2022 Global Gas Flaring Tracker Report

12

2022 Global Gas Flaring Tracker Report

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 2022 Global Gas Flaring Tracker Report

2022 Global Gas Flaring Tracker Report

2021 was yet another turbulent year for the oil and gas industry,

with rising oil prices, tight oil and gas markets, high energy prices,

and the ongoing recovery from the Covid-19 pandemic. However,

despite these challenges, the UN Climate Change Conference

of the Parties (COP26) and Global Methane Pledge (GMP)

underscored once again the growing urgency for governments,

companies, and development organizations to accelerate

decarbonizing the global economy. This is a pressing need, brought

to the fore by the Russian invasion of Ukraine earlier this year and

its dramatic impact on energy security across the world.

In 2021, 144 billion cubic meters (bcm) of gas was needlessly

flared at upstream oil and gas facilities across the globe. We

estimate that this gas flaring resulted in approximately 400

million tonnes of carbon dioxide (CO2) equivalent emissions

globally last year. Ending this polluting practice must be central

to decarbonization efforts. Not only could the gas wasted displace

dirtier fuels and increase energy access in some of the world’s

poorest countries, but by utilizing the gas that is currently being

flared, the world could make significant progress towards much-

needed energy security. For example, the volume of gas flared

worldwide is greater than the European Union's 27 member states

gas imports from Russia.

Flaring reduction also plays a critical role in mitigating methane

emissions, by eliminating a direct source of methane released

un-combusted from flares and enabling the gas successfully

conserved through reductions in venting and fugitive emissions

to be utilized rather than flared. This raises the often-overlooked

importance of integrating the decarbonization of the oil and gas

sector into wider climate initiatives and discussions.

With this in mind, we’re keen to understand not only how much

gas was flared in 2021, but where countries have made progress

and where the greatest opportunities for flaring abatement

remain. GGFR’s 2022 Global Gas Flaring Tracker, a leading global

and independent indicator of gas flaring, found that despite

strong early progress, reductions in both absolute flare volumes

and flaring intensity have plateaued over the last decade;

impressive reductions in some countries have unfortunately been

offset by concerning increases in others.

We explore several oil-producing countries where absolute flare

volumes have decreased and some where they have increased,

despite commitments and efforts to end flaring. Unfortunately,

flaring increases are not limited to those countries highlighted in

this report. We urge all governments and operators to carefully

assess how they are producing oil and to identify and seize

opportunities for effective decarbonization.

With less than a decade to go until the global ambition of Zero

Routine Flaring by 2030, it is time for swift and determined

action. Our team at the World Bank will continue to support

this effort, especially in developing countries, and work closely

with governments and oil companies to overcome the barriers to

flaring reduction.

Zubin BamjiProgram Manager

Global Gas Flaring Reduction Partnership

World Bank

Foreword

© 2022 International Bank for Reconstruction and Development / The World Bank1818 H Street NWWashington DC 20433Telephone: 202-473-1000Internet: www.worldbank.org

This work is a product of the staff of The World Bank with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent.

The World Bank does not guarantee the accuracy, completeness, or currency of the data included in this work and does not assume responsibility for any errors, omissions, or discrepancies in the information, or liability with respect to the use of or failure to use the information, methods, processes, or conclusions set forth. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Nothing herein shall constitute or be construed or considered to be a limitation upon or waiver of the privileges and immunities of The World Bank, all of which are specifically reserved.

Rights and Permissions

The material in this work is subject to copyright. Because The World Bank encourages dissemination of its knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes as long as full attribution to this work is given.

Any queries on rights and licenses, including subsidiary rights, should be addressed to

World Bank Publications, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA

Fax: 202-522-2625; e-mail: [email protected].

Cover Photo: Leonid Ikan/ShutterstockUsed with the permission.Further permission required for reuse.

2022 Global Gas Flaring Tracker Report 32022 Global Gas Flaring Tracker Report2

Plateau at a Time for Progress

Despite strong early progress since satellite observations began in 1996, reductions in flaring have plateaued over the last decade, marking a period of disappointing progress during a time of increased international focus on the urgency of greenhouse gas emissions reduction and the energy transition.

Global gas flaring volumes have remained largely static over the last 10 years, plateauing at around 144 bcm. During this same period, global oil production levels rose slightly before dropping in 2020 due to the impacts of the Covid pandemic, averaging around 80 million barrels of oil per day. However, the global perspective obscures the significant flare reduction progress made by some countries – with the reduction achieved only to be offset by increases in flaring by others.

A similar story emerges when we consider flaring intensity, the volume of gas flared per barrel of oil produced; the initial improvements are evident, only to plateau again over the last decade.

Oil

prod

ucti

on (m

ln b

bl/d

)

Gas flaring Oil production

50

75

100

125

150

175

200

225

25

0

20

30

10

40

50

60

70

80

90

100

Flar

e vo

lum

e (b

cm)

0

1996 2001 2006 2011 2016 2021

Global gas flaring and oil production 1996 to 2021 (flaring only at upstream oil & gas and LNG plants)

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

1996 2001 2006 2011 2016 2021

GGFR partner countriesGlobal Non GGFR partner countries

-50%

-45%

-25%

-30%

-35%

-40%

-20%

-15%

-10%

-5%

0

-55%

Cha

nge

in fl

arin

g in

tens

ity

-60%

Percentage reductions in flaring intensity 1996 to 2021: global average, GGFR and non-GGFR partner countries

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR

Increase Decrease Total

0

20

18

14

16

12

10

8

6

4

2

6.3

5.1

3.0

2.20.6

-0.7-0.7

-0.7

-1.2

-1.4

-1.4

-1.9

-2.5

-2.5

-3.0

1.3

Flar

e vo

lum

e ch

ange

20

12 -

20

21 (b

cm)

Iran

Uni

ted

Sta

tes

Iraq

Rus

sia

Mex

ico

Col

ombi

a

Bra

zil

Ang

ola

Indo

nesi

a

Kaz

akha

stan

Turk

men

ista

n

Uzb

ekis

tan

Arg

enti

na

Tota

l

Res

t of

Wor

ld

Nig

eria

Change in flare volume between 2012 and 2021 (individual countries with most significant change (+ or – 0.6 bcm) indicated, rest of world combined, overall global change of +1.3 bcm)

Phot

o cr

edit

: © B

ulat

Iskh

akov

/ S

hutt

erSt

ock

2022 Global Gas Flaring Tracker Report 52022 Global Gas Flaring Tracker Report4

Top Ten Countries Account for 75 percent of all Flaring

In 2021, the top 10 flaring countries (on an absolute volume basis)

accounted for 75 percent of all gas flaring and 50 percent of

global oil production.

Seven of the top 10 flaring countries have held this position

consistently for the last 10 years: Russia, Iraq, Iran, the United

States, Venezuela, Algeria, and Nigeria. The remaining three;

Mexico, Libya, and China, have shown significant flaring increases

in recent years.

When we consider flaring intensity, fragile, conflict-affected,

and insecure countries, such as Venezuela, Syria, and Yemen are

among the worst performers, flaring more gas per barrel of oil

produced than any other country. The intensity perspective also

suggests there are opportunities to improve flaring performance in

oil-producing countries such as Algeria, the Republic of the Congo,

Gabon, and Turkmenistan.

Considering again the top 10 flaring countries on a volume basis,

Russia, Iraq, the United States, Nigeria, and Mexico have all

committed to the World Bank’s Zero Routine Flaring by 2030 (ZRF)

Initiative, which commits governments and companies to (a) not

routinely flare gas in any new oil field development, and (b) to end

routine flaring in existing oil fields as soon as possible and no later

than 2030. However, over the past decade, only the United States

has successfully improved the flaring intensity of its oil production.

Phot

o cr

edit

: © O

psor

man

/ S

hutt

erst

ock

0.0

2016 2017 2018 2019 2020 20212012 2013 2014 2015

27,500

25,000

22,500

20,000

Flar

e vo

lum

e (b

cm) 17,500

15,000

12,500

10,000

7,500

5,000

2,500

Iraq

Uni

ted

Stat

es

Nig

eria

Liby

a

Om

an

Vene

zuel

a

Iran

Alg

eria

Mex

ico

Chi

na

Egyp

t

Saud

i Ara

bia

Ang

ola

Mal

aysi

a

Indo

nesi

a

Kaz

akha

stan

Gab

on

Can

ada

Rep

of t

he C

ongo

Indi

a

Turk

men

ista

n

Qat

ar

Ecua

dor

Arg

enti

na

Syri

a

Yem

en

UA

E

Bra

zil

Uni

ted

Kin

gdom

Rus

sia

Flare volumes for the top 30 flaring countries from 2012 to 2021 (sorted by 2021 volume, shown in red)

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

0

2016 2017 2018 2019 2020 20212012 2013 2014 2015

90

80

Flar

ing

inte

nsit

y (m

³/bb

l)

70

60

50

40

30

20

10

Iraq

Uni

ted

Stat

es

Nig

eria

Liby

a

Om

an

Vene

zuel

a

Iran

Alg

eria

Mex

ico

Chi

na

Egyp

t

Saud

i Ara

bia

Ang

ola

Mal

aysi

a

Indo

nesi

a

Kaz

akha

stan

Gab

on

Can

ada

Rep

of t

he C

ongo

Indi

a

Turk

men

ista

n

Qat

ar

Ecua

dor

Arg

enti

na

Syri

a

Yem

en

UA

E

Bra

zil

Uni

ted

Kin

gdom

Rus

sia

Flaring intensity for the top 30 flaring countries from 2012 to 2021 (sorted by 2021 volume, shown in red)

2022 Global Gas Flaring Tracker Report 72022 Global Gas Flaring Tracker Report6

Key Trends

Promising Reductions

In this report, we explore promising progress in a few case study

countries and connect those findings to those of our Global

Flaring and Venting Regulations: A Comparative Review of Policies

study where relevant. We also share some worrying trends in

two countries. It should be noted that these case studies are not

intended to present a comprehensive analysis of progress (or lack

thereof) in flaring reduction.

Kazakhstan has achieved the largest overall flare reduction of all

countries during the last 10 years, reducing absolute flaring from

4 bcm in 2012 to 1.5 bcm in 2021. In addition to reducing routine

flaring over these years, anecdotal evidence suggests there have

also been improvements in equipment reliability and production

efficiency leading to a reduction in non-routine flaring. This

progress has been enabled by strictly enforced regulations that

apply financial penalties for gas flaring, coupled with a well-

established domestic gas market and integrated gas value chain

to incentivize flare gas recovery. The case study for Kazakhstan

in Global Flaring and Venting Regulations: A Comparative Review of

Policies provides more details on the regulatory frameworks in

the country.

5

4

3

2

1

0

Flare volume Flare intensity

20132012 2016 2018 2019 2020 20212017201520140

1

2

3

4

5

6

7

8

Flar

ing

inte

nsit

y (m

³/bb

l)

Flar

e vo

lum

e (b

cm)

Kazakhstan flare volume versus flare intensity, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

5

4

3

2

1

0

Flaring volume Oil production

20132012 2016 2018 2019 2020 20212017201520140

0.5

1.0

1.5

2.0

Oil

prod

ucti

on (m

ln b

bl/d

)

Flar

e vo

lum

e (b

cm)

Kazakhstan flare volume versus oil production, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR, EIA

The United States is the only one of the top 10 flaring countries to

have successfully reduced absolute flare volumes while increasing

production over the last decade—decreasing its flaring intensity

by 46 percent. However, in terms of absolute volume reductions,

the United States achieved an 8 percent reduction over the last

decade, which somewhat masks the recent progress made to

reduce flaring in the shale oil basins of the Permian, Bakken, and

Eagleford. These fields represented 89 percent of all US flaring in

2021, and flaring has reduced by 51 percent since 2019, when oil

production from these regions peaked. This reduction appears to

have been achieved by increasing domestic gas utilization and the

export of natural gas in the form of liquefied natural gas (LNG),

enabled by increased pipeline infrastructure and capacity.

Our just-released Global Flaring and Venting Regulations: A

Comparative Review of Policies study explores the regulatory

context in the main flaring regions, specifically Texas (Permian,

Eagleford) and North Dakota (Bakken). In Texas, in particular, there

has been significantly increased pressure by multiple stakeholders

to reduce flaring over recent years. While regulators made flaring

and venting regulation more stringent in 2020, there is evidence

that application and enforcement of the regulations could be more

rigorous to support the positive trend in reduced flaring.

20

15

10

5

0

Flare volume Flare intensity

20132012 2016 2018 2019 2020 20212017201520140

1

2

3

4

5

6

7

8

Flar

ing

inte

nsit

y (m

³/bb

l)

Flar

e vo

lum

e (b

cm)

United States flare volume versus flare intensity, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

20

15

10

5

0

Flaring volume Oil production

20132012 2016 2018 2019 2020 20212017201520140

2

4

6

8

10

12

14

Oil

prod

ucti

on (m

ln b

bl/d

)

Flar

e vo

lum

e (b

cm)

United States flare volume versus oil production, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR, EIA

400

300

200

100

0

-100

-200

Imports Exports Total final consumption

19951990 2010 2020201520052000

Flar

e vo

lum

e (b

cm)

United States gas import, export and total final consumption indicting increase in both export and total final consumption over last decade (modified data, taken from IEA, 2021)

Source: IEA

Kazakhstan

2021 Flare volume rank:

2012-2021

62%reductionin flaring

2012-2021

67%reduction in

flaring intensity

18th

The United States

2021 Flare volume rank:

2012-2021

8%*reductionin flaring

2012-2021

46%reduction in

flaring intensity

4th

*51 percent reduction in Shale oil basins between 2019 and 2021 alone

2022 Global Gas Flaring Tracker Report 92022 Global Gas Flaring Tracker Report8

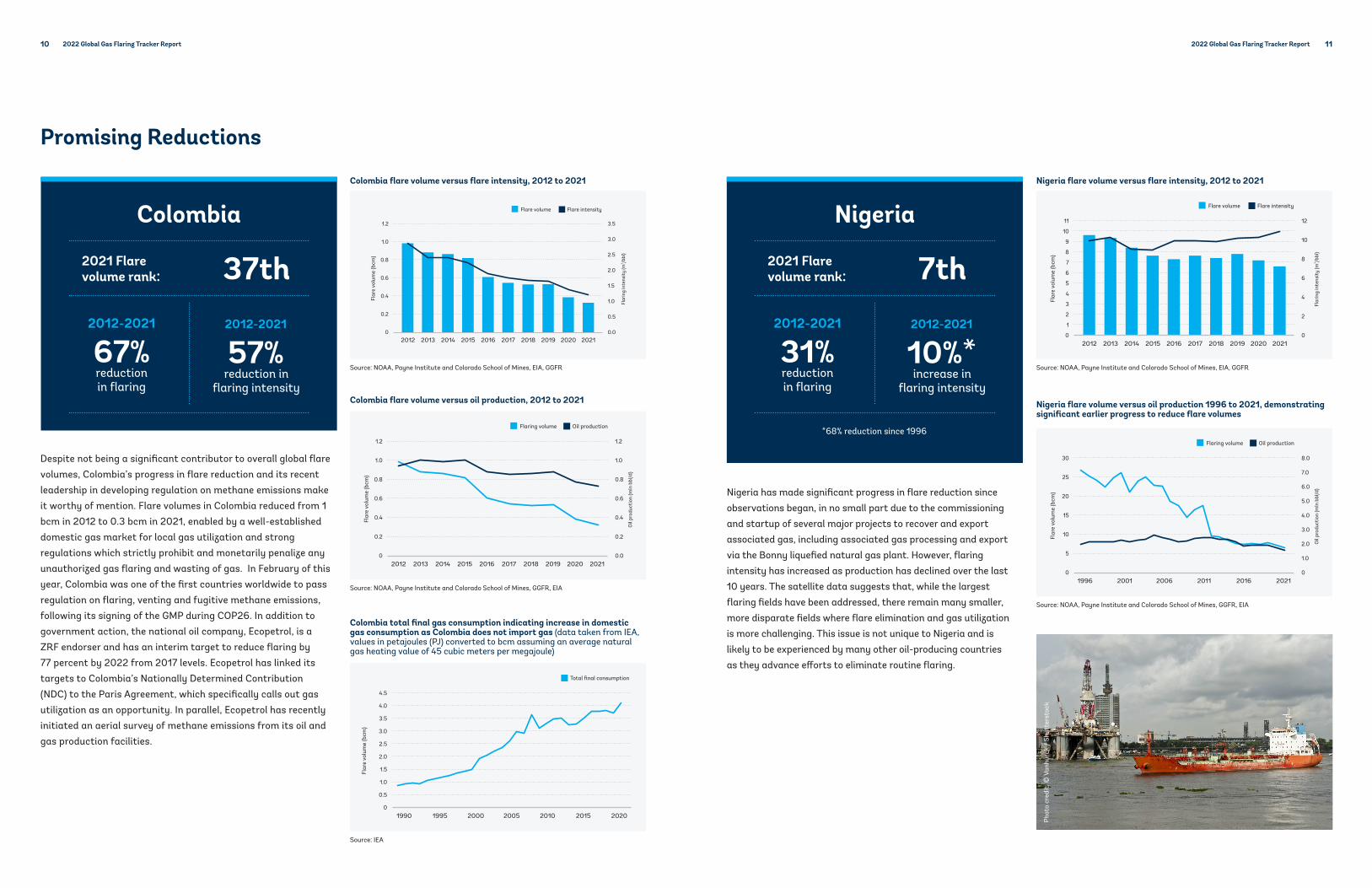

Despite not being a significant contributor to overall global flare

volumes, Colombia’s progress in flare reduction and its recent

leadership in developing regulation on methane emissions make

it worthy of mention. Flare volumes in Colombia reduced from 1

bcm in 2012 to 0.3 bcm in 2021, enabled by a well-established

domestic gas market for local gas utilization and strong

regulations which strictly prohibit and monetarily penalize any

unauthorized gas flaring and wasting of gas. In February of this

year, Colombia was one of the first countries worldwide to pass

regulation on flaring, venting and fugitive methane emissions,

following its signing of the GMP during COP26. In addition to

government action, the national oil company, Ecopetrol, is a

ZRF endorser and has an interim target to reduce flaring by

77 percent by 2022 from 2017 levels. Ecopetrol has linked its

targets to Colombia’s Nationally Determined Contribution

(NDC) to the Paris Agreement, which specifically calls out gas

utilization as an opportunity. In parallel, Ecopetrol has recently

initiated an aerial survey of methane emissions from its oil and

gas production facilities.

1.2

1.0

0.8

0.6

0.4

0.2

0

Flare volume Flare intensity

20132012 2016 2018 2019 2020 20212017201520140.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Flar

ing

inte

nsit

y (m

³/bb

l)

Flar

e vo

lum

e (b

cm)

Colombia flare volume versus flare intensity, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

1.2

1.0

0.8

0.6

0.4

0.2

0

Flaring volume Oil production

20132012 2016 2018 2019 2020 20212017201520140.0

0.2

0.4

0.6

0.8

1.0

1.2

Oil

prod

ucti

on (m

ln b

bl/d

)

Flar

e vo

lum

e (b

cm)

Colombia flare volume versus oil production, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR, EIA

4.5

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0

Total final consumption

19951990 2010 2020201520052000

Flar

e vo

lum

e (b

cm)

Colombia total final gas consumption indicating increase in domestic gas consumption as Colombia does not import gas (data taken from IEA, values in petajoules (PJ) converted to bcm assuming an average natural gas heating value of 45 cubic meters per megajoule)

Source: IEA

Nigeria has made significant progress in flare reduction since

observations began, in no small part due to the commissioning

and startup of several major projects to recover and export

associated gas, including associated gas processing and export

via the Bonny liquefied natural gas plant. However, flaring

intensity has increased as production has declined over the last

10 years. The satellite data suggests that, while the largest

flaring fields have been addressed, there remain many smaller,

more disparate fields where flare elimination and gas utilization

is more challenging. This issue is not unique to Nigeria and is

likely to be experienced by many other oil-producing countries

as they advance efforts to eliminate routine flaring.

11

10

9

1

2

3

4

5

6

7

8

0

Flare volume Flare intensity

20132012 2016 2018 2019 2020 20212017201520140

2

4

6

8

10

12

Flar

ing

inte

nsit

y (m

³/bb

l)

Flar

e vo

lum

e (b

cm)

Nigeria flare volume versus flare intensity, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

30

25

20

15

10

5

0

Flaring volume Oil production

20011996 2016 2021201120060

5.0

6.0

7.0

8.0

1.0

2.0

3.0

4.0

Oil

prod

ucti

on (m

ln b

bl/d

)

Flar

e vo

lum

e (b

cm)

Nigeria flare volume versus oil production 1996 to 2021, demonstrating significant earlier progress to reduce flare volumes

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR, EIA

Colombia

2021 Flare volume rank:

2012-2021

67%reductionin flaring

2012-2021

57%reduction in

flaring intensity

37th

Nigeria

2021 Flare volume rank:

2012-2021

31%reductionin flaring

2012-2021

10%*increase in

flaring intensity

7th

*68% reduction since 1996

Phot

o cr

edit

: © V

anhu

rck

/ Sh

utte

rsto

ck

Promising Reductions

2022 Global Gas Flaring Tracker Report 112022 Global Gas Flaring Tracker Report10

Worrying Increases

Despite oil production declining over the last 10 years, Mexico

has increased flaring by over 50 percent, with a sharp uptick

since 2018, rising from 3.8 bcm to 6.5 bcm in 2021. This increase

suggests oil production is occurring at wells with higher gas-

to-oil ratios and, with no outlet for the gas, the additional gas

produced is flared. Additionally, in the Marine Region, where the

highest gas volumes are flared, the use of nitrogen for artificial

lift results in the production of gas with a high nitrogen content,

which cannot be accepted in the domestic gas network. As a

result, a large amount of this gas is flared both offshore and at

onshore gas processing plants. Mexico’s focus over the last few

years has been on energy security, however the increase in gas

flaring has occurred while Mexico has also steadily increased

natural gas imports, highlighting the potential flare gas recovery

could play in its energy independence.

8

7

6

4

3

5

2

1

0

Flare volume Flare intensity

20132012 2016 2018 2019 2020 20212017201520140

2

4

6

8

10

12

Flar

ing

inte

nsit

y (m

³/bb

l)

Flar

e vo

lum

e (b

cm)

Mexico flare volume versus flare intensity, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0

Flaring volume Oil production

20132012 2016 2018 2019 2020 20212017201520140

0.5

1.0

1.5

2.0

2.5

3.0

Oil

prod

ucti

on (m

ln b

bl/d

)

Flar

e vo

lum

e (b

cm)

Mexico flare volume versus oil production, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR, EIA

80

70

60

50

40

30

20

10

0

Gas importsGas productionTotal gas supply

19951990 2010 2020201520052000

Nat

ural

gas

vol

ume

(bcm

)

Mexico domestic gas production, import and total final consumption 1990 to 2020, indicating increase in gas export and decrease in production (data taken from IEA, values in petajoules (PJ) converted to bcm assuming an average natural gas heating value of 45 cubic meters per megajoule, 2020 values provisional)

Source: IEA

Over the last decade, flaring has steadily increased in Iraq, with

volumes rising from 13 bcm in 2012 to almost 18 bcm in 2021,

accounting for around 12 percent of total global flaring. At the

same time, Iraq is importing natural gas; about 10 bcm in 2020.

Flare gas recovery and associated gas utilization are significant

opportunities for Iraq, which is both a GGFR partner and

endorser of the ZRF initiative and has gas utilization reduction

cited in its NDC.

20

14

16

18

8

2

10

4

12

6

0

Flare volume Flare intensity

20132012 2016 2018 2019 2020 20212017201520140

4

2

6

8

10

12

14

16

18

Flar

ing

inte

nsit

y (m

³/bb

l)

Flar

e vo

lum

e (b

cm)

Iraq flare volume versus flare intensity, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

20

18

16

14

12

10

8

6

4

2

0

Flaring volume Oil production

20132012 2016 2018 2019 2020 20212017201520140

1.0

2.0

1.5

2.5

3.0

3.5

4.0

4.5

5.0

Oil

prod

ucti

on (m

ln b

bl/d

)

Flar

e vo

lum

e (b

cm)

Iraq flare volume versus oil production, 2012 to 2021

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR, EIA

25

20

15

10

5

0

Natural gas importsDry natural gas productionDry natural gas consumption

2005 2010 20202015

Nat

ural

gas

vol

ume

(bcm

)

Iraq natural gas production, import and total consumption (data taken from bp Statistical Review of World Energy, July 2021)

Source: IEA, bp Statistical Review of World Energy, July 2021

Mexico

2021 Flare volume rank:

2012-2021

53%increasein flaring

2012-2021

126%increase in

flaring intensity

8th

Iraq

2021 Flare volume rank:

2012-2021

41%increasein flaring

2012-2021

3%increase in

flaring intensity

2nd

Phot

o cr

edit

: © G

GFR

2022 Global Gas Flaring Tracker Report 132022 Global Gas Flaring Tracker Report12

A Wasteful Practice, Crucial to Tackling Methane Emissions

Gas flaring is a wasteful practice that burns a valuable energy source that could be used to enhance economic development, provide increased energy security, and potentially displace dirtier energy sources. The 144 bcmof natural gas flared in 2021 could have potentially generated some 1,800 Terawatt hours (TWh) of energy, almost two-thirds of the European Union’s net domestic electricity generation.

Tackling gas flaring is also critical, given its role in global methane emissions. Methane is a more potent greenhouse gas than CO2 but has a shorter atmospheric lifetime. Therefore, reducing methane emissions is one of the fastest, most effective ways to slow the rate of climate change.

Gas flaring is a direct source of methane (see box below) and efforts to eliminate flaring also eliminate the associated methane emissions.

However, flare elimination efforts also support methane reductions from other sources, such as venting and fugitive releases. Without an outlet to export or utilize the gas, any methane conserved from these sources will ultimately be sent to flare and while there may be an overall emissions reduction, methane is still released, and this valuable energy source is still wasted.

This highlights the importance of flare reduction and gas management to overall oil and gas decarbonization strategies.

Why is flaring a source of methane?Methane is emitted from flares as flares do not completely combust all the hydrocarbons in the gas stream.

In our estimates, we assume:

• A flare destruction efficiency of 98 percent, assuming 2 percent methane is released uncombusted.

• The gas flared has a composition comprising 81 percent methane, with the remaining comprising heavier hydrocarbons (e.g. ethane, propane, butane).

• Methane has a global warming potential 25 times greater than CO2on a 100-year basis, consistent with the IPCC Fourth Assessment Report.

With these assumptions, we estimate that 2021 flaring resulted in 400 million tonnes of CO2 equivalent emissions (MMtCO2e), of which 361 MMtCO2e was in the form of CO2 and 39 MMtCO2e was in the form of uncombusted methane.

Methane

39

CO₂

361

Estimated emissions from gas flaring in 2021 in million tonnes of CO2 equivalants

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR

Phot

o cr

edit

: © L

eoni

d Ik

an /

Shu

tter

stoc

k

2022 Global Gas Flaring Tracker Report 152022 Global Gas Flaring Tracker Report14

-50%

0%

50%

100%

-50% 0% 50% 100% 150%

% Change Flare 2016-2021

% C

hang

e Fl

are

Inte

nsit

y 20

16-2

021

ZRF endosers Non-ZRF endosers

% Change Flare 2016-2021

Argentina

Syria

China

Libya

Iran

Algeria

IndiaTurkmenistan

Mexico

Kazakhstan

Canada

Malaysia

Indonesia

Rep of the Congo

United States

Angola

Egypt

Gabon

Saudi Arabia

Nigeria

Iraq

Oman

Ecuador

Russia

Better performance to date:these countries have decreased both flare volumes and flaring intensity since 2016

Poor performance to date:these countries have increased both flare volumes and flaring intensity since 2016

Percentage change in flare volume versus flaring intensity between 2016 and 2021, top 30 flaring countries only, ZRF endorsing countries indicated. Bubble size is 2021 flare volume

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

Mixed Progress Towards Zero Routine Flaring

In 2015, the World Bank launched the ZRF initiative, which

commits endorsing governments and companies to end routine

flaring by 2030. 2022 marks an important mid-point on this

journey, so we take an opportunity to reflect on progress to date.

Although 34 governments have endorsed the ZRF initiative,

and committed to creating an enabling environment for flare

reduction investments, there has been mixed progress to date.

Some endorsing governments have successfully achieved both

a reduction in absolute flare volume and flaring intensity since

2016, which indicates that flare reductions are not solely due to

a decline in production. However, tremendous opportunities for

improvement remain for some of the largest flaring countries,

such as Russia, Iraq, and Mexico, all of whom were endorsers of

the initiative in 2016 and have since experienced an increase in

absolute flare volumes and flaring intensity.

Non-endorsingcountries

39% Endorsingcountries

61%

Percentage of 2021 flare volumes occurring in ZRF endorsing countries

Source: NOAA, Payne Institute and Colorado School of Mines, GGFR

0%

5%

10%

15%

20%

-5%

2016 2017 2018 2019 2020 2021-10%

Global ZRF endosers Non-ZRF endosers

Change in flaring intensity 2016 to 2021: global average, ZRF endorsing countries and non-ZRF endorsing countries

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, GGFR

Phot

o cr

edit

: © O

psor

man

/ S

hutt

erst

ock

2022 Global Gas Flaring Tracker Report 172022 Global Gas Flaring Tracker Report16

Imported Flare Gas Index

In last year’s report, we introduced a new metric, the Imported

Flare Gas (IFG) Index, to infer the flaring associated with the

crude oil imported by various countries around the world. This

new metric highlights the flaring consequences of certain crude

imports and shares the burden of responsibility for flaring

reduction between both countries that produce and the countries

that import the crude oil. It is based on the premise that if a

country is importing crude oil from producing countries, it is also

importing the flaring intensity of these producing countries in

proportion to the amount of crude oil imported.

The IFG Index can help oil-importing countries assess where flaring

hotspots are in their fossil fuel supply chain. This should lead

to a dialogue with the countries from which they import oil and

potentially to assist in implementing flaring reduction initiatives,

thereby significantly improving the carbon emissions intensity of

the oil they consume.

Analysis of 2021 data suggests that many large crude oil-

importing countries, such as Spain, Italy, and the Netherlands,

are ‘exposed’ to high levels of gas flaring as they import crude

from countries with a high flaring intensity, such as Russia, Libya,

Algeria, Iraq, and Mexico.

Russian Federation Libya United Kingdom

Nigeria Iraq Gabon

Algeria United States Egypt

Kazakhstan Malaysia Tunisa

Mexico Cameroon Others

Esto

nia

Aus

tral

ia

Swit

zerl

and

Gre

ece

Spai

n

Slov

akia

Nor

way

Ital

y

Impo

rted

Fla

re G

as (I

FG) I

ndex

(m3/

bbl)

0

Aus

tria

Bel

arus

Rom

ania

Fran

ce

Finl

and

Lith

uani

a

Bul

gari

a

Pola

nd

Hun

gary

Cze

ch R

epub

lic

Ger

mna

y

Port

ugal

Net

herl

ands

Uni

ted

Kin

gdom

Can

ada

Uni

ted

Stat

es

Den

mar

k

Cro

atia

Swed

en

New

Zea

land

Irel

and

Japa

n

Bel

gium

Icel

and

Luxe

mbo

urg

Latv

ia

14

13

12

11

10

9

8

7

6

5

4

3

2

1

Rus

sian

Fed

erat

ion

2021 IFG Index Results

China

United States

India

Japan

South Korea

GermanyNetherlands

Thailand

France

United Kingdom

Singapore

Belgium

Poland

Greece

Italy

Spain

Canada

Sweden

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

0 1000 2000 3000 4000

Crude Import (Kbbl/day)

Impo

rted

Fla

re G

as (I

FG) I

ndex

(m3/

bbl)

International AverageFlaring Intensity

5000 6000 11000

Countries exposed to high flaring

IFG Index of Largest Crude Importing Countries (> 250 K bbl/day)

Source: NOAA, Payne Institute and Colorado School of Mines, EIA, UN Comtrade, GGFR

Source: NOAA, Payne Institute and Colorado School of Mines,, EIA, UN Comtrade, GGFR

Phot

o cr

edit

: © R

ed_S

hado

w /

Shu

tter

stoc

k.2022 Global Gas Flaring Tracker Report 192022 Global Gas Flaring Tracker Report18

While global flare volumes have remained largely static over the

last decade, the very significant reductions achieved by some

countries are encouraging and set an example for others.

Given the growing international focus on methane emissions and

acknowledging the important role the oil and gas industry could

play towards achieving climate goals, we call on governments

and companies to increase their focus and accelerate their

commitment to ending this wasteful industry practice by 2030.

On technology: while technology and innovation have an

important role to play, it is important to note that most flaring

is not due to a lack of available technology; it is due to a lack of

political will and leadership in developing appropriate markets and

infrastructure to recover and utilize the gas.

On regulation: effective regulation and strong enforcement

are paramount; our Global Flaring and Venting Regulations: A

Comparative Review of Policies study explores the many, and varied,

policy mechanisms that can be leveraged to both penalize gas

flaring and incentivize gas utilization.

On methane: eliminating routine flaring can offer a double win in

the shared endeavor to reduce global methane emissions by:

• eliminating a direct source of methane released un-combusted

from flares; and

• enabling the gas successfully conserved through reductions in

venting and fugitive emissions to be utilized rather than flared.

On decarbonization: the utilization of flared gas presents an

opportunity to put a valuable, wasted energy source to beneficial

use. Natural gas can help reduce the carbon intensity of the global

energy mix, with the ability to replace coal and liquid fuels quickly,

allowing time for the development and implementation of low and

no carbon sources such as renewables and green hydrogen.

On timing: Infrastructure projects needed to connect flares to

markets can take years to be developed and operational. If Zero

Routine Flaring by 2030 is to be achieved, action must be swift

and determined.

Despite the 10-year plateau in flaring, we remain hopeful that

significant progress on flaring can be made over the next few

years, but this will require strong regulation and effective

collaboration between the public and private sectors.

Concluding Reflections

Phot

o cr

edit

: © e

leon

imag

es /

Shu

tter

stoc

k.

Phot

o cr

edit

: © E

ssam

al-

Suda

ni /

Shu

tter

stoc

k.2022 Global Gas Flaring Tracker Report 212022 Global Gas Flaring Tracker Report20

Global Gas Flaring Reduction Partnership (GGFR) Multi-Donor Trust Fund

1850 I Street NW, Washington, DC 20006

MethodologyThe 2022 Global Gas Flaring Tracker Report is produced on an annual basis

by the World Bank’s GGFR, comprised of governments, oil companies,

and international institutions working to end routine gas flaring at oil

production sites around the world. GGFR, in partnership with the US NOAA

and The Payne Institute for Public Policy at the Colorado School of Mines,

has developed global gas flaring estimates based upon observations from

satellites launched in 2012 and 2017. The advanced sensors of this satellite

detect the heat emitted by gas flares as infrared emissions at global

upstream oil and gas facilities.

The Colorado School of Mines and GGFR quantify these infrared emissions

and calibrate them using country-level data collected by a third-party data

supplier, Cedigaz, to produce robust estimates of global gas flaring volumes.

The satellite data for estimating flare gas volumes is collected by NOAA’s

satellite-mounted Visual and Infrared Radiometer Suite of detectors (VIIRS).

VIIRS has a multispectral set of infrared detectors which:

• at nighttime respond only to heat emissions and hence are not affected by

sunlight, moonlight or other light sources

• respond to wavelengths where emissions from flares are at a maximum

• overfly every flare several times per night

• have excellent spatial resolution.

The ability of VIIRS to detect and discriminate hot sources, such as

gas flares, enables flares to be detected automatically with minimal

manual intervention. Emissions from non-flare hot sources (e.g. biomass

burning) can be removed from the data by selecting only emissions with

temperatures above 1100C; other hot sources burn at lower temperatures.

Indeed, flares burn hotter than any other terrestrial hot sources, including

volcanos. Since the first year of year of operation in 2012, VIIRS has

automatically detected ~10,000 flares annually around the globe.

The World Bank’s role in gas flaring reduction

The World Bank’s GGFR works closely with

governments and oil companies to help assess

technologies, develop policies and regulations,

and build capacity to end routine flaring

by 2030. We are also continuing to secure

commitments for the Zero Routine Flaring by

2030 initiative, Zero Routine Flaring by 2030

initiative, building upon the 87 government

and oil company endorsers that, together,

account for close to 60 percent of global

flaring. Ending routine gas flaring is critical

if governments and companies are to deliver

their products in the cleanest manner possible,

meet net-zero targets, and maintain their

license to operate, especially in developing

countries where millions lack access to energy.

To do this, we must test and scale innovative

approaches, while considering new solutions

that treat associated gas as an asset, not

a waste product. Such approaches must

also be tailored to the unique circumstances

and context of a particular country, or even

a specific oil production site. We need to

work collaboratively with governments and

oil companies to develop holistic policies,

considering a range of incentives and

penalties, to finally put an end to this practice.

References: Elvidge, C.D.; Zhizhin, M.; Hsu, F.-C.; Baugh, K.E. VIIRS Nightfire: Satellite Pyrometry at Night. Remote Sens. 2013, 5, 4423-4449. https://doi.org/10.3390/rs5094423 Elvidge, C.D.; Zhizhin, M.; Baugh, K.; Hsu, F.-C.; Ghosh, T. Methods for Global Survey of Natural Gas Flaring from Visible Infrared Imaging Radiometer Suite Data. Energies 2016, 9, 14. https://doi.org/10.3390/en9010014