IAB interview

40

The Accountant A VRL publication EstablishEd 1875: thE profEssion’s oldEst nEws sourcE 02-03 NEWS n druckman takes on trucost challenge n calls increase for isa adoption in Europe n audit firm registration under review 04 INTERVIEW: GHOLAMHOSSEIN DAVANI the iranian accounting profession has been developing as rapidly as the profession in western countries in recent years. an industry figure speaks with carolyn canham about the state of the industry and its global successes and ambitions 08-09 FEATURE: TAIWAN taiwan’s accounting profession is beset by regulatory changes and fierce competition. but improved relations with china could lead to more opportunities 10-15 COUNTRY SURVEY: UNITED KINGDOM it’s all about the f inancial crisis for the uK’s professional accounting bodies again this year and no doubt that topic will remain good for at least the next 12 months. the crisis is affecting the institutes in different ways, but all are positive the relevance of their qualifications remains true October 2009 Issue 6071 PEOPLE Profession braces for EC endorsement news STANDARD-SETTING The world will be watching next month to see how the International Accounting Stand- ards Board’s (IASB) new financial instruments classification and measurement standard is received in Europe. The rules will replace part of IAS 39 – Financial Instruments Recognition and Meas- urement, a standard so contentious it has been discussed and criticised by European national leaders and the G20. Once the standard is released, it will be in the hands of European politicians to decide whether it will be applied in the EU. Europe triggered a worldwide trend to adopt IFRS when it mandated the use of the standards for listed companies from 2005. But European Financial Reporting Adviso- ry Group chair Stig Enevoldsen said recently that if Europe does not endorse the classifica- tion and measurement standard, the question could be asked ‘is Europe still using IFRS?’ Several high profile figures in the UK pro- fession have said the EC could easily move either way. An indicator towards the EC not endorsing the standard is the chilly reception to the IASB’s work from European finance ministers, particularly those from France and Germany. Indicators towards EC endorse- ment include pressure from the G20 for a single set of global standards and news the US Securities and Exchange Commission is working on its proposed road map for IFRS adoption with renewed purpose. IASB chairman David Tweedie addressed EU finance minsters recently, saying the board has made changes since the exposure draft that respond to concerns from the EC. The changes include allowing reclassifica- tion of financial instruments when business models change, which the EC says is essen- tial. Another EC concern that has been addressed was extended use of fair value measurement. Tweedie said the new standard will probably result in financial institutions that undertake traditional banking activities applying less fair value accounting. The IASB has a delicate balance to strike in terms of pleasing Europe and maintaining independence. November will be an interest- ing month. < Carolyn Canham Jimmy Buffet’s Changes in Latitude, Changes in Attitude is one of Robert Harris’s favourite songs and the title the new chairman of the world’s largest accounting body chose for his inauguration speech. Harris focused on four main points as he embarked on his one-year term as chair of the American Institute of Certified Public Accountants (AICPA): globalisation, sustain- ability, re-regulation of financial services, and getting more CPAs actively involved in the profession. Sustainability and the globalisation of the CPA profession, particularly in terms of accounting standards, have been two areas the US has lagged on, but this is changing. At the highest level of politics, former US President George W Bush is infamous for his denial of issues such as climate change, while awareness of these issues is growing under the Obama administration. Sustainability is also high on Harris’s agen- da and he told The Accountant the AICPA is taking a leadership role by becoming involved in the Prince of Wales’ Accounting for Sus- tainability project. “There are no official rules on how an organisation would report sustainability. The CPA profession can play a critical role by cre- ating the measures and furnishing the proof that businesses can be profitable and, at the same time, environmentally responsible,” Harris said. The US is the last of the world’s major economies with no firm timeline for allowing or mandating the use of IFRS for large listed companies. This too, could soon change. “It’s essential to have a date certain for future adoption if the United States is going to gather any real momentum towards adopt- ing IFRS,” Harris said. The US Securities and Exchange Com- mission’s draft road map for IFRS adoption envisioned US adoption by 2014. But Harris said AICPA membership surveys have shown the majority think it would take three to five years to adopt IFRS and 2015 is a more real- istic date. Harris said convergence in other areas, such as auditing standards and regulation, is also important. Audit oversight reliance between the EU and the US hit a snag recently, with the EC excluding the US from a proposal that audit regulators in EU member states co-operate with certain other national regulators in the exchange of audit working papers. One condition was reciprocity, which the US cannot grant due to national law. Harris said the Public Company Accounting Over- sight Board is working with US politicians and foreign counterparts to find a solution. “There is correcting language in pending legislation in the House of Representatives that would expand the production of audit information and provide for exchanges with foreign counterparts,” Harris added. AICPA veteran Harris has a lengthy history of service with the AICPA, including time on the board of directors and the governing council. He was chair of the National Accreditation Commis- sion between 2003 and 2008, and has been involved with committees covering issues as diverse as women’s initiatives, disability insur- ance, state legislation and finance. Harris is also managing director of Harris, Cotherman, Jones, Price & Associates, a local CPA firm based in Vero Beach, Florida. < Carolyn Canham New AICPA president welcomes changing times in the US Robert Harris, AICPA

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of IAB interview

The

Accountant

A VRL publication Es tablishEd 1875: thE profEssion’s oldEs t nEws sourcE

02-03 NEWS

n druckman takes on trucost challengen calls increase for isa adoption in Europen audit firm registration under review

04 INTERVIEW: GHOLAMHOSSEIN DAVANI

the iranian accounting profession has been developing as rapidly as the profession in western countries in recent years. an industry figure speaks with carolyn canham about the state of the industry and its global successes and ambitions

08-09 FEATURE: TAIWAN

taiwan’s accounting profession is beset by regulatory changes and fierce competition. but improved relations with china could lead to more opportunities

10-15 COUNTRY SURVEY: UNITED KINGDOM

it’s all about the financial crisis for the uK’s professional accounting bodies again this year and no doubt that topic will remain good for at least the next 12 months. the crisis is affecting the institutes in different ways, but all are positive the relevance of their qualifications remains true

October 2009 Issue 6071

PEOPLE

Profession braces for EC endorsement news

STANDARD-SETTING

The world will be watching next month to see how the International Accounting Stand-ards Board’s (IASB) new financial instruments classification and measurement standard is received in Europe.

The rules will replace part of IAS 39 – Financial Instruments Recognition and Meas-urement, a standard so contentious it has been discussed and criticised by European national leaders and the G20.

Once the standard is released, it will be in the hands of European politicians to decide whether it will be applied in the EU.

Europe triggered a worldwide trend to adopt IFRS when it mandated the use of the standards for listed companies from 2005.

But European Financial Reporting Adviso-ry Group chair Stig Enevoldsen said recently that if Europe does not endorse the classifica-tion and measurement standard, the question could be asked ‘is Europe still using IFRS?’

Several high profile figures in the UK pro-fession have said the EC could easily move either way. An indicator towards the EC not endorsing the standard is the chilly reception to the IASB’s work from European finance ministers, particularly those from France and Germany. Indicators towards EC endorse-ment include pressure from the G20 for a single set of global standards and news the US Securities and Exchange Commission is working on its proposed road map for IFRS adoption with renewed purpose.

IASB chairman David Tweedie addressed EU finance minsters recently, saying the board has made changes since the exposure draft that respond to concerns from the EC.

The changes include allowing reclassifica-tion of financial instruments when business models change, which the EC says is essen-tial.

Another EC concern that has been addressed was extended use of fair value measurement. Tweedie said the new standard will probably result in financial institutions that undertake traditional banking activities applying less fair value accounting.

The IASB has a delicate balance to strike in terms of pleasing Europe and maintaining independence. November will be an interest-ing month. <

Carolyn Canham

Jimmy Buffet’s Changes in Latitude, Changes in Attitude is one of Robert Harris’s favourite songs and the title the new chairman of the world’s largest accounting body chose for his inauguration speech.

Harris focused on four main points as he embarked on his one-year term as chair of the American Institute of Certified Public Accountants (AICPA): globalisation, sustain-ability, re-regulation of financial services, and getting more CPAs actively involved in the profession.

Sustainability and the globalisation of the CPA profession, particularly in terms of accounting standards, have been two areas the US has lagged on, but this is changing.

At the highest level of politics, former US President George W Bush is infamous for his denial of issues such as climate change, while awareness of these issues is growing under the Obama administration.

Sustainability is also high on Harris’s agen-da and he told The Accountant the AICPA is taking a leadership role by becoming involved in the Prince of Wales’ Accounting for Sus-tainability project.

“There are no official rules on how an organisation would report sustainability. The CPA profession can play a critical role by cre-ating the measures and furnishing the proof that businesses can be profitable and, at the same time, environmentally responsible,” Harris said.

The US is the last of the world’s major economies with no firm timeline for allowing or mandating the use of IFRS for large listed companies. This too, could soon change.

“It’s essential to have a date certain for future adoption if the United States is going to gather any real momentum towards adopt-ing IFRS,” Harris said.

The US Securities and Exchange Com-mission’s draft road map for IFRS adoption envisioned US adoption by 2014. But Harris said AICPA membership surveys have shown the majority think it would take three to five years to adopt IFRS and 2015 is a more real-istic date.

Harris said convergence in other areas, such as auditing standards and regulation, is also important.

Audit oversight reliance between the EU and the US hit a snag recently, with the EC excluding the US from a proposal that audit regulators in EU member states co-operate with certain other national regulators in the exchange of audit working papers.

One condition was reciprocity, which the US cannot grant due to national law. Harris said the Public Company Accounting Over-sight Board is working with US politicians and foreign counterparts to find a solution.

“There is correcting language in pending legislation in the House of Representatives that would expand the production of audit information and provide for exchanges with foreign counterparts,” Harris added.

AICPA veteranHarris has a lengthy history of service with the AICPA, including time on the board of directors and the governing council. He was chair of the National Accreditation Commis-sion between 2003 and 2008, and has been involved with committees covering issues as diverse as women’s initiatives, disability insur-ance, state legislation and finance.

Harris is also managing director of Harris, Cotherman, Jones, Price & Associates, a local CPA firm based in Vero Beach, Florida. <

Carolyn Canham

New AICPA president welcomes changing times in the US

Robert Harris, AICPA

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

2

The Accountant October 2009

www.WorldAccountingIntelligence.com

One of the UK’s foremost figures in account-ing for sustainability has taken on a new challenge leading an environmental data company.

Paul Druckman is a past president of the Institute of Chartered Accountants in Eng-land and Wales, chairman of the Federa-tion of European Accountants sustainability policy group and chairman of the executive board of the Prince of Wales Accounting for Sustainability project.

Adding to his raft of positions, he recently became chairman of environmental data com-pany Trucost. Trucost maintains a data base with information on 4,500 global companies, including the world’s largest.

There are two sides to the business. One is selling the data and services based on the data to investors; the other is providing the data to companies so they can see their own environmental footprints and impacts.

Druckman said he believes Trucost occu-pies a niche spot in the market.

“There are no other organisations doing what we do,” he told The Accountant. “There are other organisations that provide data, but it is not the same concept because we are maintaining, validating, standardising and monetising the data that we have.

“We have the data and the model to have a complete environmental footprint, it’s more than just about carbon. Some companies are doing different pieces of that, but not the overall complete set.”

Environmental performanceTo date, much of Trucost’s emphasis has been on the investor side of the business, for exam-ple informing investors who want to know if a fund is low carbon.

“[Trucost can find] the best performing companies or the worst performing compa-nies in terms of their environmental impact,” Druckman said. “If you want to build a low carbon fund, how do you know which com-panies are low carbon? It may not be that you only invest in the lowest, but at least you will see the ranking and make an informed deci-sion.”

The company is making inroads into the public sector as well as the corporate sector.

“We have contracts on the supply chain side with local authorities and health care organisations,” Druckman explained.

“Some of them have incentives to do that through government schemes and incentives. Others just want to be best practice.”

Druckman’s role at Trucost combines the

three areas of specialisation he has developed during the past 10 years – technology, sus-tainability and the accounting profession.

First, Trucost is essentially a technology solution. Second, its provision of environmen-tal data hits the sustainability mark. Finally, Trucost converts non-financial environmental information into financial information.

“Trucost has the ability to make the accounting profession understand what all this is about because of the quantitative nature of the data,” Druckman explained.

Druckman said this financial data is a raw material that businesses can use to build sus-tainability issues into financial models.

“It has always been possible [to embed sustainability into investment decision mak-ing], but it is still a big learning curve for an accountant,” Druckman added.

“Accountants in normal practice must start looking at these externalities rather than just the financial return because they need to understand that the world is changing and there are other pressures on the behaviour of a company that will affect its value, and not just in an altruistic sense. Now here is some-thing they can actually grab hold of and use with a clearer understanding.”

Druckman said one opportunity for Tru-cost is to move beyond being a separate data source and become embedded in what other organisations do.

“Accounting software houses could have Trucost environmental data associated with their accounting systems,” Druckman said.

“Going back to the accounting side of it, there is no reason why management accounts should not now include an environmental footprint.” <

Carolyn Canham

Group Editor: arvind hickman tel: +44 (0)20 7563 5631Email: [email protected]

Editor: carolyn canhamtel: +44 (0)20 7563 5679Email: [email protected]

Senior Reporter: nicholas Moodytel: +44 (0)20 7563 5673Email: [email protected]

Surveys Researcher: nicola Maher tel: +44 (0)20 7563 5618Email: [email protected]

Contributors: david hayes

Chief Sub-editor: Mark armitageSub-editor: brooke balza

Editorial Director: hugh fasken tel: +44 (0)20 7563 5616Email: [email protected]

Head of Global Sales: Joseph alvarez tel: +44 (0)20 7563 5650Email: [email protected]

Advertising Manager: Edith piekarz tel: +44 (0)20 7563 5634Email: [email protected]

Sales Executive: Kinnor bhattacharya tel: +44 (0)20 7563 5638Email: [email protected]

Customer Services: Kirsten lamb tel: +44 (0)20 7563 5688 Email: [email protected]

for more information on Vrl, visit our website at www.vrlfinancialnews.comfor more information on accessing The Accountant content online, including a five-year archive, please telephone +44 (0)20 7563 5688 or email [email protected]

London Office34 porchester road, london w2 6Es, united Kingdomtel: +44 (0)20 7563 5600fax: +44 (0)20 7563 5601

Asia Office20 Maxwell road#09-01a, Maxwell housesingapore 069113tel: +65 6383 4688fax: +65 6383 5433Email: [email protected]

financial news publishing ltd, 2009registered in the uK no 6931627issn 0001-4710

unauthorised photocopying is illegal. the contents of this publication, either in whole or part, may not be reproduced, stored in a data retrieval system or transmitted by any form or means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publishers.

The

Accountant

NEWS

SUSTAINABILITY

Druckman takes Trucost challenge

Paul Druckman

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

3

October 2009 The Accountant

www.WorldAccountingIntelligence.com NEWS

PEOPLE

Schapiro voices support for global accounting standardsthe chairman of the us securities and Exchange commission (sEc) has said she remains committed to the goal of a global set of high-quality accounting standards.speaking at an international organization of securities commissions conference in switzerland this month, Mary schapiro said the financial crisis has highlighted the importance of implementing and enforcing high quality and consistent accounting standards around the world.“i remain committed to the goal of a global set of high-quality accounting standards,” she said. “i also believe that there are issues that will be critical to address as we at the sEc consider the input we have received on last year’s proposed road map on the role of international standards in the us.”

ASSURANCE

IAASB launches consultation on greenhouse gas standardthe international auditing and assurance standards board (iaasb) is seeking views on the development of a new assurance standard on green house gas (GhG) statements. the project seeks to enhance the consistency and quality of performance by practitioners on assurance engagements to report on this information, whether produced for regulators, legislators or investors.Assurance on a Greenhouse Gas Statement asks a series of questions addressing such matters as the form of assurance report that users would find most useful, the nature and extent of requirements, how a standard should best integrate with regulatory requirements, and technical aspects of applying the assurance process to GhG emissions.an exposure draft is scheduled for release next year.

FAIR VALUE

IASB and FASB hold out hope for fair value convergencethe international accounting standards board and the us financial accounting standards board were unable to resolve their differing opinions on the extent that financial instruments are measured at fair value at a meeting in the us this week.according to us media reports, the boards agreed to explore ways to facilitate easy comparisons if the rules in ifrs and us Gaap differ.iasb chair david tweedie also claimed that if the rules are not identical by 2010 they should be “appreciably together”. <

NEWS BRIEFS

The close of an EC consultation on the adop-tion of ISAs in Europe has heralded increased statements in their favour.

The UK Auditing Practices Board (APB) issued 33 clarified ISAs as audit standards for the UK and Ireland on 13 October, becoming one of the first major jurisdictions to do so.

APB chairman Richard Fleck said the new ISAs are more rigorous and clearer than exist-ing auditing standards in any country.

“The APB hopes that these standards will be mandated for use within the European Union in the near future,” Fleck added.

The Committee of European Securities Reg-ulators (CESR) also supports the introduction of ISAs in Europe.

CESR has said there is growing interna-tional acceptance of ISAs and many potential benefits of harmonised auditing standards in the EU.

CESR supports a European endorsement process but says this should be used with pre-caution and changes made only in “highly rare circumstances”, otherwise it could erode the coherence of the standards and their inter-national acceptability.

The Institute of Chartered Accountants in England and Wales (ICAEW) is also in favour of mandating ISAs in Europe. How-ever, ICAEW executive director Robert Hodgkinson said the institute disagrees with

an endorsement process that allows for “add-ons or carve-outs”.

Hodgkinson said if there is a “seed of doubt” regarding what exact standards have been used, it can have an adverse effect on the ability to take an audit report at face value.

The EC consultation suggested three options for the scope of an adoption: only the statu-tory audits of listed companies; the statutory audits of all limited companies except small companies; or, all statutory audits in the EU.

The ICAEW wants ISAs applied to all audits.

“Having two or more sets of standards would make it expensive for the audit market and also a bit confusing because inevitably one will be thought of as better than the other and certain audits will be seen as second rate,” Hodgkinson said.

Hodgkinson said infrastructure must be in place to ensure audits are not unnecessarily onerous.

“It is about making sure that the training, software, commercial packages and working paper packages are there for firms that can’t afford to develop their own,” he explained.

Hodgkinson said while the standards them-selves are important, having the practical tools needed to deliver audits is just as vital. The ISAs come with this complete package. <

Carolyn Canham

India’s audit regulator plans to limit the number of audit firms a network can be affiliated with in a post-Satyam shake-up that could have wide implications for the Big Four. This follows questions over the extent of PricewaterhouseCoopers (PwC) affiliates’ involvement in the Satyam accounting fraud.

Global networks such as PwC are affiliated with multiple audit firms registered in the country to overcome Indian laws that restrict the number of partners a firm may have to 20. There are nine offices in India affiliated with PwC. These operate in partnership but are mostly structured as separate legal enti-ties. Many carry variations of the name Price Waterhouse.

The Institute of Chartered Accountants of India’s (ICAI) proposal is to allow only two registered audit firms from the “same entity”.

This would affect all the Big Four networks.The proposal is designed to prevent global

networks from washing their hands of errone-ous work carried out by affiliated firms.

Opponents of the ICAI proposal argue that firms will set up new partnerships under dif-ferent names and the rules could restrict the ability of large audit firms to serve their cli-ents, having a detrimental effect on capital markets.

The Indian government recently said it could take action within a couple of months against the firms Price Waterhouse Banga-lore, Price Waterhouse New Delhi and Price Waterhouse Kolkata, four Price Waterhouse Bangalore auditors and two former Satyam Computer Services employees implicated in the Satyam accounting scandal. <

Arvind Hickman and Nicholas Moody

Calls increase for ISA adoption in Europe following EC consultation

Audit firm registration under review

AUDIT

SATYAM

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

4

The Accountant October 2009

www.WorldAccountingIntelligence.com

the relationship between Iran and the West has produced news headlines for decades. The most contentious recent issues have been the republic’s nuclear

programme and election results disputed loud-ly both at home and abroad. But in the face of high-level political wrangling, Iran’s account-ing profession is moving ever more closely in step with the rest of the world.

The Iranian Accounting Association (IAA) is holding Iran’s second international account-ing conference in December, following a suc-cessful inaugural event in 2008.

Conference board member Gholamhos-sein Davani says the issues on the conference agenda are similar to those reverberating around the rest of the world. Specific areas to be covered include accounting education, international accounting standards, corporate governance, corporate social responsibility and capital markets development.

Accounting education is one area where Iran has particularly close international ties. Davani lists at least three Iranian accounting professors teaching in the US and the UK, including University of Memphis professor Zabihollah Rezaee, who is expected to appear at the upcoming conference.

The IIA is one of three professional account-ing bodies in Iran. The oldest is the Iranian Institute of Certified Accountants (IICA), which was established in 1972 by a group of Iranians who were members of UK accounting institutes. The IICA is member of the Interna-tional Federation of Accountants (IFAC).

The second is the official Iranian Associa-tion of Certified Public Accountants (IACPA), which was established by the government in 1999 and is an associate member of IFAC. The third is the IAA, which Davani compares with the American Accounting Association in its role of promoting excellence in accounting education, research and practice.

The IACPA currently has about 1,600 members. As of January 2008, it listed 173 registered member firms.

Davani estimates there are about 45 active audit firms and the fee income of the largest in 2008 was about $1.5 million. This minute size reflects a profession that is heavily govern-ment-controlled and in need of development.

Of the world’s 10 largest accounting net-works, just four have member or correspond-ent firms listed on their global websites. None of the Big Four do.

Davani is managing partner of Dayarayan Auditing & Financial Services, an RSM Inter-national correspondent firm, which Davani says has been the top ranking firm in terms of fee income twice in the past five years.

Davani explains that prior to the Islamic Revolution in 1979, all the large international organisations were represented in Iran. But following the revolution, many private enter-prises were confiscated or came under direct government supervision. Subsequently, three audit organisations were formed within the public sector to audit and performing statu-tory services for these newly state-owned enterprises.

A 1983 Act of Parliament merged the three organisations and an earlier government audit organisation to form the Audit Organization.

Today, the Audit Organization is a finan-cially independent legal entity affiliated with the Ministry of Economic Affairs and Finance. Davani says its revenue forms about 50 per-cent of the Iranian audit market’s total reve-nue, which in 2008 was about $100 million.

Davani says audit fees in Iran are very low and the market needs support to help it devel-op.

“Iranian auditors have demonstrated, through the development of audit and consult-ing practices and tax services lines, that they will continue to invest in new service capabili-ties when they see demand,” Davani says.

However, he warns if audit policy does not

change in line with wider privatisation proc-esses the nation will find it hard to compete globally.

“Demand for certified public accountants in Iran is progressive and the future outlook for auditing and professional services depends on opening the market to foreigners and inter-national accounting firms,” Davani says, add-ing there are many opportunities for the local profession to partner with foreign investors to help build the Iranian economy.

He estimates the Iranian audit market has the potential to be worth more than $200 mil-lion.

The Audit Organization is also the official standard setter, authorising the audit and accounting standards that the profession must follow. Davani says accounting standards are about 95 percent in line with IFRS.

One critically important role for the audit and accounting profession moving forward is fostering accountability, transparency and responsibility. Davani says accountability in Iran is unfortunately weak as 90 percent of the economy is in the hands of government.

“I believe all governments try to run away from accountability and transparency, espe-cially when they are not accountable.

“However, I think under-developed coun-tries must support accounting and auditing to fight with corruption and develop transpar-ency to stabilise accountable and responsibil-ity,” he says. <

INTERVIEW: GHOLAMHOSSEIN DAVANI

practice in audit firms 44%

do not practice 30%audit organization employees 16%

sole practitioners 10%

source: The Accountant

n IACPA MEMBERSHIP 2009

Breakdown of the IACPA’s 1,600 members

“I think under-developed countries must support accounting and auditing to fight with corruption and develop transparency to stabilise accountability and responsibility”Gholamhossein davani

After the revolutionthe iranian accounting profession has been developing as rapidly as the profession in western countries in recent years. industry figure Gholamhossein davani speaks with Carolyn Canham about the state of the industry, its global successes and ambitions for the future

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

5

October 2009 The Accountant

www.WorldAccountingIntelligence.com NEWS

A further delay in the implementation of Sec-tion 404(b) of the Sarbanes-Oxley Act (SOX) for small public companies is a negative move with few benefits, one US firm has warned.

At the same time, the US Institute of Man-agement Accountants (IMA), which 18 months ago was calling for the requirements to be waived or completely redesigned for small public companies, is pleased with the way they have been made more scalable.

The Securities and Exchange Commission (SEC) this month delayed the SOX imple-mentation deadline to fiscal years ending on or after 15 June 2010 for the smallest US pub-lic listed companies – those with public floats of less than $75 million – to allow extra time to design, implement and document internal control systems before auditors are required to attest to their effectiveness.

An assurance partner of a large East Coast firm believes the delay is unnecessary and embarrassing to firms who had encouraged clients to become SOX-ready by the end of this year.

“It did not make much sense to me because most companies have been complying on an internal basis as they have been doing man-agement assessments for the past two years,” Marcum assurance partner-in-charge Gregory Giugliano said. “We also lose a little faith with our clients as we have been encouraging them to start this and then it gets delayed again.”

The exemption period for small compa-nies was previously due to end for fiscal years ending on or after 15 December 2009, which means most small listed companies had either prepared for implementation or chosen to de-register their listing.

The SEC extended the date so it could com-plete a study on whether additional guidance provided to company managers and auditors in 2007 was effective in reducing the costs of compliance.

More relevantBruce Pounder chairs the IMA’s small busi-ness financial and regulatory affairs commit-tee. He said the IMA is happy with the addi-tional guidance provided in 2007 because it made the internal and external audits of internal controls over financial reporting more scalable and risk-based. The guidance helps management and auditors to establish what is important to stakeholders and adjust procedures accordingly.

Giugliano estimates client audit fees increase

by between 20 percent and 40 percent due to SOX implementation, and additional cost can vary from $10,000 to $200,000.

“Clients also have to absorb internal expenses, which can include internal staff time or the use of external consultants,” he said.

The added costs are one reason Pounder said small companies that have not yet com-plied with 404(b) must act now.

“There is going to be a new cost hit, there is no question about it and one of the things that came out in an SEC study released earlier this month about the cost and benefits of 404 compliance is the costs are clearly proportion-ately higher for smaller companies than for larger companies,” Pounder said.

“It is absolutely a bigger issue for smaller companies to think about how they are going to pay for this, where the money is going to come from and how they can make sure this is not a financial disaster.”

Companies preparing for compliance must also evaluate whether they are happy with their current external auditor as the same auditor must be used for 404(b) requirements, Pounder added

“If you are thinking about changing audi-tors, now is the time to do that, before you get into the more involved requirements for 404(b),” Pounder said.

Grant Thornton US national managing partner of public policy and corporate govern-ance Trent Gazzaway also warned companies against delaying implementation any longer.

“An organisation’s efforts to prepare for compliance often uncovers costly inefficien-cies and potentially damaging risks. Compa-nies that wait for another delay could also be delaying opportunities to make enhancements that could improve their bottom lines,” he said.

Gazzaway’s comments follow a recent sur-vey of senior financial executives by Grant Thornton that found 74 percent of respond-ents thought small listed companies should not be forced to comply with Section 404(b).

Marlene Hutcheson, a partner at Las Vegas-based firm De Joya Griffith & Company, believes the extension is positive.

“Some filers were (also) thinking of ceasing being a reporting company because they were not ready but with the extension some of these companies will rethink and may revisit their business plan to incorporate becoming SOX compliant and continue to file,” she said. <

Nicola Maher and Carolyn Canham

Opinion divided over SOX delay for small companies in the US

REGULATION

STANDARDS

EFRAG to fast track financial instruments advicethe European financial reporting advisory Group (EfraG) will fast track endorsement advice on a new global accounting standard for classifying and measuring financial instruments. the decision is based on a European commission request to have a standard in place for listed companies to apply for 2009 year end reports. the international accounting standards board’s project to replace ias 39 financial instruments – recognition and Measurement has three phases and the board plans to issue this first standard early next month. EfraG plans to finalise Ec endorsement advice by 17 november.

STANDARDS

Islamic finance group plans framework updatethe accounting and auditing organisation for islamic financial institutions (aaoifi) plans to update standards on the conceptual framework for financial reporting and accounting for investments for the international islamic finance industry. Exposure drafts were expected to be distributed before the end of october.“aaoifi has developed the updated standards to further support the expansion of islamic finance industry and promote international best practices,” aaoifi secretary general Mohamad nedal alchaar said.

STANDARDS

Mixed response to IFRS in UStwo in five us chief financial officers and senior comptrollers do not believe us companies should ever have to use ifrs, according to new research from Grant thornton us. another 39 percent said us companies should start using ifrs in three to five years. only 7 percent want to start using it immediately. the biannual study surveyed 846 chief financial officers and senior comptrollers from 21 september to 2 october.

STANDARD-SETTING

FASB initiates non-for-profit groupthe us financial accounting standards board is to create a not-for-profit advisory committee (nac). the nac will seek comment from the not-for-profit sector on existing guidance, current and proposed technical agenda projects, and longer-term issues affecting those organisations. the 12 to 15 member committee will be formed from the not-for-profit sector early next year, with its first meeting taking place in the middle of 2010. <

NEWS BRIEFS

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

6

The Accountant October 2009

www.WorldAccountingIntelligence.comREGION ROUND-UP

• American Institute of Certified Public Accountants (AICPA) president and chief executive Barry Melancon has told the US President’s Economic Recovery Advisory Board that a comprehensive tax reform is needed.

“The dynamic American economy is rebounding slowly and, we believe, is bur-dened by an unnecessarily cumbersome and somewhat outdated income tax system,” Melancon said.

“In particular, we see significant problems for small businesses arising from the increas-ing complexity of the tax law.”

The AICPA said the US Congress is likely to take up tax reform as a major legislative challenge beginning in January.

• The US Federal Accounting Standards Advisory Board (FASAB) has issued a new standard for estimating the historical cost of general property, plant and equipment.

Statement of Federal Financial Account-ing Standards (SFFAS) 35 amends SFFAS 6 and 23 and clarifies that reasonable esti-mates of original transaction data historical cost may be used to value general property, plant and equipment.

The FASAB is responsible for setting accounting standards for the US Federal Government.

• The national average salary for US finance and accounting positions is expect-ed to decline less than 1 percent next year,

according to a survey from recruiters Ajilon.

Chief financial officers and treasurers are among the positions that will witness a sharp wage decrease, with the national aver-age salary expected to drop almost 8 percent next year, compared with 2009.

The survey was compiled by combin-ing national salary data from hundreds of Ajilon’s staff recruiting for finance and accounting positions at companies in 75 major markets across North America.

• The US Public Company Accounting Oversight Board (PCAOB) has changed the effective date of new rules that require reporting by registered public accounting firms and provide for succeeding to the reg-istration status of a predecessor firm.

The postponement will allow the PCAOB to resolve technical issues related to deploy-ing its new online system for processing and publishing filings on the new forms.

It will not affect the timing of the first annual reports required from registered firms, which will still be due on 30 June 2010 for the 12 months ending 31 March 2010.

• Almost three-quarters of US execu-tives want the US Securities and Exchange Commission (SEC) to approve its proposed IFRS road map or a modified version of it, according to a survey by Deloitte US.

The study found 51 percent of respond-

ents thought the SEC should approve the proposed road map but consider pushing back the mandatory deadline by a year, and 19 percent believe the SEC should approve its proposed road map “as is”.

Opinions were split on the approach to convergence.

Thirty-nine percent of respondents want-ed the International Accounting Standards Board and Financial Accounting Standards Board to achieve as much convergence as possible between now and 2011, and then focus on IFRS conversion.

The same number wanted the two groups to extend the convergence plan over the next 5 to 10 years.

• More than 47 percent of Canadians who hold the chartered financial analyst designa-tion are not very confident that they have a full understanding of what the impact of IFRS will be on the companies they invest or follow, according to a survey by PricewaterhouseCoopers Canada. Twenty percent were not at all confident.

Canada is due to complete its transition to IFRS by January 2011. <

• The Hong Kong Institute of Certified Public Accountants (HKICPA) will continue to liaise with Hong Kong’s Financial Report-ing Council (FRC) and Ernst & Young (E&Y) during investigations into the Big Four firm’s auditing of Akai Holdings.

Last month, Hong Kong police searched E&Y’s local offices and seized original work-ing papers in connection with the suspected forgery of Akai’s audit documents.

The Big Four firm was in court last month facing allegations it was negligent in its audits of Akai from 1997 to 1999.

E&Y settled with the liquidator of the Chinese consumer electronics company for an undisclosed amount and suspended one of its partners after finding some of the docu-ments in the audits of Akai could “no longer be relied on”.

The HKICPA said once sufficient evidence emerged from the FRC and police investiga-tions to show that institute members may have been involved in the falsification of

documents, it would initiate its disciplinary process.

• The Korean Institute of Certified Pub-lic Accountants will train accounting staff at central government agencies and public organisations as part of an agreement with the Ministry of Strategy and Finance.

The agreement was signed after Korea adopted accrual accounting and double-entry bookkeeping for governmental accounting on 1 January 2009.

The institute said more than 1,000 people have signed up for the training but due to budget constraints, only 740 will be able to participate.

They include accounting personnel from 48 major government agencies.

• New Zealand has become one of the first countries to apply the full set of clarified International Standards on Auditing (ISAs), according to the local professional account-

ancy body. For audits of financial statements covering periods beginning on or after 1 October 2009, auditors complying with New Zealand auditing standards will also be able to assert compliance with ISAs.

New Zealand Institute of Chartered Accountants general manager for standards and advocacy Bruce Bennett said this change will complete a process of strengthening auditing and financial reporting in New Zea-land that began in 2005.

“Over the past four years, we have been progressively adopting the international standards and educating our members on these new standards,” he said. <

asia -pacific

nor th aMEric a, l atin aMEric a

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

7

October 2009 The Accountant

www.WorldAccountingIntelligence.com REGION ROUND-UP

• Supervision of the financial sector in Europe is set to be revamped through the for-mation of a series of new regulatory organi-sations. The EC has adopted draft legisla-tion that aims to reinforce financial stability throughout the EU, identify systematic risks at an early stage and foster cohesion and co-operation in emergency situations.

The legislation will create a new European Systemic Risk Board (ESRB) to detect risks to the financial system as a whole.

It would also set up a European System of Financial Supervisors, composed of national supervisors and new authorities to oversee the banking, securities, insurance and occu-pational pensions sectors.

Three new European supervisory authori-ties will be created by transforming existing committees. The Committee of European Banking Supervisors will become the Euro-pean Banking Authority, the Committee of European Insurance and Occupational Pensions Committee will become the Euro-pean Insurance and Occupational Pensions Authority and the Committee of European Securities Regulators will become the Euro-pean Securities and Markets Authority.

In addition to assuming the existing func-tions of the committees, the new authorities will be responsible for developing proposals for technical standards; resolving cases of disagreement between national supervisors, where legislation requires them to co-operate or agree; and contributing to ensuring con-sistent application of technical community rules.

• The UK Audit Practice Board (APB) has issued updated guidance on the auditing of complex financial instruments. The updated practice note (PN) 23 modernises an earlier version created in 2002.

It is aimed at assisting auditors address current considerations that are relevant in the audit of financial statements of entities that use complex financial instruments.

The guidance widens the scope of PN 23 to cover other complex financial instruments, as well as derivatives, as many of the audit considerations are the same, the APB said.

• A recent survey of UK accountants found 86 percent regularly work past normal work-ing hours and 52 percent do so every day.

The study, by online accounting provider e-conomic, also found 38 percent of respond-ents regularly work past 10pm, and 22 per-cent of those that have children said it is quite normal for them to not get home in time to see their children before bedtime.

The most popular response when asked what single thing would most improve their work life balance was ‘less work for a higher margin’ and 28 percent thought they were over-worked and under-paid.

The e-conomic survey was conducted this month among 2,000 accountants.

• Des Hudson has been appointed chair-man of the Taxation Disciplinary Board by the Chartered Institute of Taxation (CIOT) and the Association of Taxation Technicians. Hudson is currently chief executive of the Law Society of England and Wales and was previously chief executive of the Institute of Chartered Accountants of Scotland. His four-year term begins on 1 November 2009.

• There is no case for any significant changes in the UK’s governance rules in the wake of the financial crisis, according to a recent study by the Institute of Chartered Accountants of England and Wales (ICAEW) Foundation.

The report, Getting it Right, found that over the past few years more effort has been made to strengthen risk identification proc-esses and ensure board committees spend more time overseeing risk management.

Most of the non-financial company boards are satisfied that their risk management is working well thus there is no need for new governance structures and processes.

• The Institute of Chartered Accountants in England and Wales has launched a register that is intended to give courts greater confi-dence in the evidence presented by members of the accounting profession. The forensic accountant and expert witness accreditation scheme was developed in response to pres-sure from the UK Government for improved credibility of evidence presented to the legal system.

• The UK Financial Reporting Council (FRC) has updated guidance to assist direc-tors of UK companies when making assess-ments of going concern. The guidance is based on three principles: the process direc-tors should follow when assessing going con-cern; the period covered by the assessment; and the disclosures on going concern and liquidity risk.

The guidance takes into account feedback from market participants on a series of docu-ments published by the FRC in the past 12 months. <

• Claims the Indian government has tightened its control over the Institute of Chartered Accountants in India (ICAI) and diluted the power of the institute’s president have been refuted by the institute.

Earlier this month, Indian media reports suggested one rule change, approved by the ICAI’s financial committee, would require all financial issues at the ICAI to be cleared consensually by members of the committee. The committee is made up of three govern-ment nominees, the president and the vice-president.

Previously, the ICAI president had the authority to approve spending. The ICAI said there has been no change in the com-

position of the finance committee since last year. The rumours of efforts to curb the ICAI presidential powers follow criticism from ICAI past president Sunil Talati about reckless spending by current ICAI president Uttam Agarwal. Last month, Talati called for a rethink of the extensive powers granted to ICAI presidents when they take office.

• The Institute of Chartered Accountants in England and Wales (ICAEW) and the Institute of Chartered Accountants of Bang-ladesh (ICAB) have signed a memorandum of understanding (MoU) to work together to develop the accounting and auditing profes-sions in Bangladesh. The two institutes will

continue their work to develop a new ICAB qualification, look at examination require-ments allowing members of one body to access membership of the other, co-operate on developing membership support and liaise on technical matters. The agreement between the two bodies was signed on 26 October by ICAEW president Martin Hagen and ICAB president Nasir Ahmed. <

afric a, MiddlE Eas t, south asia

EuropE

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

8

The Accountant October 2009

www.WorldAccountingIntelligence.comFEATURE: TAIWAN

taiwan’s accounting profession has entered a challenging period follow-ing the recent announcement of a timetable for the adoption of IFRS

and an approaching deadline for accounting firms to decide their public liability status.

New standards and changes in tax laws are expected to generate additional work for accountants, yet there is increasing com-petition among the large number of small practices due to a trend for manufacturing clients to move operations out of Taiwan.

The Big Four and mid-sized accounting firms are poised to benefit from improved relations between Taiwan and Mainland China following the election of the Taiwan Nationalist Party (Kuomintang) president Ma Ying-Jeou last year on a pro-growth platform.

Ma, a Hong Kong-born former mayor of Taipei, won votes with plans for economic expansion after years of relatively slow eco-nomic growth under former president Chen Shui Bian, who failed to develop co-opera-tion with Beijing.

Warming relations between Taiwan and China have lifted Taiwan’s economic out-look since the beginning of this year and given the local stock market an important boost.

Taiwan’s estimated 2,100 accountants could see a 25 percent increase in demand for their services within the next three years, according to the local newspaper Economic Daily News. The report forecasts a further 5 percent increase during this period if another 250 companies list on the Taiwan Stock Exchange in response to government tax incentives and other initiatives to per-suade Taiwanese companies in China to list in Taiwan.

Big Four dominanceThe Big Four audit about 84 percent of Tai-wan’s public listed companies, according to the National Federation of CPA Associa-tions of the Republic of China (NFCPAA). Medium-sized accounting firms audit the remainder as local regulations specify audit firms must employ a minimum of three CPAs to audit a public company.

Big Four firms employ about 18 percent of CPAs in Taiwan. Second-tier accounting firms employ about 15 percent of CPAs and sole proprietors account for the remaining 67 percent.

Taiwan’s planned adoption of IFRS will present accounting firms, especially sole practitioners, with new challenges.

In May, Taiwan’s Financial Supervisory Commission (FSC) announced a two-phase timetable for listed and non-listed companies to adopt IFRS.

Local companies listed on the Taiwan Stock Exchange or the Gre Tai Securities Market and financial institutions under FSC’s supervision must adopt IFRS by 2013.

Non-listed companies, credit co-operatives, credit card companies and insurance compa-nies must adopt IFRS by 2015.

The Taiwanese government previously hes-itated on IFRS adoption due to uncertainty over whether the US would adopt the interna-tional standards.

The Big Four encouraged the government to proceed due to increased foreign shareholding in Taiwanese companies, which has resulted in demands for higher standards of financial reporting. However, small businesses opposed IFRS adoption, saying they do not have the resources to meet the requirements.

“IFRS has recently become a hot topic between the government, academics and prac-ticing accountants,” says Roger Shih, an inter-national affairs and audit committee member at Taipei Provincial CPA Association, one of

the three bodies that form the NFCPAA.Amendments to Taiwan’s Certified Public

Accountants Law that were passed on 1 Janu-ary 2008 are expected to boost the quality of accounting services and bring Taiwanese accounting rules in line with international standards.

One amendment aims to ensure auditors play their part in preventing corporate fraud similar to that which occurred in the collapse of hardware manufacturer Procomp Infor-matics in 2005 and the Rebar Group in 2006-2007.

But the most important change clarifies accounting firm liability. This could cause a wave of mergers among small and medium accounting firms as they seek to achieve the economies of scale needed to operate viable practices. These mergers would be a new phe-nomenon in Taiwan where most businessmen want to retain their autonomy.

Final details of the amendments are still being sorted out between the FSC and NFCPAA, but the revised law is expected to have a greater impact on mid-tier and small firms than the Big Four.

“Under the new CPA Law, accounting firms are allowed until the end of 2009 to decide which status they will take,” Shih remarks. “Accounting firms are waiting, no one has made any announcements yet. They are think-ing of their taxation exposure as they could be liable to pay business tax. At present account-ants just pay personal income tax.”

The NFCPAA is currently campaigning for the government to waive business income tax.

Neighbourly relationsMeanwhile, Taiwan’s policy of developing closer relations with China is encouraging the growth of closer ties between the Taiwanese and Chinese accounting professions.

This process is expected to continue as economic co-operation between Taiwan and the mainland expands. An economic co-oper-ation agreement between the two countries is due to be signed this year.

The government is also reviewing Taiwan’s taxation system, including corporate tax rates and incentives. Corporate tax will be reduced

Warming relations bring promisetaiwan’s accounting profession is beset by challenging regulatory changes and fierce competition. but David Hayes discovers improved relations with china could lead to a more fertile business environment and new opportunities

“At present it is not possible for Taiwanese and mainland accounting firms to join or merge, but some accounting firms in Taiwan and China have co-operation arrangements for client referral, information sharing and other matters”roger shih nfcpaa

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

9

October 2009 The Accountant

www.WorldAccountingIntelligence.com FEATURE: TAIWAN

from 25 percent to 20 percent from 1 January 2010 as part of government efforts to attract investment to Taiwan and encourage Taiwan-ese companies to list their China operations in Taiwan.

Cross-border tiesThe Big Four and some mid-tier account-ing firms in Taiwan and China already offer cross-border services to clients with business activities in both territories. Development of ties by Taiwan and China’s accounting professions is one of the topics discussed by NFCPAA and its CPA association members during regular meetings with the Chinese Institute of Chartered Public Accountants (CICPA) and the provincial CPA organisa-tions across China.

“At present it is not possible for Taiwan-ese and mainland accounting firms to join or merge, but some accounting firms in Taiwan and China have co-operation arrangements for client referral, information sharing and other matters,” Shih explains. “Some Tai-wanese accounting firms doing this are linked to a mid-tier international practice.”

The Taiwanese government has no restric-tion on Taiwanese accounting firms’ relations with mainland Chinese accounting firms but

the Taiwanese government does not accept Chinese accounting firms’ audit reports except from the Big Four, Shih says.

Of Taiwan’s estimated 2,100 CPAs, about 1,800 work in the capital, Taipei. Most of the remaining 300 are in Kaohsiung.

Almost 95 percent of CPAs are thought to be in public practice. The Ministry of Finance, Ministry of Justice and other gov-ernment departments employ a combined total of about 100 accountants. Relatively few qualified CPAs work for industrial or commercial organisations.

As a large number of manufacturing com-panies have moved operations from Taiwan to China during the past decade, the account-ing profession’s workload has declined.

“There is an oversupply of accountants in Taiwan,” Shih notes.

“Sole practitioner accounting firms now do various jobs – they consult for private compa-nies, do tax work, also personal finance, teach in schools and other things.

“They do not specialise in one area. They do many things.”

Another reason competition among accounting practices has intensified is accountants in Taiwan share the accounting market with bookkeeping specialists who do

bookkeeping, tax work and accounting.“They cannot do audit but they can do

consulting for tax and accounting. Their market share is growing as they are cheaper than accountants,” Shih explains.

Many bookkeepers are early retirees from government departments who have good connections with government agencies and find it easy to attract private clients.

“Their clients think they can solve prob-lems for them because of their connections in government. Since 2003 they must be licensed. They were not licensed before,” Shih says.

Qualification requirementsMost prospective accountants study account-ing at local universities. About 40 universities offer accounting courses. Graduates then join an accounting firm for a minimum of two years in an accounting related position to get a CPA licence. The final CPA exam pass rate is about 16 percent each year.

With a pass rate that low, the profession may be over staffed and under-worked, but at least there are no floods of new entrants.

The profession will be looking forward with hope that the improved business envi-ronment will give them room to grow. <

The Taiwanese accounting profession is represented by three associations operat-ing under an umbrella federation. There are local government plans to consolidate this into one body, but this is receiving opposi-tion from China.

The umbrella organisation is the Nation-al Federation of CPA Associations of the Republic of China (NFCPAA), which was founded in Nanjing, China, in 1946.

The three groups the NFCPAA is com-prised of are the Taiwan Provincial CPA Association, Taipei City CPA Association and Kaohsiung City CPA Association.

CPA members pay an annual fee to the associations, which in turn fund the NFCPAA. There is no government fund-ing. The three associations also appoint del-egates to the NFCPAA’s committees.

The Taiwan Provincial CPA Association was set up in 1950 and covers the whole of Taiwan including the capital, Taipei, in the north and the second-largest city, Kaohsi-ung, in the south.

Following two decades of economic development that caused rapid growth in Taipei and Kaohsiung, Taipei CPA Associa-tion was set up in 1970 followed by Kaoh-

siung CPA Association in 1979. Practising CPAs must register with two of the three associations, which allows them to practice either in Taipei and other areas excluding Kaohsiung, or Kaohsiung and other areas excluding Taipei.

CPAs must register with all three associa-tions to practice throughout the whole of Taiwan.

The role of NFCPAA includes oversee-ing the education of accountants and acting as a communications channel between the accounting profession and the government.

The associations provide staff for serv-ice centres in the offices of the Ministry of Finance, the Ministry of Economic Affairs, the Taipei and Kaohsiung national tax administration offices, and the main nation-al tax administration offices throughout Taiwan.

Practising accountants are regulated by the Commercial Department of the Ministry of Economic Affairs. In addition, the gov-ernment’s Financial Commission controls CPAs that audit listed companies. Conse-quently, some accountants are regulated by two organisations.

The Taiwanese government has plans to

reorganise the accounting profession’s cur-rent structure, replacing the NFCPAA and three CPA associations with a single unified body representing Taiwan’s accounting pro-fession. However, this remains stalled due to opposition from Beijing.

“It is impossible to merge as we have to have relations with China’s accounting pro-fession and China wants to deal with three local accountant associations in Taiwan and not one island-wide body,” explained Roger Shih, an international affairs and audit com-mittee member at Taipei Provincial CPA Association.

Staying in favour with the Chinese profes-sion is important as the Taiwanese organisa-tions undertake joint activities with the Chi-nese Institute of CPAs (CICPA) and want this to continue, Shih said.

The NFCPAA meets with the CICPA annually and also meets regularly with CICPA provincial associations.

“Most of the issues we discuss are how we should co-operate in business to serve Taiwanese companies in China; also, the tax situation, labour laws, customs regulations and other matters, and their impact on busi-ness,” Shih said. <

n TAIWAN

The changing shape of the profession

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

10

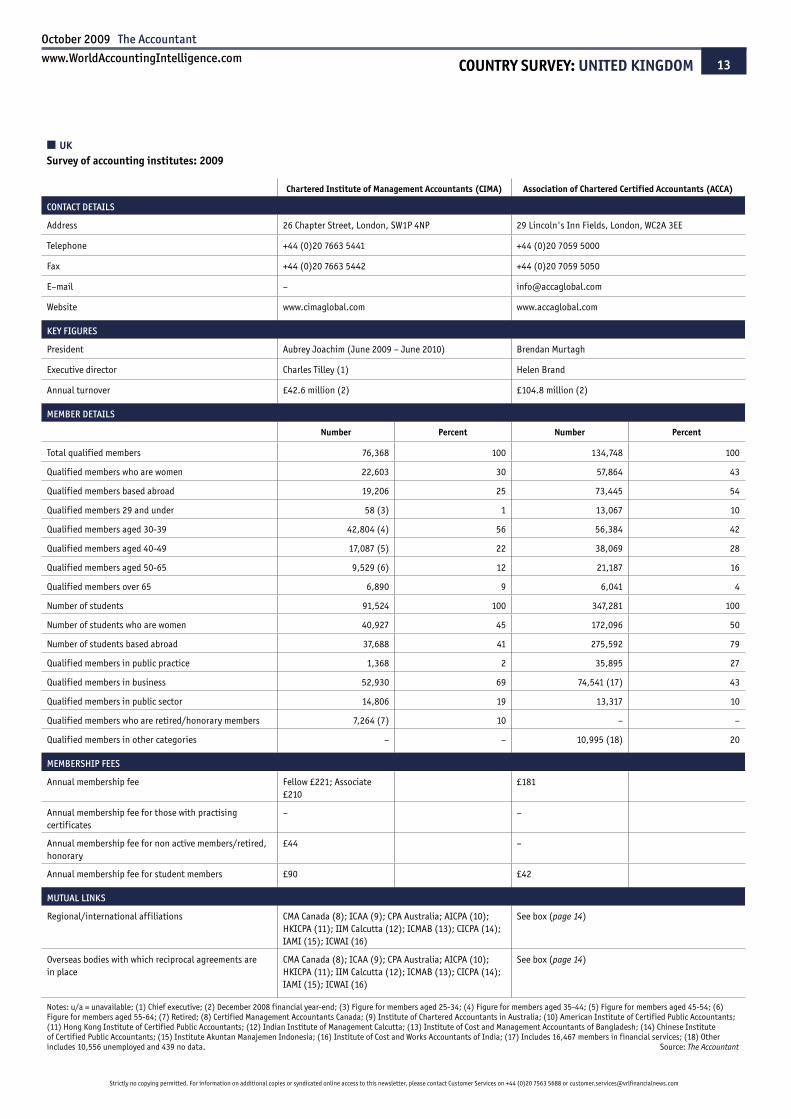

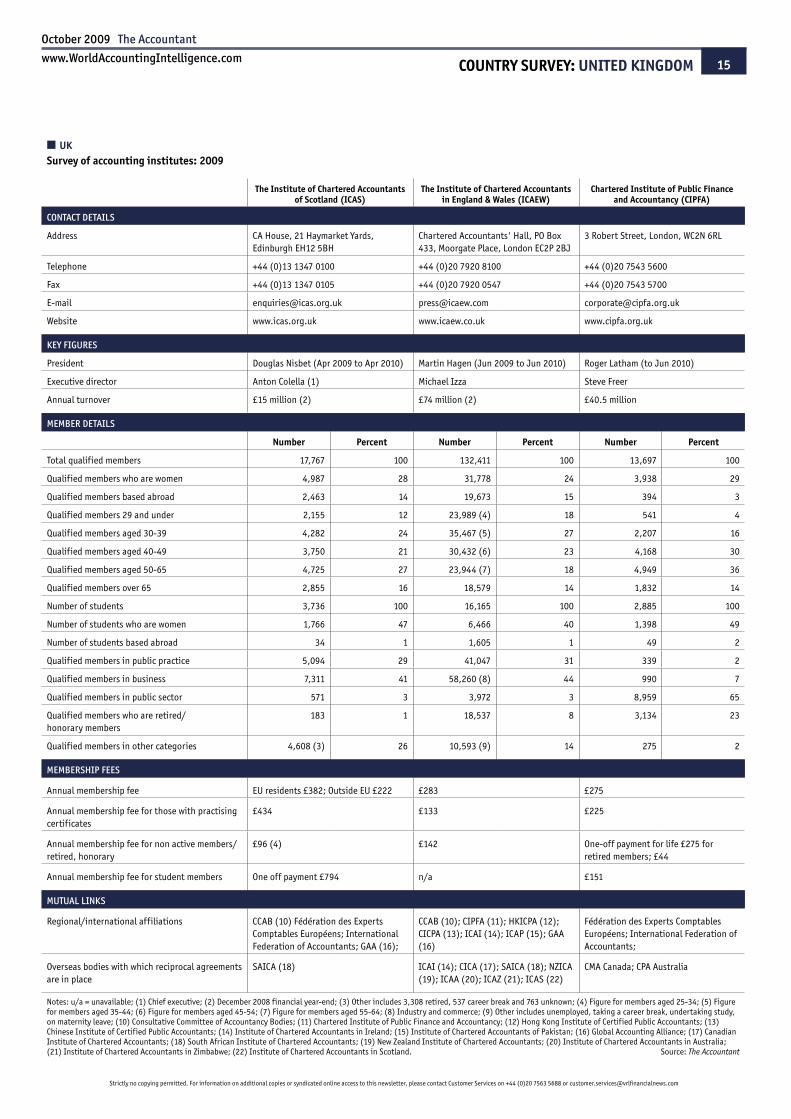

The Accountant October 2009

www.WorldAccountingIntelligence.comCOUNTRY SURVEY: UNITED KINGDOM

the recession has dominated the activi-ties of the UK’s five major professional services bodies for the second year in a row.

But while the tough economic times have dealt some challenges to the profession, they have also provided the institutes with increased opportunities to develop public policy agendas and make their voices heard on issues relating to business and the economy at large.

All five institutes have international pres-ences and the Association of Chartered Cer-tified Accountants (ACCA), the Chartered Institute of Management Accountants (CIMA) – and increasingly the Institute of Chartered Accountants in England and Wales (ICAEW) – are more global than national bodies.

Consequently, their international activities have featured prominently in The Account-ant’s UK country surveys for many years. This year, however, The Accountant will feature a global survey in December (issue 7073) so this month’s report will focus on activities and issues affecting the UK.

Higher public awarenessThe institutes report that one benefit of the eco-nomic crisis has been increased public aware-ness of the importance of professionalism and the value of professional qualifications.

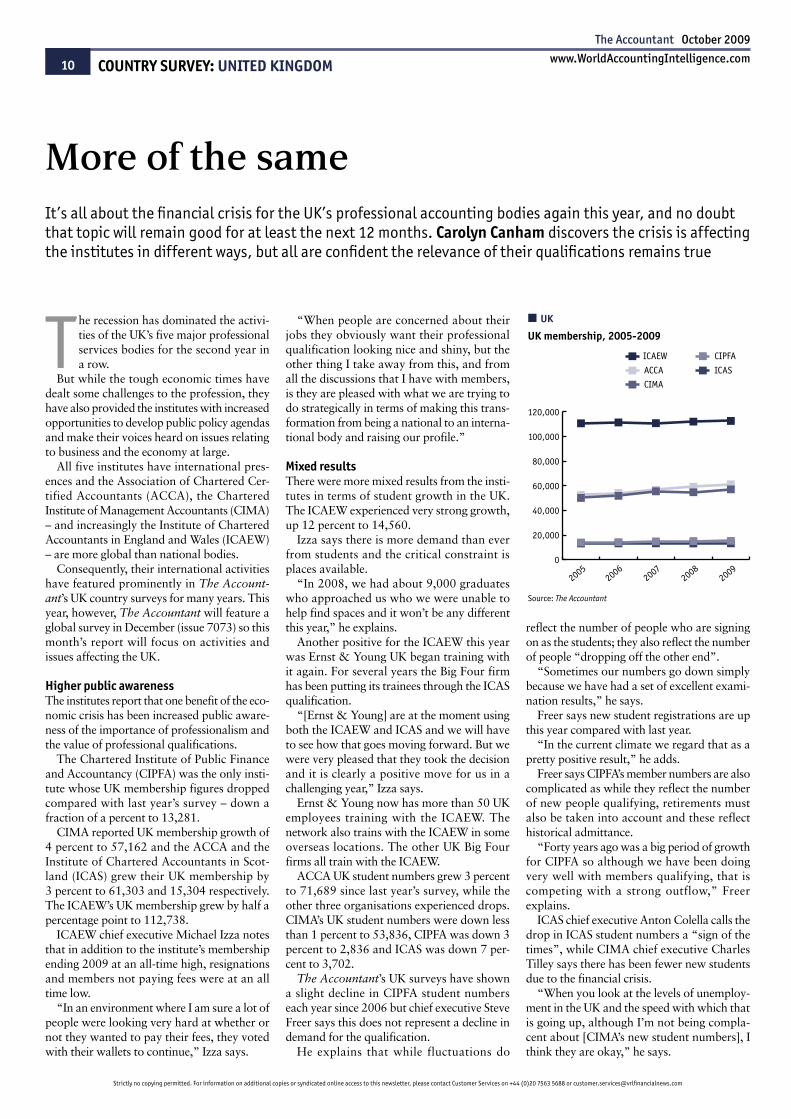

The Chartered Institute of Public Finance and Accountancy (CIPFA) was the only insti-tute whose UK membership figures dropped compared with last year’s survey – down a fraction of a percent to 13,281.

CIMA reported UK membership growth of 4 percent to 57,162 and the ACCA and the Institute of Chartered Accountants in Scot-land (ICAS) grew their UK membership by 3 percent to 61,303 and 15,304 respectively. The ICAEW’s UK membership grew by half a percentage point to 112,738.

ICAEW chief executive Michael Izza notes that in addition to the institute’s membership ending 2009 at an all-time high, resignations and members not paying fees were at an all time low.

“In an environment where I am sure a lot of people were looking very hard at whether or not they wanted to pay their fees, they voted with their wallets to continue,” Izza says.

“When people are concerned about their jobs they obviously want their professional qualification looking nice and shiny, but the other thing I take away from this, and from all the discussions that I have with members, is they are pleased with what we are trying to do strategically in terms of making this trans-formation from being a national to an interna-tional body and raising our profile.”

Mixed resultsThere were more mixed results from the insti-tutes in terms of student growth in the UK. The ICAEW experienced very strong growth, up 12 percent to 14,560.

Izza says there is more demand than ever from students and the critical constraint is places available.

“In 2008, we had about 9,000 graduates who approached us who we were unable to help find spaces and it won’t be any different this year,” he explains.

Another positive for the ICAEW this year was Ernst & Young UK began training with it again. For several years the Big Four firm has been putting its trainees through the ICAS qualification.

“[Ernst & Young] are at the moment using both the ICAEW and ICAS and we will have to see how that goes moving forward. But we were very pleased that they took the decision and it is clearly a positive move for us in a challenging year,” Izza says.

Ernst & Young now has more than 50 UK employees training with the ICAEW. The network also trains with the ICAEW in some overseas locations. The other UK Big Four firms all train with the ICAEW.

ACCA UK student numbers grew 3 percent to 71,689 since last year’s survey, while the other three organisations experienced drops. CIMA’s UK student numbers were down less than 1 percent to 53,836, CIPFA was down 3 percent to 2,836 and ICAS was down 7 per-cent to 3,702.

The Accountant’s UK surveys have shown a slight decline in CIPFA student numbers each year since 2006 but chief executive Steve Freer says this does not represent a decline in demand for the qualification.

He explains that while fluctuations do

reflect the number of people who are signing on as the students; they also reflect the number of people “dropping off the other end”.

“Sometimes our numbers go down simply because we have had a set of excellent exami-nation results,” he says.

Freer says new student registrations are up this year compared with last year.

“In the current climate we regard that as a pretty positive result,” he adds.

Freer says CIPFA’s member numbers are also complicated as while they reflect the number of new people qualifying, retirements must also be taken into account and these reflect historical admittance.

“Forty years ago was a big period of growth for CIPFA so although we have been doing very well with members qualifying, that is competing with a strong outflow,” Freer explains.

ICAS chief executive Anton Colella calls the drop in ICAS student numbers a “sign of the times”, while CIMA chief executive Charles Tilley says there has been fewer new students due to the financial crisis.

“When you look at the levels of unemploy-ment in the UK and the speed with which that is going up, although I’m not being compla-cent about [CIMA’s new student numbers], I think they are okay,” he says.

n UK

UK membership, 2005-2009

source: The Accountant

More of the sameit’s all about the financial crisis for the uK’s professional accounting bodies again this year, and no doubt that topic will remain good for at least the next 12 months. Carolyn Canham discovers the crisis is affecting the institutes in different ways, but all are confident the relevance of their qualifications remains true

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

11

October 2009 The Accountant

www.WorldAccountingIntelligence.com COUNTRY SURVEY: UNITED KINGDOM

CIMA, in partnership with professional education provider BPP, has initiated a new programme to assist recent graduates who have been unable to find full-time work.

Called Yes You Can, the programme allows students in the UK who graduated from uni-versity at the end of the most recent academic year and are working less than 20 hours a week to undertake CIMA training and exams at half the normal price.

The programme represents a departure from normal proceedings in the UK where candi-dates for the CIMA programme traditionally had to be working in a finance function.

Yes You Can is one of many programmes and initiatives the UK institutes have intro-duced to assist students and members through the recession. For example, both the ACCA and the ICAEW set up micro-websites. ACCA UK director Wyn Mears says the ACCA’s offering looks to guide members through the challenges of being made redundant and the pressures on their businesses as a result of los-ing clients and contracts.

CIPFA is a unique organisation in the UK, being the only professional accountancy body that specialises solely in the public sector. Freer says the institute found itself in a particularly interesting position this year as public finances have “been in very sharp focus”.

Most CIPFA members work in public sector organisations and are anticipating significant funding reductions following next year’s UK general election, irrespective of the outcome.

To help members deal with this, CIPFA has been developing a guide that looks at a number of different economic scenarios, con-sidering how long the recession may last, how deep it may be and what impact these factors could have on public finances.

Managing through the crisisThe institute has also been trying to identify the levers organisations can pull in order to effectively manage through what Freer says is going to be the “most difficult period for public sector organisations in our lifetime, cer-tainly in our working lifetime”.

The financial crisis has provided the insti-tutes with greater opportunity to enter public debates.

Izza says that as the crisis unfolded in the past 12 months, the ICAEW has been asked at various stages to get involved. This has includ-ed evaluating the crisis as it unfolded, suggest-ing corrective actions and justifying what the profession did or didn’t do at various stages.

An example of something the profession did well was demonstrate an improvement in audit quality and financial reporting fol-lowing the scandals at Enron and Worldcom, while one area it could improve is its ability to “see into the future”, particularly for financial institutions where situations can change very quickly, Izza says.

“In the UK, the audit profession has offered to talk to the financial regulators to see how additional things might be added to the audit that could perhaps be more helpful,” Izza says, adding that these discussions are ongoing.

“Nothing is happening very quickly,” he continues. “One of the things we are con-cerned about as a professional body sitting here in the City of London, is that nine months ago there were lots of discussions taking place about the changes that needed to be made, the lessons we must learn from the financial crisis, but all of a sudden we seem to be going back to business as usual before any of these changes have come into effect.

“That is very worrying because people who

are older than I am and who have seen this kind of thing before will say that the seeds of the next crisis are sown in the solutions to the last.”

The ICAEW developed two new faculties in the past two years, the Financial Services Faculty and the Financial Reporting Faculty. Izza says these groups “really came into their own” in terms of contributing to debate.

“I would not have liked to have been in the position we found ourselves in 2009 if we hadn’t had those groupings constituted with the member support around them because we were being asked to comment in very short order on some quite technical things,” Izza says.

Other activities the ICAEW undertook to support members and students hit by the cri-sis included working with HR departments to support those being made redundant, and in the case of students, finding them new roles as quickly as possible.

Another member request the ICAEW addressed was raising awareness that banks were changing the rules of lending to busi-nesses. The institute prepared a report on financing, concentrating specifically on SMEs, which it presented to the UK government and the Bank of England.

ICAS too has helped members deal with the changed lending environment. The institute supported members in practice who had to help their clients learn a new language of lending, and supported members in business to get a bet-ter understanding of the new lending reality.

The public policy agenda for the ACCA during the past 12 months included pushing for improvements to regulation surrounding governance. A specific issue the institute com-mented on was the Walker Review of Corpo-rate Governance of the UK Banking Industry, which the ACCA did not think addressed the root causes of bank failure. Mears says further

The financial crisis has had a variety of impacts on UK professional services insti-tutes’ continuing professional development (CPD) offerings.

Chartered Institute of Management Accountants (CIMA) chief executive Charles Tilley said CIMA has experienced less take-up of its post-qualification CPD training.

“[While this] is disappointing, it is one of the things that always happens. Training is cut back before many other things, it is one of the easier cuts,” Tilley said.

The CPD members are required to complete to retain CIMA membership is assessed on an annual basis so Tilley can-not say whether members are fulfilling their

requirements as yet, but he said he suspects more self study is being done.

Alternately, the Institute of Chartered Accountants in Scotland has reported it is experiencing more demand for CPD cours-es relevant to the immediate issues mem-bers are facing.

Examples of relevant CPD include refreshing the CA training of members working in the financial services sector, who have faced the prospect of changing or potentially losing their jobs.

Institute of Chartered Accountants in England and Wales chief executive Michael Izza said the ICAEW has not noticed any drop in members undertaking CPD, or change in demand for CPD. <

n CONTINUING PROFESSIONAL DEVELOPMENT

CPD in the spotlight

n UK

UK student membership, 2005-2009

source: The Accountant

4

strictly no copying permitted. for information on additional copies or syndicated online access to this newsletter, please contact customer services on +44 (0)20 7563 5688 or [email protected]

12

The Accountant October 2009

www.WorldAccountingIntelligence.comCOUNTRY SURVEY: UNITED KINGDOM

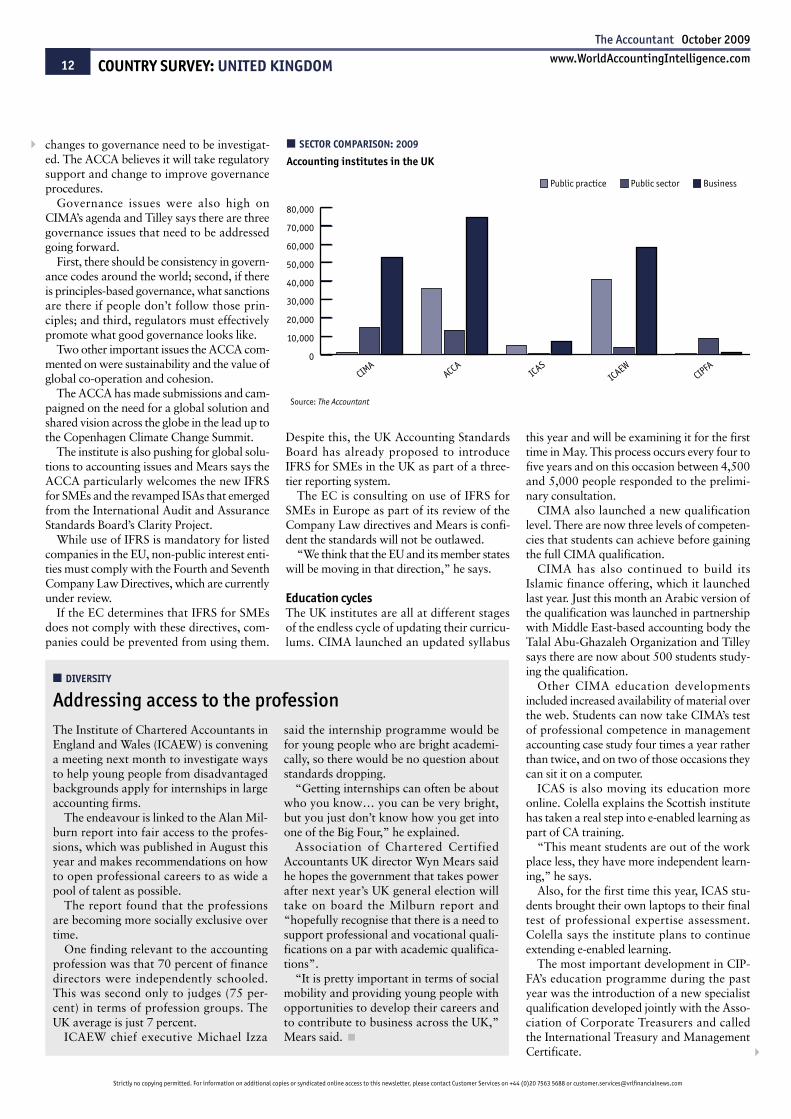

changes to governance need to be investigat-ed. The ACCA believes it will take regulatory support and change to improve governance procedures.

Governance issues were also high on CIMA’s agenda and Tilley says there are three governance issues that need to be addressed going forward.