.

The minister of finance at that point Shri Deshmukh, whereas introducing the bill, draw the

objectives of LIC therefore to carry out the operations with the economical and a lot of

economically, and a strength of trusteeship to indict a premium no above bonded by firm

calculator consideration to take a position the money for exploit most yield for the insurers

according to protection of the capital to deliver correct and economical services to insurers, by

this means creating insurance widespread. Since nationalization, LIC has designed up a large set

of connections of 2049 branches, one hundred divisions and seven zonal offices meet the state.

The insurance Corporation of Republic of India also' operates business in overseas and has

offices and branches in country, Mauritius and GB. LIC is related to joint ventures within the

field of insurance with alternative countries, viz, Ken-India, Nairobi, United Oriental Assurance

10

Company restricted, Assurance Company restricted, Kuala Lumpur and insurance Corporation

(International) .

The LIC has noncommissioned a joint endeavor organization within the year 2000 in national

capital, Kingdom of Nepal for the sake of Insurance policy Company (Nepal) forced during a

joint effort with Vishal Bunch Restricted, a part trendy Gathering. A seaward organization L.I.C.

(Mauritius) Seaward Restricted has in addition been started in 2001 to faucet the African policy

market.

History of Life Insurance Corporation of India

India Insurance agency (1896) was likewise one in every of such organizations enlivened by

loyalty. The Swadeshi development of 1905-1907 offered ascends to additional insurance

agencies. The United Bharat in Madras, National Indian and National Policy in Calcutta and

therefore the Co-agent Certification at metropolis was discovered in 1906. In 1907, geographic

area Co-agent Insurance agency took its introduction to the globe in one in every of the rooms of

the Jorasanko, place of the large author Tagore, in Calcutta. The Indian business, General

Affirmation and Swadeshi Life (later metropolis Life) were a share of the organizations

discovered amid an equivalent amount. Before 1912 Bharat had no enactment to manage policy

business.

Insurance agencies Act, therefore the Provident quality Act were passed. The policy

Organizations Act, 1912 created it essential that the premium charge table and periodical

valuation of organizations need to be confirmed by a statistician. In any case, the Demonstration

unintegrated within the middle of out of doors and Indian organizations on varied records, golf

stroke the Indian organizations off guard.

The ab initio a few years of the 20 th century saw a part of development in policy business. From

forty four organizations with mixture business-in-power as Rs.22.34 crore, it rise to 176

organizations with mixture business-in-power as Rs.296 large integer in 1938. Amid the growing

of insurance agencies varied monetarily unsafe considerations were in addition glided that

fizzled dispiritedly. The Policy Demonstration 1938 was the principal enactment overseeing

11

additional security moreover as non-Insurance policy to convey strict state management over

policy business. The interest for nationalization of additional security business was remodeled

and once more within the past but it accumulated force in 1944 once a bill to change the policy

Act 1938 was given within the Authoritative Gathering. yet, it had been abundant shortly the

nineteenth of Gregorian calendar month, 1956, that policy in Bharat was nationalized. Around

153 Indian insurance agencies, sixteen foreign organizations and seventy five provident were in

service in Bharat at the season of nationalization. Nationalization was good in 2 stages originally

the administration of the organizations was assumed management by methodology for a Statute,

and later, the possession too by methodology for a way reaching bill. The Parliament of Bharat

passed the Life coverage Organization Follow abreast of the nineteenth of June 1956, and

therefore the policy Company of Bharat was created on 1st Sep, 1956, with the target of

scattering additional security a good deal all the additional usually and specifically to the country

territories with a perspective to attain each single insured individual within the nation, giving

them satisfactory monetary fund unfold at a wise expense.

LIC had five zonal workplaces, thirty two divisional workplaces and 209 branch workplaces,

except for its company workplace within the year 1956. Since insurance contracts area unit end

of the day contracts and amid the money of the strategy it needs an assortment of administrations

want was felt within the later on years to increase the activities and spot a branch workplace at

every region head quarters. Re-association of LIC occurred and enormous quantities of latest

branch workplaces were opened, as a delayed consequence of re-affiliation change limits were

listed to the branches and branches were created bookkeeping units. It worked considers with the

execution of the association. it'd be seen that from around 200 crores of latest Business in 1957

the corporate reached a 2000 crores simply within the year 1969-70, and it took a further ten

years for LIC to cross 2000 large integer sign of latest business. Yet, with re-association

occurrence within the middle eighties, by 1985-86 LIC had effectively crossed 7000 large integer

mixture secure on new approaches.

Today LIC capacities with 2048 utterly mechanized branch workplaces, one hundred divisional

workplaces, seven zonal workplaces and therefore the company workplace. LIC's Wide Region

System covers one hundred divisional workplaces and interfaces each one of the branches

12

through a subway vary System. LIC has pledged with a number of Banks and Administration

Suppliers to supply on-line premium assemblage workplace in picked urban areas. LIC's ATM

premium portion workplace is an improvement to consumer comfort. Beside on-line Stands and

IVRS, info Focuses are licensed at Pune, Mumbai, Bangalore, Ahmedabad, Chennai, Kolkata,

Hyderabad New Delhi and various completely different urban areas. With a dream of giving

simple access to its insurer, LIC have emotional its settlement workplaces. The satellite

operating environments area unit humbler, throw and nearer to the consumer. The digitalized

proceedings of the satellite operating environments can support where change and various

completely different accommodations afterward.

LIC keeps on being the prevailing life safety web supplier even within the modified scenario of

Indian policy and is stirring fast on another development direction surpassing its own specific

past records. LIC have issued over one large integer ways amid this year. it's crossed the point of

reference of supply one,01,32,955 new methods by fifteenth Gregorian calendar month, 2005,

posting a solid development rate of sixteen.66% over the relating time of the sooner year.

From that time to currently, LIC have crossed varied developments and has set exceptional

execution records in numerous components of policy business. constant thought processes that

roused our progenitors to amass policy into presence this nation move U.S. at LIC to require this

message of insurance to light-weight the lights of security in no matter range homes as may be

expected underneath the circumstances and to push the overall population in giving protection to

their family.

2.3 VISION AND MISSION

2.3.1 Vision

"A Trans-nationally competitive financial conglomerate of significance to societies and pride of

India"

13

2.3.2 Mission

"Ensure and enhance the quality of life of people through financial security by providing

products and services of aspired attributes with competitive returns, by rendering resources for

economic development".

2.4 INFRASTRUCTURE AND NETWORK

LIC has a good base and network. because the association has 2048 fully automatic branch

workplaces, a hundred divisional workplaces, seven zonal workplaces and therefore the company

workplace. LIC's Wide Zone System covers a hundred divisional workplaces and interfaces each

one of the branches through a subway Region System. LIC has betrothed with some banks and

administration suppliers to supply on-line premium gathering workplace in chosen cities. The

Organization specifically works through its Branch workplaces at national capital in Mauritius,

Suva and Lautoka in country and at Wembley within the uk. Amid the year 2008-09, these 3

outside Branches along issued one,073 arrangements with Total bonded of US$ eighty five.1

million and 1st premium pay of US$ four.52 million.

PRODUTS AND SUBSIDIARIES

LIC renders different services like Life Insurance, Mutual fund, Investment Management and

Health Insurance.

LIC is having the accompanying subsidiaries.

LIC Housing Finance

LIC Nomura Mutual fund

LIC International

LIC Pension Plan

14

LIC Card Subsidiaries

2.5 COMPETITORS

SBI Life Insurance

SBI Insurance policy is a joint endeavor between State Bank of India and BNP Paribas Cardif.

SBI possesses 74 for each penny of the aggregate capital and BNP Paribas Cardif the remaining

26 for every penny. SBI insurance policy has an approved capital of Rs 2,000 crores (US$

332.96 million) and a paid up capital of Rs 1,000 crores (US$ 166.56 million).

SBI Life has a special multi-appropriation model enveloping dynamic Bancassurance, Retail

Organization, Institutional Union and Corporate Arrangements conveyance channels.

SBI Life broadly influences the State Bank Bunch relationship as a stage for cross-offering

policy items alongside its various keeping money item bundles, for example, lodging credits and

individual advances. SBI's entrance to more than 100 million records the nation over gives a

dynamic base to policy infiltration over each district and monetary strata in the nation,

accordingly guaranteeing genuine budgetary incorporation. Office Channel, involving the most

gainful power of more than 80,000 Policy Counselors, offers way to entryway policy answers for

clients.

Sahara Life Insurance

SILICL is today’s primary and completely nation-possessed Life coverage Organization within

the non-public dispense with further security Infiltration in India at just about twenty second of

the insured population and premium wage of twenty-two of Gross domestic product, the

gathering considers it to be a high development division of Indian economy. They propelled their

operations on thirty Oct 2004 within the wake of being conceded allow to figure as associate

existence copy arrange in Asian nation by Policy body and Improvement Power on half dozen

February 2004.

ICICI Prudential Life Insurance Company

15

ICICI prudent life insurance business is also a joint endeavor between ICICI Bank, a chief

monetary powerhouse, and prudent plc, a main worldwide cash connected administrations group

headquartered among the UK. ICICI prudent was amongst the foremost private insurance

agencies to start operation in Gregorian calendar month 2000 behind acceptive endorsement

from IRDA.

ICICI prudent life's capital stands rupees 4786 crores (of Walk thirty one, 2014) with ICICI

Bank and prudent holding seventy four and twenty sixth stake on a personal basis. For the money

connected year 2014, the organization has accumulated combination premium of Rs.12419

crores. The organization has resources at a lower place administration of over Rs. 80,100 crores

as on Walk thirty one, 2014.

For as long as decade, ICICI prudent Life coverage has preserved its predominant position (on

new business retail weighted premise) amongst private life keep a duplicate plans among the

state, with Associate in Nursing comprehensive variety of pliant things that address the issues of

the Indian shopper at each progression in life Corporation of India.

2.6 Some Areas of Future Growth

Life Insurance

The traditional life insurance operations as been a little more than a savings policy of the

insurance premium of the LIC. For the new life insurance companies, the Life insurance will

emerge main line business to start.

Health Insurance

Health insurance expenditure in Republic of India is about 6 June 1944 of value, that is far

beyond alternative countries with similar level of economic development in those countries. Of

those, 4.8% is personal and remaining is public. What’s even additional shocking is that 4.7%

square measure out of pocket expenditure. The health care system republic of India has been

principally failure and this creates a chance for insurance corporations to grow in insurance.

16

Thus, personal insurance players have bigger market to sell insurance to a additional variety of

family teams World Health Organization would really like to own health care cowl however

don't have it.

Pension

The rente framework in Asian country is in its early stages. There ar for the foremost half 3

varieties of arrangements: provident assets, tips and advantages stores. an oversized portion of

the rente plans ar certain to government representatives (and some huge organizations). far and

away most of labourers within the casual phase. later on, most laborers do not have any

retirement blessings to fall back on when retirement. All out resources of all the rente arranges in

Asian country add up to not precisely USD forty billion.

In this manner, there is an enormous extension for the advancement of benefits assets in India.

The fund pastor of India has more than once affirmed that a Latin American style change of the

privatized benefits framework in India would be welcome (Roy, 1997). Given every one of the

advantages and disadvantages, it is not clear whether such wholesale privatization would really

advantage India or not (Sinha, 2000).

2.7 SWOT ANALYSIS

STRENGHTS

Largest state-claimed insurance policy organization in India, furthermore the nation's

biggest financial specialist.

Has more than 2000 branches over all parts of India and more than 1000000 specialists.

With Biggest asset base it is the greatest financial specialist in India

Trust Research Advisory's trust report has positioned insurance policy Enterprise of India

(LIC) as the nation's most trusted brand in the managing an account and money related

foundation (BFSI) space, for the second continuous time.

Solid money related position, because of both beneficial business development and

speculation administration LIC monetary record is solid with zero obligation and

17

proceeded with year-over-year development in both shareholders' assets and approach

holders' assets

WEAKNESS

It has a picture of an Administration organization and consequently needs advancement

and innovation

Being an Administration organization, formality and administration causes and issues

like red tape and bureaucracy

Dealing with an immense workforce amid financial emergency implied overburdened to

pay salaries.

OPPURTUNITIES

Utilization of Innovation to give successful administrations to take into account urban

population.

Government plans execution.

THREATS

Financial emergency.

Passage of new NBFCs in the division will affect the market share of the LIC

Differing government policies.

18

CHAPTER-03

THEORETICAL BACKGROUND OF THE STUDY

3.1 Meaning of life Insurance:

Life insurance could be a policy against the loss of financial gain that may result if the insured

died. The named beneficiary receives the issue and is thereby safeguarded from the money

impact of the death of the insured.

3.2 Features of Life insurance:

You get to decide on the simplest coverage possibility, due in cheap premiums.

Based on your life-style, desires and preference, you'll be able to choose from a spread of life

assurance choices starting from pure insurance to hybrid insurance merchandise like ULIPs and

endowment plans wherever you get maturity edges.

Life insurance provides monetary security of your dependents just in case of any contingency.

Additionally, you furthermore may fancy tax edges on differing types of policies beneath

completely different sections of the tax Act, 1961

3.3 DIFEERENT TYPES OF INSURANCE POLICES AT LIC

3.3.1 PENSION PLANS OF LIC

Introduction to Pension plans.

Pension plan are single person plans that look keen on the future and predict money related

strength amid your seniority. This policy is mainly suitable for the older nationals and those are

arranging a future protection, so as to not abandon the best belongings in a living

19

1. JEEVAN NIDHI

This plan is a benefit deferred annuity plan. On living of the insurer past period of the

arrangement the aggregated sum (i.e. amount assured+ bonuses + assured accompaniments) is

utilized to create benefits for the policyholder. The plan additionally gives a risk wrap

throughout the postponement period. The USP of the arrangement being the annuity can initiate

at 40 years. The premium paid is exempt under Sec 80CCC of IT Act.

Silent Features:

A. Definite additions at Rs.50 per 1000 sum guaranteed for every finished year, for the initial

5 years.

B. Involvement in profits: The policy might take an interest in benefits of the Corporation as

of the sixth year onwards and should be qualified for get rewards pronounced according to the

practice of the business.

Benefits of vesting:

1. Choice to go up to 1/3 of the total obtainable on vesting, which could incorporate the total

promised beneath the essential arrange alongside gathered bonded additions, easy stake bonus

and terminal bonus, if any

2. Annuity according to the choice: annuity on the equalization amount if substitution is

worked out, or else annuity on everything.

Annuity Options:

On vesting, the annuity portion, methodology of annuity installment and sort of annuity that

ought to be created accessible to the annuitant can consider the then existing instant annuity

20

arrangement of the life assurance Corporation of Republic of India and its provisions and

conditions. Presently the subsequent choices square measure obtainable below

LIC’s immediate annuities:

1. Annuity for life: Annuity quantity is paid to the life assured till the person is living.

2. The annuity bonded sure as shooting periods: The annuity will be paid to the life assured for

term of five, ten, fifteen, twenty years as selected by him/her, whether or not he/she lives that

amount. When the selected amount, the annuity is paid to the life assured as long as he/she is

living.

3. The annuity with come of damage on death: The annuity is compensated to the life assured as

long the person is alive. On the bereavement of the life assured, the acquisition price of the

payment is paid as compensation. the acquisition price include the full assured to a lower place

the essential set up, the increased secure accompaniments and any increased bonuses, exclusive

of the commuted worth, if any.

4. Increasing regular payment: The annuity will be paid to the life assured untill he/she is living.

The number of regular payment will increase per annum at an easy rate of three each year.

5. Joint life, last survivor annuity: Regular payment is made to the insurers untill him/she is

living. On bereavement of life assured, five hundredth of the regular payment is owed to the

nominative better half as long because the better half is living.

2. JEEVAN AKSHAY VI

About the Plan:

This is an instant annuity arrangement, which will be bought by paying a singular amount. The

arrangement accommodates annuity installments of an expressed sum for the duration of the life

period of the annuitant. Different choices are accessible for the sort and method of installment of

annuities.

21

Alternatives:

The accompanying alternatives are accessible under the arrangement

• Annuity to be paid until the death of the person at identical rate.

• Annuity is to be paid in 5, 10, and 15 or 20 years definite and from that point the length of ilfe.

• The annuity for life with profit of value tag for death of an annuitant.

• Annuity payable forever expanding at a basic rate of 3% p.a.

• Annuity for the life with a procurement of half of the annuity payable to life partner amid

his/her lifetime on death of the annuitant.

• Annuity for life with a procurement of 100% of the annuity to be paid to life partner amid

his/her life span on death of an annuitant.

You might pick any one. When picked, the choice can't be modified.

Conditions of the policy

Mode Minimum Amount (Rs)

Every month 500

Every 4 months 1000

Every 6 months 2000

Every 12

months 3000

22

There is no need of medical examination under this policy.

3. JEEVAN SURAKSHA –I

Product information:

This is deferred annuity plan that permits the policyholder to create provision for subsequent

income later than the chosen period.

Premiums:

Premiums square measure owed every 12, 6, 3 months or during wage subtraction, as chosen by

the insured, all through the period of the policy or until prior to death. Or else, the premium

could also be paid in one payment.

Tax Benefits:

Tax aid under the Sec 80ccc is out there on premiums paid below Jeevan Suraksha I. The

premiums compensated below New JeevanDhara I qualify for tax aid in Sec eighty eight.

Bonuses:

These area unit with-profits plans and participate within the profits of the Corporation’s regular

payment / pension business. Policies get a share of the profits within the variety of bonuses. easy

interest Bonuses area unit declared per thousand total Assured annually at the top of every fiscal

year. Once declared, they type a part of the secured advantages of the set up. Final (Additional)

Bonuses may be collectible provided policy has endured a particular minimum amount.

23

3.3.2 CHILDREN PLANS

1. JEEVAN ANURAG:

Jeevan ANURAG is with benefits arrangement particularly intended to deal with the educational

wants of children. The arrangement can be taken by a guardian on his/her individual life.

Advantages under the arrangement are payable at pre-determined term of time regardless of what

so ever the life assured makes due to the finish of the approach term or kicks the bucket amid the

term of the strategy. Furthermore, this arrangement likewise accommodates a prompt installment

of basic amount assured on death of the life assured amid the period of the approach.

Eligibility and Conditions of the policy

Minimum(Amount in Rs) Maximum

Minimum amount to be assured 50000 No limit

Entry Age of policy holder 20 60

Maturity - 70

Payment Every month, Every Four, Six and Twelve months

Sample Illustration

Premium = 60000

Age =25

24

Policy Term= 25years, Yearly mode

Sum Assured=13,50000

Total Investment= Rs 60000*25= 15,00,000

Bonus Assumptions:

Regular Bonus - Rs.21 per 1000 sum assured at 6% rate of return

Rs.55 per 1000sum assured at 10% rate of return

Terminal Bonus- Rs. 170 per 1000sum assured at 6% rate of return

Rs. 450 1000sum assured at 10% rate of return

Guaranteed Returns:

Beginning of Year 23 = Rs 2,70,000/-

Beginning of Year 24 = Rs 2,70,000/-

Beginning of Year 25 = Rs 2,70,000/-

Maturity Benefit at the End of Year 25 = Rs540000/- + Bonus (Variable)

2. CHILD CAREER PLAN

Child Career it is a reimbursement Endowment Plan for the advantage of a toddler specified total

Assured additionally to Bonus is paid instantly to candidate on death of the Life Insured when

starting of risk. Be that because it might, if the kid outlasts the complete maturity amount, then

he/she can get a hundred and fifth of the total Assured. He/she would get half-hour of the total

Assured aboard unconditional easy interest Bonuses five years before the date of termination of

arrangement period. At that time he/she would get V-day of the total assured within the most up-

to-date four years, 3 years, a pair of years and one year before Maturity of the arrangement.

25

Likewise, once the arrangement develops, he/she would get the remaining V-day of the total

Assured and Final Addition Bonus, if any.

Eligibility and conditions of the policy

Minimum Maximum

Sum Assured 1,00,000 1 crore

Policy period (years) 11 27

Entry age of life to be Insured (years) 0 12

Premium Payment Term (years) 6 Policy Term- 5

Age at maturity (years) 23 27

Payment mode Quarterly, Half Yearly, Yearly

3. CHILDREN DEFERRED ENDOWMENT ASSURANCE PLAN VESTING AT 21

CDA Plan Vesting at 21 is a child policy approach such that the premium is paid till the child

attains the age of 21 years and afterwards child becomes the proprietor of the insurance. if in

case child dies before the policy has been matured, then the Sum Assured alongside Guaranteed

Additions are paid and the policy will be come to end.

26

Eligibility and conditions of policy

Minimum Maximum

Sum Assured 50,000 1 Crore

Policy period (years) 13 50

Entry age of child (Life insured) 0 17

Maturity (years) 30 60

Single premium Not Applicable

Payment modes Quarterly, Half-yearly, Yearly

4. JEEVAN KISHORE SCHEME

Jeevan Kishore policy is an endowment policy for a children such that the amount assured in

addition bonus will be paid for the child advantage on the terms of term maturity. The

parent/guardian can also safeguard his/her child future by deciding on premium waiver

advantage, so that on the off chance that he bites the dust before the approach develops, then the

future premiums will be waived. there are extra rider advantages like premium waiver profit, on

one occasion if the child reaches maturity period, the policy will be transformed to his/her name

and after that he/she can decide on accidental death provision by paying extra amount of

premium.

Eligibility and conditions of the policy

Minimum Maximum

Sum to be assured (in

Rupees) 50,000 40,00,000

Policy period (years) 15 35

Entry age of insured (years) 0 12

Age at maturity (years) 20 45

Payment modes

Quarterly, Half-Yearly, Yearly,

Single

Premium payment period

(years) Equal to Policy Term

27

5. Marriage Endowment or Education Annuity Plan

Marriage endowment or education annuity plan is a child policy such that total assured and in

additionally bonus will be paid for the child advantage on the terms of maturity regardless of the

fact that if the child dies before the maturity. Therefore, nothing is collectable quickly to the

chosen one on death of the life insured, unless unintentional, just the future premiums are waived

and paid by the organization such that the maturity benefit of the total amount assured in addition

to bonus is properly paid.

Eligibility and conditions of the policy

Minimum Maximum

Sum assured (Rupees) 50,000 No Limit

Policy period (years) 5 25

Premium payment period

(years) Equal to Policy Term

Entry age of insurer (years) 18 60

Age at maturity (years) - 70

Payment mode Monthly, Quarterly, Half-Yearly and Yearly

3.3.3 WHOLE LIFE INSURANCE POLICIES

1. THE WHOLE LIFE POLICY

The whole life policy is a straightforward frequent payment whole life policy and with bonus

benefit.

28

In this policy, the premium will be paid for a long time or till the age of 80 years. The life

insured can pull back the amount assured + accumulated bonuses announced below this plan

whenever subsequent of 40 years from the date of commencement of the plan provided that the

life insured have accomplished a base age of 80 years. Be that as it may, if the life insured passes

away, after that his/her dependent will be given the amount assured + accumulated bonuses and

the plan will come to end.

Eligibility and conditions of the policy

Minimum Maximum

Sum to be assured (Rupees) 50,000 No Limit

Policy period (years) Whole Life

Age at maturity (years 80 Whole Life

Payment modes Monthly, Quarterly, Half-Yearly and Yearly

Entry age of insured 15 60

2. JEEVAN ANAND

Jeevan anand is an endowment semen whole life scheme in conjunction with bonus gift. This can

be a 2 times set up if the insured person survives until the tip of the maturity period of the policy.

This policy has an average premium amount, lofty bonus rate and nice liquidity options.

In this set up, the Insured person obtains the guaranteed + bonus as term maturity profit however

the life cowl selected will continue until his/her death. Once more a further adds assured is

compensated at any time the insured dies. So this set up is each endowment set up and an entire

life set up.

However, if the insured he/she dies ahead of the finishing point of premium paying period, i.e. at

intervals the policy term, the whole add assured in conjunction with accumulated bonus is

rewarded to the dependent and also the policy will come to end.

29

There is additionally a further unintentional death and benefit is owed until seventy years elderly

of the life insured.

Eligibility and conditions of the policy

Minimum Maximum

Sum to be assured (Rupees) 1,00,000 No Limit

Policy period (years) 5 57

Premium payment period (years) 5 57

Entry age of insured 18 65

Payment modes Monthly, Quarterly, Half-Yearly and Yearly

Age at maturity - 75

3. JEEVANTARANG

Jeevan Anand is Associate in Nursing endowment seed whole life policy at the side of bonus

advantage. This is often a 2 times benefit arrange if the insured lives until the top of the policy

period. This arranges has regular premium, lofty bonus charge and nice liquidity options.

In this arrange, the life insured obtains the add assured + bonus as term maturity profit however

the life cowl selected continues until his death. once more a further add assured is paid whenever

the life insured passes away. So this arrange is each Associate in Nursing endowment arrange

and an entire life arrange.

On the other hand, if the insured passes away before the completion of premium paying time, i.e.

before the policy term maturity, the complete add assured at the side of increased bonus is paid

to the politico and therefore the policy would come to end.

30

There is conjointly a further unintentional death i.e. accidental and benefit is due until seventy

years older of the life insured

Eligibility and conditions of the policy

Minimum Maximum

Sum to be assured (Rupees) 1,00,000 No Limit

Policy period (years) Whole Life

Age for end of premium payment period (years) - 70

Age at the complation of the accumulated term

(years) 18 -

Payment modes

Monthly, Quarterly, Half-Yearly and

Yearly

Entry Age of Policyholder 0 60

Age at maturity ( years) - 100

3.3.5 PLANS FOR HIGH NET WORTH INDIVIDUALS

1. JEEVAN SHREE-1

Jeevan Shree-I arrange may be a special class arrange because it may be a life assurance policy

particularly for the high web price people. it's essentially AN endowment arrange with restricted

premium paying term that caters to the necessities of high web price people.

In this arrange, premium must be obtained a most amount of sixteen years however the life cowl

continues for the whole policy term of a most of twenty five years. The total assured +

accumulated interest bonus + secure additions would be paid to the life insured on the policy

maturity or to his politico on earlier death of the life insured.

31

Hence this arranges may be a easy Endowment arrange in conjunction with bonus and secure

additions. This arranges caters to the high web price people as a result of the minimum total

assured is Rs 5lakhs.

Eligibility and conditions of the policy

Least amount/years Maximum

Sum to be assured (Rupees) 5,00,000 There is no limit

Policy period (Years) 5 25

Age at maturity - 75

Payment mode Monthly, Quarterly, Half-yearly and Yearly

Premium payment period (Years) 1 16

Entry age of insured 18 65

2.AMULYA JEEVAN-1

Amulya Jeevan is a clean word insurance plan for lofty amount to be assured which is mainly

for policy only. In this scheme, if the insured passes away, the dependent will get the whole

amount assured but not anything else will be paid on the term matured. This policy is only for

lofty amount assured necessities.

Eligibility and conditions of the policy

Minimum Maximum

Sum to be assured (Rupees) 25,00,000 No Limit

Policy period (Years) 5 35

Entry age of policyholder

(years) 18 60

Age at maturity (Years) - 70

Payment mode Single, Half-Yearly and Yearly.

Premium payment

period(Years) Single(premium)

32

3.3.6 Money back policies

1. JEEVAN VARSHA

Jeevan Varsha is truly associate endowment policy with plenty of flexibilities that's sometimes

accessible solely with unit coupled insurance plans. thene it's classified beneath Special Plans.

this can be a non-unit-linked insurance set up with 2 times benefit of add Assured + come of

premium.

During the set up, the premium quantity is determined by the client and he gets 200 times the

monthly premium as add Assured. If the insured lives until the term the whole term, then he/she

will receive maturity sum + loyalty additions. The maturity adds assured depends on totally

different entry ages and policy term and is nominative at the start of the policy.

Now, if insured dies at intervals the policy tenure then his/her pol would receive the add

Assured + come of premiums excluding extra/rider premium and 1st year premium + Loyalty

Addition, if any. Thus, the benefit would be an equivalent regardless of age of entry and policy

term since it depends solely on chosen premium quantity however the Maturity profit would take

issue per varied age of entry and policy term.

Eligibility and conditions of the policy

Minimum Maximum

Sum to be assured (Rupees) 200 times of monthly premium

Policy period (Years) 10 35

Premium payment period (Years) 10 35

Entry age of the insurer 12 60

Age at maturity - 70

Monthly premium (Rupees) Age from 12 to 49 years = Rs250 Rs 10,000/-

Age from 50 to 60 years=Rs400

Payment modes Yearly, Half-yearly, Quarterly, Monthly

33

2. JEEVAN SURABHI PLAN

Jeevan surabhi arrangement of fifteen years is truly a refund arrangement, that is technically

called Associate in Nursing predictable endowment plan. This is often a non-unit connected

insurance ancient arrange wherever the cash is compensated as pre-determined class interval.

The premium is bought solely twelve years however the quilt will be carried out for the whole

term of fifteen years. If the Insured is going to live until the maturity of the policy, then he

would receive half-half of the add assured at the top of four and eight years and also the

outstanding four-hundredth of the add assured at the top of twelve years and life cowl continues

until the policy term will be matured. However, if the insured dies before the policy

term/maturity, then the nominee can obtain the assured amount, that keeps growing up by five

hundredth one time in each 5 years.

Eligibility and conditions of the policy

Minimum Maximum

Sum to be assured (Rupees) 50,000 No Limit

Policy period (Years) 15

Premium payment period (Years) 12

Age at maturity - 70

Payment method Yearly, Half-yearly, Quarterly, Monthly

Entry age of the Insured (Years) 14 55

3 .BIMA BACHAT PLAN

Bima Bachat set up is really one premium a refund set up. This can be a non-unit-linked

insurance ancient set up wherever an exact quantity of cash is paid as pre-decided intervals.

34

during this set up the premium is rewarded one time and V-day of the add assured is paid when

each three years and also the completely single premium paid and loyalty accompaniments are

paid on period maturity. on the other hand, if the life insured passes away before the policy term,

the whole assured amount is compensated regardless of the number of cash compensated as

survival profit.

Eligibility and conditions of the policy

Minimum Maximum

Sum to be assured (Rupees) 20,000 No Limit

Policy period (Years) 9 15

Entry age of the Insurer 15 66

Age at maturity - 75

Payment modes Every month and For every 3,6,12 months

Premium Single premium

35

3.4 CLAIM SETTLEMENT PROCESS

The Claimant/Nominee has to look in to the following details before initiating the claim.

Whether policy is been in force?

Whether insurer has performed his/her obligations?

The policy position as to installment of premium, age of admission, exceptional credit and hobby

if any, legitimate confinements if any.

Whether the occasion has occurred?

What are the commitments accepted under the agreement? Is there any task done under the

approach?

Whether the premium has been paid as on outstanding date with regard to all premiums?

3.4.1 CLAIM SETTLEMENT PROCESS

Passing claim

Stage 01:

The petitioner has to be present the composed implication at the earliest opportunity to empower

the insurance agency to start the case preparing. The case implication ought to comprise of

essential data, for example, approach number, name of the protected, date of death, reason for

death, spot of death, name of the petitioner and so forth .Claim suggestion structure will be

profited from closest branch of the insurance agency or/and by downloading it from the

organization site.

36

Step 02:

The inquirer will be obligatory to give the accompanying reports alongside a petitioner's

announcement:

1. Death Certificate

2. For confirmation of age of the life assured, a proof must be submitted (if not officially given)

3. Deeds of task/reassignments (if required)

4. The original policy document must be there.

5. Whatever other record according to necessity of the safety net provider before of schedule

passing Claim, (If the case has gathered inside of three years from the earliest starting point of

the policy).

The accompanying extra prerequisites might be called for:

1. Explanation from the healing centre if the perished had been admitted to doctor's facility

2. Testament of therapeutic orderly of the expired giving subtle elements of his/her last disease

3. Declaration of internment to be specified by a man of known personality and obligation

attended the cremation or entombment of the dead body of the perished.

4. Authentication by business if the perished was a representative In exceptional cases

according to taking after the poof of death will be not quite the same as the standard particular if

there should arise an occurrence of an air crash the declaration from the aircraft powers would be

fundamental ensuring the guaranteed was a traveller on the plane. If there should arise an

occurrence of boat mishap an ensured extricate from the daybook of the boat is required. In the

event of death from therapeutic causes, the specialists' testament and/or management records

might be required. On the off chance that the life guaranteed had a passing because of

mischance, homicide, obscure/suicide cause the police investigation report, panchanama, after

death report, and so forth would be essential.

37

Step 3:

Accommodation of required documents for claim dispensation for quicker claim handling, it is

vital to that the inquirer submits entire documents as right on time as could be expected under the

circumstances.

Step 4:

Settlement of the claim according to the guidelines of 8 of the IRDA (Policy holder's interest)

Regulations 2002, the backup plan is essential to settle a case inside of 30 days of acceptance of

all archives including illumination looked for by the safety net provider. In the event that the

case requires further examination, the safety net provider needs to finish its systems inside of six

months from accepting the composed implication of case. In the wake of getting the required

reports the organization computes the sum payable as per the arrangement. For this reason, a

structure is filled in which the information of the policy, reward, designation, task and so on

ought to be entered by suggestion to the policy ledger slip. In the event that an advance exists

under the arrangement, then the area managing advance is reached to give the subtle elements of

extraordinary advance and intrigue sum, which will be deducted from the gross approach add up

to ascertain net payable case sum. For the most part all case installments would be made through

the electronic asset exchange. Development and survival claims: The installments by the

guarantor to the safeguarded on the date of development is called development installment. The

sum payable at the season of the development incorporates an entirety guaranteed and

extra/impetuses, if any. The backup plan sends ahead of time them suggestion to the safeguarded

with a clear release structure for filling different points of interest in it. It is to be come back to

the workplace alongside Original policy archive, identification evidence, age confirmation if age

is not as of now submit, obligation/reassignment, if any and copy of inquirer's bank passbook

and cancelled Check. Settlement technique for development case is straightforward following

receipt of finished and stamped release structure from the individual qualified for the approach

cash alongside arrangement records, claim sum will be paid by record payee check. With respect

to guarantees certain focuses are to be recollected. If the life guaranteed is accounted for to have

38

kicked the bucket after the date of development however before the receipt is released, the case

is to be dealt with as the development case and paid to the legitimate beneficiaries. For this

situation demise testament and confirmation of title is essential. Where the guaranteed is known

not rationally unhinged, a declaration from the court of law under the Indian Lunacy Act

delegating a man to go about as watchman to deal with the properties of the insane person ought

to be called. For the survival benefit claim, Policy bond and release voucher is required. Rider

Claims: The life coverage policy can be joined with various riders such as unplanned rider,

Critical ailment Rider, Hospital money Rider, waiver of Premium Rider and so forth. For various

Riders diverse procedures will be picked claim settlement. Now and again the case might

continue and additionally with the passing claim (Like waiver of premium, unintentional demise

Rider and so on). Be that as it may, in some different cases diverse records can be required for

alongside the appropriately filled claim structure and policy copy: For critical sickness,

important therapeutic archives, for example, first examination report, Doctor's remedy,

Discharge summery and so on are required for accidental handicap rider, Attested duplicate of

FIR, Doctor certificate of inability, Photograph of an harmed with reflecting disablement,

Original medical bills with solutions/treatment papers and so on are required. For Hospital

money rider restorative archives are required, for example, medical and examination report,

prescription, medical and examination bill, discharge certificate and so forth.

Conclusion:

Importance of appropriate documents in claim processing:

It has been noticed that much of the time the life coverage claim has been denied by the safety

net provider in light of the fact that the petitioner has neglected to take after some stride or not

ready to present the vital data to the organization. So it is prescribed that when you assert for

disaster policy, make appropriate strides and documentation so you can gather your advantage

immediately.

39

4.0 DATA ANALYSIS AND INTERPRETATION

TABLE NO: 4.1

TABLE SHOWING FIRST YEAR PREMIUM IN INDIVIDUAL ASSURANCE

YEAR INDIVIDUAL ASSURANCE

(AMOUNT IN CRORES) PERCENTAGE

INCREASE OR

DECREASE IN

PERCENTAGE

2010-11 21756.38 100 -

2011-12 28681.37 131.8 31.8

2012-13 27905.85 128.3 28.3

2013-14 27010.36 124.1 24.1

2014-15 19432.44 89.3 - 10.7

ANALYSIS:

From the above table we can analyze that the individual premium in the year 2011-12 was

increased by 31.8%, in 2012-13 it was increased by 28.3%, in 2013-14 it was has been increased

by 24.1% and in the concluding year it was decreased by 10.7%.

40

GRAPH NO: 4.1

GRAPH SHOWING THE FIRST YEAR PREMIUM

INTERPRETATION:

From the above chart it’s very clear that the company’s first premium has been decreasing from

year to year consecutively and in the concluding year it decreased by 10.7%, this is because the

number of policies has been decreased in individual assurances.

21756.38

28681.37 27905.85

27010.36

19432.44

0

5000

10000

15000

20000

25000

30000

35000

2010-11 2011-12 2012-13 2013-14 2014-15

First Year Premium (Rs in crores)

First Year Premium

41

TABLE NO: 4.2

TABLE SHOWING NET PREMIUM INCOME

YEARS NET PREMIUM INCOME

(RS IN LAKHS) PERCENTAGE

INCREASE OR

DECREASE IN

PERCENTAGE

2010-11 20335804.75 100 -

2011-12 20280290.33 99.7 -0.3

2012-13 20858972.06 102.9 2.9

2013-14 23679807.36 113.5 13.5

2014-15 23948277.17 117.8 17.8

Analysis:

From the above table we can clearly understand that the net premium income has been increasing

year by year except for 2011-12 which was reduced to 99.7% and coming to the concluding year

it is 117.8 which is highest compare to any other financial years.

42

GRAPH NO: 4.2

GRAPH SHOWING NET PREMIUM INCOME

INTERPRETATION:

The company’s net revenue has been increasing year by year, so it very good to the company

which the revenue has been continuously increasing and in the concluding year it was 117.8.

This is because the company has been introduced some of the new plans like jeevan tarun plan,

LIC new online term plan and etc.

20335804.75 20280290.33

20858972.06

23679807.36 23948277.17

18000000

19000000

20000000

21000000

22000000

23000000

24000000

25000000

2010-11 2011-12 2012-13 2013-14 2014-15

Net Premium Income (Rs in Lakhs)

Net Premium Income (Rs in Lakhs)

43

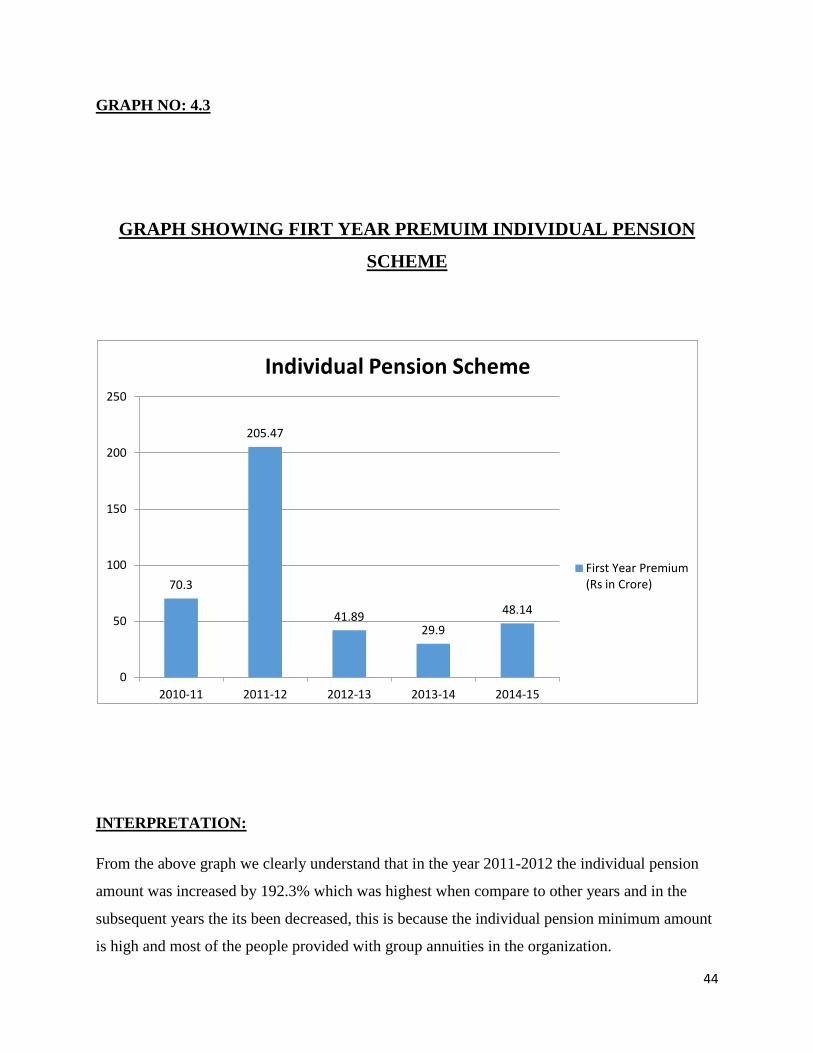

Table No: 4.3

TABLE SHOWING FIRST YEAR PREMIUM OF INDIVIDUAL PENSION SCHEMES

INDIVIDUAL

PENSION SCHEMES

FIRST YEAR

PREMIUM

(RS IN CRORE)

PERCENTAGE INCREASE OR

DECREASE IN

PERCENTAGE

2010-11 70.3 100 -

2011-12 205.47 292.3 192.3

2012-13 41.89 59.6 - 40.4

2013-14 29.9 42.5 - 47.5

2014-15 48.14 68.5 - 31.5

Analysis:

The above table gives a clear picture that the individual pension scheme in the year 2011-12 has

been increased by 192.3%, in 2012-13 it was decreased by 40.4%, in 2013-14 I has been

decreased by 47.5% and in the concluding year it decreased by 31.5%.

44

GRAPH NO: 4.3

GRAPH SHOWING FIRT YEAR PREMUIM INDIVIDUAL PENSION

SCHEME

INTERPRETATION:

From the above graph we clearly understand that in the year 2011-2012 the individual pension

amount was increased by 192.3% which was highest when compare to other years and in the

subsequent years the its been decreased, this is because the individual pension minimum amount

is high and most of the people provided with group annuities in the organization.

70.3

205.47

41.89 29.9

48.14

0

50

100

150

200

250

2010-11 2011-12 2012-13 2013-14 2014-15

Individual Pension Scheme

First Year Premium (Rs in Crore)

45

TABLE NO: 4.4

TABLE SHOWING GROUP INSURANCE PREMIUMS

YEARS

GROUP INSURANCE

PREMIUM (RS IN

CRORES)

PERCENTAGE

INCREASE OR

DECREASE IN

PERCENTAGE

2010-11 24338.8 100 -

2011-12 18135.9 74.5 - 25.5

2012-13 17567.2 72.2 - 27.8

2013-14 20720.3 85.1 - 14.9

2014-15 19409.2 79.7 - 20.3

ANALYSIS:

From the above table it is observed that in the year 2011-12 it was decreased by 25.5%, in 2012-

13 it was still reduced by 27.8%, 14.9% was decreased in the year 2013-14 and in the concluding

year it is decreased by 20.3%.

46

GRAPH NO: 4.4

GRAPH SHOWING GROUP INSURANCE PREMIUM

INTERPRETATION:

From the above graph we can understand the group insurance has been fluctuating from year to

year, in the concluding it was decreased by 20.3%. This is because of competition from ICICI

Prudential Life which attracted policy holders with new life insurance plans.

24338.82

18135.93 17567.17

20720.27 19409.17

0

5000

10000

15000

20000

25000

30000

2010-11 2011-12 2012-13 2013-14 2014-15

Group Insurance Premium (Rs in Crores)

Group Insurance Premium (Rs in Crores)

47

TABLE NO: 4.5

TABLE SHOWING GROUP SUPERANNUATION PREMIUM

YEARS

GROUP SUPERANNUATION

PREMIUM

(AMOUNT IN CRORES)

PERCENTAGE

INCREASE OR

DECREASE IN

PERCENTAGE

2010-11 14962.6 100 -

2011-12 25875.4 172.9 72.9

2012-13 22316 149.1 49.1

2013-14 31699.7 211.9 111.9

2014-15 33775.4 225.7 125.7

ANALYSIS:

The above table we can determine that the group pension plan in the year 2011-12 was increased

by 172.9, in 2012-13 it was increased by 49.1%, in 2013-14 it was increased by 111.9% and in

the concluding year it was increased by 125.7%.

48

GRAPH NO: 4.5

GRAPH SHOWING GROUP SUPERANNUATION PREMUIM

INTERPRETATION:

From the above chart we can understand that the superannuation premium is been increased in

the last two years, since most of the MNC companies are creating security for their employees to

work for longer period in the organization, so the group pension plan has been increased in the

last two years.

0

5000

10000

15000

20000

25000

30000

35000

40000

2010-11 2011-12 2012-13 2013-14 2014-15

Group Superannuation Premium(Rs in crores)

Group Superannuation Premium(Rs in crores)

49

Table No: 4.6

TABLE SHOWING JEEVAN AROGYA

YEARS JEEVAN AROGYA

(AMOUNT IN LAKHS) PERCENTAGE

INCREASE OR

DECREASE IN

PERCENTAGE

2011-12 220271 100 -

2012-13 348148 158.1 58.1

2013-14 233698 106.1 6.1

2014-15 167371 76 -24

ANALYSIS:

From the above table we determine that in the year 2012-13 the premium was increased by

58.1%, in 2013-14 it was increased by only 6.1% and in the concluding year it was decreased by

24.0%.

50

GRAPH N0: 4.6

GRAPH SHOWING JEEVAN AROGYA

INTERPREATION:

From the above graph we interpret that the jeevan arogya plan, a health care plan has been

decreased in the concluding year, this is because of competition where they providing better

features and it have a limitation of only one claim in a year.

0

50000

100000

150000

200000

250000

300000

350000

400000

2011-12 2012-13 2013-14 2014-15

Jeevan Arogya

Jeevan Arogya

51

Table No: 4.7

TABLE SHOWING HEALTH PROTECTION PLUS

YEARS HEALTH POLICY PLAN

(NO OF POLICIES) PERCENTAGE

INCREASE OR

DECREASE IN

PERCENTAGE

2010-11 36645 100 -

2011-12 12806 18.9 - 80.1

2012-13 4287 6.3 - 93.7

2013-14 1299 1.9 - 98.1

2014-15 570 0.4 - 96.6

ANALYSIS:

From the above table can understand that the health policy is being decreased by 80.1 % in 2011-

12, in 2012-13 it was decreased by 93.7%, in 2013-14 it was still reduced by 98.1% and in the

concluding it is decreased by 96.6%.

52

GRAPH NO: 4.7

GRAPH SHOWING HEALTH PROTECTION PLUS

INTERPRETATION:

Form above graph we can understand that the health protection plan is being decreasing every

year at high percentage. This is because the company has introduced more of new health

insurance policies.

36645

12806

4287

1299 570

0

5000

10000

15000

20000

25000

30000

35000

40000

2010-11 2011-12 2012-13 2013-14 2014-15

HEALTH PROTECTTION PLUS

HEALTH PROTECTTION PLUS

53

TABLE NO: 4.8

TABLE SHOWING MATURITY AND DEATH CLAIMS

YEAR MATURITY

( AMOUNT IN CRORES)

DEATH

( AMOUNT IN CRORES)

2010-11 49412.63 8077.66

2011-12 63346.03 8147.14

2012-13 64630.13 9447.71

2013-14 81112.89 10289.25

2014-15 79365.7 11092.45

ANAYISIS:

From the above table we understand that the claims settlement has been increasing every year

and claims settled by maturity is more than the claims settled by death, but in the concluding

year the claims settled by death is decreased.

54

GRAPH NO: 4.8

GRAPH SHOWING MATURITY AND DEATH CLAIMS

INTERPRETATION:

The claim settlement will not be in the hands of the company, since the claims will settled as per

maturity or death, and maturity claims will be pre-determined, but the claims settled by death is

unpredictable. It’s been increasing as more the accident rates have been increasing every year. So

in this case the company will be maintaining certain amount of provision for settlement.

49412.63

63346.03 64630.13

81112.89 79365.7

8077.66 8147.14 9447.71 10289.25 11092.45

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

2010-11 2011-12 2012-13 2013-14 2014-15

Maturity

Death

55

TABLE NO: 4.9

DISCONTINUED POLICIES IN THE YEAR 2014-15

DISCONTINUED POLICIES NO OF POLICIES

Pension plus 503

Endowment plus 1766

Samriddhi plus 3859

Flexi plus 260

Analysis:

It is very clear from the above table that Samriddhi plus policy have been discontinued by the