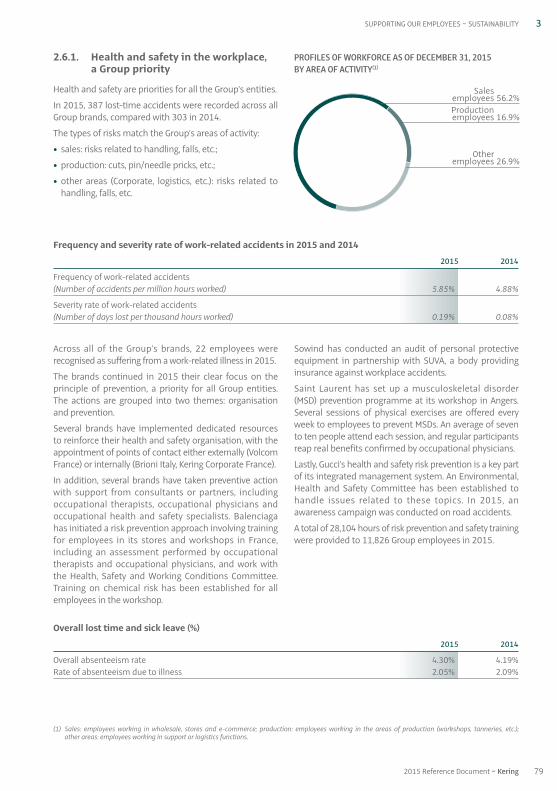

The influence of customer brand identification on hotel brand ...

Upload

khangminh22Category

view

0download

0

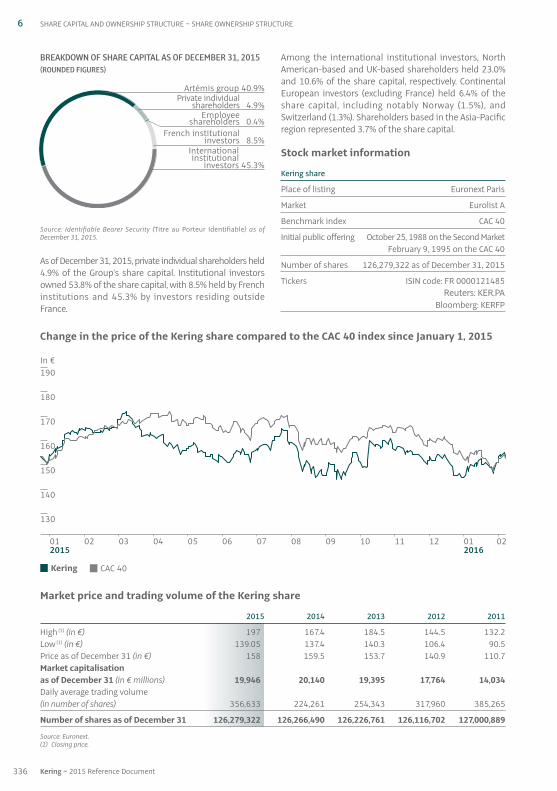

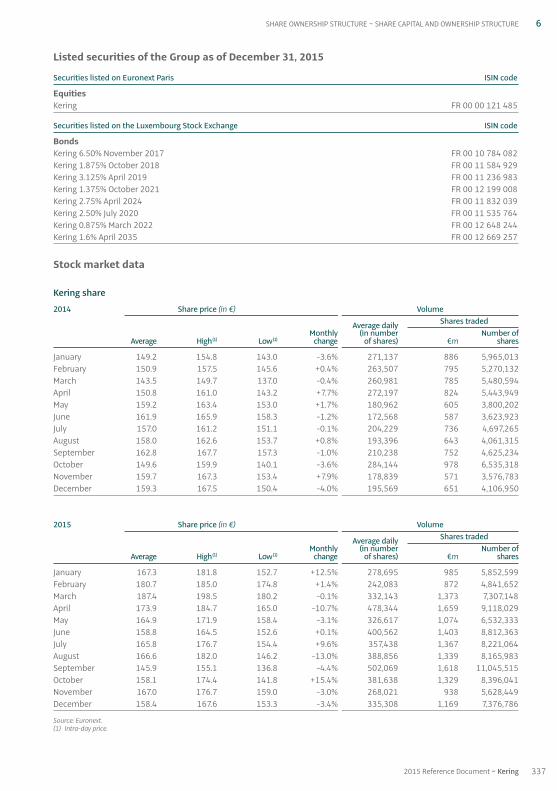

12015 Reference Document ~ Kering

TABLE OF CONTENTS

CHAPTER 1Kering in 2015 3

CHAPTER 2Our activities 15

CHAPTER 3Sustainability 57

CHAPTER 4Corporate governance 133

CHAPTER 5Financial information 175

CHAPTER 6Share capital and ownership structure 327

CHAPTER 7Additional information 339

This is a free translation into English of the 2015 Reference Document issued in French and is provided solely for the convenience of English speaking users.

01_VA_V5 07/04/2016 10:31 Page1

2 Kering ~ 2015 Reference Document

01_VA_V5 06/04/2016 17:31 Page2

32015 Reference Document ~ Kering

Chapter 1

Kering in 2015

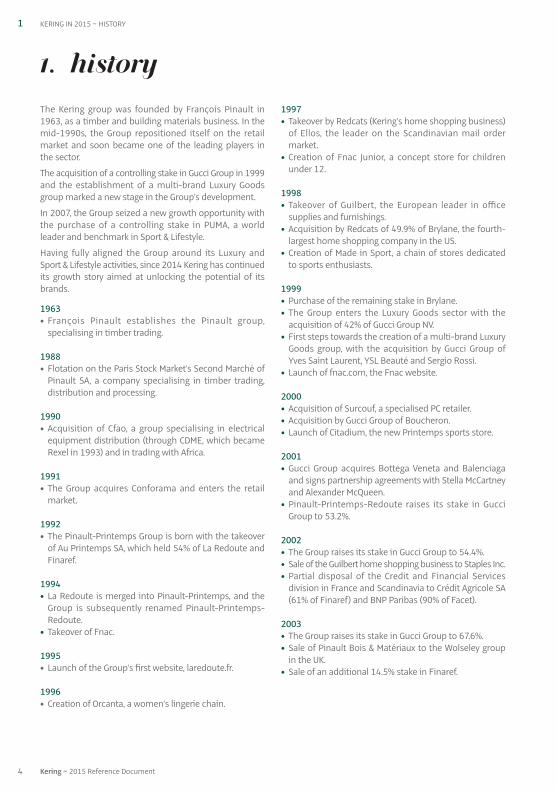

1. History 4

2. Key consolidated figures 6

3. Kering Empowering Imagination 8

4. Kering Group Simplified Organisational Chart as of December 31, 2015 14

01_VA_V5 06/04/2016 17:31 Page3

The Kering group was founded by François Pinault in1963, as a timber and building materials business. In themid-1990s, the Group repositioned itself on the retailmarket and soon became one of the leading players inthe sector.

The acquisition of a controlling stake in Gucci Group in 1999and the establishment of a multi-brand Luxury Goodsgroup marked a new stage in the Group’s development.

In 2007, the Group seized a new growth opportunity withthe purchase of a controlling stake in PUMA, a worldleader and benchmark in Sport & Lifestyle.

Having fully aligned the Group around its Luxury andSport & Lifestyle activities, since 2014 Kering has continuedits growth story aimed at unlocking the potential of itsbrands.

1963• François Pinault establishes the Pinault group,

specialising in timber trading.

1988• Flotation on the Paris Stock Market’s Second Marché of

Pinault SA, a company specialising in timber trading,distribution and processing.

1990• Acquisition of Cfao, a group specialising in electrical

equipment distribution (through CDME, which becameRexel in 1993) and in trading with Africa.

1991• The Group acquires Conforama and enters the retail

market.

1992• The Pinault-Printemps Group is born with the takeover

of Au Printemps SA, which held 54% of La Redoute andFinaref.

1994• La Redoute is merged into Pinault-Printemps, and the

Group is subsequently renamed Pinault-Printemps-Redoute.

• Takeover of Fnac.

1995• Launch of the Group’s first website, laredoute.fr.

1996• Creation of Orcanta, a women’s lingerie chain.

1997• Takeover by Redcats (Kering’s home shopping business)

of Ellos, the leader on the Scandinavian mail ordermarket.

• Creation of Fnac Junior, a concept store for childrenunder 12.

1998• Takeover of Guilbert, the European leader in office

supplies and furnishings.• Acquisition by Redcats of 49.9% of Brylane, the fourth-

largest home shopping company in the US.• Creation of Made in Sport, a chain of stores dedicated

to sports enthusiasts.

1999• Purchase of the remaining stake in Brylane.• The Group enters the Luxury Goods sector with the

acquisition of 42% of Gucci Group NV.• First steps towards the creation of a multi-brand Luxury

Goods group, with the acquisition by Gucci Group ofYves Saint Laurent, YSL Beauté and Sergio Rossi.

• Launch of fnac.com, the Fnac website.

2000• Acquisition of Surcouf, a specialised PC retailer.• Acquisition by Gucci Group of Boucheron.• Launch of Citadium, the new Printemps sports store.

2001• Gucci Group acquires Bottega Veneta and Balenciaga

and signs partnership agreements with Stella McCartneyand Alexander McQueen.

• Pinault-Printemps-Redoute raises its stake in GucciGroup to 53.2%.

2002• The Group raises its stake in Gucci Group to 54.4%.• Sale of the Guilbert home shopping business to Staples Inc.• Partial disposal of the Credit and Financial Services

division in France and Scandinavia to Crédit Agricole SA(61% of Finaref) and BNP Paribas (90% of Facet).

2003• The Group raises its stake in Gucci Group to 67.6%.• Sale of Pinault Bois & Matériaux to the Wolseley group

in the UK.• Sale of an additional 14.5% stake in Finaref.

1. HISTORy

1 KERING IN 2015 ~ HISTORY

4 Kering ~ 2015 Reference Document

01_VA_V5 06/04/2016 17:31 Page4

2004• The Group raises its stake in Gucci Group to 99.4%

further to a tender offer.• Sale of Rexel.• Sale of the residual 24.5% stake in Finaref.

2005• Change of corporate name: Pinault-Printemps-Redoute

becomes PPR.• Sale of the residual 10% stake in Facet.

2006• Sale of 51% of France Printemps to RREEF and the

Borletti group.• Sale of Orcanta to the Chantelle group.• Sale of the Bernay industrial site (YSL Beauté Recherche

et Industrie).• Discontinuation of Fnac Service’s activities.• Acquisition by Conforama of a majority stake in Sodice

Expansion.• Acquisition by Redcats group of The Sportsman’s

Guide, Inc.

2007• Sale of the residual 49% stake in France Printemps to

RREEF and the Borletti group.• Sale of Kadéos to the Accor group.• Acquisition of a 27.1% controlling stake in PUMA. This

stake was increased to 62.1% further to a tender offer.

2008• Sale of YSL Beauté to L’Oréal.• Sale of Conforama Poland.• Sale by Redcats UK of Empire Stores and by Redcats

USA of the Missy division.• Acquisition of a 23% stake in Girard-Perregaux.

2009• Acquisition by PUMA of Dobotex International BV.• Acquisition by PUMA of Brandon AB.• Sale of Bédat & Co.• Sale of Surcouf.• Flotation of 58% of Cfao.

2010• Acquisition by PUMA of a 20% stake in Wilderness

Holdings Ltd.• Acquisition by PUMA of COBRA.• Sale of Fnac éveil & jeux.• Sale of the controlling stake in Conforama to Steinhoff.

2011• Closing of the sale of Conforama to Steinhoff.• New organisation of the Luxury Division.• Acquisition of Volcom.• Increased stake (50.1%) in Sowind Group (Girard-

Perregaux and JEANRICHARD).• Announced acquisition of Brioni.

2012• Closing of the acquisition of Brioni.• Sale of the remaining 42% stake in Cfao to TTC.• Creation of a joint venture with Yoox S.p.A. dedicated to

e-commerce for several brands of the Luxury Division.• Announced project to demerge and list Fnac.• Sale of Fnac Italy.• Sale of Redcats USA business (The Sportsman’s Guide and

The Golf Warehouse, announced sale of OneStopPlus).• Announced acquisition of a majority stake in Chinese

fine jewellery brand Qeelin.

2013• Closing of the acquisition of a majority stake in Chinese

fine jewellery brand Qeelin.• Acquisition of a majority stake in the luxury designer

brand Christopher Kane.• Closing of the sale of OneStopPlus.• Sale of the Children and Family division of Redcats,

Cyrillus and Vertbaudet.• Acquisition of a majority stake in tannery France Croco.• Sale of the Nordic brands of Redcats, Ellos and Jotex.• Listing of Groupe Fnac.• Change of corporate name: PPR becomes Kering.• Acquisition of a majority stake in Italian jewellery group

Pomellato.• Kering enters into exclusive negotiations for the disposal

of La Redoute and Relais Colis.

2014• Closing of the sale of La Redoute and Relais Colis.• Announced project of internalisation of the Eyewear

business value chain.• Acquisition of the haute horlogerie brand Ulysse Nardin.

2015• Sale of the industrial property rights of the Tretorn

group (which include trademark rights, patents anddesigns) by PUMA (June 2015).

• Launch of Kering Eyewear (June 2015).• Sale of the Italian luxury shoemaker Sergio Rossi

(December 2015).

1HISTORY ~ KERING IN 2015

52015 Reference Document ~ Kering

01_VA_V5 06/04/2016 17:31 Page5

1 KERING IN 2015 ~ KEY CONSOLIDATED FIGURES

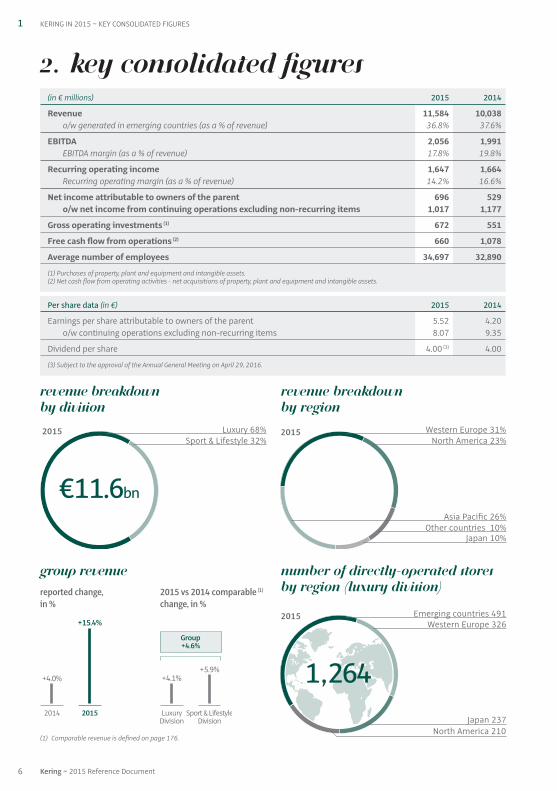

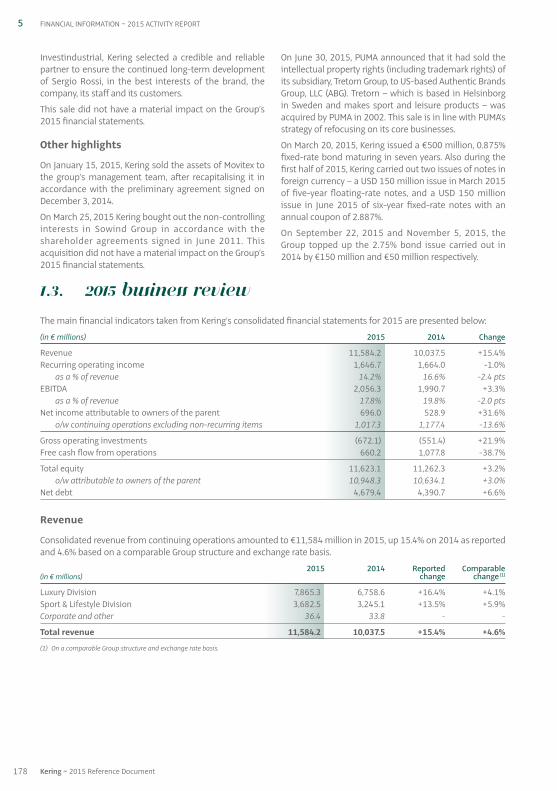

2. Key consolidated figures(in € millions) 2015 2014

Revenue 11,584 10,038o/w generated in emerging countries (as a % of revenue) 36.8% 37.6%

EBITDA 2,056 1,991EBITDA margin (as a % of revenue) 17.8% 19.8%

Recurring operating income 1,647 1,664Recurring operating margin (as a % of revenue) 14.2% 16.6%

Net income attributable to owners of the parent 696 529o/w net income from continuing operations excluding non-recurring items 1,017 1,177

Gross operating investments (1) 672 551

Free cash flow from operations (2) 660 1,078

Average number of employees 34,697 32,890

(1) Purchases of property, plant and equipment and intangible assets.(2) Net cash flow from operating activities - net acquisitions of property, plant and equipment and intangible assets.

Per share data (in €) 2015 2014

Earnings per share attributable to owners of the parent 5.52 4.20o/w continuing operations excluding non-recurring items 8.07 9.35

Dividend per share 4.00 (3) 4.00

(3) Subject to the approval of the Annual General Meeting on April 29, 2016.

6 Kering ~ 2015 Reference Document

Luxury 68%2015Sport & Lifestyle 32%

€11.6bn

Western Europe 31%North America 23%

Asia Pacific 26%Other countries 10%

Japan 10%

2015

Emerging countries 491

Japan 237North America 210

Western Europe 326

1,264

2015

Revenue breakdown by Division

Revenue breakdown by region

Number of directly-operated storesby region (luxury division)

Group revenue

2014 2015

+15.4%

+4.0%

LuxuryDivision

Sport & LifestyleDivision

+5.9%+4.1%

Group+4.6%

reported change,in %

2015 vs 2014 comparable (1)

change, in %

(1) Comparable revenue is defined on page 176.

01_VA_V5 06/04/2016 17:31 Page6

1KEY CONSOLIDATED FIGURES ~ KERING IN 2015

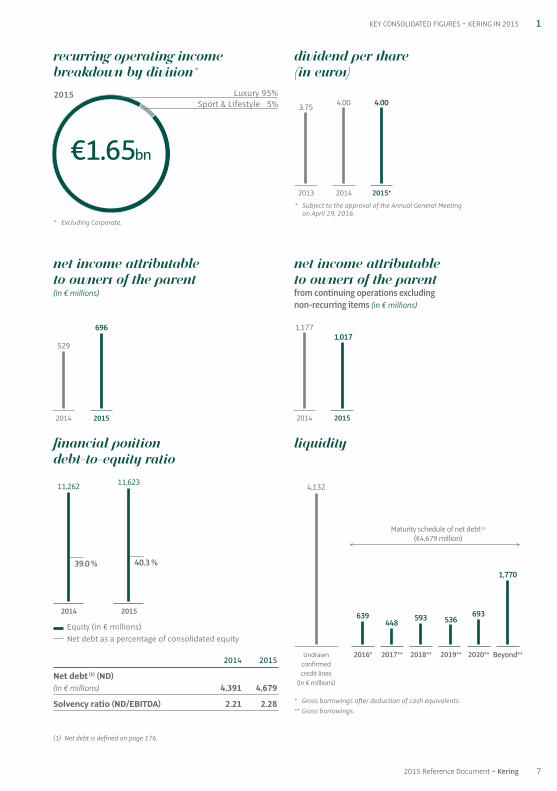

(1) Net debt is defined on page 176.

72015 Reference Document ~ Kering

Undrawnconfirmedcredit lines

(in € millions)

Maturity schedule of net debt (1)

(€4,679 million)

2016* 2017** 2018** 2019** 2020** Beyond**

* Gross borrowings after deduction of cash equivalents.** Gross borrowings.

639

4,132

448 593 536693

1,770

Liquidity

* Excluding Corporate.

Luxury 95%2015Sport & Lifestyle 5%

€1.65bn

Recurring operating incomeBreakdown by Division *

Net income attributable to owners of the parentfrom continuing operations excluding non-recurring items (in € millions)

Dividend per share(in euros)

Equity (in € millions)

2014

Net debt as a percentage of consolidated equity

2015

40.3 %

11,623

39.0 %

11,262

2014 2015

1,0171,177

Net income attributable to owners of the parent(in € millions)

2014 2015

696

529

* Subject to the approval of the Annual General Meeting on April 29, 2016.

2013

3.75

2014 2015*

4.004.00

Financial position debt-to-equity ratio

2014 2015

Net debt (1) (ND) (in € millions) 4,391 4,679

Solvency ratio (ND/EBITDA) 2.21 2.28

01_VA_V5 06/04/2016 17:31 Page7

The first phase of the Group’s transformation, through 2015,involved expanding and strengthening Kering’s brandportfolio, both through organic growth and targetedacquisitions, with the aim of building a complementaryensemble of powerful brands.

Adopting a multi-brand strategy is virtuous in manyregards. Taken individually, each brand has its owndistinctive identity, know-how, positioning and growthpotential enabling it to reach critical mass at a globallevel. Together, they form a coherent and complementaryensemble, particularly in terms of market segments,

stages of maturity and geographic base. There is nocompetition between the brands but rather a focus onidentifying and harnessing synergies.

From a financial and operational standpoint, Kering’sbalanced and diversified business model helps the Groupresist changes in the economic environment affecting agiven activity or region. It combines growth and profitability,as the Group allocates operating investments on the basisof each brand’s business cycle, enabling them to preserveexclusivity while maximising growth – what the Groupcalls “Empowering Imagination”.

A COMPLEMENTARY ENSEMBLE OF POWERfuL BRANDS AND A VIRtuOUS GROWTH MODEL

1

8 Kering ~ 2015 Reference Document

The Group began transforming its portfolio of assets andactivities in 2005 with the aim of gradually phasing outits legacy mass-retail businesses located mainly in Franceand Europe, in order to become a front-ranking group ofglobal brands in the Luxury and Sport & Lifestyle segments.

These changes are in line with the Group’s strategic visionof focusing future development on new growth drivers bycapitalising on changes in the global economy andharnessing the potential and growth cycles in emergingand mature markets. These growth drivers include:

• a global economy, which will continue to be led bymature markets but will also be shaped by the growinginfluence of emerging markets;

• growth in emerging markets, underpinned by demographictrends and rapid urbanisation, creating a middle classwith levels of income that will gradually drive updiscretionary consumer spending;

• a gradual convergence in consumer patterns, propelledby growing aspirational demand in new markets forworld-renowned brands, and supported by thedevelopment of international tourism and the digitaleconomy;

• robust demand in both mature and emerging marketsfor branded Sport & Lifestyle and Luxury products, asegment in which the Group has been well positionedsince its 1999 acquisition of Gucci Group.

From 2005 onwards, the Group began refocusing itsactivities, gradually withdrawing from mass-marketretailing activities with the sale of Printemps, Cfao,Conforama, Surcouf, certain international businesses, thechildren’s division of Redcats and La Redoute, as well aslisting Fnac on the stock market.

At the same time, the Group embarked upon an ambitiousexpansion programme to grow its portfolio of Luxury andSport & Lifestyle brands.

frOM PPR TO Kering: BUILDING A GROUP ON A GLOBAL SCALE

Since its inception in 1963, Kering (then PPR) has continuouslytransformed itself, constantly seeking growth andcreating value with an entrepreneurial spirit.

Between 2005 and 2014, Kering undertook an in-depthstrategic transformation, from a diverse conglomerate intoa cohesive international group entirely dedicated to acomplementary ensemble of apparel and accessories brands.

The change in the name of the Group from PPR to Keringin 2013 reflects this new identity. Pronounced “caring”, thenew corporate identity symbolises the way in which theGroup nurtures its brands, employees and customers, aswell as the environment.

KERING IN 2015 ~ KERING EMPOWERING IMAGINATION

3. Kering Empowering Imagination

01_VA_V5 06/04/2016 17:31 Page8

1. The organic growth of the Group’s brands

The brands’ worldwide standing, desirability and hugeconsumer appeal are key assets, which drive their organicgrowth potential.

The growth of Kering’s brands is underpinned by a seriesof clearly identified drivers:

(i) Launching new product categories and refining existing lines

The Group’s brands work continuously to produce creative,attractive and innovative products for existing ranges andto introduce new product lines with untapped potential.They are careful to constantly adapt and improve thestructure and performance of their collections to meet thespecific needs of their clientele in terms of functionality,trends and price, and to draw in new generations ofcustomers.

(ii) Improving performance in existing sales networks

In their network of directly-operated stores, the brandsdeploy initiatives to boost sales performance, capitalisingon increasingly effective merchandising, in-storeoperational excellence, an in-depth knowledge of theircustomers, customer loyalty and development programmes,and targeted communications.

(iii) Strengthening distribution channels through the selective expansion of directly-operated storenetworks, close relationships with third-party retailers, and the implementation of a dynamic e-commerce strategy

The Group is permanently fine-tuning its network ofdirectly-operated stores to optimise the distribution of itsbrands and seize growth opportunities around the globe.Taking into account the characteristics and maturity ofeach brand, this strategy translates into targeted storeopenings to broaden penetration in certain markets, or storerelocations to occupy the very best locations available.Adapting the Group’s retail network also entails storerenovation and expansion projects, as well as occasional

store closures when brand criteria are no longer met. Inaddition, the Group’s brands are constantly seeking toenhance the quality of their third-party distribution, achannel that has particular strategic significance forSport & Lifestyle activities. Kering has also invested indigital platforms alongside traditional channels in responseto new consumer and purchasing practices. Lastly, thegrowth potential in the Travel Retail channel is graduallybeing tapped.

2. A portfolio of brands rounded out by targeted acquisitions

While focusing on organic growth, Kering has strengthenedits portfolio in recent years through the acquisition ofbrands set to play a key role in the Group’s future growthand value creation. As part of this strategy, Brioni,Pomellato group, Qeelin, Christopher Kane and UlysseNardin have joined the Group.

Strict criteria are applied to these acquisitions:

• Potential targets must enjoy exceptional brand identity,strong values and a sought-after heritage; a unique scopeof expression through lasting codes and language –often referred to as their “DNA”; and an ability to broadentheir geographic footprint and to gradually expand theirmarket coverage.

• Targets must have genuine potential for significantimprovements in financial performance that Kering isable to identify and deploy in the long term, above andbeyond their potential prior to joining the Group. Aswell as seeking revenue synergies derived from theincreased capacity of newly acquired brands to expandtheir geographic presence or product categories oncethey join the Group, Kering also looks for synergies arisingfrom brand expertise in terms of technical, commercialand innovation know-how. Finally, the Group evaluatesthe potential for savings at operational (purchasing,supply chain, real estate, etc.) and financial levels. Thesesynergies are analysed and appraised during theacquisition process, giving rise to a financial andoperational roadmap to value creation drawn up at theoutset of the integration process.

1

92015 Reference Document ~ Kering

KERING EMPOWERING IMAGINATION ~ KERING IN 2015

01_VA_V5 06/04/2016 17:31 Page9

Kering sets the strategic and financial framework withinwhich the brands operate, and provides the structures,organisations and means to protect and support thesustainable growth of its brands.

Kering first deployed a number of horizontal functionsand services for its Luxury brands, including real estate, e-commerce, indirect purchasing, intellectual property,strategic marketing and media buying, to allow them tofocus on their individual business objectives and supporttheir growth, especially internationally.

Shared services platforms have been set up in the Group’sthree biggest regions – Europe, America, and Asia-Pacific.These centres employ experts in communications, audit,human resources, tax, property, legal affairs, IT systems,accounting and cash management, providing brandswith appropriate support for the local context.

More recently, important new steps have been taken on theroad to becoming an integrated Group. The finalisation ofthe Group’s transformation, combined with recent changesin its markets, consumer trends and the competitiveenvironment, have led Kering to set new milestones.

(i) In 2014 and 2015, Kering adapted its organisation tobetter reflect the areas of activity of the Group’s Luxurybrands and strengthen the operational oversight of itsbusinesses. Two new divisions were set up:

• Luxury – Couture & Leather Goods, comprising Gucci,Bottega Veneta, Saint Laurent, as well as emerging brandsAlexander McQueen, Balenciaga, Brioni, ChristopherKane, McQ, Stella McCartney and Tomas Maier;

• Luxury – Watches & Jewellery, encompassing Boucheron,Girard-Perregaux, JEANRICHARD, Pomellato, Dodo, Qeelinand Ulysse Nardin.

(ii) From 2013, the Group strengthened its upstreampositioning in the Luxury value chain, with the targetedacquisition of leather tanneries to secure raw materialssourcing. Logistics activities for its Couture & LeatherGoods brands have long been centralised, much likeready-to-wear prototyping, which is pooled in a sharedunit in Italy. In order to make this vertical integration evenmore effective and efficient in terms of services, synergiesand scale, in 2015 all of these operations were placedunder the direct governance and oversight of Kering.

(iii) In 2014, Kering also launched a key strategic initiativeaimed at growing in-house expertise in Eyewear for itsLuxury and Sport & Lifestyle brands. The worldwide marketfor frames and sunglasses is vast and its premium segment

is enjoying substantial growth. To maximise thedevelopment of its portfolio of brands in this importantcategory, Kering has decided to internalise the valuechain for its Eyewear activities, from product creation anddevelopment to supply chain management, brandstrategy, sales and marketing. This innovative managementmodel will give rise to significant value creationopportunities and help the Eyewear brands step up thepace of growth. In June 2015, Kering Eyewear unveiled itsfirst collections under brand licences that are nowdirectly managed.

(iv) The digital challenge: e-commerce is a strategic priorityfor Kering, not only for the business the Group’s brandsconduct online but also because it influences demandacross all sales channels. Gucci is a pioneer in Luxury e-commerce. Launched in 2002, its website has set thestandard in this field and the brand’s digital know-how iswidely recognised. Since the Other Luxury brands did notenjoy internal capabilities comparable to Gucci’s, in 2012the Group set up a Kering e-commerce platform toprovide the Couture & Leather Goods division brands withthe necessary technical competence to develop theironline business and digital strategy. All the brand sitesnow feature mobile- and tablet-optimised browsing,shared performance-measurement tools and a dedicatedteam of specialists to help continually improve siteperformance, conversion rates and customer satisfaction.

Our customers are increasingly connected, geographicallymobile and sensitive to the fluidity of their shoppingexperience spanning traditional physical stores andonline. In this context, the Group’s e-commerce teamshave set out a cross-channel services strategy adapted tothe characteristics of each brand. The Group now benefitsfrom several cross-channel service features, such asonline visibility of retail inventory (geo-localised for Gucci)and online sales, which are gradually being extended toin-store pickup and online reservation. A host of additionalfeatures are in the pipeline. Kering is encouraging itsbrands to try out new solutions, with pilot projects to testnew technologies such as a new online fitting solution forready-to-wear and shoes, and to share the results withthe brands as a prelude to Group-wide rollout.

With the aim of ultimately offering a seamless omni-channelapproach covering both bricks and mortar and onlineboutiques, Kering is currently assessing a large-scale projectto establish a single shared customer database acrossdistribution channels and to modernise, harmonise andoptimise its information systems and operational processes.

AN INTEGRATED GROUP, StrUCtuRED TO TAP INTO GROWTH POTENtiAL

1

10 Kering ~ 2015 Reference Document

KERING IN 2015 ~ KERING EMPOWERING IMAGINATION

01_VA_V5 06/04/2016 17:31 Page10

Kering believes that sustainable business is smartbusiness. Sustainability is both a business and leadershipopportunity for Kering, allowing the Group to create value.It stimulates growth, innovation and competitiveadvantage in the medium to long term, whilst simultaneouslyreducing costs. It also constitutes a motivational factorfor employees, enabling the Group to attract and retainthe best talents.

Sustainability is a key component of the Group brands’strategy. Kering empowers all of its brands to developproducts that meet the utmost standards of innovation,quality and sustainability.

Kering Corporate’s Sustainability Department supportseach of the Group’s brands with the development andoperational roll-out of their brand-specific action plans.Comprising around 15 experts, the team’s expertiseincludes everything from environmental footprintanalysis, raw material sourcing, ecosystem conservation,energy efficiency as well as social compliance. Thedepartment drives change within the Group by providingthe brands with the necessary know-how, guidance,collaboration and economies of scale needed in orderto develop more sustainable business models. The ChiefSustainability Officer sits on Kering’s Executive Committeeand ensures a cohesive and integrated approach tosustainability across the Group.

Kering’s sustainability strategy centres on a series of self-imposed targets, which the Group has publicly committedto achieving by 2016. Deliberately ambitious, thesetargets focus on the specific challenges of the Group’sbusiness: from the sustainable sourcing of leather, goldand diamonds to the reduction of carbon emissions, water,waste and hazardous chemicals.

Another integral part of the Group’s strategy is itsEnvironmental Profit & Loss account (E P&L), which nowcovers all the Group’s brands and their respective supplychains. Over the course of 2015, the 2013 and 2014 resultsof the group-wide E P&L were published. This innovativemanagement tool, developed by Kering, monitors andmeasures in € value the environmental impact of theGroup’s operations and those of its supply chain; from thesource of raw materials right up to the boutique floor.

Insights gathered from the Group’s E P&L serve to fortifyKering’s sourcing strategy, highlight environmental risksand economic opportunities within the supply chain,whilst also enabling the Group to track progress towardsits 2016 targets. The Group has now open-sourced its E P&L methodology (available on www.kering.com) so asto encourage other corporations to start taking accountfor their activities’ reliance on natural capital.

Collaboration is seen a key lever of sustainable innovationwithin the Group, a case in point being the MaterialsInnovation Lab. This internal research hub offers the Group’sbrands a comprehensive library of over 2,000 sustainablefabrics and a team of experts to support the integrationof these materials into their product offerings. Kering hasalso established partnerships with suppliers andinternational NGOs, so as to develop more responsiblesourcing methods for the Group’s key raw materials,including precious skins, furs and gold. An internal ethicalgold purchasing platform was also launched in 2015, viawhich Luxury Division brands have already managed toacquire 220 kilograms of ethical gold.

With regards to social compliance, a new worldwidesupplier management programme was also launched inthe past twelve months. The system is designed toimprove supplier relations, be it with regards to contracts,invoicing, traceability or auditing. With the support of thesustainability department, this programme will alsoenable the Group’s brands to monitor compliance withsocial, environmental and ethical issues, be it at suppliers’or their sub-contractors’.

Convinced that sustainability will play an ever moreprominent role in fashion going forward, Kering iscommitted to nurturing young talents and upcomingdesigners. Reflective of this, the Group launched a five-year partnership with the London College of Fashion’sCentre for Sustainable Fashion to promote sustainabledesign and innovation within the fashion industry. Similareducation programmes have also been launched withTsinghua University in China, and the Parsons School ofDesign and the Fashion Institute of Technology in theUnited States.

SUSTAINABILIty AT THE HEART OF Kering’S GROUP AND BRAND StrATEGY

1

112015 Reference Document ~ Kering

The Sport & Lifestyle brands are also working on optimisingand revitalising e-commerce, against the backdrop ofextremely rapid online growth in the sector.

(v) Recognising that its teams are the driving force behindits future success, Kering has developed an ambitious,

integrated, worldwide human resources framework, basedon ever-greater mobility across the brands. The ideabehind the HR strategy is to help brands flourish by givingthem access to shared talent pools, expertise, standards,information systems and best practices.

KERING EMPOWERING IMAGINATION ~ KERING IN 2015

01_VA_V5 06/04/2016 17:31 Page11

Against a backdrop of slower economic growth in certainkey emerging markets, notably China, and a modestrecovery in Europe, and despite a satisfactory economicperformance in the US, the global economy postedmoderate growth in 2015.

In this unfavourable environment, intensified by sharpcurrency fluctuations, Kering has demonstrated therelevance of its multi-brand model. The Group’s strategyis consistent: to nurture each brand’s long-term potential,with priority given to organic growth and operating cashflow generation.

True to its entrepreneurial and responsible vision, Keringwill continue to promote long-term value-creation,combining boldness and imagination, creativity andmeasured risk-taking, adaptability and agility.

The Group intends to leverage these values as Keringenters a new phase of its development, with a brandportfolio that now covers all key segments of its markets.

In a worldwide Luxury market: (i) where growth is normalising,(ii) shaped by more changeable and less predictableconsumer habits and locations (tourism, internet), (iii) and by significant increases in investments andoperating costs for all players in recent years as part of thedevelopment of directly-operated distribution networks;Kering possesses a number of strengths to help it unlockthe potential value and profitability of each of its brands.

Structured and organised to bring more expertise, valueand operational support to its brands, Kering focuses onincreasing return on capital employed by enhancingprofit margins and optimising capital allocation forinvestments as well as working capital.

Concrete action plans are implemented at brand level.Gucci undertook a major transformation programme inearly 2015 to overhaul its creative drive, organisation andcollections, and early indicators suggest that the brand,soon-to-be 100 year old, has lost none of its agility orability to reinvent itself and climb back to the forefront ofthe worldwide Luxury industry. PUMA, under the directionof a new management team since 2013, continues to deployof its strategic plan, aimed at renewing and streamliningits product line-up and refocusing its positioning aroundSport Performance. The results of these initiatives arealready apparent in PUMA’s top-line performance andshould gradually make a mark on profitability.

Across all Group brands, a range of cross-businessinitiatives has been drawn up with the support of Keringand dedicated teams to optimise comparable-storesales performance. The emphasis is on strengtheningstore productivity through a series of upstream anddownstream initiatives, including: improving supplychain capacity and the efficiency of product allocationcriteria by region and type; redefining ranges and theirdepth and breadth; training sales staff in best practicesfor customer service; loyalty and experience; and

IN AN ECONOMIC ENVIRONMENT THAT REMAINS UNSEttLEDIN THE SHORT TERM, Kering IS CONfiDENT IN ITS OUTLOOK

1

12 Kering ~ 2015 Reference Document

Embodying the Group’s social commitment, the KeringFoundation was launched in 2009 by François-HenriPinault. The Foundation combats violence against womenvia projects run by NGOs and social entrepreneurs and theengagement of the Group’s employees. The Foundation’sactions focus on three regions and are helping to fightagainst:

• sexual violence in America (the United States, Brazil andArgentina);

• harmful traditional practices in Western Europe(France, Italy and the United Kingdom);

• domestic violence in Asia (China).

Also central to the Foundation’s combat is awarenessraising, via campaigns including “White Ribbon forWomen” which was launched in 2012 as a call to actionon the occasion of the International Day for theElimination of Violence against Women on November 25.The campaign’s 2015 edition saw 125,000 White Ribbonbrooches distributed in over 800 stores operated by

Kering brands across 41 countries. In parallel, the Foundationran digital campaign #BeHerVoice across social mediaand reached nearly 320 million internet users.

In recognition of the Group’s continued efforts, Kering isreferenced as a leader by several bodies including theDow Jones Sustainability Index, which has ranked Keringin first place within the Textiles, Apparel & Luxury Goodsindustry for the past two years. This index tracks the best-in-class sustainability performers amongst the 2,500 largest companies in the Dow Jones Global TotalStock Market Index. Each year, participating companiesare assessed based on a specific questionnaire for eachbusiness sector, with only the top 10% in terms ofsustainability performance listed in the ranking.

In 2015, Kering was also named one of the Global 100 mostsustainable companies in the world for the first time,ranking 43rd. Compiled by Corporate Knights since 2005,the Global 100 is unveiled annually at the World EconomicForum in Davos.

KERING IN 2015 ~ KERING EMPOWERING IMAGINATION

01_VA_V5 06/04/2016 17:31 Page12

1

132015 Reference Document ~ Kering

developing CRM and clienteling tools. These initiativeswill generate cost reductions, improve profitability andoptimise capital employed. Complementing this effort,directly-operated store networks will be reviewed brand bybrand, and consolidated as necessary, as part of a broaderalignment of the allocation of investments to strictreturn guidelines. These initiatives will also be roundedout by the realisation of additional revenue and costsynergies, especially in terms of sourcing, productionand logistics. Lastly, Kering continues to promote itsbrands’ digital strategies by coordinating e-commerceprojects, encouraging knowledge sharing and drivingnew ambitious developments with the aim of increasingthe share of internet sales in the brands’ revenue andleveraging e-commerce to drive growth.

In a more volatile and unsettled short-term environment,the Group is moving into this new phase with confidenceand determination. Kering remains fully committed toenvironmental and social sustainability and diversity, allof which are crucial to its business objectives and to itslong-term performance.

KERING EMPOWERING IMAGINATION ~ KERING IN 2015

01_VA_V5 06/04/2016 17:31 Page13

1

14 Kering ~ 2015 Reference Document

KERING IN 2015 ~ KERING GROUP SIMPLIFIED ORGANISATIONAL CHART AS OF DECEMBER 31, 2015

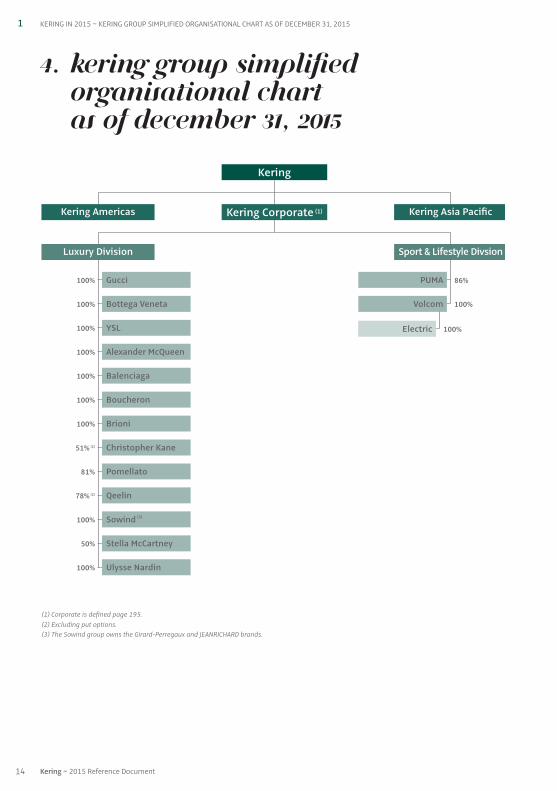

4. Kering Group SimplifiedOrganisational Chart as of December 31, 2015

Luxury Division

Gucci100%

Sport & Lifestyle Divsion

Kering

Kering Americas Kering Asia Pacific

Bottega Veneta100%

PUMA 86%

Volcom 100%

Electric 100%YSL100%

Alexander McQueen100%

Balenciaga100%

Boucheron100%

Brioni100%

51% (2) Christopher Kane

Pomellato

Qeelin

81%

78% (2)

100%

(1) Corporate is defined page 195.(2) Excluding put options.(3) The Sowind group owns the Girard-Perregaux and JEANRICHARD brands.

Ulysse Nardin

Sowind (3)

Stella McCartney50%

100%

Kering Corporate (1)

01_VA_V5 06/04/2016 17:31 Page14

CHAPTer 2

Our activities

1. Worldwide personal Luxury Goods market overview 16

2. Luxury Division 22Gucci 24Bottega Veneta 27Saint Laurent 30Other brands 33

3. Worldwide Sport & Lifestyle market overview 44

4. Sport & Lifestyle Division 48PUMA 50Other brands 54

152015 Reference Document ~ Kering

02_VA_V5 07/04/2016 10:37 Page15

2 OUR ACTIVITIES ~ WORLDWIDE PERSONAL LUXURY GOODS MARKET OVERVIEW

MARKET OVERVIEW: SIZE, trENDS AND MAINGROWTH DRIVERS

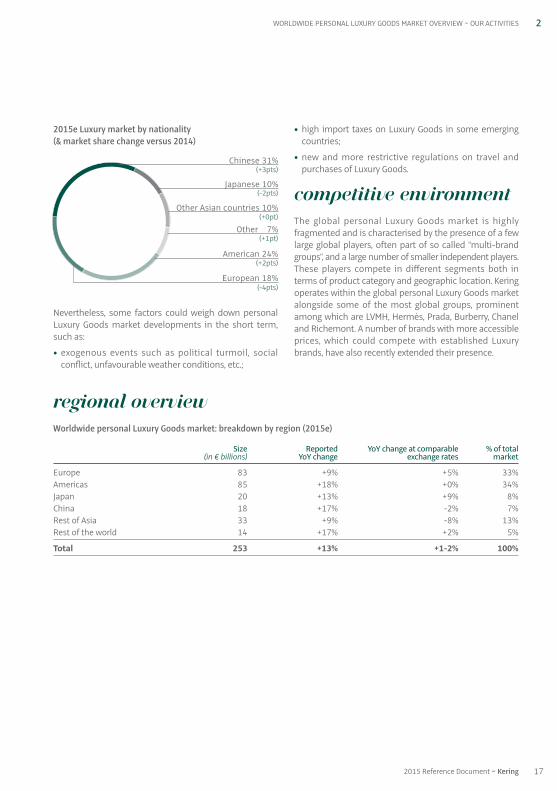

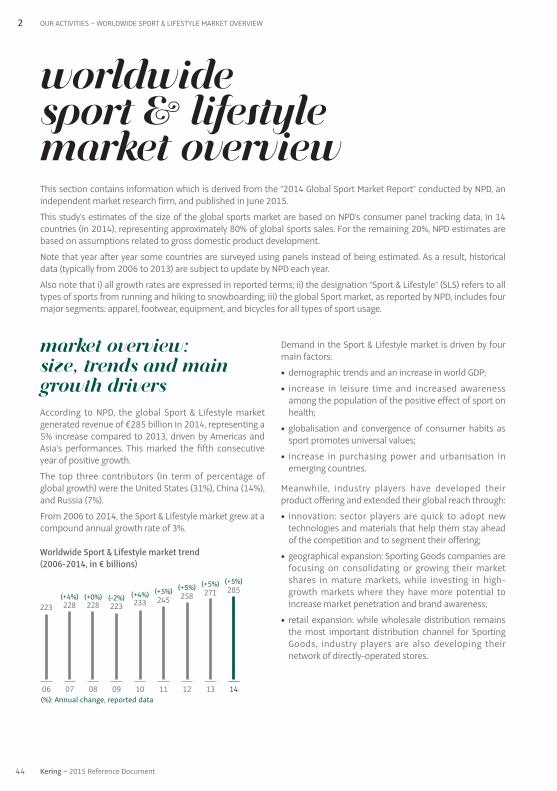

The global personal Luxury Goods market has enjoyedsignificant growth over the past few years (double-digitgrowth in 2010, 2011 and 2012). Since 2013, the markethas decelerated and entered a more “normalised” growthphase. In 2015, it generated revenue of €253 billion, up 13% reported and up 1 to 2% at comparable exchange rates.

In 2015, exogenous factors, especially strong currencyvolatility and moves, have created major challenges forthe luxury market. Euro weakening has led price gapsbetween regions to reach new heights, with a strongimpact on tourism flows and local consumption trends.Price differentials have contributed to boosting for exampleChinese customers’ spending abroad, somewhat at theexpense of the domestic market.

Worldwide personal Luxury Goods market trend (2007-2015e, in € billions)

Although the personal Luxury Goods market has seenstrong growth since 2010, outpacing the global economy,it is however tied to changes in worldwide GDP, asevidenced by the fall seen in the luxury market in 2009.

In addition to economic factors, structural factors arealso impacting demand and growth on the personalLuxury Goods market, including:

• positive demographic trends, especially in emergingmarkets;

• the emerging middle-class in these countries, wherethe average disposable income and purchasing powerof consumers has continued to grow;

• rising number of super-rich consumers;

• increased tourism flows and the growing relevance oftourist spending on Luxury Goods. As an example, Chineseoutbound tourist flows increased from c. 5 million a yearin 1995 to 116 million in 2014.

By destination, the weight of tourism spending differs:Europe is a market where luxury purchases are made bylocals but also by tourists. In Asia, Mainland Chineseconsumers tend to purchase luxury personal goods bothin Greater China and also abroad, notably in Japan, and toa lesser extent in the Americas, where purchases are stillmade mainly by locals.

In 2015, currency fluctuations changed the picture withincreasing price differentials leading “globe-shoppers” toadapt their consuming habits and spending patterns withMainland Chinese favouring Europe, Japan and to a lesserextent South Korea as main destinations. The Chinesenationality now accounts for 31% of the total market (up3ppts vs 2014).

This section contains information derived from studies conducted by organisations, such as Altagamma andBain & Company. Unless otherwise indicated, all historical and forecast statistical information, including trends, sales,market shares and growth levels, comes from the Bain Luxury Study – Altagamma Worldwide Market Monitor, publishedin October 2015. Luxury Goods industry segments and product categories correspond to the definitions used in theBain Luxury Study – Altagamma Worldwide Market Monitor.

In this document the global personal Luxury Goods market includes the “soft luxury” area such as apparel, accessories,perfumes and cosmetics, and the “hard luxury” area such as watches and jewellery.

Worldwide personalLuxury Goods marketoverview

(%): Annual change at reported exchange rates(%): Change at currency-neutral growth

15e

253(+13%)(+1-2%)

14

224(+3%)

07

170

08

167

09

153

10

173

11

192

12

212

13

218(+3%)(+10%)

(+11%)(+13%)

(+3%)(+7%)(+5%)(+13%)

(+8%)

16 Kering ~ 2015 Reference Document

02_VA_V5 06/04/2016 17:31 Page16

REGIONAL OVERVIEW

Worldwide personal Luxury Goods market: breakdown by region (2015e)

Size Reported YoY change at comparable % of total(in € billions) YoY change exchange rates market

Europe 83 +9% +5% 33%Americas 85 +18% +0% 34%Japan 20 +13% +9% 8%China 18 +17% -2% 7%Rest of Asia 33 +9% -8% 13%Rest of the world 14 +17% +2% 5%

Total 253 +13% +1-2% 100%

2015e Luxury market by nationality (& market share change versus 2014)

Nevertheless, some factors could weigh down personalLuxury Goods market developments in the short term,such as:

• exogenous events such as political turmoil, socialconflict, unfavourable weather conditions, etc.;

• high import taxes on Luxury Goods in some emergingcountries;

• new and more restrictive regulations on travel andpurchases of Luxury Goods.

COMPEtitiVE ENVIRONMENT

The global personal Luxury Goods market is highlyfragmented and is characterised by the presence of a fewlarge global players, often part of so called “multi-brandgroups”, and a large number of smaller independent players.These players compete in different segments both interms of product category and geographic location. Keringoperates within the global personal Luxury Goods marketalongside some of the most global groups, prominentamong which are LVMH, Hermès, Prada, Burberry, Chaneland Richemont. A number of brands with more accessibleprices, which could compete with established Luxurybrands, have also recently extended their presence.

2WORLDWIDE PERSONAL LUXURY GOODS MARKET OVERVIEW ~ OUR ACTIVITIES

172015 Reference Document ~ Kering

Chinese 31%

Japanese 10%

Other 7%

European 18%

American 24%

Other Asian countries 10%

(-2pts)

(+3pts)

(+2pts)

(+1pt)

(+0pt)

(-4pts)

02_VA_V5 06/04/2016 17:31 Page17

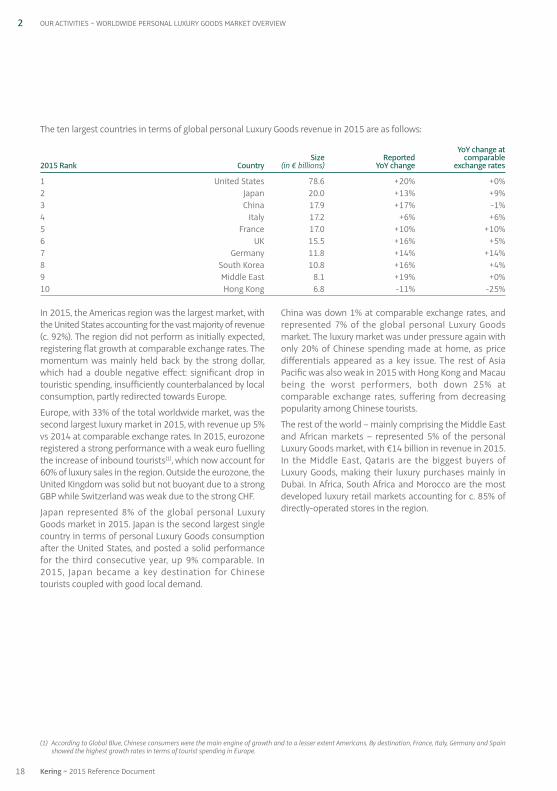

In 2015, the Americas region was the largest market, withthe United States accounting for the vast majority of revenue(c. 92%). The region did not perform as initially expected,registering flat growth at comparable exchange rates. Themomentum was mainly held back by the strong dollar,which had a double negative effect: significant drop intouristic spending, insufficiently counterbalanced by localconsumption, partly redirected towards Europe.

Europe, with 33% of the total worldwide market, was thesecond largest luxury market in 2015, with revenue up 5%vs 2014 at comparable exchange rates. In 2015, eurozoneregistered a strong performance with a weak euro fuellingthe increase of inbound tourists(1), which now account for60% of luxury sales in the region. Outside the eurozone, theUnited Kingdom was solid but not buoyant due to a strongGBP while Switzerland was weak due to the strong CHF.

Japan represented 8% of the global personal LuxuryGoods market in 2015. Japan is the second largest singlecountry in terms of personal Luxury Goods consumptionafter the United States, and posted a solid performancefor the third consecutive year, up 9% comparable. In2015, Japan became a key destination for Chinesetourists coupled with good local demand.

China was down 1% at comparable exchange rates, andrepresented 7% of the global personal Luxury Goodsmarket. The luxury market was under pressure again withonly 20% of Chinese spending made at home, as pricedifferentials appeared as a key issue. The rest of AsiaPacific was also weak in 2015 with Hong Kong and Macaubeing the worst performers, both down 25% atcomparable exchange rates, suffering from decreasingpopularity among Chinese tourists.

The rest of the world – mainly comprising the Middle Eastand African markets – represented 5% of the personalLuxury Goods market, with €14 billion in revenue in 2015.In the Middle East, Qataris are the biggest buyers ofLuxury Goods, making their luxury purchases mainly inDubai. In Africa, South Africa and Morocco are the mostdeveloped luxury retail markets accounting for c. 85% ofdirectly-operated stores in the region.

2 OUR ACTIVITIES ~ WORLDWIDE PERSONAL LUXURY GOODS MARKET OVERVIEW

The ten largest countries in terms of global personal Luxury Goods revenue in 2015 are as follows:

YoY change atSize Reported comparable

2015 Rank Country (in € billions) YoY change exchange rates

1 United States 78.6 +20% +0%2 Japan 20.0 +13% +9%3 China 17.9 +17% -1%4 Italy 17.2 +6% +6%5 France 17.0 +10% +10%6 UK 15.5 +16% +5%7 Germany 11.8 +14% +14%8 South Korea 10.8 +16% +4%9 Middle East 8.1 +19% +0%10 Hong Kong 6.8 -11% -25%

18 Kering ~ 2015 Reference Document

(1) According to Global Blue, Chinese consumers were the main engine of growth and to a lesser extent Americans. By destination, France, Italy, Germany and Spainshowed the highest growth rates in terms of tourist spending in Europe.

02_VA_V5 06/04/2016 17:31 Page18

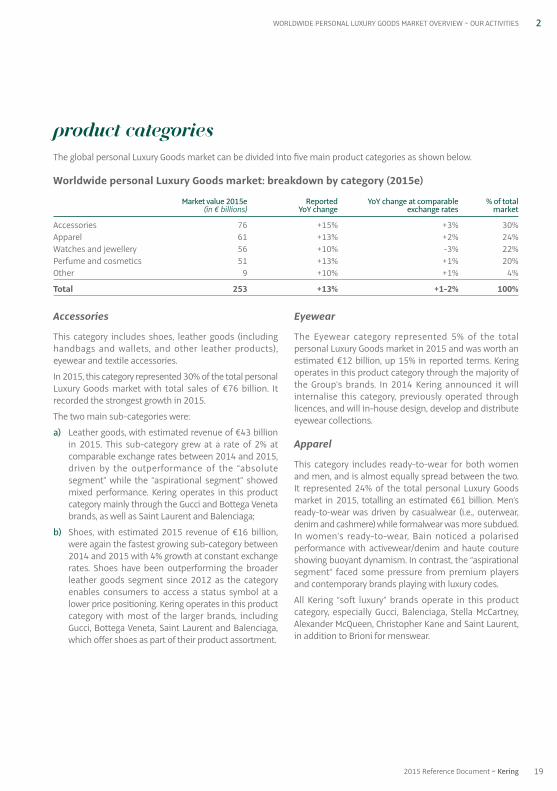

Accessories

This category includes shoes, leather goods (includinghandbags and wallets, and other leather products),eyewear and textile accessories.

In 2015, this category represented 30% of the total personalLuxury Goods market with total sales of €76 billion. Itrecorded the strongest growth in 2015.

The two main sub-categories were:

a) Leather goods, with estimated revenue of €43 billionin 2015. This sub-category grew at a rate of 2% atcomparable exchange rates between 2014 and 2015,driven by the outperformance of the “absolutesegment” while the “aspirational segment” showedmixed performance. Kering operates in this productcategory mainly through the Gucci and Bottega Venetabrands, as well as Saint Laurent and Balenciaga;

b) Shoes, with estimated 2015 revenue of €16 billion,were again the fastest growing sub-category between2014 and 2015 with 4% growth at constant exchangerates. Shoes have been outperforming the broaderleather goods segment since 2012 as the categoryenables consumers to access a status symbol at alower price positioning. Kering operates in this productcategory with most of the larger brands, includingGucci, Bottega Veneta, Saint Laurent and Balenciaga,which offer shoes as part of their product assortment.

Eyewear

The Eyewear category represented 5% of the totalpersonal Luxury Goods market in 2015 and was worth anestimated €12 billion, up 15% in reported terms. Keringoperates in this product category through the majority ofthe Group’s brands. In 2014 Kering announced it willinternalise this category, previously operated throughlicences, and will in-house design, develop and distributeeyewear collections.

Apparel

This category includes ready-to-wear for both womenand men, and is almost equally spread between the two.It represented 24% of the total personal Luxury Goodsmarket in 2015, totalling an estimated €61 billion. Men’sready-to-wear was driven by casualwear (i.e., outerwear,denim and cashmere) while formalwear was more subdued.In women’s ready-to-wear, Bain noticed a polarisedperformance with activewear / denim and haute coutureshowing buoyant dynamism. In contrast, the “aspirationalsegment” faced some pressure from premium playersand contemporary brands playing with luxury codes.

All Kering “soft luxury” brands operate in this productcategory, especially Gucci, Balenciaga, Stella McCartney,Alexander McQueen, Christopher Kane and Saint Laurent,in addition to Brioni for menswear.

PRODUCT CATEGORIES

The global personal Luxury Goods market can be divided into five main product categories as shown below.

Worldwide personal Luxury Goods market: breakdown by category (2015e)

Market value 2015e Reported YoY change at comparable % of total(in € billions) YoY change exchange rates market

Accessories 76 +15% +3% 30%Apparel 61 +13% +2% 24%Watches and jewellery 56 +10% -3% 22%Perfume and cosmetics 51 +13% +1% 20%Other 9 +10% +1% 4%

Total 253 +13% +1-2% 100%

2WORLDWIDE PERSONAL LUXURY GOODS MARKET OVERVIEW ~ OUR ACTIVITIES

192015 Reference Document ~ Kering

02_VA_V5 06/04/2016 17:31 Page19

Watches and jewellery

The watches and jewellery category generated revenue of€56 billion in 2015, representing 22% of the totalpersonal Luxury Goods market, and decreased by 3%between 2014 and 2015 at comparable exchange rates.In 2015, there was a significant polarised performanceacross the two main sub-categories with watches down6% and jewellery up 6% at comparable exchange rates.High-end watches were hit by negative Asian performancewhile jewellery was driven by high-ticket items as it isperceived as a safe investment in the context of a toughmacro environment.

Kering operates in this category across different pricepoints with Gucci Timepieces, Girard-Perregaux, andUlysse Nardin for watches, and Boucheron, Pomellatoand Qeelin for jewellery.

Perfume and cosmetics

The perfume and cosmetics category represented 20% ofthe total personal Luxury Goods market in 2015 and wasworth an estimated €51 billion.

Kering operates in this product category through royaltylicencing agreements between its main brands andleading industry players such as L’Oréal, Coty (incl. P&GPrestige) and Interparfums to develop and sell fragrancesand cosmetics.

DIStrIBUtiON CHANNELS

Worldwide personal Luxury Goods market: breakdown by distribution channel (2013-2015e)

Retail channel

A strong directly-operated store network is important forthe success of a luxury brand as it allows greater controlover the consumer shopping experience and overproduct assortment, merchandising and customerservice. In 2015 the retail channel accounted for salesamounting to 34% of the total global personal LuxuryGoods market.

In the case of Kering Luxury brands, share of retail sales isfar higher (70.6%), reflecting both the maturity of some ofthe brands and the Group’s strategic commitment to growits directly operated network. This also reflects Keringbrands’ product mix, as the higher share of leather goodsand accessories typically translates into a more prominentshare of retail sales in the channel mix.

Wholesale channel

The wholesale channel typically includes departmentstores, travel retail, independent high-end multi-brandstores and franchise stores, and accounted forapproximately 66% of the total global personal LuxuryGoods market in 2015. The wholesale channel can thusbe multi-brand or mono-brand. The share of wholesalesales is typically higher in ready-to-wear and hard luxury,and is also more important than retail in the channel mixfor a brand that stands at an earlier stage of maturity.

These two distribution channels can also be split intosix sales formats. Each of these formats could beoperated through retail or wholesale.

20 Kering ~ 2015 Reference Document

2 OUR ACTIVITIES ~ WORLDWIDE PERSONAL LUXURY GOODS MARKET OVERVIEW

RetailWholesale2015e

€253 bn

34%

66%

2013 2014

€224 bn

32%

68%

€218 bn

31%

69%

Mono-brand stores 29%

Outlets 10%

Speciality stores 23%

Airport stores 6%

Online 7 %

Department stores 25%

(+2pts)

(+1pt)

(+1pt)

(+0pt)

(-2pts)

(-2pts)

(pts): Market share change (2015e vs 2014)

02_VA_V5 06/04/2016 17:31 Page20

E-commerceOnline sales of Luxury Goods reached a record of around€17 billion in 2015 (up 22% at comparable exchangerates), representing about 7% of total global personal LuxuryGoods sales. This penetration is especially driven by therapid development of online business of wholesalers(department stores) and e-commerce pure players (e-tailers).

All Kering brands are directly present online with theirown e-commerce websites, either operated internally, asis the case for Gucci, or through a joint venture.

Kering brands are also distributed online by selectedpartners.

MARKET OUTLOOK

For 2016, Bain and Altagamma forecast overall growth of 3% to 3.5% excluding currency effects for the personalLuxury Goods markets, with the sector entering a phaseof “new normal” growth.

Growth should be driven by:

• new emerging countries: in addition to South EastAsian countries (Indonesia, Thailand, etc.), Brazil, Australia,Africa and India are expected to be increasingly key tothe growth of the global personal Luxury Goods market;

• emerging consumers: a booming upper-middle classespecially benefiting the accessible luxury segment,particularly in China. In fact, according to McKinsey, by2022, the Chinese upper-middle class should accountfor 54% of urban households and 56% of urban privateconsumption (up from 14% and 20% in 2012 respectively);

• the continued expansion of tourism flows with theemergence of new winners (Japan, South Korea, etc.),which could, however, come partly at the expense ofsome of the more traditional destinations;

• the development of key distribution channels such asoutlets, travel retail or e-commerce. The latter generated€17 billion in revenue in 2015, and is expected to growat an annual average rate of 24% over the 2013-2020period;

• an increase in high-spending consumer classes such ashigh-net-worth individuals (HNWIs);

• the development of new high-end products and services;

• the potential of the American market due to the under-penetration of European luxury brands in the region.

21

2

2015 Reference Document ~ Kering

WORLDWIDE PERSONAL LUXURY GOODS MARKET OVERVIEW ~ OUR ACTIVITIES

02_VA_V5 06/04/2016 17:31 Page21

22 Kering ~ 2015 Reference Document

2 OUR ACTIVITIES ~ LUXURY DIVISION

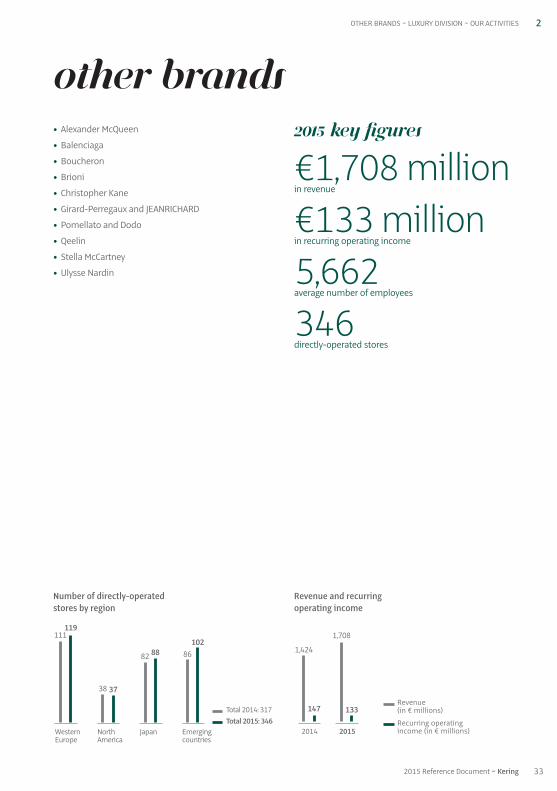

Gucci 24Bottega Veneta 27Saint Laurent 30Other brands 33

Alexander McQueenBalenciagaBoucheronBrioniChristopher KaneGirard-Perregaux and JEANRICHARDPomellato and DodoQeelinStella McCartneyUlysse Nardin

Luxury Division

02_VA_V5 06/04/2016 17:31 Page22

2LUXURY DIVISION ~ OUR ACTIVITIES

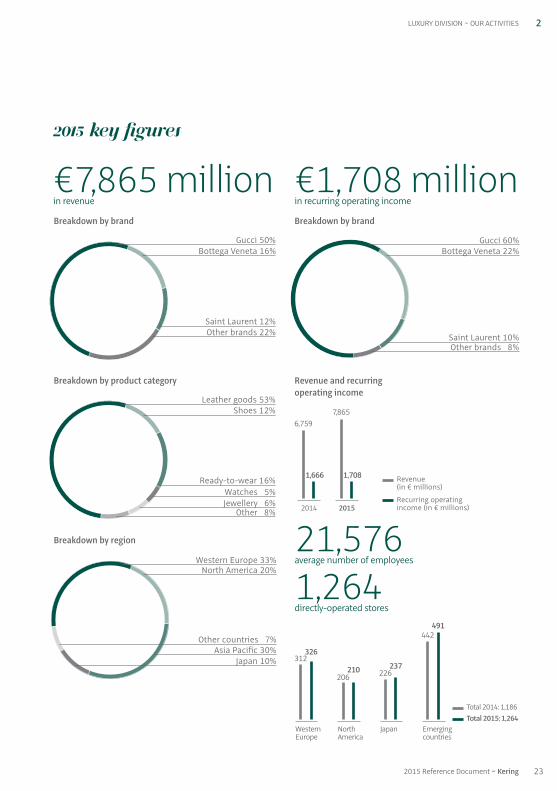

Breakdown by brand

Revenue and recurringoperating income

€7,865 millionin revenue

21,576average number of employees

1,264directly-operated stores

€1,708 millionin recurring operating income

Breakdown by brand

Breakdown by product category

Breakdown by region

Gucci 50%Bottega Veneta 16%

Saint Laurent 12%Other brands 22%

Leather goods 53%Shoes 12%

Ready-to-wear 16%Watches 5%Jewellery 6%

Other 8%

Western Europe 33%North America 20%

Japan 10%Asia Pacific 30%

Other countries 7%

2015 key figures

Gucci 60%Bottega Veneta 22%

Saint Laurent 10%Other brands 8%

Revenue (in € millions)

Recurring operating income (in € millions)2015

7,865

1,708

2014

6,759

1,666

WesternEurope

NorthAmerica

Japan Emergingcountries

Total 2014: 1,186Total 2015: 1,264

237210

326

491

226206

312

442

232015 Reference Document ~ Kering

02_VA_V5 06/04/2016 17:31 Page23

2

2015 key figures

€3,898 millionin revenue

€1,032 millionin recurring operating income

10,570average number of employees

525directly-operated stores

Breakdown of 2015 revenueby product category

Breakdown of 2015 revenueby region

Leather goods 57%Shoes 14%

Ready-to-wear 11%Watches 5%Jewellery 2%

Other 11%

Western Europe 26%North America 22%

Other countries 7%Japan 10%

Asia Pacific 35%

BUSINESS CONCEPT

Founded in Florence in 1921, Gucci is one of the world’sleading luxury fashion brands.

From its origins in the 1920s through to the late 1970s,the brand stayed loyal to its values of superior Italiancraftsmanship and innovation, and as a result Gucci soonbecame the expression of Italian-made luxury.

Throughout the 1950s, 1960s and 1970s, Gucci’s reputationbegan to grow around the world thanks in large part tothe “jet set”, socialites and celebrities, particularly fromHollywood, who wore the brand internationally. It was inthe 1990s, under the creative direction of Tom Ford, thatGucci became synonymous with fashion and acquired thereputation of being a true fashion authority and leader.

Early in the new Millennium, against the backdrop of theworld economic crisis, consumers once again began to turnto traditional luxury values. It was at this time that Gucciintroduced its “Forever Now” philosophy, emphasisingboth its fashion authority and its Florentine heritage andcraftsmanship.

At the beginning of 2015, Gucci embarked on the nextchapter in its history, with the introduction of a newcontemporary vision, which is re-establishing its reputationas one of the world’s most influential luxury fashionbrands. Eclectic, romantic, and above all contemporary,Gucci is currently inventing a wholly modern approach tofashion and thereby redefining luxury for the 21st century.

Gucci products continue to represent the pinnacle ofItalian craftsmanship and are unsurpassed in terms oftheir quality and attention to detail. They are soldexclusively through a network of 525 directly-operatedboutiques, a directly-operated online store (in 28 markets),a limited number of franchises and selected departmentand specialty stores.

At the end of the year, Gucci retail sales representedapproximately 82% of the brand’s total revenue (up fromapproximately 70% in 2009).

OUR ACTIVITIES ~ LUXURY DIVISION ~ GUCCI

24 Kering ~ 2015 Reference Document

02_VA_V5 06/04/2016 17:31 Page24

2

COMPEtitiVE ENVIRONMENT

Gucci is one of the few luxury brands with truly worldwideoperations, alongside Hermès, Dior, Chanel, Louis Vuittonand Prada. Gucci is maintaining its leadership position asone of the world’s leading luxury fashion brands both interms of revenue and profitability.

StrATEGY

With the ambition of re-establishing Gucci’s position as apivotal Italian luxury fashion brand – leading the industryby setting the tone with innovative runway collectionsand ground-breaking creativity – the strategic visionconceived by Marco Bizzarri, the brand’s new Presidentand CEO, aims to identify a new image for Gucci, more inline with the world of today, more relevant, and moreattractive for new, younger luxury consumers.

The product offering will be fully repositioned over two orthree seasons, gradually substituting all the units that arenot consistent with the new creative direction, reducingthe number of models and variations of product in eachstore, while balancing the price range by rationalisingentry prices and exploiting opportunities in the high range.

The GG signature is considered a highly valuable assetwith unlimited potential. The reinvention, in line with thecontemporary vision of Gucci’s new Creative Director,Alessandro Michele, will allow it to regain the strong andcontemporary stature it deserves.

In terms of distribution, the focus will be on optimisingthe existing store network and the online experience, withthe implementation of a program of initiatives designedto achieve retail excellence and, as a consequence,enhanced productivity.

GUCCI ~ LUXURY DIVISION ~ OUR ACTIVITIES

2015 HIGHLIGHTS AND OUTLOOK FOR 2016

For Gucci, this has been a year of reinvention. New CEOMarco Bizzarri was tasked with reinvigorating the brand,and under his leadership Gucci is now undergoing acomprehensive transformation.

Bizzarri’s first decision upon taking on this role inJanuary 2015 was to appoint Alessandro Michele,previously Associate Creative Director and AccessoriesDesigner, as Gucci’s new Creative Director. Michele’s new,contemporary vision for the brand has been criticallyacclaimed, quickly establishing him as one of the mostinfluential creative directors in the industry today – whichwas affirmed by the British Fashion Council’s decision topresent him with its 2015 International Designer of theYear award. This is a remarkable achievement after justten months in the role.

Press and buyers alike from around the world haveresponded enthusiastically to Michele’s collections,heralding them as indicative of a fresh, new direction forGucci that remoulds the brand’s legacy into a new styleand aesthetic.

Following the Fall / Winter 2015 fashion shows, AlessandroMichele presented his Cruise 2016 collection with anunprecedented fashion show in New York’s Chelseadistrict, in what has been acknowledged as the seminalmoment in the emergence of the reinvented Gucci.

Alessandro Michele’s first full collection – Cruise 2016 –began to arrive in selected stores from mid-September,two months ahead of the usual timing for the industry. Atthe same time, Michele’s new store concept was unveiledat the house’s Montenapoleone flagship store duringMilan Fashion Week. Striking new windows, visualdisplays and packaging all help bring the brand’s new,contemporary vision to life.

In terms of products, the assortment was rationalisedand given more clarity through consistent and concisemerchandising. New lines were introduced featuringcontemporary interpretations of the GG signature, andother iconic symbols and house motifs. The Dionysus –launched at the Fall / Winter 2015 fashion show – isalready on its way to becoming an iconic bag.

252015 Reference Document ~ Kering

02_VA_V5 06/04/2016 17:31 Page25

2 OUR ACTIVITIES ~ LUXURY DIVISION ~ GUCCI

On the distribution side, during the year Gucci opened 20 net directly-operated stores, mainly located in Asia-Pacific and America. The new store concept wasprogressively rolled out (in more than 30 stores) duringthe last semester of the year, and this process will continuenext year.

In October, a completely re-designed and re-platformedversion of gucci.com was launched in the US and Canada,and this will be rolled out in other regions during 2016.The site brings Alessandro Michele’s new aesthetic to lifethrough beautiful design, rich imagery, engagingstorytelling and exclusive brand content, combined with asmart user experience. With over 100 million visitors peryear, gucci.com represents the most important customertouch-point for the brand, offering significant potentialfor continued dynamic growth in online revenue.

In the second part of the year, a series of new strategiccollaborations with specialty stores including DoverStreet Market (in Tokyo, New York, London and Beijing),Boon the Shop (Seoul, Korea), Antonia (Milan, Italy) andColette (Paris, France) were finalised. Representing someof the most fashion-forward retail destinations, thepresence of Alessandro Michele’s collections within theseunique locations has created further excitement andinterest around the brand in its new direction.

A series of strategic organisational changes wereimplemented in the first months of the year, with the aimof creating a simpler and leaner structure and acceleratingthe decision-making process, while providing a promptand effective support system for the regions fromcorporate headquarters. Meanwhile, a new omni-channeldepartment was established to further increase theproximity of the brand to all of its customers.

A number of key executives joined the company duringthe year, including the new Executive Vice President andChief Merchandising and Licensing Officer, with the aimof implementing an effective merchandising strategy thatperfectly matches the creative spirit of the collectionswith market needs.

The initial dynamic trend for new Creative DirectorAlessandro Michele’s highly acclaimed Cruise 2016 andSpring / Summer 2016 collections confirms the brand’srenewed momentum. At the same time, key drivers toimprove store productivity have been identified, andduring the year management put in place the foundationsnecessary for Gucci to return to sustained growth in theyears ahead.

Revenue and recurringoperating income

Revenue (in € millions)

Recurring operating income (in € millions)2014 2015

3,898

1,032

3,497

1,056

Number of directly-operatedstores by region

WesternEurope

NorthAmerica

Japan Emergingcountries

Total 2014: 505Total 2015: 525

66

122119

218

65

117116

207

26 Kering ~ 2015 Reference Document

02_VA_V5 06/04/2016 17:31 Page26

2BOTTEGA VENETA ~ LUXURY DIVISION ~ OUR ACTIVITIES

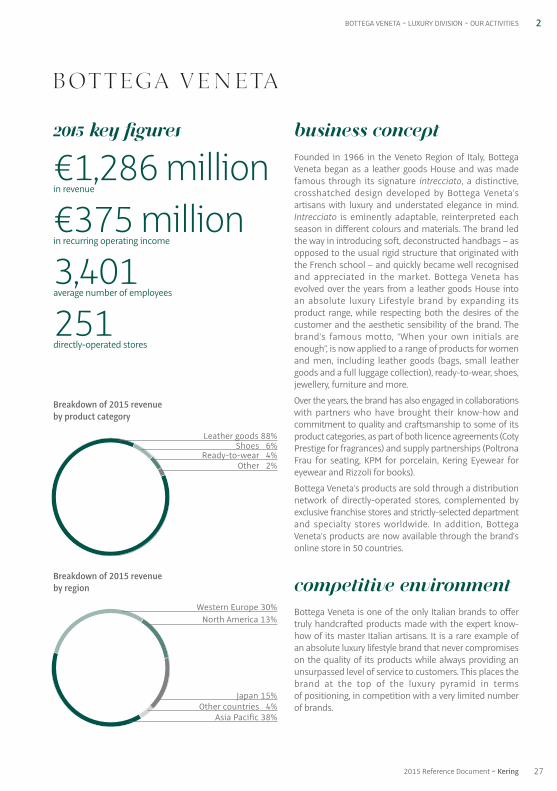

2015 key figures

€1,286 millionin revenue

€375 millionin recurring operating income

3,401average number of employees

251directly-operated stores

Breakdown of 2015 revenueby product category

Breakdown of 2015 revenueby region

Leather goods 88%Shoes 6%

Ready-to-wear 4%Other 2%

Western Europe 30%North America 13%

Asia Pacific 38%

Japan 15%Other countries 4%

BUSINESS CONCEPT

Founded in 1966 in the Veneto Region of Italy, BottegaVeneta began as a leather goods House and was madefamous through its signature intrecciato, a distinctive,crosshatched design developed by Bottega Veneta’sartisans with luxury and understated elegance in mind.Intrecciato is eminently adaptable, reinterpreted eachseason in different colours and materials. The brand ledthe way in introducing soft, deconstructed handbags – asopposed to the usual rigid structure that originated withthe French school – and quickly became well recognisedand appreciated in the market. Bottega Veneta hasevolved over the years from a leather goods House intoan absolute luxury Lifestyle brand by expanding itsproduct range, while respecting both the desires of thecustomer and the aesthetic sensibility of the brand. Thebrand’s famous motto, “When your own initials areenough”, is now applied to a range of products for womenand men, including leather goods (bags, small leathergoods and a full luggage collection), ready-to-wear, shoes,jewellery, furniture and more.

Over the years, the brand has also engaged in collaborationswith partners who have brought their know-how andcommitment to quality and craftsmanship to some of itsproduct categories, as part of both licence agreements (CotyPrestige for fragrances) and supply partnerships (PoltronaFrau for seating, KPM for porcelain, Kering Eyewear foreyewear and Rizzoli for books).

Bottega Veneta’s products are sold through a distributionnetwork of directly-operated stores, complemented byexclusive franchise stores and strictly-selected departmentand specialty stores worldwide. In addition, BottegaVeneta’s products are now available through the brand’sonline store in 50 countries.

COMPEtitiVE ENVIRONMENT

Bottega Veneta is one of the only Italian brands to offertruly handcrafted products made with the expert know-how of its master Italian artisans. It is a rare example ofan absolute luxury lifestyle brand that never compromiseson the quality of its products while always providing anunsurpassed level of service to customers. This places thebrand at the top of the luxury pyramid in terms of positioning, in competition with a very limited numberof brands.

272015 Reference Document ~ Kering

02_VA_V5 06/04/2016 17:31 Page27

StrATEGY

Bottega Veneta’s strategy, implemented under thecreative direction of Tomas Maier and the businessleadership of Carlo Alberto Beretta who joined thecompany in January 2015, aims to reinforce BottegaVeneta’s position as a high-end and exclusive luxurylifestyle brand, for which consistency and continuity arethe key elements to maintaining differentiation in theindustry. Business and creativity will continue to worktogether as an essential part of Bottega Veneta’s success,as they always have in the past.

Historically, the brand’s core business was leather goods(88% of sales), characterised by attention to detail andthe use of the highest quality materials. A wider range ofproducts appealing to an international clientele of menand women was gradually integrated, with the emphasison contemporary functionality and timeless yetinnovative design.

The brand’s predominant trait of exclusivity has beentransferred to the distribution network. Through itsworldwide expansion, Bottega Veneta has consolidatedits presence in emerging markets, without compromisingits investments in mature markets, particularly the US,but also Europe, where Bottega Veneta’s story andcraftsmanship began.

2015 HIGHLIGHTS AND OUTLOOK FOR 2016

In 2015, the careful execution of its international growthstrategy, consistent with the exclusive positioning of thebrand, resulted in full-year growth (with mature marketsaccounting for 58% of total sales) for both retail andwholesale channels, which respectively account for about80% and 20% of total sales.

Iconic leather goods products, including new seasonalvariations and plain leather, continued to represent a veryimportant part of the business in 2015.

Throughout 2015, Bottega Veneta focused on consolidatingits existing retail network, continuing its efforts toenhance its boutiques through both refurbishments andexpansions to ensure the best possible experience. It alsopursued selective store openings, bringing its totalnetwork up to 251, compared to 236 at the end of 2014. Thenew stores were distributed between emerging and

mature markets (seven new stores in Asia Pacific, six newstores in EMEA and two new stores in America).

In April, during the Salone del Mobile 2015 in Milan,Bottega Veneta celebrated the opening of its HomeCollection boutique in Via Borgospesso highlighting itsgrowing commitment to the furniture category.

During the year, Bottega Veneta opened its newly expandedboutique at Harbour City in Hong Kong originallyinaugurated in 2002, its first boutiques in Frankfurt andin lower Manhattan’s Financial District in New York atBrookfield Place. In December Bottega Veneta moved itsNew York flagship from 699 Fifth Avenue to a temporarylocation at 650 Madison Avenue in anticipation of itsMaison opening scheduled for 2017.

Starting in January 2015, La Scuola dei Maestri Pellettieridi Bottega Veneta, located within the company’s Atelier inMontebello Vicentino, embarked upon a collaborationwith the University IUAV of Venice to create a three monthpost-graduate level course in advanced handbag designand product development, honouring its commitment toensuring the future of Italian know-how and continuingthe artisanal tradition of the Veneto region.

Confirming its ongoing commitment to its roots andartisanal excellence, Bottega Veneta supported the creationof a third cooperative of artisans specialised in intrecciatoleather in Rotzo. The laboratory was inaugurated inOctober and currently employs 20 artisans, selected andtrained by Bottega Veneta master leather craftsmen. It joinsthe two Women’s Mountain cooperatives established in2011 with the joint support of Bottega Veneta and localauthorities in the Astico and Posina valleys – in Arsieroand Pedemonte.

For the second year in a row Bottega Veneta was rankedin the prestigious Great Place to Work® classification inthe Best Large Company Workplaces 2015 category. Thisaccomplishment is the result of constant efforts andinitiatives to promote employee welfare.

In addition, the company has taken the first steps into anew era of digital and social strategy starting with thedevelopment of the new www.bottegaveneta.com mobilesite and the launch of WeChat. Further developmentsand new projects are expected to be introduced in 2016to make all Bottega Veneta owned platforms a place ofdiscovery and engagement for existing and potentialcustomers.

28 Kering ~ 2015 Reference Document

2 OUR ACTIVITIES ~ LUXURY DIVISION ~ BOTTEGA VENETA

02_VA_V5 06/04/2016 17:31 Page28

Lastly, in October Bottega Veneta introduced its secondbook, “Bottega Veneta: Art of Collaboration”, which isdedicated to honouring the collaborations between TomasMaier and the artists who have contributed to the creationof the brand’s advertising portfolio season after season.

In 2016, Bottega Veneta will continue to build on itsachievements and positioning, supported by furtherstrategic retail openings worldwide.

Particularly in the US, further investments will be made toreinforce the existing retail network. Moreover in AsiaPacific, especially in China, some reshuffling andconsolidation of the network will be implemented inorder to increase the dimension of the stores and to hostthe complete range of product categories. The objective

is to grow through all product categories such as shoes,ready-to-wear, jewellery and eyewear, which have in thepast been seen as merely complementing the BottegaVeneta offering, and give them the same standing as thecore leather goods business.

Finally, Bottega Veneta will continue to focus onstrengthening and pursuing the execution of retailexcellence through further reinforcement of the bestpractices already implemented at worldwide level,conscious that guaranteeing the best luxury experiencein stores – from the selling ceremony to customer service,from windows to events – is key to maintaining theuniqueness of the brand and achieving its long-termobjectives.

29

2

2015 Reference Document ~ Kering

BOTTEGA VENETA ~ LUXURY DIVISION ~ OUR ACTIVITIES

Revenue and recurringoperating income

Revenue (in € millions)

Recurring operating income (in € millions)2014 2015

1,286

375

1,131

357

Number of directly-operatedstores by region

WesternEurope

NorthAmerica

Japan Emergingcountries

Total 2014: 236Total 2015: 251

58

30

53

110

58

29

52

97

02_VA_V5 06/04/2016 17:31 Page29

2 OUR ACTIVITIES ~ LUXURY DIVISION ~ SAINT LAURENT

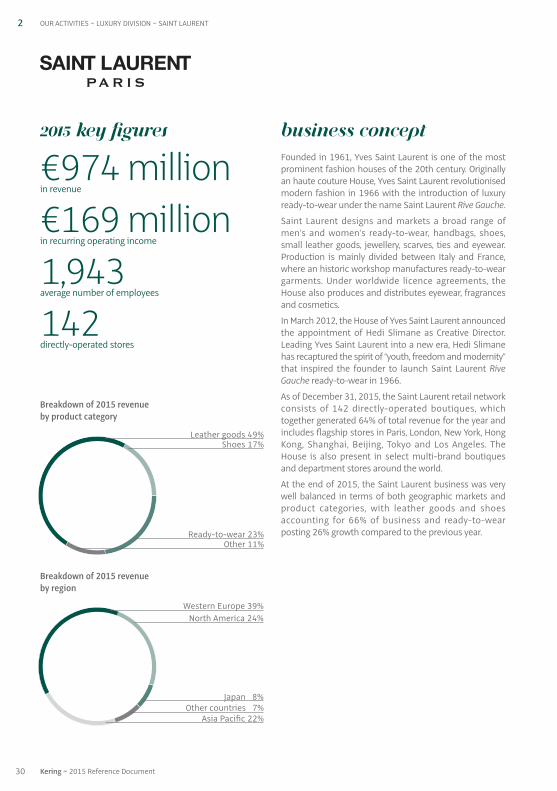

2015 key figures

€974 millionin revenue

€169 millionin recurring operating income

1,943average number of employees

142directly-operated stores

Breakdown of 2015 revenueby product category

Breakdown of 2015 revenueby region

Leather goods 49%Shoes 17%

Ready-to-wear 23%Other 11%

Western Europe 39%North America 24%

Asia Pacific 22%

Japan 8%Other countries 7%

BUSINESS CONCEPT

Founded in 1961, Yves Saint Laurent is one of the mostprominent fashion houses of the 20th century. Originallyan haute couture House, Yves Saint Laurent revolutionisedmodern fashion in 1966 with the introduction of luxuryready-to-wear under the name Saint Laurent Rive Gauche.

Saint Laurent designs and markets a broad range ofmen’s and women’s ready-to-wear, handbags, shoes,small leather goods, jewellery, scarves, ties and eyewear.Production is mainly divided between Italy and France,where an historic workshop manufactures ready-to-weargarments. Under worldwide licence agreements, theHouse also produces and distributes eyewear, fragrancesand cosmetics.

In March 2012, the House of Yves Saint Laurent announcedthe appointment of Hedi Slimane as Creative Director.Leading Yves Saint Laurent into a new era, Hedi Slimanehas recaptured the spirit of “youth, freedom and modernity”that inspired the founder to launch Saint Laurent RiveGauche ready-to-wear in 1966.

As of December 31, 2015, the Saint Laurent retail networkconsists of 142 directly-operated boutiques, whichtogether generated 64% of total revenue for the year andincludes flagship stores in Paris, London, New York, HongKong, Shanghai, Beijing, Tokyo and Los Angeles. TheHouse is also present in select multi-brand boutiquesand department stores around the world.

At the end of 2015, the Saint Laurent business was verywell balanced in terms of both geographic markets andproduct categories, with leather goods and shoesaccounting for 66% of business and ready-to-wearposting 26% growth compared to the previous year.

30 Kering ~ 2015 Reference Document

02_VA_V5 06/04/2016 17:31 Page30

31

2

2015 Reference Document ~ Kering

SAINT LAURENT ~ LUXURY DIVISION ~ OUR ACTIVITIES

COMPEtitiVE ENVIRONMENT

Since its inception, Yves Saint Laurent has held enormousinfluence both within and outside the fashion industry.Over the years, its founder, the couturier Yves SaintLaurent secured a reputation as one of the 20th century’sforemost designers and personalities.

Saint Laurent now competes globally with other Frenchhigh-end exclusive luxury brands and occupies a leadingposition in ready-to-wear, fashion and leather goods sectors.

StrATEGY

Saint Laurent’s primary objective is to create and markethighly desirable products, which embody the core valuesof the brand through innovation and unparalleled qualityand design.

Since his arrival, Hedi Slimane has entirely redefined themen’s and women’s collections and worked on new linesfor all categories. The men’s and women’s collectionshave been repositioned and made even in terms of depthof offer and product ranges, making a strong move on men’scategories including ready-to-wear, shoes and luggage.This repositioning was accompanied by a rejuvenation ofthe style, in line with Yves Saint Laurent’s originalmessage when creating the Saint Laurent Rive Gauche“Prêt-à-Porter” brand in 1966. Ready-to-wear is thereforeonce again a strong component of Saint Laurent’s overallproduct offering, across both genders. At the same time,Saint Laurent aims to further strengthen the growth of itsleather goods, shoes and other accessories offerings.

2015 HIGHLIGHTS AND OUTLOOK FOR 2016

Under the leadership of Hedi Slimane and FrancescaBellettini, the company’s CEO, 2015 has been another veryrich year for Saint Laurent, with a particular focus on theintroduction of new collections and new store openings.

During the year, the brand’s sales were fuelled by extremelystrong growth figures across the main product categories,which fully transitioned into the new brand aesthetic. Overallgrowth was driven by the success of both permanent lines(including the Sac de Jour and Monogram handbags andParis and Janis shoes), and new, successful introductionsacross all channels and categories.

Recognised as a great success, Saint Laurent’s advertisingcampaigns and fashion collections won critical acclaimand the collections received significant exposure fromeditorials and global celebrities throughout the year.

Saint Laurent also made 2015 another year of investment,enhancing its retail network with selective store openingsworldwide, in both emerging and mature markets, andkey refurbishments and relocations.