A SUMMER TRAINING REPORT ON MARKETING IN GENERAL INSURANCE OF ICICI LOMBARD SUBMITTED IN PARTIAL...

113

A SUMMER TRAINING REPORT ON MARKETING IN GENERAL INSURANCE OF ICICI LOMBARD SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENT OF BACHELOR OF BUSINESS ADMINISTRATION (BBA) Under Supervision of: Submitted by: Mr. Ankur Bhupender Sales Manager Roll No. HCL SESSION 2008-2011

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of A SUMMER TRAINING REPORT ON MARKETING IN GENERAL INSURANCE OF ICICI LOMBARD SUBMITTED IN PARTIAL...

A SUMMER TRAINING REPORT

ON

MARKETING IN GENERALINSURANCE OF ICICI

LOMBARD

SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENT OFBACHELOR OF BUSINESS ADMINISTRATION (BBA)

Under Supervision of: Submitted by:

Mr. Ankur Bhupender

Sales Manager Roll No.

HCL

SESSION 2008-2011

GURU JAMBHESHWAR UNIVERSITY OFSCIENCE & TECHNOLOGY

HISAR

ACKNOWLEDGEMENT

I take this opportunity to thank all the people who helped

me with valuable inputs, guidance and suggestions during my

tenure of project, without which this report would not have

taken its final shape.

I thank Mr. Ankur, Manager of ICICI Lombard who spared his

valuable time and gave me opportunity to work and undertake

this project and guided me through out this project.

This acknowledgement would be incomplete without thanking

Mr. Sales Consultant & Mr. Rajesh Singh, Senior Sales

Executive, ICICI Pvt. Ltd. who helped me in all possible

manner at all possible time during the course of this

project and all the above I would like to give my heartiest

regards & my Institute faculty & my internal guide whose

timely guidance and support at crucial junctures made the

undertaking of this project an enriching learning

experience. I would also like to thank all the people who

participated in this project directly or indirectly. Last

but not least I would like to thank all my friends who have

been a great help in this project with their innovative

ideas and suggestions

BHUPENDER

CONTENTS

TOPIC PAGE NO.

1. COMPANY PROFILE

2. INTRODUCTION

3. OBJECTIVE OF THE STUDY

4. RESEARCH METHODOLOGY

5. ANALYSIS AND INTERPRETATION OF DATA

6. FINDINGS / CONCLUSIONS AND SUGGESTIONS

BIBLIOGRAPHY

EXECUTIVE SUMMARY

Insurance is one of the fastest growing industry. Insurance

is basically divided into two heads one is Life Insurance

and other is General Insurance. In the beginning there was

one insurer that was LIC, but after 2000 insurance industry

was open for the private players. As of now there are 12

private and 1 public insurance company that is LIC.

This Project is prepared with the aim that the person who

read this project will come to know about the different

strategies of ICICI Lombard which is # 1 Private insurance

company and also help the consumer to choose the right

policies for themselves.

The basic objective of the study is to get adequate

knowledge of regarding the entire process of recruitment and

buying behavior of customers who are dealing with private

concern like ICICI Lombard.

The conclusion drawn and recommendation are being presented

towards the end of project.

With excessive competition prevailing in the market, it

becomes important on the part of organization to keep itself

updated on the changing trends in the market regarding to

the need of people.

CHAPTER-1

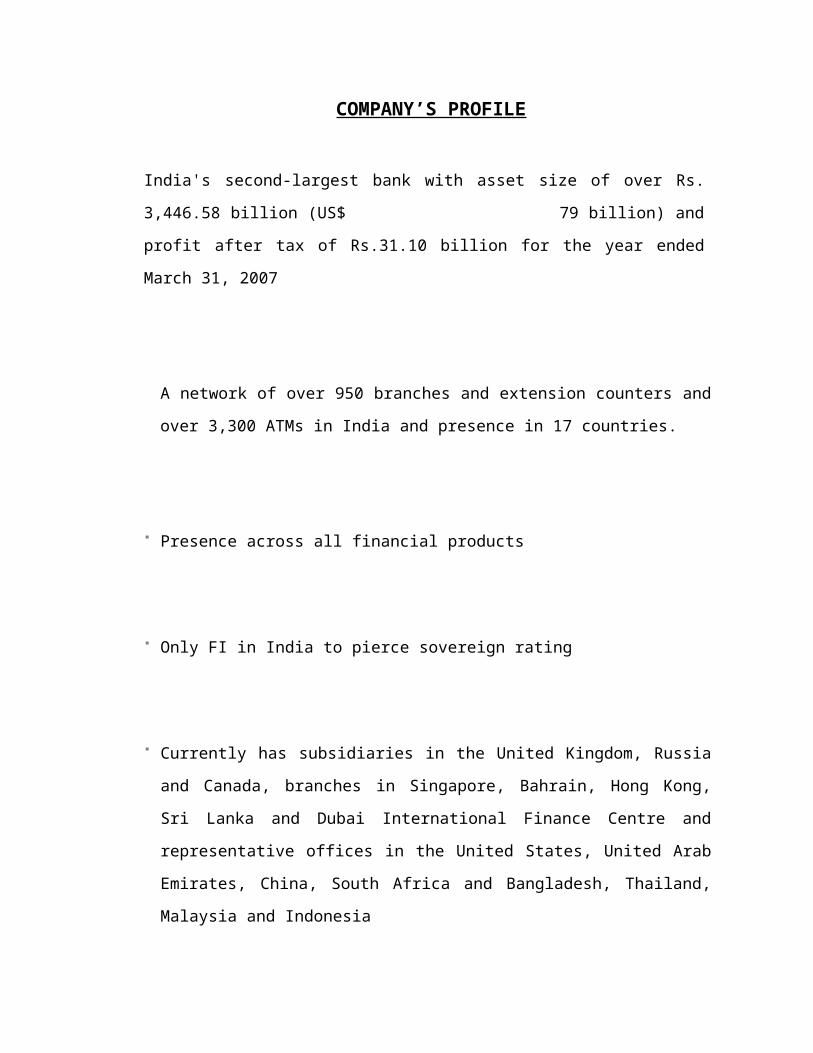

COMPANY’S PROFILE

COMPANY’S PROFILE

India's second-largest bank with asset size of over Rs.

3,446.58 billion (US$ 79 billion) and

profit after tax of Rs.31.10 billion for the year ended

March 31, 2007

A network of over 950 branches and extension counters and

over 3,300 ATMs in India and presence in 17 countries.

Presence across all financial products

Only FI in India to pierce sovereign rating

Currently has subsidiaries in the United Kingdom, Russia

and Canada, branches in Singapore, Bahrain, Hong Kong,

Sri Lanka and Dubai International Finance Centre and

representative offices in the United States, United Arab

Emirates, China, South Africa and Bangladesh, Thailand,

Malaysia and Indonesia

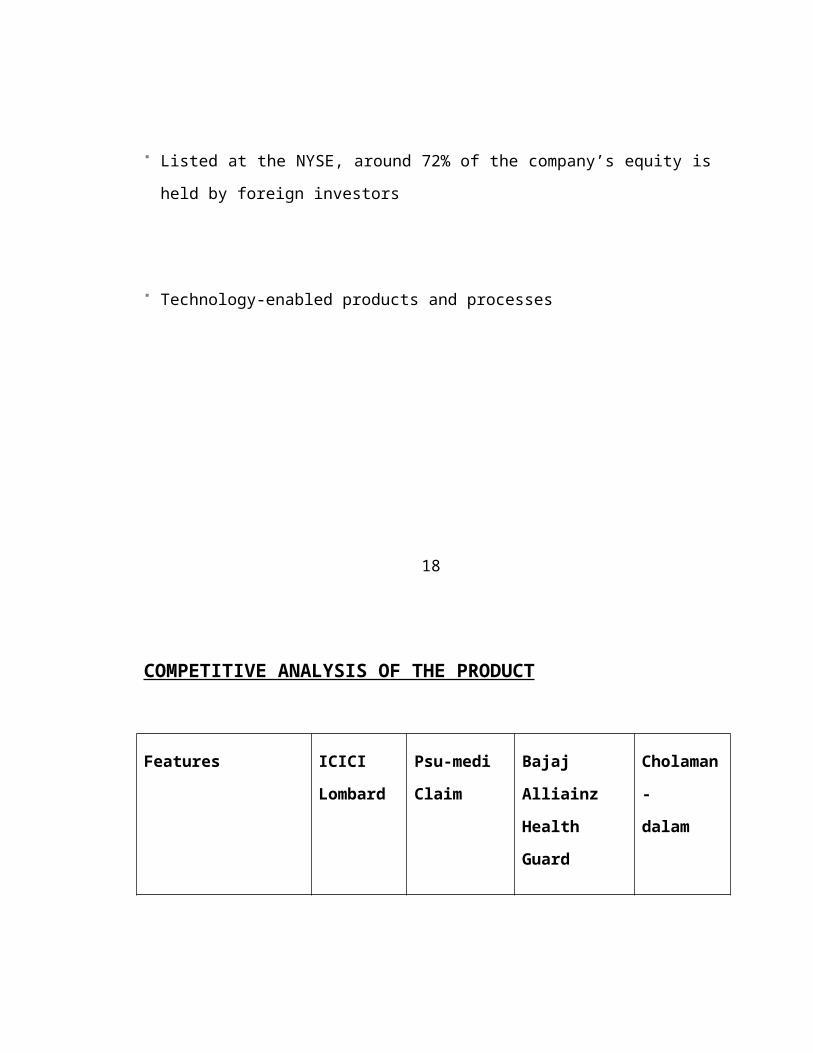

Listed at the NYSE, around 72% of the company’s equity is

held by foreign investors

Technology-enabled products and processes

18

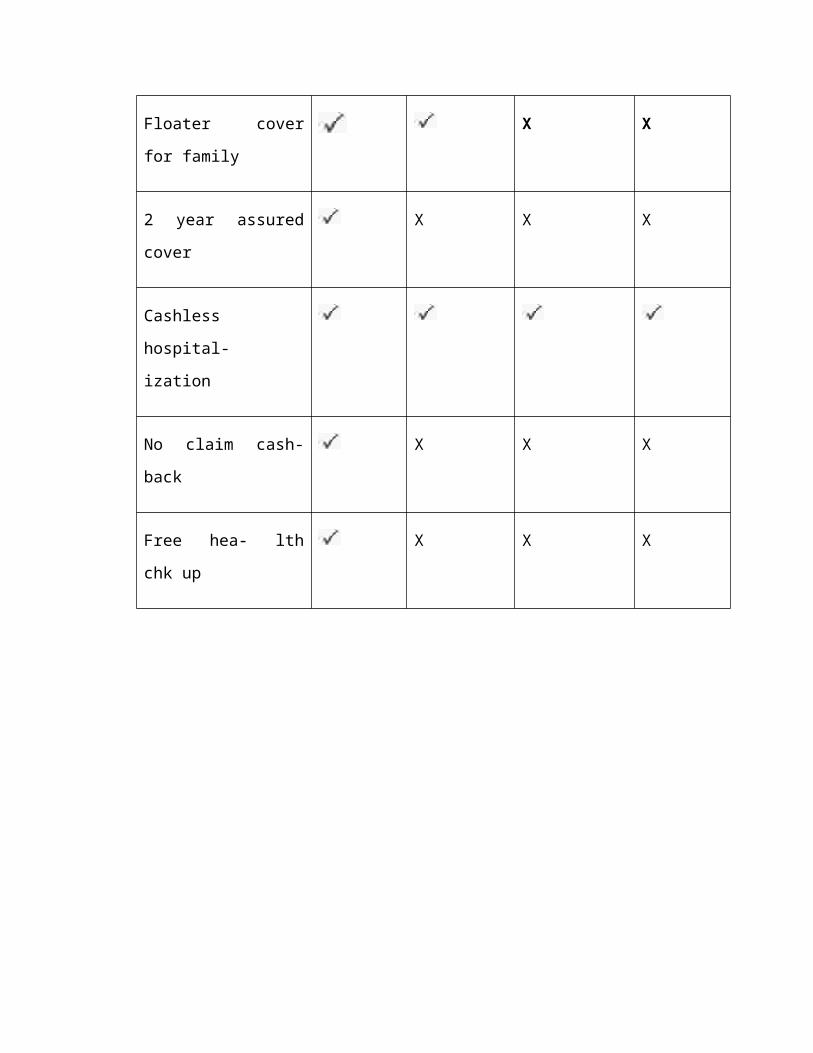

COMPETITIVE ANALYSIS OF THE PRODUCT

Features ICICI

Lombard

Psu-medi

Claim

Bajaj

Alliainz

Health

Guard

Cholaman

-

dalam

Floater cover

for family

X X

2 year assured

cover

X X X

Cashless

hospital-

ization

No claim cash-

back

X X X

Free hea- lth

chk up

X X X

19

SWOT ANALYSIS OF ICICI LOMBARD

ICICI Lombard is one of the most powerful, world class Life

Insurance Co., gaining appreciation for their strong work

ethics, excellent performance, professionalism and team work

which led them to progress in today’s challenging

environment . Though with its excellence performance and

every efforts has been made to present the most authentic

and truly representative finding, but some uncontrollable

factors do affect the performance and thus bring about some

deviation and hurdles in progress. So with its strengths and

good quality, the company is having some weaknesses, and

threats and opportunities its SWOT analysis is as below:

Strengths

1. ICICI Lombard is the largest private player in the

insurance industry in India Excellent services.

2. Customization of Product as per customer’s needs

3. Brand Image

4. Business Experience.

5. Strong financial Base.

6. Innovative products, Technology, Organization culture

and climate.

7. The company has a large network of branches, which is

helpful to customer for the payment.

20

Weakness

1. Target only higher income group whereas other companies

are trying to catch middle – lower level people.

2. Lot of competitors are in the market offer same product

by the title difference in the premium and offering.

3. Higher premium as compared to the other companies.

4. Clients face problems to get insured due to large

number of formalities.

Opportunities

Huge market is literally untapped. Out of 320 million

insurable markets only 20% of the population is insured. In

a conservative society of India where people are more

inclined towards risk free investment such as bank Fad’s and

saving rather than equity and high risk investments

insurance offers the best of both worlds – the security with

high returns. So there exist high potential for insurance

company like ICICI Lombard.

In the pension field where people want good life after their

retirement. Indian people are more emotional towards their

child that’s why children plans are selling like hot cakes.

Health insurance and pension schemes, an estimated market

potential of approximately $15 billion.

21

Threats

1. Week perception of private players in the minds of

Indian people due to frequent financial scams.

2. Large number of insurance players.

3. Existing wrong business practices of companies like LIC

first premium is paid by their agents where –as IRDA

suggests that even forms to be filled by the clients

themselves.

4. Entry of many other private companies with equally

strong experience and financial strength of foreign

partners making the competition difficult and

saturating the urban markets.

5. LIC has woken up from sleep and is following

competitive strategies. Its huge surplus in life fund

gives a capability to lodge price war.

6. Current government policies do not encourage gross

domestic saving. If the tax liability of the service

class rises, the customer will have little money to

invest.

7. For the insurance sector government set the authority

that is IRDA (insurance regulatory and development

authority) which is undertaken to track record of all

the companies and change rule day by day more rigid

which is very difficult for the companies.

22

1What is General Insurance?

Insurance other than ‘Life Insurance’ falls under thecategory of General Insurance. General Insurance comprisesof insurance of property against fire, burglary etc,personal insurance such as Accident and Health Insurance,and liability insurance which covers legal liabilities.There are also other covers such as Errors and Omissionsinsurance for professionals, credit insurance etc.

Non-life insurance companies have products that coverproperty against Fire and allied perils, flood storm andinundation, earthquake and so on. There are products thatcover property against burglary, theft etc. The non-lifecompanies also offer policies covering machinery againstbreakdown, there are policies that cover the hull of shipsand so on. A Marine Cargo policy covers goods in transitincluding by sea, air and road. Further, insurance of motorvehicles against damages and theft forms a major chunk ofnon-life insurance business.

In respect of insurance of property, it is important thatthe cover is taken for the actual value of the property toavoid being imposed a penalty should there be a claim. Wherea property is undervalued for the purposes of insurance, theinsured will have to bear a ratable proportion of the loss.For instance if the value of a property is Rs.100 and it isinsured for Rs.50/-, in the event of a loss to the extent of

say Rs.50/-, the maximum claim amount payable would beRs.25/- ( 50% of the loss being borne by the insured forunderinsuring the property by 50% ). This concept is quiteoften not understood by most insured.

Personal insurance covers include policies for Accident,Health etc. Products offering Personal Accident cover arebenefit policies. Health insurance covers offered by non-life insurers are mainly hospitalization covers either onreimbursement or cashless basis. The cashless service isoffered through Third Party Administrators who havearrangements with various service providers, i.e.,hospitals. The Third Party Administrators also provideservice for reimbursement claims. Sometimes the insurersthemselves process reimbursement claims.

Accident and health insurance policies are available forindividuals as well as groups. A group could be a group ofemployees of an organization or holders of credit cards ordeposit holders in a bank etc. Normally when a group iscovered, insurers offer group discounts.

2

Liability insurance covers such as Motor Third PartyLiability Insurance, Workmen’s Compensation Policy etc offercover against legal liabilities that may arise under therespective statutes— Motor Vehicles Act, The Workmen’sCompensation Act etc. Some of the covers such as theforegoing (Motor Third Party and Workmen’s Compensationpolicy ) are compulsory by statute. Liability Insurance notcompulsory by statute is also gaining popularity these days.

Many industries insure against Public liability. There areliability covers available for Products as well.

There are general insurance products that are in the natureof package policies offering a combination of the coversmentioned above. For instance, there are package policiesavailable for householders, shop keepers and also forprofessionals such as doctors, chartered accountants etc.Apart from offering standard covers, insurers also offercustomized or tailor-made ones.

Suitable general Insurance covers are necessary for everyfamily. It is important to protect one’s property, which onemight have acquired from one’s hard earned income. A loss ordamage to one’s property can leave one shattered. Lossescreated by catastrophes such as the tsunami, earthquakes,cyclones etc have left many homeless and penniless. Suchlosses can be devastating but insurance could help mitigatethem. Property can be covered, so also the people againstPersonal Accident. A Health Insurance policy can providefinancial relief to a person undergoing medical treatmentwhether due to a disease or an injury.

Industries also need to protect themselves by obtaininginsurance covers to protect their building, machinery,stocks etc. They need to cover their liabilities as well.Financiers insist on insurance. So, most industries orbusinesses that are financed by banks and other institutionsdo obtain covers. But are they obtaining the right covers?And are they insuring adequately are questions that need tobe given some thought. Also organizations or industries thatare self-financed should ensure that they are protected byinsurance.

Most general insurance covers are annual contracts. However,there are few products that are long-term.

It is important for proposes to read and understand theterms and conditions of a policy before they enter into an

insurance contract. The proposal form needs to be filled incompletely and correctly by a proposer to ensure that thecover is adequate and the right one.

3

We face a lot of risks in our daily lives. Some of theselead to financial losses. Insurance is a way of protectingagainst these financial losses. For a payment (premium), aninsurance company will take the responsibility ofcompensating your financial losses.

Anyone who owns an asset can buy insurance to protect itagainst losses due to fire or theft and so on. Each one ofus can insure our and our dependents’ health and well beingthrough hospitalization and personal accident policies. Tobuy a policy the person should be the one who will bearfinancial losses if they occur. This is called insurableinterest.

One of the main reasons one should insure is to protectone’s belongings and assets against financial loss. When onehas earned and accumulated property, protecting it isprudent. The law also requires us to be insured against someliabilities. That is, in case we should cause a loss toanother person, that person is entitled to compensation. Toensure that we can afford to pay that compensation, the lawrequires us to buy liability insurance so that theresponsibility of paying the compensation is transferred toan insurance company.

Insuring anything other than human life is called generalinsurance. Examples are insuring property like house andbelongings against fire and theft or vehicles againstaccidental damage or theft. Injury due to accident orhospitalization for illness and surgery can also be insured.Your liabilities to others arising out of the law can also

be insured and is compulsory in some cases like motor thirdparty insurance.

4 TYPES OF INSURANCE

Insurance may be classified as:

1. LIFE INSURANCE

2. NON-LIFE INSURANCE

LIFE INSURANCE:

Term life insurance provides coverage for a limited period

of time, the relevant term. After that period, the insured

can drop the policy or pay annually increasing premiums to

continue the coverage. If the insured dies during the term,

the death benefit will be paid to the beneficiary. Term

insurance is often the most inexpensive way to purchase a

substantial death benefit on a coverage amount per premium

dollar basis.

Term insurance functions in a manner similar to most other

types of insurance in that it satisfies claims against what

is insured if the premiums are up to date and the contract

has not expired, and does not expect a return of Premium

dollars if no claims are filed. As an example, auto

insurance will satisfy claims against the insured in the

event of an accident and a home owner policy will satisfy

claims against the home if it is damaged or destroyed by,

for example, an earthquake or fire. Whether or not these

events will occur is uncertain, and if the policy holder

discontinues coverage because he has sold the insured car or

home the insurance company will not refund the premium. This

is purely risk protection.

5

Life insurance or life assurance is a contract between the

policy owner and the insurer, where the insurer agrees to

pay a sum of money upon the occurrence of the policy owner's

death. In return, the policy owner (or policy payer) agrees

to pay a stipulated amount called a premium at regular

intervals.

NON-LIFE INSURANCE / GENERAL INSURANCE

Basically non-life or general insurance is all about making

things insured which are other than life.

All insurance excluding life insurance comes under general

insurance. General Insurance is, broadly, insurance, which

does not include any investment element, and covers risk of

other natural, individual, political and economic risks. The

general insurance products for individuals include health,

home, travel, student, motor, accident and other business

insurance.

Buying general insurance policies are a provision in case of

any uncertain loss that might come up during the normal

course of activities. Hence an insurance cover rids you of

the tension and the financial burden that you would suffer

in case of a calamity.

The non life insurance industry in India has grown above

80% within the last five years. With 81% contribution,

public sector companies accounted for almost the entire

market share. However, the private sector companies had to

content with a meager 19% of market share.

6

As per a recent market research report named, “Indian

Insurance Industry Forecast (2007-2009)” published by

RNCOS, “The present growth in the non life insurance sector

is anticipated to continue in the years to come. Growing at

the Compound Annual Growth Rate of 13%, the insurance

market in India shall touch the mark of $9 billion by

2009”.

“In spite of the entry of new companies and nationalized

banks in the insurance sector in India, the Public Sector

Life Insurance Corporation still holds a substantial share

of 72%”, as per experts at RNCOS.

PRINCIPLES OF GENERAL INSURANCE

Business, as indeed life in general, is subject to varioustypes of risk and uncertainty. It is difficult to know whenany loss by way of accident or death might befall a person.Insurance is means of providing against loss caused bynatural or man made factors. Insurance has cone to occupy animportant place in the smooth running of the business.

1. SECURITY: Insurance secures the insured person againstrisk of loss due to happening of an uncertain event.This means that a businessman can carry on hisoperations without worrying about a possible loss. Hecan even take calculated risk in running anddevelopment of his business.

2. DISTRIBUTION OF RISK: In case of loss to the insuredfrom any risk covered under the contract of insurance,he is paid by the insurer the amount of loss upto thesum assured but he himself bear the effect of such. Heonly distribute the loss suffered and insured personamong others who are exposed to similar risk and whohave insured against such risk. Thus, insurance is anattempt at pooling of risk under which a large numberof people contribute to a fund out of whichcompensation is paid to the persons suffering aparticular type of loss.

7

3. COMPETITIVENESS: A businessman who has insured againsta possible loss in business can be more confident inhandling its affairs. He knows that even if hiscompensate and save him from possible ruin. Thus, thebusinessman can afford to be bold and unconventional indecision to meet and beat competition.

4. SPECIALIZATION: Insurance enables the businessman togive undivided time

and attention to successful running of hisbusiness. If the risk of loss are duly

covered, there will be nothing to disturb thepeace of mind of the businessman in planning and accomplishing ambitious projects.The insurer, who is himself an expert in the business of risk bearing willalways be there to rescue the businessman from loss of any kind

5. OPTIMUM USE OF AVAILABLE CAPITAL: If a business isadequately

insured, there is no need to set apart capital foruse in case of a business loss. This is because in the event of loss, the business willreceive sufficient money from the insurer to cope with the loss of capital. In otherwords, entire capital at the disposal of the business can be utilize in itsoperations to earn higher profits.

6. PROMOTION OF FOREIGN TRADE: transport of goods from onecountry to

another is beset with various risks. Insuranceplays an important role in covering these risks to boost foreign trade.

7. LOAN FACILITY: Insurance companies offers loans againstthe security of

policies issued by them. Buying a house,construction of house etc. are the few Examples. Insurance companies also provideunderwriting facility in case of issue of shares, debentures etc.

8. SOCIAL WELFARE: Insurance is a small well-wearingeffort to promote social

good. It encourages people to provide for thefuture, such as old age, education and marriage of children.

8

CHAPTER- 2

RESEARCH METHODOLOGY

9Research methodology is understood as a science of studying

how research is done scientifically. In various steps are

studied that are generally adopted by a researcher in

studying his research problems along with the logic behind.

Thus research methodology includes not only research methods

also consider the logic behind the methods we use in the

context of our research studies and explain why we are using

this particular method.

Scope of StudyThe scope of my study begins with the study of history of

ICICI Lombard and it further extends to various issues

related to marketing strategies of the company.

Time frameIn the whole process time taken was 2 months that is 26th

may 07- 26th july 07 .

OBJECTIVE

Projects are basically carried out to find out any

appropriate solution of any particular problem. It helps in

the proper grooming of our analytical skill. While dealing

with any project we can understand various aspect of any

case

The main objective behind the projects are such as:

1. To improve our analytical skill.

2. To make a comparative analysis of documentation

process.

10

3. To find out the area where ICICI Lombard can get

competitive age in their documentation

process.

4. To conduct a deep research for getting and

appropriate out comes.

5. To judge the satisfaction level of customers

DATA COLLECTION

Data has been collected both from primary as well as

secondary described below:

Primary Sources

The primary sources of data were interview conducted as part

of survey this data forms the backbone of the analysis of

the customer’s requirements. As I have collected all the

data mainly from customers and internet. Everybody had

different responses regarding the various policies of the

company. Few people were more interested in public sector

rather than private sector.

.

Secondary Sources

The secondary sources of data were the various websites and

insurance manuals.

Secondary data- Secondary data is already available and

published. It could be external and internal source of data.

Internal source- It is the one which originates from

specific field or area where research is carried out.

Example- public brochure, official reports etc.

External source- this originates outside the field of study

like books, periodicals, journals and internet etc.

11

LIMITATIONS

The main limitation of my project is as follows:-

Time Constraints

Behaviour of the people

Primary data collection

OJT work pressure

Time Constraints: - I have less time to work on project

because all the time I have to work on OJT to complete my

OJT targets.

Behave of the people: - People of Delhi are not so much co-

operative as I approached to the office of other Life

Insurance Companies they refused me to give information

about the project.

Primary data collection: - It’s a tough job to collect

primary data from market and we have to collect data from

the main source and it is not an easy task.

OJT work pressure: - I have to complete my OJT targets also

so I have to adjust my time according to OJT as well as for

Project work.

12

CHAPTER-3

INTRODUCTION OF ICICI LOMBARD

13

ICICI BANK

ICICI Bank means ICICI Bank Limited, a company incorporated

under the Companies Act, 1956 and having its registered

office at Landmark, Race Course Circle, Vadodara 390 007.

ICICI Bank is India's second-largest bank with total assets

of Rs. 3,446.58 billion (US$ 79 billion) at March 31, 2007

and profit after tax of Rs. 31.10 billion for fiscal 2007.

ICICI Bank is the most valuable bank in India in terms of

market capitalization and is ranked third amongst all the

companies listed on the Indian stock exchanges in terms of

free float market capitalization*. The Bank has a network of

about 950 branches and 3,300 ATMs in

India and presence in 17 countries. ICICI Bank offers a wide

range of banking products and financial services to

corporate and retail customers through a variety of delivery

channels and through its specialized subsidiaries and

affiliates in the areas of investment banking, life and non-

life insurance, venture capital and asset management. The

Bank currently has subsidiaries in the United Kingdom,

Russia and Canada, branches in Singapore, Bahrain, Hong

Kong, Sri Lanka and Dubai International Finance Centre and

representative offices in the United States, United Arab

Emirates, China, South Africa, Bangladesh, Thailand,

Malaysia and Indonesia. Our UK subsidiary has established a

branch in Belgium.

ICICI Bank's equity shares are listed in India on Bombay

Stock Exchange and the National Stock Exchange of India

Limited and its American Depositary Receipts (ADRs) are

listed on the New York Stock Exchange (NYSE).

14

ICICI Lombard

ICICI Lombard General Insurance Company Limited, a company

incorporated under the Companies Act, 1956 and licensed

under and in terms of the Insurance Act, 1938 and the

Insurance Regulatory and Development Authority Act, 1999 to

carry out the business of general insurance and having its

registered office at ICICI Bank

Lightning fast claims settlement

Instant online policy issuance

Comprehensive product line

Highest security level offered through 128-bit encryption

in case of online data exchange

First company to provide digitally signed documents

through an online interface

Achieved financial breakeven in first full year of

operations

Achieved underwriting breakeven in second year of

operations

Awarded the NDTV Profit Business Leadership Awards 2007

in the General Insurance category on July 27, 2007

Adjudged as the most Customer Responsive Company in the

Insurance category at the Economic Times Avaya Global

Connect Customer Responsiveness Award 2006

Awarded the Best Housing Insurance in the Smart Living

Awards by 360 degrees, a Times of India Group subsidiary,

in Nov 2006.

15

Awarded the Gold Shield for "Excellence in Financial

Reporting" by the ICAI (Institute of Chartered

Accountants of India) for the year ended March 31, 2006

Among the top three General Insurance Companies to be

awarded the "General Insurance Company of the Year" at

the 10th Asia Insurance Industry Awards

Adjudged amongst the top three in the Insurance Website

of the Year category at the 9th Asia Insurance Industry

Awards function held in Singapore during Septembe2005.

16

HISTORY

ICICI Lombard General Insurance Company Limited is a 74:26

joint venture between ICICI Bank Limited and the Canada

based $ 26 billion Fairfax Financial Holdings Limited. ICICI

Bank is India's second largest bank, while Fairfax Financial

Holdings is a diversified financial corporate engaged in

general insurance, reinsurance, insurance claims management

and investment management.

Lombard Canada Ltd, a group company of Fairfax Financial

Holdings Limited, is one of Canada's oldest property and

casualty insurers. ICICI Lombard General Insurance Company

received regulatory approvals to commence general insurance

business in August 2001.

The principal objective was to create a development

financial institution for providing medium-term and long-

term project financing to Indian businesses. In the 1990s,

ICICI transformed its business from a development financial

institution offering only project finance to a diversified

financial services group offering a wide variety of products

and services, both directly and through a number of

subsidiaries and affiliates like ICICI Bank.

17

CHAPTER- 4

PRODUCT PROFILE

23

1. HEALTH INSURANCE

Illnesses can weaken your financial stability. Adding

to the already existing emotional stress. In order to

reduce the risk of unexpected medical costs, ICICI

Lombard, known for their innovative insurance products

has thoughtfully structured a Health Product Suite. The

plans under the suite vary widely in terms of coverage,

costs and benefits. So that you are well prepared in

the face of any health crisis.

1.1 Critical Care

Lump-sum benefit on diagnosis of Critical Illness/Major

Medical Illnesses and Procedures, Personal Accident and

Permanent Total Disablement (PTD)

Critical Care Insurance

Critical Care protects you or your spouse against loss

of income on diagnosis of any of the 9 major medical

illnesses and procedures. The first of its kind, it

offers a lump sum benefit on diagnosis of Cancer,

Bypass Surgery, Heart Attack, Kidney Failure, Major

Organ Transplant, Stroke, Paralysis, Heart Valve

Replacement Surgery or Multiple Sclerosis. Critical

Care Insurance also provides cover against accidental

death and permanent total disablement (PTD).

1.1.1 Critical Illness Cover

The Critical Care Insurance shall cover, subsequent to

90 days from the policy start date, the following major

medical illnesses and procedures:

1. Cancer

2. Coronary Artery Bypass Graft Surgery

3. Myocardial Infarction (Heart Attack)

24

4. Kidney Failure (End Stage Renal Failure)

5. Major Organ Transplant

6. Stroke

7. Paralysis

8. Heart Valve Replacement Surgery

9. Multiple Scleros

PRICE CHART

Critical Care Sum Insured Table

Covers Sum Insured Options

Critical Illness/Major Medical

Illness Diagnosis

Rs. 6,00,000 or Rs.

12,00,000

Accidental Death

Permanent Total Disability

(PTD)

25

Critical Care Premium Table

Policy

Tenure/Age

Groups

(Years)

Sum Insured = Rs. 6 Lakh Sum Insured = Rs. 12

Lakh

3 Years

(Rs.)

5 Years

(Rs.)

3 Years

(Rs.)

5 Years

(Rs.)

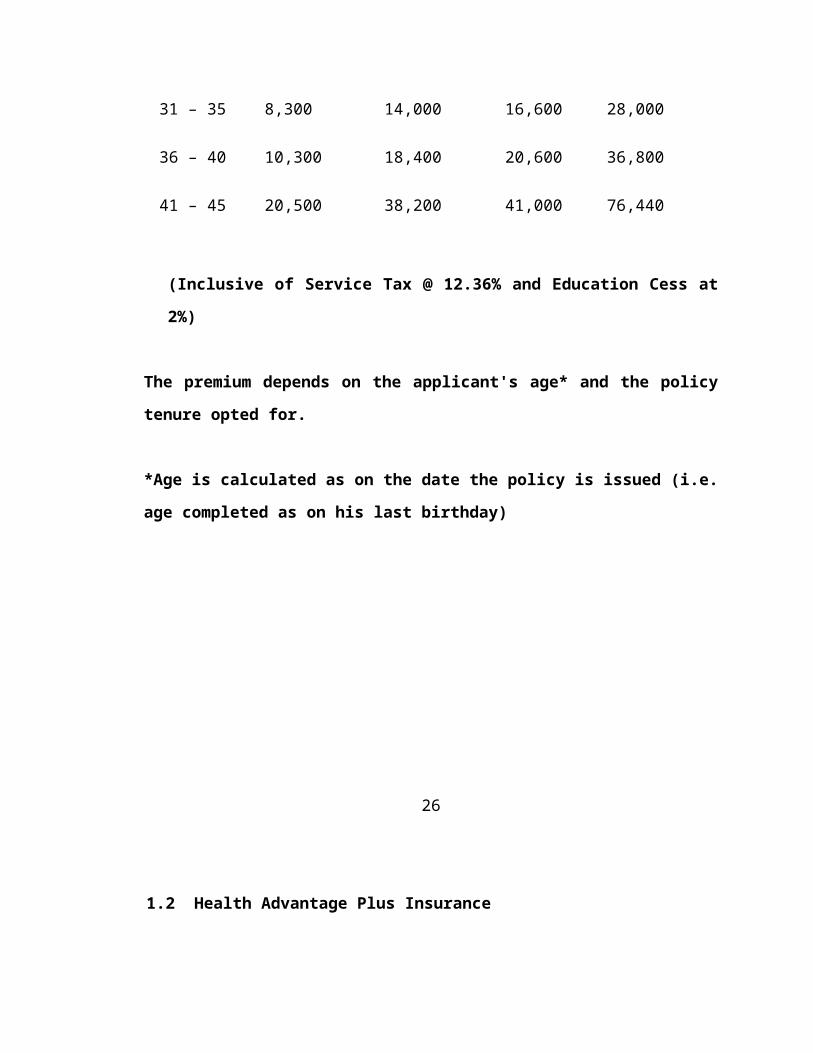

20 – 25 5,800 9,700 11,600 19,400

26 – 30 6,600 11,280 13,200 22,600

31 – 35 8,300 14,000 16,600 28,000

36 – 40 10,300 18,400 20,600 36,800

41 – 45 20,500 38,200 41,000 76,440

(Inclusive of Service Tax @ 12.36% and Education Cess at

2%)

The premium depends on the applicant's age* and the policy

tenure opted for.

*Age is calculated as on the date the policy is issued (i.e.

age completed as on his last birthday)

26

1.2 Health Advantage Plus Insurance

A unique policy that covers hospitalization and

Outpatient Department Expenses (including Dental

treatment, cost of medicines and drugs) and enables

optimum tax savings of up to Rs. 5099 u/s 80D

The `Health Advantage Plus Health Insurance Policy’ is aunique health insurance policy that covers unexpectedmedical emergencies like hospitalization costs as well asOutpatient Treatment Expenses (OPD) in the form ofreimbursement of cost of medicines, drugs, ambulance chargesand dental expenses. You avail optimum tax-saving benefit,this policy enables you to save up to Rs. 5099* underSection 80 D of the Income Tax Act.

Moreover, the 45 year age limit for ‘no health check-up’ forpolicy issuance is now extended to 55 years of age.

This Plan is available for all ages between 5-65 years and senior citizens aged 66 and above (renewable up to 70 years).

Basic Hospitalization Cover

This covers inpatient hospitalization expenses up to sum insured of Rs. 2 or Rs. 3 Lakhs (depending on the plan chosen). You can avail the cashless claim facility in any ofthe 4000+ network hospitals across India.

Basic Hospitalization cover includes:

Medical expenses incurred as an inpatient during hospitalization for more than 24 hours, including room charges, doctor’s / surgeon’s fee, medicines, diagnostic tests, etc.

27

30 days prior to hospitalization

60 days post hospitalization

Pre-existing disease can be covered after the 2nd year

provided the policy is renewed with us for three

consecutive years.

Technologically advanced treatment that do not need 24-hour hospitalisation but are covered under this policy are:-

- Cataract- Lithotripsy (Kidney Stone Removal)

Tonsillectomy

- Eye Surgery

- Dialysis

- Dilatation & Curettage

- Chemotherapy

- Radiotherapy

- Coronary Angiography’s

- Cardiac Catheterization

28

1.3 Family Floater Plan

A single policy that secures the hospitalization

expenses of your entire

family.

For the first time in India, one single policy takes

care of the hospitalization expenses of your entire

family. Family Floater Health Plan takes care of all

the medical expenses during sudden illness, surgeries

and accidents

Policy Coverage

The policy covers medical expenses:

Incurred as an inpatient during hospitalisation for more

than 24 hours, including room charges, doctor/ surgeon's

fee, medicines, etc.

30 days prior to hospitalisation.

60 days post hospitalisation.

Day Care expenses incurred on advanced technological

surgeries and procedures like Dialysis, Radiotherapy, and

Chemotherapy, requiring less than 24 hours of

hospitalisation.

Pre-existing disease can be covered after the 4th year

provided the policy is renewed with us for four

consecutive years.

29

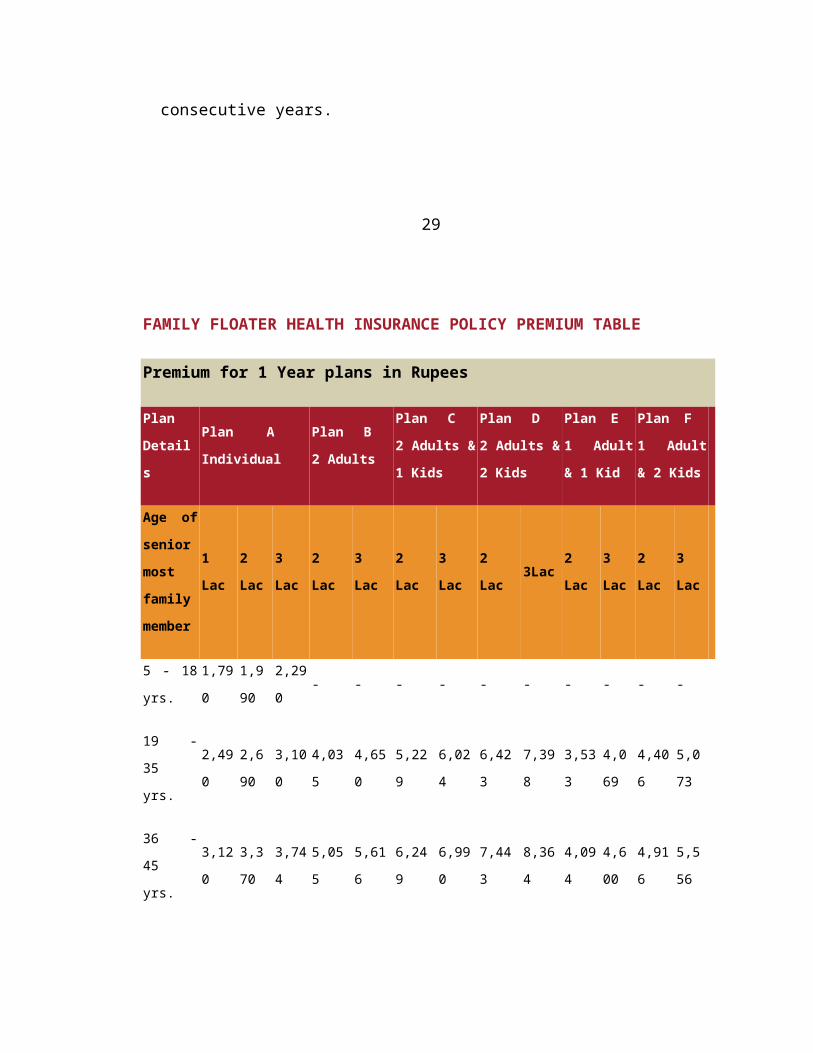

FAMILY FLOATER HEALTH INSURANCE POLICY PREMIUM TABLE

Premium for 1 Year plans in Rupees

Plan

Detail

s

Plan A

Individual

Plan B

2 Adults

Plan C

2 Adults &

1 Kids

Plan D

2 Adults &

2 Kids

Plan E

1 Adult

& 1 Kid

Plan F

1 Adult

& 2 Kids

Age of

senior

most

family

member

1

Lac

2

Lac

3

Lac

2

Lac

3

Lac

2

Lac

3

Lac

2

Lac3Lac

2

Lac

3

Lac

2

Lac

3

Lac

5 - 18

yrs.

1,79

0

1,9

90

2,29

0- - - - - - - - - -

19 -

35

yrs.

2,49

0

2,6

90

3,10

0

4,03

5

4,65

0

5,22

9

6,02

4

6,42

3

7,39

8

3,53

3

4,0

69

4,40

6

5,0

73

36 -

45

yrs.

3,12

0

3,3

70

3,74

4

5,05

5

5,61

6

6,24

9

6,99

0

7,44

3

8,36

4

4,09

4

4,6

00

4,91

6

5,5

56

46 -

55

yrs.

5,70

0

6,0

00

6,66

7

9,60

0

10,6

67

10,7

94

12,0

41

11,9

88

13,4

15

6,59

3

7,3

78

7,18

8

8,0

82

56 -

60

yrs.

8,16

7

11,7

60

13,0

67

12,9

54

14,4

41

14,1

48

15,8

15

7,78

2

8,6

98

8,26

8

9,2

82

30

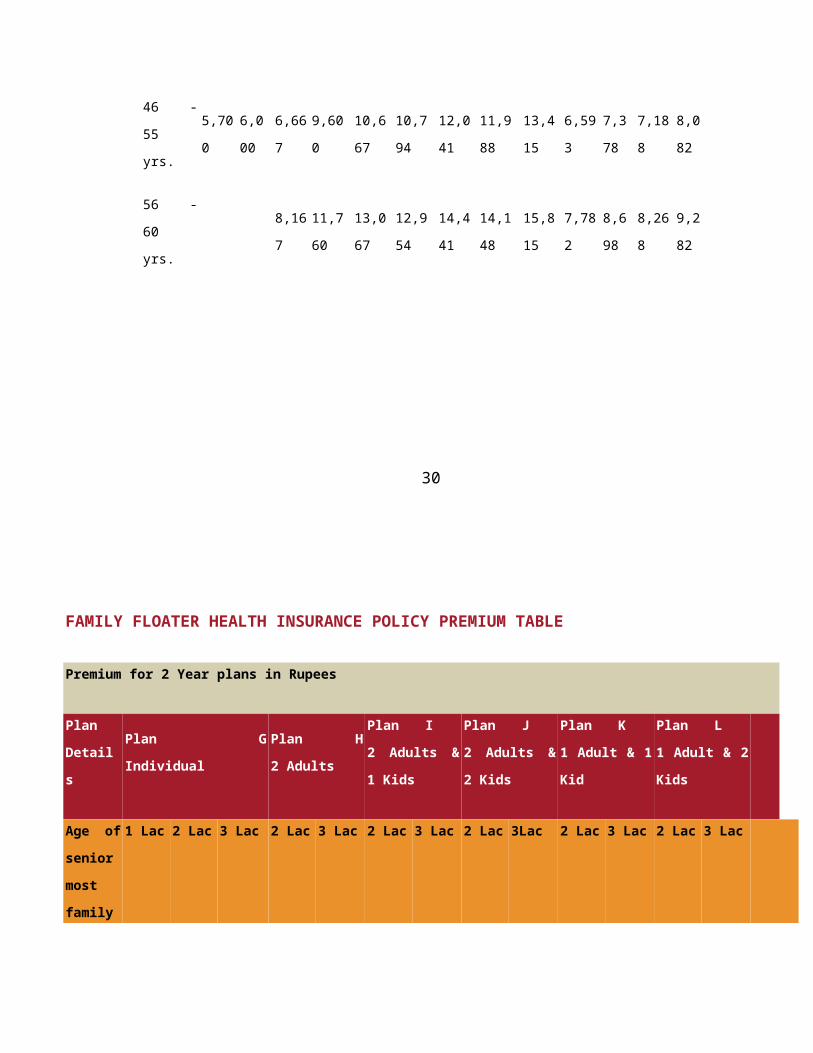

FAMILY FLOATER HEALTH INSURANCE POLICY PREMIUM TABLE

Premium for 2 Year plans in Rupees

Plan

Detail

s

Plan G

Individual

Plan H

2 Adults

Plan I

2 Adults &

1 Kids

Plan J

2 Adults &

2 Kids

Plan K

1 Adult & 1

Kid

Plan L

1 Adult & 2

Kids

Age of

senior

most

family

1 Lac 2 Lac 3 Lac 2 Lac 3 Lac 2 Lac 3 Lac 2 Lac 3Lac 2 Lac 3 Lac 2 Lac 3 Lac

member

5 - 18

yrs.3,222 3,582 4,122 - - - - - - - - - -

19 -

35

yrs.

4,482 4,842 5,580 7,263 8,370 9,41210,84

3

11,56

1

13,31

66,359 7,324 7,930 9,131

36 -

45

yrs.

5,616 6,066 6,739 9,09910,10

9

11,24

8

12,58

2

13,39

7

15,05

57,369 8,280 8,848

10,00

1

46 -

55

yrs.

10,83

0

11,40

0

12,66

7

18,24

0

20,26

8

20,50

9

22,87

8

22,77

7

25,48

9

12,52

7

14,01

9

13,65

7

15,35

5

56 -

60

yrs.

16,33

4

23,52

0

26,13

4

25,90

8

28,88

2

28,29

6

31,63

0

15,56

3

17,39

7

16,53

6

18,56

3

31

1.4 Personal Accident Insurance

A Policy that covers personal accident, permanent total

disablement (PTD) and loss due to terrorism.

ICICI Lombard Personal Accident Insurance policy covers

you against Accidental Death, Permanent Total

Disablement (PTD) and Permanent Partial Disablement

(PPD). As a special offer, we now bring 3 new Personal

Accident flexible plan options (Accidental Death &

Permanent Total Disablement cover only) with a sum

insured of Rs. 3, 5 and Rs. 10 Lakh.

Personal Accident Comprehensive Plan:

Amount of Cover Rs. 2,000,000

This is a comprehensive Personal Accident Plan

that shall cover the insured

for:

Death of the Insured person

Permanent Total Disablement (PTD)

Permanent Partial Disablement (PPD)

Carriage of Dead Body

32

PRICE CHART

Accidental Death & Permanent Total Disablement Cover

Capital Sum Insured (Rs.)

Policy Period 3,00,000 5,00,000 10,00,000

3 years Premium

(Rs.)

1125 1875 3750

4 years Premium

(Rs.)

1500 2500 5000

5 years Premium

(Rs.)

1875 3125 6250

33

2. MOTOR INSURANCE

MOTOR INSURANCE IS OF 3 TYPES:

2.1 Car Insurance

A comprehensive policy that not only covers you against

third party but also against accidents, damage, injury

and much more.

ICICI Lombard brings to you a comprehensive Package

Policy for your four-

wheelers, which covers Third Party Liability (TPL)

for bodily injury and/or

death, Personal Accident cover for owner-driver and

loss or damage to

the vehicle insured (Own Damage or OD).

-

Policy Coverage

Our Motor insurance Policy is governed by the Indian Motor

Tariff. It covers you for:

Loss or damage to your vehicle: The policy covers you

against any loss or damage caused to the vehicle or its

accessories due to the following natural and man made

calamities.

Natural Calamities – Fire, explosion, self-ignition or

lightning, earthquake, flood, typhoon, hurricane, storm,

tempest, inundation, cyclone, hailstorm, frost,

landslide,rockslide.

Man made Calamities – Burglary, theft, riot, strike,

malicious act, accident by external means, terrorist

activity, any damage in transit by road, rail, inland

waterway, lift, elevator or air.

The rates of the vehicle and its parts are subject to

depreciation as per the schedule provided by the Indian

Motor Tariff.

34

Personal accident cover: The motor insurance provides

compulsory personal accident cover for individual owners

of the vehicle while driving. You can also opt for a

personal accident cover for passengers.

Third party legal liability: This protects you against

legal liability arising due to accidental damages.

- Any permanent injury/ death of a person

- Any damage caused to the property.

2.2 Two Wheeler Insurance

A composite policy that protects you

against unfortunate accidents, third party liability,

injuries and damages.

Two- wheeler riding calls for a constant alertness from

theft and accidents. Two-wheeler policy guarantees

safety for your vehicle and yourself, thereby making

your ride stress- free.

Policy Coverage

Two-wheeler insurance policy is governed by the Indian

Motor Tariff. It covers you for:

Loss or damage to your vehicle: The policy covers

you against any loss or

damage caused to the vehicle or its accessories

due to the following natural

and man made calamities.

35

Natural Calamities – Fire, explosion, self-

ignition or lightning,

earthquake, flood, typhoon, hurricane, storm,

tempest, inundation, cyclone,

hailstorm,frost,landslide,rockslide.

Man made Calamities – Burglary, theft, riot,

strike, malicious act, accident

by external means, terrorist activity, any

damage in transit by road, rail,

inland waterway, lift, elevator or air. The

rates of the vehicle and its parts

are subject to depreciation as per the schedule

provided by the Indian

Motor Tariff.

Personal accident cover: The motor insurance

provides compulsory

personal accident cover for individual owners of

the vehicle while driving.

You can also opt for a personal accident cover

for passengers.

Third party legal liability: This protects you

against legal liability arising

due to accidental damages

- Any permanent injury/ death of a person

- Any damage caused to the property

Sum Insured

The vehicles are insured at a fixed value called the

Insured’s Declared Value (IDV). IDV is calculated on

the basis of the manufacturer’s listed selling price of

the vehicle (plus the listed price of any accessories)

after deducting the depreciation for every year as per

the schedule provided by the Indian Motor Tariff. If

the price of any electrical and / or electronic item

installed in the vehicle is not included in the

manufacturer’s listed selling price, then the actual

value (after depreciation) of this item can be added to

the sum insured over and above the IDV.

36

2.3 Commercial Vehicle Insurance

ICICI Lombard brings you Commercial Vehicle Insurance

offering the most crucial cover of Third Party Liability

(TPL). A specialised cover for Goods-carrying Vehicles –

be it Public or Private Carriers. You can now rest

assured that your vehicle is covered and your business

stays protected against liability due to accidental

death or injury to third parties or passenger(s).

Policy Coverage

ICICI Lombard Commercial Vehicle insurance offers Third

Party only cover for Goods-carrying Commercial vehicles.

This cover is applicable to Public and Private Carriers

including Motorized Three Wheelers and Motorized Pedal

Cycles.

Our Commercial Vehicle insurance Policy is governed by

the Indian Motor Tariff. It defines Goods-carrying

Commercial Vehicle as:

Public Carriers (other than three wheelers)

Private Carriers (other than three wheelers)

Goods Carrying Motorized Three Wheelers and Motorized Pedal Cycles. (Public Carriers)

Goods Carrying Motorized Three Wheelers and Motorized Pedal Cycles. (Private Carriers)

It covers you for:

a) Personal Injury

b) Property damage.

37

3. TRAVEL INSURANCE

3.1 Individual Overseas Plan

All overseas travel policies charge premium on a slab

basis. Which means if you are on a 16 day trip, you end

up paying for 21 days, as the slab is 14 to 21 days.

But with us you ‘pay per day’

Overseas Travel Insurance Policy Features

Eligibility: Insurance policy available for all ages

between 1 – 70 years and senior citizens between 71 to 85

years

Policy Duration: Cover trips from as short as 7 days to

180 days. Can be extended online

Policy Maximum: The Plans offer various coverage options

(US $ 50,000 to US $ 250,000)

Premium: Premium is payable on a pay per day basis and

not slab rates, pay at 0% EMI on ICICI Bank Credit Cards

Pre-existing diseases: Pre-existing ailments and

maternity are excluded except in case of life-threatening

situations i.e. until the insured's heath is stable

A (Excellent) Rating: ICICI Lombard has received an A

(Excellent) rating from General Insurance Company of

India and iAAA rating from ICRA signifying highest claims

paying ability

Deductible/Policy Excess: There is a Deductible/Policy

Excess of US $ 100. This implies for any claim the first

$100 are to be borne by the insured.

38

Additional Coverage: Coverage’s include Dental Treatment,

Medical Evacuation, Repatriation, Baggage Loss/Delay,

Trip Cancellation and Interruption, etc.

Insurance Direct: Buy insurance online or Dial-A-Policy

at 1800 222 555 to buy your policy over the phone

Claim: In order to make a claim, please contact our TPA

(Third Party Administrator) SOS International, which has

tie-ups with network hospitals worldwide

3.2 Student Medical Insurance

A comprehensive cover, which insures you against

unfortunate incidents or unexpected expenses abroad and

provides timely assistance and support when you need it

the most.

COMPARE PLANS (Click on Plan names to know more)

Coverageamount

GoldPlan

BronzePlan

Plus Plan

1)

MedicalExpenses*(includesMedical evacuationcost)

US$50,000to US $500,000

-

The Plus Planis an add - onplan that canbe bought inaddition to theGold or theSilver plan.

2) Dental Treatment* US$ 250 -

3)Checked Baggageloss

US$1,000

4) Personal Liability US$100,000

5) Bail Bond US$5,000

6) Study Interruption US$7,500

7) Sponsor Protection US$10,000

8)2Way CompassionateVisit

US$7,500

9) Passport Loss** US$ 200

10) Personal Accident US$25,000

US$10,000

39

11)Repatriation ofremains

Up toMedical SumInsured

-

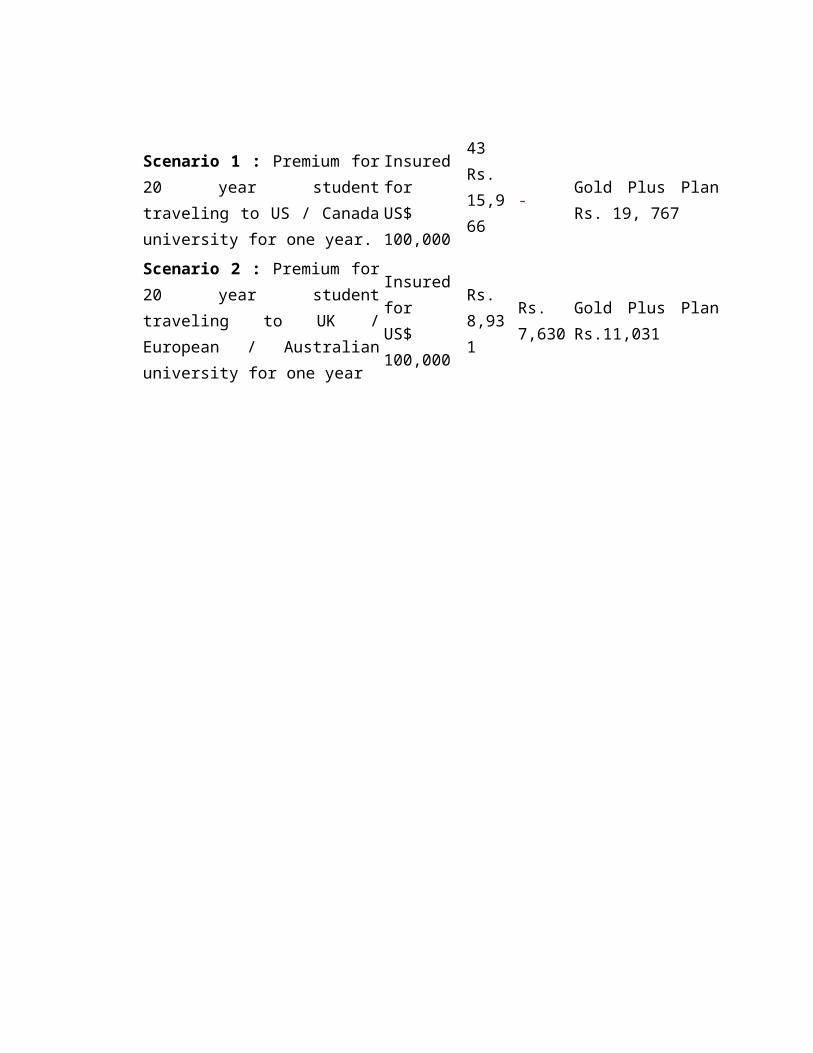

Scenario 1 : Premium for20 year studenttraveling to US / Canadauniversity for one year.

InsuredforUS$100,000

43Rs.15,966

-Gold Plus PlanRs. 19, 767

Scenario 2 : Premium for20 year studenttraveling to UK /European / Australianuniversity for one year

InsuredforUS$100,000

Rs.8,931

Rs.7,630

Gold Plus PlanRs.11,031

40

4. Home InsuranceIt is imperative that you secure your home from natural

and man-made catastrophes. Our Home Insurance Plan

ensures you peace of mind by protecting the structure

and the contents of your home

The calamities covered are:

- Fire

- Riot, strike & malicious damage

- Explosion & implosion

- Earthquake

- Lightning

- Storm, cyclone, tempest, tornado, hurricane, flood

& inundation

- Damage due to impact by vehicle

- Missile testing operation

- Subsidence, landslides and rockslides

- Leakage from automatic Sprinkler installation

- Aircraft damage

- Bursting and/or overflowing of water tanks,

apparatus and pipes

Key Benefits

Comprehensive cover - Covers both structure and contents

of your home.

Avail 15% discount on a 3 years home insurance policy and

25% discount on 5 years policy.

Optional covers available - Terrorism and Additional

expenses of rent for alternative accommodation.

Need for Policy

1. Protect your single largest investment against losses

due to natural or man-made calamities like fire,

floods, burglary, earthquake.

41

2. Cover your household contents including furniture,

durables, clothes, utensils, jewellery, at market value

to accommodate inflation.

4.1 Householder’s Insurance

4.1.1 Risk covered under this policy: Section-1: Deals with fire and allied Perils. This section insures your house and the contents of your ouse against fire, lightning, explosion of gas cylinders, bursting and overflowing of water tanks and pipes, earthquake, flood, storm, cyclone, landslide, damage by aircrafts or articles dropped

from an aircraft,and it even takes care of damage by riots, strikes and malicious acts, Terrorism.

4.1.2 Types of construction covered:Only buildings of CLASS ‘A’ construction are covered.

CLASS ‘A’ construction –building shouldfulfill the following conditions.

(i). External walls of stone, bricks, blokes,etc.(ii) Roof of R.C.C./masonry/asbestos/concretesheet or boarding on R.C.C/steel/wooden frame work.

4.1.3 Others sections of this policy:

Section2: Damage of property: this sections covers losses ordamage to the property arising out of burglary,housebreaking, larceny or theft

If the clients desires to specifically insure items ofjewellery and valuables under this section, please ensurethat they are also covered under Section 1 for the samevalue.

Section3: all risks: this section insures your jewellery andvaluables against loss or damage by accident or misfortunewhile you are traveling anywhere in India. However, it issubject to certain limitations.

Section 4:plate glass: this policy covers accidentalbreakage/such glass.

42Section 5: break down of domestic appliances damage cause todomestic electrical, electronic or mechanical appliance bymechanical or electrical breakdown are covered.

Section 6: covers TV sets and VCR against fire, lightningexplosion of the domestic appliances bursting and overflowing of water tanks, apparatus and pipes, air-crafts orarticles dropped there from, earthquake, fire or shock,flood inundation, hurricane, cyclone, theft etc.

BURGLARY INSURANCE

Burglary Insurance policy covers property contained in business premises, stocks owned, or for which insured is responsible or held in trust and/or commission. It also covers cash, valuables, securities kept in a locked safe or cash box in locked steel cupboard on specific request.

What does this Policy cover ?

This Burglary Insurance covers loss or damage caused by Burglary and Theft (i.e. theft following upon an actual forcible and violent entry of and / or exit from the premises).

Robbery : In respect of contents of offices, warehouses, shops, etc. and cash in safe or strong room and also damage caused to the premisesExtensions

It is possible to extend the policy to include loss ofthe insured property to cover burglary as a result of

riot & strike risks.

It is possible to extend the cover to include theft andlarceny not accompanied by violent ingress or exit. Theextension does not cover losses detected during routinestock taking/ checking.

43Benefits

Costs for changing locks and cost for repair of damage caused to the insured premises after an insured event up to10 % of the total sum insured. This extension is available regardless of whether the Insured is a tenant responsible for such repairs or owner of the premises.

Loss minimisation expenses up to 10 % of the total sum insured

Expenses towards restoring paper files, plans, records and drawings, data and installation costs for computer programsup to Rs 10000

Expenses towards clearance of debris and movement and protection up to 10 % of the loss subject to a maximum of Rs 10,000

Loss or damage to the properties of the employees of the Insured up to Rs 5,000

44

CHAPTER- 5

DISTRIBUTION CHANNEL

45

MEANING

Today’s Indian insurance market, the challenge to insurers

and intermediaries is two-pronged:

1. Building faith about the company in the mind of the

client

2. Intermediaries being able to build personal

credibility with the clients

Traditionally tied agents have been the primary channels for

insurance distribution in the Indian market; the public

sector insurance companies have their branches in almost all

parts of the country and have attracted local people to

become their agents. The agents are from various segments

in society and collectively cover the entire spectrum of

society. A person who has lived in the locality for many

years sells the products of the insurance company with a

local branch nearby. This ensures the last mile touch point

being closer to the customer. Of course, the profile of the

people who acted as agents suggests they may not have been

sufficiently knowledgeable about the different products

offered, and may not have sold the best possible product to

the client. Nonetheless, the customer trusted the agent and

company. This arrangement worked adequately in the absence

of competition.

In today's scenario agents continue as the prime channel for

insurance distribution in India, as is the case in most

markets, supported by call centers to a small extent. Almost

all the new players follow this model primarily because the

regulations for other channels are yet to be put in place.

However there is great excitement in the industry over the

impending broker regulations and companies are planning

possible channels in their enthusiasm to increase volumes.

The belief that all these channels will grow and seamlessly

integrate to bring in business seems a fallacy.

46

What have emerged is a much more difficult and evolving

market scene with existing players, more new players coming

in, and global marketing practices and ideas being tested.

But none of this has changed the fundamental character of

the market, which we believe will take more time than

expected.

What should the companies look at?

Basically companies have to take a look at the

intermediaries they are using, whether it is optimal to use

them, and what are the alternatives?

The new companies have attempted appealing only to the

middle, upper middle and elite classes in the major cities.

Contrasted with Public sector insurance companies, with

their offices across the country, the new companies have

miles to go before they reach anywhere. They must overcome

the mindset of the customer that life insurance is Life

Insurance Corporation of India (LIC) and general insurance

is General Insurance Corporation of India (GIC) if they hope

to grow in the market. Meanwhile, the public sector

companies are going to great lengths to revamp their image

to look and feel more contemporary. Both the public and new

private sector companies are fighting their own battles from

the perspective of customer perception management:

NEED FOR ALTERNATIVE DISTRIBUTION CHANNEL

Financial Liberation

The liberalization of national financial and capital

markets; coupled with the globalization of national

economies has catalyzed financial innovation and spurred the

growth of cross- border capital movements. The regulatory

authorities in many countries have altered rules governing

financial intermediation to allow a broader range of

institutions to provide financial services and thus new

classes of non-bank financial institutions have emerged. The

Insurance (amendment) Bill, 2002 passed on 23.09.2002

provides for setting up of Cooperatives exclusively for

carrying on Insurance business.

47

The cooperatives would be subject to some paid up capital

requirements, deposits with RBI and other regulations

concerning accounts and audit.

Cost Advantage

The existing two-tier structure needed a relook and use of

technology with agency channel was poor and inadequate.

Besides, the levels of service were poor not consistent with

the costs. To maximize reach in the market place, many

insurers are aiming to derive channel advantage because each

channel has unique strengths. For e.g., a direct sales force

is usually optimal for complex, high cost transactions where

face-to-face interaction is expected and required. Brokers

and Corporate Agents can dramatically expand market reach

through local access and penetration. The Internet can be

used to get the message out to untold millions, at an

extremely low cost.

The companies that choose and cleverly integrate the rightmix of channels can build market systems that respondoptimally to each of the requirements of the products andmarkets. They can, for example, use expensive sales forcerepresentatives only to acquire and grow the most importantkey accounts. They can then use brokers to reach dispersed

groups of smaller customers and to provide local salessupport. They can use call centers to close simple sales,generate sales leads for other channels and follow up ondirect mail campaigns. They can use the Internet to reachcustomers who prefer to serve themselves and want to savemoney. These efforts add up to a huge competitive advantagein terms of revenue growth, market reach, customer loyallyand higher productivity. Experience shows better averages interms of policy size, first premium per policy and firstpremium per Rs.1000 sum assured.

48

Advances in Information and Computer Technologies The integration of voice and data enabled entry ofinteractive voice response system (IVRS). The policyholdercan manage his policies through his facility. The website,though initially started as a spin of, became interactiveenabling the policyholders to know product information,calculate the premium quotes, know the premium position andvarious other benefits and redress grievances. The touchscreen kiosks have been introduced to create awareness ofthe products and for servicing. The metro area networks and

the wide area networks facilitated payment of premiumanywhere and provided access to policy information anywherein the country. As a result of the above initiatives thecustomer has become ever more informed, demanding andintervening in the purchase decision-making. The marketbecame highly segmented and warranted multiple channels toexploit it.

AGENTS

Today's insurance agent has to know which product will

appeal to the customer, and also know his competitor's

products in the same space to be an effective salesman who

can sell his company, the product, and himself to the

customer. To the average customer, every new company is the

same. Perceptions about the public sector companies are also

cemented in his mind. The new companies are looking for

educated, aware individuals with marketing flair, an elite

group who can be attracted only with high remuneration and

the lure of a fashionable job, all of which may not be

possible in this business with its price pressures and the

complexity of selling insurance. Unable to attract this

segment, they have started easing recruitment conditions as

against the stringent norms they had earlier, thereby

diluting the process.

While the public sector companies are able to attract

agents, they continue to suffer from high attrition rates

due to indiscriminate agent appointment. The most

successful of these companies' tied agents are hardly of the

elite variety of salesman.

49

They are still the neighborhood do gooders -- the postman,

the schoolteacher, and the shopkeeper -- who know the people

and are themselves known in the community. The challenge

here is the lack of knowledge of the competitive market and

the inability to do intelligent comparisons with the

competitor's products. Educating and training these agents

is a serious challenge for the insurance company.

The relevance of this kind of agent continues even today as

agents are sought or contacted by families by word of mouth.

Insurance companies are advised not to follow the path of

FMCG's/credit card companies, believing that a suited and

booted customer care consultant or financial consultant will

necessarily appeal to the average Indian customer. Another

social feature in the market is the considerable respect for

age in Indian society and a belief that an older person

knows better. A very young up-market agent who is a typical

salesman may not appeal to a large segment of the middle

class, which is looking for a solid trustworthy person from

whom they can buy insurance. In this context it might be a

rewarding exercise to recruit some older people (who have

taken VRS2 from banks and other financial institutions) to

sell some lines of products like pension plans, annuities

etc.

50

MARKETING STRATEGIES

Marketing Strategy #1: Gain Customer Confidence. Customerindecisiveness, skepticism, indifference, or confusion areamong the top sales killers in the business world. It's upto you to project an image of experience, quality,dependability, excellent customer service, and/or added

value to your prospective customers in order to win theirconfidence. If you haven't clearly communicated theadvantages and solid reasons for them to do business withyou, then they'll be hesitant to commit and the sale will goto your competitor.

Marketing Strategy #2: Penetrate awareness of your targetaudience by using some form of integrated marketing. Inother words, the more ways the public hears about you, thebetter your chances are for achieving brand recognition,credibility, and greater market share. Effective marketingis partly the result of exposing your target audience toyour name and your selling points (unique sellingproposition) as often as possible(frequency), in as manyways as possible, and as cost-effectively as possible.

Marketing Strategy #3: Sincere enthusiasm, in both print andin person, is contagious (and I'm not talking about usingmultiple exclamation points after sentences!!! That detractsfrom your credibility and perceived professionalism.) If youdeeply believe in your products, services, your company, andyourself, then your prospects will pick up on thatpassionate attitude and feel confident and optimistic aboutdoing business with you.

Marketing Strategy #4: Purchasing is an emotional decision.Instill in your prospects good feelings about your company,your business relationship with them, and how you canimprove their lives or solve their problem. Accomplishingthat is at least as important in the sales and marketingprocess as focusing attention on product features andbenefits.

Marketing Strategy #5: Dispel distrust. Gain customerconfidence and overcome potential feelings of distrust byoffering written guarantees of satisfaction wheneverpossible, customer testimonials, references, and by joiningrespected and well-known professional organizations, such asthe Better Business Bureau, Chambers of Commerce, andindustry associations.

51

Marketing Strategy #6: Impose a deadline.Counteract one ofthe biggest obstacles to closing a sale known to mankind:procrastination. To overcome the natural human tendancy todeliberate, postpone, and delay, it's often necessary toinject a sense of urgency into your ads, salespresentations, and marketing messages. Whether supplies arelimited or prices are going up at the end of the month, someprospects need to have a deadline or an incentive tomotivate them to take action now.

Marketing Strategy #7: Create a business marketing plan toidentify and capitalize on your strengths and opportunities.Your marketing strategies should also take into accountfactors such as your weaknesses (and possible remedies),external threats (competition, economic factors, etc.), yourmarketing mix strategy (products/services, promotionalgoals, pricing strategy, and distribution decisions), mediastrategy, sales and expense budgets, target market analysis(know your customers), and readily available marketingtools, as well as marketing tools that you need to researchor acquire.

52

CHAPTER- 6

JOB PROFILE

53

JOB DESCRIPTION

After the product training and initial understanding of the

policies, we were required to generate leads by doing

telecalling. In the RO department, there are no separate

telecallers and the ROs are supposed to generate their own

leads and do the sales. Initially we were supported by a

database given to us, but later we were asked to generate

own database. Thus we generated the data base through

internet search mainly and some other through directories of

certain specific areas in Delhi. The database and leads were

generated through both in- office work as well as field

work. It is described in the following sections:

6.1 TELECALLING

The telecalling was done not to pitch the product on

phone but the main idea was to convince the prospective

customers to listen to us, about the blank, the

services provided, get him interested in the wealth

management area and convince him for an appointment.

The telecalling function included all the following

things: -

6.1.1 Conforming the person’s name

6.1.2 Greeting the person

6.1.3 Introducing myself with my name and bank’s

name.

6.1.4 Telling him about the investment services

provided by the bank

6.1.5 Convince him for appointment.

6.1.6 Note down the time and address of the

appointment.

6.1.7 If the person asks to call later, ask for his

preferred time.

54

DIFICULTIES FACED DURING THE TELECALLING PROCESS

6.1 Person or contact number

6.2 Person that moment

6.3 Person not interested at all.

6.4 Person asking for the details, but not ready

to give appointment.

6.2 DATABASE GENERATION IN FIELD WORK

1. Database generation for motor insurance

In between there was surge of activities related the

ICICI Lombard general insurance sales. There were more

of training on general insurance products and also for

generating more leads for the sales of general

insurance. For the generation of leads, all the

summer’s trainees were given a form seeking information

about the four-wheeler owner {for the purpose of motor

insurance}

A one page form was used which sought the following

information:

The vehicle model

The month and year of purchase

The name and contact number

2. Cold Calling

We also did cold calling for the purpose of lead

generation and so as to get experience of facing the

prospective customers personally and handling the

client objections all by myself.

55

3. Cross selling of Credit Cards

Meanwhile our summer training the newly launched credit

cards of CBOP known by the name of miracle card, was

floated in the wealth management department also for

cross selling.

During the cold calling, we used to pitch the credit

cards and sold some of the credit cards. For the credit

cards to be granted to the customers, the verifications

of documents was a crucial step and thus we learnt

about the know your customers norms by RBI for credit

cards, which is a list of the required documents for a

credit card sale. The credit card sale pften required

two or three visits to the customers for complete

documentation.

56

CHAPTER- 7

OBJECTIONS

57

QUESTION 1: Am I too young to invest?

The power of compounding: the last moment. Longer you

delay the greater will be the financial burden on you to

meet your goals. On the other hand, you will b surprised

by what you can achieve by saving a small sum of money

regularly at an early age. Moreover the earliar you

invest; the longer your money works for you and greater

will be the power of compounding.

QUESTION 2: I don’t want to invest in private insurance

companies.

Insurance is a long term business entered into by

companies only after very careful deliberation and

recognizing a deep commitment to a market. Aviva combines

the financial powers and integrity of the dabur group,

with the international expertise and financial strength

of aviva.

QUESTION 3: Does Aviva guarantees returns like LIC?

The returns of Aviva policies are not guaranteed. The

rate of return would vary as per the product and the fund

chosen by the customers. You would also have noticed that

the most companies are moving away from the guaranteed

products. Many guaranteed return product have been

withdrawn from the market. Take example of Jeevan Shree,

Bima Nivesh, children’s money back , Jeevan Suraksha. All

these products have been withdrawn one after the another

in few last years.

58

QUESTION 4: What if the company winds up operations afterfew years? who will be responsible for my policy?

The philosophy of the insurance is the long term

commitment by the insurers to the policyholders, more

particularly in case of life insurance business. The

insurers can carry out insurance business in India only

after being registered with IRDA. Prior to grant of this

registration, the authority does an examination of the

credibility, financial strength and commitment of the

applicants to the Indian market. Only in suitable cases

will the authority grant the registration to the

applicant. As a policy, the authority looks into the

business projections of an applicant for 10 years to

ensure that the business plan to be carried out by the

applicant would be on a sound basis and there would not

be any attempt to under cut the interests of or under

price a product of a competitor which will affect the

strength and solvency of the insurer.

QUESTION 5: If my agent offers me a discount, can Iaccept it or is discounting illegal?

The agent is bound by law not to offer a rebate from out

of commission he gets; if he gives the discount to the

customer from the commission that he receives from the

insurance company, it will be an offence under the

insurance act, 1938.

59

OBSERVATIONS DURING SELLING EXPERIENCE

Disinterest in insurance – people are not very much

interested in the concept of insurance. They think the

risk coverage part to just a liability on their

returns. Even in the ULIP plans, they are more

interested in the investment part they take ULIP plans

for tax benefits. The ‘insurance’ in insurance has a

less weightage than the investment in insurance.

Lack of awareness about ULIP – people do not fully

understand what ULIP is all about and they tent to

think it is yet another mutual fund. During my calls,

to my surprise I found that a good number of investors

were not even aware that they have already taken ULIP

policy previously which they think to be as ‘some

fund’.

Reluctance towards long term plans- people are keen to

invest in short term like mutual funds and direct

equity market. They are reluctant to make a long term

commitment. This is another reason why people shy away

from insurance. Even in mutual funds, they are more

interested in short term. They also prefer liquidity.

Lack of knowledge about investments- I saw that many

people are not aware about mutual funds, demat system

of securities etc. the sales offer in that case should

strive to make him understand first about all the

investment avenues before his making a decision.

60

Apathy towards investment planning- some people I found

out were not even interested in planning how their own

money should be invested. They just rely on

intermediaries for their investment and do their

investment as and when there is a surplus.

Customers interested in discounts- some clients are

more interested in dealing with brokers and agents who

give out some of their own commission to the client as

a payback.

61

CHAPTER – 8

SUGESSTIONS AND RECOMMENDATIONS

62

Two months of our Summer Training proved to be a great

learning experience for us. However during these two months

of tenure we noticed some areas which may need small

improvements which are as follows:

i. More of Tellecalling

As there is no tellecalling department, more focus is

required to do telecalling by ROs. For this they must be

supported by a quality of database. Also training on

telecalling requires attention. Setting up a telecalling

department though is practiced in other banks but it has

also got its own demerits.

ii. Large Product Mix

As of now ROs are selling only two products life long and

saveguard since they provide maximum revenue to the banks.

But bank can offer more products of aviva under its

contract. So allowing and encouraging ROs to also sell other

products will enable them to offer large mix of products to

their clients.

iii. Realistic Targets

tough setting high targets are always practiced but setting

them too high may sometime also be a source of demotivation.

iv. Increase in advertisement and promotional campaigns

Till now there is no ad on TV or other media. There is lack

of awareness about the bank. The canopies put up by us

helped in promotional campaign. In future too, the

objectives of such activities should not be restricted to

database collection, but the focus should be long term brand

building for the bank.

63

v. Focus on portfolio designing

Currently the focus of employees is mainly on selling of

life insurance of products only. This focus should be

changed to whole of portfolio designing. This will require

training from expert in this field. For example Financial

planning Model can be used.

64

CHAPTER- 9

CONCLUSIONS

65Our summer training provided us valuable learning about the

industry, The product insurance and mutual funds and the

work experience of selling investment tools, especially life

insurance.

Banking industry and insurance industry today has enormous

scope in the form of bank assurance. Insurance industry has

seen enormous changes in the form of innovations. The

innovation of ULIP has brought a major change and has

revolutionized the growth of insurance industry. ULIP has

turned out to be a flexible, customer centric financial tool

having the advantage of both insurance and an investment.

We learned about technical features of the product and at

the same time, learned the soft skills needed to sell

investment tools. Especially selling of life insurance

involve a lot of relationship building, empathizing and

developing trust with the customers. It involves a lot of

patience as well.

We found that there is a gross lack of awareness about the

investment tools, especially the ULIP products, which can

greatly be improved by the sales peoples’ effort to educate

the customers about all the investment tools. The effort

should be to equip them with knowledge to let them make

better decision, rather than making decision on their

behalf. The latter is a short term approach to selling,

while the former will go a long way in building the faith of

the customer and thus the strong client.

We could generate some leads for the bank and the database

that we hope would materialize into sales. We learned

greatly from this experience and we tried to put in the best

of our effort to achieve our targets.

66

CHAPTER - 10

ANNEXURE

67

FAQ’s OF MARKETING

Q1. WHO Might YOU Choose to Reach With a Prudent Marketing-

Inspired Approach?

UNORGANIZED WORKERS

This would entail the clear identification of the target