Optimizing Rubberized Open-graded Friction ... - eScholarship

Upload

khangminh22Category

view

2download

0

A MARKET ANALYSIS OF STRENGTH

GRADED TIMBER PRODUCTS FOR THE

UNITED KINGDOM

LAB UNIVERSITY OF APPLIED SCIENCES LTD Bachelor of Engineering, Wood Technology Bachelor’s Thesis Spring 2022 Alexander McIntyre

Abstract

Author(s)

McIntyre, Alexander

Type of publication

Bachelor’s thesis

Published

Spring 2022

Number of pages

56

Title of publication

Title

A market analysis of strength graded timber products for the United Kingdom

Name of Degree

Bachelor of Engineering, Wood Technology

Abstract

The thesis work studied the timber market in the United Kingdom and Ireland, specifi-cally investigating possibilities of increasing the added value for strength graded tim-ber products. The thesis work was conducted with MM Wood Oy, a Finnish planing mill supplying the Finnish and European markets including the United Kingdom.

The thesis work identified background information on MM Wood and the historic trends in the timber trades in the United Kingdom and Ireland. The requirement for im-ported timber volumes was highlighted with the main demand coming from the con-struction industry and shortage of suitable domestic supply.

The thesis looked at the dynamics of products currently produced for the timber trade in the United Kingdom as well as possible new approaches to specialist timber prod-ucts. The thesis work introduced each product option with background information and established the end uses and working conditions for each product. The market was analysed to understand the factors affecting MM Wood’s competitiveness, fol-lowed by a comprehensive SWOT analysis focusing on the production efforts of each product and market sector.

The thesis identified products that would bring MM Wood a natural advantage with re-gards to competition and specification availability. The thesis also identified possible investments to improve the competitiveness of current products and looking at new products with growing demand for the future.

Keywords

Construction, Engineered wood products, Finger-jointed products, Precision end

trimmed products, Strength graded timber, Supply and demand, Timber Frame

CONTENTS

1 INTRODUCTION ....................................................................................................... 1

2 MM WOOD OY .......................................................................................................... 2

3 UNITED KINGDOM & IRISH TIMBER TRADES ........................................................ 5

4 ROOF TRUSSES - TR26 ........................................................................................... 8

4.1 TR26 introduction .............................................................................................. 8

4.2 The TR26 market and possibilities ....................................................................10

4.3 TR26 analysis...................................................................................................11

5 CANADIAN LUMBER STANDARD - CLS .................................................................14

5.1 CLS introduction ...............................................................................................14

5.2 Market potential ................................................................................................17

5.3 CLS analysis ....................................................................................................18

6 CONSTRUCTION CARCASSING.............................................................................22

6.1 Carcassing introduction ....................................................................................22

6.2 Market potential ................................................................................................23

6.3 Carcassing analysis..........................................................................................27

7 PRECISION END TRIMMED - PET ..........................................................................31

7.1 PET introduction ...............................................................................................31

7.2 TR26 and C24 Carcassing ...............................................................................31

7.3 CLS ..................................................................................................................32

7.4 PET analysis ....................................................................................................32

8 FINGER JOINTED PRODUCTS ...............................................................................35

8.1 Introduction to finger jointed products ...............................................................35

8.2 TR26 ................................................................................................................35

8.3 CLS & Carcassing ............................................................................................36

9 ENGINEERED WOOD PRODUCTS - EWP ..............................................................37

9.1 EWP introduction ..............................................................................................37

9.2 Konstruktionsvollholz - KVH .............................................................................37

9.2.1 Market potential ............................................................................................37

9.2.2 Konstruktionsvollholz – KVH analysis ...........................................................38

9.3 I-Joists ..............................................................................................................40

9.3.1 Market potential ............................................................................................40

9.3.2 I-Joist analysis ..............................................................................................41

10 COMPARISON AND EVALUATION .........................................................................44

10.1 Product comparison..........................................................................................44

10.2 Boston Consulting Group Matrix .......................................................................47

11 CONCLUSIONS .......................................................................................................50

LIST OF REFERENCES ..................................................................................................51

1

1 INTRODUCTION

This thesis report is a market investigation into further processed timber products pro-

duced from spruce and pine. The market investigation is based on the timber trades in the

United Kingdom and Ireland, as these markets have a strong history of importing timber

products. The focus of this report is on further processed timber products used in the

United Kingdom, primarily in the construction industry and establishing which products

would be worth developing further for a strength graded timber producer and supplier.

This thesis was conducted with MM Wood Oy, a Finnish independent planing mill, looking

to expand their current timber production. The aim of this thesis is to provide information

to MM Wood regarding the timber market in United Kingdom, and which timber products

could add the most value. When the log in the forest moves through the supply chain, ini-

tially to the sawmill’s various processes and ends with delivery as a pack of strength

graded timber to a construction site, each step in the supply chain should add value to the

product. (Waters 2009, 9). This thesis is designed to identify the products that will maxim-

ise the potential added value for MM Wood.

Each product will be introduced with background information about the product, what the

primary applications are and how the customer base is built. Market potential has been

analysed through research based on information gained while working in the timber trade

as an importer and an agent. Interviews with importers & distributors and builder’s mer-

chants operating in the United Kingdom have been conducted to justify findings. Each

product is then analysed using SWOT analysis to identify the benefits and drawbacks that

MM Wood would face by developing production of each product. The products being fo-

cused on in include traditional planed products such as roof truss materials, Canadian

lumber standard used for timber frame houses and carcassing for general building appli-

cations. These are products that MM Wood have a history of producing, and the investiga-

tion will develop into newer market segments such as engineered wood products that

could increase the added value for MM Wood even further. Comparisons are drawn be-

tween the different production options based on the customer demand and production

possibilities at MM Wood. This thesis will give MM Wood a direction on which products to

focus developments on.

2

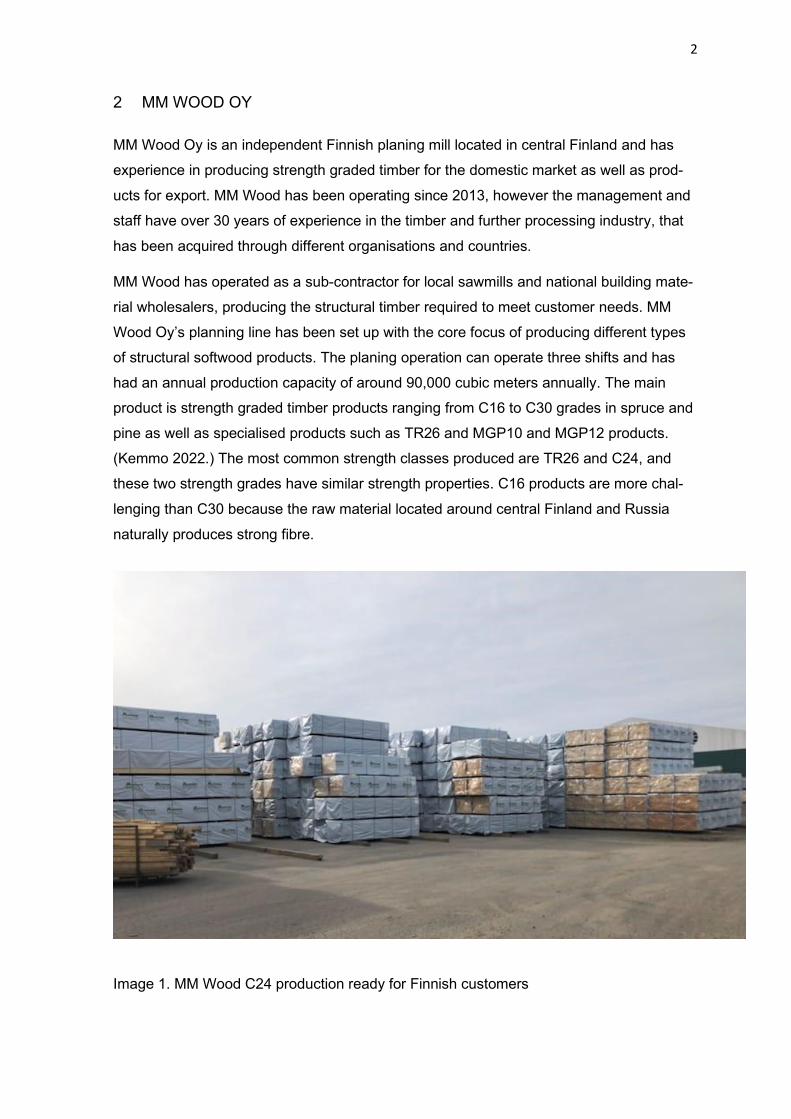

2 MM WOOD OY

MM Wood Oy is an independent Finnish planing mill located in central Finland and has

experience in producing strength graded timber for the domestic market as well as prod-

ucts for export. MM Wood has been operating since 2013, however the management and

staff have over 30 years of experience in the timber and further processing industry, that

has been acquired through different organisations and countries.

MM Wood has operated as a sub-contractor for local sawmills and national building mate-

rial wholesalers, producing the structural timber required to meet customer needs. MM

Wood Oy’s planning line has been set up with the core focus of producing different types

of structural softwood products. The planing operation can operate three shifts and has

had an annual production capacity of around 90,000 cubic meters annually. The main

product is strength graded timber products ranging from C16 to C30 grades in spruce and

pine as well as specialised products such as TR26 and MGP10 and MGP12 products.

(Kemmo 2022.) The most common strength classes produced are TR26 and C24, and

these two strength grades have similar strength properties. C16 products are more chal-

lenging than C30 because the raw material located around central Finland and Russia

naturally produces strong fibre.

Image 1. MM Wood C24 production ready for Finnish customers

3

MM Wood have been using sawn timber as their raw material coming from sawmills in

both Finland and Russia. MM Wood only work with fully certified raw materials in both

PEFC and FSC certifications and MM Wood have their own PEFC certification. MM Wood

is developing its procurement of with a focus on Finnish raw materials and has put a stop

to inbound raw material from Russia.

MM Wood are only operating planing services and currently do not offer any raw material

procurement or sales functions. The majority of the 90,000 cubic meter production capac-

ity is being exported to the United Kingdom, Benelux and other European markets for roof

truss applications and other construction products. The factory layout of the planing mill

includes a Dynagrade DG319 machine strength grading line. The Dynagrade calculates

the strength of each timber plank with a hammer at one end of the line and an acoustic

sensor at the other end. The acoustic sensor calculates the time for the sound waves to

travel through the timber and measures the result. The result of every timber plank is then

compared with the strength grade standards and criteria for the product in question and

either passes to become for example C24, or it is rejected. MM Wood have also incorpo-

rated visual strength grading practises alongside machine strength grading. The planer

operator monitors the production runs and the possible issues and problems in each piece

and where they are located. Any problem pieces that are identified are rejected. If the

planer operator has identified a piece that needs to be rejected but the Dynagrade ma-

chine allows the piece through, the piece will be rejected. The same applies, that if a piece

of timber passes visual grading but the Dynagrade machine rejects it, then the piece will

be rejected because each piece of timber requires a pass from both machine and visual

grading to go into the final strength grade. (Kemmo 2022.)

4

Image 2. MM Wood production line (Kemmo 2022)

MM Wood are a key part of the supply chain for structural softwood products, and they

have been working with Hartman Rauta Oy. Hartman Rauta Oy are a Finnish wholesaler

and distributor in Finland, producing Hartman’s timber products. Hartman do not have any

sawmilling facilities of their own and are supplying MM Wood’s planning mill with sawn

timber as raw material for their own added value product requirements. A unique selling

point of Hartman is the ability to supply long lengths in both redwood, pine and whitewood,

spruce, which are often in the range of 80% - 90% between 5,4m to 6,0m. Hartman is a

family-owned business that was founded in 1986, and in 2020 had a turnover of almost

164 million euros. (Finder.fi 2020.) Hartman use a combination of their own wood division

sales team as well as agents in export markets. The timber agent in the UK is Polar Tim-

ber Ltd, who have a representing presence in Finland and in the United Kingdom. Polar

Timber have years of experience of working in the timber trades and supplying timber to

Nordic countries as well as the United Kingdom.

5

3 UNITED KINGDOM & IRISH TIMBER TRADES

In 2012, the United Kingdom, a total sawn softwood production capacity of around 3.5 mil-

lion cubic meters. (Ward 2014a, 2.3.7). The split of this volume was determined to be 34%

for fencing products, 32% for the packaging and pallet industry and 29% going into the

construction industry by the Forestry Commission in 2013. (Ward 2014b, 2.4.3). We can

see from graph 1 below, that the share of softwood imports is considerable compared to

British softwood production.

Graph 1. UK Softwood production and imports compared (Timber Trade Federation

2020a)

The total consumption of sawn softwood in the United Kingdom was 10.1 million cubic

meters in 2014. The projected volumes required by the construction industry was just un-

der 6 million cubic meters, of which 83% was required in the form of imports. (Egan Con-

sulting Ltd 2016, 13.) Graph 2 below shows the developments of the imported volumes of

softwood between 2016 and 2021.

The United Kingdom has had growing demand for softwood from private house building

activity as well as repair, maintenance, and improvement projects. In July 2021 the

6

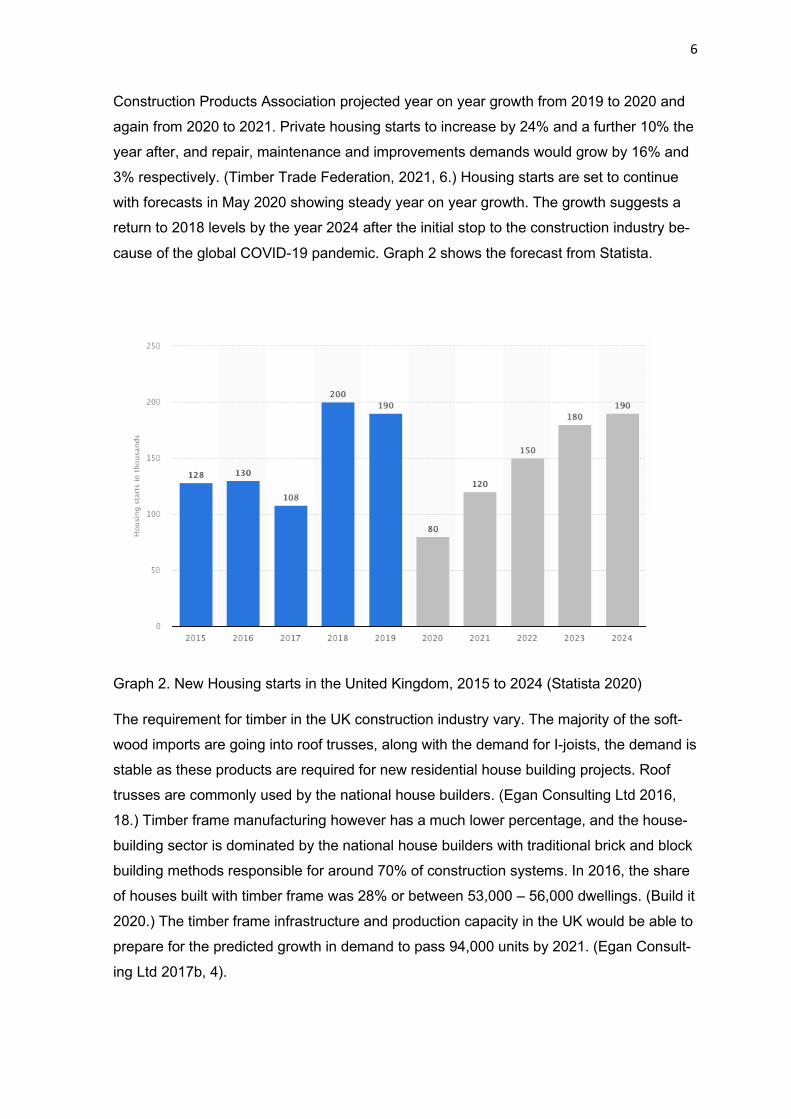

Construction Products Association projected year on year growth from 2019 to 2020 and

again from 2020 to 2021. Private housing starts to increase by 24% and a further 10% the

year after, and repair, maintenance and improvements demands would grow by 16% and

3% respectively. (Timber Trade Federation, 2021, 6.) Housing starts are set to continue

with forecasts in May 2020 showing steady year on year growth. The growth suggests a

return to 2018 levels by the year 2024 after the initial stop to the construction industry be-

cause of the global COVID-19 pandemic. Graph 2 shows the forecast from Statista.

Graph 2. New Housing starts in the United Kingdom, 2015 to 2024 (Statista 2020)

The requirement for timber in the UK construction industry vary. The majority of the soft-

wood imports are going into roof trusses, along with the demand for I-joists, the demand is

stable as these products are required for new residential house building projects. Roof

trusses are commonly used by the national house builders. (Egan Consulting Ltd 2016,

18.) Timber frame manufacturing however has a much lower percentage, and the house-

building sector is dominated by the national house builders with traditional brick and block

building methods responsible for around 70% of construction systems. In 2016, the share

of houses built with timber frame was 28% or between 53,000 – 56,000 dwellings. (Build it

2020.) The timber frame infrastructure and production capacity in the UK would be able to

prepare for the predicted growth in demand to pass 94,000 units by 2021. (Egan Consult-

ing Ltd 2017b, 4).

7

Statistics form May 2021 show that Finnish exports of sawn and planed softwood had a

total increase from the previous year of 109% with a total volume of 5.8 million cubic me-

ters. The resulting split of this total volume increase is 25% from sawn spruce, 52% from

sawn redwood and 23% from planed volumes. (Sahateollisuus ry 2021.) Similar infor-

mation was shared at the Wood From Finland Conference in 2020, when the highest

share of planed volumes from the top 20 export countries of Finnish production was the

United Kingdom. (Wood From Finland Conference 2020a, 11). This data shows that the

volumes have been increasing from Finland to the UK with high demand from all sectors,

including the construction industry using planed volumes. Graph 3 below shows the export

volumes to the United Kingdom for sawn and planed softwood and how the trend has de-

veloped between 2012 and 2018.

Graph 3. Export to the United Kingdom (Wood From Finland Conference 2020b, 25)

8

4 ROOF TRUSSES - TR26

4.1 TR26 introduction

TR26 is the name given to strength graded timber that meets roof truss requirements.

TR26 is a unique grade of timber to the United Kingdom and as a result adheres to British

Standard BS5268. TR26 is different from standard strength classes in multiple other coun-

tries, which are C14, C18, C24, C30, and relate to standard EN338. Because TR26 is

used in roof structures and subject to demanding conditions, the strength grade must

therefore meet a higher standard to ensure the correct properties suitability. (Mikkonen

2021).

TR26 comes in two standard thicknesses, which are nominal 36mm (35mm actual) and

47mm (46,5mm actual). Table 1 shows the full specification of TR26 that importers in the

UK would be expected to stock and supply to roof truss manufacturers. The 36mm thick-

ness are for traditional A frame roof truss designs, as can be seen in image 3. The thicker

47mm timber trusses are for designs with living space added into the roof. These are re-

ferred to as attic trusses or ‘room in the roof’ trusses and are shown in image 4.

Table 1. The full TR26 specification.

Roof trusses are designed and held together with metal plates. These plates can be seen

in images 3 & 4, where two TR26 pieces come together. Most roof truss manufacturers

use optimising technology during the design phase of projects of roof trusses to minimise

waste. As the design of the roof truss changes with each project, a timber merchant or im-

porter in the United Kingdom will have to hold the appropriate lengths in each section size,

as showing in table 1, to meet customer requirements and projects.

9

Image 3. Roof truss design using TR26 (Ridley-Ellis, D 2015)

Image 4. Example of ‘room in the roof’ trussed rafters (Cheshire Roof Trusses & Floor

Joists)

10

4.2 The TR26 market and possibilities

TR26 and roof trusses can be seen on most building sites in the United Kingdom. The de-

mand for roof trusses is linked to the construction of new homes, and as suggested in the

forecast show in Graph 3, the demand for new housing starts will return to 200,000 homes

in the next couple of years. However, the current UK Conservative government pledged to

build 300,000 to meet the demand for housing. With the situation over the last few years

with building material shortages in many countries, meeting the target may prove difficult.

(Savage, M 2021.) The demand for new houses has been argued to even be increased to

340,000 new homes per year. However, information is now available showing the projec-

tions from 2020 by the UK’s office for National Statistics showing an increase of 3.7 million

in the number of households in England by 2043. (Barton, C & Wilson, W 2022, 10). This

figure suggests the need for additional houses year after year will continue to grow.

TR26 products are imported from Swedish and Finnish sawmills, with the Swedish mills

responsible for the short to mid-range lengths and the Finnish mills for the mid and longer

lengths. These supply countries can supply TR26 because of the growing conditions of

these Scandinavian and Nordic forests. In a comparison, the UK are only able to supply

around 27% of sawn timber to the construction industry, and the timber would not meet

the strength graded requirements for TR26. This is because in the United Kingdom a Sitka

spruce tree reaches maturity in around 40 years. This is the time taken from planting the

seedling to harvesting the logs. (University of Oxford 2017). The speed of the tree growth

has a direct influence on the strength properties of the timber and as a rule the longer the

tree has grown, the stronger the resulting timber will be. In comparison to British grown

Sitka spruce, spruce in Finland will reach maturity 70 - 90 years after the planting.

(Puuproffa). The faster the trees grow, the lower the density and the strength will be of the

resulting timber product. To get the same TR26 strength properties and features from tim-

ber sourced from Britain, it would require a much bigger section size to meet the same

standards as the Nordic equivalent. When the stock holding requirements are considered

and the need for two separate products and double the space, the appeal will decrease

for stock holders and the economic viability would decrease. TR26 is a grade unique to

the United Kingdom and is the equivalent of C27 materials. (Trussed Rafter Association

2021). This difference shows that TR26 produced from Finnish spruce and even pine will

be needed to meet the future demand from national house builders as domestic supply is

not possible.

Because of the requirements for timber importers and distributors to hold the full range of

lengths, Hartman and MM Wood are currently able to supply TR26 to the UK in the range

11

between 2,500 and 3,000 cubic meters per month. Producing TR26 for the UK allows MM

Wood to produce long runs with minimal changes to the planing machines set up. This al-

lows MM Wood to efficiently produce TR26 and plan the production in such a way to max-

imise the volumes, minimise stoppages and down time. The value of the TR26 would de-

pend on the raw material availability, price and market situation. Being able to differentiate

its product offering through availability of longer lengths when compared against other

sawmill operations in the supplying markets, MM Wood would be able to get a better price

for the overall specification.

The UK market currently applies a premium for long lengths, which are 5,7m and 6,0m

lengths due to the lower availability. Providing that key lengths in 4,8m, 5,4m and 6,0m

are available, these items would allow MM Wood to create a better overall price for each

TR26 shipment. The UK market has also got some critical dimensions that are commonly

required by many roof truss manufacturers. Having spoken to the trade, the share of 36 x

75mm is significant and if the volume in this size could be increased, so could the overall

volume per shipment. 36 x 75 is a critical item with high demand because it is used for

webbing applications. The importance of 36 x 75mm is high and is accountable for around

30 - 40% of the total TR26 specification. (Customer A 2022.) The raw material availability

becomes the key to increase the share of 36 x 75mm. However, MM Wood and Hartman

have the customer base and infrastructure to utilise a potential increase in production ca-

pacity to focus on TR26, where MM Wood and Hartman have a competitive advantage

against other suppliers through their length specification.

Engineered Wood Products have become well established in the construction industry.

These products from timber include items such as Laminated Veneer Lumber (LVL), Glu-

lam beams, I-Beams and I-Joists. Other building materials such as metal, concrete and

composites materials may provide competition for TR26 in the future if supply is not able

to meet the demand.

4.3 TR26 analysis

Looking closer at the TR26 market, and a possible increase of MM Wood production in

TR26 will require a SWOT analysis. This tool will enable a better understanding of in-

creasing MM Wood’s production capacity with TR26 volumes. The overall TR26 market

size is estimated to be around 400,000 – 500,000 cubic meters annually. (Customer A

2022.)

12

Table 2 shows a SWOT analysis for increasing the production capacity towards TR26 vol-

umes. The strengths are possibly the largest for MM Wood because of the limited number

of TR26 suppliers available and therefore fewer competitors. Many of the sawmills in Fin-

land have investigated the possibilities of producing TR26 however the outcome has re-

sulted in a significant impact on their other production possibilities and a decision to not

produce TR26. In order to be competitive with TR26, in normal market conditions in the

United Kingdom, the sawmill must be dedicated to producing TR26 and allow sufficient

raw material for this product. However, the raw material availability is not enough and the

decision about producing TR26 also requires the correct infrastructure. The sawmill layout

will require grading possibilities after splitting, to be able to produce the key smaller

widths, for example splitting 150mm into 2 x 75 mm. Reasons like these have contributed

to Finnish mills deciding to focus on sawn production rather than added value. This has

pushed the majority of further processing production out of Finland and in to countries

such as Estonia. The demand for TR26 has been reliable and stable in recent years com-

pared to other timber products. TR26 allows MM Wood to take advantage of added value

by producing the lengths that others cannot, not only giving a better price for long lengths,

but increasing the price of the whole specification. MM Wood also already has all the cer-

tificates and licenses required by BM Trada to produce TR26.

On the other hand, the weaknesses of increasing the TR26 volumes for MM Wood is the

requirement from importers for a balanced specification. MM Wood and Hartman must be

able to balance the sizes and lengths being offered. A specification of purely long lengths

is not realistic from a raw material procurement viewpoint and might reduce the value of

the 5,4m, 5,7m and 6,0m lengths. A balanced specification allows the total volume to be

increased. The potential customers, who are operating as importers and distributors in the

United Kingdom are limited, with three main organisations holding most of the market

share. The customer base that can accept regular full cargos is therefore limited. The

ABC analysis concept suggest that 80% of the business volume goes to 20% of custom-

ers. Any higher than 80% of the volume and the risks start to rapidly increase. TR26 as a

product has the potential to go over the 80% mark especially when compared to other tim-

ber products because of the layout of the market, suppliers and customers. (Jenkins, A

2020.) Finnish suppliers have higher logistic costs than Swedish competitors, and the dif-

ference in currency between the Swedish Krona and the Euro also has an impact on the

price of TR26, which has an influence on the final profitability for MM Wood and Hartman.

The opportunities for developing and focusing on increasing TR26 volumes for the con-

struction industry in the United Kingdom is the unique supplier relationship. Because MM

Wood is not a sawmill and needs to procure the correct raw material from numerous

13

external sawmills means that the specification can be enhanced with communication with

the customer. Working with a dedicated importer or importers to define the specification

will enable growth of the monthly volumes. With the market for TR26 growing, as per the

forecasts for housing starts and TR26 dominating the market as the accepted material for

roof trusses, Hartman are in a good position for the future with a smaller amount of com-

petition than many other timber sectors. MM Wood might also be able to develop their

own branded roof truss material that would go beyond the strength requirements for

TR26, as the raw material could meet C30 strength requirements. This could open new

trade options for roof designs with an even more demanding applications and load bearing

requirements, finding a niche in the current market.

The threats that MM Wood face could include a decision by the market to accept other

material because of the limited number of suppliers. This could be either in the form of

substitute products as Laminated Veneer Lumber, or some wood composite products. In

this case TR26 would have a price advantage over engineered wood products. The other

possibility is that the grade requirements and standards are lowered to allow other suppli-

ers, for example in Central Europe to be included. This would result in a reduction in value

from the current level as the strength requirement is reduced.

Figure 1. TR26 SWOT analysis

14

5 CANADIAN LUMBER STANDARD - CLS

5.1 CLS introduction

In the United Kingdom, CLS comes in two different strength grades, C16 and C24. Tradi-

tionally C16 grades have been offered by British sawmills and C24 have come from Cen-

tral Europe, Sweden and Finland to name a few supplying countries. CLS is all kiln dried

to meet ISPM15 standards as part of the processing stage, and CLS also comes ma-

chined as planed all round or PAR with eased edges.

Image 5. CLS sections 38x63mm & 38x89mm with eased edges (Wickes)

C16 grades are mainly for builders’ merchants designed to sell volumes less than a full

pack to customers. Private builders and Do-It-Yourself enthusiasts can pick the items for

individual projects and jobs. The C16 specification is usually in the smaller section sizes

as the load bearing requirements are not as demanding in the end applications. The most

common size of CLS for builders’ merchants is 38 x 63 mm actual (50 x 75 mm nominal),

38 x 89 mm (50 x 100 mm nominal) is also used. CLS is commonly referred to by the ac-

tual size and volume, in comparison TR26 is nominal. The lengths of the CLS in the mer-

chant sector are typically 2,4m and 3,0m. Builders merchants have their infrastructure ar-

ranged so that the timber is available for customers in racks and as a result the lengths

are restricted and need to be 2,4m with some 3,0m lengths. Images 6 and 7 show a good

visual example of how the lengths are held in the rack and why other lengths other than

those requested not accepted by the builders’ merchant.

15

Image 6. CLS 38x89 Builders’ Merchant stocks (Fulham timber Building Supplies)

Image 7. Builders’ merchant racking (Fort Builders’ Merchants)

16

The other half of the CLS market is strength graded to C24 grade and is used in timber

frame housing. The timber frames are manufactured in factories off-site before being de-

livered to the building site. Timber frame manufacturing centres are able to produce differ-

ent elements, be that floor cassettes or wall elements. Further processed and added value

can be offered by certain manufactures that includes full finished floors and windows in-

cluded. Donaldson Timber Systems are able to offer up to 10,000 timber frame homes per

year. Donaldson use Modern Methods of Construction (MMC) and have been looking at

ways to develop timber frame homes which already is a quick and efficient method of de-

livering homes. The need for houses has already been mentioned and with a shortfall of

around 120,000 homes needed annually to meet the housing crisis and shortage, timber

frame could be a solution. Advanced Industrial Methods for the Construction of Homes

(AIMCH) would take the Modern Methods of Construction further by increasing the ad-

vantages of timber frame off-site manufacturing through standardisation. Panellised sys-

tems would be introduced from a manufacturing led approach in order to increase the effi-

ciency of production. A key here would also be the integrated supply chain in order to

meet demand. (Dalgarno 2020.)

In 2018, the share of new homes being built with timber frame was 1 in 4. Scotland has

the highest share with 70% of house construction using off-site timber frame manufactur-

ing. The forecast for 2019-2020 predicted that the share in England and Wales could de-

velop to 1 in 3. (Davies 2018, 32.) In 2016 the share of timber frame construction rose in

England, Scotland and Northern Ireland grew at 22.8%, 83.0% & 17.4% respectively with

the share in Wales remaining stable at 30.7%. The speed of construction and impact on

the environment from a waste reduction perspective are all shedding a positive light on

off-site manufacturing systems. (Egan Consulting Ltd 2017a, 3-4). The main section sizes

are 38 x 89 mm actual (nominal 50 x 100 mm), 38 x 140 mm actual (nominal 50 x 150

mm), and larger section sizes are available for larger projects designed typically for

schools and hospitals. These sizes are actual 38 x 184 mm and 38 x 235 mm.

17

Image 8. Timber frame systems (Donaldson Timber Systems)

5.2 Market potential

The CLS market in the United Kingdom currently looks to be around 600,000 – 700,000

actual cubic meters per year. The vast majority of the share of C24 material is in 38 x 89

and 38 x 140 dimensions. The lengths for CLS tend to be more specific, with some import-

ers working with their customers and deciding to only accept even lengths. (Customer B

2022). The same importer revealed that with limited space at customers yards and facili-

ties, the majority of timber frame manufacturers in the UK are taking advantage of Just-in-

Time setups with importers holding the stock and looking to turn full loads to customers

within 48 hours from order. The outcome is customers and importers in the UK looking to

purchase volumes from Finland in much more length specific manners. Sometimes even

looking for a single length to be delivered. (Customer B 2022.) This sort of demand from

importers is a challenge for sawmills to offer supply possibilities.

38 x 89 mm is generally used for internal applications and 38 x 140 is for external. The ex-

ternal share of the CLS market is around 40 - 50%. (Customer A 2022). The demand for

18

CLS can also be related back to the demand for new housing starts in the UK as the end

application is construction. In 2019, the number of new homes in the UK was 170,000

units, which is the highest number in the previous 11 years, however still 70,000 - 170,000

units shy of the require level. Merger and acquisition activity can be seen in the timber

frame housing sector which will hopefully be the start of a trend with the national house

builders. This recent activity involved Oregon Timber Frame Ltd and Barratt’s. (Wallace

2021, 6-7.)

Unlike TR26, CLS is a product that is in standard use around the world and the strength

grade of C24 is universally known. CLS suppliers are able to supply high volumes to Euro-

pean markets, but a large market for CLS is the United States of America. With plenty of

markets to supply, the volumes need to be assigned and allocated according to develop-

ments and price. Imperial measurements are used in markets like Japan and the United

States causing differences to European markets, for instance 2,4m meters are actually

2,44m. This difference requires a change to log harvesting in the forests to allow an addi-

tional, up to 10cm in log lengths in the procurement process. This adds the requirement

for a second stock if raw material in the same dimensions, however the alternative is to

only source 5,0m lengths rather than 4,9m but would result in waste for products being

delivered to the United Kingdom adding to competition. (Mikkonen 2022.) This can result

in changes from one quarter to the next as has been the case in recent memory when

lumber prices hit an all-time high and volumes of CLS were moved to North America by

producers in 2020. When the price in the US fell in 2021, volumes were transferred back

to the UK which lead to oversupply and affected the market price. (Timber Trade Journal

Online 2021). The supply and demand balance will affect the price and again the specifi-

cation will play a large part in successful quarterly business.

5.3 CLS analysis

A SWOT analysis model was used to analyse suitability of increasing the CLS production

at MM Wood in C24 strength grade class for the United Kingdom. An initial strength would

be the large market potential, with importers in the United Kingdom carrying some sort of

landed stock operation for the timber frame manufacturing sector as well as supplying

builders’ merchants nationwide. Especially when compared to TR26, higher volumes

could be utilised through different customers and taking advantage of the alternative lo-

gistic routes allowing access a few different ports in the United Kingdom. CLS is a stand-

ardised product and known by importers, builder merchants and their customers, and MM

Wood have the knowledge and experience of producing CLS and as a result increasing

19

the production with CLS should be possible with limited risks at the mill. CLS would de-

velop MM Wood’s product range and in doing so diversify MM Wood and Hartman’s prod-

uct portfolio to become in line with other markets. The raw material for the planing mill is a

juggling act with over 30 sawmills responsible for producing the overall specification re-

quired. The raw material for 38mm CLS is important to utilise and from this perspective

developing CLS sales to the United Kingdom would be a logical decision.

The argument and weaknesses against developing CLS volumes start with the length

specification. Not only are the length requirements in the UK challenging for sawmills and

suppliers with access to long lengths, but procurement would need to be developed to

source single lengths in some cases. Some mills would not be able to accommodate this

demand and the risk to other raw materials volumes would increase. The main lengths

that are needed to trade successfully in the UK are the same that are needed in other Eu-

ropean markets. With availability in certain lengths challenging, the competition from MM

Wood and Hartman’s customers for the allocations would also make the situation chal-

lenging. On top of this would be the competition from other suppliers in Russia, Sweden

and central Europe and the supply and demand would further influence the price and prof-

itability. The price of MM Wood’s C24 can often face competition from C16 alternative

products especially in 38 x 89 mm and 38 x 63 mm. Due to the location of the planing mill

and the supplying sawmills, C16 is not a grade that is readily available and MM Wood are

not able to be produced large volumes. The pine and spruce trees grow slowly and the

lowest realistic strength grade is C24, and the raw material could and actually does meet

higher strength grades.

Another issue is the competitive advantage that supplying countries have over Finnish

suppliers through logistics. Central European countries are able to deliver full loads by

trailer to the United Kingdom in a few days. Sawmills in South Sweden could deliver by

trailer through Europe, or by break bulk vessel. Finnish mills rely on break bulk vessels

and RoRo vessels to get their products to the United Kingdom. The lead time for delivery

from Finland is longer and more expensive than that of other countries due to the distance

to travel, which affects the price of the products and competitiveness.

Looking at the opportunities, MM Wood already have the existing infrastructure and expe-

rience to produce CLS for multiple markets and develop their UK allocations. With devel-

opments to the raw material availability and a focus on correct length specification, CLS

possibilities could be developed. In a similar way to TR26, Hartman would need to find

customers that are importing from multiple sawmills and offer a select part of the length

specification. MM Wood would be able to efficiently plan their production schedules to

20

optimise the planing series to meet customers specific length requirements. MM Wood

would need to identify customers in the UK that can fit into the supply matrix and effec-

tively allocating volume and lengths so customers whose requirements complement each

other. Hartman Rauta and MM Wood have been developing a long and shorts concept for

European markets, where longer lengths than are cross cut to meet the needs of the short

lengths that otherwise would not be possible to source correct raw material lengths.

(Rasanen 2022).

Image 9. MM Wood and Hartman C24 CLS (Rasanen 2021)

MM Wood have the infrastructure as well as the supply chain network to procure raw ma-

terial suitable for 38 x 184 mm and 38 x 235 mm. Through discussions with current cus-

tomers, the share of these products will increase in the future. By being able to supply

these larger section sizes to the United Kingdom market, and the importance of the

longer lengths, 4,8m, 5,4m and 6,0m, MM Wood and Hartman could include other vol-

umes in 38 x 140 mm and 38 x 89 mm in to offers, all of which are in C24 grade.

However, some threats are on the horizon for MM Wood, as a result of the United King-

dom leaving the European Union due to the Brexit vote. Construction products among oth-

ers, will require a UKCA marking to appear on products. UKCA markings and the

21

European Union’s CE markings will not mutually recognise one another. Products that will

require the UKCA marking, which for the construction industry include roof trusses, timber

frame products as well as visual and machine strength graded products, will need the

marking to be visible to allow any trading. (BM Trada 2022, 5). The European Union have

accepted that both UKCA and CE markings may appear on products, however at the mo-

ment it is not fully confirmed that all countries in the European Union are accepting both

markings. The second issue with the joint marking is that marking must be kept separate,

require separate audits, separate declaration of performance certificates and have sepa-

rate factory production control certification systems. (TTF UKCA Guide 2021,10.) These

additional requirements will require investment in audits as well as space for storing and

keeping dual stocks separate.

Another complication for MM Wood is the competition from suppliers that can produce

certain volumes of CLS in the required lengths that MM Wood cannot. As a result, MM

Wood’s specification, despite the fibre quality, is analysed and directly compared to other

suppliers. This comparison will highlight the different in lengths and suitability, and through

this, the price level as importers will not want to pay full price for lengths that are not re-

quested or as desirable.

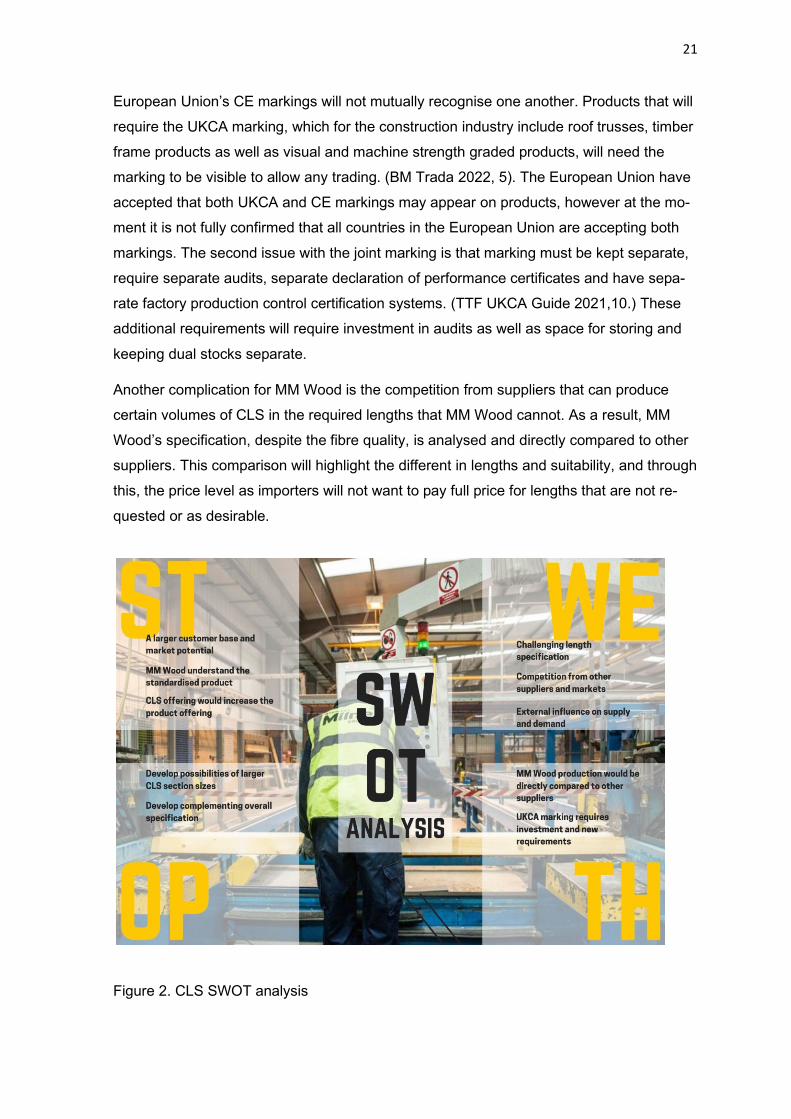

Figure 2. CLS SWOT analysis

22

6 CONSTRUCTION CARCASSING

6.1 Carcassing introduction

Carcassing is a form of strength graded timber that is designed to be used in different

structural and general applications. Carcassing comes in C16 and C24 grades and the

most common thickness is 47 mm. Carcassing is designed to be used in load bearing

end uses in wooden housing structures and as a result meets the strength properties and

requirements of British Standard BS EN 14081. (Timber Trade Federation 2020b).

C16 grade is a cheaper product and can be used for internal applications, especially if the

spans are shorter. Generally, C16 carcassing can be used as studs, partition walls shut-

tering and joists among other applications. C24 strength graded timbers can be used for

the same applications as well as floor joists general joinery and structural applications and

rafters that require higher load bearing capabilities and is needed for wider spans. (El-

liotts). In the United Kingdom, C24 carcassing can be treated or untreated with some im-

porters and land stock operators holding dual stocks.

C24 carcassing usually comes in lengths from 2,4m to 4,8m with a small amount in 5,4m

and 6,0m in 60cm increments. Sometimes the offering can include 6,6m and 7,2m in cer-

tain larger section sizes. (Customer C 2022). The main nominal thicknesses are 47 mm

and 75 mm, which are 45 mm and 73 mm actual thickness. The nominal widths in 47 mm

are commonly 75 / 100 / 125 / 150 / 175 / 200 / 225 while 75 mm are offered by importers

in widths of 100 / 150 / 200 / 225. Image 10 below shows an example of carcassing used

as ceiling joists in the wooden skeleton of a house build.

23

Image 10. Carcassing used for general construction (WEL Timber & Builder’s Depot)

6.2 Market potential

The carcassing C24 market in the United Kingdom has been geared up to supply the mer-

chant sector and with strict length requirements, buyers and suppliers must work together

to agree a workable specification to ensure the correct lengths are supplied. The standard

lengths for Carcassing include 2,4m, 3,0m, 3,6m, 4,2m, 4,8m, 5,4m and sometimes 6,0m.

The demand for other sizes seems to have been growing since 2018 with the need for

long lengths in carcassing. The Timber Trade Federation highlighted that Wardell Long

Lengths can supply up to 7.8m. The maximum section size of 300 x 300 mm, while others

supply the so called ‘wides and longs’ which are usually 6.6m and 7.2m lengths. (Timber

Trade Federation 2018). An alternative comes in the form of long lengths possibly through

finger jointed C24 grade carcassing. Finger-jointed spruce for the construction industry

has the potential to create demand of longer lengths in the United Kingdom, if builders can

accept it as a building material. Having spoken to builders' merchants in the United King-

dom, their customers can still be sceptical of finger jointed products because of a lack of

24

trust in the product. Even if the finger-jointed C24 has passed strength grade criteria, the

builder lacks 100% faith in the joints. Changing this perception has already started but

there is still a long way to go for the trade to see finger-jointed materials on the same level

as solid planed and regularised timber. (Customer C 2022.)

Finger-jointing would allow much longer carcassing to be produced. Effectively filling the

full length of a trailer for simple logistics reasons and importers such as Jordeson timber

for example, have been working with supplying mills to invests in capacity to create 13.6m

C24 carcassing. The actual finger-joint in the C24 product has been proved to be strong

enough to meet the strength grade requirements of C24. The majority of carcassing is

coming from Swedish suppliers who have typically got short lengths, up to 4,8m and some

options in 5,4m. Finger-jointed C24 gives the possibility to increase the length offering that

is otherwise not possible. Finger jointing can also improve the products features which in-

clude the straightness of each piece and as is the case in the joinery industry could be

used to cut out defects such as knots to improve the actual grade. (Scarborough 2018).

These benefits could help increase an importers market share, however by further pro-

cessing C24 carcassing through finger-jointing, is the market ready to pay for the added

value that finger jointing brings?

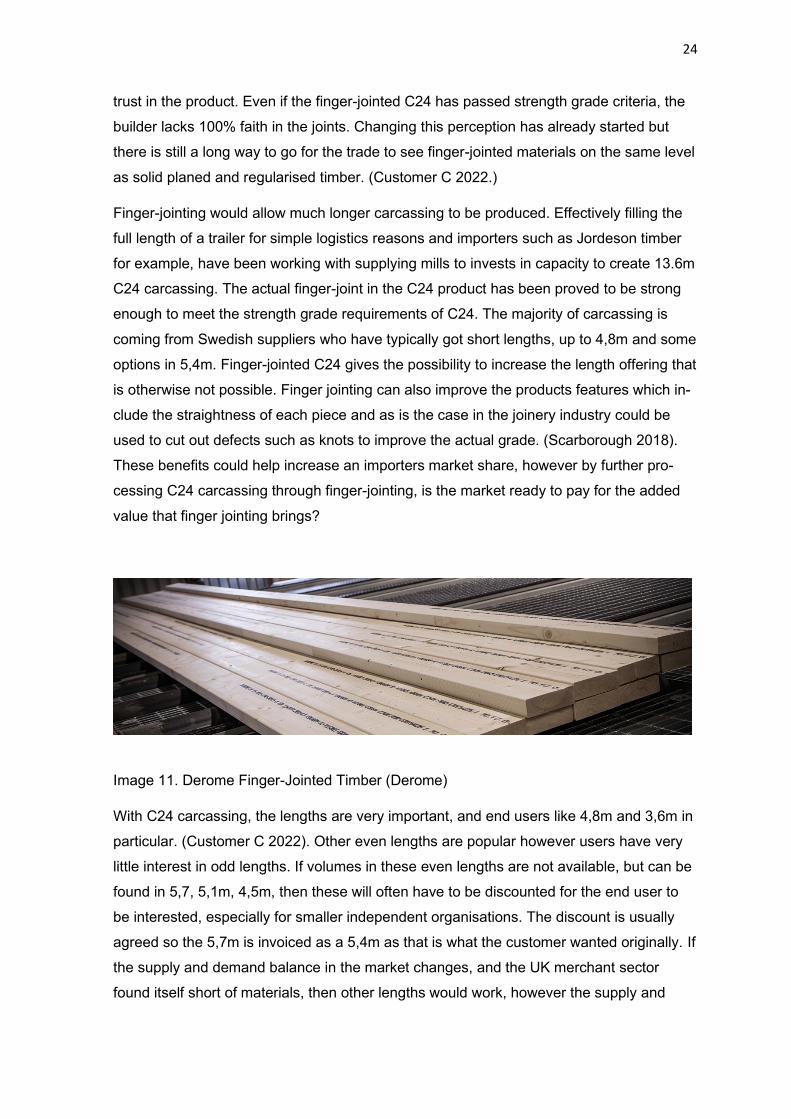

Image 11. Derome Finger-Jointed Timber (Derome)

With C24 carcassing, the lengths are very important, and end users like 4,8m and 3,6m in

particular. (Customer C 2022). Other even lengths are popular however users have very

little interest in odd lengths. If volumes in these even lengths are not available, but can be

found in 5,7, 5,1m, 4,5m, then these will often have to be discounted for the end user to

be interested, especially for smaller independent organisations. The discount is usually

agreed so the 5,7m is invoiced as a 5,4m as that is what the customer wanted originally. If

the supply and demand balance in the market changes, and the UK merchant sector

found itself short of materials, then other lengths would work, however the supply and

25

demand balance would need a large shortage for this be the case. Looking at recent

trends, with the volatility of the market between 2019 and 2021, the C24 market experi-

enced both over supply and shortages as a result of global demand and the Covid-19

pandemic. After these shortages, the timber trade in the United Kingdom returned to a

‘normal’ state of only looking to purchase the accepted even lengths.

Some of the larger national builders' merchants will not accept any deviation in the lengths

on contract due to the setup and layout of the timber yards and stocks. These builders’

merchants will hold certain lengths in stock and use IT systems to showing real time

stocks and the locations of products. If lengths like 5,1m are delivered, these would re-

quire their own new product code and storage location with racks to be created. Often

space is not available and therefore builders’ merchants will not willingly accept lengths

outside the specification and will refuse a delivery and send a trailer back to the supplier.

However not all sawmills are able to offer length specific volumes to customers and leav-

ing out all odd lengths. (Customer C 2022.)

MM Wood are currently producing C24 carcassing for customer in Europe with a long and

short concept. With access to raw material with longer average lengths than other Finnish

and Swedish suppliers from Hartman Rauta, MM Wood are able to cut the long lengths to

produce different shorter lengths for customer. 6,0m can be split to 2x 3,0m lengths with

other combinations in 5,7 and 5,4m lengths. (Rasanen 2022.) The issue for the UK market

is that the length requirements are very specific with regards to getting contracts agreed.

In recent interviews, ‘Customer B’ acknowledged that their purchase orders will often

specify volumes in a single length, and ‘Customer C’ confirming that for carcassing, only

3,6m and 4,8m lengths are of interest. Image 12 below shows MM Wood’s C24 carcas-

sing that has been produced for Hartman Rauta customers in Europe.

26

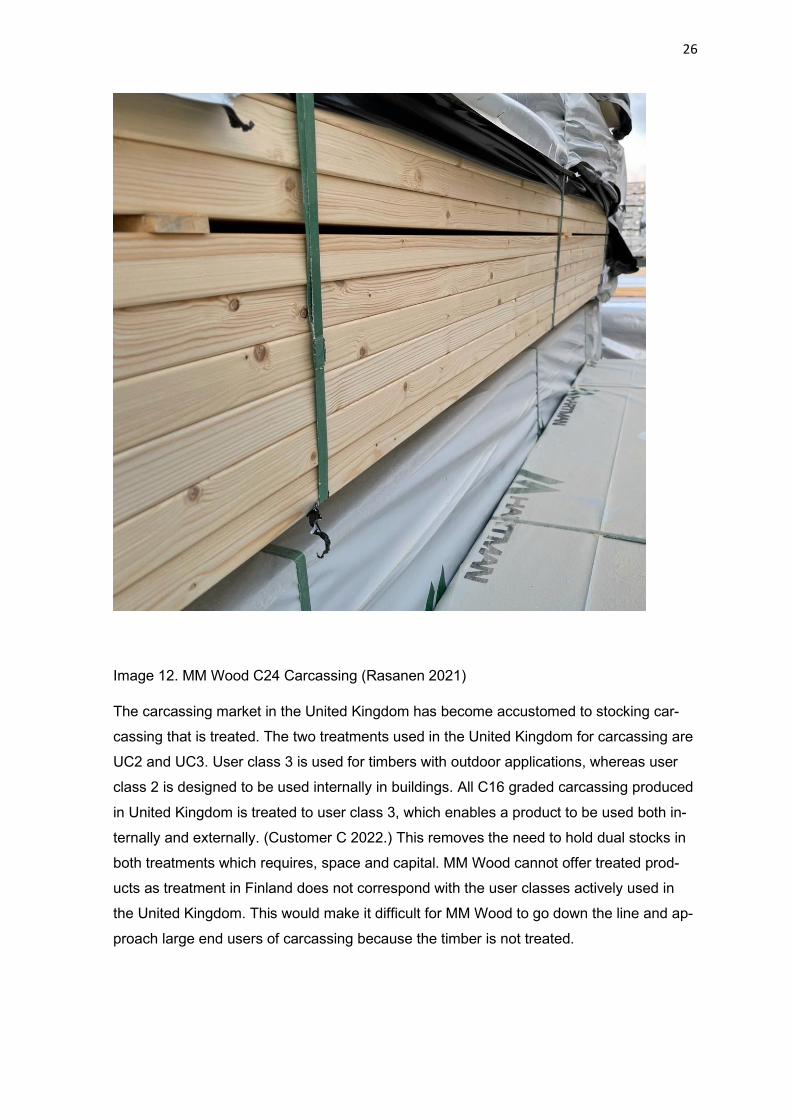

Image 12. MM Wood C24 Carcassing (Rasanen 2021)

The carcassing market in the United Kingdom has become accustomed to stocking car-

cassing that is treated. The two treatments used in the United Kingdom for carcassing are

UC2 and UC3. User class 3 is used for timbers with outdoor applications, whereas user

class 2 is designed to be used internally in buildings. All C16 graded carcassing produced

in United Kingdom is treated to user class 3, which enables a product to be used both in-

ternally and externally. (Customer C 2022.) This removes the need to hold dual stocks in

both treatments which requires, space and capital. MM Wood cannot offer treated prod-

ucts as treatment in Finland does not correspond with the user classes actively used in

the United Kingdom. This would make it difficult for MM Wood to go down the line and ap-

proach large end users of carcassing because the timber is not treated.

27

6.3 Carcassing analysis

A SWOT analysis model will help show the strengths, weaknesses, opportunities and

threats with regards to looking at increasing volumes in C24 carcassing. Looking at the

strengths, MM Wood have experience of producing C24 Carcassing for multiple markets

and also have an understanding of the specification that works with regards to the section

size and the lengths. Another strength for MM Wood is the addition to the product portfo-

lio. The importers who are able to accept large cargo vessels are often using a stock hold-

ing operation at ports for multiple timber products. By offering C24, MM Wood would be

able to negotiate a product package to include other products such as CLS and TR26.

This would allow the possibility of monthly volumes to increase. Carcassing is regularised

product, and as a result Hartman can work with the supply chain to access the raw mate-

rial requirements for carcassing on a continuous basis. This will help MM Wood’s produc-

tion planning to increase efficiency with their production.

A clear weakness for MM Wood and Hartman Rauta is the lengths of raw material that are

available. With heavy demand for the 4,8m volumes Hartman and MM Wood’s specifica-

tion does not naturally meet the demands of C24 carcassing and multiple lengths that are

not useable would be left in the raw material stocks. These lengths are unlikely to be in-

cluded in the specification based on conversations with Customer A and Customer B,

along with a handful of other importers who only show even lengths on their stock lists.

MM Wood face competition from C16 ‘home grown’ British timber as well as C24 products

from Swedish mills and Central European mills who are producing high volumes of prod-

ucts that are planed and graded to C24. From a price perspective this makes the appeal

of Carcassing challenging for MM Wood as the price and grade are already above other

suppliers' levels. Other supplying countries are also closer to the United Kingdom and

have an logistic cost advantage over MM Wood and Hartman.

MM Wood would only be able to supply the larger importers and distributors in the United

Kingdom with landed stock operations. Working with customers who are end users or

merchants will not work because of the infrastructure layout and space available for in-

bound volumes. These inbound volumes are heavily reliant on specific lengths that MM

Wood currently would struggle to supply. The timber trade in the United Kingdom has also

become dependent on Just-in-Time procedures where the end user will not hold the stock

on their premises and instead, call off orders from builders’ merchants as and when they

are needed. The builders’ merchants are passing these on to importers and this can even

be seen to be passed to some extent and affect the specifications with suppliers as every

28

stop in the supply chain wants to pass the costs of holding the stock down the line. (Wa-

ters 2009, 285).

A possible opportunity for MM Wood would be that the raw material could be utilised for

either C24 or TR26, as well as other strength grades for other markets, such as MGP10.

This would allow MM Wood to have the stock with flexibility to produce a more reliable

specification based on the strict lengths in contracts. For example, with sawn timber with

the dimensions of 47/50 x 150 mm as the raw material, MM Wood would be able to pro-

duce TR26 in sizes 46,5 mm x 147 mm which can be split to produce 46,5 mm x 72 mm.

The same raw material can produce C24 45 mm x 145 mm, which again could be split to

produce 45 mm x 70 mm. MGP10 in 45 mm x 70 mm for the Australia market can also be

produced from the same raw material, because the fibre has grown so slowly that the

properties can comfortably meet the strength criteria of TR26, C24 and MGP10. (Kemmo

2022.) MGP10 in the first half of 2022, has a good price because of global market trends.

Finnish spruce is able to compete with Radiata Pine from New Zealand as it has superior

properties. However, the supply and demand balance can be affected by purchasing deci-

sions involving China and supplying decision involving Russia that could have an influ-

ence on future volumes and competitiveness. (Mikkonen 2022.) The remaining possibili-

ties are C24 48 mm x 148 mm and split possibilities of 48 mm x 73 mm. This works in the

same way as material requirements planning and allows MM Wood to calculate the overall

gross requirements by combing all the demands. (Waters 2009, 280). Nonetheless, this

could also be a possible threat, because all the products here will require volumes in the

key sizes, 4,8m, 5,4m and 6,0m to make the full specifications as attractive as possible.

Through internal competition for the raw materials, limitations may occur with the possible

volumes of one product group, or it may leave volumes that customers will not accept in

any product group. The worst-case scenario is for MM Wood and Hartman to end up with

high stocks of ready products in 5,1 and 5,7m for example without a sales contract.

Another opportunity for MM Wood would be to differentiate themselves from other com-

petitors in the market. Working with Hartman, MM Wood have been able to stand out from

the market with a unique selling point of producing a specification consisting of a high

share of long lengths. Finger-jointed C24 is growing in popularity over the last few years,

particularly with carcassing. (Timber Trade Federation 2020c). MM Wood could take ad-

vantage of the new shift in demand for longer lengths in C24 by offering C24 carcassing

as long lengths. MM Wood would be able to be competitive and offer the solid C24 at a

lower price compared to finger-jointed alternatives as the production does not include the

further processes stages. This concept can be further developed with the lengths that are

29

not suitable for UK carcassing customers used as a combination of short lengths and raw

material for further processed finger-jointed products.

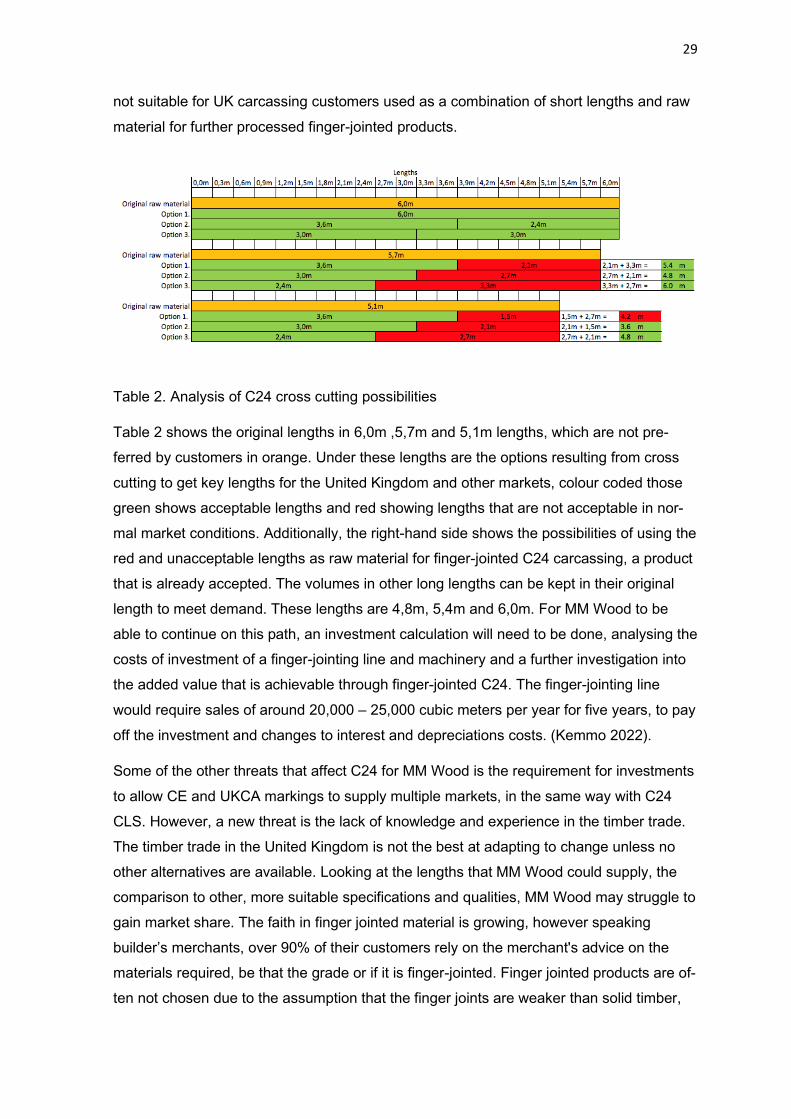

Table 2. Analysis of C24 cross cutting possibilities

Table 2 shows the original lengths in 6,0m ,5,7m and 5,1m lengths, which are not pre-

ferred by customers in orange. Under these lengths are the options resulting from cross

cutting to get key lengths for the United Kingdom and other markets, colour coded those

green shows acceptable lengths and red showing lengths that are not acceptable in nor-

mal market conditions. Additionally, the right-hand side shows the possibilities of using the

red and unacceptable lengths as raw material for finger-jointed C24 carcassing, a product

that is already accepted. The volumes in other long lengths can be kept in their original

length to meet demand. These lengths are 4,8m, 5,4m and 6,0m. For MM Wood to be

able to continue on this path, an investment calculation will need to be done, analysing the

costs of investment of a finger-jointing line and machinery and a further investigation into

the added value that is achievable through finger-jointed C24. The finger-jointing line

would require sales of around 20,000 – 25,000 cubic meters per year for five years, to pay

off the investment and changes to interest and depreciations costs. (Kemmo 2022).

Some of the other threats that affect C24 for MM Wood is the requirement for investments

to allow CE and UKCA markings to supply multiple markets, in the same way with C24

CLS. However, a new threat is the lack of knowledge and experience in the timber trade.

The timber trade in the United Kingdom is not the best at adapting to change unless no

other alternatives are available. Looking at the lengths that MM Wood could supply, the

comparison to other, more suitable specifications and qualities, MM Wood may struggle to

gain market share. The faith in finger jointed material is growing, however speaking

builder’s merchants, over 90% of their customers rely on the merchant's advice on the

materials required, be that the grade or if it is finger-jointed. Finger jointed products are of-

ten not chosen due to the assumption that the finger joints are weaker than solid timber,

30

which is not the case. (Customer C 2022.) Market materials would be required to try and

educate the trade, potentially with testing conducted at LAB University of Applied Sci-

ences. These laboratory tests could demonstrate and prove that finger-jointed products

can improve the quality and strength when compared to solid structural softwood.

Figure 3. Carcassing SWOT analysis

31

7 PRECISION END TRIMMED - PET

7.1 PET introduction

Precision end trimmed, or PET refers to products being sold in unique and very accurate

lengths. PET lengths are usually requested by customers and industrial end users. Unlike

the products presented so far, TR26, CLS and Carcassing, PET is a further processing

action that is designed to add value to the strength graded products already produced.

PET lengths are not a stock item and are usually required by customers to get rid of the

need for further processing at their own factory. For this reason, the PET possibilities and

demand are driven by the industrial end users and often by the dimensions that are re-

quired for specific wall kits. (Customer B 2022). PET lengths need to be negotiated on a

case by case basis with the customer and supplier as most sawmills and planing facilities

would not choose to produce PET, and some suppliers do not have the possibility to offer

a non-standard product. The production includes tight tolerances which adds a level of dif-

ficulty to the supply operation. (Kulmanen 2022.) MM Wood have been able to supply PET

lengths for customers however the demand has been sporadic with demand effectively

only coming from the United Kingdom.

With the timber trade in the United Kingdom operating a Just-in-Time model, customers

looking for PET materials is to be expected. Customers are expecting to see their suppli-

ers hold their stock and deliver goods as and when they are required and minimising the

need to have their own stockholding. (Waters 2009. 285). With deliveries at the right loca-

tion and at the right time, suppliers are the key to consistency and failure to meet availabil-

ity deadlines will cause stoppages on manufacturers production lines. (Waters 2009, 291).

Just-in-Time has been pushed down the supply chain with builder’s merchants and im-

porters looking for Just-in-Time delivers from their suppliers and has been seen through

regular prompt enquiries. PET lengths offer similar benefits to the customers as Just-in-

Time with lower stocks as the finished goods are imported with reduced operation on site.

Removing the internal operation will reduce administration and paperwork with works or-

ders and increase productivity. (Waters 2009, 293).

7.2 TR26 and C24 Carcassing

TR26 requires a complete range of both, dimensions and lengths in the specification with

0.3 m increments from 3,0m to 6,0m. Technology used at roof truss manufactures facili-

ties analyses and optimises the buyer’s requirements, and identifies the length of packs

32

that are required for a truss design while minimising waste. This optimising technology

has proved sufficient to date, and with high demand for long lengths of TR26 in 4,8m,

5,4m and 6,0m, PET lengths are therefore not required.

TR26 is used to create roof trusses in a variety of designs however for the most part, the

design of trusses very often produces triangular forms. TR26 is very rarely cut at 90 de-

grees and because the shapes are triangular but with many different variations, PET

would not bring any advantage. The requirement is constantly changing based on the re-

quired dimension of TR26, be that in 36 mm or 47 mm. (Customer D 2022.)

Carcassing on the other hand is a structural softwood with many different applications.

Because the end use is not known at the production stage, adding PET lengths would

simply limit the UK importers or distributors ability to sell volumes as a non-standard

length. Requirements for joists are very different to wall studs, but both applications may

look to use C24 carcassing.

7.3 CLS

PET requirements are the most common in CLS, with demand driven in particular by

house builders and timber frame manufacturers. Some of the national house builders are

using C24 CLS with the end application being wall studs that are 2,4m in length. Timber

frame manufacturers can choose the ceiling height and use this as a standard in many of

their kits ready for site. In this situation, the timber frame manufacturer can pass the fur-

ther processing to the supplying sawmill or planing mill and use CLS studs that are cut to

length with very higher accuracy, in fact, to the millimetre. Without PET, the timber frame

manufacturer would have an additional production process at their stop in the supply

chain. PET lengths allow a much more efficient operation for the manufacturer as the

packages can be opened and sent straight to the assembly line. The customer is able to

optimise their production and increase efficiency. (Customer D 2022.) Sales of PET CLS

currently can reflect up to around 4,5 – 9,0 % of an average months CLS sales. (Cus-

tomer A 2022).

7.4 PET analysis

Not many sawmills and planing operations have the facilities that enable supply of PET

lengths. By offering PET lengths, MM Wood’s reputation will grow among timber frame

33

manufacturers. With volumes high enough for timber frame manufactures to send their

suppliers requests for quotations, the potential for continuous volumes may present its self

to MM Wood.

The supply and demand balance on a global scale will also have an impact on the deci-

sion to produce PET lengths. The United States of America are known for taking large vol-

umes of CLS, and with developments in trade balances between suppliers and buyers,

the attractiveness for both parties can change quickly and question the added value of-

fered. Lengths of raw material are very important for accessing the potential of PET possi-

bilities as 4,8m would be the preferred length as it can be used to produce double the PET

measures of 2,4m sections, however as seen, 4,8m is an important length for all products

and markets. The availability of these lengths will play an important part both with invest-

ment decisions and future production planning. MM Wood may be fighting for allocations

with domestic traders in the form of merchants and DIY traders for the same raw materi-

als.

After discussion with Customer A and Customer B, the consensus was a lack of added

value by offering PET lengths in the UK timber trade. (Customer A 2022; Customer B

2022). By supplying PET lengths, it is a method of guaranteeing a certain product and vol-

ume to a specific customer. Very specific, lengths will not be stocked in a standard landed

stock operation. Based on this trend, MM Wood would be further processing their prod-

ucts, however would not see any value themselves for the added production. By offering

PET lengths, MM Wood would potential also see a reduction in their own production effi-

ciency. The trade-off in this scenario is the potential to grow the overall specification by of-

fering PET lengths to win a tender with a new customer and introduce other lengths and

even products to offers while increasing the overall volumes.

The tolerances are acceptable and these can be met by MM Wood. The tolerances for

PET tend to be +/- 1.0 mm in the United Kingdom. Timber frame manufactures in Finland

have used slightly different tolerances as + 1.0 mm / - 0.0 mm. The tolerances need to be

discussed but should be achievable. (Kulmanen 2022.) The challenges of meeting toler-

ances can be overcome, but a weakness may develop if the service of providing PET is

not reflected by a higher price for the added value. PET requirements may take resources

away from other products and finding appropriate raw material, especially as lengths

shorter than 2,4m may cause problems. The raw material procurement should be consid-

ered at an early stage to increase efficiency and productivity but is not always possible.

With a track record and providing evidence of producing PET within agreed tolerances,

MM Wood could work with importers and even some timber frame manufacturers to

34

develop PET specifications. This applies to customers and buyers in the United Kingdom

as well as other European markets that might not be aware of PET possibilities. MM

Wood may also be able to increase the value of supplying PET lengths to timber frame

manufactures by negotiating with customers individually and accessing the benefits on a

case by case basis. These negotiations would discover what savings the buyer could ex-

pect, be that from replacing the need for the operation, labour and stock holding of raw

material and finished goods.

MM Wood might cause future problems for themselves by looking and operating down the

value chain and discussing supply possibilities directly with timber frame manufactures.

This could damage and jeopardise the supplying relationship with current importers. This

could also affect volumes of CLS as well as potentially other volumes of other products

that is agreed with larger importers rather than smaller end users. Additionally, the poten-

tial problem with supplying timber frame manufactures directly is that they have be accus-

tomed to calling off orders of full loads from importers being delivered in 48 hours. The

Just in-Time supply may also cause problems when supplying direct from Finland to the

United Kingdom.

Figure 4. PET SWOT analysis

35

8 FINGER JOINTED PRODUCTS

8.1 Introduction to finger jointed products

Finger-jointing has long been accepted in the United Kingdom, especially with redwood for

the joinery industry. Knots and other defects can be removed to create desirable raw ma-

terial for joinery applications that are both aesthetically pleasing as well as structurally

sound. Finger jointing can also be produced to combine long components together to cre-

ate larger wood structures such as glulam beams. (Varis 2018, 259.)

8.2 TR26

Studies have considered the substitute of finger-jointed timber to help replace some of the

TR26 demand and in particular improving the availability of long lengths. This would help

both the customer, minimise waste in their manufacturing facility as well as help the im-

porter and distributor who would be able reduce some lengths in stock holding by allowing

customers to utilise full 12-13m lengths. However, with MUF glue, that is used in other en-

gineered timber products such as LVL and Glulam beams, the glue used in the finger

joints would be too strong and cause problems when metal plates need to be positioned

and pressed into the truss.

Image 13. TR26 pressing process (Pasquill)

Due to the nature of roof trusses, the shapes, sizes and design does vary between pro-

jects. This means that although machinery and CAD simulators can calculate the optimal

36

lengths required for each project, the location of the metal webs are not known in ad-

vance. Potentially in the future with research into other gluing alternatives, a practical so-

lution will be found with a glue that is softer after the curing stage. Research has been un-

der way looking into glueing alternatives and in particular increasing the environmental as-

pects of glue by using lignin. The results are a significantly reduced carbon footprint for

products using the adhesive without reducing or affecting the properties of the glue. (Stora

Enso 2020). Despite being aimed at the wood-based panel industry, this would have po-

tential for other timber products as well. The solution would need to keep the finger joints

stable and strong though the product life cycle as well as allowing further work to be car-

ried out on the actual location of the joints. (Customer A 2022).

8.3 CLS & Carcassing

CLS in the United Kingdom has been subject to strong competition, with numerous sup-

plying markets battling for market share. Added pressure from C16 grade against C24 has

had an impact on price developments and kept the competition high for the supplying

mills. As a result, adding a further processed finger-jointed product to the market that

would require a higher price would struggle to be the product of choice for buyers.

Some importers and customers in the United Kingdom have accepted finger-jointed C24

graded carcassing. Carcassing is a key structural product in the United Kingdom and in-

troducing finger-jointed products to MM Wood can help bring a new added value to their

production. Finger-Jointed C24 could also bring benefits for shorter lengths as well as the

longer lengths that are not common from Swedish suppliers.

Customers have consistent demand for 2,4m, 3,0m and 3,6m lengths in 45 mm C24 prod-

ucts. These products can accept finger jointed material as the increased stability is pre-

ferred by customers and end users, which is why the share of this specification is so high

in the C24 carcassing. (Customer B 2022.) Engineered wood products tend to be more

stable with regards to the price than solid timber alternatives, and with finger jointed prod-

ucts, they would be approaching this engineered wood product category. A supply of fin-

ger-jointed C24 could potentially represent 13-25% added value over solid timber equiva-

lents. (Customer B 2022.) Finding a producer like MM Wood that can supply these smaller

section sizes, reliably is key, and the reward is high volumes for an added value product

with limited competition. Finger-jointing is a key part of the production of engineered wood

products and will be included in the next chapter.

37

9 ENGINEERED WOOD PRODUCTS - EWP

9.1 EWP introduction

Engineered wood products have been a growing sector in the timber trade over the last 10

– 15 years in the United Kingdom. Engineered wood products referrers to timber products

that have been enchanted to increase their strength properties when compared to solid

constructional softwood. These products include glulam, glue laminated beams, Lami-

nated Veneer Lumber (LVL) as well as different types of I-Beams and other products.

Glulam has been around for quite some time with large Austrian and German producers

supplying the UK market. The Austrian and German glulam production capacities from

2020 highlights demand for EWP products. The top two producers were producing com-

fortably over 200,000 cubic meters per annum each and all of the organisations in the top

10 had figures at least starting at 100,000. The total volume for the top 10 was around 3

million cubic meters at the time of the survey was predicted for 2021. (Holzkurier 2021.)

Recently, Cross Laminated Timber (CLT) has also been increasing as awareness grows

in the United Kingdom and production capacity in Sweden grows to meet that of Austria.

(Global Wood Markets Info 2021).

9.2 Konstruktionsvollholz - KVH

9.2.1 Market potential

Analysing the potential of incorporating engineered wood products to MM Wood’s produc-

tion is not completely suitable at present. The main products require their own production

process. LVL requires a peeling line and requires logs as their raw material, something

not suitable for an independent planing operation. Glulam requires presses and space to

operate, which presents a problem for MM Wood in their current facility and factory layout.

All of the engineered wood possibilities will require a finger jointing line.

However, looking closer at engineered wood products, KVH or Konstruktionsvollholz is

traditionally a Central European product. The timber trade in the United Kingdom has a

history of trading and using KVH in their structures, and lengths are usually 12-13m so