a study on financial analysis of nestle india pvt. ltd for past five ...

72

“A STUDY ON FINANCIAL ANALYSIS OF NESTLE INDIA PVT. LTD FOR PAST FIVE YEARS” Project Report submitted to UNIVERSITY OF CALICUT In partial fulfillment of the requirement for the award of the degree of BACHELOR OF COMMERCE (PROFESSIONAL) Submitted by SHYAMILY K.S (CCASBCP039) Under the supervision of Asst. Prof. PRASSY VISWAMBHARAN DEPARTMENT OF COMMERCE CHRIST COLLEGE (AUTONOMOUS), IRINJALAKUDA MARCH 2021

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of a study on financial analysis of nestle india pvt. ltd for past five ...

“A STUDY ON FINANCIAL ANALYSIS OF NESTLE INDIA

PVT. LTD FOR PAST FIVE YEARS”

Project Report submitted to

UNIVERSITY OF CALICUT

In partial fulfillment of the requirement for the award of the degree of

BACHELOR OF COMMERCE (PROFESSIONAL)

Submitted by

SHYAMILY K.S

(CCASBCP039)

Under the supervision of

Asst. Prof. PRASSY VISWAMBHARAN

DEPARTMENT OF COMMERCE

CHRIST COLLEGE (AUTONOMOUS), IRINJALAKUDA

MARCH 2021

CHRIST COLLEGE (AUTONOMOUS), IRINJALAKUDA

CALICUT UNIVERSITY

DEPARTMENT OF COMMERCE

CERTIFICATE

This is to certify that the project report entitled “A STUDY ON

FINANCIAL ANALYSIS OF NESTLE INDIA PVT. LTD FOR

PAST FIVE YEARS” is a bonafide record of project done by SHYAMILY

K.S, Reg. No. CCASBCP039, under my guidance and supervision in partial

fulfillment of the requirement for the award of the degree of BACHELOR OF

COMMERCE (PROFESSIONAL) and it has not previously formed the basis for

any Degree, Diploma and Associateship or Fellowship.

PROF. K.O.FRANCIS Asst. prof. PRASSY VISWAMBHARAN

Co-ordinator Project Guide

DECLARATION

I, SHYAMILY K.S, hereby declare that the project work entitled

“A STUDY ON FINANCIAL ANANLYSIS OF NESTLE INDIA

PVT. LTD FOR PAST FIVE YEARS” is a record of independent and

bonafide project work carried out by me under the supervision and guidance of

Asst. Prof. PRASSY VISWAMBHARAN, Department of Commerce and

management studies, Christ College, Irinjalakuda.

The information and data given in the report is authentic to the best of my

knowledge. The report has not been previously submitted for the award of any

Degree, Diploma, Associateship or other similar title of any other university or

institute.

Place: Irinjalakuda SHYAMILY K.S

Date: CCASBCP039

ACKNOWLEDGEMENT

I would like to take the opportunity to express my sincere gratitude to all people who have helped me with sound advice and able guidance.

Above all, I express my eternal gratitude to the Lord Almighty under whose divine guidance; I have been able to complete this work successfully.

I would like to express my sincere obligation to Rev. Dr. Jolly Andrews, Principal-in-Charge, Christ college Irinjalakuda for providing various facilities.

I am thankful to Prof. K.O.Francis, Co-ordinator of B.Com (Professional), for providing proper help and encouragement in the preparation of this report.

I am thankful to Ms. Teena Thomas, Class teacher for her cordial support, valuable information and guidance, which helped me in completing this task through various stages.

I express my sincere gratitude to Ms. Prassy viswambharan, Assistant Professor, whose guidance and support throughout the training period helped me to complete this work successfully.

I would like to express my gratitude to all the faculties of the Department for their interest and cooperation in this regard.

I extend my hearty gratitude to the librarian and other library staffs of my college for their wholehearted cooperation.

I express my sincere thanks to my friends and family for their support in completing this report successfully.

TABLES OF CONTENTS

CHAPTER NO. CONTENTS PAGE NO:

LIST OF TABLES

LIST OF FIGURES

CHAPTER 1 INTRODUCTION 1 – 3

CHAPTER 2 REVIEW OF LITERATURE 4 – 17

CHAPTER 3 INDUSTRY AND

COMPANY PROFILE 18 – 25

CHAPTER 4 DATA ANALYSIS AND

INTERPRETATION 26 – 41

CHAPTER 5 FINDINGS, SUGGESTIONS

& CONCLUSION 42 – 45

BIBLIOGRAPHY

ANNEXURE

LIST OF TABLES

TABLE NO:

TITLE PAGE NO:

4.1 Table showing current ratio 27

4.2 Table showing liquid ratio 28

4.3 Table showing debt-equity ratio 29

4.4 Table showing solvency ratio 30

4.5 Table showing proprietary ratio 31

4.6 Table showing fixed assets to net worth ratio 32

4.7 Table showing fixed assets turnover ratio 33

4.8 Table showing net profit ratio 34

4.9 Table showing working capital turnover ratio 35

4.10 Table showing total assets turnover ratio 36

4.11 Table showing return on shareholder’s equity 37

4.12 Table showing total liability to total assets ratio 38

4.13 Table showing operating profit ratio 39

4.14 Table showing operating ratio 40

4.15 Table showing common size statement 41

LIST OF CHARTS

FIGURE NO:

TITLE PAGE NO:

4.1 Chart showing current ratio 27

4.2 Chart showing liquid ratio 28

4.3 Chart showing debt-equity ratio 29

4.4 Chart showing solvency ratio 30

4.5 Chart showing proprietary ratio 31

4.6 Chart showing fixed assets to networth ratio 32

4.7 Chart showing fixed assets turnover ratio 33

4.8 Chart showing net profit ratio 34

4.9 Chart showing working capital turnover ratio 35

4.10 Chart showing total assets turnover ratio 36

4.11 Chart showing return on equity shareholders fund 37

4.12 Chart showing total liability to total asset ratio 38

4.13 Chart showing operating profit ratio 39

4.14 Chart showing operating ratio 40

CHAPTER Ⅰ

INTRODUCTION

1

1.1 Introduction

A healthy vibrant economy provides channels to transfer fund from

individual and groups who have saved money to individual and group who

want to borrow money. The financial system is complex in both function and

structure throughout the world.

Finance is regarded as life blood of business and it is the basic foundation of

all kinds of economic activities. Finance is defined as procurement of funds

and effective utilisation of funds. Finance is very essential for smooth

running of business. Finance is needed to promote or establish the business,

acquire fixed assets and to conduct business studies.

Financial statement analysis is the process of examining relationship among

financial statement elements and making comparisons with relevant

information. The purpose of financial analysis is to diagnose the information

contained in financial statements so as to judge profitability and financial

soundness of the firm. It is a valuable tool by investor, creditors, financial

analysts and others in their decision making process related to stocks, bonds,

other financial instruments. A financial analyst analysis the financial

statements with various tools of analysis before commenting upon the

financial health or weakness of an enterprise. The process of analysing

financial statement involves the rearranging, comparing and measuring the

significance of financial and operating data.

Financial statement analysis helps in comparing companies of different size

with each other and the most important benefit is that it provides an idea to

the investors about deciding on investing their funds in a particular company.

Financial statement analysis involves reviewing the financial statements of

an organization to gain an understanding of its financial situation. Financial

statements usually include a balance sheet, income statement, statement of

cash flows and supplementary notes. An internal analysis is conducted by

employees, executives or other individuals with access to a business firms

internal accounting records. In contrast an external analysis is conducted by

outsiders with access to published financial statements. These outsiders may

2

include creditors, investors, credit agencies, government agencies or the

general public. Tools and techniques used in financial analysis include cash

flow analysis, common-size statement analysis, cost-volume-profit analysis,

fund flow analysis, networking capital analysis and trend analysis.

Financial analysis can be conducted using either horizontal/vertical analysis

or analysis that uses ratios. Analysis by using ratio is used to calculate the

relative size of one figure in relation to another which can then be compared

to ratio for a prior period. Financial statement analysis involves careful

selection of data from financial statement for the primary purpose of

forecasting the financial health of the company. This is accomplished by

examining trends in key financial data across companies, and analysing key

financial ratio. This project entitled “A study on financial analysis of Nestle

India Limited” is mainly focusing on financial performance of Nestle India

limited for past five years.

1.2 Statement of the problem:

Financial analysis of company helps in identifying profit and in predicting

the risk of bankruptcy. Money is considered as life of an economy. The

subject matter of study is concerned with the financial performance of nestle

company. Company has diverse manufacturing of food products. In this

study analyse the last 5 year total sales, shareholders fund, Borrowings and

financial position of the Nestle India limited.

1.3 Significance of the study:

The COVID-19 pandemic crisis results in reduction in consumption of food

products as well as disrupted supply chains. Management should assess the

existing and anticipated effects of COVID-19 on the company’s activities,

financial performance and the position of the company. In scenario of this

recession stage, company should be able to provide products with more

offers or in less price.

1.4 Objective of the study:

Following are the important objectives of the study:-

To find out liquidity and solvency position of company

3

To know the profitability of company

To find out financial position of company

1.5 Research Design:

1.5.1 Nature of study:-

This is an analytical study

1.5.2 Nature of data:-

Secondary data is used in the study. Secondary data include financial

variables and accounting such as yearly net profit, dividend, book value

per share, earnings per share, market price of share, beta, book value of

equity, number of outstanding shares, etc., of each company.

1.5.3 Sources of data:-

The study used secondary data. Secondary sources include annual

reports of Nestle India, journals and other published sources

1.5.4 Period of study:-

Financial data is collected for a period of 5 years from 2015- 2019

1.6 Tools of study:

Ratio analysis is used for comparing for 5 year.

Common size statements is used for 2 year

1.7 Limitations:

The study was limited to only 5 year financial data

Resource available for data is limited

1.8 Chapterization:

Chapter 1- Introduction

Chapter 2- Review of literature

Chapter 3- Industry profile and company profile

Chapter 4- Data analysis and interpretation

Chapter 5- Findings, suggestions and conclusions

CHAPTER Ⅱ

REVIEW OF LITERATURE

4

2.1 Introduction

A literature review discusses published information in a particular subject area,

and sometimes information in a particular subject area within a certain time

period. A literature review can be just a simple summary of the source, but is

usually as an organizational pattern and combines both summary and synthesis.

It helps in clarifying and defining the problem, stating the objectives, formulating

hypothesis, selecting an appropriate design and methodology of research as well

as interpreting the result in the light of research work already undertaken in the

previous studies. In this chapter an endeavour has been made to provide and

present an overview of various aspects of this study through the review of

existing literature. The sources referred include journals, books, working papers,

report related to human resources etc.

Empirical research is published in books and in scholarly, peer-reviewed

journals. However, most library database does not offer straight forward ways to

locate empirical research.

2.2 Conceptual Review

The review of literature guides the researchers for getting better understanding

of methodology used, limitation of various available estimation procedures and

database, and lucid interpretation and reconciliation of the conflicting results.

Besides this, the review of empirical studies explores the avenues for future and

present research efforts related to the subject matter. In case of conflicting and

unexpected results, the research can take the advantage of knowledge of their

researchers simply through the medium of their published works. A number of

research studies have been carried out on different aspects of performance

appraisal by the researchers, economists and academicians in India and abroad.

Different authors have analysed performance in different perspectives. The

analysis of financial statements is a process of evaluating the relationship

between component parts of financial statements to obtain a better understanding

of the firm’s position and performance.

5

Financial statement analysis is largely a study of relationship among the various

financial factors in a business as disclosed by a single set of statements. It is a

process of evaluating the relationships component parts of a financial statement

to obtain a better understanding of a firm’s positions and performance. Financial

statements analysis is an attempt to determine the significance and meaning of

the financial data so that forecast may be made of the future ability to pay interest

and debt maturities a (both current and long term) and profitability of a sound

policy. The five key elements of financial analysis is Revenues, Profits,

operational efficiency, Capital efficiency, solvency and liquidity.

Financial statement present the financial activities and health of the business in

clear and concise manner. However the further disclosure are made as per

relevant laws, regulations and as required by accounting standard that is used.

Financial statement analysis is the process of evaluating business, projects,

budgets, and other finance related transactions to determine their performance

suitability. The main advantages of financial statement analysis is helpful to the

government agencies in analysing the taxation owed by the firm, company is

able to analyse its own performance over a specific time period, budget outline

in real- time, pattern detection and forecasting, communicate with shareholders.

The main disadvantages of financial statement analysis is making strategic

decisions based on figures and data pertaining to the current market conditions

which may fluctuate, analysis of at-one-time basis, ignores the price level

changes, influence of personal judgement.

2.3 Tools or Techniques of Financial Statements

2.3.1 Ratio Analysis

A ratio is a simple arithmetical expression of the relationship of one number to

another number. Ratio analysis can be defined as the process of ascertaining the

financial ratios that are used for indicating the ongoing financial performance of

a company. Ratio analysis is a widely used tool of financial analysis. It can be

used to compare the risk and return relationships of firms of different sizes. Ratio

6

analysis was perhaps the financial tools developed to analysis and interpret the

financial statement and is still used widely for this purpose. It is one of the most

prevalent method of analysing a balance sheet. Any number of ratio can be

prepared by comparing any two figures available in the balance sheet on profit

and loss account or both.

2.3.2 Classification of Ratios

Accounting ratio can be classified in several ways, in general accounting ratios

may be classified on the following basis;

Liquidity Ratios

Leverage Ratios

Activity Ratios

Profitability Ratios

Market Test Ratio

2.3.2.1 Liquidity Ratios

The term liquidity refers to the firm's ability to pay its current liabilities out of

it’s currently assets. Liquidity ratios are used to measure the liquidity position or

short term debt paying ability of a firm. These ratios are highly useful to creditors

and commercial banks that provide short term credit important liquidity ratios

are:

1. Current Ratio

Current Ratio is one of the oldest of all financial ratios. It was first used in 1891.

Current ratio is defined as the ratio of current assets to current liabilities. It shows

the relationship between total current assets and total current liabilities. It is the

measure of firm’s short term solvency. That is, its ability to meet short-term

obligations. In sound business a current ratio of 2:1 is considered as an ideal one.

Current Assets = Current assets

Current liabilities

7

2. Liquid Ratio or Quick Ratio

Liquid ratio is the ratio of liquid assets (or quick assets) to current liabilities. It

establishes the relationship between quick assets and current liabilities. It is the

measure of the instant debt paying ability of the business enterprise. It is also

called acid test ratio. An acid test ratio of 1:1 is considered to be satisfactory as

a firm can easily meet all its current liabilities. Inventory are considered to be

less liquid. It is computed as follows:

Liquid ratio = Liquid Assets

Current liabilities

3. Absolute Liquid Ratio or Cash Ratio

Cash ratio of absolute liquid ratio show the relationship between cash and current

liabilities. Absolute liquid asset includes cash in hand and cash at bank and

marketable securities are temporary investments. The acceptable norm for this

ratio is 0.75:1.

Absolute liquid ratio= cash and bank+ short term securities/current liabilities

2.3.2.2 Leverage Ratios

The term solvency means the ability of a firm to meet its long-term obligations.

The long-term creditors of firms are primary interested in knowing firms ability

to pay interest on long term borrowings, repayment of principle amount of

maturity etc. So this ratio indicates a firm's ability to meet with interest, cost and

repayment schedule associated with this long term borrowings. These ratios are:

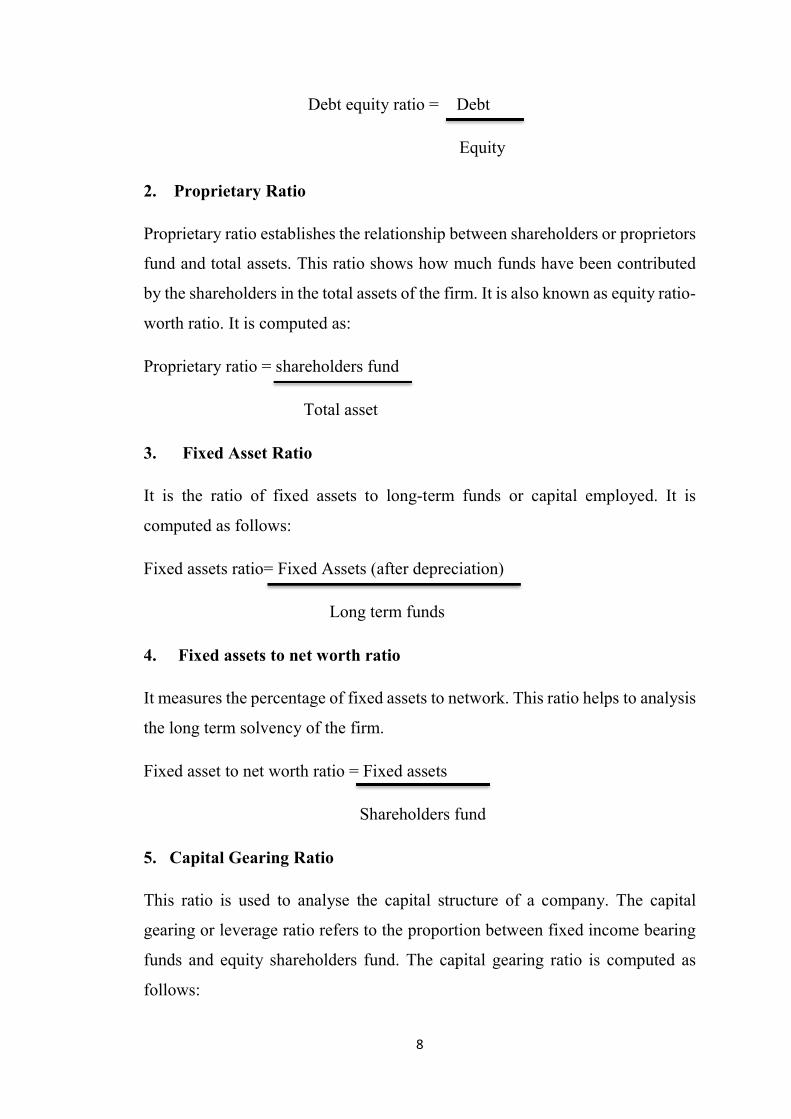

1. Debt Equity Ratio

It shows the relationship between total debt and owned debt. It is the ratio of the

amount invested by the shareholders. This ratio reflects the relative claim of

shareholders and creditors against the Assets of the company. This ratio is also

known as external-internal equity ratio. It is computed as:

8

Debt equity ratio = Debt

Equity

2. Proprietary Ratio

Proprietary ratio establishes the relationship between shareholders or proprietors

fund and total assets. This ratio shows how much funds have been contributed

by the shareholders in the total assets of the firm. It is also known as equity ratio-

worth ratio. It is computed as:

Proprietary ratio = shareholders fund

Total asset

3. Fixed Asset Ratio

It is the ratio of fixed assets to long-term funds or capital employed. It is

computed as follows:

Fixed assets ratio= Fixed Assets (after depreciation)

Long term funds

4. Fixed assets to net worth ratio

It measures the percentage of fixed assets to network. This ratio helps to analysis

the long term solvency of the firm.

Fixed asset to net worth ratio = Fixed assets

Shareholders fund

5. Capital Gearing Ratio

This ratio is used to analyse the capital structure of a company. The capital

gearing or leverage ratio refers to the proportion between fixed income bearing

funds and equity shareholders fund. The capital gearing ratio is computed as

follows:

9

Capital gearing ratio = fixed income bearing funds Equity/ shareholders fund

i.e., Preference share capital + debentures + long term loans

Equity Shareholders fund

6. Solvency Ratio

This ratio expresses the relationship between total Assets and total liabilities of

a business. It measures the solvency of the business. This ratio is known as

solvency ratio. This ratio is generally expressed as a proportion. The following

formula is used for computing solvency and ratio.

Solvency ratio = Total assets

Total debt

Interest coverage ratio

The interest coverage ratio is a debt ratio and profitability ratio used to determine

how easily a company can pay interest on its outstanding debt. The interest

coverage ratio may be calculated by dividing a company's earnings before

interest and tax (EBIT) by its interest expense during a given period by the

company's interest payments due within the same period.

The interest coverage ratio is sometimes called the times interest earned (TIE)

ratio. Lenders, investors, and creditors often use this formula to determine a

company's riskiness relative to its current debt or for future borrowing

Interest coverage ratio = EBIT

Interest

10

2.3.2.3 Activity Ratio

These ratios indicate efficiency in Asset Management. These ratios are also

known as efficiency ratios or performance ratios of assets utilization ratios. The

ratio indicates the cash elasticity of current assets. This ratio indicates the speed

with which the resources are turned over or converted into cash. These ratios are

also known as turnover ratios. It should be noted that turnover ratios are always

expressed in number of times, i.e., rate of turning over. Important activity or

turnover ratios are:

1. Inventory Turnover Ratio

Inventory or stock turnover ratio shows the relationship between cost of goods

sold and average inventory on stock. It is also called merchandise turnover ratio,

it is obtained by dividing cost of goods sold by average stock. Stock turnover

ratio is computed by the following formula:

Stock turnover ratio = Cost of goods sold

Average stock

2. Debtors Turnover Ratio

Debtors‟ turnover ratio explain the relationship between net credit sales and

average debtors including bills receivable. This ratio shows how quickly debtors

are realized or converted into cash. It is also known as receivables turnover ratio.

The following formula used for calculating debtor’s turnover ratio:

Debtors turnover ratio = Net credit sales

Debtors including B/R

3. Creditors Turnover Ratio

It shows the relationship between net credit purchase and average creditors

including bills payable. This ratio indicates the number of times the creditors are

11

paid. It is also called payable turnover ratio, it is computed by the following

formula:

Creditors turnover ratio= Net Credit Purchase

Average Creditors including B/P

4. Working capital turnover ratio

Current asset will change with change in sales. This means working capital is

related with States. The relation between sales and working capital is called

working capital turnover ratio. This ratio shows how many times the working

capital is turned over to produce sales. Working capital turnover ratio is

computed by the following formula:

Working capital turnover ratio = Net sales

Working capital

5. Fixed asset turnover ratio

For knowing whether fixed asset or effectively utilized or not, fixed asset

turnover ratio is used. Fixed asset turnover ratio establishes the relationship

between net sales and fixed asset. It measures the efficiency with which a firm

is utilizing its fixed assets in producing sales. It is computed as follows:

Fixed asset turnover ratio = Net sales

Net fixed assets

2.3.2.4 Profitability Ratios

The term profitability refers to the ability of a firm to earn income. The

profitability of a firm can be easily measured by its profitability ratios.

Profitability ratios are always based on sales. Important profitability ratios are:

12

1. Gross profit ratio :

Gross profit or sales profit or gross margin is the difference between revenue and

the cost of making a product. This is the ratio of gross profit to sales expressed

as percentage. It is also known as gross margin. It is calculated as follows:

G/P ratio = Gross profit x100

Net sales

2. Operating ratio

Operating ratio expresses the relationship between operating cost and sales. It

indicates the overall efficiency in operating the business. The formula for

computing operating ratio is as follows:

Operating ratio = Cost of goods sold + operating expenses x 100

Sales

3. .Net profit ratio

Net profit ratio is the ratio of net profit earned by a business and its net sales. It

measures overall profitability. It is calculated as follows

N/P Ratio= Net profit x 100

Net Sales

4. Operating profit ratio

Operating profit ratio Explain the relationship between operating profit and net

sales. It is calculated by the following formula:

Operating profit ratio= operating profit x 100

Net sales

13

5. Return on investment (ROI)

ROI measures the overall profitability. It establishes the relationship between

profit or return and investment. It is also called the accounting rate of return. It

is computed as follows:

ROI = Profit before interest and tax x 100 /Capital employed

6. Return on shareholders fund

This is the ratio of net profit to shareholders fund or net-worth. It measures the

profitability from the shareholders point of view. It is calculated as follows:

Return on shareholders fund = Net profit after interest and tax x 100 Shareholders

fund

2.3.2.5 Market Test Ratio

Market test ratio are used for evaluating the shares and stocks which are traded

in the market. The value of shares in the stock exchange depends upon a number

of factors like book value of shares, future profitability of company, return on

equity shares, earnings per share, Dividend policy, dividend per share, dividend

pay-out ratio etc. Important Market test ratio are as follows:

1. Dividend per share

The dividend paid to equity shareholders on a per share basis is DPS. In other

words, it is a dividend paid to equity shareholder divided by the number of equity

shares outstanding. The formula is

DPS = Dividend paid to equity shareholders

No. of equity shares

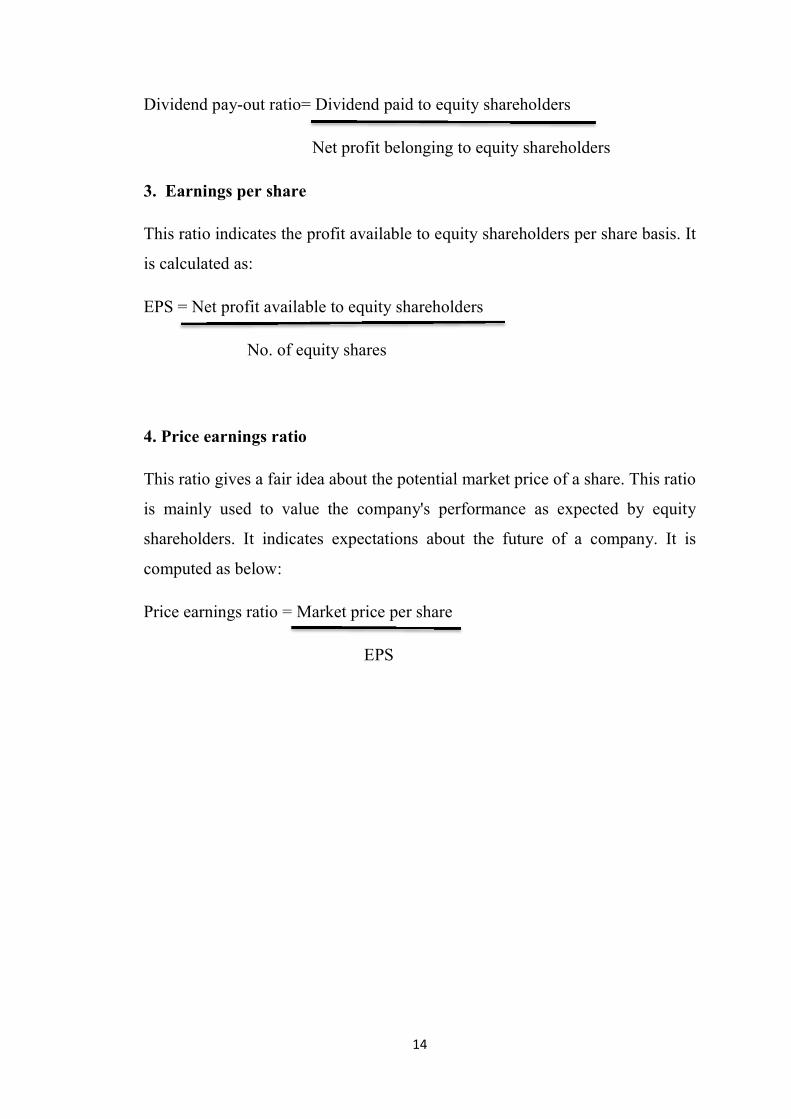

2. Dividend pay-out ratio

Dividend pay-out ratio measures the relationship between the dividend

paid to equity shareholders and the earnings belonging to them. It may be

expressed as follows:

14

Dividend pay-out ratio= Dividend paid to equity shareholders

Net profit belonging to equity shareholders

3. Earnings per share

This ratio indicates the profit available to equity shareholders per share basis. It

is calculated as:

EPS = Net profit available to equity shareholders

No. of equity shares

4. Price earnings ratio

This ratio gives a fair idea about the potential market price of a share. This ratio

is mainly used to value the company's performance as expected by equity

shareholders. It indicates expectations about the future of a company. It is

computed as below:

Price earnings ratio = Market price per share

EPS

15

2.3 Empirical Literature

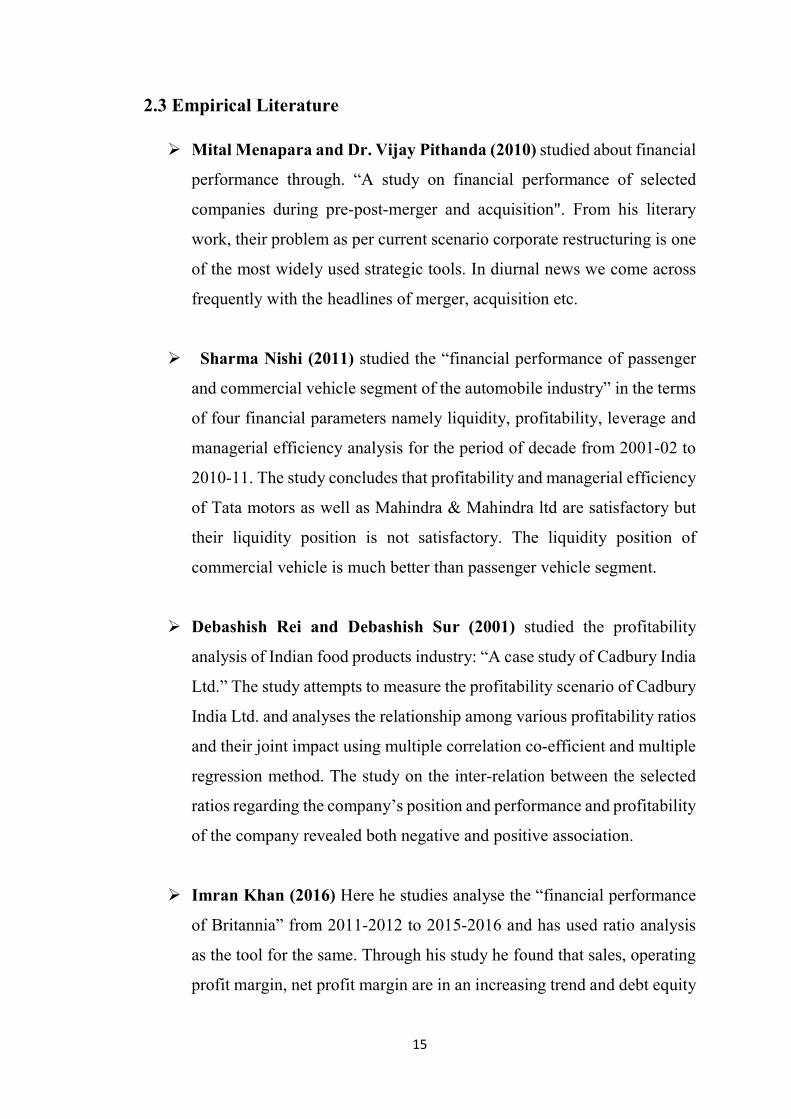

Mital Menapara and Dr. Vijay Pithanda (2010) studied about financial

performance through. “A study on financial performance of selected

companies during pre-post-merger and acquisition". From his literary

work, their problem as per current scenario corporate restructuring is one

of the most widely used strategic tools. In diurnal news we come across

frequently with the headlines of merger, acquisition etc.

Sharma Nishi (2011) studied the “financial performance of passenger

and commercial vehicle segment of the automobile industry” in the terms

of four financial parameters namely liquidity, profitability, leverage and

managerial efficiency analysis for the period of decade from 2001-02 to

2010-11. The study concludes that profitability and managerial efficiency

of Tata motors as well as Mahindra & Mahindra ltd are satisfactory but

their liquidity position is not satisfactory. The liquidity position of

commercial vehicle is much better than passenger vehicle segment.

Debashish Rei and Debashish Sur (2001) studied the profitability

analysis of Indian food products industry: “A case study of Cadbury India

Ltd.” The study attempts to measure the profitability scenario of Cadbury

India Ltd. and analyses the relationship among various profitability ratios

and their joint impact using multiple correlation co-efficient and multiple

regression method. The study on the inter-relation between the selected

ratios regarding the company’s position and performance and profitability

of the company revealed both negative and positive association.

Imran Khan (2016) Here he studies analyse the “financial performance

of Britannia” from 2011-2012 to 2015-2016 and has used ratio analysis

as the tool for the same. Through his study he found that sales, operating

profit margin, net profit margin are in an increasing trend and debt equity

16

ratio and return on assets how decrease. He also put up some suggestions

like current asset should be increased, debt capital should be increased.

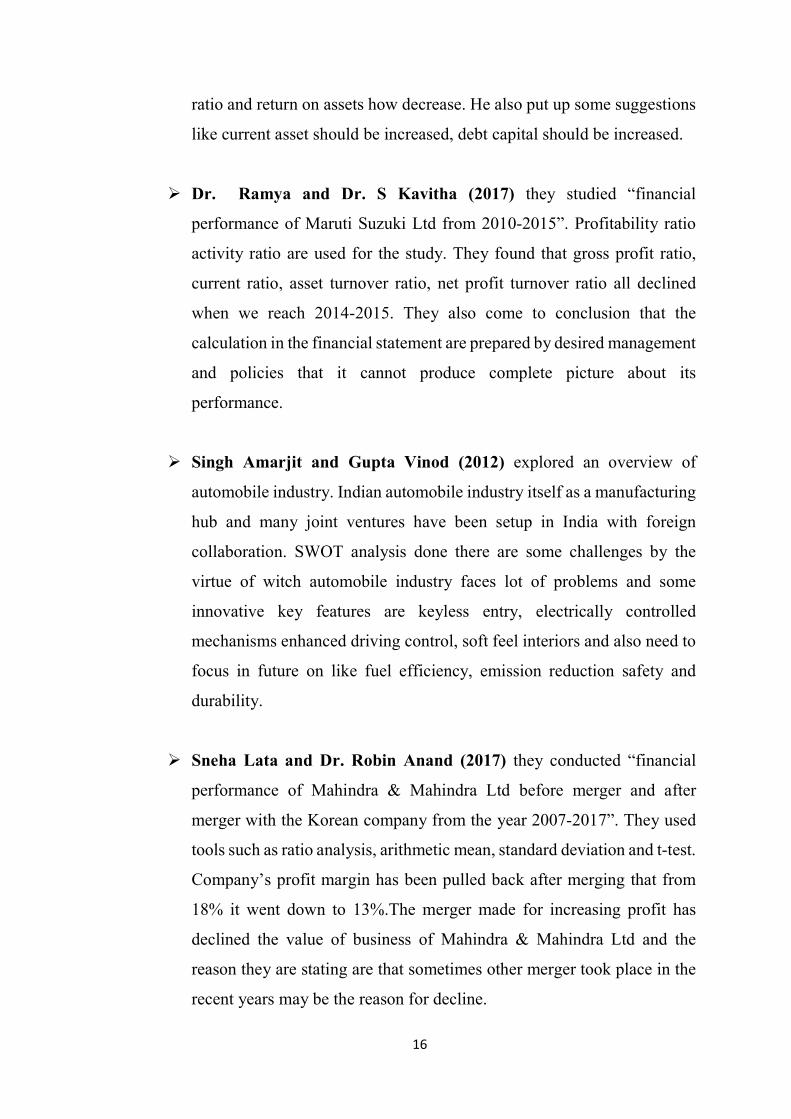

Dr. Ramya and Dr. S Kavitha (2017) they studied “financial

performance of Maruti Suzuki Ltd from 2010-2015”. Profitability ratio

activity ratio are used for the study. They found that gross profit ratio,

current ratio, asset turnover ratio, net profit turnover ratio all declined

when we reach 2014-2015. They also come to conclusion that the

calculation in the financial statement are prepared by desired management

and policies that it cannot produce complete picture about its

performance.

Singh Amarjit and Gupta Vinod (2012) explored an overview of

automobile industry. Indian automobile industry itself as a manufacturing

hub and many joint ventures have been setup in India with foreign

collaboration. SWOT analysis done there are some challenges by the

virtue of witch automobile industry faces lot of problems and some

innovative key features are keyless entry, electrically controlled

mechanisms enhanced driving control, soft feel interiors and also need to

focus in future on like fuel efficiency, emission reduction safety and

durability.

Sneha Lata and Dr. Robin Anand (2017) they conducted “financial

performance of Mahindra & Mahindra Ltd before merger and after

merger with the Korean company from the year 2007-2017”. They used

tools such as ratio analysis, arithmetic mean, standard deviation and t-test.

Company’s profit margin has been pulled back after merging that from

18% it went down to 13%.The merger made for increasing profit has

declined the value of business of Mahindra & Mahindra Ltd and the

reason they are stating are that sometimes other merger took place in the

recent years may be the reason for decline.

17

Huda Salhe Meften and Manish Roy Tirkey (2014) have studied the

“financial analysis of Hindustan petroleum corporation ltd.” The study is

based on secondary data. The company has got excellent gross profit ratio

and trend is rising in with is appreciable indicating efficiency in

production cost. The net profit for the year 2010-11 is excellent & it is 8

times past year indicating reduction in operating reduction in operating

expenses and large proportion of net sales available to the shareholders of

company.

Dr. M Ravichandran& M Venkat Subramanian (2016) studied on

Force Motors formerly known as Bajaj Tempo from 2010-2015. They

used ratio analysis, comparative financial statement analysis. The

company’s financial performance is good that it shows an increase in

reserve and surplus and decrease in borrowings. They suggest that it can

further improve by concentrates on its operating, administrative and

selling expenses and by reducing the expenses.

Vijayakumar A. (1996) has studied about "Assessment of Corporate

liquidity a discriminate analysis approach" in this research he has revealed

that the growth rate of sales, leverage, current ratio, operating expense to

sales and vertical integration was the important variables which determine

the profitability of Companies. In this study discriminating Z' scores have

been calculated with the help of discriminate function and according to

the 'Z' is scores the companies are ranked in order of liquidity.

CHAPTER Ⅲ

INDUSTRY AND COMPANY

PROFILE

18

3.1 Industry Profile

India is the world's second largest producer of food and has the potential of being

the biggest with the food and agricultural sector. The food industry is a complex,

global network of diverse business that supplies most of the food consumed by

the world's population. The term food industries covers a series of industrial

activities directed at the production, distribution, processing, conversion,

preparation, preservation, transport, certification and packaging of foodstuffs.

The food industry today has become highly diversified, with manufacturing

ranging from small, traditional, family-run activities that are highly labour-

intensive, to large, capital-intensive and highly mechanized industrial processes.

Many food industries depend almost entirely on local agriculture produce or

fishing. The Indian food industry is poised for huge growth, increasing its

contribution to world food trade every year. In India, the food sector has emerged

as a high-growth and high-profit sector due to its immense potential for value

addition, particularly within the food processing industry. The total food

production in India is likely to double in the next ten years and there is an

opportunity for large investments in food and food processing technologies,

skills and equipment, especially in areas of Canning, Dairy and Food Processing,

Specialty Processing, Packaging, Frozen Food/Refrigeration and Thermo

Processing. Fruits & Vegetables, Fisheries, Milk & Milk Products, Meat &

Poultry, Packaged/Convenience Foods, Alcoholic Beverages & Soft Drinks and

Grains are important sub-sectors of the food processing industry. The Indian food

and grocery market is the world’s sixth largest, with retail contributing 70 per

cent of the sales. The Indian food processing industry accounts for 32 per cent

of the country’s total food market, one of the largest industries in India and is

ranked fifth in terms of production, consumption, export and expected growth.

According to Ministry of Food Processing India, Food Processing Industry

accounts for about 32% of the country’s total food market, the Food Processing

Industry is one of the largest industries in India and is ranked fifth in terms of

production, consumption, export and expected growth. The Indian Food

19

Processing Industry has grown by 11% in the last decade and is expected to reach

$480 billion by 2020. The industry contributes to 14% of the country’s

manufacturing GDP, 13% of exports and 6% of total industrial investment. The

food industry has a large influence on consumerism. Food Processing Industry is

not only the need of the hour but also has the potential to bring prosperity in rural

economy and contribute to the socio economic development of the country. It is

certainly the pathway of a new future for India. However, the real challenge is

to develop industry in a way which takes care of small scale industry along with

attracting big ticket domestic and foreign investments. Indian food processing

industry is primarily export oriented. With the export growth rate of around 15%,

its share in the international market is only 1.7%. Again, only 2% of the total

food produced in India is processed for further consumption. Food consumption

drives demand, and this depends on population growth. The profitability of

individual companies depends on efficient operations, because products are

commodities subject to intense price competition. Companies compete largely

based on cost and their ability to distribute the finished product. Large companies

have economies of scale in purchasing and distribution. Small companies can

compete effectively in local or regional markets and by developing popular

products. The Indian food processing industry accounts for 32 per cent of the

country’s total food market, one of the largest industries in India and is ranked

fifth in terms of production, consumption, export and expected growth.

The Ministry of Food Processing Industries is a ministry of the Government of

India responsible for formulation and administration of the rules and regulations

and laws relating to food processing in India. The ministry was set up in the year

1988, with a view to develop a strong and vibrant food processing industry, to

create increased employment in rural sector and enable farmers to reap the

benefits of modern technology and to create a surplus for exports and stimulating

demand for processed food. The ministry is currently headed by Narendra Singh

20

Tomar, a Cabinet Minister who is also the Minister of Agriculture & Farmers

Welfare and Minister of Rural Development.

Reasons for the growth of the food industry

Increased urbanization in the country has given a boost to the food industry in

India.

Majority of the women in the country are working as a result of which families

have extra income which they are spending in buying food.

The standard of living in the country has improved as a result of which there

has been an increased demand for food.

Supermarkets and malls have opened all over the country and this has helped

in making shopping for food a pleasurable experience.

The consumers can select, inspect and pick up food items that they like in an

ambience that is comfortable. This too has helped to boost the sale of food

products in the country.

3.2 Company Profile

Nestle India Limited, is the Indian subsidiary of Nestle which is a Swiss

multinational company. Nestle was founded in 1867 in Geneva, Switzerland by

Henri Nestle. Nestle's first product was "Farine Lactee Nestle", an infant cereal.

In 1905, Nestle acquired the Anglo-Swiss Condensed Milk Company. Nestle’s

relationship with India started 1912, when it began trading as The Nestle Anglo-

Swiss Condensed Milk Company (Export) Limited, importing and selling

finished products in the Indian market. The company is headquartered in

Gurgaon, Haryana. The company's products include food, beverages, chocolate,

and confectioneries. The company was incorporated on 28 March 1959 and was

21

promoted by Nestle Alimentana S.A. via a subsidiary, Nestle Holdings Ltd. As

of 2020, the parent company Nestle owns 62.76% of Nestlé India. The company

has 8 production facilities in various locations across India. With eight factories

and a large number of co-packers, Nestle India is a vibrant Company that

provides consumers in India with products of global standards and is committed

to long-term sustainable growth and shareholder satisfaction. The Company

insists on honesty, integrity and fairness in all aspects of its business and expects

the same in its relationships. This has earned it the trust and respect of every

strata of society that it comes in contact with and is acknowledged amongst

India's 'Most Respected Companies' and amongst the 'Top Wealth Creators of

India'. Nestlé India, one the biggest players in FMCG segment, has a presence in

milk & nutrition, beverages, prepared dishes & cooking aids & chocolate &

confectionery segments. Nestle India manufactures products of truly

international quality under internationally famous brand names such as

NESCAFE, MAGGI, MILKYBAR, KIT KAT, BAR-ONE, MILKMAID and

NESTEA and in recent years the Company has also introduced products of daily

consumption and use such as NESTLE MILK, NESTLE SLIM MILK, NESTLE

Dahi and NESTLE Jeera Raita. Nestle has created brands like Nestle Milkmaid,

Nestle Everyday, Maggi Noodles, Maggi Soups, Polo, Kit Kat, Nescafe & many

more. The objective of Nestle is “We unlock the power of food to enhance

quality of life for everyone, today and for generations to come” and their motto

is ‘Good food, Good life’. As per the market-wise position Nestlé India stands

first in instant noodles & ketchups, second in healthy soups, No.1 in instant

coffee, & No.2 in overall chocolate category. The company innovates new

product & renovates existing one providing high quality, safe food products at

affordable prices. In June 2015, Nestle India's instant noodles product 'Maggi

Noodles' was banned by the Government of Delhi for a 15 day period after lead

and monosodium glutamate in samples of the product were found to be beyond

permissible limits. On 5 June 2015 Maggi noodles were banned nationwide by

the Food Safety and Standards Authority of India (FSSAI). The ban was

overturned on 13 August 2015 following the Bombay High Court's order and

22

samples of Maggi Noodles were ordered to be retested within 6 weeks by three

labs authorized by the National Accreditation Board for Testing and Calibration

Laboratories. Nestle was fined ₹45 lakh for the incident by the district

administration. Between 5 June 2015 when the noodles were first banned and 1

September 2015, Nestle recalled 38,000 tonnes of Maggi Noodles from stores

and incinerated them at 11 cement plants across India Nestle eventually cleared

the Bombay High Court mandated lab tests and Maggi Noodles were allowed to

be manufactured and sold again.

It’s 1867 in Switzerland, and a premature baby cannot breastfeed, which is

worrying in an era when many infants die of malnutrition due to a lack of

effective breast milk alternatives. Henri Nestle learns about the case and feeds

the child his new ‘farine lactee’ infant food. It is the only product that the boy

can digest, and he survives. Word of Nestle’s success spreads rapidly, and

through determination, commitment and a pioneering spirit he builds a thriving

business. His life-saving innovation is the model for all those that follow

throughout Nestle’s 150 years, which show the company’s skill in meeting and

anticipating consumers’ changing needs. Worldwide, people now consume more

than one billion servings of Nestle products per day. The company operates in

over 197 countries and employs almost 340,000 people. It’s a far cry from the

small-scale business that Henri Nestle founded in Vevey, Switzerland. But

Nestlé still embraces his values, his famous ‘Nest’ logo, and its headquarters in

the city. The company’s early success was due to its investment in science-based

products and modern factories to produce them efficiently. Railways and

steamships gave Nestle & Anglo-Swiss access to new urban markets worldwide,

and it made savvy use of modern advertising media – newspapers, magazines,

billboards – to educate people on product benefits. Namely, nutrition, quality,

safety, affordability and taste. It’s a blueprint for success that, bar a few

necessary updates, still applies today. One other benefit that Nestle products have

always offered is convenience, and this became especially important after World

War Two, when more women entered the workplace, and people demanded

foods that were easy to prepare. By 1938, people could ‘start the day with a

23

Nescafé’, the world’s first great-tasting instant coffee, simply by adding hot

water. By 1948 they could enjoy Nesquik, a cocoa-based powder that dissolves

easily in cold milk. And by 1957, they could finish the day with Maggi pasta

‘ready meals’ in cans, which were hugely successful. Cans weren’t new, but

nutritious meals in cans were, and this quickly became a high-growth segment

for Nestle. Such foods had a long shelf life, were easy to heat then eat, and you

could even enjoy them cold. Cans were also simple to transport, so you could

consume them on a camping trip, for instance, along with your cup of Nescafe.

Such products helped to shape our modern world, and life would never be the

same. From the 1960s, you could also enjoy the convenience of Nestle frozen

foods and ice creams, which the company entered as domestic fridges and

freezers grew in popularity. In 1986 Nestle went one step further by creating its

own breakthrough Nespresso system, which changed the way we experience

premium coffee. Nespresso is another Nestle innovation that enhances people’s

quality of life, everywhere, every day. In doing so it brings pleasure, an emotion

we associate strongly with chocolate. Nestle first entered this key business in

1904 when it took on export sales for Peter & Kohler, later adding brands such

as Cailler and KitKat. Today Nestle business spans beverages, waters, dairy,

confectionery, petcare, even skincare. In 2011 the company extended its

leadership in Nutrition, Health and Wellness by creating Nestle Health Science,

to develop nutritional healthcare products that target optimal brain health, for

example, or healthy aging. Such innovations will help Nestlé address the global

challenges of malnutrition, growing and aging populations and obesity. This

same passion for nutrition underpins a commitment to improve products by

reducing salt, sugar and saturated fats, and fortify them with vitamins, minerals,

vegetables and whole grains. The main objectives of Nestle India ltd is to

manufacture and market the company’s products in such a way so as to create

value that can be sustained over the long term for consumers, shareholders,

employees and business partners. Nestle aims to create value for consumers that

can be sustained over the long term by offering a wide variety of high quality,

safe food products at affordable prices. The company continuously focuses its

24

efforts to better understand the changing lifestyles of modern India and anticipate

consumer needs in order to provide convenience, taste, nutrition and wellness

through its product offerings. Achievements of Nestle India ltd are CNBC

Awaaz Consumer Awards has honoured Nescafe as the most preferred coffee

brand., Business India has rated Nestle India as No.1 on Return On Capital

Employed amongst Super 100 companies, In 2006-2007 Nestlé India was

awarded the ‘Best Exporter of Instant Coffee’ ‟Highest Exporter to Russia and

CIS”, ‘Highest Exporter to Far East Countries’, In 2009 Nestle India Board

approved Proposal to acquire Healthcare Nutrition Business of Speciality.

3.2.1 Mission of the company

Nestle is the world's leading nutrition, health and wellness company. Innovation

foundation mission is "Good Food, Good Life" is to provide consumers with the

best tasting, most nutritious choices in a wide range of food and beverage

categories and eating occasions, from morning to night.

3.2.2 Vision and value of the company

To be a leading, competitive, Nutrition, Health and Wellness Company

delivering improved shareholder value by being a preferred corporate citizen,

preferred employer, preferred supplier selling preferred products.

3.2.3 Shareholding and Listing

Nestle India shares are listed on Bombay stock exchange, Cochin stock exchange

limited, National stock exchange of India limited and MCX stock exchange.

Type Public

Traded as: BSE

NSE

500790

NESTLEIND

Industry Food processing

Founded 28 March 1959

25

Headquarters Nestle house, jacaranda Marg, ‘M’

Block, Gurgaon, Haryana, India

Area served World wide

Key People Suresh narayanan(CMD)

David steven Mc Daniel(CFO)

Martin Roemkens(executive Director)

Products Maggi

Nescafe

Milkmaid

Cerelac

KitKat

Nestea

Polo

Number of employees 7649

Parent Nestle

Website https://www.nestle.in/

CHAPTER Ⅳ

DATA ANALYSIS AND

INTERPRETATION

26

Data analysis and interpretation

Data analysis and interpretation is the main heart of the study. It is the process

of inspecting, cleansing and transforming and modelling data with the goal of

discovering useful information, suggestion, conclusion and supporting decision

making. For this purpose, secondary sources are mainly used in this study. The

collection of secondary data was done by examination of relevant information

from the companies already published sources. The main tool used for data

analysis and interpretation is ratio analysis.

After identifying a research topic, doing a literature background research,

establishing philosophical assumptions and focus problem, deciding on an

appropriate research paradigm and methodology with specific purpose,

designing a research plan and collecting sufficient data, the next step in the

research process is data analysis and interpretation, which precedes reporting of

research. Data analysis is a process that involves examining and moulding

collected data for interpretation to discover relevant information, draw or

propose conclusions and support decision-making to solve a research problem.

meaning are identified and information is interpreted.

The ratio analysis is one of the most powerful tools of financial analysis. It is

the process of establishing and interpreting various ratios. The ratio analysis is

used to study the liquidity, profitability and solvency position of the company. It

is with the help of ratios that the financial statements can be analysed more

clearly and decision making can be made from such analysis

27

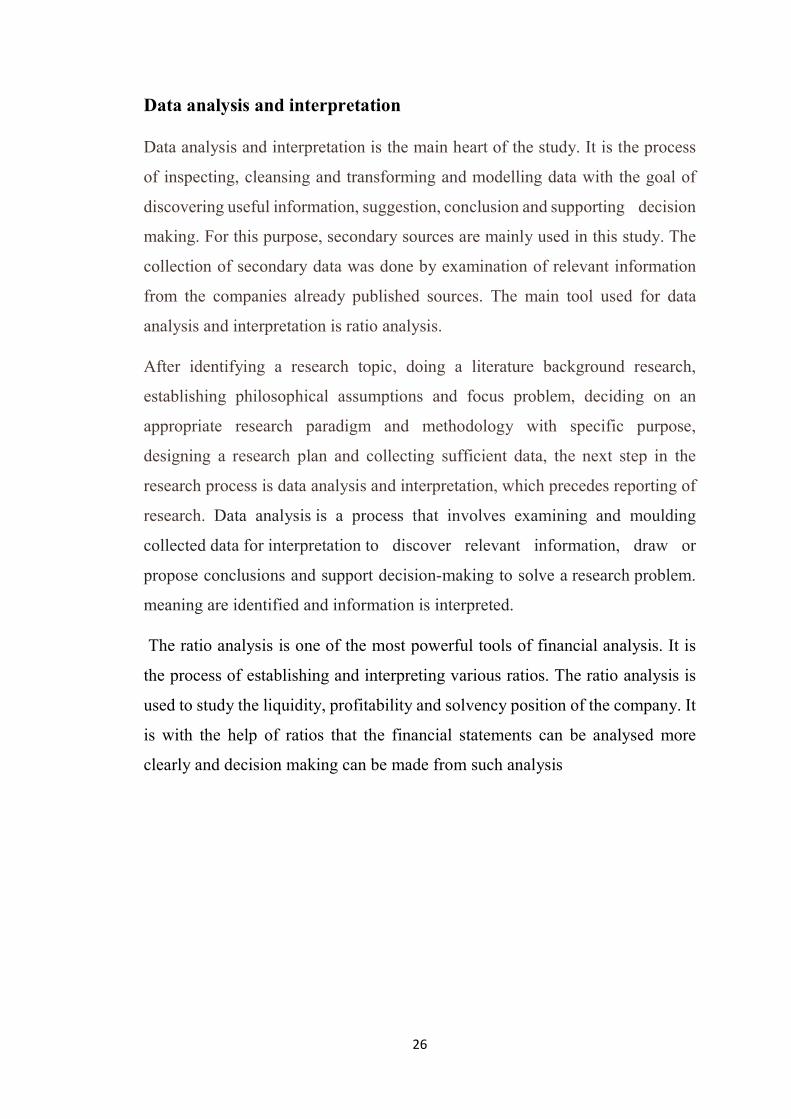

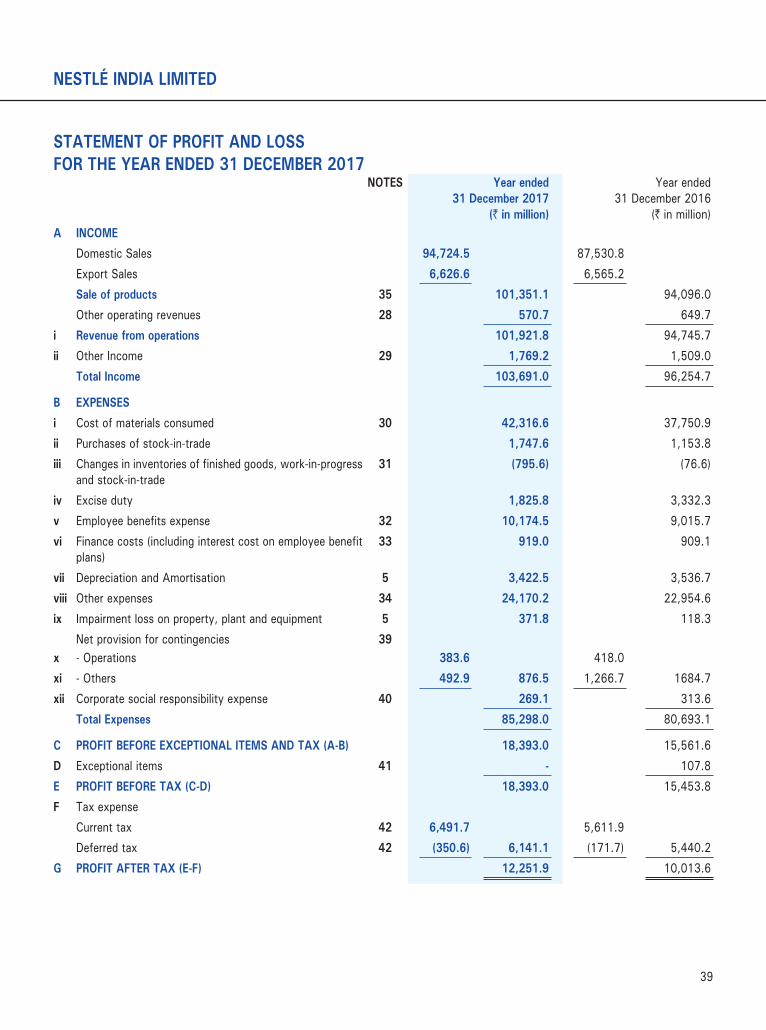

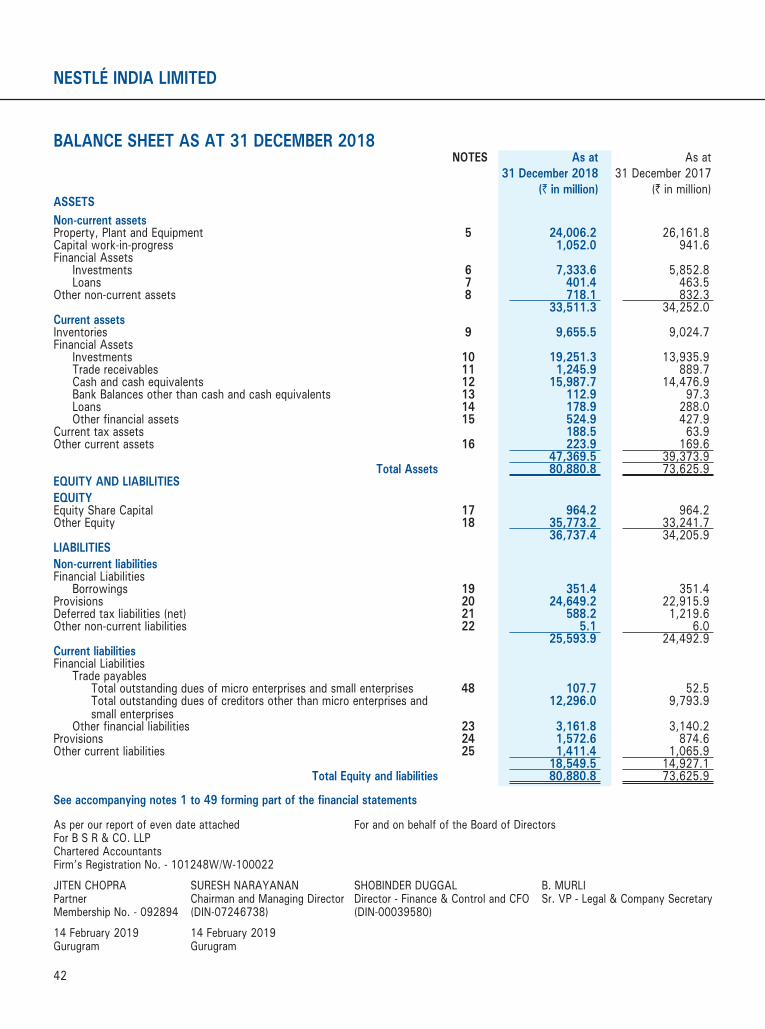

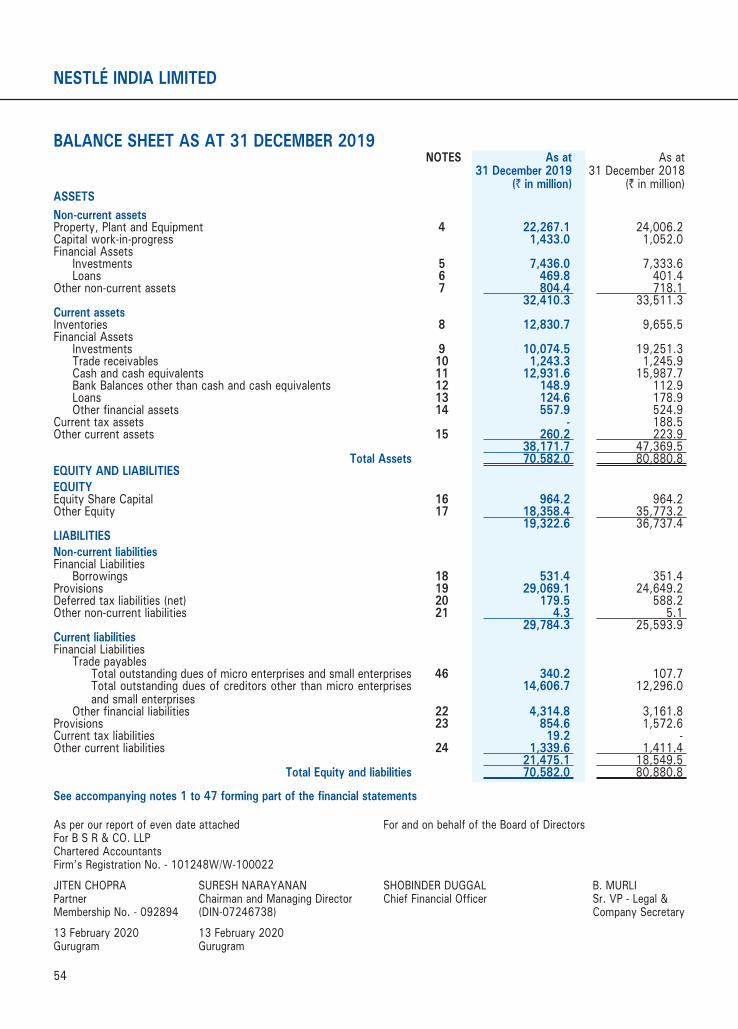

Table 4.1 Showing Current Ratio

YEAR CURRENT

ASSET

CURRENT

LIABILITY

CURRENT

RATIO

2015-2016 24,796.10 14,757.30 1.68

2016-2017 32,789.90 16,327.00 2

2017-2018 39,373.90 14,927.10 2.63

2018-2019 47,369.50 18,549.50 2.58

2019-2020 38,171.70 21,475.10 1.77

(Source: company data)

As conventional rule, a current ratio of 2:1 is considered as satisfactory. The

current ratio above 2 is considered as adequate. The above table shows that the

company has attained the ideal current ratio in the year 2016 - 2.00, 2017 – 2.63,

2018- 2.58. Current ratio measures the adequacy or inadequacy of working

capital.

Figure: 4.1 showing Current Ratio

0

0.5

1

1.5

2

2.5

3

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

CURRENT RATIO

28

Table 4.2 showing Liquid ratio

YEAR LIQUID ASSETS CURRENT

LIABILITIES

CURRENT

RATIOS

2015-2016 24701.5 14757.3 1.673

2016-2017 32692.2 16327 2.002

2017-2018 38851.9 14927.1 2.602

2018-2019 47309.4 18549.5 2.55

2019-2020 36468.9 21475.1 1.698

(Source: company data)

The above table shows the liquid ratio of the company. This ratio is used for

analysing liquidity or short term financial position of a firm. The ideal liquid

ratio is 1:1 or parity is considered as adequate. The liquid ratio of the company

increased from the year 2015-16 (1.673) to 2019-20 (1.698)

Figure: 4.2 showing Liquid Ratio

0

0.5

1

1.5

2

2.5

3

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

LIQUID RATIO

29

Table 4.3 Showing Debt Equity Ratio

YEAR TOTAL DEBT OWNED FUND DEBTEQUITY

RATIO

2015-2016 16139.6 28178.4 0.572

2016-2017 20053.6 30137 0.665

2017-2018 23266.4 34205.9 0.680

2018-2019 25000.6 36737.4 0.680

2019-2020 29600.5 19322.6 1.531

(Source: company data)

Above table shows the debt equity ratio of the company. The standard norms of

debt equity ratio is 1:1 for public sector and 2:1 for private sector. The lowest

ratio is in the year 2015-2016 and the highest ratio is in the year 2019-20. Low

ratio indicates smallest claim of creditors.

Figure: 4.3 showing Debt-Equity Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

DEBT-EQUITY RATIO

30

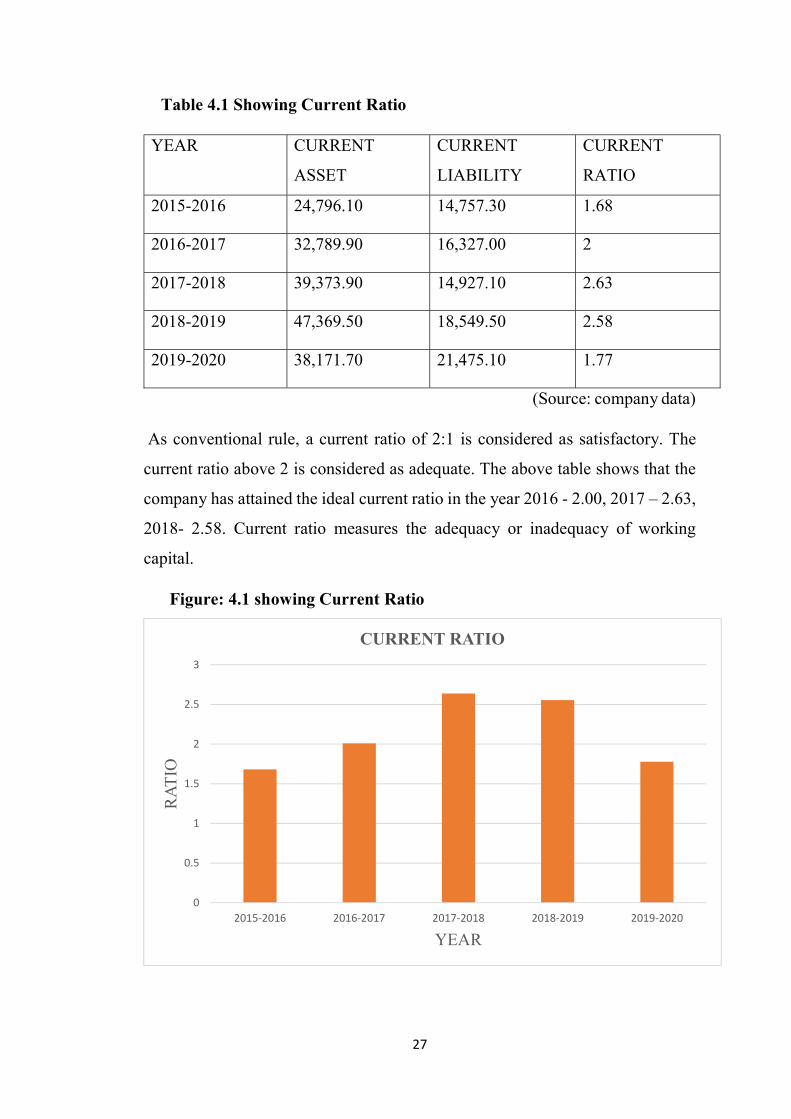

Table 4.4 showing Solvency Ratio

YEAR TOTAL ASSETS

TOTAL

LIABILTY

RATIOS

2015-2016 60804.6 32626.2 1.863

2016-2017 68059.7 37922.7 1.794

2017-2018 73625.9 39420 1.867

2018-2019 80880.8 44143.4 1.832

2019-2020 70582 51259.4 1.376

(Source: company data)

The above table shows solvency ratio of the company. The highest solvency ratio

is in the year 2017-2018 and lowest solvency ratio is in the year 2019-20. Data

indicates that the firm is financially sound

Figure 4.4 showing solvency ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

SOLVENCY RATIOS

31

Table 4.5 showing Proprietary ratio

YEAR SHAREHOLDERS

FUND

TOTAL ASSETS RATIOS

2015-2016 28178.4 24796.1 1.1364

2016-2017 30137 68059.7 0.4428

2017-2018 34205.9 73625.9 0.4645

2018-2019 36737.4 80880.8 0.4542

2019-2020 19322.6 70582 0.2737

(Source: company data)

The above table shows the proprietary ratio of the company. The standard norm

of proprietary ratio is 0.5:1. The proprietary ratio in 2015-16 is 1.136 which

decreased to 0.2737 in 2019-20. It meant that more dependence on borrowed

fund and greater risk for creditors.

Figure 4.5 showing proprietary ratio

0

0.2

0.4

0.6

0.8

1

1.2

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

PROPRIETARY RATIO

32

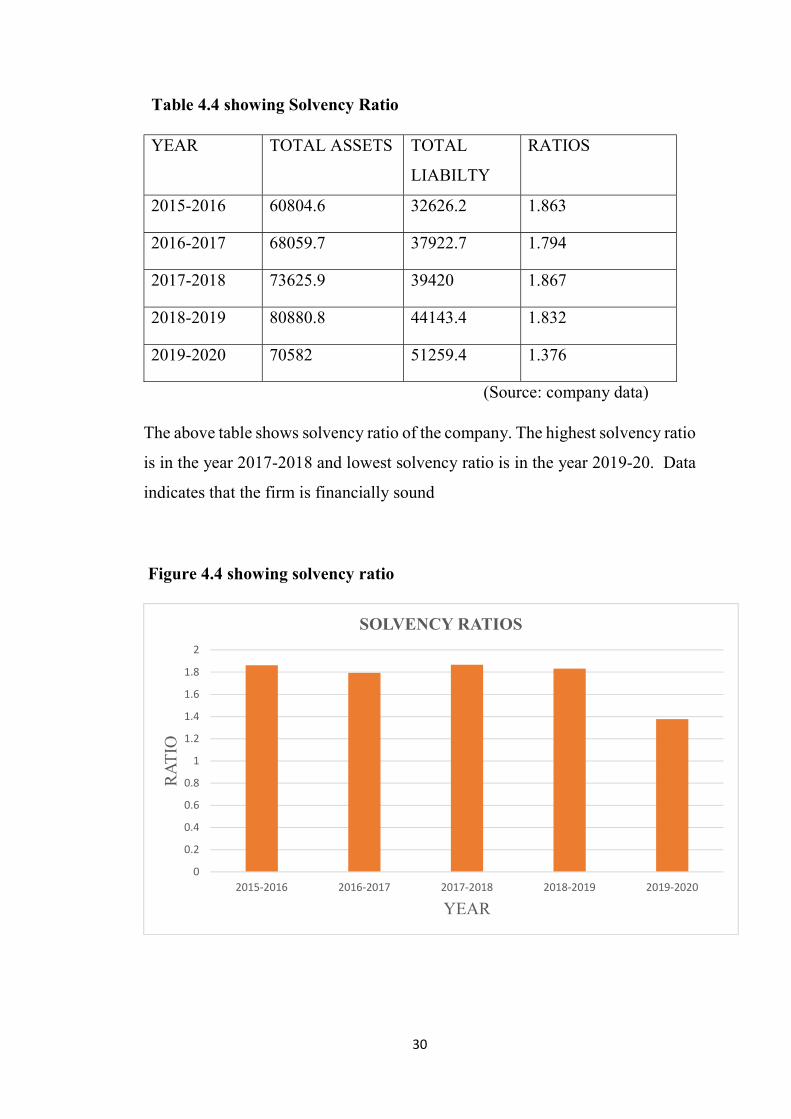

Table 4.6 showing Fixed Assets to net worth ratio

YEAR FIXED ASSETS PROPRIETORS

FUND

RATIOS

2015-2016 36008.5 28178.4 1.277

2016-2017 35269.8 30137 1.170

2017-2018 34252 34205.9 1.001

2018-2019 33511.3 36737.4 0.912

2019-2020 32410.3 19322.6 1.677

(Source: company data)

The above table shows the fixed assets to net worth ratio of the company. The

standard ratio is 0.62:0.65. In 2015-16 the ratio is 1.277 which increases to 1.677

in 2019-20. If the ratio is less than one it is considered as ideal. If ratio is more

than one, indicates part of fixed asset is financed using borrowed fund.

Figure: 4.6 showing Fixed Assets to Net worth Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

FIXED ASSETS TO NETWORTH RATIO

33

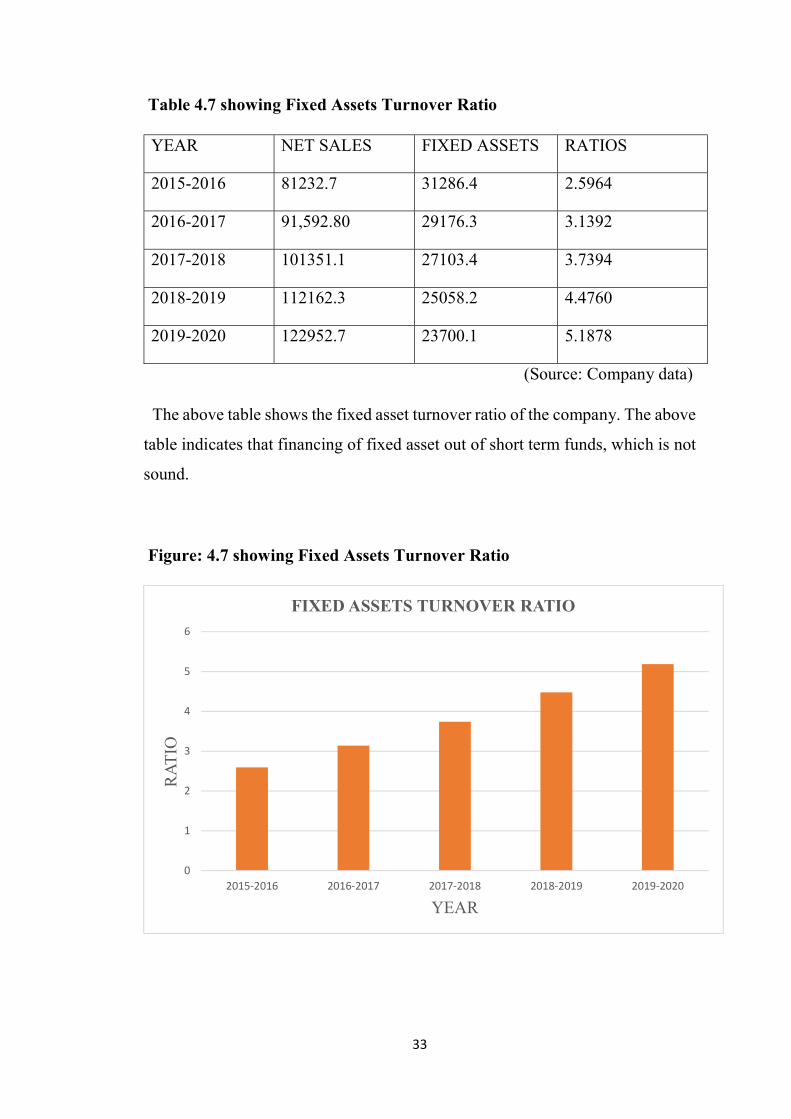

Table 4.7 showing Fixed Assets Turnover Ratio

YEAR NET SALES FIXED ASSETS RATIOS

2015-2016 81232.7 31286.4 2.5964

2016-2017 91,592.80 29176.3 3.1392

2017-2018 101351.1 27103.4 3.7394

2018-2019 112162.3 25058.2 4.4760

2019-2020 122952.7 23700.1 5.1878

(Source: Company data)

The above table shows the fixed asset turnover ratio of the company. The above

table indicates that financing of fixed asset out of short term funds, which is not

sound.

Figure: 4.7 showing Fixed Assets Turnover Ratio

0

1

2

3

4

5

6

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

FIXED ASSETS TURNOVER RATIO

34

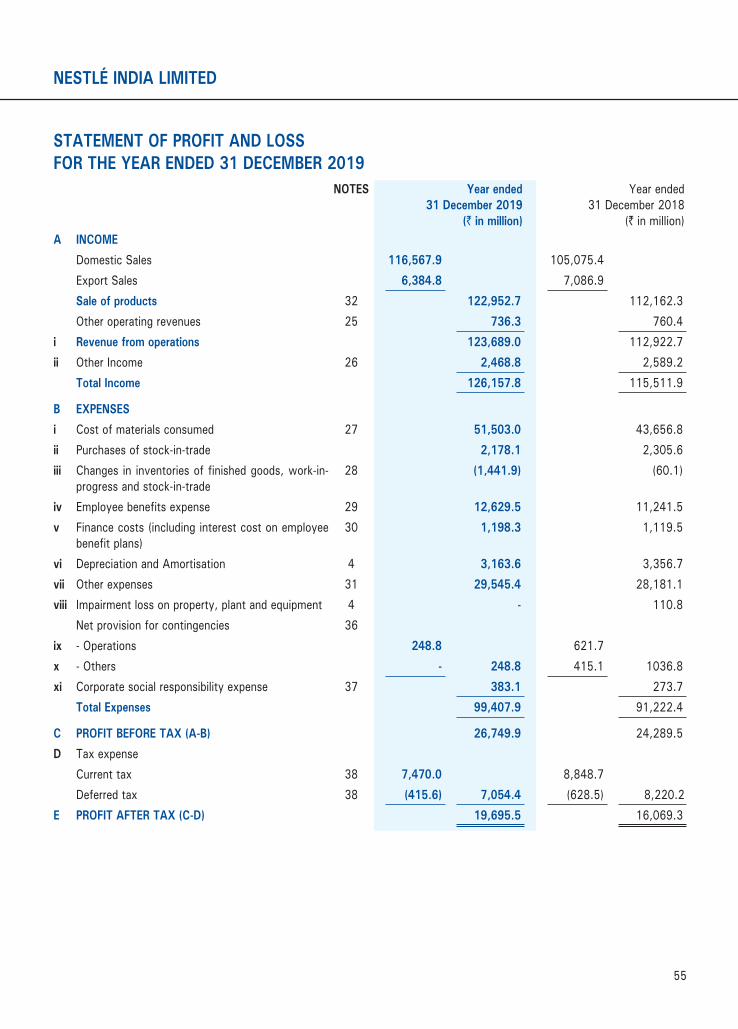

Table 4.8 showing Net Profit Ratio

YEAR NET PROFIT SALES RATIOS

2015-2016 5633 81237 0.069

2016-2017 10014 91593 0.109

2017-2018 12252 101351 0.120

2018-2019 16069 112162 0.143

2019-2020 19696 122953 0.160

(Source: company data)

The above table shows the net profit of the company. The highest net profit

ratio is in the year 2019-2020. The lowest net profit ratio is in the year 2015-16.

Higher the N/P ratio, better is the profitability. This means higher returns to

shareholders.

Figure 4.8 showing Net Profit Ratio

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

NET PROFIT RATIO

35

Table 4.9 Working Capital Turnover Ratio

YEAR REVENUE WORKING

CAPITAL

RATIO

2015-2016 81753.1 10038.8 8.143

2016-2017 92238 16462.9 5.602

2017-2018 101921 24468.8 4.165

2018-2019 112922.7 28820 3.918

2019-2020 123689 8387.4 14.747

(Source: Company data)

The above table shows the working capital turnover ratio. The highest ratio is in

the year 2019-20 and lowest ratio is in the year 2018-19. Higher the ratio better

the efficiency in utilization of resources

Figure 4.9 showing Working Capital Turnover Ratio

0

2

4

6

8

10

12

14

16

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

WORKING CAPITAL TURNOVER RATIO

36

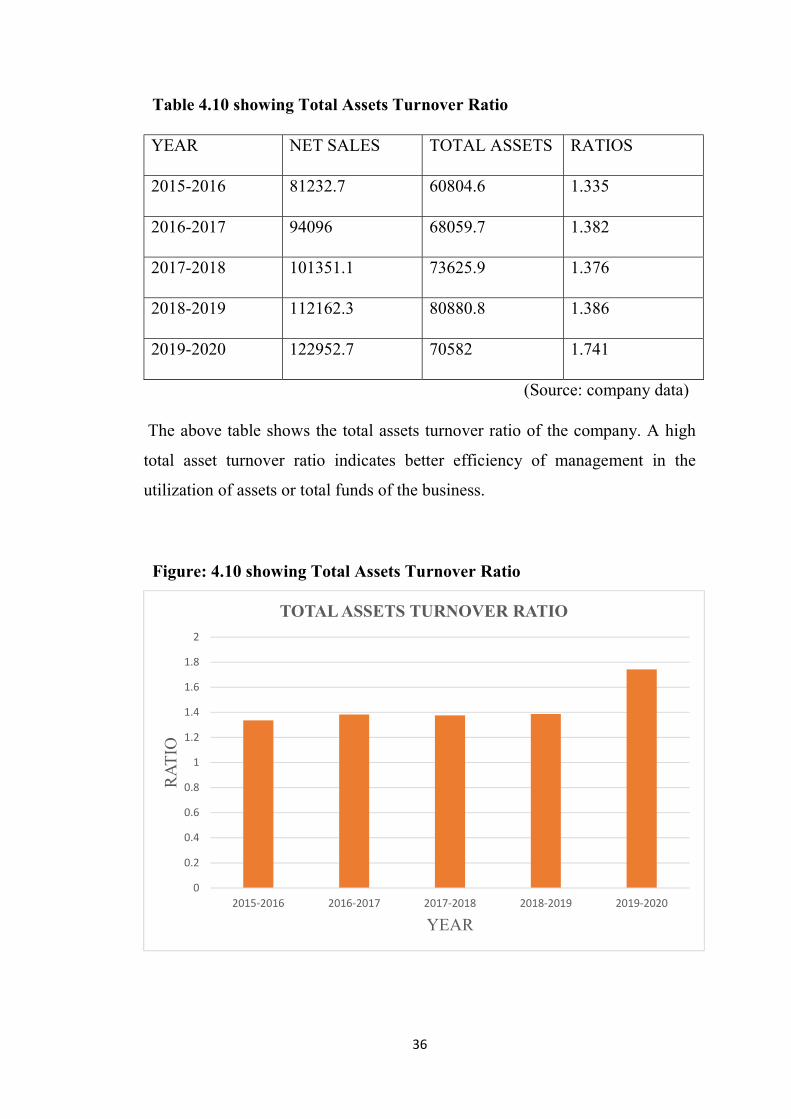

Table 4.10 showing Total Assets Turnover Ratio

YEAR NET SALES TOTAL ASSETS RATIOS

2015-2016 81232.7 60804.6 1.335

2016-2017 94096 68059.7 1.382

2017-2018 101351.1 73625.9 1.376

2018-2019 112162.3 80880.8 1.386

2019-2020 122952.7 70582 1.741

(Source: company data)

The above table shows the total assets turnover ratio of the company. A high

total asset turnover ratio indicates better efficiency of management in the

utilization of assets or total funds of the business.

Figure: 4.10 showing Total Assets Turnover Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

TOTAL ASSETS TURNOVER RATIO

37

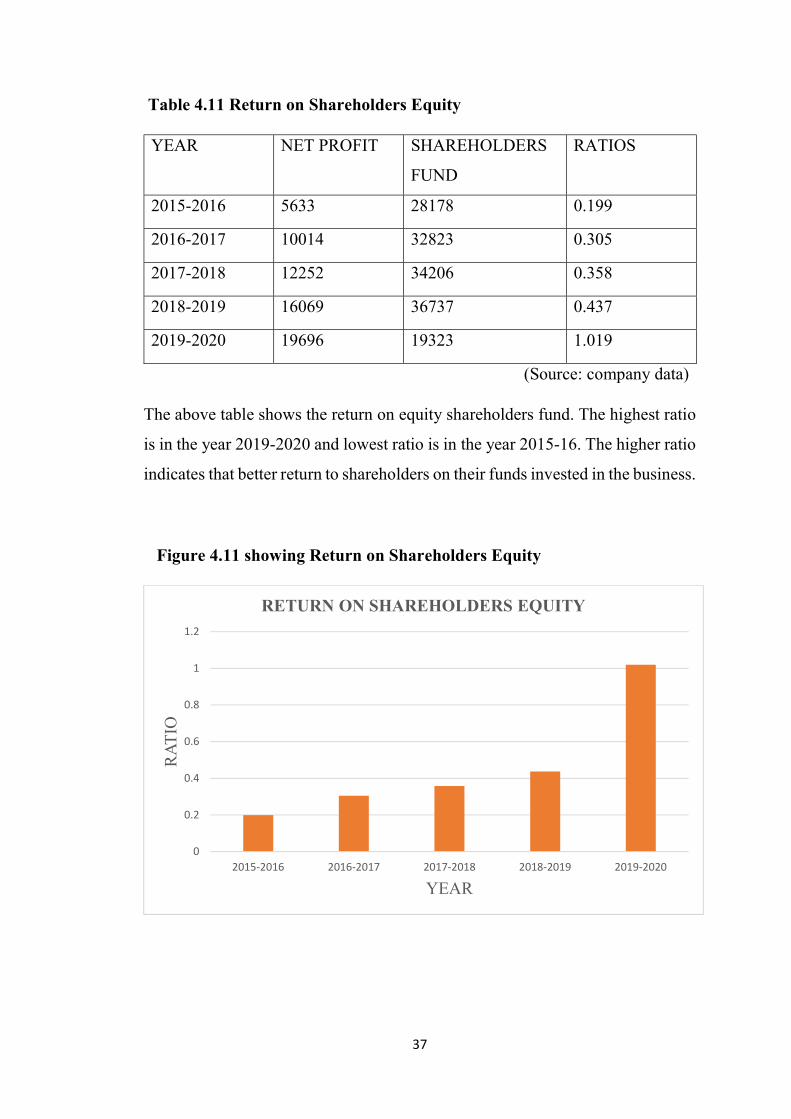

Table 4.11 Return on Shareholders Equity

YEAR NET PROFIT SHAREHOLDERS

FUND

RATIOS

2015-2016 5633 28178 0.199

2016-2017 10014 32823 0.305

2017-2018 12252 34206 0.358

2018-2019 16069 36737 0.437

2019-2020 19696 19323 1.019

(Source: company data)

The above table shows the return on equity shareholders fund. The highest ratio

is in the year 2019-2020 and lowest ratio is in the year 2015-16. The higher ratio

indicates that better return to shareholders on their funds invested in the business.

Figure 4.11 showing Return on Shareholders Equity

0

0.2

0.4

0.6

0.8

1

1.2

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

RETURN ON SHAREHOLDERS EQUITY

38

Table 4.12 Showing Total Liability to Total Asset Ratio

YEAR LIABILITY ASSET RATIO

2015-2016 16327 68059.7 0.239

2016-2017 14757.3 60804.6 0.242

2017-2018 14927 73625.9 0.202

2018-2019 18549.5 80880.8 0.229

2019-2020 21475.1 70582 0.304

(Source: Company data)

The above table shows current liability to asset ratio. Here the lower ratio

indicates that the assets are not funded by debt. High ratio indicates that a

company itself putting a risk of defaulting on its loan, if interest rates were to

rise suddenly.

Figure 4.12 showing Total liability To Total Asset Ratio

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

TOTAL LIABILITY TO TOTAL ASSET RATIO

39

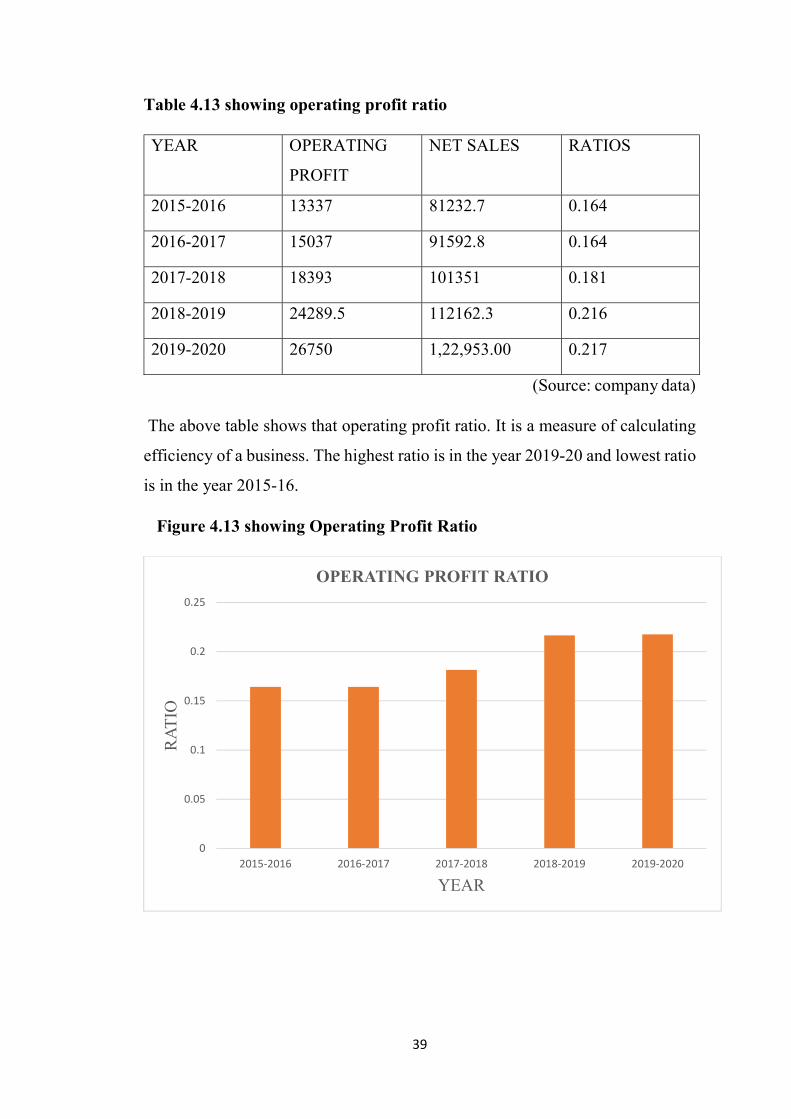

Table 4.13 showing operating profit ratio

YEAR OPERATING

PROFIT

NET SALES RATIOS

2015-2016 13337 81232.7 0.164

2016-2017 15037 91592.8 0.164

2017-2018 18393 101351 0.181

2018-2019 24289.5 112162.3 0.216

2019-2020 26750 1,22,953.00 0.217

(Source: company data)

The above table shows that operating profit ratio. It is a measure of calculating

efficiency of a business. The highest ratio is in the year 2019-20 and lowest ratio

is in the year 2015-16.

Figure 4.13 showing Operating Profit Ratio

0

0.05

0.1

0.15

0.2

0.25

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

RA

TIO

YEAR

OPERATING PROFIT RATIO

40

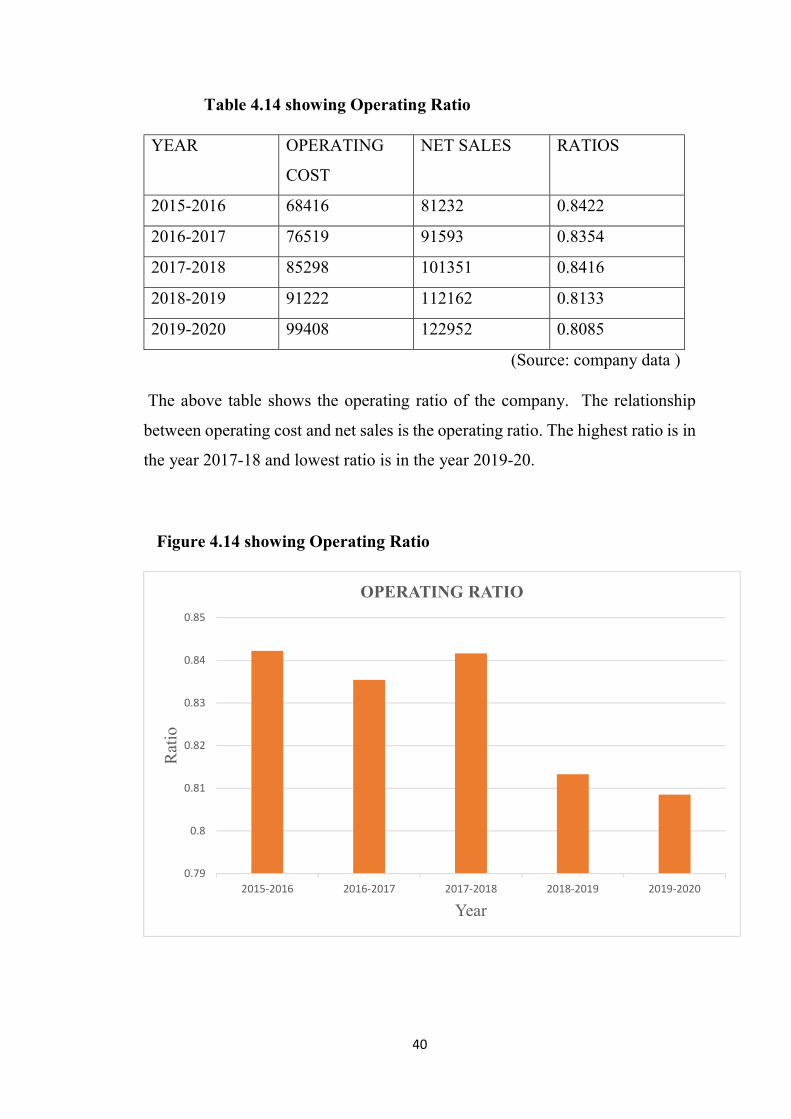

Table 4.14 showing Operating Ratio

YEAR OPERATING

COST

NET SALES RATIOS

2015-2016 68416 81232 0.8422

2016-2017 76519 91593 0.8354

2017-2018 85298 101351 0.8416

2018-2019 91222 112162 0.8133

2019-2020 99408 122952 0.8085

(Source: company data )

The above table shows the operating ratio of the company. The relationship

between operating cost and net sales is the operating ratio. The highest ratio is in

the year 2017-18 and lowest ratio is in the year 2019-20.

Figure 4.14 showing Operating Ratio

0.79

0.8

0.81

0.82

0.83

0.84

0.85

2015-2016 2016-2017 2017-2018 2018-2019 2019-2020

Rat

io

Year

OPERATING RATIO

41

4.15 Common Size Balance Sheet

Common size balance sheet for the year 2018-19, 2019-20

(Source: company data)

Non-current assets have increased from 41.43 in 2018-19 to 45.92 in 2019-20.

The current assets had decreased from 58.57 in 2018-19 to 54.08 in 2019-20.

Total equity in the year 2018-19 is 45.43 which decreased to 27.38 in the year

2019-20. The non-current liability during the year 2018-19 is 31.64 which

increased to 42.20 in 2019-20. The current liabilities have increased from 22.93

in 2018-19 to 30.42 in 2019-20.

Particulars Absolute amount Percentages 2018-19 2019-20 2018-2019 2019-20

I. Assets Non-current Assets 33511.3 32410.3 41.43 45.92

Current Assets 47369.5 38171.7 58.57 54.08 Total Assets 80880.8 70582 100 100

II. Equity and

Liabilities

Total Equity 36737.4 19322.6 45.43 27.38 Non-current Liabilities

25593.9 29784.3 31.64 42.20

Current liabilities 18549.5 21475.1 22.93 30.42 Total Equity and

Liability 80880.8 70582 100 100

CHAPTER Ⅴ

FINDINGS, SUGGESTIONS AND

CONCLUSION

42

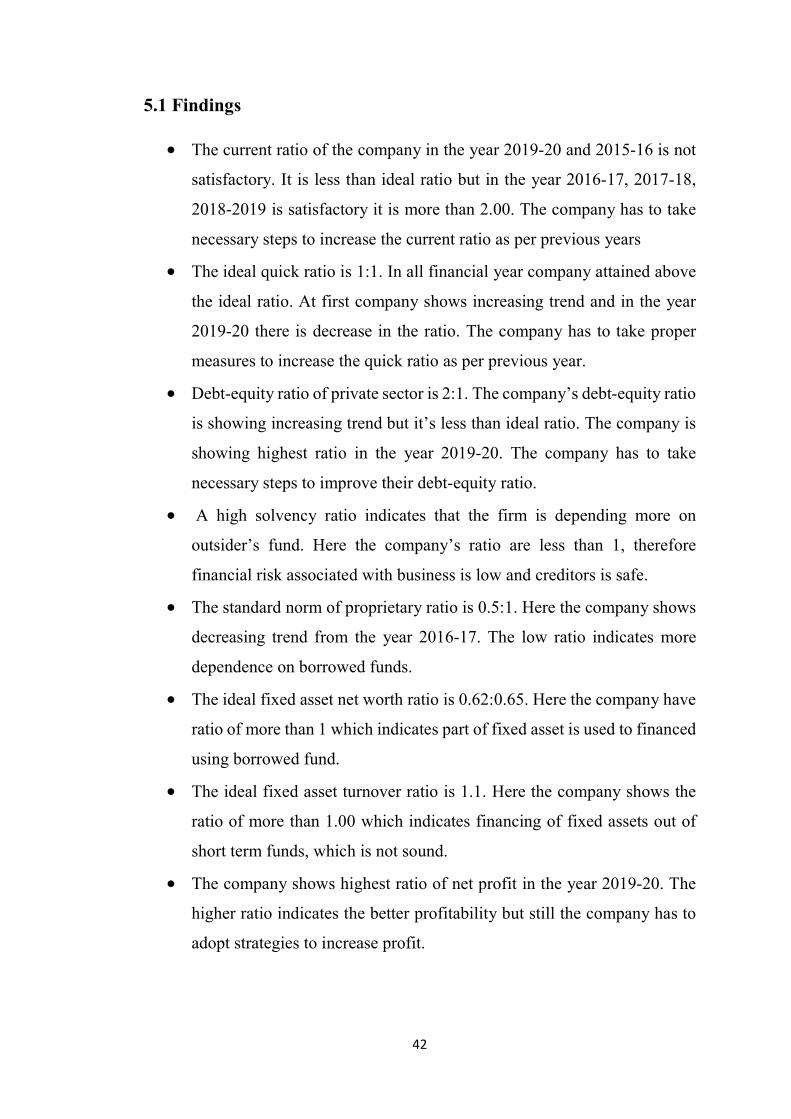

5.1 Findings

The current ratio of the company in the year 2019-20 and 2015-16 is not

satisfactory. It is less than ideal ratio but in the year 2016-17, 2017-18,

2018-2019 is satisfactory it is more than 2.00. The company has to take

necessary steps to increase the current ratio as per previous years

The ideal quick ratio is 1:1. In all financial year company attained above

the ideal ratio. At first company shows increasing trend and in the year

2019-20 there is decrease in the ratio. The company has to take proper

measures to increase the quick ratio as per previous year.

Debt-equity ratio of private sector is 2:1. The company’s debt-equity ratio

is showing increasing trend but it’s less than ideal ratio. The company is

showing highest ratio in the year 2019-20. The company has to take

necessary steps to improve their debt-equity ratio.

A high solvency ratio indicates that the firm is depending more on

outsider’s fund. Here the company’s ratio are less than 1, therefore

financial risk associated with business is low and creditors is safe.

The standard norm of proprietary ratio is 0.5:1. Here the company shows

decreasing trend from the year 2016-17. The low ratio indicates more

dependence on borrowed funds.

The ideal fixed asset net worth ratio is 0.62:0.65. Here the company have

ratio of more than 1 which indicates part of fixed asset is used to financed

using borrowed fund.

The ideal fixed asset turnover ratio is 1.1. Here the company shows the

ratio of more than 1.00 which indicates financing of fixed assets out of

short term funds, which is not sound.

The company shows highest ratio of net profit in the year 2019-20. The

higher ratio indicates the better profitability but still the company has to

adopt strategies to increase profit.

43

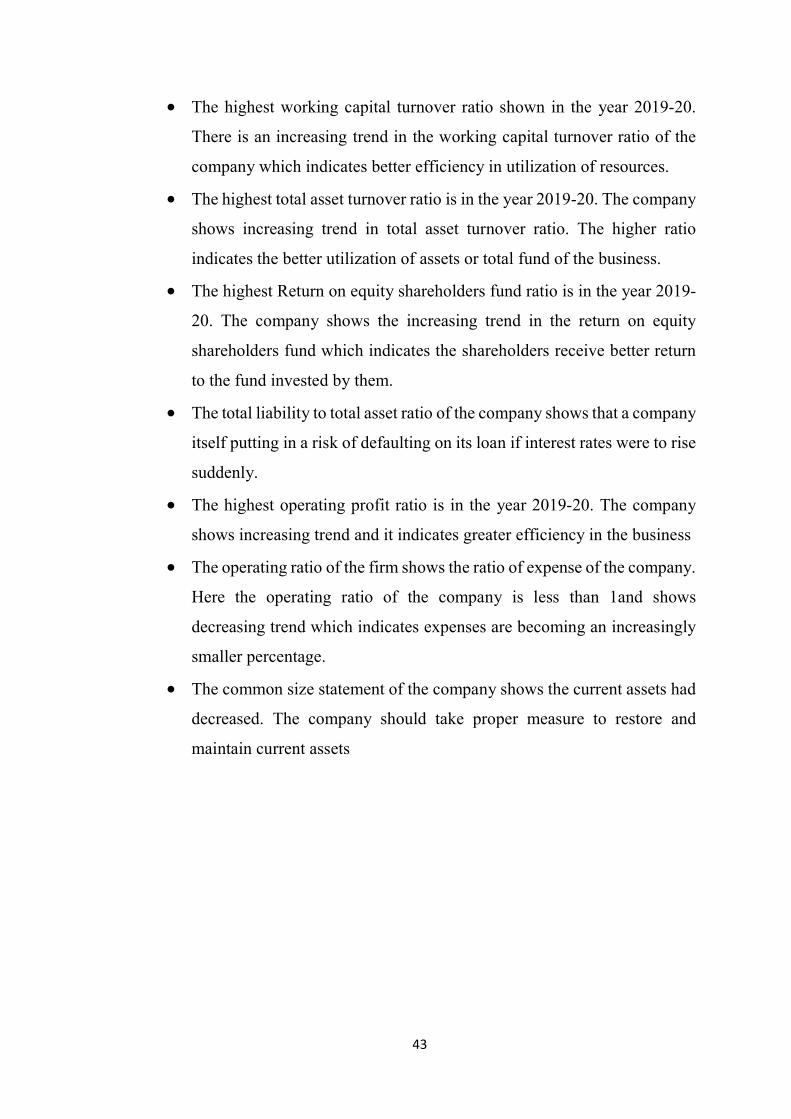

The highest working capital turnover ratio shown in the year 2019-20.

There is an increasing trend in the working capital turnover ratio of the

company which indicates better efficiency in utilization of resources.

The highest total asset turnover ratio is in the year 2019-20. The company

shows increasing trend in total asset turnover ratio. The higher ratio

indicates the better utilization of assets or total fund of the business.

The highest Return on equity shareholders fund ratio is in the year 2019-

20. The company shows the increasing trend in the return on equity

shareholders fund which indicates the shareholders receive better return

to the fund invested by them.

The total liability to total asset ratio of the company shows that a company

itself putting in a risk of defaulting on its loan if interest rates were to rise

suddenly.

The highest operating profit ratio is in the year 2019-20. The company

shows increasing trend and it indicates greater efficiency in the business

The operating ratio of the firm shows the ratio of expense of the company.

Here the operating ratio of the company is less than 1and shows

decreasing trend which indicates expenses are becoming an increasingly

smaller percentage.

The common size statement of the company shows the current assets had

decreased. The company should take proper measure to restore and

maintain current assets

44

5.2 Suggestions

Based on the above mentioned findings the following are the suggestions:-

By analysing composition of current assets and liquid assets, it is found

that the amount of liquid cash kept in the company is low, so the company

has to keep an adequate amount as cash and bank balance. So as to meet

various short term liabilities.

Fluctuations in the ratios show that there are some kind of management

problems or production problems that exist in Nestle India pvt ltd. the top

management should take necessary step to assemble the management and

workers in best way.

The pricing strategies should be in such a way that it should be affordable

to all kinds of customers and to improve supply chain policies.

In order to improve it’s solvency as well as liquidity, the company has an

opportunity of trading on equity even to the legitimate extent, the

company may request bank to convert a part of the overdraft in to the

medium term loan, which would ultimately the financial health of the

company.

It is advisable to take more efforts to increase the overall efficiency of the

business.

It’s advisable to reduce inventory, reduce overheads, reduce overall

direct costs and adopt strategies to increase profit

45

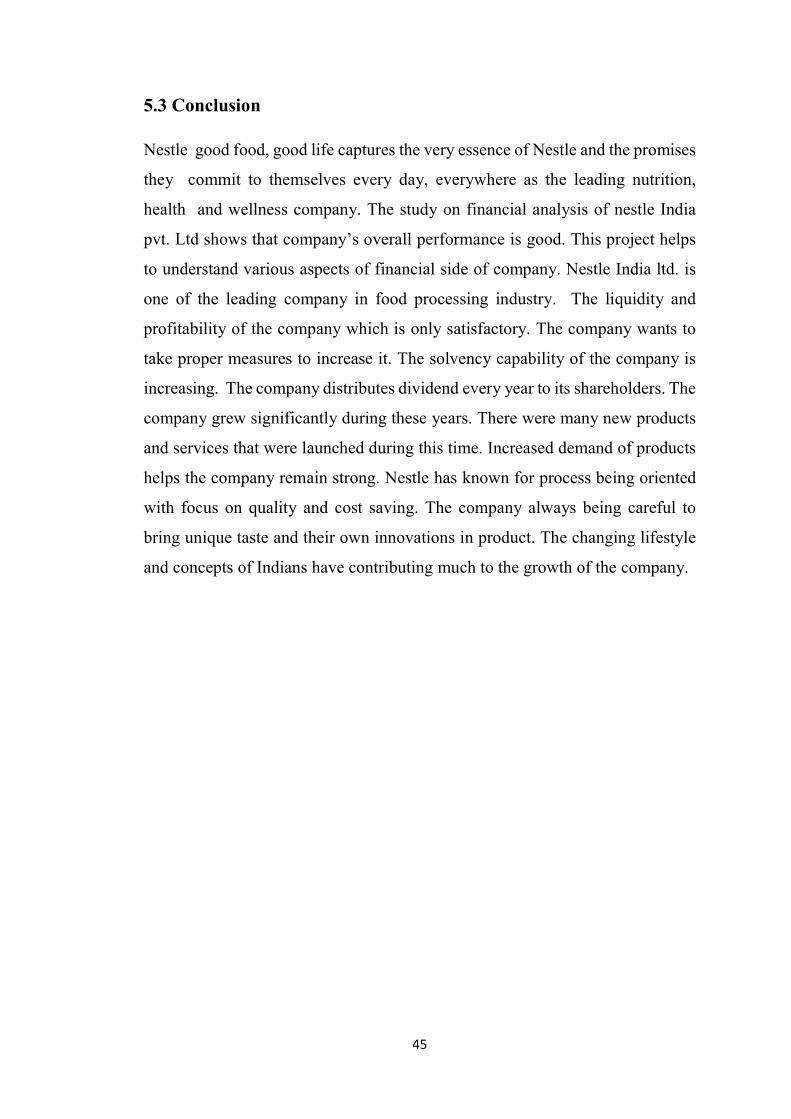

5.3 Conclusion

Nestle good food, good life captures the very essence of Nestle and the promises

they commit to themselves every day, everywhere as the leading nutrition,

health and wellness company. The study on financial analysis of nestle India

pvt. Ltd shows that company’s overall performance is good. This project helps

to understand various aspects of financial side of company. Nestle India ltd. is

one of the leading company in food processing industry. The liquidity and

profitability of the company which is only satisfactory. The company wants to

take proper measures to increase it. The solvency capability of the company is

increasing. The company distributes dividend every year to its shareholders. The

company grew significantly during these years. There were many new products

and services that were launched during this time. Increased demand of products

helps the company remain strong. Nestle has known for process being oriented

with focus on quality and cost saving. The company always being careful to

bring unique taste and their own innovations in product. The changing lifestyle

and concepts of Indians have contributing much to the growth of the company.

BIBLIOGRAPHY

JOURNALS

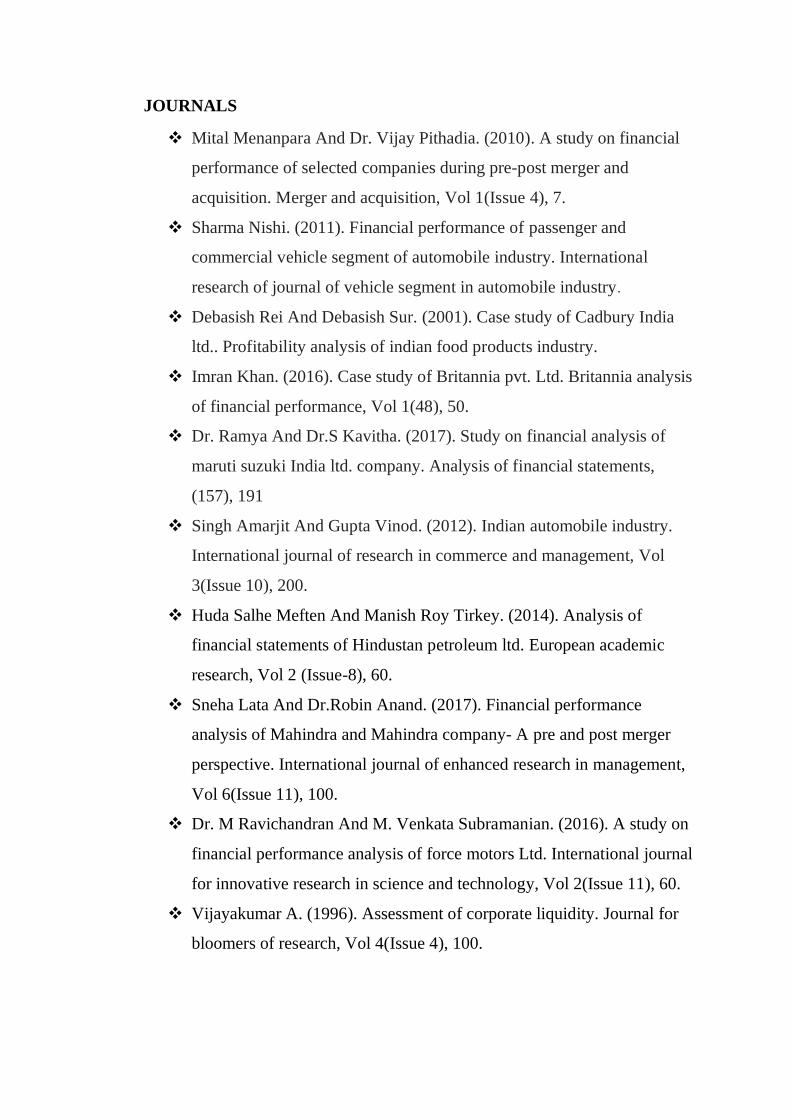

❖ Mital Menanpara And Dr. Vijay Pithadia. (2010). A study on financial

performance of selected companies during pre-post merger and

acquisition. Merger and acquisition, Vol 1(Issue 4), 7.

❖ Sharma Nishi. (2011). Financial performance of passenger and

commercial vehicle segment of automobile industry. International

research of journal of vehicle segment in automobile industry.

❖ Debasish Rei And Debasish Sur. (2001). Case study of Cadbury India

ltd.. Profitability analysis of indian food products industry.

❖ Imran Khan. (2016). Case study of Britannia pvt. Ltd. Britannia analysis

of financial performance, Vol 1(48), 50.

❖ Dr. Ramya And Dr.S Kavitha. (2017). Study on financial analysis of

maruti suzuki India ltd. company. Analysis of financial statements,

(157), 191

❖ Singh Amarjit And Gupta Vinod. (2012). Indian automobile industry.

International journal of research in commerce and management, Vol

3(Issue 10), 200.

❖ Huda Salhe Meften And Manish Roy Tirkey. (2014). Analysis of

financial statements of Hindustan petroleum ltd. European academic

research, Vol 2 (Issue-8), 60.

❖ Sneha Lata And Dr.Robin Anand. (2017). Financial performance

analysis of Mahindra and Mahindra company- A pre and post merger

perspective. International journal of enhanced research in management,

Vol 6(Issue 11), 100.

❖ Dr. M Ravichandran And M. Venkata Subramanian. (2016). A study on

financial performance analysis of force motors Ltd. International journal

for innovative research in science and technology, Vol 2(Issue 11), 60.

❖ Vijayakumar A. (1996). Assessment of corporate liquidity. Journal for

bloomers of research, Vol 4(Issue 4), 100.

BOOKS

❖ Bhattacharyya debarshi (2011). Management Accounting. New delhi:

Dorling Kindersley Pvt.Ltd.

❖ Shashi k Gupta & R k sharma “Management Accounting”, kalyani

publications,11th revised edition.

❖ A Vinod “Accounting for management”, Calicut university, revised

edition 2017.

❖ Dr. K venugopalan, “Business Research Methods”, Calicut university

Central co-operative stories ltd. No.4347 Calicut University, 2016.

WEBSITES

❖ www.nestle.in

❖ www.wikipedia.org

❖ www.investopedia.com

ANNEXURE

38

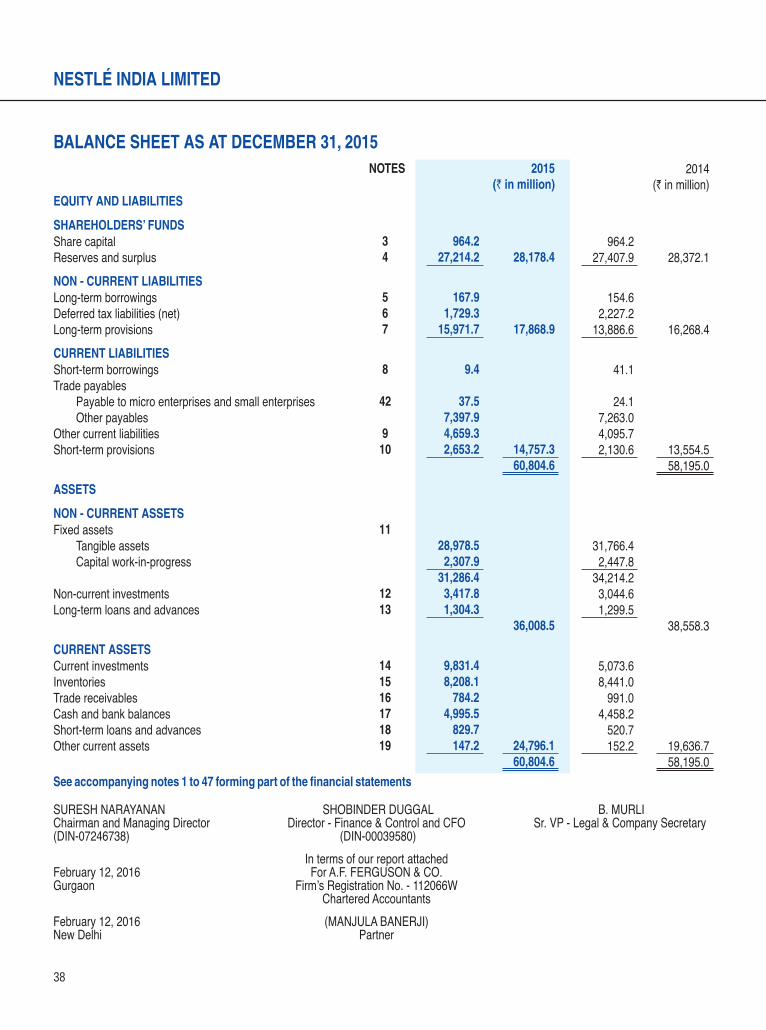

NESTLÉ INDIA LIMITED

BALANCE SHEET AS AT DECEMBER 31, 2015NOTES 2015

(` in million)2014

(` in million)EQUITY AND LIABILITIES

SHAREHOLDERS’ FUNDSShare capital 3 964.2 964.2 Reserves and surplus 4 27,214.2 28,178.4 27,407.9 28,372.1 NON - CURRENT LIABILITIES Long-term borrowings 5 167.9 154.6 Deferred tax liabilities (net) 6 1,729.3 2,227.2 Long-term provisions 7 15,971.7 17,868.9 13,886.6 16,268.4 CURRENT LIABILITIES Short-term borrowings 8 9.4 41.1 Trade payables

Payable to micro enterprises and small enterprises 42 37.5 24.1 Other payables 7,397.9 7,263.0

Other current liabilities 9 4,659.3 4,095.7 Short-term provisions 10 2,653.2 14,757.3 2,130.6 13,554.5

60,804.6 58,195.0 ASSETS

NON - CURRENT ASSETS Fixed assets 11

Tangible assets 28,978.5 31,766.4 Capital work-in-progress 2,307.9 2,447.8

31,286.4 34,214.2 Non-current investments 12 3,417.8 3,044.6 Long-term loans and advances 13 1,304.3 1,299.5

36,008.5 38,558.3CURRENT ASSETS Current investments 14 9,831.4 5,073.6 Inventories 15 8,208.1 8,441.0 Trade receivables 16 784.2 991.0 Cash and bank balances 17 4,995.5 4,458.2 Short-term loans and advances 18 829.7 520.7 Other current assets 19 147.2 24,796.1 152.2 19,636.7

60,804.6 58,195.0See accompanying notes 1 to 47 forming part of the financial statements

SURESH NARAYANAN SHOBINDER DUGGAL B. MURLI Chairman and Managing Director Director - Finance & Control and CFO Sr. VP - Legal & Company Secretary (DIN-07246738) (DIN-00039580) In terms of our report attachedFebruary 12, 2016 For A.F. FERGUSON & CO.Gurgaon Firm’s Registration No. - 112066W Chartered AccountantsFebruary 12, 2016 (MANJULA BANERJI)New Delhi Partner

2 Nestle AR 2015-16.indd 38 3/28/2016 7:18:24 PM

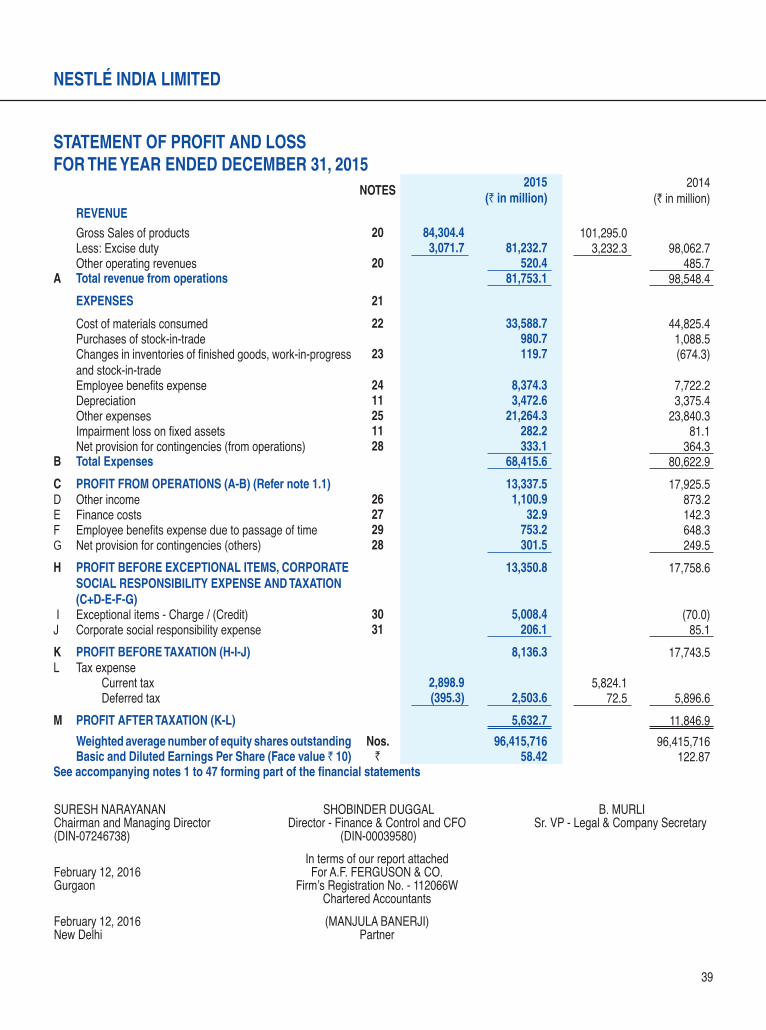

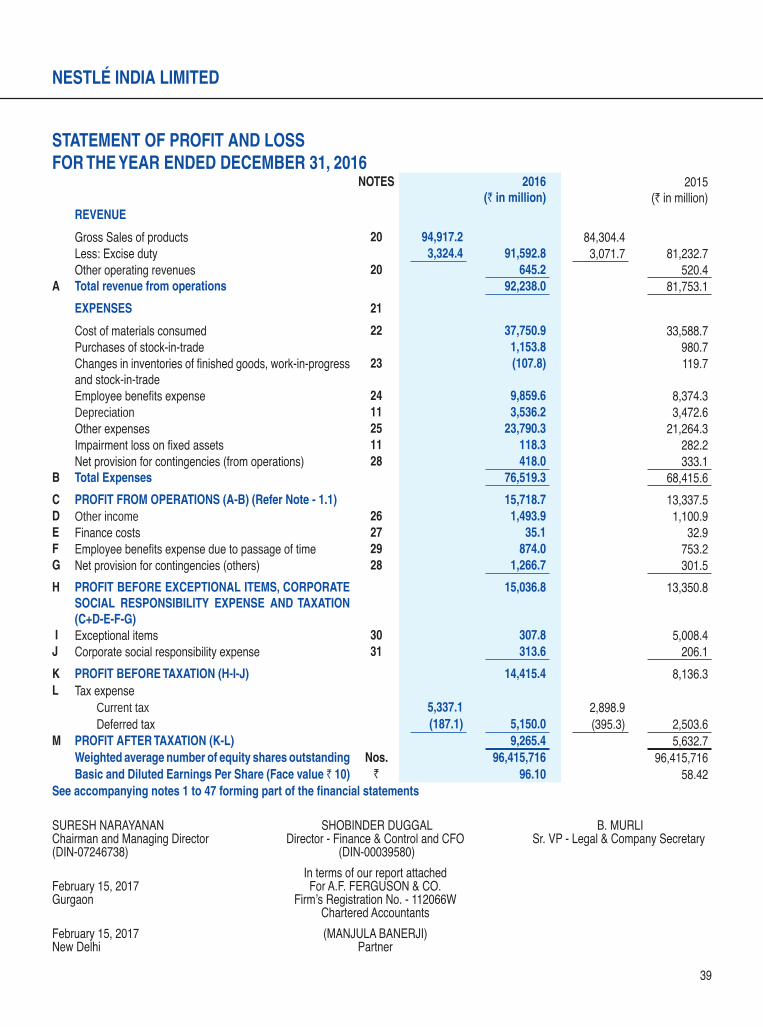

39

STATEMENT OF PROFIT AND LOSSFOR THE YEAR ENDED DECEMBER 31, 2015

NOTES2015

(` in million)2014

(` in million)REVENUEGross Sales of products 20 84,304.4 101,295.0Less: Excise duty 3,071.7 81,232.7 3,232.3 98,062.7 Other operating revenues 20 520.4 485.7

A Total revenue from operations 81,753.1 98,548.4 EXPENSES 21

Cost of materials consumed 22 33,588.7 44,825.4 Purchases of stock-in-trade 980.7 1,088.5 Changes in inventories of finished goods, work-in-progress and stock-in-trade

23 119.7 (674.3)

Employee benefits expense 24 8,374.3 7,722.2 Depreciation 11 3,472.6 3,375.4 Other expenses 25 21,264.3 23,840.3 Impairment loss on fixed assets 11 282.2 81.1 Net provision for contingencies (from operations) 28 333.1 364.3

B Total Expenses 68,415.6 80,622.9 C PROFIT FROM OPERATIONS (A-B) (Refer note 1.1) 13,337.5 17,925.5 D Other income 26 1,100.9 873.2 E Finance costs 27 32.9 142.3 F Employee benefits expense due to passage of time 29 753.2 648.3 G Net provision for contingencies (others) 28 301.5 249.5 H PROFIT BEFORE EXCEPTIONAL ITEMS, CORPORATE

SOCIAL RESPONSIBILITY EXPENSE AND TAXATION (C+D-E-F-G)

13,350.8 17,758.6

I Exceptional items - Charge / (Credit) 30 5,008.4 (70.0)J Corporate social responsibility expense 31 206.1 85.1 K PROFIT BEFORE TAXATION (H-I-J) 8,136.3 17,743.5 L Tax expense

Current tax 2,898.9 5,824.1 Deferred tax (395.3) 2,503.6 72.5 5,896.6

M PROFIT AFTER TAXATION (K-L) 5,632.7 11,846.9 Weighted average number of equity shares outstanding Nos. 96,415,716 96,415,716 Basic and Diluted Earnings Per Share (Face value ` 10) ` 58.42 122.87

See accompanying notes 1 to 47 forming part of the financial statements

NESTLÉ INDIA LIMITED

SURESH NARAYANAN SHOBINDER DUGGAL B. MURLI Chairman and Managing Director Director - Finance & Control and CFO Sr. VP - Legal & Company Secretary (DIN-07246738) (DIN-00039580) In terms of our report attachedFebruary 12, 2016 For A.F. FERGUSON & CO.Gurgaon Firm’s Registration No. - 112066W Chartered AccountantsFebruary 12, 2016 (MANJULA BANERJI)New Delhi Partner

2 Nestle AR 2015-16.indd 39 3/28/2016 7:18:24 PM

38

NESTLÉ INDIA LIMITED

BALANCE SHEET AS AT DECEMBER 31, 2016NOTES 2016

(` in million)2015

(` in million)EQUITY AND LIABILITIES

SHAREHOLDERS’ FUNDSShare capital 3 964.2 964.2Reserves and surplus 4 29,172.8 30,137.0 27,214.2 28,178.4NON - CURRENT LIABILITIESLong-term borrowings 5 331.5 167.9Deferred tax liabilities (net) 6 1,542.1 1,729.3Long-term provisions 7 19,722.1 21,595.7 15,971.7 17,868.9CURRENT LIABILITIESShort-term borrowings 8 - 9.4Trade payables

Payable to micro enterprises and small enterprises 42 48.8 37.5Other payables 7,942.8 7,456.6

Other current liabilities 9 5,128.4 4,659.3Short-term provisions 10 3,207.0 16,327.0 2,653.2 14,816.0

68,059.7 60,863.3ASSETS

NON - CURRENT ASSETSFixed assets 11

Tangible assets 27,294.6 28,978.5Capital work-in-progress 1,881.7 2,307.9

29,176.3 31,286.4Non-current investments 12 4,743.1 3,417.8Long-term loans and advances 13 1,350.4 1,304.3

35,269.8 36,008.5CURRENT ASSETSCurrent investments 14 12,750.4 9,831.4Inventories 15 9,431.8 8,208.1Trade receivables 16 979.3 784.2Cash and bank balances 17 8,800.0 4,995.5Short-term loans and advances 18 570.2 888.4Other current assets 19 258.2 32,789.9 147.2 24,854.8

68,059.7 60,863.3See accompanying notes 1 to 47 forming part of the financial statements