A guide to accounting for business combinations - Fourth Edition

321

A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Fourth Edition AUDIT For information about developments since June 2020. Click here

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of A guide to accounting for business combinations - Fourth Edition

A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONSFourth Edition

AUDIT

For information about developments since June 2020. Click here

A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONSFOURTH EDITION June 2020

For information about developments since June 2020. Click here

A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS

Prepared by:

Brian H. Marshall, Partner, National Professional Standards Group, RSM US LLP [email protected], +1 203 312 9329

Teresa Dimattia, Senior Director, National Professional Standards Group, RSM US LLP [email protected], +1 312 634 3467

June 2020

The FASB material is copyrighted by the Financial Accounting Foundation, 401 Merritt 7, Norwalk, CT 06856, and is reproduced with permission.

For information about developments since June 2020. Click here

i

AUDIT | JUNE 2020

TABLE OF CONTENTS

Executive summary ................................................................................................................. 1

General ....................................................................................................................................14 1.1 Information about the guide .......................................................................................................... 14

1.1.1 Purpose of the guide .......................................................................................................... 14 1.1.2 Topics covered in the guide ............................................................................................... 14 1.1.3 Tips on using the guide ...................................................................................................... 15 1.1.4 Acronyms and literature references ................................................................................... 15

1.1.4.1 Acronym legend................................................................................................. 15 1.1.4.2 Background on Codification and titles for topics and subtopics referred to

in the guide ........................................................................................................ 17 1.1.4.3 Other relevant literature ..................................................................................... 20 1.1.4.4 Our technical accounting guides ....................................................................... 22

1.1.5 Updates and enhancements incorporated into this edition of the guide ............................ 22 1.2 Background information on ASC 805 ........................................................................................... 24 2.1 Definition of a business combination ........................................................................................... 24

2.1.1 Private-company consolidation alternative ......................................................................... 25 2.2 Key steps in applying the acquisition method ............................................................................ 26 3.1 Scope of transactions affected by ASC 805 ................................................................................ 26

3.1.1 General ............................................................................................................................... 26 3.1.2 Business combination achieved without transferring consideration................................... 28 3.1.3 Initial consolidation of a VIE ............................................................................................... 28

3.2 Combinations or transfers between entities under common control ....................................... 29 3.2.1 What is common control for purposes of determining whether there has been a

combination or transfer between entities under common control? .................................... 29 3.2.2 Accounting for combinations or transfers between entities under common control ........... 31

3.2.2.1 Transfers between entities with a high degree of common ownership, but

that are not under common control ................................................................... 34 3.3 Not-for-profit entities ...................................................................................................................... 36 3.4 Joint venturer’s acquisition of other joint venturer’s interest ................................................... 36 4.1 Determining whether a business was acquired .......................................................................... 36

4.1.1 General ............................................................................................................................... 36 4.1.2 Definition of a business and related framework ................................................................. 37 4.1.3 Screen ................................................................................................................................ 39 4.1.4 Inputs and processes ......................................................................................................... 42 4.1.5 Outputs ............................................................................................................................... 43 4.1.6 Acquired set includes outputs ............................................................................................ 44 4.1.7 Acquired set does not include outputs ............................................................................... 47

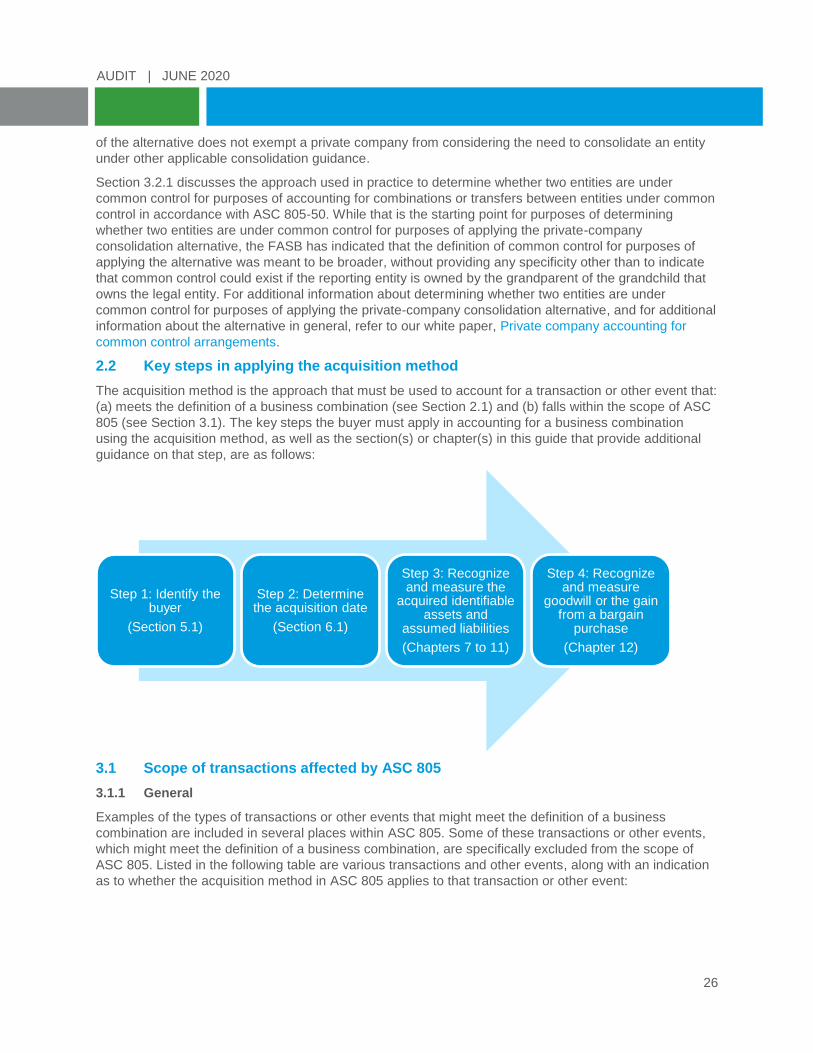

4.2 Other guidance that relies on the definition of a business used in ASC 805........................... 48 4.3 Timing of determining whether a business was acquired ......................................................... 48 5.1 Identifying the buyer ...................................................................................................................... 49 5.2 Reverse acquisitions ...................................................................................................................... 50 6.1 Determining the acquisition date .................................................................................................. 51

ii

AUDIT | JUNE 2020

General guidance on recognition and measurement of assets acquired, liabilities assumed and NCI ....................................................................................................................52 7.1 Initial recognition of assets, liabilities and any NCI .................................................................... 52

7.1.1 General ............................................................................................................................... 52 7.1.2 Definitions of assets and liabilities ..................................................................................... 52 7.1.3 Part of business combination or separate transaction? ..................................................... 53

8.1 Initial measurement of assets, liabilities and any NCI ................................................................ 53 8.1.1 General ............................................................................................................................... 53 8.1.2 Definition of fair value ......................................................................................................... 54

8.2 Subsequent accounting guidance ................................................................................................ 55 9.1 Buyer’s classification or designation of acquired assets and assumed liabilities ................. 55

Specific application of general recognition and (or) measurement guidance ....................57 10.1 Application of general recognition and measurement principles ............................................. 57 10.2 Application of measurement guidance: Fair value of assets based on highest and

best use ........................................................................................................................................... 57 10.3 Accounts and loans receivable ..................................................................................................... 60

10.3.1 General ............................................................................................................................... 60 10.3.2 ASC 326: General information and effective date .............................................................. 60 10.3.3 Additional considerations related to measuring accounts and loans receivable

acquired in a business combination prior to the adoption of ASC 326 .............................. 61 10.3.3.1 Subsequent accounting for accounts or loans receivable acquired in a

business combination prior to the adoption of ASC 326 ................................... 61 10.3.4 Additional considerations related to measuring accounts and loans receivable

acquired in a business combination after the adoption of ASC 326 .................................. 62 10.3.5 Mixed bases in accounts and loans receivable after acquisition in a business

combination ........................................................................................................................ 63 10.4 Servicing rights not contractually separated from the related financial assets ...................... 64 10.5 Investments in debt securities ...................................................................................................... 64

10.5.1 General ............................................................................................................................... 64 10.5.2 Initial measurement of investments in debt securities acquired in a business

combination ........................................................................................................................ 64 10.5.2.1 Additional considerations related to measuring investments in debt

securities acquired in a business combination prior to the adoption of

ASC 326 ............................................................................................................ 65 10.5.2.2 Additional considerations related to measuring investments in debt

securities acquired in a business combination after the adoption of

ASC 326 ............................................................................................................ 65 10.5.3 Subsequent accounting for investments in debt securities acquired in a business

combination ........................................................................................................................ 66 10.6 Customer contracts and customer relationships ....................................................................... 66

10.6.1 General ............................................................................................................................... 66 10.6.1.1 Effective date of ASC 606 ................................................................................. 67

10.6.2 Recognition of assets and liabilities related to customer contracts (including

deferred revenue) ............................................................................................................... 67 10.6.2.1 Contract liabilities acquired in a business combination ..................................... 69

10.6.3 Recognition of noncontractual customer relationships ...................................................... 70 10.6.4 Fair value measurement ..................................................................................................... 70

10.6.4.1 Measuring the fair value of contract assets and contract liabilities ................... 71

iii

AUDIT | JUNE 2020

10.6.5 Post-acquisition accounting for assets and liabilities related to customer contracts

recognized in the accounting for a business combination ................................................. 73 10.6.5.1 Derecognition of assets and liabilities related to customer contracts other

than customer relationship intangible assets .................................................... 73 10.6.5.2 Amortization of customer relationship intangible assets ................................... 77

10.6.6 Buyer is a customer of the target ....................................................................................... 78 10.6.7 Incremental costs to obtain a customer contract................................................................ 79

10.7 Inventory .......................................................................................................................................... 79 10.8 Identification of intangible assets that are separate from goodwill .......................................... 80

10.8.1 General ............................................................................................................................... 80 10.8.2 Analysis of various situations to determine whether intangible assets exist ...................... 81

10.9 Intangible assets ............................................................................................................................. 84 10.10 Defensive intangible assets .......................................................................................................... 87 10.11 Assembled workforce .................................................................................................................... 88 10.12 R&D .................................................................................................................................................. 88

10.12.1 Initial recognition of R&D assets acquired in a business combination ............................... 88 10.12.2 Subsequent accounting for R&D assets acquired, and accounted for, in a business

combination ........................................................................................................................ 89 10.12.2.1 Acquired intangible R&D assets ........................................................................ 89 10.12.2.2 Acquired R&D assets related to computer software to be sold, leased or

otherwise marketed ........................................................................................... 89 10.12.2.3 Acquired tangible R&D assets ........................................................................... 90

10.12.3 Accounting for R&D costs incurred after the business combination .................................. 90 10.13 Leases .............................................................................................................................................. 90

10.13.1 General ............................................................................................................................... 90 10.13.1.1 Effective date of ASC 842 ................................................................................. 90

10.13.2 Accounting for acquired leases in a business combination prior to the adoption of

ASC 842 ............................................................................................................................. 91 10.13.2.1 Classifying the target’s acquired leases prior to the adoption of ASC 842 ....... 91 10.13.2.2 Accounting for acquired operating leases in the business combination

prior to the adoption of ASC 842 ....................................................................... 91 10.13.2.3 Accounting for acquired leases other than operating leases in the

business combination prior to the adoption of ASC 842 ................................... 93 10.13.3 Accounting for acquired leases in a business combination after the adoption of

ASC 842 ............................................................................................................................. 94 10.13.3.1 Initial consideration when the target is the lessee after the adoption of

ASC 842 ............................................................................................................ 94 10.13.3.2 Classifying the acquired leases after the adoption of ASC 842 ........................ 94 10.13.3.3 Determining whether an acquired operating lease is favorable or

unfavorable after the adoption of ASC 842 ....................................................... 95 10.13.3.4 Determining whether an identifiable intangible asset arises from the

acquired lease after the adoption of ASC 842 .................................................. 95 10.13.3.5 Recognition and measurement for lessees after the adoption of ASC 842 ...... 95 10.13.3.6 Recognition and measurement for lessors under ASC 842 .............................. 99

10.14 Accounts payable and accrued liabilities .................................................................................... 99 10.15 Anticipated restructuring activities involving the target .......................................................... 100 10.16 AROs .............................................................................................................................................. 101 10.17 Assumed debt ............................................................................................................................... 101

iv

AUDIT | JUNE 2020

10.18 Insurance and reinsurance contracts ......................................................................................... 102 10.19 Recognition and measurement of an NCI .................................................................................. 103

10.19.1 General ............................................................................................................................. 103 10.19.2 Identification of the NCI in a target ................................................................................... 103 10.19.3 Considerations involved in estimating the fair value of an NCI ........................................ 105

10.19.3.1 General ............................................................................................................. 105 10.19.3.2 Extrapolation of an NCI’s fair value using the consideration transferred

by a buyer for its controlling interest................................................................ 106 10.19.3.3 Concurrent purchases of part of an NCI ......................................................... 106 10.19.3.4 Discounts ......................................................................................................... 107 10.19.3.5 Additional resources ......................................................................................... 110

10.19.4 Presentation of an NCI in the balance sheet .................................................................... 110 10.19.5 Disclosures about the NCI ................................................................................................ 111

Exceptions to the general recognition and (or) measurement guidance .......................... 112 11.1 Exceptions to overall recognition and measurement principles ............................................. 112 11.2 Preacquisition contingencies ...................................................................................................... 112

11.2.1 General ............................................................................................................................. 112 11.2.2 Initial accounting ............................................................................................................... 113 11.2.3 Measurement period accounting ...................................................................................... 113 11.2.4 Subsequent accounting .................................................................................................... 114 11.2.5 Income tax effects ............................................................................................................ 115 11.2.6 Disclosures ....................................................................................................................... 115

11.3 Indemnification assets ................................................................................................................. 116 11.3.1 Initial recognition and measurement ................................................................................ 116 11.3.2 Measurement period adjustments .................................................................................... 117 11.3.3 Subsequent measurement ............................................................................................... 117 11.3.4 Collectibility and contractual limitations ............................................................................ 118 11.3.5 Derecognition ................................................................................................................... 118 11.3.6 Disclosures ....................................................................................................................... 118

11.4 Income taxes ................................................................................................................................. 118 11.4.1 General ............................................................................................................................. 118

11.4.1.1 Acquisition treated as taxable or nontaxable transaction ................................ 119 11.4.2 Acquisition-date accounting: Acquired temporary differences and loss or credit

carryforwards .................................................................................................................... 120 11.4.2.1 Recognition of valuation allowances on deferred tax assets, including

consideration of deferred tax assets and liabilities with indefinite

reversal patterns .............................................................................................. 122 11.4.3 Acquisition-date accounting: Change in buyer’s preexisting valuation allowance ........... 125 11.4.4 Acquisition-date and subsequent accounting: Tax treatment of contingent

consideration .................................................................................................................... 126 11.4.4.1 Acquisition-date accounting: Contingent consideration in a taxable

transaction ....................................................................................................... 126 11.4.4.2 Subsequent accounting: Contingent consideration in a taxable

transaction ....................................................................................................... 126 11.4.4.3 Contingent consideration in a nontaxable transaction .................................... 129 11.4.4.4 Tax issue related to resolution of a specific tax position that could give

rise to contingent consideration ....................................................................... 129

v

AUDIT | JUNE 2020

11.4.4.5 Tax issue related to 338 election that should not give rise to contingent

consideration ................................................................................................... 129 11.4.5 Acquisition-date accounting: Difference between tax-deductible goodwill and

goodwill for book purposes ............................................................................................... 130 11.4.6 Acquisition-date accounting: Tax treatment of transaction costs ..................................... 132 11.4.7 Subsequent accounting: Change in valuation allowance or uncertain tax positions

that were recorded in the acquisition-date accounting ..................................................... 133 11.4.7.1 Change in valuation allowance recorded on acquisition date ......................... 133 11.4.7.2 Change in uncertain tax positions ................................................................... 134

11.5 Employee benefits ........................................................................................................................ 134 11.5.1 Defined benefit pension and postretirement plans ........................................................... 134 11.5.2 Other employee benefits .................................................................................................. 135

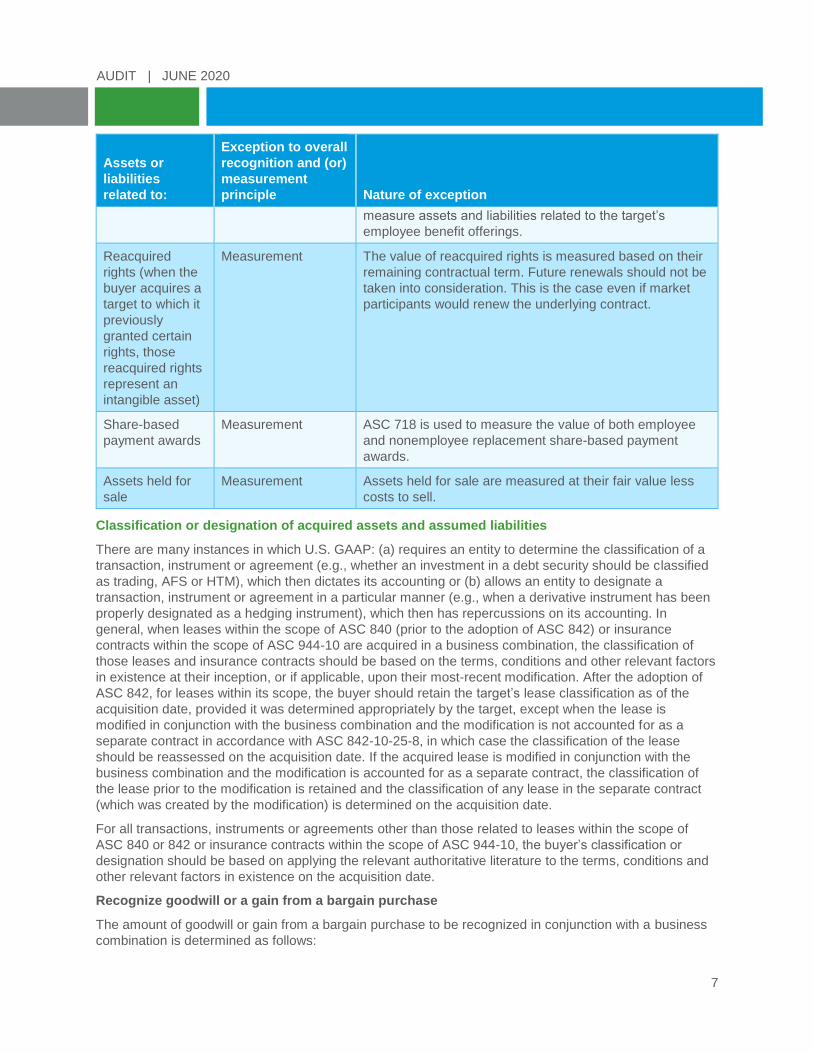

11.6 Reacquired rights ......................................................................................................................... 136 11.6.1 Definition ........................................................................................................................... 136 11.6.2 Initial accounting ............................................................................................................... 136 11.6.3 Subsequent accounting .................................................................................................... 136

11.7 Share-based payment awards ..................................................................................................... 136 11.8 Assets held for sale ...................................................................................................................... 137

Elements and results of goodwill calculation ..................................................................... 138 12.1 Determining whether goodwill or a bargain purchase exists and the related amount ......... 138 12.2 Additional considerations in a bargain purchase ..................................................................... 140

12.2.1 General ............................................................................................................................. 140 12.2.2 Frequency of bargain purchases ...................................................................................... 141

12.3 Consideration transferred............................................................................................................ 141 12.3.1 General ............................................................................................................................. 141

12.3.1.1 Buyer pays off seller’s debt ............................................................................. 142 12.3.1.2 Consideration transferred held in escrow ........................................................ 143

12.3.2 Measurement basis .......................................................................................................... 144 12.3.3 Equity securities transferred ............................................................................................. 145

12.3.3.1 Rollover equity ................................................................................................. 146 12.3.3.2 Preferred shares .............................................................................................. 148

12.3.4 Consideration is paid before control is obtained .............................................................. 148 12.4 Contingent consideration ............................................................................................................ 149

12.4.1 General ............................................................................................................................. 149 12.4.2 Initial accounting and classification .................................................................................. 149 12.4.3 Reassessment of classification ........................................................................................ 152 12.4.4 Ongoing accounting ......................................................................................................... 152

12.4.4.1 Measurement period adjustments affecting contingent consideration ............ 152 12.4.4.2 Subsequent accounting guidance applicable to contingent

consideration ................................................................................................... 153 12.4.4.3 Removal of a contingent consideration liability from the buyer’s books.......... 153

12.4.5 Income tax effects ............................................................................................................ 153 12.4.6 Classification of cash payment for contingent consideration on the cash flow

statement .......................................................................................................................... 154 12.4.7 Disclosures ....................................................................................................................... 155 12.4.8 Counterintuitive nature of subsequent accounting guidance applicable to contingent

consideration .................................................................................................................... 157

vi

AUDIT | JUNE 2020

12.4.9 Contingent consideration arrangements of the target ...................................................... 158 12.4.10 Seller’s accounting for contingent consideration .............................................................. 158

12.5 No consideration is transferred .................................................................................................. 160 12.6 Business combinations achieved in stages (i.e., step acquisitions) ...................................... 163

12.6.1 General ............................................................................................................................. 163 12.6.2 Determining fair value of buyer’s PHEI in target .............................................................. 164

12.7 Provisional amounts and measurement period adjustments .................................................. 166 12.7.1 General ............................................................................................................................. 166

12.7.1.1 What are provisional amounts, the measurement period and

measurement period adjustments? ................................................................. 166 12.7.1.2 What disclosures should be provided for provisional amounts and

measurement period adjustments and why are those disclosures

important? ........................................................................................................ 168 12.7.1.3 What are the financial reporting implications of recording a

measurement period adjustment? ................................................................... 168 12.7.1.4 Which items could be the subject of a measurement period

adjustment? ..................................................................................................... 169 12.7.2 Thought process ............................................................................................................... 169 12.7.3 Accounting consequences ............................................................................................... 170 12.7.4 Additional examples ......................................................................................................... 172 12.7.5 Disclosures ....................................................................................................................... 172

12.8 Assigning goodwill to reporting units ........................................................................................ 172 12.9 Assigning goodwill and intangible assets to foreign subsidiaries ......................................... 173 12.10 Working capital adjustments ....................................................................................................... 173

12.10.1 Description and example .................................................................................................. 173 12.10.2 Accounting guidance ........................................................................................................ 174

Determining what is part of the business combination ...................................................... 176 13.1 Determining what is or is not part of the business combination ............................................ 176 13.2 Effective settlement of preexisting relationship between buyer and target and (or)

sellers............................................................................................................................................. 178 13.3 Arrangements with employees and sellers of target ................................................................ 181

13.3.1 General ............................................................................................................................. 181 13.3.1.1 Payment is forfeited upon termination of employment .................................... 182 13.3.1.2 Payment is not forfeited upon termination of employment .............................. 182

13.3.2 Disclosures ....................................................................................................................... 186 13.4 Apportioning replacement awards between consideration transferred and

compensation and other costs for goods or services .............................................................. 187 13.4.1 Grantee is an employee ................................................................................................... 187 13.4.2 Grantee is a nonemployee ............................................................................................... 190 13.4.3 Treatment of forfeitures in replacement share-based payment awards .......................... 192

13.5 Transaction costs ......................................................................................................................... 193 13.5.1 General ............................................................................................................................. 193 13.5.2 Transaction costs paid by the seller or target .................................................................. 194 13.5.3 Transaction costs paid by related party ........................................................................... 194 13.5.4 Fees for multiple services ................................................................................................. 195 13.5.5 Acquisition services provided by related party ................................................................. 197 13.5.6 Buyer pays sellers’ transaction costs ............................................................................... 198

vii

AUDIT | JUNE 2020

13.6 Determining whether a restructuring is part of a business combination ............................... 199

Disclosures ........................................................................................................................... 203 14.1 Disclosure principles ................................................................................................................... 203 14.2 Disclosures for business combinations occurring during the reporting period ................... 203

14.2.1 Overview ........................................................................................................................... 203 14.2.2 General information .......................................................................................................... 204 14.2.3 Goodwill or a gain from a bargain purchase .................................................................... 204 14.2.4 Consideration transferred ................................................................................................. 205 14.2.5 Specific assets, liabilities and any NCI ............................................................................. 206 14.2.6 Provisional amounts ......................................................................................................... 208 14.2.7 Reduction in the buyer’s preexisting deferred tax asset valuation allowance .................. 209 14.2.8 Separate transactions ...................................................................................................... 209 14.2.9 Step acquisitions .............................................................................................................. 209 14.2.10 Public company ................................................................................................................ 210

14.3 Disclosures when a business combination occurs after the end of the reporting

period, but before the financial statements are issued or available to be issued ................. 210 14.4 Disclosures about adjustments made to amounts recorded in the accounting for

business combinations ................................................................................................................ 210 14.4.1 General ............................................................................................................................. 210 14.4.2 Measurement period adjustments .................................................................................... 211 14.4.3 Contingent consideration adjustments ............................................................................. 211 14.4.4 Goodwill adjustments ....................................................................................................... 211

14.5 Disclosure illustrations ................................................................................................................ 212 14.6 Disclosures upon initial consolidation of a VIE ........................................................................ 213 14.7 Fair value disclosures .................................................................................................................. 213

Other topics ........................................................................................................................... 215 15.1 Asset acquisitions ........................................................................................................................ 215

15.1.1 Overview ........................................................................................................................... 215 15.1.2 Determine the cost of the acquisition ............................................................................... 218

15.1.2.1 Acquirer incurs liabilities or issues equity ....................................................... 218 15.1.2.2 Acquirer surrenders nonfinancial assets or in substance nonfinancial

assets .............................................................................................................. 218 15.1.2.3 Contingent consideration ................................................................................. 218 15.1.2.4 Transaction costs ............................................................................................ 218

15.1.3 Identify and measure the assets acquired and liabilities assumed .................................. 218 15.1.3.1 Intangible assets (including an assembled workforce).................................... 219 15.1.3.2 Defensive intangible assets ............................................................................. 219 15.1.3.3 IPR&D .............................................................................................................. 219 15.1.3.4 Contingencies .................................................................................................. 220 15.1.3.5 Indemnifications............................................................................................... 220 15.1.3.6 Deferred taxes ................................................................................................. 220

15.1.4 Allocate the cost of the acquisition to the acquired assets and assumed liabilities ......... 221 15.1.5 Presentation and disclosure ............................................................................................. 223

16.1 Changes in buyer’s ownership interest in target after a business combination ................... 223 16.1.1 Increases in parent’s ownership interest in subsidiary ..................................................... 224 16.1.2 Decreases in parent’s ownership interest in subsidiary ................................................... 224

viii

AUDIT | JUNE 2020

17.1 Private-company intangible asset alternative ........................................................................... 228 17.1.1 General ............................................................................................................................. 228 17.1.2 Scope ............................................................................................................................... 228 17.1.3 CRI assets ........................................................................................................................ 229 17.1.4 Assets arising from NCAs ................................................................................................ 234 17.1.5 Disclosures ....................................................................................................................... 234 17.1.6 Effective date and transition ............................................................................................. 235 17.1.7 Considerations related to the election of the intangible asset alternative ........................ 235

18.1 Private-company goodwill alternative ........................................................................................ 235 18.1.1 General ............................................................................................................................. 235

18.1.1.1 ASU 2017-04 ................................................................................................... 236 18.1.2 Scope ............................................................................................................................... 237 18.1.3 Amortization...................................................................................................................... 237 18.1.4 Unit of account for impairment testing .............................................................................. 238 18.1.5 Frequency of impairment testing ...................................................................................... 238 18.1.6 Impairment testing and recognition .................................................................................. 238

18.1.6.1 Deferred taxes ................................................................................................. 239 18.1.7 Sequencing of impairment testing .................................................................................... 240 18.1.8 Derecognition ................................................................................................................... 240 18.1.9 Presentation ..................................................................................................................... 240 18.1.10 Disclosure ......................................................................................................................... 241 18.1.11 Effective date and transition ............................................................................................. 241 18.1.12 Considerations related to the election of the goodwill alternative .................................... 241

Appendix A: Application checklist for ASC 805 ................................................................. 243

Appendix B: ASC 805 disclosure checklists and illustration ............................................ 271

Appendix C: Pushdown accounting .................................................................................... 287

Appendix D: Audit implications of business combinations ............................................... 294

EXAMPLES

Example 3-1: Determining whether entities are under common control ................................................. 30 Example 3-2: Transfer between entities under common control ............................................................. 32 Example 3-3: Determining whether entities have a high degree of common ownership ........................ 35 Example 4-1: Acquisition of homes with in-place leases ........................................................................ 40 Example 4-2: Quantitative application of the screen ............................................................................... 41 Example 4-3: Acquisition of homes and an office park, both with in-place leases (without

employees) ........................................................................................................................ 44 Example 4-4: Acquisition of homes and office park, both with in-place leases (with employees) .......... 45 Example 4-5: Acquisition of brands ......................................................................................................... 46 Example 4-6: Acquisition of a manufacturing facility ............................................................................... 47 Example 10-1: Land acquired in a business combination ......................................................................... 58 Example 10-2: IPR&D acquired in a business combination ...................................................................... 59 Example 10-3: Recognition of a contract liability for a customer contract acquired in a business

combination ....................................................................................................................... 72 Example 10-4: Construction contract acquired in a business combination .............................................. 74 Example 10-5: Straight-line rent liability prior to the adoption of ASC 842 ............................................... 92

ix

AUDIT | JUNE 2020

Example 10-6: Accounting for an operating lease acquired in a business combination in which the

target is the lessee after the adoption of ASC 842 ........................................................... 98 Example 10-7: Fair value of NCI ............................................................................................................. 106 Example 11-1: Litigation contingency ..................................................................................................... 115 Example 11-2: Accounting for an acquired temporary difference related to a preacquisition

contingency ..................................................................................................................... 121 Example 11-3: Accounting for an acquired NOL carryforward ................................................................ 122 Example 11-4: Recognizing a valuation allowance on deferred tax assets, including consideration

of deferred tax assets and liabilities with indefinite reversal patterns ............................. 123 Example 11-5: Calculation of deferred tax asset and goodwill when there is contingent

consideration ................................................................................................................... 126 Example 11-6: Accounting for the deferred tax effects of subsequent adjustments to contingent

consideration ................................................................................................................... 127 Example 11-7: Calculation of deferred tax asset and goodwill for book purposes when there is an

excess of tax-deductible goodwill over goodwill for book purposes ............................... 131 Example 11-8: Accounting for the tax effects of nondeductible transaction costs .................................. 132 Example 11-9: Change in a deferred tax asset valuation allowance recognized in the accounting

for the business combination .......................................................................................... 133 Example 12-1: Determination of goodwill ................................................................................................ 139 Example 12-2: Effects of seller-financed debt on the accounting for a business combination ............... 144 Example 12-3: Classification of payment for contingent consideration in the cash flow statement

when the amount ultimately paid is more than what was recognized in the

accounting for the business combination ........................................................................ 154 Example 12-4: Classification of payment for contingent consideration in the cash flow statement

when the amount ultimately paid is less than what was recognized in the

accounting for the business combination ........................................................................ 155 Example 12-5: Adjustments to contingent consideration ........................................................................ 155 Example 12-6: Buyer obtains control as a result of Target’s acquisition of its own shares .................... 161 Example 12-7: Buyer obtains control through contract alone ................................................................. 162 Example 12-8: Step acquisition ............................................................................................................... 165 Example 12-9: Provisional and measurement period accounting for manufacturing facility................... 170 Example 13-1: Settlement of preexisting noncontractual relationship for which an asset or liability

had not been recognized by the buyer............................................................................ 179 Example 13-2: Settlement of preexisting noncontractual relationship for which an asset or liability

had been recognized by the buyer .................................................................................. 179 Example 13-3: Settlement of preexisting supply agreement (loss for unfavorable amount)................... 180 Example 13-4: Settlement of preexisting supply agreement (loss for contract cancellation fee) ........... 181 Example 13-5: Payments to employee in connection with acquisition.................................................... 185 Example 13-6: Payments to employee and other shareholders in connection with acquisition ............. 185 Example 13-7: Sales agreement entered into with sellers on the acquisition date ................................. 186 Example 13-8: Various replacement awards granted to employees ....................................................... 188 Example 13-9: Various replacement awards granted to nonemployees ................................................. 191 Example 13-10: Transaction costs paid by buyer and transaction costs paid by seller ............................ 194 Example 13-11: Fees for multiple services ............................................................................................... 196 Example 13-12: Parent pays subsidiary’s transaction costs ..................................................................... 198 Example 13-13: Buyer pays Sellers’ transaction costs ............................................................................. 198 Example 13-14: Restructuring activities in three scenarios ...................................................................... 199 Example 15-1: Accounting for an asset acquisition ................................................................................ 222

x

AUDIT | JUNE 2020

Example 16-1: Increase in parent’s ownership interest in existing subsidiary ........................................ 224 Example 16-2: Decrease in parent’s ownership interest in existing subsidiary while maintaining

control ............................................................................................................................. 226 Example 16-3: Parent loses control of subsidiary ................................................................................... 227 Example C-1: Pushdown accounting ..................................................................................................... 292

QUESTIONS

4Q.1.2.1 If the seller did not operate the acquired set as a business, does that mean the acquired

set is not a business? .............................................................................................................. 38

4Q.1.2.2 If the buyer does not intend to operate the acquired set as a business, can it assume it

is not a business? .................................................................................................................... 38

4Q.1.2.3 Must the acquisition result in the recognition of goodwill for the acquired set to be

considered a business? ........................................................................................................... 39

4Q.1.2.4 Could the purchase of an individual franchise by the franchisor be considered a

business? ................................................................................................................................. 39

4Q.1.4.1 Must the acquired set include employees to be considered a business? ............................... 42

4Q.1.4.2 Must the acquired set have liabilities to be a business? ......................................................... 42

4Q.1.4.3 Must the acquired set include all of the inputs and processes necessary to produce

outputs? ................................................................................................................................... 42

5Q.1.1 Are there additional factors to consider in determining who the buyer is in a business

combination that involves more than two combining entities? ................................................ 50

5Q.1.2 If a new entity is formed to achieve a business combination (through its acquisition of a

target), should that new entity be considered the buyer? ....................................................... 50

5Q.1.3 Can one of the combining entities in a business combination be identified as the buyer

for legal purposes and the target for accounting purposes? ................................................... 50

5Q.1.4 Does ASC 805 provide any additional factors that should be considered in determining

who the buyer is in a combination involving mutual entities? .................................................. 50

10Q.6.2.1 Is it appropriate to combine a receivable related to a customer contract acquired in a

business combination with a contract asset or other intangible asset recognized related

to that customer contract? ....................................................................................................... 69

10Q.6.2.2 Is it appropriate to combine a customer relationship intangible asset with another

intangible asset recognized for the customer contract in the accounting for the business

combination? ........................................................................................................................... 69

10Q.6.2.3 Should an off-market contract intangible asset or a backlog intangible asset be

recognized even if the underlying customer contract or backlog of sales or purchase

orders cannot be transferred to another party? ....................................................................... 69

10Q.6.2.4 What is the effect of the target’s order or production backlog being cancelable? ................... 69

10Q.8.1.1 How does the buyer’s intention with respect to selling, transferring, licensing, leasing or

otherwise exchanging the intangible asset affect the determination as to whether that

asset is separable? .................................................................................................................. 81

10Q.8.1.2 What type of support demonstrates that an intangible asset is actually separable? .............. 81

xi

AUDIT | JUNE 2020

10Q.8.1.3 Why is an asset that can only be sold along with a related contract, asset or liability

considered separable? ............................................................................................................ 81

10Q.8.1.4 If an intangible asset is recognized for a license that gives the target the right to own

and operate a particular type of facility (e.g., license to own and operate a nuclear

power plant), when the buyer recognizes the intangible asset for that license may it

recognize one asset for the combined fair values of the facility and the license? .................. 81

10Q.8.1.5 If the buyer concludes on the date of acquisition that an identifiable intangible asset

does not exist for a particular item, but shortly after that date there is a change in

circumstances and an identifiable intangible asset does exist for that item, should the

buyer reclassify the fair value of the identifiable intangible asset out of goodwill? ................. 81

10Q.9.1 What is the effect of one of the identifiable intangible assets in the list having

characteristics of assets other than those of intangible assets? ............................................. 87

10Q.9.2 If the target has a group of complementary identifiable intangible assets, such as: (a) a

trademark, trade name and formulas or (b) a copyright and any related assignments or

license agreements, may those individual assets be accounted for as a single asset? ......... 87

10Q.9.3 Could some of the items in this list result in a liability being recognized instead of an

identifiable intangible asset? ................................................................................................... 87

10Q.17.1 If the buyer in a business combination assumes the target’s debt, should the target’s

unamortized debt issuance costs be recognized in the buyer’s accounting for the

business combination? .......................................................................................................... 102

10Q.17.2 If a target issues standalone financial statements subsequent to being acquired, how

is the amount of debt included in those standalone financial statements affected by the

business combination? .......................................................................................................... 102

11Q.2.1.1 Does the accounting for a warranty obligation acquired in a business combination

depend on whether it is an assurance-type or service-type warranty? ................................. 112

11Q.2.4.1 What accounting policies could the buyer use with respect to the subsequent

accounting for contingent liabilities initially recognized at fair value in the accounting

for a business combination? .................................................................................................. 114

11Q.2.4.2 When a contingent liability is initially recognized at fair value in the accounting for a

business combination, may the subsequent accounting policy for that liability be based

on ASC 450? ......................................................................................................................... 114

11Q.2.4.3 When a contingent liability is initially recognized at fair value in the accounting for a

business combination, may the buyer subsequently account for the contingent liability

at fair value? .......................................................................................................................... 114

11Q.2.4.4 When a contingent liability is initially recognized at its reasonably estimable amount in

the accounting for a business combination, should the buyer subsequently account for

that contingent liability using the guidance in ASC 450? ...................................................... 115

15Q.1.1.1 If the net assets acquired in an asset acquisition are in a legal entity that was

purchased by the acquirer for which separate financial statements will be prepared,

may the asset acquisition be pushed down to the separate financial statements of the

acquired legal entity? ............................................................................................................. 217

15Q.1.1.2 What are the accounting implications for an asset acquisition between parties under

common control? ................................................................................................................... 217

xii

AUDIT | JUNE 2020

17Q.1.3.1 What is the difference between the recognition criterion for CRI assets under the

intangible asset alternative and the general recognition criteria for CRI assets in

ASC 805? .............................................................................................................................. 229

17Q.1.3.2 Why did the FASB exclude contract assets from the scope of the intangible asset

alternative (indicating that such assets should continue to be recognized as otherwise

appropriate)? ......................................................................................................................... 230

17Q.1.3.3 Should contractual-legal CRI assets (e.g., backlog, above-market customer contracts)

continue to be recognized if a private company elects the intangible asset alternative?...... 230

17Q.1.3.4 What does it mean to say that a CRI asset can be sold or licensed separate from other

assets of the business? ......................................................................................................... 230

17Q.1.3.5 What are examples of CRI assets that can be sold or licensed separate from other

assets of the business? ......................................................................................................... 231

17Q.1.3.6 How are the recognition of intangible assets for customer relationships and customer

information (e.g., customer lists) interrelated? ...................................................................... 231

17Q.1.3.7 Should a customer relationship intangible asset be recognized under the intangible

asset alternative when the target has a history of entering into contracts with a

customer (even though no contracts with the customer exist at the acquisition date)? ........ 231

17Q.1.3.8 Does a private company still have to recognize a liability for a below-market (i.e.,

unfavorable) customer contract if it elects the intangible asset alternative? ......................... 232

17Q.1.3.9 Given that paragraph BC17 of ASU 2014-18 indicates that “[c]ustomer-related

intangible assets often will not meet the criterion for recognition,” is it appropriate to

forgo the analysis of customer contracts and the identification of CRI assets when

accounting for a business combination? In other words, is it acceptable to assume

that a private company has not acquired any CRI assets that should be recognized

when it has elected the intangible asset alternative? ............................................................ 232

17Q.1.3.10 Given that paragraph BC21 of ASU 2014-18 indicates that “it is inappropriate to

classify a contract asset as a customer-related intangible asset at the acquisition

date when the contract asset will eventually be reclassified as a receivable,” should a

backlog intangible asset not be classified as a CRI asset (which would make it

ineligible to be subsumed into goodwill under the intangible asset alternative) because

it will eventually lead to a receivable? ................................................................................... 232

17Q.1.3.11 How should a private company evaluate noncontractual customer relationships for

recognition under the intangible asset alternative? ............................................................... 232

17Q.1.3.12 Can a private-company lessor apply the intangible asset alternative to its leases? ............. 233

17Q.1.3.13 How does the intangible asset alternative affect the recognition of a bargain purchase

gain? ...................................................................................................................................... 233

17Q.1.3.14 Does a private company’s election of the intangible asset alternative mean it no longer

has to perform valuations (or have valuations performed) for purposes of accounting

for a business combination? .................................................................................................. 233

17Q.1.3.15 When valuing other assets acquired in the business combination, will it be necessary

to estimate the fair value of CRI assets that are being subsumed into goodwill under

the intangible asset alternative? ............................................................................................ 233

xiii

AUDIT | JUNE 2020

CQ.3.1 If the target does not make the election to apply pushdown accounting before it

issues or makes available for issuance its financial statements for the reporting period

in which the buyer obtained control, is it precluded from electing pushdown accounting

at a later point in time? .......................................................................................................... 288

CQ.3.2 May one of the target’s subsidiaries apply pushdown accounting in its standalone

financial statements? ............................................................................................................. 289

CQ.3.3 If the target or one of its subsidiaries elects to apply pushdown accounting, may it later

decide to reverse its election? ............................................................................................... 289

CQ.3.4 If control of the target has changed hands multiple times, is the target allowed to apply

pushdown accounting in only some (i.e., not all) cases in which a buyer obtains

control? .................................................................................................................................. 289

CQ.3.5 May the target apply pushdown accounting if the owner of target sells its controlling

financial interest to multiple unrelated buyers such that no one buyer obtains control

over the target? ..................................................................................................................... 289

CQ.4.1 Does the goodwill recognized by the buyer get pushed down to the target’s

standalone financial statements? .......................................................................................... 290

CQ.4.2 Does a bargain purchase gain recognized by the buyer get pushed down to the

target’s standalone financial statements? ............................................................................. 290

CQ.4.3 Should the buyer’s transaction costs be pushed down to the target? ................................... 290

CQ.4.4 What does the equity section of the target’s standalone balance sheet consist of after

pushdown accounting is applied?.......................................................................................... 290

CQ.4.5 How should the effects of pushdown accounting on the target’s equity be reflected in

its standalone statement of stockholders’ equity? ................................................................. 290

1

AUDIT | JUNE 2020

Executive summary

Introduction

The current guidance on accounting for business combinations is captured in ASC 805. Some of the

complexities involved in applying ASC 805 include the following:

The required use of a fair-value model to account for business combinations often requires the

involvement of valuation specialists—both related to management’s accounting for a business

combination and the auditor’s testing of the amounts recognized.

It is extremely important for the buyer to determine as early in the acquisition process as possible

whether it has acquired a business within the scope of the business combination accounting

guidance, because whether a business has been acquired or not has significant accounting

implications.

The definition of a business is one of the more challenging aspects of the business combination

accounting guidance to implement in practice because that definition encompasses much more than

just a group of assets or net assets that could function together as a standalone business. A

significant amount of judgment may need to be exercised in determining whether a business has

been acquired.

The accounting for contingent consideration involves a number of potentially complex steps, including

measuring it at fair value initially, classifying it appropriately as either an asset, liability or equity and

subsequently adjusting it to fair value if it is classified as an asset or liability.

These observations and many others underscore the importance of a buyer familiarizing itself with the

business combination accounting guidance before a business combination occurs. Doing so will allow the

buyer to prepare for the accounting challenges that await. This summary provides the buyer with the start

it needs—an overview of the accounting guidance applicable to business combinations entered into by

for-profit entities.

To locate additional information on specific aspects of the business combination accounting guidance,

refer to the table of contents. In addition, refer to Section 1.1.4 of the guide for definitions of acronyms

and titles for authoritative and other literature references utilized throughout the guide, including this

summary.

Scope

A business combination occurs when the buyer obtains control of a business through a transaction or

other event. The three key elements in the definition of a business combination are the following:

1. That which is being acquired must meet the definition of a business. ASC 805-10-55-3A defines a

business as “an integrated set of activities and assets that is capable of being conducted and

managed for the purpose of providing a return in the form of dividends, lower costs, or other

economic benefits directly to investors or other owners, members, or participants.” The framework

provided to determine whether a business (rather than a group of assets or net assets) was acquired

requires consideration of whether substantially all of the fair value of the gross assets acquired are

concentrated in a single identifiable asset or a group of similar identifiable assets. If that is the case,

then a business was not acquired. If that is not the case, the framework requires consideration as to

whether the acquired set has at least one input and one substantive process. If that is not the case, a

business was not acquired. If that is the case, then the specific criteria that must be considered to

determine whether the acquired set is a business depend on whether the acquired set has outputs.

The threshold for concluding the acquired set is a business is higher when the acquired set does not

have outputs because the acquired set must include employees that form an organized workforce

when that is the case. Employees that form an organized workforce do not necessarily have to be in

2

AUDIT | JUNE 2020

the acquired set to conclude it is a business when that set includes outputs. While employees that

form an organized workforce may play a critical role in determining whether an acquired set is a

business, it is important to keep in mind that an intangible asset for an assembled workforce is not

recognized in the accounting for a business combination

2. The buyer must obtain control of a business. To evaluate whether control of a business has been

obtained when the buyer is a for-profit entity, it must first determine whether the business is a VIE. If

so, the buyer must apply the guidance in ASC 810-10 to determine whether it has a controlling

financial interest in the VIE. If the buyer obtains a controlling financial interest in a business that is a

VIE, the transaction or other event giving rise to that controlling financial interest should be accounted

for as a business combination. If the business is not a VIE (e.g., it is a voting interest entity), the

buyer must determine whether it has obtained control over the business using the same definition of

control that is used in determining whether a voting interest entity should be consolidated. Under this

definition, depending on the facts and circumstances, control may be obtained in several ways,

including through the acquisition of a majority ownership interest in the target or as a result of minority

veto rights lapsing. In addition, when the target is a limited partnership, the buyer must consider

whether it holds a majority of the partnership’s kick-out rights as a result of its acquisition of voting

interests in that partnership.

3. Control can be obtained by the buyer through a transaction or other event. An event other than a

transaction may occur through no direct action of the buyer. For example, the buyer may obtain

control of an investee as a result of that investee acquiring its own shares, which has the effect of

increasing the buyer’s ownership interest to that of a controlling interest. Assume that an investor

owns 60,000 shares in a business and the business has 150,000 shares outstanding. In this situation,

the investor owns a 40% interest in the business and accounts for its investment using the equity

method. If the business buys or redeems 50,000 of its own shares from other investors, those shares

are retired or become treasury shares and are no longer considered outstanding. As a result, the

investor’s ownership interest in the business increases to 60% (the investor’s 60,000 shares in the

business divided by 100,000 shares outstanding). This example illustrates that an investor can

become a buyer by obtaining control without transferring consideration and without undertaking any

other direct action on its own behalf and be subject to the business combination accounting guidance.

Transactions that meet the definition of a business combination include, but are not limited to: (a)

leveraged buyouts, (b) combinations between two or more mutual entities and (c) initial consolidation of a

VIE when the VIE and PB are not under common control and the VIE is a business. Even if a transaction

or other event satisfies the definition of a business combination, there are specific types of transactions

explicitly excluded from the scope of the business combination accounting guidance in ASC 805.

Examples include combinations between not-for-profit entities and combinations between entities under

common control. Accounting for mergers and acquisitions of not-for-profit entities is covered in ASC 954-

805 and 958-805. Accounting for combinations or transfers between entities under common control is

covered in ASC 805-50.

Determining whether a transaction or other event should be accounted for as a business combination or

an asset acquisition has significant accounting repercussions. For example:

Goodwill is recognized in a business combination, but not in an asset acquisition.

Transaction costs are generally expensed as incurred and when the related services have been

received by the buyer in a business combination, while the same costs are generally considered part

of the cost of the assets (or net assets) in an asset acquisition.

Assets acquired and liabilities assumed in a business combination are measured predominantly at

fair value, while assets acquired and liabilities assumed in an asset acquisition are measured by

allocating the total cost of the acquisition to the assets acquired and liabilities assumed on a relative

fair value (or other appropriate amount) basis.

3

AUDIT | JUNE 2020

These are but a few of the reasons why it is important to draw the appropriate conclusion about whether a

business combination occurred.

It is also important to note that the definition of a business used for purposes of determining whether a

business combination has occurred is also used in other accounting determinations. For example, the

definition of a business discussed herein is also used in determining:

What constitutes a reporting unit for purposes of goodwill impairment testing (unless goodwill

impairment testing is performed at the entity level as permitted under the private-company goodwill

alternative [see Section 18.1 of the guide])

What constitutes a business for purposes of a scope exception to the guidance on VIEs included in

ASC 810-10

Whether the guidance in ASC 810-10 on how to account for decreases in a parent’s ownership

interest in a subsidiary (including decreases that result in deconsolidation) is applicable

Whether the guidance in ASC 610-20 on how to account for the derecognition of nonfinancial or in

substance nonfinancial assets is applicable to the sale of such assets

Whether a specific type of transaction is a spinoff

An entity must consistently apply the definition of a business in these and other places in U.S. GAAP in

which it is used.

Overall accounting model

The overall accounting model used to account for a business combination consists of the following four

steps:

1. Identify the buyer

2. Determine the acquisition date

3. Recognize and measure, predominantly at fair value, the assets acquired, liabilities assumed and any

NCI

4. Recognize and measure the goodwill or a gain from a bargain purchase

Identify the buyer

If the business over which control has been obtained is a VIE, the buyer is always the PB of the VIE as

determined under the VIE consolidation model. If the business over which control has been obtained is