A fractional perspective to the bond graph modelling of world economies

16

This article was downloaded by: [b-on: Biblioteca do conhecimento online UNL] On: 24 September 2013, At: 04:57 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK Business History Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/fbsh20 From finance to management: Rui Ennes Ulrich, a Portuguese scholar of the early twentieth century Maria Eugénia Mata a & J.C. Rodrigues da Costa b a Faculdade de Economia, Campus de Campolide , Universidade Nova de Lisboa , Lisbon , Portugal b Instituto Superior de Ciências do Trabalho e da Empresa , Lisbon , Portugal Published online: 12 Sep 2013. To cite this article: Maria Eugénia Mata & J.C. Rodrigues da Costa , Business History (2013): From finance to management: Rui Ennes Ulrich, a Portuguese scholar of the early twentieth century, Business History, DOI: 10.1080/00076791.2013.809525 To link to this article: http://dx.doi.org/10.1080/00076791.2013.809525 PLEASE SCROLL DOWN FOR ARTICLE Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) contained in the publications on our platform. However, Taylor & Francis, our agents, and our licensors make no representations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of the Content. Any opinions and views expressed in this publication are the opinions and views of the authors, and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon and should be independently verified with primary sources of information. Taylor and Francis shall not be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use of the Content. This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms- and-conditions

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of A fractional perspective to the bond graph modelling of world economies

This article was downloaded by: [b-on: Biblioteca do conhecimento online UNL]On: 24 September 2013, At: 04:57Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Business HistoryPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/fbsh20

From finance to management: RuiEnnes Ulrich, a Portuguese scholar ofthe early twentieth centuryMaria Eugénia Mata a & J.C. Rodrigues da Costa ba Faculdade de Economia, Campus de Campolide , UniversidadeNova de Lisboa , Lisbon , Portugalb Instituto Superior de Ciências do Trabalho e da Empresa ,Lisbon , PortugalPublished online: 12 Sep 2013.

To cite this article: Maria Eugénia Mata & J.C. Rodrigues da Costa , Business History (2013): Fromfinance to management: Rui Ennes Ulrich, a Portuguese scholar of the early twentieth century,Business History, DOI: 10.1080/00076791.2013.809525

To link to this article: http://dx.doi.org/10.1080/00076791.2013.809525

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoeveror howsoever caused arising directly or indirectly in connection with, in relation to orarising out of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

From finance to management: Rui Ennes Ulrich, a Portuguese scholarof the early twentieth century

Maria Eugenia Mataa* and J.C. Rodrigues da Costab

aFaculdade de Economia, Campus de Campolide, Universidade Nova de Lisboa, Lisbon, Portugal;bInstituto Superior de Ciencias do Trabalho e da Empresa, Lisbon, Portugal

Finance is usually considered to be a complex science, made up of unsatisfactoryexplanations interpreting the mystery and volatility of financial markets. Expectations,the mood of the market, as well as investment strategies to manage diversifiedportfolios, are intimidating issues for most people even today. This paper describeshow early twentieth-century globalisation framed a network of stock exchanges, fromlocal to regional and national scale, stimulating scientific knowledge on equities,shares, securities, bonds, debentures, transactions, and risk premiums. Both individualsand institutional investors needed financial education. In Portugal Ruy Ennes Ullrichwrote his doctoral dissertation on stock exchanges and financial markets. His bookwas published in Coimbra in 1906, by the University Press. This paper analyseshis contributions in the context of the available literature, and his managementperformance.

Keywords: finance; stock exchanges; management; social elites; Portugal

1. Introduction

The early twentieth century was a very special moment for Europe regarding its capacity

to lead world trade, export capital to all continents, and advance a number of free-standing

companies to operate in the global context.1 British leadership in industrialisation and the

catching-up process followed by other nations dominated the international scene and

contributed mightily to the expanding globalisation process.2 Railways already crossed all

continents, sail and steam shipping connected all main seaports, trade fuelled the

international division of labour, and the adoption of the gold standard provided an accurate

system for international payments. Main actors were private corporations, operating in all

sectors, both in Europe and elsewhere.3 From mining to farming, transportation to

commerce, and industrial production to the provision of utilities, private corporations

raised large amounts of capital from a multitude of small-pocket savers who sought to

maximise their rewards in stock markets through investment as shareholders.4 Local,

regional, and national stock exchanges were part of a world network of financial

relationships, in which London and New York were the leading markets.5

Erudition and financial literature are the issues of this paper, to demonstrate how

academics soon embraced the need to formulate technical approaches for teaching and

disseminating useful, empirical knowledge. These issues were widely shared among the

community of experts, although the profession of ‘economist’ did not yet exist as a job

q 2013 Taylor & Francis

*Corresponding author. Email: [email protected]

Business History, 2013

http://dx.doi.org/10.1080/00076791.2013.809525

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

description. The sophisticated financial culture of the time resulted from an accumulated

expertise in domestic production and trade, in international commercial links, insurance

contracts, currency transactions, share trading, bond issuance, and time operations.6 A vast

financial elite operated businesses, commanding the urban centres and their role in the

large networking system of information, expectations, investment, and transactions.7

Dealers, accountants, brokers, bankers, and finance experts in general formed a technical

staff that operated according to behavioural rules derived from codes of honour intended to

inspire confidence, transparency, and trust, as the Daily Bulletins of stock markets

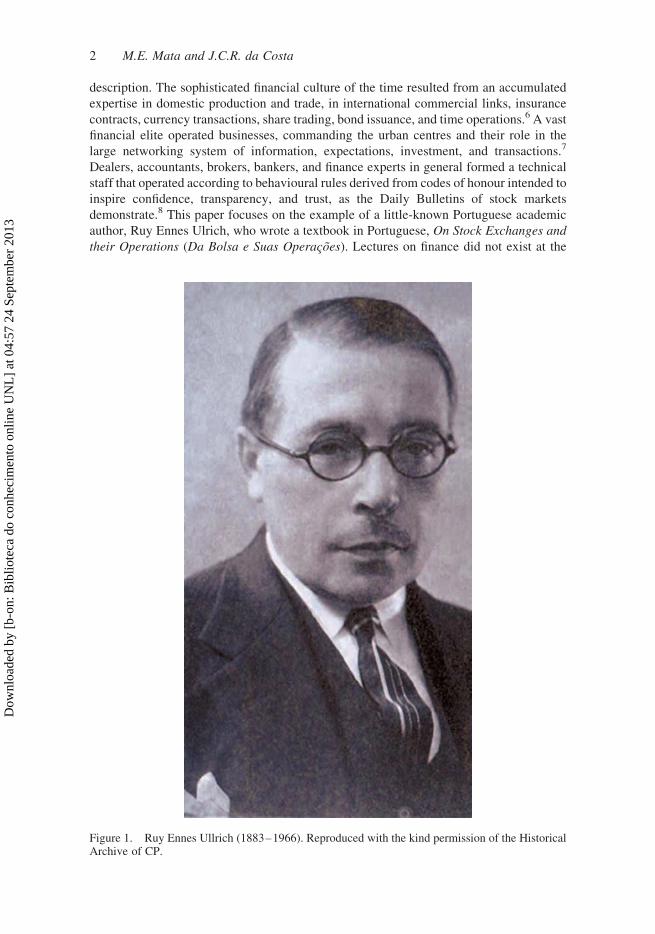

demonstrate.8 This paper focuses on the example of a little-known Portuguese academic

author, Ruy Ennes Ulrich, who wrote a textbook in Portuguese, On Stock Exchanges and

their Operations (Da Bolsa e Suas Operac�oes). Lectures on finance did not exist at the

Figure 1. Ruy Ennes Ullrich (1883–1966). Reproduced with the kind permission of the HistoricalArchive of CP.

2 M.E. Mata and J.C.R. da Costa

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

University of Coimbra (the only university that existed in Portugal), but when working

toward his PhD in 1906 at that institution, he chose stock exchanges as his dissertation

topic, with the aim of subsequently teaching a course in finance in the Law School. This

dissertation – in the form of a textbook – mentions a number of important books then

available in France, Italy, Spain, Germany, and the UK, intending to show in a simple and

pedagogical way how capital markets worked, how they were organised, how useful they

were for current life, and how they had evolved from past to present (the early 1900s).9

This article seeks to demonstrate how well-informed Ulrich was, and how

sophisticated the science of finance was at that time throughout Europe, in terms of

concepts, organisation, and empirical knowledge.

2. Finance in the early twentieth century

It is difficult to say that professional economics was already established in the early

twentieth century. The profession was populated by academic professors, but also

included businessmen (and journalists, and even public servants). Professionalisation and

professoralisation were on-going, but often teaching was not specialised.10 Recent

contributions in economics at the time were related to the theory of markets in general, and

it was possible to distinguish the Marshallian approach11 from the Austrian perspectives

provided by Menger, Wiser, and Bohm-Bawerk; while, in Switzerland, Pareto followed

Walras in framing the general equilibrium theory at the University of Lausanne.12 Thus

financial knowledge was not yet a central issue for scholars. However, it is possible to find

literature on finance, capital markets, and stock exchanges. The literature available in the

early twentieth century on stock exchanges13 had to do with legal matters: law,

government regulations, shareholders’ rights, juridical codes, and legal proceedings:14

‘We must remember that both in England and the United States the professional study of

economics was still something new that had to fight its way . . . , and that in some other

countries economics remained . . . a very minor adjunct of the study of law.’15

The early book by the Italian politician and Professor of Commercial Law, David

Supino, Le operazioni di borsa seconda la pratica, la legge e l’economia politica (1875),

is a major reference, but remains largely descriptive in character. It lists laws and decrees

regulating the Italian Stock Exchange, and includes a glossary for the main words in use.16

This means that the dominant perspective on stock exchanges was descriptive or

normative, but not explicative.17 Only a few books adopted an economic perspective, and

Ullrich’s contribution also embraces connected sociological aspects. In the years before

Ulrich’s book was published there were some exceptions, however. In 1904, Alphonse

Courtois published the Traite des operations de bourse et de change in Paris, which is

more analytical, and Chevilliard’s second edition of Le Stock-Exchange was also

published in Paris in 1904. Both were important sources for Ulrich’s interest in the issue of

stock exchanges, and he quotes both liberally in his dissertation.

Ulrich’s book was published in Coimbra in 1906 by the local University Press. It is a

scientific work presenting a complete view of stock exchanges and their operations, to

stress the important financial role they perform in economic life throughout the world. For

Ulrich a stock exchange is a market. The dominant influence on Ulrich is the French

bibliography. This is quite normal for the time in Portugal. Not only was French the

dominant global language, but Portugal was closely aligned to continental Europe, the

French culture and intellect. In spite of the close commercial connections between

Portugal and the UK at the time, French was the major international language at school,

and the Portuguese people, in particular, were far more literate in French than in English.

Business History 3

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

The French influence also has to do with scientific work organisation, which was more

centralised in France than in other countries (Germany included).18 Curiously, there are

very few references to authors from Spain,19 Germany,20 the United Kingdom,21 or the

United States of America.22 Thirty-six French authors are quoted in the text, and in his

final list of references 21 are included for the study of stock exchanges,23 six for political

economy,24 five for commercial law,25 and four for history in general.26 The influence of

Italian authors is also clear, as there are 11 Italian names quoted in the book.27

Because it was written as a dissertation on law, Ulrich’s book seems at first glance to

be a purely academic work. However, a closer examination reveals that it does not follow a

strict juridical approach. He covers both the economic and business aspects of stock

exchanges, and includes a fair treatment of some organisational features of stock

exchanges in Portugal and elsewhere in Europe. He also makes an excursion into ways to

improve the Lisbon Stock Exchange that would make it more efficient, up-to-date, and

competitive with the other European capital-city markets, so that its economic and

financial functions could more properly serve the needs of savers, investors, and customers

in general. Everyday life operations are described along with the institutional aspects, but

separating the case of operations in securities (such as shares and debt instruments) from

the case of commodities (such as foodstuffs, mineral ores, and other goods). On the

importance of stock exchanges for securities trading, Ulrich says explicitly that ‘although

it is rare to trade securities outside Exchanges, it is common to sell commodities outside of

them’.28 The book describes the open-outcry system (‘feitas em voz alta’) in use at the

time, notably in the Lisbon Stock Exchange, and presents the empirical aspects of

negotiations as market equilibrium points.29 Ulrich’s concept of equilibrium stems from

some fields of physics, such as mechanics, a new science on the eve of the First World War

that brought considerable inspiration to social sciences in general, and to the market theory

in particular. Recall how Walras had developed the Theory of General Equilibrium at the

University of Lausanne, followed by Pareto’s contributions to its re-formulation.30 Recall

too how Irving Fisher used mechanics in his 1892 doctoral dissertation at Yale to describe

market adjustments (applying them to finance, financial economics, and Wall Street in the

1920s).31

The book reveals refined legal erudition, and most of the issues of law pertaining to the

stock exchanges of the largest European cities are described. It also provides deep

economic and financial analyses. Actually, the nineteenth century had been the period of

most rapid industrialisation in many European countries, had ushered in intensified trading

networks among European nations and the rest of the world, and had witnessed important

migration flows of people leaving Europe, in the context of far-reaching globalisation of

capital flows among capital markets. Large corporations and multinationals were founded,

thanks to the principles of limited liability and capital sharing, in the most diversified

sectors of economic activity, from industry to transportation, from agriculture to trading,

and from mining to insurance, prompting the multiplication of regional and global stock

exchanges for supporting the needs of international business in the Old and New Worlds.

The book devotes special attention to the evolution of markets from antiquity to the

present (1906), discussing the origins and needs leading to their organisation. Beginning

with the Portuguese case and expanding to Europe, it covers a large time span and a wide

geographical area, in order to make possible some theorising on the role of stock

exchanges and capitalism in support of sophisticated modern societies. The book never

uses the term ‘transaction costs’, but the author presents all transactions (be they on

commodities or on securities) as the top expression of alternative uses for capital

(including transfers among shareholders’ hands in the vast world of business), in order to

4 M.E. Mata and J.C.R. da Costa

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

remark on the role of the wealth contained in tradable securities and its impact on

collective prosperity and economic growth.

Ulrich’s book speaks clearly to any educated citizen. Anyone can read it, but it is also

deep enough to be classified as a real handbook on finance. It is, in fact, a masterpiece that

deserves to be quoted as essential reading on the issues it addresses. Ulrich presents for the

first time the legal features of the Portuguese capital market, in presenting the set of laws

and decrees that framed and supported all the financial activities at the time, including

Veiga Beirao’s Commercial Code of 1888, which regulated all these aspects in Portugal.32

Another important document, the Decree of 10 October 1901, accompanied it and includes

two important Regulations, one on the brokerage profession (Regimento do Ofıcio de

Corretor), the other on the daily operations of exchanges (Regulamento do Servic�o e

Operac�oes das Bolsas de fundos publicos e particulares e outros papeis de credito). The

Decree of 24 December 1901 on the stock exchange operations calendar and opening hours

also received a meticulous analysis in relation to the legal features it laid out for Portuguese

brokers as members of a well-respected profession. The organisation, registration, and

management of all the operations by them were carefully described and appraised.

Stock exchanges are described as versatile markets for all of the segments they may

cover, including currency exchanges, debt instruments, shares of corporations,

government bonds, issue of new public loans, and spot and time operations (futures and

options).33 Stock exchanges are treated as multi-polar spaces with respect to the clients

they serve (from individual savers to institutional partners, corporations, and governments

as issuers of public debt), always having the mission of matching the interests and plans of

all these economic agents, in all of the operations in which they are involved. In effect,

therefore, Ulrich is close to the current notion of platform markets that economics

introduced, and is used in both the microeconomic perspective and the management and

logistics perspectives, in order to study markets’ equilibrium.

A sociological vision to describe stock exchanges is also used. The monopolistic

character of brokerage as a profession is discussed at length, as well as the legitimate

character of its revenues. To justify them, Ulrich takes the perspective of the users’ costs,

as well as the guarantee of honesty, transparency, honouring of contracts, safety, accuracy,

and professional discretion,34 to conclude that in this profession ‘monopoly, being always

preferred to any other system, is, without any doubt, the only one that really is appropriate

for our economic environment’.35 State roles as a regulator agent and permanent inspector

of brokers’ activities to defend the interest of corporations, of the national economy, and of

society in general, are explored meticulously.36 Although the book never mentions the

stock exchange as a ‘public good’, all the conceptual framework that it develops on

accessibility, schedules, control, transparency, and efficiency is established as a set of

advantages for economic activities and the common good, and as an expression of the

interests of all citizens in general. The only feature missing is to actually call them

‘positive externalities’.

The benefits derived from technological facilities such as the telegraph and

telephone are frequently referred to in the book, to clearly express the cost-decreasing

character of communications. The mandatory publication of quotations in a daily

bulletin and newspapers is presented as necessary for the public, in order to reduce financial

information costs, on the one hand, and to achieve market transparency, on the other.

In contributing to the spread of financial literacy among its readers, this book is an

instrument of good practices in itself, and is also an instrument to evoke the responsibility

of all partners and agents in the market. The author does not avoid the discussion on

innovative aspects of the time, such as the netting of both physical and financial flows

Business History 5

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

before final settlement of all transactions. Nor does he avoid polemical interpretations of

theory coming from the schools of socialism, such as Karl Marx, or the socialism of state,

such as Adolphe Wagner and Karl Rodbertus, or from the schools of anarchism, such as

Pierre-Joseph Proudhon. Looking at all of them, Ulrich uses their contributions and

interpretations, and also uses many more authors and international experts, whom he

carefully quotes, in order to establish common features among all stock markets through

comparative law of many countries.37

A final aspect on this book deserves to be stressed: its pedagogical quality in parallel

with its didactic character, not only because of the clarity of its language but also because

of the frequent use of numerical examples to better explain concrete cases. Typically, the

author requires the reader to follow the example of Mr. A, a prospective seller of a number

of shares, and Mr. B, who goes to his broker to buy the same securities, in order to explain

that, with the intervention of Mr. C, who is a broker, pressures from demand and from

supply can reach an equilibrium point through the compensation mechanism.38 Probably

this inspiration for examples comes from Alphonse Courtois and his disciple Emmanuel

Vidal.39 Although it was common at this time to criticise both capital markets and stock

exchanges due to their speculative behaviour, Ulrich does not promote the idea that

irresponsible persons inflict pernicious losses to society because of greed. There is an

elegant balance between the use of scientific erudition made of abstraction and wide

theoretical horizons, and the simultaneous use of concrete explanations, depicted in

practical examples drawn from real life.

As for today’s readers who are versed in finance and will note the absence of Louis

Bachelier, the founding father of financial mathematics and of any interpretation for the

behaviour of share prices as a stochastic process, it is important to mention the pioneering

work The Theory of Speculation40 in stock markets. It is a seminal introduction of the

concept of stochastic processes to mathematically describe stock price evolution. For this

reason, Bachelier is recognised as the founding father of financial mathematics; his book

appeared in 1900 in Paris. Based on his doctoral dissertation at the University of Sorbonne,

Bachelier’s book opened the way to the Brownian motion model to evaluate stock options.

However, Ulrich’s book ignores this mathematical contribution. Some details on

Bachelier’s career need to be provided. Perhaps they can explain this lacuna. First of all,

Bachelier presented this contribution in his doctoral dissertation on the Theory of

Speculation, from the Sorbonne, published in 1900, but Ulrich’s book is not devoted to this

issue, although he mentions the matter of speculation in stock markets. The main point,

however, is the fact that Bachelier’s theory was far from being a success in the French

academic environment of the time.41 He was granted his PhD, but simply approved,

without distinction. He only managed to obtain a teaching position in 1909, and only

secured a permanent position in 1927 (and only in Besanc�on), having received little notice

as an author by the time of Ulrich’s publication in 1906.

Ulrich’s book addresses a void that was completely unfilled in Portugal at the time. In

fact there are no citations of Portuguese works on the stock exchange, although there is

extensive reference to books on commercial law,42 history,43 political economy, and

statistical geography.44 This means that a book written in Portuguese and revealing the

character and the regulations of the Portuguese stock exchanges was a very useful

instrument, for both students and practitioners. This fact may be surprising, because the

complexity of finance and the deep analysis demonstrates the author’s juridical

preparation, as well as his empirical expertise in capital markets, their peculiar features,

the character of their operations, and his knowledge of the economic role they perform in

modern capitalist economies and societies.

6 M.E. Mata and J.C.R. da Costa

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

3. The local environment and the need of a professional move

Ruy Ennes Ulrich belonged to a family of bankers and high-finance businessmen of

German origin that moved from Hamburg to Lisbon following the Lisbon earthquake

of 1755, when the reconstruction of the Portuguese capital, spearheaded by the

Prime Minister, Marquis of Pombal (Sebastiao Jose de Carvalho e Malo), offered

good opportunities for investment and business. The family spread their interests to

Porto, Coimbra, and to the (then) Brazilian capital city, Rio de Janeiro. Family

financial culture and erudition are important aspects in forming Ulrich’s interest in

financial markets, stocks, and the operation of stock exchanges.

Curiously, Ulrich was a very young man when he wrote this book, and was only 23

years old when it was published in 1906. He was born in Lisbon on 20 April 1883, and his

father, Joao Henrique Ulrich, sent him to attend the School of Law of the University of

Coimbra in the academic year of 1899–1900, when he was only 16;45 he was student

number 138. He proved his abilities immediately, as stated in the 1902–03 University

Yearbook, which records him as a fourth-year student who was awarded the Accessit

Prize.46 He continued to demonstrate his academic potential by publishing his first book,

on the Portuguese economy and the Portuguese economic crises, in 1902.

He then graduated according to the University Yearbook of 1904–05, which includes

his name in the list of graduates.47 He graduated on 30 March 1905 and achieved the

highest possible mark with the classification of Very Good, 19 values (on a scale 0–20),

thanks to a work he published in 1905.48 The Dean awarded him the diploma.49 At the time

the sixth year of study had been eliminated as a requirement for admission to graduate and

doctoral studies,50 as it was considered to be redundant instruction. Only students who

graduated with the highest classification could apply for doctoral studies. Moreover, as the

doctorate was sought only by students wishing to pursue an academic career, this change

reduced students’ spending and focused on the most talented candidates, independent of

their financial capacity to support their fees.51

With his dissertation entitled ‘Stock Exchanges and their Operations’ (‘Da Bolsa e

suas Operac�oes’), Ulrich completed his PhD on 13 May 1906.52 This step entitled him to

apply for a full professorship in December of that year.53 He was a full professor at the

School of Law of the University of Coimbra from 1906 to 1910, teaching a course on

colonial administration to fourth-year students.54

In 1907 he married Genoveva Lima Mayer,55 who came from a wealthy business

family of Lisbon. During the nineteenth century her family had owned the ship-towing

service in the port of Lisbon, developed banking activities, and was the representative

and agent of foreign freighter companies that operated in Portuguese ports in the

import–export sector, as well as in the maritime insurance field.56 She was also a writer,

and her father was a philosopher of intellectual romanticism, who in the 1870s participated

in the group ‘Vencidos da Vida’, made up of the most prestigious writers and philosophers

in the country. Ulrich’s wife was raised as a Lisbon socialite, but marriage took her out

of this milieu of cultural evening parties, to Coimbra, where she bore Ulrich a daughter

in 1908.57

Ulrich was a monarchist, but the Constitutional monarchy was ousted on 5 October

1910 by a revolution that installed the Republican regime in Portugal. The echoes of the

political turmoil also involved the University of Coimbra, with claims against supporters

of the monarchy. Prompted by the so-called Academic Question (Questao Academica),

Ulrich resigned from the University of Coimbra and moved to Lisbon with his family,58 to

attend to different pursuits.

Business History 7

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

4. Scientific knowledge on finance, management, and other professional

applications

At this time the Portuguese capital city was in turmoil in the aftermath of the political

transition, but in 1911 Ulrich was elected for a top position at the Ministry of Finance

Board of Public Credit, Junta de Credito Publico (caring for the public debt).59 According

to Reis he kept this position until 1914, when he moved to the Board of the Portuguese

central bank, the Bank of Portugal (Banco de Portugal), where he remained until 1928.60

His professional career adds much to the understanding of the importance of financial

expertise for corporate management and efficiency in firm portfolio management. While

remaining in the Bank of Portugal, which assumed the functions of central banking after

the monetary reform of 1933, he also worked as director and CEO of some large

Portuguese corporations, such as the colonial Company of Mozambique, Companhia de

Moc�ambique (1920 to 1933),61 and the domestic railway Caminhos-de-ferro Portugueses

(CP) (1922 to 1933). The colonial Company of Mozambique was one of the most

profitable corporations in all of the Portuguese economy, while the railway CP was the

largest Portuguese firm of the time, if scale is defined by the number of employees.62 This

was a very special period in his life, as the 1920s was the time of the European

reconstruction and the payment of German reparations following the First World War.

Significant foreign exchange fluctuations due to the large international flows of hot money

searching for the highest returns and exchange-rate swings provided good opportunities

for speculation, while transactions on commodities also led to a specialisation of that part

of the Lisbon Exchange dedicated to trading in colonial foodstuffs.

Ulrich’s high management positions also highlight his good relationship with three

political regimes in the country. Serving as a university professor at Coimbra during the last

years of the monarchy, and his new jobs at the Ministry of Finance Board of Public Credit

and the Bank of Portugal, demonstrate howmuch the Portuguese job market was in need of

qualified staff with a special expertise in finance during the First Republic period of 1910–

26. When the military coup of 1926 brought a newly inspired political regime, another

expert in finance and professor from the University of Coimbra, Oliveira Salazar, assumed

a decisive role as Minister of Finance, first, and as Prime Minister from 1932 on. Ulrich’s

good relationship with Salazar’s political regime is also quite clear (Salazar, too, had some

sympathy towards monarchist regimes). Ulrich’s house in Lisbon became a literary salon

open to the social elite of the Portuguese capital city. The following decade and the global

crisis after 1929 were challenging times for corporate management and financial activities,

but Ulrich spent the whole period maintaining high-responsibility tasks in the wake of the

separation between ownership and daily control being adopted in large corporations in

Portugal.63 From 1933 to 1935 he lived in London as Portuguese special ambassador to the

UK, a coveted position for career diplomats, which was not even his case.64

Regarding academia, he returned to lecturing in 1935, immediately after his post in

London.65 He was invited to teach at the University of Coimbra, a position he accepted for

a while, and to lecture the course on political economy at the School of Law of the

University of Lisbon. Here he was later the president of the Centre for Economic Studies

(Centro de Estudos Economicos)66 and became the Dean of the school in 1937, where he

remained until 1950. Supporting his teaching, his textbooks on political economy were

published in 1937, 1938, 1940, 1943, 1947, and 1949, illustrating how influential Ulrich

was in educating a generation of lawyers and intellectuals for Portuguese society.

From 1936 to 1942 Ulrich also took a political position as Procurador a Camara

Corporativa.67 Actually, he combined his teaching, research, and political activities

8 M.E. Mata and J.C.R. da Costa

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

with high management positions, which may be related to his family shareholding

interests. He was the President of the Board of the Portuguese shipping corporation

Companhia Nacional de Navegac�ao from 1936 on, a member of the Board of the

corporate institutional regulator Junta Nacional da Marinha Mercante in 1940, member

of the Board of the international gas company Companhias Reunidas de Gas e

Electricidade, of the Angolan railway company Companhia de Caminho de Ferro de

Benguela (CFB), and of the insurance company Companhia de Seguros Ultramarina.

Like American economists such as Jeremiah Jenks and William Ripley, his influence on

local society was considerable. His devotion to academics was never affected, and

this is one more lesson to be learned, as he wrote extensively on wages and labour

economics (1949), and on the economics of transport (1938, 1945, 1950). These

two issues clearly reflect his reasoning and professional expertise in transportation

firms as well as in human resources management, in both local and geographically

distant large-scale corporations.

In 1950 he received a new invitation from Salazar’s government to go back to London

for three years as Portuguese ambassador to the UK.68 This was the challenge that moved

him away from academia until his retirement in 1953. In this phase, as a Portuguese

diplomat, he participated in the NATO Supplementary Board, Conselho dos Suplentes do

Pacto do Atlantico Norte (from 1950 to 1952),69 where he represented Portugal on many

formal occasions, including the signing of the agreement to allow Greece and Turkey to

enter the NATO alliance, on 22 October 1951. After his retirement he maintained for a

short period (1958) the presidency of the General Assembly of the Portuguese Central

Bank, Banco de Portugal. Ulrich lived for 83 years, passing away on 20 January 1966.70

Throughout his long professional life he used his financial knowledge in many

positions. For years he practised as a highly qualified economist and as a finance expert,

thanks to his academic preparation in these fields. A member of many scientific societies,

such as the International Colonial Office (Instituto Colonial Internacional) or the

International Diplomacy Academy (Academia Diplomatica Internacional), Ulrich also

headed the prestigious Lisbon Geography Society, and was the vice-president of the

Portuguese Academy of Science, where he gave and published some historical and

political addresses. For a life so devoted to important functions in Portugal, Ulrich was

recognised and decorated with the highest Portuguese honours and decorations (Gra-cruz

da Ordem de Cristo, Gra-cruz da Ordem de Sant’Iago da Espada, and from RomaniaGra-

cruz da Ordem da Coroa).

While choosing crafts and decorative arts for adorning Ulrich’s home, according to

the prevailing art nouveau style of the inter-war period, his wife Genoveva published

several books (under the pen name Veva Mayer), often contributing her writings to the

newspapers of the capital city. She also participated in radio debates and promoted

some theatre productions.71 High society in Lisbon was populated with literati,

diplomats, and conferences, and was rich in music and arts, as was usual throughout

Europe. Elegance, erudition, and arts, coupled with the inter-war period of extravagance

and glamour, were all marks of exoticism in the Ulrichs’ literary salon; it was an

intellectual atmosphere that social history has not yet fully appreciated in sound studies

on the Portuguese elites.

5. Conclusions

Ulrich’s case illustrates that Portugal was not excluded from the mainstream knowledge

on financial markets in the early twentieth century. His book covers all of Portugal’s

Business History 9

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

commercial and financial life, and is a textbook of wide practical and educational interest.

In spite of being in a small and peripheral country, the Portuguese universities of Coimbra

(and Lisbon from 1911 onward), could provide scientific teaching on these issues to their

students, thanks to his highly qualified knowledge on these matters.

Ruy Ennes Ulrich, the young PhD student who devoted his dissertation to the issues of

stock exchanges using a scientific perspective on finance, is largely overlooked. The

History of Portuguese Economic Thought72 does not even mention his name, but he

deserves to be recognised as an expert on these issues, and his book is an important piece

of analytical thought on stock markets and their mechanisms. His main contributions were

the diffusion of his personal knowledge on these matters, thanks to a long-term family

expertise in capital markets, and also his highly qualified performance in managing the

largest and most important Portuguese companies during the four decades of his

professional life.

Unfortunately he could not pursue his academic career at the University of Coimbra as

Professor of Finance. As a consequence, Ulrich pursued a management career, was CEO at

the most important Portuguese companies, Professor of Political Economy in Lisbon, and

proved to be a hard-working and prolific author.

Ulrich’s textbook on stock markets is not well known internationally, as it is written in

Portuguese, and it is therefore not listed in specialised bibliographies.73 Note that his goal

was to ‘nationalise’ financial knowledge due to the lack of alternatives in Portuguese. In

any case, his proficiency was not wasted, as he was one of the most sought-after and

successful experts in finance in Portugal, and was later called upon to manage large

Portuguese corporations, putting his academic and scientific knowledge to direct practical

use. As his other books demonstrate, corporate governance, financial management,

organisational behaviour, and scientific control were important instruments that were

made available in the largest Portuguese corporations throughout the first half of the

twentieth century, in spite of the turbulence of the markets and the difficult political

conditions related to the two world wars and the Great Depression. His contributions in

these fields deserve further research and analysis.

Acknowledgements

This paper results from a three-year research project on The Cost of Capital in Portugal, funded bythe Portuguese Science Foundation. We are grateful for the facilities we received from FEUNL, andto John Huffstot for correcting our English. Of course, any errors are our own.

Notes

1. Amatori and Jones, Business History around the World.2. Rodrik, The New Global Economy and Developing Countries.3. Jones, Merchants to Multinationals.4. Bauer, Pool, and Dexter, American Business and Public Policy.5. Chandler, Strategy and Structure.6. Courtois, Traite d’Operations de Bourse et de Change, 80–90.7. Cassis, Capitals of Capital.8. In Lisbon as in London, for example: London Stock Exchange Intelligence, Burdett’s Official

Intelligence.9. Mata, da Costa, and Justino, “Justificac�ao da Nova Edic�ao da Obra,” “Prefacio.”10. Schumpeter, History of Economic Analysis, 754. In the School of Law of the University of

Coimbra Marnoco e Sousa taught Ullrich the course of political economy.11. Marshall, Economics of Industry.12. Ekelund and Hebert, History of Economic Theory and Method.

10 M.E. Mata and J.C.R. da Costa

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

13. Not to mention the singular case of ‘Confusion de Confusiones’ written in 1688 by Joseph de laVega, a Portuguese Jew in Amsterdam where the workings of the local exchange are explainedunder the form of a trialogue between a merchant, a philosopher, and a shareholder. It isconsidered as the first text on such matters.

14. Cosack, Traite de droit commercial; Hayaux, Du marche financier; Sayous, Les bourses;Vivant, Trattato; Fontaine, La bourse; Moysen, Le coulissier; Thaler, Traite; Weil, L’impot;Franchi, Manuale; Marghieri, Il diritto; Lambert, Dictionnaire; Lyon-Caen and Renault,Traite; Pfleger and Gschwindt, La riforma; Passos, A Treatise; Say, Agents; Scherer, Labourse; Vidal, Agents; Guilmard, De la vente; Guillard, 1877; Tedeschi, Dei contrati.

15. Schumpeter, History of Economic Analysis, 755.16. Ulrich quotes Lafargue’s article “La fonction economique de la bourse,” 7, as well as Supino’s

La borsa e il capitale improduttivo.17. Bedarride, Des bourses de commerce, and Buriat, Le comissionaire contre-partiste en bourse,

are good examples.18. Schumpeter, History of Economic Analysis, 510.19. Carreras and Gonc�alez on stock exchanges and Eduardo Perez Pujol on history.20. F.J. Peleger, L. Gschwindt.21. On the UK stock exchanges, only Passos, A Treatise on the Law of Stock-brokers, is quoted.22. Before 1914 the American universities depended on the income flow of European experts, and

‘Teaching fedmainly onMcCulloch and Say’ (Schumpeter,History of Economic Analysis, 515).23. Alphonse Courtois, Ambroise Buchere, Andre Moysen, Andre Sayous, Arthur Raffalovich,

Buriat, Emanuel Vidal, Jean Bedarride, Jeannotte Bozerian, Charles Scherer, C. Colson,Boudon, G. Chevilliard, Henri Fontaine, Henri Oulman, Horace Say, Jean Hayaux du Tilly,J. G. Courcelle-Seneuil, Lafargue, Prosper, and Rambaud.

24. Abel Waldeman, C. Cosack, Edmond Weil, Edmond Guilard, Georges Boudon, and J. BaptisteSay.

25. A. Bouche-Leclerq, Eliezer Lambert, Ch. Lyon-Caen, L. Renault, and Emile Laveleye.26. Eugene Petit, E. Thaler, Joachim Marquardt, and Paul Frederic Girard.27. Alberto Marghieri, Augusto Graziani, Camilo Supino, David Supino, Ferdinando Piccinelli,

and Prof. Grunhut, on Stock Exchanges; Ferrari on Political Economy, and Ercole Vidari, LuigiFranchi, David Supino, and Dott Errico Thol, for Law.

28. In Portuguese: ‘Sendo rarıssima a venda de valores fora da Bolsa, e vulgarıssima a venda demercadorias fora d’ella’, 6.

29. Pages 6–7, 16.30. Schumpeter, History of Economic Analysis, 998–1026, on the Walrasian system, and 858–861

on the Paretian school.31. Pressman, Fifty Major Economists, 92.32. The Code had been approved by a law of 28 June, 1888, and was enacted from 1 January 1889.33. Pages 433–503 and 507–542.34. Oulmann, De l’etendue, 265, 286, 342, 346, 370, 384.35. ‘o monopolio, sendo sempre preferıvel a qualquer outro systema, e incontestavelmente o unico

que se harmoniza com as circunstancias proprias do nosso meio economico’, 383.36. Pages 125–130.37. Let us recall the book by Proudhon, Manuel du speculateur a la bourse, 387–417.38. See Ulrich, Da Bolsa, 467–471, for example.39. In 1902, Emanuel Vidal re-published Alph. Courtois’ book Traite des Operations de Bourse et

de Change, after 10 editions from the first in 1850, and in the Preface he describes Alph.Courtois as his master.

40. Louis Jean-Baptiste Alphonse Bachelier (11 March 1870–28 April 1946).41. As many others in academia, Besanc�on was scientifically flawed. Other mathematical authors

in economics also had to wait a long time to see their theories praised. Recall Cournot’spioneering contribution to the study of market equilibrium, Recherches. Published in 1838, fewunderstood its importance at the date of his death in 1877 (Ekelund and Herbert, History ofEconomic Theory and Method, 209).

42. Such as Diogo Pereira Forjaz Pimentel, Joaquim Pedro Martins, Jose Ferreira Borges, Jose daSilva Lisboa, and M. A. Coelho da Rocha.

43. Such as Arnaldo Gama, Costa Lobo, Gama Barros, Jose Anastacio de Figueiredo, PinheiroChagas, and Rebelo da Silva.

Business History 11

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

44. Adrien Balbi, Jose Alberto dos Reis and Marnoco e Sousa.45. University Yearbook (Anuario da Universidade de Coimbra) 1899–1900, 57.46. Along with another colleague Jose Caeiro da Matta, born in 1877, page 131, who also would be

a distinguished intellectual.47. The 1903–04 University Yearbook already registers him as a fifth-year student (Universidade

de Coimbra, Anuario, 1903–04, 128), adding his address (Arco do Bispo n8 3).48. Estudos sobre a condic�ao legal das ordens e congregac�oes religiosas em Portugal. De 1834 a

1901, Coimbra, 1905.49. Universidade de Coimbra, Anuario, 1904–05, 25.50. Art 5, Decree of 15-06-1870, Diario do Governo n8 155, 14 July 1871.51. Preamble to the Decree of 15-06-1870, Diario do Governo n8 155, 14 July 1871, 375.52. Universidade de Coimbra, Anuario, 1906–07, 25–27.53. For this purpose Ulrich presented another work, ‘Do Reporte no Direito Comercial Portugues’

as his ‘Dissertac�ao para o concurso ao magisterio na Faculdade de Direito da Universidadede Coimbra, o primeiro despacho para o magisterio de Professor Cathedratico’. Universidadede Coimbra, Anuario, 1907–08, 10–11. Reis, Uma Elite Financeira, is wrong in quoting thiswork as Ulrich’s PhD dissertation.

54. Universidade de Coimbra, Anuario, 1909–10, 160. One may associate this position to his bookon Science of Colonial Administration (Ciencia e Administrac�ao Colonial) that he published inCoimbra, in 1908. His lessons were published in 1909 and 1910, and he went on publishing oncolonial issues in 1911 and 1912, namely on the colonial monetary regime and colonialfinances, after leaving the University of Coimbra.

55. Born in 1886, died in 1963.56. The Companhia el Fenix Espanol, headquartered in Madrid for life, maritime and fire

insurance, and the French L’Atlantique, from the Havre, with Fr. 1,000,000 equity. Mata, “AForgotten Country in Globalisation?,” 189.

57. Maria, who would found the pre-school care and Kindergarten system in Portugal in the 1960s.58. A son was born there in 1912, Jorge Lima Mayer Ulrich.59. ‘On August 21, 1911 he was elected the first member by legal substitute for the Board of Public

Credit for three years 1911–1914, and was called to replace a full member of that Board onSeptember 7, serving up to 5 November. Called again on the 25th of that month, he stayed untilJanuary 6, 1912’. http://www.arqnet.pt/dicionario/ulrichre.html (accessed 26 July 2012).

60. Reis, Uma elite.61. Recall his teaching on colonial administration at the University of Coimbra, and his published

works on monetary colonial subjects and colonial finances.62. Mata, “Large Portuguese Firms from the Marshall Plan to EFTA,” 126.63. This period, however, was crowned by the most dramatic family event, as Ullrich’s son

committed suicide in 1932, following the example of his grandfather Carlos LimaMayer in 1910.http://www1.ionline.pt/conteudo/5895-a-excentrica-das-amoreiras (accessed 26 August 2012).

64. He replaced General Tomaz Garcia Rosado, who reached retirement age. On the reasons forUlrich’s replacement in London, because of a Republican campaign against him in Portuguesenewspapers, for having invited the pretender to the Portuguese crown, D. Duarte Nuno, todinner, see Brandao, A demissao de Rui Ulrich, 125–137.

65. Ulrich, ‘Relac�oes economicas luso-britanicas’ (1936), reflects his diplomatic activity onPortuguese–British economic relations in foreign markets.

66. Brandao, A demissao de Rui Ulrich, 135. He was also on the Board of the scholarly journal ofthe school, Revista da Faculdade de Direito.

67. From the 1st to the 4th Parliamentary terms (Legislaturas).68. To compensate Ulrich for his unfair dismissal from this position in 1935, according to Brandao,

A demissao de Rui Ulrich, 136 (quoting an elegant letter from Salazar to Genoveva LimaMayer): Ironically, the Portuguese Foreign Office Minister, Armindo Monteiro, who recalledUlrich from London in 1935, was the new ambassador in London in 1936.

69. Raquel Sofia Lemos, Ficha bio-bibliografica de Rui Ennes Ulrich (1883–1966), available inthe following site of the School of Law of UNL university: http://www.fd.unl.pt/ConteudosAreasDetalhe_DT.asp?I¼1&ID ¼ 1372.

70. As there were no grandchildren, the family patrimony was devoted to two Foundations, both ofthem located in Ulrich’s Lisbon house: The Veva Mayer Foundation, to honour his wife’sprofessional name, and the Maria Ulrich Foundation, after their daughter’s death, in 1988.

12 M.E. Mata and J.C.R. da Costa

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

71. The Coimbra artist Lourenc�o Chaves de Almeida mentions Mrs Ulrich as a patron of his worksof forged iron in his book of memoirs (Mendes, ‘Prefacio,’ in Almeida, Memorias). In 1935more silver, decorations and furniture were added to the house, amounting to £3000, comingfrom London, where they were bought for the Portuguese Embassy (but rejected for publicexpenditure by the Lisbon Foreign Office). Brandao, A demissao de Rui Ulrich, 135.

72. Almodovar and Cardoso, A History of Portuguese Economic Thought.73. Ibid.

Notes on contributors

Jose Rodrigues da Costa is Professor of Finance at the Instituto Superior de Ciencias do Trabalho eda Empresa, and advisor of EURONEXT-NYSE.

Maria Eugenia Mata is Associate Professor of Economic History and History of Economic Thoughtat Nova SBE. Oliveira Marques Prize 2010, by the Association of Spanish and Portuguese

References

Almeida, Lourenc�o Chaves de. Memorias de um Ferreiro. Coimbra: Imprensa da Universidade deCoimbra, 2007.

Almodovar, Antonio, and Jose Luıs Cardoso. A History of Portuguese Economic Thought. London:Routledge, 1998.

Amatori, F, and Geoffrey Jones, eds. Business History around the World. Cambridge: CambridgeUniversity Press, 2003.

Bauer, R., I. Pool, and L. Dexter. American Business and Public Policy. Chicago: Aldine Atherton,1972.

Bedarride, J.Des bourses de commerce, agents de change et courtiers. Paris: Arthur Rousseau, 1901.Brandao, Fernando de Castro. A demissao de Rui Ulrich, Embaixador em Londres (1935), Biblioteca

InfoEuropa, Negocios Estrangeiros, n8 7 Setembro de 2004, 125–137.Buriat, Emile. Le comissionaire contre-partiste en bourse et specialement en marchandises. Paris:

Henri Janne, 1903.Cassis, Youssef. Capitals of Capital. Cambridge: Cambridge University Press, 2006.Chandler, Alfred. Strategy and Structure, Chapters in the History of the American Industrial

Enterprise. Cambridge, MA: MIT Press, 1962/1998.Chevilliard, G. Le Stock-Exchange. Paris: Boyveau et Chevilet, 1904.Cosack, C. Traite de droit commercial.Vol. II – Traduit de 1’allemand par Leon Mis. Paris: Giard et

Briere, 1905.Cournot, Antoine. Recherches dans les Prıncipes Mathematiques de la Theorie des Richesses. Paris:

L. Hachette, 1838.Courtois, Alphonse. Traite d’Operations de Bourse et de Change. 12eme edition par Emmanuel

Vidal. Paris: Garnier Freres, 1902.Ekelund, Robert, and Robert Hebert.History of Economic Theory and Method. New York: McGraw-

Hill, 1975.Fontaine, Henri. La bourse et ses operations legales. Paris: Pedone, 1905.Franchi, Luigi. Manuale del diritto commerciale italiano, Vol. I. Torino: Unione Typografica

Editrice, 1890.Guillard, Edmond, Les operations de bourse, Paris: Guillaumin et Cie and Durand, Pedone Louriel,

1877.Guilmard, E. De la vente directe des valeurs de bourse sans intermediaire. Paris: Guillaumin et C.ie,

1904.Jean, Hayaux du Tilly. Du marche financier et de sa reglementation. Paris: L. Larose, 1901.Jones, Geoffrey. Merchants to Multinationals. Oxford: Oxford University Press, 2000.Lafargue, Paul. “La fonction economique de la bourse.” Devenir Social (April 1897).Lambert, Eliezer. Dictionnaire de legislation et de jurisprudence sur les operations de bourse. Paris:

Giard et Briere, 1902.London Stock Exchange Intelligence. Burdett’s Official Intelligence. (several issues). London:

British Library of Political and Economic Science, BLPES, London School of Economics.Lyon-Caen, C., and L. Renault. Traite de droit commercial. Tom. IV. Paris: F. Pichon, 1901.

Business History 13

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

Marghieri, Alberto. II diritto commerciale italiano esposto sistematicamente, Vol. I. Napoli: RicardoMarghieri di Gius, 1886.

Marshall, Alfred. Economics of Industry. London: Edward Elgar, 1879, 2002.Mata, Maria Eugenia. “A Forgotten Country in Globalisation? The Role of Foreign Capital in

Nineteenth-century Portugal.” In In Small European Countries responding to Globalisation andDe-globalisation, edited by Margrit Muller, and Timo Myllyntaus, 177–208. Bern: Peter Lang,2007.

Mata, Maria Eugenia. “Large Portuguese Firms from the Marshall Plan to EFTA: Early Stirrings ofManagerial Capitalism?” Imprese e Storia 38 (2009): 121–153.

Mata, Maria Eugenia, Jose Rodrigues da Costa, and David Justino. “Justificac�ao da Nova Edic�ao daObra,” “Prefacio.” InDa Bolsa e Suas Operac�oes, edited by Ruy Ennes Ulrich. 2nd ed. reviewedand augmented Coimbra: Imprensa da Universidade de Coimbra, 2011 (1st ed. 1906).

Mendes, J. A. “Prefacio.” In Memorias de um Ferreiro, edited by Lourenc�o Chaves de Almeida,11–22. Coimbra: Imprensa da Universidade de Coimbra, 2007.

Moysen, Andre. Le coulissier contre-partiste en bourse devant la loi penale. Paris: E. Cassegrain,1904.

Oulman, Henri. De letendue du monopole des agents de change et de la reorganisation du marchefinancier. Paris: L. de Saye et fils, 1902.

Passos, John R. dos. A Treatise on the Law of Stock-brokers and Stock-exchanges, Vol. 1. New York:The Banks Law Publishing Co, 1905.

Pfleger, F. J., and L. Gschwindt. La riforma delle borse in Germania.Biblioteca dell’economista. 4thSeries, Vol. II. Part II, Torino: Unione Tipografico-Editrice Torinese, 1899.

Pressman, Steven. Fifty Major Economists. London: Routledge, 1999.Proudhon, P. J. Manuel du speculateur a la bourse. Paris: Garnier freres, 1857.Reis, Jaime. Uma Elite Financeira, Os Corpos Sociais do Banco de Portugal 1846–1914. Lisbon:

Banco de Portugal, 2011.Rodrik, Dani. The New Global Economy and Developing Countries: Making Openness Work.

Washington, DC: Overseas Development Council, 1999.Say, Horace. Agents de change. Paris: Guillaumin et C.ie, 1854.Sayous, (AndreL.). Les bourses allemandes de valeurs et de commerce et les lois imperiales des 22

Juin et 5 Juillet 1896. Paris: Arthur Rousseau, 1898.Scherer, Charles. La bourse de Paris. Paris: Librarie Nouvelle, 1886.Schumpeter, Joseph. History of Economic Analysis. Cambridge, MA: Allen and Unwin, 1954.Supino, Camilo. La borsa e il capitale improdutivo. Milano: Ulrico Hoepli, 1898.Tedeschi, Felice. Dei contrati di borsa detti diferenziali in Italia ed all’ Estero. Torino: Frateli

Bocca, 1897.Thaler, E. Traite elementaire de droit commercial. Paris: Arthur Rousseau, 1900.Ulrich, Ruy Ennes. Da Bolsa e Suas Operac�oes. Coimbra: Imprensa da Universidade, 1906.Universidade de Coimbra. Anuario da Universidade de Coimbra para o ano lectivo de 1899–1900

(and others until 1905–06). Coimbra: Imprensa da Universidade, several years.Vidal. Agents de change. Entry in Dictionnaire du commerce, de l’industrie et de la banque, edited

by Yves Guyot, and A. Raffalovich, T.I. Paris: Guillaumin et C.ie, 1901.Vivante, Cesare. Trattato di diritto commerciale, Vol. I. Torino: Fratelli Bocca, 1902.Weil, Edmond. L’impot sur les operations de bourse. Paris: Rousseau, 1902.

Appendix. Works by Ruy Ennes Ulrich

– (1901) Estudos sobre a condic�ao legal das ordens e congregac�oes religiosas em Portugal. De1834 a Coimbra, 1905.

– (1902) Estudos de economia nacional, Crises economicas portuguesas, Coimbra.– (1906) Da Bolsa e suas operac�oes, Coimbra.– (1906) Estudos de Economia Nacional, Legislac�ao Operaria Portuguesa, Coimbra.– (1908) Ciencia e Administrac�ao Colonial, Coimbra.– (1909) Polıtica Colonial, Lic�oes, Coimbra.– (1910) Economia Colonial – Lic�oes feitas ao curso do 4.8 ano jurıdico no ano de 1909, Coimbra.– (1912) “Regime monetario colonial.” Boletim da Sociedade de Geografia de Lisboa, 1911–1912.

14 M.E. Mata and J.C.R. da Costa

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013

– (1912) Financ�as Coloniais, Coimbra.– (1914) Teoria economica das reservas bancarias, Coimbra.– (1916) “Colonizac�oes ibericas.” A questao Iberica, Lisboa.– (1936) Relac�oes economicas luso-britanicas em mercados externos.– (1937) Lic�oes de Economia Polıtica, Lisboa.– (1938) Economia Polıtica (Moeda, prec�o, credito), Lisboa.– (1938) Transportes;– (1939) “O caso da Cooperativa Auto-Mecanica de Portugal (parecer).” Jornal do Foro 3, no. 40,

pp. 66–69.– (1940) A antiga Bolsa do Porto, Porto.– (1940) Crıtica do Socialismo utopico dos idealistas e do socialismo revolucionario dos

marxistas, separata de O Ocidente, Lisboa.– (1940) Economia polıtica (Bancos de emissao, cambios. comercio) Lic�oes proferidas ao curso do

48 ano jurıdico nos anos de 1938–39 e 1939–40, Lisboa.– (1940) Os diplomatas do Portugal restaurado, Lisboa.– (1941) Discurso na Academia das Ciencias de Lisboa em homenagem ao Brasil, Academia das

Ciencias de Lisboa, Lisboa.– (1941) “Sociedades anonimas e sua fiscalizac�ao (1940).”Revista daOrdem dos Advogados 1, no. 1.– (1943) Economia polıtica (Repartic�ao – Propriedade – Renda – Juro).– (1945) Aspectos gerais do problema dos transportes em Portugal.– (1947) Discurso na sessao da Academia das Ciencias comemorativa do cinquentenario do governo

colonial de Antonio Enes.– (1947) Introduc�ao ao estudo do Economia Politica.– (1948) Manipulac�oes monetarias e prec�os, Coimbra.– (1949) “Novas concepc�oes em materia de salarios.” Revista do Faculdade de Direito do

Universidade de Lisboa VI, pp. 7–26.– (1949a) Economia polıtica – O salario.– (1950) “Doutor Manuel Rodrigues.” Revista da Faculdade de Direito da Universidade de Lisboa

VII, pp. 337–347.– (1950) Economia polıtica – Os transportes.– (1954) El-Rei Dom Manuel e o Marques de Soveral em Londres.– (1954) Conferencia, A conjuntura economica actual de Portugal, Vila Vic�osa.– (1954) Discurso na sessao comemorativa do centenario de Almeida Garrett na Academia das

Ciencias.

Business History 15

Dow

nloa

ded

by [

b-on

: Bib

liote

ca d

o co

nhec

imen

to o

nlin

e U

NL

] at

04:

57 2

4 Se

ptem

ber

2013