A taxonomy of performance metrics in executive incentives ...

124

What to reward executives for? A taxonomy of performance metrics in executive incentives supplemented by an overview of business practice Authors Baeten, Xavier; Van Hove, Marthe Download date 27/01/2022 09:01:49 Link to Item http://hdl.handle.net/20.500.12127/6655

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of A taxonomy of performance metrics in executive incentives ...

What to reward executives for? A taxonomy ofperformance metrics in executive incentives

supplemented by an overview of business practice

Authors Baeten, Xavier; Van Hove, Marthe

Download date 27/01/2022 09:01:49

Link to Item http://hdl.handle.net/20.500.12127/6655

Marthe Van Hove

Prof. Xavier Baeten

Executive Remuneration Research Centre

A taxonomy of performance metrics

in executive incentives supplemented by an overview of business practice.

Prime Foundation Partner:

2

CONTENTS Introduction 3

How to read this paper? 5

KPI categorisation 6

Framework 6 Taking stock: use of performance metrics 9 Number of key performance indicators 11

Taxonomy 12

Financial key performance indicators 12

Share-based 13

Sales 13

Gross profit 14

EBITDA 14

EBIT 14

Profit before taxes 14

Net profit 15

Cash flow 15

Relative return 15

Cost 16

Debt 16

Economic profit 16

Non-financial key performance indicators 17

Strategy 18

Innovation 18

Legal and compliance 18

Risk management and internal control 19

Quality and efficiency 19

Sustainability index 19

Environment 20

Customer 20

Employee 21

Top management team 21

Supplier 22

Examples 23

Examples financial key performance indicators 23

Examples non-financial key performance indicators 59

References 116

References annual/remuneration reports 117

Hungry for more? Contact us! 122

3

Executive target-setting and linking it to

incentive systems proves to be a complex

process. Moreover, boards are under

increasing pressure to use a balanced set

of (strategic) performance metrics and to

look beyond financial indicators1. Key

performance indicators (KPIs) are defined

as critical indicators demonstrating a

company’s progress towards its key

business objectives2. The challenge many

boards and companies are facing is two-

fold.

On the one hand, there is an increased

focus on the use of non-financial

performance metrics to be included as a

driver in executive incentive systems. This

is caused by the following:

• An increased focus on

sustainability, which implies a

broader view than just accounting

measures. Today, more and more

companies feel the challenge and

responsibility to clarify which of the

United Nations’ Sustainable

Development Goals are key for

them and on which they have the

biggest impact. Also, from a risk

perspective, investors are more

and more looking at the extent to

which companies take this into

account, including in their reward

systems.

• From a regulatory perspective, the

European Commission’s

Shareholder Rights Directive asks

firms to include both financial and

non-financial performance criteria3.

• The fact that, in addition to lagging

indicators (such as accounting

measures), it can also be beneficial

to include leading indicators that

are more forward-looking and

concretely aligned with the

company’s strategy.

1 Gopalan, R., Horn, J., & Milbourn, T. (2017). Comp targets

that work. Harvard Business Review, 95(5), 102-107. 2 PricewaterhouseCoopers. (2007). Guide to key

performance indicators: Communicating the measures that

matter. Retrieved January 4, 2020, from 1316_UK KPI

2007_030907.indd (pwc.com)

On the other hand, companies are also

having difficulties finding the right set of

financial KPIs. They often tend to use

easy-to-measure data, while the real

challenge is to find the more critical KPIs,

taking into account shareholder

structures, business cycles, level in

organisational hierarchy, while also being

aware of the drawbacks caused by at least

some financial KPIs4.

Vlerick Business School’s Executive

Remuneration Research Centre has

developed this paper in order to inspire

practitioners looking for the ‘right’

financial and non-financial KPIs,

underlying both short-term incentives and

long-term incentives. This paper provides

a taxonomy of different indicators that can

be used. On top of this, the reader will be

inspired by the inclusion of a large set of

real-life examples (more than 100!) found

in the remuneration reports of STOXX

Europe 600 companies5 and grouped by

type of KPI.

The objective of our paper is not to

prescribe by providing the ultimate set of

KPIs – which would be ‘mission

impossible’, as this is highly dependent on

each firm’s specific situation. Rather, the

objective is to take a broad and non-

prescribing perspective by providing an

encompassing overview and inventory of

performance metrics used in executive

remuneration. As such, the paper offers a

guide to improving the choice of key

performance indicators by summarising

examples and inspiring practices. Of

course, KPIs need to be deduced from the

firm’s strategy and the objectives the firm

wants to achieve.

3 See art. 9a, 6 of the Directive (EU) 2017/828 of the

European Commission 4 Marr, B. (2012). Key Performance Indicators (KPI): The 75

measures every manager needs to know. Pearson UK.

5 For an overview of the companies currently included in the

STOXX Europe 600, see: https://www.stoxx.com/index-

details?symbol=SXXP

Introduction

4

COPYRIGHT © 2021 VLERICK BUSINESS SCHOOL, BELGIUM

No part of this publication may be copied, stored, transmitted, reproduced or distributed in any form or medium whatsoever without the permission of the copyright owner.

What to reward executives for? A taxonomy of performance metrics in executive

incentives supplemented by an overview of

business practice.

5

The paper is organised as follows:

• It starts with categorising KPIs into

the main performance dimensions

involved, which is a unique

categorisation developed by Vlerick

Business School’s Executive

Remuneration Research Centre, based

on both research and business

practice.

• Next, it provides an overview of the

use of each of these performance

dimensions in incentive systems, as

well as the number of KPIs

determining CEO incentives.

• Last but not least, numerous

examples of concrete performance

metrics used for each of the

performance categories are provided.

It is important to note that we do not

take into account sector-specific

metrics6.

Concretely, the paper consists of three

parts:

• KPI categorisation. In the first part

of the paper, the overall typology of

performance metrics used in executive

incentive contracts is presented and

explained. Moreover, we ‘take stock’

by providing an overview of the use of

performance metrics in incentive

contracts (both short- and long-term

incentives), from both the perspective

of the types of KPIs and the number of

KPIs used.

• Taxonomy. The core part of this

paper includes the taxonomy of

performance metrics. Here, the

remuneration reports of STOXX Europe

600 companies served as the source of

inspiration. In this part, an overview is

provided of the concrete KPIs used,

grouped into the different categories

(e.g., EBITDA, cash flow, environment,

etc.). Next to the concrete KPIs,

reference is made to examples

6 E.g., solvency ratio for banks, occupancy rate for real

estate, innovation milestone in pharmaceutical industry, etc.

included for some of the underlying

metrics (e.g., highlighted below):

• Examples. The third part of the paper

contains the examples mentioned

under the taxonomy, which provide

more specific information about the

underlying metric (e.g., Example 1

share-based: TSR compared to peer

group).

To conclude: the optimal way to read this

paper is to first go through the lists of

underlying metrics and then select the

examples you want to have more

information about. The reader can easily

navigate through the paper by clicking on

the examples in the taxonomy (e.g., by

clicking on Example 1, you will

automatically go to the example of

Schroders). You can go back to the

taxonomy by clicking on the KPI category

mentioned above the example (e.g.,

Share-based: STI).

How to read this paper?

6

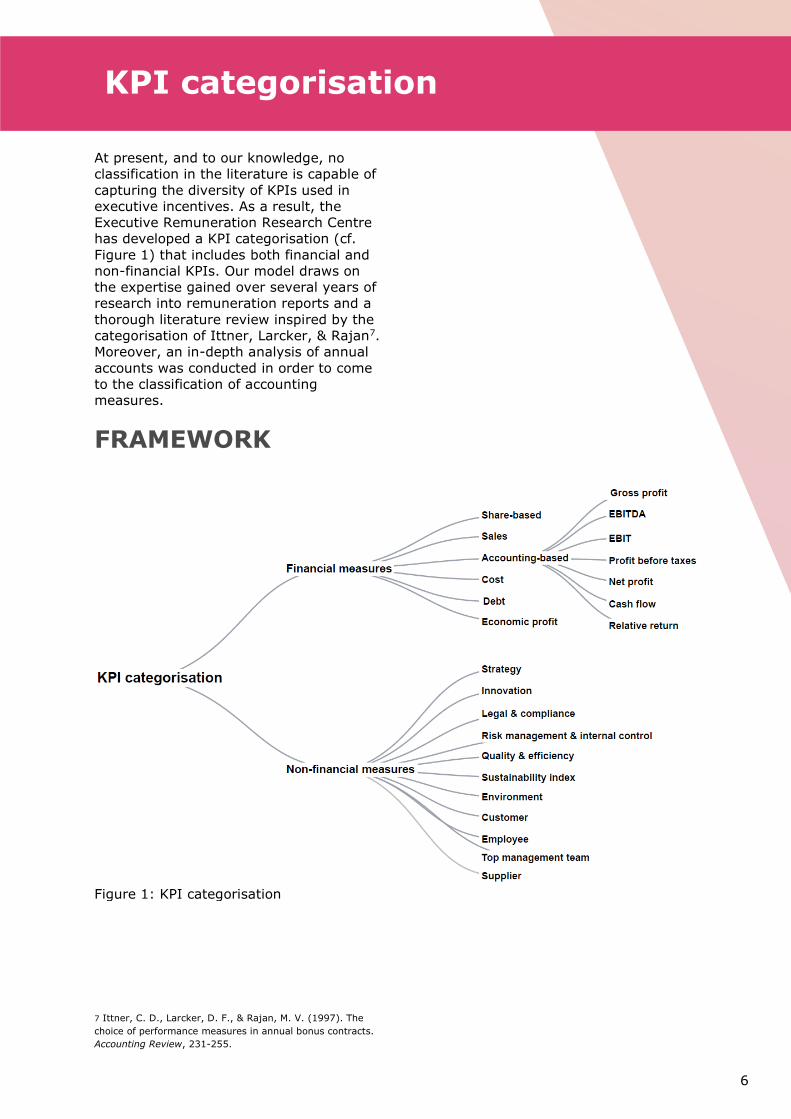

At present, and to our knowledge, no

classification in the literature is capable of

capturing the diversity of KPIs used in

executive incentives. As a result, the

Executive Remuneration Research Centre

has developed a KPI categorisation (cf.

Figure 1) that includes both financial and

non-financial KPIs. Our model draws on

the expertise gained over several years of

research into remuneration reports and a

thorough literature review inspired by the

categorisation of Ittner, Larcker, & Rajan7.

Moreover, an in-depth analysis of annual

accounts was conducted in order to come

to the classification of accounting

measures.

FRAMEWORK

7 Ittner, C. D., Larcker, D. F., & Rajan, M. V. (1997). The

choice of performance measures in annual bonus contracts.

Accounting Review, 231-255.

KPI categorisation

Figure 1: KPI categorisation

7

As mentioned in the Introduction, key

performance indicators (KPIs) are defined

as critical indicators demonstrating a

company’s progress towards its key

business objectives. Our model of KPIs

consists of 3 layers (cf. Figure 1).

The first layer distinguishes between

financial (lagging) and non-financial

(leading) performance metrics. Financial

KPIs are measures that indicate a

company's financial performance in order

to achieve financial objectives.

Conversely, non-financial KPIs are

measures defining what actions are

necessary to successfully meet overall

business objectives.

The second layer provides the different

dimensions underlying financial and non-

financial KPIs8.

The dimensions underlying financial

KPIs include:

• Share-based: based on the

company’s stock price.

• Sales: based on the company’s

revenues/sales.

• Accounting-based: based on the

company’s profit & loss statement.

• Cost: criteria measuring cost-

reduction, -management, and -

effectiveness.

• Debt: criteria to determine the

proportion of a company's assets

that is financed through debt.

• Economic profit: criteria designed

to measure value creation at the

most basic level of a corporation’s

operations9.

8 Each of these dimensions will be further explained in this

paper by the means of concrete examples. 9 Economic Value Added. Stern Value Management.

https://sternvaluemanagement.com/economic-value-added-

eva 10 Sustainability Accounting Standards Board. (2020). Bases

for conclusions & invitation to comment on exposure drafts.

https://www.sasb.org/wp-

The dimensions underlying

non-financial KPIs include:

• Strategy: metrics that define

strategic success.

• Innovation: criteria measuring new

developments/products and market

success in a company.

• Legal & compliance: metrics

defining the performance of a

company’s compliance efforts and

legal requirements.

• Risk management & internal

control: criteria measuring internal

control and risks that the business

is exposed to.

• Quality & efficiency: measures

used to monitor a company’s

quality and efficiency performance

by means of pre-established

standards.

• Environment: measures related to

the firm’s environmental impact as

a consequence of its activities10.

• Customer: criteria tracking the

progress on specific business

objectives regarding customer

service.

• Employee: metrics related to the

company’s workforce, addressing

issues such as health and safety,

labour practices, employee

satisfaction and engagement, and

diversity and inclusion11.

• Top management team: criteria

designed to measure top

management abilities and

competences.

• Supplier: metrics tracking supply

chain performance and monitoring

supplier relationships.

content/uploads/2020/08/Invitation-to-Comment-SASB-CF-

RoP.pdf 11 Sustainability Accounting Standards Board. (2020). Bases

for conclusions & invitation to comment on exposure drafts.

https://www.sasb.org/wp-

content/uploads/2020/08/Invitation-to-Comment-SASB-CF-

RoP.pdf

8

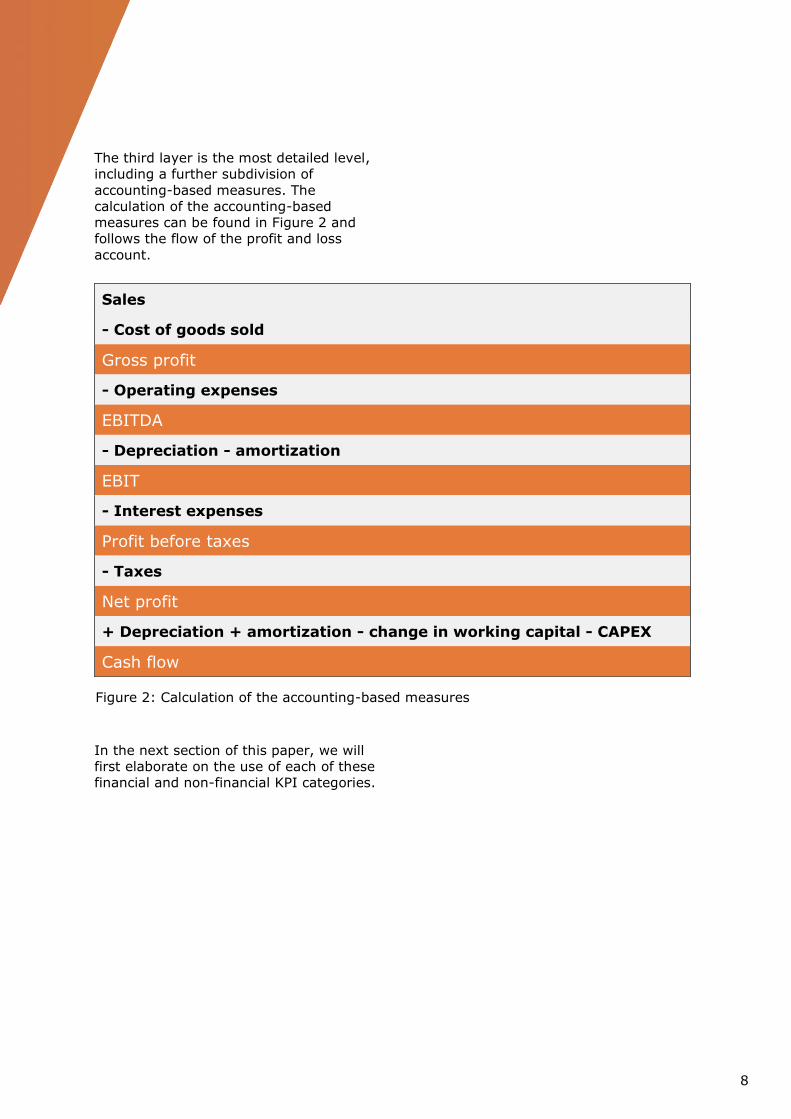

The third layer is the most detailed level,

including a further subdivision of

accounting-based measures. The

calculation of the accounting-based

measures can be found in Figure 2 and

follows the flow of the profit and loss

account.

In the next section of this paper, we will

first elaborate on the use of each of these

financial and non-financial KPI categories.

Sales

- Cost of goods sold

Gross profit

- Operating expenses

EBITDA

- Depreciation - amortization

EBIT

- Interest expenses

Profit before taxes

- Taxes

Net profit

+ Depreciation + amortization - change in working capital - CAPEX

Cash flow

Figure 2: Calculation of the accounting-based measures

9

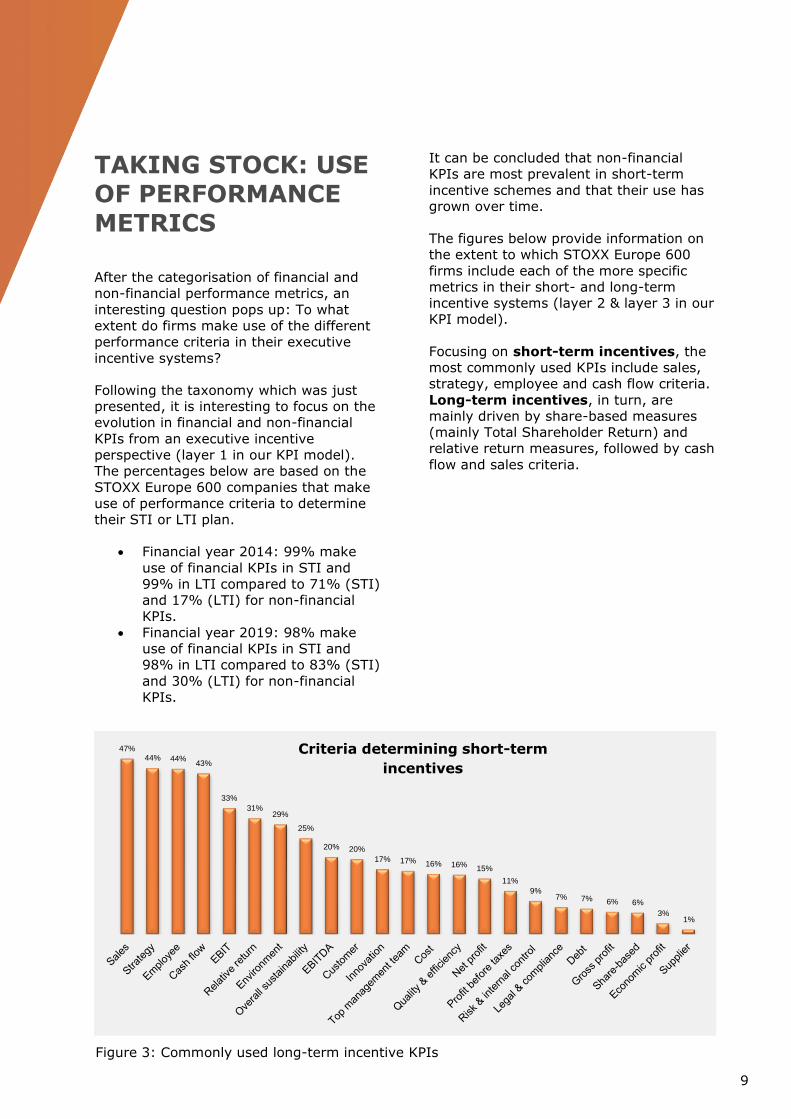

TAKING STOCK: USE OF PERFORMANCE

METRICS

After the categorisation of financial and

non-financial performance metrics, an

interesting question pops up: To what

extent do firms make use of the different

performance criteria in their executive

incentive systems?

Following the taxonomy which was just

presented, it is interesting to focus on the

evolution in financial and non-financial

KPIs from an executive incentive

perspective (layer 1 in our KPI model).

The percentages below are based on the

STOXX Europe 600 companies that make

use of performance criteria to determine

their STI or LTI plan.

• Financial year 2014: 99% make

use of financial KPIs in STI and

99% in LTI compared to 71% (STI)

and 17% (LTI) for non-financial

KPIs.

• Financial year 2019: 98% make

use of financial KPIs in STI and

98% in LTI compared to 83% (STI)

and 30% (LTI) for non-financial

KPIs.

It can be concluded that non-financial

KPIs are most prevalent in short-term

incentive schemes and that their use has

grown over time.

The figures below provide information on

the extent to which STOXX Europe 600

firms include each of the more specific

metrics in their short- and long-term

incentive systems (layer 2 & layer 3 in our

KPI model).

Focusing on short-term incentives, the

most commonly used KPIs include sales,

strategy, employee and cash flow criteria.

Long-term incentives, in turn, are

mainly driven by share-based measures

(mainly Total Shareholder Return) and

relative return measures, followed by cash

flow and sales criteria.

47%44% 44%

43%

33%

31%29%

25%

20% 20%

17% 17% 16% 16%15%

11%

9%7% 7% 6% 6%

3%1%

Criteria determining short-term

incentives

Figure 3: Commonly used long-term incentive KPIs

10

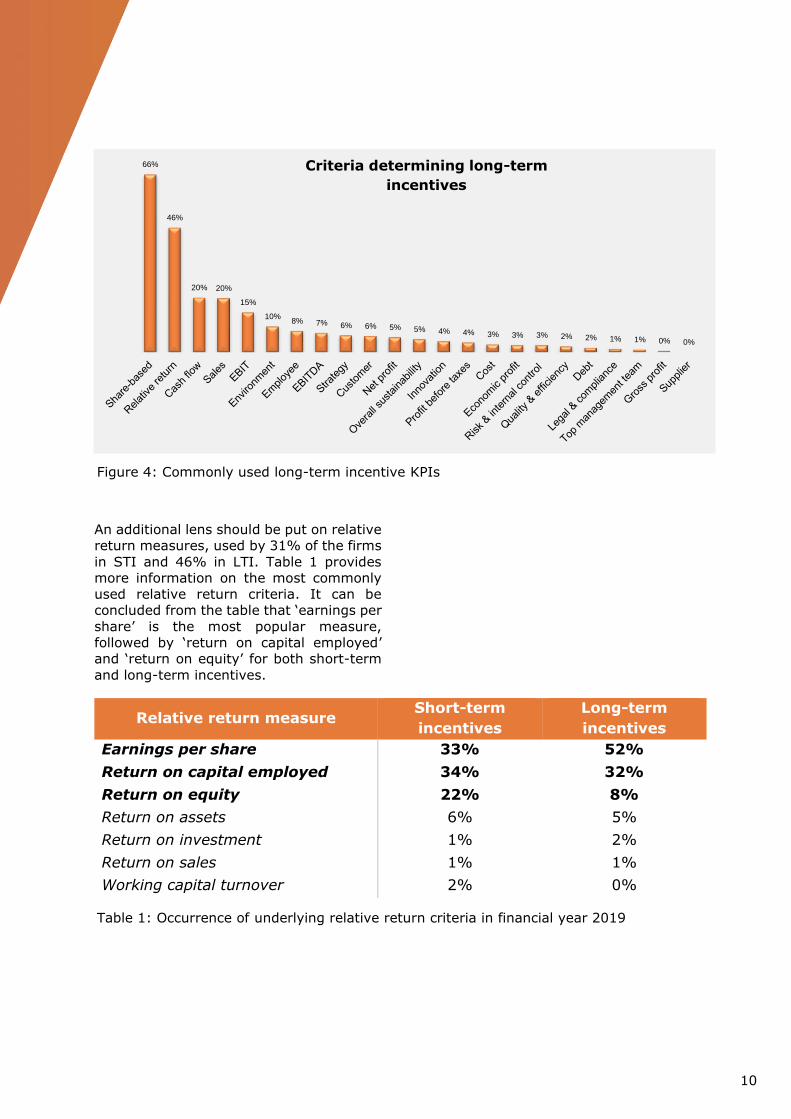

An additional lens should be put on relative

return measures, used by 31% of the firms

in STI and 46% in LTI. Table 1 provides

more information on the most commonly

used relative return criteria. It can be

concluded from the table that ‘earnings per

share’ is the most popular measure,

followed by ‘return on capital employed’

and ‘return on equity’ for both short-term

and long-term incentives.

Relative return measure Short-term

incentives

Long-term

incentives

Earnings per share 33% 52%

Return on capital employed 34% 32%

Return on equity 22% 8%

Return on assets 6% 5%

Return on investment 1% 2%

Return on sales 1% 1%

Working capital turnover 2% 0%

Figure 4: Commonly used long-term incentive KPIs

66%

46%

20% 20%

15%

10%8% 7% 6% 6% 5% 5% 4% 4% 3% 3% 3% 2% 2% 1% 1% 0% 0%

Criteria determining long-term

incentives

Table 1: Occurrence of underlying relative return criteria in financial year 2019

11

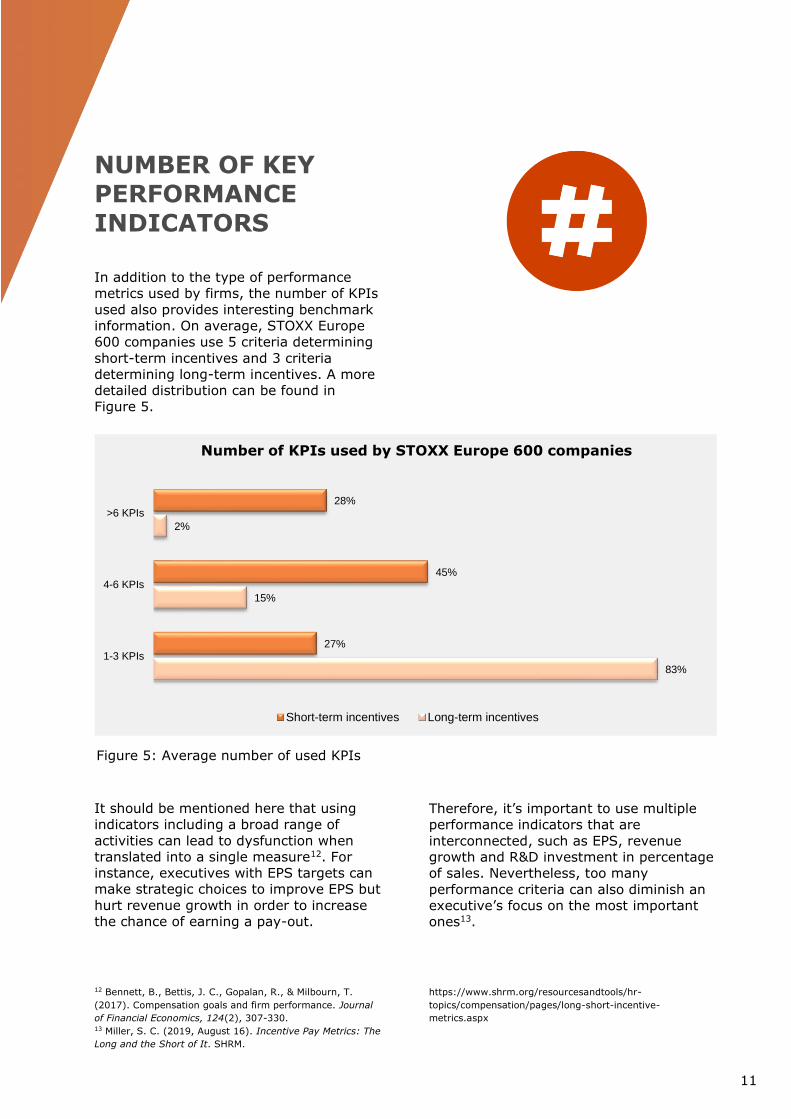

NUMBER OF KEY PERFORMANCE

INDICATORS

In addition to the type of performance

metrics used by firms, the number of KPIs

used also provides interesting benchmark

information. On average, STOXX Europe

600 companies use 5 criteria determining

short-term incentives and 3 criteria

determining long-term incentives. A more

detailed distribution can be found in

Figure 5.

It should be mentioned here that using

indicators including a broad range of

activities can lead to dysfunction when

translated into a single measure12. For

instance, executives with EPS targets can

make strategic choices to improve EPS but

hurt revenue growth in order to increase

the chance of earning a pay-out.

12 Bennett, B., Bettis, J. C., Gopalan, R., & Milbourn, T.

(2017). Compensation goals and firm performance. Journal

of Financial Economics, 124(2), 307-330. 13 Miller, S. C. (2019, August 16). Incentive Pay Metrics: The

Long and the Short of It. SHRM.

Therefore, it’s important to use multiple

performance indicators that are

interconnected, such as EPS, revenue

growth and R&D investment in percentage

of sales. Nevertheless, too many

performance criteria can also diminish an

executive’s focus on the most important

ones13.

https://www.shrm.org/resourcesandtools/hr-

topics/compensation/pages/long-short-incentive-

metrics.aspx

83%

15%

2%

27%

45%

28%

1-3 KPIs

4-6 KPIs

>6 KPIs

Short-term incentives Long-term incentives

Number of KPIs used by STOXX Europe 600 companies

Figure 5: Average number of used KPIs

12

As mentioned, the core part of this paper

consists in providing the reader with

concrete information on the exact

meaning of each of the KPI categories, as

well as examples for each of the

performance metrics outlined above. For

each of the KPI categories, metrics will be

presented.

The order follows the structure of KPIs

outlined above. As far as the order of

examples is concerned, examples of the

use of the metrics in short-term incentives

will be provided first, followed by

examples of use in long-term incentives.

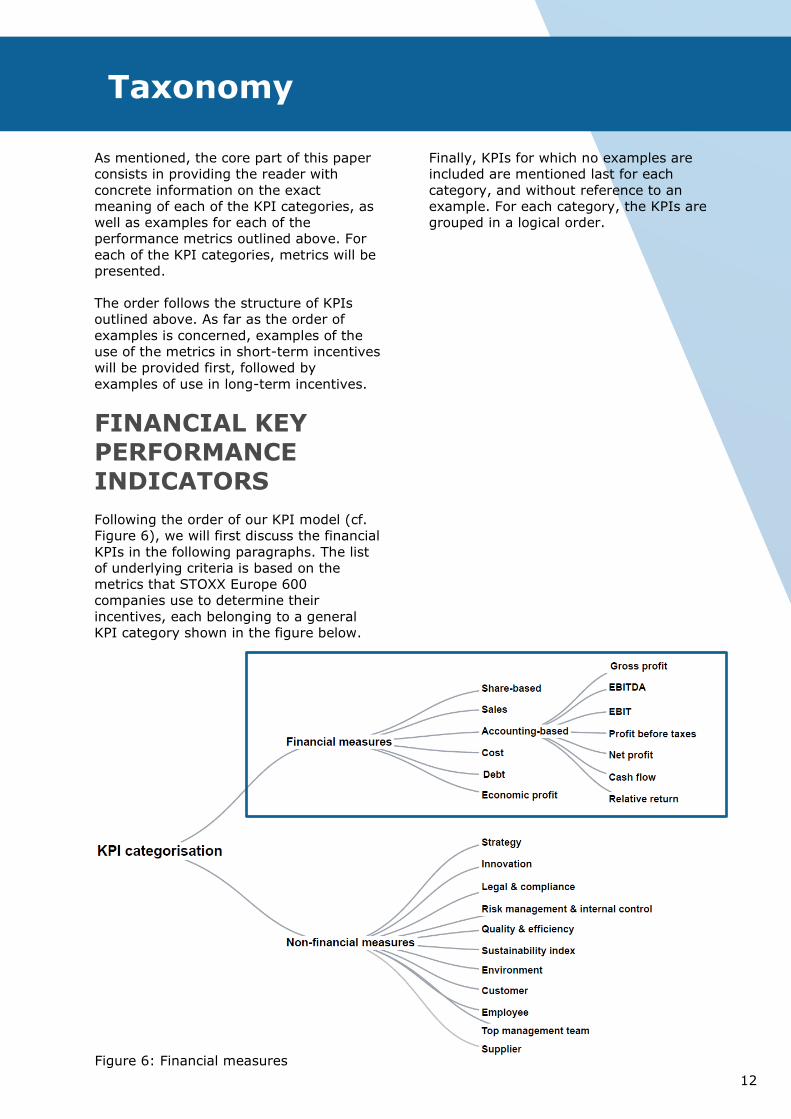

FINANCIAL KEY PERFORMANCE INDICATORS

Following the order of our KPI model (cf.

Figure 6), we will first discuss the financial

KPIs in the following paragraphs. The list

of underlying criteria is based on the

metrics that STOXX Europe 600

companies use to determine their

incentives, each belonging to a general

KPI category shown in the figure below.

Finally, KPIs for which no examples are

included are mentioned last for each

category, and without reference to an

example. For each category, the KPIs are

grouped in a logical order.

Figure 6: Financial measures

Taxonomy

13

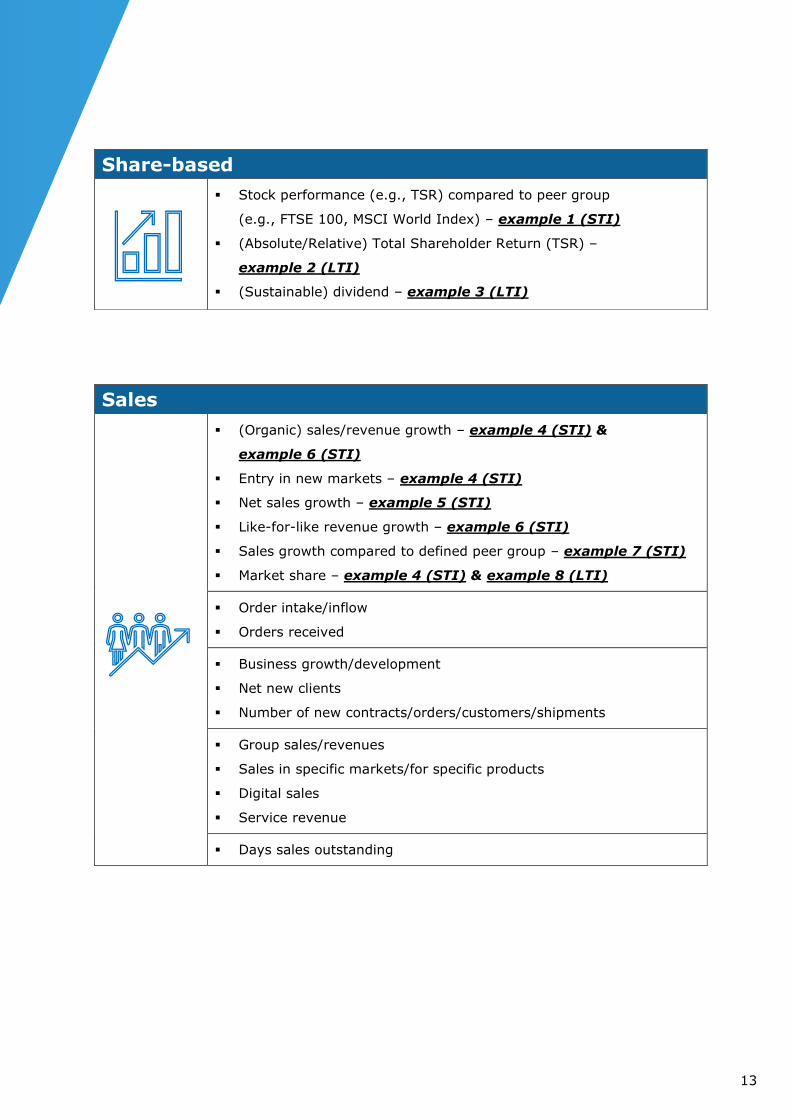

Share-based

▪ Stock performance (e.g., TSR) compared to peer group

(e.g., FTSE 100, MSCI World Index) – example 1 (STI)

▪ (Absolute/Relative) Total Shareholder Return (TSR) –

example 2 (LTI)

▪ (Sustainable) dividend – example 3 (LTI)

Sales

▪ (Organic) sales/revenue growth – example 4 (STI) &

example 6 (STI)

▪ Entry in new markets – example 4 (STI)

▪ Net sales growth – example 5 (STI)

▪ Like-for-like revenue growth – example 6 (STI)

▪ Sales growth compared to defined peer group – example 7 (STI)

▪ Market share – example 4 (STI) & example 8 (LTI)

▪ Order intake/inflow

▪ Orders received

▪ Business growth/development

▪ Net new clients

▪ Number of new contracts/orders/customers/shipments

▪ Group sales/revenues

▪ Sales in specific markets/for specific products

▪ Digital sales

▪ Service revenue

▪ Days sales outstanding

14

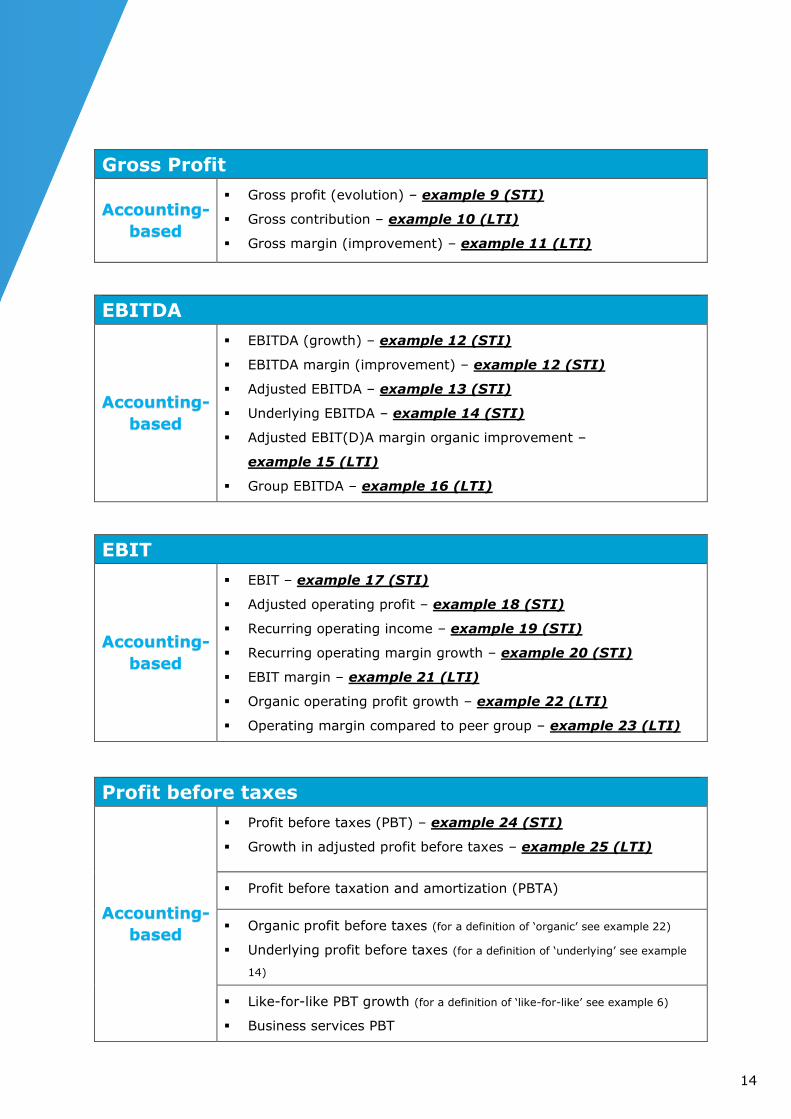

Gross Profit

Accounting-

based

▪ Gross profit (evolution) – example 9 (STI)

▪ Gross contribution – example 10 (LTI)

▪ Gross margin (improvement) – example 11 (LTI)

EBITDA

Accounting-

based

▪ EBITDA (growth) – example 12 (STI)

▪ EBITDA margin (improvement) – example 12 (STI)

▪ Adjusted EBITDA – example 13 (STI)

▪ Underlying EBITDA – example 14 (STI)

▪ Adjusted EBIT(D)A margin organic improvement –

example 15 (LTI)

▪ Group EBITDA – example 16 (LTI)

EBIT

Accounting-

based

▪ EBIT – example 17 (STI)

▪ Adjusted operating profit – example 18 (STI)

▪ Recurring operating income – example 19 (STI)

▪ Recurring operating margin growth – example 20 (STI)

▪ EBIT margin – example 21 (LTI)

▪ Organic operating profit growth – example 22 (LTI)

▪ Operating margin compared to peer group – example 23 (LTI)

Profit before taxes

Accounting-

based

▪ Profit before taxes (PBT) – example 24 (STI)

▪ Growth in adjusted profit before taxes – example 25 (LTI)

▪ Profit before taxation and amortization (PBTA)

▪ Organic profit before taxes (for a definition of ‘organic’ see example 22)

▪ Underlying profit before taxes (for a definition of ‘underlying’ see example

14)

▪ Like-for-like PBT growth (for a definition of ‘like-for-like’ see example 6)

▪ Business services PBT

15

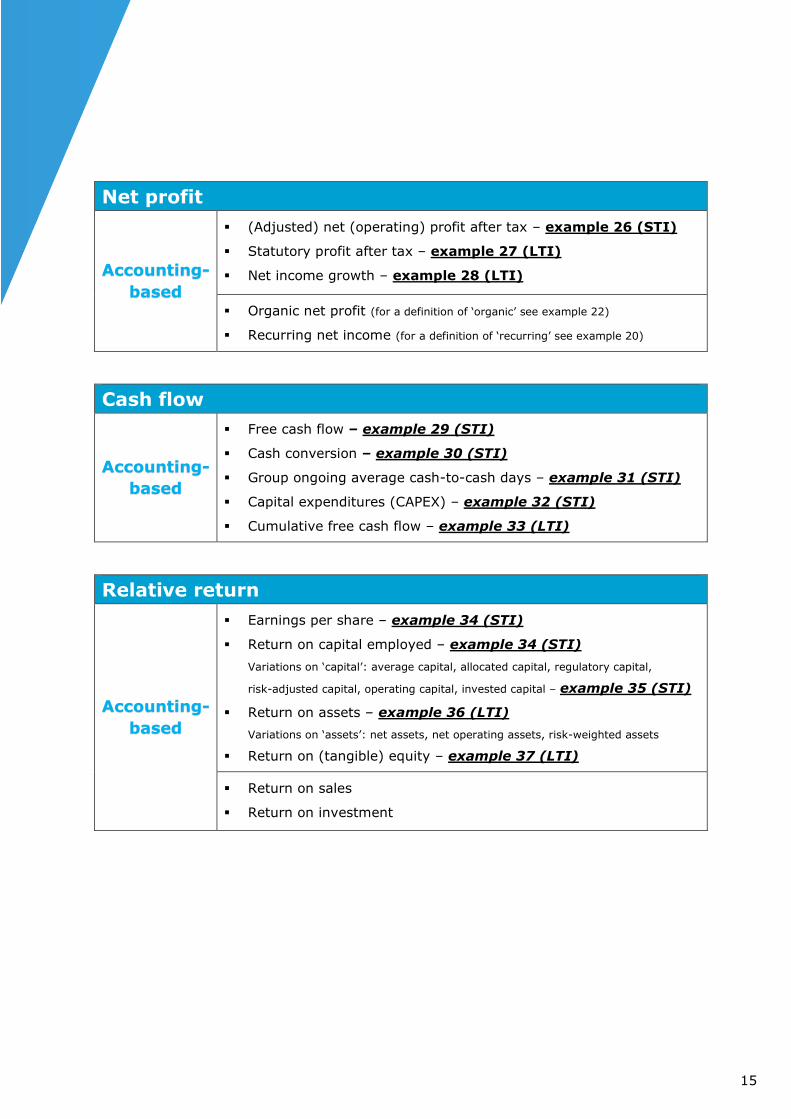

Net profit

Accounting-

based

▪ (Adjusted) net (operating) profit after tax – example 26 (STI)

▪ Statutory profit after tax – example 27 (LTI)

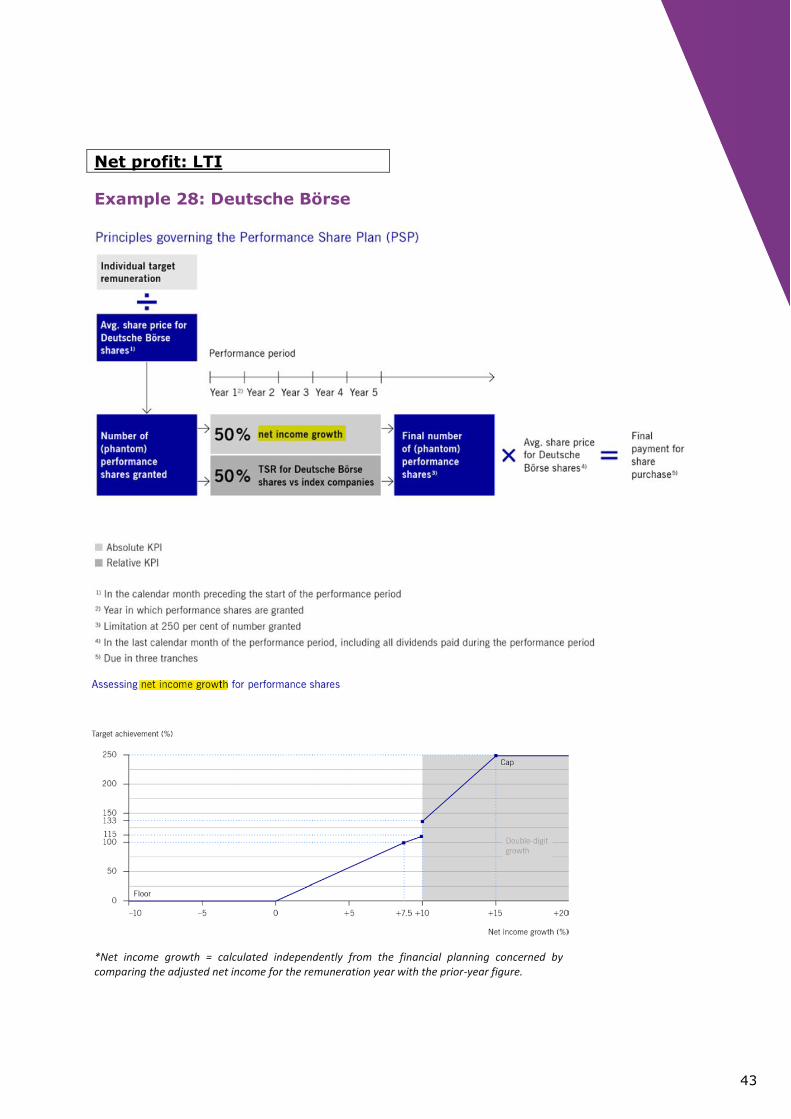

▪ Net income growth – example 28 (LTI)

▪ Organic net profit (for a definition of ‘organic’ see example 22)

▪ Recurring net income (for a definition of ‘recurring’ see example 20)

Cash flow

Accounting-

based

▪ Free cash flow – example 29 (STI)

▪ Cash conversion – example 30 (STI)

▪ Group ongoing average cash-to-cash days – example 31 (STI)

▪ Capital expenditures (CAPEX) – example 32 (STI)

▪ Cumulative free cash flow – example 33 (LTI)

Relative return

Accounting-

based

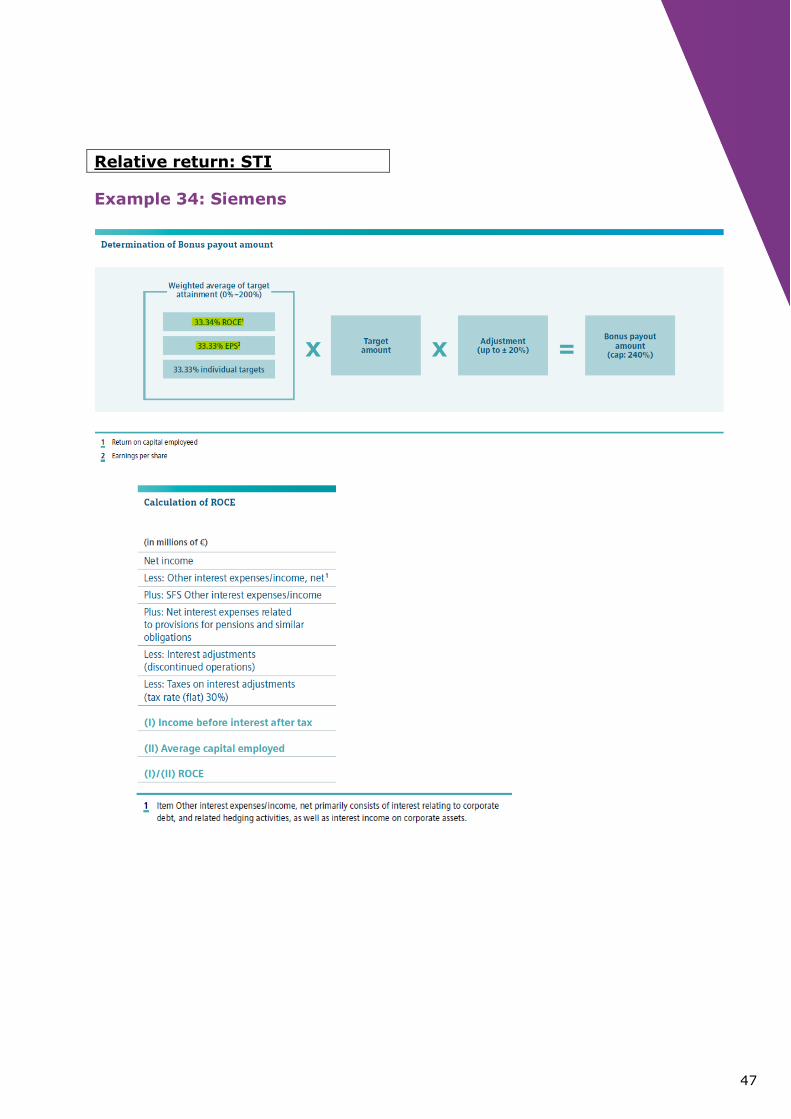

▪ Earnings per share – example 34 (STI)

▪ Return on capital employed – example 34 (STI)

Variations on ‘capital’: average capital, allocated capital, regulatory capital,

risk-adjusted capital, operating capital, invested capital – example 35 (STI)

▪ Return on assets – example 36 (LTI)

Variations on ‘assets’: net assets, net operating assets, risk-weighted assets

▪ Return on (tangible) equity – example 37 (LTI)

▪ Return on sales

▪ Return on investment

16

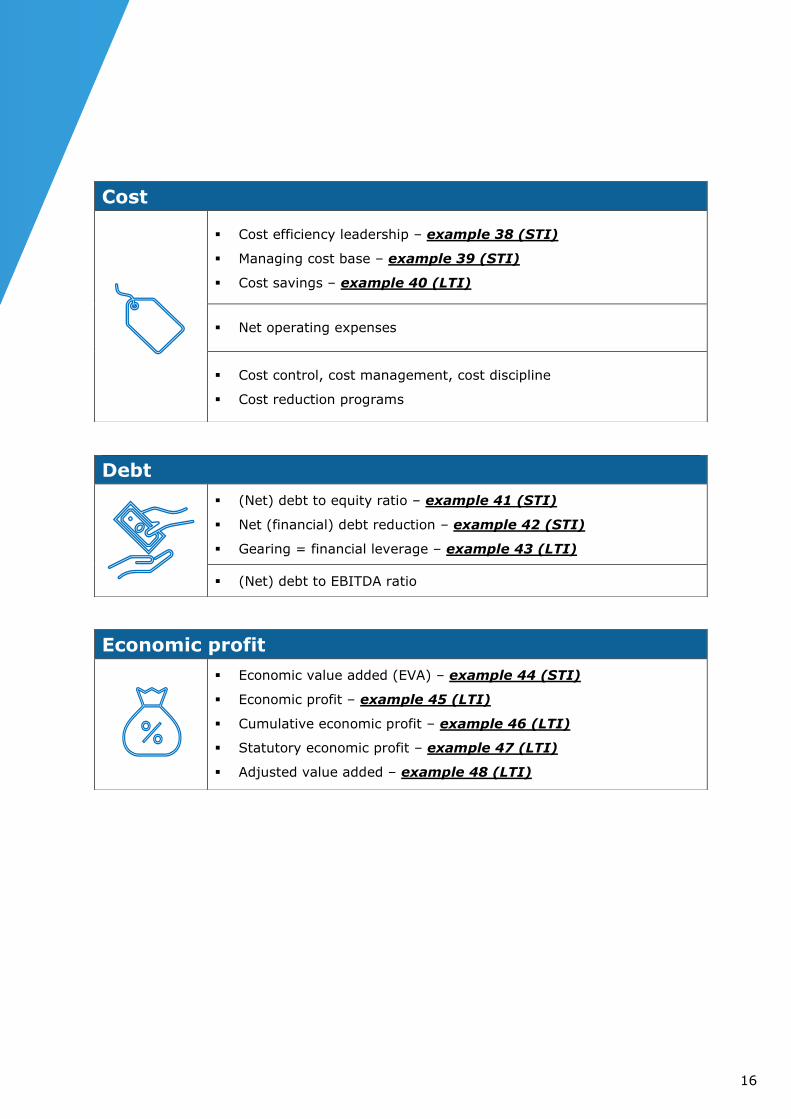

Cost

▪ Cost efficiency leadership – example 38 (STI)

▪ Managing cost base – example 39 (STI)

▪ Cost savings – example 40 (LTI)

▪ Net operating expenses

▪ Cost control, cost management, cost discipline

▪ Cost reduction programs

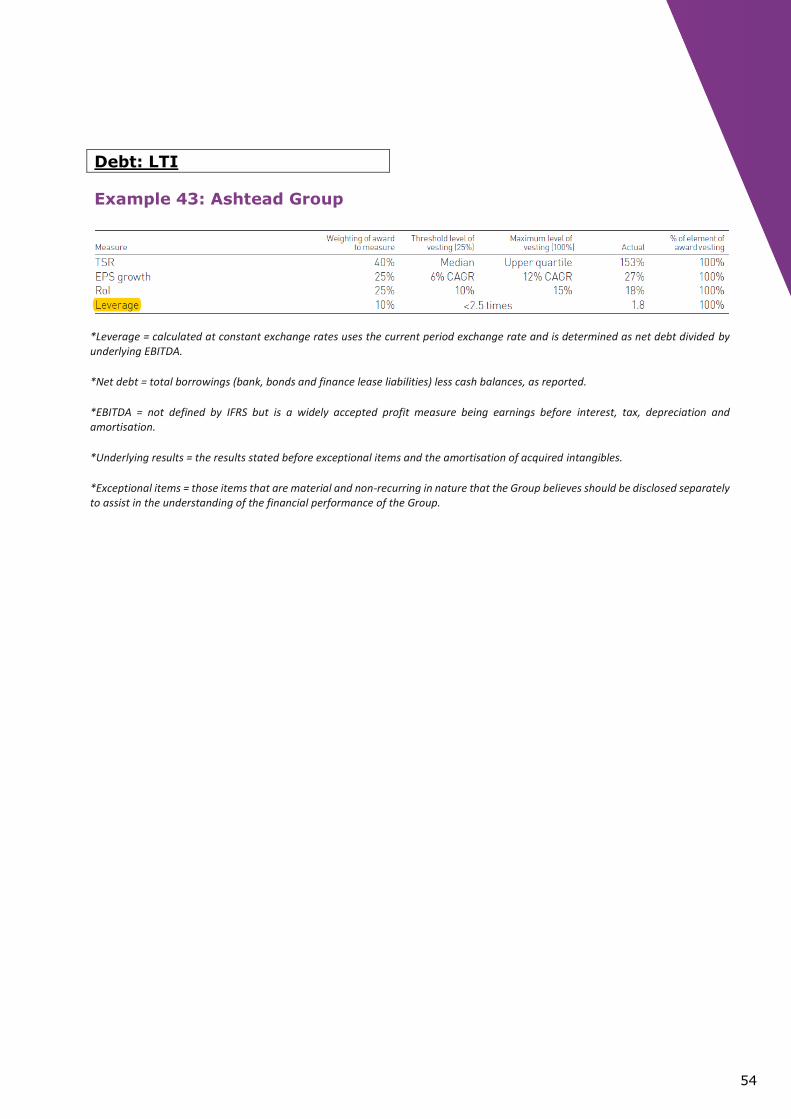

Debt

▪ (Net) debt to equity ratio – example 41 (STI)

▪ Net (financial) debt reduction – example 42 (STI)

▪ Gearing = financial leverage – example 43 (LTI)

▪ (Net) debt to EBITDA ratio

Economic profit

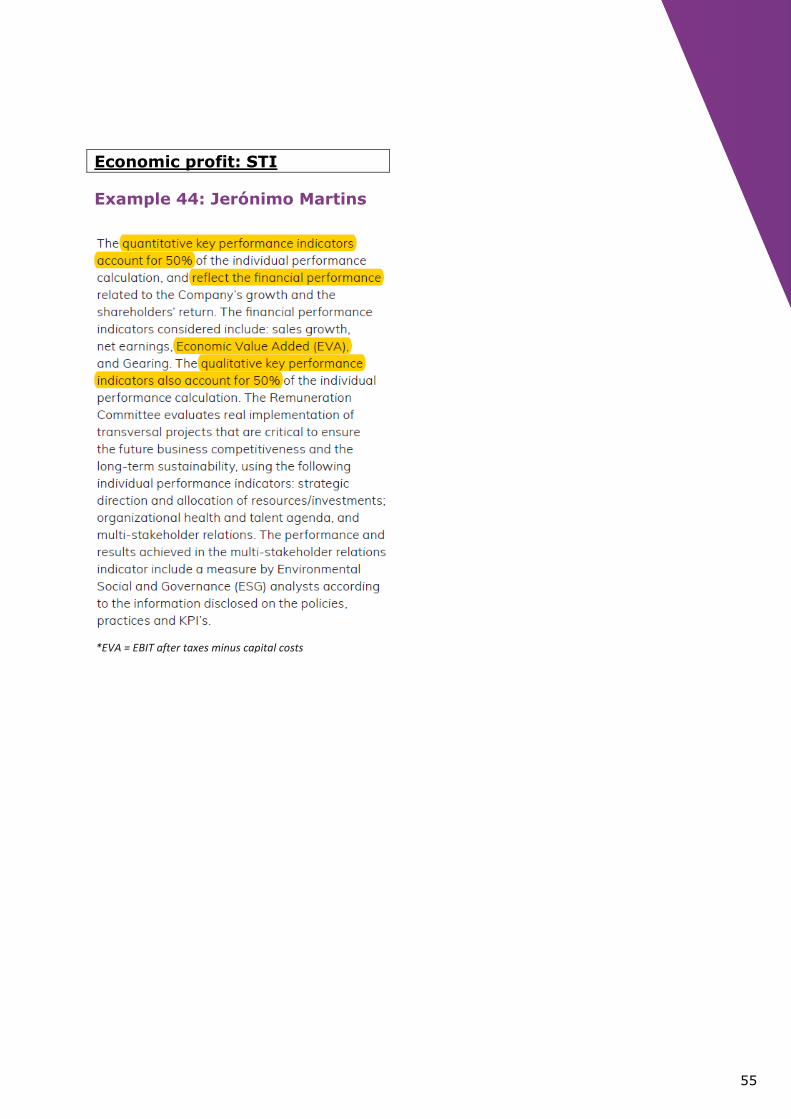

▪ Economic value added (EVA) – example 44 (STI)

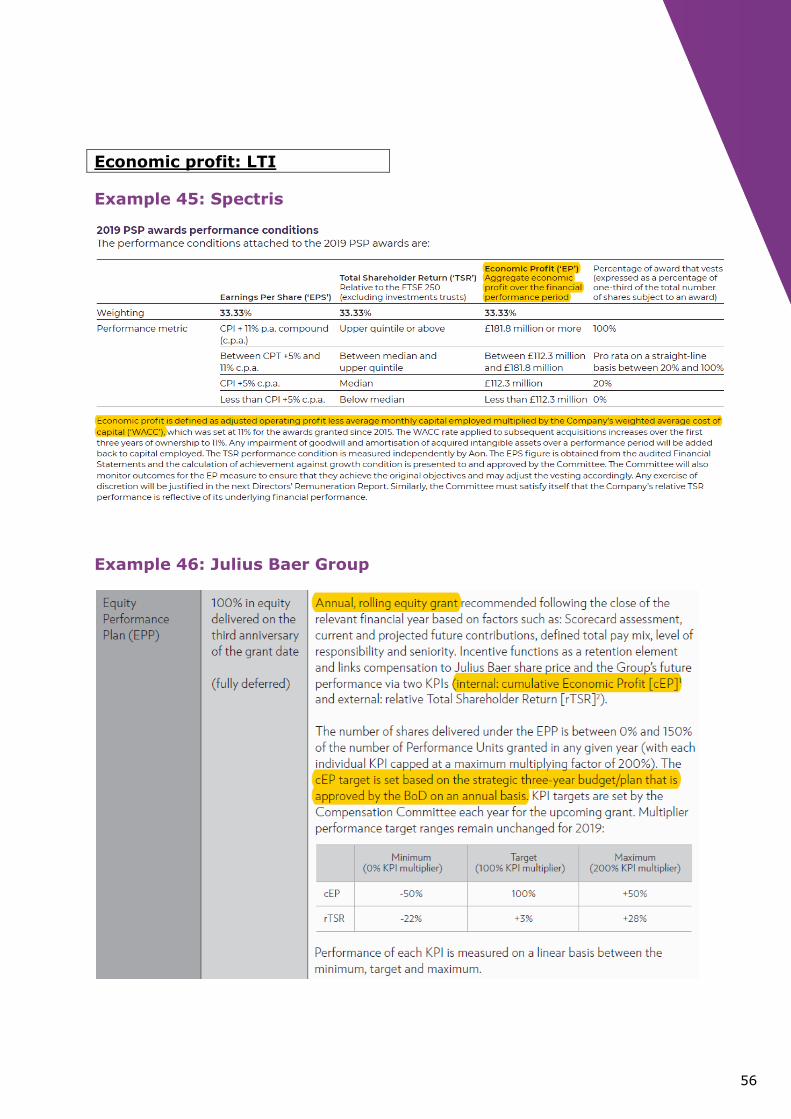

▪ Economic profit – example 45 (LTI)

▪ Cumulative economic profit – example 46 (LTI)

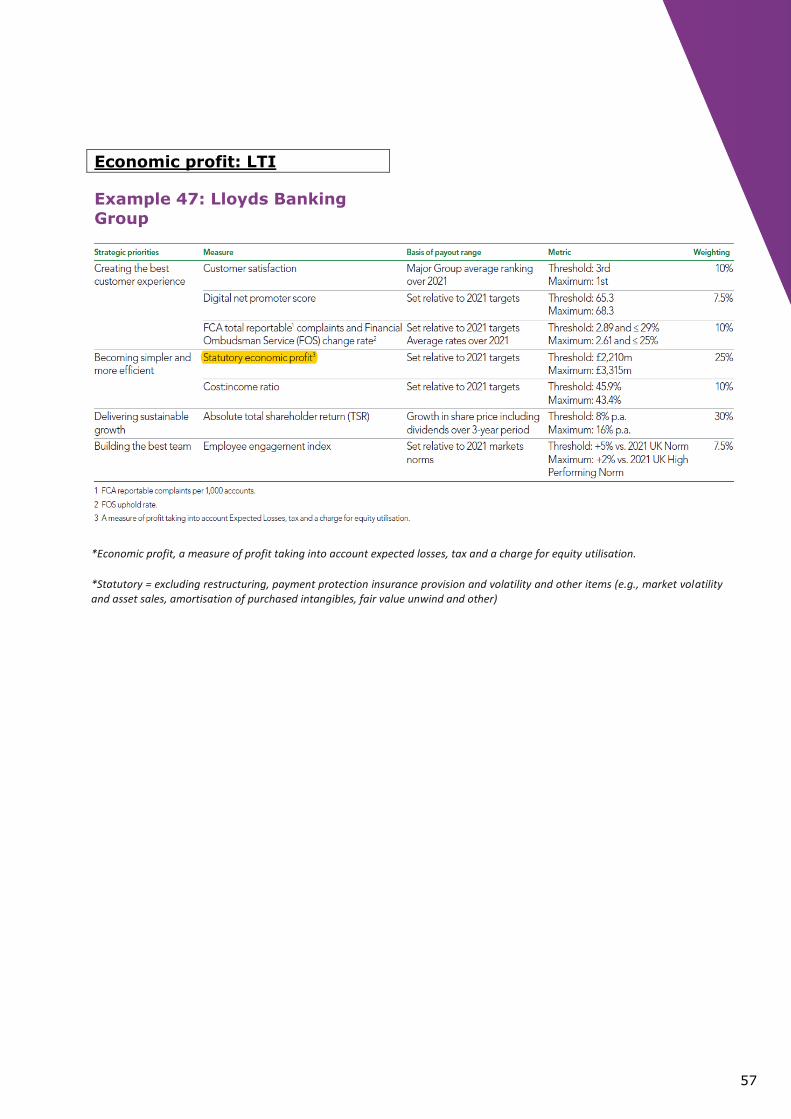

▪ Statutory economic profit – example 47 (LTI)

▪ Adjusted value added – example 48 (LTI)

17

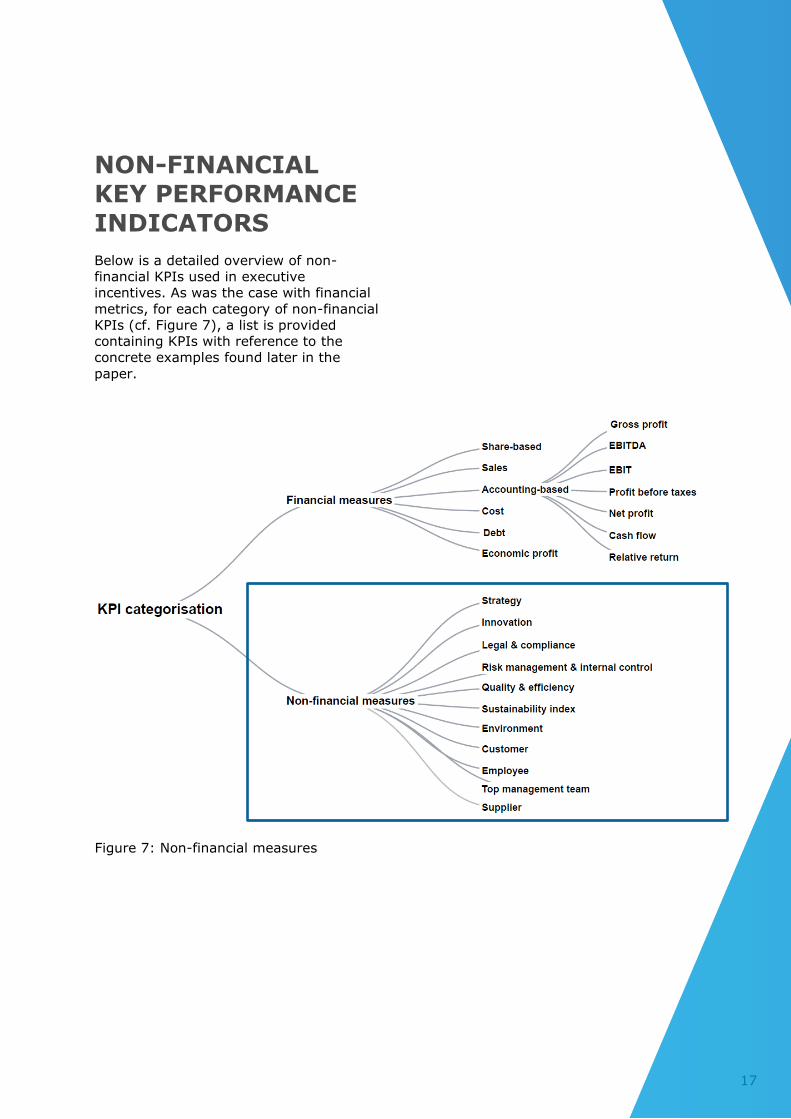

NON-FINANCIAL KEY PERFORMANCE

INDICATORS

Below is a detailed overview of non-

financial KPIs used in executive

incentives. As was the case with financial

metrics, for each category of non-financial

KPIs (cf. Figure 7), a list is provided

containing KPIs with reference to the

concrete examples found later in the

paper.

Figure 7: Non-financial measures

18

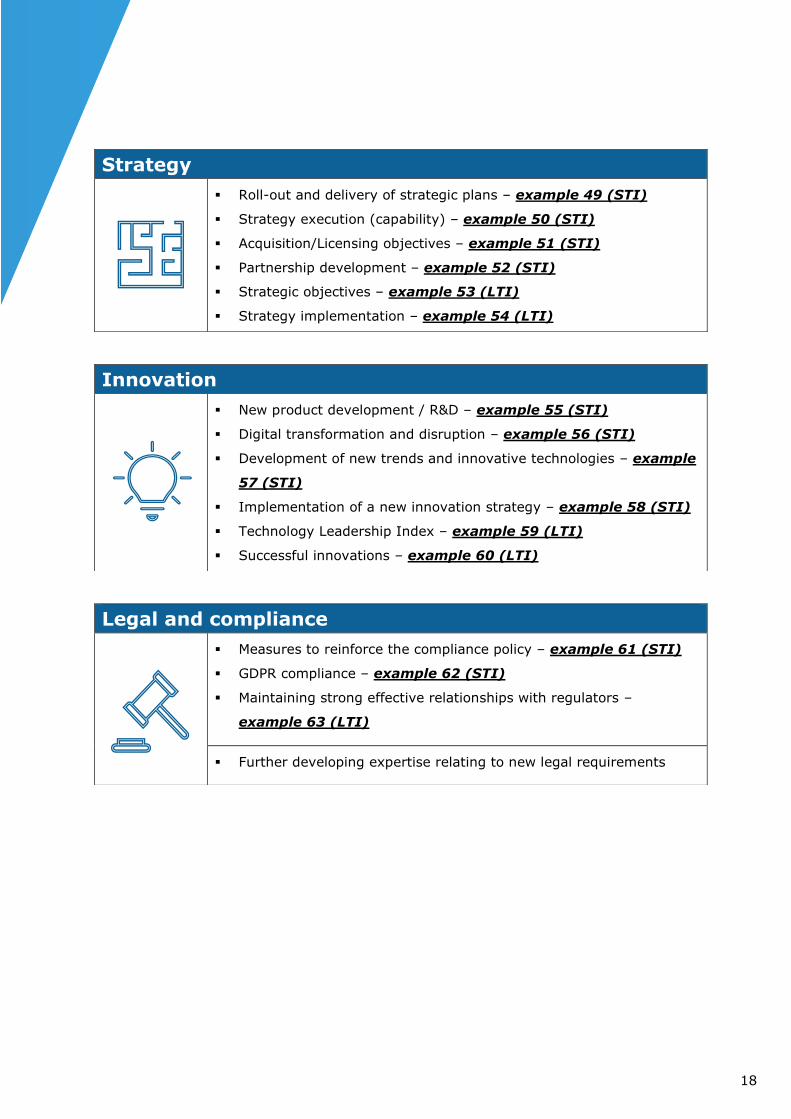

Strategy

▪ Roll-out and delivery of strategic plans – example 49 (STI)

▪ Strategy execution (capability) – example 50 (STI)

▪ Acquisition/Licensing objectives – example 51 (STI)

▪ Partnership development – example 52 (STI)

▪ Strategic objectives – example 53 (LTI)

▪ Strategy implementation – example 54 (LTI)

Innovation

▪ New product development / R&D – example 55 (STI)

▪ Digital transformation and disruption – example 56 (STI)

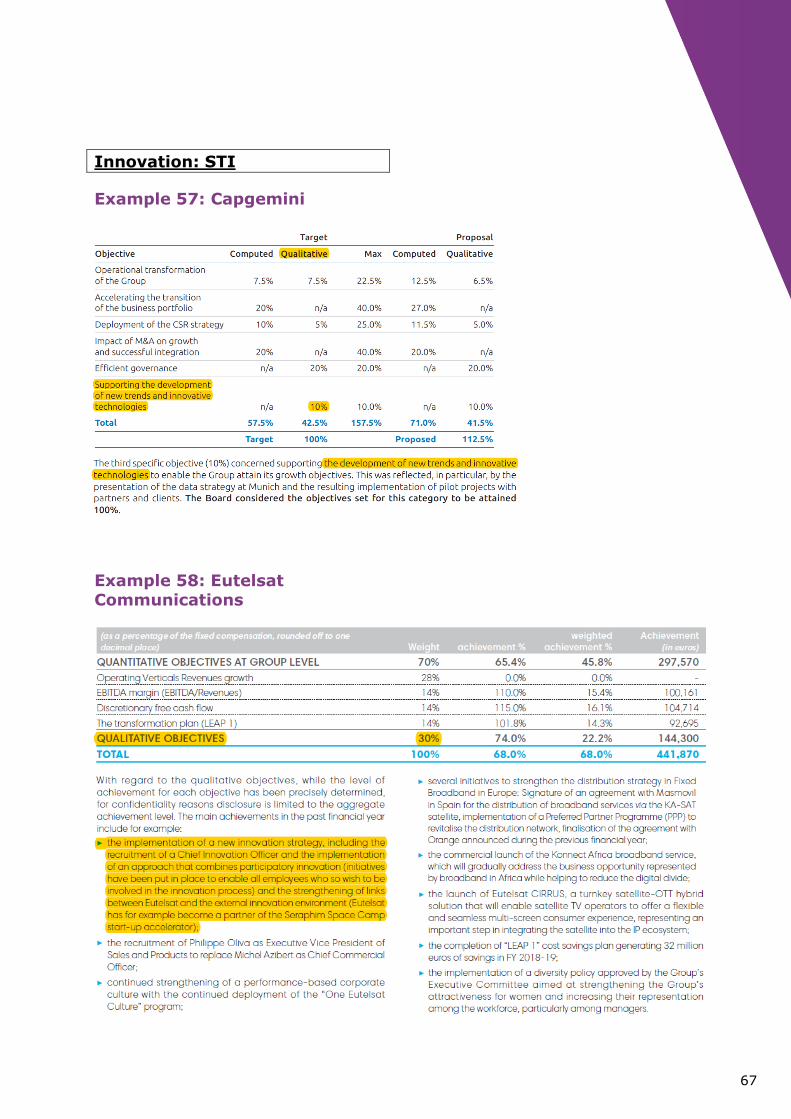

▪ Development of new trends and innovative technologies – example

57 (STI)

▪ Implementation of a new innovation strategy – example 58 (STI)

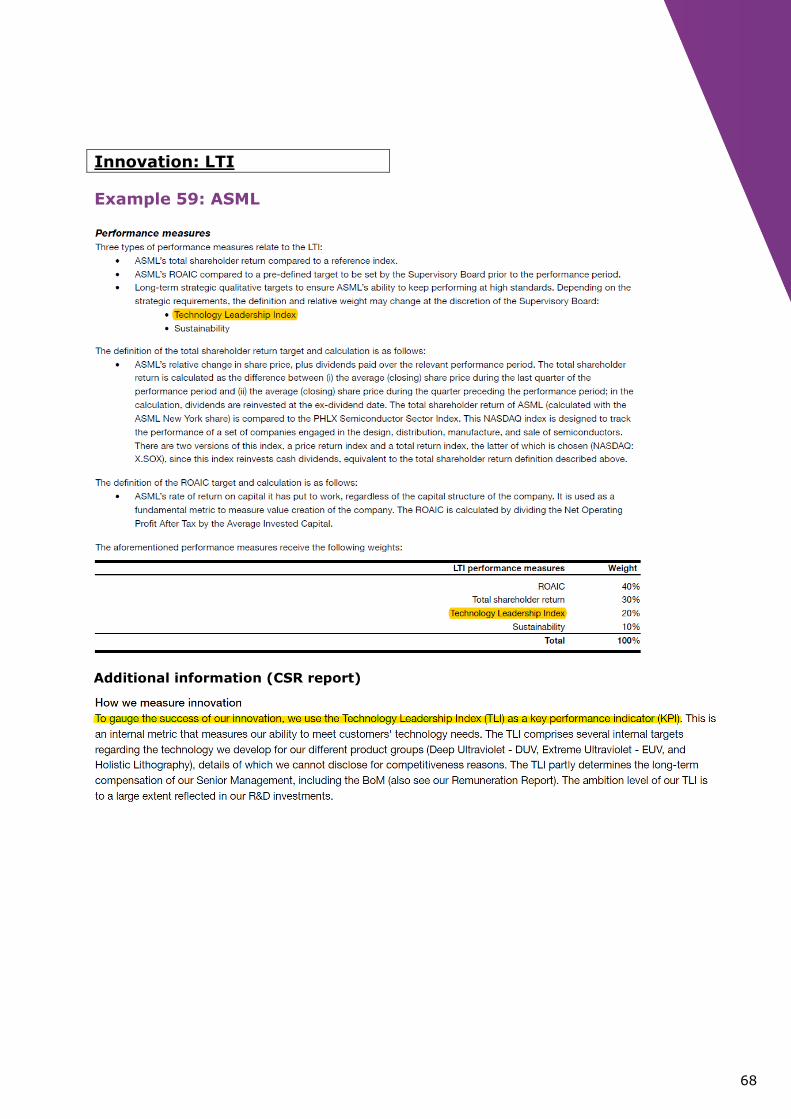

▪ Technology Leadership Index – example 59 (LTI)

▪ Successful innovations – example 60 (LTI)

Legal and compliance

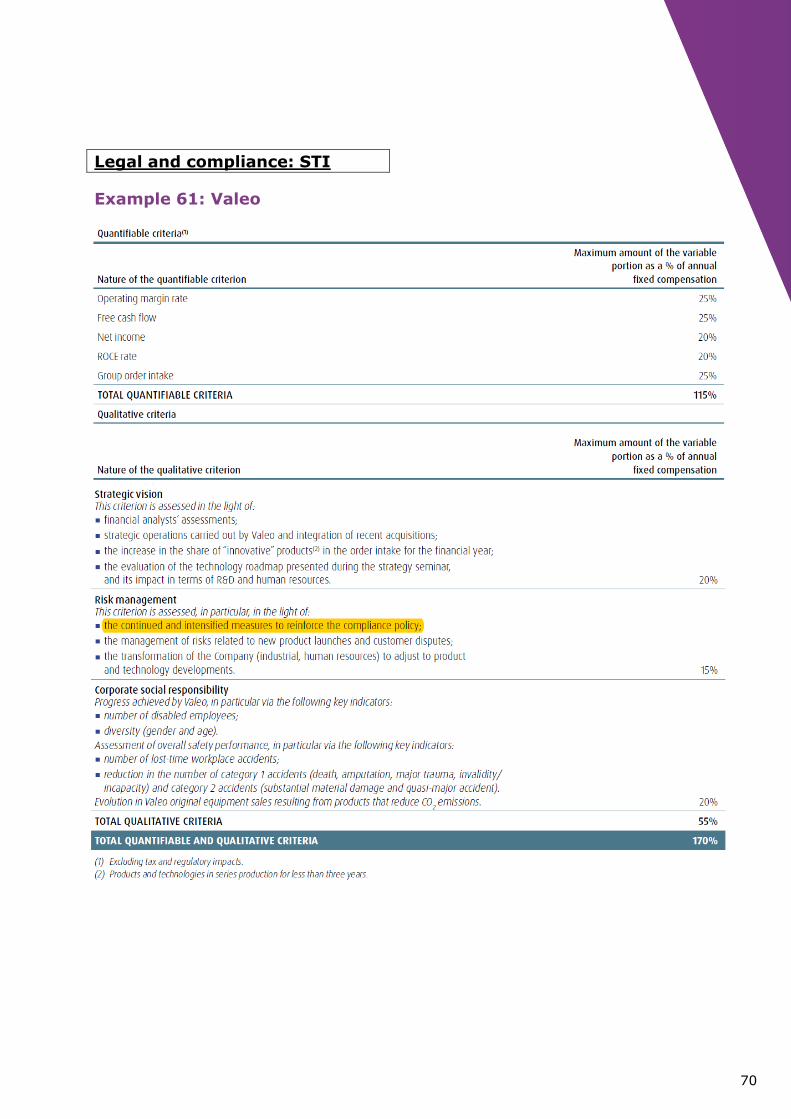

▪ Measures to reinforce the compliance policy – example 61 (STI)

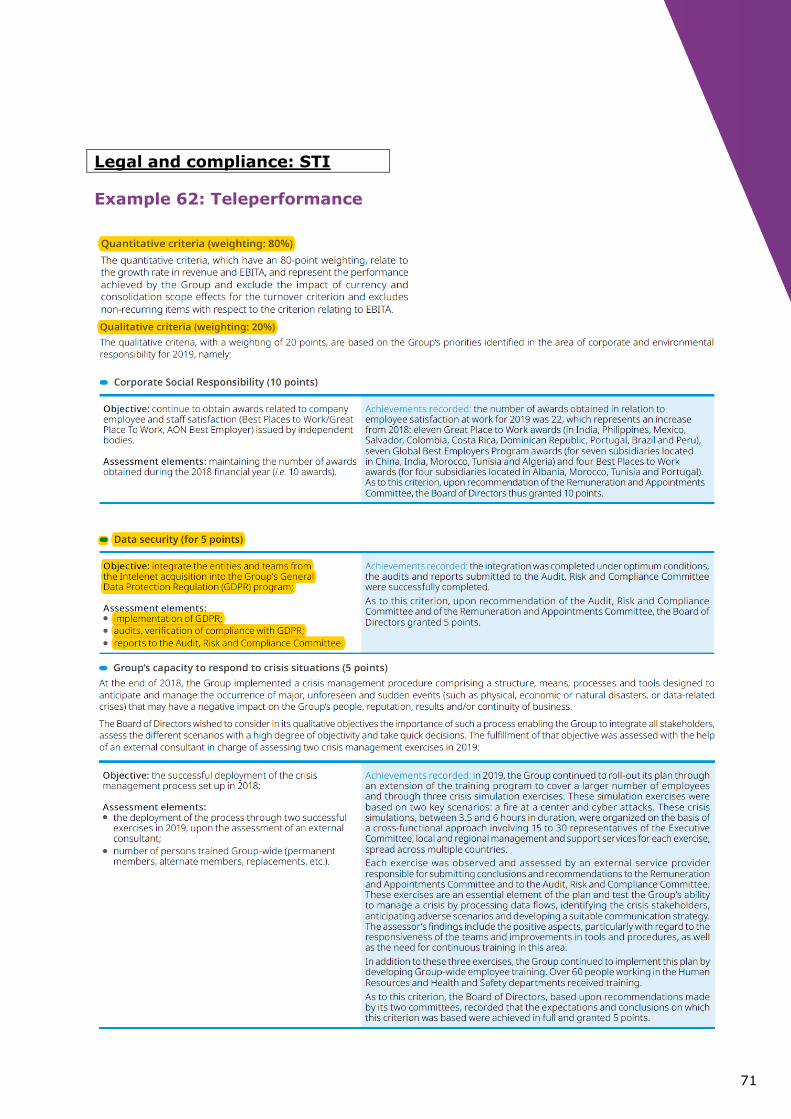

▪ GDPR compliance – example 62 (STI)

▪ Maintaining strong effective relationships with regulators –

example 63 (LTI)

▪ Further developing expertise relating to new legal requirements

19

Risk management and internal control

▪ Risk & control objectives – example 64 (STI)

▪ Risk mitigation – example 65 (STI)

▪ Risk management framework – example 66 (STI)

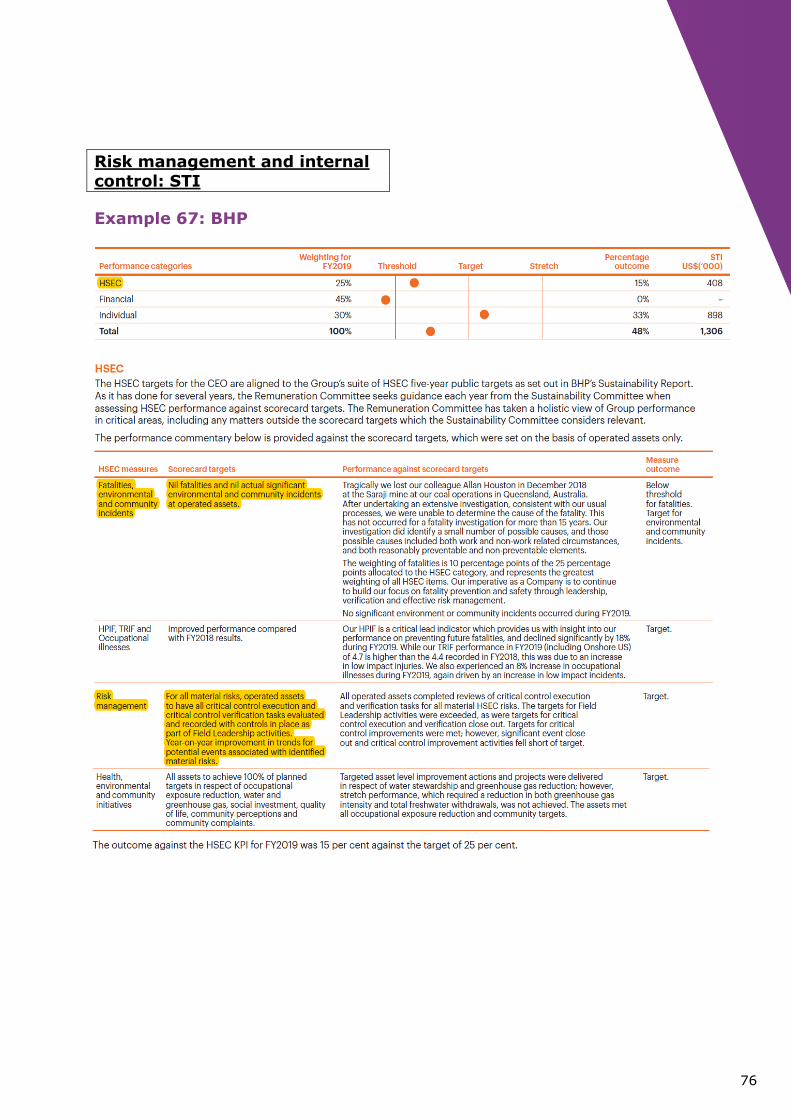

▪ Risk management – example 67 (STI)

▪ Environmental and community incidents – example 67 (STI)

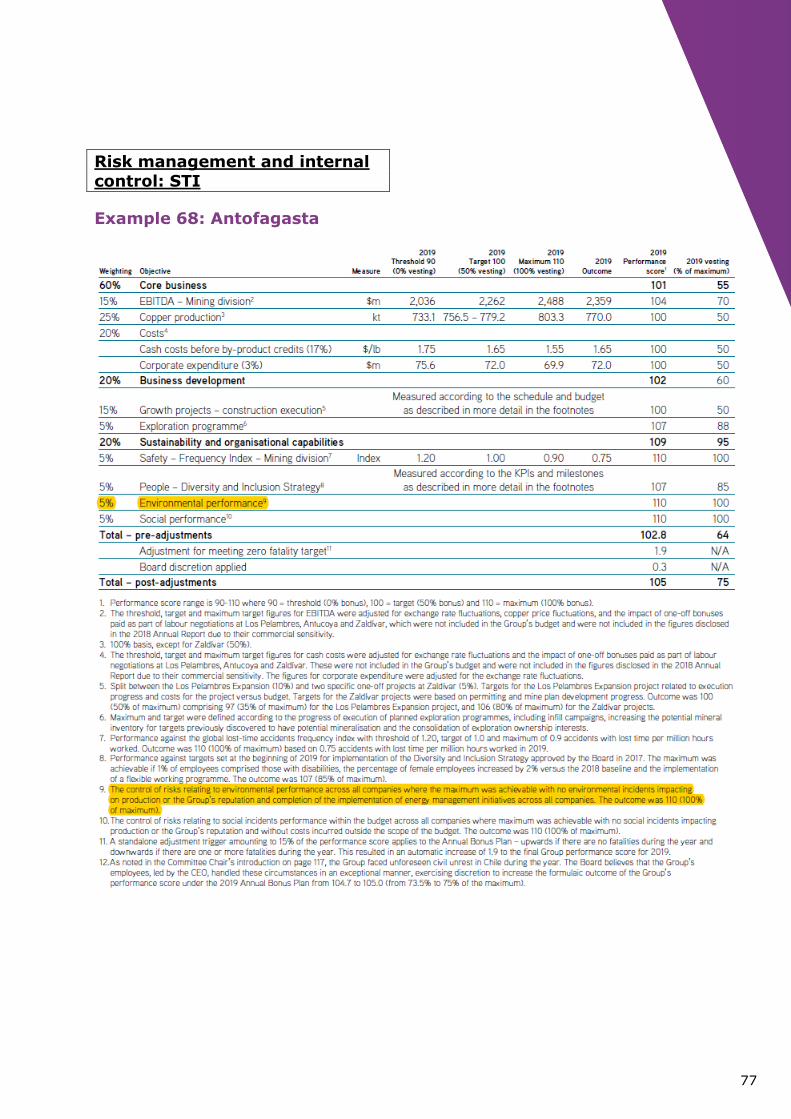

▪ The control of risks relating to environmental performance –

example 68 (STI)

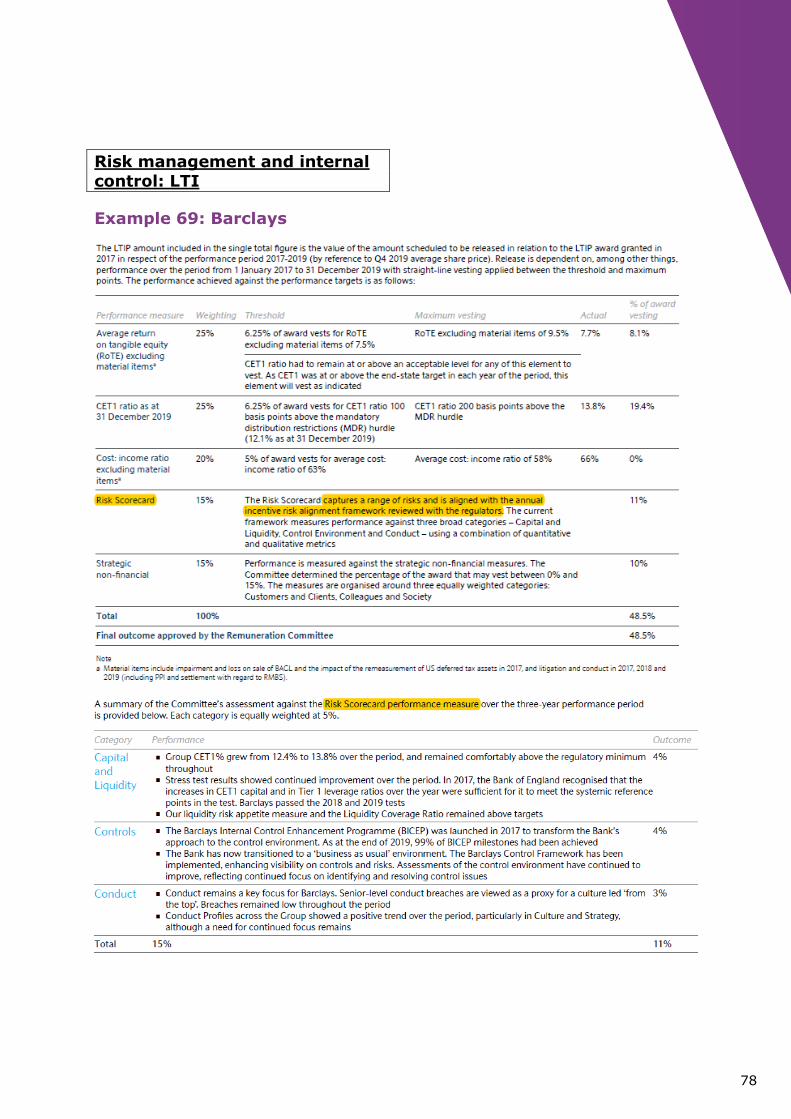

▪ Risk scorecard – example 69 (LTI)

▪ Cyber security (trainings)

▪ Training provided to employees by the Compliance Department

Regular Risk Committee

Quality and efficiency

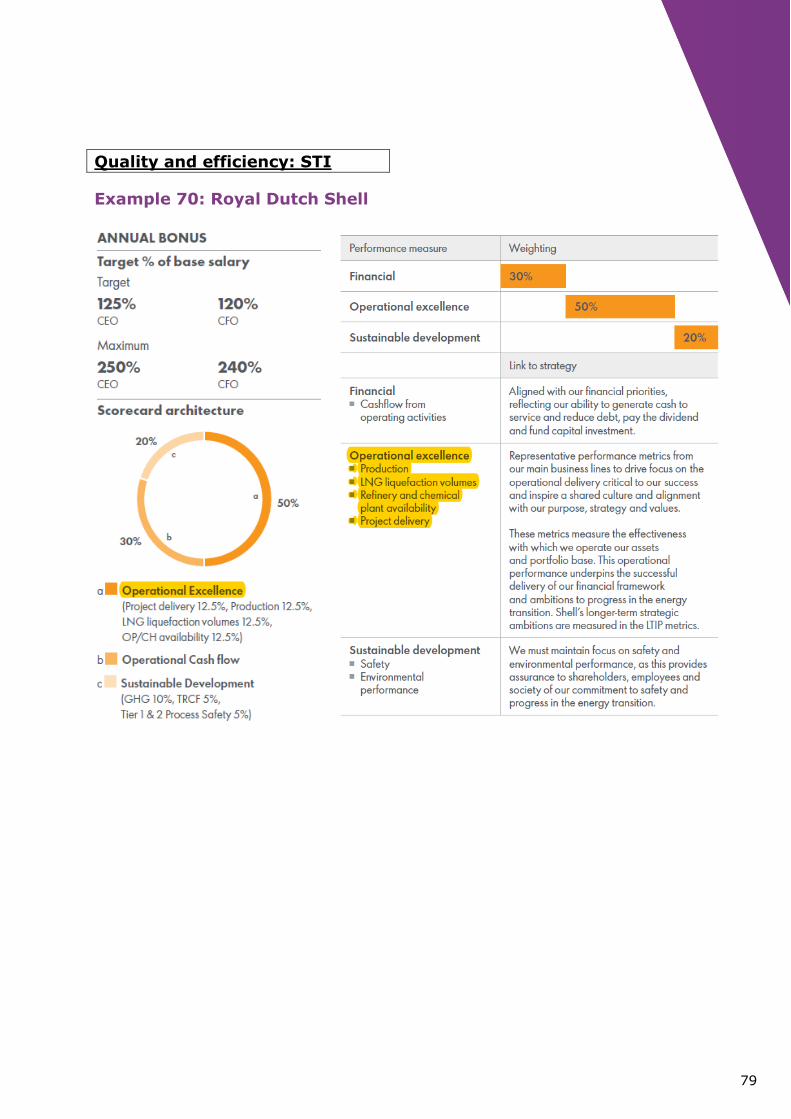

▪ Operational excellence – example 70 (STI) & example 71

(STI)

▪ Process digitisation – example 71 (STI)

▪ Resource management – example 72 (STI)

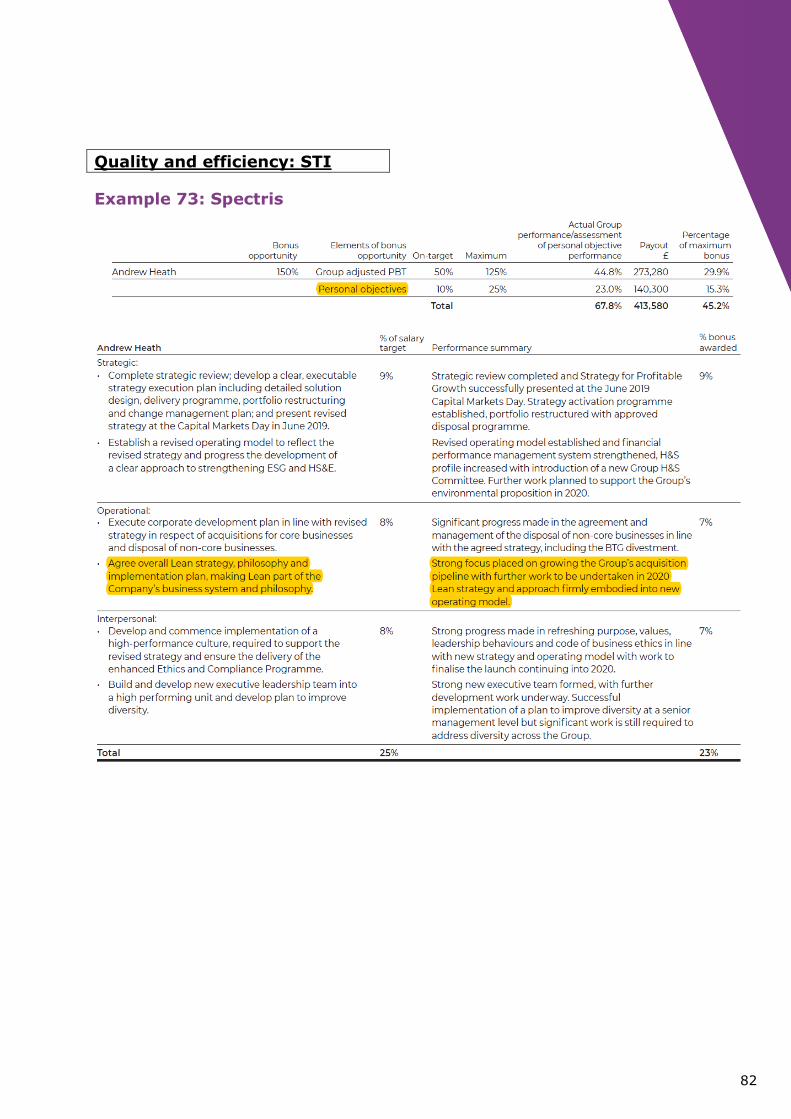

▪ Lean strategy – example 73 (STI)

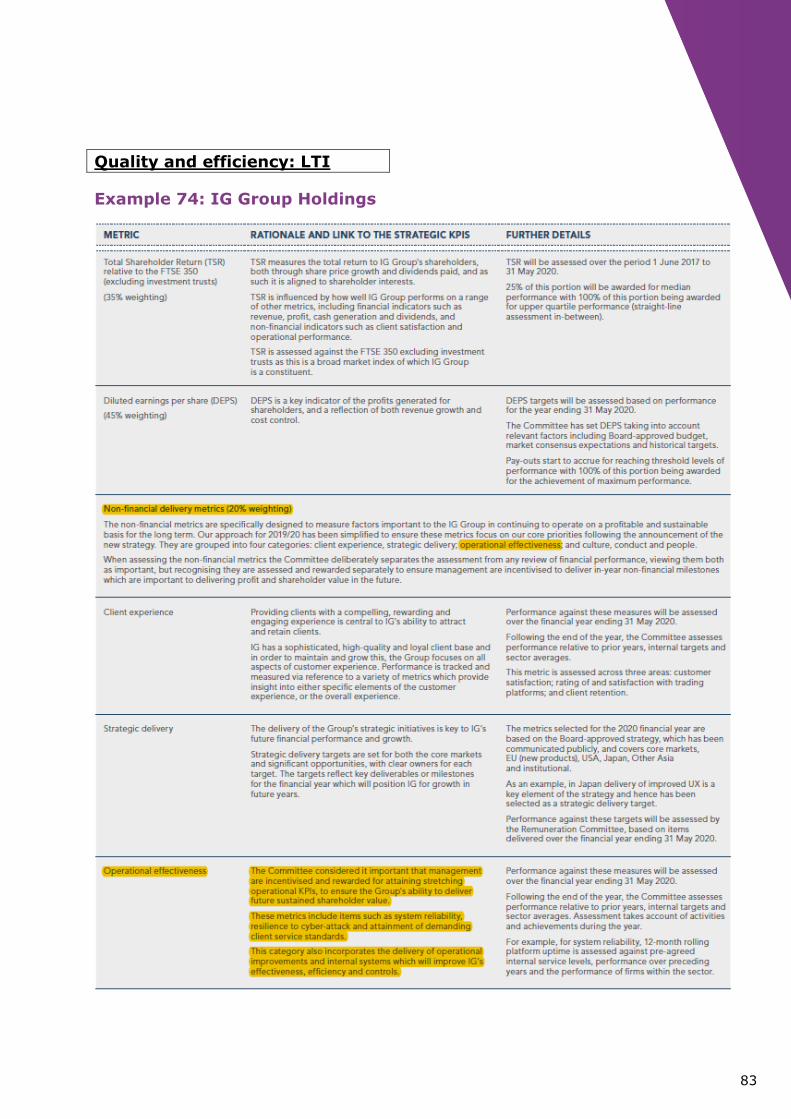

▪ Operational effectiveness – example 74 (LTI)

▪ On-time performance

▪ Inventory turnover

▪ Product quality

▪ Product and service delivery and improvement

▪ Synergies

Sustainability index

▪ Sustainability scorecard/impact – example 75 (STI)

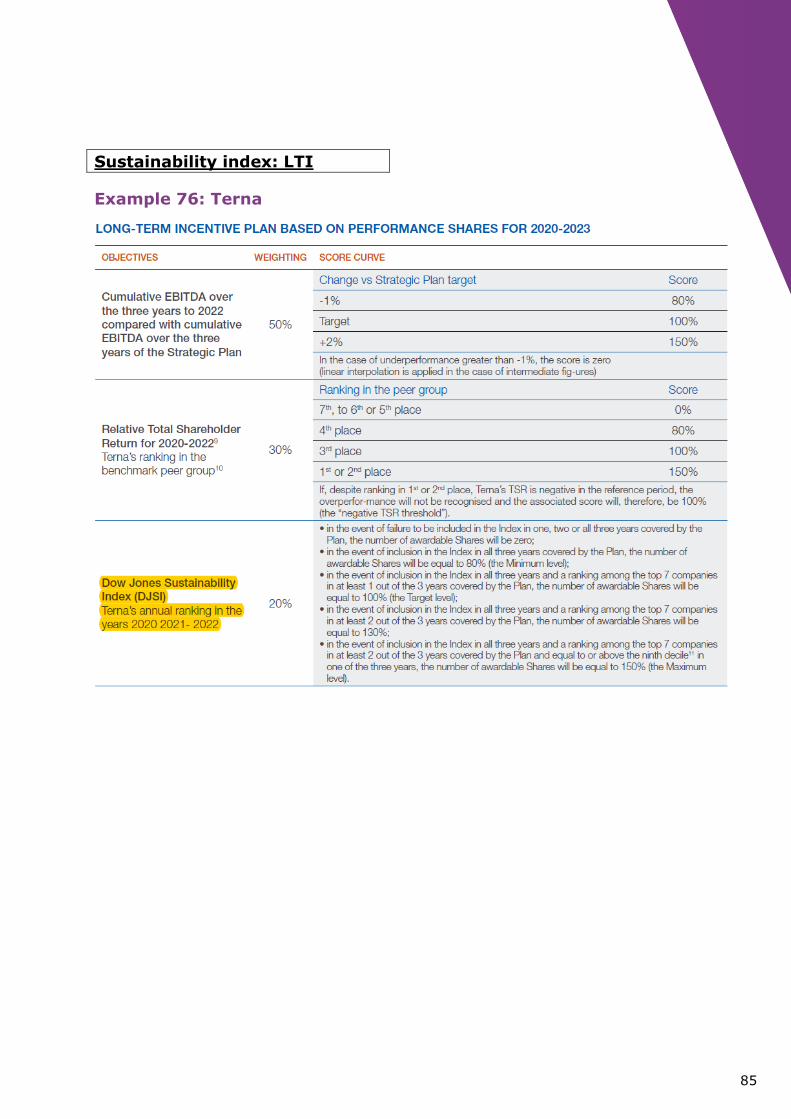

▪ Dow Jones Sustainability Index – example 76 (LTI)

20

Environment

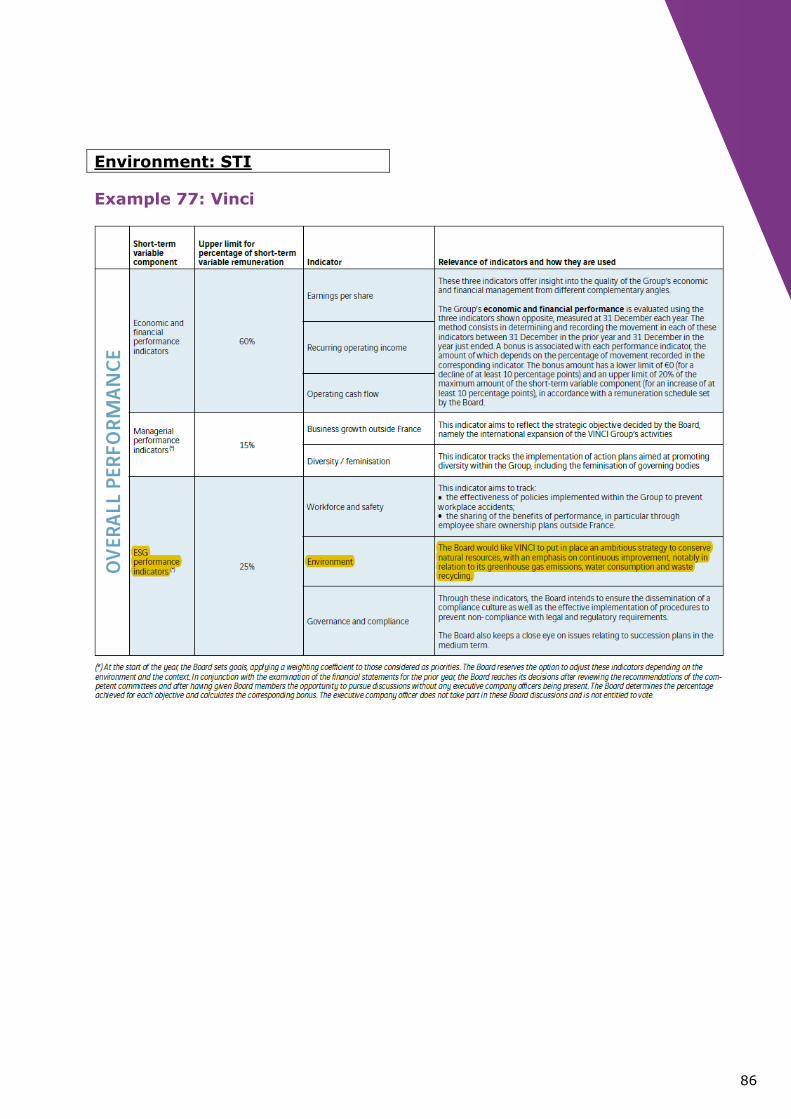

▪ Ambitious environmental strategy – example 77 (STI)

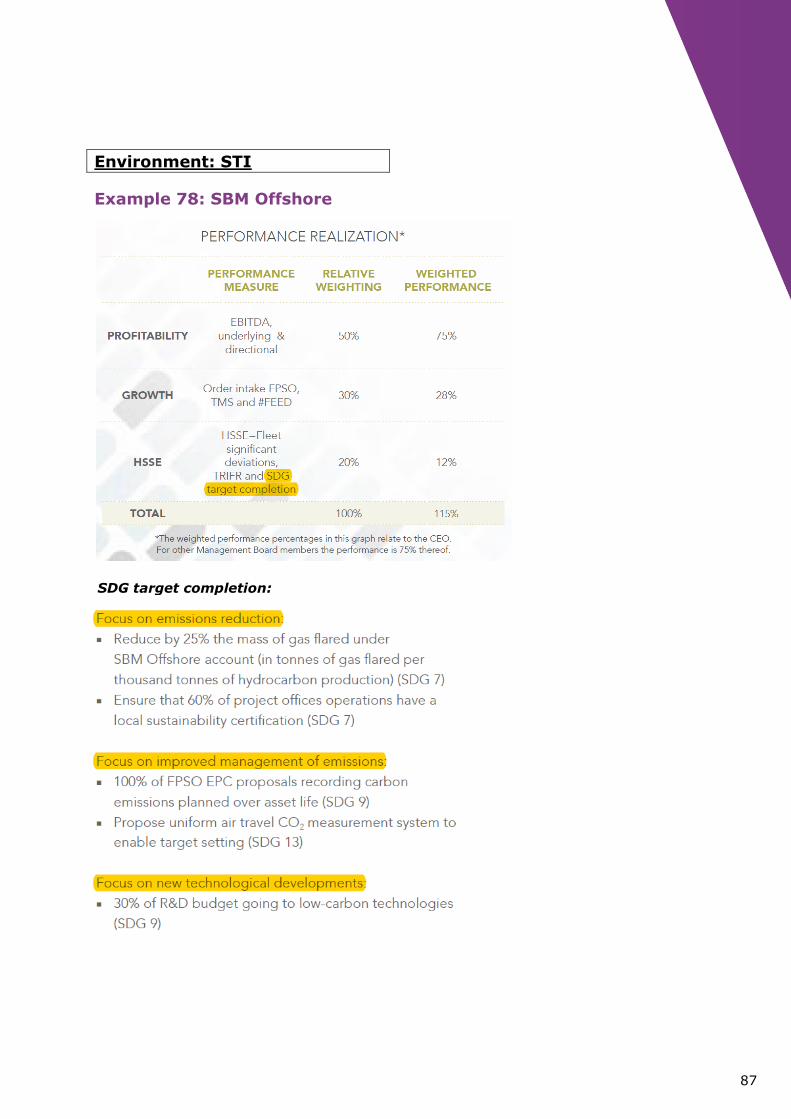

▪ Emissions – example 78 (STI)

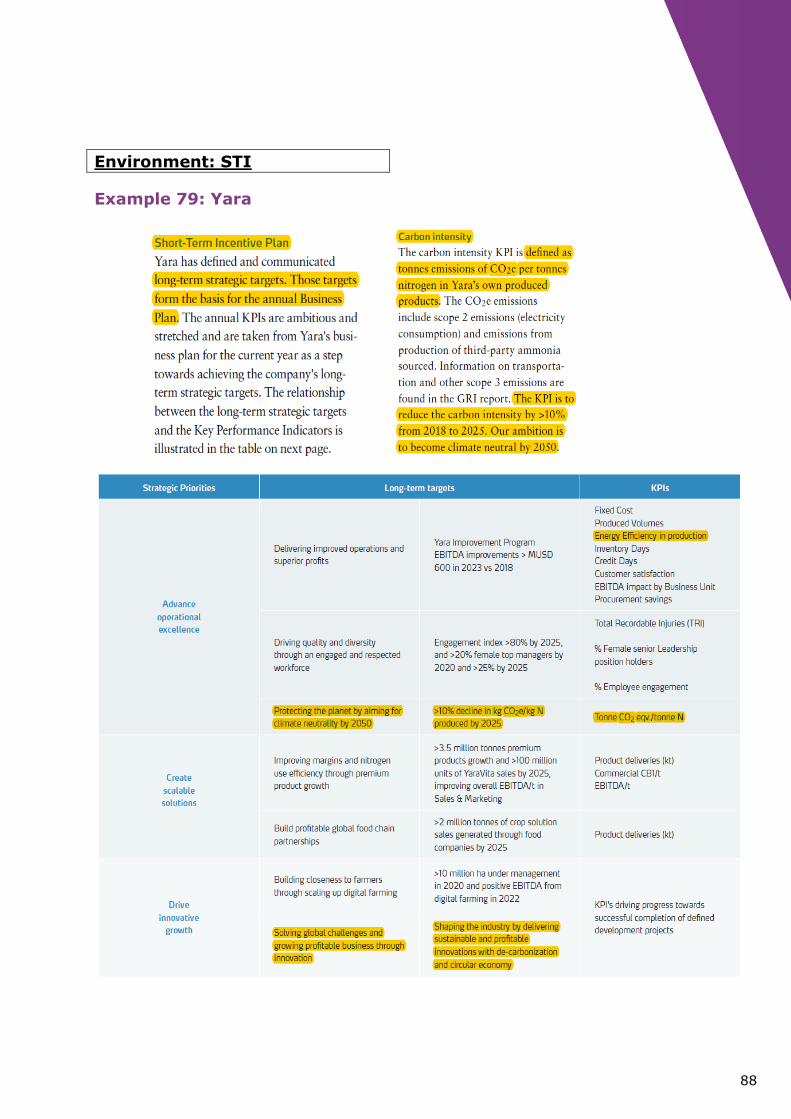

▪ Climate neutrality by 2050 – example 79 (STI)

▪ Energy efficiency in production – example 79 (STI)

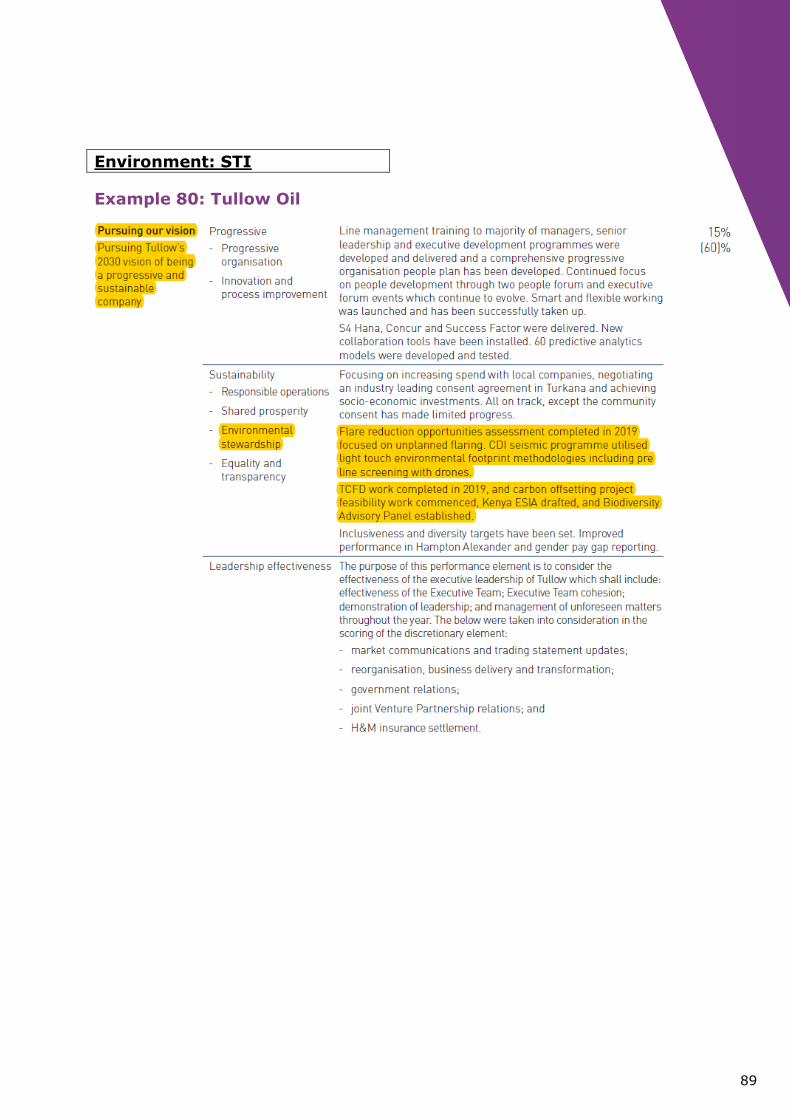

▪ Environmental stewardship – example 80 (STI)

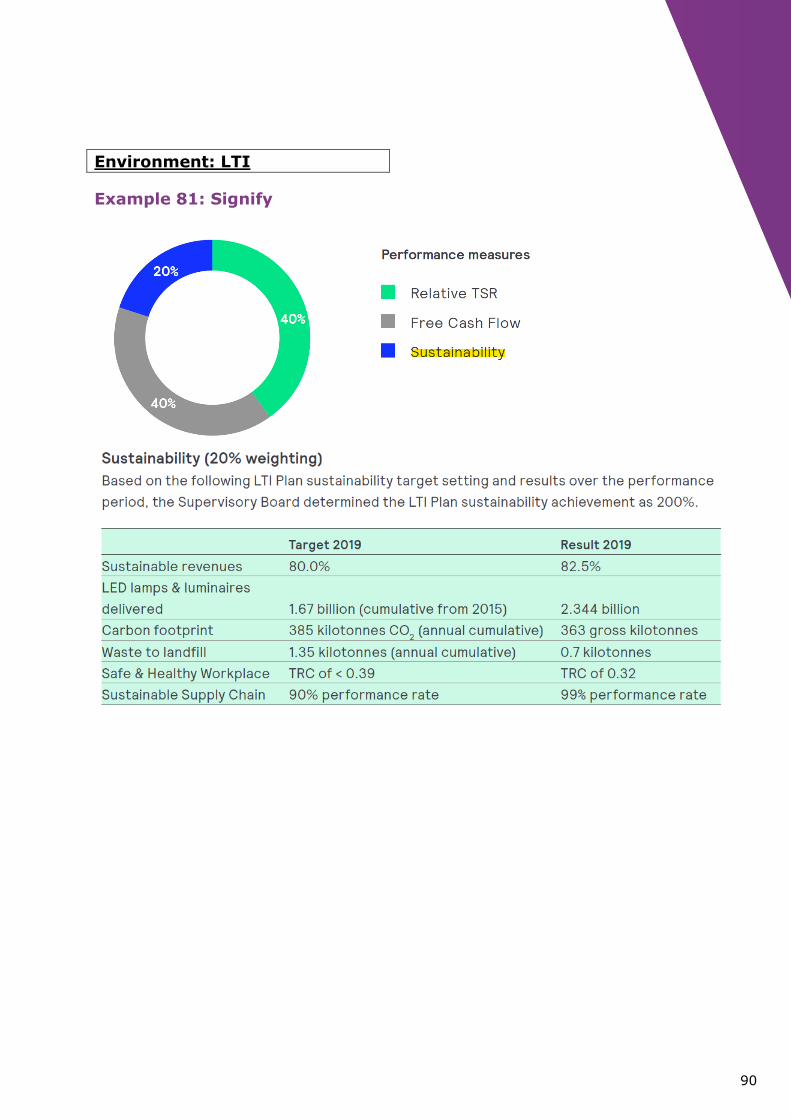

▪ Carbon/environmental footprint – example 81 (LTI)

▪ Renewable raw materials and energy funding

▪ Reduction in emissions per employee

▪ Renewable electricity as % of global consumption

▪ Undertaking a strategic review of the recycling businesses in light of

the Government’s waste strategy

▪ Promote and use the Environmental Profit & Loss account (EP&L)

▪ EcoVadis rating: obtaining gold level

▪ LEED/BREEAM certification

▪ Climate Change score received from Carbon Disclosure Project

(CDP) Worldwide

Customer

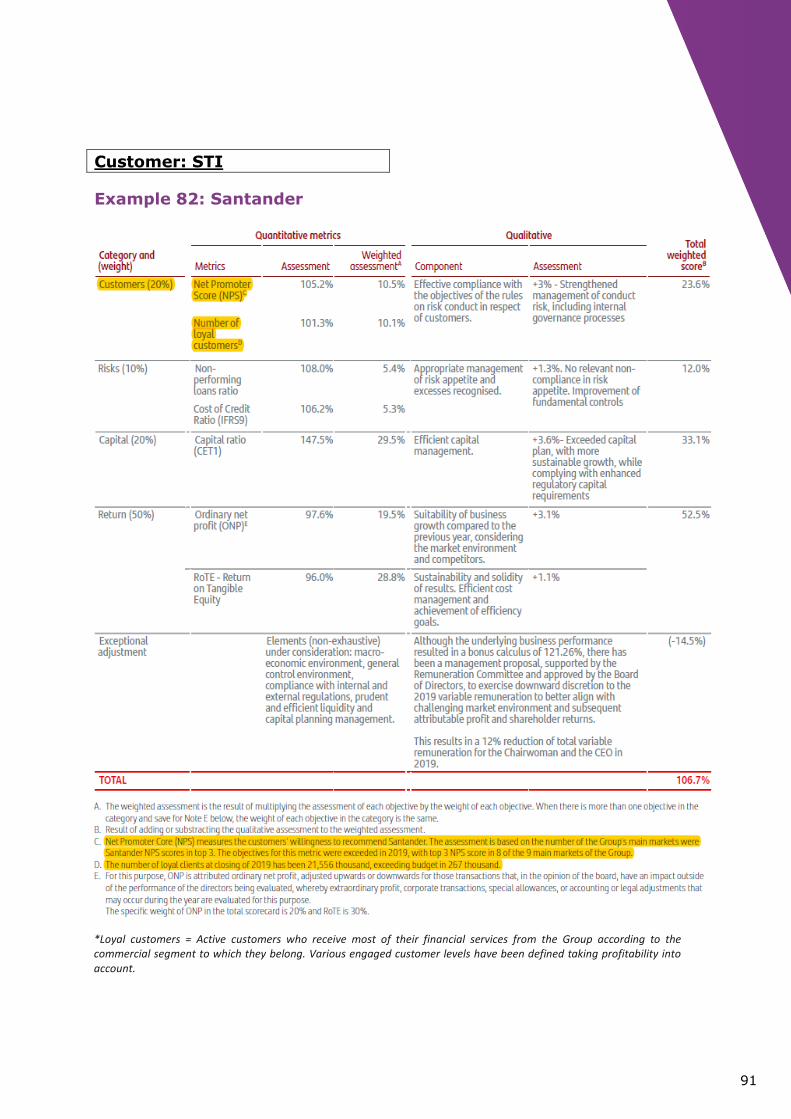

▪ Net promoter score – example 82 (STI)

▪ Number of loyal customers – example 82 (STI)

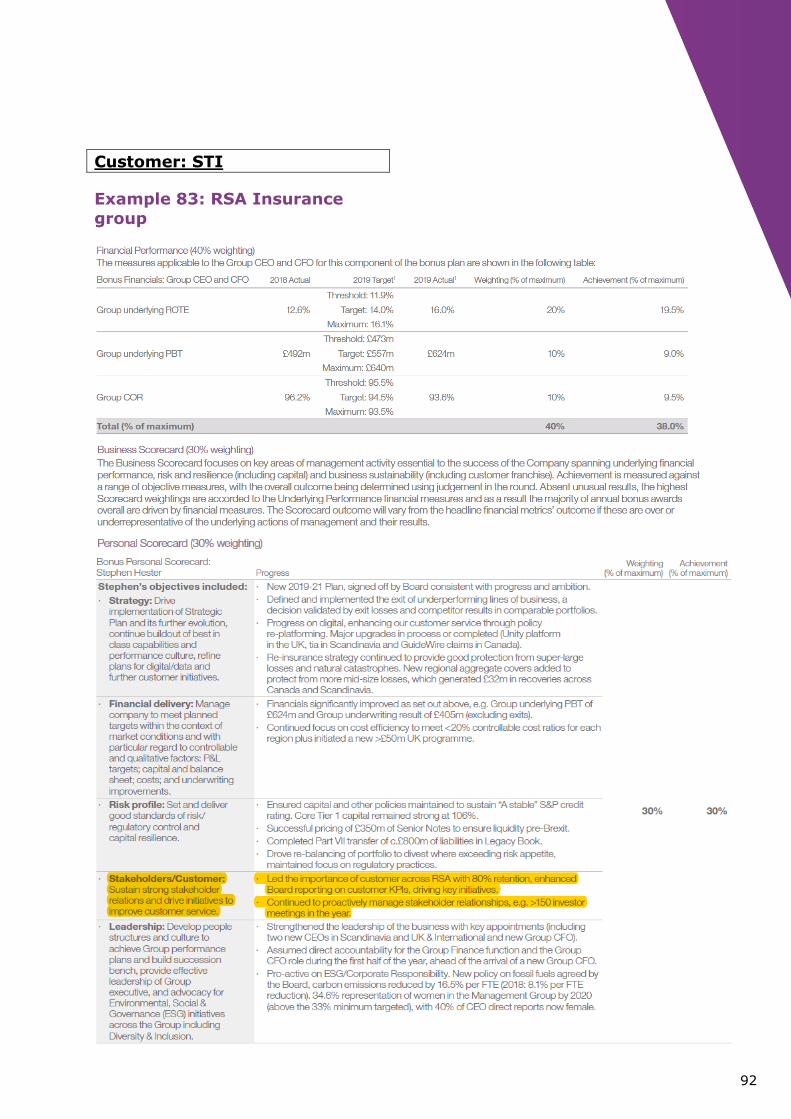

▪ Drive initiatives to improve customer service – example 83 (STI)

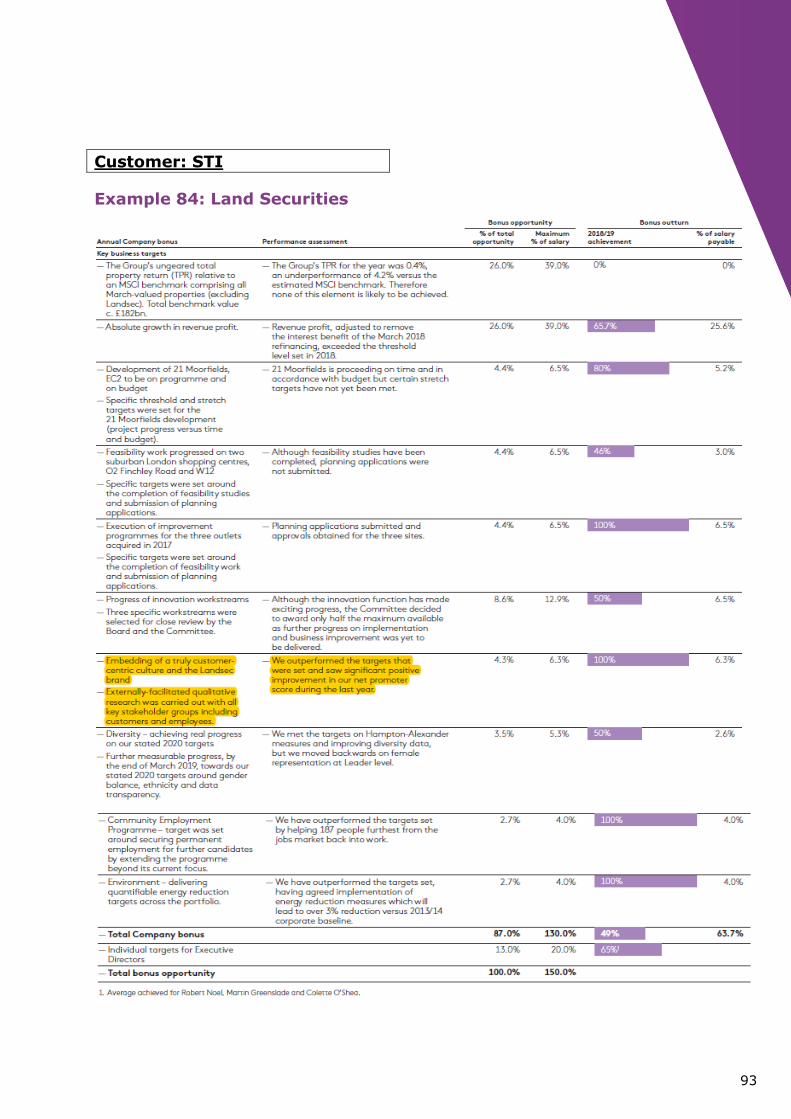

▪ Embedding a truly customer-centric culture – example 84 (STI)

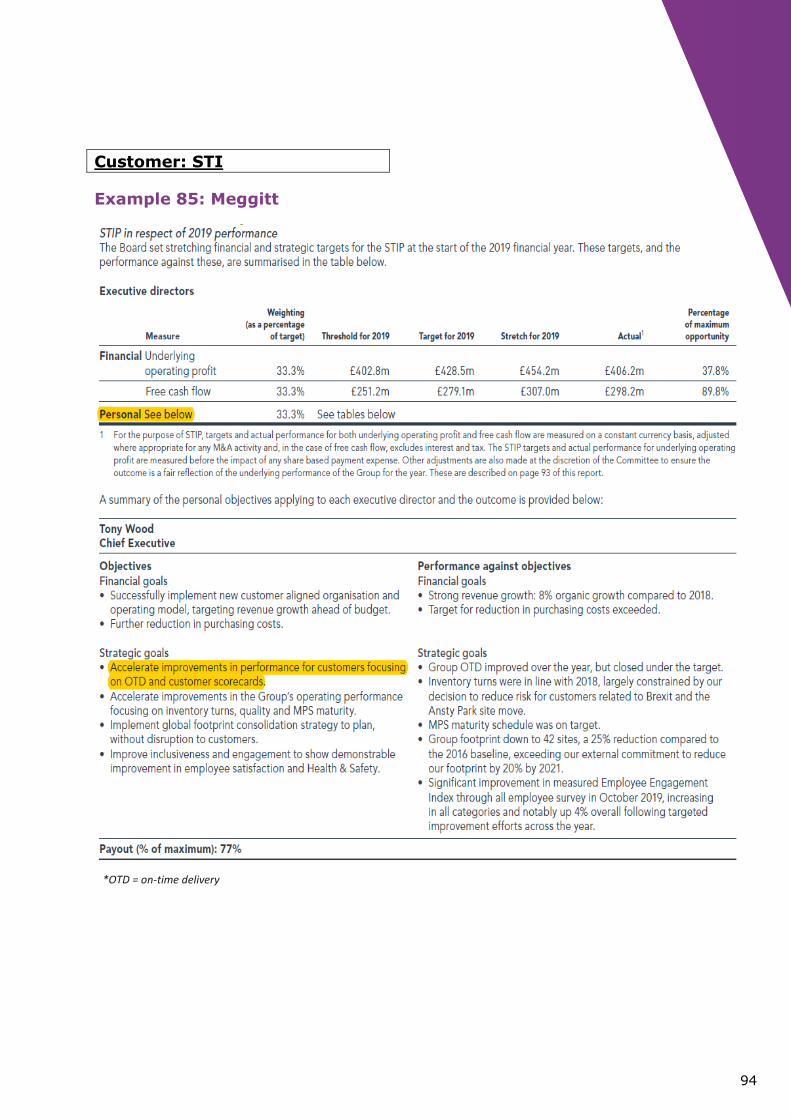

▪ Improvements in performance for customers – example 85 (STI)

▪ Improving customer engagement – example 86 (STI)

▪ Total customer heartbeat – example 87 (STI)

▪ Leading customer experience – example 88 (LTI)

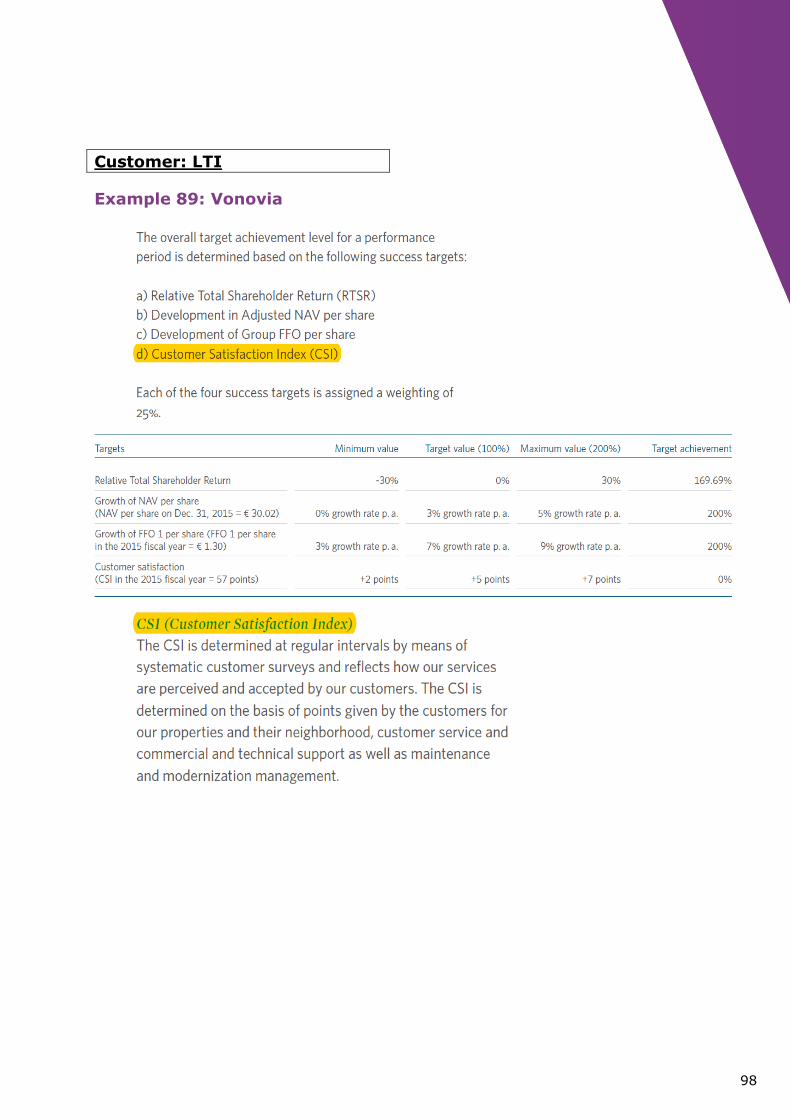

▪ Customer Satisfaction Index (CSI) – example 89 (LTI)

▪ Net new clients

▪ Customer churn rate

▪ Enhance Voice of Customer (VoC) (launch and roll-out of CRM

surveys)

21

Employee

▪ Social – employee aspects – example 90 (STI)

▪ People and culture – example 91 (STI)

▪ Diversity, inclusion and gender balance – example 92 (STI),

example 93 (STI) & example 96 (LTI)

▪ Employee engagement – example 93 (STI)

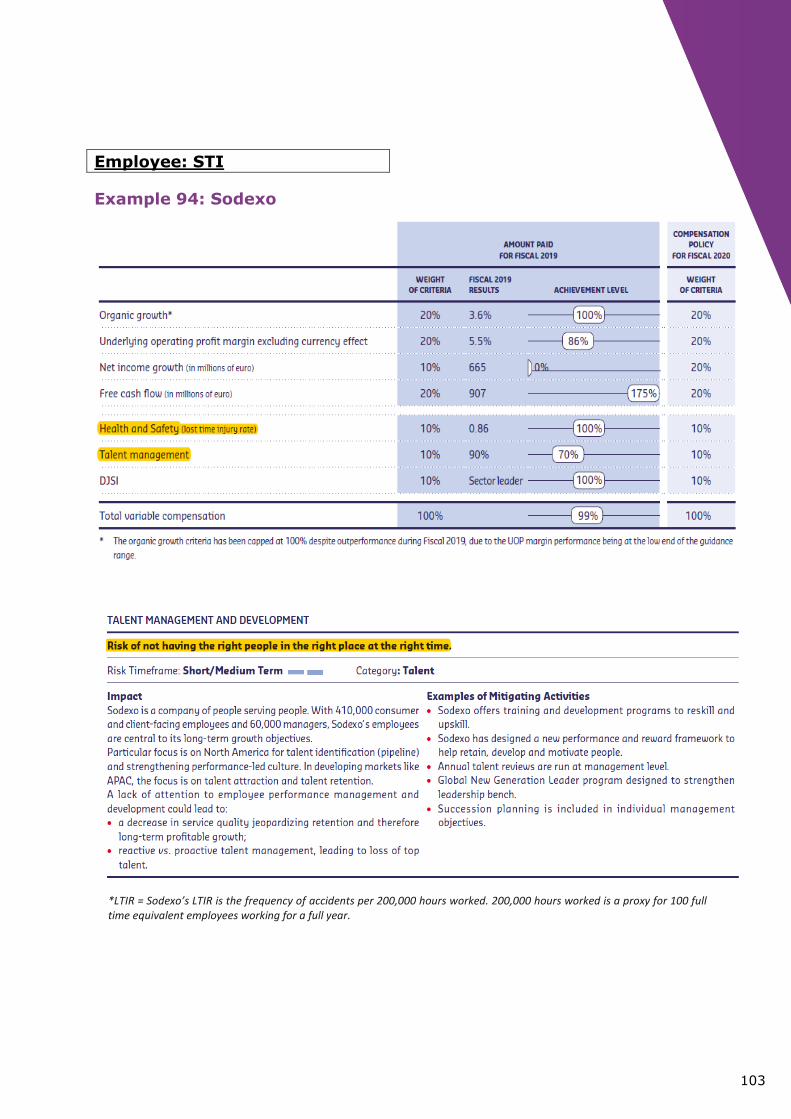

▪ Talent management/development – example 94 (STI)

▪ Lost Time Injury Rate (LTIR) – example 94 (STI)

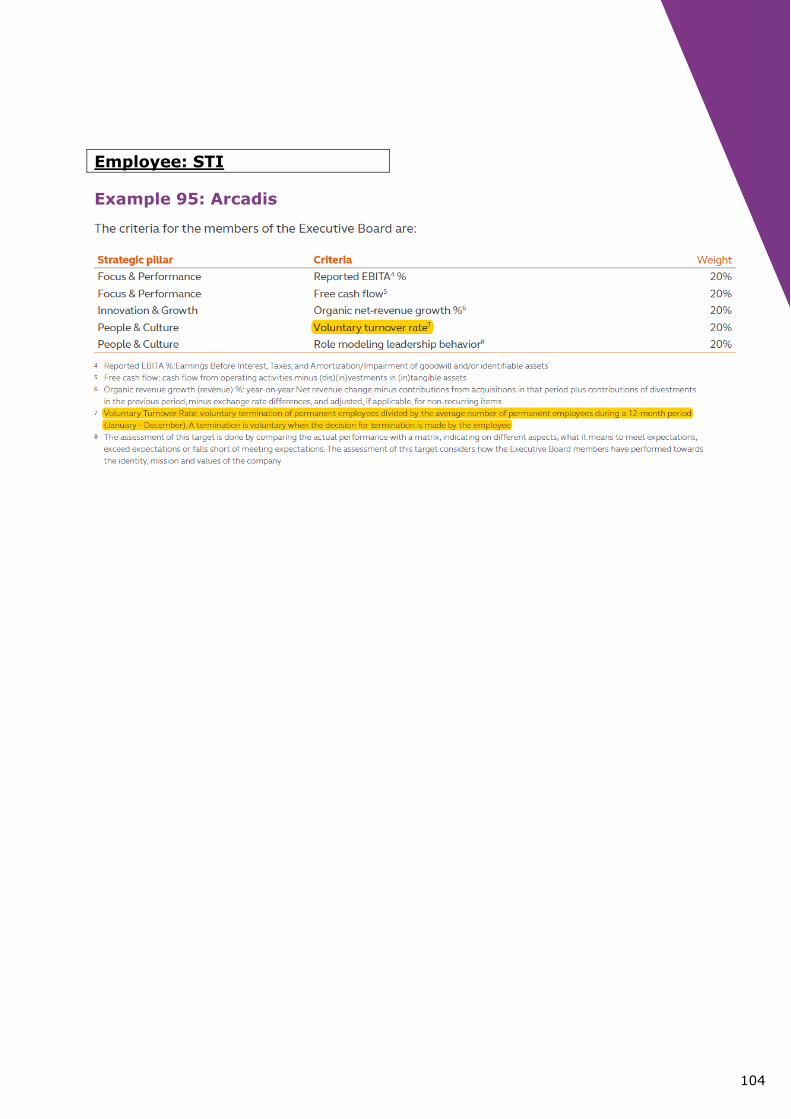

▪ Voluntary Turnover Rate – example 95 (STI)

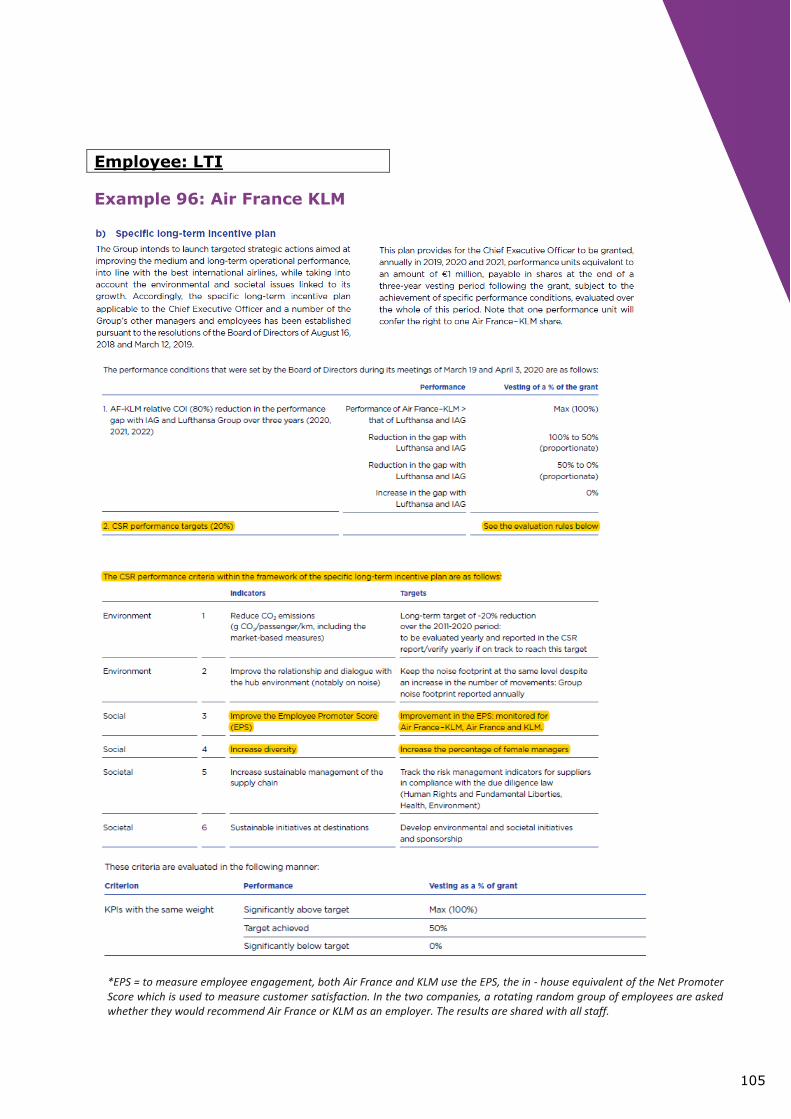

▪ Employee promotor score – example 96 (LTI)

▪ Training hours per employee

▪ Absenteeism

▪ Total Recordable Case Frequency (TRCF)

▪ Accident Frequency Rate (AFR)

Top management team

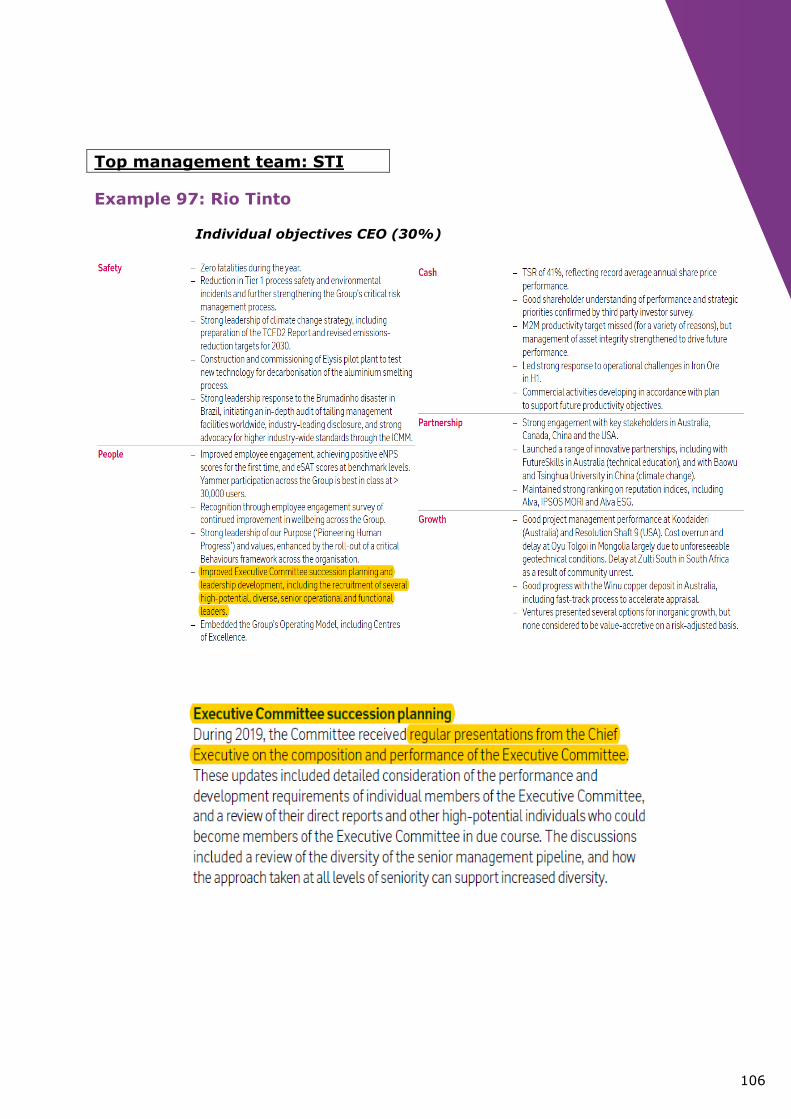

▪ Succession planning and leadership development –

example 97 (STI)

▪ Leadership effectiveness – example 98 (STI)

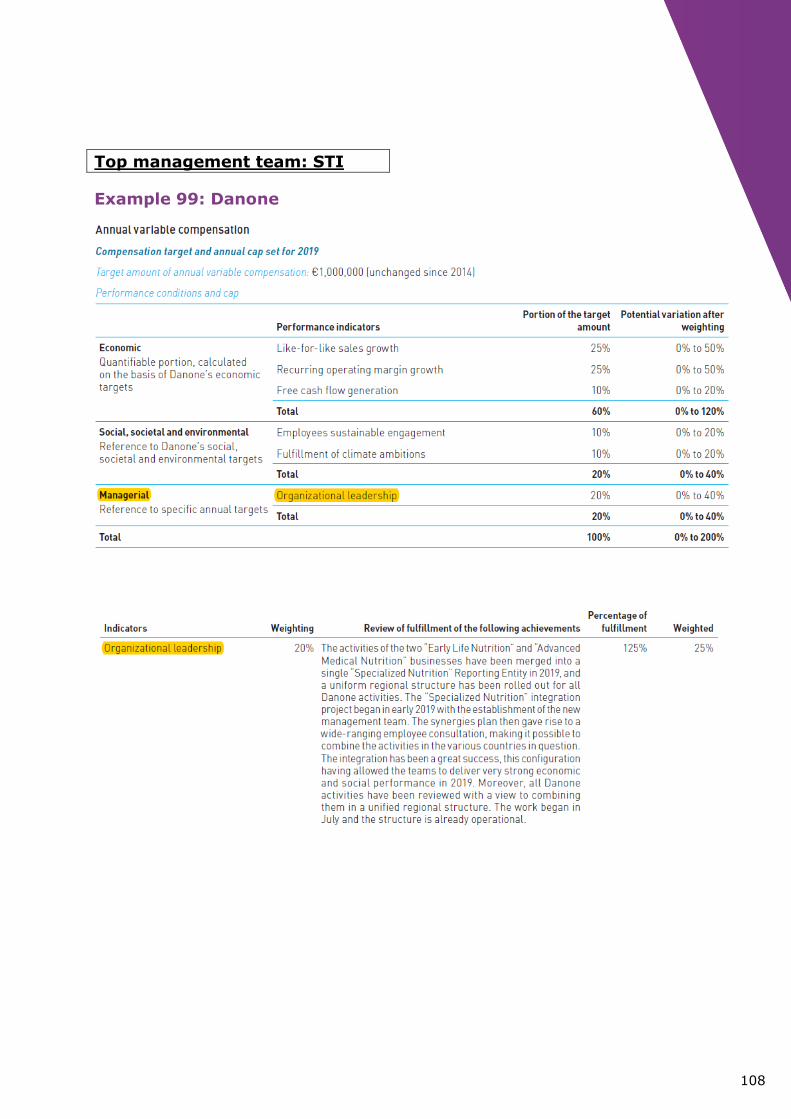

▪ Organisational leadership – example 99 (STI)

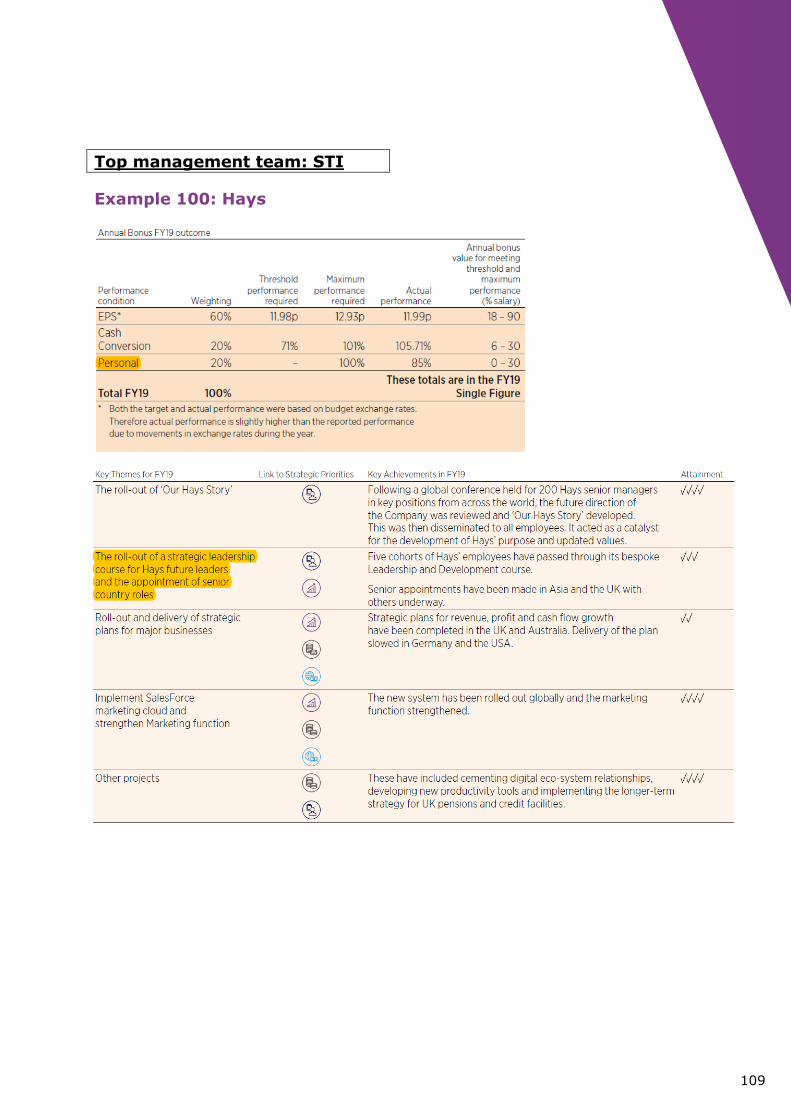

▪ Roll-out of strategic leadership course – example 100 (STI)

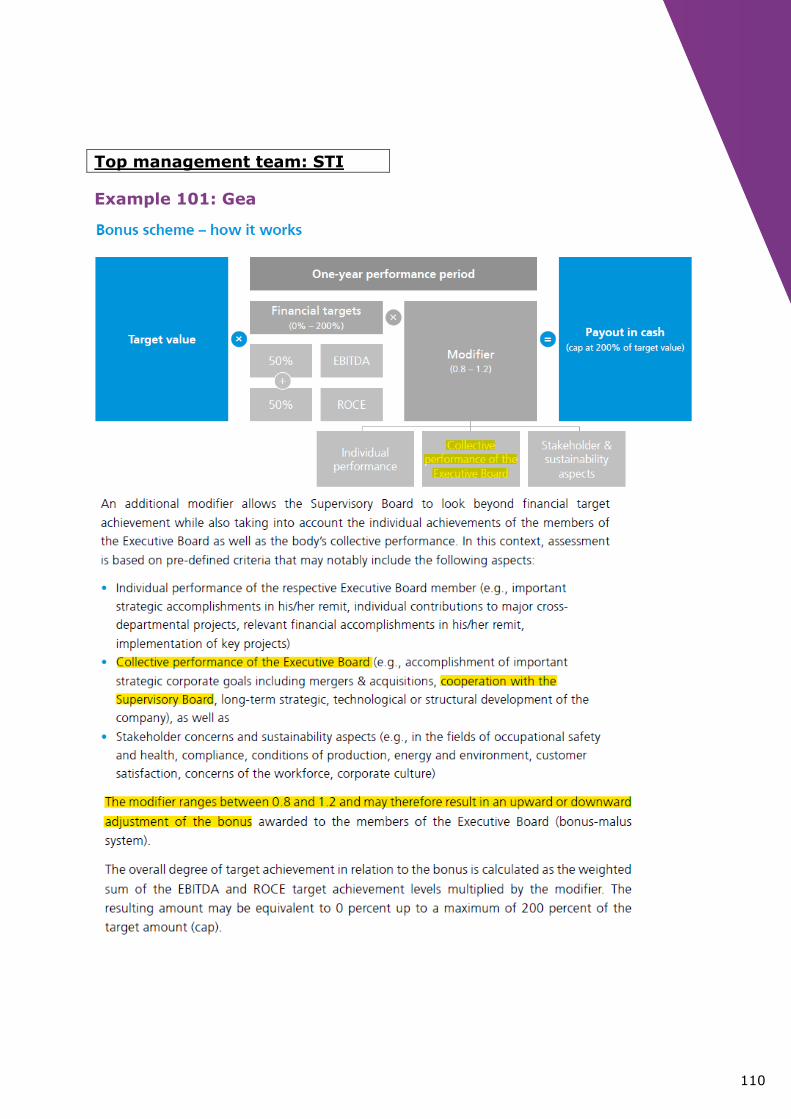

▪ Cooperation with supervisory board – example 101 (STI)

▪ Professional and personal development of each Corporate

Executive Committee's member – example 102 (STI)

▪ Conduct – example 103 (LTI)

▪ Reporting and communication

▪ Board effectiveness in discussion and decision making

▪ Teamwork and team leadership effectiveness

▪ Clear management structure

▪ Building a trustful relation with the Board and its Committees

▪ Smooth running of the new Executive Committee

22

e

Supplier

▪ Maintaining good supplier relationships – example 104 (STI)

▪ Supply chain monitoring – example 105 (STI)

▪ Supply chain transformation plans – example 106 (STI)

▪ Supply chain improvement – example 107 (STI)

▪ Supplier code of conduct – example 108 (STI)

▪ Audits to ensure supplier performance and compliance – example

108 (STI)

▪ Supplier diversity and inclusion program – example 108 (STI)

23

The previous chapter provided a

taxonomy of performance metrics used by

European companies in their executive

incentive systems, which serves as a

source of inspiration. Explicit reference

was made by including ‘example x’,

referring to where a concrete example

could be found.

All of these examples are grouped in this

chapter. For each example, the relevant

KPI that is referred to is highlighted in the

text. For each category, we first provide

examples of its use in short-term

incentives, followed by long-term

incentives14.

EXAMPLES

FINANCIAL KEY PERFORMANCE INDICATORS

Share-based: STI

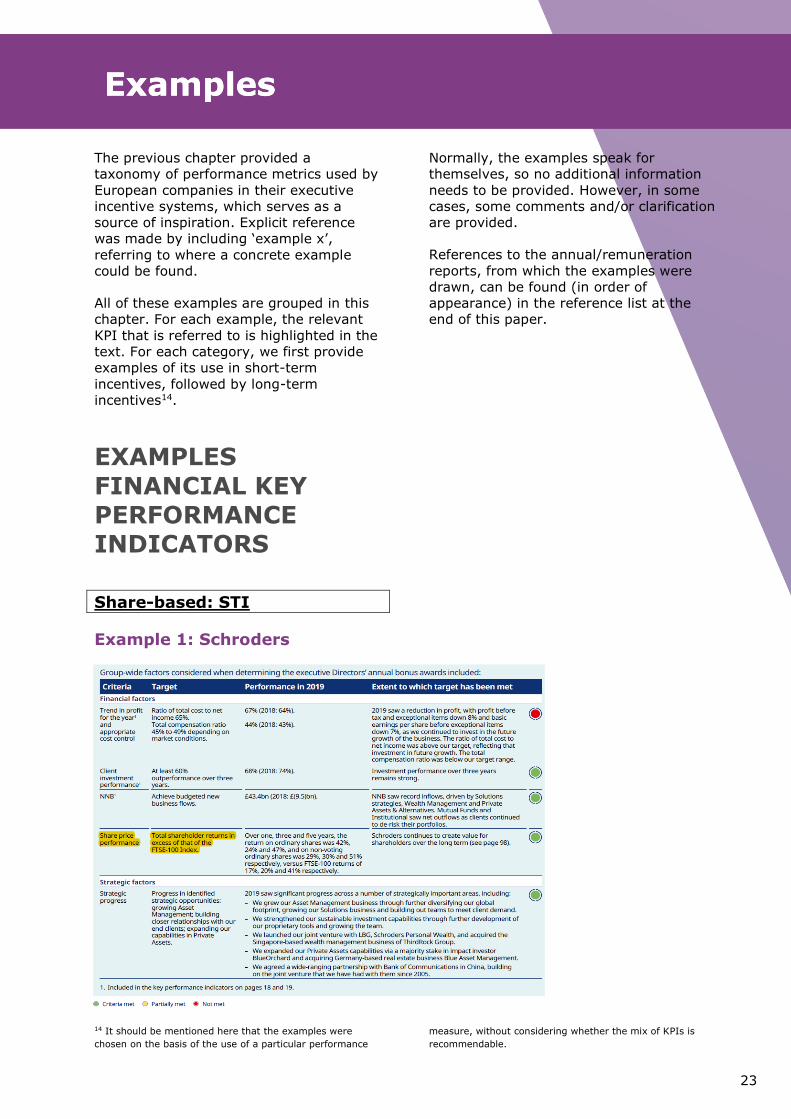

Example 1: Schroders

14 It should be mentioned here that the examples were

chosen on the basis of the use of a particular performance

Normally, the examples speak for

themselves, so no additional information

needs to be provided. However, in some

cases, some comments and/or clarification

are provided.

References to the annual/remuneration

reports, from which the examples were

drawn, can be found (in order of

appearance) in the reference list at the

end of this paper.

measure, without considering whether the mix of KPIs is

recommendable.

Examples Examples

24

Share-based: LTI

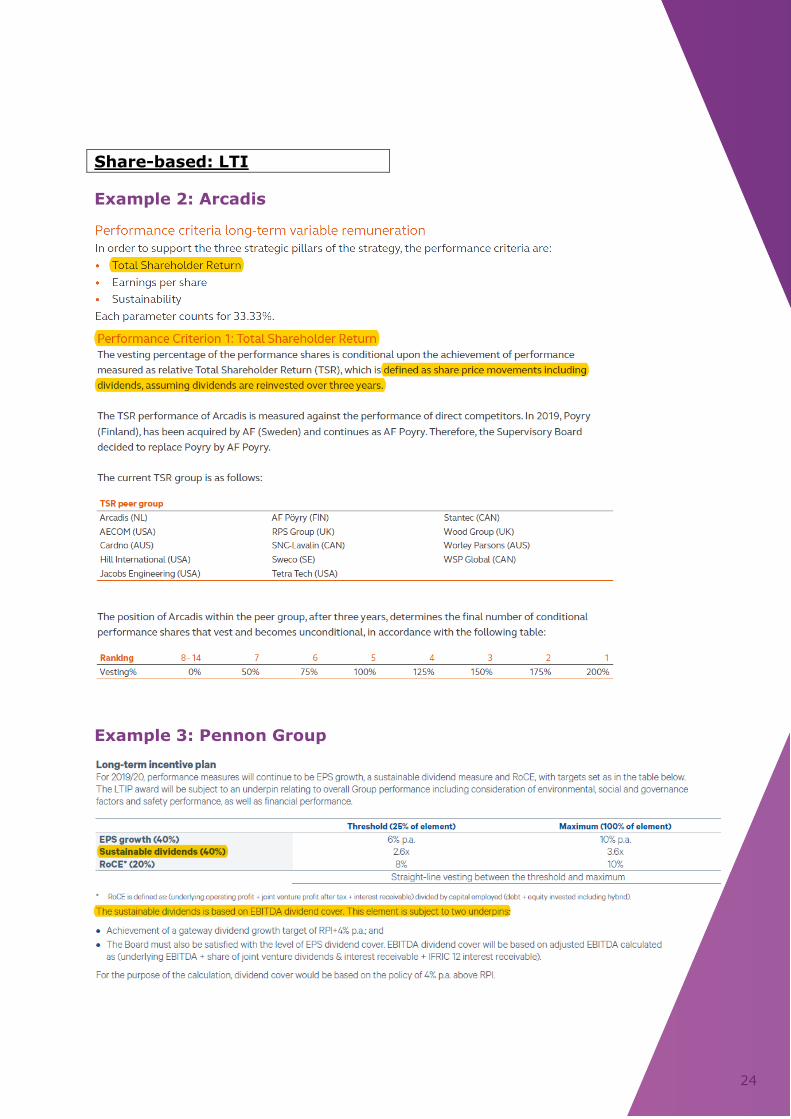

Example 2: Arcadis

Example 3: Pennon Group

25

Sales: STI

Example 4: Legrand

Quantitative Qualitative

26

Sales: STI

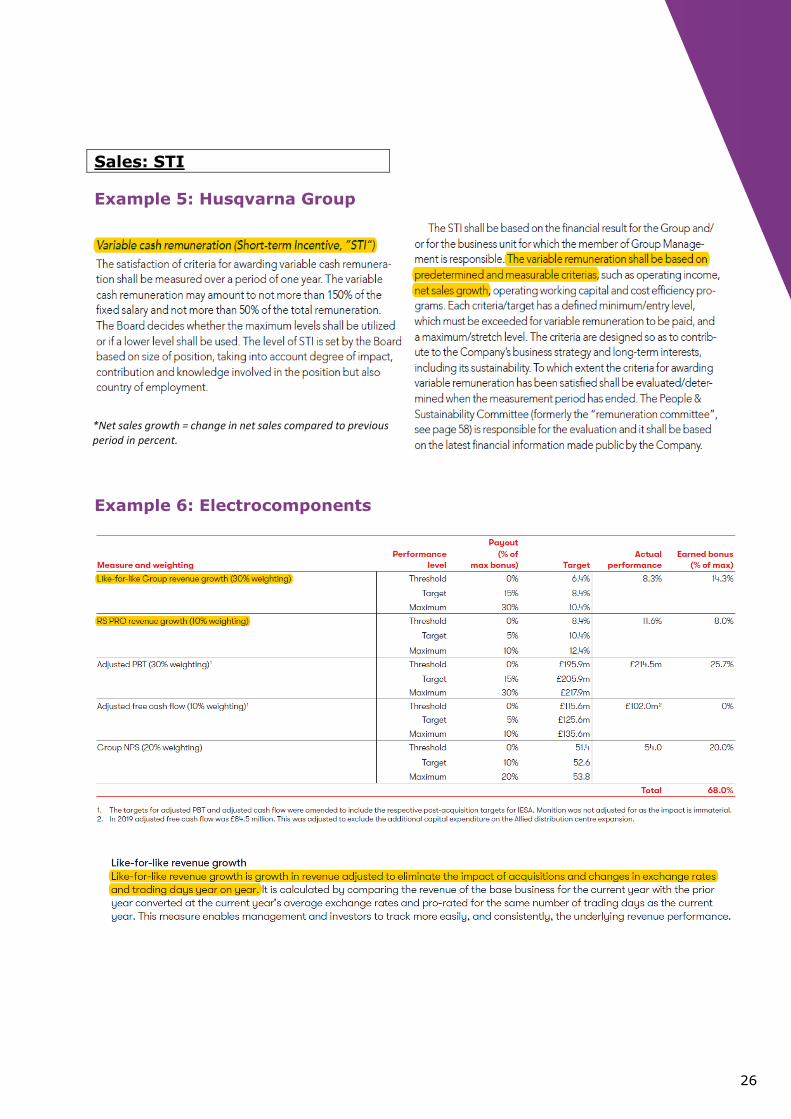

Example 5: Husqvarna Group

Example 6: Electrocomponents

*Net sales growth = change in net sales compared to previous period in percent.

27

Sales: STI

Example 7: Sika

28

Sales: LTI

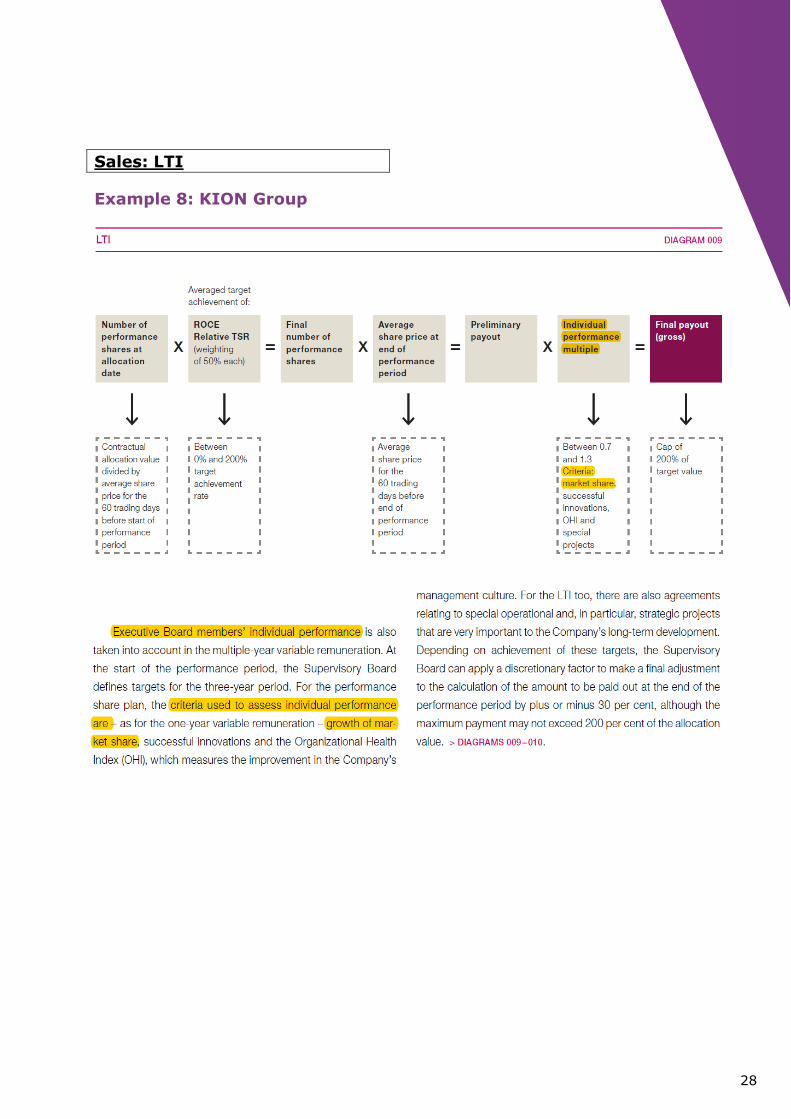

Example 8: KION Group

29

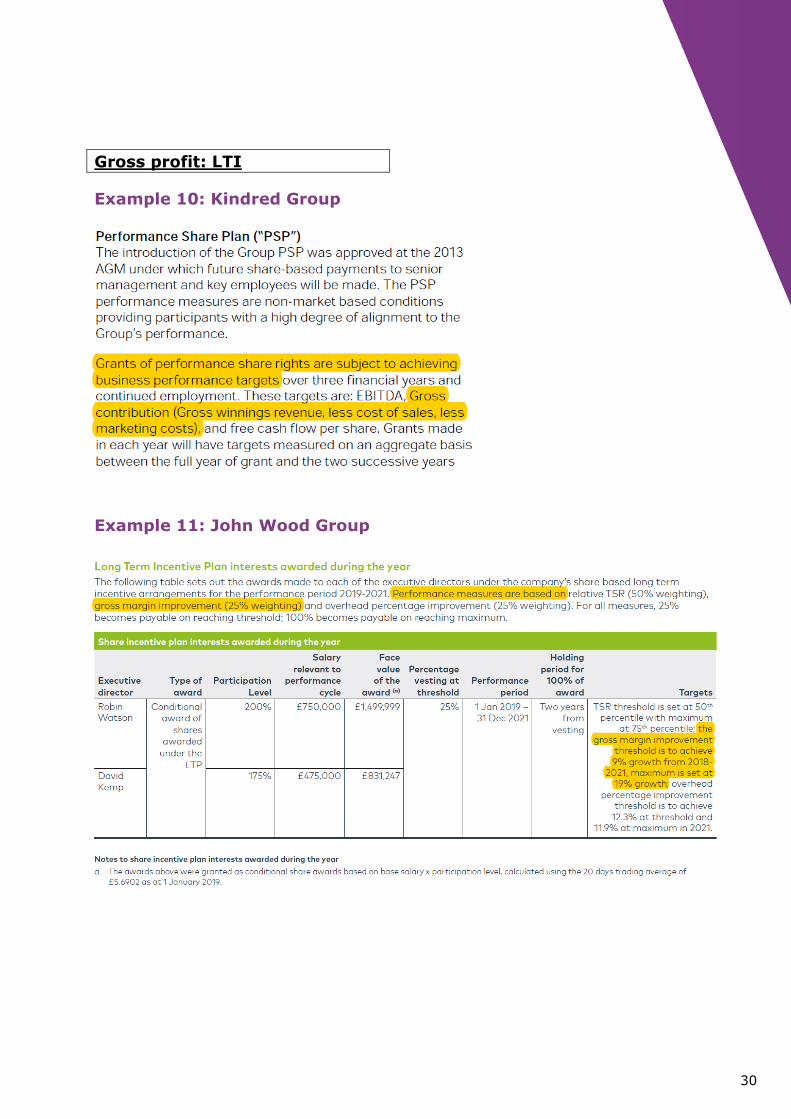

Gross profit: STI

Example 9: Sunrise

30

Gross profit: LTI

Example 10: Kindred Group

Example 11: John Wood Group

31

EBITDA: STI

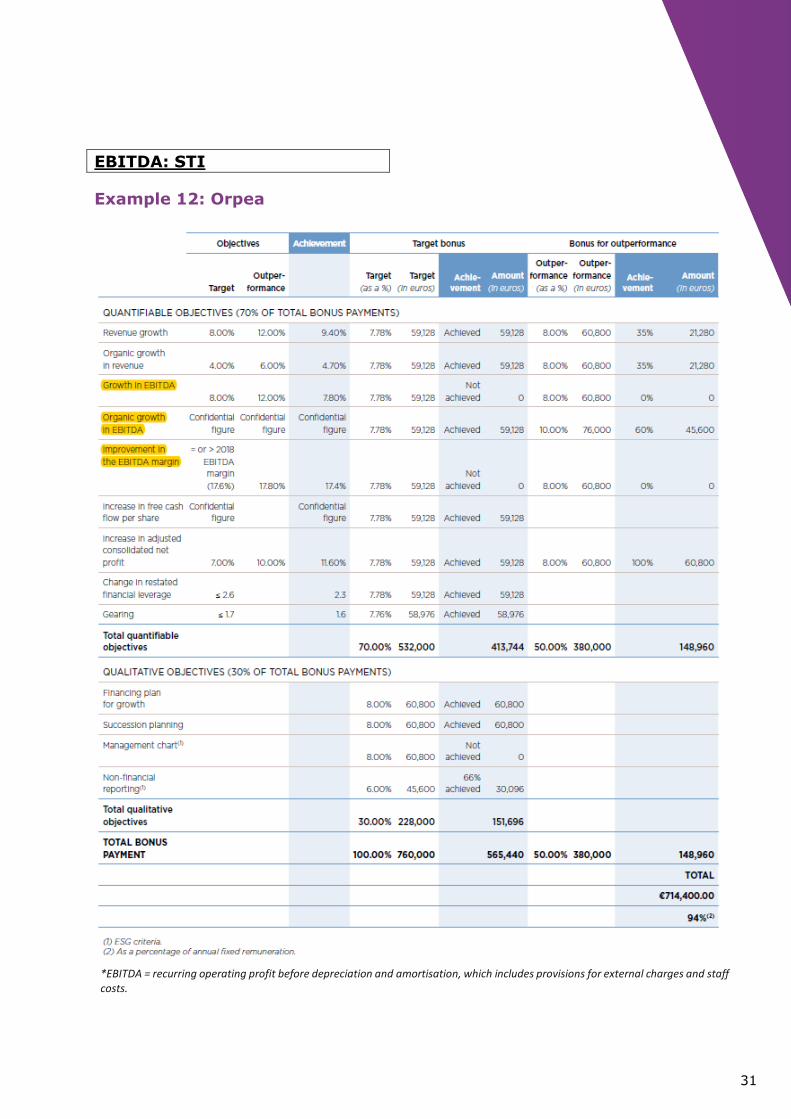

Example 12: Orpea

*EBITDA = recurring operating profit before depreciation and amortisation, which includes provisions for external charges and staff costs.

32

EBITDA: STI

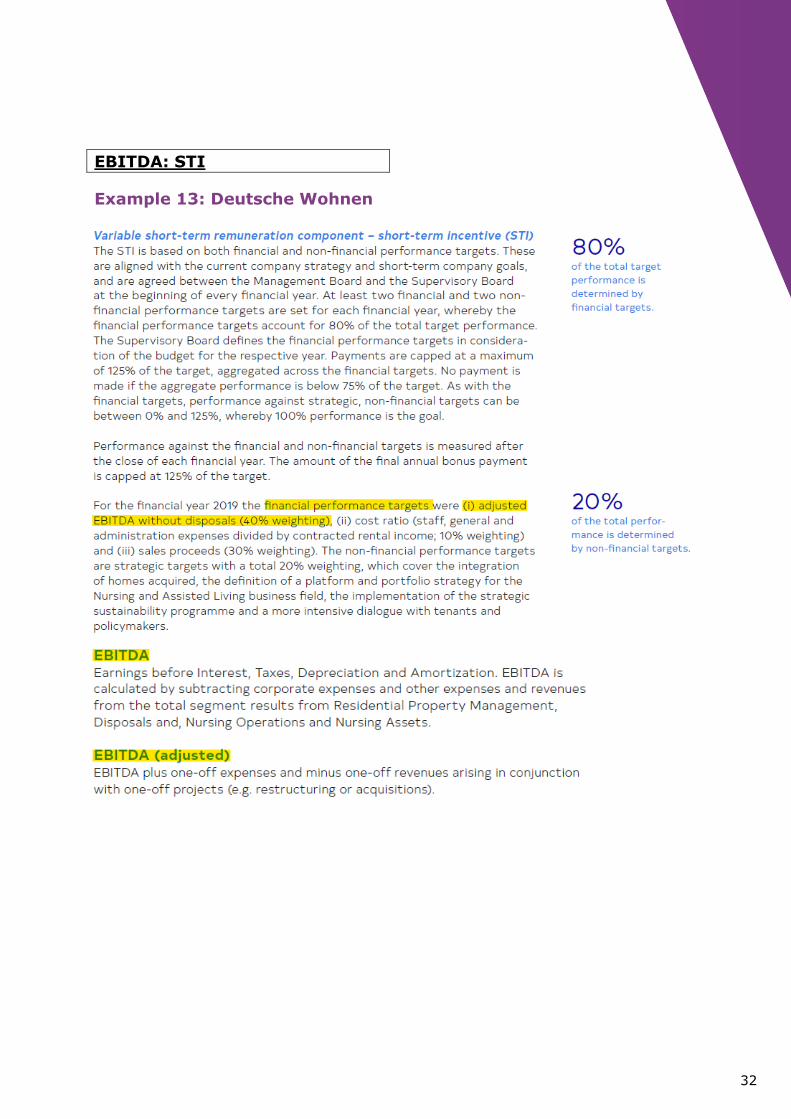

Example 13: Deutsche Wohnen

33

EBITDA: STI

Example 14: Mondi

*Underlying EBITDA = operating profit before special items, depreciation, amortisation and impairments not recorded as special items. Underlying EBITDA provides a measure of the cash generating ability of the business that is comparable from year to year.

34

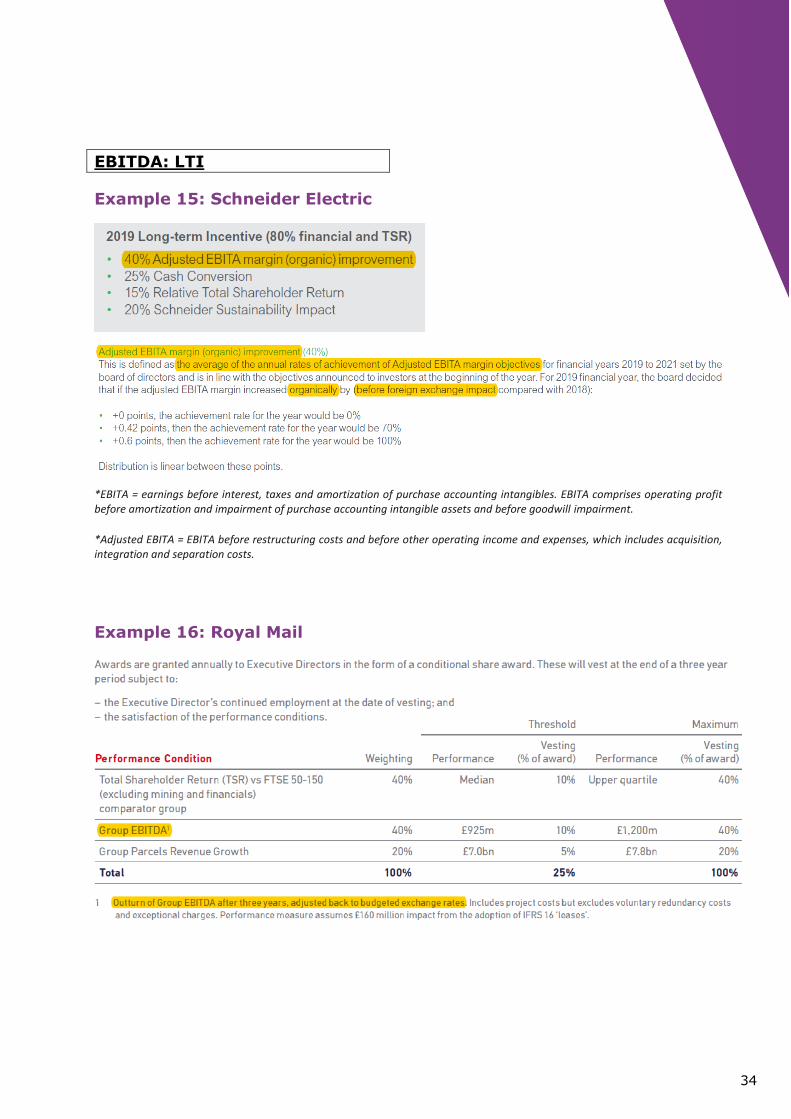

EBITDA: LTI

Example 15: Schneider Electric

Example 16: Royal Mail

*EBITA = earnings before interest, taxes and amortization of purchase accounting intangibles. EBITA comprises operating profit before amortization and impairment of purchase accounting intangible assets and before goodwill impairment.

*Adjusted EBITA = EBITA before restructuring costs and before other operating income and expenses, which includes acquisition, integration and separation costs.

35

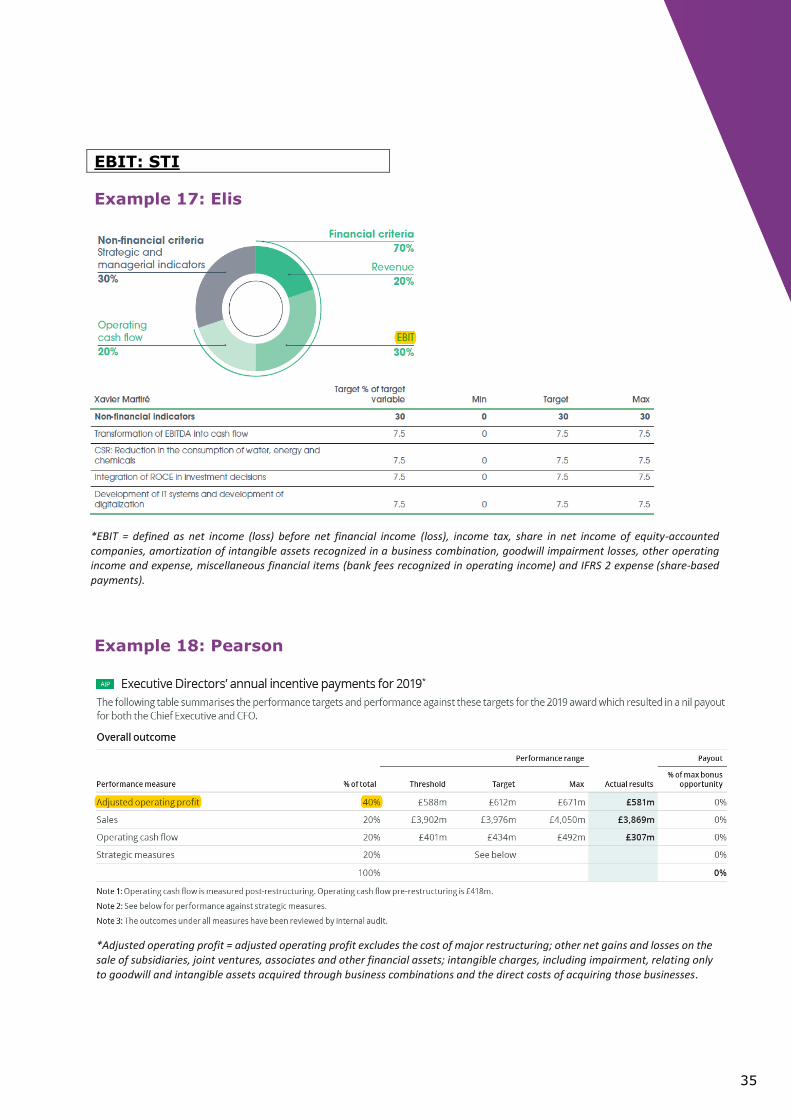

EBIT: STI

Example 17: Elis

Example 18: Pearson

*EBIT = defined as net income (loss) before net financial income (loss), income tax, share in net income of equity-accounted companies, amortization of intangible assets recognized in a business combination, goodwill impairment losses, other operating income and expense, miscellaneous financial items (bank fees recognized in operating income) and IFRS 2 expense (share-based payments).

*Adjusted operating profit = adjusted operating profit excludes the cost of major restructuring; other net gains and losses on the sale of subsidiaries, joint ventures, associates and other financial assets; intangible charges, including impairment, relating only to goodwill and intangible assets acquired through business combinations and the direct costs of acquiring those businesses.

36

EBIT: STI

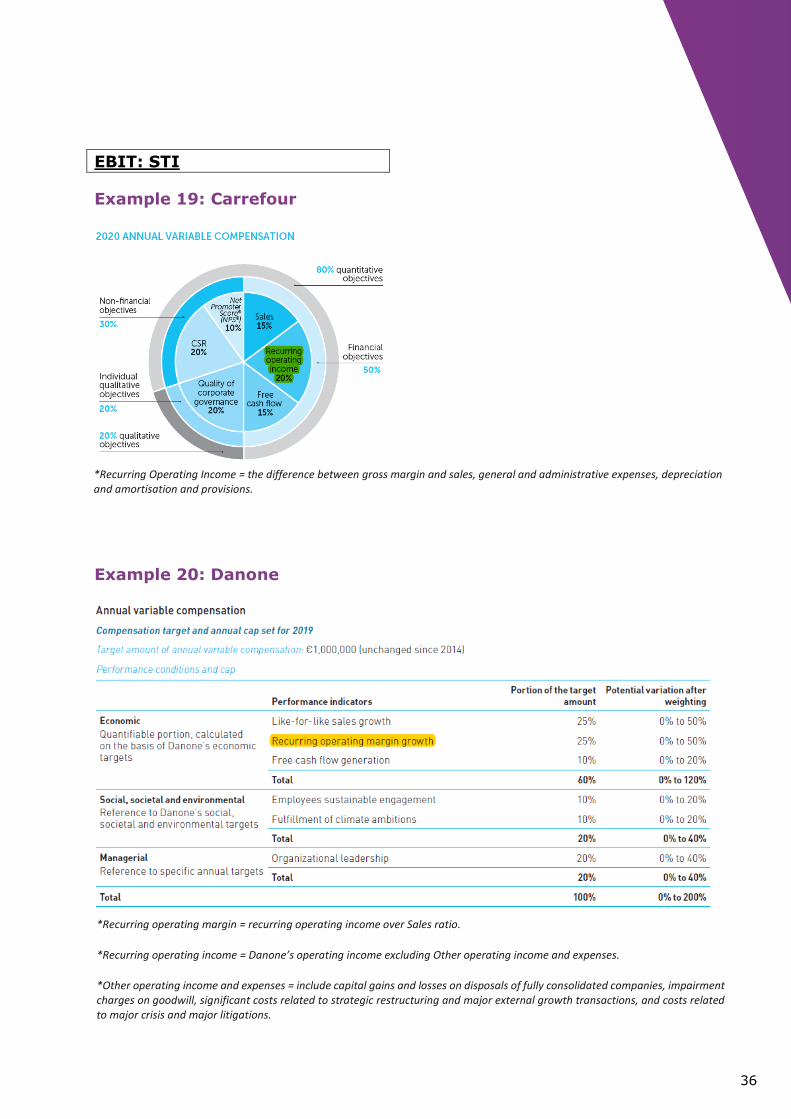

Example 19: Carrefour

Example 20: Danone

*Recurring Operating Income = the difference between gross margin and sales, general and administrative expenses, depreciation and amortisation and provisions.

*Recurring operating margin = recurring operating income over Sales ratio.

*Recurring operating income = Danone’s operating income excluding Other operating income and expenses.

*Other operating income and expenses = include capital gains and losses on disposals of fully consolidated companies, impairment charges on goodwill, significant costs related to strategic restructuring and major external growth transactions, and costs related to major crisis and major litigations.

37

EBIT: LTI

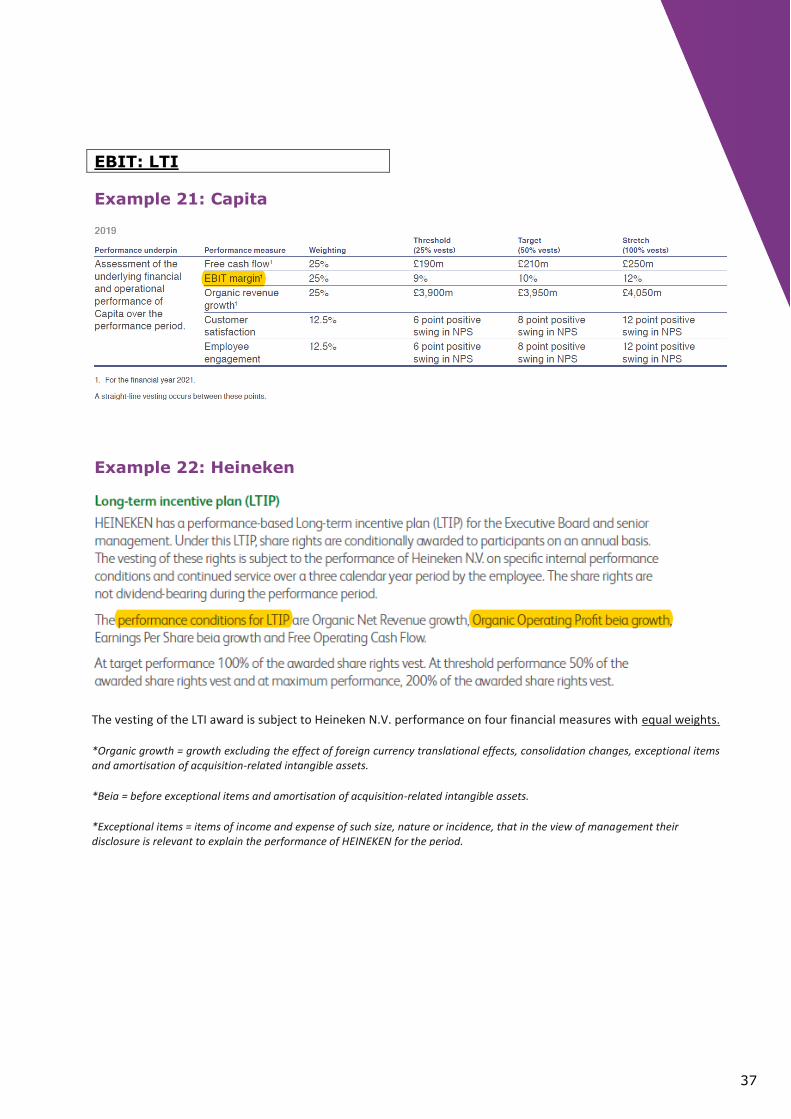

Example 21: Capita

Example 22: Heineken

The vesting of the LTI award is subject to Heineken N.V. performance on four financial measures with equal weights.

*Organic growth = growth excluding the effect of foreign currency translational effects, consolidation changes, exceptional items and amortisation of acquisition-related intangible assets.

*Beia = before exceptional items and amortisation of acquisition-related intangible assets.

*Exceptional items = items of income and expense of such size, nature or incidence, that in the view of management their disclosure is relevant to explain the performance of HEINEKEN for the period.

38

EBIT: LTI

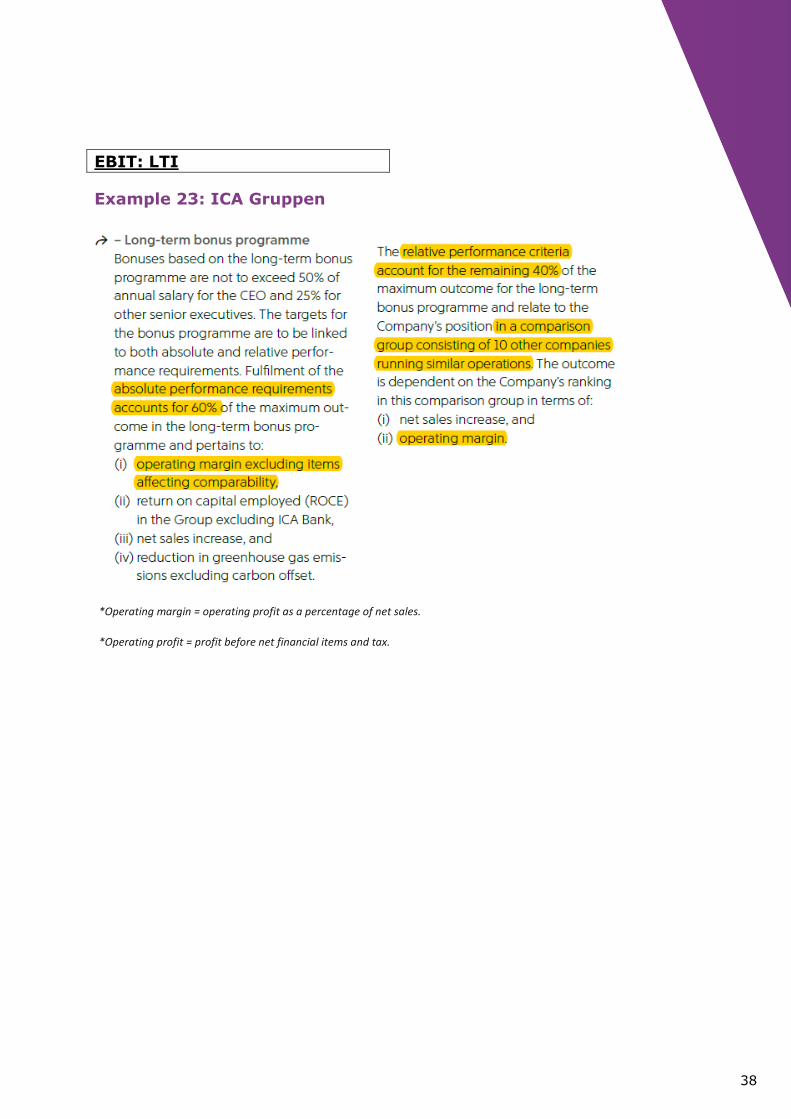

Example 23: ICA Gruppen

*Operating margin = operating profit as a percentage of net sales.

*Operating profit = profit before net financial items and tax.

39

Profit before taxes: STI

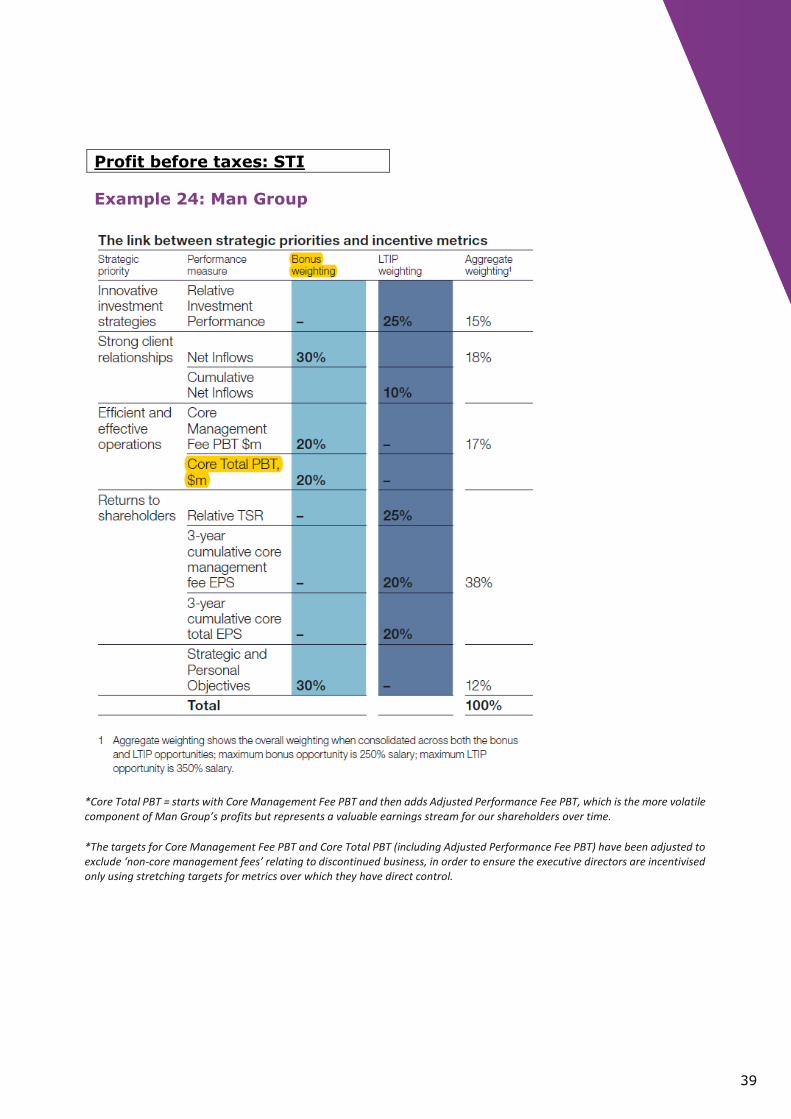

Example 24: Man Group

*Core Total PBT = starts with Core Management Fee PBT and then adds Adjusted Performance Fee PBT, which is the more volatile component of Man Group’s profits but represents a valuable earnings stream for our shareholders over time.

*The targets for Core Management Fee PBT and Core Total PBT (including Adjusted Performance Fee PBT) have been adjusted to exclude ‘non-core management fees’ relating to discontinued business, in order to ensure the executive directors are incentivised only using stretching targets for metrics over which they have direct control.

40

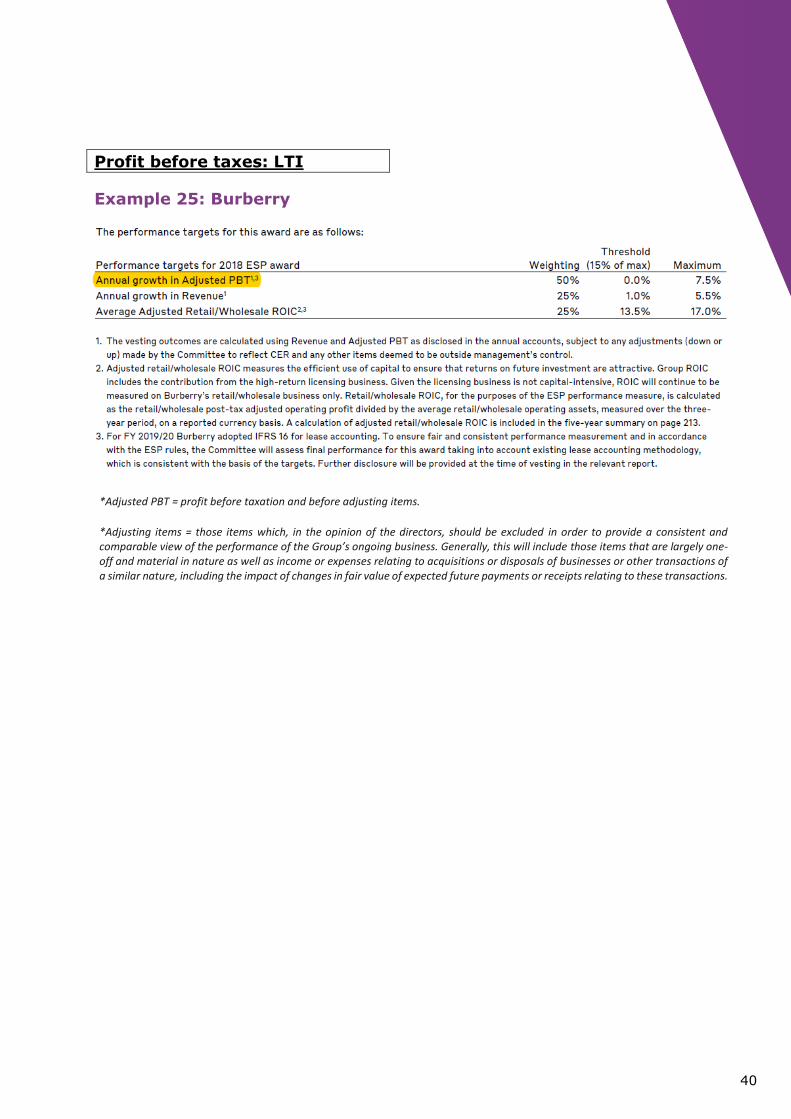

Profit before taxes: LTI

Example 25: Burberry

*Adjusted PBT = profit before taxation and before adjusting items.

*Adjusting items = those items which, in the opinion of the directors, should be excluded in order to provide a consistent and comparable view of the performance of the Group’s ongoing business. Generally, this will include those items that are largely one-off and material in nature as well as income or expenses relating to acquisitions or disposals of businesses or other transactions of a similar nature, including the impact of changes in fair value of expected future payments or receipts relating to these transactions.

41

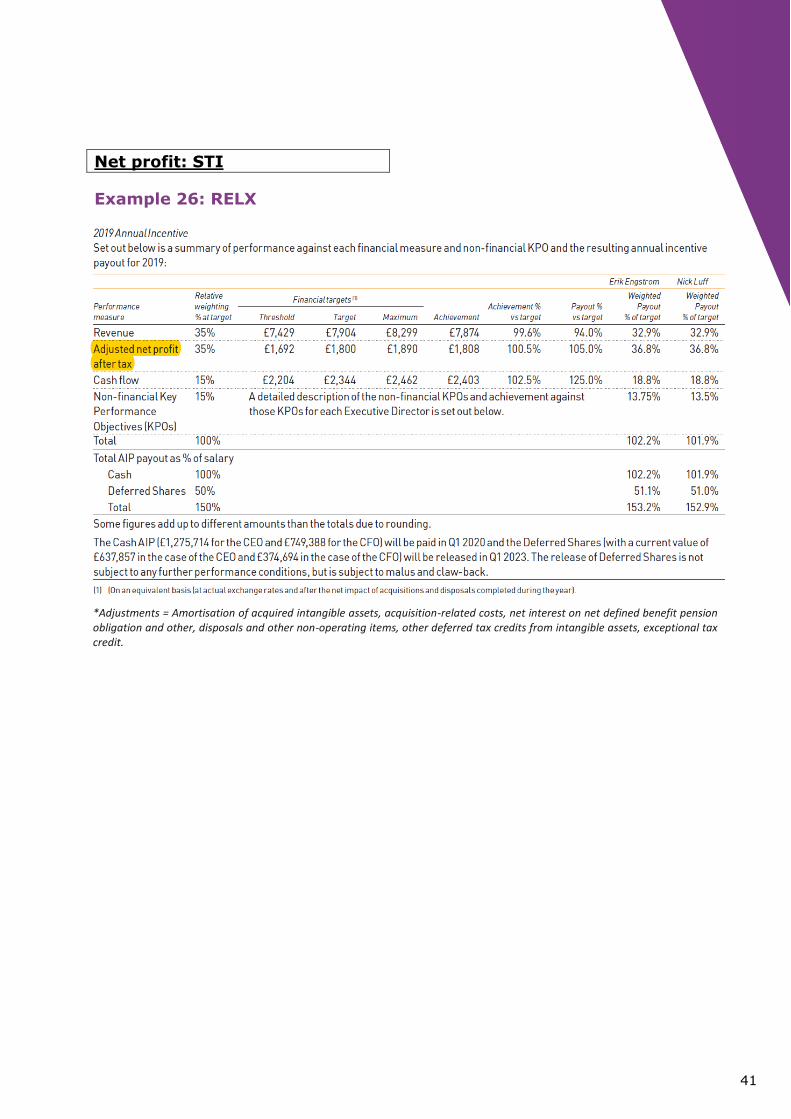

Net profit: STI

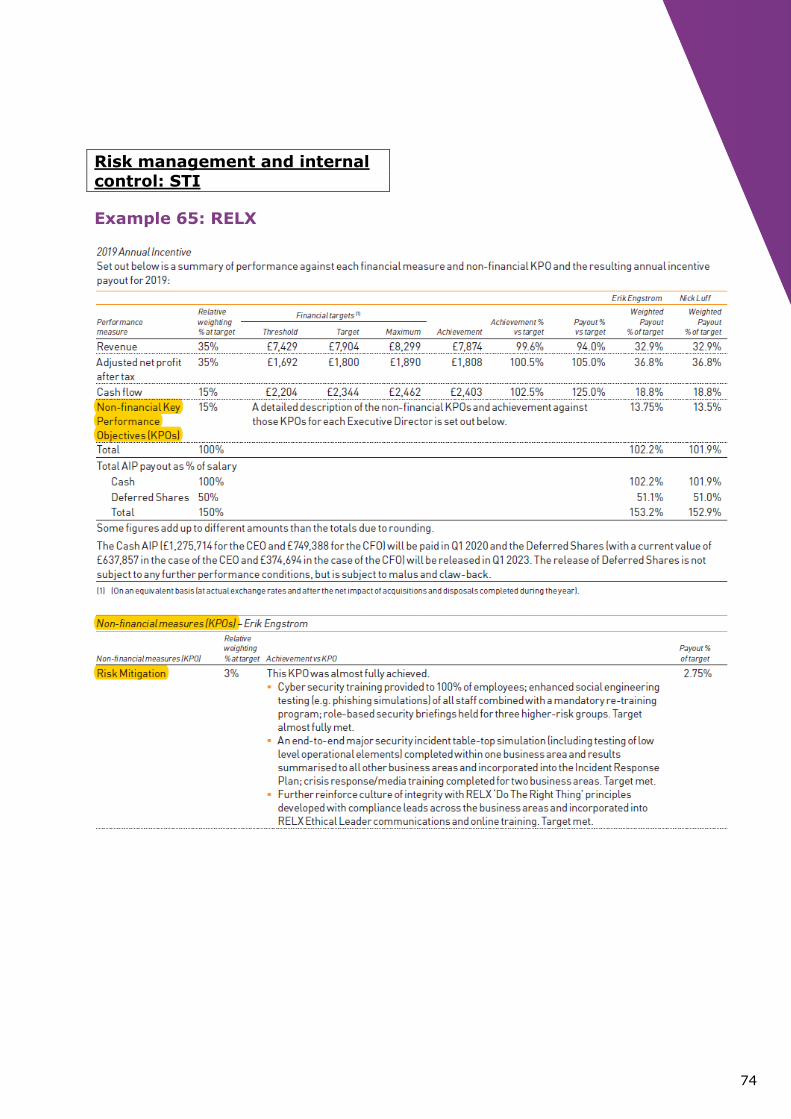

Example 26: RELX

*Adjustments = Amortisation of acquired intangible assets, acquisition-related costs, net interest on net defined benefit pension obligation and other, disposals and other non-operating items, other deferred tax credits from intangible assets, exceptional tax credit.

42

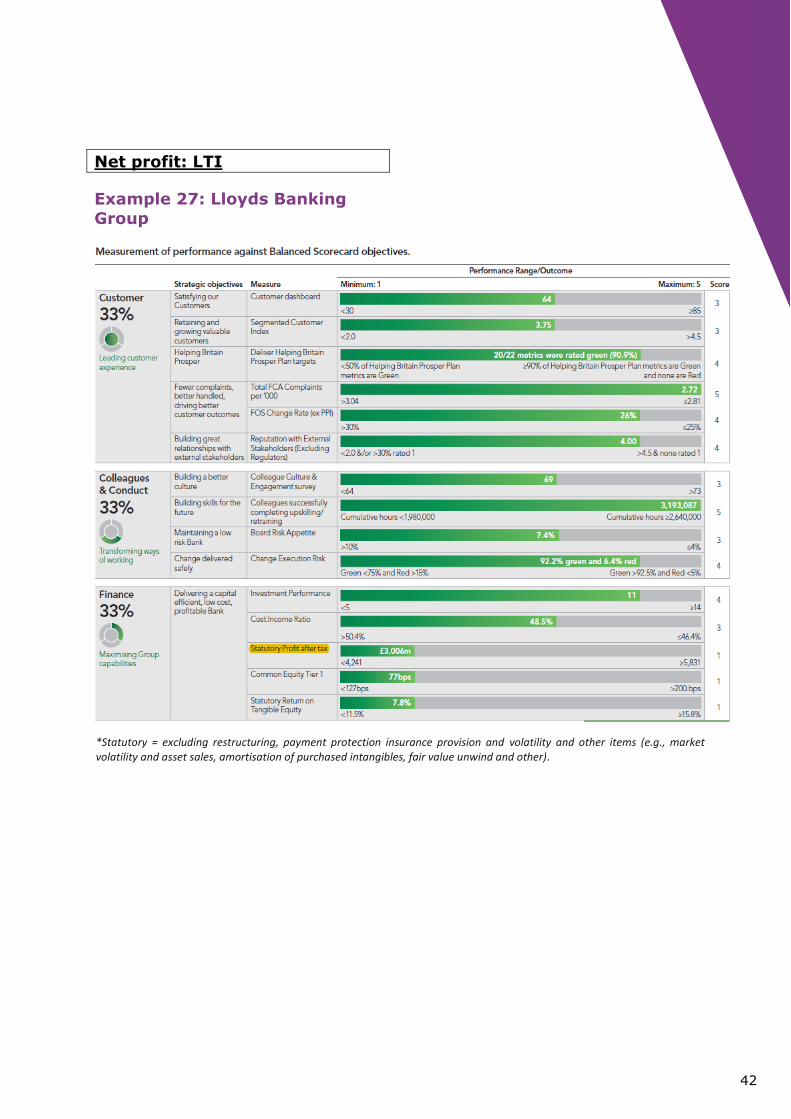

Net profit: LTI

Example 27: Lloyds Banking

Group

*Statutory = excluding restructuring, payment protection insurance provision and volatility and other items (e.g., market volatility and asset sales, amortisation of purchased intangibles, fair value unwind and other).

43

Net profit: LTI

Example 28: Deutsche Börse

*Net income growth = calculated independently from the financial planning concerned by comparing the adjusted net income for the remuneration year with the prior-year figure.

44

Cash flow: STI

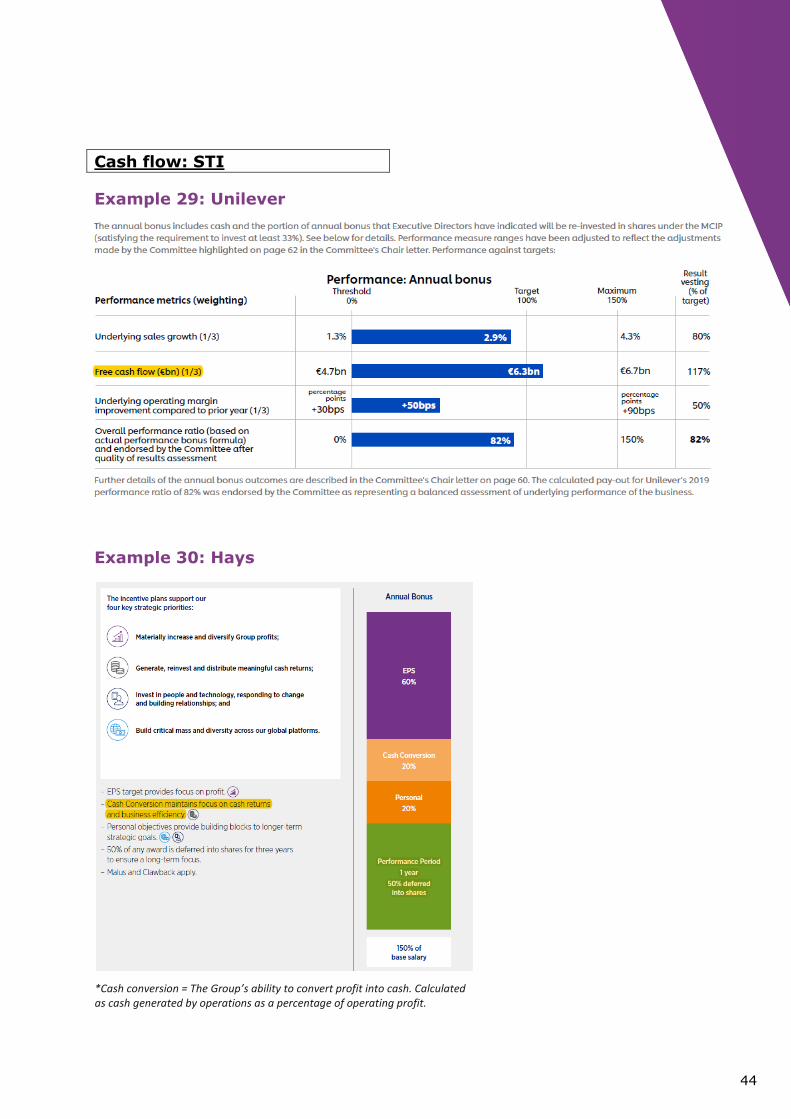

Example 29: Unilever

Example 30: Hays

*Cash conversion = The Group’s ability to convert profit into cash. Calculated as cash generated by operations as a percentage of operating profit.

45

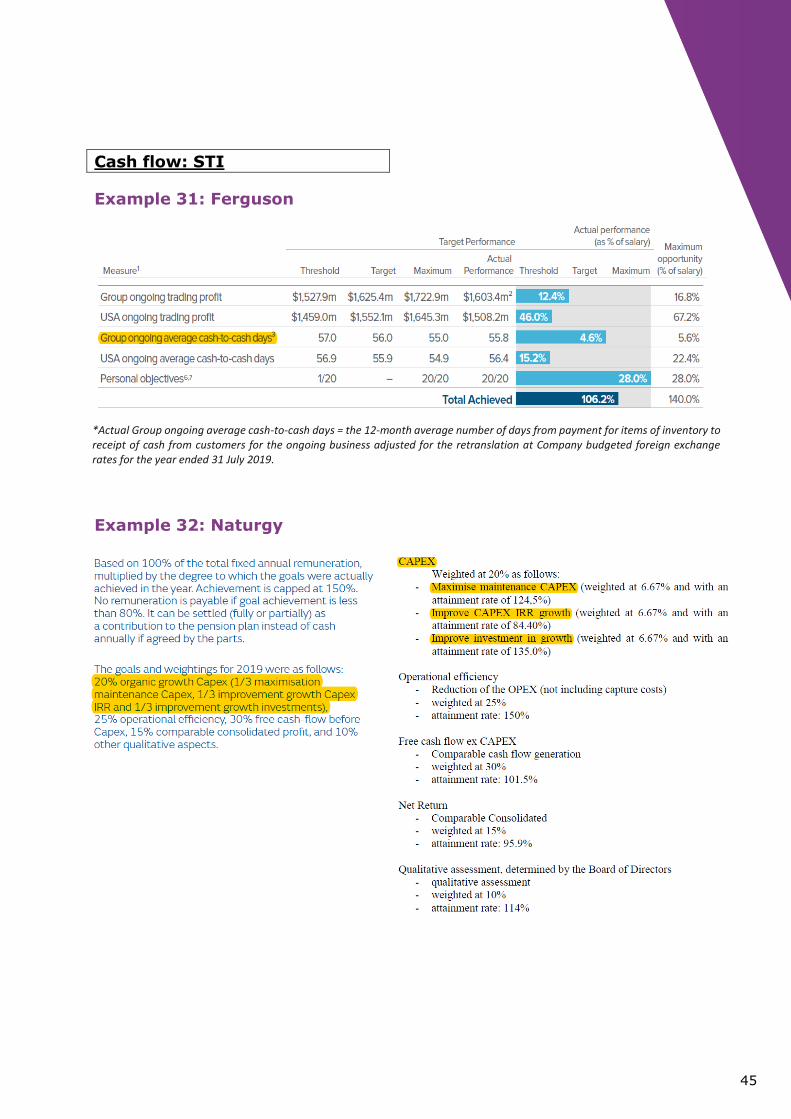

Cash flow: STI

Example 31: Ferguson

Example 32: Naturgy

*Actual Group ongoing average cash-to-cash days = the 12-month average number of days from payment for items of inventory to receipt of cash from customers for the ongoing business adjusted for the retranslation at Company budgeted foreign exchange rates for the year ended 31 July 2019.

46

Cash flow: LTI

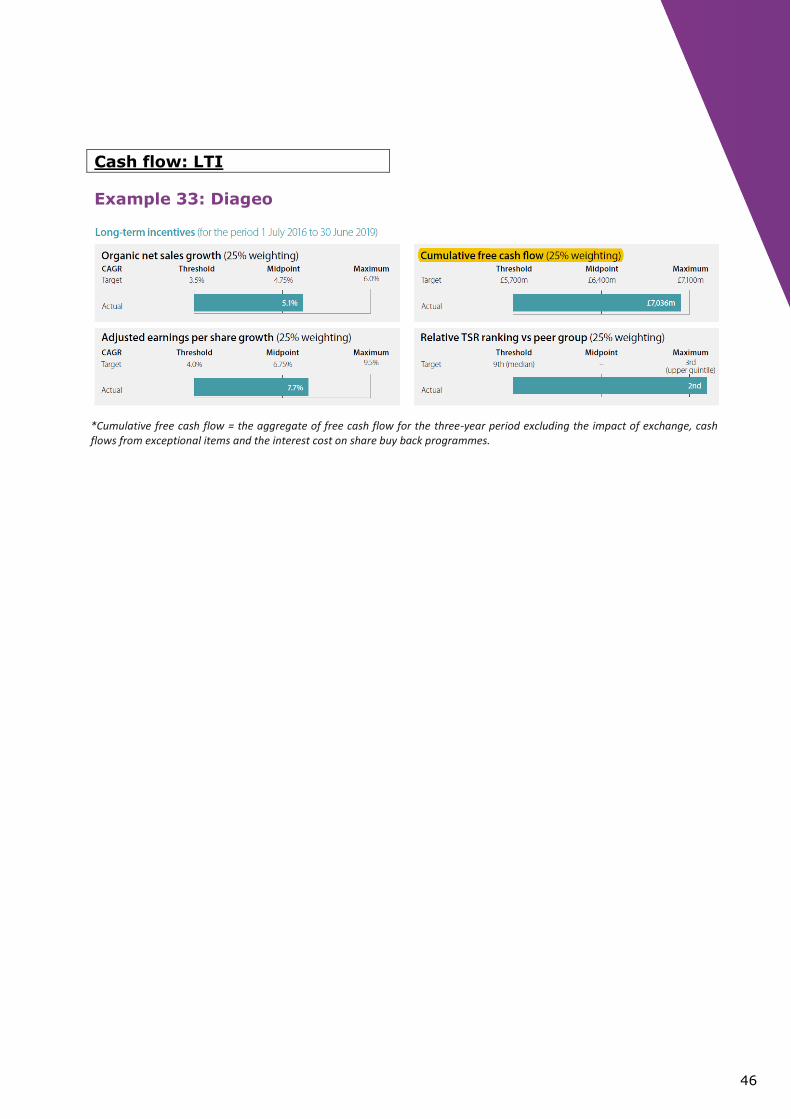

Example 33: Diageo

*Cumulative free cash flow = the aggregate of free cash flow for the three-year period excluding the impact of exchange, cash flows from exceptional items and the interest cost on share buy back programmes.

47

Relative return: STI

Example 34: Siemens

48

Relative return: STI

Example 35: Intertek

*ROIC = Adjusted profit after tax divided by invested capital.

*Invested capital = Net assets excluding tax balances, net financial debt and net pension liabilities.

*Adjusted = Before Separately Disclosed Items (‘SDIs’) = include amortisation of acquisition intangibles; impairment of goodwill and other assets; the profit or loss on disposals of businesses or other significant fixed assets; costs related to acquisition activity; the cost of any fundamental restructuring of a business; material claims and settlements; significant recycling of amounts from equity to the income statement; unrealised market or fair value gains or losses on financial assets or liabilities, including contingent consideration; and significant legislative changes.

49

Relative return: LTI

Example 36: Valeo

Example 37: Scor

50

Cost: STI

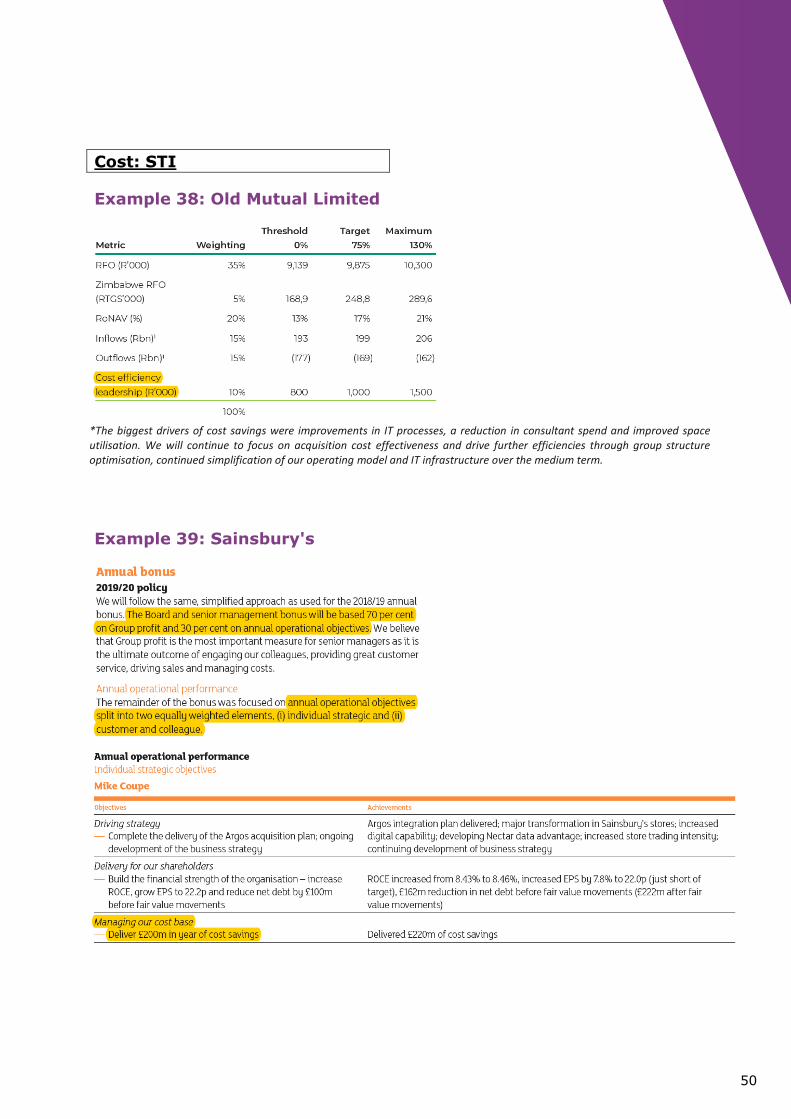

Example 38: Old Mutual Limited

Example 39: Sainsbury's

*The biggest drivers of cost savings were improvements in IT processes, a reduction in consultant spend and improved space utilisation. We will continue to focus on acquisition cost effectiveness and drive further efficiencies through group structure optimisation, continued simplification of our operating model and IT infrastructure over the medium term.

51

Cost: LTI

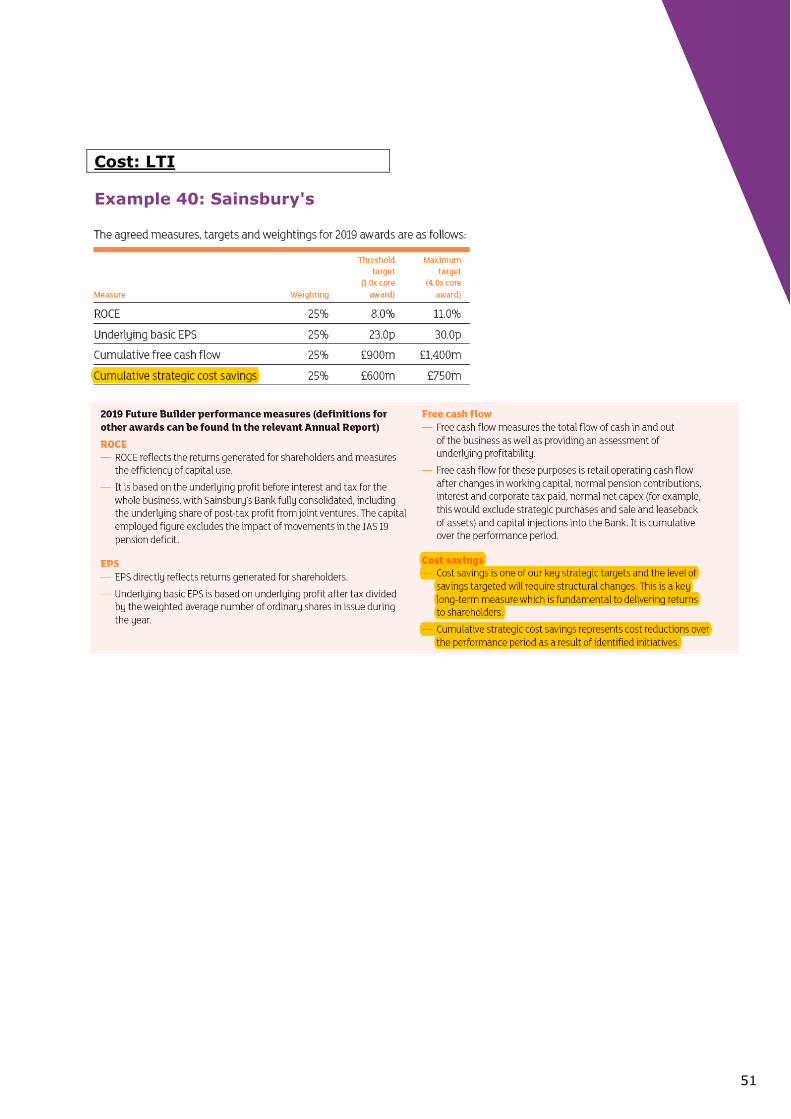

Example 40: Sainsbury's

52

Debt: STI

Example 41: Total S.A.

*Net-debt-to-equity ratio = Net debt/Equity

*Net financial debts = see figure below

53

Debt: STI

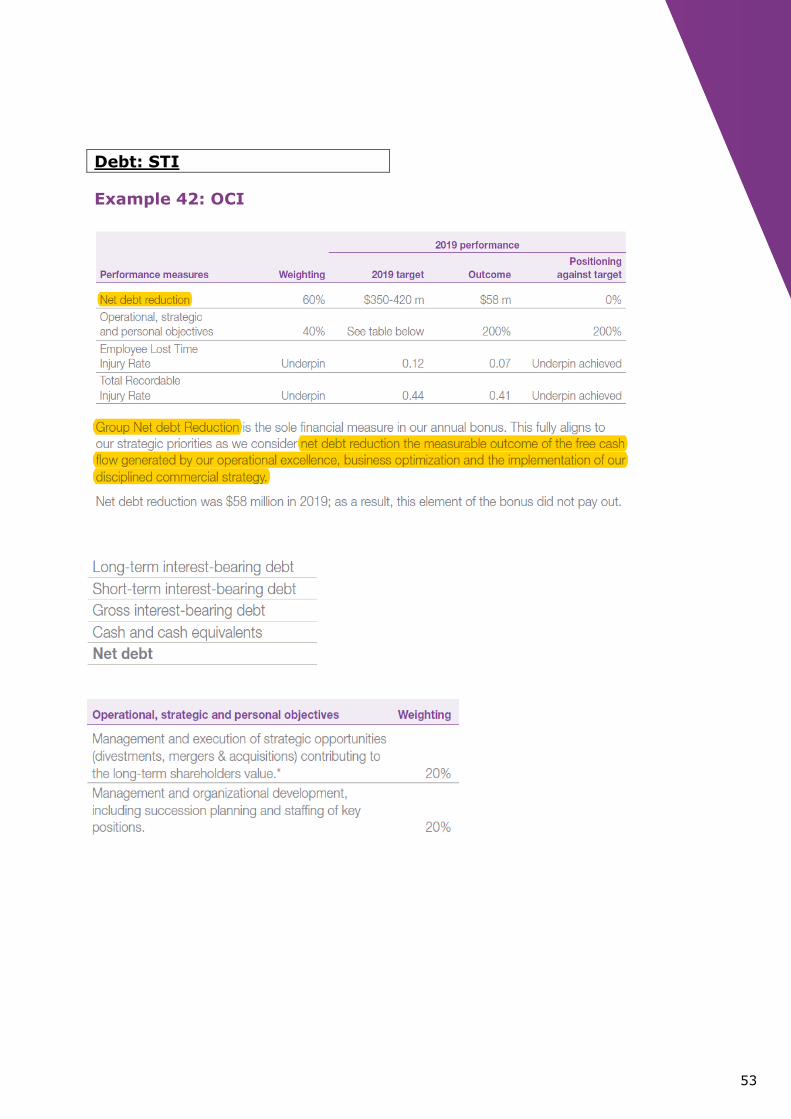

Example 42: OCI

54

Debt: LTI

Example 43: Ashtead Group

*Leverage = calculated at constant exchange rates uses the current period exchange rate and is determined as net debt divided by underlying EBITDA.

*Net debt = total borrowings (bank, bonds and finance lease liabilities) less cash balances, as reported.

*EBITDA = not defined by IFRS but is a widely accepted profit measure being earnings before interest, tax, depreciation and amortisation.

*Underlying results = the results stated before exceptional items and the amortisation of acquired intangibles.

*Exceptional items = those items that are material and non-recurring in nature that the Group believes should be disclosed separately to assist in the understanding of the financial performance of the Group.

55

Economic profit: STI

Example 44: Jerónimo Martins

*EVA = EBIT after taxes minus capital costs

56

Economic profit: LTI

Example 45: Spectris

Example 46: Julius Baer Group

57

Economic profit: LTI

Example 47: Lloyds Banking

Group

*Economic profit, a measure of profit taking into account expected losses, tax and a charge for equity utilisation.

*Statutory = excluding restructuring, payment protection insurance provision and volatility and other items (e.g., market volatility and asset sales, amortisation of purchased intangibles, fair value unwind and other)

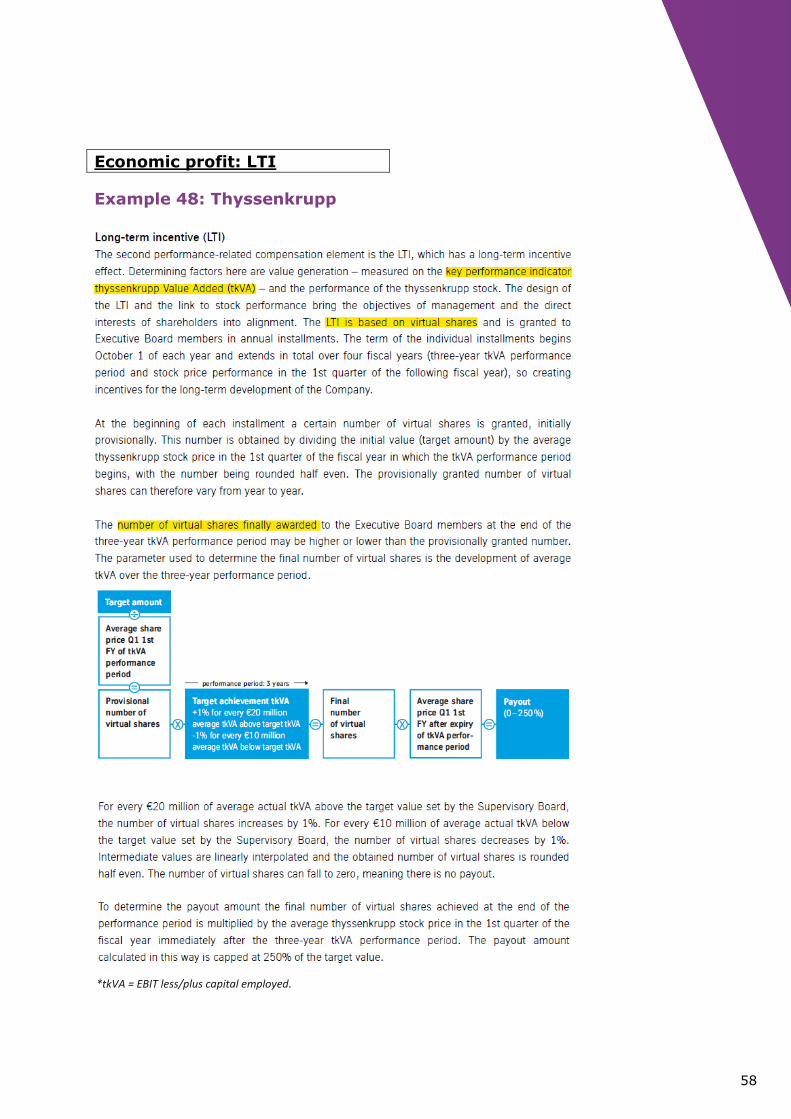

58

Economic profit: LTI

Example 48: Thyssenkrupp

*tkVA = EBIT less/plus capital employed.

59

EXAMPLES NON-FINANCIAL KEY

PERFORMANCE INDICATORS

Strategy: STI

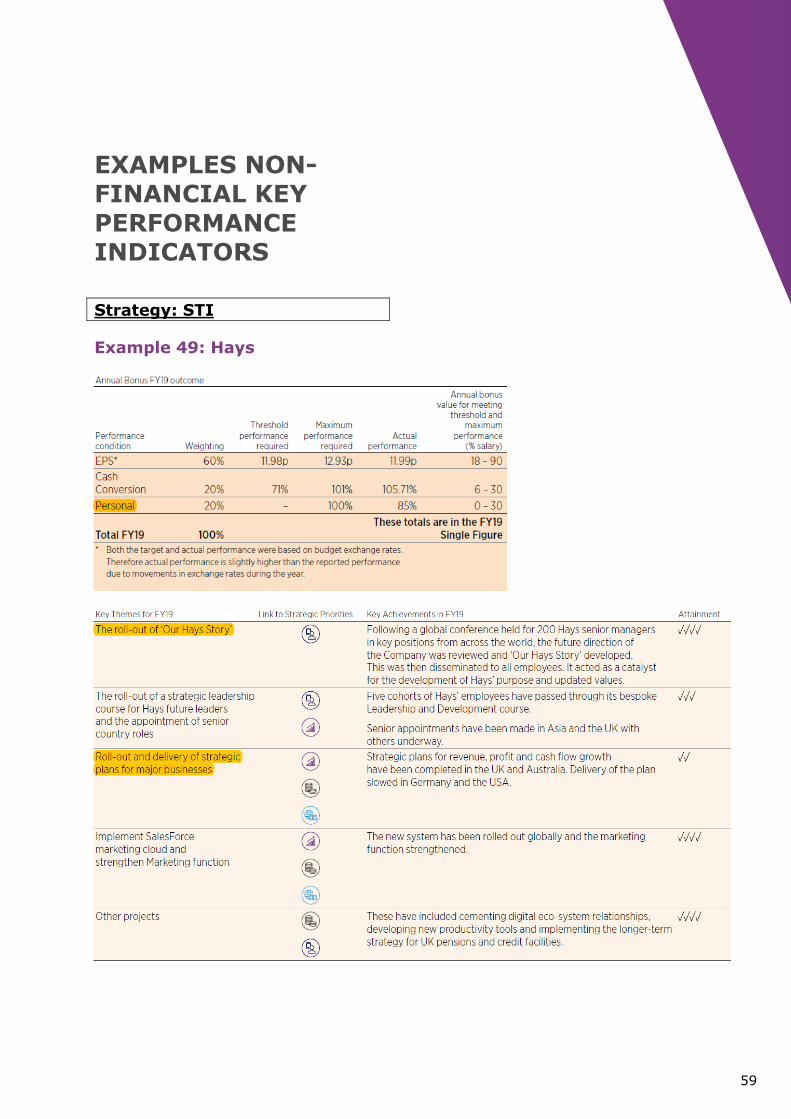

Example 49: Hays

60

Strategy: STI

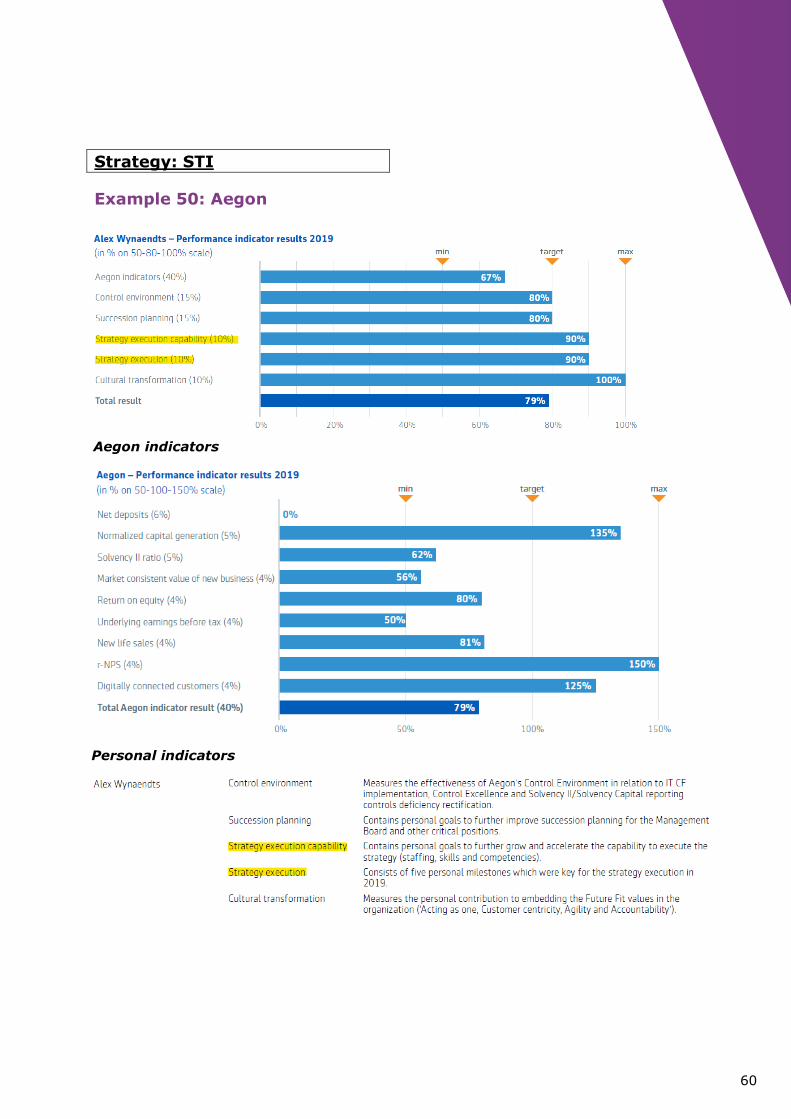

Example 50: Aegon

Aegon indicators

Personal indicators

61

Strategy: STI

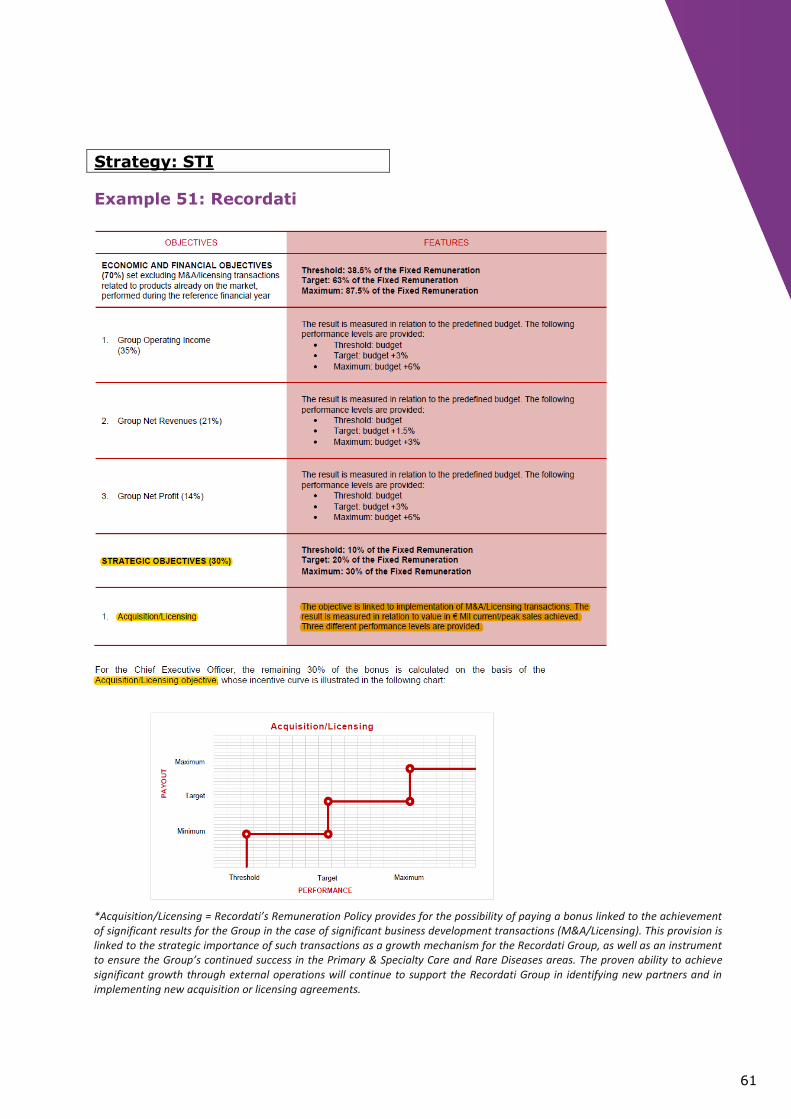

Example 51: Recordati

*Acquisition/Licensing = Recordati’s Remuneration Policy provides for the possibility of paying a bonus linked to the achievement of significant results for the Group in the case of significant business development transactions (M&A/Licensing). This provision is linked to the strategic importance of such transactions as a growth mechanism for the Recordati Group, as well as an instrument to ensure the Group’s continued success in the Primary & Specialty Care and Rare Diseases areas. The proven ability to achieve significant growth through external operations will continue to support the Recordati Group in identifying new partners and in implementing new acquisition or licensing agreements.

62

Strategy: STI

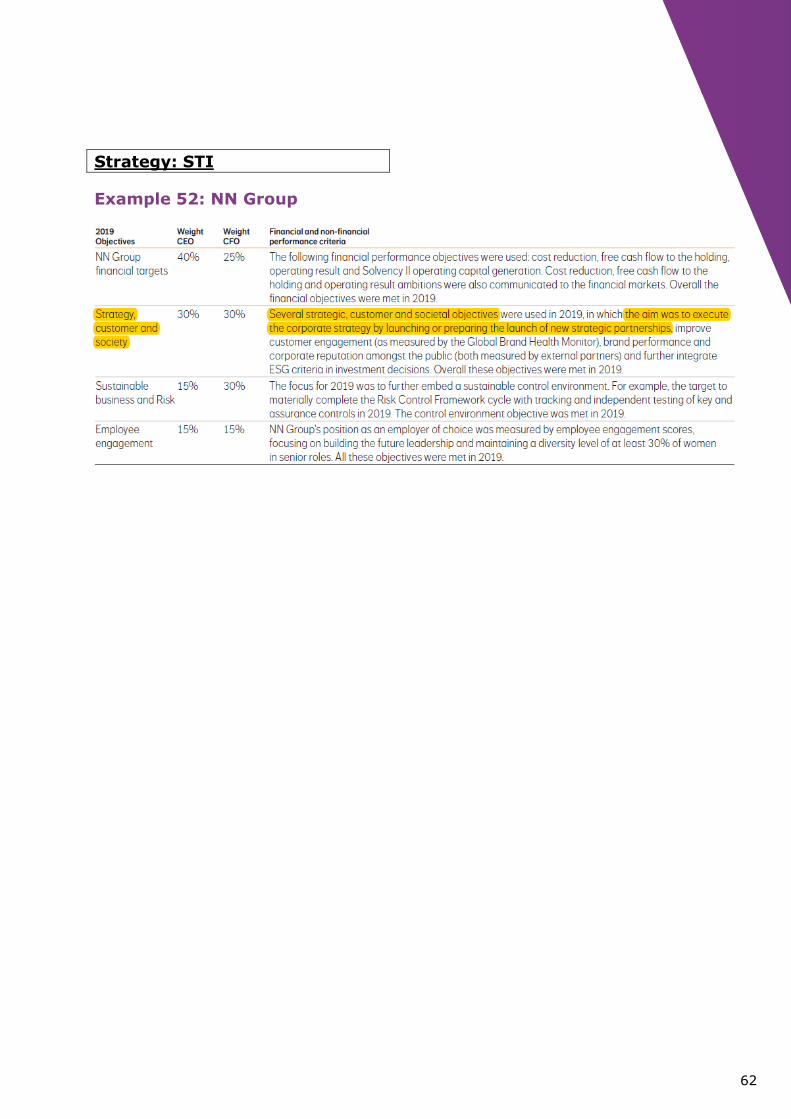

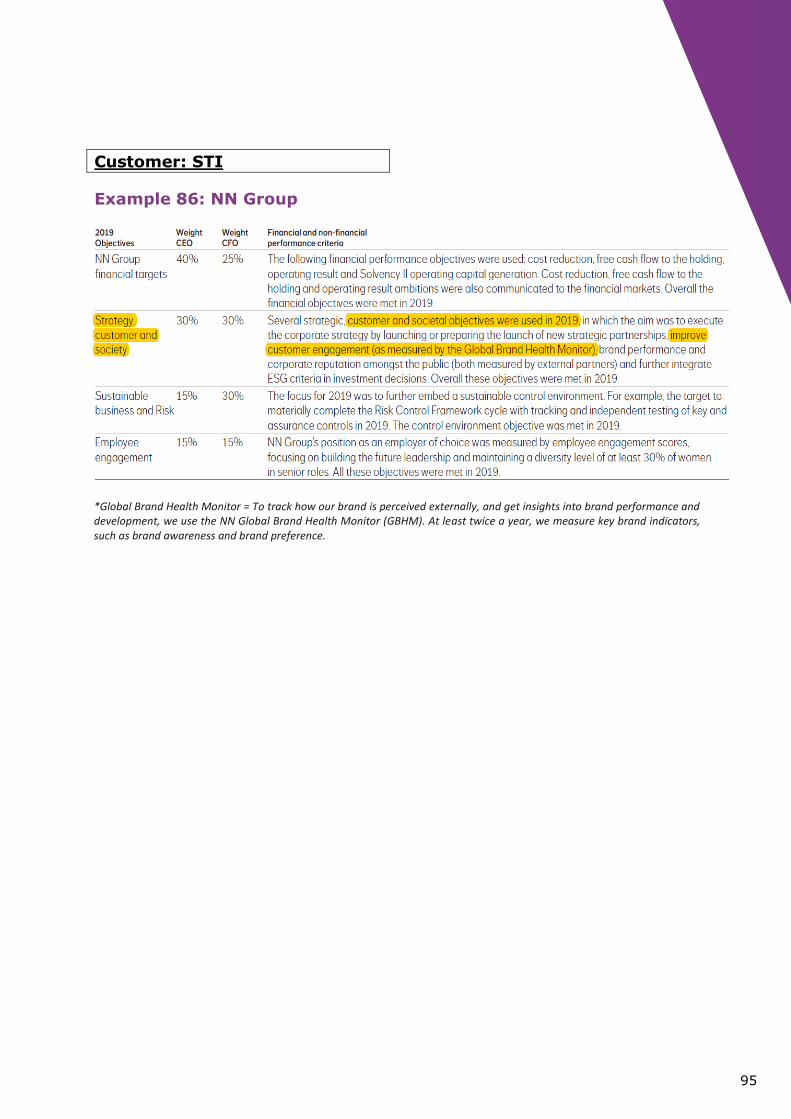

Example 52: NN Group

63

Strategy: LTI

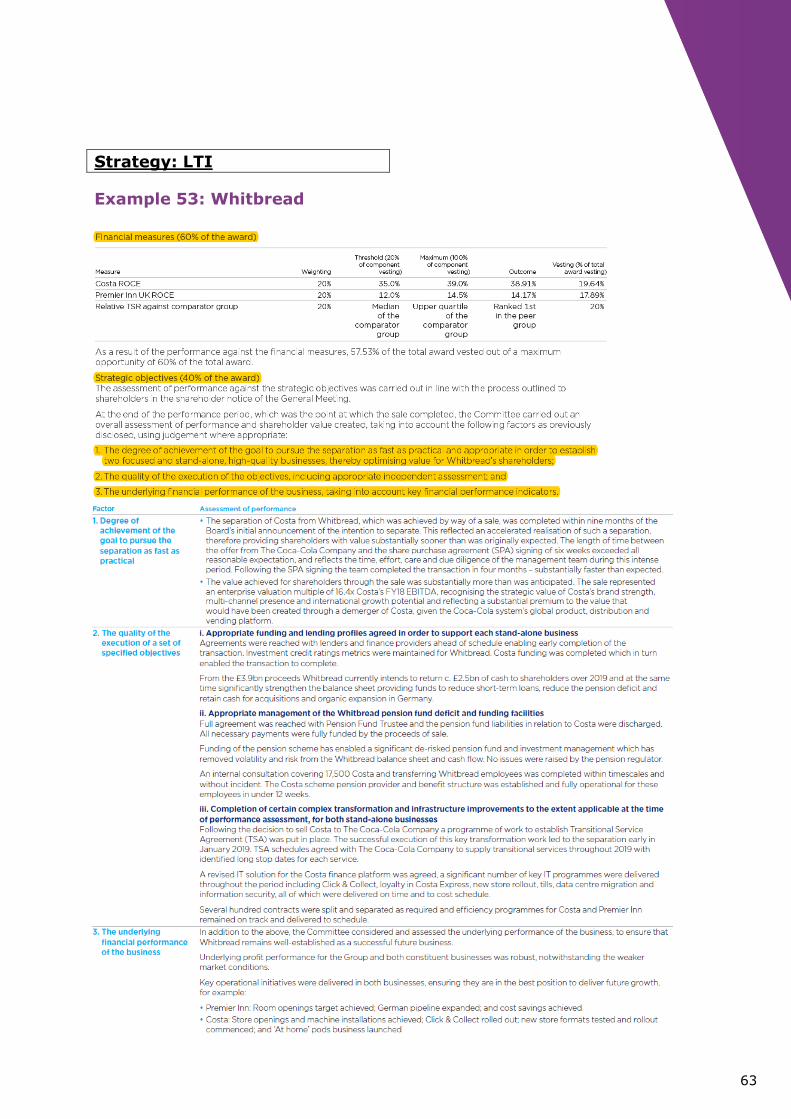

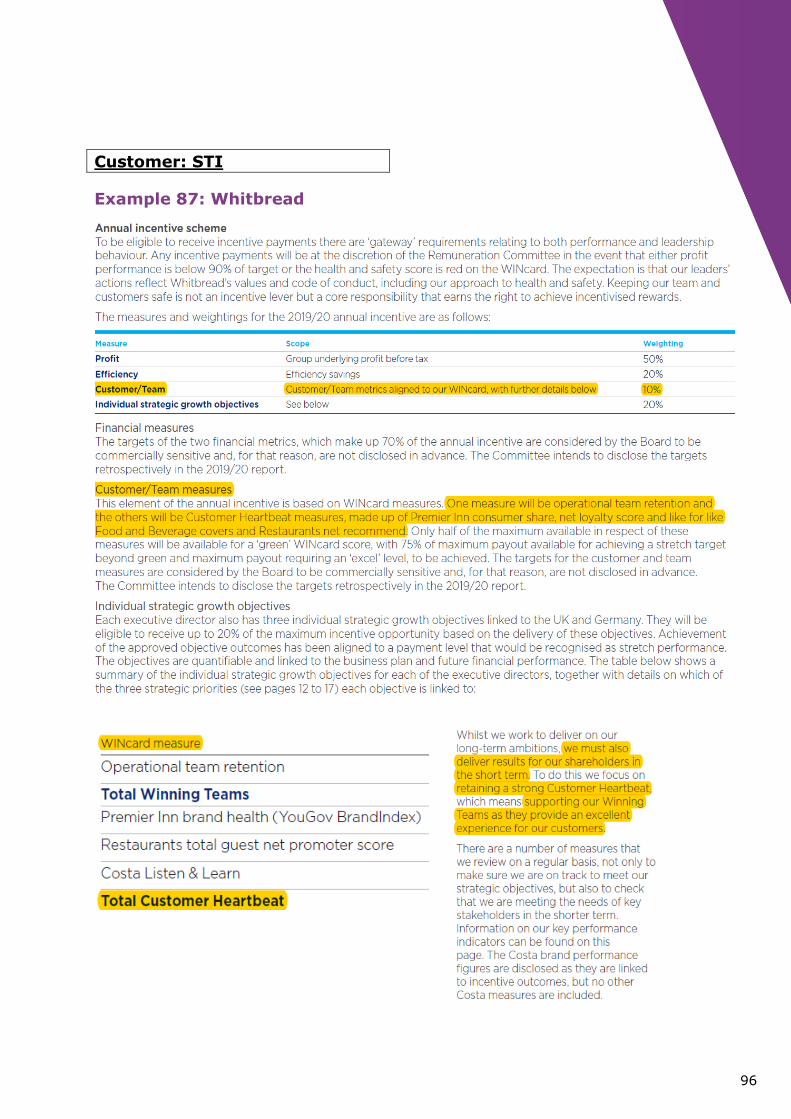

Example 53: Whitbread

64

Strategy: LTI

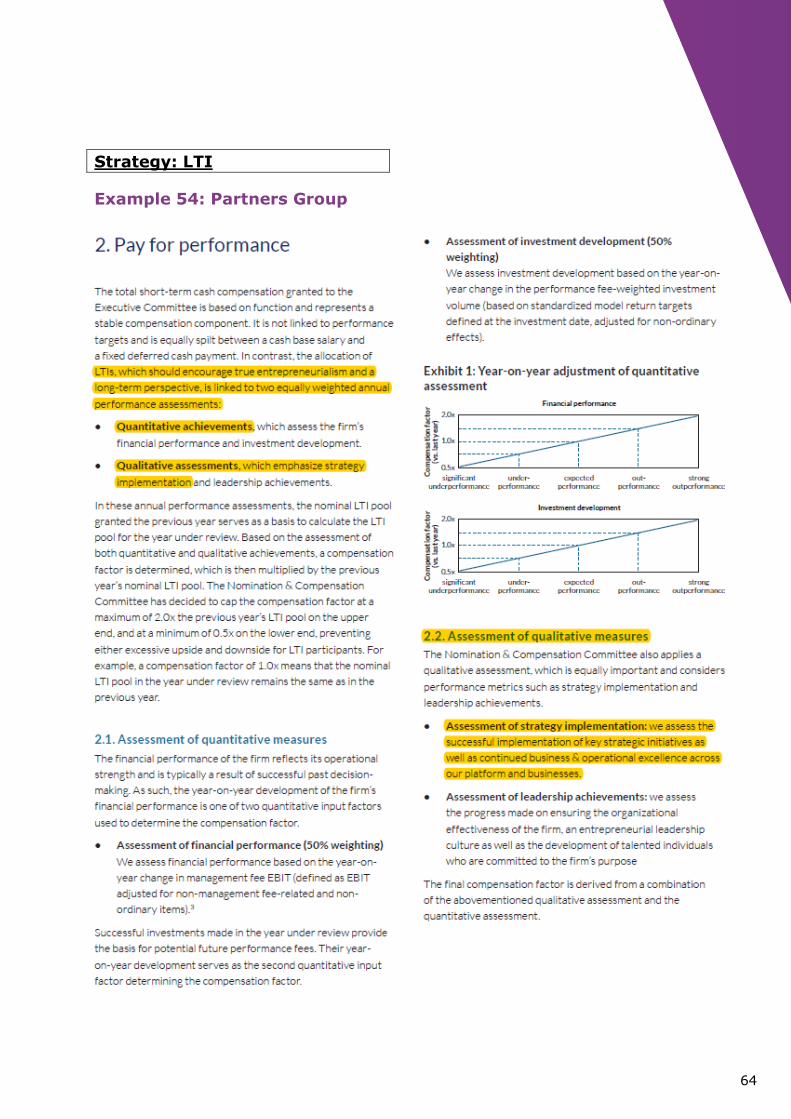

Example 54: Partners Group

65

Innovation: STI

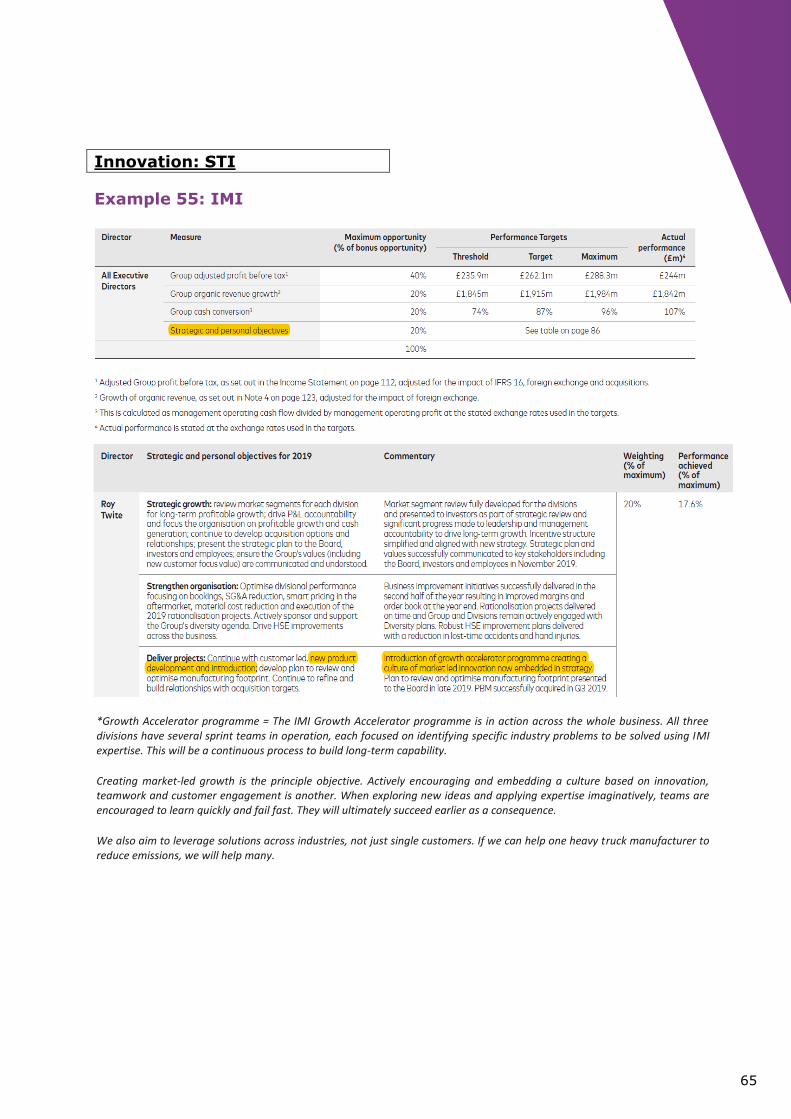

Example 55: IMI

*Growth Accelerator programme = The IMI Growth Accelerator programme is in action across the whole business. All three divisions have several sprint teams in operation, each focused on identifying specific industry problems to be solved using IMI expertise. This will be a continuous process to build long-term capability.

Creating market-led growth is the principle objective. Actively encouraging and embedding a culture based on innovation, teamwork and customer engagement is another. When exploring new ideas and applying expertise imaginatively, teams are encouraged to learn quickly and fail fast. They will ultimately succeed earlier as a consequence.

We also aim to leverage solutions across industries, not just single customers. If we can help one heavy truck manufacturer to reduce emissions, we will help many.

66

Innovation: STI

Example 56: Standard

Chartered

67

Innovation: STI

Example 57: Capgemini

Example 58: Eutelsat Communications

68

Innovation: LTI

Example 59: ASML

Additional information (CSR report)

69

Innovation: LTI

Example 60: Kion Group

70

Legal and compliance: STI

Example 61: Valeo

71

Legal and compliance: STI

Example 62: Teleperformance

72

Legal and compliance: LTI

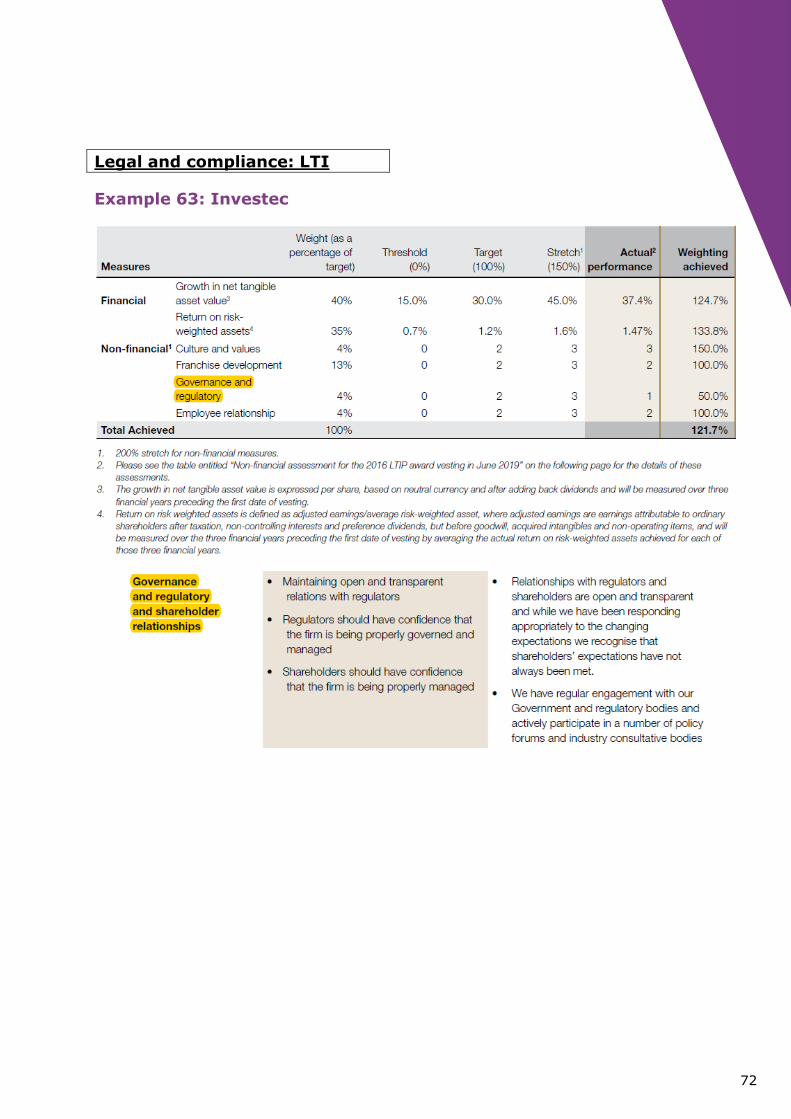

Example 63: Investec

73

Risk management and internal

control: STI

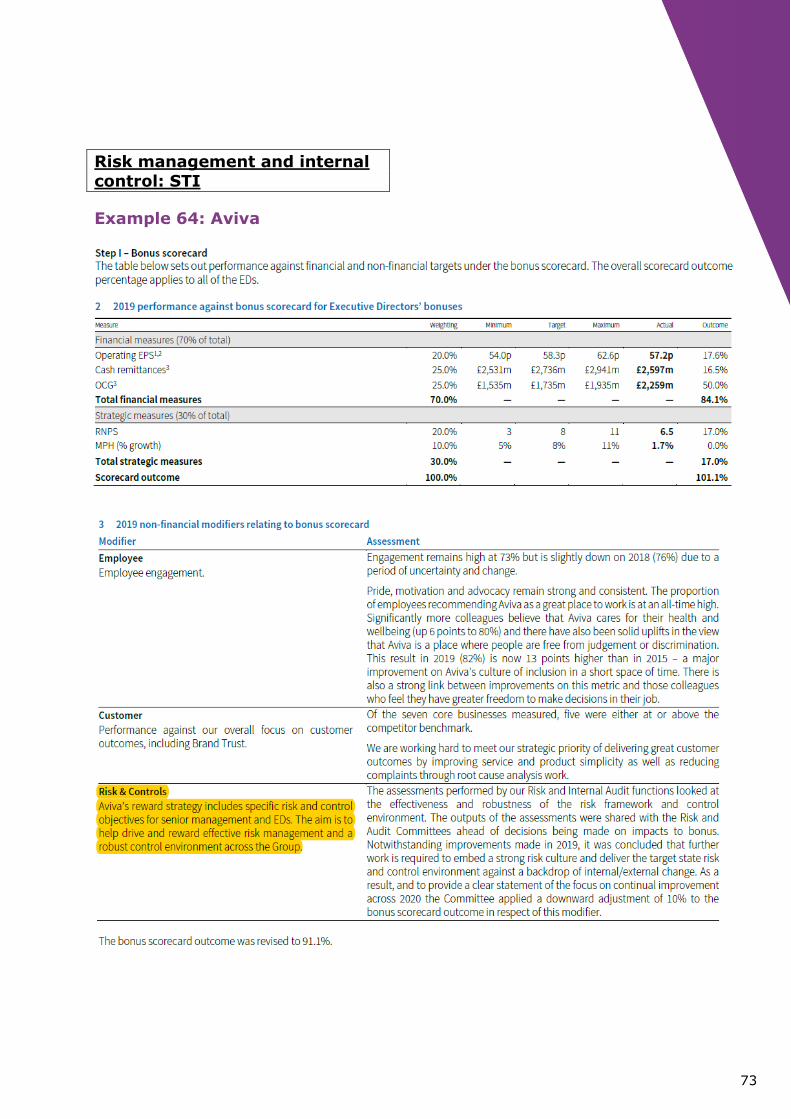

Example 64: Aviva

74

Risk management and internal

control: STI

Example 65: RELX

75

Risk management and internal

control: STI

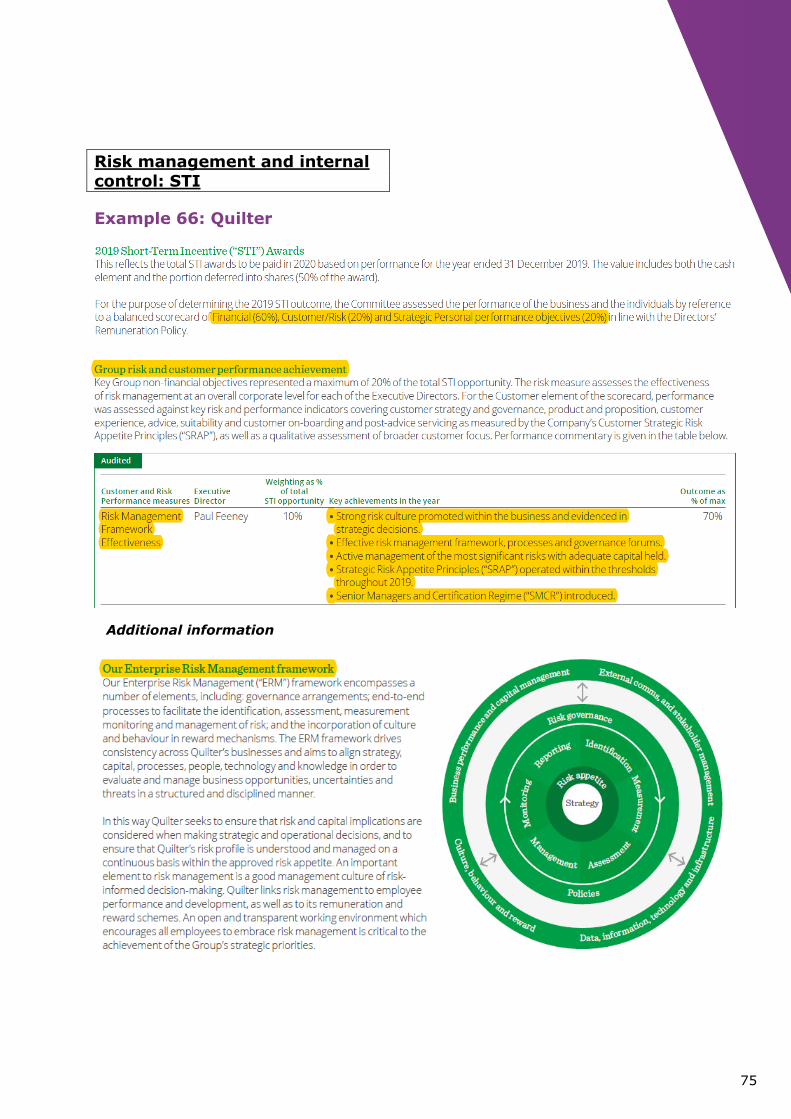

Example 66: Quilter

Additional information

76

Risk management and internal

control: STI

Example 67: BHP

77

Risk management and internal

control: STI

Example 68: Antofagasta

78

Risk management and internal

control: LTI

Example 69: Barclays

79

Quality and efficiency: STI

Example 70: Royal Dutch Shell

80

Quality and efficiency: STI

Example 71: CNP Assurances

81

Quality and efficiency: STI

Example 72: Société Générale

82

Quality and efficiency: STI

Example 73: Spectris

83

Quality and efficiency: LTI

Example 74: IG Group Holdings

84

Sustainability index: STI

Example 75: Schneider Electric

85

Sustainability index: LTI

Example 76: Terna

86

Environment: STI

Example 77: Vinci

87

Environment: STI

Example 78: SBM Offshore

SDG target completion:

88

Environment: STI

Example 79: Yara

89

Environment: STI

Example 80: Tullow Oil

90

Environment: LTI

Example 81: Signify

91

Customer: STI

Example 82: Santander

*Loyal customers = Active customers who receive most of their financial services from the Group according to the commercial segment to which they belong. Various engaged customer levels have been defined taking profitability into account.

92

Customer: STI

Example 83: RSA Insurance

group

93

Customer: STI

Example 84: Land Securities

94

Customer: STI

Example 85: Meggitt

*OTD = on-time delivery

95

Customer: STI

Example 86: NN Group

*Global Brand Health Monitor = To track how our brand is perceived externally, and get insights into brand performance and development, we use the NN Global Brand Health Monitor (GBHM). At least twice a year, we measure key brand indicators, such as brand awareness and brand preference.

96

Customer: STI

Example 87: Whitbread

97

Customer: LTI

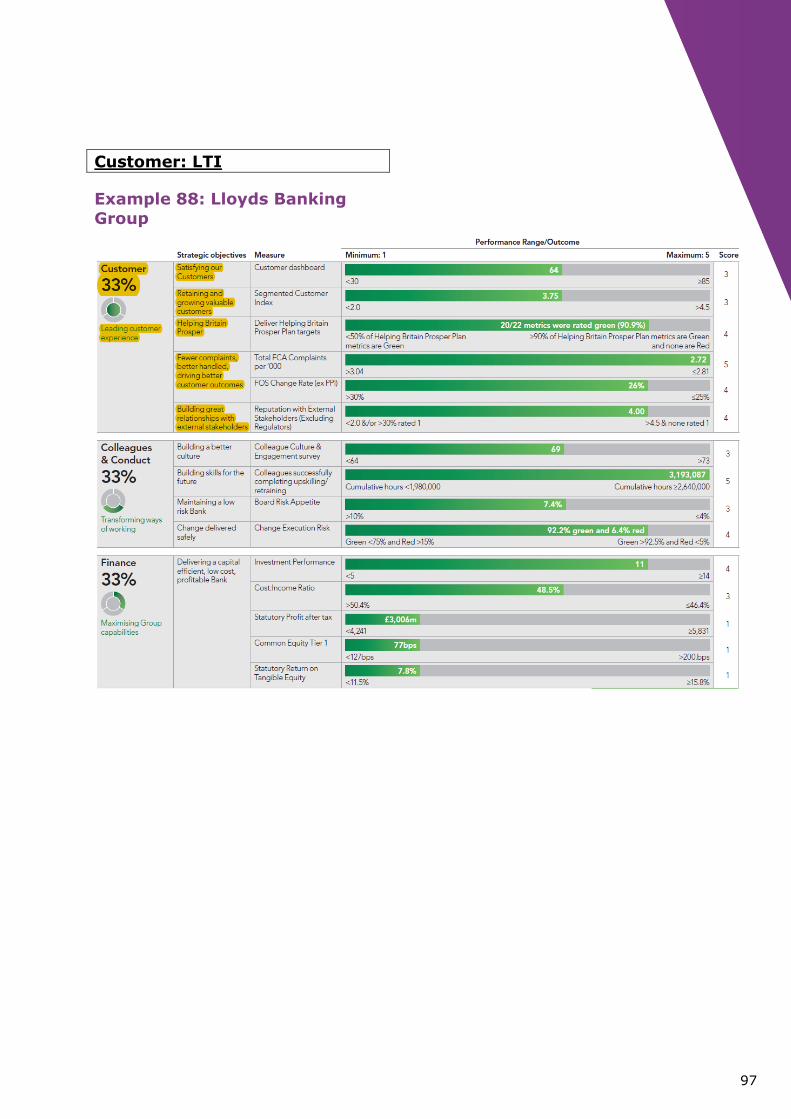

Example 88: Lloyds Banking

Group

98

Customer: LTI

Example 89: Vonovia

99

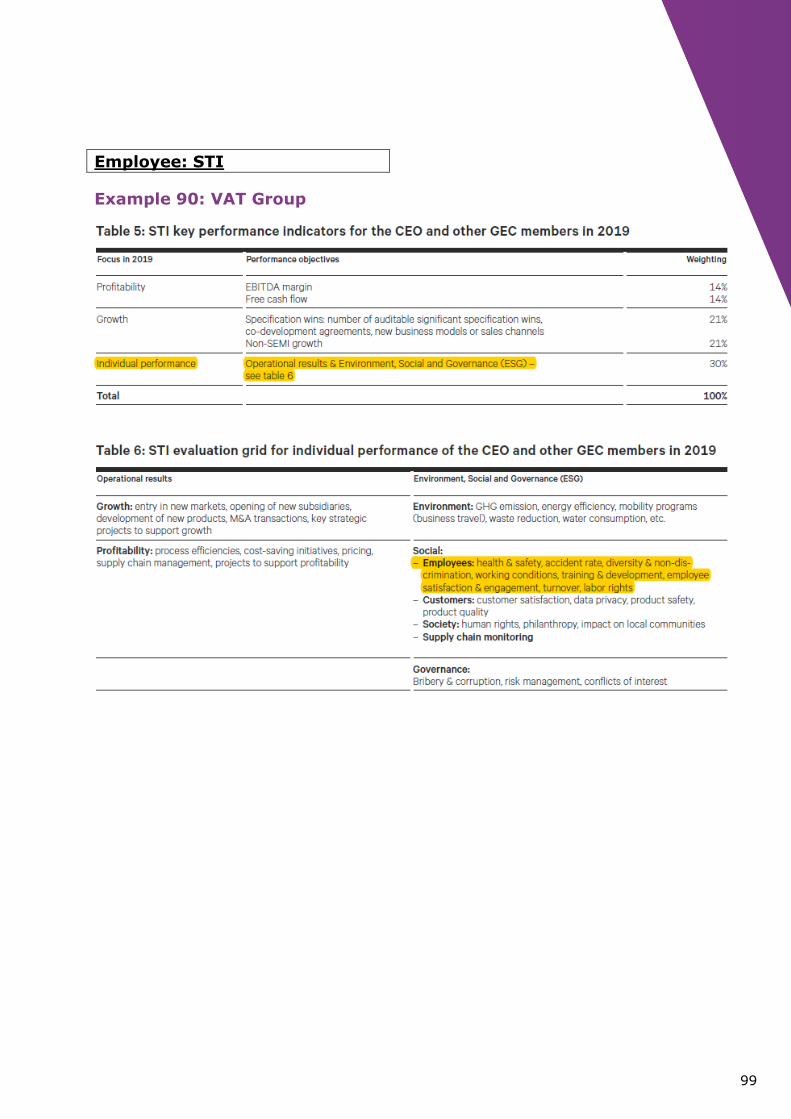

Employee: STI

Example 90: VAT Group

100

Employee: STI

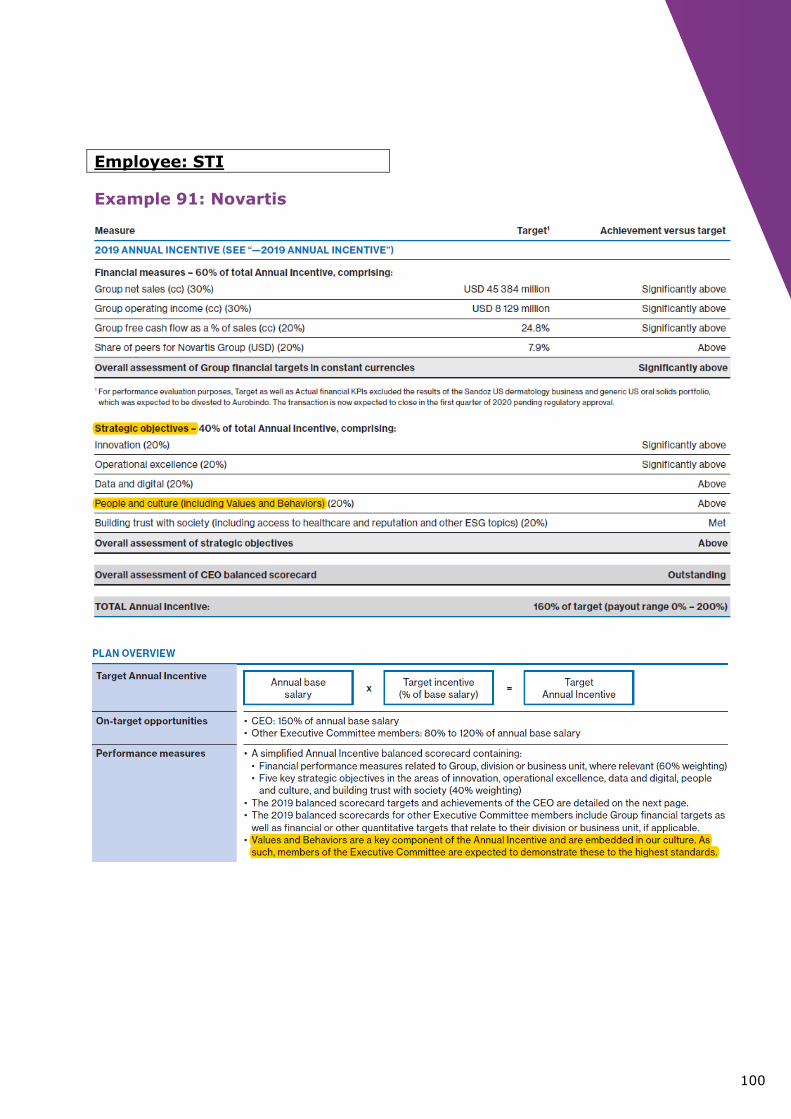

Example 91: Novartis

101

Employee: STI

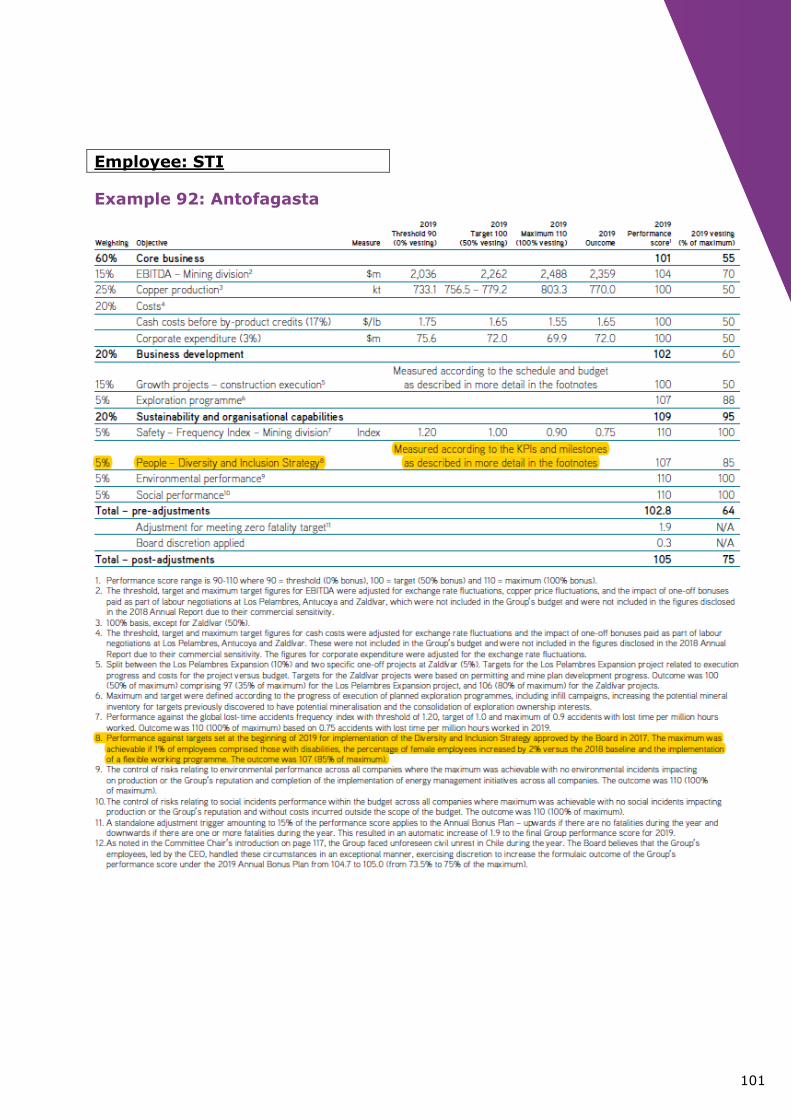

Example 92: Antofagasta

102

Employee: STI

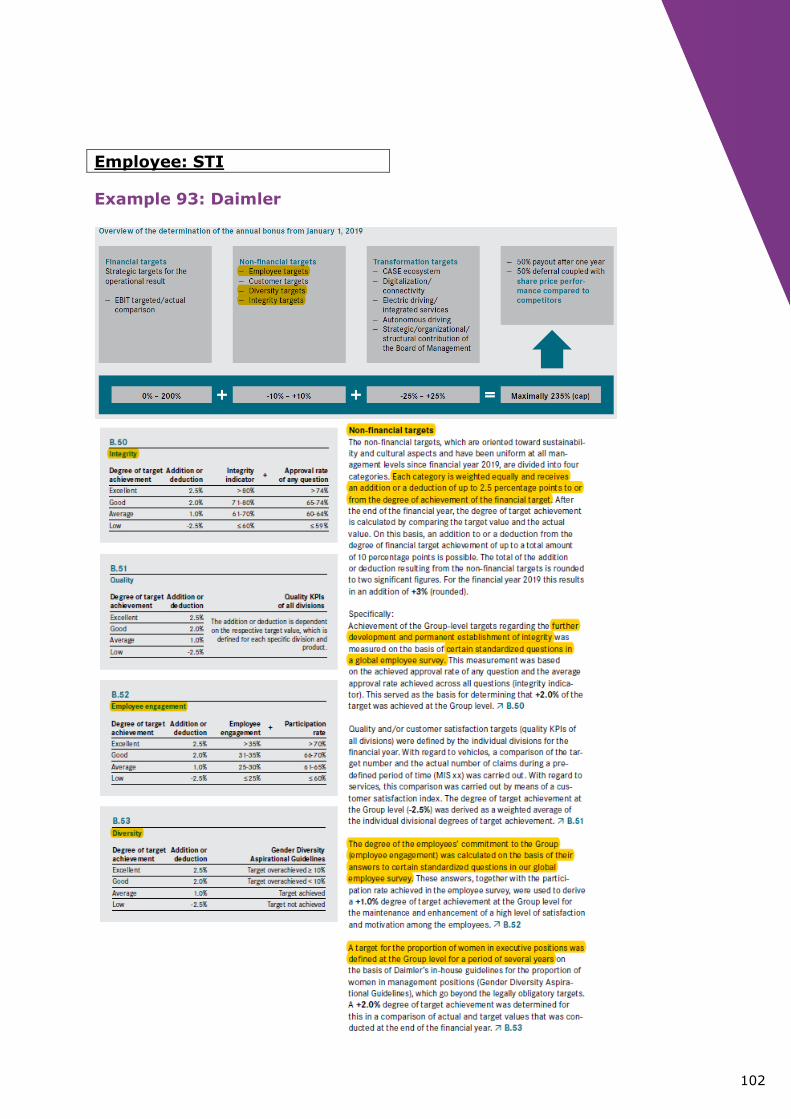

Example 93: Daimler

103

Employee: STI

Example 94: Sodexo

*LTIR = Sodexo’s LTIR is the frequency of accidents per 200,000 hours worked. 200,000 hours worked is a proxy for 100 full time equivalent employees working for a full year.

104

Employee: STI

Example 95: Arcadis

105

Employee: LTI

Example 96: Air France KLM

*EPS = to measure employee engagement, both Air France and KLM use the EPS, the in - house equivalent of the Net Promoter Score which is used to measure customer satisfaction. In the two companies, a rotating random group of employees are asked whether they would recommend Air France or KLM as an employer. The results are shared with all staff.

106

Top management team: STI

Example 97: Rio Tinto

Individual objectives CEO (30%)

107

Top management team: STI

Example 98: Tullow Oil

108

Top management team: STI

Example 99: Danone

109

Top management team: STI

Example 100: Hays

110

Top management team: STI

Example 101: Gea

111

Top management team: STI

Example 102: Baloise Holding

112

Top management team: LTI

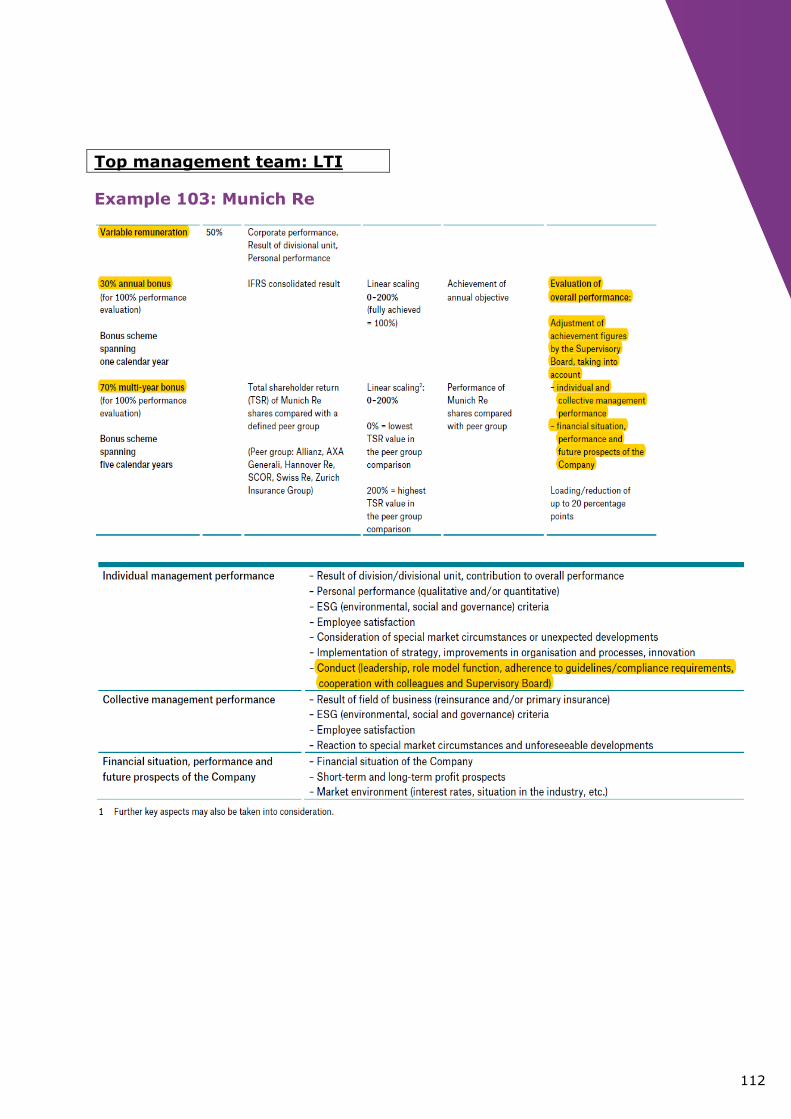

Example 103: Munich Re

113

Supplier: STI

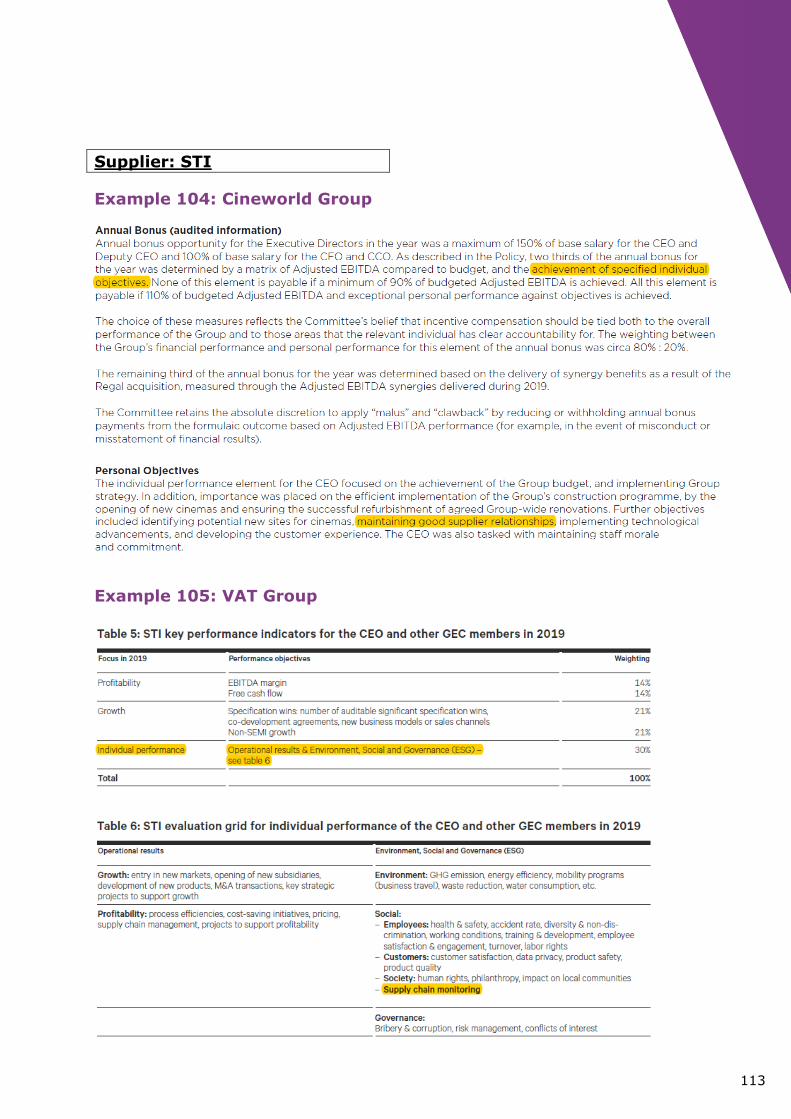

Example 104: Cineworld Group

Example 105: VAT Group

114

Supplier: STI

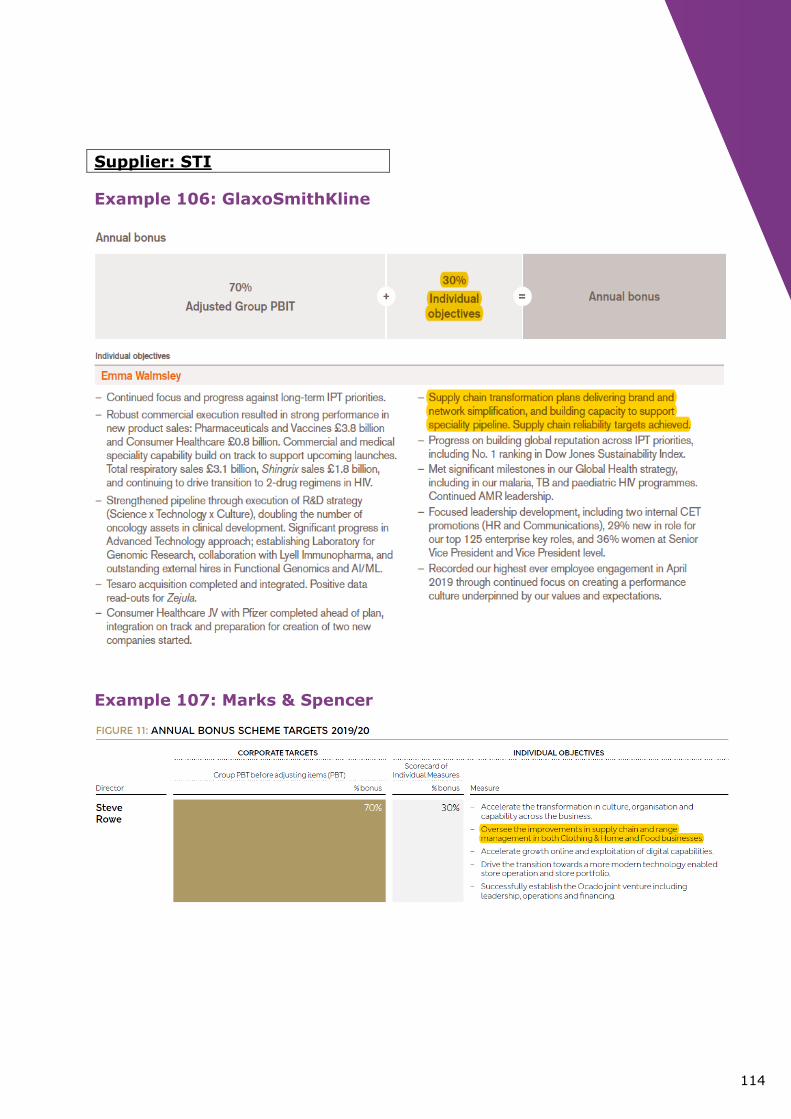

Example 106: GlaxoSmithKline

Example 107: Marks & Spencer

115

Supplier: STI

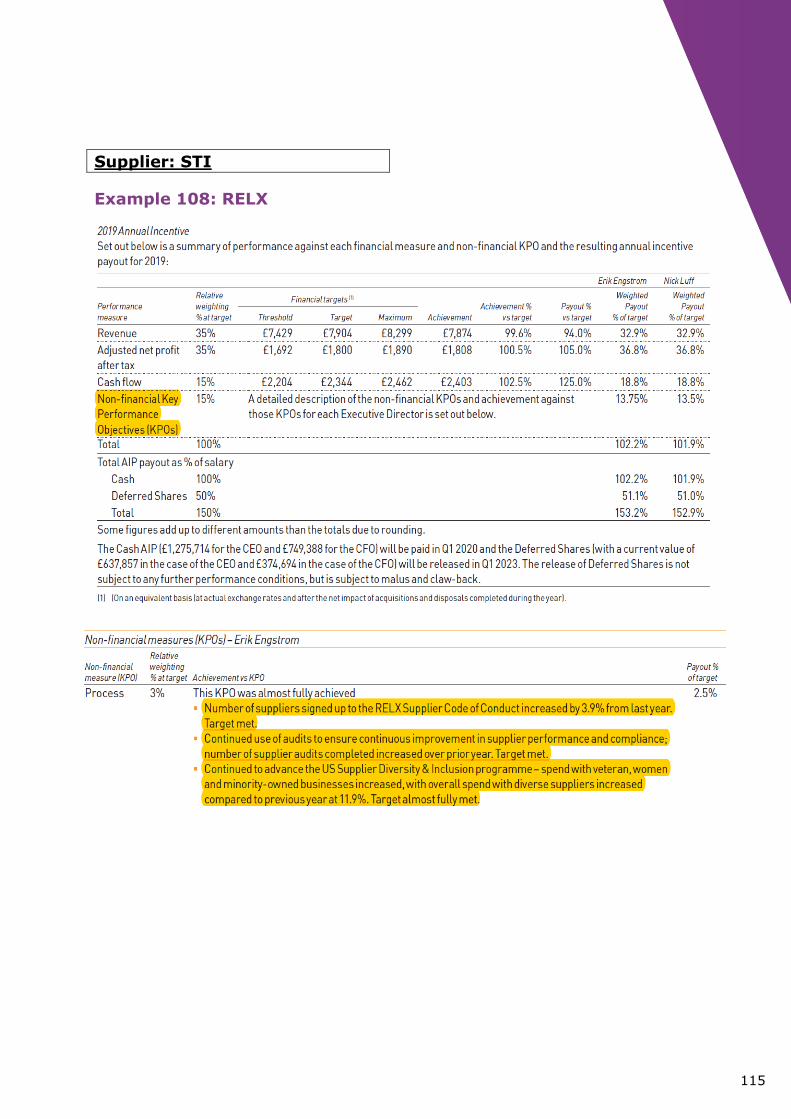

Example 108: RELX

116

• Bennett, B., Bettis, J. C., Gopalan, R., & Milbourn, T. (2017). Compensation goals

and firm performance. Journal of Financial Economics, 124(2), 307-330.

• Economic Value Added. Stern Value Management.

https://sternvaluemanagement.com/economic-value-added-eva

• European Commission. (2019, July). Guidelines on the standardised presentation of

the remuneration report under Directive 2007/36/EC, as amended by Directive (EU)

2017/828, as regards the encouragement of long-term shareholder engagement.

• Gopalan, R., Horn, J., & Milbourn, T. (2017). Comp targets that work. Harvard

Business Review, 95(5), 102-107.

• Ittner, C. D., Larcker, D. F., & Rajan, M. V. (1997). The choice of performance

measures in annual bonus contracts. Accounting Review, 231-255.

• Marr, B. (2012). Key Performance Indicators (KPI): The 75 measures every manager

needs to know. Pearson UK.

• Miller, S. C. (2019, August 16). Incentive Pay Metrics: The Long and the Short of It.

SHRM. https://www.shrm.org/resourcesandtools/hr-

topics/compensation/pages/long-short-incentive-metrics.aspx

• PricewaterhouseCoopers. (2007). Guide to key performance indicators:

Communicating the measures that matter. Retrieved January 4, 2020, from

1316_UK KPI 2007_030907.indd (pwc.com)

• Qontigo. STOXX Europe 600. STOXX. https://www.stoxx.com/index-

details?symbol=SXXP

• Sustainability Accounting Standards Board. (2020). Bases for conclusions & invitation

to comment on exposure drafts. https://www.sasb.org/wp-

content/uploads/2020/08/Invitation-to-Comment-SASB-CF-RoP.pdf

• Vlerick Executive Remuneration Research Centre dataset (STOXX Europe 600)

References

How to cite this paper: Baeten, X., & Van Hove, M. (2021). What to Reward Executives for?

A Taxonomy of Performance Metrics in Executive Incentives Supplemented by an Overview of

Business Practice. Vlerick Business School. http://hdl.handle.net/20.500.12127/6655

License: What to Reward Executives for? A Taxonomy of Performance Metrics in Executive Incentives

Supplemented by an Overview of Business Practice by Xavier, B., & Van Hove, M. is licensed under CC BY-NC-ND

4.0

117

We hereby provide the weblinks to the annual/remuneration reports where the examples

were drawn from (in order of appearance).

Share-based

• Example 1: https://www.schroders.com/en/investor-relations/results-and-reports/annual-report-and-accounts-2019/

• Example 2: https://www.arcadis.com/en/global/investors/publications-presentationsdownload-center/

• Example 3: https://annualreport.pennon-group.co.uk/2019/index.html

Sales

• Example 4: https://www.legrandgroup.com/sites/default/files/Documents_PDF_Legrand/Finance/2020/autres/Legrand-URD_2019_1589441384.pdf

• Example 5: https://www.husqvarnagroup.com/en/report/husqvarna-groups-annual-report-2019 • Example 6: https://www.electrocomponents.com/investors/annual-report-2019

• Example 7: https://www.sika.com/en/annual-report/annual-report-2019.html • Example 8: https://reports.kiongroup.com/2019/ar/

Gross profit

• Example 9: https://www.sunrise.ch/content/dam/sunrise/corporate/documents/ir-reports-presentations/2020/Sunrise_Annual%20Report%202019.pdf

• Example 10: https://www.kindredgroup.com/globalassets/documents/investor-relations-related-

documents/financial-reports/kindred-annual-report-2019-eng.pdf • Example 11: https://www.woodplc.com/annual-report-2019

EBITDA

• Example 12: https://www.orpea-corp.com/images/orpeafinance/pdf/Documentation/EN/2020/ORPEA_URD_2019_UK.pdf

• Example 13: https://ir.deutsche-wohnen.com/download/companies/dewohnen/Annual%20Reports/DW_Annual_Report_2019.pdf

• Example 14: https://www.mondigroup.com/en/investors/results-and-reports/ • Example 15: https://www.se.com/ww/en/about-us/investor-relations/regulatory-

information/annual-reports.jsp • Example 16: https://www.royalmailgroup.com/en/investors/annual-reports/

EBIT

• Example 17: https://fr.elis.com/sites/fr.elis.com/files/2020/04/14/Elis%20-%202019%20Universal%20Registration%20Document.pdf

• Example 18: https://www.pearson.com/content/dam/one-dot-com/one-dot-com/global/standalone/ar2019/2019-ar.pdf

• Example 19: https://www.carrefour.com/sites/default/files/2020-07/Carrefour%20-%20Universal%20Registration%20Document%202019.pdf

• Example 20: https://www.danone.com/content/dam/danone-corp/danone-com/investors/en-all-publications/2019/registrationdocuments/URD_2019_ENG_VA.pdf

• Example 21: https://www.capita.com/sites/g/files/nginej291/files/2020-03/capita-annual-report-2019_0.pdf

• Example 22: https://www.theheinekencompany.com/sites/theheinekencompany/files/Investors/financial-information/results-reports-presentations/heineken-nv-2019-annual-report.pdf

• Example 23: https://www.icagruppen.se/globalassets/3.-investerare/5.-rapporter/arkiv---finansiellt/engelska/2020/02.-annual-report-2019/icagruppen-annual-report-2019.pdf/

References annual/remuneration

reports

https://www.schroders.com/en/investor-relations/results-and-reports/annual-report-and-accounts-2019/

118

Profit before taxes

• Example 24: https://www.man.com/document-archive?name=Corporate+Annual+Report+-+For+the+year+ended+31+December+2019

• Example 25: https://www.burberryplc.com/en/investors/annual-report-19-20.html

Net profit

• Example 26: https://www.relx.com/~/media/Files/R/RELX-Group/documents/reports/annual-reports/2019-annual-report.pdf

• Example 27: https://www.lloydsbankinggroup.com/assets/pdfs/investors/annual-report/2019-download-links/2019_lbg_annual_report.pdf

• Example 28: https://deutsche-boerse.com/dbg-en/investor-relations/financial-reports/annual-

reports/annual-report-2019

Cash flow

• Example 29: https://www.unilever.com/Images/unilever-annual-report-and-accounts-2019_tcm244-547893_en.pdf

• Example 30: https://www.haysplc.com/investors/annual-report-2019

• Example 31: https://www.fergusonplc.com/content/dam/ferguson/corporate/investors_and_media/anual-report/ferguson_plc_annual_report_2019.pdf

• Example 32: https://annualreport2019.naturgy.com/en/?_ga=2.169138470.643344134.1614698550-72736002.1614698550

• Example 33: https://www.diageo.com/en/investors/financial-results-and-presentations/annual-

report-2019/

Relative return

• Example 34: https://assets.new.siemens.com/siemens/assets/api/uuid:0389873c-aed9-444d-9780-4b14b1b7ce57/2019-annual-report.pdf

• Example 35: https://investors.intertek.com/assets/pdf/Intertek-AR-2019-full-WEB.pdf • Example 36: https://www.valeo.com/wp-content/uploads/2020/06/2019-Integrated-Report.pdf

• Example 37: https://www.scor.com/sites/default/files/scor_universal_registration_document_2019.pdf

Cost

• Example 38: https://www.oldmutual.com/investor-relations/2019-annual-results • Example 39 + 40:

https://www.about.sainsburys.co.uk/~/media/Files/S/Sainsburys/documents/reports-and-

presentations/annual-reports/sainsburys-ar2019.pdf

Debt

• Example 41: https://www.total.com/sites/g/files/nytnzq111/files/atoms/files/2019_total_universal_registration_document.pdf

• Example 42: https://www.oci.nl/media/1779/oci-annual-report-2019.pdf • Example 43: https://www.ashtead-group.com/files/downloads/reports/ashtead-ara-2019.pdf

Economic profit

• Example 44: https://www.jeronimomartins.com/wp-content/uploads/01-DOCUMENTS/Investor/Reports/AnnualReportJeronimoMartins2019.pdf

• Example 45: https://www.spectris.com/sites/spectris-corp/files/report/2019/annual-report-

2019.pdf

119

• Example 46: https://www.juliusbaer.com/fileadmin/about/Julius_Baer_Foundation_Annual_Report_2019_Web.pdf

• Example 47: https://www.lloydsbankinggroup.com/assets/pdfs/investors/annual-report/2019-

download-links/2019_lbg_annual_report.pdf • Example 48:

https://ucpcdn.thyssenkrupp.com/_legacy/UCPthyssenkruppAG/assets.files/media/investoren/berichterstattung-publikationen/update-21.11.2019/en/thyssenkrupp-gb-2018-2019-en-web_neu.pdf

Strategy

• Example 49: https://www.haysplc.com/investors/annual-report-2019

• Example 50: https://www.aegon.com/about/integrated-annual-report-2019/

• Example 51: https://www.recordati.com/resources/Pubblicazione/___eb9a60f3bad5457a9b3ebf9813dc19e1_/annual-report-2019.pdf

• Example 52: https://www.nn-group.com/nn-group/file?uuid=55caeb72-5699-4d50-b540-d191328f5880&owner=84c25534-c28a-4a64-9c78-5cc1388e4766&contentid=10852

• Example 53: https://www.whitbread.co.uk/~/media/Files/W/Whitbread/report-and%20presentations/2019/Whitbread_18-19%20Full%20Report_Final_Final.pdf

• Example 54: https://report.partnersgroup.com/2019/app/uploads/Annual_Report_2019_Web.pdf

Innovation

• Example 55: https://www.imiplc.com/sites/imi-corp/files/2020/annualreport-2019.pdf • Example 56: https://av.sc.com/corp-en/content/docs/standard-chartered-plc-full-year-2019-

report.pdf • Example 57: https://investors.capgemini.com/en/publication/2019-universal-registration-

document/ • Example 58: https://www.eutelsat.com/files/PDF/fr/investisseurs/ETL%20COM_URD%202018-

19_UK_web.pdf • Example 59: https://www.asml.com/en/investors/annual-report/2019 • Example 60: https://reports.kiongroup.com/2019/ar/

Legal and compliance

• Example 61: https://www.valeo.com/wp-content/uploads/2020/06/2019-Integrated-Report.pdf • Example 62:

https://www.teleperformanceinvestorrelations.com/media/5470402/Teleperformance-2019-Universal-registration-document.pdf

• Example 63: https://www.investec.com/content/dam/investor-relations/financial-information/group-financial-results/2019/investec-dlc-vol-1-annual-report-2019.pdf

Risk management and internal control

• Example 64: https://www.aviva.com/investors/annual-report-2019/

• Example 65: https://www.relx.com/~/media/Files/R/RELX-Group/documents/reports/annual-reports/2019-annual-report.pdf

• Example 66: https://www.quilter.com/siteassets/quilter/investor-relations/reporting-centre/reports/quilter_ar_2019.pdf

• Example 67: https://www.bhp.com/investor-centre/annual-report-2019/ • Example 68: https://www.antofagasta.co.uk/investors/annual-report-2019/ • Example 69: https://home.barclays/investor-relations/reports-and-events/annual-reports/annual-

report-2019/

Quality and efficiency

• Example 70: https://reports.shell.com/annual-report/2019/

120

• Example 71: https://www.cnp.fr/cnp/content/download/8837/file/CNP%20Assurances%20URD%202019%20English%20Version.pdf?inLanguage=eng-GB

• Example 72: https://www.societegenerale.com/sites/default/files/documents/2020-

10/sg_urd_eng_2020.pdf • Example 73: https://www.spectris.com/sites/spectris-corp/files/report/2019/annual-report-

2019.pdf • Example 74: https://www.iggroup.com/sites/ig-group/files/fy19-ig-annual-report.pdf

Sustainability index

• Example 75: https://www.se.com/ww/en/about-us/investor-relations/regulatory-

information/annual-reports.jsp

• Example 76: https://download.terna.it/terna/TERNA_INTEGRATO_2019_ENG_8d7e862fd8fb0a9.pdf

Environment

• Example 77: https://www.vinci.com/publi/vinci/2019-vinci-annual-report.pdf

• Example 78: https://www.sbmoffshore.com/wp-content/uploads/2020/02/SBM-Offshore_Annual-Report-2019.pdf

• Example 79: https://www.yara.com/siteassets/investors/057-reports-and-presentations/annual-reports/2019/yara-annual-report-2019-web.pdf/

• Example 80: https://www.tullowoil.com/application/files/5815/8636/0065/2019_Annual_Report_and_Accounts.pdf

• Example 81: https://www.signify.com/static/2019/signify-annual-report-2019.pdf

Customer

• Example 82: https://www.santander.com/en/shareholders-and-investors/financial-and-economic-information/annual-report/2019-online-report#santander-bank-s-2019

• Example 83: https://www.rsagroup.com/investors/reports/annual-report-2019/ • Example 84: https://landsec.com/annual-report-2019

• Example 85: https://www.meggitt.com/wp-content/uploads/2020/03/Meggitt_Annual_Report_and_Accounts_2019.pdf

• Example 86: https://www.nn-group.com/nn-group/file?uuid=55caeb72-5699-4d50-b540-d191328f5880&owner=84c25534-c28a-4a64-9c78-5cc1388e4766&contentid=10852

• Example 87: https://www.whitbread.co.uk/~/media/Files/W/Whitbread/report-and%20presentations/2019/Whitbread_18-19%20Full%20Report_Final_Final.pdf

• Example 88: https://www.lloydsbankinggroup.com/assets/pdfs/investors/annual-report/2019-download-links/2019_lbg_annual_report.pdf

• Example 89: https://reports.vonovia.de/2019/annual-report/

Employee

• Example 90: https://ir.vatvalve.com/ar2019/home.html • Example 91: https://www.novartis.com/sites/www.novartis.com/files/novartis-annual-report-

2019.pdf • Example 92: https://www.antofagasta.co.uk/investors/annual-report-2019/ • Example 93: https://www.daimler.com/documents/investors/reports/annual-

report/daimler/daimler-ir-annual-report-2019-incl-combined-management-report-daimler-ag.pdf • Example 94: https://www.sodexo.com/files/live/sites/sdxcom-

global/files/PDF/Finance/20191121_Sodexo-Fiscal-2019-Universal-Registration-Document_EN.pdf • Example 95: https://www.arcadis.com/en/global/investors/publications-presentationsdownload-

center/ • Example 96: https://www.airfranceklm.com/en/publications/universal-registration-document-

2019

121

Top management team

• Example 97: https://www.riotinto.com/-/media/Content/Documents/Invest/Reports/Annual-reports/RT-Annual-report-financial-statements-2019.pdf

• Example 98:

https://www.tullowoil.com/application/files/5815/8636/0065/2019_Annual_Report_and_Accounts.pdf

• Example 99: https://www.danone.com/content/dam/danone-corp/danone-com/investors/en-all-publications/2019/registrationdocuments/URD_2019_ENG_VA.pdf

• Example 100: https://www.haysplc.com/investors/annual-report-2019 • Example 101: https://www.gea.com/nl/binaries/gea-annual-report-2019_tcm26-66349.pdf • Example 102: https://www.baloise.com/dam/baloise-

com/documents/de/publikationen/jahresabschluss/2019/annual-report-baloise-group-2019.pdf • Example 103: https://www.munichre.com/content/dam/munichre/mrwebsiteslaunches/2019-

annual-report/MunichRe-Group-Annual-Report-2019-en.pdf/_jcr_content/renditions/original./MunichRe-Group-Annual-Report-2019-en.pdf

Supplier

• Example 104: https://www.cineworldplc.com/sites/cineworld-plc/files/2020-03/cineworld-ar2019.pdf

• Example 105: https://ir.vatvalve.com/ar2019/home.html • Example 106: https://www.gsk.com/media/5894/annual-report.pdf • Example 107: https://corporate.marksandspencer.com/documents/msar-2019/full-annual-

report.pdf • Example 108: https://www.relx.com/~/media/Files/R/RELX-Group/documents/reports/annual-

reports/2019-annual-report.pdf

122

Hungry for more? Contact us!

The Executive Remuneration Research Centre (ERRC) is a knowledge-driven network

in the field of executive reward management. The centre’s main topics of interest

include:

• Strategic alignment of executive rewards

• Sustainable executive rewards

• Transparency & disclosure on executive reward

• Stakeholder engagement on executive reward

• Behavioural outcomes of executive reward

The centre is grateful to Deloitte, its Prime Foundation Partner, and its research

members.

For more information, please contact:

XAVIER BAETEN

Professor in Reward & Sustainability

T: + 32 9 210 98 97

ANGIE VAN STEERTHEM

Senior Researcher & Coordinator Vlerick Reward Centre

T: + 32 9 210 97 38

WWW.VLERICK.COM/ERRC

123