$25,760,000 INDIANAPOLIS AIRPORT AUTHORITY Siebert ...

196

NEW ISSUE RATINGS: See “CREDIT RATINGS” Book-Entry-Only In the opinion of Ice Miller LLP, Indianapolis, Indiana, and Gonzalez Saggio & Harlan LLP, Indianapolis, Indiana (together, “Co‑Bond Counsel”), under existing laws, regulations, judicial decisions and rulings, interest on the 2010 Bonds (hereinafter defined) is excludable from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, as amended and in effect on the date of issuance of the 2010 Bonds (the “Code”), except for interest on any 2010 Bond for any period during which such 2010 Bond is owned by a person who is a “substantial user” of the Airport System (hereinafter defined) or a “related person” as defined in Section 147(a) of the Code. Such exclusion is conditioned on continuing compliance with the Tax Covenants (hereinafter defined). Interest on the 2010 Bonds is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations and is not taken into account in determining adjusted current earnings for the purpose of computing the federal alternative minimum tax imposed on certain corporations. In addition, in the opinion of Co‑Bond Counsel, under existing laws, regulations, judicial decisions and rulings, interest on the 2010 Bonds is exempt from income taxation in the State of Indiana. $25,760,000 INDIANAPOLIS AIRPORT AUTHORITY AIRPORT REVENUE BONDS, SERIES 2010A (Non-AMT) Dated: Date of delivery Due: January 1, as shown on the inside cover page The Indianapolis Airport Authority (the “Authority”) will issue its Airport Revenue Bonds, Series 2010A (the “2010 Bonds”), pursuant to the Ordinance, as defined and described herein. The 2010 Bonds will be dated the date of delivery and will bear interest from that date to their respective maturity dates in the amounts and at the rates set forth on the inside cover page hereof. The 2010 Bonds are issuable only as fully registered bonds and, when issued, will be registered in the name of Cede & Co., as nominee for The Depository Trust Company, New York, New York (“DTC”). Purchases of beneficial interests in the 2010 Bonds will be made in book-entry-only form, in denominations of $5,000 or any integral multiple thereof. Purchasers of beneficial interests in the 2010 Bonds (the “Beneficial Owners”) will not receive physical delivery of certificates representing their interests in the 2010 Bonds. Interest on the 2010 Bonds is payable on January 1 and July 1 of each year, commencing July 1, 2010. Interest, together with the principal and redemption premium, if any, of the 2010 Bonds, will be paid directly to DTC by The Bank of New York Mellon Trust Company, N.A., Indianapolis, Indiana, as paying agent under the Ordinance (hereinafter defined), so long as DTC or its nominee is the registered owner of the 2010 Bonds. The final disbursement of such payments to the Beneficial Owners of the 2010 Bonds will be the responsibility of DTC, the DTC Participants and the Indirect Participants, all as defined and more fully described in APPENDIX F—“BOOK-ENTRY-ONLY SYSTEM.” The 2010 Bonds are being issued by the Authority for the principal purposes of providing moneys to (i) refund the Authority's outstanding commercial paper and (ii) pay costs of issuing the 2010 Bonds, all as more fully described herein. See “PLAN OF FINANCING.” The 2010 Bonds are subject to optional and mandatory sinking fund redemption prior to maturity as described herein under “2010 BONDS—Mandatory Sinking Fund Redemption” and “—Optional Redemption.” The 2010 Bonds are special obligations of the Authority and are payable solely from and secured exclusively by a lien upon certain revenues of the Airport System administered by the Authority, on a parity with certain bonds previously issued by the Authority and outstanding pursuant to the Ordinance. The 2010 Bonds do not constitute a debt, liability, general obligation or loan of the credit of the State of Indiana (the “State”) or any political subdivision thereof, including the City of Indianapolis, Indiana (the “City”) and the Authority, under the constitution and laws of the State, or a pledge of the faith, credit and taxing power of the State or any political subdivision thereof, including the City and the Authority. The sources of payment of, and security for, the 2010 Bonds are more fully described herein. The 2010 Bonds are not payable from property taxation. See “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS.” The 2010 Bonds are further secured by a debt service reserve fund as described herein under “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS—Revenue Bond Reserve Fund.” A detailed maturity schedule for the 2010 Bonds is set forth on the inside cover page of this Official Statement. This cover page contains information for quick reference only and is not a summary of this issue. Investors must read the entire Official Statement, including the appendices hereto, to obtain information essential to making an informed investment decision, paying particular attention to the matters discussed under “BONDHOLDER RISKS.” The 2010 Bonds are offered when, as and if issued by the Authority and received by the Underwriters and subject to prior sale, withdrawal or modification of the offer without notice, and to the approval of legality by Ice Miller LLP and Gonzalez Saggio & Harlan LLP, Co-Bond Counsel. Certain legal matters will be passed on for the Authority by its Counsel, Erika Davis, Esq., Indianapolis, Indiana, and for the Underwriters by their counsel, Baker & Daniels LLP, Indianapolis, Indiana. It is expected that the 2010 Bonds will be available for delivery through the facilities of DTC in New York, New York, on or about January 27, 2010. Siebert Brandford Shank & Co., L.L.C. BofA Merrill Lynch City Securities Corporation Goldman, Sachs & Co. J.P. Morgan January 15, 2010

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of $25,760,000 INDIANAPOLIS AIRPORT AUTHORITY Siebert ...

NEW ISSUE RATINGS: See “CREDIT RATINGS”Book-Entry-Only

In the opinion of Ice Miller LLP, Indianapolis, Indiana, and Gonzalez Saggio & Harlan LLP, Indianapolis, Indiana (together, “Co‑Bond Counsel”), under existing laws, regulations, judicial decisions and rulings, interest on the 2010 Bonds (hereinafter defined) is excludable from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, as amended and in effect on the date of issuance of the 2010 Bonds (the “Code”), except for interest on any 2010 Bond for any period during which such 2010 Bond is owned by a person who is a “substantial user” of the Airport System (hereinafter defined) or a “related person” as defined in Section 147(a) of the Code. Such exclusion is conditioned on continuing compliance with the Tax Covenants (hereinafter defined). Interest on the 2010 Bonds is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations and is not taken into account in determining adjusted current earnings for the purpose of computing the federal alternative minimum tax imposed on certain corporations. In addition, in the opinion of Co‑Bond Counsel, under existing laws, regulations, judicial decisions and rulings, interest on the 2010 Bonds is exempt from income taxation in the State of Indiana.

$25,760,000INDIANAPOLIS AIRPORT AUTHORITYAIRPORT REVENUE BONDS, SERIES 2010A

(Non-AMT)

Dated: Date of delivery Due: January 1, as shown on the inside cover page

The Indianapolis Airport Authority (the “Authority”) will issue its Airport Revenue Bonds, Series 2010A (the “2010 Bonds”), pursuant to the Ordinance, as defined and described herein.

The 2010 Bonds will be dated the date of delivery and will bear interest from that date to their respective maturity dates in the amounts and at the rates set forth on the inside cover page hereof. The 2010 Bonds are issuable only as fully registered bonds and, when issued, will be registered in the name of Cede & Co., as nominee for The Depository Trust Company, New York, New York (“DTC”). Purchases of beneficial interests in the 2010 Bonds will be made in book-entry-only form, in denominations of $5,000 or any integral multiple thereof. Purchasers of beneficial interests in the 2010 Bonds (the “Beneficial Owners”) will not receive physical delivery of certificates representing their interests in the 2010 Bonds. Interest on the 2010 Bonds is payable on January 1 and July 1 of each year, commencing July 1, 2010. Interest, together with the principal and redemption premium, if any, of the 2010 Bonds, will be paid directly to DTC by The Bank of New York Mellon Trust Company, N.A., Indianapolis, Indiana, as paying agent under the Ordinance (hereinafter defined), so long as DTC or its nominee is the registered owner of the 2010 Bonds. The final disbursement of such payments to the Beneficial Owners of the 2010 Bonds will be the responsibility of DTC, the DTC Participants and the Indirect Participants, all as defined and more fully described in APPENDIX F—“BOOK-ENTRY-ONLY SYSTEM.”

The 2010 Bonds are being issued by the Authority for the principal purposes of providing moneys to (i) refund the Authority's outstanding commercial paper and (ii) pay costs of issuing the 2010 Bonds, all as more fully described herein. See “PLAN OF FINANCING.”

The 2010 Bonds are subject to optional and mandatory sinking fund redemption prior to maturity as described herein under “2010 BONDS—Mandatory Sinking Fund Redemption” and “—Optional Redemption.”

The 2010 Bonds are special obligations of the Authority and are payable solely from and secured exclusively by a lien upon certain revenues of the Airport System administered by the Authority, on a parity with certain bonds previously issued by the Authority and outstanding pursuant to the Ordinance. The 2010 Bonds do not constitute a debt, liability, general obligation or loan of the credit of the State of Indiana (the “State”) or any political subdivision thereof, including the City of Indianapolis, Indiana (the “City”) and the Authority, under the constitution and laws of the State, or a pledge of the faith, credit and taxing power of the State or any political subdivision thereof, including the City and the Authority. The sources of payment of, and security for, the 2010 Bonds are more fully described herein. The 2010 Bonds are not payable from property taxation. See “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS.”

The 2010 Bonds are further secured by a debt service reserve fund as described herein under “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS—Revenue Bond Reserve Fund.”

A detailed maturity schedule for the 2010 Bonds is set forth on the inside cover page of this Official Statement.

This cover page contains information for quick reference only and is not a summary of this issue. Investors must read the entire Official Statement, including the appendices hereto, to obtain information essential to making an informed investment decision, paying particular attention to the matters discussed under “BONDHOLDER RISKS.”

The 2010 Bonds are offered when, as and if issued by the Authority and received by the Underwriters and subject to prior sale, withdrawal or modification of the offer without notice, and to the approval of legality by Ice Miller LLP and Gonzalez Saggio & Harlan LLP, Co-Bond Counsel. Certain legal matters will be passed on for the Authority by its Counsel, Erika Davis, Esq., Indianapolis, Indiana, and for the Underwriters by their counsel, Baker & Daniels LLP, Indianapolis, Indiana. It is expected that the 2010 Bonds will be available for delivery through the facilities of DTC in New York, New York, on or about January 27, 2010.

Siebert Brandford Shank & Co., L.L.C.BofA Merrill Lynch City Securities CorporationGoldman, Sachs & Co. J.P. Morgan

January 15, 2010

MATURITY SCHEDULE

$25,760,000 INDIANAPOLIS AIRPORT AUTHORITY

AIRPORT REVENUE BONDS, SERIES 2010A

(Non-AMT)

Dated: Date of delivery Due: January 1, as shown below

Year Principal Amount Interest Rate Yield CUSIP

2011 $ 510,000 3.000% 0.930% 455254FG2 2012 570,000 3.000 1.410 455254FH0 2013 585,000 3.000 1.800 455254FJ6 2014 600,000 3.000 2.260 455254FK3 2015 620,000 4.000 2.750 455254FL1 2016 645,000 4.000 3.260 455254FM9 2017 670,000 4.000 3.590 455254FN7 2018 695,000 4.000 3.850 455254FP2 2019 725,000 4.000 4.070 455254FQ0 2020 755,000 4.000 4.220 455254FR8 2021 785,000 4.000 4.310 455254FS6 2022 815,000 4.125 4.390 455254FT4 2023 850,000 4.250 4.470 455254FU1 2024 885,000 4.250 4.540 455254FV9 2025 925,000 4.375 4.610 455254FW7 2026 965,000 4.500 4.680 455254FZ0 2027 1,005,000 4.500 4.750 455254GA4

4.750% $3,305,000 Term Bonds due January 1, 2030, to Yield 4.940%; CUSIP: 455254FY3

5.000% $9,850,000 Term Bonds due January 1, 2037, to Yield 5.100%; CUSIP: 455254FX5

No dealer, broker, salesperson or other person has been authorized by the Authority or the Underwriters to give any information or to make any representations other than those contained in this Official Statement in connection with the offering of the 2010 Bonds, and if given or made, such information or representations must not be relied upon as having been authorized by any of the foregoing. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the 2010 Bonds by any person, in any jurisdiction in which it is unlawful for such person to make such offer, solicitation or sale. The information set forth herein has been obtained from sources which are believed to be reliable. The Underwriters have provided the following sentence for inclusion in this Official Statement. The Underwriters have reviewed the information in this Official Statement in accordance with, and as part of, their responsibilities to investors under the federal securities law as applied to the facts and circumstances of this transaction, but the Underwriters do not guarantee the accuracy or completeness of such information. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there have been no changes in the information presented herein since the date hereof.

* * *

The 2010 Bonds have not been registered with the Securities and Exchange Commission under the Securities Act of 1933, as amended. In making an investment decision, investors must rely on their own examination of the Authority, the Airport System and the terms of the offering, including the merit and risk involved. THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED OR DISAPPROVED OF THE 2010 BONDS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THIS OFFICIAL STATEMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

REGISTRATION OR QUALIFICATION OF THE 2010 BONDS IN ACCORDANCE WITH APPLICABLE PROVISIONS OF LAWS OF THE STATES IN WHICH 2010 BONDS HAVE BEEN REGISTERED OR QUALIFIED AND THE EXEMPTION FROM REGISTRATION OR QUALIFICATION IN OTHER STATES CANNOT BE REGARDED AS A RECOMMENDATION THEREOF. NEITHER THESE STATES NOR ANY OF THEIR AGENCIES HAVE PASSED UPON THE MERITS OF THE 2010 BONDS OR THE ACCURACY OR COMPLETENESS OF THIS OFFICIAL STATEMENT. ANY REPRESENTATION TO THE CONTRARY MAY BE A CRIMINAL OFFENSE.

* * *

IN CONNECTION WITH THIS OFFERING, THE UNDERWRITERS MAY OVER-ALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE 2010 BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME.

THE 2010 BONDS MAY BE OFFERED AND SOLD TO CERTAIN DEALERS, INCLUDING

DEALERS DEPOSITING THE 2010 BONDS INTO INVESTMENT ACCOUNTS, AND TO OTHERS AT PRICES LOWER THAN THE PUBLIC OFFERING PRICES SET FORTH ON THE COVER PAGE OF THIS OFFICIAL STATEMENT. AFTER THE 2010 BONDS ARE RELEASED FOR SALE TO THE PUBLIC, THE PUBLIC OFFERING PRICES AND OTHER SELLING TERMS MAY FROM TIME TO TIME BE VARIED BY THE UNDERWRITERS.

INDIANAPOLIS AIRPORT AUTHORITY

BOARD OF DIRECTORS

Michael B. Stayton, President Lacy M. Johnson, Vice President

Alfred R. Bennett, Secretary Alex M. Azar II, Member Kelly J. Flynn, Member Andrew Miller, Member Jean Wojtowicz, Member

Steven Dillinger, Advisory Member Lynn T. Gordon, Advisory Member

Jack Morton, Advisory Member

SENIOR MANAGEMENT

John D. Clark, III, Executive Director and Chief Executive Officer Marsha A. Stone, Chief Financial Officer

Robert A. Duncan, Chief Operating Officer

CO-BOND COUNSEL

Ice Miller LLP Gonzalez Saggio & Harlan LLP

CO-FINANCIAL ADVISORS

Jefferies & Company, Inc. Backstrom McCarley Berry & Co., LLC

AIRPORT CONSULTANT

Ricondo & Associates, Inc.

TRUSTEE

The Bank of New York Mellon Trust Company, N.A.

INDIANAPOLIS AIRPORT AUTHORITY AIRPORT REVENUE BONDS, SERIES 2010A

INTRODUCTION ........................................................................................................................................................................................................... 1

2010 Bonds ............................................................................................................................................................................................... 1 Security and Sources of Payment for 2010 Bonds .................................................................................................................................... 2 Indianapolis Airport Authority .................................................................................................................................................................. 3 Bondholder Risks ...................................................................................................................................................................................... 3 Official Statement; Additional Information .............................................................................................................................................. 3

PLAN OF FINANCING ................................................................................................................................................................................................. 4 Introduction .............................................................................................................................................................................................. 4 PFCs and CFCs ......................................................................................................................................................................................... 4 Dedicated Revenues .................................................................................................................................................................................. 5 Estimated Sources and Uses of Funds....................................................................................................................................................... 6 Revenue Bond Debt Service ..................................................................................................................................................................... 7 Variable Rate Bonds ................................................................................................................................................................................. 8 Qualified Derivative Agreements ............................................................................................................................................................. 8 Subordinate Securities .............................................................................................................................................................................. 9 Commercial Paper .................................................................................................................................................................................. 10 Other Obligations .................................................................................................................................................................................... 11

2010 BONDS ................................................................................................................................................................................................................ 11 General Description ................................................................................................................................................................................ 11 Mandatory Sinking Fund Redemption .................................................................................................................................................... 12 Optional Redemption .............................................................................................................................................................................. 13 Selection of Bonds to Be Redeemed ....................................................................................................................................................... 13 Notice of Redemption ............................................................................................................................................................................. 13

SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS ........................................................................................................................... 14 2010 Bonds ............................................................................................................................................................................................. 14 Pledge of Net Revenues .......................................................................................................................................................................... 14 Qualified Derivative Agreements, Repayment Obligations .................................................................................................................... 15 Funds and Accounts ................................................................................................................................................................................ 16 Revenue Bond Reserve Fund .................................................................................................................................................................. 18 Rate Covenant ......................................................................................................................................................................................... 19 Additional Bonds .................................................................................................................................................................................... 21 Events of Default and Remedies; No Acceleration ................................................................................................................................. 22

INDIANAPOLIS AIRPORT AUTHORITY ................................................................................................................................................................ 22 Powers and Purposes .............................................................................................................................................................................. 22 Authority Board ...................................................................................................................................................................................... 23 Management of Authority ....................................................................................................................................................................... 24

THE AIRPORT AND AIRPORT SYSTEM ................................................................................................................................................................ 26 Overview ................................................................................................................................................................................................ 26 Facilities ................................................................................................................................................................................................. 27 Authority Agreements ............................................................................................................................................................................. 29 Environmental Matters ........................................................................................................................................................................... 32

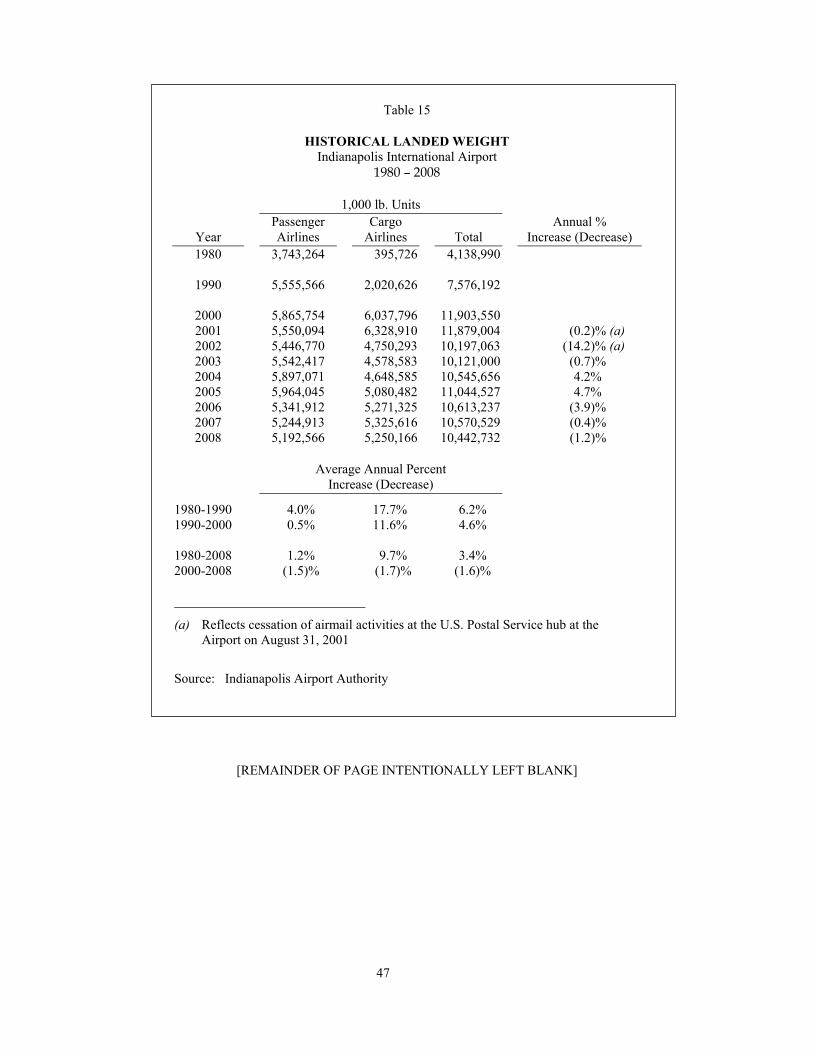

HISTORICAL AIRPORT ACTIVITY ......................................................................................................................................................................... 34 Introduction ............................................................................................................................................................................................ 34 Airline Service ........................................................................................................................................................................................ 35 Historical Airline Traffic ........................................................................................................................................................................ 35 Recent Trends in Airline Traffic ............................................................................................................................................................. 35 Seat Capacity .......................................................................................................................................................................................... 35 Airline Fares ........................................................................................................................................................................................... 37 Airline Market Shares of Enplaned Passengers....................................................................................................................................... 39 O&D Markets ......................................................................................................................................................................................... 41 Air Cargo Activity .................................................................................................................................................................................. 43 Landed Weight ....................................................................................................................................................................................... 45 Aircraft Operations ................................................................................................................................................................................. 48

AIRPORT FINANCIAL INFORMATION .................................................................................................................................................................. 48 Historical Operating Results ................................................................................................................................................................... 48 Management's Discussion and Analysis of Results of Operations .......................................................................................................... 50 Nine Months Ended September 2009 Unaudited Results ........................................................................................................................ 50

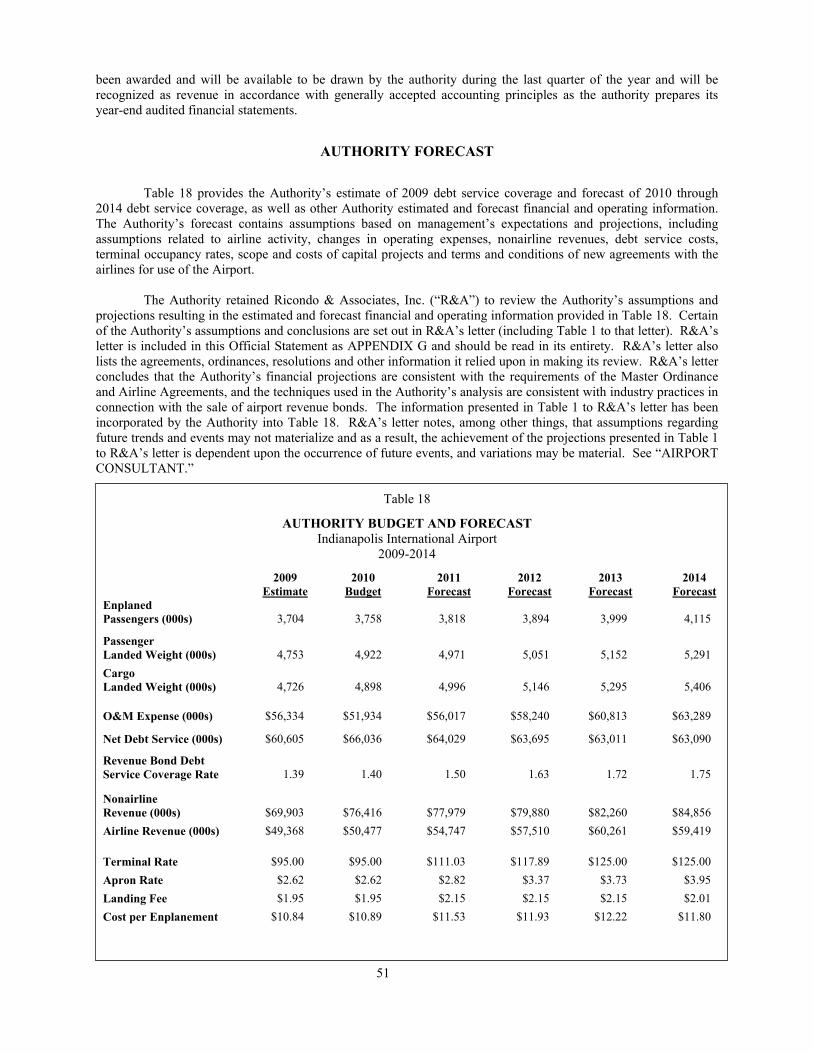

AUTHORITY FORECAST .......................................................................................................................................................................................... 51 CAPITAL IMPROVEMENT PROGRAM .................................................................................................................................................................. 52

Plan of Funding for Five Year Capital Program (2010-2014) ................................................................................................................. 52 BONDHOLDER RISKS ............................................................................................................................................................................................... 53

Factors Affecting Air Transportation Industry and Airport System ........................................................................................................ 53 Cost of Aviation Fuel .............................................................................................................................................................................. 54 Airline Consolidation and Mergers ......................................................................................................................................................... 54 Effect of Airline Bankruptcies ................................................................................................................................................................ 54 Airline Agreements ................................................................................................................................................................................. 56 Geopolitical Risks ................................................................................................................................................................................... 56 Aviation Security Concerns and Related Costs ....................................................................................................................................... 56 Regulations and Restrictions Affecting Airport ...................................................................................................................................... 57 Loss of PFCs ........................................................................................................................................................................................... 57 Travel Substitutes ................................................................................................................................................................................... 58 Five Year Capital Program (2010-2014) ................................................................................................................................................. 58 Variable Rate Bonds, Hedge Agreements ............................................................................................................................................... 58 Limitations on Bondholders’ Remedies .................................................................................................................................................. 58 Assumptions by Authority ...................................................................................................................................................................... 58 Forward-Looking Statements .................................................................................................................................................................. 59

LITIGATION ................................................................................................................................................................................................................ 59 No Litigation Relating to 2010 Bonds .................................................................................................................................................... 59 Other Litigation ...................................................................................................................................................................................... 59

TAX MATTERS ........................................................................................................................................................................................................... 60 AMORTIZABLE BOND PREMIUM .......................................................................................................................................................................... 61 ORIGINAL ISSUE DISCOUNT .................................................................................................................................................................................. 61 ENFORCEABILITY OF REMEDIES ......................................................................................................................................................................... 62 APPROVAL OF LEGAL PROCEEDINGS ................................................................................................................................................................. 62 CREDIT RATINGS ...................................................................................................................................................................................................... 63 INDEPENDENT AUDITORS ...................................................................................................................................................................................... 63 UNDERWRITING ........................................................................................................................................................................................................ 63 CERTAIN RELATIONSHIPS ..................................................................................................................................................................................... 63 CO-FINANCIAL ADVISORS ..................................................................................................................................................................................... 63 AIRPORT CONSULTANT .......................................................................................................................................................................................... 64 CONTINUING DISCLOSURE .................................................................................................................................................................................... 64 MISCELLANEOUS ..................................................................................................................................................................................................... 65 APPENDIX A ECONOMY OF AIRPORT SERVICE REGION ........................................................................................................................... A-1 APPENDIX B AUDITED FINANCIAL STATEMENTS ...................................................................................................................................... B-1 APPENDIX C FORM OF APPROVING OPINION OF CO-BOND COUNSEL .................................................................................................. C-1 APPENDIX D SUMMARY OF ORDINANCE ...................................................................................................................................................... D-1 APPENDIX E SUMMARY OF AIRLINE AGREEMENTS .................................................................................................................................. E-1 APPENDIX F BOOK-ENTRY-ONLY SYSTEM .................................................................................................................................................... F-1 APPENDIX G LETTER OF AIRPORT CONSULTANT ....................................................................................................................................... G-1

OFFICIAL STATEMENT

$25,760,000 Indianapolis Airport Authority

Airport Revenue Bonds, Series 2010A

(Non-AMT)

INTRODUCTION

The purpose of this Official Statement, including the cover page, inside cover page, preliminary pages and appendices, is to set forth certain information concerning the issuance and sale by the Indianapolis Airport Authority (the “Authority”) of its Airport Revenue Bonds, Series 2010A, in the aggregate principal amount of $25,760,000 (the “2010 Bonds”).

The 2010 Bonds are being issued under Indiana Code 8-22-3, as amended and in effect on the issue date of the 2010 Bonds (the “Act”), and pursuant to Authority's General Ordinance No. 4-2002, as previously amended and supplemented (the “Master Ordinance”), as further amended by General Ordinance No. 7-2005 and General Ordinance No. 1-2008, and as further supplemented by General Ordinance No. 4-2009 (the “2010 Supplemental Ordinance”; and together with the Master Ordinance, the “Ordinance”). The 2010 Supplemental Ordinance was adopted by the Authority on December 18, 2009, and provides for the specific terms of and security for the 2010 Bonds.

Proceeds of the 2010 Bonds are expected to be used by the Authority to:

• refund the Authority's outstanding commercial paper, and

• pay costs of issuing the 2010 Bonds.

See “PLAN OF FINANCING.” Terms used but not defined in this INTRODUCTION are used with the meanings ascribed to such terms elsewhere in this Official Statement.

2010 Bonds

The 2010 Bonds will mature on the dates and in the principal amounts set forth on the inside cover page of this Official Statement, and will be dated the date of their delivery. Interest on the 2010 Bonds will be payable on each January 1 and July 1, commencing July 1, 2010. The 2010 Bonds are issuable as fully registered bonds in authorized denominations of $5,000 and any integral multiple of $5,000. See “2010 BONDS.”

The 2010 Bonds will be registered in the name of Cede & Co., as nominee for The Depository Trust Company, New York, New York (“DTC”). Purchases of beneficial interests in the 2010 Bonds will be made in book-entry-only form. Purchasers of beneficial interests in the 2010 Bonds (the “Beneficial Owners”) will not receive physical delivery of certificates representing their interest in the 2010 Bonds. Interest on the 2010 Bonds, together with principal of the 2010 Bonds, will be paid by the Paying Agent directly to DTC, so long as DTC or its nominee is the registered owner of the 2010 Bonds. The final disbursement of such payments to Beneficial Owners of the 2010 Bonds will be the responsibility of the DTC Participants and Indirect Participants, all as defined and more fully described in APPENDIX F—“BOOK-ENTRY-ONLY SYSTEM.”

The 2010 Bonds are subject to optional and mandatory redemption prior to maturity as described herein under the captions “2010 BONDS—Mandatory Sinking Fund Redemption” and “—Optional Redemption.” The Bank of New York Mellon Trust Company, N.A. will serve as Trustee, Paying Agent and Registrar for the 2010 Bonds.

2

Security and Sources of Payment for 2010 Bonds

Under the Master Ordinance, the Authority has outstanding $1,226,145,000 aggregate principal amount of Revenue Bonds (defined herein), including its:

• Airport Revenue Bonds, Series 2003A (the “2003 Bonds”), outstanding in the aggregate principal amount of $96,835,000;

• Airport Revenue Bonds, Series 2004A (the “2004 Bonds”), outstanding in the aggregate principal amount of $205,540,000;

• Airport Revenue Bonds, Series 2005A (the “2005 Bonds”), outstanding in the aggregate principal amount of $197,385,000;

• Airport Revenue Bonds, Series 2006A (the “2006A Bonds”), outstanding in the aggregate principal amount of $345,205,000; and Airport Revenue Bonds, Series 2006B, outstanding in the aggregate principal amount of $31,180,000 (the “2006B Bonds” and together with the 2006A Bonds, the “2006 Bonds”); and

• Variable Rate Airport Revenue Bonds, Series 2008A (the “2008 Bonds”), outstanding in the aggregate principal amount of $350,000,000.

The 2003 Bonds, the 2004 Bonds, the 2005 Bonds, the 2006 Bonds and the 2008 Bonds are collectively referred to as the “Prior Bonds.” All the Prior Bonds were purchased and are held by The Indianapolis Local Public Improvement Bond Bank (the “Bond Bank”), a body corporate and public, with proceeds of limited obligation revenue bonds issued by the Bond Bank for such purpose. The Bond Bank holds the Prior Bonds as the principal security and source of payment for such limited obligation bonds. See “PLAN OF FINANCING—Variable Rate Bonds.”

The 2010 Bonds will be secured by a pledge of the Net Revenues (defined herein) of the Airport System on

parity with the Prior Bonds and any additional Revenue Bonds issued by the Authority under the Master Ordinance, as further supplemented and amended (together with the 2010 Bonds, the “Revenue Bonds”). Payments under Qualified Derivative Agreements (defined herein), excluding any termination payments, and payments on any Repayment Obligations (defined herein) also will be payable from Net Revenues of the Airport System on parity with the Revenue Bonds. See “PLAN OF FINANCING—Qualified Derivative Agreements.”

The 2010 Bonds will be further secured by an account of the Revenue Bond Reserve Fund (the “2010 Account”). The 2010 Account and the account of the Revenue Bond Reserve Fund established when the Authority issued the 2003 Bonds (the “2003 Account”) will secure, on parity, all 2010 Bonds and 2003 Bonds, with funds currently on deposit in the 2003 Account. The 2010 Bonds will not be secured by or payable from the accounts established for any of the Prior Bonds other than the 2003 Bonds. In the future, the Authority may issue Additional Revenue Bonds secured on parity with the 2010 Account and the 2003 Account.

The Revenue Bonds are special limited obligations of the Authority payable solely from and secured exclusively by a lien upon the Net Revenues of the Airport System and moneys in certain funds established under the Ordinance, and neither the Authority, the Board of the Authority (the “Authority Board”), the City of Indianapolis, Marion or any other county, nor any of their officers, agents or employees, is under any obligation to pay the Revenue Bonds except from those revenues and moneys. The Revenue Bonds, and interest on the Revenue Bonds, are not a debt or a general obligation of the Authority, the City of Indianapolis, Marion or any other county, or the State of Indiana, nor a charge, a lien or an encumbrance, legal or equitable, upon property of the Authority or the Authority Board or upon income, receipts or revenues of the Authority or the Authority Board, other than those revenues and moneys that have been specifically pledged to the payment of the Revenue Bonds. The Revenue Bonds are not payable from funds raised or to be raised by taxation. See “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS.”

3

Indianapolis Airport Authority

The Authority is a municipal corporation, separate from the City of Indianapolis and Marion and other counties, organized and existing under the Act, with the power to own and operate public airports. The Authority owns and operates Indianapolis International Airport (the “Airport”), as well as the Downtown Heliport, Eagle Creek Airpark, Metropolitan Airport, Mt. Comfort Airport and Hendricks County Airport-Gordon Graham Field (collectively with the Airport, the “Airport System”). See “INDIANAPOLIS AIRPORT AUTHORITY” and “THE AIRPORT AND AIRPORT SYSTEM” for information concerning the Authority and its assets and operations.

Bondholder Risks

General. The 2010 Bonds may not be suitable for all investors. Prospective purchasers of the 2010 Bonds should read this entire Official Statement, including information under “BONDHOLDER RISKS.”

Factors Affecting Air Transportation Industry. During the past nine years, specific incidents and general trends, some of which are continuing, have had an adverse impact on air travel and the air transportation industry. Among these are financial difficulties of many airlines, including the bankruptcy of airlines, mergers and acquisitions and restructurings, significant fluctuations in fuel prices, economic decline and recession, terrorist attacks in the United States and other parts of the world, heightened concern over security in air transportation and conflicts in Iraq and Afghanistan and elsewhere in the world. The Authority cannot predict the duration or extent to which these factors will continue to impact air travel and the air transportation industry, nor can the Authority predict the likelihood of similar future incidents and trends or future air transportation disruptions. See “BONDHOLDER RISKS—Certain Factors Affecting Air Transportation Industry and Airport System.”

Airline Agreements. The Authority has entered into Airline Agreements (defined herein) with passenger and air cargo carriers under which the Signatory Airlines (defined herein) are obligated to make payments for use of Airport System facilities sufficient in the aggregate to pay Operation and Maintenance Expenses (defined herein) and debt service on Revenue Bonds, among other things, taking into account other revenues and moneys available to the Authority for such purposes. The Airline Agreements will expire on December 31, 2010, and the Authority and the Signatory Airlines have begun discussions regarding new airline agreements; however, new agreements may not be consummated by January 1, 2011. The Authority’s financial projections for 2011 through 2014, which are included in this Official Statement under “AUTHORITY FORECAST,” are based on rate-setting and other provisions substantially similar to the Authority’s practice under the current Airline Agreements. Any new Airline Agreements or, in the absence of such agreements, an ordinance of the Authority, may include rate-setting and other provisions that differ from those in the current Airline Agreements. These differences may be material and may materially adversely affect the likelihood of achieving the Authority’s financial projections. In any event, the Authority has covenanted to charge rates that are sufficient to generate Gross Revenues sufficient to pay Operation and Maintenance Expenses as well as debt service and required debt service coverage on Revenue Bonds, taking into account other available revenues and funds. See “THE AIRPORT AND AIRPORT SYSTEM—Authority Agreements—Airline Agreements” and “BONDHOLDER RISKS—Airline Agreements.”

Official Statement; Additional Information

This Official Statement speaks only as of its date, and the information contained herein is subject to change.

The information contained in this INTRODUCTION is qualified by reference to this entire Official Statement (including the cover page, the inside cover page, the preliminary pages and the appendices). This INTRODUCTION is only a brief description and a full review should be made of this entire Official Statement (including the appendices), as well as the documents summarized or described in this Official Statement. The summaries of and references to all documents, statutes and other instruments referred to in this Official Statement do not purport to be complete and are qualified in their entirety by reference to the full text of each such document, statute or instrument.

4

Additional information with respect to the Authority, and copies of the Ordinance, may be obtained from Jeremiah Wise, Treasurer, Indianapolis Airport Authority, 7800 Col. H. Weir Cook Memorial Drive, Suite 100, Indianapolis, IN 46241; telephone (317) 487-5258.

PLAN OF FINANCING

Introduction

The Authority is issuing the 2010 Bonds to refinance capital improvements to the Airport System. From 2003 through 2008, the Authority issued six series of Revenue Bonds to finance and refinance a portion of the costs of its 2001-2010 Capital Improvement Program. Under that program, the Authority constructed the new $1.07 billion Col. H. Weir Cook Terminal and associated capital improvements to the Airport, as more fully described in this Official Statement. These improvements are sometimes referred to as “The New Indianapolis Airport” or the “Midfield Project.” The new terminal opened November 11, 2008.

Proceeds of the 2010 Bonds are expected to be used to (i) refund the outstanding commercial paper issued by the Authority to finance capital improvements (the “Commercial Paper”), and (ii) pay costs of issuing the 2010 Bonds.

With the substantial completion of The New Indianapolis Airport, the Authority continues to upgrade, repair, modify and add to its existing facilities. The capital projects and associated costs budgeted for fiscal years 2010 through 2014 are referred to as the “Five Year Capital Program (2010-2014)” or the “Five Year Capital Program.” The Authority will not use 2010 Bond proceeds to fund costs of the Five Year Capital Program (2010-2014). The Authority expects to fund such costs with federal and state grants and any other available revenues and funds of the Authority. However, the Authority may determine in the future to fund such costs with Additional Revenue Bonds and Commercial Paper or similar obligations. See “THE AIRPORT AND AIRPORT SYSTEM” and “CAPITAL IMPROVEMENT PROGRAM.”

PFCs and CFCs

PFCs. The Authority is authorized by the Federal Aviation Administration (“FAA”) to collect a passenger facility charge (“PFC”) of $4.50 per eligible enplaned passenger. From September 1993 through March 2001, the Authority collected a PFC of $3.00 per eligible enplaned passenger, as authorized by the FAA. The Authority increased its PFC to $4.50, as authorized by the FAA on January 17, 2001. On August 25, 2003, the Authority received “use approval” from the FAA for $524.5 million of PFC revenue for eligible project costs of The New Indianapolis Airport, including $387.5 million to pay debt service on Revenue Bonds issued to finance and refinance The New Indianapolis Airport. As of November 1, 2009, the Authority had $324.6 million of PFC use authority remaining to pay debt service on Revenue Bonds, a portion of which are or will be designated as Dedicated Revenues.

In the five years from 2004 through 2008, the Authority collected PFC revenue (excluding interest income) in the following amounts:

Year

PFCs

2004 $16,722,9392005 17,460,3592006 17,479,699 2007 16,774,356 2008 16,852,737

From 2009 through 2014, the Authority estimates that it will collect approximately $104.6 million of additional PFC revenue, some of which has been designated as Dedicated Revenues, as described below.

5

CFCs. On March 17, 2006, the Authority adopted an ordinance establishing a customer facility charge (“CFC”) to be collected by rental car companies serving the Airport. Effective May 1, 2006, the rental car companies began to collect a $3.00 CFC per contract day (up to a maximum of 14 contract days) to be remitted to the Authority. Under the Authority’s current rate ordinance, the Authority may modify the CFC rate upon 60 days notice to the rental car companies to a maximum of $4.00 per contract day (up to a maximum of 14 contract days). The Authority’s forecast assumes this increase will occur in 2010. To date, the Authority has used all its CFC revenue for payment of debt service on Revenue Bonds.

From May 2006 through December 2008, the Authority collected CFC revenue (excluding interest income) of approximately $13.8 million. From 2009 through 2014, the Authority estimates that it will collect $34.9 million of additional CFC revenue.

See “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS—Rate Covenant” and “—Additional Bonds—Revenue Bonds” and “AUTHORITY FORECAST.”

Dedicated Revenues

Pursuant to the Ordinance, the Authority adopted resolutions irrevocably designating approximately $13.25 million per year of PFC revenue, to the extent collected, as Dedicated Revenues (defined in the Master Ordinance), to be used exclusively to pay debt service on Revenue Bonds through 2014. The Authority also adopted resolutions irrevocably designating approximately $31.6 million of CFC revenue, in amounts ranging from approximately $5.9 million per year to approximately $7.0 million per year, to the extent collected, as Dedicated Revenues to be used exclusively to pay debt service on Revenue Bonds through 2014.

The effect of the dedication of PFC revenue and CFC revenue is to exclude principal of and interest on Revenue Bonds equal to such Dedicated Revenues for purposes of demonstrating debt service coverage under the Rate Covenant and satisfying requirements for issuance of Additional Revenue Bonds, including the 2010 Bonds.

To the extent the Authority collects less PFC revenue or CFC revenue than dedicated, the Authority must use other revenues to pay debt service on Revenue Bonds.

The Authority’s forecast assumes that the Authority will dedicate an additional $24.6 million of PFC revenue to pay debt service on Revenue Bonds from 2010 through 2014; however, the Authority has not yet designated such additional PFC revenue as Dedicated Revenues.

See “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS—Rate Covenant” and “—Additional Bonds—Revenue Bonds” and “AUTHORITY FORECAST.”

[REMAINDER OF PAGE INTENTIONALLY LEFT BLANK]

6

Estimated Sources and Uses of Funds

Estimated sources and uses of the 2010 Bond proceeds are as follows:

SOURCES:

Par Amount of 2010 Bonds $25,760,000.00 Net Original Issue Discount (249,271.85)

Total Sources $25,510,728.15 USES:

Deposit to 2010 Construction Fund (1) $25,000,513.59 Fees and Costs Related to 2010 Bonds (2) 510,214.56

Total Uses $25,510,728.15 ________________

(1) Substantially all the proceeds of the 2010 Bonds deposited in the 2010 Construction Fund will be used to pay the principal of all the outstanding Commercial Paper at maturity, which is not later than 90 days from the date of issuance of the 2010 Bonds. Interest on the outstanding Commercial Paper will be paid from 2010 Bond proceeds and Net Revenues of the Authority. See “—Commercial Paper.”

(2) Includes underwriters' discount of $182,266.99 and costs of issuance, including legal, fiduciary, financial advisory, credit rating and printing fees and expenses. See “UNDERWRITING.”

[REMAINDER OF PAGE INTENTIONALLY LEFT BLANK]

7

Revenue Bond Debt Service

See Table 1 for the scheduled principal and interest due on the outstanding Revenue Bonds and the 2010 Bonds:

Table 1

REVENUE BOND DEBT SERVICE Indianapolis International Airport

Outstanding

Revenue Bonds

2010 Bonds(1) (2)

Fiscal Year

Ended

December 31

Principal/Sinking Fund Installment

and

Interest (1)(2)(3)

Principal/Sinking Fund

Installment

Interest

Total Debt

Service(2)(3)

2009 $ 74,346,452 $ — $ — $ 74,346,452

2010 83,691,492 510,000 1,066,678 85,268,170

2011 85,746,606 570,000 1,134,413 87,451,019

2012 84,768,173 585,000 1,117,313 86,470,486

2013 84,888,384 600,000 1,099,763 86,588,147

2014 84,877,678 620,000 1,081,763 86,579,441

2015 84,867,587 645,000 1,056,963 86,569,550

2016 85,106,708 670,000 1,031,163 86,807,871

2017 85,097,976 695,000 1,004,363 86,797,339

2018 85,072,911 725,000 976,563 86,774,474

2019 85,060,504 755,000 947,563 86,763,067

2020 85,046,810 785,000 917,363 86,749,173

2021 85,027,422 815,000 885,963 86,728,385

2022 85,450,505 850,000 852,344 87,152,849

2023 88,569,328 885,000 816,219 90,270,547

2024 88,650,687 925,000 778,606 90,354,293

2025 88,739,192 965,000 738,138 90,442,330

2026 88,844,895 1,005,000 694,713 90,544,608

2027 87,476,231 1,050,000 649,488 89,175,719

2028 87,599,285 1,100,000 599,613 89,298,898

2029 87,705,976 1,155,000 547,363 89,408,339

2030 87,830,885 1,210,000 492,500 89,533,385

2031 87,955,801 1,270,000 432,000 89,657,801

2032 88,088,679 1,335,000 368,500 89,792,179

2033 77,185,749 1,400,000 301,750 78,887,499

2034 59,395,069 1,470,000 231,750 61,096,819

2035 59,361,798 1,545,000 158,250 61,065,048

2036 56,378,750 1,620,000 81,000 58,079,750

Total $2,312,831,533

$25,760,000 $20,062,105 $2,358,653,638

(1) Amounts due January 1 are shown as debt service for the preceding Fiscal Year ended December 31 (that is, the amounts actually required to be set aside in that Fiscal Year). For example, a debt service payment with regard to the 2010 Bonds due on January 1, 2012, is shown in the Fiscal Year ended December 31, 2011.

(2) This table reflects all principal and interest due on the outstanding Revenue Bonds and the 2010 Bonds. However, a portion of principal and interest due on the outstanding Revenue Bonds is expected to be paid with PFCs and CFCs. See “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS—Pledge of Net Revenues.” Totals may not add due to rounding.

(3) The interest rate assumed to be borne by the 2008 Bonds included in the Outstanding Revenue Bonds column is 5.21%, which reflects the fixed rates payable by the Authority under the Hedge Agreements (defined herein), an assumed 100 basis point basis mismatch between the underlying variable rate bonds and the variable rate to be received by the Authority under the Hedge Agreements, and the annual fees owed to the bank providing liquidity support for the 2008 Bonds and the remarketing agents therefor.

Source: Indianapolis Airport Authority

8

Variable Rate Bonds As described under “INTRODUCTION,” $350.0 million of the approximately $1.238 billion of Prior Bonds are variable rate demand bonds. The 2008 Bonds were purchased by the Bond Bank, also as described under “INTRODUCTION,” which issued its own variable rate demand limited obligation bonds to provide the moneys necessary to do so and to pay costs of issuance and related costs (the “2008 Bond Bank Bonds”). Payment of principal of and interest on the 2008 Bond Bank Bonds when due is guaranteed under an insurance policy issued by Financial Security Assurance, Inc. In addition, under a standby bond purchase agreement, Dexia Credit Local, acting through its New York Branch, has agreed to purchase any 2008 Bond Bank Bonds bearing interest at a Daily Interest Rate or a Weekly Interest Rate (as defined in such agreement) that have been tendered by their owners, but not remarketed. That standby bond purchase agreement will expire on June 25, 2011, unless terminated, suspended or extended prior to such date. The credit ratings for Financial Security Assurance, Inc. are Aa3, Moody’s; AAA, S&P; and AA, Fitch. The long-term / short- term credit ratings for Dexia Credit Local are A1 / P-1, Moody’s; A / A1, S&P; and A+ / F1+, Fitch. The Authority’s obligations to Dexia Credit Local with respect to the standby bond purchase agreement are on parity with the Revenue Bonds, including the 2010 Bonds. See “INTRODUCTION—Security and Sources of Payment for 2010 Bonds” and “BONDHOLDER RISKS—Variable Rate Bonds.” Qualified Derivative Agreements

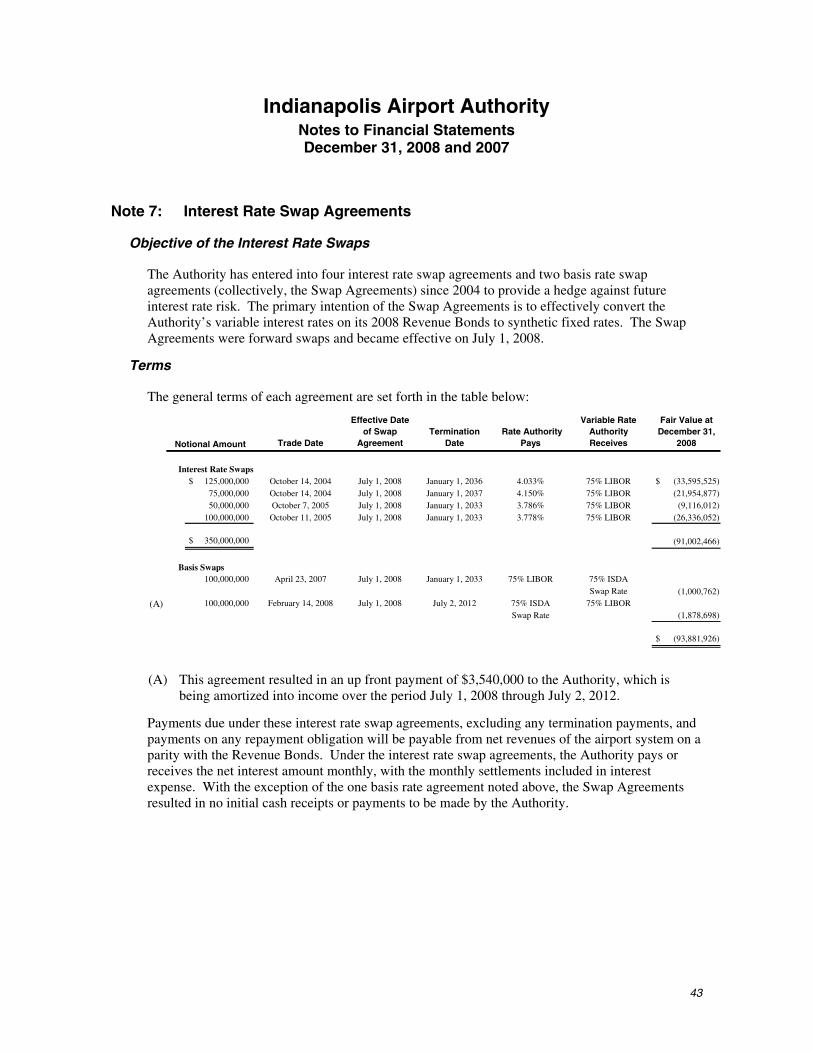

The Authority has entered into four floating-to-fixed interest rate swap agreements in an effort to provide a synthetic fixed rate for the variable rate 2008 Bonds. The counterparties (each a “Counterparty”) are J. P. Morgan Chase Bank, N.A. (“JP Morgan Chase”), UBS AG (“UBS”), and SBS Financial Products Company, LLC (“SBS”). Such agreements are “Qualified Derivative Agreements” as defined under “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS”; and certain of the Authority's payment obligations under such agreements are on parity with the 2010 Bonds and other Revenue Bonds.

The terms of these swap agreements, other than the fixed-rate payer portion, are substantially similar and provide for payments to or from the applicable Counterparty equal to the difference between the fixed rate payable by the Authority to the applicable Counterparty and 75% of one-month LIBOR payable by such Counterparty to the Authority. The Counterparties, notional amounts, fixed rates of interest payable by the Authority to the Counterparties under such agreements, termination dates and credit ratings of the Counterparties are shown on Table 2. See “CREDIT RATINGS” for definitions of “Moody's,” “S&P” and “Fitch.”

[REMAINDER OF PAGE INTENTIONALLY LEFT BLANK]

9

Table 2

QUALIFIED DERIVATIVE AGREEMENTS Indianapolis International Airport

Counterparty

JP Morgan Chase

JP Morgan Chase

UBS*

SBS*

Notional Amount

$125.0 million

$75.0 million

$100.0 million

$50.0 million

Fixed Rate

4.0325%

4.1500%

3.775%

3.7860%

Termination Date

January 1, 2036

January 1, 2037

January 1, 2033

January 1, 2033

Moody's Aa1 Aa1 Aa3 A2** S&P AA- AA- A+ A** Fitch AA- AA- A+ A+** Sources: Indianapolis Airport Authority; credit rating agencies

In addition, the Authority is a party to two additional interest rate swap agreements with UBS, the net effect of which is that beginning after July 1, 2012, the Authority will receive 75% of the ten-year LIBOR and pay 75% of one-month LIBOR on a notional amount of $100.0 million. The first additional interest rate swap agreement, with an effective date of July 1, 2008 and a termination date of July 1, 2033, provides that the Authority will receive 75% of the ten-year LIBOR less 43.7 basis points and pay 75% of the one-month LIBOR. The second additional interest rate swap agreement, with an effective date of July 1, 2008 and a termination date of July 1, 2012, effectively reversed the first additional interest rate swap agreement through July 1, 2012 and, in exchange, required UBS to pay the Authority $3,540,000 on February 19, 2008. (The Bond Bank is also a party to one of these interest rate swap agreements.)

All the swap agreements referred to under “—Qualified Derivative Agreements” are collectively referred to as the “Hedge Agreements”) and will be treated by the Authority as Qualified Derivative Agreements (defined herein) under the Ordinance. As a result, payments other than termination payments, if any, under the Hedge Agreements will be made by the Authority from the Net Revenues in the Revenue Bond Interest and Principal Fund on parity with payments on the Revenue Bonds. See “SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS—Pledge of Net Revenues” and “—Qualified Derivative Agreements, Repayment Obligations” and “BONDHOLDER RISKS—Hedge Agreements.”

Subordinate Securities

Under the Ordinance, the Authority may issue for any lawful Airport System purpose one or more series of revenue bonds, notes or other obligations secured in whole or in part by a lien on Net Revenues junior and

* The Bond Bank, which issued variable rate limited obligations to finance the purchase of the variable rate 2008

Bonds, is also a party to the UBS and SBS swaps identified on Table 2. ** These credit ratings are the credit ratings of Merrill Lynch & Co., the credit support provider for SBS’s

obligations under this swap agreement.

10

subordinate to the lien on Net Revenues securing payment of the 2010 Bonds and other Revenue Bonds (“Subordinate Securities”). Subordinate Securities may be further secured by any other lawfully available source of payment and need not be issued on parity with one another. Agreements for issuance of Subordinate Securities cannot require that a default or an event of default under such agreements will create an event of default under the Ordinance.

Commercial Paper constitutes a Subordinate Security under the Ordinance and is payable from and secured by a lien on Net Revenues of the Airport System that is junior and subordinate to the lien of the 2010 Bonds and other Revenue Bonds. From time to time, the Authority has issued, and may continue to issue in the future, Commercial Paper to provide interim financing for capital improvements to the Airport System. To mitigate the risk of unsuccessful placement or remarketing of Commercial Paper following maturity, the Authority has procured letters of credit from banks and entered into reimbursement agreements with such banks to provide for repayment of draws to buy Commercial Paper under certain circumstances. The Authority’s obligations under such reimbursement agreements also constitute Subordinate Securities.

Commercial Paper

The Authority is authorized to issue up to $245.0 million aggregate principal amount of commercial paper under two separate Commercial Paper programs, the $45.0 million 1999 Commercial Paper program (the “1999 CP Program”) and the $200.0 million 2007 Commercial Paper program (the “2007 CP Program”). The 1999 CP Program is supported by a letter of credit issued by J.P. Morgan Chase Bank, N.A. (“JP Morgan Chase”), and the 2007 CP Program is supported by letters of credit issued by State Street Bank and Trust Company (“State Street Bank”) and Fortis Bank, S.A./N.V., acting by and through its New York Branch (“Fortis Bank”). As of December 1, 2009, $25.0 million of Commercial Paper was outstanding under the 1999 CP Program, and no Commercial Paper was outstanding under the 2007 CP Program.

The Authority plans to repay the Commercial Paper outstanding from time to time (including any related reimbursement obligations to the issuers of letters of credit supporting such Commercial Paper) from Net Revenues, other available funds of the Authority and/or proceeds of Additional Revenue Bonds. The Authority may continue to use Commercial Paper or similar obligations as a means of providing interim financing for capital improvements to the Airport System. See “CAPITAL IMPROVEMENT PROGRAM—Plan of Funding for Five Year Capital Program (2010-2014).”

Published long-term and short-term credit ratings for the banks providing letters of credit for the 1999 CP Program and the 2007 CP Program, together with the stated termination dates for such letters of credit, are set forth on Table 3. See “CREDIT RATINGS” for definitions of “Moody's,” “S&P” and “Fitch.”

The Authority may decrease (or increase) the amount of Commercial Paper that may be issued from time to time, although the Authority has no plans to do so.

Table 3

COMMERCIAL PAPER Indianapolis International Airport

1999 CP Program 2007 CP Program

Bank JP Morgan Chase Fortis Bank State Street Bank

Moody's Aa1, P-1 A1, P-1 Aa2, P-1

S&P AA-, A1+ AA-, A1+ AA-, A1+

Fitch AA-, F1+ AA-, F1+ A+, F1+

Stated Termination May 17, 2012 June 19, 2012 June 19, 2012

Sources: Indianapolis Airport Authority; credit rating agencies

11

Other Obligations

General Obligation Bonds. The Act permits the Authority Board to authorize the issuance of general obligation bonds of the Authority (“General Obligation Bonds”) for the purpose of procuring funds to pay the costs of acquiring real property, or constructing, enlarging, improving, remodeling, repairing or equipping buildings, structures, runways or other facilities, for use as or in connection with or for administrative purposes of the Airport System. To raise money to pay all General Obligation Bonds and any interest on them, the Authority Board may levy each year a special tax upon all of the property, both real and personal, located within the territorial limits of the County, in a manner and in an amount to meet and pay the principal of the General Obligation Bonds as they severally mature, together with all interest accruing on them. Any taxes collected for the purpose of paying principal and interest on General Obligation Bonds are not Gross Revenues and are not pledged to payment of Authority Revenue Bonds. The Ordinance provides that after funding of the Revenue Bond Interest and Principal Fund and the Revenue Bond Reserve Fund, Net Revenues may be deposited into the General Obligation Bond Interest and Principal Fund to pay debt service on General Obligation Bonds.

Although the Authority has no General Obligation Bonds outstanding and has no plans to issue General Obligation Bonds, the Authority may issue General Obligation Bonds in the future.

Special Purpose Facilities Bonds. Under the Ordinance, the Authority reserves the right to issue one or more series of bonds to finance and refinance the cost of any Special Purpose Facilities (“Special Purpose Facilities Bonds”), including all reserves required therefor, all related costs of issuance and other amounts reasonably relating thereto; provided, that such Special Purpose Facilities Bonds will be payable solely from payments by Special Purpose Facilities lessees and other security not provided by the Authority. Each Special Purpose Facilities lease must provide that an Airport System improvement or facility is leased by the Authority to a lessee which agrees to pay (i) all of the debt service requirements for the Special Purpose Facilities Bonds issued to finance the Special Purpose Facility and (ii) all administrative expenses allocable to the Special Purpose Facility. No Gross Revenues or Net Revenues or any other amounts held in any other fund or account maintained by the Authority as security for the Revenue Bonds or for the construction, operation, maintenance or repair of the Airport System are pledged to payment of Special Purpose Facilities Bonds or to payment of lessee expenses of operation and maintenance of Special Purpose Facilities. The Authority has issued and, in the future, may issue one or more additional series of Special Purpose Facilities Bonds for one or more airlines or entities which conduct operations at the Airport System. See “THE AIRPORT AND AIRPORT SYSTEM—Facilities—Maintenance Facilities.”

2010 BONDS

General Description

The 2010 Bonds are issuable as fully registered bonds in denominations of $5,000 or any integral multiple thereof. The 2010 Bonds will be dated as of the date of their delivery.

Interest on the 2010 Bonds will be payable on January 1 and July 1 of each year, commencing July 1, 2010 (each an “Interest Payment Date”). The 2010 Bonds will bear interest (calculated on the basis of twelve 30-day months for a 360-day year) at the rates and will mature on the dates and in the principal amounts set forth on the inside cover page of this Official Statement. Each 2010 Bond will bear interest from the Interest Payment Date next preceding the date on which it is authenticated unless it is (a) authenticated prior to the closing of business on June 15, 2010, in which event it will bear interest from the date of delivery, or (b) authenticated after the fifteenth day immediately preceding an Interest Payment Date (a “Record Date”), in which event it will bear interest from such Interest Payment Date; provided, however, that if, at the time of authentication of any 2010 Bond, interest is in default, such 2010 Bond will bear interest from the date to which interest has been paid.

When issued, all 2010 Bonds will be registered in the name of and held by Cede & Co., as nominee for DTC. Purchases of beneficial interests from DTC in the 2010 Bonds will be made in book-entry-only form (without certificates) in denominations of $5,000 or any integral multiple thereof. So long as DTC or its nominee is the registered owner of the 2010 Bonds, payments of the principal of and interest on the 2010 Bonds will be made directly by the Paying Agent by wire transfer of funds to Cede & Co., as nominee for DTC. Disbursement of such

12

payments to the participants of DTC (the “DTC Participants”) will be the sole responsibility of DTC, and the ultimate disbursement of such payments to the Beneficial Owners of the 2010 Bonds will be the responsibility of the DTC Participants and the Indirect Participants (defined herein). See APPENDIX F—“BOOK-ENTRY-ONLY SYSTEM.”

If DTC or its nominee is not the registered owner of the 2010 Bonds, principal of and premium, if any, on all the 2010 Bonds will be payable at maturity upon the surrender thereof at the delivery office of the Paying Agent. Interest on the 2010 Bonds, when due and payable, will be paid by check dated the due date and mailed by the Paying Agent to the persons in whose names such 2010 Bonds are registered, at their addresses as they appear on the bond registration books maintained by the Registrar on the Record Date, irrespective of any transfer or exchange of such 2010 Bonds subsequent to such Record Date and prior to such Interest Payment Date, unless the Authority shall default in payment of interest due on such Interest Payment Date.

Except as described in APPENDIX F—“BOOK-ENTRY-ONLY SYSTEM,” in all cases in which the privilege of exchanging or transferring 2010 Bonds is exercised, the Authority will execute and the Registrar will deliver 2010 Bonds in accordance with the Ordinance. The 2010 Bonds will be exchanged or transferred at the designated corporate trust office of the Registrar only for 2010 Bonds of the same tenor and maturity. In connection with any transfer or exchange of 2010 Bonds, the Authority, the Registrar and Paying Agent or the Trustee may impose a charge for any applicable tax, fee or other governmental charge incurred in connection with such transfer or exchange, which sums are payable by the person requesting such transfer or exchange.

The person in whose name a 2010 Bond is registered will be deemed and regarded as its absolute owner for all purposes, and payment of principal and interest thereon will be made only to or upon the order of the registered owner or its legal representative, but such registration may be changed as provided above. All such payments shall be valid to satisfy and discharge the liability upon such 2010 Bond to the extent of the sum or sums so paid.

Mandatory Sinking Fund Redemption

2010 Bonds maturing January 1, 2030 (the “2030 Term Bonds”) are subject to mandatory sinking fund redemption prior to maturity at the redemption price of 100% of the principal amount thereof, plus accrued interest to the date of redemption, and will be redeemed on January 1 of the respective years and in the respective principal amounts set forth below:

2030 Term Bonds Year Principal Amount

2028 $1,050,000 2029 1,100,000

2030(1) 1,155,000 ____________ (1) Final maturity

[REMAINDER OF PAGE INTENTIONALLY LEFT BLANK]

13

2010 Bonds maturing January 1, 2037 (the “2037 Term Bonds”) are subject to mandatory sinking fund redemption prior to maturity at the redemption price of 100% of the principal amount thereof, plus accrued interest to the date of redemption, and will be redeemed on January 1 of the respective years and in the respective principal amounts set forth below:

2037 Term Bonds Year Principal Amount

2031 $1,210,000 2032 1,270,000 2033 1,335,000 2034 1,400,000 2035 1,470,000 2036 1,545,000

2037(1) 1,620,000 ____________ (1) Final maturity

Optional Redemption

The 2010 Bonds maturing on or after January 1, 2021, are subject to redemption prior to maturity in whole or in part on January 1, 2020, or at any time thereafter, at the redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption.

Selection of Bonds to Be Redeemed

If fewer than all the 2010 Bonds shall be called for redemption, the principal amount and maturity of the particular 2010 Bonds to be redeemed shall be selected by the Authority, provided that the 2010 Bonds shall be redeemed only in integral multiples of $5,000 principal amount. If the 2010 Bonds are held in a book-entry-only system, the 2010 Bonds within a maturity to be redeemed shall be selected by the depository company in such manner as the depository company may determine. If the 2010 Bonds are not held in the book-entry-only system, the Registrar shall, in selecting portion of 2010 Bonds for redemption, treat each such 2010 Bond as representing that number of 2010 Bonds of $5,000 denominations which is obtained by dividing the principal amount of such 2010 Bond by $5,000.

Notice of Redemption

In the case of redemption of the 2010 Bonds, notice of the call for any such redemption identifying the 2010 Bond or portions of fully registered 2010 Bond to be redeemed shall be given by the Registrar by mailing a copy of the redemption notice by first class mail at least 30 days but not more than 60 days prior to the date fixed for redemption to the registered owner of each 2010 Bond to be redeemed at the address shown on the registration books. Any notice of redemption given by the Registrar may provide that, if at the time of mailing the notice of redemption, there shall not have been deposited with the Trustee moneys sufficient to redeem all 2010 Bonds called for redemption, such notice may state that it is conditional, that it is subject to the deposit of the redemption moneys with the Trustee not later than the date of redemption of such 2010 Bonds, and that such notice shall be of no effect unless such moneys are so deposited. In the event sufficient redemption moneys are not on deposit on the required date, then the redemption shall be cancelled and notice shall be mailed to the holders of such 2010 Bonds to be redeemed, in the manner provided above. Failure to give such notice by mailing to any bondholder, or any defect in the notice, shall not affect the validity of any proceeding for the redemption of any other 2010 Bonds. On and after the redemption date specified in the aforementioned notices, such 2010 Bonds, or portions thereof, thus called (provided funds for their redemption are on deposit at the place of payment) shall not bear interest, shall no longer

14

be protected by the Ordinance and shall not be deemed to be outstanding under the Ordinance, and the owners thereof shall have the right only to receive the redemption price thereof plus accrued interest thereon to the date fixed for redemption from the funds deposited with the Trustee for the redemption of such 2010 Bonds.

SECURITY AND SOURCES OF PAYMENT FOR 2010 BONDS

2010 Bonds