Adex BenchmArk 2012 - IAB France

52

ADEX BENCHMARK 2012 EUROPEAN ONLINE ADVERTISING EXPENDITURE Published 28th August 2013

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Adex BenchmArk 2012 - IAB France

Adex BenchmArk

2012EUROPEAN ONLINE

ADVERTISING EXPENDITURE

Published 28th August 2013

IAB Europe AdEx Benchmark 20122

CONTENTS3 Introduction

4 About this report

5 Executive summary

Section 1 – AdEx Benchmark 2012 analysis

6 Online advertising growth over time

8 Online advertising in a macroeconomic context

10 26 markets in perspective

10 Volume

12 Growth

14 Share of total media

16 Ad spend per capita

18 Share of formats

Section 2 – Online advertising overview by sector

19 Display

22 Classifieds & Directories

25 Search

28 Mobile

30 Video

32 Video & Mobile

Section 3 – Overview by country

33 Top 10

35 Rest of Europe

Section 4 – Background market data

37 Top properties December 2012

42 Internet penetration in Europe 2012

Section 5 – Appendices

43 Appendix i: Definition of formats

44 Appendix ii: Participating IABs

45 Appendix iii: Methodology and adjusted data

45 Appendix iv: Adjustments by country

Section 6 – About us

49 Our research partners

50 About IAB Europe

51 And finally

© IAB Europe 3

IAB Europe in collaboration with IHS is pleased to publish the

7th edition of the AdEx Benchmark report, the definitive guide to

online advertising spend across Europe and reference point for

understanding the state and potential of the online advertising

market. This year’s report reveals that 2012 has been a

remarkable year for online which earned the best performer spot

in the advertising market, with an overall growth of 11.5 per cent.

In spite of macroeconomic volatility and high unemployment rates

in Europe, this strong upward trend continues with one in four

advertising Euros now being allocated to online.

The AdEx Benchmark report splits the online ad market into

three top level segments: Display, Classifieds and Directories and

Search. In 2012, the Display Ad market experienced a like-for-

like growth of 8.9 per cent giving it a total value of €7.9 billion,

mainly driven by mobile and online video. Spend on Classifieds

and Directories were underpinned by strong redistribution from

print to online and valued at €4.5 billion. While Search experienced

the strongest like-for-like growth of 15.5 per cent with a market

value of €11.9 billion.

Mobile display advertising continued an impressive surge growing

78.3 per cent to nearly €392m in total value – now accounting for

5 per cent of all online display spend in Europe. Meanwhile, online

video advertising has increasingly acted as a major draw for brand

advertisers, grabbing double-digit portion of display advertising

for the first time, with a share of 12.9 per cent. This is the first

time in Europe that online video has grabbed double-digit share of

display advertising.

The importance of neighbouring markets has also become more

obvious this year with Turkey, Russia and Slovakia registering the

biggest individual market growth (Slovakia 36.3 per cent, Russia

34.0 per cent, and Turkey 30.4 per cent). Russia also moved up a

notch to 4th position in the top ten largest online market rankings

falling behind the UK, Germany and France.

Since it was first published in 2006 the AdEx Benchmark report

has become a valuable tool for people seeking to navigate the

evolution of the online advertising sector. It is also extremely

relevant for companies seeking to make effective advertising

investment decisions, accurately access market opportunities

and maximise market potential.

IAB Europe remains committed to building its collaboration with

IHS and to delivering broader and deeper analysis in the years to

come. Next year in response to demand, we will extend our AdEx

reports to offer further data and analysis on a commercial basis.

INTrOduCTION

Digital advertising again shows its resilience in a year

of instability for the wider ad market. Whilst individual

markets have shown varying growth levels reflecting

economic pressures, the overall double-digit increase

confirms the sector’s ability to thrive on innovation, crea-

tivity and technology. Our contribution of over €24 billion

to the European economy grows ever more significant

and worthy of protection and development.

Constantine Kamaras, Vice-Chairman, 24 Media Group

Kimon Zorbas, CEO, IAB Europe

IAB Europe AdEx Benchmark 20124

ABOuT ThIS rEpOrT

The sources of the online advertising spend data contained within

this report are the annual industry benchmarking studies run by

each national Interactive Advertising Bureau (IAB) in Europe. The

national benchmarking studies represent the income of thousands

of websites and online advertising businesses.

The reported results are considered the closest measurement on

online advertising revenues across Europe as the data is compiled

directly by local IABs based on information supplied by companies

selling advertising online in each country. This year the AdEx

Benchmark covered 26 local IABs, double the amount since its

inception in 2006.

The data for this report is stated on the basis of actual gross

income (the amount of actual spend invoiced by the publisher

including any agency commission). To avoid any double-counting,

production costs and pan-regional ad spend are taken out of the

figures provided by the local IABs.

The report incorporated data from the following online

advertising formats:

• Display

• Classifieds&Directories

• Search

In 2012, the IAB Europe Research Committee in conjunction with

IHS held working groups to standardise and improve definitions

and measurement across markets for emerging formats. For the

first time, the AdEx Benchmark has systematically and consistently

incorporated data for spend on:

• Onlinevideoadvertisingdefinedasin-streamvideo

advertising (pre-rolls, mid-rolls, post-rolls) as agreed by the

IAB Europe AdEx Benchmark Video Working Group

• MobiledisplayadvertisingasagreedbytheIABEuropeAdEx

Benchmark Mobile Working Group

IAB Europe in partnership with IHS collates and aggregates the

data and makes the adjustments necessary to enable the data to

be comparable. Full details of this process for each country are

provided in Appendix iv.

The result is comparable data based on actual revenues from

across Europe. This is the seventh edition of the report and

therefore once again we are able to include year-on-year

comparisons for those countries that have provided data for at

least two years.

IHS does not audit the information or the data from local IABs and

provides no opinion or other form of assurance with respect to the

information. Only aggregate results are published and individual

company information is held in strict confidence by the audit

partners of local IAB studies.

2012: 26 countries

2008: 19 countries

2006: 13 countries

© IAB Europe 5

On an aggregate level across the 26 countries studied, Search

outperformed the other formats with a year-on-year increase in

spend of 15.5 per cent. It also is the largest single format in terms

of spend. Generating spend of €11.9 billion, it accounted for

48.8 per cent of all online advertising spend in 2012. As a purely

performance-driven format, Search has proven to be relatively

resilient to the weakening economy in Europe.

Display grew by 8.9 per cent year-on-year, underperforming

overall online advertising growth. In terms of spend, it generated

€7.9 billion, or 32.4 per cent of European online ad spend.

Display growth was fuelled by a burgeoning online video and

mobile advertising market. However, it was also held back by the

commoditisation of banner display advertising inventory, especially

in the long-tail, as well as exposure to economic headwinds which

cause brand advertising budgets to suffer.

The growth in both Search and Display spend slowed down in 2012

compared to the growth in 2011. For Classifieds and Directories,

the story is different. Although growth also underperformed

the overall rate of 11.5 per cent, the pace of growth picked up

nevertheless. Whereas spend on Classifieds and Directories grew

by 5.7 per cent in 2011, growth accelerated to 6.3 per cent in

2012. Growth came from the Classifieds component in particular,

outperforming Directories. Recent years have seen ongoing

consolidation in the online Classifieds markets, both on a national

and a pan-European level. This consolidation, driven by large print

publishers, was a key contributor to 2012 market growth.

The European online advertising market recorded spend of €24.3

billion in 2012. This is a year-on-year increase of 11.5 per cent

from €21.9 billion in 2011. In 2012, online advertising accounted

for 25.6 per cent of all advertising spend, surpassing newspapers

to become the second biggest media category in Europe after TV.

The 2012 double-digit growth took place despite weak

macroeconomic stimulus. Flat or declining GDP in most markets

had an adverse effect on the advertising market and most

traditional media suffered. Across Europe, total media advertising

revenue fell by 2.7 per cent, according to IHS estimates.

The 11.5 per cent growth for European online advertising is derived

from aggregated revenues across all 26 countries represented in

this study. Individual growth rates varied across countries. Eleven

markets grew above the European 11.5 per cent. Seven of these

markets were from Central and Eastern Europe (CEE). Russia,

Slovakia and Turkey grew fastest with rates above 30.0 per cent.

The fast-growing CEE markets are emerging markets with low

ad spend per capita and a low online share of advertising in a

European context. Yet, above-average growth also came from

some of the most mature online advertising markets in Europe

with high ad spend per capita. Online advertising spend grew by

12.5 per cent year-on-year in Denmark, by 13.3 per cent in the UK

and by 20.0 per cent in Sweden.

The variance in growth is not only reflected in different national

trends, it also varied across formats. This study tracks online

ad spend across Display (including video and mobile), Search

(including mobile) and Classifieds and Directories.

0

5

10

15

20

25

20122011

€bn

€21.9bn11.5%

€24.3bn

Online grows 11.5% in 2012

ExECuTIvE SummAry

European online advertising: year-on-year growth (%)

0

5

10

15

2040.0%

15.5%

%

Paid-for-search

2012

Display Classifieds &Directories

Total

8.9%

15.4%

6.3%5.7%

11.5%

14.5%

17.9%

2011

1. Year-on-year growth is calculated excluding the ‘Other’ category to maintain comparability across countries. The growth reported is also like-for-like and hence excludes online ad formats and market entrants newly introduced in 2012.

2. At constant 2012 exchange rates.

IAB Europe AdEx Benchmark 2012

Section 1 - AdEx Benchmark 2012 Analysis

6

Online advertising growth over time

Since IAB Europe began documenting the size of the European online advertising market in 2006, spend has grown every year. In 2006,

the value at the market stood at €9.4 billion, versus €24.3 billion in 2012. This is an increase in spend of €14.9 billion and translates into a

2012 GrOwTh IN CONTExT

Online ad spend in Europe over time (€bn)

0

5

10

15

20

25

30

2012201120102009200820072006

compound annual growth rate of 17.2 per cent, or €2.5 billion per annum. Growth rates, drivers and inhibitors varied between 2006 and

2012.

In 2007, spend was up 40 per cent year-on-year. Principal drivers were France, Germany and the UK as some of the earliest adopter

markets of online advertising and three largest overall advertising markets in Europe.

In 2008, the three biggest European markets matured and their growth clustered around the 20 per cent mark. The main impetus now

came from emerging markets in Poland and Slovenia. Yet, their absolute market size stood behind those of the big three and the European

effect of Polish and Slovenian developments were more modest in consequence.

2009 market conditions were characterised by the global economic recession. All media were affected, including online. Yet, 2009 also

demonstrated that online advertising was more resilient against economic volatility. Whereas all other media were flat or down, online ad-

vertising achieved 4.5 per cent growth across Europe. Some emerging markets saw drops in online advertising as the sector was still small

and underdeveloped. Advertisers chose to relocate budgets to traditional media channels which at that time were more tried and tested.

Search in particular stood out in 2009, growing by 10.8 per cent as advertisers were reassured by the return-on-investment provided by

search’s direct response pricing model.

7© IAB Europe

Section 1 - AdEx Benchmark 2012 Analysis

2012 GrOwTh IN CONTExT

Online advertising growth over time

0

5

10

15

20

25

30

35

40

201220112010200920082007

%

40.0%

20.2%

15.3% 14.5%

4.5%

11.5%

Europe’s online advertising market rebounded from the 2009 slump a year later. In 2010, growth was back at double-digit (15.3 per cent).

Display led this surge with growth of 21.3 per cent. Innovations in targeting, format standardisation, and the proliferation of online video

advertising increased confidence in the display format and triggered new spend from brand advertisers, especially the fast-moving con-

sumer goods sector.

Online advertising spend maintained double-digit growth in 2011, increasing by 14.5 per cent year-on-year. Display (+15.3 per cent) and

Search (+17.9 per cent) performed similarly.

Economically, 2012 was the toughest advertising year since 2009. Many European economies suffered both GDP and advertising spend

declines. In contrast, online advertising experienced double-digit growth for the third year in a row, up 11.5 per cent. This was primarily

helped by advertiser confidence in the performance-based nature of search, the brand-friendly online video format, as well as the increased

scalability of mobile advertising.

Online advertising in a macroeconomic context

Advertising markets are in general very susceptible to changes in the macroeconomic environment. 2012 has been a tough year for

European economies, and the Eurozone in particular. After the 2008 and 2009 recession, Eurozone GDP showed eight quarters of year-on-

year growth. Yet, after a Q1 2011 peak, growth rates have slowed down. Since Q1 2012, Eurozone GDP has been on a decline throughout

2012. In the context of the European sovereign debt crisis, high unemployment and cutbacks in consumer spending, advertising markets

suffered in 2012.

Total advertising across all media declined -0.4 per cent in Europe1 last year, but would have experienced a steeper fall at -4.0 per cent

without the contribution of online. In Western Europe, total advertising excluding online would have declined by -5.2 per cent but with

the 9.1 per cent surge in online ad markets, the region ended the year with a drop of -1.8 per cent. Online also lifted CEE markets from

what would have been a mere 2.9 per cent growth in ad markets excluding online to a 7.2 per cent total media advertising growth rate

year-on-year.

IAB Europe AdEx Benchmark 2011

Section 1 - AdEx Benchmark 2012 Analysis

8

2012 GrOwTh IN CONTExT

1 Europe entails only the 26 countries participating in the study

Real GDP growth in Europe (%)

-8

-6

-4

-2

0

2

4

6

2013

Q4

2013

Q3

2013

Q2

2013

Q1

2012

Q4

2012

Q3

2012

Q2

2012

Q1

2011

Q4

2011

Q3

2011

Q2

2011

Q1

2010

Q4

2010

Q3

2010

Q2

2010

Q1

2009

Q4

2009

Q3

2009

Q2

2009

Q1

2008

Q4

2008

Q3

2008

Q2

2008

Q1

2007

Q4

2007

Q3

2007

Q2

2007

Q1

2006

Q4

2006

Q3

2006

Q2

2006

Q1

2005

Q4

2005

Q3

2005

Q2

2005

Q1

2004

Q4

2004

Q3

2004

Q2

2004

Q1

Germany GDP Growth Italy GDP GrowthFrance GDP GrowthEurozone GDP Growth

9© IAB Europe

Section 1 - AdEx Benchmark 2012 Analysis

2012: economic & advertising growth (%)

-10

-5

0

5

10

15

20

25

30

Total EuropeCEEWE

%

0.2%

-5.2%

-1.8%

2.9%

7.2%

26.6%

9.1%

0.4%

-4.0%

11.5%

-0.4%

2.0%

Real GDPReal GDP All media advertisingexcl. online

Online advertising All media advertising

2012 GrOwTh IN CONTExT

Online advertising has been more resilient against macroeconomic turmoil than other media. This is due to a number of factors:

• Performance-based models of online advertising. Search advertising in particular has a clearly measureable return-on-

investment in form of the cost-per-click metric on which it is priced. Search spend usually comes from direct marketing budgets,

which focus on sales-driven advertising. This type of advertising is used especially when consumer budgets are tight. Search

prices, measured in cost-per-click, have been falling in 2012. However, this could be compensated by a growth in volume of search

advertising. This volume growth in 2012 mainly came from small and medium-sized business upping their search investments.

The rise of real-time-bidding trading mechanisms also improves the return-on-investment for performance-based online display

campaigns.

• The move of brand advertising spend online. Video advertising and premium display (e.g. large-scale banners) in particular are

increasingly attracting brand advertisers to online. Video advertising resembles TV advertising in terms of creative format, campaign

objectives and measurement metrics. European video advertising spend grew by 50.7 per cent in 2012 and is now 12.9 per cent of

all online display advertising spend.

• The use of data-driven targeting and automation. The increased use of demographic, behavioural and other types of consumer

data in online display advertising, paired with algorithmic processing, allows for more accurate and cost-efficient targeting.

IAB Europe AdEx Benchmark 2012

Section 1 - AdEx Benchmark 2012 Analysis

10

26 mArKETS IN pErSpECTIvE

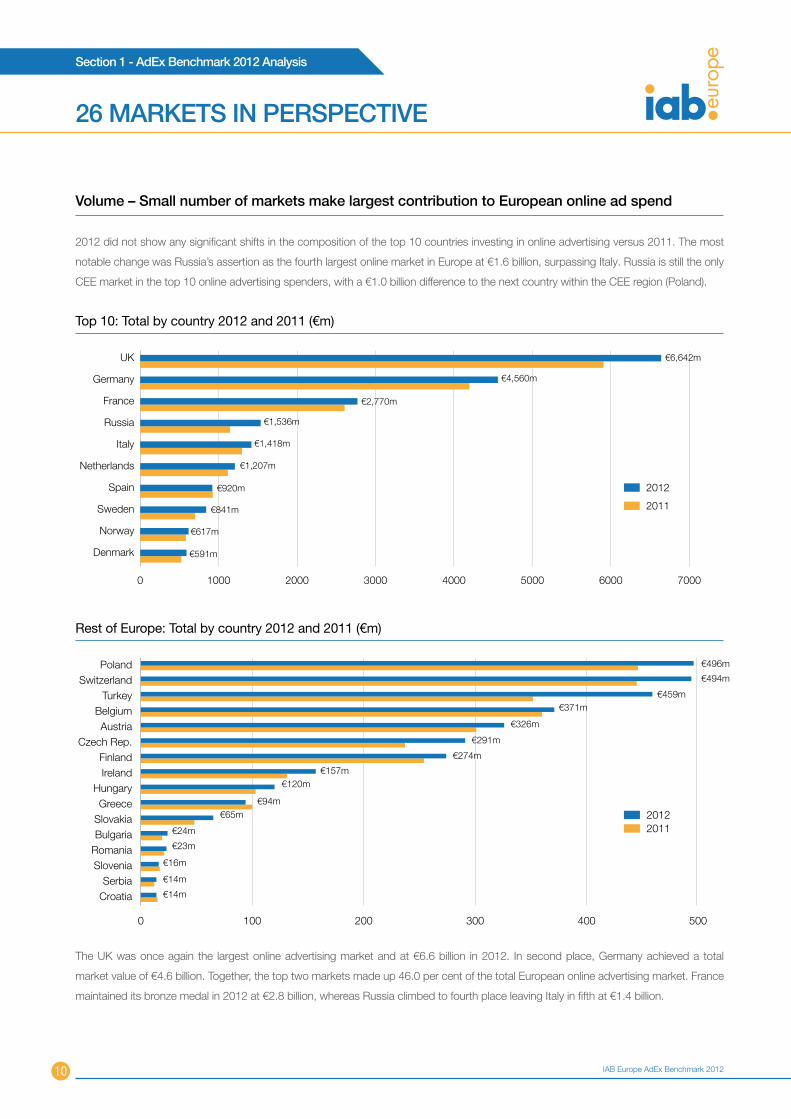

volume – Small number of markets make largest contribution to European online ad spend

2012 did not show any significant shifts in the composition of the top 10 countries investing in online advertising versus 2011. The most

notable change was Russia’s assertion as the fourth largest online market in Europe at €1.6 billion, surpassing Italy. Russia is still the only

CEE market in the top 10 online advertising spenders, with a €1.0 billion difference to the next country within the CEE region (Poland).

The UK was once again the largest online advertising market and at €6.6 billion in 2012. In second place, Germany achieved a total

market value of €4.6 billion. Together, the top two markets made up 46.0 per cent of the total European online advertising market. France

maintained its bronze medal in 2012 at €2.8 billion, whereas Russia climbed to fourth place leaving Italy in fifth at €1.4 billion.

Top 10: Total by country 2012 and 2011 (€m)

0 1000 2000 3000 4000 5000 6000 7000

Denmark

Norway

Sweden

Spain

Netherlands

Italy

Russia

France

Germany

UK

2012

2011

€6,642m

€4,560m

€2,770m

€1,418m

€1,536m

€1,207m

€920m

€841m

€617m

€591m

Rest of Europe: Total by country 2012 and 2011 (€m)

0 100 200 300 400 500

CroatiaSerbia

SloveniaRomaniaBulgariaSlovakiaGreece

HungaryIrelandFinland

Czech Rep.Austria

BelgiumTurkey

SwitzerlandPoland

20112012

€496m

€494m

€459m€371m

€326m

€291m

€274m

€157m€120m

€94m€65m

€24m

€23m

€16m

€14m

€14m

11© IAB Europe

Section 1 - AdEx Benchmark 2012 Analysis

26 mArKETS IN pErSpECTIvE

Share of European online ad revenue by market

0

20

40

60

80

100

Top 15Top 10Top 7Top 5Top 2

Source: IAB Europe/IHS Screen Digest

46.0%

69.5%

78.3%

86.7%

95.5%

The remaining countries of the European top 10 maintained their position in the ranking, with Italy followed by the Netherlands, Spain,

Sweden, Norway and Denmark. Similarly to 2011, it is still a small number of markets making the largest contribution. The top five markets

accounted for 69.5 per cent of all online ad revenue in Europe and the top 10 are responsible for 86.7 per cent of all online advertising in

Europe.

IAB Europe AdEx Benchmark 2012

Section 1 - AdEx Benchmark 2012 Analysis

12

26 mArKETS IN pErSpECTIvE

Growth: double-digit increase in emerging economies and mature online ad markets show the sustainability of the online medium

In 2012, CEE markets led growth with seven countries outpacing the European average of 11.5 per cent. Czech Republic and Bulgaria

experienced strong growth over 20 per cent and the online ad markets of Turkey, Slovakia and Russia rose above 30 per cent. This was

due to the fast expanding Search business in the CEE region, which grew 38.7 per cent year-on-year, but also to a strongly evolving Display

business, which saw a strong increase of 16.7 per cent from 2011 to 2012. As more households become connected in the region, the

addressable audience continues to increase, providing opportunity for further investment in the online medium by advertisers.

Year-on-year growth in 2012 (%)

-10

-5

0

5

10

15

20

25

30

35

40

36.3

%

34.0

%

30.4

%

23.2

%

22.8

%

20.0

%

16.9

%

16.5

%

13.3

%

12.5

%

12.3

%

11.5

%

11.1

%

11.1

%

9.2%

8.6%

-6.2

%

-4.6

%

-4.4

%

-0.6

%3.0%

5.8%6.3%8.

1%

8.1%8.5%9.

2%

Greece

Croati

a

Sloven

ia

Spain

Belgium

Norway

Fran

ce

Netherl

ands

Finlan

d

Austria

German

y

Roman

iaIta

ly

Poland

Switzerl

and

Total

Euro

pe

Irelan

d

DenmarkUK

Hunga

ry

Serbia

Sweden

Czech

Rep

ublic

Bulgari

a

Turke

y

Russia

Slovak

ia

In addition to the CEE markets, strong growth also came from the most mature markets in Europe. The UK, Sweden and Denmark

increased above the European average in 2012 experiencing a double-digit increase, despite being in the top five most mature markets

in Europe (as measured by online ad spend per capita). The relationship between ad growth and ad spend per capita is illustrated in the

bubble chart with emerging markets on the left of the graph and mature markets on the right. The size of the bubbles corresponds to the

size of the online ad market. Strong growth is observed on both sides of the growth demonstrating the sustainability and the continued

advertiser confidence in online as an advertising medium.

13© IAB Europe

Section 1 - AdEx Benchmark 2012 Analysis

26 mArKETS IN pErSpECTIvE

Benchmark: growth and maturity of online ad markets in Europe

UK

Turkey

Switzerland

Sweden

Slovenia

Serbia

Russia

Romania

Poland

Norway

Netherlands

Italy

Ireland

Hungary

Greece

Germany

France

Finland

Denmark

Czech Republic

Bulgaria

Austria

Spain

Croatia

20 40 60 80 100 120

-10

-5

0

5

10

15

20

25

30

35

40

Online ad spend per capita (€)

Onl

ine

ad g

row

th (%

)

Belgium

IAB Europe AdEx Benchmark 2012

Section 1 - AdEx Benchmark 2012 Analysis

14

Europe: online market share of total media ad spend

0

5

10

15

20

25

30

201220092006

%

Source: IAB Europe/IHS

10.3%

19.0%

25.6%

26 mArKETS IN pErSpECTIvE

Share of Total media: Online becomes second biggest media category in Europe

Pairing online advertising data provided in this report with IHS valuations for all other media (television, print, cinema, radio, and out-of-

home) reveals substantial variations in the online advertising market share across Europe.

Higher market share indicates a more developed market, where the majority of advertisers invest in online in some way, and where

advertisers have a wide variety of formats and online channels from which to choose. Low market share for online advertising suggests

that a market has headroom for growth, as it indicates that there are still plenty of advertisers in the market who have not yet devoted

themselves to the online medium.

Since the inception of the Adex Benchmark in 2006, online has more than doubled its share of all media revenue. From 10.3 per cent in

2006, online market share of total advertising spend in Europe reached 25.6 per cent in 2012.

The consistent growth of online during an adverse economic environment and a declining or flat traditional media market placed online in

second place in terms of ad spend in 2012. For the first time, online overtook newspapers at €24.3 billion trailing only behind TV.

15© IAB Europe

Section 1 - AdEx Benchmark 2012 Analysis

2012: European advertising market share by medium (€bn)

0 5 10 15 20 25 30

Cinema

Radio

OOH

Magazines

Newspapers

Online

TV

€0.6bn

€4.6bn

€8.7bn

€19.3bn

€24.3bn

€28.1bn

€6.3bn

Source: IAB Europe/IHS

Market shares calculated from IAB Europe and IHS data may vary from those published in the local markets by the national IABs. That is

because the national IABs have used a source other than IHS for the valuation of the total advertising market in that country.

26 mArKETS IN pErSpECTIvE

IAB Europe AdEx Benchmark 2011

Section 1 - AdEx Benchmark 2012 Analysis

16

Online ad spend per capita in 2012 (€)

0

20

40

60

80

100

120

Onl

ine

ad s

pend

/cap

ita (€

)

Roman

ia

Serbia

Bulgari

a

Turke

y

Croati

a

Russia

Slovak

ia

Greece

Hunga

ry

Poland

Sloven

iaSpa

inIta

ly

Czech

Rep

Irelan

d

Europe

an A

vg

Belgium

Austria

Fran

ce

Finlan

d

German

y

Switzerl

and

Netherl

ands

SwedenUK

Denmark

Norway

€117

.4

€93.

8

€93.

4

€73.

9

€66.

8

€55.

6

€51.

3

€47.

0

€41.

0

€35.

5

€33.

4

€30.

1

€28.

7

€22.

5

€21.

3

€19.

6

€11.

6

€10.

3

€8.9

€8.8

€8.1

€8.0

€4.7

€3.4

€2.6

€1.7

€1.0

Ad spend per capita: online shows linear growth trajectory

Using IHS population numbers, ad markets exhibit variation in online spend per capita across the region.

Online ad spend per capita is a metric that helps to evaluate the maturity and scope for development of a market. It shows how much an

online consumer is worth in terms of advertising in a given market. By use of population data, online ad spend per capita uses a normalised

basis and is therefore well-suited to compare and benchmark online advertising markets. It highlights the maturity of an online market

irrespective of its size or absolute revenues incurred.

The most mature online markets in Europe in 2012 continue to be the Scandinavian countries, the UK and the Netherlands. Norway led

at €117.4 per capita indicating the advanced development of the online medium as an advertising vehicle. Mature online markets typically

see single-digit growth rates year-on-year and are more susceptible to macroeconomic fluctuations. This is reflective in the 2012 online ad

markets in Norway and the Netherlands, which grew 5.8 and 8.1 per cent year-on-year, respectively.

The remaining top five most mature markets in Europe (the UK, Denmark and Sweden), in contrast to Norway and the Netherlands

experienced double-digit growth in 2012, above the European average. This demonstrates the sustainability of online advertising, which

continues to attract more spend and new advertisers.

26 mArKETS IN pErSpECTIvE

Monetisation lags behind in the CEE region, with online ad spend per capita ranging from €1.0 in Romania to €22.5 in the Czech Republic.

The average online ad spend per capita in Europe in 2012 was €30.1, below which value we find the high growth markets of Russia, Turkey

and Slovakia.

17© IAB Europe

Section 1 - AdEx Benchmark 2012 Analysis

Ad spend per capita by medium: Europe (€)

0

20

40

60

80

100

120

140

2012201120102009200820072006

Source: IHS based on IAB Europe data

40.0%

Online TV

Ad

spen

d/ca

pita

(€)

Total Media

Print and Online ad spend per capita: Europe

0

10

20

30

40

50

60

70

2012201120102009200820072006

40.0%

Online Print

Ad

spen

d/ca

pita

(€)

Source: IHS based on IAB Europe data

26 mArKETS IN pErSpECTIvE

In order to deepen understanding of the maturity of the online medium, it is important to place this metric in context of other media. Over

time in Europe, TV is resilient in its ad spend per capita, total media is volatile contingent on economic conditions and online shows a linear

growth trajectory. This points to an improved monetisation of online audiences over time.

In contrast, print advertising per capita has been consistently declining since 2006 from €57.2 to €38.9 in 2012, as online grew from just

over €10.0 in 2006 to €30.1 in 2012. Although it is erroneous to assume that online is absorbing all of print ad spend, budgets are migrating

from one medium to the other.

IAB Europe AdEx Benchmark 2012

Section 1 - AdEx Benchmark 2012 Analysis

18

ShArE OF FOrmATS

In 2012, in terms of composition of ad revenue, Search remained

the largest segment of online advertising. The performance-based

format increased its share of online advertising from 47.1 per

cent in 2011 to 48.8 per cent in 2012. Display was fairly stable,

decreasing 0.7 per cent from 33.1 per cent in 2011 to 32.4 per

cent in 2012. The small decline is due to the outperformance of

Search, which grew 15.5 per cent in 2012, compared to Display’s

8.9 per cent increase. Classifieds and Directories also decreased

its share of online ad spend at 18.5 per cent, from 19.3 per cent

in the previous year.

In Western Europe, the split is very similar to that of total Europe.

Search dominated online ad spend at 48.4 per cent, followed

by Display at 30.9 per cent and Classifieds & Directories at

20.3 per cent.

The CEE region appears to have a much stronger Search market

at 51.8 per cent of all online ad spend, with Display trailing at

42.6 per cent and Classifieds and Directories at 5.5 per cent. This

is however largely skewed by the strong Russian search market.

When excluding Russia, Search makes up only 37.7 per cent of

total online ad spend in CEE, with Display as the leading format

at 51.0 per cent.

Share of formats : Europe

Western Europe: Share of formats 2012

0102030405060708090

100

20122011Other

%

Classifieds & DirectoriesSearchDisplay

19.3%

33.1%

47.1%

18.5%

32.4%

48.8%

0.5% 0.3%

Display

SearchClassifieds & DirectoriesOther

Western Europe: share of formats in 2012 CEE: share of formats in 2012 CEE excl Russia: share of formats in 2012

42.6%

5.5%

51.8% 51.0%

11.1%

37.7%

30.9%

20.3%

48.4%

Display

SearchClassifieds & DirectoriesOther

Display

SearchClassifieds & DirectoriesOther

CEE excl. Russia: Share of formats 2012

CEE: Share of formats 2012

Display

SearchClassifieds & DirectoriesOther

Western Europe: share of formats in 2012 CEE: share of formats in 2012 CEE excl Russia: share of formats in 2012

42.6%

5.5%

51.8% 51.0%

11.1%

37.7%

30.9%

20.3%

48.4%

Display

SearchClassifieds & DirectoriesOther

Display

SearchClassifieds & DirectoriesOther

Display

SearchClassifieds & DirectoriesOther

Western Europe: share of formats in 2012 CEE: share of formats in 2012 CEE excl Russia: share of formats in 2012

42.6%

5.5%

51.8% 51.0%

11.1%

37.7%

30.9%

20.3%

48.4%

Display

SearchClassifieds & DirectoriesOther

Display

SearchClassifieds & DirectoriesOther

19© IAB Europe

Section 2 - AdEx Benchmark 2012 Analysis

dISplAy

display grows strong single-digit in 2012

• Value:€7.9billion

• Accountsfor32.4percentofallonlineadvertisingspend

• YoYgrowthof8.9percent

• Topfivecountriesbyvalue:UK,Germany,France,

Italy, Russia

• Topfivebygrowth:Turkey,Slovakia,Bulgaria,Russia,

Czech Republic

Despite the adverse economic environment, Display ad spend

grew strong single-digit at 8.9 per cent, in 2012. In a declining

economy, where advertising budgets are shrinking across media,

Display tends to suffer more than performance-based formats.

In 2009, when advertisers were cutting down spending, Display

only grew 0.3 per cent. In 2012, with many European ad markets

declining double-digit, an 8.9 per cent growth demonstrates the

increased strength of the format.

There are a number of trends behind this development.

Firstly, growth was driven by the increased investment of

advertisers in social media. As Facebook and local social media

players began to pursue a more aggressive advertising strategy

in the second half of 2012, social media ad spend increased

strong double-digit, pushing the Display growth rate upward. This

was true in the developed European markets, but social media

advertising was particularly strong in the CEE region, contributing

between 10.0 to 26.7 per cent of all Display ad spend.

Year-on-year growth in Display ad spend 2007 - 2012

05

1015202530354045

201220112010200920082007

%

39.0%

15.1%

0.3%

21.3%

15.4%

8.9%

Secondly, Display growth was propelled by the expansion of

the online video and mobile formats. As more brand advertisers

become interested in online, video, the format which most

resembles TV as a brand messenger is becoming an increasingly

significant proportion of Display. Please see the Mobile and Video

sections for further insights.

Lastly, Display advertising growth was also boosted by the

continued development of online ad technology. As data is not

just more easily available, but also better analysed, the targeting

of ads and measurement of campaign effectiveness could make

online advertising more transparent and more accountable. If

executed correctly, programmatic buying could be a significant

driver of online advertising growth in the next five years.

The trend towards pan regional digital and TV brand

campaigns is ever-increasing as consumers confirm

their desire for great content irrespective of platform.

This means that clients are able to increase reach and

engagement taking advantage of technology advances,

maturing industry systems and focus on digital creativity.

Rapid growth in mobile advertising confirms this trend

and video goes from strength to strength. The luxury

sector continues to show resilient growth within wider

market turmoil and pan-European digital campaigns are

broadening from their strong base in Western Europe to

include the surging digital markets of Russia and Turkey.

Tom Bowman, VP Strategy, Solutions and Sales

Operations, BBC Advertising

Programmatic buying is one of the key drivers reshaping

our industry. In the US, about 1/3 of all display cam-

paigns are already bought through RTB and algorithmic

type of technologies. Europe, driven by its Western Euro-

pean markets, will experience a similar growth in the next

three to five years. This change is, literally, a fundamental

one. It will progressively span across all digital channels

– and beyond, as offline media are increasingly turn-

ing digital – to become the standardised way of trading

media: after search, display and video, the frontier today

is mobile. TV, radio and outdoor will be next in line.

Marc Panic, COO, GroupM Interaction EMEA

IAB Europe AdEx Benchmark 2012

Section 2 - Online advertising overview by sector

20

dISplAy

Rest of Europe: Display value by country 2012 and 2011 (€m)

0 50 100 150 200 250

Croatia

Serbia

Slovenia

Bulgaria

Romania

Slovakia

Greece

Ireland

Hungary

Switzerland

Belgium

Finland

Austria

Czech Rep.

Denmark

Norway

20112012

€208m

€203m

€168m

€124m

€107m

€113m

€84m

€60m

€59m

€34m

€31m

€22m

€19m

€10m

€8m

€7m

Top 10: Display value by country 2012 and 2011 (€m)

0 500 1000 1500 2000

Turkey

Poland

Sweden

Spain

Netherlands

Russia

Italy

France

Germany

UK

20112012

€1,514m

€1,608m

€847m

€639m

€526m

€370m

€387m

€281m

€229m

€224m

© IAB Europe

Section 2 - Online advertising overview by sector

21

Rest of Europe: 2012 Year-on-year Display growth by country

Top 10: 2012 Year-on-year Display growth by country

0 5 10 15 20 25 30 35

Sweden

Italy

Serbia

Hungary

UK

Czech Rep.

Russia

Bulgaria

Turkey

Slovakia

%

-15 -12 -9 -6 -3 0 3 6 9 12

Slovenia

Croatia

Spain

Switzerland

Greece

Netherlands

Norway

Belgium

Ireland

France

Austria

Germany

Denmark

Poland

Finland

Romania

%

dISplAy

IAB Europe AdEx Benchmark 2012

Section 2 - Online advertising overview by sector

22

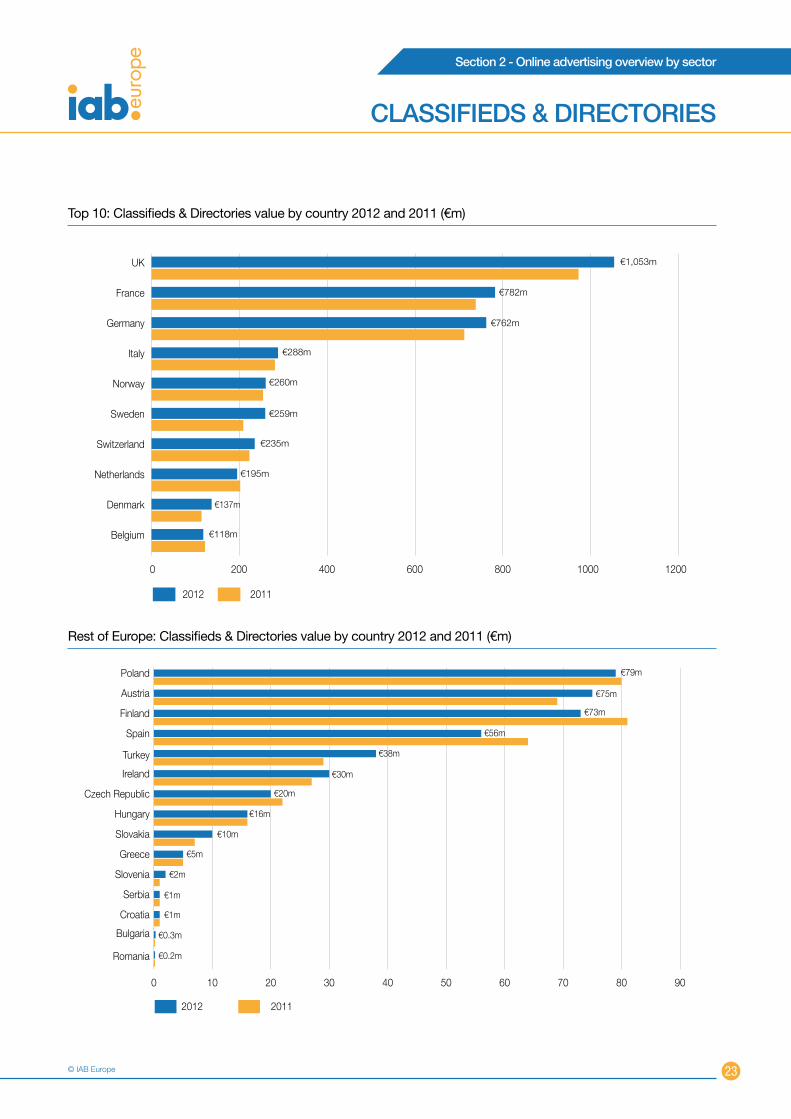

ClASSIFIEdS & dIrECTOrIES

Classifieds & directories 1 sees an acceleration to its growth rate in 2012

• Value:€4.5billion

• Accountsfor18.5percentofallonlineadvertisingspend

• YoYgrowthof6.3percent

• Topfivecountriesbyvalue:UK,France,Germany,Italy,Norway

• Topfivebygrowth:Turkey,Slovenia,Slovakia,Sweden,Denmark

Classifieds and Directories grew 6.3 per cent in 2012. The format was the only one which saw an acceleration in its growth rate year-on-

year. In adverse economic conditions, this was unusual, as Classifieds and Directories are highly dependent on the state of the job, real-

estate and automotive markets and hence more at risk during economic downturns.

There were three forces acting on Classifieds and Directories in 2012 showing great discrepancy in growth rates across Europe.

Firstly, there has been an emergence of regional players who have invested and acquired into the Classifieds market across Europe.

Companies which traditionally operated in one or two countries are now becoming European ventures and operating transnationally.

Secondly and in conjunction with the first point, there is a continued shift of print ad spend to the online medium. As publishers move online

more systematically they are expanding their Classifieds and Directories ad business online.

Lastly, and counter to the previous two points, the weakening of the economy has had a negative effect on Classifieds and Directories as

there were fewer jobs, houses and cars to advertise. As a result, in seven markets Classifieds and Directories declined, with Spain and

Finland decreasing double-digit.

1. Classifieds & Directories ad spend is available for 25 countries. Russia has not been included in this category on instructions by IAB Russia.

© IAB Europe

Section 2 - Online advertising overview by sector

23

ClASSIFIEdS & dIrECTOrIES

Top 10: Classifieds & Directories value by country 2012 and 2011 (€m)

0 200 400 600 800 1000 1200

Belgium

Denmark

Netherlands

Switzerland

Sweden

Norway

Italy

Germany

France

UK €1,053m

€782m

€762m

€288m

€260m

€235m

€259m

€195m

€118m

€137m

20112012

Rest of Europe: Classifieds & Directories value by country 2012 and 2011 (€m)

0 10 20 30 40 50 60 70 80 90

Romania

Bulgaria

Croatia

Serbia

Slovenia

Greece

Slovakia

Hungary

Czech Republic

Ireland

Turkey

Spain

Finland

Austria

Poland €79m

€75m

€73m

€56m

€38m

€30m

€20m

€16m

€10m

€5m

2012 2011

€2m

€1m

€1m

€0.3m

€0.2m

IAB Europe AdEx Benchmark 2012

Section 2 - Online advertising overview by sector

24

Top 10: 2012 year-on-year Classifieds & Directories growth by country

Rest of Europe: 2012 year-on-year Classifieds & Directories growth by country

0 5 10 15 20 25 30 35 40

Germany

UK

Austria

Ireland

Serbia

Denmark

Sweden

Slovenia

Turkey

Slovakia

%

-15 -10 -5 0 5 10

Spain

Finland

Czech Republic

Belgium

Netherlands

Poland

Hungary

Croatia

Italy

Norway

Romania

Greece

Switzerland

France

Bulgaria

%

ClASSIFIEdS & dIrECTOrIES

© IAB Europe

Section 2 - Online advertising overview by sector

25

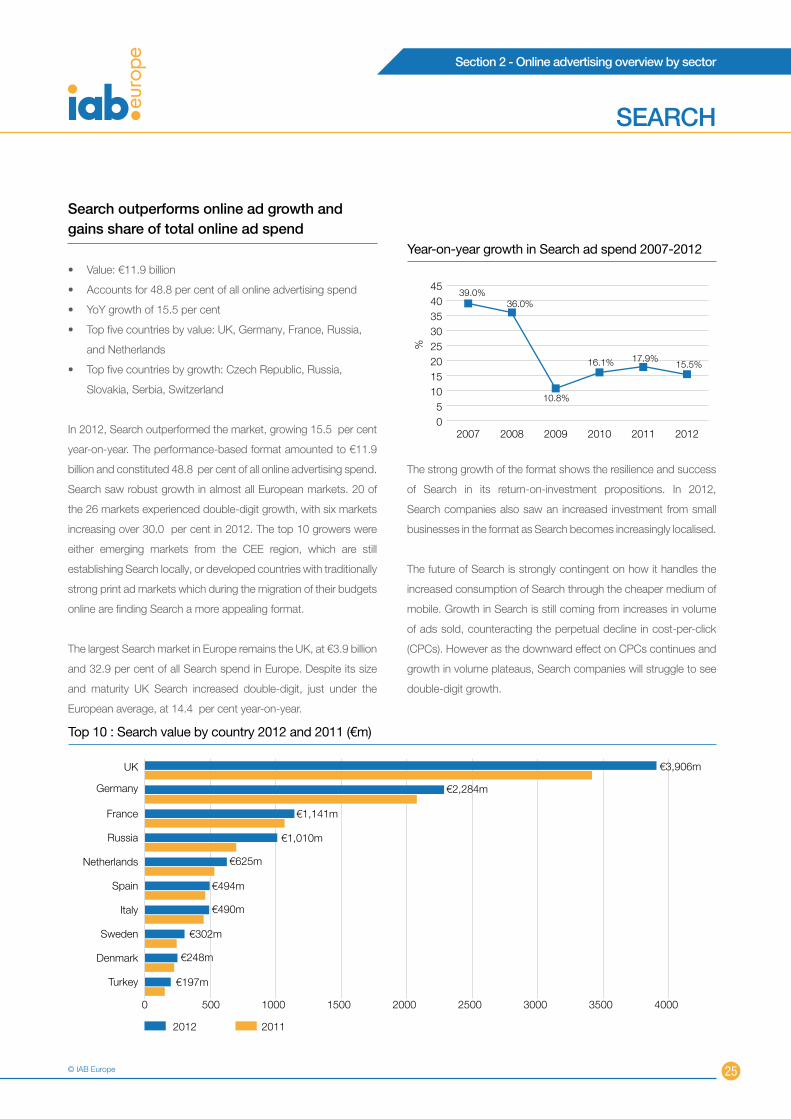

SEArCh

Top 10 : Search value by country 2012 and 2011 (€m)

0 500 1000 1500 2000 2500 3000 3500 4000

Turkey

Denmark

Sweden

Italy

Spain

Netherlands

Russia

France

Germany

UK €3,906m

€2,284m

€1,141m

€1,010m

€625m

€494m

€490m

€302m

€248m

€197m

2012 2011

Year-on-year growth in Search ad spend 2007-2012

05

1015202530354045

201220112010200920082007

%

39.0%36.0%

16.1% 17.9%

10.8%

15.5%

Search outperforms online ad growth and gains share of total online ad spend

• Value:€11.9billion

• Accountsfor48.8percentofallonlineadvertisingspend

• YoYgrowthof15.5percent

• Topfivecountriesbyvalue:UK,Germany,France,Russia,

and Netherlands

• Topfivecountriesbygrowth:CzechRepublic,Russia,

Slovakia, Serbia, Switzerland

In 2012, Search outperformed the market, growing 15.5 per cent

year-on-year. The performance-based format amounted to €11.9

billion and constituted 48.8 per cent of all online advertising spend.

Search saw robust growth in almost all European markets. 20 of

the 26 markets experienced double-digit growth, with six markets

increasing over 30.0 per cent in 2012. The top 10 growers were

either emerging markets from the CEE region, which are still

establishing Search locally, or developed countries with traditionally

strong print ad markets which during the migration of their budgets

online are finding Search a more appealing format.

The largest Search market in Europe remains the UK, at €3.9 billion

and 32.9 per cent of all Search spend in Europe. Despite its size

and maturity UK Search increased double-digit, just under the

European average, at 14.4 per cent year-on-year.

The strong growth of the format shows the resilience and success

of Search in its return-on-investment propositions. In 2012,

Search companies also saw an increased investment from small

businesses in the format as Search becomes increasingly localised.

The future of Search is strongly contingent on how it handles the

increased consumption of Search through the cheaper medium of

mobile. Growth in Search is still coming from increases in volume

of ads sold, counteracting the perpetual decline in cost-per-click

(CPCs). However as the downward effect on CPCs continues and

growth in volume plateaus, Search companies will struggle to see

double-digit growth.

IAB Europe AdEx Benchmark 2012

Section 2 - Online advertising overview by sector

26

Top 10: 2012 Year-on-year search growth by country

0 10 20 30 40 50 60

Finland

Sweden

Bulgaria

Hungary

Turkey

Switzerland

Serbia

Slovakia

Russia

Czech Rep.

%

Rest of Europe: Search value by country 2012 and 2011 (€m)

0 50 100 150 200

Romania

Serbia

Slovenia

Bulgaria

Croatia

Slovakia

Hungary

Greece

Ireland

Finland

Czech Rep.

Austria

Belgium

Norway

Switzerland

Poland €188m

€148m

€147m

€127m

€103m

€89m

€68m

€55m

€44m

€24m

2012 2011

€6m

€5m

€4m

€2m

€1m

€175m

SEArCh

© IAB Europe

Section 2 - Online advertising overview by sector

27

-30 -20 -10 0 10 20 30

Romania

Greece

Croatia

France

Spain

Italy

Germany

Belgium

Austria

Denmark

Slovenia

UK

Netherlands

Ireland

Poland

Norway

%

Rest of Europe: 2012 Year-on-year search growth by country

Online advertising continues to grow faster than any other advertising channel in Russia. More and more brands which had been

focused on TV start to pay more attention to the internet in order to reach and interact with their target audience. This trend

will continue, fuelled by the growth of the internet population - Russian having the largest now in Europe. Furthermore, Yandex

and other publishers are developing new targeting features to help advertisers reach very precise audiences, which could move

incremental AD budgets online.

Bernard Lukey, General Director, Yandex

SEArCh

IAB Europe AdEx Benchmark 2012

Section 2 - Online advertising overview by sector

28

mOBIlE

mobile ad spend still lags behind consumption

In 2012, the IAB Europe AdEx Benchmark received mobile advertising spend from 21 markets up from 14 in 2011. This indicates the

increasing prominence of the medium and its establishment as a legitimate medium for advertising. Mobile display advertising ranged in

volume across Europe from €0.1 million in Romania to €184.9 million in the UK, with mature markets investing more in mobile display than

the CEE region (with the exception of Russia).

0

25

50

75

100

125

150

175

200

€m

€184

.9m

€47.

8m

€43.

0m

€24.

0m

€20.

6m

€15.

0m

€13.

3m

€11.

9m

€8.7

m

€5.8

m

€5.6

m

€4.2

m

€3.3

m

€1.9

m

€1.5

m

€0.4

m

€0.3

m

€0.2

m

€0.2

m

€0.1

m

€0.1

m

UK

German

y

Fran

ceSpa

in

Russia Ita

ly

Sweden

Netherl

ands

Irelan

d

Denmark

Turke

y

Austria

Poland

Hunga

ry

Czech

Rep

ublic

Sloven

ia

Slovak

ia

Bulgari

a

Serbia

Croati

a

Roman

ia

Mobile display ad spend in 2012 (€m)

Mobile display as a share of online display in 2012

0

2

4

6

8

10

12

14

2011 2012

11.5

%

6.5%

5.1%

5.0%

4.7%

4.2%

3.9%

3.4%

3.2%

3.1%

3.1%

2.8%

2.5%

2.3%

1.9%

1.8%

1.4%

1.1%

0.9%

Czech

Rep

ublic

Bulgari

a

Poland

Croati

a

Serbia

Italy

Turke

y

Denmark

Netherl

ands

Hunga

ry

German

y

Austria

Russia

Sloven

ia

Sweden

Europe

Fran

ceSpa

inUK

A small number of markets also supplied data for mobile search advertising from both Western Europe and the CEE. In Western Europe,

mobile search was led by the UK at €450.0 million, followed by Germany at €109.6 million. In the CEE, Hungary reported a mobile search

figure of €1.2 million, followed by the Czech Republic at €0.4 million.

© IAB Europe

Section 2 - Online advertising overview by sector

29

Proliferation of devices and technology advances have

continued to grow digital audiences across Europe.

These increasingly sophisticated and empowered con-

sumers are constantly demanding content and services

which allow the digital industry to offer opportunities

for advertisers to reach and engage them in a variety of

innovative ways and with increased efficiency. At the

same time we see multi-screening confirm the need for

advertisers to increase the synergy between their offline

and digital campaigns. These factors are helping to drive

growth in digital spend.

Stephanie Hospital, Executive Vice President,

Orange Digital

Smartphone penetration Western Europe

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

0

10

20

30

40

50

60

70

80

90

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

%

2005

Source: IHS

Mobile display advertising grew strongly in 2012 (with eight markets growing triple-digit), however it remains a small proportion of online

Display. In 2012, mobile made up 5.0 per cent of Display ad spend. With the exception of the UK, whose mobile share of Display is over

10.0 per cent, all European markets are still very small.

mOBIlE

0

100

200

300

400

500

600

700

580%

200%

150%

142%

135%

132%

114%

107%

83%

80%

61%

51%

33%

29%

25%

4% 1% -22%

Czech

Rep

.

Bulgari

a

Poland

Croati

a

Serbia

Italy

Turke

y

Denmark

Netherl

ands

Hunga

ry

German

y

Austria

Russia

Sloven

ia

Sweden

Fran

ceSpa

inUK

As smartphone penetration continues to rise and with it the addressable market for mobile advertising, investment will fol-

low. According to IHS, from 32.0 per cent in 2012, smartphone penetration is expected to grow to 77.0 per cent in Europe

by 2016.

Mobile display ad spend: 2012 year-on-year growth (%)

IAB Europe AdEx Benchmark 2012

Section 2 - Online advertising overview by sector

30

video accounts for 13 per cent of online display

AdEx Benchmark 2012 includes online video advertising figures for 19 markets. In 2012, we have standardised definitions across all

countries to include only in-stream advertising (pre-rolls, mid-rolls and post-rolls) as agreed by the IAB AdEx Benchmark Video Working

Committee. Where such a distinction was not provided in a local market, IHS modelled the figure based on local market knowledge and

regional averages.

On average, video represented 12.9 per cent of the total online Display market value in Europe in 2012, up from 9.7 per cent in 2011. In

many markets across the continent, broadcasters and publishers have expanded their online presence, offering more premium inventory

online. This has attracted traditional TV advertisers to the online medium and provides a good entry point for brand investment online.

vIdEO

Video as a share of online display in 2012

0

5

10

15

20

25

30

35

Bulgar

ia

Hunga

ry

Roman

ia

Slovak

ia

Denm

ark

Czech

Rep

.

Austri

a

Germ

any

Nethe

rland

s

Irelan

d

Turk

ey

Sweden

Russia

Finlan

dUK

Poland

Europ

e

Spain

Italy

Sloven

ia

31.6

%

20.0

%

17.3

%

12.9

%

11.6

%

10.5

%

9.1%

8.9%

8.9%

8.8%

8.8%

8.2%

7.3%

6.8%

3.2%

2.8%

2.4%

2.2%

1.6%

1.4%

%

Online video advertising grew 50.7 per cent in Europe in 2012. Seven markets grew triple-digit from 2011 and ten countries above the

European average. However, growth rates vary across markets. For instance, Spain saw an increase 204.0 per cent year-on-year largely

due to the undersupply of TV inventory. Online video was used for advertising to satisfy excess demand for TV advertising. In contrast,

the Netherlands experienced a decline of -0.6 per cent in video ad spend in 2012, due to decrease in prices of video ads, as the supply of

online video inventory increased year-on-year.

It is also important to note the difference in the volumes of online video ad spend. Most investment originates from Western Europe with

just Russia and Poland reporting double-digit online video ad spend in 2012, from the CEE region. The UK, Italy and Germany were the

only markets with online video ad spend above €100.0 million.

© IAB Europe

Section 2 - Online advertising overview by sector

31

2012 Year-on-year growth in Video by country

-50

0

50

100

150

200

250

Netherl

ands

Sloven

ia

Slovak

ia

Bulgari

a

Sweden

German

y

Finlan

d

Irelan

dUK

Europe

Czech

Rep

.

Poland

Italy

Russia

Turke

y

Roman

ia

Austria

Denmark

Hunga

ry

Spain

204.

0%

181.

1%

160.

0%

146.

8%

115.

6%

104.

5%

100.

0%

75.0

%

64.9

%

58.1

%

50.7

%

43.2

%

20.4

%

20.0

%

16.9

%

16.1

%

11.4

%

2.0%

-0.7

%

-10.

6%

%

Total Video ad spend in 2012 (€m)

0

20

40

60

80

100

120

140

160

180 €168

.5m

€128

.0m

€110

.0m

€64.

2m

€47.

0m

€31.

8m

€26.

4m

€25.

0m

€19.

8m

€10.

2m

€8.5

m

€5.6

m

€5.4

m

€5.2

m

€3.2

m

€1.0

m

€0.7

m

€0.5

m

€0.3

m

Netherl

ands

Sloven

ia

Slovak

ia

Bulgari

a

Sweden

German

yFin

land

Irelan

dUK

Czech

Rep

.

Poland

Italy

Russia

Turke

y

Roman

ia

Austria

Denmark

Hunga

ry

Spain

vIdEO

Online will obviously continue to grow, but the main drivers in the coming years will be the new digital channels. When we

exclude video or mobile we find that classical display advertising is only growing slowly and the continuing fragmentation of

media channels poses a significant challenge for the industry and how we measure their audience and effectiveness.

Arndt Groth, CEO, Publigroupe

IAB Europe AdEx Benchmark 2012

Section 2 - Online advertising overview by sector

32

Display ad spend: 2012 year-on-year growth (%)

-30

-20

-10

0

10

20

30

40

Sloven

ia

Croati

a

Spain

Netherl

ands

Austria

German

y

Denmark

Poland

Roman

ia

SwedenIta

ly

Hunga

ryUK

Czech

Rep

ublic

Russia

Bulgari

a

Turke

y

Display Display excl. Video

25.1

%

22.1

%

10.6

%

12.9

%

3.0%

10.9

%

4.1%

8.4% 9.9%

4.0% 6.

9%

5.6%

- 0.2

%

1.7%

-22.

9%

-12.

5%

-19.

4%

Display excl. Video & Mobile

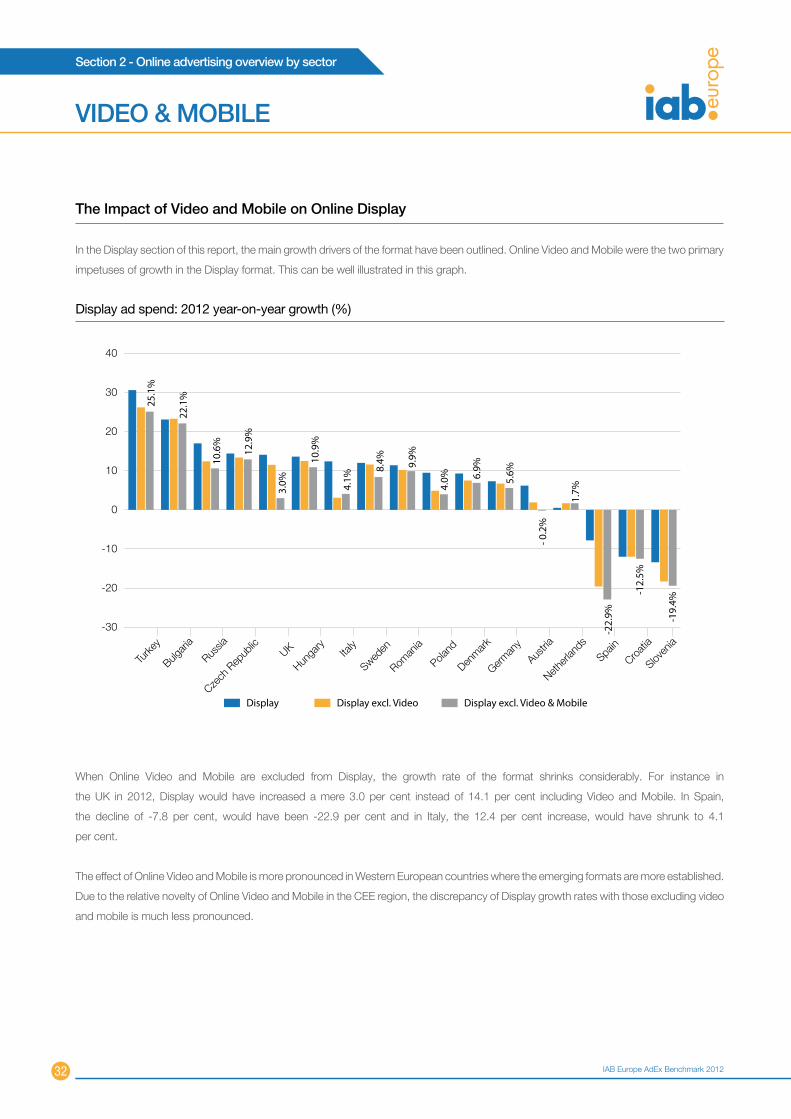

The Impact of video and mobile on Online display

In the Display section of this report, the main growth drivers of the format have been outlined. Online Video and Mobile were the two primary

impetuses of growth in the Display format. This can be well illustrated in this graph.

When Online Video and Mobile are excluded from Display, the growth rate of the format shrinks considerably. For instance in

the UK in 2012, Display would have increased a mere 3.0 per cent instead of 14.1 per cent including Video and Mobile. In Spain,

the decline of -7.8 per cent, would have been -22.9 per cent and in Italy, the 12.4 per cent increase, would have shrunk to 4.1

per cent.

The effect of Online Video and Mobile is more pronounced in Western European countries where the emerging formats are more established.

Due to the relative novelty of Online Video and Mobile in the CEE region, the discrepancy of Display growth rates with those excluding video

and mobile is much less pronounced.

vIdEO & mOBIlE

© IAB Europe

Section 3 - Overview by country

33

TOp 10

0

1000

2000

3000

4000

5000

6000

7000

Denmark

Norway

Sweden

Spain

Netherl

andsIta

ly

Russia

Fran

ce

German

yUK

OtherClassifieds & DirectoriesSearchDisplay

Spend by format and by country: Top 10 (€m)

Display 1,608 1,514 847 526 639 387 370 281 208 203

Classifieds 1,053 762 782 0 288 195 56 259 260 137

Search 3,906 2,284 1,141 1,010 490 625 494 302 148 248

Other 75 0 0 0 0 0 0 0 0 2

uK:

2012 Online Ad Spend €6,642m

2012 YoY growth 13.3%

Online ad spend per capita €93.4

Germany:

2012 Online Ad Spend €4,560m

2012 YoY growth 8.6%

Online ad spend per capita €51.3

France:

2012 Online Ad Spend €2,770m

2012 YoY growth 6.3%

Online ad spend per capita €41.0

russia:

2012 Online Ad Spend €1,536m

2012 YoY growth 34.0%

Online ad spend per capita €8.0

Italy:

2012 Online Ad Spend €1,418m

2012 YoY growth 9.2%

Online ad spend per capita €21.3

Netherlands:

2012 Online Ad Spend €1,207m

2012 YoY growth 8.1%

Online ad spend per capita €66.8

IAB Europe AdEx Benchmark 2012

Section 3 - Overview by country

34

Russia has the largest online audience in Europe, ac-

cording to some estimates up to 70 million people. Pen-

etration of 55 per cent of the audience will grow. High

and stable prices for oil and gas fuelled consumption in

Russia and stimulate the economy and the advertising

industry as a whole. Internet as a media in Russia is sec-

ond only to TV with a share of 19 per cent and is invest-

ing in infrastructure RTB, Big Data and On-line Video.

These factors explain why the Russian market for online

advertising in 2012, up more than 30 per cent and came

in fourth place in Europe and we expect continued

double-digit growth in the next 3-5 years.

Boris Omelnitskiy, President, IAB Russia

TOp 10

Spain:

2012 Online Ad Spend €920m

2012 YoY growth -0.6%

Online ad spend per capita €19.6

Sweden:

2012 Online Ad Spend €841m

2012 YoY growth 20.0%

Online ad spend per capita €73.9

Norway:

2012 Online Ad Spend €617m

2012 YoY growth 5.8%

Online ad spend per capita €117.4

denmark:

2012 Online Ad Spend €591m

2012 YoY growth 12.6%

Online ad spend per capita €93.8

In the UK, one in three Euros spent on advertising goes

online and on mobile. And it’s the mobile sector which

has experienced the most impressive year-on-year

growth - of +158 per cent - to reach one tenth of the

overall digital pie. The rise in smartphone ownership has

been exponential – ending the year at 64 per cent of

the entire population, and still growing fast. And we can

already see the tablet going mainstream in 2013. These

developments have major implications for advertisers,

agencies and publishers, as the majority of ad impres-

sions migrate to mobile devices in the short term!

The UK is, arguably, the most mature digital advertising

economy in the world, so it’s pleasing to see overall ad

spend growth two points ahead of the curve at +13.3 per

cent. The key UK market drivers in 2012 were undoubt-

edly search (+14.4 per cent), mobile (+158 per cent) and

video (+43 per cent) – with marketers increasingly turning

to online to enhance their brand campaigns. Indeed the

packaged goods sector consolidated its position as the

number one spender in display, accounting for 16 per

cent of the total. Forecasts for 2013 indicate that the UK’s

contribution to 2013 AdEx will easily surpass €7 billion.

Guy Phillipson, CEO, IAB UK

© IAB Europe

Section 3 - Overview by country

35

rEST OF EurOpE

0

100

200

300

400

500

600

Croati

a

Serbia

Sloven

ia

Roman

ia

Bulgari

a

Slovak

ia

Greece

Hunga

ry

Irelan

d

Finlan

d

Czech

Rep

ublic

Austria

Belgium

Turke

y

Switzerl

and

Poland

OtherClassifieds & DirectoriesPaid-for-searchDisplay

Spend by format and by country: Rest of Europe (€m)

Display 229 84 224 107 124 168 113 59 60 34 31 19 22 10 8 7

Classifieds 79 235 38 118 75 20 73 30 16 5 10 0 0 2 1 1

Search 188 175 197 147 127 103 89 68 44 55 24 5 1 4 2 6

Other 0 0 0 0 0 0 0 0 0 0 0 1 0 0 3 0

poland:

2012 Online Ad Spend €496m

2012 YoY growth 11.1%

Online ad spend per capita €11.6

Switzerland:

2012 Online Ad Spend €494m

2012 YoY growth 11.1%

Online ad spend per capita €55.6

Turkey:

2012 Online Ad Spend €459m

2012 YoY growth 30.4%

Online ad spend per capita €4.7

Belgium:

2012 Online Ad Spend €371m

2012 YoY growth 3.0%

Online ad spend per capita €33.4

Austria:

2012 Online Ad Spend €326m

2012 YoY growth 8.5%

Online ad spend per capita €35.5

Czech republic:

2012 Online Ad Spend €291m

2012 YoY growth 22.8%

Online ad spend per capita €22.5

Finland:

2012 Online Ad Spend €274m

2012 YoY growth 8.1%

Online ad spend per capita €47.0

Ireland:

2012 Online Ad Spend €157m

2012 YoY growth 12.3%

Online ad spend per capita €28.7

IAB Europe AdEx Benchmark 2012

Section 3 - Overview by country

36

In 2012 the composition of the top 10 digital advertising

spenders was very similar to the previous year. UK, Ger-

many and France retained their top three positions and

achieved again around two thirds of total top-10 value,

reaching €14 billion (~57 per cent of the European online

ad market). Russia overtook Italy and Netherlands, and

rose to the fourth spot as a result of the successive high

double-digit growth index. The order of other countries

completing top 10 remained the same, however growth

trends observed in 2012 may have a crucial impact on

potential shifts between bottom 4 of the top 10 spenders

in 2013.

Pawel Kolenda, Market Research Manager, IAB Poland

Digital media ad spend in Turkey has a growth rate of

30 per cent over the previous year. DigitalMedia has be-

come the third media in terms of advertising investment.

In media consumption digital media comes second when

ranked by reach and time spent. Digital media invest-

ments will soon catch up with print media and overtake

to assume second place behind TV.

There is a prominent growth in digital video and mobile

advertising matching the increasing time spent on those

platforms.

Neslihan Mesutoglu, General Manager, Turkuvaz Reklam

Pazarlama Danişmanlik/Dijital&Radio Reklam Satış / IAB

Turkey Board Member

rEST OF EurOpE

hungary:

2012 Online Ad Spend €120m

2012 YoY growth 16.5%

Online ad spend per capita €10.3

Greece:

2012 Online Ad Spend €94m

2012 YoY growth -6.2%

Online ad spend per capita €8.8

Slovakia:

2012 Online Ad Spend €65m

2012 YoY growth 36.3%

Online ad spend per capita €8.9

Bulgaria:

2012 Online Ad Spend €24m

2012 YoY growth 23.2%

Online ad spend per capita €2.6

romania:

2012 Online Ad Spend €23m

2012 YoY growth 9.2%

Online ad spend per capita €1.0

Slovenia:

2012 Online Ad Spend €16m

2012 YoY growth -4.4%

Online ad spend per capita €8.1

Serbia:

2012 Online Ad Spend €14m

2012 YoY growth 16.9%

Online ad spend per capita €1.7

Croatia:

2012 Online Ad Spend €14m

2012 YoY growth -4.6%

Online ad spend per capita €3.4

© IAB Europe

Section 4 - Background Data

37

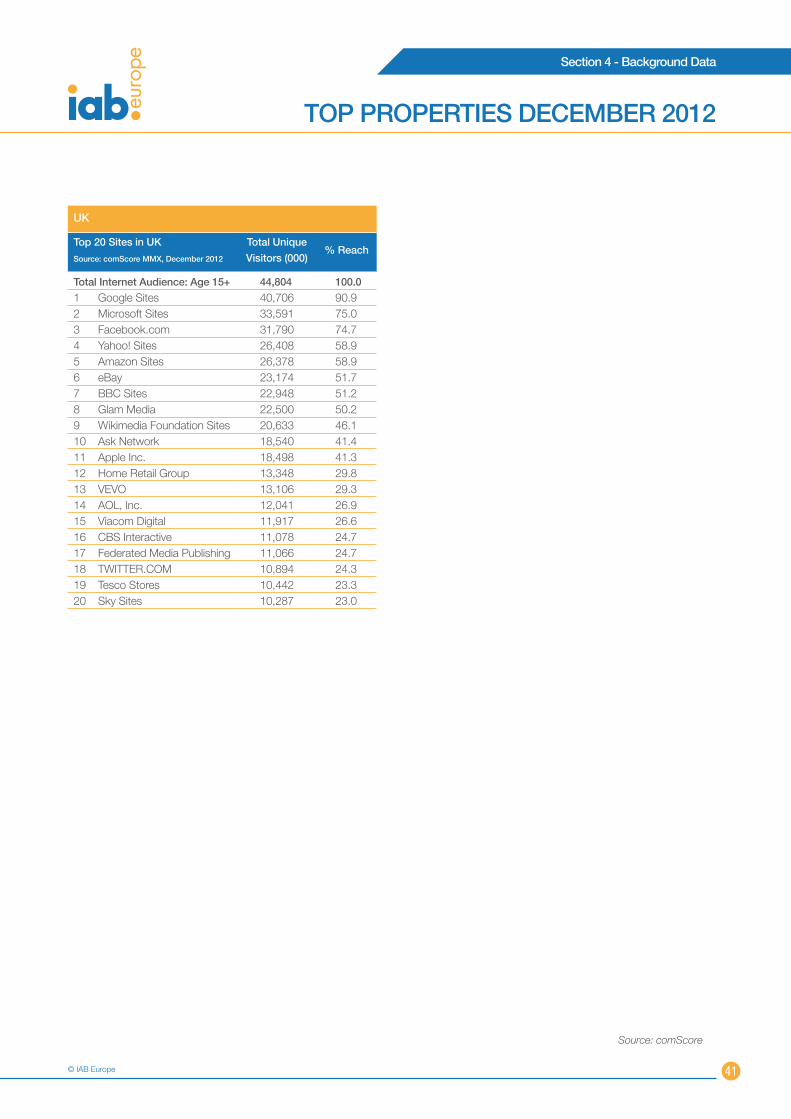

TOp prOpErTIES dECEmBEr 2012

Austria

Top 20 Sites in Austria

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 5,027 100.0

1 Google Sites 4,763 94.7

2 Facebook.com 3,344 66.5

3 Microsoft Sites 2,612 52.0

4 Amazon Sites 2,437 48.5

5 Wikimedia Foundation Sites 2,193 43.6

6 Styria Media Group 1,635 32.5

7 Glam Media 1,602 31.9

8 eBay 1,575 31.3

9 Yahoo! Sites 1,560 31.0

10 Axel Springer AG 1,514 30.1

11 United-Internet Sites 1,485 29.5

12 Hubert Burda Media 1,342 26.7

13 ORF.at Network 1,260 25.1

14 VEVO 1,258 25.0

15 Ask Network 1,235 24.6

16 Apple Inc. 1,141 22.7

17 gutefrage.net GmbH 1,005 20.0

18 ProSiebenSat1 Sites 969 19.3

19 Deutsche Telekom 949 18.9

20 Herold Sites 947 18.8

Belgium

Top 20 Sites in Belgium

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 6,371 100.0 1 Google Sites 6,102 95.82 Microsoft Sites 5,432 85.33 Facebook.com 5,176 81.24 Wikimedia Foundation Sites 2,667 41.95 Corelio Publishing 2,451 38.56 Yahoo! Sites 2,341 36.77 VEVO 2,277 35.78 Belgacom Group 2,029 31.99 Apple Inc. 1,720 27.010 VRT Sites 1,646 25.811 Ask Network 1,538 24.112 Viacom Digital 1,506 23.613 De Persgroep 1,497 23.514 Amazon Sites 1,461 22.915 Groupe Rossel 1,393 21.916 eBay 1,380 21.717 Sanoma Group 1,373 21.618 Truvo International 1,333 20.919 2dehands 1,298 20.420 Telenet Sites 1,252 19.6

denmark

Top 20 Sites in denmark

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 3,772 100.0 1 Google Sites 3,533 93.72 Microsoft Sites 2,896 76.83 Facebook.com 2,733 72.54 JP Politiken Hus 1,362 36.15 Wikimedia Foundation Sites 1,292 34.26 DR.DK 1,229 32.67 Yahoo! Sites 1,160 30.78 TV2 Danmark 1,137 30.29 eBay 1,125 29.810 Apple Inc. 1,097 29.111 VEVO 1,076 28.512 Eniro Group 1,048 27.813 Amazon Sites 943 25.014 Berlingske Media 929 24.615 Spotify 842 22.316 Ask Network 768 20.417 Linkedin 754 20.018 Valve Corporation 751 19.919 Glam Media 739 19.620 Viacom Digital 714 18.9

Finland

Top 20 Sites in Finland

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 3,476 100.0

1 Google Sites 3,336 96.02 Sanoma Group 3,332 95.93 Microsoft Sites 2,839 81.74 Facebook.com 2,794 80.45 Alma Media 2,680 77.16 Yleisradio Oy 2,597 74.77 Otavamedia 2,548 73.38 MTV3 Internet 2,436 70.19 Wikimedia Foundation Sites 1,853 53.310 Aller Media 1,397 40.211 VEVO 1,234 35.512 Viacom Digital 1,173 33.713 Foreca 1,164 33.514 Glam Media 1,100 31.615 Yahoo! Sites 1,072 30.816 Kesko Sites 1,043 30.017 Rohea 999 28.718 Elisa Oyj 938 27.019 OP-Pohjola 921 26.520 Amazon Sites 920 26.5

Source: comScore

IAB Europe AdEx Benchmark 2012

Section 4 - Background Data

38

TOp prOpErTIES dECEmBEr 2012

France

Top 20 Sites in France

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 48,017 100.0

1 Google Sites 44,654 93.02 Microsoft Sites 37,048 77.23 Facebook.com 34,258 71.34 Orange Sites 22,062 45.95 Yahoo! Sites 21,289 44.36 CCM-Benchmark 20,876 43.57 Wikimedia Foundation Sites 20,765 43.28 Iliad - Free.fr Sites 18,567 38.79 Axel Springer AG 18,194 37.910 Amazon Sites 18,123 37.711 Kering 17,648 36.812 Solocal Group 17,423 36.313 Schibsted (Anuntis-Infojobs-20minutos) 17,400 36.214 Groupe Lagardere 16,868 35.115 Vivendi 16,062 33.516 Ebuzzing 15,187 31.617 DAILYMOTION.COM 13,836 28.818 Apple Inc. 13,662 28.519 Groupe M6 13,419 27.920 Groupe Casino 12,731 26.5

Germany

Top 20 Sites in Germany

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 57,389 100.0

1 Google Sites 53,610 93.42 Facebook.com 38,569 67.23 Amazon Sites 35,215 61.44 eBay 33,659 58.75 Microsoft Sites 32,374 56.46 Deutsche Telekom 29,252 51.07 Axel Springer AG 27,357 47.78 United-Internet Sites 26,974 47.09 Wikimedia Foundation Sites 26,436 46.110 Hubert Burda Media 23,800 41.511 ProSiebenSat1 Sites 21,021 36.612 Yahoo! Sites 19,912 34.713 gutefrage.net GmbH 19,481 33.914 RTL Group Sites 16,248 28.315 Glam Media 16,242 28.316 Otto Gruppe 15,352 26.817 Apple Inc. 13,911 24.218 Ask Network 11,181 19.519 Sparkassen-Finanzgruppe 10,440 18.220 METRO Group 10,318 18.0

Ireland

Top 20 Sites in Ireland

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 2,598 100.0 1 Google Sites 2,414 92.92 Yahoo! Sites 1,942 74.73 Facebook.com 1,876 72.24 Microsoft Sites 1,785 68.75 Distilled Media 1,346 51.86 Glam Media 1,277 49.27 RTE.IE 1,246 48.08 Ask Network 1,232 47.49 Amazon Sites 1,077 41.510 Wikimedia Foundation Sites 969 37.311 Independent News & Media 919 35.412 BBC Sites 878 33.813 AOL, Inc. 832 32.014 Apple Inc. 816 31.415 Irish Times Group 794 30.616 DoneDeal 785 30.217 VEVO 777 29.918 Viacom Digital 754 29.019 CBS Interactive 704 27.120 eBay 656 25.3

Italy

Top 20 Sites in Italy

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 28,722 100.0 1 Google Sites 26,902 93.72 Facebook.com 22,398 78.03 Microsoft Sites 17,827 62.14 Yahoo! Sites 17,277 60.25 ItaliaOnline 15,107 52.66 Telecom Italia 13,254 46.17 Wikimedia Foundation Sites 11,216 39.08 eBay 9,635 33.59 Banzai 8,636 30.110 Ask Network 8,455 29.411 Populis 8,328 29.012 ForumCommunity 7,662 26.713 VEVO 7,644 26.614 RCS Media Group 7,613 26.515 ALTERVISTA.ORG 7,425 25.916 Amazon Sites 6,322 22.017 Apple Inc. 6,001 20.918 Gruppo Mediaset 5,871 20.419 Gruppo Editoriale Espresso 5,624 19.620 Axel Springer AG 5,467 19.0

Source: comScore

© IAB Europe

Section 4 - Background Data

39

TOp prOpErTIES dECEmBEr 2012

Netherlands

Top 20 Sites in Netherlands

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 12,006 100.0

1 Google Sites 11,610 96.72 Microsoft Sites 10,671 88.93 Facebook.com 9,018 75.14 Sanoma Group 7,853 65.45 Telegraaf Media Groep 6,174 51.46 eBay 6,124 51.07 Wikimedia Foundation Sites 5,876 48.98 Publieke Omroep 5,403 45.09 RTL Group Sites 4,942 41.210 Ahold Sites 4,898 40.811 ING Group 4,046 33.712 Rabobank Group 4,013 33.413 VEVO 3,961 33.014 Apple Inc. 3,933 32.815 Yahoo! Sites 3,912 32.616 TWITTER.COM 3,805 31.717 Linkedin 3,631 30.218 KPN 3,231 26.919 Ask Network 3,165 26.420 De Persgroep 2,969 24.7

Norway

Top 20 Sites in Norway

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 3,336 100.0

1 Google Sites 3,020 90.52 Facebook.com 2,573 77.13 Microsoft Sites 2,552 76.54 Schibsted (Anuntis-Infojobs-20minutos) 2,244 67.35 A-Pressen Group 1,489 44.66 Wikimedia Foundation Sites 1,403 42.17 Spotify 1,264 37.98 AS Avishuset Dagbladet 1,247 37.49 Telenor 1,216 36.510 Yahoo! Sites 1,182 35.411 Eniro Group 1,142 34.212 NRK Sites 1,023 30.713 Edda Media 968 29.014 TV2 Sites 912 27.415 Amazon Sites 876 26.316 VEVO 873 26.217 Apple Inc. 859 25.718 YR.NO 855 25.619 Federated Media Publishing 807 24.220 Aller Media 790 23.7

poland

Top 20 Sites in poland

Source: comScore mmx, december 2012

Total unique

visitors (000)% reach

Total Internet Audience: Age 15+ 19,350 100.0