A SURVEY OF BANKS IN NAKURU COUNTY. Rael Cherobon

91

EFFECTS OF CORPORATE SOCIAL RESPONSIBILITY SPENDING ON A FIRM’S PERFORMANCE: A SURVEY OF BANKS IN NAKURU COUNTY. Rael Cherobon (CBM12/10281/12). A Research Thesis Submitted to the Graduate School in Partial Fulfillment of the Requirement for the Conferment of Master of Business Administration Degree, Faculty of Commerce. Kisii University December 2014.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of A SURVEY OF BANKS IN NAKURU COUNTY. Rael Cherobon

EFFECTS OF CORPORATE SOCIAL RESPONSIBILITY SPENDING ON A

FIRM’S PERFORMANCE: A SURVEY OF BANKS IN NAKURU COUNTY.

Rael Cherobon

(CBM12/10281/12).

A Research Thesis Submitted to the Graduate School in Partial Fulfillment of the

Requirement for the Conferment of Master of Business Administration Degree,

Faculty of Commerce.

Kisii University

December 2014.

i

DECLARATION

This research thesisis my original work and has not been presented for examination in

any other university or institution of higher learning.

………………… ……………………………

Sign Date

Rael Cherobon,

Reg. No. CBM12/10281/12

RECOMENDATION

This research has been submitted for examination with our approval as the University

supervisors. It represents the work carried out by the candidate under our supervision.

………………………………… ……………………………

Dr. Jared Bogonko,

Lecturer, Kisii University,

Faculty of Commerce.

………………………………… ……………………………

Sign Date

Dr. Ronald Bonuke,

Lecturer, Kisii University,

Faculty of Commerce.

ii

DEDICATION

This work is dedicated to my parents and all the other family members, who supported

me throughout the entire time that I was working on this piece of work. Thank you all for

your support, love and understanding.

iii

ACKNOWLEDGEMENT

I sincerely acknowledge the contributions of my supervisors Dr. Bogonko and Dr.

Bonuke, for their guidance and invaluable advice throughout the entire period when I was

writing this thesis. Your efforts have come a long way in making this work presentable. I

acknowledge your time and effort with gratitude.

Many thanks also go to my classmates Justus, Moraa, Dianah, Beatrice and Grace. It is

through the continuous support and encouragement that we had for each other that this

piece of work has come to completion. Thank you all and I wish you well in your future

endeavors.

iv

ABSTRACT

Research findings have provided support for the benefits that CSR spending yield to

companies, particularly in terms of enhanced consumer perceptions of the company.

However, understanding of the different CSR spending associated with bank performance

is still limited especially in developing countries. Even though there have been earlier

researches on the effects of CSR on business performance, little has been done and

reported on Kenyan firms. The main focus of this study was to understand whether or not

there exists any relationship between CSR spending and the performances of firms

thereof, within the banking industry in Nakuru County. The study objectives were to

determine the effect of ethical spending on bank performance, effect of economic

spending on bank performance, effect of legal spending on bank performance and effect

discretionary spending on bank performance. The study was developed and guided by the

stakeholder theory, which obligates corporate directors to appeal to all sides and balance

everyone‘s interests and welfare in a bid to maximize benefits across the spectrum of

those whose lives are touched by the business. Edward Freeman, the main proponent of

this theory with other scholars, views it as the mirror image of corporate social

responsibility, and they hold the view that the more socially responsible the firm is, the

better its performance. The study targeted all the bank staff in Nakuru County. Nassiuma

sample size formula was used to obtain 144 respondents. The study adopted explanatory

research design. This design focuses on why questions. In answering the 'why' questions,

the study was involved in developing causal explanations. Stratified random sampling

technique was used to select the respondents. A 5 likert scale structured questionnaire

was used for data collection. The validity and reliability of the questionnaire was checked

by use of pilot testing and Cronbach alpha test respectively. Data collected was coded

and analyzed using both descriptive statistics (means, standard deviation, Skewness and

kurtosis) and inferential statistics (Multiple regression and Pearson correlation).The study

findings point out that CSR ought to be adopted and executed smartly by firms so as to

avoid the imbalances of performing and not performing by only achieving its advantages

and avoiding its disadvantages.

v

TABLE OF CONTENTS

DECLARATION ............................................................................................................i

RECOMENDATION .....................................................................................................i

DEDICATION .............................................................................................................. ii

ACKNOWLEDGEMENT ........................................................................................... iii

ABSTRACT .................................................................................................................. iv

TABLE OF CONTENTS .............................................................................................. v

LIST OF FIGURES .....................................................................................................vii

LIST OF TABLES ..................................................................................................... viii

LIST OF ABBREVIATIONS ....................................................................................... ix

CHAPTER ONE ............................................................................................................ 1

INTRODUCTION ......................................................................................................... 1

1.1 Background of the study ............................................................................... 1

1.2 Statement of the Problem .............................................................................. 4

1.3 Objectives of the study .................................................................................. 5

1.3.1 General objective .......................................................................................... 5

1.3.2 Specific objectives ........................................................................................ 5

1.4 Research Hypotheses .................................................................................... 6

1.5 Significance of the Study .............................................................................. 6

1.6 Scope of the Study ........................................................................................ 7

1.7 Operational Definition of Terms ................................................................... 8

CHAPTER TWO ......................................................................................................... 10

LITERATURE REVIEW............................................................................................ 10 2.1 Theoretical Review ..................................................................................... 10

2.1.1 CSR Literature Territory ............................................................................. 10

2.1.2 Milton Friedman‘s shareholder view on CSR .............................................. 11

2.1.3 Edward Freeman‘s stakeholder view on CSR .............................................. 12

2.1.4 Reconciling Freeman‘s and Friedman‘s Views: Carroll‘s CSR Pyramid ...... 13

2.1.5 Galbreath‘s Four CSR Strategies ................................................................. 15

2.1.6 Criticism of Theories .................................................................................. 17

2.1.6.1 Edward Freeman‘s stakeholder Theory ....................................................... 17

2.1.6.2 Milton Friedman‘s Shareholder Theory ....................................................... 19

2.1.6.3 Conclusion on CSR Theories ...................................................................... 20

2.2 Empirical Review ....................................................................................... 22

2.2.1 Concept of Corporate Social Responsibility ................................................ 22

2.2.2 Link between CSR and Bank Performance .................................................. 24

2.2.3 Economic Spending and Bank Performance ................................................ 25

2.2.4 Legal Spending and Bank Performance ....................................................... 27

2.2.5 Discretional Spending and Bank Performance ............................................. 29

2.2.6 Ethical Spending and Bank Performance..................................................... 30

2.3 Critical Review ........................................................................................... 32

2.4 Conceptual Framework ............................................................................... 33

CHAPTER THREE ..................................................................................................... 34

RESEARCH METHODOLOGY ................................................................................ 34

3.1 Research Design ......................................................................................... 34

vi

3.2 Study Area .................................................................................................. 35

3.3 Target Population ....................................................................................... 37

3.4 Sample size and Sampling Procedures ........................................................ 37

3.5 Data Collection Procedures ......................................................................... 39

3.5.1 Questionnaire .............................................................................................. 39

3.5.2 Documentary Analysis ................................................................................ 40

3.6 Instrumentation ........................................................................................... 40

3.6.1 Validity of the Instruments .......................................................................... 40

3.6.2 Reliability of the Instruments ...................................................................... 41

3.7 Measurement of Variables .......................................................................... 41

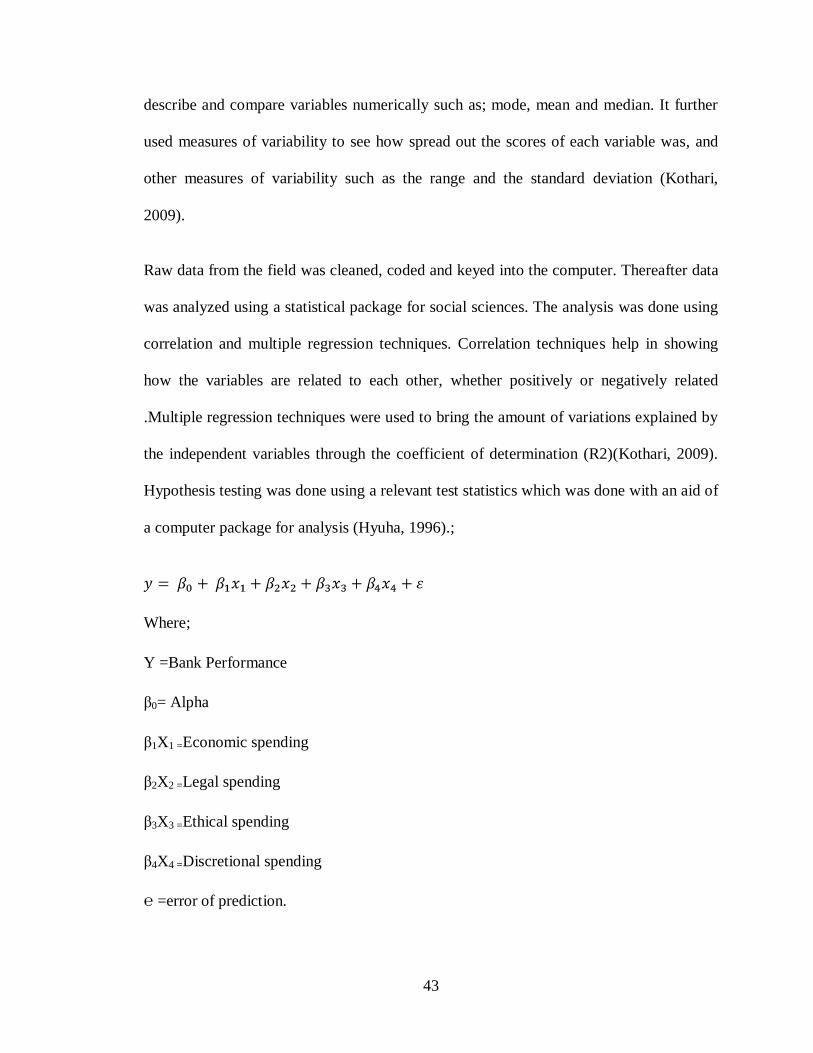

3.8 Data Analysis and Presentation ................................................................... 42

3.9 Assumption of Regression Model ............................................................... 44

3.10 Ethical Consideration .................................................................................. 44

CHAPTER FOUR ....................................................................................................... 46

DATA ANALYSIS, PRESENTATION AND INTERPRETATION ......................... 46 4.1 Response Rates ........................................................................................... 46

4.2 Background Information ............................................................................. 46

4.2.1 Demographic Information ........................................................................... 46

4.3 Specific Research Findings ......................................................................... 47

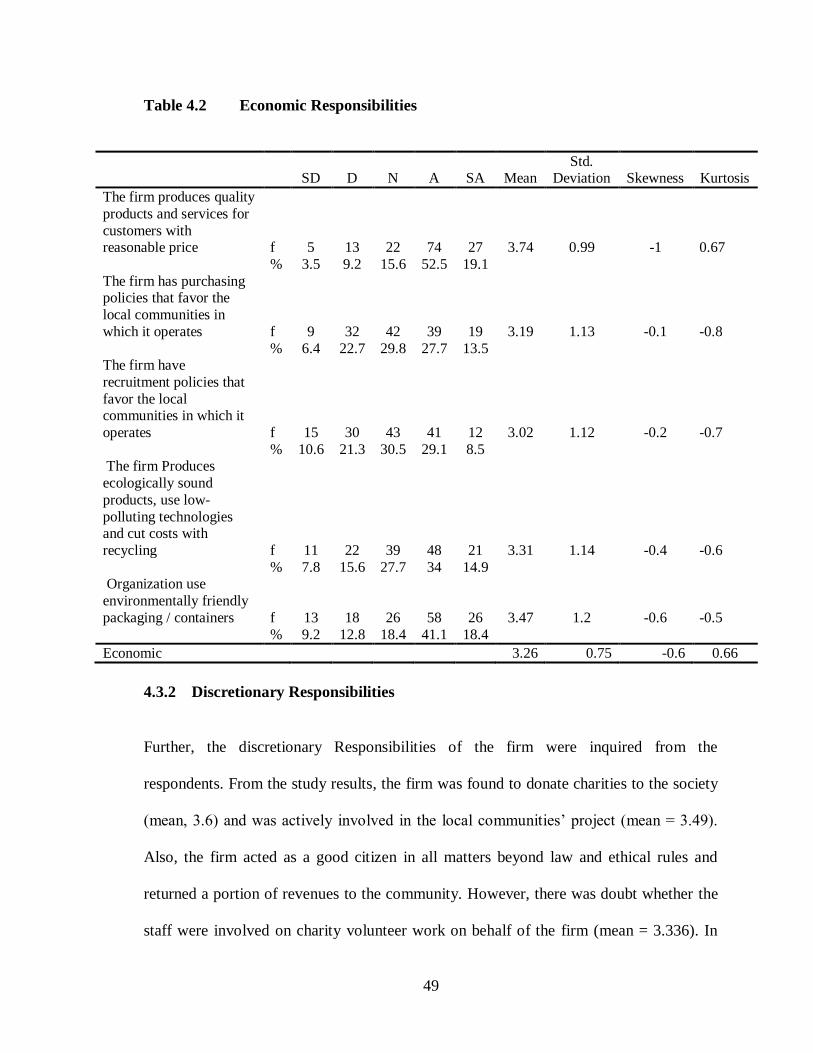

4.3.1 Economic Responsibilities .......................................................................... 48

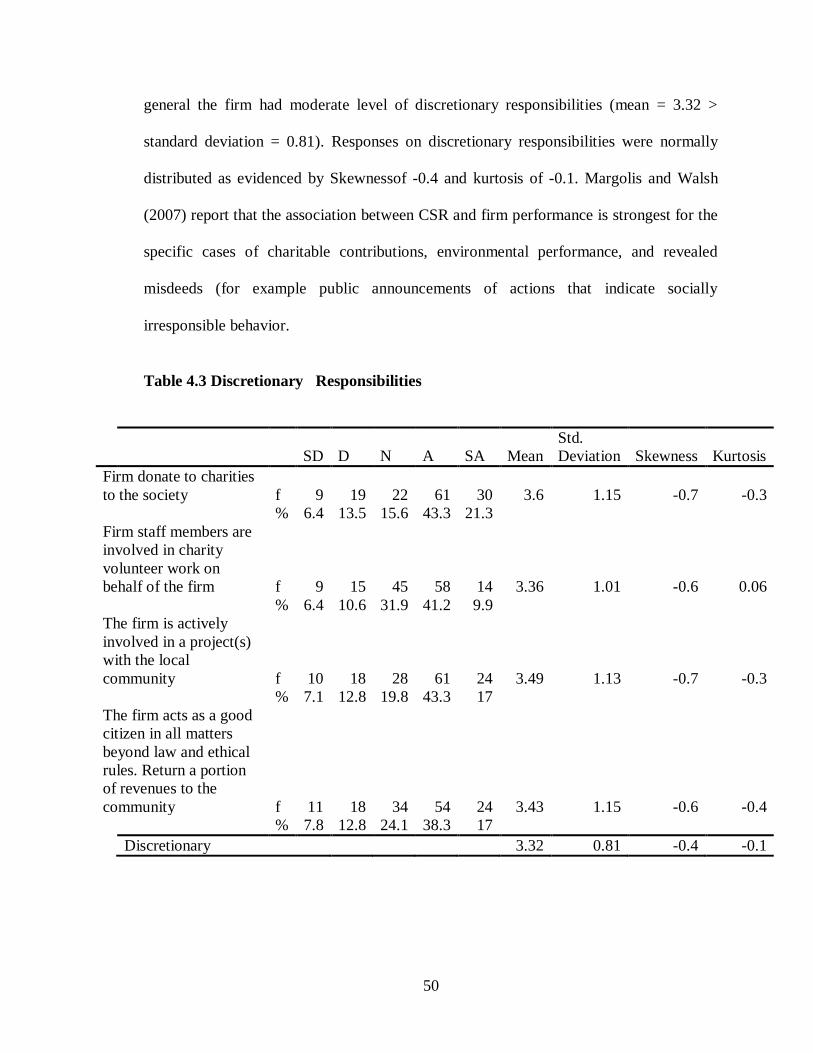

4.3.2 Discretionary Responsibilities ..................................................................... 49

4.3.3 Legal Responsibilities ................................................................................. 51

4.3.4 Ethical Responsibilities ............................................................................... 52

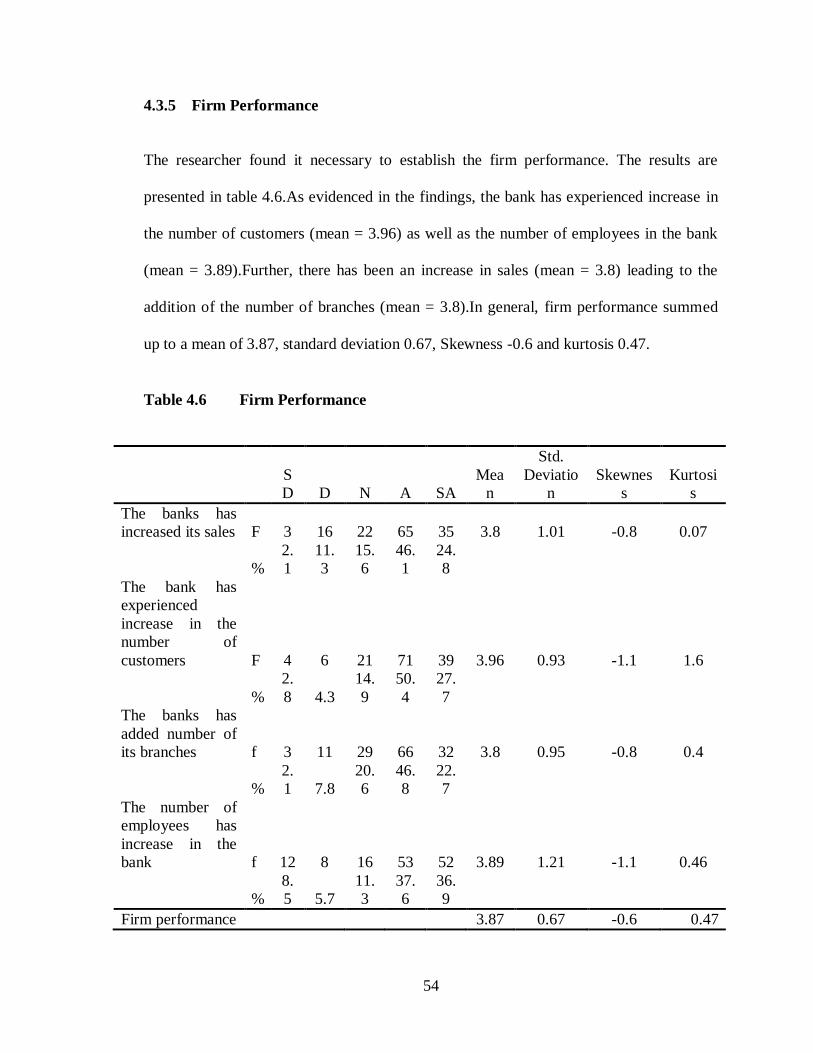

4.3.5 Firm Performance ....................................................................................... 54

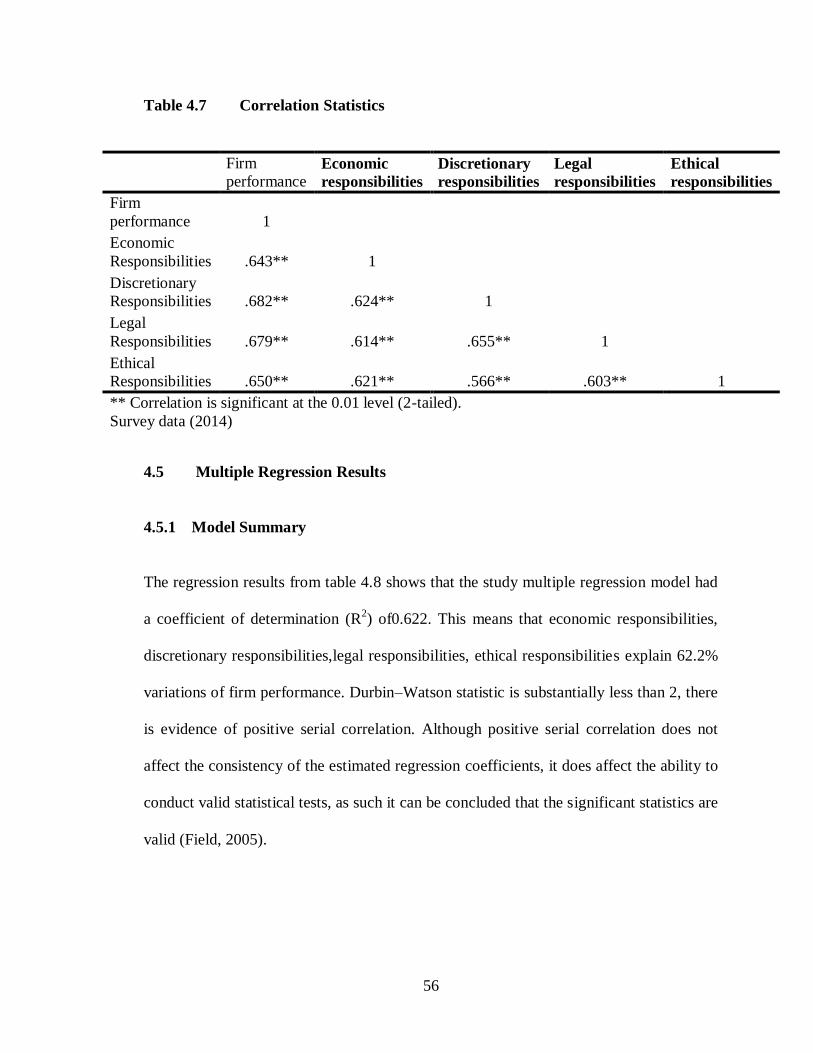

4.4 Correlation Statistics ................................................................................... 55

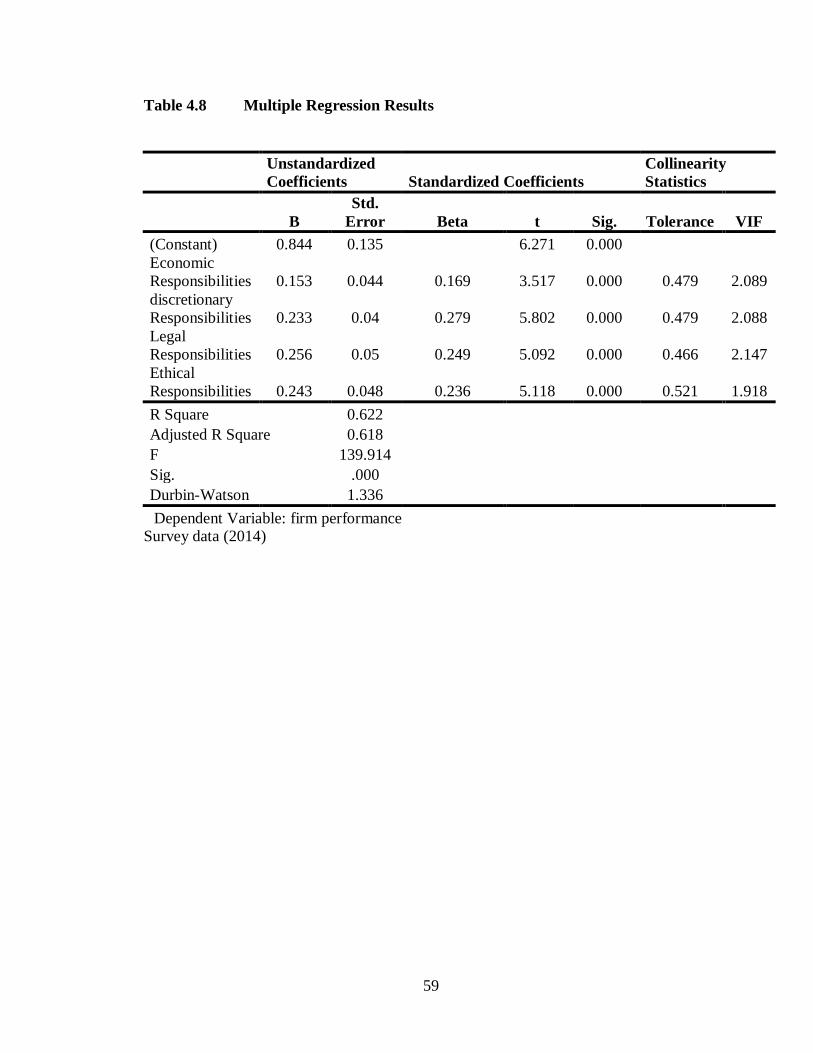

4.5 Multiple Regression Results ....................................................................... 56

4.5.1 Model Summary ......................................................................................... 56

4.5.2 Test of Multi-Collinearity ........................................................................... 57

4.5.3 Test of Hypothesis ...................................................................................... 57

CHAPTER FIVE ......................................................................................................... 60

SUMMARY, CONCLUSION AND RECOMMENDATIONS .................................. 60 5.1 Summary of the Findings ............................................................................ 60

5.2 Conclusions ................................................................................................ 62

5.3 Recommendations....................................................................................... 63

5.4 Suggestions for Further Studies................................................................... 64

REFERENCES ............................................................................................................ 66

APPENDIX I: INTRODUCTION LETTER .............................................................. 74

APPENDIX II: QUESTIONNAIRE ........................................................................... 75

APPENDIX III: RESEARCH PERMIT ..................................................................... 79

APPENDIX IV: RESEARCH AUTHORIZATION LETTER (NACOSTI) ............. 80

APPENDIX V: RESEARCH AUTHORIZATION LETTER .................................... 81

vii

LIST OF FIGURES

Figure 2.1 Conceptualization of CSR ...................................................................... 14

Figure 2.2 Conceptual Framework of Effects of CSR Spending on Bank Performance33

Figure 3.1 Study Area ............................................................................................. 36

viii

LIST OF TABLES

Table 3.1 Target Population ................................................................................... 37

Table 3.2 Sample Size ............................................................................................ 39

Table 3.1 Reliability of the Instruments .................................................................. 41

Table 4.1 Demographic Information ....................................................................... 47

Table 4.2 Economic Responsibilities ...................................................................... 49

Table 4.3 Discretionary Responsibilities .............................................................. 50

Table 4.4 Legal Responsibilities............................................................................. 52

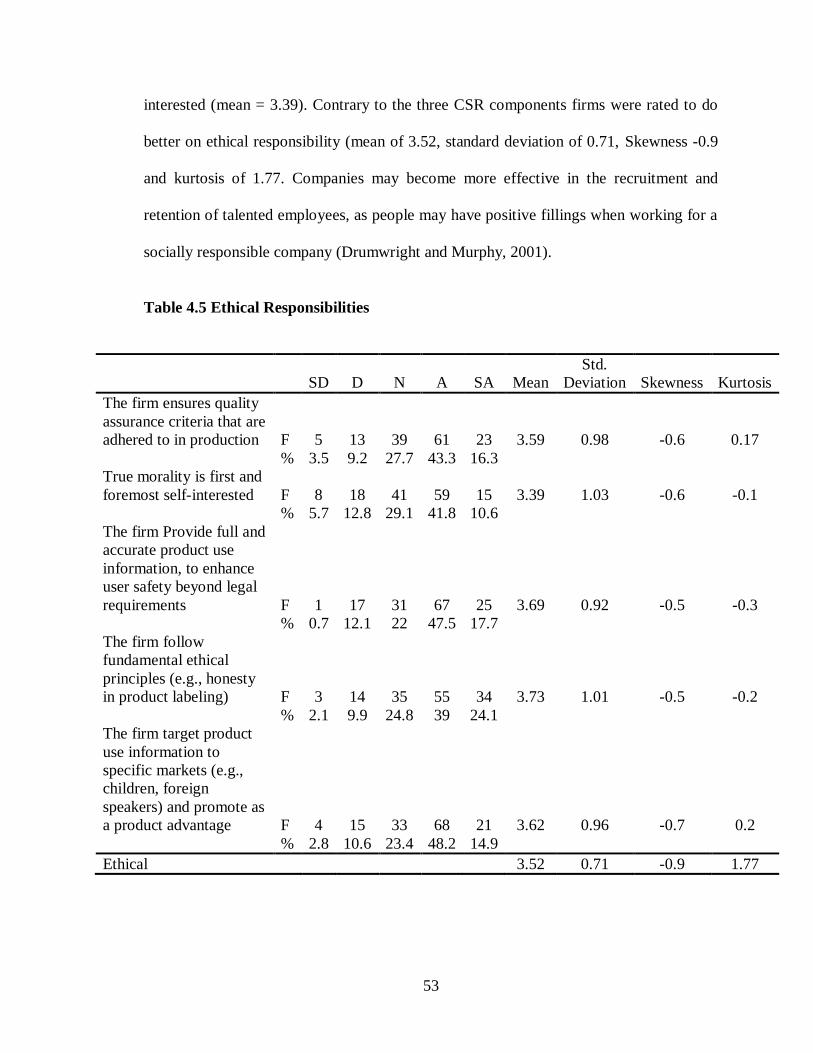

Table 4.5 Ethical Responsibilities .......................................................................... 53

Table 4.6 Firm Performance ................................................................................... 54

Table 4.7 Correlation Statistics .............................................................................. 56

Table 4.8 Multiple Regression Results ................................................................... 59

ix

LIST OF ABBREVIATIONS

CSR Corporate Social Responsibility

EAI Environmental Impact Assessment

KCB Kenya Commercial Bank

WBCSD World Business Council for Sustainable Development

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the study

Corporate Social Responsibility (CSR) has become an emerging issue in the recent

business world. It is a known fact that the main reason for a firm‘s existence is that of

profit maximization. In a bid to achieve this goal, firm‘s processes have not been able to

avoid leading to the degeneration of the environment within and around it. The result has

been unhealthy workplaces and the surrounding environment through emission of toxic

substances and other similar issues (Lindgreen, Swaen and Johnston, 2009). This has not

spared such firms sharp criticisms for their actions. Through this pressure, firms have

come to the realization that without adopting CSR, they will not be able to thrive in this

competitive arena. The result has been an immense involvement of firms in varied ranges

of CSR activities, if only to win and retain the confidence of investors and that of the

other stakeholders (Lee, 2008). In this regard, education, health care, human resource

development, conservation of nature, creation of social awareness, rehabilitation of

destitute people, addressing human sufferings arising from manmade and natural causes

are some of the important areas where Kenyan banks have been carrying out their social

and philanthropic activities.

Globally, CSR has emerged as a high-profile notion that has strategic importance to many

companies. Companies are taking direct and visible steps to communicate their CSR

spending to consumers (Luo and Bhattacharya, 2006). Bhattacharya and Sen (2004)

2

argue that many marketing studies have found that social responsibility programs have a

significant influence on several performance outcomes, thus a company with good

reputation on CSR creates a favorable context that positively boosts firm performance

(Giirhan - Canli and Batra, 2004).

The practice of CSR has been dominated by developments in Western and developed

countries, such as the United States of America (USA) and the United Kingdom (UK)

(Cheers, 2011) and it is unclear whether it translates easily into developing and non-

Western countries. These specific circumstances have been discussed by several scholars

who have identified the gaps between developed and developing countries when CSR is

implemented (Visser, 2007). Khan, (2005), suggested that different cultural models and

traditional customs may mean that a great deal of what is currently understood about CSR

may not be applicable in developing countries such as Kenya.

Researchers in developing countries are now beginning to examine the concept of CSR in

more depth. Of particular interest is whether, and to what extent (Dobers and Halme

2009), prevailing Western notions of CSR can be implemented in developing countries

and whether CSR has positive business benefits(Jamali, 2007). Although various

stakeholders have pushed companies to implement CSR in developing countries, it seems

many firms do not have sufficient knowledge to actualize it (Fombrun, 1996).Moreover,

there are no accepted rules in developing countries to enforce stakeholder demands

(Visser, 2008). Others suggest that managers‘ lack of understanding about the benefits of

CSR inhibits its implementation (Agarwal, 2008).

3

Previous studies have majored on the aspect of finding a link between CSR spending and

Corporate Performance. In the process, a number of inconsistent relationships have been

found. Scholars within the neoclassical economics school of thought argued theoretically

that CSR strategies unnecessarily raise a firm‘s costs, thus creating a competitive

disadvantage when compared to their competitors (Friedman, 1970; Aupperle, Carroll

and Hatfield, 1985; McWilliams and Siegel, 1997; Jensen, 2002). While arguing from the

agency theory point of view on one hand, other studies have suggested that employing

valuable firm resources for positive social performance strategies results in significant

managerial benefits rather than financial benefits to shareholders (Brammer and

Millington, 2008). On the other hand, other scholars have argued that enhanced social

performance may lead to obtaining better resources (Cochran and Wood, 1984; Waddock

and Graves, 1997), higher quality employees (Turban and Greening, 1996; Greening and

Turban, 2000), better marketing of products and services Moskowitz, 1972; Fombrun,

1996) and it may even lead to the creation of unforeseen opportunities (Fombrun,

Gardberg and Barnett, 2002).

From the above findings, it is clear that no real consensus has been arrived at, as regards

the link between these two variables. A recent review of seven earlier empirical studies

concluded that ―economic performance is not directly linked, in either a positive or

negative way, to social responsiveness‖ (Arlow& Gannon, 1982).Whether or not a

relationship exists clearly is an important issue for corporate management in this business

world. Certain actions (classified as socially responsible) tend to be negatively correlated

with performance of firms, then managers might be advised to be cautious in this area.On

the other hand, a positive relationship can be shown to exist, then management might be

4

encouraged to pursue such activities with increased vigor. Critics of CSR reject the role

of CSR, while they argue that the primary responsibility of a business is seen as creating

financial returns for its shareholders and the larger economy. Thus, any social or

environmental initiative that does not simultaneously create profit for a company is

deemed to be a waste of corporate resources.

Based on these arguments, this thesis aimed at bringing out the relationship between

CSR spending and firm‘s performances (if any exists), as well as aim at understanding if

really CSR is a necessity or is it just an avenue to waste corporate resources, as already

put forth by CSR critics.

Chapter one starts with a development of an insight into the background of the study,

where scholarly researches on the problem are briefly reviewed. The chapter further

provides the statement of the problem, objectives of the study, research hypotheses based

on the research objectives, significance of the study, and finally, the scope of the study.

1.2 Statement of the Problem

With growing scrutiny of business operations, organizations are increasingly being driven

to satisfy the expectations of opinion formers, governments and customers in order to

thrive. In essence, businesses adopting CSR principles believe that by operating ethically

and responsibly, they have a greater chance of success. Businesses are demonstrating that

well managed corporate responsibility actually supports business objectives, especially

amongst large corporates where improved compliance, reputation and relationships have

been shown to increase shareholder value and profitability.

5

The overall research problem that this study addressed is that despite the many

boardroom talks held on CSR, implying that CSR is a prerequisite for good corporate

leadership and governance, little has been done to establish whether indeed there is any

relationship between CSR spending and the corresponding performance of firms adopting

these CSR practices. Is CSR centered on improving the financial performance, which is

the underlying reason for a firm‘s existence or is it all about creating value to the society?

What parameters depict a socially responsible firm? What are the drivers for embracing

CSR? and further still, what aspects of CSR should a firm embrace most? If these issues

are not looked at and analyzed, then firms could just be indulging themselves in activities

that result in a waste of the ever limited corporate resources.

1.3 Objectives of the study

1.3.1 General objective

To examine effects of corporate social responsibility spending on a firm‘s performance, a

survey of banks in Nakuru County.

1.3.2 Specific objectives

i. To establish the effect of ethical spending on bank performance in Nakuru

County.

ii. To determine the effect of economic spending on bank performance in Nakuru

County.

iii. To establish the effect of legal spending on bank performance in Nakuru County.

6

iv. To determine the effect of discretionary spending on bank performance in Nakuru

County.

1.4 Research Hypotheses

H01: Ethical spending has no significant effect on bank performance.

H02: Economic spending has no significant effect on bank performance.

H03: Legal spending has no significant effect on bank performance.

H04: Discretionary spending has no significant effect on bank performance.

1.5 Significance of the Study

At the end of this study, it is expected that the findings will be of benefit to the firms

under study on helping them realize the impact of it‘s spending on CSR activities, on its

performance, and that it will be able to know whether or not they are on the right track by

engaging itself in CSR activities.

Secondly, the findings will assist in pointing out the major aspects of CSR that impact

well on the industry, so that it directs greater efforts on those areas.

Thirdly, the study will help the general public get informed on the various approaches

that banks can use to improve the quality of life in the community, at the workplace,

market place and in giving back to the society in general.

Lastly, it is expected that the findings will add to the existing reservoir of knowledge on

CSR versus firms‘ performances. It will help to provide insights to support future

research regarding strategic guidance for organizations in engaging in socially

7

responsible behavior. It is hoped that it will assist in bridging any knowledge gaps in this

subject, which has attracted numerous scholarly debates over the years.

1.6 Scope of the Study

This paper aimed at specifically examining the effects of the various aspects of CSR

spending on bank performance in the banking sector. It targeted the employees of 12

banks in Nakuru County. The study was conducted on a constructed cohort of 144 staff

drawn from all the banks in the county. The study was limited to the use of

questionnaires as a method of data collection. Although this required a lot of time when

distributing them, the method was still preferred as it ensured adequate information was

obtained from the respondents.

8

1.7 Operational Definition of Terms

In the field of Corporate Social Responsibility, several terminologies are often used

interchangeably. The following distinctions have however been made in the terms below,

for the purpose of this research.

Corporate Social Responsibility, (CSR) Refers to the economic spending, legal

spending, ethical spending and discretionary spending

expectations that society has for a given organization at a given

point in time.

Corporate stakeholder Is a party that can affect or be affected by the actions of the

business as a whole.

Corporate philanthropyRefers to an activity above and beyond what is required of an

organization and which can have a significant impact on the

communities in which a company operates.

Discretionary responsibility Entails voluntary social involvement, including activities

such as philanthropic contributions. These activities are

purely voluntary, guided only by the firm‘s desire to

engage in social activities that are not mandated, not

required by law and not generally expected of business.

Economic responsibility Refers to producing quality products and services for

customers with reasonable price and providing good jobs

for employees.

Ethical responsibility Refers to a firm being expected to act beyond legal requirements

by considering its standards, norms, and expectations which in

turn reflect an obligation to do what is right, just, fair and to avoid

harm to others.

9

Firm performance Refers to the ability of an enterprise to achieve such objectives as

high profit, quality products, large market share, a highly

motivated employee workforce, good financial results, and

survival at a pre-determined time using relevant strategy for

action.

Legal component Refers to a company complying with the laws and regulations

within which they operate.

Stakeholder Any person or organization perceived to have a legitimate interest

in a given project or entity.

10

CHAPTER TWO

LITERATURE REVIEW

2.1 Theoretical Review

2.1.1 CSR Literature Territory

The Corporate Social Responsibility (CSR) field presents not only a number of theories,

but also a proliferation of approaches, which are controversial, complex and unclear‘‘

Garriga&Mele 2004:51). This statement calls for the need to have a map of the CSR

landscape. Garriga and Mele provide this map in their Corporate Social Responsibilities

Theories: Mapping the Territory. The authors outline four main types of theories:

instrumental theories, ethical theories, integrative theories, and political theories. This

paper will define the first three theories, which are deemed relevant to the study. Thus the

political theories will not be defined.

Instrumental Theories of CSR: These focus on achieving economic objectives of the firm

through social activities. There are three main approaches to this. First is through

maximization of shareholder value as proposed by Friedman (1970) and Jensen (2000) in

Garriga and Mele 2004:63. The second approach is the strategies for competitive

advantage, which include social investments in a competitive context, strategies based on

the natural resource view of the firm and the dynamic capabilities of the firm, and finally

strategies for the bottom of the pyramid as proposed by Prahalad (2002, 2003) in Garriga

and Mele 2004:63). The third instrumental approach is cause-related marketing.

11

Integrative Theories of CSR: These focus on the integration of social demands. They

include four approaches: issues management, public responsibility, stakeholder

management, and corporate social performance.

Ethical Theories of CSR: Under these theories, focus is on doing the right thing to

achieve a good society. The approaches to this theory include: stakeholder normative

theory, universal rights, sustainable development, and the common good.

2.1.2 Milton Friedman’s shareholder view on CSR

In his commonly cited article in the New York Times Magazine, (1970), The Social

Responsibility of Business is to Increase its Profits . Milton Friedman argued that ―there

is one and only one social responsibility of business – to use its resources to engage in

activities designed to increase its profits so long as it stays within the rules of the game,

which is to say, engages in open and free competition without deception or fraud‖

(Friedman, 1970:6). Friedman, in concurrence with Adam Smith, argued that the pursuit

of economic self-interest (within legal and ethical bounds) leads to efficient markets.

Further still, Friedman views the corporate executive as an employee of the owners of the

business, whose responsibility is to conduct business in accordance with the desires of

these owners. The executive is the agent serving the owners (shareholders) as the

principals. It would therefore, be considered as a case of mismanagement of the

company, if the executive were to allocate the company‘s funds in ways other than that of

maximizing shareholder value. If, however, the executive wished to contribute his own

means to a charitable cause, he would be his own principal then, and would be free of the

agent‘s responsibilities. Friedman further expounds on this by describing how the

12

company and its executives are ill-equipped to pick the best causes for charity, and that

this is the domain of taxes and government, and not of business (Friedman, 1970).

2.1.3 Edward Freeman’s stakeholder view on CSR

On the other hand, while opposing Friedman‘s views that ―the business of business is

business‖, Freeman proposed a stakeholder approach to strategic management (Freeman,

1984). At the heart of this view is the stakeholder, a spin on the word shareholder, which

is ―any group or individual who can affect or is affected by the achievement of the

organization‘s objectives‖. Freeman argues that ―stakeholder theory begins with the

assumption that values are necessarily and explicitly a part of doing business. It asks

managers to articulate the shared sense of the value they create, and what brings its core

stakeholders together. Further, it pushes managers to be clear about how they want to do

business, specifically what kinds of relationships they want and need to create with their

stakeholders to deliver on their purpose‘‘ Freeman, Wicks, & Parmar,2004:364). Hence,

Freeman‘s stakeholder theory counters that of Friedman‘s shareholder views and opines

that the businesses are responsible for more than profit maximization for shareholders.

Stakeholder theory was brought forward by R. Edward. This theory is concerned with

evaluating the various stakeholders that the firm is perceived to be responsible to, thus

it‘s a theory of organizational management and business ethics. It‘s mainly concerned

with morals and values while managing an organization. According to this theory, a firm

has various stakeholders to whom it is responsible to. It aims at evaluating the various

parties that have a claim over the firm. A firm is a collection of various stakeholders who

have diverse requirements from the firm (Freeman 1984). This theory models the various

13

stakeholders into groups with diverse interests who are to be taken into consideration by

the company while devising some ways of incorporating their various interests. A

stakeholder refers to any person or organization perceived to have a legitimate interest in

a given project or entity. A corporate stakeholder is a party that can affect or be affected

by the actions of the business as a whole. The term has been broadened to include

anyone who has an interest in a matter.

On one side of the argument are those who believe in providing for society‘s

discretionary spending expectations. In addition to making a profit and obeying the law, a

company should attempt to alleviate or solve social problems. This view is commonly

advocated through stakeholder theory. This theory maintains that corporations should

consider the effects of their actions upon the customers, suppliers, general public,

employees, and others who have a stake or interest in the corporation (Jensen, 2002;

Smith, 2003a; Freeman, Wicks, &Parmar, 2004; Lee, 2008; Schaefer, 2008). Supporters

of this theory reason that by providing for the needs of stakeholders, corporations ensure

their continued success. A renowned company that exhibits the stakeholder view is

Johnson and Johnson. They list the corporation‘s responsibilities in the following order:

customers, employees, management, communities, and stockholders (Seglin, 2000/2002).

2.1.4 Reconciling Freeman’s and Friedman’s Views: Carroll’s CSR Pyramid

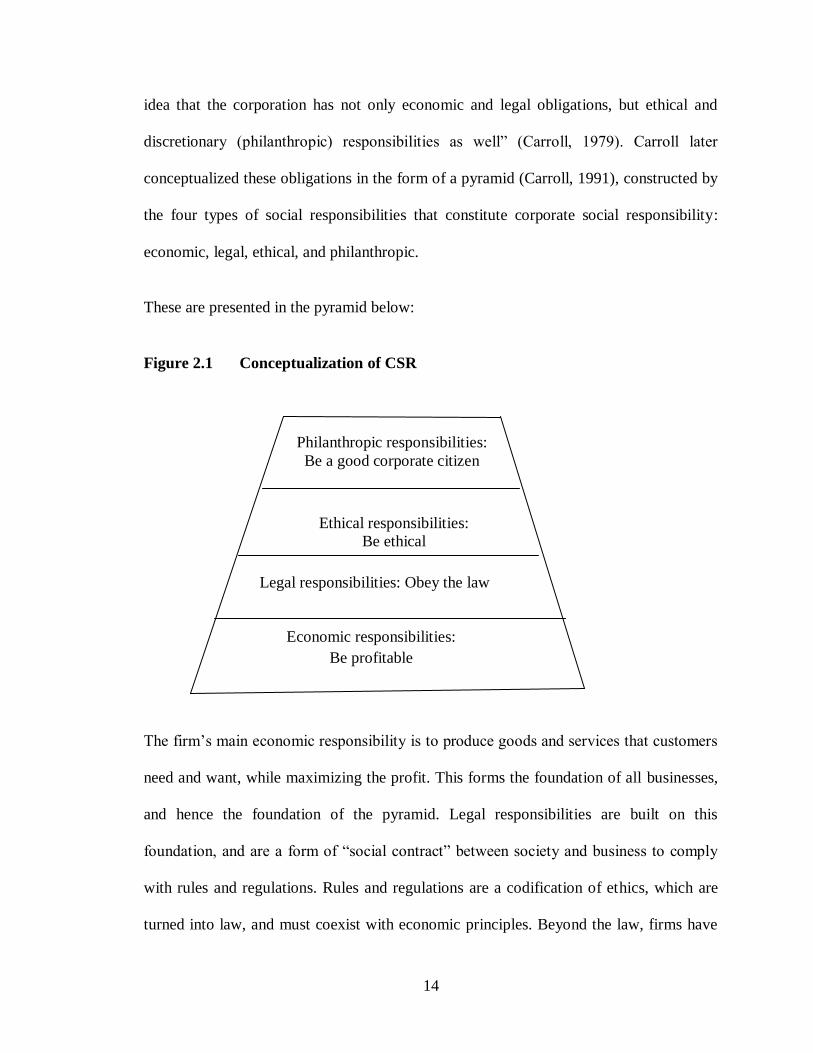

A renowned researcher in the CSR field, Archie B. Carroll, has made an attempt to

reconcile the firm‘s economic orientation with its social orientation, or the shareholder

and stakeholder perspectives described above. In an effort to give a comprehensive

definition of CSR, Carroll created ―a four part conceptualization of CSR, to include the

14

idea that the corporation has not only economic and legal obligations, but ethical and

discretionary (philanthropic) responsibilities as well‖ (Carroll, 1979). Carroll later

conceptualized these obligations in the form of a pyramid (Carroll, 1991), constructed by

the four types of social responsibilities that constitute corporate social responsibility:

economic, legal, ethical, and philanthropic.

These are presented in the pyramid below:

Figure 2.1 Conceptualization of CSR

The firm‘s main economic responsibility is to produce goods and services that customers

need and want, while maximizing the profit. This forms the foundation of all businesses,

and hence the foundation of the pyramid. Legal responsibilities are built on this

foundation, and are a form of ―social contract‖ between society and business to comply

with rules and regulations. Rules and regulations are a codification of ethics, which are

turned into law, and must coexist with economic principles. Beyond the law, firms have

Philanthropic responsibilities:

Be a good corporate citizen

Ethical responsibilities:

Be ethical

Legal responsibilities: Obey the law

Economic responsibilities:

Be profitable

15

certain ethical responsibilities which are standards, norms and expectations that reflect

concern for consumers, employees, and shareholders. At the top of the pyramid are the

philanthropic responsibilities. These are for business leaders to act as good corporate

citizens, by promoting human welfare or goodwill, of which Carroll emphasizes that this

is not expected in an ethical or moral sense.

In conclusion, Carroll argues that the first three tiers of his pyramid address the same

issues that Friedman embraces, i.e. economics, legalities, and ethics. This leaves only the

philanthropic issue for Friedman to reject. Therefore, Carroll‘s CSR Pyramid can be seen

as an attempt to reconcile the two views on CSR, as opined by Friedman and Freeman.

2.1.5 Galbreath’s Four CSR Strategies

Another scholar, Jeremy Galbreath, has described four options of strategies that a firm

might choose in its pursuit of implementing its CSR activities (Galbreath, 2006).

Galbreath is of the view that CSR is ultimately a strategic issue, one that cannot be

separated from a firm‘s overall strategy. He conceptualizes the four strategies, while

setting a benchmark to evaluate their implementation across firms. These are the

strategies:

CSR Strategic option 1: The Shareholder Strategy

Under this strategy, CSR is held as a component of the overall profit motive, in tandem

with Friedman‘s views. The firm works towards maximizing the shareholder returns, has

a short- term vision and measurements and benefits are purely financial in nature.

16

CSR Strategy Option 2: The Altruistic Strategy

In this strategy, Galbreath is of the view that CSR falls on the managers who guide the

firm‘s social responsiveness. The interwoven nature of the relationship between the firm

and the community is acknowledged. The firm is ―doing the right thing‖. The

philanthropy comes from the surplus, and donations are made to the community

endlessly.

CSR Strategy Option 3: The Reciprocal Strategy

Here, CSR is seen as being necessary to the firm‘s survival. The goal is mutual benefits,

societal benefits to the community and economic benefits to the firm. This is more of a

proactive strategy. It focuses on partnerships like cause-related marketing, and is of

medium to long-term range.

CSR Strategic Option 4: The Citizenship Strategy

The Citizenship Strategy is based on Freeman‘s stakeholder view, and the goal of the

strategy is built up of responsibility, transparency, sustainability, and accountability. The

citizenship strategy views the internal and external constituents as stakeholders, and the

firm must address their needs. The time frame for this strategy is long-term, and its

success can be measured by a holistic, triple –bottom line analysis.

17

2.1.6 Criticism of Theories

2.1.6.1 Edward Freeman’s stakeholder Theory

Political philosopher Charles Blattberg has criticized stakeholder theory on the grounds

of assuming that the interests of the various stakeholders can be, at best, compromised or

balanced against each other (Blattberg, 2004). He argues that this is a product of its

emphasis on negotiation as the chief mode of dialogue for dealing with conflicts between

stakeholder interests. He further recommends conversation instead and this leads him to

defend what he calls a 'patriotic' conception of the corporation as an alternative to that

associated with stakeholder theory.

Proponents of stakeholder theory maintain that increasing shareholder wealth is too

myopic a view. According to stakeholder theory, increased CSR makes firms more

attractive to consumers. Therefore, CSR should be undertaken by all firms. However,

Stakeholder theory has some significant disadvantages. For instance, stakeholder theory

runs directly counter to corporate governance. Since shareholders are owners of the firm,

the firm should be operated to maximize their returns. Stakeholder theory transfers the

corporation‘s focus from shareholders to the needs of stakeholders. By implementing

unprofitable CSR programs, firms are denying their fiduciary responsibility to

shareholders (Cheers, 2011).

On the other hand, Stakeholder theory succeeds in becoming famous not only in the

business ethics fields. It is used as one of the frameworks in corporate social

responsibility methods. In fields such as law, management and human resource,

18

stakeholder theory succeeded in challenging the usual analysis frameworks, by

suggesting putting stakeholders' needs at the beginning of any action.

Stakeholder theory provides an inadequate explanation of the firm's behavior within its

environment. Key to theory development is providing an explanatory logic for the

relationships under observation. Beyond the concept of ``affect/affected by'', Freeman's

work does not sufficiently address the dynamics which link the firm to the stake holders

which are identified. While it may be correct to suggest that the firm's survival be linked

to external others as other theorists have done, (e.g. resource dependency and population

ecology theory), the motivating description of this linkage needs to be more clearly

addressed. His categorization involving power and stake or interest lay the groundwork

for a way that this might be achieved.

He does identify processes eliciting stakeholder maps (rational level), environmental

scanning (process level), and exchanges with stakeholders (transactional level). The

motivating force of these processes is not specifically identified. The reader might guess

that Freeman is relying on rationality but this is not adequately explored. Thus, Freeman

may be suggesting that a particular value such as profit and efficiency as suggested by the

economic model explains firm behavior within society, and thus in turn explains its

relationship to stakeholders.

19

2.1.6.2 Milton Friedman’s Shareholder Theory

Friedman believed that ―There is one and only one social responsibility of business – to

use its resources and engage in activities designed to increase its profits‖ (Friedman,

1970)

He famously argued that the „business of business is business‟, reasoning that the sole

responsibility of the organization was its shareholders, providing profits for them. He

acknowledged legal and ethical constraints on business activity, emphasizing that the

organization should not harm society, but he denied that it should assume any wider

social responsibility for its maintenance and improvement.

Friedman's critics have argued that his own reasoning is flawed. His assertions about the

difference between actively seeking to do good (which he regards as being beyond the

duty of business) and merely avoiding doing harm (which he advocates) are unclear,

often illustrating instead that the choice is between doing good, or by default, doing evil

(Somerville, 2006).

One of Friedman's principle arguments was against the idea that the good being done

must be a non-profit exercise, not undertaken for self-interest. If self-interest were the

motivation, Friedman would not oppose it. (Somerville, 2006).

This again suggests misunderstanding of the CSR concept, as self-interest is never

necessarily excluded from these policies. CSR involves establishing all the

responsibilities of the organization to its associated communities and environment, and

consideration of the impact being made by the organization on society (Tench, 2006).

20

This is not necessarily performed to the exclusion of the organization‘s needs; “Doing

Well by Doing Good" is a frequently cited CSR slogan (CSR Europe, 2007), along with

„Enlightened self-interest‟ (Tench, 2006). Both phrases suggest that organizations acting

to further the interests of others (or the interests of the community (ies) which they are

part of), ultimately do so for their own long term self-interest.

In fact, it may be harder to pinpoint policies that never consider self- interest on some

level, although often in the long term. Companies may at times receive little recognition

for their actions and could be seen to be acting altruistically, but the author argues that

they would not deny their involvement should the media express an interest, and certainly

most companies like to receive such coverage for any CSR policies they introduce. If

achieved, this immediately serves to raise their profile, with associated benefits of a

short-term nature.

2.1.6.3 Conclusion on CSR Theories

Focus on CSR engagement has during the last decade increased but there are those who

criticize it, claiming that CSR is not a company issue. Putting focus on CSR will only

take the eye from the real goal; to increase their shareholders wealth, is to confuse the

essence of what corporations should do (Henderson, 2001). Corporation‘s sole

responsibility is to increase profits by legal means, donating to charities, is detrimental to

firms since it may decrease profitability or increase product prices or both (Pinkston &

Carroll 1996 cited in Snider, Hill & Martin, 2003). CSR reduce the focus on profit and

should therefore be a cost outside the scope of legitimate corporate concern. Corporations

21

and managers might not in addition be competent to engage in social issues (Friedman,

1970)

CSR rests upon a false view of the world that CSR is oversimplified, taking for granted

―the idea that the problems and solutions of today have known and agreed solutions‖

(Henderson, 2001). Business should focus on what they are best at, increase shareholders

wealth and create job opportunities. Corporations are not responsible for the world.

Private interest, must be separated from the public, they should have nothing to do with

CSR. It is politicians that should speak for society, not business people (Henderson,

2001).

A scrutiny of all the four approaches above brings us to almost one item.Garriga and

Mele provide a mapping of the CSR territories, which basically encompass the profit

motive, the ethical responsibility as well as the legal responsibility. Friedman on his side

decided to dwell on the economic side of CSR, which is that of profit making. Freeman

on the contrary took a holistic approach and brought in all the other stakeholders.

Galbreath breaks down his views into four strategies, almost fitting them into Carroll‘s

model. Carroll sums them all in the form of a pyramid, famously known as the CSR

pyramid. In conclusion, all the scholars have the same view in mind, in their attempt to

discuss CSR.

22

2.2 Empirical Review

2.2.1 Concept of Corporate Social Responsibility

CSR is rapidly becoming a corporate priority. Franklin (2008) argues that by 2011, the

percentage of executives giving high priority to CSR had increased to 70%. CSR can take

many forms (Vlachos, 2011).There are many definitions of CSR by various scholars

basing on the area they are tackling. This study focuses on external CSR which relates to

customer loyalty.

According to the World Business Council for Sustainable Development,(WBCD), CSR is

regarded as the continuous process of firms acting by ethically spending in the society,

management acting responsibly in its relationships with the various stakeholders who

have a legitimate interest in the business and contributing to economic spending

development while improving the quality of life of the workforce and their families as

well as of the local community and society at large. The company's responsibility is to be

fair and honest, trustworthy and respectful, in dealing with all its constituents (Johnson &

Johnson, 2000).

CSR is viewed as the ability of a company to incorporate its responsibility to society to

develop solutions for economic spending and social problems (Volkswagen, 2000). It is

also regarded as the impact of assessing the various contributions of the business to the

society and ensuring that there‘s a balance between the economic spending ,

environmental and social aspects (Moody-Stuart, 1999).

23

Burke (1996) stated that CSR is the positive outcome a company provides while it

manages its normal business trade. CSR is said to provide a long term commitment to

social contribution be it towards the society or for the development of a particular

company's workers. In doing so, a company as a whole, can organize its business ethical

spending in order to directly contribute to the betterment of the society as a whole (Soni,

2009; Verhoeff, 2009; Verma, 2010).

CSR was viewed as a social obligation first by (Carroll, 1979, in Maignan and Ferrell,

2000). Who developed one of the best-known CSR pyramid. This model views the

various compositions encompassing the social responsibilities of the business which

include; economic spending, legal spending, ethical spending and philanthropic

responsibilities. Businesses are creations which are driven by profit motive, thus the main

reasons why firms are in a constant struggle of maintaining customers and creating new

ones by engaging in various responsibilities. Legal spending responsibility involves

businesses complying with federal, state and local government laws and regulations by

providing a safe product for consumption to customers, firms complying with the tax

department, using resources in the best interest of the society and enhancing fair

competition. Ethical spending responsibilities are regarded as those standards, norms and

expectations that reflect a concern for what consumers, employees, shareholders and the

community regard as fair, just and respectful of stakeholders‘ moral rights. Philanthropic

responsibility was viewed as the expectation that businesses will be good corporate

citizens, by actively engaging in programs to promote human welfare and goodwill

(Carroll, 1991).

24

This study will be employing the various variables adopted from the Carroll‘s model to

assess their effects on bank performance. These variables are examined below;

2.2.2 Link between CSR and Bank Performance

Researchers have shown that CSR-related reactions to a company are determined not

only by its actions in this domain, but also by those of its stakeholder groups (for instance

customers ), which are typically beyond the company's control (Bhattacharya &Sen,

2003; Brown, Dacin, Pratt, &Whetten, 2006 as cited in Pramanik et al, 2007,). CSR

moves beyond the often rare field of controlled empirical contexts to paint more

externally valid picture of the forces determining consumer reactions to CSR

spending(Pramanik et al, 2007). In other words, in as much as the competitive context

impacts the marketing mix, a company, in formulating its CSR strategy, needs to

understand how consumers perceive and react to its CSR actions not in isolation but in

the context of different CSR actions, if any, taken by its competitors. (Bhattacharya

&Sen, 2004).Onlaor and Rotchanakitumnuai (2010) argue that organizations should

realize and invest in corporate social responsibility schemes in order to enhance their

relationships with customers by initiating robust corporate strategy particularly in social

concerns such as setting reasonable price, improving their services, developing

innovation, and implementing privacy policy. Moreover, organizations should

communicate CSR ways to the general public. Several marketing studies have reported

that CSR behaviors can positively affect consumer attitudes towards the firm and its

offerings (Bhattacharya and Sen, 2003; Folkes and Kamins, 1999; Lichtenstein et al.,

2004; Luo and Bhattacharya, 2006).

25

2.2.3 Economic Spending and Bank Performance

Economic spending component is an important responsibility to stakeholders for example

customers, societies, employees (Ramasamy and Yeung, 2009). This is fundamental for

business growth (Shahin and Zairi, 2007). Previous studies have revealed that economic

spending responsibilities are done through producing quality products and services for

customers with reasonable price and providing good jobs for employees (for example,

Lindgreenet al, 2009, Lantos,2002, Swaen and Chumptaz, 2008).

The economic spending aspects of CSR consist of understanding the economic spending

impacts of the company‘s operations. Economic spending issues have long been

overlooked in the discussion on corporate social responsibility. For many years, the

aspect has been widely assumed to be well managed. It is however, the least understood

by many of those shaping the corporate and public policy agendas, and underrepresented

by the corporate responsibility agenda.

A company is, first of all, an economic setup with making profits as its goal and it has the

status of legal entity with independent economic interests. When looking at the social

responsibilities that a company should take, those scholars in the economic circle and

who are in favor of this opinion believe that corporate objectives lie in creating good

conditions of existence and sound development prospect for a company. The managers of

a company should become concerned with the optimal long-term capital gains of the

company in order to achieve corporate goals; if to achieve the optimal long-term profits,

a company will have to take up social responsibilities as well as the social cost thus

incurred. When studying on the relationship between social responsibilities and economic

26

performance and efficiency, the focus is given on the research of the relationship between

social responsibilities and economic performance and efficiency during the long-term

development process of a company so that a positive correlation of the two can be

derived.

Economic spending dimension considers the direct and indirect economic spending

impacts that the organization‘s operations have on the surrounding community and on the

company‘s stakeholders. That is what makes up corporate economic spending

responsibility (Uddin, 2008).Economic spending responsibility activities fuel the local

service industry, government programs and the community activities. This multiplier

effect becomes all the more important if the company is one of the largest employers in

the communities.

From among the economic spending benefits the company will have, some authors name

benefits of financial nature, increased company visibility, preference of consumers for the

products of socially responsible companies, increased internal cohesion of the team

involved in developing the project within the respective company, etc.(Coord,2007).

From an economic spending point of view ―CSR adds value because it allows companies

to reflect the needs and concerns of their various stakeholder groups (William, 2006)

The main concern of a business is to make profits. Traditionally this was the main

concern of a given business organization. The owners of a concern are also interested in

getting value for their investments. The profit motive acts as the basis for expanding the

firms‘ activities, remunerating the workforce and also providing other services to both the

employee and the customers (Saleemi, 2010). A firm which has high profits i.e. favorable

27

economic spending condition is more likely to engage in social activities. The economic

spending perspective of the firm is the main determinant whether or not a business should

undertake CSR, and the forms that should be adopted. According to the neo classical

view, the firm is responsible for provision of employment and payment of taxes, thus

forming the basis of acting in a socially responsible manner.

In periods of high inflations the profits of the firm are generally low thus the firms may

be less likely to act in socially responsible manner since consumer confidence is weak

and productivity growth is low. In a stable economic spending environment coupled with

stability in profits firms are more likely to engage in CSR. Also, in a stiff competing

environment firms are less likely to act in a socially responsible manner since more

resources are channeled to wasteful competition through advertising. On the other hand

stiff competition may be of great benefit to the consumer since they may obtain a product

and/or a service at a cheaper price. For example stiff competition involving the price war

between the various mobile providers in Kenya early this year caused the mobile calling

rates to fall. This kind of competition may at times be viewed as an unethical spending

way of some firms trying to get customers.

2.2.4 Legal Spending and Bank Performance

Legal spending component refers to a company complying with the laws and regulations

within which they operate (Swaen and Chumptaz, 2008). The most widely accepted

position on the legal spending purpose of the corporation—known as shareholder

primacy (Springer 1999; Fisch 2006; Ehrlich 2005)—was articulated by Milton Friedman

in 1970.He stated that in a free-enterprise, private-property system, a corporate executive

28

is an employee of the owners of the business. He has direct responsibility to his

employers. That responsibility is to conduct the business in accordance with their desires,

which generally will be to make as much money as possible while conforming to the

basic rules of the society, both those embodied in law and those embodied in ethical

spending custom (Friedman 1970 as cited in Reinhardt.et al, 2008)

The criterion of regulating the various contradictions of relationships of interests is to

prioritize efficiency while giving consideration to justice, which means when efficiency

contradicts with justice, efficiency overtakes as the dominating factor

As far as civil law is concerned, a company, as a legal entity, is the principal of civil law.

The principle of public order and good conducts is one of the most basic principles of

modern civil law, which requires that the principals of civil cases shall not violate the

public orders and good conducts when engaged in civil activities, which also requires

companies to undertake non-performance liabilities on any behaviors prohibited by law

when engaged in civil activities. As far as companies are concerned, they should also

make their shift from the self-centered business profits to the promotion of social benefits

as a whole and take up certain social responsibilities while not sacrificing self-profit-

making opportunities.

Tax laws acts as a motivating tool toward a firm acting in a socially responsible manner.

Deductions allowable from the taxable income on philanthropic responsibilities

encourage many firms to engage in CSR since that income will not attract any tax.

Researchers have tried to investigate the effect of tax law deductions on corporate

philanthropy. Tax laws acts as a determinant on how firms are to engage CSR (Campbell,

29

2004). Therefore, state regulation in form of taxes affects the extent to which

corporations behave in socially responsible ways.

If companies seek ruthlessly high efficiency and high profitability and therefore damage

the justice and fair rules of the society, all the individuals in the society will ultimately

have to pay a heavy price (Saleemi,2010).

2.2.5 Discretional Spending and Bank Performance

Firms ‗discretionary spending responsibilities entail voluntary social involvement,

including activities such as philanthropic contributions. These activities are

purelyvoluntary, guided only by business desire to engage in social activities that are not

mandated, not required by law and not generally expected of business. They include such

things as providing a day care centre for working mothers and providing charitable

donations (Maignan and Ferrell, 2000).

The competing environment has necessitated the company to not only continue in

provision of better products but to go an extra mile in acting in a philanthropic manner in

order to woo customers. This entails building of schools, hospitals, engaging in societal

projects and engagement in sporting activities etc. These acts of contributing more than

the legal spending expectation to the society has increased transactional effect by

customers continually in demand for the products and/or services of the company

(Lichtenstein et al. 2004). Philanthropic contributions are associated with creating

psychological perceptions in the mind of the customers by viewing the company in a

30

positive manner (Sen&Bhattacharya, 2001). This act of the company makes customers to

be attached psychologically with the company and its products and/or services.

For managers to act responsibly, they may have created that culture through involvement

in some culture. This culture involves the company/ its managers joining a given

associations which prompts its members to act in a socially responsible manner by

creating proper set of incentives for such behavior (Galaskiewicz ,1991). When managers

or corporations belonging to professional associations are dedicated to charitable giving,

it will encourage those corporations/managers to engage in philanthropy giving.

Membership in such organizations act as a driving force for managers or corporations to

act in a more ethical spending manner. The seminars provided by such memberships

instills in members the virtues and benefits of corporate giving. This is strengthened by

the peer pressure accruing from how others are contributing to the society in other

localities.

2.2.6 Ethical Spending and Bank Performance

Ethical spending responsibility goes beyond legal spending requirements in terms of

standards, norms, and expectations which in turn reflect a concern for doing what is right,

just, fair and to avoid harms to others (Shahin and Zairi, 2007). Vogel (2008) argued that

consumers are more concerned about ethical spending products which are a niche market

where all goods and services continue to be purchased on the basis of price, convenience

and quality. However, even in the niche market for ethical spending products, consumers

may find it difficult to decide which firms to support (Cheers, 2011).

31

Society is an organic whole. Companies (enterprises) are components making up the

organic whole. To look at the relationship of society and companies, companies cannot

survive in isolation from a society. Social development relies on the growth of

companies. This interdependency decides that society and companies interplay with each

other, and at the same time they are restricted by their respective development rules; what

is more, companies, as a social setup, have their independent interests; social benefits is

of public welfares. The development objectives of companies lie in maximizing their

corporate profits, whereas social development objectives are for increment of common

benefits of its members in a society. Also, companies, as one tier of a society, require that

corporate interests are put under constraint of social benefits and company‘s objectives

should comply with those of social benefits. Thus, it is made known quite obviously that

companies should undertake their respective social responsibilities.

Ethical spending duties require that businesses abide by moral rules which define

appropriate behaviours in society. They entail acting in a moral manner, doing what is

right, just and fair; respecting people‘s moral rights; and avoiding harm or social injury as

well as preventing harm caused by others. Ethical spending duties embrace those

activities and practices that are expected or prohibited by society even though they are

not codified into law (Carroll, 1991).

Williams (2006) argues that throughout time, corporations have often broken the rules of

ethical spending conduct in business, which led to mistrust in their activity. A CSR

approach may lead to an improvement of company‘s relation with interested groups, to a

greater transparency and to higher ethical spending standards;

32

Carrigan and Attalla (2001) argue that although consumers may express a desire to

support ethical spending companies and punish unethical spending firms, their actual

purchase behavior often remains unaffected by ethical spending concerns

2.3 Critical Review

Though much literature does not link CSR with bank performance directly, they have

provided considerable knowledge to the various responsibilities a company has to the

various stakeholders. The economic spending , ethical spending , philanthropic and legal

spending variables used on the Carroll model which tries to explain the various

responsibilities a firm has to its various stakeholders are the main concern of this study.

Theories used in this study assist to analysis the various conflicting interests among

stakeholders.

If managers understand the various contributions of CSR, they will engage more in it so

as to gain strategic advantage over their rivals. It is also essential for firms to treat its

employees in a better manner since they are also customers of the company. A company

which engages in CSR creates a relational behavior that is associated to go beyond the

purchase of a product (Lichtenstein et al., 2004) to consumer loyalty to the company‘s

existing product, willingness of the consumer to buy new products that the firm might

offer, favorable word of mouth and resilience in the face of negative information about

the company, such as in a product-harm crisis. When the firm is perceived to undertake

CSR in a proper manner by customers it will strengthen the brand relationship leading to

better bank performance.

33

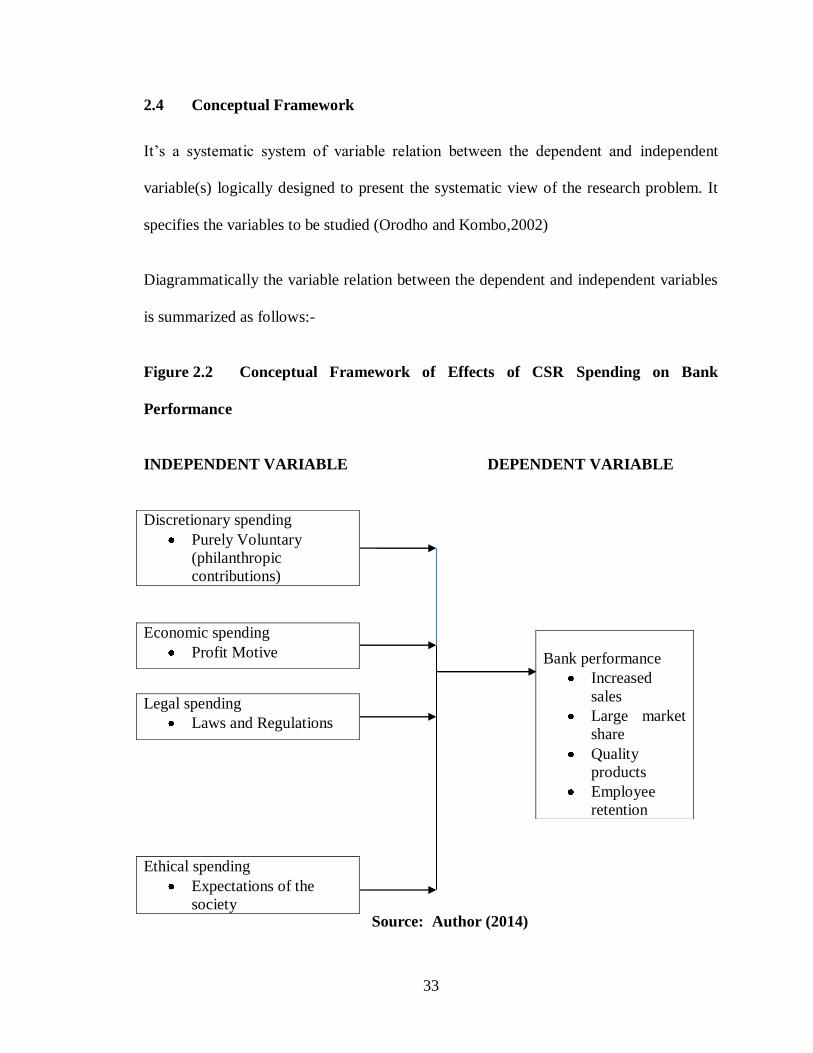

2.4 Conceptual Framework

It‘s a systematic system of variable relation between the dependent and independent

variable(s) logically designed to present the systematic view of the research problem. It

specifies the variables to be studied (Orodho and Kombo,2002)

Diagrammatically the variable relation between the dependent and independent variables

is summarized as follows:-

Figure 2.2 Conceptual Framework of Effects of CSR Spending on Bank

Performance

INDEPENDENT VARIABLE DEPENDENT VARIABLE

Source: Author (2014)

Discretionary spending

Purely Voluntary

(philanthropic

contributions)

Economic spending

Profit Motive

Bank performance

Increased

sales

Large market

share

Quality

products

Employee

retention

Legal spending

Laws and Regulations

Ethical spending

Expectations of the

society

34

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Research Design

Research design represents the master plan that specifies the methods and procedures for

collecting and analyzing data in order to achieve research objectives. The study adopted

explanatory research design.Explanatory research focuses on ‗why‘ questions. In

answering the 'why' questions, the study was involved in developing causal explanations.

Causal explanations argue that phenomenon Y (For example Bank performance) is

affected by factor X (For example CSR economic spending initiative). An explanatory

study goes beyond description and attempts to explain the reasons for the phenomena that

the descriptive study only observed (Cooper and Schindler, 2003) by seeking to establish

a causal relationship between variables (Saunders, M., Lewis, P. and Thornhill, A, 2007).

This design was chosen because it applied closely to the research objectives of the study,

and hence proved practical in testing the study hypothesis.

The method can be used when collecting information about people‘s attitudes, opinions,

habits or any variety of education or social issues (Orodho and Kombo, 2002).This

approach is thus appropriate for this kind of study in that data generation techniques

majorly involved the use of questionnaires.

35

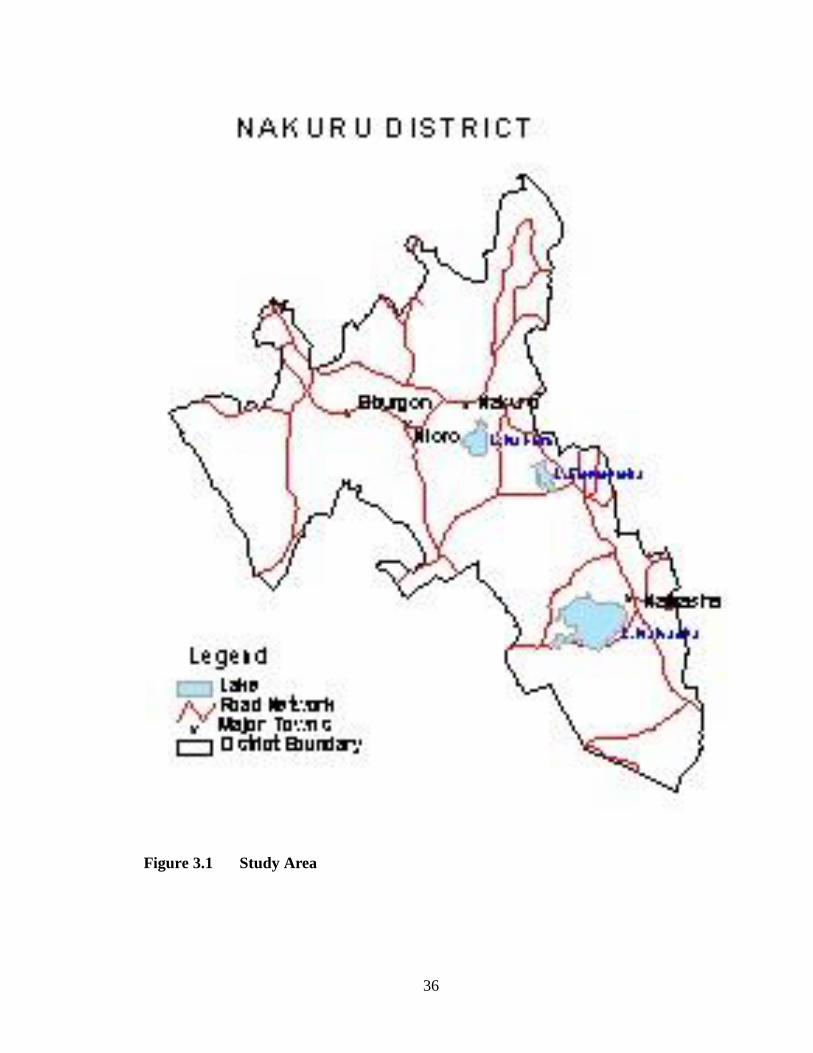

3.2 Study Area

The study was carried out in Nakuru County in Kenya. The surface area of Nakuru

County is estimated to be 1320 square Kilometers. The area of the study was chosen

since there many banks are being established and are offering lending services to

business people. The main economic activity of the residents is that of engaging in varied

types of businesses. There are also many companies in Nakuru, hence large business

transactions go on a daily basis (Kenya National Bureau of Statistics, 2009). There are

currently 12 banks within this area.

36

Figure 3.1 Study Area

37

3.3 Target Population

The total population was 12 banks within Nakuru County namely; KCB, Barclays,

Equity, Transnational, National, CFC Stanbic, Commercial Bank of Africa, Diamond

Trust bank, Imperial bank, Bank of Baroda, Family Bank and Cooperative Bank.From the

12 banks‘ database, there were a total 404 employees.

Table 3.1 Target Population

Banks Names No. Of Employees

KCB, 38

Barclays 42

Equity, 56

Transnational, 29

National, 30

CFC Stanbic, 32

Commercial Bank of Africa, 28

Diamond Trust bank, 27

Imperial bank, 28

Bank of Baroda, 25

Family Bank 27

Cooperative Bank 42

Total 404

Source: Bank Database, (2014)

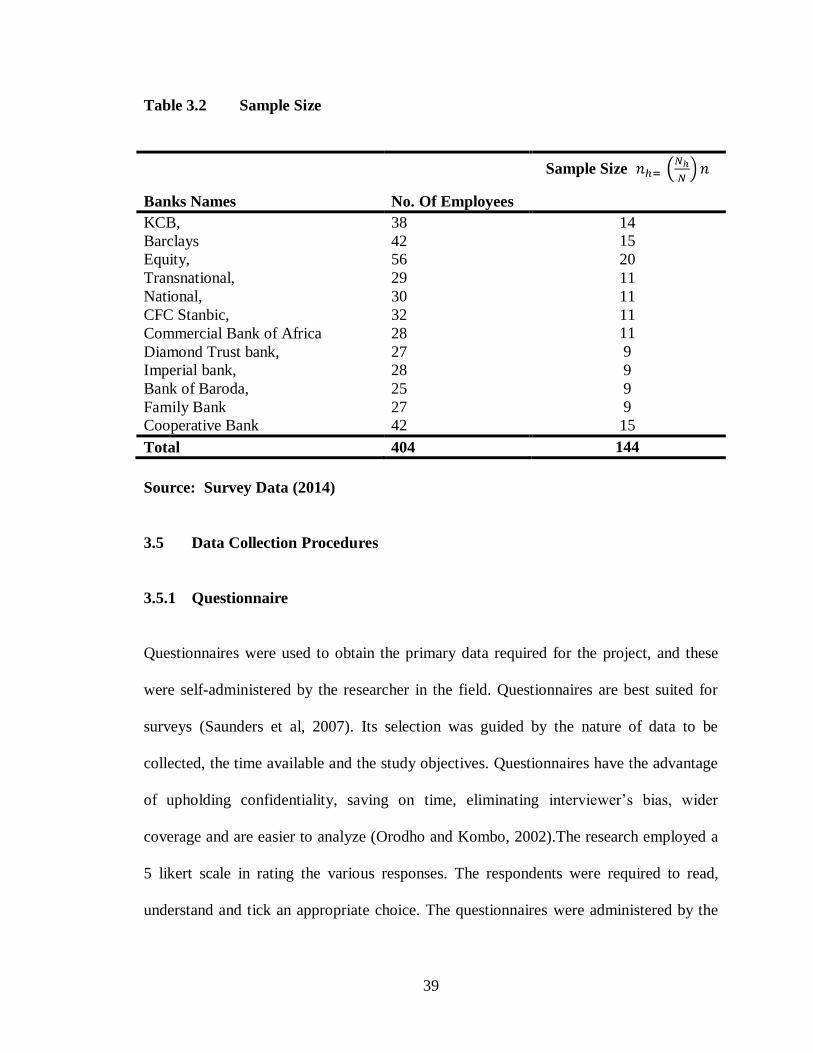

3.4 Sample size and Sampling Procedures

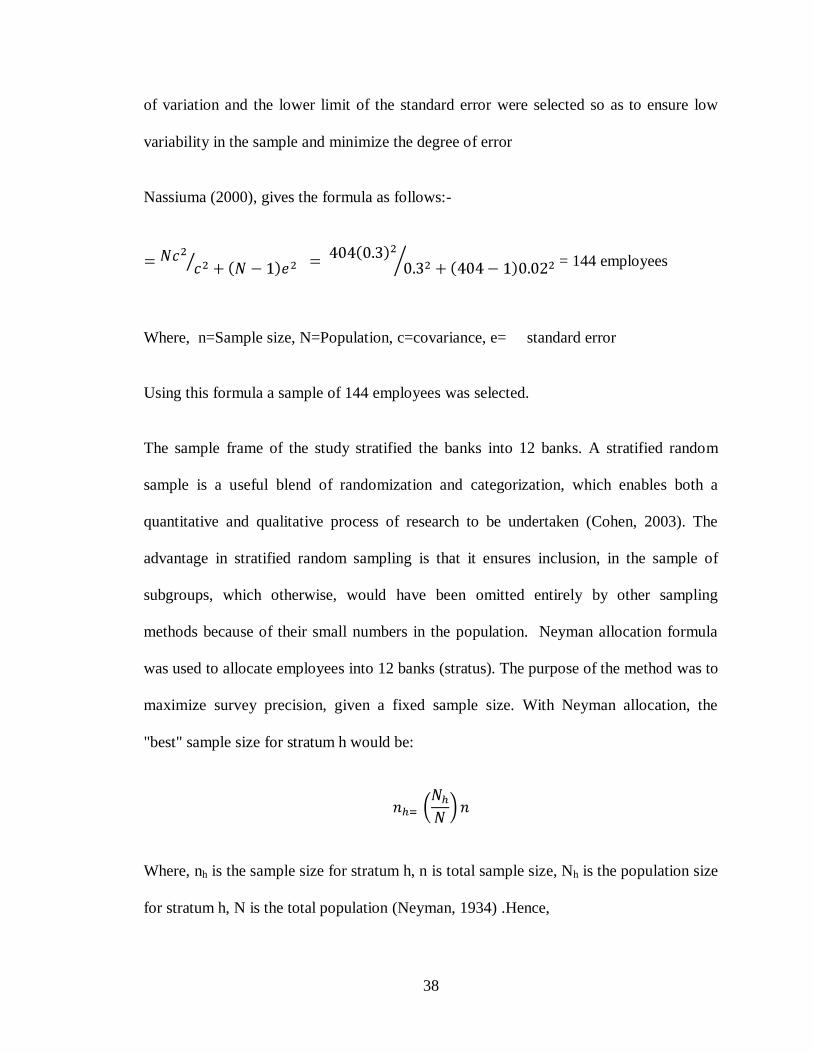

The sample was obtained using coefficient of variation. Nassiuma, (2000) asserts that in

most surveys, a coefficient of variation in the range of 21%≤ c≤ 30% and a standard error

in the range of 2%≤ e ≤ 5% is usually acceptable. Therefore, a coefficient variation of

30% and a standard error of 2% were used respectively. The higher limit for coefficient

38

of variation and the lower limit of the standard error were selected so as to ensure low

variability in the sample and minimize the degree of error

Nassiuma (2000), gives the formula as follows:-

= 144 employees

Where, n=Sample size, N=Population, c=covariance, e= standard error

Using this formula a sample of 144 employees was selected.

The sample frame of the study stratified the banks into 12 banks. A stratified random

sample is a useful blend of randomization and categorization, which enables both a

quantitative and qualitative process of research to be undertaken (Cohen, 2003). The

advantage in stratified random sampling is that it ensures inclusion, in the sample of

subgroups, which otherwise, would have been omitted entirely by other sampling

methods because of their small numbers in the population. Neyman allocation formula

was used to allocate employees into 12 banks (stratus). The purpose of the method was to

maximize survey precision, given a fixed sample size. With Neyman allocation, the

"best" sample size for stratum h would be:

Where, nh is the sample size for stratum h, n is total sample size, Nh is the population size

for stratum h, N is the total population (Neyman, 1934) .Hence,

39

Table 3.2 Sample Size

Banks Names No. Of Employees

Sample Size

KCB, 38 14

Barclays 42 15

Equity, 56 20

Transnational, 29 11

National, 30 11

CFC Stanbic, 32 11

Commercial Bank of Africa 28 11

Diamond Trust bank, 27 9

Imperial bank, 28 9

Bank of Baroda, 25 9

Family Bank 27 9

Cooperative Bank 42 15

Total 404 144

Source: Survey Data (2014)

3.5 Data Collection Procedures

3.5.1 Questionnaire

Questionnaires were used to obtain the primary data required for the project, and these

were self-administered by the researcher in the field. Questionnaires are best suited for

surveys (Saunders et al, 2007). Its selection was guided by the nature of data to be

collected, the time available and the study objectives. Questionnaires have the advantage

of upholding confidentiality, saving on time, eliminating interviewer‘s bias, wider

coverage and are easier to analyze (Orodho and Kombo, 2002).The research employed a

5 likert scale in rating the various responses. The respondents were required to read,

understand and tick an appropriate choice. The questionnaires were administered by the

40

researcher so as to obtain more information and also obtain clarity of information

obtained from the respondents.

3.5.2 Documentary Analysis

Secondary data was obtained from textbooks related to the study, magazines, journals,

presented conferences and previous reports as well as the internet. The primary data on

the other hand was obtained from questionnaires adopted for the study.

3.6 Instrumentation

3.6.1 Validity of the Instruments

According to Panton (2000), validity is the quality attributed to proposition or measures

of the degree to which they conform to establish the truth.The purpose of construct

validity is to show that the items measure and are correlated with what they purport to

measure, and that the items do not correlate with other constructs.

For this study, validity was achieved by conducting a pilot test on 5 individuals in the

population, but did not form part of the study sample. Their feedback was used to

determine: whether the questions measured what they were supposed to measure, whether

the wording was flowing, if all the questions were interpreted in the same way by

respondents and what overall response was provoked by the questions.

Necessary amendments on the questions were then made on receiving the responses and

an evaluation of the revised questions was done to ensure their clarity and check on their

balance.

41

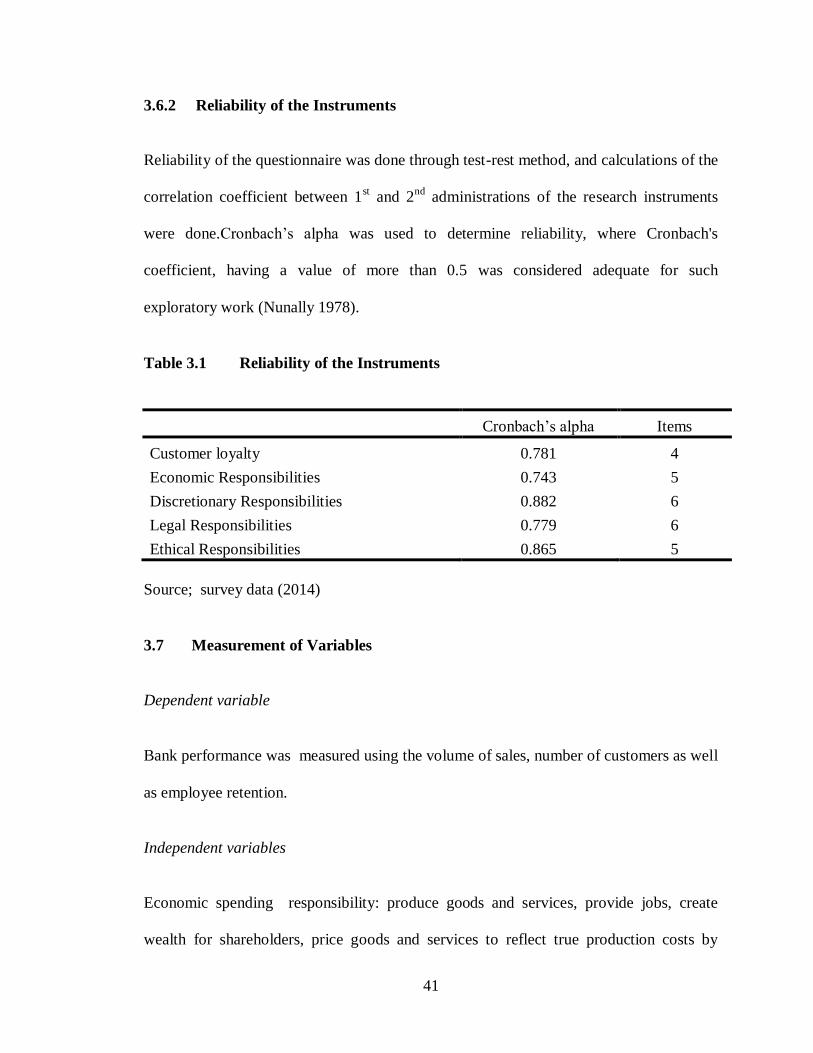

3.6.2 Reliability of the Instruments

Reliability of the questionnaire was done through test-rest method, and calculations of the

correlation coefficient between 1st and 2

nd administrations of the research instruments

were done.Cronbach‘s alpha was used to determine reliability, where Cronbach's

coefficient, having a value of more than 0.5 was considered adequate for such

exploratory work (Nunally 1978).

Table 3.1 Reliability of the Instruments

Cronbach‘s alpha Items

Customer loyalty 0.781 4

Economic Responsibilities 0.743 5

Discretionary Responsibilities 0.882 6

Legal Responsibilities 0.779 6

Ethical Responsibilities 0.865 5

Source; survey data (2014)

3.7 Measurement of Variables

Dependent variable

Bank performance was measured using the volume of sales, number of customers as well

as employee retention.

Independent variables

Economic spending responsibility: produce goods and services, provide jobs, create

wealth for shareholders, price goods and services to reflect true production costs by

42