A real options reasoning approach to hybrid vehicle investments

13

A real options reasoning approach to hybrid vehicle investments Arman Avadikyan ⁎, Patrick Llerena PEGE/BETA (Université de Strasbourg, UMR 7522 CNRS), 61 avenue de la Forêt Noire, 67 085 Strasbourg, France article info abstract Article history: Received 25 July 2009 Received in revised form 19 November 2009 Accepted 2 December 2009 Long term increases of petrol prices and the threat of a global climate change have created in the automotive industry a new competitive environment based on the development of more sustainable technologies. Using the real option reasoning lens we provide a theoretical framework to better account for the technological and market uncertainties and irreversibilities that impact the investment and innovation decisions of automotive firms supporting the development of more sustainable vehicle technologies. We investigate the case of hybrid vehicles in a transitional perspective by insisting on their potential to influence the dynamic shaping of investment decisions of firms in the car industry. We consider the hybridization strategy as intra-project and inter-project compound growth options to manage the flexibilities and irreversibilities of investment decisions during the transition process. We provide four different–sometimes conflicting–strategic rationales structuring the investment efforts of firms in hybrid vehicles and illustrate them with numerous examples from the automotive industry. © 2009 Elsevier Inc. All rights reserved. Keywords: Sustainable transport Technological transition Real options Investment strategy Hybrid vehicle 1. Introduction Long term petrol price increases and the threat of climate change have created in the automotive industry a new competitive environment based on the development of more sustainable technologies. Using the real option reasoning lens we provide a theoretical framework to better account for the technological uncertainties and irreversibilities that impact the investment and innovation decisions of automotive firms supporting the development of more sustainable vehicles. We investigate the case of hybrid vehicles (HVs) in a transitional perspective by insisting on their potential to influence the dynamic shaping of firms' investment decisions. By combining an internal combustion engine (ICE) and an electric motor, HVs have attracted increasing interest by the automotive industry. They are in fact considered in the short term as the most viable alternative propulsion system improving significantly vehicle fuel efficiency and emissions without sacrificing traditional vehicle performance criteria. Furthermore, HVs possess in the long term the potential to facilitate the transition to more disruptive technologies such as fuel cell vehicles (FCVs) and battery electric vehicles (BEVs) because of important spillovers among different technical components and systems which are common to all alternatives. Several contributions have already addressed the role of hybrid technologies from a transitional perspective [1–3]. The originality of our research with respect to existing contributions consists in characterizing investment strategies of firms in the Technological Forecasting & Social Change 77 (2010) 649–661 Abbreviations: ADEME, Agence de l'Environnement et de la Maîtrise de l'Energie; APU, Auxiliary Power Unit; BEV, Battery Electric Vehicle; BMW, Bayerische Motor Werke; CO 2 , Carbon Dioxide; DEV, Diesel Engine Vehicle; DoE, Department of Energy; FCV, Fuel Cell Vehicle; GM, General Motors; HSD, Hybrid Synergy Drive; HV, Hybrid Vehicle; ICEV, Internal Combustion Engine Vehicle; IEA, International Energy Agency; IMA, Integrated Motor Assist; JAMA, Japan Automobile Manufacturers Association; Li-ion, Lithium-ion; NiCd, Nickel Cadmium; NiMH, Nickel Metal Hydride; NPV, Net Present Value; PEMFC, Proton Exchange Membrane Fuel Cell; PHV, Plug-in Hybrid Vehicle; RE, Range Extender; RITA, Research and Innovative Technology Administration; SOFC, Solid Oxide Fuel Cell; SUV, Sport Utility Vehicle; THS, Toyota Hybrid System. ⁎ Corresponding author. Tel.: +33 368852192. E-mail addresses: [email protected] (A. Avadikyan), [email protected] (P. Llerena). 0040-1625/$ – see front matter © 2009 Elsevier Inc. All rights reserved. doi:10.1016/j.techfore.2009.12.002 Contents lists available at ScienceDirect Technological Forecasting & Social Change

Transcript of A real options reasoning approach to hybrid vehicle investments

Technological Forecasting & Social Change 77 (2010) 649–661

Contents lists available at ScienceDirect

Technological Forecasting & Social Change

A real options reasoning approach to hybrid vehicle investments

Arman Avadikyan⁎, Patrick LlerenaPEGE/BETA (Université de Strasbourg, UMR 7522 CNRS), 61 avenue de la Forêt Noire, 67 085 Strasbourg, France

a r t i c l e i n f o

Abbreviations: ADEME, Agence de l'EnvironnemenMotor Werke; CO2, Carbon Dioxide; DEV, Diesel EnginDrive; HV, Hybrid Vehicle; ICEV, Internal CombustionManufacturers Association; Li-ion, Lithium-ion; NiCd, NFuel Cell; PHV, Plug-in Hybrid Vehicle; RE, Range ExtUtility Vehicle; THS, Toyota Hybrid System.⁎ Corresponding author. Tel.: +33 368852192.

E-mail addresses: [email protected] (A. Avadikyan)

0040-1625/$ – see front matter © 2009 Elsevier Inc.doi:10.1016/j.techfore.2009.12.002

a b s t r a c t

Article history:Received 25 July 2009Received in revised form 19 November 2009Accepted 2 December 2009

Long term increases of petrol prices and the threat of a global climate change have created inthe automotive industry a new competitive environment based on the development of moresustainable technologies. Using the real option reasoning lens we provide a theoreticalframework to better account for the technological and market uncertainties andirreversibilities that impact the investment and innovation decisions of automotive firmssupporting the development of more sustainable vehicle technologies. We investigate the caseof hybrid vehicles in a transitional perspective by insisting on their potential to influence thedynamic shaping of investment decisions of firms in the car industry. We consider thehybridization strategy as intra-project and inter-project compound growth options to managethe flexibilities and irreversibilities of investment decisions during the transition process. Weprovide four different–sometimes conflicting–strategic rationales structuring the investmentefforts of firms in hybrid vehicles and illustrate them with numerous examples from theautomotive industry.

© 2009 Elsevier Inc. All rights reserved.

Keywords:Sustainable transportTechnological transitionReal optionsInvestment strategyHybrid vehicle

1. Introduction

Long term petrol price increases and the threat of climate change have created in the automotive industry a new competitiveenvironment based on the development of more sustainable technologies. Using the real option reasoning lens we provide atheoretical framework to better account for the technological uncertainties and irreversibilities that impact the investment andinnovation decisions of automotive firms supporting the development of more sustainable vehicles. We investigate the case ofhybrid vehicles (HVs) in a transitional perspective by insisting on their potential to influence the dynamic shaping of firms'investment decisions.

By combining an internal combustion engine (ICE) and an electric motor, HVs have attracted increasing interest by theautomotive industry. They are in fact considered in the short term as the most viable alternative propulsion system improvingsignificantly vehicle fuel efficiency and emissions without sacrificing traditional vehicle performance criteria. Furthermore, HVspossess in the long term the potential to facilitate the transition to more disruptive technologies such as fuel cell vehicles (FCVs)and battery electric vehicles (BEVs) because of important spillovers among different technical components and systems which arecommon to all alternatives.

Several contributions have already addressed the role of hybrid technologies from a transitional perspective [1–3]. Theoriginality of our research with respect to existing contributions consists in characterizing investment strategies of firms in the

t et de la Maîtrise de l'Energie; APU, Auxiliary Power Unit; BEV, Battery Electric Vehicle; BMW, Bayerischee Vehicle; DoE, Department of Energy; FCV, Fuel Cell Vehicle; GM, General Motors; HSD, Hybrid SynergyEngine Vehicle; IEA, International Energy Agency; IMA, Integrated Motor Assist; JAMA, Japan Automobileickel Cadmium; NiMH, Nickel Metal Hydride; NPV, Net Present Value; PEMFC, Proton Exchange Membrane

ender; RITA, Research and Innovative Technology Administration; SOFC, Solid Oxide Fuel Cell; SUV, Spor

, [email protected] (P. Llerena).

All rights reserved.

t

650 A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

light of the uncertainties that punctuate the transition process towards disruptive technologies. Our contribution is thus mainlyinterested in clarifying the effect of technological uncertainties on the investment behavior of firms during the transition process.

We adopt for this purpose a real options reasoning approach [4–6] where the investment behavior of firms is influenced bothby the uncertainties they are confrontedwith and the irreversibilities of the existing technical system and those theywant to avoidto remain flexible. Real option models show that the will to preserve flexibility in the presence of uncertainty and irreversibilityinduces investment strategies which are different from those advocated by traditional net present value calculus. An importantcontribution of the real option theory is to show that investment behavior is not confined to a binary choice between ‘invest’ and‘do not invest’. Rather, decisions are guided by the strategic exploitation of flexibilities and irreversibilities proper to the sequentiallogic of investments. It is this tension between flexibility and irreversibility that shapes the investment decisions of firms withinthe transition process.

More specifically, by assimilating investment strategies in HVs to compound growth options we provide four strategicrationales structuring the investment efforts of firms in hybrid vehicles and illustrate them with several examples from theautomotive industry. These four rationales reflect the different and sometimes divergent perceptions firms can have in the shortand the long term potential (option value) of hybrid vehicles and they explain the disparity of strategic postures within theautomotive industry.

Our paper is structured as follows. Section 2 presents the real option reasoning approach. Section 3 focuses on the simplegrowth option characteristics of HVs. Subsequent sections investigate the four strategic rationales structuring firms' investmentefforts in HVs as compound growth options. First, investments in HVs can be justified as an opportunity to improve the optionvalue to maintain the incumbent paradigm by improving its environmental performance, and act at the same time as a hedgingoption against the uncertainties which characterize the improvement potential of both the ICE andmore disruptive solutions suchas FCVs or BEVs (Section 4). A second rationale relates to the uncertainties that affect the very potential of HVs. Under acompetitive context, these uncertainties explain the differentiated investment strategies within the automotive industry whichpursue either a sequential or architectural logic to innovation (Section 5). A third motivation to invest in hybridization refers to itscapacity to contribute to the option value to diversify on a larger set of technological alternatives by changing the way to managethe technology portfolio (Section 6). Finally, we consider HVs from a transitional perspective as a generic investment platformwith built-in flexibility to facilitate the deployment of more sustainable disruptive technologies such as EVs (Section 7). Section 8concludes.

2. Real options reasoning

The real options approach [7–9] constitutes a fruitful framework to better understand investment decisions in the presence ofuncertainty and irreversibility. Contrasting with traditional investment rules based on the net present value (NPV), thisperspective takes into account the value to react flexibly to environmental changes and stresses the impact of varying uncertaintylevels and sources on investment decisions. In this sense the real options lens provides a methodology to assess the opportunitiesand benefits associated to flexible investments.

The value of a real option depends on six variables: (1) the present value of risky assets (called underlying assets) to beacquired in order to realize the project on which an option is held; (2) the cost of holding the option (the expenses to hold theoption to invest in the project); (3) the cost of exercising the option (expenses to acquire the assets of the project); (4) theduration of the option until its expiration date (decision date until which the option stays open before being exercised); (5) thevolatility of the underlying assets; (6) the riskless interest rate during option duration.

If there is no volatility, there is no reason to adopt an option strategy since flexibility has no value. In return, for a given level ofirreversibility, the option value (of flexibility) increases with uncertainty. Since an option is defined as a right but not an obligationto acquire an asset, holding an option creates an asymmetric risk profile: an option to invest benefits from risky events whenuncertainty gets resolved in favor of the investment under consideration by giving a preferential right to exercise the option. Ifconditions are unfavorable, the option is not exercised and the only cost borne is the one of holding the option (assumed to belargely inferior to the investment cost).

Several types of options have been highlighted in the literature, including i.e. the options to wait, to stage, to expand, toabandon, to switch and to grow. Whereas earlier contributions on real options have mainly insisted on the value associated to theoption to wait or to defer investments [10], several contributions have recently considered more proactive option strategies suchas growth options giving firms a competitive advantage [11]. Even if the logic that underlies both deferral and growth options isbased on the value of flexibility, this value does not derive from the same source for each option. Deferral stresses the value todelay investment in order to benefit from the arrival of new information. Growth options insist on the value of early investment inorder to develop the capabilities necessary to facilitate preferential access to future opportunities [4,6].

Both options advocate a different investment strategy if we take the NPV as a reference. An investment which could be justifiedby the NPV rule (NPVN0) may not be engaged if firms consider the deferral option. According to this option, a firm only invests ifthe revenues expected from the uncertain project cover not only the investment cost but also the additional option (flexibility)value of waiting. In the case of growth options, an investment can be initiated even if the NPV rule advocates not to invest(NPVb0). Some irreversibility may be accepted in order to create access to potential opportunities. An early investment is hereconsidered as the opportunity price to participate in the sequence of future expected projects. This ambiguity about theinvestment behavior of firms compels us to have a closer look at uncertainty sources and to differentiate the role of differentenvironmental and competitive contingencies in order to better understand firms' option choices [12,13].

651A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

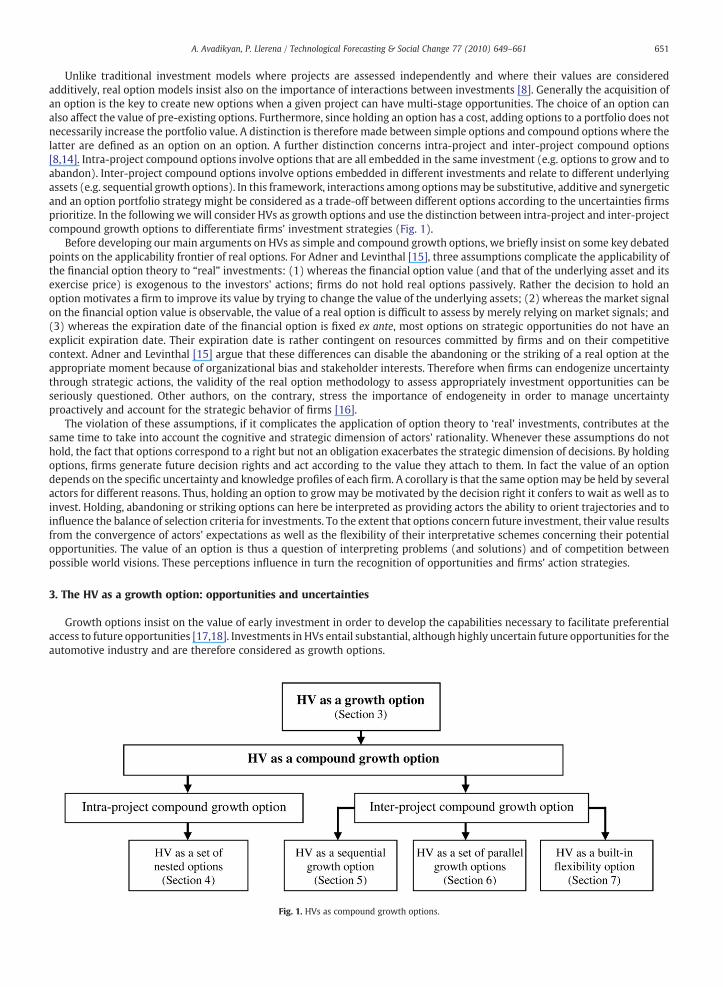

Unlike traditional investment models where projects are assessed independently and where their values are consideredadditively, real option models insist also on the importance of interactions between investments [8]. Generally the acquisition ofan option is the key to create new options when a given project can have multi-stage opportunities. The choice of an option canalso affect the value of pre-existing options. Furthermore, since holding an option has a cost, adding options to a portfolio does notnecessarily increase the portfolio value. A distinction is therefore made between simple options and compound options where thelatter are defined as an option on an option. A further distinction concerns intra-project and inter-project compound options[8,14]. Intra-project compound options involve options that are all embedded in the same investment (e.g. options to grow and toabandon). Inter-project compound options involve options embedded in different investments and relate to different underlyingassets (e.g. sequential growth options). In this framework, interactions among optionsmay be substitutive, additive and synergeticand an option portfolio strategy might be considered as a trade-off between different options according to the uncertainties firmsprioritize. In the following we will consider HVs as growth options and use the distinction between intra-project and inter-projectcompound growth options to differentiate firms' investment strategies (Fig. 1).

Before developing our main arguments on HVs as simple and compound growth options, we briefly insist on some key debatedpoints on the applicability frontier of real options. For Adner and Levinthal [15], three assumptions complicate the applicability ofthe financial option theory to “real” investments: (1) whereas the financial option value (and that of the underlying asset and itsexercise price) is exogenous to the investors' actions; firms do not hold real options passively. Rather the decision to hold anoption motivates a firm to improve its value by trying to change the value of the underlying assets; (2) whereas the market signalon the financial option value is observable, the value of a real option is difficult to assess by merely relying on market signals; and(3) whereas the expiration date of the financial option is fixed ex ante, most options on strategic opportunities do not have anexplicit expiration date. Their expiration date is rather contingent on resources committed by firms and on their competitivecontext. Adner and Levinthal [15] argue that these differences can disable the abandoning or the striking of a real option at theappropriate moment because of organizational bias and stakeholder interests. Therefore when firms can endogenize uncertaintythrough strategic actions, the validity of the real option methodology to assess appropriately investment opportunities can beseriously questioned. Other authors, on the contrary, stress the importance of endogeneity in order to manage uncertaintyproactively and account for the strategic behavior of firms [16].

The violation of these assumptions, if it complicates the application of option theory to ‘real’ investments, contributes at thesame time to take into account the cognitive and strategic dimension of actors' rationality. Whenever these assumptions do nothold, the fact that options correspond to a right but not an obligation exacerbates the strategic dimension of decisions. By holdingoptions, firms generate future decision rights and act according to the value they attach to them. In fact the value of an optiondepends on the specific uncertainty and knowledge profiles of each firm. A corollary is that the same optionmay be held by severalactors for different reasons. Thus, holding an option to growmay be motivated by the decision right it confers to wait as well as toinvest. Holding, abandoning or striking options can here be interpreted as providing actors the ability to orient trajectories and toinfluence the balance of selection criteria for investments. To the extent that options concern future investment, their value resultsfrom the convergence of actors' expectations as well as the flexibility of their interpretative schemes concerning their potentialopportunities. The value of an option is thus a question of interpreting problems (and solutions) and of competition betweenpossible world visions. These perceptions influence in turn the recognition of opportunities and firms' action strategies.

3. The HV as a growth option: opportunities and uncertainties

Growth options insist on the value of early investment in order to develop the capabilities necessary to facilitate preferentialaccess to future opportunities [17,18]. Investments in HVs entail substantial, although highly uncertain future opportunities for theautomotive industry and are therefore considered as growth options.

Fig. 1. HVs as compound growth options.

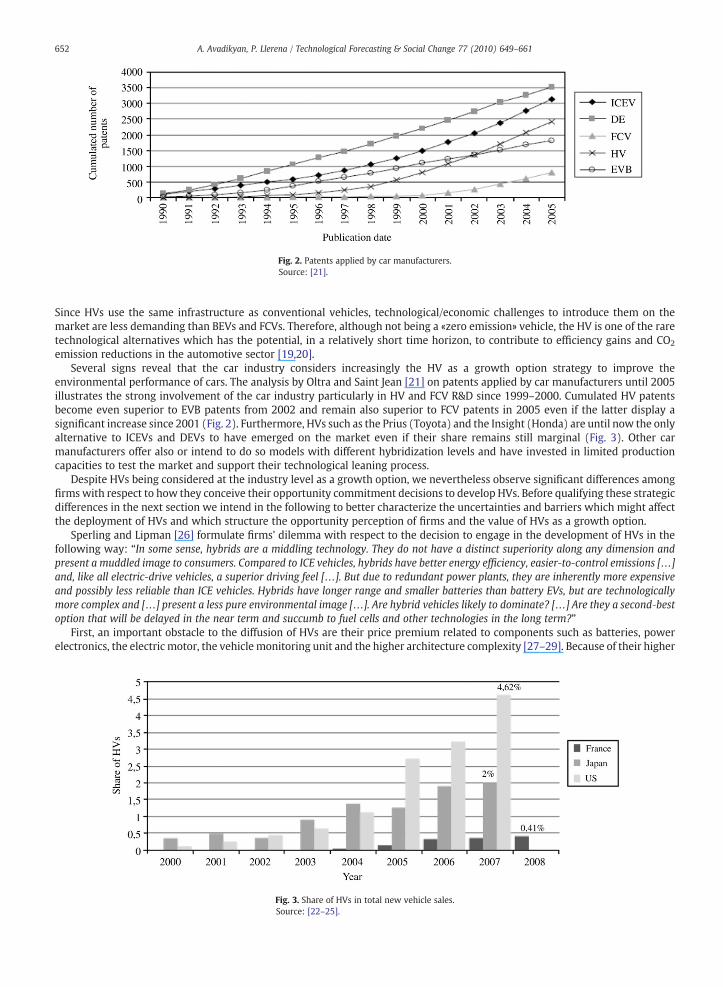

Fig. 2. Patents applied by car manufacturers.Source: [21].

Fig. 3. Share of HVs in total new vehicle sales.Source: [22–25].

652 A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

Since HVs use the same infrastructure as conventional vehicles, technological/economic challenges to introduce them on themarket are less demanding than BEVs and FCVs. Therefore, although not being a «zero emission» vehicle, the HV is one of the raretechnological alternatives which has the potential, in a relatively short time horizon, to contribute to efficiency gains and CO2

emission reductions in the automotive sector [19,20].Several signs reveal that the car industry considers increasingly the HV as a growth option strategy to improve the

environmental performance of cars. The analysis by Oltra and Saint Jean [21] on patents applied by car manufacturers until 2005illustrates the strong involvement of the car industry particularly in HV and FCV R&D since 1999–2000. Cumulated HV patentsbecome even superior to EVB patents from 2002 and remain also superior to FCV patents in 2005 even if the latter display asignificant increase since 2001 (Fig. 2). Furthermore, HVs such as the Prius (Toyota) and the Insight (Honda) are until now the onlyalternative to ICEVs and DEVs to have emerged on the market even if their share remains still marginal (Fig. 3). Other carmanufacturers offer also or intend to do so models with different hybridization levels and have invested in limited productioncapacities to test the market and support their technological leaning process.

Despite HVs being considered at the industry level as a growth option, we nevertheless observe significant differences amongfirms with respect to how they conceive their opportunity commitment decisions to develop HVs. Before qualifying these strategicdifferences in the next section we intend in the following to better characterize the uncertainties and barriers which might affectthe deployment of HVs and which structure the opportunity perception of firms and the value of HVs as a growth option.

Sperling and Lipman [26] formulate firms' dilemma with respect to the decision to engage in the development of HVs in thefollowing way: “In some sense, hybrids are a middling technology. They do not have a distinct superiority along any dimension andpresent a muddled image to consumers. Compared to ICE vehicles, hybrids have better energy efficiency, easier‐to‐control emissions […]and, like all electric‐drive vehicles, a superior driving feel […]. But due to redundant power plants, they are inherently more expensiveand possibly less reliable than ICE vehicles. Hybrids have longer range and smaller batteries than battery EVs, but are technologicallymore complex and […] present a less pure environmental image […]. Are hybrid vehicles likely to dominate? […] Are they a second‐bestoption that will be delayed in the near term and succumb to fuel cells and other technologies in the long term?”

First, an important obstacle to the diffusion of HVs are their price premium related to components such as batteries, powerelectronics, the electric motor, the vehicle monitoring unit and the higher architecture complexity [27–29]. Because of their higher

653A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

cost, HVs have only captured a negligible market share since their introduction a decade ago. Even if the cost of HVs can drop bytechnological learning and mass production, the very principle of hybridization consisting in combining several technologicalinnovations is likely to keep their cost high. This cost can hardly be borne by compact vehicle segments which represent the largemajority of the vehicle fleet and the HV might in this case only concern some niche segments such as SUVs.

The second uncertainty is related to the fuel efficiency of HVs. In most cases the fuel economies achieved by HVs during realdriving conditions are lower than those observed during test driving conditions. It turns out that, more than for conventional cars,the efficiency of HVs is dependent on usage patterns [30]. The use of energy intensive auxiliary units such as air conditioningonboard vehicles reduces also significantly the efficiency of HVs [31]. Furthermore since the promotion of HVs is based upon their«lack of compromise», one important risk is related to rebound effects through the power increase of cars to justify the premiumprice and limiting thus their benefits in terms of fuel efficiency [19].

A third uncertainty relates to the short and long term competitiveness of HVs. In the short term, competition might be fierceless between ICEVs and FCVs or BEVs than between hybrid and advanced diesel engine vehicles. The preference for gasoline hybridrather than diesel vehicles in the US and Japan is mostly explained by the more severe legislation on pollutant emissions in thesecountries compared to Europe. For the latter, the generalization of the diesel car fleet and the cost advantages of advanced dieselengines compared to HVs make the market breakthrough of HVs less likely [32,33]. In the long term, technological advances thatfavor the diffusion of HVs might also benefit EVs. This would make the hybrid alternative only a transitional investment,questioning the development of a dedicated HV industry. Advances made on lithium-ion (Li-ion) batteries which provide bothhigh power and high energy densities, make them relevant not only for HVs but also for plug-in rechargeable HVs (PHVs) and BEVs[34,35]. Li-ion batteries are likely to favor in some segments such as urban vehicles, where HVs are the most beneficial in terms offuel economy, the development of BEVs with the sufficient range for urban drives.

The above opportunities and uncertainties confer to the HV an optional character which is exemplified by the increasing patentrace at the industry level and the introduction on some niche markets of such vehicles. Having in mind these uncertainties andopportunities, we will in the rest of the paper qualify more precisely firms' investment and resource commitment strategies onHVs as compound options.

4. The HV as a hedging strategy and the option value to maintain the ICE

In this section, we show that the HV has the properties of an intra-project compound growth option, that is a set of nestedoptions embedded in the same investment. As shown by the real options literature most option strategies embedmultiple optionsand the value of an option generally depends on the value of other options it is built upon and the value it confers to them.Wewillshow that growth options on the HV derive partly their value from on the one hand the option value tomaintain the ICE and on theother hand from being a hedging option against several uncertainty sources.

Since one of the distinctive features of HVs is the synergy between the ICE and other alternative technologies, growth optionson HVs derive part of their value from the option to maintain the ICE. HVs create in fact a new perception for both the dominantand the alternative paradigms. The increase in the option value to maintain results from the interdependency created by HVsbetween emerging and existing technologies. The growth option value of HVs is derived from the higher margin created tooptimise the ICE by being progressively associated with the innovations and functionalities of emerging technologies. But,advances on HVs also depend on incremental and cumulative innovations on the ICE and thewhole vehicle. Thus, the benefits fromhybridising rest also upon the importance of technological innovations on advanced ICEs.

First, the value of the option to maintain the ICE relates to the path dependencies that structure the automotive industries'investment behavior (technological and mass production competencies accumulated on ICEVs, network complementarities andfuel infrastructures). When organizational change is disruptive, regime actors may hesitate to shift radically the system, hopingthat future states of the world will allow the incumbent regime to become more attractive. Actors may thus delay exit, even if theNPV of ICE projects becomes negative and investments on the incumbent regime may continue until the economic losses exceedthe option value to keep the incumbent system [36].

Second the value of the option to keep the ICE derives from the fact that the environmental performance of ICEs represents arelatively recent concern in the history of the automotive industry where innovation efforts have traditionally been guided byattributes such as engine power, autonomy, security and reliability. Investment strategies aim thus to exploit the ICE by exploringsolutions to improve its environmental performance. The option to keep the existing system may thus be justified because of theperception that its technological frontier has not yet been exhausted. As Chi and Nystrom [37] argue, a higher uncertainty on theevolution of the dominant technologymeans a higher learning potential andmay conduce firms to exploit it more intensively untilthe cost of such learning becomes higher than the benefits expected.

Third, the value of the option to keep the ICE derives from the uncertainties relative to the technical and commercial feasibilityof long term alternatives such as FCVs and BEVs. In fact, the more important uncertainties on future technological alternatives andtheir adoption costs, the more regime actors might rationally choose to persist on technologies that might prove inferior in thelong term. In other words, the higher the uncertainty level, the more firms will be keen to lengthen the life span of existingsolutions with a low capital cost. Inertia in this case mirrors the expectations concerning the value of present and futuretechnologies and the cost of change. This inertia increases with uncertainty since firms are rationally hesitant to support the cost ofchange towards competences whichmight become obsolete if the environment returns back to its previous state or because of therisk to choose the wrong alternative.

654 A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

The growth option value of HVs apart being highly dependent on the option value to maintain the ICE derives also its value byacting as a hedging option to moderate different uncertainties firms are faced with. The hedging option value of the HV stems forinstance from its capacity to compensate theweaknesses of the ICE in caseswhere it makes limited progress. But the hybrid systemas a hedging option can additionally increase the flexibility of the existing fossil fuel paradigm. In fact the fuel economies obtainedwith HVs can notably smoothen the pressures brought upon the diversification and usage of other primary sources than petroleumfor the production of liquid fuels.

In the same way the growth option value of HVs derives from being envisaged as a hedging strategy against uncertainties withregard to the long term evolution of BEVs and FCVs. In fact the deployment of HVs does not depend on the development of a newhydrogen infrastructure for FCV and/or an electric network to charge the batteries. Instead the success of FCs and batteries but alsothe use of hydrogen and electricity as energy vectors in vehicles are tributary on a number of complementary factors which maketheir adoption highly uncertain. In the case of batteries, uncertainties concern their cost, reliability, security, autonomy, lifeexpectancy, their recharge time [35,38]. These uncertainties and repeated failures to introduce in the past BEVs [39,40] in themarket have led some authors to qualify them as an “eternally emergent” technology [41].

The challenges are of the same order for FCs and concern their cost, duration, life span, operation under low temperatures, thepossibility to substitute in FCs precious metals such as the platinum. As for batteries for the electricity storage, the storage ofhydrogen on board vehicles remains a critical factor for the success of FCV [42,43].

5. The HV in a competitive context: sequential vs. architectural growth options

In the preceding section we interpreted the HV as an intra-project compound growth option deriving its value from being a setof nested options embedded in the same investment. In this sectionwe show that the HV has also the properties of an inter-projectcompound option deriving its value from the flexibility it gives to car manufacturers to structure their investments sequentially.

Although HVs are considered industry-wide as a growth option, it is important to take into account the competitive context ofthe automotive industry and firms' specific perception of uncertainties and opportunities concerning this technological trajectoryin order to better specify option management strategies. In fact, competitive dynamics can have effects on option choice, optioncreation and exercise [11,12]. Although an increase in uncertainty raises the value of the investment deferral option, when there isstrategic interaction first-mover advantages canmake early investment (growth option) more valuable and prompt early exerciseof the option. However, under circumstances where delayed market introduction is beneficial, such as when there are second-mover advantages [44] or when a new product may cannibalize existing or other promising products of the firm [45], a companymay adopt a more cautious behavior and follow an incremental investment process [4].

The HV case is a rich illustration of the way an emerging trajectory can provide in a highly competitive context actors withopportunities not only to exploit it but also to create and explore new growth option strategies. It shows how the commitment ofsome firms on the hybrid solution has created at the industry level a new focal competition field. Within this field, firms have onthe one hand engaged efforts to participate to the standard competition at the architectural level of HVs. But they have at the sametime privileged a more sequential and incremental growth option logic to reduce the risk of making early commitments given theuncertain prospects of HVs.

One should notice that HV projects by Japanese firms, particularly by Toyota [46], have from the outset considered toincorporate all the functionalities offered by the hybrid solution to improve the efficiency of cars. The project launched by Toyotain 1992 has led to the commercialization in 1997 of the first full HV (the Prius) based on an architectural innovation, theparticularity of which was to go beyond the dichotomy between two architectures generally used separately for hybrid motors:the serial and parallel architectures. Called the Toyota Hybrid System (THS) this new serial-parallel architecture was based on thedevelopment of a new transmission principle taking advantage of both architectures. Important revisions took also place for thesecond Prius II version (commercialized in 2003) based on the Hybrid Synergy Drive (HSD) which enabled the electric motor toacquire a larger role to support the performance of the vehicle.

The early commitment by Toyota, as illustrated by its growth option choice on the HV shows both the importance given by theJapanese firm to the hybrid concept in its long term strategy and the efforts made as a first-mover to define a dominant standardfor the HV architecture. Selling its first HV production series at a loss is also in line with the desire of Toyota to speed up thelearning process on its technology and to promote its proprietary technology as a standard.

Since the dynamics initiated by Toyota most car manufacturers consider the architectural choice as a key part of theirhybridization strategy. One can distinguish, at this level, noteworthy differences among firms. Honda has chosen a parallel onlyarchitecture by developing a new transmission system, the Integrated Motor Assist, used for its Insight, Civic and Accord hybridmodels. As opposed to Toyota, the hybrid by Honda belongs to themild category and has thus a lower premium cost. As for Nissan,after mixed results on its own proprietary full hybrid Tinomodel, the company acquired a license on the Toyota technology for itsAltima model. A similar strategy is carried on by Ford who concluded a license agreement with Toyota and still continues todevelop its own system. While adopting the Toyota technology such a strategy enables car manufacturers to accelerate their HVmarket growth. A third group of firms including GM, Chrysler, Daimler and BMW has initiated an alliance which successfullydeveloped its own parallel architecture called «2‐mode hybrid» most appropriate for the high power SUV segment. Finally, some carmanufacturers as Peugeot and Daimler are more interested in the long term potential of diesel HVs. Although these strategies maydiffer, all car manufacturers aim to catch up with Toyota, either by developing new architectural variants around the parallelarchitecture or by accelerating their market introduction in a differentiated way.

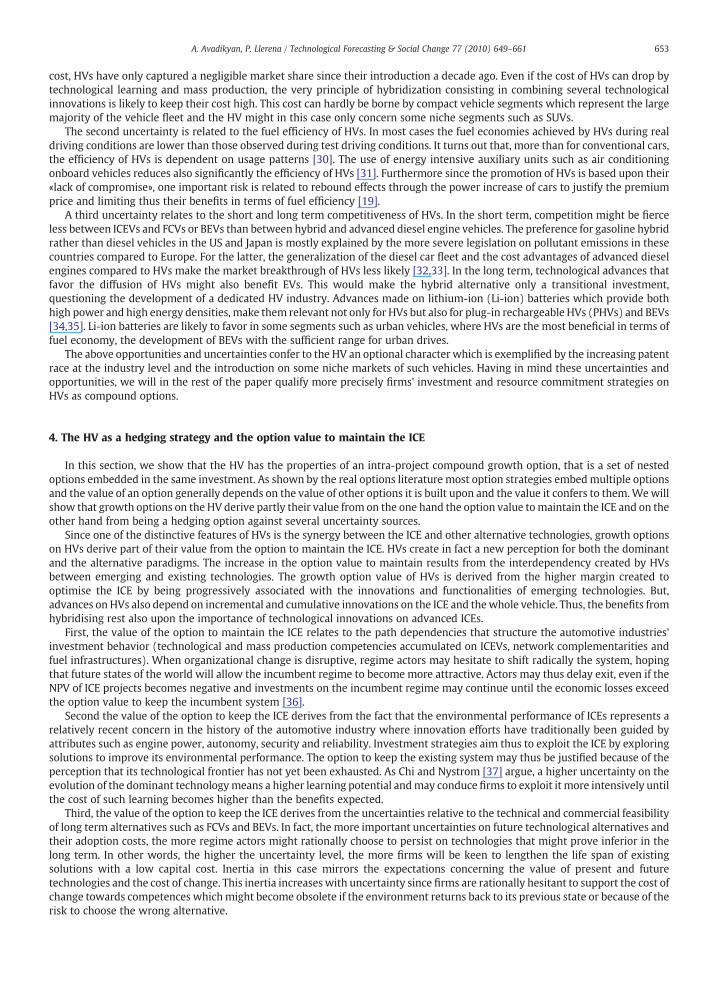

Fig. 4. HV characteristics and functionalities according to their electrification level.Sources: [33,34,48].

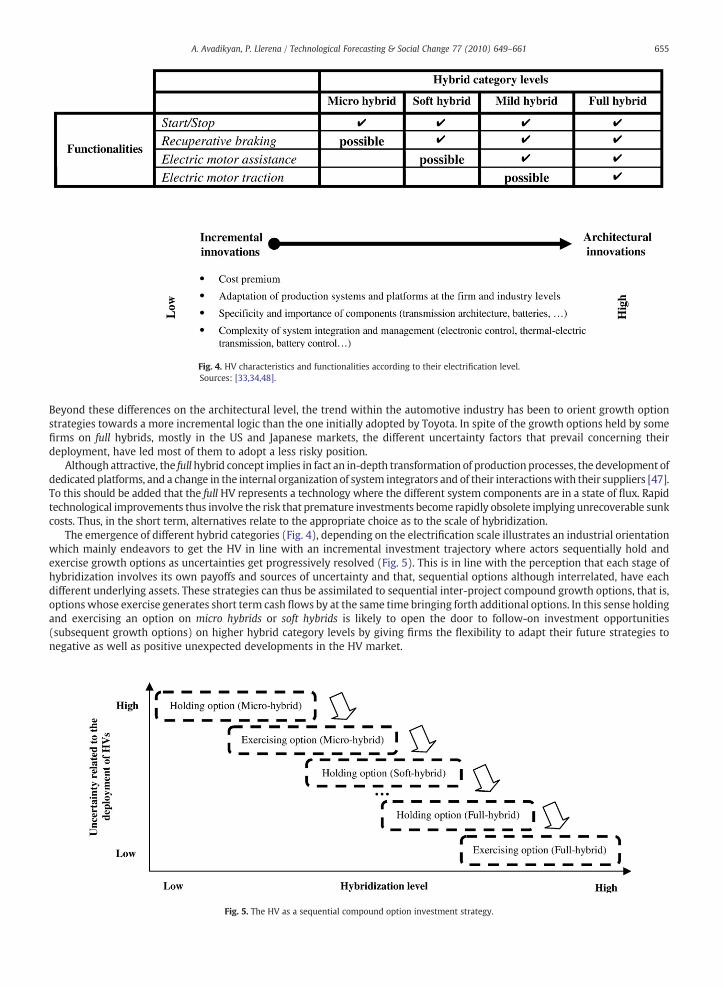

Fig. 5. The HV as a sequential compound option investment strategy.

655A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

Beyond these differences on the architectural level, the trend within the automotive industry has been to orient growth optionstrategies towards a more incremental logic than the one initially adopted by Toyota. In spite of the growth options held by somefirms on full hybrids, mostly in the US and Japanese markets, the different uncertainty factors that prevail concerning theirdeployment, have led most of them to adopt a less risky position.

Although attractive, the full hybrid concept implies in fact an in-depth transformation of production processes, the development ofdedicated platforms, and a change in the internal organization of system integrators and of their interactionswith their suppliers [47].To this should be added that the full HV represents a technology where the different system components are in a state of flux. Rapidtechnological improvements thus involve the risk that premature investments become rapidly obsolete implying unrecoverable sunkcosts. Thus, in the short term, alternatives relate to the appropriate choice as to the scale of hybridization.

The emergence of different hybrid categories (Fig. 4), depending on the electrification scale illustrates an industrial orientationwhich mainly endeavors to get the HV in line with an incremental investment trajectory where actors sequentially hold andexercise growth options as uncertainties get progressively resolved (Fig. 5). This is in line with the perception that each stage ofhybridization involves its own payoffs and sources of uncertainty and that, sequential options although interrelated, have eachdifferent underlying assets. These strategies can thus be assimilated to sequential inter-project compound growth options, that is,optionswhose exercise generates short term cash flows by at the same time bringing forth additional options. In this sense holdingand exercising an option on micro hybrids or soft hybrids is likely to open the door to follow-on investment opportunities(subsequent growth options) on higher hybrid category levels by giving firms the flexibility to adapt their future strategies tonegative as well as positive unexpected developments in the HV market.

656 A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

For most car manufacturers micro and soft hybrids possess the potential to provide up to 80% of the efficiency of full hybrids by atthe same time avoiding their high cost premium [49]. These two categories represent therefore an attractive solution to improvesignificantly vehicle efficiency without taking prematurely risky and costly development efforts on full hybrids. We thus observewithin the industry a variety of approaches exploiting and exploring more intensively the potentials of low hybrid categories.

One should notice that according to the regions considered, firms' investment behavior reveals different growth optionstrategies. Car manufacturers established mainly on the European market aim to introduce HVs on the mass market segment byfocusing their growth efforts in the short term on micro and soft hybrids conceivable also for diesel engines. Firms mainlyoperational in the US market, focus principally on the full HV by adopting a niche growth strategy aiming at luxury and SUVsegments (Daimler, Ford and GM). A third group of firms, mainly the Japanese, whose markets are more diversified, adopt anintermediary position. Honda aims the mass market segment with its mild HV and Toyota although having pioneered the full HVoffers also different hybrid categories including both micro hybrids (Toyota Witz) and soft hybrids (Toyota Crown).

6. Hybridization and the option value to diversify

Up to nowwe have approached the hybrid concept as a growth option strategy to contribute to the flexibility of and the optionvalue to maintain the dominant paradigm around the ICE. This section considers the hybridization strategy as a set of parallelgrowth options focusing on its role as a vector for technological diversification. We show that the hybrid concept can beapproached as a strategy contributing to the preservation as well as the creation of technological diversity for vehicle propulsionsystems by affecting the resource allocation structure among technologies [50,51]. We assimilate HVs to a technology portfoliomanagement strategy influencing positively the value of growth options on a larger set of alternative technologies.

The portfolio diversity resulting from the hybrid concept derives principally from the different combinations possible betweentechnologies in order to create new improvement potentials. An important feature of HVs is that they pave the way for a moresynergistic approach between technologies [52]. Such synergies transcend the antinomy between radical and incrementalinnovation approaches and modify the interaction dynamics between technologies. In so doing hybridization favors theemergence and the creation of new concepts and functionalities. It also facilitates the variety of trial–error processes which arenecessary to sustain exploration activities by at the same time providing emerging technologies an exploitation base [53]. Inevolutionary terms, hybridization changes the selection environment of innovation activities and promotes the coexistence oftechnologies [54] in the sense that it proceeds by combination to get around the limits of technologies taken separately.Hybridization alters in fact the investment conditions on alternative technologies and hence the value of their growth options andcreates portfolio effects where holding or exercising a growth option on HVs influences the value to introduce, hold or exerciseother options in the portfolio.

Portfolio diversification effects of holding HV growth options can be defined on the one hand through correlations existingbetween underlying assets (correlation effect) and on the other hand through the constraints which hang over exercising someoptions (constraint effect) such that if there are n growth options in the portfolio only m may be exercised (with mbn) [55].

First, hybridization increases the positive correlation between different underlying assets since it creates complementaritiesamong technologies. This increase in correlation through technological clustering affects in turn positively the growth option valueon a larger set of alternative technologies and justifies introducing them in the portfolio, keeping them open or exercising them.

A case worth mentioning is the diversification of different battery types for HVs [27]. HVs have in fact become in recent years aplatform to experiment different established battery technologies such as advanced lead-acid batteries as well as new generationbatteries including NiMH, NiCd and Li-ion batteries. It is mainly through its use within HVs that for instance the NiMH battery hasbeenmore largely diffused in the automotivemarket. Next generation HVs represent also an opportunity to introduce in transportapplications the Li-ion battery, alreadymassively used in portable electronics, andwhich is considered in the long term as themostappropriate choice–because of its high power and energy densities–for plug-in or grid-connected HVs and BEVs.

Another example is given by the association of batteries and fuel cells. Jeong and Oh [56] show that if the cost of fuel cellsremains high, hybridization can reduce the life-cycle cost of fuel cell vehicles, increasing thus their growth option value. Thisexplains the increasing orientation of car manufacturers towards hybrid FCV prototypes [57]. Since, on their own, the cost-performance of FCs do not allow them to satisfy the market selection criteria, their combination with other technologies createsbetter prospects for their market introduction.

A similar path can be observed for BEVs. To overcome the performance and range limits of batteries car manufacturers combinethem with other alternative technologies. A first association envisaged is the use of ultra-capacitors for power assist alongsidebatteries. A second association considers using batteries with a secondary energy source as a range extender (RE) producingelectric power to increase the autonomy of the car. A third alternative resides in installing solar cells at the roof of cars to provideenergy for dashboard electronics to allow for smaller capacity batteries [58]. Each combination increases respectively the growthoption value of ultra-capacitors, of solar cells in automotive applications and of the RE technology.

The second effect of hybridization on diversity is related to the constraint which bears upon the possibility to exercise optionsheld in the portfolio. In fact, when there is a strong constraint on exercising several options as in the case when at the end of theselection process only one technological system is likely to dominate, each new growth option added to the portfolio has adecreasing marginal value since it has a lower likelihood to be exercised. However, by creating new combination opportunities,hybridization has a relaxing effect on the exercise constraint and increases thus the option value to diversify.

We can illustrate this effect through the variety of new functionalities endorsed by several technologies in HVs. Thehybridization pattern relaxes in fact the exercise constraint on growth options in that it gives the possibility to alternative

657A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

technologies to perform functionalities which are more suited to their technical characteristics at a given moment in time. Bycreating new functionalities hybridization generates new potential markets for alternative technologies. It allows exploringdifferent market segments by exploiting their differentiated needs.

Whereas FCs have been used generally as a primary energy source in vehicles, their hybridization with other technologiesallows them also to function as an auxiliary power unit (APU) or a RE. For instance BMW which has explicitly expressed itsskepticism on FCs as the main energy source for cars, is actively involved in R&D on this application not only to built-up itstechnological position and develop absorptive capabilities but also because the company aims (in partnership with Renault) atusing FCs principally as an APU. Recently, vehicle prototypes have also been developedwhere the RE function in BEVs is performedby FCs. Among car manufacturers, Peugeot has been one of the first to focus on FCs as REs to overcome the limited range ofbatteries. Such a hybrid concept, beyond overcoming the limits of batteries, makes the exploitation of FCs easier since they uselower power and lower cost FCs. Furthermore in such a system the quantity of hydrogen carried on board the vehicle remains quitelow and facilitates refueling by using exchangeable hydrogen tanks. Recently Ford and GM have presented prototypes where theFC system functions as a RE. Also while the PEM trajectory has since the beginning been considered as the dominant choice fortransport applications, the application of FCs as APUs and REs has led the car industry to consider the SOFC trajectory, traditionallydeveloped for stationary applications, for transport applications [59–61]. Also keeping and continuing to innovate on the ICE couldbe critical to the acceptance of BEVs. Given the limited autonomy of batteries, the use of the ICE as a RE in a BEV requires to developand to explore dedicated motors for this new usage pattern [62]. Contrary to the hybridization trajectory presented in thepreceding sections the role of the ICE is here more in line with a logic where it supports and contributes to the acceptance of theBEV or the hydrogen ICE vehicle.

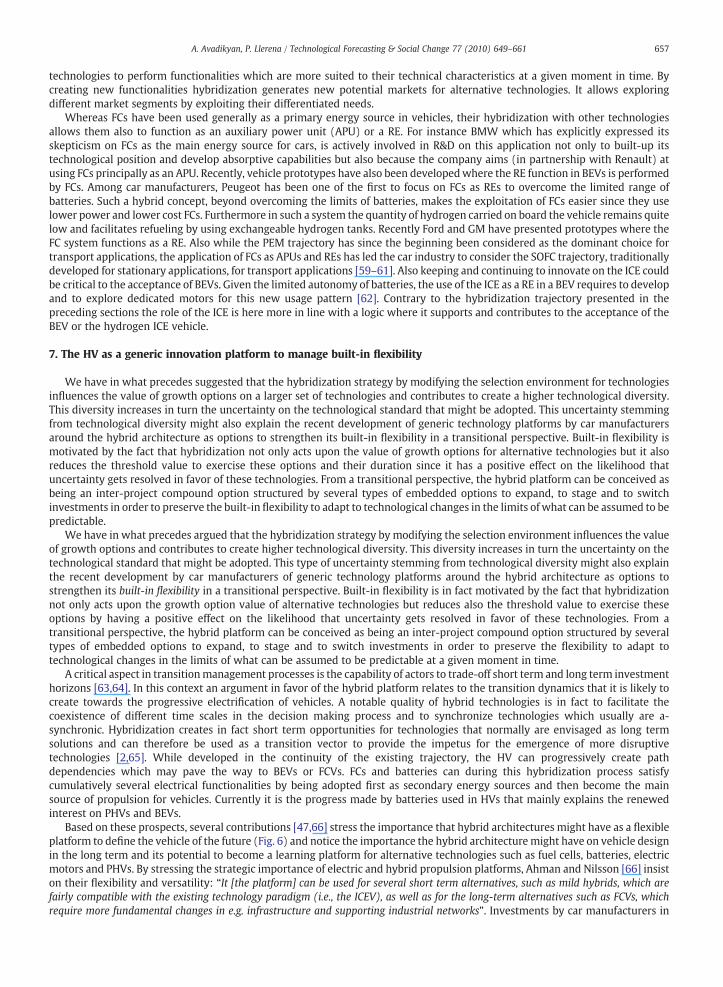

7. The HV as a generic innovation platform to manage built-in flexibility

We have in what precedes suggested that the hybridization strategy by modifying the selection environment for technologiesinfluences the value of growth options on a larger set of technologies and contributes to create a higher technological diversity.This diversity increases in turn the uncertainty on the technological standard that might be adopted. This uncertainty stemmingfrom technological diversity might also explain the recent development of generic technology platforms by car manufacturersaround the hybrid architecture as options to strengthen its built-in flexibility in a transitional perspective. Built-in flexibility ismotivated by the fact that hybridization not only acts upon the value of growth options for alternative technologies but it alsoreduces the threshold value to exercise these options and their duration since it has a positive effect on the likelihood thatuncertainty gets resolved in favor of these technologies. From a transitional perspective, the hybrid platform can be conceived asbeing an inter-project compound option structured by several types of embedded options to expand, to stage and to switchinvestments in order to preserve the built-in flexibility to adapt to technological changes in the limits of what can be assumed to bepredictable.

We have in what precedes argued that the hybridization strategy by modifying the selection environment influences the valueof growth options and contributes to create higher technological diversity. This diversity increases in turn the uncertainty on thetechnological standard that might be adopted. This type of uncertainty stemming from technological diversity might also explainthe recent development by car manufacturers of generic technology platforms around the hybrid architecture as options tostrengthen its built-in flexibility in a transitional perspective. Built-in flexibility is in fact motivated by the fact that hybridizationnot only acts upon the growth option value of alternative technologies but reduces also the threshold value to exercise theseoptions by having a positive effect on the likelihood that uncertainty gets resolved in favor of these technologies. From atransitional perspective, the hybrid platform can be conceived as being an inter-project compound option structured by severaltypes of embedded options to expand, to stage and to switch investments in order to preserve the flexibility to adapt totechnological changes in the limits of what can be assumed to be predictable at a given moment in time.

A critical aspect in transitionmanagement processes is the capability of actors to trade-off short term and long term investmenthorizons [63,64]. In this context an argument in favor of the hybrid platform relates to the transition dynamics that it is likely tocreate towards the progressive electrification of vehicles. A notable quality of hybrid technologies is in fact to facilitate thecoexistence of different time scales in the decision making process and to synchronize technologies which usually are a-synchronic. Hybridization creates in fact short term opportunities for technologies that normally are envisaged as long termsolutions and can therefore be used as a transition vector to provide the impetus for the emergence of more disruptivetechnologies [2,65]. While developed in the continuity of the existing trajectory, the HV can progressively create pathdependencies which may pave the way to BEVs or FCVs. FCs and batteries can during this hybridization process satisfycumulatively several electrical functionalities by being adopted first as secondary energy sources and then become the mainsource of propulsion for vehicles. Currently it is the progress made by batteries used in HVs that mainly explains the renewedinterest on PHVs and BEVs.

Based on these prospects, several contributions [47,66] stress the importance that hybrid architectures might have as a flexibleplatform to define the vehicle of the future (Fig. 6) and notice the importance the hybrid architecturemight have on vehicle designin the long term and its potential to become a learning platform for alternative technologies such as fuel cells, batteries, electricmotors and PHVs. By stressing the strategic importance of electric and hybrid propulsion platforms, Ahman and Nilsson [66] insiston their flexibility and versatility: “It [the platform] can be used for several short term alternatives, such as mild hybrids, which arefairly compatible with the existing technology paradigm (i.e., the ICEV), as well as for the long-term alternatives such as FCVs, whichrequire more fundamental changes in e.g. infrastructure and supporting industrial networks”. Investments by car manufacturers in

Fig. 6. The HV as a flexible and generic innovation platform.

658 A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

hybrid architectures may here be motivated by the will of using more quickly a larger set of knowledge created in differenttechnological fields in order to feed continuously and keep vivid their innovation process.

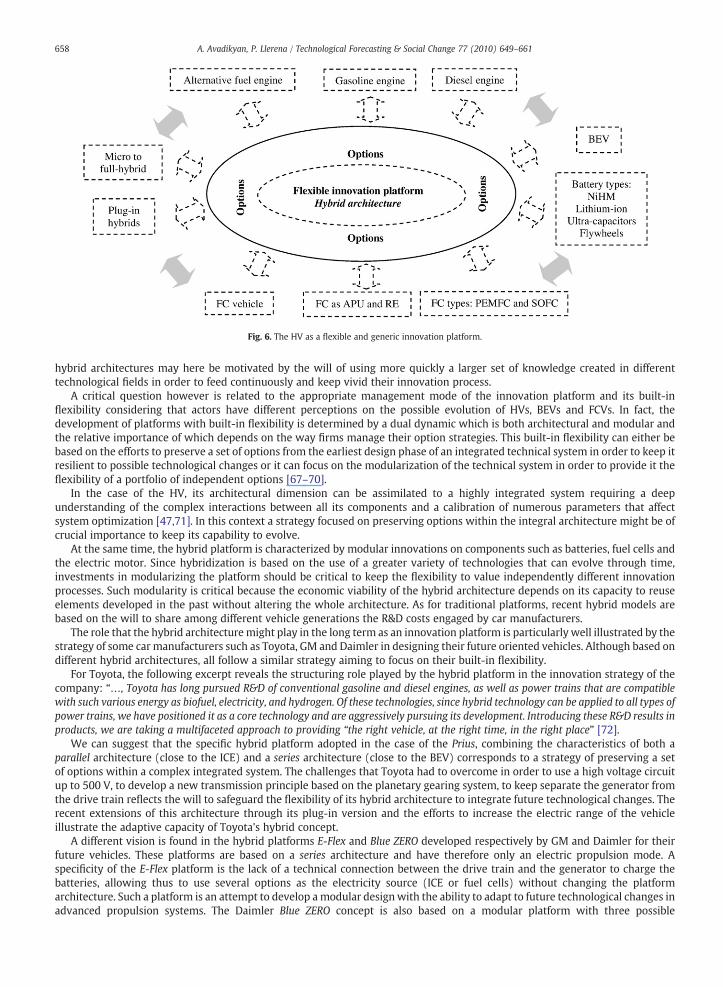

A critical question however is related to the appropriate management mode of the innovation platform and its built-inflexibility considering that actors have different perceptions on the possible evolution of HVs, BEVs and FCVs. In fact, thedevelopment of platforms with built-in flexibility is determined by a dual dynamic which is both architectural and modular andthe relative importance of which depends on the way firms manage their option strategies. This built-in flexibility can either bebased on the efforts to preserve a set of options from the earliest design phase of an integrated technical system in order to keep itresilient to possible technological changes or it can focus on the modularization of the technical system in order to provide it theflexibility of a portfolio of independent options [67–70].

In the case of the HV, its architectural dimension can be assimilated to a highly integrated system requiring a deepunderstanding of the complex interactions between all its components and a calibration of numerous parameters that affectsystem optimization [47,71]. In this context a strategy focused on preserving options within the integral architecture might be ofcrucial importance to keep its capability to evolve.

At the same time, the hybrid platform is characterized by modular innovations on components such as batteries, fuel cells andthe electric motor. Since hybridization is based on the use of a greater variety of technologies that can evolve through time,investments in modularizing the platform should be critical to keep the flexibility to value independently different innovationprocesses. Such modularity is critical because the economic viability of the hybrid architecture depends on its capacity to reuseelements developed in the past without altering the whole architecture. As for traditional platforms, recent hybrid models arebased on the will to share among different vehicle generations the R&D costs engaged by car manufacturers.

The role that the hybrid architecturemight play in the long term as an innovation platform is particularly well illustrated by thestrategy of some car manufacturers such as Toyota, GM and Daimler in designing their future oriented vehicles. Although based ondifferent hybrid architectures, all follow a similar strategy aiming to focus on their built-in flexibility.

For Toyota, the following excerpt reveals the structuring role played by the hybrid platform in the innovation strategy of thecompany: “…, Toyota has long pursued R&D of conventional gasoline and diesel engines, as well as power trains that are compatiblewith such various energy as biofuel, electricity, and hydrogen. Of these technologies, since hybrid technology can be applied to all types ofpower trains, we have positioned it as a core technology and are aggressively pursuing its development. Introducing these R&D results inproducts, we are taking a multifaceted approach to providing “the right vehicle, at the right time, in the right place” [72].

We can suggest that the specific hybrid platform adopted in the case of the Prius, combining the characteristics of both aparallel architecture (close to the ICE) and a series architecture (close to the BEV) corresponds to a strategy of preserving a setof options within a complex integrated system. The challenges that Toyota had to overcome in order to use a high voltage circuitup to 500 V, to develop a new transmission principle based on the planetary gearing system, to keep separate the generator fromthe drive train reflects the will to safeguard the flexibility of its hybrid architecture to integrate future technological changes. Therecent extensions of this architecture through its plug-in version and the efforts to increase the electric range of the vehicleillustrate the adaptive capacity of Toyota's hybrid concept.

A different vision is found in the hybrid platforms E-Flex and Blue ZERO developed respectively by GM and Daimler for theirfuture vehicles. These platforms are based on a series architecture and have therefore only an electric propulsion mode. Aspecificity of the E-Flex platform is the lack of a technical connection between the drive train and the generator to charge thebatteries, allowing thus to use several options as the electricity source (ICE or fuel cells) without changing the platformarchitecture. Such a platform is an attempt to develop amodular designwith the ability to adapt to future technological changes inadvanced propulsion systems. The Daimler Blue ZERO concept is also based on a modular platform with three possible

659A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

configurations according to the electric propulsion system envisaged: (1) batteries; (2) fuel cells; and (3) an electric motor usingthe ICE as a generator. Nevertheless, contrary to the Prius platform which positions itself in the continuity of the existing ICEparadigm and which integrates the possibility of a trajectory with an increasing electrification of vehicles, the GM and Daimlerplatforms adopt straightaway the EV paradigm by at the same time taking into account the uncertainty as to the choice betweenalternative electric propulsion modes.

8. Conclusion

By adopting a real options reasoning approach we tried to provide a more qualified explanation of firms' investment decisionsand patterns on HVs as a technological strategy to remain flexible and manage proactively technological, market and policyuncertainties. By assimilating investments in HVs to compound growth options we suggested possible rationales structuring thestrategic positioning of firms on this technology and illustrated them with several examples from the automotive industry. Theserationales reflect the different and sometimes divergent perceptions firms can have in the short and the long term potential(option value) of hybrid vehicles and they explain the disparity of strategic postures within the automotive industry.

In fact although HVs are considered industry-wide as a growth option strategy, a closer look on their technologicalcharacteristics reveals that such vehicles can be assimilated to compound growth options embedding a series of embeddedoptions. Considering these second order options allows in our paper to differentiate four types of growth option strategies. Growthoptions on HVs can in fact be motivated by being: (1) an option to maintain the existing technological paradigm and a hedgingstrategy against long term uncertainties; (2) an option to act sequentially to limit HV project risks; (3) an option to diversify and(4) a platform with built-in flexibility option. The choice and intensity of each of these growth options may depend on theperception of firm specific as well as industry-wide uncertainties that may be different and even divergent among firms and overtime as new information is revealed and new knowledge is acquired.

The four compound option strategies may also display conflicting and synergetic interactions among each other. The options tohedge and to maintain the ICE (the HV as set of nested options) and the sequential investment options are complementary andreinforce each other. They contribute all to improve and perpetuate the existing regime. Also the option to diversify (the HV as aset of parallel growth options) and the built-in flexibility platform option reinforce each other. But they see their value increasebecause of their potential to support the transition process towards more disruptive technologies. Consequently, a HV growthoption which derives its value from the option to maintain the ICE and acts as a hedging option might be in conflict with both theoption value to diversify and the option value of platforms with built-in flexibility. As a matter of fact, since increasinghybridization narrows the environmental performance and efficiency gap between the ICE, the BEV and the FCV, the HVmay affectnegatively the possibility for other alternative technologies to be marketed autonomously.

Policy support schemes have evidently contributed to influence firms' investment efforts in developing andmarketing alternativevehicles, including HVs. Public R&D subsidies for fuel cells and batteries have intensified firms' long term efforts to advance electricvehicles. Nevertheless taking into account uncertainties with regard to these alternatives, regulations on the reduction of CO2

emissions have overall pursued, in line with the market oriented innovation logic of the car industry a progressive trend favoringmostly the commercialization of more efficient ICEVs and HVs. In view however of the compound option characteristics of HVs, animportant policy implication is to consider and examine the long termprospects of HVs through their technology diversification effectand as built-in flexibility platforms. Policy decisions to push and pull technological development and support transitions raise in factconcerns about technology selection and the risk of creating new technology lock-ins. In this context HVs can provide governments apossible alternative to combine short term and long term technology policies by taking into account their compound optioncharacteristics and factoring in their limits and potentials to contribute to the transition towards ‘zero emission’ vehicles.

Acknowledgments

The authors would like to thank two anonymous referees for their constructive comments on an earlier draft of this paper.We would also like to thank the PREDIT which is a program of research, experimentation and innovation in land transport,implemented by the French ministries in charge of research, transport, environment and industry, the ADEME and the OSEOInnovation.

References

[1] M. Hekkert, R. Van den Hoed, Competing technologies and the struggle towards a new dominant design: the emergence of the hybrid vehicle at the expenseof the fuel cell vehicle, Greener Management International 47 (2006) 29–47.

[2] R. Raven, Niche accumulation and hybridisation strategies in transition processes towards a sustainable energy system: an assessment of differences andpitfalls, Energy Policy 35 (4) (2007) 2390–2400.

[3] F.W. Geels, J. Schot, Typology of socio‐technical transition pathways, Research Policy 36 (3) (2007) 399–417.[4] E.H. Bowman, D. Hurry, Strategy through the option lens: an integrated view of resource investments and the incremental choice process, Academy of

Management Review 18 (4) (1993) 760–782.[5] R.G. McGrath, A real options logic for initiating technology positioning investments, Academy of Management Review 22 (4) (1997) 974–996.[6] B. Kogut, N. Kulatilaka, Capabilities as real options, Organization Science 12 (6) (2001) 744–758.[7] A.K. Dixit, R.S. Pindyck, Investment Under Uncertainty, Princton University Press, Princton, NJ, 1994.[8] L. Trigeorgis, Real Options: Managerial Flexibility and Strategy in Resource Allocation, MIT Press, Cambridge, 1996.[9] Y. Li, B.E. James, R. Madhavan, J.T. Mahoney, Real options: taking stock and looking ahead, in: J.J. Reuer, T.W. Tong (Eds.), Real Options Theory, Advances in

Strategic Management, Elsevier Ltd, 2007.

660 A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

[10] R.L. McDonald, D. Siegel, The value of waiting to invest, Quarterly Journal of Economics 10 (4) (1986) 707–727.[11] N. Kulatilaka, E.C. Perotti, Strategic growth options, Management Science 44 (8) (1998) 1021–1031.[12] T.B. Folta, J.P. O'Brien, Entry in the presence of dueling options, Strategic Management Journal 25 (2) (2004) 121–138.[13] M.J. Leiblein, A.A. Ziedonis, Deferral and growth options under sequential innovation, in: J.J. Reuer, T.W. Tong (Eds.), Real Options Theory, Advances in

Strategic Management, Elsevier Ltd, 2007.[14] M. Benaroch, Option-based management of technology investment risk, IEEE Transactions on Engineering Management 48 (4) (2001) 428–444.[15] R. Adner, D.A. Levinthal, What is not a real option: considering boundaries for the application of real options to business strategy, Academy of Management

Review 29 (1) (2004) 74–85.[16] R.G. McGrath, W.J. Ferrier, A.L. Mendelow, Real options as engines of choice and heterogeneity, Academy of Management Review 29 (1) (2004) 86–101.[17] W.C. Kester, Today's options for tomorrow's growth, Harvard Business Review 62 (2) (1984) 153–160.[18] R.S. Vassolo, F. Ravara, J.M. Connor, Valuing strategic growth options: a portfolio approach, Management Research 3 (1) (2005) 87–99.[19] IEA, Energy technology perspectives: scenarios and strategies to 2050, Support of the G8 Plan of Action, Ed. OECD-IEA, Paris, 2006.[20] Toyota, Sustainability Report, 2008.[21] V. Oltra, M. Saint Jean, Variety of technological trajectories in low emission vehicles (LEVs): a patent data analysis, Journal of Cleaner Production 17 (2) (2009)

201–213.[22] ADEME, Véhicules particuliers en France: 2003–2009, athttp://www2.ademe.fr/servlet/getDoc?cid=96&m=3&id=52819&p1=02&p2=12&ref=17597

(accessed July 24th 2009).[23] JAMA, The Motor Industry of Japan — 2009, at http://www.jama-english.jp/publications/index.html(accessed November 11th 2009).[24] DoE, US Hybrid Electric Vehicle Sales by Model: 1999–2008, at http://www.afdc.energy.gov/afdc/data/vehicles.html(accessed November 11th 2009).[25] RITA, National Transportation Statistics, Bureau of Transportation Statistics, 2009http://www.bts.gov/publications/national_transportation_statistics

(accessed November 11th 2009).[26] D. Sperling, T. Lipman, International Assessment of Electric‐Drive Vehicles: Policies, Markets, and Technologies, The University of California Transportation

Center (UCTC, 2000, p. 619.[27] O. Bitsche, G. Gutmann, Systems for hybrid cars, Journal of Power Sources 127 (1–2) (2004) 8–15.[28] A. Raskin, S. Shah, The Emergence of Hybrid Vehicles, Research on Strategic Change, Alliance Bernstein, 2006.[29] UBS-Ricardo report, is diesel set to boom in the US? UBS Investment Research Q Series®: Global Autos Research, May 24 2007.[30] J.B. Heywood, M.A. Weiss, A. Schafer, S.A. Bassene, V.K. Natarajan, The performance of future ICE and fuel cell powered vehicles and their potential fleet

impact, MIT‐LFEE‐2003‐004 RP, Paper n° 04P‐25, MIT Laboratory for Energy and Environment, 2004.[31] D. Karner, J. Francfort, Hybrid and plug‐in hybrid electric vehicle performance testing by the US Department of Energy Advanced Vehicle Testing Activity,

Journal of Power Sources 174 (1) (2007) 69–75.[32] C. Berggren, T. Magnusson, D. Sushandoyo, Hybrids, diesel or both? The forgotten technological competition for sustainable solutions in the global automotive

industry, International Journal of Automotive Technology and Management 9 (2) (2009) 148–173.[33] F. Vangraefschepe, F. Menegazzi, Véhicules Hybrides: Quel Avenir ?, IFP Panorama 2005, IFP, Diffusion et Connaissances, Paris, 2005.[34] E. Karden, S. Ploumen, B. Fricke, T. Miller, K. Snyder, Energy storage devices for future hybrid electric vehicles, Journal of Power Sources 168 (1) (2007) 2–11.[35] F.R. Kalhammer, B.M. Kopf, D.H. Swan, V.P. Roan, M.P. Walsh, Status and prospects for zero emissions vehicle technology, Report of the ARB Independent

Expert Panel 2007, Prepared for the State of California Air Resources Board, Sacramento, California, 2007.[36] A. Dixit, Investment and hysteresis, Journal of Economic Perspectives 6 (1) (1992) 107–132.[37] T. Chi, P.C. Nystrom, Decision dilemmas facing managers: recognizing the value of learning while making sequential decisions, Omega— International Journal

of Management Science 23 (3) (1995) 303–312.[38] C.J. Murray, Auto industry working hard to make an electric vehicle battery, Design News April 2008, at http://www.designnews.com/article/

10574Auto_Industry_Working_Hard_to_Make_an_Electric_Vehicle_Battery.php (accessed July 24th 2009).[39] R. Cowan, S. Hulten, Escaping lock‐in: the case of the electric vehicle, Technological Forecasting and Social Change 53 (1) (1996) 61–79.[40] D. Calef, R. Goble, The allure of technology: how France and California promoted electric and hybrid vehicles to reduce urban air pollution, Policy Sciences 40

(1) (2006) 1–34.[41] F. Fréry, Un cas d'amnésie stratégique: l'éternelle émergence de la voiture électrique, Montpellier, IXème Conférence Internationale de Management

Stratégique, 2000.[42] M.L. Wald, Questions about a hydrogen economy, Scientific American 290 (5) (2004) 66–73.[43] R. Romm, The car and fuel of the future, Energy Policy 34 (17) (2006) 2609–2614.[44] G.J. Tellis, P.N. Golder, First to market, first to fail? Real causes of enduring market leadership, Sloan Management Review 37 (2) (1996) 65–75.[45] K.R. Conner, Strategies for product cannibalism, Strategic Management Journal 9 (1) (1988) 9–26.[46] H. Itazaki, The PRIUS that Shook the World, Nikkan Kogyo Shimbun, Tokyo, Japan, 1999.[47] K. Blumenröder, G. Buschmann, C. von Essen, O.C. Mehler, B. Voss, The Hybrid Drive — An Engineering Spearhead, MTZ Special Edition, 2005.[48] N. Owen, R. Gordon, Carbon to Hydrogen Roadmaps for Passenger Cars, a Study for the Department for Transport and the Department of Trade and Industry,

RD. 02/3280, Ricardo Consulting Engineers Ltd, 2002.[49] L. Brooke, High value hybrids, Automotive Engineering International (April 2008) 25–27.[50] I.C. MacMillan, R.G. McGrath, Crafting R&D project portfolios, Research Technology Management 45 (5) (2002) 48–60.[51] T.A. Luehrman, Strategy as a portfolio of real options, Harvard Business Review 76 (5) (1998) 89–99.[52] C.W.I. Pistorius, J.M. Utterback, Multi‐mode interaction among technologies, Research Policy 26 (1) (1997) 67–84.[53] R. Adner, D.A. Levinthal, The emergence of emerging technologies, California Management Review 45 (1) (2002) 50–66.[54] A. Nair, D. Ahlstrom, Delayed creative destruction and the coexistence of technologies, Journal of Engineering and Technology Management 20 (4) (2003)

345–365.[55] J. Anand, R. Oriani, R.S. Vassolo, Managing a portfolio of real options, in J.J. Reuer, T.W. Tong (Eds), Real Options Theory, Advances in Strategic Management,

Elsevier, JAI Press, Oxford, 2007.[56] K.S. Jeong, B.S. Oh, Fuel economy and life‐cycle cost analysis of a fuel cell hybrid vehicle, Journal of Power Sources 105 (1) (2002) 58–65.[57] S. Bakker, H. van Lente, F. Prager, M. Meeus, Prototyping hydrogen futures, Paper presented at DIME International Conference, Innovation, Sustainability and

Policy, 11‐13 September 2008, GRETHa, University Bordeaux, France, 2008.[58] P. Grumberg, M. Fontez, Automobile: la révolution électrique, Science & Vie 1096 (January 2009) 45–61.[59] U. Bossel, Does a hydrogen economy make sense? Proceedings of the IEEE 94 (10) (2006) 1826–1837.[60] J.J. Botti, M.J. Grieve, J.A. MacBain, Electric vehicle range extension using an SOFC APU, SAE Technical Paper Series, SAEWorld Congress Detroit, Michigan, April

2005.[61] K. Rajashekara, J.A. MacBain, M.J. Grieve, Evaluation of SOFC hybrid systems for automotive propulsion applications, Industry Applications Conference, 41st

IAS Annual Meeting, Conference Record of the EEE, 2006.[62] ERTRAC, The electrification approach to urban mobility and transport, Strategy Paper, Draft Version, September 2008.[63] P. del Rio González, Policy implications of potential conflicts between short-term and long-term efficiency in CO2 emissions abatement, Ecological Economics

65 (2) (2008) 292–303.[64] B.A. Sandén, C. Azar, Near‐term technology policies for long term climate targets: economywide versus technology specific approaches, Energy Policy 33 (12)

(2005) 1557–1576.[65] R. Kemp, Sustainable technologies do not exist! Paper presented at DIME International Conference, Innovation, Sustainability and Policy, 11‐13 September

2008, GRETHa, University Bordeaux, France, 2008.[66] M. Ahman, L.J. Nilsson, Path dependency and the future of advanced vehicles and biofuels, Utilities Policy 16 (2) (2008) 80–89.

661A. Avadikyan, P. Llerena / Technological Forecasting & Social Change 77 (2010) 649–661

[67] N. Gil, On the value of project safeguards: embedding real options in complex products and systems, Research Policy 36 (7) (2007) 980–999.[68] C.Y. Baldwin, K.B. Clark, Design Rules: The Power of Modularity, Vol. I, MIT Press, Cambridge, MA, 2000.[69] K.T. Ulrich, The role of product architecture in the manufacturing firm, Research Policy 24 (3) (1995) 419–440.[70] B. Kogut, N. Kulatilaka, Options thinking and platform investments: investing in opportunity, California Management Review 36 (2) (1994) 52–71.[71] T. Magnusson, C. Berggren, Knowledge integration as a key competence: contrasting technology and sourcing strategies for the development of hybrid‐

electric vehicles, KITE RADMA Advanced Workshop, September, 2008.[72] Toyota, Annual Report: Sustainability in Three Areas — Special Feature, 2008.

Arman Avadikyan has a Ph.D in economics. He is a research engineer at the Bureau of Theoretical and Applied Economics, a research unit of the University ofStrasbourg, University Nancy 2 and the CNRS (France). His current research work focuses on innovation management/marketing and sustainable transporttechnologies.

Patrick llerena is Professor at the Faculty of Economics and Management (University of Strasbourg, France) and a member of the Bureau of Theoretical andApplied Economics (BETA). He was the director of the BETA from 2003 to 2008. His main research fields are innovation and science policy.