Adopted FY 2021 Budget

614

Adopted FY 2021 Budget ARLINGTON COUNTY budget.arlingtonva.us

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Adopted FY 2021 Budget

Adopted FY 2021 Budget

ARLINGTON COUNTY

budget.arlingtonva.us

Department of Management and Finance2100 Clarendon Boulevard, Suite 501

Arlington, VA 22201703-228-3415

budget.arlingtonva.us

ARLINGTON COUNTY VISION

Arlington will be a diverse and inclusive world-class urban community with secure, attractive

residential and commercial neighborhoods where people unite to form a caring, learning, participating, sustainable community in which

each person is important.

COUNTY BOARD MEMBERS

County Board Members

Libby Garvey Chair

Katie Cristol

Matt de Ferranti Christian Dorsey

This page intentionally left blank

ARLINGTON COUNTY VISION

"Arlington will be a diverse and

inclusive world-class urban community with secure, attractive residential and

commercial neighborhoods where people unite to form a caring,

learning, participating, sustainable community in which each person is

important."

— Adopted by the Arlington County Board January 26, 2002

The FY 2021 Adopted Budget is printed on paper consisting of 30% recycled content (post-consumer fiber) and SSI certified.

CONTENTS GUIDE TO READING THE ADOPTED BUDGET ...................................................................... 1 TRANSMITTAL LETTER ....................................................................................................... 3 ARLINGTON COUNTY PROFILE .......................................................................................... 9 BUDGET SUMMARY County Budget Resolution ............................................................................................... 21 Budget Decisions ............................................................................................................. 25 FY 2021 Revised Proposed Budget .................................................................................. 29 Expenditure Summary (All Funds) .................................................................................. 47 All Funds Revenue and Expenditure Detail ...................................................................... 48 General Fund Summary ................................................................................................... 50 General Fund Expenditure and Revenue Pie Charts ......................................................... 51 County Government Summary ......................................................................................... 52 Expenditure Comparison ................................................................................................. 53 Adopted Budget Position Changes ................................................................................... 54 COMPENSATION SUMMARY Budgeted Compensation – General Fund and All Funds ................................................... 59 Pay Enhancements, Retirement Rates, and Health Insurance Rates ............................... 60 REVENUE SUMMARY ........................................................................................................ 67 GENERAL FUND County Board Office ...................................................................................................... 127 County Manager’s Office ............................................................................................... 133 Department of Management and Finance ...................................................................... 139 Department of Technology Services .............................................................................. 145

CONTENTS

Human Resources Department ...................................................................................... 153 Office of the County Attorney ........................................................................................ 159 Circuit Court .................................................................................................................. 163 Clerk of the Circuit Court ............................................................................................... 169 General District Court .................................................................................................... 175 Juvenile and Domestic Relations District Court ............................................................. 179 Office of the Magistrate ................................................................................................. 185 Office of the Public Defender ......................................................................................... 189 Commonwealth's Attorney ............................................................................................ 193 Sheriff's Office .............................................................................................................. 199 Office of the Commissioner of Revenue ......................................................................... 207 Office of the Treasurer .................................................................................................. 213 Office of the Electoral Board and Voter Registration ..................................................... 219 Department of Public Safety Communications and Emergency Management ................. 225 Police Department ......................................................................................................... 233 Fire Department ............................................................................................................ 243 Department of Environmental Services ......................................................................... 251 Department of Human Services ..................................................................................... 273 Department of Libraries ................................................................................................ 295 Department of Parks and Recreation ............................................................................. 301 Arlington Economic Development .................................................................................. 317 Department of Community Planning, Housing and Development................................... 325 Non-Departmental......................................................................................................... 333 Debt Service .................................................................................................................. 337 Regionals/Contributions ............................................................................................... 343 Washington Metropolitan Area Transit Authority - Metro .............................................. 353

CONTENTS

ENTERPRISE, SPECIAL REVENUE and INTERNAL SERVICE FUNDS

Ballston Quarter Tax Increment Financing Area Fund ................................................... 359

Travel and Tourism Promotion Fund.............................................................................. 363

Ballston Business Improvement District ....................................................................... 369

Rosslyn Business Improvement District ........................................................................ 373

Crystal City Business Improvement District .................................................................. 377

Housing and Community Development Fund ................................................................ 381

Housing Choice Voucher Fund ....................................................................................... 397

Stormwater Management Fund ..................................................................................... 405

Transportation Capital Fund .......................................................................................... 415

Crystal City, Potomac Yard, and Pentagon City Tax Increment Financing Area Fund ..... 425

Columbia Pike Tax Increment Financing Area Fund ....................................................... 433

Utilities Fund ................................................................................................................. 439

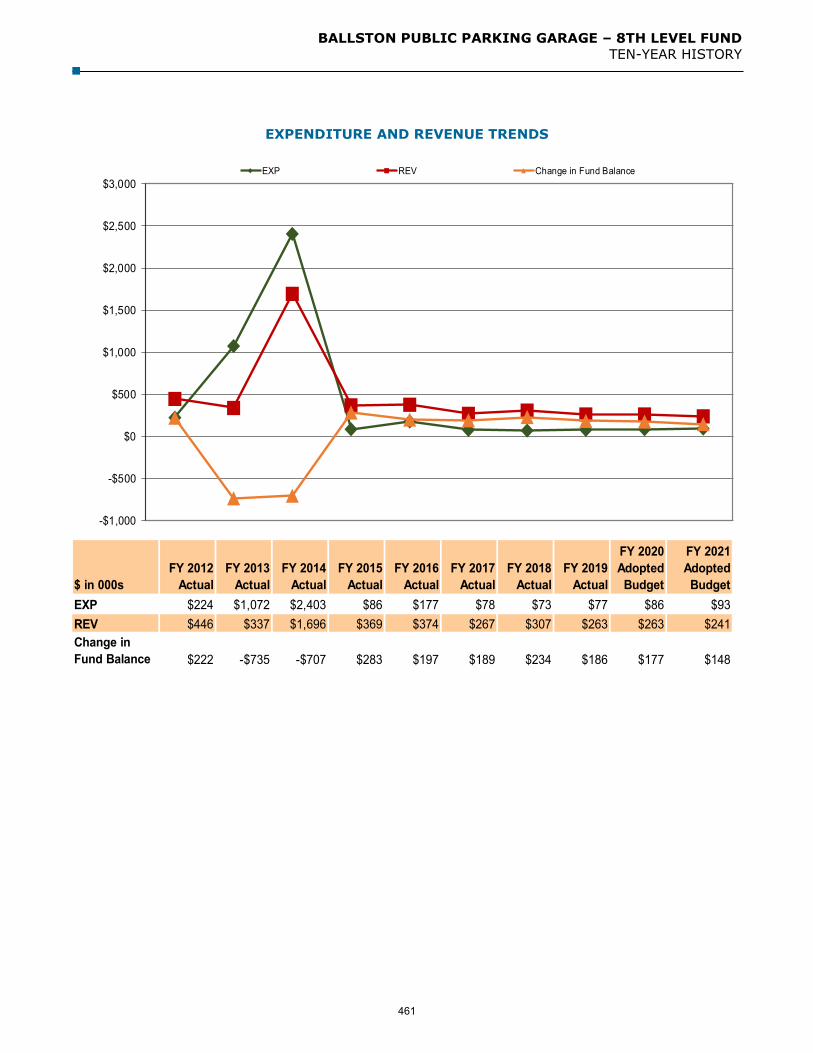

Ballston Public Parking Garage ..................................................................................... 453

Ballston Public Parking Garage – Eighth Level ............................................................. 459

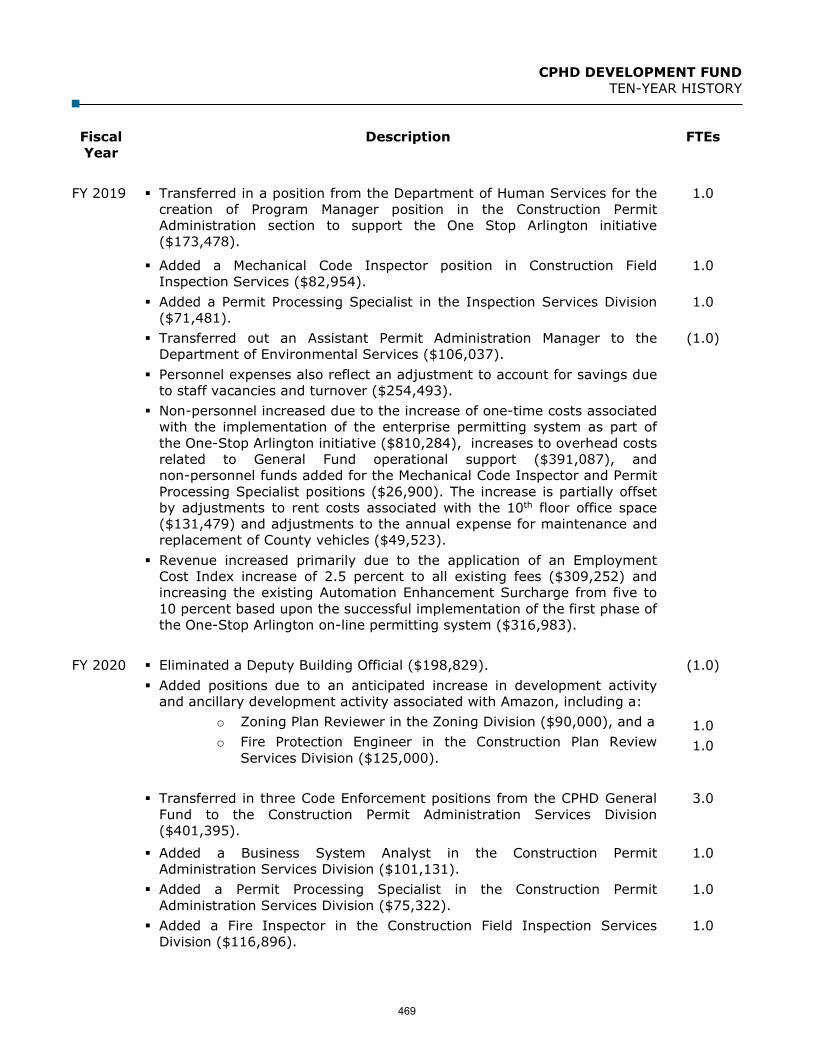

CPHD Development Fund ............................................................................................... 463

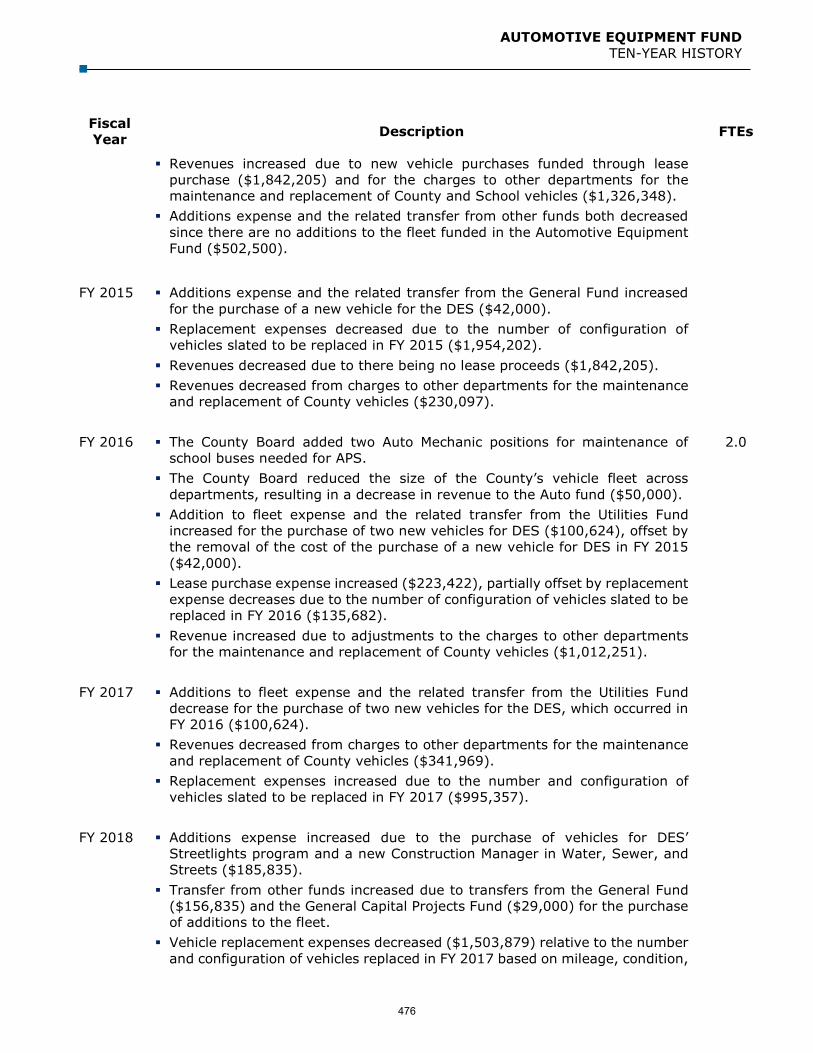

Automotive Equipment Fund ......................................................................................... 471

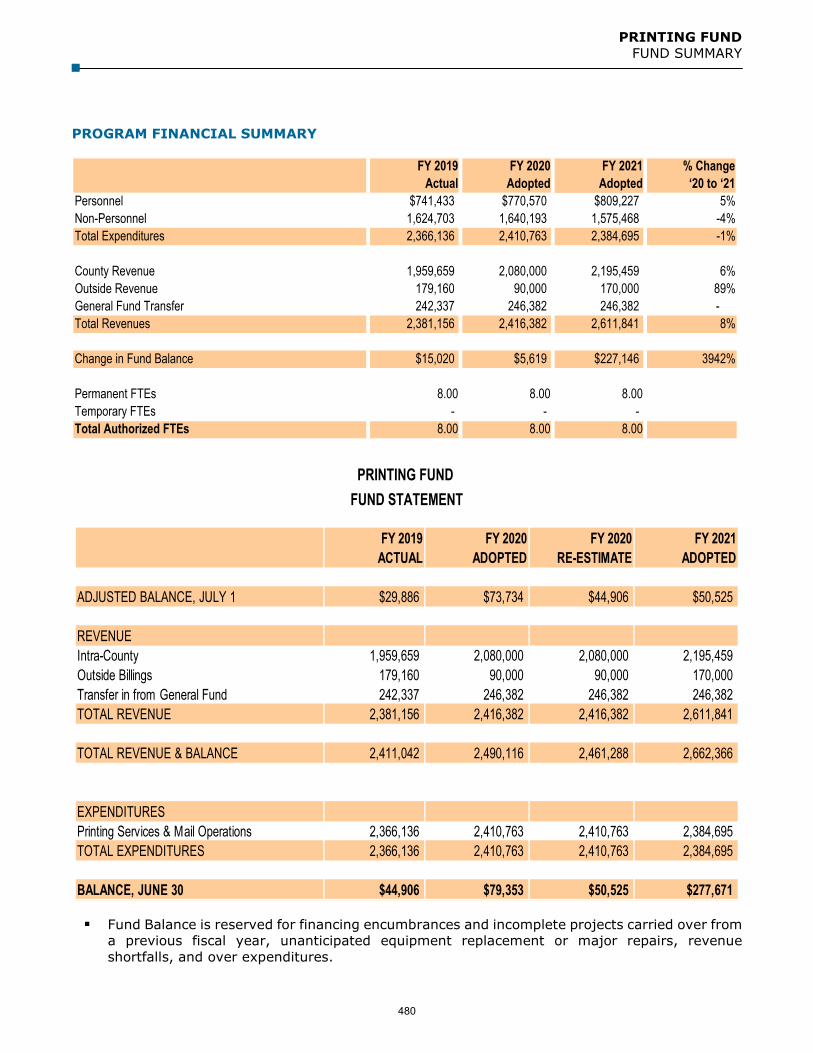

Printing Fund ................................................................................................................ 479

PAY-AS-YOU-GO CAPITAL BUDGET AND SHORT-TERM FINANCING

General Capital Projects Fund ....................................................................................... 487

General Obligation (GO) Bonds ..................................................................................... 499

Capital Program Project Lists ........................................................................................ 501

Short-Term Financing .................................................................................................... 509

Utility Capital Projects Fund .......................................................................................... 513

PAY PLAN FOR COUNTY EMPLOYEES ............................................................................. 519

GLOSSARY AND APPENDIX

Budget Calendar ............................................................................................................ 559

CONTENTS

Budget Process ............................................................................................................. 561 Selected Fiscal Indicators ............................................................................................. 565 Governmental Operating Fund Summaries .................................................................... 566 One-time Funding Summary .......................................................................................... 571 Prior Year Closeout (FY 2019) & Fund Balance Carryover Summary ............................. 573 Financial and Debt Management Policies ....................................................................... 575 Comprehensive Plan Summary ...................................................................................... 583 Housing Summary ......................................................................................................... 591 Tax and Fee Compendium…………………………………………………………………………………… 595 Glossary ........................................................................................................................ 597

GUIDE TO READING THE ADOPTED BUDGET

The Adopted Budget is presented in a format that provides several levels of financial detail. The focus of the Adopted Budget Document is to summarize major policy and program directions and initiatives that are funded in departmental budgets. More detailed descriptions of the various programs and activities in the County are included in the County Manager’s Proposed Budget, which is available on Arlington County’s web site, Department of Management and Finance https://budget.arlingtonva.us/

The Transmittal Letter, starting on the ivory pages, provides an overview of the Adopted Budget, highlighting strategic priorities for the upcoming fiscal year, major revenue and expenditure decisions made to implement those priorities, and changes affecting County staff.

Following the Transmittal Letter is a brief Profile of Arlington County, which includes both organizational and demographic information.

The Budget Summary section includes the Budget Resolution, budget decisions made by the County Board after the proposed budget was presented, summary charts and comparisons, and the County Manager’s Revised Proposed Budget, which was released at the beginning of April to respond to changing conditions resulting from the coronavirus pandemic.

The Compensation Summary includes highlights of the compensation changes included in the adopted budget, the total budget for salaries and fringe benefits, and additional information about pay enhancements, health insurance changes, and retirement rate changes in recent fiscal years.

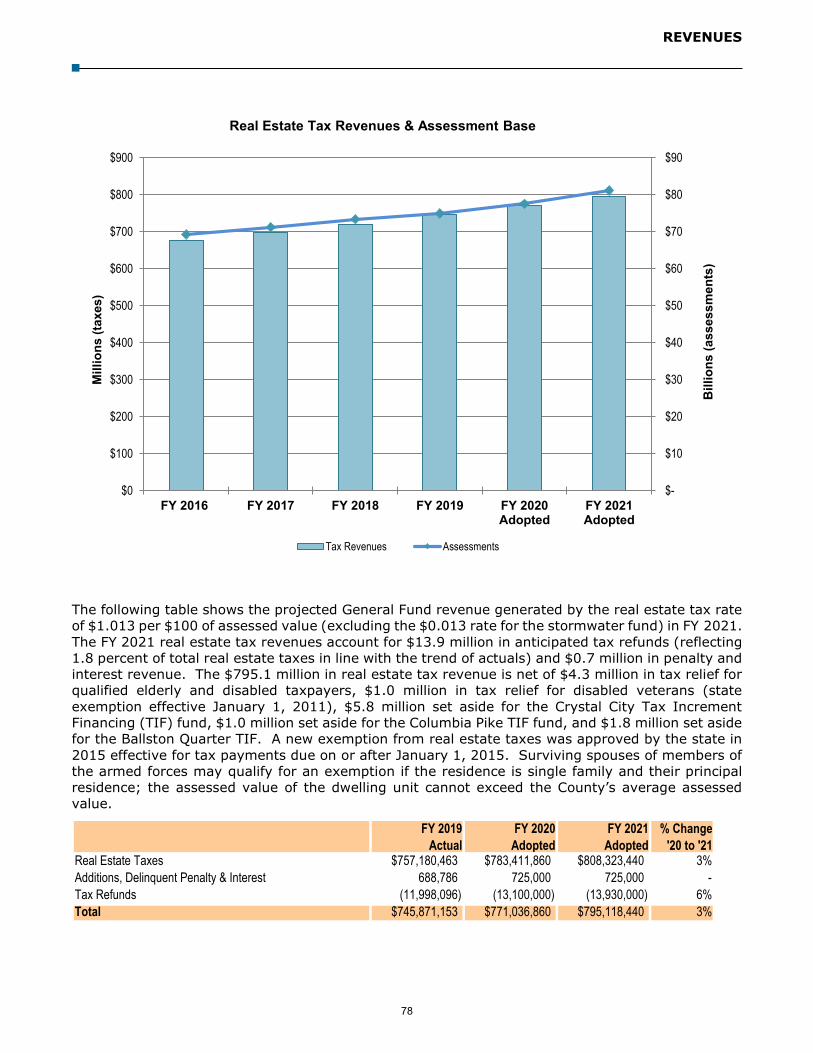

The Revenue Summary section follows on the ivory pages. The tables included in this section provide historical and current year data, in addition to the approved revenue budget. Descriptions of the revenue sources are also provided.

General Fund departmental budget summaries start on the white pages. For each department, a mission statement is presented, along with a budget description explaining significant budget changes from FY 2020 to FY 2021.

Departmental financial summaries detail expenditure, revenue, net tax support and staffing levels for FY 2019 (Actual); current year FY 2020 (Adopted Budget); and FY 2021 (Adopted Budget). Aggregation of expenses and revenues by category are defined as follows:

Personnel - This category includes expenses for salaries, wages, and employee fringe benefits such as retirement, health, and life insurance.

Non-Personnel - This category includes expenses for goods or services provided to the County by vendors or by County internal service funds (see Glossary for definition of internal service funds); expenses for items that are used or consumed in the course of operation of the program or department; and expenses for initial, additional, or replacement items of office or operating equipment not funded through the capital budget.

Intra-County Charges and Inter-Departmental Credit - These categories represent charges by one unit of County government to support another unit's activities.

Fees - These are monies received by the County as payment for services, goods, or use of a facility. Examples are residential refuse disposal fees, user fees for recreation facilities, and various permit and inspection fees.

1

FY 2021 ADOPTED BUDGET GUIDE TO READING THE ADOPTED BUDGET

Grants - Grants are a contribution of funding, usually from state or federal agencies, to be used for a specific purpose or activity. Examples include state highway aid and the HIDTA (High Intensity Drug Trafficking Area) grant.

Net Tax Support - The funds that the County Board may allocate from local tax revenues to fully finance or to supplement revenues received by a department or program. Net tax support is the remainder determined by subtracting all department specific state and federal aid, fees, and charges from the total cost of the programs.

The Position Summary (FTEs) shows authorized permanent positions and temporary positions by full-time equivalent (see glossary for further information on how FTEs are calculated).

Except in the smallest departments, the department summary narrative also includes a table which summarizes the breakout of the departmental expenditure budget by lines of business, reflecting FY 2019 actual expenditures, FY 2020 adopted budget, FY 2021 adopted budget, and FY 2021 Adopted FTE count.

The Ten-Year History for each department reflects actual expenses and revenues prior to FY 2020 and adopted budget amounts for FY 2020 and FY 2021. The program history summarizes significant budget changes over a ten-year period.

Other operating funds (non-General Fund) are presented on the blue pages.

Summaries and project detail for Pay-As-You-Go Capital are exhibited on the grey pages.

The FY 2021 pay schedule for County employees is on the yellow pages.

The Appendix, on the white pages, includes the Budget Calendar, Budget Process, One-Time Funding Summary, Governmental Operating Fund Summaries, Selected Fiscal Indicators, Prior Year Closeout & Fund Balance Carryover Summary, Financial and Debt Management Policies, Comprehensive Plan Summary, the Housing Summary, which provides information in one place about the wide variety of housing-related programs provided in the County, and the Glossary.

2

TRANSMITTAL LETTER:

Coming soon!

3

This page intentionally left blank

4

ARLINGTON COUNTY PROFILE

9

This page intentionally left blank

10

ARLINGTON COUNTY PROFILE

OVERVIEW OF ARLINGTON

Arlington County is located in northern Virginia, directly across the Potomac River from Washington, D.C. The County encompasses 25.8 square miles of land, which was originally split off from Fairfax County in 1801 and ceded by Virginia to be included in the ten-mile square Federal District. In 1847, however, Congress allowed the land to return to the jurisdiction of Virginia following a vote in favor of retrocession by its members. This area was then known as Alexandria City and Alexandria County. In 1920, to avoid confusion, the county was renamed Arlington County.

Annexation of any part of Arlington County by neighboring jurisdictions is prohibited by present law unless the entire County is annexed with the approval of County voters. There are no jurisdictions with overlapping debt or taxing powers. The water and sewage systems are operated on a self-supporting basis by the County government.

Arlington’s location in the center of the Washington metropolitan region, just five minutes from Washington by car or Metrorail, has made the County a highly desirable business and residential location. Arlington has maintained high-quality residential neighborhoods while supporting well-managed growth. High-density commercial and residential development is focused around Metro stations in the Rosslyn-Ballston corridor and the Richmond Highway corridor, which includes both Pentagon City and Crystal City.

Arlington County has an estimated 2020 population of 228,400, an increase of 10 percent over the 2010 population. Additionally, Arlington is home to an estimated 234,800 jobs, as of January 1, 2020.

Almost all land in Arlington County has been developed. This development consists of extensive single-family residential areas, as well as commercial, office, and multi-family residential structures.

Economic activity in Arlington County has historically been closely associated with numerous governmental activities of the Washington Metropolitan region. In 2020 about 20.9 percent (or about 49,000) of the jobs in Arlington County are with the numerous federal, state or local government agencies. In recent years, however, the private employment base, particularly in the service sector, has increased substantially. The 2020 estimates show that sectors of the professional and technical services (24.3 percent and 57,000 jobs) and other services (22.4 percent and 52,500 jobs) have become the top industries for employment in Arlington County.

11

ARLINGTON COUNTY PROFILE

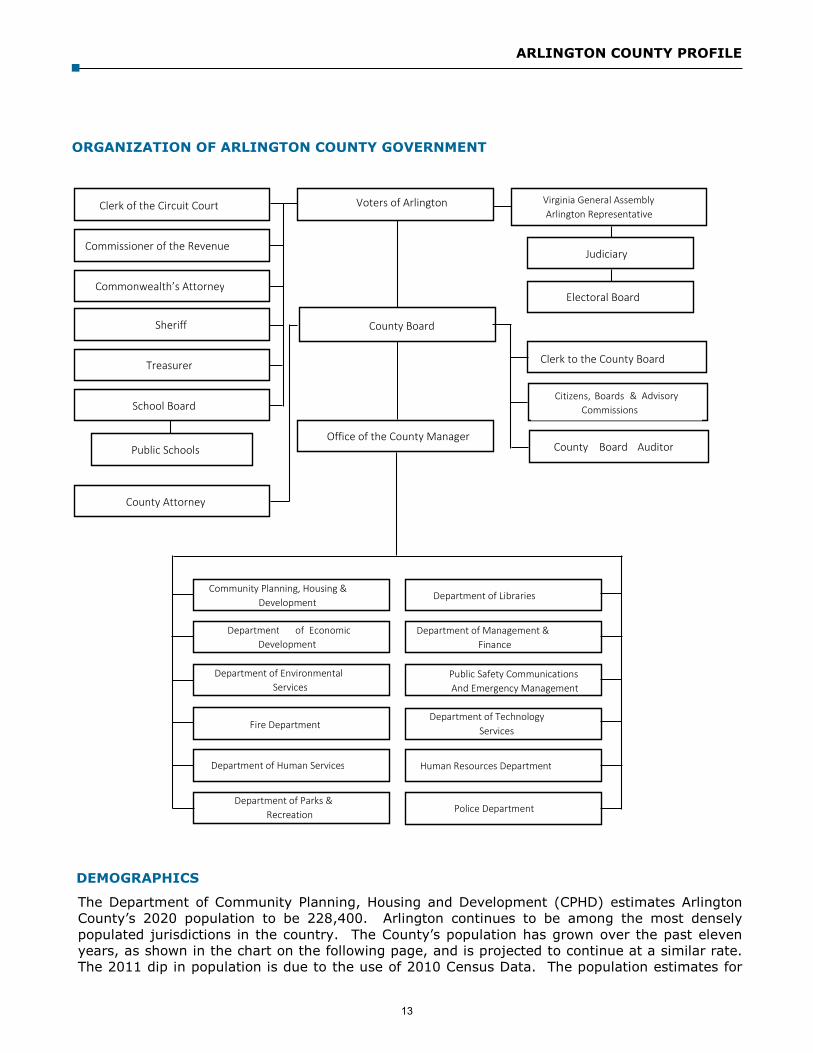

ORGANIZATION OF ARLINGTON COUNTY GOVERNMENT

The government of Arlington County has been organized according to the County Manager Plan of Government since 1932. Arlington County was the first jurisdiction in the United States to adopt a manager form of government by popular vote.

The five members of the County Board are elected at large for staggered, four-year terms. No more than two members are elected at one time. The Chairman of the County Board is elected annually by the members.

The County Board is responsible for several appointments. The County Board appoints a County Manager to serve as the chief executive and administrator of the County. The County Manager serves at the pleasure of the County Board, implements its policies, directs business and administrative procedures, and appoints department directors.

Assisting the County Manager are four Deputy County Managers, three Assistant County Managers and the Directors of 12 departments: Fire; Police; Public Safety Communications and Emergency Management; Environmental Services; Human Services; Economic Development; Community Planning, Housing and Development; Parks and Recreation; Management and Finance; Libraries; Human Resources; and Technology Services.

The County Board also appoints an Auditor to complement and augment the County’s existing internal auditing program. The auditor, and an advisory committee, report directly to the County Board and focuses on tightening financial oversight and deepening program performance review.

Finally, the County Board appoints a County Attorney. The County Attorney provides legal services to the County Board, County agencies and personnel, elected County officials, independent County boards and commissions, and the Arlington School Board.

The operation of public schools in Arlington County is the responsibility of a five-member School Board. School Board members serve staggered, four-year terms in a sequence similar to that of County Board members.

A 1992 revision of the State Code provided a local option to elect the School Board; Arlington voters chose to exercise that option via a November 1993 referendum. As of November 1994 and continuing each year thereafter, School Board members are elected.

The Superintendent of Schools is appointed by the School Board for a four-year term; the Superintendent administers the operations of the County’s public schools. The local share of the cost of operating public schools in the County is met with an appropriation and transfer by the County Board from the County’s General Fund. Operations of the School Board, however, are independent of the County Board and the County administration as prescribed by Virginia law.

In addition to the County Board, other elected County officials include the Commonwealth’s Attorney, Sheriff, Commissioner of the Revenue, Treasurer, and Clerk of the Circuit Court. The Judges of the Circuit Court, the General District Court and the Juvenile and Domestic Relations District Court are appointed by the State legislature.

The structure of Arlington County’s Government is depicted in an organizational chart on the following page.

12

ARLINGTON COUNTY PROFILE

ORGANIZATION OF ARLINGTON COUNTY GOVERNMENT

DEMOGRAPHICS

The Department of Community Planning, Housing and Development (CPHD) estimates Arlington County’s 2020 population to be 228,400. Arlington continues to be among the most densely populated jurisdictions in the country. The County’s population has grown over the past eleven years, as shown in the chart on the following page, and is projected to continue at a similar rate. The 2011 dip in population is due to the use of 2010 Census Data. The population estimates for

County Board

Voters of Arlington Virginia General Assembly Arlington Representative

Office of the County Manager

Clerk of the Circuit Court

Commissioner of the Revenue

Commonwealth’s Attorney

Sheriff

Treasurer

School Board

County Attorney

Public Schools

Judiciary

Electoral Board

Clerk to the County Board

Citizens, Boards & Advisory Commissions

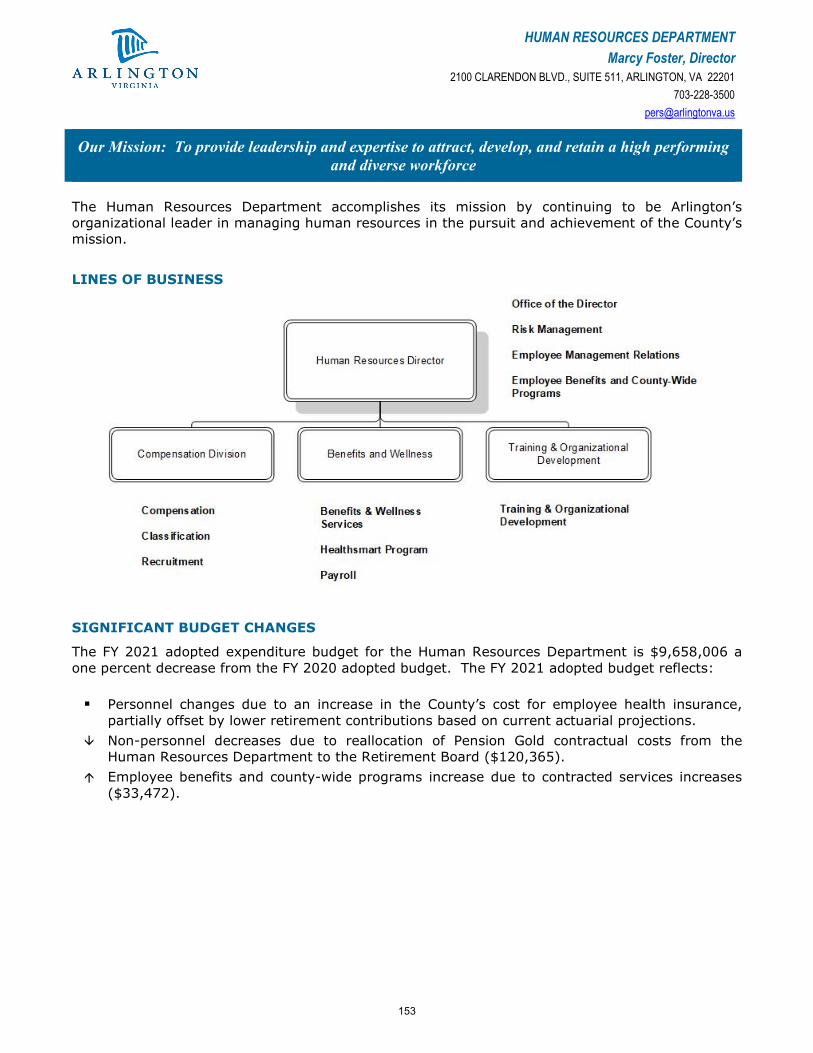

County Board Auditor

Community Planning, Housing & Development

Department of Economic Development

Department of Environmental Services

Fire Department

Department of Human Services

Department of Parks & Recreation

Department of Libraries

Department of Management & Finance

Public Safety Communications And Emergency Management

Department of Technology Services

Human Resources Department

Police Department

13

ARLINGTON COUNTY PROFILE

2002-2009 used the 2000 Census as a base. The new 2010 Census data were used to recalibrate the CPHD’s method for estimating Arlington’s population for 2011 and beyond. Estimates for 2007-2009 and 2011-2020 are provided by CPHD and are based on new residential construction and estimates of average household size and vacancy rates. The 2010 number is based on the 2010 Census. CPHD estimates that 19.5 percent (43,530 persons) of the population are under the age 20. Individuals between the ages of 20-24 make up 6.8 percent or 15,590 persons. Those between the ages of 25-34 make up the largest share of the population at 24.1 percent or 54,960 persons. Persons between the ages of 35-44 represent 16.6 percent of the population (or 38,020 persons), those between the ages 45-64 make up 22.4 percent (or 51,060), those between the ages of 65-84 include 9.3 percent (or 21,280 persons) and those 85 and over represent 1.3 percent of the population (or 2,960 persons).

RACIAL/ETHNIC COMPOSITION

Arlington County takes pride in, and gains vitality from, the diversity of its population. According to the 2010 Census, 64.0 percent of Arlington residents are white, 15.1 percent are Hispanic, 8.2 percent are black or African-American, 9.6 percent are Asian or Other Pacific Islanders, and 3.0 percent identified as another race or two or more races. (Note: percentages may not add due to rounding.)

CPHD estimates that the aggregate population of Arlington increased by 9.6 percent between 2000 and 2010. (Note that staff believes the Census 2000 figure to be a bit lower than the actual population.) From 2000 to 2010 the largest increase in population among the racial/ethnic groups was an increase of about 18,472 among the white population. Among other groups, the Asian-Pacific Islander population also increased substantially, by 3,549 persons. The Hispanic population decreased by 3,886 persons and the African-American population decreased by 156 persons between 2000 and 2010. The following table shows the change in population among various racial/ethnic groups from 2000 to 2010. The 2000 and 2010 figures are from the Decennial Censuses. Race and ethnicity data from the 2020 Census will be included in this section once available.

195,000

200,000

205,000

210,000

215,000

220,000

225,000

230,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Population

14

ARLINGTON COUNTY PROFILE

Racial/Ethnic Group 2000 2010 % Change

Non-Hispanic/Latino White alone 114,489 132,961 16.1% Black or African American alone 17,244 17,088 -0.9% Asian/Pacific Islander 16,346 19,895 21.7% Other/MultiRacial 6,106 6,301 3.2%

Total Non-Hispanic/Latino 154,185 176,245 14.3%

Hispanic/Latino 35,268 31,382 -11.0%

TOTAL 189,453 207,627 9.6%

EDUCATION

Arlington’s population is among the most highly educated in the country. According to the U.S. Census Bureau 2018 American Community Survey, 94.5 percent of all household residents age 25 and older were high school graduates, 74.6 percent were college graduates, and 39.7 percent had graduate or professional degrees. Of the Arlington Public School (APS) class of 2019-2020, 88 percent planned to pursue higher education, and the average expenditure per pupil was expected to be $19,921 in the 2020 fiscal year.

PERSONAL INCOME

The educational achievements of Arlington’s population are reflected in the County’s income statistics as well. In 2018, the Bureau of Economic Analysis reported that Arlington’s per capita personal income was $95,198. According to the U.S. Census American Community Survey, the median household income in Arlington County in 2018 was $117,374. The Per Capita Income graph above shows the growth in per capita personal income since 2002. Income figures for 2004 through 2018 are from the U.S. Bureau of Economic Analysis.

HOUSING

According to CPHD estimates, there are 117,300 total housing units in Arlington as of January 2020. A housing unit is a multi-family dwelling or a single-family dwelling attached to other dwellings or a single-family detached dwelling. The majority (66.1 percent or 77,500) of housing units in Arlington are multi-family. There are an estimated 28,500 single-family detached (24.3 percent), 11,200 single-family attached housing units (9.2 percent) and 100 other types of housing units in Arlington. Since 2000, growth in housing units has been largely due to multi-family development. Between 2000 and January 2020, 25,167 new multi-family units have been completed (an increase of 48.0 percent), compared to 918 single family attached units. There has been a net gain of 851 single family detached units during the same time span. According to the

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Per Capita Income

15

ARLINGTON COUNTY PROFILE

2018 American Community Survey, owners occupy 43.5 percent and renters occupy 56.5 percent of occupied housing units.

HOUSEHOLD COMPOSITION

All persons living in a housing unit are termed a household. As of January 2020, CPHD estimates that there are 108,000 households in Arlington County. According to the 2010 Census the average household size is 2.09 persons. The 2010 Census also reports that an estimated 42.4 percent of Arlington households were family households and 57.6 percent were non-family households.

COMMUNITY FACILITIES IN ARLINGTON

County Owned Parkland 925 acres

Synthetic Fields 15

NOVA Parks 136 acres

Libraries 8

Multi-Use Trails (Off-Street) 52 Nature Centers 3 County Owned Parks 148 Senior Centers 5 Tennis and Basketball Courts 180 Community Centers 13 Natural Grass Fields 82 Fire Stations 10

AT-PLACE EMPLOYMENT

According to Arlington County estimates, the total number of jobs in the County increased by about 16.7 percent between 2000 and 2020. The service sector comprises a significant share of jobs in Arlington. About 24.3 percent of all jobs are in the professional and technical services sector. Another 22.4 percent of jobs are in other service sectors, including administrative, education, and health. The government sector also continues to comprise a large share of Arlington jobs. About 20.9 percent (49,000 jobs) of the County’s January 2020 employment is estimated to be in government. 2017 was the first year in which a sector (professional and technical services) other than government held the highest percentage of at-place jobs in Arlington County.

16

ARLINGTON COUNTY PROFILE

At-Place Employment Construction 3,800 Retail Trade 10,800 Transportation and Warehousing 13,200 Information 6,800 Finance Insurance 6,400 Real Estate and Rental/Leasing 9,100 Professional and Technical Services 57,000 Hospitality and Food Services 17,200 Other Services 52,500 Government 49,000 All Other 9,000

TOTAL 234,800

Source: Sector employment are Arlington County CPHD estimates based on data from the U.S. Bureau ofEconomic Analysis for the year 2018 (most current available). Unemployment data is from the U.S.Bureau of Labor Statistics Local Area Unemployment Statistics (LAUS).

Note: Jobs by sector may not add due to rounding.

17

ARLINGTON COUNTY PROFILE

TOP 10 PRINCIPAL PRIVATE EMPLOYERS

COMPANY NATURE OF BUSINESS ARLINGTON EMPLOYEES

1 Accenture Consulting Services 2,500 – 4,999 2 Deloitte Consulting Services 2,500 – 4,999 3 Virginia Hospital Center Healthcare 2,500-4,999 4 Booz Allen Hamilton Consulting Services 1,000 – 2,499 5 Gartner Consulting Services 1,000 – 2,499 6 Bloomberg BNA Information Services 750-9997 LIDL Supermarket 750-9998 Marriott International, Inc. Hotel 750-9999 CACI Consulting Services 500-749

10 Marymount University Education 500-749

TOTAL 12,750-24,490

Source: QCEW 2Q 2019

SELECTED SERVICE INDICATORS

FY 2019 FY 2020 FY 2021Actual Estimate Estimate

General Obligation Bond Rating Aaa/AAA/AAA Aaa/AAA/AAA Aaa/AAA/AAANew Voters Registered by Electoral Board (Calendar Year) 11,905 25,000 12,000Inspections Conducted for Fire Code Enforcement, fireprotection system, and hazardous materials inspections 3,159 3,400 3,400Percentage of Fire Emergencies Reached Within Four Minutesof Dispatch 60% 60% 60%Fire/EMS/Public Service Responses 60,851 63,000 63,000Refuse Collected on County and Contracted Routes (Tons) 27,367 28,534 29,675Total Curbside Recycling Tonnage Collected 12,968 10,437 10,437Licensed Child Care Facilities (Family Day Care Homes) 138 138 138Number of registrations in Parks and Recreation programs 60,260 61,000 61,000Number of individuals registered with the Office for Senior Adult Programs (OSAP) 6,905 7,000 7,200Police response time for Priority 1 calls (minutes from dispatch to arrival) 4:55 4:50 5:00

18

BUDGET SUMMARY

19

This page intentionally left blank

20

ATTACHMENT I

GENERAL FUND:

County Board 1,704,263

County Manager 5,134,115

Management and Finance 8,569,554

Technology Services 26,039,370

Human Resources 9,658,006

County Attorney 3,264,500

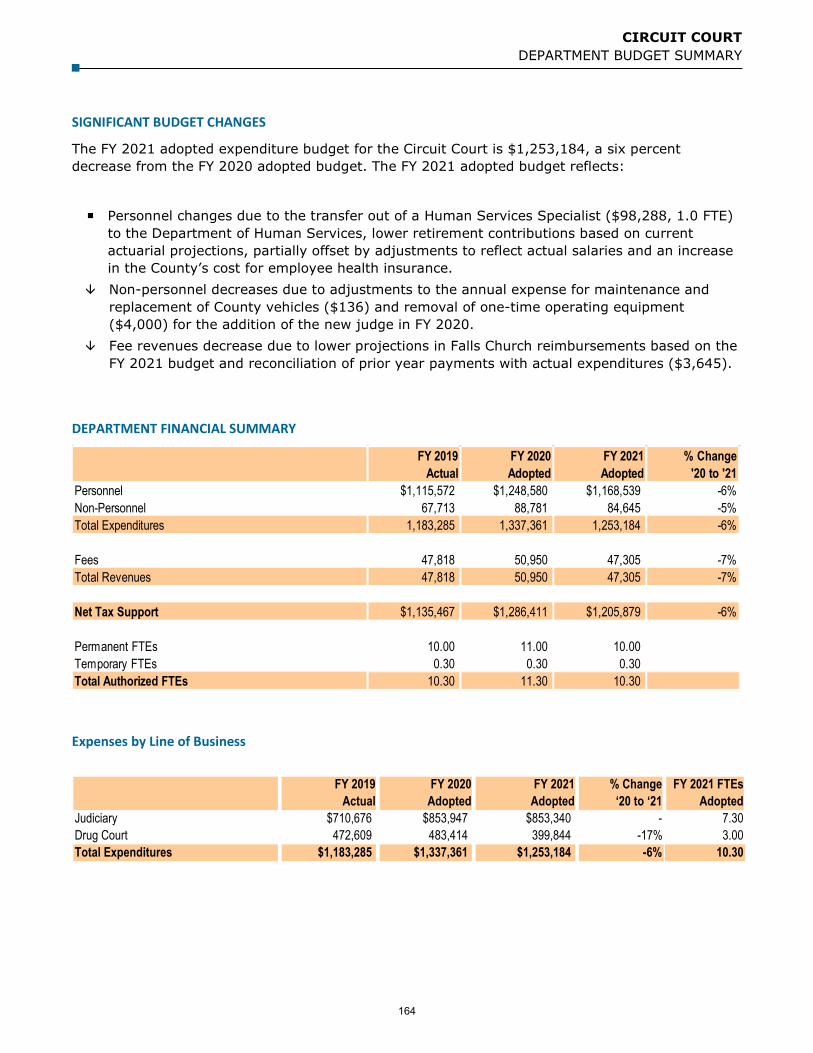

Circuit Court 1,253,184

Clerk of the Circuit Court 3,492,403

General District Court 406,355

Juvenile and Domestic Relations Court 7,335,007

Commonwealth's Attorney 4,632,228

Office of the Magistrate 29,986

Office of the Public Defender 181,239

Sheriff 46,192,674

Commissioner of the Revenue 5,949,123

Treasurer 7,298,502

Electoral Board 1,835,477

Public Safety Communications and Emergency Management 13,629,582

Police 72,274,292

Fire 66,430,066

Environmental Services 109,182,243

Human Services 146,126,784

Libraries 14,758,386

Economic Development 8,669,102

Community Planning, Housing & Development 11,624,696

Parks and Recreation 44,685,251

Non‐Departmental 54,235,363

Debt Service 68,962,748

Regionals / Contributions 6,724,786

METRO 47,808,764

TOTAL GENERAL FUND BUDGET: $798,088,049

OTHER FUNDS:

Ballston Quarter Tax Increment Financing 2,018,464

Travel and Tourism 1,209,582

Ballston Business Improvement District 1,569,935

Rosslyn Business Improvement District 4,053,393

Crystal City Business Improvement District 4,739,568

Community Development 3,378,470

Section 8 Housing Assistance 19,473,520

General Capital PAYG 24,274,441

General Obligation Bonds (Street & Highway,

Neighborhood Conservation, Government Facility,

Public Recreation, & Transit Facilities Bonds) 14,500,000

Stormwater Management 11,729,047

FISCAL YEAR 2021 COUNTY BUDGET RESOLUTION

Be it resolved by the County Board of Arlington County, Virginia, that the

following Budget is hereby adopted for the Fiscal Year 2021 and that any surplus

for general County purposes remaining at the end of the Fiscal Year shall return

to the General Fund of the County.

21

ATTACHMENT I

Transportation 34,436,800

Crystal City Tax Increment Financing 5,759,940

Columbia Pike Tax Increment Financing 1,014,000

Utilities 103,667,295

Utilities Capital 23,422,000

Ballston Public Parking Garage 4,144,996

Ballston Public Parking Garage ‐ 8th Level 92,841

CPHD Development 24,200,894

Automotive Equipment 18,574,340

Printing 2,384,695

TOTAL OTHER OPERATING FUNDS BUDGET: $304,644,221

TOTAL COUNTY GOVERNMENT BUDGET: $1,102,732,270

Facilities to be expended on order of the School Board

School Operating Fund 560,562,109

School Children's Services Act Fund 4,225,000

School Capital Projects Fund 2,040,843

School Debt Service Fund 56,905,740

School Food Services Fund 11,325,152

School Grants & Restricted Programs Fund 16,245,544

Total School and other funds appropriations $651,304,388

Total Community Activities Fund $19,756,037

TOTAL BUDGET FOR COUNTY $1,773,792,694

GENERAL FUND REVENUES:

Real Estate Tax 795,118,440

Personal Property Tax 120,052,147

Business License Tax 63,000,000

Other Local Taxes 138,065,778

Licenses, Permits and Fees 13,115,693

Fines 8,211,282

Interest, Rents 13,303,309

Charges for Services 64,253,949

Miscellaneous 1,855,329

State Revenue 79,146,009

Federal Revenue 16,145,620

Other Transfers In 10,937,655

Prior Year Balance (Revenue & County Exp. Savings) 22,239,239

TOTAL GENERAL FUND REVENUES: $1,345,444,450

Total Other Operating Fund Revenues $428,348,244

TOTAL REVENUES FOR COUNTY $1,773,792,694

For the operation and maintenance of Public Schools and Community Activities

22

ATTACHMENT II

GENERAL FUND:

County Board 1,704,263

County Manager 5,134,115

Management and Finance 8,569,554

Technology Services 26,039,370

Human Resources 9,658,006

County Attorney 3,264,500

Circuit Court 1,253,184

Clerk of the Circuit Court 3,492,403

General District Court 406,355

Juvenile and Domestic Relations Court 7,335,007

Commonwealth's Attorney 4,632,228

Office of the Magistrate 29,986

Office of the Public Defender 181,239

Sheriff 46,192,674

Commissioner of the Revenue 5,949,123

Treasurer 7,298,502

Electoral Board 1,835,477

Public Safety Communications and Emergency Management 13,629,582

Police 72,274,292

Fire 66,430,066

Environmental Services 109,182,243

Human Services 146,126,784

Libraries 14,758,386

Economic Development 8,669,102

Community Planning, Housing & Development 11,624,696

Parks and Recreation 44,685,251

Non‐Departmental 54,235,363

Debt Service 68,962,748

Regionals / Contributions 6,724,786

METRO 47,808,764

TOTAL GENERAL FUND APPROPRIATIONS: 798,088,049

FISCAL YEAR 2021 COUNTY APPROPRIATIONS RESOLUTION

Be it resolved by the County Board of Arlington County, Virginia, that the following

appropriations are hereby made for the Fiscal Year 2021, and that any surplus for general

County purposes remaining at the end of the Fiscal Year shall return to the General Fund

of the County. For other funds, such as capital funds and certain restricted funds, the

appropriations designated for these funds, unexpended as of June 30, 2020, are hereby

reappropriated to those funds to the following fiscal year. The reappropriation of the

funds is in addition to the appropriations listed in Attachment II. This section applies to all

existing appropriations for the capital and restricted funds on June 30, 2020 noted below

with an asterisk (*) and for all Bond Funds and the Urban Area Security Initiative (UASI)

fund.

23

ATTACHMENT II

OTHER FUNDS:

Ballston Quarter Tax Increment Financing $2,018,464

Travel and Tourism 1,209,582

Ballston Business Improvement District 1,569,935

Rosslyn Business Improvement District 4,053,393

Crystal City Business Improvement Dist. 4,739,568

Community Development 3,378,470

Section 8 Housing Assistance 19,473,520

* General Capital PAYG 24,274,441

* Stormwater Management 11,729,047

* Transportation 34,436,800

* Crystal City Tax Increment Financing 5,759,940

* Columbia Pike Tax Increment Financing 1,014,000

Utilities 103,667,295

* Utilities Capital 23,422,000

* Ballston Public Parking Garage 4,144,996

* Ballston Public Parking Garage ‐ 8th Level 92,841

CPHD Development 24,200,894

Automotive Equipment 18,574,340

Printing 2,384,695

TOTAL OTHER OPERATING FUNDS APPROPRIATIONS: $290,144,221

TOTAL COUNTY GOVERNMENT APPROPRIATIONS: $1,088,232,270

Facilities to be expended on order of the School Board

School Operating Fund $560,562,109

School Children's Services Act Fund 4,225,000

School Capital Projects Fund 2,040,843

School Debt Service Fund 56,905,740

School Food Services Fund 11,325,152

School Grants & Restricted Programs Fund 16,245,544

Total School and other funds appropriations $651,304,388

Total Community Activities Fund $19,756,037

TOTAL APPROPRIATIONS FOR COUNTY $1,759,292,694

For the operation and maintenance of Public Schools and Community Activities

24

FY 2021 BUDGET DECISIONS

FY 2021 BUDGET DECISIONS

The FY 2021 Adopted Budget incorporates funding levels for County programs and services which were determined after a detailed review of revenue and expenditure options contained in the FY 2021 Revised Proposed Budget. A summary of County Board actions is provided on the following pages. This list details expenditure and revenue changes between the FY 2021 Revised Proposed and the FY 2021 Adopted Budgets, as well as all changes in tax and fee rates from the FY 2020 adopted levels (including those previously cited in the FY 2021 Proposed and FY 2021 Revised Proposed Budgets).

TAXES

The base real estate tax rate remains at the CY 2019 rate of $1.013 per one hundred dollars of assessed value, no change.

A County-wide sanitary district tax for stormwater management, originally adopted in CY 2008, is reaffirmed at a rate of $0.013, bringing the combined base and sanitary real estate rate to $1.026 per one hundred dollars of assessed value.

An additional real estate tax, originally adopted in CY 2008, is reaffirmed at a rate of $0.125 per one hundred dollars of assessed value on properties used for or zoned to permit commercial and industrial purposes. Revenue from this tax is used to fund transportation initiatives.

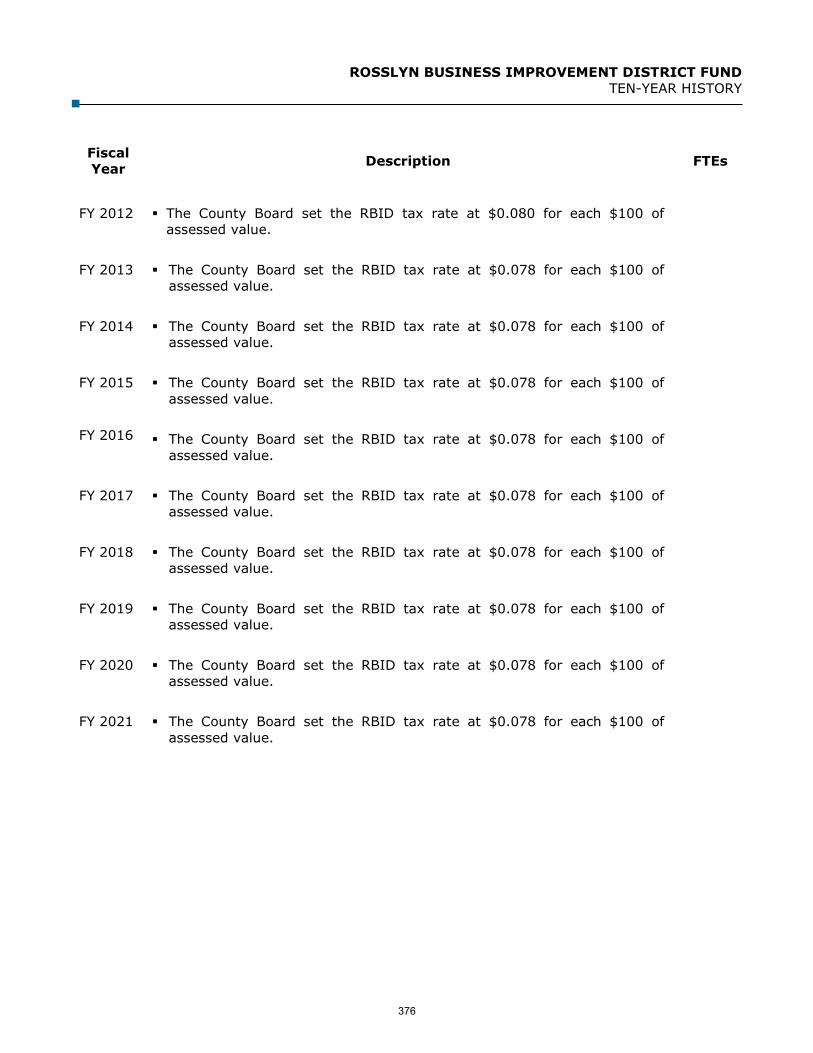

The Rosslyn Business Improvement Service District tax rate remains unchanged at $0.078 per one hundred dollars of assessed value. This service district tax rate is in addition to the real estate tax rate.

The Crystal City Business Improvement Service District tax rate remains unchanged at $0.043 per one hundred dollars of assessed value. This service district tax rate is in addition to the real estate tax rate.

The Ballston Business Improvement Service District tax rate remains unchanged at $0.045 per one hundred dollars of assessed value. This service district tax rate is in addition to the real estate tax rate.

The Crystal City, Potomac Yard, and Pentagon City Tax Increment Financing District is projected to total $5,759,940 based on 25 percent of the incremental tax payments generated by the projected assessment tax base increase for properties in the defined Crystal City, Potomac Yard and Pentagon City area.

The Columbia Pike Tax Increment Financing District funding is projected to total $1,014,000 based on the increment of real estate tax revenue generated above the CY 2018 baseline.

The Ballston Quarter Tax Increment Financing District funding is projected to total $2,018,464 based on incremental tax growth of real property values as well as sales and meals taxes in the TIF district compared to the 2015 base year. Funding in an amount up to 65 percent of the incremental base value will be transferred to the trustee for the Ballston Quarter Community Development Authority (CDA) to fund the project stabilization fund as part of the Ballston Quarter CDA Series 2016A & Series 2016 B bond issuance.

25

FY 2021 BUDGET DECISIONS

Other local tax rates, including Personal Property, Business Professional & Occupational License (BPOL), meals, utility, and transient occupancy taxes remain unchanged.

REVENUES - GENERAL FUND

In the Department of Environmental Services (DES), the household solid waste rate increases from $306 to $319.03. The fee is charged per refuse unit and achieves the County’s objective of 100 percent recovery of household refuse collection, disposal and recycling costs, leaf collection costs, and overtime costs associated with brush and metal collection.

The Department of Human Services (DHS) is implementing new fees for new course offerings from the Arlington Employment Center related to childcare and computer training and certifications and new fees for newly offered certified vital event (eg. birth, death, marriage, divorce) certificates.

In the Department of Libraries, fines for overdue materials have been eliminated to make the collections more accessible to all library users.

In the Police Department, new fees have been established for alarm registrations and false alarm fines have been increased.

In the Department of Parks and Recreation (DPR), new fees have been adopted for nature summer camps extended day options, adult 3-verses-3 basketball tournaments, and lifeguard classes. Other fee adjustments have been made to more accurately reflect costs and DPR fee policy. These changes include fee adjustments for aquatics and gymnastics teams, creative arts programs, summer camps, and youth sports leagues.

In the Department of Community Planning, Housing and Development, development services fees including site plan fees have been increased by 2.5 percent.

In Arlington Economic Development (AED), Scenic Studio use fees have been increased.

REVENUES - OTHER FUNDS

In the Utilities Fund the water/sewer rate increased to $14.20 per thousand gallons. The rate represents an increase of $0.40 per thousand gallons, or 2.9 percent, above the current rate. At the new rate, the average single-family house will pay $24 more per year for water and sewer service based on an estimated household consumption of 60,000 gallons of water per year.

The FY 2021 adopted budget includes a 2.5 percent inflationary increase to all Development Fund fees to reflect increases to the costs of employee wages and benefits.

EXPENDITURES/OTHER ADJUSTMENTS

NOTE: All funding is ongoing unless otherwise noted. Reductions are changes to net tax support unless otherwise noted.

NON-DEPARTMENTAL/REGIONALS/OTHER Increased funding for Arlington Independent Media ($70,000 one-time) bringing total support for that organization to $397,978.

Allocated $25,000 in one-time funding for Lee Highway Alliance bringing total support for that organization to $85,500.

26

FY 2021 BUDGET DECISIONS

SCHOOLS The FY 2021 adopted transfer is $524,631,091 in ongoing funding. The revenue sharing percentage remains at 47.0 percent of ongoing local tax revenues.

27

This page intentionally left blank

28

COUNTY MANAGER’S OFFICE

2100 Clarendon Boulevard, Suite 314, Arlington, VA 22201 TEL 703.228.3120 FAX 703.228.3218 www.arlingtonva.us

Revised FY 2021 Budget MemorandumTo: County Board of Arlington, Virginia Date: April 6, 2020

From: Mark Schwartz, County Manager

Subject: Revised FY 2021 Proposed Budget

Members of the Board: Given the extraordinary circumstances facing our community, I am providing, for your consideration, a revised Fiscal Year (FY) 2021 Proposed budget.

With the COVID-19 virus altering our way of life, we have seen the personal toll borne by countless Americans and many here in Arlington. Our community’s physical and mental health has been challenged as never before. The economic impact has been unprecedented.

What was unthinkable two months ago is now in front of us. Businesses have laid off staff, residents have lost jobs, schools have closed and only the most essential functions continue. In over 30 years of my public service, I have seen nothing like this.

Our amazing staff have, in less than two weeks, prepared a new budget for your consideration. These same staff have juggled this work with their own concerns for their health and the need to care for their families. In the pages that follow, we have done our best to assess our anticipated revenues and expenditures. I know that I will be back to you many times in the coming months with revisions to today’s proposal. I fear that we are all being too optimistic. As actual receipts and expenses are tallied, we will have a better sense of the choices in front of us.

Under the Code of Virginia, we are still required to submit a budget and the Board must adopt one for the year beginning July 1. To ensure that real estate tax bills can be provided to residents in May, the proposed budget should serve as a good guide through at least the first few months of FY 2021 (July, August, September).

Update on FY 2020

Before moving into my revised proposal for FY 2021, I wanted to give you an update on the COVID efforts made to date and that are on the horizon for the next few days and weeks and the initial budget impacts.

This crisis hit with close to 75% of the fiscal year complete. As described in more detail below, we remain concerned about those economically sensitive tax sources, specifically sales, meals and transient occupancy taxes. We also recognize that we will experience declines in non-tax sources such as parking meter revenues, fees for services, among others. Much of this data is reported on a lagging basis, so we will not have a better sense of these impacts until late April / early May.

29

Memorandum Page 2 of 17

That said, we have many levers to address these near-term impacts (and the investments noted below) to ensure that we do not face a shortfall for the last three months of the fiscal year.

• We have instituted a hiring slowdown that will continue into FY 2021.• We have contingents available:

o The County Manager’s Contingent of which approximately $0.75 million remainsunallocated.

o Stabilization Reserve – while I am proposing that $4.0 million of this reserve beutilized in FY 2021, a balance of $7.8 million remains that could be available inFY 2020 or later in a worst-case scenario.

• Capital projects could be deferred or cancelled beyond what I have already recommendeddoing for FY 2021 as noted below.

We are monitoring revenues and expenditures on a daily basis and will provide periodic reports as data becomes available.

Initial Investments to Address COVID-19

While mindful of the financial impacts, over the last month, we have taken a series of actions critical to addressing the pandemic:

• Purchase of personal protective equipment (PPE) and additional cleaning supplies for ourfront-line employees and non-profit partners.

• Invested in technology (laptops, etc.) to move as much of the workforce to telework aspossible with a focus on standing up virtual call centers for COVID-19 response and forremote ECC call intake and dispatch and allowing case workers and other services to beprovided remotely.

• Provided initial support to front-line non-profits:o Set up telehealth capabilities to connect the Virginia Hospital Center and the

Arlington Free Clinic.o Provided $100,000 for food purchases to the Arlington Food Assistance Center.

• Stood up the COVID-19 testing center with Virginia Hospital Center, including technology,facilities and logistical assistance.

• Identified back-up quarantine housing for congregate care settings.

In the coming days and weeks, I will also be proposing other initiatives:

• Premium pay for those front-line employees who cannot work remotely and must be on-site.The City of Alexandria and the State of Maryland have implemented similar hourlypremiums.

• Small business support through a grant program and exploring the possibility of a revolvingloan fund. The remaining balance of the Gazelle grant program (approximately $650,000)can be reallocated to at least partially fund this business support.

• Delaying required repayments by recipients of County AHIF loans.

30

Memorandum Page 3 of 17

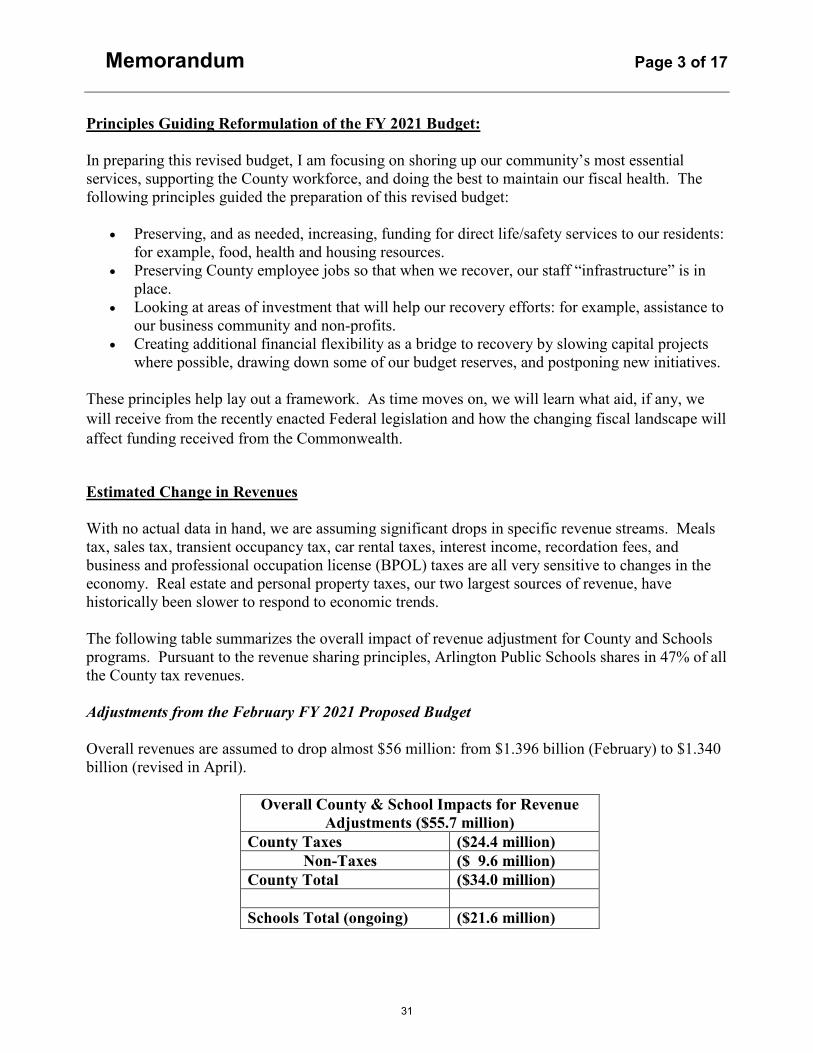

Principles Guiding Reformulation of the FY 2021 Budget:

In preparing this revised budget, I am focusing on shoring up our community’s most essential services, supporting the County workforce, and doing the best to maintain our fiscal health. The following principles guided the preparation of this revised budget:

• Preserving, and as needed, increasing, funding for direct life/safety services to our residents:for example, food, health and housing resources.

• Preserving County employee jobs so that when we recover, our staff “infrastructure” is inplace.

• Looking at areas of investment that will help our recovery efforts: for example, assistance toour business community and non-profits.

• Creating additional financial flexibility as a bridge to recovery by slowing capital projectswhere possible, drawing down some of our budget reserves, and postponing new initiatives.

These principles help lay out a framework. As time moves on, we will learn what aid, if any, we will receive from the recently enacted Federal legislation and how the changing fiscal landscape will affect funding received from the Commonwealth.

Estimated Change in Revenues

With no actual data in hand, we are assuming significant drops in specific revenue streams. Meals tax, sales tax, transient occupancy tax, car rental taxes, interest income, recordation fees, and business and professional occupation license (BPOL) taxes are all very sensitive to changes in the economy. Real estate and personal property taxes, our two largest sources of revenue, have historically been slower to respond to economic trends.

The following table summarizes the overall impact of revenue adjustment for County and Schools programs. Pursuant to the revenue sharing principles, Arlington Public Schools shares in 47% of all the County tax revenues.

Adjustments from the February FY 2021 Proposed Budget

Overall revenues are assumed to drop almost $56 million: from $1.396 billion (February) to $1.340 billion (revised in April).

Overall County & School Impacts for Revenue Adjustments ($55.7 million)

County Taxes ($24.4 million) Non-Taxes ($ 9.6 million) County Total ($34.0 million)

Schools Total (ongoing) ($21.6 million)

31

Memorandum Page 4 of 17

Schools: In the February Proposed budget, Arlington Public Schools would have received $546.3 million in ongoing funding based on the Principles of Revenue Sharing for the split of local tax dollars, an increase of $23.9 million from the adopted FY 2020 level. With that revenue transfer, the Schools proposed a needs-based budget which created a funding gap of over $27 million; however, APS outlined a variety of program and compensation choices to balance the School budget for FY 2021. The revised revenue projections outlined in this memo reduce the projected School transfer by $21.6 million to a total of $524.6 million in ongoing funding. Similar to the County, the Schools will need to make some very difficult choices due to the pandemic crisis.

Comparison to the FY 2020 Adopted Budget

With this revised Proposed Budget, overall revenues are assumed to drop almost $16 million below the FY 2020 adopted totals. The events of this spring are significantly impacting FY 2020 and FY 2021. Updates on the FY 2020 budget, both revenue and expense, will be provided later this month as a part of the 3rd Quarter review.

Revised assumptions for both FY 2020 and FY 2021 assume a variety of impacts on our revenue sources. Depending on the timing of revenue receipts to the County, revenue sources are impacted differently. Generally, for revenue received on a daily or monthly basis (e.g., sales, meals, and transient occupancy tax), drops in anticipated revenue receipts are assumed beginning in mid-March and continuing through June where a recovery period is expected until activity resumes to normal. This impact and curve to recovery varies based on the tax source. It will impact sales, meals, and transient occupancy tax (hotel tax) most immediately. Hotel taxes (Transient Occupancy Tax, or TOT) will see the most significant declines in FY 2020 with up to 75% loss in monthly revenue.

Business license taxes (BPOL) in the spring of CY 2020 (impacting FY 2021 revenue) will see significant impacts with recovery beginning in the first quarter of FY 2021. For other tax revenue received annually or bi-annually (e.g., real estate and personal property taxes) different assumptions are made.

Our expectations of recovery change from day to day. The estimates in this revised budget proposal may be too optimistic and as I mentioned earlier, I will likely be back to the County Board and community with revisions to this proposal.

32

Memorandum Page 5 of 17

Revenue

FY 2020 Adopted Budget

FY 2021 Originally Proposed Budget

FY 2021 Revised

Proposed Budget

FY 2021 Percent Change (original

to revised)

FY 2021 $ Change

(original to revised)

FY 2020 Adopted to

Revised FY 2021

% Change

Real Estate Tax $771,036,860 $806,680,276 $795,118,440 -1.4% ($11,561,836) 3.1% Personal Property Tax 119,052,147 122,252,147 120,052,147 -1.8% (2,200,000) 0.9% BPOL Tax 69,020,000 74,860,000 63,000,000 -15.8% (11,860,000) -8.7%Sales Tax 44,700,000 47,500,000 43,127,695 -9.2% (4,372,305) -3.5%Meals Tax 40,900,000 42,310,000 36,772,563 -13.1% (5,537,437) -10.1%Transient Occupancy Tax 26,000,000 26,000,000 19,257,639 -25.9% (6,742,361) -25.9%Car Rental Tax 6,300,000 6,300,000 4,342,881 -31.1% (1,957,119) -31.1%Recordation Tax 5,500,000 6,000,000 4,200,000 -30.0% (1,800,000) -23.6%Other Taxes 29,112,000 30,365,000 30,365,000 0.0% - 4.3% Total Taxes 1,111,621,007 1,162,267,423 1,116,236,365 -4.0% (46,031,058) 0.4%

License, Permits & Fees 12,382,803 14,330,893 13,115,693 -8.5% (1,215,200) 5.9% Fines, Interest & Leases 23,663,266 26,354,543 21,542,350 -18.3% (4,812,193) -9.0%Charges for Service 64,252,642 66,035,658 64,231,949 -2.7% (1,803,709) 0.0% State & Federal 92,063,641 95,861,629 95,291,629 -0.6% (570,000) 3.5% Other 11,153,921 9,342,428 8,096,333 -13.3% (1,246,095) -27.4%Fund Balance 41,108,294 21,978,940 21,978,940 0.0% - -46.5% Non-Tax Revenue 244,624,567 233,904,091 224,256,894 -4.1% (9,647,197) -8.3%

TOTAL REVENUE BUDGET 1,356,245,574 1,396,171,514 1,340,493,259 -4.0% (55,678,255) -1.2%

SCHOOL TRANSFER (ongoing funding) $522,426,668 $546,265,689 $524,631,091 -3.9% ($21,634,597) -0.7%

Fiscal Year 2021 revised proposed revenues are estimated to be $56 million lower than the originally proposed FY 2021 budget and $16 million lower than the Fiscal Year 2020 adopted budget due to the lingering impacts of social distancing and state-imposed business restrictions amid the COVID-19 outbreak, along with the greater macroeconomic effects from the global pandemic and potential future waves of the virus.

Real Estate – Real estate tax revenue is forecasted to be $11.6 million lower than originally budgeted due to changes in assumptions related to the growth of the County’s real estate assessment tax base in January 2021. The original proposed budget assumed a three percent growth rate for property values for CY 2021. The current revision assumes no growth in the tax base.

33

Memorandum Page 6 of 17

Personal Property – Personal property tax revenue is composed of vehicle personal property and business tangibles. A slightly lower assumption is being made to business tangible revenue as a result of slower business equipment purchases through the remainder of the calendar year. Total tax revenue is forecasted to be $2.2 million (1.8%) lower than originally budgeted.

Business, Professional and Occupational License Tax (BPOL) – BPOL tax revenue is expected to see a significant decline in FY 2021. BPOL tax is calculated based on gross receipts from the previous calendar year. For FY 2021, these will include the business receipts from this spring and summer (CY 2020), significantly impacted by the slowdown of business operations. The original estimate was based on a trend of steady growth in revenue receipts, including an 11 percent increase in FY 2019. The revised lower tax projection is almost a $12 million decrease from the originally proposed projections.

Sales – Business closures and social distancing measures have also impacted the sales tax revenue estimate as in-person purchases begin to slowly recover while online sales remain relatively more stable. Revised sales tax revenue is forecasted to be $4.4 million lower than the original estimate.

Meals – Meals tax receipts are expected to follow a similar pattern to sales tax but decease slightly more as restaurants begin to build back up from temporary partial or full closures. This tax revenue is forecasted to decrease $5.5 million from the original estimate.

Transient Occupancy (TOT) – TOT is expected to see the most significant impact from the COVID-19 outbreak due to sudden decreases in both business and personal travel. Hotel occupancy rates have plunged since the beginning of March. So, while receipts for FY 2021 are expected to rebound some, they are forecasted to remain well below FY 2020 levels. This tax revenue is forecasted to decrease $6.7 million from the original estimate.

Car Rental – Car rental tax income is in large part related to travel and tourism. With the decline in travel and tourism expected to continue into the fall of CY 2020, this revenue tax source has been reduced $2.0 million from the original proposed budget projections.

Recordation – Recordation taxes are received by the County on the transfer and refinancing of residential and commercial properties. With the uncertain economic environment, sale transactions, specifically large commercial properties, is expected to slow. This tax revenue is forecasted to decrease $1.8 million from the original estimate.

Other Local Taxes – The remaining tax categories (utility taxes, communication, cigarette, bank stock) are expected to remain at the original FY 2021 budget projection levels.

County Non-Tax revenues are projected to be $9.6 million lower than originally proposed. Highlights include:

• License, Permits & Fees: There are a variety of fees that deal with development relatedactivity which are expected to slow during the beginning of the fiscal year. They include,among others, right of way fees, highway permits, site plan fees, and assembly permits.

34

Memorandum Page 7 of 17

• Fines, Interest, and Leases: Fine revenues that will be impacted include parking ticketsand photo red light due to changes in traffic patterns. Interest income may see a decline dueto the reduction in interest rates resulting from the Federal Reserve lowering rates in March2020. Depending on the length of the economic recovery at the national level, a lowerinterest rate environment will result in lower interest income on cash balances invested bythe Treasurer.

• Charges for Services: A variety of Charges for Service revenues will be impacted due tothe revised service and programming offered throughout a number of County agencies. Parkand Recreation program changes, ART transportation ridership, and parking meter revenuewill all be affected through the first quarter of the fiscal year.

• State and Federal Revenue have been held steady with the expectation that moreinformation will be forthcoming from various state and federal agencies. One adjustmentwas made to Grantor’s tax revenue. This revenue is received as a percentage of real estatetransactions similar to the County’s receipt of Recordation taxes noted above.

Proposed Expense Changes in the Revised FY 2021 Proposed Budget

In order to balance declining revenues and fund critical needs, my revised budget makes expenditure adjustments in several areas as described below.

The most difficult choice was foregoing compensation increases for our workforce, but I make this recommendation in order to preserve jobs for our employees. I have not made any changes to benefit levels but will be deferring the Consumer Driven High Deductible health insurance plan until the middle of FY 2021. Preservation of jobs is the surest way, in my mind to ensure that we lessen the shocks to the economy and that we have a reliable framework in place once we escape the grip of the pandemic. I watch with dismay the furloughs in other local governments in the Commonwealth and we are fortunate that we are not yet at that point.

This revised proposed budget keeps most service levels intact.

35

Memorandum Page 8 of 17

FY 2020 Adopted

Level

FY 2021 Proposed

Level

FY 2021 New Level

$ Change - Original

Proposed to New Level

Compensation Increase n/a $16.0 million $2.7 million ($13.3 million) Delay in Opening Long Bridge & Lubber Run

- $4.2 million in new funding

$1.0 million in new funding

($3.2 million)

New or Augmentation of Existing Programs

n/a $14.7 million $7.3 million ($7.4 million)

Metro $47.6 million $49.3 million $47.8 million ($1.5 million) Debt Service $72.2 million $75.0 million $69.0 million ($6.0 million) Transfer to Capital (Ongoing)*

$6.8 million $6.8 million $3.8 million ($3.0 million)

Stabilization Reserve** $4.0 million $13.5 million $7.8 million ($5.7 million) Contingents for added services or additional loss in revenue

n/a n/a $10.2 million $10.2 million

*In addition to the reallocation of $3.0 million of FY 2021 funding for PAYG, this revised budgetalso proposes the redirection of $5.0 million of capital projects deferrals and project balanceswhere the funding was provided in multiple prior fiscal years.**Stabilization Reserve is 1.0% of the General Fund. Some funding was utilized for emergencytechnology needs after the February proposed budget. This revised budget utilizes an additional$4.0 million.

What Hasn’t Changed from the Proposed Budget

My revised budget proposal continues support in the following areas:

Compensation, Recruitment & Benefits

While I am proposing no compensation increase at this time, I am not proposing any changes to the County’s pension, health care program or other existing benefits (I am delaying the new health care option of the Consumer Driven Health Plan (CDHP)).

There are several compensation enhancements which remain in the FY 2021 revised budget. • Continued hiring for our public safety agencies: recruitment funding for Police ($129,000,

one-time) and Sheriff ($75,000, one-time)• Increase to Fire staffing (9 FTEs) to continue the implementation of Fire’s Kelly Day and a

second recruit class ($2.4 million). Continuation of this effort is extremely important sowhen we exit from these difficult times, Arlington’s Fire Service will continue to beappropriately staffed.

36

Memorandum Page 9 of 17

• Increase in dependent care subsidy ($500 to $1,000), increase to vacation leave accrual fornew/recent hires, increase in paid parental leave from 4 to 6 weeks, one-time Election Dayholiday, and an additional floating holiday.

Affordable Housing

• Housing Grants: $10.1 million total, including an $0.8 million increase, to meet theestimated increase in demand prior to COVID.

• Permanent Supportive Housing: $2.5 million, including an $0.4 million increase, to meetthe estimated increase in demand. In addition, two additional positions were added tosupport this at-risk population and the growing demand in this program ($200k). Theprogram has grown 9% since 2018 and approximately 46% over the last five years.

• Affordable Housing Investment Fund: Revised budget matches the FY 2020 level of $16.0million.

Safety Net Non-Profits: Continuing to fund the same level of support as in the proposed budget, including contractual services levels for the Residential Program Center, the Homeless Services Center and various group homes as well as other base budget contributions for organizations like Offender Aid & Restoration (OAR) and others.

Other Services and Programs: The rest of my revised budget assumes continuing the same level of day to day services as provided prior to COVID. This may be overly optimistic depending on the recovery trajectory, but it is too early to consider full-scale program and service reductions.

I did want to highlight areas where my original budget included additional funding to: 1) meet contract increases due to the results of new procurements; 2) areas where we have been experiencing an increase in demand or we were falling behind; or 3) maintaining filled staff positions that had been funded with one-time funds in prior years; and 4) prior commitments or legally mandated new programs that are underway and likely cannot be eliminated, like election funding. These include:

• Contractual cost increases: A number of base budget increases remain due to the increasedcost of procured services. One of the most significant increases in FY 2021 was due to thenew operator contract for the County’s ART bus service ($4.4 million full year impact).Other increases include rent costs for the County occupying leased space, technologysoftware increases, and other services provided to County residents and businesses.

• Service demand & County infrastructure:o Additional staffing for Transportation Engineering and Operations: $0.2 milliono Procurement: $0.1 milliono Concrete maintenance: $0.3 milliono Facilities maintenance: $0.1 million

• Maintaining filled staff positions in Cultural Affairs, Human Services, Parks & Recreation,CPHD, Technology Services and Commonwealth Attorney’s Office: $1.4 million, 13.5FTEs

• Prior commitments or legally required:

37

Memorandum Page 10 of 17

o New Mental health docket positions: $0.2 milliono One-time funds for the November election: $0.3 milliono Commitments to regional partners (e.g. NOVA Park Authority, COG)

Proposed Reductions: In February, I proposed a budget that added back targeted investments in areas that were falling behind after two years of reductions. My revised budget now proposes that $10.5 million of program adjustments be postponed: $4.8 million in new services and $5.7 million in enhancements to existing programs. The following tables outline those items.

Dept. Expense Adjustment Ongoing One-time Total AED Signature Costume Shop Management $ 70,000 $ 70,000 Clerk CCT Marriage license request portal $ 75,000 $ 75,000 CMO Innovation funding $ 200,000 $ 200,000 CPHD Historic Preservation Master Plan $ 35,000 $ 35,000

DES Pilot low cost flood sensors for 300 high risk homes $ 9,000 $ 9,000

DHS Housing Support to those aging out of foster care $ 251,736 $ 251,736 DHS Case Manager for Housing Support for foster care $ 91,923 $ 91,923 DPR & DES Lubber Run Community Center* $ 1,141,000 $ 180,000 $ 1,321,000 DPR Long Bridge Aquatics and Fitness Center** $ 1,600,000 $ 285,000 $ 1,885,000 DPR Community Engagement Position $ 100,000 $ 100,000 LIB Courthouse Library staffing & materials $ 75,000 $ 75,000 POL Traffic Control Officers $ 453,992 $ 104,012 $ 558,004

Non-DGARE equity training($25,000 remains)

$ 75,000 $ 75,000

Non-D Northern VA Economic Development Consortium $ 75,000 $ 75,000 $ 3,838,651 $ 983,012 $ 4,821,663

Postponed Program Adjustments: New Programs

* Note: $0.3 million of new funding remains in the revised budget for Lubber Run Community Center to cover basic building maintenance and to fund the maintenance of the outdoor park.

**Note: Elimination of funding for Long Bridge Aquatics & Fitness Center does not result in net tax support savings, as these operations were offset by program revenue and Boeing grant funding. $0.7 million of new funding remains in the revised budget for the General Manager & Maintenance Tech positions for facility management, minimal cleaning and utilities, pool chemicals, and outdoor park maintenance

38

Memorandum Page 11 of 17

Dept. Expense Adjustment Ongoing One-time Total Remaining Services AED Lee Highway Alliance $ 25,500 $ 25,500 Base budget of $60,500 included in revised budget AED Clarendon Alliance $ 15,000 $ 10,000 $ 25,000 Base budget of $80,000 included in revised budget AED Columbia Pike Revitalization $ 60,000 $ 60,000 Base budget of $350,000 included in revised budget

AED Arts Grants $ 30,000 $ 30,000 Arts Grants funding will remain at the base budget level of approximately $215,810.

CBO Audit consulting funds $ 60,000 $ 60,000 The Board Auditor base budget of $235,000 remains funded.

CBO Salary increase $ 58,480 $ 58,480 Salaries remain flat, consistent with staff compensation

Clerk CCT

Court Clerk $ 68,000 $ 68,000 The Court will continue to operate with four Court Clerks.

CPHD Housing Arlington $ 248,750 $ 248,750

CPHD Principle Planner, Housing $ 147,000 $ 147,000

CPHD Principle Planner $ 147,000 $ 147,000 Comprehensive Planning staffing will only increase by 0.5 FTE, which fully funds an existing position.

DES Facilities Planner/Architect $ 81,254 $ 81,254 DES Facilities Planning base budget remains at the FY 2020 Adopted level.

DESWater/Sewer/Streets Training Specialist

$ 28,020 $ 28,020 Admin and training work for the Water/Sewer/Streets Bureau will continue to be supported centrally within DES.

DES Streetlight Support $ 111,643 $ 23,000 $ 134,643 Major repairs remain at 45 days instead of improving to 30 days, and minor repairs remain at 14 days instead of improving to 7 days.

DMFCommercial Real Estate Appraiser

$ 103,846 $ 103,846 Existing Commercial Real Estate Appraisal team (4.0 FTEs) remains unchanged.

DMF Internal Audit $ 50,000 $ 50,000 Revised proposal retains 1.5 FTEs and consulting support.

DPRRestructure Roving Monitor Program

$ 70,000 $ 70,000 Roving monitor program will be restructured by reallocating existing budget

DPR Additional Urban Forester $ 135,000 $ 53,000 $ 188,000 Urban Forestry team remains at 3.0 FTEs. DPR Tree Maintenance (pruning) $ 200,000 $ 200,000

DPRDisease/Pest Maintenance for trees

$ 50,000 $ 50,000

DPR Temp Employee Conversion $ 596,875 $ 596,875 Existing staff will remain temporary employees.

HRD Business Partner $ 121,366 $ 121,366

Human Resources and the departments impacted will continue handling human resources issues although less optimally than would be possible with this additional resource.

HRD Class & Compensation position $ 140,000 $ 140,000

With the pause in classification studies, Classification & Compensation will continue studying positions although they will not be completed as quickly without this additional resource.

LIB Collections materials $ 100,000 $ 100,000 Libraries collection budget increases from $1.5 million in FY 20 adopted budget to $1.6 million in revised proposal (instead of $1.7 million).

Non-D AHIF $ 2,700,000 $ 2,700,000 AHIF funding remains at the FY 20 Adopted Budget level of $16.0 million.

Non-DProbation & Parole: increase supplement to 15%

$ 97,225 $ 97,225 Supplement for Probation and Parole remains at 7.5%.

Non-D Transfer to Capital $ 119,795 $ 119,795 In addition to this reduction in PAYG funding, the base is reduced by an additional $3 million resulting in total FY 21 funding of $3.8 million.

$ 2,196,209 $ 3,454,545 $ 5,650,754

TOTAL EXPENSE ADJUSTMENT $ 6,034,860 $ 4,437,557 $ 10,472,417

Tree pruning cycle remains unchanged at 17 years instead of improving to 10 years.

The Housing Arlington staff budget remains unchanged from the FY 2020 Adopted budget.

Postponed Program Adjustments: Enhancements of Existing Programs

39

Memorandum Page 12 of 17

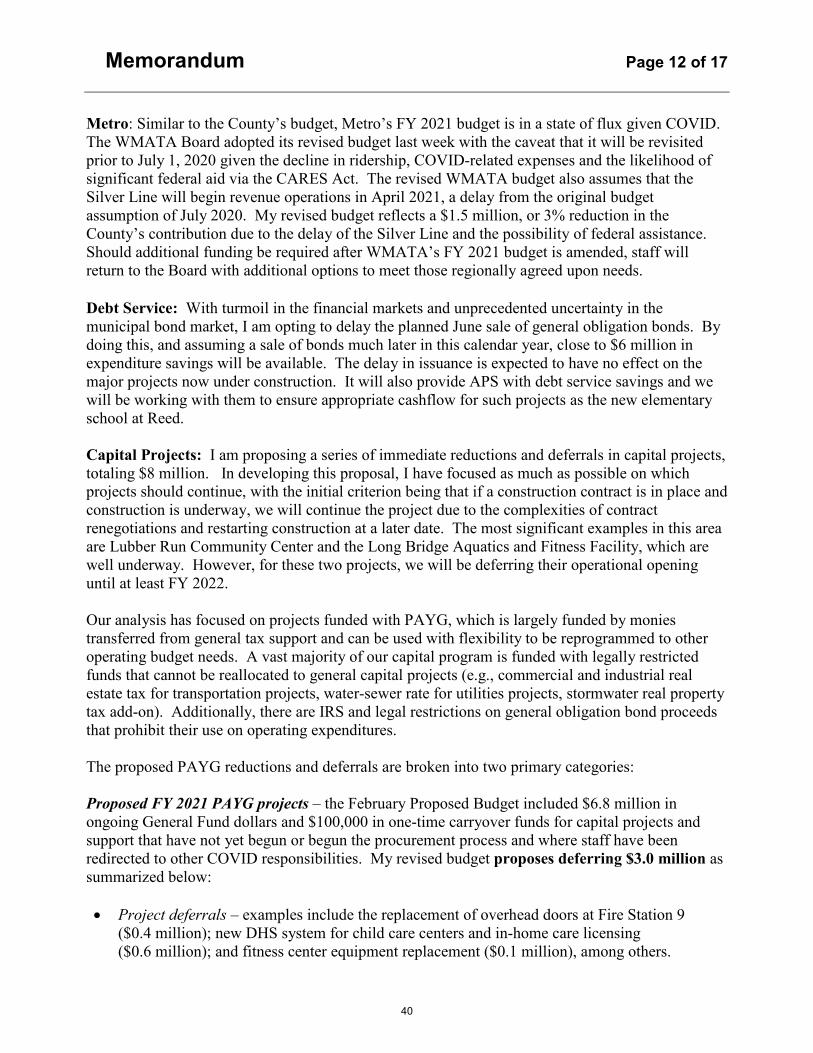

Metro: Similar to the County’s budget, Metro’s FY 2021 budget is in a state of flux given COVID. The WMATA Board adopted its revised budget last week with the caveat that it will be revisited prior to July 1, 2020 given the decline in ridership, COVID-related expenses and the likelihood of significant federal aid via the CARES Act. The revised WMATA budget also assumes that the Silver Line will begin revenue operations in April 2021, a delay from the original budget assumption of July 2020. My revised budget reflects a $1.5 million, or 3% reduction in the County’s contribution due to the delay of the Silver Line and the possibility of federal assistance. Should additional funding be required after WMATA’s FY 2021 budget is amended, staff will return to the Board with additional options to meet those regionally agreed upon needs.

Debt Service: With turmoil in the financial markets and unprecedented uncertainty in the municipal bond market, I am opting to delay the planned June sale of general obligation bonds. By doing this, and assuming a sale of bonds much later in this calendar year, close to $6 million in expenditure savings will be available. The delay in issuance is expected to have no effect on the major projects now under construction. It will also provide APS with debt service savings and we will be working with them to ensure appropriate cashflow for such projects as the new elementary school at Reed.

Capital Projects: I am proposing a series of immediate reductions and deferrals in capital projects, totaling $8 million. In developing this proposal, I have focused as much as possible on which projects should continue, with the initial criterion being that if a construction contract is in place and construction is underway, we will continue the project due to the complexities of contract renegotiations and restarting construction at a later date. The most significant examples in this area are Lubber Run Community Center and the Long Bridge Aquatics and Fitness Facility, which are well underway. However, for these two projects, we will be deferring their operational opening until at least FY 2022.

Our analysis has focused on projects funded with PAYG, which is largely funded by monies transferred from general tax support and can be used with flexibility to be reprogrammed to other operating budget needs. A vast majority of our capital program is funded with legally restricted funds that cannot be reallocated to general capital projects (e.g., commercial and industrial real estate tax for transportation projects, water-sewer rate for utilities projects, stormwater real property tax add-on). Additionally, there are IRS and legal restrictions on general obligation bond proceeds that prohibit their use on operating expenditures.

The proposed PAYG reductions and deferrals are broken into two primary categories:

Proposed FY 2021 PAYG projects – the February Proposed Budget included $6.8 million in ongoing General Fund dollars and $100,000 in one-time carryover funds for capital projects and support that have not yet begun or begun the procurement process and where staff have been redirected to other COVID responsibilities. My revised budget proposes deferring $3.0 million as summarized below: