A short masters level course in public economics (for public administration students)

121

1 A SHORT COURSE ON MASTERS LEVEL ECONOMICS FOR PUBLIC ADMINISTRATION STUDENTS Cameron Gordon, PhD Associate Professor of Economics University of Canberra [email protected] February 14, 2014 This is a short course on economics based on lecture notes for an MPA class on Public Managerial Economics I taught while on the faculty of the School of Public Administration (and then later the School of Policy, Planning and Development) at the University of Southern California in the late 1990s/early 2000s.

Transcript of A short masters level course in public economics (for public administration students)

1

A SHORT COURSE ON MASTERS LEVEL ECONOMICS FOR PUBLIC ADMINISTRATION STUDENTS Cameron Gordon, PhD Associate Professor of Economics University of Canberra [email protected] February 14, 2014 This is a short course on economics based on lecture notes for an MPA class on Public Managerial Economics I taught while on the faculty of the School of Public Administration (and then later the School of Policy, Planning and Development) at the University of Southern California in the late 1990s/early 2000s.

2

Concepts: Economic reasoning, general equilibrium and economic systems

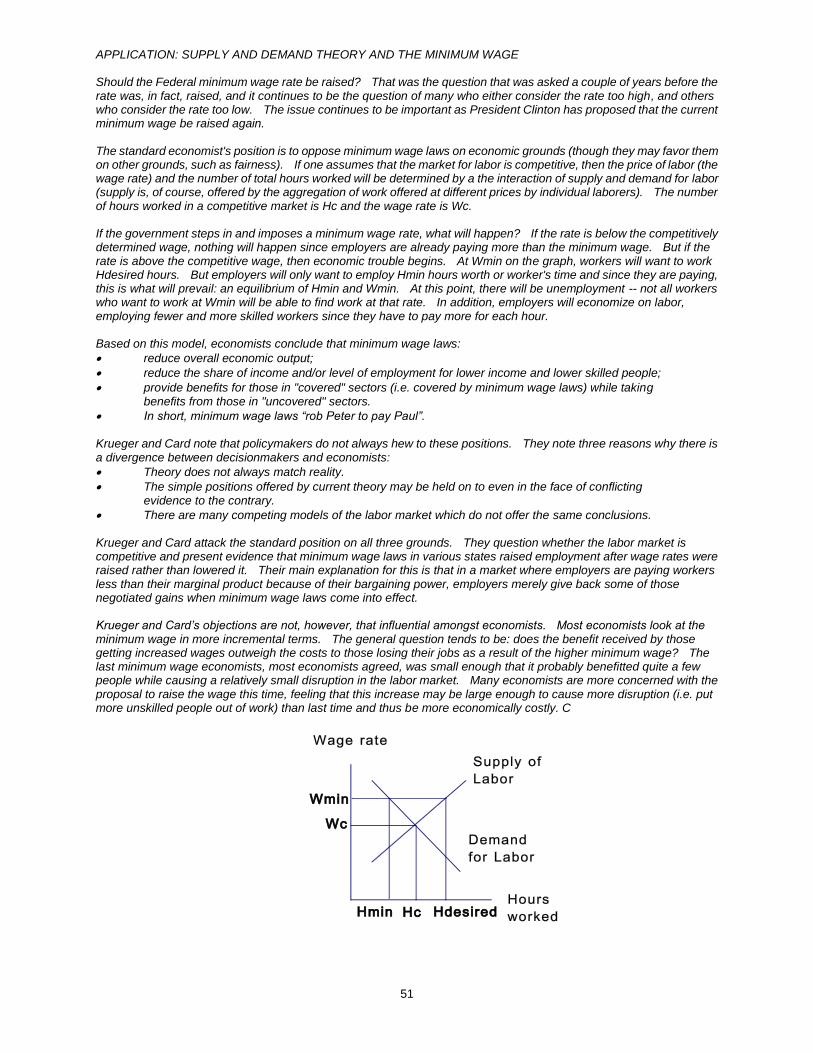

Scarcity and constrained optimization (scarcity (noun)) scarce: 1. Infrequently seen or found. 2. Not plentiful or abundant. The major question for economics tends to be: "How are resources best allocated given scarcity?" Economics captures this notion of scarcity in the budget constraint. A budget constraint shows all the different combinations of goods and services that a consumer can purchase given the resources (income) under his/her command. It is possible to graph a budget constraint, although to do this in two dimensions, one needs to limit one's attention to two goods. Suppose that a consumer wants only to buy apples and oranges and wants to spend all their income on those two things. In this case the budget constraint line shows all the combinations of apples and oranges that can be bought with a given income. What is an optimum? The American Heritage dictionary defines it as: “The best or most favorable condition, degree, or amount for a particular situation.” To “optimize” is “to make the most effective use of”. So economics is a discipline which focuses on attainment of optima (the plural of optimum) in a setting where scarcity prevails. This scarcity acts as a central constraint on the system. Hence economics is often referred to as an analysis of constrained optimization. Optimizing along the budget constraint When an economist sees a budget constraint, what does s/he do? First, an economist will tell you to get on to the line. In other words, assuming that you want to spend all your income on apples and oranges (and it is important that it be known exactly what your objectives are) then you should choose a point somewhere along the budget constraint (a point like A). Points above the constraint (like C) are unattainable given existing resources, while points like B are attainable but are not making full use of your available resources given your chosen objectives. This is the essence of constrained optimization. We know that point B is not an optimal point and that point C is unattainable and hence irrelevant to our decisionmaking. However, how does one choose between point A and point D, both of which are along the constraint? This issue will be encountered again later on. Suffice it to say that to know which point is an optimal point, one needs to know what it is one wants. In other words, there is a need to know objectives and a need to know preferences among those objectives. The neo-classical paradigm A very coherent and powerful world-view which is often referred to as the neoclassical paradigm. This paradigm assumes that the economy works in very set ways along very set lines. There are some who believe that this model can explain many or most noneconomic phenomena, including war, revolution and crime. Such people are often called economic imperialists because they want the neoclassical paradigm to take over all social science. Elements of the Neo-classical Paradigm

All actors in the system are rational, or behave as if they were. “Rational” here means that people act consistently and in a well-ordered fashion.

All actors are self-interested. This does not mean that they think of no one else but that they ultimately choose to make themselves better off and will not seek to make themselves worse off.

The goal of actors is to maximize their desired objective. Put another way, whatever "good" (as opposed to "bad") you want, more is always better.

People respond to incentives, and price is the best incentive.

Markets generally clear, that is desired quantities will be traded at agreed upon prices.

The economic system is generally self-equilibrating, i.e. if left to its own devices, it will find a stable equilibrium.

3

The economic system is efficient, i.e. the forces of competition will always lead to lowest production cost and maximum consumer utility or satisfaction.

“Economic Imperialism” and the “Chicago School” As mentioned above, “economic imperialists” believe that the neoclassical paradigm could and should take over all social science. The neoclassical paradigm lends itself to economic imperialism quite well because it is a theory with (a) a coherent structure; (b) concepts which are general in nature and very generalizable (i.e. can be easily extended, in a logical sense, beyond their immediate and intended domain); (c) a compelling internal logic and ease for generating "stories" and explanations of why things happen. In addition, in many noneconomic areas where economic thinking has become pervasive, other disciplines often offer conflicting theories of phenomena in those areas, or offer no theory at all. Thus it is that Nobel Laureate Gary Becker has argued that "it takes a theory to beat a theory" and that economic thinking "wins" in many cases because other disciplines do not offer competing and testable theories of their own. The University of Chicago has become known for its intensive development of the neoclassical paradigm and its extension of that paradigm into many noneconomic areas in the true spirit of economic imperialism. This distinctive approach to economics has become known as the Chicago School. As a logical game, it is easy to play with extend the neoclassical paradigm far beyond its original boundaries. But in the real world, many of the basic premises of the model -- perfectly clearing markets, perfect information, rational maximizing individuals -- often do not seem to accord with the observed facts. Now a given theory will always deviate from the facts in some way since a theory is by definition a simplification of reality. How do economic imperialists tend to deal with uncooperative facts? In his article on Chicago School economics, Reder lists at least 4 possible responses a theoretician can take when observed facts do not match the predictions or premises of the neoclassical paradigm:

Reexamine the data until the findings match the model's predictions

Redefine or augment the variables in the model to account for the data

Alter the theory to accomodate behavior inconsistent with rationality

Place findings on research agenda as a researchable anomoly Chicago School thinking tends to do all but the third item. The other options tend to preserve and extend the neoclassical paradigm and allow it to extend to more hostile settings. The third option tends to undermine the paradigm.

APPLICATION: THE THEORY OF RATIONAL ADDICTION One seeming challenge to this paradigm is addictive behavior, which seems to be irrational and self-defeating. However, Nobel Laureates Gary Becker and George Stigler have developed a theory of so-called “rational addiction”

The argument goes something like so:

Each individual has a “utility function” through which they get satisfaction (more on this concept a little later on). A typical utility function can be written in general form like so:

Utility of Consumer A = f(good 1, good 2...good n)

“Inputs” into this utility function are goods which people consume. The “output” of this utility function is “utility” which is a measure of consumer satisfaction. It is not directly observable, but people desire as much satisfaction as they can get and organize their behavior accordingly to maximize satisfaction within the constraints of time, money, etc. which they find themselves presented with. The function itself — “f(..)” — represents a “technology” which the consumer has for transforming raw inputs into the useful output of satisfaction. As economic observers, we cannot observe this technology directly. The best that we can do is to see how many inputs a consumer consumes and then, by observing the consumer’s actions over time, make some guess about the output of utility being produced.

In a world with only one good, the economist might observe the following pattern

Consumer A is offered 1 unit of good X and is asked how much s/he is willing to pay and the consumer says

4

$1. If offered 2 units, the consumer is willing to pay $2. If 3 units, $3 and so on. If we equate the dollar amounts to utility received, the economist might assume a “technology” which relates inputs to output like this:

Utility of Consumer A = (X), i.e., 1 unit of X yields 1unit of utility, 2 yields 2 units and so forth.

With respect to addiction, Becker and Stigler come up with some generalizations about addictive behavior, and then worked backwards, using neoclassical postulates, to arrive at an explanation of such behavior.

They describe addicts as (1) being willing to pay increasingly greater amounts for a given unit of an addictive substance over time and thus (2) deriving ever less utility from that unit over time.

This behavior pattern they claim can be explained as rational maximizing behavior because the addictive substance causes changes in the consumption technology which make the utility function less “efficient” over time in transforming the good into utility.

Thus one might observe the following utility function for beer consumption in period 1

U (of consumer A) = 3(number of beers) - 1.5^(number of beers)

In that period, consumer A will receive 1.5 units of utility by consuming 1 beer, 3.75 units by consuming 2, 5.63 units from 3, 6.94 from 4, 7.41 from 5, and then diminishing returns set in at 6 beers when utility is only 6.61. (“Diminishing returns’” is a pervasive concept in economics and refers to the pattern whereby an activity is first associated with big payoffs and then increasingly small payoffs as that activity increases. A typical textbook example is, in fact, beer consumption — the first one tastes really great, the second one less so, and the third one might begin to get one sick).

This is what happens at time 1. But suppose beer is like dirty water in a paper manufacturing plant. Just as dirty water will begin to gum up the works in such a plant and make it less efficient with time, beer may be a substance, at least for some consumers, that degrades the consumption technology. Thus in period 2, the consumer may find his/her utility function looking like so: U = [4(number of beers)-1.5^(number of beers)]-5.2

It’s a subtle difference, but now the consumer must drink 6 beers instead of 5 to get that 7.41 units of utility. If the function continues to deteriorate like this, the consumer will have to drink more and more beers each time to get that same level of satisfaction. And at some point, even that original “high” may not be achievable no matter how many beers are consumed.

The main point of this model is that there is no need to assume that the consumer is being irrational or not maximizing in order to derive behavioral conclusions which mimic certain behaviors that are seen in addicts.

Are the objections to this model? Of course there are, but these will be considered later on.

5

Concepts: Supply and demand, elasticity

Supply and Demand Demand and supply, given a number of assumptions, can be drawn as curves (here as straight lines) which relate a a particular quantity of something (e.g. good "X") to a particular price. Thus the demand curve shows how much X is demanded at various prices and the supply curve shows how much X is provided at the same array of prices. Such curves are shown in Figure 3. Note that the demand curve slopes downward from left to right. This means that at high prices relatively little X is demanded while at low prices relatively more X is sought. The supply curve, by contrast, slopes upward from left to right. Thus at low prices, relatively little X is offered by the supplier while at high prices, relatively more X is provided. Although there are exceptions, demand curves slope downward so often that this pattern has been referred to as the law of demand. Similarly, the law of supply holds that the supply curve almost always slopes upward. Why does the demand curve slope downward and the supply curve slope upward? Economists generally assume that people are rational maximizers. In other words, there is some logical structure to a person's actions (it does not move about wildly or randomly) and that person prefers more to less ceteris parabus (i.e. if I can get more of something without paying anything more for it, I will take it). Thus the lower the price of a good, the more that I will take of it because for a given dollar amount, I can get more of it and will want more of it. Similarly, the higher the price of a good, the more willing I am to sell it because for a given amount of the good, I can get more money as the price goes up. Shifts in demand/supply versus moves along them The fact that I am willing to buy more of a good as price goes down, and sell more as the price goes up is indicated graphically by a movement up or down the supply or demand curve. The curve simply shows how my demand changes as price changes, everything else being equal (including tastes and income). This movement is indicated by the arrows pointing to one another below. If I suddenly lose my taste for chocolate, this will change my demand curve. Such a change is represented by a shift in the demand schedule, in this case a shift downwards in the demand curve. In other words, if I lose my taste for chocolate then I want to buy less at every price and this is shown by a downward shift in the curve (from Demand to Demand*). Supply and Demand Schedules Underlying supply and demand curves, at least conceptually, are supply and demand schedules. Two representations of supply and demand are shown here. The table shows supply and demand schedules which indicate how much a person, firm or other entity either demands of a particular something at a range of prices or how much they are willing to supply at a range of prices. The graph shows that the same schedule are graphed and the resulting supply and demand curves are shown (here they are straight lines). Of course the average Joe is unlikely to have a demand schedule in mind and the average firm may not have an actual supply schedule. But economists assume that people behave as if they do and further these curves summarize propositions about human behavior. e.g. that people will demand more of a good as its price falls.

6

Price

Quantity demanded (demand)

Quantity supplied (supply)

$2

5

1

$3

4

2

$4

3

3

$5

2

4

$6

1

5

Supply and Demand Functions Behind curves and schedules are mathematical relationships known as functions. An example of a function is Y= f(X) which in words can be stated as "Y is a function of X". The function is defined as any relationship such that, given a value for X, a corresponding value of Y, and only one value, is returned. X and Y are thus said to have a one-to-one relationship or mapping. X is the "independent" variable while Y is the "dependent" variable, i.e. Y's value depends, through the functional relationship, on X. An Example of Supply and Demand Functions Recall the supply and demand schedules used before. These values can be summarized even more succinctly with an equation which reproduces the value of "Y" (quantity supplied or demanded) for each corresponding value of "X" (price). As shown earlier, these schedules are graphed as straight lines so the functional relationship will have a form of "mx+b" where m is the slope of the line and b is the point on the Y-axis where the line intercepts it. D = -X+7 (or D = 7-X) S = X-1 Note that D is downward sloping (its slope = -1) and S is upward sloping (=+1) Market Equilibrium Supply and demand intersecting indicates an equilibrium in a market. The graph shows such an equilibrium. Note how the equilibrium resembles the two blades of a scissors, following the metaphor used earlier. In this case the demand for good X and the supply for good X match up at only one point in the middle. This point is an equilibrium in the market for good X. At prices lower than the equilibrium, demand for X will exceed supply and at prices higher than that supply will exceed demand.

7

General Equilibrium Where there is one market, there is only one equilibrium. But there are typically many markets in a developed economy -- markets for food, manufactures, etc; in this case, equilibrium in one market, or lack thereof, may cause equilibrium or lack thereof in one or more other markets. The presence of equilibrium in all markets is known as general equilibrium. Formally, general equilibrium is simply the analysis of many interrelated markets as depicted below. In such a case, equilibrium in one market will affect the equilibrium outcome in another one (or in a set of other ones). Of course, if markets are unrelated to one another, there is no meaningful general equilibrium since the status of one market has no bearing on any other and we could study each single market in isolation from the others. A General Equilibrium Example Imagine now that the markets being studied are the markets which include the supply and demand for (1) steel; (2) plastics; (3) glass; and (4) automobiles. It is easy to see that the equilibrium of demand and supply in the market for automobiles will affect the equilibrium in the other markets and that equilibrium in the other markets will affect the equilibrium in the market for automobiles. This comes about in this case because the first three markets represent inputs into the process for making automobiles. Thus the amount of autos that a society creates will have a major impact on the amount of steel, plastics and glass that will be created and vice-versa. Substitutes and Complements Markets are not only related by the fact that one market provides inputs to a production process relevant to another as with the automobiles example. Markets are also related to one another by patterns in consumption. For example, consider the markets below for tea, coffee, sugar and crumpets. Purchase of sugar is related to purchase of tea and coffee because many people consume those two goods with sugar. In this case the goods are complements -- that is one good tends to be used or consumed with the other. Tea and crumpets are also complements. On the other hand, tea and coffee are also related to one another through consumption patterns except that they are substitutes -- one is consumed or used in lieu of the other. Other Market Interrelationships There are yet other relationships between markets. For example, the market for Starbuck's stock is related to the market for coffee in part through financial mechanisms since the market for such stock depends on the health of Starbucks which depends on the coffee market. Adjustments between these multiple markets tend to occur through price -- e.g. a strong demand for steel will drive up the price of steel (unless supply increases) which will then tend to drive up the price of autos. Of course a change in price will affect final quantities traded. Income and Substitution Effects Demand in particular can be broken down into two components. As the price of a good changes, this affects both the amount of that particular good that a person can buy ( the income effect) and it also changes the incentives to buy that good ( the price

8

effect). Say a good falls in price. This fall in price (1) allows a person to buy more of another good should they choose to do so because some of the income they devoted to buying the original good is now "released" for other purposes. Thus they have more disposable income as a result of the price change and this is the income effect. At the same time, the lowered price itself makes the good cheaper relative to other goods and this alone makes the good a more attractive buy (the price effect). How much a consumer actually buys of the newly priced good depends, in part, on their tastes. Elasticity Supply and demand can both be summarized by an elasticity. An elasticity is equal to the percentage change in one quantity divided by the percentage change in another quantity. For supply and demand, one typically wants to know the price elasticity. That is the equal to: [(% change in quantity of a good supplied or demanded)/(% change in price of that good).] For demand only, the whole division has a minus sign before it. This is simply a convention of economics to ensure that the elasticity of demand is nonnegative. Types of Elasticity Economists use some elasticities more than others. Some of the more common ones are: Price elasticity: The change in quantity of X demanded or supplied in response to a change in the price of X. Income elasticity: The change in quantity of X demanded or supplied as income of the party doing the demanding or supplying changes. Cross-price elasticity: The change in quantity of Y demanded or supplied in response to a change in the price of some other good Y. Elasticity of Output: The change in an entity's output in response to a change in a given input. Elastic and Inelastic “Elastic," means something is highly responsive to changes in something else. For example, elastic demand means that the quantity demanded changes a lot when the price changes. Inelastic demand means that the quantity demanded does not change much when the price changes. The qualitative idea is that: Elastic = Responsive Inelastic = Unresponsive The terms "elastic" and "inelastic" can be given a precise meaning in terms of the number that comes out of the elasticity fraction. The divider between elastic and inelastic is -1, for demand elasticities. (For elasticities where you expect a positive relationship between Q and P, such as for elasticities of supply, the divider is +1.) If the demand elasticity is more negative than -1, the demand is elastic.If the demand elasticity is between -1 and 0, the demand is inelastic. Elastic demand -- elasticity more negative than -1 -- means if the price goes up, the total amount customers spend goes down.Inelastic demand -- elasticity between -1 and 0 -- means if the price goes up, the total amount customers spend goes up.If the elasticity is exactly -1, the amount customers spend stays the same as the price changes. Price elasticity is a measure of responsiveness. It tells how much one thing changes when you change something else that affects it. For example, the elasticity of demand tells us how much the quantity demanded changes when the price changes. The elasticity of demand measures the responsiveness of quantity demanded to changes in the price charged.

9

Inelastic Demand Consider the following graph and table. INELASTIC DEMAND

Price

6| F

5| E

4| D

3| C

2| B

1| A

:....:....:....:....:....:....:....:....:....:....:....:....:

0 5 10 15 20 25 30 35 40 45 50 55 60 Quantity

A B C D E F

Price $1 $2 $3 $4 $5 $6

Quantity 40 40 40 40 40 40

Regardless of whether the price is $1 or $6 or anything between, the amount sold will be the same, 40 units. This is an example of completely inelastic demand, i.e. completely unresponsive to price changes. This is an extreme case. The traditional medical model implies completely inelastic demand. If health care professionals provide what they judge that the patient "needs" regardless of cost, and if the patient is unable to object or is fully insured or both, then demand will be inelastic. Note in this case the relationship of elasticity to revenues: A B C D E F

Price $1 $2 $3 $4 $5 $6

Quantity 40 40 40 40 40 40

------------------------------------------------------

Revenue $ 40 $ 80 $120 $160 $200 $240

Revenue equals Price times Quantity. So If your demand is inelastic, the more you charge, the more revenue you take in, since the amount you sell doesn't go down. Therefore, if profit is your goal, you should raise price when demand is inelastic. This leads directly to the standard. Demand becomes elastic if consumers are price conscious and if they have an alternative. Suppose that the market in the example above gets a new competitor, who charges $3.50. Suppose also that price is the consumer's only consideration (no quality difference, no customer loyalty to a particular company). Then the demand might look like this. Demand -- One Competitor Who Charges $3.50 -- Price Only Consideration

Price

6|F

5|E

4|D

3| C

2| B

1| A

:....:....:....:....:....:....:....:....:....:....:....:....:

0 5 10 15 20 25 30 35 40 45 50 55 60 Quantity

A B C D E F

Price $1 $2 $3 $4 $5 $6

Quantity 40 40 40 0 0 0

If you charge less than your competitor's price, you get all of the business. If you charge more than $3.50, you get no business. Your demand is now highly elastic near the competitor's price. This can be a highly unstable market because your competitor faces the same situation. You can cut your price to $3.49 and take away all of the business. Your competitor can then charge $3.48 and take it all back. Each of you has the temptation to cut price on the other until one of you goes broke. You see something like this when neighboring gasoline stations have a price war. One thing is for sure: If there is a competitor in your market, and if the consumers care about price, then there's a definite limit to how high you can raise your price.

10

Of course completely elastic demand is the opposite of completely inelastic demand: If one were to draw the demand curve in this case it would be completely horizontal rather than vertical. Analogous arguments can be made for supply curves. Elasticity. Substitutability and Complementarity Cross-elasticities refer to the change in the demand for good X when the price of Y changes. Such relationships are interesting as a measure of whether one good is a substitute or complement to another. For example, one would expect that a rise in the price of tea would cause an increase in the consumption of coffee. This is one of many important elasticities -- one could invent any one that one sees as useful. Normal and Inferior Goods Another relationship which is summarized by elasticity refers to the change in consumption of a good when a person's income changes. A normal good is one whose consumption relative to income increases as income increases. An inferior good is one whose consumption relative to income falls as income rises. Thus the richer one gets, the less iceberg lettuce (it is an inferior good) one may consume and the more arugula one eats (it is a normal good).

APPLICATION 1: THE PUZZLE OF ECONOMIC DEVELOPMENT: A review of Bairoch, Paul, Economic and World History: Myths and Paradoxes (University of Chicago Press, 1993)

This book could be titled: “What determines economic growth?” for much of the discussion centers on factors which cause some countries to grow and others not to. Bairoch starts with the Depression, but one could start with a larger theme in his book which is the impact that trade has on economic growth.

One of the seven “minor” myths that he ends with is “Was trade an engine of economic growth?” Here is one of the first suspects on the usual list of causes of economic development.

Much of Bairoch’s work focuses on determining whether free trade prevailed in the first place. Of course mercantilism and protectionism predominated before the 19

th century although this was due more to various

interests protecting their perceived turfs rather than a result of the influence of mercantilist theories. (17-18). But was that century a golden age of free trade? Bairoch thinks not.

The United Kingdom did become increasingly liberal in trade matters but not really before 1842. The Corn Laws were not abolished before 1846 and other trade restrictions were relaxed only in a piecemeal fashion — in 1825, with an act allowing emigration of some skilled laborers and with reduction of some import duties in 1833. The Corn Laws themselves were successfully repealed by a coalition of manufacturers and others who used the high food prices and low wages from such laws to make an issue of worker poverty. It was indeed a free trade watershed. But it must be kept in mind that free trade only took hold as the UK established commanding leads in almost all industries and in per capita income (20-21).

From 1846-1860, the UK aggressively pursued free trade and via the example set by this and through the increasing volumes of international trade, free trade began to take hold on the Continent as well. At first this was limited to small economies such as Holland, Portugal, Denmark and Switzerland, though with some degree of protectionism as well. Then between 1860 and 1879, free trade became dominant in Europe, but not elsewhere in the world, especially the U.S. (21-23). Then protectionism began a resurgence in Europe that continued until the beginning of World War 1. Here, though, the UK’s free trade policies became more entrenched. At the same time, the U.K. became less important economically and less robust as well (23-29)

Looking at the rest of the world, the picture is more complicated still. Japan and China, often seen as the closed and mysterious East, in fact had open trade regimes at various times before the 1800's. The U.S. conducted a protectionist trade policy before the beginning of the Civil War. And while there were twists and turns in that policy, it grew more protectionist after the Civil War. Here, though, the justification for such policies changed from protection of infant industries, a viable rationale when the U.S. economy was young, to protection of wages (31-37). Protectionism also reigned in other parts of the developed world, especially in the British Commonwealth countries of primarily European descent — Canada, Australia and New Zealand. For the latter half of the nineteenth century in to the early part of the twentieth, the developed world was a bastion of protectionism with an island of liberalism — the U.K. (41). It is only in the so-called “future third world” that free trade was a rule and there it was enforced by colonial masters, except in the Ottoman Empire which had a free trade policy already and whose example of economic decline was sometimes used as an argument against unfettered free trade, especially by Disraeli. (41-42)

This history raises a related question which is if free trade did not always predominate in the high-growth 19

th

11

century, was protectionism always a burden? One clue is found by the fact that the rise of free trade which started around 1870 was accompanied by the great depression of 1873 while the rise of protectionism in the early 1890's saw the end of this depression. This is obviously too simplistic a case by itself but what seems to be happening during this time is that differing stages of economic development and different external circumstances imply different results for the same policy regime. When Britain adopted free trade for agriculture in 1846, the hundred years prior had already seen a marked shift in the proportion of the labor force employed in manufacturing relative to agriculture — England’s ratio of industrial workers to farm workers was much higher than that of Europe at the time. In addition, non-European sources of grain became much more important and much cheaper as the nineteenth century progressed. Thus free trade, especially in agricultural products, had a much harsher effect on European economies in the 1860's and 1870's than it would in England at that time and the relaxation of those policies would have a more salutary effect in Europe than England. (47-49). The case “against” free trade is even stronger if one looks at correlations of per capita output growth and free trade policy, which move inversely, both in Europe and even more so in the U.S. (50-53)

So was trade an engine of economic growth? For the most part, the answer seems to be “no”, at least for all other than small countries where external trade to begin with represents a much higher proportion of economic activity. To be more precise, the mechanistic model of free trade as a spur to economic growth must be resisted for it depends on the circumstances. (136-138). If not trade, then what? Another alternative is that Europe and the developed world relied on the exploit of third world resources to grow. If so, this is a bad story for the current third world since they have no such hinterland to exploit. But Bairoch says that this too is not an economic prime mover. For if one looks at various raw materials, Europe and the developed world were either exporters of such goods or primarily self-sufficient, often on the order of producing 90 to close to 100% of their needs of various basic inputs. (60-68). However, for the third world this meant that the overwhelming bulk of their exports were raw materials. However, one needs to distinguish between raw materials, such as oil, which often require a large amount of processing, and primary goods, such as fruit and salt, which undergo little real transformation before being shipped). (68-69)

So the Third World was not a crucial source of raw materials during a critical period of economic growth in the developed world. Was it a crucial outlet for colonialist goods? In a global sense, the answer is no for overall the share of exports going from the West to the underdeveloped nations remained small until the twentieth century. However, the picture varies by nation. The U.K. textile industry became especially dependent on third world outlets by the turn of the century, although it must be remembered that the country at this point had a good six decades of modern economic development behind it. Even so, relatively small outlets can be critical for the profitability of an industrial sector. At the same time, easy colonial outlets can have a negative effect as well as domestic producers become “lazy” and uncompetitive. (74-75) Loose evidence that colonial empires may be negative influences on growth rather than positive ones comes from the correlation of lower economic growth with presence of such empires. Empires can be costly both in terms of direct expenditures and diversion of entreprenurial resources (77-78)

Perhaps colonial possessions did not feed ongoing economic growth, but were they a trigger to the industrial revolution itself, or mare particularly, to the more colony-oriented economy of Great Britain? There is an immediate problem with this hypothesis since the industrial revolution in England started before its empire was either that large or important in terms of trade — that came later. (80-82) More generally, it seems to be the case that colonial empires were not an especially significant source of riches or development for Europeans, though it is not to be treated likely. However, the impacts of colonial de-industrialization on the Third World is much more negative, accounting for a lot of the slow income growth characteristic of those regions between 1800 and 1950. (88-98)

Perhaps history matters here, for it is often assumed that Europe was much richer and much more urbanized at the outset of the industrial revolution and that these factors accounted for Europe’s take-off and the Third World’s persistent stagnation (though these differentials themselves need to be explained). There is a lot of uncertainty with regards to this question but as to wealth, Bairoch says that the future Third World and Europe were at roughly similar per capita income levels at the beginning of, say, 1700. (101-108). As for urbanization, Bairoch says that the pre-industrial world, on average, was more urbanized than commonly believed, consistent with levels seen during the Greek and Roman Empires. These levels are, it is true, far below those necessary to sustain industrialization; but the main point here is that differentials between urbanization may not be a very robust explanation for economic growth [this last point is really mine, not the author’s]. (142-144)

How about population growth? It has been argued that the impact of population growth early in the West’s economic growth was positive. However, the rate of this growth is critical — current rates in the third world

12

are much higher than those witnessed during the early 1800's in Europe or anywhere else for that matter. (127-128) In addition, Europe’s experience in this matter does not suggest such a simple correlation. In particular, high increases in both private and social investment, particularly in education, are necessary to provide for increased population. (130-131). One big difference also in current third world urbanization and early European urbanization is that the latter is taking place largely as a concentration of people without a concomitant urban and economic development (132).

Indeed, this issue of causality crops up again and again in economic history. Bairoch suggests, for example, that growth drives trade and not the other way around. And so it can be for urbanization — growth driving population concentration can be a good thing, but population concentration by itself does not necessarily drive growth.

One can turn this economic development question on its head and ask what drives underdevelopment. Bairoch tackles these issues as well. One of these myths is that a reliance on export of primary goods leads to backwardness. The evidence does not support this for many nations in the 1800's were exporters of primary goods, including New Zealand, Argentina, and, most of all, the United States, and they had very high levels of per capita income. Thus a reliance on primary goods as a main export is not by itself a road to underdevelopment. However industrialization at some point seems to be necessary to reach the next level of economic growth. This is what happened in Argentina which was a very rich country before World War 1 but because of a lack of industrialization as time went on and very low growth in agricultural productivity sunk to a much lower rank in the modern period. (140-141)

It also used to be argued, though much less so now, that a deterioration in the relative price of raw materials to manufactured goods throughout the 19

th century led to the current fix of Third World countries since they are

primary exporters of raw materials. In fact, such terms of trade seemed to have improved during the period with one very important exception: sugar, a key import for many colonial nations. (111-113)

APPLICATION 2: RAILROADS AND AMERICAN ECONOMIC GROWTH AFTER THE CIVIL WAR

Take-off thesis: The railroad caused America to industrialize rapidly and suddenly, increasing the rate of per capita output growth dramatically in a very short period of time (Rostow, 1960). The take-off thesis relied on forward and backwards linkages.

Backward and forward linkages Forward linkages refer to the use of the outputs of the leading sector, in this case railroads, as inputs into production by other sectors.

Backward linkages refer to the use of the outputs of other sectors as inputs into production of the leading sector.

Thus railways provide improved transportation services which are used by, say, agricultural producers to get

goods to market faster (a forward linkage) and railways require steel; which increases demand for the product and stimulates the growth of the steel industry (a backwards linkage). The Fogel argument/Counterfactual Fogel looked at the economy up until 1890, with the railroads available and then, in 1890, suddenly eliminated them from the economy, requiring the use of alternative, and more expensive transport methods such as canals. He then measured the effect on Gross National Product (GNP) in that year, under a number of simplifying assumptions described below, and called that effect social saving railroad's impact.

Social Saving

His measure of indispensability was the "social saving" due to railroads. Social saving generally refers to the resources saved by a society, and hence available for other purposes, when it has the use of a technology or other innovation as compared to the situation which would prevail if it did not have the use of that technology or innovation.

13

The general definition can be better understood by using a diagram of a simplified economy (adapted from Coatsworth, 1981). Two aggregate supply curves and one aggregate demand curve for transportation are pictured below.

For simplicity, the transportation supply curves are horizontal, the transportation demand curve, vertical. S

w/rail is the supply of transport available in the presence of railroads. Sw/o rails is the supply curve of transportation when railroads are unavailable and when only alternatives, such as canals, can be used. The amount spent on transport is equal to the appropriate price times quantity (which I have not labeled above). With railroads available, the amount spent on transportation equals area 1. Without railroads, the amount spent on transportation equals area 1 plus area 2. The social saving, that is, the resources which railroads free up for social uses other than transportation, is equal to the resources which would have been spent on transport without railroads minus the resources which are spent on transport with railroads. It should be clear that this difference is area 2.

Social saving thus defined is both a net measure and a gross measure of the economic impact of the railroads. It is a net measure, because it compares one circumstance, the actual historic, or "factual" circumstance where railroads are operating, with another hypothetical, or "counterfactual" circumstance where railroads are not operating, and then subtracts the difference in transportation costs between the factual and counterfactual to arrive at a net change in transportation costs. It is a gross figure because it consolidates a whole range of impacts into a single index and measures the absolute impact on overall resources available to society, rather than relative changes to resource allocations within that society.

Embodied/Disembodied Effects Fogel himself referred to the social saving as a disembodied effect, due to the fact that any transport innovation lowers costs and hence results in savings to society. Railroads delivered these savings in a very particular form, and the form which savings due to railroads, as opposed to a different transport innovation which might have occurred, are the embodied effects (Fogel, 1979, pp. 38-39). Thus a relatively insignificant social saving might result in otherwise dramatic changes in a society. In other words, while total output might have remained fairly similar in the absence of railroads, the social fabric might have changed dramatically.

John Coatsworth has summarized this complex web of impacts well: "The most celebrated technological innovation of the nineteenth century industrial revolution was the railroad. Since nearly every product of industry, agriculture, and mining used transport, and railroads reduced transport costs, the effects of the new technology were felt throughout entire economies. Since railroads quickly came to be major consumers of iron and steel, they were credited with stimulating the development of basic industries. As large enterprises with heavy capital requirements, they pioneered the development of modern management techniques and had considerable impact on the evolution of modern capital markets. The social effects of cheap, rapid transport provided drama for historians of labor struggles, elite behavior, and migratory patterns. Military historians have noted the difference that railroads made in strategic and tactical planning (Coatsworth, 1981, p.7)."

Oliver Williamson and Alfred Chandler have argued that railroads produced not only transportation efficiencies, bur organizational and institutional innovations which, when combined with the delivery of speedier and more regular goods and passenger carriage, made a system of mass distribution possible, promoted the growth of mass manufacturing and led to the development of the large, vertically-integrated corporation(Chandler, 1977; Williamson). Williamson also noted that the geographic broadening of the market may have led as well to quality debasement as local manufacturers had to oversee increasingly distant distributors. While these effects can be discussed, and even observed and understood, they are difficult to formalize and disentangle analytically (James, 1984, pp. 241-242).

Pros and Cons of Fogel Some of these criticisms of Fogel become clearer by returning to Figure 1 above. For simplicity, the transport supply and demand curves are drawn with infinite and zero price elasticities respectively. These clearly are unrealistic assumptions. The assumption of zero elasticity of demand has the effect of maximizing the amount of social saving. This can be seen by imagining a slant to the demand curve, which causes area 2 to be reduced. Fogel desired such an outcome since he wanted to show that, even using a measure with an upward bias, social saving was still modest. Fogel was attacked by many authors for using a zero demand elasticity, with many authors arguing that passenger demand elasticities at least, were much greater than zero, and that available evidence was sufficiently detailed to be used to estimate actual price elasticities (Boyd and Walton, 1972; Fogel, 1979). The unrealism of the assumption of zero demand elasticity is further seen by restating it: when transport prices go up, shippers are assumed not to respond, shipping the same volume of goods to the same points over the

14

same distances. For Fogel's purpose of debunking railroad indispensability, this may be a reasonable stratagem, since if shippers were allowed to adjust, social saving would be even less, but for a "true" counterhistorical picture, this may constitute an unreasonable compromise. It also makes different estimates of social saving, based on differing demand elasticity assumptions, difficult to compare (Fogel, 1979, pp. 10-12). Transportation supply elasticities will also affect the social saving estimate. Fogel assumed, like many authors, that the long-run marginal cost was constant: hence the horizontal supply curve in the diagram. But unlike the zero demand elasticity assumption, which overstates social saving, this assumption may have the effect of understating social saving. If, for example, canals have a rising marginal cost structure, then when the hypothetical shut-down of railroads throws a large volume of traffic on to the canal network, prices of canal transport will presumably rise much more than observed canal tariffs, and the assumption of constant marginal cost, would suggest. The amount of resources diverted to transportation in the absence of railroads, and hence the social saving due to railroads, will be much greater than otherwise assumed. All of this suggests, as Fogel himself conceded later in the debate, that careful specification and understanding of the transportation sector is a prerequisite to understanding the impacts that a transport innovation might have on costs and prices (Fogel, 1979). Additionally, inferences based on available evidence, which may seem obvious, must be carefully defended and supported. Besides the obvious problem of adjusting observed canal and railroad tariffs to equate with true marginal cost by adjusting for government subsidies and monopoly power, one has to understand how prices would have reacted in response to a major shift in demand for transport. Although observed canal rates and railroad rates in 1890 might be fairly similar on average, if the only way that canals could meet additional demand was to pull in less efficient and more expensive operators, price would increase more than these 1890 rates would suggest. Fogel makes another point, namely that the ownership of both railroads and canals might make a difference in pricing policy. Thus government-owned canals would tend to charge below marginal cost, or at least not above it, in response to a surge in demand, while privately owned canals would tend to charge more than marginal cost in such a case. Fogel argues that the former was the case in postbellum America, where many canals were publicly owned, while the latter was the case in England, where most canals were privately owned (Fogel, 1979; Hawke 1970). Less obvious from the diagram is the relationship of industrial structure of nontransport sectors to social saving induced by changes in the transport sector. As mentioned earlier, social saving represents the amount of resources that railroads made available to society for alternative uses. However, whether a society could or would actually make good alternative use of these savings depends largely on the strength and quality of the backwards and forward linkages which exist. This fact is particularly important in underdeveloped economies where structural and institutional barriers to efficient allocation of resources (such as concentration of wealth, illiteracy, and state intervention) often means that any savings due to less costly transportation fails to result in overall savings to society because weak forward linkages cause these transportation economies to be squandered. Conversely, if a railroad is built mainly with foreign capital and foreign labor, benefits from backward linkages, such as the development of a domestic steel industry, may also fail to come to pass (Coatsworth, pp. 201-203).

Main Results of the Analysis of Railroads and Economic Growth

Railroads were not indispensable in most European countries and America. That is, shutting down the rails for one year in England, the U.S., Russia, France, Germany and Belgium would have resulted in a GNP loss no greater than 11% and as low as 2.5%, clustering closer to 5%. Only in Mexico and Spain were GNP losses truly catastrophic, closer to 20%, much of that having to do with the lack of viable alternatives (O'Brien, 1983, pp. 9-11). Even more dynamic simulations such as Jeffrey Williamson's have shown relatively modest, though higher, social saving (WIlliamson, 1974, 1975; Fogel, 1979; James, 1984).

Social saving due to rails was generally greatest over shorter hauls where wagons and roads were the main alternative rather than longer hauls where waterways were often quite competitive and where productivity continued to improve over the late 19th century. Indeed, in this period canals continued to be built in Belgium, France and Germany (11). Thus social saving was greatest in countries which relied most on roads - productivity in this sector remained low until the development of the internal combustion engine - and lowest where there were many navigable rivers, terrain well-suited to building canals, and good facilities for coastal trade. In general, railways alleviated

15

poor natural endowments. Where these endowments were rich, rails had relatively little impact. Where these endowments were poor, railroads saved society more in terms of transport costs (O'Brien, 1983, pp. 11-14).

While many societies would perhaps have been only moderately worse off without railroads in terms of measured output, all societies would have looked significantly different without them. Beyond lowering transport costs, railroads had some of their greatest impacts in developed societies on corporate organization, capital markets, market structure, labor markets, and regional distribution of output mix (Chandler, 1977; Williamson, 1974). In less developed societies such as Mexico, railroads had significant impact on land ownership as well (Coatsworth, 1981).

Concepts: Marginal Analysis, Cost, Economies of Scale, Monopoly, competition and market structure

Marginal Analysis: Three dimensions to every problem One can view a system from its overall behavior, i.e. the sum of all the outcomes arising from that system. One could say that this is a total perspective.

One could also try to look at the behavior of the system over repeated workings of the system. One way of doing this is look at the averages, i.e. if the system produces outcome "t" in "n" instances, the average outcome is t/n.

Or one could look at how the system has changed since the last time the system was examined. Thus if the system is in some state "a" at time 1 and then at a different state "b" at time 2, one could subtract a from b to get (b-a), a measure of the net change from one time to another. Such net changes are called marginal changes or changes at the margin.

A marginal analysis table

# of times or units (N)

Total X (T)

Average X (A) = T/N

Marginal X (M)=(T(n)-T(n-1))

0

0

----

0

1

80

80

80

2

180

90

100

3

270

90

90

4

280

70

10

5

250

50

-30

Here is a table presenting total, average and marginal outputs of some process. The outputs could be anything and the process could be anything. For illustration, assume that this is a table of profits associated with production of can openers. But literally, the arithmetic relationships will hold regardless of what you are examining. Look at the "Total X" column first. At 0 units, total X is 0. Then 1 unit (here, a can opener) is produced. Total X (which is assumed to be profits from that can opener) is 80. With production of 2 units, total profit clips to 180; with 3 units, to 270; with 4 units to 280. And with 5 units, total profit falls back down to 250. Now one can already tell a great deal about this system just by looking at the total. For one thing, this outfit should only produce 4 can openers if it wants to maximize profit. The firm may also be interested in knowing its unit profit, also known as average profit per unit of output. This quantity is provided in the "average x" column which is simply "total x" divided by the "# of times or units." Note that the average is undefined for 0 (since T/0 is undefined).

16

Here average revenues start falling between the 3rd and 4th unit. This also indicates that production beyond the 4th unit are not sensible from a profit point of view. Finally, look at the "marginal x" column. Marginal quantities indicate the net change from one total level to another. Thus when the firm moves from a total profit of 0 at 0 can openers to a total profit of 80 at 1 can opener, the marginal profit is equal to 80, i.e. (80-0). At the second can opener, total profit is 180. The net change in profit between the first and second unit is 180-80=100. Marginal profit climbs then falls but remains positive until after the 4th can opener is produced.

Marginal Analysis in Graphs Here are the same relationships shown graphically. A number of things become clear when examining it, all of which are arithmetical relationships.

1. When the marginal quantity is negative, i.e. when each additional unit is negative, the total quantity starts declining. This makes sense since negative increments are being added to an accumulated total. One can look at the converse too -- if the total is declining, the marginal quantity must be negative. 2. It should also be clear that the average rises when each increment (marginal quantity) is above the average (i.e. is pulling the average up) and that the average falls when each increment is below the average (i.e. is pulling the average down). In fact, there are many such arithmetical "laws": 3. Total, average and marginal quantities are equal for the first unit (so long as total x=0 at 0 units). 4. The scale of an activity should be expanded as long as its marginal net yield (however that is properly measured, e.g. profit) is positive and carried on until it marginal net yield is zero. 5. Separate activity levels should, wherever possible, be carried to levels where they all yield the same marginal returns per unit of effort

17

Rules 4 and 5 are especially important for they help any entity set optimal activity levels. Moreover they are allow such decisions to be made on the basis of only partial information -- the marginal quantities. In other words, one often need keep track off of only one piece of information -- ignore the rest -- to make optimal decisions. Intuition of marginal analysis It might seem odd at first to keep an activity going until its net contribution -- its marginal yield -- is zero. For example, for the can opener firm, doesn't it seem like they should quit while they're ahead, i.e. stop producing at some positive profit per unit? It might seem that way, but if the firm stops producing at a level where each unit is providing positive profit, that means that it is giving up the opportunity to make even more profit. As long as each unit provides something -- anything -- in terms of net contribution to an organization, the entity's total net gain is increased. Similarly, for different activities: their marginal net yields should be equalized until each one is equal to zero. Otherwise, activity could be shifted from one place to another with resulting net gains. These marginal rules crop up again and again in economics. Memorize them. Production Functions and the theory of the firm The production function is meant to summarize the technology which allows a given input or inputs (such as labor and capital) to be transformed into a given output (such as a can opener). A simple production function might look something like the following: Y = 0.5(K/L) where Y = output, K=units of capital and L=units of labor. The resulting output from different inputs of K, holding L constant, are shown below.

units of K

units of L

resulting output (Y)

1

1

0.5

2

1

1

3

1

1.5

4

1

2

It is important to note that a production function traces out the output resulting from different combinations of inputs. When graphing this relationship, one has to hold all but one of the inputs constant, while varying the other one to see how output changes. Below L is held at 1 unit, while K is varied and the resulting output relationship is graphed as a straight line. Firms and Profit Maximization Every firm which produces something has a production function. But a production function only captures the technology of the firm. The decisions that a firm makes will also depend on the firm's objectives and that, in turn, will depend on the utility functions of those who own the firm. In addition, of course, the firm has to be worried about being "a going concern," i.e. can it make a profit, sell all that it makes, meet the payroll, etc. The classic assumption about firms is that they exist to maximize profits. Maximizing profits can be shown to be equivalent to maximizing the value of the shares of a corporation and since a firm is ultimately owned by somebody, this means that maximizing profits will lead to maximizing shareholder wealth.

18

Now money can't buy happiness, but it can buy things which lead to satisfaction, or utility. Assuming that firm owners are utility maximizers, they are also likely to be profit maximizers. There are two ways in which it is possible that firms will choose to maximize something other than profits. One is that the firm owners will derive utility from things other than profits, or at least that this is not the exclusive focus of their enterprises. For example, the firm owner's utility function may look like: U = f(profits, firm size, prestige) In this case, the firm owner gets utility from three things: profits, the size of the firm -- the bigger, the better -- and prestige attached to being a CEO of a big firm, like going to Republican fund-raisers, or sleeping in the Lincoln Bedroom. Of course one limitation to this strategy is that firm has to be a going concern. Firms which focus on more than profits may be driven out of business by leaner, meaner competitors. Some firms may behave this way but they may not last long on average. The other main deviation from profit maximization tends to come about when the owners of the firm and the managers are different people (i.e. the owners hire managers to take care of business). In this setup, there may be an agency problem whereby those hired to run the store may act in ways at variance with the interests of those who own it. For example, managers may pay themselves more than they're worth, pour money into big cushy offices rather than into the business, or hire incompetent cronies. All of this drives down profits. The limitation here, besides competitive pressures, is that owners are not stupid. Eventually they wise up to mismanagement and presumably take action to change it. Cost and Pricing Underlying both consumption and production is scarcity. If goods and services fell down like manna from heaven, there would be little need for theories of production and consumption. However, with scarcity there is an issue of not getting everything that we want and having to make choices. Scarcity is captured by the concept of cost. Cost indicates what you would have to give up to get what you want. In economics, cost is usually synonymous with opportunity cost which indicates the value of the next best available opportunity in lieu of the desired good, service or investment. Economists focus on opportunity costs, a concept which is meant to capture the true value of foregoing something. In the real world, most costs are accounting costs. Accounting costs usually diverge from opportunity costs because (1) they are based on accounting, and not economic conventions and (2) the objectives of those doing the accounting are not interested primarily in economic concepts (e.g. a troubled firm may want to understate costs to fool auditors or shareholders). When economists put forth hypotheses with respect to costs, they are almost always speaking of economic, not accounting costs. In an economic system, one of the central problems revolves around allocating scarce resources to competing uses. At one extreme a central planner could make such decisions. Most of economics deals with some version of the other extreme, namely completely decentralized decision-making with completely autonomous, though interdependent, decisionmakers. In a decentralized system, price is used to guide actors toward decisions which are both optimal for them and for the system. More will be said on this point later, but price is meant to act as a signal of the true opportunity costs of different decisions. Cost and Revenue Relationships Just as there are demand, supply, utility and production functions, there are also cost functions. These functions behave in certain ways regular enough that there is a whole theory of their behavior. There are two basic types of costs. Fixed cost, also known as sunk cost, does not vary with the level of activity but is constant for every level of activity. An example is the cost of investing in factory. The cost of building the factory does not vary with how much that factory runs. Contrasted with this is variable cost which does vary with the level of activity. An example are operating costs associated with running the factory. Just like there is marginal, average and total everything else, there is also marginal, average and total cost. Some important identities include: TC = TVC + TFC where TC= total cost, TVC= total variable cost and TFC=total fixed cost.

19

AC= TC/N, where N is the number of instances of the activity. Or one can state AC as AC=AVC+AFC where AC=average cost, AVC=average variable cost which is equal to TVC/N and AFC=average fixed cost which is equal to TFC/N. Note that as the level of activity rises, AFC falls (TFC remains constant while N increases). MC=(change in TC)/(change in N). Or, MC=MVC where MC=marginal cost and MVC=marginal variable cost. Note that there is no marginal fixed cost since fixed costs are a one-time thing completely unrelated to the level of activity. What is sauce for the goose is sauce for the gander. There aer similar (though not identical) relationships for revenues as there are for costs. Some important identities include: TR = P x N, where P is the unit price of whatever is being sold and N is the number of things sold. AR= TR/N MR=(change in TR)/(change in N). Generally speaking, there is no "fixed revenue" as a counterpart to "fixed cost". That is because while some investment costs may be fixed irrespective of firm or market activity, revenues generally cannot be so fixed. Cost and Revenue Curves and Profit Maximization This graph should be familiar -- it is simply the graph of the total, average and marginal quantity curves except this time applied to costs. All the arithmetical relationships which apply to any other quantity apply here as well. Costs, of course, are critical to a firm's profit maximization. A firm's total profit is defined as: TP = TR-TC where TP=total profit, TR=total revenue and TC=total cost. It turns out that profit is maximized where: MC=MR, where MC=marginal cost and MR=marginal revenue. Before this point is reached, the firm is clearing more revenue on each unit than it costs to make it. Therefore the firm can make more profit by producing more units. After this point, of course, the firm is losing money on each unit and should cut back production. Note that where marginal cost and marginal revenue intersect, there too total profits are maximized. Beyond that point, profits fall and where TR=TC total profits are zero. Returns to and Economies of Scale Some of the elements of production include technology; management and institutions; price; and cost. All of these elements come together on some scale of production, e.g. large-scale production at the level of a major conglomerate or small-scale production at the level of a single entrepreneur. Does the average or unit output per unit of input increase, fall, or remain the same as a given production activity moves from

20

small-scale production to large-scale production? The answer to this question depends on many factors. The question itself is summarized with the concept of economies of scale. If one is examining only the way that technology of production affects output, this is a narrower concept referred to as returns to scale. One of the basic determinants of economies of scale is production technology. Graphed below are three different production functions: (PF1) Y=X (PF2) Y=1/X (PF3) Y=X^2 This is the simplest case where there is only one input , X, which goes into producing the output Y. PF1 has constant returns to scale, i.e. if the input X is doubled, say from 1 to 2, output Y also doubles from 1 to 2. PF2 has decreasing returns to scale, i.e. if X is doubled from 1 to 2, Y increases proportionately less than that, from 1 to 0.5 (and this is a special case where returns are negative). Decreasing returns only require that output increases proportionately less than input. Finally, PF3 has increasing returns to scale, i.e. if X is raised from 1 to 2, Y increases proportionately more than that, from 1 to 4. Note that technologies may have different returns to scale over different ranges, e.g. have increasing returns at low levels, constant returns at medium levels and decreasing returns at high levels of output. As mentioned before, return to scale is a technological relationship between input and output. Economy of scale is a broader concept which includes the effects of factors such as market prices and managerial capacity. For example, steel may technically increasing returns to scale. Does that mean that ultimately only one big firm will dominate production? Not necessarily, because a huge firm is subject to management control limitations -- it gets too big and it gets inefficient due to difficulty of managing the enterprise itself. Also a big firm may drive up prices of scarce inputs (although it could also drive them down -- more on that later) and this may mean that at high levels of production its costs are higher even though its technology is more efficient. One way to assess economies of scale is to look at the relationship between unit, or average costs of production and the scale of production. Stigler proposes looking at average cost against market share of a company (i.e. how much of the total output of a market is accounted for by a particular firm. The graphical relationship might look like that below. The graph indicates that there are increasing economies over small scales of production (i.e. firms with relatively small but increasing market share have declining unit costs), then roughly constant economies to scale over medium scales, and then decreasing economies at high scales. Remember that costs of production, which include but are not limited to technical relationships, are being graphed. Hence this is an attempt to measure economies not just returns. Market Structure There are many different types of markets. In a nutshell, here are the major types:

Perfect Competition: many firms, many consumers, homogenous products, firms and consumers act autonomously and do not collude, free "exit and entry" (i.e. firms can move into and out of the market at will), firms and consumers are "price-takers", i.e. do not have market power sufficient to influence price by themselves.

Pure Monopoly: Only one firm, restricted exit and entry, firm has market power to set price.

Discriminating Monopoly: Same as monopoly but firm can charge different classes of consumers different prices for same good.

Oligopoly: Few firms, may or may not collude, firms have market power constrained by actions of competitors.

Duopoly: Special case of oligopoly with only two firms.

Monopsony: Only one buyer

Bilateral Monopoly: Monopsonist trading with a monopolist (i.e. one buyer dominating a market buying from one seller dominating the market).

Monopolistic Competition: Same as perfect competition except products are not homogenous.

21

The Classic Case of Perfect Competition To understand the perfectly competitive market, one must look at it from two perspectives: (1) from the perspective of the individual firm and (2) from the perspective of the market as a whole with all firms (suppliers) aggregated and all consumers (demanders) aggregated. From the firm perspective, demand is infinitely elastic (horizontal) which means that the firm can sell as much as it wants at the market price: it is a price taker. The demand curve for the firm in a perfectly competitive market is also equivalent to the firm's unit or average revenue (AR). That is because AR=PQ/Q and in this market all units will be sold at one price and there will be no unsold units. Thus AR will simply equal the price that is received for each unit. Since AR is constant, the rules of marginal analysis indicate that marginal revenue (MR) is equal to AR (the per unit revenue is always equal to P and so the revenue on the next unit sold -- the MR -- is also equal to P).

The firm also faces some cost for the production of each unit. The marginal cost (MC) curve can have many shapes; a typical one is drawn in the graph. Recall that profit is maximized where MR=MC and where the appropriate second order conditions hold. Both these conditions hold at point B, but not point A (which, in fact, is a minimum profit point, not a maximum one). Recall that in a perfectly competitive markets, D=MR=P. Firms maximize profits at the point where MR=MC. In a perfectly competitive market then P=MC. This is known as the fundamental rule of perfectly competitive markets. It shows that perfectly competitive markets are the most efficient means of production and consumption because the price that consumers pay for the 'last" unit of a good exactly equals the cost of producing that last unit (MC). Other market structures deviate from this outcome. Profit in a Perfectly Competitive Market While a firm will set output at the point where MR=MC, and this point maximizes profit, one needs information on average costs and average revenues (i.e. per unit costs and revenues) to be able to estimate total profit. The AC curve is derived from the MC curve and total profit is equal to (Q*AR)-(Q*AC) and that difference is shown as the shaded area. This is only a short-run equilibrium however; in the long-run, economic profit is zero, i.e. the firm just covers the opportunity costs of its inputs (including the cost of the entrepreneur's time). This long-rum equilibrium is pictured in the second panel. Note that there is no total profit, i.e. "excess" returns to the firms above its costs. The competitive equilibrium of the market (not the firm) Of course if one aggregates all the firms and all the consumers in the market, one gets the familiar supply and demand cross. Shifts in the supply and demand curves will, of course, effect equilibrium price. However no individual firm or consumer can affect the price by themselves and must take that price as given. As with the firm, there is both a short-run equilibrium (which

is defined as a period during which most economic parameters are fixed) and a long-run equilibrium (a period when all parameters, such as production capacity, could in principle be varied). In the long run, competition will drive out less efficient, higher cost firms. Those firms left over will all have the same (lowest) costs.

22

Pure Monopoly If a monopolist were to take over a perfectly competitive market, what would happen? The supply curve would no longer be the sum of individual firm supply curves but the AC curve of the monopolist (for the firm would want to cover unit costs and would determine how much it was willing to supply at different prices by looking at those unit costs). The firm's AR curve is the Demand curve, which is, of course, the demand curve of the whole market. MR and MC curves would be derived from those average curves and the firm would produce where MR=MC. Whereas the competitive equilibrium would be at S=D, the monopolist's equilibrium is at the industry MC=MR. Thus price (Pm Vs Pc) is higher and quantity lower (Qm Vs Qc) than under perfect competition. Note also that P does not equal MC. The firm charges what the market will bear at the point where MR=MC, but this P is higher than the firm's MC.

APPLICATION: HENRY FORD AND THE $5 DOLLAR DAY

(basic information for this discussion taken from “The $5 Day” by Stephen W. Sears in Audacity, Summer 1997, pp. 11-19)

On January 5, 1914, Henry Ford announced that his flagship Highland Park auto plant would operate on 8-hour rather than 9-hour shifts and that all workers at that plant would be paid 5 dollars a day for their work, a more than doubling of their current wages.

On it’s face the changes were extraordinary, and not just in comparison to current labor policy within Ford. The doubling of daily wages meant that the average Ford worker would be earning $1,500 a year. Here is what other types of worker were earning annually in that same year, on average across the United States:

Average manufacturing worker — $578

23

Average teacher — $547

Average coal miner — $631

Average railroad worker — $760

Average federal employee — $1,136

James Couzen’s, Ford’s head of the firm’s business side estimated that the new policy would cost $10 million a year, a staggering amount compared to the net profit that General Motors, Ford’s largest competitor, earned in 1913 — $7.5 million.

Workers swamped the Highland Park plant, at many as 15,000 at a time. A fire-hose had to be trained on these job-seekers at one point to calm a rising disturbance. 14,000 applications were sent by mail to the plant within one week, far more than the available openings.

The question arose: Was Henry Ford crazy?

The answer is: “crazy like a fox”.

Ford, of course, had good business reasons for taking his gamble, a gamble which, by the way, paid off handsomely for him. Here are some of the key strategic elements of his decision:

Economies of Scale: Automobile manufacturing was the fastest-growing business in the U.S. in 1914 and Ford was the leader of that growth. In 1899 the industry placed 150

th in the rank among all American industries.

By 1914 it had climbed to 7th

place. In 1913, 485,000 cars and trucks rolled off the assembly lines, 28% more than produced in 1912. When Ford announced his new wage policy, there were over 1.25 million motor vehicles on the nation’s roads, 6 times more than were on the road in 1909.

Ford had a lot to do with this growth when he created the Model T in 1907. The car was much cheaper than any other available touring car with a price of $850 as it went into production in 1908. In 1909, Ford ensured that these cheap prices would remain by announcing that the Model T would be the company’s only model with several body styles offered on a common chassis. No other competitor produced this way.

This is where the Highland Park plant came in. Opened in 1910 on a sixty-acre plot that was the site of a race-track outside Detroit, Ford instituted a regime of assembly-line mass production. Ford installed moving conveyer belts which moved a car chassis part past worker’s stations at a steady six feet per minute. This automation allowed one Model T to come out of the plant every 24 seconds by 1914, much faster than previous times.

Labor Productivity: The weak link in this system however was labor: workers could be much more unreliable than machines. In 1912, monthly labor turnover was a huge 48%. Other manufacturers had large absentee problems as well, but none as big as Ford.

So Ford moved in to try to solve the problem. His first move was to have his personnel manager, John R. Lee, devise reforms in pay equalization, end the arbitrary firing power of foremen, and make it company policy to find jobs in other departments for supposed misfits. These reforms had dramatic results with labor turnover falling to 6.7% in 1913. The Additional Dimension of Product Demand: With results like these, why go farther? Why the dramatic wage increase?