A Foreign currency options pricing model and application for the Zimbabwean market

68

Here is to the crazy ones, the misfits, the rebels, the troublemakers, the round pegs in the square holes, the ones who see things differently, you can quote them, disagree with them, glorify them or vilify them, but the only one thing you can’t do is ignore them because they change things... they push the human race forward and while some may see them as the crazy ones, we see genius, because the ones who are crazy enough to think that they can change the world, are the ones who do. By Steve Jobs. i

Transcript of A Foreign currency options pricing model and application for the Zimbabwean market

Here is to the crazy ones, the misfits, the rebels, the troublemakers, theround pegs in the square holes, the ones who see things differently, you canquote them, disagree with them, glorify them or vilify them, but the onlyone thing you can’t do is ignore them because they change things... theypush the human race forward and while some may see them as the crazyones, we see genius, because the ones who are crazy enough to think thatthey can change the world, are the ones who do. By Steve Jobs.

i

Abstract

This study involves the developement of a foreign currency option pricing applica-

tion from the Heston model and the Garman-Kohlhagen model in Visual Basic and

Excel. The Garman-Kohlhagen model has been adopted as the standard model for

pricing foreign currency options as it is a modification of the famous, Black-Scholes

(1973). However, we outline the limitations of the Garman-Kohlhagen model and

propose a better foreign currency pricing model, the Heston model. In the Hes-

ton model, instead of holding the volatility of exchange rate constant, volatility is

assumed to be stochastic and is defined by a stochastic differential equation. The

success of the Heston model is based on the calibration of its parameters, in this

regard, we employ the inverse problem model to calibrate the Heston model using

Excel Solver. After having calibrated the model, we evaluate the performance of

the Heston model against that of the Garman-Kohlhagen model. Furthermore we

perform sensitivity analysis to ascert the effect of the Heston model parameters

on option prices and also if the Heston model is able to account for flactuations in

exchange rates.

ii

AcknowledgementsI would like to take this opportunity to thank the Department of Statistics and

Operations Research who gave me this rare opportunity not only to learn but a

platform for me to apply all that I had acquired both in and out of University.

My greatest gratitude goes to my project supervisor Mr. Edward Chiyaka for his

time, patience, advice and guidance. I would also like to thank Mr. Xolani Ndlovu

from Old Mutual Zimbabwe, Mr Kgopotso Mosako from the Reserve bank of South

Africa, for helping with the data for this project and for their input in this re-

search. To my friends Joanna Mhlanga, Chengetai Chitungo, Siyanai Zhou, Moth-

abisi Nare, Diana Gasa, Caroline Makoni and Ntokozo Ndlovu thank you for your

support and loyalty. Above all to my friend Constantine Chideme who gave me the

idea behind this project, thank you so much for the support, for listening to me and

helping me polish up my ideas. Finally I thank God, who is my source of strength

and believing His word in James 1 verse 17, “ Every desirable and beneficial gift

comes out of heaven. The gifts are rivers of lights cascading from the Father of

light. There is nothing deceitful in God, nothing two faced, nothing fickle!!!!”

iii

Contents

1 Introduction 11.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2. Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

1.2.1. Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.2.2. Uses of Derivatives Instruments . . . . . . . . . . . . . . . . . 51.2.3. Importance of a derivatives market . . . . . . . . . . . . . . . . 71.2.4. Foreign Currency Option Pricing Models Fundamentals . . . 8

1.3. Statement of the Problem . . . . . . . . . . . . . . . . . . . . . . . . . 81.4. Aim of Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81.5. Research Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.6. Importance of Currency Options . . . . . . . . . . . . . . . . . . . . . 91.7. Scope of Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.8. Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2 Literature Review 112.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112.2. Foreign Currency Pricing Models . . . . . . . . . . . . . . . . . . . . . 12

2.2.1. The Garman-Kohlhagen Model . . . . . . . . . . . . . . . . . . 132.2.2. Other foreign currency pricing models . . . . . . . . . . . . . . 16

2.3. Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

3 Methodology 243.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243.2. Stochastic Differential Equations (SDEs) . . . . . . . . . . . . . . . . 25

3.2.1. Geometric Brownian motion (GBM) . . . . . . . . . . . . . . . 263.2.2. Ornstein-Uhlenberk Process . . . . . . . . . . . . . . . . . . . . 273.2.3. Square-root Process . . . . . . . . . . . . . . . . . . . . . . . . 27

3.3. The Heston Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.3.1. Examination of the Heston model parameters . . . . . . . . . 293.3.2. Risk Neutralized approach to option pricing . . . . . . . . . . 303.3.3. Numerical Solution for the Heston Model . . . . . . . . . . . 30

3.4. Visual Basic and Excel in obtaining a closed form solution for theHeston model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

3.5. Model Calibration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 323.6. Comparison between the Heston Model and the Garman-Kohlhagen

model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 333.6.1. Model accuracy . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

iv

3.6.2. Model Fairness . . . . . . . . . . . . . . . . . . . . . . . . . . . 333.7. Sensitivity Analysis of Heston model parameters . . . . . . . . . . . . 343.8. Option Pricing Application . . . . . . . . . . . . . . . . . . . . . . . . . 343.9. Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

4 Data Analysis, Simulations and Results 364.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 364.2. Data and data sources . . . . . . . . . . . . . . . . . . . . . . . . . . . 374.3. Heston Model Calibration Results . . . . . . . . . . . . . . . . . . . . 384.4. Comparison of the Heston model to the Garman Kohlhagen model . 39

4.4.1. Interpretation of the table . . . . . . . . . . . . . . . . . . . . . 404.5. Sensitivity analysis of Heston model parameters . . . . . . . . . . . . 41

4.5.1. Changes to the correlation parameter ρ . . . . . . . . . . . . . 424.5.2. Changes in the value of the Correlation coefficient . . . . . . . 424.5.3. Changes in the value of volatility of the volatility process . . . 444.5.4. Analysis of the Volatility graph . . . . . . . . . . . . . . . . . . 45

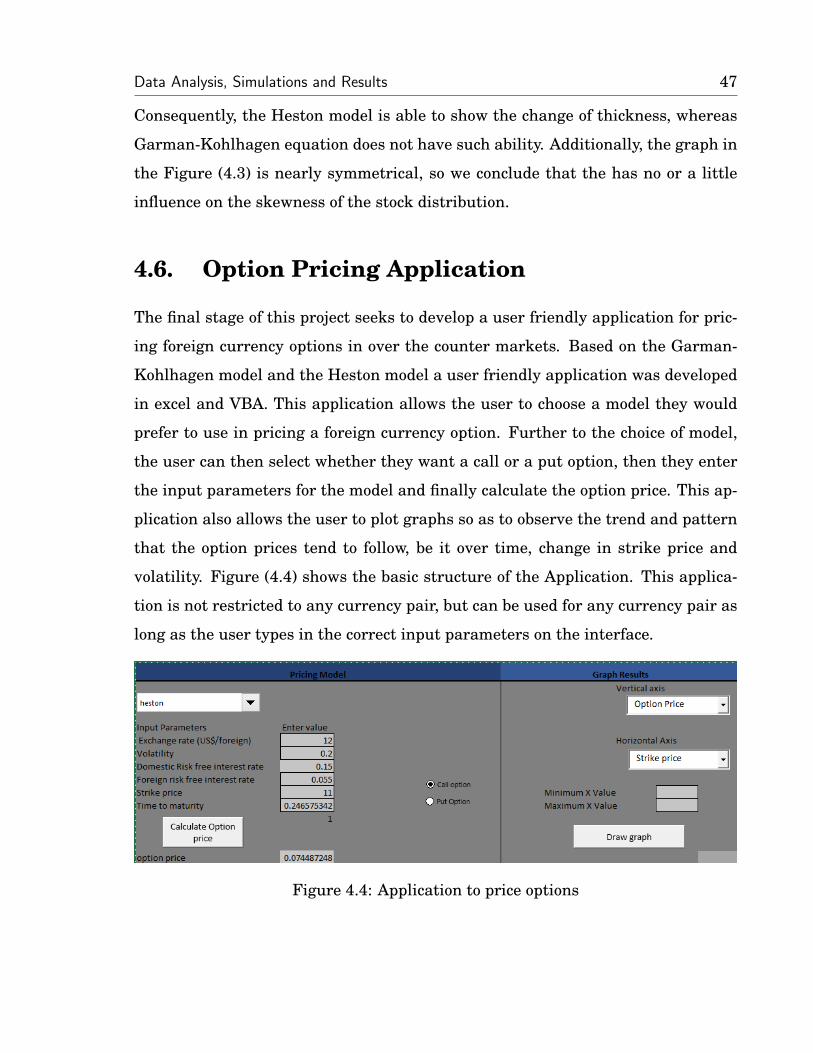

4.6. Option Pricing Application . . . . . . . . . . . . . . . . . . . . . . . . 474.7. Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

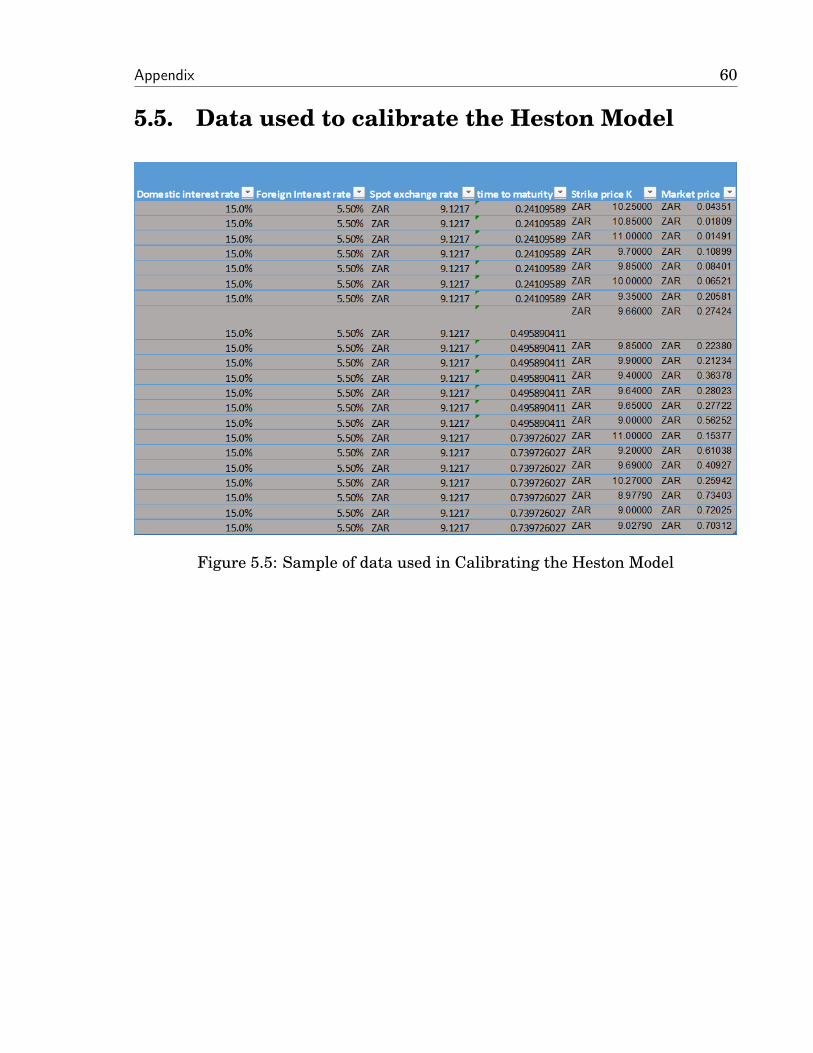

5 Conclusions and Recommendations 495.1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 495.2. Conclusions and Recommendations from the study . . . . . . . . . . . 505.3. Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 515.4. Visual basic Application code for the Garman Kohlhagen model . . . 585.5. Data used to calibrate the Heston Model . . . . . . . . . . . . . . . . . 605.6. Generalised Reduced Gradient Optimization Method . . . . . . . . . 61

v

List of Figures

1.1 Volatility of the rand against the US dollar . . . . . . . . . . . . . . . 3

3.1 Methodology framework . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.1 Differences in Option prices between the Garman Kohlhagen, Realmarket Option prices and the Heston model prices . . . . . . . . . . . 41

4.2 Graphical representation of the differences between the Heston Modeland Garman Kohlhagen model as a result of the correlation coeffi-cient ρ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

4.3 Graphical representation of the differences between the Heston Modeland Garman Kohlhagen model as a result of the variance of volatility 46

4.4 Application to price options . . . . . . . . . . . . . . . . . . . . . . . . 47

5.1 Heston model Excel VB code page 1 . . . . . . . . . . . . . . . . . . . 575.2 Heston model Excel VB code page 2 . . . . . . . . . . . . . . . . . . . 585.3 Heston model Excel VB code page 3 . . . . . . . . . . . . . . . . . . . 595.4 Excel VB code Garman Kohlhagen Model . . . . . . . . . . . . . . . . 595.5 Sample of data used in Calibrating the Heston Model . . . . . . . . . 60

vi

List of Tables

4.1 Calibration results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 384.2 A comparison between the Heston and the Garman Kohlhagen model 394.3 Calibration results when ρ is fixed at 0.5 and -0.5 . . . . . . . . . . . 424.4 Sample data of correletaion coefficient ρ sensitivity analysis . . . . . 434.5 Calibration results when σ is fixed at 0.1 and 0.2 . . . . . . . . . . . 454.6 Sample data of variance of volatility σ sensitivity analysis . . . . . . 46

vii

Chapter 1

Introduction

1.1. Introduction

Currency is the creation of a circulating medium of exchange based on a store of

value. It evolved from two basic innovations: the use of counters to assure that

shipments arrived with the same goods that were sent, and the use of silver ingots

to represent value; both of these developments had occurred by 2000BC. Foreign

exchange refers to money denominated in the currency of another nation. A foreign

exchange rate is therefore a price at which two currencies can be exchanged against

each other (Cross, 1998). The exchange rate, is a major determinant of a nations

economic health and hence the well-being of all the people residing in it. Central

banks play two roles in the foreign exchange market. They intervene in the market

by buying or selling foreign currencies, and they also may be in the market as

agents for other central banks.

Introduction 2

1.2. Background

Since the dollarization from 2008 to the present date, Zimbabwean companies have

had the privilege of using the US dollar. Due to easy access of this currency, local

companies can now easily trade with other firms in South Africa, Botswana, Asia

and other countries. In trading with other countries, companies face the risk of for-

eign exchange rates flactuations, which can result in the value of their investments

decreasing and them making losses in the process. Rodgers (2013) reveals that a

large number of Zimbabwean companies that are predominantly import-oriented

were losing value on their imports because they were allowing their South African

suppliers to give them prices in US dollars instead of South African Rand. Accord-

ing to him, Zimbabwean companies are essentially being cheated by their South

African suppliers when they get priced in US dollars because the South African

company will be buying a hedge on the value of the transaction. Zimbabwean

trading companies should not take it for granted that just because they have been

offered a price in US dollars it is the best deal. They should ask for a rand price

and then shop for a hedging product that will immunise them from exchange rate

movements.

Recent observations on the US dollar and the Rand trading patterns reveal

that the rand has been very volatile against the US dollar since December 2009

to December 2013 as shown in Figure 1.1. The graph shows spot exchange rates

of the rand/US dollar against time and we observe that there has been a general

increase in the exchange rate between the rand and the dollar as shown by the

trend line. We also notice the frequent flactuations in exchange rate proving the

volatility of the rand against the dollar.

Although Zimbabwe is using a stable currency, the development of derivative

instruments has been very stunted and the community’s understanding of these

products is very shallow to a certain extent that the general traders don’t under-

stand these at all. According to Dodd, (2004) and Tian, (2005), derivatives are a

Introduction 3

Figure 1.1: Volatility of the rand against the US dollar

requirement to strengthen the financial market. Derivative instruments can help

companies hedge against foreign currency risks.

1.2.1. Options

Derivative markets are populated with a vast range of instruments, and amongst

these, options are perhaps the most interesting, mathematically and financially,

in terms of complexity and scope. Black and Scholes (1973) define an option as a

security giving the right to buy or sell an asset, subject to certain conditions, within

a specified period of time. When in possession of an options contract, the holder has

the right but not the obligation to trade an underlying asset at a predetermined

date in the future and at a predetermined price, regardless of where the underlying

market is trading. There are two types of options: call options and put options. A

call option grants its holder the right, but not the obligation, to buy the underlying

Introduction 4

asset(s) at a specified price on, and in some cases before, the date the option expires.

The specified price is called the strike price (or exercise price), the date the option

expires is called the maturity (or expiration date), and the premium (i.e. option

price) is the price paid to acquire the option. A put option is similar, but with the

right to sell the underlying asset(s).

Call and put options are further categorised in various ways based on their

additional features. These features include:

1. Underlying asset

Due to the enormous growth in financial markets, the use of options has be-

come increasingly popular and are available on many assets. Currently, op-

tions are actively traded on stocks, commodities, indices, foreign exchange

rates (of particular relevance to this study), futures, and even on weather

and electricity.

2. Exercise frequency

Options that can only be exercised at maturity are called European options

while those that can be exercised at any time up to maturity are called Amer-

ican options. Variants include Bermudan options, which can also be exercised

before maturity, but only on a fixed number of pre-determined dates during

the contract life.

3. Payoff functions

New types of options may be devised by changing the payoff function for the

option. For example, binary options have payoffs of either a fixed amount or

zero, rather than being linearly related to underlying asset value at maturity.

Whether the payoffs are achieved at all may be made to depend on the path

followed by the underlying asset. A barrier option, for instance, may cause

the payoff to be knocked out (alternatively, knocked in), dependent on path.

The payoffs from lookback options depend on the maximum or minimum as-

set price reached during their contract life. For Asian options, the payoffs

depends on the average price of the underlying asset during the life of the

contract.

Introduction 5

4. Moneyness (i.e. Intrinsic value)

This classification is mainly important in option price analysis. When the

strike price is equal to the spot price of the underlying asset, the option is

called an at-the-money option. When the strike price is greater than the spot

price of the underlying asset, the option is called an out-of-the-money call

option or an in-the-money put option. If the strike price is less than the spot

price of the underlying asset, the option is called an in-the-money call option

or an out-of-the-money put option.

Although regulated trading of options has not been done yet in Zimbabwe, regu-

lated options trading began in 1973 at the Chicago Board Options Exchange.

1.2.2. Uses of Derivatives Instruments

There are four main uses of derivative instruments which are Hedging, Specula-

tion, Arbitrage and Leverage (Chisholm, 2004). In his study, Chisholm outlined

the importance of derivative instruments through their application in asset man-

agement firms.

• Hedging refers to the action taken to protect an existing market position or

asset from an adverse market move for example a stock market crush that

could erode the value of a portfolio. The hedge is a position that would react

in an opposite manner, if the adverse market movement occurs. The idea will

be to offset the loss of value in the position being hedged. Chisholm (2004)

postulates that Asset Management Firms could hedge a share portfolio by

selling Futures that represent the portfolio held. He further asserts that not

only investing institutions like asset management firms, but also corpora-

tions, banks and governments can use derivative products to hedge or reduce

their exposures to market variables such as, share values, bond prices, cur-

rency exchange rates, interest rates and commodity prices.

• Hull (2001) defines speculation as entering a contract with the purpose of

making a profit. Portfolio managers in the form of speculators can take a fu-

ture position if they believe that they could make a profit. If they are bullish

Introduction 6

on the price of the underlying asset for example stock, they would buy the fu-

ture and then sell again once the price of the underlying asset had increased

sufficiently, making the future price rise. Similarly, if they feel that the un-

derlying asset is overpriced, they can sell the future and then buy back the

asset once the price has fallen. Chisholm (2004) asserts that derivatives in-

struments are very well suited to speculating on the prices of commodities

and financial assets and on key market variables such as interest rates, stock

market indices and currency exchange rates. It is much less expensive to

create a speculative position using derivatives than by actually trading the

underlying commodity or asset. As a result, the potential returns are that

much greater.

An arbitrage is a deal that produces risk free profits by exploiting a mispricing

in the market. A simple example occurs when a trader can purchase an asset

like Old Mutual shares which are dual listed both on ZSE and Johannesburg

Stock Exchange. The Old Mutual share is cheaper in one exchange and the

purchaser simultaneously arranges to sell it in another at a higher price.

Such opportunities are unlikely to persist for very long, since arbitrageurs

would rush in to buy the asset in the ‘cheap location, thus closing the pricing

gap.

• Leverage enables a greater gain (loss) to be made for a given amount of initial

capital employed-higher risk for higher returns. In this sense, derivatives

can be used as an efficient avenue to obtain leverage in financial markets.

For example, if a speculator in the form of asset mangers thinks a stock will

rise, they can purchase a call option on the stock. They use less capital than

buying the stock outright, since less money is required on the initiation of the

contract. In the case of the forward contract no money changes hands, while

with the option only the premium is paid. The leverage that can be acquired

in derivatives markets is also a highly attractive feature to those looking to

hedge, as it allows a smaller amount of money to be put up front in order to

Introduction 7

gain protection against changes in the asset price.

1.2.3. Importance of a derivatives market

Effenberger (2004) asserts that the volatility of financial markets can affect a firm,

thus managers should seek to avoid it. Initially many asset management firms

tried to build better forecasting models so that if they could predict price changes,

they could avoid the risk. Hamilton (1998) postulated that derivatives can be used

to combat the adverse effects of volatile commodity prices on the economies of de-

veloping countries because forward prices tend to be less volatile than spot prices,

giving commodity producers an opportunity to reduce the volatility of the price of

their output through hedging.

The Deustche Bundesbank report (2006) states that an active derivatives ex-

change plays an important role in facilitating an efficient determination of prices

in the underlying cash (or spot) market by providing improved and transparent

information on both current and future prices for an asset. For example, in com-

modity markets, spot prices are often pegged to futures prices because the futures

market provides excellent pricing information for the underlying product. Prices on

derivatives markets reflect anticipated supply and demand, and derivatives mar-

kets thus enhance the ability of market participants to make decisions about future

production processing, and trade.

Derivatives can be used to generate and deliver abnormal performance that can

be packaged within a core-satellite approach to portfolio management, that option

portfolios can be used to enhance the performance of tactical asset allocation pro-

grammes and that fixed-income derivatives offer significant risk reduction benefits.

Introduction 8

1.2.4. Foreign Currency Option Pricing Models Fundamen-

tals

The development of Nobel-prize winning Black Scholes (1973) model on pricing an

option rejuvenated modern quantitative finance in the early 1970s. Based on the

Black Scholes Model, a standard approach to pricing foreign currency options was

developed by Garman-Kohlhagen (1983). This approach took into consideration

six fundamental variables in determining the price of an option on an exchange

rate. These variables include: the current (spot) price, the strike price, the time

to expiration, the foreign currency interest rate, the domestic currency interest

rate, and volatility. Most models that have been developed to price options, seek to

quantify the magnitude in which these individual variables affect the price of an

option. For instance, on volatility, the Garman Kohlhagen model assumes volatility

to be constant, whereas Melino and Turnbull (1990) considered the existence of

stochastic volatility.

1.3. Statement of the Problem

This study seeks to develop a foreign currency options pricing model that can be

used by various players (investment banks, brokers, arbitrageurs) in the Zimbab-

wean financial markets. There is need for a foreign exchange options market where

Zimbabwean companies and individual traders can hedge themselves against for-

eign currency risks. These instruments have not been traded in Zimbabwe, hence

this study will be based on the assumption that a trading system similar to the one

used on the Johannesburg Stock Exchange (JSE) will be used by the Zimbabwe

Stock Exchange (ZSE) in trading these instruments.

1.4. Aim of Study

This study seeks to develop an application for pricing foreign currency options.

Introduction 9

1.5. Research Objectives

The main objectives of this study are as follows:

• Analyse the effect of stochastic volatility on foreign currency options with

particular interest being on the significant difference between the Heston and

the Black Scholes (Garman Kohlhagen, 1983) model.

• Modify and calibrate the Heston model, to make it a better suited foreign

currency option pricing model for the Zimbabwean market.

• To develop a user friendly foreign currency option pricing application that can

be used in Over the Counter markets.

1.6. Importance of Currency Options

Currency options are widely used to hedge foreign exchange risk for a future date.

They provide foreign exchange risk managers, investors and traders with a wide

array of capabilities for controlling the risks inherent in foreign exchange exposure,

and for participating in market movements and implementing investment research

decisions related to exchange rate flactuations. In academic research, currency

options are important in measuring the value of other international financial in-

struments, such as currency option bonds, currency future options, currency option

forwards and so on. As international financial markets further develop, currency

options will play an increasingly important role as a major international financial

instrument.

1.7. Scope of Study

This project will encampass studies on Foreign currency option pricing. A num-

ber of models have been developed in the past to price foreign currency options,

these include the Garman Kohlhagen (1983) model, stochastic volatility models

and jump diffusion option pricing models. In this study we focus on the Garman

Introduction 10

Kohlhagen model and stochastic volatility models with particular interest being on

the Heston model for Stochastic volatility models. When determining a closed form

solution for the Heston model, a number of variables are used. To estimate the

exact value of these variables, optimisation techniques are applied. This is called

calibration of the Heston model. To calibrate the Heston model we use the inverse

method from a number of methods which will be highlighted in the chapter 3. The

inverse problem can be solved by a number of optimisation tools like Matlab, Lingo

and Microsoft excel. In this study we use Microsoft excel as it is very user friendly,

accessible, easy to understand and produces fairly accurate results.

Furthermore through this study, the researcher develops an application that

seeks to determine the premium value of an option. This application should allow

the user to choose a pricing model they want to use in determining the option price.

Among the models to be chosen from will be the Garman Kohlhagen model and the

Heston model.

The main African countries that Zimbabwe trades with are Botswana and South

Africa of which the later has got a higher trade ratio than the former. In this regard

this study will focus on the following currency pairs:

• USD/ZAR,

• USD/GBP, and

• USD/BWP.

1.8. Summary

This chapter gives a basic overview of foreign currency derivatives. The researcher

highlights the basic need for foreign currency derivatives in Zimbabwe, further-

more the researcher seeks to unravel what foreign currency options are, the struc-

ture and role of the foreign exchange market and finally the fundamentals of for-

eign currency options pricing.

Chapter 2

Literature Review

2.1. Introduction

In this chapter, we consider aspects surrounding foreign currency options pricing.

According to Chensey and Scott (1989), when developing an option pricing model,

financial engineers seek to achieve two objectives:

1. Deteremine a fair price for an option, and

2. Develop an accurate model comparing model values to observed values.

Various models have been developed to price options, the famous of them all being

the Nobel Prize winning Black Scholes model 1973. The Black Scholes model laid

a foundation to stock option pricing and has been widely used in over the counter

markets and organised exchanges to determine the fair prices of a stock option.

The main advantages of the Black Scholes model that have ensured its continuous

recognition in the financial markets is that it is fast and easy to use. By providing

a way of calculating hedge ratios and more efficient portfolios, the Black Scholes

model also helps investors understand the sensitivity of option prizes to stock price

movements, thereby helping investors maximize the efficiency of their portfolios.

Literature Review 12

Finally the Black Scholes steadies the market because of its ability to measure

equilibrium pricing relationships.

However inspite of its successes and advantages, Rubinstein (1985) asserts that

the Black Scholes model has known biases. These biases include:

1. Constant volatility assumption

The Black Scholes model assumes constant volatility of stock prices, of which

this assumption is strongly violated in financial markets. In financial mar-

kets, volatility tends to exhibit consistently the following traits:

• Volatility tends to revert around some long term value.

• Volatility clusters with time: large (small) changes tend to follow large

(small) price changes.

• Volatility is correlated to stock return.

2. The leverage effect

The Black Scholes model can not account for the leverage effect which is but

just the tendency for stock prices to be negatively correlated with changes in

volaltility.

Meisner and Labuszewski (1984) illustrate how the Black Scholes model can be

modified to tailor make it for the pricing of various assets options, for example, the

Garman-Kohlhagen model (1983) modified the Black Scholes model to price foreign

currency options.

2.2. Foreign Currency Pricing Models

Jarrow (1991), defines a European foreign currency call (put) option as a derivative

instrument that gives the holder the right to buy (sell) a fixed amount of the foreign

currency or currency futures, respectively, at a predetermined price only at the

fixed expiration date. The corresponding American options can be exercised at any

time until the expiration date.

Currency options pricing models are dependant mainly on the following factors:

Literature Review 13

• Exchange rate,

• Interest rate, and

• Anticipated volatility of the exchange and interest rates.

We review literature on models that have been developed to pricing foreign cur-

rency options. Much attention is given to the Garman-Kohlhagen model (1983)

which is a direct modification of the Black-Scholes model and has been widely used

in foreign currency options pricing across counters.

2.2.1. The Garman-Kohlhagen Model

According to Garman-Kohlhagen (1983) a model for pricing foreign currency op-

tions can be developed from the Black-Scholes formula. This model is based on the

following assumptions:

1. No transaction costs, no differential taxes, no borrowing or lending restric-

tions, and trading takes place continuously.

2. The term-structure of interest rates in both the domestic and foreign country

are flat and non-stochastic.

3. The underlying state variable is the spot exchange rate

4. The exchange rate S can be described by the stochastic process

dS = BSdt+ σSdZ, (2.1)

where B is the instantaneous mean, σ2 is the instantaneous variance; and Z

is a standard Wiener process. It is also assumed that B and σ are constants,

implying that the stochastic process describing the evolution of the spot rate

over time is log-normal.

Literature Review 14

Given the above assumptions and further referring to Merton (1973), Garman

and Kohlhagen (1983) value an European option by the following formula:

C = exp(−rFT )SN(d1)− exp(−rDT )KN(d2), and (2.2)

P = −exp(−rFT )SN(−d1) + exp(−rDT )KN(−d2), (2.3)

where:

• C is the Call option price and P is the Put option price.

• rD (rF ) is the domestic (foreign) risk free interest rate per unit time.

• T is the maturity of the option: T ≡ T1 − t where T1 is the date the option

matures and t the current time.

• K is the exercise price.

• d1 ≡ ln(S/K)+((rD−rF )+σ2/2)Tσ√

T.

• d2 ≡ d1 − σ√T .

• N(.) is the cumulative normal distribution function.

Drawbacks of the Garman-Kohlhagen Model

Underlying the Garman-Kohlhagen options valuation formula are a number of as-

sumptions. To the extent that the world deviates from these assumptions, the

Garman-Kohlhagen model will be biased in certain, often predictable ways. This

subsection explores the pricing biases introduced by two major simplifying assump-

tions of the Garman-Kohlhagen model: constant volatility and a normal (or lognor-

mal) distribution of price changes. The Garman-Kohlhagen may not be a perfect

model of options valuation, but as long as market participants understand these

and other problems with the model, then it is useful in practice.

The Garman-Kohlhagen model assumes that an exchange rate’s volatility is

known and never changes. However, causal observation reveals exchange rate

Literature Review 15

volatility is not constant. This fact has a major impact on the values of certain

options, especially those options that are away from the money, because the dy-

namics of the volatility process rapidly change the probability that a given out

of the money option can reach the exercise price. The Garman-Kohlhagen model

consistently underestimates the value of an option to the extent that volatility is

stochastic rather than constant as assumed.

A second major assumption of the Garman-Kohlhagen model is that exchange

rate returns are normally (or lognormally) distributed with a variance proportional

to the length of time over which the asset trades. However, a number of academic

studies show that exchange rate movements are neither normally nor lognormally

distributed. Empirically, exchange rates experience big moves with a frequency

that exceeds what one would expect theoretically. This could be a result of herd

like behaviour among currency speculators or it could be due to the intervention of

central banks. Once again, this problem with the distributional assumption of the

Black-Scholes model means that it generally underestimates currency option val-

ues because the likelihood of having an extreme price movement is greater than the

model expects. As with the Black-Scholes (1973) model, the Garman-Kohlhagen

formula has been a popular practical choice for currency option pricing over the

years, despite the fact that interest rate and volatility are not constant in practice.

Biger and Hull (1983) again used the Black-Scholes (1973) methodology includ-

ing dividends, and obtained comparable results based on the same assumptions

as employed by Garman and Kohlhagen (1983). In the same year, Grabbe (1983)

presented a model for European options, which relaxes the assumption of constant

interest rates. He assumed that the processes of interest rates in the domestic

currency and the foreign currency are deterministic functions of time, using an

arbitrage-free approach to obtain a partial differential equation (PDE) and con-

sequently the European call price. However, the model is not supported by the

empirical evidence of Adams and Wyatt (1987a), who showed that the interest rate

risk is an important element in the valuation of currency options.

Literature Review 16

2.2.2. Other foreign currency pricing models

Hull and White (1987) introduced a second stochastic differential equation to model

the volatility process of asset prices. In their study, the derivative asset has a price

that depends on the security price, S, and its instantaneous variance, V = σ2,

which obeys the following stochastic process:

dS = ϕSdt+ σSdW, and (2.4)

dV = µV dt+ ξV dZ, (2.5)

where ϕ is dependent on S, σ, t. The variables µ and ξ depend on σ and t. The

Weiner processes dW and dZ are correlated.

Hull and White make a number of assumptions in developing their model above.

These include:

1. S and σ2 are the only two variables that affect the price of an option.

2. The risk free interest rate r is constant.

3. The volatility V is uncorrelated with the stock price.

4. The volatility V has no sytematic risk, where sytematic risk is defined as the

risk that affects the entire market and cannot be avoided through portfolio

diversification.

Melino and Turnbull (1990) investigated the consequences of stochastic volatility

in foreign currency option pricing. In their study, they relaxed the assumption

about the stochastic process describing the evolution of the exchange rates. Draw-

ing from the work of Marsh and Rosenfield (1983) who addressed the issue of mod-

elling different types of stochastic processes for interest rates, Melino and Turnbull

(1990) assumed that the stochastic process for the exchange rate is of the form

dS = (A′S−(1−β) +B′S)dt+ σSβ2 dZ, (2.6)

Literature Review 17

where A′, B′ and β are constants and 0 ≤ β ≤ 2 and S ≥ 0.

Note that the different values of β give different probability distributions of the un-

derlying asset. These are normal distributions for β = 0, chi-square distributions

for β = 1 and lognormal distributions for β = 2. According to their empirical work

on the market data, Melino and Turnbull also assumed the stochastic volatility

was described by the following Stochastic differential equation (SDE):

d ln ν = (A′ + θ ln ν)dt+ γdZt. (2.7)

However, they held both the domestic interest rate and foreign interest rate con-

stant. They argued that neither the lognormal probability distribution for ex-

change rates nor constant volatility fit empirical data. By simply setting the in-

terest rates as constant, Melino and Turnbull used Equation (2.6) with historical

data, then used this SDE for the volatility of the exchange rate process. They

did find that making volatility stochastic gave a much better fit to the Canada-U.S.

exchange rate distribution and more accurate predictions of observed option prices.

Based on the assumption that the volatility, reverting to a long-run mean, fol-

lows an arithmetic Ornstein-Uhlenberk process, Stein and Stein (1991) developed

a model for pricing options. Unlike Hull and White (1987) where the processes

determining the stock price and volatility are uncorrelated, in this case they are

assumed to be independent. The assumption of volatility being governed by an

arithmetic Ornstein-Uhlenberk process has a possibility to have negative values.

Although they were able to come up with a closed solution for their model, the

technical problem they encountered was in defining the distribution of the average

variance of the underlying asset.

A simple approach to price European currency options under stochastic inter-

est rates, and the assumption that domestic and foreign bond prices have local

variances depending only on time and not on otherstate variables was proposed by

(Hilliard etal., 1991). By constructing a delta-hedging strategy following Grabbe

Literature Review 18

(1983), invoking the risk-neutrality argument of Cox and Ross (1976), and by

identifying Vasicek’s (1977) term structure model as the appropriate bond pric-

ing model, (Hilliard etal., 1991) derived a closed-form European currency-option

pricing model under stochastic interest rates. Unfortunately, the Vasicek model al-

lows the occurrence of negative interest rates, which is unreasonable,and moreover,

these models cannot be extended to American option pricing analytically. (Hilliard

etal., 1991) model is competitive for currencies with highly volatile interest rates

and for long-lived options. (Hilliard etal., 1991), and Amin and Bodurtha (1995)

indicated that allowing for stochastic interest rates leads to a more accurate val-

uation of currency options with longer maturities than the constant interest rates

alternative.

Tucker (1991) suggested that foreign exchange rates follow a jump-diffusion

process, and that an option pricing model, that takes this process into account, is

likely to be more accurate. Many other authors also demonstrate that these large

jumps exist in foreign exchange price movements, which are responsible for the

leptokurtic distribution on price returns (i.e. the inflation of peak and tails as the

result of the occurrence of more frequent small and large price changes than nor-

mal). Unfortunately, Tucker also assumes that interest rates are non-stochastic.

A general framework for valuing a European option on a foreign currency with

stochastic interest rates was introduced by Amin and Jarrow (1991). Their model

allowed domestic and foreign term structures of interest rates to follow the stochas-

tic processes of the (Heath etal., 1992) (hereafter, HJM) structure. Amin and Jar-

row (1991) also obtained closed-form solutions for European options by assuming

the market is complete and the volatility functions governing the term structure

are deterministic. The Amin and Jarrow (1991) model is a multi-factor model in

which there are at least three different sources of uncertainty, those associated

with the domestic interest rate, the foreign interest rate, and the exchange rate.

To find a risk-free equivalent martingale measure, they chose the domestic current

account (i.e. the cash account) as the numeraire and calibrated the domestic bond,

Literature Review 19

the foreign bond and the exchange rate into the new equivalent martingale mea-

sure, and obtained an analytic solution for European-style options. However, the

complexity of the assumptions of the Amin and Jarrow model make it applicable

only to European-type options. Even using numerical approaches, it is diffcult to

implement the HJM framework.

The first highly stochastic currency-option model allowing American-style (i.e.

early exercise) feature was produced by Amin and Bodurtha (1995). In their model

they considered an arbitrage-free discrete time implementation of the Amin and

Jarrow (1991) framework, using a multinomial version of the lattice technique of

(Cox etal., 1979). They derived a path-dependent model with specific interest-rate

functions. A property of path dependence is that the outcome of a process depends

on its past history, which implies the tree cannot recombine. Therefore it is diffi-

cult to obtain an accurate result due to the vast computational cost. In Amin and

Bodurtha’s model, a simplified HJM model is adopted. They assumed the volatil-

ities of both the domestic and the foreign forward rates are constant (i.e. the Ho

and Lee, 1986 model). Moreover, they only managed to obtain up to 12 time steps

for a five-year American put option value. The multinomial tree with only 12 time

steps applied to a three-factor model is rather unsatisfactory, although it is stated

in their paper:

“... for option maturities up to five years, path-dependent models with

fewer than 12 steps can still yield option values that are accurate to

within one or two percent of their continuous-time limiting values.”

Since there is no benchmark for the American option price with stochastic interest

rates, they adopted a path-independent model in their paper, with a recombining

tree. However, the accuracy of the recombine tree is rather poor, there remains

much scope for improvement in early-exercise currency option pricing which sub-

sequent work has not adequately addressed.

Literature Review 20

Bakshi, Cao and Chen (1997) stated that many assumptions can be made con-

cerning the distribution of the underlying asset, the interest rates components and

the market price of risk. They used a generalised least-squares technique to esti-

mate the parameters, essentially minimising an error term each day of the sample.

This approach, although straight forward to implement, is somewhat contrary to

the assumptions of the model, as it allows the parameters to take on a different

value every day. Moreover, obtaining parameters using cross-sectional information

may result in an excellent fit at the current date, but does not provide any infor-

mation about the dynamics of the system.

Chang (2001) extended Geske and Johnson’s (1984) approach to a stochastic

interest-rate economy. He used only the values of once and twice exercisable op-

tions and described how stochastic interest rates affect the option value. He built a

tree of forward exchange rate process StBf

Bdwhere St was the spot exchange rate at

time t, Bf was a foreign bond and Bd was a domestic bond. However, Chang’s paper

suffers the disadvantage of tree methods, as mentioned for Amin and Bodurtha’s

(1995) model, which is computationally inefficient and is difficult to apply to Amer-

ican options.

A numerical improvement to Amin and Bodurtha’s (1995) model was made by

Choi and Marcozzi (2001). They used a radial basis function (RBF) methodology

to approximate the PDE for currency options. Choi and Marcozzi transformed the

HJM framework into a short-rate version to obtain a Partial differential equation

and established a risk-neutral measure by using the domestic interest rate as a

risk-free numeraire. However, they presented numerical results for a one-year

option with merely five steps for both the foreign interest rate and the domestic

interest rate processes, 31 steps for the exchange rate and 360 time steps for a

one-year option.

Choi and Marcozzi (2003) managed to obtain an analytic solution for European

currency-options. They considered the state variables to be the short rates of in-

Literature Review 21

terest and the exchange rate, as opposed to the forward rates as proposed in Amin

and Jarrow (1991) and utilised in Amin and Bodurtha (1995), in which case the as-

sociative diffusion representing the global economy possesses a coercive diffusion

matrix.

A model that focused on the exchange-rate process with jump diffusion was

proposed by Chesney and Jeanblanc (2004). In their model they obtained a Par-

tial differential equation for a European option, then claimed, “If the American

and European option values satisfied the same linear PDE (in the continuation re-

gion), their difference ∆C, the American premium, must also satisfy this Partial

differential equation in the same region.” Unfortunately, the sign of the jump size

significantly affects the pricing model. Only negative-jump processes can be priced

and furthermore, Partial differential equations describing American options are

inherently nonlinear and, as a consequence, the quantity ∆C cannot satisfy the

same Partial differential equation.

A two dimensional random diffussion proces to model the dynamics of an as-

set price is exploited by Parello, etal (2008). They assume that the stock price

is governed by a log-Brownian motion and that the Ornstein Uhlernberk process

describes the randomness of the log-volatilty and that the two Weinner processes

are correlated. Although the derivation process of a closed form solution to their

model is tedious and laborious, after making a number of assumptions and using

the Fokker-Planck Equation, they come up with a closed form solution. The key

in obtaining an accurate pricing model through their approach is in calibrating for

the parameters that were used in the derivation process.

Dupoyet (2006) undertook an empirical investigation into Japanese Yen/U.S.

Dollar currency-options traded on the Philadelphia stock exchange during March

29th, 1996 to December 31st, 1999, with the aim of determining the information

content of European option prices (for which analytic solutions are available). The

models tested were Black-Scholes (1973) and three others, using stochastic volatil-

Literature Review 22

ity, stochastic interest rates and stochastic volatility with jumps. In order to in-

crease the sample size, both European calls and American calls were studied, in

a stochastic interest-rate environment where American call values could be safely

approximated by corresponding European call values (with the Japanese interest

rate much lower than U.S. interest rate). The greatest improvement over Black-

Scholes in pricing and hedging was found by using stochastic volatility. Stochastic

interest rates improved pricing only for in-the-money long-term options, with in-

significant effect on hedging; including jumps improved pricing and the volatility

smile, but again contributed little to hedging.

Although there is a wide concensus that volatility plays a key role in the dy-

namics of financial markets, there still seem to be no acceptable model which can

realy predict volatility as it is unobservable.

In this study we will use the Heston model (1993). Heston (1993) pioneered the

developement of stochastic volatility in currency option models. As volatility is an

unobservable yet very important parameter, Heston applied a mean-reverting fea-

ture to the volatility process. Thus the model is composed of a stochastic domestic

zero-coupon bond, a foreign zero-coupon bond, an exchange rate, and the volatility

of the exchange rate process. Heston obtained a partial differential equation by

delta-hedging two different maturity portfolios in the model, and then obtained an

analytic solution by invoking the Black-Scholes (1973) formula. Although Heston’s

model has been influential, he assumed interest rates are non-stochastic, which

is somewhat inconsistent with the stochastic bond prices in the model. Also it

is heuristic since he separated Garman-Kohlhagen’s formula into two probability

parts and assumed these satisfy the partial differential equation independently in

order to obtain the option price. Despite its limitations stated above we use the

Heston (1993) model because it has the following advantages:

• It provides a closed-form solution for a European call option.

• It is able to explain the property of stock price when its distribution is non-

Literature Review 23

Gaussian.

• It fits the implied volatility surface of the option prices in the market.

• It allows the correlation between stock price and volatility to be negative.

The number of option pricing models that can be derived is virtually unlimited

because of the many combinations of assumptions that are possible. A number of

models have attempted to capture many processes simultaneously (see Nawalkha

and Chambers, 1995). Such models include the stochastic volatility and stochastic

interest rate models of Amin and Ng (1993), Bakshi and Chen (1997), the stochastic

volatility and jump models of Bates (1996), and the stochastic interest rates and

jump-diffusion models of Doffou and Hilliard (2001).

2.3. Summary

Throughout this chapter, we reviewed literature on foreign currency option pricing.

An overview of the standard Black-Scholes model (1973) was done,thereafter we

reviewed the Garman-Kohlhagen model (1983) which is a direct evolution of the

Black-Scholes model (1973). Although successful in pricing foreign currency op-

tions, the Garman-Kohlhagen model (1983) assumes constant volatility of interest

and exchange rates, and this has resulted in other researchers developing stochas-

tic volatility models so as to account for flactuations in volatility. The researcher

thereby reviewed literature on stochastic volatility models and finally settles on

the Heston model which will be used in pricing foreign currency options in this

research project. The success and significance of the Heston model is based on the

calibration for its input parameters, in the next chapter, methodology, a great deal

of effort will be made to establish a better suited method for calibrating the Heston

model.

Chapter 3

Methodology

3.1. Introduction

In this study, the Heston model (1993) is applied to determine the price of a foreign

currency option. Past studies that have been conducted on option pricing stand to

prove that the Garman-Kohlhagen model (1983) has got a lot of biases as a result

of the assumptions on which it is built upon. One of these assumptions is that

it assumes constant volatility of exchange rates, this assumption results in the

Garman-Kohlhagen model not meeting the common phenomenon in option pricing

which is the volatility smile.

After having applied the Heston model to price an option, we then compare its

performance to the Garman-Kohlhagen model. Two main foundations of option

pricing are used as a basis for comparison, and these include the fairness of the op-

tion price and the accuracy of the model as compared to real market values. There

are a number of steps that are taken in doing so, and this process involves the use

of Visual basic and Optimisation models to calibrate the Heston model. Once this

process is done a user friendly application that allows the user to price a foreign

Methodology 25

currency option is developed. This application will be able to determine the option

price for the ZAR/USD, BWP/USD, GBP/USD and finally the Euro/USD currency

pairs. Various counters have different risk appetites. In this regard, both the He-

ston model and the Garman-Kohlhagen model will be used as the main models in

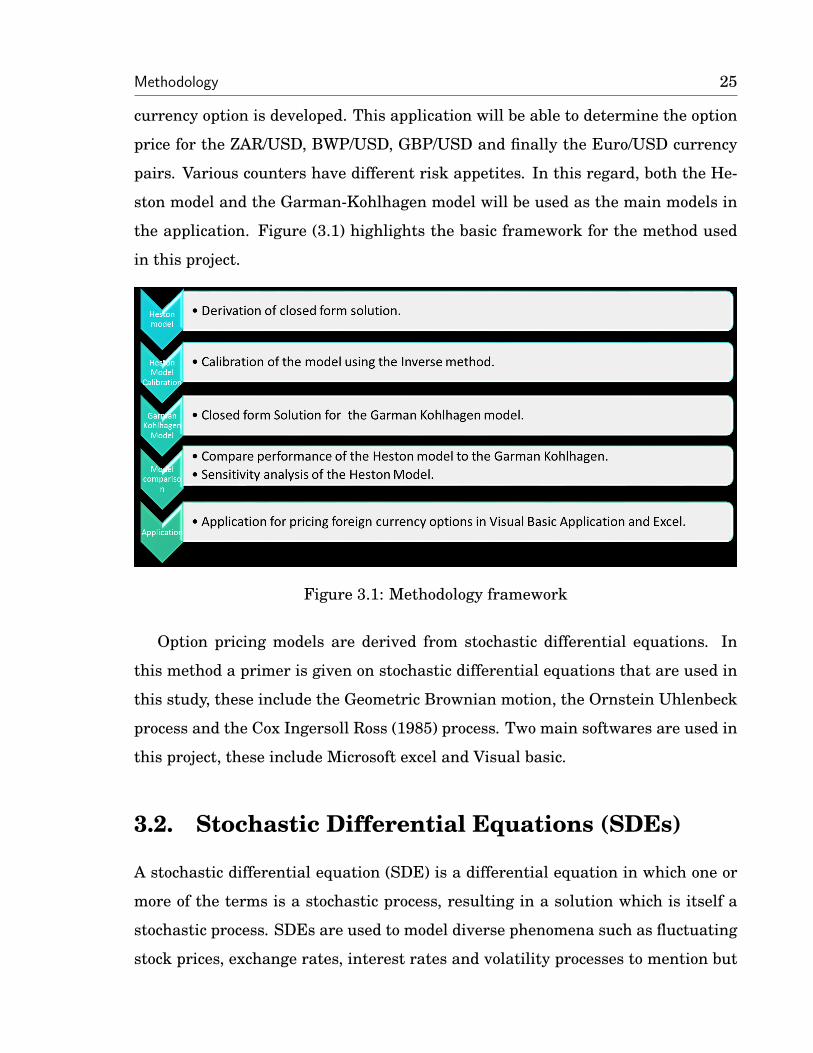

the application. Figure (3.1) highlights the basic framework for the method used

in this project.

Figure 3.1: Methodology framework

Option pricing models are derived from stochastic differential equations. In

this method a primer is given on stochastic differential equations that are used in

this study, these include the Geometric Brownian motion, the Ornstein Uhlenbeck

process and the Cox Ingersoll Ross (1985) process. Two main softwares are used in

this project, these include Microsoft excel and Visual basic.

3.2. Stochastic Differential Equations (SDEs)

A stochastic differential equation (SDE) is a differential equation in which one or

more of the terms is a stochastic process, resulting in a solution which is itself a

stochastic process. SDEs are used to model diverse phenomena such as fluctuating

stock prices, exchange rates, interest rates and volatility processes to mention but

Methodology 26

a few.

The theory of stochastic differential equations is a framework for expressing

dynamical models that include both random and deterministic components; the

theory being based on the Ito integral. The solution to an SDE is a stochastic pro-

cess which is expressed in terms of a stochastic integral with respect to Brownian

motion. Stochastic differential equations form the basis of option pricing. In this

study we use stochastic differential equations to:

1. Determine the foreign currency option price, and to

2. Model volatility of exchange rates.

3.2.1. Geometric Brownian motion (GBM)

A Geometric Brownian motion is the most common process utilised in financial

market modelling, and can be used to model the uncertain return of an asset, such

as a stock. The SDE of a Geometric Brownian motion is defined as

dXt

Xt

= µdt+ σdBt, (3.1)

with initial values X0 = x0 where µ ∈ < and σ ≥ 0.

In this model, σ is the volatility and µ is the mean return. Bt is the Weiner process

and Xt is the asset price

The solution to the GBM is:

Xt = X0eµ−σ2

2t + σBt. (3.2)

It is clear that Xt has a normal distribution with expectation and variance condi-

tioned on X0 = x0 given by

E[Xt|x0] = x0eµt, and (3.3)

V ar[Xt|x0] = x20e

2µt(1− eσ2t). (3.4)

Methodology 27

respectively. Equation (3.1) is used to model the exchange rate process for the

Garman-Kohlhagen model because it has a desirable memoryless property, i.e, to

make a prediction of the value of X at time t we only need to know the value of X

now, not anything about the path it took to get to the present value.

3.2.2. Ornstein-Uhlenberk Process

A stochastic process is called an Ornstein-Uhlenberk process if the SDE has the

form

dXt = κ(θ −Xt)dt+ σdBt, (3.5)

where κ is the rate of mean reversion, θ is the long term mean of asset price and

σ is the volatility, and Bt is a Weiner process with the initial value X0 = x0. The

solution to the Ornstein-Uhlenberk process is

Xt = θ + (x0 − θ)e−κt + σ

∫e−θ(t−s))dBs. (3.6)

Note that Xt has a normal distribution with the expectation and variance, condi-

tioned on X0 = x0 given by

E[Xt|x0] = θ + (x0 − θ)e−κt, and (3.7)

V ar[Xt|x0] =σ2

2κ(1− e−2κt). (3.8)

In finance, the Ornstein Uhlenberk process is a widely used for the term structure

model of interest rates, including the Vasicek (1977) model because its drift com-

ponent is not constant as in the GBM but is dependant on the current value of the

process Xt, if the current value is less than the long term mean θ, then the drift will

be positive, if it is greater than the long term mean, then the drift will be negative.

3.2.3. Square-root Process

A process

dXt = κ(θ −Xt)dt+ σ√XtdBt (3.9)

Methodology 28

with the initial value X0 = x0 is classified as a square-root process. The SDE has

no explicit solution generally, although its transition density can be defined as

E[Xt|x0] = x0e−κt +

1− eκt

κ, and (3.10)

V ar[Xt|x0] =σ2

κ(1− e−κt)(x0e

−κt +1

2κ(1− e−κt)). (3.11)

This is also known as a Cox, Ingersoll and Ross (1985) model which is often used for

interest rate, volatility, and other financial models because it has a non-negative

mean-reverting feature.

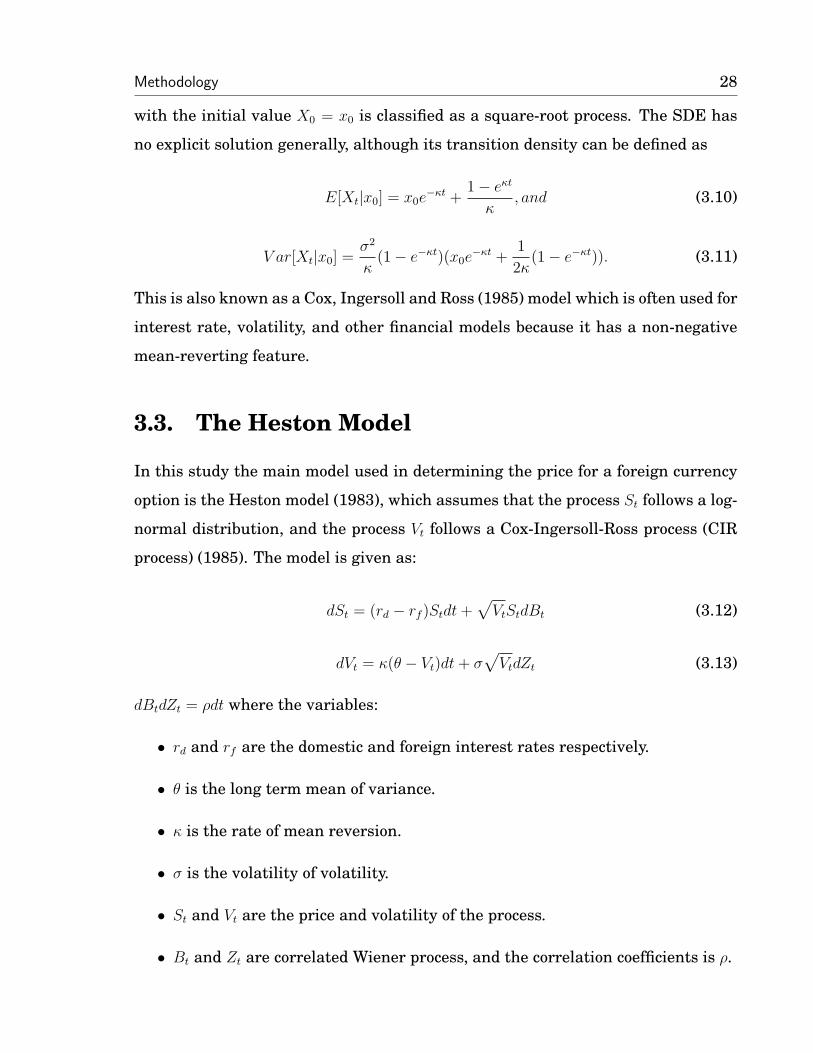

3.3. The Heston Model

In this study the main model used in determining the price for a foreign currency

option is the Heston model (1983), which assumes that the process St follows a log-

normal distribution, and the process Vt follows a Cox-Ingersoll-Ross process (CIR

process) (1985). The model is given as:

dSt = (rd − rf )Stdt+√VtStdBt (3.12)

dVt = κ(θ − Vt)dt+ σ√VtdZt (3.13)

dBtdZt = ρdt where the variables:

• rd and rf are the domestic and foreign interest rates respectively.

• θ is the long term mean of variance.

• κ is the rate of mean reversion.

• σ is the volatility of volatility.

• St and Vt are the price and volatility of the process.

• Bt and Zt are correlated Wiener process, and the correlation coefficients is ρ.

Methodology 29

The variance of the of the CIR process is always positive and if 2κθ > σ2 , then it

cannot reach zero.

It is assumed that the interest rate is a constant, hence rd and rf are fixed

values.

3.3.1. Examination of the Heston model parameters

Correlation coefficient (ρ)

The correlation coefficient ρ is defined as the correlation between the shock to the

log exchange rate and the shock to the volatility. If ρ > 0, then the volatility will

increase as the exchange rate increases. If ρ < 0, then the volatility will increase

while the exchange rate decreases. If ρ = 0, there is no effect to the skewness of

distribution.

Volatility of volatility (σ)

σ controls the volatility of volatility, and it affects the kurtosis of the probability

density distribution. When σ is zero, the volatility is deterministic, so the distri-

bution of exchange rate follows the normal distribution, otherwise, increasing σ

causes the kurtosis to increase. Note that higher σ means that the volatility is

more volatile, which states that the market has a greater chance of extreme move-

ments, (Heston, 1993).

The rate of mean reversion κ and the long run mean of variance θ

The mean reversion speed κ is considered as representing the degree of volatility

cluster. It defines how fast the variance process reverts to its long term mean, and it

can be found in the real market. Generally speaking, a large price variation is more

likely to be followed by a large volatility, and a large volatility more likely follows

a small κ . The variance drifts toward a long run mean of θ, with mean-reversion

rate κ. The mean reversion determines the relative weights of the current variance

and the long-run variance on option pricing. When mean reversion is positive, the

Methodology 30

variance has a steady-state distribution with mean θ (Cox et al., 1985). These two

parameters account for the mean reversion property of the Heston model.

3.3.2. Risk Neutralized approach to option pricing

For the stochastic volatility model defined above a risk neutralised approach, also

known as the Equivalent Martingale Measure (EMM), is widely used in the pricing

of financial derivatives. It is based on the Girsanov’s theorem of asset pricing. The

basic way is to set up a new model that replaces the drift µ by the risk-free interest

rate r and transforms the drift in the volatility equation. In a complete market, the

discounted expected value of the future payoff under the unique risk-neutralized

measure in particular assuming a constant risk free domestic and foreign interest

rate rd and rf respectively is given by:

E∗[St|S] = Se(rd−rf )t,

where S = S0.

Under the equivalent martingale measure, the dynamics of the Heston model equa-

tion defined by equations (3.12) and (3.13) are given by the following set of stochas-

tic differential equations

dSt = (rd − rf )Stdt+√VtStdBt, and (3.14)

dVt = κ∗(θ∗ − Vt)dt+ σ√VtdZt, (3.15)

where dBtdZt = ρdt.

3.3.3. Numerical Solution for the Heston Model

The Numerical solution for the Heston call option after solving equations (3.14)

and (3.15) is given by:

Methodology 31

C(S, υ, t) = Se−rf τP1 −KerdτP2 (3.16)

where τ = T−t, P1 and P2 can be defined via the Fourier Inversion Transformation:

Pj =1

2+

1

π

∫ ∞

0

Re[e−iψ lnKfj(x, υ, τ, ψ)

iψ]dψ

where j = 1, 2. The characteristic function for the logarithm of exchange rate,

x = lnSt is given by:

fj(x, υ, τ, ψ) = eC(τ,φ)+D(τ,φ)υt+iφx,

where:

C(τ, φ) = (rd − rf )φiτ +a

σ2[(bj − ρσφi+ d)τ − 2 ln(

1− gedτ

1− g)] (3.17)

D(τ, φ) =bj − ρσφi+ d

σ2(

1− edτ

1− gedτ) (3.18)

g =bj − ρσφi+ d

bj − ρσφi− d(3.19)

d =√

(ρσφi− bj)2 − σ2(2ujφi− φ2) (3.20)

u1 = 12,u2 = −1

2,a = κθ,b1 = κλ− ρσ, b2 = κ+ λ

To find the price for a put option we use the call/put parity theorem and the

price of the option is

P (S, υ, t) = C(S, υ, t)− Se−rf τP1 +KerdτP2 (3.21)

where P (S, υ, t) is the put option price and C(S, υ, t) is the call option price.

Methodology 32

3.4. Visual Basic and Excel in obtaining a closed

form solution for the Heston model

We use Visual Basic and Excel to fit the Heston model closed form solution. Evalu-

ating P1 and P2 involves the use of complex numbers which may be generally diffi-

cult to code in excel and VBA. For the numerical integration method, the Simpson

rule instead of the Gauss Quadrature is employed, which is relatively accurate and

is not hard to program in Excel-VBA. The input variables for the closed form includ-

ing stock spot price ST , strike price K, risk-free interest rate rd and rf , time step

which need to do integration and the five parameters υ, κ, θ, σ and ρ that needed to

be estimated. The VBA code for the Heston Model is found in the appendix.

3.5. Model Calibration

There are five parameters υ, κ, θ, σ and ρ that need to be estimated in the Heston

model. The change for each parameter will bring a big impact on the correctness

of the model, so the estimation of parameters becomes very important. A variety

of methods can be chosen. For instance, one can observe the real market data,

and use statistic tool to fit data in the Heston model (Ait-Sahila & Kimmel, 2005).

Monte Carlo simulation is another famous method to do the calibration, Alexander

(2010).

In this study we use a commonly used method called the Inverse Problem, which

means that the data is collected from the real market first, and then used to esti-

mate parameters. The most popular approach to solving this inverse problem is to

minimise the error or discrepancy between Heston model prices and real market

prices. This usually turns out to be a non-linear least-squares optimisation prob-

lem. More specifically, the squared differences between European option market

prices and that of the model are minimised over the parameter space. Assume Ω is

a set of realization for the parameters in the Heston model. For a call option that

is calculated from the Heston model, the optimization problem can be described as:

Methodology 33

MinS(Ω) = min(Ω)∑n

i=1(CHi − CM

i )2

Subject to:

2κθ > σ2

−1 < ρ < 1

κ > 0

0 < θ < 1

0 < σ < 1.

where CHi and CM

i are the ith call option price, respectively, calculated by the

Heston model and collected from the real market. N is the number of options that

are used to calibrate the model. Various softwares can be used in calibrating the

Heston model using the Inverse problem model. One of these is Matlab, however in

this study Excel solver was used as it is quick and produces fairly accurate results.

Excel Solver turns out to be very robust and reliable among all kinds of local op-

timizers, Mikhailov (2008). The method employed by Excel Solver is Generalized

Reduce Gradient (GRG) method. More detail on the Generalized reduced gradient

method is found in the appendix.

3.6. Comparison between the Heston Model and

the Garman-Kohlhagen model

3.6.1. Model accuracy

To check for model accuracy, the average relative percentage (ARP) method is em-

ployed. Respective ARP for the Heston and the Garman-Kohlhagen model are

computed. The model which has a small percentage error to six decimal places

is taken to be the better model. The mathematical expression for the percentage

error is given as:

Error =|Modelprice−Realprice|

|Realprice|× 100. (3.22)

Methodology 34

3.6.2. Model Fairness

Studies on the Garman-Kohlhagen reveal that the model tends to:

1. Overprice at the money options, that is where St ≈ K.

2. Underprice options at the ends in the money, St >> K or deep out of the

money St << K.

This is an indication that security price processes have “fat tails” ,i.e, a distribution

which has the probability of large changes in price St greater than those predicted

by the lognormal distribution. Further research shows that stochastic volatility

models address this limitation. We compare the option prices for the Heston model

and the Garman-Kohlhagen model to determine the model that produces fairer

results. The price for comparison with real market prices is determined from the

heston model after the model has been calibrated to find the approximate values

for its parametres.

3.7. Sensitivity Analysis of Heston model parame-

ters

For the Heston model to converge to the Garman-Kohlhagen model, volatility, σGK ,

should be equivalent to the square root of the volatility process, Vt, in the Heston

model. Once this condition is held constant we perform sensitivity analysis deter-

mine the impact of the Heston model parameters on option prices. One common

phenomenon is that the Garman-Kohlhagen model cannot account for variation in

exchange rates, in this regard, through sensitivity analysis we seek to determine if

the correlation coefficient, ρ can explain the skewness in exchange rates and also

if the volatility of volatility, σHeston, can explain the kurtosis of exchange rates. To

doing so, we hold ρ and σHeston constant respectively and observe if any significant

difference exist in between the Garman-Kohlhagen model and the Heston model.

Methodology 35

3.8. Option Pricing Application

Finally we develop a user friendly application for pricing foreign currency option.

The main tools used in developing the application are Visual basic and Microsoft

excel. The application developed should allow the user to choose a model to use in

determining the price of an option between the Garman-Kohlhagen model and the

Heston model.

3.9. Summary

Stochastic differential equations play a huge role in pricing foreign currency op-

tions. We will use stochastic differential equations to determine the foreign cur-

rency option prices as defined by the Heston model and the Garman-Kohlhagen

model (1983). The first part of this chapter served as an introduction to stochas-

tic differential equations and their application in option pricing. Furthermore we

will apply fourier transformations in solving the Heston model partial differential

equation so as to come up with a closed form solution for the Heston model. The for-

eign currency put option will be derived using the call/put parity principle. After

having found the closed solution, the Heston model is then callibrated using the

inverse problem method that is then solved using Excel Solver while employing

the Generalized Reduce Gradient (GRG) method. Another method we will employ

in pricing options in this project is the Garman Kohlhagen model, so included in

this chapter is a section that shows how the closed form solution for a call option

according to the Garman Kohlahagen is obtained. We will then perform a compar-

ison between the Heston model and the Garman Kohlhagen model to determine

a model that is better in giving accurate option prices and also in producing fair

option prices was done. Finally explained in this chapter is the use of excel and

Visual basic in developing an application for pricing foreign currency options in

Zimbabwe.

Chapter 4

Data Analysis, Simulations and

Results

4.1. Introduction

The Garman-Kohlhagen model has long been used to price foreign currency options

in both organised exchanges and over the counter markets. The main reason for

its adoption as the main foreign currency option pricing model is not because of its

accuracy or ability to explain flactuations in exchange rate, but beacuse of its sim-

plicity. Several researches have been done to determine a better pricing model than

the Garman-Kohlhagen model. In our case we use the Heston model. The Heston

model assumes that the volatility process for the model follows a stochastic process

which is modelled as a stochastic differential equation. Past studies have shown

that this assumption tends to produce better results than the Garman-Kohlhagen

model which assumes that the volatility process is constant. The main motiva-

tion of this chapter is to ascertain whether these studies have been true or not.

Furthermore after having produced the results for the comparison of both models

against the market option price, we then develop a user friendly application for

Data Analysis, Simulations and Results 37

pricing foreign currency options.

4.2. Data and data sources

In order to produce fairly accurate results the Heston model needs to be calibrated

so as to estimate numerical values for its parameters. In calibrating the Heston

model, the USD/ZAR pair was used to estimate ρ, σ, θ, υ and κ.

In determining the foreign currency option price using either the Heston model

or the Garman-Kohlhagen model, the following prevailing market data had to be

extracted from the foreign currency market. This data includes:

1. Exchange rate,

2. Domestic and Foreign interest rate, and

3. Strike price.

Daily exchange rates data from 2009 to 2013 was obtained from Old Mutual Zim-

babwe. This data contained the, opening, highest, lowest and closing price recorded

on that day. To obtain the prevailing exchange rate for the day we used the closing

price. Instead of using the whole dataset from 2009 to 2013, we extracted data for

the year 2013.

The US Treasury produces data for daily risk free interest rates. These rates are

used to determine the domestic interest rates used in this study. Foreign interest

rates, in this case the foreign currency being the South African rand, were obtained

from the Reserve bank of South Africa. The South African reserve bank produces

risk free interest rate on an annual basis, in this regard the foreign interest rate

for 2013 had a constant value of 5.5% per annum.

The Strike price data was obtained from the Johannesburg Stock Exchange’s for-

eign currency options market. European options are traded and exercised on spe-

cific dates. We used options with the following expiry dates:

• options that expire in 3 months,

Data Analysis, Simulations and Results 38

• 6 months currency options,

• 9 months currency options, and

• options that expire after 12 months.

Considering that this is raw data, we treated the data to ensure that it helped us

achieve our objectives.

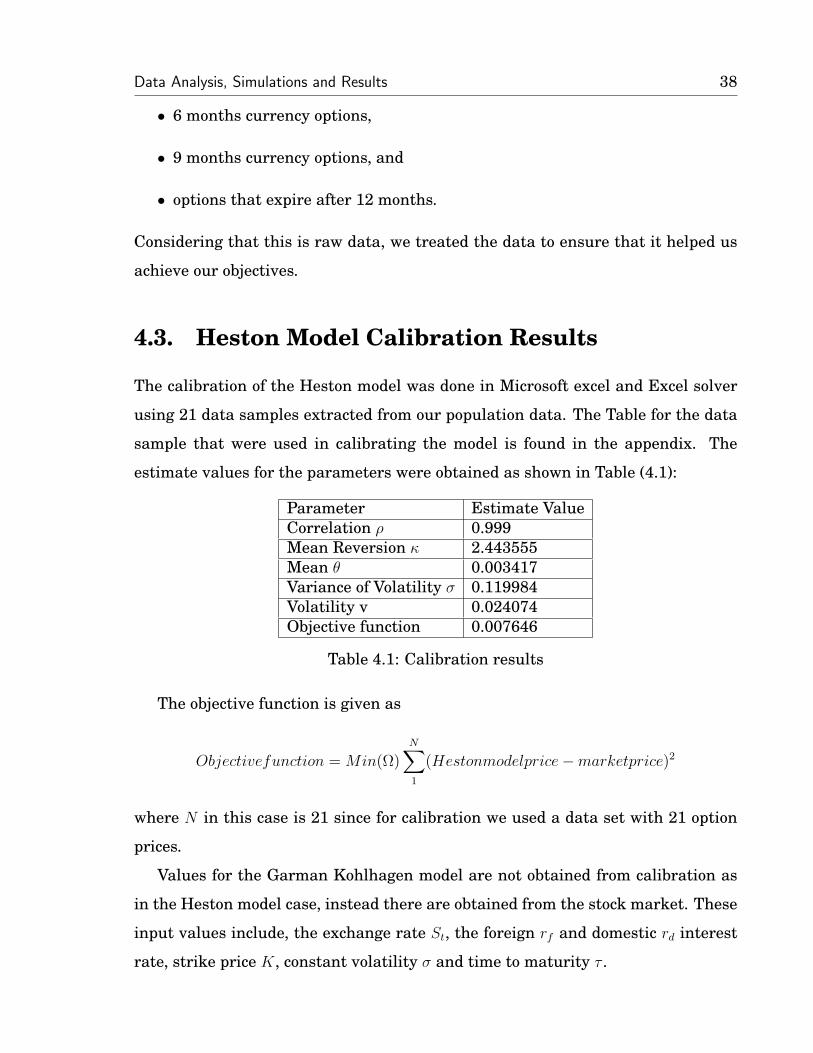

4.3. Heston Model Calibration Results

The calibration of the Heston model was done in Microsoft excel and Excel solver

using 21 data samples extracted from our population data. The Table for the data

sample that were used in calibrating the model is found in the appendix. The

estimate values for the parameters were obtained as shown in Table (4.1):

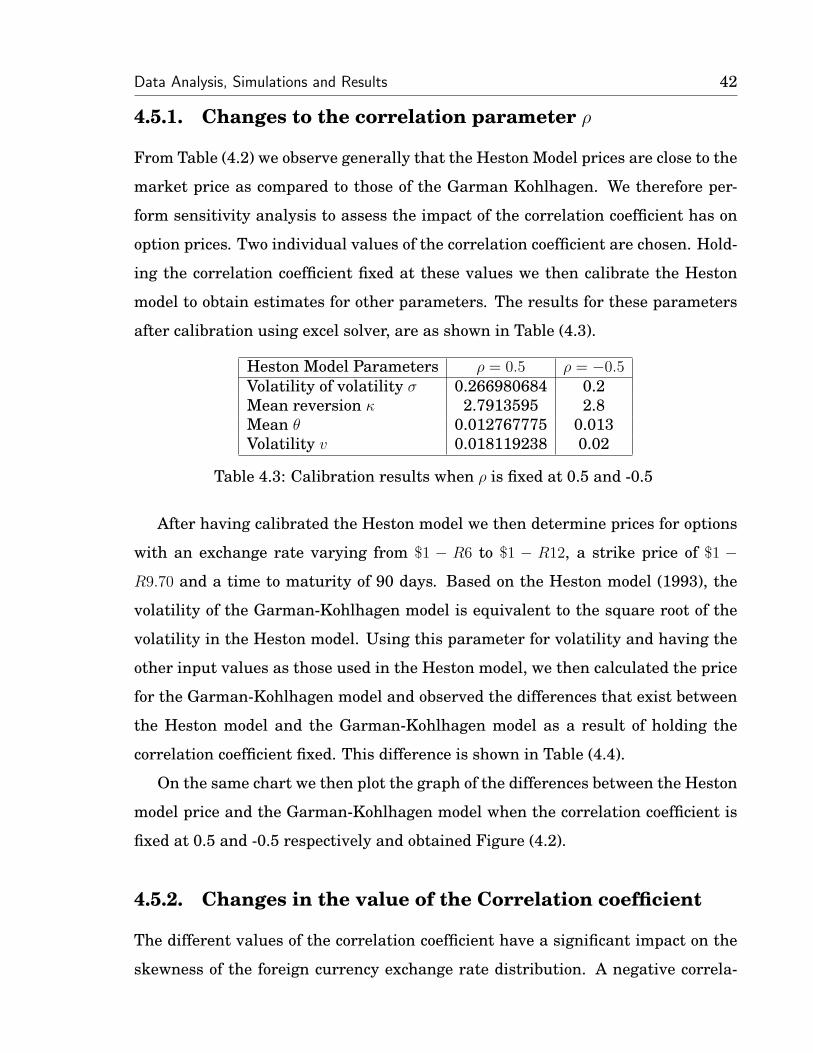

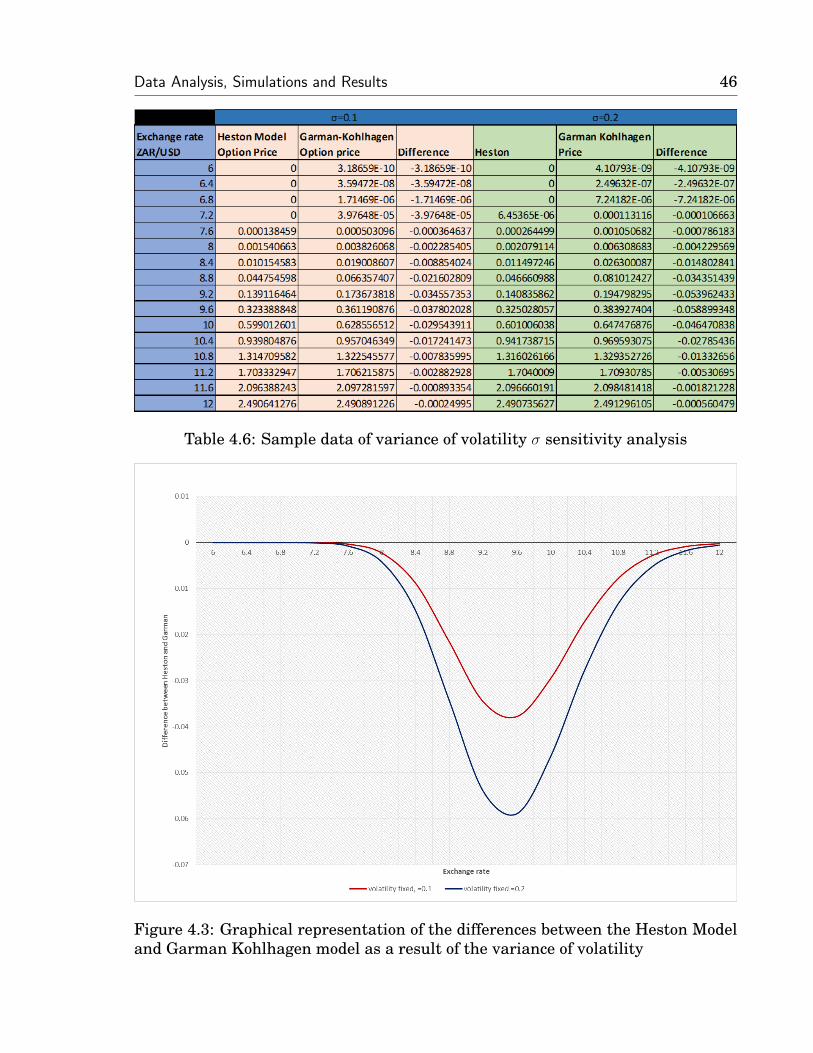

Parameter Estimate ValueCorrelation ρ 0.999Mean Reversion κ 2.443555Mean θ 0.003417Variance of Volatility σ 0.119984Volatility v 0.024074Objective function 0.007646

Table 4.1: Calibration results

The objective function is given as

Objectivefunction = Min(Ω)N∑1

(Hestonmodelprice−marketprice)2

where N in this case is 21 since for calibration we used a data set with 21 option

prices.

Values for the Garman Kohlhagen model are not obtained from calibration as

in the Heston model case, instead there are obtained from the stock market. These

input values include, the exchange rate St, the foreign rf and domestic rd interest

rate, strike price K, constant volatility σ and time to maturity τ .

Data Analysis, Simulations and Results 39

4.4. Comparison of the Heston model to the Gar-

man Kohlhagen model

As outlined in chapter three, one of the main objective of this project is to deter-

mine which model is more accurate in estimating option prices between the Heston

model and the Garman-Kohlhagen model. In comparing 36 data samples we ob-

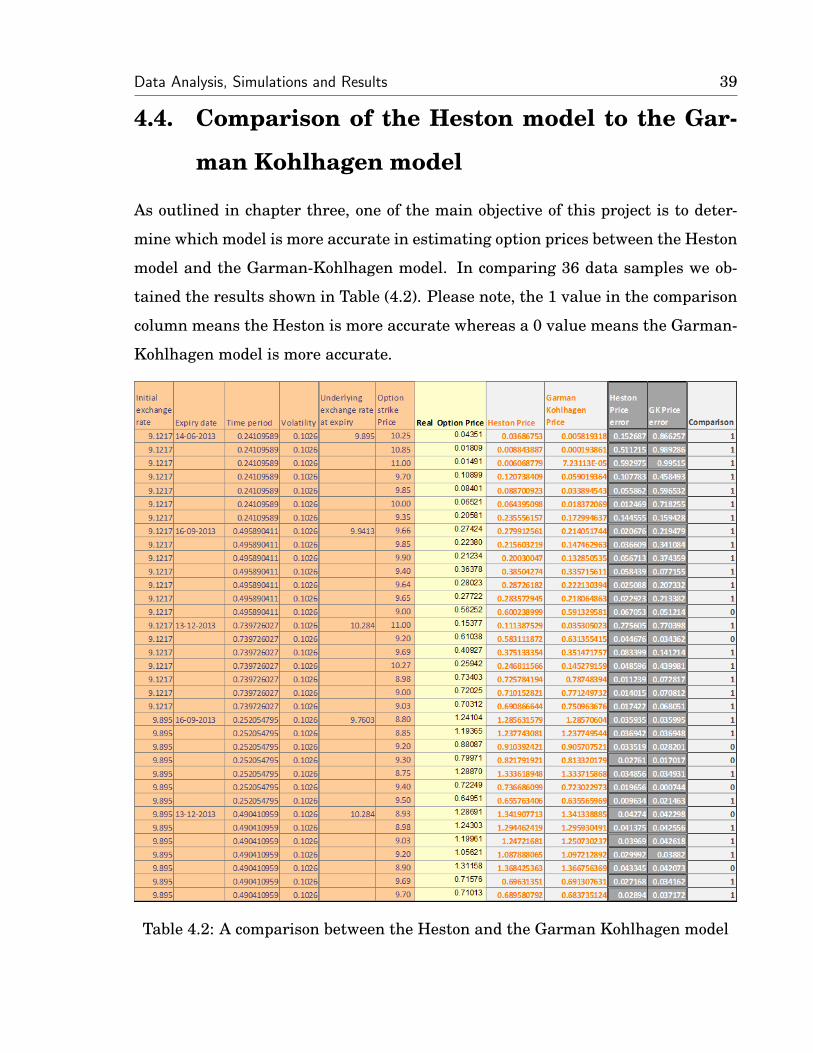

tained the results shown in Table (4.2). Please note, the 1 value in the comparison

column means the Heston is more accurate whereas a 0 value means the Garman-

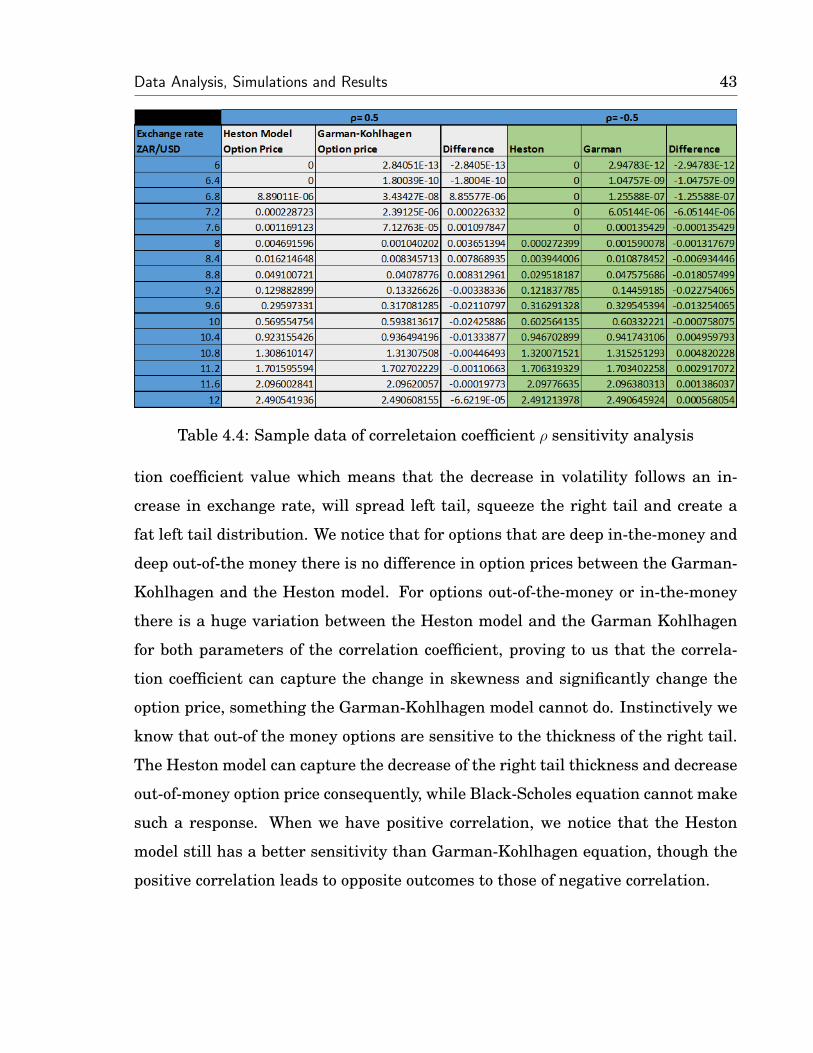

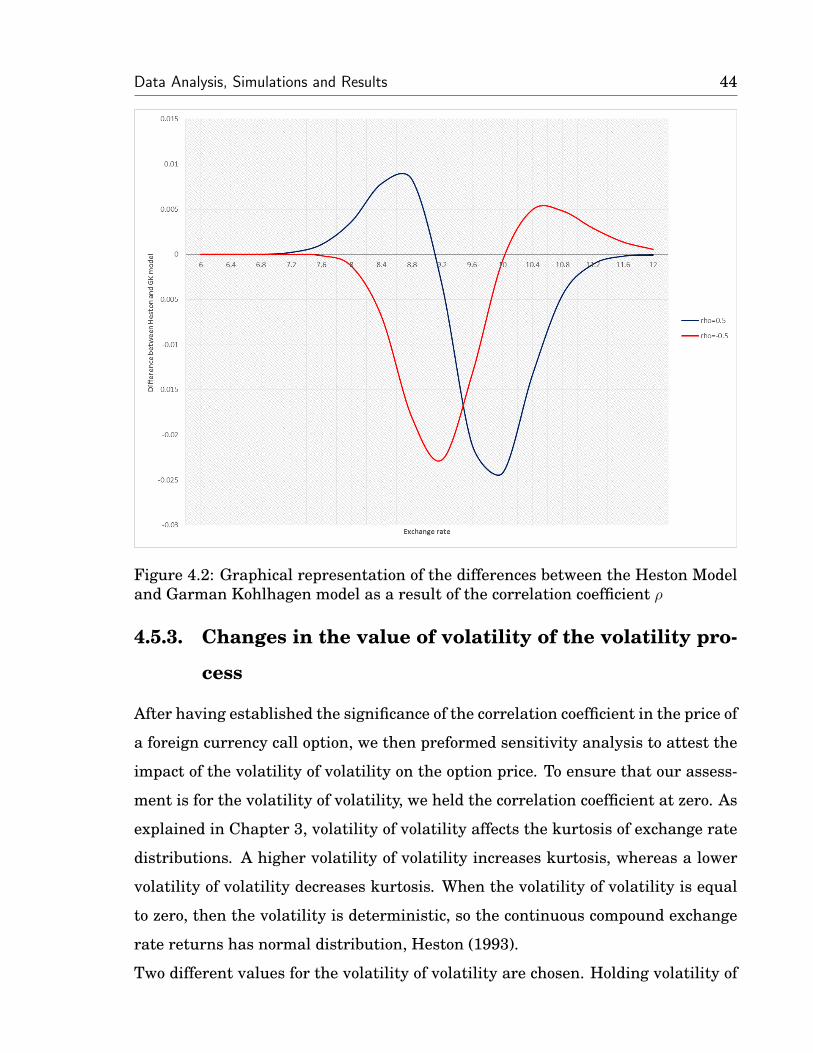

Kohlhagen model is more accurate.

Table 4.2: A comparison between the Heston and the Garman Kohlhagen model

Data Analysis, Simulations and Results 40

4.4.1. Interpretation of the table

Comparison between the Heston and Garman-Kohlhagen model

From the Table (4.2) we notice that generally the Heston model produces better

results than the Garman-Kohlhagen model in both in-the-money and out-of-the-

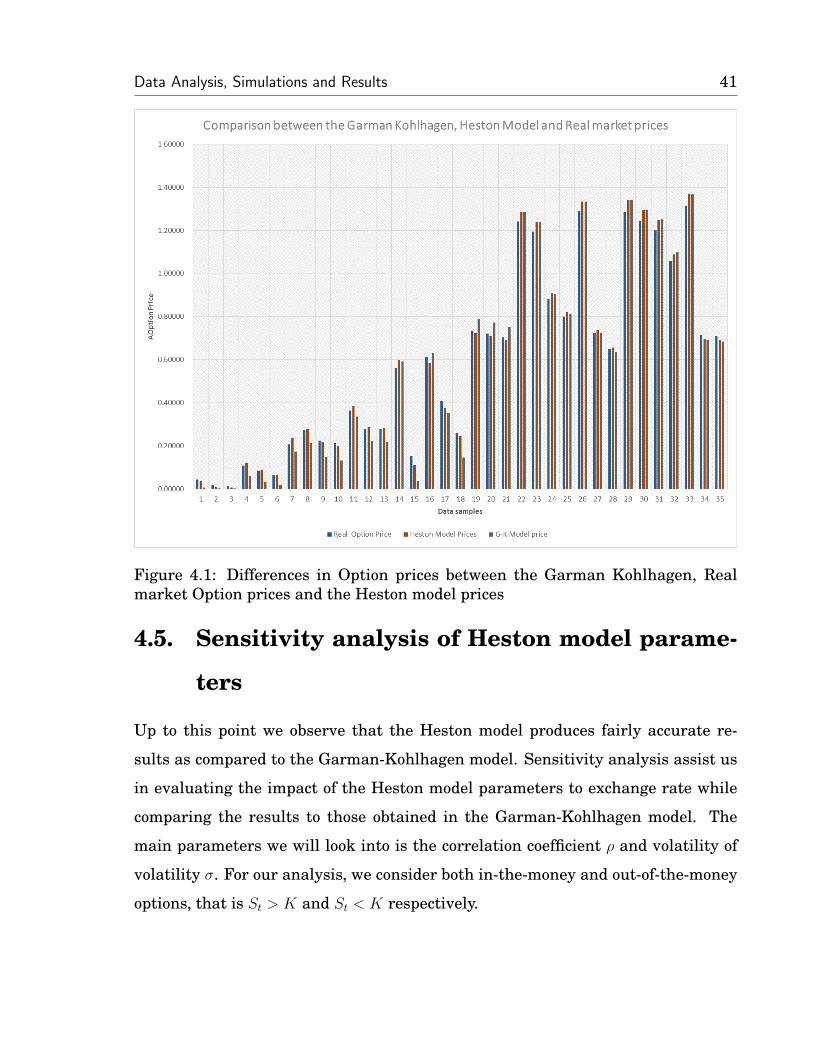

money call options. There are a few instances when the Garman-Kohlhagen pro-

duces results that are closer to the market price than the Heston model. In all

these instances the option is deep in the money. A clear representation of the dif-

ference in option prices as calculated by the Heston Model, the Garman-Kohlhagen

and the observed real market price is shown in Figure (4.1).

There are a number of reasons why the Heston model could be perfoming better

than the Garman-Kohlhagen model, for one it could be as a result of the volatility

process which is assumed to be a stochastic differential equation. In the follow-

ing section sensitivity analysis we analyse the impact of changing the parameter

values of the Heston model, so as to assert the factors that result in it producing

better results than the Garman-Kohlhagen.

Limitations of our data

As the time period for the option increases we observe from Table (4.2) that there

is an improvement in the accuracy of the option prices obtained from the Garman-