A MULTIPLE CASE STUDY EXAMINATION OF MUNICIPAL FINANCIAL DISTRESS IN PENNSYLVANIA

276

A MULTIPLE CASE STUDY EXAMINATION OF MUNICIPAL FINANCIAL DISTRESS IN PENNSYLVANIA By Donna J. Piper Rupert ANTHONY PIZUR, PhD, Faculty Mentor and Chair CLIFFORD BUTLER, PhD, Committee Member MARY JANE KUFFNER HIRT, PhD, Committee Member William A. Reed, PhD, Dean, School of Business and Technology A Dissertation Presented in Partial Fulfillment Of the Requirements for the Degree Doctor of Philosophy Capella University October 2012

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of A MULTIPLE CASE STUDY EXAMINATION OF MUNICIPAL FINANCIAL DISTRESS IN PENNSYLVANIA

A MULTIPLE CASE STUDY EXAMINATION OF MUNICIPAL

FINANCIAL DISTRESS IN PENNSYLVANIA

By

Donna J. Piper Rupert

ANTHONY PIZUR, PhD, Faculty Mentor and Chair

CLIFFORD BUTLER, PhD, Committee Member

MARY JANE KUFFNER HIRT, PhD, Committee Member

William A. Reed, PhD, Dean, School of Business and Technology

A Dissertation Presented in Partial Fulfillment

Of the Requirements for the Degree

Doctor of Philosophy

Capella University

October 2012

All rights reserved

INFORMATION TO ALL USERSThe quality of this reproduction is dependent upon the quality of the copy submitted.

In the unlikely event that the author did not send a complete manuscriptand there are missing pages, these will be noted. Also, if material had to be removed,

a note will indicate the deletion.

Microform Edition © ProQuest LLC.All rights reserved. This work is protected against

unauthorized copying under Title 17, United States Code

ProQuest LLC.789 East Eisenhower Parkway

P.O. Box 1346Ann Arbor, MI 48106 - 1346

UMI 3544057

Published by ProQuest LLC (2012). Copyright in the Dissertation held by the Author.

UMI Number: 3544057

© Donna J. Rupert, 2012

Abstract

In 1987, the Pennsylvania Legislature enacted the Financially Distressed

Municipalities Act, commonly known as Act 47, which was meant to address financial

distress by providing assistance to municipalities that were suffering from declining

economies, financial mismanagement, and administrative inefficiencies (PA Legislature,

1987). Since 1987, 27 municipalities in Pennsylvania have been declared financially

distressed pursuant to Act 47 (PA Department of Community and Economic

Development, 2012). Currently, 21 municipalities operate under the financial distress

declaration while only six of the 27 have had the declaration rescinded (PA Department

of Community and Economic Development, 2012).

This research examines four (the boroughs of East Pittsburgh, Homestead, North

Braddock, and Wilkinsburg) of the six municipalities that have had a financial distress

declaration rescinded by the Secretary of the Pennsylvania Department of Community

and Economic Development using a mixed method case study approach.

The purpose of this research is to determine whether patterns and trends exist

among the four cases and to determine how, based upon the patterns and trends, each of

the case municipalities were able to have their financial distress declaration rescinded.

Subsequently, the ultimate purpose of this research is to apply the answers to how, to

other financially distressed municipalities across the Pennsylvania Commonwealth. In

addition, identified patterns and trends during the pre-distress study period may also be

applied to other Pennsylvania municipalities and may act as an early warning system for

municipal financial distress in Pennsylvania.

iii

Dedication

To my: daughter, Melissa, sons Ryan and Dylan; and granddaughters Laikyn and

Leah, and grandson Bryson. You are my shining stars – my reasons for being.

iv

Acknowledgements

My deepest appreciation is extended to my former Committee Chairperson, Dr.

Valerie Coxon. Her encouragement and guidance gave me the courage to continue.

I would also like to thank my dear friend Dr. Mary Jane Hirt for her expert advice

and guidance through this process.

Finally, I would like to acknowledge my family and friends and all who have

listened, smiled, and asked how things are coming along. I very much appreciated the

encouraging words.

v

Table of Contents

Acknowledgements iv

List of Tables ix

List of Figures xi

CHAPTER 1. INTRODUCTION 1

Background of the Study 2

Statement of the Problem 3

Purpose of the Study 6

Rationale for the Study 7

Research Management Framework 8

Research Questions 10

Research Study Conceptual Model 11

Significance of the Study 13

Definition of Terms 14

Assumptions and Limitations 20

Nature of the Study 21

Organization of the Remainder of the Study 21

CHAPTER 2. LITERATURE REVIEW 23

Municipal Bankruptcy 23

Municipal Solvency 25

Insolvency: Financial Distress 26

The Municipal Financial Distress Cycle 31

The State’s Roles 34

vi

Pennsylvania’s Approach 39

Causal Factors 43

Stress Factors 46

Measuring Municipal Financial Distress 47

Financial Monitoring Systems 49

Summary 53

CHAPTER 3. METHODOLOGY 55

Purpose of the Study 55

Research Questions 55

Research Design 57

Description of the Population and Sample Characteristics 58

Measurement Plan 59

Data Collection Plan. 59

Data Analysis and Display 66

Validity and Reliability 67

Ethical Considerations 68

Conclusion 69

CHAPTER 4. RESEARCH FINDINGS 71

Research Questions 71

Data Collection 73

Data Presentation and Analysis 74

Socioeconomic Characteristics 74

Organizational Structure 84

vii

Financial Analysis 103

Summary of Findings 150

CHAPTER 5. DISCUSSION, LIMITATIONS AND RECOMMENDATIONS FOR

FUTURE RESEARCH 170

Discussion of the Results 173

Conclusions 182

Limitations 184

Recommendations for Future Research 188

REFERENCES 190

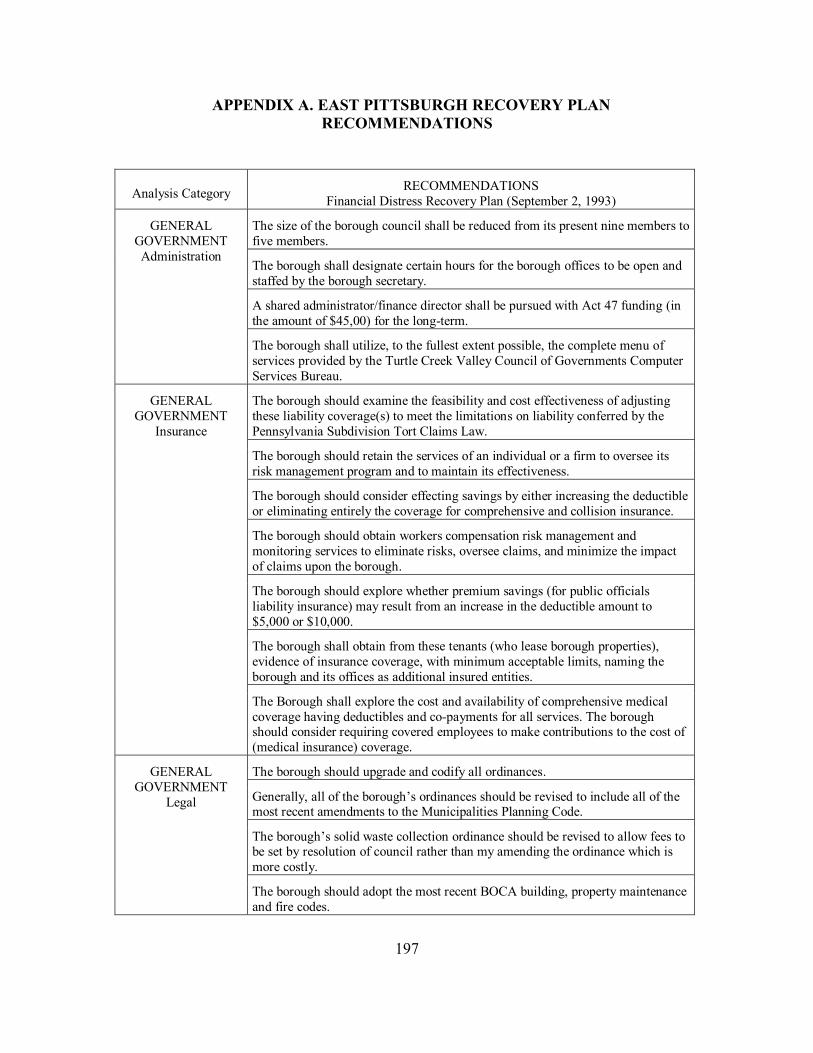

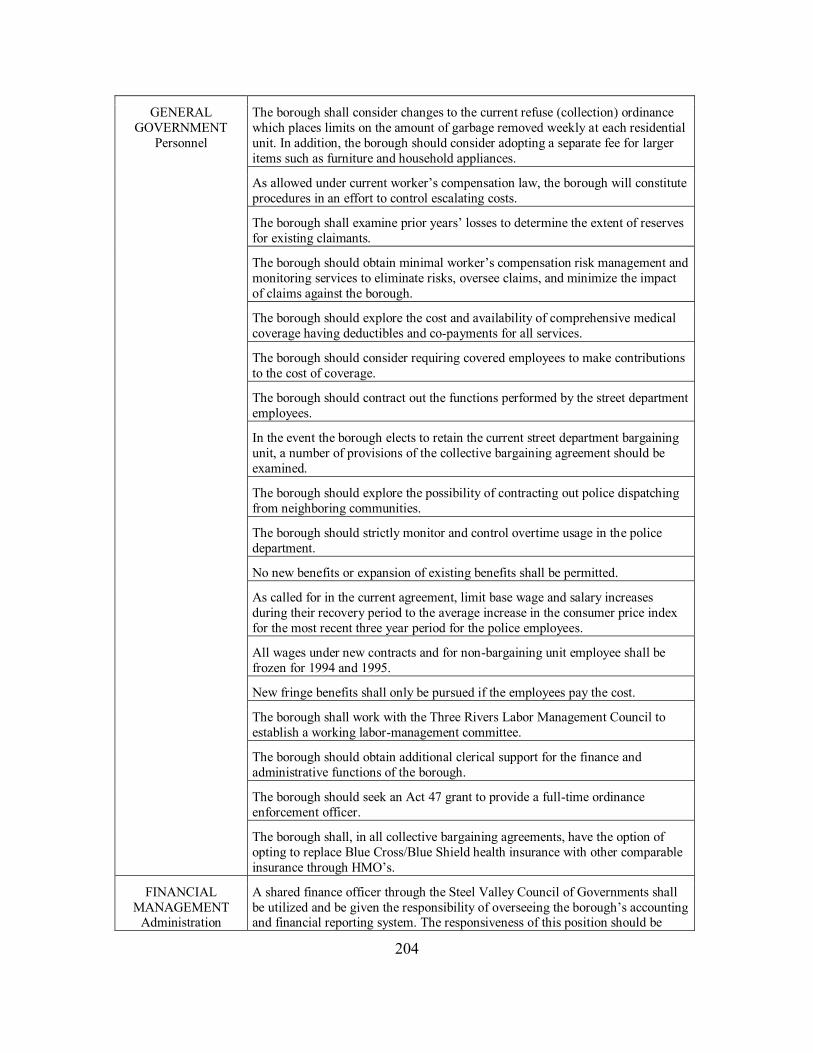

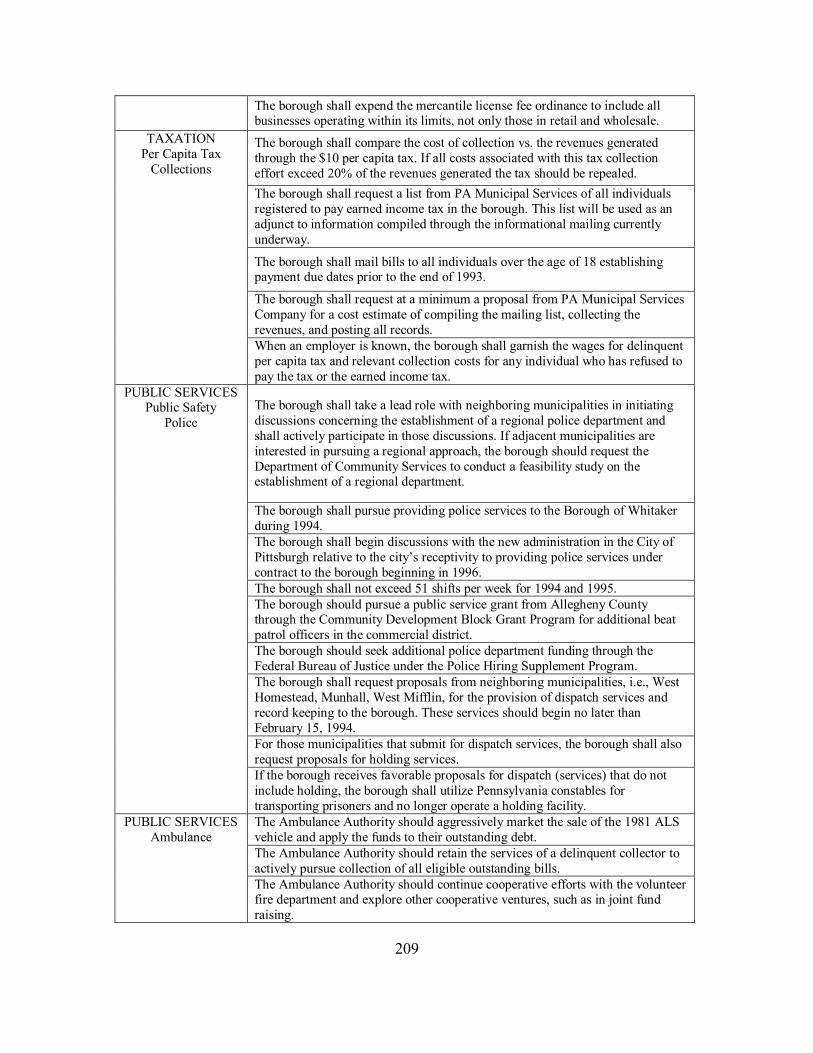

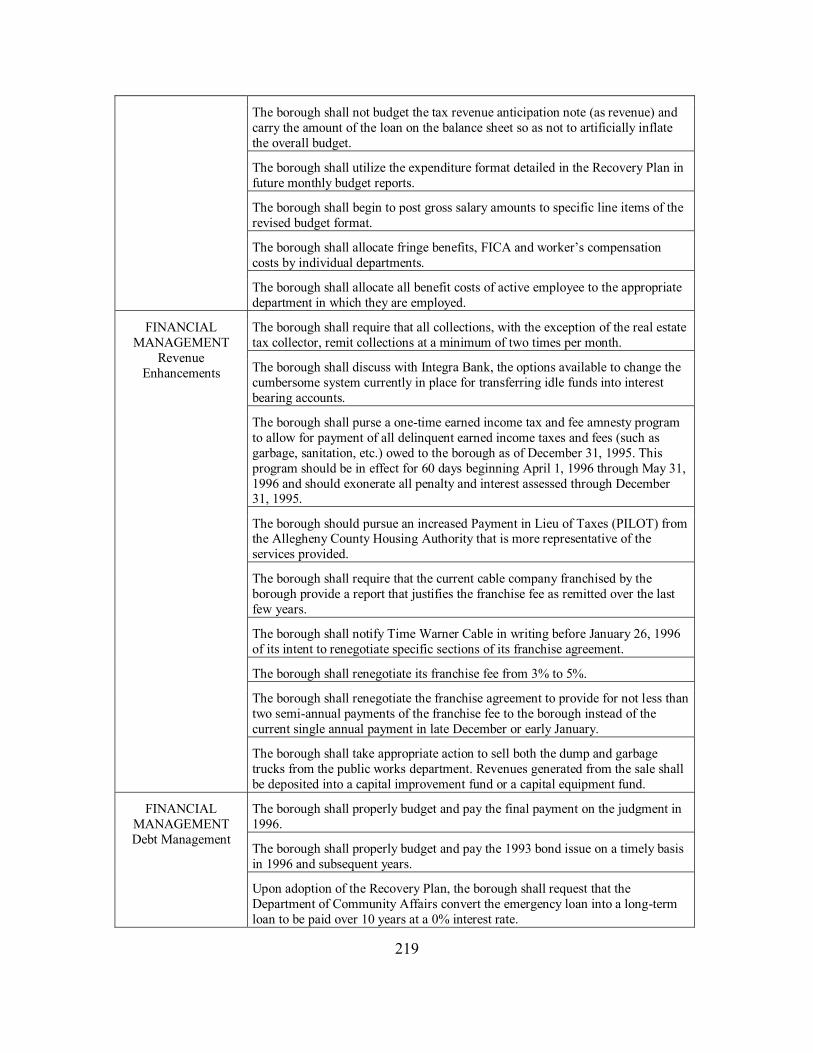

APPENDIX A. EAST PITTSBURGH RECOVERY PLAN

RECOMMENDATIONS 197

APPENDIX B. HOMESTEAD RECOVERY PLAN RECOMMENDATIONS 203

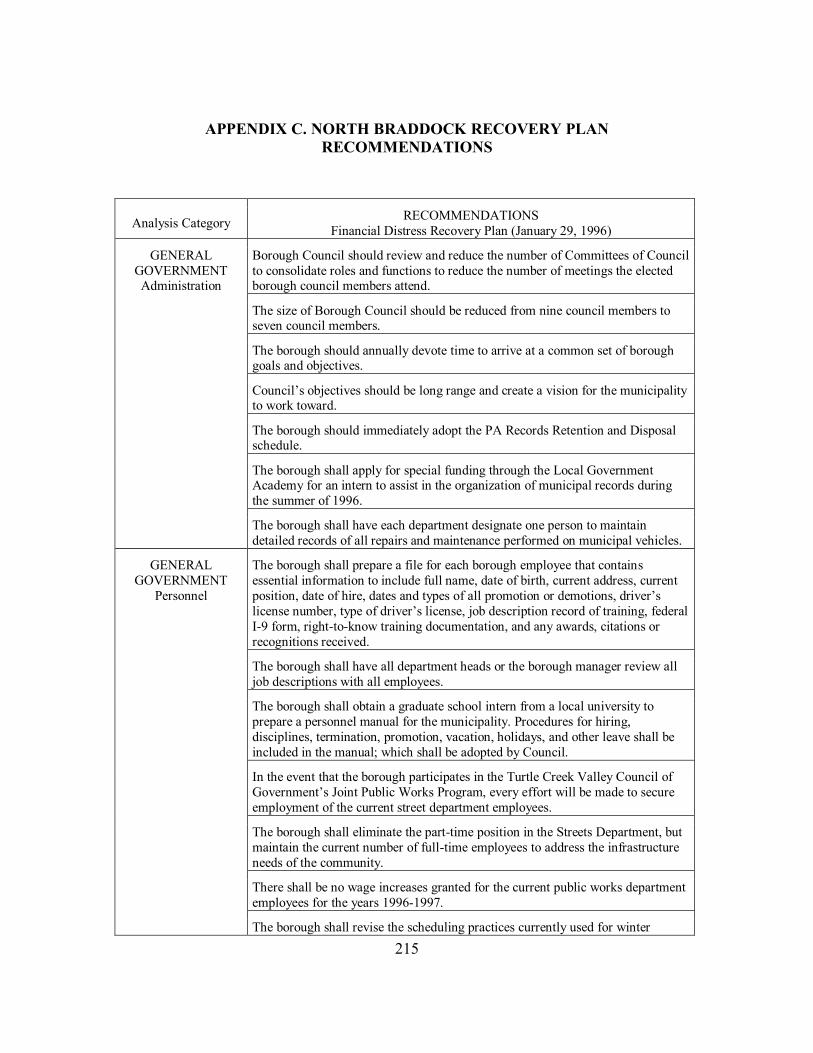

APPENDIX C. NORTH BRADDOCK RECOVERY PLAN

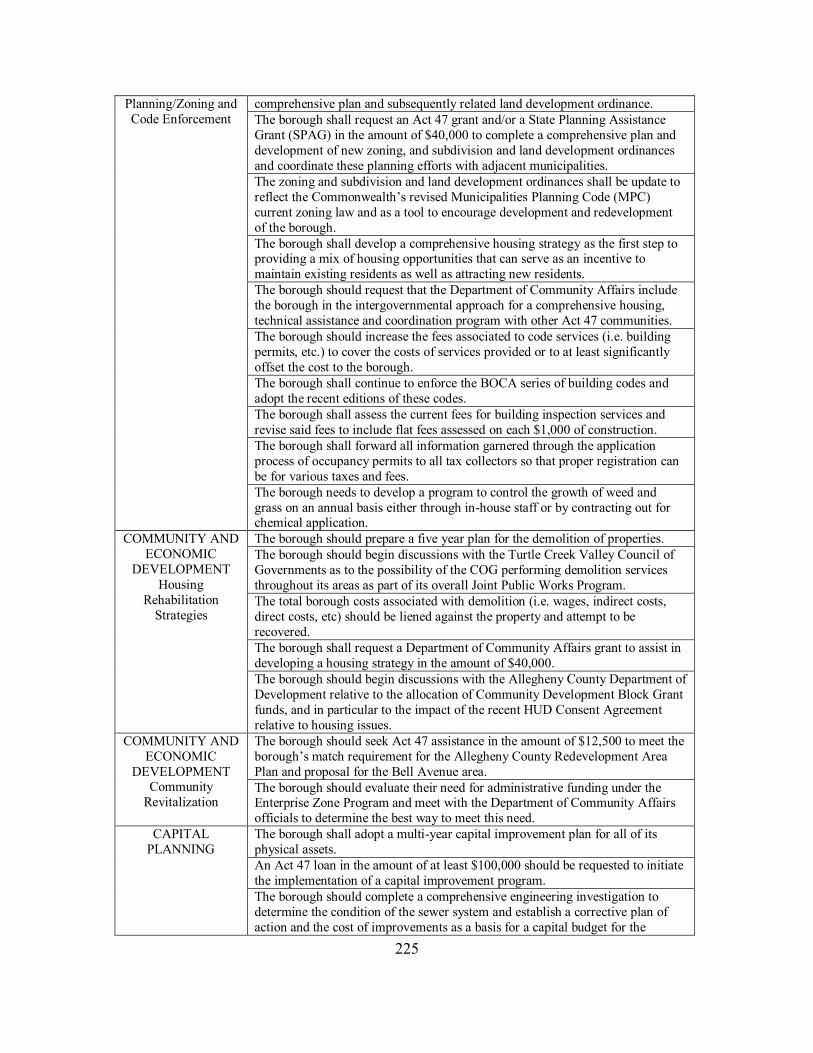

RECOMMENDATIONS 215

APPENDIX D. WILKINSBURG RECOVERY PLAN RECOMMENDATIONS 227

APPENDIX E. FINANCIAL DISTRESS IN WILKINSBURG BOROUGH 230

APPENDIX F. FINANCIAL DISTRESS IN NORTH BRADDOCK BOROUGH 239

APPENDIX G. PUBLIC SERVICE DEPARTMENTS AND APPOINTED

OFFICIALS BY CASE MUNICIPALITY 246

APPENDIX H. TAXES LEVIED BY CASE MUNICIPALITY 248

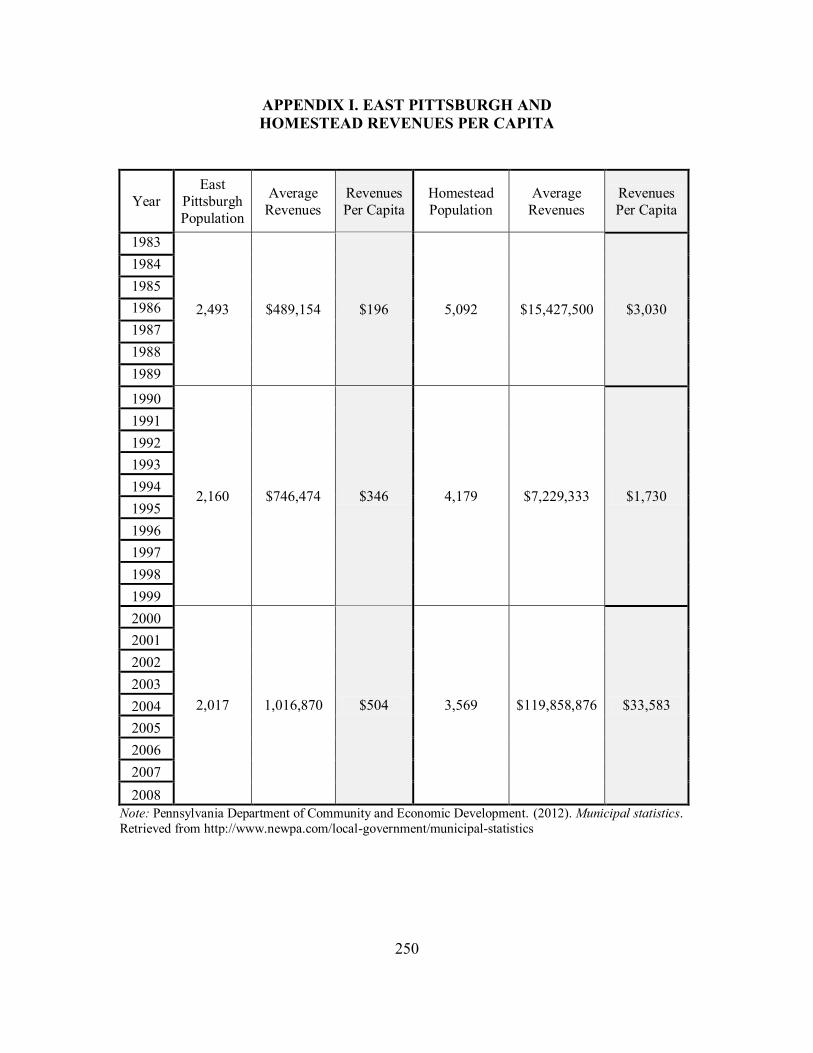

APPENDIX I. EAST PITTSBURGH AND HOMESTEAD REVENUES PER

CAPITA 250

APPENDIX J. NORTH BRADDOCK AND WILKINSBURG REVENUES PER

CAPITA 251

APPENDIX K. EAST PITTSBURGH TAX REVENUES 252

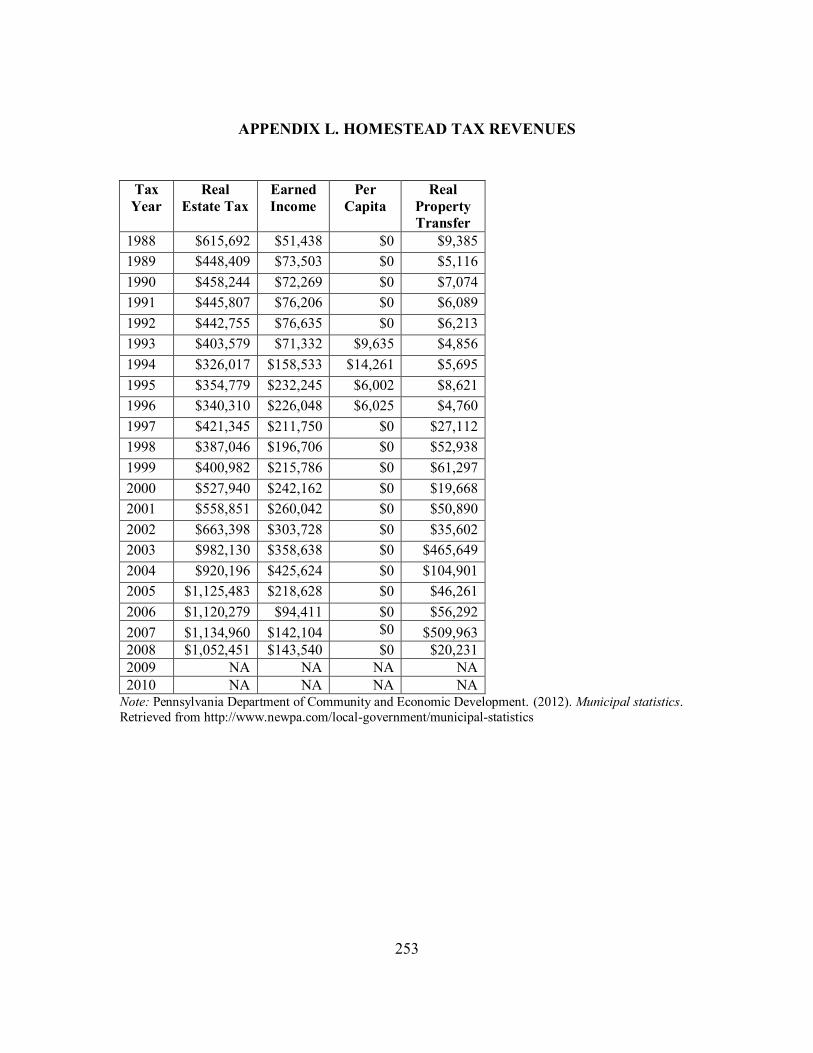

APPENDIX L. HOMESTEAD TAX REVENUES 253

viii

APPENDIX M. NORTH BRADDOCK TAX REVENUES 255

APPENDIX N. WILKINSBURG TAX REVENUES 256

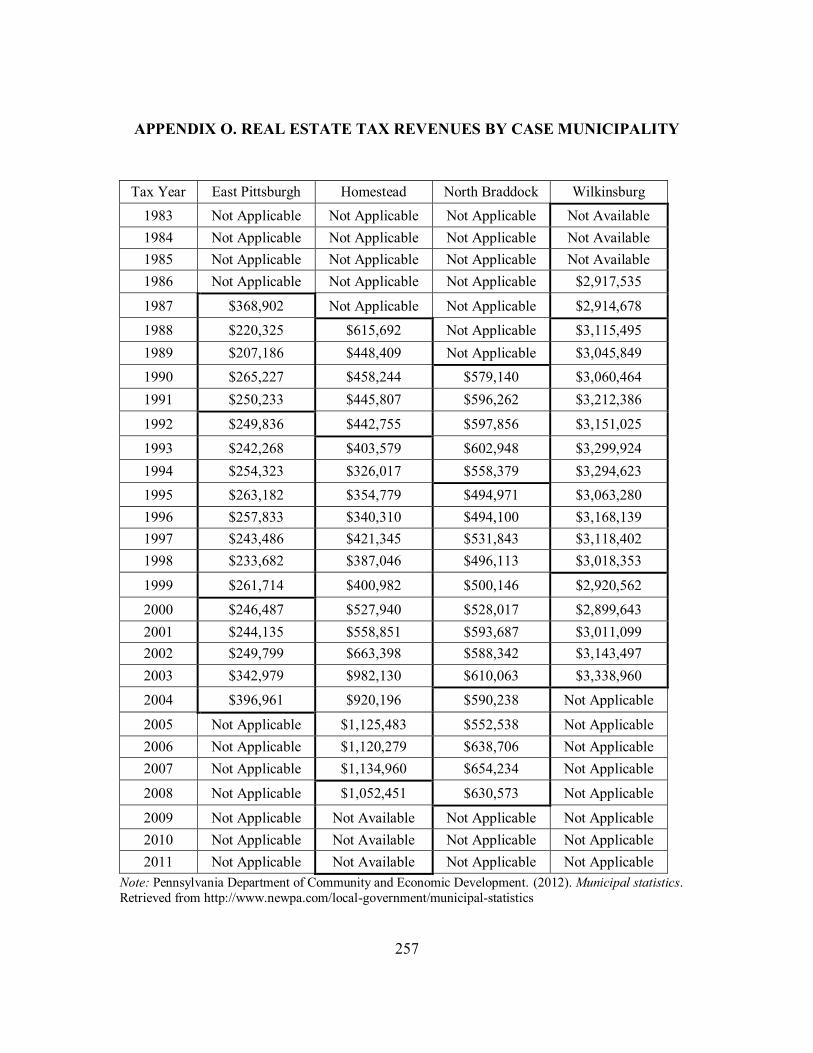

APPENDIX O. REAL ESTATE TAX REVENUES BY CASE MUNICIPALITY 257

APPENDIX P. TOTAL EXPENDITURES BY CASE MUNICIPALITY 258

APPENDIX Q. EAST PITTSBURGH DEPARTMENTAL EXPENDITURES 259

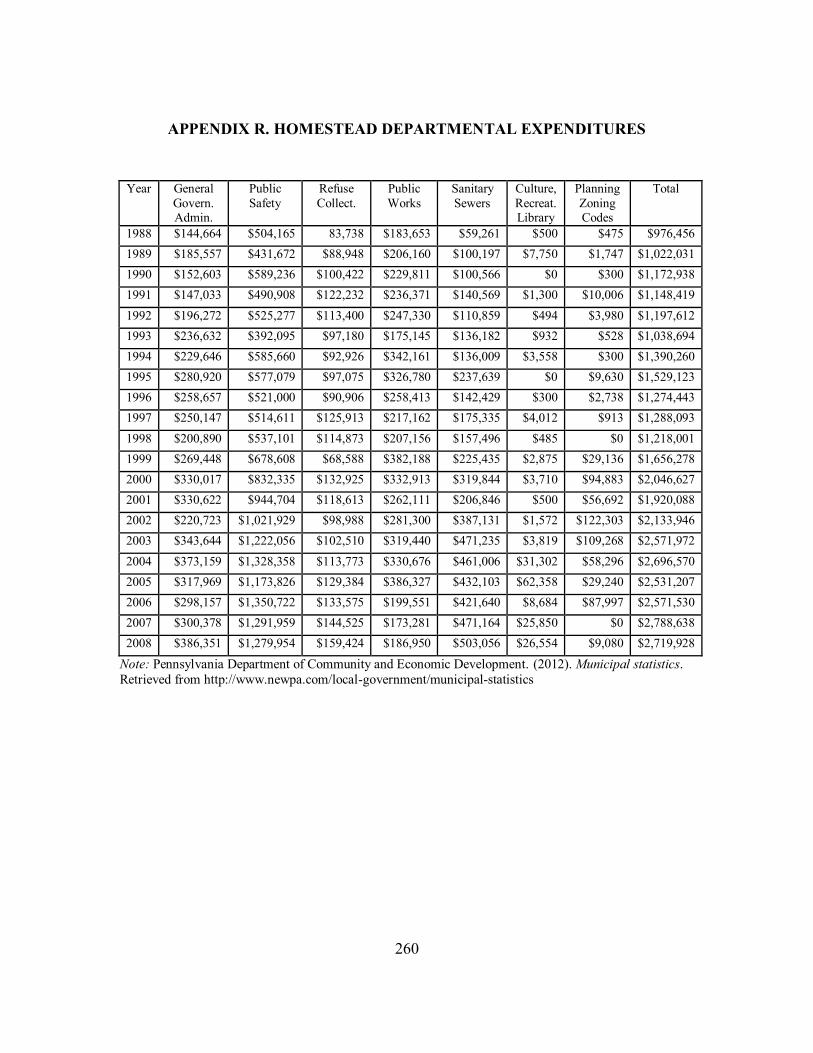

APPENDIX R. HOMESTEAD DEPARTMENTAL EXPENDITURES 260

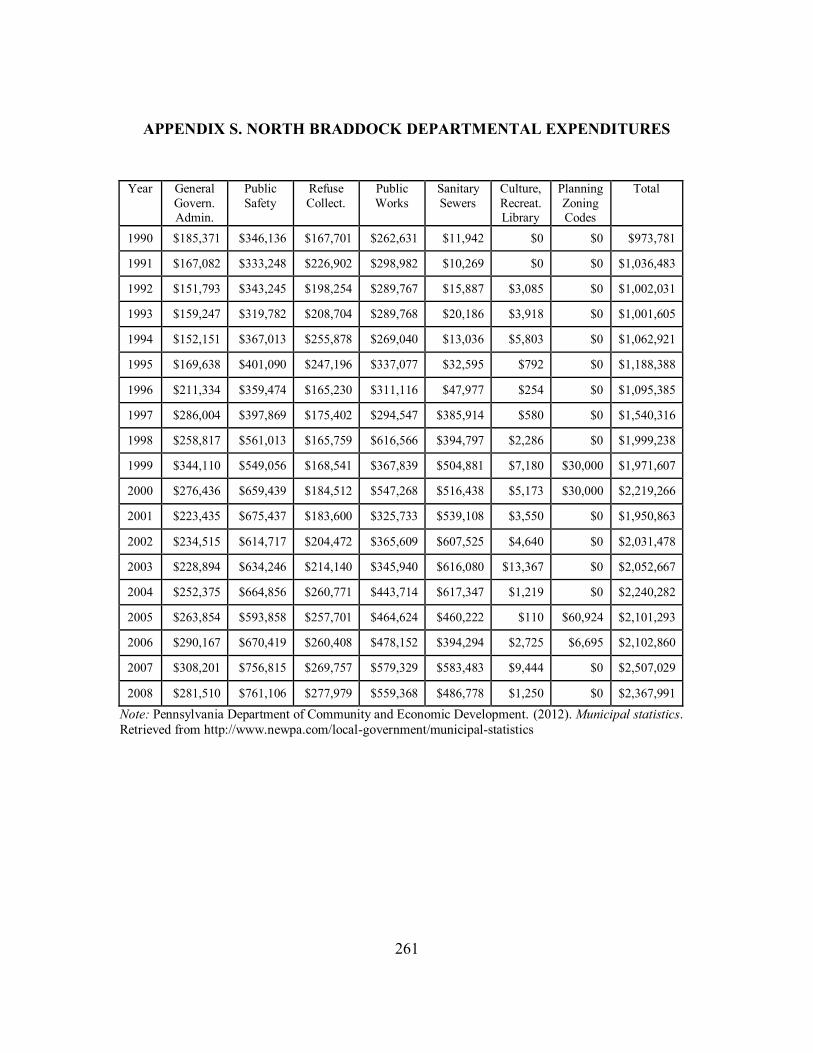

APPENDIX S. NORTH BRADDOCK DEPARTMENTAL EXPENDITURES 261

APPENDIX T. WILKINSBURG DEPARTMENTAL EXPENDITURES 262

ix

List of Tables

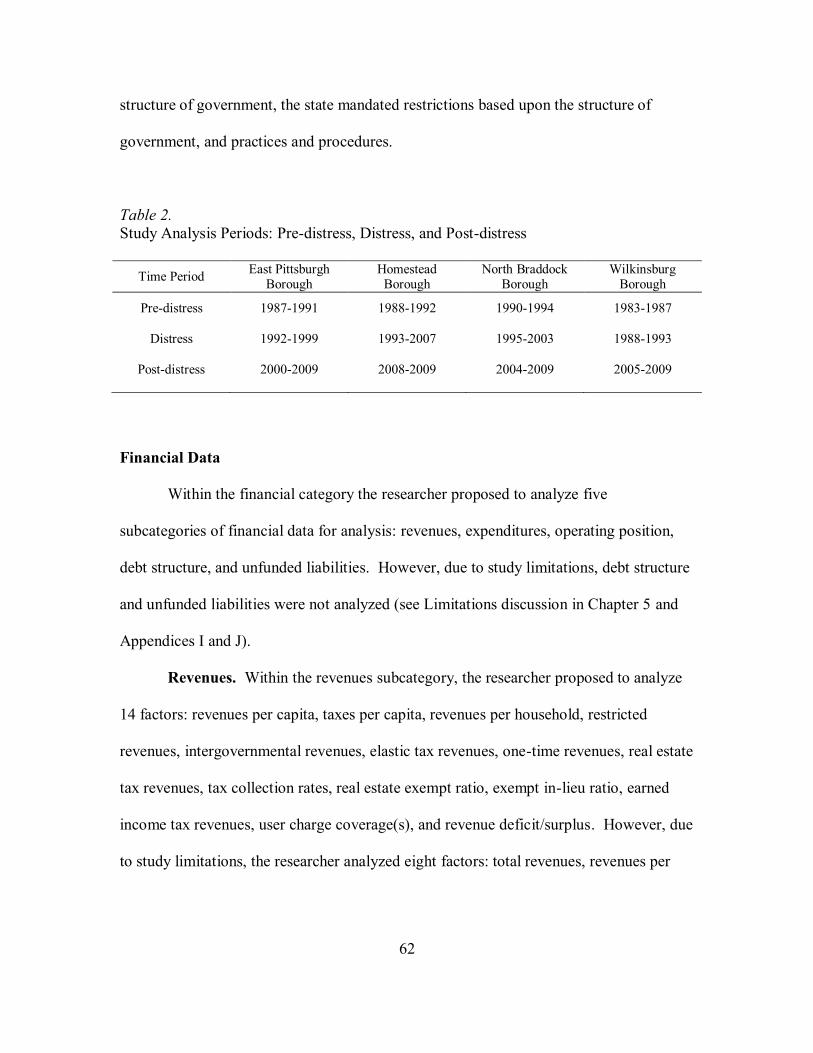

Table 1. Secondary Data Sources 61

Table 2. Study Analysis Periods: Pre-distress, Distress, and Post-distress 62

Table 3. East Pittsburgh Total Population (1970-2010) 76

Table 4. East Pittsburgh Population Characteristics (1970-2010) 76

Table 5. East Pittsburgh Housing Characteristics (1970-2010) 77

Table 6. East Pittsburgh Housing Occupancy Characteristics (1970-2010) 77

Table 7. Homestead Total Population (1970-2010) 78

Table 8. Homestead Population Characteristics (1970-2010) 79

Table 9. Homestead Housing Characteristics (1970-2010) 79

Table 10. Homestead Housing Occupancy Characteristics (1970-2010) 80

Table 11. North Braddock Total Population (1970-2010) 81

Table 12. North Braddock Population Characteristics (1970-2010) 81

Table 13. Wilkinsburg Total Population (1970-2010) 83

Table 14. Tax Revenue Comparison by Case Municipality 94

Table 15. Financial Distress Criterion Found to be Evident in East Pittsburgh 107

Table 16. Financial Distress Criterion Found to be Evident in Homestead 108

Table 17. Financial Distress Criterion Found to be Evident in North Braddock 110

Table 18. Financial Distress Criterion Found to be Evident in Wilkinsburg 111

Table 19. Assessed Valuation by Case Municipality. 114

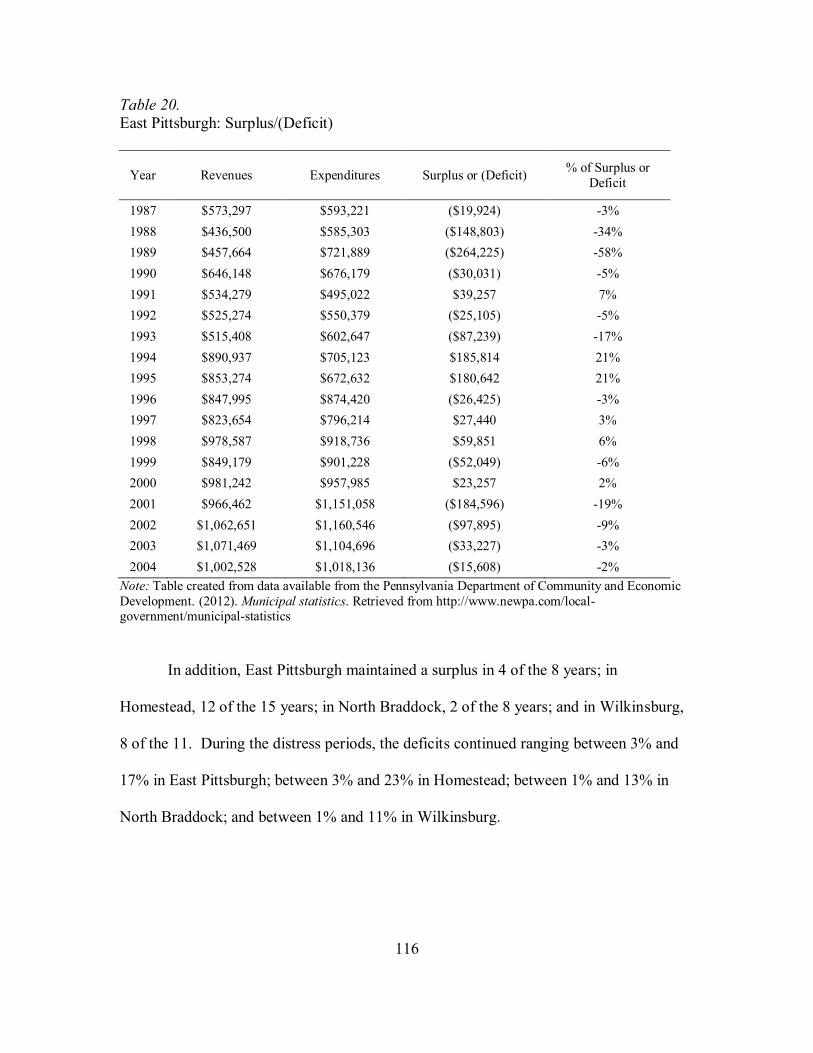

Table 20. East Pittsburgh Surplus/ (Deficit) 116

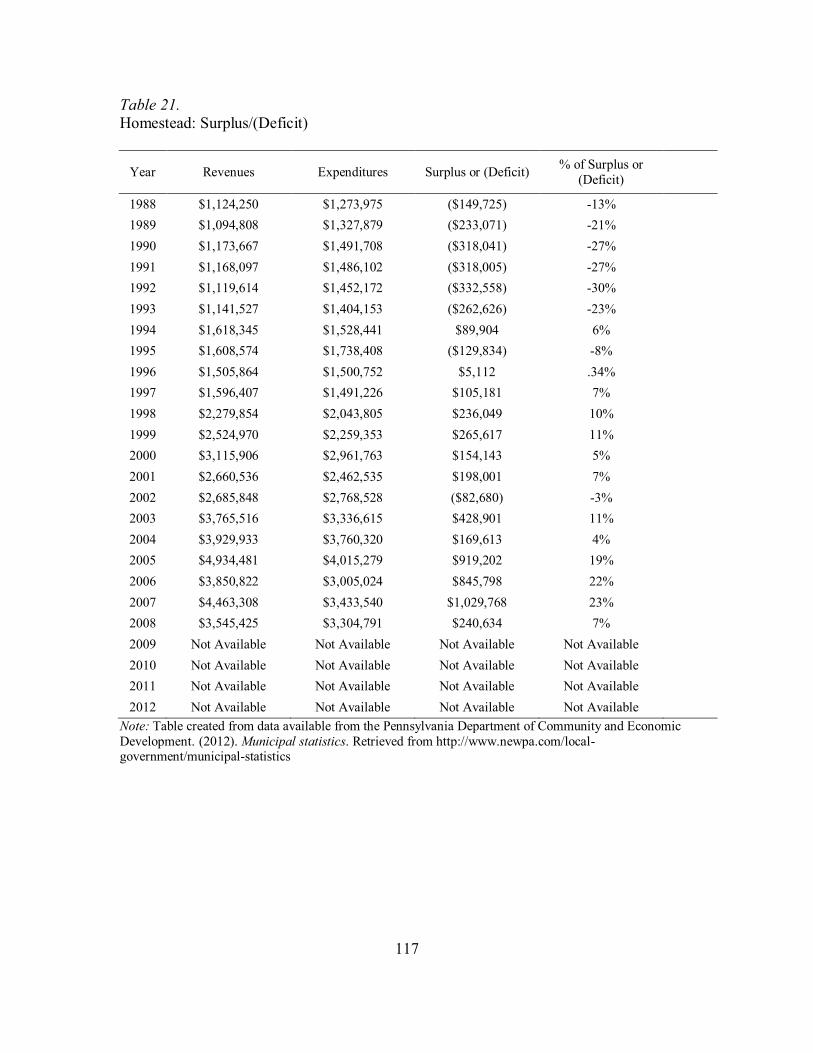

Table 21. Homestead Surplus/ (Deficit) 117

x

Table 22. North Braddock Surplus/ (Deficit) 118

Table 23. Wilkinsburg Surplus/ (Deficit) 119

Table 24. Revenues by Case Municipality 122

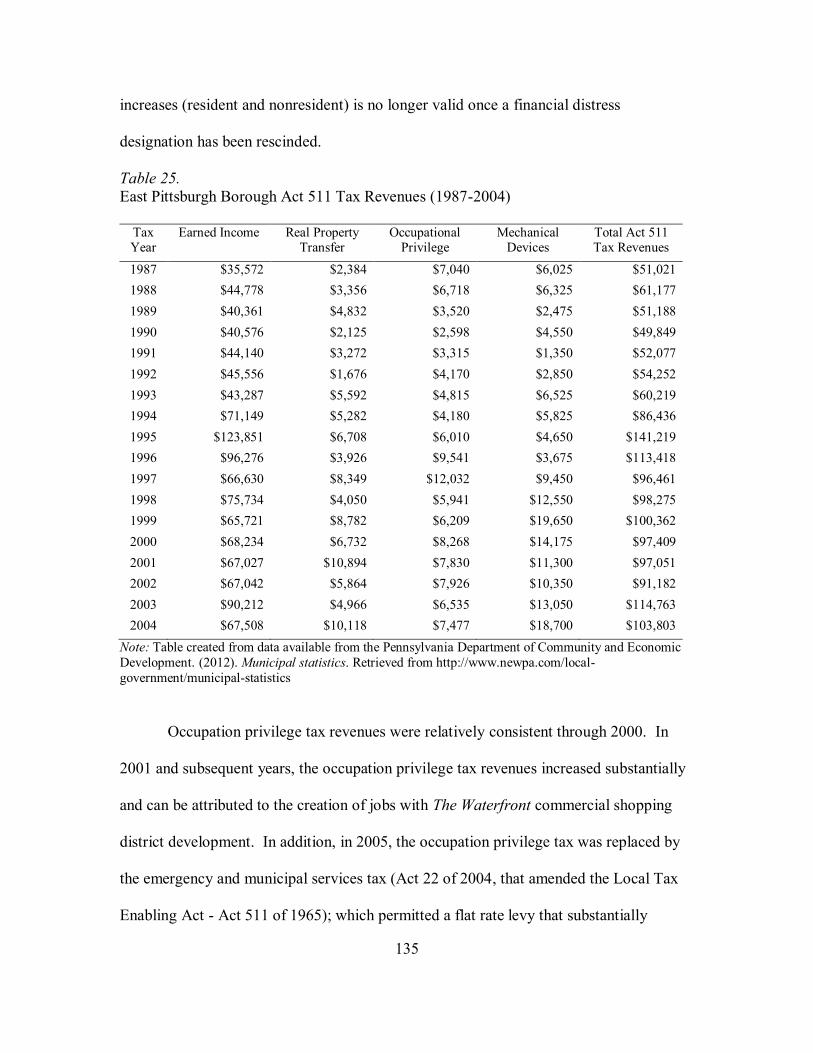

Table 25. East Pittsburgh Borough Act 511 Tax Revenues (1987-2004) 135

Table 26. Homestead Borough Act 511 Tax Revenues (1988-2010) 137

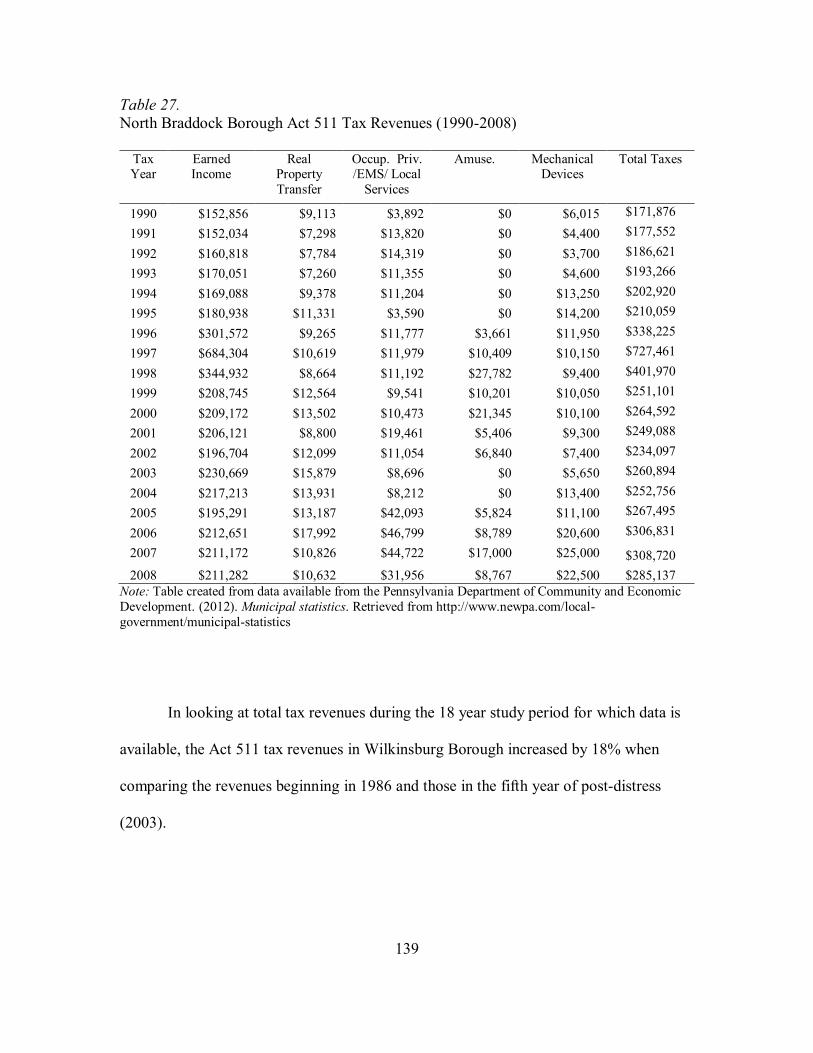

Table 27. North Braddock Borough Act 511 Tax Revenues (1990-2008) 139

Table 28. Wilkinsburg Borough Act 511 Tax Revenues (1983-2003) 140

Table 29. Annual Average of Regional Asset District Revenues by Municipality

(1994-2005) 141

Table 30. East Pittsburgh Borough State Funding Assistance 142

Table 31. Homestead Borough State Funding Assistance 143

Table 32. North Braddock Borough State Funding Assistance 143

Table 33. Wilkinsburg Borough State Funding Assistance 144

Table 34. East Pittsburgh Borough Departmental Function Expenditures (1987-1991) 147

xi

List of Figures

Figure 1. Research study conceptual model 34

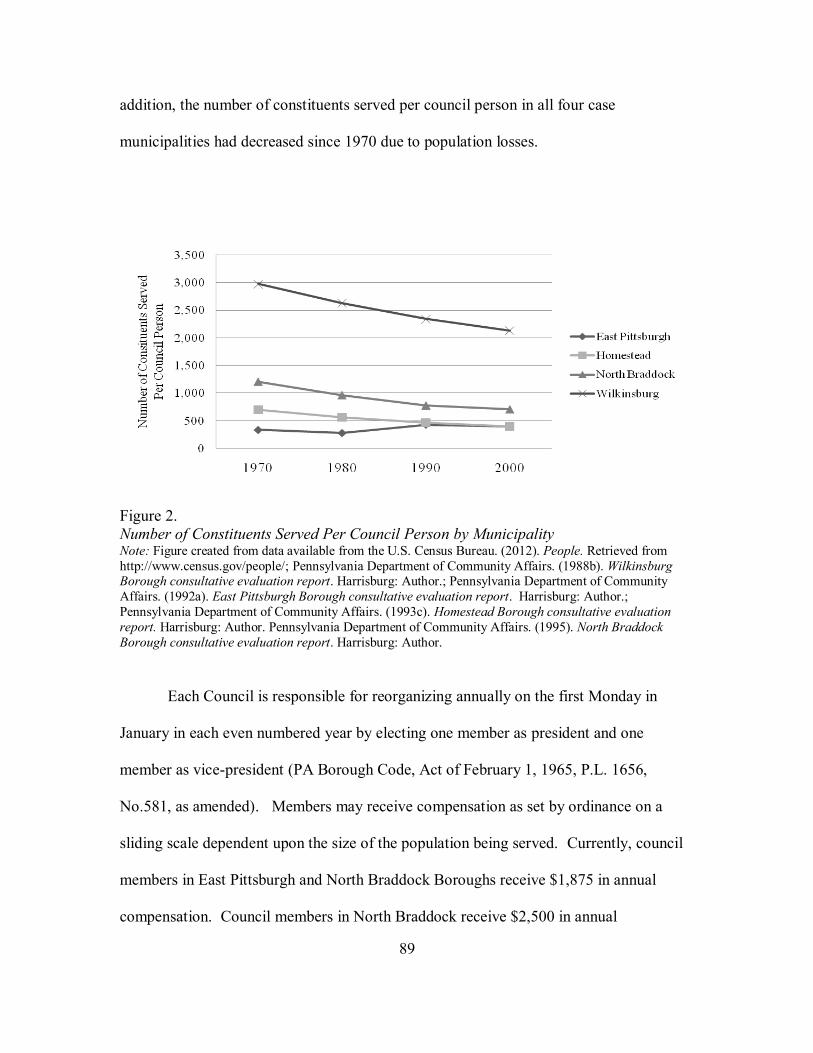

Figure 2. Number of constituents served per council person by municipality 89

Figure 3. Plan recommendations by function as a percent of total recommendations

across cases 98

Figure 4. Plan recommendations by topic within the functional area of general

government 99

Figure 5. Plan recommendations by topic within the functional area of financial

Management 100

Figure 6. Plan recommendations by topic within the functional area of taxation 101

Figure 7. Plan Recommendations by topic within the functional area of public

Services… 102

Figure 8. Plan recommendations by topic within the functional area of community

and economic development 103

Figure 9. Revenue trends by case municipality 120

Figure 10. Revenues per capita (1980-2009) 123

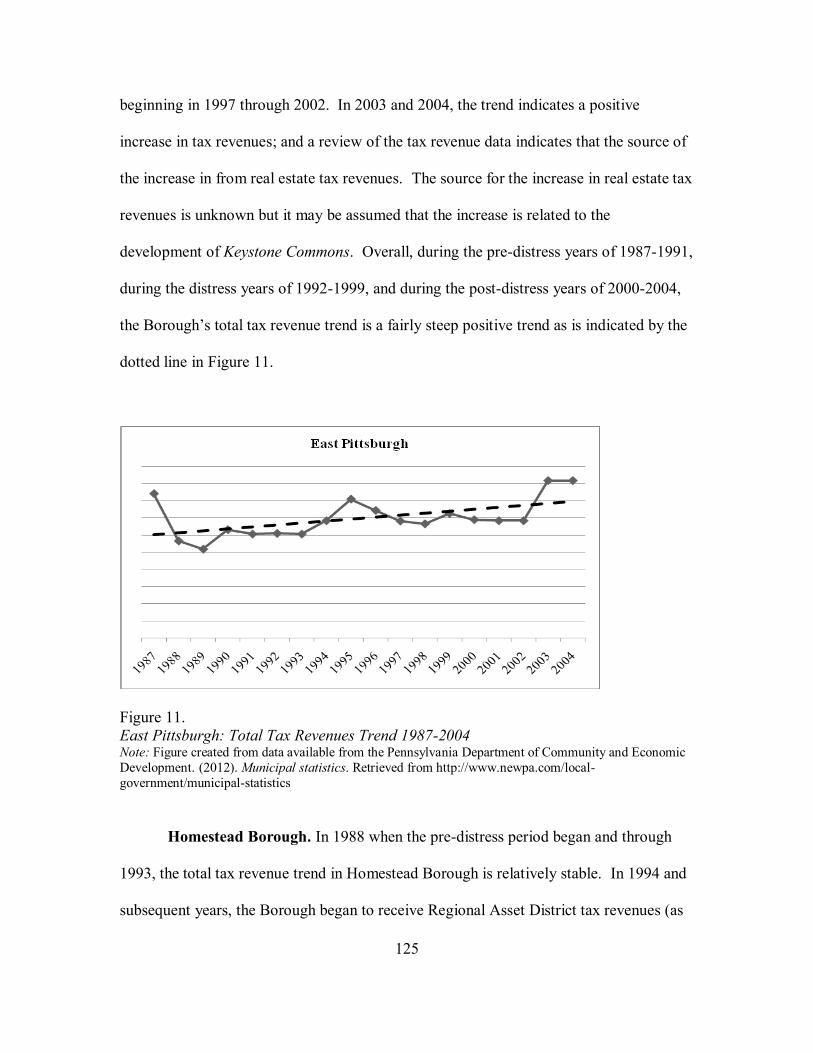

Figure 11. East Pittsburgh total tax revenues trend (1987-2004 125

Figure 12. Homestead total tax revenues (1988-2008) 127

Figure 13. North Braddock total tax revenues (1990-2008) 128

Figure 14. Wilkinsburg total tax revenues (1986-2003) 130

Figure 15. East Pittsburgh real estate tax revenue trend 131

Figure 16. Homestead real estate tax revenue trend 132

Figure 17. North Braddock real estate tax revenue trend 132

Figure 18. Wilkinsburg real estate tax revenue trend 133

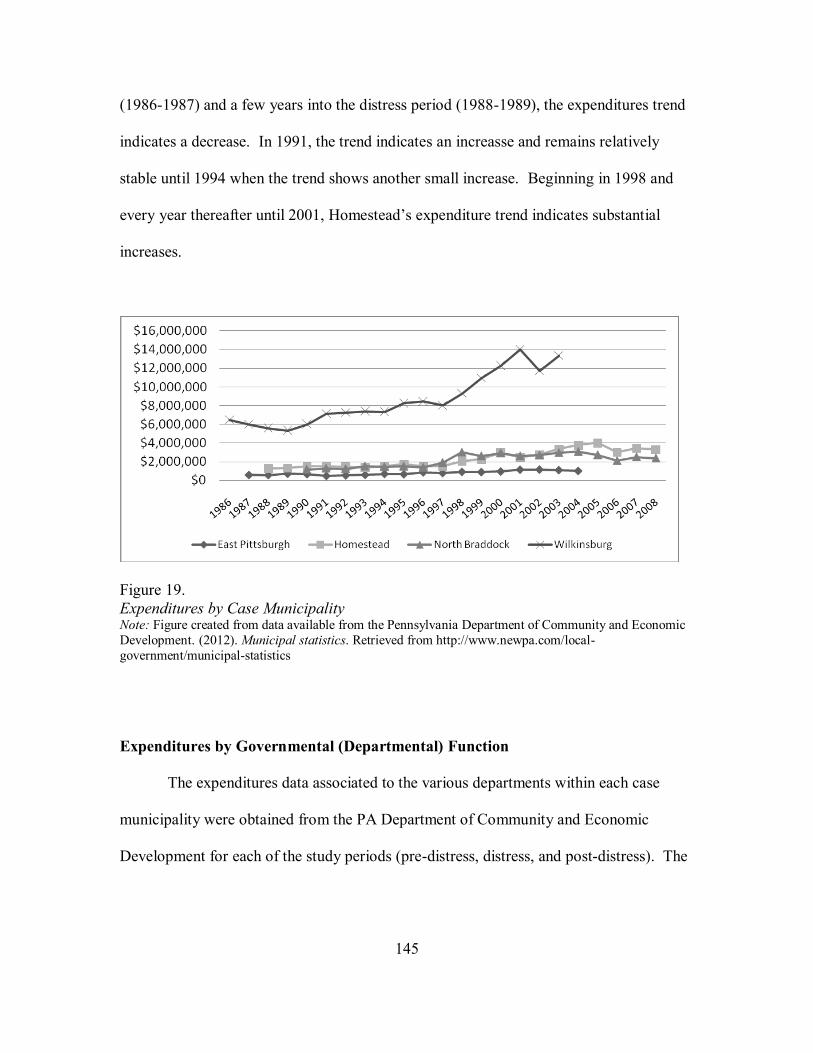

Figure 19. Expenditures by case municipality 145

xii

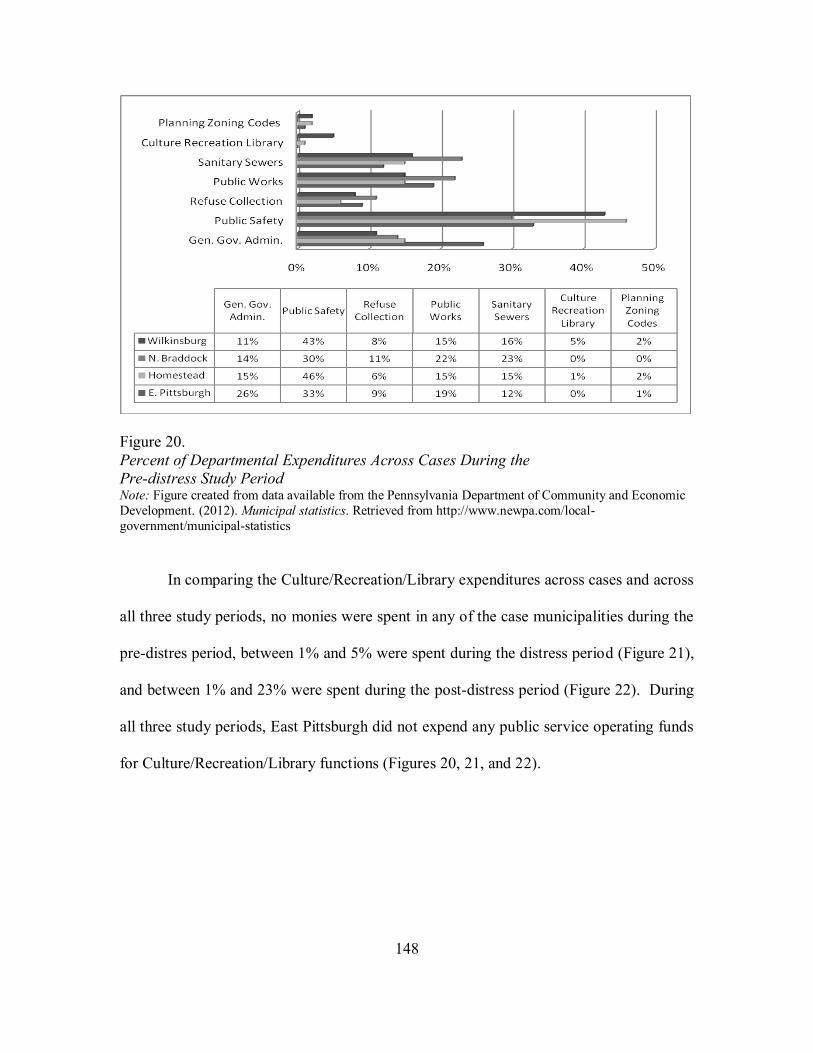

Figure 20. Percent of departmental expenditures across cases during the pre-distress

study period 148

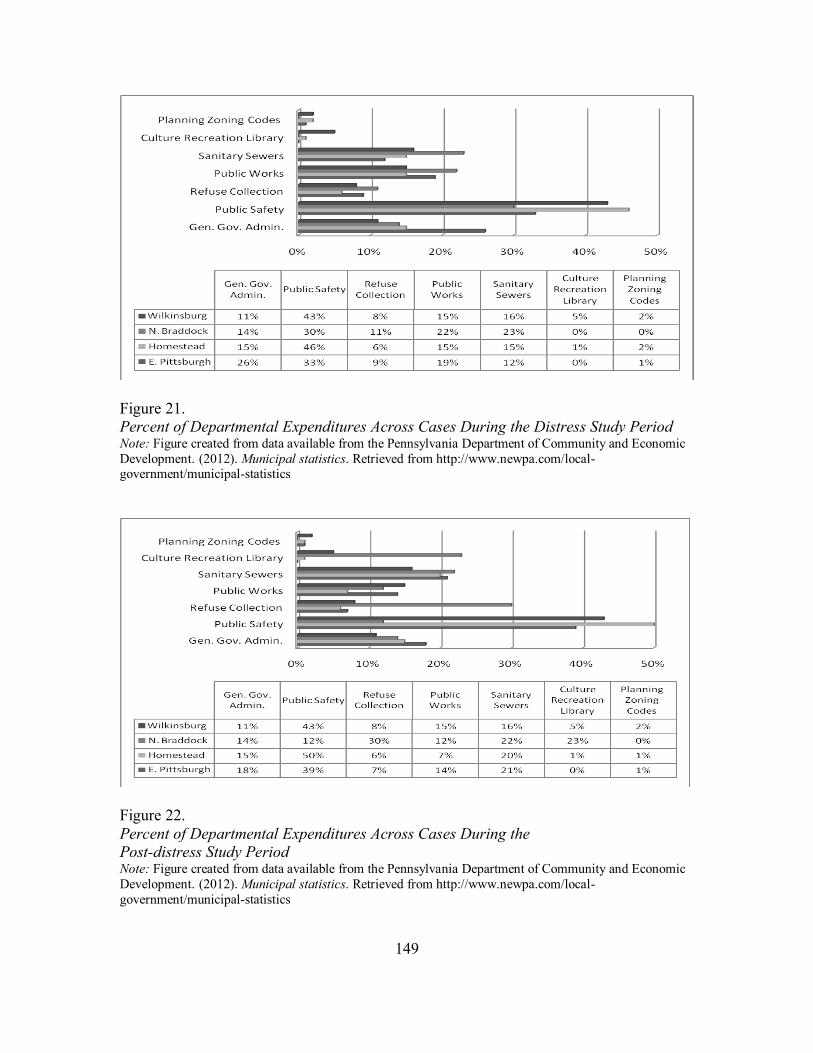

Figure 21. Percent of department expenditures across cases during the distress study

Period 149

Figure 22. Percent of departmental expenditures across cases during the post-distress

study period 149

Figure 23. Recommendations by (departmental) functional area by case

Municipality 155

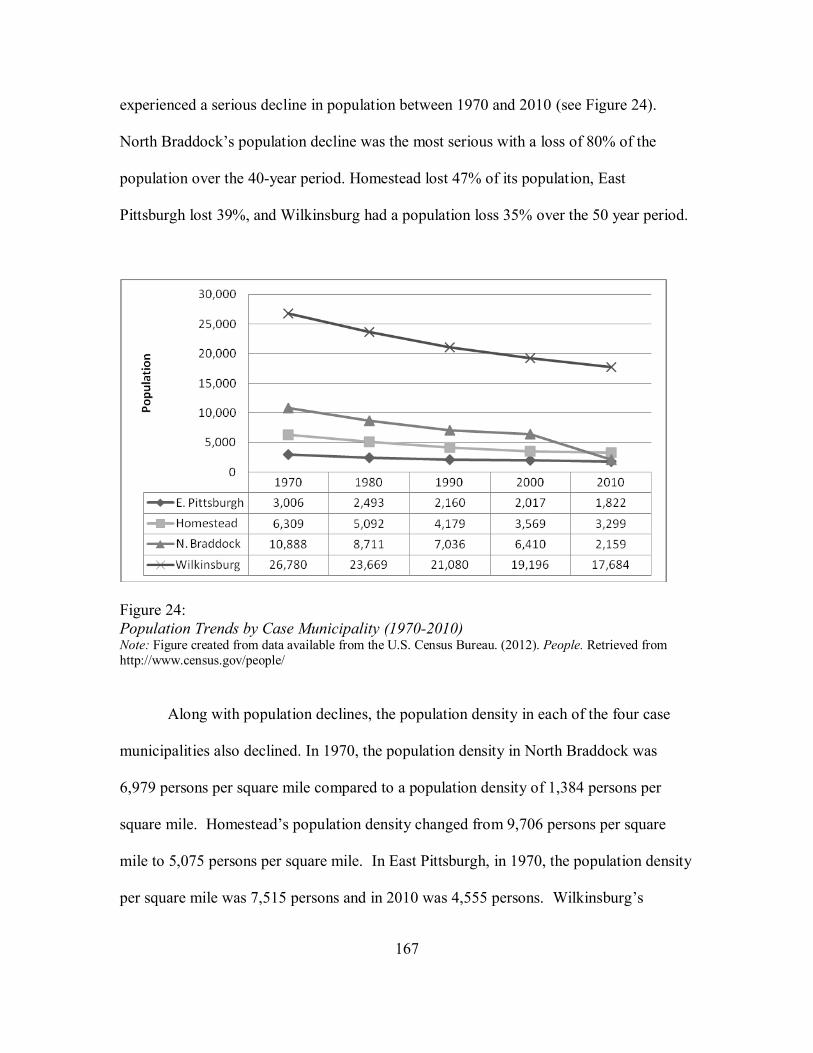

Figure 24. Population trends by case municipality (1970-2010) 167

1

CHAPTER 1. INTRODUCTION

Financial distress is not a new problem as it is evident in municipal government in

many states as far back as the late 1800s (Dession, 1936). In Pennsylvania, there is a

long history of municipal financial distress; as examples, the City of Philadelphia

defaulted in 1857, and the City of Pittsburgh defaulted in 1867 and 1877 (Dession, 1936).

Over the past 25 years, financial pressures within municipal government have increased

to a point where many are on the verge of financial distress (Pennsylvania Economy

League, 2007). As a result, health, safety, welfare, and public services may be

compromised as municipalities face continuous financial pressures due to external

political pressures. These pressures are caused by legislative mandates with regard to

organizational structure of municipal government in Pennsylvania and declining external

socioeconomic characteristics that effect revenue generation (Cahill & James, 1992).

In 1987, the Pennsylvania General Legislative Assembly enacted the

Municipalities Financial Recovery Act-commonly referred to as Act 47 (Act 47 of 1987,

P.L. 246; 53 P.S. § 11701.101). The Act was a reactive response to the financial effects

that the collapse of the steel industry had on municipal governments in Beaver and

Allegheny Counties in southwest Pennsylvania (Cahill & James, 1991). Within the first

five years after passage of Act 47, nine Pennsylvania municipalities were declared as

financially distressed under the Act by the Secretary of the Pennsylvania Department of

Community Affairs (PA DCA)-now known as the Pennsylvania Department of

Community and Economic Development (PA DCED, 2012). Seven of the initial nine

municipalities declared financially distressed within the first five years were located in

southwestern Pennsylvania (PA DCED, 2012). Further, since enactment of Act 47 in

2

1987, 27 Pennsylvania municipalities have been declared financially distressed; and to

date, only six of those municipalities have had their financial distress declaration

rescinded (PA DCED, 2012). As shown, municipal financial distress in the

Commonwealth of Pennsylvania is not a new phenomenon nor is it a temporary situation.

Municipal financial distress is probable given current economic circumstances; and

according to the Pennsylvania Economy League (1999) will become stressed by financial

pressures caused by factors associated with organizational structure, mismanagement,

and socioeconomic characteristics.

Background of the Study

Based upon the literature review for this research study, the literature prior to the

1970s on municipal financial distress is limited and focused on governmental units that

defaulted on bonded debt service payments wherein the only recourse was municipal

bankruptcy; and it was not until the 1970s that the United States Advisory Commission

on Intergovernmental Regulations (ACIR) recognized financial distress as an important

topic on the national level. However, even then the focus was on big cities, central cities,

and urban and metropolitan areas (ACIR, 1980). In 1973, the ACIR, recognizing the

magnitude of municipal financial distress, conducted a study on governmental financial

emergencies (ACIR, 1973). Although the focus of the 1973, ACIR study was on big

cities, the study adopted a broad definition of government financial emergency

concluding that these emergencies exist when a governmental unit reaches the point at

which it can no longer perform its existing levels of services, is unable to meet payroll,

3

cannot pay current bills and amounts due to other government agencies, and is unable to

pay debt service on bonds and or short-term notes.

In the 1980s, although big cities remained the focus of further studies, it was

becoming more evident that small municipalities were also struggling (ACIR, 1981). In

1980, the ACIR completed an exploratory study on the types of aid and assistance

provided by each of the 50 states to local units of government identified as experiencing

some form of distress (ACIR, 1980). The importance of that study was that it did not

limit the focus of municipal financial distress to big cities or urban areas, but looked at

each state as a whole to identify the programs in effect that addressed municipal financial

distress for all municipalities and instruments within each state.

Based upon the literature review for this research, there is no literature on

municipal financial distress specific to Pennsylvania prior to 1980; and subsequent to

1980, the literature on municipal financial distress specific to Pennsylvania is limited and

focuses on three areas: a call for municipal financial distress legislation, assessments of

Act 47 of 1987, and studies that focused on regional and state economic outlooks.

Further, since the adoption of Act 47 in 1987, there has been no research on financial

distressed municipalities that have had the financial distress declaration rescinded.

Statement of the Problem

Based upon a review of the literature wherein it was found that Philadelphia

defaulted on bond payments in 1867 and 1877 (Dession, 1936), municipal financial

distress in Pennsylvania has been a long-standing issue. Municipalities face continuous

external political pressures due to the legislatively mandated organizational structures for

4

municipal governments in Pennsylvania (Bradbury, 1983); and socioeconomic trends that

diminish financial resources (Sacks and Callahan, 1970). In Pennsylvania specifically,

local government units (municipalities) are creatures of the state and are governed by the

state constitution and municipal codes based upon their structure of local government

(PA DCED, 2010). The Pennsylvania Constitution places the responsibility for the

health, safety, welfare, and basic quality of life of the citizens with municipal

government; and in Pennsylvania, municipal government is the provider of basic services

that support the local quality of life (PA DCED, 2010). Such basic services provided by

municipal government include police services, fire protection, emergency management,

water, sanitary sewer, solid waste collection, construction and maintenance of public

streets/roads, public health services to include planning/zoning, general code and building

code oversight and enforcement, and recreation and culture including such amenities as

public parks, playgrounds, and public libraries (PA DCED, 2010). The ability of

municipal government to provide for the health, safety, welfare, and basic quality of life

is dependent on financial resources, the capacity of leadership (management), the

capacity of personnel, and sound financial management practices (Pennsylvania

Southwest Planning Commission, n.d.).

Across the Commonwealth of Pennsylvania, there are 67 counties (PA DCED,

2010). Distributed across those 67 units of county government, according to PA DCED

in 2010, there are 2,553 incorporated municipal jurisdictions (56 cities; 958 boroughs; 1

incorporated town; and 1,547 townships). Each of the different structures (cities,

boroughs, towns, and townships) is governed by a separate state code that determines the

municipality’s organizational structure and powers (PA DCED, 2010). Due to the fact

5

that Pennsylvania municipalities are creatures of the state, the state is ultimately

responsible for the financial welfare of every municipality; therefore, the financial health

of municipal government is not only the responsibility of any given municipality, but it is

also a responsibility of the state (PA DCED, 2010).

In 1987, the Pennsylvania Legislature enacted Act 47 to address municipal

financial distress by providing assistance to financially distressed municipalities that were

suffering from declining economies in addition to problems resulting from financial

mismanagement and administrative inefficiency (Gannon, 1993). To be declared

financially distressed under Act 47, a municipality must undergo an assessment by PA

DCED that is based upon 11 financial stability criteria (PA Legislature, 1987). Provided

one or more criteria are found, PA DCED shall exercise its powers and duties to declare

the municipality as financially distressed pursuant to Act 47 (PA Legislature, 1987).

Since 1987, 27 municipalities across the Pennsylvania Commonwealth have been

declared as financially distressed (PA DCED, 2012). At present, 21 municipalities

remain financially distressed, while six municipalities have had the financial distress

declaration rescinded (PA DCED, 2012). The literature available on the causes of

municipal financial distress specific to Pennsylvania provides only broad categories of

causal factors designated as internal and environmental (ACIR, 1973), internal and

structural (Bradbury, 1983; Cahill & James, 1991), administrative and structural (Wolff,

2004); and cyclical and structural (ACIR, 1985; Gasbarre & Hobbs, 1987). Internal

factors are those factors that are under the control of the decision-making practices of

leadership such as the failure to control spending, a history of overestimating revenues

during the budgeting process, or abuse of borrowing (Bradbury, 1983; Cahill & James,

6

1991). External factors, also referred to as structural factors, are economic and/or socio-

demographic factors associated to municipal financial distress that are beyond the direct

control of the decision-making of leadership such as a loss in the economic tax base

within a community and the resulting demographic shifts (ACIR, 1985; Bradbury, 1983;

Cahill & James, 1991; and Gasbarre & Hobbs, 1987).

Given that the scholarly research on municipal financial distress in Pennsylvania

is limited, and that there is a near absence of scholarly research that examines financially

distressed municipalities and there is a gap in knowledge that examines financial distress

from a case study approach. A case study approach allows the researcher to become

immersed within the municipal setting and explore the meaning and understanding of

problems and issues pertaining to municipal financial distress.

Purpose of the Study

This research examines four (the boroughs of East Pittsburgh, Homestead, North

Braddock, and Wilkinsburg) of the six municipalities that have had a financial distress

declaration rescinded by the Secretary of the Pennsylvania Department of Community

and Economic Development using a mixed-method, multiple case study approach to

determine whether patterns and trends exist within and among the four municipalities

over time in regard to organizational structure, financial condition, and socioeconomic

characteristics during their respective periods of pre-distress, distress, and post-distress.

The purpose of this research is to determine whether patterns and trends exist

among the four cases and to determine how, based upon the patterns and trends, each of

the case municipalities were able to have their financial distress declaration rescinded.

7

Subsequently, the answer(s) to how may be applied to other financial distressed

municipalities across the Pennsylvania Commonwealth. In addition, identified patterns

and trends may also be applied to other Pennsylvania municipalities and may act as an

early warning system for financial distress.

For the purposes of this research study, the pre-distress, distress, and post-distress

time periods are dependent upon the year in which each municipality was declared as

financially distressed by the Secretary of the Pennsylvania Department of Community

and Economic Development. For each municipality, the pre-distress years are the five

years priors to their financial distress declaration, the distress years are those years each

municipality remained financially distressed pursuant to Act 47, and the post-distress

years are up to five years after the municipality’s financial distress declaration was

rescinded by the Secretary of the Pennsylvania Department of Community and Economic

Development.

Rationale for the Study

Municipal financial distress compromises the health, safety, welfare, and quality

of life in a community. The issue of municipal financial distress is not a new

phenomenon (Dession, 1936). At one time, financial distress was mainly associated to

urban areas and large cities. Today, municipal financial distress may occur in even the

smallest of communities (Pennsylvania Economy League - PEL, 2007). Important to

understand is the phenomena associated with municipal financial distress in order to

adequately and efficiently address circumstances that contribute to distress (financial

8

disparity/lack of funds) without compromising a community’s health safety, welfare, and

quality of life.

Research Management Framework

Municipal financial distress is not a new problem, as it is evident in municipal

government in many states as far back as the late 1800s (Dession, 1936). Over the past

25 years, financial pressures within municipal government have increased to a point

where many are on the verge of financial distress (Pennsylvania Economy League, 2007).

As a result, health, safety, welfare, and public services (service delivery) may be

compromised as municipalities face continuous financial pressures. These pressures may

be caused by legislative mandates with regard to organizational structure of municipal

government in Pennsylvania and declining external socioeconomic characteristics that

affect revenue generation (Cahill, James, & Levigne, 1994).

This research provided an extensive assessment of how organizational structure,

financial condition, and socioeconomic characteristics have affected municipalities that

were once declared distressed, but have had that distress declaration rescinded by

answering the following management questions (see Figure 1):

• Why are some financially distressed municipalities able to overcome financial

distress while other financially distressed municipalities remain in distress for

many years?

• How can financially distressed municipalities overcome financial distress?

• Does organizational structure affect municipal financial distress?

• Is financial distress a result of state mandated structures of government?

9

• Is financial distress a result of state mandated taxation provisions?

• Is financial distress a result of the established policies and procedures within the

municipality?

• How does financial condition affect municipal financial distress?

• Is financial distress related to changes in assessed real estate valuations?

• Is financial distress related to revenues?

• Is financial distress related to expenditures?

• Is financial distress related to operating position?

• How do socioeconomic characteristics affect municipal financial distress?

• Is financial distress related to changing demographics?

• Is financial distress related to changing social characteristics?

• Is financial distress related to changes in housing characteristics?

• Is financial distress related to changes in economic development characteristics?

The following general research questions provided a starting point for research

into the causal factors of municipal financial distress and the causal factors that remedy

municipal financial distress in Pennsylvania:

• Organizational Structure - In those municipalities wherein a financial distress

designation has been rescinded, are there common identifiable patterns and

trends in organization structure over-time?

• Financial Condition - In those municipalities wherein a financial distress

designation has been rescinded, are there common identifiable patterns and

trends in financial condition over-time?

10

• Socioeconomic Characteristics - In those municipalities wherein a financial

distress designation has been rescinded, are there common identifiable patterns

and trends in the socioeconomic characteristics over-time?

Research Questions

This study address three main research areas (organizational structure, financial

condition, and socioeconomic characteristics) using a case study approach in four

municipalities in Allegheny County, Pennsylvania during their respective periods of pre-

distress, distress, and post-distress by asking three general questions.

General Questions

• Do common patterns and trends in organizational structure exist in North

Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during their

respective periods of pre-distress, distress, and post-distress?

• Do common patterns and trends in financial condition exist in North Braddock,

East Pittsburgh, Wilkinsburg, and Homestead boroughs during their respective

periods of pre-distress, distress, and post-distress?

• Do common patterns and trends in socioeconomic characteristics exist in North

Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during their

respective periods of pre-distress, distress, and post-distress?

11

Conceptual Framework

Figure 1.

Research Study Conceptual Model

Detailed Questions

Based upon on the findings within the existing body of literature and the

constructed conceptual framework, the three general questions posed may be

methodically narrowed into more explicit questions within the three main areas

(organizational structure, financial condition, and socioeconomic characteristics).

Narrowed and more explicit questions will assist in maintaining the structure of the

Organizational Financial Socioeconomic

Borough Structure

State Mandated

Tax Limitations

Practice/Procedures

Assessed Valuation

Revenues

Expenditures

Operating Position

Demographics

Housing

Economic

Development

Pennsylvania Municipalities

Declared as Financially Distressed

Allegheny County

Rescission of Financial Distress Declaration

12

research design and assist the researcher by providing a tight and detailed research

framework as follows:

Organizational Structure

• Do common patterns and trends in the structure of borough government exist in

North Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during

their respective periods of pre-distress, distress, and post-distress?

• Do common patterns and trends exist due to state mandated taxing provisions in

North Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during

their respective periods of pre-distress, distress, and post-distress?

• Do common patterns and trends exist in practices/procedures in North

Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during their

respective periods of pre-distress, distress, and post-distress?

Financial Condition

• Do common patterns and trends exist in assessed real estate valuation in North

Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during their

respective periods of pre-distress, distress, and post-distress?

• Do common patterns and trends exist in revenue(s) collections in North

Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during their

respective periods of pre-distress, distress, and post-distress?

• Do common patterns and trends exist in expenditure(s) management in North

Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during their

respective periods of pre-distress, distress, and post-distress?

13

Socioeconomic Characteristics

• Do common patterns and trends exist in demographic characteristics in North

Braddock, East Pittsburgh, Wilkinsburg, and Homestead boroughs during their

respective periods of pre-distress, distress, and post-distress?

• Do common patterns and trends in housing characteristics in North Braddock,

East Pittsburgh, Wilkinsburg, and Homestead boroughs during their respective

periods of pre-distress, distress, and post-distress?

• Do common patterns and trends exist in community and economic development

characteristics in North Braddock, East Pittsburgh, Wilkinsburg, and Homestead

boroughs during their respective periods of pre-distress, distress, and post-

distress?

Significance of the Study

In 2003, Carmeli identified theoretical gaps in the literature on fiscal and financial

crises by asking (a) “What are the effects of political, sociological, and economic

structures and processes?”, (b) “How can financially poor local mechanisms break

through the vicious cycle of this phenomenon?”, (c) “What mechanisms must be

established to handle this phenomenon more efficiently and effectively?”, (d) “How can

accountability be applied?” (p. 1428). This study addressed Carmeli’s first two identified

gaps and sought to identify and understand relationships among political, sociological,

and economic phenomenon. The identification of such may reveal the underlying causal

factors of financial distress, which may be generalized across the Commonwealth of

Pennsylvania to serve as early warning signs of financial distress. Such identification,

14

understanding, and generalization will assist in avoiding or alleviating financial distress.

By examining and understanding phenomenon associated with moving from a pre-

distress stage to a distress determination stage, commonalities may be generalized across

the Commonwealth of Pennsylvania that may prevent municipalities from moving from

pre-distress to distress. Additionally, by examining and understanding the phenomenon

associated with moving from a distress stage to a post-distress stage, commonalities may

be observed and generalized across the Commonwealth of Pennsylvania that may be

identified as strategies to emerge from financial distress. Finally, the study will begin a

new direction in scholarly literature with regard to municipal financial distress in the

Commonwealth of Pennsylvania.

Definition of Terms

The following are definitions of key terms that appear frequently in the study.

Advisory Commission on Intergovernmental Relations (ACIR). A permanent,

bipartisan body of 26 members established in 1959 by the 86th Congress for the purpose

of giving continuing study to the relationship among local, state, and national levels of

government (U.S. Code, Title 42, Chapter 53, The Public Health and Welfare, Section

42; Public Law 86-380; 73 Stat 703). The functions of the ACIR were terminated by the

104th Congress effective September 30, 1996, Treasury, Postal Service, and Government

Appropriations Act of 1996 (P.L. 104-52, 109 Stat 514, 248, 480 of 1995).

Amusement Tax. The amusement tax is a tax levied on the privilege of engaging

in an amusement such as the admissions price to places of amusement, entertainment, and

15

recreation; and may include such things as craft shows, bowling alleys, golf courses, ski

facilities, or county fairs. (PA DCED, 2004).

Assets. Assets refer to property owned by a government, which has monetary

value (Rosenberg & Stallings, 1978).

Basics Services. Basic services refer to those services provided by public

organizations as part of tax dollar revenues or fees for services such as fire and police

protection, public water and public sewer services, road maintenance services, and solid

waste collection services (PA DCED, 2010).

Bond. A bond is a written promise to pay (debts) a specified sum of money,

called principle of face value, at a specified future date, called the maturity dates, along

with periodic interest paid at a specified percentage of the principle; and are typically

used for long-term debt (Rosenberg & Stallings, 1978).

Budget (Operating). Operating budget refers to a plan of financial operation

embodying an estimate of proposed expenditures for a given period (typically a financial

year) and the proposed means of financing them (revenue estimates; Rosenberg &

Stallings, 1978).

Capital Assets. Capital assets are those with significant value and having a useful

life of several years (Rosenberg & Stallings, 1978).

Capital Outlays. Capital outlays are expenditures for the acquisition of capital

assets (Rosenberg & Stallings, 1978).

Capital Projects. Capital projects are projects that purchase or construct capital

assets; and typically, are projects that encompass a purchase of land and/or the

construction of a building or a facility (Rosenberg & Stallings, 1978).

16

Debt Service. Debt service is the total of principal and interest paid annually on

all the municipality’s long-term bonds and notes (Rosenberg & Stallings, 1978).

Deficit. Deficit refers to the excess of an entity’s liabilities over its assets (see

also fund balance), or the excess of expenditures over revenues during a single

accounting period (Rosenberg & Stallings, 1978).

Department. Department refers to the Pennsylvania Department of Community

and Economic Development (PA DCED)-formerly known as Pennsylvania Department

of Community Affairs (Pennsylvania Legislature, 1987).

Earned Income Tax. Local income taxes in Pennsylvania are variously termed

earned income taxes, wage taxes or net profits taxes or a combination of these terms and

is levied on the wages, salaries, commissions, net profits or other compensation of

persons subject to the jurisdiction of the taxing body In general, all other jurisdictions

adopting income taxes under the Local Tax Enabling Act are limited to one percent

(where both municipality and school district levy the tax, the one percent limit must be

shared on a 50/50 basis, unless otherwise agreed to by the taxing bodies) (PA DCED,

2004).

Expenditures. Expenditures are the disbursement of revenues or assets of a

municipality (Rosenberg & Stallings, 1978).

Financial Condition. Financial condition refers to a governmental unit’s short-

term and long-term ability and willingness to generate sufficient revenue to meet its

financial obligations as they come due on an ongoing basis and to provide services at the

level the citizen’s desire and at the quality that is necessary to provide for the health,

17

safety, and welfare of the community (International City/County Management

Association, 2003).

Fiscal Capacity. Fiscal capacity is the government’s ability and willingness to

meet its financial obligations as they come due on an ongoing basis (Rosenberg &

Stallings, 1978).

Fund. An independent fiscal and accounting entity with a self-balance set of

accounts recording cash and/or other resources together with all related liabilities,

obligations, reserves, and equities which are segregated for the purpose of carrying on

specific activities or attaining certain objectives (Rosenberg & Stallings, 1978).

Fund balance. Fund balance is the excess of an entity’s assets over its liabilities

(Rosenberg & Stallings, 1978).

Fugitive Document. Fugitive document refers to nonpublished research, typically

written at the request of a state legislative committee or commission, that is difficult to

access either due to a lack of a central repository, index, or policies of confidentiality

standards in many legislatively based research and analysis offices in state legislatures,

which are commonly released only on the authorization of the legislator and/or after a

period of time (Cahill & James, 1992).

General Fund. The fund of the municipality that accounts for all activity not

specifically accounted for in other funds (Rosenberg & Stallings, 1978).

Government Funds. Funds that provide general government services are

government funds and include the general fund, special revenue funds, capital projects

funds, and debt service funds (Rosenberg & Stallings, 1978).

18

Governing Body. For the purpose of this research study, the governing body is

the Borough Council.

Leader/leadership. For the purpose of this research study, a leader shall be any

elected or appointed official.

Liability. Liability refers to debt or other legal obligations arising out of

transactions in the past that must be liquidated, renewed, or refunded at some future date,

but does not include encumbrances (Rosenberg & Stallings, 1978).

Mechanical Device Tax. Mechanical device tax is a tax on coin-operated

machines of amusement such as jukeboxes, pinball machines, video games, and pool

tables (PA DCED, 2004).

Mercantile Tax. Mercantile tax (also referred to as the business gross receipts tax

or business privilege tax) is a tax that is levied on the gross receipts of local businesses;

and may be levied on wholesale and retail trade as well as restaurant receipts (the Local

Tax Reform Act of 1988 prohibited imposing any new mercantile taxes after November

30, 1988, although local units of government that were using the mercantile tax as a

source of revenue are permitted to continue to levy the tax) (PA DCED, 2004).

Municipality. Municipal refers to any political subdivision or similar general

purpose unit of government created by the Pennsylvania General Assembly

(Pennsylvania Legislature, 1968).

Municipal Financial Distress. For the purposes of this research, municipal

financial distress shall be defined in accordance with Pennsylvania Act 47 (Pennsylvania

Legislature, 1987).

19

Municipal Record. For the purposes of this research, municipal records refer to

all documents of a municipality but excluding confidential information relating to

personnel matters and matters relating to the initiation and conduct of investigations of

violations of law.

PA Act 47. The Financially Distressed Municipalities Act of 1987 is commonly

referred to as the Municipalities Financial Recovery Act or Act 47 (Pennsylvania

Department of Community and Economic Development, 2001).

Official. A person who occupies a municipal legislative, quasi-judicial,

administrative, executive or enforcement position (PA DCED, 2010).

Operating Expenditures. For the purposes of this research, operating

expenditures refer to the combination of local, state, and federal dollars spent for

operating purposes.

PA Commonwealth Agency. The PA Commonwealth Agency is the Governor and

the departments, boards, commissions, authorities, and other officers and agencies of the

Commonwealth, whether or not they are subject to policy supervision and control of the

Governor (Pennsylvania Department of Community and Economic Development, 2001).

Public Official. For the purposes of this research study, a public official shall be

any person serving as an elected or appointed government official.

Real Estate (Real Property) Tax. Taxes levied based on the value of real property

(land, buildings, and other improvements) owned by a taxpayer (PA DCED, 2004).

Realty Transfer Tax. A tax on the sale of real estate (PA DCED, 2004).

20

Revenue. A term that designates an increase to a fund’s assets such as proceeds

from a loan, a repayment of an expenditure already made, a cancellation of certain

liabilities, and an increase in contributed capital (Rosenberg & Stallings, 1978).

Secretary. The Secretary of the Department of Community and Economic

Development who is responsible for: declaring a municipality to be in distress,

appointing a financial recovery plan coordinator, commenting on a financial plan

formulated by a coordinator, withholding state funds from a distressed municipality

which refuses to adopt a financial plan, and determining whether a municipality ceases to

be distressed (PA DCED, 2001).

SocioEconomic Characteristics. For the purposes of this research, socioeconomic

characteristics refer to those community characteristics that have interrelationships

between social, economic, and demographic aspects.

Tax Rate Limit. The tax rate limit is the maximum legal rate that a municipality

may levy a tax; and may apply to taxes raised for a particular purpose or for general

purposes (Rosenberg & Stallings, 1978).

Assumptions and Limitations

Assumptions

The study is confined to the geographic boundaries of the state of Pennsylvania

and the municipal governments that operate under the PA Constitution and includes only

those municipalities that have been declared financially distressed by the Secretary of the

PA Department of Community and Economic Development (PA DCED). Further, this

study includes only those municipalities in Allegheny County Pennsylvania that have had

21

their financial distress declaration rescinded by the Secretary of the PA DCED.

Therefore, this research may not be generalized to municipalities in other states and is

limited to only those municipalities in Pennsylvania that have been declared financially

distressed pursuant to PA Act 47.

Limitations

Some data collected that was necessary for this research study was archived and

not easily retrieved. Additionally, some documents that contained necessary data were

not easily reproduced and required extensive and accurate note-taking by the researcher.

Nature of the Study

This research is a multi-case descriptive study that examined organizational

structure, financial condition, service delivery, and socioeconomic characteristics in four

municipalities in Allegheny County, Pennsylvania during their respective periods of pre-

financial distress, financial distress, and post-financial distress. A content analysis of

public documents and reports was used to collect qualitative data. The data was analyzed

on a case-by-case basis and across cases for relationships and similarities using

quantitative descriptive statistics in chart and graph formats and, where necessary,

qualitative narratives depicted in tables were added.

Organization of the Remainder of the Study

This research follows the traditional organization of a doctoral thesis. The

introductory Chapter 1 provides an introduction to the topic, background information on

the topic, and statements of problem, purpose, and rationale for the study. Chapter 2

22

provides a comprehensive literature review necessary to establish the theoretical

foundation for answering the research questions. This necessary framework involves

municipal financial distress as a single distinct body of theoretical knowledge beginning

with a history of municipal financial distress in the United States, and then the literature

proceeds to examine the history of municipal financial distress specific to the

Commonwealth of Pennsylvania. Chapter 3, Methodology, details the research

methodology (design and ethical considerations) and data collection procedures (sample,

instrumentation/measures, analysis, validity, and reliability) of the study. Chapter 4,

Results, provides a summary of the data collected and illustrates how the data was treated

and analyzed. Chapter 5, Discussion, Implications, and Recommendations, summarizes

the study’s findings and limitations, provides implications specific to the objectives for

this research, and provides recommendations for further research in the conclusion.

23

CHAPTER 2. LITERATURE REVIEW

The literature review provides an historical perspective of the evolution of

municipal financial distress beginning with municipal defaults as far back as the 1800s

and the Federal government’s solution with inclusion of Chapter IX in the United States

Bankruptcy Act. An important discussion on Dillon’s Rule is included to explain the

differing methods and approaches the states have taken with regard to municipal financial

distress. A large amount of content is devoted to describing and defining municipal

financial distress, which in-part is due to the varying responsibilities of state government

and restrictions within state constitutions and their resulting approaches (proactive,

reactive, and ad-hoc) to municipal financial distress.

Additionally, the literature review discusses the conceptual and theoretical

frameworks that link causal factors (internal versus external), but more importantly the

review describes the stress factors associated to causal factors, and how such are

intertwined within cycles of municipal financial distress. Important to municipal

financial distress is the actual process by which financial distress can be measured–the

financial indicators. A review of scholarly studies, institutional studies, and financial

monitoring systems developed by organizations reinforced the conclusions in the

literature that the financial distress indicators used to measure municipal financial distress

is dependent upon the focus and intended use for measurement (Honadle, 2003).

Municipal Bankruptcy

Prior to 1934, state and federal bankruptcy legislation pertaining to municipalities

in the United States did not exist (McConnell & Picker, 1993); although, municipal

24

financial distress (default) is documented by the Advisory Commission on

Intergovernmental Relations (ACIR, 1973) and others (Dession, 1936) as occurring in the

United States since the mid 1800s. During the 1920s and early 1930s, municipal

financial distress defaults became more prevalent and were the impetus for emergency

legislation enacted by Congress in 1934 to add Chapter IX to the Bankruptcy Act of

1898; and in 1936, Chapter IX was declared unconstitutional (Wells and Swanson, 1986).

In 1937, again proposed as emergency legislation, Congress adopted a revised Chapter IX

(as amended in 1938, 1940, 1942, and 1946) (Wells & Swanson, 1986).

Municipal financial distress and municipal defaults reached an all-time high

during the 1930s and 1040s (ACIR, 1973) even though the provisions of Chapter IX of

the Bankruptcy Act were infrequently used due to constitutional inadequacies (Wells &

Swanson, 1986). The U.S. Congress, to address the inadequacies of the Bankruptcy Act,

established a Commission on Bankruptcy Laws in 1970; and was charged with providing

a complete revision of the United States Bankruptcy Code (ACIR, 1973). Subsequently,

Congress enacted Chapter 9 in 1978 (as amended in1994 and 2005), specifically, to

address the unique aspects of municipal defaults (Deal, 2007).

The purpose of Chapter 9 of the U.S. Bankruptcy Code is to provide financially

distressed municipalities with protection from creditors while the municipalities develop

and negotiate plans for adjusting and repayment of debt; and although Chapter 9

Bankruptcy may be used as a tool for municipalities to buy time to stave-off creditors

while developing a debt recovery plan, the option is only available to a municipality

when permitted by the state constitution (Honadle, 2003). Across the 50 states, according

to Honadle (2003) various scenarios are found within state constitutions wherein some

25

permitted municipal bankruptcy, some permitted it with special conditions, some

prohibited municipal bankruptcy, and some state constitutions did not address it one way

or another.

The ACIR, while researching municipal bankruptcy in 1973, concluded that the

recovery performance of municipal units in or near financial crises that are located within

States that have court or administrative assistance options are considerably better off than

those in States in which no provisions have been made. The ACIR study further

concluded that because a State is the creator of local government, it must assume the

responsibility for technical assistance, financial controls, and overseeing debt adjustments

for municipal units in financial distress and further recommended that all States enact

laws providing for a state agency that would be responsible for at least the supervision of

municipal units in times of financial distress (ACIR, 1973).

Municipal Solvency

According to Chapter IX of the U.S. Bankruptcy Code of 1937, municipal units of

government were permitted to file under Chapter IX provided they are found to be

insolvent. Insolvent, according to Chapter IX of the U.S. Bankruptcy Code of 1937, is

defined as when liabilities exceed expenditures. Terms closely related to fiscal health

and solvency are financial condition and financial position. Rabin (2005) differentiates

the two terms by defining financial position as a “shorter-run concept when compared to

financial condition–a more long term concept (p. 106). Maher and Nollenberger (2009)

define financial condition as “an organization’s ability to maintain existing service levels,

withstand economic disruption, and meet the demands of growth and decline” (p.62).

26

The ICMA defined financial condition as being financially solvent in four areas: cash,

budget, long-run, and service-level (ICMA, 2003). According to the ICMA (2003), cash

solvency refers to the ability to pay 30 day obligations on time; budgetary solvency refers

to the ability to generate revenues to cover 12 month budgetary obligations; and long-run

solvency refers to the ability to pay all obligations timely (including long-term debt and

pension obligations); and service-level solvency refers to the ability to provide general

services at the level appropriate to ensure health, safety, and welfare.

Insolvency: Financial Distress

The literature demonstrated that there is no agreement as to the terminology of

insolvent municipal financial condition. Based upon the literature review for this

research, the terms found to be used interchangeably when describing a condition of

municipal insolvency are: municipal default, unsound financial condition, financial

emergency, financial crises, fiscal crises, fiscal stress, and fiscal distress. Further, a

scholarly discussion has only recently ensued as to a single relevant term to be used; and

the literature does not demonstrate any specific agreement as to the definition of

insolvent municipal financial condition.

In 1938, the State of New Jersey with the enactment of the Fiscal Supervision Act

put forth a definition of unsound municipal financial condition through the Act’s five

tests of financial unsoundness (Marion, 1942). According to the state of New Jersey, a

municipal unit is in a position of unsound financial condition when: (a) it defaults on the

payment of principal of bonded or bond anticipation obligations; (b) is indebted to a

special district, school district, county or the state for two preceding years; (c) has a year-

27

end cash deficit situation in the preceding year; (d) has poor real estate and personal

property collection rates-a large percentage of revenues being turned over to delinquent

collection processes; (e) has an excess amount of debt compared to revenues at year end-

excluding dedicated debt service expenditures, and revenues (Marion, 1942).

Prior to the 1970s, there was no universal term or distinction between insolvency

and municipal fiscal distress, municipal defaults, municipal financial emergencies, and

municipal financial crises–all terms found in the literature that address municipal

financial distress. At approximately the same time, Congress realized the inadequacies of

the Bankruptcy Code in the 1960s; the Advisory Commission on Intergovernmental

Relations began to study municipal financial distress and employed municipal defaults

and municipal financial emergencies interchangeably (ACIR, 1973, 1977, 1978, 1980,

1981, 1985). Further, the ACIR term municipal default is not necessarily meant to mean

municipal bankruptcy. According to the ACIR, between 1839 and 1969, there were over

6,000 recorded municipal defaults, but only the largest of the municipalities in default

actually filed under Chapter IX of the Bankruptcy Code (ACIR, 1973). The use of

Chapter IX and Chapter 9 under the U.S. Bankruptcy Code is in fact quite rare (Deal,

2007). As of 2010, research indicated that approximately 500-600 municipal bankruptcy

filings have actually occurred since 1937 (The Allegheny Institute for Public Policy,

2010).

The ACIR report of 1973 provided a broad definition of financial emergency.

This is important because until the 1970s (with the exception of the state of New Jersey),

the literature does not attempt to define a financial emergency situation (other than the

28

implied–when a municipality is unable to meet its current obligations; Marion, 1942).

In 1973, the ACIR defined financial emergency

Situations in which a city reaches the point at which it can no longer perform its

existing levels of service because of an inability to meet payrolls, pay current

bills, pay amounts due other government agencies, or pay debt service on bonds

or maturing short-term notes because it lacks either cash or appropriations

authority. (p. 3)

In 1981, Ronca acknowledged the ACIR (1973) definition of financial emergency

while comparing Pennsylvania’s local government financial control programs with those

in other states. In 1986, Wells and Swanson, while writing recommendations for

legislative action on Pennsylvania municipal bankruptcy, provided an extensive

definition of a local financial emergency that encompassed an excessive decline in

revenues and/or expenditures, excess deficits in the current year, excessive long-term

debt, default in payments of principle or interest on bonds or notes, failure to make

payroll, failure to make payment to other governmental units, failure to comply with

applicable municipal finance accounting standards, and the filing of a petition to adjust

debt under Chapter 9 on the U.S. Bankruptcy Code.

In 1981, the ACIR defined financially distressed communities as those where

residents bear substantially higher tax burdens to support levels of public services

comparable to better-off communities. In 1991, in a report to the Local Government

Commission of the General Assembly of Pennsylvania, Cahill and James defined

financial distress as “a persistent shortfall in cash flows experienced by a government,

resulting from an imbalance between revenues and expenditures for given service levels”

29

(p.7). Hirsch and Rufolo (1990) defined fiscal crises as when a government no longer

has the budgetary flexibility to make additional expenditure cuts, increase revenues, or

continue to borrow. Inman (1995) defines fiscal crises as when revenue potential is

insufficient to cover expenditures.

In 2003, Honadle conducted a National Survey of state programs relating to fiscal

crises and found that only ten states had formal definitions for local government fiscal

crises. Although Honadle’s purpose for the study was to explore the roles of states when

dealing with local government fiscal crises, the research is important to the literature

because it provides a distinction between fiscal stress and fiscal crises, which have been

used interchangeably in the literature. Honadle makes the distinction that a fiscal stress

situation threatens the status quo of the continued operation of a governmental unit and a

fiscal crises situation is when the governmental unit is unable to meet its obligations of

payroll, bills, and debt repayment.

Carmeli (2003) further refined Honadle’s (2003) explanations of fiscal crises

versus fiscal stress by stating that fiscal stress and fiscal crises are one in the same; the

indicators for fiscal stress are actually indicators of fiscal crises. Further, Carmeli made a

distinction between fiscal crises and financial crises-a fiscal crisis is when a negative gap

between revenues and expenditures exist, and a financial crisis is when an organization

does not make timely payment of financial obligations. In 2005, Kloha, Weissert, and

Kleine further refine the work of Honadle (2003) and Carmeli (2003) by providing a

definition that included long-term considerations; fiscal distress is defined as failure to

make payment and meet community needs over successive years. Jones and Walker

30

(2007) defined distress as a local government unit’s “inability to maintain preexisting

levels of services to the community” (p. 396).

Although there is no identifiable agreement in terminology as to the definition of

insolvent municipal financial condition, numerous common characteristics in defining

distress have emerged from the literature:

• When a municipal government unit’s expenditures exceed revenues (Carmeli,

2003; Inman, 1995; Wells & Swanson, 1984)

• When a municipal government unit does not have the ability to pay obligations

(of any type including indebtedness to other governmental units) when due

(ACIR, 1973; Carmeli, 2003; Marion, 1942; Wells & Swanson, 1984).

• When a municipal governmental unit struggles to maintain status quo service

levels (ACIR, 1973; ACIR, 1981; Cahill & James, 1991; Kloha, Weisert &

Kleine, 2005; Marion, 1942).

• When a municipal government unit exhibits a year-end cash deficit (Marion,

1942; Wells and Swanson, 1984).

• When a municipal government demonstrates an excessive amount of long-term

debt (Marion, 1942; Wells and Swanson, 1984).

• When a municipal government unit displays a pattern of low tax revenue

collection (Marion, 1942).

• When a municipal government petitions to file Chapter 9 Bankruptcy (U.S.

Bankruptcy Code, Chapter 9, Section 101, 32, C, i. and ii.).

31

For the purposes of this research study, insolvent municipal financial condition

herein referred to as municipal financial distress shall be defined in accordance with the

Pennsylvania Municipalities Financial Recovery Act (Pennsylvania Legislature, 1987).

The Municipal Financial Distress Cycle

Just as “changes in community needs and resources are interrelated in a

continuous cumulative cycle of cause and effect” (Groves & Valente, 1994, p. 112), so

are the effects of community needs and resources related to municipal financial distress

and distress cycles. Community factors that trigger distress cycles are specifically related

to the characteristics of community population such as decline, a rapid increase, density,

age, income and employment, and other community factors such as housing

characteristics (owner occupied versus renter occupied), vacancy rates, property values,

crime rates, and economic activities (ICMA, 2003). For example, a decrease in

population places a decreased demand on housing, which in-turn decreases the value of

housing. Decreases in housing values negatively affect tax assessment valuations.

Decreased assessments are directly related to decreased real estate tax collections. A

decrease in tax collections brings a decrease in real estate tax revenues. Additionally, a

decrease in population typically decreases the average household income across the

municipality, which results in decreased earned income tax collections (and for some

municipalities, decreased per capita tax revenues). A decrease in household income

typically coincides with a decrease in the vitality of the local economy (people don’t have

money to spend). Decreases in tax revenues make it difficult for the municipality to

continue to provide services at status quo levels, which are directly related to quality of

32

life and population shifts (people want to live where the quality of life if good). In order

to maintain services delivery at status quo, it may be necessary for the municipality to

increase the real estate tax levy to make-up for the loss

in tax revenues, which may result in further decreases in population (people want to live

where taxes are low). This is just one example of a distress cycle.

Distress cycles do not necessarily have to begin with decreases in population. A

municipal distress cycle may actually begin prior to a decrease in population where a

decrease in population is precipitated by loss of industry and/or employment

opportunities (PEL, 2007). For example, during times of economic recession, a distress

cycle may begin as a result of a high unemployment rate that causes a decrease in earned

income revenues. In addition, because the population is not earning a wage, the housing

begins to deteriorate that causes a decrease in assessed valuations and decreases in real

estate property tax collections.

Distress cycles may also begin with rapid population growth that places financial

pressures on the municipality for increased service delivery or costs associated to capital

improvements such as public water and sewer extensions and additional road

construction and maintenance costs in new developments (ACIR, 1973). As a final

example, a distress cycle may begin at any time as a consequence of inadequate

accounting and reporting practices and overall administrative mismanagement including

poor decision making as a result of poor accounting practices and/or the lack of

management capacity. For example, legal compliance with balanced budgets and audits

requirements is not enough to understand the true financial condition of a municipality

(Hendrick, 2004). Management must have the capacity to further analyze the effects of

33

an annual budget in regard to program costs (cost benefit analysis) over time and be able

to measure long-term financial condition (Groves & Valente, 1994).

In 2007, the Pennsylvania Economy League (PEL) completed a study on the

financial health of Pennsylvania’s municipalities and proposed five stages of municipal

financial decline. The PEL study indicated that over half of the municipal government

units in Pennsylvania are in stages three through five of financial decline; and concluded

that there is a mismatch between the organizational structure of local government in

Pennsylvania and the movement of resources. Further, PEL (2007) concluded that it is

difficult for local government units to maintain status quo or move–up the pyramid to a

higher stage of viability. Although the five stages are not cyclic in nature, the five stages

are important to the literature because they provide an additional model of municipal

financial distress decline. In addition, there is no steadfast beginning to PEL’s five

stages, but the causal factors, losses in tax revenues and a declining population associated

to PEL’s end-stage are found in Grove’s and Valente’s (1994) distress cycle. An

advantage of PEL’s (2007) model is its ease of use as municipal government leaders can

easily discern their municipality’s stage of distress. The disadvantage of PEL’s model is

that it does not associate specific causal factors to each stage; for example, PEL identifies

decreased tax revenues as a factor associated with Stage 4 distress, but does not give

reason as to why tax revenues are decreasing.

Also contained within the literature is reference to a distress cycle that takes on an

entirely different meaning compared to the two previous models. In a 1991 report to the

Local Government Commission of the General Assembly of Pennsylvania, Cahill and

James referred to a fiscal distress cycle as when municipal government experiences fiscal

34

distress and with State assistance and intervention is able to overcome distress. The state

subsequently withdraws and within a few years the municipality again finds itself

experiencing fiscal distress. Cahill and James based their discussion on a particular

municipality in Michigan, but writing in 1991, just four years after enactment of

Pennsylvania Act 47, it was not known whether this type of distress cycle would appear

in Pennsylvania. Cahill and James referred to this distress cycle as a “vicious cycle of

repeated state interventions” (p. 46). The Pennsylvania Economy League (1999) referred

to it as “perpetual life support to severely distressed local governments” (p. 29).

The State’s Roles

The United States Constitution does not recognize the powers or authority of a

municipal government unit. Therefore, while the U.S. Constitution directs powers to

State government, a municipal government unit receives its powers and authority from its

State Constitution. The cornerstone court decision that applies to state and municipal

powers and authorities is derived from Judge John F. Dillon of Iowa in 1865–known and

commonly referred to as Dillon’s Rule (Clark v. City of Des Moines, 19 Iowa 199, 208,

1865); wherein, according to Judge Dillion, a local government unit within a state has

only the power that is granted to it by the state. In a landmark case (Clinton v. Cedar

Rapids & Missouri River R.R. Co., 24 Iowa 455, 1868), Judge Dillon wrote on the

powers of municipal government as sanctioned by the state and concluded: (a) that a state

only has the authority to exercise the powers that are expressly stated, implied, and those

essential to accomplish the express objectives and purposes of the organization; and (b) if

by action of the courts, a doubt exists, then the power is denied.

35

In a 2003 discussion paper prepared by Richardson, Gough, and Puentes (2003)

for the Brookings Institution Center on Urban and Metropolitan Policy, four categories of

implementation of the court ruling of Judge Dillon in 1865 were identified: (a) 31 states

have implemented the ruling in-full, (b) eight states have only partially implemented the

ruling, c) ten states have rejected the ruling in-full, (d) one state has conflicting case law

on the authority and powers of the state and local government units.

Specific to Pennsylvania, the principles of Dillon’s Rule are well established and

the responsibility for the health, safety, welfare, and basic quality of life of the citizens on

municipal government (Gasbarre & Hobbs, 1987). Municipal governments in

Pennsylvania are the providers of public services (PA DCED, 2010). The ability of

municipal government in Pennsylvania to provide for the health, safety, welfare, and

public services is dependent on the incorporated structure and the municipal code by

which it is governed; and a municipality’s financial capacity is limited to only those

aspects permitted in the municipal code under which it operates (Bradbury, 1983). Such

limitations may include allowable forms of taxation and specific limits associated to

those forms of taxation, debt and spending limits, tax levy limits, and financial reporting

requirements (Bradbury, 1983). As a result, a municipality has no legal recourse when it

finds itself in a situation of fiscal distress due to restrictive taxing or debt limitations; it

has no powers or authority to remedy financial problems (Ronca, 1981).

In 1973, the ACIR completed a study that looked at how each of the fifty states

provided oversight to its governmental units in the areas of budgeting, accounting,

financial reporting, the issuance of short-term operating debt, and the programs, and

agencies in place charged with exercising control over their local government unit

36

finances. ACIR found a wide variety of local government unit and state relationships

ranging from no administrative supervision of municipal finance to complete supervision

of virtually every aspect of municipal finance. ACIR then placed each of the 50 states

into three distinct categories: (a) No Substantive State Administrative Control, (b)

Limited State Administrative Control, (c) Complete State Administrative Control (ACIR,

1973). The ACIR concluded that “states have neglected their overall responsibility for

supervising and assisting in the improvement of local financial management” (p. 69).

The ACIR report (1973) provided four recommendations on how a State may

structure an agency or program to provide at least minimal oversight of their local

government units in the area of municipal finance. The purposes for such oversight

included: to preserve local autonomy to the fullest extent possible, but with the consistent

goal of promoting sound financial management; to provide a system that is flexible

enough to promote continued education for the improvement of financial practices; and to

enable state officials to detect symptoms of financial difficulty in the earliest possible

stages (ACIR, 1973). Also according to the ACIR (1973), the most directive approach to

achieve minimal oversight of local government units, would be for a State to place the

responsibility of oversight with the State’s department of community affairs or the State

Auditor’s Office. The ACIR report further provided additional alternatives in achieving

minimal oversight: (a) for a State to create a small board composed of State officials such

as the governor, attorney general, and auditor and a small team of full-time professionals;

(b) for the State to create a bi-level, bipartisan board (from local official’s associations

and other interest groups; and (c) for the State/Governor to appoint a small board of

professionals with experience in local government finance.

37

The ACIR finding of 1973 specific to the Commonwealth of Pennsylvania were

(a) the Commonwealth did have administrative oversight and controls in place for short-

term municipal operating debt, and (b) the Department of Community Affairs (DCA –

now the Department of Community and Economic Development) was the responsible

state agency for receiving and reviewing the adopted budgets (submitted on uniform

forms) of all local government units with the exceptions of the cities of Philadelphia,

Pittsburgh, and Scranton (ACIR, 1973).

In 1999, the Pennsylvania Economy League (PEL) in making the

recommendation that Pennsylvania’s “Act 47 should contain provisions for a fiscal

recovery board with authority to exercise all the rights, powers, privileges, prerogatives

and duties of municipal governing bodies” (p. 17) questioned whether Article III, Section

31 of the Pennsylvania Constitution does in fact prohibit the General Assembly from

establishing a fiscal recovery board with said powers in financially distressed

municipalities. In an attempt to answer this question, PEL consulted with a law firm in

Pittsburgh, Pennsylvania; which suggested that the Pennsylvania Constitution would not

prohibit the General Assembly from establishing a financial recovery board and could be

justified on three grounds: (a) voluntary acceptance by the financially distressed

municipality, (b) established limits in exercising legislative taxing powers, and (c) a state

agency is not considered a commission per the provisions of the Pennsylvania

Constitution, Article III, Section 31 of 1874. According to PEL (1999), the consulting

law firm concluded that the provisions of the Pennsylvania Constitution (Article III,

Section 31 of 1874) were intended to prevent independent commissions from taking

38

control of the decision making processes in municipal government and more specifically

to expend revenues without public accountability in order to achieve their own goals.

State Approaches: Proactive, Reactive, and Others

In 2003, Honadle studied the roles of states when dealing specifically with local

government fiscal crises. The research concluded that only 10 states had formal

definitions of local government fiscal crises and the remainder of states varied between

having a working definition of fiscal crises to having no definition of fiscal crises

(Honadle, 2003). Honadle further developed a theoretical framework of the potential

roles that states take before, during, and/or after fiscal distress occurs that consisted of

four broad categories or roles that states take when dealing with local government fiscal

crisis’s. The first role is that of prediction wherein the state has established controls such

as financial reporting requirements and fiscal distress indicators that would allow an

assigned state agency to be able to predict a potential fiscal crises situation (Honadle,

2003). The second role is to avert wherein the state has established programs that would

assist the local government in avoiding (or averting) the fiscal crises (Honadle, 2003).