Accounting Measurement Intensity - Rady School of ...

78

Accounting Measurement Intensity * Ionela Andreicovici † Laurence van Lent ‡ Valeri Nikolaev § Ruishen Zhang ¶ December 2020 Abstract We propose an empirical measure of firms’ metering problems. We build on the notion that metering problems are reflected in the intensity with which firms apply Generally Accepted Accounting Principles (GAAP) to map economic transactions onto financial statements. We develop an algorithm to identify textual patterns that uniquely signify the use of accounting measurements, and construct firm-level scores of accounting mea- surement intensity, AMI . Metering problems are an important source of transaction costs that affect firm boundaries and productivity; we show that firms with higher AMI exhibit lower levels of investment and hiring. Furthermore, we provide evidence that metering problems are associated with lower total factor productivity and with lower firm growth, as measured by Tobin’s Q. We then examine metering frictions that reduce firms’ access to capital. Specifically, we show that AMI is positively associ- ated with the cost of debt as well as with measures of information asymmetry among equity investors, including the probability of informed trade (PIN) and the coverage of a firm by financial analysts. Finally, we present evidence that metering problems influence firms’ contracts, and show that these problems link to non-price terms in debt contracts and to the pay-performance sensitivity of CEO compensation contracts. Together, these findings are consistent with the predictions in Alchian and Demsetz (1972) that metering problems affect firms’ boundaries and contracts with outsiders. Keywords: metering problems, accounting measurement, stewardship, theory of the firm, productivity, contracts JEL codes: D22, D23, D24, G12, J23, M40 * The dataset described in the paper is publicly available at https://doi.org/10.17605/OSF.IO/5ZGK3. We thank John Barrios, Frank Ecker, Christian Leuz, and Ahmed Tahoun for constructive comments. Work- shop participants at Fudan University and Shanghai University of Finance and Economics provided useful feedback. Van Lent and Zhang gratefully acknowledge funding from the Deutsche Forschungsgemeinschaft Project ID 403041268 - TRR 266. † Frankfurt School of Finance and Management; Postal Address: Adickesallee 32-34, 60322 Frank- furt am Main, Germany; E-mail: [email protected]. ‡ Frankfurt School of Finance and Management; Postal Address: Adickesallee 32-34, 60322 Frank- furt am Main, Germany; E-mail: [email protected]. § The University of Chicago; Postal Address: Booth School of Business, 5807 South Woodlawn Avenue, Chicago, IL 60637; E-mail: [email protected]. ¶ Shanghai University of Finance and Economics; Postal Address: Guoding Road 777, 200433, Shanghai, China; E-mail: [email protected].

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Accounting Measurement Intensity - Rady School of ...

Accounting Measurement Intensity∗

Ionela Andreicovici†

Laurence van Lent‡

Valeri Nikolaev§

Ruishen Zhang¶

December 2020

Abstract

We propose an empirical measure of firms’ metering problems. We build on the notionthat metering problems are reflected in the intensity with which firms apply GenerallyAccepted Accounting Principles (GAAP) to map economic transactions onto financialstatements. We develop an algorithm to identify textual patterns that uniquely signifythe use of accounting measurements, and construct firm-level scores of accounting mea-surement intensity, AMI. Metering problems are an important source of transactioncosts that affect firm boundaries and productivity; we show that firms with higherAMI exhibit lower levels of investment and hiring. Furthermore, we provide evidencethat metering problems are associated with lower total factor productivity and withlower firm growth, as measured by Tobin’s Q. We then examine metering frictions thatreduce firms’ access to capital. Specifically, we show that AMI is positively associ-ated with the cost of debt as well as with measures of information asymmetry amongequity investors, including the probability of informed trade (PIN) and the coverageof a firm by financial analysts. Finally, we present evidence that metering problemsinfluence firms’ contracts, and show that these problems link to non-price terms indebt contracts and to the pay-performance sensitivity of CEO compensation contracts.Together, these findings are consistent with the predictions in Alchian and Demsetz(1972) that metering problems affect firms’ boundaries and contracts with outsiders.

Keywords: metering problems, accounting measurement, stewardship, theory of the firm,productivity, contractsJEL codes: D22, D23, D24, G12, J23, M40

∗The dataset described in the paper is publicly available at https://doi.org/10.17605/OSF.IO/5ZGK3.We thank John Barrios, Frank Ecker, Christian Leuz, and Ahmed Tahoun for constructive comments. Work-shop participants at Fudan University and Shanghai University of Finance and Economics provided usefulfeedback. Van Lent and Zhang gratefully acknowledge funding from the Deutsche ForschungsgemeinschaftProject ID 403041268 - TRR 266.†Frankfurt School of Finance and Management; Postal Address: Adickesallee 32-34, 60322 Frank-

furt am Main, Germany; E-mail: [email protected].‡Frankfurt School of Finance and Management; Postal Address: Adickesallee 32-34, 60322 Frank-

furt am Main, Germany; E-mail: [email protected].§The University of Chicago; Postal Address: Booth School of Business, 5807 South Woodlawn Avenue,

Chicago, IL 60637; E-mail: [email protected].¶Shanghai University of Finance and Economics; Postal Address: Guoding Road 777, 200433,

Shanghai, China; E-mail: [email protected].

1. Introduction

When Alchian and Demsetz (1972) characterized the key problem of economic organization

as “the economical means of metering input productivity and metering rewards” (p. 778),

they placed accounting squarely at the heart of the theory of the firm (Ball, 1989). This

theory views firms as a nexus of contracts that coordinate cooperation and the allocation of

economic resources (see also: Coase (1937); Jensen and Meckling (1976); Demsetz (1988)).

Firms’ boundaries and productivity are directly affected by informational costs that are re-

lated to the metering of production inputs and to the metering of subsequent productivity

(Holmstrom and Milgrom, 1994; Kanodia, 2007). Despite the early recognition of the im-

portance of accounting in the theory of the firm, quantifying “the metering problem” and its

effect on firms has been hampered by the lack of a validated, large-sample metric of firms’

production of information using the accounting measurement system (Gao, 2013). To this

point, little guidance has been offered, even conceptually, on how such a measure could be

constructed in order to determine the (intensity of the) firm’s metering.

In this paper, we use a simple machine-learning algorithm to construct a new firm-

level, time-varying metric of accounting measurement intensity (henceforth, AMI). The

metric capitalizes on the idea that accounting uses rules to convert a firm’s transactions

into information that meters these transactions’ economic substance. We use a two-step

procedure to quantify the degree of such metering. First, we rely on the textual analysis of

US Generally Accepted Accounting Principles (GAAP) to identify unique language (word

combinations) used to discuss the rules of converting transactions into accounting reports.

Specifically, we identify language that is particular to the measurement process, such as the

use of judgments, assumptions, or estimates. We then quantify the level of measurement-

related language in a firm’s annual reports (10-K filings), adjusted by total length of report,

to obtain a measure of the “intensity” of accounting measurement in a firm’s disclosures.

As far back as Coase (1937), the literature examining the firm through the lens of con-

1

tracts has emphasized the importance of transactions as the unit of analysis. Coase’s fun-

damental insight is that certain transactions are more efficiently organized and coordinated

by a firm than by market mechanisms. Thus, understanding the salient dimensions of a

transaction is imperative to understanding a firm. Frequency, specificity, and uncertainty

are important sources of transaction costs that directly affect firm boundaries and contracts.

For example, asset specificity in the presence of unforeseen contingencies explains owner-

ship structure and integration decisions (Grossman and Hart, 1986). Alchian and Demsetz

(1972) emphasize the additional important transaction characteristic of metering problems.

These metering problems are considered a primitive source of transaction costs that shape

the organization of economic resources and that influence firm boundaries.

Obtaining a broad-based measure of primitive metering problems presents a non-trivial

challenge to researchers. Ideally, one would need to open up a firm’s black box and assess the

measurement complexities related to specific transactions. These measurement complexities

can stem from considerations about applicable accounting rules and from accountants’ de-

cisions on transaction classification, choice of assumptions, and on whether future estimates

are required. While such an approach might be feasible for individual cases, it is unworkable

for providing large-sample evidence.

We address the challenge of large-sample evidence by building on the insight that firms

likely use the same (GAAP) procedures for internally metering transactions as for preparing

financial statements (Hemmer and Labro, 2008). It is possible that firms invest in infor-

mation systems or accounting expertise to improve measurement, or that managers exercise

discretion over reported numbers. However, we assume that when firms communicate fi-

nancial information to outside investors, they have incentives, due to mandatory disclosure

requirements or to other, voluntary motives, to sufficiently explain the accounting principles

and procedures used to construct the reported numbers (Drymiotes and Hemmer, 2013).

Thus, these explanations should be a reliable base for approximating the size of a firm’s ex

ante primitive metering problems.

2

We conduct comprehensive analyses that strengthen our interpretation that AMI mean-

ingfully captures ex ante metering problems. For example, we list the top bigrams (two-word

combinations) from US GAAP in order to identify accounting measurement discussions in

financial statements. We observe that these bigrams correspond to an accountant’s notion

of measurement-related issues. Prime examples include word combinations such as “intangi-

ble asset,” “estimate future,” “business combination,” “tax position,” and “discount rate.”

We also identify top-scoring 10-Ks, and verify that they feature extensive discussions of

measurement-related issues.

We also show that our measure varies over time and across sectors. Across firms, the

mean of AMI increases significantly between 2000 and 2008, coinciding with US GAAP

relying more on fair value-based measurement (as opposed to historical cost measurement).

From 2009, the mean AMI varies somewhat but appears to have reached an overall plateau.

We find high mean AMI for financial services and several manufacturing industries (paper,

textiles), but low mean accounting measurement intensity in tobacco and coal.1

Our validation exercises include an examination of the firm-level associations between

AMI and firm characteristics that are commonly thought to be associated with accounting

measurement issues (Francis et al., 2008).2 More importantly, we demonstrate that auditors

respond to accounting measurement intensity when pricing their certification services. In

line with auditing effort and associated risk depending on the extent of a firm’s ex ante

metering problems, we show that auditors charge significantly higher audit premiums when

a company has elevated levels of accounting measurement intensity.

Taken together, the evidence suggests that we capture economically meaningful varia-

tion in firm-level accounting measurement intensity, i.e., in the magnitude of a firm’s ex

1The financial services sector has the highest across-sector AMI score. For this reason, and given that themetering problems are likely qualitatively different from other sectors, we exclude it from further analyses.

2For example, frequent changes in a firm’s business model and the volatility of a firm’s operating envi-ronment are both expected to add to the magnitude of the metering problem. Furthermore, we examine theassociations between AMI and key accounting properties, e.g., earnings persistence and predictability (see,for example, Francis et al. (2008)). We conclude that traditional accounting properties are conceptually andempirically distinct from our concept of accounting measurement intensity.

3

ante primitive metering problems. Our metric allows us to address a question of central

importance in the theory of the firm, more specifically, whether metering problems influence

an organization’s boundaries, productivity, and growth (Coase, 1937; Alchian and Demsetz,

1972; Jensen and Meckling, 1976). Coase argues that as firm size and complexity increase,

efficiency gains shrink, effectively defining firm boundaries. While firms are generally better

than markets at dealing with metering problems (i.e., when monitoring employees and co-

ordinating hard to observe inputs), firms’ advantages are likely to diminish as measurement

complexities grow (Alchian and Demsetz, 1972). Thus, a firm’s growth is tempered. This

theory motivates our first set of tests.

We examine the relation between metering problems and firm growth, and show that

firms with higher accounting measurement intensity exhibit significantly lower levels of cap-

ital expenditures, investments in intangible assets, and employment growth. These associ-

ations have considerable economic magnitudes and are robust across various specifications.

To shed further light on the correlation between AMI and firm growth, we examine two

potential explanations for this baseline result. First, Alchian and Demsetz (1972) predict

that metering problems result in a looser link between rewards and employee productivity.

Consequently, frictions in providing incentives will lower firm-level productivity directly or

from the distortions in resource allocation. Consistent with these predictions, we show that

AMI is associated with the erosion of firm-level total-factor productivity. We also show that

Tobin’s Q, a measure of firms’ profitable investment opportunities, is negatively associated

with AMI, which suggests that higher accounting measurement intensity is correlated with

lower firm growth. The second explanation is that metering problems introduce financial

frictions, decreasing firm access to capital markets. In Alchian and Demsetz (1972), and

mirrored in the predictions of classic agency theory (Jensen and Meckling, 1976), metering

problems complicate the selling of promises of future returns to prospective capital providers

by introducing barriers to effective monitoring by outsiders. To test this idea, we examine

the role of AMI on capital markets and show that accounting measurement intensity is

4

associated with informational frictions in equity markets. Specifically, AMI is positively

associated with the probability of informed trade (PIN), while higher AMI is connected

with the reduced coverage of the firm by financial analysts; both of these correlates are of-

ten interpreted as measures of information asymmetry. Turning to debt markets, we next

show that AMI has a positive and statistically significant association with the cost of debt.

Finally, consistent with primitive metering problems as a source of financing frictions, we

provide evidence that higher accounting measurement intensity is positively correlated with

the sensitivity of investment to a firm’s internal cash flows.

Having shown that accounting measurement intensity is associated with firm access to

capital markets, we next establish how contracts vary with AMI. Two major contractual

arrangements are plausibly impacted by the rise of metering problems: 1) (the non-price

terms of) debt contracts and 2) compensation contracts. As metering problems become

more pronounced, lenders tighten their grip on a firm by adding a more encompassing array

of covenants to the contract. We show evidence of a positive association between the use of

control rights and AMI. Alchian and Demsetz (1972) also suggest that one way to address

the metering problem is to make the rewards of top management depend on fluctuations

in the residual value of the firm, and we do find that CEO compensation varies with stock

performance. However, to the extent that accounting measurement produces precise, sen-

sitive signals that are informative about residual value, compensation should also respond

to accounting performance measures (Lambert and Larcker, 1987; Banker and Datar, 1989;

Barclay et al., 2005). In line with this conjecture, we find that lower AMI scores (that indi-

cate fewer metering problems) are associated with a higher sensitivity of CEO compensation

to accounting performance measures, whereas the sensitivity of contracts to stock prices

remains unaffected.

We make several contributions to the literature. First, we introduce and empirically val-

idate a new measure that quantifies the intensity of the mapping between economic trans-

actions and financial statements. As such, our measure captures the primitive metering

5

problems that are manifested in the degree to which GAAP is used in converting a firm’s

transactions into reported numbers. Second, based on the proposed measure, we are able

to test several predictions that follow from the theory of the firm and from transaction cost

economics. We establish a link between primitive metering problems, resource allocation,

firm productivity and growth, and access to capital markets. Our evidence suggests that

measurement is a significant determinant of firms’ emergence and growth, as well as their

allocation of resources. The caveat here is that our analysis does not establish causal links.

Future research can take advantage of our proposed AMI measure, but would need to find a

source of exogenous variation, which is beyond the scope of the current study. However, our

results are of general interest as they establish a baseline set of associations that are con-

sistent with the first-order role of accounting measurement in understanding the economic

performance of organizations.

Following Li (2008), a branch of literature has examined how investors process complex

financial reports. The main focus in this literature is the readability and the length of finan-

cial reports as measured dimensions of disclosure complexity that are related to investors’

cognitive and information-processing abilities. We rely on an entirely different approach to

engage with the text of annual reports, and do not analyze linguistic complexity or use the

document’s length to infer human processing costs. Instead of emphasizing the complexity of

the disclosure document, we use the text of annual reports to infer a primitive characteristic

of the firm, namely, the magnitude of its metering problems. Our findings also have more

specific implications for the financial statement complexity literature: As firms use GAAP

to turn hard-to-meter transactions into accounting numbers, investors will likely face more

difficulties in processing the information in financial statements.

The importance of accounting measurement for understanding the organization of pro-

duction and the allocation of resources is well recognized in the accounting literature (Kan-

odia, 2007; Kanodia and Sapra, 2016). The empirical work on this subject remains lim-

ited, however. In recent work, Barrios et al. (2019) examine the relation between financial

6

measurement practices and firm-level productivity. These authors conceptualize a firm’s

investment in audited GAAP-based financial statements as a managerial practice that aids

in executive decision-making, and thus increases productivity. Breuer (2018) examines the

effect of tough financial reporting regulation on resource allocation in product and capital

markets. Both these important studies focus on private (or limited liability) firms, and rely

on stark differences between firms that do and do not have audited financial statements to

measure reporting quality. Adding to these studies, we offer a metric (based on an algorithm)

that can be applied to any sample of firms with publicly available disclosures, complement-

ing the research based on the (proprietary) data sets of private firms. Our measure does

not reflect reporting quality, but centers on metering problems in firms; these problems are

conceptualized as the root cause for inefficiencies in productivity. Furthermore, instead of

focusing on how measurement helps managers improve productivity, we highlight the role

of accounting measurement in reflecting a firm’s primitive metering problems. Understand-

ing these problems is important in view of Choi (2018), whose general equilibrium analysis

suggests that (accrual) accounting systems improve resource allocation and aggregate pro-

ductivity. However, we think that the driving force is not the firm’s choice of accounting

system, but the underlying primitive metering problems at play in a given firm.

Early work on the “stewardship” role of accounting aims to describe how different ac-

counting measurement rules are related to governance outcomes (Gjesdal, 1981; Paul, 1992;

Bushman et al., 2006; Bushman and Indjejikian, 1993). These studies also generally dis-

tinguish between the role of accounting in addressing the “metering problem” (i.e., how to

measure the marginal productivity of inputs and how to appropriately reward the owners

of those inputs) and providing information to decision-making investors. We show that ac-

counting measurement intensity is associated with contracting frictions that manifest in the

performance sensitivity of compensation contracts and in the terms of debt contracts. In

addition, we provide evidence that metering problems are priced in equity and debt mar-

kets, suggesting a valuation role and another potential mechanism through which accounting

7

measurement might be implicated in the scope of the firm (namely, the funding of the firm’s

operations). Our approach is consistent with the ideas in Kanodia (2007), which emphasizes

that alternative accounting measurements have real effects, as the ways in which accountants

measure and report a firm’s economic transactions in capital markets matters for decisions

within the firm and thus for resource allocation in the economy.

2. Measuring Accounting Measurement Intensity

Our method of obtaining a metric of accounting measurement intensity builds on the insight

that the process of transforming transactions into accounting data has been described in a

purposeful vocabulary in the pronouncements of standard setting bodies. Thus, the degree

to which companies use a similar vocabulary to describe their accounting practices should

be a valid measure of the intensity of the process that transforms business transactions into

meaningful accounting reports, and hence of the level of a firm’s metering problems.

While our premise is intuitive, we face three distinct challenges to practical implementa-

tion. First, when identifying uniquely-accounting vocabulary, we must identify expressions

that are used much more frequently in accounting documents than in everyday language.

Following Hassan et al. (2019), we achieve this objective by comparing two-word combi-

nations (bigrams) in a comprehensive set (“a library” A) of FASB pronouncements with a

library of documents capturing non-business English.

We use a large set of (open source) English language novels to build our non-business

English library. However, removing non-business English from our set of bigrams is unlikely

to be sufficient to obtain the metering-specific bigrams in which we are interested. Compli-

cated transactions such as M&A deals can give rise to metering problems, but the two are

still distinct. Thus, we supplement our non-accounting training library (N) with texts that

reflect the non-accounting language used to discuss business-related issues. This is a not

straightforward process, as accounting is the language of business and many non-accounting

texts are steeped in accounting language. Including such “contaminated” texts into the

8

training library would amount to “throwing the baby out with the bathwater.” Thus, we

augment our non-business English library with a collection of texts from a BBC news dataset

(Greene and Cunningham, 2006) and from Webhose Datasets.3 These texts capture a broad

range of topics that span entertainment, sports, technology, and politics. While the texts

likely include business-related words, they also cater to a generalist audience and are likely

to avoid accounting-specific terms. Together, this collection of text documents forms our

non-accounting training library N.

Our third challenge is that conceptually, AMI should reflect variation in metering prob-

lems between firms while a substantial proportion of transactions is common to all firms

and/or pose few measurement issues. The transactions are routine, the implications well

understood, and little judgment is needed to capture them in accounting terms. Thus, these

transactions should have little (if any) contribution to a metric of accounting measurement

intensity. Our choices for pre-processing the text data in the A training library reflect these

considerations. Specifically, we remove bigrams that appear in more than 90 percent of 10-Ks

in an effort to filter out “boilerplate” accounting terminology. Additionally, in accordance

with best-practice in textual analysis, we first lemmatize and stem the texts, removing digits,

punctuation, and stop words.

Having constructed the libraries N and A, we now define the set of uniquely-accounting

bigrams as A \ N. This set forms the basis for computing our AMI metric. We then count

the number of A \ N bigrams in a given firm’s annual report (10-K). We scale each count

by the total number of bigrams in a 10-K, yielding a statistic that represents the degree of

accounting measurement intensity of a firm. We follow this process for every 10-K in our

sample, which we obtain from the SEC Edgar database for all US publicly listed firms with

a 10-K filed between 2001 and 2018. Thus,

(1) AMIit =1

Bit

Bit∑b

(1[b ∈ A \ N]),

3Webhose is a web data provider turning unstructured web content into machine-readable data feeds.

9

where b = 0, 1, ...Bit are the bigrams contained in the 10-K of firm i in year t, and where 1[·]

is the indicator function. We equally weigh bigrams in the construction of AMI, though we

experiment with several alternative weighting schemes.4 We equal weight to avoid largely

capturing a few frequent terms; instead, in line with our objective, we are able to emphasize

the ‘long tail’ of heterogeneous measurement-specific terminology in annual reports. To

facilitate interpretation, we standardize AMI by subtracting its sample mean and dividing

by the sample standard deviation, so that a one-unit change in AMI represents a single

standard deviation.5

2.1. Training libraries

The validity of AMI, which we extensively test below, depends on the effective identifica-

tion of the set of uniquely-accounting (A \ N) bigrams. We identify these bigrams using a

procedure that requires minimal human involvement in order to avoid contaminating the

measure with researcher biases. The only subjective intervention is the researcher’s choice

of training libraries. We more fully justify our choices next.

Accounting training library. We use a comprehensive set of statements issued by

the Financial Accounting Standards Board to capture the unique vocabulary that accoun-

tants use to transfer economic transactions into financial reports. We use the Financial

Accounting Standards Original Pronouncements and Updates (“as amended” and “as is-

sued”), the FASB Interpretations (as amended and as issued), FASB staff position papers,

and the Emerging Issues Task Force Abstracts (including Other Technical Matters) from

1973 to 2019. Collectively, this library contains 70.2 MB of documents (more specifically,

4.7 million unique bigrams excluding digits, punctuation, and stop words) outlining and dis-

4In particular, weighing by a bigram’s tf-idf is common practice in the textual analysis literature (seeLoughran and McDonald (2011)). The “term frequency-inverse document frequency” weighs a bigram by itsfrequency in the training library (tf) and is scaled by discriminatory power across training libraries (idf). Inour setting with only two training libraries, the idf term reduces to a constant scalar, which means that wewould effectively be weighing by the term frequency of the bigram. This method yields very similar AMIrankings and our inferences are not materially impacted.

5When standardizing and throughout most of the analysis, we drop observations from the FinancialServices industry, as they typically have very high raw AMI scores.

10

cussing GAAP in the United States; taken together, these documents shape the then-current

accounting practices of firms.6

Non-accounting training library. To define the non-accounting library N, we start by

taking a set of English-language novels from Project Gutenberg.7 We supplement this base

library with news articles about sports, entertainment, politics, and technology.These texts

include bigrams like “investment economics,” “share price,” “equity owner,” and “credit

financial,” illustrating the texts’ effectiveness at identifying generic business language. Al-

ternatively, we could supplement our base library with news articles that are more directly

related to business (i.e., stories from the finance and economics pages of newspapers). Such

a strategy, however, would likely remove important measurement-related phrases from our

ultimate A\N set of bigrams, as business news is often steeped in accounting language. Our

preferred method, on the other hand, errs on the side of leaving too many business-related

but not uniquely-accounting bigrams in our ultimate set of uniquely-identified accounting bi-

grams. Nevertheless, the overlap between the two alternative N libraries is about 90 percent,

which leads us to conclude that the set of A \ N bigrams is not particularly sensitive to the

choice of non-accounting training libraries. Ultimately, we adopt the non-accounting training

library with news articles aimed at a lay audience. After removing non-accounting bigrams,

our library of uniquely-identified accounting bigrams (A \ N) contains 490,397 terms.

2.2. Validation of AMI as a metric for accounting measurement intensity

In this section, we start validating the output of our method by evaluating the patterns of

bigrams in A \ N. This is an important step, as without the face validity of our building

blocks for the AMI score, we cannot hope to develop an economically meaningful statistic.

6The corresponding pdf files that are transformed into txt format for use in our machine learning algorithmare 211.7 MB.

7We provide a list of the selected novels in Appendix Table 1.

11

2.2.1. Face validity of AMI

We list the top 200 bigrams (measured by occurrence in 10-Ks across the sample period)

in Appendix Table 2. Reassuringly, we find that the top bigrams are generally word com-

binations that reflect the presence of metering problems in the transformation of business

transactions to financial reports. Prominent examples include “intangible asset,” “business

combination,” “loan loss,”“measure fair,” “deferred income,”“unrecognized tax,” and “vari-

able rate.” Indeed, in this list of 200 bigrams, there is very little evidence of clear-cut “false

positives,” i.e., bigrams that fail to capture accounting measurement intensity. Perhaps the

only exception are the bigrams referring to corporate officers (such as“officer principal” and

“director officer”). Interestingly, some top bigrams capture an important aspect of account-

ing measurement intensity, namely, the managerial judgment that is required to adequately

reflect the economics of the transactions mapped into accounting reports. For example,

frequently used bigrams are “management estimate,” “measure fair,” and “company deter-

mine.”

We provide further texture by listing the top-10 bigrams for each sample year in Appendix

Table 3. These lists reveal interesting patterns in the frequency of certain bigrams that

appear to mirror the time-series patterns in accounting standard setters’ concerns. For

example, between 2001 and 2004, two top bigrams were “option plan” and “stock purchase,”

consistent with the FASB’s stated intent to regulate stock option plans and other executive

compensation instruments in response to the 2001 internet bubble crash. Appendix Table 4

records the top-10 bigrams by industry (using the Fama-French 17 industry classification).

Again, the patterns in the bigrams make intuitive sense. In the Financial Services Industry,

top bigrams include “loan loss,” “mortgage loan,” and “capital requirement,” while in the

Oil and Gas Industry, signature bigrams are “gas reserve,” “prove reserve,” and “asset

retirement.”

While establishing the face validity of specific word combinations is useful, individual

bigrams can be misleading as each only contributes a small amount to the final AMI score

12

for a firm’s 10-K (recall that we weight bigrams equally). What should be evaluated is

whether these uniquely-accounting bigrams lead to a AMI score that accurately portrays

the heterogeneity in accounting measurement intensity across firms (and within a given firm

over time). More specifically, we wish to examine the properties of the AMI measure created

by our algorithm. To that end, we test the face validity of the AMI score. This analysis

is particularly important, as some individual bigrams could reflect the nature of a firm’s

business model and economic transactions in addition to capturing accounting measurement.

Our algorithm’s selection of these bigrams might increase measurement error, but given the

sheer volume of bigrams used to compute AMI, their individual effect is likely to be very

small.

We aggregate AMI scores for each firm-year by taking the yearly cross-sectional means

and plotting them over time in Fig. 1. We then compute average AMI scores by industry

(across years), and present the results in Fig. 2. Fig. 1 shows the longitudinal development

of accounting measurement intensity during our sample period. The upward trend of yearly

mean AMI scores is clearly visible, particularly until the start of the Great Recession in 2008,

after which the mean AMI plateaus at about 0.1. The pattern could reflect the increased

attention on “measurement intensive” fair-value accounting in the early 2000s, as well as the

subsequent reduction in emphasis during the financial crisis in 2008. At the industry-level, we

observe high AMI values for Oil, Machinery, and Construction, while Consumer Goods and

Mining are on the opposite side of the spectrum. Variation across industries is perhaps more

important than the difference in mean AMI scores.8 As expected, our proposed measure

captures between-industry heterogeneity in measurement intensity.

We probe the relative contributions of aggregate (i.e., time series), sectoral, and firm-level

accounting measurement intensity more systematically by performing a variance decompo-

sition, reported in Table 1. This analysis examines how much of the variation in AMIit

stems from various sets of fixed effects. We find that time fixed effects explain a modest

8Note that we drop observations from the Financial Services industry.

13

degree of variation in AMI. The trend in aggregate AMI shown in Fig. 1 accounts for

only 5.53 percent of the total variation. Sector fixed effects (at the three-digit SIC level)

and the interaction of sector and time fixed effects account for another 21.29 percent and 4.2

percent, respectively. The remaining variation in AMI scores, 69.98 percent, plays out at

the firm-level rather than at the level of the sector or the economy as a whole. Only 21.01

percent of this variation is not explained by time or firm fixed effects. As expected, adding

granularity to our sector definition increases the explanatory power of sector fixed effects

(which range between 19.74 and 22.81 percent, and moves from SIC 2 to 4 digit precision).

This increase in power is mirrored by a decrease in the explanatory power of firm fixed effects

(from 54.49 to 45.46 percent), putting bounds on the amount of firm-level variation in AMI.

The aggregate patterns above are reassuring as they confirm our priors of the longitu-

dinal trends in accounting measurement and the heterogeneity in the degree of metering

problems across industries. The identity of S&P500 firms with AMI scores in the top 15

is also comforting. Appendix Table 5 presents an overview; the table also includes the top

bigrams in a firm’s 10-K, as well as a top-scoring “snippet” with the highest number of ac-

counting bigrams (scaled by sentence length). A number of noteworthy observations follow

from the table. First, top bigrams include “measurement heavy” concepts such as “value

hierarchy,” “remeasurement gain,” “impairment charge,” and “defer compensation.” Fur-

thermore, consistent with measurement intensity stemming from the measurement of inputs

and from metering rewards, bigrams associated with these rewards are prominent: “post

retirement,” “compensation expense,” and “performance cash.” Third, the snippets capture

prime instances of measurement. For example, the top snippet for the supermarket chain

Kroger reads: “the company assesses, both at the inception of the hedge and on an ongoing

basis, whether derivatives used as hedging instruments are highly effective in offsetting the

changes in the fair value of cash flow of the hedged items.” This excerpt highlights the mea-

surement issues surrounding the use of derivative instruments. The snippet from the truck

manufacturer Paccar deals with the complications of loss reserves: “small balance impaired

14

receivables with similar risk characteristics are evaluated as a separate pool to determine the

appropriate reserve for losses using the historical loss information discussed below.”

2.2.2. AMI and audit premiums

Our next validation exercise moves beyond face validity and builds on the idea that

auditors, experts who specialize in the accounting measurement process, recognize firms with

high accounting measurement intensity and price their certification services accordingly. If

this assumption is valid, we expect a positive association between audit fees (i.e., the price

charged by auditors to client firms) and AMI when controlling for other determinants of

audit fees. To examine this prediction, we compute AMI for 10-Ks filed between 2001 and

2018, which means that our sample of AMI covers firms with fiscal years ending between 2000

to 2018. Next, we match the AMI data set with accounting information from Compustat

using the linking table from WRDS SEC Analytics Suite. This AMI-Compustat sample

serves as the primary dataset for all following analyses. We provide descriptive statistics for

all variables in Table 2 and variable definitions and the data sources in Appendix A.

We use the intersection of the AMI-Compustat sample and the sample of firms with

audit fee information between 2000 and 2018 available on Audit Analytics to estimate the

following regression:

(2) Auditfeeit = δi + δt × δs + αAMIit + βEAi,t−1 + γXi,t−1 + εit

where the dependent variable is Audit fee, AMI is our firm and time-varying proxy for

accounting measurement intensity, and the vector X consists of a standard set of controls,

including the log of total assets to approximate firm scale, sales growth as a measure of

performance, and leverage (debt over total assets) to account for capital structure. All

control variables are lagged by one period. Standard errors are clustered by firm throughout

the paper unless we state otherwise.9 Prior work has shown that auditors charge a premium

9All of our inferences are unaffected by clustering standard errors by firm-year. Further, we conductextensive analysis on the appropriate standard errors in Section 7.2 below.

15

for client firms with poor accounting quality, so we also add controls for accounting attributes

(EA) like earnings persistence and predictability, as well as indicator variables for firms

with restated financial statements and with going concern qualifications. To the extent

that auditors recognize “accounting measurement intensity” as a unique feature of a firm’s

accounting system 10, AMI should be correlated with higher fees even in the presence of our

controls. In our preferred specification in column 2, we add (δt) and (δs), which represent a

full set of time and sector fixed effects; in column 3, we include firm fixed effects (δi) with

the year fixed effect.

Our evidence in Table 3 shows that AMI is positively and significantly correlated with

audit fees. When we build our preferred specification with all the controls (including controls

for the four accounting properties) and with year and firm fixed-effects, we find an estimated

coefficient of 0.034 (std. err. = 0.007) on AMI in column 3. This estimate is somewhat

more attenuated than the estimate using within-sector and time variation in column 2, but

still implies an economically meaningful role for over-time within-firm changes in AMI in

explaining audit fees. Based on the estimate in column 2, a one standard deviation change

in AMI increases audit fees by about seven percent of the sample mean.11 These findings

indicate that AMI is priced by auditors and that this effect cannot be explained by the

correlation of AMI with firm characteristics or with accounting attributes.

2.2.3. Additional validity checks

We report additional validation checks in Online Appendix Table 6. We summarize these

efforts here. We start by systematically examining firm characteristics that are correlated

with AMI. Our intuition is that AMI varies with the firm’s business model and operating

environment (Francis et al., 2008). Our evidence is consistent with this intuition, as AMI is

positively associated with the volatility of a firm’s operating environment, its size, and the

10We provide evidence consistent with AMI and earnings quality attributes being empirically distinct inmore detail in Appendix Table 6

11As we standardize AMI by its panel standard deviation, we compute the economic magnitude usingthe estimated coefficient from column 2, which includes sector-year fixed effects. Using estimates from thefirm fixed effect regression would be inappropriate, as over-time within-firm changes of one (panel) standarddeviation are rare (Mummolo and Peterson, 2018).

16

length of its operating cycle; AMI is also positively associated with a firm’s intangible and

capital intensity.

Accounting quality proxies. We also examine whether and to what extent accounting

measurement intensity is empirically distinct from proxies for well-know earnings attributes,

such as earnings persistence, earnings predictability, or a restated financial statement. We

find a correlation between AMI and these earnings attributes, which is expected given that

they are subject to how well GAAP rules reflect the economic substance of transactions.

Importantly, however, we find little evidence of an “overlap” between AMI and the various

earnings attributes, and conclude that there is little reason to suspect that AMI inadver-

tently picks up firm heterogeneity in earnings attributes rather than in primitive metering

problems.

To this point, our validation strategy has shown that our algorithm identifies bigrams that

are intuitively associated with metering problems and that the frequency of these bigrams

varies over time and across sectors. Consistent with these observations, bigrams produce ac-

counting measurement intensity scores that vary (on average) in an economically meaningful

way, both longitudinally and in the cross-section. The AMI scores are associated with firm

characteristics suggesting more complex business models and operating environments, and

with attributes of accounting information. Furthermore, accounting measurement intensity

is reflected in the pricing decisions of auditors.

3. Metering and Firm Growth

Our validation tests provide first evidence that AMI is a valid firm and time-specific measure

of metering problems. This measure allows us to address fundamental questions about the

role of accounting measurement in the theory of the firm. Recall that this theory views or-

ganizations as a nexus of contracts coordinating economic activities and alleviating metering

problems (Coase, 1937; Alchian and Demsetz, 1972; Demsetz, 1988; Jensen and Meckling,

1976).

17

Coase (1937) argues that firm boundaries are determined by the costs and benefits of or-

ganizing and coordinating economic transactions inside organizations versus in the markets.

Building on this insight, Alchian and Demsetz (1972) argue that the presence of metering

problems associated with economic transactions can explain the rise of firms and can de-

termine their boundaries. Firms are more efficient than market mechanisms at addressing

metering problems because they can resort to direct monitoring or to the use of sophisticated

contracts. However, in line with Coase’s finding that firms have boundaries, increases in me-

tering problems associated with firms’ growth and expansion could temper the efficiency

gains and impose limits on firms’ organizing activities. For example, the problem of (who

is) “monitoring the monitors” worsens as firms grow and ownership disperses. Ultimately,

the metering costs of coordinating transactions in firms (from the monitoring of inputs and

the writing of contracts) can exceed the benefits. Theory implies that in such cases, firms

will stop growing.

We use the data to explore the relation between AMI and a firm’s expansion via capital

and R&D investment decisions as well as its hiring decisions. If metering problems create

contracting frictions inside the firm or in contracting with external parties, the marginal

benefit of investing in physical or human capital diminishes. As a result, we expect that

firms with greater AMI will invest less.12

To test this prediction using the AMI-Compustat sample, our specification regresses

proxies for investments and hiring onto AMI, the standard set of controls (Xi,t−1), and a

full set of fixed effects:

(3) Invit = δi + δt × δs + αAMIit + γXi,t−1 + εit

where Invit is one of our two proxies for investment decisions or net hiring. The capital

investment rate is the ratio Ii,t/Ki,t, which is measured recursively using the perpetual-

12This prediction, however, is not completely straightforward, given that some theoretical models predictan indirect relation between measurement issues and investments; see, e.g., Kanodia et al. (2005).

18

inventory method described in Stein and Stone (2013). We also use Ri,t/Gi,t, which is R&D

expense scaled by the “knowledge stock” (Stein and Stone, 2013)13. Net hiring, Net hiringi,t,

is the change in year-to-year employment divided by last year’s value.

The findings in Table 4, panel A (column 2) suggest that a one standard deviation in

AMI is associated with a 2.2 percentage point decrease in the capital investment rate (std.

err. = 0.002). Similarly, in panels B and C, we find that a one standard deviation change

in AMI decreases the R&D investment rate by 2.4 percentage points (std. err. = 0.003),

and lowers the employment growth rate by 1.9 percentage points (std. err. = 0.002). To

evaluate these magnitudes, it is helpful to compare the effects to the sample mean, so that

the reported coefficients translate to decreases of 10 percent, 11 percent, and 38 percent of

the sample mean, respectively. The results are robust to the use of industry × year and

firm fixed effects, which is is noteworthy, as it suggests that over-time variation in AMI is

economically important.

There are two channels through which metering problems can affect firm expansion. First,

as suggested by Alchian and Demsetz (1972), metering problems are expected to reduce a

firm’s productivity. Second, investment and hiring can be constrained by limited access to

external capital. We explore each of these possibilities in the following sections.

4. Metering and Firm Productivity

The frictions created by metering problems can impair a firm’s ability to efficiently allocate

resources and to contract with employees, and can ultimately impact firm productivity. For

example, better metering helps managers make more informed decisions (Choi, 2018) and

offers opportunities to tie rewards more closely to decision outcomes.

13Stein and Stone (2013) estimate the knowledge stock by assuming that the first year of reported R&Dis consistent with a growth of five percent net a depreciation of 15 percent. The estimation of these capitalstocks involves assigning initial values; for this, we use the complete Compustat history (going back to 1966)and obtain the earliest net value of PPE.

19

4.1. Total factor productivity

Our next test considers whether metering problems (measured by AMI) are related to firm-

level total-factor productivity. Such an outcome is predicted given that metering problems

distort the measured marginal product of capital and labor and/or change the measured

marginal product of one factor relative to the other (Hsieh and Klenow (2009); Barrios et al.

(2019)).

Our tests rely on two alternative metrics for firm-level TFP: tfp1 and tfp2, where tfp2

includes firm age, labor, and capital in the production function. Specifically, the production

function is given by yi,t = β0 + β1li,t + β2ki,t + ωi,t + ηi,t, where yi,t is the log output of the

firm measured as sales minus material expenses. li,t and ki,t are the log values of labor costs

and firm capital, respectively. ωi,t is productivity and ηi,t is the error term. The productivity

ωi,t is recovered by the Olley-Pakes (1996) estimator, which uses investments to proxy for

unobserved productivity shocks. We compute firm-level TFP metrics following Imrohoroglu

and Tuzel (2014), which produces Olley-Pakes (1996) estimates of firm-level TFP that are

free from the effect of industry and aggregate TFP in any given year and that control for

several other econometric problems that hamper the estimation of production functions at

the firm-level.

We regress each alternative proxy onto AMI, the standard set of control variables, and

a full set of fixed effects:

(4) tfpit = δi + δt × δs + αAMIit + γXi,t−1 + εit

where tfpit is one of the two alternative metrics for firm-level total-factor productivity, and

where X (as before) includes the log of a firm’s assets, leverage (debt/assets), and sales

growth as a measure of firm performance, all of which are measured in the previous period.

We report our estimates in Table 5. After accounting for sector-and-year fixed effects in

column 2, we find a negative and significant association between AMI and tfp1 (in panel A)

20

and tfp2 (in panel B). Most of the variation in TFP appears to play out within the sector-year

dimension, as including firm fixed effects in column 3 attenuates the estimated coefficient

on the variable of interest. Overall, we find evidence that AMI -related information frictions

are correlated with over-time within-firm changes in productivity, but the evidence points

more strongly towards the impact of cross-sectional variation in measurement frictions on

resource allocation and productivity within a given sector-year.

A valid potential concern about the data that we (along with others in the literature)

use to measure total factor productivity is that the data itself is based on accounting num-

bers and thus subject to “metering problems” (i.e., measurement error) in capital and labor

inputs. This measurement error could bias the estimates of productivity and lead to a me-

chanical relation between AMI and TFP. Earlier research on the empirical estimation of

production functions has recognized these potential issues (Bartelsman and Doms, 2000;

Syverson, 2011), and has pointed out that such issues result in a downward bias of the

coefficient on capital in the production function (Collard-Wexler and De Loecker, 2016).

This underestimation of the share of capital affects the residual, and consequently overstates

measured productivity(Collard-Wexler and De Loecker, 2016). Together, this yields a posi-

tive (mechanical) correlation between AMI and TFP, but the bias works to understate the

negative effect of AMI on productivity.

4.2. Tobin’s Q

As an alternative market-based measure of productivity, we examine Tobin’s Q, which is de-

fined as the ratio of the market value of equity plus the book value of liabilities to the book

value of assets. Intuitively, Tobin’s Q is thought to reflect the average value generated by

one dollar of investment in assets and hence is closely related to productivity and investment

opportunities. We use the same model as in equation 5, replace total factor productivity

with Tobin’s Q, and report our estimates in Table 6. We find a significant negative associa-

tion between AMI and Tobin’s Q in all three columns. Including firm and year fixed effects

21

in column 3, we find a coefficient estimate of -0.239 that is significant at the one percent

level (std.err. = 0.078). Thus, over-time within-firm increases in accounting measurement

intensity are associated with a lower Tobin’s Q, consistent with the idea that a firm’s pro-

ductivity declines with an increase in metering problems. As before, we use the coefficient

estimate on AMI from the regression with sector-by-year fixed effects to compute economic

effect sizes, and find that a one standard deviation increase in AMI reduces Tobin’s Q by

0.16, which is a considerable economic magnitude.

To summarize, we examine the association between a firm’s metering problems, invest-

ment and hiring decisions, and productivity. We find systematic patterns suggesting that

firms with higher levels of accounting-measurement intensity make lower investments in

fixed assets and intangible capital, hire fewer employees, and record lower factor productiv-

ity. While we do not interpret these findings causally, they offer a tantalizing glimpse of how

metering problems limit a firm’s scope. Theory suggests that the correlation of metering

problems and productivity and investments is related to the ways in which metering prob-

lems hinder a firm’s access to capital markets and its ability to write contracts. We examine

these suggestions next.

5. Accounting Measurement Intensity in Capital Markets

Metering problems create contracting frictions within organizations, but also between firms

and the outside world, e.g., external capital providers. It is likely that financing frictions

are partly responsible for the relatively depressed investment levels in high AMI firms doc-

umented above. In this section, we investigate the link between accounting measurement

intensity and capital market outcomes (such as the cost of capital). Because the cost of

equity capital is not directly observable, we focus on measures of information asymmetry

between investors in equity markets. In addition, in credit markets, we examine the asso-

ciation between AMI and the contractual interest rates charged by lenders in private debt

contracts.

22

5.1. Information asymmetry in equity markets

Metering problems may hinder the ability of investors to judge the economic performance of a

firm and could increase the information asymmetry between firm “insiders” and “outsiders”

as well as among outside investors. We offer two sets of results consistent with this idea. First,

we examine the correlation between AMI and the probability of informed trade (PIN), which

is a common statistic for the level of information asymmetry among (equity) investors Brown

and Hillegeist (2007). Second, as an alternative measure of informational frictions in equity

markets, we examine whether metering problems are correlated with a firm’s coverage by

equity analysts. These professional information intermediaries may help overcome problems

in conveying firm performance in the presence of metering problems. However, these analysts’

ability to mitigate problems is plausibly compromised for measurement intensive firms, e.g.,

buy/sell recommendations are less likely to be informative. We thus expect lower coverage

for firms with high levels of AMI.

We begin by estimating PIN following Easley et al. (2002, 2010) for all firms on the

intersection of NYSE Trade and Quote and Compustat from 2000 to 2018. From IBES, we

collect the number of analysts covering a given firm in each fiscal year ending between 2000

and 2018. We then merge our AMI-Compustat sample with the PIN and analyst data. We

use this merged data to estimate a specification similar to equation 3, but using either the

PIN or the number of analysts covering the firm (Coverage) as the dependent variable.

Table 7 presents our estimates. In panel A, we find that AMI is positively associated with

the probability of informed trading, consistent with the prediction that high measurement

intensity increases information asymmetry in equity markets. The coefficient of interest

drops from 0.007 (std. err. = 0.001) to 0.003 (std. err. = 0.001) as we move from year to

firm and year fixed effects, suggesting that some variation is driven by differences between

firms (within a sector) in a given year. However, the association remains significant at the

one percent level.

In panel B, we examine the association between AMI and Coverage. Our preferred

23

estimate in the most stringent specification in column 3 is equal to -0.039 (std. err. = 0.007)

and is significant at the one percent level. Firms with higher accounting measurement

intensity have a lower following of financial analysts. The drop in the estimate of interest

is about 53 percent from column 2, again indicating that significant variation in AMI plays

out at the sector-year level.

5.2. Debt markets

Next, we examine the extent to which the cost-of-debt capital varies with the degree of

metering problems. We report the association between AMI and the cost of debt based on

a sample of private loans issued from 2000 to 2018 and available in the Dealscan database.

We then use the intersection of Dealscan data and our firm-level AMI-Compustat sample,

aligned by year of loan issuance. Our regression specification is given as:

(5) CoDit = δi + δt × δs + αAMIit + γXi,t−1 + εit,

where CoD is our proxy for the cost of debt, and where X includes the set of previously used

(one period lagged) control variables augmented by contemporaneous controls for contract

characteristics: Maturity and Facility amount.

We use an all-in-drawn spread to proxy for the cost of debt; this spread describes the

amount the borrower pays in basis points over LIBOR for each drawn down dollar. As

reported in Table 8, we find a positive association between AMI and the all-in-drawn spread;

the estimated coefficient ranges between 5.3 and 8.9, and depends on whether we include

time fixed effects or time and firm fixed effects. Using the sector-and-time fixed effects

specification in column 2, we estimate the economic magnitude of a one standard deviation

increase in AMI to be associated with an approximately 7.1 bps increase in the cost-of-debt.

Taken together, our findings on the association between AMI and pricing in capital

markets suggests that firms with elevated metering problems are impeded in their ability to

24

access credit and equity markets.

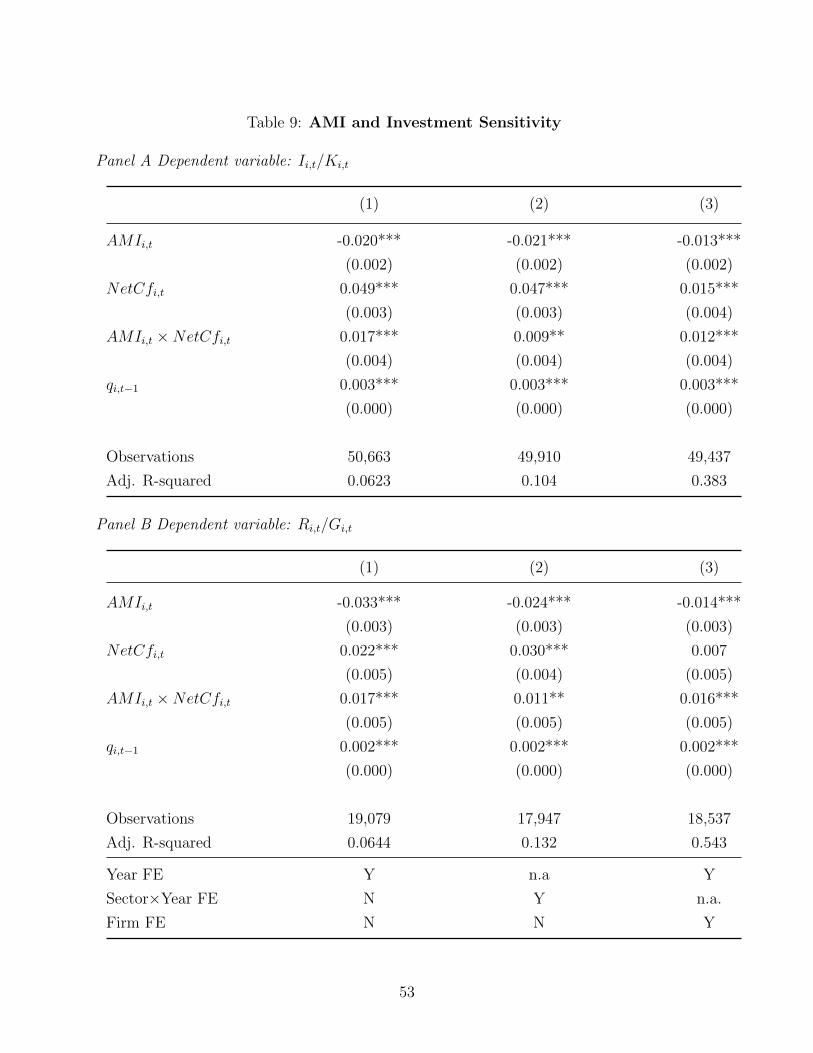

5.3. Investment-cash-flow sensitivity

In this subsection, we investigate whether the external financing channel can help explain why

firms invest less when they have greater AMI. The classic q-theory of investment (Hayashi,

1982; Erickson and Whited, 2000) suggests that the investment rate It/Kt−1 should only be

a function of the marginal productivity q; the availability of internal funds, in particular,

plays no role in investment decisions. Accordingly, when regressing the capital investment

rate on proxies for q and internal funds (i.e., cash flows) in a world with frictionless capital

markets, the estimated coefficient should be insignificant. Empirically, it is well known that

financial constraints are an important determinant of a firm’s investment decisions. Thus,

investment does depend on the availability of liquid funds (Whited, 1992; Fazzari et al., 1987;

Biddle et al., 2009). If metering problems further limit a firm’s access to cheap capital, as

our findings suggest, a firm’s response to improvements in growth opportunities is expected

to be less elastic, as reflected in an increased sensitivity of investment and hiring decisions to

internally generated cash flows. Thus, we can “triangulate” our findings on capital market

access and information asymmetry by showing that firms’ investment decisions become more

sensitive to internally generated cash flows in the presence of higher AMI.

Our main specification examining whether AMI distorts resource allocation in firms

takes the form:

yi,t = δi + δt × δs + β1AMIi,t + β2qi,t + β3NetCfi,t + β4AMIi,t ×NetCfi,t + ε(6)

where y represents the capital investment rate (Ii,t/Ki,t), the R&D investment rate (Ri,t/Gi,t),

or the employment growth rate (Net hiringi,t). We include qi,t, the proxy for the marginal

benefit of investing an extra dollar, and NetCfi,t, the net cash flow, as well as the interac-

tion of NetCfi,t with AMIi,t. We also include a full set of fixed effects, but otherwise follow

25

Fazzari et al. (1987) and choose not to include further controls.14

Based on the discussion above, we expect that metering problems increase the sensitivity

of investments to internal cash flow. Hence, we expect a positive estimate of β4, which

is the coefficient on the interaction between AMI and NetCf . We test this prediction in

Table 9, and find that accounting measurement intensity is associated with greater sensitivity

of investments and hiring to the availability of internal funds. Specifically, across all three

panels (showing the capital investment rate, the intangible investment rate, and firm hiring),

we observe positive and statistically significant coefficients on the interaction of AMI and

NetCf . This conclusion holds in the within-firm estimation in column 3, implying that

the dynamics in a firm’s metering issues drive a significant part of the observed increase in

investment-cash flow sensitivity. This increased reliance on internal funding can be construed

as evidence of heightened investment distortion in the presence of metering problems.

6. Metering and the Writing of Contracts

Having documented that metering issues are associated with lower investments, lower produc-

tivity, and reduced access to capital markets, we examine the economic mechanism broadly

connecting our results. Specifically, the key prediction from Alchian and Demsetz (1972) is

that metering problems impair an entrepreneur’s ability to write effective contracts. In turn,

we examine whether metering problems, proxied for by AMI, influence the design of two

important types of contracts. First, we examine the link between AMI and the allocation

of control rights in debt contracts. Second, we examine the pay-for-performance sensitivity

in CEO compensation contracts.

14Fazzari et al. (1987) suggests that internal finance might be correlated with sales and with cash flows.If so, controlling for sales growth would subsume part of the relation of interest. However, the tenor of ourresults does not change when we add total assets and leverage as additional controls.

26

6.1. Control rights in debt contracts

Debt contracts represent a useful laboratory to test the idea that metering problems create

a demand for control rights. Indeed, the theory of the firm suggests that firms substitute

price mechanisms for more direct control over employee action. In the context of metering

problems, control is beneficial as it allows management to monitor and influence the direction

of employee action. It is well known, however, that control rights serve a similar purpose

in financial contracting (Aghion and Bolton, 1992). Thus, it follows that elevated metering

problems will create creditor demand for control over managerial decisions, and theoretical

work does suggest that lenders respond to information frictions (poor measurement) by

demanding tighter control rights (Sridhar and Magee, 1996; Garleanu and Zwiebel, 2009).

We expect that lenders favor heavier use of control rights and demand a more comprehen-

sive package of accounting-based covenants in debt contracts. We investigate this prediction

in Table 8 using a sample at the intersection of the Dealscan and AMI-Compustat datasets.

The results indicate a significant positive association between AMI and the number of fi-

nancial covenants. Our estimates suggest that a one-standard deviation increase in AMI

increases the number of covenants by about 0.06, or by 4.9 percent compared to the sample

mean. We conclude that metering problems create a demand for control, in line with the

predictions from the theory of the firm.

6.2. Compensation contracts

Motivated by Alchian and Demsetz’ (1972) characterization of the metering of rewards, which

includes activities like measuring output performance, apportioning rewards, and detecting

and estimating the marginal productivity of employees, we turn to the question of how

AMI correlates with the use of accounting performance measures in compensation contracts.

To the extent that metering problems (indicated by high AMI scores) complicate efficient

contracting with employees, we expect that firms rely less on accounting-based performance

measures. In theory, this can happen if metering problems are associated with greater noise

27

in accounting performance measures (Banker and Datar (1989)), or if these problems stem

from the presence of accounting manipulations (Baker (1992)). Stock price-based measures,

on the other hand, should be unaffected by metering problems (Lambert and Larcker, 1987).

We test this prediction in a standard performance sensitivity framework (see, e.g., Morse

et al. (2011)), where we regress the (log of) total compensation onto two summary measures of

performance: accounting return on assets (ROA) and stock returns (Ret). For this analysis,

we supplement our AMI-Compustat sample with data taken from Execucomp on total CEO

compensation. We then allow the compensation sensitivity to depend on AMI and estimate

the following regression:

(7) Compensationi,t = δi + δs × δt + β1AMIi,t + β2zROAi,t

+ β3AMIi,t × zROAi,t + β4zReti,t + β5(AMIi,t × zReti,t) + γXi,t−1 + ε,

where, following (Morse et al., 2011), z indicates that the variable is standardized by sub-

tracting the mean of each two-digit SIC-year group and dividing by the group’s standard

deviation. Compensation is the log of total CEO compensation and X is our standard set

of controls.

If metering problems reduce the usefulness of accounting performance measures in reward-

ing executives, we expect that β3 < 0. We also expect that the compensation-sensitivity

of stock prices is not significantly affected by the accounting measurement intensity, i.e.,

β5 = 0. We report our estimates in Table 11. The three columns in the table present

estimates based on regressions that include increasingly stringent fixed effects structures.

Regardless of the specification, we find negative and significant estimates on the interaction

term AMI × zROA. Thus, our evidence is consistent with the conjecture that as AMI

increases and metering problems are exacerbated, compensation contracts become less sen-

sitive to measured accounting performance. In fact, we find little evidence that metering

problems (increased AMI) are correlated with the sensitivity of performance to stock re-

28

turns, consistent with the contracting-usefulness of these metrics remaining unaffected by

accounting measurement intensity. The estimated coefficient on AMI × zRet is only signifi-

cant in columns 1 and 2, and then only at the ten percent level. The generally insignificant

coefficient suggests that the interaction between accounting performance and AMI is un-

likely to be explained by an omitted factor correlated with both AMI and the sensitivity of

performance measurement; in such a case, we would expect both sensitivities to behave in a

similar fashion.

In sum, the findings in this section are consistent with the idea that metering problems

provide obstacles to efficient contracting within the firm and with outside investors.

7. Falsification and Alternative Explanations

To this point, we have presented our evidence largely without discussing possible alternative

explanations for our findings. In this section, we consider several alternative explanations in

more detail. We also address the possibly of overstated statistical significance levels.

7.1. Controlling for disclosure complexity, accounting quality, and fair value topics

In our validation of AMI, we argue that accounting measurement intensity is conceptually

different from conventional earnings properties (such as persistence and predictability), and

does not depend on the general complexity of a firm’s disclosure. This allows us to rule out

three possible alternative explanations for our results.

7.1.1. Disclosure complexity

We start by verifying the robustness of our results to a common measure of general

disclosure complexity. Following Li (2010), we use a natural log of the file size of 10-Ks

as a proxy for disclosure complexity.15 We repeat all our tests and summarize our findings

in panel A of Table 12. For the sake of brevity, we only report the coefficient on the

15Another popular disclosure metric is the number of words and/or tables used in a firm’s 10-K (Miller,2010; You and Zhang, 2009; Chakraborty et al., 2019). We avoid this proxy given that the (word) length ofthe 10-K is used to scale AMI.

29

main independent variable of interest, i.e., AMI, AMI × NetCf , or AMI × zROA, using

our preferred specification that includes sector-and-year fixed effects and the original set of

control variables.

The findings indicate that our results are robust to controlling for disclosure complex-

ity, consistent with AMI and report size being empirically distinct constructs. Untabulated

results suggest that while Filesize is often statistically significant, consistent with prior liter-

ature and the notion that accounting disclosures are correlated with capital market outcomes,

file size associations are considerably different from those based on AMI. Specifically, AMI

and File size, which are modestly but significantly positively correlated (ρ = 0.19, p < .01),

tend to enter the model with opposite signs. For example, while AMI increases the proba-

bility of informed trade and decreases coverage by financial analysts, the association between

these dependent variables and File size is exactly opposite, consistent with more disclosure

reducing information asymmetry and attracting analyst coverage. Similar observations hold

for tests on investment rate and hiring. It is also worth noting that including File size does

not materially attenuate the coefficient estimate on AMI, which reassures us that AMI is

not inadvertently subsuming the effect of other accounting-related variables not included in

the specification.

7.1.2. Accounting quality

We also verify the robustness of our inferences to controlling for a set of proxies for

accounting quality. Specifically, we control for (1) an unsigned discretionary accruals proxy,

(2) earnings persistence, and (3) earnings predictability, all of which are constructed following

Francis et al. (2008) (see Appendix A for additional details). As previously, we only report

the coefficient on the main independent variable of interest, i.e., AMI, AMI × NetCf , or

AMI × zROA, using our preferred specification that includes sector-and-year fixed effects

and the original set of control variables. The analysis is reported in panel B of Table 12.

The results indicate that our inferences are largely equivalent to our main results when we

control for accounting quality, consistent with AMI being a conceptually different construct.

30

7.1.3. Fair value measurement

Finally, we examine whether our results are driven by the discussion of fair-value-related

topics and disclosures. The use of fair value accounting standards has increased over the

past decades, and can involve considerable measurement complexities. However, we aim to

construct a general measure that is not primarily driven by fair-value measurement, which

we do by reconstructing our measure of accounting measurement intensity after removing

bigrams related to fair value-related topics.16 The results of this analysis are reported in

panel C of Table 12. Again, we find that our results hold up to the exclusion of fair value-

related topics. We conclude that our results are not driven by fair value measurement.

7.2. Placebo tests

We conduct a series of placebo tests to help dispel the concern that our findings may be

explained by the understatement of standard errors (Noreen, 1989). We randomize (with

replacement) the AMI score assigned to each firm-year, and re-estimate our main regressions

with sector-year fixed effects on the newly created sample using pseudo-AMI scores. We

repeat this procedure 500 times, saving the estimated coefficient of interest and its t-statistic

for each regression. The coefficient estimate on the randomized AMI score is nearly identical

to zero (unreported). In Appendix fig. 1, we report the empirical distribution of t-statistics

to better assess how false positives and negatives affect our inferences. In most of our tests,

these incidences appear to be low and close to the critical value of 2.5 percent. In a few

cases, however, the number of false positives or false negatives is slightly higher, suggesting

that evaluating significance at the 2.5 percent level might be appropriate. So doing, however,

does not affect our inferences materially, as in most cases, the estimated coefficient on AMI

is significant at the one percent level.