An alternative to stochastic ALM models

16

November 2014 Frédéric Sart

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of An alternative to stochastic ALM models

November 2014

Frédéric Sart

1. Overview

2. Investment strategy

3. Fair replicating portfolio

4. Potential applications

2

3

The fair replication method (FRM) is a computationally efficient alternative to traditional stochastic modeling

It is designed to value liabilities whose profit sharing mechanism is endogenous, i.e. based on the performance of the backing assets

The basic idea is to construct a hypothetical portfolio, the fair replicating portfolio (FRP), whose cash flows are scenario-invariant

4

2.1. Traditional stochastic modeling

In stochastic ALM models, the investment strategy consists of buy and sell rules

This results in high computational complexity

DSC1,1 * CF1 + DSC1,2 * CF2 + … + DSC1,T * CFT

BEL = (DSC1 * $ + DSC2 * $ + … + DSCn * $)/n

Stochastic setting

5

2.2. Rule-based vs. principle-based approach

Is this complexity really necessary?

Why not derive the investment strategy from a risk minimization principle?

This would drastically reduce the computational complexity of the problem, at least when the profit sharing mechanism is endogenous

BEL = (DSC1 * $ + DSC2 * $ + … + DSCn * $)/n

= (DSC1 + DSC2 + … + DSCn)/n * $

= DSCCE * $

Stochastic setting

6

2.3. Fair replication method

The fair replication strategy is an investment strategy that makes the liability cash flows scenario-invariant

This is achieved by instantaneously switching from the current backing assets to the fair replicating portfolio

7

3.2. Comparison with the Black-Scholes model

In both cases, the valuation problem reduces to a deterministic problem (by choosing the investment strategy that eliminates risk)

A partial differential equation is derived in the Black-Scholes model and a fixed-point equation in the present case

3.1. Valuation technique

The fair replicating portfolio is a static replicating portfolio of zero-coupon bonds

This means that the liability can be valued using only (1) the fair path, i.e. the book return path of the fair replicating portfolio, to project the cash flows and (2) the certainty equivalent scenario to discount them

8

3.3. Construction (1)

Start from the fixed-income portion of the current backing assets

The fixed-income outflows are assumed to be adjusted for credit risk

-40

-20

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10

Liability outflows *

Adjusted fixed-income outflows

* For any time t, the liability outflow at t is defined as the sum of the cash flow at t and the profit at t

9

3.3. Construction (2)

Where necessary, cap these adjusted outflows

-40

-20

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10

10

3.3. Construction (3)

Where necessary, complete these adjusted outflows with new zero-coupon bonds

-40

-20

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10

-2%

0%

2%

4%

6%

-50

0

50

100

150

1 2 3 4 5 6 7 8 9 10

-2%

0%

2%

4%

6%

-50

0

50

100

150

1 2 3 4 5 6 7 8 9 10

11

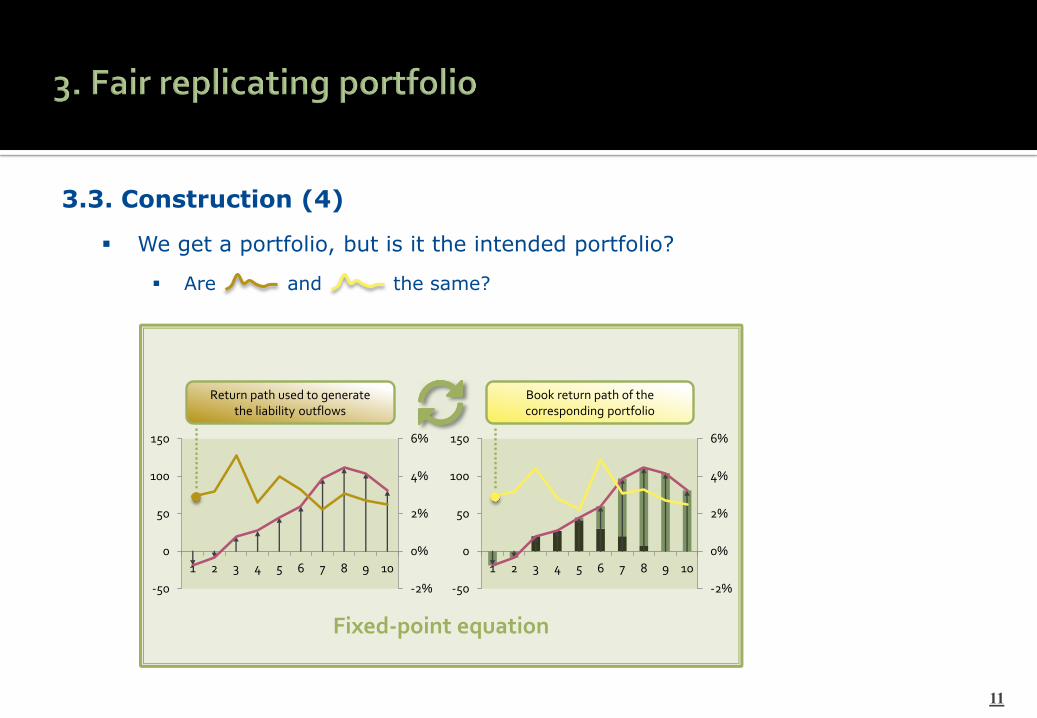

3.3. Construction (4)

We get a portfolio, but is it the intended portfolio?

Are and the same?

Return path used to generatethe liability outflows

Book return path of the corresponding portfolio

Fixed-point equation

1. Start with a zero return path

12

3.3. Construction (5)

The fair replicating portfolio is the one for which they are the same

How to find it?

3. Use as return path the book return path of the 1st portfolio

5. Use as return path the book return path of the 2nd portfolio

2. You get a 1st portfolio

4. You get a 2nd portfolio

6. And so on

13

3.3. Construction (6)

The sequence of portfolios converges very fast to the fair replicating portfolio

Typically, three iterations are sufficient to obtain an accurate result

14

4.1. In the short run

The fair replication method could be used as a basis for validating stochastic ALM models

15

4.2. In the medium to long run

The fair replication method could be used as a substitute for stochastic ALM models (e.g. to avoid nested simulations when calculating the SCR)

FRP1

FRP2

FRPi

FRPn

…

Outer + inner scenarios Outer scenarios + FRPs

16

Kalberer, T. (2013). Why so complicated? Life is easy!. Unpublished manuscript.

Sart, F. (2010). Fair valuation of universal life policies via a replicating portfolio. Journal of Applied Analysis, 16(1), 95-105.