An Exploratory Study of Family Member Characteristics and Involvement: Effects on Entrepreneurial...

14

An Exploratory Study of Family Member Characteristics and Involvement: Effects on Entrepreneurial Behavior in the Family Firm Franz W. Kellermanns, Kimberly A. Eddleston, Tim Barnett, Allison Pearson Family firms are essential for economic growth and development through new business startups and growth of existing family firms. Entrepreneurial behavior by the CEO is essential for such growth to occur. Entrepreneurial behavior can be influenced by inher- ent characteristics of the CEO, such as age and tenure, as well as by the degree of family influence in the firm, as indicated by the number of generations involved in the business. We assess the empirical relationships of these variables to both entrepreneurial behavior and subsequent firm growth. Introduction Entrepreneurial behavior can be a critically impor- tant factor in a firm’s profitability and growth (Lumpkin & Dess, 1996; Zahra, 1991, 1996). Firm- level entrepreneurship may be particularly crucial to a family firm as it strives to identify and take advantage of opportunities in the dynamic and uncertain competitive environment of the 21st century (Sirmon & Hitt, 2003). Indeed, family firms that engage in the innovative, proactive, and risk- taking behaviors that characterize firm-level entre- preneurship (Miller, 1983) are major contributors to economic development and growth in the U.S. and world economies (Zahra, Hayton, & Salvato, 2004). In spite of this, a consideration of the poten- tial effects of family characteristics and family involvement is largely absent from the general entrepreneurship literature (Aldrich & Cliff, 2003). Indeed, since the seminal work of Miller (1983), much of the entrepreneurship literature has instead focused on the impact of environmental, strategic, and organizational contingencies on firm-level entrepreneurship (Zahra, Jennings, & Kuratko, 1999). Miller (1983) suggests, however, that the unique characteristics of different types of firms must be considered by researchers as they study firm-level entrepreneurship. A burgeoning litera- ture suggests that family firms are indeed different from other firms due to the unique interplay among individual family members, the family “system,” and the business “system” (e.g., Gersick, Davis, Hampton,& Lansberg,1997; Tagiuri & Davis,1996). Further, a more complete understanding of the family firm CEO is necessary because family firms tend to be overly dependent on a single decision maker (Feltham, Feltham, & Barnett, 2005) and senior executives are key in promoting a firm’s commitment and support of entrepreneurship (Zahra, Neubaum, & Huse, 2000). Thus, it would seem that researchers interested in entrepreneurial behavior in family firms should address (1) how the characteristics of family firm CEOs affect entrepreneurial behavior within those firms, (2) how different levels of family involvement in family firms affect entrepreneurial behavior within those firms, and (3) how entrepreneurial behavior affects organizational growth. There seems to be little doubt that, worldwide, family businesses are critical in spurring FAMILY BUSINESS REVIEW, vol. XXI, no. 1, March 2008 © Family Firm Institute, Inc. 1 at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.com Downloaded from

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of An Exploratory Study of Family Member Characteristics and Involvement: Effects on Entrepreneurial...

An Exploratory Study of Family MemberCharacteristics and Involvement: Effects onEntrepreneurial Behavior in the Family FirmFranz W. Kellermanns, Kimberly A. Eddleston, Tim Barnett, Allison Pearson

Family firms are essential for economic growth and development through new businessstartups and growth of existing family firms. Entrepreneurial behavior by the CEO isessential for such growth to occur. Entrepreneurial behavior can be influenced by inher-ent characteristics of the CEO, such as age and tenure, as well as by the degree of familyinfluence in the firm, as indicated by the number of generations involved in the business.We assess the empirical relationships of these variables to both entrepreneurial behaviorand subsequent firm growth.

Introduction

Entrepreneurial behavior can be a critically impor-tant factor in a firm’s profitability and growth(Lumpkin & Dess, 1996; Zahra, 1991, 1996). Firm-level entrepreneurship may be particularly crucialto a family firm as it strives to identify and takeadvantage of opportunities in the dynamic anduncertain competitive environment of the 21stcentury (Sirmon & Hitt,2003).Indeed,family firmsthat engage in the innovative, proactive, and risk-taking behaviors that characterize firm-level entre-preneurship (Miller, 1983) are major contributorsto economic development and growth in the U.S.and world economies (Zahra, Hayton, & Salvato,2004). In spite of this, a consideration of the poten-tial effects of family characteristics and familyinvolvement is largely absent from the generalentrepreneurship literature (Aldrich & Cliff, 2003).

Indeed, since the seminal work of Miller (1983),muchof theentrepreneurship literaturehas insteadfocused on the impact of environmental, strategic,and organizational contingencies on firm-levelentrepreneurship (Zahra, Jennings, & Kuratko,1999). Miller (1983) suggests, however, that the

unique characteristics of different types of firmsmust be considered by researchers as they studyfirm-level entrepreneurship. A burgeoning litera-ture suggests that family firms are indeed differentfrom other firms due to the unique interplay amongindividual family members, the family “system,”and the business “system” (e.g., Gersick, Davis,Hampton,& Lansberg,1997; Tagiuri & Davis,1996).Further, a more complete understanding of thefamily firm CEO is necessary because family firmstend to be overly dependent on a single decisionmaker (Feltham, Feltham, & Barnett, 2005) andsenior executives are key in promoting a firm’scommitment and support of entrepreneurship(Zahra, Neubaum, & Huse, 2000). Thus, it wouldseem that researchers interested in entrepreneurialbehavior in family firms should address (1) howthe characteristics of family firm CEOs affectentrepreneurial behavior within those firms, (2)how different levels of family involvement infamily firms affect entrepreneurial behaviorwithin those firms, and (3) how entrepreneurialbehavior affects organizational growth.

There seems to be little doubt that, worldwide,family businesses are critical in spurring

FAMILY BUSINESS REVIEW, vol. XXI, no. 1, March 2008 © Family Firm Institute, Inc. 1

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

economic development and growth by creatingand funding new businesses as well as growingexisting firms (Astrachan, Zahra, & Sharma, 2003).However, the impact of family involvement onentrepreneurial behavior is uncertain. Manyresearchers suggest that family firms provide par-ticularly fertile grounds for essential entrepre-neurial behavior needed in firm creation andgrowth (Aldrich & Cliff, 2003). Zahra (2005) iden-tifies a variety of reasons that family firms may beadept at entrepreneurial behaviors, including (1)goal congruency between the firm and ownersand (2) goal continuity across multiple genera-tions involved in the firm. Family ownership alsopromotes a long-term planning perspective, nec-essary for the firm to continue successfully acrossmultiple generations of the family (Zahra et al.,2004). Finally, family firms are often in a uniqueposition to create valuable social capital in theform of lasting relationships with critical organi-zational stakeholders via the stability of key deci-sion makers in the family (De Carolis & Saparito,2006). Aligned, continuous goals, long-term per-spectives, and valuable social relationships canpotentially foster entrepreneurial behavior in thefirm.

However, in spite of the seemingly rich condi-tions for entrepreneurial behaviors in familyfirms, some have argued that the family businesscontext can be a distinct liability for entrepreneur-ial behavior (e.g., Schulze, Lubatkin, Dino, & Buch-holtz, 2001). Perhaps the greatest concern is that inorder to protect the firm over the long run, familyleaders may become too strategically conserva-tive, thereby minimizing entrepreneurial behav-iors. Indeed, because many entrepreneurialventures fail or take several years to be profitable,entrepreneurship poses substantial risks that canthreaten the success, wealth, and survival of thefirm (Zahra et al., 2000). Risk aversion, stagnation,or strategic comfort zones represent status quobehaviors that are indicative of diminished entre-preneurial behaviors needed to grow the familyfirm.

Thus, the impact of individual family membersand overall family involvement in the family firmmay be critical to entrepreneurial behavior and

firm success (Astrachan, 2003). But, as Aldrich andCliff (2003, p. 574) suggest, “very little attentionhas been paid to how family dynamics affect fun-damental entrepreneurial processes.” They go onto state:

We need more research on how family systems affectopportunity emergence and recognition, the newventure creation decision, and the resource mobiliza-tion process. We need to learn more about the rolethat family characteristics and dynamics play in why,when, and how some people, but not others, identifyentrepreneurial opportunities. (Aldrich & Cliff, 2003,p. 593).

What triggers some family firms to embraceand aggressively pursue continued entrepreneur-ial behaviors while other family organizationsbecome entrenched and stagnant? We set out toaddress this important question by examiningpotential antecedents of entrepreneurial behaviorin family firms, including the personal character-istics of the CEO (age and tenure), as well as theinfluence of the family over time, as indicated bythe number of generations involved in the firm.CEO age and tenure may be particularly salientinfluences on family firm entrepreneurial behav-ior because family firm CEOs tend to remain inpower much longer than CEOs in nonfamily firms(Gersick et al., 1997), and thus have an enduringimpact on the firm’s organizational culture andentrepreneurial disposition. Generational involve-ment may also be a key predictor of family firmentrepreneurial behavior given that founder-centered firms often lose their innovative momen-tum until the second or third generations join thefirm, reviving and fostering entrepreneurship(Salvato, 2004). Hereby it is also very important tounderstand the consequences of entrepreneurialbehavior. Although it has often been argued thatentrepreneurial behavior affects employmentgrowth at the macro and micro levels (e.g., Chang,2007; Kirchhoff, Newbert, Hasan, & Armington,2007), research has yet to show this as a conse-quence in family firms. However, we believe that asentrepreneurial behavior increases in familyfirms, organizational growth will likely follow.Indeed, entrepreneurship is believed to be anecessary component of family firm survival,

Kellermans, Eddleston, Barnett, Pearson

2

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

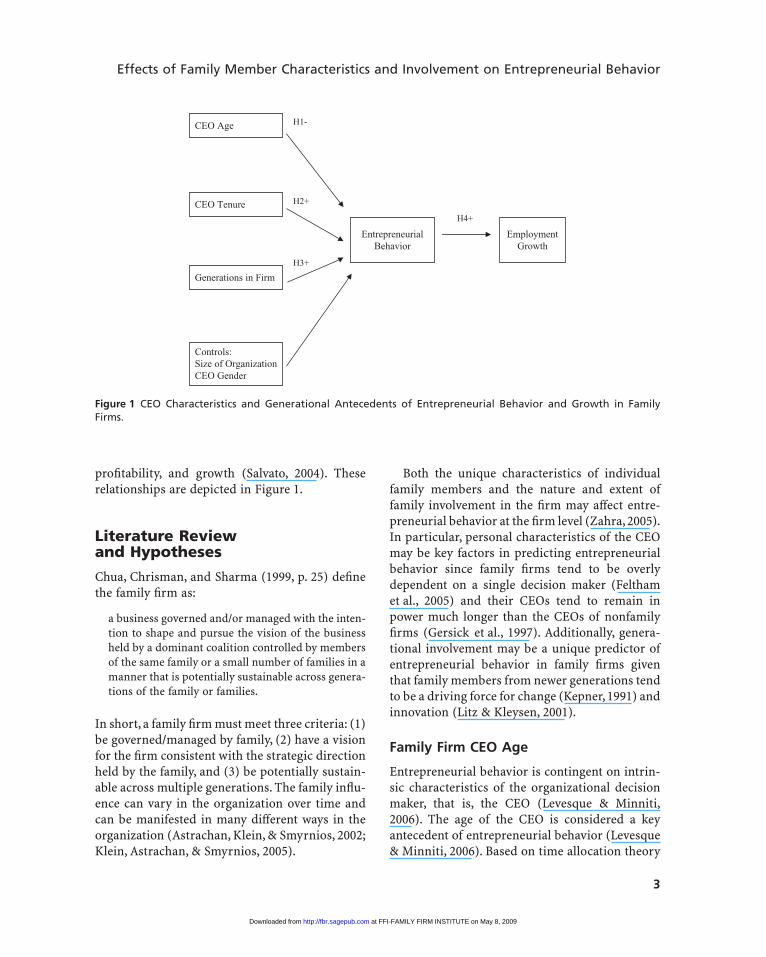

profitability, and growth (Salvato, 2004). Theserelationships are depicted in Figure 1.

Literature Reviewand Hypotheses

Chua, Chrisman, and Sharma (1999, p. 25) definethe family firm as:

a business governed and/or managed with the inten-tion to shape and pursue the vision of the businessheld by a dominant coalition controlled by membersof the same family or a small number of families in amanner that is potentially sustainable across genera-tions of the family or families.

In short, a family firm must meet three criteria: (1)be governed/managed by family, (2) have a visionfor the firm consistent with the strategic directionheld by the family, and (3) be potentially sustain-able across multiple generations. The family influ-ence can vary in the organization over time andcan be manifested in many different ways in theorganization (Astrachan, Klein, & Smyrnios, 2002;Klein, Astrachan, & Smyrnios, 2005).

Both the unique characteristics of individualfamily members and the nature and extent offamily involvement in the firm may affect entre-preneurial behavior at the firm level (Zahra, 2005).In particular, personal characteristics of the CEOmay be key factors in predicting entrepreneurialbehavior since family firms tend to be overlydependent on a single decision maker (Felthamet al., 2005) and their CEOs tend to remain inpower much longer than the CEOs of nonfamilyfirms (Gersick et al., 1997). Additionally, genera-tional involvement may be a unique predictor ofentrepreneurial behavior in family firms giventhat family members from newer generations tendto be a driving force for change (Kepner, 1991) andinnovation (Litz & Kleysen, 2001).

Family Firm CEO Age

Entrepreneurial behavior is contingent on intrin-sic characteristics of the organizational decisionmaker, that is, the CEO (Levesque & Minniti,2006). The age of the CEO is considered a keyantecedent of entrepreneurial behavior (Levesque& Minniti, 2006). Based on time allocation theory

CEO Age H1-

CEO Tenure

Generations in Firm

EntrepreneurialBehavior

EmploymentGrowth

Controls:Size of OrganizationCEO Gender

H2+

H3+

H4+

Figure 1 CEO Characteristics and Generational Antecedents of Entrepreneurial Behavior and Growth in FamilyFirms.

Effects of Family Member Characteristics and Involvement on Entrepreneurial Behavior

3

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

(Becker, 1965), Levesque and Minniti (2006)argued that a CEO’s entrepreneurial efforts willdecline over time. As CEOs grow older, they maylimit decision making to commonly held norms ofindustry behavior, rather than seeking unique, yetrisky, strategic directions (Hambrick & Finkel-stein, 1987). Younger entrepreneurs have beenfound to adjust their expectations faster inresponse to new information than do older entre-preneurs, supporting the notion that older entre-preneurs are more complacent than their youngercounterparts (Parker, 2006). For example, age hasbeen found to be significantly negatively corre-lated with innovation and risk taking (Stewart,Watson, Carland, & Carland, 1999).

Age may be a particularly salient predictor ofentrepreneurial behavior in family firms sincetheir CEOs often become preoccupied with suc-cession issues as they age (Feltham et al., 2005). Assuccession grows nearer, the aging CEO may placegreater importance on a smooth, seamless transi-tion than on the need to pursue entrepreneurialendeavors. Further, because leaders of familyfirms are often motivated to build a lasting legacyfor their children, they often become conservativein their decisions because of the high risk ofentrepreneurial ventures (Morris, 1998) and theirfear of losing family wealth (Sharma, Chrisman, &Chua, 1997). Therefore, as CEOs of family firmsage, they may naturally become less innovativeand risky and also become more focused onsuccession issues and maintaining family wealth,thereby reducing their entrepreneurial behavior.

Hypothesis 1. The age of the family firm CEO willbe negatively related to entrepreneurial behavior.

Family Firm CEO Tenure

Will the tenure of the CEO in the organization bebeneficial or harmful to the pursuit of entrepre-neurial behaviors in the family firm? There issome argument that long CEO tenures inspireentrepreneurial behavior. This perspective isbased on the belief that long tenures allow theCEO to accumulate a wealth of knowledge andexperience, making him or her better able to select

appropriate entrepreneurial behaviors, therebyreducing risk while also pursing aggressivechange (Levesque & Minniti, 2006). Long CEOtenure may also allow the CEO to build valuablerelationships among organizational constituents.These relationships may give the CEO moreknowledge and comfort to pursue the risky deci-sions necessary to entrepreneurship.

Alternatively, dominant, singular leadershipover long tenures may make employees less likelyto question ideas and practices (Zahra et al.,2004). Long tenures may create an internal orga-nizational environment that stifles the creativityand innovativeness that result from cognitive con-flict, the much needed and healthy questioning ofideas and concepts (Kellermanns & Eddleston,2004). For example, CEOs with longer tenure havebeen found to be more likely to conform to indus-try norms, presumably because their firm-specifichuman capital keeps them from compromisingthe comfortable status quo (Finkelstein & Ham-brick, 1990). Indeed, in a canonical analysis offamily firm variables, Zahra (2005) found thatCEO tenure was negatively related to innovative-ness in his study of more than 200 family firms.Zahra (2005) also found that CEO tenure in familyfirms was inversely associated with risk taking. Itappears that when family businesses are highlydependent on the CEO, suboptimal decisions canresult because the family business has not plannedfor change or the leader dominates decisionmaking (Feltham et al., 2005). The identity ofCEOs with long tenure may become so interwovenwith the family firm that the objectivity of thedecision-making process is strained (Daily &Dollinger, 1992). Indeed, entrepreneurial familyfirms appear to continuously question and changetheir cultural patterns and ways of doing business(Hall, Melin, & Nordqvist, 2001). In contrast, theexecutive succession literature has shown thatnew top management is positively related to stra-tegic change and innovation (Kesner, Shapiro, &Sharma, 1994). Therefore, family firm CEOs withlong tenure may display less entrepreneurialbehavior than their newer counterparts becauseof their resistance to change and support for thestatus quo.

Kellermans, Eddleston, Barnett, Pearson

4

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

Hypothesis 2. The tenure of the family firm CEOwill be negatively related to entrepreneurialbehavior.

Generations Involved in the Family Firm

When multiple generations are involved in thefamily firm, the organization has greater input anda variety of individual perspectives—both valu-able assets for entrepreneurial ideas. Newergenerations tend to push for new ways of doingthings (Kepner, 1991) and are often the drivingforce behind innovation (Litz & Kleysen, 2001)and entrepreneurial activities (Salvato, 2004).Although founders of family firms often basetheir firms on innovative ideas, over time they maylose their entrepreneurial edge (Corbetta, 1995;Salvato, 2004). The involvement of subsequentgenerations increases the firm’s chance that entre-preneurial opportunities will be identified andpursued (Salvato, 2004). As Salvato explains, “thefounder alone may find it difficult to have innova-tive ideas without the fresh momentum addedto the firm by second-generation members” (2004,p. 73).

Several researchers suggest that multi-generational family involvement increases thechances that entrepreneurial opportunities will berecognized (Salvato, 2004) and entrepreneurialbehavior fostered (Gersick et al., 1997). Indeed, astewardship theory lens would suggest that thecohesion between the family is fostered andopportunities are sought out to provide for cross-generational sustainability and growth (e.g.,Davis, Schoorman, & Donaldson, 1997; Eddleston& Kellermanns, 2007). A recent empirical study(Zahra, 2005) is consistent with this view, findingthat the more generations of the family involved ina family firm, the more the firm focused on inno-vative behaviors. The involvement of multiplegenerations may foster entrepreneurial behaviorbecause newer generations may put greateremphasis on enhancing business growth so asto ensure the firm’s survival. Indeed, family firmsurvival through multiple generations requiresrenewal through innovation (Hoy, 2006) and

greater focus on maintaining and enhancingbusiness growth (McConaughy & Phillips, 1999).Multiple-generation firms must adapt to changesin their environments by rejuvenating and rein-venting themselves over time if they are tosustain the same level of growth and financialinheritance of the previous generation (Jaffe &Lane, 2004). Furthermore, serial business fami-lies, families that repeatedly recreate new familybusiness ventures, appear to be able to harnessthe fresh motivation and entrepreneurial spiritof each generation (Kenyon-Rouvinez, 2001).Accordingly, the involvement of multiple genera-tions may increase entrepreneurial behaviorbecause newer generations may be a drivingforce for change and innovation and they mayalso be more likely to perceive the importance ofentrepreneurial behavior to the long-term sur-vival of the firm.

Hypothesis 3. The number of generations involvedin the family firm will be positively related to entre-preneurial behavior.

Entrepreneurial Behavior andFirm Growth

Entrepreneurship involves innovation and newventure creation (Steier, Chrisman, & Chua,2004). More specifically,“entrepreneurship centerson recognizing and exploiting opportunities byreconfiguring existing and new resources in waysthat create an advantage” (Zahra, 2005, p. 25).Entrepreneurial behavior is essential for firms toadapt and respond to environmental changes,such as consumer preferences, competitor actions,and technological developments. For example,Zahra and colleagues (2000) discussed how entre-preneurship can help a firm acquire new capabili-ties, launch new businesses, develop new revenuestreams, and improve firm performance, profit-ability, and growth. In this way, entrepreneurialbehavior is seen as an important element in thesurvival and growth of family firms because ithelps create jobs and wealth for family members(Kellermanns & Eddleston, 2006a).

Effects of Family Member Characteristics and Involvement on Entrepreneurial Behavior

5

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

For example, an innovative strategy has beenfound to benefit a family firm’s competitivemarket position (McCann, Leon-Guerrero, &Haley, 2001). Entrepreneurial behavior maypromote the continuity and success of the familyfirm by increasing revenue streams and profitabil-ity that thereby encourage growth in employment(Kellermanns & Eddleston, 2006a). Indeed, Salvato(2004) argues that entrepreneurial behavior isimportant to family firm survival, profitability,and growth. Without entrepreneurial behavior,family firms will likely become stagnant, therebylimiting the potential for firm success and growthin the future.

Hypothesis 4. Entrepreneurial behavior will bepositively related to firm growth.

Method

Our sample frame consisted of 232 family firmsassociated with the family business centers of twoU.S. universities in the Northeast. The surveyswere directed to the CEO, and as part of a largerdata-collection effort the CEO was asked todistribute the questionnaires to other familymembers within the family firm. Overall, 50 CEOsreturned surveys, representing a 21.4% responserate at the CEO level of analysis.

Measures

All items and the associated alphas of the con-structs are reported in the Appendix.

Dependent variable. Employment growth wasmeasured via a subjective self-reported assess-ment since objective measures relating to growthor other performance dimensions are often notavailable or obtainable from smaller, privatelyowned firms (Love, Priem, & Lumpkin, 2002).Prior research has shown that such subjective self-assessments are highly correlated with objectivedata (Dess & Robinson, 1984; Love et al., 2002;Venkatraman & Ramanujam, 1987). The respon-

dents were given multiple options relatedto growth, ranging from a decrease in growth toincreases in 2% increments up to 12% or more.Indeed, not only has entrepreneurial behavior ingeneral been associated with employment growthat the macro and micro levels (e.g., Chang, 2007;Kirchhoff et al., 2007), it is widely utilized in mea-suring the success of small-scale businesses (e.g.,Rauch, Frese, & Utsch, 2005).

Independent variables. Entrepreneurial beha-vior was assessed with four items on a 7-pointLikert scale. The measures were adapted from aseven-item scale developed by Miller (1983).Although other measures of entrepreneurialbehavior exist in the literature (e.g., Zahra, 1996),we chose to utilize an adaptation of the Millermeasure due to its better fit to the family firmcontext and its ability to produce meaningfulinferences for smaller organizations (Kellermanns& Eddleston, 2006a). The measure demonstratedacceptable reliability, with an alpha of 0.86.

Tenure was measured via a self-report questionasking how many years the individual had workedin the family firm. Age was similarly assessed viaself-report. Lastly, we asked CEOs to indicate thenumber of generations currently working inthe family firm (Kellermanns & Eddleston, 2006a).

Control variables. Two controls were used inthis study. First, we controlled for CEO gendersince entrepreneurial roles are more often associ-ated with men than women (Olson, Zuiker, Danes,Stafford, Heck et al., 2003). Second, we controlledfor organizational size based on sales, since largersales may allow the family firm to accumulatemore organizational slack, which in turn maypositively affect the ability to engage in entrepre-neurship.

Results

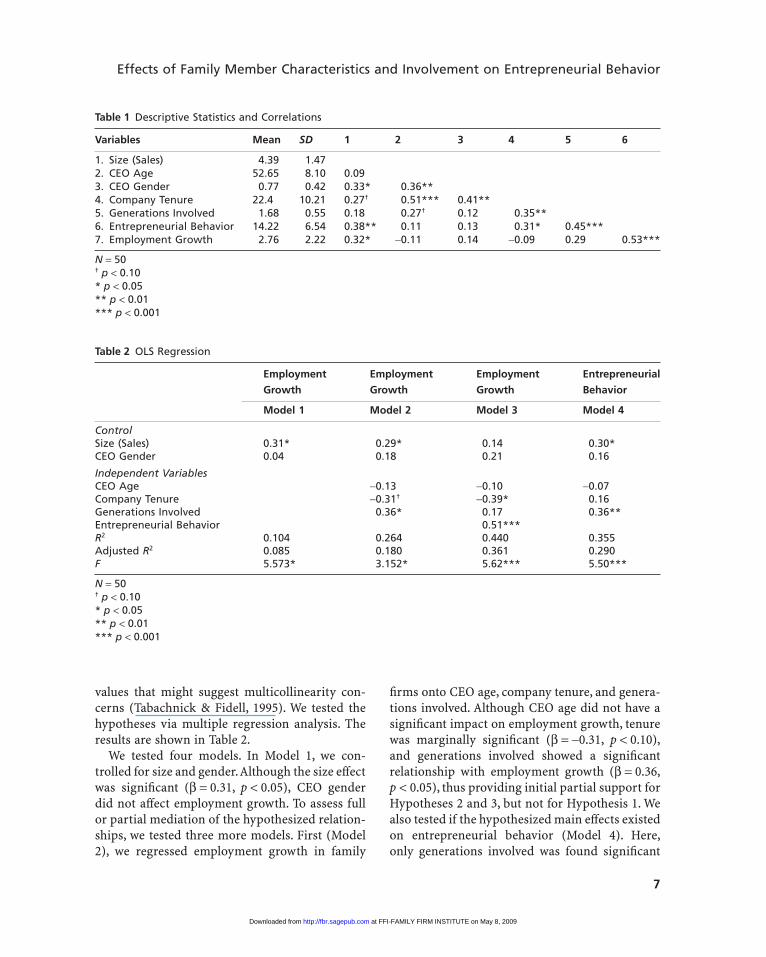

The means, standard deviations, and zero-ordercorrelations are shown in Table 1. The highestobserved VIF equaled 1.64 and the highest valueof the condition index equaled 24.84, far below

Kellermans, Eddleston, Barnett, Pearson

6

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

values that might suggest multicollinearity con-cerns (Tabachnick & Fidell, 1995). We tested thehypotheses via multiple regression analysis. Theresults are shown in Table 2.

We tested four models. In Model 1, we con-trolled for size and gender.Although the size effectwas significant (b = 0.31, p < 0.05), CEO genderdid not affect employment growth. To assess fullor partial mediation of the hypothesized relation-ships, we tested three more models. First (Model2), we regressed employment growth in family

firms onto CEO age, company tenure, and genera-tions involved. Although CEO age did not have asignificant impact on employment growth, tenurewas marginally significant (b = -0.31, p < 0.10),and generations involved showed a significantrelationship with employment growth (b = 0.36,p < 0.05), thus providing initial partial support forHypotheses 2 and 3, but not for Hypothesis 1. Wealso tested if the hypothesized main effects existedon entrepreneurial behavior (Model 4). Here,only generations involved was found significant

Table 1 Descriptive Statistics and Correlations

Variables Mean SD 1 2 3 4 5 6

1. Size (Sales) 4.39 1.472. CEO Age 52.65 8.10 0.093. CEO Gender 0.77 0.42 0.33* 0.36**4. Company Tenure 22.4 10.21 0.27† 0.51*** 0.41**5. Generations Involved 1.68 0.55 0.18 0.27† 0.12 0.35**6. Entrepreneurial Behavior 14.22 6.54 0.38** 0.11 0.13 0.31* 0.45***7. Employment Growth 2.76 2.22 0.32* -0.11 0.14 -0.09 0.29 0.53***

N = 50† p < 0.10* p < 0.05** p < 0.01*** p < 0.001

Table 2 OLS Regression

Employment

Growth

Employment

Growth

Employment

Growth

Entrepreneurial

Behavior

Model 1 Model 2 Model 3 Model 4

ControlSize (Sales) 0.31* 0.29* 0.14 0.30*CEO Gender 0.04 0.18 0.21 0.16

Independent VariablesCEO Age -0.13 -0.10 -0.07Company Tenure -0.31† -0.39* 0.16Generations Involved 0.36* 0.17 0.36**Entrepreneurial Behavior 0.51***R2 0.104 0.264 0.440 0.355Adjusted R2 0.085 0.180 0.361 0.290F 5.573* 3.152* 5.62*** 5.50***

N = 50† p < 0.10* p < 0.05** p < 0.01*** p < 0.001

Effects of Family Member Characteristics and Involvement on Entrepreneurial Behavior

7

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

(b = 0.36, p < 0.01), while both CEO age (b = -0.07,ns) and company tenure (b = 0.16, ns) were not.This suggested that only the relationship betweengenerational involvement and employmentgrowth was mediated by entrepreneurial behav-ior, which did not support Hypothesis 1 and onlypartially supported Hypothesis 2. Indeed, Model3 confirms full mediation, supporting Hypothe-sis 3. When entrepreneurial behavior (b = 0.51,p < 0.001) is added to the main effects (supportingHypothesis 4), generational involvement loses itssignificance (b = 0.17, ns) indicating full media-tion. In addition, company tenure was significantin this step (b = -0.39, p < 0.05).

Since the data were collected via a cross-sectional survey design, common method biaswas a potential problem. To address this concern,we performed a test suggested by Podsakoff andOrgan (1986) and entered all items of the maineffect variables in a factor analysis. Two factorsemerged that explained 67.8% of the variance. Thefirst factor consisted of the four entrepreneurialbehavior items and explained 47.5% of the vari-ance, while the remaining three single indicatoritems explained 20.3% of the variance. Since nosingle method factor emerged, common methodvariance did not appear to be a significantproblem.

In addition, we performed checks for potentialnonresponse biases by dividing our respondentsinto early and late respondents. This procedure isperformed under the assumption that late res-pondents are more similar in nature to nonre-spondents than early respondents. No statisticaldifferences between the early and late respondentswere observed, which suggests that nonresponsebias was not a major problem (e.g., Kanuk & Ber-enson, 1975).

To further mitigate concerns, we compared ouroverall sample with two national samples in termsof respondent age, gender, and size. A comparisonwith the 1997 National Family Business Survey(NFBS) (Winter, Danes, Koh, Fredericks, & Paul,2004) and the Federal Reserve Board’s 2003Survey of Small Business Finances (SSBF) (Winter,Fitzgerald, Heck, Haynes, & Danes, 1998) revealedthat our respondents were similar in age and

gender composition to CEOs in the nationalsample. However, the respondent firms tended tobe significantly larger in size. Since we control forsize effects, however, we do not believe this to be asignificant concern in our study.

Discussion

Our study provided the first empirical test infamily firms of the age hypothesis proposed byLevesque and Minniti (2006) and expands onwork from Zahra (2005) by testing antecedents ofentrepreneurial behavior as well as its growthconsequences in a holistic model. Our findingswere mixed. Overall, the entrepreneurial behav-ior of family firm CEOs was strongly related toour performance variable, employment growth.As such, this study adds to findings in the familyfirm literature that have linked corporate entre-preneurship to important outcome variables likefinancial performance in family firms in particu-lar and nonfamily firms in general (e.g., Barrett& Weinstein, 1998; Gudmundson, Tower, &Hartman, 2003; Lumpkin & Dess, 1996; Zahra,1996, 2005).

Contrary to expectations, we did not find a sig-nificant relationship of CEO age with either entre-preneurial behavior or employment growth. It ispossible that this may be a unique finding forfamily firms. Although entrepreneurial behaviorin general may be strongly associated with age, itis possible that pressures in family firms maymitigate such an effect. So even if a family firmmember becomes a CEO at a young age, he or shemay not have the power to enact entrepreneurialbehavior; such may be the case in family firmsorganized as cousin consortiums (Gersick et al.,1997). Accordingly, future research may want toexamine the effect of the ownership share of theCEO on entrepreneurial behavior. Alternatively,because the welfare of the entire family is at stake,the family firm CEO may not lose the desire forentrepreneurial behavior as he or she ages.Knowing that the benefits of his or her behaviorwill accrue to future generations of the family, theCEO may be highly motivated to continue topursue entrepreneurial ventures.

Kellermans, Eddleston, Barnett, Pearson

8

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

Our findings pertaining to CEO tenure in theorganization only partly supported our hypoth-eses. Organizational tenure was not related toentrepreneurial behavior by the CEO. However,organizational tenure of the CEO was negativelyrelated to employment growth. Our findings arethus somewhat consistent with Zahra (2005), whofound CEO tenure to be negatively related to invest-ments in new technologies and innovation. A pos-sible explanation for the finding is that the behaviorof longer-tenured CEOs may be reflecting greatercaution as they focus on succession issues,which inturn would lead to lower growth. The nonsignifi-cant main effect on entrepreneurial behaviorfurther suggests that many constraints may beimposed on the CEO by the family,which may limithis or her engagement in such behavior.

Our hypothesis relating to generational involve-ment received strong support. Indeed, the rela-tionship between generational involvement andemployment growth was fully mediated by entre-preneurial behavior in family firms. As such,generational involvement was the only strongpredictor of entrepreneurial behavior in ourfamily firm sample. This is an important finding,since the main effect of generational involvementon corporate entrepreneurship has been foundnonsignificant at the firm level (Kellermanns &Eddleston, 2006a), indicating the importance ofindividuals to make innovation in organizations areality (Kanter, 1983).

Indeed, some researchers suggest that theinvolvement of family in the firm can cause poten-tial agency conflicts resulting from the ongoingpaternalistic care some family members receive,regardless of their contribution to the firm (e.g.,Schulze et al., 2001). If, indeed, examples of dys-functional altruism exist in the family firm, thiscould be even more problematic in multi-generational family firms. Here, excessive altruismmay result in free riding and shirking that couldsubstantially hinder the entrepreneurial efforts ofthe family firm. However, this is not what we foundin this study. Generational involvement increasedentrepreneurial behavior. As such, our findingsadd to the growing evidence that although agencycosts in family firms exist, they may be lower than

agency costs in nonfamily firms (Chrisman, Chua,& Litz, 2004). Indeed, if reciprocal altruism andstewardship behavior are present in family firms(e.g., Davis et al., 1997; Eddleston & Kellermanns,2007), a positive impact on entrepreneurial behav-ior, growth, and success of the family firm can beexpected.

Our study therefore contributed to the litera-ture in two ways. First, we added to the growingcorporate entrepreneurship literature (e.g.,Barrett & Weinstein, 1998; Levesque & Minniti,2006; Lumpkin & Dess, 1996; Sharma & Chrisman,1999; Zahra, 1996) by following Miller’s (1983)early call for research into the impact of firm typeson entrepreneurial behavior. Indeed, we wereable to show that unique family firm characteri-stics impact entrepreneurial behavior. Second,we added to the literature on entrepreneurialbehavior in family firms (e.g., Hall et al., 2001;Kellermanns & Eddleston, 2006a; Zahra, 2005).Specifically, we contributed to initial researchfocusing on CEO behavior (Zahra, 2005).

Limitations and Implications

Before discussing the implications of our findings,a few limitations of our study should be noted.As mentioned in the method section, our studyemployed a cross-sectional design. Accordingly,we cannot infer causality in our study. Commonmethod bias is also a limitation of our study,although the test for common method bias did notindicate significant concerns (Podsakoff & Organ,1986) and the unambiguous nature of the self-reports for age, tenure, and generational involve-ment should reduce the potential for commonmethod bias. However, future studies shouldinvestigate the relationship between entrepre-neurial behavior and growth via a longitudinaldesign. Additional measures of growth shouldalso be examined, such as growth in market shareand profit margins.

A further limitation of our study is the smallsample size and the sample origination in thenortheastern United States. A small sample sizemay always cause a Type II error (Mazen, Graf,Kellogg, & Hemmasi, 1987). However, since the

Effects of Family Member Characteristics and Involvement on Entrepreneurial Behavior

9

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

majority of our hypotheses were supported, thisdoes not seem to be a significant concern inthis study. Furthermore, we compared our samplewith larger national studies and found that theorganizations in our sample were larger thanthe national average; thus, our generalizabilitymay be more prevalent for larger family firms.

Entrepreneurial behavior has been identified tobe of paramount importance for the U.S. economy(e.g., Chang, Kellermanns, & Chrisman, 2007), andgiven the dominance of family firms in the UnitedStates and other economies (e.g., Chua, Chrisman,& Chang, 2004), it is crucial to understand entre-preneurial behavior in family firms. Indeed, ourstudy adds to the developing research in this area(Kellermanns & Eddleston, 2006a; Zahra, 2005).However, future research needs to develop a betterunderstanding of the facilitating conditions infamily firms that allow such behavior. In thisregard, future research may want to extend thecurrent research by initially focusing on moreorganizational-level predictors. Furthermore, fut-ure empirical research needs to expand the contentdomain of corporate entrepreneurship. Althoughour article focuses exclusively on entrepreneurialbehavior within the firm, this area of investigationneeds to be expanded to include new ventures thatare facilitated by the family (Steier, in press).

In addition, other variables such as familysupport and norms (Chang et al., 2007) and finan-cial, contact, and resource support (Dyer &Handler, 1994) could be investigated as anteced-ents of entrepreneurial behavior in family firms. Itwould also be beneficial to identify and under-stand inhibitors that curb entrepreneurial behav-ior. For example, Kellermanns and Eddleston(2004) and Eddleston and Kellermanns (2007)identified relationship conflict as a devastatingstrategy process. Indeed, it is likely that such nega-tive forms of conflict and the lack of its propermanagement (Kellermanns & Eddleston, 2006b)would significantly reduce entrepreneurial behav-ior. In addition, constraints such as financial andtime pressures may mitigate entrepreneurialbehavior in family firms (Dyer, 1992).

In particular, succession and its managementmay be a potential avenue of future research per-

taining to entrepreneurial behavior in familyfirms (Sharma, Chua, & Chrisman, 2005; Stavrou,1999). If there are multiple potential successorswithin the family firm, or if it is foreseeable thatthe family firm will need to generate revenue andprovide employment for future generations, entre-preneurial behavior may be more likely. However,if no successor is available, the CEO may lackincentives beyond his or her personal motivationto engage in such behavior.

Future research may also want to consider thetype of entrepreneurial behavior that is initiatedby the CEO. Although initial research on radicalchange has been conducted in family firms (Hallet al., 2001), more research on incremental change(Quinn, 1980) and strategic initiatives is needed(Floyd, Ortiz-Walters, Wooldridge, & F., forthcom-ing). Indeed, no studies to date have addressedthis topic in family firms.

Lastly, we need to discuss the implications ofour study to the growing body of literature onfamily-based social capital in family firms(Arregle, Hitt, Sirmon, & Very, 2007; Bubolz, 2001;Dyer, 2006). Particularly, our finding pertaining tothe direct effect of generational involvement onentrepreneurial behavior of the CEO suggeststhat the family can be the source of social capital(Bubolz, 2001) and innovation. By having multiplegenerations involved, the family is in a position ofpower that allows the family to better control deci-sion making and implementation (Arregle et al.,2007) and may thus facilitate entrepreneurialbehavior. As such, generational involvement canbe seen as an integral component that allows forthe creation of “familiness” in family firms (Hab-bershon & Williams, 1999; Habbershon, Williams,& MacMillan, 2003).

In conclusion, the study of entrepreneurialbehavior of family firm CEOs can provide addi-tional insights in understanding why some familyfirms grow while other family firms stagnate.Our study showed that organizational tenure andgenerations involved were important predictorsof entrepreneurial behavior and employmentgrowth. Indeed, our study suggests that the entre-preneurial behavior of CEOs is a key factor inexplaining employment growth in family firms.

Kellermans, Eddleston, Barnett, Pearson

10

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

Appendix: Scale Items and Reliabilities

Construct Items a

Independent VariablesEntrepreneurial Behavior Over the past three years, our firm has pioneered the development

of breakthrough innovations in its industry0.86

Our firm has introduced many new products or services over the pastthree years

Our firm has emphasized making major innovations in its productsand services over the past three years

Our firm has emphasized taking bold, wide-ranging actions inpositioning itself and its products or services over the past threeyears

Generations Involved How many generations are currently working in the family firm (onegeneration, two generations, three generations)

Tenure Worked in the family firm since: ____ (fill in)

Age Age: ____ years

Gender Gender: ____ Male ____ Female

Dependent VariableEmployment Growth Please indicate growth in employment over the past three years:

____ No growth or decrease in growth____ Less than 2%____ 2.00%–3.99%____ 4.00%–5.99%____ 6.00%–7.99%____ 8.00%–9.99%____ 10.00%–11.99%____ 12.00% or more

References

Aldrich, H. E., & Cliff, J. E. (2003). The pervasive effectsof family on entrepreneurship: Toward a familyembeddedness perspective. Journal of Business Ven-turing, 18, 573–596.

Arregle, J.-L., Hitt, M.A., Sirmon, D. G., & Very, P. (2007).The development of organizational social capital:Attributes of family firms. Journal of ManagementStudies, 44, 72–95.

Astrachan, J. H. (2003). Commentary on the specialissue: The emergence of a field. Journal of BusinessVenturing, 18, 567–572.

Astrachan, J. H., Klein, S. B., & Smyrnios, K. X. (2002).The F-PEC scale of family influence: A proposal forsolving the family business definition problem.Family Business Review, 15(1), 45–58.

Astrachan, J. H., Zahra, S. A., & Sharma, P. (2003).Family-sponsored ventures. Kansas City, MO: Kauff-man Foundation.

Barrett, H., & Weinstein, A. (1998). The effect of marketorientation and organizational flexibility on corpo-rate entrepreneurship. Entrepreneurship Theory andPractice, 23(1), 57–70.

Becker, G. (1965). A theory of the allocation of time.Economic Journal, 75, 493–517.

Bubolz, M. (2001). Family as source, user, and builder ofsocial capital.Journal of Socio-Economics,30,129–131.

Chang, E. P. C. (2007). Entrepreneurship and economicdevelopment and growth in America: An investigationat the county level. Unpublished dissertation. Missis-sippi State University.

Chang, E. P. C., Kellermanns, F. W., & Chrisman, J. J.(2007). From intentions to venture creation: Plannedentrepreneurial behavior among Hispanics in theU.S. In T. Habbershon & M. Rice (Eds.), Perspectiveson entrepreneurship (Vol. 3, pp. 119–145). Westport,CT: Praeger.

Chrisman, J. J., Chua, J. H., & Litz, R. (2004). Comparingthe agency costs of family and non-family firms:

Effects of Family Member Characteristics and Involvement on Entrepreneurial Behavior

11

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

Conceptual issues and exploratory evidence. Entre-preneurship Theory and Practice, 28(4), 335–354.

Chua, J. H., Chrisman, J. J., & Chang, E. P. C. (2004). Arefamily firms born or made? An exploratory investi-gation. Family Business Review, 17, 37–54.

Chua, J. H., Chrisman, J. J., & Sharma, P. (1999). Definingthe family business by behavior. EntrepreneurshipTheory and Practice, 23(4), 19–39.

Corbetta, G. (1995). Patterns of development of familybusinesses in Italy. Family Business Review, 8(4), 255–265.

Daily, C. M., & Dollinger, M. J. (1992). An empiricalexamination of ownership structure in family andprofessionally managed firms. Family BusinessReview, 5(2), 117–136.

Davis, J. H., Schoorman, F. D., & Donaldson, L. (1997).Toward a stewardship theory of management.Academy of Management Review, 22(1), 20–47.

De Carolis, D. M., & Saparito, P. (2006). Social capital,cognition, and entrepreneurial opportunities: A theo-retical framework. Entrepreneurship Theory andPractice, 30(1), 41–56.

Dess, G. G., & Robinson, R. B. (1984). Industry effectsand strategic management research. Journal of Man-agement, 16(7), 7–27.

Dyer, W. G. (1992). The entrepreneurial experience. SanFrancisco, CA: Jossey-Bass.

Dyer, W. G. (2006). Examining the“family effect”on firmperformance. Family Business Review, 19(4), 253–273.

Dyer, W. G., & Handler, W. (1994). Entrepreneurship andfamily business: Exploring the connections. Entrepre-neurship Theory and Practice, 19, 71–83.

Eddleston, K., & Kellermanns, F. W. (2007). Destructiveand productive family relationships: A stewardshiptheory perspective Journal of Business Venturing,22(4), 545–565.

Feltham, T. S., Feltham, F., & Barnett, J. J. (2005). Thedependence of family businesses on a singledecision-maker. Journal of Small Business Manage-ment, 17, 258–270.

Finkelstein, S., & Hambrick, D. C. (1990). Top manage-ment team tenure and organizational outcomes: Themoderating role of managerial discretion. Adminis-trative Science Quarterly, 35, 484–503.

Floyd, S., Ortiz-Walters, R., Wooldridge, B., & Keller-manns, F. W. (forthcoming). Aligning internal andexternal selection environments: Effects of socialcontext on strategic renewal. In S. A. Zahra (Ed.),Handbook of corporate entrepreneurship.

Gersick, K. E., Davis, J. A., Hampton, M. M., & Lansberg,I. (1997). Generation to generation: Life cycles of thefamily business. Cambridge, MA: Harvard BusinessSchool Press.

Gudmundson, D., Tower, C. B., & Hartman, F. A. (2003).Innovation in small businesses: Culture and owner-ship structure do matter. Journal of DevelopmentalEntrepreneurship, 8(1), 1–17.

Habbershon, T. G., & Williams, M. (1999). A resource-based framework for assessing the strategic advan-tage of family firms. Family Business Review, 12, 1–25.

Habbershon, T. G., Williams, M., & MacMillan, I. C.(2003). A unified systems perspective of family firmperformance. Journal of Business Venturing, 18, 451–465.

Hall, A., Melin, L., & Nordqvist, M. (2001). Entrepreneur-ship as radical change in the family business: Explor-ing the role of cultural patterns. Family BusinessReview, 14(3), 193–208.

Hambrick, D. C., & Finkelstein, S. (1987). Managerialdiscretion: A bridge between polar views on organi-zations. In L. L. Cummings & B. M. Staw (Eds.),Research in organizational behavior (Vol. 9, pp. 369–406). Greenwich, CT: JAI Press.

Hoy, F. (2006). The complicating factor of life cycles incorporate venturing. Entrepreneurship Theory andPractice, 30(6), 831–836.

Jaffe, D. T., & Lane, S. H. (2004). Sustaining a familydynasty: Key issues facing complex multigenera-tional business- and investment-owning families.Family Business Review, 69, 85–98.

Kanter, R. M. (1983). The change masters. New York:Simon and Schuster.

Kanuk, L., & Berenson, C. (1975). Mail surveys andresponse rate: A literature review. Journal of Market-ing Research, 22, 440–453.

Kellermanns,F.W.,& Eddleston,K. (2004).Feuding fami-lies: When conflict does a family firm good. Entrepre-neurship Theory and Practice, 28(3), 209–228.

Kellermanns, F. W., & Eddleston, K. (2006a). Corporateventuring in family firms: Does the family matter?Entrepreneurship Theory and Practice,30(6),837–854.

Kellermanns, F. W., & Eddleston, K. (2006b). Feudingfamilies: The management of conflict in family firms.In P. Poutziouris, K. Smyrnios, & B. Klein (Eds.),Family business research handbook (pp. 358–368).Northampton, MA: Edward Elgar Publishing.

Kenyon-Rouvinez, D. (2001). Patterns in serial businessfamilies: Theory building through global case studyresearch. Family Business Review, 14(3), 175–192.

Kepner, E. (1991). The family and the firm: A coevolu-tionary perspective. Family Business Review, 4, 445–461.

Kesner, I. F., Shapiro, D. L., & Sharma, A. (1994). Broker-ing mergers: An agency theory perspective on therole of representatives. Academy of ManagementJournal, 37(3), 703–721.

Kellermans, Eddleston, Barnett, Pearson

12

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

Kirchhoff, B. A., Newbert, S. L., Hasan, I., & Armington,C. (2007). The influence of university R&D expendi-tures on new business formations and employmentgrowth. Entrepreneurship Theory and Practice, 31(4),543–559.

Klein, S. B., Astrachan, J. H., & Smyrnios, K. X. (2005).The F-PEC scale of family influence: Construct vali-dation, and further implication for theory. Entrepre-neurship Theory and Practice, 29(3), 321–339.

Levesque, M., & Minniti, M. (2006). The effect of agingon entrepreneurial behavior. Journal of Business Ven-turing, 21, 177–194.

Litz, R. A., & Kleysen, R. F. (2001). Your old men shalldream dreams, your young men shall see visons:Toward a theory of family firm innovation with helpfrom the Brubeck family. Family Business Review,14(4), 335–351.

Love, L. G., Priem, R. L., & Lumpkin, G. T. (2002). Explic-itly articulated strategy and firm performance underalternative levels of centralization. Journal of Man-agement, 28(5), 611–627.

Lumpkin, G. T., & Dess, G. G. (1996). Clarifying theentrepreneurial orientation construct and linking itto performance. Academy of Management Review,21(1), 135–172.

Mazen, A. M., Graf, L. A., Kellogg, C. E., & Hemmasi, M.(1987). Statistical power in contemporary manage-ment research. Academy of Management Journal,30(2), 369–380.

McCann, J. E., Leon-Guerrero, A.Y., & Haley, J. D. (2001).Strategic goals and practices of innovative familybusinesses. Journal of Small Business Management,39(1), 50–59.

McConaughy, D., & Phillips, G. (1999). Founders versusdescendants: The profitability, efficiency, growthcharacteristics, and financing in large, public,founding-family-controlled firms. Family BusinessReview, 12(2), 123–132.

Miller, D. (1983). The correlates of entrepreneurship inthree types of firms. Management Science, 29(7), 770–791.

Morris, M. H. (1998). Entrepreneurial intensity. West-port, CT: Quorum Books.

Olson, P. D., Zuiker, V. S., Danes, S. M., Stafford, K.,Heck, R. K. Z., & Duncan, K. A. (2003). The impact ofthe family and the business on family business sus-tainability. Journal of Business Venturing, 18, 639–666.

Parker, S. C. (2006). Learning about the unknown: Howfast do entrepreneurs adjust their beliefs? Journal ofBusiness Venturing, 21, 1–26.

Podsakoff, P. M., & Organ, D. W. (1986). Self-reports inorganizational research: Problems and perspectives.Journal of Management, 12, 531–544.

Quinn, J. B. (1980). Strategies for change: Logical incre-mentalism. Homewood, IL: Richard D. Irwin, Inc.

Rauch, A., Frese, M., & Utsch, A. (2005). Effects ofhuman capital and long-term human resourcesdevelopment and utilization on employment growthof small-scale businesses: A causal analysis. Entrepre-neurship Theory and Practice, 29(6), 681–698.

Salvato, C. (2004). Predictors of entrepreneurship infamily firms. Journal of Private Equity, 7(3), 68–76.

Schulze, W. S., Lubatkin, M. H., Dino, R. N., & Buchholtz,A. K. (2001). Agency relationship in family firms:Theory and evidence. Organization Science, 12(9),99–116.

Sharma, P., & Chrisman, J. J. (1999). Toward a reconcili-ation of the definitional issues in the field of corpo-rate entrepreneurship. Entrepreneurship Theory andPractice, 23(3), 11–27.

Sharma, P., Chrisman, J. J., & Chua, J. H. (1997). Strategicmanagement of the family business: Past researchand future challenges. Family Business Review, 10(1),1–36.

Sharma, P., Chua, J. H., & Chrisman, J. J. (2005). Succes-sion planning. In M. A. Hitt, & R. D. Ireland (Eds.),The Blackwell encyclopedic dictionary of entrepre-neurship. Oxford: Blackwell.

Sirmon, D. G., & Hitt, M. A. (2003). Managing resources:Linking unique resources, management and wealthcreation in family firms. Entrepreneurship Theoryand Practice, 27(4), 339–358.

Stavrou, E. T. (1999). Succession in family businesses:Exploring the effects of demographic factors onoffspring intentions to join and take over the busi-ness. Journal of Small Business Management, 37(3),43–61.

Steier, L. (in press). New venture creation and organiza-tion: A familial sub-narrative. Journal of BusinessResearch.

Steier, L., Chrisman, J. J., & Chua, J. H. (2004). Entrepre-neurial management and governance in family firms:An introduction. Entrepreneurship Theory and Prac-tice, 28, 295–303.

Stewart, W. H., Watson, W. E., Carland, J. A., & Carland, J.W. (1999). A proclivity for entrepreneurship: A com-parison of entrepreneurs, small business owners, andcorporate managers. Journal of Business Venturing,14, 189–214.

Tabachnick, B. G., & Fidell, L. S. (1995). Using multivari-ate statistics (3rd ed.). New York: HarperCollinsCollege Publishers.

Tagiuri, R., & Davis, J. A. (1996). Bivalent attributes ofthe family firm. Family Business Review, 9(2), 199–208.

Effects of Family Member Characteristics and Involvement on Entrepreneurial Behavior

13

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from

Venkatraman, N., & Ramanujam, V. (1987). Measure-ment of business performance in strategy research: Acomparison of approaches. Academy of ManagementReview, 11(4), 801–814.

Winter, M., Danes, S. M., Koh, S., Fredericks, K., & Paul,J. J. (2004). Tracking family businesses and theirowners over time: Panel attrition, manager depar-ture, and business demise. Journal of Business Ventur-ing, 19, 535–559.

Winter, M., Fitzgerald, M. A., Heck, R. K. Z., Haynes, G.W., & Danes, S. M. (1998). Revisiting the study offamily businesses: Methodological challenges, dilem-mas, and approaches. Family Business Review, 11(3),239–252.

Zahra, S.A. (1991). Predictors and financial outcomes ofcorporate entrepreneurship as firm behavior: A cri-tique and extension. Journal of Business Venturing, 6,259–285.

Zahra, S. A. (1996). Governance, ownership, and corpo-rate entrepreneurship: The moderating impact ofindustry technological opportunities. Academy ofManagement Journal, 39(6), 1713–1735.

Zahra, S.A. (2005). Entrepreneurial risk taking in familyfirms. Family Business Review, 18(1), 23–40.

Zahra, S. A., Hayton, J. C., & Salvato, C. (2004). Entrepre-neurship in family vs. non-family firms: A resource-

based analysis of the effect of organizational culture.Entrepreneurship Theory and Practice,28(4),363–381.

Zahra, S. A., Jennings, D., & Kuratko, D. (1999). Theantecedents and consequences of firm-level entrepre-neurship: The state of the field. EntrepreneurshipTheory and Practice, 24(2), 45–65.

Zahra, S. A., Neubaum, D. O., & Huse, M. (2000). Entre-preneurship in medium-size companies: Exploringthe effects of ownership and governance systems.Journal of Management, 26(5), 947–976.

Dr. Franz W. Kellermanns, Mississippi State Uni-versity, PO Box 9581, Mississippi State, MS 39762;[email protected]. Kimberly A. Eddleston, College of BusinessAdministration, Northeastern University, 319Hayden Hall, Boston, MA 02115-5000;[email protected]. Tim Barnett, Mississippi State University,PO Box 9581, Mississippi State, MS 39762;[email protected]. Allison Pearson, Mississippi State University,PO Box 9581, Mississippi State, MS 39762;[email protected].

Kellermans, Eddleston, Barnett, Pearson

14

at FFI-FAMILY FIRM INSTITUTE on May 8, 2009 http://fbr.sagepub.comDownloaded from