Takaful ‒ Foundations and Standardization of Islamic Insurance by ...

Upload

khangminh22Category

view

0download

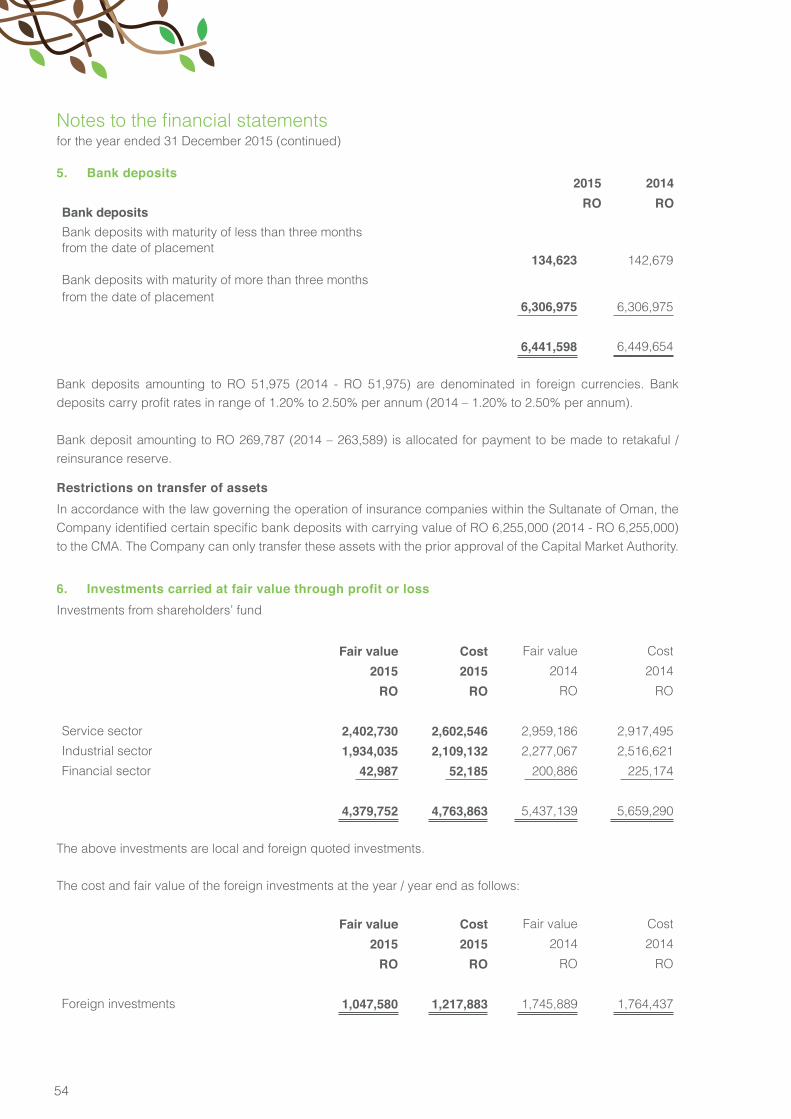

0

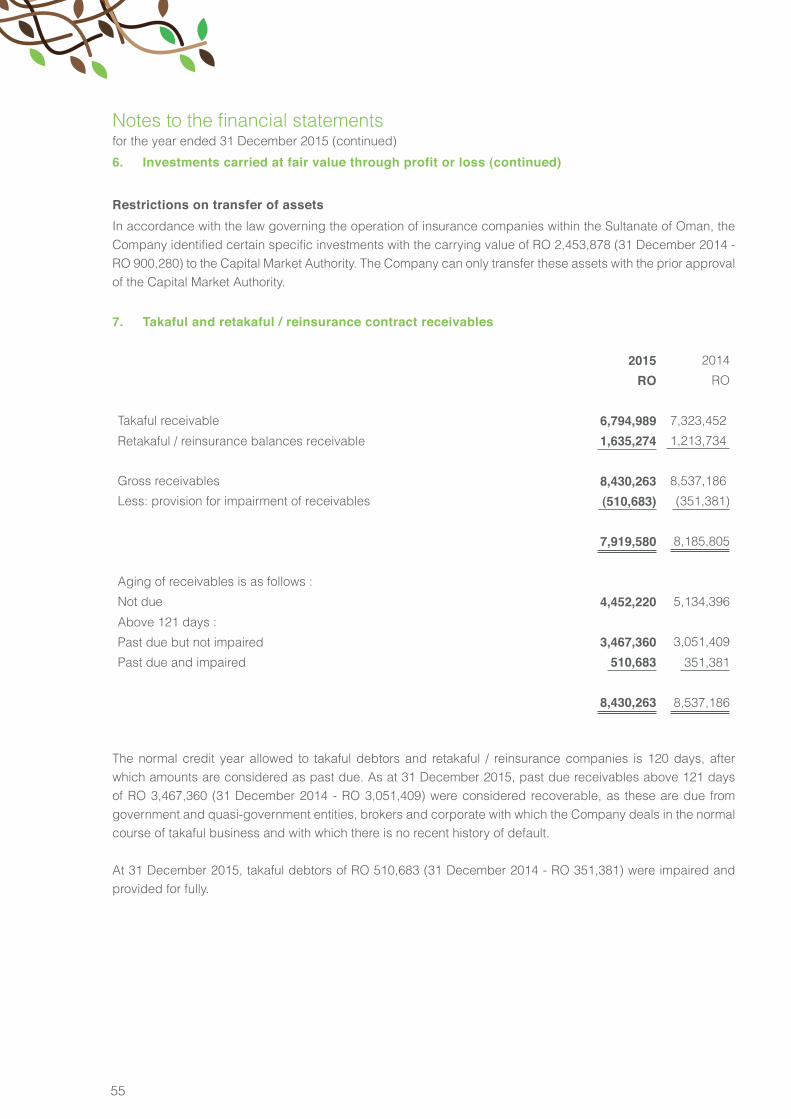

1

3

4

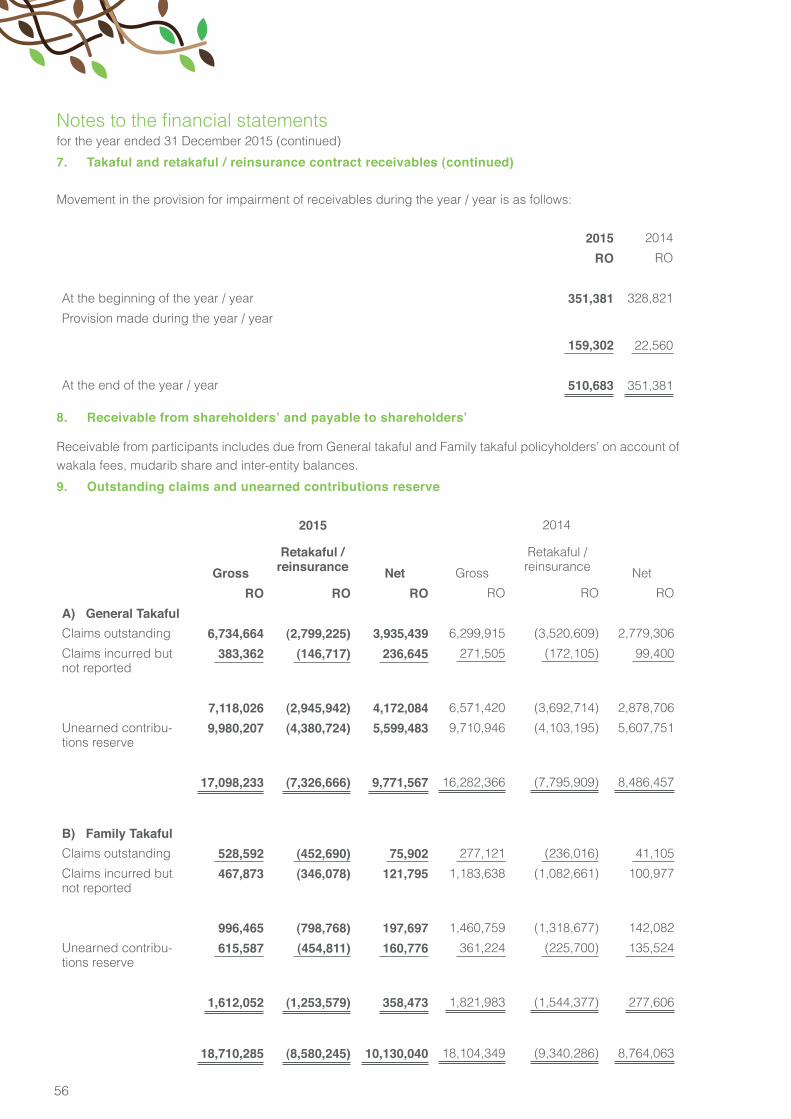

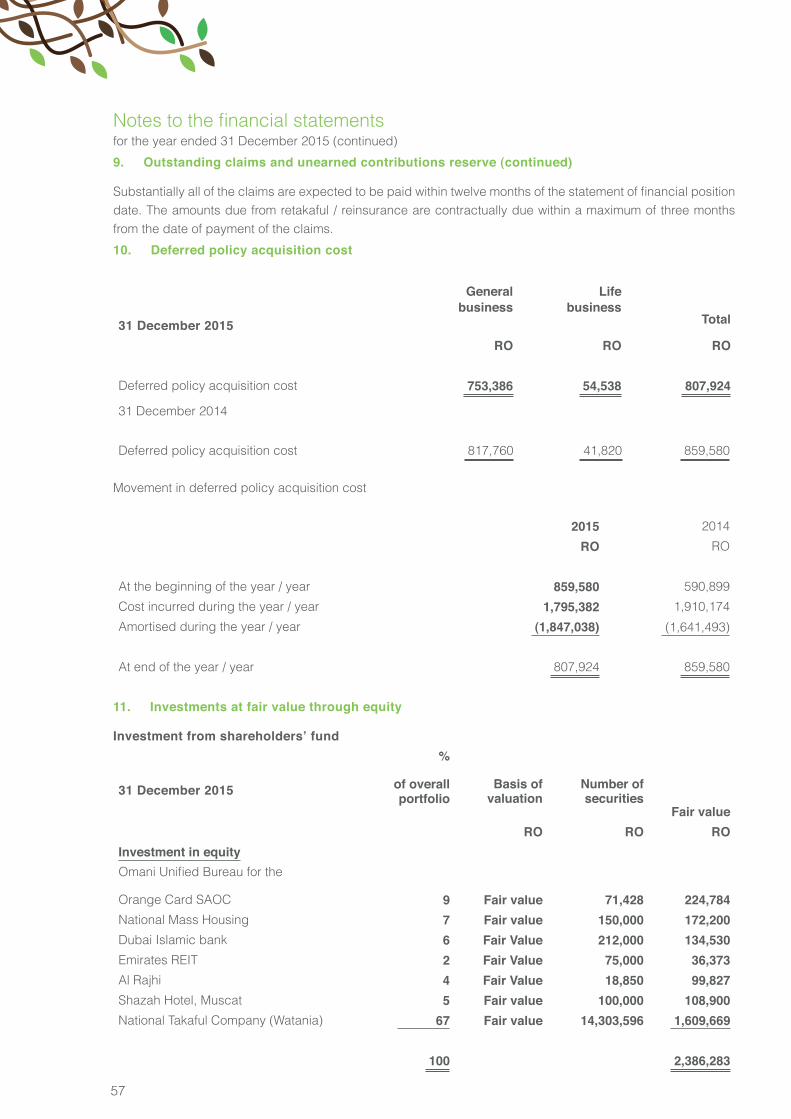

Contents

5

Chairman's Report

Management Discussion and Analysis Report

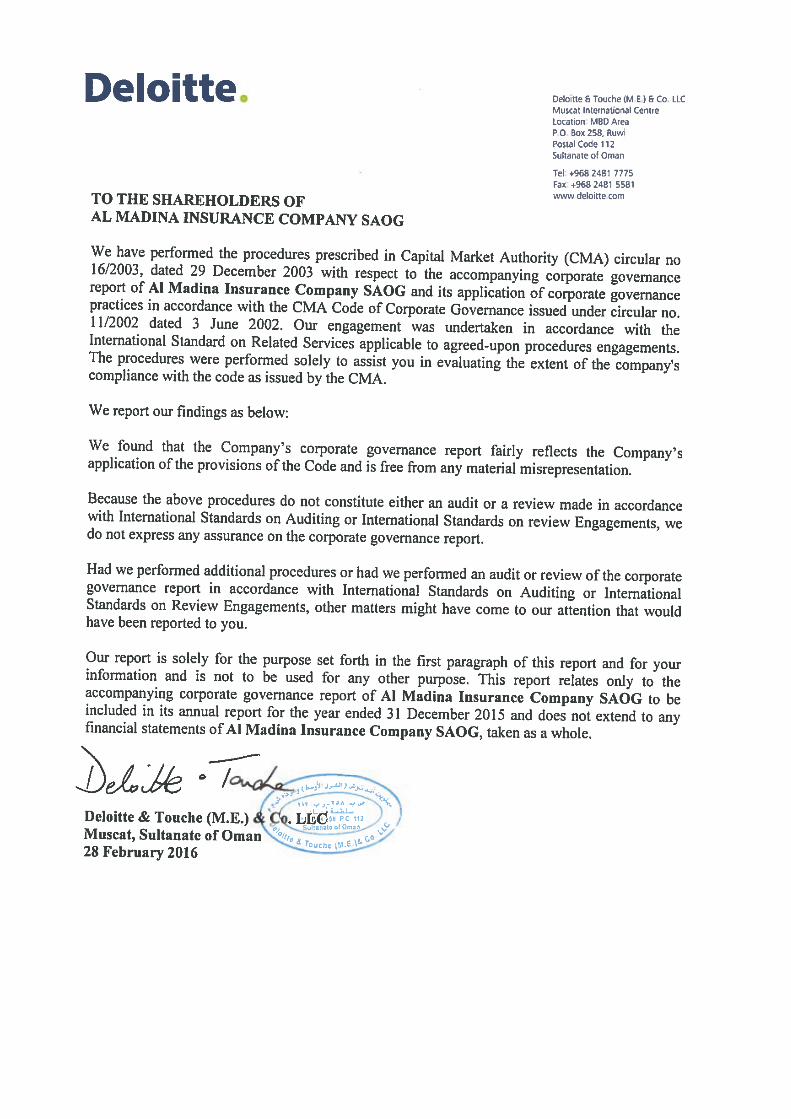

Auditor's Report on Corporate Governance

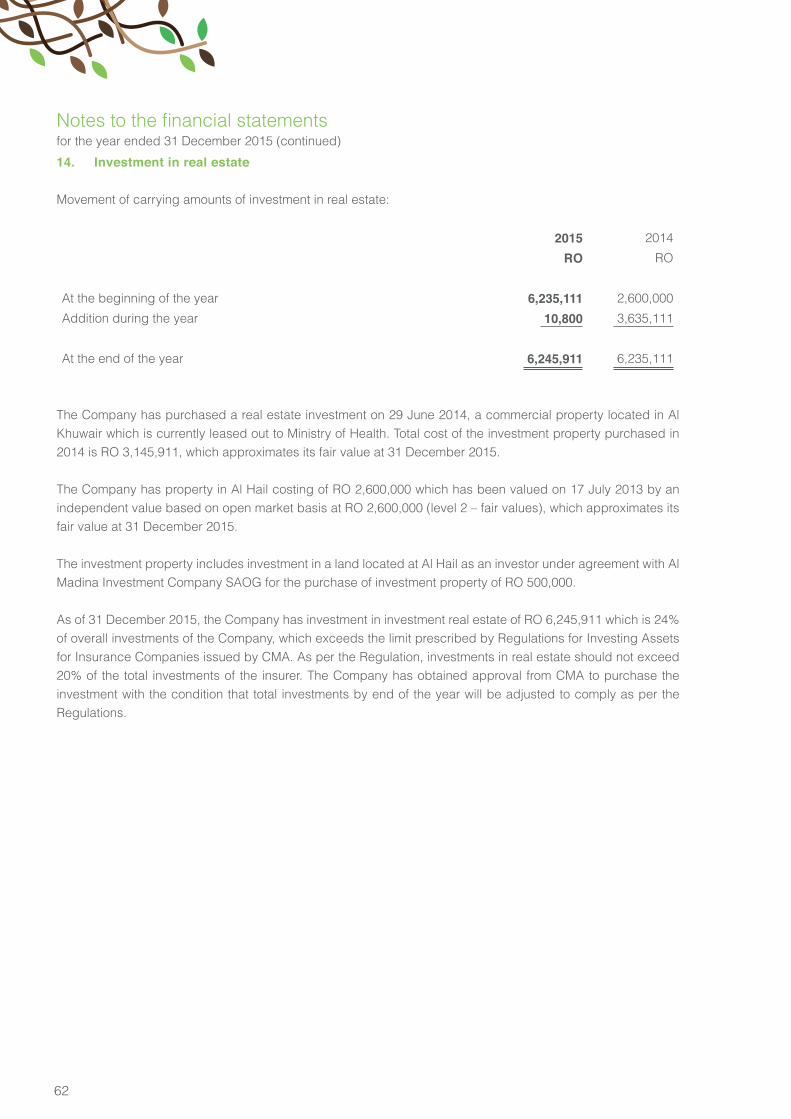

Report on Corporate Governance

Shari'ah Supervisory Board's Report

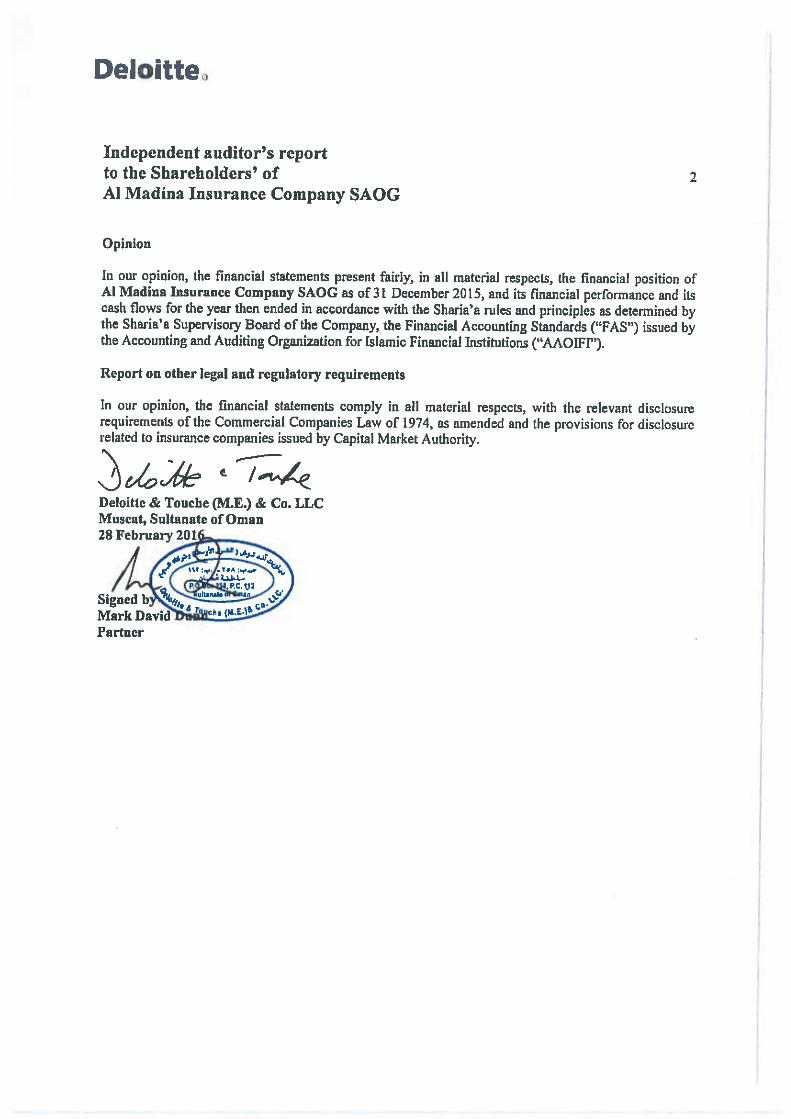

Auditor's Report to shareholders

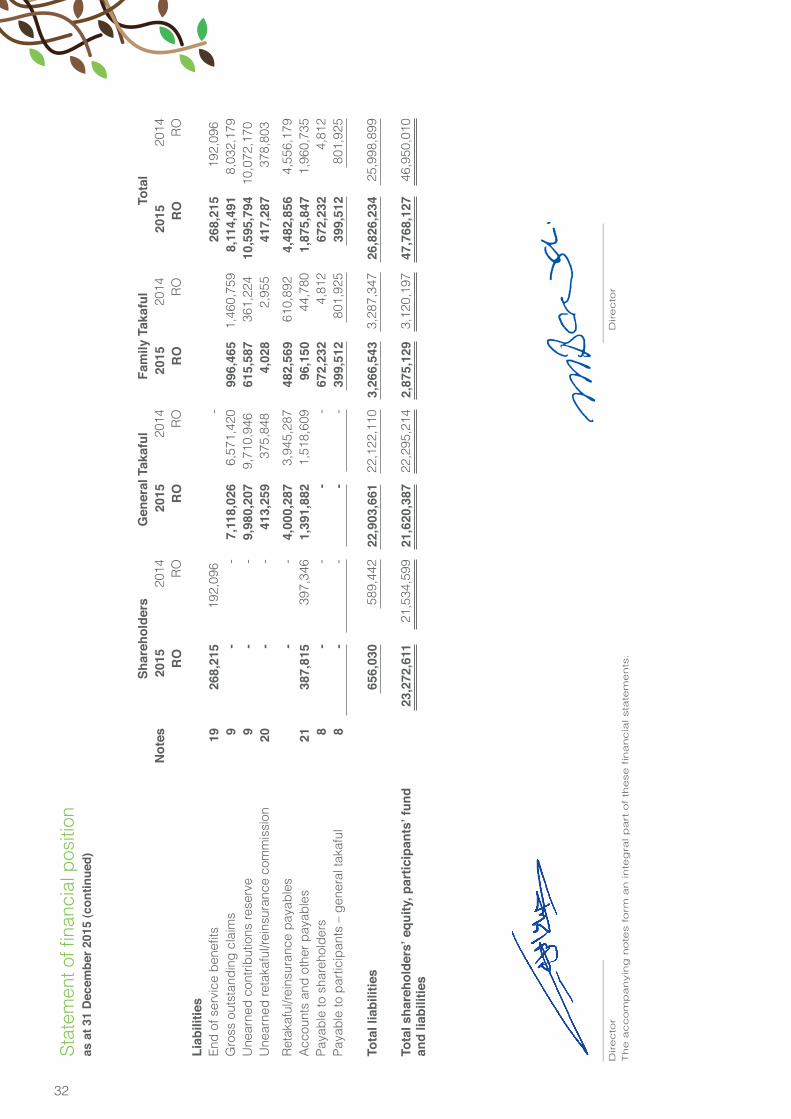

Statement of Financial Position

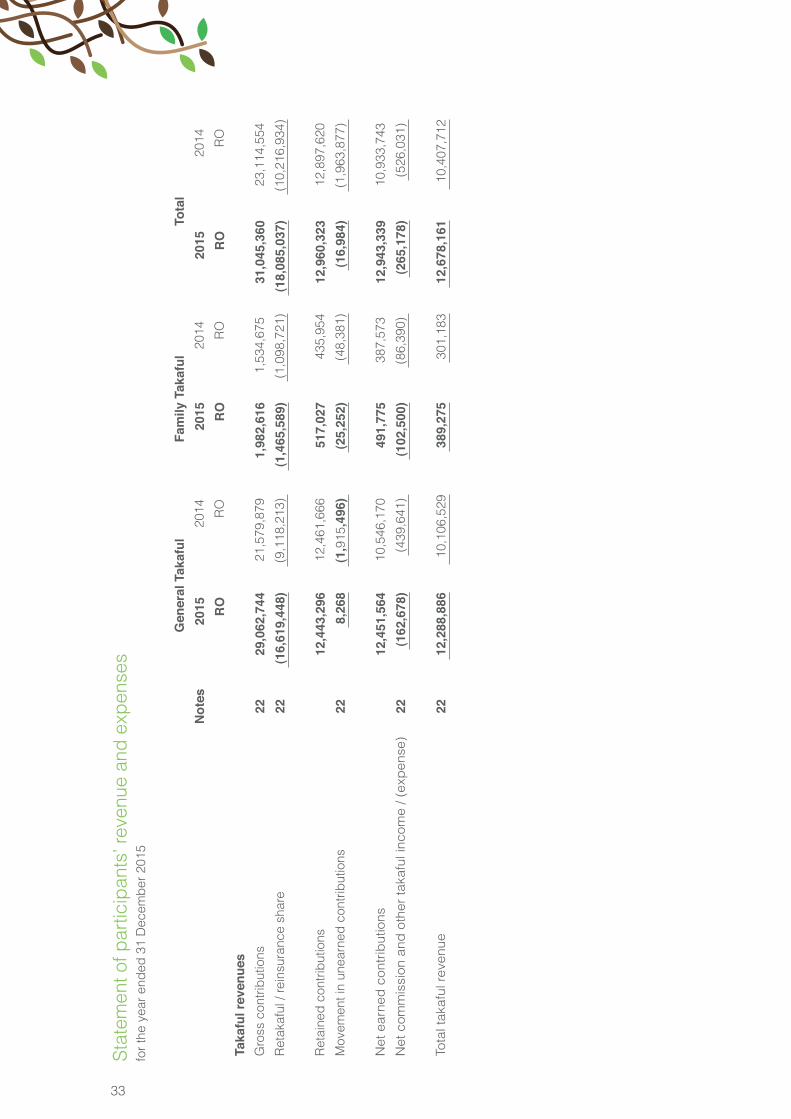

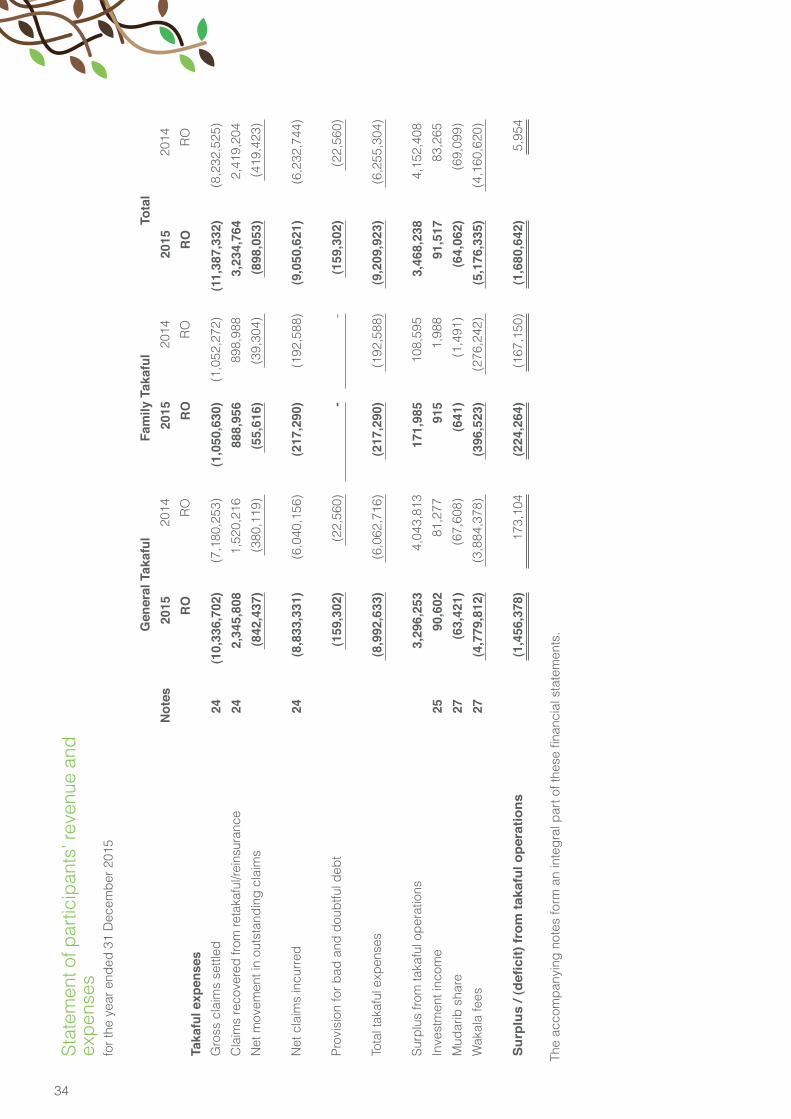

Statement of Participants' Revenue and Expenses

Statement of Comprehensive Income

Statement of Changes in Equity

Statement of Cash Flows

Notes to the Financial Statements

9

12

16

17

26

27

30

33

35

36

39

41

6

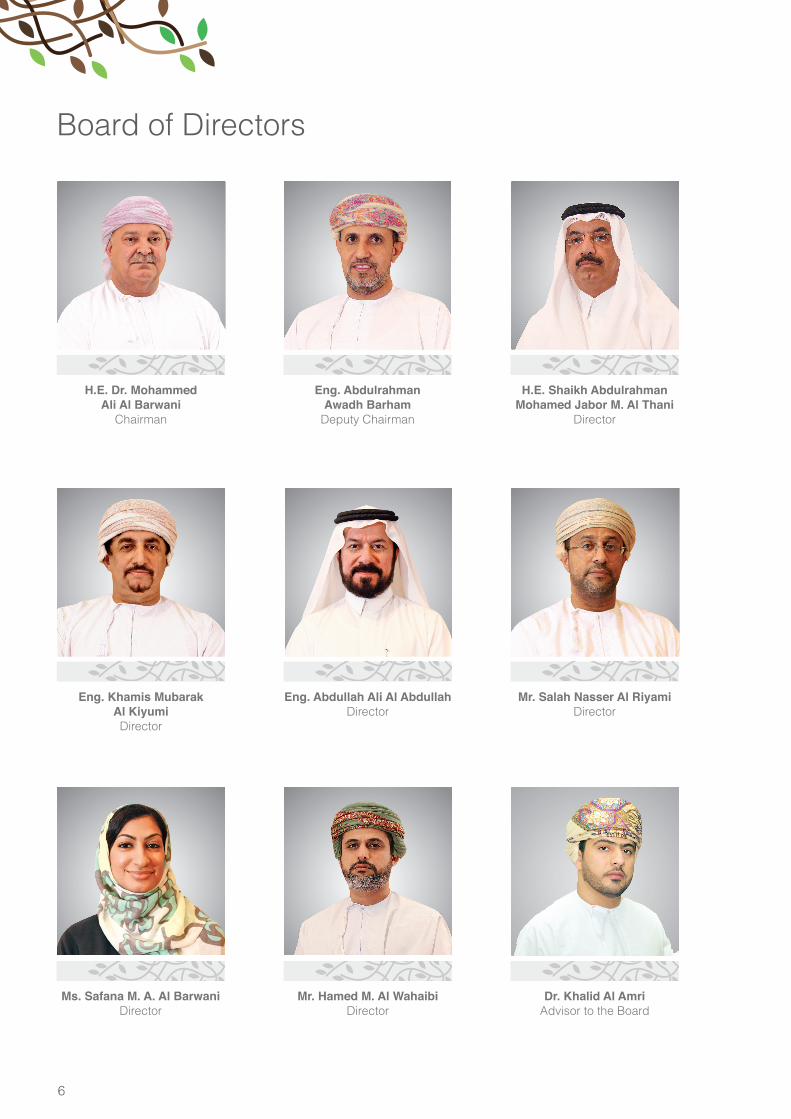

Board of Directors

7

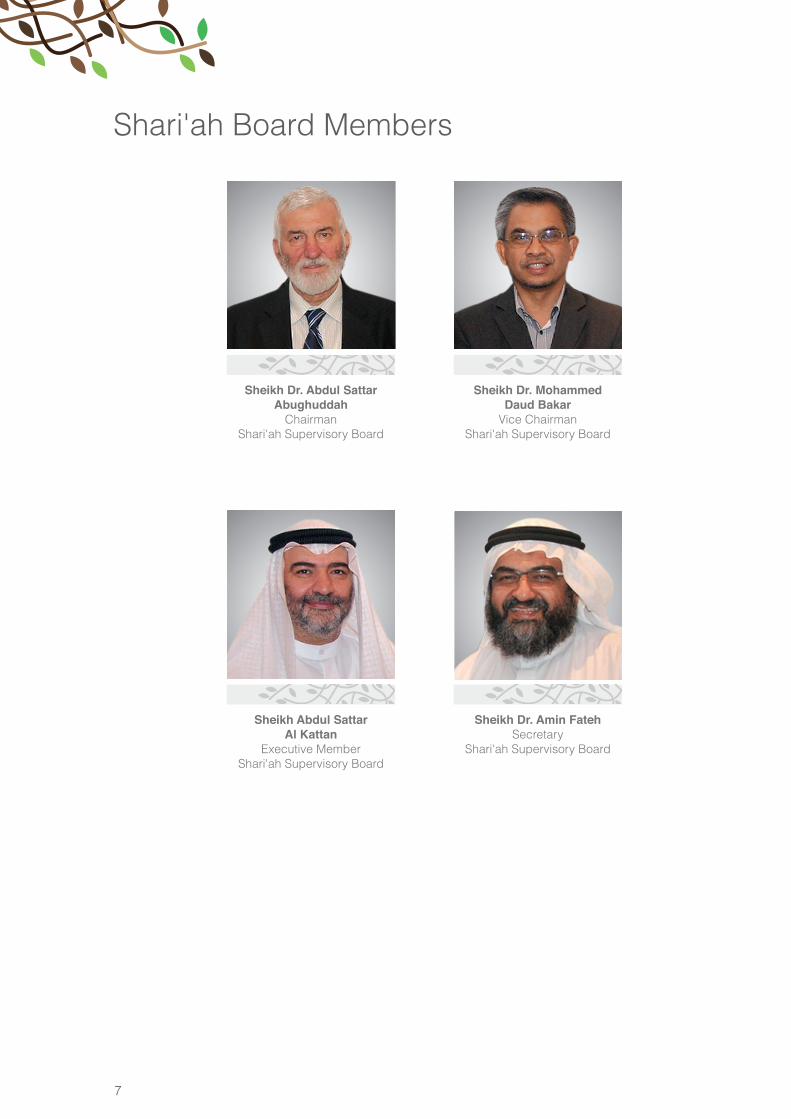

Shari'ah Board Members

8

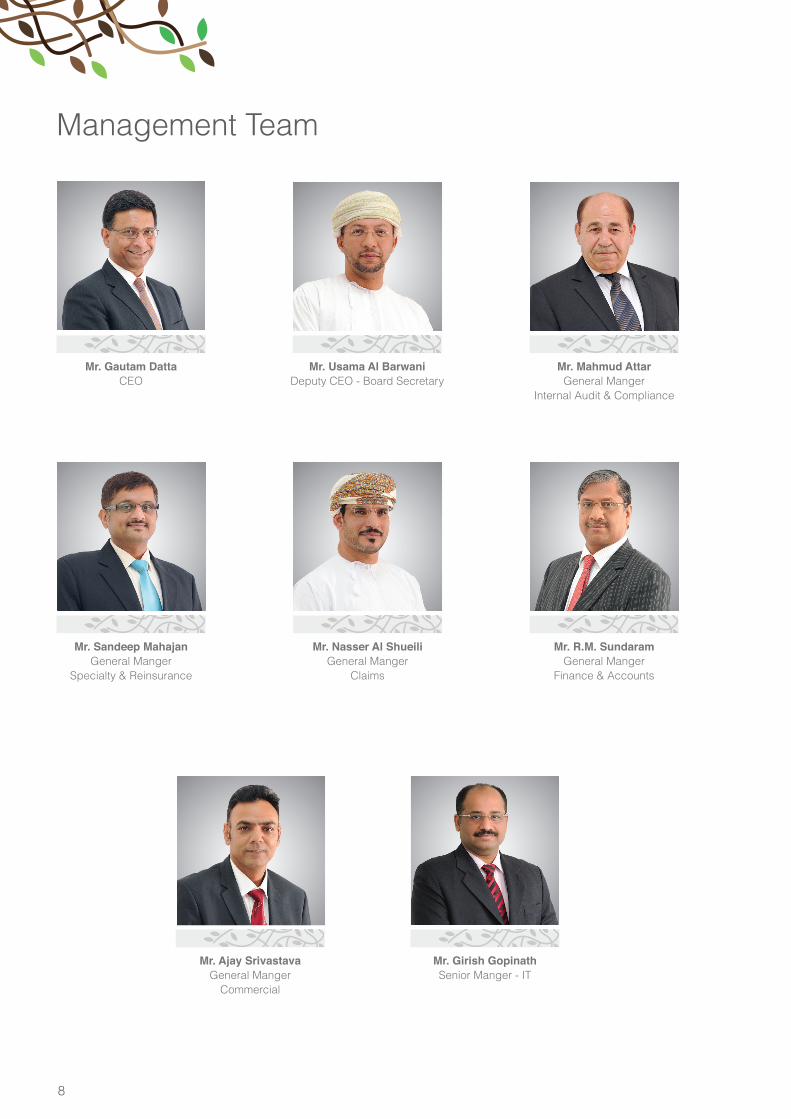

Management Team

9

Chairman's Report

10

Dear Shareholders,

May the Peace, Mercy and Blessing of Allah be with

you.

On behalf of the Board of Directors, and Management

team of Al Madina Insurance Co, I am pleased to

present to you a report on the detailed financial year

2015.

The 2015 financial results delivered by your Company

reflect our intent, capacity and expectations and

I believe that the company is steadily poised to

continue to reward both you as shareholders and as

policyholders (customers) as we go into the future.

The growth in gross contribution was over 34%.

The Company had to take a onetime impairment in

respect of its investment in National Takaful Company

(Watania) in UAE which has resulted in lower profit for

2015.

The management in Watania has taken steps to

improve its performance and synergies in the

operations of both the companies will help in reducing

cost and increasing profitability. Due to increase in

legal awards our motor portfolio experienced a slight

setback this year. It also contributed to the increase

in over all claims experience from 60% to 71%. The

management has taken corrective measures and its

positive impact will be evident in 2016. This will help

in getting Policyholder’s Fund back in surplus in the

current year.

As a leader in the Takaful industry in Oman, it has

been both an opportunity and a challenge for your

company to propel growth and continue to gain

share of the market. After a period of high growth, the

Oman insurance industry is now in the realm of steady

performance in 2015. While the market is registering

growth, the relative growth in revenues continues to

be impacted by several factors such as the increase

in the number of players and the resultant over

capacity, the competitive nature of the business, and

the overwhelming challenges in the larger economic

and fiscal context.

The momentum that we gained in 2014 was quickly

contested by the steady decline in oil prices and its

negative impact on the overall fiscal environment as

the year unfolded. Our preparedness for the situation

and our philosophy of looking at every challenge as

an opportunity helped us to consolidate our position,

and look at new ways to deliver success.

The year saw us to continue to inspire our customers,

business partners and stakeholders with our

innovative approach towards growth of businesses,

overall profitability and strengthening the presence of

Takaful in the Sultanate.

The company launched mInsurance: Oman’s first

mobile app for Insurance, supported by a dedicated

24/7 Call Center. It is a matter of pride that the software

backbone for our digital offerings are developed

in-house at Al Madina, under the name ‘Tameenet’.

We also recognized the increasing need for us to be

closer to our customers prompting us to arrive at a

strategic model of adopting kiosks at malls, placing

us in the everyday lives of our customers.

We continued our partnership with corporate Oman

by conducting workshops with key clients and

collaborating with them to develop bespoke Takaful

solutions for their needs, whilst enabling them to get

an understanding of Takaful and its principles.

Among the many initiatives that we engaged with the

11

community, our presence at the students’ career fair

stands out as it served well to increase the awareness

of Takaful amongst the young audience.

We also continued to build on the success of ‘Connect’

our internal newsletter, which has grown from being

an information tool to one that helps us engage with

all stakeholders, form employees, customers, to

regulators and media and increase the awareness for

Takaful.

The year also saw us initiate a series of internal email

campaigns for employee well-being and awareness

at the workplace, contributing to our healthy people

and HR strategy.

As you will know, the global economy, and especially

the region, continues to reel under the steady decline

of oil prices. It is important to recognise that the

situation is here to stay, and the recovery will be slow.

As a result, Government spending in the economy is

expected to be considerably lower which will have

negative impact on growth.

Adverse as it may sound, at Al Madina we have

always remained optimistic about our approach. I

believe that cyclical downturns is a time to introspect,

becoming more focused, disciplined and look out for

opportunities.

Becoming more cost efficient, enhancing our focus on

customer service, retaining our talented employees

are some of the ways in which we can come out of

these challenging conditions tougher, smarter and

profitable.

Innovation has never been more important to

organistions, and we need to work in synergy in the

areas of finding newer segments such as the growing

SME base, product development, distribution and

leveraging technology to elevate our levels of service

to customers.

With businesses becoming more cautious, insurance

will occupy a bigger role in the economy and the

changing regulations will mean companies that are

better managed and are financially strong will have a

key advantage going into the future.

Our successful journey as the flagbearer of the

Takaful industry in Oman is a consolidated effort

of all stakeholders. We particularly recognize the

continuous support of the CMA and their committed

people.

As a testimony to our leadership position and strong

governance, we proudly received two coveted

recognitions. Al Madina Takaful was named ‘General

Takaful Company of the Year’ at the 2nd Middle East

Insurance Industry Awards 2015 which attracted

close to 280 nominations in different categories from

across the region. In quick succession, we were

named the ‘Oman Insurer of the Year’ at the MENAIR

Insurance Awards 2016, which was even more special

to us as it was heavily contested by both Takaful

and conventional insurance providers operating in

Oman. Al Madina Takaful was named finalist in three

categories and was the only insurance company

from Oman, both local and global, to be recognized

at this year’s MENAIR Awards programme. Oman is

a relatively new entrant into the world of Takaful, and

securing these awards in the nascent stages of the

industry will give all the players confidence and the

encouragement to go further.

On behalf of the Board of Directors, I take this

opportunity to thank the Insurance community, both in

Oman and overseas, for the confidence reposed in the

company. I would also like to thank the Management

Team and all our employees for their dedication and

commitment to press ahead amid the challenging situation to reach higher levels of excellence.

The Board of Directors is deeply grateful to His Majesty

Sultan Qaboos Bin Said for his vision and guidance,

which has helped the country along its path of growth

and prosperity.

May the Peace, Mercy and Blessing of Allah be with

you. May God Bless you all.

Dr. Mohammed Ali Al BarwaniChairman of the Board

12

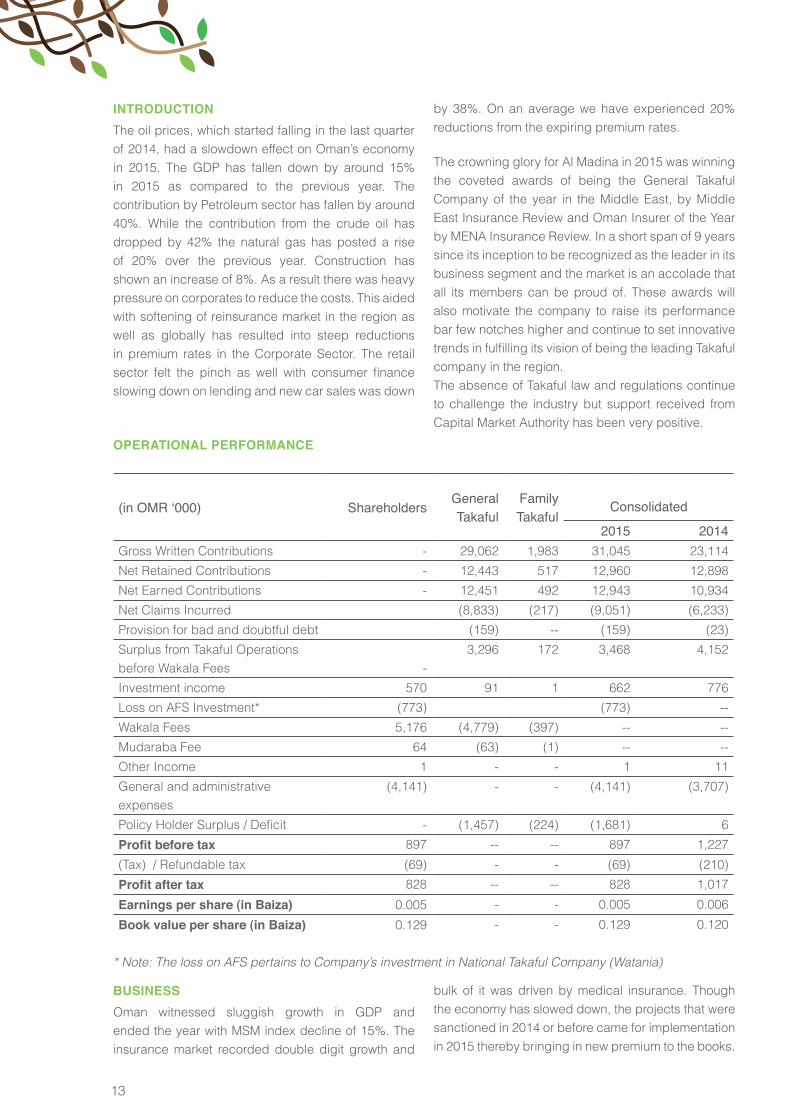

Management Discussion &Analysis Reportfor the financial year ended 31 December 2015

13

INTRODUCTIONThe oil prices, which started falling in the last quarter of 2014, had a slowdown effect on Oman’s economy in 2015. The GDP has fallen down by around 15% in 2015 as compared to the previous year. The contribution by Petroleum sector has fallen by around 40%. While the contribution from the crude oil has dropped by 42% the natural gas has posted a rise of 20% over the previous year. Construction has shown an increase of 8%. As a result there was heavy pressure on corporates to reduce the costs. This aided with softening of reinsurance market in the region as well as globally has resulted into steep reductions in premium rates in the Corporate Sector. The retail sector felt the pinch as well with consumer finance slowing down on lending and new car sales was down

OPERATIONAL PERFORMANCE

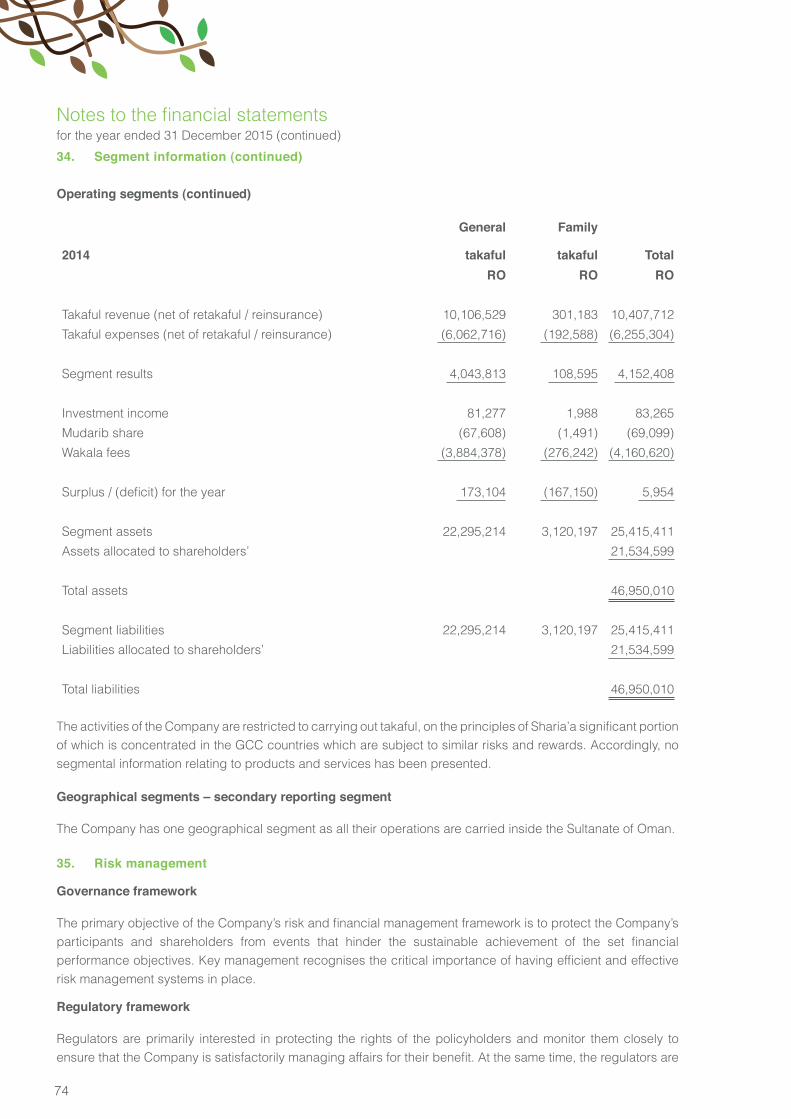

(in OMR ‘000) Shareholders General Takaful

Family Takaful

Consolidated

2015 2014Gross Written Contributions - 29,062 1,983 31,045 23,114

Net Retained Contributions - 12,443 517 12,960 12,898

Net Earned Contributions - 12,451 492 12,943 10,934

Net Claims Incurred (8,833) (217) (9,051) (6,233)

Provision for bad and doubtful debt (159) -- (159) (23)

Surplus from Takaful Operations before Wakala Fees -

3,296 172 3,468 4,152

Investment income 570 91 1 662 776

Loss on AFS Investment* (773) (773) --

Wakala Fees 5,176 (4,779) (397) -- --

Mudaraba Fee 64 (63) (1) -- --

Other Income 1 - - 1 11

General and administrative expenses

(4,141) - - (4,141) (3,707)

Policy Holder Surplus / Deficit - (1,457) (224) (1,681) 6

Profit before tax 897 -- -- 897 1,227

(Tax) / Refundable tax (69) - - (69) (210)

Profit after tax 828 -- -- 828 1,017

Earnings per share (in Baiza) 0.005 - - 0.005 0.006

Book value per share (in Baiza) 0.129 - - 0.129 0.120

* Note: The loss on AFS pertains to Company’s investment in National Takaful Company (Watania)

by 38%. On an average we have experienced 20% reductions from the expiring premium rates.

The crowning glory for Al Madina in 2015 was winning the coveted awards of being the General Takaful Company of the year in the Middle East, by Middle East Insurance Review and Oman Insurer of the Year by MENA Insurance Review. In a short span of 9 years since its inception to be recognized as the leader in its business segment and the market is an accolade that all its members can be proud of. These awards will also motivate the company to raise its performance bar few notches higher and continue to set innovative trends in fulfilling its vision of being the leading Takaful company in the region. The absence of Takaful law and regulations continue to challenge the industry but support received from Capital Market Authority has been very positive.

BUSINESSOman witnessed sluggish growth in GDP and ended the year with MSM index decline of 15%. The insurance market recorded double digit growth and

bulk of it was driven by medical insurance. Though the economy has slowed down, the projects that were sanctioned in 2014 or before came for implementation in 2015 thereby bringing in new premium to the books.

14

Al Madina was successful in getting some key projects as well as large operational accounts. We could succeed in striking a balance due to our favorable positioning in the regional and global markets based on our excellent underwriting strength, high retentions and a good branding. We have maintained our placements with A and above rated reinsurers.The Company continued to focus on building awareness in the community on Takaful through its Knowledge Forum. It sponsored in partnership with CMA and Deloitte a symposium to discuss the development of Takaful.

The Company continued to innovate by using technology in distribution and customer service. It launched mInsurance the first mobile insurance application offering products and claims services to its customers on their mobile phones. It also launched self-service Kiosks, which will be deployed across the country more and more in the coming years.

INVESTMENTSPerformance of the Company’s investment book was negatively impacted by the fall in the regional equity markets in the 4th quarter of 2015. Benchmark index (MSM Sharia index) for the company fell by 11.5% in 2015 impacting the performance of company’s equity portfolio. Although company’s fixed income generating assets provided some stability to the overall investment performance, still the total investment income fell well short of its budget. The company generated total investment income of RO 0.56 million in 2015 (before an impairment loss of RO 0.77 which the company had to take on a strategic investment, Watania) as against RO .78 million in 2014.

The equity markets are expected to remain volatile in 2016 due to looming uncertainty over the fate of the oil prices and its impact on the regional economies. The company plans to focus on diversifying its investment book into more stable investment portfolio and at the same time look for profitable opportunities in the equity segment.

CLAIMSThe first three quarters of the year witnessed higher accidents and slowly the fourth quarter witnessed lower accident rates due to ROP conducting awareness programs and laying stringent rules on the use of mobile phones during drive and Traffic fines on speed.

The trends of court awards for injury compensations have taken a higher level of awards which the country witnessed RO 230,000 awarded for a permanent disability which is the highest award for a single injury as far as the market is concerned , the increase in awards have significant hit in the financials of insurance companies which is a growing concern for the Industry .The accident death rate during 2013 was 913 , 816 during 2014 and same has fallen to 502 as of Sep 2015 which is 21 % fall in the average / month compared to the previous year.

The agencies continued to cut their discount rates which were offered previously and have parked their participation on participating in consolidated repairs due to growing complaints on repair quality to PACP .The effect on this we witnessed an increase of 8% increase in our agency repairs over the previous year.

New claim intimation process was implemented during the second half of the year where quality audit been put place to monitor the process quality, documentation and turnaround time to enhance the service standards to the clients along with operations centralized to process the claims intimated across Oman under one head . To mitigate the incurred claims new empanelment of garages across the branches being driven along with a new look on exploring of salvages through our counterpart in Abu Dhabi.

Proposal on handling recovery claims through Watniah being presented to the management considering the past cooperation issues with the UAE market and to ease the recovery procedures going forward with an outlook to ease the service facilitation to our mutual clients and trim the recoveries.

MANPOWER AND HRHR team launched an automated Performance Management System to align the corporate goals and objectives to individual goals. The system facilitates to monitor performance “As it Happens” and empowers performance monitoring at individual, departmental, and organizational levels.

HRA team launched a learning management system during 2015 which is aimed to facilitate self-paced learning and enabling employees to review their learning processes.

As a result of these initiatives, the HR team has been contributing to further a positive and performance

15

based culture in the organization. HR has embarked on the process of empowering employees to be able to understand how their individual performances contribute to the overall achievement of business objectives on one side, and on the other, it also empowers them to review their learning and development progresses. HRA team shall stay focused on these aspects for the year 2016.

Omanization percentage of 68.24% was achieved for the year 2015.

IT SERVICESThe management has recognized the need that utilization of innovative technological advancement in IT services can act as the driver to bring about great improvements in the quality of service rendered. Accordingly the management has continued to increase its investment in this domain which has resulted in the following:--Unique E Initiatives includes Product offering and Customer Services through Internet, Mobile devices and Interactive Kiosks as part of fulfilling our mission “to provide cost effective insurance and superior customer service in a manner that takes into account the culture, social ethos and needs of the community”. With these applications one can: -

• Know about us and the way how we work by ‘Takaful’ model

• Contact the team for assistance• Check offers, insurance packages and special

pricing • Buy a featured policy• Get assisted when met with an accident;• Get notified on claim movements• Sit back at home and track the claim• Identify our nearest branch and agency network• Identify the Garage and Hospital network

Internal Audit & ComplianceAl Madina Insurance Company continued to focus on the Internal Audit and Compliance Department through:

• Supporting and developing the Company’s internal audit function through identifying operational, financial, and administrative risks of the company.

• Supporting and developing the Company’s compliance function through consistent follow up on the Company’s operations to be according to

the rules and regulations governing the Sultanate of Oman.

• Supporting and developing of the Company’s complaints department through contacting the company’s clients and coordination with the Capital Market Authority.

• Audit & follow up commitment to the decisions & instructions of the Sharia’a Board with respect to all operational, financial, and administrative activities of the company.

• Supporting and developing the continuous training of the department’s staff members and encourage them to get professional certificates to compliment the Company’s progress.

FUTURE OUTLOOKWe anticipate a further slow down in 2016 but expect Government spending on infrastructure to be on track, thereby giving positive outlook on project insurances. There will be significant cutbacks in budgets and what is deemed as non-essential expenditures. There will be withdrawal of various subsidies like petrol, diesel, gas, water and electricity. Oil price will continue to fluctuate which will result in a volatile equity market for the region. Lower investments, reduction in subsidies, cutting back on benefits will have a negative impact on consumer spending and insurance price will be under severe pressure. Reinsurance markets, in the absence of major catastrophe losses continues to be soft and competitive which will act as a catalyst in keeping premiums low. In this kind of scenario companies will do well to hold their market share and maintain underwriting surplus after meeting all expenses. Focusing on profitable segments and discipline in keeping costs low will be key to success. Notwithstanding the economic prognosis we are optimistic about our future. Over the years we have invested in technology to increase our penetration in distribution, in sophisticated MIS to identify and competitively price the profitable segments and innovative applications that enhances customer experience and increases productivity. The Company has also invested in territorial diversification through its sister company Watania in Abu Dhabi. This will help in bringing down the cost of its reinsurance by building scale and share the cost of highly skilled resources ensuring quality in its offerings and at the same time reducing its expenses. We believe 2016 will be challenging but with the right mix of effort, focus and discipline there will be opportunities for the company that will have a positive outcome.

17

Report on CorporateGovernance

18

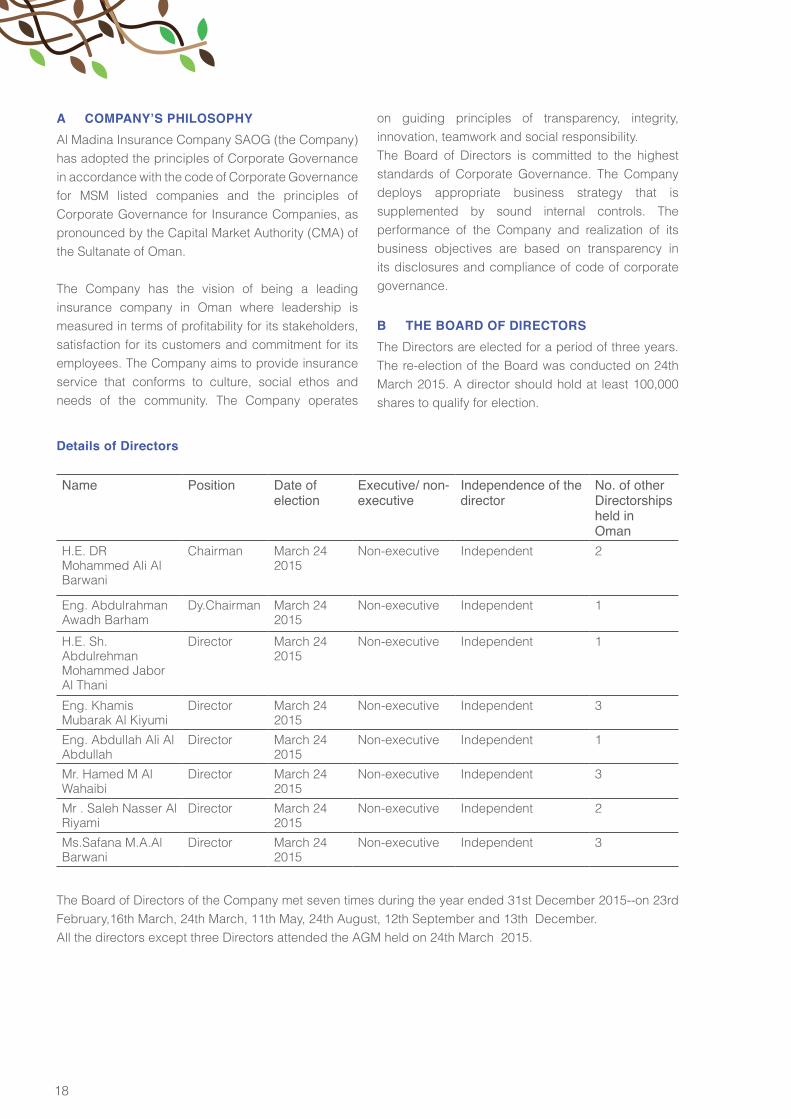

A COMPANY’S PHILOSOPHYAl Madina Insurance Company SAOG (the Company) has adopted the principles of Corporate Governance in accordance with the code of Corporate Governance for MSM listed companies and the principles of Corporate Governance for Insurance Companies, as pronounced by the Capital Market Authority (CMA) of the Sultanate of Oman.

The Company has the vision of being a leading insurance company in Oman where leadership is measured in terms of profitability for its stakeholders, satisfaction for its customers and commitment for its employees. The Company aims to provide insurance service that conforms to culture, social ethos and needs of the community. The Company operates

on guiding principles of transparency, integrity, innovation, teamwork and social responsibility.The Board of Directors is committed to the highest standards of Corporate Governance. The Company deploys appropriate business strategy that is supplemented by sound internal controls. The performance of the Company and realization of its business objectives are based on transparency in its disclosures and compliance of code of corporate governance.

B THE BOARD OF DIRECTORSThe Directors are elected for a period of three years. The re-election of the Board was conducted on 24th March 2015. A director should hold at least 100,000 shares to qualify for election.

Details of Directors

Name Position Date ofelection

Executive/ non-executive

Independence of thedirector

No. of other Directorships held inOman

H.E. DR Mohammed Ali AlBarwani

Chairman March 242015

Non-executive Independent 2

Eng. AbdulrahmanAwadh Barham

Dy.Chairman March 242015

Non-executive Independent 1

H.E. Sh. Abdulrehman Mohammed JaborAl Thani

Director March 242015

Non-executive Independent 1

Eng. KhamisMubarak Al Kiyumi

Director March 242015

Non-executive Independent 3

Eng. Abdullah Ali AlAbdullah

Director March 242015

Non-executive Independent 1

Mr. Hamed M AlWahaibi

Director March 242015

Non-executive Independent 3

Mr . Saleh Nasser AlRiyami

Director March 242015

Non-executive Independent 2

Ms.Safana M.A.AlBarwani

Director March 242015

Non-executive Independent 3

The Board of Directors of the Company met seven times during the year ended 31st December 2015--on 23rd February,16th March, 24th March, 11th May, 24th August, 12th September and 13th December.All the directors except three Directors attended the AGM held on 24th March 2015.

19

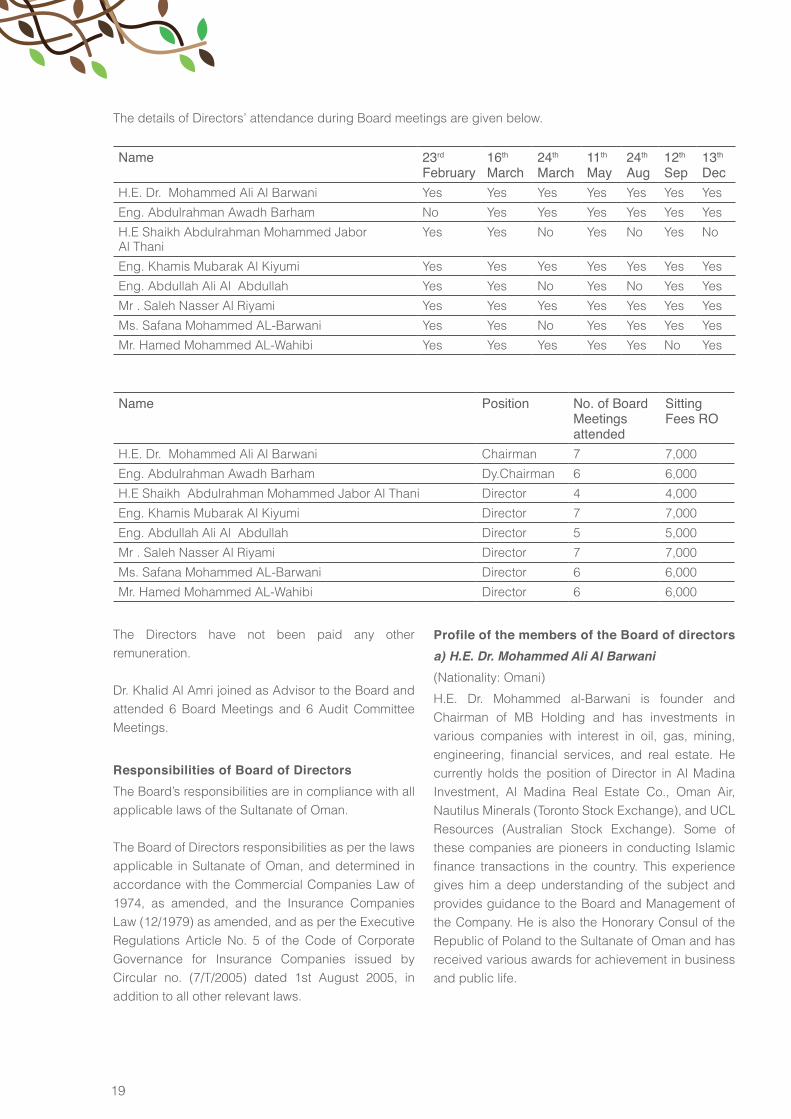

The details of Directors’ attendance during Board meetings are given below.

Name 23rd

February 16th

March 24th

March 11th

May 24th

Aug 12th

Sep 13th

DecH.E. Dr. Mohammed Ali Al Barwani Yes Yes Yes Yes Yes Yes Yes

Eng. Abdulrahman Awadh Barham No Yes Yes Yes Yes Yes Yes

H.E Shaikh Abdulrahman Mohammed JaborAl Thani

Yes Yes No Yes No Yes No

Eng. Khamis Mubarak Al Kiyumi Yes Yes Yes Yes Yes Yes Yes

Eng. Abdullah Ali Al Abdullah Yes Yes No Yes No Yes Yes

Mr . Saleh Nasser Al Riyami Yes Yes Yes Yes Yes Yes Yes

Ms. Safana Mohammed AL-Barwani Yes Yes No Yes Yes Yes Yes

Mr. Hamed Mohammed AL-Wahibi Yes Yes Yes Yes Yes No Yes

Name Position No. of Board Meetingsattended

SittingFees RO

H.E. Dr. Mohammed Ali Al Barwani Chairman 7 7,000

Eng. Abdulrahman Awadh Barham Dy.Chairman 6 6,000

H.E Shaikh Abdulrahman Mohammed Jabor Al Thani Director 4 4,000

Eng. Khamis Mubarak Al Kiyumi Director 7 7,000

Eng. Abdullah Ali Al Abdullah Director 5 5,000

Mr . Saleh Nasser Al Riyami Director 7 7,000

Ms. Safana Mohammed AL-Barwani Director 6 6,000

Mr. Hamed Mohammed AL-Wahibi Director 6 6,000

The Directors have not been paid any other remuneration.

Dr. Khalid Al Amri joined as Advisor to the Board and attended 6 Board Meetings and 6 Audit Committee Meetings.

Responsibilities of Board of DirectorsThe Board’s responsibilities are in compliance with all applicable laws of the Sultanate of Oman.

The Board of Directors responsibilities as per the laws applicable in Sultanate of Oman, and determined in accordance with the Commercial Companies Law of 1974, as amended, and the Insurance Companies Law (12/1979) as amended, and as per the Executive Regulations Article No. 5 of the Code of Corporate Governance for Insurance Companies issued by Circular no. (7/T/2005) dated 1st August 2005, in addition to all other relevant laws.

Profile of the members of the Board of directorsa) H.E. Dr. Mohammed Ali Al Barwani(Nationality: Omani)

H.E. Dr. Mohammed al-Barwani is founder and Chairman of MB Holding and has investments in various companies with interest in oil, gas, mining, engineering, financial services, and real estate. He currently holds the position of Director in Al Madina Investment, Al Madina Real Estate Co., Oman Air, Nautilus Minerals (Toronto Stock Exchange), and UCL Resources (Australian Stock Exchange). Some of these companies are pioneers in conducting Islamic finance transactions in the country. This experience gives him a deep understanding of the subject and provides guidance to the Board and Management of the Company. He is also the Honorary Consul of the Republic of Poland to the Sultanate of Oman and has received various awards for achievement in business and public life.

20

b) Eng. Abdulrehman Awadh Barham(Nationality: Omani)

Eng. Barham is the Vice Chairman of the Company and has over 25 years of experience in handling and planning projects. He currently holds the position of CEO and investment committee member in Al Madina Real Estate. He has a profound understanding of the products relevant to finance real estate projects. He also holds the position of Director in Salalah Mills Company SAOG, Tilal Development Company SAOC, Shaden Development Company SAOC and Shaza Muscat Hotel Company SAOC.

c) H.E. Sheikh Abdulrehman Mohammed JabrAl Thani (Nationality: Qatari)

H.E. Sheikh Al Thani has over 35 years of experience in industrial investments and private sector. He currently holds the position of Vice Chairman in Al Madina investment, Director in Oman & Qatar Company and Qatar Industrial Manufacturing. He is involved closely with Islamic financial institutions in Qatar and is able to provide guidance based on his knowledge and expertise gained from these institutions.

d) Eng. Khamis Mubarak Al Kiyumi(Nationality: Omani)

Eng. Kiyumi, an Industrial Engineer, has over 30 years of experience in industrial investments and private sector.He is one of the pioneers in introducing Islamic finance services in the country. His close relationship with leading experts in Islamic Financial Services in Malaysia helps him to bring the changes in the global Islamic financial services industry to Oman. He currently holds the position of CEO and Director in Al Madina Investment He also holds the position of Chairman in Gulf Mushroom Products Company SAOG, Al Madina Real Estate Company SAOC and Shaden Development Company SAOC.

e) Eng. Abdullah Ali Abdullah (Nationality: Qatari)

Eng. Abdullah has over 35 years of experience in investments. He currently holds the position of Director in Trans Gulf Investment Holding, Al Madina Investment Finance and Al Madina Real State. He is closely associated with leading Islamic financial institutions in Qatar and brings a wealth of experience and knowledge gained from his dealings with such institutions.

f) Saleh Nasser Sulaiman Al Riyami(Nationality: Omani)Mr. Riyami has more than 15 years of experience as an investment expert. He currently holds the position of Vice Chairman at Oman Ceramics and Taageer Finance. Mr. Riyami has put in an effort to attract key Islamic Shariah scholars who are experts in Islamic financial services in the GCC region to provide consultation in the field of Islamic financial services in coordination with Omani consulting firms.

g) Safana Mohammed Ali Al Barwani(Nationality: Omani)

Ms. Safana has 10 years of experience in investment, insurance and real estate. She holds the position of Director in Mazoon Petro Gas, Risk Management Services and Interior Hotels.

h) Hamed Mohammed Al Wahaibi(Nationality: Omani)

Mr. Hamad Mohammad Hamood Al Wahaibi has been the Director of Investment at Ministry of Defense Pension Fund for the last seven years. He also serves as a board member of Galfar Engineering and Contracting Company and Voltamp Energy Company. Al Wahaibi holds an MBA, specializing in Finance, and is a Chartered Financial Analyst (CFA) and Chartered Alternative Investment Analyst (CAIA) charterholder.

i) Khalid Al Amri (Nationality: Omani)

Dr. Khalid Al Amri PhD, has joined as an Advisor to the Board of Directors of Al Madina Insurance Co. SAOG . Dr. Khalid has done his PhD in Risk Management and Insurance (Major) and Finance (2nd Major) from the Temple University – Fox School of Business Philadelphia, USA. He is a Msc. In Actuarial Science from Boston University, USA and is currently Assistant Professor at the College of Economics and Political Science, Sultan Qaboos University.

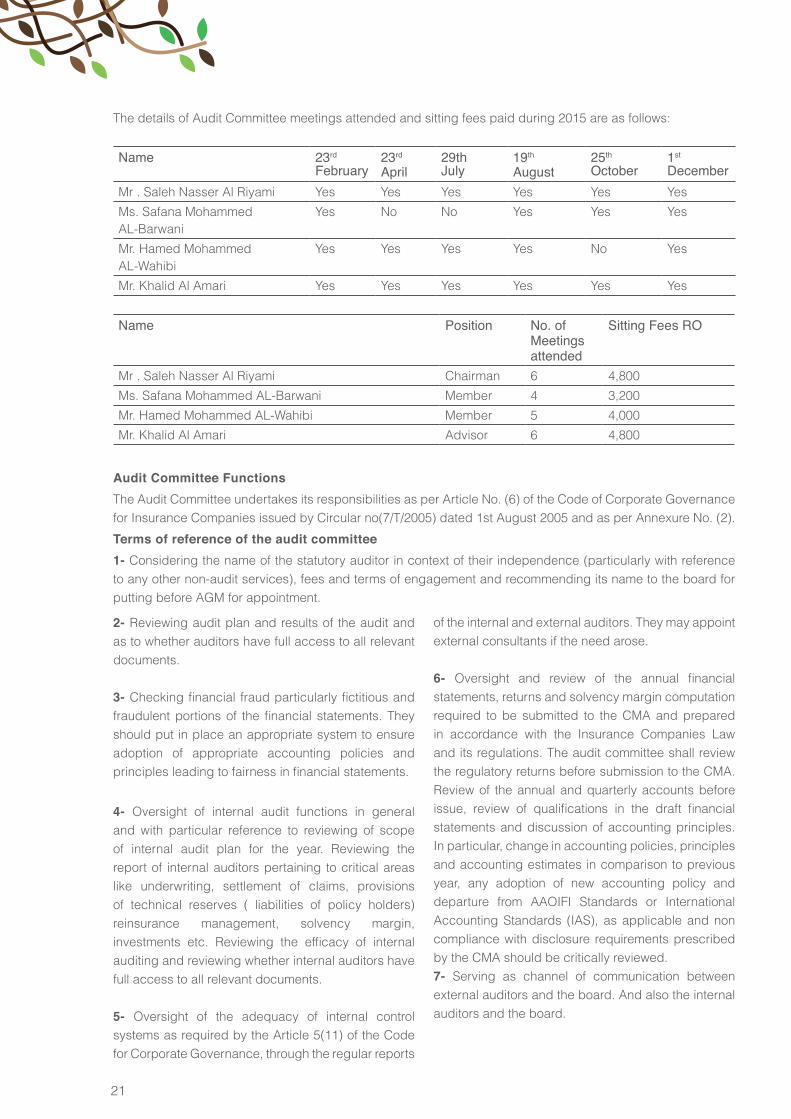

C AUDIT COMMITTEE The Audit Committee comprising of three non-executive and independent members is constituted by the Board, to guide the Finance, Audit and Accounting functions and to ensure adherence to best practices. The Audit Committee met six times during the year ended 31st December 2015 on 23rd February, 23rd April, 29th July, 19th August, 25th October and 1st December 2015.

21

The details of Audit Committee meetings attended and sitting fees paid during 2015 are as follows:

Name 23rd

February 23rd

April29thJuly

19th

August 25th

October 1st

DecemberMr . Saleh Nasser Al Riyami Yes Yes Yes Yes Yes Yes

Ms. Safana MohammedAL-Barwani

Yes No No Yes Yes Yes

Mr. Hamed MohammedAL-Wahibi

Yes Yes Yes Yes No Yes

Mr. Khalid Al Amari Yes Yes Yes Yes Yes Yes

Name Position No. of Meetingsattended

Sitting Fees RO

Mr . Saleh Nasser Al Riyami Chairman 6 4,800

Ms. Safana Mohammed AL-Barwani Member 4 3,200

Mr. Hamed Mohammed AL-Wahibi Member 5 4,000

Mr. Khalid Al Amari Advisor 6 4,800

Audit Committee FunctionsThe Audit Committee undertakes its responsibilities as per Article No. (6) of the Code of Corporate Governance for Insurance Companies issued by Circular no(7/T/2005) dated 1st August 2005 and as per Annexure No. (2).

Terms of reference of the audit committee1- Considering the name of the statutory auditor in context of their independence (particularly with reference to any other non-audit services), fees and terms of engagement and recommending its name to the board for putting before AGM for appointment.

2- Reviewing audit plan and results of the audit and as to whether auditors have full access to all relevant documents.

3- Checking financial fraud particularly fictitious and fraudulent portions of the financial statements. They should put in place an appropriate system to ensure adoption of appropriate accounting policies and principles leading to fairness in financial statements.

4- Oversight of internal audit functions in general and with particular reference to reviewing of scope of internal audit plan for the year. Reviewing the report of internal auditors pertaining to critical areas like underwriting, settlement of claims, provisions of technical reserves ( liabilities of policy holders) reinsurance management, solvency margin, investments etc. Reviewing the efficacy of internal auditing and reviewing whether internal auditors have full access to all relevant documents.

5- Oversight of the adequacy of internal control systems as required by the Article 5(11) of the Code for Corporate Governance, through the regular reports

of the internal and external auditors. They may appoint external consultants if the need arose.

6- Oversight and review of the annual financial statements, returns and solvency margin computation required to be submitted to the CMA and prepared in accordance with the Insurance Companies Law and its regulations. The audit committee shall review the regulatory returns before submission to the CMA. Review of the annual and quarterly accounts before issue, review of qualifications in the draft financial statements and discussion of accounting principles. In particular, change in accounting policies, principles and accounting estimates in comparison to previous year, any adoption of new accounting policy and departure from AAOIFI Standards or International Accounting Standards (IAS), as applicable and non compliance with disclosure requirements prescribed by the CMA should be critically reviewed.7- Serving as channel of communication between external auditors and the board. And also the internal auditors and the board.

22

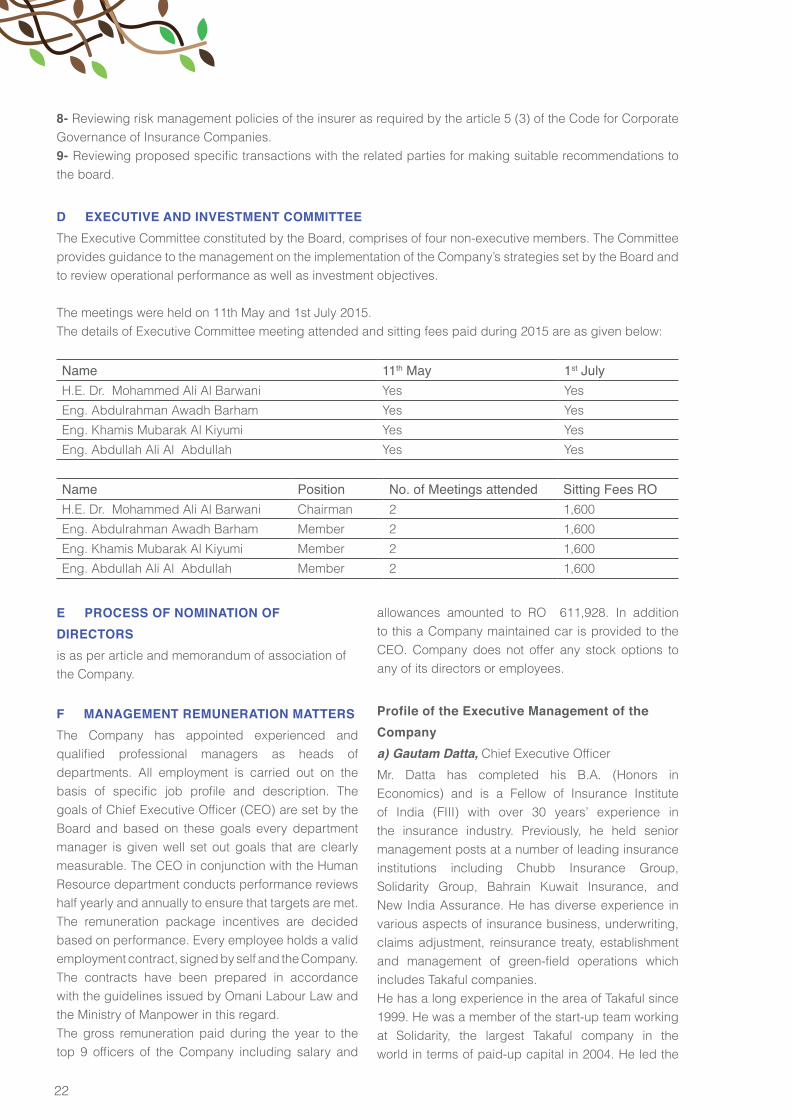

8- Reviewing risk management policies of the insurer as required by the article 5 (3) of the Code for Corporate Governance of Insurance Companies.9- Reviewing proposed specific transactions with the related parties for making suitable recommendations to the board.

D EXECUTIVE AND INVESTMENT COMMITTEE The Executive Committee constituted by the Board, comprises of four non-executive members. The Committee provides guidance to the management on the implementation of the Company’s strategies set by the Board and to review operational performance as well as investment objectives.

The meetings were held on 11th May and 1st July 2015.The details of Executive Committee meeting attended and sitting fees paid during 2015 are as given below:

Name 11th May 1st JulyH.E. Dr. Mohammed Ali Al Barwani Yes Yes

Eng. Abdulrahman Awadh Barham Yes Yes

Eng. Khamis Mubarak Al Kiyumi Yes Yes

Eng. Abdullah Ali Al Abdullah Yes Yes

Name Position No. of Meetings attended Sitting Fees ROH.E. Dr. Mohammed Ali Al Barwani Chairman 2 1,600

Eng. Abdulrahman Awadh Barham Member 2 1,600

Eng. Khamis Mubarak Al Kiyumi Member 2 1,600

Eng. Abdullah Ali Al Abdullah Member 2 1,600

E PROCESS OF NOMINATION OF DIRECTORSis as per article and memorandum of association of the Company.

F MANAGEMENT REMUNERATION MATTERSThe Company has appointed experienced and qualified professional managers as heads of departments. All employment is carried out on the basis of specific job profile and description. The goals of Chief Executive Officer (CEO) are set by the Board and based on these goals every department manager is given well set out goals that are clearly measurable. The CEO in conjunction with the Human Resource department conducts performance reviews half yearly and annually to ensure that targets are met. The remuneration package incentives are decided based on performance. Every employee holds a valid employment contract, signed by self and the Company. The contracts have been prepared in accordance with the guidelines issued by Omani Labour Law and the Ministry of Manpower in this regard. The gross remuneration paid during the year to the top 9 officers of the Company including salary and

allowances amounted to RO 611,928. In addition to this a Company maintained car is provided to the CEO. Company does not offer any stock options to any of its directors or employees.

Profile of the Executive Management of the Companya) Gautam Datta, Chief Executive Officer

Mr. Datta has completed his B.A. (Honors in Economics) and is a Fellow of Insurance Institute of India (FIII) with over 30 years’ experience in the insurance industry. Previously, he held senior management posts at a number of leading insurance institutions including Chubb Insurance Group, Solidarity Group, Bahrain Kuwait Insurance, and New India Assurance. He has diverse experience in various aspects of insurance business, underwriting, claims adjustment, reinsurance treaty, establishment and management of green-field operations which includes Takaful companies.He has a long experience in the area of Takaful since 1999. He was a member of the start-up team working at Solidarity, the largest Takaful company in the world in terms of paid-up capital in 2004. He led the

23

initiative to obtain a license for the company in KSA. He participated actively with members of the Shariah Board in the process of establishing structures for Wakala fees and wrote a number of essays in tackling this topic. The Company was established as a joint project with Solidarity with all its systems created by the latter to be compatible with the Takaful system. He joined as the CEO of the Company to help it understand the model of Takaful business and operations.

b) Usama Al Barwani, Deputy CEO

Mr. Usama is pursuing his MBA and has completed his Postgraduate Diploma in HRM and Diploma in Information System Management and Education. He is a Certified Islamic Specialist in Islamic Insurance and a Certified Compliance Officer. He has over 23 years of experience in HR and Administration. He is involved in the meetings held with specialists in Shariah consulting services in respect of transforming the Company’s activities into Takaful based insurance.

c) Ajay Srivastava, General Manager – Commercial

Mr. Srivastava has completed his Bachelor of Science (Honors). He has a Bachelor’s degree in Law and is an Associate of Insurance Institute of India (AIII), with over 24 years of insurance experience in Indian & London Insurance markets. Amongst his experiences, he has been involved in one of India’s largest petrochemical plant (ONGC) and with one of the large auto manufacturer of India (Daewoo Motors). He developed and serviced one of UK’s largest furnishing Chain (ROSEBYS) and Hotel Chains (Aurora group) during his career.

d) Sandeep Mahajan, General Manager – Specialty

Mr. Mahajan has completed his BE (Mechanical), MBA (Finance) & is a Fellow of Insurance Institute of India (FIII). He has over 20 years’ experience in technical departments of various local and multinational insurance companies in India and GCC including AIG and Oriental Insurance. As a loss control engineer, he has more than 500 risk surveys to the credit, including petrochemicals and major properties like Zuari Agro Chemicals, Deepak Fertilizers, Tata Motors, etc. Over the period, he moved to underwriting and reinsurance and has handled major programs including Sohar Aluminum, Ministry of Defence and Oman Gas amongst others. He has been dealing with major international reinsurers and brokers in the current role.

e) R. M. Sundaram, General Manager - Finance and

Accounts

Mr. Sundaram has completed his Bachelors in Science. He is also an Associate of Institute of Cost & Works Accountants of India and Certified Management Accountant, issued by the Institute of Certified Management Accountants, New Jersey, USA, with over 30 years of experience in Insurance and Banking in India and the GCC.

f) Nasser Al Shueili, General Manager – Claims

Mr. Nasser has completed his Diploma in Insurance (CIII). He has over 18 years of experience in underwriting, audit, non-motor and motor claims in Omani and multinational insurance companies in the region.

g) Mahmud Attar, General Manager - Compliance

and Internal Audit

Mr. Mahmud has completed his Bachelor in Administrative Science & Accounting. He has over 30 years of experience in Islamic Banking and retail sector in the Gulf, expertise in audit and compliance functions.

Whilst at Bahrain Islamic Bank, he was instrumental in defining audit manual and overseeing the audit programs, risk assessments criteria and risk assessment audits. He was a key member of the team that was responsible for changing the Company’s activities to the Takaful insurance system and its obtainment of the necessary license from the CMA.

h) Girish Gopinath, Senior Manager – IT

Mr. Gopinath has more than 23 years of experience in software product development. He is the Chief architect for the Company’s own brand ‘Tameenet’ which supports retail product development, customer services and online delivery. Prior to joining the Company, Mr. Girish has worked for Oman United Insurance and Veritas DGC Ltd. He has completed his Bachelor in Computer Science and Masters in Banking and Insurance from India.

G AREAS OF NON COMPLIANCEDuring the year there have been no strictures or penalties imposed on the Company by the Muscat Security Market or Capital Market Authority for non-compliance with the code of Corporate Governance For Insurance Companies.

24

H MEANS OF COMMUNICATION WITH SHAREHOLDERSAs per the legal requirements, a notice is sent to the shareholders for the Annual General Meeting together with the annual audited financial statements including details of related party transactions (which are entered into on an arm’s length basis) along with the Chairman’s Report and MD & A Report. The nature and value of related party transactions are disclosed by way of a note to the financial statements.

The Company has become a public joint stock company in December 2013. The quarterly results of the company are disclosed to the public through announcements in MSM website as per statutory requirements.

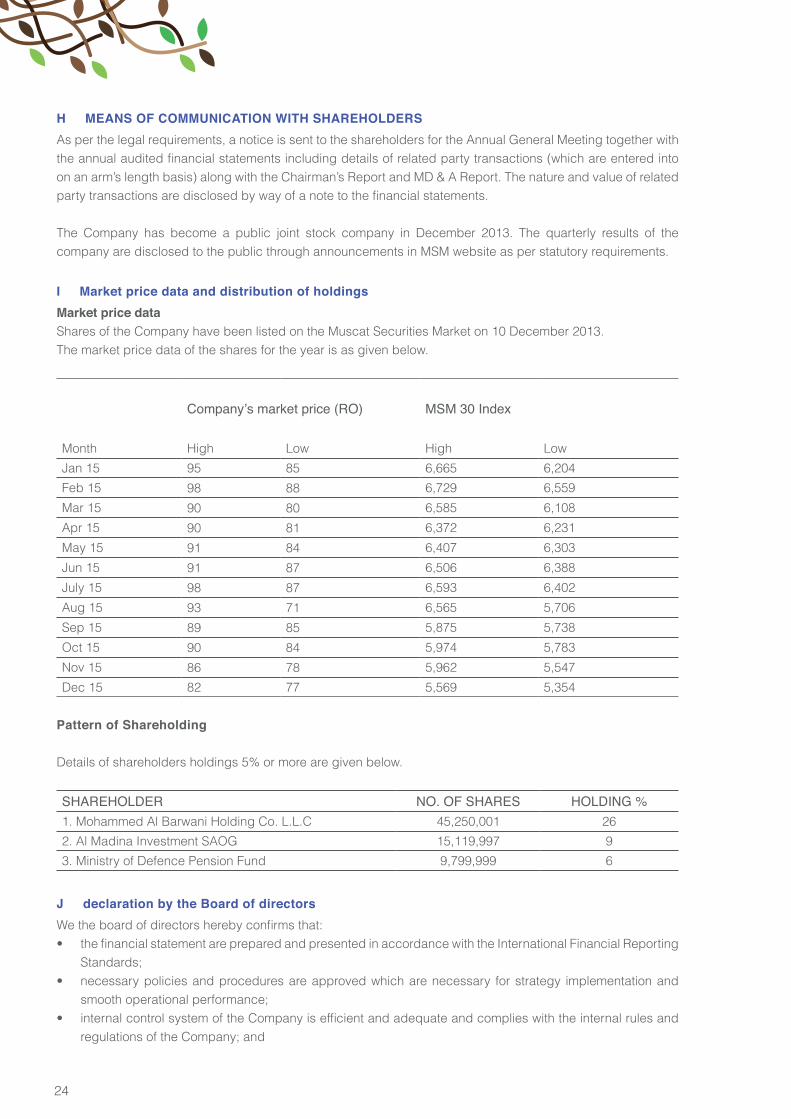

I Market price data and distribution of holdingsMarket price dataShares of the Company have been listed on the Muscat Securities Market on 10 December 2013.The market price data of the shares for the year is as given below.

Company’s market price (RO) MSM 30 Index

Month High Low High Low

Jan 15 95 85 6,665 6,204

Feb 15 98 88 6,729 6,559

Mar 15 90 80 6,585 6,108

Apr 15 90 81 6,372 6,231

May 15 91 84 6,407 6,303

Jun 15 91 87 6,506 6,388

July 15 98 87 6,593 6,402

Aug 15 93 71 6,565 5,706

Sep 15 89 85 5,875 5,738

Oct 15 90 84 5,974 5,783

Nov 15 86 78 5,962 5,547

Dec 15 82 77 5,569 5,354

Pattern of Shareholding

Details of shareholders holdings 5% or more are given below.

SHAREHOLDER NO. OF SHARES HOLDING %1. Mohammed Al Barwani Holding Co. L.L.C 45,250,001 26

2. Al Madina Investment SAOG 15,119,997 9

3. Ministry of Defence Pension Fund 9,799,999 6

J declaration by the Board of directorsWe the board of directors hereby confirms that:• the financial statement are prepared and presented in accordance with the International Financial Reporting

Standards;• necessary policies and procedures are approved which are necessary for strategy implementation and

smooth operational performance;• internal control system of the Company is efficient and adequate and complies with the internal rules and

regulations of the Company; and

25

• there are no material matters, which will affect the Company’s ability to continue its operations in the coming financial years.

K PROFILE OF THE STATUTORY AUDITORSAbout DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about/ for a more detailed description of DTTL and its member firms.Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 220,000 professionals are committed to making an impact that matters.

About Deloitte & Touche (M.E.)Deloitte & Touche (M.E.) is a member firm of Deloitte Touche Tohmatsu Limited (DTTL) and is a leading professional services firm established in the Middle East region with uninterrupted presence since 1926.Deloitte provides audit, tax, consulting, and financial advisory services through 26 offices in 15 countries with more than 3,300 partners, directors and staff. It is a Tier 1 Tax advisor in the GCC region since 2010 (according to the International Tax Review World Tax Rankings). It has also received numerous awards in the last few years which include best employer in the Middle East, best consulting firm, the Middle East Training & Development Excellence Award by the Institute of Chartered Accountants in England and Wales (ICAEW), as well as the best CSR integrated organization.

For the year 2015, professional fee (Statutory Audit RO 10,250 and other services RO 5,650) has been charged for RO 15,900 by them to the organization.

For Al Madina Insurance Company SAOG

26

27

28

29

Financial Statementsfor the financial year ended 31 December 2015

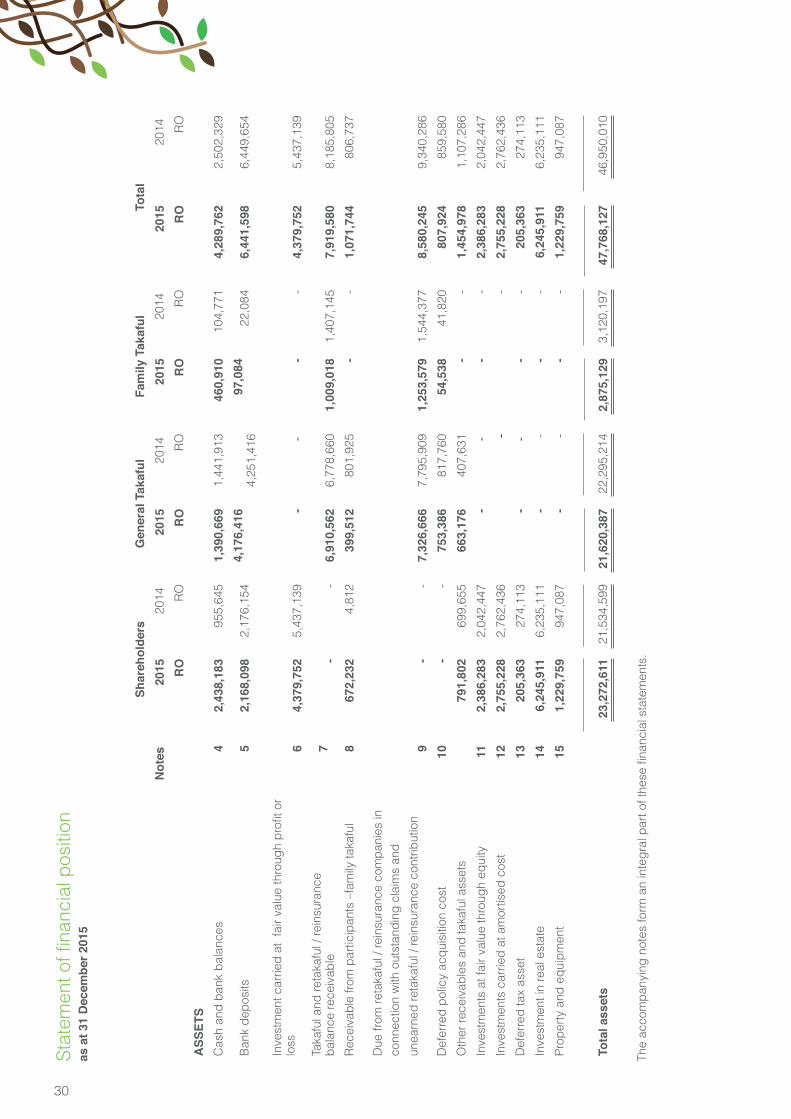

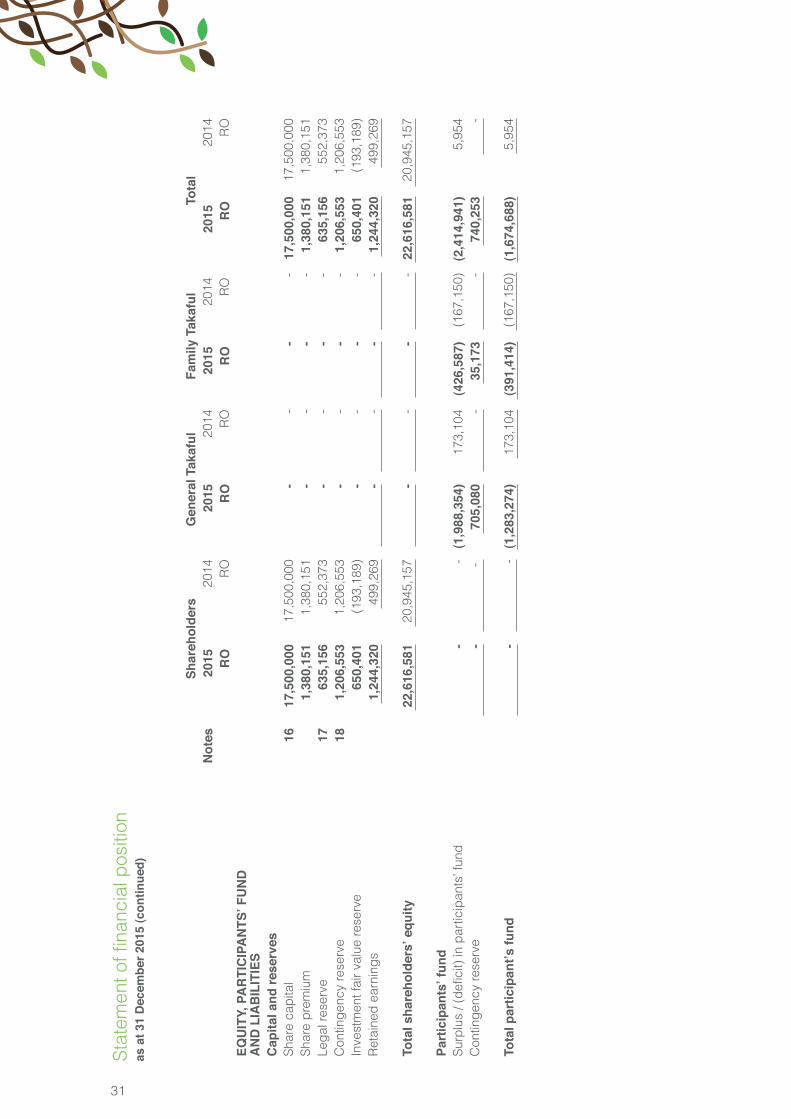

30

Stat

emen

t of fi

nanc

ial p

ositi

on

as a

t 31

Dec

embe

r 201

5

Shar

ehol

ders

Gen

eral

Tak

aful

Fam

ily T

akaf

ulTo

tal

Not

es20

1520

14

2015

2014

20

1520

14

2015

2014

RO

RO

RO

RO

RO

RO

RO

RO

ASS

ETS

Cas

h an

d ba

nk b

alan

ces

42,

438,

183

955,

645

1,39

0,66

91,

441,

913

460,

910

104,

771

4,28

9,76

2 2

,502

,329

Ban

k de

posi

ts5

2,16

8,09

82,

176,

154

4,17

6,41

6

4

,251

,416

97,0

8422

,084

6,44

1,59

8 6

,449

,654

Inve

stm

ent c

arrie

d at

fai

r val

ue th

roug

h pr

ofit o

rlo

ss6

4,37

9,75

25,

437,

139

- -

--

4,37

9,75

2 5

,437

,139

Tak

aful

and

reta

kafu

l / re

insu

ranc

eba

lanc

e re

ceiv

able

7-

-6,

910,

562

6,77

8,66

01,

009,

018

1,40

7,14

57,

919,

580

8,18

5,80

5

Rec

eiva

ble

from

par

ticip

ants

–fa

mily

taka

ful

867

2,23

24,

812

399,

512

801,

925

--

1,07

1,74

480

6,73

7

Due

from

reta

kafu

l / re

insu

ranc

e co

mpa

nies

in c

onne

ctio

n w

ith o

utst

andi

ng c

laim

s an

d

unea

rned

reta

kafu

l / re

insu

ranc

e co

ntrib

utio

n 9

--

7,32

6,66

6 7

,795

,909

1,25

3,57

91,

544,

377

8,58

0,24

5 9

,340

,286

Def

erre

d po

licy

acqu

isiti

on c

ost

10-

-75

3,38

681

7,76

054

,538

41,8

2080

7,92

485

9,58

0

Oth

er re

ceiv

able

s an

d ta

kafu

l ass

ets

791,

802

699,

655

663,

176

407,

631

--

1,45

4,97

81,

107,

286

Inve

stm

ents

at f

air v

alue

thro

ugh

equi

ty11

2,38

6,28

32,

042,

447

- -

--

2,38

6,28

3 2

,042

,447

Inve

stm

ents

car

ried

at a

mor

tised

cos

t12

2,75

5,22

82,

762,

436

--

2,75

5,22

8 2

,762

,436

Def

erre

d ta

x as

set

1320

5,36

327

4,11

3-

- -

-20

5,36

327

4,11

3

Inve

stm

ent i

n re

al e

stat

e14

6,24

5,91

16,

235,

111

--

--

6,24

5,91

1 6

,235

,111

Prop

erty

and

equ

ipm

ent

151,

229,

759

947,

087

--

--

1,22

9,75

994

7,08

7

Tota

l ass

ets

23,2

72,6

11 2

1,53

4,59

921

,620

,387

22,2

95,2

142,

875,

129

3,12

0,19

747

,768

,127

46,9

50,0

10

The

acco

mpa

nyin

g no

tes

form

an

inte

gral

par

t of t

hese

fina

ncia

l sta

tem

ents

.

31

Stat

emen

t of fi

nanc

ial p

ositi

on

as a

t 31

Dec

embe

r 201

5 (c

ontin

ued)

Shar

ehol

ders

Gen

eral

Tak

aful

Fam

ily T

akaf

ulTo

tal

Not

es20

1520

1420

1520

1420

1520

1420

15

2014

RO

RO

RO

RO

RO

RO

RO

RO

EQU

ITY,

PA

RTI

CIP

AN

TS’ F

UN

DA

ND

LIA

BIL

ITIE

SC

apita

l and

rese

rves

Shar

e ca

pita

l16

17,5

00,0

0017

,500

,000

--

--

17,5

00,0

00 1

7,50

0,00

0Sh

are

prem

ium

1,38

0,15

11,

380,

151

--

--

1,38

0,15

1 1

,380

,151

Lega

l res

erve

1763

5,15

655

2,37

3-

--

-63

5,15

655

2,37

3C

ontin

genc

y re

serv

e18

1,20

6,55

31,

206,

553

--

--

1,20

6,55

3 1

,206

,553

Inve

stm

ent f

air v

alue

rese

rve

650,

401

(193

,189

)-

--

-65

0,40

1(1

93,1

89)

Ret

aine

d ea

rnin

gs1,

244,

320

499,

269

-

-

-

-1,

244,

320

499,

269

Tota

l sha

reho

lder

s’ e

quity

22,6

16,5

8120

,945

,157

-

-

-

-

22,6

16,5

81 2

0,94

5,15

7

Part

icip

ants

’ fun

dSu

rplu

s / (

defic

it) in

par

ticip

ants

’ fun

d-

-(1

,988

,354

)17

3,10

4(4

26,5

87)

(167

,150

)(2

,414

,941

)5,

954

Con

tinge

ncy

rese

rve

-

-

705,

080

-35

,173

-74

0,25

3

-

Tota

l par

ticip

ant’s

fund

-

-

(1,2

83,2

74)

173,

104

(391

,414

)(1

67,1

50)

(1,6

74,6

88)

5,95

4

32

Stat

emen

t of fi

nanc

ial p

ositi

on

as a

t 31

Dec

embe

r 201

5 (c

ontin

ued)

Liab

ilitie

sEn

d of

ser

vice

ben

efits

1926

8,21

5 1

92,0

96

-26

8,21

5 1

92,0

96

Gro

ss o

utst

andi

ng c

laim

s9

--

7,11

8,02

66,

571,

420

996,

465

1,4

60,7

598,

114,

491

8,03

2,17

9U

near

ned

cont

ribut

ions

rese

rve

9-

-9,

980,

207

9,7

10,9

46

615,

587

361

,224

10

,595

,794

10,

072,

170

Une

arne

d re

taka

ful/r

eins

uran

ce c

omm

issi

on20

--

413,

259

375

,848

4,

028

2,9

55

417,

287

378

,803

Ret

akaf

ul/re

insu

ranc

e pa

yabl

es-

-4,

000,

287

3,94

5,28

748

2,56

9 6

10,8

92

4,48

2,85

64,

556,

179

Acc

ount

s an

d ot

her p

ayab

les

2138

7,81

539

7,34

61,

391,

882

1,5

18,6

0996

,150

44,

780

1,87

5,84

71,

960,

735

Paya

ble

to s

hare

hold

ers

8-

--

-67

2,23

24,

812

672,

232

4,81

2Pa

yabl

e to

par

ticip

ants

– g

ener

al ta

kafu

l8

-

-

-

-

399,

512

801,

925

399,

512

801,

925

Tota

l lia

bilit

ies

656,

030

589,

442

22,9

03,6

6122

,122

,110

3,26

6,54

33,

287,

347

26,8

26,2

3425

,998

,899

Tot

al s

hare

hold

ers’

equ

ity, p

artic

ipan

ts’ f

und

and

liabi

litie

s23

,272

,611

21,

534,

599

21,6

20,3

8722

,295

,214

2,87

5,12

93,

120,

197

47,7

68,1

2746

,950

,010

_________________

____________________

Directo

r

D

irecto

r The a

ccom

panyin

g n

ote

s f

orm

an inte

gra

l p

art

of

these

fin

an

cia

l sta

tem

en

ts.

Shar

ehol

ders

Gen

eral

Tak

aful

Fam

ily T

akaf

ulTo

tal

Not

es20

1520

1420

1520

1420

1520

1420

15

2014

RO

RO

RO

RO

RO

RO

RO

RO

33

Stat

emen

t of p

artic

ipan

ts’ r

even

ue a

nd e

xpen

ses

for t

he y

ear e

nded

31

Dec

embe

r 201

5

Gen

eral

Tak

aful

Fam

ily T

akaf

ulTo

tal

Not

es20

1520

1420

1520

1420

1520

14

RO

RO

RO

RO

RO

RO

Taka

ful r

even

ues

Gro

ss c

ontri

butio

ns22

29,0

62,7

44 2

1,57

9,87

9 1,

982,

616

1,5

34,6

75

31,0

45,3

60 2

3,11

4,55

4

Ret

akaf

ul /

rein

sura

nce

shar

e22

(16,

619,

448)

(9,1

18,2

13)

(1,4

65,5

89)

(1,0

98,7

21)

(18,

085,

037)

(10,

216,

934)

Ret

aine

d co

ntrib

utio

ns12

,443

,296

12,

461,

666

517,

027

435

,954

12,9

60,3

23 1

2,89

7,62

0

Mov

emen

t in

unea

rned

con

tribu

tions

228,

268

(1,9

15,4

96)

(25,

252)

(48,

381)

(16,

984)

(1,9

63,8

77)

Net

ear

ned

con

trib

utio

ns12

,451

,564

10,

546,

170

491,

775

387

,573

12

,943

,339

10,

933,

743

Net

com

mis

sion

and

oth

er ta

kafu

l inc

ome

/ (ex

pen

se)

22(1

62,6

78)

(439

,641

) (1

02,5

00)

(86,

390)

(2

65,1

78)

(526

,031

)

Tota

l tak

aful

rev

enue

2212

,288

,886

10,

106,

529

389,

275

301,

183

12,6

78,1

61 1

0,40

7,71

2

34

Gen

eral

Tak

aful

Fam

ily T

akaf

ulTo

tal

Not

es20

1520

1420

1520

1420

1520

14

RO

RO

RO

RO

RO

RO

Stat

emen

t of p

artic

ipan

ts’ r

even

ue a

nd

expe

nses

for t

he y

ear e

nded

31

Dec

embe

r 201

5

Tak

aful

exp

ense

sG

ross

cla

ims

settl

ed24

(10,

336,

702)

(7,1

80,2

53)

(1,0

50,6

30)

(1,0

52,2

72)

(11,

387,

332)

(8,2

32,5

25)

Cla

ims

reco

vere

d fro

m re

taka

ful/r

eins

uran

ce24

2,34

5,80

8 1

,520

,216

88

8,95

6 8

98,9

88

3,23

4,76

4 2

,419

,204

Net

mov

emen

t in

outs

tand

ing

clai

ms

(842

,437

)(3

80,1

19)

(55,

616)

(39,

304)

(8

98,0

53)

(419

,423

)

Net

cla

ims

incu

rred

24(8

,833

,331

)(6

,040

,156

)(2

17,2

90)

(192

,588

)(9

,050

,621

)(6

,232

,744

)

Prov

isio

n fo

r bad

and

dou

btfu

l deb

t(1

59,3

02)

(22,

560)

-

-

(159

,302

)(2

2,56

0)

Tota

l tak

aful

exp

ense

s(8

,992

,633

)(6

,062

,716

)(2

17,2

90)

(192

,588

)(9

,209

,923

)(6

,255

,304

)

Sur

plus

from

taka

ful o

pera

tions

3,29

6,25

34,

043,

813

171,

985

108,

595

3,46

8,23

8 4

,152

,408

Inve

stm

ent i

ncom

e25

90,6

02 8

1,27

7 91

5 1

,988

91

,517

83,

265

Mud

arib

sha

re27

(63,

421)

(67,

608)

(6

41)

(1,4

91)

(64,

062)

(69,

099)

Wak

ala

fees

27(4

,779

,812

)(3

,884

,378

) (3

96,5

23)

(276

,242

) (5

,176

,335

)(4

,160

,620

)

Sur

plus

/ (d

efici

t) fr

om ta

kafu

l ope

ratio

ns(1

,456

,378

)

1

73,1

04(2

24,2

64)

(167

,150

)(1

,680

,642

)5,

954

The

acco

mpa

nyin

g no

tes

form

an

inte

gral

par

t of t

hese

fina

ncia

l sta

tem

ents

.

35

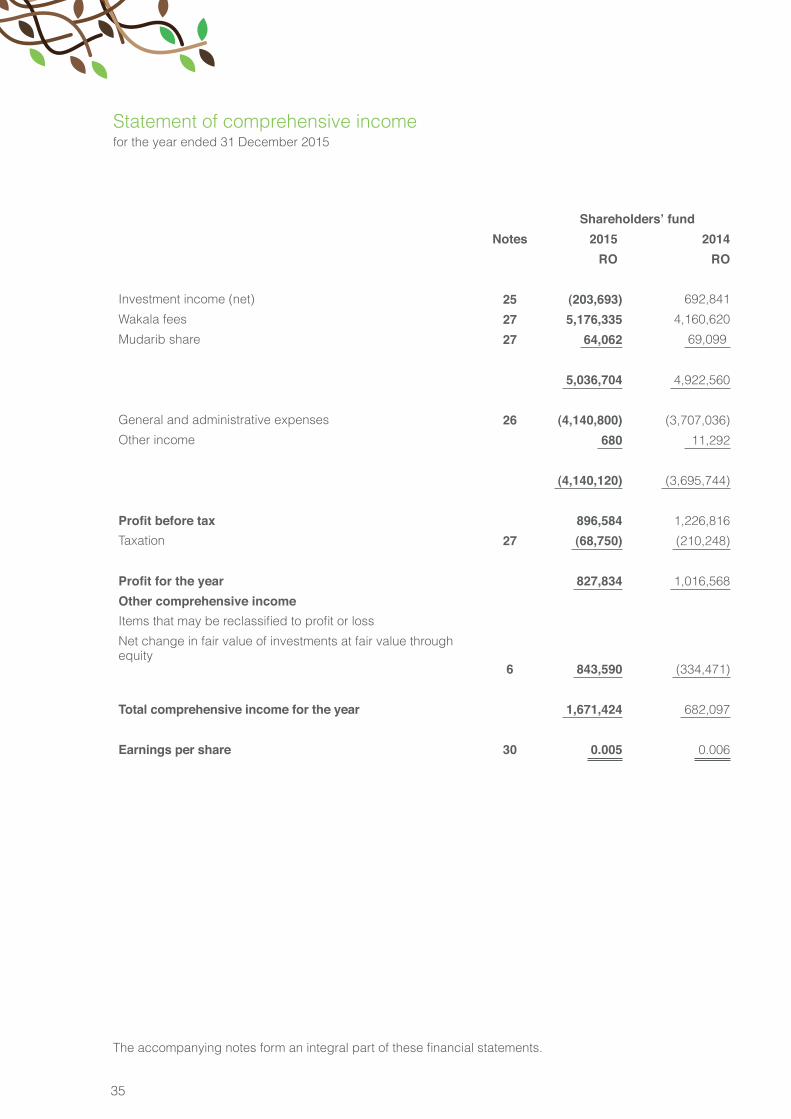

Statement of comprehensive income for the year ended 31 December 2015

Shareholders’ fundNotes 2015 2014

RO RO

Investment income (net) 25 (203,693) 692,841

Wakala fees 27 5,176,335 4,160,620

Mudarib share 27 64,062 69,099

5,036,704 4,922,560

General and administrative expenses 26 (4,140,800) (3,707,036)

Other income 680 11,292

(4,140,120) (3,695,744)

Profit before tax 896,584 1,226,816

Taxation 27 (68,750) (210,248)

Profit for the year 827,834 1,016,568

Other comprehensive incomeItems that may be reclassified to profit or loss

Net change in fair value of investments at fair value throughequity

6 843,590 (334,471)

Total comprehensive income for the year 1,671,424 682,097

Earnings per share 30 0.005 0.006

The accompanying notes form an integral part of these financial statements.

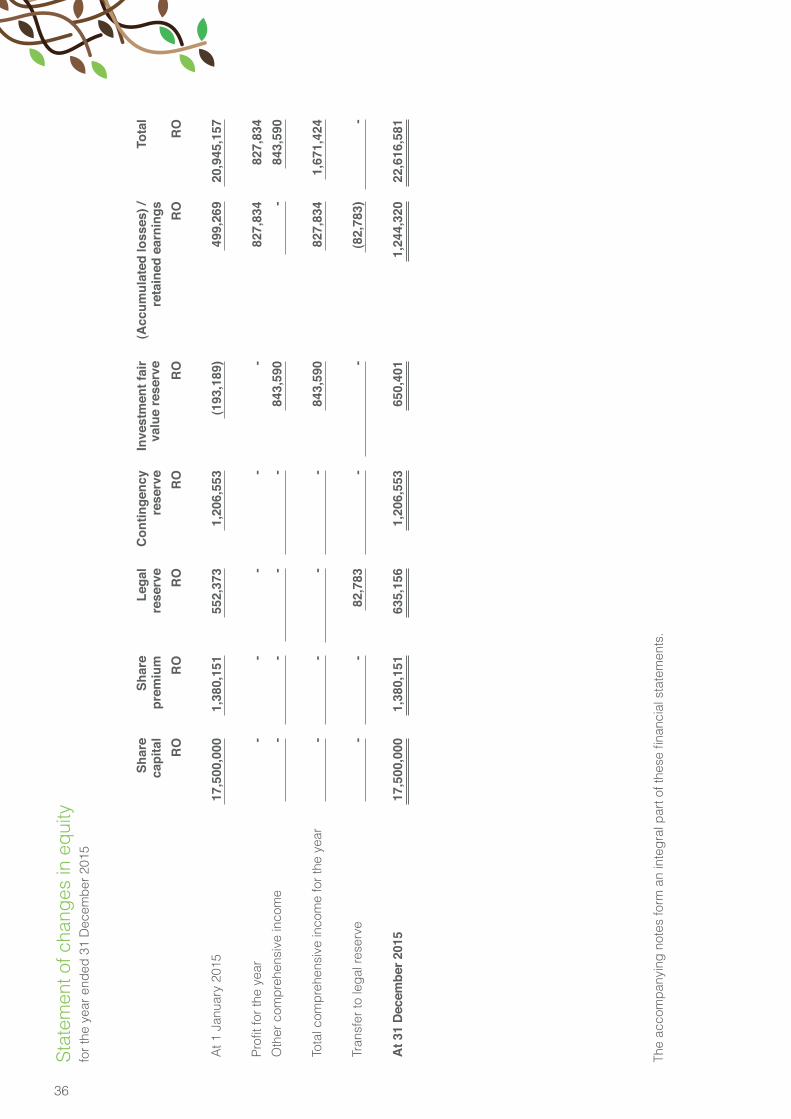

36

Stat

emen

t of c

hang

es in

equ

ityfo

r the

yea

r end

ed 3

1 D

ecem

ber 2

015

Shar

eca

pita

l S

hare

prem

ium

Leg

alre

serv

e C

ontin

genc

yre

serv

e In

vest

men

t fai

rva

lue

rese

rve

(Acc

umul

ated

loss

es) /

reta

ined

ear

ning

sTo

tal

RO

RO

RO

RO

RO

RO

RO

At 1

Jan

uary

201

517

,500

,000

1,38

0,15

155

2,37

31,

206,

553

(193

,189

)49

9,26

920

,945

,157

Profi

t for

the

year

--

--

-82

7,83

482

7,83

4O

ther

com

preh

ensi

ve in

com

e

-

-

-

-

843,

590

-84

3,59

0

Tota

l com

preh

ensi

ve in

com

e fo

r the

yea

r

-

-

-

-

843,

590

827,

834

1,67

1,42

4

Tra

nsfe

r to

lega

l res

erve

-

-82

,783

-

-(8

2,78

3)

-

At 3

1 De

cem

ber 2

015

17,5

00,0

001,

380,

151

635,

156

1,20

6,55

365

0,40

11,

244,

320

22,6

16,5

81

The

acco

mpa

nyin

g no

tes

form

an

inte

gral

par

t of t

hese

fina

ncia

l sta

tem

ents

.

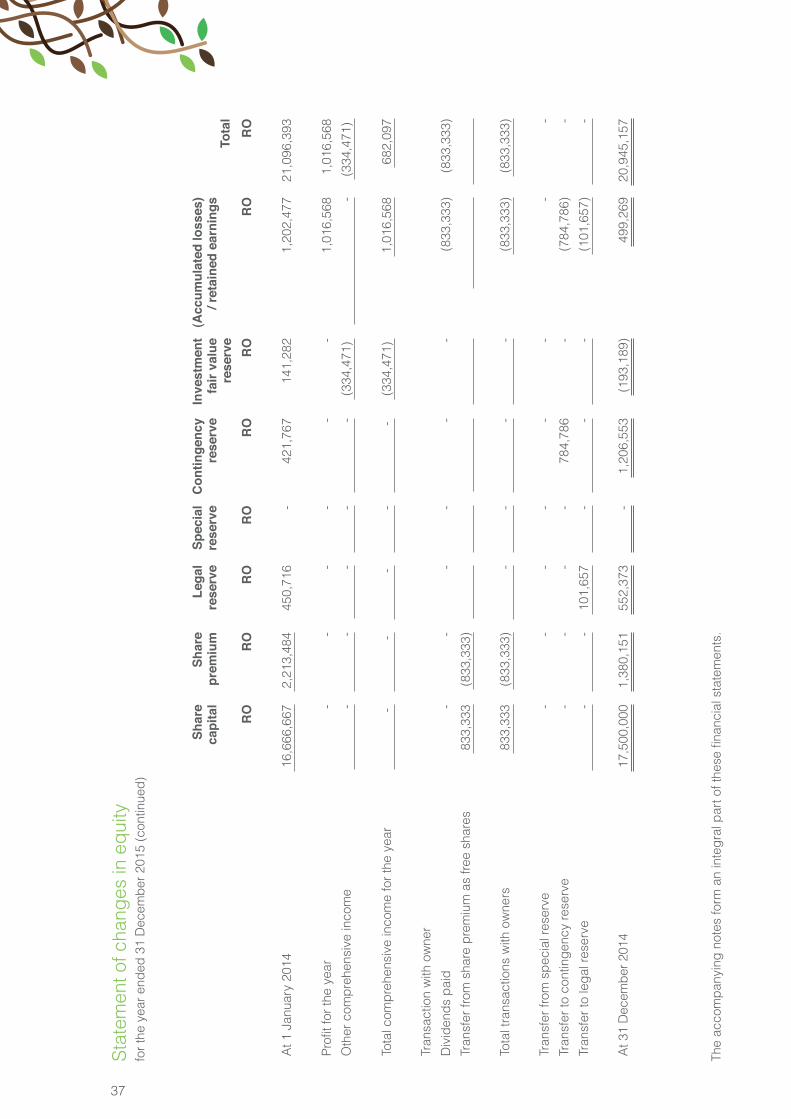

37

Stat

emen

t of c

hang

es in

equ

ityfo

r the

yea

r end

ed 3

1 D

ecem

ber 2

015

(con

tinue

d)

Shar

eca

pita

l S

hare

prem

ium

Leg

alre

serv

e S

peci

alre

serv

e C

ontin

genc

yre

serv

e In

vest

men

t fa

ir va

lue

rese

rve

(Acc

umul

ated

loss

es)

/ ret

aine

d ea

rnin

gsTo

tal

RO

RO

RO

RO

RO

RO

RO

RO

At 1

Jan

uary

201

416

,666

,667

2,21

3,48

445

0,71

6-

421,

767

141,

282

1,20

2,47

721

,096

,393

Profi

t for

the

year

--

--

--

1,01

6,56

81,

016,

568

Oth

er c

ompr

ehen

sive

inco

me

-

-

-

-

-(3

34,4

71)

-(3

34,4

71)

Tota

l com

preh

ensi

ve in

com

e fo

r the

yea

r

-

-

-

-

-

(334

,471

) 1,

016,

568

682,

097

Tran

sact

ion

with

ow

ner

Div

iden

ds p

aid

--

--

--

(833

,333

)(8

33,3

33)

Tran

sfer

from

sha

re p

rem

ium

as

free

shar

es83

3,33

3(8

33,3

33)

Tota

l tra

nsac

tions

with

ow

ners

833,

333

(833

,333

)

-

-

-

-

(833

,333

)(8

33,3

33)

Tran

sfer

from

spe

cial

rese

rve

--

--

--

--

Tran

sfer

to c

ontin

genc

y re

serv

e-

--

-78

4,78

6-

(784

,786

)-

Tran

sfer

to le

gal r

eser

ve

-

-

101,

657

-

-

-

(101

,657

)

-

At 3

1 D

ecem

ber 2

014

17,5

00,0

001,

380,

151

552,

373

-1,

206,

553

(193

,189

)49

9,26

920

,945

,157

The

acco

mpa

nyin

g no

tes

form

an

inte

gral

par

t of t

hese

fina

ncia

l sta

tem

ents

.

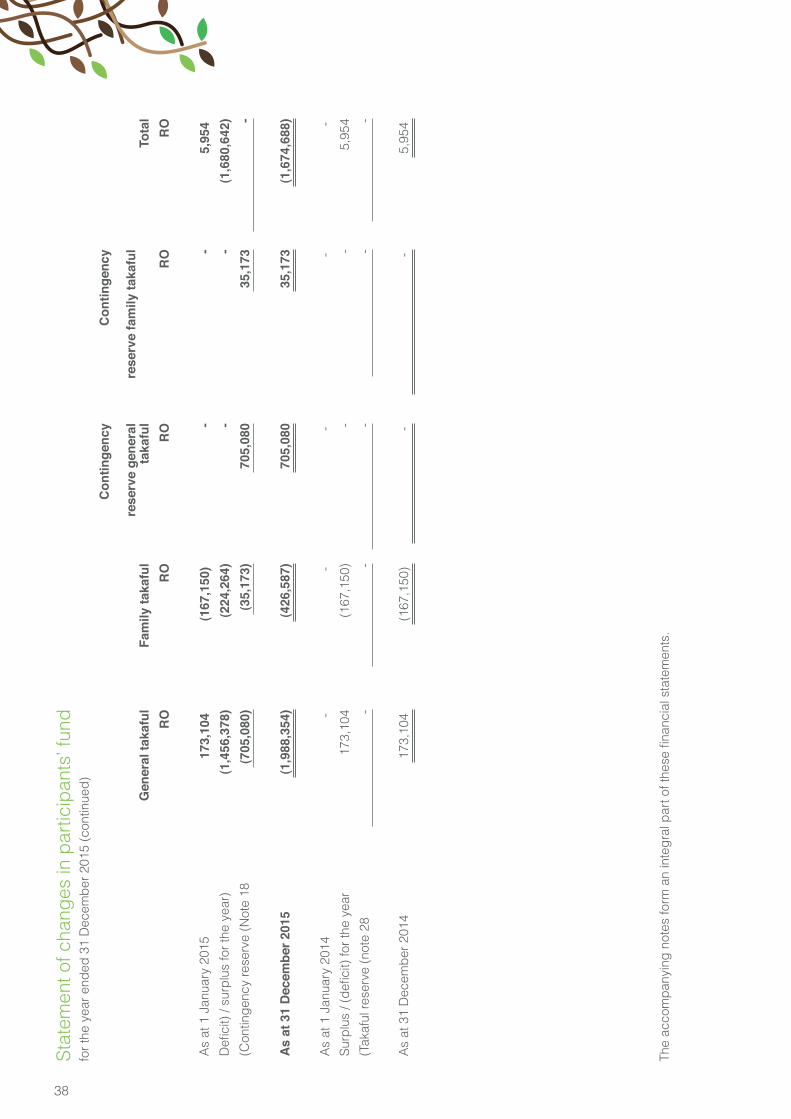

38

Stat

emen

t of c

hang

es in

par

ticip

ants

’ fun

dfo

r the

yea

r end

ed 3

1 D

ecem

ber 2

015

(con

tinue

d)

Gen

eral

taka

ful

Fam

ily ta

kafu

l

Con

tinge

ncy

rese

rve

gene

ral

taka

ful

Con

tinge

ncy

rese

rve

fam

ily ta

kafu

lTo

tal

RO

RO

RO

RO

RO

As

at 1

Jan

uary

201

5 1

73,1

04

(167

,150

)

-

- 5

,954

D

efici

t) / s

urpl

us fo

r the

yea

r)(1

,456

,378

)(2

24,2

64)

--

(1,6

80,6

42)

(Con

tinge

ncy

rese

rve

(Not

e 18

(705

,080

)(3

5,17

3)70

5,08

035

,173

-

As

at 3

1 D

ecem

ber 2

015

(1,9

88,3

54)

(426

,587

)70

5,08

035

,173

(1,6

74,6

88)

As

at 1

Jan

uary

201

4

-

-

-

-

-

Surp

lus

/ (de

ficit)

for t

he y

ear

173,

104

(167

,150

)-

-5,

954

(Tak

aful

rese

rve

(not

e 28

-

-

-

-

-

As

at 3

1 D

ecem

ber 2

014

173,

104

(167

,150

)

-

- 5,

954

The

acco

mpa

nyin

g no

tes

form

an

inte

gral

par

t of t

hese

fina

ncia

l sta

tem

ents

.

39

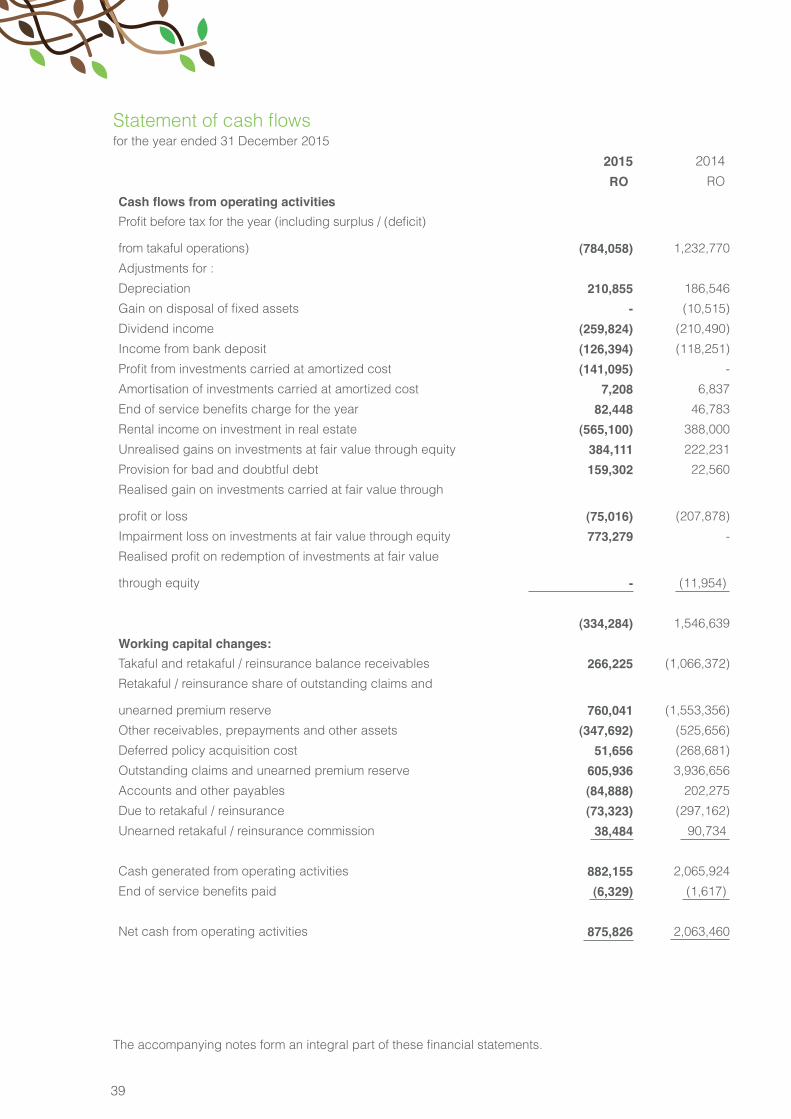

Statement of cash flows for the year ended 31 December 2015

2015 2014

RO RO

Cash flows from operating activities Profit before tax for the year (including surplus / (deficit)

from takaful operations) (784,058) 1,232,770

Adjustments for :

Depreciation 210,855 186,546

Gain on disposal of fixed assets - (10,515)

Dividend income (259,824) (210,490)

Income from bank deposit (126,394) (118,251)

Profit from investments carried at amortized cost (141,095) -

Amortisation of investments carried at amortized cost 7,208 6,837

End of service benefits charge for the year 82,448 46,783

Rental income on investment in real estate (565,100) 388,000

Unrealised gains on investments at fair value through equity 384,111 222,231

Provision for bad and doubtful debt 159,302 22,560

Realised gain on investments carried at fair value through

profit or loss (75,016) (207,878)

Impairment loss on investments at fair value through equity 773,279 -

Realised profit on redemption of investments at fair value

through equity - (11,954)

(334,284) 1,546,639

Working capital changes:Takaful and retakaful / reinsurance balance receivables 266,225 (1,066,372)

Retakaful / reinsurance share of outstanding claims and

unearned premium reserve 760,041 (1,553,356)

Other receivables, prepayments and other assets (347,692) (525,656)

Deferred policy acquisition cost 51,656 (268,681)

Outstanding claims and unearned premium reserve 605,936 3,936,656

Accounts and other payables (84,888) 202,275

Due to retakaful / reinsurance (73,323) (297,162)

Unearned retakaful / reinsurance commission 38,484 90,734

Cash generated from operating activities 882,155 2,065,924

End of service benefits paid (6,329) (1,617)

Net cash from operating activities 875,826 2,063,460

The accompanying notes form an integral part of these financial statements.

40

Statement of cash flows for the year ended 31 December 2015 (continued)

Notes 2015 2014

RO RO

Cash flows from investing activitiesPurchase of property and equipment 15 (492,967) (222,859)

Purchases of investments carried at fair value through

profit or loss (122,364)

(4,958,923)

Purchase of investments at fair value through equity (280,318) 12,503

Proceeds from disposal of fixed assets - (1,890,207)

Proceeds from investment in real estate (10,800) -

Proceeds from disposal of investments carried at fair

value through profit or loss 875,328 3,464,652

Proceeds from redemption of investment at fair value

through equity 6,793 154,688

Movement in bank deposits 8,056 118,828

Rent on investment in real estate received 565,100 (388,000)

Profit from investments carried at amortized cost 114,655 -

Purchase of investment in real estate - (3,635,111)

Purchase of investments carried at amortized cost – net of income - (1,015,161)

Dividends received 240,068 210,490

Net cash (used in) / generated from investing activities 903,551 (8,149,100)

Cash flows from financing activitiesDividends paid - (833,333)

Net cash (used in) / from financing activities - (833,333)

Net (decrease) / increase in cash and cash equivalents 1,779,377 (6,918,973)

Cash and cash equivalents at the beginning of the year 31 2,645,008 9,563,981

Cash and cash equivalents at the end of year 31 4,424,385 2,645,008

The accompanying notes form an integral part of these financial statements.

41

Notes to the financial statementsfor the year ended 31 December 2015

1. General Al Madina Insurance Company SAOG (formerly Al Madina Insurance Company SAOC) (the “Company”) was incorporated on 15 May 2006 as a closed joint stock company in the Sultanate of Oman. On 10 December 2013, the Company has become a public joint stock company. The Company operates in Oman and is engaged in the business of General and Family Takaful activities by adopting a Wakala model. The Company also adopts a Mudarabha model for its investments, on behalf of the participants in accordance with the Islamic Sharia’a principles. The retakaful / reinsurance activities organised on an underwriting year basis with the participants pooling their contributions to cover for losses suffered in the pool on occurrence of a defined event.

The Company commenced commercial operations from 1 August 2006. The Company was granted license from Capital Market Authority (CMA) on 15 July 2006. The Company started Takaful operations on 1 January 2014 after being granted the Takaful license by the CMA.

2. Summary of significant accounting policies Statement of complianceThe financial statements have been prepared in accordance with the Financial Accounting Standards (“FAS”) issued by the Accounting and Auditing Organization for Islamic Financial Institutions (“AAOIFI”), for the matters which are not covered by AAOIFI standards, International Financial Reporting Standards (“IFRS”) have been applied. The financial statements comply with the disclosure related to insurance companies issued by Capital Market Authority and the requirements of the Commercial Companies Law of 1974, as amended.

AAOIFI standards have been applied prospectively from the date of the 1 January 2014 as allowed under such standards. The application of AAOIFI has resulted in the additional disclosures relating to General Takaful and Family Takaful Business, Shareholders’ Fund and Participants’ Fund. The statement of profit or loss and other comprehensive income has been divided into two statements namely “Statement of Participants’ Revenues and Expenses” and “Statement of Profit or Loss and Other Comprehensive Income”. Further, statement of change in equity has been divided into two statements namely “Statement of changes in Participants’ Fund” and “Statement of change in Shareholders’ Equity”.

CMA has issued the Draft Takaful Law which is under final stages of approval. As and when any new regulations and instructions are issued by CMA regarding Takaful Business management will ensure that the basis of preparation of financial statements complies with such regulations.

Basis of preparation The financial statements are prepared under the historical cost convention and using going concern assumption, except for the measurement of financial assets classified as held for trading and Equity type instruments carried at fair value through equity investments and investment property which are measured at fair value.

Historical cost is generally based on the fair value of the consideration given in exchange for goods and services.

The financial statements are presented in Rials Omani (“RO”), which is the Company’s functional and presentation currency.

The Company presents its statement of financial position broadly in order of liquidity.

The preparation of financial statements in conformity with FAS requires the use of certain critical accounting estimates.

42

Notes to the financial statementfor the year ended 31 December 2015 (continued)

2. Summary of significant accounting policies (continued) Basis of preparation (continued)

It also requires management to exercise its judgment in the process of applying the Company’s accounting policies.

The accounting policies have been consistently applied by the Company and are consistent with those used in the previous year. The principal accounting policies are set out as below:

Foreign currencyFunctional and presentation currencyItems included in the financial statements of the Company are measured and presented in Rial Omani (“RO”) being the currency of the primary economic environment in which the Company operates (functional currency).

Transactions and balancesForeign currency transactions are translated into Rial Omani at the exchange rate prevailing on the transaction date. Foreign currency assets and liabilities are translated into Rial Omani at the exchange rate prevailing at the statement of financial position date. Differences on exchange are dealt with in profit or loss as they arise

Takaful operationsAs an Islamic insurance (takaful) provider, the Company issues contracts that are based on co-operative activity by risk sharing or financial risk, or both. The Company classifies all its contracts individually as either takaful contracts or investment contracts.