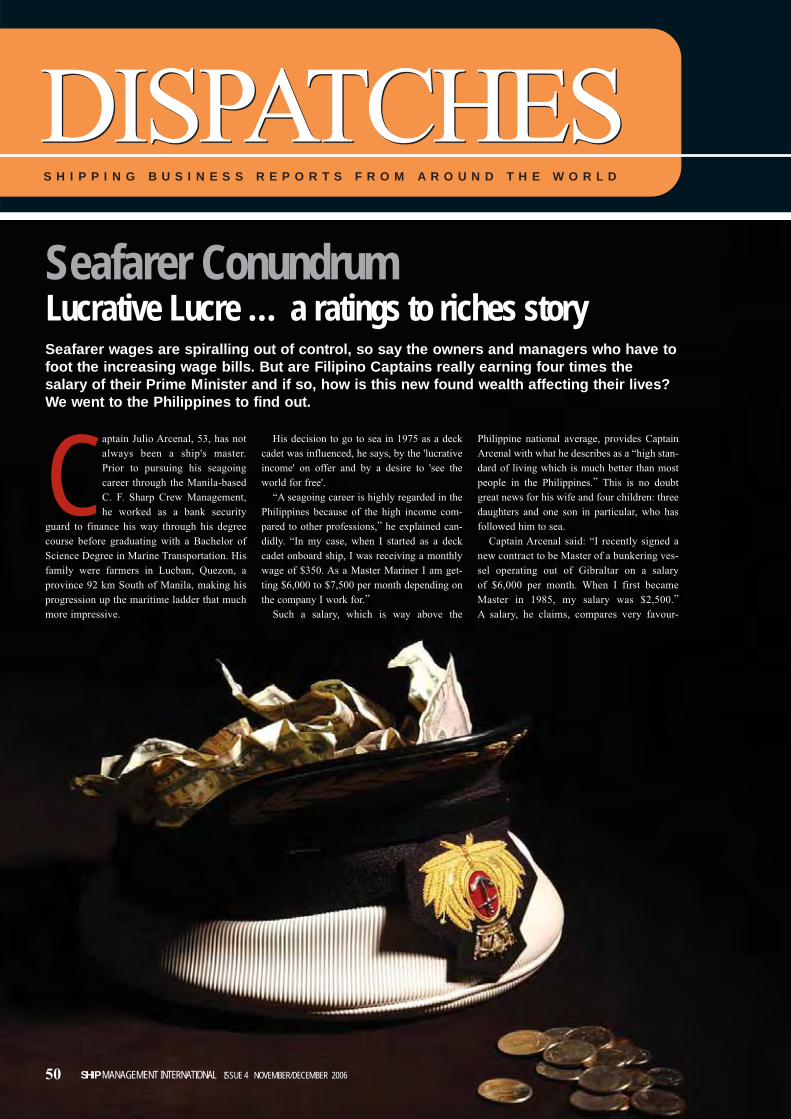

50 Lucrative Lucre - Ship Management International

100

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 50 Lucrative Lucre - Ship Management International

NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL 3

50 Lucrative Lucre …a ratings to riches storyAre Filipino Captains really earning four times the salary of their Prime Minister and if so,how is this new found wealth affecting their lives?

COVER STORY

SHIPMANAGEMENT FEATURES

16 How I WorkSMI talks to two industryachievers and asks the question: How do you keep up with the rigours of the shipping industry?

21 Training for the task aheadAs Chief Executive Officer ofV.Ships’ Shipmanagement division, Bob Bishop is chargedwith steering an industry juggernaut. He spoke to SeanMoloney about the challengesahead

24 On My MindOle Stene is Managing Director of Aboitiz Jebsen Bulk Transport Corporation and Chief Operating Officer of Jebsen Management AS. He is also the newly appointedPresident of InterManager

T H E M A G A Z I N E O F T H E W O R L D ’ S S H I P M A N A G E M E N T C O M M U N I T Y ISSUE 4 NOV/DEC 2006

NOTEBOOK

6 STRAIGHT TALK

9 Pedersen swaps Thome for TESMASvein Pedersen has joined Eitzen Maritime Services as President for EMS Ship Management

10 V.Ships to triple seafarer pool Company unveils plans to boost crew numbers to 60,000

10 Phew! What a relief!Professionalism and operational integrity is alive and well in the V.Ships camp even if it does means losing an owners' fleet

11 No ‘free lunch’ for IMOThe bunkering industry has reacted angrily to IMO’s decision to phase out residual fuels in an attempt to tackle the growingproblem of ship emissions

13 Executive stressWasting office time!

13 Dot com intrigue on the P&I frontInsurers remain non-plussed over P&I internet-based alternative

13 Suez Canal to expandEgypt is planning to spend $1bn to expandthe Suez Canal by 2010, but analysts arequestioning its economic viability

14 Box vessel calls top the restContainer shipping proves its 10 year dominance

16

16

21

24

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 20064

TRADE ANALYSIS

LIFESTYLE

REGIONAL FOCUS

MARKET SECTOR

BUSINESS VIEWPOINT

SPOTLIGHT

83 European and Asian newbuilding roundup

29 Teekay Shipping

LETTERS

20 Mailbox

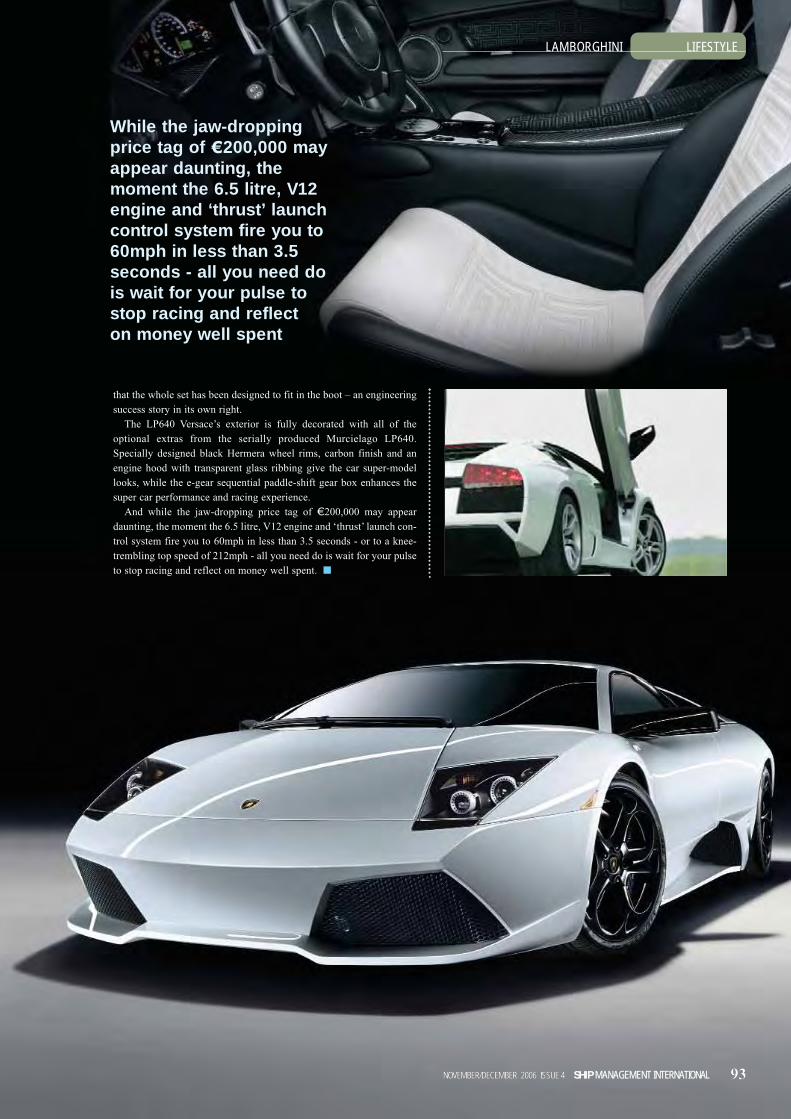

92 On the catwalkThe Murcielago LP640 was already the fastest Lamborghini everbuilt. Now it has been given a professional make-over just in time forChristmas…

94 Skiing in styleSki resorts the world over are heaving under the force of people but,as Andy Pierce discovered, winter paradise is not too far away

BUSINESS OF SHIPPING

30 Burning objectivesSulphur emissions are a hot topic, but the debate is set to continuewith increased scientific understanding and new ideas providing morequestions than answers

76 AdHocDigitally Exposed!Papalexis: getting intellectualGun tottin' trainers end up inchoppy waterSounding offISSA glitz in Singapore

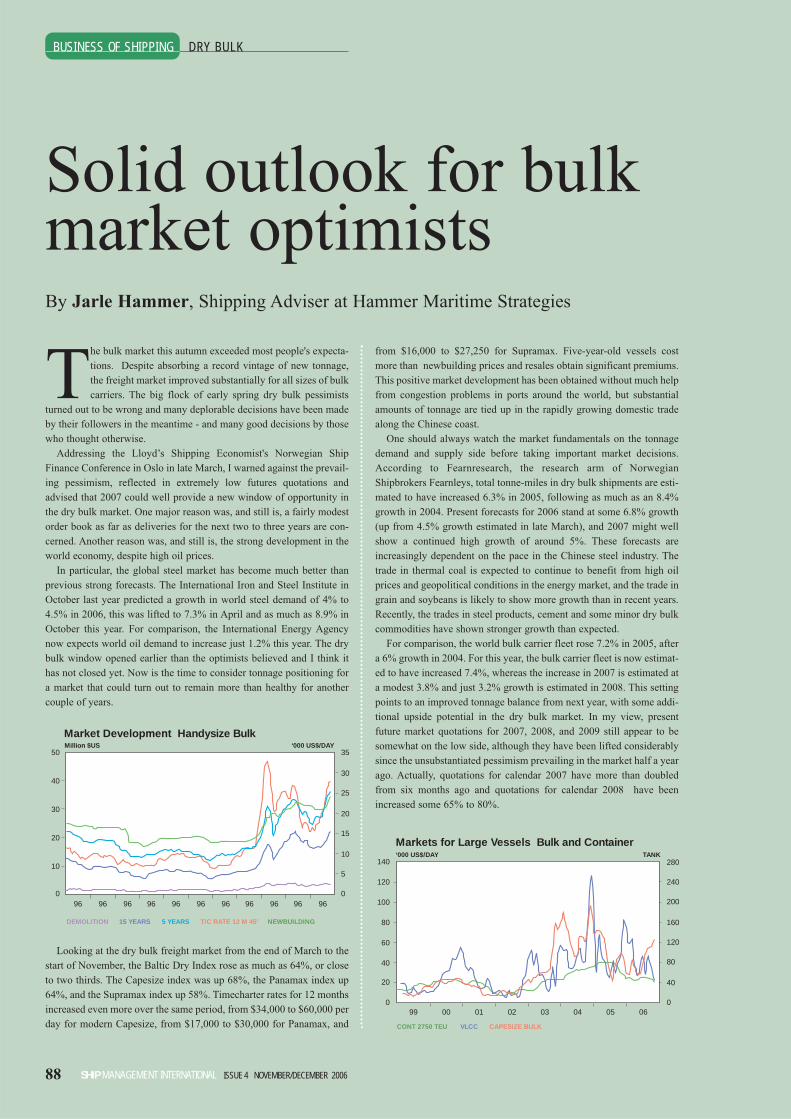

88 Solid outlook for bulkmarket optimistsAnalysis by Jarle Hammer, Shipping Adviser at Hammer MaritimeStrategies

26 Agents - Swimming against the tideThe perennial issues of falling income due to downward pressure onagency fees and increasing workload, due to the agent’s enhanced rolein the exchange of information between the ship and shore, continue toimpact on the health of the port agency industry

58 Dun & Bradstreet Country Riskline Report for SINGAPORE

72 Stripping-out one product from anotherWith implementation of the revised MARPOL Annex II and IBC Codejust weeks away, owners, operators, managers and charterers of prod-ucts and chemical carriers should have got their act together by now

LIVE

80 Objects of desire Things that make you go oooh!

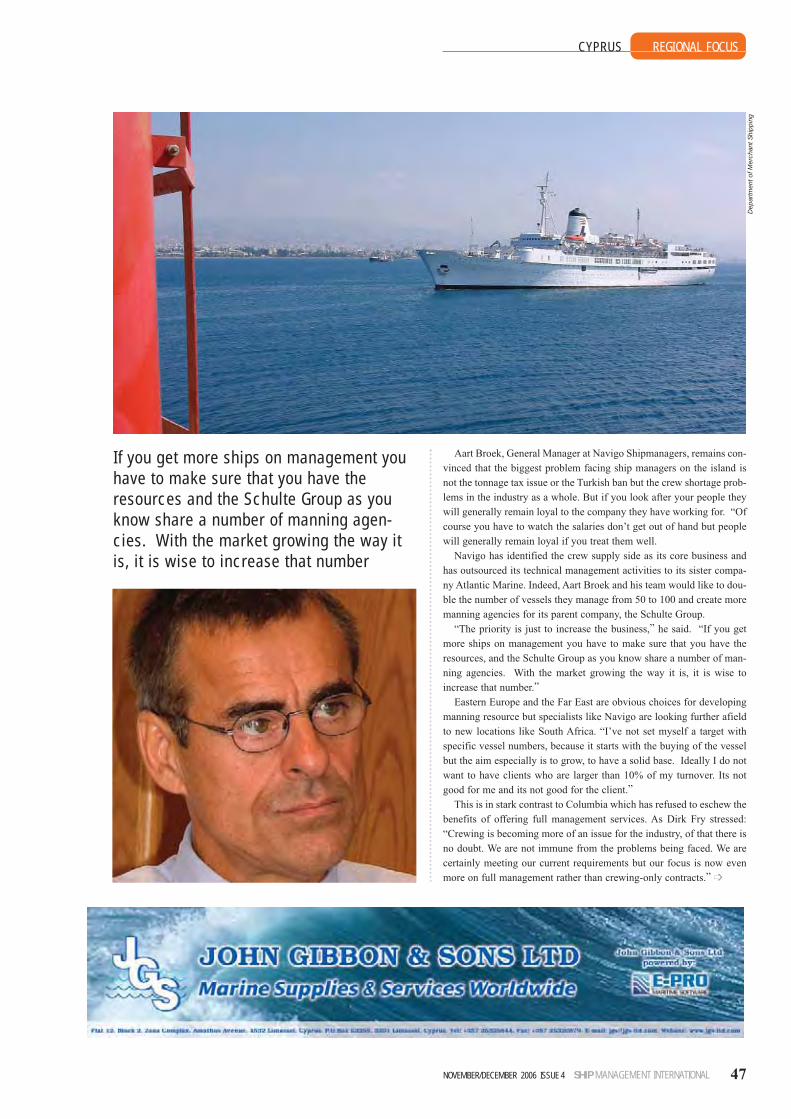

38 Cyprus - Striding for growthThe admonishment of Turkey by Brussels in early November for failing to lift its ban on Cyprus-flagged ships was largely expected butwill have been greeted with nothing more than passing interest in thecorridors of power in Nicosia and the shipping offices in Limassol

60 Hong Kong/SingaporeA force to be reckoned withDespite soaring office rents and risingwages it is still business as usual for theshipmanagement industry in Hong Kong.And any attempt by Singapore to establisha position of strength in the tanker manage-ment market will only go to underline thestrength of the region in helping to dominate this market sector

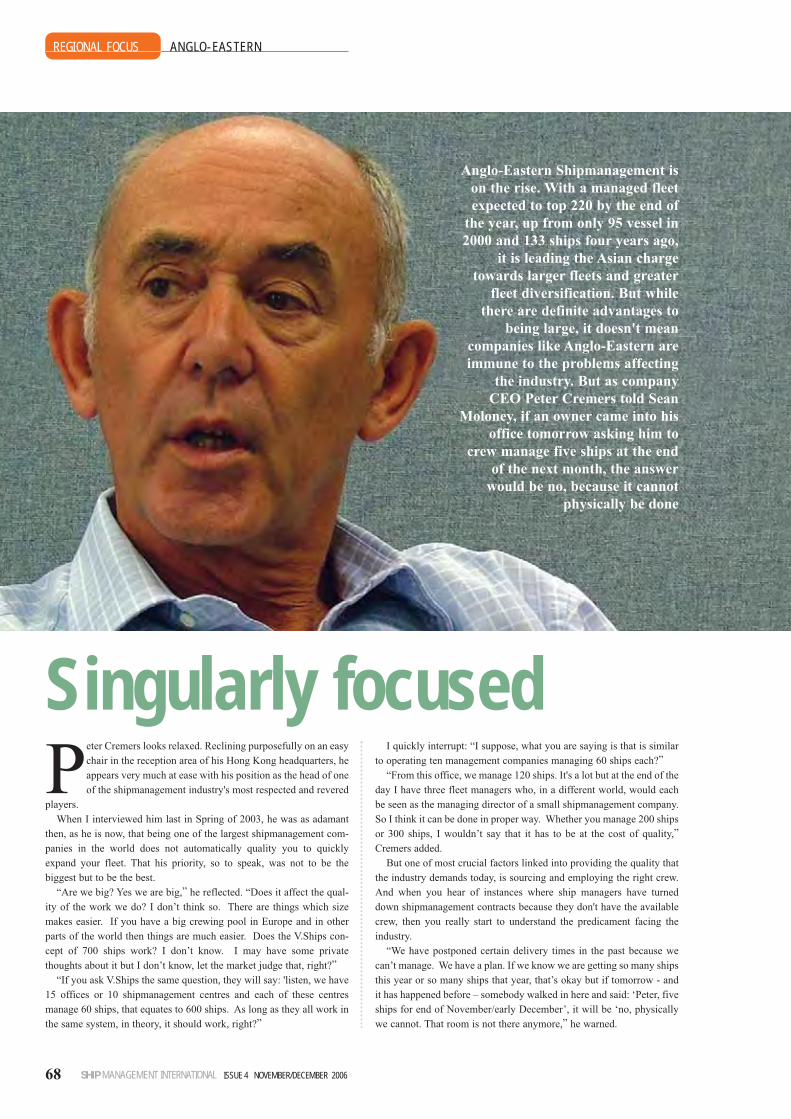

68 Anglo-Eastern - Singularly focussedWhile there are definite advantages to being large, it doesn't meancompanies like Anglo-Eastern are immune to the problems affectingthe industry

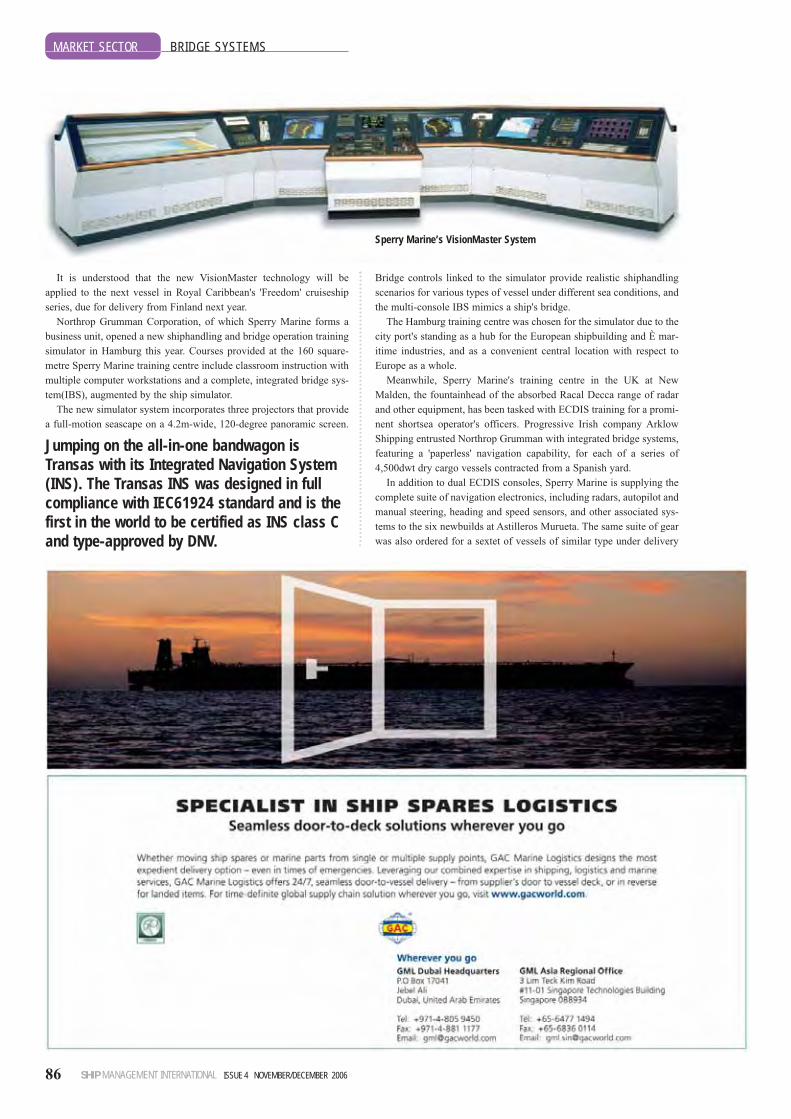

84 Bridge Systems - Offering the navigator a helping handAdvances for bridge watchkeepers' technological and practical needs

NEWBUILDING

Hair Oil - Mopping-up!

DISPATCHES

50 Lucrative Lucre … a ratings to riches storyAre Filipino Captains really earning four times the salary of theirPrime Minister and if so, how is this new found wealth affectingtheir lives?

54 A new kind of warfare By Emmanuel VordonisNew ships are coming onto the market: owners are taking deliv-ery of huge fleets and in order for the ships to be staffed we’regoing to get into warfare on prices and wage increases

56 A day in the mind of a PSC inspectorPort state control detentions can put a black mark on a ship operator's profit as well as its reputation. But are inspections reallysomething to be feared? Andy Pierce joined a vessel inspection tofind out what today's inspectors are really looking for

BOOK REVIEW

82 What I’m readingWith Douglas Lang, MD, Anglo-Eastern (UK) plus reviews ofEngland’s Mistress and Box Boats: The Story of Container Ships

The Shipping BusinessMagazine today’s owners andmanagers have been waiting for

Inever really thought that size mattered!Indeed, there are those stalwarts who believethat small really is beautiful because it pro-motes greater understanding of what you

have and what you can give. It is preferable to theexistence of larger shipmanagement combinesthey say, because there is never any compromiseover personal service. The Customer is King andwe should be there 24/7, at the drop of a hat, totell him that in whatever way he wants telling.

The business ethics, I agree with. The cus-tomer is always right and as a service industrythird party managers should be mindful not onlyof his needs but of the needs of the customers heis trying to satisfy. But for the size issue: I am notso sure.

Because while I am constantly reminded aboutthe need for personal service within the industryand the downsides associated with the conse-quences of consolidation through mergers andacquisitions, the whole industry is besotted withexpansion. There is a determined effort by someof the smaller and medium-sized third party man-agers to take advantage of the growth in popular-ity of their sector and grow their fleets exponen-tially. It is as if they are proud to be known assmall enough to care and deliver but only as longas they are at the vanguard of a drive for growth.I suppose it's not really being a small fish in asmall sea but being a medium sized fish in anocean.

Oslo-based Barber Ship Management wentpublic in the summer by claiming it wanted a20% share of the global third party shipmanage-ment market by 2011. And a handful of compa-nies we have spoken to at random, haveannounced restructuring plans that are part of ageneral strategy to at least double their managedfleets within this period. So the race is on and,while the stakes might not be that high, therewards are certainly worth investing for.

But on the flip side, and there is always a flipside, how can we really expect the industry to

cope with this extra business. After all, the scep-tics amongst us could be excused for clinging tothe notion that one of the main reasons shipown-ers are interested in third party managers isbecause they believe they have the resources toman and crew their ever expanding fleets.

But they don't! We all know the problems fac-ing the crewing sector and if owners think a thirdparty ship manager can man his vessels with amonth's notice, without having to rob Peter to payPaul, then he is largely mistaken. Many of thelargest and most respected ship managers haveadmitted such and have even turned down busi-ness because they can't cope at such short notice.

So it is clear that crewing remains at the heartof the expansionary thrust driving this industryforward. But any quality third party managerworth his salt knows this and will have surelytaken it onboard as part of his overall strategy forgrowth. V.Ships have. They claim in this maga-zine that they have a strategy to near triple theirseafarer pool to 60,000 by 2010 and they havehired a head hunter to help them achieve thisgoal. It would seem that the gloves are off in thefight for predominance.

Whatever it says for the machinations betweenthe major players as far as the growth of managedfleets and managed crewing pools is concerned,remains to be seen. What is clear is that the sea-farer is now clearly king! Lets hope he doesn’t letthis new found attraction and interest mask thereasons why he really joined this fine industry.

Sean Moloney

STRAIGHT TALK

6 SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 2006

Printed in the UK by Cambrian Printers. Although every effort hasbeen made to ensure that the information contained in this publi-cation is correct, Elaborate Communications accepts no responsi-bility or liability for any inaccuracies that may occur or their con-sequences. The opinions expressed in this publication are not nec-essarily those of the publishers. All rights reserved. No part of thispublication may be reproduced whole, or in part, stored in aretrieval system or transmitted in any form or by any means with-out prior permission from Elaborate Communications.

ABC application approved March 2006

Ship Management International is published six timesa year and is entirely devoted to reporting on thedynamic and diverse in-house and third party shipmanagement industry. Subscriptions UK and ROW – 1 year: £85 ($153); 2 years: £160 ($288).

Download a subscription form fromwww.shipmanagementinternational.com or

Send subscription enquiries and/or address corrections to:

Elaborate Communications, Acorn Farm BusinessCentre, Cublington Road, Wing, Leighton Buzzard,Bedfordshire LU7 0LB, United Kingdom. Tel: +44 (0)1296 682051/682241/682403

Editorial Director: Sean Moloney

Assistant Editor: Andy Pierce

Technical Editor: David Tinsley

Advertisement Director: Jean Winfield

Sales Manager: Mark Howe

Sales Support: Martine Frost

Research Manager: Roger Morley

Accounts: Irene Morley

Design & Layout: Phil Macaulay

Cover Photography: Martin Bou Mansour

Editorial contributors: The best and most informed writers currently servingthe global shipmanagement and shipowning industry.

Ship Management International Editorial Board

Rajaish Bajpaee (Eurasia Group of Companies)

Stephen Chapman (InterManager)

Nigel Cleave (EPIC)

Andreas Droussiotis (Hanseatic Shipping Company)

Dirk Fry (Columbia Ship Management)

Sean Moloney (Elaborate Communications)

Svein Pedersen (Thome Ship Management)

Published by

Elaborate CommunicationsAcorn Farm Business CentreCublington Road, Wing, Leighton Buzzard, Bedfordshire LU7 0LBUnited Kingdom

Sales/Accounts +44 (0) 1296 682241/682051Editorial +44 (0) 1296 682356 Fax: +44 (0) 1296 682156Email: [email protected]/[email protected]

Approved and Supported by

November/December 2006 Issue No. 4

www.shipmanagementinternational.com

Long Live the King!

Welcome to Ship Management International

9NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL

NOTEBOOKSHIPMANAGEMENT NEWS AND REPORTS FROM AROUND THE WORLD

The Singaporean shipmanagement communityhas lost one of its staunchest leaders followingthe resignation of Svein Pedersen as ManagingDirector of Thome Ship Management.

Confusion surrounded the reasons behindhis decision to leave which was swift in itsnature but SMI can confirm that he has joinedEitzen Maritime Services as President for EMSShip Management, a group more commonlyknown as TESMA.

TESMA's decision to snap up Pedersen issomething of a shrewd move as he is viewed as

a quality and well-connected operator in theshipmanagement sector. One other very largeship management competitor was known to beinterested in contacting him after hearing of hisdecision to leave Thome, SMI can reveal.

Pedersen will join TESMA during the firstquarter of next year and will move toCopenhagen with the task of spearheading itsdrive to strengthen its position within the third

party shipmanagement market. He will stream-line the operation of six offices in Europe, onein India and one in Singapore. TESMA is theworld's third biggest chemical vessel ownerwith approximately 80 chemical carriers inaddition to LPG and approx 30 vessels on thirdparty ship management. A total of 120 vesselsare managed with an additional 200 vessels oncrew management.

He will report to Annette Malm Justad whotook over as CEO of Eitzen Maritime Servicesfrom April 1st this year.

She told SMI that growth was very muchpart of TESMA’s reorganisational plans at themoment and that it wanted to “maintain astronger position in the third party managementsector.” She did not rule out TESMA acquiringone of its competitors as part of its drive forgrowth. “We want to be part of the consolida-tion move,” she said.

Svein Pedersen believes in the personal sideof shipmanagement and deems it important tobe approachable. He recently told SMI: “Ibelieve in people and the empowerment of peo-ple, that’s very important for me. There are somany different aspects to this industry andthere is a need for so much focus so if youbelieve you can do it all by yourself then I thinkyou have to rethink.” ■

Pedersen swaps Thome for TESMA

SMI can confirm that SveinPedersen has joined EitzenMaritime Services as Presidentfor EMS Ship Management, agroup that is more commonlyknown as TESMA. He will bemoving to Denmark as a result

TESMA is the world's thirdbiggest chemical vessel ownerwith approximately 80 chemicalcarriers in addition to LPG andapprox 30 vessels on third partyship management. A total of 120vessels are managed with anadditional 200 vessels on crewmanagement

NOTEBOOK

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 200610

The sigh of relief emanating fromV.Ships' Avenue de Fontvieille HQmust have been as loud as thewhoops and hollers coming from the

board rooms of the Monaco ship manager'soil major clients: professionalism and opera-tional integrity is alive and well in theV.Ships camp even if it does means losing anowners' fleet.

High costs and disputes over technicalissues were reported to be behind the deci-sion by Italian ship owner Enrico Bogazzi todrop V.Ships as manager of around 50 ves-sels, almost exactly a year after the arrange-ment began. However, it appears the splitmay have been forced through an allegedreluctance by V.Ships to reduce the level ofmanagement service it offered.

Mr Bogazzi has a very close relationshipwith V.Ships supremo Tullio Biggi: indeedthey went to school together and have seen each other's careers flourish since. So itwas hardly surprising that V.Ships ended upmanaging the Bogazzi fleet.

While the divorce was very amicable,Enrico Bogazzi was reported as saying, iron-ically, “we were not happy. Probably.”

“V.Ships is a verysophisticated companyand we have very old scrapvessels. But it wasn’t justabout price. It was veryexpensive, but technicallywe also had some argu-ments,” he told the press.

This was a point echoedby a source very close to the deal who toldSMI: “It takes two to tango and putting theinitial enthusiasm aside, you can't upgradethings that are scrap, for nothing. You need acommitment to finish the project.”

Sources close to Bogazzi say the first 10ships under crew and technical managementwere handed back to Bogazzi in September.The process will continue at around 10 shipsper month for practical purposes, with expec-tations that the entire fleet will be broughtback under Bogazzi's management by the endof the year.

V.Ships President Roberto Giorgi said thetwo companies had “different strategies andpriorities”, while declining further commenton the reasons behind Bogazzi’s decision.

He also sought to downplay the loss of

the sizeable Bogazzi fleet as part of the normal course of business, adding that“every year we have 150-160 ships comingin and a churn of about 100 ships for variousreasons.” He claimed that even with the loss of Bogazzi, the company’s roughly 900-vessel fleet was still 43 ships up on last year.

Still on the V.Ships front, the much publi-cised decision by major investor CloseBrothers to realise its gains in the Monaco-based ship manager is unlikely to be conclud-ed until next Spring, we hear. And there willbe reluctance from other shareholders deter-mined to 'stay for the ride' to accept any newinvestor with less than acceptable motives.Likely interested parties? Another equityinvestor! Let's see! ■

Phew! What a relief!

V.Ships to triple seafarer pool by 2010V.Ships has nailed its crew development plansfirmly to the expansionary mast by announc-ing a strategy to near triple its global seafarerpool within the next three years and it hashired a head hunter to spearhead this growth.

The world’s largest ship manager currentlyboasts a seafarer pool of 23,500 but confirmedit has set a target of 60,000 seafarers by 2010,to be achieved by recruiting from inside aswell as outside the industry.

Bob Bishop, V.Ships ShipmanagementChief Executive Officer, told SMI: “One ofthe things we did last year was to employ ahead hunter and just as you have head hunters

for accountancy, why wouldn’t you apply thesame facilities and procedures for crew. Theirsole job is to increase the number of seafarersavailable to V Ships.

He dismissed any accusation that V.Shipsmay ultimately be adding to the poachingproblem gripping the industry.

“If you look at the issue of poaching I don’tthink that can ever be seriously levelled atV.Ships. We have masters who have been withus for a number of years but who have beenpoached by companies prepared to upset thewhole process across the industry for theirown short-term needs. And this is in actual

fact, making the problem evenworse going forward, becauseincreasingly you are seeing the sea-farers earn more than PrimeMinisters of their country,” he said.

V.Ships will also add to itsgrowing seafarer pool by tradition-al means. “We are going to sourcethem from the usual sorts of placesthat you would expect, but alsosome new ones,” said Bob Bishop.

“We have opened five new crew

management offices this year, and we haveopened up in areas that we weren’t in beforesuch as Myanmar, so it’s more of the same interms of the locations, but it is more focusedwithin those locations. This is where therecruitment drive is helping.”

He added: “I think people are attracted towork for V.Ships for all the reasons we wellunderstand ourselves. But if you just take theLNG sector alone, 160 plus ships are poised tocome into the market, so consider the sea staffthat will be required for these ships.

“Sadly a lot of people haven’t given seriousthought to this, they have just assumed theywill be there. Given the volume required, weare one of the few companies which can offerthe security of supply because there is aninevitable flow of people from dry cargo totankers, to LPG and from LPG to LNG. Andone can bury one’s head in the sand and pre-tend it won’t happen and that people will stayin their sectors, but the guy standing on thetanker sees what the LPG master is getting,who in turn sees what the LNG master is get-ting and guess where they want to go,” hestressed. ■

NOTEBOOK

The bunkering industry has reacted angrily to an IMO decision to press forward with theidea to phase out residual fuels in an attempt totackle the growing problem of ship emissions.

Don Gregory, Chairman of the InternationalBunker Industry Association, argued that in thecomplex world surrounding emissions “therewas no such thing as a free lunch”, and stressedthat technology may offer a better alternative.

“We do recognise with reducing emissionsthat one way to help is to have a lower sulphurfuel. But it isn’t the only solution and you canget better results by doing it in different ways.Would you close down coal fired power stations just because they have sulphur in them and they produce soot? No, you say theyshould have a stack treatment system to catchthe soot and wash out the sulphur,” he reasoned.

The move to adopt distillates in favour ofresidual fuel was one of four proposalsapproved by the Bulk Liquids and Gasses(BLG) Subcommittee as IMO seeks to updateMarpol Annex VI regulations.

Don Gregory said it would not be possiblefor refineries to convert all of the existingresidual fuels to distillates, stressing such a move could aid global warming and have

serious health implications.“From a greenhouse gas point of view it has

serious implications,” he said. “Running ondiesel fuel will produce more fine particulates,and it is generally agreed by the experts that it isthe fine particles that get ingested into your lungsand cause cancer. It’s the fine particles that causethe majority of the damage and if we go over todiesel we will be producing more of them.”

Despite the criticism Intertanko - which putforward the proposal - believes it is making animportant contribution to the debate surround-ing the Annex VI update.

“Very little is controlled or regulated on thefuel that the ship is using,” said Dragos Rauta,Intertanko Technical Director. “We feel thatgreener fuel specifications can’t be ignored –it has to be part of the discussion.” ■

No ‘free lunch’ for IMO

“We do recognise with reducingemissions that one way to help is to have a lower sulphur fuel. But itisn’t the only solution and you canget better results by doing it in different ways”

NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL 13

NOTEBOOK

According to a survey by America Online andSalary.com, the average worker admits to frit-tering away 2.09 hours per eight-hour workingday doing nothing that could benefit hisemployer. And this does not include lunchtimes and scheduled tea breaks.

Top of the list at 44.7% of the time wasted issurfing the internet for personal gain, followedby socialising with co-workers at a worrying23.4%. The average worker feels it importantto spend at least nine minutes a day conductingpersonal business, while they will spend atleast half that amount just staring into space.

If you see your salesman speeding off in hiscar, mid-morning, don't worry, he is just exer-cising his personally-believed right to spend3.1% of his wasted time at work running per-sonal errands. As for planning his personal

social diary, employers should leave theirprized employee alone for two minutes a day torealise this need.

As for arriving late and going home early,that is the least of your problems.

Employees say they're not always to blamefor this wasted time. As many as 33.2% ofrespondents cited lack of work as their biggestreason for wasting time, while 23.4% said theywasted time at work because they believe theywere underpaid.

Sole employees even divulged other waysthey wasted their time at work, such as primp-ing in the bathroom mirror and having runningraces up the staircase with co-workers. Onerespondent said: “The hurried walk around theoffice is not only a great way to look like youare busy, but also a good cardio exercise.” ■

STRESSEXECUTIVE

The insurance market appeared confused andnon-plussed about an innovative new projectwhich it is claimed will revolutionise the marineinsurance market by among other things usingthe powers of the internet to capture some of themarket share currently dominated by the P&IClub establishment.

The joint Hull and P&I venture, which isunderstood to be nearing finalisation under thebanner of Vega Marine, is reported to be thebrainchild of Terje Adolfsen, a former insurancemanager with Bergsen Marine, and KareFranseth, who held a similar position withTorvald Klaveness.

When questioned by SMI, Terje Adolfsenadded to the confusion by confirming that VegaMarine had already been established and he wasinvolved in it but added: “We are working onvarious ideas in various directions in insuranceactivities but there is a very long way to go. I amnot denying anything but I cannot confirm any-thing either at this stage.”

Somewhat reassuringly, he did promise fur-ther information when something was 'for-malised'. Previous reports have suggested thepair have big ideas to use the internet to changethe face of existing hull insurance practices.

Bjørn Hildan Managing Director and CEO ofleading Norwegian company BluewaterInsurance revealed he was aware of market gos-sip regarding the new company and stressed hewas very interested to see how the pair intendedto employ the internet as a means of doing busi-ness. But as he opined, even in today’s technol-ogy-obsessed world previous attempts by hullinsurers to utilise the internet have been blightedwith technical and communication difficulties.

“I know the individuals concerned,” BjornHildan said. “They are both very professional

people with extensive market knowledge andexperience. If anybody can pull it off it is them.”

A fixed premium scheme offering wealthyoperators a reported $1bn cover is said to be thefundamental aim of the P&I branch of the busi-ness but only if they are prepared to risk bigdeductibles.

Clear details have yet to emerge, with keyplayers in the insurance market seemingly igno-rant to the plans of the Norwegian pair, butstressing a desire to know more.

The news will come as a blow to existingP&I players who are already under pressure fol-lowing accusations that smaller companies arepaying for the honour of sharing a Club withsome of the industry’s main players.

“Those ship owners who make up the Clubs’boards of directors, and so set the level ofincrease, appear to have a tendency to avoidpaying it themselves,” according to the annualP&I report of the brokering group Tysers.

“If each Club’s largest 20 members all paidthe premium required by their records, Clubswould return underwriting surpluses and gener-al increases of the magnitude seen in recentyears would be consigned to history,” the reportconcluded. ■

Dot com intrigue on the P&I front Suez Canal toexpandEGYPT is planning to spend $1bn to expandthe Suez Canal by 2010, but analysts arequestioning the economic viability of thisgrand project, latest news reports have sug-gested.

The Suez Canal Authority is contemplat-ing making this investment to attract moretanker and container traffic as vessels onlong haul are getting larger. Under the plansthe canal would be deepened by 10 ft to han-dle ships with a 72-ft draught and widenedby 17% to around 365 m.

“We want to deepen and widen the canaland create more bypasses to handle futurehuge tankers,” Admiral Ahmed Fadel, chair-man of the Suez Canal Authority reportedlytold Bloomberg.

It follows swiftly on the heels of the deci-sion by Panama to expand the size of thePanama Canal. Some 78% Panamaniansvoted in October to support a $5.25bn projectto build a third set of locks capable of han-dling 12,000 teu containerships, suezmaxtankers and capesize bulkers.

The Suez Canal Authority is keen toattract very large and ultra large crude carri-ers that carry Middle East crude to Europeand the US. But with more Middle Eastcrude cargoes going to Asia and the Sumedpipeline operating through Egypt carrying oilto the Mediterranean, there may not be thedemand from tanker markets for a widercanal, said analysts.

Others suggested the canal’s wideningcould benefit container shipping better,allowing larger ships to got through takingAsian cargo to Europe. ■

NOTEBOOK

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 200614

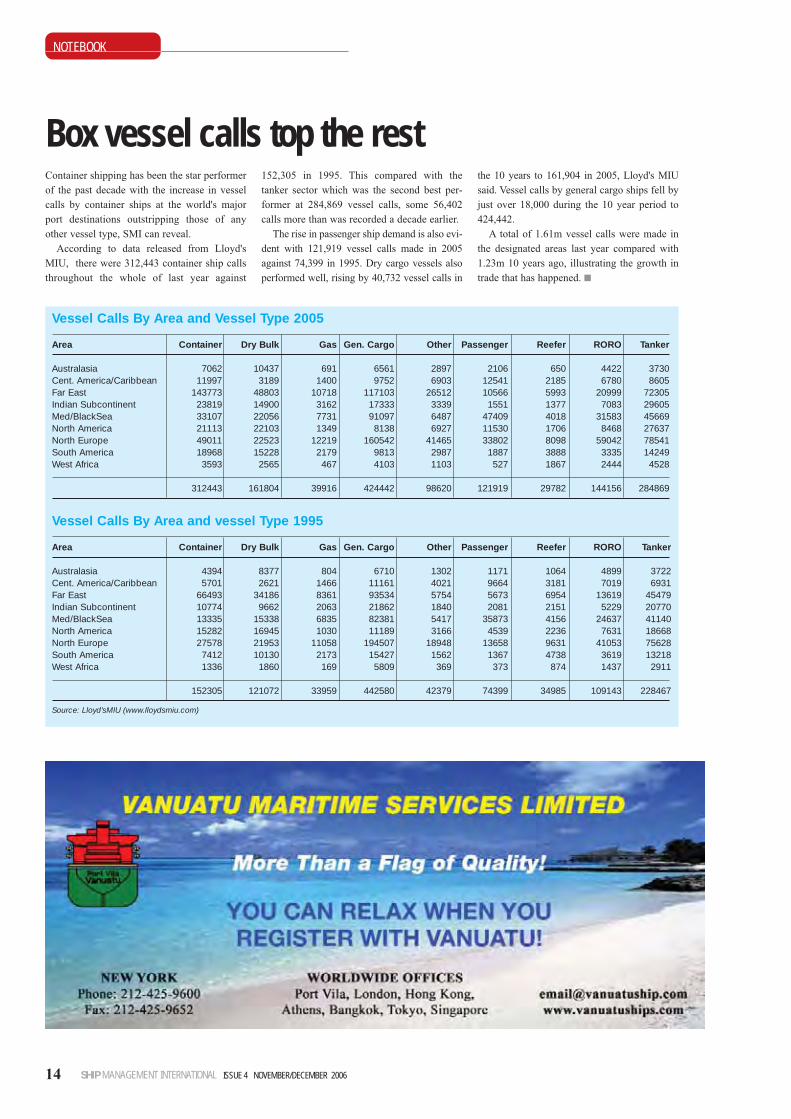

Container shipping has been the star performerof the past decade with the increase in vesselcalls by container ships at the world's majorport destinations outstripping those of anyother vessel type, SMI can reveal.

According to data released from Lloyd'sMIU, there were 312,443 container ship callsthroughout the whole of last year against

152,305 in 1995. This compared with thetanker sector which was the second best per-former at 284,869 vessel calls, some 56,402calls more than was recorded a decade earlier.

The rise in passenger ship demand is also evi-dent with 121,919 vessel calls made in 2005against 74,399 in 1995. Dry cargo vessels alsoperformed well, rising by 40,732 vessel calls in

the 10 years to 161,904 in 2005, Lloyd's MIUsaid. Vessel calls by general cargo ships fell byjust over 18,000 during the 10 year period to424,442.

A total of 1.61m vessel calls were made inthe designated areas last year compared with1.23m 10 years ago, illustrating the growth intrade that has happened. ■

Vessel Calls By Area and Vessel Type 2005

Area Container Dry Bulk Gas Gen. Cargo Other Passenger Reefer RORO Tanker

Australasia 7062 10437 691 6561 2897 2106 650 4422 3730Cent. America/Caribbean 11997 3189 1400 9752 6903 12541 2185 6780 8605Far East 143773 48803 10718 117103 26512 10566 5993 20999 72305Indian Subcontinent 23819 14900 3162 17333 3339 1551 1377 7083 29605Med/BlackSea 33107 22056 7731 91097 6487 47409 4018 31583 45669North America 21113 22103 1349 8138 6927 11530 1706 8468 27637North Europe 49011 22523 12219 160542 41465 33802 8098 59042 78541South America 18968 15228 2179 9813 2987 1887 3888 3335 14249West Africa 3593 2565 467 4103 1103 527 1867 2444 4528

312443 161804 39916 424442 98620 121919 29782 144156 284869

Vessel Calls By Area and vessel Type 1995

Area Container Dry Bulk Gas Gen. Cargo Other Passenger Reefer RORO Tanker

Australasia 4394 8377 804 6710 1302 1171 1064 4899 3722Cent. America/Caribbean 5701 2621 1466 11161 4021 9664 3181 7019 6931Far East 66493 34186 8361 93534 5754 5673 6954 13619 45479Indian Subcontinent 10774 9662 2063 21862 1840 2081 2151 5229 20770Med/BlackSea 13335 15338 6835 82381 5417 35873 4156 24637 41140North America 15282 16945 1030 11189 3166 4539 2236 7631 18668North Europe 27578 21953 11058 194507 18948 13658 9631 41053 75628South America 7412 10130 2173 15427 1562 1367 4738 3619 13218West Africa 1336 1860 169 5809 369 373 874 1437 2911

152305 121072 33959 442580 42379 74399 34985 109143 228467

Source: Lloyd'sMIU (www.lloydsmiu.com)

Box vessel calls top the rest

HARRY GILBERTChairman, International Transport Intermediaries Club (ITIC), andformer CEO of The Wallem Group, Hong Kong

“I have the interaction and the interests, but I can work from home if I

wish. I can also work on my own interests, so it’s a good compromise

as far as I’m concerned.”

Restoring classic cars and motorbikes in the idyllic Cheshire country-side is quite literally a world apart from the municipal hustle and bustleof Hong Kong. And when Harry Gilbert retired from Wallem, a life inrural England seemed like a dream come true.

But after leaving the Wallem hot-seat, Harry soon missed the day-to-day contact with the industry he joined as a 16-year-old cadet. “When Iwas working full-time I didn’t think I would take up anything resem-bling full-time employment [after I retired]. But if you can only playgolf on a Saturday morning for all of your working life and then some-body says: ‘You can play golf seven days a week’, you get fed up withplaying golf after a couple of weeks,” he explained. “It isn’t quite aseasy to switch off as one imagines.”

Now, four years after returning home to England, Harry remains onthe board of Wallem UK. He is also chairman of ITIC and CEO of thediversified marine service company the Charente Group. “I think I havethe best of both worlds now,” he said. “I have the interaction and theinterests, but I can work from home if I wish. I can also work on myown interests, so it’s a good compromise as far as I’m concerned.”

However, Harry admits working from home creates its own chal-lenges. “You have to be very organised. You have to devote a certainamount of the day to the job. It’s very easy to get sidetracked and notdo that, but I find I’m spending quite a bit of time visiting variousoffices. My week is largely split between working a couple of days athome and visiting one of the offices. Although I could be away for theentire week if we have board and management meetings scheduled.”

Despite the challenge of balancing his various commitments, Harryis sure working from home helps him when making key decisions.“When I was with Wallem, I was responsible, on a day-to-day basis, forthe entire organisation. The pressures were more intense. Now, becauseI have this overarching responsibility, but not on a 'day-to-day sittingbehind the desk moving the paperwork backwards and forwards basis',

the pressure is certainly less. This gives [me] the opportunity to think alot more – to actually consider where the company should be going. Ihave the opportunity to take a distant, ‘helicopter view’ and make moremeasured and considered decisions,” he said.

Harry has a chief operating officer at Charente who runs the compa-ny on a day-to-day basis. However, his role is still hands-on andrequires him to travel in the UK and abroad. Fortunately, his businesstrips are less rushed than they once were allowing him to mix businesswith a little pleasure. “My family has now grown up and flown the nest,so my wife can often come with me. If I have a couple of days inLondon, she can come down with me and flex the credit card while I’mdoing what I need to do,” he joked.

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 200616

workHow I

SMI talks to two industry achievers, and asks the question: How do they keepup with the rigours of the shipping industry?

SHIPMANAGEMENT HOW I WORK

“It wasn’t too bad in Hong Kong, my wife could come with me, butoften I was in Taiwan for a day, then Tokyo the following day, and per-haps, Shanghai on the way back. Living out of a suitcase and checkinginto a hotel at five at night, and checking out again to catch a flight atfive in the morning doesn’t thrill my wife a great deal,” he continued.

Having spent his working life travelling the world - first onboardships and later as a leading ship management figure - Harry is wellplaced to comment on the issues facing the industry today. “Legislationcontinues to pile up. I am concerned for the seafarers themselves,because I feel disappointed at the potential amount of litigation that cancome down on the shoulders of the seafarer - nine times out of 10through no fault of their own. The move towards the criminalisation ofthe seafarer is a very, very bad one. It puts more and more pressure onpeople.

“I think people don’t look at seafaring as a long-term career any-more. They see it as a chance to make money for a few years and thenleave, which I think is causing its own problems in the industry.” Whenquestioned, he agreed that a lot of things had changed the perception ofa life at sea, “but obviously ships are not getting as much time in portas the used to, therefore the senior officers in particular don’t get theopportunity to have a break. There are many more inspections and thereis more work to do in port, in a shorter amount of time. The potentiallitigation against the seafarer is a problem that has to be taken into con-sideration. All of these pressures build up – especially in this day andage where going away from home, particularly when you have a wifeand family, is a difficult thing to do.”

Fortunately for Harry Gilbert, ‘retirement’ has allowed him timeaway from shipping to dedicate to the other love of his life – restoringclassic cars and motorbikes. One of his first jobs when he returned toEngland was to build a workshop in his garden, complete with a small

office to store technical drawings. “I have got a 1954 MG TF which isin need of restoration. But about 18 months ago I brought an AC Cobrareplica, which I’m generally refurbishing and am busy transplanting anew engine and gear box into. That’s the winter project in the hope ofgetting it on the road again for next spring,” Harry explained.

“It’s nice to be able to pick those interests up and put them downagain. This is what I like about the mixture of work and retirement.After a few days working underneath a car, to put a suit on again andtravel up to Liverpool makes a pleasant change.”

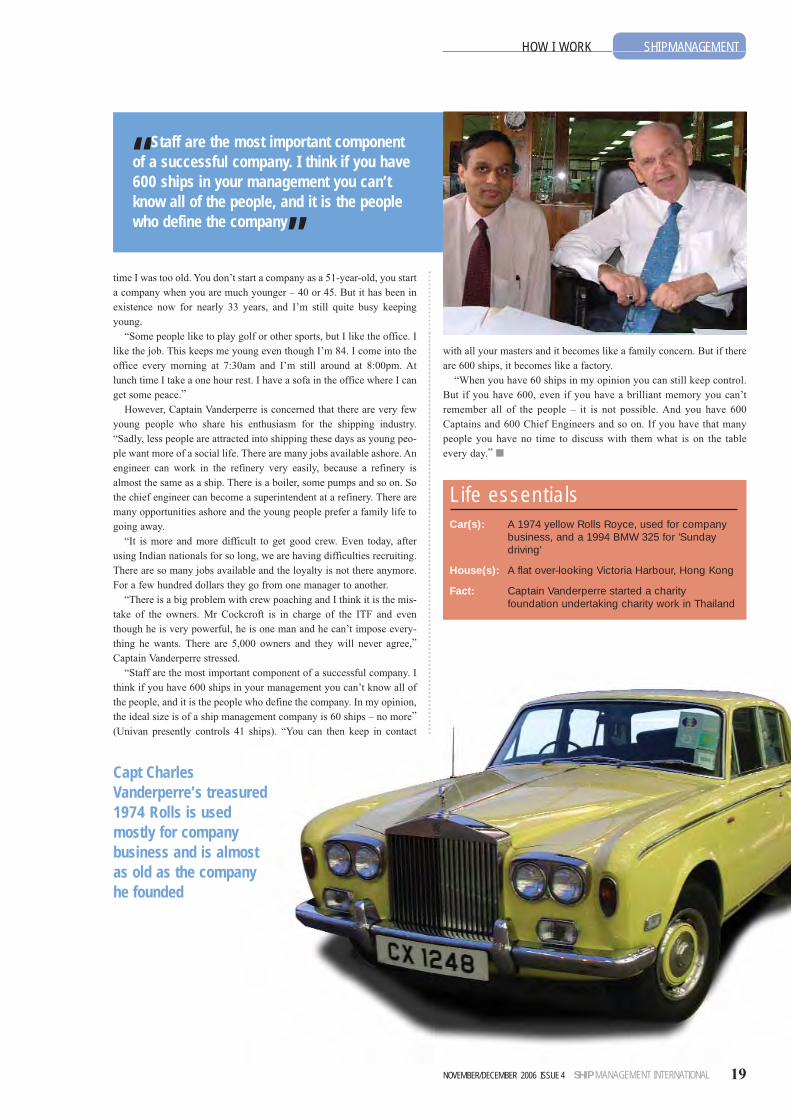

CAPTAIN CHARLES VANDERPERRE Founder and Chairman, Univan Ship Management

“Some people like to play golf or other sports, but I like the office.

I like the job. This keeps me young even though I’m 84.”

Captain Charles Vanderperre recently fuelled speculation that he wasset to retire when he revealed he had sold a 50% stake in his companyto the Clipper Group. Now those same tongues are set to be wagging onoverdrive following his announcement that current Univan ChiefAccountant Mr AS Maniyar has been chosen as heir to the UnivanCrown.

However, Captain Vanderperre has ruled out the prospect of retire-ment, and is determined to continue in his current position as one of theship management industry’s most colourful characters. Ship manage-ments’ very own Godfather still has no plans to voluntarily step-down.

“There will be no change to what I do at the moment,” CaptainVanderperre said when questioned whether his role would change inwake of the Clipper deal. “There are no plans to retire – work is mypleasure. I have a friend in Holland who was asked when she was plan-ning to retire. She said: ‘it depends on God’. But it also depends on peo-ple who work with you and their motivation.”

This is not a surprising stance for a man who leaves home at 6:45 inthe morning and walks the 45 minute journey to work, six days a week,and only allows himself an extra 30 minutes in bed on a Sunday beforeheading to the office.

“I like the job, it keeps me young – it’s as simple as that,” CaptainVanderperre explained. “If you are active all your life and you retire,then I should say frankly, you die. There is a banker in Belgium whosaid: ‘The older I get the more work becomes the most important thingin my life – even more important than love.’ As long as you can walkand talk there is a job for you somewhere, I believe.

“I started Univan in 1973 when I was already in my 50s. At that ➩

SHIPMANAGEMENTHOW I WORK

NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL 17

Life essentialsCar(s): A 1954 MG TF, an AC Cobra (Replica) and

seven classic motorcycles “in need of tender loving care”

House(s): Family home in Cheshire, UK

Fact: During his time at Denholm, Harry went from Chief Engineer to Chief Executive in 11 years

“about 18 months ago I brought an ACCobra replica, which I’m generally refurbishing and am busy transplanting a new engine and gear box into. That’s the winter project”

time I was too old. You don’t start a company as a 51-year-old, you starta company when you are much younger – 40 or 45. But it has been inexistence now for nearly 33 years, and I’m still quite busy keepingyoung.

“Some people like to play golf or other sports, but I like the office. Ilike the job. This keeps me young even though I’m 84. I come into theoffice every morning at 7:30am and I’m still around at 8:00pm. Atlunch time I take a one hour rest. I have a sofa in the office where I canget some peace.”

However, Captain Vanderperre is concerned that there are very fewyoung people who share his enthusiasm for the shipping industry.“Sadly, less people are attracted into shipping these days as young peo-ple want more of a social life. There are many jobs available ashore. Anengineer can work in the refinery very easily, because a refinery isalmost the same as a ship. There is a boiler, some pumps and so on. Sothe chief engineer can become a superintendent at a refinery. There aremany opportunities ashore and the young people prefer a family life togoing away.

“It is more and more difficult to get good crew. Even today, afterusing Indian nationals for so long, we are having difficulties recruiting.There are so many jobs available and the loyalty is not there anymore.For a few hundred dollars they go from one manager to another.

“There is a big problem with crew poaching and I think it is the mis-take of the owners. Mr Cockcroft is in charge of the ITF and eventhough he is very powerful, he is one man and he can’t impose every-thing he wants. There are 5,000 owners and they will never agree,”Captain Vanderperre stressed.

“Staff are the most important component of a successful company. Ithink if you have 600 ships in your management you can’t know all ofthe people, and it is the people who define the company. In my opinion,the ideal size is of a ship management company is 60 ships – no more”(Univan presently controls 41 ships). “You can then keep in contact

with all your masters and it becomes like a family concern. But if thereare 600 ships, it becomes like a factory.

“When you have 60 ships in my opinion you can still keep control.But if you have 600, even if you have a brilliant memory you can’tremember all of the people – it is not possible. And you have 600Captains and 600 Chief Engineers and so on. If you have that manypeople you have no time to discuss with them what is on the tableevery day.” ■

NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL 19

SHIPMANAGEMENTHOW I WORK

Capt CharlesVanderperre’s treasured1974 Rolls is used mostly for companybusiness and is almostas old as the companyhe founded

Life essentialsCar(s): A 1974 yellow Rolls Royce, used for company

business, and a 1994 BMW 325 for 'Sunday driving'

House(s): A flat over-looking Victoria Harbour, Hong Kong

Fact: Captain Vanderperre started a charity foundation undertaking charity work in Thailand

“Staff are the most important componentof a successful company. I think if you have600 ships in your management you can’tknow all of the people, and it is the peoplewho define the company”

SIR. In relation to your edition of September/October of 2006 (Issue 3),regarding the news on page 51 “Not what it says on the tin”. As anowner of a chemical blender company located in Brazil - a “third worldcountry” - I must declare my unpleasantness against this text. My com-pany, as an ISO 9001:2000 certified company, has controlled and doc-umented processes to ensure that what it produces is exactly what isAGREED and REQUESTED by the Customer (major chemical compa-nies world-wide). Our company prays for the quality and takes it to thesame level that serious “first world” companies do. We use equipmentof the latest technology to blend the chemicals, maybe better than theone that is made at the “main” plant.

This way it is not right to generalise all third world blenders due to afew cowboy companies. I believe that the responsibility for this problemlies with the “first world” chemical companies who are giving opportuni-ty for the cowboys to work. The best solution to avoid this type of worryis for these companies, at the time of signing contracts with any blenderfrom the “third world”, to perform a local inspection on the facilities andassure that they will be dealing with a trustful company. I would like tohave my view forwarded to your magazine readers; this type of irrespon-sible text can directly affect serious companies like ours.

Fabio RodriguesDSF Services and Ship Supplier, Santos, Brazil

Editor's replyThe intention of the article was to raise awareness surrounding theexistence of so-called cowboy blenders and not to label all third worldcompanies as cowboys. As you quite rightly say, something needs to bedone to ensure high standards are met by all.

LETTERS

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 200620

SIR. Like industry awards, I’m not a big fan of round table discus-sions. Somehow they appear very stilted and not particularly insight-ful. However, I must congratulate Sean Moloney of ShipManagement International for changing my opinion. In your last edi-tion (September/ October) you presented the findings of a recent dis-cussion between some of the leading lights of the younger Greekshipping generation. The write up of the discussion between messrsPistiolis (Top), Vafias (Stealth), Molaris (Quintana), Varouxakis

(FreeSeas) and Kassiotis (Omega), who have successfully used thepublic equity markets to build up a fleet of over 100 ships betweenthem, is certainly worth a read.

The topics covered were familiar ones but nonetheless interesting,particularly given the polite interplay between the ‘players’. The rel-ative merits of young versus old ships, the appetite for risk amongequity investors and the increasingly regulated markets all get an air-ing in a frank manner.

Certainly no punches are pulled when the subject of outsourcing isintroduced.. The opinions aired are mixed, ranging from some gener-al concerns about handing over an older vessel to a third party man-ager and reservations about using a generalist manager like V.Shipsas opposed to a smaller specialist, to the benefits which companieslike Frontline enjoy from outsourcing. These include the manager’sability to find crew now that traditional sources have dried up, theneed to import expertise and the flexibility it can bring strategically.

What does come across stronger than anything else is the confi-dence of this new generation which has made an important mark inshipping in such a small space of time. Certainly, these guys havestrong opinions and whether you agree with them or not they areworth listening to.

Malcolm WillingaleGroup Services Director, V.Holdings

POWERFUL INTERPLAY

MAILBOX

NOT WHAT IT SAYS ON THE TIN?

Ihave always been fascinated with people in authority. Notbecause I crave such status, although my friends would prob-ably disagree, but I find them interesting. I suppose under-standing how they got to where they are and how they runtheir lives to ensure they maintain their positions in the peck-

ing order is what really fascinates. One thing is for sure, the trappingsand symbols of power and authority do nothing for me. I am not theslightest bit interested in owning a Ferrari or a racehorse. Quite theopposite, give me a car that gets me from A to B and a good round ofgolf and I am happy.

Bob Bishop is a little like me – only a little, mind. He likes to golf andhe likes to drive an old car too – old estate car, although he is probablynot too happy talking about it. With two children and two dogs to ferryaround he can be excused for harking back to his old cargo officer days.He is also single minded and focused – after all, he completed the gru-elling shipping industry-sponsored bike race 'Tour Pour La Mer' last yeardespite only jumping on a bike previously for fun! As far as being a person of authority, as Chief Executive Officer of V.Ships’

Shipmanagement division he cer-tainly commands a great deal ofrespect.

“I trained regularly for the raceand I have continued bike ridingsince. Although I have boughtmyself something rather moreexpensive than I was riding regu-larly before I went on the bike ride.So I do try and continue to cyclealthough Glasgow in the autumn is

not conducive to nipping out on your bike before going to work.”Smiling, he continues: “I’m lucky as there is a cycle track on an old

converted railway line about half a mile from my house so I can have agood blast up and down there if I want to and as a result, I do feel moreinvigorated when I then get into the office. But putting on your cyclinggear just after getting out of bed can be a little tough sometimes,” he said.

I first really got to know Bob Bishop when he left his post as MarineDirector of Intertanko to join the Glasgow-based shipmanagement teamat Acomarit under the stewardship of Peter Cooney. He soon became acrucial member of the enlarged ship management team when Acomaritmerged with V.Ships and now heads up V.Ship’s shipmanagement oper-ations, albeit still from his Glasgow base.

He is a staunch believer in the effectiveness of third party shipman-agement and believes the sector has a strong future ahead even if thereare only really a few managers actually managing ships in a qualityway. His words, not mine.

“I think third party ship management is becoming increasinglyattractive for large ship owners, for a number of reasons. One: The reg-ulatory regime that ship operators now operate in means that they can

put themselves slightly at arms length. The second factor is crewing. Ifyou have 50 ships in a newbuilding programme you probably haven’tgot the crew to man them.

“I think if owners are managing all their ships in-house, just as theymight have a crew problem, they will have a shore staff problem too.And, depending where they are located, that can be quite costly.Because of these reasons, we are now starting to see significant out-sourcing by people who wouldn’t have generally considered third partymanagement in the past,” he opined.

Ask any owner to name a third party ship manager and they willprobably say V. Ships because it is acknowledged by most as the mar-ket leader in terms of size and influence. And with an interest in 900ships the company is a force to be reckoned with. But, as Bob Bishopcontends, while it is large it does have a significant client base with60% of its clients owning between one and three ships.

“Don’t forget that there really are very few independent ship man-agers like V.Ships around. I think this is an important issue for some-body considering outsourcing, because we all know that a manager thatis not truly independent will put the best crew on his own ships.”

Quality is a buzz word in the shipmanagement industry at themoment and companies like V.Ships are tending to veer towards a sec-tor of the market that is embracing high quality. But, according to BobBishop, there is a practical reason for this.

“By and large the more problematic ships tend to have other prob-lems associated with them like lack of funding which means that theyrequire more management time in dealing with suppliers etc. Whereasin many ways, it is an easier proposition to manage quality tonnage ina quality way,” he added.

Bob does raise a finger against those who believe that old vessels,purely because of their age, can fall into this category of problematical ➩

SHIPMANAGEMENTFOCUS

NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL 21

Training for the task ahead

Ask any owner to name a third party ship managerand they will probably say V. Ships because it isacknowledged by most as the market leader in termsof size and influence. And with 900 ships reputed to be under its full or partial management, the company is a force to be reckoned with

By Sean Moloney

vessels when it comes to their effective management. “Just because you have an old ship doesn’t mean you will automati-

cally have management problems with it. There is absolutely nothingwrong with an older vessel that gets the attention it deserves. The prob-lem is when people feel the vessel is no longer worthwhile and that’sdispiriting, both to the crew and the people managing the vessels.

“I think, in actual fact, that’s where ship managers have a skill setthat may not be so readily found in an owners’ office. I think we arevery used to dealing with more elderly and problematic vessels; wehave the skills to do that. So in going forward, we are not necessarilylooking for a fleet of less than five-years-old, we are looking across therange, but what we are looking for are clients who share our vision ofoperating at the quality end of the market,” he said.

As the drive for quality in the industry intensifies, there are many inthe industry who believe this will accelerate the attraction of the quali-ty third party manager. After all, a quality reputation can mean the dif-ference between successful oil major vettings or poor port state controldetentions records.

Bob Bishop continued: “If you take tankers: wet, LPG and all the restof it, I think there is a drive towards quality operation which has just goneup a gear as TMSA has come in, or as the cogence of quality and robustship management is better understood by the likes of EMSA. Gettingapproval for a vessel means you have to be right on top of your game.

“We are getting audited all the time. We have even got an office setaside for the auditors. We are being audited by oil majors, we are beingaudited by class, we are getting audited by flag states, we are gettingaudited by owners’ financial people, so there is always somebody inauditing us.

“There are two things I would say about regulation: one is that theIMO has meetings 25 weeks a year, 160+ nations come to London and

determine the regulations. They are not about to give that up. They havealmost exhausted all the possibilities they have for the technical regula-tion of ships, so increasingly we are seeing attention moving into thesoft side starting with the ISM Code and the ISPS Code,” he added.This will increasingly lead to more regulation coming into the manage-ment office.

By far the biggest issue affecting the shipping industry at the momentis crewing and companies like V.Ships are looked upon as the maindriving forces behind increasing the seafarer pool through more focusedrecruitment, better retention and even more training.

“One of the advantages of V.Ships size is that we can give a careerstructure to people. We actively tell people that if they want to come towork for us, we can give them a career for life because, if you are fedup of going to sea, there is always an office somewhere where you cansettle down to a shore-based job. Equally, we can attract people who areambitious and enthusiastic. [We have] promotion prospects that are justnot available in a smaller organisation. So, on that basis we can keeppeople that might otherwise be gone,” he stressed.

V.Ships currently boasts a seafarer-pool of 23,500 seafarers butaccording to Bob Bishop the company has set itself a target of increas-ing this to 60,000 by 2010 – a daunting task by anyone’s standards. Thisnear tripling of its ship-based workforce will be achieved by the tradi-tional recruitment and training methods as well as normal human

SHIPMANAGEMENT FOCUS

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 200622

By far the biggest issue affecting the shipping indus-try at the moment is crewing and companies likeV.Ships are looked upon as the main driving forcesbehind increasing the seafarer pool through morefocused recruitment, better retention and even more training

resource practices of advertising and recruiting for existing talent with-in the industry.

“One of the things we did last year was to employ a head hunter andjust as you have head hunters for accountancy, why wouldn’t you applythe same facilities and procedures for crew. Their sole job is to increasethe number of seafarers available to V Ships,” he said.

But is this not adding to the whole issue of poaching? “If you look at the issue of poaching I don’t think that can ever be

seriously levelled at V.Ships. We have masters who have been with usfor a number of years who have been poached by companies who areprepared to upset the whole process across the industry for their ownshort-term needs. And this is in actual fact making the problem even

worse going forward, because increasingly you are seeing the seafarersearn more than Prime Minister of their country,” said Bob Bishop.

“With that sort of salary differential they don’t need to stay at sea forvery long, they can come ashore and buy a hotel. So they are lost to theindustry and these people who are playing the high salaries, coinciden-tally, don’t appear to have the regime to develop their own sea staff.

“At V.Ships we hold the power and the means to encourage our sea-farers to stay. It’s not just about money, although we need to be there orthere abouts; there are other features like job security, which is also veryimportant,” he added.

According to Bob Bishop, V.Ships takes its training responsibilitiesvery seriously. “We have 765 cadets currently being trained and wewant to increase this number to 1,000 then eventually 2,000. So there is a huge influx of people coming into the industry but that alone doesn’t get us to our goal of 60,000 seafarers. That is why we haveemployed these people out there to encourage people to take up available positions.”

Having spent two hours talking to Bob Bishop I realised that perhapsthe reason why people like him are respected is because they are able toset themselves tough targets and have the presence and determination tomake them happen. ■

SHIPMANAGEMENTFOCUS

If you take tankers: wet, LPG and all the rest of it, I think that there is a drive towards quality operation which has just gone up a gear as TMSAhas come in, or as the cogence of quality and robust ship management is better understood by the likes of EMSA

You have just started a two-year-term as InterManagerPresident. What is your strategy for the association and howwould you like to see it develop under your leadership?The strategic goal of InterManager is quite clear: to make it the unques-tioned and unchallenged representative body or reference for allinvolved in the quality operation, management and crewing of ships.We want to make InterManager an association so powerful as to havethe ability to influence the decisions that are relevant to the industry, itsstandards and the conditions of work for the people it employs.

We are opening InterManager to ALL people involved in the opera-tion, management and crewing of ships, meaning shipowners/operators,in-house managers as well as third party managers, i.e. technical man-agers as well as crewing managers, because the issues facing the shipoperators is the same. The strategy over the next two years will be tobuild the powerbase of InterManager and to involve it in all issues ofrelevance to the profession. We will achieve this through the systemat-ic increase of its membership of the association. All people of good willand quality will be welcomed, because the more members we have thebetter we can defend our association.

This systematic search for new members will require some resource,but with the full support of our members, we will reach our goals. Butat the same time we have to make sure we serve our members' needs byunderstanding their needs and responding to them. This will beachieved through systematic discussions with them about issues such ascrew shortages, the image of the industry and lobbying relevant partiesto defend whatever shipmanagement cases need defending.

What is the big issue facing the industry at the moment?KPIs as we know are an important issue facing ship managers today andInterManager has been, and will continue to be, at the vanguard of thisdrive for a pan-industry set of measurable KPIs for the industry. But I

don't want InterManager to be totally synonymous with KPIs or viceversa as there are a number of other important issues we need tobecome involved in.

A huge challenge for the future is the recruitment and competence ofcadets and crew coming into the industry. We do know from statistics -depending on how much you believe in statistics – that there is a lack oftrained officers qualified to meet the national fleet and if we do not dosomething there will be a huge undersupply of officers in the future. It isclear that there needs to be much closer co-operation between the crewmanager, the ship manager and the ship owner on this issue.

But is the shipping industry undergoing change?I believe it is, in the sense that it’s more likely a supply chain manage-ment scenario where the ship is part of a delivery chain, a productionchain. If part of the chain breaks down that will hurt the whole supplychain and that means that the crew and we as managers have to under-stand what the requirement is from the ship owners when it comes tocompetence of the crew. The master manages the running of the shipbut how can he be a manager or director of a ship if he doesn’t under-stand how each individual ship owner prefers to do business. The crewonboard has to understand what will happen if I don’t manage the shipthe way my customer, the owner, wants me to.

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 200624

SHIPMANAGEMENT ON MY MIND

The strategy over the next two years willbe to build the powerbase of InterManagerand to involve it in all issues of relevancefor the profession. We will achieve thisthrough the systematic increase of itsmembership of the association

ONMYMINDOle B. SteneOle Stene is Managing Director of Aboitiz JebsenBulk Transport Corporation and Chief OperatingOfficer of Jebsen Management AS. He is also thenewly appointed President of InterManager, the tradeAssociation for in-house and third party ship man-agers. A graduate of the University of Bergen LawSchool, he also holds a commercial degree from theAnt. Johannessen Handelsskole in Bergen as well asa postgraduate degree in building and construction.He lists Alternate Member of Germanischer Lloyd'sAsian Committee; Member of Lloyd's Register's AsiaShipowners' Committee; ex-member of the SkuldCommittee and ex-member of the Board of BergenHull Club among the past and present positions hehas held

So do you think that the onboard management team has tofully embrace the needs, wishes and desires of the owner andof his customer?I think we have to accept that the most important people in a shippingcompany are the crew. I don’t think we should forget that we are sup-porting staff. The guys onboard a ship are meeting the problems,they’re meeting the customers first and they’re meeting a lot of chal-lenges that they have to solve there and then.

We are there to support them so we have to build up self confidencein the officers so they have the support and understand what they haveto do to solve this problem there and then and not to forget to ask ques-tions. So in addition to the technical competences of the officers, we are

beginning to require difference competencies than were there beforesuch as leadership and management skills.

Are you concerned that the level of competency onboardships is not up to the standard it should be?Well that’s what you see in a lot of trades now because together withthe ship owners we have not been clever enough to foresee therequirements coming through with respect to training and competen-cy. Ships today are worth $80m or $100m+. If you build a factoryashore for that kind of money you will be dead sure that the peopleyou are employing will be trained to be able to manage the factorywell. But because we have this strange scenario in shipping where youhave the signing on/signing off system for seaborne staff we are deal-ing with a different set of challenges. We have to focus on buildingup loyality and developing closer co-operation between us as suppli-ers of services together with our customers, the ship owners, to reallyget the people to understand where they affect the system. ■

SEPTEMBER/OCTOBER 2006 ISSUE 3 SHIP MANAGEMENT INTERNATIONAL 25

SHIPMANAGEMENTON MY MIND

“Are you concerned that the level of competencyonboard ships is not up to the standard it should be?”

“Well that’s what you see in a lot of trades now because together with the shipowners we have not been clever enough to foresee the requirements comingthrough with respect to training and competency.”aQ

The guys onboard a ship are meetingthe problems, they’re meeting the cus-tomersfirst and they’re meeting a lot ofchallenges that they have to solve thereand then. We are here to support them

NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL 25

The perennial issues of falling income due todownward pressure on agency fees and increas-ing workload, due to the agent’s enhanced rolein the exchange of information between the shipand shore, continue to impact on the health of

the port agency industry. So significant is the situation, believes Jonathan

Williams, General Secretary of The Federation ofNational Associations of Ship Brokers and Agents(FONASBA), that intense competition within the indus-try is forcing agents to offer ever-lower fees in order tosecure business and so rates are being driven furtherdown. “Fees have now reached the levels at which agentsfind it increasingly difficult to provide the required levelof resources, to maintain infrastructure and to provide forthe future,” he said.

“The future of the agency industry is also threatenedby the extremely low profile of the industry, the anti-social hours that agency staff are required to keep andcompetition from other industries,” he warned.

With the introduction of the ISPS Code, the Europeanship-generated waste disposal directive and the US 24hour Advance Cargo Declaration Rule, as well as otherproposed measures, most of which are security related,agents are becoming ever more involved in the exchangeof information between the ship and shore. Significantamounts of data now require to be requested, collected,collated and passed on to the correct recipients with a high degree of accu-racy and in most cases within very tight deadlines. The agency communi-ty has absorbed and carries out these additional tasks with equanimity butit is a further service that the agent is required to provide to his principalsbut in most cases does not get paid for.

The issue of fees and remuneration was a point recently echoed byPeter Titchener, Secretary General of the Multiport Ship AgenciesNetwork, who was quoted as claiming that all agents continue to seedownward pressure on fees and commissions, despite the boom in ship-ping that has been enjoyed in all sectors.

There is also a trend, he claimed, for principals in the liner business toset up their own regional and local offices. “We are seeing instances wherethey begin to regret the extent of such offices when they realise they havetaken on direct fixed costs, whereas had they used a regional office work-ing with independent agents they would have had variable costs, and inmost cases, better local market knowledge,” he was reported as saying.

Jonathan Williams cited the container industry as central in the grow-ing issue of consolidation in the agency sector.

“Almost inevitably when two container lines merge, there is a corre-sponding consolidation of agents and in many cases one agent loses out.The merits of dedicated, usually line-owned, agents compared to inde-pendent agents have been argued for many years and there is no set answerto which is best.

“While a dedicated agent will only work for one line, the independentagent, who relies for his income on a commission from the line, may bemore active in seeking, and more competitive in securing, business thanan inhouse agent securing business from the line itself. This process tends,however to by cyclical. In a number of cases lines, burdened with all thecosts of running their own operations, have closed their own offices andhave returned to using an independent agent,” he stressed.

The problems this creates can be significant with key staff being headhunted by shipping lines and locally-based members of the workforcelosing their jobs. The choice between a line opening up its own agencynetwork or using independent agents is influenced by a number of factorsthat are individual to its own requirements, the size of its business or the area in which it is operating so there are plusses and minuses on both sides.

According to Christer Sjodoff, Regional Director of the global agencyoperation Gulf Agency Company, the sector is very fragmented. We areamong the top three agents in the world when it comes to vessel calls andwe handle between 33,000 and 35,000 port calls a year. The top threeagents put together probably only account for between 6%-8% of the totalnumber of port calls in the world. So the biggest competitors are not among the top three, the biggest competitors are actually the smallerplayers,” her added.

“But serious ship owners will want to deal with an agent who has good

BUSINESS VIEWPOINT AGENTS

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 200626

Swimmingagainst the tide

With the introduction of the ISPS Code, the European ship-generated waste disposal directive and the US 24 hourAdvance Cargo Declaration Rule, as well as other proposedmeasures, most of which are security related, agents arebecoming ever more involved in the exchange of informationbetween the ship and shore

cover; who has the right assurances in place and who employ well trainedstaff alongside quality systems,” emphasised Christer Sjodoff.

“Our strategy as a major player in the agency market is to provideadded value services for the ships berth side and custom clearance whichmeans not only clearing the ship in and out but clearing the cargo in andout. Again I think we can take it all a lot further but we have to talk a lotmore to the owners, operators, managers and port authorities to see howwe can do more for them than we do today,” he said.

Ivo Verheyen, Managing Director of GAC's Singapore office, agreedthat a lot of the shipping lines were looking at their own agency set ups.As they set up regional offices there was a tendency to pull their ownagency operations in-house, he stressed.

“We are protected from that here in Singapore as we have a very strongfocus on supply services that are related to the needs of the owner, such asship supplies to crew changes to delivery of spare parts and bringingsuperintendents on board etc,” he added.

“Because Singapore is a transit point, there are a lot of ships coming by

not for cargo operations but for the other owner-related matters: that iswhy we see synergies between our logistics set up and our role as a ship-ping agent,” he added.

“When you look at the make up of our operating income you’ll find that45% of that is today made up from logistic business, 11% is what we termas marine services, the operation of crew boats, supply boats, tugs, bargesand then the balance is 44% made up of ship agency services,” said ChrisSteibelt, Director of Logistics at GAC marine Logistics.

“As a shipping agency part of the function is to clear spares and putthem on board the vessel. As we received what we felt were very poorlymanaged freight movements we said we should have a logistics capabili-ty. We questioned why we weren't harnessing that capability and putting ittogether with our ship agency business to offer our clients a single pointof contact for getting the spares from the origin through to delivered onboard the vessel,” he said. ■

BUSINESS VIEWPOINTAGENTS

NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL 27

“Because Singapore is a transit point, there area lot of ships coming by not for cargo operations

but for the other owner-related matters: that iswhy we see synergies between our logistics set

up and our role as a shipping agent”

“Serious ship owners will want to deal withan agent who has good cover; who has theright assurances in place and who employwell trained staff alongside quality systems”

Ivo Verheyen

Christer Sjodoff

NOVEMBER/DECEMBER 2006 ISSUE 4 SHIP MANAGEMENT INTERNATIONAL 29

Teekay Shipping

Managing Director, Teekay Marine Services

What do you think is the answer to the industry’s crewingproblems?

I think companies need to have a vision. We need to have a fiveyear, or more likely a ten year plan, looking at the business in thelonger term. We have to continue to invest in training and moni-tor the demographics of the industry – being sure to focus onwhere we are currently recruiting while assessing where that maybe in the future and investing accordingly.

What role can third party managers play in tackling theproblem?

I think there are a lot of reputable ship managers and they stillhave a role to play for those owners who wish to outsource thatpart of their operation. But I can only speak for Teekay and weare owners and operators. We prefer to manage that risk internal-ly, in terms of an operational risk, and manage all of the humanresource risks as well.

Why do you prefer to keep things in-house instead ofusing a third party manager?

It’s what we call the Operational Leadership Programme and thishas helped build our brand – our reputation – to where it is today.I should explain to you that there are four business units atTeekay. One is focused on gas, one on shuttle tankers and off-shore services and one on conventional tankers. The other busi-ness unit is what we call Teekay Marine Services. We regardTeekay Marine Services as the engine room of the company andone of its key responsibilities is retaining our high standards. Bydoing this we know what standards of performance we need, weknow what the customers expect and therefore we have to man-age that in-house.

John Adams

FRANKLYSPEAKINGRecognised as an international leader in energy shipping,Teekay has recently expanded into the LNG sector andundertaken a major relocation programme to establish a plat-form for future growth.

The fresh activity, which was encouraged by customer feedback,saw three of the company’s conventional ship teams move in order toencourage interaction between the teams and their customers; andhelp the company establish a stronger presence in regions with largepools of skilled marine personnel.

The multi-functional teams, who are responsible for the day-to-dayrunning of Teekay’s conventional vessels, are viewed as the heart ofTeekay’s operations. Three ship teams have relocated to Glasgow,Houston and Singapore. The Glasgow team overseas the fleet in theAtlantic and the Mediterranean, Houston is responsible for the fleet inthe US Gulf and Singapore manages the fleet in the Indo-Pacific region.

David Robinson, Vice President, Fleet Operations said: “This is thestart of a new era for us. We have evolved into a global player in sev-eral different markets. In addition to bringing ship teams closer totheir fleet and to customers, the regionalisation is a key component ofTeekay’s growth strategy. By taking our ship teams into differentregions we continue to establish ourselves as a global organisationwith a regional, customer focused operating bases.”

This year has certainly been an active one for Teekay, which hasbeen involved in the energy sector since it was established in 1973.In February 2006 it announced an agreement with PGS ProductionAS, a subsidiary of Petroleum Geo-Services ASA, to develop solu-tions through floating production storage and offloading units.

Teekay Shipping transports more than 10% of the world’s seaborneoil and boasts a fleet of more than 145 tankers. The recent move intothe lucrative LNG sector came through the company’s publicly-listedsubsidiary, Teekay LNG Partners L.P.

With offices in 17 countries, and employing more than 5,100seaborne and shore-based staff, Teekay provides a comprehensive setof services to the world’s oil and gas companies. It is the world leaderin the shuttle tanker business, has one of the largest aframax andsuezmax fleets, and has an emerging product carrier division. ■

Looking down on the industrial outline of the dock, the effects ofsulphur emissions scar the sky. A yellow haze hangs in the warmmorning air, casting a suffocating blanket across the roof tops ofthe town towards the ocean. But this is not a view of a third worldmetropolis, it is an every day occurrence in ports around the

Baltic, the North Sea and other parts of the industrialised world as a directresult of sulphur emissions from ships.

The inhalation of sulphur affects the human respiratory system, and it iswell known that sulphur emissions cause acid rain. “Sulphur is in theatmosphere in very limited quantities. It has a very high greenhouse factor,so a small quantity of sulphur is significant to the greenhouse effect,”explained Vinchenzo Grecco, Technical Manager for the Marine Divisionof Greenpeace. “Ships burn hundreds of tonnes of residual fuel per day andsome of this stuff is liquid asphalt, basically.”

The need for the industry to address sulphur emissions was highlightedby Dr Johann Jungclaus of the Max-Planck-Instutut Für Mererologie. Hesaid: “We have to make an effort to reduce emissions. An 80% reductionin emissions would be required to halt global warming at two degrees fromnow. Ships contribute a lot of sulphur and nitrous oxide and these particlescreate changes in local climate.

“The thing you have to understand with sulphur emissions is they areessentially regional problems,” added Robert Ashdown, Manager ofOffshore and Environmental Affairs at the International Chamber ofShipping. “There are some very specific areas in the world that happen tohave a sulphur problem. What we need to do is bring the sulphur limitsdown in these places, as we have with SECAs (Sulphur Emissions ControlAreas) in the Baltic and the North Sea.”

However, while tackling the problem on a regional scale appears to bescientifically sound, having different sulphur limits around the world caus-es many practical difficulties for ship owners and managers. And the prob-lems are set to get worse as states prepare to follow California’s lead andintroduce strict local limits on sulphur emissions which go beyond the1.5% maximum sulphur content of marine bunker fuel oil required to oper-ate in existing SECAs.

“Different sulphur limits in different ports are potentially problematic asships may have to carry three different fuel types, requiring separate tanksand piping, and the potential for human errors during fuel quality changesmight also present a potential safety hazard,” explained Jean-ClaudeSainlos, Director, Marine Environment Division, IMO Secretariat. Andwith the EU set to introduce 0.1% sulphur emissions at berth in 2010, thesituation will only get worse, with some predicting as many as five or sixfuel types will be required on a single vessel in the near future.

SHIP MANAGEMENT INTERNATIONAL ISSUE 4 NOVEMBER/DECEMBER 200630